Embed Size (px)

Citation preview

Domestic Demand And Regional Growth To Transform Brazilian Chemical Industry- A Closer

Look At The Catalysts

Binu P. Paul, Senior Research Analyst

Economic Research and Analytics

Chemicals Materials and Food

16th October 2008

2

Focus Points

1. Country Profile and Macro Economic outlook

2. Industry Coverage

4. Drivers and Restraints

5. Growth Opportunities

3. Industry Performance and Analysis of Segments

3

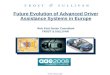

Brazil - Country Profile

Political Scenario

Economy

Monetary Outlook

Fiscal Outlook

• President - Luiz Inacio Lula Da Silva • Political outlook – Stable

• Manufacturing constituted 35 % of GDP in 2007• Privatization and Financial Assistance from the IMF – steady flow of

investments• Investors confidence and increase in consumption• PDP announced in May 2008

• Tax cuts amounting to $ 12.5 billion announced in May 2008• The tax burden on chemicals industry is approximately 70% of the

value added by the industry• Public debt around 41 percent of GDP in 2007

• Flexible exchange rate regime combined with inflation targeting• Inflationary pressures expected

4

Brazil - Promising Macro Economic Outlook

Expected macro economic outlook

• The economy is expected to grow at an average of 4.7 % during the period 2008-2013

• The inflation in the economy is expected to be in the range of 4 % to 5% during the period 2008-2013

• Total investment expected to be 21% of GDP by 2010

Factors driving the economy

• Sustained growth in domestic demand

• Increased foreign direct investment

• Stable consumer and investor confidence

0.00

300.00

600.00

900.00

1200.00

1500.00

1800.00

2100.00

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013

$ B

illi

on

s

0

3

6

9

12

15

18

Perc

enta

ge

GDP at Current Prices

Inflation

Source: IMF and Frost and Sullivan

5

Brazilian Chemicals Industry

Basic Chemicals

Pharmaceuticals

Consumer Chemicals

Fertilizers and Agricultural Chemicals

Synthetics and Fibers

Materials

Other Chemicals

Brazilian Chemical Industry- Industry Coverage

6

Energy and feedstock shortages

Globalization and

Privatization induce

investment Regulatory barriers

remain high

Higher Investors Confidence

Competitiveness depend on exchange rate stability and wagesChemical

Industry

Economic growth to support demand

Brazilian Chemical Industry- Key Features Of The Industry

Contribution to the total GDP was 3.2 percent in 2007.

Average capacity utilization in 2007 was 87 %

The industry provides 340 thousand direct employment opportunities.

Net revenues in 2007- $103.5 Billion

Share of exports- 6.6%

Share of imports- 19.8%2007

7

Growth Acceleration Programme (PAC)

Construction

Energy

Healthcare

Agriculture

End user Industries

PROFARMA

Agro Energy plan

PRONAF

Initiatives

Policy Initiatives And End User Industries

Transportation

Productive Development Policy Package (PDP)

Perfumes

8

Sectoral Composition of the Brazilian Chemical Industry (2007)

Brazilian Chemical Industry- Key Industry Segments In 2007

• Chemical products for industrial use, is the biggest segment in the Brazilian chemical industry and accounted for 53.2 percent of the total sales in the industry

• Sales in industrial chemicals segment was $ 55.1 billion in 2007

• The pharmaceutical products segment accounted for 14.6% of the total sale in chemical industry

• The remaining segments such as perfumes and cosmetics, fertilizers, soaps and detergents, crop protection, paints and varnishes and others together, accounted for 32.2% of the total sales in 2007

