Embed Size (px)

Citation preview

August 16th, 2013

2Q13 Results

2

Disclaimer

The stand-alone and consolidated financial statements were prepared in accordance with the accounting

principles adopted in Brazil, which include corporation law, the pronouncements, instructions and

interpretations issued by the Accounting Pronouncements Committee (CPC) and the regulations of the

Securities and Exchange Commission of Brazil (CVM), combined with specific legislation issued by the

National Electric Power Agency (ANEEL). As the industry regulator, ANEEL has powers to regulate the

concessions. The results are usually presented in both IFRS and former formats in order to permit

comparisons with other periods. However, the results presented in “Regulatory” format are not audited.

ALUPAR uses the audited results based on the IFRS principles to declare dividends.

The forward-looking statements contained in this document relating to the business outlook, projections of

operational and financial results and the growth prospects of ALUPAR are merely projections, and as such

are based exclusively on management’s expectations for the future of the business. These expectations

depend materially on changes in market conditions and the performance of the Brazilian economy, the

sector and international markets and therefore are subject to change without prior notice.

3

RS

SC

PR

SP

MG

GO

MT

AC

AM

RR

ROBA

PI

MAPA

AP

TO

CE RN

PE

AL

SE

MS

RJ

ES

DF

PB

Colômbia

Brasil

Chile

Alupar at a Glance Alupar is the only listed company in Brazil operating in transmission and generation segments

Geographic Footprint of the Assets

Operational Under construction

Portfolio of 27 long-term

concessions, starting to expire

in 2030 (transmission) and

2034 (generation)

Transmission

Generation

Begin Concession End

2000

2001

2001

2002

2002

2004

2004

2005

2005

2004

2006

2007

2005

2008

2009

2010

2010

2009

2012

2012

2004

2004

2006

2006

2010

2011

2012

2030

2031

2031

2032

2032

2034

2034

2035

2035

2034

2036

2037

2038

2039

2040

2040

2039

2042

2042

2034

2034

2041

2041

2047

Type Asset

Alupar Concession – Transmission and Generation

Today

Lifetime

Lifetime

Transmission

Transmission

Transmission

Transmission

Transmission

Transmission

Transmission

Transmission

Transmission

Transmission

Transmission

Transmission

Transmission

Transmission

Transmission

Transmission

Transmission

Transmission

Transmission

Transmission

Generation

Generation

Generation

Generation

Generation

Generation

Generation

Transchile

Operating Under Construction

2045

4

Company’s Assets

Nota:

(1) TBE holds 10 transmission assets: EATE, EBTE, ECTE, ENTE, ERTE, ESDE, ETEP; ETSE, LUMITRANS e STC.

V 50.01%

T 35.01%

100%

50.01% V 50.02%

T 50.02%

V 100%

T 50.01%

70.02%

V 50.01%

T 35.01%

99.90%

41.00%

41.00%

41.00%

Transminas

Lavrinhas

47.51%

50.99%

V 50.02%

T 50.02%

51.00%

80.00% 15.00% 80.00% 20.00%

Transirapé

Transleste

Rio Claro

Ijuí

Queluz

STC

EBTE

Transudeste

Lumitrans

ETES

50.01%

V 100%

T 50.01%

STN ENTE EATE

ECTE

ERTE

ETEP

ETEM 62.6%

ETVG

ESDE Ferreira

Gomes

100%

TNE 51.00%

Risaralda 99.86%

100%

ETSE 100%

46.00%

TME

50.99% Energia

dos Ventos

51.00% Transchile

TBE

TBE

TBE

TBE

TBE TBE TBE

TBE TBE

TBE

10.00%

10.00%

10.00%

Alupar is a holding Company with a portfolio of 27 long-term concessions

Transmission

Generation

Under Construction

TBE TBE group’s assets

5

Alupar’s Business Culture

Financial Discipline

Responsible and Sustainable Growth

Efficient Capital Structure

Corporate Governance and Transparency

Skilled and Motivated Team

6

• BM&FBovespa – Level 2 Listing

• UNITs (1 common share + 2 preferred shares ) Securities

• 100% Primary Offering

Breakdown

• 44,390,600 units Shares Issued

• Investments to support Company’s growth in transmission and generation activities Use of Proceeds

