Embed Size (px)

DESCRIPTION

BASF Performance Products including an overview of BASF's Dispersions & Pigments, Paper Chemicals, Performance Chemicals and Care Chemicals.

Citation preview

1BASF Performance Products Investor Day 2010

Growth. Value. Sustainability.

BASF Performance ProductsOutperforming: Growth. Value. Sustainability.Dr. John Feldmann

2BASF Performance Products Investor Day 2010

Growth. Value. Sustainability.

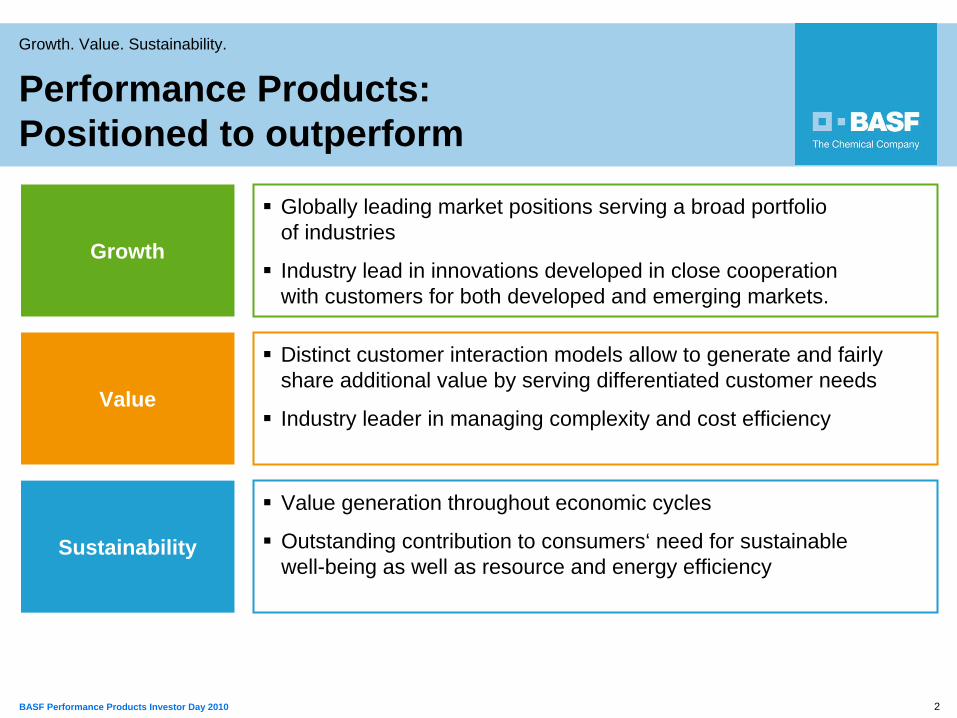

Distinct customer interaction models allow to generate and fairly share additional value by serving differentiated customer needs

Industry leader in managing complexity and cost efficiency

Globally leading market positions serving a broad portfolio of industries

Industry lead in innovations developed in close cooperation with customers for both developed and emerging markets.

Growth

Value

Sustainability

Performance Products: Positioned to outperform

Value generation throughout economic cycles

Outstanding contribution to consumers‘ need for sustainable well-being as well as resource and energy efficiency

3BASF Performance Products Investor Day 2010

Growth. Value. Sustainability.

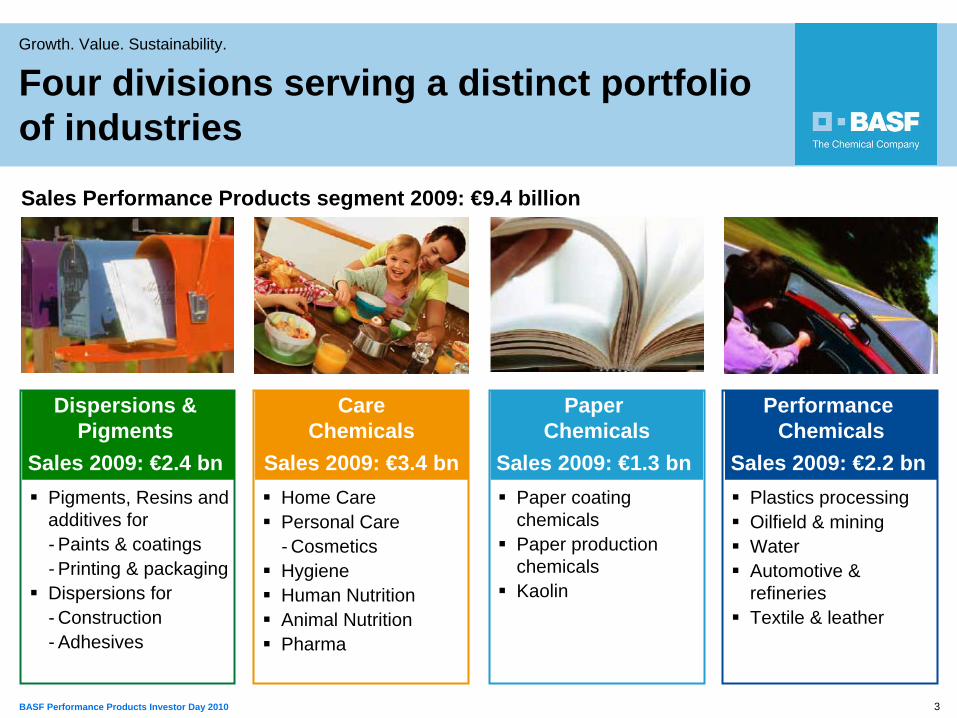

Four divisions serving a distinct portfolio of industries

Sales Performance Products segment 2009: €9.4 billion

Paper coating chemicals Paper production chemicals Kaolin

Paper Chemicals

Sales 2009: €1.3 bnPigments, Resins and additives for- Paints & coatings- Printing & packagingDispersions for- Construction- Adhesives

Dispersions & Pigments

Sales 2009: €2.4 bnHome CarePersonal Care- CosmeticsHygieneHuman NutritionAnimal NutritionPharma

Care Chemicals

Sales 2009: €3.4 bnPlastics processingOilfield & miningWaterAutomotive & refineries Textile & leather

Performance Chemicals

Sales 2009: €2.2 bn

4BASF Performance Products Investor Day 2010

Growth. Value. Sustainability.

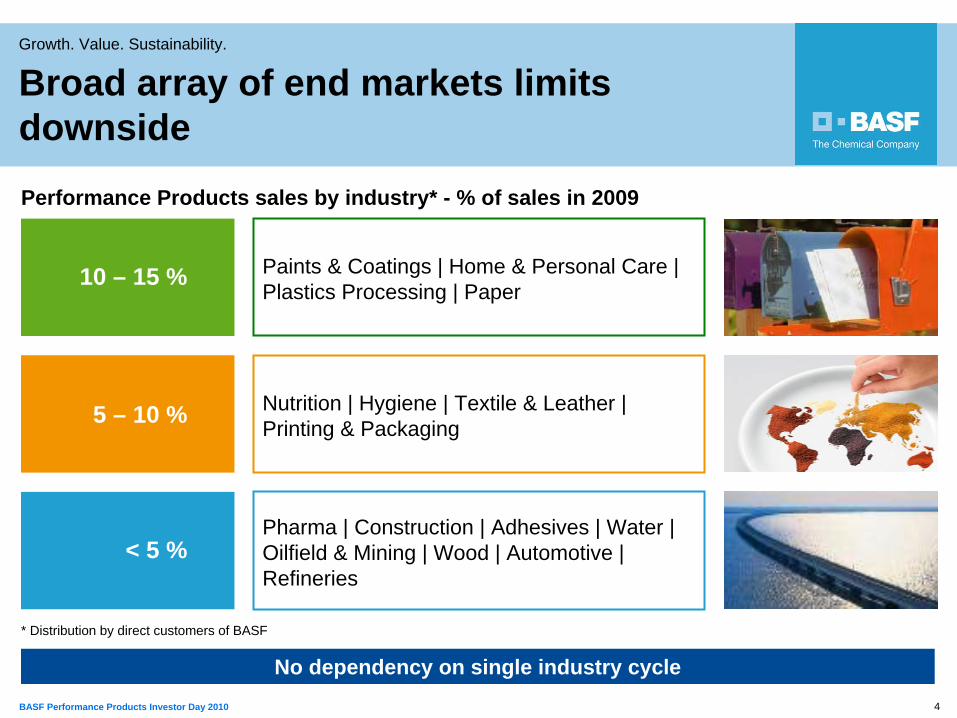

Nutrition | Hygiene | Textile & Leather | Printing & Packaging

10 – 15 %

5 – 10 %

< 5 %Pharma | Construction | Adhesives | Water | Oilfield & Mining | Wood | Automotive | Refineries

Paints & Coatings | Home & Personal Care | Plastics Processing | Paper

No dependency on single industry cycle

Performance Products sales by industry* - % of sales in 2009

* Distribution by direct customers of BASF

Broad array of end markets limits downside

5BASF Performance Products Investor Day 2010

Growth. Value. Sustainability.

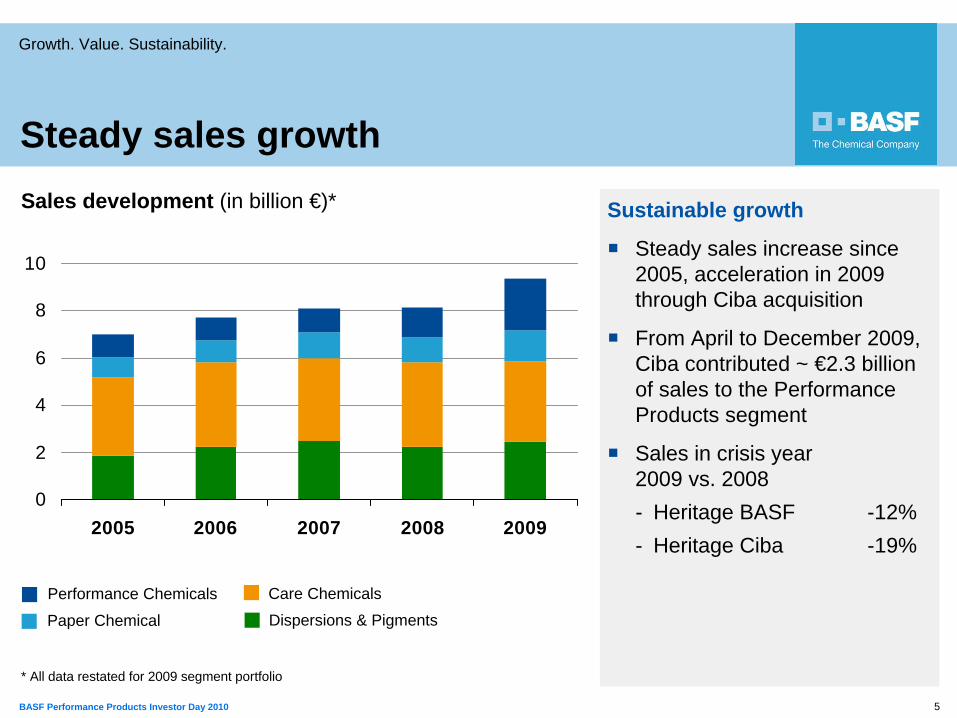

Sales development (in billion €)*

0

2

4

6

8

10

2005 2006 2007 2008 2009

Steady sales growth

Sustainable growth

Steady sales increase since 2005, acceleration in 2009 through Ciba acquisition

From April to December 2009, Ciba contributed ~ €2.3 billion of sales to the Performance Products segment

Sales in crisis year 2009 vs. 2008 - Heritage BASF -12%- Heritage Ciba -19%

Dispersions & PigmentsPaper Chemical

Care ChemicalsPerformance Chemicals

* All data restated for 2009 segment portfolio

6BASF Performance Products Investor Day 2010

Growth. Value. Sustainability.

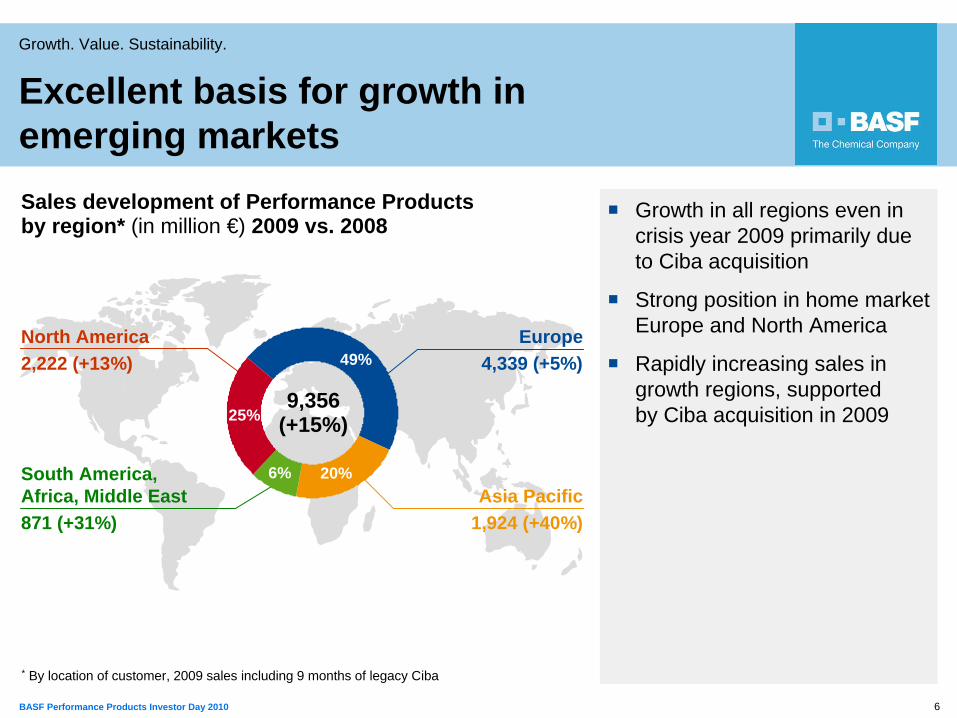

Sales development of Performance Products by region* (in million €) 2009 vs. 2008

25%

Growth in all regions even in crisis year 2009 primarily due to Ciba acquisition

Strong position in home market Europe and North America

Rapidly increasing sales in growth regions, supported by Ciba acquisition in 2009

Excellent basis for growth in emerging markets

North America2,222 (+13%)

Europe4,339 (+5%)

Asia Pacific1,924 (+40%)

South America, Africa, Middle East871 (+31%)

49%

20%6%

25%

* By location of customer, 2009 sales including 9 months of legacy Ciba

9,356(+15%)

7BASF Performance Products Investor Day 2010

Growth. Value. Sustainability.

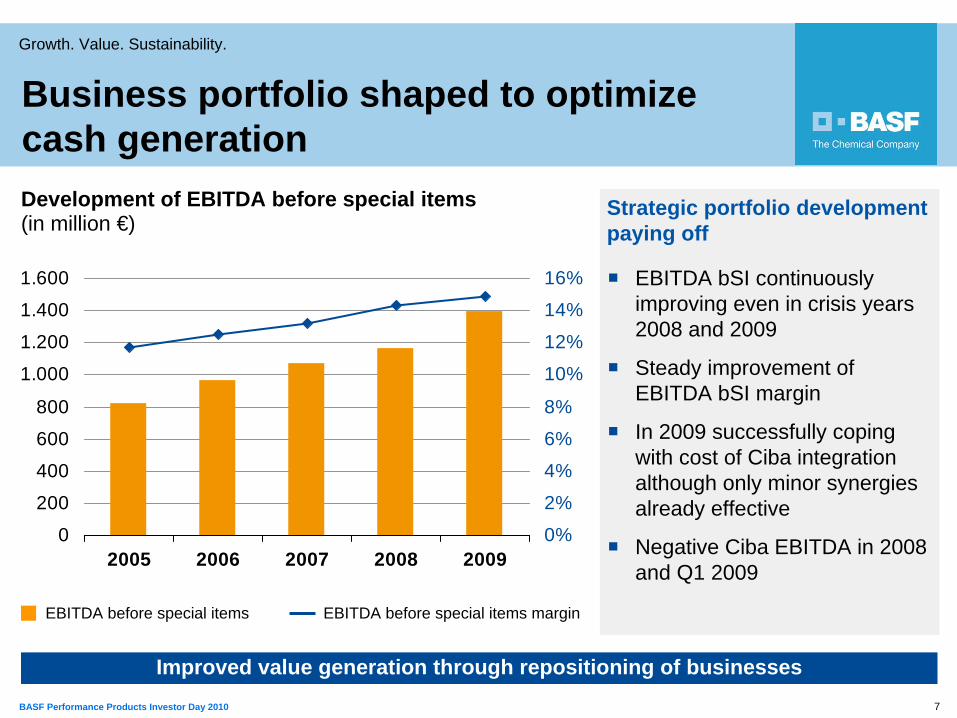

Development of EBITDA before special items (in million €)

Business portfolio shaped to optimize cash generation

EBITDA bSI continuously improving even in crisis years 2008 and 2009

Steady improvement of EBITDA bSI margin

In 2009 successfully coping with cost of Ciba integration although only minor synergies already effective

Negative Ciba EBITDA in 2008 and Q1 2009

Strategic portfolio development paying off

Improved value generation through repositioning of businesses

EBITDA before special items EBITDA before special items margin

0

200

400

600

800

1.000

1.200

1.400

1.600

2005 2006 2007 2008 20090%

2%

4%

6%

8%

10%

12%

14%

16%

8BASF Performance Products Investor Day 2010

Growth. Value. Sustainability.

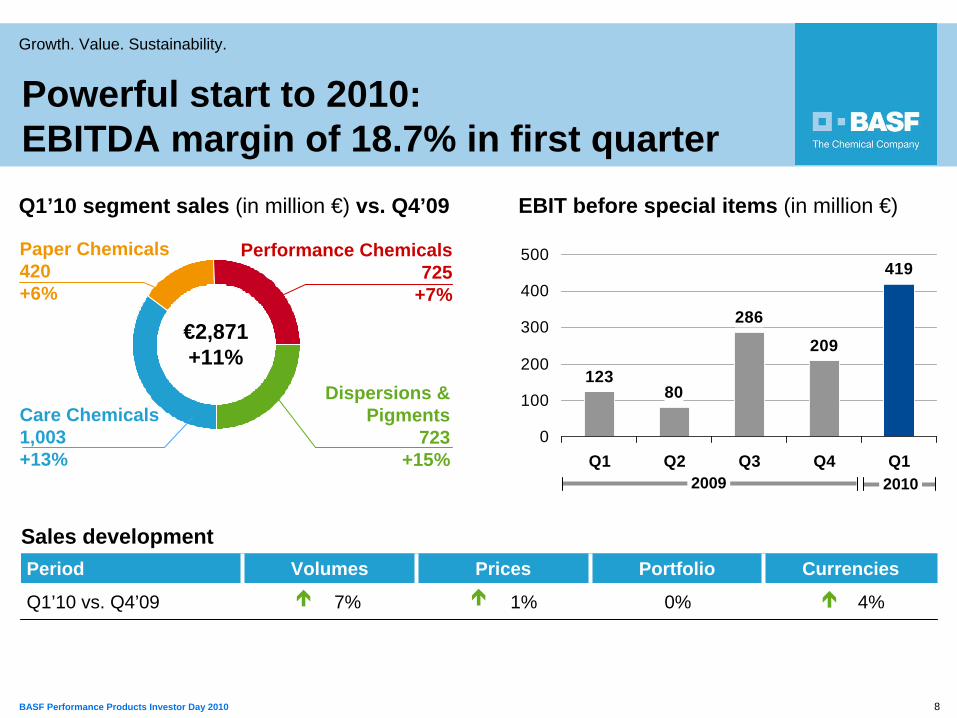

419

123

209

286

80

0

100

200

300

400

500

Q1 Q2 Q3 Q4 Q1

Sales developmentPeriod Volumes Prices Portfolio Currencies

Q1’10 vs. Q4’09 7% 1% 0% 4%

Dispersions & Pigments

723+15%

Performance Chemicals725

+7%

Paper Chemicals420+6%

€2,871 +11%

Care Chemicals1,003+13%

Q1’10 segment sales (in million €) vs. Q4’09 EBIT before special items (in million €)

20102009

Powerful start to 2010: EBITDA margin of 18.7% in first quarter

9BASF Performance Products Investor Day 2010

Growth. Value. Sustainability.

