Embed Size (px)

Citation preview

Corporate Presentation

September 2016

Daimler AG

Contents

Page 2

Results for Q2 2016

Outlook for 2016

Daimler Group Strategy

Divisional information

China

Appendix

Daimler Corporate Presentation / September 2016 /

Daimler AG

Highlights of Q2 2016

Strong growth in Group unit sales 761,300 + 7 %

Highest quarterly unit sales so far at Mercedes-Benz Cars 546,500 + 9 %

EBIT adjusted for special items € 4.0bn + 6 %

World premiere of the new Mercedes-Benz E-Class station wagon

Start of production of new Mercedes-Benz C-Class Cabriolet, GLC Coupé and long-wheelbase E-Class in China

World premiere of the Mercedes-Benz Future Bus with CityPilot – a milestone on the way to autonomous driving

Successful start of car2go services in the Chinese metropolis Chongqing

Transfer of shares in Renault/Nissan strengthens pension assets by €1.8 billion

Launch of six regional sales centers for Daimler commercial vehicles completed

Page 3 Daimler Corporate Presentation / September 2016 /

Daimler AG

Key financials

Q2 2015 Q2 2016

Revenue 37.5 38.6

EBIT

as reported 3.7 3.3

adjusted for special items 3.8 4.0

Net profit 2.4 2.5

Earnings per share (in euros) 2.12 2.27

Net liquidity industrial business (2015: year-end) 18.6 17.4

Free cash flow of the industrial business (January-June) 3.4 2.1

in billions of euros

Page 4 Daimler Corporate Presentation / September 2016 /

Daimler AG

Key balance sheet and financial figures

Daimler Group Dec. 31, 2015 June 30, 2016

Equity ratio 23.6% 22.7%

Gross liquidity 18.2 22.9

Industrial business

Equity ratio 44.2% 41.2%

Net liquidity 18.6 17.4

in billions of euros

Page 5 Daimler Corporate Presentation / September 2016 /

Daimler AG

Net industrial liquidity: development in H1 2016

Free cash flow industrial business

H1 2016: €2.1bn

Net industrial

liquidity

12/31/2015

Earnings and

other cash flow

impact

Working capital

impact

Other Net industrial

liquidity

6/30/2016

+0.0

17.4 +0.2 18.6

+2.1

- in billions of euros -

Dividend payment

Daimler AG

-3.5

Page 6 Daimler Corporate Presentation / September 2016 /

Daimler AG

Unit sales

Q2 2015 Q2 2016 % change

Daimler Group 714.8 761.3 +7

of which

Mercedes-Benz Cars 500.7 546.5 +9

Daimler Trucks 125.1 108.3 -13

Mercedes-Benz Vans 81.6 99.6 +22

Daimler Buses 7.3 7.0 -5

in thousands of units

Page 7 Daimler Corporate Presentation / September 2016 /

Daimler AG

Revenue by region

Page 8

Q2 2015 Q2 2016 % change

Daimler Group 37.5 38.6 +3

of which

Western Europe 12.0 14.0 +16

of which Germany 5.5 6.2 +12

NAFTA 12.1 11.5 -5

of which United States 10.6 10.0 -6

Asia 8.5 8.4 -0

of which China* 3.8 3.9 +4

Other markets 4.9 4.7 -3

in billions of euros

* excluding revenue of not fully consolidated companies

Daimler Corporate Presentation / September 2016 /

Daimler AG

Revenue by division

Q2 2015 Q2 2016 % change

Daimler Group 37.5 38.6 +3

of which

Mercedes-Benz Cars 21.1 22.1 +5

Daimler Trucks 9.4 8.7 -8

Mercedes-Benz Vans 2.8 3.4 +22

Daimler Buses 1.0 1.1 +8

Daimler Financial Services 4.8 5.0 +5

Contract volume of Daimler Financial Services* 116.7 120.3 +3

in billions of euros

* figures as of December 31, 2015 and June 30, 2016

Page 9 Daimler Corporate Presentation / September 2016 /

Daimler AG

EBIT by division

Q2 2015 Q2 2016

- EBIT in millions of euros; RoS in % - EBIT RoS* EBIT RoS*

Daimler Group 3,718 10.0 3,258 8.3

of which

Mercedes-Benz Cars 2,227 10.5 1,410 6.4

Daimler Trucks 682 7.2 621 7.2

Mercedes-Benz Vans 234 8.3 401 11.7

Daimler Buses 57 5.5 88 7.8

Daimler Financial Services 445 – 479 –

Reconciliation 73 – 259 –

* Return on sales; Daimler Group excluding Daimler Financial Services

Page 10 Daimler Corporate Presentation / September 2016 /

Daimler AG

EBIT adjusted for special items

Q2 2015 Q2 2016

- EBIT in millions of euros; RoS in % - EBIT RoS* EBIT RoS*

Daimler Group 3,764 10.1 3,973 10.4

of which

Mercedes-Benz Cars 2,234 10.6 2,209 10.0

Daimler Trucks 717 7.6 661 7.6

Mercedes-Benz Vans 238 8.4 462 13.4

Daimler Buses 57 5.5 89 7.9

Daimler Financial Services 445 – 479 –

Reconciliation 73 – 73 –

* Return on sales; Daimler Group excluding Daimler Financial Services

Page 11 Daimler Corporate Presentation / September 2016 /

Daimler AG

Contents

Results for Q2 2016

Outlook for 2016

Daimler Group Strategy

Divisional information

China

Appendix

Page 12 Daimler Corporate Presentation / September 2016 /

Daimler AG

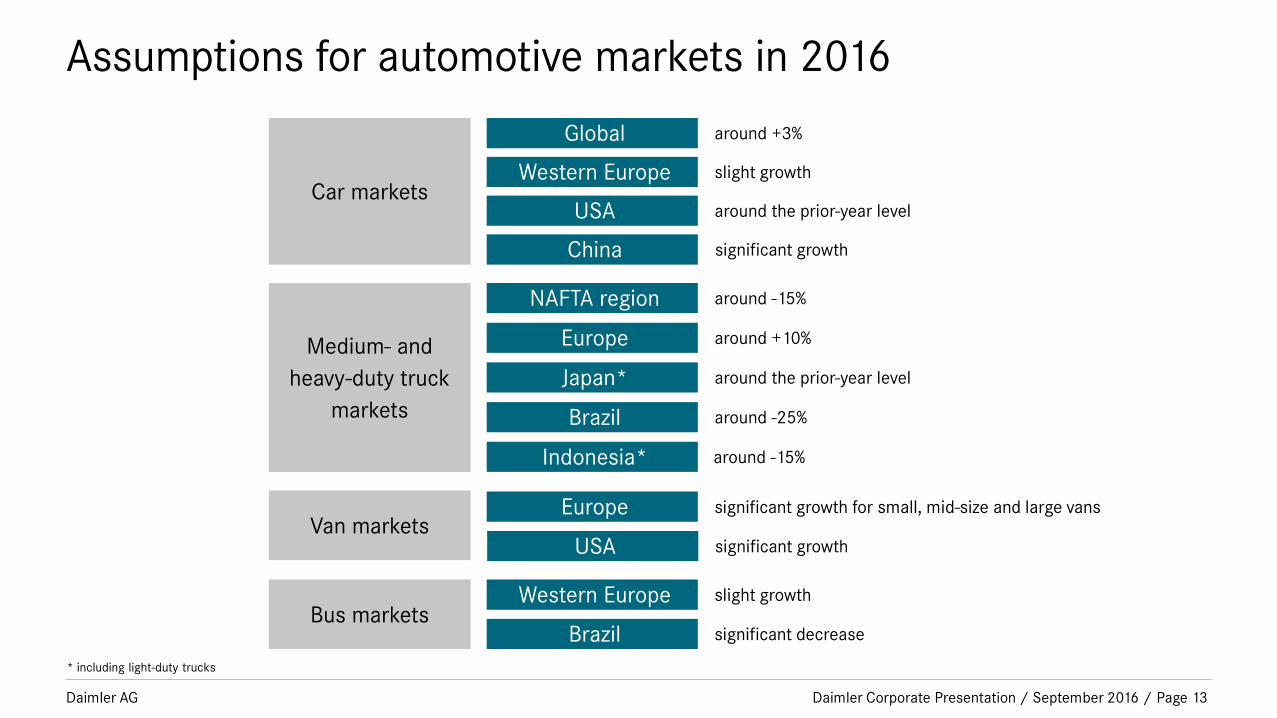

Assumptions for automotive markets in 2016

Car markets

Global

Western Europe

Medium- and

heavy-duty truck

markets

NAFTA region

Europe

Japan*

Brazil

Europe

Bus markets Western Europe

Brazil

around +3%

slight growth

around -15%

around +10%

around the prior-year level

around -25%

significant growth for small, mid-size and large vans

slight growth

significant decrease

USA around the prior-year level

Van markets

Indonesia* around -15%

China significant growth

* including light-duty trucks

USA significant growth

Page 13 Daimler Corporate Presentation / September 2016 /

Daimler AG

2016 sales outlook

Significantly higher unit sales

Strong momentum from renewed SUV portfolio and further plug-in hybrid models

Launch of all-new E-Class, C-Class Coupé, S-Class Cabriolet and smart fortwo cabrio

Unit sales significantly below the prior-year level

Worsened situation of global truck markets; weakening NAFTA market can be only

partially offset by the market development in Europe

Significantly higher unit sales

Significant growth in core market Western Europe

Continued momentum from “Mercedes-Benz Vans goes global” strategy

Unit sales slightly below the prior-year level

Maintain market leadership in core markets

Significant growth in Western Europe, significantly lower demand in Brazil

Mercedes-Benz Cars

Daimler Trucks

Mercedes-Benz Vans

Daimler Buses

Page 14 Daimler Corporate Presentation / September 2016 /

Daimler AG

2016 outlook for EBIT adjusted for special items

Slightly above the prior-year level

Significantly above the prior-year level

Slightly above the prior-year level

Significantly below the prior-year level

Slightly above the prior-year level

We expect Group EBIT for FY 2016 to increase slightly

based on the following expectations for divisional EBIT:

Mercedes-Benz Cars

Daimler Trucks

Mercedes-Benz Vans

Daimler Buses

Daimler Financial Services

Page 15 Daimler Corporate Presentation / September 2016 /

Daimler AG

Contents

Page 16

Results for Q2 2016

Outlook for 2016

Daimler Group Strategy

Divisional information

China

Appendix

Daimler Corporate Presentation / September 2016 /

Daimler AG

Clear aspiration for all our divisions

17

Daimler Buses Daimler Trucks Mercedes-Benz

Vans Daimler Financial

Services

“Most successful

premium

manufacturer”

Mercedes-Benz Cars

“No 1 in

the global truck

business”

“Best financial

and mobility

services provider”

“No 1 in the

global bus

business”

“Most successful

player in

worldwide van

business”

Page 17 Daimler Corporate Presentation / September 2016 /

Daimler AG

The four strategic focus areas of Daimler

Page 18 Daimler Corporate Presentation / September 2016 /

Daimler AG

Digitalization puts the focus on the customer

Digital target picture Daimler

1) Industry 4.0

„Shaping the future of safe and sustainable mobility“

We are among the leaders in our industry regarding digital work

environment and culture. Our customers perceive us as the most innovative

digital automotive manufacturer.

Vision

Mission statement

DigitalLife@Daimler

Success factors

Indirect customer perception

Direct customer perception

Key digital

levers

Products & Services

Processes and Structures Management system Digital skills & Corporate culture

Digitalization of the value chain1)

Page 19 Daimler Corporate Presentation / September 2016 /

Daimler AG

Profit targets

Return on sales-target for the automotive business : 9 percent

9 6 17 10

Mercedes-Benz

Cars

8 Daimler

Trucks

Mercedes-Benz

Vans

Daimler

Buses

Daimler

Financial Services

Profit targets [Return on Sales / Return on Equity1) in %]

Page 20

1) Daimler Financial Services

Daimler Corporate Presentation / September 2016 /

Daimler AG

Contents

Page 21

Results for Q2 2016

Outlook for 2016

Daimler Group Strategy

Divisional information

China

Appendix

Daimler Corporate Presentation / September 2016 /

Daimler AG Page 22

Mercedes-Benz Cars

Daimler Corporate Presentation / September 2016 /

Daimler AG

Mercedes-Benz Cars: product highlights

Mercedes-Benz Concept IAA New Mercedes-Benz S-Class Cabriolet

New smart cabrio New Mercedes-Benz GLC Coupé New Mercedes-Benz E-Class station wagon

New Mercedes-AMG GT R New Mercedes-Benz C-Class Cabriolet

Page 23 Daimler Corporate Presentation / September 2016 /

Daimler AG

Mercedes-Benz Cars and Vans: continued product offensive

S-Class Cabriolet

SLC facelift SL facelift

CLA facelift

E-Class station wagon

smart cabrio

GLS facelift E-Class sedan

C-Class Cabriolet

GLC Coupé

E-Class (long wheelbase)

smart fortwo EV

GT R Coupé

E-Class All Terrain

E-Class Coupé

GLA facelift

GT C Roadster

S-Class facelift

E-Class Cabriolet

GT C Coupé

Pickup

2016 2017

V-Class China

smart cabrio EV

smart forfour EV

Vito China

Page 24 Daimler Corporate Presentation / September 2016 /

Daimler AG

Product offensive to fuel our sales offensive

2015 1992 2025

Current Product

offensive

Mercedes-Benz sales development

First product

offensive

530 k

1.63 m

Schematic

representation

Current Product

offensive

First product

offensive

Page 25 Daimler Corporate Presentation / September 2016 /

Daimler AG

smart: Summer in the city

Page 26 Daimler Corporate Presentation / September 2016 /

Daimler AG

We are on our way to emission-free driving

Example: MBC fleet consumption in Europe

230

220

210

200

190

180

170

160

150

140

2009

173

2008

183

0 2007

158

1995

120

2011 2010

130

160

CO

2-e

mis

sio

ns

(g/

km

)

