Embed Size (px)

Citation preview

GE CapitalFranchise Finance

2014Canadian ChainRestaurantIndustry Review

Research Partners

GE CapitalFranchise Finance

2014Canadian ChainRestaurantIndustry Review1 Preface . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 22 Introduction . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 53 Foodservice Industry Profile . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 64 Top-of-Mind: What CEOs Think . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .185 Trends Impacting Restaurants . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .246 Finance . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .327 Cost of Doing Business . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .428 Top Chains . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .629 Notes . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .64

Research Partners

Insightful and Trustworthy Data to Help Grow our Businesses

Welcome to GE Capital’s third annual Canadian Chain Restaurant Industry Review . I am pleased to bring you this extensive research report on the state of chain foodservice in this country with the goal of providing insight into key factors affecting our Canadian industry.

The Review is a comprehensive analysis and factual overview of market shares, revenue trends, costs, hot (and not-so-hot) products, consumer behaviour and the overall state of chain foodservice in Canada. These findings have implications for job growth, construction activity and other factors that will impact the economic health of Canada for 2014 and for several years to come . GE Capital wishes to thank fsSTRATEGY and NPD Group Canada for their great work at compiling and analyzing these results .

As our economy keeps on improving, the Review shows that Canadians continue to spend more and more at restaurants, with a year-over-year increase of 2% . In fact, total Canadian foodservice industry sales are expected to increase by 4 .4%, or almost $3 .2 billion, to $71 .1 billion in 2014 .

I find this data very encouraging for the future of our industry. Reading through the Review will undoubtedly give you food for thought . Our market insights will also assist you in building forward-looking plans to help grow your business .

The Canadian chain foodservice industry has gotten stronger in the past years and it’s thanks to your passion and dedication . I wish you all continued success in your endeavours .

Ed KhediguianGE Capital, CanadaFranchise Finance

GE CapitalFranchise Finance

Preface1

2

GE Capital, Franchise Finance Canada

We’re More Than Just Bankers, We’re Builders

GE Capital, Franchise Finance is a leading lender to the restaurant and hospitality industries in Canada. We specialize in financing regional and national restaurant businesses of all sizes across the country. In the past 12 years, we’ve financed more than 750 restaurant customers with upwards of 1,525 property locations . That’s in excess of $1 .35 billion that we’ve invested in the Canadian restaurant space .

In addition to financing at the franchisee and franchisor levels, we lend money for new developments, recapitalizations of existing businesses, mergers and acquisitions, and management-led buyouts .

But we offer our clients more than money.

At GE Capital, we’re not just bankers, we’re builders. On top of smart financing, we provide the know-how of GE to help your capital go further and do more . We’re excited that you’re building something great . It takes money, along with knowledge and expertise . That’s where we come in .

Here are some reasons to consider financing with us:

� A vast portfolio of national and regional restaurant relationships – in a variety of quick service and casual formats – that we’ve maintained through economic ups and downs;

� Deep expertise in the franchise business and a special understanding of the brands that operate in this market;

� A cash flow-based lending model that allows us to value a business based on performance, while taking into account seasonality and other operation issues that specifically affect restaurants; and

� The Access GE program, through which we bring the tools, resources, insights and expertise of GE to help business leaders with their most pressing challenges .

We look forward to working with you as you continue to grow and succeed .

GE CapitalFranchise Finance

1 | Preface

3

Now in its fifth year, the Canadian RestauRant investment summit has solidly established itself as the

annual business conference that brings the industry

into focus.

Operators, chain executives, franchise operators, investors,

lenders and key suppliers from across the country agree

that this is the event that delivers what they need—insight,

information and opportunity—all with meaningful content

and a tight focus that is uniquely Canadian.

Each year, the Summit presents topical issues and noted

thought leaders who share opinions, stimulate discussion

and create new directions. The entire conference program

is designed to yield authoritative information and the latest

data from across the country. When combined with the

powerful networking opportunities it presents, the Summit

is an experience that is unequalled anywhere in Canada.

maY 6+7, 2014EATON CHELSEA TOrONTO HOTEL

rESTAUrANTINVEST.CA rESTAUrANTINVEST.CA rESTAUrANTINVEST.CA rESTAUrANTINVEST.CA

TOP NAME INDUSTrY SPEAKErS.SErIOUS NETWOrKING.THANK YOU fOr jOINING THE DISCUSSION.

*Confirmed Sponsors as of March 21, 2014

Canadian RestauRantinvestment summit

PArTNErS & SPONSOrS

4

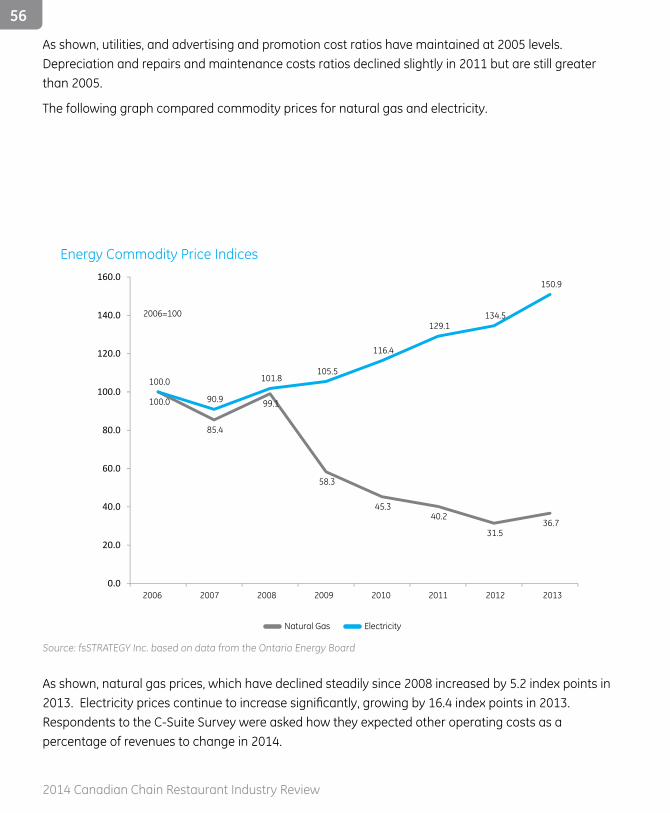

fsSTRATEGY Inc . (“fsSTRATEGY”) and The NPD Group, Inc . (“NPD”) are pleased to release this 2014 Canadian Chain Restaurant Review as part of the 2014 Canadian Restaurant Investment Summit .

This report is the culmination of extensive primary and secondary research conducted by fsSTRATEGY and NPD . Sources include:

� Research and data provided by Restaurants Canada, formerly the Canadian Restaurant and Foodservices Association (“CRFA”) .

� C-Suite Survey in January and February, 2014 conducted by fsSTRATEGY and sent to over 94 CEOs and CFOs in the Canadian chain foodservice market .

� Detailed data from NPD’s Future of Foodservice . � Interviews with selected food grower associations, foodservice distributors and landlords .

� Information prepared by GE Canada on the state of money markets and chain restaurant financing.

� Secondary research data from other sources such as Statistics Canada, PKF Consulting, TD Economics, the Conference Board of Canada, University of Guelph, Human Resources and Skills Development Canada, Canada Ministry of Labour, Ontario Energy Board, International Monetary Fund and RSMeans .

For further information, please contact:

Geoff Wilson or Jeff Dover Robert CarterfsSTRATEGY Inc . The NPD Group (Canada), Inc .gwilson@fsSTRATEGY .com robert .carter@npd .com jdover@fsSTRATEGY .com (647) 723-7767(416) 229-2290

Introduction2

5

2 | Introduction

FoodserviceIndustryProfile3.1 Canadian Foodservice Industry Sales3.2 Chain versus Independent Operator Sales 3.3 Provincial Sales Trends3.4 Same Store Sales Growth3.5 C-Suite Expectations for Sales and Traffic

3

6

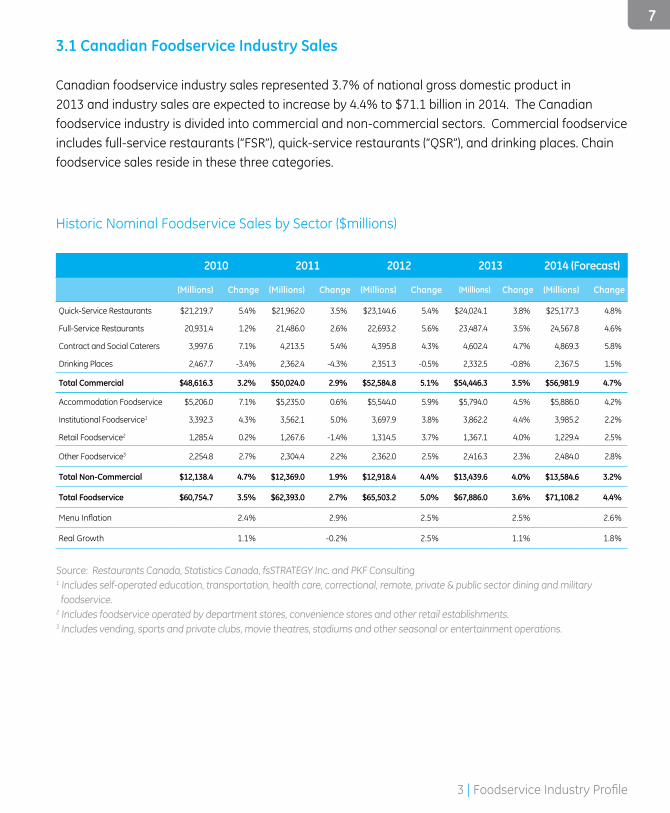

3.1 Canadian Foodservice Industry Sales

Canadian foodservice industry sales represented 3 .7% of national gross domestic product in 2013 and industry sales are expected to increase by 4 .4% to $71 .1 billion in 2014 . The Canadian foodservice industry is divided into commercial and non-commercial sectors . Commercial foodservice includes full-service restaurants (“FSR”), quick-service restaurants (“QSR”), and drinking places . Chain foodservice sales reside in these three categories .

Source: Restaurants Canada, Statistics Canada, fsSTRATEGY Inc . and PKF Consulting1 Includes self-operated education, transportation, health care, correctional, remote, private & public sector dining and military foodservice .2 Includes foodservice operated by department stores, convenience stores and other retail establishments .3 Includes vending, sports and private clubs, movie theatres, stadiums and other seasonal or entertainment operations .

Historic Nominal Foodservice Sales by Sector ($millions)

2010 2011 2012 2013 2014 (Forecast)

(Millions) Change (Millions) Change (Millions) Change (Millions) Change (Millions) Change

Quick-Service Restaurants $21,219 .7 5 .4% $21,962 .0 3 .5% $23,144 .6 5 .4% $24,024 .1 3 .8% $25,177 .3 4 .8%

Full-Service Restaurants 20,931 .4 1 .2% 21,486 .0 2 .6% 22,693 .2 5 .6% 23,487 .4 3 .5% 24,567 .8 4 .6%

Contract and Social Caterers 3,997 .6 7 .1% 4,213 .5 5 .4% 4,395 .8 4 .3% 4,602 .4 4 .7% 4,869 .3 5 .8%

Drinking Places 2,467 .7 -3 .4% 2,362 .4 -4 .3% 2,351 .3 -0 .5% 2,332 .5 -0 .8% 2,367 .5 1 .5%

Total Commercial $48,616.3 3.2% $50,024.0 2.9% $52,584.8 5.1% $54,446.3 3.5% $56,981.9 4.7%

Accommodation Foodservice $5,206 .0 7 .1% $5,235 .0 0 .6% $5,544 .0 5 .9% $5,794 .0 4 .5% $5,886 .0 4 .2%

Institutional Foodservice1 3,392 .3 4 .3% 3,562 .1 5 .0% 3,697 .9 3 .8% 3,862 .2 4 .4% 3,985 .2 2 .2%

Retail Foodservice2 1,285 .4 0 .2% 1,267 .6 -1 .4% 1,314 .5 3 .7% 1,367 .1 4 .0% 1,229 .4 2 .5%

Other Foodservice3 2,254 .8 2 .7% 2,304 .4 2 .2% 2,362 .0 2 .5% 2,416 .3 2 .3% 2,484 .0 2 .8%

Total Non-Commercial $12,138.4 4.7% $12,369.0 1.9% $12,918.4 4.4% $13,439.6 4.0% $13,584.6 3.2%

Total Foodservice $60,754.7 3.5% $62,393.0 2.7% $65,503.2 5.0% $67,886.0 3.6% $71,108.2 4.4%

Menu Inflation 2 .4% 2 .9% 2 .5% 2 .5% 2 .6%

Real Growth 1 .1% -0 .2% 2 .5% 1 .1% 1 .8%

7

3 | Foodservice Industry Profile

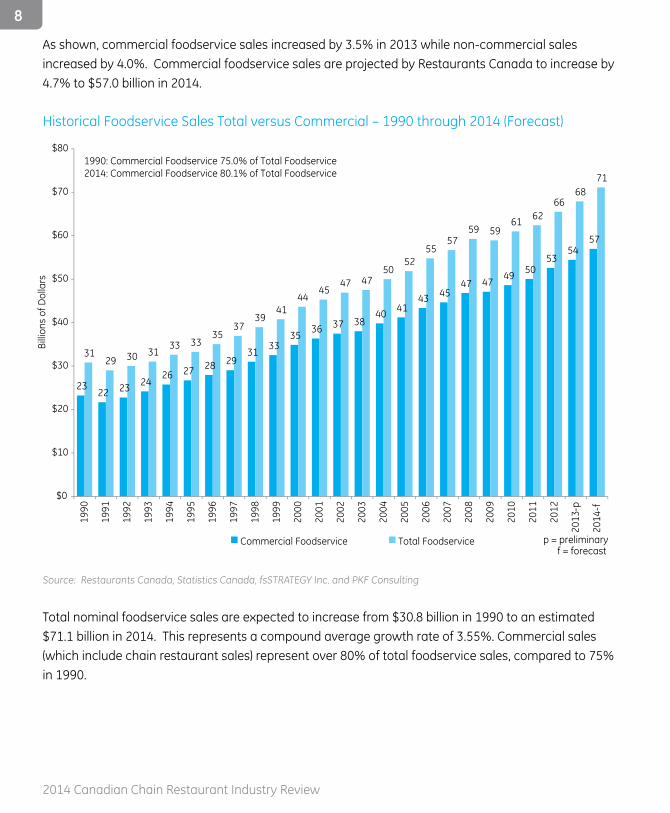

As shown, commercial foodservice sales increased by 3 .5% in 2013 while non-commercial sales increased by 4 .0% . Commercial foodservice sales are projected by Restaurants Canada to increase by 4 .7% to $57 .0 billion in 2014 .

Historical Foodservice Sales Total versus Commercial – 1990 through 2014 (Forecast)

Source: Restaurants Canada, Statistics Canada, fsSTRATEGY Inc . and PKF Consulting

Total nominal foodservice sales are expected to increase from $30 .8 billion in 1990 to an estimated $71 .1 billion in 2014 . This represents a compound average growth rate of 3 .55% . Commercial sales (which include chain restaurant sales) represent over 80% of total foodservice sales, compared to 75% in 1990 .

Billi

ons

of D

olla

rs

23 22 23 24

26 27 28 29 31

33 35 36 37 38

40 41 43 45

47 47 49 50

53 54

57

31 29 30 31

33 33 35

37 39

41 44

45 47 47

50 52

55 57

59 59 61 62

66 68

71

$0

$10

$20

$30

$40

$50

$60

$70

$80

1990

1991

1992

1993

1994

1995

1996

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

2013

-p

2014

-f

1990: Commercial Foodservice 75.0% of Total Foodservice2014: Commercial Foodservice 80.1% of Total Foodservice

Commercial Foodservice Total Foodservice p = preliminaryf = forecast

8

2014 Canadian Chain Restaurant Industry Review

2013 Forecasted Share of Foodservice Sales by Sector ($millions)

Total Foodservice Commercial Foodservice

Source: Restaurants Canada, Statistics Canada, fsSTRATEGY Inc . and PKF Consulting

QSRs and FSRs generate relatively similar sales (about $25 billion each annually) and together represent 87 .3% of commercial foodservice sales and 70 .0% of total foodservice sales .