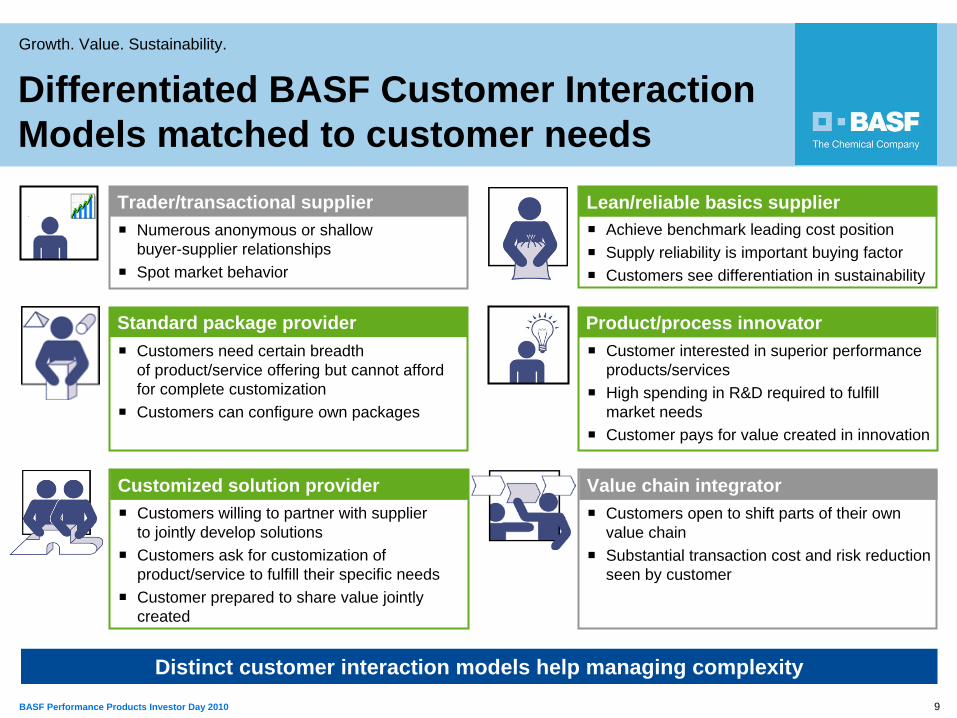

Customers need certain breadth of product/service offering but cannot afford for complete customizationCustomers can configure own packages

Numerous anonymous or shallow buyer-supplier relationshipsSpot market behavior

Customers willing to partner with supplier to jointly develop solutionsCustomers ask for customization of product/service to fulfill their specific needsCustomer prepared to share value jointly created

Achieve benchmark leading cost positionSupply reliability is important buying factorCustomers see differentiation in sustainability

Differentiated BASF Customer Interaction Models matched to customer needs

Distinct customer interaction models help managing complexity

Trader/transactional supplier

Standard package provider

Customized solution provider

Lean/reliable basics supplier

Customers open to shift parts of their own value chain Substantial transaction cost and risk reduction seen by customer

Value chain integrator

Customer interested in superior performance products/servicesHigh spending in R&D required to fulfill market needsCustomer pays for value created in innovation

Product/process innovator

10BASF Performance Products Investor Day 2010

Growth. Value. Sustainability.

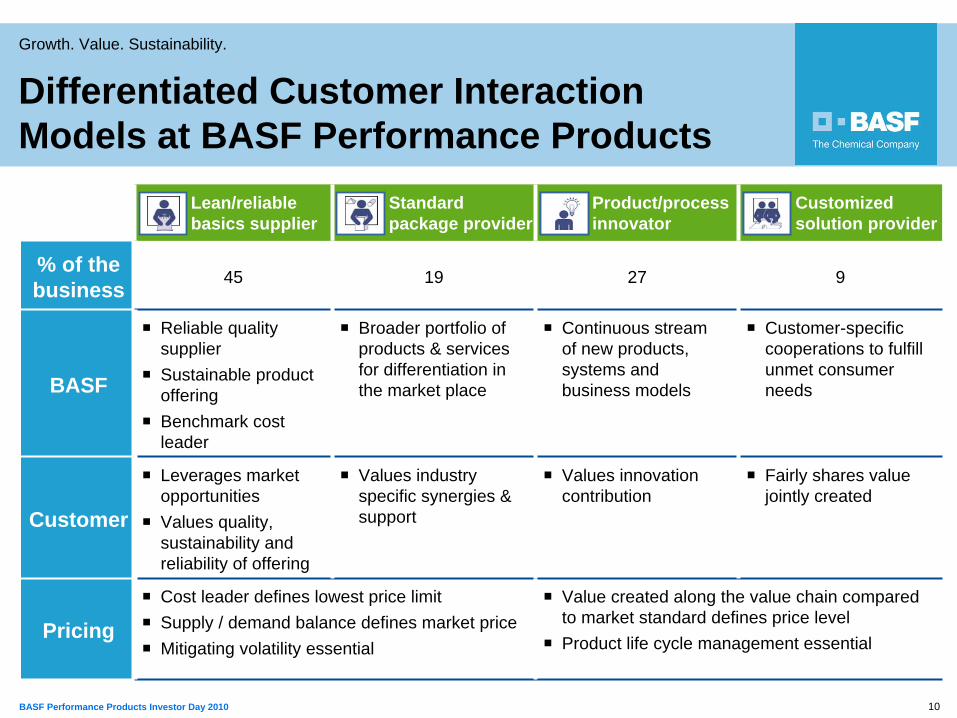

Differentiated Customer Interaction Models at BASF Performance Products

Lean/reliable basics supplier

Standard package provider

Product/process innovator

Customized solution provider

% of the business 45 19 27 9

BASF

Reliable quality supplierSustainable product offering Benchmark cost leader

Broader portfolio of products & services for differentiation in the market place

Continuous stream of new products, systems and business models

Customer-specific cooperations to fulfill unmet consumer needs

Customer

Leverages market opportunitiesValues quality, sustainability and reliability of offering

Values industry specific synergies & support

Values innovation contribution

Fairly shares value jointly created

PricingCost leader defines lowest price limit Supply / demand balance defines market priceMitigating volatility essential

Value created along the value chain compared to market standard defines price level Product life cycle management essential

11BASF Performance Products Investor Day 2010

Growth. Value. Sustainability.

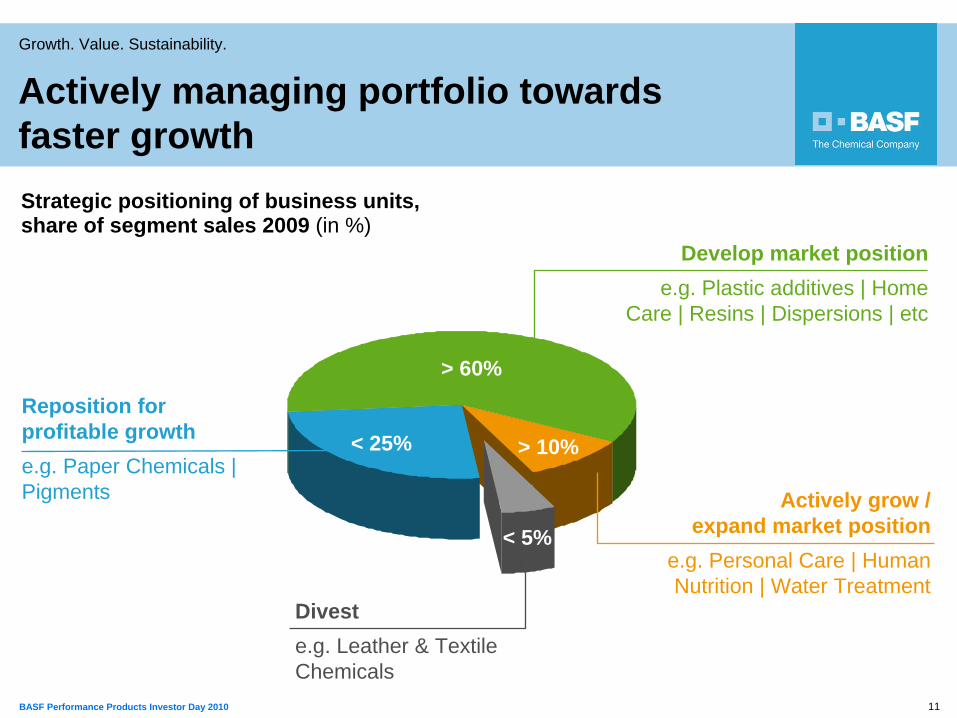

> 60%

Diveste.g. Leather & Textile Chemicals

Reposition for profitable growthe.g. Paper Chemicals | Pigments

Develop market positione.g. Plastic additives | Home

Care | Resins | Dispersions | etc

Actively grow / expand market position

e.g. Personal Care | Human Nutrition | Water Treatment

< 5%

< 25% > 10%

Actively managing portfolio towards faster growthStrategic positioning of business units, share of segment sales 2009 (in %)

12BASF Performance Products Investor Day 2010

Growth. Value. Sustainability.

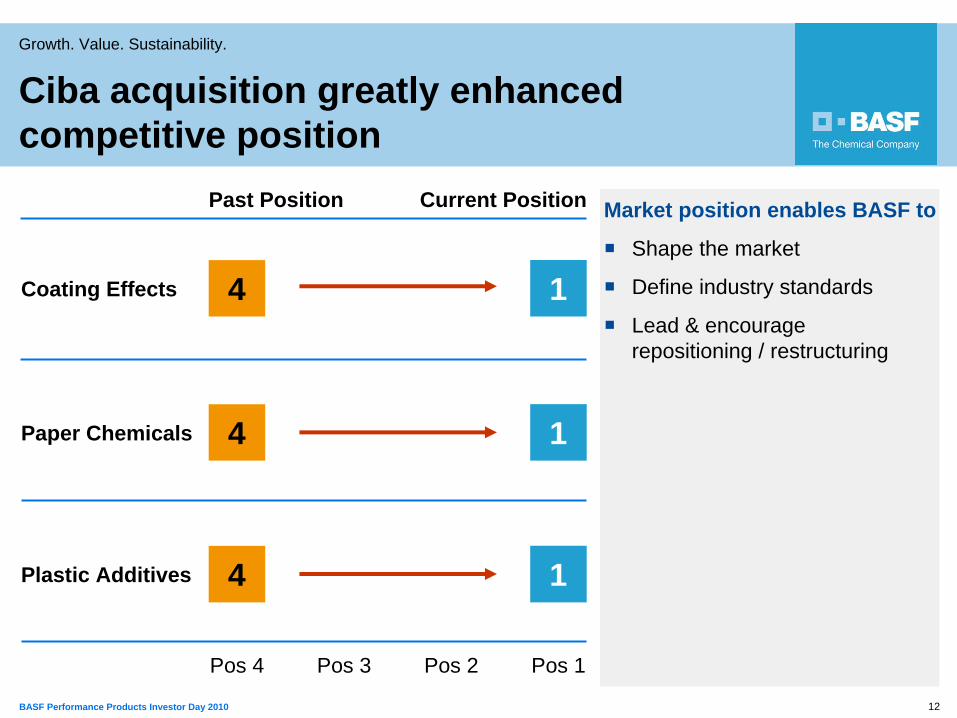

Market position enables BASF to

Shape the market

Define industry standards

Lead & encourage repositioning / restructuring

Coating Effects 1

Paper Chemicals

Past Position

Plastic Additives

Current Position

Ciba acquisition greatly enhanced competitive position

4

1

1

4

4

Pos 4 Pos 1Pos 3 Pos 2

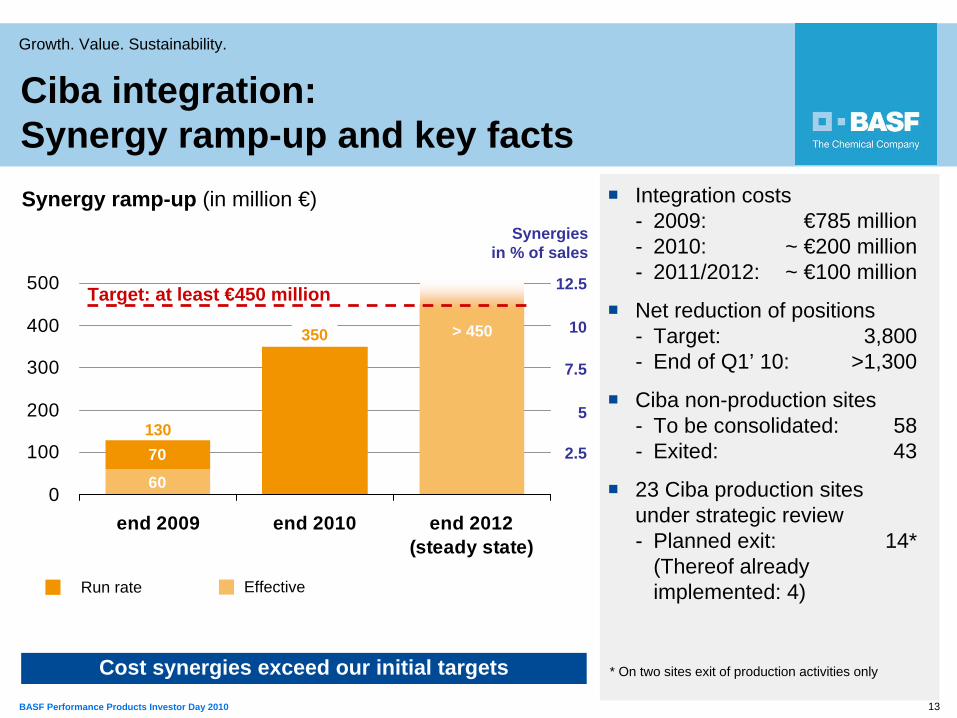

13BASF Performance Products Investor Day 2010

Growth. Value. Sustainability.

Synergy ramp-up (in million €)

70

600

100

200

300

400

500

end 2009 end 2010 end 2012(steady state)

Target: at least €450 million

Synergies in % of sales

10

5

7.5

2.5

12.5

130

Cost synergies exceed our initial targets

> 450

Ciba integration: Synergy ramp-up and key facts

Integration costs- 2009: €785 million- 2010: ~ €200 million- 2011/2012: ~ €100 million

Net reduction of positions- Target: 3,800- End of Q1’ 10: >1,300

Ciba non-production sites- To be consolidated: 58- Exited: 43

23 Ciba production sites under strategic review- Planned exit: 14*

(Thereof already implemented: 4)

* On two sites exit of production activities only

350

EffectiveRun rate

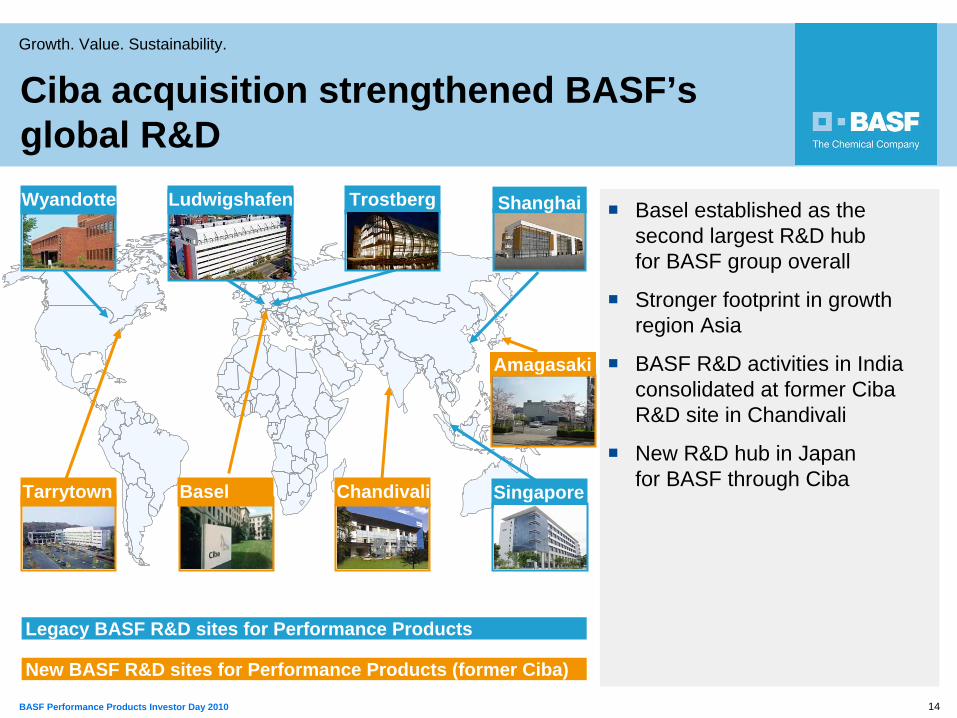

14BASF Performance Products Investor Day 2010

Growth. Value. Sustainability.

Amagasaki

Singapore

Trostberg

Legacy BASF R&D sites for Performance Products

New BASF R&D sites for Performance Products (former Ciba)

Ciba acquisition strengthened BASF’s global R&D

Basel established as the second largest R&D hub for BASF group overall

Stronger footprint in growth region Asia

BASF R&D activities in India consolidated at former Ciba R&D site in Chandivali

New R&D hub in Japan for BASF through CibaTarrytown Chandivali

Wyandotte Ludwigshafen Shanghai

Basel

15BASF Performance Products Investor Day 2010

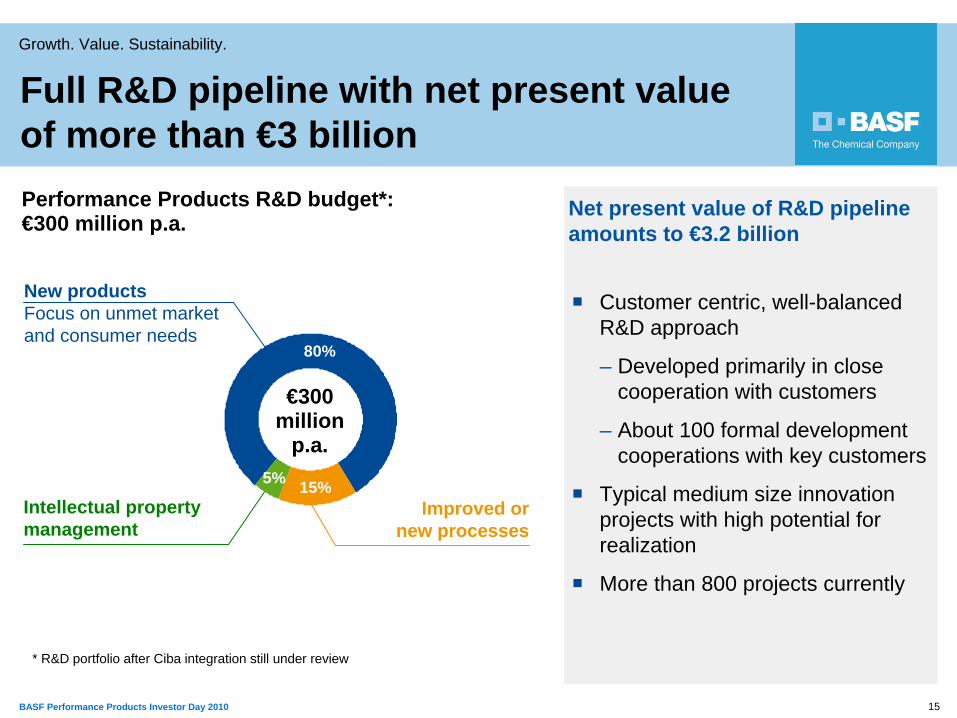

Growth. Value. Sustainability.

