Embed Size (px)

Citation preview

ADDRESSING WEAKNESSES AND STEREOTYPES

IN MODERN ISLAMIC BANKING:

HELPING REACH CRITICAL MASS

by

Ms. Shagufta Ahmad

Open University Malaysia 2012

II

ADDRESSING WEAKNESSES AND STEREOTYPES

IN MODERN ISLAMIC BANKING:

HELPING REACH CRITICAL MASS

by

Ms. Shagufta Ahmad

Project Paper Submitted in Partial fulfillment of the Requirement for the Degree of

Master of Business Administration in Islamic Finance

Open University Malaysia 2012

III

DECLARATION

Name : Shagufta Ahmad

Matric Number : 51090183

I hereby declare that this project paper is the result of my own work, except

for quotations and summaries which have been duly acknowledged.

Signature: _________________________ Date: May 11, 2012

IV

APPLICATION TO CONDUCT RESEARCH PAPER

PART A: STUDENT’S PARTICULARS

Student’s Name : Shagufta Ahmad

Matric Number : 51090183

PART B: PARTICULARS ABOUT THE PROJECT

1. Title of the project: “Addressing Weaknesses And Stereotypes In

Modern Islamic Banking: Helping Reach Critical Mass”

2. Research Objectives:

1. To identify the existing weaknesses in the Islamic finance industry

2. To identify the prevailing stereotypes in the Islamic finance industry

3. To identify the methods to remove the above

3. Proposed Research Method: “qualitative (descriptive and analytical)

and quantitative approaches”

PART C: FACULTY’S INPUTS

1. Topic Chosen: Accepted/Not Accepted

2. Supervisor for the student: Dr. Shaban M. Islam Barwari

V

RESEARCH PAPER SUBMISSION FORM

Student’s Name : Shagufta Ahmad Matric Number : 51090183

Director Open University of Malaysia (OUM) Bahrain Branch Dear Sir,

Attached are the following documents for your evaluation and approval

Chapter 1: Introduction

Chapter 2: Literature Review

Chapter 3: Research Methodology

Chapter 4: Findings - Weaknesses

Chapter 5: Findings - Stereotypes

Chapter 6: Conclusion and Recommendations

I have thoroughly checked my work and I am confident that it is free from major grammatical errors, weaknesses in sentence constructions, spelling mistakes, referencing mistakes and others. I have checked with CGS Guideline for Writing Project Papers and I am satisfied that my project paper proposal satisfies most of its requirements. Thank You,

Student’s Signature: __________________________________

I have read the student’s research proposal and I am satisfied that it is in line with the CGS Guideline for writing project proposal. It is also free from major grammatical errors, sentence construction weaknesses, citation and others.

Supervisor’s Signature: _______________________________

VI

DEDICATION

I dedicate this paper to all those seeking their way to the

“waterhole,” i.e. the Shari’ah.

VII

ACKNOWLEDGEMENT

First of all I thank Allah Almighty, the Most Exalted, for granting me the taufeeq to

specialize in Islamic finance – a branch of the most needed yet most misunderstood

system in the world today – the Shari’ah. Then I send countless and choicest blessings

and salutations upon our last and final and most beloved Prophet Muhammad (peace be

upon him) who taught us and gave us the shining example of how to implement the

Shari’ah in our lives and communities.

I would then thank my parents, family and friends for their prayers. A special note of

thanks to my parents without whose constant support I would not have been able to

complete my Masters degree. I would also like to thank my brother for his guidance and

networking and to colleagues at the Arab Open University, Bahrain as well as my

spiritual mentors and friends at the Islamic Educational and Cultural Research Center,

USA and Canada.

And last but not least, I would like to thank the Open University Malaysia for giving me

the chance to present this research subject in order to help me get my Masters Degree.

And many thanks to my supervisor Dr. Shaban Barwari for his excellent introduction and

insight into this dynamic field and for his guidance and support.

VIII

ABSTRACT

Although Islamic finance has seen tremendous growth and exposure over the past few

decades, nevertheless there are still some prevailing misconceptions about some of the

fundamental concepts underlying this dynamic and viable alternative to the ailing

conventional system. These misconceptions along with some developmental weaknesses

are being bottlenecks to its even more far reaching growth and impact. This paper seeks

to identify these stereotypes through a survey sample of 1080 respondents with a profile

that reflects world demographics to a large degree in gender, age, nationality and religion.

It also seeks to identify weaknesses within the system as stated by seasoned professionals

within the Islamic finance industry in Bahrain. The worldwide survey has revealed that

an overwhelming majority of the population is unaware of the fundamental concepts of

Islamic finance such as the nature of usury. Almost a third of those surveyed (holding

only conventional bank accounts) had either not heard of Islamic Banking or knew very

little about it. And almost half of these were not even interested in this field. To echo the

findings of the external survey, the veterans within the industry are also calling for

fundamental improvements stating research and development as the key area of weakness

so that Islamic finance instruments are truly Shari’ah based and not just Shari’ah

compliant. This paper presents a practical plan to address these weaknesses and

stereotypes and exhorts all IFIs to implement it in full to mitigate the effects of these

external and internal drawbacks in order to help the industry reach critical mass.

IX

Table of Contents

List of Tables ............................................................................................................................. X

List of Figures ........................................................................................................................... XI

Glossary of Arabic Terms and Abbreviations .......................................................................... XII

Chapter 1: Introduction ............................................................................................................... 1

1.1 Problem Statement ........................................................................................................ 1

1.2 Objectives of the Study ................................................................................................. 3

1.3 Limitations of the Study ................................................................................................ 3 Chapter 2: Literature Review ....................................................................................................... 4

2.1 What is a Finance System? ............................................................................................ 4

2.2 The History of Money ................................................................................................... 7

2.3 The History of Interest / Usury (Riba) ........................................................................... 9

2.4 Basics of Islamic Finance ............................................................................................ 10

2.5 Weaknesses and Stereotypes ....................................................................................... 16 Chapter 3: Research Methodology ............................................................................................. 18

3.1 Weakness identification .............................................................................................. 18

3.2 Stereotype Identification ............................................................................................. 20 Chapter 4: Findings - Weaknesses ............................................................................................. 22

Chapter 5: Findings - Stereotypes .............................................................................................. 34

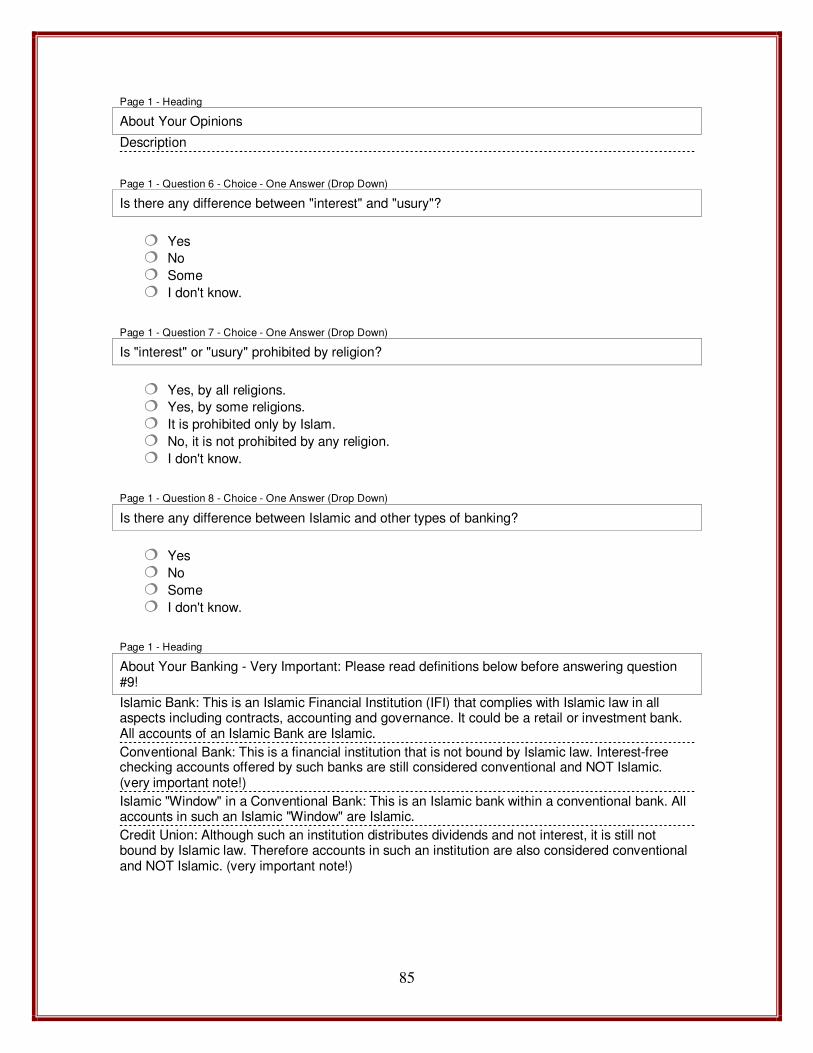

5.1 Stereotype #1: “Interest and Usury are different.” ........................................................ 34

5.2 Stereotype #2: “Interest/Usury is prohibited only by some religions.” .......................... 39

5.3 Stereotype #3: “Islamic banking appears the same as conventional banking.” .............. 41

5.4 Stereotype #4: “Every increase is wrong.” ................................................................... 46

5.5 Stereotype #5: “Everything fixed is wrong.” ................................................................ 46

5.6 Stereotype #6: “Risk taking is wrong.” ........................................................................ 47

5.7 Summary of interesting statistical findings from worldwide survey ............................. 54 Chapter 6: Conclusion and Recommendations ........................................................................... 55

6.1 Conclusion .................................................................................................................. 55

6.2 Recommendations - Action Plan ................................................................................. 57 Bibliography ............................................................................................................................. 63

Appendix A - IFI Professionals Responses on Critical Mass ...................................................... 66

Appendix B - Advantages of the Islamic Finance system as per IFI Professionals ...................... 67

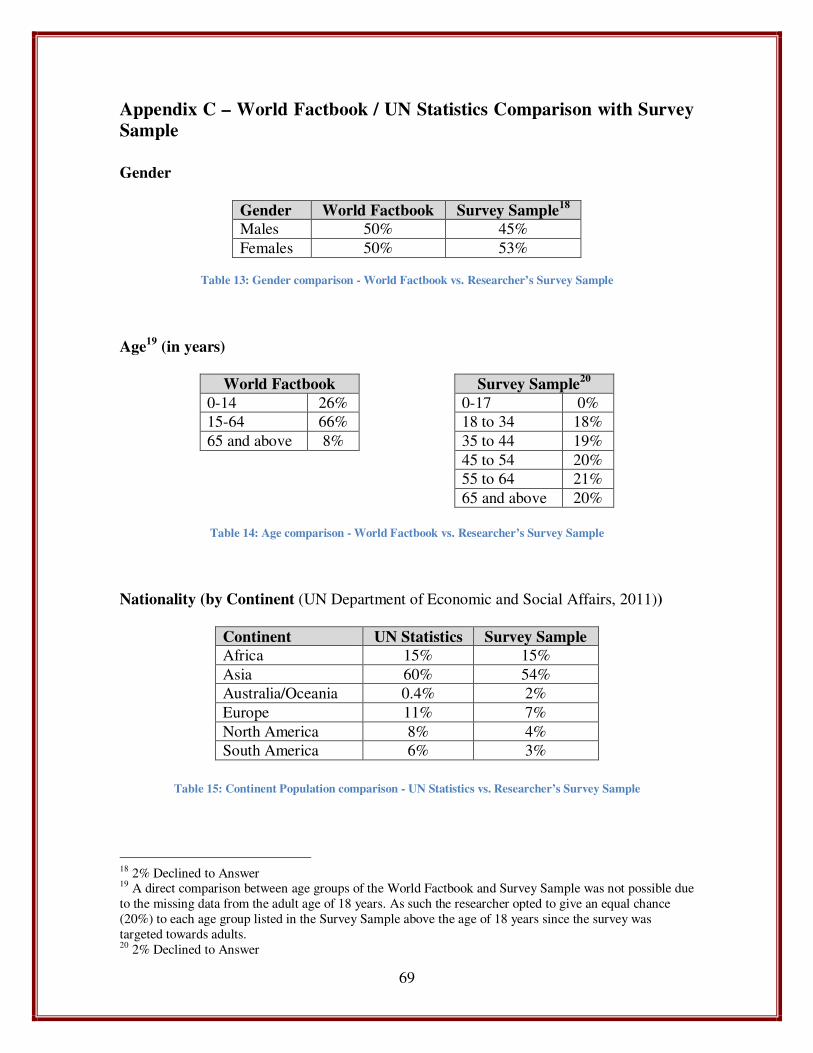

Appendix C – World Factbook / UN Statistics Comparison with Survey Sample ....................... 69

Appendix D – Islamic Finance Survey 2012 (for IFI Professionals) ........................................... 71

Appendix E – Worldwide Islamic Banking Survey 2011-2012 (GSM) ....................................... 74

X

List of Tables

Table 1: List of IFIs Invited to Participate in Survey ...................................................... 19

Table 2: Weaknesses within IFIs as stated by Industry Professionals ............................. 25

Table 3: Categories of Weaknesses within IFIs Identified in Order of Severity .............. 27

Table 4: Adequacy of Islamic financial products as per IFI Professionals ...................... 28

Table 5: Suggestions to improve IFIs as stated by Industry Professionals ...................... 31

Table 6: Categories of Suggestions to improve IFIs Offered by Industry Professionals in

Order of Popularity........................................................................................................ 32

Table 7: IFI Responses on lay people’s understanding of difference between Islamic and

Conventional Finance .................................................................................................... 42

