Embed Size (px)

Citation preview

1

Malaysia CCTV / E-surveillance

July 2009

Analyst Day Presentation

Developed for

2

Table of Contents

22

33

Malaysia - Market Dynamics, Size & ForecastMalaysia - Market Dynamics, Size & Forecast

Outlooks – Risks & Opportunities and Key Take AwayOutlooks – Risks & Opportunities and Key Take Away

11 Overview: Current Scenario & Global SecurityOverview: Current Scenario & Global Security

3

Table of Contents

11 Overview: Current Scenario & Global SecurityOverview: Current Scenario & Global Security

4

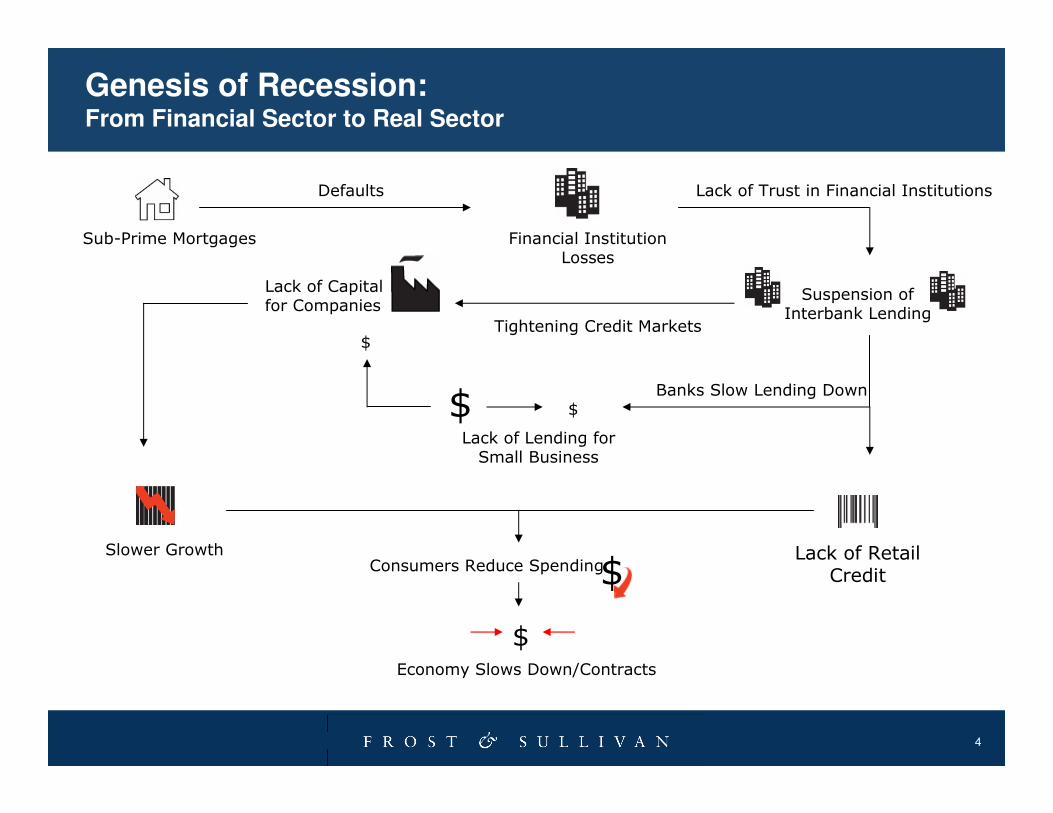

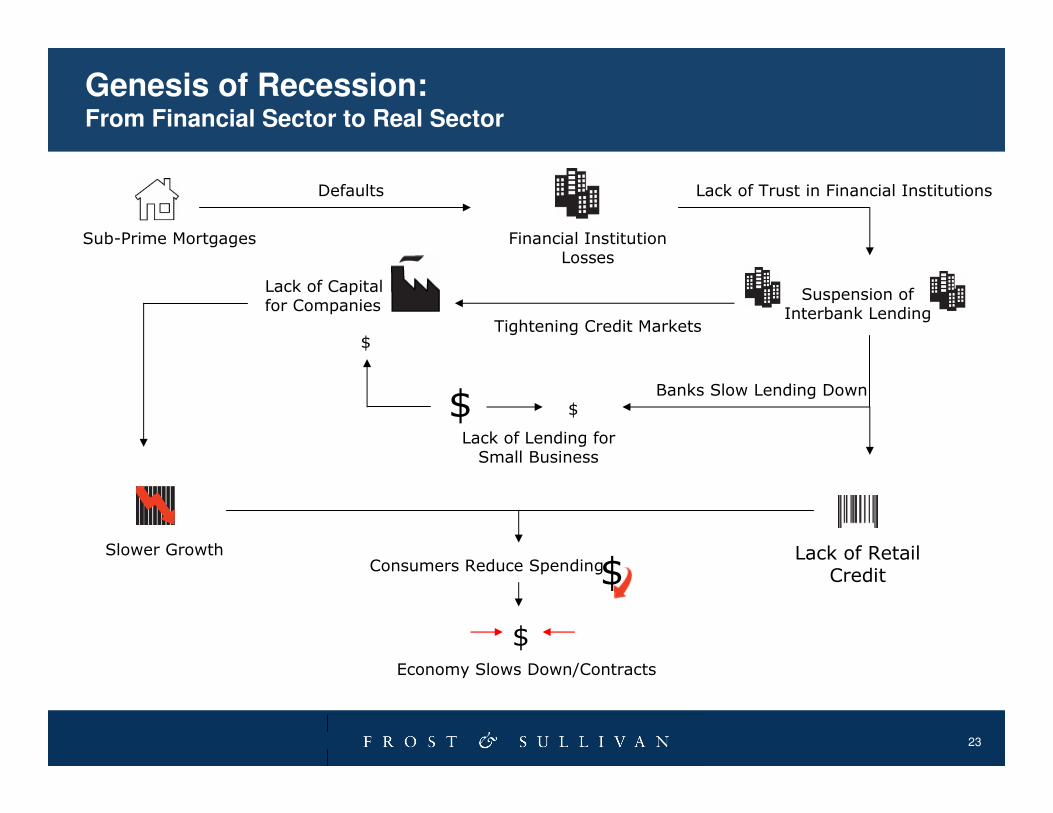

Genesis of Recession: From Financial Sector to Real Sector

Defaults Lack of Trust in Financial Institutions

Tightening Credit Markets

Banks Slow Lending Down

Slower Growth

Financial InstitutionLosses

Lack of Lending forSmall Business

Lack of RetailCredit

Consumers Reduce Spending

Economy Slows Down/Contracts

Sub-Prime Mortgages

$

Lack of Capitalfor Companies

Suspension of Interbank Lending

$

$

$

$

5

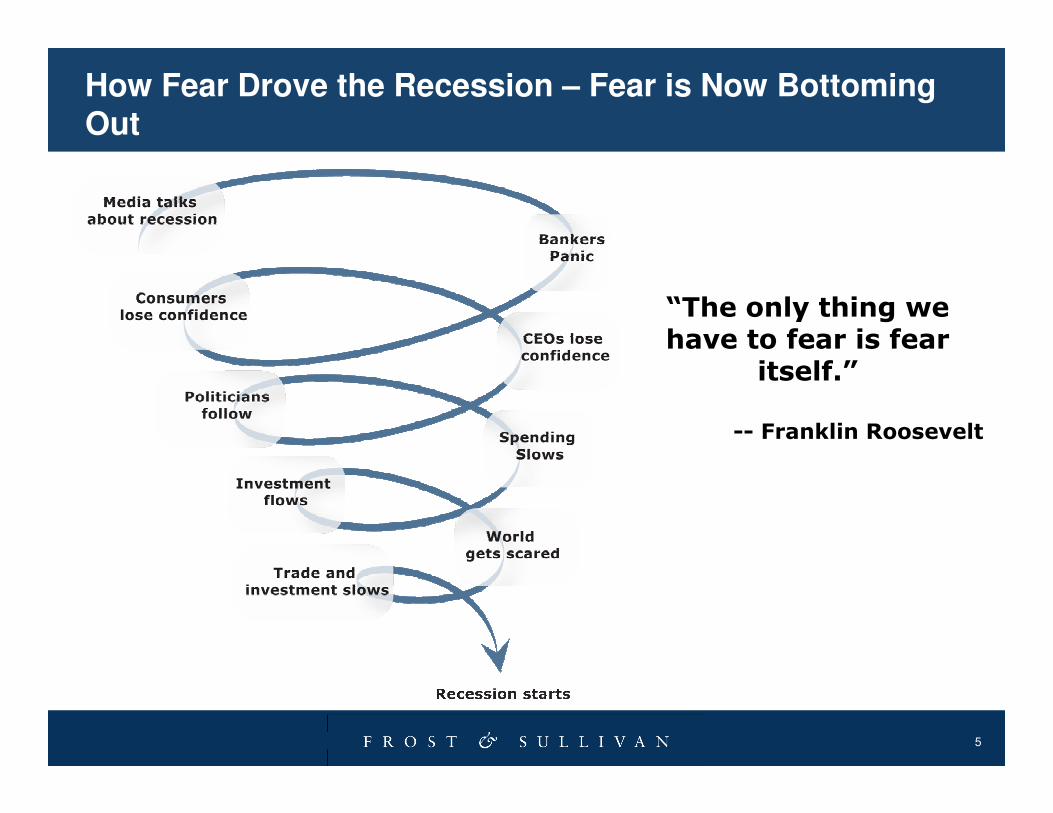

How Fear Drove the Recession – Fear is Now Bottoming Out

“The only thing we have to fear is fear

itself.”

-- Franklin Roosevelt

6

Global Security Threats

• Economic decline in the region has attracted various global threats.• Translated to more potential of cyber crimes, thefts, security threats and so on.