Customer centric, well-balanced R&D approach

– Developed primarily in close cooperation with customers

– About 100 formal development cooperations with key customers

Typical medium size innovation projects with high potential for realization

More than 800 projects currently

Net present value of R&D pipeline amounts to €3.2 billion

New products Focus on unmet market and consumer needs

Improved or new processes

Intellectual property management

80%

15%5%

€300million

p.a.

Performance Products R&D budget*: €300 million p.a.

* R&D portfolio after Ciba integration still under review

Full R&D pipeline with net present value of more than €3 billion

16BASF Performance Products Investor Day 2010

Growth. Value. Sustainability.

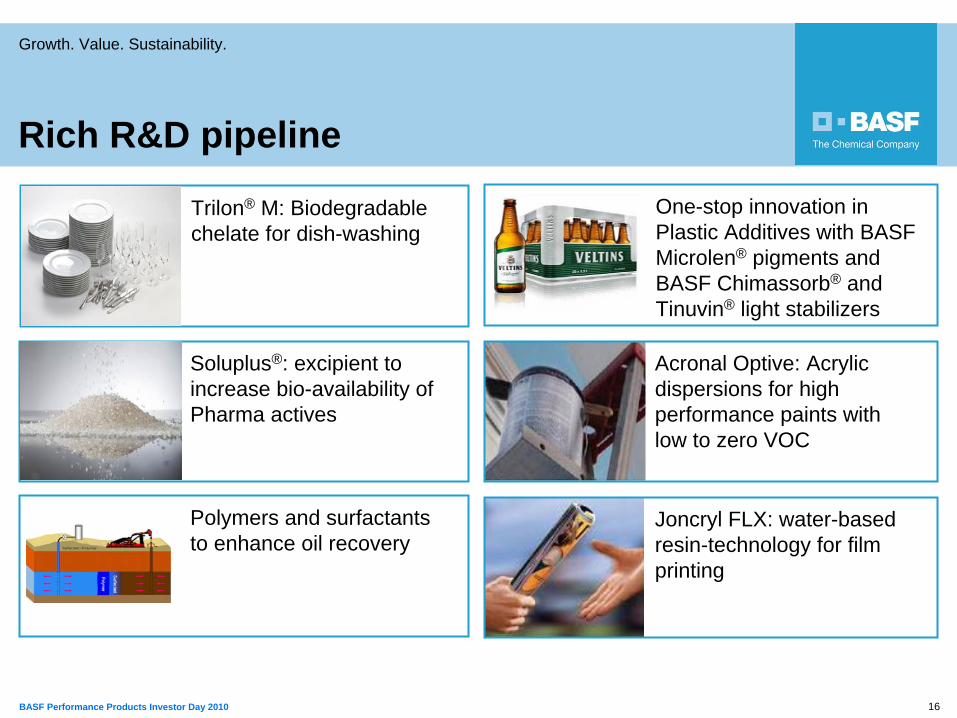

Trilon® M: Biodegradable chelate for dish-washing

Joncryl FLX: water-based resin-technology for film printing

One-stop innovation in Plastic Additives with BASF Microlen® pigments and BASF Chimassorb® and Tinuvin® light stabilizers

Soluplus®: excipient to increase bio-availability of Pharma actives

Polymers and surfactantsto enhance oil recovery

Acronal Optive: Acrylic dispersions for high performance paints with low to zero VOC

Rich R&D pipeline

17BASF Performance Products Investor Day 2010

Growth. Value. Sustainability.

Performance Products: today and into the future

Vision 20202009

17

Chemical industry leader to improve quality of life

Preferred partner for all performance & innovation driven customers

Comprehensive portfolio of value-adding and sustainable products and services

Earning a substantial premium on cost of capital every year in each division

EBITDA margin of minimum 20%

Growth: 2% points above relevant markets

Value: EBITDA margin of minimum 18% -consistently earning a premium on cost of capital

Sustainability: Value generation throughout business cycles

Leading innovator for sustainable solutions

Sales to 3rd parties € 9,4 billion

EBITDA bSI margin of 15%

CIBA integration cost of € 785 million

EBIT after cost of capital € - 930 million

Roadmap 2012

1BASF Performance Products Investor Day 2010

Growth. Value. Sustainability.

1 | Dispersions & Pigments Markus Kramer

2 | Paper Chemicals Fred Baumgartner

3 | Performance Chemicals Hans W. Reiners

4 | Care Chemicals Gabriel Tanbourgi

1

2BASF Performance Products Investor Day 2010

Growth. Value. Sustainability.

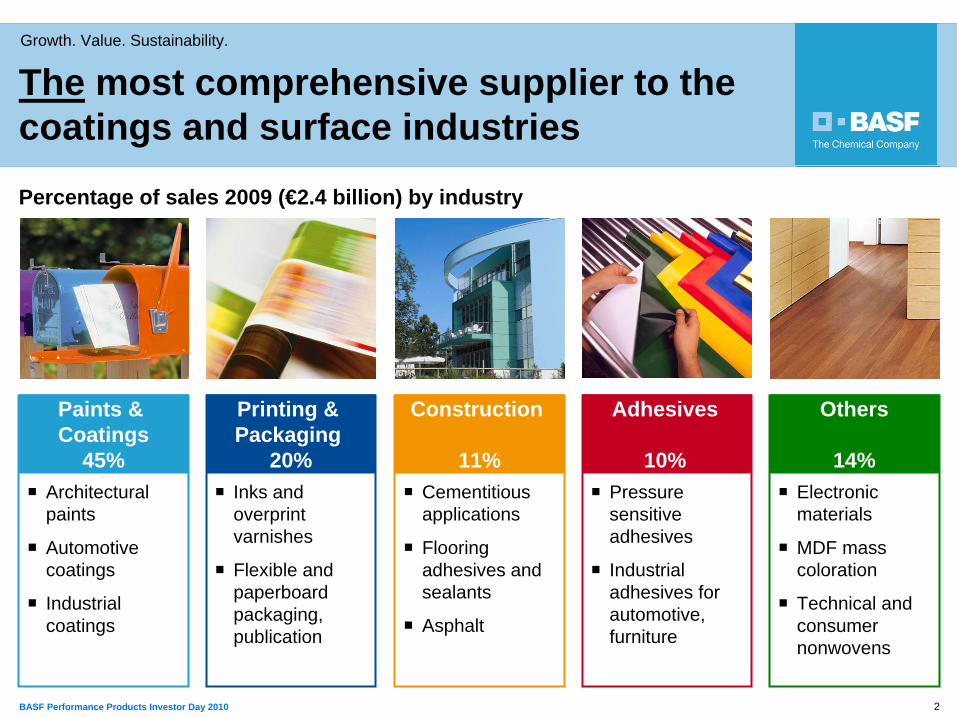

Architectural paints

Automotive coatings

Industrial coatings

Cementitious applications

Flooring adhesives and sealants

Asphalt

Pressure sensitive adhesives

Industrial adhesives for automotive, furniture

Electronic materials

MDF mass coloration

Technical and consumer nonwovens

Inks and overprint varnishes

Flexible and paperboard packaging, publication

Paints & Coatings

45%

Construction

11%

Adhesives

10%

Others

14%

Printing & Packaging

20%

Percentage of sales 2009 (€2.4 billion) by industry

The most comprehensive supplier to the coatings and surface industries

3BASF Performance Products Investor Day 2010

Growth. Value. Sustainability.

Full range of solutions from one supplier: Automotive sector

Ingredients* BASF offering Effect

Binders & Crosslinkers ~70%

Acrylic resins and dispersionsUV resins and photo initiatorsPolyisocyanatesAmino resins

Shaping coating properties, e.g. scratch & stain resistance, glossy finish, fast curing

Pigments ~10%

Complete portfolio of organic and inorganic pigmentsPreparations and dyes

ColorationEmotion & appearance

Protecting Additives ~2%

Light stabilizersAnti-oxidants

Preserving coatings quality against severe conditions, e.g. bleaching

Formulation Additives ~2%

DispersantsRheology modifiersSlip/leveling agents

Optimize processabilityProvide the finishing touch for a Coatings system

* Rest: solvent ~15%

4BASF Performance Products Investor Day 2010

Growth. Value. Sustainability.

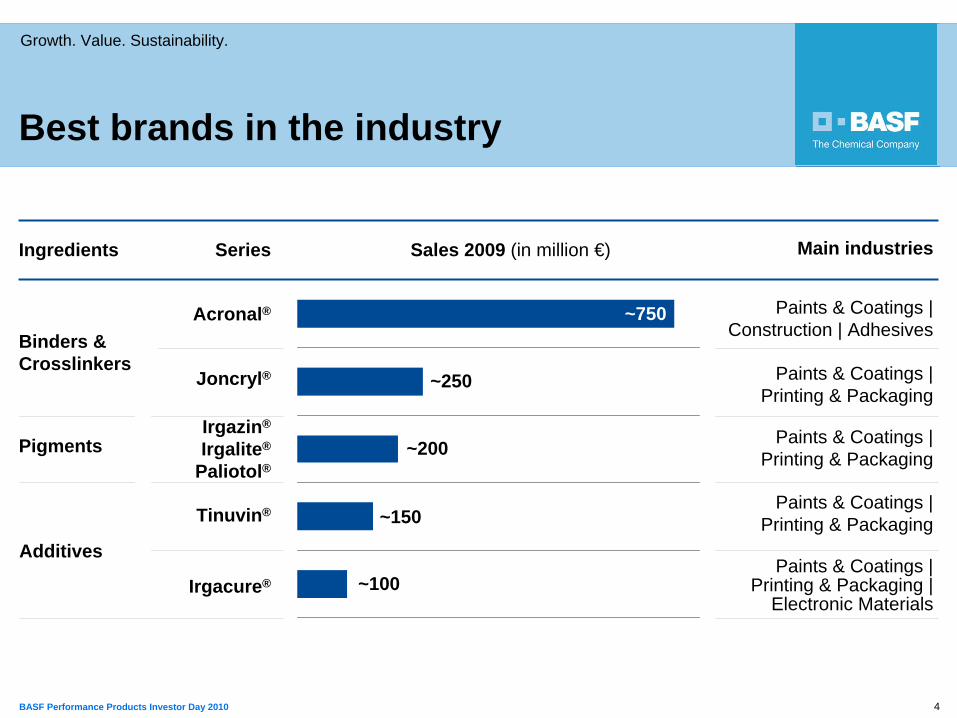

Binders & Crosslinkers

Pigments

0 100 200 300 400 500 600 700 800

Series Sales 2009 (in million €)

Paints & Coatings | Construction | Adhesives

Paints & Coatings | Printing & Packaging

Paints & Coatings | Printing & Packaging

Paints & Coatings | Printing & Packaging

Paints & Coatings | Printing & Packaging |

Electronic MaterialsIrgacure®

Joncryl®

Tinuvin®

Acronal®

Ingredients

Irgazin®

Irgalite®

Paliotol®

Main industries

~750

~250

~200

~150

~100

Additives

Best brands in the industry

5BASF Performance Products Investor Day 2010

Growth. Value. Sustainability.

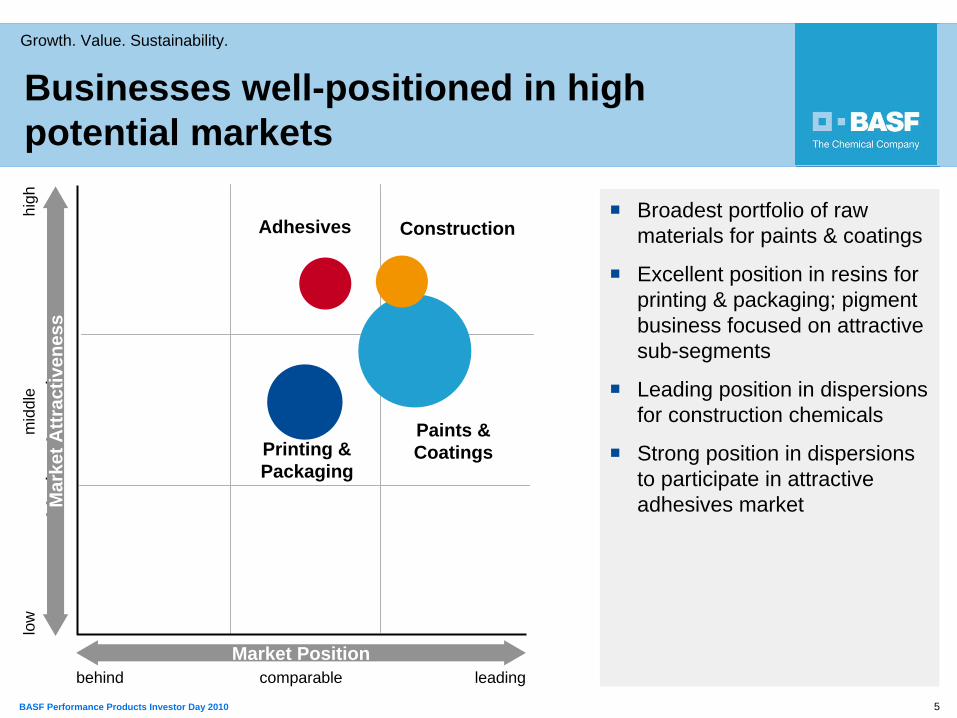

Businesses well-positioned in high potential markets

Mar

ket A

ttrac

tiven

ess

Paints & CoatingsPrinting &

Packaging

Adhesives ConstructionBroadest portfolio of raw materials for paints & coatings

Excellent position in resins for printing & packaging; pigment business focused on attractive sub-segments

Leading position in dispersions for construction chemicals

Strong position in dispersions to participate in attractive adhesives market

low

mid

dle

high

Mar

ket A

ttrac

tiven

ess

leadingcomparablebehindMarket Position

6BASF Performance Products Investor Day 2010

Growth. Value. Sustainability.

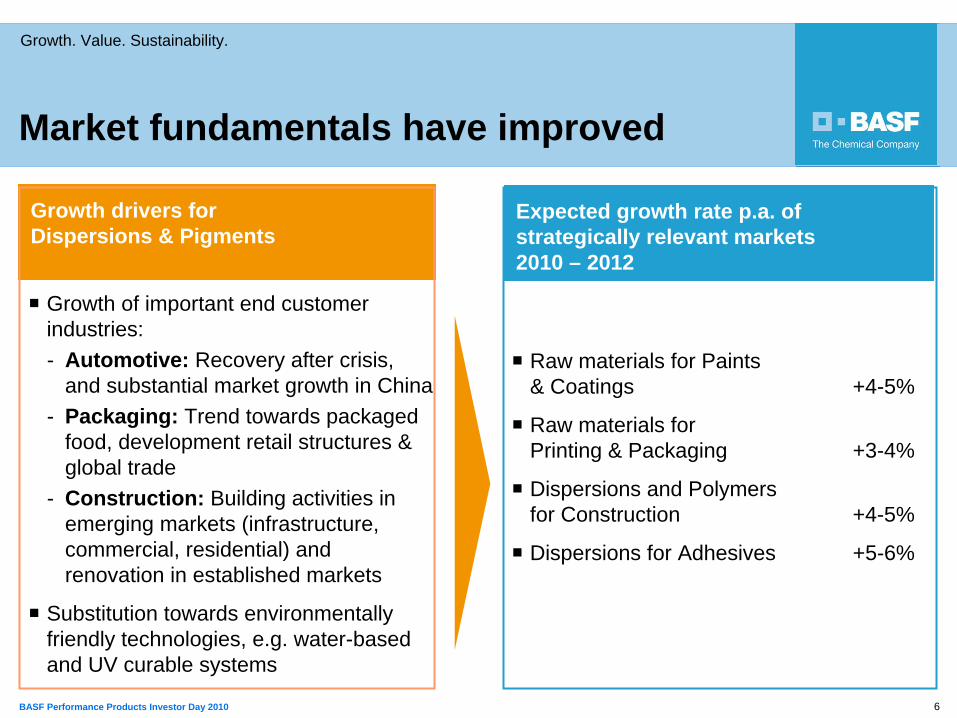

Growth drivers forDispersions & Pigments

Expected growth rate p.a. of strategically relevant markets 2010 – 2012

Growth of important end customer industries:- Automotive: Recovery after crisis,

and substantial market growth in China - Packaging: Trend towards packaged

food, development retail structures & global trade

- Construction: Building activities in emerging markets (infrastructure, commercial, residential) and renovation in established markets

Substitution towards environmentally friendly technologies, e.g. water-based and UV curable systems

Raw materials for Paints & Coatings +4-5%

Raw materials for Printing & Packaging +3-4%

Dispersions and Polymers for Construction +4-5%

Dispersions for Adhesives +5-6%

Market fundamentals have improved

7BASF Performance Products Investor Day 2010

Growth. Value. Sustainability.

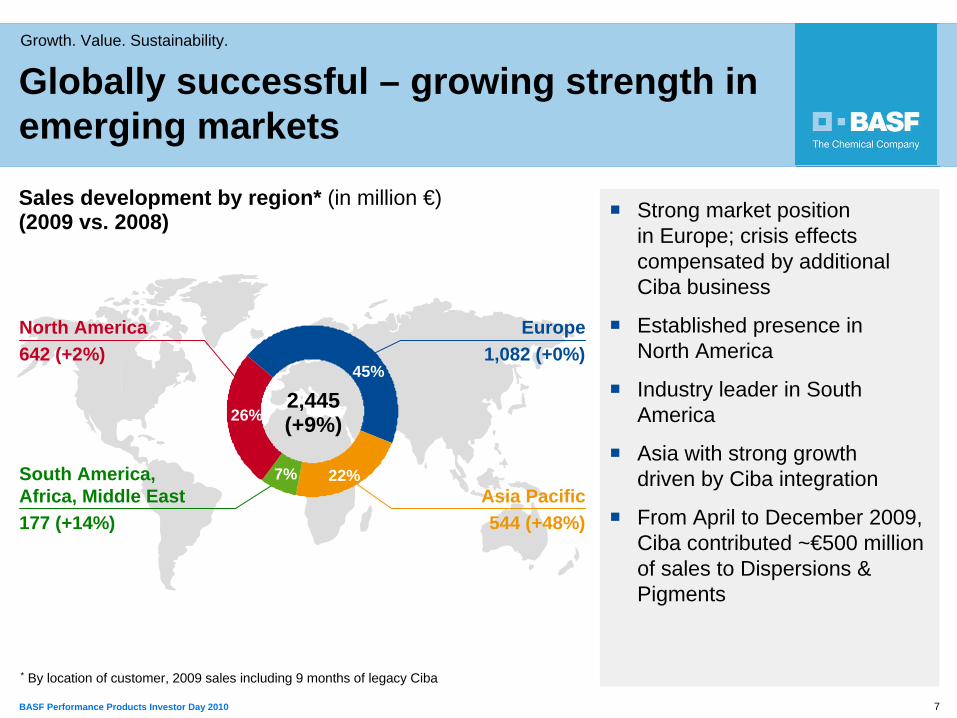

Sales development by region* (in million €) (2009 vs. 2008)

* By location of customer, 2009 sales including 9 months of legacy Ciba

25%

Strong market position in Europe; crisis effects compensated by additional Ciba business

Established presence in North America

Industry leader in South America

Asia with strong growth driven by Ciba integration

From April to December 2009, Ciba contributed ~€500 million of sales to Dispersions & Pigments

Globally successful – growing strength in emerging markets

North America642 (+2%)

Europe1,082 (+0%)

Asia Pacific544 (+48%)

South America, Africa, Middle East177 (+14%)

45%

22%7%

26%2,445(+9%)

8BASF Performance Products Investor Day 2010

Growth. Value. Sustainability.

