Embed Size (px)

Citation preview

Airline Industry Economics Advisory Workshop 2016 1

Outlook for growth,

traffic and airline profits

Brian Pearce,

Chief Economist,

IATA

www.iata.org/economics

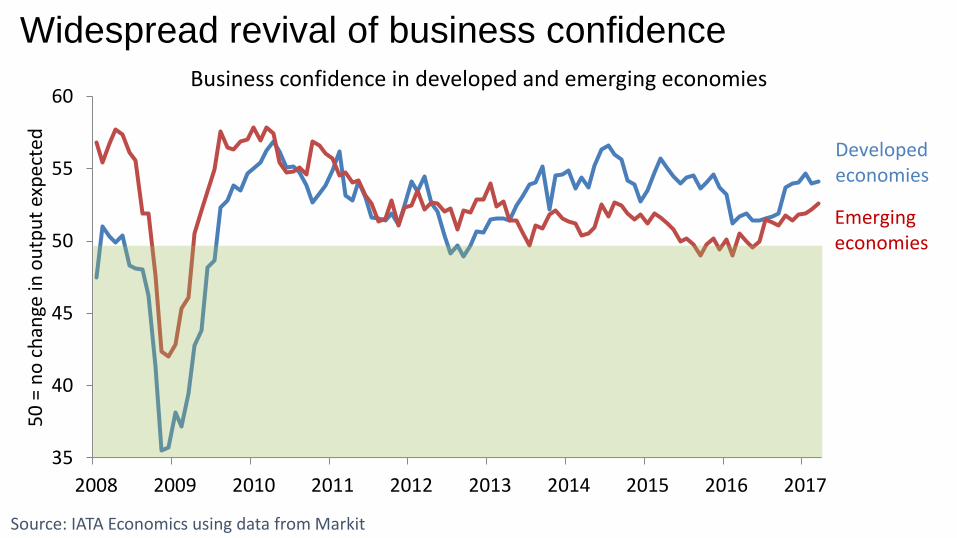

Widespread revival of business confidence

Source: IATA Economics using data from Markit

35

40

45

50

55

60

2008 2009 2010 2011 2012 2013 2014 2015 2016 2017

50

= n

o c

han

ge in

ou

tpu

t ex

pec

ted

Business confidence in developed and emerging economies

Developedeconomies

Emerging economies

Consumers have become more confident too

Source: IATA Economics using data from Datastream

96

97

98

99

100

101

102

2008 2009 2010 2011 2012 2013 2014 2015 2016 2017

Worldwide average consumer confidence

Donald Trump Vows to Rip Up

Trade Deals and Confront ChinaThe New York Times

28 June 2016

Perhaps surprisingly given political shocks

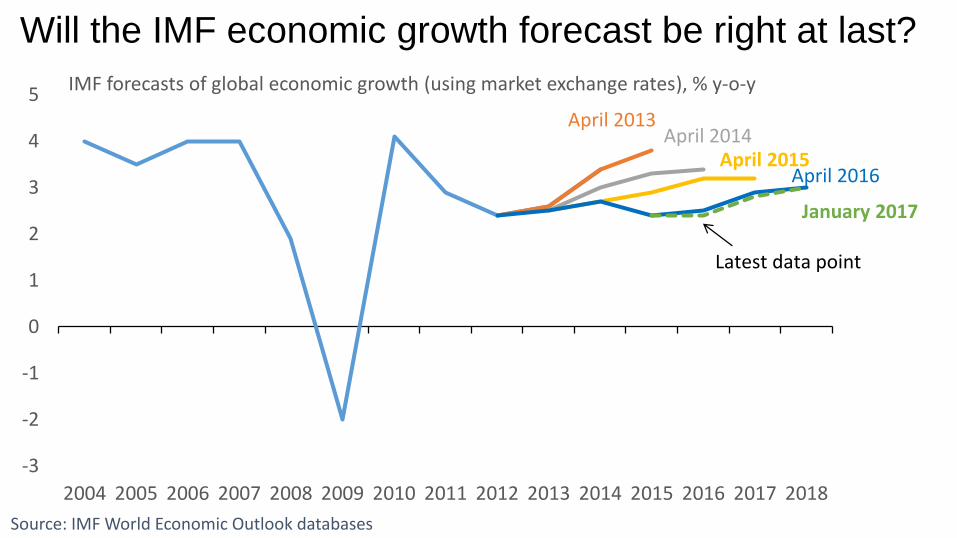

Will the IMF economic growth forecast be right at last?