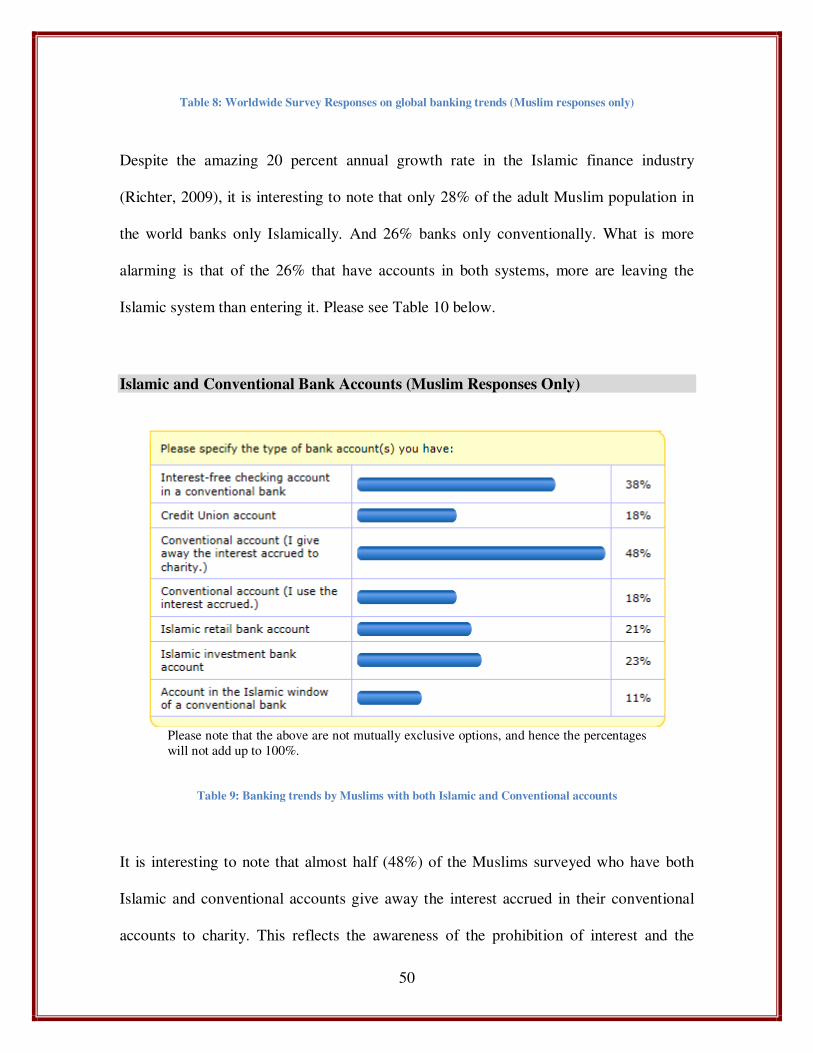

Table 8: Worldwide Survey Responses on global banking trends (Muslim responses only)

...................................................................................................................................... 50

Table 9: Banking trends by Muslims with both Islamic and Conventional accounts ....... 50

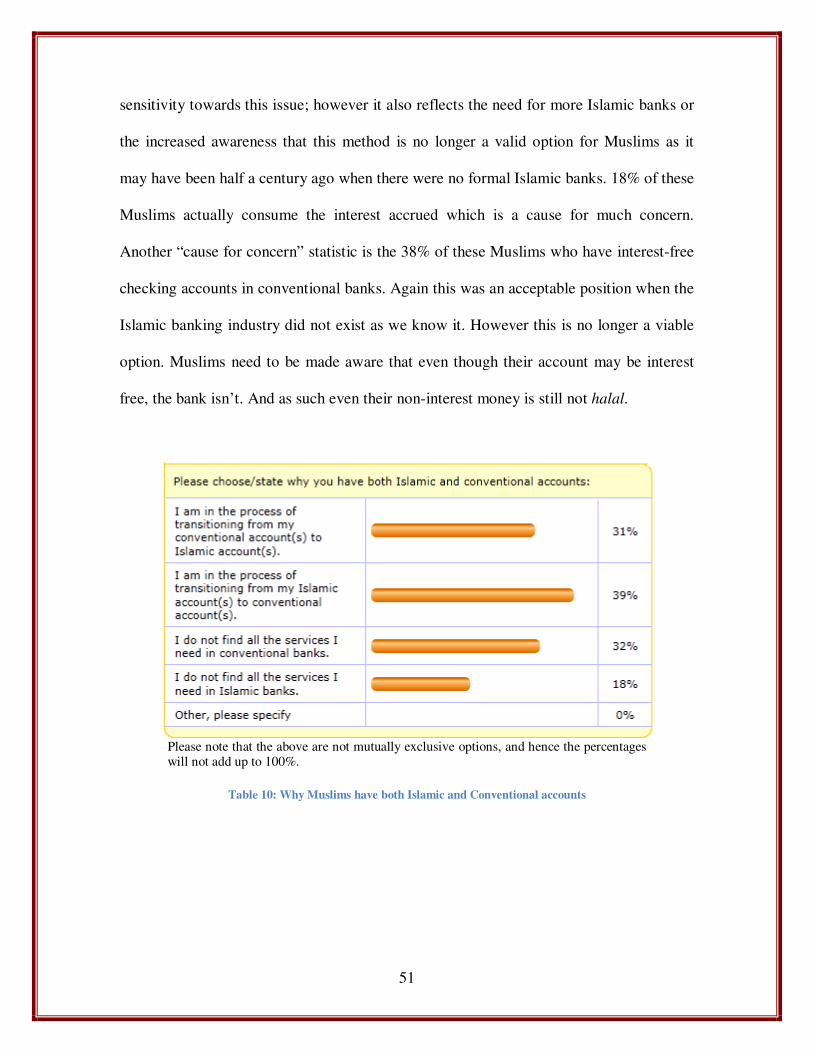

Table 10: Why Muslims have both Islamic and Conventional accounts ......................... 51

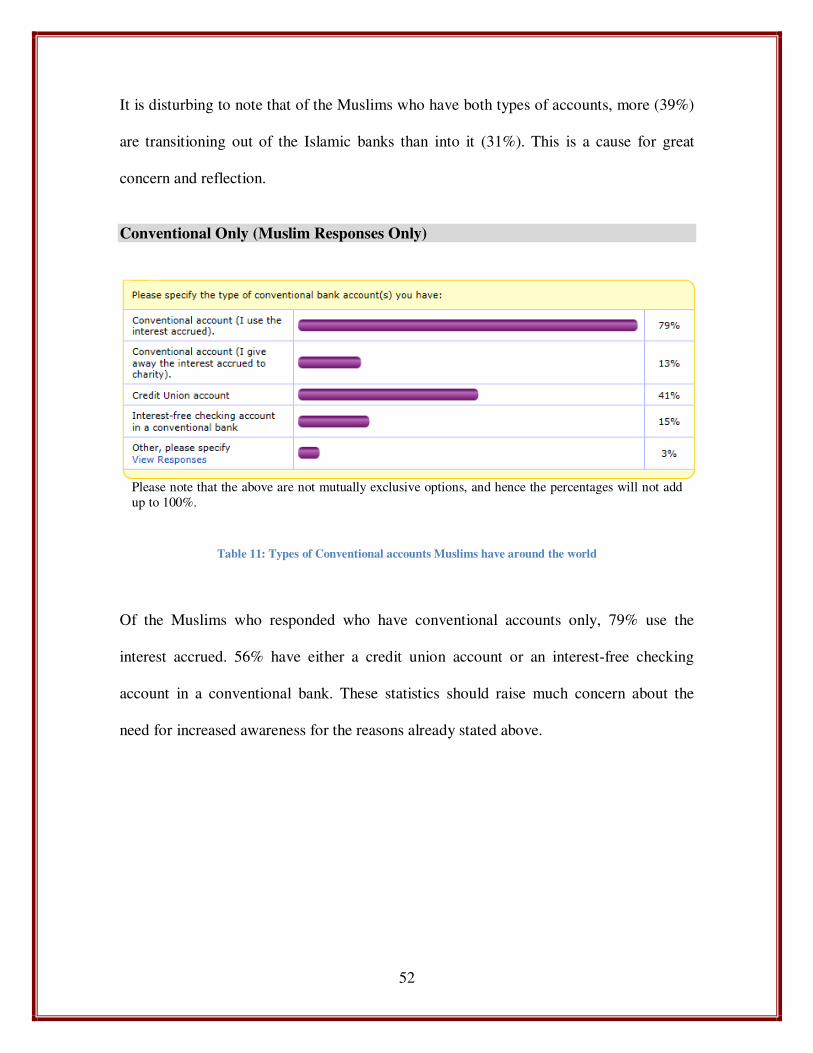

Table 11: Types of Conventional accounts Muslims have around the world ................... 52

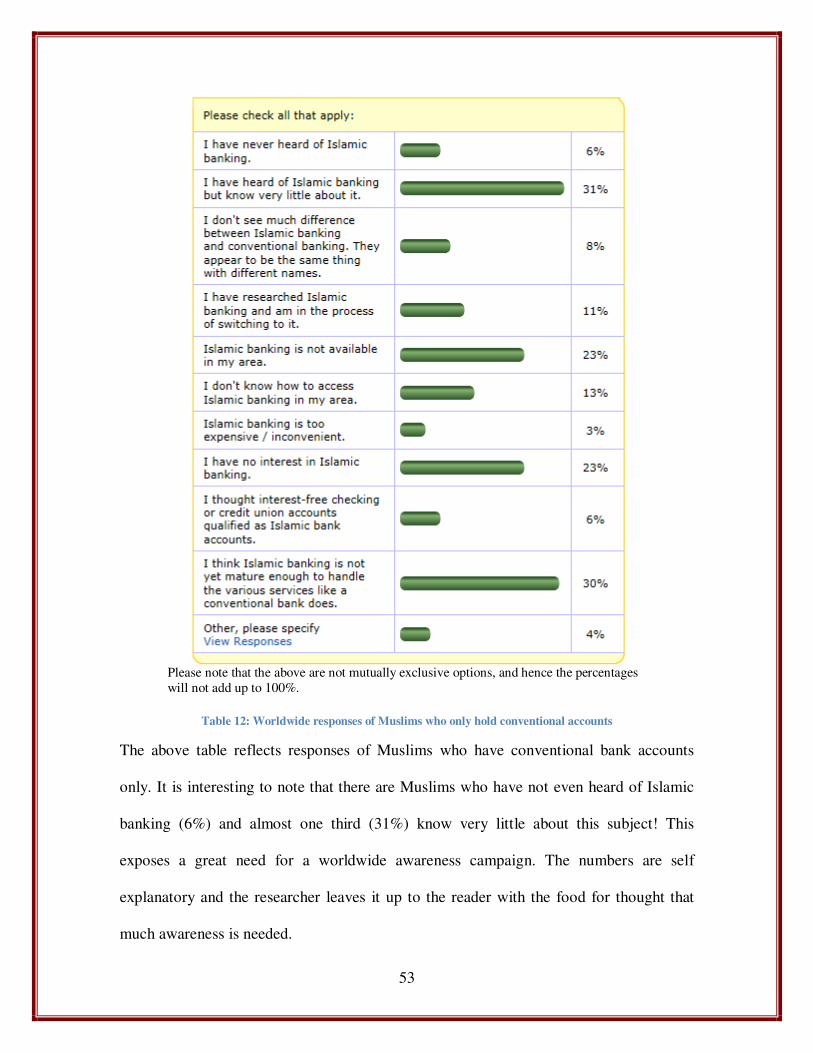

Table 12: Worldwide responses of Muslims who only hold conventional accounts ........ 53

Table 13: Gender comparison - World Factbook vs. Researcher’s Survey Sample ......... 69

Table 14: Age comparison - World Factbook vs. Researcher’s Survey Sample .............. 69

Table 15: Continent Population comparison - UN Statistics vs. Researcher’s Survey

Sample .......................................................................................................................... 69

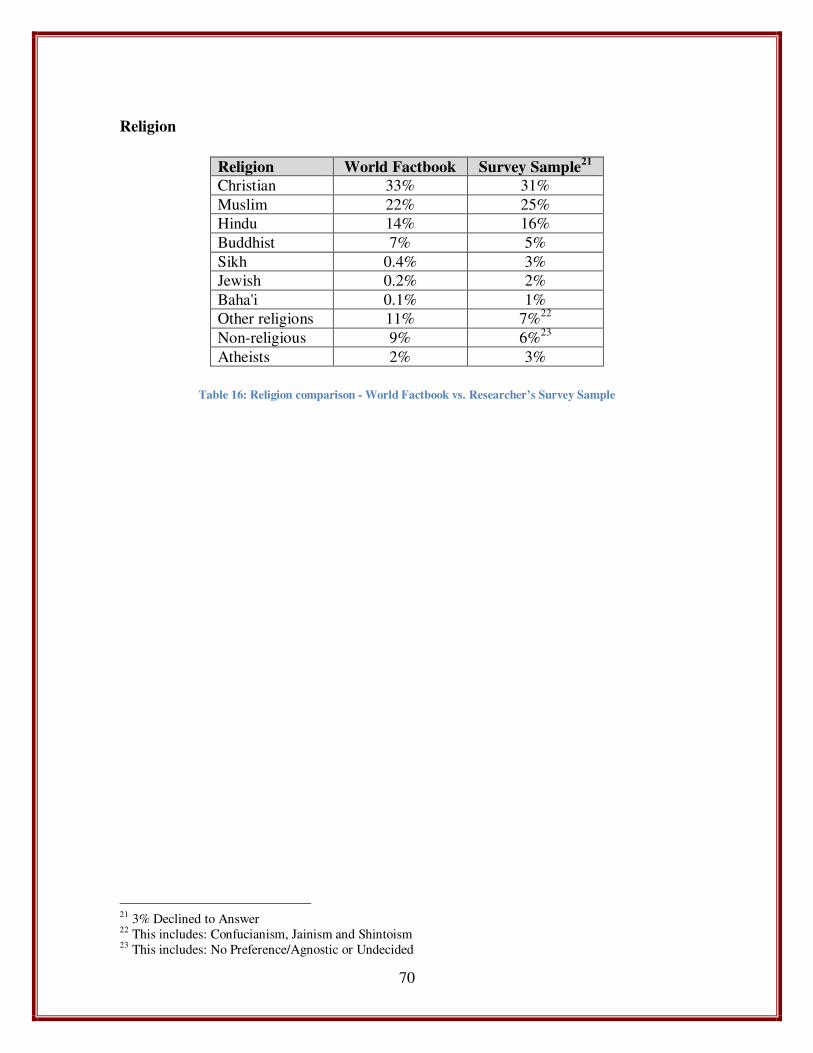

Table 16: Religion comparison - World Factbook vs. Researcher’s Survey Sample ....... 70

XI

List of Figures

Figure 1: Categories of Weaknesses within IFIs as Identified by Industry Professionals 27

Figure 2: Categories of Suggestions to improve IFIs Offered by Industry Professionals . 32

Figure 3: Researcher’s Worldwide Survey responses on difference between ‘interest’ and

‘usury’ ........................................................................................................................... 34

Figure 4: Researcher’s Worldwide Survey response on prohibition of interest/usury by

religion .......................................................................................................................... 39

Figure 5: Researcher’s Worldwide Survey response on difference between Islamic and

Conventional banking .................................................................................................... 41

