Embed Size (px)

Citation preview

Steffen RisagerChief Operating Officer

Regional Ports ConferenceCairns

THE ROLE OF TOWAGE IN PORT EFFICIENCY

2

DRAFT

Melbourne

Newcastle

Cairns

MourilyanLucinda

Bowen – Abbott Point

Brisbane

Sydney

Port Kembla

WesternportGeelong

Port Adelaide

Whyalla

Port Pirie

Ardrossan

Port Giles

Project MagnetPort Bonython

Port LincolnThevenard

Albany

Kwinana

Fremantle

Geraldton

Koolan Island

Cockatoo IslandDarwin

Darwin LNG

Eden

Bunbury

Australia

Gorgon LNG

Wheatstone

LNG

Harbour towage

Terminal towage

Aabenraa

EsbjergFredericia

Oxelosund Nynashamn

Norrkoping

Stenungsund

Brofjorden

GothenburgWalhamm

Uddevalla

CopenhagenMalmo

Sweden

Denmark

Frederikshavn

Aalborg

StigsnæsKalundborg

Avonmouth

Belfast

Felixstowe

Greenock

ImminghamLiverpool

London Medway

Port Talbot

Southampton

Tees

Tyne

Felixarc

Forth

South Hook LNGDragon LNG

SCANDINAVIAUK

SVITZER HARBOR TOWAGE… … LEADER IN EUROPE AND AUSTRALIA

3

DRAFT

EACH PORT MUST ENSUREIT’S OWN SUCCESS

• A safe and healthy workplace

in which all employees are

looking out for each other

• A working environment built

on mutual respect where

everyone understands the

challenges, contributes to the

solutions and shares in the