7

Security Threat Targets

Source : Frost & Sullivan

• Residential

• Retail Stores

• Banks

• Shopping Malls

• Office Complexes and so on

TARGETS

• Individual Parties

• Localized region

• Organizations or Private Parties

• Localized region

Standard Security Threats

SyndicatedSecurity Threats

GLOBAL THREATS• Large populated areas

• Targets that have global coverage• Terrorist organizations

8

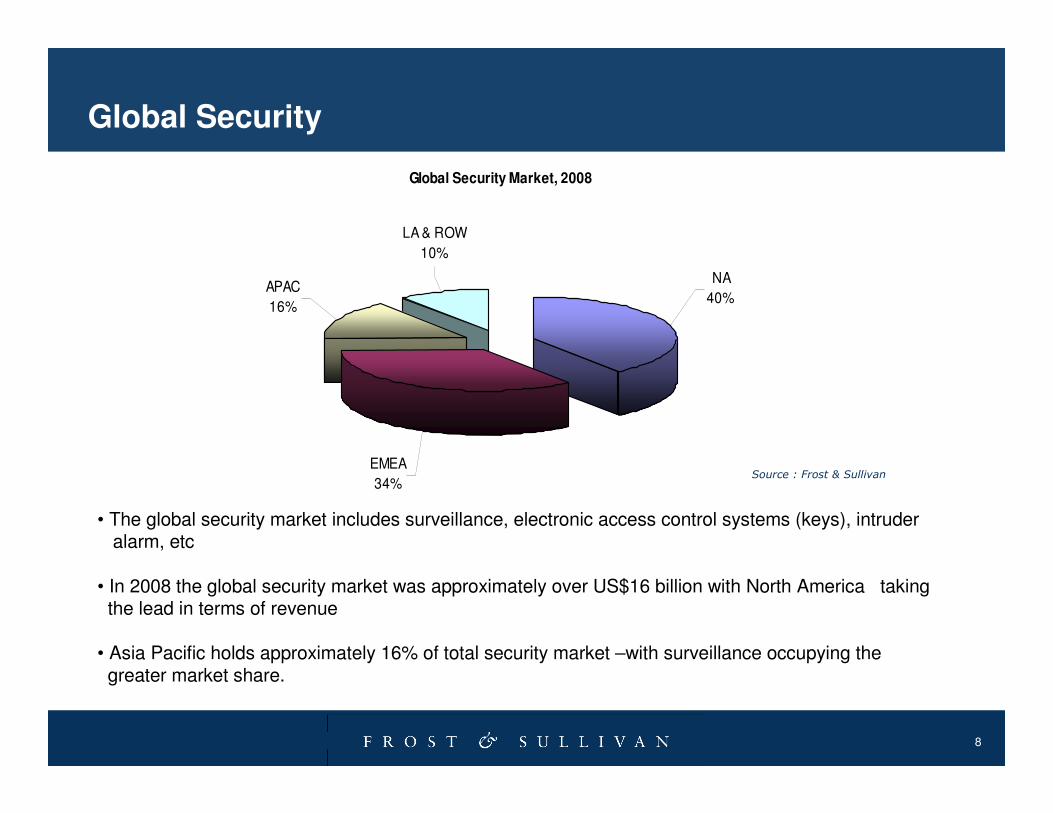

Global Security Market, 2008

EMEA

34%

APAC

16%

LA & ROW

10%

NA

40%

Global Security

Source : Frost & Sullivan

• The global security market includes surveillance, electronic access control systems (keys), intruder alarm, etc

• In 2008 the global security market was approximately over US$16 billion with North America taking the lead in terms of revenue

• Asia Pacific holds approximately 16% of total security market –with surveillance occupying the greater market share.

9

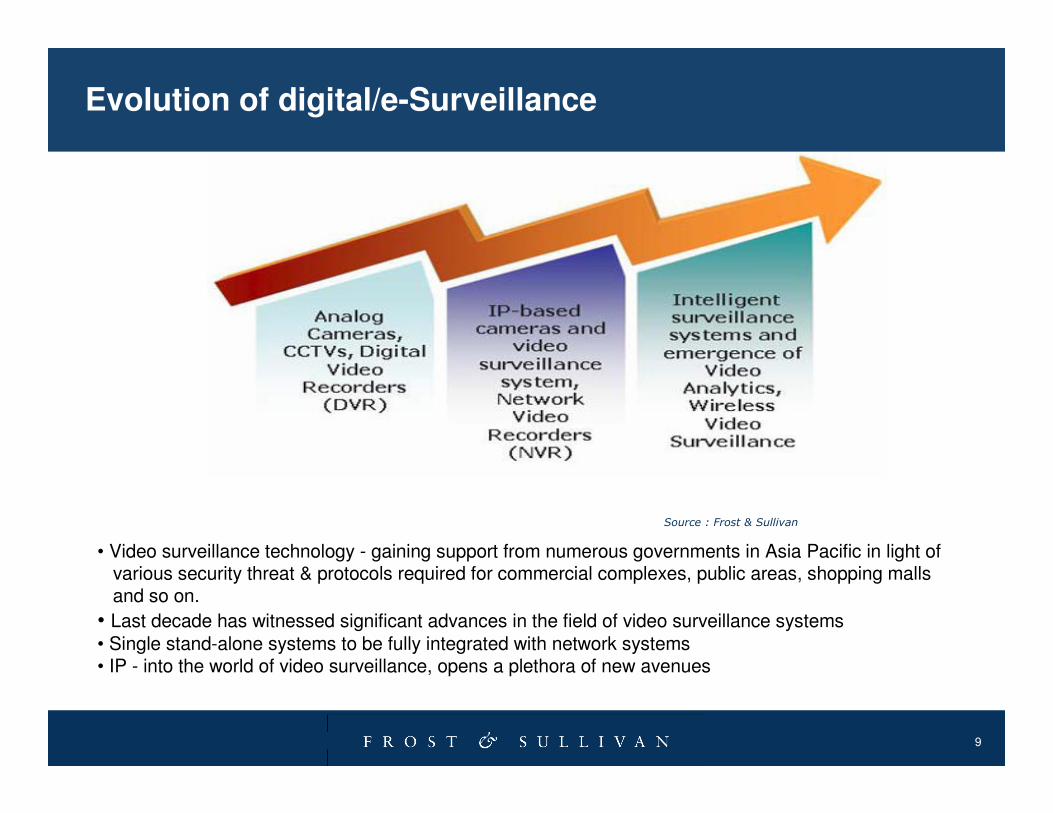

Evolution of digital/e-Surveillance

Source : Frost & Sullivan

• Video surveillance technology - gaining support from numerous governments in Asia Pacific in light of various security threat & protocols required for commercial complexes, public areas, shopping malls and so on.

