Embed Size (px)

Citation preview

1999 Annual Report

A StrongerCompany

Better Positioned

United Dominion Realty Trust

10 South Sixth Street

Richmond, Virginia 23219-3802

804.780.2691

www.udrt.com

Un

ited Do

min

ion

Realty Tru

st A Stro

nger Co

mpany—

Better Po

sition

ed1999 An

nual R

eport

De

sig

n:

Fra

nk

lin

Str

ee

t M

ark

eti

ng

& A

dve

rtis

ing

P

ho

tog

rap

hy

: C

hip

Mit

che

ll

United Dominion Realty Trust, Inc., founded in 1972, is a leading

national apartment operating company with a strong focus on service

to its residents. United Dominion owns 82,000 completed apartment

homes in 301 communities, has 1,800 additional apartment homes

under development and employs approximately 2,400 associates.

The company acquires, repositions, develops, owns, manages and

selectively sells apartment communities nationwide. | United

Dominion’s goal is to provide an annual average shareholder return

of at least 15%. The company has a long and successful history as

a publicly traded real estate investment trust, having increased its

dividend every year for the past 23 years. | Over the past three years,

United Dominion has strategically repositioned itself to increase

long-term profitability. This process has entailed diversifying into

new markets in the West, Northwest and Midwest, upgrading the

quality of the portfolio, building development capability and

investing in systems and other technology. | United Dominion’s

common stock is traded on the New York Stock Exchange under

the symbol UDR.

U N I T E D D O M I N I O N R E A LT Y T R U S T, I N C .

C o n t e n t s

1 FINANCIAL HIGHLIGHTS

2 LETTER TO SHAREHOLDERS

8 OUR ASSETS

14 DEVELOPMENT

16 RESIDENT SATISFACTION

18 TECHNOLOGY

20 FINANCIAL SECTION

44 GENERAL INFORMATION

1

Years Ended December 31, 1999 1998 1997

Dollars in millions, except per share amounts and apartment homes owned

For the YearRental income $ 618.7 $ 478.7 $ 386.7Income from property operations excluding depreciation (NOI) 371.5 279.2 222.9Income before gains on sales of investments,

minority interests and extraordinary item 60.4 47.3 57.8Net income 93.6 72.3 70.1Distributions to preferred shareholders 37.7 23.6 17.3Net income available to common shareholders 55.9 48.7 52.8Funds from operations* 176.4 139.3 117.2Common distributions declared 109.6 107.8 88.6

Per ShareEarnings per common share-diluted $ 0.54 $ 0.49 $ 0.60Funds from operations-diluted 1.42 1.34 1.34Common distributions declared 1.06 1.05 1.01

At Year EndReal estate owned** $3,953.0 $3,952.8 $2,517.4Secured debt 1,000.1 1,072.2 417.3Unsecured debt 1,127.2 1,045.6 738.9Shareholders’ equity 1,310.2 1,374.1 1,058.4Number of common shares outstanding 102.7 103.6 89.2Number of completed apartment homes owned 82,154 86,893 62,789

* Funds from operations is defined as income before gains (losses) on sales of investments, minority interests of unitholders in operating partnership and extraordinary items (computed in accordance with generally accepted accounting principles) plus real estate depreciation, less preferred dividends and after adjustment for significant non-recurring items, if any.

** Includes real estate held for investment, real estate held for disposition and real estate under development, at cost.

F I N A N C I A L H I G H L I G H T S

I am pleased to report that the

changes to United Dominion

that began at the end of 1996 are

substantially complete. During 1999,

for the first time in our history,

we operated a national apartment

portfolio with excellent regional and market diversification. We continued

to upgrade our portfolio and narrow our product mix by selling an additional

7,400 non-core apartment homes during the year. In the process, we exited

some markets with limited growth prospects. We completed the development

of seven projects, six new communities and one second phase. Our increased

development capability, with acquisitions, gives us more investment options.

We continued to strengthen our management team, both at the senior level

and throughout our organization. Additionally, we invested in state-of-the-

art accounting and information systems that will provide operating and

marketing advantages as well as better tools to enhance decision making.

D E A R S H A R E H O L D E R S

2

Most importantly over the past three years, we

have become better apartment operators, more

focused on our resident customers. We are now

beginning to realize the benefits which come from

being a better positioned and stronger company,

including consistent net operating income (NOI)

growth, expanding operating margins, strong

expense control, operating efficiencies, lower

recurring capital expenditures and more cash flow

per apartment home. As a consequence, we

reported improved results for the year.

3

1 9 9 9 A C C O M P L I S H M E N T S

• Same community NOI growth of more than

5% for the third consecutive year.

• Recurring capital expenditures per apartment

down 20% from the average of the past three

years.

• Return on investment for the first year on

American Apartment Communities II

properties (AAC) of 9.1%.

• Seven development completions in five

different markets, with lease-ups generally

ahead of projected absorption.

• Apartment sales of $241 million as a key part

of upgrading the portfolio.

• A stock buyback program that resulted in

repurchasing $38 million of common stock

and OP units.

• Funds from operations (FFO) per share

growing at an increasing rate each quarter

compared to last year and 5.8% for the

full year.

• Systems upgrades and technology initiatives

that make us a technology leader among

apartment companies.

• Higher resident satisfaction than ever before,

as indicated on our resident surveys.

JOHN MCCANN,

CHAIRMAN & CHIEF EXECUTIVE OFFICER

(Center)

JOHN SCHNEIDER,

PRESIDENT & CHIEF OPERATING OFFICER

(Left)

BILL HAMILL,

EXECUTIVE VICE PRESIDENT &

CHIEF FINANCIAL OFFICER

(Right)

Results of Operations

For 1999, FFO, our primary earnings measure, was $176.4 million or

$1.42 per diluted share, compared with $139.3 million or $1.34 per

diluted share in 1998. The company reported total rental income of

$618.7 million, NOI of $371.5 million and net income available to

common shareholders of $55.9 million or $.54 per diluted share.

Our key earnings driver was same community NOI growth. In

1999, same community NOI grew 5.6% at the 51,316 apartments

owned throughout both years. NOI growth resulted from a 3.4%

increase in average rental rates, a 0.1% increase in economic occu-

pancy and a 0.6% decline in operating expenses. We enjoyed solid

rent growth in all but one of our ten largest markets, led by Orlando,

Houston, Dallas, Richmond and Tampa, where rent growth exceeded

4%. Occupancy climbed in all of our Mid-Atlantic markets, while

declines in Dallas, Houston, and Orlando were very modest. Much of

the decline in operating expenses was the result of the transfer of

water and sewer costs to our residents, the impact of economies of

scale and initiatives to do more of our apartment turnover work

in-house. With growing revenues and a modest decline in expenses,

our gross operating margin climbed 1.5%. We have been able to

consistently grow same community results year over year.

Primarily as a result of our significant acquisition activity over

the past two years to create a national apartment portfolio, non-

mature communities provided 40% of our revenues. The AAC port-

folio, our largest 1998 acquisition, provided a first-year return on

investment of 9.1%, slightly above the projected return. However,

our 1999 FFO per share growth was moder-

ated by disappointing returns from other

1998 acquisitions and costs associated with

the company’s repositioning, including

dispositions, increased development and

technology investments.

Financial Flexibility/Stock Buyback

United Dominion’s significant 1998 acquisition activity was financed

primarily with debt and, to a lesser extent, preferred stock. Since

completing the acquisitions, we have been committed to increasing

our financing flexibility by reducing debt and maintaining Baa2/ BBB

investment grade debt ratings. By doing so, our financing costs will

decrease, and our financing options will

increase.

During 1999, we used $141 million,

or 59%, of the proceeds from apartment

sales to repay outstanding debt. In 2000,

we will again use most of our divestiture

proceeds to repay debt.

In equity markets, the stock prices of

REITs continued to trade down in 1999.

Most REITs, including our company, are

trading at material discounts to the under-

lying net asset value (NAV) of their real

estate. For the benefit of our shareholders,

we took advantage of this opportunity and

bought back stock and operating partner-

ship units at a significant discount to our

NAV. Consistent with our commitment

to increase our financial flexibility, we

limited the repurchases to approximately

$38 million, which was 16% of the

proceeds from our divestitures in 1999.

LA PRIVADA, PHOENIX, AZ

KELLY CROSSING, DALLAS, TX

4

In 2000, we may repurchase additional shares of our common

stock and operating partnership units. Our board has authorized

the repurchase of up to 5.5 million shares, and by the end of 1999,

only 3.3 million shares and OP units had been repurchased. Any

such repurchases, however, will only be undertaken if our financial

flexibility would be sufficient to maintain Baa2/BBB debt ratings.

Looking Ahead

As a result of the changes made over the past three years, we

believe United Dominion is now much better positioned. We

upgraded our portfolio by selling more than 15,000 apartment

homes, added features to core communities to better position them

to compete in their markets and developed approximately 3,500

new homes, with another 700 nearing completion. We exited some

slower growing Southeast markets and invested in markets where

growth opportunities are better.

