Embed Size (px)

Citation preview

The Saturday Economist - we always keep you in the picture …

On Brexit …

?

April 2016 …

The Saturday Economist - we always keep you in the picture …

The Saturday Economist on Brexit

At the Saturday Economist we always like to keep you in the picture. In this April report, we endeavour to deliver an objective and dispassionate analysis of the pros and cons of Brexit.

We provide the facts and information to assist the decision making process for all our readers. No polemics just the facts.

We assess the implications of leaving the EU and outline the alternative relationships that could ensue - the Danish model, the Swiss Model, the Icelandic model and the Turkish option.

In addition we will consider the impact on UK growth, investment, trade, Sterling, immigration, sovereignty and security of the in-out decision. Don’t miss this important update … all the information you need to make an informed decision.

The Saturday Economist - we always keep you in the picture …

On Brexit … The Spectrum of Issues …

?Business Economic

Social PoliticalImmigration NHS

We think it is important to differentiate the main issues into business, economic, political and social …

Trade Investment Uncertainty

Sovereignty … Who governs Britain …

Growth Jobs Inflation Trade

Deficits Current Account Borrowing Sterling

The Saturday Economist … we always keep you in the picture.

12th March 2016Who governs Britain …

Avoiding jingoism and post imperial calls to action …

The Saturday Economist - we always keep you in the picture …

The Key Question …

?

Should the UK remain a member of the EU or leave the EU …

Should the UK remain a member of the EU or leave the EU …

The Key Question …

The polls suggest the outcome will be pretty close on the 23rd June ….

The Saturday Economist - we always keep you in the picture …

Should the UK remain a member of the EU or leave the EU …

The Key Question …

The FT poll is rather more supportive of the “Remain” case …

The Saturday Economist - we always keep you in the picture …

The Key Question …It is not, or should not be a choice between Europe and the Rest of the World …. we need to trade with both …

The Saturday Economist - we always keep you in the picture …

The Saturday Economist - we always keep you in the picture …

Geographically we are part of Europe like it or not … “Gravitational pull” has a significant impact on trade flows …

Eurozone

The Saturday Economist … we always keep you in the picture.

The EU is not a “basket case”

Eurozone Q4 2015 Latest Data GDP 1.5%

Growth Rate

20151.6%2016

2013Q1

2013Q2

2013Q3

2013Q4

2014Q1

2014Q2

2014Q3

2014Q4

2015Q1

2015Q2

2015Q3

2015Q4

-0.1 1.3 -0.3 0.5 0.2 0.4 0.8 0.9 1.0 1.4 1.7 1.97

Our Forecasts - Euro GDP Growth this year

2014 0.9%

2015

1.5% … and by quarter %

Growth Rate

Data

-2.0

-1.0

0.0

1.0

2.0

3.0

2010 2011 2012 2013 2014 2015 2016 2017

1.71.61.50.9

-0.4-0.6

1.61.9

Euro GDP Eurozone GDP Change year on year … Eurozone Inflation …

Date of Next Update :

-2.0

-1.0

0.0

1.0

2.0

3.0

2010 2011 2012 2013 2014 2015 2016 2017

1.2

0.50.00.4

1.3

2.52.7

1.6

Euro Inflation

Release Date14th August

A slow recovery is taking place. Growth in Ireland was 7.5% and in Spain it was 4.5% in 2015 …

The Saturday Economist - we always keep you in the picture …

On monetary policy …Mario Draghi is set to do whatever it takes …

The Saturday Economist - we always keep you in the picture …

How difficult is it to leave …

?

So how difficult is it to leave?…

The Saturday Economist - we always keep you in the picture …

Article 50

Simple really, we invoke Article 50 … An Article with 5 clauses and about 270 words …

The Saturday Economist - we always keep you in the picture …

How long will it take …

?

How long will it take to exit?We have no idea. it has never been done before. Exit could take up to two years to organise but it could take even longer. Then we still have to negotiate a new trade deal …

How long will a trade deal take?That could take a further five to ten years at least …

Canada and the EU “CETA” The Trade deal with Canada and the EU has taken almost ten years to negotiate … it could take a similar period to determine the UK : EU deal …

USA and the EU “TTIP”The Trade deal with USA and the EU is an ongoing negotiation which began in 2013 … there is no guarantee of the US commitment to a Free Trade Deal on the scale envisaged by the EU …

USA and the UK …There is no reason why the UK would be able to jump the UK in bilateral talks prior to a satisfactory out turn for a “TTIP” deal …

Trans Pacific Partnership…The Trans-Pacific Partnership (TPP) is a trade agreement among twelve Pacific Rim countries signed on 4 February 2016 in Auckland, New Zealand, after seven years of negotiations.

Historically, the TPP is an expansion of the Trans-Pacific Strategic Economic Partnership Agreement (TPSEP or P4), which was signed by Brunei, Chile, New Zealand, and Singapore in 2005

Ten Years

Ten Years

Ten Years?

The Saturday Economist - we always keep you in the picture …

How long will it take … The “Leave” deal is an impossible ask!

?

Basis of ”Leave Camp” Deal ..The Leave Camp appear to want …Free trade in goods …Free trade in Services …Free movement of Capital …Free from payments into the EU …Free from commitment to Free movement of Labour … Free from product and labour regulation …

That could take forever … And an impossible “give”

The Saturday Economist - we always keep you in the picture …

And what of free trade deals with the rest of the world …

?

Iceland and China Iceland negotiated a Free Trade deal with China. It took six years for trade flows valued at $180 million largely confined to fish, Ice and Igloos.

Even then there were restrictions on paper products to China and food products into Iceland …

Six Years

The Saturday Economist - we always keep you in the picture …

Be careful what you wish for … the deficits could just get worse

?