• Last decade has witnessed significant advances in the field of video surveillance systems • Single stand-alone systems to be fully integrated with network systems • IP - into the world of video surveillance, opens a plethora of new avenues

10

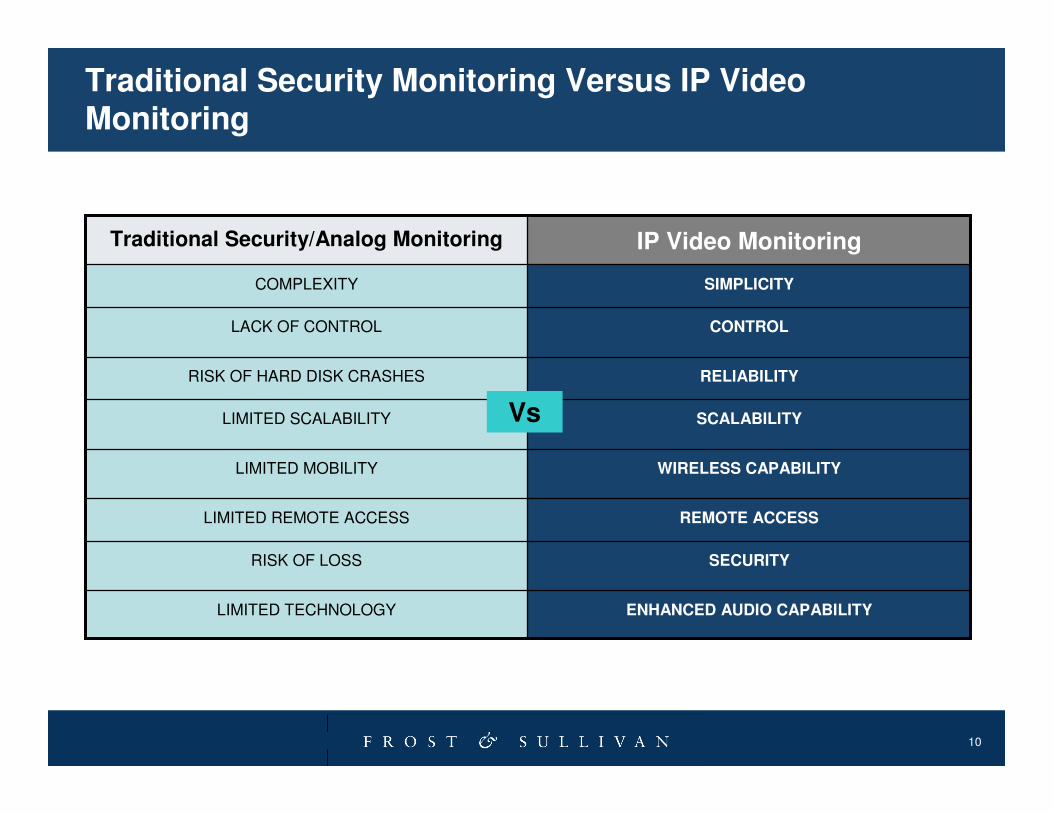

Traditional Security Monitoring Versus IP Video Monitoring

ENHANCED AUDIO CAPABILITYLIMITED TECHNOLOGY

SECURITYRISK OF LOSS

REMOTE ACCESSLIMITED REMOTE ACCESS

WIRELESS CAPABILITYLIMITED MOBILITY

SCALABILITYLIMITED SCALABILITY

RELIABILITYRISK OF HARD DISK CRASHES

CONTROLLACK OF CONTROL

SIMPLICITYCOMPLEXITY

IP Video MonitoringTraditional Security/Analog Monitoring

Vs

11

Traditional Security Monitoring Versus IP Video Monitoring (Contd.)

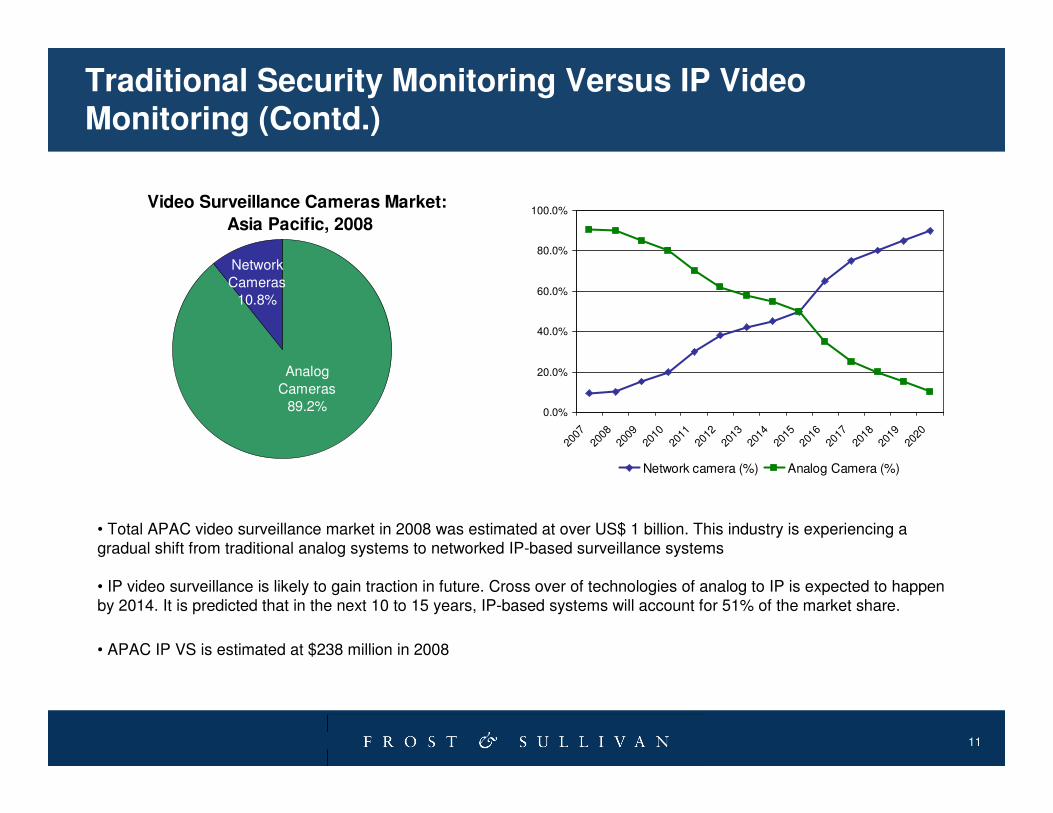

Video Surveillance Cameras Market:

Asia Pacific, 2008

Network

Cameras10.8%

Analog

Cameras89.2% 0.0%

20.0%

40.0%

60.0%

80.0%

100.0%

2007

2008

2009

2010

2011

2012

2013

2014

2015

2016

2017

2018

2019

2020

Network camera (%) Analog Camera (%)

• Total APAC video surveillance market in 2008 was estimated at over US$ 1 billion. This industry is experiencing a gradual shift from traditional analog systems to networked IP-based surveillance systems

• IP video surveillance is likely to gain traction in future. Cross over of technologies of analog to IP is expected to happen by 2014. It is predicted that in the next 10 to 15 years, IP-based systems will account for 51% of the market share.