A key element for 2000 will be our success in growing average

occupancy during a time when economic growth may slow slightly,

and new apartment home completions remain near the levels

where they have been the past two years. We believe that occu-

pancy gains are achievable through a number of enhanced pro-

grams including renting more apartments over the Internet and

greater use of revenue maintenance tools to manage vacant inven-

tory. Assuming the national economy continues to grow, we’re

confident that we can deliver same community NOI growth in

2000 when our same communities will produce more than 90% of

company revenues.

While we expect consistent NOI

growth to once again drive our earnings

growth, expected higher interest rates, the

use of disposition proceeds to reduce debt,

and technology investments will offset

some of the NOI growth.

The combination of lower capital

expenditures plus steady NOI growth over

the three year period has increased cash

flow per apartment home approximately

30%, compared to 1996. Higher cash flow

and lowering our dividend payout ratio

allowed the company to internally generate

and retain more cash flow. Over the next

two years, we hope to increase retained

cash flow from a continuing decline in

capital expenditures and lowering our

dividend payout ratio, as FFO growth

outpaces dividend growth.

5

Over the past three years, the company has invested in both

the systems and people necessary to make us a more efficient and

better apartment operating company. Our stronger team and

enhanced systems provide us with longer-term operating and

marketing advantages and make us a technological leader in

our business.

While we have improved United Dominion’s positioning,

the external environment in which we operate is continuing to

change, and we must continue to change with it. Even though we

are a technology leader in the apartment business, we can only begin

to anticipate the impact that technology, including e-commerce, will

have on our business longer-term.

Technology-based opportunities, as well as other new initia-

tives, will be easier to pursue since Congress recently approved the

REIT Modernization Act that will become effective in 2001. These

new regulations will allow us to offer our residents additional services

and enable us to invest in synergistic businesses. As a result, these

regulations provide new ways for us to increase our profitability.

As we repositioned our company over the past few years, we

made substantial changes. Since we first embarked on our reposi-

tioning, the housing markets and financial environment have

changed significantly. Soon, the range of activities open to REITs will

expand. In view of all these changes, we believe that it is appropriate

to review and refine our business strategy. In the first half of 2000,

we will be undertaking a comprehensive assessment of the various

market segments in which we operate as well as an evaluation of

alternative investment opportunities avail-

able to us. We expect to complete this

process by the end of the summer.

Whatever refinements we make to our

business strategy will be done with the goal

of further improving the company’s long-

term earnings outlook and increasing the

level of returns generated for our share-

holders. We are excited about the prospects for United Dominion,

and we look forward to reporting to you on the strategy review.

In closing, I want to recognize and thank Jeff Bane, one of the

founders of United Dominion, who will retire from our Board of

Directors at the May annual shareholders’ meeting. Jeff has served

our company and shareholders very well as a director for almost 28

years, and his wise counsel will be missed.

I want to recognize our professional and hardworking associates

across the country, at our communities, in our area and regional

offices, and in our corporate headquarters for their dedication,

hard work, commitment to our customers, and willingness to

accept change to make us better. Thanks for all that you accom-

plished in 1999.

Finally, I want to thank our shareholders for their support. The

repositioning of United Dominion has been a substantial undertaking.

As a stronger and better positioned company, United Dominion has

greater opportunities to create value for our shareholders.

Sincerely,

John P. McCann

Chairman and CEO

February 11, 2000

PROVIDENCE COURT, CHARLOTTE, NC

ARBORS AT LEE VISTA, ORLANDO, FL

6

7

We have 82,000 quality apartment homes from

Baltimore to Fort Lauderdale to San Diego to

Seattle. Our 301 communities are an excellent

growth platform for generating increasing cash flow

and creating new sources of revenue by providing

other services for our more than 200,000 resident

customers. We have a deep and creative

management team and experienced

associates committed to continuous improvement.

We have made and will continue making financing

changes to increase our financing flexibility.

Change for the better has been a constant at

United Dominion over the past few years.

Our Assets

RANCHO VALLECITOS, SAN DIEGO, CA

8

9

Our Apartment Homes

Upgraded Portfolio

Over the past three years, in order to meet

our key operating objectives, including

more predictable NOI growth, lower capital

expenditures and greater management effi-

ciencies, we began narrowing our apartment

product focus to A and B grade communities.

Part of the impetus to do this was what we

saw as the evolution of the apartment industry

into a service business with opportunities to deliver additional

services to our residents and generate income in addition to rents.

To take full advantage of this, we needed to serve a resident

customer with more household income. We began the process

of upgrading our apartment portfolio through several initiatives:

• The sale of more than 15,000 of our older, slower growing apartments

where there was greater capital expenditure exposure. Dispositions

entailed exiting some markets, the largest being Greenville/Spartanburg,

South Carolina, which historically had been a slow growth market.

• The completion of the development of 3,500 new B+ and A apartment

homes during the past three years and assembling a development

pipeline as a source of further new product.

• The acquisition of B grade and above communities, many in markets

that offer better prospects for NOI growth.

• The addition of new features and enhanced amenities

including interior upgrades, security features,

garages, carports, storage units, water and sewer

submeters, business centers, and enlarged fitness

centers.

As a result of our upgrade program, we have

improved the overall quality of our portfolio.

Today, we have significantly higher average

rents and NOI, lower recurring and non-recurring

capital expenditures and consequently more

cash flow per apartment home.

A feature of better, higher rent communities is resident

customers with greater discretionary income. To capitalize on this,

we are introducing new resident services at our communities to

generate more non-rental income.

Geographical Diversity

Our objective has been to operate a national portfolio with both

regional and market diversification to minimize the risk of local

oversupply and economic cycles. For the first time in our history,

we are operating a truly national portfolio. On the West Coast,

Seattle, Portland, Sacramento, San Francisco, the Monterey

Peninsula, and Southern California became important markets

for us. Other new markets included Denver,

and in the Midwest, Columbus, Detroit and

Indianapolis. By the fourth quarter, western

markets were providing almost 20% of our

NOI and midwest markets another 8%.

As a result of the geographic diversifi-

cation achieved in 1998 and 1999, no single

market will provide more than 10% of our

NOI in 2000, and our 20 largest markets, which

include San Francisco, Columbus, the Monterey

Peninsula, and Southern California, will provide

76% of our 2000 NOI.

LEGACY HILL, NASHVILLE, TN

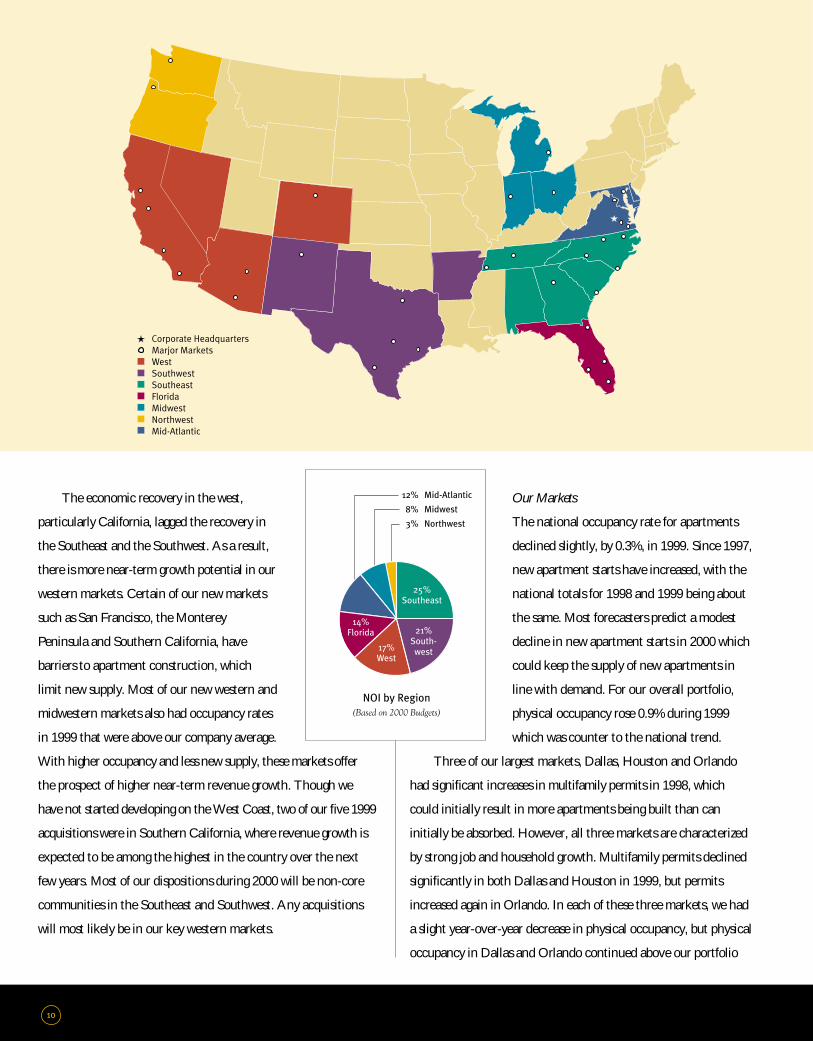

The economic recovery in the west,

particularly California, lagged the recovery in

the Southeast and the Southwest. As a result,

there is more near-term growth potential in our

western markets. Certain of our new markets

such as San Francisco, the Monterey

Peninsula and Southern California, have

barriers to apartment construction, which

limit new supply. Most of our new western and

midwestern markets also had occupancy rates

in 1999 that were above our company average.

