Embed Size (px)

Citation preview

4th Quarter 2016 First Financial

Bankshares, Inc.

2

Forward Looking Statement

The numbers, as of and for the quarter and year ended December 31, 2016, contained within this presentation are unaudited. Certain statements contained herein may be considered “forward-looking statements” as defined in the Private Securities Litigation Reform Act of 1995. These statements are based upon the belief of the Company’s management, as well as assumptions made beyond information currently available to the Company’s management and, may be, but not necessarily are identified by such words as “expect”, “plan”, “anticipate”, “target”, “forecast” and “goal”. Because such “forward-looking statements” are subject to risks and uncertainties, actual results may differ materially from those expressed or implied by such forward-looking statements. Factors that could cause actual results to differ materially from the Company’s expectations include competition from other financial institutions and financial holding companies; the effects of and changes in trade, monetary and fiscal policies and laws, including interest rate policies of the Federal Reserve Board; changes in the demand for loans; fluctuations in value of collateral and loan reserves; inflation, interest rate, market and monetary fluctuations; changes in consumer spending, borrowing and savings habits; and acquisitions and integration of acquired businesses, and similar variables. Other key risks are described in the Company’s reports filed with the Securities and Exchange Commission, which may be obtained under “Investor Relations-Documents/Filings” on the Company’s web site or by writing or calling the Company at 325.627.7155. The Company does not undertake any obligation to update publicly or revise any forward-looking statements herein because of new information, future events or otherwise.

