Embed Size (px)

DESCRIPTION

The Saturday Economist, UK Economics news and market updates from the best UK Economics blogs

Citation preview

The Saturday Economist johnashcroft.co.uk

Saturday, 8 September 2012Draghi saves the euro and the worldOTHER NEWSManufacturingJuly output bounces back in the month but 0.5% down in 2011. --------------------------------Producer PricesOutput prices rise by 2.2% as input costs increase 1.4%. ------------------------------Money SupplyNarrow money, notes and coins increase by 5.1% August --------------------------------- Base RatesMPC votes to keep base rates on hold, no more QE for now. -----------------------------Base RatesWhy the next move will be up and much sooner than expected

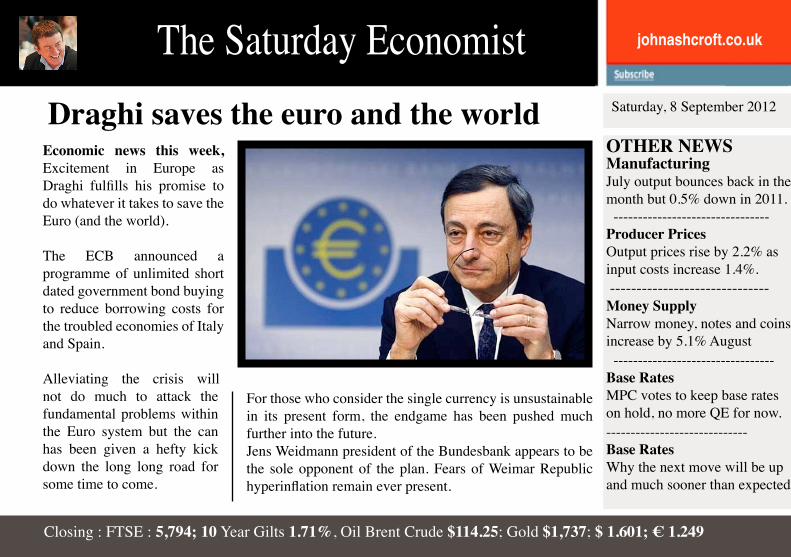

Economic news this week, Excitement in Europe as Draghi fulfills his promise to do whatever it takes to save the Euro (and the world).

The ECB announced a programme of unlimited short dated government bond buying to reduce borrowing costs for the troubled economies of Italy and Spain.

Alleviating the crisis will not do much to attack the fundamental problems within the Euro system but the can has been given a hefty kick down the long long road for some time to come.

Closing : FTSE : 5,794; 10 Year Gilts 1.71%, Oil Brent Crude $114.25; Gold $1,737; $ 1.601; € 1.249

For those who consider the single currency is unsustainable in its present form, the endgame has been pushed much further into the future.Jens Weidmann president of the Bundesbank appears to be the sole opponent of the plan. Fears of Weimar Republic hyperinflation remain ever present.

The Saturday Economist johnashcroft.co.uk

Saturday, 8 September 2012ECB moves to mop up Euro bondsThe ECB made the critical move to save the Euro and mop up the bonds on the olive branch of the Southern states.

Draghi fulfilled his promise to do whatever it takes to save the Euro (and the world). The ECB announced a programme of unlimited short dated government bond buying to reduce borrowing costs for the troubled economies of Italy, Spain and Greece.

Alleviating the short term crisis will not do much to attack the fundamental

problems within the Euro system but the can has been given a hefty kick down the long long road.

For those who consider the single currency is unsustainable in its present form, the endgame has been pushed much further into the future.

Jens Weidmann president of the Bundesbank appears to be the sole critic of the plan.

Fears of Weimar Republic hyperinflation remain ever present. The Germans begin large scale production of the wheelbarrow industry. Perhaps this accounts for the 1.3% increase in German manufacturing output in July!