UK and China …The UK trade deficit with China was £25 billion in 2015. The UK exported £13 billion worth of goods into China …

China exported £38 billion of goods into the UK even with EU tariffs in place …

The deficit could just get worse …

UK and Norway …The UK trade deficit with Norway was £10 billion in 2015. The UK exported £3 billion worth of goods into Norway in 2015.

Norway exported £13 billion of goods into the UK even with EU restrictions in place …

The deficit could just get worse …

UK and Canada …The UK trade deficit with Canada was £3 billion in 2015. The UK exported £4 billion worth of goods into Norway in 2015.

Canada exported £7 billion of goods into the UK even with EU restrictions in place …

The deficit could just get worse …

UK and Japan …The UK trade deficit with Japan was over £2 billion in 2015. The UK exported £5 billion worth of goods into Japan in 2015.

Japan exported £7 billion of goods into the UK even with EU restrictions in place …

The deficit could just get worse …

ChinaTrade deficit£25 billion

NorwayTrade deficit£10 billion Canada

Trade deficit£ 4 billion

JapanTrade deficit£ 2 billion

The Saturday Economist - we always keep you in the picture …

How important is the EU to the UK and vice versa …

?

Comparative Sizes

Size of economies (GDP, $bn)

The EU is the largest trading block in the world … excluding the UK it would be the second largest trading block in the world after the USA ….

The Saturday Economist - we always keep you in the picture …

Comparative Sizes

Size of economies (GDP, $bn)

3,860

2,836

German

y

Fran

ce

4,616

Japa

n

2,597

The UK is the fifth (or sixth) largest economy in the world … after USA. China, Germany, Japan and possibly France …

The Saturday Economist - we always keep you in the picture …

0%

10%

20%

30%

40%

2010 2011 2012 2013 2014 2015 2016 2017 2018 2019 2020 2021 2022 2023 2024 2025 2030

North America

Asean

China

Japan

Europe

Share of World GDP

It is true to say, Europe’s share of world GDP is declining as the ASEAN block expands …

The Saturday Economist - we always keep you in the picture …

China China will dominate the world growth story in the years ahead …

It is the second largest economy in the world …

With a population of 1.3 billion …

China struggles to enter the world top eighty in terms of GDP per capital …

The Saturday Economist - we always keep you in the picture …

The Saturday Economist - we always keep you in the picture

6th February 2016

China

Return of the Middle Kingdom …We talk of the return of the Middle Kingdom …

China - Return of the Middle Kingdom

0.0%

10.0%

20.0%

30.0%

40.0%

1000 1500 1600 1700 1820 1870 1913 1950 1973 2003 2014

22%

25%

29%

22%

33%

17%

9%

5% 5%

15%13%

22%24%

29%

23%

37%

28%

24%

22% 23%21%

18%

Share Share of World Population

Share of World GDP

Data : Maddison A. Contours of the World Economy 1 - 2030 AD OUP

In the 17th century and in the early 19th century … China was the largest economy in the world …

The Saturday Economist - we always keep you in the picture …

The Saturday Economist - we always keep you in the picture

6th February 2016

The importance of being ASEAN …The ASEAN trade block is of critical importance to China …

The Saturday Economist - we always keep you in the picture

6th February 2016

China

Return of the Middle Kingdom …Collect ive ly the ASEAN block accounts for 50% of world population and 30% of World GDP …

Growing at 4.5% per annum …

The Saturday Economist - we always keep you in the picture

6th February 2016

China

Return of the Middle Kingdom …

The UK is not guaranteed a trade slot in the ASEAN trade group …

The ASEAN block accounts for just 16% of UK exports …

The Saturday Economist - we always keep you in the picture …

How important is the EU to the UK and vice versa …

?

Share of EU Exports

Others 38%

4%6% 5%3%2%3%

China 8%

USA 15%

UK 16%

UK USA China Japan Korea NorwayRussia Switzerland Turkey Others

The Saturday Economist - we always keep you in the picture …

The UK accounts for 16% of EU exports …

Share of UK Exports

3%2%5%7%

ASEAN 16%

North America 20%

EU 47%

EU North America ASEAN MENAOther Europe South America Other nc

The Saturday Economist - we always keep you in the picture …

The EU accounts for 47% of UK exports …

A wider Europe accounts for 52% of UK exports …Europe

52%

Trade Data 2015

£ billion UK to EU % GDP EU to UK % GDP Deficit /Surplus

ExportsGoods £134.4 7.2% £223.4 1.6% -£89.0

ExportsServices £85.7 4.6% £65.7 0.4% + £20.0

ExportsTotal £220.1 11.8% £289.1 2.0% -£69.0

Trade Data : ONS 2015

The Saturday Economist - we always keep you in the picture …

EU trade with UK accounts for 2% of

EU GDP …UK trade with EU accounts for 12% of

UK GDP …

Share of UK Exports

North America

Europe

The Saturday Economist - we always keep you in the picture …

It is true to say, the EU share of UK exports is falling …

Share of Trade

30%

40%

50%

60%

70%

2000 2002 2004 2006 2008 2010 2012 2014 2016 2018 2020

UK Share of Trade with EU … Trade in Goods

Share of Exports

The Saturday Economist - we always keep you in the picture …

We expect the trend to continue in the years ahead, whilst the EU share of imports is likely to be maintained at around 55% …Share of Imports

Remain basis

Share Trade

30%

40%

50%

60%

2000 2002 2004 2006 2008 2010 2012 2014 2016 2018 2020

UK Share of Trade with EU … Trade in Services

Share of Exports

The Saturday Economist - we always keep you in the picture …

Trade in services are expected to be much more stable … EU 48% of service sector imports

