Embed Size (px)

Citation preview

A Perspective on Market Leadership A Perspective on Market Leadership in Today’s Marketin Today’s Market

July 20, 2011

2

Agenda

I. Introduction

II. Case Studies to Support Our View

III. Gridley’s Advice for the Audience

3

I. Introduction

4

Introduction

• Industry leaders today are highly vulnerable

• Increasingly tough to compete with new, innovative entrants

Unprecedented opportunity for new leaders to emerge across all sectors of Information Services

5

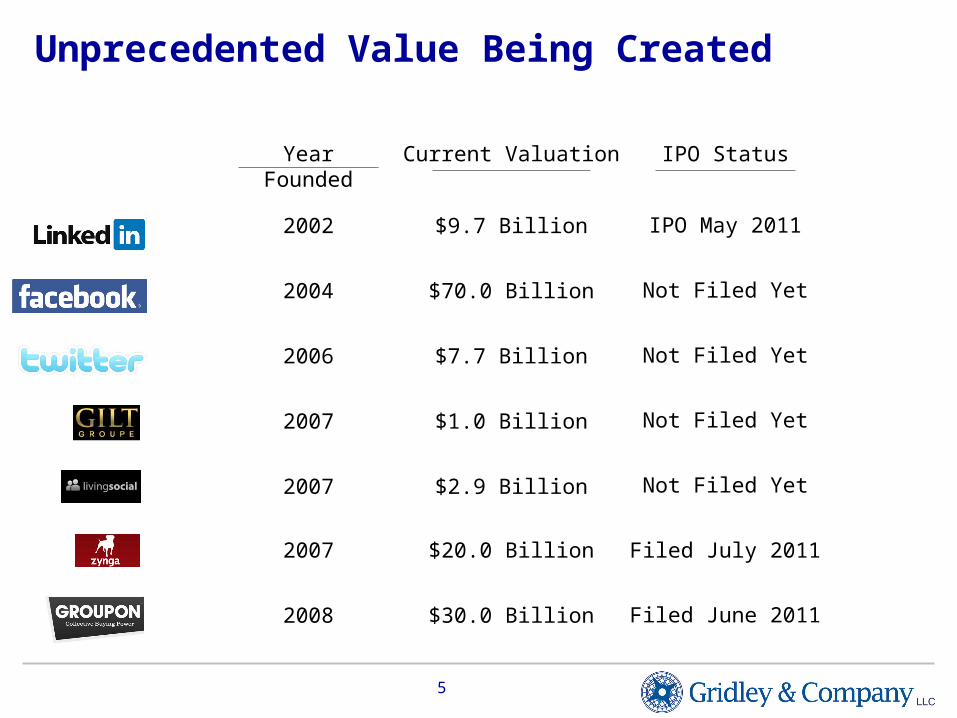

Unprecedented Value Being Created

Year Founded Current Valuation IPO Status

2002

2004

2006

2007

2007

2007

2008

$9.7 Billion IPO May 2011

Not Filed Yet

Filed July 2011

Filed June 2011

$70.0 Billion

$7.7 Billion

$1.0 Billion

$2.9 Billion

$20.0 Billion

$30.0 Billion

Not Filed Yet

Not Filed Yet

Not Filed Yet

6

II. Case Studies to Support Our View

7

Traditional Ad Agencies

vs.

Performance Based Marketing

8

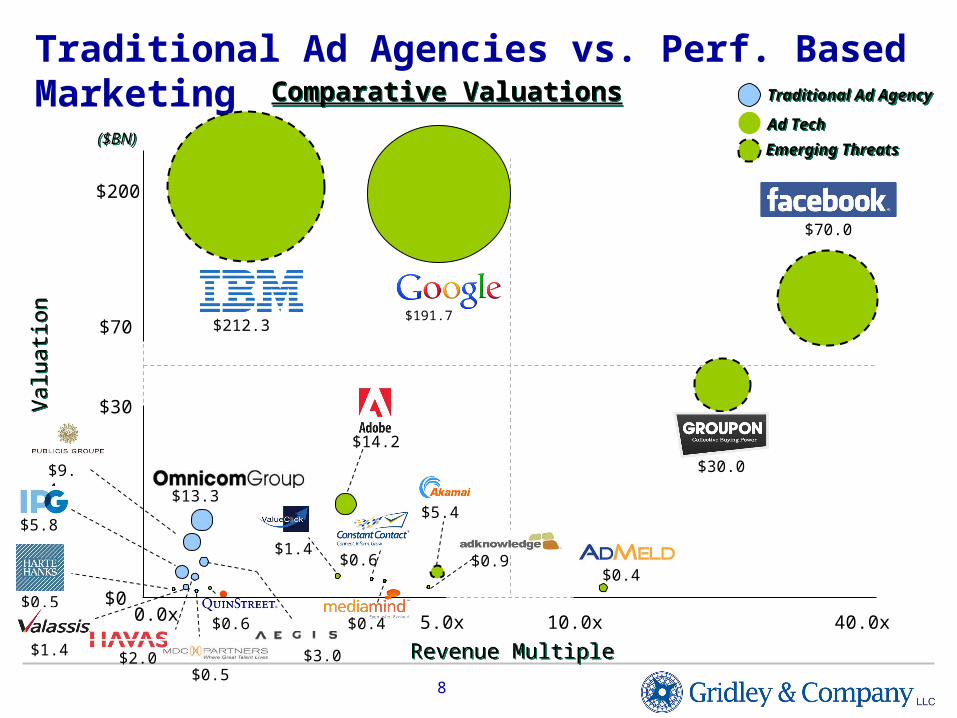

Traditional Ad Agencies vs. Perf. Based Marketing

Revenue MultipleRevenue Multiple

($BN)($BN)