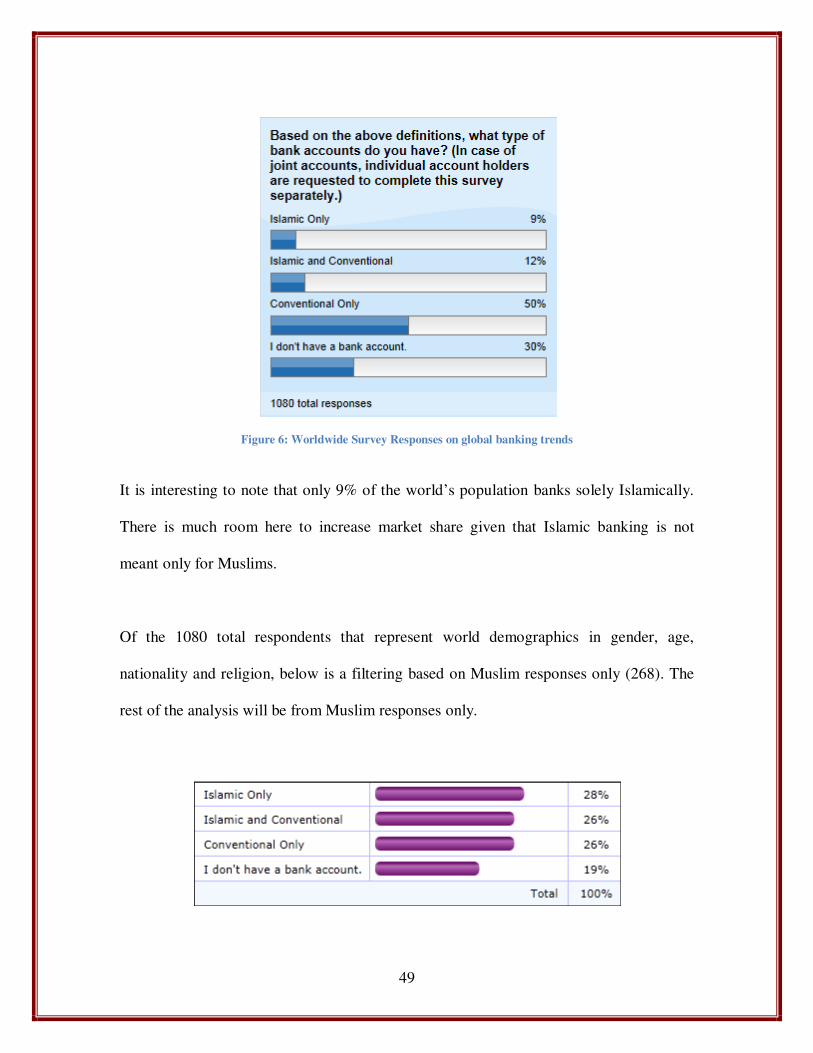

Figure 6: Worldwide Survey Responses on global banking trends ................................. 49

Figure 7: Snapshot of Awareness Video Tutorial #1 on fundamentals of Islamic Finance

(Profit vs. Interest)......................................................................................................... 60

XII

Glossary of Arabic Terms and Abbreviations

Gharar Any uncertainty or ambiguity created by the lack of information or

control in a contract.

GSM Global Survey Market (Online Survey Company)

Hadith Blessed Saying of the Holy Prophet (peace be upon him)

Halal An act permissible in Islamic law

Haram An act impermissible in Islamic law

Hijab Head covering

IFI Islamic Financial Institution

Ijarah

A sale contract which is not the sale of a tangible asset but rather a sale

of the usufruct (the right to use the object) for a specified period of

time.

Mudarabah

An economic agent with capital (rabbul-mal) can develop a partnership

with another agent (mudarib), with skills to form a partnership, with the

agreement to share profits. Although losses are borne only by the capital

owner, the mudarib may be liable for loss, in case of misconduct or

negligence on his part.

Mudarib Economic agent, with entrepreneurial and management skills, who

partners with rabbul-mal (owner of capital) in a Mudarabah contract.

Murabaha

A cost-plus-sale contract where a financier purchases a product, i.e.

commodity, raw material or supplied, for an entrepreneur who does

have his/her own capital to do so. The financier and the entrepreneur

agree on a profit margin, often referred to mark-up which is added to

the cost of the product. The payment is delayed for a specific period of

time.

Musharakah Equity partnership … combining the act of investment and management

Riba

The premium (interest/usury) that must be paid by the borrower to the

lender along with the principal amount as a condition for the loan or for

an extension.

Shareek One of the economic partners in a Musharakah contract

Shari’ah Islamic Law

Sukuk Plural of the Arabic word Sakk meaning certificate, reflects

participation rights in the underlying assets.

Taufeeq Help by God, success

Ummah Nation/People (generally Muslims)

UN United Nations

Islamic Finance related Arabic Terms Extracted from (Iqbal & Mirakhor, 2007)

1

Chapter 1: Introduction

1.1 Problem Statement

Even though the Islamic finance industry has seen astounding growth over the past

decades and is being sought by western countries as a viable alternative to its ailing

conventional counterpart, nevertheless there prevail misconceptions about the industry

not just to those outside Islam but to the adherents of the faith as well. In about 40 years,

the Islamic finance industry has grown to a “total asset base of $1 trillion [but] is still less

than one per cent of global banking assets.” (Banking & Finance, 2012) Given that

Islamic finance is not just for Muslims, but it offers a modus operandi that all ethical

people seek, this percentage is an anomaly that must be addressed. At the least, given that

Muslims are 22% of the world’s population, its banking assets should mirror a similar

percentage.

No doubt the formal Islamic finance industry has been in existence for a very short time

compared to its centuries’ old conventional counterpart. Nevertheless it is imperative

upon the reflective community to analyze the weaknesses within and without the system

for more effective and efficient delivery of its goals. Weaknesses are internal and real.

Stereotypes, on the other hand, are viewed from the outside and are generally wrong

perceptions. Merriam Webster defines the term as “a standardized mental picture that is

held in common by members of a group and that represents an oversimplified opinion,

prejudiced attitude, or uncritical judgment.” (Merriam-Webster, 2012) Stereotypes are

2

perceptions made by outsiders based on either wrong information or judgments. It is

important to address both internal weaknesses and external stereotypes in order to assure

the quality of any system that is attempting to achieve a pre-determined set of goals.

The fundamental concept of the prohibition of Riba (interest/usury) is an elusive concept

to most Muslims. The aversion is from a religious perspective without an in-depth

understanding of the implications of this cancerous element that has taken over the

finance world. The prohibition of large amounts or even small amounts of alcohol doesn’t

baffle the Muslim mind, but many Muslims ask what is wrong with making money out of

money. Isn’t that what business is all about? In addition to Riba, this study attempts to

address the several stereotypes related to Islamic banking and finance to increase

awareness about this holistic approach with the intention that it clears the dust and clouds

around the topic encouraging Muslims as well as non-Muslims away from the dangerous

conventional system which has proven its destructive capabilities time and time again. It

is only when the real and perceived weaknesses from a system are identified and

systematically eliminated, that the system moves towards increased strength, quality and

sustainability. As the Islamic finance system gains more clarity in the minds of people, it

is hoped that more will shift out of the conventional and into the Islamic system creating

critical mass. It is only when a critical mass is achieved in the realm of Islamic finance

that a global affect can be seen of this just and equitable method of distribution of

resources.

3

1.2 Objectives of the Study

The objectives of the study are three fold:

1. To identify the existing weaknesses in the Islamic finance industry

2. To identify the prevailing stereotypes in the Islamic finance industry

3. To identify the methods to remove the above

The study attempts to glean existing weaknesses in the system as stated by professionals

within the Islamic finance industry in Bahrain. And the stereotypes are determined

through a worldwide survey of 1080 individuals who match world demographics in age,

gender, nationality and religion.

1.3 Limitations of the Study

• The study was unable to get responses from every single IFI in Bahrain.

• For the worldwide survey, four criteria were chosen: age, gender, nationality and

religion. Household income and education level were two other factors that could

have been considered but were beyond the scope of this study.

4

Chapter 2: Literature Review

In order to understand the workings of the Islamic finance system, it is important to know

what goals it is trying to accomplish. It is important to understand the spirit before one

delves into its myriad forms which sometimes lead people to confusion given the

unfamiliar terminology involved. But before we explore the Islamic finance system, let us

try to understand what a finance system in general is meant to achieve.

2.1 What is a Finance System?

The systems of any society are eventually designed to fulfill human needs, be they of the

mind, body or soul. In the Islamic worldview, the human being is then responsible for

taking care of the rest of creation be they the animals or the environment because they

have been created as “Khalifa” or vicegerent on this earth. (The Holy Quran, 2:30) It is

important to understand here that this doesn’t represent an anthropocentric view where

Islam considers human beings as the egotistical center of the universe. On the contrary,

centrality or leadership in Islam is not about authority. It is about responsibility and

accountability to Allah Almighty in all matters. So even though human beings have been

given the title of “Ashraful Makhluqat,” (most noble of creation) that is on the premise

that they truly fulfill the archetype of “ahsani taqweem” (best of stature) (The Holy

Quran, 95:4) and carry out the duties of taking care of everything in their jurisdiction. If

they don’t, then they stand the chance of being relegated to the “asfala saafileen” (lowest

of the low) (The Holy Quran, 95:5).

5

Human needs according to Maslow (1970) can be divided into physiological, safety,

belongingness, esteem and self-actualization. Others have added another level which is

self-transcendence, i.e. to go beyond the self which is a very high Islamic principle of

spirituality as well. The systems in a society that service these needs are healthcare, food

and water, municipality, finance, education, political, justice and defense to name the

fundamental ones. The topic of discussion of this paper is the financial system. The term

“finance” is often used interchangeably with “economics” and “banking” It is important

to spell out the difference between these three terms. “The word economy can be traced

back to the Greek word oikonomos, … derived from oikos, ‘house,’ and nemein, ‘to

manage.’ (The Free Dictionary, 2012) Economics therefore means to “manage house.”

Since a home is the microcosm of society, it would then lead us to infer that economics is

the management of all homes. But what is it that is being managed? It is indeed the

resources, be they human, monetary or natural that make up the homes or society.

Economics is therefore defined as a social science “that deals with the production,

distribution, and consumption of goods and services, or the material welfare of

humankind.” (Dictionary.com, 2012) At the macro level it deals with higher level societal

factors such as unemployment, inflation and policies. At the micro level it deals with

individual decisions of home and firms which affects supply, demand, pricing and so

forth.

An interesting contrast between conventional economics and Islamic economics is the

concept of scarcity. Conventional economics based on the definition of many modern

economists is the science of competing for scarce resources.

6

From the conventional economics standpoint the fundamental concept is

scarcity. This is based on the initial assumptions that whereas human

economic wants (i.e. the desire for goods and services) is unlimited the

actual means to satisfy these wants (i.e. economic resources) is limited by

nature. (Collins, 2004)

In the Islamic worldview, although resources are acknowledged as scarce, i.e.

diminishing, however there is a fundamental concept central to the Islamic tradition

which is the concept of “barakah” which literally means “increase” (opposite of scarcity)

or “blessings” which is a special favor from Allah Almighty in the experience of these

resources depending on one’s inner harmony and spiritual alignment with Allah

Almighty as manifested through commitment to the Shari’ah. Another central element in

the Islamic spiritual tradition is the concept of “qana’ah” which is to be satiated with the

fulfillment of needs and not have the constant want for more. This worldview lends

adherents to a more collaborative sentiment rather than the competitive emotions that the

conventional version evokes.

Although Adam Smith is considered the father of economics, it is argued that the laurel is

deserved by Ibn Khaldun, his almost 4 century predecessor:

His significant contributions to economics, however, should place him in

the history of economic thought as a major forerunner, if not the "father,"

7

of economics, a title which has been given to Adam Smith, whose great

works were published some three hundred and seventy years after Ibn

Khaldun's death. Not only did Ibn Khaldun plant the germinating seeds of

classical economics, whether in production, supply, or cost, but he also

pioneered in consumption, demand, and utility, the cornerstones of

modern economic theory. (Oweiss, 2002)

Finance is a branch of economics that deals directly with the management of monetary

resources. And banks of course are the institutions central to this management. If there is

anything central to all three it is money. Below is a discussion of the history and nature of

money.

2.2 The History of Money

Money as we know it today (paper currency and coins) is a relatively modern

occurrence in the spectrum of recorded human history (about 6000 years).

However the concept of using a standard medium of exchange evolved naturally

out of the ancient barter system going back to about 100,000 years. Preceding the

barter system was also the concept of gift economy where people gave each other

things without any expectations. The incentive if analyzed sans spiritual

considerations was possibly social status and its history dates back to the Stone

Age. However the obvious limitation of the barter system which is the lack of a

standard medium of exchange led to the adoption of certain commodities for this

purpose. In the barter system if I had a chicken farm and I needed honey, then I

8

would need to find someone who owned a bee farm but who also needed chicken.

If he did not need chicken, then I would be stuck! This is why the commodity

medium of exchange was the obvious solution and evolved naturally. Different

societies adopted different commodities such as barley, silver and even oxen and

horses. This was the first commodity money which became in use around 4000

B.C. in the Mesopotamian civilization (modern day Iraq). The natural weakness in

using perishable commodities such as barley and horses which were difficult to

store and transport led to the minting of easily storable coined money which was

often stamped for its purity and weight. However the gold coins could still

become heavy and difficult to transport. This led to the invention of representative

money which was made of much lighter metals such as copper and aluminum and

represented the actual commodity but was not the commodity itself. The money

that is in circulation today is fiat money which has been disconnected from the

commodity (gold) backing. This happened in 1971 in what is called the Nixon

Shock. Fiat money has no intrinsic value and the only reason it can be used as a

medium of exchange is because the government says so. This is one of the most

crucial turning points in the history of money because it has opened up the avenue

of printing money that has no commodity backing which leads to the serious

problem of inflation. Money the etymology of which is rooted in Roman

Mythology (money in ancient Rome was coined at the temple of Roman goddess

Juno Moneta), has therefore existed in commodity form since the time of the

ancient barter system. (Qadri, 2011)

9

As can be seen from the above discussion, money was an invention by humanity in order

to carry out necessary transactions. Therefore it has no inherent or intrinsic value. This is

why in the Islamic financial system, money cannot be bought or sold like other

commodities. Even Aristotle considered money as a means to facilitate exchange and

therefore was of the view that a piece of money cannot beget another piece. (Zarlenga,

The Usury Problem Remains, 2010) This understanding rejects the entire premise of

interest or usury where money is generated from money without the presence of other

elements of production such as labor and assets. In order to see the big picture, presented

below is a brief history of interest. This element in the modern conventional financial

system is taken very much for granted. However history tells us that charging interest too

was an innovation by humanity, and a truly destructive one.

2.3 The History of Interest / Usury (Riba)

The Arabic word for interest or usury is “Riba” which linguistically means “increase.”