Source: IMF World Economic Outlook databases

-3

-2

-1

0

1

2

3

4

5

2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017 2018

IMF forecasts of global economic growth (using market exchange rates), % y-o-y

April 2013April 2014

April 2015April 2016

January 2017

Latest data point

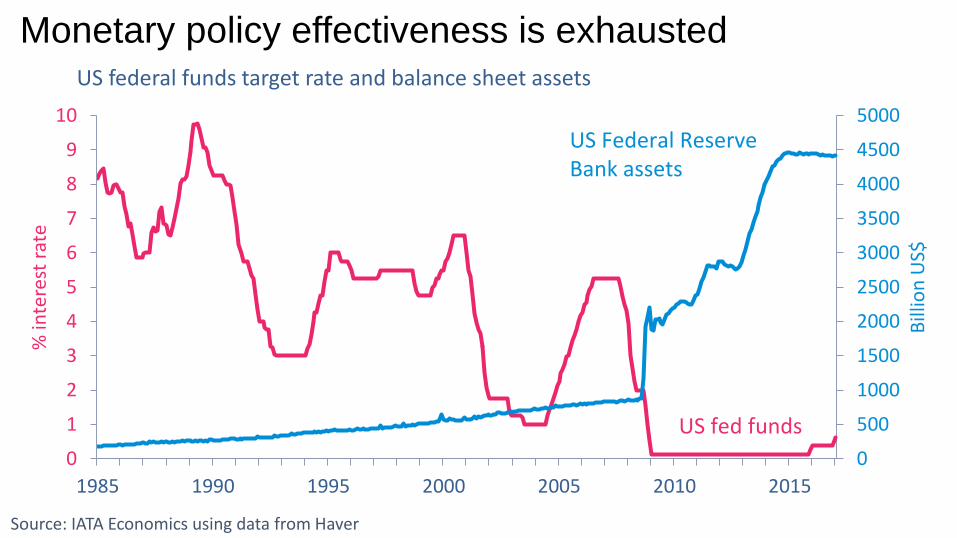

Monetary policy effectiveness is exhausted

Source: IATA Economics using data from Haver

0

500

1000

1500

2000

2500

3000

3500

4000

4500

5000

0

1

2

3

4

5

6

7

8

9

10

1985 1990 1995 2000 2005 2010 2015

Bill

ion

US$

% in

tere

st r

ate

US federal funds target rate and balance sheet assets

US fed funds

US Federal Reserve Bank assets

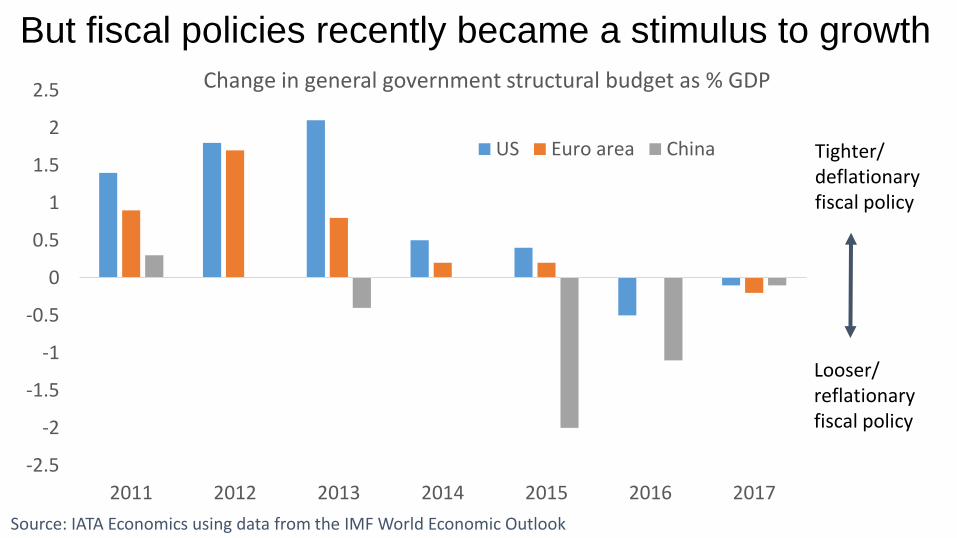

But fiscal policies recently became a stimulus to growth

Source: IATA Economics using data from the IMF World Economic Outlook

-2.5

-2

-1.5

-1

-0.5

0

0.5

1

1.5

2

2.5

2011 2012 2013 2014 2015 2016 2017

Change in general government structural budget as % GDP

US Euro area China Tighter/ deflationary fiscal policy

