Embed Size (px)

Citation preview

WORKERS’

COMPENSATION INSIDER

SECRETS

PRESENTED BY: YOUNG KIM & DOUG MEGILL

TODAY’S AGENDA

Overview of Workers’ Comp Overall statistics

What is Workers’ Comp?

Who is covered? Employees vs Independent Contractors

Employees of Independent Contractors

Statutory Employers

How is Workers’ Comp Premium determined?

Workers’ Comp applications & class codes

Experience Mod Rate What it is

Know to calculate it? Know to lower it!

What to do if you have a claim?

How to handle an audit?

WORKERS’ COMPENSATION

STATISTICS

WORKERS’ COMPENSATION

STATISTICS

WORKERS’ COMPENSATION

STATISTICS

CAUSES OF WORKPLACE

DEATHS

Top 10 Occupations With The Largest Number Of Injuries or Illnesses, 2007

1. Laborers (non-construction)

2. Truck Drivers (heavy)

3. Nursing Aides, orderlies

4. Construction Laborers

5. Truck Drivers, light

6. Retail Salespersons

7. Janitors & Cleaners

8. Carpenters

9. Maintenance & Repair Workers (general)

10. Registered Nurses

Source: Department of Labor, Bureau of Labor Statistics

DID YOU KNOW?

MORE THAN 20% OF ALL FATAL INJURIES IN 2013

WERE EMPLOYED IN CONSTRUCTION JOBS*

*According to Bureau of Labor Statistics, out of 3929 private sector worker fatalities, 796 were in

construction

294

82 71

21

0

50

100

150

200

250

300

350

Top 4 Causes Of Fatalaties in Construction

Number of Fatalaties

Type Of Fatality in Construction % of Total Mix

Falls 36.9%

Struck By Objects 10.3%

Electrocutions 8.9%

Caught-in/between 2.6%

Workers’ Comp Statistics

WHAT IS WORKERS’ COMP?

The Workers’ Compensation & Employers Liability Policy was developed by the National Council of Compensation Insurance, Inc. (NCCI)

It is the standard coverage form used to provide insurance for an employer and covers the insured’s statutory liability under the various states workers compensation laws or acts

Employers Liability (WC) covers the insured employer against its common law tort liability for employee injuries that fall outside the scope of the state laws or acts that are separate and distinguished from the liability imposed by worker compensation laws

Injuries must arise from and be related to the injured worker’s job duties

The policy also covers related costs for disease or death that occurs as the result of the accident

When was the system of Workers Compensation first established?

In which US state was Workers

Compensation first established?

2050 B.C. – City of Ur (Ancient

Mesopotamia) provided monetary

compensation for specific injuries

to workers’ body parts including

fractures

In Wisconsin, 1911

What are the 3 basic eligibility requirements for Workers’ Compensation benefits?

1. The person or company you are working for must carry workers’ compensation insurance or be legally required to do so

2. You must be an employee or person of that company

3. Your illness or injury must be work related

What Does Workers’ Comp Really

Mean?

Workers’ Compensation is a mandatory coverage which provides 100% medical benefits as well as statutory loss of wages for the employee who suffers a job related injury or disease. Employers are required by the various states to provide this coverage for their employees:

In Virginia, Statutory requirements for employers are 3 or more workers

In DC, Statutory requirement is 1 or more employee

In MD, one or more (same as DC)

What are the penalties in VA & MD for

not carrying Workers Compensation

coverage?

MARYLAND:

Not to exceed $10K

VIRGINIA:

$250 per day for non-compliance

AND

Subject to Maximum Civil Penalty up to

$50k

WHO IS COVERED?

GUIDELINES FOR CONTRACTORS & SUBCONTRACTORSNeither the Workers’ Compensation Commission nor the State Corporation Commission can provide legal advice on individual contractor/subcontractor situations. The status of an independent contractor, a subcontractor, and an employee must be determined based upon the facts of each case. The following are general guidelines only.

1. Employee vs. Independent Contractors

2. Independent contractors are NOT automatically eligible for Workers’ Compensation

3. Employees of contractors are eligible for Workers’ Compensation

4. Statutory employers

EMPLOYEE vs.

INDEPENDENT CONTRACTORS

The Workers’ Compensation Act defines an employee as:

A person under written or implied contract of hire “except one whose employment is not in the usual course of the trade, business, occupation and profession of the employer.”

