Embed Size (px)

Citation preview

0

1H05 Analysts and investors meeting

Localiza Rent a Car S.A.

1

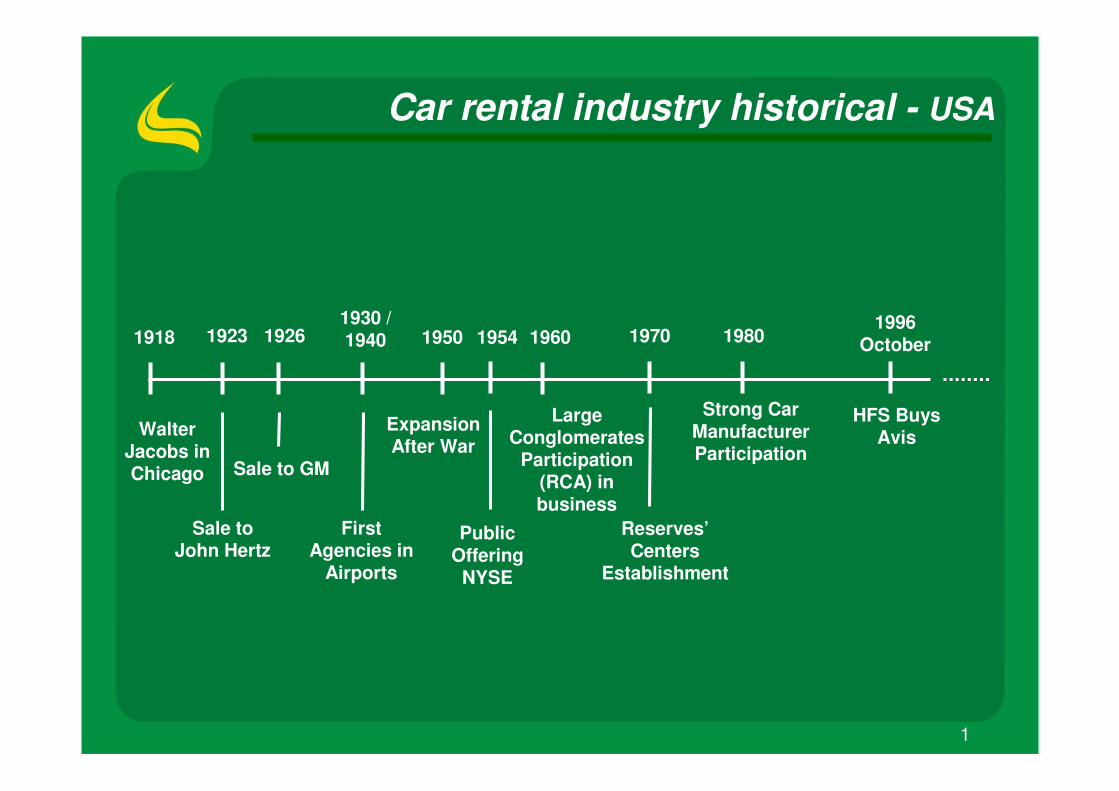

Car rental industry historical - USA

Walter Jacobs in Chicago

1918 1923

Sale to John Hertz

1926

Sale to GM

1930 / 1940

FirstAgencies in

Airports

1950

ExpansionAfter War

1954

PublicOffering

NYSE

1960

LargeConglomerates

Participation(RCA) in business

Reserves’ Centers

Establishment

1970 1980

Strong Car ManufacturerParticipation

1996October

HFS BuysAvis

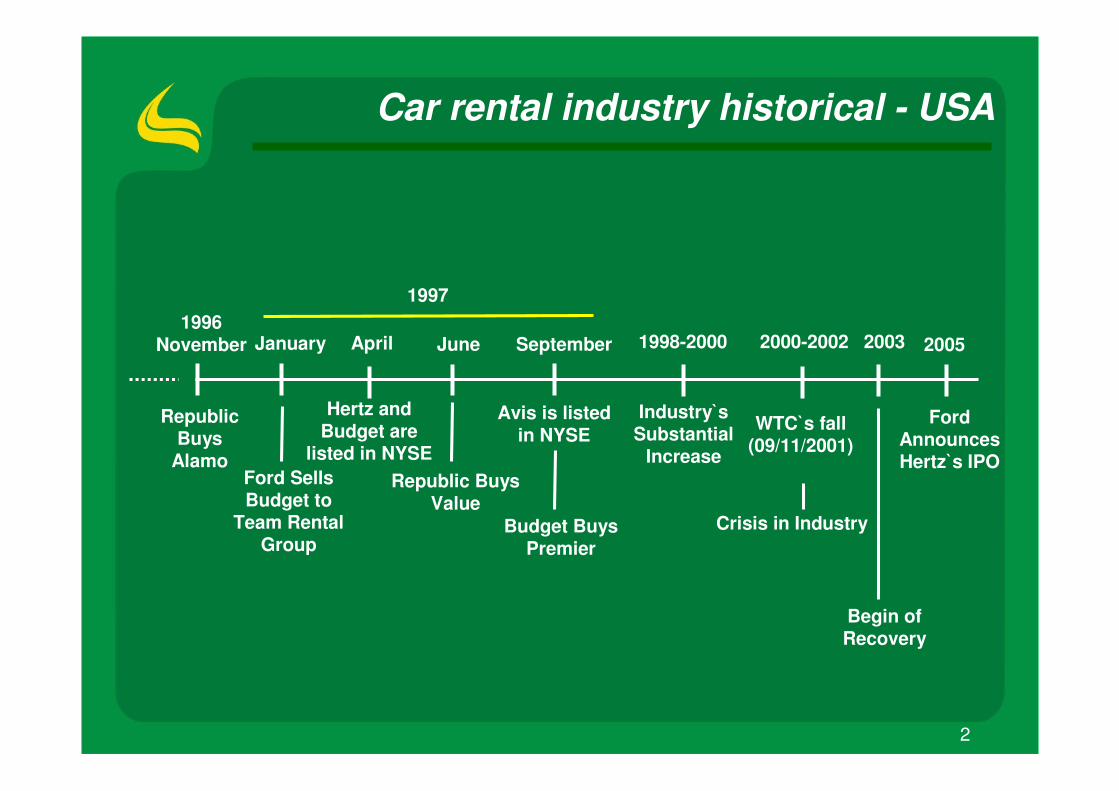

2

1996November

RepublicBuys

Alamo

1998-2000January April

Ford SellsBudget to

Team RentalGroup

Hertz andBudget are

listed in NYSE

June

Republic BuysValue

September

Avis is listedin NYSE

Budget BuysPremier

2005

Ford AnnouncesHertz`s IPO

1997

Industry`s Substantial

Increase

2000-2002

WTC`s fall(09/11/2001)

Crisis in Industry

2003

Begin ofRecovery

Car rental industry historical - USA

3

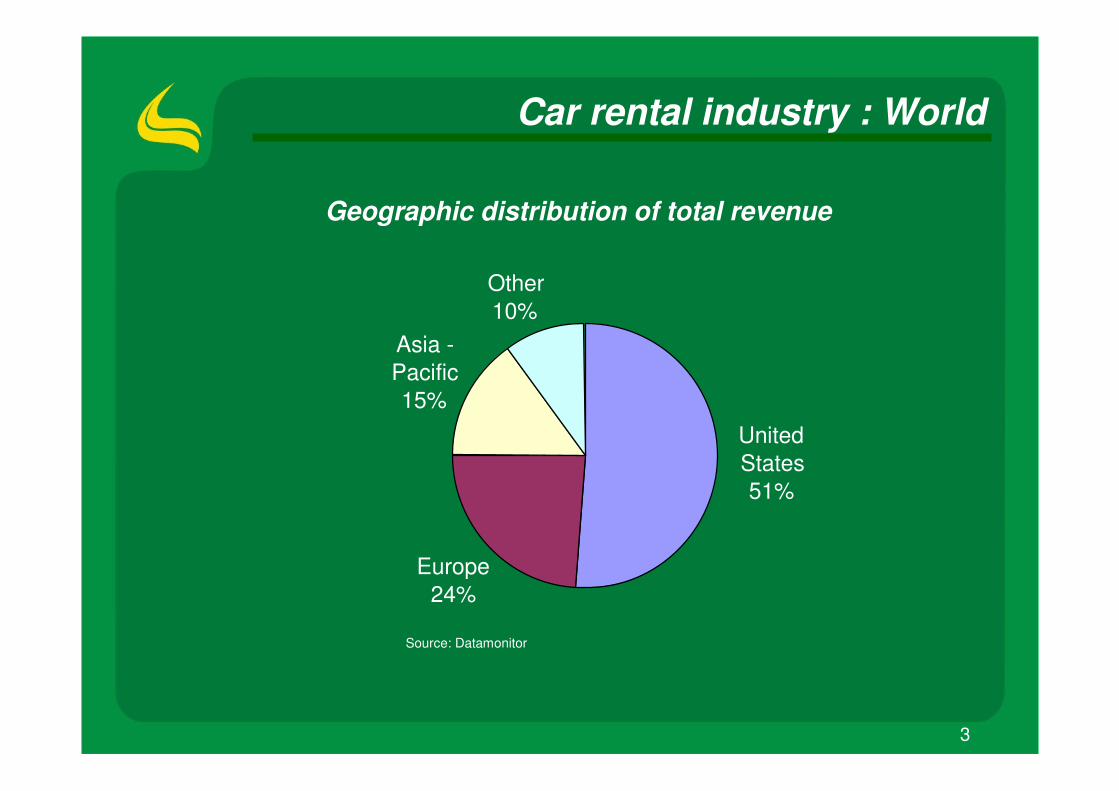

Car rental industry : World

Geographic distribution of total revenue

Source: Datamonitor

UnitedStates51%

Europe24%

Asia -Pacific15%

Other10%

4

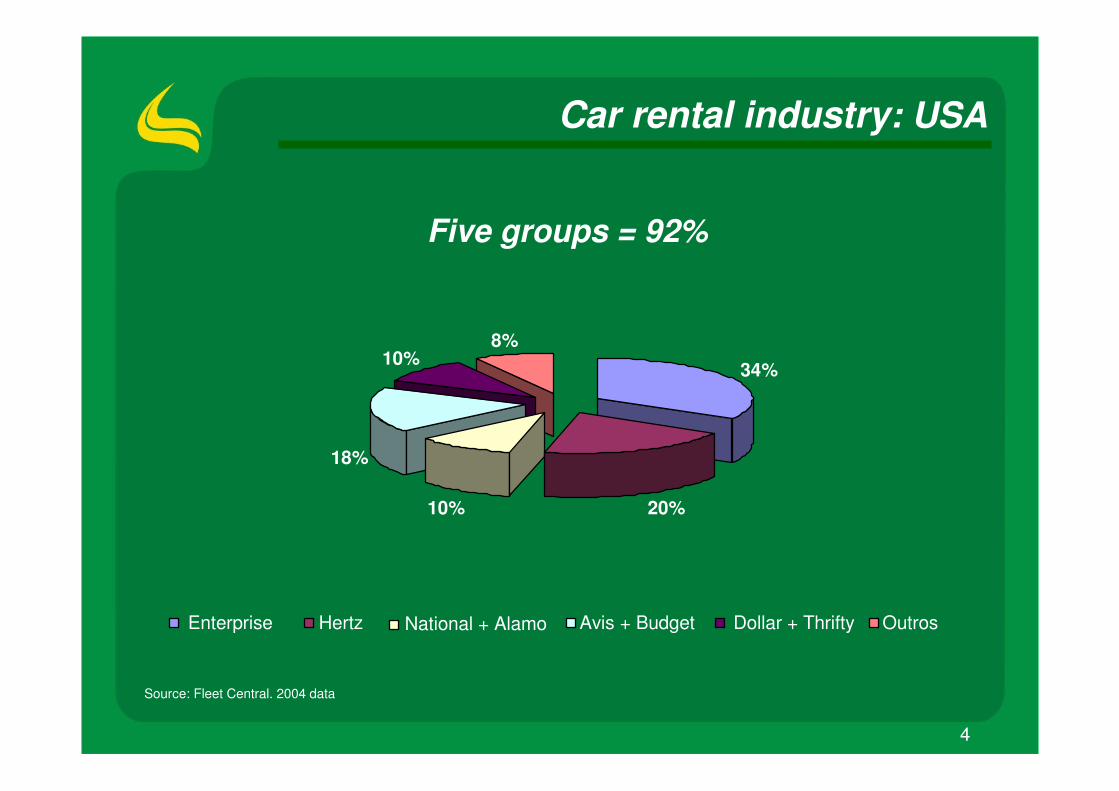

Car rental industry: USA

Source: Fleet Central. 2004 data

Five groups = 92%

34%

20%10%

18%

10%8%

Enterprise Hertz National + Alamo Avis + Budget Dollar + Thrifty Outros

5

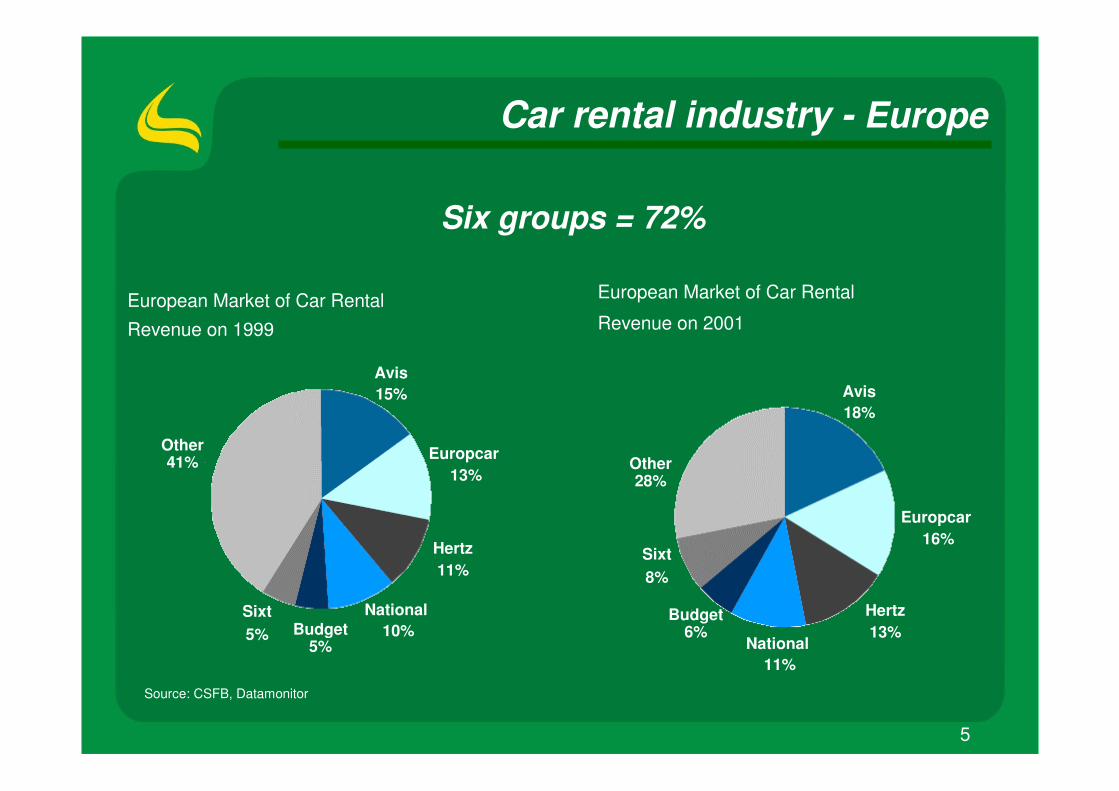

Car rental industry - Europe

Source: CSFB, Datamonitor

European Market of Car RentalRevenue on 1999

Other41%

Sixt5%

Hertz11%

National10%

Avis 15%

Budget 5%

Europcar13%

European Market of Car Rental

Revenue on 2001

Other28%

Sixt8%

Hertz13%

National11%

Avis 18%

Budget 6%

Europcar16%

Six groups = 72%

6

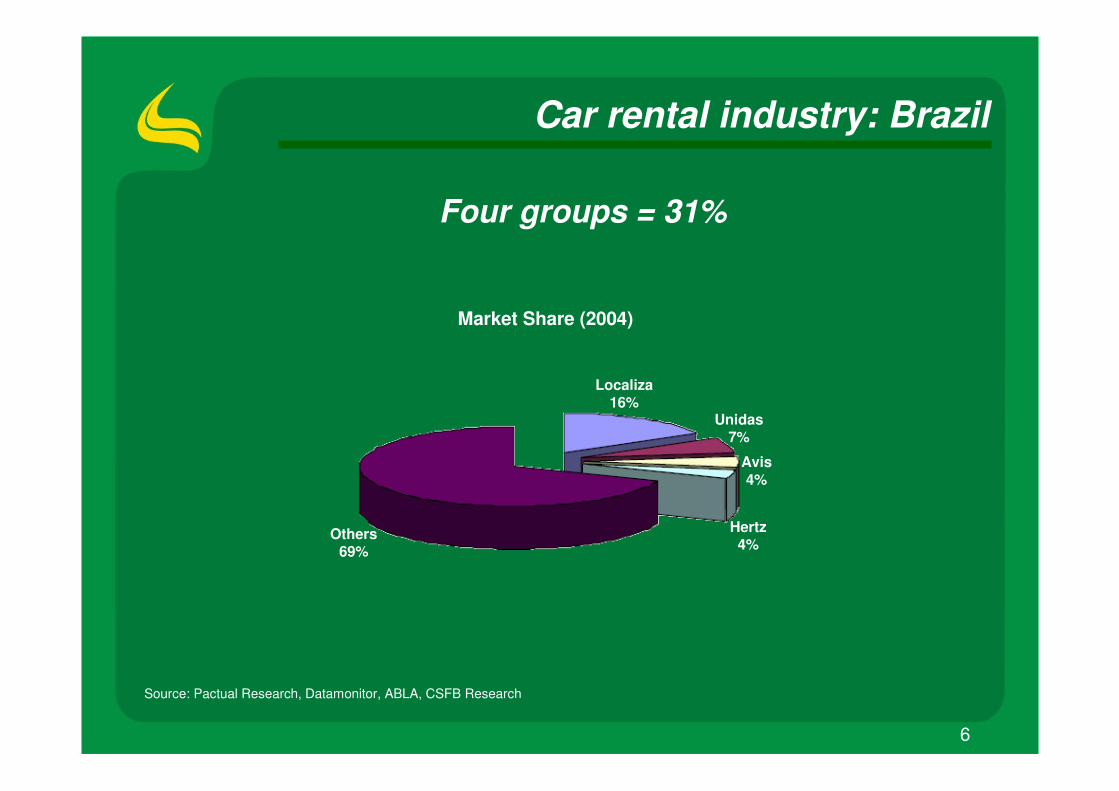

Car rental industry: Brazil

Source: Pactual Research, Datamonitor, ABLA, CSFB Research

Market Share (2004)