9.2 l 7.3 l 6.9 l 6.3 l 6.4 l

150

6.0 l

2012

123

Actual

2015

100

110

140

5.6 l

230

-44%

until 2020

95

<4.0 l

EU Legislation

2013

134

5.4 l

-6g

129

5.2 l

2014

125

Target

2016

Page 27

5.0 l

Daimler Corporate Presentation / September 2016 /

Daimler AG

Our roadmap for sustainable mobility

28

Mercedes-AMG GT S: Fuel consumption urban/extra-urban/combined: 12,5-12,2/7,9-7,8/9,6-9,4 l/100 km,

CO2 emissions combined: 224-219 g/km. High-tech

combustion engines

Plug-in

hybrids

Electric vehicles

with battery or fuel-cell

Page 28 Daimler Corporate Presentation / September 2016 /

Daimler AG Page 29

24% friction reduction

11% faster acceleration

13% CO₂ reduction

-80% NOx emissions

17% weight reduction

18 kW more power

The new diesel engine OM654 …

… the first member of a complete new engine family

Daimler Corporate Presentation / September 2016 /

Daimler AG Page 30

2015 2014

2016 2017

C-Class Estate

S-Class

GLE

C-Class

E-Class

GLC

C-Class LWB

Introduction of 10 Plug-in Hybrid vehicles by 2017

Our Plug-In Hybrid Rollout is at full speed

Daimler Corporate Presentation / September 2016 /

Daimler AG Page 31

< 50 g/km CO2-Emissions

> 30 km electric operating range

Market introduction in 09/2016

Plug-In Hybrid Rollout - The upcoming E 350 e

Daimler Corporate Presentation / September 2016 /

Daimler AG

Autonomous driving goes far beyond technology

Page 32 Daimler Corporate Presentation / September 2016 /

Daimler AG

Beltbag

PRE-SAFE®

Impulse Side

Active Blind Spot Assist

Active Lane Keeping Assist

Evasive Steering Assist MULTIBEAM LED Headlights with Adaptive High Beam Assist

Remote

Park-Pilot

Active Braking Assist with Pedestrian Detection, Cross-Traffic

Function and Congestion Emergency Braking

Function

DRIVE PILOT with Distance Pilot DISTRONIC, Steering

Pilot, Active Lane Change Assist,

Active Emergency Stop Assist,

Speed Limit Pilot PRE-SAFE®

Page 33

Car-to-X-Communication PRE-SAFE® PLUS

The new E-Class takes autonomous and accident-free driving

to the next level

Daimler Corporate Presentation / September 2016 /

Daimler AG Daimler Corporate Presentation / September 2016 / Page 34

Development steps towards fully autonomous driving

Singe control functions

such as speed selection,

braking or lane keeping

are automated.

Driver in charge.

Level 1 Driver

Assistance

Vehicle can perform the

dynamic driving task in

certain modes.

Driver expected to

respond to requests to

take control.

Vehicle can perform

the dynamic driving

task in all modes that

can also be managed

by a human driver.

No driver needed.

Vehicle can perform

the dynamic driving

task in certain

modes.

Driver not expected to

respond to requests to

take control.

Autonomous Driving

Level 2 Partial

Automation

Level 3 ConditionalAutomation

Level 4 High

Automation

Level 5 Full

Automation

+ enabler for new & complementary mobility services

More than one control

function is automated.

Driver expected to take

care of all remaining

aspects of the dynamic

driving task.

- Currently offered by MB

& legally permissible -

Daimler AG

Connectivity as ‘enabling technology’ is the core of…

EVs

Charging Station Search

Range on Map

Remote Services

Examples

Safety

Live Traffic Information

Car-2-X Warnings

Emergency Call

Examples

Autonomous

Driving

Car-2-Car Communication

Intelligent Parking Assist

Smart Routing

Examples

Infotainment

Navigation

Radio/ Media

Internet/ Apps

Examples

Page 35 Daimler Corporate Presentation / September 2016 /

Daimler AG

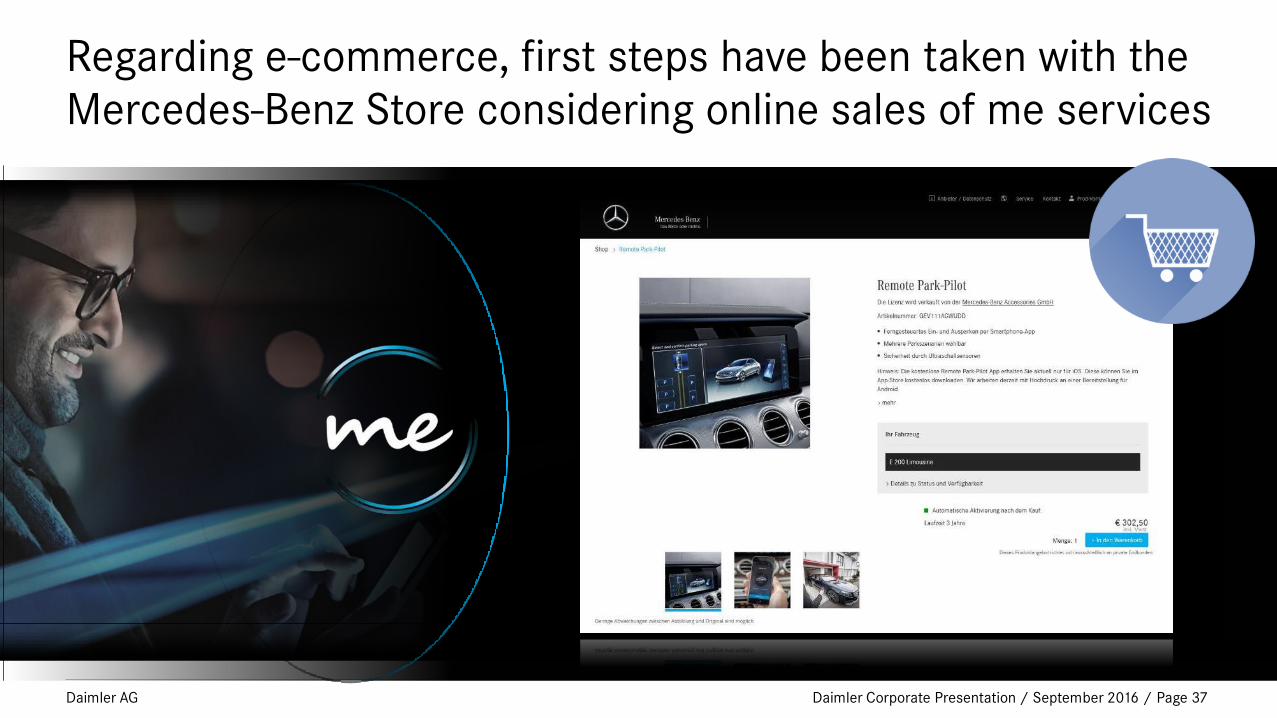

We want to become digital champion of the automotive industry

with the help of Mercedes me and the Mercedes-Benz Store

Digital Car Key Online Service

Appointment

Integration

Mobility Offers

in Mercedes me (App)

Contract- & Document

Management

Remote

Park Pilot

Lifestyle

Configurator

• Launch of the Mercedes-Benz Store for all Mercedes me connect markets

• Customer can purchase services directly online

(Starting with Remote Park Pilot)

Page 36 Daimler Corporate Presentation / September 2016 /

Daimler AG

Regarding e-commerce, first steps have been taken with the

Mercedes-Benz Store considering online sales of me services

Page 37 Daimler Corporate Presentation / September 2016 /

Daimler AG

But Mercedes me is more than just digital...

...it’s an innovative sales approach

Page 38

Opening of the world-wide 6th

Mercedes me store in Beijing.

Daimler Corporate Presentation / September 2016 /

Daimler AG

Fit for Leadership was designed as long-term profit

optimization of „MB 2020“-strategy. „Next Stage“ will focus

on structural improvement

Page 39

2020 2013 2015 2016 2012 2014

Growth Strategy MB 2020 „Fit For Leadership“

Optimized business

structures Measurement

implementation for cost

improvement

2 bn. €

until 2014

Fit for Leadership

Next Stage

„Fire Fighting“ „Fire Prevention“

Daimler Corporate Presentation / September 2016 /

Daimler AG

Our target: No.1 premium car manufacturer

Sales target In thousand units

Profitability target Return on Sales in %

on a sustainable basis

2,001

2015

significantly

higher

than 2015

2016

No. 1

2020

Page 40 Daimler Corporate Presentation / September 2016 /

Daimler AG

Daimler Trucks

Page 41 Daimler Corporate Presentation / September 2016 /

Daimler AG

Broadest and strongest truck portfolio in our history

Page 42 Daimler Corporate Presentation / September 2016 /

Daimler AG

Our strategy works out. We keep on developing it.

Technology Leadership in efficiency, safety and

connectivity

Global Market Presence in traditional and

emerging markets

Intelligent Platforms for tailored products and

decisive economies of scale

Page 43 Daimler Corporate Presentation / September 2016 /

Daimler AG

Efficiency: the most efficient trucks are Daimler Trucks

~13% ~7% ~5%

Mercedes-Benz Actros Freightliner Cascadia Evolution Fuso Super Great V

less fuel than previous model less fuel than previous model

less fuel than previous model

Page 44 Daimler Corporate Presentation / September 2016 /

Daimler AG

Efficiency: we are pioneering alternative drivetrains

Page 45

2000 2002 2006 2010 2014 2015 2016 1970

Unimog

E-Drive

Introduction

Canter Eco

Hybrid Portugal

Hybrid

Technology

Center

FUSO Canter

E-Cell@IAA

Atego with hybrid

drivetrain

2nd Generation

Canter E-Cell Stuttgart

Fleet test

Daimler Corporate Presentation / September 2016 /

Daimler AG

Our EBIT drivers: Push captive component strategy to

strengthen undisputed market leadership in NAFTA

Page 46

Penetration rate integrated powertrain US/CAN in % Built and scheduled

Heavy Duty Engines

HDEP

Automated Manual Transmission

DT12

86.0 94.0

As of June 2016 Year End 2015

39.0

65.0

As of June 2016 Year End 2015

Daimler Corporate Presentation / September 2016 /

Daimler AG

2001

Electronic Stability Program (ESP)

1981 Anti-lock Braking System

(ABS)

2006 Active Break Assist (ABA)

Safety: many firsts on our record

Page 47 Daimler Corporate Presentation / September 2016 /

Daimler AG

Safety: new Blind Spot Monitor improves active safety further

Page 48 Daimler Corporate Presentation / September 2016 /

Daimler AG

We are pioneering autonomous driving

Page 49

2016 2015 2014

Highway Pilot Connect world premiere of platooning

Inspiration Truck premiere on US highway

Highway Pilot test licence for German autobahn

Future Truck world premiere

Daimler Corporate Presentation / September 2016 /

Daimler AG

• Less fuel: ~7% savings/entire platoon

• More safety: shorter reaction time

(< 0,1 sec. vs. 1.4 sec. driver)

• Less space: 3 trucks span 80m vs. 150m

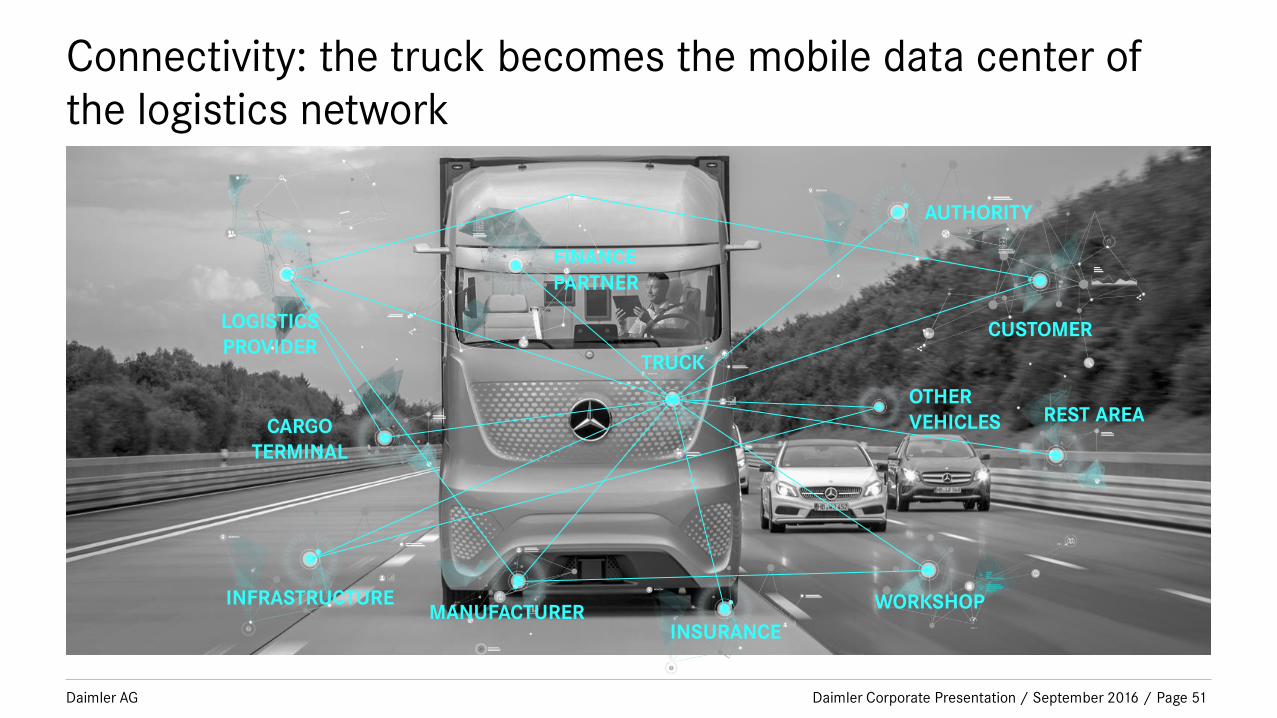

We will lead in connectivity like we do in autonomous driving

Page 50 Daimler Corporate Presentation / September 2016 /

Daimler AG

TRUCK

FINANCE

PARTNER

LOGISTICS

PROVIDER

CARGO

TERMINAL

MANUFACTURER WORKSHOP

AUTHORITY

OTHER

VEHICLES REST AREA

INSURANCE

CUSTOMER

INFRASTRUCTURE

Connectivity: the truck becomes the mobile data center of

the logistics network

Page 51 Daimler Corporate Presentation / September 2016 /

Daimler AG

NO MORE

TRAFFIC JAMS

Real-time data from

infrastructure & vehicles

NO MORE

EMPTY RUNS

Ride sharing

platforms for cargo

NO MORE WAITING TIME

All information

transmitted digitally

in advance (e.g. toll)

