Embed Size (px)

Citation preview

ISG Confidential. © 2017 Information Services Group, Inc. All Rights Reserved.

Proprietary and Confidential. No part of this document may be reproduced in any form or by any electronic

or mechanical means, including information storage and retrieval devices or systems, without prior written

permission from Information Services Group, Inc.

Global Sourcing and As-a-Service Market Insights

Hosted by:

John King, Bank of America, Merrill Lynch

17 October 2017

THIRD QUARTER 2017

ISG Confidential. © 2017 Information Services Group, Inc. All Rights Reserved 2EMEA 3Q17

Covering the state of the

combined Traditional

Sourcing and As-a-Service

industry for the EMEA

commercial market.

Welcome to the 60th Quarterly EMEA ISG Index

Barry Matthews Partner, UK

Wayne ButterfieldDirector – Cognitive & AI Innovation and Automation

Friedrich LoeerPartner, DACH

ISG Confidential. © 2017 Information Services Group, Inc. All Rights Reserved 3EMEA 3Q17

‘‘

*Contracts with ACV ≥ €4M from the ISG Contracts Knowledgebase™

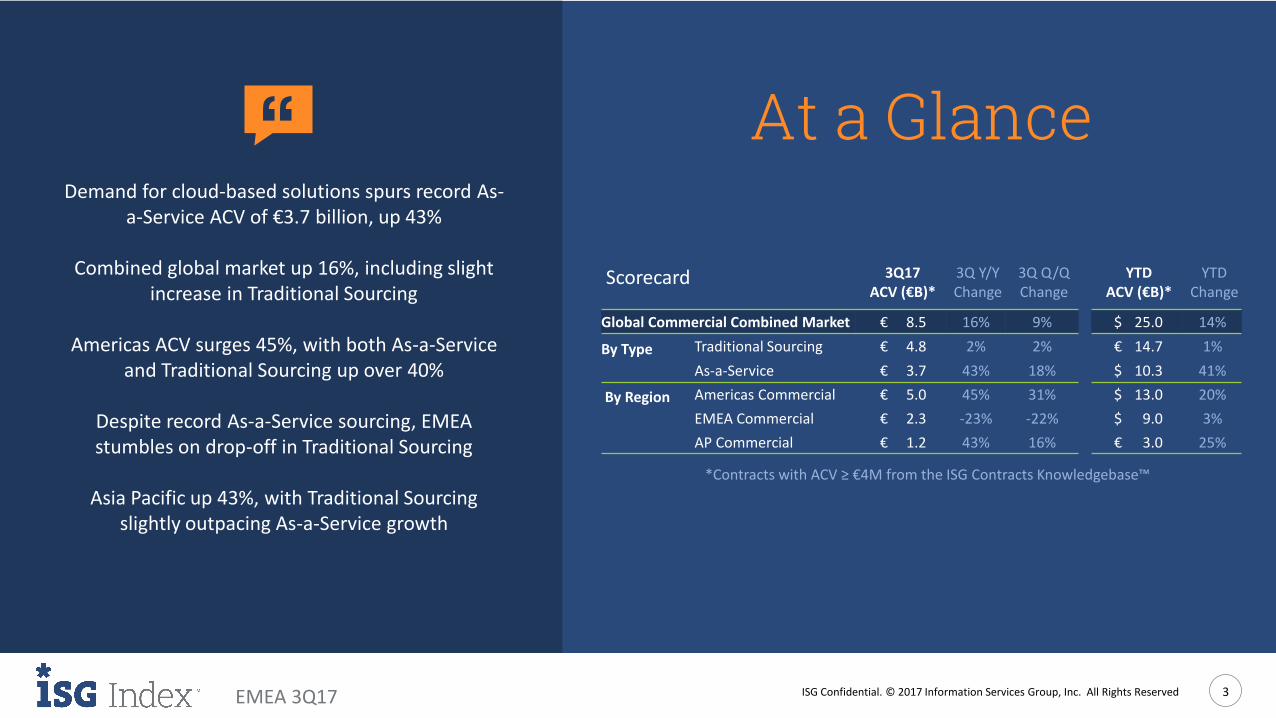

At a GlanceDemand for cloud-based solutions spurs record As-

a-Service ACV of €3.7 billion, up 43%

Combined global market up 16%, including slight increase in Traditional Sourcing

Americas ACV surges 45%, with both As-a-Service and Traditional Sourcing up over 40%

Despite record As-a-Service sourcing, EMEA stumbles on drop-off in Traditional Sourcing

Asia Pacific up 43%, with Traditional Sourcing slightly outpacing As-a-Service growth

Scorecard 3Q17 3Q Y/Y 3Q Q/Q YTD YTD ACV (€B)* Change Change ACV (€B)* Change

Global Commercial Combined Market € 8.5 16% 9% $ 25.0 14%

By Type Traditional Sourcing € 4.8 2% 2% € 14.7 1%

As-a-Service € 3.7 43% 18% $ 10.3 41%

By Region Americas Commercial € 5.0 45% 31% $ 13.0 20%

EMEA Commercial € 2.3 -23% -22% $ 9.0 3%

AP Commercial € 1.2 43% 16% € 3.0 25%

ISG Confidential. © 2017 Information Services Group, Inc. All Rights Reserved 4EMEA 3Q17

Global Commercial Sector Contracting Trends3Q17 Combined Market ACV up 16% Y/Y on record high As-a-Service ACV;

YTD, Traditional Sourcing remains static but with record high contracting activity (based on number of awards).