Increase is the foundation of production which is the cornerstone of economics. However

how this increase occurs is of prime importance. Organic commodities when borrowed

have the inherent ability to produce. For example in ancient societies “when tools were

borrowed, the produce which the tools had helped to create were shared or used to ‘pay

back’ for the use of the tool” (Zarlenga, http://www.monetary.org, 2000). The same

applied to seeds or animals borrowed, as seeds can naturally “produce” and animals can

give birth. So the payback was natural and it didn’t cause any unnatural stress in the

system of transfer of resources.

10

However, it was the Ancient Orient (Egypt, Assyria, Sumeria) which made a

momentous innovation, allowing usury to be charged on loans of metals, with the

interest to be paid in more metal. This conceptual error treated inorganic materials

as if they were living organisms with the means of reproduction. This is the

beginning of the charging of usury/interest and is attributed to the Pharaohs who

as the central authority were the largest lenders and chargers of interest and who

manipulated market prices in order to offset the negative effects of usury on the

market. Even they realized the harmful effects of their innovation and

consequently stepped in to try to mitigate it. (Zarlenga, http://www.monetary.org,

2000)

2.4 Basics of Islamic Finance

With this fundamental understanding about finance, money and interest let us turn

towards understanding Islamic finance. People think of it as a conventional system

without interest and without certain sector involvement such as alcohol, pork, weapons,

pornography and the like. However Islamic finance is much more than that. It is a system

of social justice where the resources within the economy are made available to those who

truly need it and who can develop it for the betterment of the rest. There is no reek of

socialism as Islamic Law fully allows individual ownership rights to property. However

there is the understanding that this ownership is under the vice regency of the Almighty.

No ownership is absolute. In the Shari’ah one doesn’t even truly own one’s body so an

11

individual has no right to harm oneself. This is the basis of the prohibition of suicide in

Islamic Law. Additionally, profit generation is not a faux pas, provided nobody’s rights

are violated in its pursuit. Therefore in Islamic finance, Corporate Social Responsibility is

not a nice-to-have, but a fundamental element of the structural makeup of any

transaction. A firm claiming to adhere to the Shari’ah cannot for example exploit child

labor, or pollute the environment or knowingly use harmful ingredients while attempting

to make the bottom line. A balance must be struck where everyone and everything

including the environment is given its due right (haq). It is important to understand some

fundamental principles related to Islamic finance before one delves into the many

branches. Below are listed a few fundamentals starting with the goals of the Shari’ah

itself:

• Goals of the Shari’ah: It is crucial that those seeking to understand Islamic

finance understand the goals of the Shari’ah or what is called Maqaasid As-

Shar’i. This is because Islamic finance is a branch of the Shari’ah. Understanding

universals (usool) before specifics (furoo’), and spirit before form is critical to the

path of understanding any discipline. All too often we find people confused and

entangled in the branches because there is no clear understanding of the root. The

Shari’ah has often been personified in Islamic literature as a tree the roots of

which are very deep and stable and the branches of which are very wide and

flexible. It is only such a system that can survive because it continues to provide

dynamic and viable solutions to contemporary issues based on wise principles that

have stood the test of time. Unfortunately today many do not understand the

12

Shari’ah and view the actions of certain cultures who are actually carrying out

very anti-Shari’ah activities and have labeled them as Shar’i. This is a fine

example of lack of knowledge of the usool or the Maqaasid As-Shar’i. The

Shari’ah has both universal as well as specific goals. The universal goals

(Maqaasid-ul kulliyya) is to further benefit and prevent harm which is a direct

heed to the verse in the Holy Quran that calls upon the rising of a people who

invite everyone to all that is good, enjoining what is right and forbidding what is

wrong. (The Holy Quran, 3:104). The specific goals (Maqaasid-ul juziyya) are the

protection of religion (deen), life (hayaa), intellect (‘aql), progeny (nasb) and

wealth (maal). With this overarching view in mind, one can then proceed towards

any of the branches of the Shari’ah – in our case Islamic finance.

• Nature of Money – As discussed earlier, in the Islamic worldview, money is not a

commodity but a means of exchange. Hence it cannot be traded. People tend to

think of interest as the “price” you pay for borrowing money. However, one

cannot think of interest as the “price” paid for something like a glass of lemonade

which is used to quench ones thirst. Money in itself does not fulfill a human need.

One cannot eat it to satiate hunger pangs or use it as a blanket on a cold night.

However one can buy some bread and a blanket with it. It is a means to an end

and not the end in itself. As Aristotle correctly argued, money is not a commodity.

He rejected the justification for charging interest on this ground, arguing “that

money is sterile; it doesn’t beget more money the way cows beget more cows. He

13

knew that ‘Money exists not by nature but by law’” (Zarlenga, The Usury

Problem Remains, 2010).

“The most hated sort (of wealth getting) and with the greatest reason, is

usury, which makes a gain out of money itself and not from the natural

object of it. For money was intended to be used in exchange but not to

increase at interest. And this term interest (tokos), which means the birth

of money from money, is applied to the breeding of money because the

offspring resembles the parent. Wherefore of all modes of getting wealth,

this is the most unnatural.” (1258b, POLITICS) (Zarlenga, The Usury

Problem Remains, 2010)

This universal truth is stated by the Holy Prophet Muhammad (peace be upon

him) on the authority of Syedna Abu Hurayrah (may Allah be pleased with him):

"Riba has seventy [degrees] of sin, the easiest [least] of which is that [equivalent

to] a man marries [commits adultery with] his mother." (Ibn Majah) This is how

serious and detrimental the workings of interest/usury are and its practical

implications can be seen in the world today with the continuous increase in the

rich-poor divide, man-made famines, global poverty and the overwhelming debt

crisis which is the direct result of usury.

14

• Nature of Increase: Often people are unable to see the difference between the

increase in money that occurs due to interest from a bank account and that due to

profit from a successful business venture. The key difference is in the factors of

production. If money is the only element involved in producing an increase then it

is like the above mentioned Hadith and is rejected by the Shari’ah. Not only is it

unnatural, it leads to the chronic problem in our economies today and that is

inflation. In a business venture profit is made naturally due to beneficial

transactions which include labor and assets as factors of production in addition to

money. In the interest scenario due to the absence of labor and assets, there is no

economic activity associated with the production. This is the formula for an

unnatural stagnation and other artificial methods are adopted to “fix” this. More

money is printed leading to the problem of inflation. And given the human

tendency to not take risk and obtain “easy” money, the interest/usury system lures

people away from the more holistic community investment projects into what

they think is a “guaranteed” return on their hard earned money. It is a trick that

takes advantage of the greed (hirs) element of the human self (nafs).

• Nature of Debt/Credit: The Shari’ah system makes every attempt that a human

being is free from debt at all times unless there is a dire necessity. Debt is looked

upon as a state of disequilibrium. The Prophet Muhammad (peace be upon him)

said, “…best amongst you are those who are best in paying off debt.” (reported by

Muslim) and “Procrastination (delay) in paying debts by a wealthy person is

injustice…” (reported by Bukhari). Khan & Mould (2008) continue to report that

15

“Debt is one of the principal causes of poverty; it has hampered the economic

development of indebted countries and has prevented them from investing in

essential services such as healthcare and education.” This cycle of poverty is the

direct result of the interest required to service the debt. Additionally, Khan &

Mould state that “Indeed, indebted countries are paying approximately $118

million every day in interest and principal payments to rich countries - although

payments far greater than the original loan amount have already been made.”

• Risk and Return: “It is the established Hadith ‘liability justifies utility or return’.”

(Al-Suwailem, 2000) Hence this breaks the stereotype that Islamic finance is

against risk or risk-averse. It is indeed the risk one takes when investing in a

business venture as a Mudarib or Shareek that entitles one to the profits of that

venture. When Islamic finance is known as risk-averse it is in reality uncertainty

or Gharar-averse. In other words it does not participate in transactions that are

ambiguous or whose elements are unclear such as selling birds in the sky.

However, legitimate hardships or “unchartered territory” explored and endured

during a business transaction are the responsibility of all community members to

partake in so that risk is shared. What Islamic finance does not allow is risk being

borne only by some segments such as an entrepreneur would have to bear in a

usurious lending scenario with a bank. Islamic finance is more risk-diverse than

risk-averse.

16

2.5 Weaknesses and Stereotypes

Past surveys investigating images about Islamic finance have revealed similar

stereotypes. However the conclusion was that of non-viability of this system instead of a

constructive criticism for increased sustainability as is the purpose of this study.

A recent survey of European and American bankers revealed that a majority were

only vaguely aware of the existence of Islamic finance… One was the view that

Islamic financial institutions, being interest-free, cannot possibly work. (The

interviewer would invariably find himself on the receiving end of a lecture on the

role of interest rates in finance.) A variation on that theme – and one also leading

to the conclusion of non-viability – was the equation of ‘interest-free’ with ‘non-

profit’. The other common set of attitudes was that Islamic financial institutions

were no different from conventional ones, since interest, albeit under different

names and guises, was used. (Warde, 2000)

Weaknesses of the system in terms of dearth of Shari’ah scholars have also been

identified. “The controversy over the Goldman sukuk illustrates some of the weaknesses

of the Islamic finance industry… ‘The big problem is that there just aren't enough of

them [Shari’ah scholars],’ said one Dubai-based banker in the industry.” (Sleiman, 2012)

A survey was conducted of corporate customers in Malaysia which has also revealed that

there exists much need for product awareness and education. “…Islamic banking

17

products and services have not done enough in educating customers and marketing their

products.” (Haron)

Other studies have also recommended structural change within the industry so its

direction can be put back on track (“Is Islamic Finance Delivering?” Ethica Institute).

However, the focus was on increasing the accountability of the industry to active

engagement in the community as is the theoretical mandate of Islamic finance. This

researcher’s study expands its suggestions to focus a great deal on awareness of the

public to raise their knowledge quotient and hence Shari’ah sensibilities of the masses in

general and scholars in particular.

Some weaknesses such as lack of Islamic interbank liquidity, legal support and so forth

have been identified in the past but were not revealed through this study. However,

“many of the questions facing those in Islamic finance turn on regulation and

governance.” (The gulf business vews & analysis, 2010) These findings were also echoed

in the researcher’s study.

Although work has been done in this area, the researcher purports that more rich data and

analysis has been added to the existing body of knowledge.

18

Chapter 3: Research Methodology

This study employs both qualitative (descriptive and analytical) and quantitative research

approaches to gather and analyze data and reach conclusions. It consists of two parts:

1. to identify the weaknesses within the IFIs through a survey of experienced

professionals within the industry

2. to identify the stereotypes perceived by the public from the outside through a

survey of a sample of all adults (individuals of age18 years and above)

The research instruments used in both cases were online surveys that were emailed to the

target audiences (or sample) as explained below. Online surveys are an acceptable part of

research methodology as “research investigators may choose to contact respondents in

person, by telephone, by mail, or on the Internet.” (Zikmund, 2003)

3.1 Weakness identification

A survey titled Islamic Finance Survey 2012 (for Islamic Financial Institution

Professionals) was designed by the researcher using an online survey tool which queried

IFI professionals on their opinions regarding the strengths, weaknesses and methods of

improving their financial institutions1. It is also included in Appendix D. The target

population was professionals within the major IFIs in the Kingdom of Bahrain.

Professionals included IFI employees at the director, manager, officer and administrator

levels. Over 70% of those who responded were at the director or manager levels.

1 This survey can be previewed here: http://www.zoomerang.com/Survey/WEB22ETP7NUUX8/Preview.

19

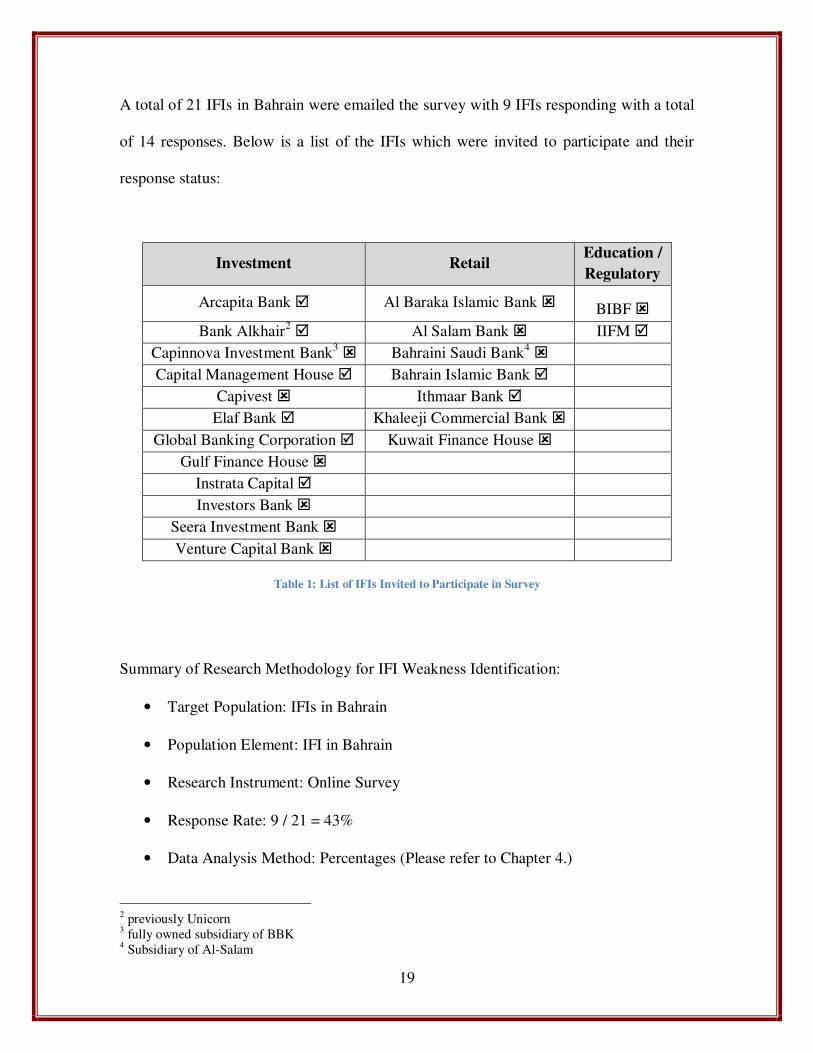

A total of 21 IFIs in Bahrain were emailed the survey with 9 IFIs responding with a total

of 14 responses. Below is a list of the IFIs which were invited to participate and their

response status:

Investment Retail Education /

Regulatory

Arcapita Bank � Al Baraka Islamic Bank �

BIBF �

Bank Alkhair2 � Al Salam Bank � IIFM �

Capinnova Investment Bank3 � Bahraini Saudi Bank4 �

Capital Management House � Bahrain Islamic Bank �

Capivest � Ithmaar Bank �

Elaf Bank � Khaleeji Commercial Bank �

Global Banking Corporation � Kuwait Finance House �

Gulf Finance House �

Instrata Capital �

Investors Bank �

Seera Investment Bank �

Venture Capital Bank �

Table 1: List of IFIs Invited to Participate in Survey

Summary of Research Methodology for IFI Weakness Identification:

• Target Population: IFIs in Bahrain

• Population Element: IFI in Bahrain

• Research Instrument: Online Survey

• Response Rate: 9 / 21 = 43%

• Data Analysis Method: Percentages (Please refer to Chapter 4.)

