Embed Size (px)

Citation preview

Africa GreenCo(Africa Green Regional Energy: Efficient, New and Creditworthy Offtaker

Copyright © 2010 by Africa GreenCo.All rights reserved. No part of this publication may be reproduced, distributed, or transmitted in any form or by any means, including photocopying, recording, or other electronic or mechanical methods, without the prior written permission of the publisher, except in the case of brief quotations embodied in critical reviews and certain other noncommercial uses permitted by copyright law. For permission requests, write to the publisher, addressed “Attention: Permissions Coordinator,” at the address below.

Ana HajdukaAfrica GreenCo Founder & CEOEmail: [email protected]: +447789204363Abidjan, PIDA Week November 2015

Mission

Benefit

Sectors

Africa GreenCo’s mission is to promote the development of a public-private partnership in the form of an independent, creditworthy, renewable energy offtaker/trader of power, acting at a regional level in Sub-Saharan Africa to purchase electricity from Independent Power Producers (IPPs) and sell via the power pools. From a financial stand-point, it will use its capital base to enhance off-taker creditworthiness. From an operations stand-point, it will coordinate government decision making, facilitate interconnection and increase power trading.

Regional and interregional power sector integration is a prerequisite for larger and more cost-effective hydro-electric, geothermal, wind, solar and biomass projects, and will savebillions of dollars in development, opera-tion and maintnance costs, enabling the expansionof energy access in Sub-Saharan Africa.This single-point power purchase agreement (PPA) counterparty would streamline development, mitigate offtake and credit risk,and catalyze private sector finance for large scale cross border renewable energy development.

Renewable and sustainable energy

Feasibility study Current status

Grant funding provided by the Rockefeller Foundation .Funded By

SE4AAll Finance Committee Report, which was presented at the Financing for Development Conference in Addis to Africa’s Heads of State, endorsed Africa Green Coas a recommendation and a call to look into the concept’s viability

Endorsed By

Ben Kioko – Former Chief Legal Advisor to the African UnionTim Nielander – Senior Legal Advisor for ARC and rom 2005 until 2010, Tim served as General Counsel and Managing Director of Corporate Services for theGAVI AllianceTantra Thakur – Former Founder and Managing Director of PTC India

Special Advisors:

SE4AAll Finance Committee Report, which was presented at the Financing for Development Conference in Addis to Africa’s Heads of State, endorsed Africa Green Coas a recommendation and a call to look into the concept’s viability

Financial AdvisorsLion’s Head Global Partners.

Project Development & Finance: Shearman & Sterling has one of the leading international legal practices in limited recourse development and acquisition financing of projects

Legal AdvisorsShearman & Sterling LLP

Working with

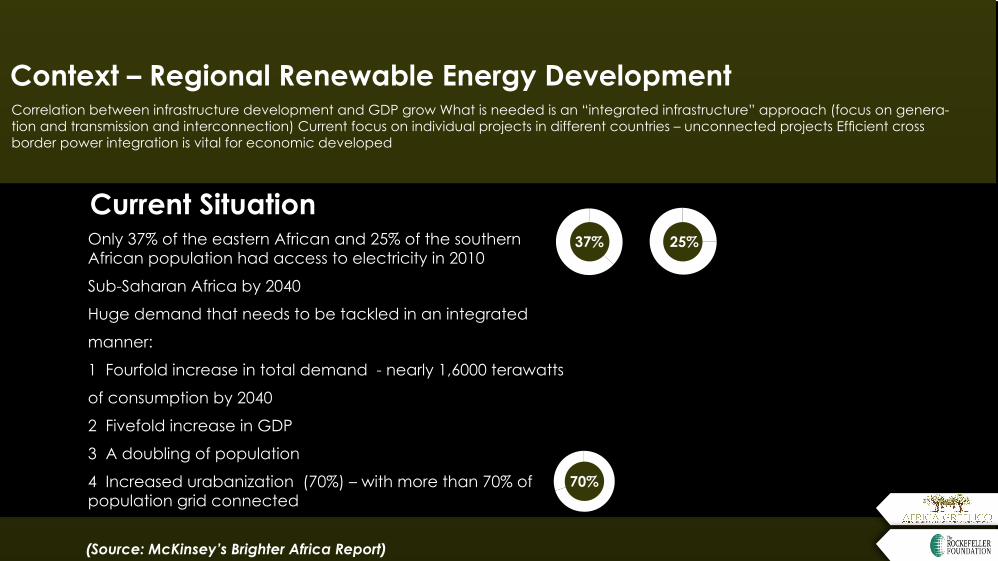

Current Situation

Correlation between infrastructure development and GDP grow What is needed is an “integrated infrastructure” approach (focus on genera-tion and transmission and interconnection) Current focus on individual projects in different countries – unconnected projects Efficient cross border power integration is vital for economic developed

(Source: McKinsey’s Brighter Africa Report)

Only 37% of the eastern African and 25% of the southern African population had access to electricity in 2010

Sub-Saharan Africa by 2040

Huge demand that needs to be tackled in an integrated

manner:

1 Fourfold increase in total demand - nearly 1,6000 terawatts

of consumption by 2040

2 Fivefold increase in GDP

3 A doubling of population

4 Increased urabanization (70%) – with more than 70% of population grid connected

Context – Regional Renewable Energy Development

25%37%

70%

(Source: McKinsey’s Brighter Africa Report)