Looser/ reflationary fiscal policy

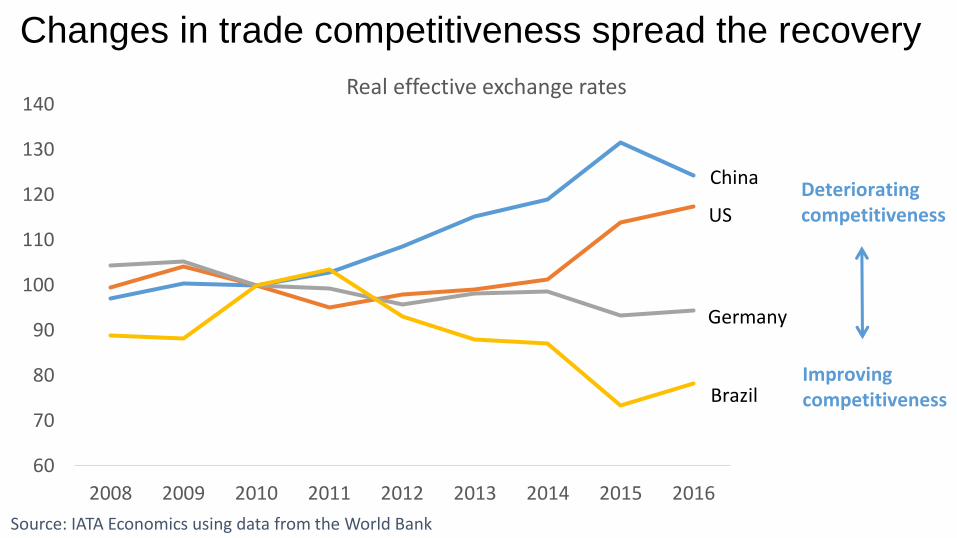

Changes in trade competitiveness spread the recovery

Source: IATA Economics using data from the World Bank

60

70

80

90

100

110

120

130

140

2008 2009 2010 2011 2012 2013 2014 2015 2016

Real effective exchange rates

China

US

Germany

Brazil

Deteriorating competitiveness

Improving competitiveness

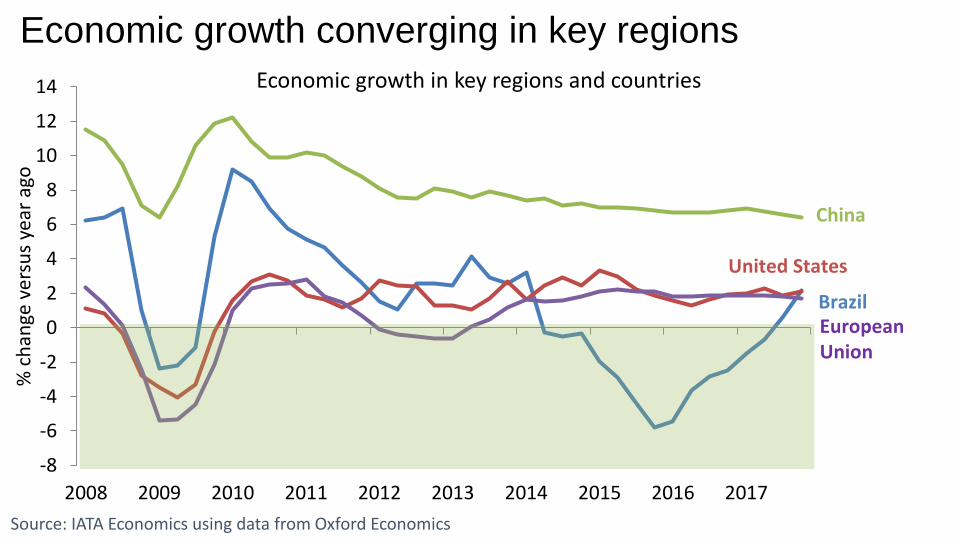

Economic growth converging in key regions

Source: IATA Economics using data from Oxford Economics

-8

-6

-4

-2

0

2

4

6

8

10

12

14

2008 2009 2010 2011 2012 2013 2014 2015 2016 2017

% c

han

ge v

ersu

s ye

ar a

go

Economic growth in key regions and countries

China

Brazil

United States

European Union

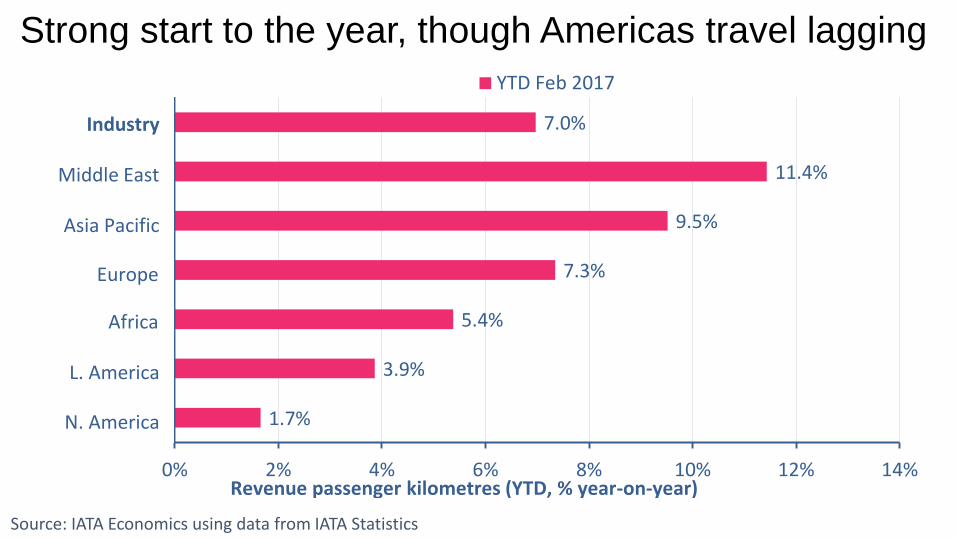

Strong start to the year, though Americas travel lagging

Source: IATA Economics using data from IATA Statistics

1.7%

3.9%

5.4%

7.3%

9.5%

11.4%

7.0%

0% 2% 4% 6% 8% 10% 12% 14%

YTD Feb 2017

Revenue passenger kilometres (YTD, % year-on-year)

