Embed Size (px)

Citation preview

Stakeholder Meeting July 10th 2013 5:00-7:00pm Corless Auditorium, URI Bay Campus

Project Goal • Through a public process help develop innovative

and practical policies and tools for managing development along shorelines vulnerable to erosion and flooding

Melissa Devine, 2012

Melissa Devine, 2012

Lynne Harrington, Pawtuxet Cove 2012

Hurricane Irene, RI Sea Grant

Thank you! • Rhode Island Bays, Rivers and Watershed

Coordination Team • URI Coastal Institute • Rhode Island Foundation • Rhode Island Sea Grant • Rhode Island Geologic Survey • Coastal Resources Management Council • URI Coastal Resources Center • URI Graduate School of Oceanography • URI College of Environmental and Life

Sciences • RI Statewide Planning (North Kingstown) • Prince Charitable Trusts and Van Buren

Charitable Foundation (Newport) • NOAA, TNC, Save the Bay, NB National

Estuarine Research Reserve , Roger Williams University (Marsh Migration) Image Credit, CRMC

Project Update April 2013- Kick off Meeting

Policy and Adaptation Review is underway

Field work, Mapping & Modeling Areas at Risk

Melissa Devine, 2012

Melissa Devine, 2012

Ongoing state and local coordination of

efforts

Audience Polling

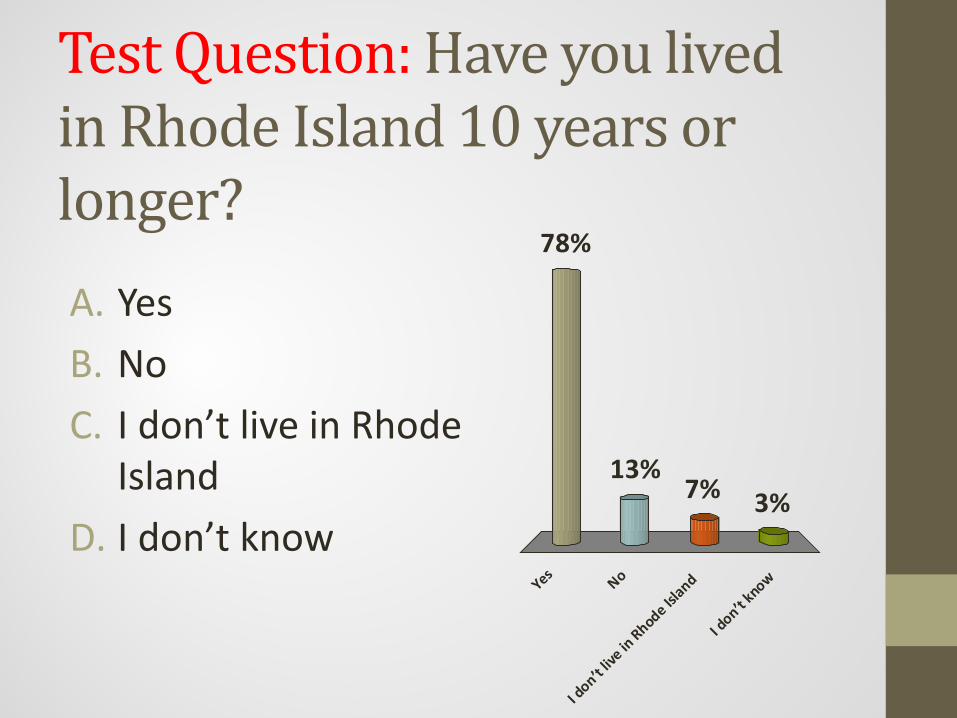

Test Question: Have you lived in Rhode Island 10 years or longer? A. Yes B. No C. I don’t live in Rhode

Island D. I don’t know

YesNo

I don’t l

ive in

Rhode Island

I don’t k

now

78%

3%7%13%

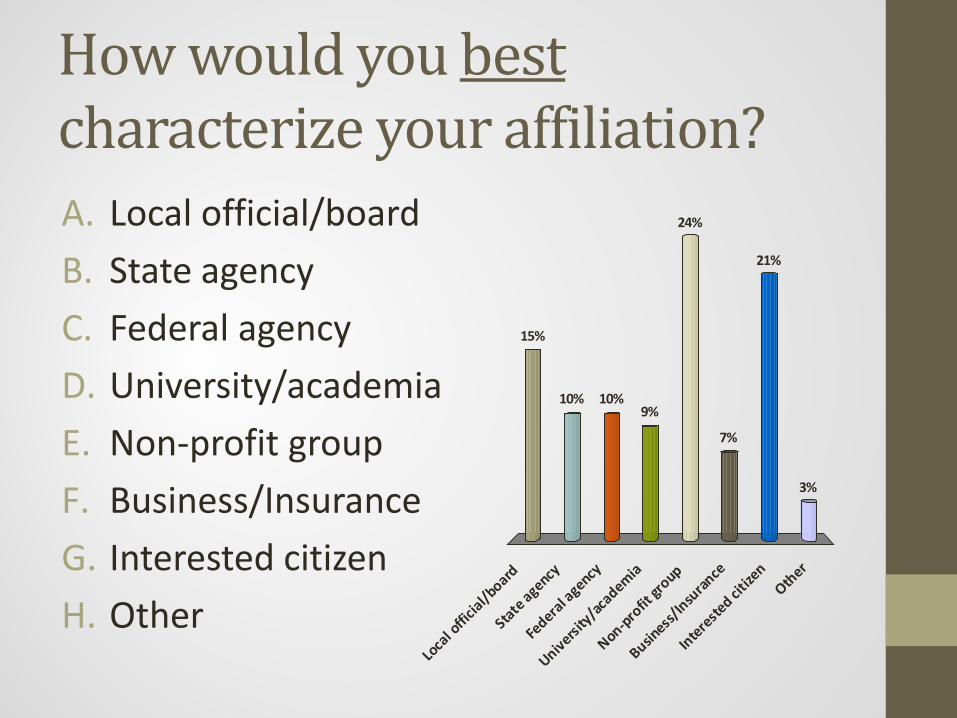

How would you best characterize your affiliation? A. Local official/board B. State agency C. Federal agency D. University/academia E. Non-profit group F. Business/Insurance G. Interested citizen H. Other

Loca

l offic

ial/board

State agency

Federal a

gency

University/ac

ademia

Non-profit

group

Business/

Insuran

ce

Interested cit

izen

Other

15%

10% 10%

3%

21%

7%

24%

9%

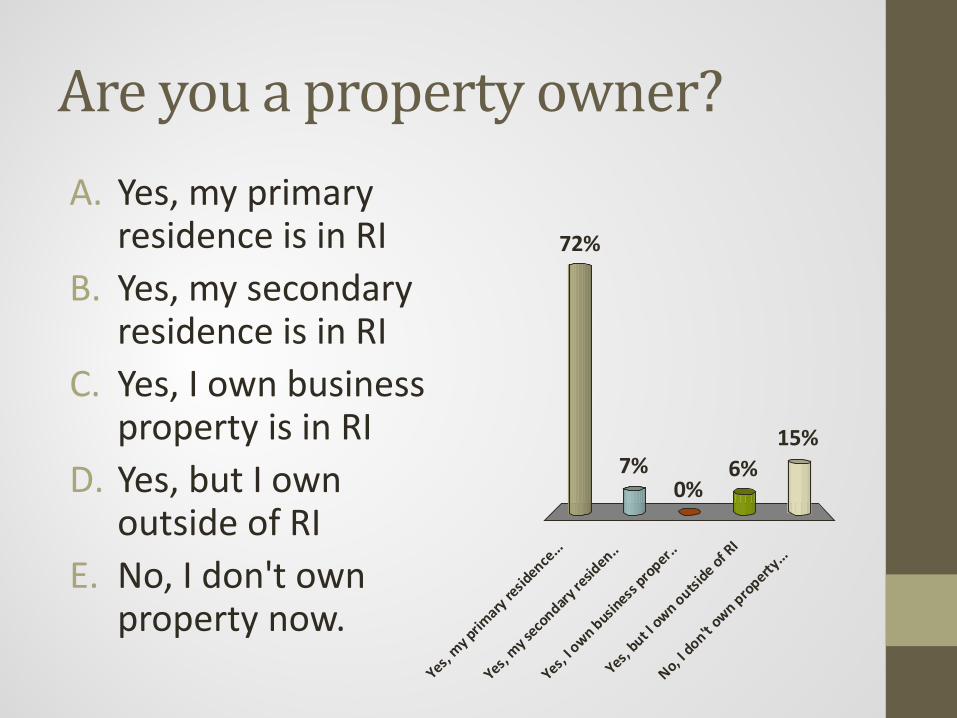

Are you a property owner? A. Yes, my primary

residence is in RI B. Yes, my secondary

residence is in RI C. Yes, I own business

property is in RI D. Yes, but I own

outside of RI E. No, I don't own

property now. Yes,

my prim

ary resid

ence...