The Saturday Economist johnashcroft.co.uk

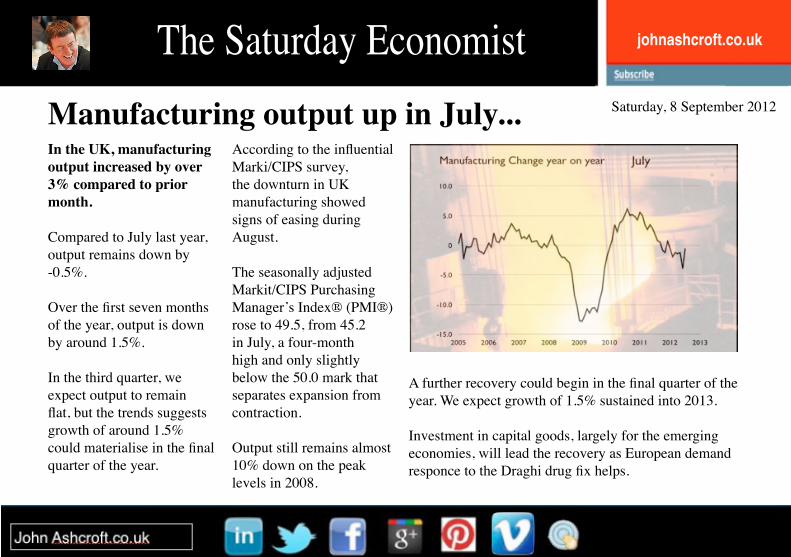

Saturday, 8 September 2012Manufacturing output up in July...In the UK, manufacturing output increased by over 3% compared to prior month.

Compared to July last year, output remains down by -0.5%.

Over the first seven months of the year, output is down by around 1.5%.

In the third quarter, we expect output to remain flat, but the trends suggests growth of around 1.5% could materialise in the final quarter of the year.

According to the influential Marki/CIPS survey, the downturn in UK manufacturing showed signs of easing during August.

The seasonally adjusted Markit/CIPS Purchasing Manager’s Index® (PMI®) rose to 49.5, from 45.2 in July, a four-month high and only slightly below the 50.0 mark that separates expansion from contraction.

Output still remains almost 10% down on the peak levels in 2008.

A further recovery could begin in the final quarter of the year. We expect growth of 1.5% sustained into 2013.

Investment in capital goods, largely for the emerging economies, will lead the recovery as European demand responce to the Draghi drug fix helps.

The Saturday Economist johnashcroft.co.uk

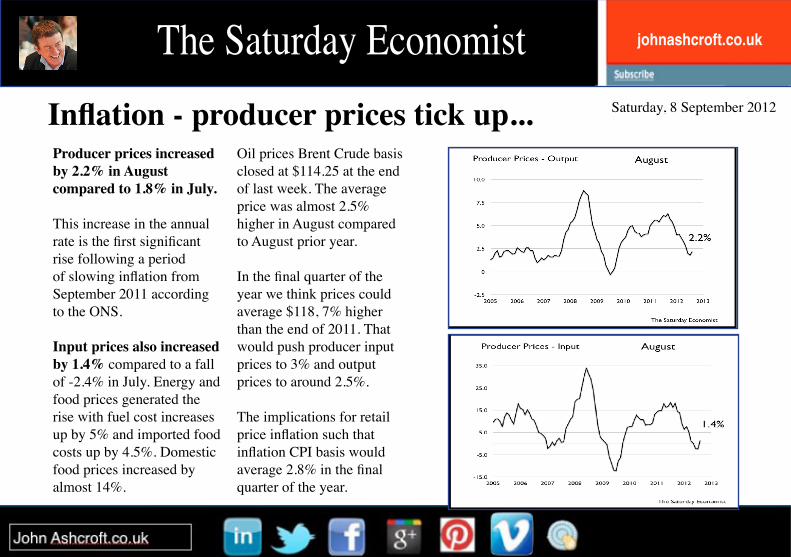

Saturday, 8 September 2012Inflation - producer prices tick up...Producer prices increased by 2.2% in August compared to 1.8% in July.

This increase in the annual rate is the first significant rise following a period of slowing inflation from September 2011 according to the ONS.

Input prices also increased by 1.4% compared to a fall of -2.4% in July. Energy and food prices generated the rise with fuel cost increases up by 5% and imported food costs up by 4.5%. Domestic food prices increased by almost 14%.

Oil prices Brent Crude basis closed at $114.25 at the end of last week. The average price was almost 2.5% higher in August compared to August prior year.

In the final quarter of the year we think prices could average $118, 7% higher than the end of 2011. That would push producer input prices to 3% and output prices to around 2.5%.

The implications for retail price inflation such that inflation CPI basis would average 2.8% in the final quarter of the year.

The Saturday Economist johnashcroft.co.uk

Saturday, 8 September 2012Interest rates kept on hold at 0.5%Thursday the Bank of England MPC voted to keep rates on hold and to contain the level of Asset Purchases at £375 billion.

No real surprise despite some calls for a cut in base rates of a further 25 basis points.

Ten year gilt yields languish at 1.7%, the buy order for APF is still not complete, the option for a cut in rates and further gilt purchases is limited.

The next rate move will be up and much sooner than is expected.