NO MORE OVERBOOKED

REST AREAS

Connected truck makes

reservation in time

Connectivity: with its real-time information, the connected

truck solves major logistics inefficiencies

Page 52 Daimler Corporate Presentation / September 2016 /

Daimler AG

With our new Regional Centers, we push sales and after

sales in emerging markets

Latin

America

Middle East/

Northern Africa

Central

Africa

Southern

Africa

Southern

Asia

Southeast

Asia

Page 53 Daimler Corporate Presentation / September 2016 /

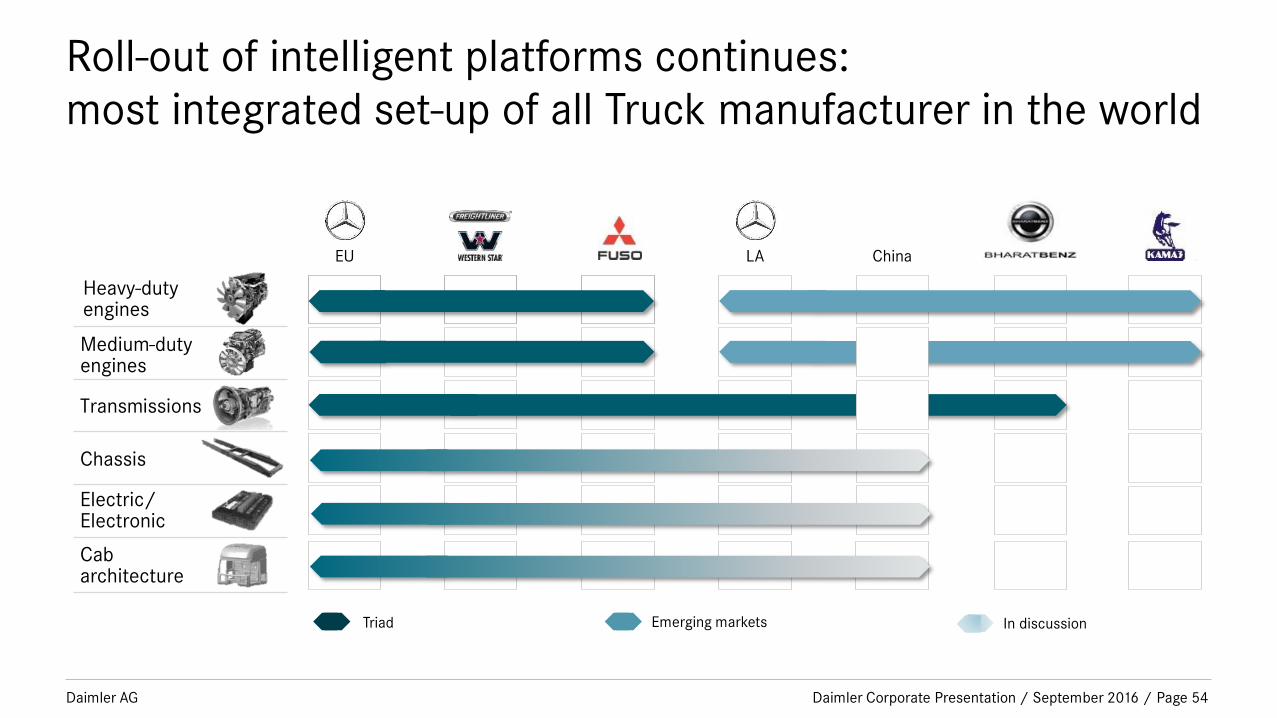

Daimler AG

Roll-out of intelligent platforms continues:

most integrated set-up of all Truck manufacturer in the world

Page 54

Transmissions

Electric/ Electronic

Chassis

Medium-duty engines

Heavy-duty engines

EU LA

Cab architecture

Triad Emerging markets

China

In discussion

Daimler Corporate Presentation / September 2016 /

Daimler AG

Global Platform Roll-out will secure pass-car-like volumes in

next decade for Daimler Trucks

Page 55

Today 2025 2020

Chassis Electrics/Electronics

Today 2020 2025 Today 2020 2025

Europe

Brazil

Russia

China Europe

NAFTA

Brazil

China

Europe

Brazil

China Japan NAFTA

Cabin

Daimler Corporate Presentation / September 2016 /

Daimler AG

Sticking to our target: undisputed leader in the truck industry

Sales target In thousand units

496

2014

>500

2015

~700

2020

Profitability target Return on Sales in %

over the cycle

Page 56 Daimler Corporate Presentation / September 2016 /

Daimler AG Page 57

Daimler Financial Services

Daimler Corporate Presentation / September 2016 /

Daimler AG

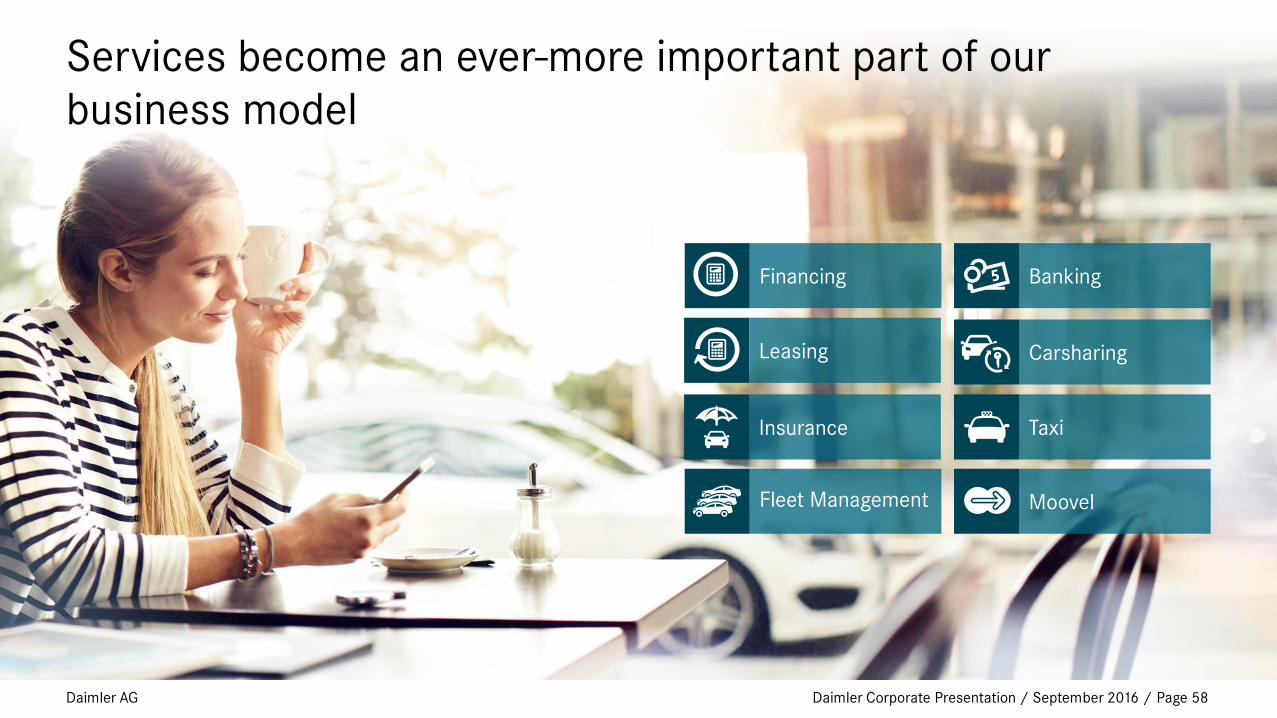

Banking

Fleet Management Moovel

Taxi

Financing

Leasing

Insurance

Carsharing

Services become an ever-more important part of our

business model

Page 58 Daimler Corporate Presentation / September 2016 /

Daimler AG Page 59

Supporting all Daimler brands

Daimler Corporate Presentation / September 2016 /

Daimler AG

We finance every second vehicle sold by Daimler

We finance every second vehicle sold by Daimler

Page 60 Daimler AG Daimler Corporate Presentation / September 2016 /

Daimler AG

Strong business growth

Page 61

Strong business growth

59

2007

63

2008

58

2009 64

2010 72

2011 80

2012

84

2013

99

2014

Contract volume (€ billion)

117

2015

28 2007

30 2008 25

2009

29 2010

34 2011

38 2012

41 2013

48 2014

New acquisitions (€ billion)