33

Who We Are

$6.8 billion financial holding company headquartered in Abilene, Texas

Group of 11 separate regions

126 year history

Growth markets include 50 mile radius of the larger cities of Texas

4

Recognitions – Financial Exploitation Prevention Program

ABA Foundation Community Commitment Award – November 2015

Texas Bankers Association 2016 Leaders in Financial Education Award – May 2016

White House Conference on Aging – July 2015

AARP Roundtable Discussion – November 2015

Texas Senate Committee on Business and Commerce – Jan. 2016

House Investments and Financial Services Committee – March 2016

5

66

Recognitions

SNL - #5 Best-Performing Regional Bank – April 2016

Raymond James Community Bankers Cup #3, One of thirty banks named– March 2016

2015 Proven Performers Award Winner – Bank Intelligence Solutions

American Banker - #15 – Based on three year average Return on Equity – May 2015

KBW Honor Roll – One of twenty five banks named – April 2015

77

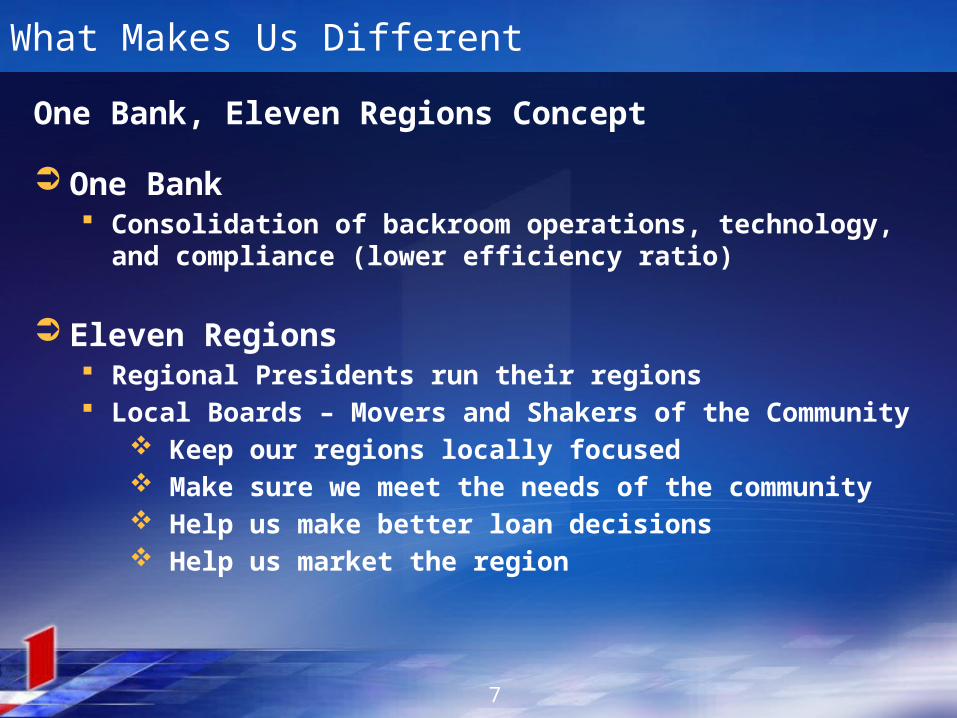

What Makes Us Different

One Bank, Eleven Regions Concept

One Bank Consolidation of backroom operations, technology, and

compliance (lower efficiency ratio)

Eleven Regions Regional Presidents run their regions Local Boards – Movers and Shakers of the Community

Keep our regions locally focused Make sure we meet the needs of the community Help us make better loan decisions Help us market the region

88

FFIN’s Unique Positioning in Texas

Bank Key MarketsComerica DFW, Austin, Houston, California, Michigan, Florida, Mexico

Green Houston, Austin, Dallas (New Public Company – August 2014)

Frost San Antonio, Austin, Corpus Christi, DFW, Rio Grande, West Texas

Independent North and Central Texas

International Bancshares Rio Grande, Houston, San Antonio, Oklahoma

Legacy Texas Dallas

Prosperity Houston, DFW, Austin, West Texas, South Central Texas, and Oklahoma

Southside East Texas

Texas Capital DFW, Austin, San Antonio, and Houston

Triumph Dallas (New Public Company – November 2014)

Veritex Dallas (New Public Company – October 2014)

99

First Bank, N.A. - Conroe Acquisition Consummated July 31, 2015 Montgomery, Walker, & Harris Counties (On I-45 North of Houston)

Exxon Mobil Headquarters in the Woodlands Montgomery County – Approximately 500,000 residents, 55% growth from 2000 to

2010, 24th fastest growing county in the United States #4 Market Share in Conroe – 10.6%

8 Branches in Conroe, Magnolia, Tomball, Cut and Shoot, Montgomery, and Huntsville; additional site on Grand Parkway in Spring, Texas to expand

$374 million in Assets at acquisition date $343 million in deposits $248 million in loans

1.06% Return on Assets in 2014 $61.0 million purchase price of our stock which represents 16x last twelve

months earnings Conroe acquisition is consistent with our acquisition model of high growth areas,

strong management and excellent earnings opportunity Provides diversification and fits well into our footprint Management and Board share same values to outstanding customer service

1010

4Trust Mortgage Acquisition Consummated – May 31, 2015

Originated $175 million in mortgage loans in 2014 – Compared to $225 million that First Financial Bank originated in 2014

15 year old Company with offices in Fort Worth, Dallas and North Richland Hills

$1.9 million purchase price

Troy Fore is now President of Mortgage Division of First Financial Bank; other owners joining First Financial as EVP’s – Tammie Harding, Kami Graves, and Ryan Craig

Considered one of the top mortgage companies in Fort Worth

Are now offering expanded mortgage products and services to customers

10

1212

Texas: Large and Growing

Five most populous states:* Growth (2005 – 2015)