UK exports to the EU around 40% of total exports …

Share of Imports

Remain basis

Share Trade

30%

40%

50%

60%

2000 2002 2004 2006 2008 2010 2012 2014 2016 2018 2020

UK Share of Trade with EU … Trade in Goods and Services

Share of Exports

Share of Imports

The Saturday Economist - we always keep you in the picture …

This is the pattern of trade in goods and services with the EU …

Import shares are steady whilst the UK develops greater trade links with the rest of the world …

Remain basis

UK Trade Total

Total Goods Trade …

0

100,000

200,000

300,000

400,000

500,000

2000 2002 2004 2006 2008 2010 2012 2014 2016 2018 2020

£ millionThe Saturday Economist - we always keep you in the picture …

This is the pattern of total trade in goods … the deficits set to continue and expand …

UK Trade Total

Total Services Trade …

0

50,000

100,000

150,000

200,000

250,000

300,000

2000 2002 2004 2006 2008 2010 2012 2014 2016 2018 2020

£ millionThe Saturday Economist - we always keep you in the picture …

This is the pattern of total trade in services … the surplus set to continue and expand …

For more information - Check out The Saturday Economist .com

Trade with EU

-150,000

-100,000

-50,000

0

2000 2002 2004 2006 2008 2010 2012 2014 2016 2018 2020

Trade in Goods Deficit with EU …

The UK has a huge deficit trade in goods with the EU … we expect a deficit of £100 billion in 2016 …

For more information - Check out The Saturday Economist .com

-10,000

0

10,000

20,000

30,000

2000 2002 2004 2006 2008 2010 2012 2014 2016 2018 2020

Trade in Services Surplus with EU …

Trade with EU

The UK has a huge surplus in services with the EU … we expect + £20 billion surplus in 2016 …

For more information - Check out The Saturday Economist .com

Trade with EU

-150,000

-100,000

-50,000

0

2000 2002 2004 2006 2008 2010 2012 2014 2016 2018 2020

Trade in Goods and Services Deficit with EU …

The UK has a huge deficit in goods and services with the EU …

For more information - Check out The Saturday Economist .com

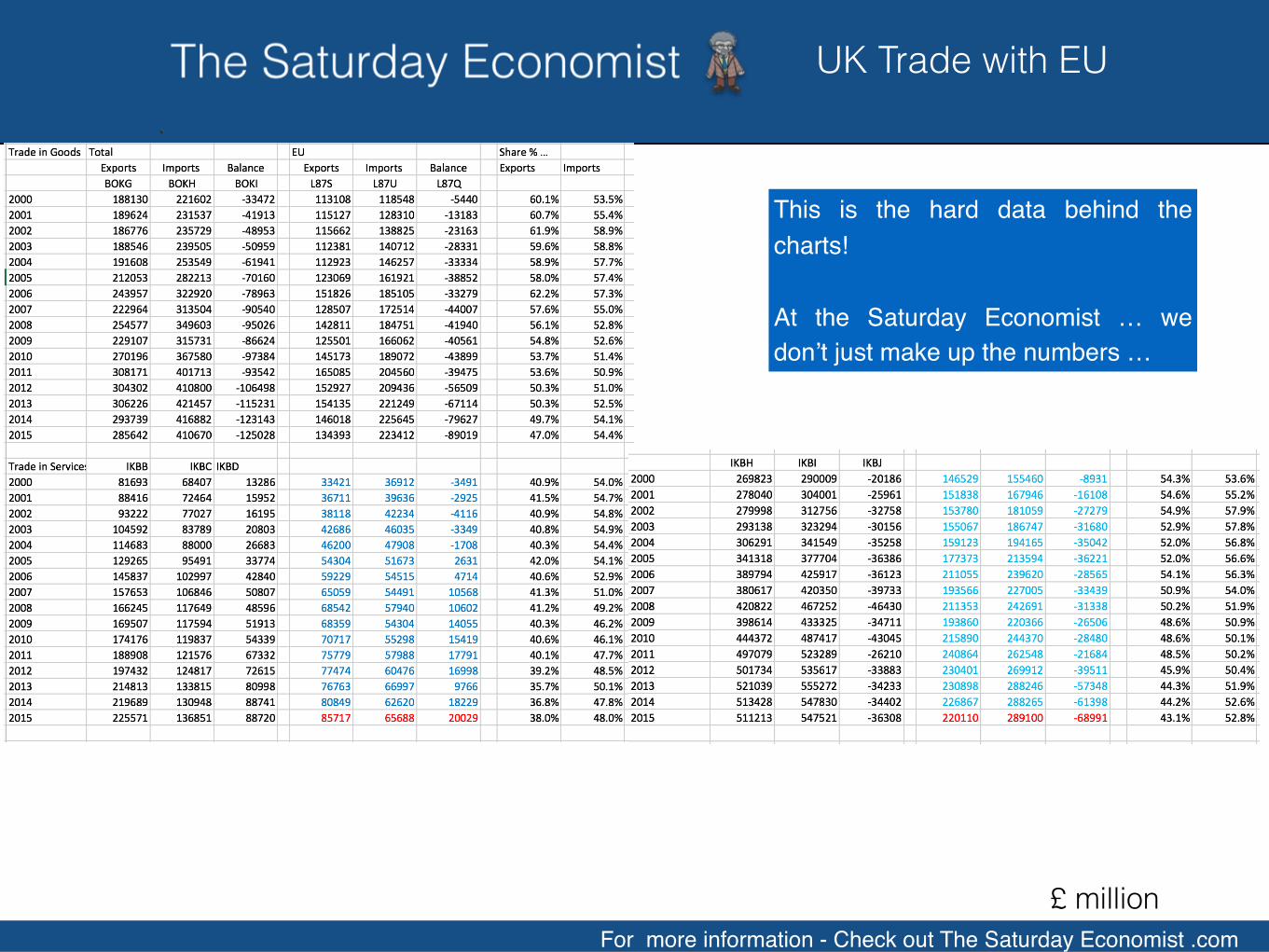

UK Trade with EU

£ million

This is the hard data behind the charts!