With higher occupancy and less new supply, these markets offer

the prospect of higher near-term revenue growth. Though we

have not started developing on the West Coast, two of our five 1999

acquisitions were in Southern California, where revenue growth is

expected to be among the highest in the country over the next

few years. Most of our dispositions during 2000 will be non-core

communities in the Southeast and Southwest. Any acquisitions

will most likely be in our key western markets.

Our Markets

The national occupancy rate for apartments

declined slightly, by 0.3%, in 1999. Since 1997,

new apartment starts have increased, with the

national totals for 1998 and 1999 being about

the same. Most forecasters predict a modest

decline in new apartment starts in 2000 which

could keep the supply of new apartments in

line with demand. For our overall portfolio,

physical occupancy rose 0.9% during 1999

which was counter to the national trend.

Three of our largest markets, Dallas, Houston and Orlando

had significant increases in multifamily permits in 1998, which

could initially result in more apartments being built than can

initially be absorbed. However, all three markets are characterized

by strong job and household growth. Multifamily permits declined

significantly in both Dallas and Houston in 1999, but permits

increased again in Orlando. In each of these three markets, we had

a slight year-over-year decrease in physical occupancy, but physical

occupancy in Dallas and Orlando continued above our portfolio

O U R A S S E T S

10

average. We had solid rent growth in all three markets and strong

NOI growth in Houston and Orlando.

Multifamily permits increased in Charlotte, Raleigh, and

Tampa in 1999, three of our major markets, so these markets

could soften in the short-term. However, if the pattern that we’ve

seen over the past five years continues, there should be a precipitous

drop in permits in these markets in 2000. With a very diversified

portfolio, each year we expect some of our markets to be strong,

some to be average, and some to be weak. Among our mature

markets, Houston, Orlando, Tampa, Richmond and Nashville

were very strong for us in 1999.

Operations

Beginning in 1997, we refocused our company on serving our

resident customers. Each year since then, the scores on our resident

satisfaction surveys have risen. These surveys indicate that we are

better serving our resident customers, and that they are more satisfied

with their living experience in our communities. We believe that

this has contributed to our above market

average rent growth over the past two years.

Our operations group, including

on-site staff, know how to grow NOI. Since

1995, same community NOI has grown

more than 5% each year except 1996.

One of our objectives in 1999 was to

reduce operating expenses, which on a

same community basis, declined 0.6%.

We were a pioneer in the transfer of water

and sewer costs to residents when we

began submetering individual apartment

usage in 1995. By 1998, we made the

decision to transfer this cost to the residents

of all of our communities and to bear the

expense of using submeters, wherever we

could. As a result of this initiative, we reduced our water and

sewer expense in 1999. We did not have full penetration at all of

our communities being billed at year-end. The ramp up of water

and sewer reimbursement will continue throughout 2000 and will

further reduce utility expense. Additionally in 1999, we were able

to reduce certain operating expenses from size efficiencies, through

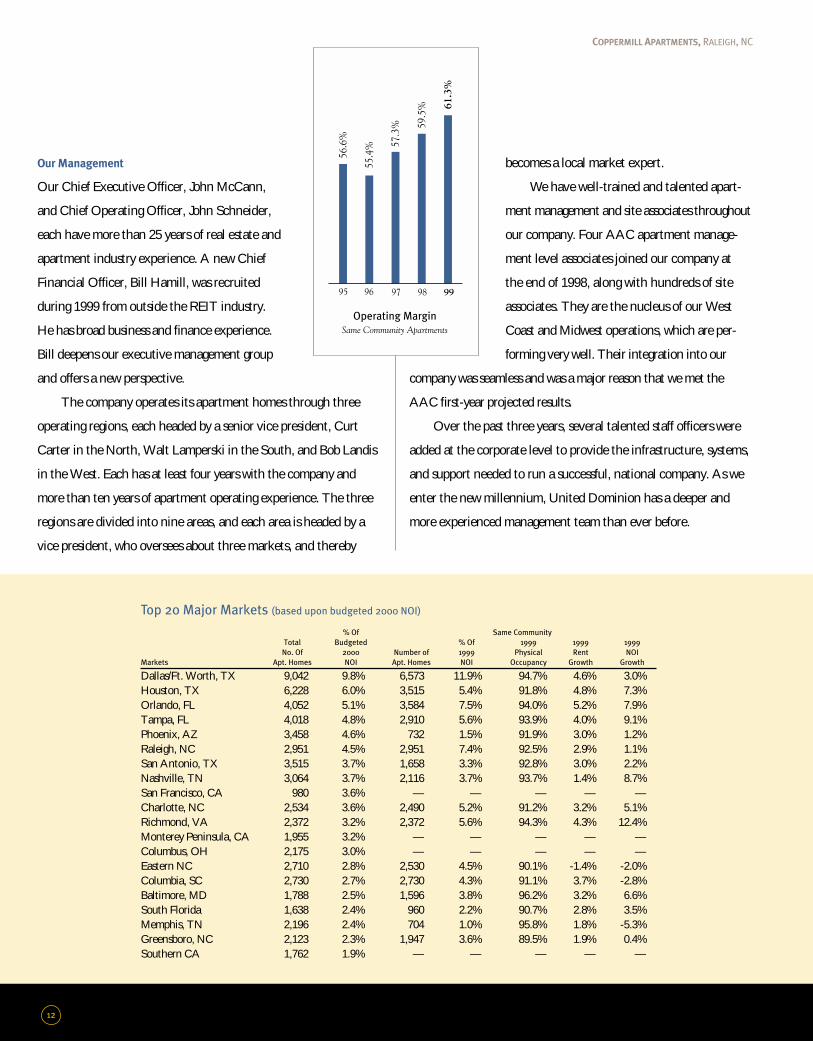

improved buying practices, and by our on-site staff doing more of

our turnover work. Since 1995, we have grown our same

community operating margin from 56.6% to 61.3% by upgrading

the portfolio, growing rents faster than expenses, adding

non-rental income, and by becoming better apartment operators.

We will undertake a number of new initiatives in 2000 to

grow non-rental income. During the year, we will roll out a

renter’s insurance product that takes advantage of volume discounts

and allows for monthly premium payments. We will also offer

high-speed Internet service at an attractive price, for the first time.

The changes in the REIT regulations that will be effective beginning

in 2001 will allow us to offer many more resident services.

2000 POST, SAN FRANCISCO, CA

Our Management

Our Chief Executive Officer, John McCann,

and Chief Operating Officer, John Schneider,

each have more than 25 years of real estate and

apartment industry experience. A new Chief

Financial Officer, Bill Hamill, was recruited

during 1999 from outside the REIT industry.

He has broad business and finance experience.

Bill deepens our executive management group

and offers a new perspective.

The company operates its apartment homes through three

operating regions, each headed by a senior vice president, Curt

Carter in the North, Walt Lamperski in the South, and Bob Landis

in the West. Each has at least four years with the company and

more than ten years of apartment operating experience. The three

regions are divided into nine areas, and each area is headed by a

vice president, who oversees about three markets, and thereby

becomes a local market expert.

We have well-trained and talented apart-

ment management and site associates throughout

our company. Four AAC apartment manage-

ment level associates joined our company at

the end of 1998, along with hundreds of site

associates. They are the nucleus of our West

Coast and Midwest operations, which are per-

forming very well. Their integration into our

company was seamless and was a major reason that we met the

AAC first-year projected results.

Over the past three years, several talented staff officers were

added at the corporate level to provide the infrastructure, systems,

and support needed to run a successful, national company. As we

enter the new millennium, United Dominion has a deeper and

more experienced management team than ever before.

