Embed Size (px)

Citation preview

When will we see MO’mentumin OLED production?

Views on development of metal-oxide TFT (e.g. IGZO) for active-matrix displays at OLEDs World Summit 2013—David Barnes, BizWitz LLC

Disclosure

n The presenter worked closely with the current CEO of LG Display on the Paju industrialization plann LGD financials provide a great amount of information for analystsn The company remains a leader and we can learn a lot from them

n The presenter has evaluated four encapsulation/barrier technologies, including IP and business valuations

n The presenter has been analyzing investments in semi-TFT capital equipment since the 1970’s

n The presenter has not made many people happy but has helped some people make money

n What follows is a personal perspective on where we’ve been and where we may go…

14 Sep 2013 When will we see MO'mentum 2

MO TFT adds to the challenge of making OLED

Choices TFT OLED Barrier/Optic

MaterialChannelDielectricPassivation

DopantsEmittersTransports

SealantPolymerGas barrier

Tool CoaterSputter

PatternedUnpatterned

LaminatorThin film encap.

MethodAnnealDepositImplant

PrintTransferEvaporate

CoatSputterCVD/ALD/MLD

Capital ConvertGreenfield

Vertical–proprietaryOutsource–supply

Vertical–proprietaryOutsource–supply

14 Sep 2013

n Panel makers face several choices for each of three major layers.n Competitive rivalry causes leaders to try proprietary approaches, which

reduces incentives for suppliers and slows development, industry-wide.n LTPS has been an easy choice as a starting point for industrialization.

When will we see MO'mentum 3

MO TFT adds less value to mainstream LCD

There are real advantages for using MO instead of silicon, but those lie at the high-end of display performance today.Array impedance is a bigger problem for large HD or UHD LCD TV sets than is TFT performance… Mainstream market needs can be met with improved copper bus technologies and circuit designs using silicon, not MO.Yes, we can imagine 8k/4k TV needing MO performance… in a few years.Until then, Taiwan and China can lever assets into LCD TV.