Localiza 16%

Unidas7%

Avis4%

Hertz4%

Four groups = 31%

Others69%

7

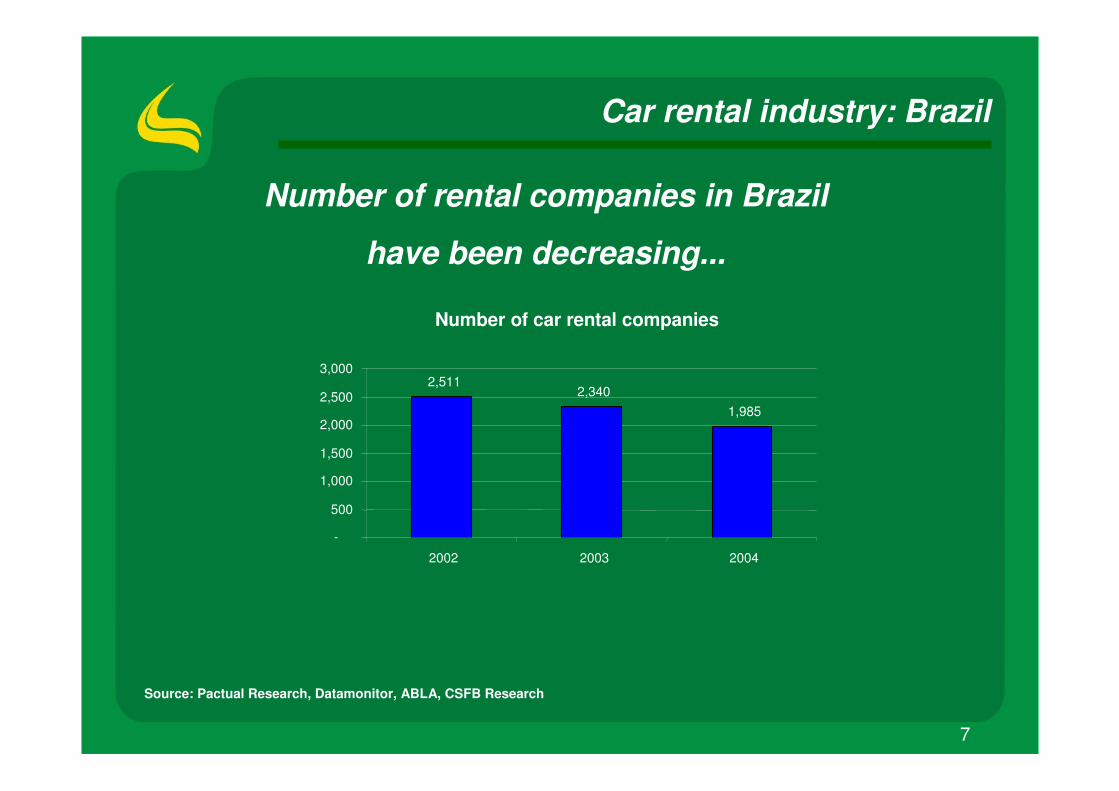

Car rental industry: Brazil

Source: Pactual Research, Datamonitor, ABLA, CSFB Research

Number of car rental companies

Number of rental companies in Brazil

have been decreasing...

2,5112,340

1,985

-

500

1,000

1,500

2,000

2,500

3,000

2002 2003 2004

8

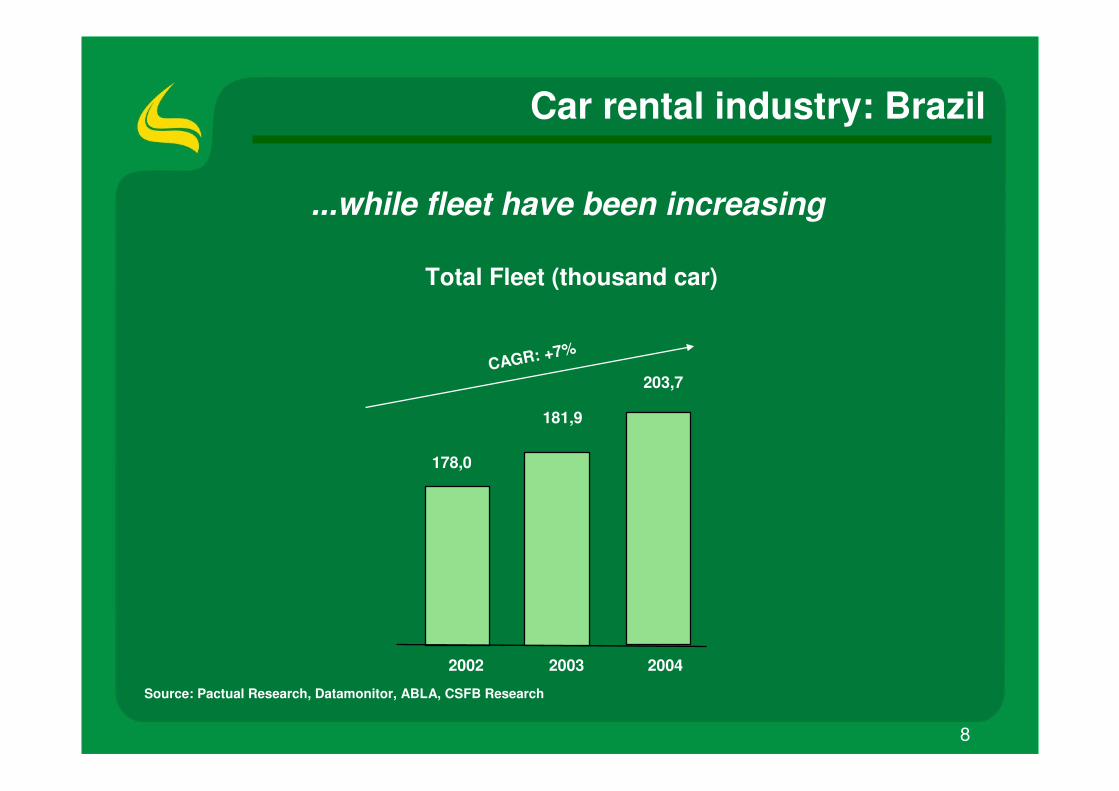

Car rental industry: Brazil

Total Fleet (thousand car)

CAGR: +7%

178,0

181,9

203,7

2002 2003 2004

...while fleet have been increasing

Source: Pactual Research, Datamonitor, ABLA, CSFB Research

9

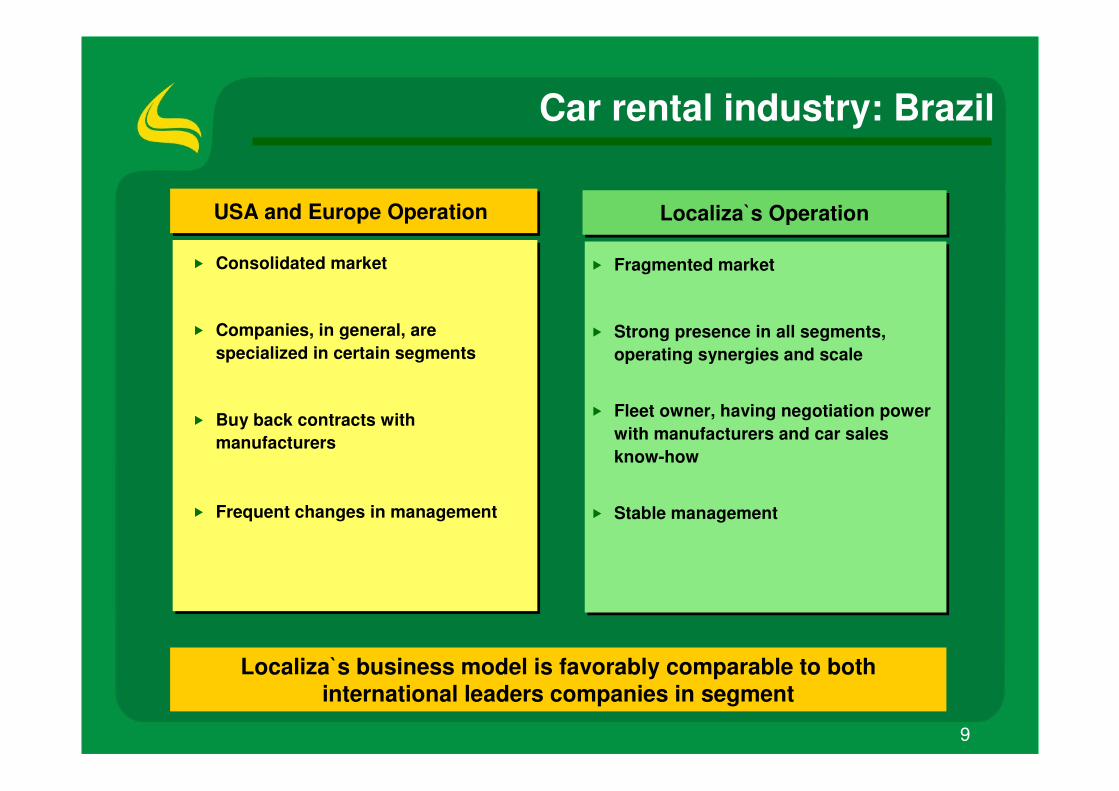

Car rental industry: Brazil

� Fragmented market

� Strong presence in all segments, operating synergies and scale

� Fleet owner, having negotiation power with manufacturers and car sales know-how

� Stable management

� Consolidated market

� Companies, in general, are specialized in certain segments

� Buy back contracts with manufacturers

� Frequent changes in management

Localiza`s OperationLocaliza`s OperationUSA and Europe Operation USA and Europe Operation

Localiza`s business model is favorably comparable to both international leaders companies in segment