Yes, my s

econdary

resid

en..

Yes, I o

wn business

proper..

Yes, but I

own outside of R

I

No, I don't o

wn property...

72%

15%6%

0%7%

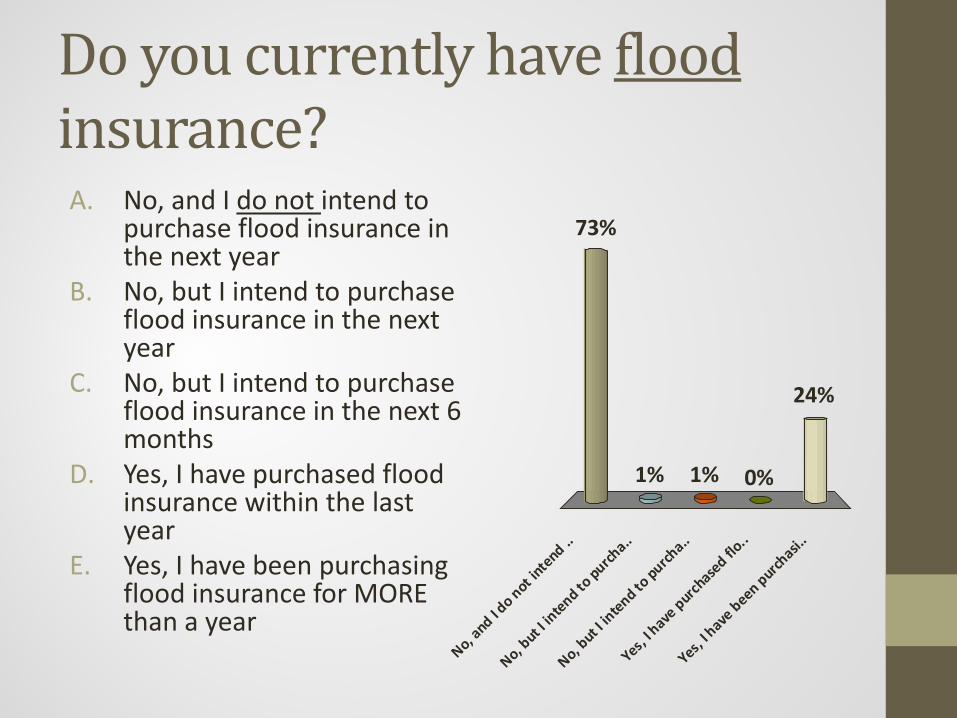

Do you currently have flood insurance? A. No, and I do not intend to

purchase flood insurance in the next year

B. No, but I intend to purchase flood insurance in the next year

C. No, but I intend to purchase flood insurance in the next 6 months

D. Yes, I have purchased flood insurance within the last year

E. Yes, I have been purchasing flood insurance for MORE than a year

No, and I d

o not intend ..

No, but I

intend to purch

a..

No, but I

intend to purch

a..

Yes, I h

ave purch

ased flo..

Yes, I h

ave been purch

asi..

73%

24%

0%1%1%

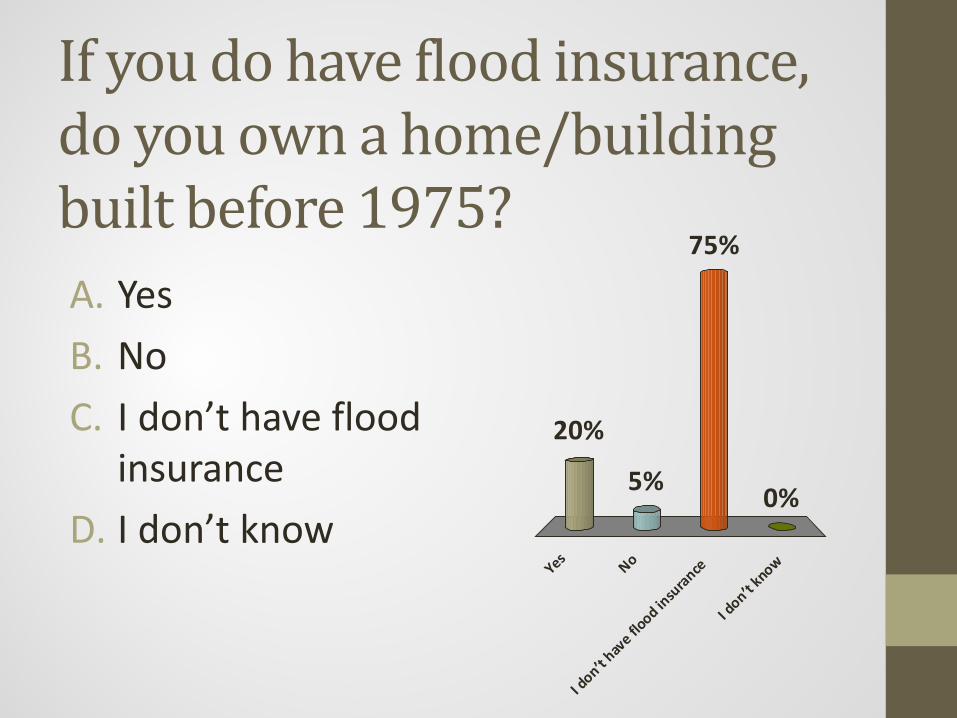

If you do have flood insurance, do you own a home/building built before 1975? A. Yes B. No C. I don’t have flood

insurance D. I don’t know

YesNo

I don’t h

ave flo

od insu

rance

I don’t k

now

20%

0%

75%

5%

RHODE ISLAND EMERGENCY MANAGEMENT AGENCY RHODE ISLAND EMERGENCY MANAGEMENT AGENCY

National Flood Insurance Reforms – What do these changes mean for Rhode Island? Impact of changes to the NFIP under Section 205 of the Biggert-Waters Act July 10, 2013

RHODE ISLAND EMERGENCY MANAGEMENT AGENCY RHODE ISLAND EMERGENCY MANAGEMENT AGENCY

National Flood Insurance Program Background

• National Flood Insurance Act of 1968 – Established the NFIP – Required mapping of flood-prone areas – Made flood insurance available to all residents of

communities that meet floodplain management requirements

– Afforded communities ability to obtain certain types of disaster assistance

RHODE ISLAND EMERGENCY MANAGEMENT AGENCY RHODE ISLAND EMERGENCY MANAGEMENT AGENCY

The NFIP: How It Works

RHODE ISLAND EMERGENCY MANAGEMENT AGENCY RHODE ISLAND EMERGENCY MANAGEMENT AGENCY

Flood Insurance Facts • Standard homeowners insurance doesn't cover flooding.

• Flood Insurance is required if you live in a Special Flood Hazard Area (SFHA) or high-risk area AND have a federally backed mortgage or other commitment (reverse mortgage, line of credit, etc.)

• A lender can require flood insurance, even if a structure is NOT in the SFHA.

• Flood insurance can be purchased through a local insurance agent.

RHODE ISLAND EMERGENCY MANAGEMENT AGENCY RHODE ISLAND EMERGENCY MANAGEMENT AGENCY

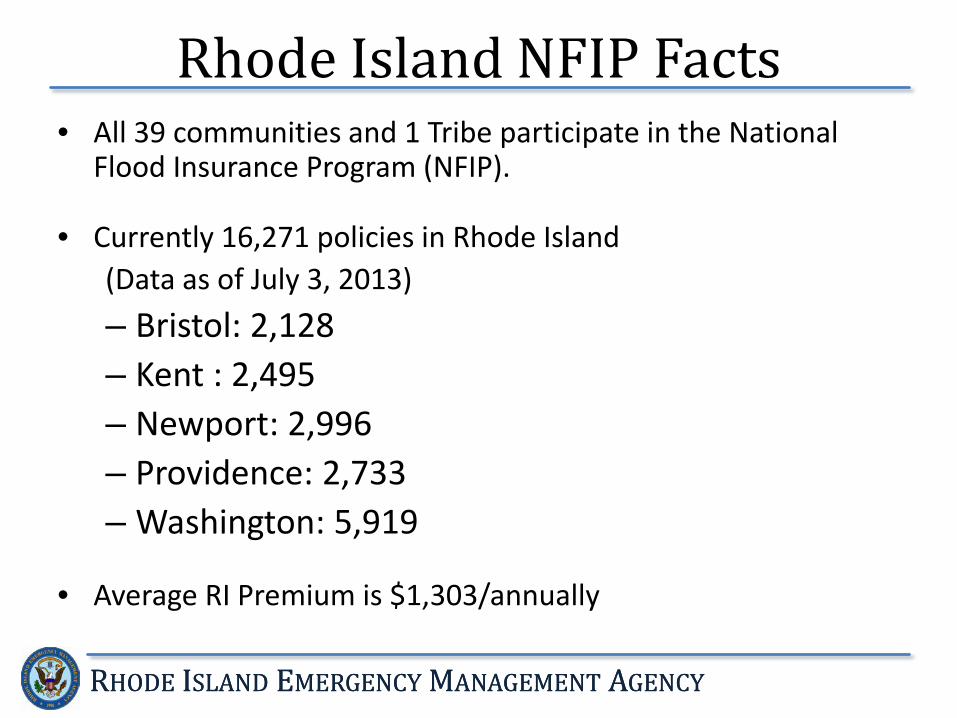

Rhode Island NFIP Facts • All 39 communities and 1 Tribe participate in the National

Flood Insurance Program (NFIP).