0.0x$0

$200

5.0x 10.0x 40.0x

$70

$30

Val

uatio

nV

alua

tion

$14.2

$13.3

$9.4

$5.8

$3.0$1.4 $2.0

$0.5

$0.5

$0.6

$1.4$0.6 $0.9

$0.4

$0.4

$30.0

$5.4

$212.3$191.7

$70.0

Comparative ValuationsComparative Valuations

Emerging ThreatsEmerging Threats

Traditional Ad AgencyTraditional Ad Agency

Ad TechAd Tech

9

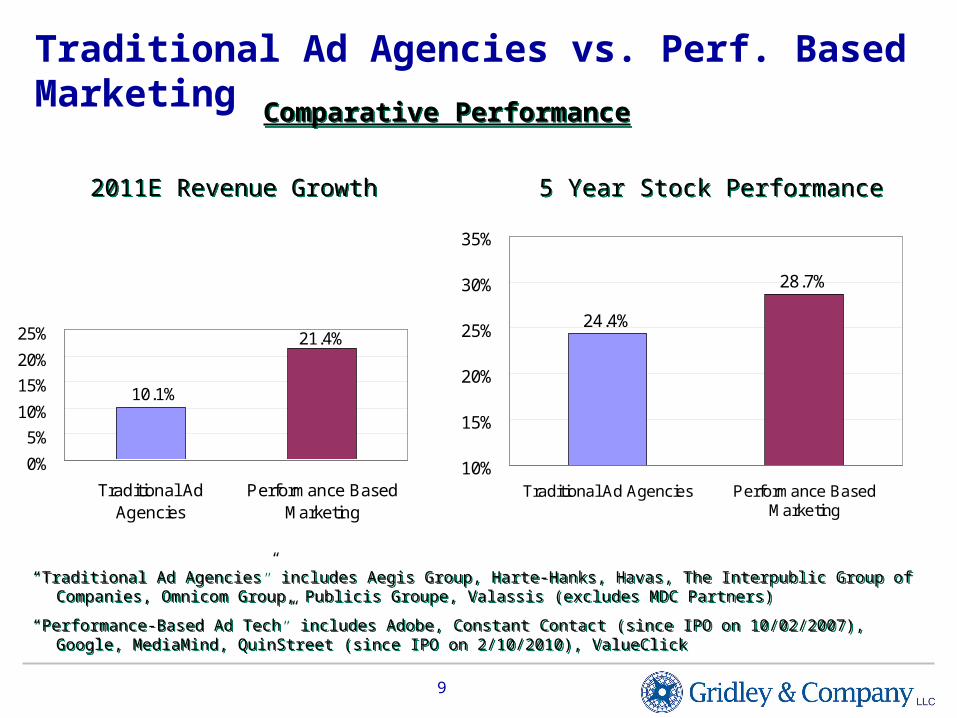

“Traditional Ad Agencies” includes Aegis Group, Harte-Hanks, Havas, The Interpublic Group of Companies, Omnicom Group, Publicis Groupe, Valassis (excludes MDC Partners)

“Performance-Based Ad Tech” includes Adobe, Constant Contact (since IPO on 10/02/2007), Google, MediaMind, QuinStreet (since IPO on 2/10/2010), ValueClick

“Traditional Ad Agencies” includes Aegis Group, Harte-Hanks, Havas, The Interpublic Group of Companies, Omnicom Group, Publicis Groupe, Valassis (excludes MDC Partners)

“Performance-Based Ad Tech” includes Adobe, Constant Contact (since IPO on 10/02/2007), Google, MediaMind, QuinStreet (since IPO on 2/10/2010), ValueClick