• APAC IP VS is estimated at $238 million in 2008

12

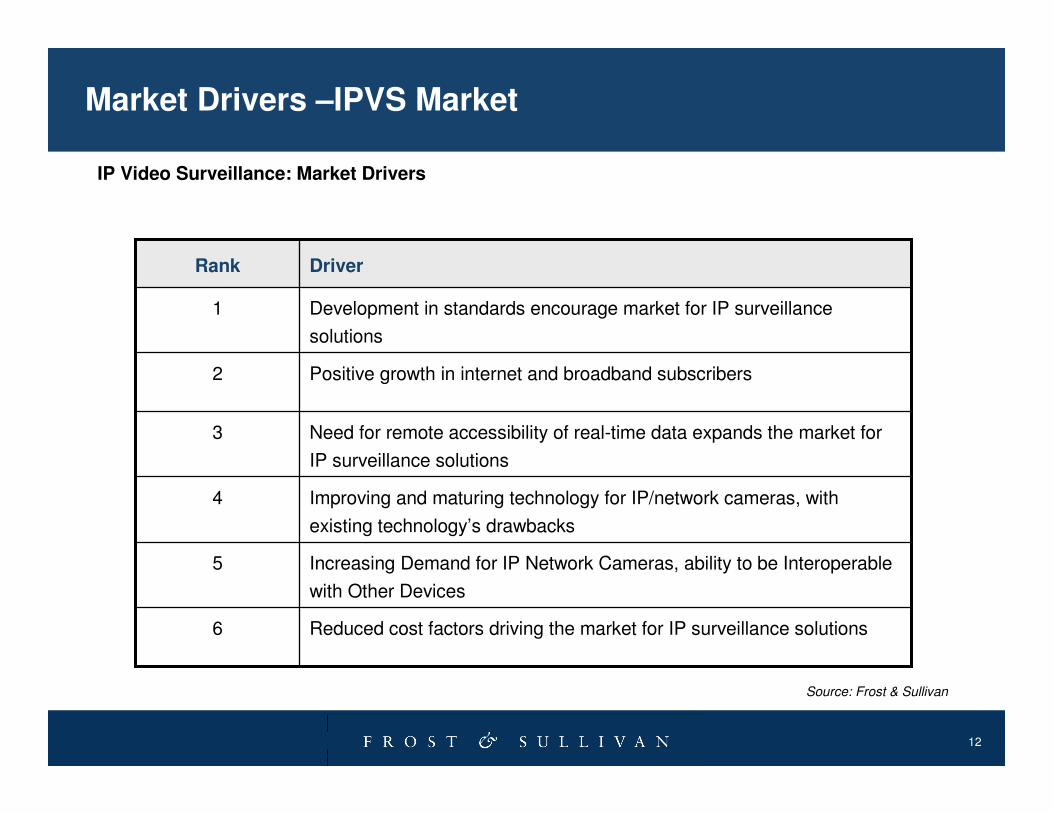

Market Drivers –IPVS Market

Increasing Demand for IP Network Cameras, ability to be Interoperable

with Other Devices

5

Development in standards encourage market for IP surveillance

solutions

1

Positive growth in internet and broadband subscribers2

Need for remote accessibility of real-time data expands the market for

IP surveillance solutions

3

Improving and maturing technology for IP/network cameras, with

existing technology’s drawbacks

4

Reduced cost factors driving the market for IP surveillance solutions6

DriverRank

Source: Frost & Sullivan

IP Video Surveillance: Market Drivers

13

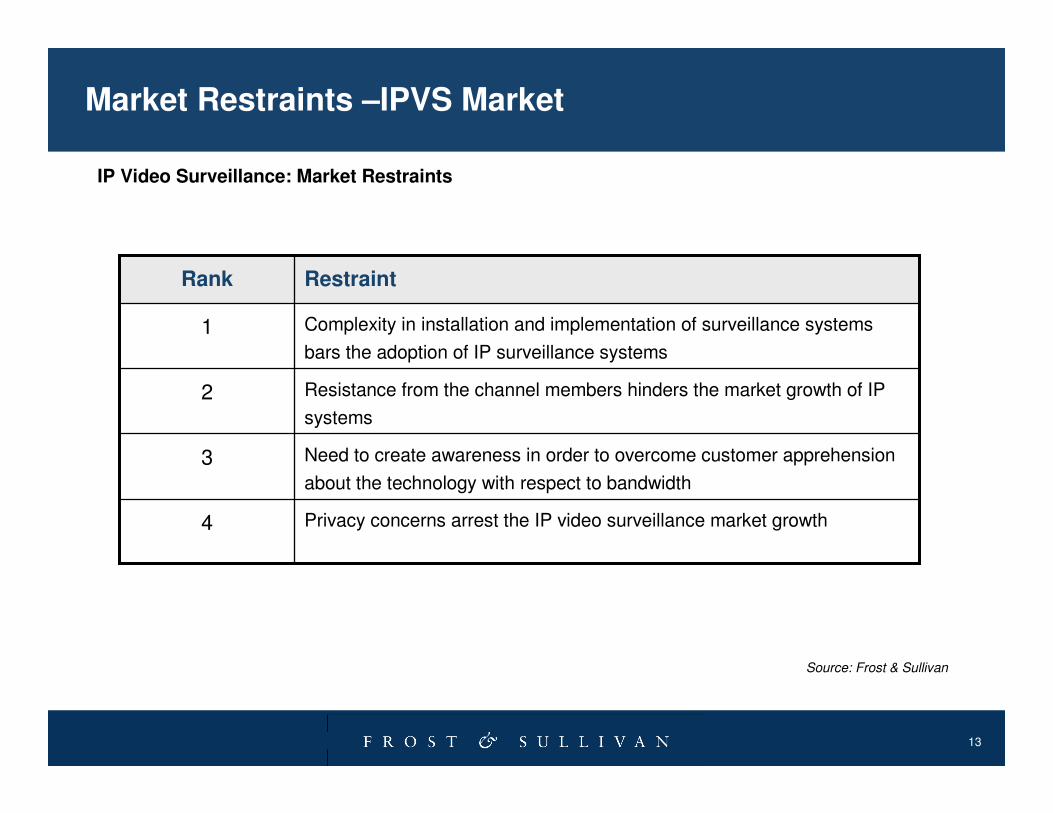

Market Restraints –IPVS Market

Privacy concerns arrest the IP video surveillance market growth4

Need to create awareness in order to overcome customer apprehension

about the technology with respect to bandwidth

3

Resistance from the channel members hinders the market growth of IP

systems

2

Complexity in installation and implementation of surveillance systems

bars the adoption of IP surveillance systems

1

RestraintRank

Source: Frost & Sullivan

IP Video Surveillance: Market Restraints

14

Table of Contents

22 Malaysia - Market Dynamics, Size & ForecastMalaysia - Market Dynamics, Size & Forecast

15

Pest Analysis of the Malaysia Video Surveillance Market

• Political :

• Government guidelines to install video surveillance cameras in commercial buildings and public areas

• Compliance & regulations in the financial services industry

• Economic & Social:

• With current economic scenario & global terrorist threats are leading to increased video surveillance

equipment but with cautious spending on video surveillance equipment/products & services

• Technological:

• Emergence of IP has helped in driving the growth of the Surveillance Market

• Advances in technology has not only led to improved features but also falling prices

• High growth & penetration of IT infrastructure is aiding the growth of VS and IPVS market in this

country

16

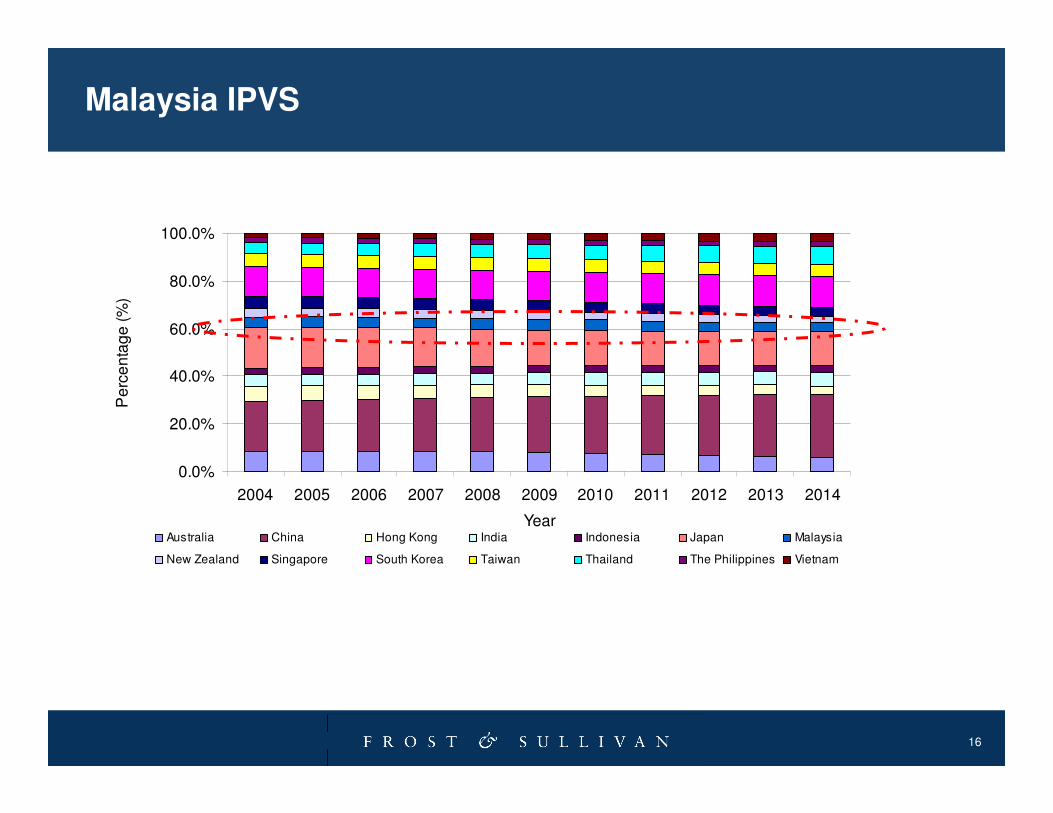

Malaysia IPVS

0.0%

20.0%

40.0%

60.0%

80.0%

100.0%

2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014

Year

Pe

rce

nta

ge

(%

)