14 Sep 2013

Distributed Impedance in Transmission Lines

Source: Dr. Wiki

When will we see MO'mentum 4

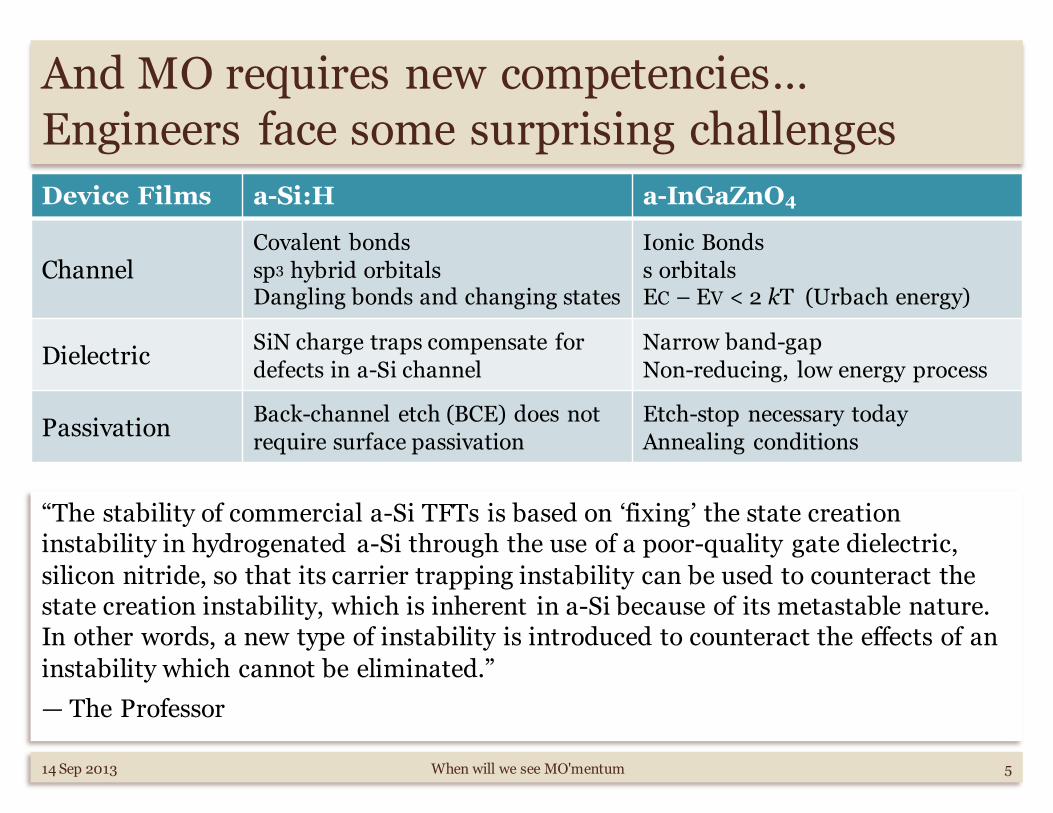

And MO requires new competencies…Engineers face some surprising challengesDevice Films a-Si:H a-InGaZnO4

ChannelCovalent bondssp3 hybrid orbitalsDangling bonds and changing states

Ionic Bondss orbitalsEC – EV < 2 kT (Urbach energy)

Dielectric SiN charge traps compensate for defects in a-Si channel

Narrow band-gapNon-reducing, low energy process

Passivation Back-channel etch (BCE) does not require surface passivation

Etch-stop necessary todayAnnealing conditions

14 Sep 2013

“The stability of commercial a-Si TFTs is based on ‘fixing’ the state creation instability in hydrogenated a-Si through the use of a poor-quality gate dielectric, silicon nitride, so that its carrier trapping instability can be used to counteract the state creation instability, which is inherent in a-Si because of its metastable nature. In other words, a new type of instability is introduced to counteract the effects of an instability which cannot be eliminated.”— The Professor

When will we see MO'mentum 5

But who cares?The industry is underwater and may stay thereEven LG Display has not generated free cash flow. They might if they slow investment… but what about AMOLED?Taken together, Taiwan’s LCD industry has accumulated a negative $19 billon of not-so free cash flow since 2001.And, one might ask, why should companies conspire to fix prices below cost?But, that was then…Now leaders need a new story and OLED is it.Otherwise, there’s nothing but new entrants in China and commoditization… what fun!

($25)

($20)

($15)

($10)

($5)

$0

2001 2003 2005 2007 2009 2011

LGD's Cumulative FCF

Taiwan's Cumulative FCF

14 Sep 2013

Cumulative Free Cash Flow in USD billions

Source: public disclosures; BizWitz analysis

When will we see MO'mentum 6

And don’t be misled by managerial accounting… corporations borrow, not their product linesDepreciation can be over appreciated in managerial accounting.It is a corporate charge, not a cost, for money spent before.A constant level of capex will create a constant charge, regardless of the schedule.Here we see depreciation falling as a portion of product cost while its charge per area out remains flat.Now that LGD is expanding again, and investing in OLED, depreciation will become a larger portion of cost, again.There is no free lunch…

