Embed Size (px)

Citation preview

5th June, New York

Business Briefing

Global Capacity

0

500

1,000

1,500

2,000

2,500

3,000

Summer2010

Summer2011

Summer2012

Summer2013

Summer2014

Summer2015

Mil

lio

ns

Approximately there are 2.8 billion seats in Summer 2015 compared

to 2.3 billion at the start of the decade; an increase of 500 million or

1.3 million seats a day.

The average capacity per scheduled flight is now at around 139

compared to 125 at the beginning of the decade.

OAG Schedules Analyser

Global Capacity

0

500

1,000

1,500

2,000

2,500

3,000

Summer 2010 Summer 2015

Mill

ion

s

Scheduled Capacity Comparison

Australasia

Middle East

Latin America

Asia

Africa

North America

Europe

In all regions capacity has increased and this is reflective of the use

of both larger aircraft types and reduced regional jet flying in some

markets, including a 13% decline in North America.

OAG Schedules Analyser

27.5% 26.8%

26.8% 23.0%

27.2% 32.0%

Global Frequency

1718181818181919191919202020

Summer2010

Summer2011

Summer2012

Summer2013

Summer2014

Summer2015

Mil

lio

ns

Scheduled Flights

19.7 million scheduled services planned for Summer 2015, representing

growth of 3% for the peak period year on year. The global picture does

however disguise some significant regional variations.

Over 1.5 million extra flights scheduled for 2015 versus 2010,

approximately 4,100 a day more.

Global Frequency

0

5

10

15

20

25

Summer 2010 Summer 2015

Mill

ion

s Scheduled Flights Comparison

Australasia

Middle East

Latin America

Asia

Africa

North America

Europe

The number of scheduled flights operated in North America has declined

by 7% over the last six years as airline consolidation has impacted

networks and regional operations have been scaled back. The

United/Continental consolidation in particular resulted in an 18%

reduction in frequency over the last five years.

34.6% 29.7%

20.8% 26.6%

25.8% 24.8%

Legacy Versus Low-cost Capacity, Intra

Region

0%10%20%30%40%50%60%70%80%90%

100%

Scheduled Frequency Comparison

Low Cost

Legacy

Low-cost carriers will account for around 27% of global capacity this

summer with Europe at 36% (39% intra Europe) leading the way and

China still at a regional level the least well served by such carriers.

With 6% and 9%, respectively, of capacity provided by LCC’s, China and

Africa appear to be the two last opportunities or challenges.

OAG Schedules Analyser

Alliances Share…

0%10%20%30%40%50%60%70%80%90%

100%

Scheduled Capacity Comparison

Star

Skyteam

OneWorld

Non Aligned

Non-aligned carriers still provide the majority of frequency in the global

market, circa 54%.

Star are the largest alliance and are particularly strong in Africa whilst

Skyteam are the strongest in Asia although that is driven by their

Chinese partnerships (China Eastern and Southern).

OAG Schedules Analyser

And in terms of key carriers…

Source:- OAG Schedules Analyser

The ‘Big Three’ North American carriers dominate the GLOBAL

landscape producing 13% of all available capacity.

EY

QR

EK CA

MU CZ

UA

DL

AA

0

50

100

150

200

250

300

Seats

(m

)

Ranked Order

Seats by Airline in 2014

Load factors at least globally suggest

spare capacity….

30

40

50

60

70

80

90

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014

Avera

ge

Glo

ba

l %

Average Load Factor By Segment

Passenger Cargo

Whilst we may think load factors are now very high (and they are in some

markets!) on average one in five seats remains empty. In the cargo

market less than half of capacity is used highlighting the real directional

challenges of cargo demand (east to west, perishables etc)

*Source: IATA 2014 Annual Report

IATA

But US airlines have been enjoying record levels…..

70

75

80

85

90

Av

era

ge P

ax L

oad

Facto

r %

Average Passenger Load Factors US Major Carriers Systemwide

American Delta Air Lines United Airlines Southwest JetBlue Alaska Spirit

US airlines have been reporting strong load factors over the last year,

with above industry averages reported by most carriers. The low-cost

carriers appear to have improved load factors in the last few months

whilst the three legacy carriers have seen slippages in their numbers.