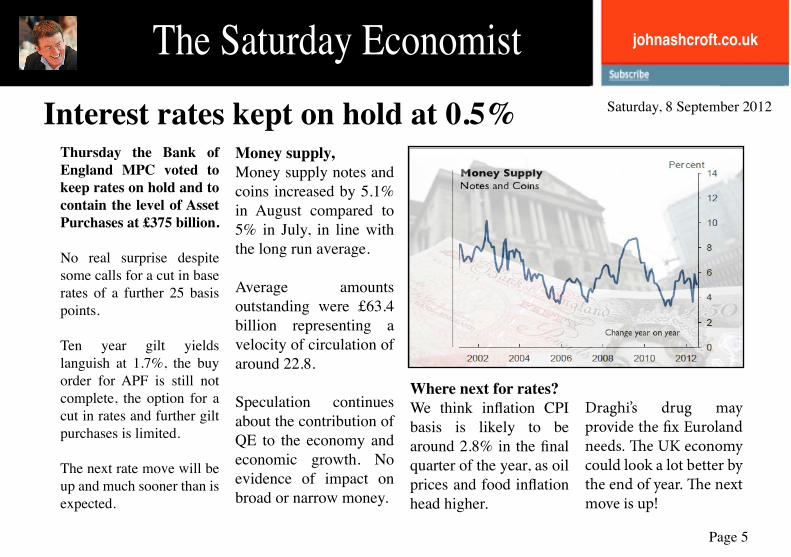

Money supply, Money supply notes and coins increased by 5.1% in August compared to 5% in July, in line with the long run average.

Average amounts outstanding were £63.4 billion representing a velocity of circulation of around 22.8.

Speculation continues about the contribution of QE to the economy and economic growth. No evidence of impact on broad or narrow money.

Where next for rates?We think inflation CPI basis is likely to be around 2.8% in the final quarter of the year, as oil prices and food inflation head higher.

Draghi’s drug may provide the fix Euroland needs. The UK economy could look a lot better by the end of year. The next move is up!

Page 5

Saturday, 8 September 2012What happened in the world this week

Draghi’s drugBond yields rallied as the ECB announced the bond purchase plan for Spain and Italian debt.

Outright monetary transactions could be “on my tab” the fear of Jens Weidmann, the president of the Bundesbank. The plan will be implemented despite German fears.

German output ralliesGerman manufacturing output rallied in July as output leapt by 1.3%.

The ECB move is significant in calling an end to the calls for the end of the Euro.

Confidence and growth should follow ECB move.

China - manufacturing In August, China’s manufacturing purchasing managers index (PMI) was 49.2 percent, down by 0.9 percentage points month-on-month.

In the first quarter of the year, the index averaged 51.5 - manufacturing output is contracting slightly.

Spanish boos The Chancellor was booed when presenting medals at the paralympics this week. There has been endless speculation as to why 80,000 booed.

That was the capacity of the stadium, the explanation.

Yeah that and economic policy perhaps.

The Saturday Economist johnashcroft.co.uk

Page 6

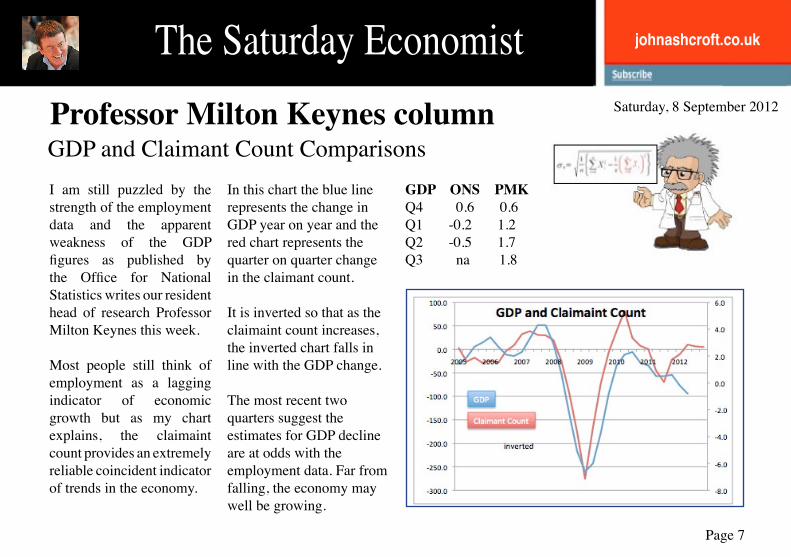

Saturday, 8 September 2012Professor Milton Keynes column

I am still puzzled by the strength of the employment data and the apparent weakness of the GDP figures as published by the Office for National Statistics writes our resident head of research Professor Milton Keynes this week.