Industry

Middle East

Asia Pacific

Europe

Africa

L. America

N. America

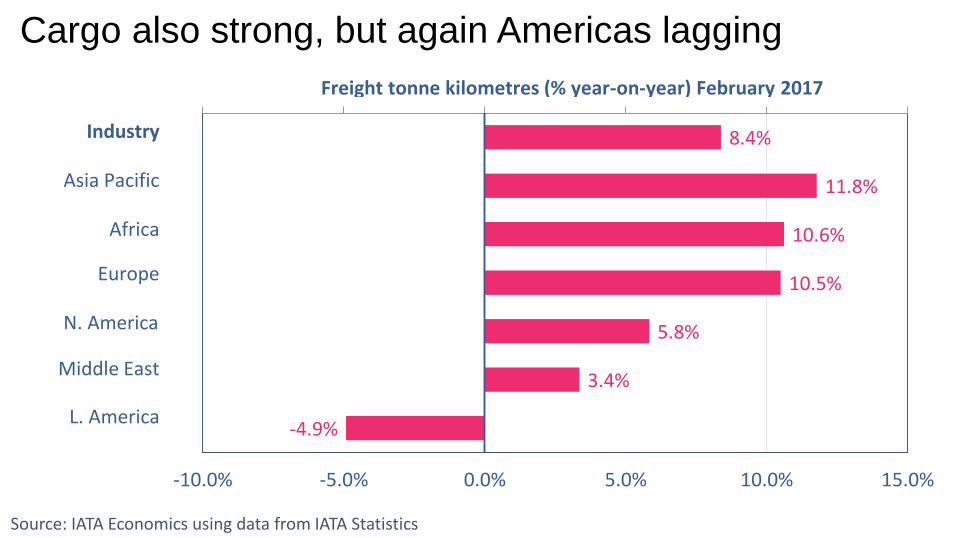

Cargo also strong, but again Americas lagging

Source: IATA Economics using data from IATA Statistics

-4.9%

3.4%

5.8%

10.5%

10.6%

11.8%

8.4%

-10.0% -5.0% 0.0% 5.0% 10.0% 15.0%

Freight tonne kilometres (% year-on-year) February 2017

Industry

Asia Pacific

Africa

Europe

N. America

Middle East

L. America

Airline Industry Economics Advisory Workshop 2016 12

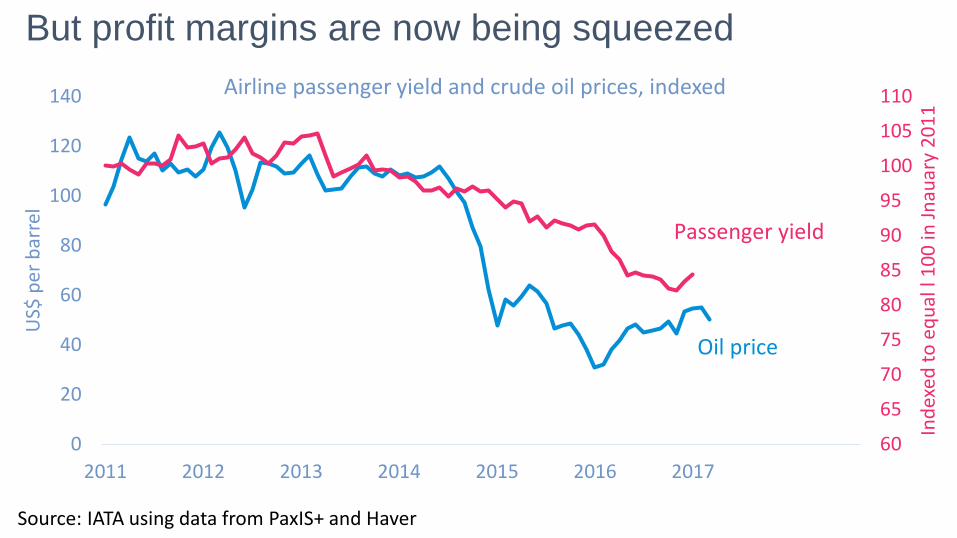

But profit margins are now being squeezed

Source: IATA using data from PaxIS+ and Haver

60

65

70

75

80

85

90

95

100

105

110

0

20

40

60

80

100

120

140

2011 2012 2013 2014 2015 2016 2017

Ind

exed

to

eq

ual

l 1

00

in J

nau

ary

20

11

US$

per

bar

rel

Airline passenger yield and crude oil prices, indexed

Oil price

Passenger yield

Airline Industry Economics Advisory Workshop 2016 13

Industry profitability peaked a year ago

Source: IATA Economic Performance of the Airline Industry – end year 2016 report

-2%

0%

2%

4%

6%

8%

10%

12%

14%

16%

2011 2012 2013 2014 2015 2016 2017

EBIT

as

% r

even

ues

Quarterly profile for airline industry operating profits (EBIT)