$56,981.9

$5,886.0 $3,985.2

$1,229.4 $2,484.0

$25,177.3

$24,567.8

$4,869.3 $2,367.5

Total Commercial

Accommodation foodserviceInstitutional foodservice

Retail foodservice

Other foodservice

Quick-service restaurants

Full-service restaurants

Contract and social caterers

Drinking places

3 | Foodservice Industry Profile

9

100.0

102.3

99.4 100.3 100.3

102.9

106.0

101.5

97.3 96.1 95.9

98.5

102.2

104.0 103.5

106.9 107.4

111.0

113.8

100.9

94.4

98.8

101.2

104.2

107.5

99.0

95.5

90.1

83.9

81.6 80.6 80.0

85.0

90.0

95.0

100.0

105.0

110.0

115.0

120.0

2007 2008 2009 2010 2011 2012 2013-p

Real Sales Index 2007 = 100

Total Commercial Full-Service Restaurants Quick-Service Restaurants Caterers Drinking Places

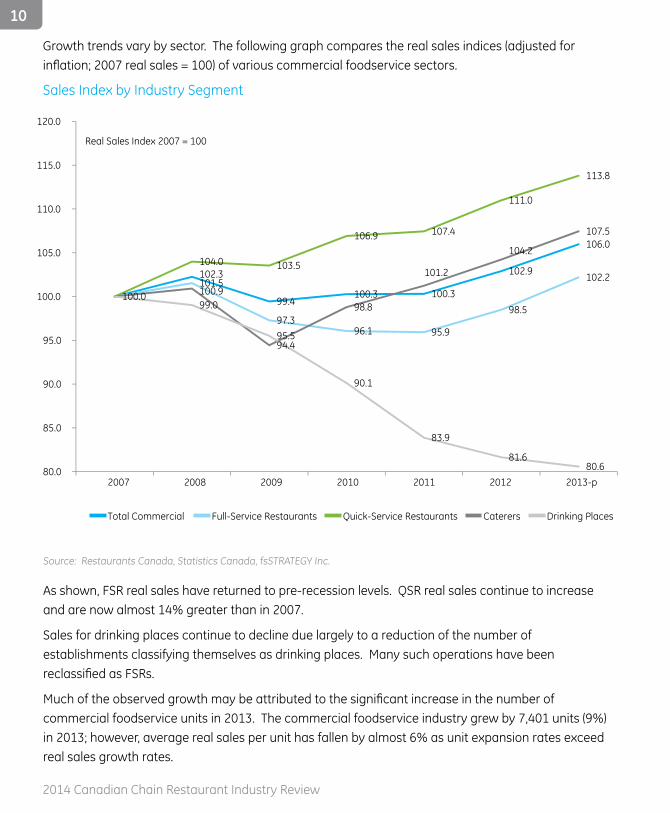

Growth trends vary by sector . The following graph compares the real sales indices (adjusted for inflation; 2007 real sales = 100) of various commercial foodservice sectors.

Sales Index by Industry Segment

Source: Restaurants Canada, Statistics Canada, fsSTRATEGY Inc .

As shown, FSR real sales have returned to pre-recession levels . QSR real sales continue to increase and are now almost 14% greater than in 2007 .

Sales for drinking places continue to decline due largely to a reduction of the number of establishments classifying themselves as drinking places . Many such operations have been reclassified as FSRs.

Much of the observed growth may be attributed to the significant increase in the number of commercial foodservice units in 2013 . The commercial foodservice industry grew by 7,401 units (9%) in 2013; however, average real sales per unit has fallen by almost 6% as unit expansion rates exceed real sales growth rates .

10

2014 Canadian Chain Restaurant Industry Review

3.2 Chain versus Independent Operator Sales

The chart below graphically depicts the share of chain and independent restaurant expenditures in various regions of Canada for 2013 .

Chain versus Independent Restaurant Expenditures – 2013

Source: The NPD Group/CREST®

As shown, 62 .2% of the expenditure in restaurants in Canada is in branded local, regional, national and international chains . Quebec has the greatest percentage of independent expenditures, with almost half of all restaurant sales unaffiliated with chains.

69.4%

51.6% 65.4% 63.2% 62.2%

30.6% 48.4%

34.6% 36.8% 37.8%

0%

20%

40%

60%

80%

100%

CanadaWestOntarioQuebecAtlantic

Chain Restaurants Independent Restaurants

11

3 | Foodservice Industry Profile

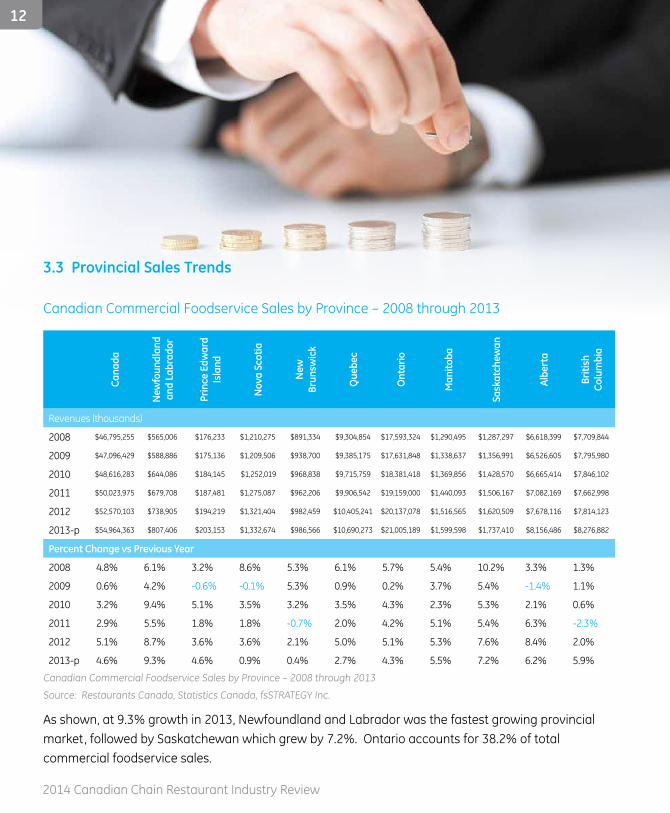

3.3 Provincial Sales Trends

Canadian Commercial Foodservice Sales by Province – 2008 through 2013

Cana

da

New

foun

dlan

d an

d La

brad

or

Prin

ce E

dwar

d Is

land

Nov

a Sc

otia

New

Br

unsw

ick

Que

bec

Ont

ario

Man

itoba

Sask

atch

ewan

Albe

rta

Briti

sh

Colu

mbi

a

Revenues (thousands)

2008 $46,795,255 $565,006 $176,233 $1,210,275 $891,334 $9,304,854 $17,593,324 $1,290,495 $1,287,297 $6,618,399 $7,709,844

2009 $47,096,429 $588,886 $175,136 $1,209,506 $938,700 $9,385,175 $17,631,848 $1,338,637 $1,356,991 $6,526,605 $7,795,980

2010 $48,616,283 $644,086 $184,145 $1,252,019 $968,838 $9,715,759 $18,381,418 $1,369,856 $1,428,570 $6,665,414 $7,846,102

2011 $50,023,975 $679,708 $187,481 $1,275,087 $962,206 $9,906,542 $19,159,000 $1,440,093 $1,506,167 $7,082,169 $7,662,998

2012 $52,570,103 $738,905 $194,219 $1,321,404 $982,459 $10,405,241 $20,137,078 $1,516,565 $1,620,509 $7,678,116 $7,814,123

2013-p $54,964,363 $807,406 $203,153 $1,332,674 $986,566 $10,690,273 $21,005,189 $1,599,598 $1,737,410 $8,156,486 $8,276,882

Percent Change vs Previous Year

2008 4 .8% 6 .1% 3 .2% 8 .6% 5 .3% 6 .1% 5 .7% 5 .4% 10 .2% 3 .3% 1 .3%

2009 0 .6% 4 .2% -0 .6% -0 .1% 5 .3% 0 .9% 0 .2% 3 .7% 5 .4% -1 .4% 1 .1%

2010 3 .2% 9 .4% 5 .1% 3 .5% 3 .2% 3 .5% 4 .3% 2 .3% 5 .3% 2 .1% 0 .6%

2011 2 .9% 5 .5% 1 .8% 1 .8% -0 .7% 2 .0% 4 .2% 5 .1% 5 .4% 6 .3% -2 .3%

2012 5 .1% 8 .7% 3 .6% 3 .6% 2 .1% 5 .0% 5 .1% 5 .3% 7 .6% 8 .4% 2 .0%

2013-p 4 .6% 9 .3% 4 .6% 0 .9% 0 .4% 2 .7% 4 .3% 5 .5% 7 .2% 6 .2% 5 .9%

Canadian Commercial Foodservice Sales by Province – 2008 through 2013

Source: Restaurants Canada, Statistics Canada, fsSTRATEGY Inc .

As shown, at 9 .3% growth in 2013, Newfoundland and Labrador was the fastest growing provincial market, followed by Saskatchewan which grew by 7 .2% . Ontario accounts for 38 .2% of total commercial foodservice sales .

12

2014 Canadian Chain Restaurant Industry Review

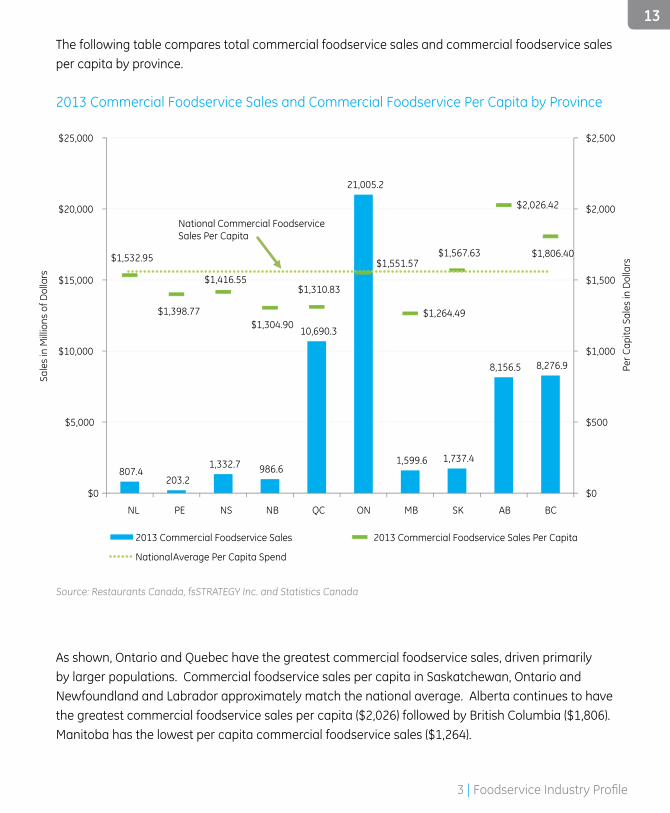

As shown, Ontario and Quebec have the greatest commercial foodservice sales, driven primarily by larger populations . Commercial foodservice sales per capita in Saskatchewan, Ontario and Newfoundland and Labrador approximately match the national average . Alberta continues to have the greatest commercial foodservice sales per capita ($2,026) followed by British Columbia ($1,806) . Manitoba has the lowest per capita commercial foodservice sales ($1,264) .

Source: Restaurants Canada, fsSTRATEGY Inc . and Statistics Canada

The following table compares total commercial foodservice sales and commercial foodservice sales per capita by province .

2013 Commercial Foodservice Sales and Commercial Foodservice Per Capita by Province

807.4 203.2

1,332.7 986.6

10,690.3

21,005.2

1,599.6 1,737.4

8,156.5 8,276.9

$1,532.95

$1,398.77

$1,304.90

$1,310.83

$1,551.57

$1,264.49

$1,567.63

$2,026.42

$1,806.40

$0

$500

$1,000

$1,500

$2,000

$2,500

$0

$5,000

$10,000

$15,000

$20,000

$25,000

National Commercial Foodservice Sales Per Capita

2013 Commercial Foodservice Sales 2013 Commercial Foodservice Sales Per Capita

National Average Per Capita Spend

NL PE NS NB QC ON MB SK AB BC

$1,416.55

Per C

apita

Sal

es in

Dol

lars

Sale

s in

Mill

ions

of D

olla

rs

13

3 | Foodservice Industry Profile

Same Store Sales Growth 2007 through 2013, Selected Publicly-Traded Restaurant Chains

3.1%

1.8%

-2.5%

1.2%

2.5%

1.3%

0.1%

-3%

-2%

-1%

0%

1%

2%

3%

4%

2007 2008 2009 20112010 2012 2013

Source: Company annual and quarterly reports .1 .Selected publicly traded Canadian chains . 2013 data year-to-date 2nd or 3rd quarter results .

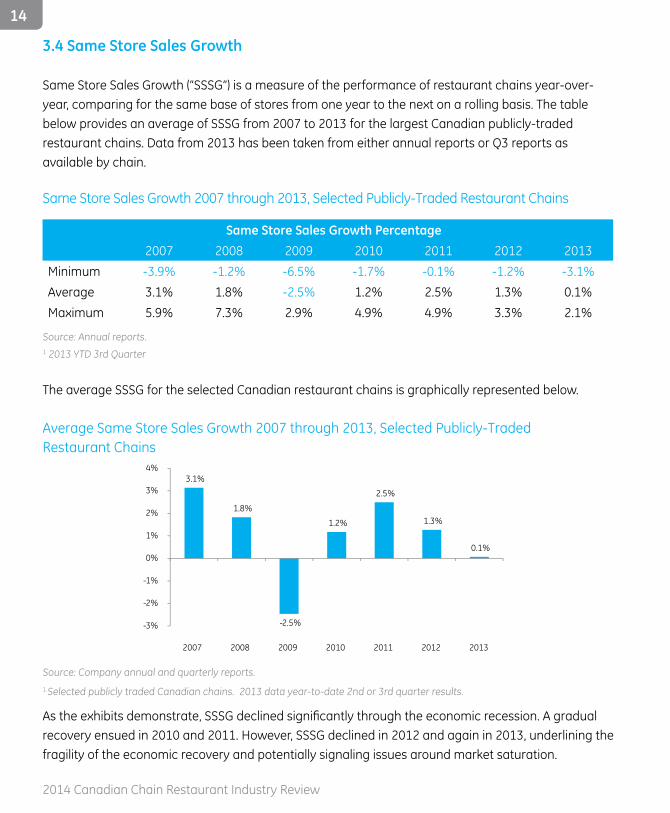

As the exhibits demonstrate, SSSG declined significantly through the economic recession. A gradual recovery ensued in 2010 and 2011 . However, SSSG declined in 2012 and again in 2013, underlining the fragility of the economic recovery and potentially signaling issues around market saturation .

Same Store Sales Growth Percentage2007 2008 2009 2010 2011 2012 2013

Minimum -3 .9% -1 .2% -6 .5% -1 .7% -0 .1% -1 .2% -3 .1%Average 3 .1% 1 .8% -2 .5% 1 .2% 2 .5% 1 .3% 0 .1%Maximum 5 .9% 7 .3% 2 .9% 4 .9% 4 .9% 3 .3% 2 .1%

Source: Annual reports .1 2013 YTD 3rd Quarter

The average SSSG for the selected Canadian restaurant chains is graphically represented below .

Average Same Store Sales Growth 2007 through 2013, Selected Publicly-Traded Restaurant Chains

3.4 Same Store Sales Growth

Same Store Sales Growth (“SSSG”) is a measure of the performance of restaurant chains year-over-year, comparing for the same base of stores from one year to the next on a rolling basis . The table below provides an average of SSSG from 2007 to 2013 for the largest Canadian publicly-traded restaurant chains . Data from 2013 has been taken from either annual reports or Q3 reports as available by chain .