• Currently 16,271 policies in Rhode Island (Data as of July 3, 2013) – Bristol: 2,128 – Kent : 2,495 – Newport: 2,996 – Providence: 2,733 – Washington: 5,919

• Average RI Premium is $1,303/annually

RHODE ISLAND EMERGENCY MANAGEMENT AGENCY RHODE ISLAND EMERGENCY MANAGEMENT AGENCY

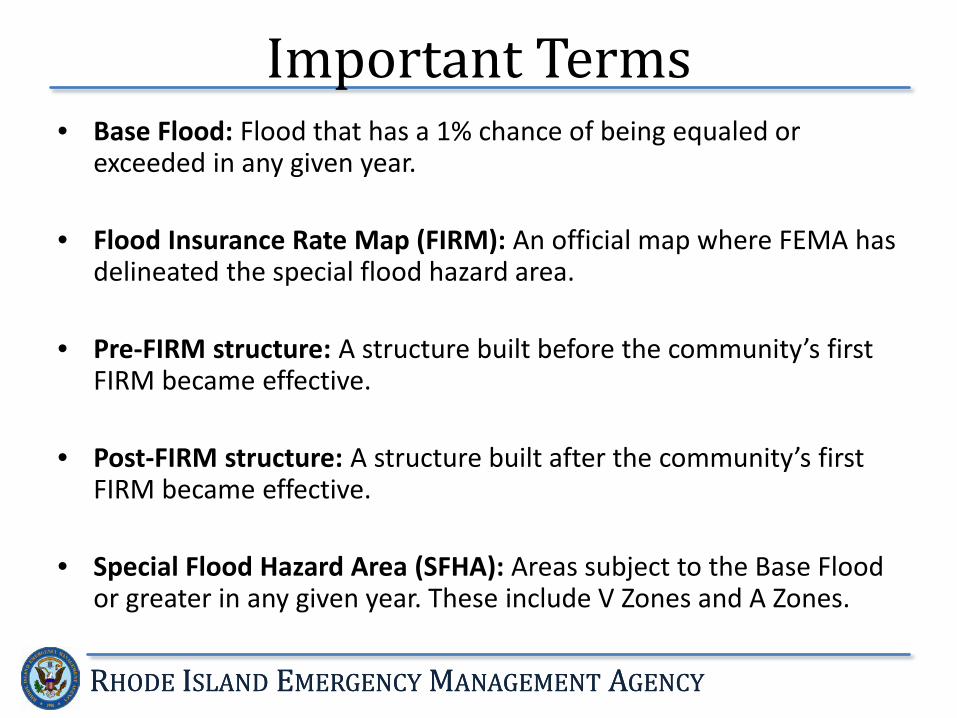

Important Terms • Base Flood: Flood that has a 1% chance of being equaled or

exceeded in any given year.

• Flood Insurance Rate Map (FIRM): An official map where FEMA has delineated the special flood hazard area.

• Pre-FIRM structure: A structure built before the community’s first FIRM became effective.

• Post-FIRM structure: A structure built after the community’s first FIRM became effective.

• Special Flood Hazard Area (SFHA): Areas subject to the Base Flood or greater in any given year. These include V Zones and A Zones.

RHODE ISLAND EMERGENCY MANAGEMENT AGENCY RHODE ISLAND EMERGENCY MANAGEMENT AGENCY

Mapping: Why New Maps? • There is a nationwide project underway to update the FEMA

FIRMs. A combination of new data and outdated maps has propelled the project.

• The maps were created by a FEMA contactor, STARR, through extensive modeling using new transects, surveys and coastal analyses.

RHODE ISLAND EMERGENCY MANAGEMENT AGENCY RHODE ISLAND EMERGENCY MANAGEMENT AGENCY

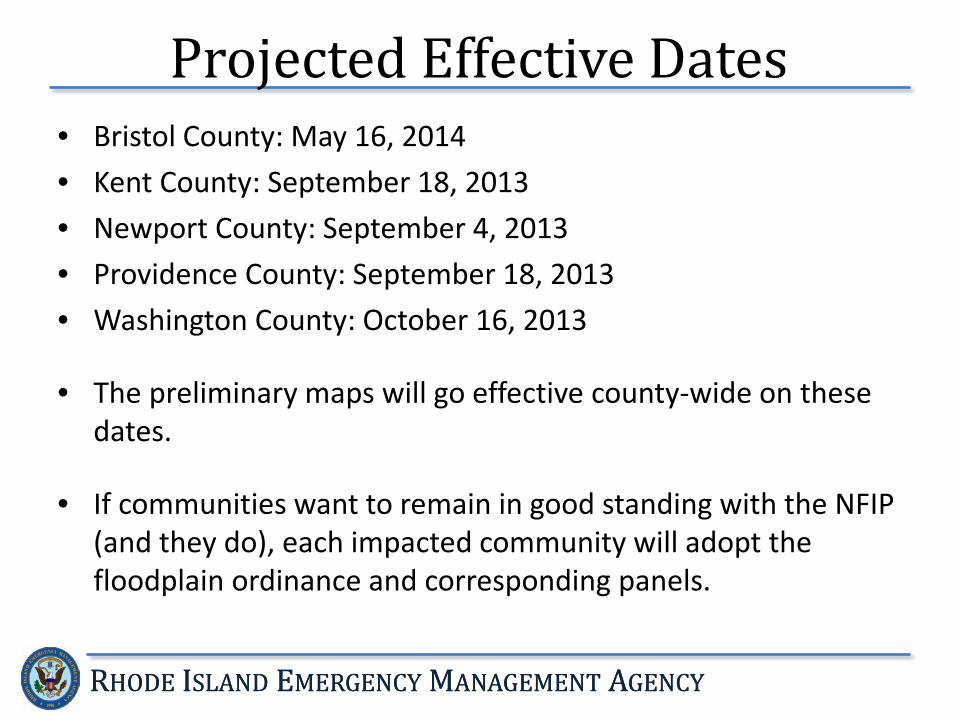

Projected Effective Dates • Bristol County: May 16, 2014 • Kent County: September 18, 2013 • Newport County: September 4, 2013 • Providence County: September 18, 2013 • Washington County: October 16, 2013

• The preliminary maps will go effective county-wide on these dates.

• If communities want to remain in good standing with the NFIP (and they do), each impacted community will adopt the floodplain ordinance and corresponding panels.

