Embed Size (px)

Citation preview

Collects, organizes and processes transaction data

Transaction is an event that results in a change of a balance sheet item.

Typically it is an exchange. (Asset, liability, stock, revenue or

expense for one another.)

201Lec03.PPTX

1

3

Step 1: Accumulate facts.

Step 2: Determine effects on accounting equationNote: Algebra requires that you keep the equality!

Steps in transaction analysis:Steps in transaction analysis:

2

Transaction AnalysisTwo or more items will always be affectedExample: (1) Owner invested $10,000 Cash in exchange for $10,000 of Common Stock

Two or more items will always be affectedExample: (1) Owner invested $10,000 Cash in exchange for $10,000 of Common Stock

3

Example: (2) Borrowed $5,000 by issuing a bond. Example: (2) Borrowed $5,000 by issuing a bond.

(2) + $5,000 + $5,000 ________ $15,000 = $5,000 +$10,000

Bonds Payable

4

Transaction Analysis

TRANSACTION ANALYSIS examples TRANSACTION ANALYSIS examples

Business buys a computer, paying cash.

Increase and Decrease

Business provides service to a customer and is paid cash.

Increase and Increases

Contractor works and business pays cash for service.

Decrease and Decreases

5

TRANSACTION ANALYSIS examples

TRANSACTION ANALYSIS examples

Business applies & gets a corporate credit card account.

Business takes out an advertisement that runs today in

the newspaper and charges the cost to the credit card.

Increase and Decreases

Business pays off credit card .

Decrease and Decrease

6

TRANSACTION ANALYSIS examples

TRANSACTION ANALYSIS examples

Business provides services to a customer but allows them

30 days to pay.

Increase and Increases

30 days later customer pays off amount due in full.

Increase and Decrease

Business pays cash dividend to Owners.

Decrease and Decreases

7

Lowest level of detail in accounting.

Records increases and decreases for a specific Asset, Liability, or Stockholders’ Equity item.

Number of accounts used depends on facts and personal desires of the accountant & management.

How much detail do they want on the financial statements?

8

Account is . . . .Account is . . . .

Account Detail exampleAccount Detail exampleConsider the options in accounts used to record the

purchase of an Apple computer:1. Equipment.

If used, other computers, printers, photocopiers, factory machines all will be grouped into one account.

2. Office Equipment.If used, other computers, printers, photocopiers will be grouped here, but factory machines go in a different account.

3. Computer related equipmentIf used, other computers and printers will be grouped here, but photocopiers, factory machines go in different accounts.