10

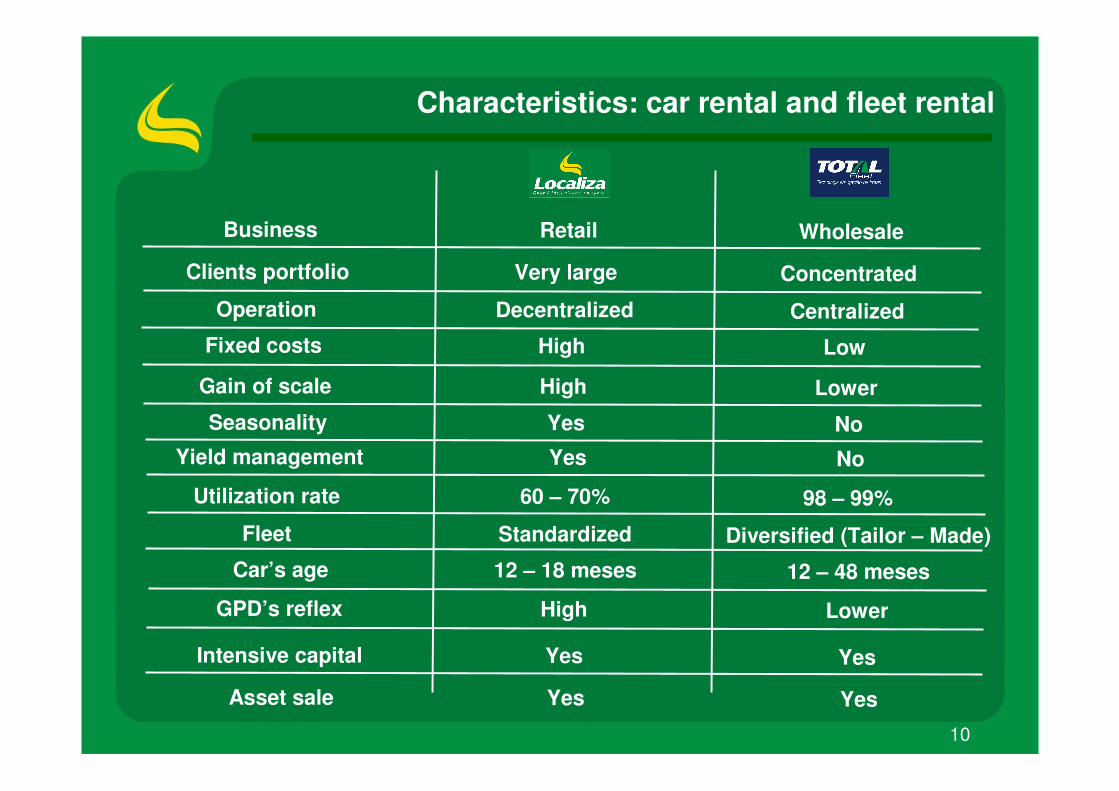

Characteristics: car rental and fleet rental

Retail WholesaleBusiness

Very large ConcentratedClients portfolio

Decentralized CentralizedOperation

High LowFixed costs

High LowerGain of scale

Yes NoSeasonality

Yes NoYield management

60 – 70% 98 – 99%Utilization rate

Standardized Diversified (Tailor – Made)Fleet

12 – 18 meses 12 – 48 mesesCar’s age

High LowerGPD’s reflex

Yes YesIntensive capital

Yes YesAsset sale

11

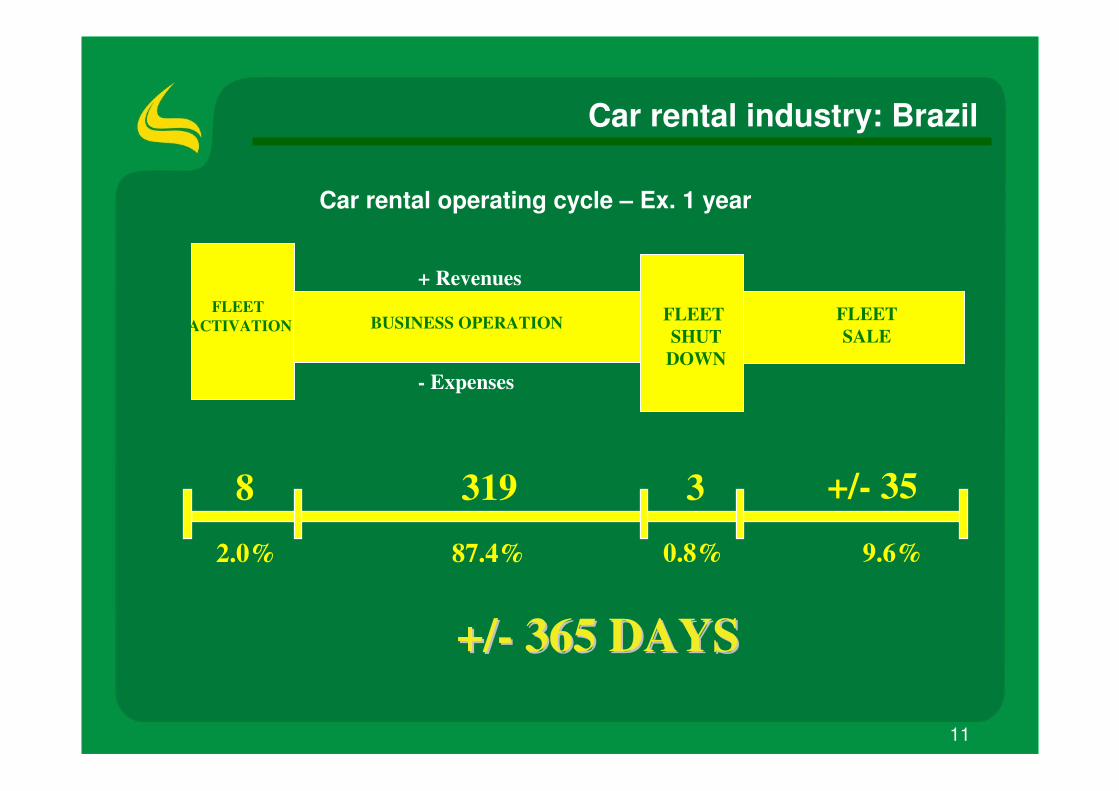

FLEET SALE

FLEET ACTIVATION BUSINESS OPERATION FLEET

SHUTDOWN

8 319 3 +/- 35

0.8% 9.6%

+/+/-- 365 DAYS365 DAYS

+ Revenues

- Expenses

2.0% 87.4%

Car rental operating cycle – Ex. 1 year

Car rental industry: Brazil

12

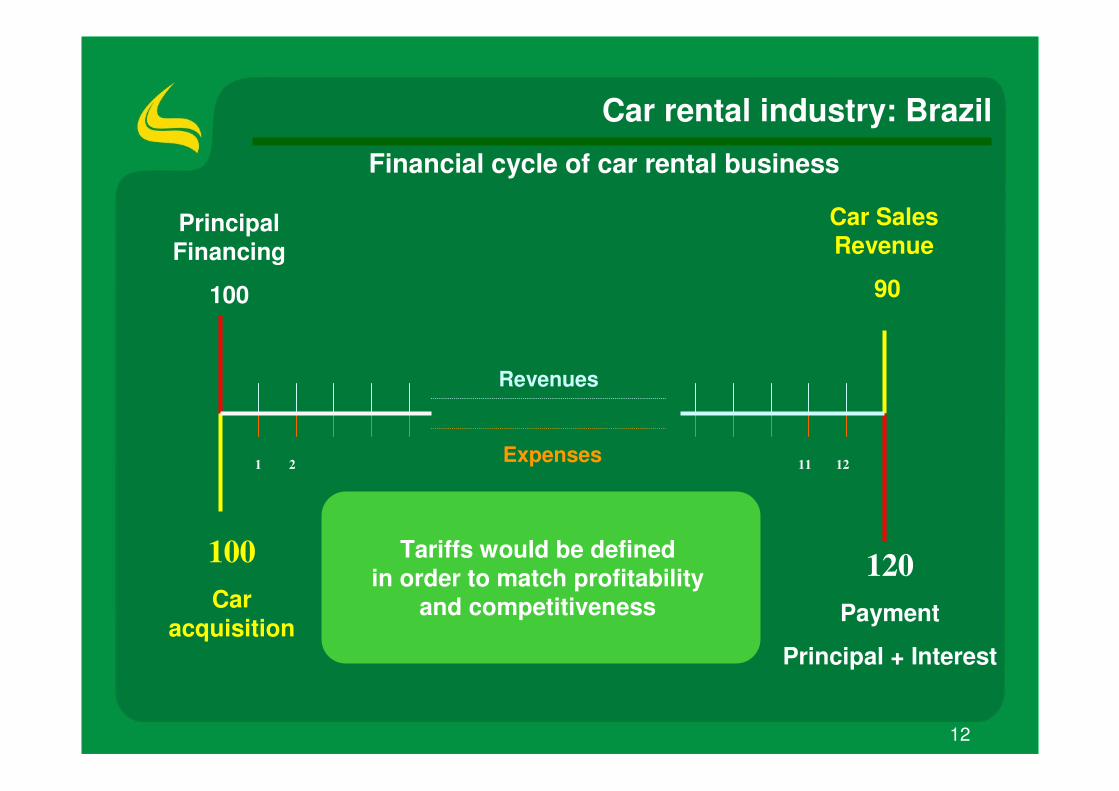

Principal Financing

100

120Payment

Principal + Interest

100Car

acquisition

Car Sales Revenue

90

Revenues

Expenses1 2 1211

Car rental industry: Brazil

Tariffs would be definedin order to match profitability

and competitiveness

Financial cycle of car rental business

13

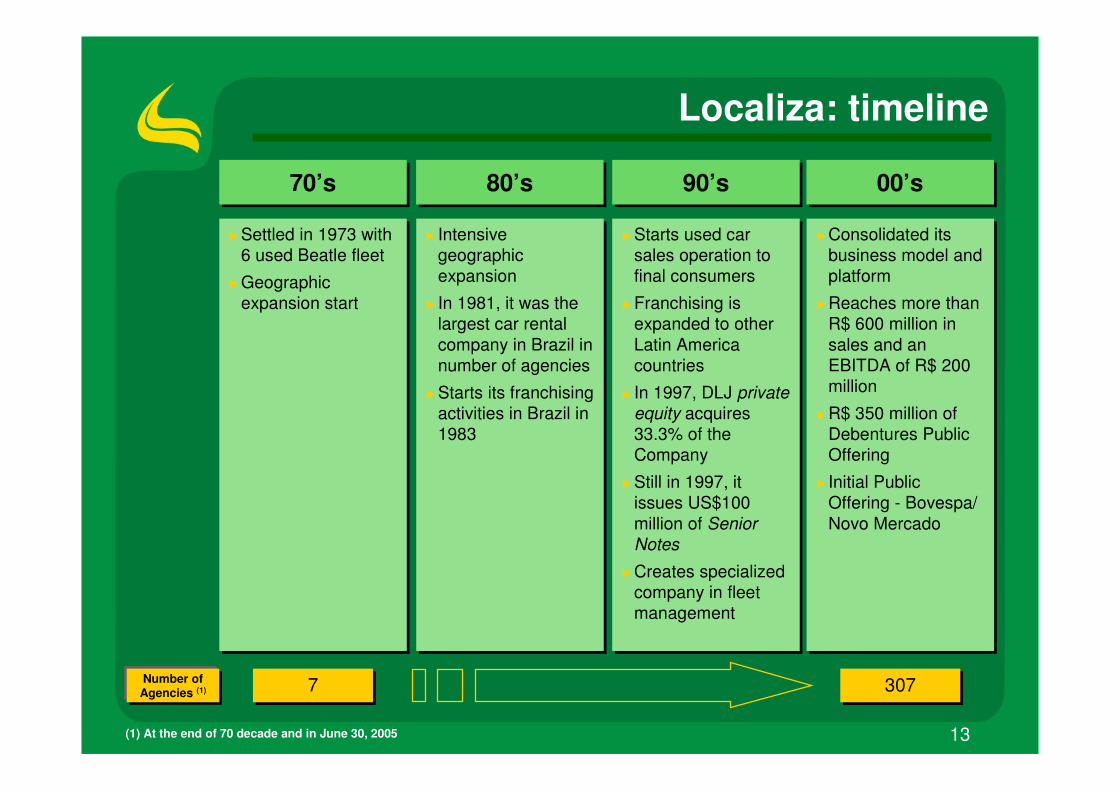

Localiza: timeline

� Settled in 1973 with 6 used Beatle fleet

� Geographic expansion start

� Settled in 1973 with 6 used Beatle fleet

� Geographic expansion start

70’s70’s 80’s80’s 90’s90’s 00’s00’s

� Intensive geographic expansion

� In 1981, it was the largest car rental company in Brazil in number of agencies

� Starts its franchising activities in Brazil in 1983

� Intensive geographic expansion

� In 1981, it was the largest car rental company in Brazil in number of agencies

� Starts its franchising activities in Brazil in 1983

� Starts used car sales operation to final consumers

� Franchising is expanded to other Latin America countries

� In 1997, DLJ private equity acquires 33.3% of the Company

� Still in 1997, it issues US$100 million of Senior Notes

� Creates specialized company in fleet management

� Starts used car sales operation to final consumers

� Franchising is expanded to other Latin America countries

� In 1997, DLJ private equity acquires 33.3% of the Company

� Still in 1997, it issues US$100 million of Senior Notes

� Creates specialized company in fleet management

� Consolidated its business model and platform

� Reaches more than R$ 600 million in sales and an EBITDA of R$ 200 million

� R$ 350 million of Debentures Public Offering

� Initial Public Offering - Bovespa/ Novo Mercado

� Consolidated its business model and platform

� Reaches more than R$ 600 million in sales and an EBITDA of R$ 200 million

� R$ 350 million of Debentures Public Offering

� Initial Public Offering - Bovespa/ Novo Mercado

77 307307

(1) At the end of 70 decade and in June 30, 2005

Number of Agencies (1)

14

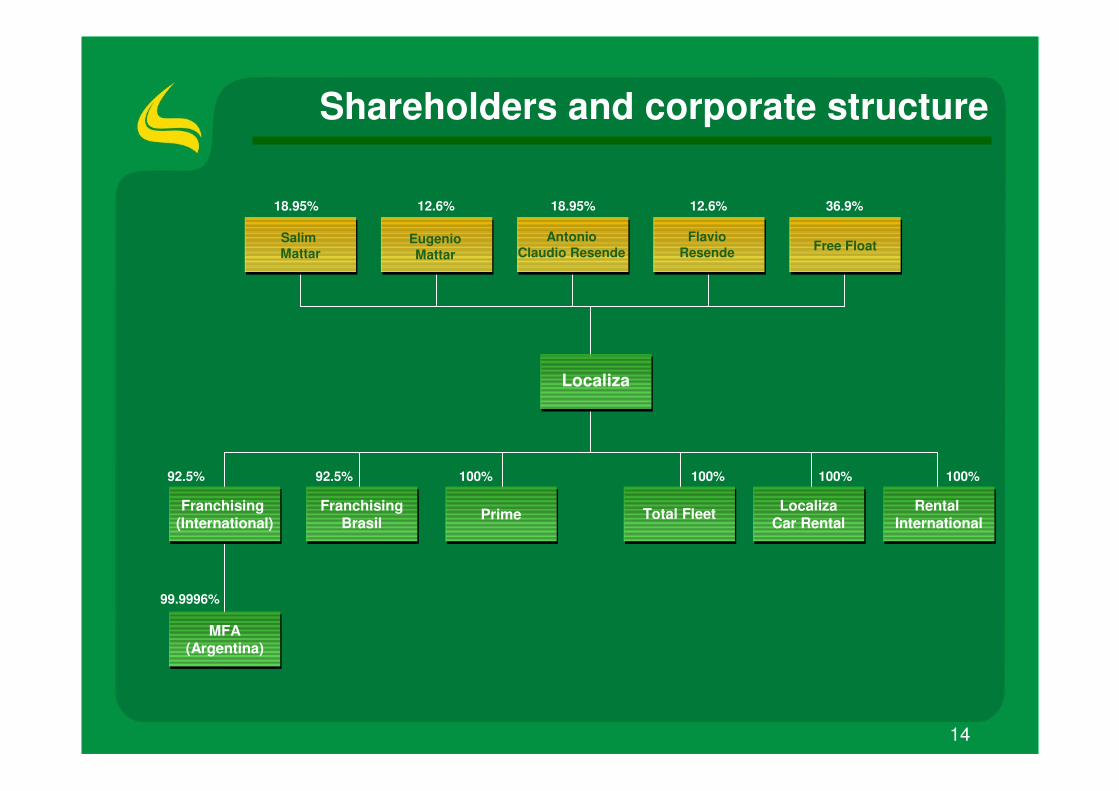

Shareholders and corporate structure

Localiza

MFA(Argentina)

99.9996%

EugenioMattar

AntonioClaudio Resende

FlavioResende Free Float

18.95% 12.6% 18.95% 12.6% 36.9%

Franchising (International) Prime Total FleetFranchising

Brasil

100%100%92.5%

LocalizaCar Rental

100%92.5%

Salim Mattar

RentalInternational

100%

15

Localiza: company’s management

* Estatutory Officers

Chief Executive Officer*Salim Mattar

Vice Chief Executive Officer*

Eugenio Mattar

Antonio Cláudio

Vice Chief Executive Officer *

Founder

Founder

Founder

Chief Financial Officer and IR*Roberto Mendes 20 years

Aristides Newton Franchising 23 years

Investors RelationsSilvio Guerra 11 years

Eugênia Rafael Car Rental 25 years

Daltro Leite Total Fleet 20 years

Marco Antônio Guimarâes Seminovos 15 years

Years in the Company

16

Company overview

Cor

e B

usin

ess

Sup

port

� #1 operator in Brazil with 91 corporate owned branches� Segments: Individuals, Corporate, Travel Industry, Replacement,

Mini Lease� Largest fleet in Brazil: 20,877 cars� EBITDA Share: 64%

� #1 operator in Brazil with a fleet of 10,514 cars� Approximately 200 corporate clients� EBITDA Share: 35%

� Presence in 8 countries: Brazil, Argentina, Bolivia, Chile, Ecuador, Mexico, Paraguay and Uruguay

� 216 Franchised agencies, with a fleet of 7.293 cars� EBITDA Share: 1%

� 13 points of sale located in the country’s largest cities � 9,856 sold cars in the first half of 2005� 76.8% cars sold to final customers

17

Localiza: integrated business platformC

ore

Bus

ines

sS

uppo

rt

Used Car SalesUsed Car Sales

Fleet ManagementFleet ManagementFranchisingFranchising

Rent a CarRent a Car

Synergy among the main business

segments- Cross-Selling

- Cost Reduction

18

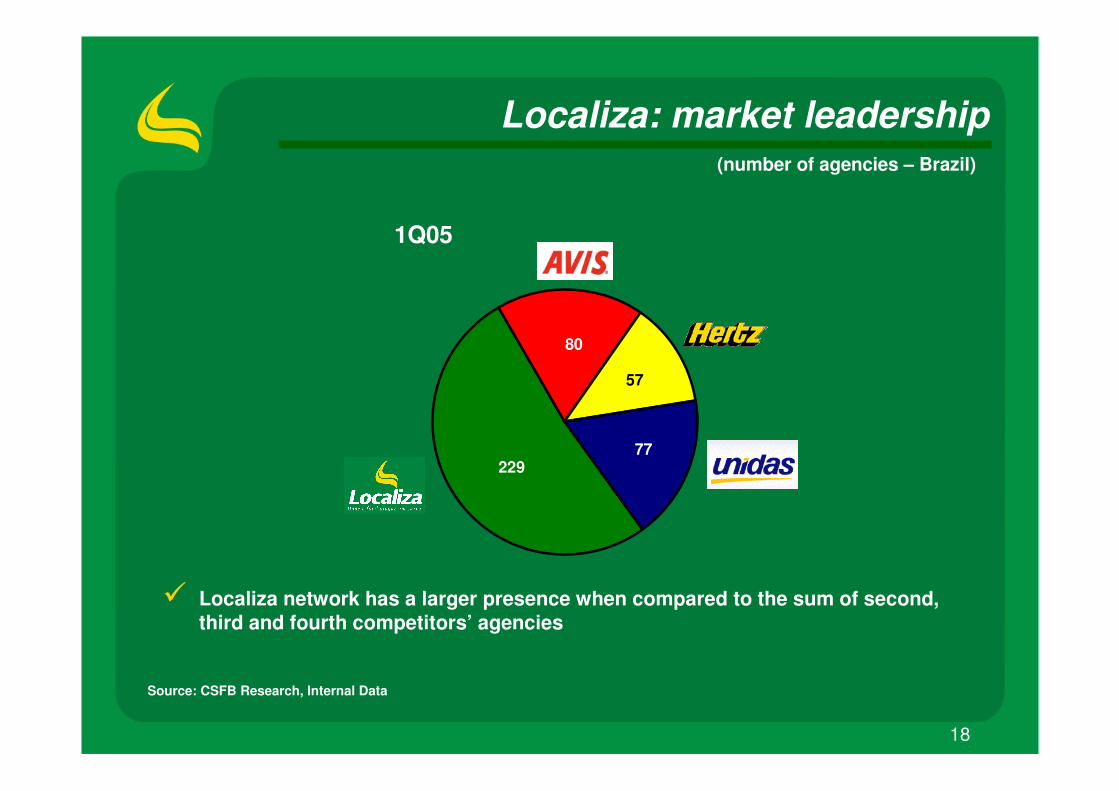

Localiza: market leadership

Source: CSFB Research, Internal Data

� Localiza network has a larger presence when compared to the sum of second, third and fourth competitors’ agencies

(number of agencies – Brazil)

80

57

77229

1Q05

19

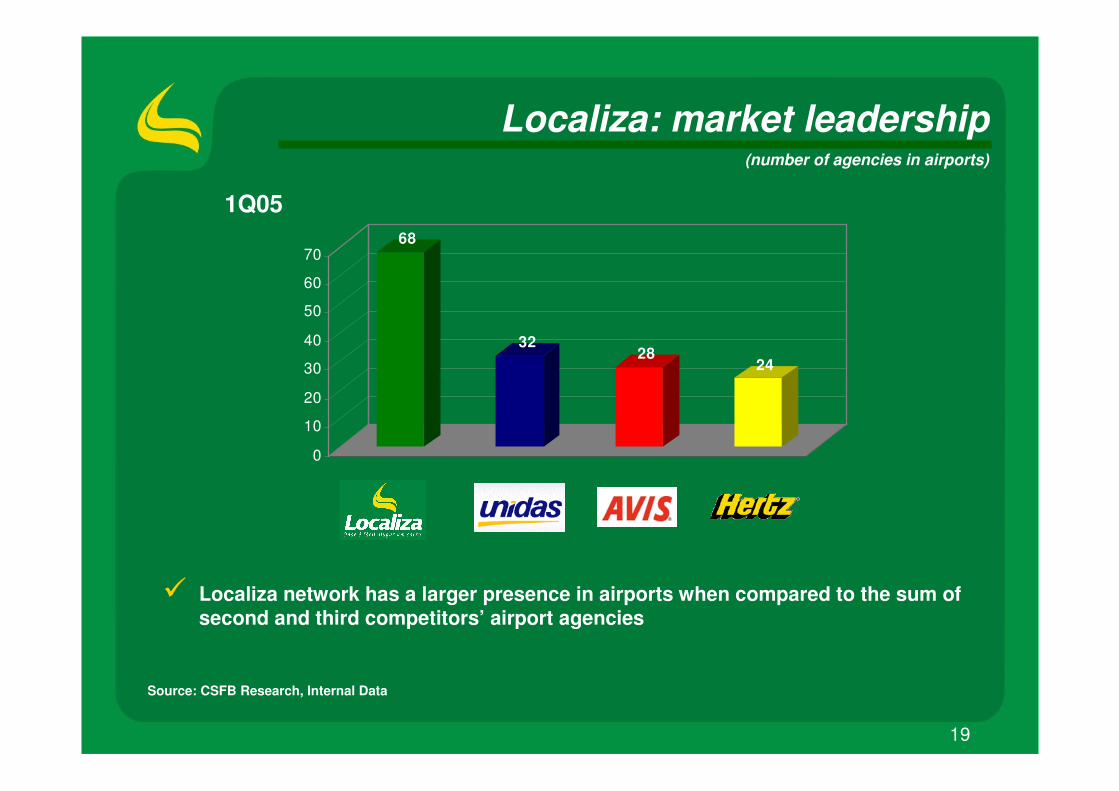

Localiza: market leadership(number of agencies in airports)