At the Saturday Economist … we don’t just make up the numbers …

Cost of Eu Contributions

Trade with EU

The Saturday Economist - we always keep you in the picture …

This is the pattern of EU trade in goods … with member companies

For more information - Check out The Saturday Economist .com

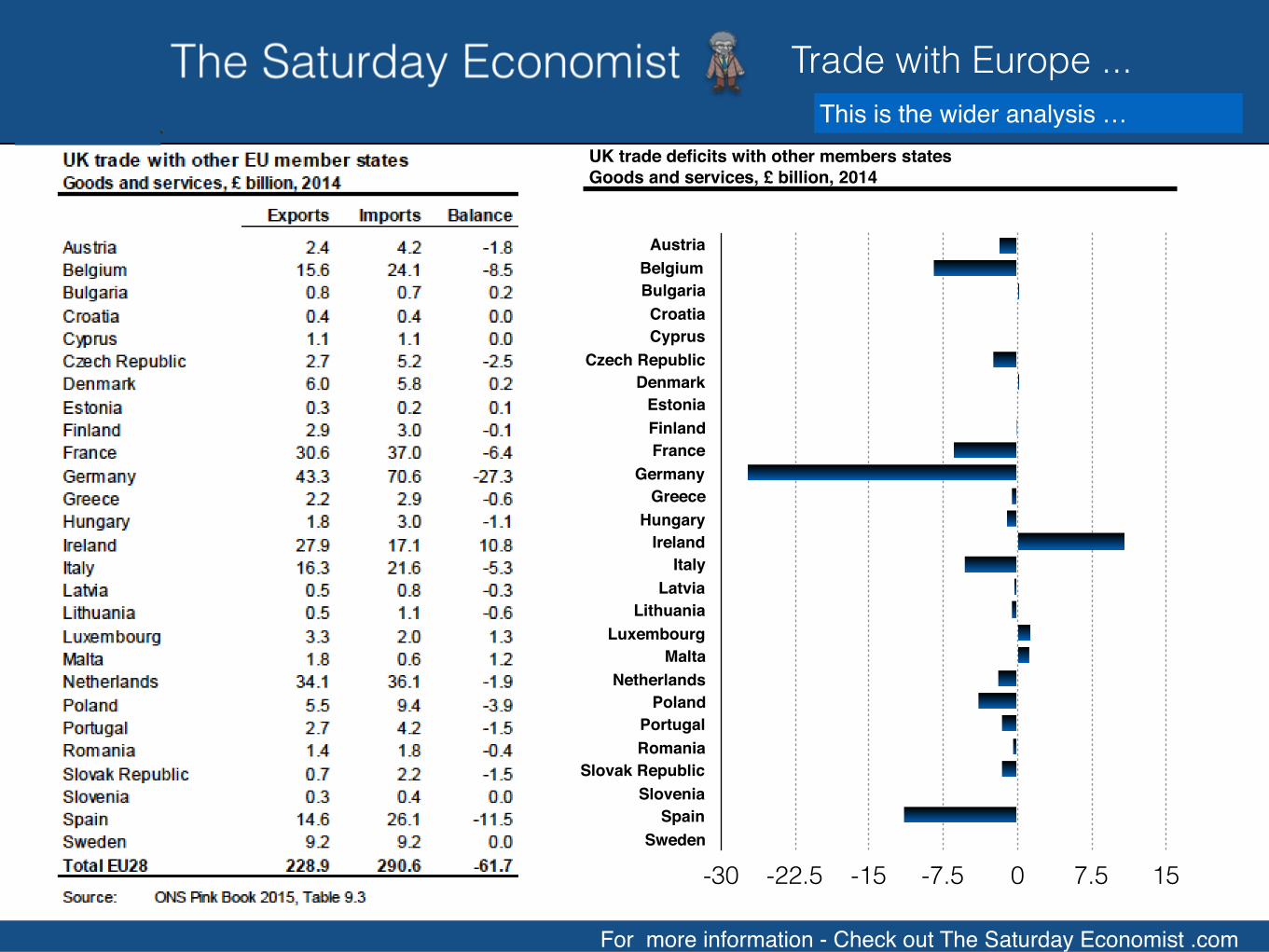

Trade with Europe ...

AustriaBelgium BulgariaCroatiaCyprus

Czech RepublicDenmark

EstoniaFinlandFrance

GermanyGreece

HungaryIreland

ItalyLatvia

LithuaniaLuxembourg

MaltaNetherlands

PolandPortugalRomania

Slovak RepublicSlovenia

SpainSweden

-30 -22.5 -15 -7.5 0 7.5 15

UK trade deficits with other members states Goods and services, £ billion, 2014

This is the wider analysis …

Trade with EU

The Saturday Economist - we always keep you in the picture …

This is the pattern of trade in goods and services by product …

For more information - Check out The Saturday Economist .com

The importance of FDI

0

100

200

300

400

500

600

2005 2006 2007 2008 2009 2010 2011 2012 2013Figure 1 and 2 Overseas net stock of assets held in the UK and earnings received

0

10

20

30

40

2005 2006 2007 2008 2009 2010 2011 2012 2013

Fig 1 EU Assets in UK … Fig 2 EU Earnings in UK …

0

120

240

360

480

600

2005 2006 2007 2008 2009 2010 2011 2012 2013

Fig 3 UK Assets in EU …

0

10

20

30

40

2005 2006 2007 2008 2009 2010 2011 2012 2013

Fig 4 UK Earnings in EU …Figure 3 and 4 UK net stock of assets held overseas and earnings received

This is the pattern of foreign investment and earnings …

The Saturday Economist - we always keep you in the picture …

How much does it cost the UK …

?