Global Commercial Sector Quarterly ACV (€B)

Global Commercial Sector YTD ACV (€B) Global Commercial Sector YTD ACV by Type (€B)

Global Commercial Sector Quarterly ACV (€B)

Global Commercial Sector YTD ACV (€B) Global Commercial Sector YTD ACV by Type (€B)

€ 4.8 € 4.7 € 5.2 € 4.5€ 4.7 € 4.6

€ 5.3 € 6.0

€ 4.7 € 5.2 € 4.2

€ 5.5 € 4.7

€ 5.6 € 5.5

€ 3.7 € 3.2 € 3.4

€ 3.2 € 2.6 € 2.3 € 2.4

€ 2.3 € 2.2 € 1.8

€ 1.7 € 1.5

€ 1.5 € 1.7 € 1.4

€ 8.5 € 7.9

€ 8.6 € 7.7 € 7.3 € 6.9

€ 7.7 € 8.3

€ 6.9 € 7.0 € 5.9

€ 7.0 € 6.2

€ 7.3 € 6.9

3Q172Q1Q4Q3Q162Q1Q4Q3Q152Q1Q4Q3Q142Q1Q14

Traditional Sourcing As-a-Service

€ 14.7 € 14.6 € 14.1 € 15.8

€ 10.3 € 7.3€ 5.7 € 4.7

€ 7.7 € 8.3 € 7.0

€ 25.0 € 29.6 € 28.1€ 27.5

2017201620152014

YTD Traditional Sourcing YTD As-a-Service Combined 4Q

€ 11.6

€ 3.1

€ 2.6

€ 7.7

€ 0

€ 5

€ 10

€ 15

ITO BPO SaaS IaaS

Range of Prior 3 YTDs Avg of Prior 3 YTDsYTD 3Q16 YTD 3Q17

ISG Confidential. © 2017 Information Services Group, Inc. All Rights Reserved 5EMEA 3Q17

EMEA Commercial Sector Contracting TrendsCombined Market in EMEA declines 23% Y/Y; record ACV levels in As-a-Service (+48%) can’t offset decline in Traditional Sourcing (-43%);

YTD, Combined Market increases 3% with strength in IaaS and a flurry of Traditional Sourcing activity from early in 2017.

EMEA Commercial Sector Quarterly ACV (€B)

EMEA Commercial Sector YTD ACV (€B) EMEA Commercial Sector YTD ACV by Type (€B)

€ 1.3

€ 2.2 € 2.8

€ 2.1 € 2.4

€ 1.9

€ 2.6 € 3.2

€ 2.3 € 2.4 € 1.9

€ 2.7 € 2.2

€ 2.7 € 2.7 € 1.0

€ 0.8 € 0.9

€ 0.9 € 0.7 € 0.6

€ 0.5€ 0.6

€ 0.6 € 0.5 € 0.5

€ 0.4 € 0.4

€ 0.4 € 0.4 € 2.3

€ 3.0 € 3.6

€ 3.0 € 3.1 € 2.5

€ 3.1€ 3.8

€ 2.9 € 2.9 € 2.4

€ 3.1 € 2.6

€ 3.1 € 3.1

3Q172Q1Q4Q3Q162Q1Q4Q3Q152Q1Q4Q3Q142Q1Q14

Traditional Sourcing As-a-Service

€ 6.3 € 6.9 € 6.6 € 7.6

€ 2.7 € 1.8 € 1.6 € 1.3 € 3.0 € 3.8 € 3.1

€ 9.0 € 11.7 € 12.0 € 12.0

2017201620152014

YTD Traditional Sourcing YTD As-a-Service Combined 4Q

€ 4.9

€ 1.4 € 0.6

€ 2.1

€0

€2

€4

€6

€8

ITO BPO SaaS IaaS

Range of 3 YTDs Avg of Prior 3 YTDsYTD 3Q16 YTD 3Q17

ISG Confidential. © 2017 Information Services Group, Inc. All Rights Reserved 6EMEA 3Q17

EMEA Commercial Sector Industry Award TrendsYTD, mixed results in many industry sectors with Financial Services leading and Manufacturing and Telecom lagging; Financial Services and mid-

sized verticals CPG and Business Services lead the way with double-digit gains in both Traditional Sourcing and As-a-Service.

Manufacturing and Retail are the exceptions.

Traditional

Sourcing

YTD ACV (€B)

EMEA

Commercial

Industries

As-a-Service

YTD ACV (€B)

EMEA

Commercial

Industries

€ 2.1

€ 0.9 € 1.1

€ 0.7 € 0.7 € 0.4

€ 0.2 € 0.1 € 0.2 € 0.0

€ 0.5

€ 1.0

€ 1.5

€ 2.0

€ 2.5

Financial Services Manufacturing Energy Telecom & Media Travel, Transport &Leisure

Business Services Healthcare &Pharma

Retail ConsumerPackaged Goods

Range of 3 YTDs Avg of Prior 3 YTDs YTD 3Q16 YTD 3Q17

€ 0.5 € 0.4

€ 0.1

€ 0.3 € 0.3

€ 0.5

€ 0.2 € 0.2 € 0.2

€ 0.0

€ 0.1

€ 0.2

€ 0.3

€ 0.4

€ 0.5

€ 0.6

Financial Services Manufacturing Energy Telecom & Media Travel, Transport &Leisure

Business Services Healthcare &Pharma

Retail ConsumerPackaged Goods

Range of 3 YTDs Avg of Prior 3 YTDs YTD 3Q16 YTD 3Q17

ISG Confidential. © 2017 Information Services Group, Inc. All Rights Reserved 7EMEA 3Q17