2 previously Unicorn 3 fully owned subsidiary of BBK 4 Subsidiary of Al-Salam

20

3.2 Stereotype Identification

A survey titled Worldwide Islamic Banking Survey 2011 - 2012 (GSM) was designed by

the researcher and administered through a reputed online survey agency. This survey

agency provided the service of emailing the researcher’s online survey5 to a sample of the

world’s population which matched it within an approximately 3-5% margin of error in

age, gender, nationality and religion. This survey can be found in Appendix E. The

statistical comparison between the profile of the world population and the survey sample

can be found in Appendix C.

The survey queried the respondents on their views about interest/usury,

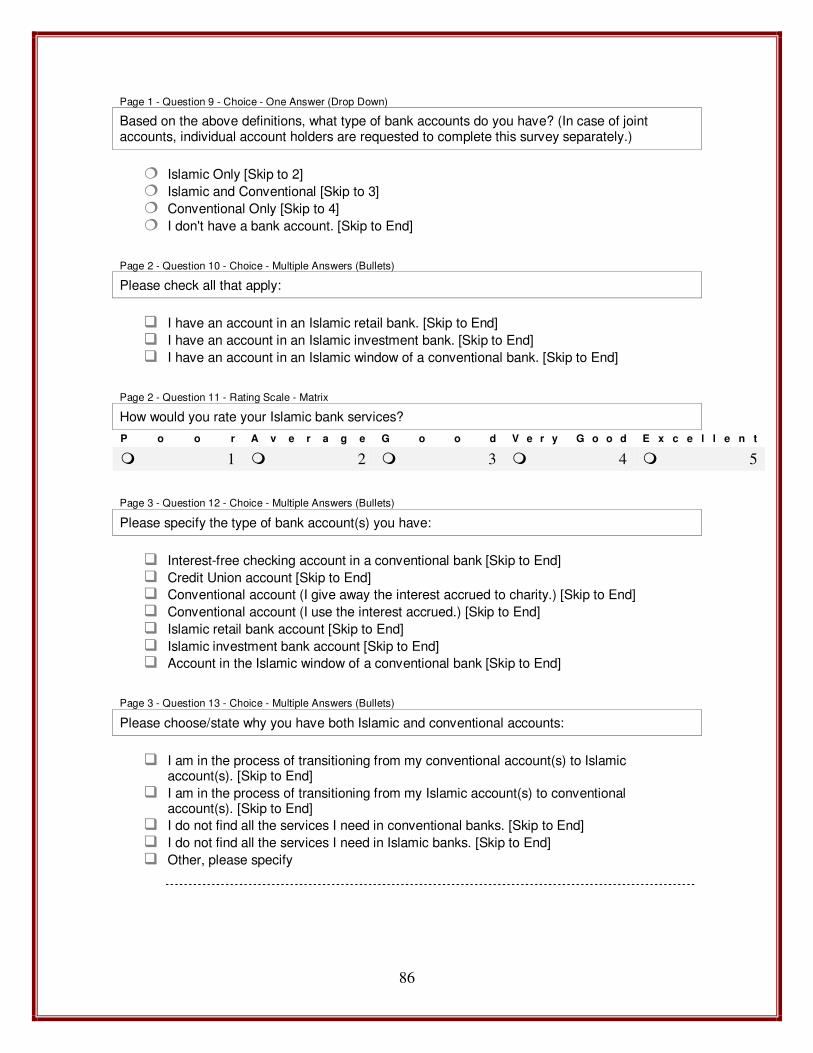

conventional/Islamic banking and their banking trends. At question number 9, the survey

branched off into three sections:

1. Respondents with Islamic accounts only

2. Respondents with Islamic and Conventional accounts

3. Respondents with Conventional accounts only

A total of 1080 respondents participated in this worldwide survey out of which 268 were

Muslims. A sample size of 1111 respondents is needed for a population greater than

100,000 with a precision error of 3%. (Israel, 1992)

Summary of Research Methodology for Stereotype Identification:

• Target Population: All adults (18 years or above) around the world

5 http://www.zoomerang.com/Survey/WEB22FEL2ZE6ML/Preview

21

• Population Element: An adult (18 years or above)

• Research Instrument: Online Survey

• Sample: 1080 adults matching world demographics in age, gender, nationality and

religion (Comparison provided in Appendix C)

• Response Rate: 1080 / 1111 = 97%

• Data Analysis Method: Percentages (Please refer to Chapter 5.)

22

Chapter 4: Findings - Weaknesses

In order to strengthen any system it is important to indentify its weaknesses with the

intention of addressing them systematically. In a survey conducted by the researcher of

major IFIs in the Kingdom of Bahrain, professionals were asked to state three current

challenges within the Islamic finance industry. Below is a table of responses with their

verbatim challenges stated as well as categorized into nine areas for ease of study and

response. Almost 60% of the respondents have over 5 years of experience within the

industry and over 20% have an experience of more than 10 years. Over 70% of the

respondents were either Managers or Directors at the IFIs. Below is a list of the

participating IFIs.

Participating IFIs (alphabetical):

1. Arcapita Bank

2. Bahrain Islamic Bank

3. Bank Alkhair

4. Capital Management House

5. Elaf Bank

6. Global Banking Corporation

7. Instrata Capital

8. International Islamic Financial Market

9. Ithmaar Bank

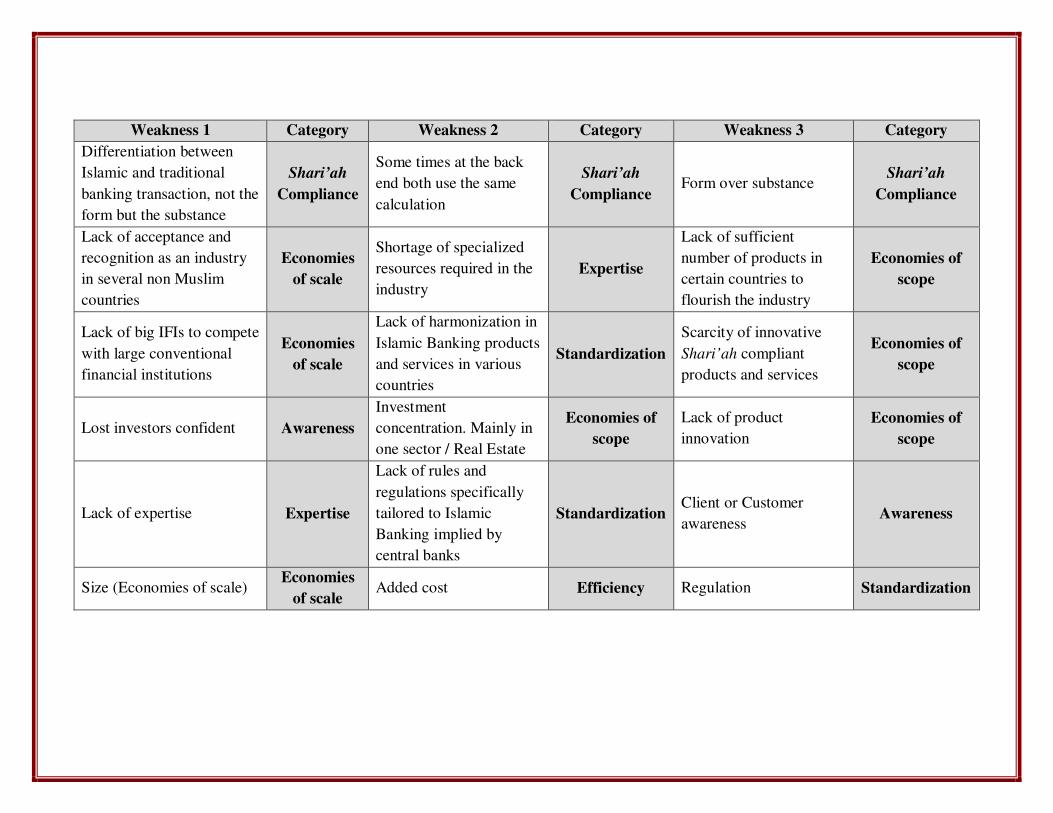

Weakness 1 Category Weakness 2 Category Weakness 3 Category

Differentiation between

Islamic and traditional

banking transaction, not the

form but the substance

Shari’ah

Compliance

Some times at the back

end both use the same

calculation

Shari’ah

Compliance Form over substance

Shari’ah

Compliance

Lack of acceptance and

recognition as an industry

in several non Muslim

countries

Economies

of scale

Shortage of specialized

resources required in the

industry

Expertise

Lack of sufficient

number of products in

certain countries to

flourish the industry

Economies of

scope

Lack of big IFIs to compete

with large conventional

financial institutions

Economies

of scale

Lack of harmonization in

Islamic Banking products

and services in various

countries

Standardization

Scarcity of innovative

Shari’ah compliant

products and services

Economies of

scope

Lost investors confident Awareness

Investment

concentration. Mainly in

one sector / Real Estate

Economies of

scope

Lack of product

innovation

Economies of

scope

Lack of expertise Expertise

Lack of rules and

regulations specifically

tailored to Islamic

Banking implied by

central banks

Standardization Client or Customer

awareness Awareness

Size (Economies of scale) Economies

of scale Added cost Efficiency Regulation Standardization

24

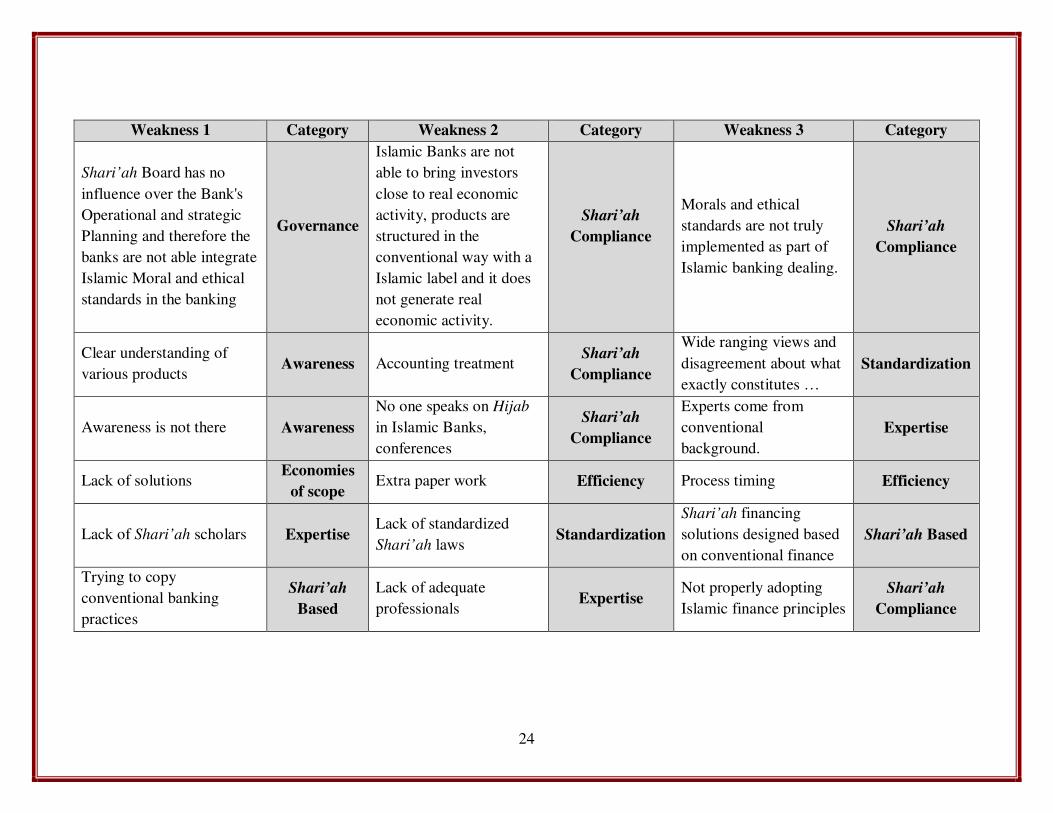

Weakness 1 Category Weakness 2 Category Weakness 3 Category

Shari’ah Board has no

influence over the Bank's

Operational and strategic

Planning and therefore the

banks are not able integrate

Islamic Moral and ethical

standards in the banking

Governance

Islamic Banks are not

able to bring investors

close to real economic

activity, products are

structured in the

conventional way with a

Islamic label and it does

not generate real

economic activity.

Shari’ah

Compliance

Morals and ethical

standards are not truly

implemented as part of

Islamic banking dealing.

Shari’ah

Compliance

Clear understanding of

various products Awareness Accounting treatment

Shari’ah

Compliance

Wide ranging views and

disagreement about what

exactly constitutes …

Standardization

Awareness is not there Awareness

No one speaks on Hijab

in Islamic Banks,

conferences

Shari’ah

Compliance

Experts come from

conventional

background.

Expertise

Lack of solutions Economies

of scope Extra paper work Efficiency Process timing Efficiency

Lack of Shari’ah scholars Expertise Lack of standardized

Shari’ah laws Standardization

Shari’ah financing

solutions designed based

on conventional finance

Shari’ah Based

Trying to copy

conventional banking

practices

Shari’ah

Based

Lack of adequate

professionals Expertise

Not properly adopting

Islamic finance principles

Shari’ah

Compliance

25

Weakness 1 Category Weakness 2 Category Weakness 3 Category

New and not competitive in

its product offering

Economies

of scope

Focus only on Shari’ah

compliant and NOT on

Shari’ah based banking

Shari’ah Based

Drive is for profitability

of the shareholders and

not to the benefit of the

Muwakkil i.e. depositors

as the returns offered are

minimal

Efficiency

Failure to follow proper

Shari’ah guidelines due to

lack of active Shari’ah

board/committees roles.

Shari’ah

Compliance

Conflict between

shareholders' vision and

management's goals.

Governance

Lack of

professionals/leaders in

Islamic banking

including Shari’ah

advisors.