14

2014 Canadian Chain Restaurant Industry Review

14

Same Store Sales Growth 2007 through 2013, Selected Publicly-Traded Restaurant Chains

15

3 | Foodservice Industry Profile

16

2014 Canadian Chain Restaurant Industry Review

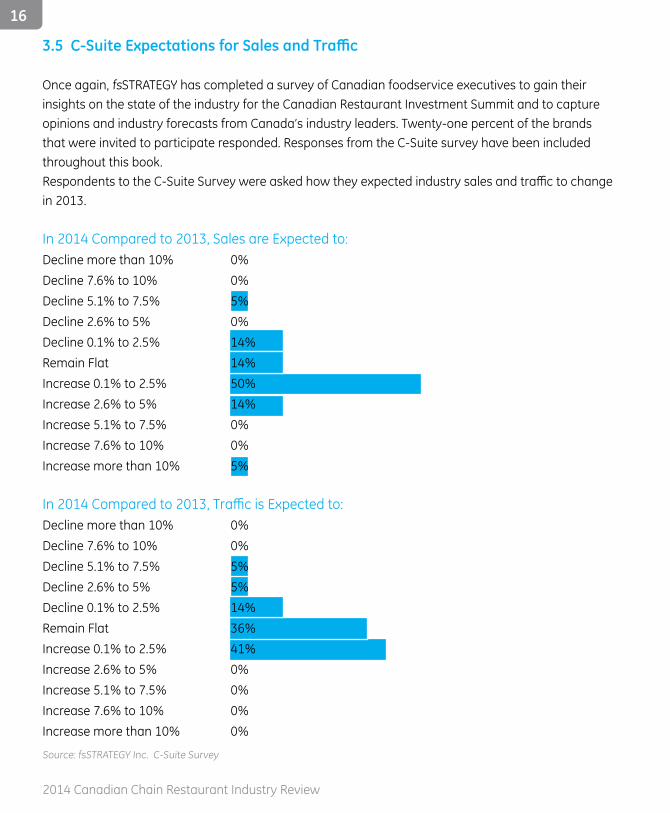

3.5 C-Suite Expectations for Sales and Traffic

Once again, fsSTRATEGY has completed a survey of Canadian foodservice executives to gain their insights on the state of the industry for the Canadian Restaurant Investment Summit and to capture opinions and industry forecasts from Canada’s industry leaders . Twenty-one percent of the brands that were invited to participate responded . Responses from the C-Suite survey have been included throughout this book .Respondents to the C-Suite Survey were asked how they expected industry sales and traffic to change in 2013 .

In 2014 Compared to 2013, Sales are Expected to: Decline more than 10% 0%Decline 7 .6% to 10% 0%Decline 5 .1% to 7 .5% 5%Decline 2 .6% to 5% 0%Decline 0 .1% to 2 .5% 14%Remain Flat 14%Increase 0 .1% to 2 .5% 50%Increase 2 .6% to 5% 14%Increase 5 .1% to 7 .5% 0%Increase 7 .6% to 10% 0%Increase more than 10% 5%

In 2014 Compared to 2013, Traffic is Expected to: Decline more than 10% 0%Decline 7 .6% to 10% 0%Decline 5 .1% to 7 .5% 5%Decline 2 .6% to 5% 5%Decline 0 .1% to 2 .5% 14%Remain Flat 36%Increase 0 .1% to 2 .5% 41%Increase 2 .6% to 5% 0%Increase 5 .1% to 7 .5% 0%Increase 7 .6% to 10% 0%Increase more than 10% 0%

Source: fsSTRATEGY Inc . C-Suite Survey

Most respondents (50%) expect industry sales to increase by up to 2 .5% in 2014 with 14% expecting growth of between 2 .6% and 5% . In last year’s study, respondents were more positive with 60% of respondents expected sales to increase by 0 .1% to 2 .5% and 30% expecting revenues to increase by 2.6% to 5% in 2013. Thirty-six percent of respondents expect industry traffic to remain flat in 2014 and 41% expect traffic to grow by up to 2.5%. Respondents to the 2014 survey were more positive than 2013 respondents with respect to industry traffic with 41% expecting traffic to increase by up to 2 .5% . Once again this year, the survey strongly suggests that revenue increases will depend on operators’ ability to increase average cheques .

Approximately 40% of respondents to Restaurant Canada’s Restaurant Outlook Survey for Q4 2013 experienced a decrease in year-over-year same store sales and one quarter of respondents feel that same store sales will decrease in the next six months; although, based on historical results, Restaurants Canada suggests this decrease may reflect seasonality.

17

3 | Foodservice Industry Profile

Top-of-Mind:What CEOsThink4.1 Opportunities4.2 Challenges4.3 Biggest Changes4.4 Sustainability

4

18

2014 Canadian Chain Restaurant Industry Review

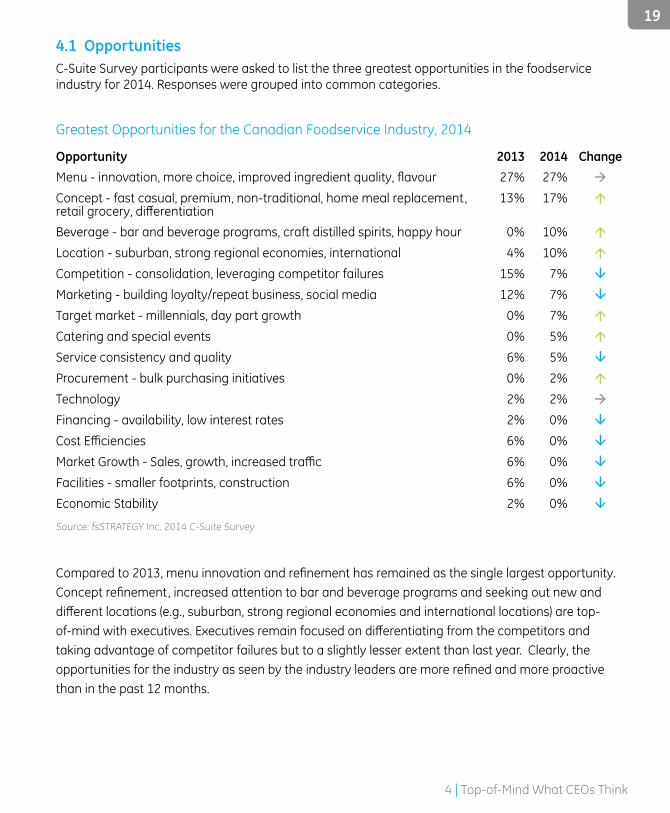

4.1 OpportunitiesC-Suite Survey participants were asked to list the three greatest opportunities in the foodservice industry for 2014 . Responses were grouped into common categories .

Greatest Opportunities for the Canadian Foodservice Industry, 2014

Opportunity 2013 2014 Change Menu - innovation, more choice, improved ingredient quality, flavour 27% 27% à

Concept - fast casual, premium, non-traditional, home meal replacement, retail grocery, differentiation

13% 17% á

Beverage - bar and beverage programs, craft distilled spirits, happy hour 0% 10% á

Location - suburban, strong regional economies, international 4% 10% á

Competition - consolidation, leveraging competitor failures 15% 7% â

Marketing - building loyalty/repeat business, social media 12% 7% â

Target market - millennials, day part growth 0% 7% á

Catering and special events 0% 5% á

Service consistency and quality 6% 5% â

Procurement - bulk purchasing initiatives 0% 2% á

Technology 2% 2% à

Financing - availability, low interest rates 2% 0% â

Cost Efficiencies 6% 0% â

Market Growth - Sales, growth, increased traffic 6% 0% â

Facilities - smaller footprints, construction 6% 0% â

Economic Stability 2% 0% â

Source: fsSTRATEGY Inc . 2014 C-Suite Survey

Compared to 2013, menu innovation and refinement has remained as the single largest opportunity. Concept refinement, increased attention to bar and beverage programs and seeking out new and different locations (e.g., suburban, strong regional economies and international locations) are top-of-mind with executives. Executives remain focused on differentiating from the competitors and taking advantage of competitor failures but to a slightly lesser extent than last year . Clearly, the opportunities for the industry as seen by the industry leaders are more refined and more proactive than in the past 12 months .

19

4 | Top-of-Mind What CEOs Think

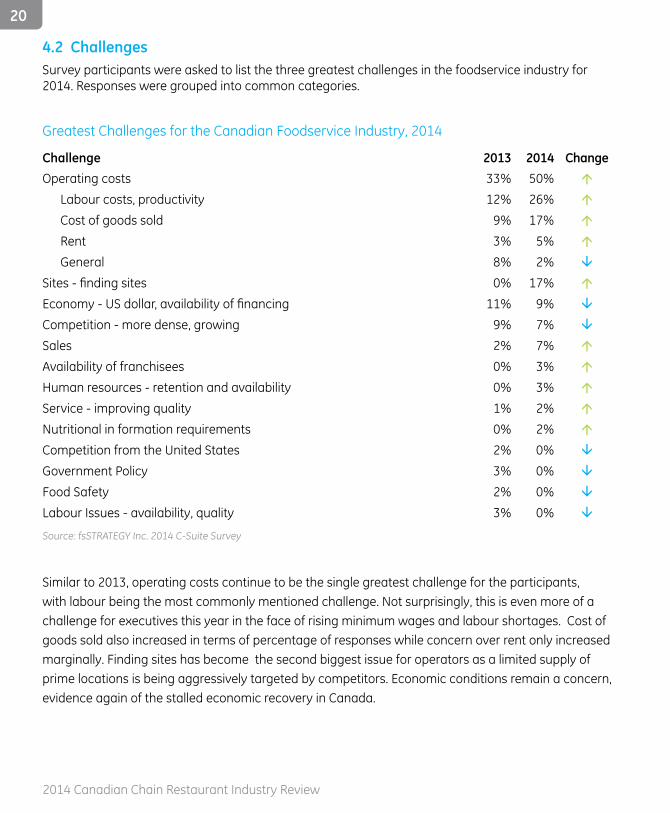

4.2 ChallengesSurvey participants were asked to list the three greatest challenges in the foodservice industry for 2014 . Responses were grouped into common categories .

Greatest Challenges for the Canadian Foodservice Industry, 2014

Challenge 2013 2014 ChangeOperating costs 33% 50% á

Labour costs, productivity 12% 26% á

Cost of goods sold 9% 17% á

Rent 3% 5% á

General 8% 2% â

Sites - finding sites 0% 17% á

Economy - US dollar, availability of financing 11% 9% â

Competition - more dense, growing 9% 7% â

Sales 2% 7% á

Availability of franchisees 0% 3% á

Human resources - retention and availability 0% 3% á

Service - improving quality 1% 2% á

Nutritional in formation requirements 0% 2% á

Competition from the United States 2% 0% â

Government Policy 3% 0% â

Food Safety 2% 0% â

Labour Issues - availability, quality 3% 0% â

Source: fsSTRATEGY Inc . 2014 C-Suite Survey

Similar to 2013, operating costs continue to be the single greatest challenge for the participants, with labour being the most commonly mentioned challenge . Not surprisingly, this is even more of a challenge for executives this year in the face of rising minimum wages and labour shortages . Cost of goods sold also increased in terms of percentage of responses while concern over rent only increased marginally . Finding sites has become the second biggest issue for operators as a limited supply of prime locations is being aggressively targeted by competitors . Economic conditions remain a concern, evidence again of the stalled economic recovery in Canada .

20

2014 Canadian Chain Restaurant Industry Review

4.3 Biggest Changes

4 .3 .1 Short-Term Changes

C-Suite Survey participants were asked what they thought would be the biggest short-term changes in the foodservice industry .

In 2013, participants cited intensifying competition, industry consolidation, increasing specialization of menus and the growth of social media as an influencer in success.

This year, participants continued the themes of intensifying competition and industry consolidation . Competition is expected to grow in smaller markets and operators continue to expect entries into the market by US chains . Participants believe there will be further mergers, acquisitions and closures in the chain restaurant industry in Canada . Some operators also suggest that independent restaurants will recapture market share they have been losing to the chains, especially in the premium casual market .

New this year, operators suggested that they expect consumer confidence to improve somewhat, yet consumers will have even higher value expectations .

Finally, operators expect labour shortages to persist, regulation to tighten, real estate costs to rise and availability to be limited and supply management to continue to burden cost of goods sold .

4 .3 .2 Long-Term Changes

C-Suite Survey participants were asked what they thought would be the biggest long-term changes in the foodservice industry .

In 2013, participants cited contraction and redefinition, concept changes, technology and changing consumer behaviour as baby boomers retire .

This year, participants reiterated their belief that the industry can expect more consolidation over the long-term, suggesting that there are too many chains doing the same thing . Participants also echoed the expectations of industry redefinition and concept changes . Of note, participants suggested the following:

� emergence of more fast casual concepts; � expansion of premium casual dining at the expense of fine and mid-scale family dining but with higher consumer expectations of premium casual dining; and

� FSRs getting out of the lunch business .This year, while demographic changes as the population ages continue to be top-of-mind, operators also mentioned growing population ethnicity as a long-term influencer of the industry.Finally, labour shortages and rising labour costs are also expected to be long-term issues for our industry .

21

4 | Top-of-Mind What CEOs Think

22

2014 Canadian Chain Restaurant Industry Review

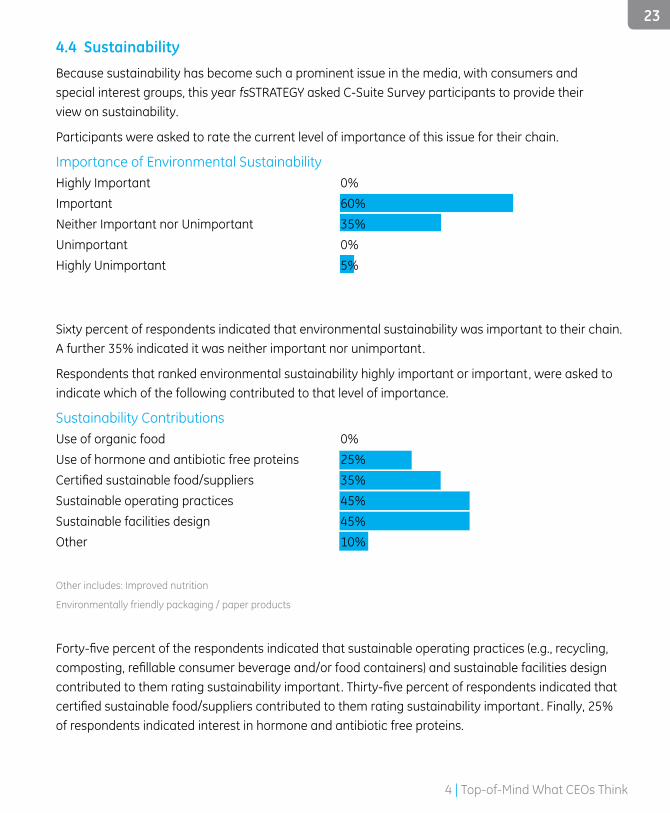

4.4 Sustainability

Because sustainability has become such a prominent issue in the media, with consumers and special interest groups, this year fsSTRATEGY asked C-Suite Survey participants to provide their view on sustainability .

Participants were asked to rate the current level of importance of this issue for their chain .

Importance of Environmental SustainabilityHighly Important 0%Important 60%Neither Important nor Unimportant 35%Unimportant 0%Highly Unimportant 5%

Sixty percent of respondents indicated that environmental sustainability was important to their chain . A further 35% indicated it was neither important nor unimportant .

Respondents that ranked environmental sustainability highly important or important, were asked to indicate which of the following contributed to that level of importance .

Sustainability ContributionsUse of organic food 0%Use of hormone and antibiotic free proteins 25%Certified sustainable food/suppliers 35%Sustainable operating practices 45%Sustainable facilities design 45%Other 10%

Other includes: Improved nutrition

Environmentally friendly packaging / paper products

Forty-five percent of the respondents indicated that sustainable operating practices (e.g., recycling, composting, refillable consumer beverage and/or food containers) and sustainable facilities design contributed to them rating sustainability important. Thirty-five percent of respondents indicated that certified sustainable food/suppliers contributed to them rating sustainability important. Finally, 25% of respondents indicated interest in hormone and antibiotic free proteins .