rewards

• A profitable and financial

sustainable business unit

3

4

DRAFT

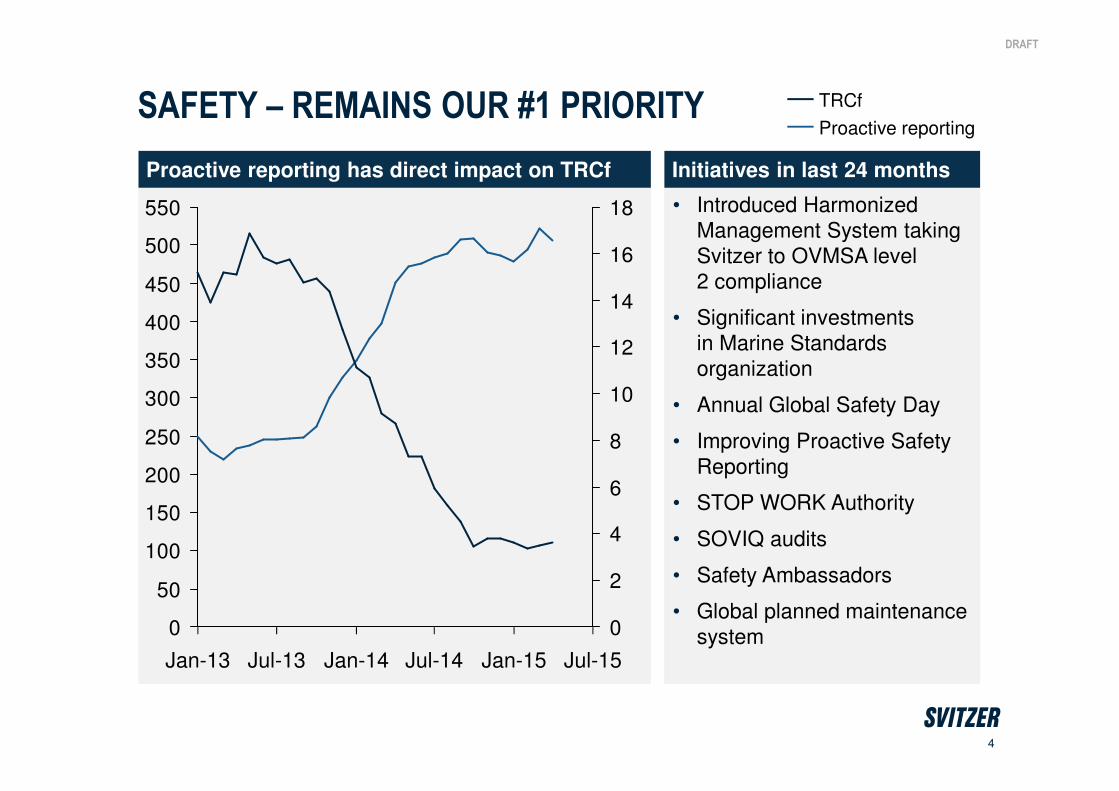

SAFETY – REMAINS OUR #1 PRIORITY

Proactive reporting has direct impact on TRCf

0

50

100

150

200

250

300

350

400

450

500

550

0

2

4

6

8

10

12

14

16

18

Jul-13 Jan-14 Jul-14Jan-13 Jul-15Jan-15

Proactive reporting

TRCf

Initiatives in last 24 months

• Introduced Harmonized

Management System taking

Svitzer to OVMSA level

2 compliance

• Significant investments

in Marine Standards

organization

• Annual Global Safety Day

• Improving Proactive Safety

Reporting

• STOP WORK Authority

• SOVIQ audits

• Safety Ambassadors

• Global planned maintenance

system

5

DRAFT

PART OF THE PORT COMMUNITY – ENGAGEMENT

Courtesy of Maersk Line

• We are partof a bigger value chain

• We are discussing optimisationswith customers and their agents

• We are similar to pilots in our optimisationchallenges and opportunities

6

DRAFT

7

DRAFT

7

8

DRAFT

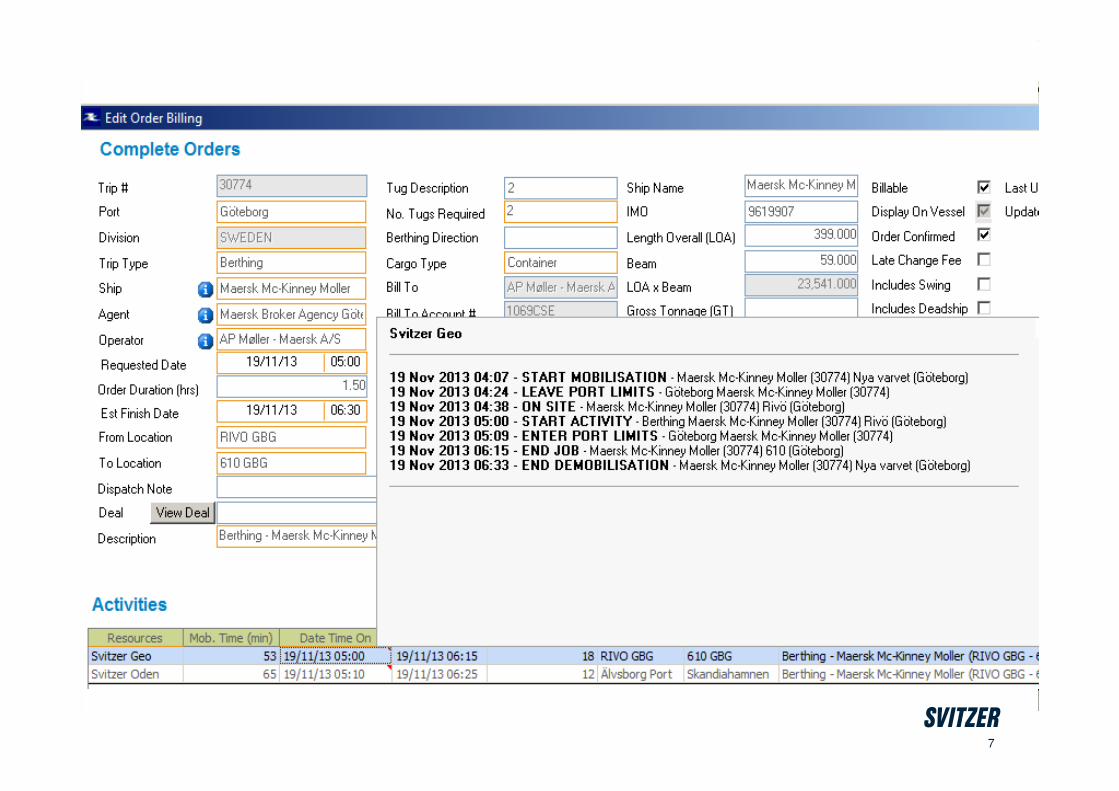

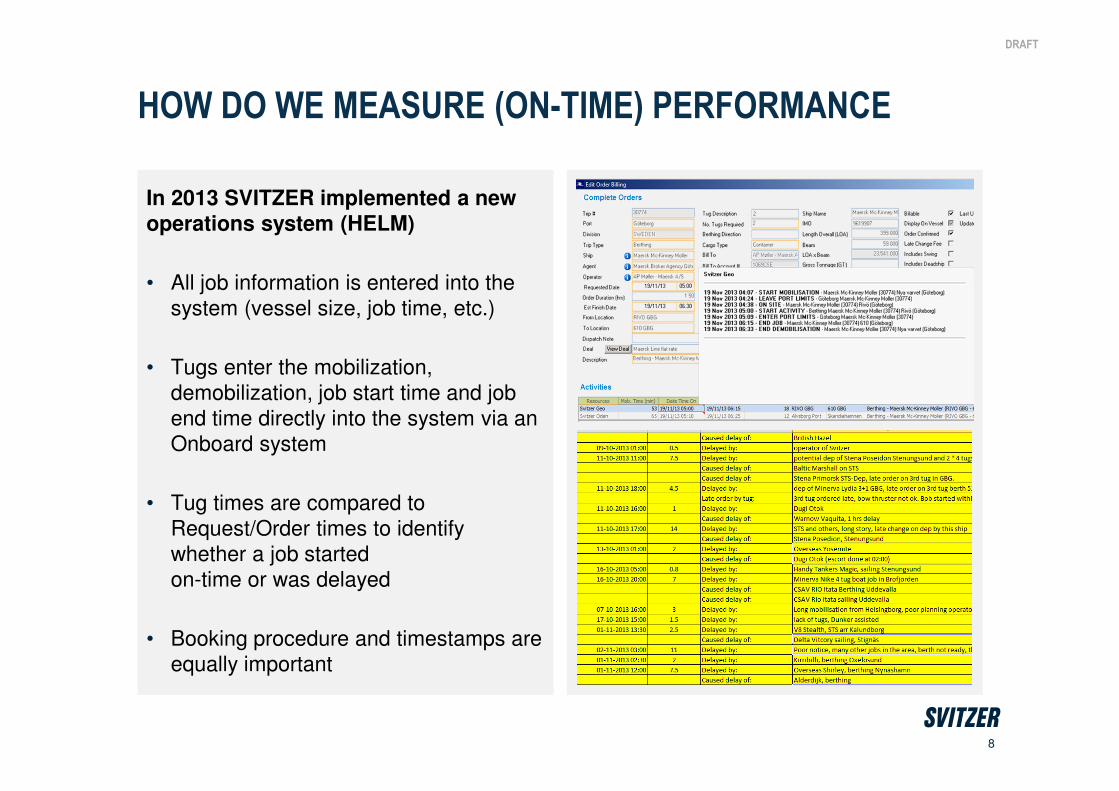

HOW DO WE MEASURE (ON-TIME) PERFORMANCE

In 2013 SVITZER implemented a new operations system (HELM)

• All job information is entered into the

system (vessel size, job time, etc.)