4. Apple Computers and so on.

9

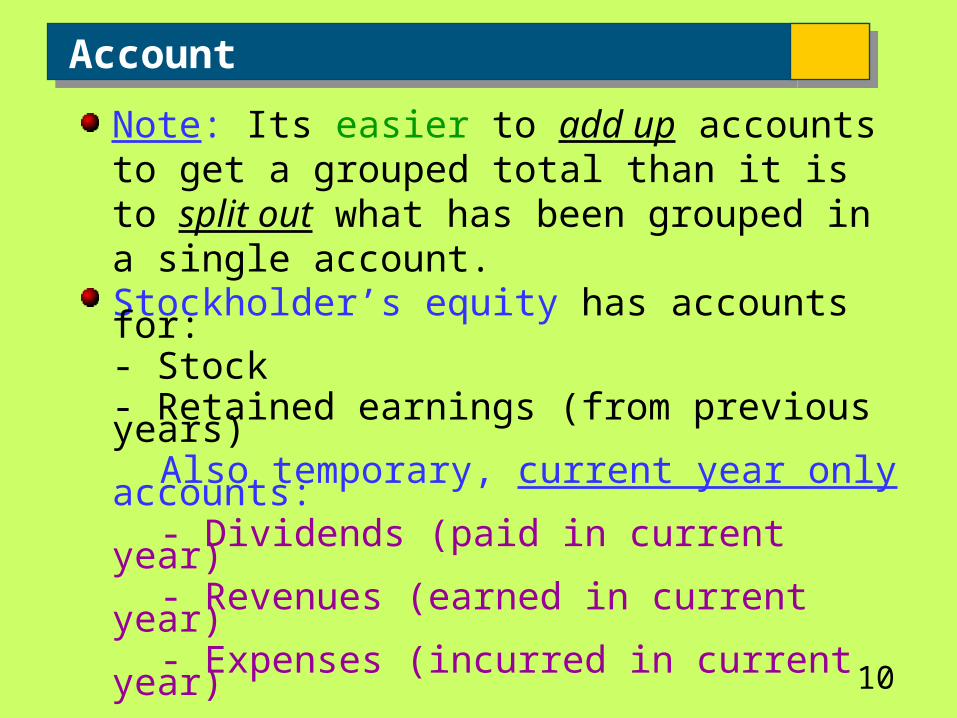

Note: Its easier to add up accounts to get a grouped total than it is to split out what has been grouped in a single account.Stockholder’s equity has accounts for:- Stock- Retained earnings (from previous years)

Also temporary, current year only accounts:

- Dividends (paid in current year)- Revenues (earned in current year)- Expenses (incurred in current year)

10

AccountAccount

Account Implementation: TABULAR summary format (Not used in the business world.)

Example: Cash in checking+50.00+100.00- 20.00+60.00- 30.00+250.00+300.00+500.00- 15.00+10.00

balance +1205.00

11

Account Implementation: ACCOUNT form (aka T-Account)

ACCOUNT NAME

Debit Side (Dr.) Credit Side (Cr.)

means LEFT means RIGHT

CASH IN CHECKING

50.00100.00 60.00250.00300.00510.00

20.00 30.00 15.00

Example:

1270.00 BALANCE 1205.00

65.00

12

ACCOUNT NAME

Date Reference or Description Debit Credit Balance

Account Implementation: Running balance format. Not in text

9/15 Cash sale 100.00 100.00dr

9/16 Pay bill 70.00 30.00dr

9/17 Buy supplies 40.00 10.00cr

13

- Algebra is the foundation.

- The accounting equation:

ASSETS = LIABILITIES + EQUITY .

EXPENSES REVENUES debit credit

+ -

debit credit

- +

14

debit credit

+ -

debit credit

- +

debit credit

- ++ means increase balance

- means decrease balance

Accounting MathematicsAccounting Mathematics

Algebra requires that you must keep the equality:

Example: 10 = 6 + 4

10 + 1 = (6 + 4) + 1

or 10+1-1= 6 + 4

Same rule in accounting states that we must use the ‘double entry’ system. This requires that:

15

EACH TRANSACTION MUST BE RECORDED SO THAT TOTAL DEBITS EQUALS

TOTAL CREDITS.

Step 1: Accumulate facts.

Step 2: Determine effects on accounting equation

STEP3: Determine accounts and amounts of required debits and credits.

16

Steps in transaction analysis:Steps in transaction analysis:

TRANSACTION ANALYSIS REVISTEDTRANSACTION ANALYSIS REVISTED

Owner’s Invest $10,000 in business and are issued stock.

Debit and Credit

Business borrows $5,000 from a bank by issuing a bond.

Debit and Credit

17

TRANSACTION ANALYSIS REVISTEDTRANSACTION ANALYSIS REVISTED

Business buys a computer, paying cash.

Debit and Credit

Business provides service to a customer and is paid cash.

Debit and Credit

Contractor works and business pays cash for service.

Debit and Credit

18

TRANSACTION ANALYSIS REVISTEDTRANSACTION ANALYSIS REVISTED

Business applies & gets a corporate credit card account.

Not a transaction. No effect on accounting equation.

Business takes out an advertisement that runs today in

the newspaper and charges the cost to the credit card.

Debit and Credit

Business pays off credit card .

Debit and Credit

19

TRANSACTION ANALYSIS REVISTEDTRANSACTION ANALYSIS REVISTED

Business provides services to a customer but allows them

30 days to pay.

Debit and Credit

30 days later customer pays off amount due in full.

Debit and Credit

Business pays cash dividend to Owners.

Debit and Credit

20

General Journal - Book used to record transactions before recording them in the accounts. - Listing of transactions by date.

General Ledger - Binder of all the accounts. (T or ledger format) - Table of contents to the general ledger is

called the “Chart of Accounts”

Information ends up being recorded twice. It’s just organized differently.

Process of copying transactions from journal to ledger is called POSTING

JOURNAL

LEDGER

21

The BOOKS in accountingThe BOOKS in accounting

What did we buy?