5 Year Stock Performance5 Year Stock Performance2011E Revenue Growth2011E Revenue Growth

Comparative PerformanceComparative Performance

Traditional Ad Agencies vs. Perf. Based Marketing

10.1%

21.4%

0%

5%

10%

15%

20%

25%

Traditional AdAgencies

Performance BasedMarketing

24.4%

28.7%

10%

15%

20%

25%

30%

35%

Traditional Ad Agencies Performance BasedMarketing

10

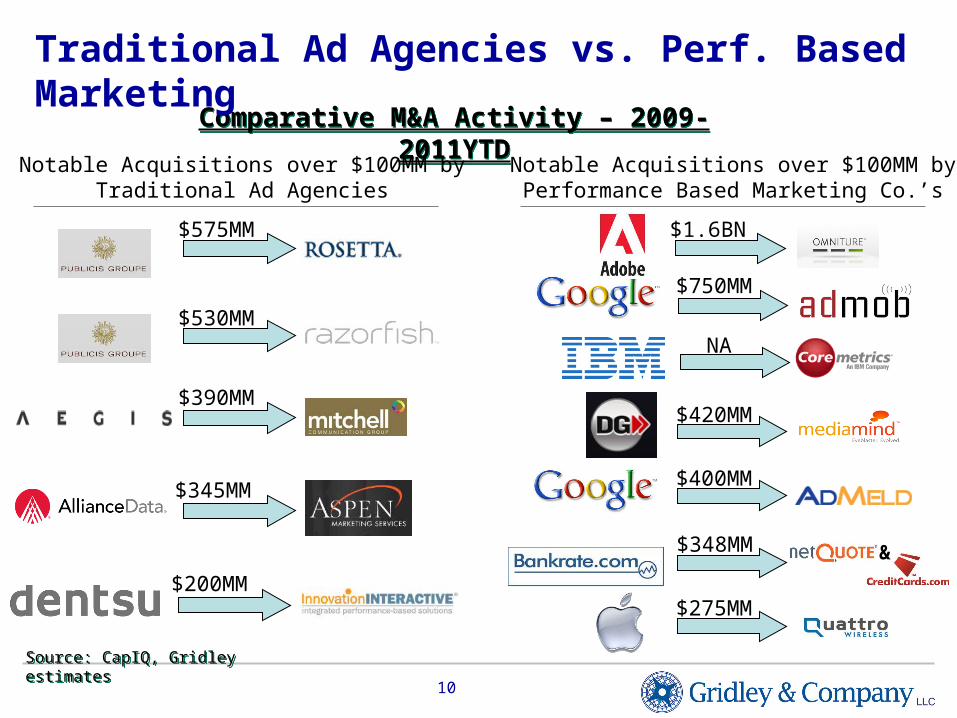

Comparative M&A Activity – 2009-2011YTDComparative M&A Activity – 2009-2011YTD

Traditional Ad Agencies vs. Perf. Based Marketing

$575MM

$530MM

$390MM

$750MM

$420MM

$400MM

$275MM

Notable Acquisitions over $100MM byTraditional Ad Agencies

Notable Acquisitions over $100MM byPerformance Based Marketing Co.’s

$348MM

$1.6BN

&

NA

$345MM

$200MM

Source: CapIQ, Gridley estimatesSource: CapIQ, Gridley estimates

11

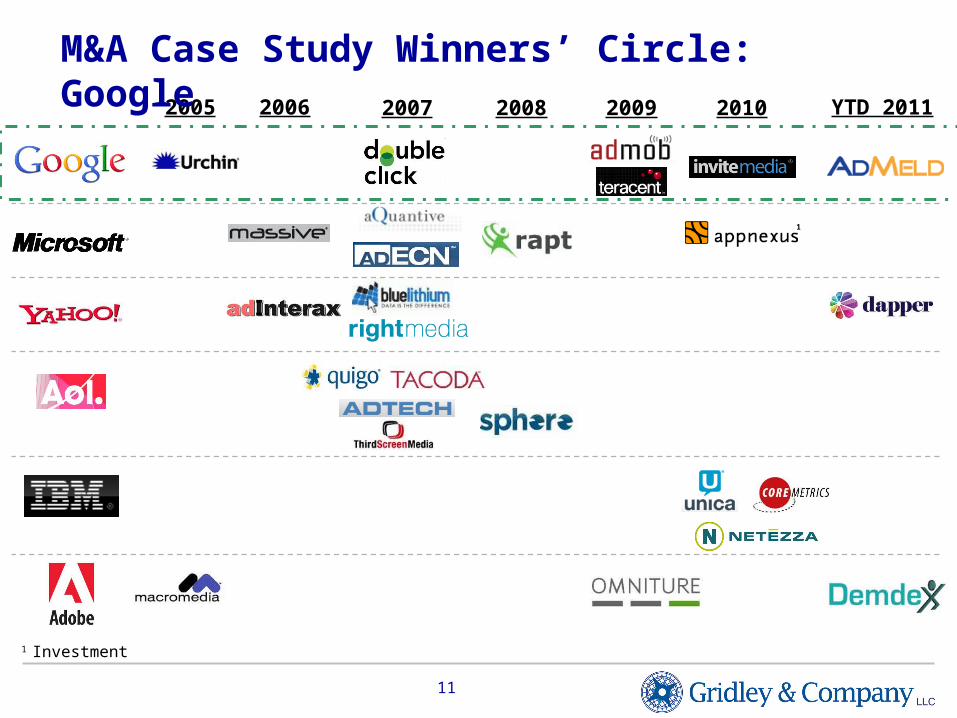

1 Investment

2006 2007 2008 2010

1

YTD 201120092005

M&A Case Study Winners’ Circle: Google

12

Traditional Media

vs.