• Tugs enter the mobilization,

demobilization, job start time and job

end time directly into the system via an

Onboard system

• Tug times are compared to

Request/Order times to identify

whether a job started

on-time or was delayed

• Booking procedure and timestamps are

equally important

9

DRAFT

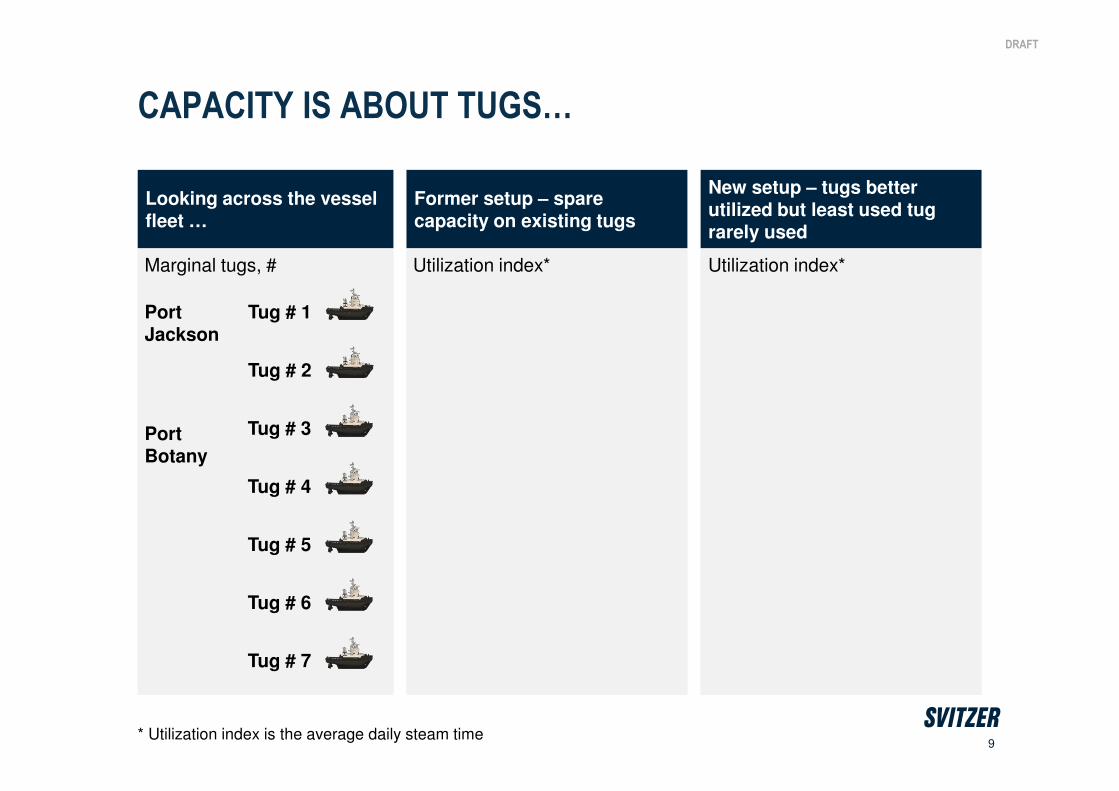

Former setup – sparecapacity on existing tugs

New setup – tugs better utilized but least used tug rarely used

CAPACITY IS ABOUT TUGS…

* Utilization index is the average daily steam time

Looking across the vessel fleet …

Marginal tugs, # Utilization index* Utilization index*

Tug # 2

Tug # 4

Tug # 5

Tug # 6

Tug # 7

Tug # 1PortJackson

Tug # 3PortBotany

10

DRAFT

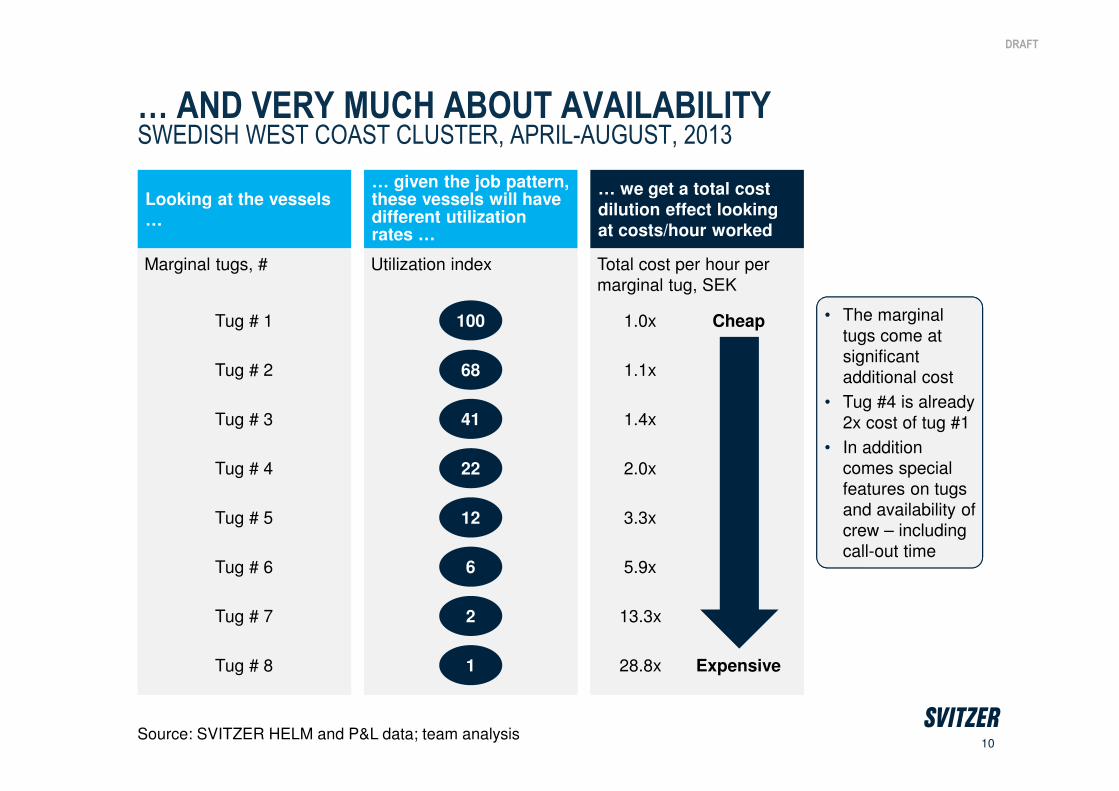

… AND VERY MUCH ABOUT AVAILABILITYSWEDISH WEST COAST CLUSTER, APRIL-AUGUST, 2013

Source: SVITZER HELM and P&L data; team analysis

• The marginal

tugs come at

significant

additional cost

• Tug #4 is already

2x cost of tug #1

• In addition

comes special

features on tugs

and availability of

crew – including

call-out time

Looking at the vessels …

… given the job pattern, these vessels will have different utilizationrates …

… we get a total cost dilution effect lookingat costs/hour worked

Marginal tugs, # Utilization index Total cost per hour per

marginal tug, SEK

100Tug # 1 Cheap1.0x

68Tug # 2 1.1x

41Tug # 3 1.4x

22Tug # 4 2.0x

12Tug # 5 3.3x

6Tug # 6 5.9x

2Tug # 7 13.3x

1Tug # 8 Expensive28.8x

11

DRAFT

TRAINING & COMPETENCY BUILDING

• SVITZER cooperates with FORCE Technology

and uses their 3600 full mission simulators in

Copenhagen, Singapore, and Brisbane

• SVITZER owns 5 mobile simulators:

– Gothenburg, Sweden

– UK (containerized)

– Dubai, UAE

– Soyo, Angola

– Miami, USA

• Trainings together with pilots and tanker

captains in specific operating conditions

• SVITZER cooperates with FORCE Technology

and uses their 3600 full mission simulators in

Copenhagen, Singapore, and Brisbane

• SVITZER owns 5 mobile simulators:

– Gothenburg, Sweden

– UK (containerized)

– Dubai, UAE

– Soyo, Angola

– Miami, USA

• Trainings together with pilots and tanker

captains in specific operating conditions

Mobile simulator in Gothenburg

International legislation requirements (IMO) STCW 2010 Flag state requirements SVITZERrequirements

International legislation requirements (IMO) STCW 2010 Flag state requirements SVITZERrequirements

Hands-on training360 deg full mission simulatorMobile simulatorsClass room trainingE-learning

Hands-on training360 deg full mission simulatorMobile simulatorsClass room trainingE-learning

CertificatesCompetenciesProficienciesSkills

CertificatesCompetenciesProficienciesSkills

12

DRAFT

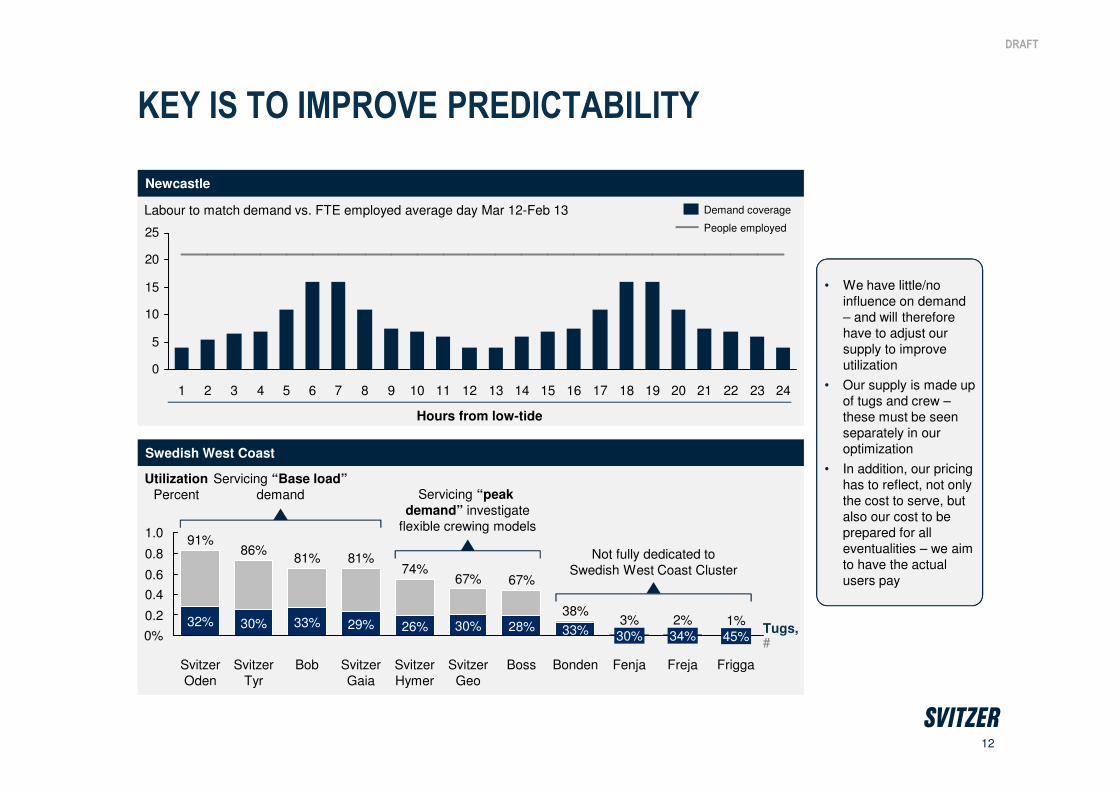

KEY IS TO IMPROVE PREDICTABILITY

• We have little/no

influence on demand

– and will therefore

have to adjust our