12

COPPERMILL APARTMENTS, RALEIGH, NC

Top 20 Major Markets (based upon budgeted 2000 NOI)

% Of Same Community

Total Budgeted % Of 1999 1999 1999

No. Of 2000 Number of 1999 Physical Rent NOI

Markets Apt. Homes NOI Apt. Homes NOI Occupancy Growth Growth

Dallas/Ft. Worth, TX 9,042 9.8% 6,573 11.9% 94.7% 4.6% 3.0%Houston, TX 6,228 6.0% 3,515 5.4% 91.8% 4.8% 7.3%Orlando, FL 4,052 5.1% 3,584 7.5% 94.0% 5.2% 7.9%Tampa, FL 4,018 4.8% 2,910 5.6% 93.9% 4.0% 9.1%Phoenix, AZ 3,458 4.6% 732 1.5% 91.9% 3.0% 1.2%Raleigh, NC 2,951 4.5% 2,951 7.4% 92.5% 2.9% 1.1%San Antonio, TX 3,515 3.7% 1,658 3.3% 92.8% 3.0% 2.2%Nashville, TN 3,064 3.7% 2,116 3.7% 93.7% 1.4% 8.7%San Francisco, CA 980 3.6% — — — — —Charlotte, NC 2,534 3.6% 2,490 5.2% 91.2% 3.2% 5.1%Richmond, VA 2,372 3.2% 2,372 5.6% 94.3% 4.3% 12.4%Monterey Peninsula, CA 1,955 3.2% — — — — —Columbus, OH 2,175 3.0% — — — — —Eastern NC 2,710 2.8% 2,530 4.5% 90.1% -1.4% -2.0%Columbia, SC 2,730 2.7% 2,730 4.3% 91.1% 3.7% -2.8%Baltimore, MD 1,788 2.5% 1,596 3.8% 96.2% 3.2% 6.6%South Florida 1,638 2.4% 960 2.2% 90.7% 2.8% 3.5%Memphis, TN 2,196 2.4% 704 1.0% 95.8% 1.8% -5.3%Greensboro, NC 2,123 2.3% 1,947 3.6% 89.5% 1.9% 0.4%Southern CA 1,762 1.9% — — — — —

13

Financing

An objective of the company is to maintain Baa2/BBB investment

grade debt ratings and to improve our financing flexibility. During

the first half of 1999, we refinanced a significant portion of the debt

that resulted from our 1998 acquisitions in order to spread maturities

and to increase our financing flexibility. During the first four months

of the year, we sold $190 million of medium-term notes at a weighted

average interest rate of 7.6% and an average maturity of 4.3 years.

For many years, we borrowed in the unsecured corporate market

rather than by mortgaging our properties because terms, including

lower transaction costs, were more favorable. For the first time since

the 1980’s, we initiated non-tax-exempt mortgage financing because

interest rates in the secured mortgage market were significantly lower

than in the unsecured market. We closed a $200 million FNMA

revolving credit facility that is secured by mortgages on 19 properties.

The facility’s flexible terms permit us to fix the rate on all or a part of

the borrowings, substitute collateral, and extend the term.

The benefits of the 1999 debt financings were longer maturities,

a balanced maturity schedule and only modest financing to do in

2000. Our only major debt maturity during 2000 is a $150 million

unsecured note that matures in November. We will, however,

renew our revolving bank credit facility during the first half of 2000.

We will also sell at least $200 million of non-core communities. A

majority of the proceeds from dispositions will be utilized to reduce

debt and further increase our financing flexibility.

During 1999, we continued to expand our

development capability, both as a way of

upgrading our portfolio and increasing our

investment options. We are now

able to make investment choices

in targeted markets between acquiring and

developing. We have more balance between

acquisition and development capabilities,

and this will help us achieve better long-

term investment returns.

Development

14

15

During the year, we completed seven

development projects containing 1,846

apartment homes at a cost of $120 million.

These communities, in five different mar-

kets, were completed between March and

December. The company acted as the

general contractor on two of the develop-

ment projects. In general, leasing activ-

ity has produced absorption at or above

the levels in our marketing plans. The

three communities completed during the

fourth quarter were each 80% leased at

the time of completion with monthly

absorption averaging 28 homes, well above expectations. Each is

expected to stabilize with occupancy above 93%, well in advance of

the proforma stabilization date. The expected stabilized return on

the completed development projects is approximately 10%.

At the end of the year, we had six development projects under

construction, consisting of three second phases, and three new com-

munities, all in different markets. As part of our development

strategy, we plan to build almost all of our new starts as our own

general contractor, which we are doing on all six of the communities

now under construction. As the general contractor, we have more

control over the schedule, including building delivery, and can better

react to subcontractor labor shortages or material delays to meet

our objectives. Meeting the construction schedule is often critical

to achieving timely lease-up, given the seasonality of leasing activity.

We have continued to develop in markets where we have a very

strong operating group who are very

involved in the planning and design of the

product that we are delivering.

Our newest communities, located in

Nashville, Ft. Myers, Columbus, Houston

and Phoenix, offer architectural details and

community features that reflect the lifestyle of the

specific markets for which they are targeted. For example, some of

our new communities offer lap pools, putting greens, and herb

gardens. Most include attached and detached garages with some

of the attached garages being direct access. All communities

include wiring for high-speed Internet access and many have

built-in computer areas.

As part of our objective to increase our financing flexibility

in 2000, we plan to undertake a development joint venture with a

financial partner that will include three of the communities under

construction at year-end 1999 and two other starts in January

2000. This development joint venture will allow us to reduce our

development capital commitment, generate fee income as the

developer, general contractor, and apartment manager, and con-

tinue to increase our development experience and capability.

We plan to continue developing on the

best sites in our target markets, where

there is demand, with a goal of achieving

development returns in excess of 10%.

ALEXANDER COURT, COLUMBUS, OH

Development SummaryTotal

Apartment Apartment Dollars

Homes Homes Invested

Year Started Completed (in millions)

1995 60 60 $ 4.61996 1,320 105 $ 9.21997 736 1,067 $ 52.21998 1,772 890 $ 97.21999 860 1,514 $114.0

THE ASHLAR, FT. MYERS, FL

16

Every United Dominion associate is moti-

vated by a common purpose: to provide

our resident customers with high quality

apartment homes, an outstanding living

environment, uncompromising service,

and exceptional value.

Our teams of community

directors, marketing associates and service

associates strive to not only meet the

expectations of our resident customers,

but to exceed them.

ResidentSatisfaction

17

It Starts With Our People

The associates of United Dominion are focused

on serving and satisfying our resident customers

and earning their trust. We have successfully

met these objectives by:

• Empowering our associates to make timely and

responsible decisions, and to take the actions

necessary to achieve exceptionally high customer

satisfaction.

• Getting to know our residents in order to under-

stand their wants and needs. Our community associates work with

our management teams to find ways to continually improve the living

experience of our residents.

• Listening to and learning from one another, sharing ideas and develop-

ing best practices.

• Providing training and performance enhancing goals that teach us to pro-

vide residents with the best in well maintained communities and homes.

Dedication To Learning

Most of our associate education is provided locally, in the markets

where our associates live and work. By providing training and edu-

cational opportunities, we facilitate job success and enrich careers.

Our Certified Training Program takes advantage of our “best of the

best” on-site people to help new associates learn the basics of com-

munity operations. This is complemented with a curriculum of 30

industry, business, and management programs, which help us devel-

op professional, thoroughly trained associates who can succeed in

their positions and have an opportunity to grow within our compa-

ny. In addition, we offer a wide array of systems and software training

programs to build individual computer

skills, ensuring that United

Dominion will continue to

benefit from the best applica-

tions of new technologies.

SuperStar ServiceSM

We are committed to providing our residents

with SuperStar ServiceSM. This means that we

back our pledge to provide exceptional service

with a unique service guarantee. For example, if

we do not respond to service requests within 48

hours, residents may live rent free for one month.

Since the introduction of this SuperStar

ServiceSM program three years ago, we have had

an outstanding response from our residents—

and our associates. From the service manager in the field to the

accountant in the corporate office, SuperStar ServiceSM has become the

United Dominion credo.

Measuring Success

Three years ago we enlisted the services of CEL & Associates, Inc.,

the nation’s largest independent customer satisfaction surveyor for

the real estate industry. Each year, CEL measures our residents’

evaluation of our performance in the eight categories of service that

are the most critical factors in successful apartment management.

CEL then compares our scores with those of our peers to establish

best practices and set benchmark standards of excellence for our

industry.

We are very proud to report that United Dominion was the

Level 1 winner of the 1999 National Multifamily Customer Service

Award for Excellence. Winning this award means that we received

the highest customer satisfaction ratings of all companies with over

100 apartment communities under

management, surveyed by CEL.

It is a mark of achievement for

our company and especially

our community-

based associates.

Overall Satisfaction Rating

999897

82.2

%

76.0

%

73.7

%

LYNN MCAULIFFE,

TECHNICAL TRAINING MANAGER

SUSAN NORTHCUTT,

TRAINING DIRECTOR

NELLCINE FORD,

H.R. DEVELOPMENT SPECIALIST

ED WELLER,

SERVICE MANAGER, GRIFFIN CROSSING

We are committed to being a technology

leader in the apartment industry in order

to continue improving the efficiency of our

operations, gain marketing

advantages and because our

residents are constantly demanding a higher

level of electronic services.

18

TechnologyImproving

An Infrastructure For The New Millennium

United Dominion has made a substantial investment over the past

two years in talented people and state-of-the-art systems to

become a technology leader in the apartment industry.

In 1999, we undertook and successfully completed, on time

and on budget, the installation of our initial PeopleSoft financial

systems. This latest generation of web-based accounting and reporting

software is already providing improved financial controls and faster

access to better management information for our associates nation-

wide, and with reduced manual input. This system is modular,

scalable and compatible with other new application technologies,

so it is readily adaptable to the changing needs of our business.