$0

$500

$1,000

$1,500

$2,000

$2,500

0%

5%

10%

15%

20%

25%

2003 2004 2005 2006 2007 2008 2009 2010 2011 2012

Depreciation / Cost of Product Depreciation / m² of Output

14 Sep 2013

Depreciation Charges for LGD

When will we see MO'mentum 7

%

$

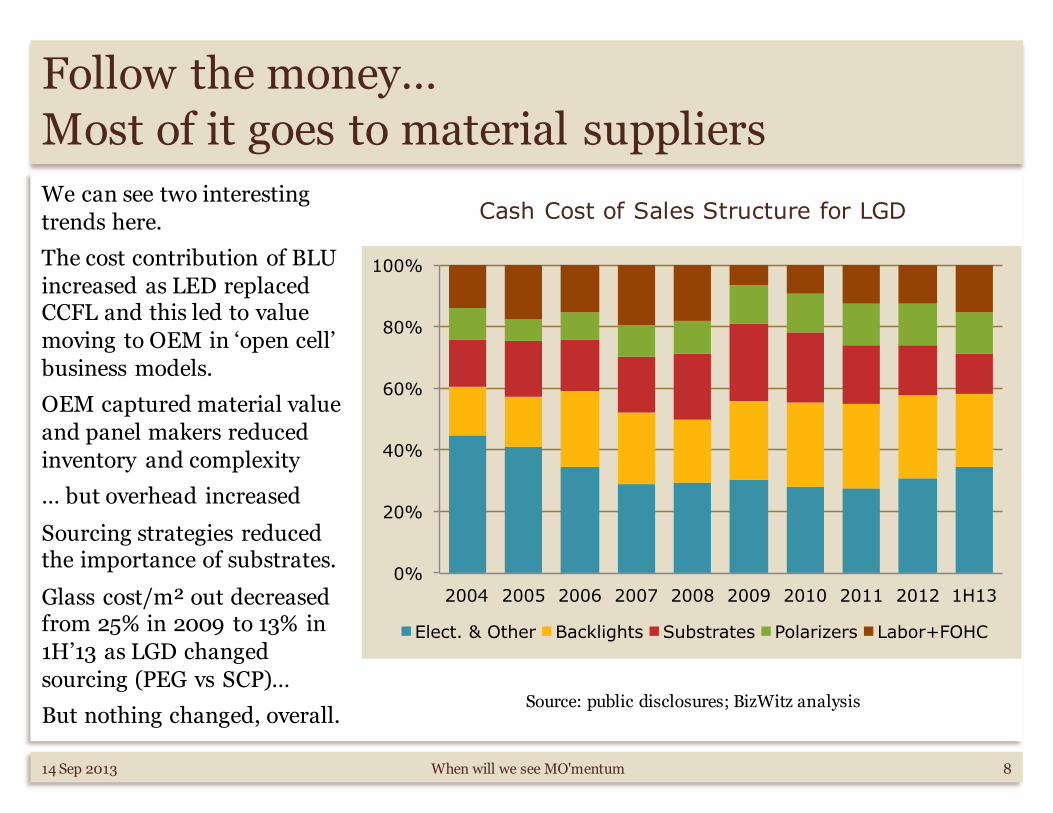

Follow the money…Most of it goes to material suppliersWe can see two interesting trends here.The cost contribution of BLU increased as LED replaced CCFL and this led to value moving to OEM in ‘open cell’ business models.OEM captured material value and panel makers reduced inventory and complexity… but overhead increasedSourcing strategies reduced the importance of substrates.Glass cost/m² out decreased from 25% in 2009 to 13% in 1H’13 as LGD changed sourcing (PEG vs SCP)…But nothing changed, overall.