53%

2%

3%5%5%

9%

9% 14%

Industrial Chemicals Pharmaceuticals

Fertilizers Personal Care and Cosmetics

Soaps and Detergents Crop Protection

Paints and Varnishes Others

Source : ABIQUIM

9

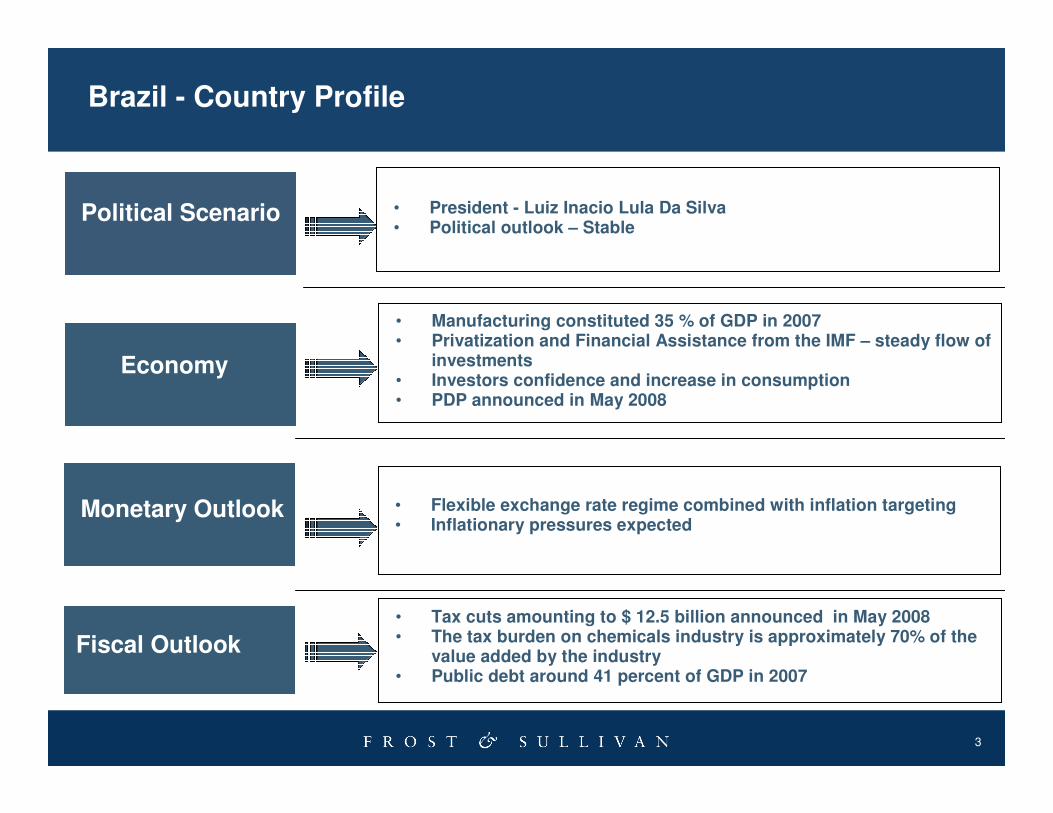

Brazilian Chemical Industry- Performance Of Some Key Industry Segments In 2007

Thermoplastic resins Glues Adhesives and Sealants

• Produced more than 4.8 million tones of thermoplastic resins in 2007.

• Imported 691.7 thousand tons of thermoplastic resins in 2007 which is 23.9 % more than 2006.

• Per capita consumption increased by 6.9% from 2006 to reach 26.09 kg.

• Imports increased 13% from 2006 and were valued at $ 514.8 million.

• Exports came down by 1% and amounted to $144.4 million

• The trade deficit in the sector was $370 million.

• Production increased 6% over 2006

• Growth in automotive, packaging, and construction

Dyes and Pigments

MaterialsPaints and Varnishes

10

• Brazilian chemical exports grew 19.6 % in 2007, and was valued at $ 10.7 billion. The country imported $ 23.9 billion worth chemicals in 2007.

• Brazilian chemical product balance of trade deficit was over US$ 13.2 billion in 2007.