RHODE ISLAND EMERGENCY MANAGEMENT AGENCY RHODE ISLAND EMERGENCY MANAGEMENT AGENCY

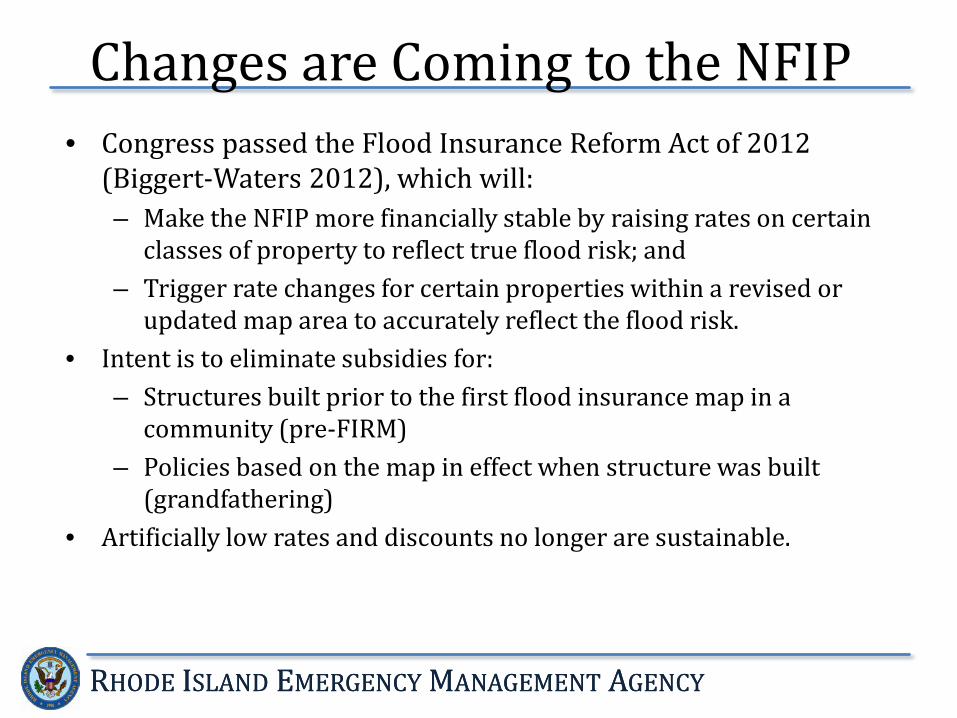

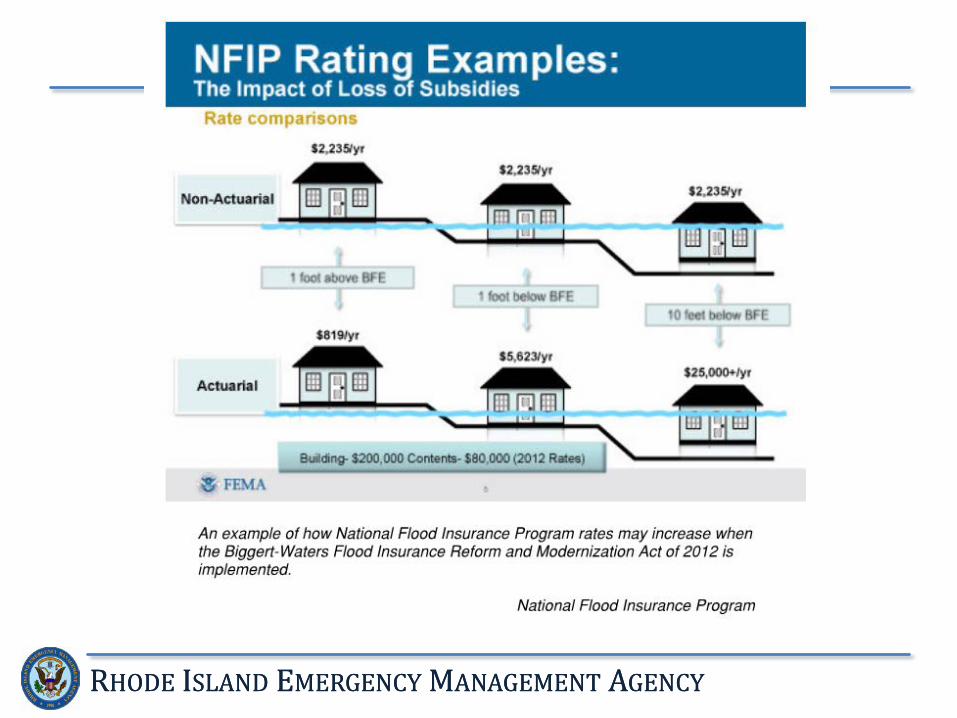

• Congress passed the Flood Insurance Reform Act of 2012 (Biggert-Waters 2012), which will: – Make the NFIP more financially stable by raising rates on certain

classes of property to reflect true flood risk; and – Trigger rate changes for certain properties within a revised or

updated map area to accurately reflect the flood risk. • Intent is to eliminate subsidies for:

– Structures built prior to the first flood insurance map in a community (pre-FIRM)

– Policies based on the map in effect when structure was built (grandfathering)

• Artificially low rates and discounts no longer are sustainable.

Changes are Coming to the NFIP

RHODE ISLAND EMERGENCY MANAGEMENT AGENCY RHODE ISLAND EMERGENCY MANAGEMENT AGENCY

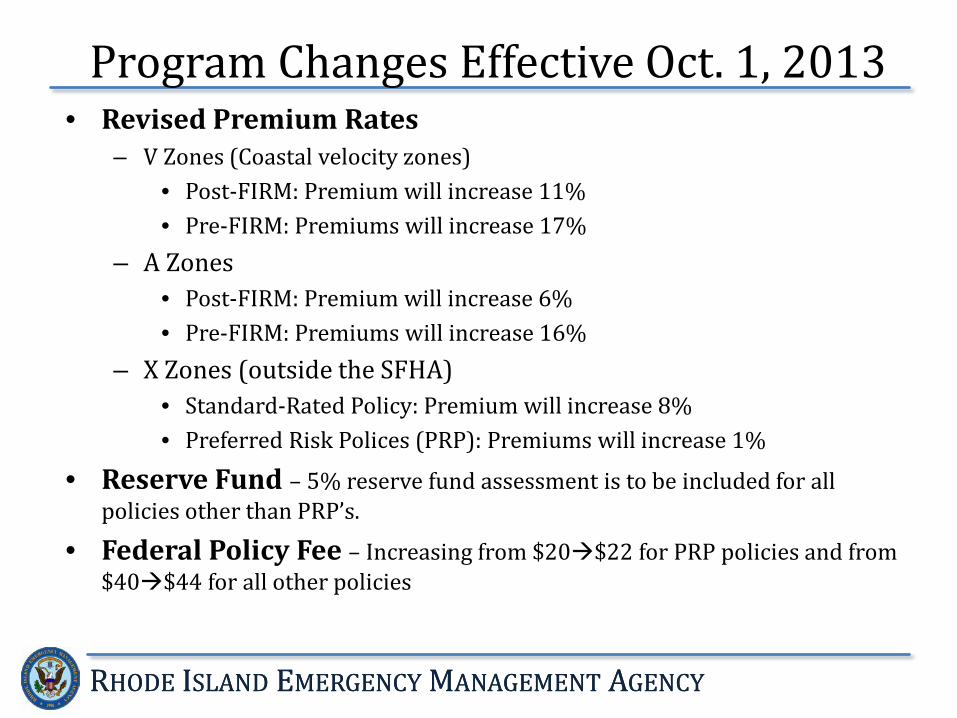

• Revised Premium Rates – V Zones (Coastal velocity zones)

• Post-FIRM: Premium will increase 11% • Pre-FIRM: Premiums will increase 17%

– A Zones • Post-FIRM: Premium will increase 6% • Pre-FIRM: Premiums will increase 16%

– X Zones (outside the SFHA) • Standard-Rated Policy: Premium will increase 8% • Preferred Risk Polices (PRP): Premiums will increase 1%

• Reserve Fund – 5% reserve fund assessment is to be included for all policies other than PRP’s.

• Federal Policy Fee – Increasing from $20$22 for PRP policies and from $40$44 for all other policies

Program Changes Effective Oct. 1, 2013

RHODE ISLAND EMERGENCY MANAGEMENT AGENCY RHODE ISLAND EMERGENCY MANAGEMENT AGENCY

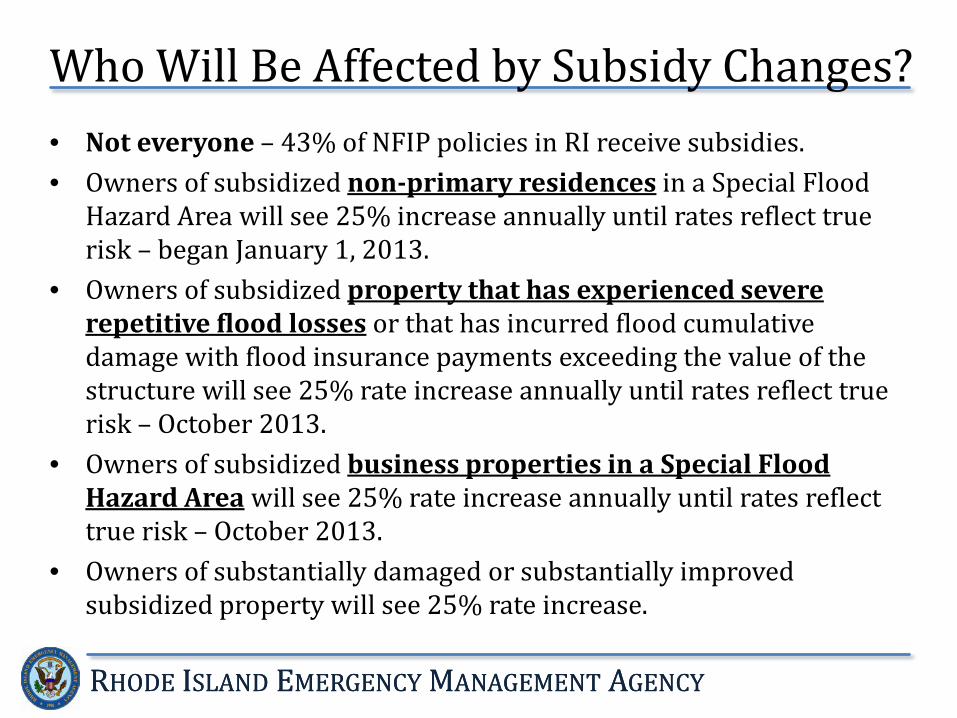

• Not everyone – 43% of NFIP policies in RI receive subsidies. • Owners of subsidized non-primary residences in a Special Flood

Hazard Area will see 25% increase annually until rates reflect true risk – began January 1, 2013.