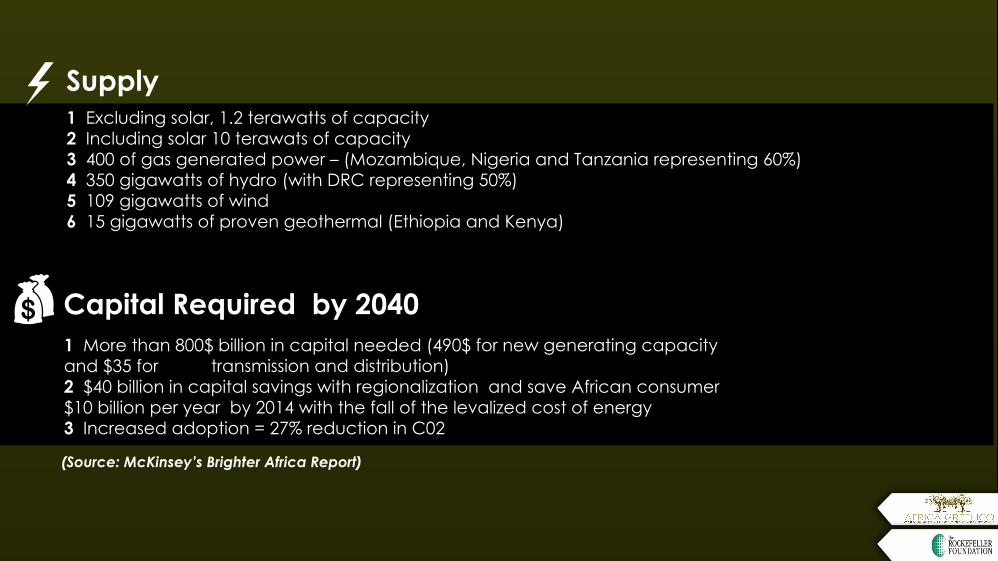

Supply1 Excluding solar, 1.2 terawatts of capacity 2 Including solar 10 terawats of capacity3 400 of gas generated power – (Mozambique, Nigeria and Tanzania representing 60%)4 350 gigawatts of hydro (with DRC representing 50%)5 109 gigawatts of wind6 15 gigawatts of proven geothermal (Ethiopia and Kenya)

Capital Required by 20401 More than 800$ billion in capital needed (490$ for new generating capacity and $35 for transmission and distribution)2 $40 billion in capital savings with regionalization and save African consumer $10 billion per year by 2014 with the fall of the levalized cost of energy3 Increased adoption = 27% reduction in C02

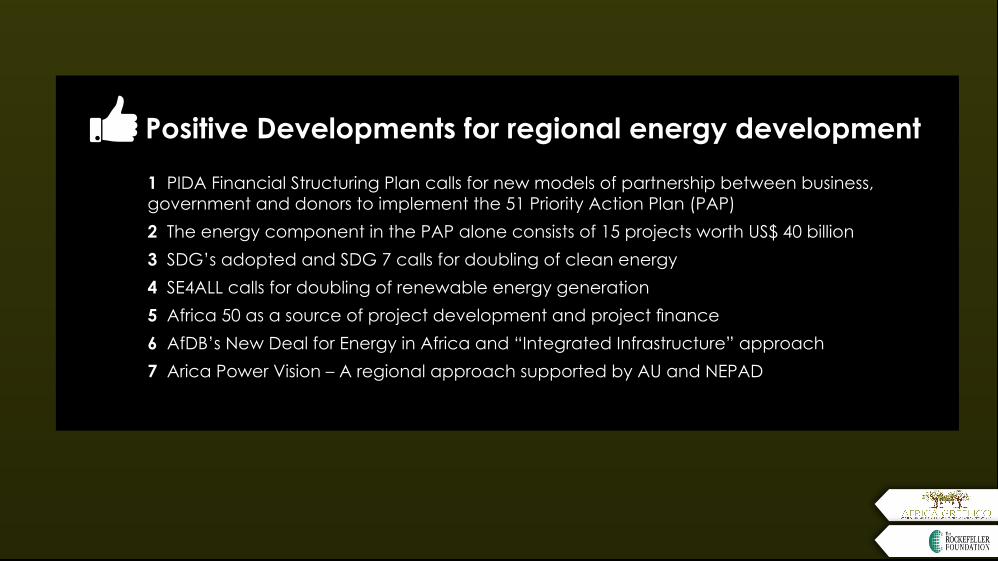

Positive Developments for regional energy development1 PIDA Financial Structuring Plan calls for new models of partnership between business, government and donors to implement the 51 Priority Action Plan (PAP) 2 The energy component in the PAP alone consists of 15 projects worth US$ 40 billion3 SDG’s adopted and SDG 7 calls for doubling of clean energy4 SE4ALL calls for doubling of renewable energy generation5 Africa 50 as a source of project development and project finance6 AfDB’s New Deal for Energy in Africa and “Integrated Infrastructure” approach7 Arica Power Vision – A regional approach supported by AU and NEPAD