supply to improve

utilization

• Our supply is made up

of tugs and crew –

these must be seen

separately in our

optimization

• In addition, our pricing

has to reflect, not only

the cost to serve, but

also our cost to be

prepared for all

eventualities – we aim

to have the actual

users pay

Newcastle

Swedish West Coast

Labour to match demand vs. FTE employed average day Mar 12-Feb 13

0

5

10

15

20

25

21 22 232016 1711 2412 1815 191410 13987654321

Demand coverage

People employed

Hours from low-tide

1.0

0.8

0.6

0.2

0.4

0% 45%

Freja

2%

34%

Frigga

1%

Fenja

3%

30%

Bonden

38%

33%

Boss

28%

Svitzer

Geo

67%

30%

Svitzer

Hymer

74%

26%

Svitzer

Gaia

81%

29%

Bob

81%

33%

Svitzer

Tyr

86%

30%

Svitzer

Oden

91%

32%

67%

Utilization

Percent

Servicing “Base load”

demand Servicing “peak

demand” investigate

flexible crewing models

Not fully dedicated to

Swedish West Coast Cluster

Tugs,#

13

DRAFT

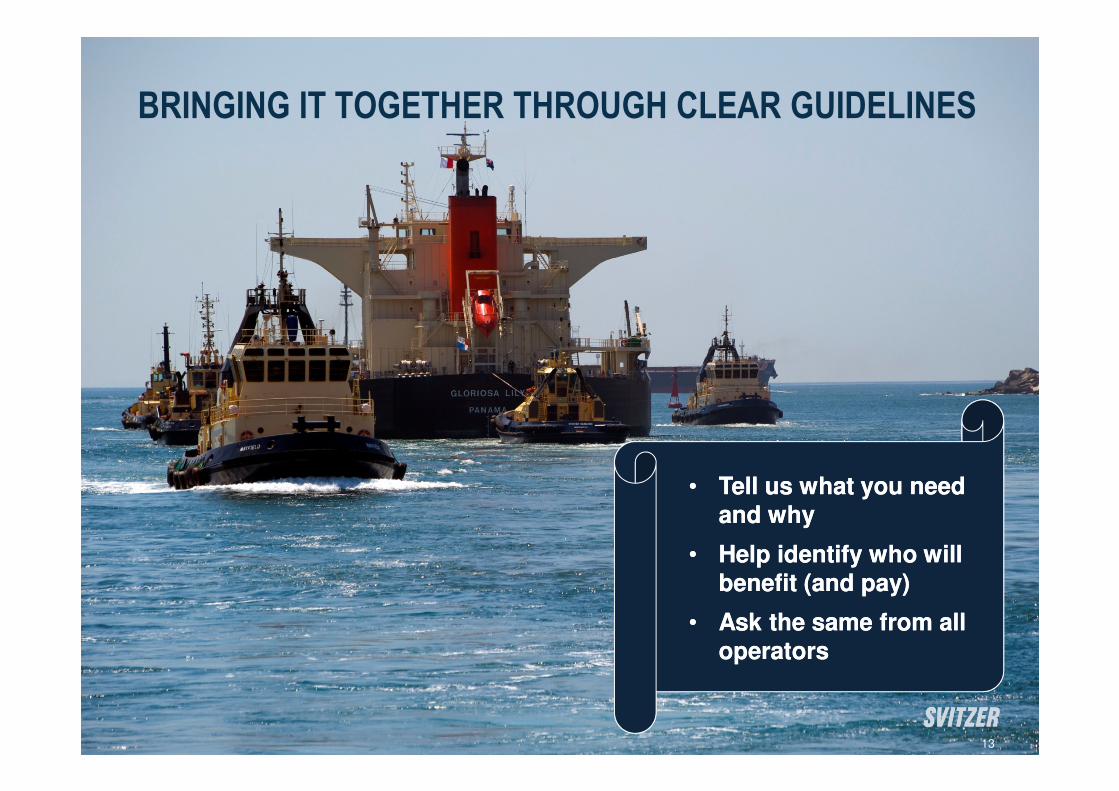

• Tell us what you need and why

• Help identify who will benefit (and pay)

• Ask the same from all operators

• Tell us what you need and why

• Help identify who will benefit (and pay)