For more information - Check out The Saturday Economist .com

Costs of EU

Cost of EU Contributions

£350 million per week?

How much does it cost the UK …

For more information - Check out The Saturday Economist .com

Costs of EU

Cost of EU Contributions

• Gross Cost £18.0 billion • Rebate £ 5.0 billion• Receipts £ 4.5 billion• Net Cost £ 8.5 billion

• Receipts relate to farming subsidies and poor area allocation. Figures are for 2015. Source HM Treasury "European Union Finances 2015. • Net cost - £23 million per day

How much does it cost the UK …

£350 million per week?

£350 million per week (£18 billion per annum) is the Gross cost before rebate and receipts …

For more information - Check out The Saturday Economist .com

Costs of EU

Cost of EU Contributions

• Full Cost £18.0 billion • Rebate £ 5.0 billion• Receipts £ 4.5 billion• Net Cost £ 8.5 billion

• Receipts relate to farming subsidies and poor area allocation. Figures are for 2015. Source HM Treasury "European Union Finances 2015. • Net cost - £23 million per day

How much does it cost the UK …

£160 million per week?

The net cost is £8.5 billion…

More like £160 million per week …

The Saturday Economist - we always keep you in the picture …

How much does the EU cost …

?

£160 million per week but is that value for money …

For more information - Check out The Saturday Economist .com

Costs of EU and Allocation

€132,961.302014c1%ofGDP

FinancingofthegeneralbudgetandEUexpenditurebymemberstate(2014)[29]

6%

14%

Internal Policies 10%

Structural Fund 30%

CAP 40%

CAP Structural FundInternal Policies Pre Accession / CompensationAdmin

The EU budget is €133 billion that’s 1% of EU GDP approximately …

Most of which is accounted for bythe common agricultural budget …

Just 6% is spent on administration …

How much does the EU cost …

For more information - Check out The Saturday Economist .com

EU Budget Who Pays

GermanyFrance

United KingdomNetherlands

ItalySwedenAustria

DenmarkFinland IrelandCyprusCroatia

MaltaSpain

EstoniaSlovenia

LatviaSlovakia

LuxembourgLithuaniaBulgariaBelgium

Czech RepublicPortugalRomania

GreeceHungary

Poland-18,000 -13,500 -9,000 -4,500 0 4,500 9,000 13,500 18,000

Winners and Losers

FinancingofthegeneralbudgetandEUexpenditurebymemberstate(2014)[29]

Germany is the largest contributor …

Po land , Hunga ry t he l a rges t beneficiaries …

The Saturday Economist - we always keep you in the picture …

The Big Issues …

?

So what are the big issues …

For more information - Check out The Saturday Economist .com

The Big Issues …

Regulation costing £27 billion!Working Time DirectiveTemporary Agency Workers DirectiveEnergy and Climate Change