23

4 | Top-of-Mind What CEOs Think

TrendsImpactingRestaurants5.1 Key Consumer Profiles5.2 Key Foodservice Industry Trends5.3 Looking Ahead

5

24

2014 Canadian Chain Restaurant Industry Review

5.1 Key Consumer Profiles

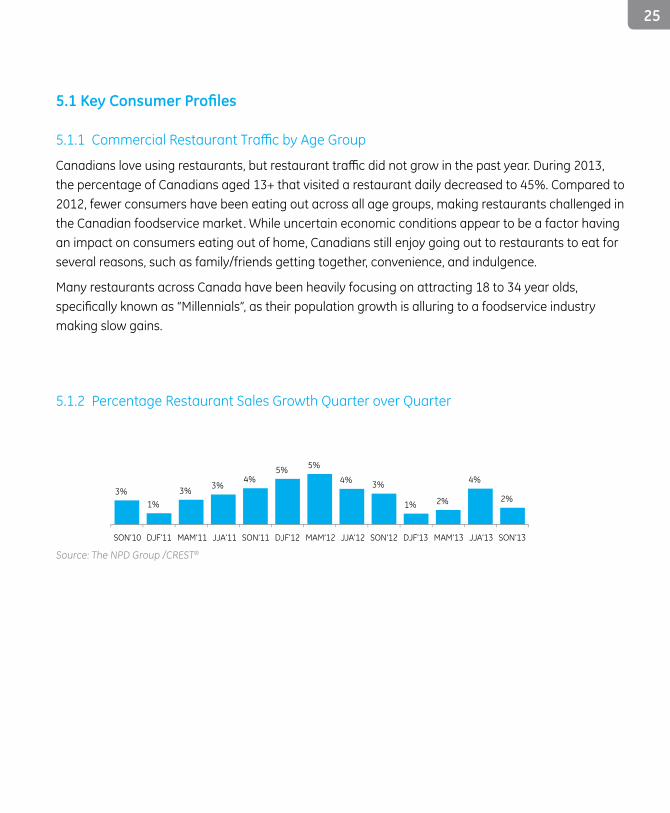

5.1.1 Commercial Restaurant Traffic by Age Group

Canadians love using restaurants, but restaurant traffic did not grow in the past year. During 2013, the percentage of Canadians aged 13+ that visited a restaurant daily decreased to 45% . Compared to 2012, fewer consumers have been eating out across all age groups, making restaurants challenged in the Canadian foodservice market . While uncertain economic conditions appear to be a factor having an impact on consumers eating out of home, Canadians still enjoy going out to restaurants to eat for several reasons, such as family/friends getting together, convenience, and indulgence .

Many restaurants across Canada have been heavily focusing on attracting 18 to 34 year olds, specifically known as “Millennials”, as their population growth is alluring to a foodservice industry making slow gains .

5 .1 .2 Percentage Restaurant Sales Growth Quarter over Quarter

SON’10 DJF’11 MAM’11 JJA’11 SON’11 DJF’12 MAM’12 JJA’12 SON’12 DJF’13 MAM’13 JJA’13 SON’13

3% 1%

3% 3% 4%

5% 5%

4% 3%

1% 2%

4%

2%

Source: The NPD Group /CREST®

25

5.2 Key Foodservice Industry Trends

While the Canadian foodservice industry is still in a fragile recovery as a result of the negative impacts of the global crisis, the ‘battle for share’ environment continues to intensify across all restaurant market segments. All provinces reflected a similar trend with visits remaining flat in the past five years.

With a +1% compound annual growth rate in foodservice visits since 2008 and -1% in the latest year, the Canadian Restaurant Market remains a challenging environment particularly for the QSR segment in Canada, which represents two thirds of visits . The QSRs that are winning in today’s market are those that have capitalized on urbanization through improvements on restaurant décor that reflects an upscale, casual image, as well as those who have an emphasis on menu innovation and promote the concept of premium menu items .

Customer traffic to the QSR segment has been soft to flat since 2008 in most provinces; Alberta is the only province exhibiting modest QSR traffic growth of +3% in the last five years.

The FSR segment, which represents 21% of all restaurant traffic continues to experience challenges in attracting customers on a regular basis . Hardest hit since 2008, all provinces continue to experience flat to declining customer traffic in this segment since.

During the past five years, Home Meal Replacement (“HMR”) has been one of the best performing segments of the Canadian foodservice industry . Today, all of the top Grocery Stores are allocating more resources to their HMR program in order to capture a greater share of consumers’ food dollar . The challenge for Grocery Stores, similar to the greater challenges faced in the overall restaurant market is that the volume of out of home prepared meals is expected to remain flat in 2014 versus last year . Published in late 2013, NPD’s Exploring Untapped Opportunities at HMR report provides a comprehensive study on how Grocery Stores can successfully increase customer traffic to their HMR programs, which highlights the strategies that have helped QSR operators realize gains in this challenging market .

Trends Analysis

Canada’s daypart sales share has experienced a slight change in distribution, which reflects the changing eating habits of Canadians over the past five years. In particular, morning meal is the fastest growing daypart in visits versus any other occasion . Success at morning meal is mainly driven by QSR as a result of convenience, with a +3% compound annual growth since 2008 . FSR faces morning meal challenges with visits down -3% in the last five years. Core offerings such as coffee, breakfast sandwiches, and muffins are supporting the morning meal success at QSR. QSR restaurants that play a dominant role in the morning meal daypart are likely to continue to penetrate the existing habitual preferences among Canadian morning meal consumers .

26

2014 Canadian Chain Restaurant Industry Review

5 | Trends Impacting Restaurants

Source: The NPD Group /CREST®

27

HMR Outpaced All Other Segments Over Last Five Years

5 | Trends Impacting Restaurants

Source: The NPD Group /CREST®

Source: The NPD Group /CREST®

27

Trends Analysis

Canada’s daypart sales share has experienced a slight change in distribution, which reflects the changing eating habits of Canadians over the past five years. In particular, morning meal is the fastest growing daypart in visits versus any other occasion . Success at morning meal is mainly driven by QSR as a result of convenience, with a +3% compound annual growth since 2008 . FSR faces morning meal challenges with visits down -3% in the last five years. Core offerings such as coffee, breakfast sandwiches, and muffins are supporting the morning meal success at QSR. QSR restaurants that play a dominant role in the morning meal daypart are likely to continue to penetrate the existing habitual preferences among Canadian morning meal consumers .

Dollars

4%

3%

-2%

1%

2%

Traffic

11

10

13

65

-2%

-1%

-6%0%

1%

PCYA PCYA

QSR

Family/Midscale

Casual Dining

Fine Dining

Prepared Food from Retail

PCYA = Percent Change vs. Year Ago

7

22

21

46

41

GrowthRate

2013 2008Traffic Volume (Millions)6.66.5

Total Market

4.34.0

QSR

1.61.7

FSR

0.50.4

HMR

0.20.3

Convenience

1% -2%2%-1%1%

Restaurant Market Segments – Share of Traffic and Dollar Sales

HMR Outpaced All Other Segments Over Last Five Years

Source: The NPD Group /CREST®

24% 26%

26% 26%

27% 25%

23% 23%

20132008

PM Snack

Supper

Lunch

Morning Meal

Daypart Distributon

28

2014 Canadian Chain Restaurant Industry Review

5.3 Looking Ahead

5 .3 .1 Population trends

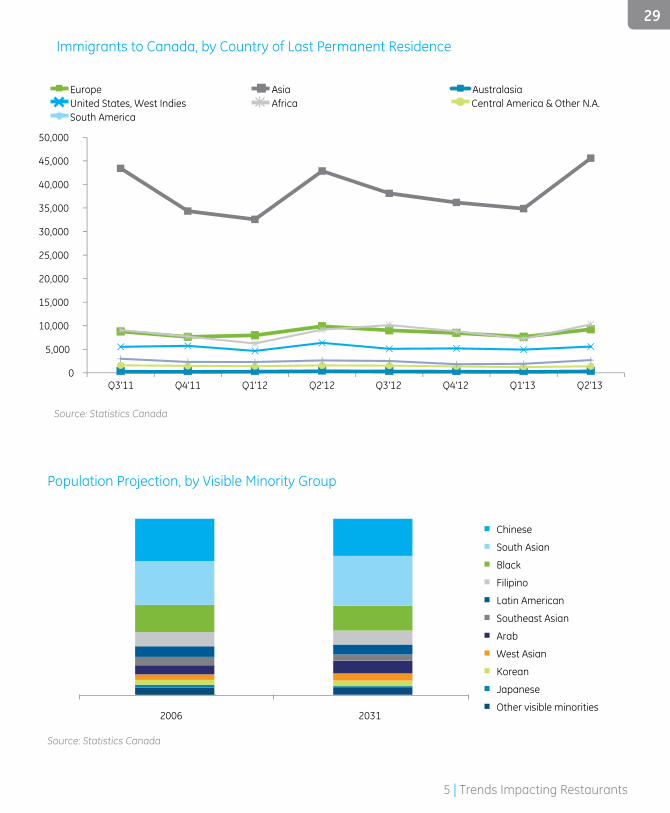

Canada’s demographic environment continues to change with much of the population growth fueled by immigration . The importance of immigration to Canada is put into context when compared to the United States . For instance, over the next ten years, the net migration rate in Canada is forecasted to be nearly 50 percent higher than our neighbours to the south . Immigration to Canada will continue to come primarily from Asia, and though this represents a varied cross-section of groups from a cultural and linguistic perspective, linkages among these groups surface when compared to the population . Visible minorities skew younger and newcomers are more likely to live in a larger household . Given the younger age and larger household size of this population segment, newcomers can be considered a prime growth target .

29

Source: Statistics Canada

0

5,000

10,000

15,000

20,000

25,000

30,000

35,000

40,000

45,000

50,000

Europe Asia Australasia United States, West Indies Africa Central America & Other N.A. South America

Q3'11 Q4'11 Q1'12 Q2'12 Q3'12 Q4'12 Q1'13 Q2'13

Population Projection, by Visible Minority Group

Immigrants to Canada, by Country of Last Permanent Residence

2006 2031

Chinese

South Asian

Black

Filipino

Latin American

Southeast Asian

Arab

West Asian

Korean

Japanese

Other visible minorities

Source: Statistics Canada

5 | Trends Impacting Restaurants

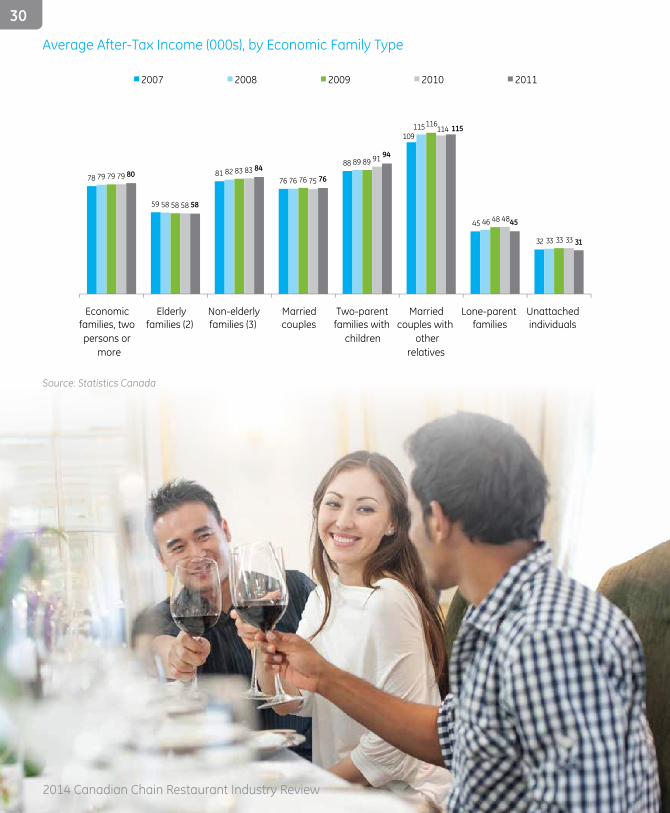

Average After-Tax Income (000s), by Economic Family Type

78

59

81 76

88

109

45

32

79

58

82 76

89

115

46

33

79

58

83 76

89

116

48

33

79

58

83 75

91

114

48

33

80

58

84 76

94

115

45

31

Economic families, two persons or

more

Elderly families (2)

Non-elderly families (3)

Married couples

Two-parent families with

children

Married couples with

other relatives

Lone-parent families

Unattached individuals

2007 2008 2009 2010 2011

Source: Statistics Canada

30

2014 Canadian Chain Restaurant Industry Review

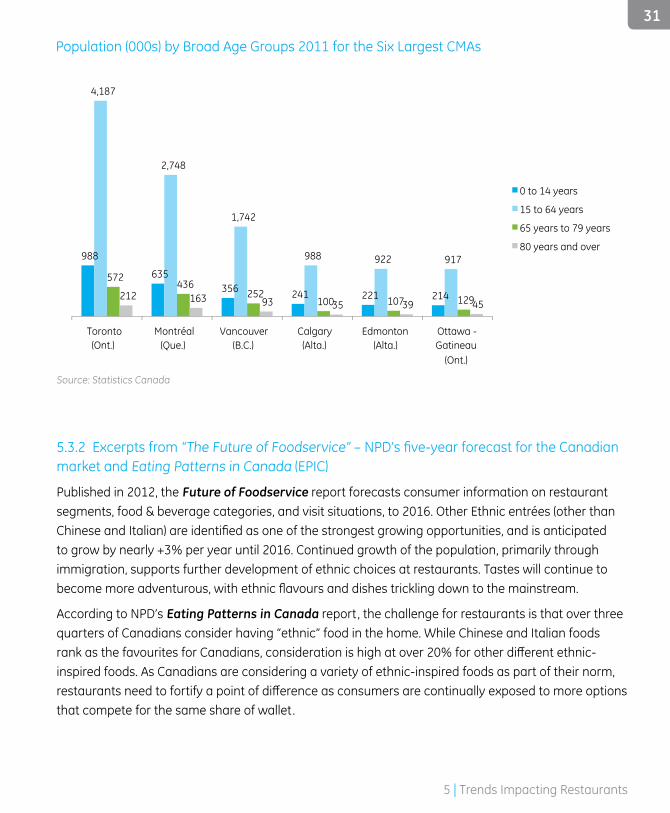

Population (000s) by Broad Age Groups 2011 for the Six Largest CMAs

5 .3 .2 Excerpts from “The Future of Foodservice” – NPD’s five-year forecast for the Canadian market and Eating Patterns in Canada (EPIC)

Published in 2012, the Future of Foodservice report forecasts consumer information on restaurant segments, food & beverage categories, and visit situations, to 2016 . Other Ethnic entrées (other than Chinese and Italian) are identified as one of the strongest growing opportunities, and is anticipated to grow by nearly +3% per year until 2016 . Continued growth of the population, primarily through immigration, supports further development of ethnic choices at restaurants . Tastes will continue to become more adventurous, with ethnic flavours and dishes trickling down to the mainstream.

According to NPD’s Eating Patterns in Canada report, the challenge for restaurants is that over three quarters of Canadians consider having “ethnic” food in the home . While Chinese and Italian foods rank as the favourites for Canadians, consideration is high at over 20% for other different ethnic-inspired foods . As Canadians are considering a variety of ethnic-inspired foods as part of their norm, restaurants need to fortify a point of difference as consumers are continually exposed to more options that compete for the same share of wallet .

Source: Statistics Canada

988

635 356 241 221 214

4,187

2,748

1,742

988 922 917

572 436

252 100 107 129 212 163 93 35 39 45

Toronto (Ont.)

Montréal (Que.)

Vancouver (B.C.)

Calgary (Alta.)

Edmonton (Alta.)

Ottawa - Gatineau

(Ont.)

0 to 14 years

15 to 64 years

65 years to 79 years

80 years and over

5 | Trends Impacting Restaurants

31

Finance 6.1 The Economy6.2 Global Financial Markets6.3 Financial Markets in Canada6.4 Total Financeable Debt Market Size and Loan Volumes

6

32

2014 Canadian Chain Restaurant Industry Review

6.1 The Economy

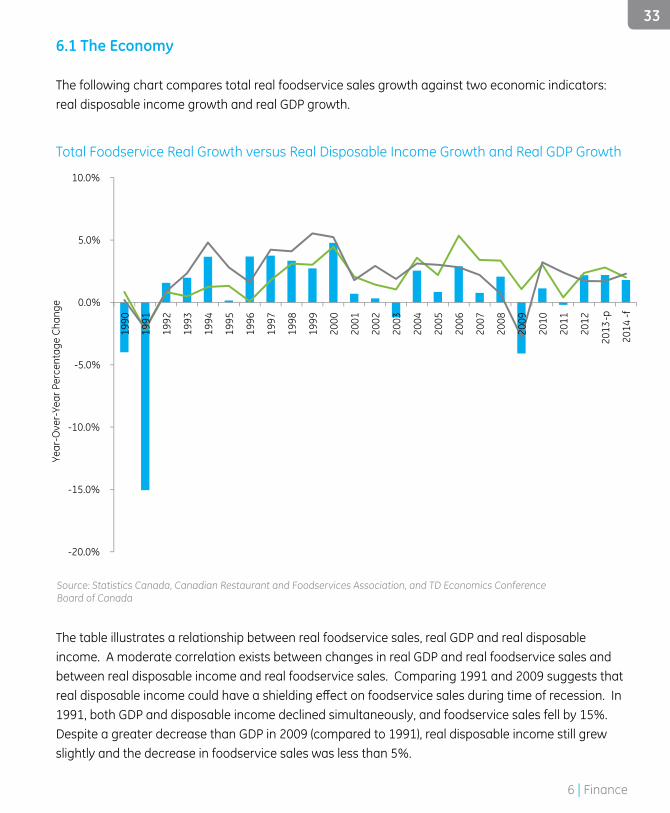

The following chart compares total real foodservice sales growth against two economic indicators: real disposable income growth and real GDP growth .