Expertise

Table 2: Weaknesses within IFIs as stated by Industry Professionals

Below is a list of definitions of the above categories and breakdown of the weaknesses in order of severity:

1. Shari’ah Compliance: This is a complaint by the industry professionals that expresses either a real or perceived violation of

Shari’ah principle(s) in the financial instrument or any other transaction within the industry.

2. Economies of scope: This is a complaint that there aren’t enough Islamic products in the market to fulfill people’s needs.

3. Expertise: This is a complaint that the industry professionals are not trained enough in Shari’ah or accounting principles. It

also encompasses the malady that Shari’ah scholars are not well versed in accounting principles.

26

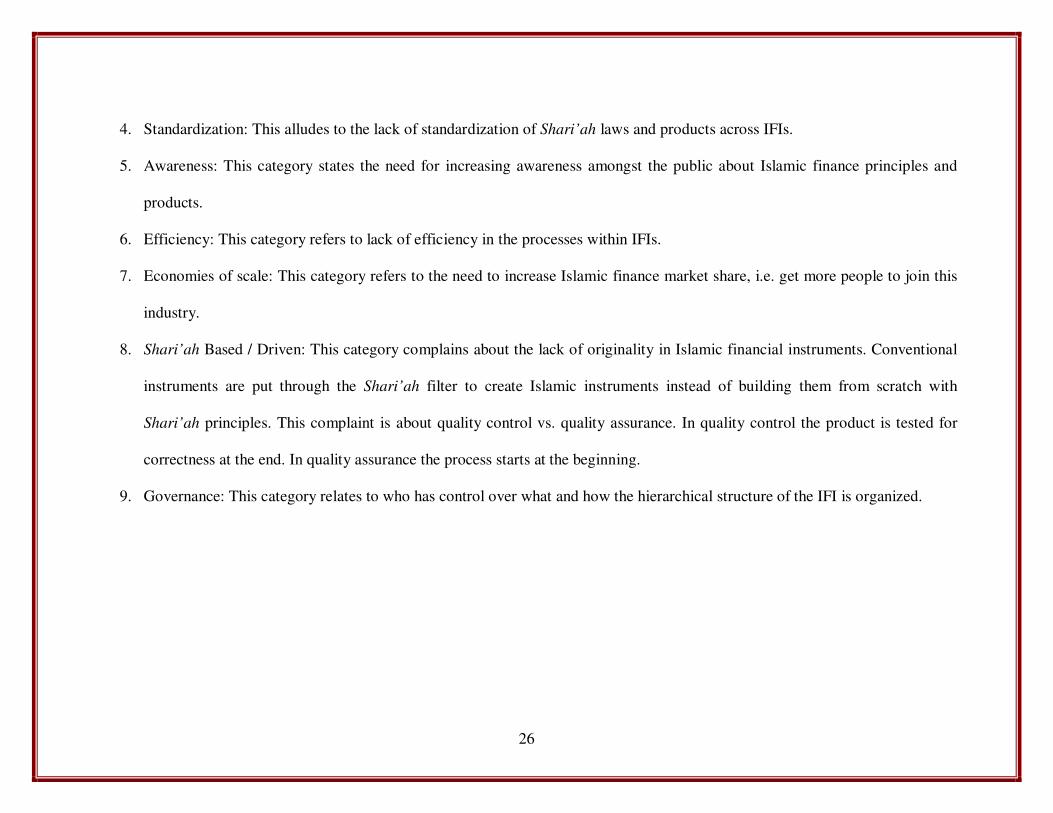

4. Standardization: This alludes to the lack of standardization of Shari’ah laws and products across IFIs.

5. Awareness: This category states the need for increasing awareness amongst the public about Islamic finance principles and

products.

6. Efficiency: This category refers to lack of efficiency in the processes within IFIs.

7. Economies of scale: This category refers to the need to increase Islamic finance market share, i.e. get more people to join this

industry.

8. Shari’ah Based / Driven: This category complains about the lack of originality in Islamic financial instruments. Conventional

instruments are put through the Shari’ah filter to create Islamic instruments instead of building them from scratch with

Shari’ah principles. This complaint is about quality control vs. quality assurance. In quality control the product is tested for

correctness at the end. In quality assurance the process starts at the beginning.

9. Governance: This category relates to who has control over what and how the hierarchical structure of the IFI is organized.

27

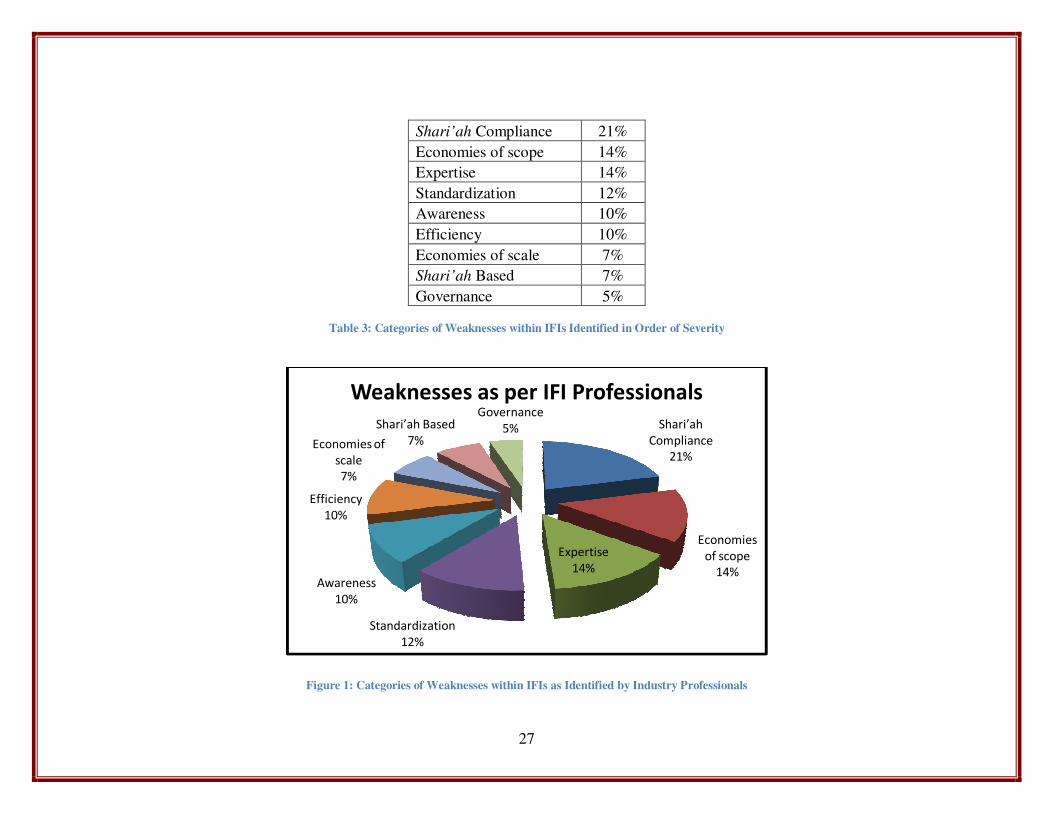

Shari’ah Compliance 21%

Economies of scope 14%

Expertise 14%

Standardization 12%

Awareness 10%

Efficiency 10%

Economies of scale 7%

Shari’ah Based 7%

Governance 5%

Table 3: Categories of Weaknesses within IFIs Identified in Order of Severity

Figure 1: Categories of Weaknesses within IFIs as Identified by Industry Professionals

Shari’ah

Compliance

21%

Economies

of scope

14%

Expertise

14%

Standardization

12%

Awareness

10%

Efficiency

10%

Economies of

scale

7%

Shari’ah Based

7%

Governance

5%

Weaknesses as per IFI Professionals

28

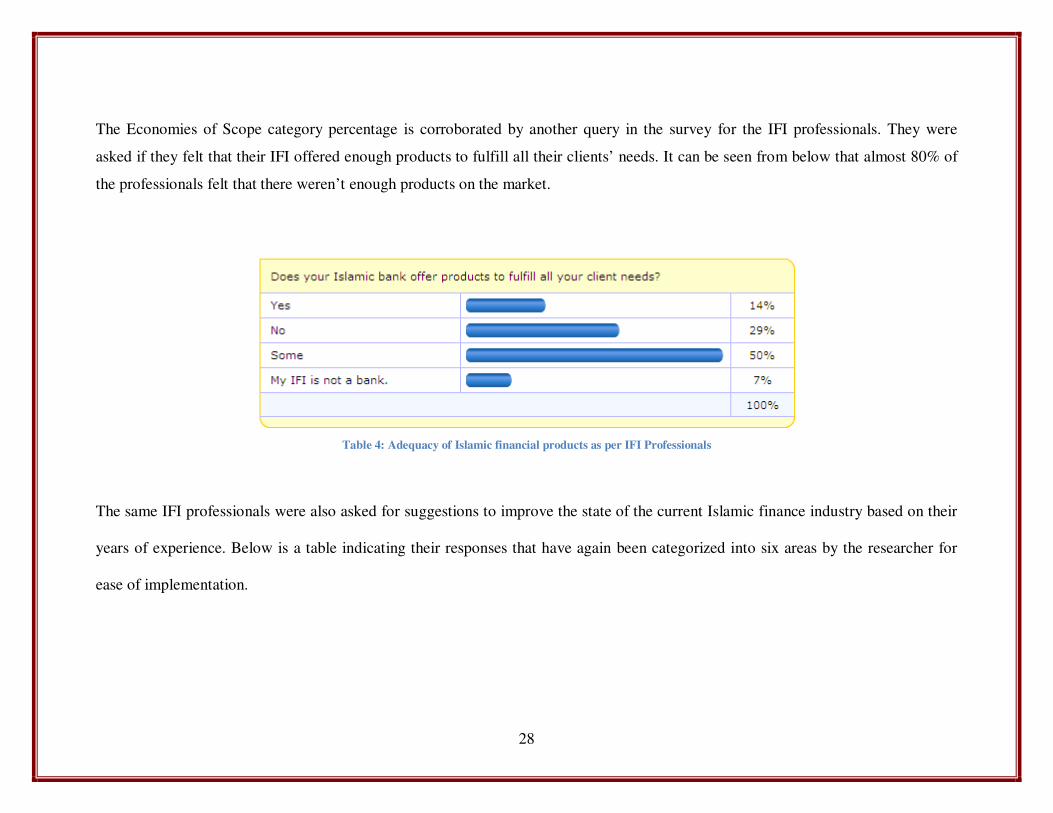

The Economies of Scope category percentage is corroborated by another query in the survey for the IFI professionals. They were

asked if they felt that their IFI offered enough products to fulfill all their clients’ needs. It can be seen from below that almost 80% of

the professionals felt that there weren’t enough products on the market.

Table 4: Adequacy of Islamic financial products as per IFI Professionals

The same IFI professionals were also asked for suggestions to improve the state of the current Islamic finance industry based on their

years of experience. Below is a table indicating their responses that have again been categorized into six areas by the researcher for

ease of implementation.

29

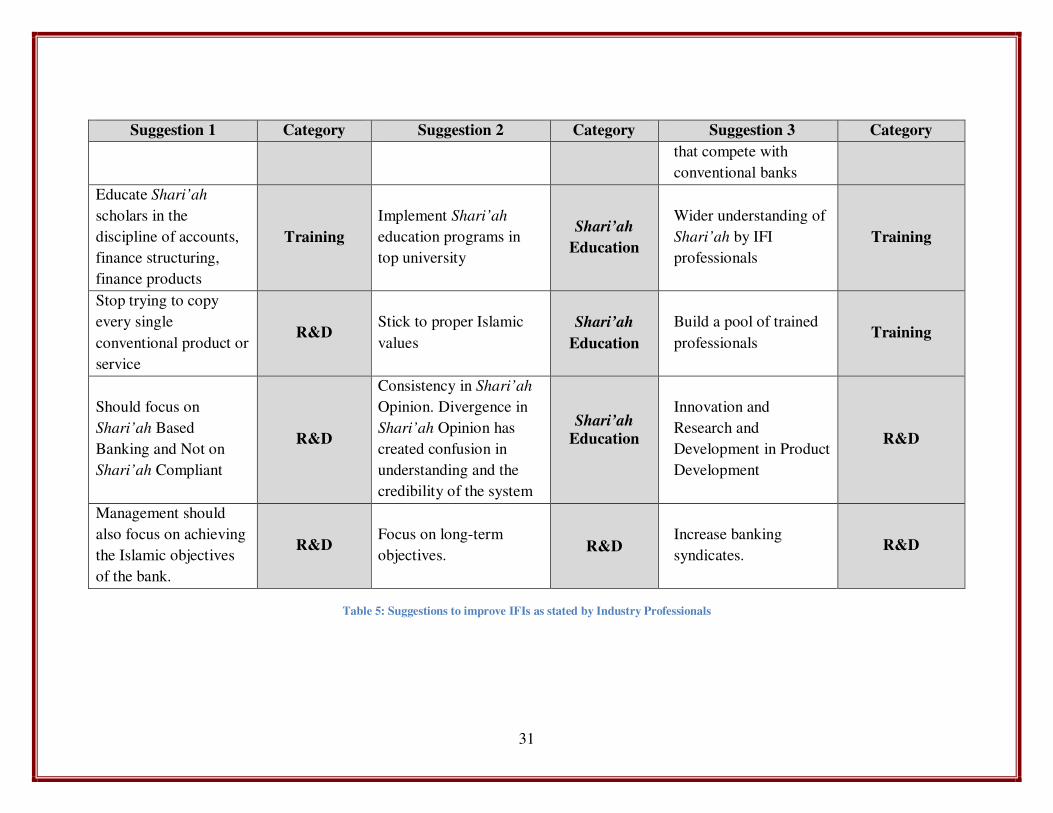

Suggestion 1 Category Suggestion 2 Category Suggestion 3 Category

Serious studies and

research to develop

products to not to use

"form over substance

concept"

R&D

Islamic banking should

be competitive / cheaper

not more expensive than

traditional banking

R&D

Strict and more

knowledgeable Shari’ah

boards

Training

Marketing of Islamic

finance be based on its

just and fair principles.

Awareness

Changing the perception

that Islamic Banking is

banking for followers of

Islam only.

Awareness

Enhancing the

Accounting principles

for Islamic Financing in

line with IFRS to the

extent possible.

R&D

Establishment of giant

IFIs Market Share

Proper marketing of

Islamic economic system

in comparison with

socialism and capitalism

Awareness

Proper training of

Islamic Banking staff

and research for

innovative products

Training /

R&D

Centralized Shari’ah

regulator. Feedback Competent regulators Feedback

Products innovation.

Now we only replicate

conventional bank

product.

R&D

Increase awareness to

differentiate between

Islamic and

conventional banking

Awareness

Specializing in creating

structured products that

cater to the large

conventional banking

consumer base.