For more information - Check out The Saturday Economist .com

The Big Issues …

Here are the claims of savings from the leave camp …

We haven’t verified these numbers …

For more information - Check out The Saturday Economist .com

The Big Issues …

And the proposals for change

For more information - Check out The Saturday Economist .com

The Big Issues …

Chemicals and Health

Emissions Trading System

Common Security and Defence Policy

The Bigger list …

The Saturday Economist - we always keep you in the picture …

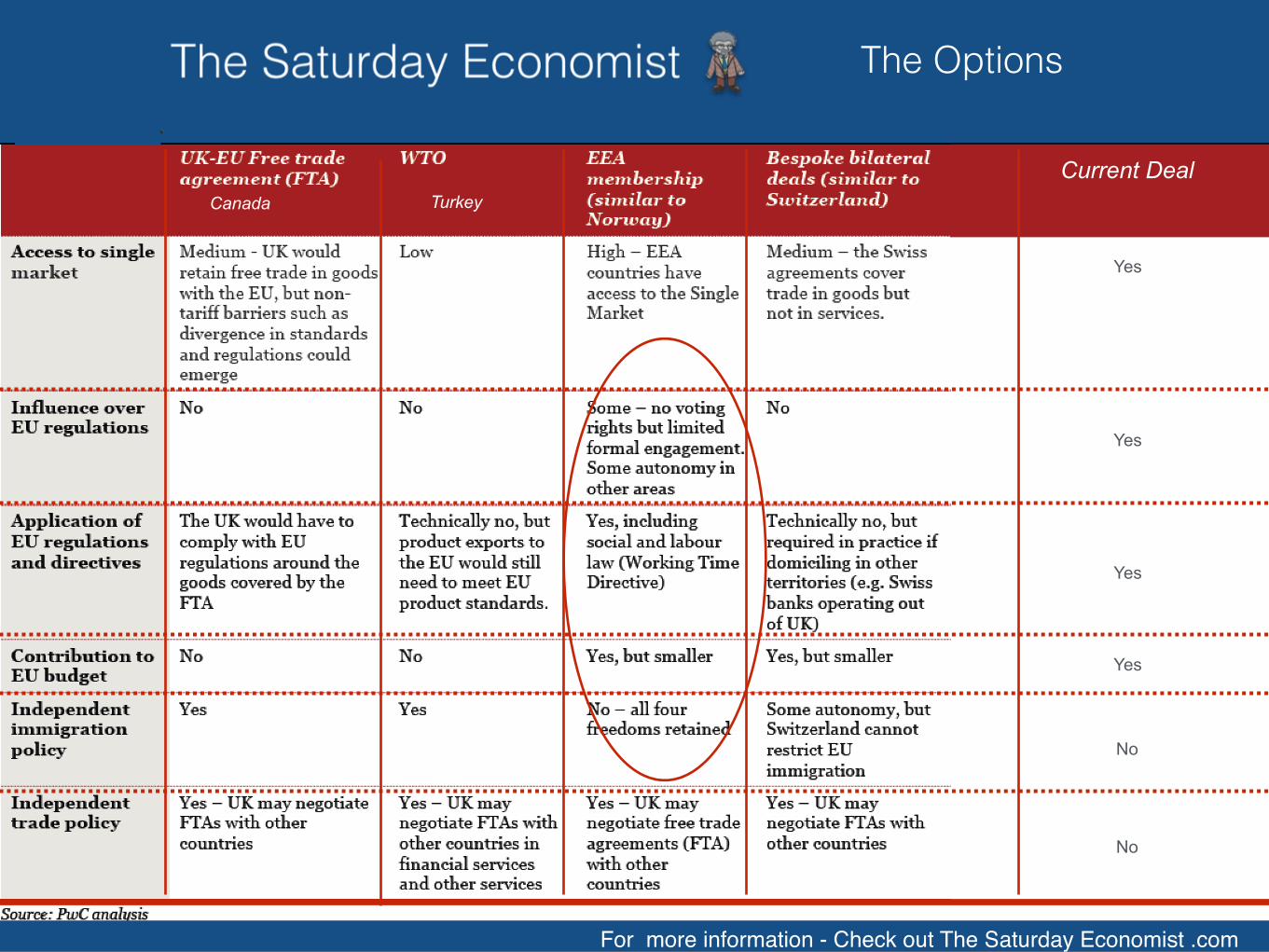

The Options …

?

For more information - Check out The Saturday Economist .com

The Options

Current Deal

Yes

No

Yes

Yes

Yes

No

Canada Turkey

For more information - Check out The Saturday Economist .com

The Options

1.1 This paper looks at the potential models for the UK’s relationship with the EuropeanUnion, if there were to be a vote to leave. It provides examples of countries that are notmembers of the EU but have other arrangements with it – specifically Norway, Switzerland,Canada and Turkey – and describes those arrangements. It also looks at a possiblerelationship based only on World Trade Organisation membership.

1.2 These models offer different balances in terms of advantages, obligations andinfluence. If the result of the referendum were a vote to leave, we would seek the best possible balance of advantage for the UK. However, regardless of the preferred outcome the UK seeks, the precedents clearly indicate that we would need to make a number of trade-offs:

•• in return for full access to the EU’s free-trade Single Market in key UK industries, wewould have to accept the free movement of people;

•• access to the Single Market would require us to implement its rules. But fromoutside, the UK would no longer have a vote on these rules. And there is noguarantee that we could fully replicate our existing cooperation in other areas, suchas cross-border action against criminals;

•• full access to the Single Market would require us to continue to contribute to the EU’sprogrammes and budget;

•• an approach based on a Free Trade Agreement would not come with the same levelof obligations, but would mean UK companies had reduced access to the SingleMarket in key sectors such as services (almost 80 per cent of the UK economy),1 andwould face higher costs;

••we would lose our preferential access to 53 markets2 outside the EU with whichthe EU has Free Trade Agreements. This would take years to renegotiate, with noguarantee that the UK would obtain terms as good as those we enjoy today; and

•• in order to maintain the rights of UK citizens living, working and travelling in other EUcountries, we would almost certainly have to accept reciprocal arrangements for theircitizens in the UK.

1.3 It would take up to a decade or more to negotiate a new agreement with the EU and toreplace our existing trade deals with other countries. Moreover, each of the alternative models would come with significant obligations and costs for the UK:

•• the Norway model has considerable access to the Single Market but not inagriculture and fisheries. It does not give access to the EU’s trade deals withcountries outside the EU and still requires customs checks on goods crossing intothe EU. It also involves making a significant contribution to EU spending, acceptingfree movement of people, and taking on EU rules without having a vote on them;

•• bilateral agreements vary, but none provide full access to services, which constitutealmost 80 per cent of the UK economy. Higher levels of access to the Single Marketinvolve implementing EU rules in domestic legislation, accepting free movement (asin the case of Switzerland), and in some cases making contributions to EU spending.The EU-Canada Trade Agreement provides reduced access to the Single Market forexample in services and agriculture; and

•• if we could not reach agreement with the EU on a new arrangement, our tradingarrangements would revert to WTO rules. This would provide the most completebreak with the EU. It does not entail accepting free movement, budgetarycontributions or implementing EU rules. But it would cause a major economic shockto the UK. WTO rules mean that the EU, and all countries with which we currentlyhave trade deals, would have no choice but to apply WTO tariffs on exports fromthe UK – putting our companies at a competitive disadvantage. Meanwhile, the UKwould face a difficult choice between either raising tariffs on imports from the EUor lowering tariffs on imports from all countries. Raising tariffs would have knockoneffects on UK jobs and incomes, as well as on the attractiveness of the UK as adestination for international investment. Lowering tariffs would deny the UK revenue,and undermine our negotiating position in future trade deals.

1.4 Under any of these alternatives, there would also be a non-economic cost, in terms ofthe UK’s security and strength. The European Arrest Warrant and the Schengen InformationSystem, for instance, allow our law-enforcement agencies to obtain and act on informationfrom their EU counterparts. Even if over time we manage to negotiate replacement bilateralagreements, there is no guarantee that we could fully replace our access to current EUmeasures for police and security cooperation. And we would no longer be able, as weare now, to use the EU as one of our major tools, like our membership of the UN or otherinternational organisations, to project UK influence in the world, or to use the EU’s economicweight to impose sanctions, such as those it has imposed on Russia or Iran.