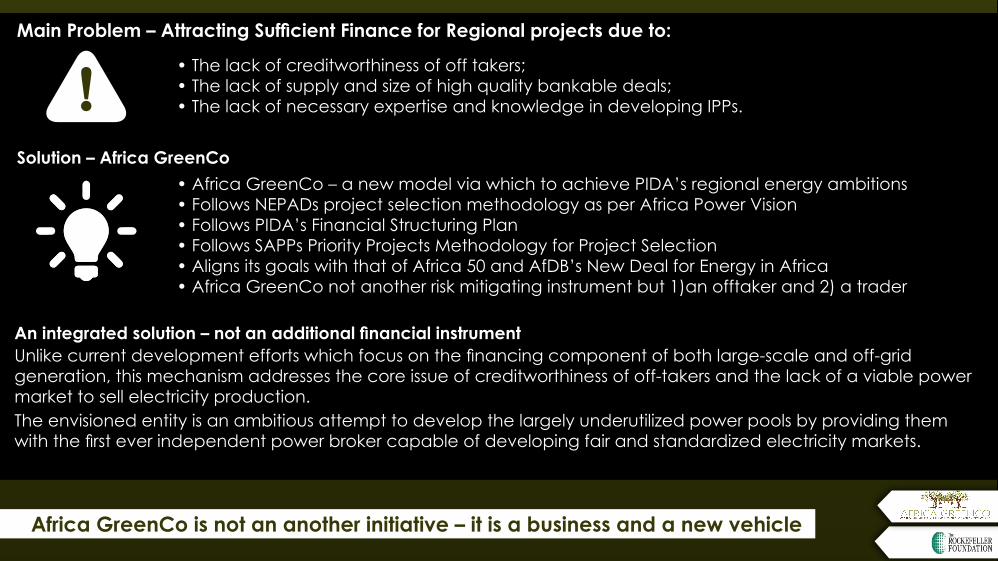

Main Problem – Attracting Sufficient Finance for Regional projects due to:

Solution – Africa GreenCo

• The lack of creditworthiness of off takers;• The lack of supply and size of high quality bankable deals;• The lack of necessary expertise and knowledge in developing IPPs.

• Africa GreenCo – a new model via which to achieve PIDA’s regional energy ambitions • Follows NEPADs project selection methodology as per Africa Power Vision• Follows PIDA’s Financial Structuring Plan• Follows SAPPs Priority Projects Methodology for Project Selection • Aligns its goals with that of Africa 50 and AfDB’s New Deal for Energy in Africa• Africa GreenCo not another risk mitigating instrument but 1)an offtaker and 2) a trader

Unlike current development efforts which focus on the financing component of both large-scale and off-gridgeneration, this mechanism addresses the core issue of creditworthiness of off-takers and the lack of a viable powermarket to sell electricity production. The envisioned entity is an ambitious attempt to develop the largely underutilized power pools by providing themwith the first ever independent power broker capable of developing fair and standardized electricity markets.