Together with our joint-venture partner, AvalonBay

Communities, Inc., we are breaking new ground with the develop-

ment of a cutting-edge, web-based property management system.

Unlike existing site-based and primarily accounts receivable

oriented software, this centralized, real-time system focuses on

improving the functionality of our business. When integrated with

PeopleSoft and our new virtual private network, later this year, it

will provide us with the most advanced operating system in the

apartment industry. It will also give us virtual rental offices seven

days a week, 24 hours a day to respond to residents and prospects.

Today our resident customers want to connect with the

Internet from their apartment homes more conveniently and at

greater speeds to meet their work, shopping and leisure activity

needs. In 1999, we partnered with CAIS Internet, one of the lead-

ing Internet access companies, to provide high-speed broadband

Internet service to all of our communities. When completed in the

fall of 2000, this network will offer exceptional value to our resi-

dent-customers and provide us with a new non-rental income

opportunity. The company will also be able to use the high-speed

access lines provided by CAIS. This will strengthen our communi-

cations network at no incremental expense, with all of our offices

and communities connected at high speed and in real time.

As a part of our commitment to continual improvement,

United Dominion is adding a Director of E-Commerce to our

professional staff. We expect to complete our first comprehensive

e-commerce business plan later this year to take further advantage

of the economic opportunities afforded by these exciting new

technologies.

We are at the forefront of our industry in having made the

commitment and the investment in the people and the systems to

have the infrastructure needed in the new millennium. Some benefits

from our early commitment to the new technology will begin to be

realized in the latter part of 2000, but particularly in 2001.

19

PATRICK GREGORY,

INFORMATION SYSTEMS DIRECTOR

CHERYL KOZLOWSKI,

LEAD DATABASE ENGINEER

KEVIN CARTER,

SOFTWARE DEVELOPMENT MANAGER

THOMAS XAYACHACK,

DESKTOP SUPPORT ANALYST

F I N A N C I A L S E C T I O N C O N T E N T S

21 SELECTED FINANCIAL DATA

22 MANAGEMENT’S DISCUSSION & ANALYSIS OF

FINANCIAL CONDITION & RESULTS OF OPERATIONS

29 REPORT OF INDEPENDENT AUDITORS

30 CONSOLIDATED BALANCE SHEETS

31 CONSOLIDATED STATEMENTS OF OPERATIONS

32 CONSOLIDATED STATEMENTS OF CASH FLOWS

33 CONSOLIDATED STATEMENTS OF SHAREHOLDERS’ EQUITY

34 NOTES TO CONSOLIDATED FINANCIAL STATEMENTS

43 BOARD OF DIRECTORS

1 9 9 9 A n n u a l R e p o r t 21

Years Ended December 31, 1999 1998 1997 1996 1995

In thousands, except per share data and apartment homes owned

Operating Data (a)

Rental income $ 618,749 $ 478,718 $ 386,672 $ 241,260 $ 194,511Income before gains on sales of investments, minority

interests and extraordinary item 60,379 47,339 57,813 33,726 28,037Gains on sales of investments 37,995 26,672 12,664 4,346 5,090Extraordinary item—early extinguishment of debt 927 (138) (50) (23) —Net income 93,622 72,332 70,149 37,991 33,127Distributions to preferred shareholders 37,714 23,593 17,345 9,713 6,637Net income available to common shareholders 55,908 48,739 52,804 28,278 26,490Common distributions declared 109,607 107,758 88,587 55,493 48,610Weighted average number of common shares outstanding-basic 103,604 99,966 87,145 57,482 52,781Weighted average number of common shares outstanding-diluted 103,639 100,062 87,339 57,655 52,972Weighted average number of common shares, OP units and common

equivalents—diluted 124,127 103,793 87,656 57,724 52,972Per share:

Basic earnings per share $ 0.54 $ .49 $ .61 $ .49 $ .50Diluted earnings per share 0.54 .49 .60 .49 .50Common distributions declared 1.06 1.05 1.01 .96 .90

Balance Sheet Data (a)

Total real estate owned, at carrying value $3,953,045 $3,952,752 $2,517,398 $2,099,641 $1,205,685Accumulated depreciation 395,864 316,630 245,367 187,909 153,026Total real estate owned, net of accumulated depreciation 3,557,181 3,636,122 2,272,031 1,911,732 1,052,659Total assets 3,688,317 3,762,940 2,313,725 1,966,904 1,080,616Secured debt 1,000,136 1,072,185 417,325 376,560 180,481Unsecured debt 1,127,169 1,045,564 738,901 668,275 349,858Total debt 2,127,305 2,117,749 1,156,226 1,044,835 530,339Shareholders’ equity 1,310,212 1,374,121 1,058,357 850,379 516,389Number of common shares outstanding 102,741 103,639 89,168 81,983 56,375

Other Data (a)

Cash Flow DataCash provided by operating activities $ 190,876 $ 152,875 $ 137,903 $ 90,064 $ 66,428Cash used in investing activities (34,294) (276,142) (342,273) (161,572) (183,930)Cash (used in)/provided by financing activities (174,985) 148,875 191,391 82,056 113,145

Funds from Operations (b)

Income before gains on sales of investments, minority interests and extraordinary item $ 60,379 $ 47,339 $ 57,813 $ 33,726 $ 28,037

Adjustments:Depreciation of real estate owned, net of outside partners’ interests 120,543 99,588 76,688 47,410 38,939Distributions to preferred shareholders (37,714) (23,593) (17,345) (9,713) (6,637)Minority interests of outside partnerships (1,245) (111) — — —Non-recurring items:

Impairment loss on real estate owned and investments 19,300 — 1,400 290 1,700Loss on termination of an interest rate risk management agreement — 15,591 — — —Prior years’ employment and other taxes — — — — 395Adjustment for internal acquisition costs (c) — (544) (1,341) (901) (587)

Funds from operations-basic $ 161,263 $ 138,270 $ 117,215 $ 70,812 $ 61,847Adjustments:

Distributions to preferred shareholders Series D (Convertible) 15,154 986 — — —Funds from operations - diluted $ 176,417 $ 139,256 $ 117,215 $ 70,812 $ 61,847

Apartment Homes OwnedTotal apartment homes owned at December 31 82,154 86,893 62,789 55,664 34,224

Weighted average number of apartment homes owned during the year 85,926 70,724 58,038 37,481 31,242

(a) From 1996 to 1998, United Dominion completed the following statutory mergers: (i) South West Property Trust, Inc. on December 31, 1996 for an aggregate purchase price of $572 million, (ii) ASR InvestmentsCorporation Inc. on March 27, 1998 for an aggregate purchase price of $323 million, and (iii) AmericanApartment Communities II on December 7, 1998, for an aggregate purchase price of $794 million.

(b) Funds from operations (“FFO”) is defined as income before gains (losses) on sales of investments, minority interests and extraordinary items (computed in accordance with generally accepted accounting principles) plus real estate depreciation, less preferred dividends and after adjustment for significant non-recurring

items, if any. This definition conforms to recommendations set forth in a White Paper adopted by the National Association of Real Estate Investment Trusts (NAREIT) in early 1995. United Dominion considers FFO in evaluating property acquisitions and its operating performance and believes that FFO should be considered along with, but not as an alternative to, net income and cash flows as a measure ofUnited Dominion’s activities in accordance with generally accepted accounting principles and is not necessarily indicative of cash available to fund cash needs.

(c) Reflects the adjustment for internal acquisition costs that were capitalized prior to March 19, 1998.

S E L E C T E D F I N A N C I A L D ATA

U n i t e d D o m i n i o n R e a l t y Tr u s t , I n c .22

OverviewThis annual report contains forward-looking statements within the meaning ofSection 27A of the Securities Act of 1993, as amended, and Section 21E ofthe Securities Exchange Act of 1934, as amended. Such forward-looking state-ments include, without limitation, statements concerning property acquisitionsand dispositions, development activity and capital expenditures, capital raisingactivities, rent growth, occupancy and rental expense growth. Such statementsinvolve known and unknown risks, uncertainties and other factors which maycause the actual results, performance or achievement of United DominionRealty Trust, Inc. (“United Dominion”) to be materially different from theresults of operations or plans expressed or implied by such forward-lookingstatements. Such factors include, among other things, unanticipated adversebusiness developments affecting United Dominion, or its properties, adversechanges in the real estate markets and general and local economies and businessconditions. Although United Dominion believes that the assumptions underlyingthe forward-looking statements contained herein are reasonable, any of theassumptions could be inaccurate, and therefore there can be no assurance thatsuch statements included in this report will prove to be accurate. In light of thesignificant uncertainties inherent in the forward-looking statements includedherein, the inclusion of such information should not be regarded as a represen-tation by United Dominion or any other person that the results or conditionsdescribed in such statements or the objectives and plans of United Dominionwill be achieved. The following discussion should be read in conjunction withthe Consolidated Financial Statements and Notes thereto of United Dominionappearing elsewhere in this annual report.