Social Networks

13

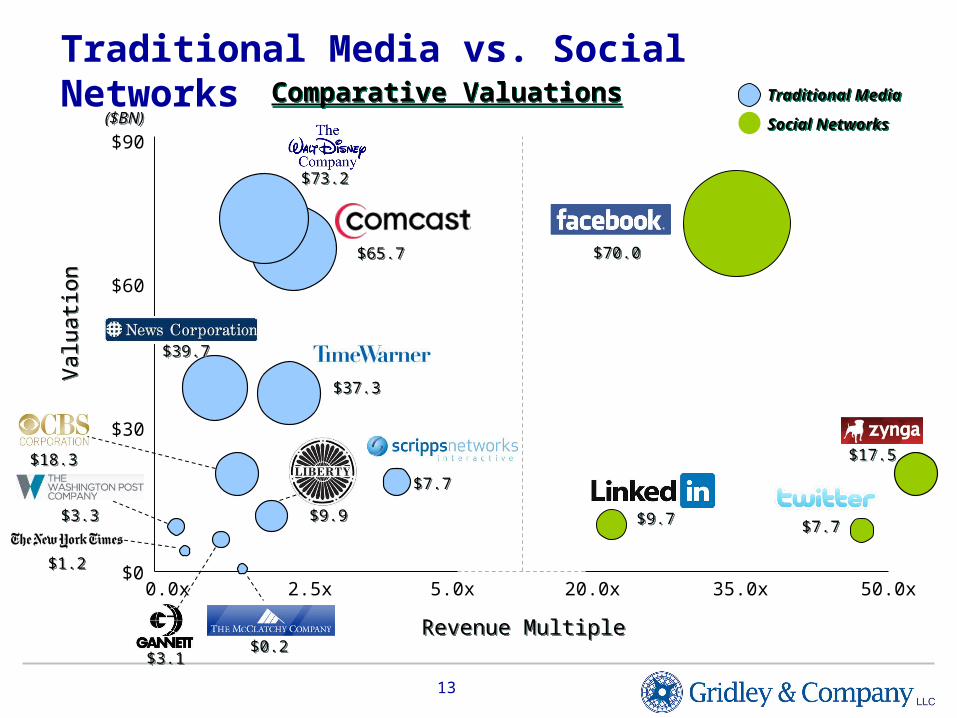

Traditional Media vs. Social NetworksComparative ValuationsComparative Valuations

Revenue MultipleRevenue Multiple

($BN)($BN)

Val

uatio

nV

alua

tion

0.0x 5.0x 20.0x 50.0x$0

$90

$30

$60

2.5x 35.0x

$70.0$70.0

$17.5$17.5

$9.7$9.7$7.7$7.7

$73.2$73.2

$65.7$65.7

$37.3$37.3

$7.7$7.7

$0.2$0.2

$9.9$9.9

$39.7$39.7

$3.1$3.1

$1.2$1.2

$3.3$3.3

$18.3$18.3

Traditional MediaTraditional Media

Social NetworksSocial Networks

14

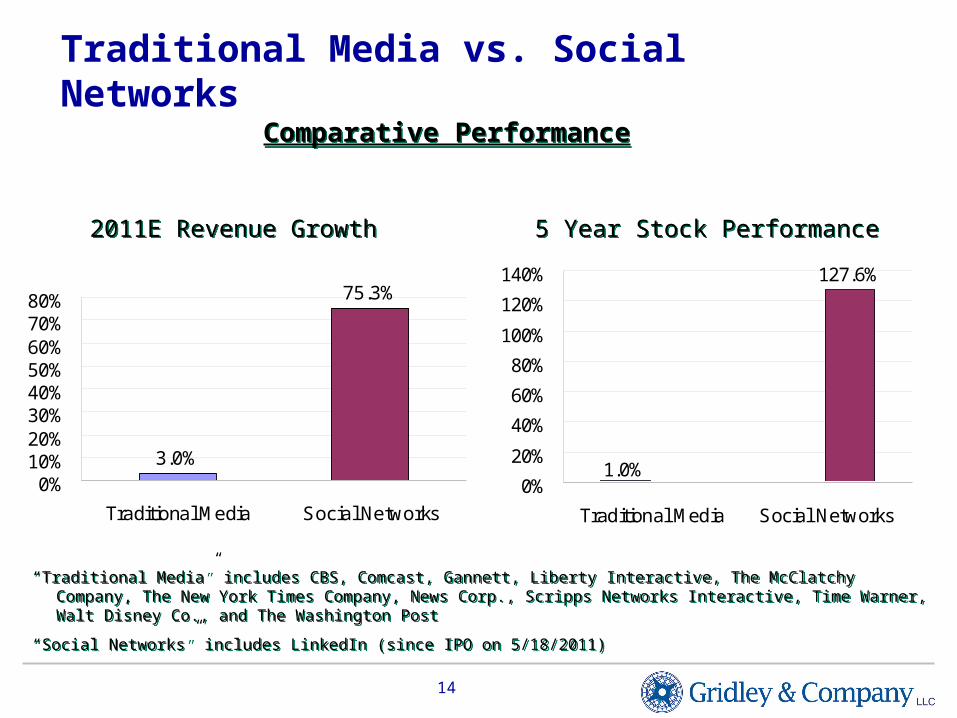

Traditional Media vs. Social Networks

5 Year Stock Performance5 Year Stock Performance2011E Revenue Growth2011E Revenue Growth

“Traditional Media” includes CBS, Comcast, Gannett, Liberty Interactive, The McClatchy Company, The New York Times Company, News Corp., Scripps Networks Interactive, Time Warner, Walt Disney Co., and The Washington Post

“Social Networks” includes LinkedIn (since IPO on 5/18/2011)

“Traditional Media” includes CBS, Comcast, Gannett, Liberty Interactive, The McClatchy Company, The New York Times Company, News Corp., Scripps Networks Interactive, Time Warner, Walt Disney Co., and The Washington Post

“Social Networks” includes LinkedIn (since IPO on 5/18/2011)