Africa GreenCo is not an another initiative – it is a business and a new vehicle

An integrated solution – not an additional financial instrument

What is Africa GreenCo

Intermediary &Creditworthy Regional

Offtaker

Power Trader via apower poolAND

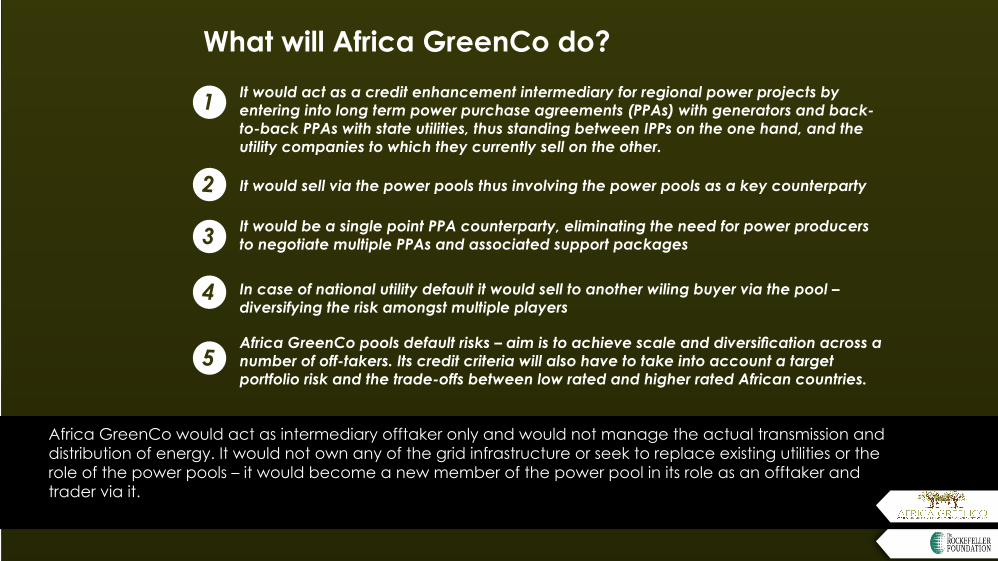

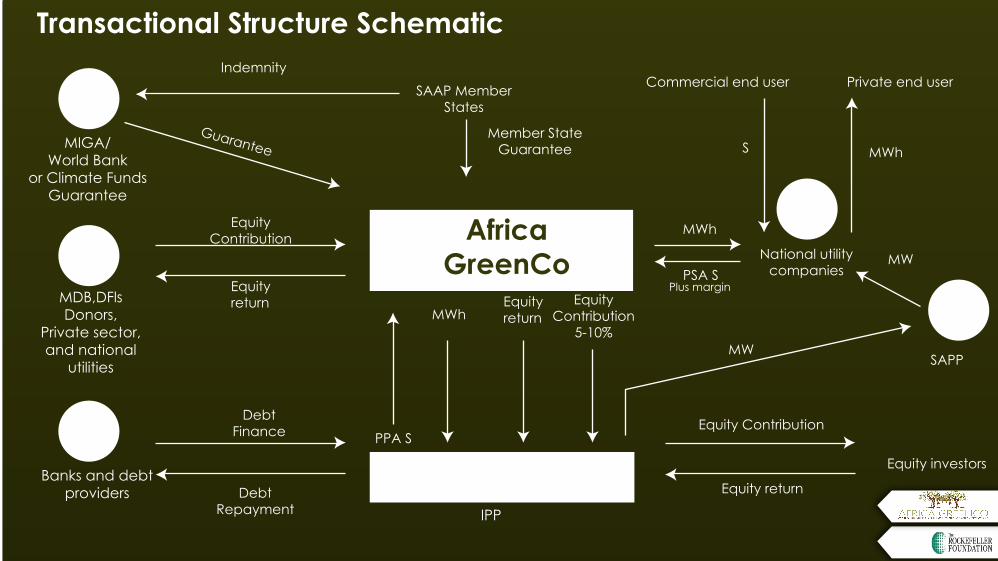

What will Africa GreenCo do?It would act as a credit enhancement intermediary for regional power projects byentering into long term power purchase agreements (PPAs) with generators and back-to-back PPAs with state utilities, thus standing between IPPs on the one hand, and theutility companies to which they currently sell on the other.

It would sell via the power pools thus involving the power pools as a key counterparty

It would be a single point PPA counterparty, eliminating the need for power producersto negotiate multiple PPAs and associated support packages

In case of national utility default it would sell to another wiling buyer via the pool –diversifying the risk amongst multiple players

Africa GreenCo pools default risks – aim is to achieve scale and diversification across anumber of off-takers. Its credit criteria will also have to take into account a targetportfolio risk and the trade-offs between low rated and higher rated African countries.

Africa GreenCo would act as intermediary offtaker only and would not manage the actual transmission and distribution of energy. It would not own any of the grid infrastructure or seek to replace existing utilities or the role of the power pools – it would become a new member of the power pool in its role as an offtaker and trader via it.

1

2

3

4

5

Transactional Structure Schematic

MIGA/World Bank

or Climate FundsGuarantee

SAAP MemberStates

Commercial end user Private end user

MDB,DFlsDonors,

Private sector,and national

utilities

Banks and debtproviders

EquityContribution

Equity Contribution

EquityContribution

5-10%

Equityreturn

Equity return

DebtFinance

DebtRepayment IPP

Equityreturn

Equity investors

National utilitycompanies

SAPP

AfricaGreenCo

Indemnity

GuaranteeMember State

Guarantee S MWh

MWh

MW

MW

MWh

PSA S

PPA S

Plus margin

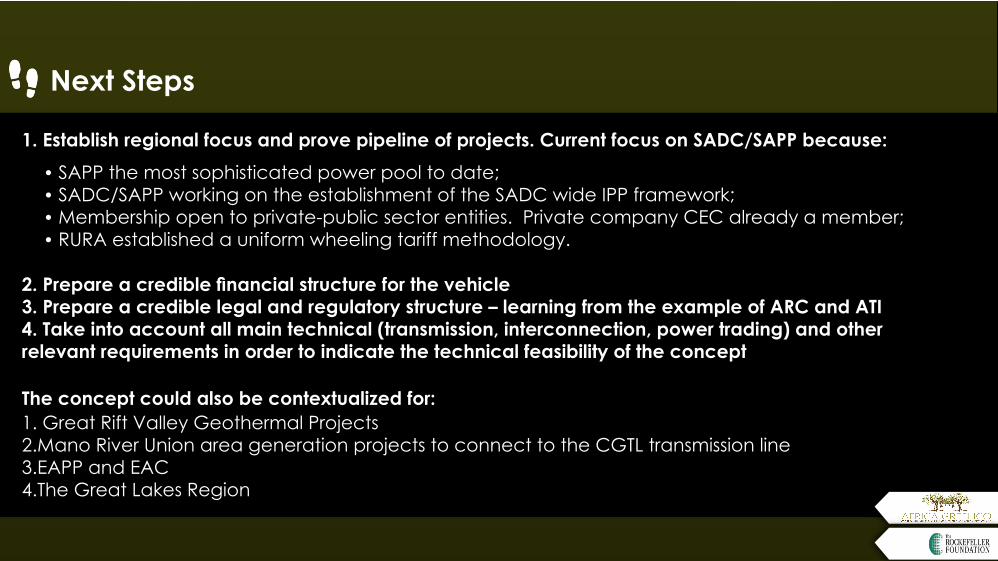

Next Steps

1. Establish regional focus and prove pipeline of projects. Current focus on SADC/SAPP because:• SAPP the most sophisticated power pool to date;• SADC/SAPP working on the establishment of the SADC wide IPP framework;• Membership open to private-public sector entities. Private company CEC already a member;• RURA established a uniform wheeling tariff methodology.