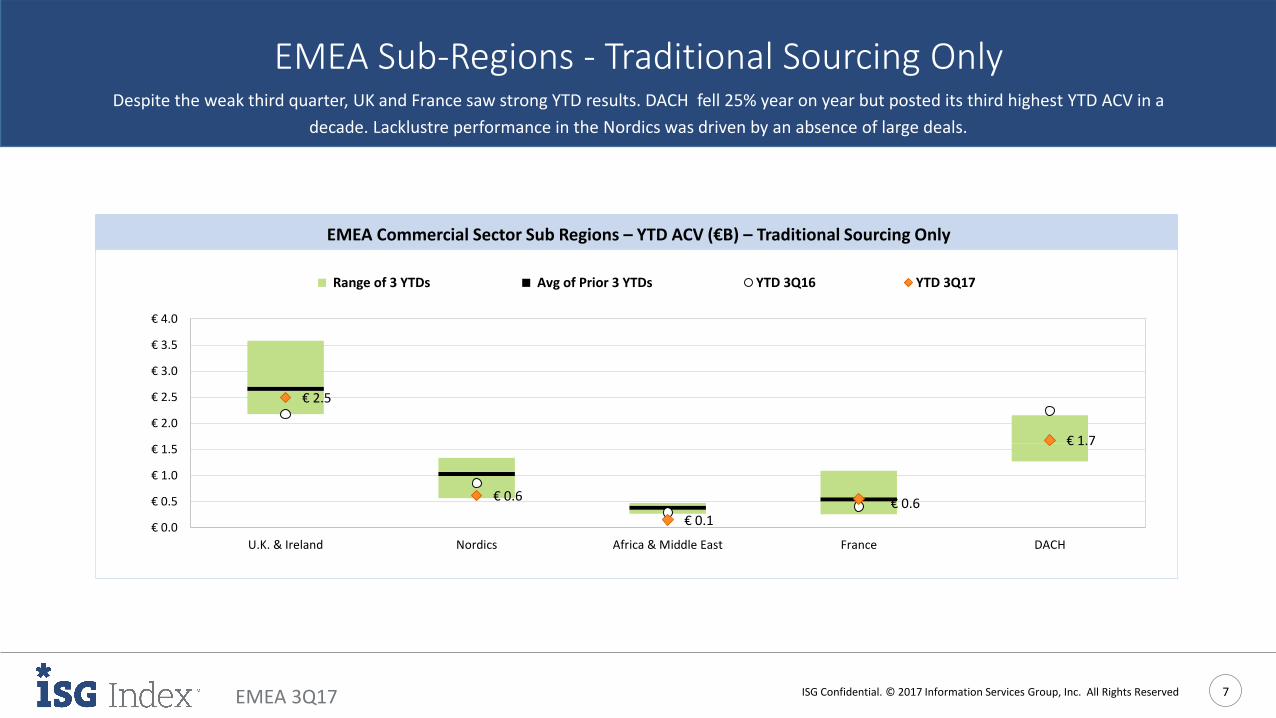

EMEA Sub-Regions - Traditional Sourcing Only Despite the weak third quarter, UK and France saw strong YTD results. DACH fell 25% year on year but posted its third highest YTD ACV in a

decade. Lacklustre performance in the Nordics was driven by an absence of large deals.

EMEA Commercial Sector Sub Regions – YTD ACV (€B) – Traditional Sourcing Only

€ 2.5

€ 0.6

€ 0.1 € 0.6

€ 1.7

€ 0.0

€ 0.5

€ 1.0

€ 1.5

€ 2.0

€ 2.5

€ 3.0

€ 3.5

€ 4.0

U.K. & Ireland Nordics Africa & Middle East France DACH

Range of 3 YTDs Avg of Prior 3 YTDs YTD 3Q16 YTD 3Q17

ISG Confidential. © 2017 Information Services Group, Inc. All Rights Reserved 8EMEA 3Q17

Our Contracts Knowledgebase™is used to determine placements

based on the annual value of commercial contracts

awarded in the past 12 months.

Traditional Sourcing MarketAdare Group

Coor Service ManagementEulen

Firstsource SolutionsHexaware

IbykusKMD

LuxoftMAYKORNNIT A/SVirtusaWNS

As-a-Service MarketInterxionLogMeIn

OVH

Traditional Sourcing MarketAtentoCapita

CarillionDiebold Nixdorf

EVRYHCL

InterserveOrange Business Services

Sopra SteriaTech Mahindra

TietoWipro

As-a-Service MarketAdobe Systems

EquinixUnited Internet

Traditional Sourcing MarketAccenture

AtosBT

CapgeminiCognizant

DXC TechnologyIBM

InfosysTCS

T-Systems

As-a-Service MarketAmazon Web Services

GoogleMicrosoft

OracleSAP

The Building 15 The Breakthrough 15The Big 15Co. Revenues > $10 BSourcing Standouts

EMEACo. Revenues $1 -10 B Co. Revenues < $1 B

Providers in alphabetical order; no rankings implied. Revenues sourced from Hoovers and individual company financial fillings.

theISG15

ISG Confidential. © 2017 Information Services Group, Inc. All Rights Reserved 9EMEA 3Q17

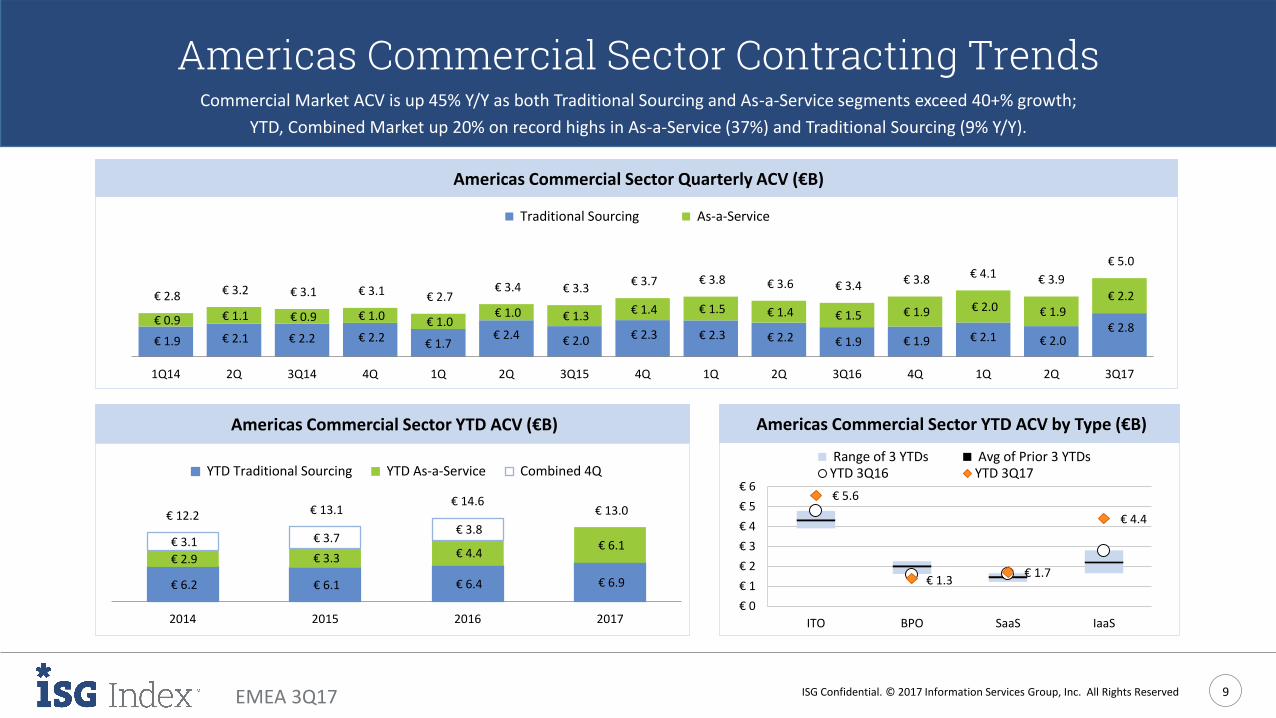

Americas Commercial Sector Contracting TrendsCommercial Market ACV is up 45% Y/Y as both Traditional Sourcing and As-a-Service segments exceed 40+% growth;

YTD, Combined Market up 20% on record highs in As-a-Service (37%) and Traditional Sourcing (9% Y/Y).