California 39.2 million 8.3%

Texas 27.7 million 21.1%

Florida 20.3 million 14.0%

New York 19.8 million 2.8%

Illinois 12.9 million 0.8%

* U.S. Census Bureau

1313

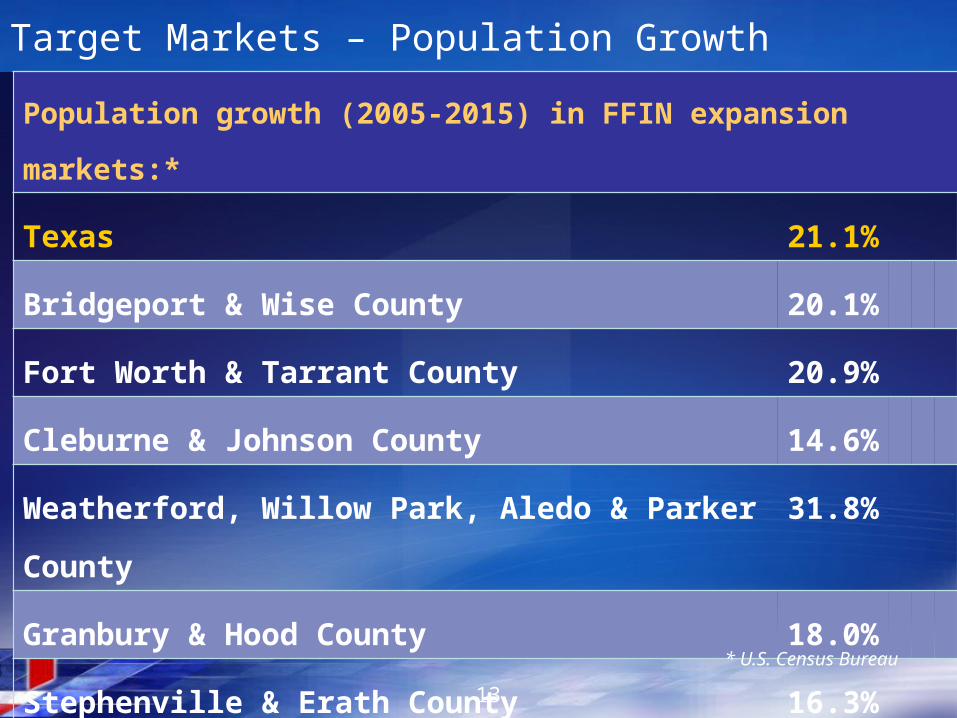

Target Markets – Population Growth

Population growth (2005-2015) in FFIN expansion markets:*

Texas 21.1%

Bridgeport & Wise County 20.1%

Fort Worth & Tarrant County 20.9%

Cleburne & Johnson County 14.6%

Weatherford, Willow Park, Aledo & Parker County 31.8%

Granbury & Hood County 18.0%

Stephenville & Erath County 16.3%

Conroe & Montgomery County 46.0%* U.S. Census Bureau

1414

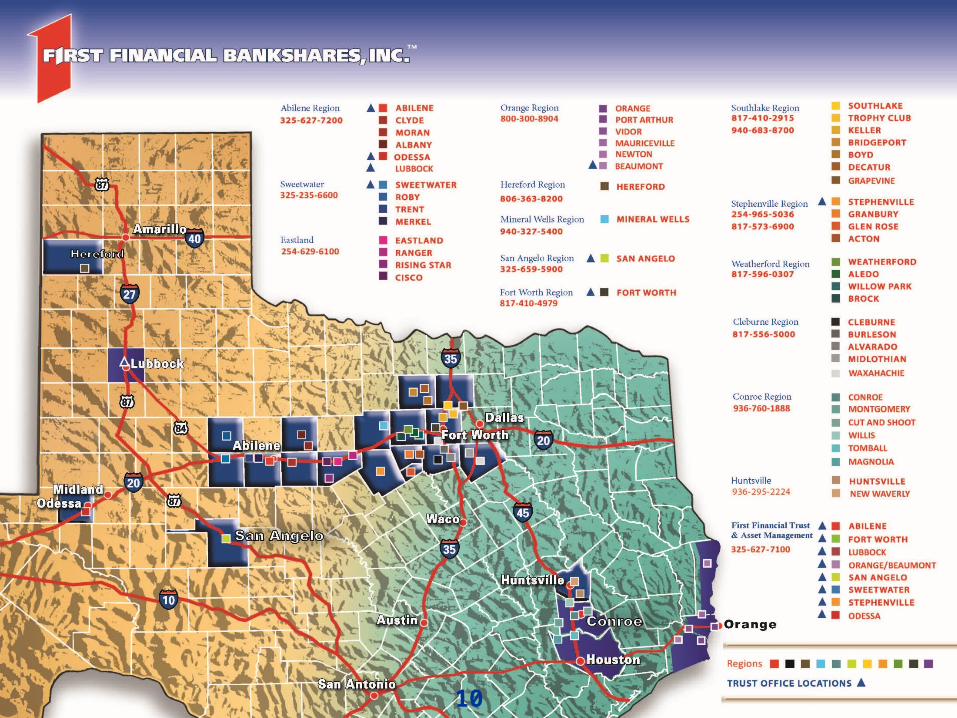

Core Markets: West Central Texas Markets served benefiting from well-established, long- time customers