2. Prepare a credible financial structure for the vehicle 3. Prepare a credible legal and regulatory structure – learning from the example of ARC and ATI4. Take into account all main technical (transmission, interconnection, power trading) and otherrelevant requirements in order to indicate the technical feasibility of the concept

The concept could also be contextualized for:1. Great Rift Valley Geothermal Projects2.Mano River Union area generation projects to connect to the CGTL transmission line3.EAPP and EAC4.The Great Lakes Region

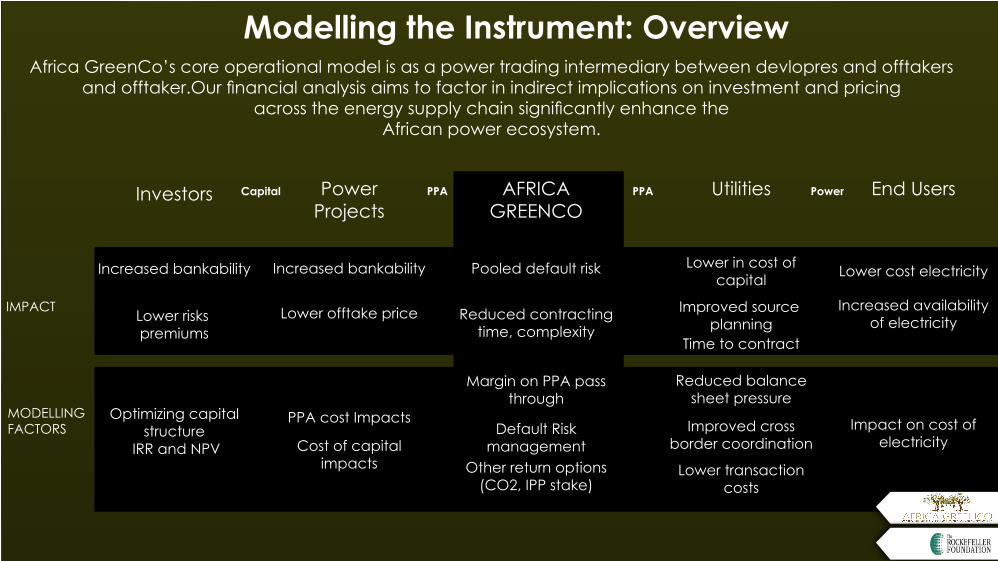

Modelling the Instrument: OverviewAfrica GreenCo’s core operational model is as a power trading intermediary between devlopres and offtakers

and offtaker.Our financial analysis aims to factor in indirect implications on investment and pricingacross the energy supply chain significantly enhance the

African power ecosystem.

Investors

IMPACT

MODELLINGFACTORS

Capital

Increased bankability

Lower risks premiums

Optimizing capitalstructure

IRR and NPV

PPA cost Impacts

Cost of capitalimpacts

Margin on PPA passthrough

Default Riskmanagement

Other return options(CO2, IPP stake)

Reduced balancesheet pressure

Improved crossborder coordination

Impact on cost ofelectricity

Lower transactioncosts

PowerProjects

AFRICAGREENCO

Utilities End UsersPPA

Increased bankability

Lower offtake price

Pooled default risk

Reduced contractingtime, complexity

Lower in cost ofcapital

Improved source planning

Time to contract

Lower cost electricity

Increased availabilityof electricity

PPA Power

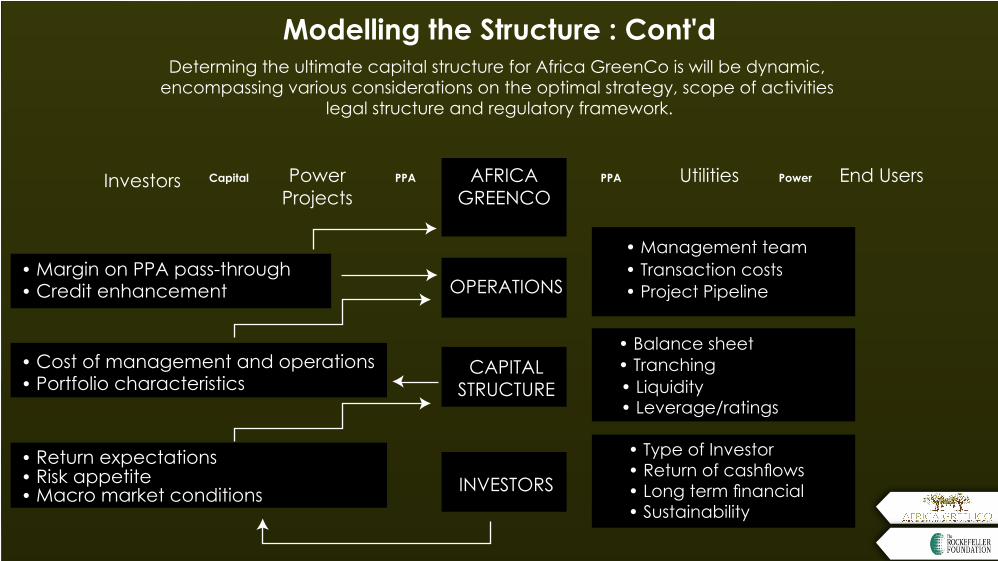

Modelling the Structure : Cont'dDeterming the ultimate capital structure for Africa GreenCo is will be dynamic,

encompassing various considerations on the optimal strategy, scope of activities legal structure and regulatory framework.