Source: CSFB Research, Internal Data

� Localiza network has a larger presence in airports when compared to the sum of second and third competitors’ airport agencies

68

3228

24

0

10

20

30

40

50

60

70

1Q05

20

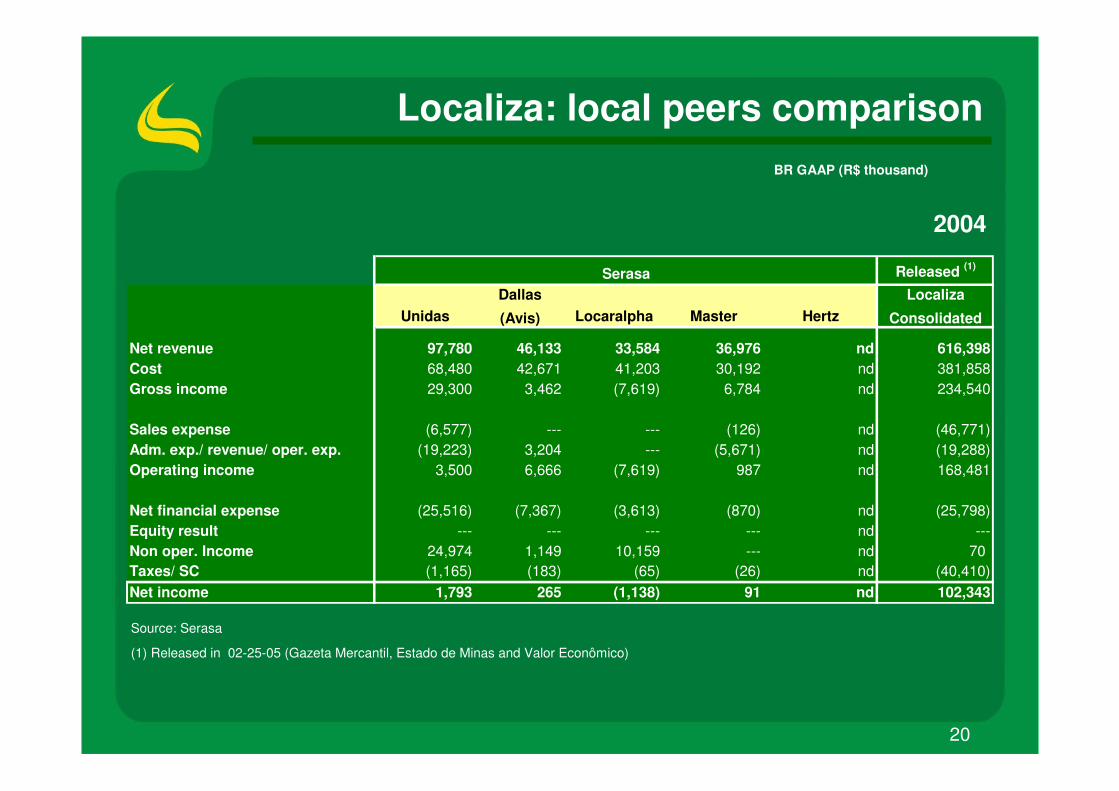

Localiza: local peers comparisonBR GAAP (R$ thousand)

Source: Serasa

(1) Released in 02-25-05 (Gazeta Mercantil, Estado de Minas and Valor Econômico)

2004

Released (1)

UnidasDallas

(Avis) Locaralpha Master HertzLocaliza

Consolidated

Net revenue 97,780 46,133 33,584 36,976 nd 616,398Cost 68,480 42,671 41,203 30,192 nd 381,858Gross income 29,300 3,462 (7,619) 6,784 nd 234,540

Sales expense (6,577) --- --- (126) nd (46,771)Adm. exp./ revenue/ oper. exp. (19,223) 3,204 --- (5,671) nd (19,288)Operating income 3,500 6,666 (7,619) 987 nd 168,481

Net financial expense (25,516) (7,367) (3,613) (870) nd (25,798)Equity result --- --- --- --- nd ---Non oper. Income 24,974 1,149 10,159 --- nd 70Taxes/ SC (1,165) (183) (65) (26) nd (40,410)Net income 1,793 265 (1,138) 91 nd 102,343

Serasa

21

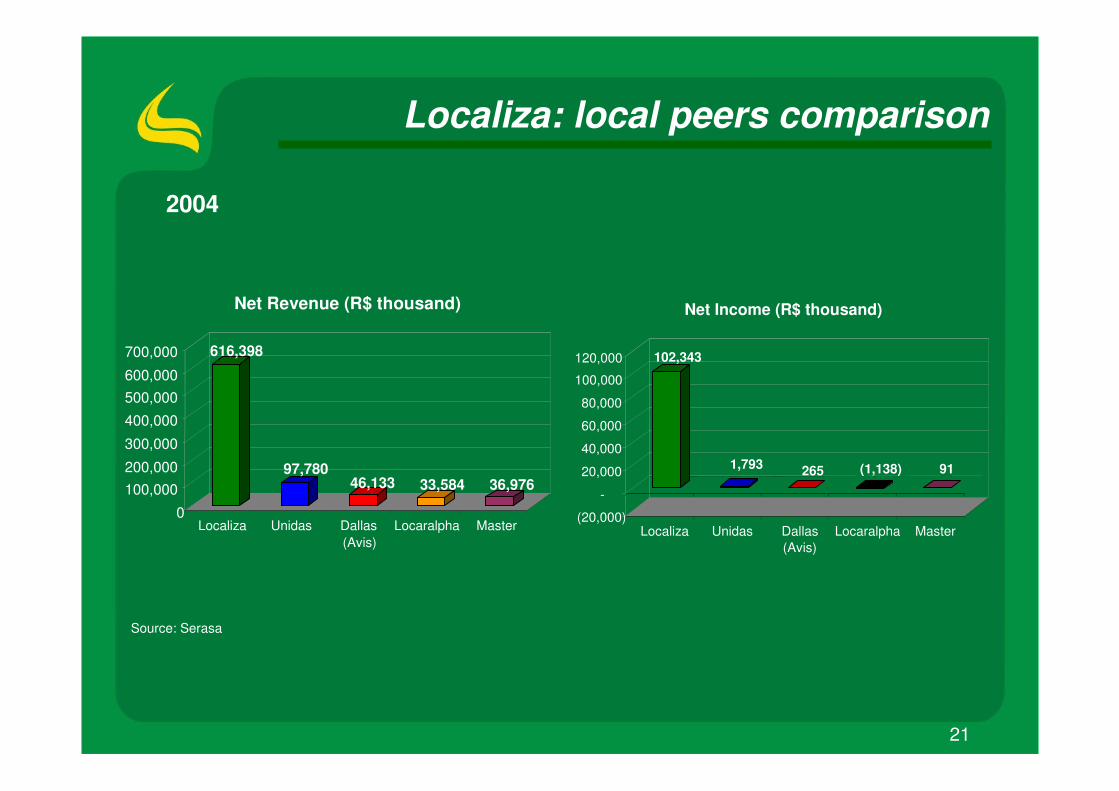

Localiza: local peers comparison

Source: Serasa

2004

616,398

97,78046,133 33,584 36,976

0

100,000200,000

300,000

400,000

500,000600,000

700,000

Localiza Unidas Dallas(Avis)

Locaralpha Master

Net Revenue (R$ thousand)

102,343

1,793 265 (1,138) 91

(20,000)

-

20,000

40,000

60,000

80,000

100,000

120,000

Localiza Unidas Dallas(Avis)

Locaralpha Master

Net Income (R$ thousand)

22

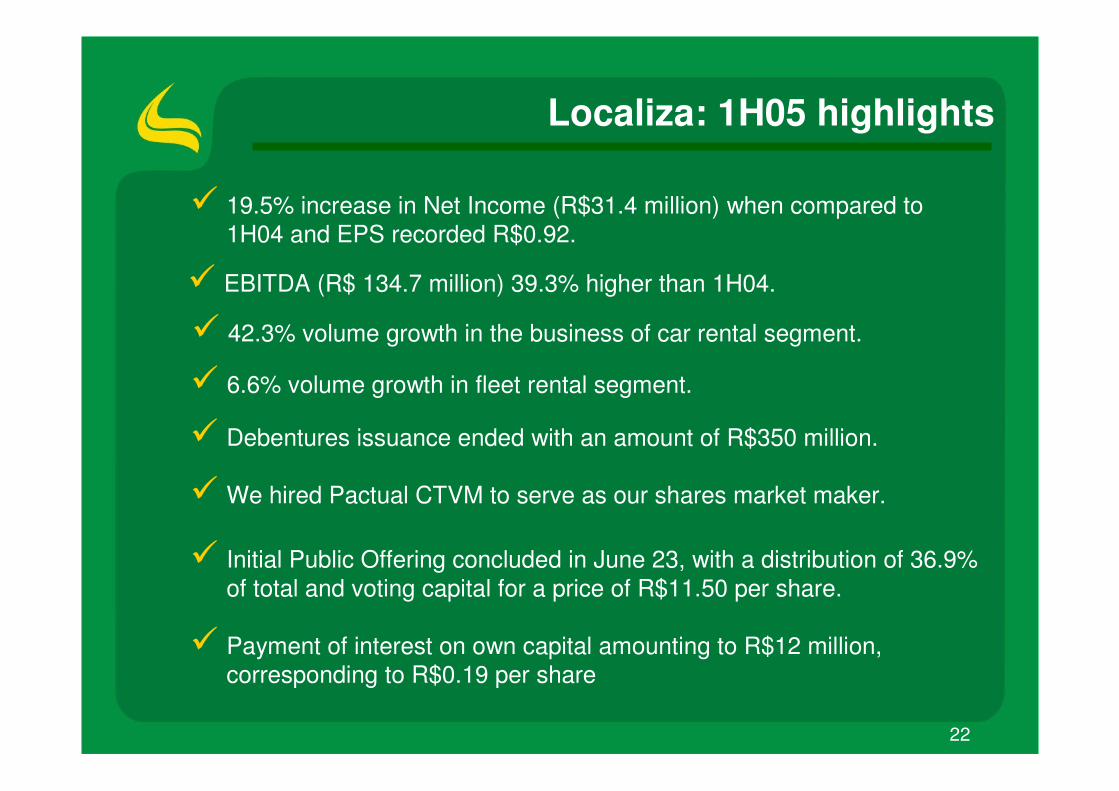

Localiza: 1H05 highlights

� 19.5% increase in Net Income (R$31.4 million) when compared to 1H04 and EPS recorded R$0.92.

� 42.3% volume growth in the business of car rental segment.

� 6.6% volume growth in fleet rental segment.

� Debentures issuance ended with an amount of R$350 million.

� We hired Pactual CTVM to serve as our shares market maker.

� Initial Public Offering concluded in June 23, with a distribution of 36.9% of total and voting capital for a price of R$11.50 per share.

� Payment of interest on own capital amounting to R$12 million, corresponding to R$0.19 per share

� EBITDA (R$ 134.7 million) 39.3% higher than 1H04.

23

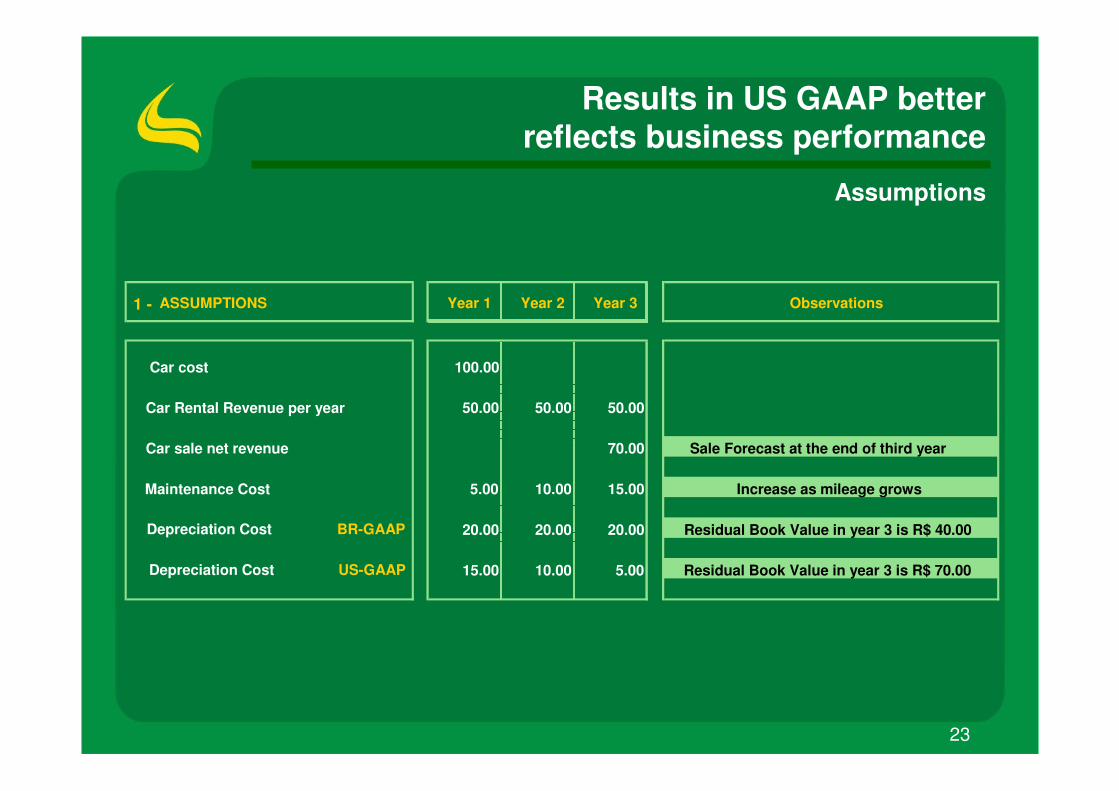

1 - ASSUMPTIONS Year 1 Year 2 Year 3 Observations

Car cost 100.00

Car Rental Revenue per year 50.00 50.00 50.00

Car sale net revenue 70.00 Sale Forecast at the end of third year

Maintenance Cost 5.00 10.00 15.00 Increase as mileage grows

Depreciation Cost BR-GAAP 20.00 20.00 20.00 Residual Book Value in year 3 is R$ 40.00

Depreciation Cost US-GAAP 15.00 10.00 5.00 Residual Book Value in year 3 is R$ 70.00

Results in US GAAP betterreflects business performance

Assumptions

24

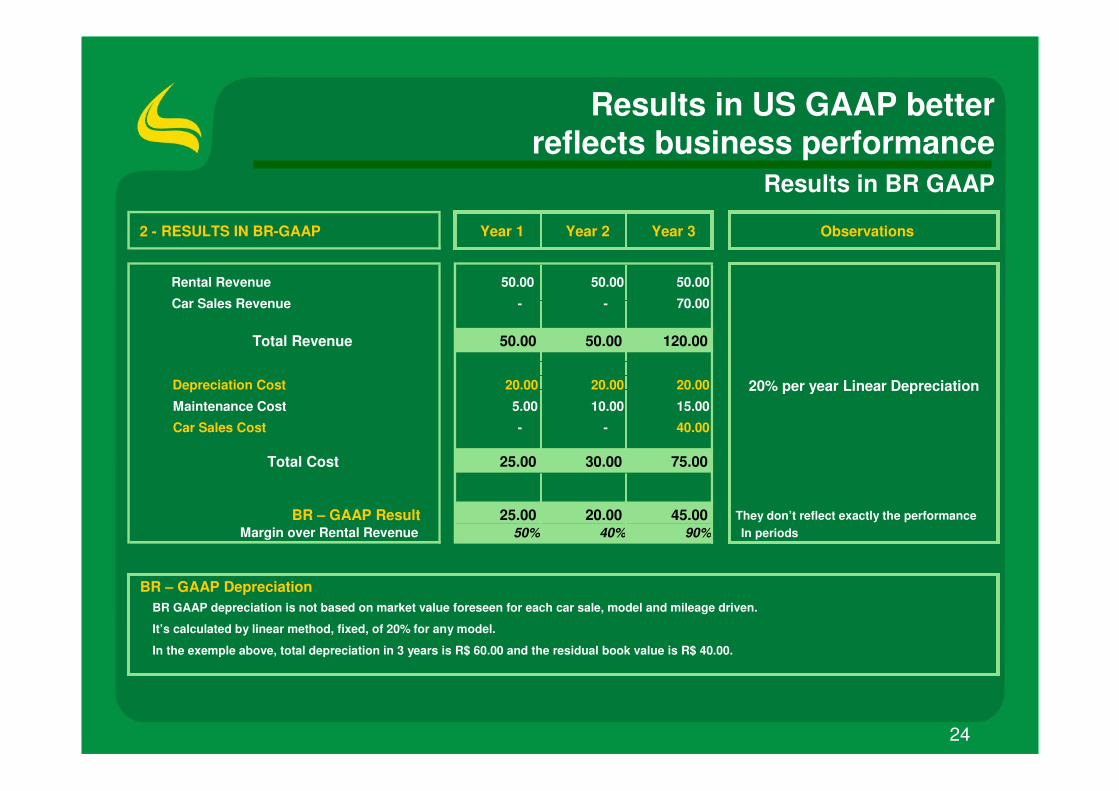

2 - RESULTS IN BR-GAAP Year 1 Year 2 Year 3 Observations

Rental Revenue 50.00 50.00 50.00

Car Sales Revenue - - 70.00

Total Revenue 50.00 50.00 120.00

Depreciation Cost 20.00 20.00 20.00 20% per year Linear DepreciationMaintenance Cost 5.00 10.00 15.00

Car Sales Cost - - 40.00

Total Cost 25.00 30.00 75.00

BR – GAAP Result 25.00 20.00 45.00 They don’t reflect exactly the performance Margin over Rental Revenue 50% 40% 90% In periods

BR – GAAP Depreciation

Results in US GAAP betterreflects business performance

Results in BR GAAP

BR GAAP depreciation is not based on market value foreseen for each car sale, model and mileage driven.