REGIONASSET SIZE*

LOCATIONSDEPOSIT

MARKET SHARE**MARKET

SHARE RANK**

First Financial Bank(Abilene, Clyde, Moran, Albany, Odessa

Eastland, Ranger, Rising Star, Cisco,

Sweetwater, Roby, Trent, Merkel)

$2,401M 23 46% 1

First Financial Bank(Hereford)

$186M 1 45% 1

First Financial Bank(San Angelo)

$710M 3 26% 1

TOTALS $3,297M 27

* Data as of 12-31-16** Data as of 06-30-16

1515

Expansion Markets REGION ASSET SIZE* LOCATIONS

DEPOSIT MARKET SHARE**

MARKET SHARE RANK**

First Financial Bank (Cleburne, Burleson, Alvarado)

(Midlothian, Waxahachie)

$524M 42

20%10%

24

First Financial Bank (Southlake, Trophy Club, Keller, Grapevine)

(Bridgeport, Decatur, Boyd)

$452M 43

4%20%

52

First Financial Bank (Stephenville, Granbury, Glen Rose, Acton)

$503M 6 24% 2

First Financial Bank(Weatherford, Aledo, Willow Park, Brock)

$494M 7 23% 1

First Financial Bank(Mineral Wells)

$261M 1 38% 1

First Financial Bank(Ft. Worth)

$64M 1 - -

First Financial Bank(Orange, Mauriceville, Vidor)

(Newton, Port Arthur, Beaumont)

$492M 33

37%3%

17

First Financial Bank (Conroe, Magnolia, Cut and Shoot, Montgomery, Huntsville, Willis, Tomball,

New Waverly)

(Market Share for Huntsville, Conroe, Magnolia, Cut and Shoot, Montgomery and Willis Only)

$587M 9 10% 5

TOTALS $3,377M 43 * Data as of 9-30-16** Data as of 06-30-16

1616

Recent De Novo Growth New Waverly: Branch of Huntsville – August 2014 Beaumont: Branch of Orange – August 2014 Weatherford: I-20 Branch – June 2013 San Angelo: HEB Branch – March 2013 Waxahachie: Branch of Cleburne – December 2012 Abilene: Antilley Road Branch – September 2012 Grapevine: Branch of Southlake – March 2012 Cisco: Branch of Eastland – September 2011 (New Building – Opened August 2016)

Lamesa: Office of Trust Company – April 2011 Odessa: Branch of Abilene – February 2010 (New Building – Opened September 2016)

Fort Worth: Branch of Weatherford – February 2010 Odessa: Office of Trust Company – April 2009 Merkel: Branch of Sweetwater – July 2008 Brock: Branch of Weatherford – March 2008 Acton: Branch of Stephenville – March 2008 Albany: Branch of Abilene – May 2007 Fort Worth: Office of Trust Company – April 2007 (New Building – Opened May 2016)

Fort Worth – Forest Park Blvd. and Rosedale (Opened May 2016)

1716

Fort Worth – Forest Park Blvd. and Rosedale (Opened May 2016)