Comparative PerformanceComparative Performance

127.6%

1.0%0%

20%

40%

60%

80%

100%

120%

140%

Traditional Media Social Networks

3.0%

75.3%

0%10%20%30%40%50%60%70%80%

Traditional Media Social Networks

15

45

47

49

51

53

55

57

59

61

63

65

1945

1948

1951

1954

1957

1960

1963

1966

1969

1972

1975

1978

1981

1984

1987

1990

1993

1996

1999

2002

2005

2008

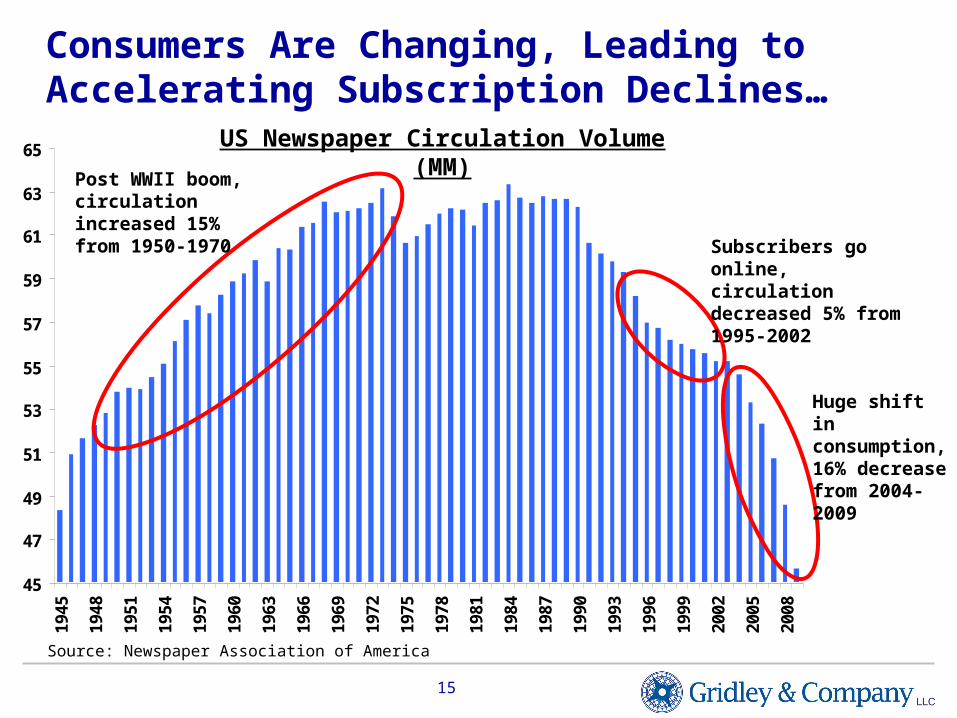

Consumers Are Changing, Leading to Accelerating Subscription Declines…

Post WWII boom, circulation increased 15% from 1950-1970

Subscribers go online, circulation decreased 5% from 1995-2002

US Newspaper Circulation Volume (MM)

Huge shift in consumption, 16% decrease from 2004-2009

Source: Newspaper Association of America

16

… And Disruption of Traditional Models

Bankrupt Newspapers

17

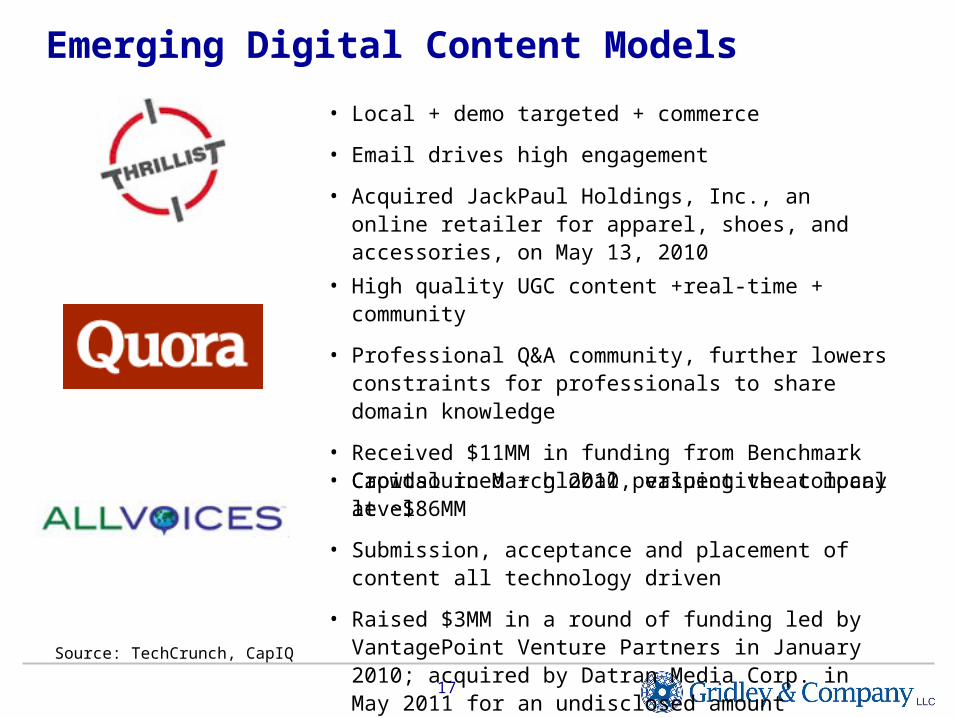

Emerging Digital Content Models

Source: TechCrunch, CapIQ

• Local + demo targeted + commerce

• Email drives high engagement

• Acquired JackPaul Holdings, Inc., an online retailer for apparel, shoes, and accessories, on May 13, 2010

• High quality UGC content +real-time + community

• Professional Q&A community, further lowers constraints for professionals to share domain knowledge

• Received $11MM in funding from Benchmark Capital in March 2010, valuing the company at ~$86MM

• Crowdsourced + global perspective at local level

• Submission, acceptance and placement of content all technology driven

• Raised $3MM in a round of funding led by VantagePoint Venture Partners in January 2010; acquired by Datran Media Corp. in May 2011 for an undisclosed amount

18

Traditional Retail

vs.