• Owners of subsidized property that has experienced severe repetitive flood losses or that has incurred flood cumulative damage with flood insurance payments exceeding the value of the structure will see 25% rate increase annually until rates reflect true risk – October 2013.

• Owners of subsidized business properties in a Special Flood Hazard Area will see 25% rate increase annually until rates reflect true risk – October 2013.

• Owners of substantially damaged or substantially improved subsidized property will see 25% rate increase.

Who Will Be Affected by Subsidy Changes?

RHODE ISLAND EMERGENCY MANAGEMENT AGENCY RHODE ISLAND EMERGENCY MANAGEMENT AGENCY

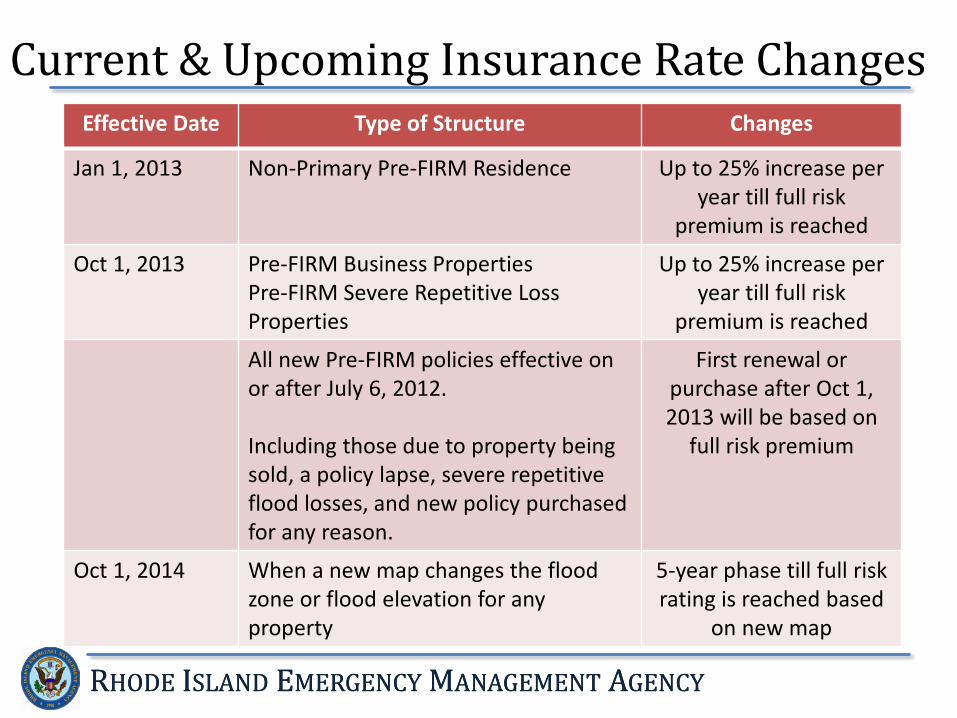

Current & Upcoming Insurance Rate Changes Effective Date Type of Structure Changes

Jan 1, 2013

Non-Primary Pre-FIRM Residence Up to 25% increase per year till full risk

premium is reached

Oct 1, 2013 Pre-FIRM Business Properties Pre-FIRM Severe Repetitive Loss Properties

Up to 25% increase per year till full risk

premium is reached

All new Pre-FIRM policies effective on or after July 6, 2012. Including those due to property being sold, a policy lapse, severe repetitive flood losses, and new policy purchased for any reason.

First renewal or purchase after Oct 1, 2013 will be based on

full risk premium

Oct 1, 2014 When a new map changes the flood zone or flood elevation for any property

5-year phase till full risk rating is reached based

on new map

RHODE ISLAND EMERGENCY MANAGEMENT AGENCY RHODE ISLAND EMERGENCY MANAGEMENT AGENCY

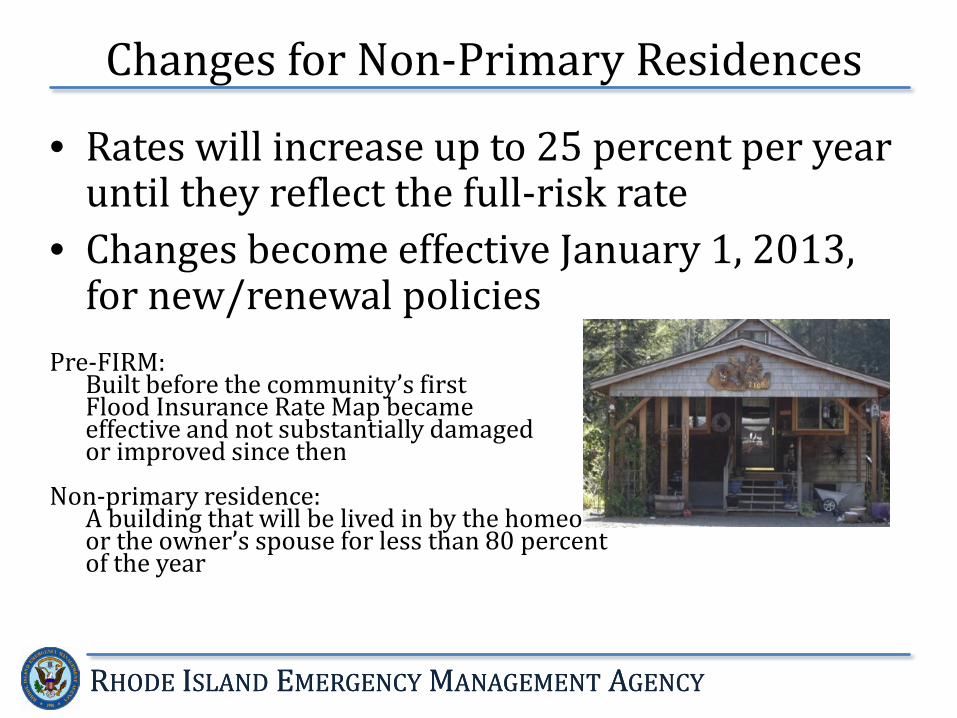

Changes for Non-Primary Residences

• Rates will increase up to 25 percent per year until they reflect the full-risk rate

• Changes become effective January 1, 2013, for new/renewal policies

Pre-FIRM: Built before the community’s first Flood Insurance Rate Map became effective and not substantially damaged or improved since then

Non-primary residence: A building that will be lived in by the homeowner or the owner’s spouse for less than 80 percent of the year

RHODE ISLAND EMERGENCY MANAGEMENT AGENCY RHODE ISLAND EMERGENCY MANAGEMENT AGENCY

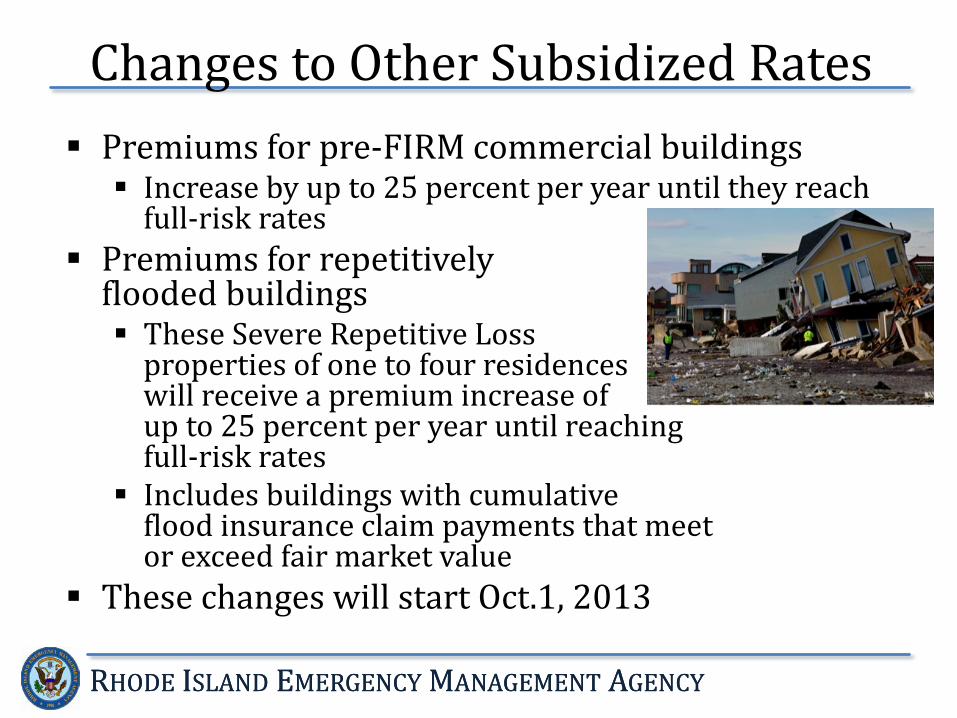

Changes to Other Subsidized Rates Premiums for pre-FIRM commercial buildings Increase by up to 25 percent per year until they reach

full-risk rates Premiums for repetitively

flooded buildings These Severe Repetitive Loss

properties of one to four residences will receive a premium increase of up to 25 percent per year until reaching full-risk rates