Americas Commercial Sector Quarterly ACV (€B)

Americas Commercial Sector YTD ACV (€B) Americas Commercial Sector YTD ACV by Type (€B)

€ 2.8 € 2.0 € 2.1€ 1.9 € 1.9 € 2.2 € 2.3 € 2.3 € 2.0 € 2.4

€ 1.7€ 2.2 € 2.2€ 2.1 € 1.9

€ 2.2 € 1.9 € 2.0 € 1.9 € 1.5 € 1.4 € 1.5 € 1.4 € 1.3 € 1.0

€ 1.0 € 1.0 € 0.9 € 1.1 € 0.9

€ 5.0

€ 3.9€ 4.1€ 3.8 € 3.4 € 3.6 € 3.8 € 3.7 € 3.3 € 3.4

€ 2.7 € 3.1 € 3.1 € 3.2 € 2.8

3Q172Q1Q4Q3Q162Q1Q4Q3Q152Q1Q4Q3Q142Q1Q14

Traditional Sourcing As-a-Service

€ 6.9 € 6.4 € 6.1 € 6.2

€ 6.1 € 4.4 € 3.3 € 2.9

€ 3.8 € 3.7 € 3.1

€ 13.0 € 14.6

€ 13.1 € 12.2

2017201620152014

YTD Traditional Sourcing YTD As-a-Service Combined 4Q

€ 5.6

€ 1.3€ 1.7

€ 4.4

€ 0

€ 1

€ 2

€ 3

€ 4

€ 5

€ 6

ITO BPO SaaS IaaS

Range of 3 YTDs Avg of Prior 3 YTDsYTD 3Q16 YTD 3Q17

ISG Confidential. © 2017 Information Services Group, Inc. All Rights Reserved 10EMEA 3Q17

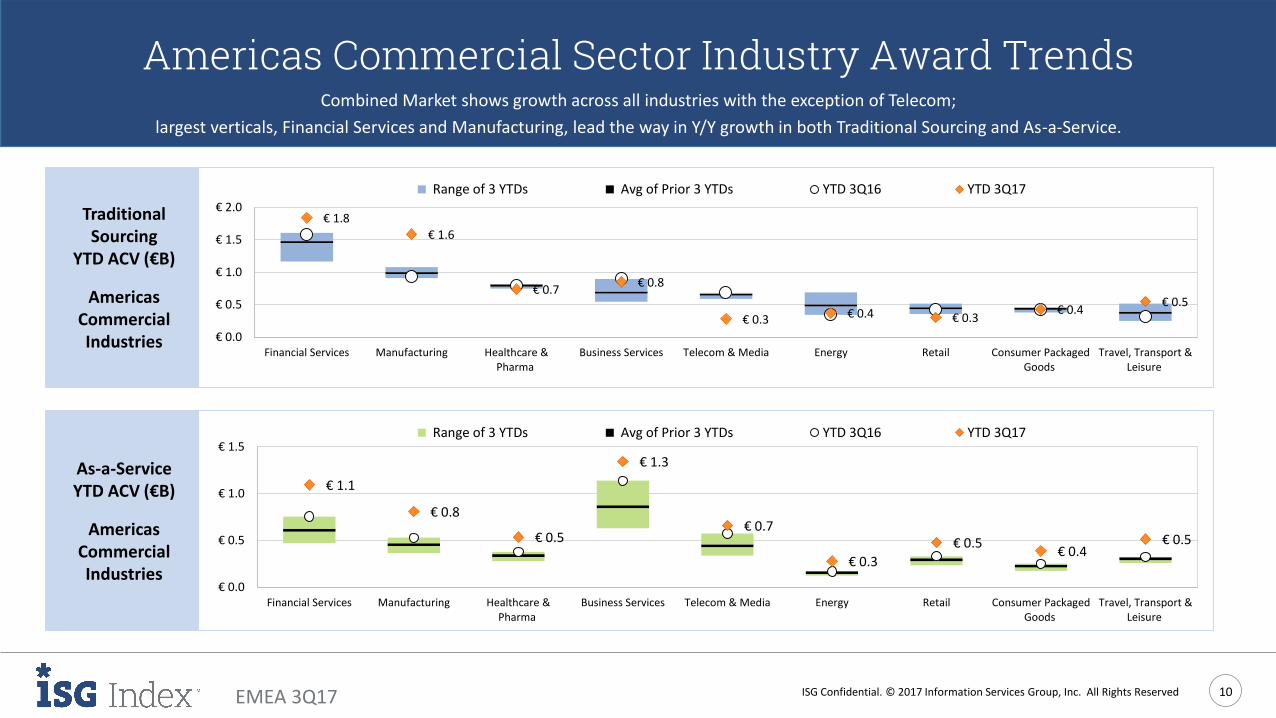

Americas Commercial Sector Industry Award TrendsCombined Market shows growth across all industries with the exception of Telecom;

largest verticals, Financial Services and Manufacturing, lead the way in Y/Y growth in both Traditional Sourcing and As-a-Service.