United Dominion is a real estate investment trust (“REIT”) with activitiesrelated to the ownership, development, acquisition, renovation, management,marketing and strategic disposition of multifamily apartment communitiesnationwide. Management’s strategy is to be a national, highly efficient providerof quality apartment homes. During the past several years, United Dominionhas implemented this strategy through the acquisition of portfolios of higherquality communities, the disposition of non-strategic communities, a greatercommitment to development and the upgrade of its core portfolio of apart-ment communities. Through a combination of dispositions and acquisitionsover the past two years, United Dominion aggressively moved the companyinto better performing markets with attractive prospects for long-term growth.During this same period, more emphasis has been placed on higher qualitydevelopment projects. This strategy resulted in the upgrade of the overall qualityand average age of United Dominion’s portfolio which is now solidly positionedwith “B” and “A” grade communities. United Dominion seeks to be a marketleader by operating a sufficiently sized portfolio of apartments within each of itstarget markets in order to drive down operating costs through economies ofscale and management efficiencies. United Dominion believes that geographicmarket diversification increases investment opportunities and decreases therisk associated with cyclical local real estate markets and economies.

At December 31, 1999, United Dominion owned 301 communities with82,154 apartment homes nationwide, including 37 communities with 7,182 completed apartment homes included in real estate held for disposition and330 recently completed apartment homes included in real estate under devel-opment (see Table I).

Liquidity and Capital ResourcesUnited Dominion expects to meet its short-term financial requirementsthrough net cash provided by operations and borrowings under its unsecuredbank lines of credit. United Dominion believes that cash provided by operationswill be adequate to meet normal operating requirements and payment of distributions by United Dominion in accordance with REIT requirements inboth the short and long-term. In addition, budgeted capital expenditures andmonthly principal amortization of debt are also expected to be funded fromnet cash provided by operating activities.

United Dominion meets certain long-term liquidity requirements, such asscheduled debt maturities, development activity and significant capitalimprovements through: (i) the issuance of long-term secured and unsecuredborrowings, (ii) proceeds from the sales of assets, (iii) common and preferred

stock offerings, (iv) retained operating cash flow and (v) the use of unusedcredit facilities. To facilitate future fund raising activities in the public capitalmarkets, management believes that it is prudent to maintain shelf registrationstatement capacity. In this regard, United Dominion filed such a shelf registra-tion statement in December 1999 providing for the issuance of up to $700million in common shares, preferred shares and debt securities.

In March 2000, United Dominion sold $100 million of senior unsecured notesdue March 2003 at an interest rate of 8.625%. The proceeds from the offeringwere used to prepay certain mortgage debt and repay revolving bank debt.

United Dominion currently plans to establish during 2000, a program for thesale of up to $150 million aggregate principal amount of medium-term notes.

United Dominion has no significant maturities of debt until the fourth quarterof 2000 at which time approximately $175 million of secured and unsecureddebt will mature. At this time, management expects to refinance the maturingdebt with debt of similar characteristics and at prevailing market rates.

The following discussion explains the changes in net cash provided byoperating activities, net cash used in investing activities and net cash used infinancing activities which are presented in United Dominion’s ConsolidatedStatements of Cash Flows.

Operating ActivitiesFor the year ended December 31, 1999, United Dominion’s cash flow fromoperating activities was $190.9 million compared to $152.9 million in 1998.The increase was primarily due to the increased operating income fromUnited Dominion’s acquired communities as well as increases in propertyoperating income achieved through higher rent growth as discussed under“Results of Operations.”

Investing ActivitiesFor the year ended December 31, 1999, net cash used in investing activitieswas $34.3 million compared to $276.1 million for 1998, a decrease of $241.8million. During 1999, United Dominion shifted its focus from the acquisitionof real estate assets to the disposition and development of real estate assets.Changes in the level of investing activities from period to period reflect thechanging levels of United Dominion’s acquisition, capital expenditure, devel-opment and disposition programs, as well as the impact of the capital marketenvironment on these activities.

Disposition of InvestmentsAs part of its strategic repositioning, United Dominion determined that itwould selectively dispose of assets that are not in core markets, have a lowernet operating income growth rate than the overall portfolio or no longer meetthe operating and investment strategies of United Dominion. The dispositionprogram allows United Dominion to reduce the age of its existing portfolio,which should result in lower operating expense and capital expendituregrowth associated with the older communities.

During 1999, United Dominion sold 36 communities with 7,443 apart-ment homes for an aggregate sales price of $241.2 million and recognizedgains for financial reporting purposes of $38.0 million. These sales allowedUnited Dominion to exit certain markets that had low growth opportunitiesand improve the average age of the company’s overall apartment portfolio by selling communities with an average age of 25 years. During 1998, 18communities with 5,318 apartment homes and an average age of 25 yearswere sold for an aggregate sales price of $156.6 million, which resulted ingains for financial reporting purposes of $26.7 million.

Proceeds from the disposition program were used to strengthen the balancesheet by paying down debt, as well as to fund new development projects andto selectively repurchase shares of United Dominion’s preferred and commonstock. Where necessary to defer capital gain taxes, disposition proceeds havebeen reinvested in strategically attractive communities.

United Dominion intends to sell 6,000 to 7,000 apartment homes during2000. Proceeds from the 2000 dispositions, expected to be at levels similar to1999, are to be used to reduce debt, repurchase preferred shares, fund devel-opment activity and acquire communities through 1031 exchanges.

M A N A G E M E N T ’ S D I S C U S S I O N & A N A LY S I S O F F I N A N C I A L C O N D I T I O N

& R E S U LT S O F O P E R AT I O N S

1 9 9 9 A n n u a l R e p o r t 23

The following table summarizes United Dominion’s apartment market information by major geographic markets and other geographic areas (including realestate under development and excluding four commercial properties):

As of December 31, 1999 December 31, 1999

No. of No. of % of Carrying Year Ended Quarter Ended

Apartment Apartment Carrying Value Physical Physical

Area Communities Homes Value (in thousands) Occupancy Occupancy

Major MarketsDallas/Fort Worth, TX 29 9,042 11% $ 415,116 94.5% 94.8%Houston, TX 25 6,228 6% 238,123 90.5% 90.3%Phoenix, AZ 10 3,458 5% 198,702 91.5% 93.3%Orlando, FL 13 4,052 5% 194,569 94.1% 94.3%Tampa, FL 12 4,018 5% 179,307 92.4% 93.2%San Antonio, TX 12 3,515 4% 171,556 92.4% 92.5%Raleigh, NC 9 2,951 4% 146,528 92.5% 92.3%Nashville, TN 11 3,064 4% 144,107 89.7% 92.4%San Francisco, CA 4 980 4% 138,681 98.8% 99.5%Charlotte, NC 10 2,534 3% 128,190 91.2% 91.1%Columbus, OH 5 2,175 3% 118,268 92.8% 95.3%Wilmington, NC 10 2,710 3% 111,709 89.8% 93.7%Monterey Peninsula, CA 13 1,955 3% 111,474 93.1% 91.2%Memphis, TN 7 2,196 3% 105,859 93.9% 94.1%South Florida 6 1,638 3% 102,349 91.1% 90.8%Richmond, VA 8 2,372 3% 102,120 94.3% 97.0%Greensboro, NC 8 2,123 3% 102,091 88.8% 90.8%Columbia, SC 9 2,730 2% 97,414 91.1% 91.2%Southern California 6 1,762 2% 95,243 93.8% 93.4%Baltimore, MD 8 1,788 2% 85,368 96.2% 97.1%Atlanta, GA 6 1,426 2% 69,239 92.7% 94.4%Seattle, WA 5 1,159 1% 57,816 93.2% 96.9%Jacksonville, FL 3 1,157 1% 56,783 90.5% 92.0%Hampton Roads, VA 6 1,437 1% 54,655 95.1% 97.4%Sacramento, CA 2 914 1% 52,758 97.8% 98.1%Denver, CO 2 876 1% 44,942 93.5% 95.1%Detroit, MI 4 744 1% 42,910 94.9% 95.0%Washington, DC 3 615 1% 35,731 97.7% 98.4%Portland, OR 3 627 1% 34,353 91.2% 91.0%Indianapolis, IN 3 875 1% 28,699 94.0% 92.7%Austin, TX 2 542 1% 23,836 94.6% 97.4%

Other AreasOther Florida 7 1,665 1% 78,929 92.1% 94.6%Eastern Shore MD and Delaware 6 1,156 1% 52,553 96.3% 95.6%Other North Carolina 4 1,052 1% 48,876 94.7% 94.5%Other Virginia 6 1,154 1% 47,984 93.8% 94.7%Other Michigan 4 1,227 1% 47,535 90.5% 95.0%Other Midwest 5 969 1% 42,780 94.5% 95.0%Arkansas 2 512 1% 22,306 93.9% 95.3%Other Washington State 3 536 1% 21,914 83.3% 93.5%Nevada 1 384 1% 20,776 93.4% 96.8%New Mexico 3 530 1% 19,972 89.4% 90.6%Other Arizona 2 408 — 13,408 91.5% 94.8%Other Georgia 1 240 — 10,413 90.8% 95.9%Alabama 1 242 — 8,780 91.8% 91.7%Other Texas 1 248 — 8,330 85.4% 91.4%Other South Carolina 1 168 — 7,428 88.7% 93.0%

Total 301 82,154 100% $3,940,480 92.6% 93.6%

Subsequent to year-end, United Dominion sold three communities forapproximately $18.5 million. In addition, United Dominion entered into con-tracts to sell two communities with 285 apartment homes for an aggregate salesprice in excess of $17 million. For financial reporting purposes, aggregate gainson the sales of investments are not expected to be material. The transactions areexpected to close during the first and second quarters of 2000; however, therecan be no assurance that these transactions will be consummated as planned.