*Source: OAG DOT Analyser

65

70

75

80

85

90

95

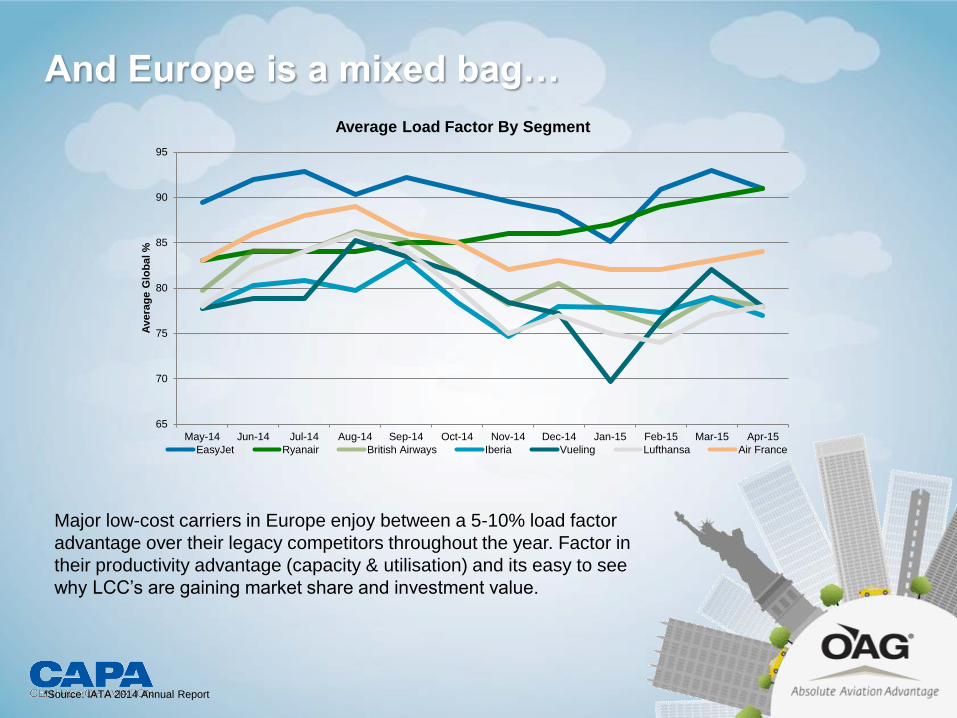

May-14 Jun-14 Jul-14 Aug-14 Sep-14 Oct-14 Nov-14 Dec-14 Jan-15 Feb-15 Mar-15 Apr-15

Avera

ge

Glo

ba

l %

Average Load Factor By Segment

EasyJet Ryanair British Airways Iberia Vueling Lufthansa Air France

Major low-cost carriers in Europe enjoy between a 5-10% load factor

advantage over their legacy competitors throughout the year. Factor in

their productivity advantage (capacity & utilisation) and its easy to see

why LCC’s are gaining market share and investment value.

*Source: IATA 2014 Annual Report

And Europe is a mixed bag…

30

40

50

60

70

80

90

2010 2011 2012 2013 2014 2015 (YTD)

Avera

ge

Glo

ba

l %

Average Load Factor By Segment

AEA Average Load Factor

AEA’s load factors over the last five years have hovered around the 80%

mark on a per annum basis. It may just be that securing load factors

above that point on a yearly basis is just too challenging for some airlines.

Association European Airlines

With Europe reflecting that average level

Capacity in Summary

The North

American

Market

North American Domiciled Carrier Capacity

Share….

0%

20%

40%

60%

80%

100%

2011 2012 2013 2014 2015

Scheduled Capacity Summer Season World

Global Capacity NAM Domiciled Carrier Capacity

21.7%

75.3% 78.3%

Over one in five seats operated by scheduled airlines this summer will be

provided by North American domiciled carriers.

Source:- OAG Schedules Analyser

24.7%

North American Domiciled Carrier Frequency

Share….

0%

20%

40%

60%

80%

100%

2011 2012 2013 2014 2015

Scheduled Frequency Summer Season World

Global Capacity NAM Domiciled Carrier Capacity

29.0%

69.1% 71.0%

Scheduled capacity has continued to grow steadily and faster than

flights, reflecting the use of larger aircraft and continued growth in

emergent markets.

AAGR over the last 5 years has been just above 5% with the strongest

growth occurring in the last two year.

Source:- OAG Schedules Analyser

30.9%

But The Rest of The World is Growing Faster!

The United States is the largest market in the World and despite the

emergence of China, will probably remain so for at least another 7-10 years.

Canada is the 15th largest market (No change) and Mexico are 19th (Down

Two) but in absolute terms, has grown by 26% in that time!