Traditional Sourcing

YTD ACV (€B)

Americas Commercial Industries

As-a-ServiceYTD ACV (€B)

Americas Commercial Industries

€ 1.8 € 1.6

€ 0.7 € 0.8

€ 0.3 € 0.4 € 0.3 € 0.4

€ 0.5

€ 0.0

€ 0.5

€ 1.0

€ 1.5

€ 2.0

Financial Services Manufacturing Healthcare &Pharma

Business Services Telecom & Media Energy Retail Consumer PackagedGoods

Travel, Transport &Leisure

Range of 3 YTDs Avg of Prior 3 YTDs YTD 3Q16 YTD 3Q17

€ 1.1

€ 0.8

€ 0.5

€ 1.3

€ 0.7

€ 0.3

€ 0.5 € 0.4

€ 0.5

€ 0.0

€ 0.5

€ 1.0

€ 1.5

Financial Services Manufacturing Healthcare &Pharma

Business Services Telecom & Media Energy Retail Consumer PackagedGoods

Travel, Transport &Leisure

Range of 3 YTDs Avg of Prior 3 YTDs YTD 3Q16 YTD 3Q17

ISG Confidential. © 2017 Information Services Group, Inc. All Rights Reserved 11EMEA 3Q17

Asia Pacific Commercial Sector Contracting TrendsCombined Market ACV rises 43% Y/Y on record high As-a-Service awards and best Traditional Sourcing ACV since 2014;

YTD, Asia Pacific ACV is up 25% as both IaaS and ITO ACV increase 30+%.

AP Commercial Sector Quarterly ACV (€B)

AP Commercial Sector YTD ACV (€B) AP Commercial Sector YTD ACV by Type (€B)

€ 1.1

€ 0.3€ 0.3

€ 1.3

€ 0.0

€ 0.5

€ 1.0

€ 1.5

€ 2.0

ITO BPO SaaS IaaS

Range of 3 YTDs Avg of Prior 3 YTDsYTD 3Q16 YTD 3Q17

€ 1.4 € 1.3 € 1.4 € 2.0

€ 1.6€ 1.1 € 0.8

€ 0.6 € 0.8

€ .07€ 0.8

€ 3.0 € 3.2 € 2.9

€ 3.4

2017201620152014

YTD Traditional Sourcing YTD As-a-Service Combined 4Q

€ 0.6 € 0.5

€ 0.3 € 0.4 € 0.4 € 0.5 € 0.4 € 0.4 € 0.5 € 0.5 € 0.5

€ 0.6 € 0.4

€ 0.8 € 0.8

€ 0.6 € 0.5

€ 0.5 € 0.5 € 0.4 € 0.4 € 0.3€ 0.3 € 0.3 € 0.2 € 0.2

€ 0.2 € 0.2

€ 0.2 € 0.2

€ 1.2 € 1.0

€ 0.8 € 0.8 € 0.8 € 0.9€ 0.7 € 0.7€ 0.8 € 0.7 € 0.7

€ 0.8 € 0.6

€ 1.0 € 1.0

3Q172Q1Q4Q3Q162Q1Q4Q3Q152Q1Q4Q3Q142Q1Q14

Traditional Sourcing As-a-Service

ISG Confidential. © 2017 Information Services Group, Inc. All Rights Reserved 12EMEA 3Q17

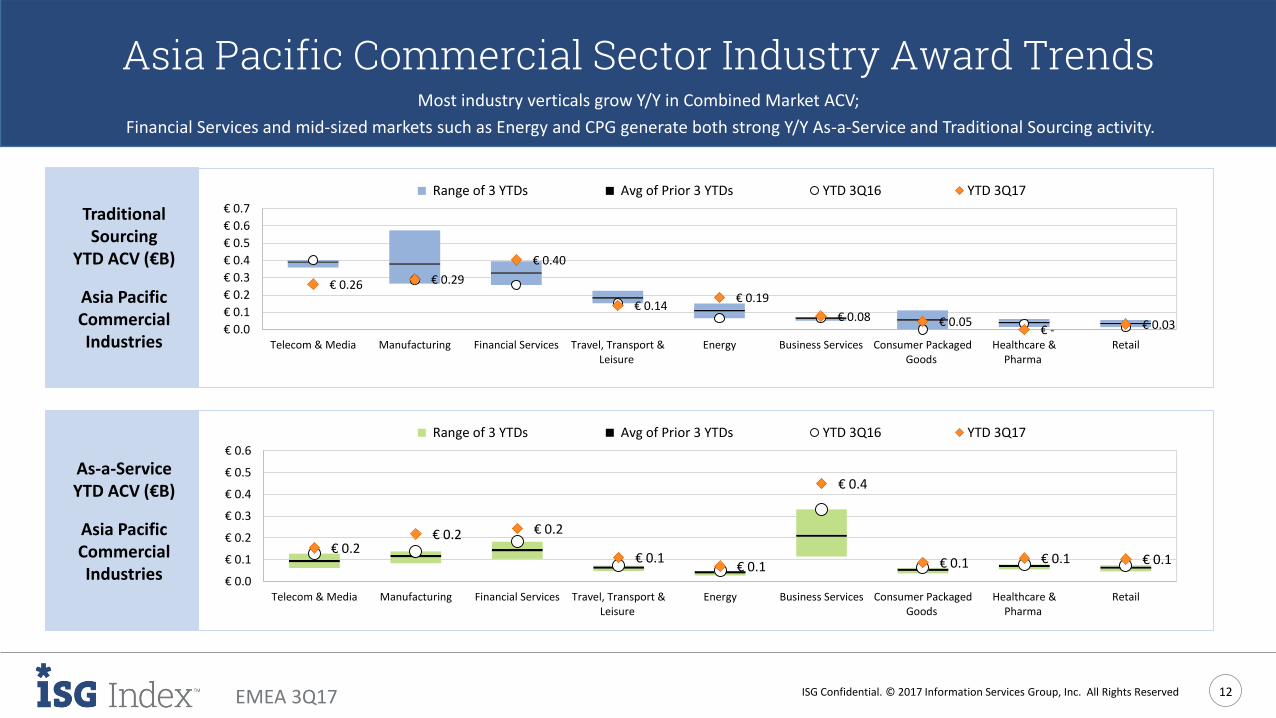

Asia Pacific Commercial Sector Industry Award TrendsMost industry verticals grow Y/Y in Combined Market ACV;

Financial Services and mid-sized markets such as Energy and CPG generate both strong Y/Y As-a-Service and Traditional Sourcing activity.