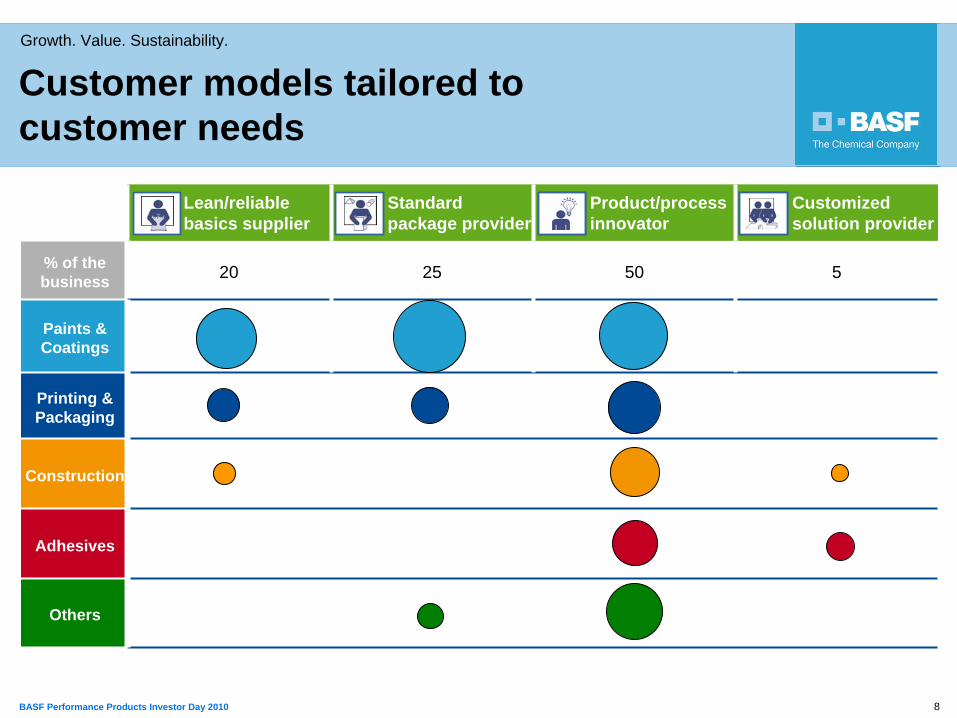

Customer models tailored to customer needs

Lean/reliable basics supplier

Standard package provider

Product/process innovator

Customized solution provider

% of the business 20 25 50 5

Paints & Coatings

Printing & Packaging

Construction

Adhesives

Others

9BASF Performance Products Investor Day 2010

Growth. Value. Sustainability.

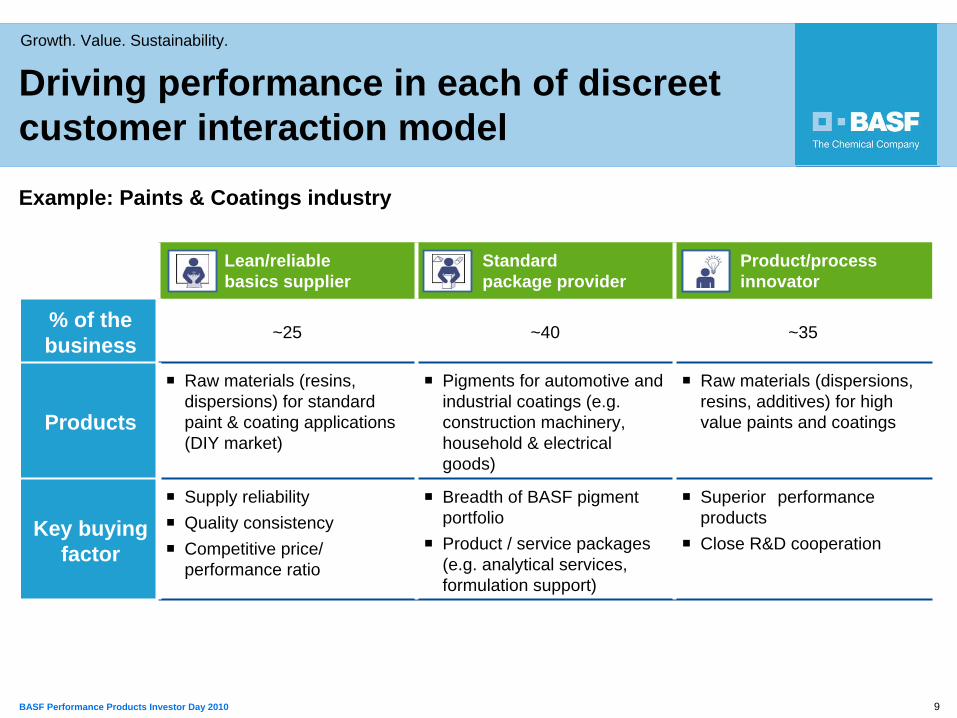

Driving performance in each of discreet customer interaction model

Lean/reliable basics supplier

Standard package provider

Product/process innovator

% of the business ~25 ~40 ~35

Products

Raw materials (resins, dispersions) for standard paint & coating applications (DIY market)

Pigments for automotive and industrial coatings (e.g. construction machinery, household & electrical goods)

Raw materials (dispersions, resins, additives) for high value paints and coatings

Key buying factor

Supply reliabilityQuality consistencyCompetitive price/ performance ratio

Breadth of BASF pigment portfolioProduct / service packages (e.g. analytical services, formulation support)

Superior performance productsClose R&D cooperation

Example: Paints & Coatings industry

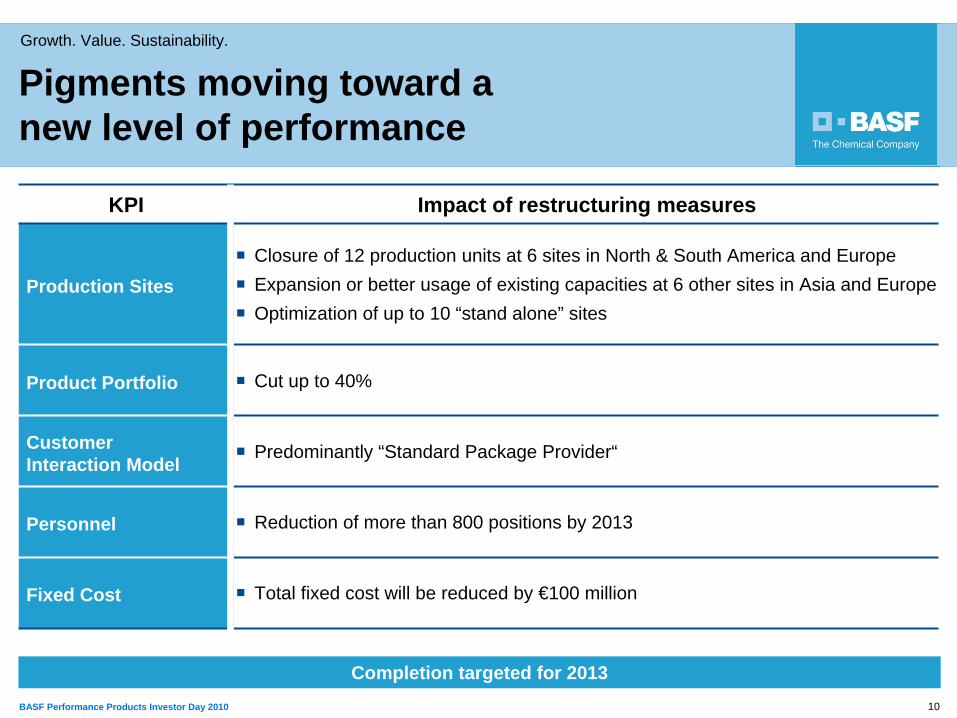

10BASF Performance Products Investor Day 2010

Growth. Value. Sustainability.

KPI Impact of restructuring measures

Production SitesClosure of 12 production units at 6 sites in North & South America and EuropeExpansion or better usage of existing capacities at 6 other sites in Asia and EuropeOptimization of up to 10 “stand alone” sites

Product Portfolio Cut up to 40%

Customer Interaction Model

Predominantly “Standard Package Provider“

Personnel Reduction of more than 800 positions by 2013

Fixed Cost Total fixed cost will be reduced by €100 million

Pigments moving toward a new level of performance

Completion targeted for 2013

11BASF Performance Products Investor Day 2010

Growth. Value. Sustainability.

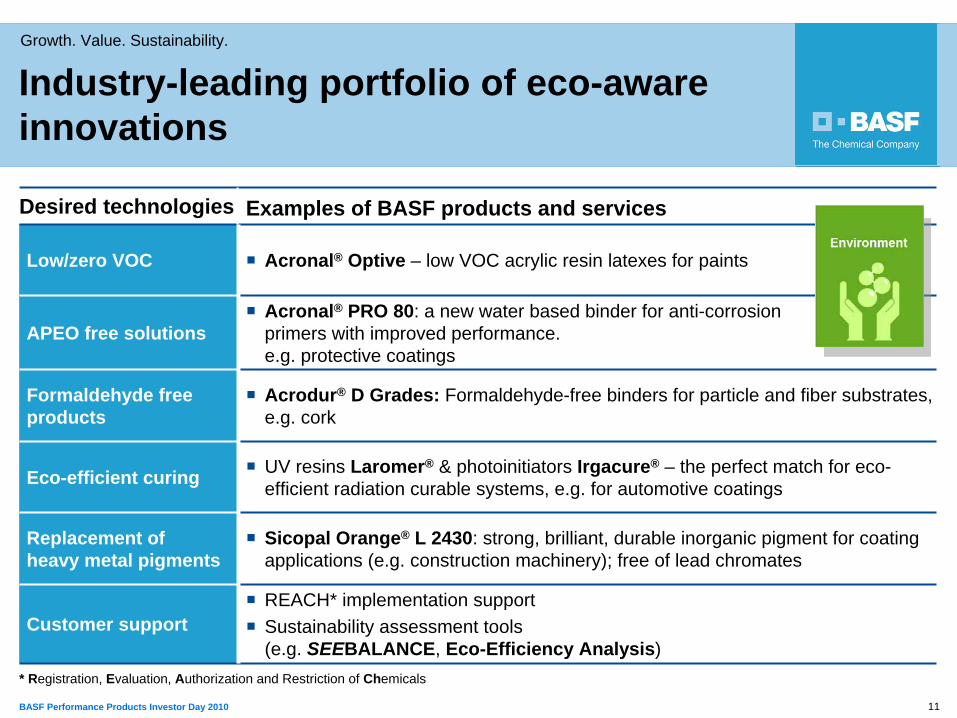

Industry-leading portfolio of eco-aware innovations

* Registration, Evaluation, Authorization and Restriction of Chemicals

Desired technologies Examples of BASF products and services

Low/zero VOC Acronal® Optive – low VOC acrylic resin latexes for paints

APEO free solutionsAcronal® PRO 80: a new water based binder for anti-corrosion primers with improved performance. e.g. protective coatings

Formaldehyde free products

Acrodur® D Grades: Formaldehyde-free binders for particle and fiber substrates, e.g. cork

Eco-efficient curing UV resins Laromer® & photoinitiators Irgacure® – the perfect match for eco-efficient radiation curable systems, e.g. for automotive coatings

Replacement of heavy metal pigments

Sicopal Orange® L 2430: strong, brilliant, durable inorganic pigment for coating applications (e.g. construction machinery); free of lead chromates

Customer supportREACH* implementation supportSustainability assessment tools(e.g. SEEBALANCE, Eco-Efficiency Analysis)

12BASF Performance Products Investor Day 2010

Growth. Value. Sustainability.

Growth. Value. Sustainability.Dispersions & Pigments

We are recognized as the comprehensive raw material supplier for the Coatings industry

We are the preferred partner for formulating innovative and sustainable coatings and printing solutions

Vision 2020Roadmap 2012Growth: We focus on attractive market segments which grow above the chemical market

Cost structure & Operational Excellence:We restructure our assets and continuously improve productivity

Life Cycle Management:We manage our businesses in line with their strategic positioning and invest in R&D and assets accordingly

Sustainability: We offer innovative, differentiated and sustainable products and solutions

We earn a premium on our cost of capital as of 2011

1BASF Performance Products Investor Day 2010

Growth. Value. Sustainability.

1 | Dispersions & Pigments Markus Kramer

2 | Paper Chemicals Fred Baumgartner

3 | Performance Chemicals Hans W. Reiners

4 | Care Chemicals Gabriel Tanbourgi

1

2BASF Performance Products Investor Day 2010

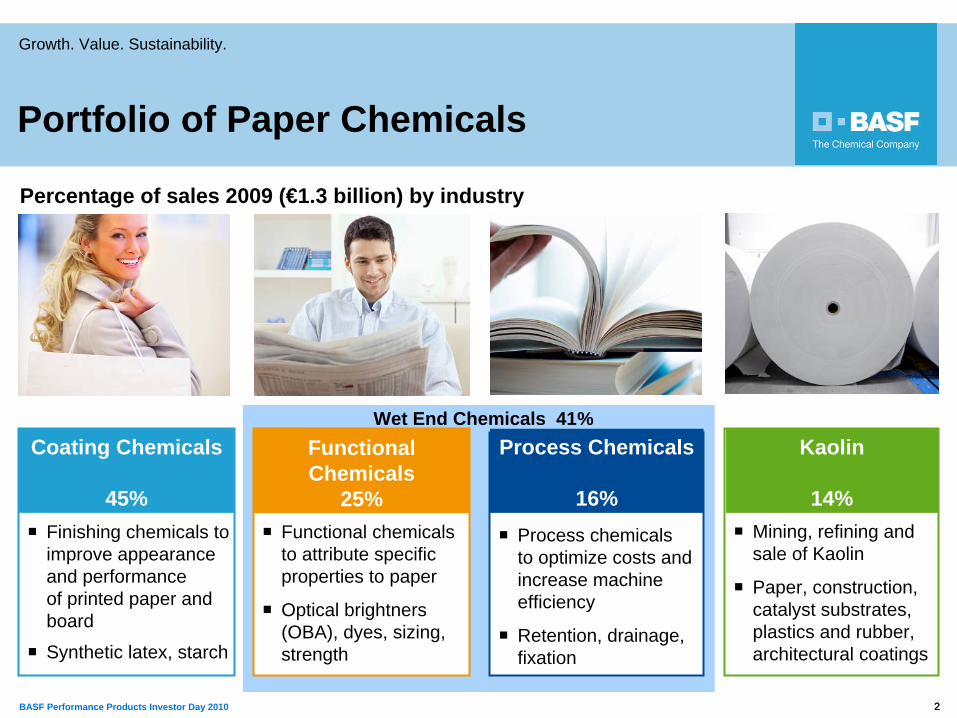

Growth. Value. Sustainability.

2

Finishing chemicals to improve appearance and performance of printed paper and board

Synthetic latex, starch

Coating Chemicals

45%Process chemicals to optimize costs and increase machine efficiency

Retention, drainage, fixation

Process Chemicals

16%Functional chemicals to attribute specific properties to paper

Optical brightners(OBA), dyes, sizing, strength

Functional Chemicals

25%

Wet End Chemicals 41%

Mining, refining and sale of Kaolin

Paper, construction, catalyst substrates, plastics and rubber, architectural coatings

Kaolin

14%

Percentage of sales 2009 (€1.3 billion) by industry

Portfolio of Paper Chemicals

3BASF Performance Products Investor Day 2010

Growth. Value. Sustainability.

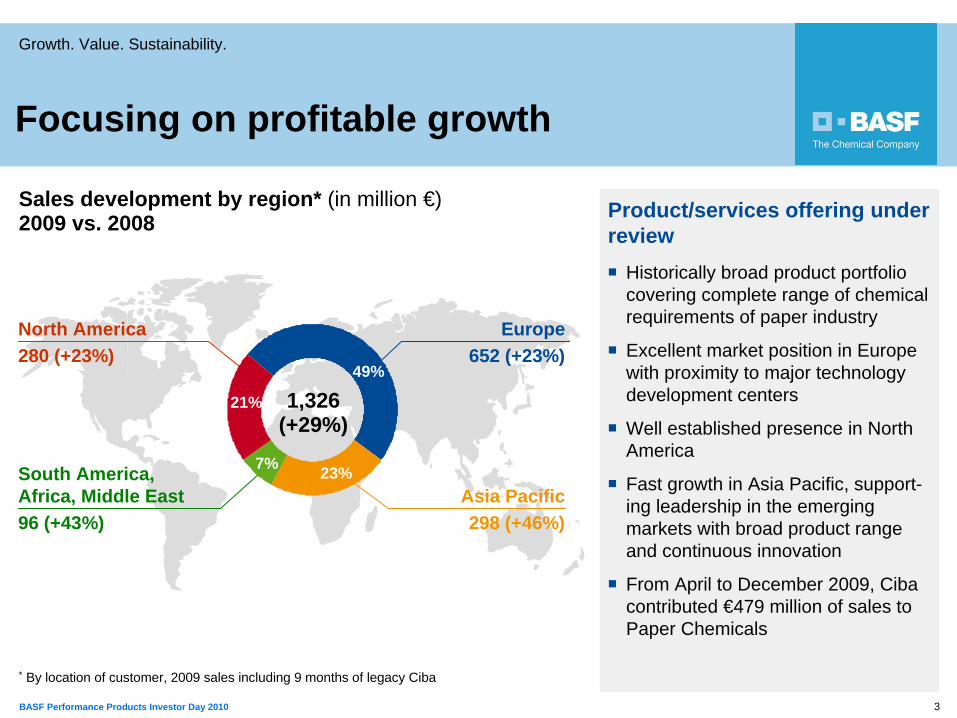

Sales development by region* (in million €) 2009 vs. 2008

25%

Focusing on profitable growth

North America280 (+23%)

Europe652 (+23%)

Asia Pacific298 (+46%)

South America, Africa, Middle East96 (+43%)

49%

23%7%

21% 1,326(+29%)

Historically broad product portfolio covering complete range of chemical requirements of paper industry

Excellent market position in Europe with proximity to major technology development centers

Well established presence in North America

Fast growth in Asia Pacific, support-ing leadership in the emerging markets with broad product range and continuous innovation

From April to December 2009, Ciba contributed €479 million of sales to Paper Chemicals

Product/services offering under review

* By location of customer, 2009 sales including 9 months of legacy Ciba

4BASF Performance Products Investor Day 2010

Growth. Value. Sustainability.