Most people still think of employment as a lagging indicator of economic growth but as my chart explains, the claimaint count provides an extremely reliable coincident indicator of trends in the economy.

In this chart the blue line represents the change in GDP year on year and the red chart represents the quarter on quarter change in the claimant count.

It is inverted so that as the claimaint count increases, the inverted chart falls in line with the GDP change.

The most recent two quarters suggest the estimates for GDP decline are at odds with the employment data. Far from falling, the economy may well be growing.

GDP ONS PMKQ4 0.6 0.6 Q1 -0.2 1.2Q2 -0.5 1.7Q3 na 1.8

The Saturday Economist johnashcroft.co.uk

Page 7

GDP and Claimant Count Comparisons

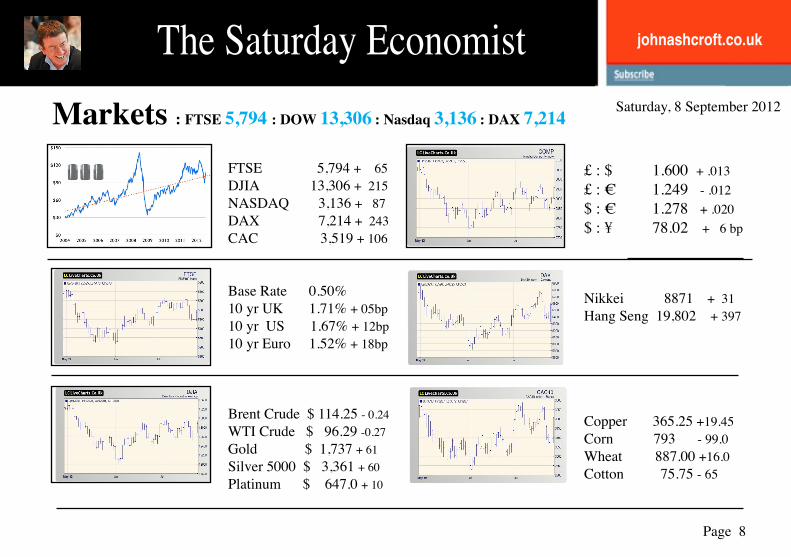

Saturday, 8 September 2012Markets : FTSE 5,794 : DOW 13,306 : Nasdaq 3,136 : DAX 7,214

The Saturday Economist johnashcroft.co.uk

FTSE 5,794 + 65DJIA 13,306 + 215NASDAQ 3,136 + 87 DAX 7,214 + 243CAC 3,519 + 106

Base Rate 0.50%10 yr UK 1.71% + 05bp10 yr US 1.67% + 12bp10 yr Euro 1.52% + 18bp

Brent Crude $ 114.25 - 0.24WTI Crude $ 96.29 -0.27Gold $ 1,737 + 61Silver 5000 $ 3,361 + 60 Platinum $ 647.0 + 10

£ : $ 1.600 + .013 £ : € 1.249 - .012$ : € 1.278 + .020 $ : ¥ 78.02 + 6 bp

Nikkei 8871 + 31Hang Seng 19,802 + 397

Copper 365.25 +19.45Corn 793 - 99.0Wheat 887.00 +16.0Cotton 75.75 - 65

Page 8

The Saturday Economist johnashcroft.co.uk

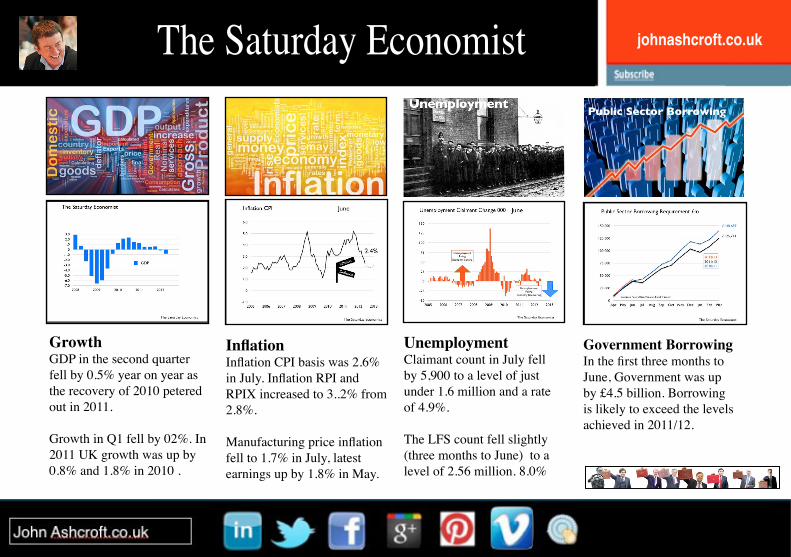

GrowthGDP in the second quarter fell by 0.5% year on year as the recovery of 2010 petered out in 2011.