It’s calculated by linear method, fixed, of 20% for any model.

In the exemple above, total depreciation in 3 years is R$ 60.00 and the residual book value is R$ 40.00.

25

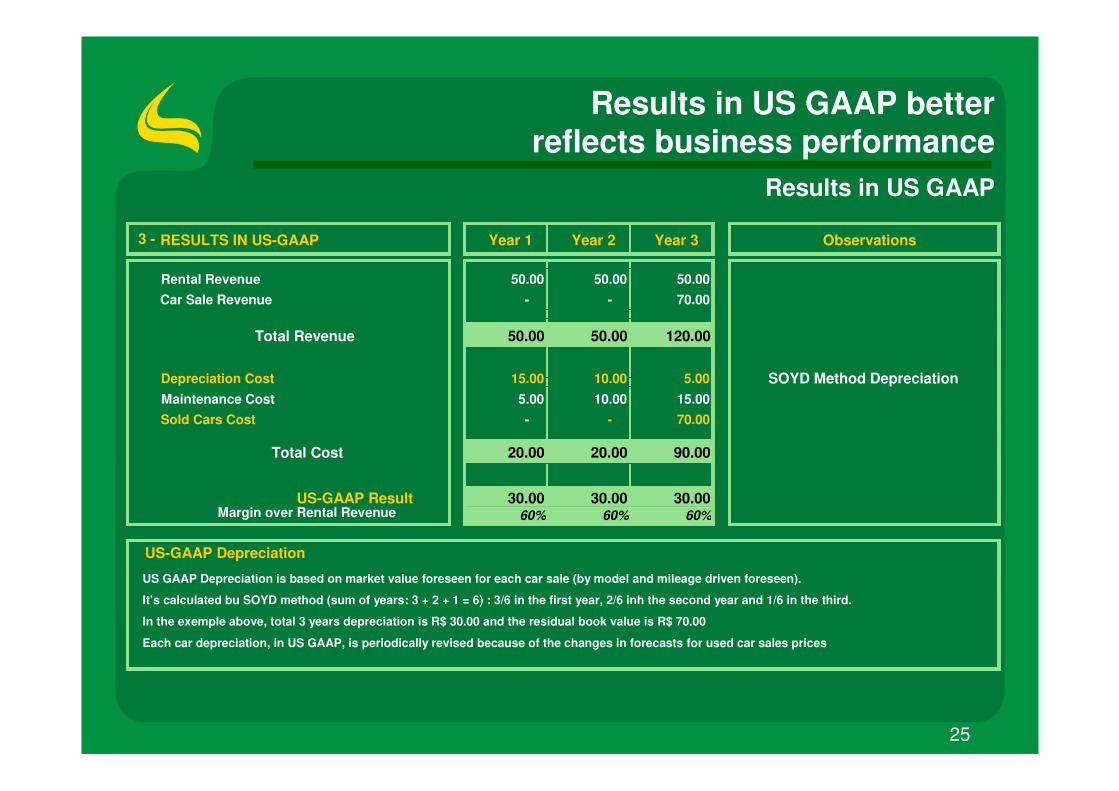

3 - RESULTS IN US-GAAP Year 1 Year 2 Year 3 Observations

Rental Revenue 50.00 50.00 50.00Car Sale Revenue - - 70.00

Total Revenue 50.00 50.00 120.00

Depreciation Cost 15.00 10.00 5.00 SOYD Method DepreciationMaintenance Cost 5.00 10.00 15.00Sold Cars Cost - - 70.00

Total Cost 20.00 20.00 90.00

US-GAAP Result 30.00 30.00 30.00Margin over Rental Revenue 60% 60% 60%

US-GAAP Depreciation

Results in US GAAP betterreflects business performance

Results in US GAAP

US GAAP Depreciation is based on market value foreseen for each car sale (by model and mileage driven foreseen).

It’s calculated bu SOYD method (sum of years: 3 + 2 + 1 = 6) : 3/6 in the first year, 2/6 inh the second year and 1/6 in the third.

In the exemple above, total 3 years depreciation is R$ 30.00 and the residual book value is R$ 70.00

Each car depreciation, in US GAAP, is periodically revised because of the changes in forecasts for used car sales prices

26

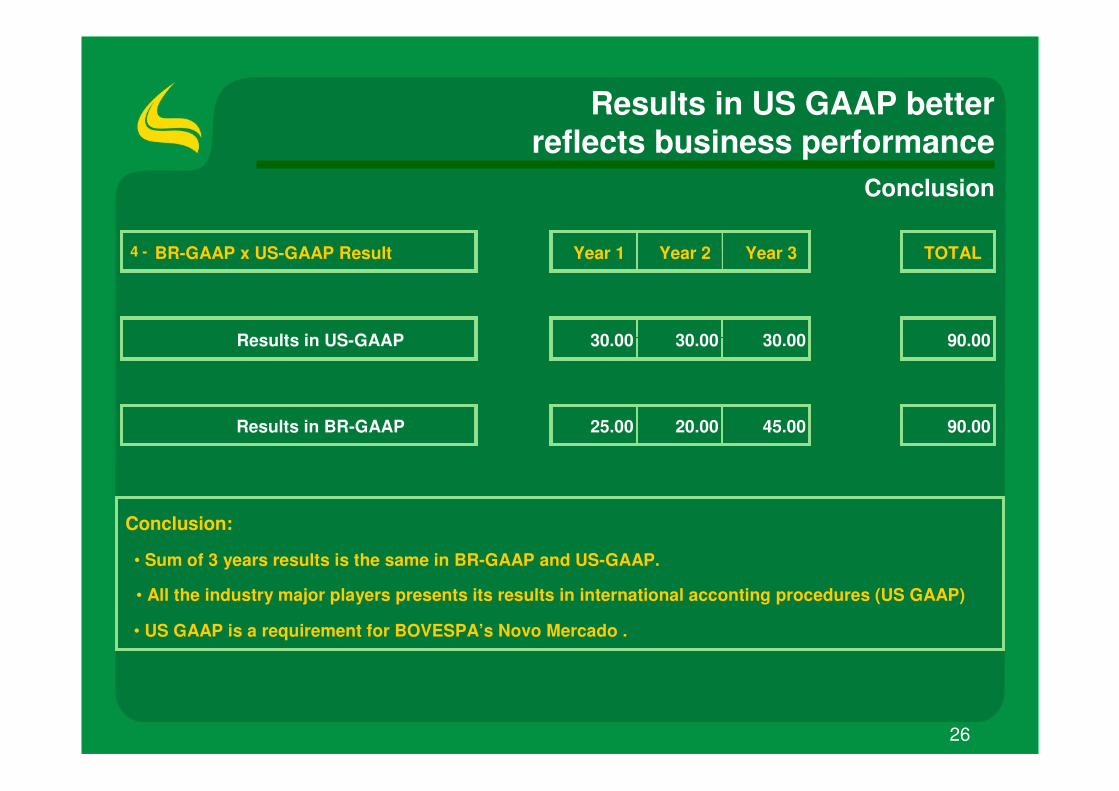

4 - BR-GAAP x US-GAAP Result Year 1 Year 2 Year 3 TOTAL

Results in US-GAAP 30.00 30.00 30.00 90.00

Results in BR-GAAP 25.00 20.00 45.00 90.00

Conclusion:

• Sum of 3 years results is the same in BR-GAAP and US-GAAP.

• All the industry major players presents its results in international acconting procedures (US GAAP)

Results in US GAAP betterreflects business performance

Conclusion

• US GAAP is a requirement for BOVESPA’s Novo Mercado .

27

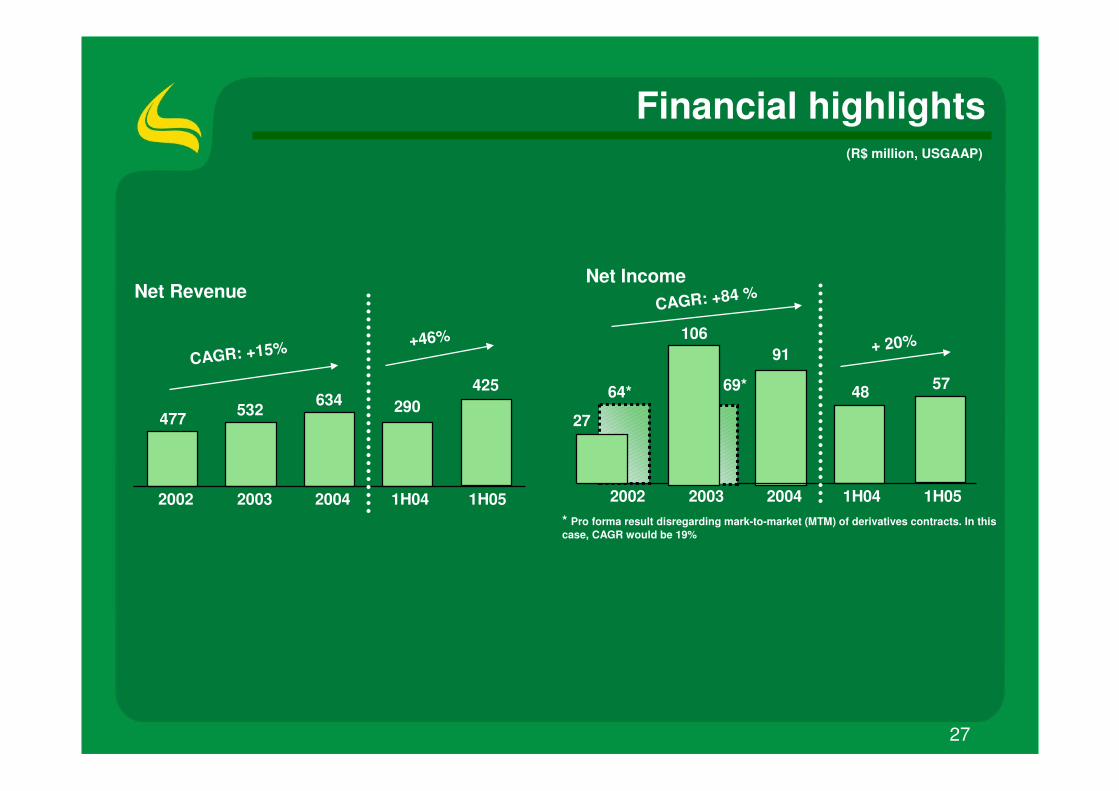

Financial highlights

634 290532477

2002 2003 2004 1H04 1H05

91

48

106

64*

2002 2003 2004 1H04 1H05

Net RevenueNet Income

425 57

CAGR: +84 %

CAGR: +15% +46% + 20%

(R$ million, USGAAP)

27

69*

* Pro forma result disregarding mark-to-market (MTM) of derivatives contracts. In this case, CAGR would be 19%

28

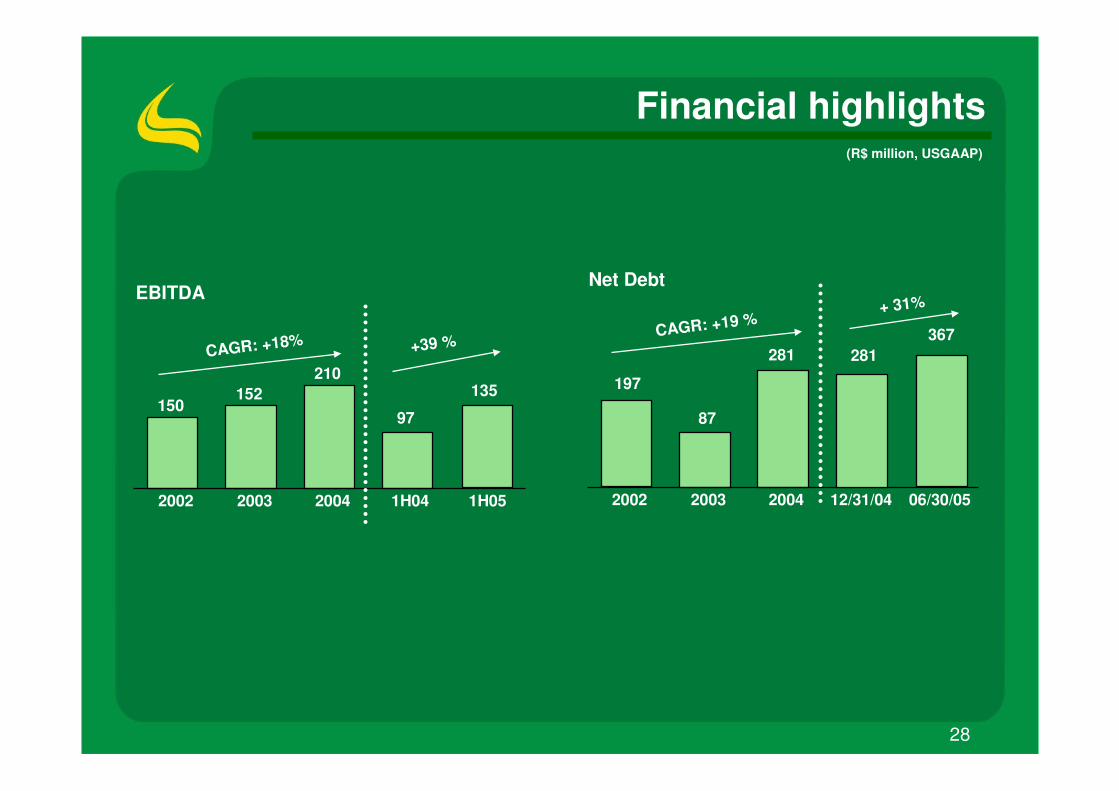

Financial highlights

210

97152

150

2002 2003 2004 1H04 1H05

281

87

2002 2003 2004 12/31/04 06/30/05

EBITDANet Debt

135

367CAGR: +18%

197

+39 %

(R$ million, USGAAP)

281CAGR: +19 %

+ 31%

29

Operating performance

(R$ million, USGAAP)

Net Revenue Fleet EBITDA

76

1H04 1H05

+86%

65

1H04 1H05

69

11,379

1H04 1H05

20,877

8,501*

1H04 1H05

10,514*

51

1H04 1H05

86

45

1H04 1H05

47

+83%

+70%

-9% +24%

+4%

80

88Car Rental

191168

313

Car Sales

54 39

119 108

Car Rental

Car Sales

39%

+6%

122

* Includes managed fleet

30

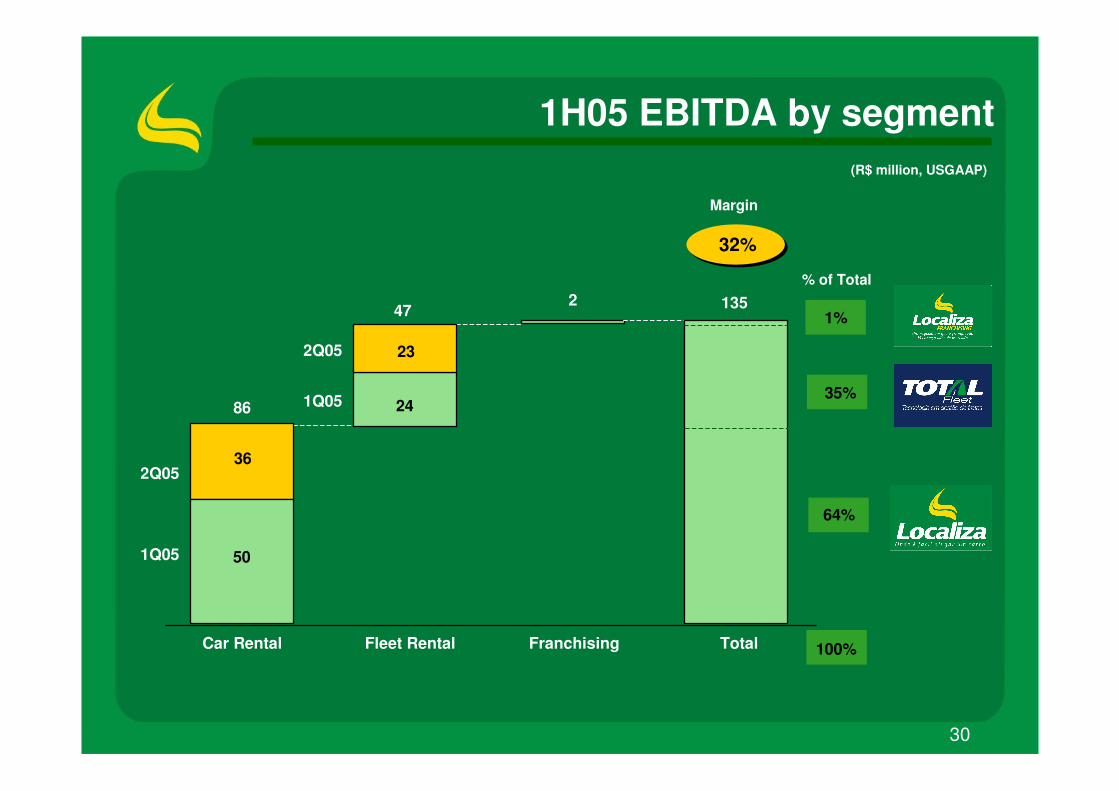

1H05 EBITDA by segment(R$ million, USGAAP)