Australia China Hong Kong India Indonesia Japan Malaysia

New Zealand Singapore South Korea Taiwan Thailand The Philippines Vietnam

17

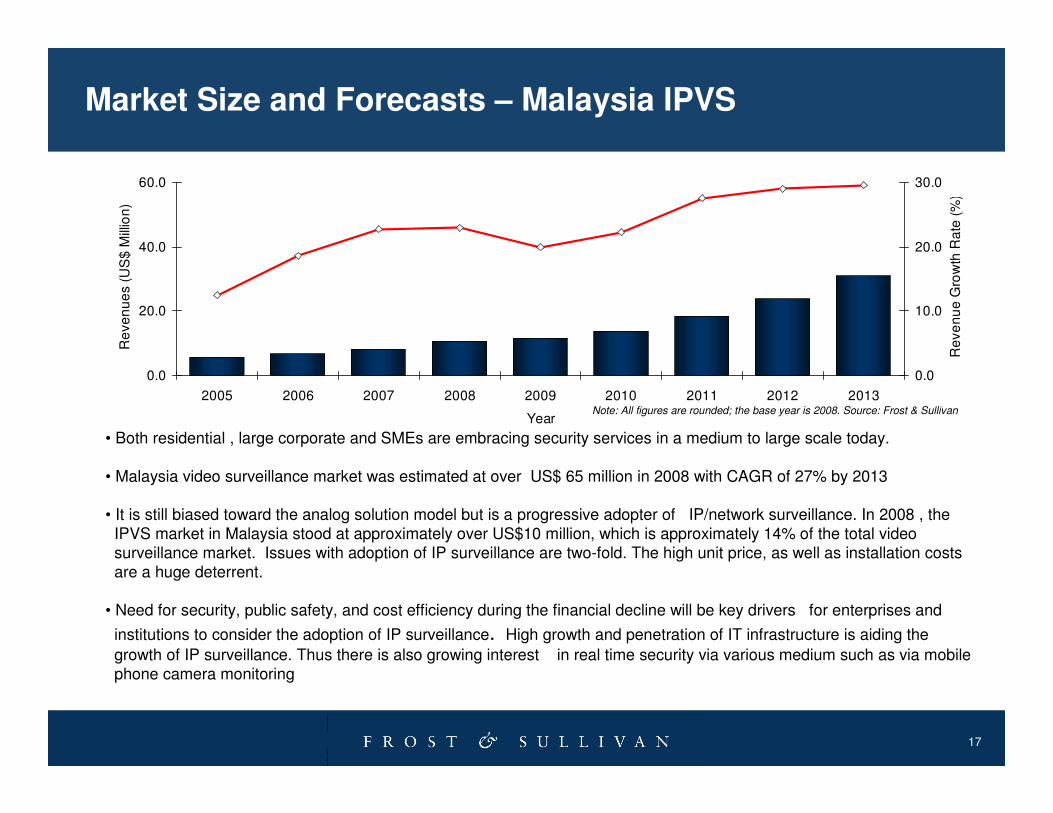

Market Size and Forecasts – Malaysia IPVS

0.0

20.0

40.0

60.0

2005 2006 2007 2008 2009 2010 2011 2012 2013

Year

Re

ve

nu

es (

US

$ M

illio

n)

0.0

10.0

20.0

30.0

Re

ve

nu

e G

row

th R

ate

(%

)

Note: All figures are rounded; the base year is 2008. Source: Frost & Sullivan

• Both residential , large corporate and SMEs are embracing security services in a medium to large scale today.

• Malaysia video surveillance market was estimated at over US$ 65 million in 2008 with CAGR of 27% by 2013

• It is still biased toward the analog solution model but is a progressive adopter of IP/network surveillance. In 2008 , the IPVS market in Malaysia stood at approximately over US$10 million, which is approximately 14% of the total video surveillance market. Issues with adoption of IP surveillance are two-fold. The high unit price, as well as installation costs are a huge deterrent.

• Need for security, public safety, and cost efficiency during the financial decline will be key drivers for enterprises and

institutions to consider the adoption of IP surveillance. High growth and penetration of IT infrastructure is aiding the

growth of IP surveillance. Thus there is also growing interest in real time security via various medium such as via mobile phone camera monitoring

18

Key Verticals

• Banks are the front runner s of IP-based solutions, as they consolidate security networks for central management nationwide

• This country’s abundant natural resources, such as oil and gas and the industry being dominated by state-run companies uses sophisticated technology such as IPVS. Given its high commercial value, interest in high-end solutions has also gone up among state and private-owned oil companies

• Tourism industry forms a vital source of IP VS revenue in Malaysia too. Implementation of such surveillance system at public gathering spots (e.g. stadiums, genting casino) brings about a more secure environment to the industry

• Government stimulus packages ensure large-scale projects. Special allocations for housing construction andrehauling basic amenities provide largely untapped markets.

• City surveillance and airports are also upgrading to IP solutions and wireless IP VS, along with health care.

• Increasing interest from education sector too – schools and campuses are able to monitor the activities and movement of persons in and out of the school on-site, as well as remotely. This vertical has a very high growth potential.

• Numerous number of incidents in parking lots of large building complexes . The Housing and Local Government Minister recently gave a directive that requires commercial buildings and public places with parking lots to install surveillance systems. This directive will lead to fruitful opportunities as many building owners still have not installed security cameras at their premises

• Similarly at child and aged care centre.

19

Competitive Landscape- of IPVS in Malaysia

• The competition is intense and polarized between the high-end Western and

Japanese participants and the low-end Taiwanese, South Korean, and Chinese

manufacturers

• IP video surveillance products in Malaysia rely heavily on imports from China,

Taiwan, and South Korea. Taiwanese products still have the upper hand in terms of

price and performance.

• Panasonic, in addition to Honeywell, also has a significant presence in the network

cameras market.

• Axis continued to dominate the IP/network camera market, closely followed by Sony

& Bosch

• Axis’ efforts to educate the market continued to help it stay ahead of the competition