OAG Schedules Analyser

Country Summer

2011

Summer

2015

Movement in

Position

USA 568,713,826 577,342,813 No Change

China 238,817,979 332,634,172 No Change

Japan 94,006,876 109,815,423 No Change

United Kingdom 92,367,240 96,916,630 No Change

Germany 85,875,118 88,065,676 Up One

Brazil 83,372,305 83,762,237 Down One

Spain 82,102,835 80,033,795 No Change

India 67,740,006 79,192,686 No Change

Indonesia 63,465,882 75,802,592 Up Three

France 57,387,294 64,039,068 No Change

Forecast Capacity Growth

0

200

400

600

800

1,000

1,200

Mil

lio

ns

Forecast Capacity Growth

United States & China, Summer Seasons

US Capacity China Capacity

Based on current growth rates we can expect China to become the

largest market in the world based on capacity by 2022, although on

which day remains unclear!

And yet frequency growth remains controlled….

0

2

4

6

8

10

12

14

16

American Delta AirLines

United Southwest AlaskaAirlines

JetBlue Spirit Allegiant

Su

mm

er

Fre

qu

en

cy

(‘

000,0

00’s

)

Frequency Growth From US Majors

Summer '13 Summer '15

12.7% 43.7% 43.0%

In absolute terms there has been no frequency growth in the US market

over the last two Summer seasons. Amongst the ‘Big Four’, no carrier has

added frequency in the last three years.

There is relatively large frequency growth from Spirit, Alaska and Allegiant

but it hardly moves the market needle.

*Source: OAG Schedules Analyser

0.0%

(3.2)% (12.1%)

(3.1%)

12.5%

And capacity hasn’t grown much either….

0

20

40

60

80

100

120

140

160

American Delta AirLines

United Southwest AlaskaAirlines

JetBlue Spirit Allegiant

Su

mm

er

Cap

acit

y S

eats

M

illio

ns

Capacity Growth From US Majors

Summer '13 Summer '15

14.5% 48.8% 42.2%

US domestic capacity has grown by some 4% since Summer’13.

3.4%

4.7%

(2.1%) 1.0%

15.8%

OAG Schedules Analyser

But yields have recently softened…..

6

8

10

12

14

16

18

20

AmericanAirlines Inc.

Delta AirLines Inc.

JetBlueAirways

SouthwestAirlines Co.

Spirit AirLines

United AirLines Inc.

US AirwaysInc.

US Majors Domestic Yields Per Available Seat Kilometre

20134 20144

In the third quarter of 2014, average US domestic yields were between 9-

15% higher than 2013. Latest data for 4th Quarter suggest that yields are

now only slightly above those reported in 2013 and in one case actually

lower.

*Source: OAG DOT Analyser

Load Factor Summary

The Big Three

Discussion

(or is it Four?)

The Big Three/Four Discussion

Direct services between the Middle East and North America have increased considerably

over the last 5 years….

In June 2011 there were 21 non-stop city pair connections with 6 operated by US

domiciled airlines, 11 by Middle East Carriers and 4 by Turkish Airlines.

The Big Three/Four Discussion

Today, some 49 city pairs are being operated….

US domiciled airlines operate 6 of those city pairs, 32 are operated by Middle East

Carriers and 11 by Turkish Airlines.

But other markets have seen similar change

During June 2011, there were 14 non-stop city pair connections from North America to China – today

there are 43 non-stop city pairs. US domiciled carriers operate 18 of those city pairs, Chinese

carriers operate 25; five years ago they operated 7.

Supply has increased, has demand?

OAG Traffic Analyser

- 100 200 300 400 500 600 700 800 900

1,000P

ax

Pe

r A

nn

um

(‘0

00

’s)

Middle East – North America Traffic

2011 2014

In four years the market has grown by 34% with some noticeable

increases in major markets such as Saudi Arabia (+131%) and Iran

(+46%).

Israel is still the largest market in the region with a 32% share of

traffic compared to 40% in 2011.

Supply has increased, has demand?

OAG Traffic Analyser

0

50

100

150

200

250

300

350

Pa

x P

er

An

nu

m (

‘00

0’s

) Middle East – North America Traffic

By Airline

2011 2014

United Airlines have the third largest market share and in the last four

years have seen their traffic increase by 91%; in comparison Emirates

traffic has only increased by some 46%. Only two carriers have seen a

reduction in traffic carried; Delta Air Lines (-29%) and Air France (-4%)

but both have also cut capacity over that time series.