E-Commerce

19

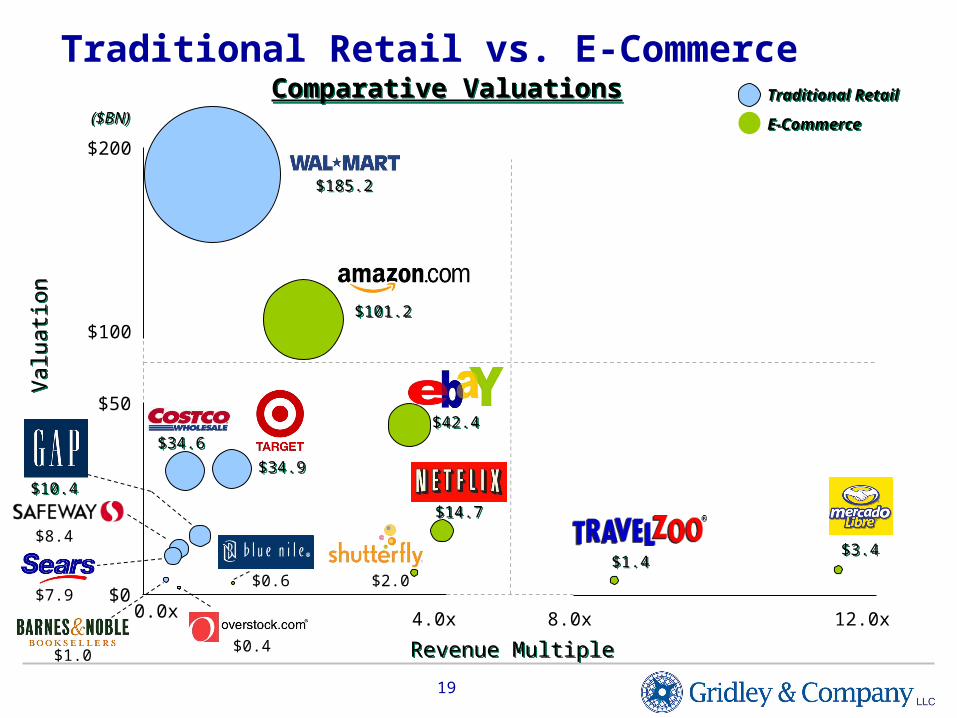

Traditional Retail vs. E-Commerce

0.0x 4.0x 8.0x 12.0x

($BN)($BN)

$0

$200

$100

$50

Val

uatio

nV

alua

tion

Revenue MultipleRevenue Multiple

$1.4$1.4$3.4$3.4

$14.7$14.7

$7.9

$1.0

$8.4

$2.0$0.6

$185.2$185.2

$101.2$101.2

$34.6$34.6

$34.9$34.9

$42.4$42.4

$10.4$10.4

$0.4

Comparative ValuationsComparative Valuations Traditional RetailTraditional Retail

E-CommerceE-Commerce

20

Traditional Retail vs. E-Commerce

5 Year Stock Performance5 Year Stock Performance2011E Revenue Growth2011E Revenue Growth

“Traditional Retail” includes Barnes & Noble, Costco, Gap, Safeway, Sears Holdings, Target, and Wal-Mart

“E-Commerce” includes Amazon.com, Blue Nile, eBay, Mercadolibre (since IPO on 08/09/2007), Netflix, Overstock.com, Shutterfly (since IPO on 9/28/2006), and Travelzoo

“Traditional Retail” includes Barnes & Noble, Costco, Gap, Safeway, Sears Holdings, Target, and Wal-Mart

“E-Commerce” includes Amazon.com, Blue Nile, eBay, Mercadolibre (since IPO on 08/09/2007), Netflix, Overstock.com, Shutterfly (since IPO on 9/28/2006), and Travelzoo