58 2015

Daimler Corporate Presentation / September 2016 /

Daimler AG

We are about to re-invent personal mobility

Selfdriving Mobility Marketplace Ride4Hire

Page 62 Daimler Corporate Presentation / September 2016 /

Daimler AG

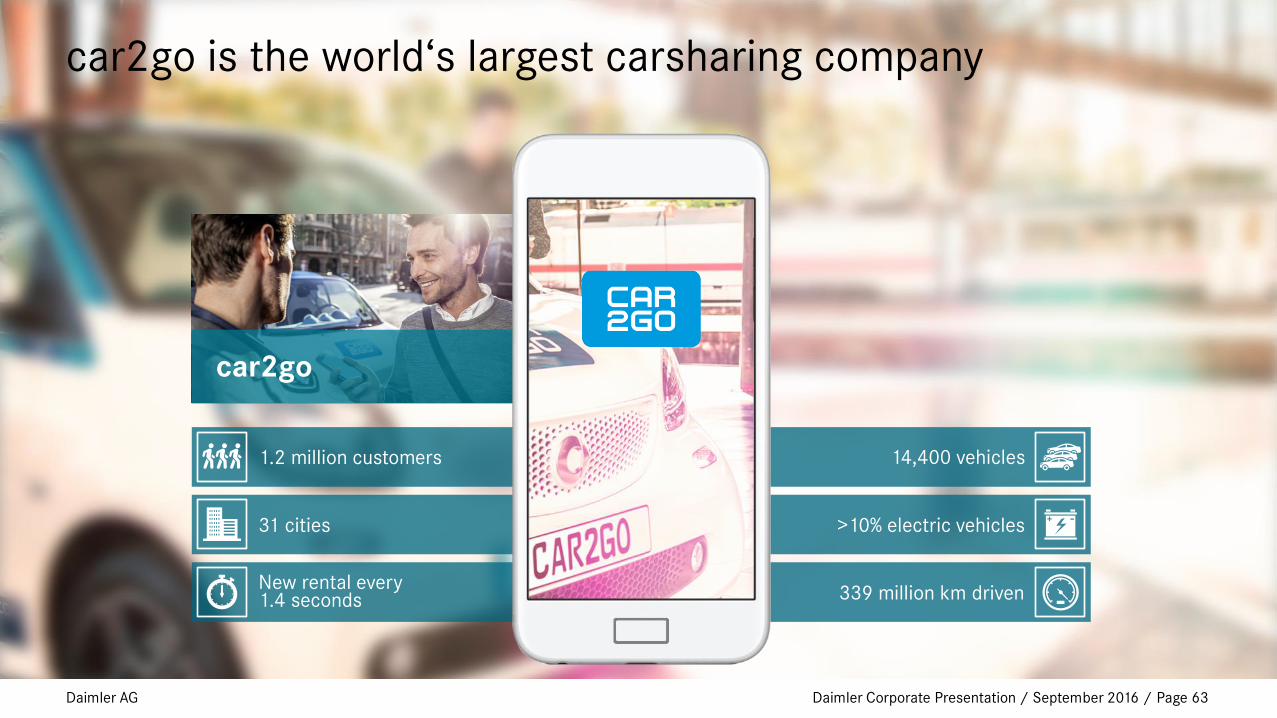

1.2 million customers

31 cities

New rental every 1.4 seconds

14,400 vehicles

>10% electric vehicles

339 million km driven

car2go

car2go is the world‘s largest carsharing company

Page 63 Daimler Corporate Presentation / September 2016 /

Daimler AG

Public transport

Carsharing

Railway

Taxi

Bikesharing

moovel

moovel – find, book and pay

Page 64 Daimler Corporate Presentation / September 2016 /

Daimler AG

3-4 minutes until arrival

40 cities

45,000 registered drivers

Number of tours tripled

> 10 million downloads

mytaxi

mytaxi – the world‘s first taxi app

Page 65 Daimler Corporate Presentation / September 2016 /

Daimler AG

Contents

Page 66

Results for Q1 2016

Outlook for 2016

Daimler Group Strategy

Divisional information

China

Appendix

Daimler Corporate Presentation / September 2016 /

Daimler AG

China

China Market

Development

Daimler in China

China Market

Development Daimler Corporate Presentation / September 2016 / Page 67

Daimler AG

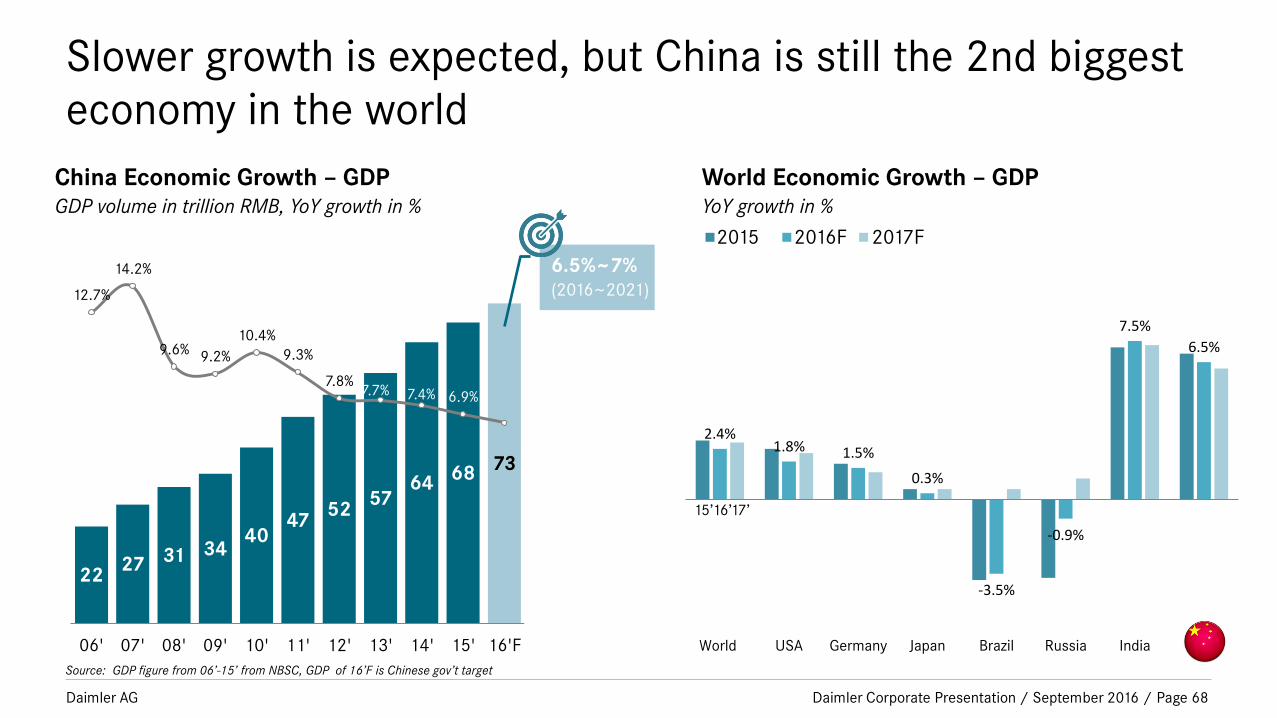

Slower growth is expected, but China is still the 2nd biggest

economy in the world

China Economic Growth – GDP GDP volume in trillion RMB, YoY growth in %

Source: GDP figure from 06’-15’ from NBSC, GDP of 16’F is Chinese gov’t target

22 27 31 34

40 47

52 57

64 68

73

12.7%

14.2%

9.6% 9.2%

10.4%

9.3%

7.8% 7.7% 7.4% 6.9%

06' 07' 08' 09' 10' 11' 12' 13' 14' 15' 16'F

6.5%~7%

(2016~2021)

2.4% 1.8% 1.5%

0.3%

-3.5%

-0.9%

7.5%

6.5%

World USA Germany Japan Brazil Russia India China

16’ 17’ 15’

World Economic Growth – GDP YoY growth in %

2015 2016F 2017F

Daimler Corporate Presentation / September 2016 / Page 68

Daimler AG

Sales of the China auto market reached over 25 million units

in 2015.

Page 69

2014

Sales Volume

2015

Sales Volume

2015

YoY Growth

Volume in thousand units

Total Market

PV

Truck

Van

Bus

thereof HDT

Sales of the China auto market reached over 25 million units

in 2015. Growth continues in 2016

Note: Segment definition according to Daimler internal division. 2014 & 2015 figures are actual domestic wholesales, with import and w/o export. 2016 figure is preliminary, which is domestic wholesale plus export

and w/o import. Source: China Automotive Industry Newsletter (CAAM) , MoC and Customs of PRC

23,819 25,004 5%

18,091 19,702 9%

2,290 2,016 -12%

655 460 -30%

3,168 3,017 -5%

270 269 0%

YTD July 2016

Sales Volume

YTD July 2016

YoY Growth

14,687 10.1%

11,490 14.1%

1,341 2.6%

390 17.2%

1,705 -6.0%

151 0.7%

Daimler Corporate Presentation / September 2016 /

Daimler AG

The fundamentals remain unchanged

814

594

580

320

199

121

24

US

Japan

German

Russia

Brazil

India

Low Car Density

Light Vehicle per1,000 people

(in units in I2015,IHS Report)

Urbanization

43% End of 2005

55.9% End of 2015

60.0% End of 2020

13 cities

Population > 10 million

101cities

Population > 5 million

274cities

Population > 1 million

By the end of 2014

Regional Potentials

Note: New Car Registration YoY Growth rate 2015

10%< YoY Growth Rate <20%

YoY Growth Rate >20%

YoY Growth Rate <10%

Source: NBSC,

Calculation by MI

Daimler Corporate Presentation / September 2016 / Page 70

Daimler AG

China

Daimler in China

China Market

Development Daimler Corporate Presentation / September 2016 / Page 71

Daimler AG

Daimler in China

Beijing

Fuzhou

Shenzhen

Trucks & Buses

Production & Distribution

Mercedes-Benz Vans

Production & Distribution

NEV Development

Production & Distribution

Mercedes-Benz Cars

Distribution

Auto Finance

R&D

Production

Daimler Corporate Presentation / September 2016 / Page 72

Daimler AG

Auman

Daimler Corporate Presentation / September 2016 / Page 73

Daimler AG

The China HDT market saw significant decrease in recent

years

China HDT Domestic Market Development Volume in thousand units

Registration figure, Source: CAAM , MoC and Customs of PRC.

Daimler Corporate Presentation / September 2016 / Page 74

Daimler AG

Auman HDT Domestic Wholesale

2012 ~ YTD 1st half 2016 Volume in thousand units

+21%

YoY

growth

Source: BFDA

Daimler Corporate Presentation / September 2016 / Page 75

Daimler AG

Market Forecast by 2023 MD/HD truck market

Daimler Corporate Presentation / September 2016 / Page 76

Daimler AG

OM457 engines production preparation in 2016

Production of China-made OM457

OM457 Engine Plant at Beijing

Daimler Corporate Presentation / September 2016 / Page 77

Daimler AG

Mercedes-Benz Truck

Daimler Corporate Presentation / September 2016 / Page 78

Daimler AG

China HDT WEU Import Segment Development

2010-2015

Despite the import segment shrank even further, MB Truck

still remains No.1 European importer.

WEU brand

SoM 2015

Firefighting

Oilfield

Logistics

Concrete Pump

Typical application of MB Truck

2010 2015 2011 2012 2013 2014

Note: Registration figure, excl. firefighting

3000

6300

Competitor 1

Competitor 2 Competitor 3

Daimler Corporate Presentation / September 2016 / Page 79

Daimler AG

Mercedes-Benz Vans

Page 80 Daimler Corporate Presentation / September 2016 /

Daimler AG Page 81

Vans sales in China

Source: FBAC

2012 2013 2014 2015 2016F

Mercedes-Benz Vans Retail Development in China

Daimler Corporate Presentation / September 2016 /

Daimler AG

The locally produced V-Class and Vito were introduced to the

China market this year

All new V-Class Launched in March

All new Vito Launched in September

Daimler Corporate Presentation / September 2016 / Page 82

Daimler AG

2012 2013 2014 2015 2016F

Mercedes-Benz Vans Retail Development in China

Page 83

Successful V-Class ramp-up

YTD July

2016:

59% YoY

increase

+46% YTD 2016

1st half

Source: FBAC

Daimler Corporate Presentation / September 2016 /

Daimler AG

DENZA

Page 84 Daimler Corporate Presentation / September 2016 /

Daimler AG

With 331K units sold, China became the world’s No.1 NEV

market in 2015

CV

PV

PHEV

PV

BEV

Source: China Automotive Industry Newsletter (CAAM)

2011-2015 NEV Sales Development

Wholesale Volume in thousand units

Page 85 Daimler Corporate Presentation / September 2016 /

Daimler AG

Most of the top selling models have an e-range < 250km &

MSRP < 250k RMB

E-Range (KM)

MSRP

14.1

3.7

29.7 18.2

10.7

8.1

3.0

16.5

15.5

10.5

17.6 10.5

model a

Source: Volume from China Automotive Industry Newsletter (CAAM); product feature from internet research

2015 NEV Sales by model

Bubble size refers to sales volume in thousand units PHEV BEV Micro BEV

Page 86

RMB 100K RMB 200K RMB 300K RMB 700K RMB 400K

model b model c

model d

model e

model f

model g

model h

model i

model j

model s

DENZA

Daimler Corporate Presentation / September 2016 /

Daimler AG

DENZA: the safest, most reliable, and most convenient

electric vehicle

Up to 300 kilometers

driving range

Over 1.2 million

kilometers testing C-NCAP 5 Stars

Daimler Corporate Presentation / September 2016 / Page 87

Daimler AG

Upgrading e-range to 400km to enhance competitiveness

Daimler Corporate Presentation / September 2016 / Page 88

Daimler AG

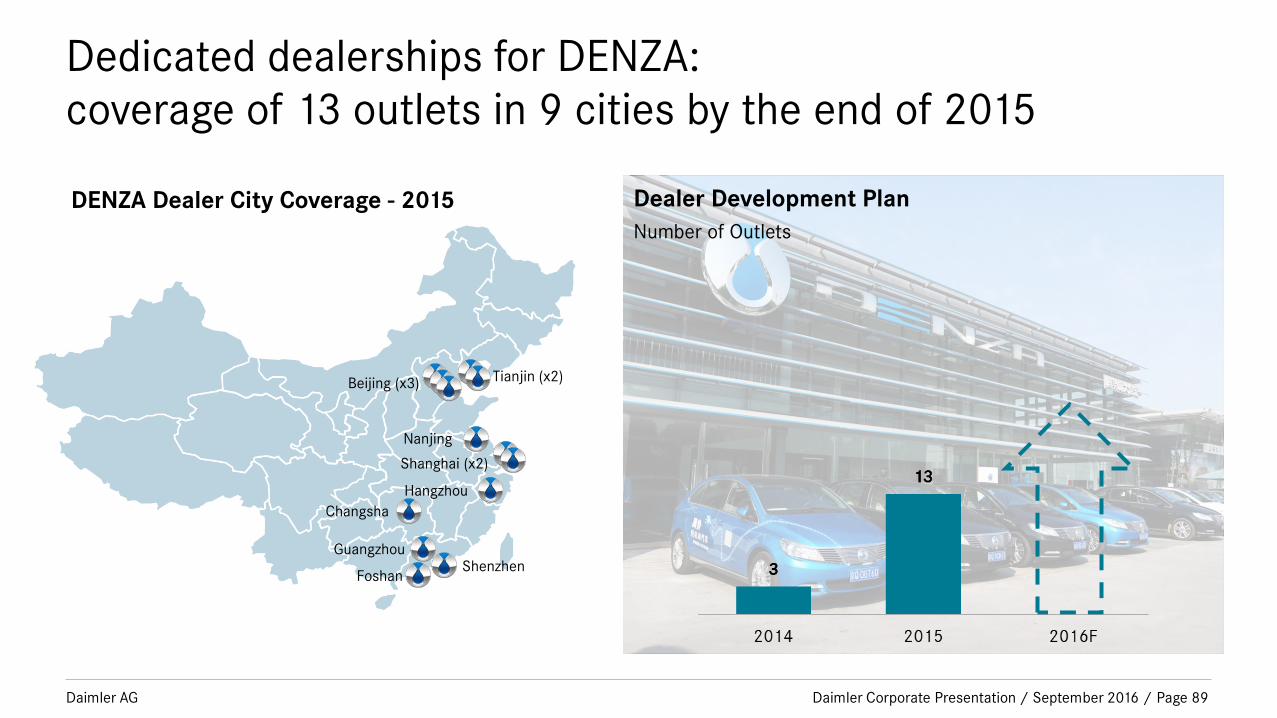

Dedicated dealerships for DENZA:

coverage of 13 outlets in 9 cities by the end of 2015

Beijing (x3)