2Q05

1Q05

Margin

247

Car Rental Fleet Rental Franchising Total

32%

1351%

35%

64%

% of Total

100%

86

50

36

24

232Q05

1Q05

31

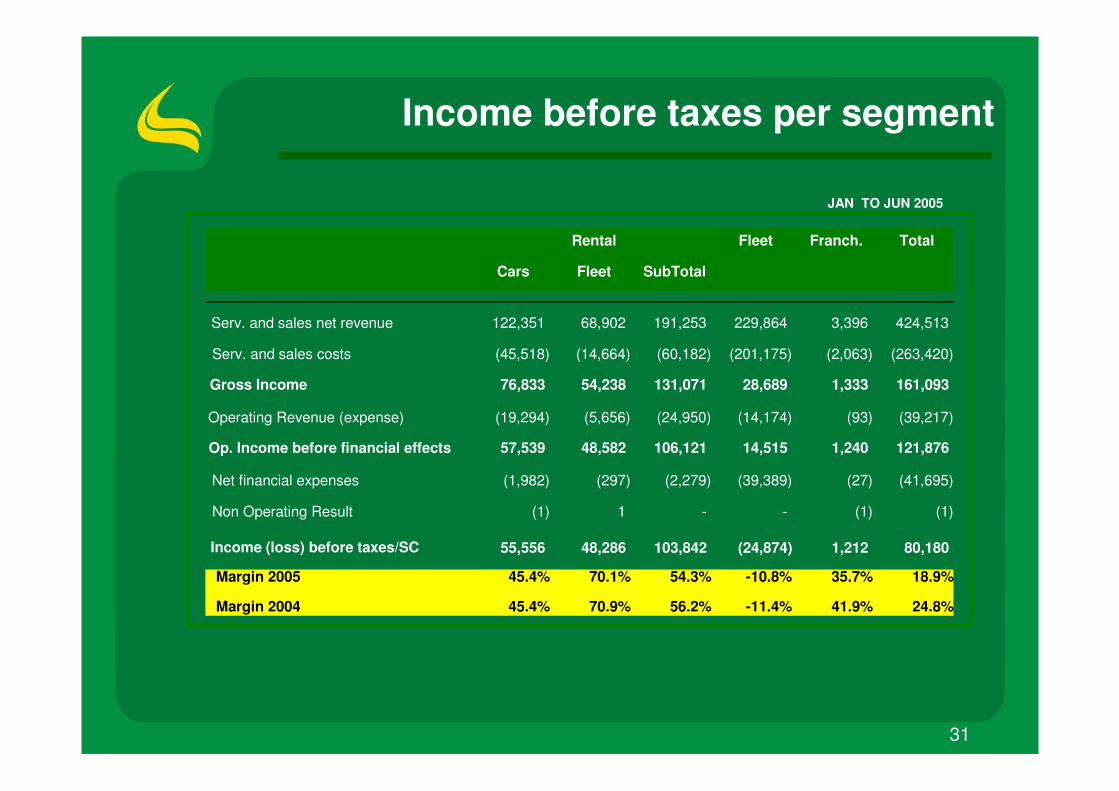

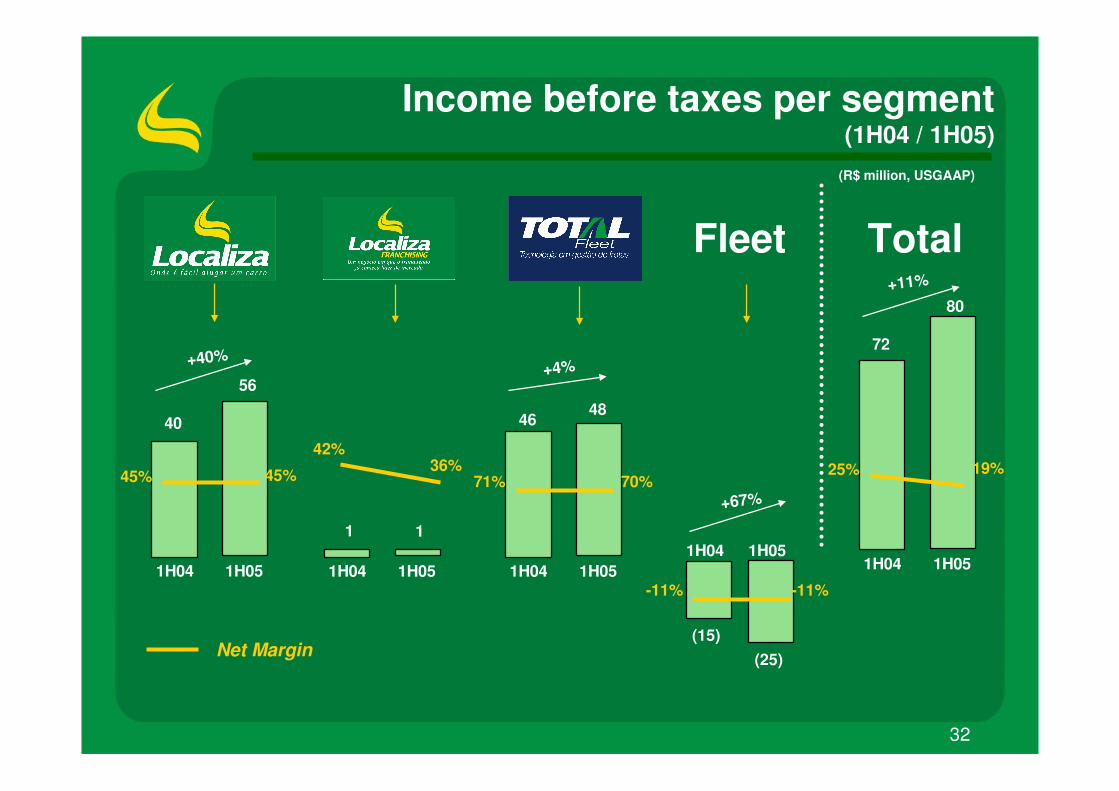

Income before taxes per segment

Fleet Franch. Total

Cars Fleet SubTotal

Serv. and sales net revenue 122,351 68,902 191,253 229,864 3,396 424,513

Serv. and sales costs (45,518) (14,664) (60,182) (201,175) (2,063) (263,420)

Gross Income 76,833 54,238 131,071 28,689 1,333 161,093

Operating Revenue (expense) (19,294) (5,656) (24,950) (14,174) (93) (39,217)

Op. Income before financial effects 57,539 48,582 106,121 14,515 1,240 121,876

Net financial expenses (1,982) (297) (2,279) (39,389) (27) (41,695)

Non Operating Result (1) 1 - - (1) (1)

Income (loss) before taxes/SC 55,556 48,286 103,842 (24,874) 1,212 80,180

Margin 2005 45.4% 70.1% 54.3% -10.8% 35.7% 18.9%

Margin 2004 45.4% 70.9% 56.2% -11.4% 41.9% 24.8%

JAN TO JUN 2005

Rental

32

Income before taxes per segment (1H04 / 1H05)

(R$ million, USGAAP)

Fleet

Net Margin

40

1H04 1H05

56

+40%

1

1H04 1H05

1

46

1H04 1H05

48

+4%

(15)

1H04 1H05

(25)

+67%

42%36%

45% 45% 71% 70%

-11% -11%

72

1H04 1H05

80+11%

25% 19%

Total

33

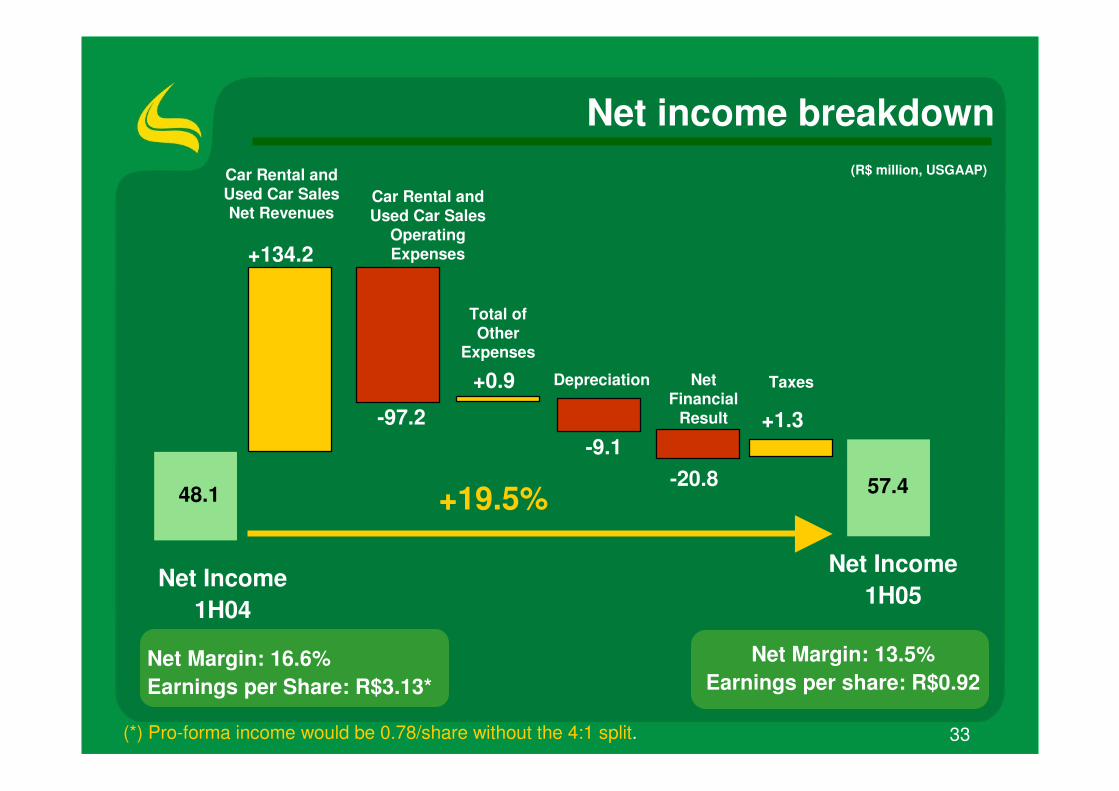

Net income breakdown

48.1

Net Income1H04

(R$ million, USGAAP)

+134.2

Car Rental and Used Car Sales Net Revenues

-97.2

Car Rental and Used Car Sales

Operating Expenses

+0.9

Total of Other

Expenses

Depreciation

-9.1-20.8

Net Financial

Result

Taxes

57.4

Net Income1H05

Net Margin: 16.6%Earnings per Share: R$3.13*

Net Margin: 13.5%Earnings per share: R$0.92

+19.5%

(*) Pro-forma income would be 0.78/share without the 4:1 split.

+1.3

34

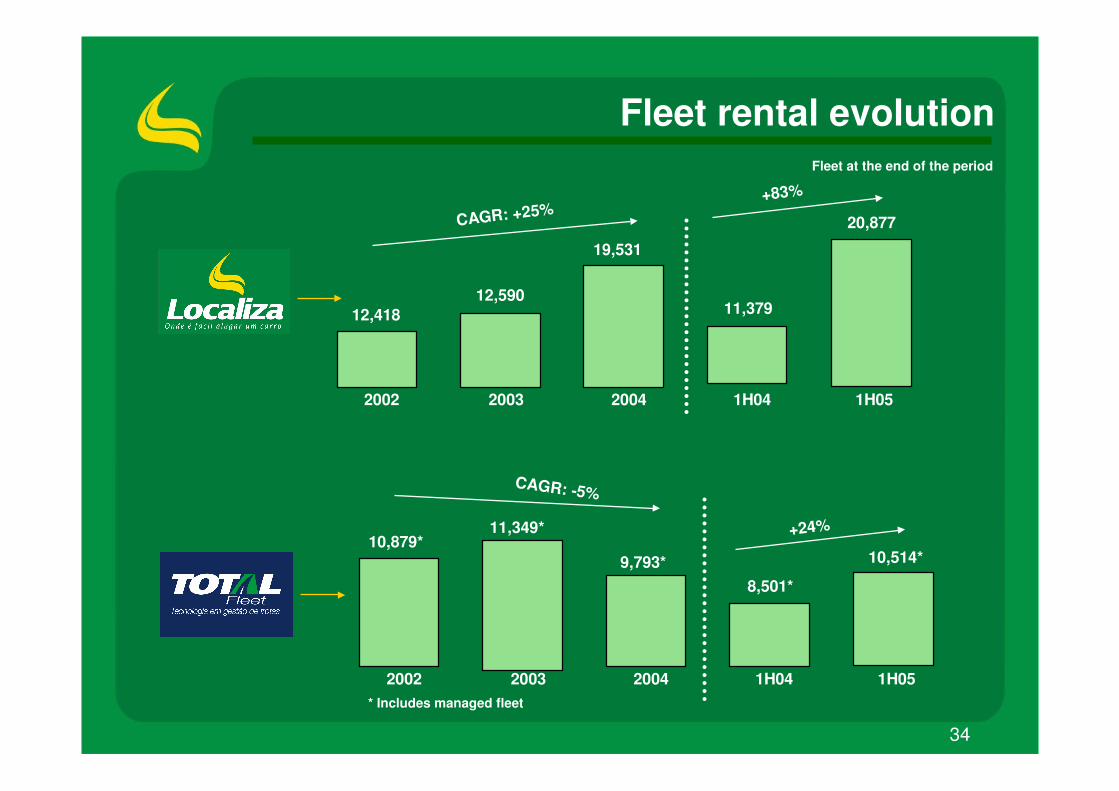

Fleet rental evolutionFleet at the end of the period

19,531

11,37912,590

12,418

2002 2003 2004 1H04 1H05

20,877CAGR: +25% +83%

* Includes managed fleet

9,793*8,501*

11,349*10,879*

2002 2003 2004 1H04 1H05

10,514*

CAGR: -5%

+24%

35

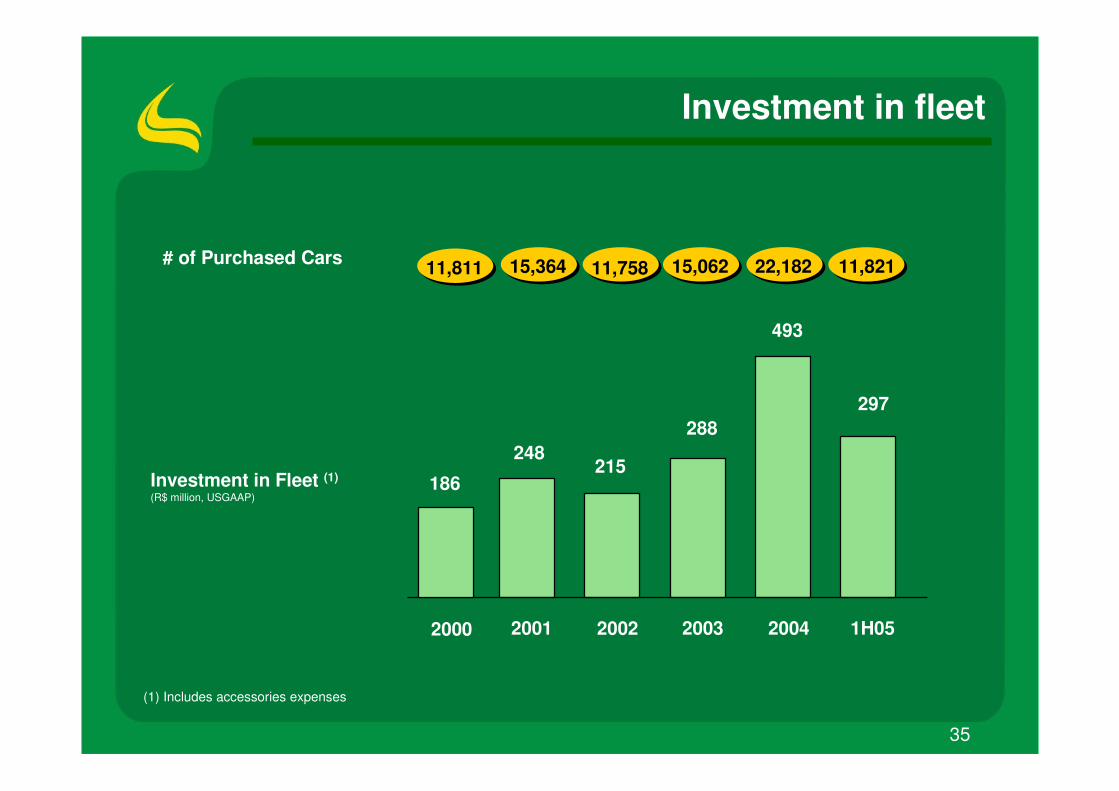

Investment in fleet

# of Purchased Cars

(1) Includes accessories expenses

Investment in Fleet (1)