Example: Use of ledger and journalCASH IN CHECKING

50.00100.00 60.00250.00300.00510.00

50.00 15.001000.00

1270.00

1065.00

Look at journal entryDate Accounts Debits Credits9/12 Computers 700.00

Supplies 300.00Cash 1000.00

(Purchased Laser printer & toner cartridges from Office Depot)

22

Steps 1, 2, 3: Accumulate facts, determine effects on accounting equation, accounts to be used, debits and credits

Step 4: Journalize (usually done daily)

Step 5: Post to Ledger (often batched, daily or weekly)

Step 6: Total all accounts in ledger and check math for errors. Total Debits = Total Credits (called trial balance).

Debit CreditCash 100Equipment 500Accounts Payable 200Retained Earnings 400Revenue 200Wage Expense 200

800 800

23

Steps in transaction analysis:Steps in transaction analysis:

Example: Assume the following 10/1/2014 ledger balances:Ret Earnings

1200Cash in Bank

1000Receivables

200Fee Revenue Rent Exp

• 10/3 Earned $300 in fees, terms net 30 days.

• 10/10 Received $100 payment on account from customers.

• 10/20 Earned $400 in fees. Cash received from customers.

• 10/31 Paid rent of $200.

24

Ret Earnings

1200Cash in Bank

1000Receivables

200Fee Revenue Rent Exp

• 10/3 Earned $300 in fees, terms net 30 days.

General Journal

10/3 Receivables 300Fee Revenue 300

25

Ret Earnings

1200Cash in Bank

1000Receivables

200Fee Revenue Rent Exp

• 10/10 Received $100 payment on account from customers.

General Journal

10/3 Receivables 300Fee Revenue 300

10/10 Cash 100Receivables 100

26

Ret Earnings

1200Cash in Bank

1000Receivables

200Fee Revenue Rent Exp

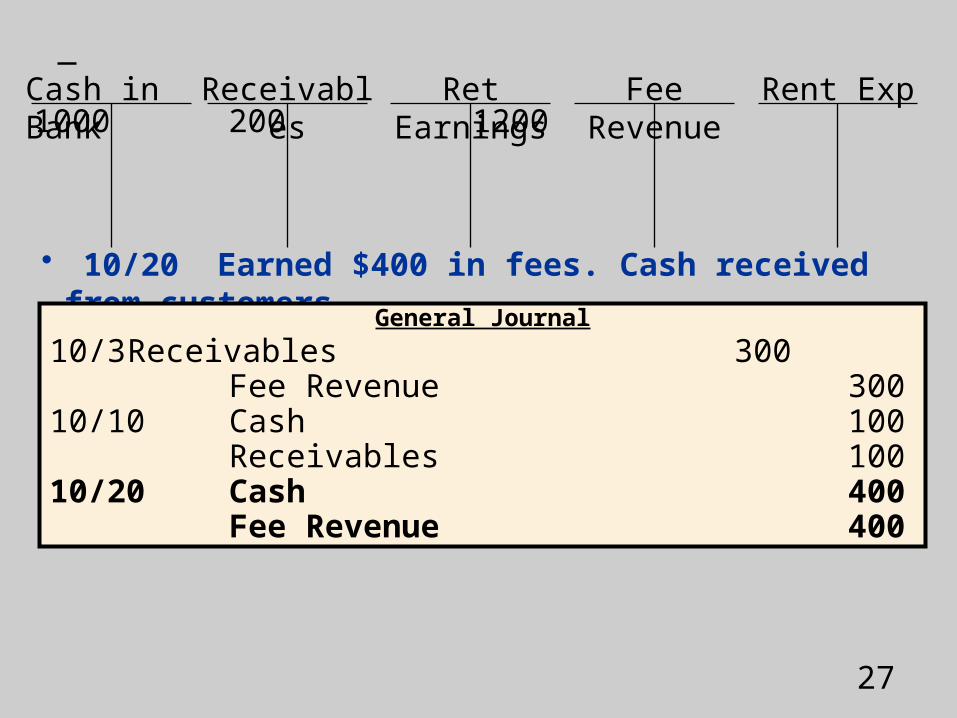

• 10/20 Earned $400 in fees. Cash received from customers.