Shanghai (x2)

Tianjin (x2)

Shenzhen

Nanjing

Hangzhou

Changsha

Foshan

Guangzhou

Dealer Development Plan

Number of Outlets

DENZA Dealer City Coverage - 2015

Daimler Corporate Presentation / September 2016 / Page 89

Daimler AG

Mercedes-Benz Cars

Page 90 Daimler Corporate Presentation / September 2016 /

Daimler AG

2014 Capital Market Day

Daimler Corporate Presentation / September 2016 / Page 91

Daimler AG

2006 2007 2008 2009 2010 2011 2012 2013 2015

~364,000

We are well on track to narrow the gap with competitor

Gap to

Brand

“B”

Mercedes-Benz Sales Development in China MBPC Retail sales in Mainland China

Daimler Corporate Presentation / September 2016 / Page 92

Daimler AG

China became the single biggest market MB Passenger Cars

in 2015, and contributed one fifth of the worldwide sales

~20%

Rest of the world

Share of Market of Mercedes-Benz PC By retail sales, in 2015

Top 3 Market of Mercedes-Benz Retail sales in 2015, in thousand units

364 343

259

Daimler Corporate Presentation / September 2016 / Page 93

Daimler AG

And we grew at a faster speed among competitors in 2015

+35% +1.8% -1.2%

2014 2015

German Premium Brands China Performance - 2015 Retail Sales, in Mainland China

~364,000

Brand “B” Brand “A”

Note: Mercedes-Benz w/o smart & V-Class, Brand “B” w/o MINI

Daimler Corporate Presentation / September 2016 / Page 94

Daimler AG

The 6 key initiatives start to pay off

Extension Product Portfolio Expansion Dealer Network

Extension Local Production Leverage Financial Services Extension Local R&D

Integrated Sales Organization

Daimler Corporate Presentation / September 2016 / Page 95

Daimler AG

The 6 key initiatives start to pay off

Extension Product Portfolio Expansion Dealer Network Integrated Sales Organization

Daimler Corporate Presentation / September 2016 / Page 96

Daimler AG

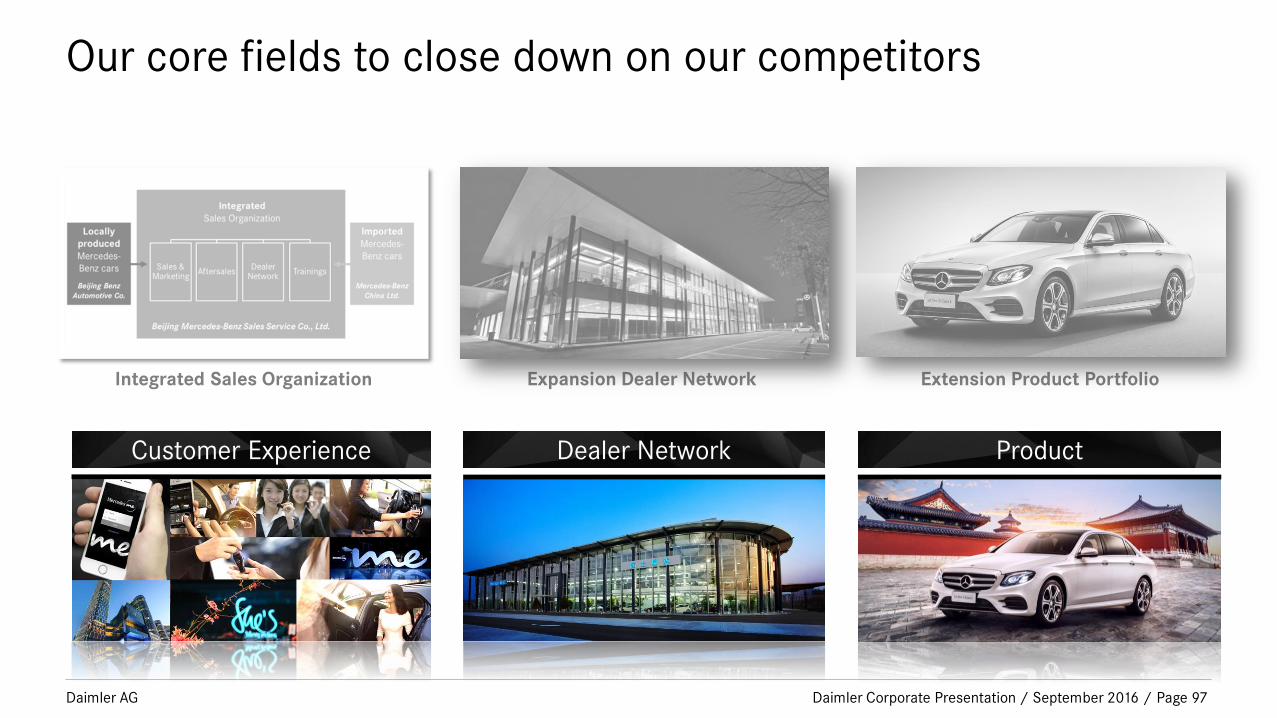

Our core fields to close down on our competitors

Integrated Sales Organization Extension Product Portfolio Expansion Dealer Network

Customer Experience Dealer Network Product

Daimler Corporate Presentation / September 2016 / Page 97

Daimler AG

Our core fields to close down on our competitors

Page 98

Product Customer Experience Dealer Network

Daimler Corporate Presentation / September 2016 /

Daimler AG

China has younger customer group who ‘live’ on-line

Page 99

Average

age

36.2 Addicted to

Social

Media

Online

Shopping

Daimler Corporate Presentation / September 2016 /

Daimler AG

We gear up for our potential customers:

E-Commerce for dealers online sales

Page 100

1

2

3

Select your car

Select your dealer

Buy your car

Daimler Corporate Presentation / September 2016 /

Daimler AG

We gear up for our existing customers:

Mercedes me Portal offers personalized online services

Page 101

Mercedes assist me Mercedes finance me

Mercedes inspire me Mercedes move me Mercedes store linkage

Mercedes connect me

Daimler Corporate Presentation / September 2016 /

Daimler AG

We gear up for the ladies:

She’s Mercedes

Page 102 Daimler Corporate Presentation / September 2016 /

Daimler AG

We gear up for everyone:

Mercedes me Sanlitun

Page 103

320k visitors in 4 months

10k customers have

joined community

in 4 months

22

60K

>500 KG of coffee beans

participants

events

Daimler Corporate Presentation / September 2016 /

Daimler AG

Our brand values are positively recognized…

Page 104

Brand Core

Brand

Values

EMOTIONAL

INTELLIGENT

Innovation

Design

Sportiness

Customer Care

Comfort

Sustainability

Safety

Quality

102

101

103

100

101

98

103

103

101

102

104

(+2)

(+1)

(+2)

(±0)

(+3)

(+1)

(+1)

(+1)

(+1)

(±0)

(+2)

THE BEST

Brand

Experiences

Index = 100 Index > 100

MB is as good as

the best competitor

MB exceeds

the best competitor

Index < 100

MB is weaker than

the best competitor

Source: Brand Monitor Report 2016

Daimler Corporate Presentation / September 2016 /

Daimler AG

…… and in our workshops

Page 105

Q3

2014

Q4

2014

Q1

2015

Q2

2015

Q3

2015

Q4

2015

Jan

2016

Feb

2016

Mar

2016

April

2016

May

2016

Jun

2016

July

2016

Source: MRA report PC China

Star

Maintenance

Menu launch

New Parts

Pricing

launch

After-Sales Retention Development 2014 Q3 – 2016 July in percentage

>75%

Daimler Corporate Presentation / September 2016 /

Daimler AG

Our core fields to close down on our competitors

Page 106

Product Customer Experience Dealer Network

Daimler Corporate Presentation / September 2016 /

Daimler AG

We have caught up on dealer outlet number and coverage

Page 107

250

300

350

400

450

500

Ou

tle

t P

lan

nin

g

2012 2013 2014 2015 2016F

Cit

y C

ov

era

ge

+79

+106 +55

+36

+47

+26

Brand A Brand A Brand B

Brand B

Brand A

Brand B

Brand A

Brand B

Brand A Brand B

Brand B

Brand A

Note: 1. City coverage counting based on MB new city tier definition

2. Data Source: MB Network Planning Project List & Timer Tracking Data (Brand A & Brand B outlet counting excl. Experience Center & Used Car Center)

Daimler Corporate Presentation / September 2016 /

Daimler AG Page 108

We are managing our network for the future: hardware

Optimizing and digitalizing our sales space

Upgrading and relocations to enhance capacities

Daimler Corporate Presentation / September 2016 /

Daimler AG

We are managing the network for the future: software

Page 109

Consistency in sales quality

Profitable growth of franchise business

Daimler Corporate Presentation / September 2016 /

Daimler AG

Our dealers = Our partners = Sustainable growth

Page 110

Product Forum March 2016

All Investor Conference July 2016

National Dealer Conference March 2016 Dealer Council Committee

Strategic Partner Conference March 2016

Daimler Corporate Presentation / September 2016 /

Daimler AG Page 111

DISS No.1 - This collaborative relationship bears fruit!

Overall Dealer Satisfaction – Development over time

2011 2012 2013 2014 2015 2016

DISS – Dealer Identification & Satisfaction Survey conducted in 2016

Brand B

Brand A

Daimler Corporate Presentation / September 2016 /

Daimler AG

Our core fields to close down on our competitors

Page 112

Customer Experience Product Dealer Network

Daimler Corporate Presentation / September 2016 /

Daimler AG

The C-Class – our first Game-Changer in August 2014

Page 113

Average

Monthly

Retail Sales

C-Class Long

Wheelbase

launched in

August 2014

C-Class Short

Wheelbase

launched in

June 2015

2014 2015

YTD Aug

2016

+131%

+39%

Daimler Corporate Presentation / September 2016 /

Daimler AG

The all new GLA SUV followed from BBAC 9 months later in

May 2015

Page 114

Average

Monthly

Retail Sales

May – Dec.

2015

YTD Aug

2016

GLA SUV

launched in

May 2015

+25%

Daimler Corporate Presentation / September 2016 /

Daimler AG

Followed by the all new GLC SUV in November 2015– setting

new standard in all dimensions

Page 115

Average

Monthly

Retail Sales

2014 2015

YTD Aug

2016

GLC SUV

launched in

Nov. 2015

+10%

+30%

Daimler Corporate Presentation / September 2016 /

Daimler AG

And the superlative new E-Class Long Wheelbase comes to

market right now!

Page 116 Daimler Corporate Presentation / September 2016 /

Daimler AG

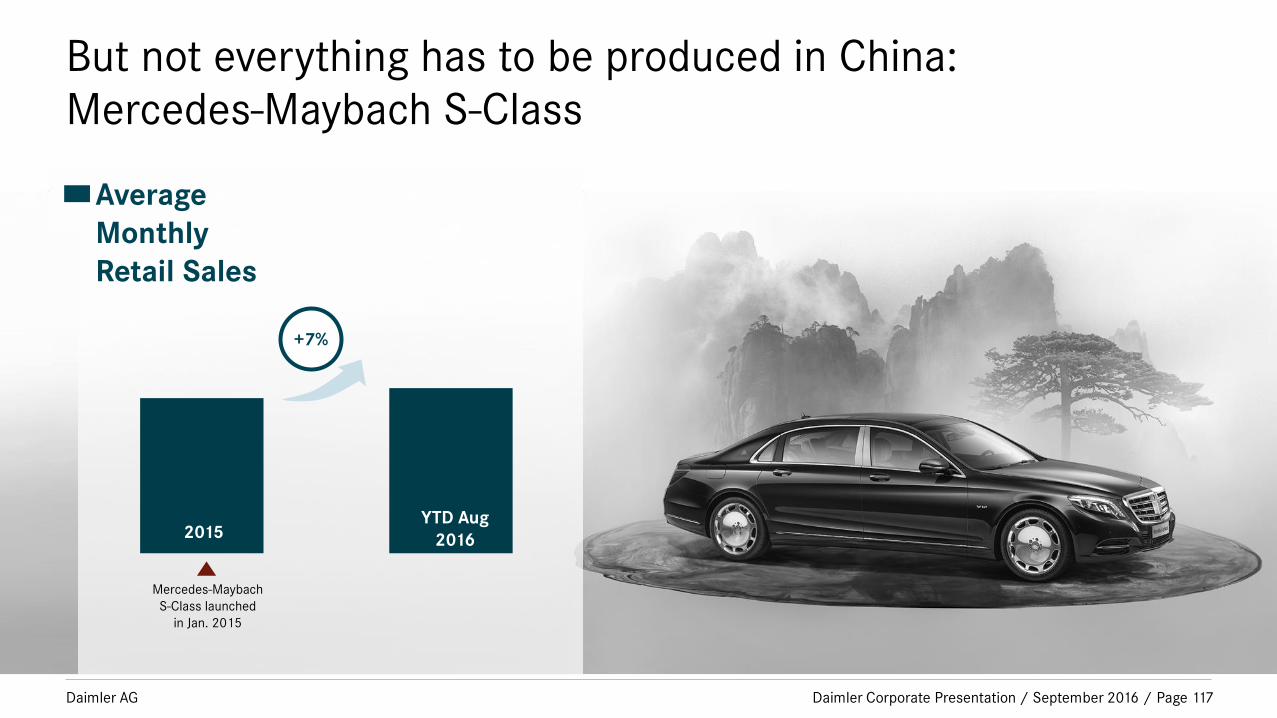

But not everything has to be produced in China:

Mercedes-Maybach S-Class

Page 117

0

100

200

300

400

500

600

700

800

900

1,000

Mercedes-Maybach

S-Class launched

in Jan. 2015

2015 YTD Aug

2016

+7%

Average

Monthly

Retail Sales

Daimler Corporate Presentation / September 2016 /

Daimler AG

Option packages for all model ranges

Page 118 Daimler Corporate Presentation / September 2016 /

Daimler AG

Mercedes me Connect 2.0 offering unique connectivity for

Chinese tastes

Page 119

Mercedes me connect

Concierge Service

Online Map Update

Parked Vehicle

Locator

Geofencing

Vehicle Tracker

Remote Retrieval of

Vehicle Status

Maintenance

Management

Wi-Fi Hotspot

Remote Parking Pilot

Software Updates

Mercedes-Benz Apps

WeChat-Mycar

Weather (AQI)

Daimler Corporate Presentation / September 2016 /

Daimler AG

Positive sales momentum with double digit growth expected

in 2016

Page 120

Source: BMBS Internal as of 2016 Aug YTD

MBC Sales Development (MB + smart)

Unit in thousand

206 229

288

364

291

2012 2013 2014 2015

2016

Aug

YTD

Double digit

growth To be updated to August

140

201

82

90 9

13

2015 Aug YTD 2016 Aug YTD

MB CBU

MB PbP

smart +32%

+11%

+44%

+36%

MBC Sales Development (MB + smart)

Unit in thousand

13

MBPC

smart

MBC 13

2016 Aug YTD

Daimler Corporate Presentation / September 2016 /

Daimler AG

6 Key Initiatives

Extension Product Portfolio Expansion Dealer Network

Extension Local Production Leverage Financial Services Extension Local R&D

Integrated Sales Organization

Daimler Corporate Presentation / September 2016 / Page 121

Daimler AG

Localized models are the key driving force to Mercedes-Benz

success in China

MB PC China Retail Sales Performance

Locally produced Imported Sales proportion of PbP over MB PC

2008 2009 2014 2015 2013 2012 2011 2010

65%

33%

49%

2/3 of

total sales

~364,000

Daimler Corporate Presentation / September 2016 / Page 122

Daimler AG

+ …

Made in China for China: we’re producing four car models

and three engine models

GLC (X253)

E-Class (V/W 213)

C-Class (V/W 205)

GLA (X156)

M270

M274

M276

Rear

wheel

drive

Engine

Front

wheel drive

Daimler Corporate Presentation / September 2016 / Page 123

Daimler AG

Continuously deepening the strategic partnership

Daimler Corporate Presentation / September 2016 / Page 124

Daimler AG

6 Key Initiatives

Extension Product Portfolio Expansion Dealer Network

Extension Local Production Leverage Financial Services Extension Local R&D

Integrated Sales Organization

Daimler Corporate Presentation / September 2016 / Page 125

Daimler AG

6 Key Initiatives

Extension Product Portfolio Expansion Dealer Network

Extension Local Production Leverage Financial Services Extension Local R&D

Integrated Sales Organization

Daimler Corporate Presentation / September 2016 / Page 126

Daimler AG

Increasing Importance of

Financial Services in China

Daimler Corporate Presentation / September 2016 / Page 127

Daimler AG

MBFS penetration rate will mature over time to the level of the global DFS penetration rate.

China

Demand for Auto Financing is increasing and we will make

sure we have our share…

12%

2011

50%

2013 2015 2018F 2020F

Daimler Corporate Presentation / September 2016 / Page 128

Daimler AG

…by covering customers’ finance, leasing & insurance

needs based on a solid shareholding structure

Mercedes-Benz Auto Finance Ltd. Mercedes-Benz Leasing Co., Ltd.

100%

Daimler

35%

65%

BAIC Daimler

As of March 2015

Portfolio as of

2016 July YTD 51 Billion RMB 3 Billion RMB

Daimler Corporate Presentation / September 2016 / Page 129

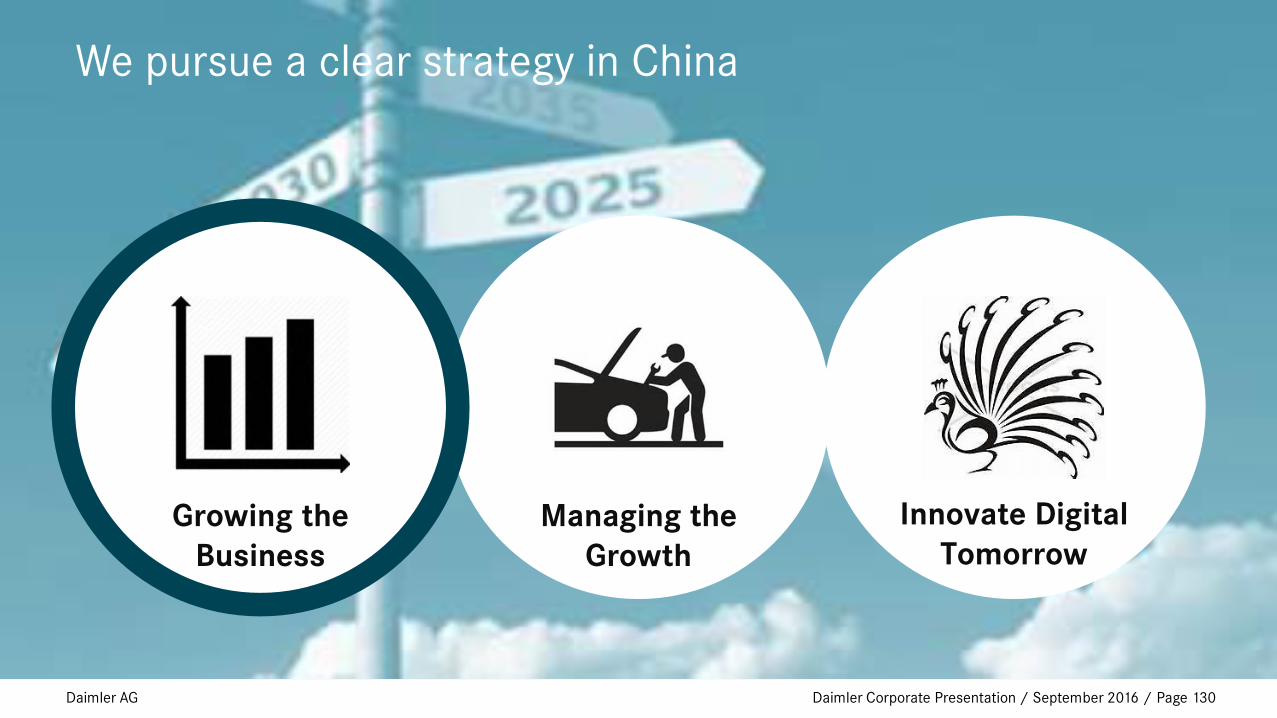

Daimler AG

Growing the

Business

Innovate Digital

Tomorrow

Managing the

Growth

We pursue a clear strategy in China

Daimler Corporate Presentation / September 2016 / Page 130

Daimler AG

16% 17%

26%

33%

2012 2013 2014 2015 2016E 2020E

Financing Leasing Wholesale

We are growing fast, and not only with a comprehensive

auto finance portfolio…

PC Penetration % & Portfolio in billion RMB

18 22 33

49

F F

Daimler Corporate Presentation / September 2016 / Page 131

Daimler AG

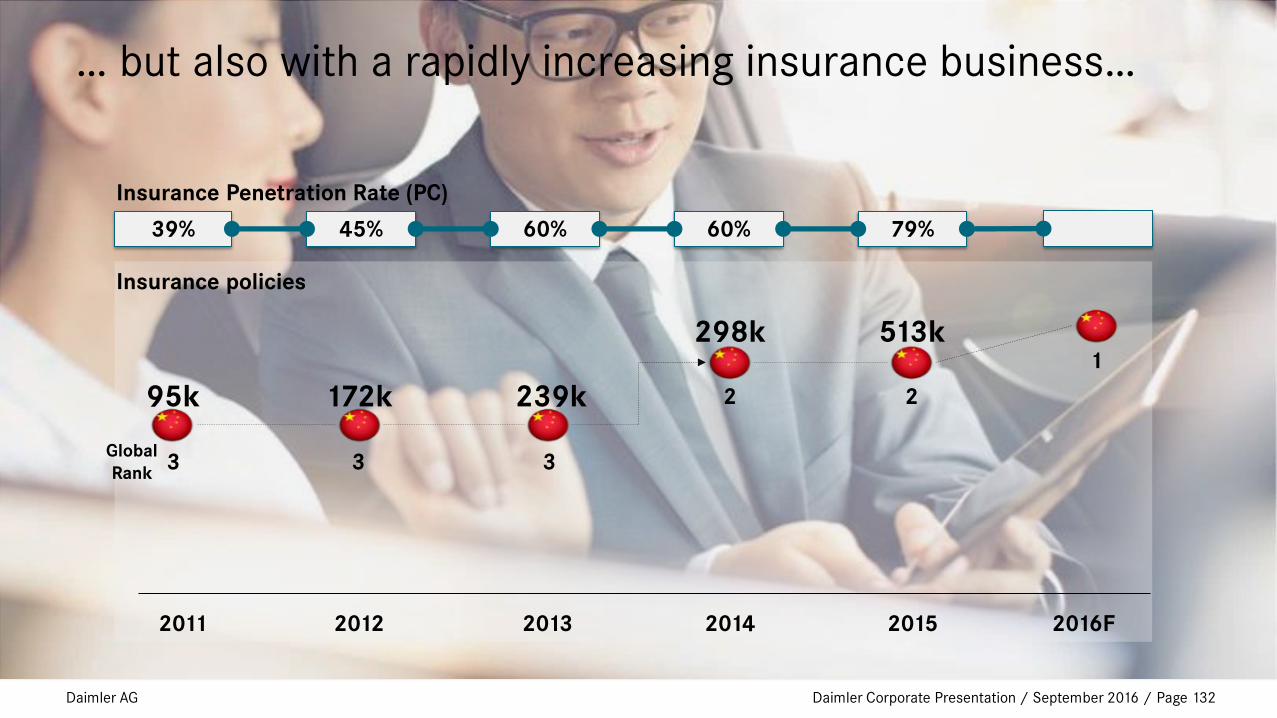

2011 2012 2013 2014 2015 2016F

… but also with a rapidly increasing insurance business…

39% 45% 60% 60% 79%

Insurance policies

298k 513k

95k 172k 239k

Insurance Penetration Rate (PC)

3 Global

Rank 3 3

2 2

1

Daimler Corporate Presentation / September 2016 / Page 132

Daimler AG

…and Newly Launched

Mobility Services in China

Daimler Corporate Presentation / September 2016 / Page 133

Daimler AG

Simple. Always. Everywhere.

Launched in 2016

78,000 members, a new rental every1.7 min

As of July 2016

Daimler Corporate Presentation / September 2016 / Page 134

Daimler AG

Growing the

Business

Innovate Digital

Tomorrow

Managing the

Growth

We pursue a clear strategy in China

Daimler Corporate Presentation / September 2016 / Page 135

Daimler AG

>450 contracts per day

We are facing the challenges of fast growth every day Average number of contracts signed by MBFS China 2014 vs. YTD 2016 [units]

From > 200 contracts per day in 2014 to

Daimler Corporate Presentation / September 2016 / Page 136

Daimler AG

To support the business growth, we actively engage

ourselves to find the right people for the right position

Employees Development MBFS China

422 427 498

594

2012 2013 2014 2015 2016EF

Daimler Corporate Presentation / September 2016 / Page 137

Daimler AG

We hire high performers, develop them into experts and

retain them with attractive career path opportunities

Talent Development and Retention Continuous Efforts in Talent Acquisition

• Dedicated Recruitment Resources

• Expanded Sourcing Channels

• Global Search

Strive for

MORE.

Daimler Corporate Presentation / September 2016 / Page 138

Daimler AG

• Auto Decision

2016 (YTD) 26% of applications are

already automatically decided,

improving our operational costs

further. This ratio is expected to be

>30% by end of this year.