R&D

Current Islamic boards

should start involving in

setting standards for

specialized industries to

cater to other sectors

needs and promote for

Islamic banking rather

than just setting rules

R&D

30

Suggestion 1 Category Suggestion 2 Category Suggestion 3 Category

and regulations in

general.

Merger between

Shari’ah institutions Market Share

Better transparency and

accountability Feedback Product diversification R&D

Shari’ah Board should

be given more power in

the bank’s business

plan and they should

not limited to

approving products.

Independent Shari’ah

Board should be fully

aware of banks

activities.

R&D

More research is

required, real economic

activity should be given

instead of focusing on

just the legal form of

transaction without

underlying real economic

activity

R&D

Clients of investment

banks should have an

access to Shari’ah

Board to raise any

ethical issues and the

memberships of

Shari’ah Board

members should be

limited so they can

focus on few

institutions and closely

work with the bank and

understand its

operations.

Feedback /

R&D

More investment

products R&D

Sophistication through

greater fundamentals R&D

Enhanced role of

Scholars R&D

Spread awareness Awareness

Establish Shari’ah /

Islamic finance schools

(economical)

Shari’ah

Education

Islamic finance studies

are made as business

and are very costly

Shari’ah

Education

Make advertisement for

new product Awareness

Give a Good service for

customer Awareness

Creating new product

and service solutions R&D

31

Suggestion 1 Category Suggestion 2 Category Suggestion 3 Category

that compete with

conventional banks

Educate Shari’ah

scholars in the

discipline of accounts,

finance structuring,

finance products

Training

Implement Shari’ah

education programs in

top university

Shari’ah

Education

Wider understanding of

Shari’ah by IFI

professionals

Training

Stop trying to copy

every single

conventional product or

service

R&D Stick to proper Islamic

values

Shari’ah

Education

Build a pool of trained

professionals Training

Should focus on

Shari’ah Based

Banking and Not on

Shari’ah Compliant

R&D

Consistency in Shari’ah

Opinion. Divergence in

Shari’ah Opinion has

created confusion in

understanding and the

credibility of the system

Shari’ah

Education

Innovation and

Research and

Development in Product

Development

R&D

Management should

also focus on achieving

the Islamic objectives

of the bank.

R&D Focus on long-term

objectives. R&D

Increase banking

syndicates. R&D

Table 5: Suggestions to improve IFIs as stated by Industry Professionals

32

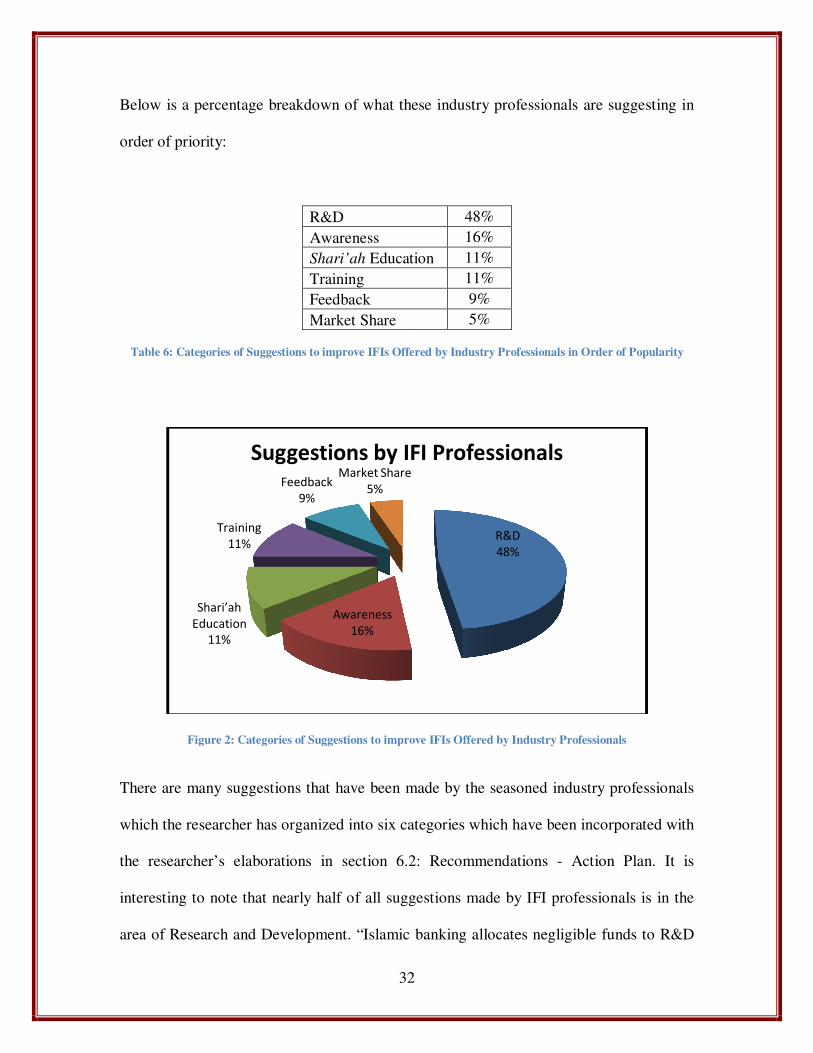

Below is a percentage breakdown of what these industry professionals are suggesting in

order of priority:

R&D 48%

Awareness 16%

Shari’ah Education 11%

Training 11%

Feedback 9%

Market Share 5%

Table 6: Categories of Suggestions to improve IFIs Offered by Industry Professionals in Order of Popularity

Figure 2: Categories of Suggestions to improve IFIs Offered by Industry Professionals

There are many suggestions that have been made by the seasoned industry professionals

which the researcher has organized into six categories which have been incorporated with

the researcher’s elaborations in section 6.2: Recommendations - Action Plan. It is

interesting to note that nearly half of all suggestions made by IFI professionals is in the

area of Research and Development. “Islamic banking allocates negligible funds to R&D

R&D

48%

Awareness

16%

Shari’ah

Education

11%

Training

11%

Feedback

9%

Market Share

5%

Suggestions by IFI Professionals

33

and does not have enough R&D qualified personnel. To set up really effective R&D is

not cheap but it can pay high dividends and more than off-set the expenditure.” (Ali,

1998) Although this remark was made a while back, most IFIs today still do not have

dedicated R&D departments. Hence it is suggested to IFIs to seriously invest in an R&D

Department which would be charged with but not be limited to the mandate suggested in

section 6.2.

34

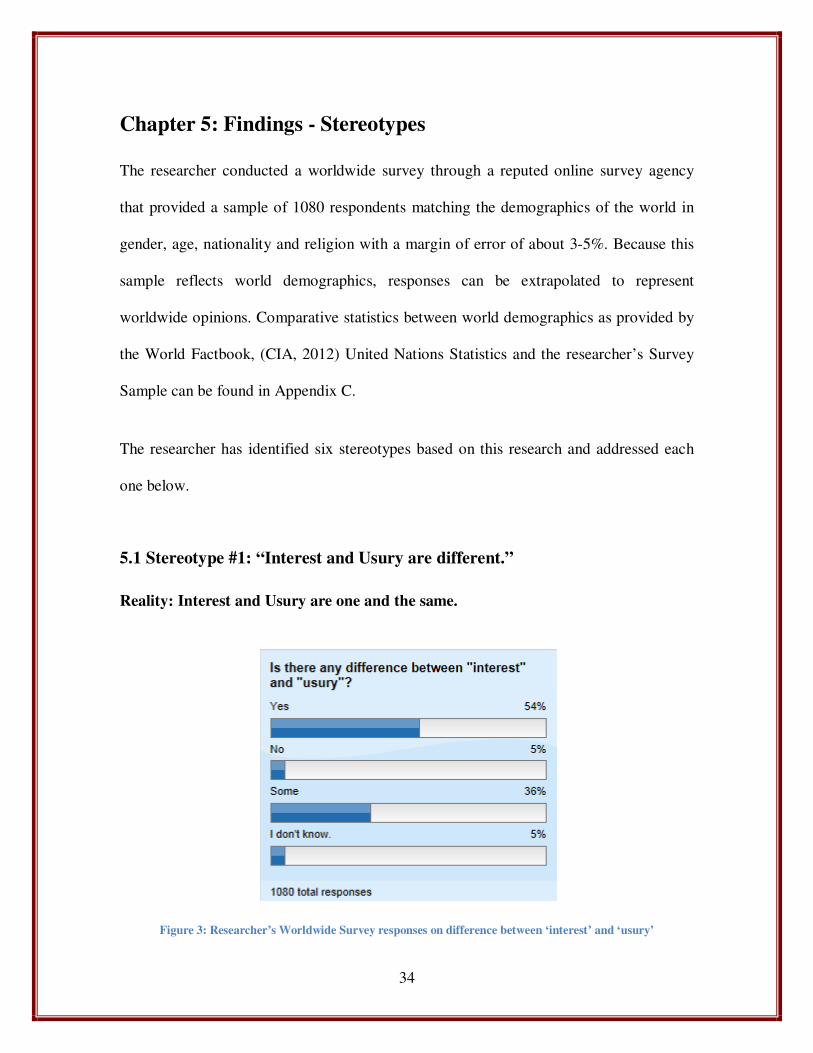

Chapter 5: Findings - Stereotypes

The researcher conducted a worldwide survey through a reputed online survey agency

that provided a sample of 1080 respondents matching the demographics of the world in

gender, age, nationality and religion with a margin of error of about 3-5%. Because this

sample reflects world demographics, responses can be extrapolated to represent

worldwide opinions. Comparative statistics between world demographics as provided by

the World Factbook, (CIA, 2012) United Nations Statistics and the researcher’s Survey

Sample can be found in Appendix C.

The researcher has identified six stereotypes based on this research and addressed each

one below.

5.1 Stereotype #1: “Interest and Usury are different.”

Reality: Interest and Usury are one and the same.

Figure 3: Researcher’s Worldwide Survey responses on difference between ‘interest’ and ‘usury’

35

The above statistics show that almost 90%6 of the respondents felt that there was a

difference between the concepts of interest and usury. Many modern definitions also

define usury as “unusually high” and “illegal” rates of interest. However the question

arises: Who defines what is “unusually high” and on what basis does a government

decide the legal rate? Another argument often made is that interest rates cover for

inflation. Surely 100 dinars today does not have the same value as 100 dinars from 100

years ago. However we need to remember that today’s money is simply representative

money which post 1971 has become fiat money after the Nixon shock. This money has

no connection with any commodity backing giving governments free hand to print as

much paper money as they want which naturally results in its devaluation i.e. inflation. If

things have to be set right, the root cause must be addressed. Instead of adding artificial

rates to money loaned, what must be determined is the purchasing power of the money on

the day that it was loaned. After all, as discussed earlier, money is nothing but a means

with the power to purchase. It has no inherent value of its own. This can practically be

done by determining how much weight in say, gold a certain amount of money can buy.

For example if I borrowed 100 dinars on January 1, 2012, I should find out how much

gold this money can buy. On my loan maturity date, i.e. the date that I have promised to

return the loan, I would then find out the monetary value of exactly that much gold in

weight. That is what I would owe back to the person I borrowed from. This is a much

more natural and just method of returning on a loan than charging artificial rates that

claim to be adjusting for inflation but can easily turn usurious. Usury is the increased

amount of money owed due to no other factor than the passage of time. This is the

essence of “Riba an-Nasi`ah [which] essentially implies that the fixing in advance of a

6 combination of the “Yes” and “Some” responses

36

positive return on a loan as a reward for waiting is not permitted by the Shari’ah.” (Iqbal

& Mirakhor, 2007) The “time value of money” is really inflation and must be addressed

as an imperative and this can be done by returning the monetary system to one that is

commodity backed. Once the inflation factor is removed, there would be no grounds

whatsoever to charge a higher amount on the loan as that would be purely usurious.

However the “interest” rate that banks charge today has all the elements of adjusting for

inflation as well as what the bank claims are risks involved in lending due to the passage

of time such as default risk, credit risk, market risk etc. The advertised rate is the nominal

interest rate which includes the inflation rate as well as the real interest rate as per the

formula below:

Real interest rate ≈ Nominal interest rate – Inflation rate

(Ross, Westerfield, Jaffe, & Jordan, 2008)

The real interest rate on the other hand includes the various risk factors that the bank

claims it has to compensate for with the passage of time, one of them being the

opportunity cost of the money loaned. This argument is flawed because it places the

entire risk of a transaction on one party (the one being charged interest) for the

“possibility” that that money “may” have earned profits if placed elsewhere. This is

inherently unjust. What if that same amount would actually have incurred a loss if placed

elsewhere? As an example, I lend $100 to person A and demand he pays me back $110,

claiming the extra $10 is the cost of a lost opportunity elsewhere. But what if I had put

that $100 in stocks and actually lost all of it? So the “lost opportunity” can go both ways

37

and it is unfair to force a fixed compensation from person A as cost of a “lost

opportunity. In Islamic banking, risk is always shared and never placed on one party

alone.

The researcher urges that an in-depth understanding of interest be introduced to the

masses so that its true elements are recognized for what they are.

It is crucial to understand the negative impact that interest/usury has on a society to

appreciate its ban by not just Islam but practically all major religions and thinkers. As

explained earlier in this paper, this destructive innovation was the work of the Pharaohs

and they too realized its artificiality and resulting harm. However the impact was felt

most by the

Greek city states where the prices of agricultural commodities were not

monetized by central authority but valued by more individually

determined markets, [and hence] charging usury on loans of coinage to

farmers quickly led to severe social problems. By about 600 BC the class

of free small farmers was vanishing, with land becoming concentrated into

the hands of the Oligarchy. (Zarlenga, http://www.monetary.org, 2000)

In the modern scenario, because interest/usury offers a “fixed” rate of return, people are

more inclined to place their money in such savings accounts rather than invest in

38

community projects which are good for humanity but are obviously riskier in terms of the

possible returns. This observation was made by

Pope Innocent IV (1250-1261) [who] noted that if usury were permitted,

rich people would prefer to put their money in a usurious loan rather than

invest in agriculture. Only the poor would do the farming and they didn’t

have the animals and tools to do it. Famine would result. (Zarlenga,

http://www.monetary.org, 2000)

It is no wonder that the famine and usury are considered two sides of the same coin:

Very commonly, the relationship of exploitation involved a notion of

"credit", with the dominant classes asserting that the handouts they gave

were "advances" which had to be repaid with augmented interest at harvest

time. If the harvest was inadequate, only a portion of the so-called "debt"

could be repaid, the rest running on enhanced by interest till the next year,

and usually beyond that. In practice, most peasants were in a condition of

perpetual "indebtedness" of this sort. In this respect, dearth and usury were

for the peasant two sides of the one coin, with dearth creating the need to

"borrow", while high "debt-repayments" ensured that dearth was never far

away and famine always a possibility. The majority of peasants were thus

trapped in a cycle of dearth and debt. (Hardiman, 2012)

39

Not only does usury exacerbate famines, it is also responsible for the great and increasing

divide between the haves and the have-nots. Due to the inherent risk skew that the

interest/usury mechanism furthers, risk is not shared justly and the result is the huge

divide we see where almost “40% of the world’s wealth is concentrated in the hands of

1% of the population.” (Usmani) Recent Arab Spring type revolutionary protests and

efforts by the Occupy Wall Street (OWS)7 movement in the United States with “We are

the 99%”8 calling out against income inequality and wealth concentration are testimony

to this fact.