General Journal

10/3 Receivables 300Fee Revenue 300

10/10 Cash 100Receivables 100

10/20 Cash 400Fee Revenue 400

27

Ret Earnings

1200Cash in Bank

1000Receivables

200Fee Revenue Rent Exp

• 10/31 Paid rent of $200.

General Journal

10/3 Receivables 300Fee Revenue 300

10/10 Cash 100Receivables 100

10/20 Cash 400Fee Revenue 400

10/31 Rent Expense 200Cash 200

28

Ret Earnings

1200Cash in Bank

1000Receivables

200Fee Revenue Rent Exp

General Journal

10/3 Receivables 300Fee Revenue 300

10/10 Cash 100Receivables 100

10/20 Cash 400Fee Revenue 400

10/31 Rent Expense 200Cash 200

300300

29

Ret Earnings

1200Cash in Bank

1000Receivables

200Fee Revenue Rent Exp

General Journal

10/3 Receivables 300Fee Revenue 300

10/10 Cash 100Receivables 100

10/20 Cash 400Fee Revenue 400

10/31 Rent Expense 200Cash 200

300300

100100

30

Ret Earnings

1200Cash in Bank

1000Receivables

200Fee Revenue Rent Exp

General Journal

10/3 Receivables 300Fee Revenue 300

10/10 Cash 100Receivables 100

10/20 Cash 400Fee Revenue 400

10/31 Rent Expense 200Cash 200

300300

100100

400400

31

Ret Earnings

1200Cash in Bank

1000Receivables

200Fee Revenue Rent Exp

General Journal

10/3 Receivables 300Fee Revenue 300

10/10 Cash 100Receivables 100

10/20 Cash 400Fee Revenue 400

10/31 Rent Expense 200Cash 200

300300

100100

400400

200200

32

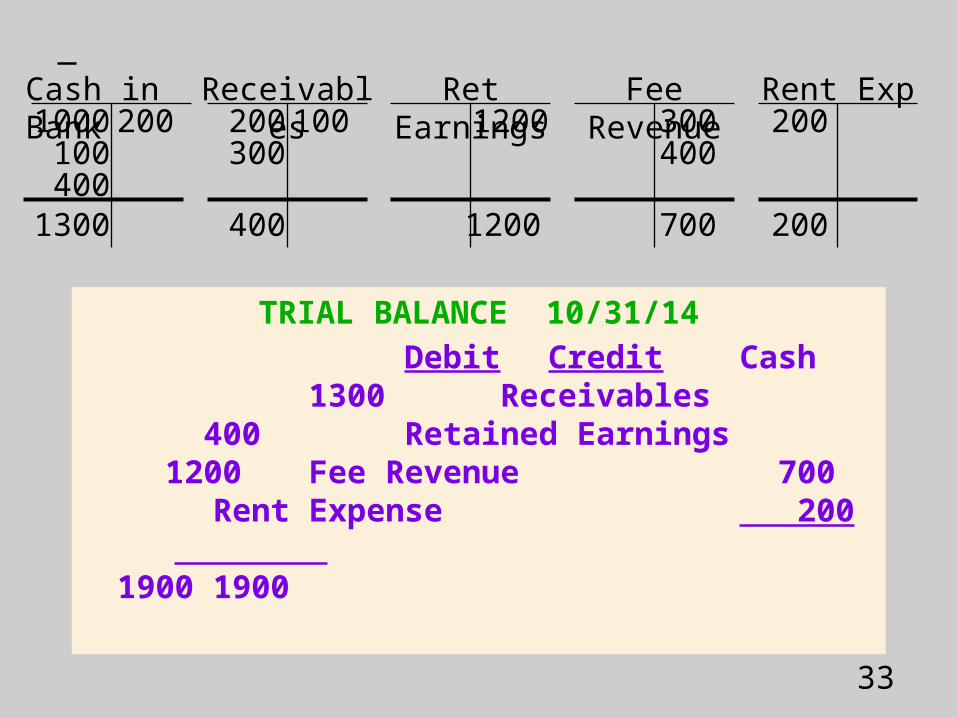

Ret Earnings

1200Cash in Bank

1000Receivables

200Fee Revenue Rent Exp

300300

100100

400400

200200

1300 400 1200 700 200

TRIAL BALANCE 10/31/14

Debit CreditCash 1300

Receivables 400 Retained Earnings

1200 Fee Revenue 700 Rent

Expense 200 1900 1900

33