• Bosch Security, on the other hand, has had good success in the Malaysian retail

sector. Bosch contributes to both cameras and video management software,

significantly

20

Table of Contents

33 Outlooks – Risks & Opportunities and Key Take AwayOutlooks – Risks & Opportunities and Key Take Away

21

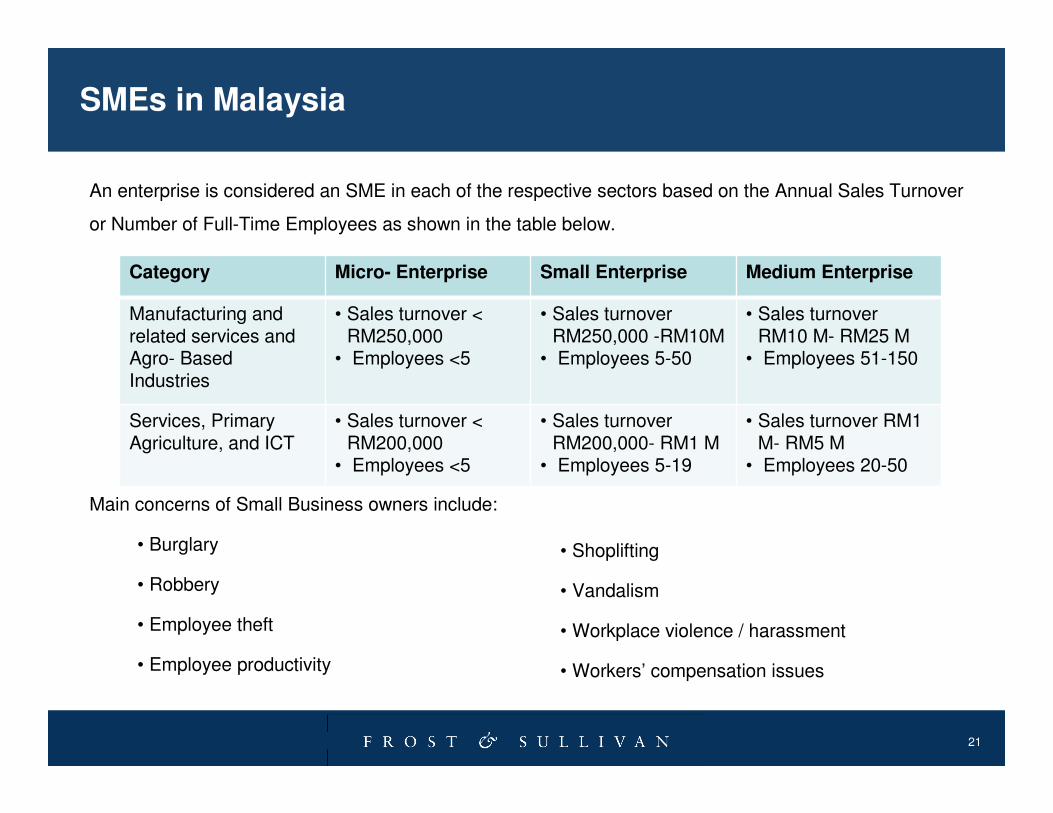

SMEs in Malaysia

Main concerns of Small Business owners include:

• Burglary

• Robbery

• Employee theft

• Employee productivity

• Shoplifting

• Vandalism

• Workplace violence / harassment

• Workers’ compensation issues

An enterprise is considered an SME in each of the respective sectors based on the Annual Sales Turnover

or Number of Full-Time Employees as shown in the table below.

Category Micro- Enterprise Small Enterprise Medium Enterprise

Manufacturing and related services and Agro- Based Industries

• Sales turnover < RM250,000

• Employees <5

• Sales turnover RM250,000 -RM10M

• Employees 5-50

• Sales turnover RM10 M- RM25 M

• Employees 51-150

Services, Primary Agriculture, and ICT

• Sales turnover < RM200,000

• Employees <5

• Sales turnover RM200,000- RM1 M

• Employees 5-19

• Sales turnover RM1 M- RM5 M

• Employees 20-50

22

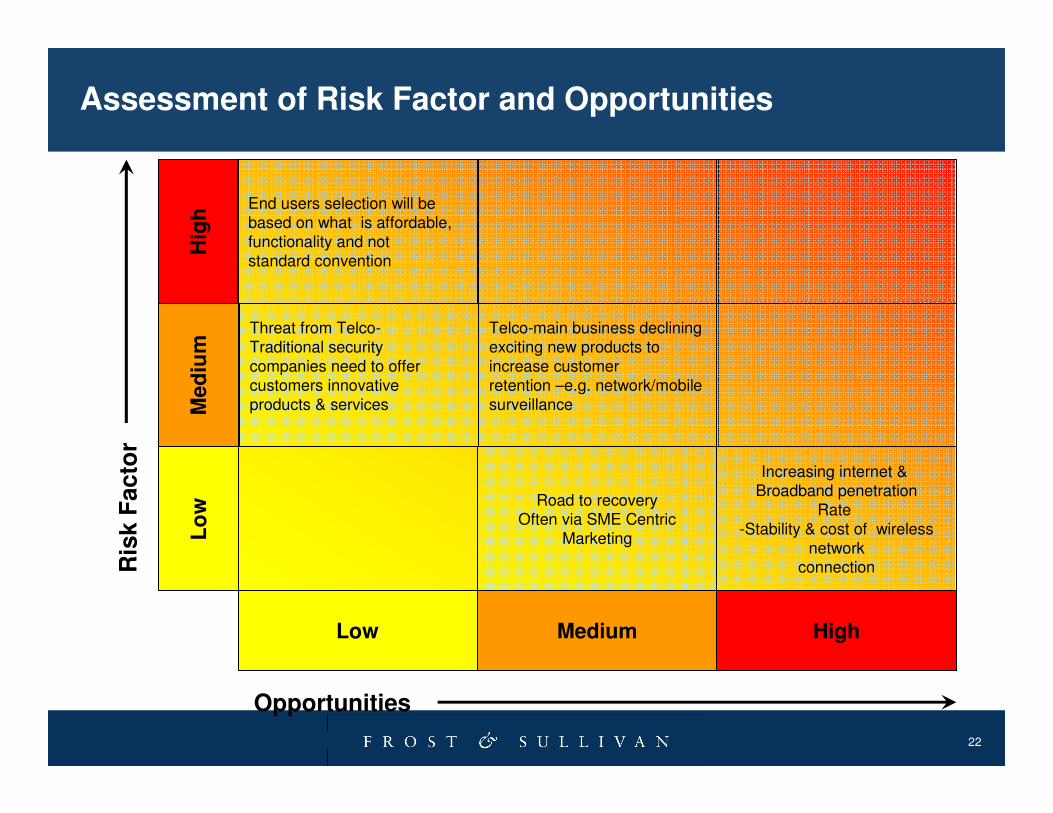

End users selection will be based on what is affordable,functionality and notstandard convention

Telco-main business decliningexciting new products to increase customerretention –e.g. network/mobilesurveillance

Threat from Telco-Traditional securitycompanies need to offercustomers innovativeproducts & services