(R$ million, USGAAP)

15,364 11,758 15,062 22,182 11,82111,811

186

248215

288

493

1H0520042003200220012000

297

36

Used car sales

Number of Sold Cars

13,33115,715

10,430

6,173

2000 2001 2002 2003 2004

15,468

1H05

9,856

37

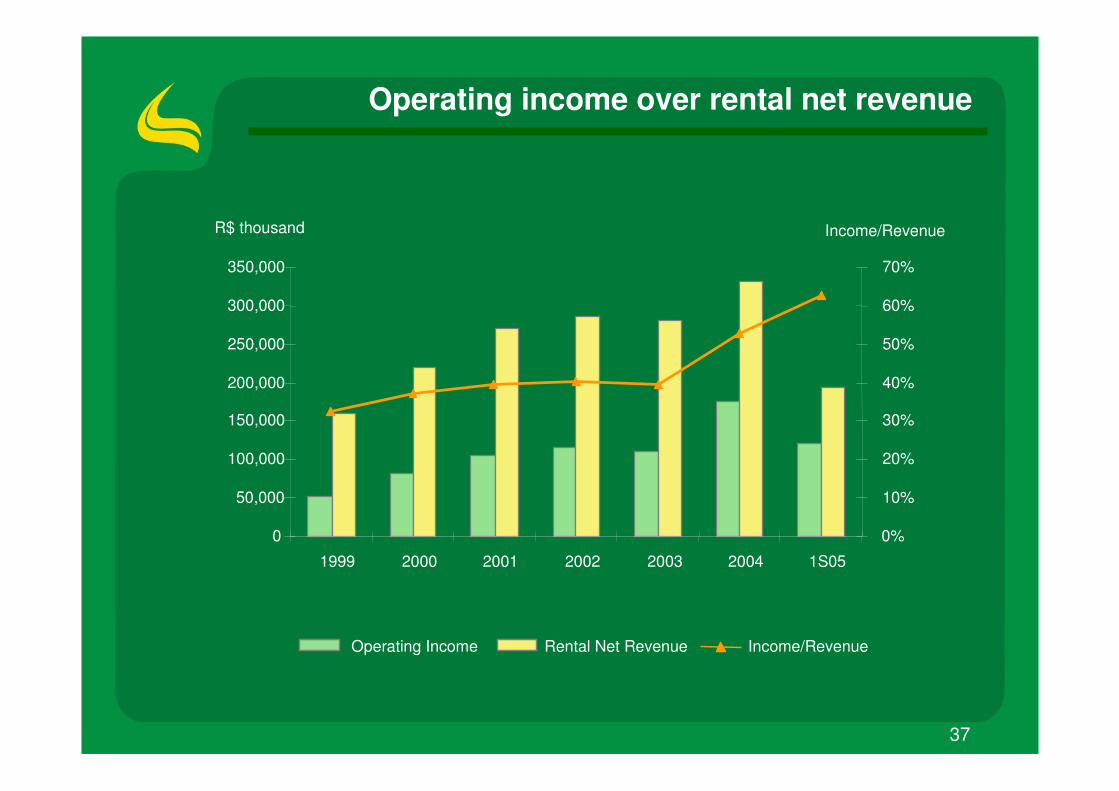

Operating income over rental net revenue

Operating Income Rental Net Revenue Income/Revenue

0

50,000

100,000

150,000

200,000

250,000

300,000

350,000

1999 2000 2001 2002 2003 2004 1S05

R$ thousand

0%

10%

20%

30%

40%

50%

60%

70%

Income/Revenue

38

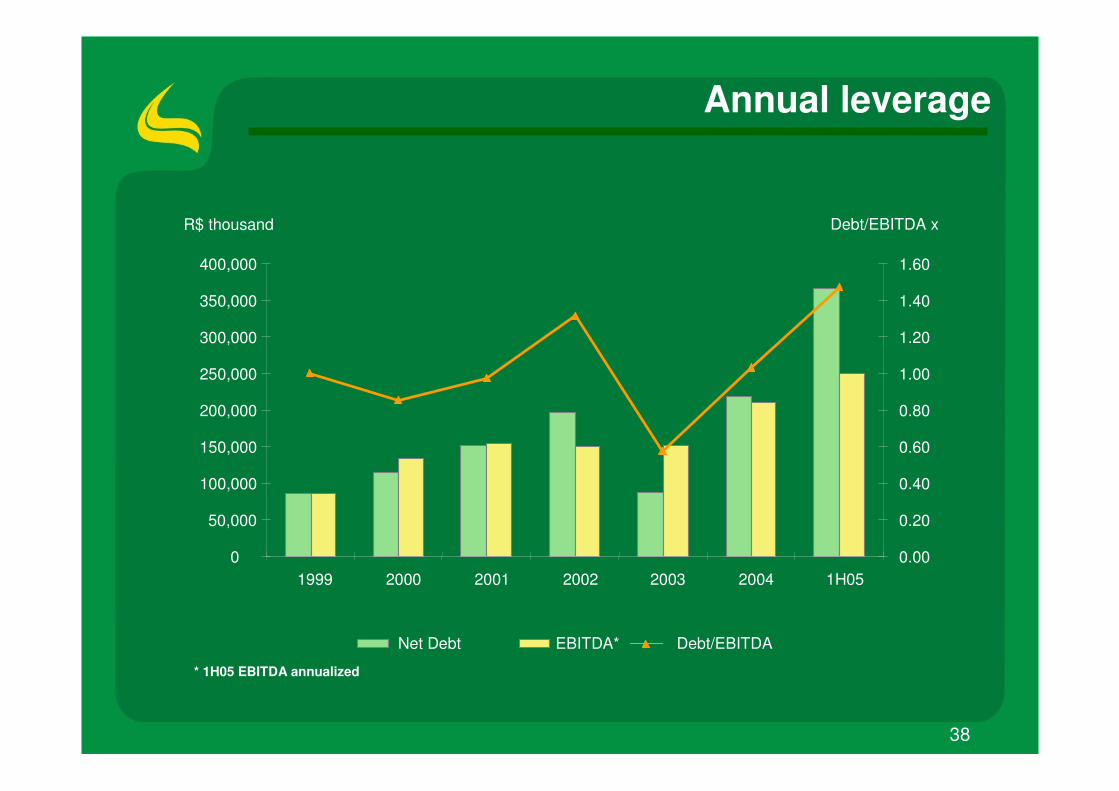

Annual leverage

0

50,000

100,000

150,000

200,000

250,000

300,000

350,000

400,000

1999 2000 2001 2002 2003 2004 1H05

R$ thousand

0.00

0.20

0.40

0.60

0.80

1.00

1.20

1.40

1.60

Debt/EBITDA x

Net Debt EBITDA* Debt/EBITDA

* 1H05 EBITDA annualized

39

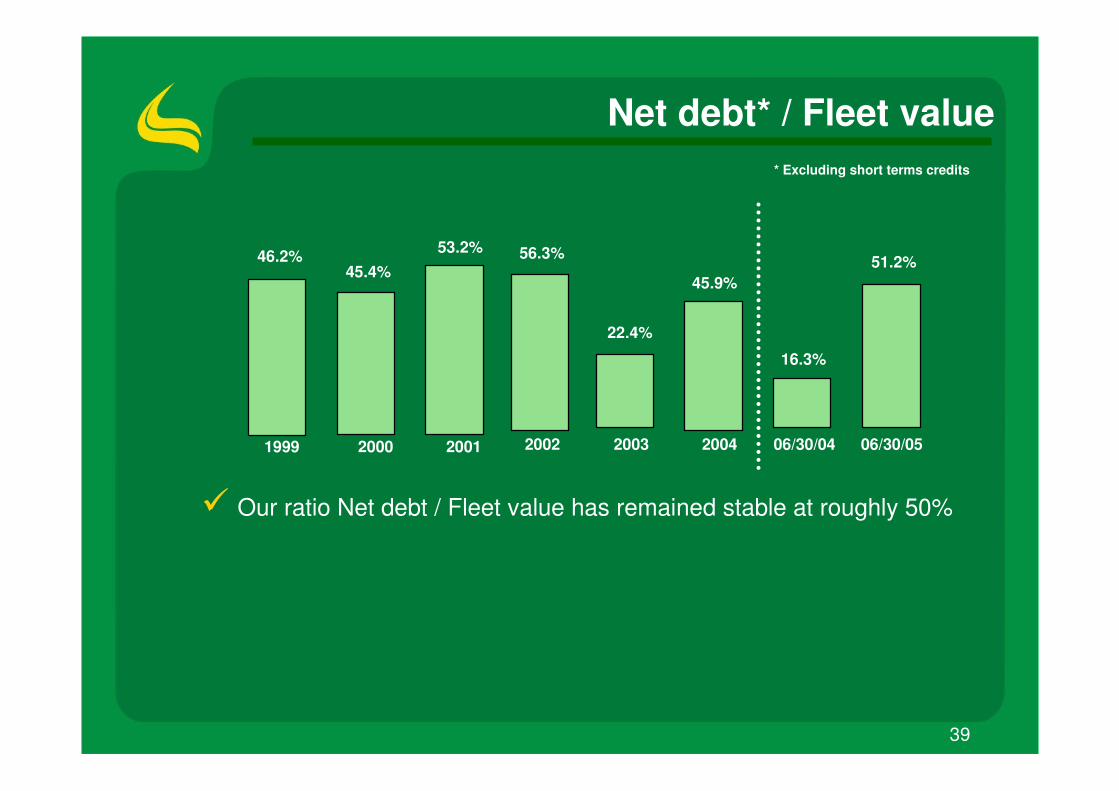

Net debt* / Fleet value

� Our ratio Net debt / Fleet value has remained stable at roughly 50%

* Excluding short terms credits

2002 2003 2004 06/30/04 06/30/051999 2000 2001

46.2%45.4%

53.2% 56.3%

22.4%

45.9%

16.3%

51.2%

40

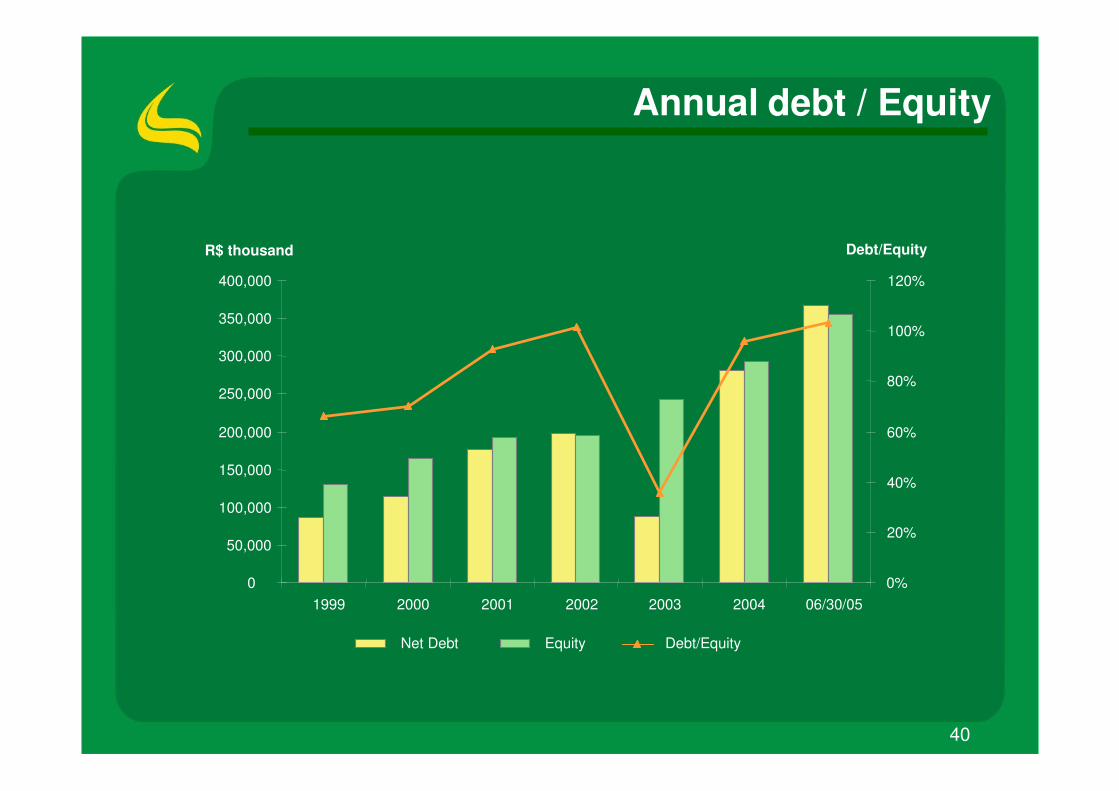

Annual debt / Equity

0

50,000

100,000

150,000

200,000

250,000

300,000

350,000

400,000

1999 2000 2001 2002 2003 2004 06/30/05

R$ thousand

0%

20%

40%

60%

80%

100%

120%

Debt/Equity

Net Debt Equity Debt/Equity

41

x1.9 - Independent Audit

x1.8 – Conflict Solution by Arbitration determined in Bylaws

x1.7 – Imediate Communication through CVM/Bovespa (ITR/IAN/DFP/IPE) andMarket (mailing to 4.200 addresses)

x1.6 – Calendar of Events

x1.5 – Disclosure Policy / Material facts

Projectx1.4 - CRM with Demand Segmentation

x1.3 - Road-shows

x1.2 – Investors Meeting

x1.1 – Portuguese and English website

NoteNoYes1- Transparency (Disclosure)

Corporate governance - Localiza

CorporateCorporate GovernanceGovernance is is notnot simplysimply meeting Bovespa’s meeting Bovespa’s requirementsrequirements, , butbut havinghavingatitudes in atitudes in lineline withwith thethe interestsinterests ofof major major shareholdersshareholders, , thethe management management andandminorityminority shareholdersshareholders..

42

x2.6 – Capital only represented by Common Shares

x2.5 - Free-Float ( Minimum of 25% of Free Float )

x2.4 - Dividends (We don’t have Automatic Reinvestment Program )

x2.3 - Tag-Along ( 100% )

x2.2 – Listed to Novo Mercado

x2.1 – Code of Ethics

NoteNoYes2 - Fairness

Corporate governance - Localiza

43

x3.14.3 – Stock Option Programs

x3.14.2 – Shareholders Agreement

x3.14.1 – Report of Related Parties Contracts

3.14 – Availability of:

x3.13 – The Company’s Main Executive and the Chairman of Board of Directors are the Same

Person

x3.12 – Board of Directors’ Payment is Structured in order to follow the Company’s Results

x3.11 – The Main Executive is Annually Evaluated by Board of Directors

Projectx3.10 - Auditing, Internal Controls ( COSO )

x3.9 –Financial Statements in International Accounting Procedures are available

x3.8 - Annual Report presents the Management’s Individual or Aggregated Compensation

x3.7 – Annual Report presents the Management Participation in the Company’s Capital

Projectx3.6 – Board of Directors with Standardized Activities as per Internal rules

x3.5 – Independent Directors Highly Qualified

x3.4 – Board of Directors members Elected by Minority Shareholders

x3.3 – One Year Terms, with reelection

x3.2 – Board of Directors composed by 5 to 9 Members (the majority is not independent)

Foreseenx3.1 – Fiscal Council Established

NoteNoYes3 - Accountability

Corporate governance - Localiza

44

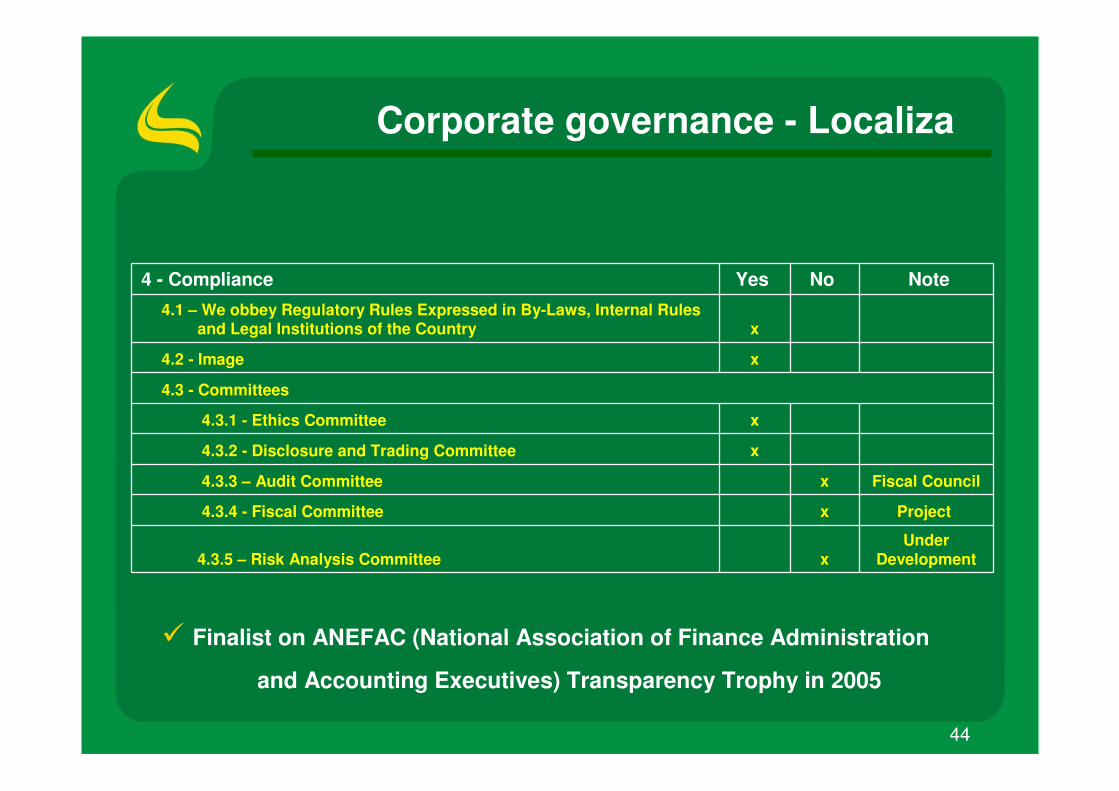

UnderDevelopmentx4.3.5 – Risk Analysis Committee

Projectx4.3.4 - Fiscal Committee

Fiscal Councilx4.3.3 – Audit Committee

x4.3.2 - Disclosure and Trading Committee

x4.3.1 - Ethics Committee

4.3 - Committees

x4.2 - Image

x4.1 – We obbey Regulatory Rules Expressed in By-Laws, Internal Rules

and Legal Institutions of the Country

NoteNoYes4 - Compliance

Corporate governance - Localiza

� Finalist on ANEFAC (National Association of Finance Administration

and Accounting Executives) Transparency Trophy in 2005

45

Total Fleet receives Valor 1000 Award

Total Fleet was chosen the best Company in SpecializedServices sector, according to a research made by Valor newspaper.