Real Estate under DevelopmentDuring 1999, United Dominion continued its commitment to development aspart of its strategic repositioning, shifting capital into development activity andaway from lower yielding acquisitions. During 1999, the development of over1,500 homes was completed, up from 890 homes completed during 1998.Development activity is focused in core markets that have locally based development teams, and strong operations managers in place.

Table I—Apartments by Market

U n i t e d D o m i n i o n R e a l t y Tr u s t , I n c .24

In addition to the apartment homes under development at December 31,1999 (see Table II), United Dominion has land held for future developmentwith a carrying value of $37.9 million. Future development activity will bebased upon the availability of capital and real estate fundamentals. Additionaldevelopment starts planned in 2000 are expected to be undertaken withfinancial partners through joint venture arrangements.

AcquisitionsDuring 1999, United Dominion curtailed its active pace of acquisitions,investing in new communities only when necessary to complete 1031exchanges in order to defer taxes on large capital gains. During 1999, usingproceeds from its disposition program, United Dominion acquired five com-munities with 1,230 apartment homes at a total cost (including closing costs)of $74.3 million or $60,400 per home during 1999. These communities arelocated in markets that are considered strategically important to UnitedDominion, such as Baltimore, Maryland, South Florida and Riverside andSan Diego, California.

During 2000, United Dominion does not anticipate acquiring communitiesexcept to reinvest a portion of the proceeds from property dispositions in orderto defer taxes on capital gains.

Capital ExpendituresUnited Dominion capitalizes those expenditures related to acquiring newassets, materially enhancing the value of an existing asset, or substantiallyextending the useful life of an existing asset. Expenditures necessary tomaintain an existing property in ordinary operating condition are expensedas incurred.

During 1999, United Dominion substantially completed the upgrade program which was part of the strategic plan to improve the overall qualityof its portfolio. Capital expenditures decreased from 1998 while the overallage and physical condition of the apartment portfolio has improved. For theyear ended December 31, 1999, $32.8 million or $639 per home was spent

on capital expenditures for United Dominion’s same communities (thoseacquired or developed prior to January 1, 1998). These capital improvementsincluded recurring capital expenditures, including floor coverings, HVACequipment, roofs, appliances, landscaping, siding, parking lots and other non-revenue enhancing capital expenditures, which aggregated $19.8 million or$386 per home. In addition, non-recurring / revenue enhancing capitalexpenditures, including water sub-metering, gating and access systems, theadditions of microwaves, washer-dryers, interior upgrades and new businessand fitness centers totaled $13.0 million or $253 per home for the year endedDecember 31, 1999. United Dominion reduced capital expenditures relatedto same communities throughout 1999, but will continue to selectively addrevenue enhancing improvements, which are budgeted to provide a highreturn on investment. Capital expenditures during 2000 are expected to beat levels similar to 1999.

In addition to capital improvements to its same communities, UnitedDominion invested approximately $42 million or $1,220 per home on itsnon-mature communities (those acquired or developed subsequent toJanuary 1, 1998) during 1999, which includes both recurring and revenueenhancing capital improvements.

Financing ActivitiesNet cash used in financing activities during 1999 was $175.0 million compared to net cash provided by financing activities of $148.9 million for1998. During 1999, as part of its strategic plan to improve its balance sheetposition, United Dominion used approximately 60% of the proceeds from itsdisposition program to pay down secured and unsecured debt. The remainingproceeds were used to acquire assets where necessary to complete 1031exchanges and, to a lesser extent, to repurchase shares of preferred and com-mon stock.

In January 1999, United Dominion established a program for the sale of up to $200 million aggregate principal amount of medium-term notes(the “MTN Program”). For the year ended December 31, 1999, United

Table II—Real Estate Under Development

During 1999, the following development projects were completed:

Total

No. Apt. Costs Cost per Date % Leased

Property Location Homes (Thousands) Home Completed at 12/31/99

New CommunitiesStone Canyon Houston, TX 216 $10,322 $47,800 3/99 89.4%Dominion Franklin Nashville, TN 360 26,347 73,200 3/99 91.4%Ashlar I Ft. Myers, FL 260 18,887 72,600 5/99 99.6%Alexander Court Columbus, OH 356 22,827 64,100 11/99 91.9%Sierra Foothills Phoenix, AZ 322 21,458 66,600 11/99 79.5%Legends at Park 10 Houston, TX 236 13,612 57,700 11/99 89.8%

1,750 113,453 64,800Additional PhasesHeritage Green II Columbus, OH 96 6,740 70,200 5/99 94.8%

Total 1,846 $120,193 $65,100

The following projects are under development at December 31, 1999:

Completed Costs Estimated Estimated Expected

No. Apt. Apt. to Date Costs Cost Completion

Property Location Homes Homes (Thousands) (Thousands) per Home Date

New Communities Ashton at Waterford Lakes Orlando, FL 292 204 $19,244 $ 21,000 $71,900 1Q00The Meridian Dallas, TX 250 82 11,403 16,500 66,000 2Q00Oaks at Weston Raleigh, NC 380 — 6,391 30,200 79,500 2Q01

922 286 37,038 67,700 73,400Additional PhasesDominion Crown Point II Charlotte, NC 220 44 10,016 14,800 67,300 1Q01Ashlar II Ft. Myers, FL 168 — 1,712 12,900 76,800 4Q00Escalante II San Antonio, TX 312 — 5,295 19,700 63,100 4Q00

700 44 17,023 47,400 67,700Total 1,622 330 $54,061 $115,100 $71,000

1 9 9 9 A n n u a l R e p o r t 25

Dominion sold an aggregate of $190 million of senior unsecured notes underthe MTN Program with a weighted average interest rate of 7.61%. Net pro-ceeds from the offerings were used to repay amortizing unsecured debt, repaymaturing mortgage debt, repay a $75 million senior unsecured note thatmatured in April 1999 and repay revolving bank debt.

During 1999, United Dominion closed on $195.7 million of a $200 millionrevolving credit facility with the Federal National Mortgage Association (the“FNMA Credit Facility”). The FNMA Credit Facility is for an initial term offive years, bears interest at a floating rate which can be fixed for periods of upto 270 days, and can be extended for an additional five or ten years at UnitedDominion’s discretion. The FNMA Credit Facility had a weighted averageinterest rate of 6.32% at December 31, 1999. United Dominion used interestrate swap agreements to limit its interest rate exposure on $57 million of thisborrowing (see Secured Credit Facilities in Note 3). The proceeds from theFNMA Credit Facility were used to repay a $91 million secured credit facilityassumed in connection with the American Apartment Communities II trans-action, to replace $58 million in maturing secured debt and the remainingproceeds were used to repay revolving bank debt.

United Dominion issued 1.6 million shares of its common stock andreceived $16.7 million under its Dividend Reinvestment and Stock PurchasePlan during 1999 that included $1.2 million in optional cash investments and$15.5 million of reinvested dividends.

For the year ended December 31, 1999, United Dominion paid distributionsto its common shareholders and unitholders in its operating partnershipsaggregating $118.8 million. The distribution to common shareholders andholders of operating partnership units equates to a dividend rate of $1.06 pershare or unit. In addition, $35.0 million of preferred dividends were paid toSeries A, B and D preferred shareholders.

In June 1999, the Board of Directors authorized the repurchase of up to 5.5million common shares, or 5% of the total common shares outstanding, usingproceeds from the disposition program. Such purchases will be made from timeto time in the open market or in privately negotiated transactions; the timing,volume and price of such purchases will be at the discretion of management and the Board of Directors. For the year ended December 31, 1999, UnitedDominion repurchased 2.6 million common shares at an average price of $11.22per share. The Board of Directors also approved the repurchase of up to $25million of United Dominion’s Series A and Series B Cumulative RedeemablePreferred Stock from time to time as market conditions permit. For the yearended December 31, 1999, United Dominion repurchased 31,440 Series A preferred shares at an average price of $19.76 per share and 53,700 Series B preferred shares at an average price of $18.35 per share. In addition, UnitedDominion redeemed one million operating partnership units for $12.0 million.

