Embed Size (px)

Citation preview

Katherine Regional Mining &

Exploration Seminar 24 May, 2016

Minerals Industry: Myths and Realities and Returns

Drew Wagner

Executive Director

Minerals Council of Australia

Who we are

• Peak industry organisation representing

Australia’s exploration, mining and minerals

processing industry

• Product coverage is base metals, precious

metals, coal, iron ore, uranium, mineral

sands, light metals

• MCA member companies produce more than

85% of Australia’s mineral output and a

greater proportion of minerals exports (close

to 100% coverage in the NT)

What we do

• Represent our members’ interests

• Promote and build coalitions for policy

reform

• Talk to politicians and officials

• Engage with industry stakeholders and

wider Australian community

Our policy focus

• Enhance productivity and industry competitiveness

• Promote open and competitive markets –

domestically and internationally

• Address capacity constraints (e.g. Export

infrastructure, transport corridors, approvals

processes)

• Long-term fiscal sustainability and stability

• Maximise industry contribution to sustainable

development and environmental management

• Enhance social licence to operate

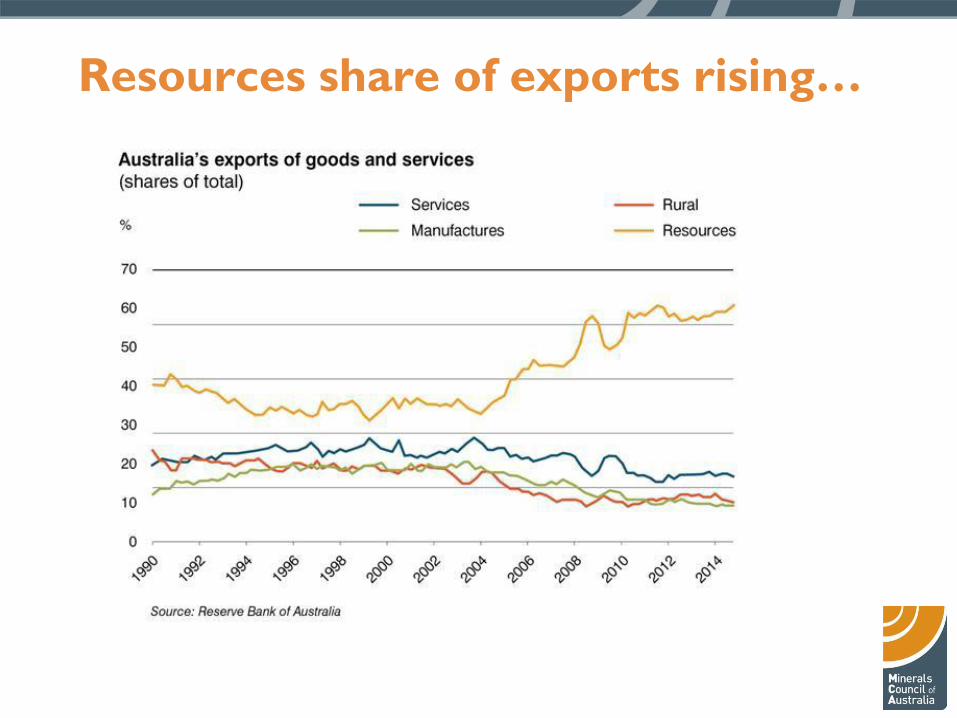

Resources share of exports rising…

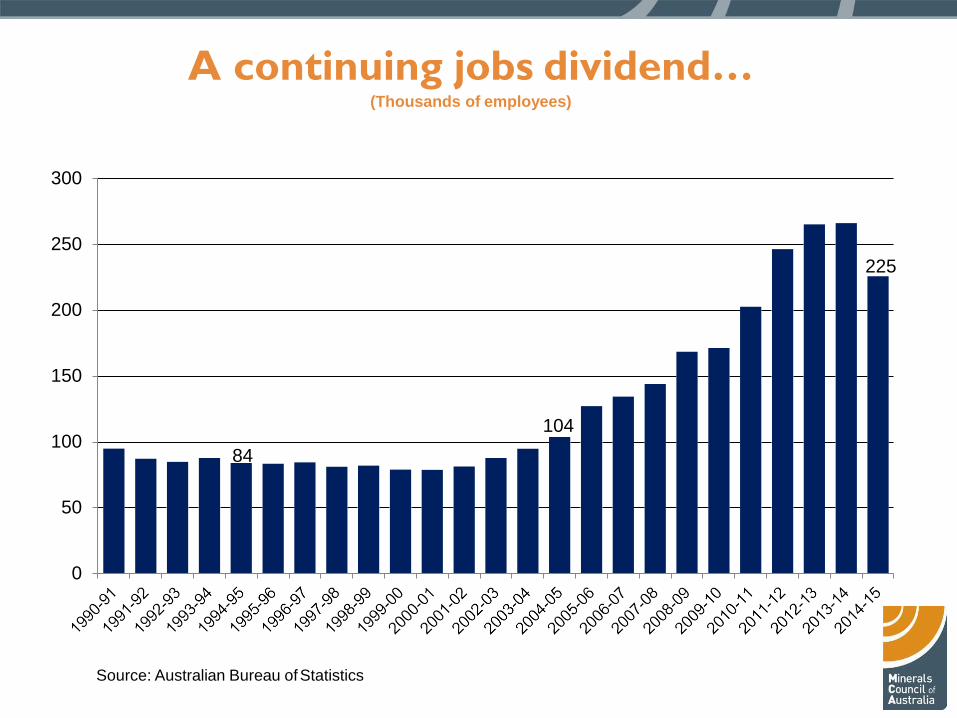

A continuing jobs dividend… (Thousands of employees)

84

104

225

0

50

100

150

200

250

300

Source: Australian Bureau of Statistics

Source: Australian Bureau of Statistics

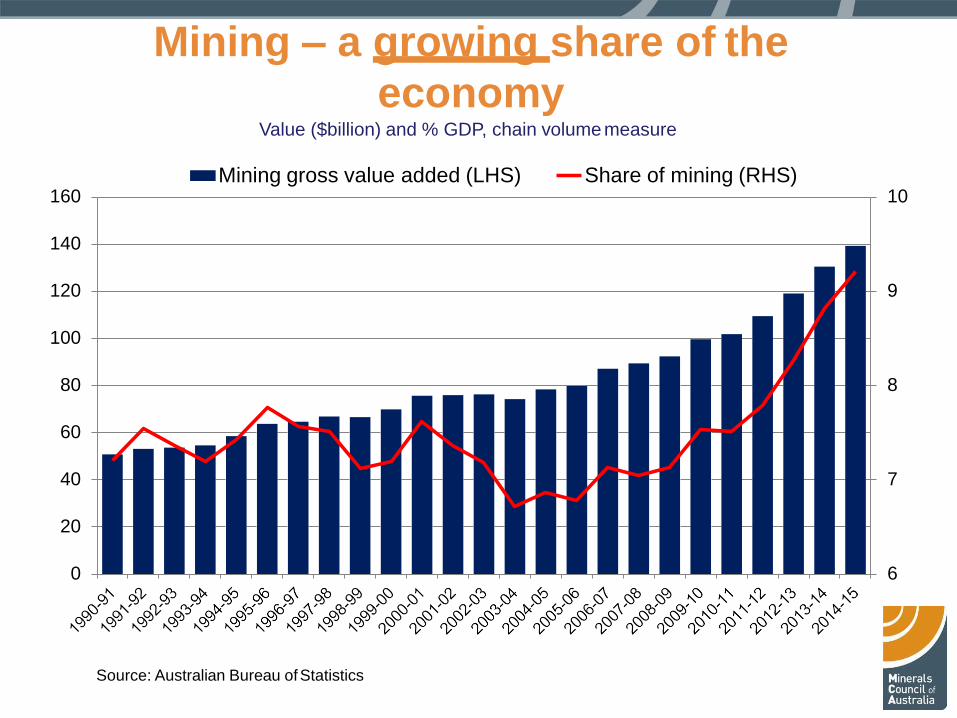

Mining – a growing share of the

economy

6

7

8

9

10

0

20

40

60

80

100

120

140

160

Value ($billion) and % GDP, chain volume measure

Mining gross value added (LHS) Share of mining (RHS)