The table illustrates a relationship between real foodservice sales, real GDP and real disposable income . A moderate correlation exists between changes in real GDP and real foodservice sales and between real disposable income and real foodservice sales . Comparing 1991 and 2009 suggests that real disposable income could have a shielding effect on foodservice sales during time of recession. In 1991, both GDP and disposable income declined simultaneously, and foodservice sales fell by 15% . Despite a greater decrease than GDP in 2009 (compared to 1991), real disposable income still grew slightly and the decrease in foodservice sales was less than 5% .

Total Foodservice Real Growth versus Real Disposable Income Growth and Real GDP Growth

Source: Statistics Canada, Canadian Restaurant and Foodservices Association, and TD Economics Conference Board of Canada

-20.0%

-15.0%

-10.0%

-5.0%

0.0%

5.0%

10.0%

1990

1991

1992

1993

1994

1995

1996

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

2013

-p

2014

-f

Year

-Ove

r-Ye

ar P

erce

ntag

e Ch

ange

Real Foodservice Sales-Total Real Disposable Income Real GDP

33

6 | Finance

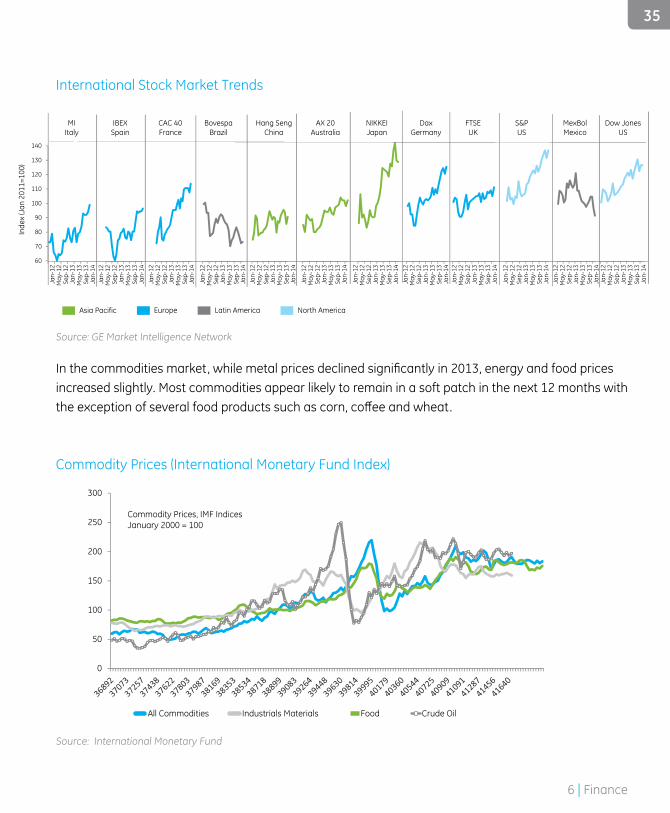

6.2 Global Financial Markets

The positive outlook of the 2014 global economy is shaped by key trends: US, Japan and the Eurozone are experiencing their first synchronized expansion since 2010, supporting global growth in 2014; consumer confidence is increasing in North America; and financial markets are stabilizing in developing economies with China’s strong 7 .5% GDP growth target for this year .

But while strong, China’s growth will be an important support for the global economy in 2014, debt has grown quickly and rebalancing the economy has a long way to go . Also, escalating geopolitical tensions in East Asia and the fast-changing new developments in Ukraine could have substantial economic repercussions that disrupt growth and trade .

Central banks will maintain loose monetary policies to combat deflationary pressures and the European Central Bank (ECB) will ease money supply further at a time when the US Fed considers tapering . The Euro is up by 3% since January, which reduces the ability of Eurozone peripheral countries to benefit from export boom to offset the decline in domestic demand.

The growing importance of liquidity of financial markets will continue to drive swings in assets and commodity prices . In 2013, commodities underperformed developed market equities for the third consecutive year, following ten years of outperformance; slowing China growth, US Fed tightening and rising supply expectations were the main factors weighing on prices . But 2014 could be a turnaround year as a slight increase in metal prices could be expected and oil and gas prices are likely to remain range-bound providing tactical trade opportunities .

Policy response such as tightening rates in emerging markets (EM) in 2013, market volatility and capital flow exposed some weaknesses, especially in India, Brazil, Indonesia, and Turkey leaving less room for fiscal stimulus; fiscal balances deteriorated in most EMs since the onset of the global financial crisis, while the social pressure to expand government spending remained.

The global equities market continues to recover, showing overall better performance in 2013 in comparison to 2012 . The best performers in last three months have been Japan, US, Germany and France . Japan boosted stock prices in the fourth quarter of 2013 supported by a stronger Yen but emerging market currencies lost ground . The broadly held view that 2014 would be the year of equities, with bonds doomed by the taper-driven rise in yields has already hit the first road bump. The following chart shows the current trends of the main stock markets by region .

34

2014 Canadian Chain Restaurant Industry Review

0

50

100

150

200

250

300

All Commodities Industrials Materials Food Crude Oil

Commodity Prices, IMF IndicesJanuary 2000 = 100

International Stock Market Trends

60

70

80

90

100

110

120

130

140

Jan-

12M

ay-1

2Se

p-12

Jan-

13M

ay-1

3Se

p-13

Jan-

14Ja

n-12

May

-12

Sep-

12Ja

n-13

May

-13

Sep-

13Ja

n-14

Jan-

12M

ay-1

2Se

p-12

Jan-

13M

ay-1

3Se

p-13

Jan-

14

Jan-

12M

ay-1

2Se

p-12

Jan-

13M

ay-1

3Se

p-13

Jan-

14Ja

n-12

May

-12

Sep-

12Ja

n-13

May

-13

Sep-

13Ja

n-14

Jan-

12M

ay-1

2Se

p-12

Jan-

13M

ay-1

3Se

p-13

Jan-

14

Jan-

12M

ay-1

2Se

p-12

Jan-

13M

ay-1

3Se

p-13

Jan-

14Ja

n-12

May

-12

Sep-

12Ja

n-13

May

-13

Sep-

13Ja

n-14

Jan-

12M

ay-1

2Se

p-12

Jan-

13M

ay-1

3Se

p-13

Jan-

14

Jan-

12M

ay-1

2Se

p-12

Jan-

13M

ay-1

3Se

p-13

Jan-

14Ja

n-12

May

-12

Sep-

12Ja

n-13

May

-13

Sep-

13Ja

n-14

Jan-

12M

ay-1

2Se

p-12

Jan-

13M

ay-1

3Se

p-13

Jan-

14

Inde

x (J

an 2

011=

100)

MIItaly

CAC 40France

Hang SengChina

BovespaBrazil

NIKKEIJapan

AX 20Australia

DaxGermany

FTSEUK

Dow JonesUS

S&PUS

MexBolMexico

IBEXSpain

North AmericaLatin AmericaEuropeAsia Pacific

Source: GE Market Intelligence Network

In the commodities market, while metal prices declined significantly in 2013, energy and food prices increased slightly . Most commodities appear likely to remain in a soft patch in the next 12 months with the exception of several food products such as corn, coffee and wheat.

Commodity Prices (International Monetary Fund Index)

Source: International Monetary Fund

35

6 | Finance

Commodities Percentage Change Year-Over-Year

Source: GE Capital

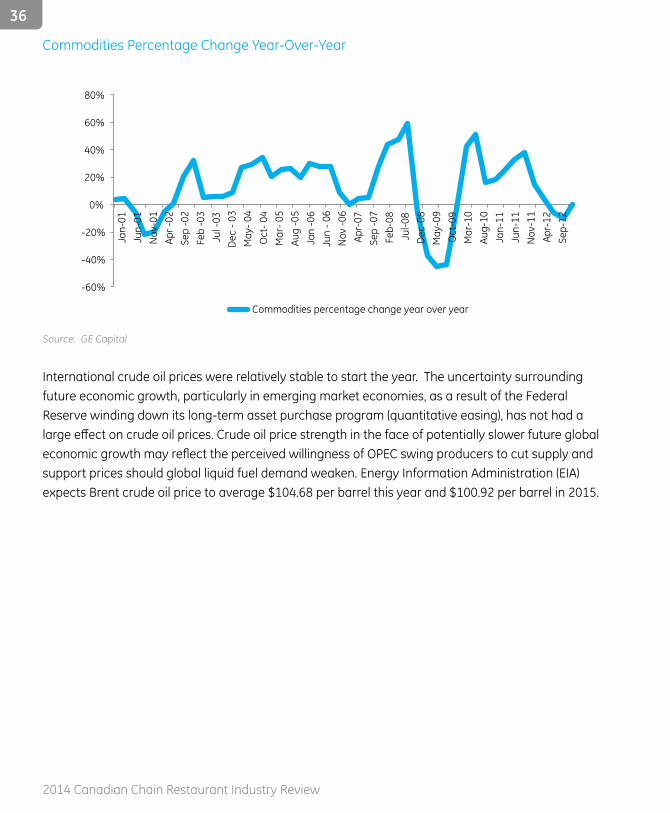

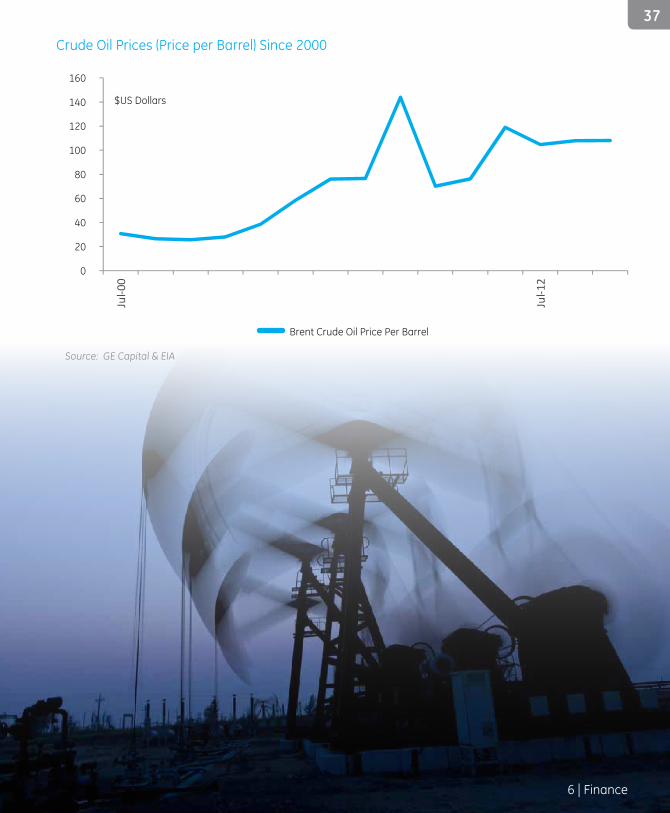

International crude oil prices were relatively stable to start the year . The uncertainty surrounding future economic growth, particularly in emerging market economies, as a result of the Federal Reserve winding down its long-term asset purchase program (quantitative easing), has not had a large effect on crude oil prices. Crude oil price strength in the face of potentially slower future global economic growth may reflect the perceived willingness of OPEC swing producers to cut supply and support prices should global liquid fuel demand weaken . Energy Information Administration (EIA) expects Brent crude oil price to average $104 .68 per barrel this year and $100 .92 per barrel in 2015 .

-60%

-40%

-20%

0%

20%

40%

60%

80%

Commodities percentage change year over year

Jan-

01

Jun-

01

Nov

-01

Apr -

02

Sep

-02

Feb

-03

Jul -

03

Dec

- 03

M

ay- 0

4 O

ct- 0

4 M

ar- 0

5 Au

g -0

5 Ja

n -0

6 Ju

n - 0

6 N

ov -0

6 Ap

r-07

Se

p -0

7 Fe

b-08

Ju

l-08

Dec

-08

May

-09

Oct

-09

Mar

-10

Aug-

10

Jan-

11

Jun-

11

Nov

-11

Apr-

12

Sep-

12

36

2014 Canadian Chain Restaurant Industry Review

Crude Oil Prices (Price per Barrel) Since 2000

Source: GE Capital & EIA

0

20

40

60

80

100

120

140

160

Jul-0

0

Jul-1

2

$US Dollars

Brent Crude Oil Price Per Barrel

37

6 | Finance

6.3 Financial Markets in Canada

Analysis

The Europe and US economic recovery will benefit Canada’s near-term economic outlook and the stability of its financial markets. The domestic demand is improving, the unemployment rate is falling, the Purchasing Manager’s index increasing and business confidence is up. However, high tensions and geopolitical uncertainty (e .g ., Ukraine) are tempering global economic optimism in 2014 .

Concerns about the high level of Canadian household debt is still persisting, so a rise in the base interest rate would be troublesome because so much debt is tied to mortgages and could cause a sudden deleveraging .

The Bank of Canada held firm on keeping its interest rate at 1% as an incentive to increase investment and exports as foreign demand strengthens and uncertainty diminishes. With an inflation rate close to 2% and the economy expanding, GE Capital expects that the Bank of Canada will hold interest rates steady until the end of 2014 .

Since October last year, the Canadian dollar lost 6 .8% against the US dollar driven by soft exports, a limited shift toward business investment, and US Fed’s stance . As the US recovery builds, and exports and investment improve, GE Capital expects the Canadian dollar to stabilize .

Forecast

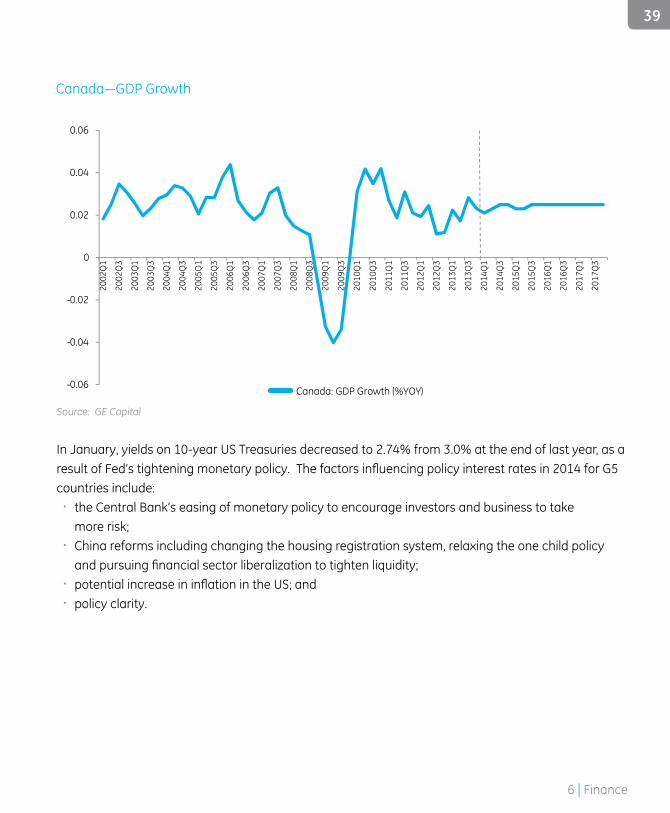

Although Canada’s overall export growth rates were below expectations in 2013, the Canadian economy rebounded at 2 .9% GDP growth on a quarter to quarter basis annualized in the fourth quarter, representing 2% on an annual basis; the oil extraction and mining sectors showed the strongest growth supporting the GDP’s increase . In 2014, strong increases in investment will be expected in transportation and warehousing, housing and public administration sectors . Geographically, total capital investment is anticipated to increase in six of 13 provinces and territories in 2014 . Alberta anticipates the largest increase to support the oil and gas industry .