Includes buildings with cumulative flood insurance claim payments that meet or exceed fair market value

These changes will start Oct.1, 2013

RHODE ISLAND EMERGENCY MANAGEMENT AGENCY RHODE ISLAND EMERGENCY MANAGEMENT AGENCY

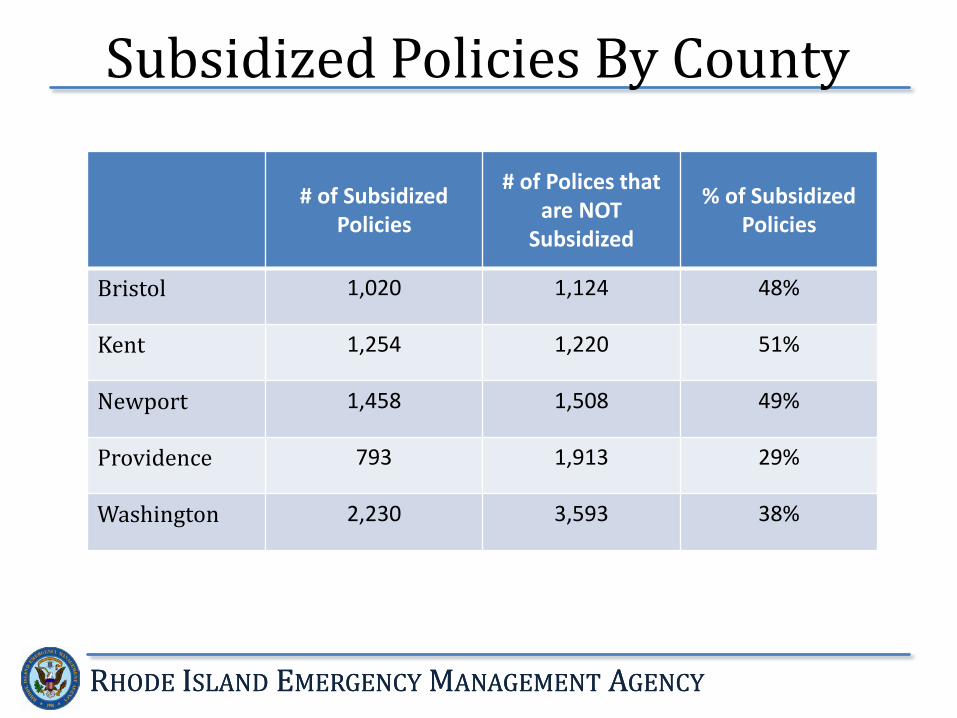

Subsidized Policies By County

# of Subsidized Policies

# of Polices that are NOT

Subsidized

% of Subsidized Policies

Bristol 1,020 1,124 48%

Kent 1,254 1,220 51%

Newport 1,458 1,508 49%

Providence 793 1,913 29%

Washington 2,230 3,593 38%

RHODE ISLAND EMERGENCY MANAGEMENT AGENCY RHODE ISLAND EMERGENCY MANAGEMENT AGENCY

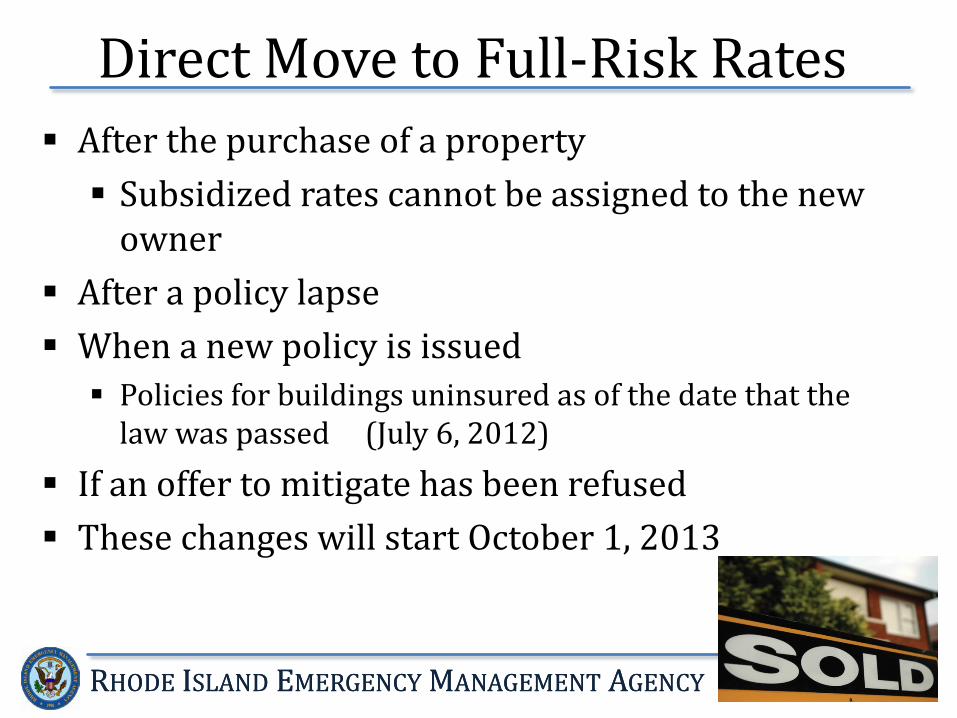

Direct Move to Full-Risk Rates After the purchase of a property Subsidized rates cannot be assigned to the new

owner After a policy lapse When a new policy is issued Policies for buildings uninsured as of the date that the

law was passed (July 6, 2012) If an offer to mitigate has been refused These changes will start October 1, 2013

RHODE ISLAND EMERGENCY MANAGEMENT AGENCY RHODE ISLAND EMERGENCY MANAGEMENT AGENCY

RHODE ISLAND EMERGENCY MANAGEMENT AGENCY RHODE ISLAND EMERGENCY MANAGEMENT AGENCY

What about when a new flood map is adopted?

• If you live in a community which adopts a new, updated Flood Insurance Rate Map (FIRM) : – Charging of insurance premiums based on a prior

FIRM -- grandfathering -- will be phased out. • The Biggert-Waters Act Section 100207 calls for a phase-

out of grandfathering discounts for properties shown on Flood Insurance Rate Maps that are updated.