Brazilian Chemical Industry- Foreign Trade

Major export destinations – Mercosur countries, United states and Canada

4.0

0

3.5

0

3.8

0

4.8

0

5.9

0

7.4

0

8.9

0

10

.70

12

.17

13

.65

15

.12

16

.59

18

.07

19

.54

10

.80

10

.70

10

.10

11

.00

14

.50

15

.30

17

.40

23

.90

25

.33

26

.75

28

.18

29

.61

31

.03

32

.46

0

5

10

15

20

25

30

35

20

00

20

01

20

02

20

03

20

04

20

05

20

06

20

07

20

08

20

09

20

10

20

11

20

12

20

13

$ B

illi

on

s

Exports Imports

Source: ABIQUIM and Frost and Sullivan

11

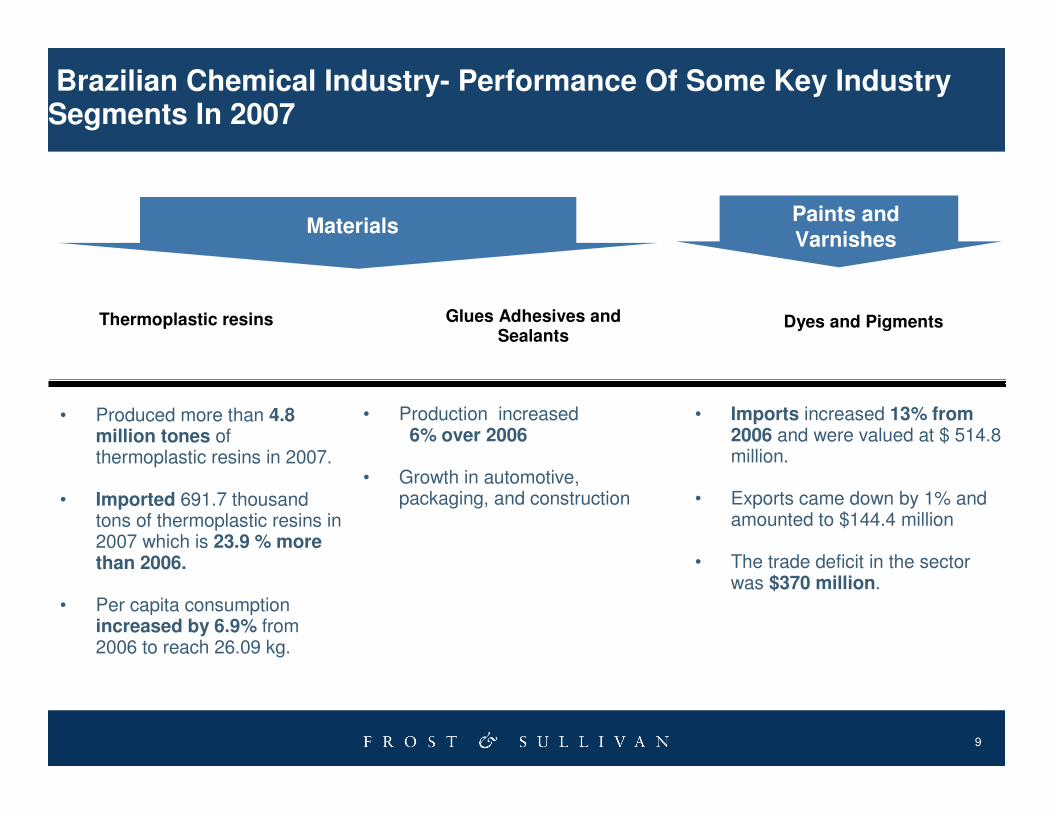

Key Trade Agreements

Mercosur(1995)

Mercosur-GCC

(2006)

Mercosur-India(2005)

Venezuela(2006)

Andean Community

(2005)Mercosur-

SACU(2004)

• The EU- Mercosur FTA is currently being negotiated.

• A proposal for an establishment of a free trade agreement between the Mercosur and the

countries of the Gulf Cooperation Council was proposed in August 2006.

• The Economic Complementation Agreement signed between the Mercosur and, Andean

Community members, went into effect in 2005.