Investors Capital PowerProjects

AFRICAGREENCO

Utilities End UsersPPA PPA Power

• Margin on PPA pass-through• Management team• Transaction costs• Project Pipeline

• Balance sheet• Tranching• Liquidity• Leverage/ratings

• Type of Investor• Return of cashflows• Long term financial• Sustainability

• Credit enhancement

• Cost of management and operations• Portfolio characteristics

• Return expectations• Risk appetite• Macro market conditions

OPERATIONS

CAPITALSTRUCTURE

INVESTORS

Investor Base: ConsiderationsAfrica GreenCo presents timely innovative financing opportunity – pooling capital from a board range of types of investors according to the quantum of capital needed, market demand and

relative risk/return profile

CONCESSIONAL InternationalDonors

• Catalytic Capital• Host/partner organisation(s)

• Non financial impacts numerous,• Health, education, trade

• Local ownership• Risk sharing

• Scalability/Marketing Depending• Long term financial sustainability

• Improved risk/ Price discovery• Direct assest class exposure

PhilanthropicInvestors

African PublicSector

African PrivateSector

InternationalCapital MarketsCOMMERCIAL

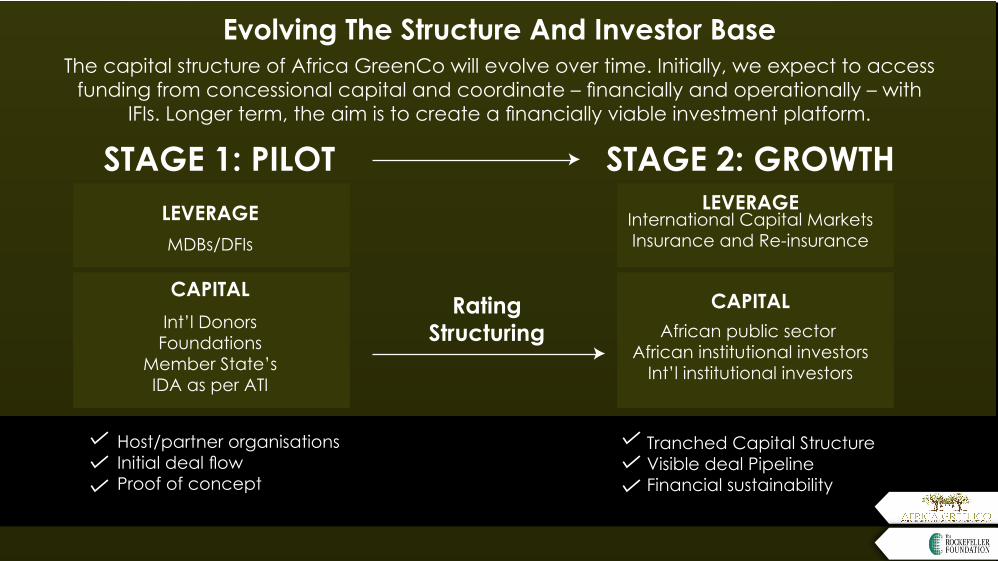

Evolving The Structure And Investor BaseThe capital structure of Africa GreenCo will evolve over time. Initially, we expect to access

funding from concessional capital and coordinate – financially and operationally – withIFIs. Longer term, the aim is to create a financially viable investment platform.