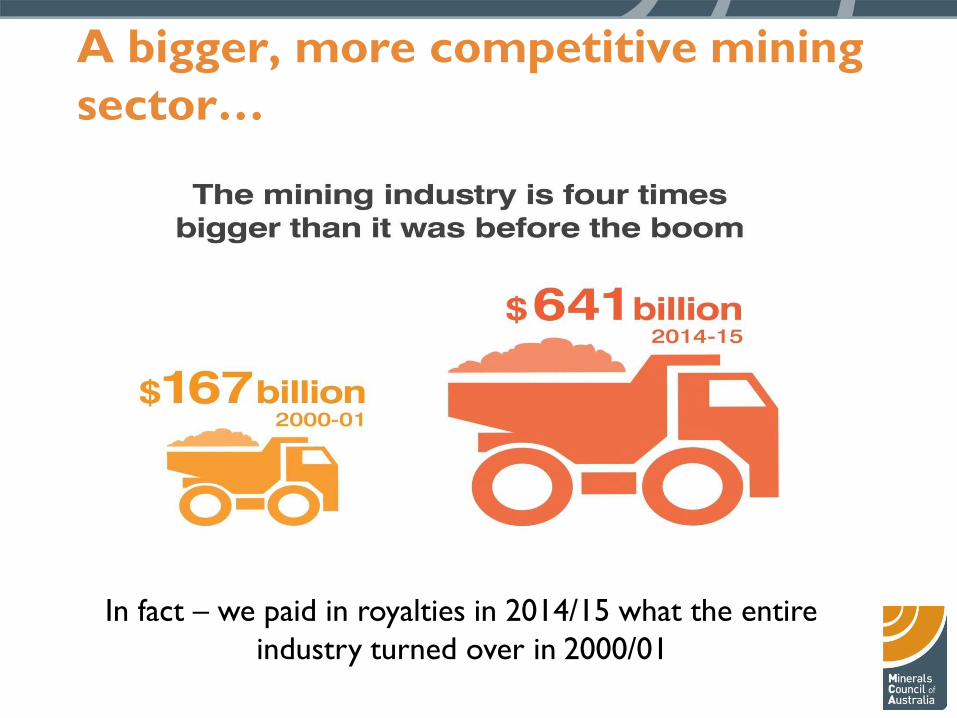

A bigger, more competitive mining

sector…

In fact – we paid in royalties in 2014/15 what the entire

industry turned over in 2000/01

Over the last decade global coal use far

outstripped renewables like wind and solar.

1500

1000

500

0

2000

2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014

Coal

Renewables

Source: BP Statistical Review (2015)

MTOE

4000

3500

3000

2500

Coal generation in East Asia will

grow strongly to 2040…

10

• On the demand side, the growth of

China has been the dominant factor.