• A Preferential Trade Agreement was signed in 2004 between Mercosur and South Africa Customs

Union (SACU)

Brazil – Trade Agreements

Mercosur- EU

Israel(2007)

12

Brazil- Investment Incentives

Incentives for Investment

• PDP to promote investments in agribusiness, bio diesel, perfume and oil and gas

• Close to $130 billion finance for machinery and infrastructure

• Equal treatment for local and foreign investors. Brazilian Congress approved an amendment to eliminate the difference between foreign and national capital

• State and local government provides investment incentives through reduction in indirect taxes

• Tax concessions including reduction in Federal Income tax is given for companies that are set up in the poorer North East and Amazon Region

• Incentives are given to companies for the promotion of export

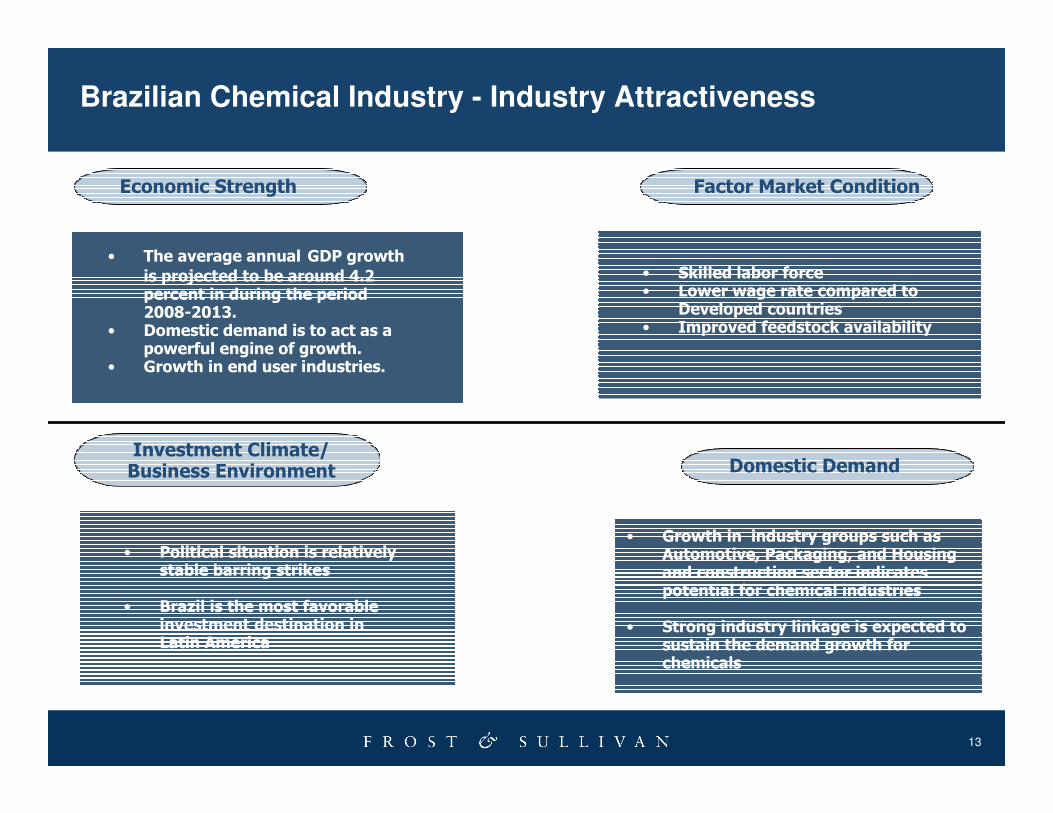

13

IndustryAttractiveness

• Skilled labor force• Lower wage rate compared to

Developed countries• Improved feedstock availability

• Growth in industry groups such as Automotive, Packaging, and Housing and construction sector indicates potential for chemical industries

• Strong industry linkage is expected to sustain the demand growth for chemicals

• Political situation is relatively stable barring strikes

• Brazil is the most favorable investment destination in Latin America

Economic Strength Factor Market Condition

Investment Climate/Business Environment Domestic Demand

Brazilian Chemical Industry - Industry Attractiveness

• The average annual GDP growth

is projected to be around 4.2 percent in during the period 2008-2013.

• Domestic demand is to act as a powerful engine of growth.

• Growth in end user industries.