Growth in Q1 fell by 02%. In 2011 UK growth was up by 0.8% and 1.8% in 2010 .

UnemploymentClaimant count in July fell by 5,900 to a level of just under 1.6 million and a rate of 4.9%.

The LFS count fell slightly (three months to June) to a level of 2.56 million. 8.0%

Government BorrowingIn the first three months to June, Government was up by £4.5 billion. Borrowing is likely to exceed the levels achieved in 2011/12.

Inflation Inflation CPI basis was 2.6% in July. Inflation RPI and RPIX increased to 3..2% from 2.8%.

Manufacturing price inflation fell to 1.7% in July, latest earnings up by 1.8% in May.

The Saturday Economist johnashcroft.co.uk

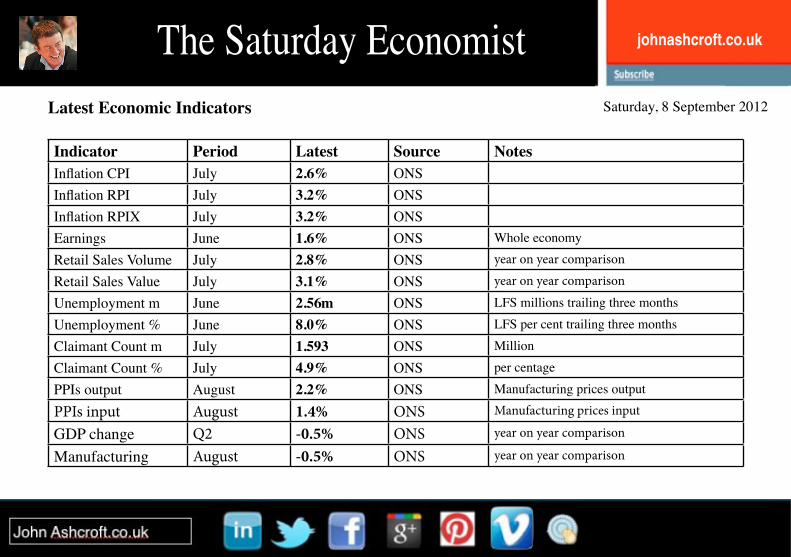

Latest Economic Indicators Saturday, 8 September 2012

Indicator Period Latest Source NotesInflation CPI July 2.6% ONSInflation RPI July 3.2% ONSInflation RPIX July 3.2% ONSEarnings June 1.6% ONS Whole economy

Retail Sales Volume July 2.8% ONS year on year comparison

Retail Sales Value July 3.1% ONS year on year comparison

Unemployment m June 2.56m ONS LFS millions trailing three months

Unemployment % June 8.0% ONS LFS per cent trailing three months

Claimant Count m July 1.593 ONS Million

Claimant Count % July 4.9% ONS per centage

PPIs output August 2.2% ONS Manufacturing prices output

PPIs input August 1.4% ONS Manufacturing prices input

GDP change Q2 -0.5% ONS year on year comparison

Manufacturing August -0.5% ONS year on year comparison

The Saturday Economist johnashcroft.co.uk

The Saturday Economist is a round up of the week’s economics news for the UK published on the web site johnashcroft.co.uk.

The information is also available as a PDF download.

The information was originally published in short form in the Sunday Times and Croissants weekly blog post and has been expanded following requests for more information.

The material in the Saturday Economist is based upon information which we consider to be reliable but we do not represent that it is accurate or complete and it should not be relied upon as such. We accept no liability for errors, or omissions of opinion or fact.

In particular, no reliance should be placed on the comments or trends in financial markets.

The publication of this document should not be construed as the giving of investment advice.

Forecasting is subject to frequent revision Please remember we are forecasting the output of the Office for National Statistics which may, of itself, be subject to revision.

All views expressed in the Saturday Economist are my own. Information is intended to provide a general outline of the subjects covered. It should neither be regarded as comprehensive nor sufficient for making decisions, nor should it be used in place of professional advice.

Neither the Saturday Economist or any representative accept any responsibility for any loss arising from any action taken or not taken by anyone using this material.

John K AshcroftData adapted from the Office for National Statistics licensed under Open Government Licence .v.1.0.

The Saturday Economist johnashcroft.co.uk