STAGE 1: PILOTLEVERAGE LEVERAGE

RatingStructuring

MDBs/DFIsInternational Capital MarketsInsurance and Re-insurance

African public sector African institutional investors

Int’l institutional investors

Int’l DonorsFoundations

Member State’sIDA as per ATI

Host/partner organisationsInitial deal flowProof of concept

Tranched Capital StructureVisible deal PipelineFinancial sustainability

CAPITAL CAPITAL

STAGE 2: GROWTH

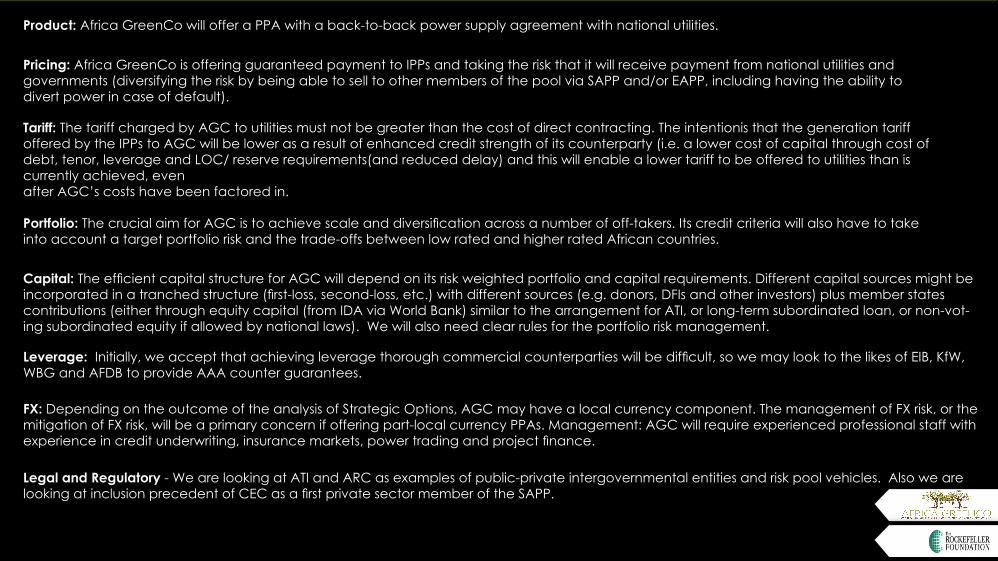

Product: Africa GreenCo will offer a PPA with a back-to-back power supply agreement with national utilities.

Pricing: Africa GreenCo is offering guaranteed payment to IPPs and taking the risk that it will receive payment from national utilities and governments (diversifying the risk by being able to sell to other members of the pool via SAPP and/or EAPP, including having the ability to divert power in case of default).

Tariff: The tariff charged by AGC to utilities must not be greater than the cost of direct contracting. The intentionis that the generation tariff offered by the IPPs to AGC will be lower as a result of enhanced credit strength of its counterparty (i.e. a lower cost of capital through cost of debt, tenor, leverage and LOC/ reserve requirements(and reduced delay) and this will enable a lower tariff to be offered to utilities than is currently achieved, evenafter AGC’s costs have been factored in.

Portfolio: The crucial aim for AGC is to achieve scale and diversification across a number of off-takers. Its credit criteria will also have to take into account a target portfolio risk and the trade-offs between low rated and higher rated African countries.

Capital: The efficient capital structure for AGC will depend on its risk weighted portfolio and capital requirements. Different capital sources might be incorporated in a tranched structure (first-loss, second-loss, etc.) with different sources (e.g. donors, DFIs and other investors) plus member states contributions (either through equity capital (from IDA via World Bank) similar to the arrangement for ATI, or long-term subordinated loan, or non-vot-ing subordinated equity if allowed by national laws). We will also need clear rules for the portfolio risk management.

Leverage: Initially, we accept that achieving leverage thorough commercial counterparties will be difficult, so we may look to the likes of EIB, KfW, WBG and AFDB to provide AAA counter guarantees.

FX: Depending on the outcome of the analysis of Strategic Options, AGC may have a local currency component. The management of FX risk, or the mitigation of FX risk, will be a primary concern if offering part-local currency PPAs. Management: AGC will require experienced professional staff with experience in credit underwriting, insurance markets, power trading and project finance.

Legal and Regulatory - We are looking at ATI and ARC as examples of public-private intergovernmental entities and risk pool vehicles. Also we are looking at inclusion precedent of CEC as a first private sector member of the SAPP.

Other return options(CO2, IPP stake)

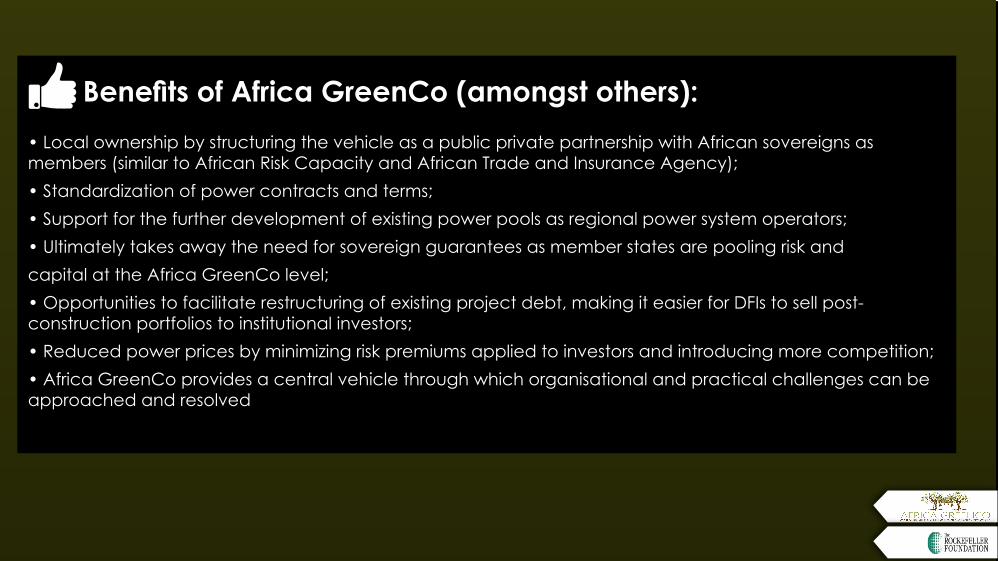

Benefits of Africa GreenCo (amongst others):• Local ownership by structuring the vehicle as a public private partnership with African sovereigns asmembers (similar to African Risk Capacity and African Trade and Insurance Agency);• Standardization of power contracts and terms;• Support for the further development of existing power pools as regional power system operators;• Ultimately takes away the need for sovereign guarantees as member states are pooling risk andcapital at the Africa GreenCo level;• Opportunities to facilitate restructuring of existing project debt, making it easier for DFIs to sell post-construction portfolios to institutional investors;• Reduced power prices by minimizing risk premiums applied to investors and introducing more competition; • Africa GreenCo provides a central vehicle through which organisational and practical challenges can beapproached and resolved