Seasonally adjusted margins

Unadjusted margins

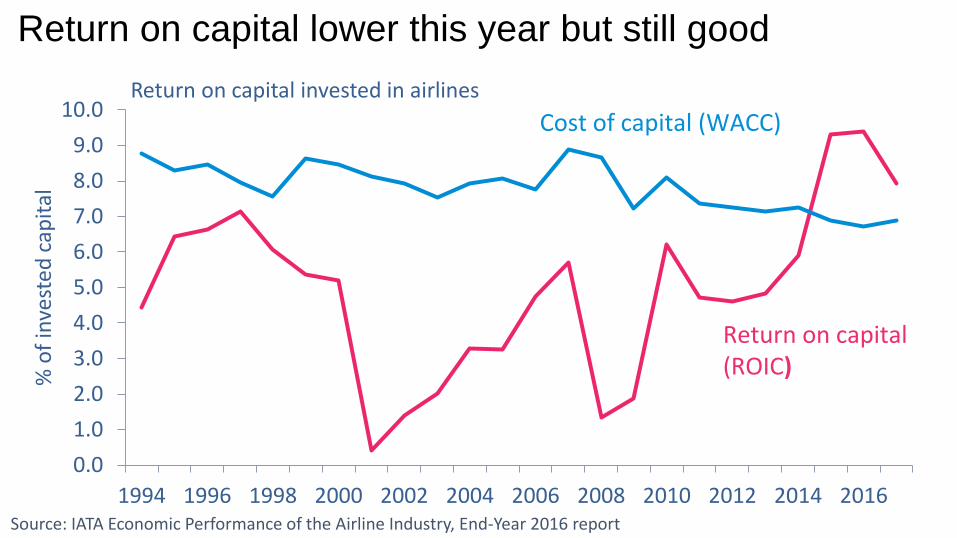

Return on capital lower this year but still good

Source: IATA Economic Performance of the Airline Industry, End-Year 2016 report

0.0

1.0

2.0

3.0

4.0

5.0

6.0

7.0

8.0

9.0

10.0

1994 1996 1998 2000 2002 2004 2006 2008 2010 2012 2014 2016

% o

f in

vest

ed c

apit

al

Return on capital invested in airlines

Cost of capital (WACC)

Return on capital (ROIC)