14 Sep 2013

Cash Cost of Sales Structure for LGD

Source: public disclosures; BizWitz analysis

0%

20%

40%

60%

80%

100%

2004 2005 2006 2007 2008 2009 2010 2011 2012 1H13

Elect. & Other Backlights Substrates Polarizers Labor+FOHC

When will we see MO'mentum 8

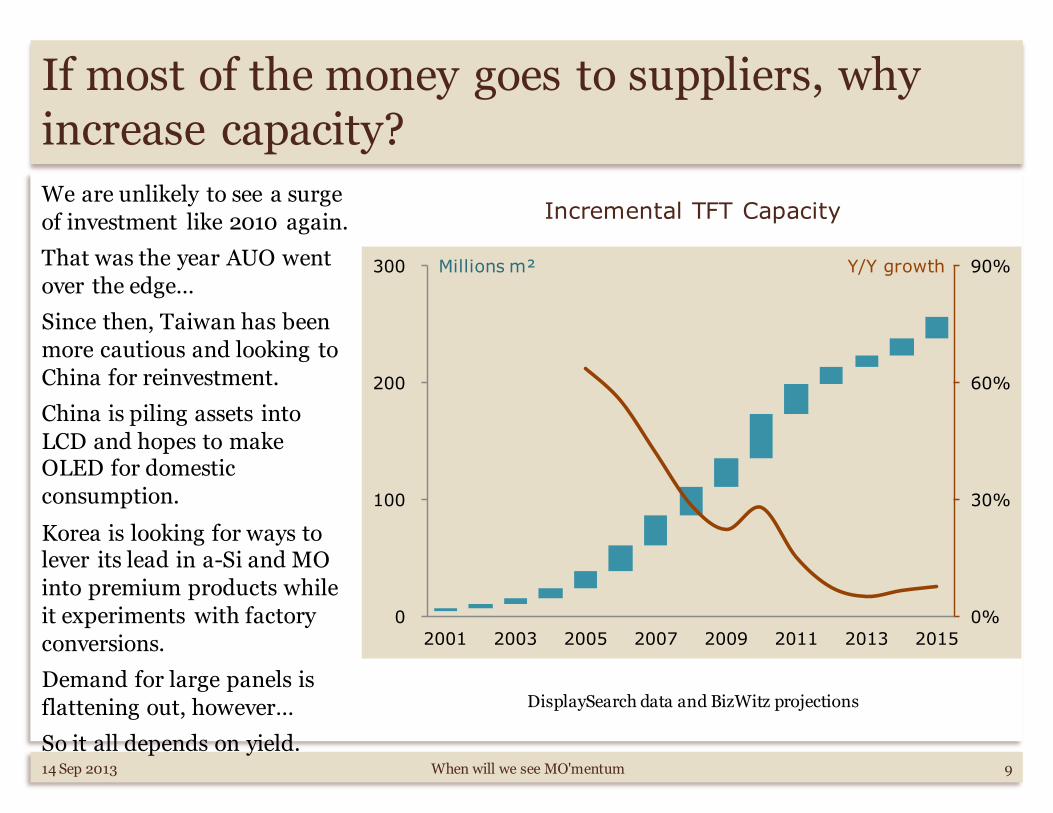

If most of the money goes to suppliers, why increase capacity?We are unlikely to see a surge of investment like 2010 again.That was the year AUO went over the edge…Since then, Taiwan has been more cautious and looking to China for reinvestment.China is piling assets into LCD and hopes to make OLED for domestic consumption.Korea is looking for ways to lever its lead in a-Si and MO into premium products while it experiments with factory conversions.Demand for large panels is flattening out, however…So it all depends on yield.