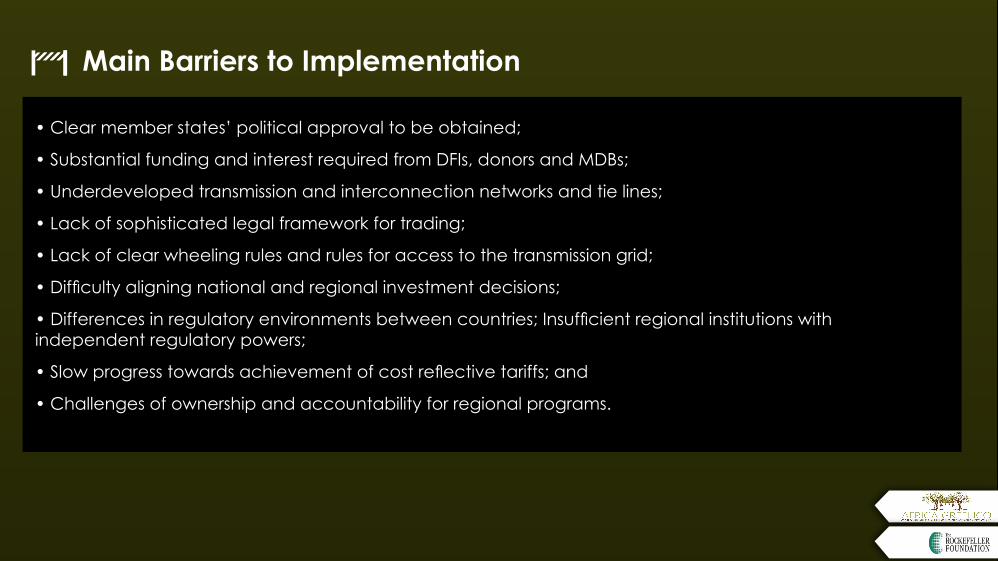

• Clear member states’ political approval to be obtained;

• Substantial funding and interest required from DFIs, donors and MDBs;

• Underdeveloped transmission and interconnection networks and tie lines;

• Lack of sophisticated legal framework for trading;

• Lack of clear wheeling rules and rules for access to the transmission grid;

• Difficulty aligning national and regional investment decisions;

• Differences in regulatory environments between countries; Insufficient regional institutions withindependent regulatory powers;

• Slow progress towards achievement of cost reflective tariffs; and

• Challenges of ownership and accountability for regional programs.

Main Barriers to Implementation

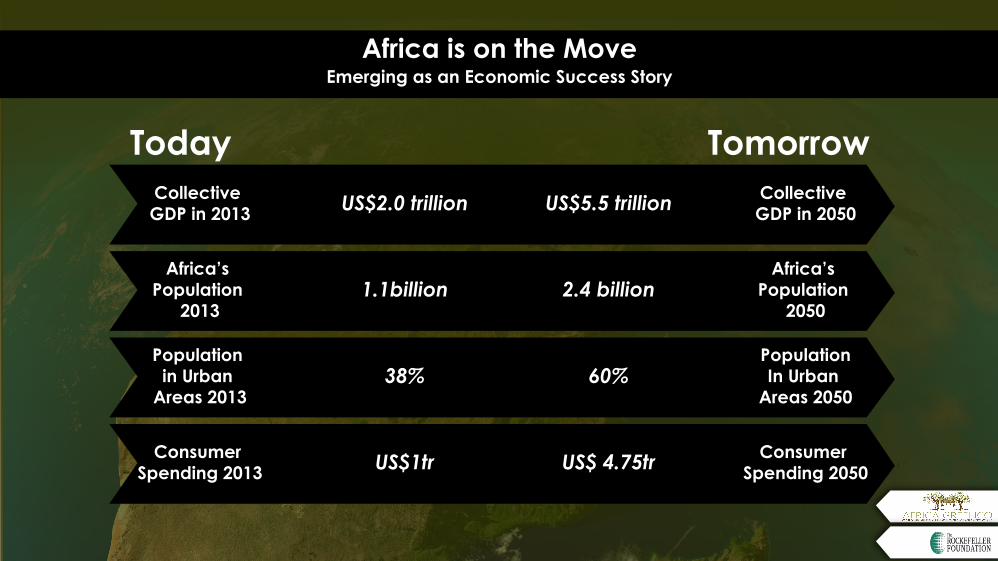

Africa is on the Move

TodayCollective GDP in 2013 US$2.0 trillion

1.1billion

38%

US$1tr

US$5.5 trillion

2.4 billion

60%

US$ 4.75tr

Africa’s Population

2013

Population in Urban

Areas 2013

Consumer Spending 2013

Collective GDP in 2050

Africa’s Population

2050

PopulationIn Urban

Areas 2050

Consumer Spending 2050

Tomorrow

Emerging as an Economic Success Story