With efficient processes and systems we form a sound

foundation for future sustainable growth

• Outsourcing of non-core processes

• Service Center & Customer Contact

Center

• Major IT infrastructure upgrades &

core system replacements

Daimler Corporate Presentation / September 2016 / Page 139

Daimler AG

Growth is managed with a reasonable risk control…

47% of our Finance

77% of our Leasing

Consumers make a

Down payment > 50%

33 Months

Average Terms

Daimler Corporate Presentation / September 2016 / Page 140

Daimler AG

…which is reflected in our low credit losses Net Credit Loss ratio in %

0.31 0.48

0.34 0.36

2012 2013 2014 2015 2016F

Daimler Corporate Presentation / September 2016 / Page 141

Daimler AG

Asset Backed Securitization is leveraged to support the

increasing capital demand

2015

Equity

15%

Bank loan

and others

85%

2016 F 2017 F

Equity

ABS

Bank Loan

and others

Equity ABS

Bank Loan

and others

49 bn RMB

Daimler Corporate Presentation / September 2016 / Page 142

Daimler AG

Growing the

Business

Innovate Digital

Tomorrow

Managing the

Growth

We pursue a clear strategy in China

Daimler Corporate Presentation / September 2016 / Page 143

Daimler AG

Digitize Business Disrupt Industry

Big Data Ecosystem

We reinvent and challenge our business before anybody

else does

Daimler Corporate Presentation / September 2016 / Page 144

Daimler AG

6 Key Initiatives

Extension Product Portfolio Expansion Dealer Network

Extension Local Production Leverage Financial Services Extension Local R&D

Integrated Sales Organization

Daimler Corporate Presentation / September 2016 / Page 145

Daimler AG

The momentum continues in 2016

German Premium Brands China Performance - YTD July 2016 Retail Sales, in Mainland China

Note: Mercedes-Benz w/o smart & V-Class, competitor 1 w/o MINI

+33%

2014 2015

2016

YTD July

>251,000

+8.7% +6.6%

Brand “B” Brand “A”

Daimler Corporate Presentation / September 2016 / Page 146

Daimler AG

Contents

Results for Q2 2016

Outlook for 2016

Daimler Group Strategy

Divisional information

China

Appendix

Page 147 Daimler Corporate Presentation / September 2016 /

Daimler AG

Group EBIT in Q2 2016 - in millions of euros -

-29 -669

3,258

+34 3,718

+93 +111

• Cars +246 • Trucks -313 • Vans +153 • Buses +25

• Cars -18 • Trucks +87 • Vans -5 • Buses +29

• Cars -252 • Trucks +169 • Vans +76 • Buses -22

of which:

• Contribution to pension plan +605

• Expenses due to Takata airbags -499

• Legal proceedings -400

• Measurement of inventories MBC -284

• Patent dispute -64

• Own dealer network +15

• Currency transactions -19

• Workforce adjustments DT -14

0

Actual

Q2 2015

Volume/

Structure/

Net pricing

Foreign

exchange

rates

Other cost

changes

Reconciliation Actual

Q2 2016

Financial

Services

Special items

affecting

EBIT

Page 148 Daimler Corporate Presentation / September 2016 /

Daimler AG

Special items affecting EBIT (I)

Mercedes-Benz Cars Q2 2015 Q2 2016 H1 2015 H1 2016

Restructuring of own dealer network -16 -11 -36 -21

Relocation of headquarters of MBUSA +9 – -11 –

Sale of real estate in the United States – – +87 –

Expenses in connection with Takata airbags – -440 – -460

Net expenses from measurement of inventories – -284 – -284

Settlement in connection with patent dispute – -64 – -64

Daimler Trucks

Workforce adjustments -20 -34 -25 -34

Restructuring of own dealer network -15 -6 -19 -7

Sale of Atlantis Foundries – – -55 –

in millions of euros

Page 149 Daimler Corporate Presentation / September 2016 /

Daimler AG

Special items affecting EBIT (II)

Mercedes-Benz Vans Q2 2015 Q2 2016 H1 2015 H1 2016

Restructuring of own dealer network -4 -2 -8 -3

Relocation of headquarters of MBUSA – – -2 –

Expenses in connection with Takata airbags – -59 – -63

Workforce adjustments in Germany – – – -30

Daimler Buses

Restructuring of own dealer network – -1 -1 -1

Reconciliation

Expenses related to legal proceedings – -400 – -400

Impairment of investment in BAIC Motor – – – -244

Losses from currency transactions (not allocated to business operations) – -19 – -241

Contribution of shares of Renault and Nissan to pension plan assets – +605 – +605

in millions of euros

Page 150 Daimler Corporate Presentation / September 2016 /

Daimler AG

Mercedes-Benz Cars: continued business growth based on

strong product portfolio

Unit sales – in thousands of units –

Q2 2015 Q2 2016

Revenue – in billions of euros –

EBIT adjusted for special items – in millions of euros –

501 547

Q2 2015 Q2 2016

21.1 22.1

Q2 2015 Q2 2016

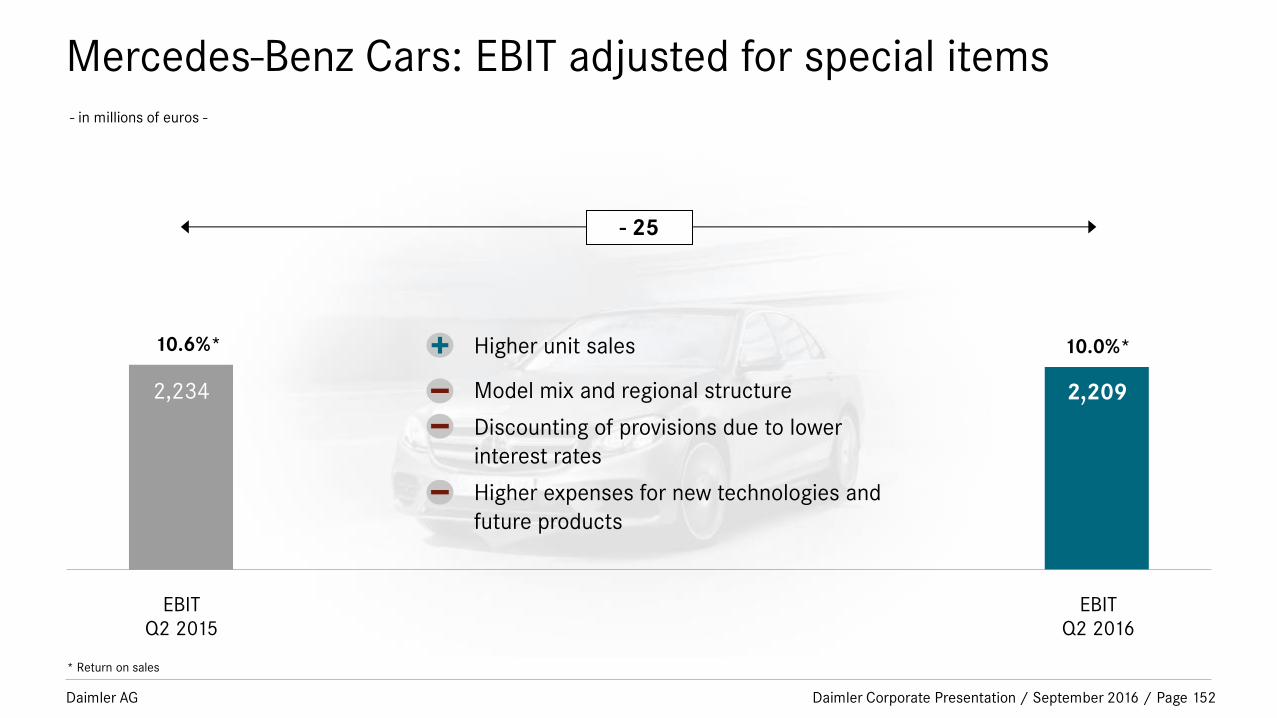

2,234 2,209 +9% +5% -1%

Page 151 Daimler Corporate Presentation / September 2016 /

Daimler AG

- in millions of euros -

* Return on sales

EBIT

Q2 2015

EBIT

Q2 2016

2,234 2,209

- 25

10.6%* 10.0%* Higher unit sales

Model mix and regional structure

Discounting of provisions due to lower

interest rates

Higher expenses for new technologies and

future products

Mercedes-Benz Cars: EBIT adjusted for special items

Page 152 Daimler Corporate Presentation / September 2016 /

Daimler AG

Mercedes-Benz Cars: sales volume above prior-year level

* incl. GLA

- in thousands of units -

Q2 2015

501

547

Q2 2016

113

128

58

23

6

110

113

80

28

8

smart

E-Class

C-Class

A-/B-Class

S-Class

Sports Cars 40

34

SUVs* 127 180

Page 153 Daimler Corporate Presentation / September 2016 /

Daimler AG

Mercedes-Benz Cars: balanced sales structure

- unit sales in thousands -

Q2 2015

501

547

Q2 2016

117

87

84

142

91

90

79

122

Rest of world

Germany

United States

China

Western Europe excl. Germany

119

117

Page 154 Daimler Corporate Presentation / September 2016 /

Daimler AG

Daimler Trucks: key figures driven by heterogeneous market

development

Unit sales – in thousands of units –

Q2 2015 Q2 2016

Revenue – in billions of euros –

EBIT adjusted for special items – in millions of euros –

125

108

Q2 2015 Q2 2016

9.4 8.7

Q2 2015 Q2 2016

717 661 -13% -8% -8%

Page 155 Daimler Corporate Presentation / September 2016 /

Daimler AG

Daimler Trucks: EBIT adjusted for special items - in millions of euros -

* Return on sales

EBIT

Q2 2015

EBIT

Q2 2016

717 661

- 56

7.6%* 7.6%*

Higher unit sales in Europe (EU30)

Efficiency enhancements

Foreign exchange rates

Lower unit sales in the NAFTA region, Turkey,

Latin America, Indonesia and Middle East

Intense competition in Europe

Page 156 Daimler Corporate Presentation / September 2016 /

Daimler AG

Daimler Trucks: decrease in unit sales driven by NAFTA

region, Turkey, Latin America, Indonesia and Middle East - in thousands of units -

Q2 2015

125

108

Q2 2016

20

41

7

30

18

49

9

35

Rest of world

Latin America

NAFTA region

EU30*

Asia

14

10

* European Union, Switzerland and Norway

Page 157 Daimler Corporate Presentation / September 2016 /

Daimler AG

Daimler Trucks: incoming orders significantly below prior-

year level - in thousands of units -

Q2 2015

124

94

Q2 2016

20

25

7

32

21

40

8

38 Rest of world

Latin America

NAFTA region

EU30*

Asia

17

10

* European Union, Switzerland and Norway

Page 158 Daimler Corporate Presentation / September 2016 /

Daimler AG

Mercedes-Benz Vans: strong development based on very

successful products

Unit sales – in thousands of units –

Q2 2015 Q2 2016

Revenue – in billions of euros –

EBIT adjusted for special items – in millions of euros –

81.6

99.6

Q2 2015 Q2 2016

2.8

3.4

Q2 2015 Q2 2016

238

462 +22% +22% +94%

Page 159 Daimler Corporate Presentation / September 2016 /

Daimler AG

Mercedes-Benz Vans: EBIT adjusted for special items - in millions of euros -

* Return on sales

EBIT

Q2 2015

EBIT

Q2 2016

238

462

+ 224

8.4%*

13.4%*

Higher unit sales

Efficiency enhancements

Page 160 Daimler Corporate Presentation / September 2016 /

Daimler AG

Mercedes-Benz Vans: market success of mid-size vans

- in thousands of units -

Q2 2015

81.6

99.6

Q2 2016

6.9

13.9

24.7

54.1

5.4

8.2

19.5

48.6

Vito

V-Class*

Citan

Sprinter

* incl. Viano

Page 161 Daimler Corporate Presentation / September 2016 /

Daimler AG

Daimler Buses: strong EBIT despite significant market

contraction in Latin America

Unit sales – in thousands of units –

Q2 2015 Q2 2016

Revenue – in billions of euros –

EBIT adjusted for special items – in millions of euros –

7.3 7.0

Q2 2015 Q2 2016

1.0 1.1

Q2 2015 Q2 2016

57

89 -5% +8% +56%

Page 162 Daimler Corporate Presentation / September 2016 /

Daimler AG

Daimler Buses: EBIT adjusted for special items - in millions of euros -

* Return on sales

EBIT

Q2 2015

EBIT

Q2 2016

57

89

+ 32

5.5%*

7.9%* Higher unit sales and better model mix

in Western Europe

Foreign exchange rates

Lower sales and cost inflation in Latin

America

Page 163 Daimler Corporate Presentation / September 2016 /

Daimler AG

Daimler Buses: lower demand for bus chassis in Latin

America - unit sales in thousands -

Q2 2015

7.3 7.0

Q2 2016

2.5

0.6

1.8

1.2

2.4

0.9

1.9

1.4

Rest of world

Brazil

Mexico

Europe

Latin America (excl. Brazil and Mexico)

0.7 0.9

Page 164 Daimler Corporate Presentation / September 2016 /

Daimler AG

Daimler Financial Services: further business growth

New business – in billions of euros –

Q2 2015 Q2 2016

Contract volume – in billions of euros –

EBIT – in millions of euros –

14.8 15.4

12/31/2015 6/30/2016

116.7 120.3

Q2 2015 Q2 2016

445 479 +4% +3% +8%

Page 165 Daimler Corporate Presentation / September 2016 /

Daimler AG

Daimler Financial Services: EBIT - in millions of euros -

* Return on equity

EBIT

Q2 2015

EBIT

Q2 2016

445 479

+ 34

20.7%* 19.3%*

Higher contract volume

Foreign exchange rates

Page 166 Daimler Corporate Presentation / September 2016 /

Daimler AG

Daimler Financial Services: growth in all regions

- contract volume in billions of euros -

12/31/2015

116.7 120.3

6/30/2016

20.9

26.3

50.9

22.2

19.8

25.8

50.8

20.2

Americas

Europe (excl. Germany)

Germany

Africa & Asia-Pacific

Page 167 Daimler Corporate Presentation / September 2016 /

Daimler AG

Daimler Financial Services: net credit losses* at low level

* as a percentage of portfolio, subject to credit risk

0.69% 0.68%

0.50%

0.61%

0.36%

0.51%

0.89% 0.83%

0.43%

0.34% 0.37% 0.31%

0.24% 0.29%

2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2016

YTD

2015

Page 168 Daimler Corporate Presentation / September 2016 /

Daimler AG

Development of dividend per share

Page 169

2.20

2.45

2.25

1.85

2.20

- in euros -

+76%

3.25

2010 2011 2012 2013 2015 2014

Daimler Corporate Presentation / September 2016 /

Daimler AG

Increased investment as a basis for profitable growth

Page 170

10.5 10.5 10.5

8.5

9.8

Actual

2010

Actual

2011

Actual

2012

Actual

2013

Actual

2014

Research and

development

expenditure

Investment in

property, plant

and equipment

Plan

2016/17

(average p.a.)