Airline Industry Economics Advisory Workshop 2016 15

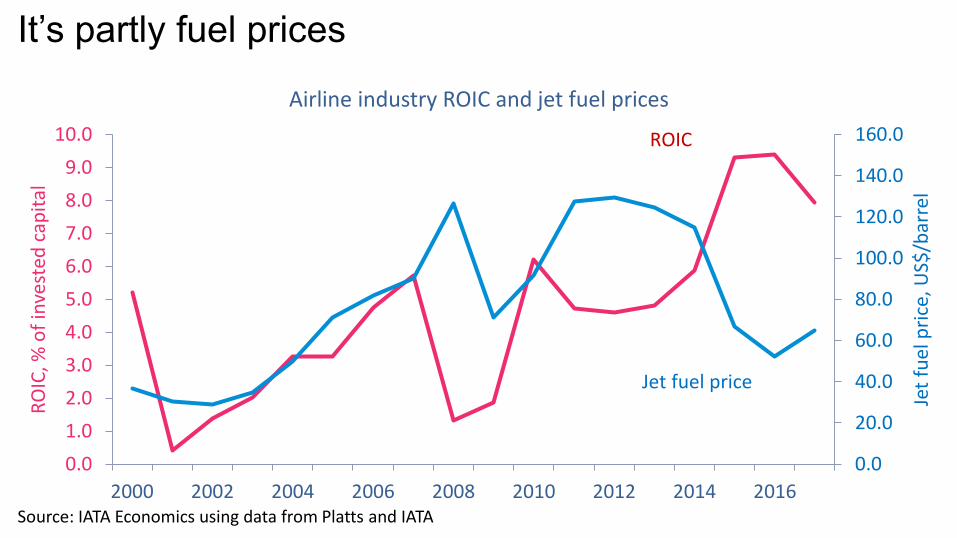

It’s partly fuel prices

Source: IATA Economics using data from Platts and IATA

0.0

20.0

40.0

60.0

80.0

100.0

120.0

140.0

160.0

0.0

1.0

2.0

3.0

4.0

5.0

6.0

7.0

8.0

9.0

10.0

2000 2002 2004 2006 2008 2010 2012 2014 2016

Jet

fuel

pri

ce, U

S$/b

arre

l

RO

IC, %

of

inve

sted

cap

ital

Airline industry ROIC and jet fuel prices

ROIC

Jet fuel price

Airline Industry Economics Advisory Workshop 2016 16

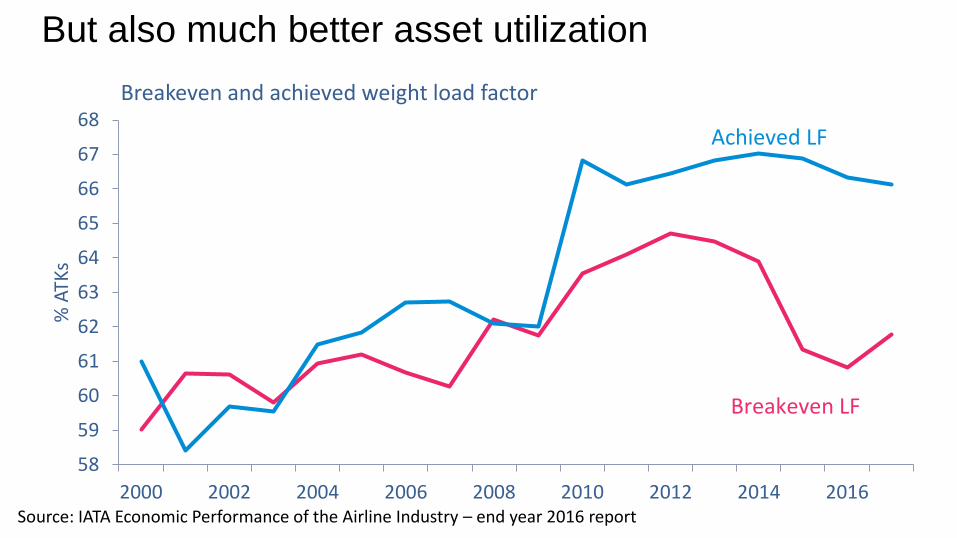

But also much better asset utilization

58

59

60

61

62

63

64

65

66

67

68

2000 2002 2004 2006 2008 2010 2012 2014 2016

% A

TKs

Breakeven and achieved weight load factor

Achieved LF

Breakeven LF

Source: IATA Economic Performance of the Airline Industry – end year 2016 report