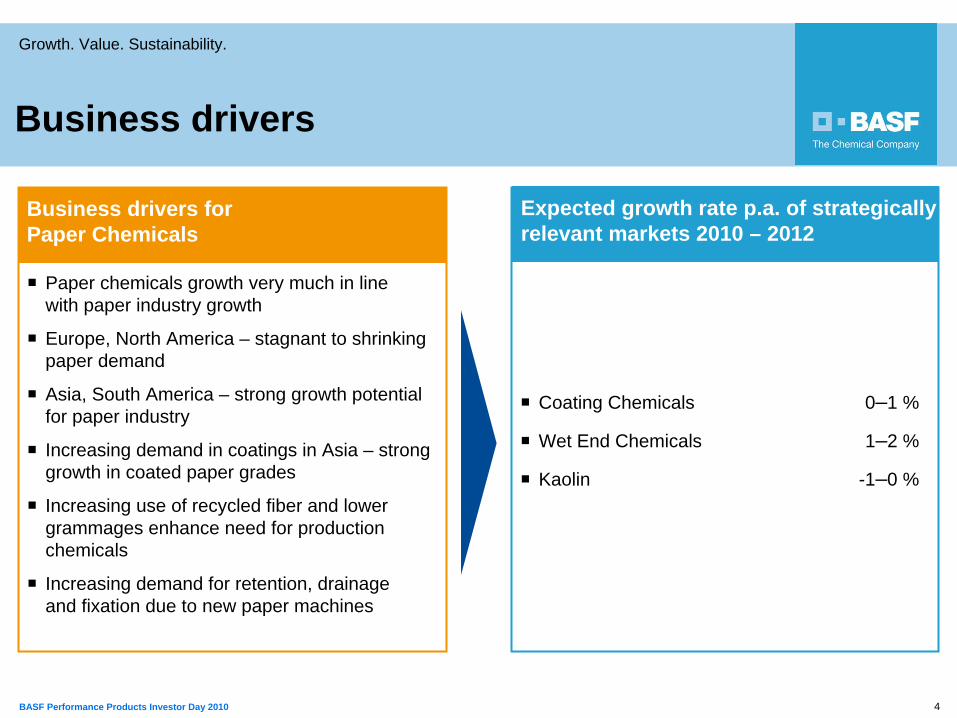

Paper chemicals growth very much in line with paper industry growth

Europe, North America – stagnant to shrinking paper demand

Asia, South America – strong growth potential for paper industry

Increasing demand in coatings in Asia – strong growth in coated paper grades

Increasing use of recycled fiber and lower grammages enhance need for production chemicals

Increasing demand for retention, drainage and fixation due to new paper machines

Coating Chemicals 0–1 %

Wet End Chemicals 1–2 %

Kaolin -1–0 %

Business drivers for Paper Chemicals

Business drivers

Expected growth rate p.a. of strategically relevant markets 2010 – 2012

5BASF Performance Products Investor Day 2010

Growth. Value. Sustainability.

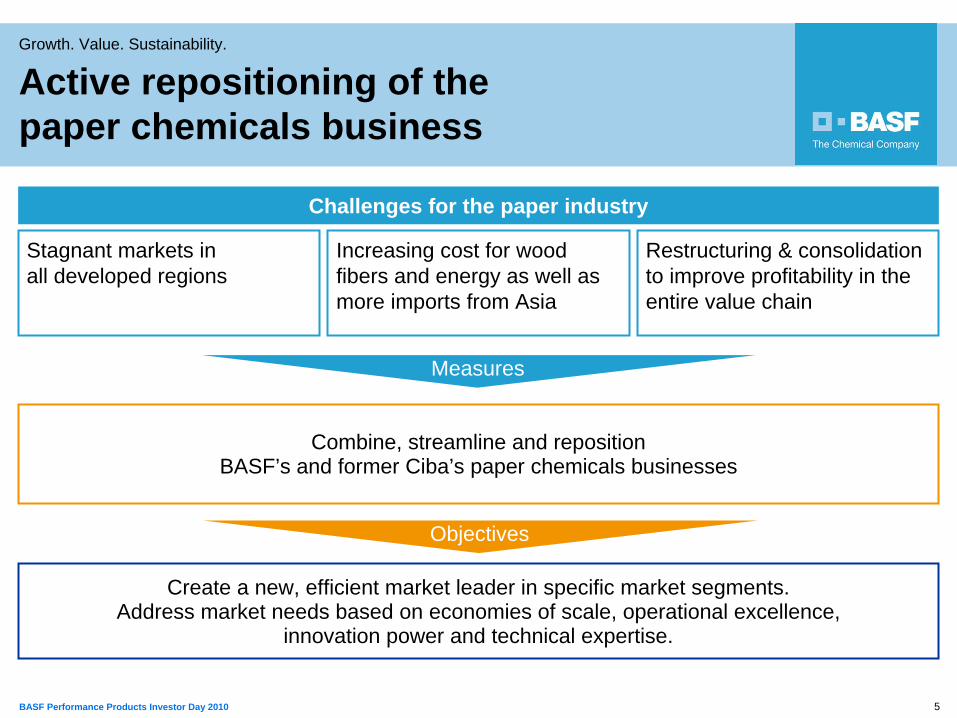

Combine, streamline and reposition BASF’s and former Ciba’s paper chemicals businesses

Challenges for the paper industry

Stagnant markets in all developed regions

Increasing cost for wood fibers and energy as well as more imports from Asia

Restructuring & consolidation to improve profitability in the entire value chain

Create a new, efficient market leader in specific market segments.Address market needs based on economies of scale, operational excellence,

innovation power and technical expertise.

Measures

Objectives

Active repositioning of the paper chemicals business

6BASF Performance Products Investor Day 2010

Growth. Value. Sustainability.

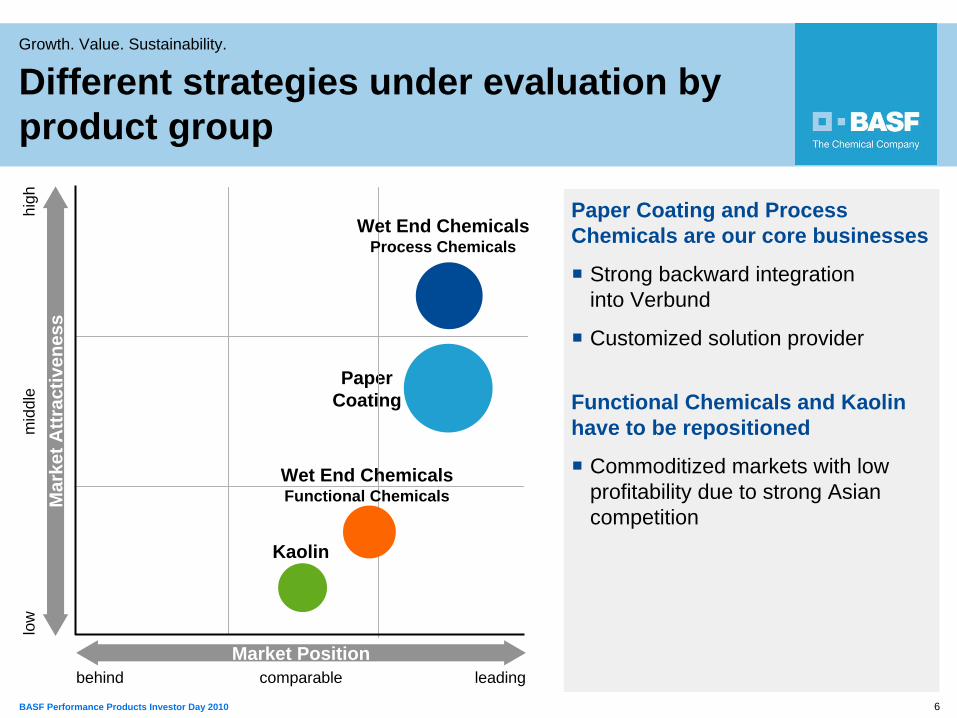

Paper Coating and Process Chemicals are our core businesses

Strong backward integration into Verbund

Customized solution provider

Functional Chemicals and Kaolin have to be repositioned

Commoditized markets with low profitability due to strong Asian competition

Paper Coating

Kaolin

low

mid

dle

high

leadingcomparablebehind

Mar

ket A

ttrac

tiven

ess

Market Position

Wet End Chemicals Process Chemicals

Wet End Chemicals Functional Chemicals

Different strategies under evaluation by product group

7BASF Performance Products Investor Day 2010

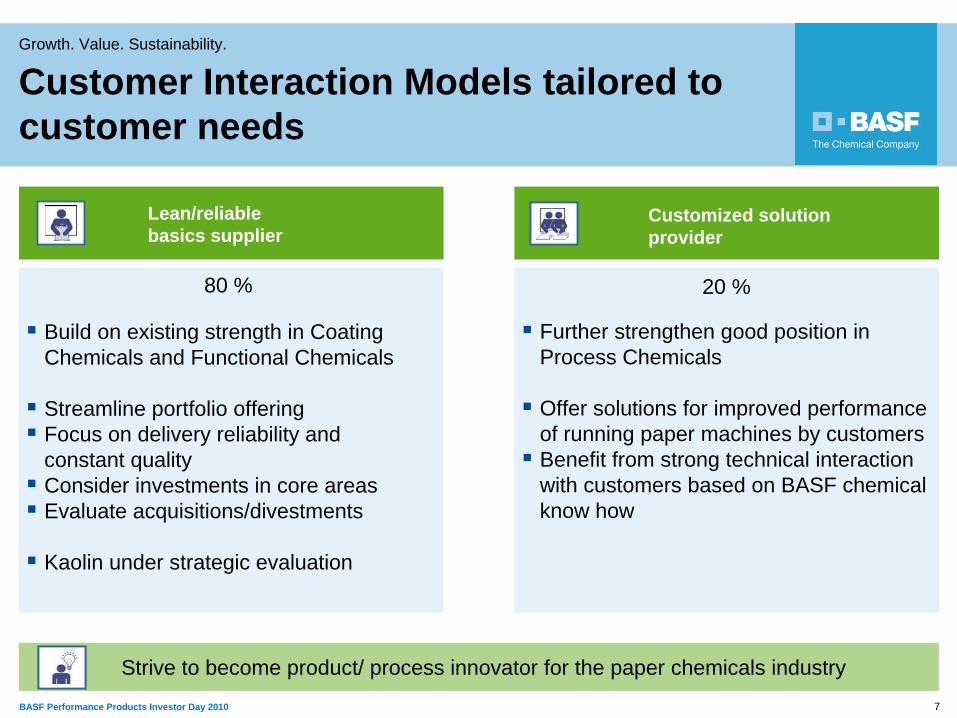

Growth. Value. Sustainability.

Customized solution provider

Lean/reliable basics supplier

80 % 20 %

Build on existing strength in Coating Chemicals and Functional Chemicals

Streamline portfolio offeringFocus on delivery reliability and constant qualityConsider investments in core areasEvaluate acquisitions/divestments

Kaolin under strategic evaluation

Further strengthen good position in Process Chemicals

Offer solutions for improved performance of running paper machines by customersBenefit from strong technical interaction with customers based on BASF chemical know how

Strive to become product/ process innovator for the paper chemicals industry

Customer Interaction Models tailored to customer needs

8BASF Performance Products Investor Day 2010

Growth. Value. Sustainability.

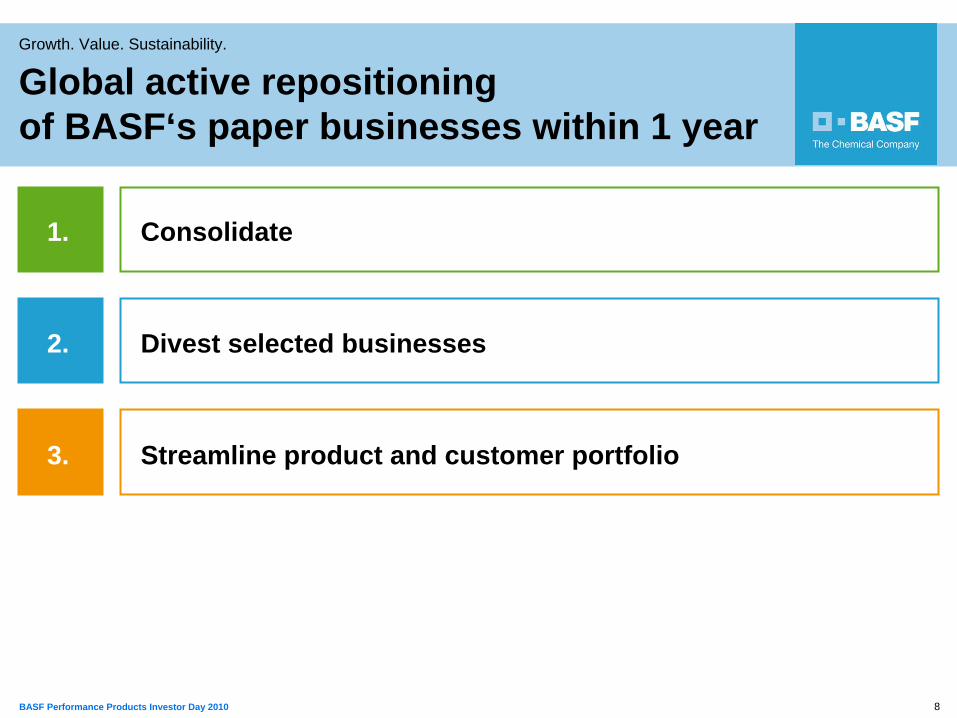

1. Consolidate

2. Divest selected businesses

3. Streamline product and customer portfolio

Global active repositioning of BASF‘s paper businesses within 1 year

9BASF Performance Products Investor Day 2010

Growth. Value. Sustainability.

1. Consolidate

Ludwigshafen

Jiangsu

Ankleshwar

GrenzachPischelsdorf

Merak

Paulinia

Hamina

BACC

Guaratingueta

Mangalore

Bradford

General Lagos

Cengkareng

Coating Chemicals

Wet End Chemicals

Kaolin

McIntosh

Altamira

AppletonMonaca

Chattanooga SuffolkWest Memphis

Middle Georgia

LapuaKokemäkiMietoinen

Estrada do Colégio

SensTolosa

Kaipiainen

GuturribayRibécourt

Berwick

SGBD - JVRokuromi

AltonaConcon

Global production sites as of closing 2009

10BASF Performance Products Investor Day 2010

Growth. Value. Sustainability.

1. Consolidate Restructuring plans well advanced

Ludwigshafen

Jiangsu

Ankleshwar

GrenzachPischelsdorf

Merak

Paulinia

Hamina

BACC

Guaratingueta

Mangalore

Bradford

General Lagos

Cengkareng

Coating Chemicals

Wet End Chemicals

Kaolin

McIntosh

Altamira

AppletonMonaca

Chattanooga SuffolkWest Memphis

Middle Georgia SGBD - JVRokuromi

AltonaConcon

10 productions consolidated in one year

11BASF Performance Products Investor Day 2010

Growth. Value. Sustainability.

11

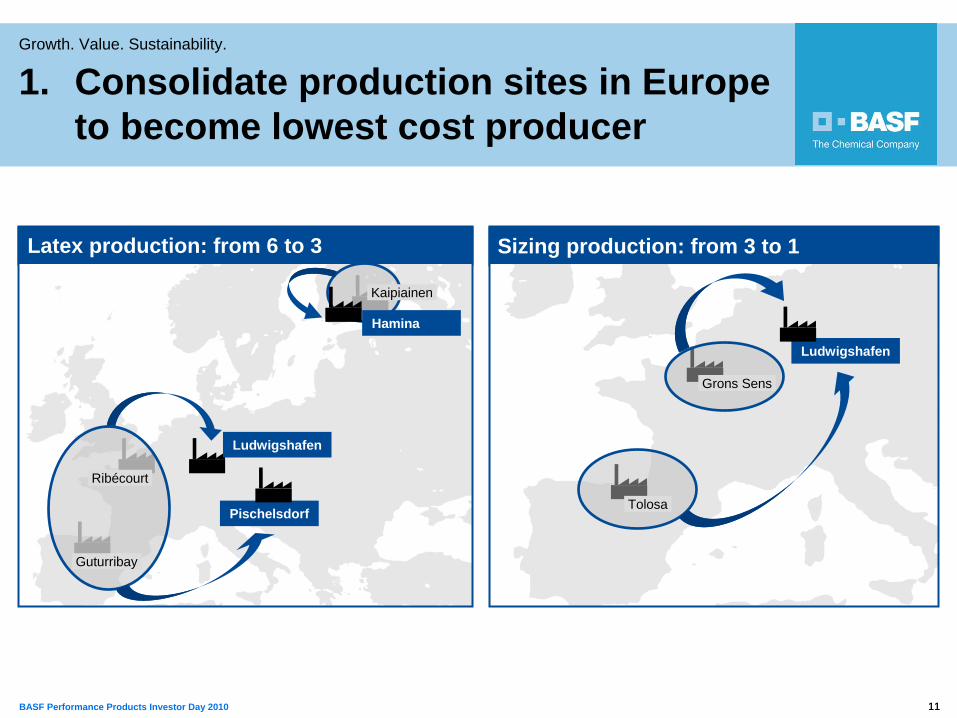

1. Consolidate production sites in Europe to become lowest cost producer

Latex production: from 6 to 3 Sizing production: from 3 to 1

Ludwigshafen

Grons Sens

Tolosa

Ludwigshafen

Ribécourt

Pischelsdorf

Kaipiainen

Hamina

Guturribay

12BASF Performance Products Investor Day 2010

Growth. Value. Sustainability.

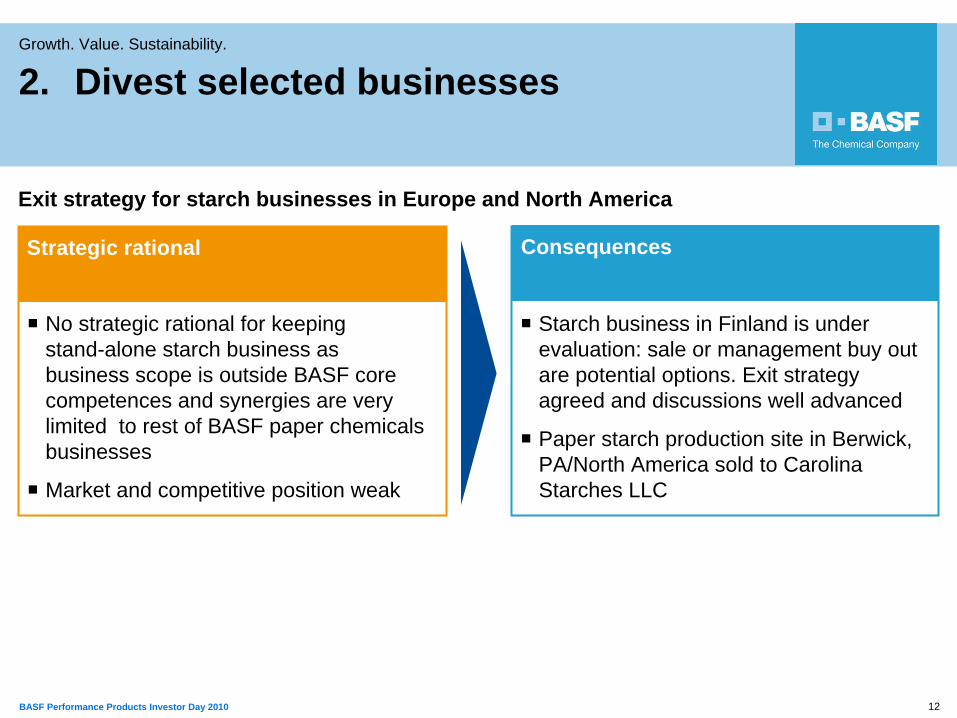

2. Divest selected businesses

No strategic rational for keeping stand-alone starch business as business scope is outside BASF core competences and synergies are very limited to rest of BASF paper chemicals businesses

Market and competitive position weak

Starch business in Finland is under evaluation: sale or management buy out are potential options. Exit strategy agreed and discussions well advanced

Paper starch production site in Berwick, PA/North America sold to Carolina Starches LLC

Strategic rational Consequences

Exit strategy for starch businesses in Europe and North America

13BASF Performance Products Investor Day 2010

Growth. Value. Sustainability.