Road to recoveryOften via SME Centric

Marketing

Increasing internet & Broadband penetration

Rate -Stability & cost of wireless

network connection

Low Medium High

Hig

hM

ed

ium

Lo

w

Opportunities

Ris

k F

acto

rAssessment of Risk Factor and Opportunities

23

Genesis of Recession: From Financial Sector to Real Sector

Defaults Lack of Trust in Financial Institutions

Tightening Credit Markets

Banks Slow Lending Down

Slower Growth

Financial InstitutionLosses

Lack of Lending forSmall Business

Lack of RetailCredit

Consumers Reduce Spending

Economy Slows Down/Contracts

Sub-Prime Mortgages

$

Lack of Capitalfor Companies

Suspension of Interbank Lending

$

$

$

$

24

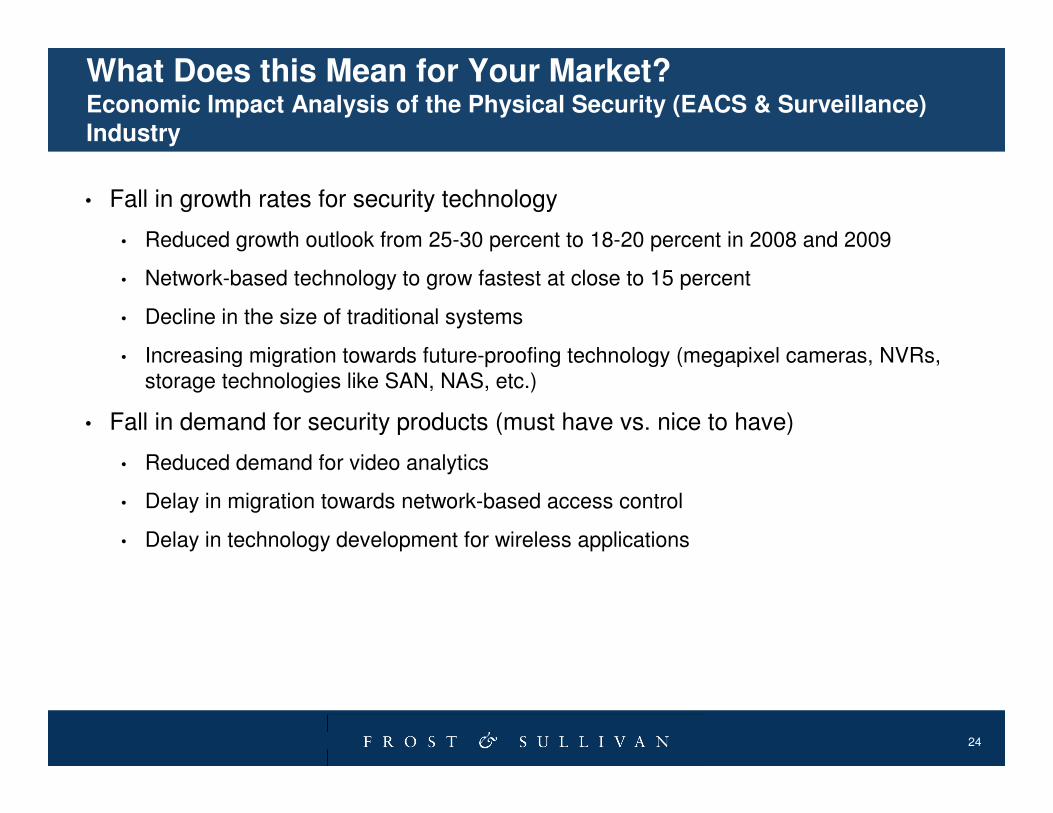

What Does this Mean for Your Market?Economic Impact Analysis of the Physical Security (EACS & Surveillance) Industry

• Fall in growth rates for security technology

• Reduced growth outlook from 25-30 percent to 18-20 percent in 2008 and 2009

• Network-based technology to grow fastest at close to 15 percent

• Decline in the size of traditional systems

• Increasing migration towards future-proofing technology (megapixel cameras, NVRs, storage technologies like SAN, NAS, etc.)

• Fall in demand for security products (must have vs. nice to have)

• Reduced demand for video analytics

• Delay in migration towards network-based access control

• Delay in technology development for wireless applications

25

What Does this Mean for Your Market? (cont.) Economic Impact

Analysis of the Physical Security Industry

• Fall in prices of security

technology

• Industry Consolidation

– Large vendors buying out small

startups to boost product/service

portfolio

• Reduced investment in emerging

technology

– Lower number of initial public

offerings (IPO’s)

– Reduced venture capital funding for

security startups

– Increased number of bankruptcy

filings in the market

26

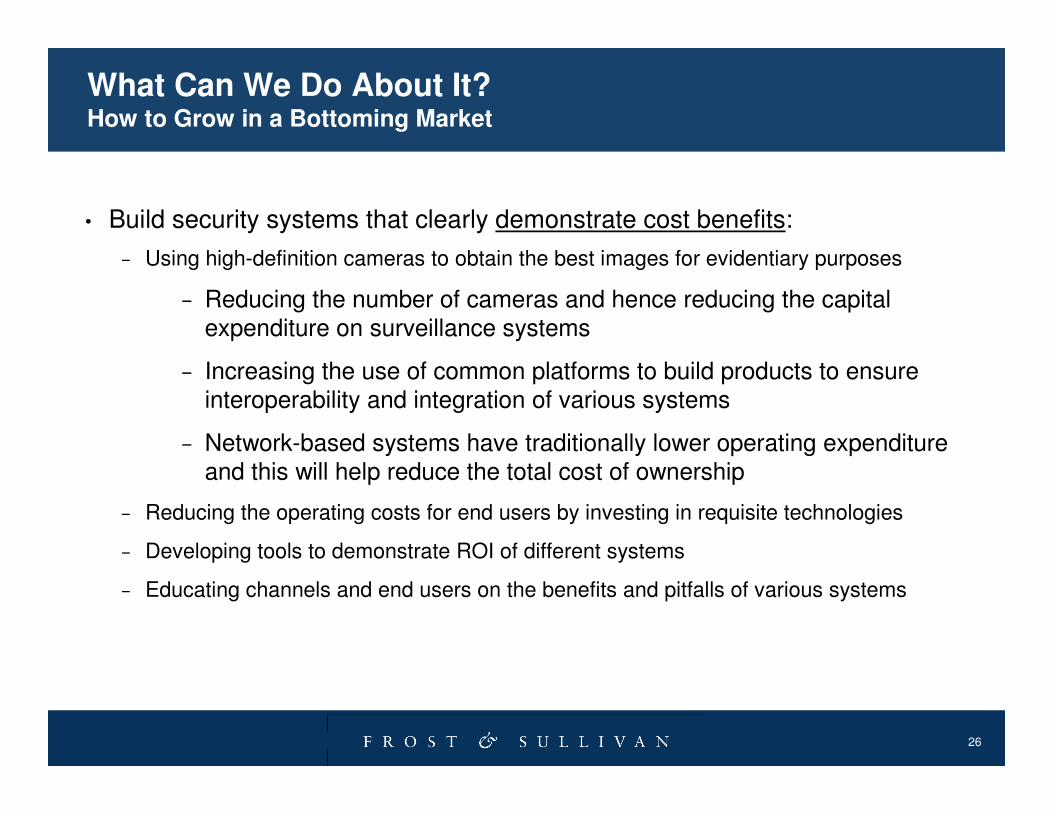

What Can We Do About It?How to Grow in a Bottoming Market

• Build security systems that clearly demonstrate cost benefits:

– Using high-definition cameras to obtain the best images for evidentiary purposes

– Reducing the number of cameras and hence reducing the capital expenditure on surveillance systems

– Increasing the use of common platforms to build products to ensure interoperability and integration of various systems

– Network-based systems have traditionally lower operating expenditure and this will help reduce the total cost of ownership

– Reducing the operating costs for end users by investing in requisite technologies

– Developing tools to demonstrate ROI of different systems

– Educating channels and end users on the benefits and pitfalls of various systems

27

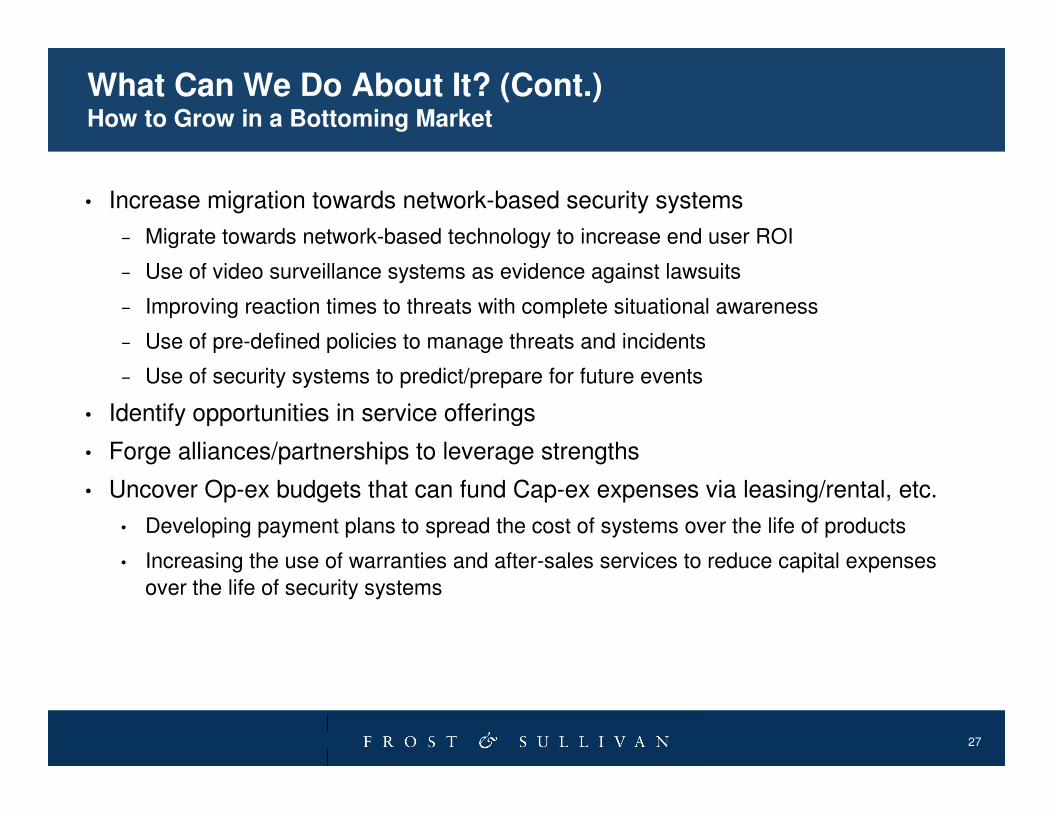

What Can We Do About It? (Cont.) How to Grow in a Bottoming Market

• Increase migration towards network-based security systems

– Migrate towards network-based technology to increase end user ROI

– Use of video surveillance systems as evidence against lawsuits

– Improving reaction times to threats with complete situational awareness

– Use of pre-defined policies to manage threats and incidents

– Use of security systems to predict/prepare for future events

• Identify opportunities in service offerings

• Forge alliances/partnerships to leverage strengths

• Uncover Op-ex budgets that can fund Cap-ex expenses via leasing/rental, etc.