Airline Industry Economics Advisory Workshop 2016 17

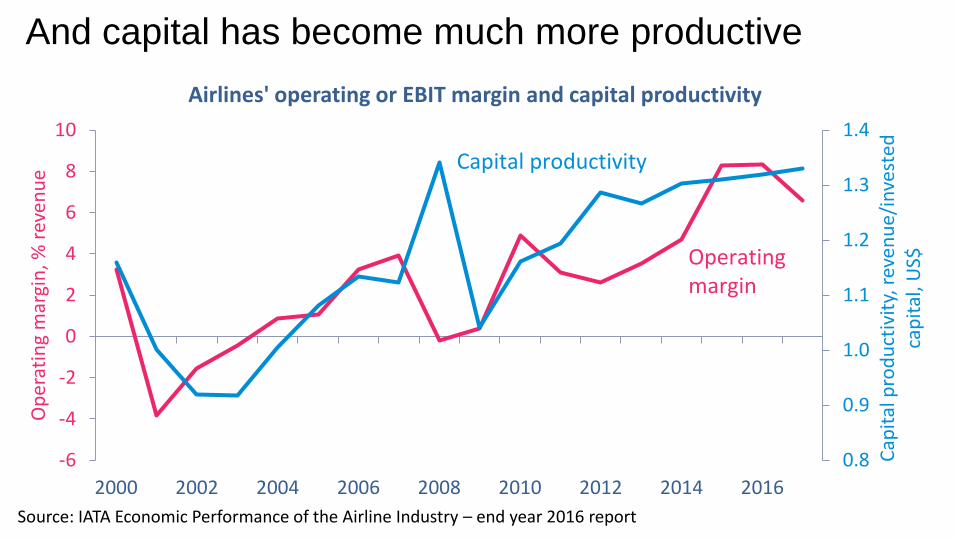

And capital has become much more productive

0.8

0.9

1.0

1.1

1.2

1.3

1.4

-6

-4

-2

0

2

4

6

8

10

2000 2002 2004 2006 2008 2010 2012 2014 2016

Cap

ital

pro

du

ctiv

ity,

rev

enu

e/in

vest

ed

cap

ital

, US$

Op

erat

ing

mar

gin

, % r

even

ue

Airlines' operating or EBIT margin and capital productivity

Capital productivity

Operating margin

Source: IATA Economic Performance of the Airline Industry – end year 2016 report

But performance is very different between regions

Source: IATA Economics using data from The Airline Analyst

0%

2%

4%

6%

8%

10%

12%

14%

16%

18%

20%

2010 2011 2012 2013 2014 2015 2016

EBIT

ad

just

ed f

or

op

erat

ing

leas

es a

s %

in

vest

ed c

apit

alReturn on invested capital

Industry average

North America