In distinguishing between an employee & an independent contractor, some important considerations are as follows:

The right to hire

The power to dismiss

The obligation to pay wages

The power of control

An employee arrives to work and is unable to enter the premises at the start of the shift. He forgot his key and doesn’t want to clock in late. If he is late one more time, he will be terminated. The employee decides to climb over the chain link fence to avoid lateness. As he is climbing the fence, he loses his footing, falls about 5-ft and lands on his right knee causing a significant contusion. He tells his employer he was injured and would like to see a doctor. What is the correct employer response?

A. The employee should not be compensated for this claim. He was late and used poor judgment in climbing the fence

B. The employee was on the employer’s premises and is therefore eligible for workers’ compensation benefits

C. The employee should be disciplined for not remembering his key. This resulted in a disruption in the workplace, lateness and causing the employer to report an avoidable injury

Correct Answer:

B and possibly C depending on your approach to employee

discipline. The claim is still compensable whether or not

injury could have been avoided by the employee exercising

better judgment.

INDEPENDENT CONTRACTORS

Independent contractors are not automatically eligible for workers’ compensation

An independent contractor who is generally a sole proprietor or partner, is not entitled to workers’ compensation benefits unless:

A formal election of coverage has been made; or

A written agreement has been reached among the independent contractor, the employer, and the insurance carrier that coverage will be provided

EMPLOYEES OF CONTRACTORS &

STATUTORY EMPLOYERS

When a sole proprietor, partnership, or

corporation contracts to perform work or provide

services that are part of the same trade,

business, or occupation of the employer, a

contractor/subcontractor relationship is

established. The contractor becomes the

statutory employer of the employees of the

subcontractor

Who is covered under Workers’ Compensation ?

Trainee & Apprentice

Cash Labor

Insured Subcontractor

Uninsured subcontractor

Officers

HOW IS WORKERS’

COMPENSATION COST

DETERMINED?

The cost of average Workers’ Compensation policy is based on payroll or remuneration.

Remuneration is pay or salary, typically monetarypayment for services rendered as an employee. It can include: Commission

Compensation

Executive Compensation

Deferred Compensation

Employee Stock Options

Fringe Benefits

Salary

Wage

WORKERS’ COMPENSATION

CLASS CODES

How is the Workers’ Compensation premium determined?

Employees are “classed” into the particular rating groups based on the type of work they do which determines the rate that the employer will pay

Ex: A person manufacturing dynamite will have a much higher rate than the person answering the phone in the office

Where are class codes found?

They are found in the NCCI Scope’s manual.

How to classify employees?

General class codes encompass a large pool of different types of workers. It is important to find the best possible class code for the particular class of workers

Can I classify employees to a category of my choosing to reduce my rate?

DO NOT misclassify employees! All Workers’ Compensation policies are “audited” at the end of the policy time and audit time. Insurance companies are very notorious for moving employees out of a particular rating group and placing them in a much higher class.

PS: All rates are based on a “per hundred” of remuneration

Volt is a Clerical Employee of Electro Electric Services, Inc. He is paid $30,000 a year to balance the books and provide clerical support. The insurance carrier rate is .18 per hundred of payroll. Thus the charge for Volt will be:

HOW IS WORKERS’

COMPENSATION COST

DETERMINED?

In the same office as Volt is Zapper. Zapper is a “Supervisor” and runs around all over the area checking on job sites but will “occasionally” fill in as an electrician. The rates for executive supervisor are $3.41 and the rates for Electrician are $5.19. Zapper is paid $72,000/yr. What class code do you use?

Although most businesses will want to put Zapper in the lower

class (Supervisor), Workers’ Compensation companies will

automatically put him into the Electrician class (higher class)

unless Zapper can break down his compensation on the books by

job classification, time and wages attributable to those

classifications.Workers’ Compensation class codes are 4 digits long.

8810 is clerical

5606 for Executive Supervisor

5190 Electricial Wiring, etc.

EXPERIENCE MOD

(Actuarial Science Version)

EXPERIENCE MOD

(Actuarial Science Version)

EXPERIENCE MOD(Simple Approach)

Claims = Experience Mod =

Claims = Experience Mod =

WHAT IS Experience

Modification Rate?