• Ask the same from all operators

BRINGING IT TOGETHER THROUGH CLEAR GUIDELINES

13

14

DRAFT

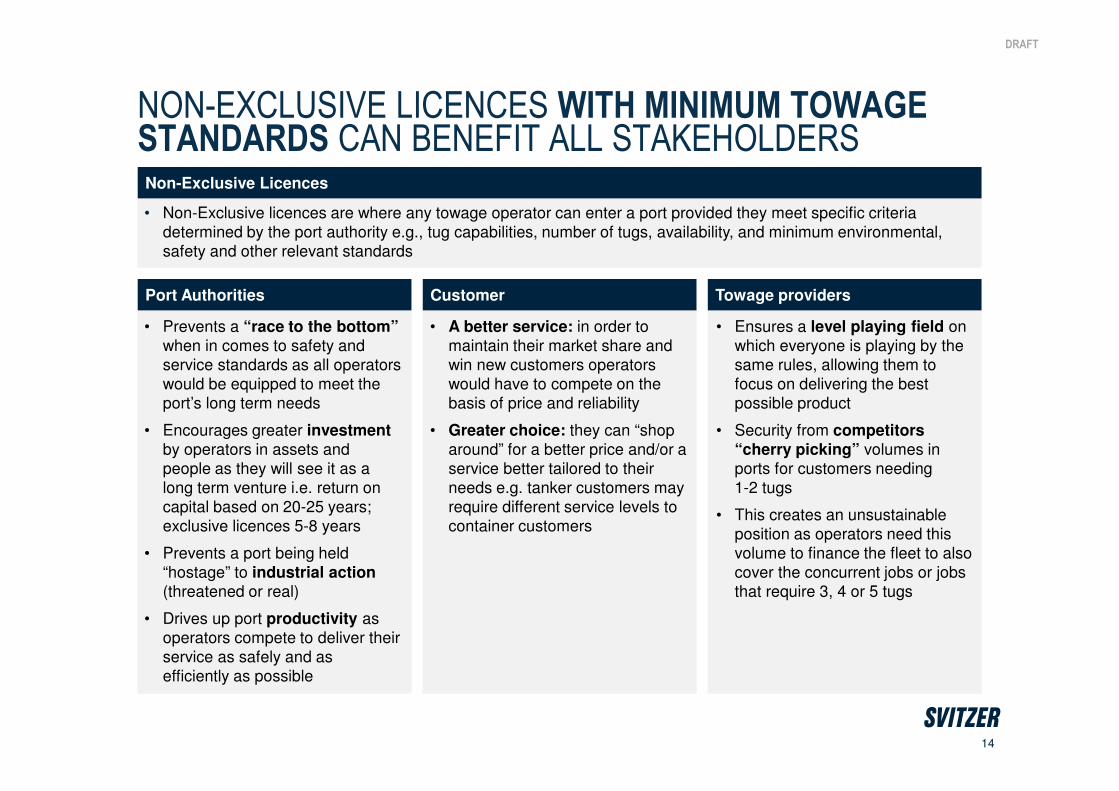

NON-EXCLUSIVE LICENCES WITH MINIMUM TOWAGE STANDARDS CAN BENEFIT ALL STAKEHOLDERSNon-Exclusive Licences

• Non-Exclusive licences are where any towage operator can enter a port provided they meet specific criteria

determined by the port authority e.g., tug capabilities, number of tugs, availability, and minimum environmental,

safety and other relevant standards

Port Authorities Customer Towage providers

• Prevents a “race to the bottom” when in comes to safety and

service standards as all operators

would be equipped to meet the

port’s long term needs

• Encourages greater investmentby operators in assets and

people as they will see it as a

long term venture i.e. return on

capital based on 20-25 years;

exclusive licences 5-8 years

• Prevents a port being held

“hostage” to industrial action (threatened or real)