14

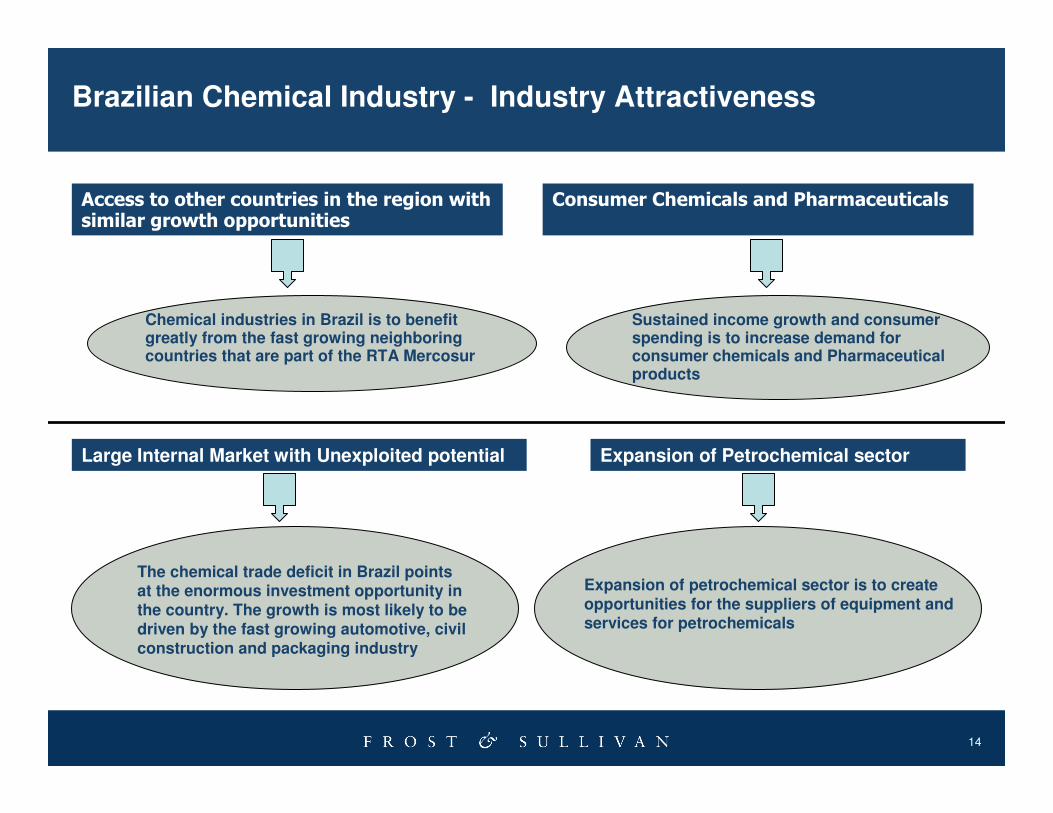

Brazilian Chemical Industry - Industry Attractiveness

Chemical industries in Brazil is to benefit greatly from the fast growing neighboring countries that are part of the RTA Mercosur

The chemical trade deficit in Brazil points at the enormous investment opportunity in the country. The growth is most likely to be driven by the fast growing automotive, civil construction and packaging industry

Sustained income growth and consumer spending is to increase demand for consumer chemicals and Pharmaceutical products

Expansion of Petrochemical sector

Consumer Chemicals and PharmaceuticalsAccess to other countries in the region with similar growth opportunities

Large Internal Market with Unexploited potential

Expansion of petrochemical sector is to create opportunities for the suppliers of equipment and services for petrochemicals

15

DRIVERS

RESTRAINTS

Regional Integration

Feed Stock Availability

Domestic Demand

Taxation

Brazilian Chemical Industry – Drivers And Restraints

Green field investment announcements in petrochemical sector

High interest rates

16

Brazilian Chemical Industry – Growth Opportunities

Fertilizers

Dyes, Pigments, Adhesives

and Thermoplastic

s

Industry chemicals

Growth Opportunities

Consumer chemicals

and Pharmaceuti

cals

17

Your Feedback is Important to Us

Growth Forecasts?

Competitive Structure?

Emerging Trends?

Strategic Recommendations?

Other?

Please inform us by taking our survey.

What would you like to see from Frost & Sullivan?

18

For Additional Information

• To leave a comment, ask the analyst a question, or receive the free audio segment that accompanies this presentation, please contact Stephanie Ochoa, Social Media Manager at (210) 247-2421, via email, [email protected], or on Twitter at http://twitter.com/stephanieochoa.