Traditional Sourcing

YTD ACV (€B)

Asia Pacific Commercial Industries

As-a-ServiceYTD ACV (€B)

Asia Pacific Commercial Industries

€ 0.26 € 0.29

€ 0.40

€ 0.14 € 0.19

€ 0.08 € 0.05 € - € 0.03 € 0.0

€ 0.1

€ 0.2

€ 0.3

€ 0.4

€ 0.5

€ 0.6

€ 0.7

Telecom & Media Manufacturing Financial Services Travel, Transport &Leisure

Energy Business Services Consumer PackagedGoods

Healthcare &Pharma

Retail

Range of 3 YTDs Avg of Prior 3 YTDs YTD 3Q16 YTD 3Q17

€ 0.2 € 0.2 € 0.2

€ 0.1 € 0.1

€ 0.4

€ 0.1 € 0.1 € 0.1

€ 0.0

€ 0.1

€ 0.2

€ 0.3

€ 0.4

€ 0.5

€ 0.6

Telecom & Media Manufacturing Financial Services Travel, Transport &Leisure

Energy Business Services Consumer PackagedGoods

Healthcare &Pharma

Retail

Range of 3 YTDs Avg of Prior 3 YTDs YTD 3Q16 YTD 3Q17

EMEA 3Q17

The Rapidly Transforming Digital Contact Center

Wayne ButterfieldDirector – Cognitive & AI Innovation and Automation

3Q17 Index Inside Track from

ISG Confidential. © 2017 Information Services Group, Inc. All Rights Reserved 14EMEA 3Q17

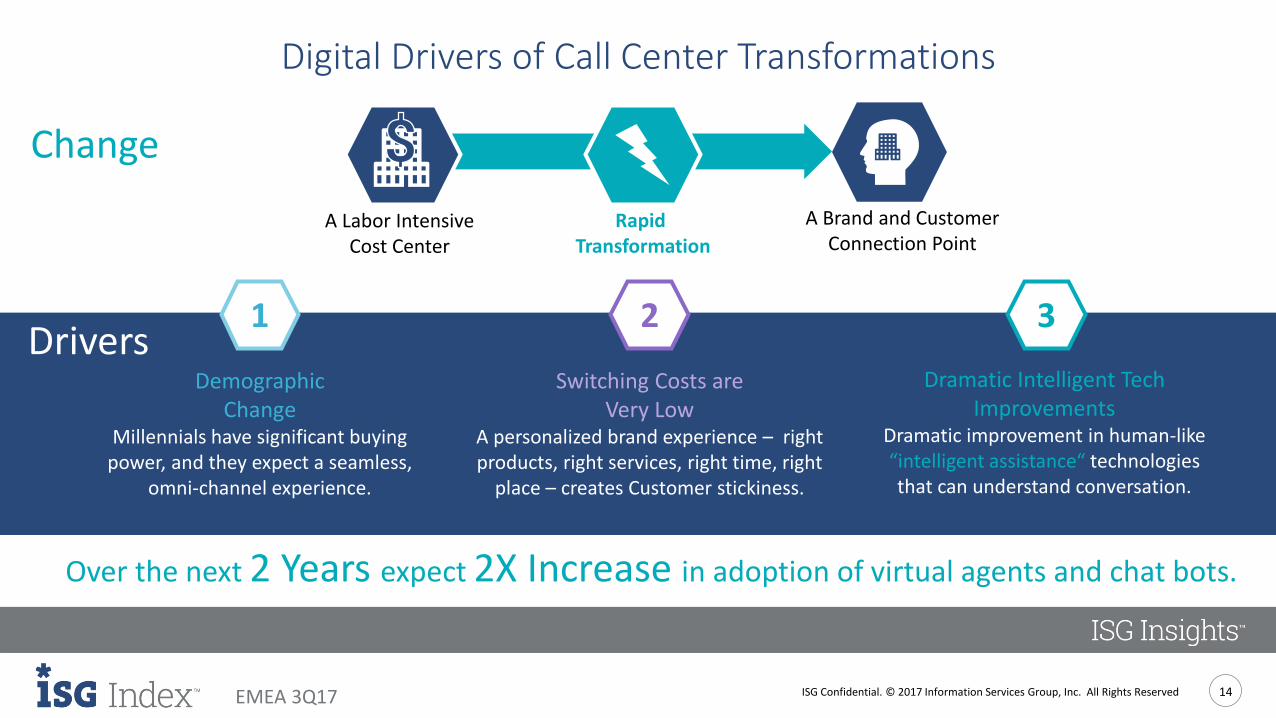

Digital Drivers of Call Center Transformations

A Labor IntensiveCost Center

A Brand and CustomerConnection Point

DemographicChange

Millennials have significant buying power, and they expect a seamless,

omni-channel experience.

Switching Costs areVery Low

A personalized brand experience – right products, right services, right time, right

place – creates Customer stickiness.

Dramatic Intelligent Tech Improvements

Dramatic improvement in human-like “intelligent assistance“ technologiesthat can understand conversation.

321

Over the next 2 Years expect 2X Increase in adoption of virtual agents and chat bots.

Rapid Transformation

Drivers

Change

ISG Confidential. © 2017 Information Services Group, Inc. All Rights Reserved 15EMEA 3Q17