Despite the unexpected decrease of employment in January, the Canadian unemployment rate will continue to be close to 7% with a moderated wage growth in the next three years that will help to keep prices in line as the Canadian government holds the interest rate steady during 2014 .

GE Capital sees Canada’s GDP growth picking up to 2 .3% in 2014 based on recovery of US, China and Europe, increased government investment and the weak Canadian dollar that will boost Canadian exports .

The US economy is forecasted to grow by almost 4% in 2014 with the labour market improving, US consumer confidence growing, steady gasoline prices and increasing US housing starts.

38

2014 Canadian Chain Restaurant Industry Review

Canada—GDP Growth

Source: GE Capital

In January, yields on 10-year US Treasuries decreased to 2 .74% from 3 .0% at the end of last year, as a result of Fed’s tightening monetary policy. The factors influencing policy interest rates in 2014 for G5 countries include:

� the Central Bank’s easing of monetary policy to encourage investors and business to take more risk;

� China reforms including changing the housing registration system, relaxing the one child policy and pursuing financial sector liberalization to tighten liquidity;

� potential increase in inflation in the US; and � policy clarity .

-0.06

-0.04

-0.02

0

0.02

0.04

0.06

2002

Q1

2002

Q3

2003

Q1

2003

Q3

2004

Q1

2004

Q3

2005

Q1

2005

Q3

2006

Q1

2006

Q3

2007

Q1

2007

Q3

2008

Q1

2008

Q3

2009

Q1

2009

Q3

2010

Q1

2010

Q3

2011

Q1

2011

Q3

2012

Q1

2012

Q3

2013

Q1

2013

Q3

2014

Q1

2014

Q3

2015

Q1

2015

Q3

2016

Q1

2016

Q3

2017

Q1

2017

Q3

Canada: GDP Growth (%YOY)

39

6 | Finance

G5 Average Policy Interest Rates

Source: GE Capital

Note: The G5 economies include the United States, the Euro Area, Japan, the United Kingdom and Canada .

0%

1%

2%

3%

4%

5%

6%M

ar-0

0

Nov

-01

Jul-0

1

Mar

-02

Nov

-02

Jul-0

3

Mar

-04

Nov

-04

Jul-0

5

Mar

-06

Nov

-06

Jul-0

7

Mar

-08

Nov

-08

Jul-0

9

Mar

-10

Nov

-10

Jul-1

1

Mar

-12

Nov

-12

Jul-1

3

Mar

-14

GE Average Policy Interest Rate

40

2014 Canadian Chain Restaurant Industry Review

6.4 Total Financeable Debt Market Size and Loan Volumes

The following charts summarize total financial debt in the Canadian restaurant industry by transaction type and segment type as prepared by GE Capital. GE Capital estimates a total financeable debt of $4.5 billion. Financeable debt is used for refinancing/renovations, acquisitions and new builds.

Total Financeable Debt by Transaction Type ($millions)

Total Financeable Debt by Transaction Type ($MM)

Source: GE Capital

Source: GE Capital

$4,488.1

$868.1

$1,077.7

$400.2 $421.5

$361.2 $351.3

$175.8 $62.6 $45.3 $12.7

TotalMarket

QSR Coffee Casual Sandwich Pizza Asian Express ChickenFamilyCasual

PremiumCasual

$4,488.1

$2,394.9

$1,655.1

$438.2

Total Market Refinance/Renovation Acquisiton New Build

41

6 | Finance

Cost ofDoing Business 7.1 Cost of Sales7.2 Labour Costs7.3 Rental and Occupancy Costs7.4 Other Operating Costs 7.5 CAPEX

7

42

2014 Canadian Chain Restaurant Industry Review

7.1 Cost of Sales

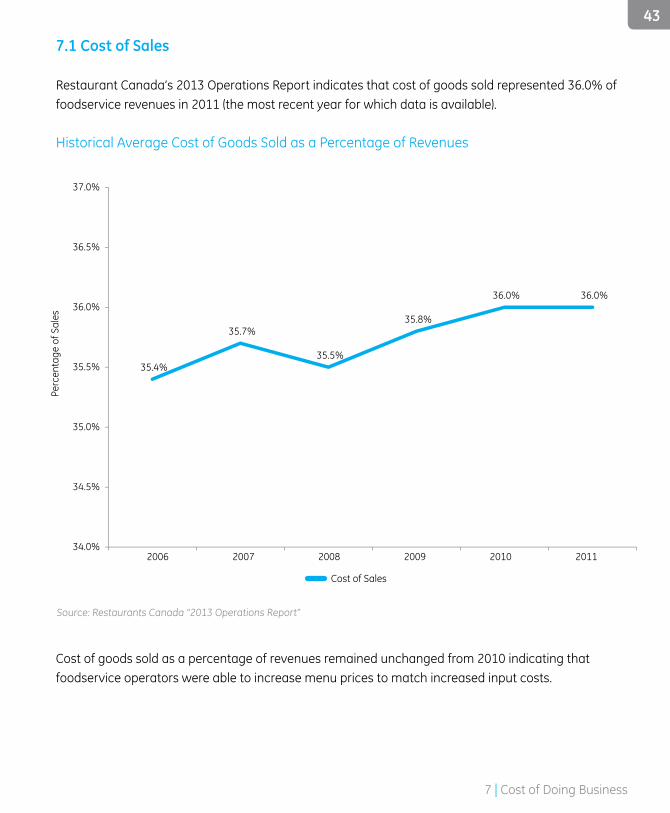

Restaurant Canada’s 2013 Operations Report indicates that cost of goods sold represented 36 .0% of foodservice revenues in 2011 (the most recent year for which data is available) .

Historical Average Cost of Goods Sold as a Percentage of Revenues

Cost of goods sold as a percentage of revenues remained unchanged from 2010 indicating that foodservice operators were able to increase menu prices to match increased input costs .

35.4%

35.7%

35.5%

35.8%

36.0% 36.0%

34.0%

34.5%

35.0%

35.5%

36.0%

36.5%

37.0%

2006 2007 2008 2009 2010 2011

Perc

enta

ge o

f Sal

es

Cost of Sales

Source: Restaurants Canada “2013 Operations Report”

43

7 | Cost of Doing Business

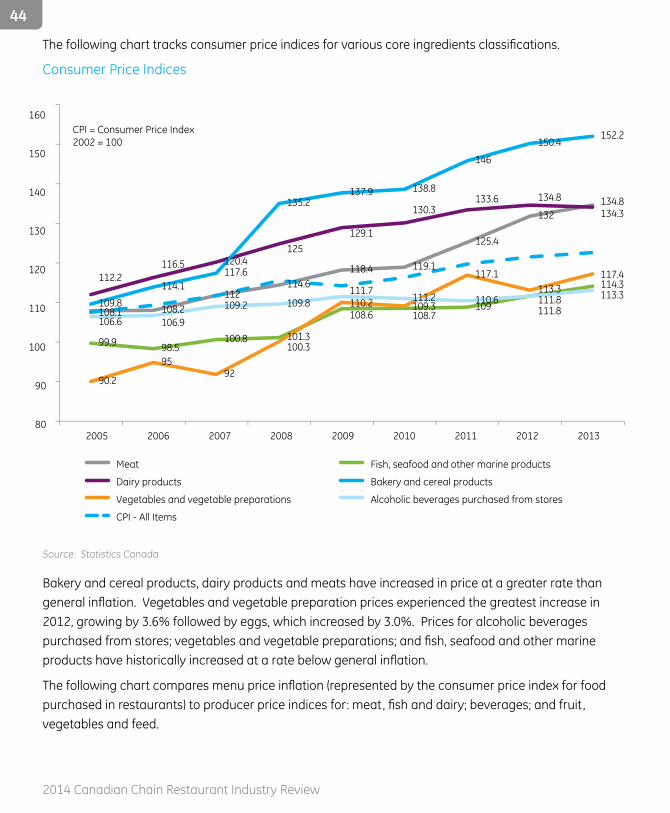

The following chart tracks consumer price indices for various core ingredients classifications.

Consumer Price Indices

Bakery and cereal products, dairy products and meats have increased in price at a greater rate than general inflation. Vegetables and vegetable preparation prices experienced the greatest increase in 2012, growing by 3 .6% followed by eggs, which increased by 3 .0% . Prices for alcoholic beverages purchased from stores; vegetables and vegetable preparations; and fish, seafood and other marine products have historically increased at a rate below general inflation.

The following chart compares menu price inflation (represented by the consumer price index for food purchased in restaurants) to producer price indices for: meat, fish and dairy; beverages; and fruit, vegetables and feed .

108.1 108.2 112

114.6 118.4 119.1

125.4

132 134.8

99.9 98.5 100.8 101.3

108.6

108.7 109 111.8

114.3 112.2

116.5

120.4 125

129.1

130.3

133.6

134.8

134.3

109.8

114.1 117.6

135.2 137.9 138.8

146

150.4 152.2

90.2

95 92

100.3

110.2 109.3

117.1 113.3

117.4

106.6 106.9

109.2 109.8 111.7 111.2 110.6

111.8 113.3

80

90

100

110

120

130

140

150

160

20062005 2007 2008 2009 2010 2011 20132012

Meat Fish, seafood and other marine products

Dairy products Bakery and cereal products

Vegetables and vegetable preparations Alcoholic beverages purchased from stores

CPI - All Items

CPI = Consumer Price Index2002 = 100

Source: Statistics Canada

44

2014 Canadian Chain Restaurant Industry Review

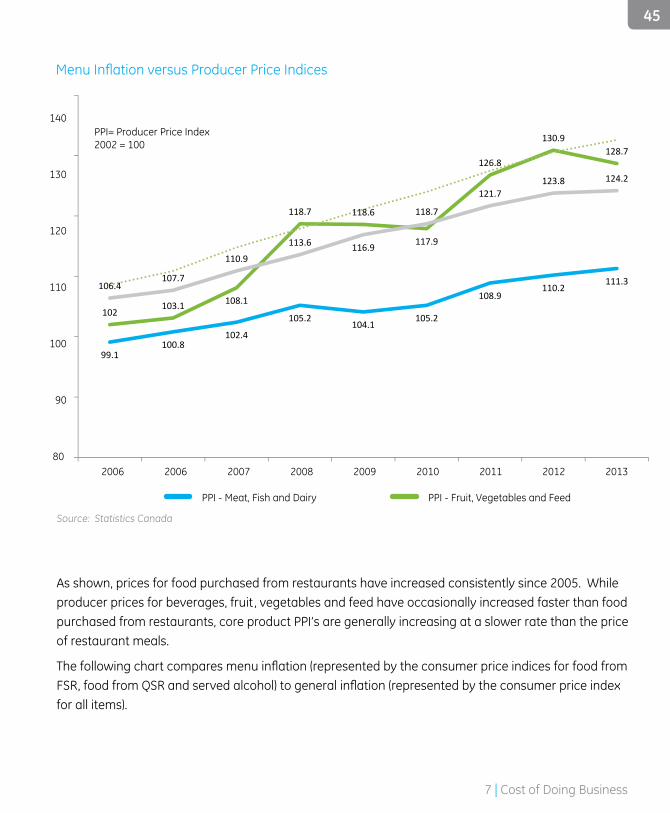

Menu Inflation versus Producer Price Indices

As shown, prices for food purchased from restaurants have increased consistently since 2005 . While producer prices for beverages, fruit, vegetables and feed have occasionally increased faster than food purchased from restaurants, core product PPI’s are generally increasing at a slower rate than the price of restaurant meals .

The following chart compares menu inflation (represented by the consumer price indices for food from FSR, food from QSR and served alcohol) to general inflation (represented by the consumer price index for all items) .

Source: Statistics Canada

99.1 100.8

102.4

105.2 104.1

105.2

108.9 110.2

111.3

102 103.1 108.1

118.7 118.6

117.9

126.8

130.9 128.7

106.4 107.7

110.9

113.6 116.9

118.7

121.7 123.8 124.2

80

90

100

110

120

130

140PPI= Producer Price Index2002 = 100

2006 2006 2007 2008 2009 2010 2011 2012 2013

PPI - Meat, Fish and Dairy PPI - Fruit, Vegetables and Feed

PPI - Beverages CPI - Food from Restaurants

45

7 | Cost of Doing Business

Menu Inflation versus General Inflation

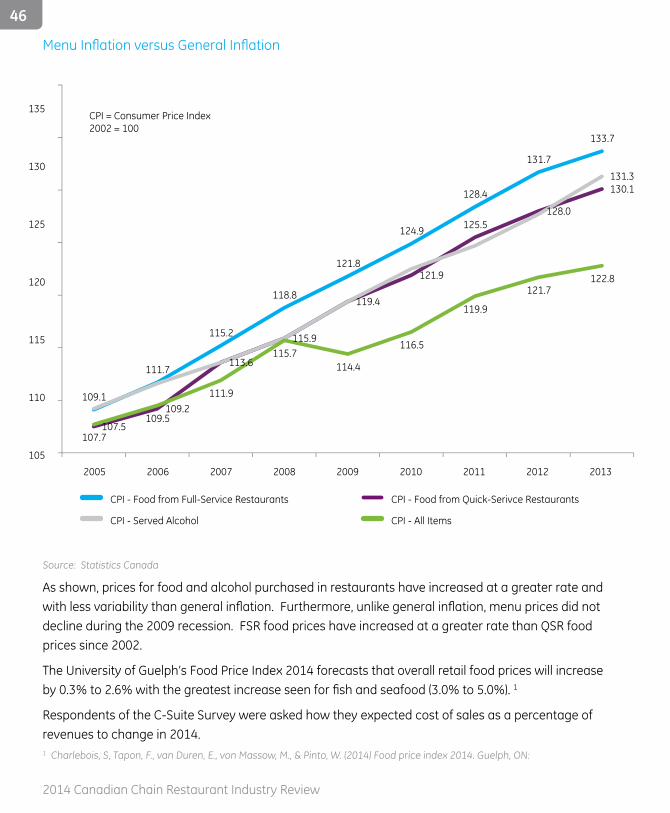

As shown, prices for food and alcohol purchased in restaurants have increased at a greater rate and with less variability than general inflation. Furthermore, unlike general inflation, menu prices did not decline during the 2009 recession . FSR food prices have increased at a greater rate than QSR food prices since 2002 .

The University of Guelph’s Food Price Index 2014 forecasts that overall retail food prices will increase by 0.3% to 2.6% with the greatest increase seen for fish and seafood (3.0% to 5.0%). 1

Respondents of the C-Suite Survey were asked how they expected cost of sales as a percentage of revenues to change in 2014 .

Source: Statistics Canada

1 Charlebois, S, Tapon, F ., van Duren, E ., von Massow, M ., & Pinto, W . (2014) Food price index 2014 . Guelph, ON:

109.1

111.7

115.2

118.8

121.8

124.9

128.4

131.7

133.7

107.5

109.2

113.6

115.9

119.4

121.9

125.5 128.0

130.1 131.3

107.7

109.5

111.9

115.7 114.4

116.5

119.9

121.7 122.8

CPI = Consumer Price Index 2002 = 100

105

110

115

120

125

130

135

2005 2006 2007 2008 2009 2010 2011 20132012

CPI - Food from Full-Service Restaurants CPI - Food from Quick-Serivce Restaurants

CPI - Served Alcohol CPI - All Items

46

2014 Canadian Chain Restaurant Industry Review

2 Growers have been liquidating their herds over last seven years . 2013 saw the lowest US calf production in North American since the 1950s . Similar declines have occurred in Canada . Several US processing facilities could close in 2014 due to low supply .