14.2

- in billions of euros -

11.6

Actual

2015

5.7

4.8

6.6

5.1

7.2

7.0

Daimler Corporate Presentation / September 2016 /

Daimler AG

Capital expenditure / Research and development

Page 171

Actual

2014

Actual

2015

4.8

Plan

2016/2017

(average p.a.)

5.1

7.0

Actual

2014

Actual

2015

5.7

6.6 7.2

Plan

2016/2017

(average p.a.)

- in billions of euros -

Investment in property, plant and equipment

Research and development expenditure

Daimler Corporate Presentation / September 2016 /

Daimler AG

Capital expenditure / Research and development

Investment in property, plant

and equipment

Research and development

expenditure

Actual

2014

Actual

2015

Plan*

2016-2017

Actual

2014

Actual

2015

Plan*

2016-2017

Daimler Group 4.8 5.1 7.0 5.7 6.6 7.2

of which

Mercedes-Benz Cars 3.6 3.6 5.0 4.0 4.7 5.4

Daimler Trucks 0.8 1.1 1.4 1.2 1.3 1.3

Mercedes-Benz Vans 0.3 0.2 0.6 0.3 0.4 0.4

Daimler Buses 0.1 0.1 0.1 0.2 0.2 0.2

Daimler Financial Services 0.02 0.03 0.02 – – –

in billions of euros * average p.a.

Page 172 Daimler Corporate Presentation / September 2016 /

Daimler AG

MBC retail sales by model Q1-2 2016

* incl. Derivatives

** incl. GLA

Retail sales Q1-2 2016 Q1-2 2015 Change in %

Mercedes-Benz 1,006,619 898,353 +12.1

of which*: A-/B-Class 220,556 202,121 +9.1

C-Class 229,872 226,082 +1.7

E-Class 135,232 149,177 -9.3

S-Class 45,299 56,606 -20.0

SUVs** 339,541 232,406 +46.1

Sports Cars 13,839 16,747 -17.4

V-Class 22,280 15,214 +46.4

smart 73,510 62,164 +18.3

Mercedes-Benz Cars 1,080,129 960,517 +12.5

Page 173

- in units -

Daimler Corporate Presentation / September 2016 /

Daimler AG

MBC retail sales by model FY 2015

* incl. Derivatives

** incl. GLA

Retail sales FY 2015 FY 2014 Change in %

Mercedes-Benz 1,871,599 1,650,007 +13.4

of which*: A-/B-Class 414,365 389,577 +6.4

C-Class 460,497 343,195 +34.2

E-Class 301,566 338,205 -10.9

S-Class 107,335 107,277 +0.1

SUVs** 525,894 415,363 +26.6

Sports Cars 30,441 31,440 -3.2

V-Class 31,501 24,950 +26.2

smart 119,382 89,844 +32.9

Mercedes-Benz Cars 1,990,981 1,739,923 +14.4

Page 174

- in units -

Daimler Corporate Presentation / September 2016 /

Daimler AG

MBC retail sales major markets Q1-2 2016

Page 175

- in units -

*Incl. Hong Kong **BRIKT: Brazil, Russia, India, South Korea and Turkey

Retail sales Q1-2 2016 Q1-2 2015 Change in %

China* 229,137 173,553 +32.0

of which locally produced vehicles 148,495 98,393 +50.9

USA 165,383 168,616 -1.9

Germany 161,271 150,648 +7.1

UK 93,745 77,979 +20.2

BRIKT** 70,931 71,777 -1.2

Italy 49,728 41,484 +19.9

Japan 34,288 32,706 +4.8

France 32,961 28,770 +14.6

South Korea 25,208 22,235 +13.4

Spain 27,019 21,479 +25.8

Russia 19,271 23,325 -17.4

Canada 21,149 19,817 +6.7

Turkey 14,509 11,846 +22.5

Rest of World 206,460 188,059 +9.8

Mercedes-Benz Cars 1,080,129 960,517 +12.5

Daimler Corporate Presentation / September 2016 /

Daimler AG

MBC retail sales major markets FY 2015

*Incl. Hong Kong **BRIKT: Brazil, Russia, India, South Korea and Turkey

Page 176

- in units -

Retail sales FY 2015 FY 2014 Change in %

China* 386,635 299,416 +29.1

of which locally produced vehicles 237,894 147,633 +61.1

USA 350,548 340,623 +2.9

Germany 309,989 282,347 +9.8

UK 152,929 127,823 +19.6

BRIKT** 149,357 131,364 +13.7

Italy 76,064 61,596 +23.5

Japan 65,983 61,768 +6.8

France 62,971 55,436 +13.6

South Korea 45,638 35,985 +26.8

Spain 45,132 34,001 +32.7

Russia 42,179 50,131 -15.9

Canada 39,696 36,474 +8.8

Turkey 30,433 23,263 +30.8

Rest of World 351,677 309,003 +13.8

Mercedes-Benz Cars 1,990,981 1,739,923 +14.4

Daimler Corporate Presentation / September 2016 /

Daimler AG

MBC regional retail sales mix Q1-2 2016

Japan

3,1%

3,2%

Italy 4,6%

BRIKT**

6,6%

UK

Rest of World

Canada

19,1%

2,0%

2,5% Spain

France

14,9%

15,3%

21,2%

8,7%

Germany

USA

China*

**BRIKT: Brazil, Russia, India, South Korea and Turkey

*Incl. Hong Kong

Page 177 Daimler Corporate Presentation / September 2016 /

Daimler AG

MBC regional retail sales mix FY 2015

17,7%

Rest of World

Canada 2,0%

2,3% Spain

3,2% France

3,3% Japan

3,8% Italy

7,5%

BRIKT**

UK Germany

7,7% 15,6%

USA 17,6%

China*

19,4%

**BRIKT: Brazil, Russia, India, South Korea and Turkey

*Incl. Hong Kong

Page 178 Daimler Corporate Presentation / September 2016 /

Daimler AG

Daimler follows a conservative Financial Policy

Page 179

Clear commitment to a single A rating

Dividend policy on a sustainable basis (40% target pay-out ratio)

No share buybacks planned, further pension contributions will be evaluated

Balanced approach between shareholder interest and credit providers

Daimler Corporate Presentation / September 2016 /

Daimler AG

Bonds total outstanding as of Q2 2016: 59.1

Bond Maturities

Page 180

- in billions of euros -

Q3 2016 Q4 2016 Q1 2017 Q2 2017

Next 12

months

Bonds

short term

-4.3 -2.1 -4.7 -2.9 -14.0

0-1 Y 1-2 Y 2-3 Y 3-4 Y 4-5 Y 5-6 Y >6 Y

Bonds

long term

-14.0 -12.5 -8.5 -9.6 -3.7 -2.1 -8.6

Daimler Corporate Presentation / September 2016 /

Daimler AG

Bonds and ABS Development 2013 - 2015

Note: Figures may not be additive due to fx effects and rounding.

Bond development

ABS development

Maturities

New deals

50,842,938,7

16,9

10,8

2015 Actual

-10,2

2014 Actual

-9,4

2013 Actual

7,46,06,1

6,2

3,5

-5,8

2014 Actual

-4,4

2013 Actual 2015 Actual

Page 181

- in billions of euros -

Daimler Corporate Presentation / September 2016 /

Daimler AG

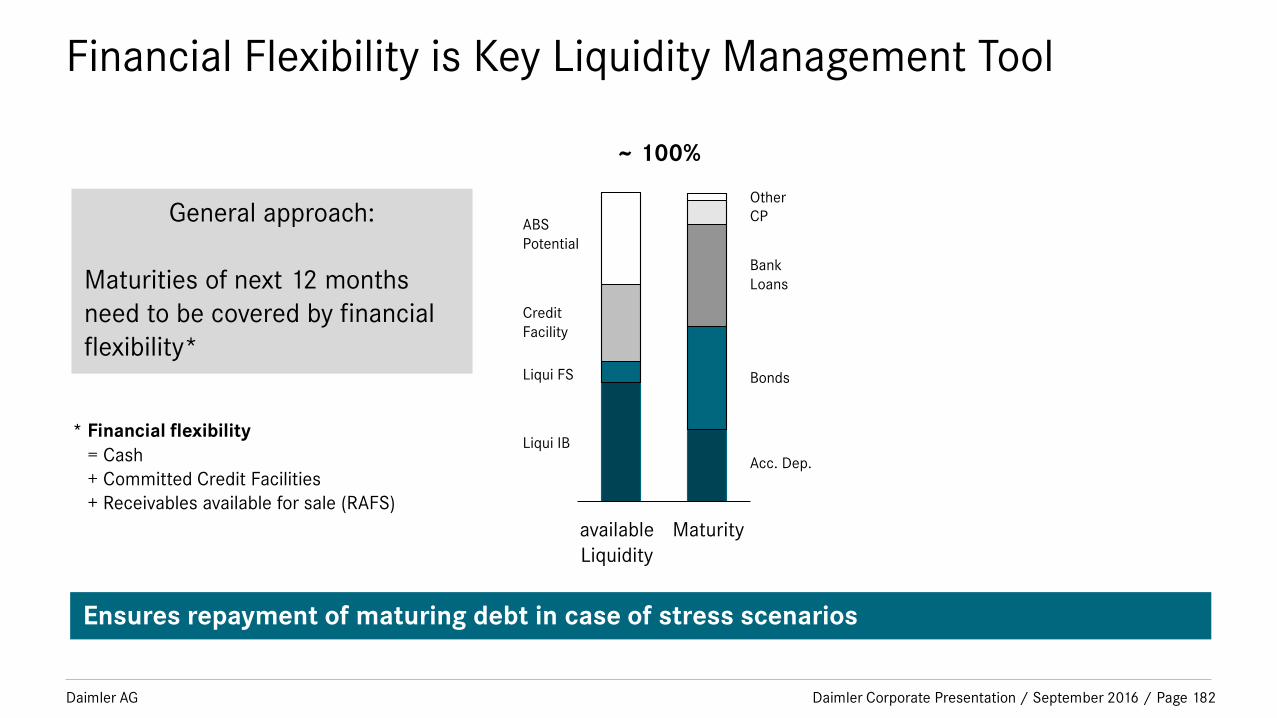

Financial Flexibility is Key Liquidity Management Tool

~ 100%

General approach:

Maturities of next 12 months

need to be covered by financial

flexibility*

* Financial flexibility

= Cash

+ Committed Credit Facilities

+ Receivables available for sale (RAFS)

available

Liquidity

Maturity

Bonds

Acc. Dep.

Bank

Loans

CP

Other

Liqui FS

Liqui IB

Credit

Facility

ABS

Potential

Ensures repayment of maturing debt in case of stress scenarios

Page 182 Daimler Corporate Presentation / September 2016 /

Daimler AG

Our funding strategy is built on prudent principles

Targeting

Financial

Independence

No dependence from single markets, instruments, banks or investors

Diversification of funding sources and instruments:

Bank Loans, Bonds, ABS, CP, Deposits

No Covenants, no MAC, no asset pledges, no CSAs

Maximizing

Financial

Flexibility Early capital market funding to save credit capacity in growth regions

New markets funded via global and local banks first

Stringent Global

Funding Policy

Liquidity matched funding

Interest rate matched funding

Currency matched funding

Country matched funding

Keeping prudent amount of Cash and Committed Credit Facility

Page 183 Daimler Corporate Presentation / September 2016 /

Daimler AG

Disclaimer

This document contains forward-looking statements that reflect our current views about future events. The words “anticipate,” “assume,” “believe,”

“estimate,” “expect,” “intend,” “may,” ”can,” “could,” “plan,” “project,” “should” and similar expressions are used to identify forward-looking statements.

These statements are subject to many risks and uncertainties, including an adverse development of global economic conditions, in particular a decline of

demand in our most important markets, caused for example by the possible exit of the United Kingdom from the European Union; a deterioration of our

refinancing possibilities on the credit and financial markets; events of force majeure including natural disasters, acts of terrorism, political unrest, armed

conflicts, industrial accidents and their effects on our sales, purchasing, production or financial services activities; changes in currency exchange rates; a

shift in consumer preferences towards smaller, lower-margin vehicles; a possible lack of acceptance of our products or services which limits our ability to

achieve prices and adequately utilize our production capacities; price increases for fuel or raw materials; disruption of production due to shortages of

materials, labor strikes or supplier insolvencies; a decline in resale prices of used vehicles; the effective implementation of cost-reduction and efficiency-

optimization measures; the business outlook for companies in which we hold a significant equity interest; the successful implementation of strategic

cooperations and joint ventures; changes in laws, regulations and government policies, particularly those relating to vehicle emissions, fuel economy and

safety; the resolution of pending government investigations or of investigations requested by governments and the conclusion of pending or threatened

future legal proceedings; and other risks and uncertainties, some of which we describe under the heading “Risk and Opportunity Report” in the current

Annual Report. If any of these risks and uncertainties materializes or if the assumptions underlying any of our forward-looking statements prove to be

incorrect, the actual results may be materially different from those we express or imply by such statements. We do not intend or assume any obligation

to update these forward-looking statements since they are based solely on the circumstances at the date of publication.

Page 184 Daimler Corporate Presentation / September 2016 /