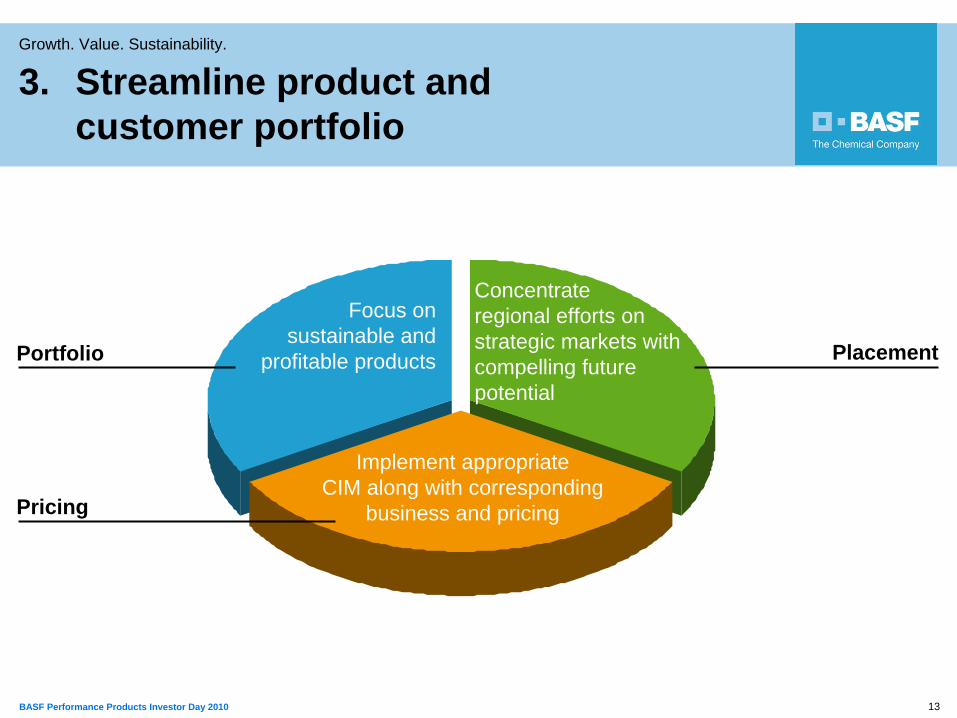

3. Streamline product and customer portfolio

Focus on sustainable and

profitable products

Concentrate regional efforts on strategic markets with compelling future potential

Implement appropriate CIM along with corresponding

business and pricing

Portfolio Placement

Pricing

14BASF Performance Products Investor Day 2010

Growth. Value. Sustainability.

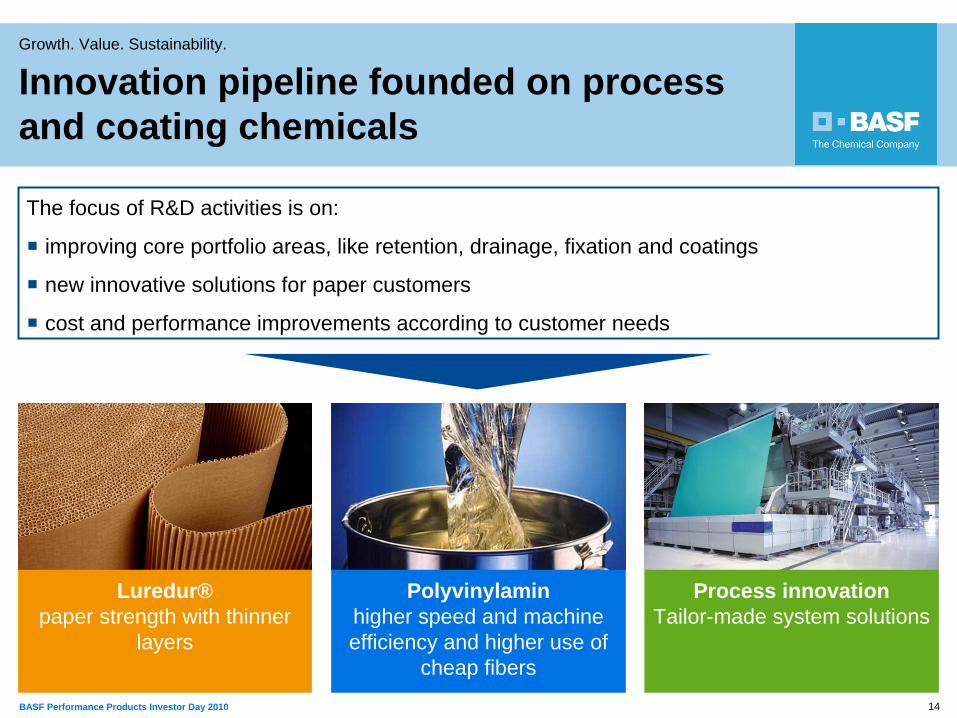

The focus of R&D activities is on:

improving core portfolio areas, like retention, drainage, fixation and coatings

new innovative solutions for paper customers

cost and performance improvements according to customer needs

Luredur® paper strength with thinner

layers

Polyvinylamin higher speed and machine efficiency and higher use of

cheap fibers

Process innovation Tailor-made system solutions

Innovation pipeline founded on process and coating chemicals

15BASF Performance Products Investor Day 2010

Growth. Value. Sustainability.

Growth. Value. Sustainability.Paper Chemicals

Globally leading and preferred supplier of chemicals to the paper industry

Successfully participate in the significant growth of Asia and South America

Deliver new innovative solutions to the paper industry serving customer needs with a clear advantage

Solidly contribute to segment profitability

Vision 2020Roadmap 2012BASF is the new #1 supplier for paper chemicals

Businesses are currently repositioned with focus on CIMs

In Europe and North America focus is on restructuring the business

In the growth regions Asia and South America BASF will exploit market potential

Our target is to earn our cost of capital by 2012 and thereafter

1BASF Performance Products Investor Day 2010

Growth. Value. Sustainability.

1 | Dispersions & Pigments Markus Kramer

2 | Paper Chemicals Fred Baumgartner

3 | Performance Chemicals Hans W. Reiners

4 | Care Chemicals Gabriel Tanbourgi

1

2BASF Performance Products Investor Day 2010

Growth. Value. Sustainability.

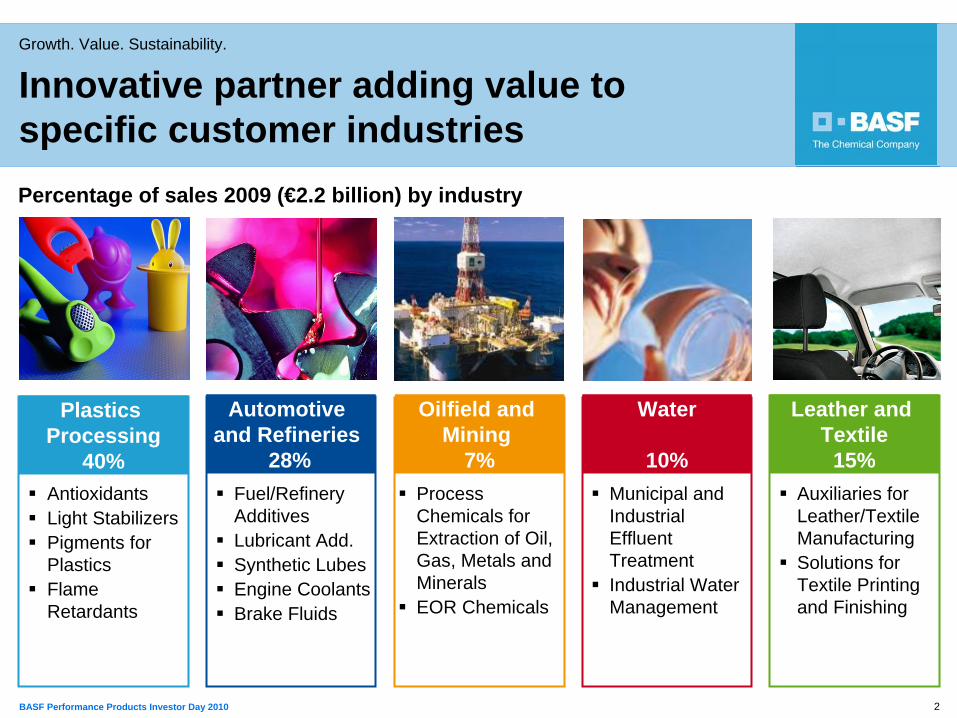

AntioxidantsLight StabilizersPigments for PlasticsFlame Retardants

Process Chemicals for Extraction of Oil, Gas, Metals and Minerals EOR Chemicals

Municipal and Industrial Effluent TreatmentIndustrial Water Management

Auxiliaries for Leather/Textile ManufacturingSolutions for Textile Printing and Finishing

Fuel/Refinery AdditivesLubricant Add.Synthetic LubesEngine CoolantsBrake Fluids

Plastics Processing

40%

Oilfield and Mining

7%

Water

10%

Leather and Textile

15%

Automotive and Refineries

28%

Percentage of sales 2009 (€2.2 billion) by industry

Innovative partner adding value to specific customer industries

3BASF Performance Products Investor Day 2010

Growth. Value. Sustainability.

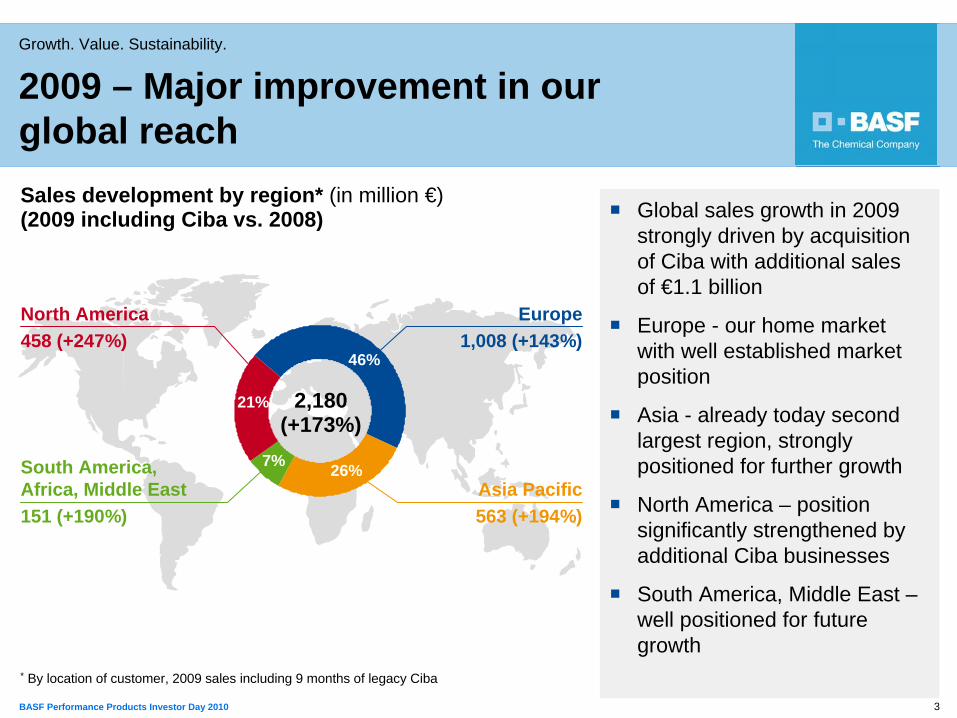

Sales development by region* (in million €) (2009 including Ciba vs. 2008)

* By location of customer, 2009 sales including 9 months of legacy Ciba

Global sales growth in 2009 strongly driven by acquisition of Ciba with additional sales of €1.1 billion

Europe - our home market with well established market position

Asia - already today second largest region, strongly positioned for further growth

North America – position significantly strengthened by additional Ciba businesses

South America, Middle East –well positioned for future growth

North America458 (+247%)

Europe1,008 (+143%)

Asia Pacific563 (+194%)

South America, Africa, Middle East151 (+190%)

2,180(+173%)

46%

26%7%

21%

2009 – Major improvement in our global reach

4BASF Performance Products Investor Day 2010

Growth. Value. Sustainability.

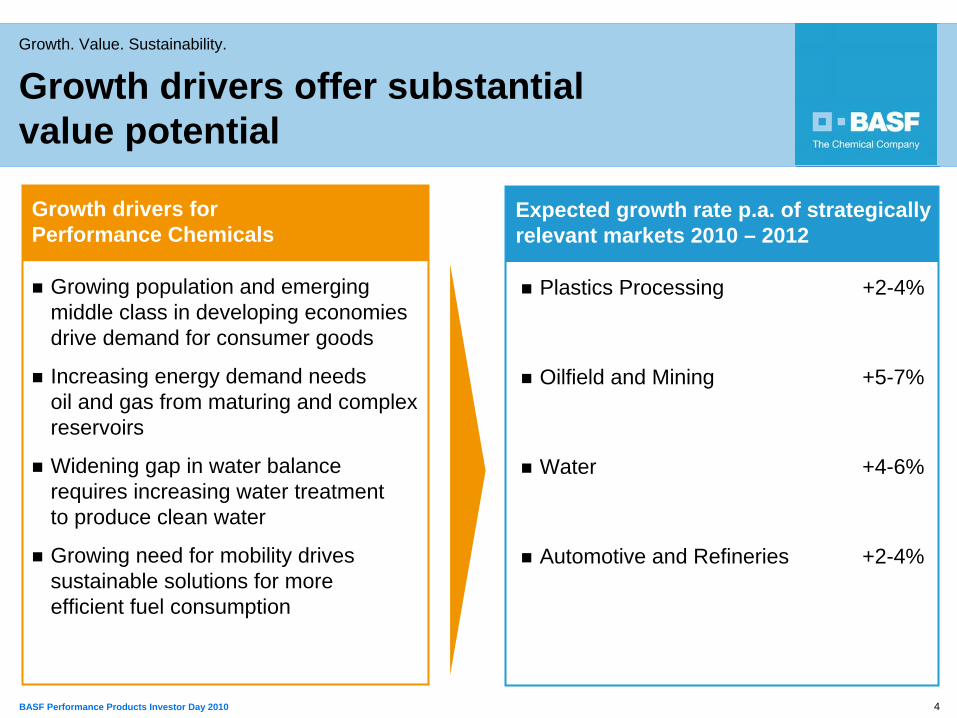

Growth drivers for Performance Chemicals

Growing population and emerging middle class in developing economies drive demand for consumer goods

Increasing energy demand needs oil and gas from maturing and complex reservoirs

Widening gap in water balance requires increasing water treatment to produce clean water

Growing need for mobility drives sustainable solutions for more efficient fuel consumption

Expected growth rate p.a. of strategically relevant markets 2010 – 2012

Plastics Processing +2-4%

Oilfield and Mining +5-7%

Water +4-6%

Automotive and Refineries +2-4%

Growth drivers offer substantial value potential

5BASF Performance Products Investor Day 2010

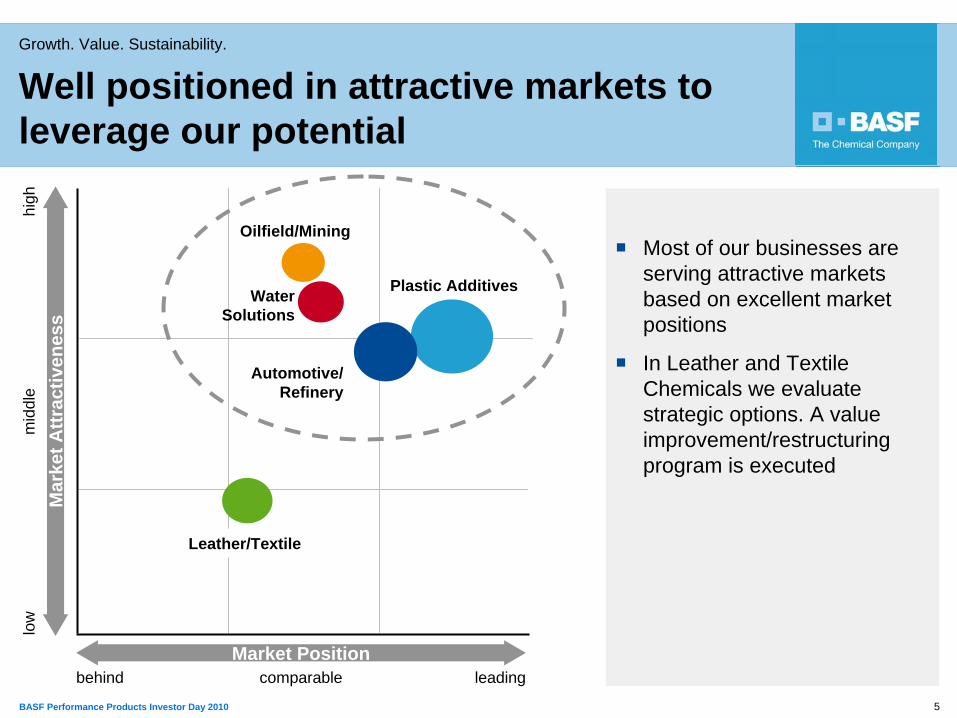

Growth. Value. Sustainability.

Automotive/ Refinery

Plastic Additives

Leather/Textile

Water Solutions

Oilfield/Mining

Well positioned in attractive markets to leverage our potential

Most of our businesses are serving attractive markets based on excellent market positions

In Leather and Textile Chemicals we evaluate strategic options. A value improvement/restructuring program is executed

low

mid

dle

high

Mar

ket A

ttrac

tiven

ess

leadingcomparablebehindMarket Position

6BASF Performance Products Investor Day 2010

Growth. Value. Sustainability.

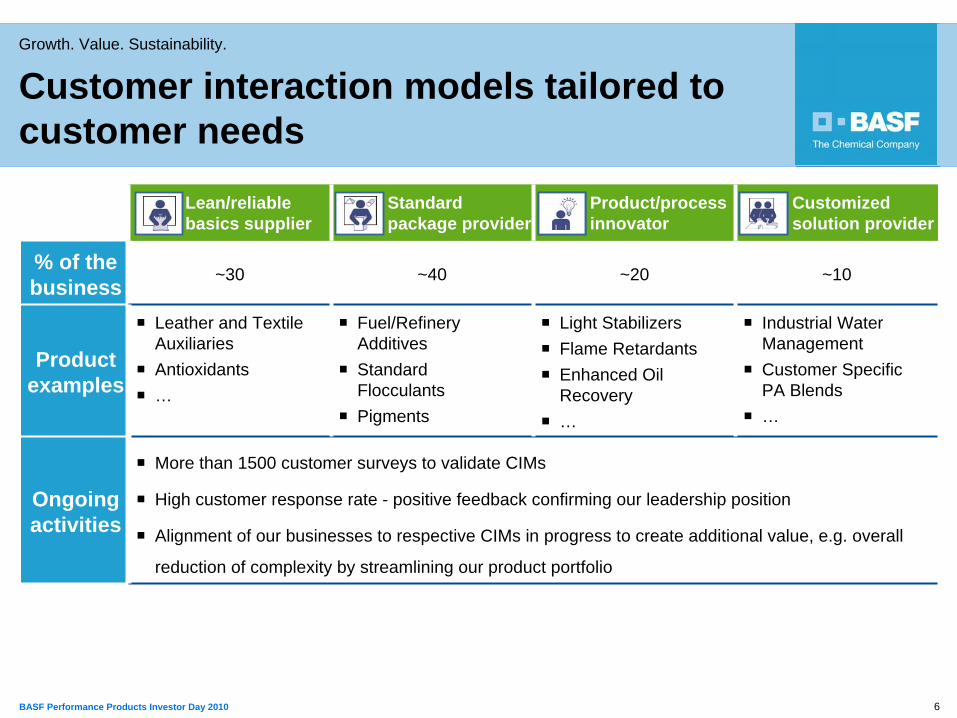

Lean/reliable basics supplier

Standard package provider

Product/process innovator

Customized solution provider

% of the business ~30 ~40 ~20 ~10

Product examples

Leather and Textile AuxiliariesAntioxidants…

Fuel/RefineryAdditivesStandard FlocculantsPigments

Light StabilizersFlame RetardantsEnhanced Oil Recovery…

Industrial Water ManagementCustomer SpecificPA Blends…

Ongoing activities

More than 1500 customer surveys to validate CIMs

High customer response rate - positive feedback confirming our leadership position

Alignment of our businesses to respective CIMs in progress to create additional value, e.g. overall

reduction of complexity by streamlining our product portfolio

Customer interaction models tailored to customer needs

7BASF Performance Products Investor Day 2010

Growth. Value. Sustainability.