• But the pain is lessened somewhat, because new rates will be gradually phased in at 20% per year for five years

• Implementation anticipated in 2014

RHODE ISLAND EMERGENCY MANAGEMENT AGENCY

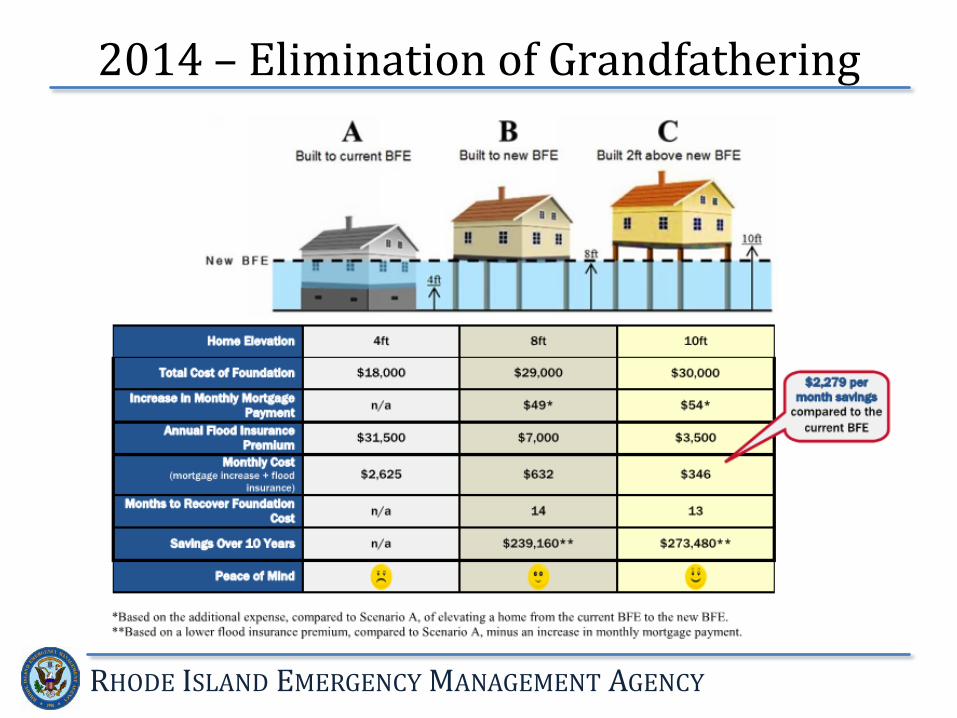

2014 – Elimination of Grandfathering

RHODE ISLAND EMERGENCY MANAGEMENT AGENCY RHODE ISLAND EMERGENCY MANAGEMENT AGENCY

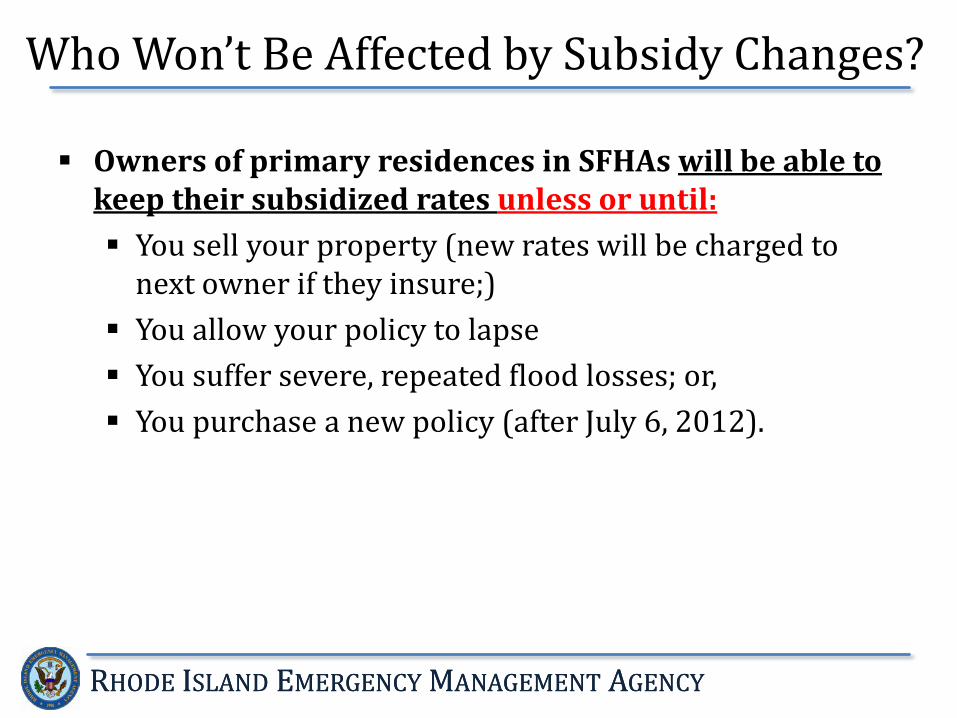

Owners of primary residences in SFHAs will be able to keep their subsidized rates unless or until: You sell your property (new rates will be charged to

next owner if they insure;) You allow your policy to lapse You suffer severe, repeated flood losses; or, You purchase a new policy (after July 6, 2012).

Who Won’t Be Affected by Subsidy Changes?

RHODE ISLAND EMERGENCY MANAGEMENT AGENCY RHODE ISLAND EMERGENCY MANAGEMENT AGENCY

Home and business owners: Talk to your insurance agent about your insurance options

You’ll probably need an Elevation Certificate to determine your correct rate Higher deductibles might lower your premium

Consider remodeling or rebuilding Building or rebuilding higher will lower your risk and could reduce your

premium Consider adding vents to your foundation or using breakaway walls

Talk with local officials about community-wide mitigation steps Community leaders:

Consider joining the Community Rating System (CRS) or increasing your CRS activities to lower premiums for residents.

Talk to your state about grants. FEMA issues grants to states which can distribute the funds to communities to help with mitigation and rebuilding.

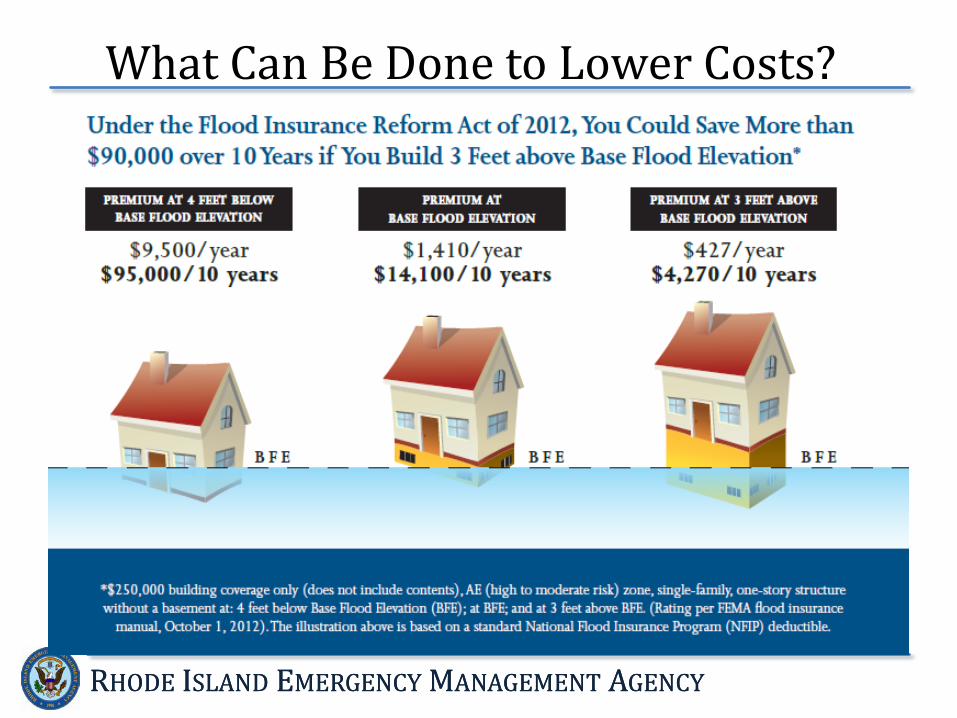

What Can Be Done to Lower Costs?

RHODE ISLAND EMERGENCY MANAGEMENT AGENCY RHODE ISLAND EMERGENCY MANAGEMENT AGENCY

• Many changes are coming to the Flood Insurance program • Congress acted to make program stronger financially.

• On many more policies, flood insurance rates will reflect full risk.

• Insurance rates will rise on some policies; and • There are specific actions which will trigger rate changes.

• Talk to your insurance agent about how changes may affect your property and flood insurance policy.

• Building or rebuilding higher can lower your flood risk and could save you money.

• FEMA can help communities lower flood risk and flood insurance premiums through: • Community Rating System program; • Various mitigation grants; and • Technical advice on building and rebuilding to mitigate future flood

damage.

What You Need to Remember

RHODE ISLAND EMERGENCY MANAGEMENT AGENCY RHODE ISLAND EMERGENCY MANAGEMENT AGENCY

Michelle Burnett Rhode Island State Floodplain Manager Rhode Island Emergency Management Agency 645 New London Avenue Cranston, RI 02920 Direct: (401) 462-7048 [email protected] Bob Desaulniers FEMA Region I – New England Insurance Specialist Direct: (617) 832-4760 [email protected]

Contact Information

Be prepared, take the survey and get tips to be more prepared for such emergencies.

http://seagrant.gso.uri.edu/climate/

Speak to your builder/designer and local building official about adding freeboard to your existing, rebuilt or new home.

Support Community Efforts

Join Stormsmart RI.stormsmart.org Use the Community Rating System to reduce rates Continue to engage in the Beach SAMP

Questions?