0%

30%

60%

90%

0

100

200

300

2001 2003 2005 2007 2009 2011 2013 2015

14 Sep 2013

Incremental TFT Capacity

DisplaySearch data and BizWitz projections

Millions m² Y/Y growth

When will we see MO'mentum 9

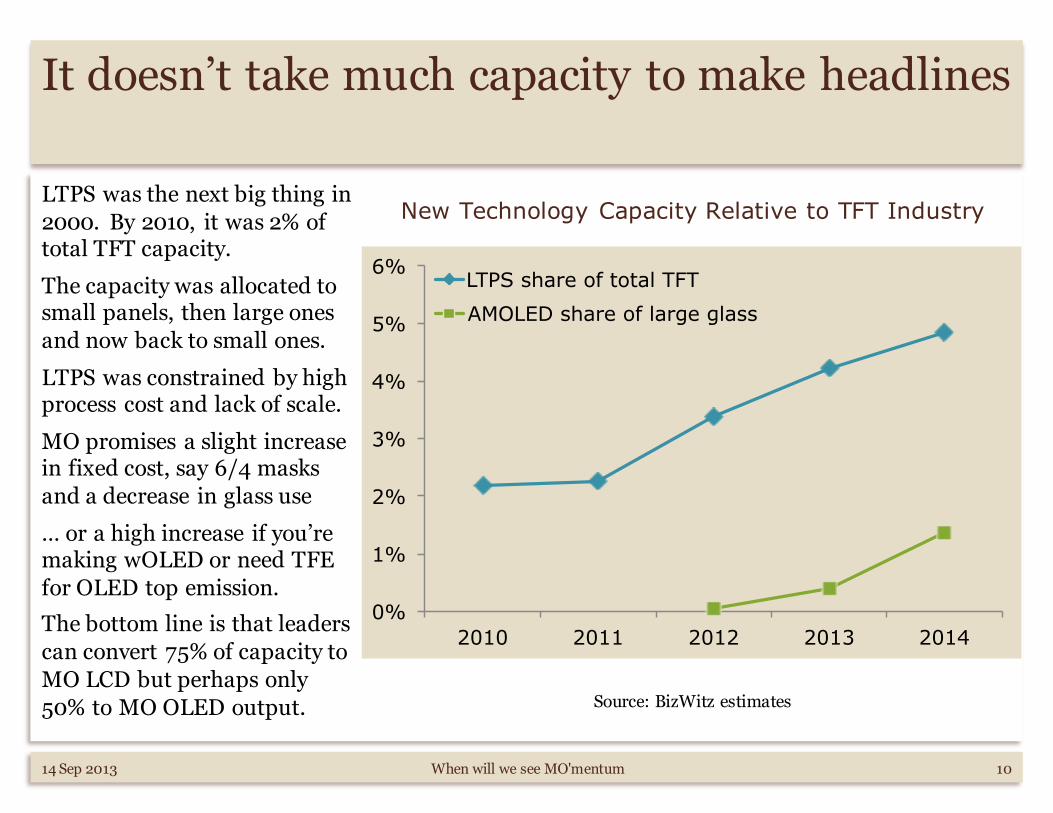

It doesn’t take much capacity to make headlines

LTPS was the next big thing in 2000. By 2010, it was 2% of total TFT capacity.The capacity was allocated to small panels, then large ones and now back to small ones.LTPS was constrained by high process cost and lack of scale.MO promises a slight increase in fixed cost, say 6/4 masks and a decrease in glass use… or a high increase if you’re making wOLED or need TFE for OLED top emission.The bottom line is that leaders can convert 75% of capacity to MO LCD but perhaps only 50% to MO OLED output.

0%

1%

2%

3%

4%

5%

6%

2010 2011 2012 2013 2014

LTPS share of total TFT AMOLED share of large glass

14 Sep 2013

New Technology Capacity Relative to TFT Industry

Source: BizWitz estimates

When will we see MO'mentum 10

It takes time to convert a fab…Look at AUO and Sharp history for evidenceForget managerial accounting games and yield forecasts…Let’s assume the new MO line is as productive, long-term, and that less output (from more process steps) is offset by premium prices.Opportunity cost becomes the main risk.Using LGD results, we can see that taking three 30k lines down for 12 months would bring consolidated EBIT over 18 months to zer0.That is assuming conditions hold that gave LGD 3% OPM over the past six quarters.Conversion is not free…

Lines 3 mo. 6 mo. 9 mo. 12 mo. 18 mo.1 3% 3% 3% 2% 2%3 3% 2% 1% 0% -2%6 2% 0% -2% -4% -9%9 1% -2% -5% -9% -20%

14 Sep 2013

18 month OPM based on 30k Line Conversions

This table is based on LG Display’s latest 18 month average performance(Jan ‘12 – Jun ‘13)

Hypothesis:u Gen-8 lines of 30k monthly input sheets are converted.u Time delay before productivity recovers is varied in 3-month increments.u Operating profit margin of remaining capacity is estimated over 18 months.

u For comparison, LGD’s OPM was 3% for the latest 18 month period.

When will we see MO'mentum 11

So panel makers will convert slowly and use the experience to justify greenfield investmentsHere we can hypothesize the safe conversion region.Looks reasonable for a panel maker to take 90k off-line for 6–9 months…More than that, longer than that, could sink the ship.We can see LGD invest in a new 30k line for MO already.Think of that as a pilot before greater investments.At the normal crystal cycle of 2½–3 years, we should expect the next round in 2016.That leaves time for several modest conversions… maybe 5% of TFT capacity by 2020.

Lines 3 mo. 6 mo. 9 mo. 12 mo. 18 mo.1 3% 3% 3% 2% 2%3 3% 2% 1% 0%6 2% 0%9

14 Sep 2013

18 month OPM based on 30k Line Conversions

This table is based on LG Display’s latest 18 month average performance(Jan ‘12 – Jun ‘13)