During 1999, using proceeds from its disposition program, United Dominionrepurchased $70.0 million of certain of its higher rate outstanding unsecured debt with a weighted average yield of 7.74%. In addition, in connection with thedisposition program, United Dominion was relieved of $57.7 million of mortgagedebt and $9.3 million of revolving bank debt.

Credit FacilitiesUnited Dominion has a $200 million three-year unsecured revolving creditfacility (the “Bank Credit Facility”) which expires in August 2000 and a $110million one-year unsecured line of credit (the “Line of Credit”) which expiresin August 2000 that are provided by a consortium of banks. Under the BankCredit Facility, pricing is based upon the higher of United Dominion’s seniorunsecured debt ratings from Standard & Poor’s Corporation and Moody’sInvestor Services that are currently BBB and Baa2, respectively. At these rat-ing levels, interest under the Bank Credit Facility is LIBOR plus 0.50% andinterest under the Line of Credit is LIBOR plus 1.0%. However, these ratesare subject to change as United Dominion’s credit ratings change. The BankCredit Facility also includes a $100 million competitive bid option, whichallows United Dominion to solicit bids from participating banks at rates belowthe contractual rate. At December 31, 1999, $277.6 million was outstandingunder these credit facilities leaving $32.4 million available for use.

The Bank Credit Facility and Line of Credit are subject to customaryfinancial covenants and limitations.

Derivative InstrumentsUnited Dominion, from time to time, uses derivative instruments to syntheticallyalter on-balance sheet liabilities or to hedge anticipated financing transactions.Derivative contracts did not have a material impact on the results of operationsduring 1999.

Market RiskUnited Dominion is exposed to market risk principally from interest rate riskassociated with variable rate notes payable and maturing debt that has to berefinanced. United Dominion does not hold financial instruments for tradingpurposes, but rather issues these financial instruments to finance owning andmanaging real estate. United Dominion’s interest rate sensitivity position ismanaged by its treasury department. Interest rate sensitivity is the relationshipbetween changes in market interest rates and the fair value of market rate sen-sitive assets and liabilities. United Dominion’s earnings are affected by changesin short-term interest rates on its variable rate debt and the repricing of fixedrate debt. A large portion of United Dominion’s market risk is exposure toshort-term interest rates from variable rate borrowings outstanding under itsbank credit facilities, which totaled $277.6 million at December 31, 1999. Theimpact on United Dominion’s financial statements of refinancing fixed ratedebt that matured during 1999 was not material.

At December 31, 1999, the notional value of United Dominion’s derivativeproducts for the purpose of managing interest rate risk was $177 million ofinterest rate swaps under which United Dominion pays a fixed rate of interestand receives a variable rate. These agreements effectively fix $177 million ofUnited Dominion’s variable rate notes payable to a weighted average fixedrate of 6.78% (see Note 5-Financial Instruments). At December 31, 1999, the aggregate fair market value of the interest rate swaps in a favorableposition to United Dominion would have been $626 thousand. If interest rateswere 100 basis points more or less at December 31, 1999, the fair marketvalue of the interest rate swaps would have increased or decreased approxi-mately $500 thousand, respectively.

If market interest rates for variable rate debt averaged 100 basis points morein 2000 than they did during 1999, United Dominion’s interest expense, afterconsidering the effects of its interest rate swap agreements, would increase, andincome before taxes would decrease by $4.0 million. Comparatively, if marketinterest rates for variable rate debt averaged 100 basis points more in 1999 thanit did in 1998, United Dominion’s interest expense, after considering the effectsof its interest rate swap agreements, would increase, and income before taxeswould decrease by $4.0 million. If market rates for fixed rate debt were 100 basispoints higher at December 31, 1999, the fair value of fixed rate debt would havedecreased from $1.55 billion to $1.50 billion. If market interest rates for fixedrate debt were 100 basis points lower at December 31, 1999, the fair value offixed rate debt would have increased from $1.55 billion to $1.62 billion.

These amounts are determined by considering the impact of the hypotheticalinterest rates on United Dominion’s borrowing cost and interest rate swap agree-ments. These analyses do not consider the effects of the reduced level of overalleconomic activity that could exist in such an environment. Further, in the eventof a change of such magnitude, management would likely take actions to furthermitigate its exposure to the change. However, due to the uncertainty of the specific actions that would be taken and their possible effects, the sensitivityanalysis assumes no change in United Dominion’s financial structure.

Results of OperationsUnited Dominion’s net income is primarily generated from the operations ofits apartment communities.

1999-vs-1998For 1999, net income available to common shareholders increased $7.2 million,with a corresponding increase of $.05 for both basic and diluted earnings pershare, compared to 1998. The increase per share was primarily attributable toaggregate gains on the sale of investments of $38.0 million ($.37 per share)for the year ended December 31, 1999, compared to $26.7 million ($.27 pershare) in 1998. However, the increases associated with the gain on sales ofinvestments were moderated in part due to the $19.3 million of impairmentlosses recorded during 1999. United Dominion’s non-mature communitieswith 31,454 apartment homes at December 31, 1999 provided a substantialportion of the increase in United Dominion’s operating income during 1999.

U n i t e d D o m i n i o n R e a l t y Tr u s t , I n c .26

1998-vs-1997For 1998, net income available to common shareholders decreased $4.1 million,with a corresponding decrease of $.12 and $.11 for basic and diluted earningsper share, respectively, compared to 1997. The decrease per share was primarilyattributable to the $15.6 million ($.15 per share) loss on the termination of aninterest rate risk management agreement during the fourth quarter of 1998.Net income available to common shareholders for the year ended December31, 1998 included aggregate gains on the sales of investments of $26.7 million($.27 per share) compared to $12.7 million ($.15 per share) in 1997.

Same Communities (See Table III)

1999-vs-1998 (51,316 apartment homes)In 1999, property rental income grew 3.1%, or approximately $11.1 million,reflecting an increase in average monthly rental rates of 3.4% while physicaloccupancy remained constant at 93.1%.

For 1999, property operating expenses at these same communities decreased0.6%, or $827 thousand. Utility expense decreased due to the continued transferof water and sewer costs to residents, repair and maintenance expense decreasedas a result of the upgrade program and taking more turnover work in-houseand property management expenses decreased due to better economies ofscale. However, these decreases were offset by an increase in personnel costsdue to higher salaries and benefit costs, an increase in real estate taxes, the addition of monitored alarms in more communities and higher technology costs.

As a result of the increase in property rental income and the decrease inproperty operating expenses, the operating margin (property operating incomedivided by property rental income) improved 1.5% to 61.3%.

1998-vs-1997 (47,875 apartment homes)Compared to the same period in 1997, property rental income from these com-munities grew 3.5%, or approximately $11.0 million, reflecting an increase inaverage monthly rental rates of 3.4%. During 1998, physical occupancy of 92.9%was the same as reported in 1997.

For 1998, property operating expenses at these communities were unchanged.Utility expenses decreased as a result of United Dominion’s water and sewersub-metering initiative and repair and maintenance expenses decreased asUnited Dominion continued to benefit from a centralized purchasing initia-tive and the upgrade program. However, these expense decreases were offsetby increases in real estate taxes primarily in certain Florida and Texas marketsand increases in personnel costs as United Dominion experienced pressure onwages due to low unemployment and tighter job markets.

Due to the increase in property rental income and the unchanged propertyoperating expenses, the operating margin improved 1.4% to 59.5%.

Non-Mature Communities (See Table IV)

1999-vs-1998Property rental income and property operating expenses increased from 1998to 1999 directly as a result of the increase in the weighted average number ofapartment homes owned during 1999. For the year ended December 31, 1999,average economic occupancy was 88.2%, and the operating margin was 58.8%for the non-mature communities.

United Dominion’s non-mature apartment portfolio can be categorized asfollows for the years ended December 31, 1999 and 1998:

1998 AcquisitionsAmerican Apartment Communities II, Inc. (AAC) On an average investment of $761 million, the AAC portfolio (13,728homes net of sales) provided a first year return on investment (property rentalincome less property operating expenses divided by the average capital investmentin real estate) of 9.1% which is slightly better than the projection of 9.0%made at the time of the acquisition. These communities achieved physicaloccupancy of 93.6%, which is higher than United Dominion’s average physicaloccupancy primarily due to the California markets included in this portfolio.For the year, these communities had an economic occupancy of 92.1% and anoperating margin of 62.7%.

1998 Acquisitions (Excluding AAC)For the 13,577 homes (net of sales) acquired in 1998, the return on investmentfor the year ended December 31, 1999, on an average investment of $611million was 8.4%. This return on investment was below amounts projectedfor 1999, however, these communities continue to be upgraded, repositionedand selectively sold, which is expected to improve overall operating resultsover the long-term. These communities had an economic occupancy of88.8% and an operating margin of 57.8%.

1999 AcquisitionsIncluded in this category are five communities with 1,230 apartment homesacquired by United Dominion during 1999 that are projected to provide afirst year return on investment of 9.0% on an initial investment of $74 million.These communities did not have a material impact on 1999 results of operations.