• April 23th, 2013 CVM Register

• ALUP11 Ticker

• R$ 787.7 million Net Proceeds

• R$ 821.2 million Gross Offering

Conclusion of Alupar IPO

Notice to the Market, June 3th, 2013

7

• ITAUVEST DTVM S.A. Market Maker

• 6 (six) months renewed automatically Period

• May 28th, 2013 Begin of

Services

Market Maker contracted

• Any time at no cost by either party by written notice with at least thirty days in advance Rescission

Terms

Notice to the Market, May 27th, 2013

8

Annual Permited Revenue - RAP 2013/2014 Cycle

Notes:

(1) Includes RBNI that are not included in the Ratificatory Decision 1559/2013

(2) Was not included in the Ratificatory Decision of previous year (calculated by Alupar)

(3) Not included in the Ratificatory Decision1559/2013 (calculated by Alupar)

(4) USD = BRL 2,20

Notice to the Market, Jul 1st, 2013

BRL million

Transmission Co. 2012/2013 Cycle 2013/2014 Cycle Reajustment

EATE 319,7 339,6 6,2%

ETEP 72,8 77,4 6,2%

ENTE 167,3 177,7 6,2%

ECTE 70,6 75,0 6,2%

ERTE 37,6 39,9 6,2%

STC 30,1 32,0 6,5%

LUMITRANS 19,8 21,0 6,2%

TRANSUDESTE 18,8 20,0 6,2%

TRANSLESTE 30,3 32,2 6,2%

TRANSIRAPE¹ 16,8 23,3 38,7%

ETES 11,1 11,9 6,5%

STN 133,9 142,2 6,2%

EBTE 34,0 36,7 7,8%

TME 33,4 35,6 6,5%

ETEM 10,0 10,7 6,5%

ETVG 3,4 3,6 6,5%

ESDE 10,1 10,8 6,5%

ETSE² 14,8 15,8 6,8%

TNE³ 126,3 134,5 6,5%

Transchile⁴ 14,8 15,4 3,9%

TOTAL 1.175,6 1.255,1 6,8%

9

Material Fact, August 8th, 2013

Transmission Assets share acquisition by EATE (direct subsidiary)

V 50.02%

T 50.02%

70.02%

Transminas

Transirapé

Transleste

Transudeste

EATE

TBE

10.00%

10.00%

10.00%

70.02%

41.00%

41.00%

41.00%

Transminas

Transirapé

Transleste

Transudeste

Before Indirect Interest

28.71%

After Indirect Interest

33.71%

R$ 34,1 million Base Price

Approving

from

Buyer

41.00%

41.00%

41.00%

Debt Holders, ANEEL e CADE

EATE

Seller ORTENG

Assets Concession Oper.

Begin Line Ext. RAP/RBNI

Inflation

Index.

Tariff

Review Begin End Km BRL mm

Transleste 2004 2034 2005 150 32,2 IGP - M No

Transudeste 2005 2035 2007 140 20,0 IGP - M No

Transirapé 2005 2035 2007 65 23,3 IGP - M No

355 km BRL 75,5 mi

10

Material Fact, August 14th, 2013

Transmission Assets share acquisition ( ECTE - direct subsidiary)

Before Direct Interest

45.01%

After Direct Interest

47.51% R$ 4,430 million Base Price

Buyer Alupar

Seller MDU Sul

Assets Concession Oper.

Begin Line Ext. RAP/RBNI

Inflation Index. Tariff

Review Begin End Km BRL mm

ECTE 2000 2030 2002 252Km 75,0 IGP - M No

11

Energy Price Hike

0

50

100

150

200

250

300

350

400

450

jan/12 fev/12 mar/12 abr/12 mai/12 jun/12 jul/12 ago/12 set/12 out/12 nov/12 dez/12 jan/13 fev/13 mar/13 abr/13 mai/13 jun/13 jul/13

PLD1 PLD F Averg. PLD1 2012 Averag. PLD1 2013

Energy Spot Prices – BRL

BRL166

BRL 262

0

10

20

30

40

50

60

70

80

90

Jan Fev Mar Abr Mai Jun Jul Ago Set Out Nov Dez

2012

2013

SE/CO Regions Reservoirs - %

12

New eletric energy price methodology due to Resolution CNPE nº03

Expectancy of higher spot prices – PLD - Difference Settlement Price;

Expectancy of reduction in Thermal Dispatch from the thermal plants outside the

order of merit;

Expectancy of reduction of ESS charges

Financial Highlights

14

Financial Highlights

R$ MM 2Q13 2Q12 Var.% 1H13 1H12 % Chg.