When will we see MO'mentum 12

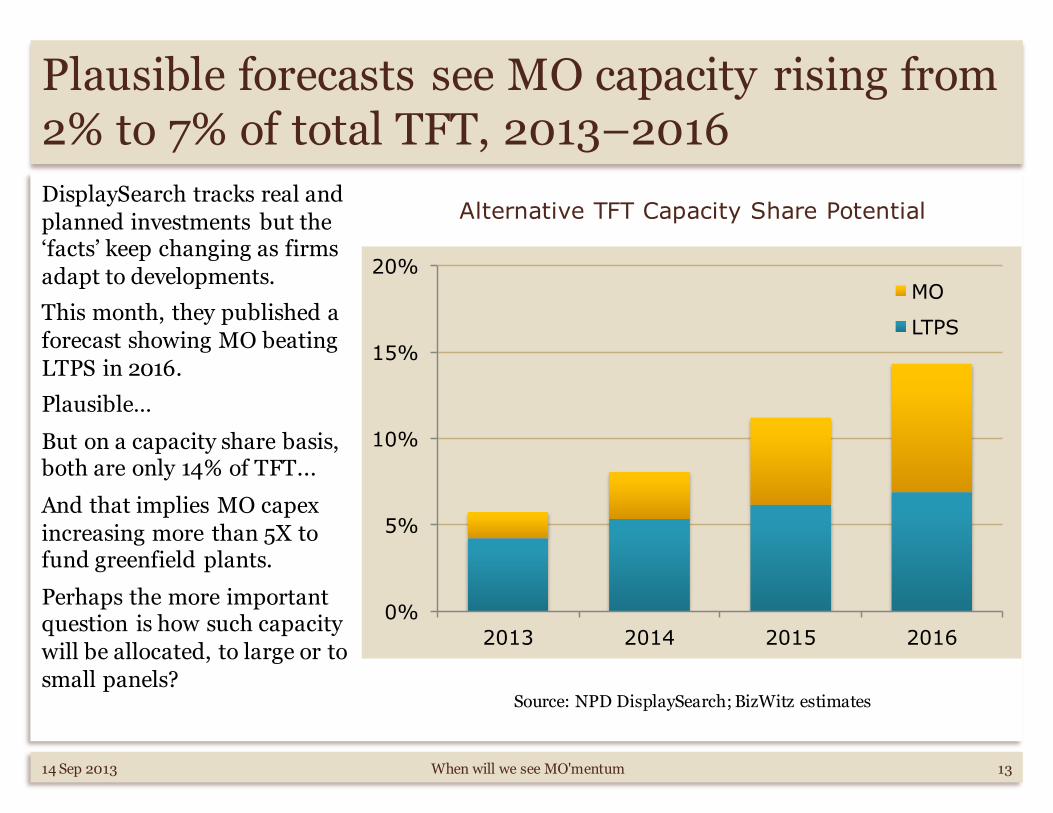

Plausible forecasts see MO capacity rising from 2% to 7% of total TFT, 2013–2016DisplaySearch tracks real and planned investments but the ‘facts’ keep changing as firms adapt to developments.This month, they published a forecast showing MO beating LTPS in 2016.Plausible…But on a capacity share basis, both are only 14% of TFT...And that implies MO capexincreasing more than 5X to fund greenfield plants.Perhaps the more important question is how such capacity will be allocated, to large or to small panels?

0%

5%

10%

15%

20%

2013 2014 2015 2016

MO

LTPS

14 Sep 2013 When will we see MO'mentum 13

Alternative TFT Capacity Share Potential

Source: NPD DisplaySearch; BizWitz estimates

Implications: expect more changes downstream than upstream

14 Sep 2013

Materials

§ Demand declines for commodity optical films as LCD goes to FFS

§ OLED material sources may be acquired or may be commoditized

§ Laminates versus TFE polymers may create new leaders

Tools

§ Deposition tools need joint dev… when will panel makers open up?

§ Little change in the leader board overall…

§ But encapsulation invites innovation; experimentation will continue

Producers

§ Koreans will go it alone

§ Taiwanese will seek investors

§ Chinese will move as fast as possible

§ Producers with affiliated brands face less risk and will be creative

Brands

§ Any UHD LCD v. OLED forecast may be a self-fulfilling prophesy

§ TV and PC prices will continue down at double-digit annual rates

§ Panel suppliers regain power over OEM/ODMs?

When will we see MO'mentum 14

FPD is a difficult business…BizWitz analysts are here to help

14 Sep 2013

Growth

§ Market entry§ Business structure§ Phase gates, R&D

Technologies

§ Market sensing§ Market & IP value§ Consortia synergy

Alliances

§ M&A candidates§ Partnerships, JVs§ Integration plans

Plans

§ Strategic audits § Investor insights§ Business valuation

Materials

§ Pricing policies§ Market strategies§ Licenses, royalties

Performance

§ Price position§ Cost reduction§ Portfolio balance

CapEx

§ Factory plans§ Tool selections§ Plant conversions

Sourcing

§ Make/buy§ Value chains§ Supplier selection

When will we see MO'mentum 15