Workers Compensation rating factor

KEY Component in the development of the final WC

premium

Regulated by NCCI (some states have own rating

bureau). All states have some form of experience

rating plan filed

Mandatory that the experience modification is

applied on WC premium

Ultimately controlled BY the insured

It is a reward or punishment based on loss history

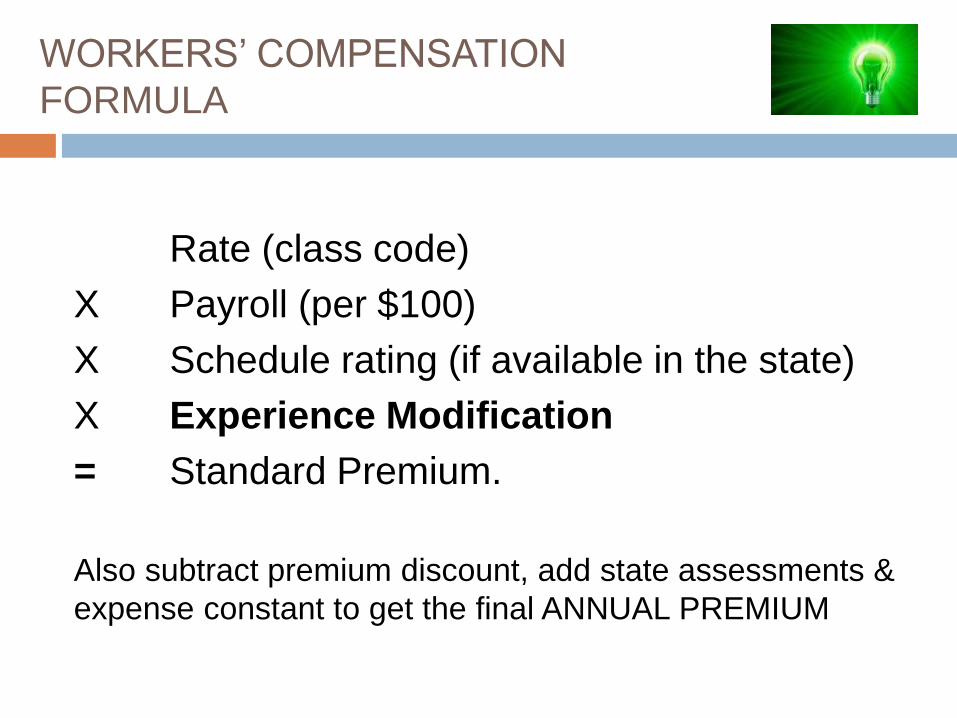

WORKERS’ COMPENSATION

FORMULA

Rate (class code)

X Payroll (per $100)

X Schedule rating (if available in the state)

X Experience Modification

= Standard Premium.

Also subtract premium discount, add state assessments &

expense constant to get the final ANNUAL PREMIUM

ELECTRO ELERCTRIC

SERVICES, INC.

Name Annual Payroll Description of Work Class Code

Mr. Volt $30,000 Clerical 8110

Mr. Zapper $50,000 Supervising & Sales 5606

Mr. Zapper $20,000 Electrical Wiring 5190

Field workers $1,150,000 Electrical Wiring 5190

Total Clerical Payroll (8110): $30,000

Total Supervisor Payroll (5606): $50,000

Total Electrical Wiring Payroll (5190): $1,200,000

Claim Free for over 3 years

ELECTRO ELECTRIC

SERVICES, INC. Scenario 1

Class Code Rate Payroll Premium

8810 (Clerical) 0.18 30,000 54

5606 (Supervisor) 3.41 50,000 1,705

5190 (Electrical Wiring) 5.19 1,200,000 62,280

Total Class Premium 64,039

Schedule Rating 1.0

Experience Mod 0.84

Standard Premium $ 53,793

Over $300K in claims since 2011

Class Code Rate Payroll Premium

8810 (Clerical) 0.18 30,000 54

5606 (Supervisor) 3.41 50,000 1,705

5190 (Electrical Wiring) 5.19 1,200,000 62,280

Total Class Premium 64,039

Schedule Rating 1.0

Experience Mod 1.60

Standard Premium $ 102,462

ELECTRO ELECTRIC

SERVICES, INC. Scenario 2

EXPERIENCE MOD

(Actuarial Science Version)

EXPERIENCE MOD

(Actuarial Science Version)