Adjusted Net Revenue 302.2 274.4 10.2% 583.3 540.3 8.0%EBITDA (CVM 527) 260.9 219.2 19.0% 488.3 444.6 9.8%Adjusted EBITDA Margin 86.3% 79.9% 6.4 p.p 83.7% 82.3% 1.4 p.pEBITDA (Excluding GSF effects) - - - 501.9 - 12.9%EBITDA Margin (Excluding GSF effects) - - - 86.0% - 3.7 p.pFinancial Result -44.2 -53.1 -16.9% -96.0 -105.6 -9.1%Consolidated Net Income 168.5 128.7 30.9% 315.6 270.2 16.8%Subsidiaries' Minority Interest 92.9 73.6 26.3% 176.0 151.6 16.1%Net Income - Alupar 75.6 55.1 37.1% 139.6 118.7 17.6%Earnings per UNIT (R$) 0.36 0.26 37.1% 0.67 0.57 17.6%Net Income - Alupar (Excluding GSF ) - - - 144.8 - 22.0%Net Debt* 2,159.7 2,501.0 -13.6% 2,159.7 2,501.0 -13.6%Net Debt / Ebitda** 2.1 2.9 -27.4% 2.2 2.8 -21.4%

Key Indicators "CORPORATE LAW(IFRS)"

R$ MM 2Q13 2Q12 Var.% 1H13 1H12 % Chg.

Net Revenue 267.0 251.6 6.1% 536.5 501.2 7.0%EBITDA (CVM 527) 222.5 194.1 14.6% 435.1 400.3 8.7%Ebitda Margin 83.3% 77.2% 6.2 p.p 81.1% 79.9% 1.2 p.pEBITDA (Excluding GSF effects) - - - 448.7 - 12.1%EBITDA Margin (Excluding GSF effects) - - - 83.6% - 3.7 p.pFinancial Result -44.2 -53.0 -16.6% -96.0 -105.5 -9.0%Consolidated Net Income 117.5 94.1 24.9% 220.0 193.3 13.8%Subsidiaries' Minority Interest 69.1 57.4 20.5% 124.5 114.9 8.3%Net Income - Alupar 48.4 36.7 31.7% 95.5 78.4 21.9%Earnings per UNIT (R$) 0.23 0.18 31.7% 0.46 0.38 21.9%Net Income - Alupar (Excluding GSF ) - - - 100.7 - 28.5%Net Debt* 2,159.7 2,501.0 -13.6% 2,159.7 2,501.0 -13.6%Net Debt / Ebitda** 2.4 3.2 -24.7% 2.5 3.1 -20.6%

* Including Securities under Non-Current Assets

**Annualized EBITDA

Key Indicators "REGULATORY"

15

Consolidated Financial Highlights- IFRS

219.2

260.9

79.9% 86.3%

2Q12 2Q13

EBITDA (R$ MM) and Margin (%)

55.1

75.6

2Q12 2Q13

Net Income Alupar (R$ MM)

274.4 302.2

2Q12 2Q13

Ajusted Net Revenues (R$ MM)

540.3 583.3

1H12 1H13

Adjusted Net Revenues (R$ MM)

444.6

488.3 501.9

13.6

1H12 1H13 GSF Adjust. Adjusted 1H13

EBITDA (R$ MM) e Margin (%)

83.7% 86.0%

82.3%

118.7

139.6 144.8 5.2

1H12 1H13 GSF Adjust. Adjusted 1H13

Net Income Alupar (R$ MM)

16

Consolidated Financial Highlights - Regulatory

194.1

222.5

77.2% 83.3%

2Q12 2Q13

EBITDA (R$ MM) e Margin (%)