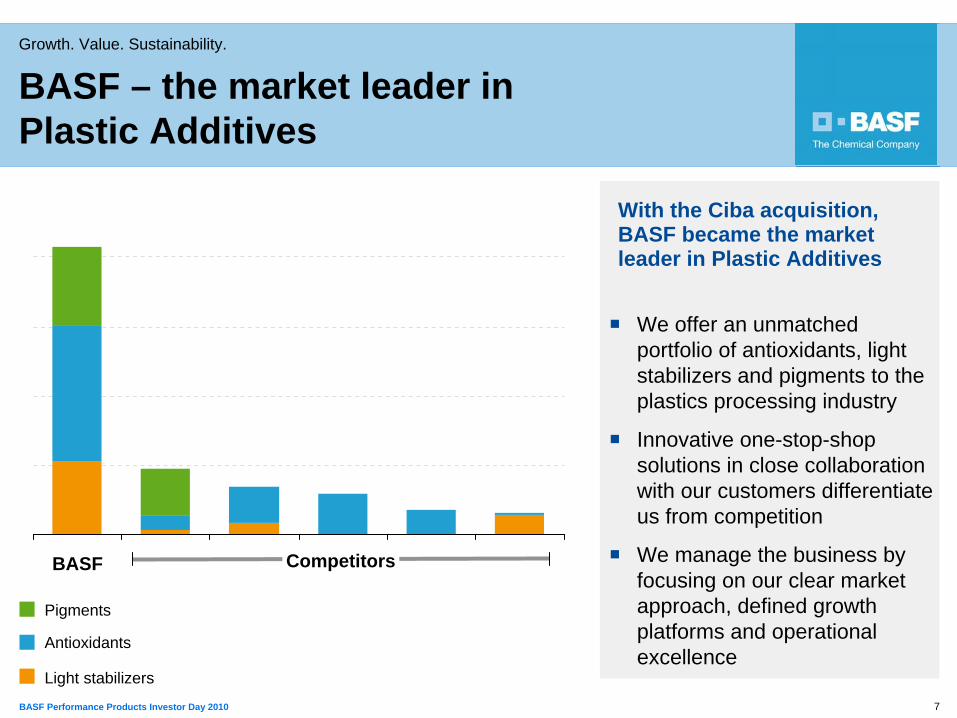

With the Ciba acquisition, BASF became the market leader in Plastic Additives

We offer an unmatched portfolio of antioxidants, light stabilizers and pigments to the plastics processing industry

Innovative one-stop-shop solutions in close collaboration with our customers differentiate us from competition

We manage the business by focusing on our clear market approach, defined growth platforms and operational excellence

BASF – the market leader in Plastic Additives

Pigments

Antioxidants

Light stabilizers

CompetitorsBASF

8BASF Performance Products Investor Day 2010

Growth. Value. Sustainability.

Differential Drive

Weir Plate Bowl Drive

Flocculant Sol.

Sludge Feed

CakeCentrate

Bowl

Scroll

Differential Drive

Weir Plate Bowl Drive

Flocculant Sol.

Sludge Feed

CakeCentrate

Bowl

Scroll

Around 75% of R&D spending dedicated to product innovation creating unique value propositions for our customers

Close to 15% of R&D spending dedicated to process innovation improving our competitiveness

Up to 10% of R&D spending dedicated to managing our intellectual property position

All legacy Ciba R&D projects are currently being validated

Capitalizing on growth drivers and addressing customer needs

Plastic Additives withOne-stop innovation

BASF innovations to enhance oil recovery

Rheomax® to increase mineral recovery

Keropur® to improve fuel economy

Zetag® 9000 S to enhancewaste water treatment

Steron® to enablenew surface textures

Innovation to foster growth and create value

9BASF Performance Products Investor Day 2010

Growth. Value. Sustainability.

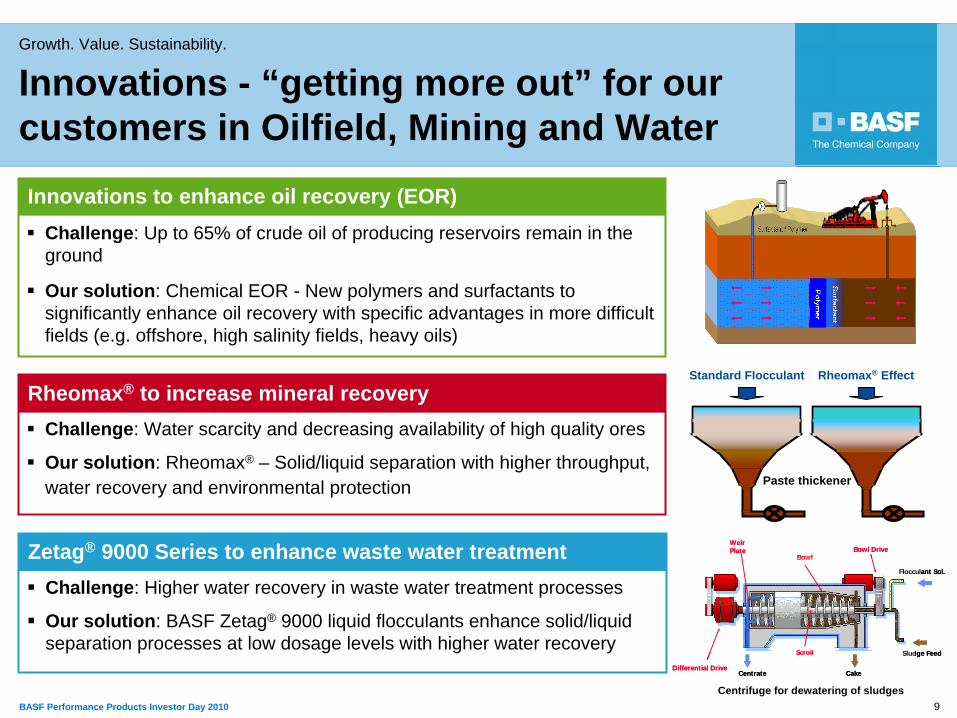

Challenge: Water scarcity and decreasing availability of high quality ores

Our solution: Rheomax® – Solid/liquid separation with higher throughput, water recovery and environmental protection

Challenge: Up to 65% of crude oil of producing reservoirs remain in the ground

Our solution: Chemical EOR - New polymers and surfactants to significantly enhance oil recovery with specific advantages in more difficult fields (e.g. offshore, high salinity fields, heavy oils)

Innovations to enhance oil recovery (EOR)

Rheomax® to increase mineral recovery

Innovations - “getting more out” for our customers in Oilfield, Mining and Water

Standard Flocculant Rheomax® Effect

Paste thickener

Differential Drive

Weir Plate Bowl Drive

Flocculant Sol.

Sludge Feed

CakeCentrate

Bowl

Scroll

Differential Drive

Weir Plate Bowl Drive

Flocculant Sol.

Sludge Feed

CakeCentrate

Bowl

Scroll

Centrifuge for dewatering of sludges

Challenge: Higher water recovery in waste water treatment processes

Our solution: BASF Zetag® 9000 liquid flocculants enhance solid/liquid separation processes at low dosage levels with higher water recovery

Zetag® 9000 Series to enhance waste water treatment

10BASF Performance Products Investor Day 2010

Growth. Value. Sustainability.

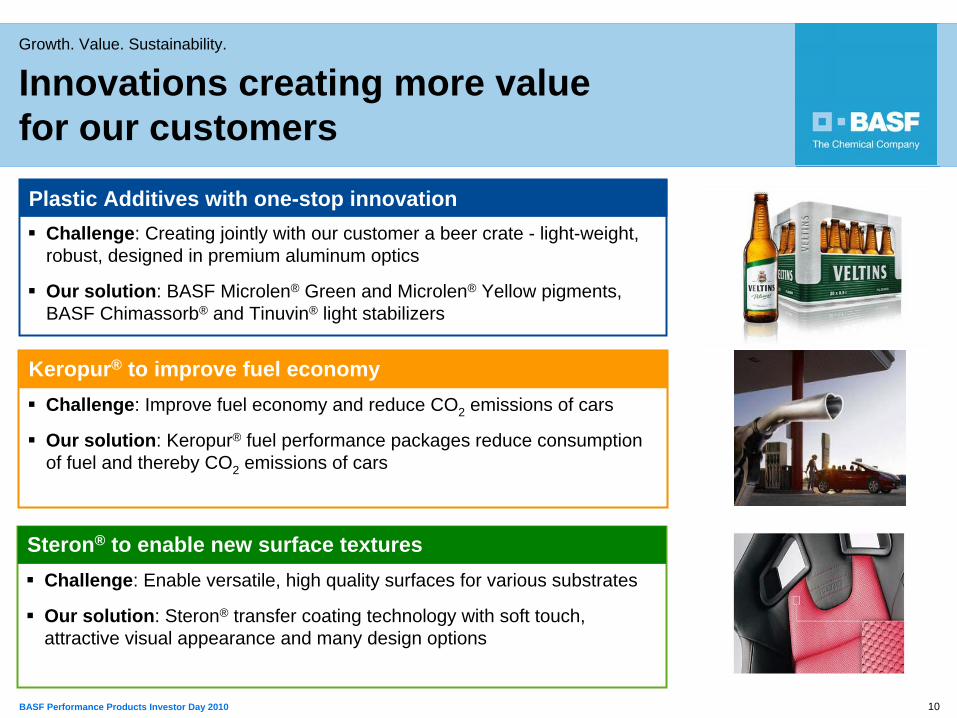

Challenge: Improve fuel economy and reduce CO2 emissions of cars

Our solution: Keropur® fuel performance packages reduce consumption of fuel and thereby CO2 emissions of cars

Keropur® to improve fuel economy

Plastic Additives with one-stop innovationChallenge: Creating jointly with our customer a beer crate - light-weight, robust, designed in premium aluminum optics

Our solution: BASF Microlen® Green and Microlen® Yellow pigments, BASF Chimassorb® and Tinuvin® light stabilizers

Innovations creating more value for our customers

Challenge: Enable versatile, high quality surfaces for various substrates

Our solution: Steron® transfer coating technology with soft touch, attractive visual appearance and many design options

Steron® to enable new surface textures

11BASF Performance Products Investor Day 2010

Growth. Value. Sustainability.

Growth. Value. Sustainability.Performance Chemicals

Leading supplier of Plastic Additives with broad portfolio and know-how

Significant player in Oilfield/Mining Chemicals creating value with innovation

Strong platform in Water Treatment offering sustainable chemical solutions and services

Leading position with Automotive and Refinery Chemicals focusing on sustainable solutions

Vision 2020Roadmap 2012Further create value by realizing Ciba synergies and striving to be best-in-class

Grow profitably 2% above our relevant markets based on

– our excellent market positions and clear strengths

– a consequent implementation of our CIMs

Create additional value with focused investment into innovation

We earn a premium on our cost of capital latest by 2012

1BASF Performance Products Investor Day 2010

Growth. Value. Sustainability.

1 | Dispersions & Pigments Markus Kramer

2 | Paper Chemicals Fred Baumgartner

3 | Performance Chemicals Hans W. Reiners

4 | Care Chemicals Gabriel Tanbourgi

1

2BASF Performance Products Investor Day 2010

Growth. Value. Sustainability.

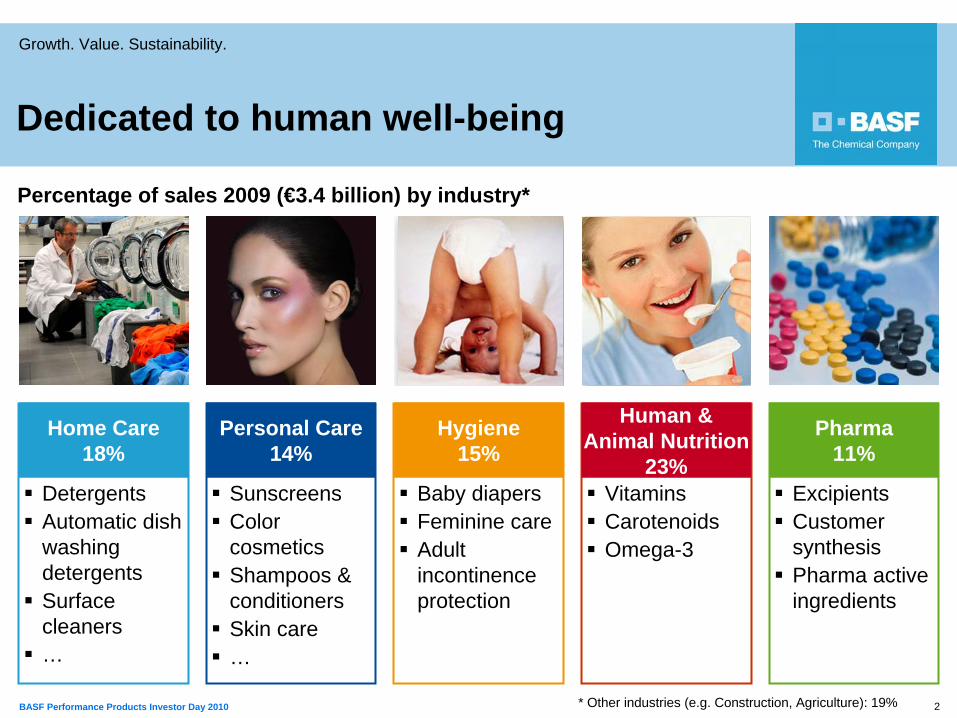

Percentage of sales 2009 (€3.4 billion) by industry*

VitaminsCarotenoidsOmega-3

Human & Animal Nutrition

23%Baby diapersFeminine careAdult incontinence protection

Hygiene15%

SunscreensColor cosmeticsShampoos & conditionersSkin care…

Personal Care14%

ExcipientsCustomer synthesisPharma active ingredients

Pharma11%

DetergentsAutomatic dish washing detergentsSurface cleaners…

Home Care18%

* Other industries (e.g. Construction, Agriculture): 19%

Dedicated to human well-being

3BASF Performance Products Investor Day 2010

Growth. Value. Sustainability.

Growth drivers for Care Chemicals

Expected growth rate p.a. of strategically relevant markets 2010 – 2012

More wealth, more choice drives end markets

Consumers’ desire for wellness, health, convenience, and comfort

Demand for consumer goods driven by rising disposable income in developing countries

Aging population taking more self-responsibility in health

Eco-friendly trend and increasing environmental awareness requiring sustainable solutions

Home Care 4-5%

Personal Care 4-5%

Hygiene 4-5%

Human Nutrition 3-4%

Animal Nutrition 2-3%

Pharma 3-6%

4BASF Performance Products Investor Day 2010

Growth. Value. Sustainability.

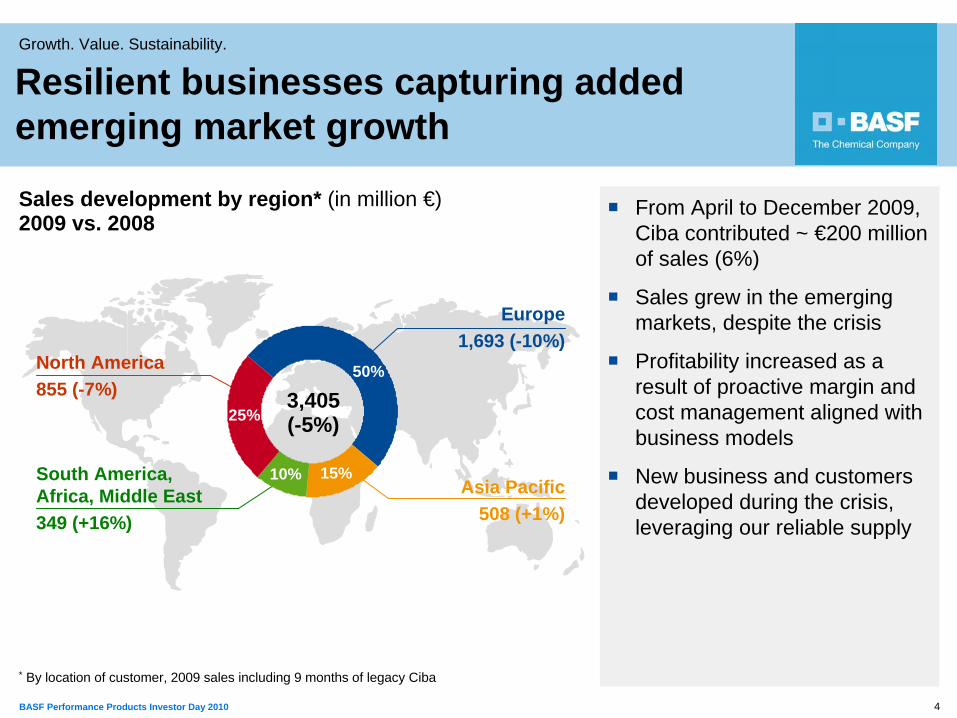

Sales development by region* (in million €) 2009 vs. 2008

* By location of customer, 2009 sales including 9 months of legacy Ciba

25%

From April to December 2009, Ciba contributed ~ €200 million of sales (6%)

Sales grew in the emerging markets, despite the crisis

Profitability increased as a result of proactive margin and cost management aligned with business models

New business and customers developed during the crisis, leveraging our reliable supply

Resilient businesses capturing added emerging market growth

North America855 (-7%)

Europe1,693 (-10%)

Asia Pacific508 (+1%)

South America, Africa, Middle East349 (+16%)

50%

15%10%

25%3,405(-5%)

5BASF Performance Products Investor Day 2010

Growth. Value. Sustainability.

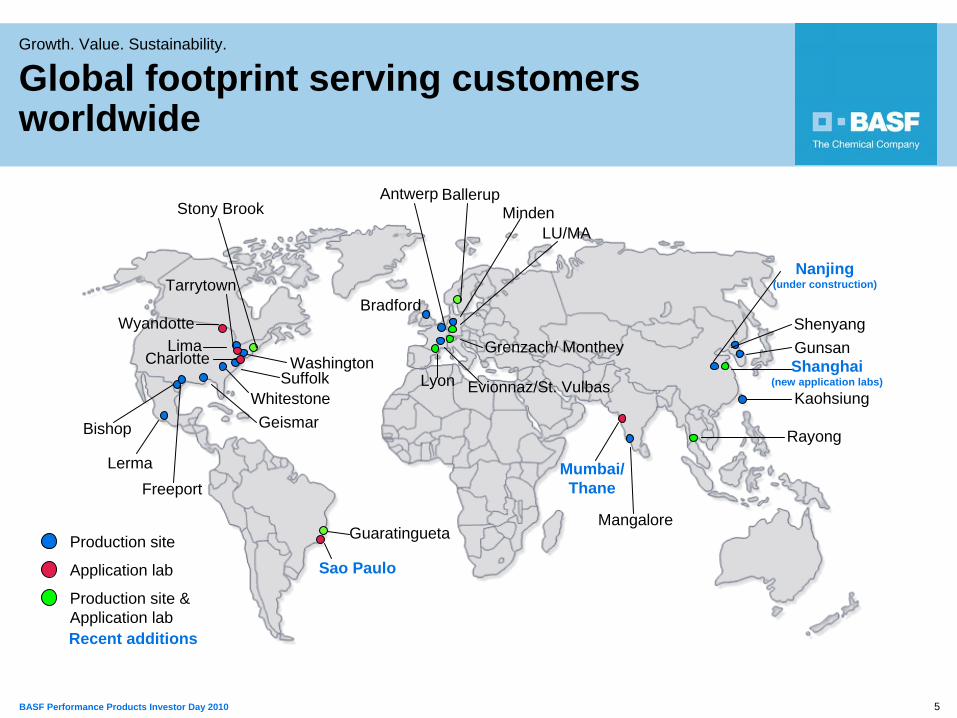

Global footprint serving customers worldwide

AntwerpMinden

Shenyang

Rayong

LU/MA

Ballerup

Lyon

Bradford

Grenzach/ Monthey

Evionnaz/St. Vulbas

Bishop Geismar

LimaWashington

SuffolkWhitestone

Stony Brook

Freeport

Production site

Application lab

Production site & Application lab

Mumbai/Thane

Tarrytown

Wyandotte

Sao Paulo

Nanjing(under construction)

GunsanShanghai

(new application labs)Kaohsiung

Guaratingueta

Lerma

Mangalore

Recent additions

Charlotte

6BASF Performance Products Investor Day 2010

Growth. Value. Sustainability.