Comparative PerformanceComparative Performance

4.4%

36.7%

0%5%

10%15%20%25%30%35%40%

Traditional Retail E-Commerce

19.1%

224.3%

0%

50%

100%

150%

200%

250%

Traditional Retail E-Commerce

21

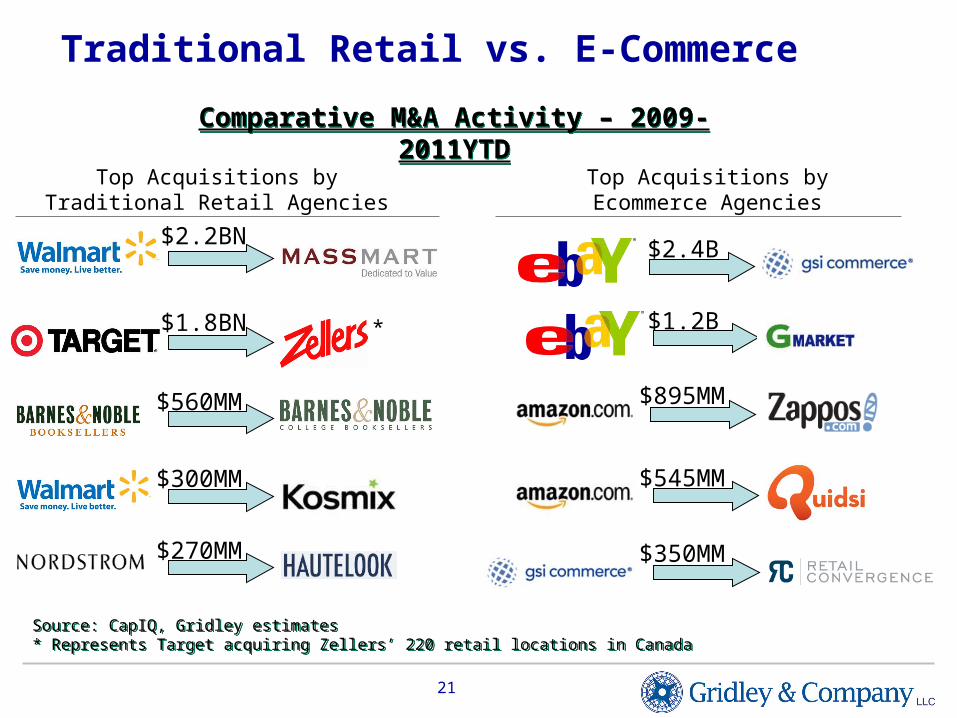

Traditional Retail vs. E-Commerce

Comparative M&A Activity – 2009-2011YTDComparative M&A Activity – 2009-2011YTD

$2.2BN

$560MM

$300MM

$270MM

$1.8BN *

$2.4B

$1.2B

$895MM

$545MM

$350MM

Top Acquisitions byTraditional Retail Agencies

Top Acquisitions byEcommerce Agencies

Source: CapIQ, Gridley estimates* Represents Target acquiring Zellers’ 220 retail locations in CanadaSource: CapIQ, Gridley estimates* Represents Target acquiring Zellers’ 220 retail locations in Canada

22

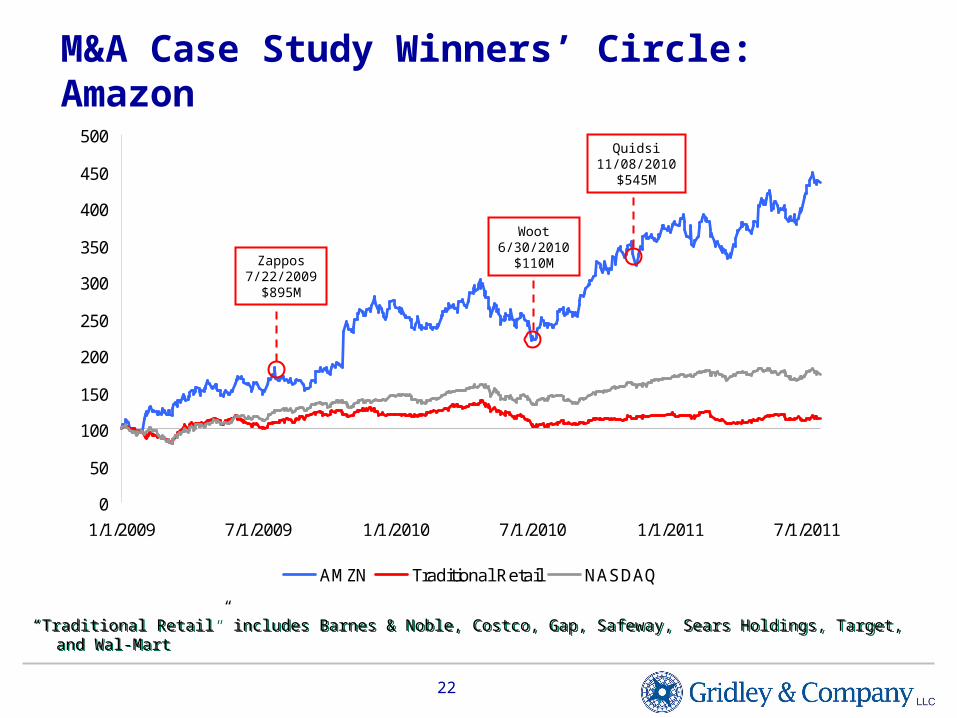

0

50

100

150

200

250

300

350

400

450

500

1/1/2009 7/1/2009 1/1/2010 7/1/2010 1/1/2011 7/1/2011

AMZN Traditional Retail NASDAQ

M&A Case Study Winners’ Circle: Amazon

Zappos7/22/2009

$895M

Woot6/30/2010

$110M

Quidsi11/08/2010

$545M

“Traditional Retail” includes Barnes & Noble, Costco, Gap, Safeway, Sears Holdings, Target, and Wal-Mart“Traditional Retail” includes Barnes & Noble, Costco, Gap, Safeway, Sears Holdings, Target, and Wal-Mart