36.7

48.4

2Q12 2Q13

Net Income Alupar (R$ MM)

251.6

267.0

2Q12 2Q13

Net Revenue (R$ MM)

501.2 536.5

1H12 1H13

Net Revenue (R$ MM)

400.3

435.1 448.7 13.6

1H12 1H13 GSF Adjust. Adjusted 1H13

EBITDA (R$ MM) e Margin (%)

81.1% 83.6%

79.9%

78.4

95.5 100.7 5.2

1H12 1H13 GSF Adjust. 1S13 Ajustado

Net Income Alupar (R$ MM)

17

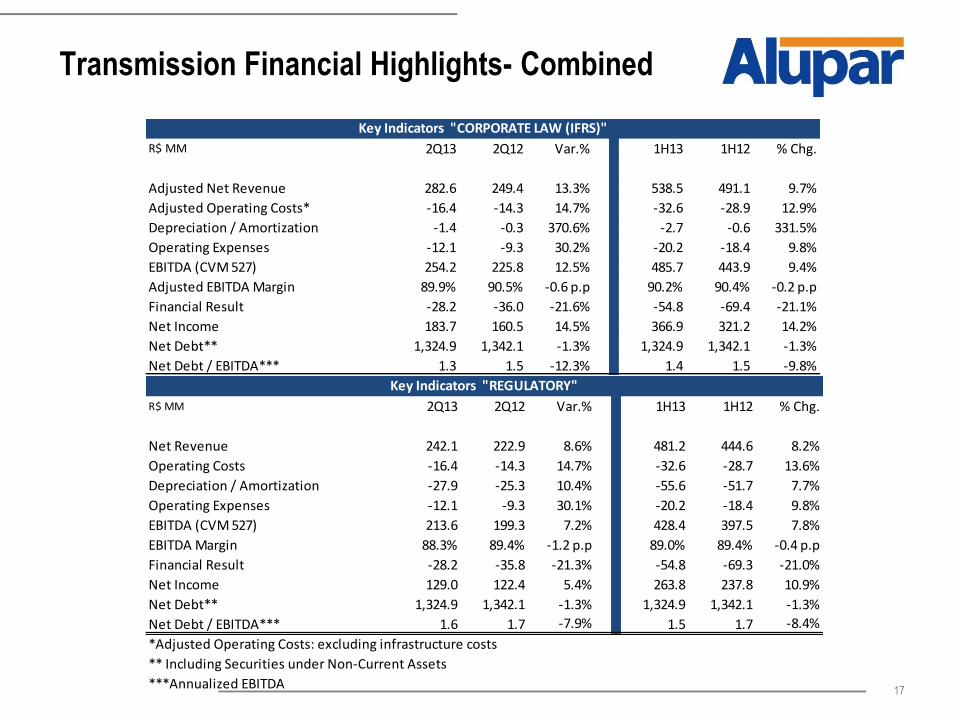

Transmission Financial Highlights- Combined

R$ MM 2Q13 2Q12 Var.% 1H13 1H12 % Chg.

Adjusted Net Revenue 282.6 249.4 13.3% 538.5 491.1 9.7%

Adjusted Operating Costs* -16.4 -14.3 14.7% -32.6 -28.9 12.9%

Depreciation / Amortization -1.4 -0.3 370.6% -2.7 -0.6 331.5%

Operating Expenses -12.1 -9.3 30.2% -20.2 -18.4 9.8%

EBITDA (CVM 527) 254.2 225.8 12.5% 485.7 443.9 9.4%

Adjusted EBITDA Margin 89.9% 90.5% -0.6 p.p 90.2% 90.4% -0.2 p.p

Financial Result -28.2 -36.0 -21.6% -54.8 -69.4 -21.1%

Net Income 183.7 160.5 14.5% 366.9 321.2 14.2%

Net Debt** 1,324.9 1,342.1 -1.3% 1,324.9 1,342.1 -1.3%

Net Debt / EBITDA*** 1.3 1.5 -12.3% 1.4 1.5 -9.8%

Key Indicators "CORPORATE LAW (IFRS)"

R$ MM 2Q13 2Q12 Var.% 1H13 1H12 % Chg.