The award, which is on its fifth edition, selects, among the 1000 largestcompanies, the sector`s winners (27) which differ from the others by theirinnovation and technical rigor.

Total Fleet`s strong financial performance, high productivity, quality andtranparency associated to committed and qualified employees were the mainaspects to conquer the award.

46

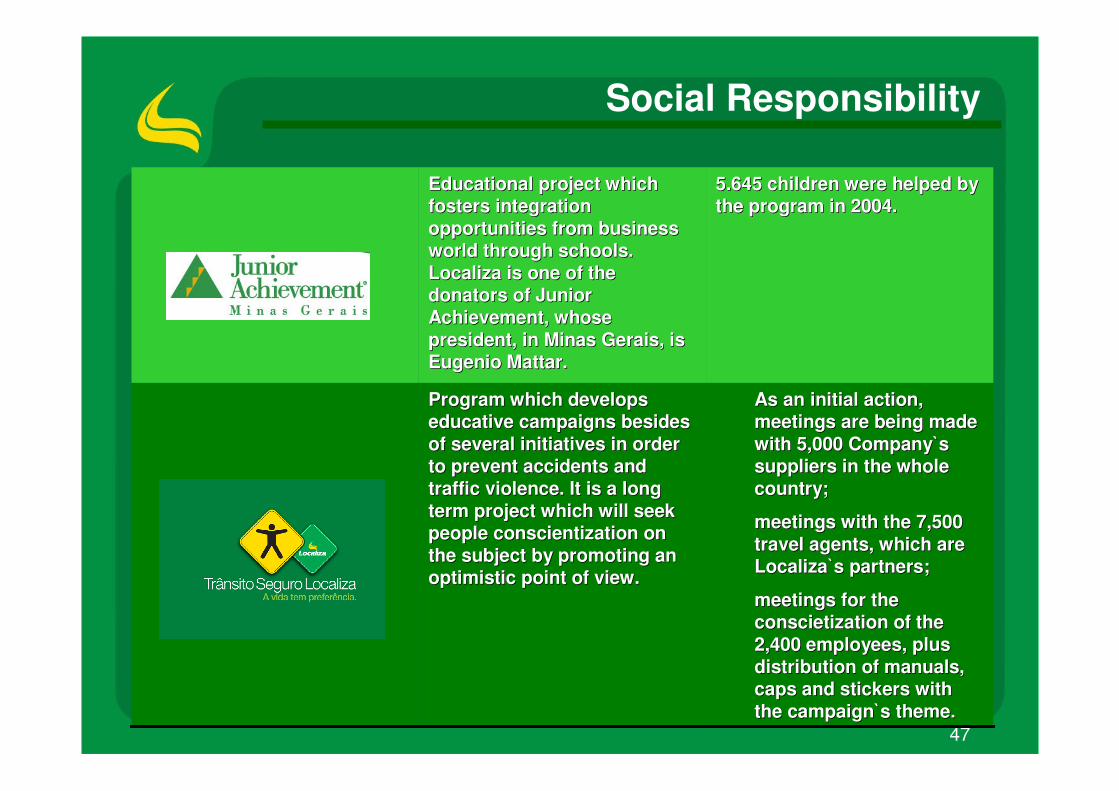

VOLUNTARYNESS: VOLUNTARYNESS: 2.3 2.3 tonton ofof foodsfoods werewerecollectedcollected besidesbesides ofofhygienicshygienics itemsitems andandeducationaleducational material for material for 55 55 childrenchildren

Social Social projectproject whichwhich aimsaimsto to supportsupport institutionsinstitutionsthroughthrough voluntarynessvoluntarynessandand donationsdonations throughthroughthethe Fundo Social da Fundo Social da Criança e Adolescente.Criança e Adolescente.

30 30 projectsprojects wereweresupportedsupported andand 6,280 6,280 peoplepeople werewerecontemplatedcontemplated byby thetheprogramprogram onlyonly in 2004.in 2004.

Cultural Cultural projectproject whichwhichsupportssupports cultureculture for more for more thanthan 20 20 yearsyears in in thethe wholewholecountry (country (BrazilBrazil).).

Social Responsibility

DONATIONS:DONATIONS:Missão Missão RamacrisnaRamacrisnaandand Cidade dos Cidade dos MeninosMeninos

47

As As anan initialinitial actionaction, , meetingsmeetings are are beingbeing mademadewithwith 5,000 5,000 CompanyCompany`s `s supplierssuppliers in in thethe wholewholecountry;country;

meetingsmeetings withwith thethe 7,500 7,500 traveltravel agentsagents, , whichwhich are are Localiza`s Localiza`s partnerspartners;;

meetingsmeetings for for thetheconscietizationconscietization ofof thethe2,400 2,400 employeesemployees, , plusplusdistributiondistribution ofof manualsmanuals, , capscaps andand stickersstickers withwiththethe campaigncampaign`s `s themetheme. .

ProgramProgram whichwhich developsdevelopseducativeeducative campaignscampaigns besidesbesidesofof severalseveral initiativesinitiatives in in orderorderto to preventprevent accidentsaccidents andandtraffictraffic violenceviolence. It is a . It is a longlongtermterm projectproject whichwhich willwill seekseekpeoplepeople conscientizationconscientization ononthethe subjectsubject byby promotingpromoting ananoptimisticoptimistic pointpoint ofof viewview. .

5.645 5.645 childrenchildren werewere helpedhelped bybythethe programprogram in 2004.in 2004.

EducationalEducational projectproject whichwhichfostersfosters integrationintegrationopportunitiesopportunities fromfrom business business worldworld throughthrough schoolsschools. . Localiza is Localiza is oneone ofof thethedonatorsdonators ofof Junior Junior AchievementAchievement, , whosewhosepresidentpresident, in Minas Gerais, is , in Minas Gerais, is Eugenio Mattar.Eugenio Mattar.

Social Responsibility

48

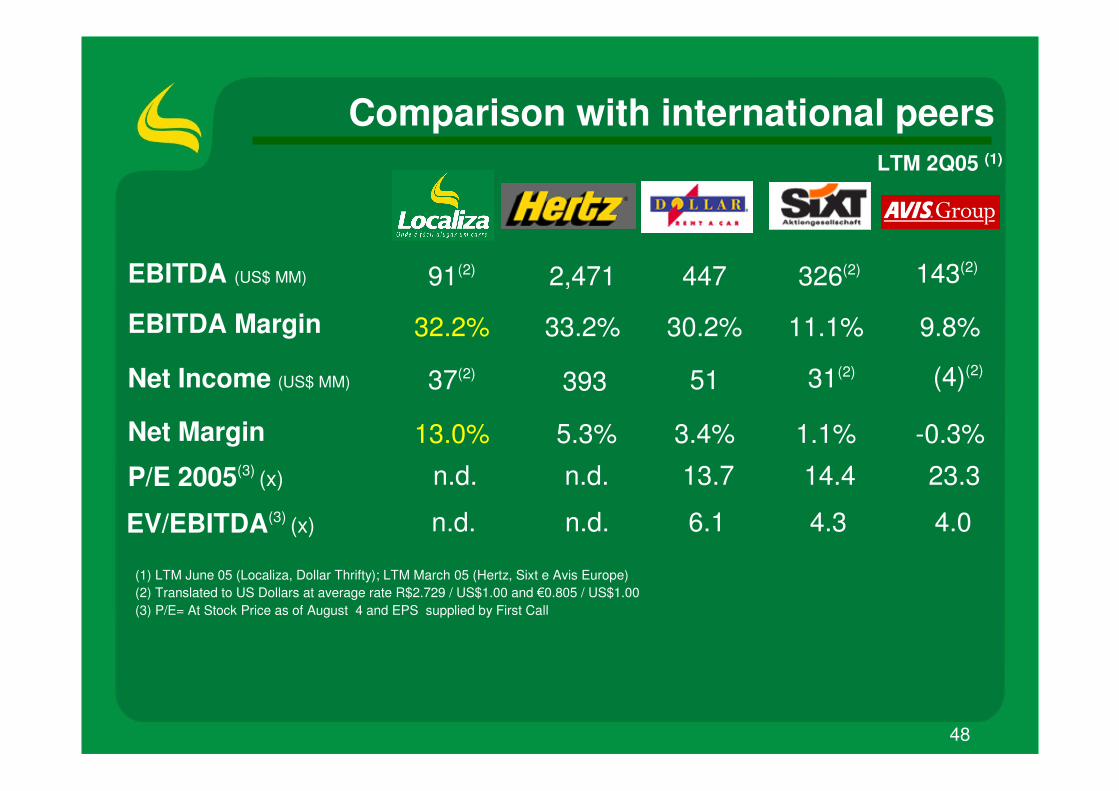

Comparison with international peers

Net Income (US$ MM)

EBITDA (US$ MM)

EBITDA Margin

P/E 2005(3) (x)

Net Margin

37(2)

91(2)

n.d.

32.2%

13.0%

14.4

11.1%

1.1%

51

447

13.7

30.2%

3.4%

393

2,471

n.d.

33.2%

5.3%

23.3

9.8%

-0.3%

EV/EBITDA(3) (x) n.d. 4.36.1n.d. 4.0

(1) LTM June 05 (Localiza, Dollar Thrifty); LTM March 05 (Hertz, Sixt e Avis Europe)(2) Translated to US Dollars at average rate R$2.729 / US$1.00 and �0.805 / US$1.00(3) P/E= At Stock Price as of August 4 and EPS supplied by First Call

143(2)

(4)(2)

326(2)

31(2)

LTM 2Q05 (1)

49

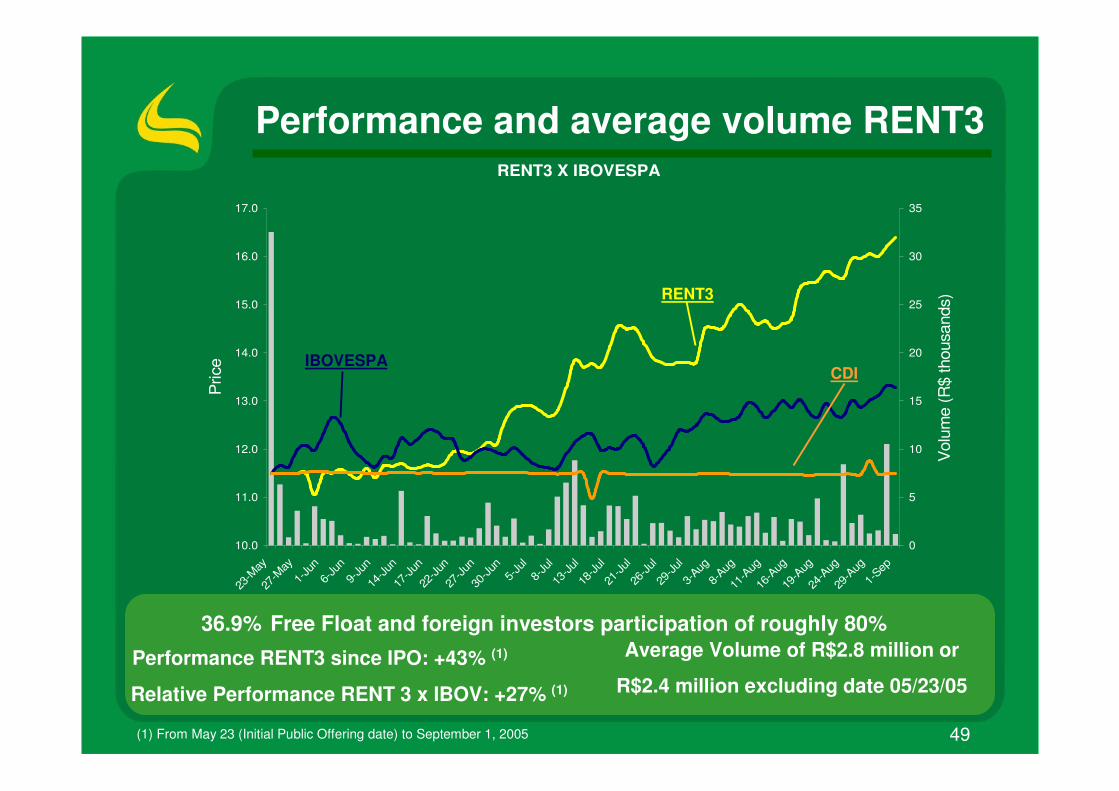

RENT3 X IBOVESPA

10.0

11.0

12.0

13.0

14.0

15.0

16.0

17.0

23-M

ay27

-May

1-Ju

n6-

Jun

9-Ju

n14

-Jun

17-Ju

n22

-Jun

27-Ju

n30

-Jun

5-Ju

l8-

Jul

13-Ju

l18

-Jul

21-Ju

l26

-Jul

29-Ju

l3-

Aug8-

Aug11

-Aug

16-A

ug19

-Aug

24-A

ug29

-Aug

1-Sep

Pric

e

0

5

10

15

20

25

30

35

Vol

ume

(R$

thou

sand

s)

Performance and average volume RENT3

36.9% Free Float and foreign investors participation of roughly 80%

Performance RENT3 since IPO: +43% (1)

Relative Performance RENT 3 x IBOV: +27% (1)

Average Volume of R$2.8 million or

R$2.4 million excluding date 05/23/05

(1) From May 23 (Initial Public Offering date) to September 1, 2005

RENT3

IBOVESPACDI

50

Disclaimer - Forward Looking Statements

The material that follows is a presentation of general background information about LOCALIZA as of the

date of the presentation. It is information in summary form and does not purport to be complete. It is not

intended to be relied upon as advice to potential investors. No representation or warranty, express or

implied, is made concerning, and no reliance should be placed on, the accuracy, fairness, or

completeness of the information presented herein.

This presentation contains statements that are forward-looking within the meaning of Section 27A of the

Securities Act of 1933 and Section 21E of the Securities Exchange Act of 1934. Such forward-looking

statements are only predictions and are not guarantees of future performance. Investors are cautioned

that any such forward-looking statements are and will be, as the case may be, subject to many risks,

uncertainties and factors relating to the operations and business environments of LOCALIZA and its

subsidiaries that may cause the actual results of the companies to be materially different from any future

results expressed or implied in such forward-looking statements.

Although LOCALIZA believes that the expectations and assumptions reflected in the forward-looking

statements are reasonable based on information currently available to LOCALIZA’s management,

LOCALIZA cannot guarantee future results or events. LOCALIZA expressly disclaims a duty to update

any of the forward-looking statement.

The material that follows is a presentation of general background information about LOCALIZA as of the

date of the presentation. It is information in summary form and does not purport to be complete. It is not

intended to be relied upon as advice to potential investors. No representation or warranty, express or

implied, is made concerning, and no reliance should be placed on, the accuracy, fairness, or

completeness of the information presented herein.

This presentation contains statements that are forward-looking within the meaning of Section 27A of the

Securities Act of 1933 and Section 21E of the Securities Exchange Act of 1934. Such forward-looking

statements are only predictions and are not guarantees of future performance. Investors are cautioned

that any such forward-looking statements are and will be, as the case may be, subject to many risks,

uncertainties and factors relating to the operations and business environments of LOCALIZA and its

subsidiaries that may cause the actual results of the companies to be materially different from any future

results expressed or implied in such forward-looking statements.

Although LOCALIZA believes that the expectations and assumptions reflected in the forward-looking

statements are reasonable based on information currently available to LOCALIZA’s management,

LOCALIZA cannot guarantee future results or events. LOCALIZA expressly disclaims a duty to update

any of the forward-looking statement.