1.5 We need to assess the benefits offered by any alternative model against what the UK’smembership of the EU gives us now. The UK Government believes that no existing modeloutside the EU comes close to providing the same balance

March 2016

The Saturday Economist - we always keep you in the picture …

The Big Ask … from the “Leave” camp …

?A Free Trade Agreement for goods and services …

A Free Trade Agreement for Capital…

Restrictions on Labour migration…

No EU budget payment …

Free from EU regulation on goods, labour and capital …

An impossible ask …An impossible give …An impossible deal …

The Saturday Economist - we always keep you in the picture …

The Big Risks …

?

The Saturday Economist - we always keep you in the picture …

The Big Risks …

?

1 Trade … 50 % of trade is at stake With no guarantee of post exit trade deals Trade deficits with China, Japan, Norway and Canada could get worse Cars, Aerospace and Financial Services particularly at risk

For more information - Check out The Saturday Economist .com

Costs of EU

Trade and Tariffs

The tariffs at issue …

The Saturday Economist - we always keep you in the picture …

The Big Risks …

?

1 Trade …

2 Investment … at risk Uncertainty … in the short term Strategic … Motor, Aerospace and financial in the medium term …

For more information - Check out The Saturday Economist .com

The Big Risks

Growth and Jobs …

CBI … 3 million jobs related to EU 1 million jobs could be lost

The Economic estimates vary widely and wildly …The CBI estimates that 3 million jobs are related to trade with the EU …Of which 1 million could be lost in the worst case …

For more information - Check out The Saturday Economist .com

Costs of EU

This is the range according to the PwC CBI sensitivities …

The Saturday Economist - we always keep you in the picture …

The Big Risks …

?

1 Trade …

2 Investment … Uncertainty short term Strategic … long term

3 Financial Services

For more information - Check out The Saturday Economist .com

Growth Financial Services … Relocation Passporting

Financial Services could be the biggest area of impact, w i t h m a n y i n s t i t u t i o n s relocating to ensure Passport access is maintained …

It will also be the toughest area of negotiation with strong competition from EU financial centres in Paris and elsewhere …

The Big Risks …

The Saturday Economist - we always keep you in the picture …

The Big Risks …

?

1 Trade …

2 Investment … Uncertainty short term Strategic … long term

3 Financial Services …

4 Trade Deficits …

For more information - Check out The Saturday Economist .comDate of Next Update : 10th October

Heading in the wrong direction …

For more information - Check out The Saturday Economist .com

The Big Risks …

Trade deficits are likely to deteriorate in a free trade world …

The Saturday Economist - we always keep you in the picture …

The Big Risks …

?1 Trade …

2 Investment … Uncertainty short term Strategic … long term

3 Financial Services …

4 Trade Deficits …

5 Capital Account “Putting more pressure on the capital account”

-7.0

-6.0

-5.0

-4.0

-3.0

-2.0

-1.0

0.0

1.0

2.0

3.0

4.0

5.0

1955 1960 1965 1970 1975 1980 1985 1990 1995 2000 2005 2010 2015

UK Current Account Deficit % of GDP

For more information - Check out The Saturday Economist .com

The UK has a significant current account deficit over 5% in 2015 …

We are already reliant on the “kindness of strangers” to finance the deficit holding 25% of UK Gilts and 50% of UK capital markets …

The Big Risks …

The Saturday Economist - we always keep you in the picture …

The Big Risks …

?

1 Trade …

2 Investment … Uncertainty short term Strategic … long term

3 Financial Services …

4 Trade Deficits …

5 Capital Account

6 Sterling

MarchLatest Data Sterling £1.4514

Dollar Spot

1.30

1.40

1.50

1.60

1.70

1.80

1.90

2.00

2.10

2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016

Sterling Dollar Daily Rate

For more information - Check out The Saturday Economist .com

Dollar Rate $Resistance

$1.6800 $1.5000

Support

$1.70 resistance level

Which way for Sterling?

$1.50 support level

Technical

Short Rates

Long Rates

Money

Capital Flows

Portfolio

-0.15 0 0.15 0.3

Sterling Dollar

18th March

T h e r e a r e s o m e suggestions Sterling could fall by 20% …

The Big Risks …

0.90

1.00

1.10

1.20

1.30

1.40

1.50

1.60

2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016

Sterling Euro Daily Rate

Latest Data Sterling €1.2853

Euro Spot

For more information - Check out The Saturday Economist .com

Euro Rate

€1.28 resistance / support level

Which way for Sterling?

€

March Resistance$1.4000 $1.2800

Support

€1.40 resistance level

Technical

Short Rates

Long Rates

Money

Capital Flows

Portfolio

-0.5 -0.25 0 0.25 0.5

Sterling Euro

18th March

In the short term as a result of uncertainty and volatility … in the long term as a result of capital outflows ..

The Big Risks …

The Saturday Economist - we always keep you in the picture …

The Big Risks …

?1 Trade …

2 Investment … Uncertainty short term Strategic … long term

3 Financial Services …

4 Trade Deficits …

5 Capital Account

6 Sterling

7 Agriculture and the CAP …

Common Agricultural PolicyCAP accounts for 40% of EU spend …

Set to fall to 30% over the next five years

N F U i s v o t i n g t o remain …

With large proportion of trade with EU at risk …

Farm subsidies £1.5 billion could be lost if Brexit happens…

But could be funded by HMG from EU payment savings …

For more information - Check out The Saturday Economist .com

NFU pro 50% incomes dependent

Key markets could be l o s t i f t a r i f f s a r e imposed …

The Big Risks …

The Saturday Economist - we always keep you in the picture …

The Big Risks …

?