• Drives up port productivity as

operators compete to deliver their

service as safely and as

efficiently as possible

• A better service: in order to

maintain their market share and

win new customers operators

would have to compete on the

basis of price and reliability

• Greater choice: they can “shop

around” for a better price and/or a

service better tailored to their

needs e.g. tanker customers may

require different service levels to

container customers

• Ensures a level playing field on

which everyone is playing by the

same rules, allowing them to

focus on delivering the best

possible product

• Security from competitors “cherry picking” volumes in

ports for customers needing

1-2 tugs

• This creates an unsustainable

position as operators need this

volume to finance the fleet to also

cover the concurrent jobs or jobs

that require 3, 4 or 5 tugs

15

DRAFT

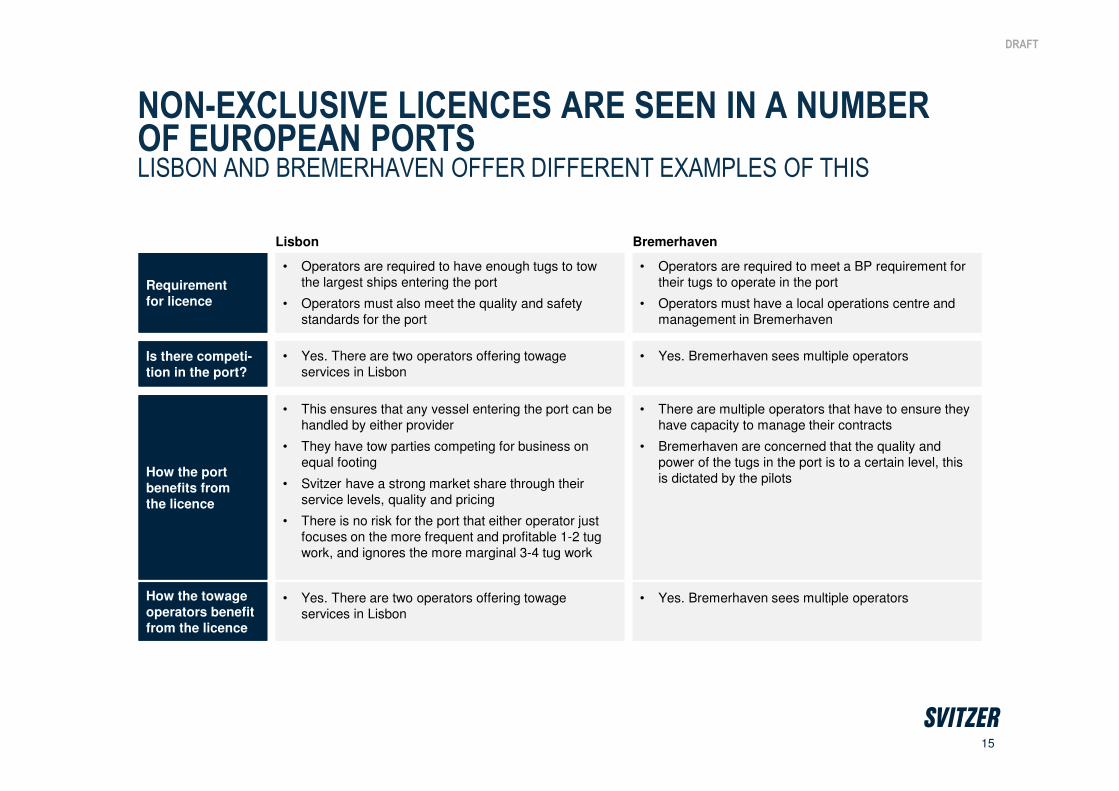

NON-EXCLUSIVE LICENCES ARE SEEN IN A NUMBEROF EUROPEAN PORTSLISBON AND BREMERHAVEN OFFER DIFFERENT EXAMPLES OF THIS

Requirement

for licence

Requirement

for licence

Bremerhaven

• Operators are required to meet a BP requirement for

their tugs to operate in the port

• Operators must have a local operations centre and

management in Bremerhaven

• Operators are required to have enough tugs to tow

the largest ships entering the port

• Operators must also meet the quality and safety

standards for the port

Lisbon

Is there competi-

tion in the port?

Is there competi-

tion in the port?

• Yes. Bremerhaven sees multiple operators• Yes. There are two operators offering towage

services in Lisbon

How the port

benefits from

the licence

How the port

benefits from

the licence

• This ensures that any vessel entering the port can be

handled by either provider

• They have tow parties competing for business on

equal footing

• Svitzer have a strong market share through their

service levels, quality and pricing

• There is no risk for the port that either operator just

focuses on the more frequent and profitable 1-2 tug

work, and ignores the more marginal 3-4 tug work

• There are multiple operators that have to ensure they

have capacity to manage their contracts

• Bremerhaven are concerned that the quality and

power of the tugs in the port is to a certain level, this

is dictated by the pilots

How the towage

operators benefit

from the licence

How the towage

operators benefit

from the licence

• Yes. Bremerhaven sees multiple operators• Yes. There are two operators offering towage

services in Lisbon

16

DRAFT

EFFICIENCIES BY GROUPING PORTS – SCANDINAVIA EXAMPLE

Aabenraa

Esbjerg

Fredericia

OxelosundNynashamn

NorrkopingStenungsundBrofjorden

Gothenburg

Walhamn

Uddevalla

Copenhagen

Malmo

Sweden

Denmark

Frederikshavn

Aalborg

Stigsnæs

Kalundborg

• Serving 20+ ports with 25 tugs, with

majority of ports requiring multiple tugs on

any one job

• Sub-clusters of tugs within the cluster

serving ”base load” with frequent sharing of

tugs within the cluster to service ”peak

demand”

• Service level commitment with

Gothenburg, Brofjorden and Fredericia

ports to be available within 20 minutes

• Benefits for ports: Few of the ports have

the towage volumes to sustain the required

number of tugs for peak volumes at an

acceptable price level, as such the ”sharing

of tugs” between ports enhances the ports

competetiveness in regards to cost as well

as service level

• Benefits for Svitzer: Keeping vessel

investments and vessel costs at a

minimum with a streamlined fleet of tugs

and through improved utilizations also

lowering crew costs per tug job.

Lindö

Aarhus

Helsingborg

3 TUGS

8 TUGS

3 TUGS

9 TUGS

2 TUGS

17

DRAFT

THANK YOU

17