1817

19

Years with Company Years in Industry

Scott Dueser Chairman of the Board, President & Chief Executive Officer

41 46

Ron Butler Executive Vice President Chief Administrative Officer

24 35

Troy Fore President First Financial Mortgage

1 35

Gary S. Gragg Executive Vice President Lending

26 38

J. Bruce Hildebrand, CPA Executive Vice President Chief Financial Officer

14 38

Monica Houston Executive Vice President Retail Banking & Training

21 21

Executive Management at First Financial

19

20

Years with Company Years in Industry

Luke Longhofer Executive Vice President & Loan Review Officer Lending

6 14

Stan Limerick Executive Vice President Chief Information Officer

2 36

Randy Roewe Executive Vice President Chief Risk Officer

1 25

Kirk Thaxton, CTFA President First Financial Trust & Asset Management

30 34

Marna Yerigan Executive Vice President Lending

6 33

Executive Management at First Financial

20

21

Years with Company Years in Industry

Brandon Harris Senior Vice President Appraisal Services

3 16

Larry Kentz Senior Vice President & Compliance Officer Compliance

3 36

Michele Stevens Senior Vice President Advertising and Marketing

17 32

Senior Management at First Financial

21

Experienced Regional CEOs & Presidents

22

Years with Company Years in Industry

Marelyn Shedd, Abilene 25 33

Mike Mauldin, Hereford 14 39

Mike Boyd, San Angelo 41 44

Tom O’Neil, Cleburne 18 37

Trent Swearengin, Stephenville 17 19

Jay Gibbs, Weatherford 15 42

Mark Jones, Southlake 16 39

Ken Williamson, Mineral Wells 15 45

Stephen Lee, Southeast Region 4 28

Sam Baker, Conroe 1 40

Martin Noto, Fort Worth 1 33

2323

2011 2012 2013 2014 2015 2016

$4,121$4,502

$5,222

$5,522

$6,665 $6,810Chart Title

Growth in Total Assets

Asset Performance

(in millions)

2424

2011 2012 2013 2014 2015 2016

$1,102 $1,312 $1,362 $1,570 $1,746 $1,718

$2,233$2,321

$2,773$3,180

$3,444 $3,761

Non Interest Bearing Interest Bearing

Deposit Growth

Growth in FFIN Total Deposits (in millions)

$5,479

$3,335$3,633

$4,135

$4,750$5,190

2525

Deposit Products

Time9.3%

Deman

d31.4%

Money

Market46.8%

Sav-ings12.5%

2626

Account Growth

Net Growth in 2012 – 1,219 Accounts

Net Growth in 2013 – 3,308 Accounts*

Net Growth in 2014 – 10,687 Accounts

Net Growth in 2015 – 5,886 Accounts**

Net Growth in 2016 – 3,015 Accounts

December 31, 2012

December 31, 2013

December 31, 2014

December 31, 2015

December 31,2016

Total Number of Accounts

205,282 208,590 234,614 251,699 254,714

*(Excluding Orange Acquisition)**(Excluding Conroe Acquisition)

2727

2011 2012 2013 2014 2015 2016$66 $68 $76 $106 $102 $84

$218 $273 $334 $361 $386 $409 $427

$510 $590 $640 $685 $674

$1,076 $1,238

$1,689 $1,831

$2,178 $2,217

Real Estate

Commercial

Consumer

Agricultural

Loan PerformanceGrowth in FFIN Total Loans (in millions)

$1,787

$2,089

$2,689

$3,384

$2,938

$3,351

2828

Overview of Loan Portfolio Commercial

19.8%Agriculture

2.5%

Consumer12.1%

Real Estate65.6%

Note: Oil & Gas Exposure 2.32%

2929

Residential Development & Construction 8.6%

1-4 Family 45.2%

Commercial Development and Construc-tion

5.3%

Commercial R/E 23.9%

Other R/E 17.0%

Chart Title

Breakdown of R/E Loan Portfolio

3030

Oil & Gas Portfolio Analysis

Oil & Gas Supplemental Information (dollars in thousands)

December 31, 2015 Dec. 31, 2016

Oil & Gas Loans 96,712 78,483

% of Total Loans 2.89% 2.32%

Classified Oil & Gas Loans 34,506 32,518

Non Accrual Oil & Gas Loans 5,404 4,093

Quarter Ended Net Charge-offs 1,370 105

ALLL of % of Oil & Gas 6.35% 6.28%

3131

2011 2012 2013 2014 2015 2016

End of Period 53.6 57.5 65.0 61.8 64.6 61.8

Average Balances

54.6 56.4 64.3 64.1 63.0 64.9

Loan to Deposit Ratio

3232

2011 2012 2013 2014 2015 2016

FirstFinancial 1.64% 1.22% 1.16% 0.74% 0.90% 0.86%

Peer Group 4.59% 3.67% 2.71% 1.92% 1.32% 1.09%**

Sound Lending Practices

Nonperforming assets as a percentage of loans + foreclosed assets (FFIN vs. Peers)