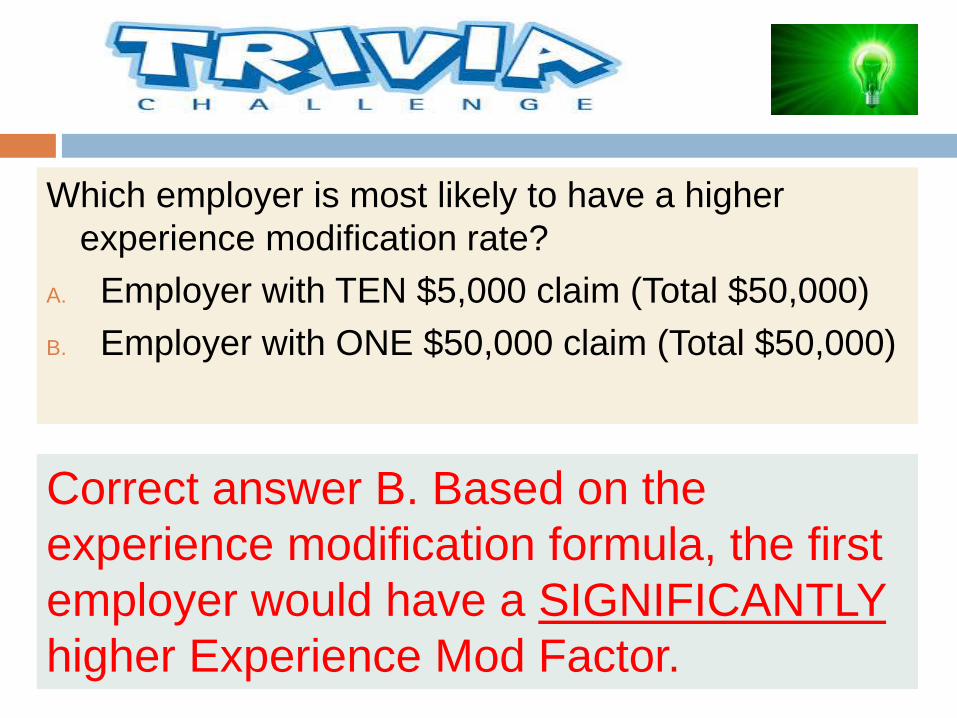

Which employer is most likely to have a higher

experience modification rate?

A. Employer with TEN $5,000 claim (Total $50,000)

B. Employer with ONE $50,000 claim (Total $50,000)

Correct answer B. Based on the

experience modification formula, the first

employer would have a SIGNIFICANTLY

higher Experience Mod Factor.

Ms. Hot Wire from Electro Electric Services

Inc has been in the Electrical industry for

over 15 years. She is a field manager

doing electrical wiring. Unfortunately, she

fell off a ladder and broke her knee.

In which of those 2 cases will Electro

Electric Services Inc end up with a

LOWER experience modification rate?

A. Case A: Employer has a Return To Work program providing Ms. Hot Wire a position in the office to pick up the phone

B. Case B: Employer has NO Return To Work program leaving Ms. Hot Wire at home until she is fully capable of doing what she did before the incident.

Correct Answer:

A. There would be less indemnity and less reserve on the

claim

WHAT TO DO IF YOU HAVE A

CLAIM?

Seek immediate medical attention for the

injured employee

Notify the insurance carrier as soon as

practical – within 24 hours for severe claims

Cooperate with the carrier and provide all

necessary information

Use carrier panel providers whenever possible

to help mitigate claim costs

WORKERS’ COMPENSATION

AUDIT

All Workers’ Compensation policies are issued with “estimated” exposures

Insurance carrier retains the right to audit your books at the end of each policy term to develop the correct policy exposure

Audits generally take place approximately 30 days after expiration

Audit can be done by paper aka “Paper Audit” or in person aka “Physical Audit”

Carriers will in some cases send the audits out to a fee company or independent firm

Have your books ready and available for review

941s

VA EEOC report

1099 tax records during the term

Have certificates of insurance on file for all

payments to subcontractors during the policy

period

Have complete job descriptions for all employees

Cooperate with the carrier

Ask for assistance from your agent

HOW TO PREPARE FOR A

WORKERS’ COMPENSATION

AUDIT?

THANK YOU

WE APPRECIATE YOUR ATTENDANCE & PARTICIPATION

If you have any questions at all, please don’t hesitate to contact McLean Insurance:

703.790.5770