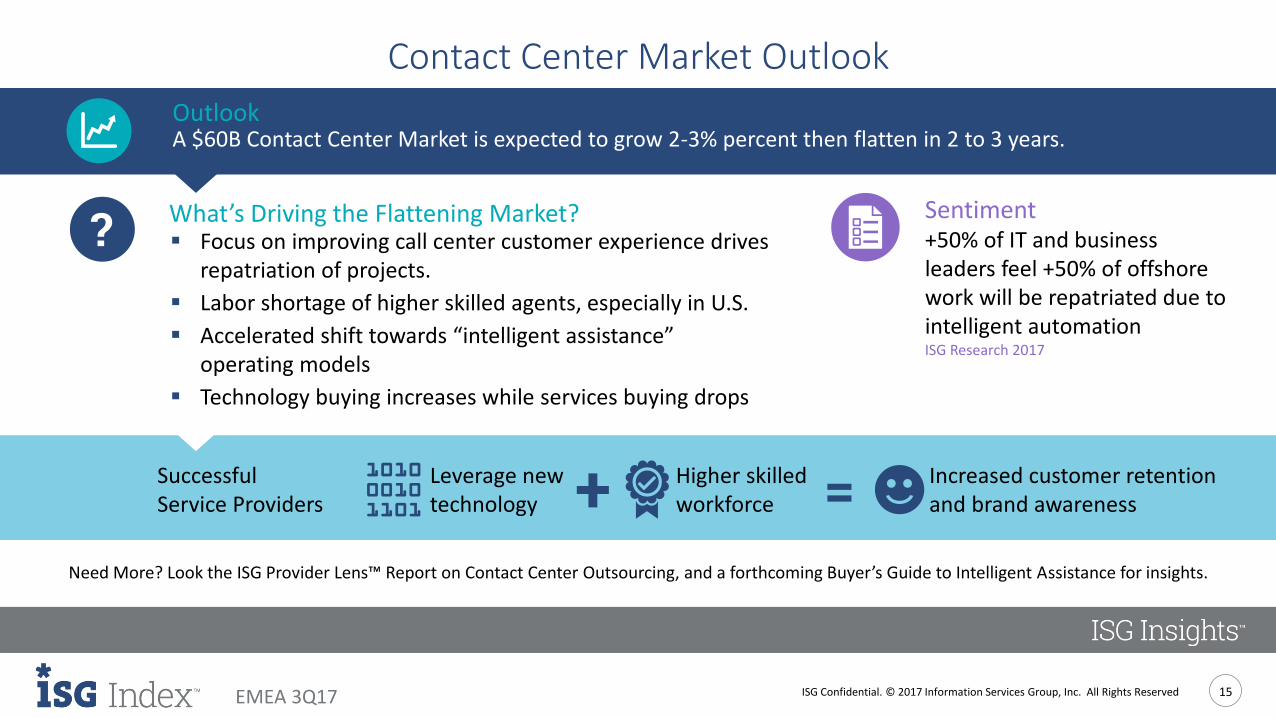

Contact Center Market Outlook

A $60B Contact Center Market is expected to grow 2-3% percent then flatten in 2 to 3 years.

Sentiment+50% of IT and business leaders feel +50% of offshore work will be repatriated due to intelligent automation ISG Research 2017

▪ Focus on improving call center customer experience drives repatriation of projects.

▪ Labor shortage of higher skilled agents, especially in U.S.

▪ Accelerated shift towards “intelligent assistance” operating models

▪ Technology buying increases while services buying drops

Higher skilledworkforce

What’s Driving the Flattening Market?

Outlook

Leverage new technology

SuccessfulService Providers

Increased customer retention and brand awareness

Need More? Look the ISG Provider Lens™ Report on Contact Center Outsourcing, and a forthcoming Buyer’s Guide to Intelligent Assistance for insights.

ISG Confidential. © 2017 Information Services Group, Inc. All Rights Reserved 16EMEA 3Q17

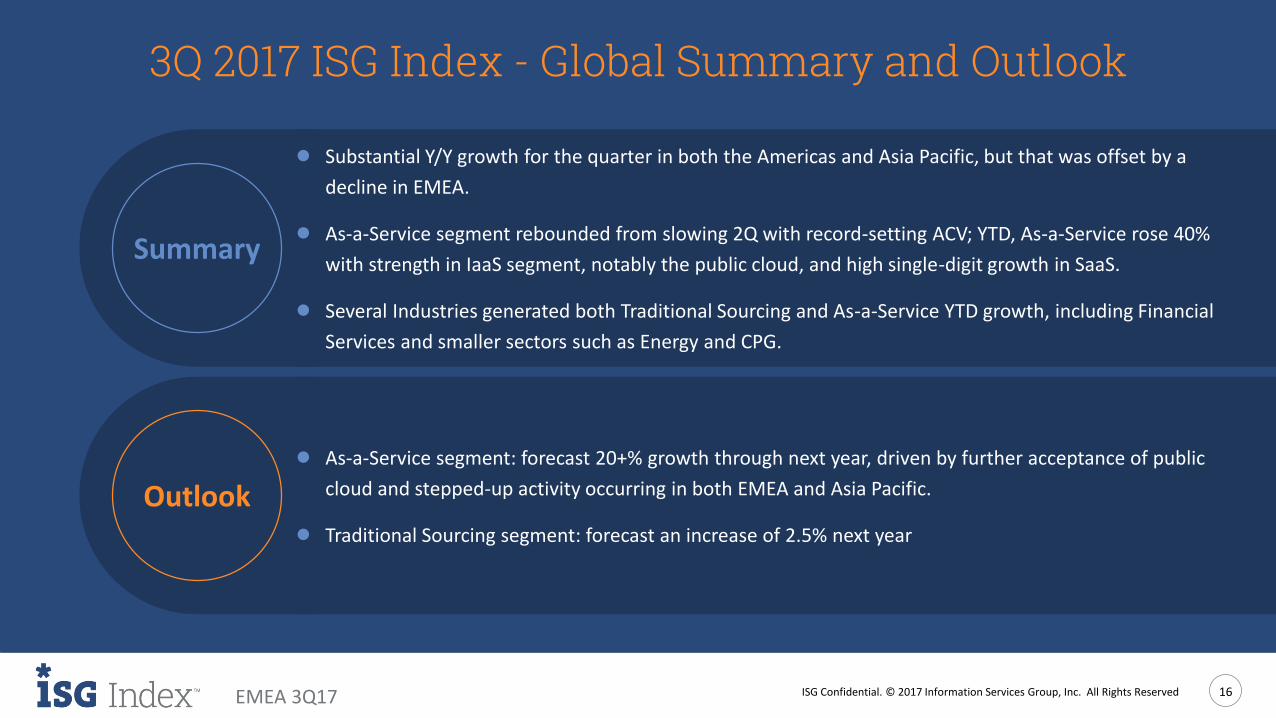

3Q 2017 ISG Index - Global Summary and Outlook

● Substantial Y/Y growth for the quarter in both the Americas and Asia Pacific, but that was offset by a

decline in EMEA.

● As-a-Service segment rebounded from slowing 2Q with record-setting ACV; YTD, As-a-Service rose 40%

with strength in IaaS segment, notably the public cloud, and high single-digit growth in SaaS.