Net Revenue 242.1 222.9 8.6% 481.2 444.6 8.2%

Operating Costs -16.4 -14.3 14.7% -32.6 -28.7 13.6%

Depreciation / Amortization -27.9 -25.3 10.4% -55.6 -51.7 7.7%

Operating Expenses -12.1 -9.3 30.1% -20.2 -18.4 9.8%

EBITDA (CVM 527) 213.6 199.3 7.2% 428.4 397.5 7.8%

EBITDA Margin 88.3% 89.4% -1.2 p.p 89.0% 89.4% -0.4 p.p

Financial Result -28.2 -35.8 -21.3% -54.8 -69.3 -21.0%

Net Income 129.0 122.4 5.4% 263.8 237.8 10.9%

Net Debt** 1,324.9 1,342.1 -1.3% 1,324.9 1,342.1 -1.3%

Net Debt / EBITDA*** 1.6 1.7 -7.9% 1.5 1.7 -8.4%

*Adjusted Operating Costs: excluding infrastructure costs

** Including Securities under Non-Current Assets

***Annualized EBITDA

Key Indicators "REGULATORY"

18

Transmission Financial Highlights- Combined

249.4 282.6

491.1 538.5

2Q12 2Q13 1H12 1H13

Adjusted Net Revenue (R$ MM)

222.9 242.1

444.6 481.2

2Q12 2Q13 1H12 1H13

Net Revenue (R$ MM)

122.4 129.0

237.8 263.8

2Q12 2Q13 1H12 1H13

Net Income (R$ MM)

Corporate Law (IFRS)

Regulatory

160.5 183.7

321.2

366.9

2Q12 2Q13 1H13 1H13

Net Income (R$ MM)

225.8 254.2

443.9 485.7

90.5% 89.9% 90.4% 90.2%

2Q12 2Q13 1H12 1H13

EBITDA (R$ MM) and Margin (%)

199,3 213,6

397,5 428,4

89.4% 88.3% 89.4% 89.0%

2Q12 2Q13 1H12 1H13

EBITDA (R$ MM) e Margin (%)

19

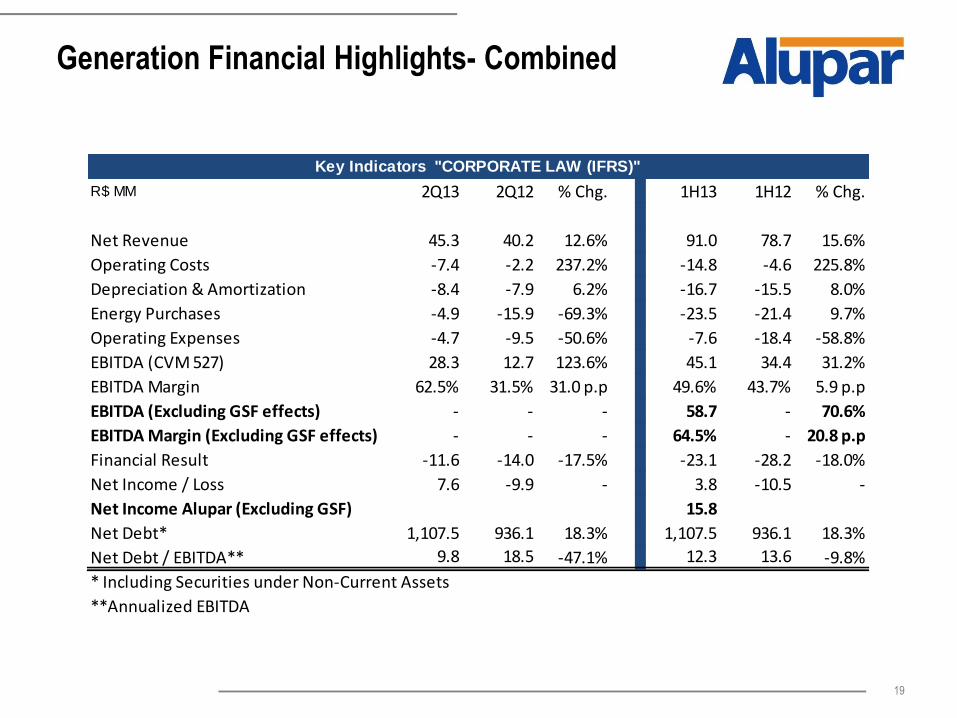

Generation Financial Highlights- Combined

R$ MM 2Q13 2Q12 % Chg. 1H13 1H12 % Chg.