Europe

Asia Pacific

Latin AmericaMiddle East

Weighted Average Cost of Capital

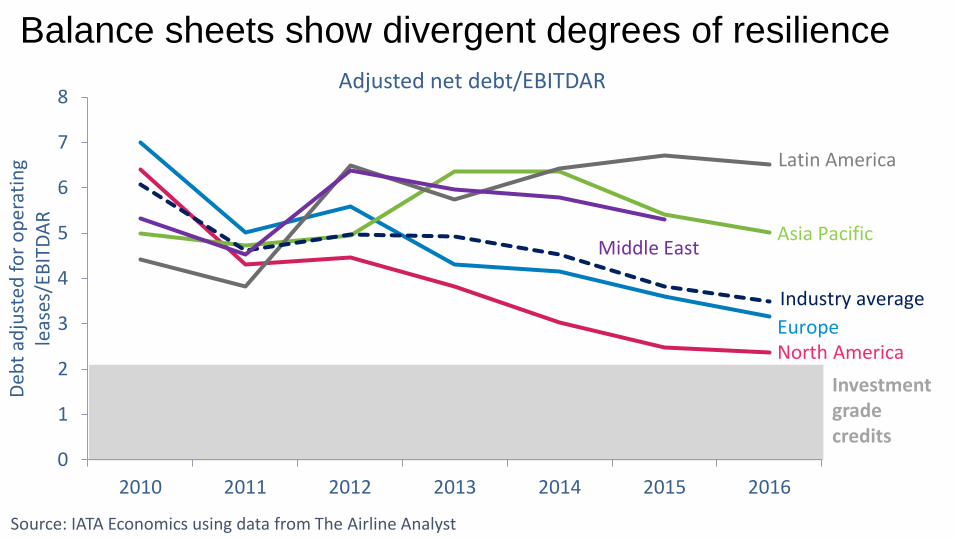

Balance sheets show divergent degrees of resilience

Source: IATA Economics using data from The Airline Analyst

0

1

2

3

4

5

6

7

8

2010 2011 2012 2013 2014 2015 2016

Deb

t ad

just

ed f

or

op

erat

ing

leas

es/E

BIT

DA

R

Adjusted net debt/EBITDAR

Latin America

Asia Pacific

Industry average

EuropeNorth America

Middle East

Investment grade credits

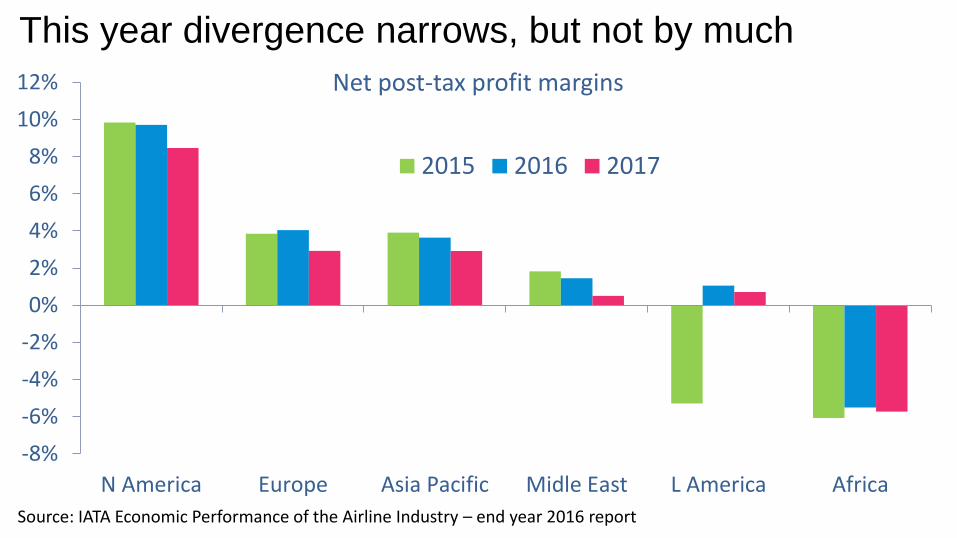

This year divergence narrows, but not by much

Source: IATA Economic Performance of the Airline Industry – end year 2016 report

-8%

-6%

-4%

-2%

0%

2%

4%

6%

8%

10%

12%

N America Europe Asia Pacific Midle East L America Africa

Net post-tax profit margins

2015 2016 2017

Airline Industry Economics Advisory Workshop 2016 21