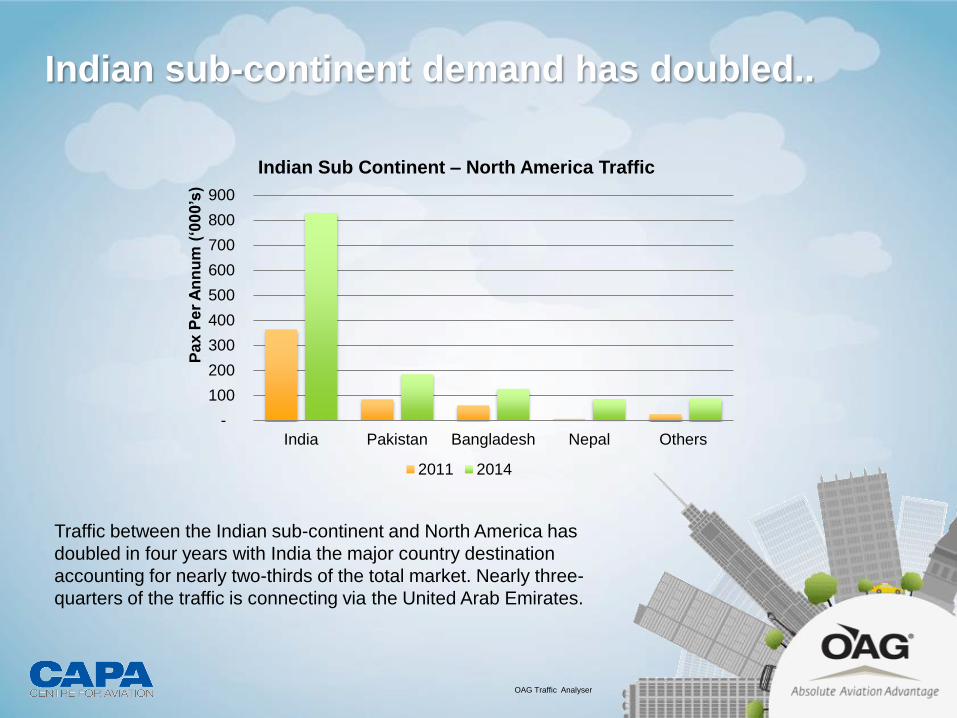

Indian sub-continent demand has doubled..

OAG Traffic Analyser

-

100

200

300

400

500

600

700

800

900

India Pakistan Bangladesh Nepal Others

Pa

x P

er

An

nu

m (

‘00

0’s

)

Indian Sub Continent – North America Traffic

2011 2014

Traffic between the Indian sub-continent and North America has

doubled in four years with India the major country destination

accounting for nearly two-thirds of the total market. Nearly three-

quarters of the traffic is connecting via the United Arab Emirates.

Supply has increased, has demand?

OAG Traffic Analyser

-

100

200

300

400

500

600

Pa

x P

er

An

nu

m (

‘00

0’s

) Indian Sub-Continent – North America Traffic

By Airline

2011 2014

Not surprisingly the Big Three Middle East carriers secure around 90%

of the traffic flow.

And those new services provide feed to US

carriers….

Over 730,000 passengers were ‘fed’ to US domiciled carriers from Emirates,

Etihad and Qatar Airways in 2014. Assume an average ‘feeder’ value of $150

per passenger and that equates to nearly $110 million of feed for little effort.

Passenger Feed …. EK EY QR Grand

Total

US/American 43,853 105,258 304,743 453,854

United Airlines 22,503 7,684 13,954 44,141

Delta Air Lines 27,629 4,410 1,799 33,838

JetBlue 80,616 31,864 23,222 135,702

Others 58,527 2,259 2,422 63,208

233,128 151,475 346,140 730,743

32% 21% 47%

US/American 62%

United Airlines 6%

Delta Air Lines 5%

JetBlue 18%

Others 9%

Carriers benefitting from connecting traffic from Gulf carriers (2014)

OAG Traffic Analyser

Whilst US Airlines ‘fed’ via major European

gateways to the Middle East Carriers….

Some 9,500 passengers were ‘fed’ to the Gulf domiciled carriers from the Big

Three US carriers in 2014 via LON, PAR or FRA. Assume an average ‘feeder’

value of $350 per passenger and that equates to under $3.3 million of ‘

reciprocal’ feed.

Passenger Feed …. AA/US DL UA Grand Total

Emirates 871 194 266 1,291

Etihad 3,598 674 799 5,071

Qatar 2,983 45 63 3,091

Total 7,452 913 1,088 9,453

OAG Traffic Analyser

Big Three Summary

Aircraft &

Market

Evolution

B787 Scheduled Network

Summer 2012 Summer 2012

Number of Scheduled

Flights

8,521

Scheduled Capacity 2,099,720

B787 Scheduled Network

Summer 2015 Summer 2015

Number of Scheduled

Flights

115,081

Scheduled Capacity 30,225,563

A380 Scheduled Network

Summer 2012

Summer 2012

Number of Scheduled

Flights

9,877

Scheduled Capacity 4,773,876

A380 Scheduled Network

Summer 2015

Summer 2015

Number of Scheduled

Flights

52,447

Scheduled Capacity 25,487,701

Thank you!