• Developing payment plans to spread the cost of systems over the life of products

• Increasing the use of warranties and after-sales services to reduce capital expenses

over the life of security systems

28

1

36

9

5

8

7

4

2

Small Large

Market Size of Vertical Markets

Low(0-5%)

High(>10%)

CAGR for Vertical Markets

Medium

Medium(5-10%)

Sectors with highest total growth potential

Banking and Financial Services1

Education

2 Corrections

3

Gaming and Casinos4

5 Government

6 Healthcare

7

8

Infrastructure

9

Retail and Commercial

Event Security

Where Will The Opportunities Be?Key End-Users in the Physical Security Industry to Focus On

29

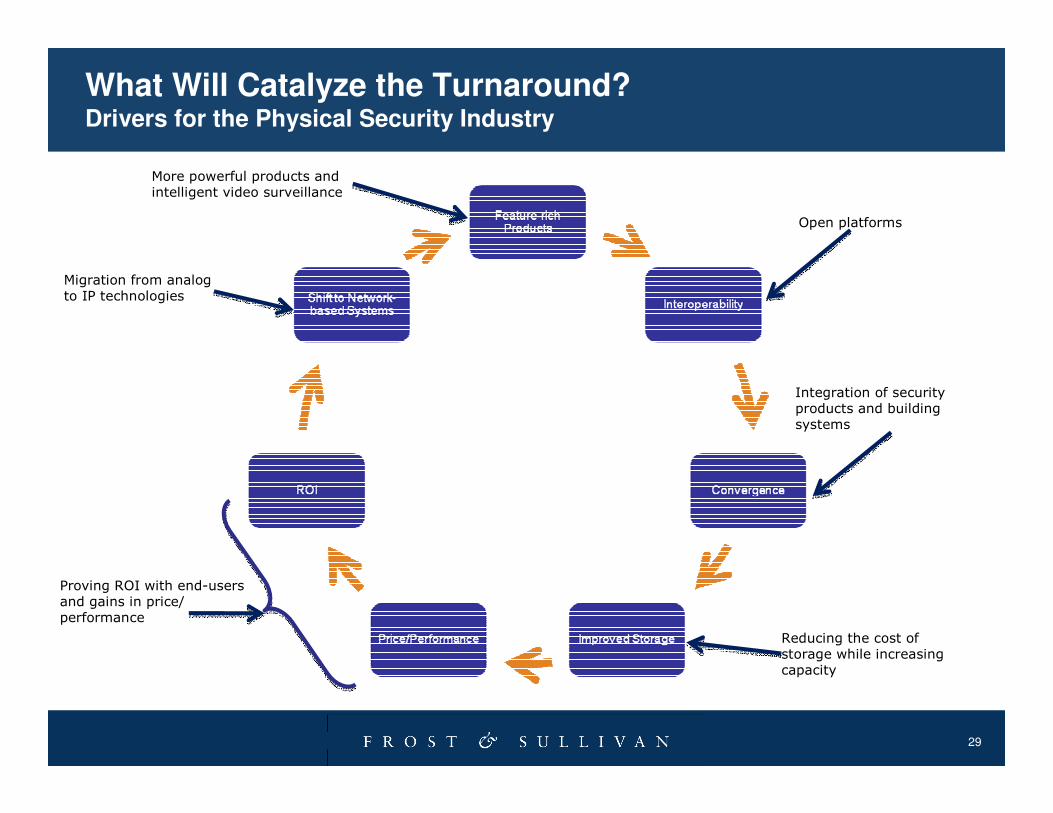

What Will Catalyze the Turnaround?Drivers for the Physical Security Industry

Migration from analog to IP technologies

More powerful products and intelligent video surveillance

Reducing the cost of storage while increasing capacity

Integration of security products and building systems

Proving ROI with end-users and gains in price/ performance

Open platforms

30

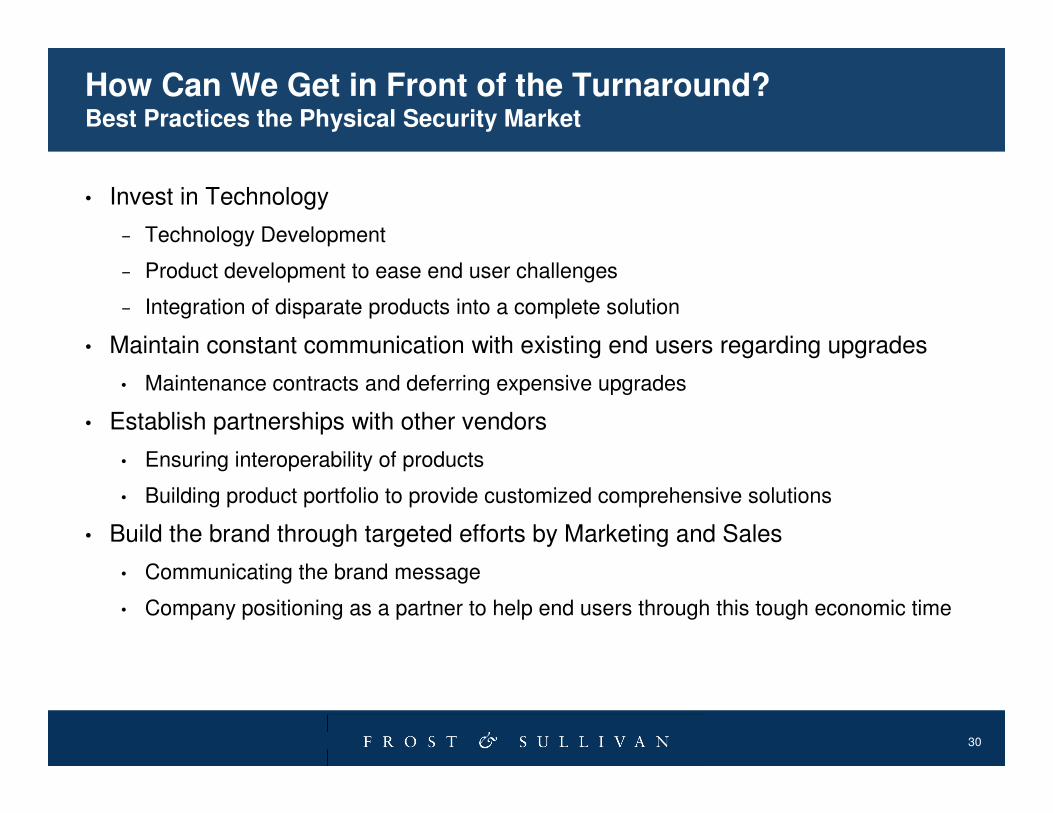

How Can We Get in Front of the Turnaround?Best Practices the Physical Security Market

• Invest in Technology

– Technology Development

– Product development to ease end user challenges

– Integration of disparate products into a complete solution

• Maintain constant communication with existing end users regarding upgrades

• Maintenance contracts and deferring expensive upgrades

• Establish partnerships with other vendors

• Ensuring interoperability of products

• Building product portfolio to provide customized comprehensive solutions

• Build the brand through targeted efforts by Marketing and Sales

• Communicating the brand message

• Company positioning as a partner to help end users through this tough economic time

31

Thank You

• Prepared by: Jafizwaty Ishahak (Research Manager, Electronics &

Security & Smart Cards, APAC)

• email ID: [email protected]