23

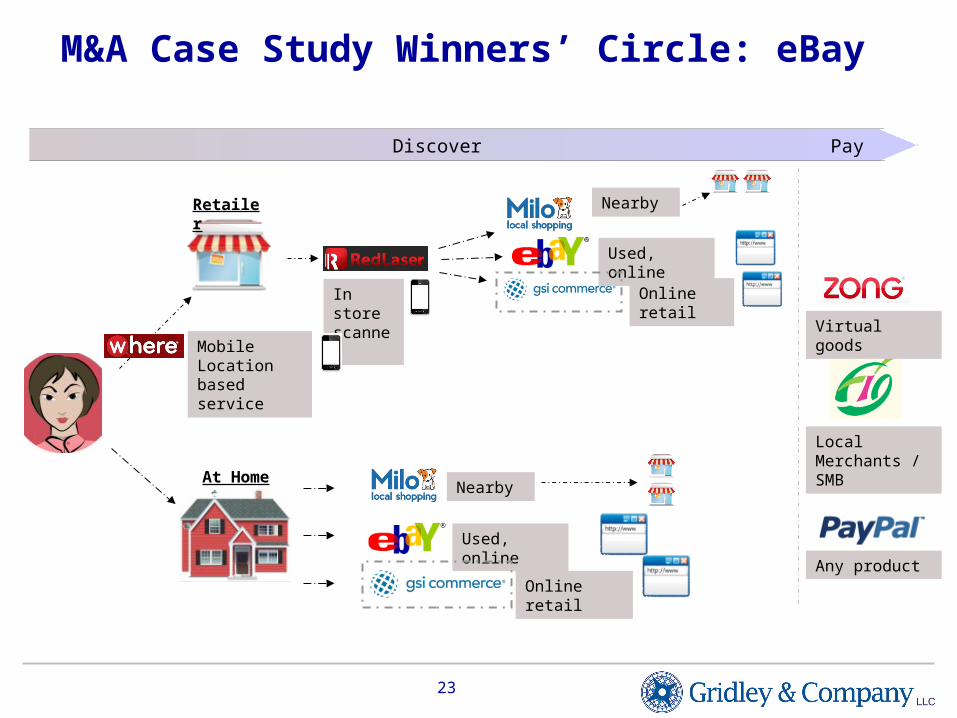

M&A Case Study Winners’ Circle: eBay

In store scanner

Nearby

Used, online

Online retail

Nearby

Used, online

Online retail

Virtual goods

Local Merchants / SMB

Any product

Discover Pay

Mobile Location based service

Retailer

At Home

24

III. Gridley’s Advice for the Audience

25

Unprecedented Agents of Change

Open SourceOpen Source Open ArchitectureOpen Architecture

Cloud ComputingCloud Computing New Business ModelsNew Business Models

26

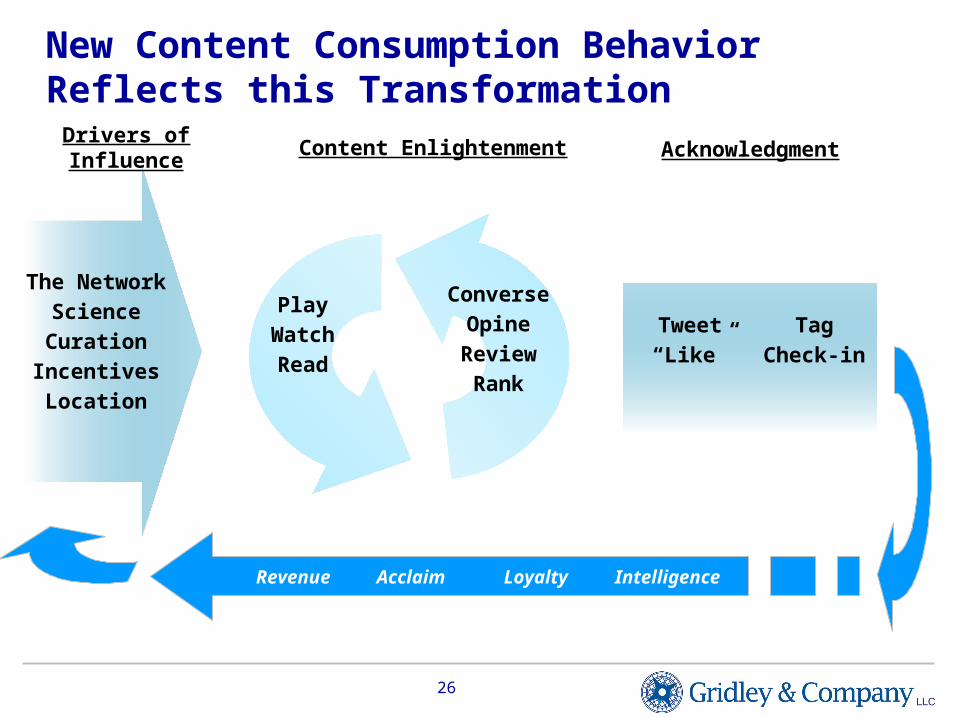

Drivers of Influence

The Network

Science

Curation

Incentives

Location

Acknowledgment

Tweet

“Like”

New Content Consumption Behavior Reflects this Transformation

Tag

Check-in

Content Enlightenment

Play

Watch

Read

Converse

Opine

Review

Rank

Revenue Acclaim Loyalty Intelligence

27

Advice to the Audience – Private Companies

• Unprecedented opportunity for new leadership

• Clear, differentiated capabilities are key

• Buyers will pay premiums for market leaders and experienced teams

• Scale and successful client case studies are key

• Watch for new buyers to emerge

28

Advice to the Audience – Public Companies

• Traditional leaders – You are more vulnerable than you think

• Think strategically about innovation and M&A

• Tremendous value being created, competitive dynamics are changing

• Watch out for disruptive business models

29

Advice to the Audience – VC / PE Investors

• "Jump In – The Water's Fine"

• Be careful about amount of $ invested

• $250MM+ exits aren't easy!

• Look for new strategic buyers to emerge

• Different companies require different exit strategies

30

Questions?

Linda GridleyGridley & Company LLC

10 East 53rd Street, 24th FloorNew York, NY 10022

212.400.9720 tel212.400.9717 fax

Twitter: @gridleycowww.gridleyco.com