● Several Industries generated both Traditional Sourcing and As-a-Service YTD growth, including Financial

Services and smaller sectors such as Energy and CPG.

● As-a-Service segment: forecast 20+% growth through next year, driven by further acceptance of public

cloud and stepped-up activity occurring in both EMEA and Asia Pacific.

● Traditional Sourcing segment: forecast an increase of 2.5% next year

Summary

Outlook

ISG Confidential. © 2017 Information Services Group, Inc. All Rights Reserved 17EMEA 3Q17

isg-one.com

Learn More

Barry Matthews Partner

+44 7881 954 [email protected]

Tara BenhamCohn & Wolfe for ISG+44 (0) 20 7331 5395

Denise Colgan EMEA and AP Media Contact

+44 1737 [email protected]

Esteban HerreraPartner, Global Leader

ISG Research+1 203 820 8987

Paul ReynoldsPartner, Chief Research Officer

ISG Momentum+1 508 625 2194

GLOBAL 4Q16

EMEA 3Q17

Appendix: Score Card for TCVTHIRD QUARTER 2017

ISG Confidential. © 2017 Information Services Group, Inc. All Rights Reserved 19EMEA 3Q17

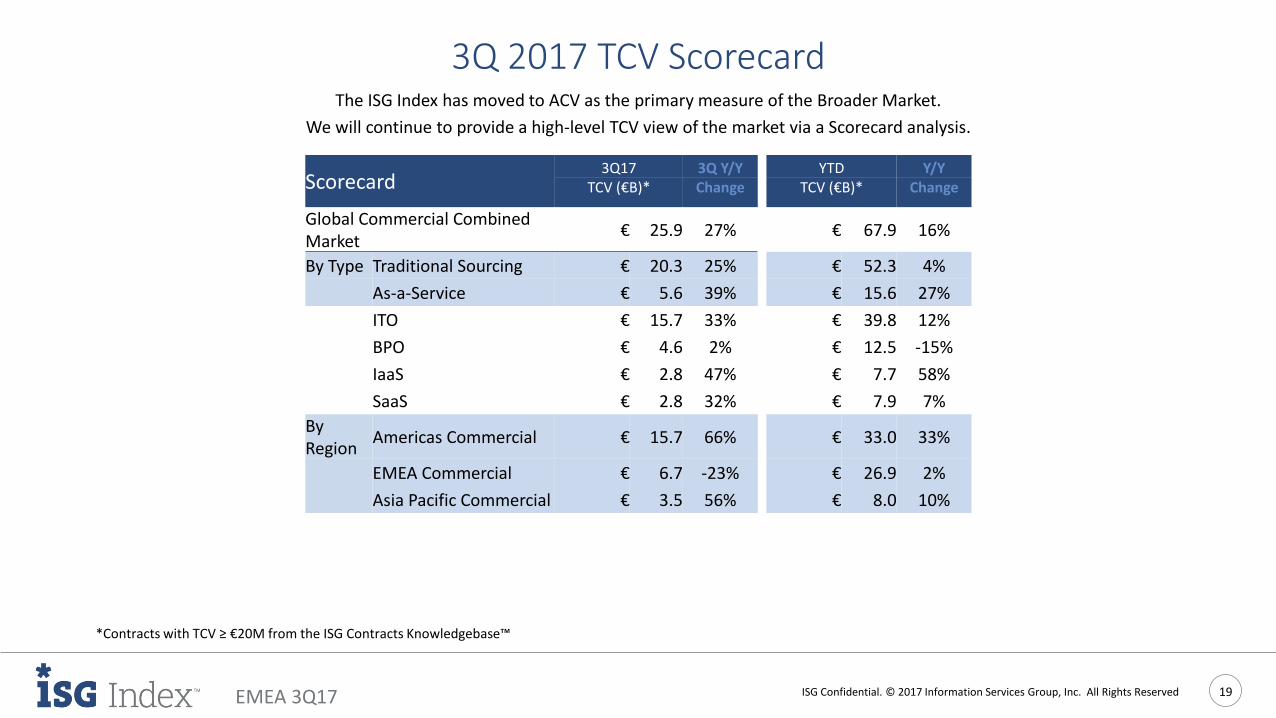

3Q 2017 TCV ScorecardThe ISG Index has moved to ACV as the primary measure of the Broader Market.

We will continue to provide a high-level TCV view of the market via a Scorecard analysis.

*Contracts with TCV ≥ €20M from the ISG Contracts Knowledgebase™

Scorecard3Q17 3Q Y/Y YTD Y/Y

TCV (€B)* Change TCV (€B)* Change

Global Commercial Combined Market

€ 25.9 27% € 67.9 16%

By Type Traditional Sourcing € 20.3 25% € 52.3 4%

As-a-Service € 5.6 39% € 15.6 27%

ITO € 15.7 33% € 39.8 12%

BPO € 4.6 2% € 12.5 -15%

IaaS € 2.8 47% € 7.7 58%

SaaS € 2.8 32% € 7.9 7%

By Region

Americas Commercial € 15.7 66% € 33.0 33%

EMEA Commercial € 6.7 -23% € 26.9 2%

Asia Pacific Commercial € 3.5 56% € 8.0 10%

ISG Confidential. © 2017 Information Services Group, Inc. All Rights Reserved.

Proprietary and Confidential. No part of this document may be reproduced in any form or by any electronic

or mechanical means, including information storage and retrieval devices or systems, without prior written

permission from Information Services Group, Inc.isg-one.com

ISG (Information Services Group) (NASDAQ: III) is a leading global technology research and advisory

firm. A trusted business partner to more than 700 clients, including 75 of the top 100 enterprises in the

world, ISG is committed to helping corporations, public sector organizations, and service and technology

providers achieve operational excellence and faster growth. The firm specializes in digital

transformation services, including automation, cloud and data analytics; sourcing advisory; managed

governance and risk services; network carrier services; technology strategy and operations design;

change management; market intelligence and technology research and analysis. Founded in 2006, and

based in Stamford, Conn., ISG employs more than 1,300 professionals operating in more than 20

countries—a global team known for its innovative thinking, market influence, deep industry and

technology expertise, and world-class research and analytical capabilities based on the industry’s most

comprehensive marketplace data.