47

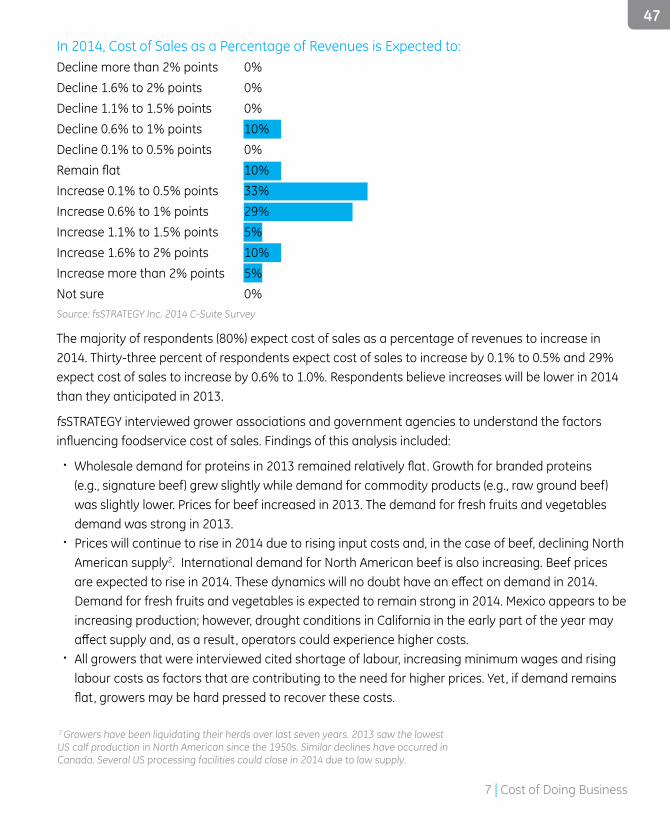

In 2014, Cost of Sales as a Percentage of Revenues is Expected to:Decline more than 2% points 0%Decline 1 .6% to 2% points 0%Decline 1 .1% to 1 .5% points 0%Decline 0 .6% to 1% points 10%Decline 0 .1% to 0 .5% points 0%Remain flat 10%Increase 0 .1% to 0 .5% points 33%Increase 0 .6% to 1% points 29%Increase 1 .1% to 1 .5% points 5%Increase 1 .6% to 2% points 10%Increase more than 2% points 5%Not sure 0%Source: fsSTRATEGY Inc . 2014 C-Suite Survey

The majority of respondents (80%) expect cost of sales as a percentage of revenues to increase in 2014 . Thirty-three percent of respondents expect cost of sales to increase by 0 .1% to 0 .5% and 29% expect cost of sales to increase by 0 .6% to 1 .0% . Respondents believe increases will be lower in 2014 than they anticipated in 2013 .

fsSTRATEGY interviewed grower associations and government agencies to understand the factors influencing foodservice cost of sales. Findings of this analysis included:

� Wholesale demand for proteins in 2013 remained relatively flat. Growth for branded proteins (e .g ., signature beef) grew slightly while demand for commodity products (e .g ., raw ground beef) was slightly lower . Prices for beef increased in 2013 . The demand for fresh fruits and vegetables demand was strong in 2013 .

� Prices will continue to rise in 2014 due to rising input costs and, in the case of beef, declining North American supply2 . International demand for North American beef is also increasing . Beef prices are expected to rise in 2014. These dynamics will no doubt have an effect on demand in 2014. Demand for fresh fruits and vegetables is expected to remain strong in 2014 . Mexico appears to be increasing production; however, drought conditions in California in the early part of the year may affect supply and, as a result, operators could experience higher costs.

� All growers that were interviewed cited shortage of labour, increasing minimum wages and rising labour costs as factors that are contributing to the need for higher prices . Yet, if demand remains flat, growers may be hard pressed to recover these costs.

7 | Cost of Doing Business

7.2 Labour Costs

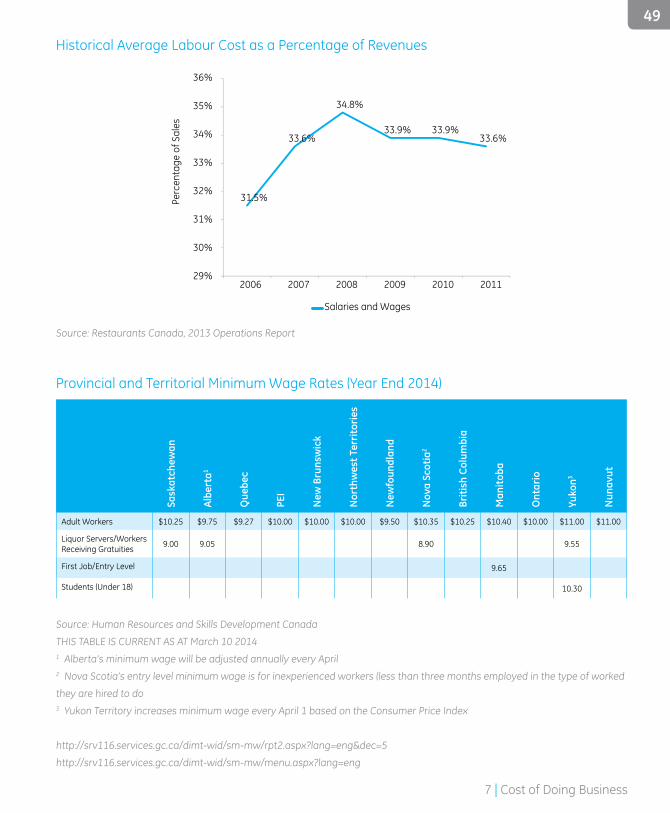

Restaurants Canada’s 2013 Operations Report indicates that salaries and wages represented 33 .6% of foodservice revenues in 2011 (the most recent year for which data is available) .

Salaries and wages as a percentage of revenues in 2011 decreased slightly from 33 .9% in 2009 and 2010 to 33 .6% in 2011 .

By the end of 2014, provincial and territorial minimum wages for adult workers will have increased by 15% from minimum wages at the end of 2009 .

3 Operators will need to innovate with existing ingredients as opposed to using new producer products .

fsSTRATEGY also interviewed foodservice distributors to understand the factors influencing foodservice cost of sales . Findings of this analysis included:

� Foodservice distributors report demand in 2013 remained relatively flat compared to 2012. The only growth experienced was from independent operators; chain demand remained flat. Distributors did not see prices increase as much as expected, as some of the dire cost increases that were predicted did not materialize from suppliers .

� Distributors expect foodservice sales to grow by two to three percent in 2014, with a small amount of traffic growth and the majority of growth coming through operator price increases. Weather conditions in the early part of 2014 have dampened restaurant traffic. Some distributors hope that the declining Canadian dollar will spur some additional cross border tourism and, therefore, foodservice demand. Distributors are facing significant labour shortage issues and rising fuel costs. Distributors expect price increases for their customers in 2014 will be at or just over inflation. Distributors are working hard to absorb rising costs by introducing greater efficiency through technological innovations and better route scheduling .

� Distributors suggest that a number of issues will affect the foodservice industry in 2014. These include:

� continuing concern over supply-managed products and their effect on foodservice operating costs;

� limited product innovation on the part of food processors, leading to some limitations on new product introduction by foodservice operators3; and

� continuing consolidation in both the food distribution and foodservice operator sectors .

48

2014 Canadian Chain Restaurant Industry Review

31.5%

33.6%

34.8%

33.9% 33.9% 33.6%

29%

30%

31%

32%

33%

34%

35%

36%

2006 2007 2008 2009 2010 2011

Perc

enta

ge o

f Sal

es

Salaries and Wages

Historical Average Labour Cost as a Percentage of Revenues

Provincial and Territorial Minimum Wage Rates (Year End 2014)

Sask

atch

ewan

Albe

rta1

Que

bec

PEI

New

Bru

nsw

ick

Nor

thw

est T

erri

tori

es

New

foun

dlan

d

Nov

a Sc

otia

2

Briti

sh C

olum

bia

Man

itoba

Ont

ario

Yuko

n3

Nun

avut

Adult Workers $10 .25 $9 .75 $9 .27 $10 .00 $10 .00 $10 .00 $9 .50 $10 .35 $10 .25 $10 .40 $10 .00 $11 .00 $11 .00

Liquor Servers/Workers Receiving Gratuities 9 .00 9 .05 8 .90 9 .55

First Job/Entry Level 9 .65

Students (Under 18) 10 .30

Source: Human Resources and Skills Development Canada

THIS TABLE IS CURRENT AS AT March 10 20141 Alberta’s minimum wage will be adjusted annually every April2 Nova Scotia’s entry level minimum wage is for inexperienced workers (less than three months employed in the type of worked

they are hired to do3 Yukon Territory increases minimum wage every April 1 based on the Consumer Price Index

http://srv116.services.gc.ca/dimt-wid/sm-mw/rpt2.aspx?lang=eng&dec=5

http://srv116.services.gc.ca/dimt-wid/sm-mw/menu.aspx?lang=eng

Source: Restaurants Canada, 2013 Operations Report

49

7 | Cost of Doing Business

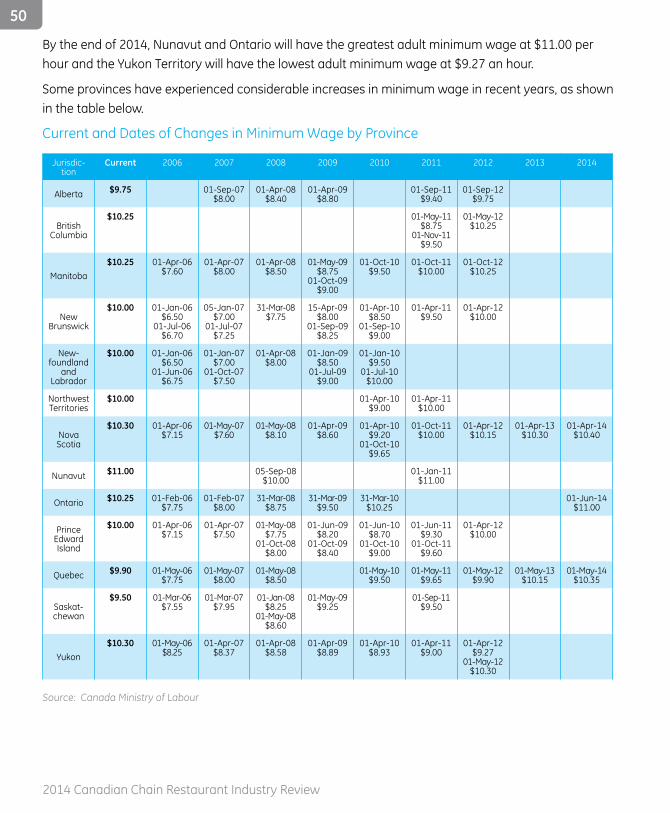

By the end of 2014, Nunavut and Ontario will have the greatest adult minimum wage at $11 .00 per hour and the Yukon Territory will have the lowest adult minimum wage at $9 .27 an hour .

Some provinces have experienced considerable increases in minimum wage in recent years, as shown in the table below .

Current and Dates of Changes in Minimum Wage by Province

Jurisdic-tion

Current 2006 2007 2008 2009 2010 2011 2012 2013 2014

Alberta $9.75 01-Sep-07$8 .00

01-Apr-08$8 .40

01-Apr-09$8 .80

01-Sep-11$9 .40

01-Sep-12$9 .75

British Columbia

$10.25 01-May-11$8 .75

01-Nov-11$9 .50

01-May-12$10 .25

Manitoba$10.25 01-Apr-06

$7 .6001-Apr-07

$8 .0001-Apr-08

$8 .5001-May-09

$8 .7501-Oct-09

$9 .00

01-Oct-10$9 .50

01-Oct-11$10 .00

01-Oct-12$10 .25

New Brunswick

$10.00 01-Jan-06$6 .50

01-Jul-06$6 .70

05-Jan-07$7 .00

01-Jul-07$7 .25

31-Mar-08$7 .75

15-Apr-09$8 .00

01-Sep-09$8 .25

01-Apr-10$8 .50

01-Sep-10$9 .00

01-Apr-11$9 .50

01-Apr-12$10 .00

New-foundland

and Labrador

$10.00 01-Jan-06$6 .50

01-Jun-06$6 .75

01-Jan-07$7 .00

01-Oct-07$7 .50

01-Apr-08$8 .00

01-Jan-09$8 .50

01-Jul-09$9 .00

01-Jan-10$9 .50

01-Jul-10$10 .00

Northwest Territories

$10.00 01-Apr-10$9 .00

01-Apr-11$10 .00

Nova Scotia

$10.30 01-Apr-06$7 .15

01-May-07$7 .60

01-May-08$8 .10

01-Apr-09$8 .60

01-Apr-10$9 .20

01-Oct-10$9 .65

01-Oct-11$10 .00

01-Apr-12$10 .15

01-Apr-13$10 .30

01-Apr-14$10 .40

Nunavut $11.00 05-Sep-08$10 .00

01-Jan-11$11 .00

Ontario $10.25 01-Feb-06$7 .75

01-Feb-07$8 .00

31-Mar-08$8 .75

31-Mar-09$9 .50

31-Mar-10$10 .25

01-Jun-14$11 .00

Prince Edward Island

$10.00 01-Apr-06$7 .15

01-Apr-07$7 .50

01-May-08$7 .75

01-Oct-08$8 .00

01-Jun-09$8 .20

01-Oct-09$8 .40

01-Jun-10$8 .70

01-Oct-10$9 .00

01-Jun-11$9 .30

01-Oct-11$9 .60

01-Apr-12$10 .00

Quebec $9.90 01-May-06$7 .75

01-May-07$8 .00

01-May-08$8 .50

01-May-10$9 .50

01-May-11$9 .65

01-May-12$9 .90

01-May-13$10 .15

01-May-14$10 .35

Saskat-chewan

$9.50 01-Mar-06$7 .55

01-Mar-07$7 .95

01-Jan-08$8 .25

01-May-08$8 .60

01-May-09$9 .25

01-Sep-11$9 .50

Yukon$10.30 01-May-06

$8 .2501-Apr-07

$8 .3701-Apr-08

$8 .5801-Apr-09

$8 .8901-Apr-10

$8 .9301-Apr-11

$9 .0001-Apr-12

$9 .2701-May-12

$10 .30

Source: Canada Ministry of Labour

50

2014 Canadian Chain Restaurant Industry Review

Employment Indices—All Industries, Foodservice and Employees per Foodservice Location

Source: Labour Force Survey, Statistics Canada

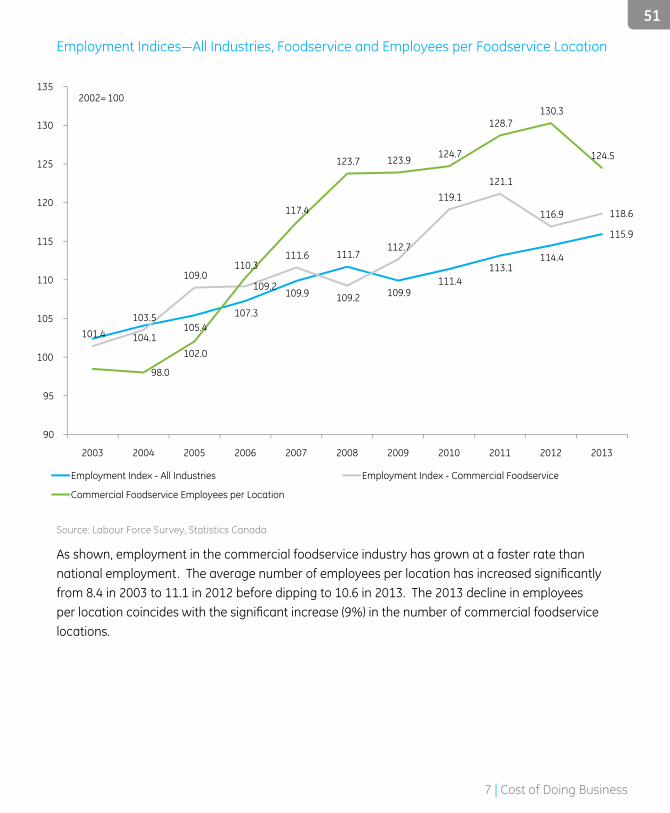

As shown, employment in the commercial foodservice industry has grown at a faster rate than national employment. The average number of employees per location has increased significantly from 8 .4 in 2003 to 11 .1 in 2012 before dipping to 10 .6 in 2013 . The 2013 decline in employees per location coincides with the significant increase (9%) in the number of commercial foodservice locations .