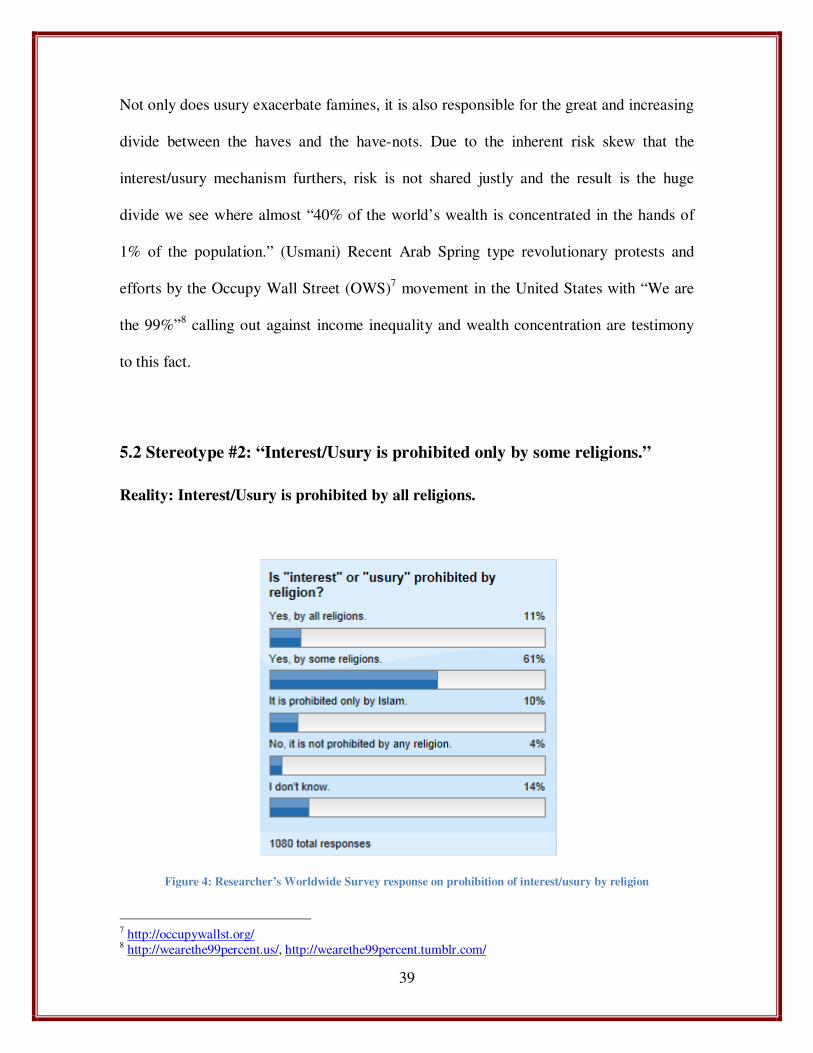

5.2 Stereotype #2: “Interest/Usury is prohibited only by some religions.”

Reality: Interest/Usury is prohibited by all religions.

Figure 4: Researcher’s Worldwide Survey response on prohibition of interest/usury by religion

7 http://occupywallst.org/ 8 http://wearethe99percent.us/, http://wearethe99percent.tumblr.com/

40

Divine injunctions as sent through the various religions and finally culminating in Islam

are meant for the good of humanity. It is no wonder that:

explicit and implicit prohibition of interest is mentioned in Hinduism, Buddhism,

Judaism, Christianity and Islam. The Hindu priests (Brahmans) and warriors

(Kshatriyas) of the higher castes were forbidden from being usurers or lenders at

interest. Also, in the Buddhist Jatakas, usury is referred to in a deprecating

manner, claiming that ‘hypocritical ascetics are accused of practicing it.’ (Iqbal &

Mirakhor, 2007)

In the Judeo-Christian-Islamic tradition there is explicit forbiddance on usury. One

example is given below from each scripture:

Judaism: “If thou lend money to any of my people that is poor by thee, thou shalt not be

to him as an usurer, neither shalt thou lay upon him usury (interest).” [Exodus 22:25]

Christianity: “He that hath not given forth upon usury (interest), neither hath taken any

increase, [he] that hath withdrawn his hand from iniquity, hath executed true judgment

between man and man …” [Ezekiel 18:8]

Islam: “O you who believe, you shall not take usury (interest), compounded over and

over. Observe God that you may succeed.” [Aal-‘Imran 3:130]

41

Given the categorical prohibition of usury/interest in all major religions it is a true

reflection of lack of knowledge on part of the people where only 11% in the researcher’s

worldwide survey responded that usury/interest is indeed prohibited by all religions.

Indeed much awareness needs to be raised amongst the public on this grave issue.

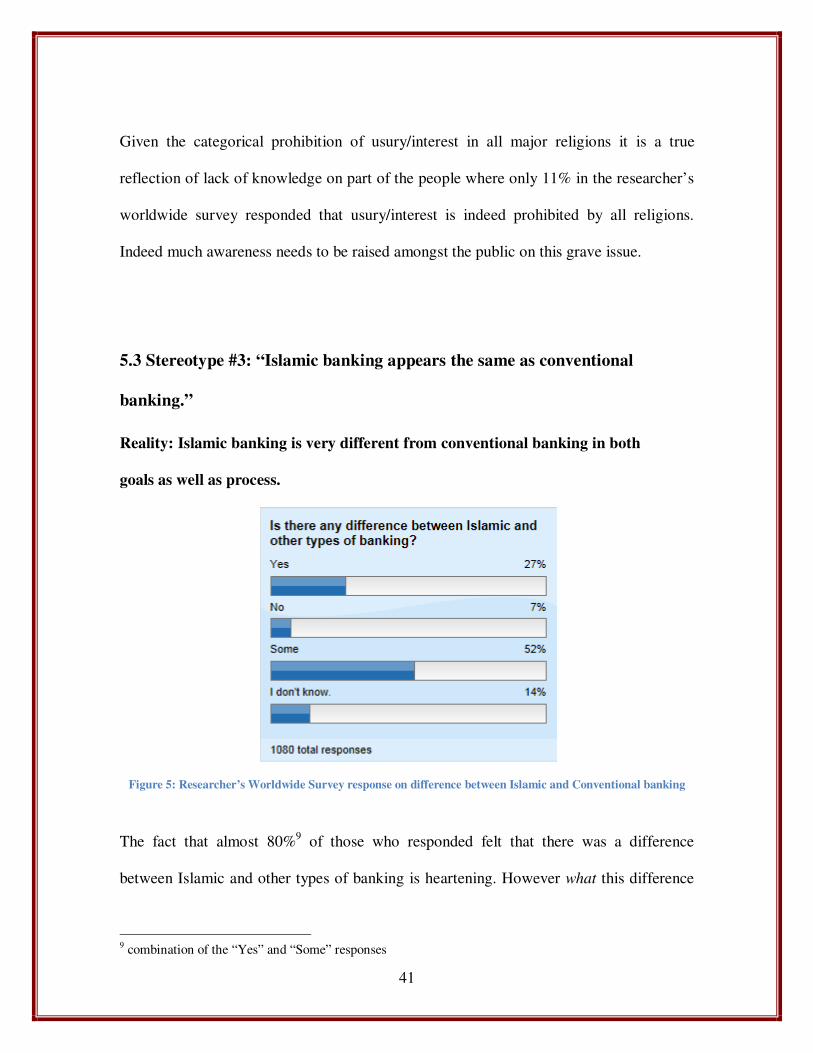

5.3 Stereotype #3: “Islamic banking appears the same as conventional

banking.”

Reality: Islamic banking is very different from conventional banking in both

goals as well as process.

Figure 5: Researcher’s Worldwide Survey response on difference between Islamic and Conventional banking

The fact that almost 80%9 of those who responded felt that there was a difference

between Islamic and other types of banking is heartening. However what this difference

9 combination of the “Yes” and “Some” responses

42

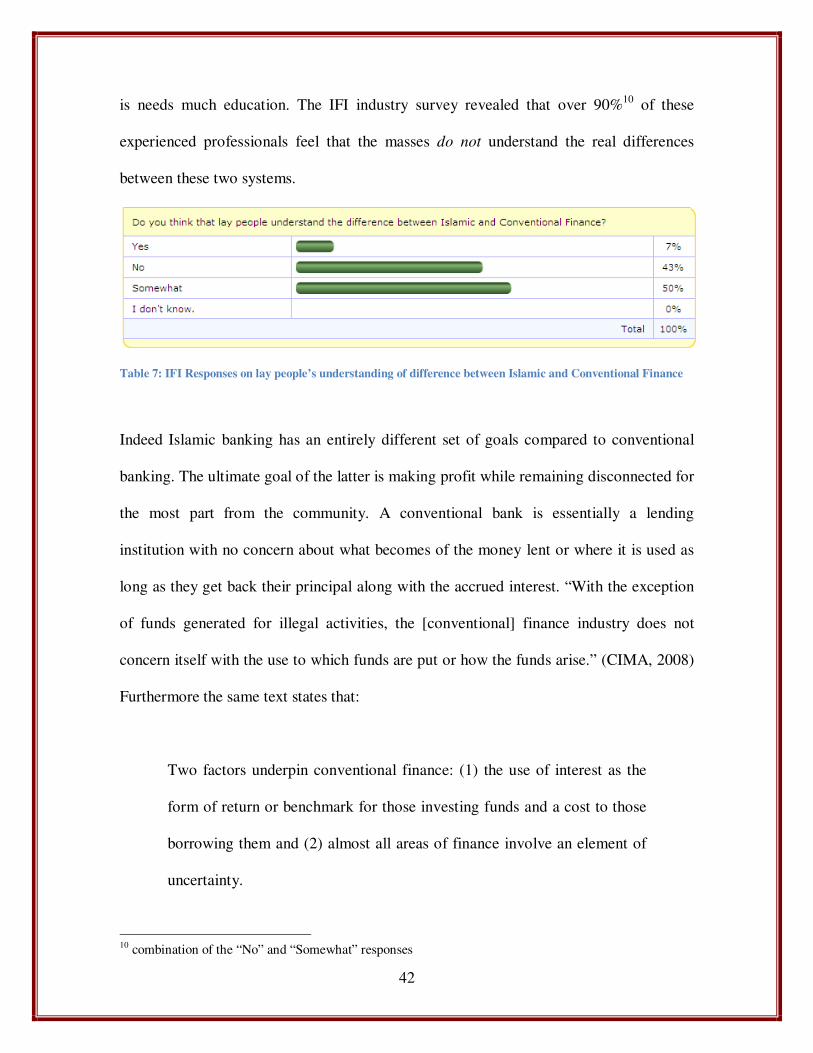

is needs much education. The IFI industry survey revealed that over 90%10 of these

experienced professionals feel that the masses do not understand the real differences

between these two systems.

Table 7: IFI Responses on lay people’s understanding of difference between Islamic and Conventional Finance

Indeed Islamic banking has an entirely different set of goals compared to conventional

banking. The ultimate goal of the latter is making profit while remaining disconnected for

the most part from the community. A conventional bank is essentially a lending

institution with no concern about what becomes of the money lent or where it is used as

long as they get back their principal along with the accrued interest. “With the exception

of funds generated for illegal activities, the [conventional] finance industry does not

concern itself with the use to which funds are put or how the funds arise.” (CIMA, 2008)

Furthermore the same text states that:

Two factors underpin conventional finance: (1) the use of interest as the

form of return or benchmark for those investing funds and a cost to those

borrowing them and (2) almost all areas of finance involve an element of

uncertainty.

10 combination of the “No” and “Somewhat” responses

43

For reasons mentioned earlier in the study, Islamic finance categorically rejects the

concept of interest/usury. And as also elucidated earlier, all other faiths reject it as well.

However:

The justification for charging interest evolved historically in works promoting

capitalism. One recurring theme was to attack Aristotle. [The French Protestant

Reformer] John Calvin finished off the usury ban in 1536. But his arguments were

shallow compared to the Scholastics [such as Aristotle]: "When I buy a field does

not money breed money?” he asked rhetorically. For centuries the Scholastics had

demonstrated the correct answer is no - it is the field not the money which grows

products. As economies became more dynamic, with real growth possibilities, it

became clear that charging interest on business loans where the borrowing

merchant prospered couldn’t be condemned as greed or lack of charity and by

1516 the idea of a lending institution charging interest for its services had been

overwhelming accepted. (Zarlenga, The Usury Problem Remains, 2010)

Whereas the ultimate goal of Islamic banking is providing the resources for

comprehensive community development which involves taking care of basic human

needs such as owning a modest house, a modest means of transportation, education,

healthcare, family and is highly concerned about what the money is being used for. Profit

making is not disallowed; however it cannot be the ultimate goal. Lending in Islamic

banks is limited to Qard Hasan (Benevolent loan) which is mostly for consumption

44

purposes. All other types of transactions are productive where the bank is an investor and

not a lender. As an investor it shares in the risk of the investment. This is the fundamental

PLS (Profit Loss Sharing) mode of an Islamic bank. However, this is an area that needs

much development and is very much in the nascent stage within the Islamic finance

industry. So much so that literature is being circulated that Islamic banking should be

subject to the same regulations as conventional banking as there isn’t much difference

between the two. Another criticism is the benchmarks used within the Islamic finance

industry – that they are still conventional for the most part such as LIBOR (London Inter

Bank Offered Rate). However, much clarification is needed here. It is wrong to state that

Islamic banking is "interest-based" if Islamic investment rates are currently benchmarked

to conventional interest rates. The intent is to stay competitive. It is like pricing halal

meat so that it stays competitive with say pork. Just because the pricing is competitive

doesn't make the halal meat haram. Nevertheless new independent benchmarks must be

sought. Additionally, it is important to understand the difference between conventional

interest rates and Islamic investment rates around which there appears to be much

confusion. The former is a function of the principal and the latter is a function of the