**As of Sept. 30, 2016

3333

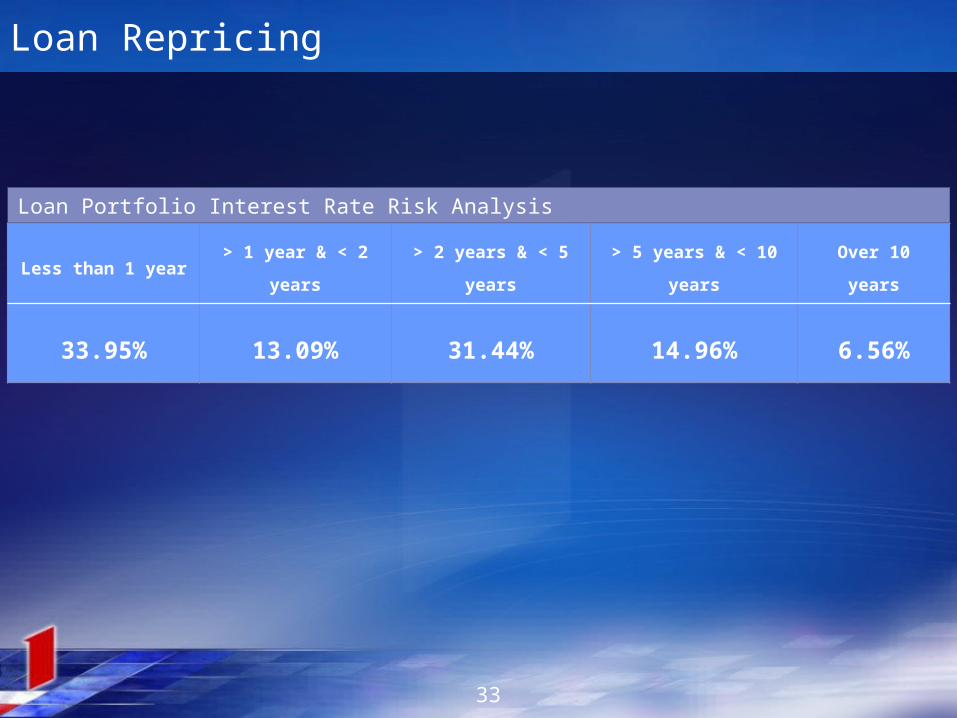

Less than 1 year > 1 year & < 2 years > 2 years & < 5 years > 5 years & < 10 years Over 10 years

33.95% 13.09% 31.44% 14.96% 6.56%

Loan Repricing

Loan Portfolio Interest Rate Risk Analysis

3434

2011 2012 2013 2014 2015 2016

$34,315 $34,839 $33,900$36,824

$41,877$45,779

$6,626$3,484 $3,753 $4,465

$9,685 $10,212

ALLL Provision

Allowance for Loan Losses and Provision for Loan Losses

(in thousands)

3535

Summary of Bond Portfolio

Agencies 4.22% Corporates 1.75%

Muni 53.80%

MBSs 19.42%

CMOs 20.42%

Treasuries 0.39%

3636

2011 2012 2013 2014 2015 2016

$1,912$2,233

$2,465$2,774

$3,060

$3,374Chart Title

Growth in Trust Assets

Total Trust Assets – Book Value (in millions)

3737

2011 2012 2013 2014 2015 2016

$12,671$14,464

$16,317

$18,766 $19,252 $19,636

Total Trust Fees

Growth in FFTAM Fees (in thousands)

3838

2011 2012 2013 2014 2015 2016

$4,176

$5,183

$6,142

$7,109$7,449 $7,190

Total Trust Net Income

Growth in FFTAM Net Income (in thousands)