• Convergence of China’s economic

development (steel and energy

consumption) and urbanisation with

developed economies is far from

complete

• Major source of demand for mineral

resources for some time to come –

together with India

The China factor

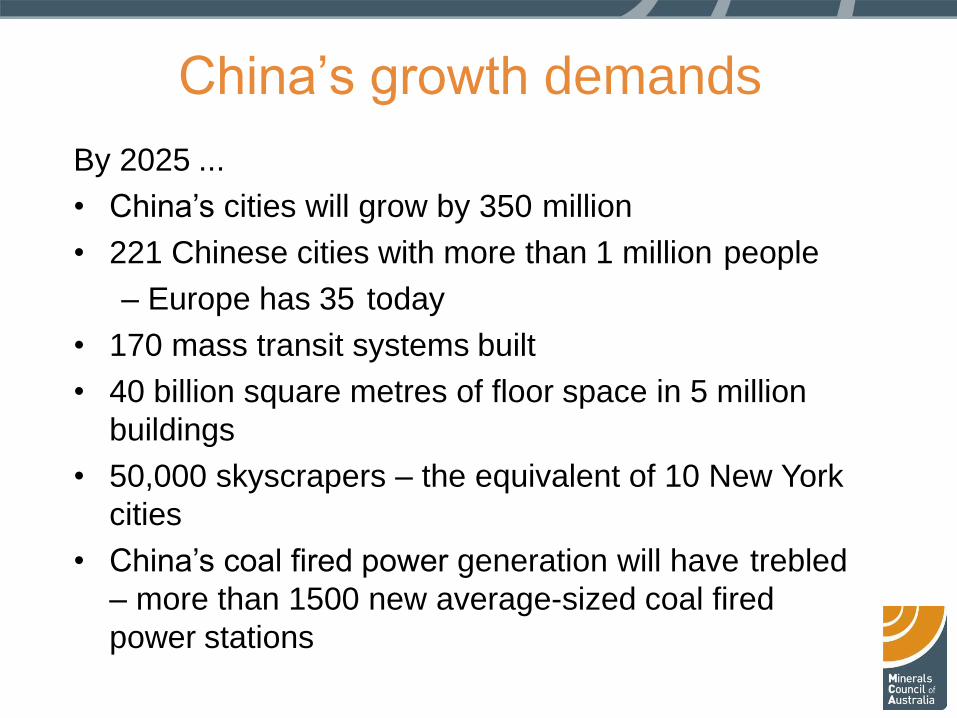

China’s growth demands

By 2025 ...