1 Trade …

2 Investment … Uncertainty short term Strategic … long term

3 Financial Services …

4 Trade Deficits …

5 Capital Account

6 Sterling

7 Agriculture and the CAP …

8 Fisheries CFP

The Saturday Economist on Brexit and Fishing …

The Big Risks …It’s not just about “our” fish …

The Saturday Economist on Brexit and Fishing …

The Big Risks …

It’s not just about “our” fish …Wor ld wide agreements are necessary

The Saturday Economist - we always keep you in the picture …

The Big Risks …

?

1 Trade …

2 Investment … Uncertainty short term Strategic … long term

3 Financial Services …

4 Trade Deficits …

5 Capital Account

6 Sterling

7 Agriculture and the CAP …

8 Fisheries CFP

9 Migration

For more information - Check out The Saturday Economist .com

ImmigrationThe Big Risks …

N e t m i g r a t i o n i s 300,000 …

For more information - Check out The Saturday Economist .com

ImmigrationThe Big Risks …

Almost 200,000 is study related …

For more information - Check out The Saturday Economist .com

ImmigrationThe Big Risks …

Almost half from the EU …

For more information - Check out The Saturday Economist .com

Immigration

Total EU immigration is 260,000 …

The Big Risks …

For more information - Check out The Saturday Economist .com

ImmigrationThe Big Risks …

We have no control over borders …

We must control EU immigration …

Puts pressure on schools and NHS

A drain on welfare …

Deflationary - low level of pay …

Taking “British” jobs

We do have control over borders …

Free movement of labour is an EU principle

NHS is reliant on immigration to maintain staff levels …

Some welfare access in place re timing and pricing …

Provides essential labour pool …

UK approaching “Full Employment” …

We have more vacancies than claimants …

Immigration a source of growth to fund Schools and NHS

Leave … Remain …

The Arguments

The Saturday Economist - we always keep you in the picture …

The Big Risks …

?

9 Migration

10 Inflation Immigration cap could push up pay Tariff reductions could lower prices

11 Timetable It will take a long time to set up ..

China - Iceland $180m Canada - EU - CETA 10 years

12 Growth … Will be hit - trade & investment

Motor, Aerospace (Airbus) & Finance 13 Jobs …

3.0 to 3.5 m jobs dependent on EU trade

14 Balance of PaymentsWill deteriorate faster

15 Government Borrowinglargely neutral

1 Trade …

2 Investment … Uncertainty short term Strategic … long term

3 Financial Services …

4 Trade Deficits …

5 Capital Account

6 Sterling

7 Agriculture and the CAP …

8 Fisheries CFP

The Saturday Economist - we always keep you in the picture …

The Big Risks …

?

9 Migration

10 Inflation Immigration cap could push up pay Tariff reductions could lower prices

11 Timetable It will take a long time to set up ..

China - Iceland $180m Canada - EU - CETA 10 years

12 Growth … Will be hit - trade & investment

Motor, Aerospace (Airbus) & Finance 13 Jobs …

3.0 to 3.5 million jobs dependent on EU trade

14 Balance of PaymentsWill deteriorate faster

15 Government Borrowinglargely neutral

16 Scotland …Threat to union?

17 Science TechNeutral - subsidies lost couldbe HMG funded

18 Security …Brexit won’t help

19 Peace …NATO and EU issuesEU is a force for peace internalNATO is a force for peace external

20 Sovereignty A political issue

1 Trade …

2 Investment … Uncertainty short term Strategic … long term

3 Financial Services …

4 Trade Deficits …

5 Capital Account

6 Sterling

7 Agriculture and the CAP …

8 Fisheries CFP

The Saturday Economist - we always keep you in the picture …

?Leave says the UK is “powerless to prevent laws that damage our country”. But the UK enjoys 12.7% of votes in the EU Council, a veto in key areas and influence on many issues.

The Big Risks … Sovereignty

In the UK data suggest that from 1997 to 2009 6.8% of primary legislation (Statutes) and 14.1% of secondary legislation (Statutory Instruments) had a role in implementing EU obligations, although the degree of involvement varied from passing reference to explicit implementation.

Source How much legislation comes from Europe?House of Commons Library October 2010

Who governs Britain?

The leave camp take exception to . The Working Time DirectiveThe Temporary Agency Workers DirectiveThe Energy and Climate Change legislation butMost of these are welcomed by progressive business

Between 1993 and 2014, 64.7 per cent of UK law can be deemed to be EU-influenced. EU regulations accounted for 59.3 per cent of all UK law. UK laws implementing EU directives accounted for 5.4 per cent.

This body of legislation consists of 49,699 exclusively ‘EU’ regulations and 4,532 UK measures which implement EU directives.

This figure is important because EU regulations are transposed into national law without passing through Parliament. Hence, they do not appear in the recent calculation by the House of Commons Library which estimates the proportion of EU legislation at 13.3 per cent.3 The 13.3 per cent

Source Business for Britain Tim Philpott

The level of influence is confused …

The Saturday Economist - we always keep you in the picture …

?The CBI

The EEF

The SMMT

The NFU

The Big Risks …

Voting to remain …

The Saturday Economist - we always keep you in the picture …

On Brexit … The Spectrum of Issues …

?Business Economic

Social PoliticalImmigration NHS

We think it is important to differentiate the main issues into business, economic, political and social …

Trade Investment Uncertainty

Sovereignty … Who governs Britain …

Growth Jobs Inflation Trade

Deficits Current Account Borrowing Sterling

“Whatever we may think of the political and social arguments …There is no “Business Case” for Brexit"

The Saturday Economist - we always keep you in the picture …

On Brexit …

?

April 2016 …