104.1 105.4

107.3

109.9

111.7

109.9 111.4

113.1 114.4

115.9

101.4

103.5

109.0 109.2

111.6

109.2

112.7

119.1 121.1

116.9 118.6

98.0

102.0

110.3

117.4

123.7 123.9 124.7

128.7 130.3

124.5

90

95

100

105

110

115

120

125

130

135

Employment Index - All Industries Employment Index - Commercial Foodservice

Commercial Foodservice Employees per Location

2002 = 100

20052003 2004 2006 2007 2008 2009 2010 2011 20132012

51

7 | Cost of Doing Business

6.8%

7.0%

7.2% 7.2%

7.6% 7.7%

6.2%

6.4%

6.6%

6.8%

7.0%

7.2%

7.4%

7.6%

7.8%

Rental and leasing

Perc

enta

ge o

f Sal

es

2006 2007 2008 2009 2010 2011

7.3 Rental and Occupancy Costs

Restaurants Canada’s 2013 Operations Report indicates that rental and leasing costs accounted for 7 .7% of foodservice revenues in 2011 (the most recent year for which data is available) .

Historical Average Rental and Leasing Cost as a Percentage of Revenues

Source: Restaurants Canada,

2012 Operations Report

52

2014 Canadian Chain Restaurant Industry Review

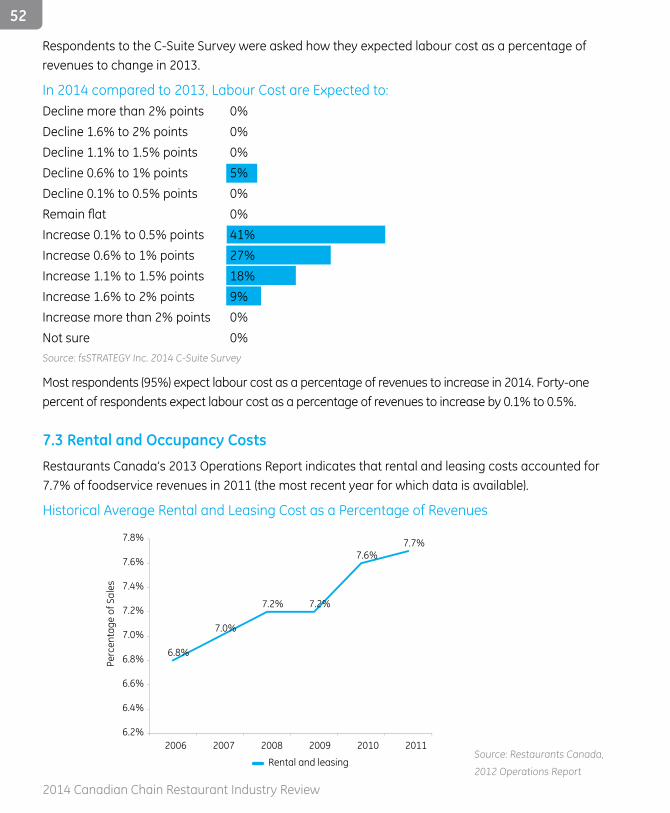

Respondents to the C-Suite Survey were asked how they expected labour cost as a percentage of revenues to change in 2013 .

In 2014 compared to 2013, Labour Cost are Expected to:Decline more than 2% points 0%Decline 1 .6% to 2% points 0%Decline 1 .1% to 1 .5% points 0%Decline 0 .6% to 1% points 5%Decline 0 .1% to 0 .5% points 0%Remain flat 0%Increase 0 .1% to 0 .5% points 41%Increase 0 .6% to 1% points 27%Increase 1 .1% to 1 .5% points 18%Increase 1 .6% to 2% points 9%Increase more than 2% points 0%Not sure 0%Source: fsSTRATEGY Inc . 2014 C-Suite Survey

Most respondents (95%) expect labour cost as a percentage of revenues to increase in 2014 . Forty-one percent of respondents expect labour cost as a percentage of revenues to increase by 0 .1% to 0 .5% .

Rental and leasing costs as a percentage of revenues increased by 0 .1 percentage points in 2011 compared to 2010 .

Respondents to the C-Suite Survey were asked how they expected rent and occupancy cost as a percentage of revenues to change in 2014 .

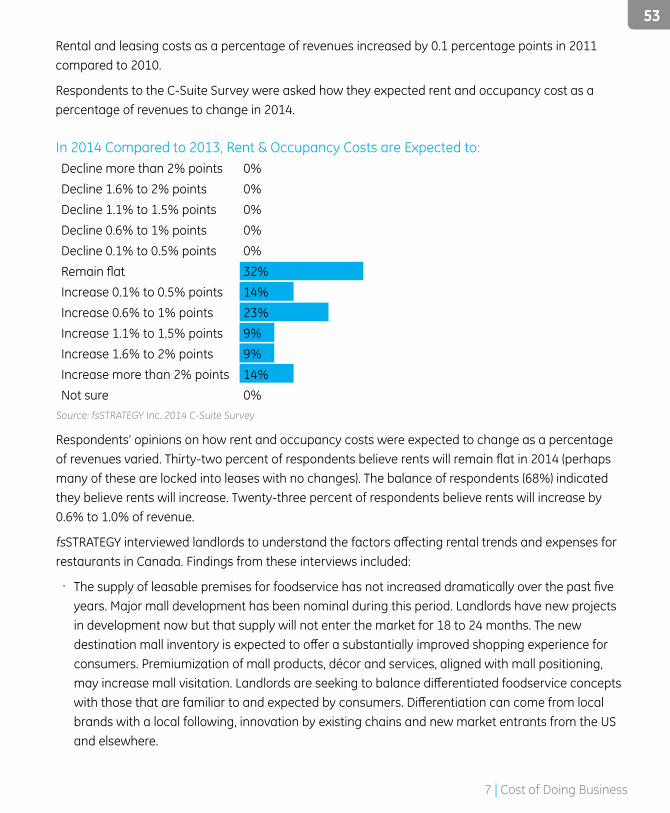

53

In 2014 Compared to 2013, Rent & Occupancy Costs are Expected to: Decline more than 2% points 0%Decline 1 .6% to 2% points 0%Decline 1 .1% to 1 .5% points 0%Decline 0 .6% to 1% points 0%Decline 0 .1% to 0 .5% points 0%Remain flat 32%Increase 0 .1% to 0 .5% points 14%Increase 0 .6% to 1% points 23%Increase 1 .1% to 1 .5% points 9%Increase 1 .6% to 2% points 9%Increase more than 2% points 14%Not sure 0%

Source: fsSTRATEGY Inc . 2014 C-Suite Survey

Respondents’ opinions on how rent and occupancy costs were expected to change as a percentage of revenues varied. Thirty-two percent of respondents believe rents will remain flat in 2014 (perhaps many of these are locked into leases with no changes) . The balance of respondents (68%) indicated they believe rents will increase . Twenty-three percent of respondents believe rents will increase by 0 .6% to 1 .0% of revenue .

fsSTRATEGY interviewed landlords to understand the factors affecting rental trends and expenses for restaurants in Canada . Findings from these interviews included:

� The supply of leasable premises for foodservice has not increased dramatically over the past five years . Major mall development has been nominal during this period . Landlords have new projects in development now but that supply will not enter the market for 18 to 24 months . The new destination mall inventory is expected to offer a substantially improved shopping experience for consumers . Premiumization of mall products, décor and services, aligned with mall positioning, may increase mall visitation. Landlords are seeking to balance differentiated foodservice concepts with those that are familiar to and expected by consumers. Differentiation can come from local brands with a local following, innovation by existing chains and new market entrants from the US and elsewhere .

53

7 | Cost of Doing Business

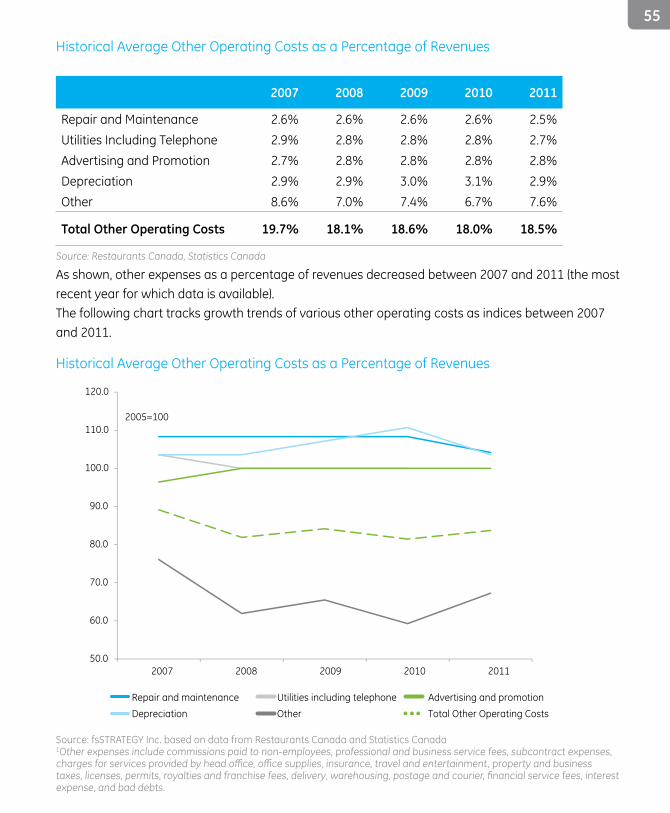

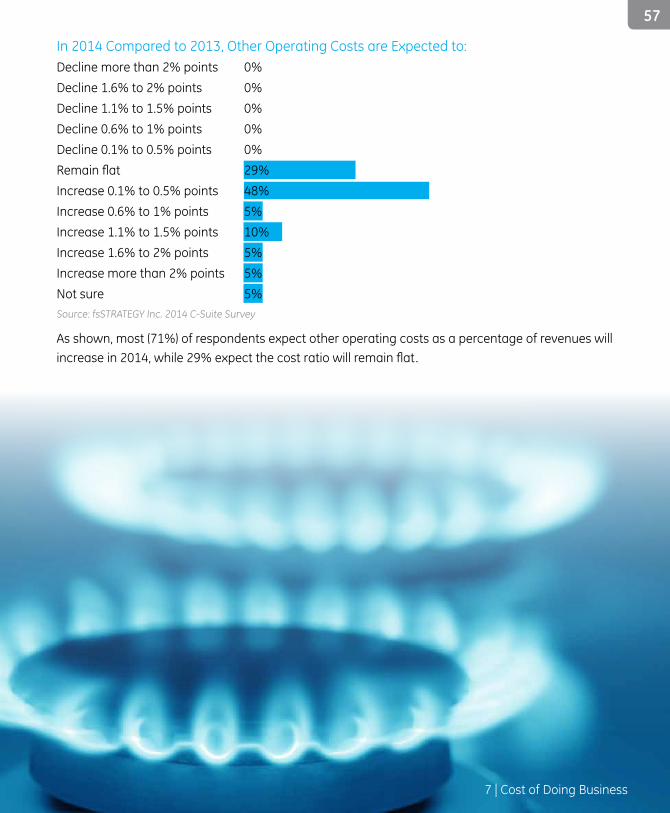

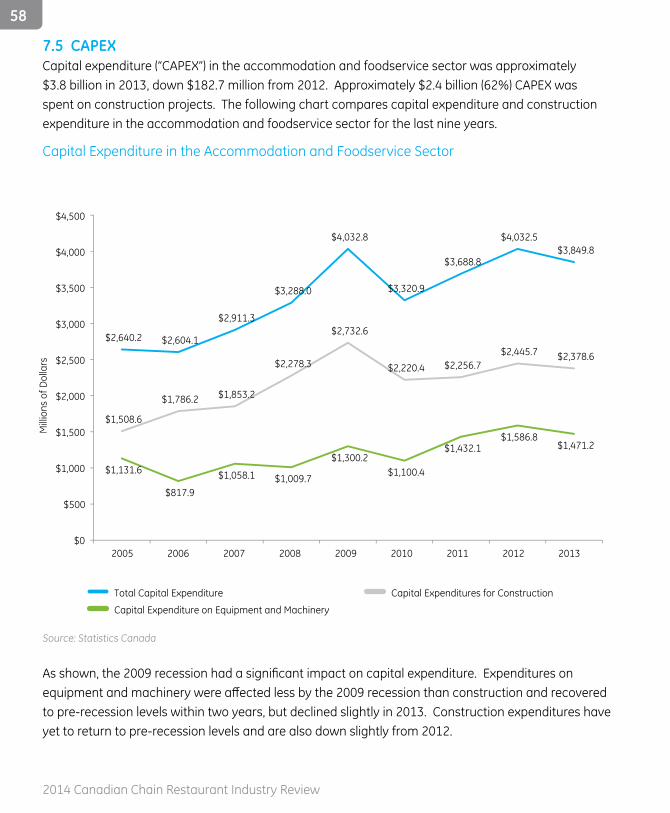

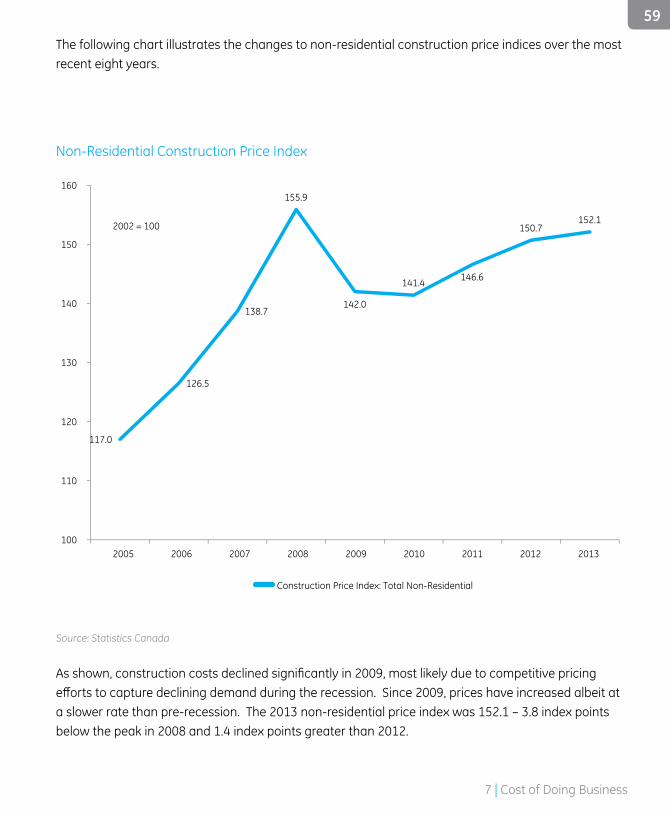

7.4 Other Operating CostsOther operating costs include utilities (including telephone), repair and maintenance, advertising and promotion, depreciation and other operating costs .Restaurants Canada’s 2013 Operations Report indicates that total other operating costs represented 18% of foodservice sales in 2011 . The following table shows the average other operating costs as a percentage of revenues for the most recent five year period available (2007 to 2011).

� Landlords report demand for foodservice space continues to rise . Demand for 1,500 to 3,000 square foot spaces from US chains testing the Canadian market is prevalent . Western Canadian chains are exploring Eastern Canada sites with greater interest . Some operators are beginning to favour the economics of regional as opposed to destination malls .

� Landlords indicate that while foodservice leasing rates are climbing due to market dynamics; compared to retail leasing, prices are relatively attractive . In addition, foodservice operators are demanding greater tenant inducements. Landlords confirm that there is very little good space left in urban areas .

� Landlords reported that leasing prices rose anywhere between 2% and 6% in 2013, depending on regional economic and market conditions . Increases in Alberta and Saskatchewan were at the higher end of the range . Landlords expect price increases in 2014 to track similarly, but perhaps slightly less in Alberta and Saskatchewan .

Time strapped consumers are aggregating their shopping and dining experiences . In addition to ongoing demand for new quick service concepts, fast casual dining (modified counter service) and premium casual dining concepts with healthy food options are in high demand from consumers . Operators able to offer differentiated concepts of these types will have an advantage in gaining lease space .While the leasing market clearly favours landlords, opportunities exist for foodservice operators who can respond to these trends .

54

2014 Canadian Chain Restaurant Industry Review

50.0

60.0

70.0

80.0

90.0

100.0

110.0

120.0

Repair and maintenance Utilities including telephone Advertising and promotion

Depreciation Other Total Other Operating Costs

2007 2008 2009 20112010

2005=100

Historical Average Other Operating Costs as a Percentage of Revenues

Historical Average Other Operating Costs as a Percentage of Revenues

2007 2008 2009 2010 2011