39

2011 2012 2013 2014 2015 2016

$68.4$74.2

$78.9

$89.6$100.4

$104.8

30th Consecutive Year of Increased Earnings

FFIN Earnings (in millions)

39

40

2011 2012 2013 2014 2015 2016

$1.1$1.2 $1.2

$1.4$1.6 $1.59

Strong Shareholder Earnings

Basic Earnings Per Share

40

41

2012 2013 2014 2015 2016

1.75%1.64% 1.65% 1.61% 1.59%

0.98% 1.04% 0.95% 0.97% 1.00%*

FFIN Outperforms Peers

Percentage Return on Average Assets

Peer

Gro

up

Firs

t Fin

anci

al

41

*As of Sept. 30, 2016

42

2012 2013 2014 2015 2016

13.85% 13.75% 14.00%13.60%

12.36%

8.56% 8.69% 8.32% 8.59% 9.12%*

Strong Return on Capital Percentage Return on Average Equity

Peer

Gro

up

Firs

t Fin

anci

al

42

*As of Sept. 30, 2016

4343

2012 2013 2014 2015 2016

Shareholders’Equity 556,963 587,647 681,537 804,986 837,885

As a Percent of Total Assets

12.37 11.25 11.65 12.08 12.30

Tangible

Capital484,990 490,163 584,178 660,537 694,282

Tier 1

Leverage Ratio10.60 9.84 9.89 9.96 10.71

Common Equity

Tier 1 Capital Ratio17.43 15.82 16.05 15.90 17.40

Tier 1 Capital Ratio 17.43 15.82 16.05 15.90 17.40

Total

Capital Ratio18.68 16.97 17.16 16.97 18.45

Capital & Capital Ratios(dollars in thousands)

44

3rd Qtr. '13

4th Qtr. '13

1st Qtr. '14

2nd Qtr. '14

3rd Qtr. '14

4th Qtr. '14

1st Qtr. '15

2nd Qtr. '15

3rd Qtr. '15

4th Qtr. '15

1st Qtr. '16

2nd Qtr. '16

3rd Qtr. '16

4th Qtr. '16

3.00%

3.25%

3.50%

3.75%

4.00%

4.25%

4.50%

4.75%

5.00%

First Financial Peer Group

Net Interest Margin

Quarterly Interest Margin

44

4545

2011 2012 2013 2014 2015 2016

FirstFinancial 48.37% 48.14% 50.20% 49.24% 47.61% 49.22%

Peer Group 65.57% 65.77% 67.80% 66.94% 63.92% 62.77%**

Working Harder and Smarter

Efficiency Ratio (FFIN vs. Peers)

**As of Sept. 30, 2016

4646

Stock cost in January 2016 $30,170

Dividend declared ($0.70 x 1,000 shares) $ 700

Increase in stock price during 2016($30.17 to $45.20 X 1,000 shares) $15,030

2016 return on investment 52.14%

2015 return on investment 3.05%

2014 return on investment -7.96%

2013 return on investment 72.11%

2012 return on investment 19.65%

5 year compound average return 12.36%

Total Return on Investment

27.79%

Assume you owned 1,000 shares of FFIN stock on January 1, 2016…

4747

Dividends Per Share

2012 2013 2014 2015 2016

$0.50 $0.52 $0.55

$0.62

$0.70

Chart Title

Annual Dividends Declared Per Share

4848

Strong Stock Performance

-100.00%

-50.00%

0.00%

50.00%

100.00%

150.00%

200.00%

250.00%

FFIN S&P 500 NASDAQ Dow JonesJan . ‘07 Dec. ’16Dec . ‘09Dec ‘07 Dec ‘08 Dec. ‘10 Dec. ’11 Dec. ’12 Dec. ’13 Dec. ’14 Dec. ’15

4949

Challenges

Regulatory reform from Washington

Stagnant national economy

Low oil & gas and commodity prices

Low interest rate environment

Maintaining net interest margin

5050

Opportunities

Loan Growth

Mortgage Lending

Trust Services

Treasury Management

Mobile Banking

Lower Efficiency Ratio

Potential Acquisitions