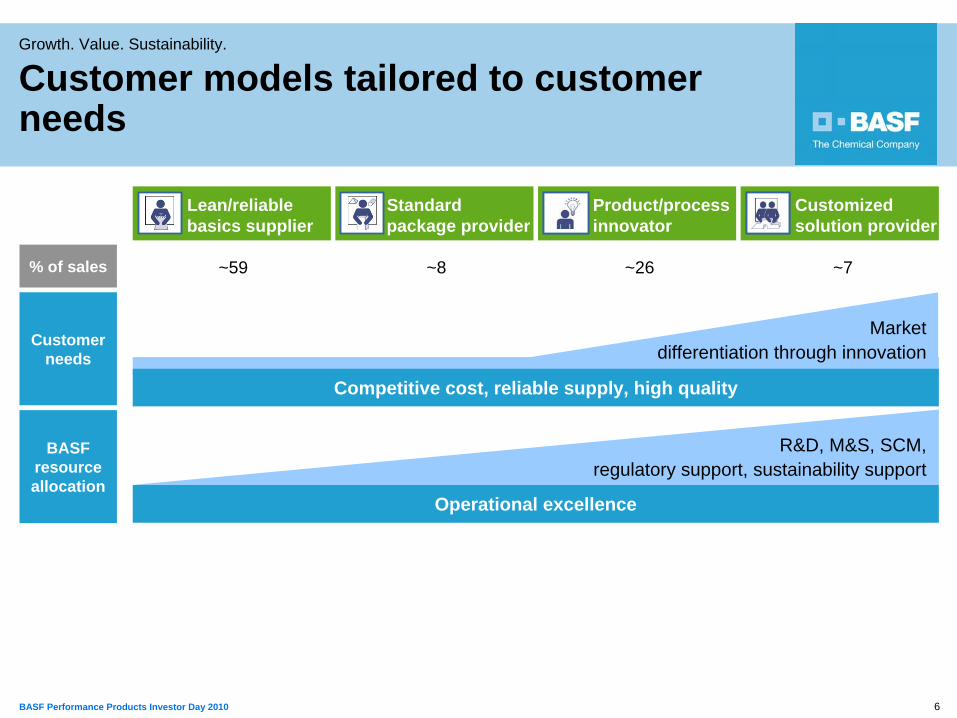

Customer models tailored to customer needs

Customized solution provider

Product/process innovator

Standard package provider

Lean/reliable basics supplier

% of sales ~59 ~8 ~26 ~7

R&D, M&S, SCM, regulatory support, sustainability support

Marketdifferentiation through innovation

Competitive cost, reliable supply, high quality

Operational excellence

Customer needs

BASF resource allocation

7BASF Performance Products Investor Day 2010

Growth. Value. Sustainability.

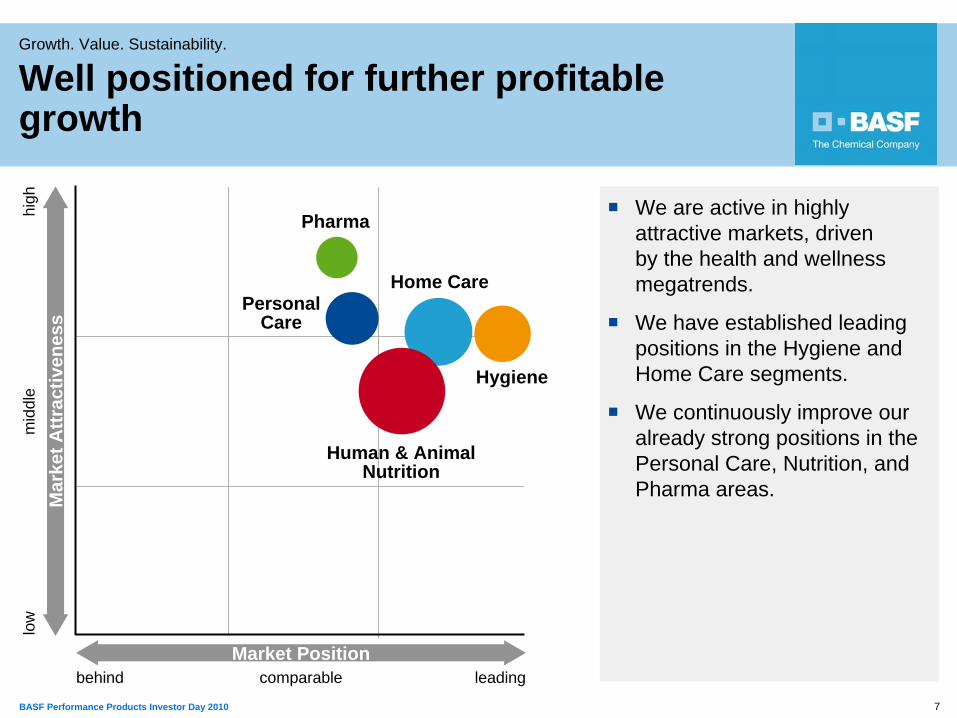

We are active in highly attractive markets, driven by the health and wellness megatrends.

We have established leading positions in the Hygiene and Home Care segments.

We continuously improve our already strong positions in the Personal Care, Nutrition, and Pharma areas.

Well positioned for further profitable growth

low

mid

dle

high

leadingcomparablebehind

Home CarePersonal

Care

Human & Animal Nutrition

Hygiene

Pharma

Mar

ket A

ttrac

tiven

ess

Market Position

8BASF Performance Products Investor Day 2010

Growth. Value. Sustainability.

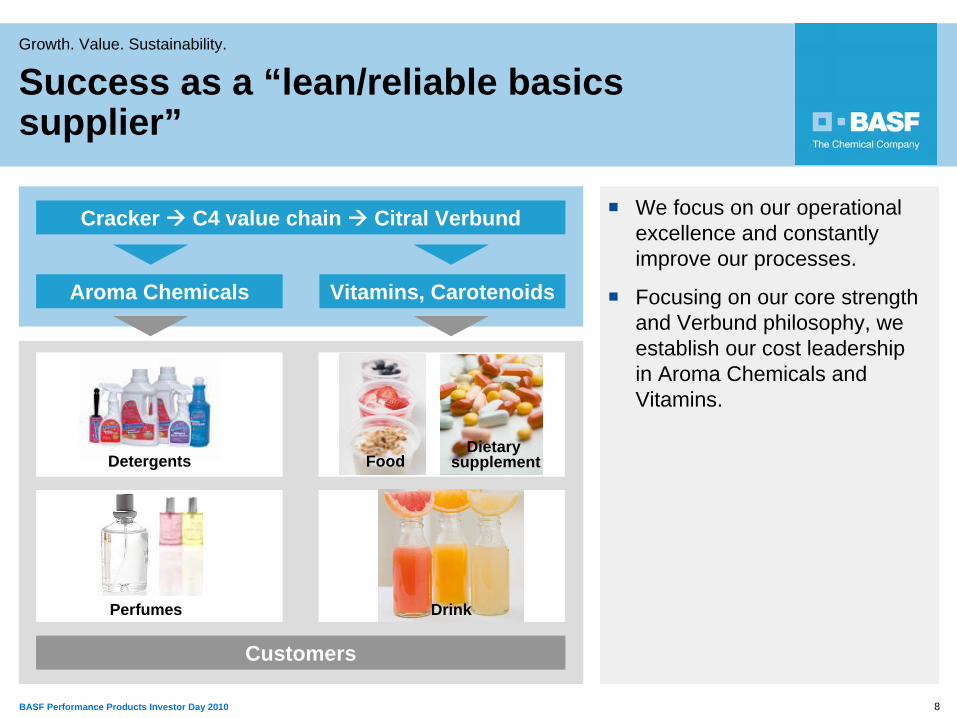

We focus on our operational excellence and constantly improve our processes.

Focusing on our core strength and Verbund philosophy, we establish our cost leadership in Aroma Chemicals and Vitamins.

Success as a “lean/reliable basics supplier”

Customers

Perfumes Drink

FoodDietary

supplement

Aroma Chemicals Vitamins, Carotenoids

Cracker C4 value chain Citral Verbund

Detergents

9BASF Performance Products Investor Day 2010

Growth. Value. Sustainability.

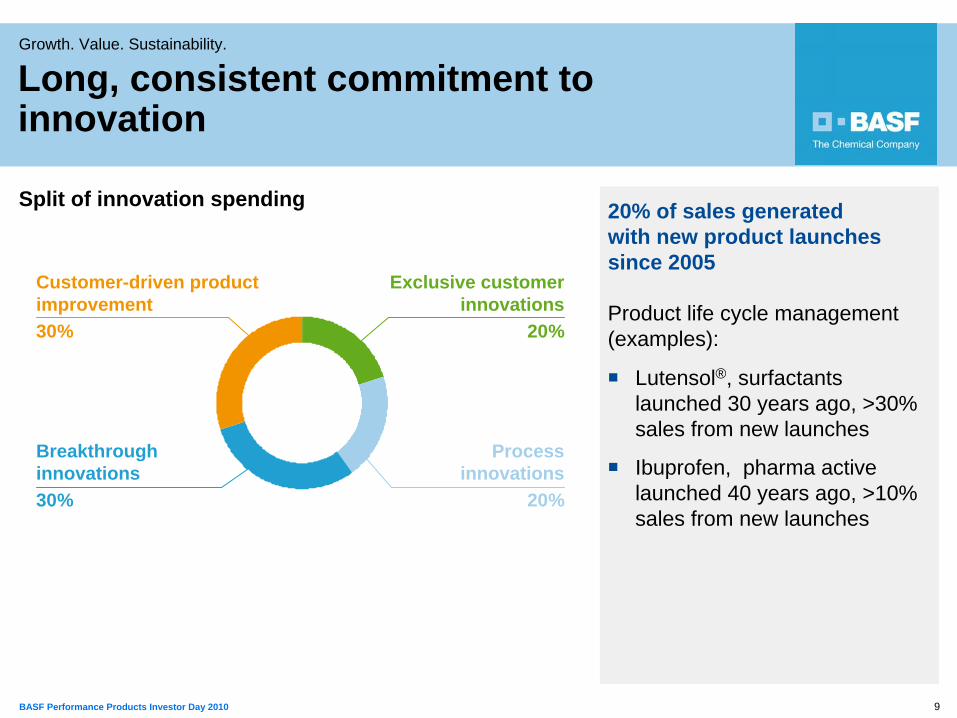

Long, consistent commitment to innovation

Lutensol®, surfactants launched 30 years ago, >30% sales from new launches

Ibuprofen, pharma active launched 40 years ago, >10% sales from new launches

Split of innovation spending

20%

30%

Customer-driven product improvement30%

Exclusive customer innovations

20%

Breakthrough innovations30%

Process innovations

20%

20% of sales generated with new product launches since 2005

Product life cycle management (examples):

10BASF Performance Products Investor Day 2010

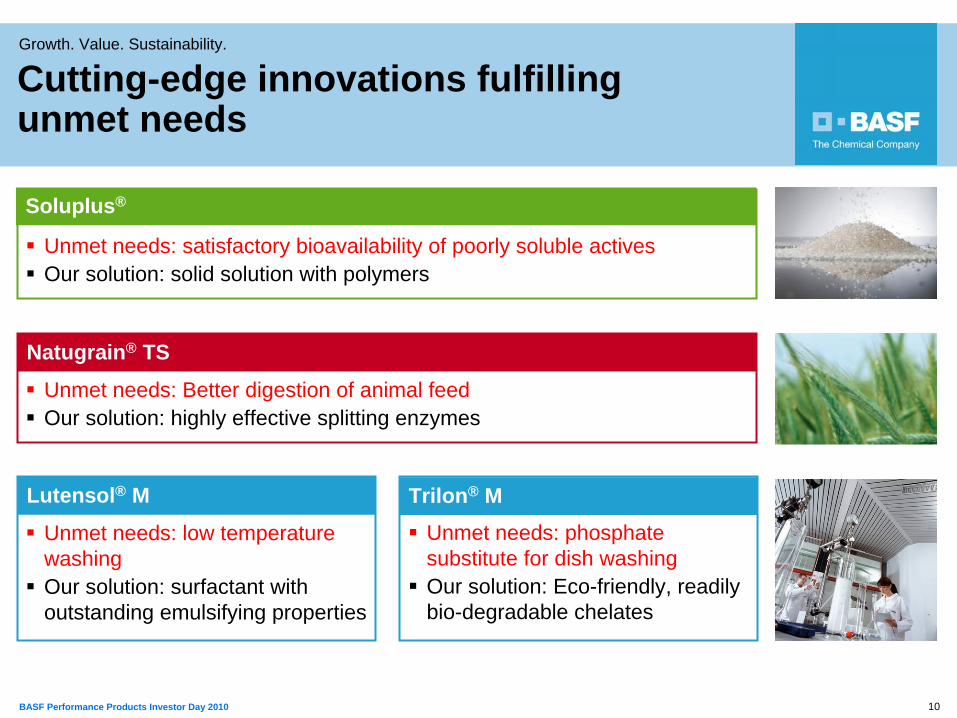

Growth. Value. Sustainability.

Unmet needs: satisfactory bioavailability of poorly soluble activesOur solution: solid solution with polymers

Soluplus®

Unmet needs: low temperature washingOur solution: surfactant with outstanding emulsifying properties

Lutensol® M

Cutting-edge innovations fulfilling unmet needs

Unmet needs: Better digestion of animal feedOur solution: highly effective splitting enzymes

Natugrain® TS

Unmet needs: phosphate substitute for dish washingOur solution: Eco-friendly, readily bio-degradable chelates

Trilon® M

11BASF Performance Products Investor Day 2010

Growth. Value. Sustainability.

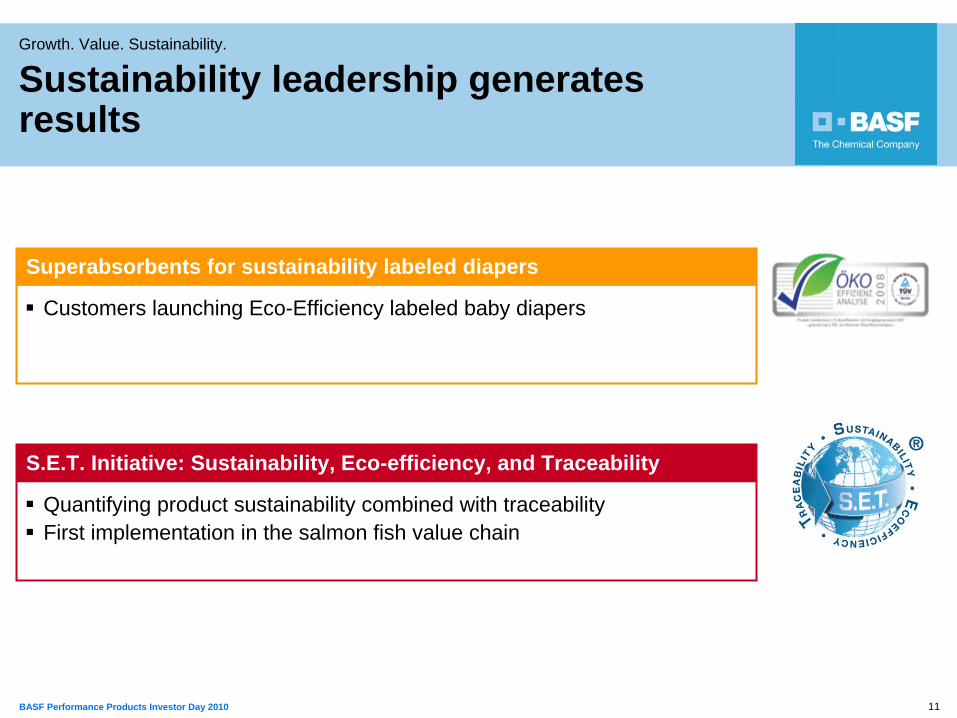

Sustainability leadership generates results

Quantifying product sustainability combined with traceabilityFirst implementation in the salmon fish value chain

S.E.T. Initiative: Sustainability, Eco-efficiency, and Traceability

Customers launching Eco-Efficiency labeled baby diapers

Superabsorbents for sustainability labeled diapers

12BASF Performance Products Investor Day 2010

Growth. Value. Sustainability.

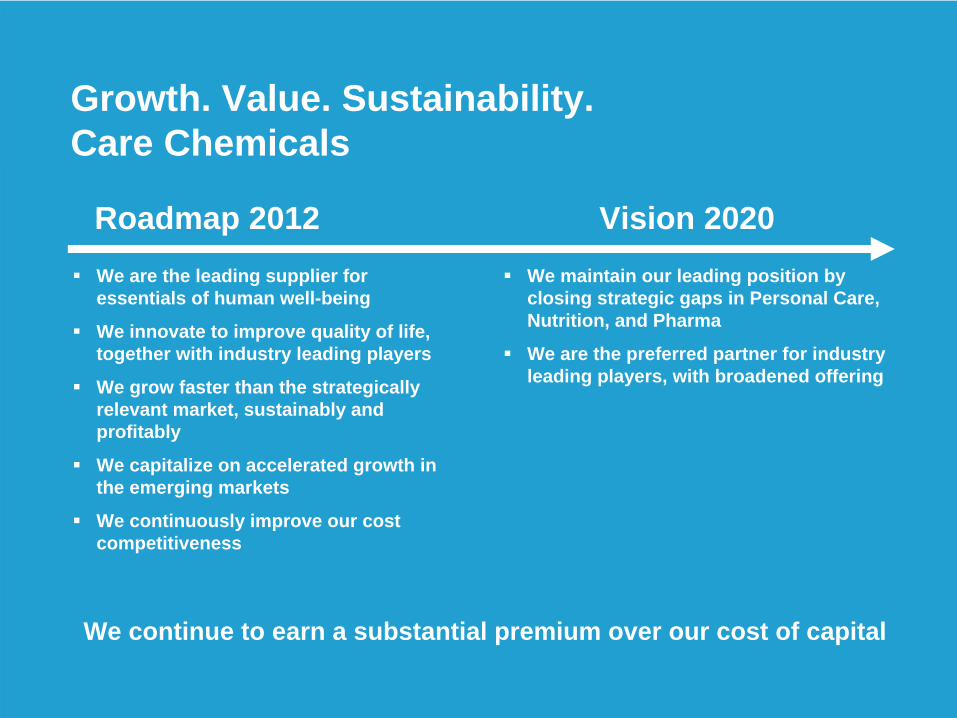

Growth. Value. Sustainability.Care Chemicals

We maintain our leading position by closing strategic gaps in Personal Care, Nutrition, and Pharma

We are the preferred partner for industry leading players, with broadened offering

Vision 2020Roadmap 2012We are the leading supplier for essentials of human well-being

We innovate to improve quality of life, together with industry leading players

We grow faster than the strategically relevant market, sustainably and profitably

We capitalize on accelerated growth in the emerging markets

We continuously improve our cost competitiveness

We continue to earn a substantial premium over our cost of capital