POST-Presentation Questions

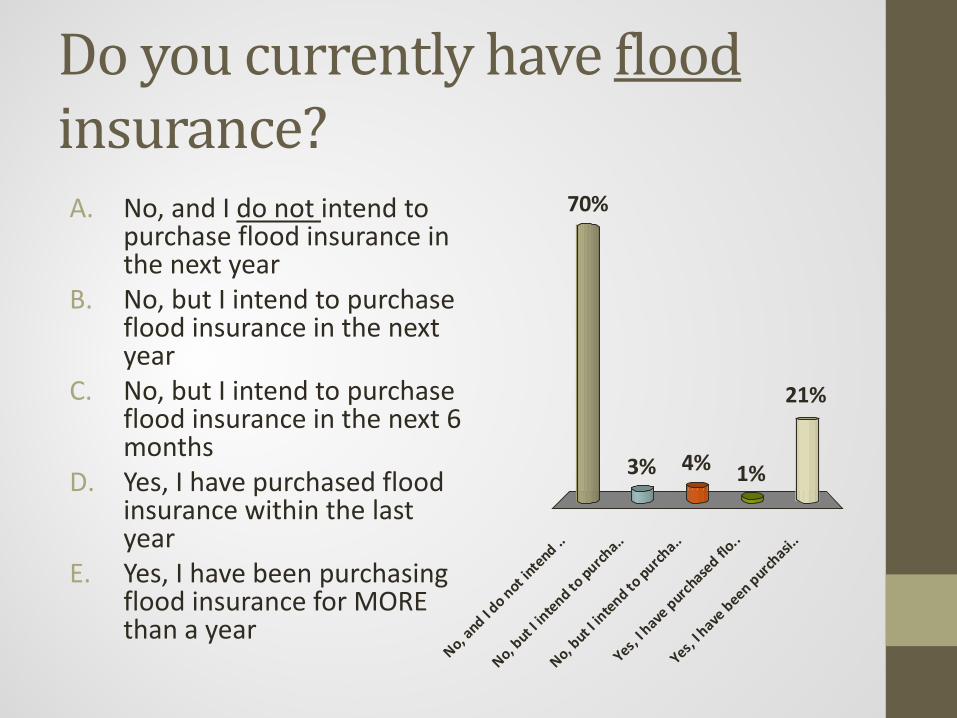

Do you currently have flood insurance? A. No, and I do not intend to

purchase flood insurance in the next year

B. No, but I intend to purchase flood insurance in the next year

C. No, but I intend to purchase flood insurance in the next 6 months

D. Yes, I have purchased flood insurance within the last year

E. Yes, I have been purchasing flood insurance for MORE than a year

No, and I d

o not intend ..

No, but I

intend to purch

a..

No, but I

intend to purch

a..

Yes, I h

ave purch

ased flo..

Yes, I h

ave been purch

asi..

70%

21%

1%4%3%

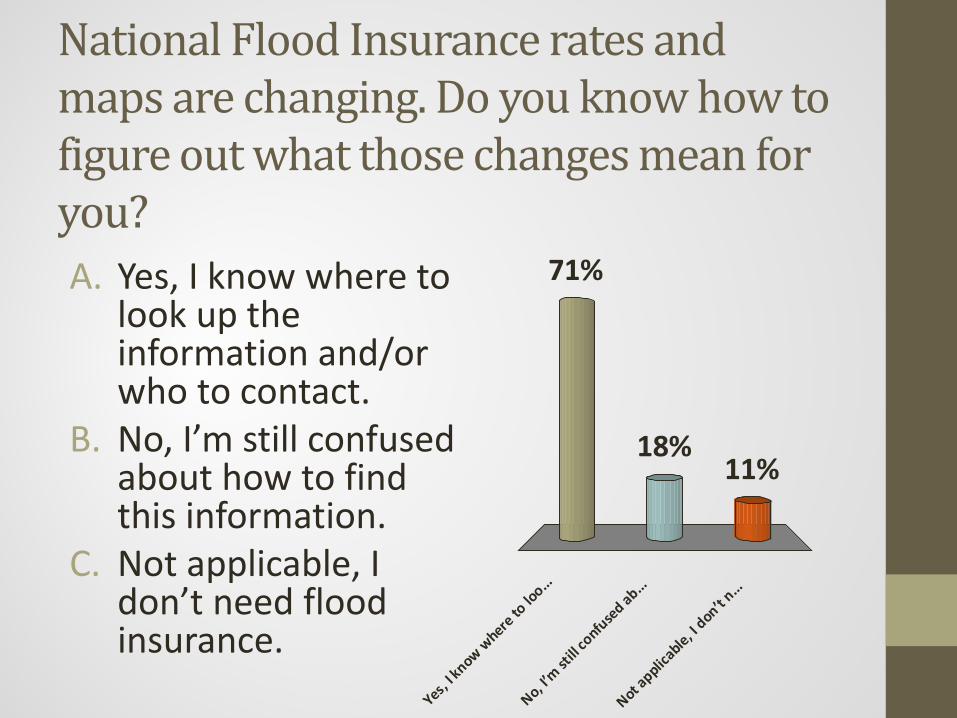

National Flood Insurance rates and maps are changing. Do you know how to figure out what those changes mean for you? A. Yes, I know where to

look up the information and/or who to contact.

B. No, I’m still confused about how to find this information.

C. Not applicable, I don’t need flood insurance.

Yes, I k

now where to

loo...

No, I’m st

ill co

nfused ab...

Not applic

able, I don’t n

...

11%18%

71%

Audience Feedback Session

Who should be involved?

What are the issues you’d like the SAMP

to respond to?

Melissa Devine, 2012 Browning Cottages, Post-Sandy

What change would you like to see? And

from who?

Butch Lombardi 2012, Warren

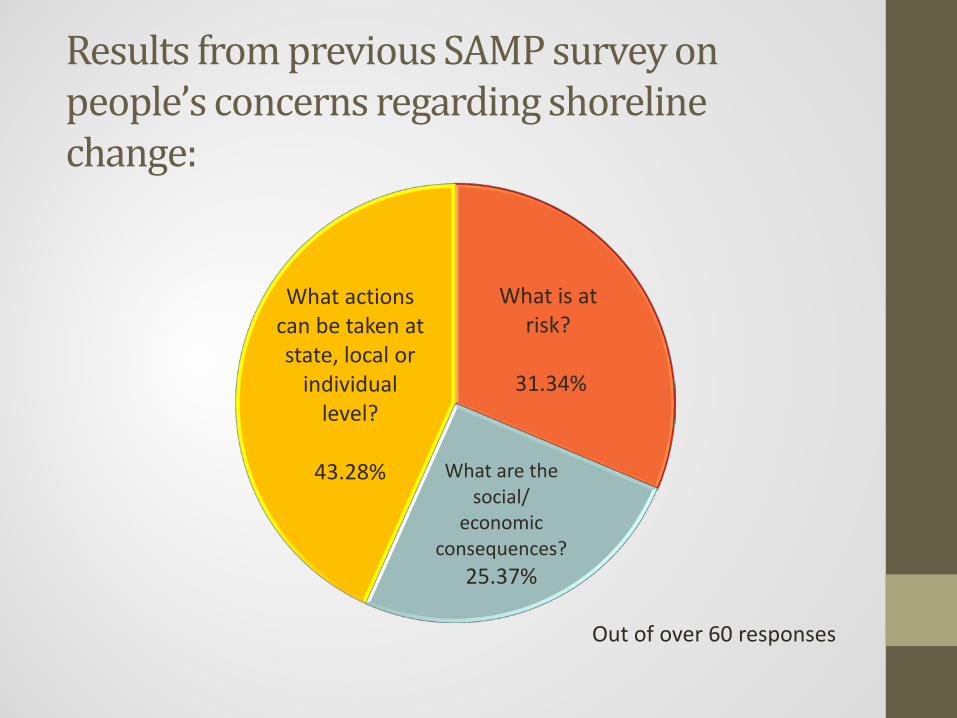

What is at risk?

31.34%

What are the social/

economic consequences?

25.37%

What actions can be taken at state, local or

individual level?

43.28%

Out of over 60 responses

Results from previous SAMP survey on people’s concerns regarding shoreline change:

Next Steps Questions we are tackling:

• How has the shoreline changed over time and how might we expect it to change in the future?

• What areas are at risk from storm surge and sea level rise? • How will our wetlands respond to rising sea levels, will

they migrate landward or drown in place? • What are other places doing to deal with these issues and

would that work in Rhode Island? • What is the cost (insurance, rebuilding, loss of tax

revenue) associated with shoreline change? (pending)

• Coordination with other state agencies

Stay involved! • Tell a neighbor,

colleague, friend about what you learned tonight

• Next stakeholder meeting will be in fall

• Visit the new website: beachsamp.org

• Join the listserv