• China’s cities will grow by 350 million

• 221 Chinese cities with more than 1 million people

– Europe has 35 today

• 170 mass transit systems built

• 40 billion square metres of floor space in 5 million

buildings

• 50,000 skyscrapers – the equivalent of 10 New York

cities

• China’s coal fired power generation will have trebled

– more than 1500 new average-sized coal fired

power stations

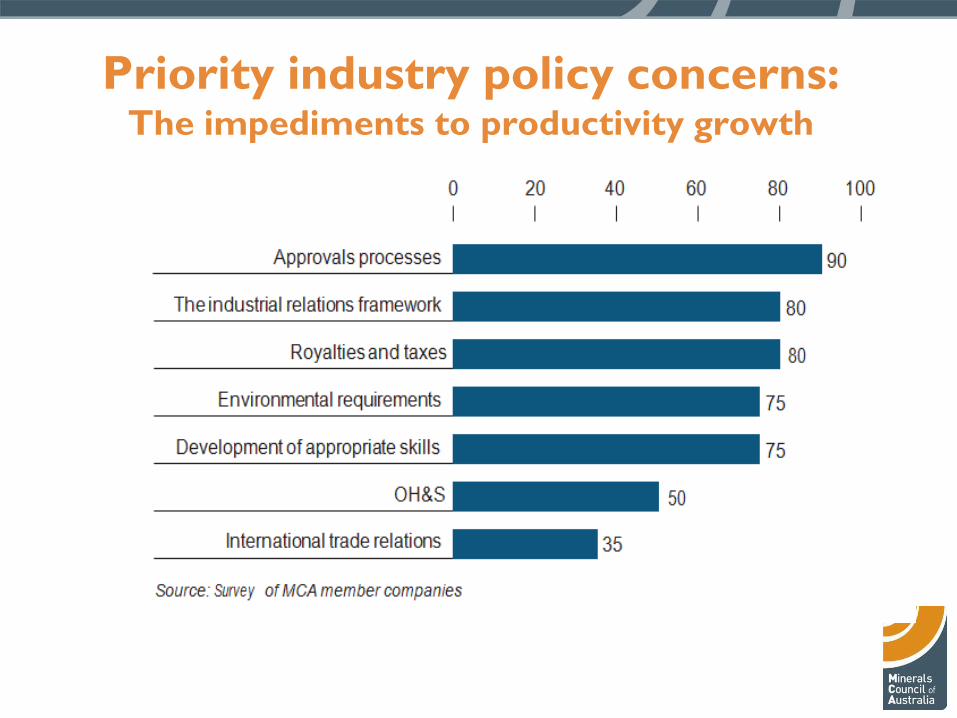

Priority industry policy concerns: The impediments to productivity growth

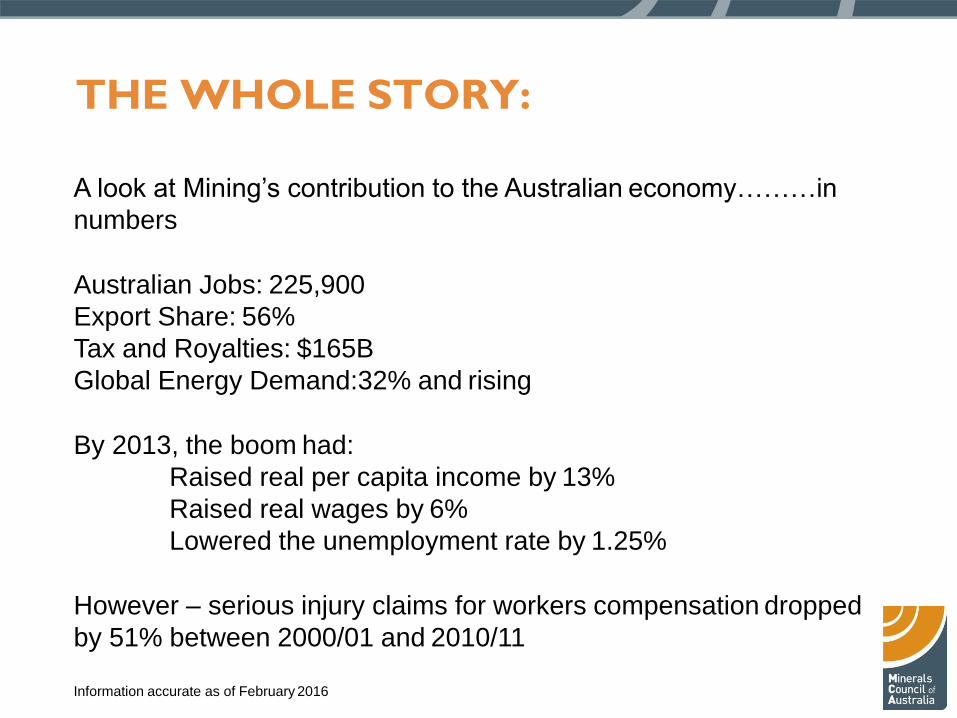

THE WHOLE STORY:

A look at Mining’s contribution to the Australian economy………in

numbers

Australian Jobs: 225,900

Export Share: 56%

Tax and Royalties: $165B

Global Energy Demand:32% and rising

By 2013, the boom had:

Raised real per capita income by 13%

Raised real wages by 6%

Lowered the unemployment rate by 1.25%

However – serious injury claims for workers compensation dropped

by 51% between 2000/01 and 2010/11

Information accurate as of February 2016

THE WHOLE STORY:

R&D spend in 2013/14 was $1.8B

6% of the entire sectors workforce is Indigenous (up

from 0.5% just two decades ago – and some Territory

companies having in excess of 20% and more)