Net Revenue 45.3 40.2 12.6% 91.0 78.7 15.6%

Operating Costs -7.4 -2.2 237.2% -14.8 -4.6 225.8%

Depreciation & Amortization -8.4 -7.9 6.2% -16.7 -15.5 8.0%

Energy Purchases -4.9 -15.9 -69.3% -23.5 -21.4 9.7%

Operating Expenses -4.7 -9.5 -50.6% -7.6 -18.4 -58.8%

EBITDA (CVM 527) 28.3 12.7 123.6% 45.1 34.4 31.2%

EBITDA Margin 62.5% 31.5% 31.0 p.p 49.6% 43.7% 5.9 p.p

EBITDA (Excluding GSF effects) - - - 58.7 - 70.6%

EBITDA Margin (Excluding GSF effects) - - - 64.5% - 20.8 p.p

Financial Result -11.6 -14.0 -17.5% -23.1 -28.2 -18.0%

Net Income / Loss 7.6 -9.9 - 3.8 -10.5 -

Net Income Alupar (Excluding GSF) 15.8

Net Debt* 1,107.5 936.1 18.3% 1,107.5 936.1 18.3%

Net Debt / EBITDA** 9.8 18.5 -47.1% 12.3 13.6 -9.8%

* Including Securities under Non-Current Assets

**Annualized EBITDA

Key Indicators "CORPORATE LAW (IFRS)"

20

34.4

45.1

58.7

13.6

1H12 1H13 GSF Adjust. 1S13 Ajustado

EBITDA (R$ MM) and Margin (%)

49.6%

64.5%

Generation Financial Highlights - Combined

40.2

45.3

2Q12 2Q13

Net Revenue (R$ MM)

78.7

91.0

1H12 1H13

Net Revenue (R$ MM)

12.7

28.3 31.5%

62.5%

2Q12 2Q13

EBITDA (R$ MM) and Margin (%)

(9.9)

7.6

2T12 2T13

Net Income (R$ MM)

(10.5)

3.8

15.8

12.0

1H12 1H13 GSF Adjust. Adjusted 1H13

Net Income (R$ mm)

43.7%

21

Indebtedness - Consolidated

33.9%

40.2%

11.0%

0.2% 14.8%

CDI

TJLP

Fixed

Foreign Currency

IPCA

Gross Debt by Index (%)

1,341.4

307.8

4.6 6.4

1,570.9

BNDES (TJLP / IGP-M)

Other Development banks

Others

Foreign Currency

Debentures

Debt Compositon (R$ MM)

3,231.1

1,071.5

2,159.7

Gross Debt Cash and Cash Equivalents Net Debt

Total Debt (R$ MM)

17%

83%

Debt Profile (%)

Short Term Long Term

22

Indebtness - Consolidated

278.9

137.3

424.0

316.3 277.9 250.4

135.2

925.1

792.5

117,1

92.1

83.8 34.1 133.1

79.9

224.9

Cash and Cash Equivalents

2013 2014 2015 2016 2017 2018 after 2018

Debt Amortization Schedule (R$ MM)

Subsidiárias Controladora Bridges

156.9

Moody’s Investors Service

Corporate (national scale) AA+ Corporate (national scale) Aa2.br Corporate (global scale) Ba1

August, 16th , 2013

IR Contacts

Marcelo Costa – IRO

IR Specialist

Guilherme Villani

Luiz Coimbra

Tel.: (011) 2184-9600

![1Q14 RESULTS PRESENTATION - NOS · 1Q14 RESULTS PRESENTATION Monthly Bill per Unique Corporate, SME and SoHo subscribers [Euros] 0 ä 200 ä 1Q13 2Q13 3Q13 4Q13 1Q14 Monthly Bill](https://img.pdfslide.net/doc/110x75/5f4bf904fbd0f2207a556b26/1q14-results-presentation-nos-1q14-results-presentation-monthly-bill-per-unique.jpg)