1,984 Indigenous Land Use Agreements negotiated –

99% involved no legal contest of rights

Coal is still predicted to be 30% of global electricity

generation demand in 2040

For original sources of the statistics please visit www.minerals.org.au

Information accurate as of February 2016

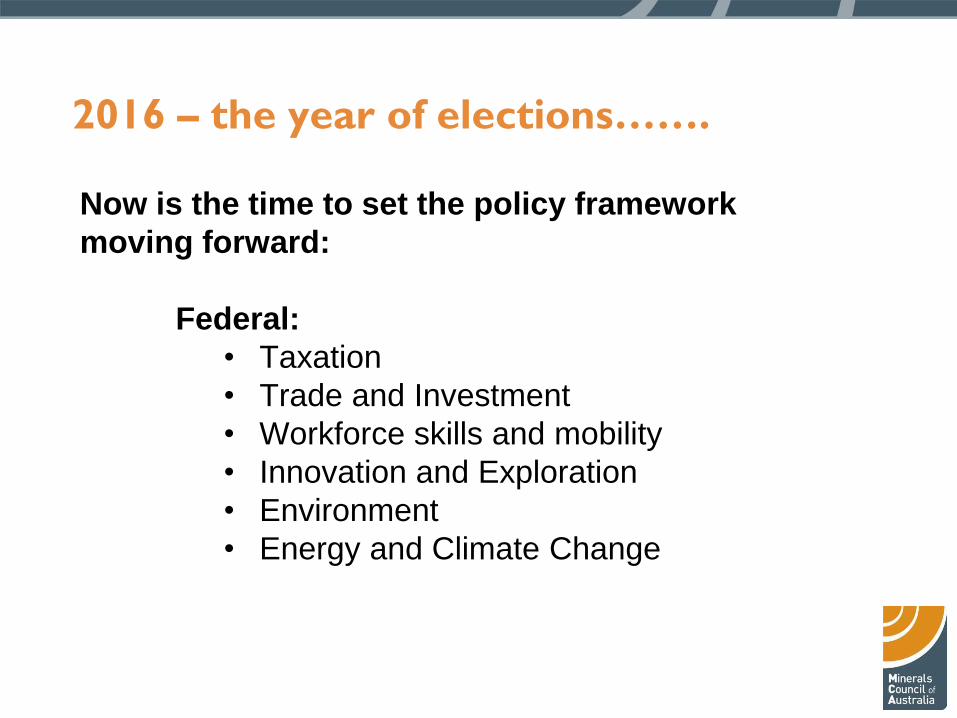

2016 – the year of elections…….

Now is the time to set the policy framework

moving forward:

Federal:

• Taxation

• Trade and Investment

• Workforce skills and mobility

• Innovation and Exploration

• Environment

• Energy and Climate Change

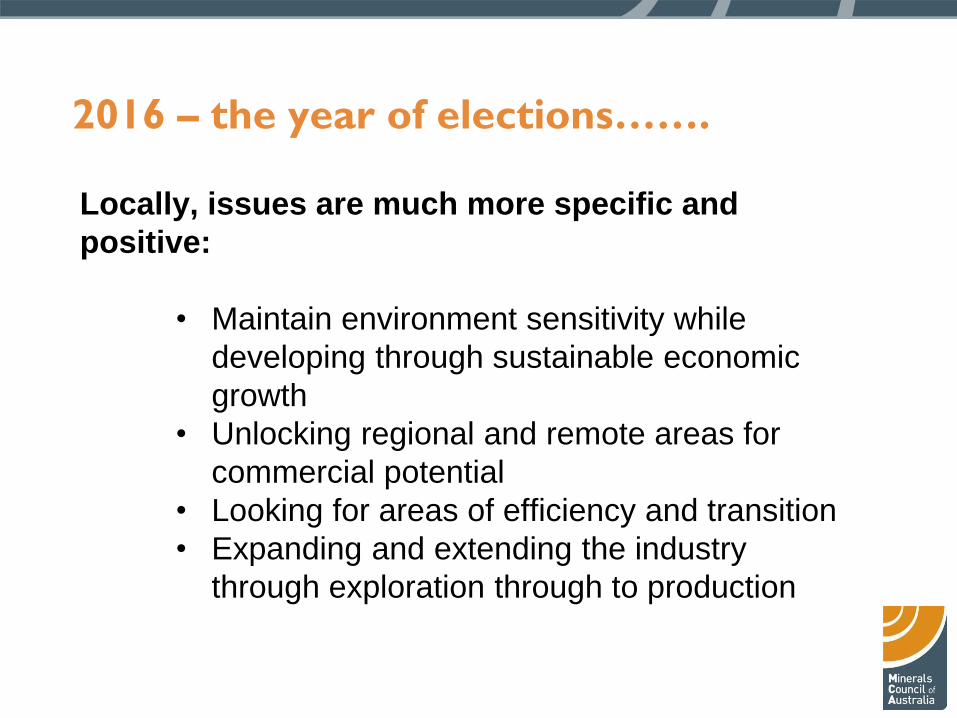

2016 – the year of elections…….

Locally, issues are much more specific and

positive:

• Maintain environment sensitivity while

developing through sustainable economic

growth

• Unlocking regional and remote areas for

commercial potential

• Looking for areas of efficiency and transition

• Expanding and extending the industry

through exploration through to production

A strong NT minerals sector leads to a

stronger NT economy – together we can

make it grow

THANK YOU.

![· Title: Concerto pour clarinette, cordes et percussions [opus 013] Author: Ortiz, Wagner - Arranger: Ortiz, Wagner - Publisher: Ortiz, Wagner : Subject: Ortiz, Wagner](https://img.pdfslide.net/doc/110x75/5e5889d9e121a130e36dd2e9/title-concerto-pour-clarinette-cordes-et-percussions-opus-013-author-ortiz.jpg)