Embed Size (px)

Citation preview

1

PAN African e-Network Project

DBMAccounting For Managers

Semester - I

Navleen Kaur

ACCOUNTING FOR MANAGERS

Learning Objectives: The Objectives of the course are:

• To develop an understanding of the importance, language and techniques of Financial, Cost , Management Accounting and Capital Budgeting.

• To develop skills for preparation and analysis of financial statements.

• To develop an understanding of cost classification, allocation and how the costing techniques are useful in the process of managerial decision making

Detailed Course Contents: Module I: Final Accounts

• Bank Reconciliation Statement, Financial Statements and their Nature, Preparation of Manufacturing, Trading and Profit & Loss Account and Balance Sheet - Matching of Revenue (AS 9) & Expenses, Fixed Assets (AS 10), Depreciation (AS 6& and other related adjustments

Module II: Company Accounts• Issue of Shares & Debentures and their

Redemption, Form and Contents of Financial Statements with reference to Indian Companies (Schedule VI)

Module III: Financial Statement Analysis • Financial Ratio Analysis, Liquidity, Activity,

Capital Structure, Profitability Ratios, Funds Flow statement and Cash Flow Statement (AS 3)

Module IV: Cost Accounting• Elements of Cost Classification and

Allocation, Cost Sheet, Methods of Inventory

Module V: Management Accounting • Emergence of Management Accounting,

Marginal Costing and Cost Volume Profit Analysis, Budgeting & Variance Analysis

Executive Summary

• Issuing securities involves the corporation in a number of decisions.

• This presentation looks at how corporations issue securities to the investing public.

• The basic procedure for selling debt and equity securities are essentially the same.

Outline• The Public Issue• The Basic Procedure for a New Issue• The Cash Offer• The Announcement of New Equity and

the Value of the Firm• The Cost of Issuing Securities• Rights• The Private Equity Market• Summary and Conclusions

The Public Issue

• Regulation of the securities market in Canada is carried out by provincial commissions.

• In the U.S., regulation is handled by a federal body (SEC).

• The regulators’ goal is to promote the efficient flow of information about securities and the smooth functioning of securities’ markets.

• All companies listed on the TSE come under the jurisdiction of the Ontario Securities Commission (OSC).

• Other provinces have similar legislation and regulating bodies

The Basic Procedure for a New Issue

Steps involved in issuing securities to the public:Management obtains approval from the board of directors.

1. The firm prepares a preliminary prospectus to the OSC.2. The OSC studies the preliminary prospectus and

notifies the company of any changes required.3. Once the revised, final prospectus meets with the

OSC’s approval, a price is determined and a full-fledged selling effort gets under way.

The Cash Offer

• Underwriters are usually involved in a cash offer.• Underwriters perform the following services:

– Formulating the method used to issue the securities.– Pricing and selling the new securities.

• The difference between underwriter’s buying price and the offering price is called the spread.

• Because underwriting involves risk, underwriters combine to form an underwriting group called a syndicate

The Cash Offer (cont.)

Types of Underwriting: two types of underwriting are involved in a cash offer.

1. Regular Underwriting• firm commitment underwriting• best efforts underwriting

2. Bought Deal• In a bought deal, the issuer sells the entire issue to

one investment dealer or to a group.

The Cash Offer (cont.)• The selling period: while the issue is being sold to the

public, the underwriting group agrees not to sell securities for less than the offering price until the syndicate dissolves.

• The over-allotment option: known as the Green Shoe provision gives members of the underwriting group the option to purchase additional shares at the offering price less fees and commissions.

• Investment Dealers:– In 2000, RBC Dominion Securities was the leading

underwriter by revenue.– TD securities was the first ranked by assets.

The Cash Offer (cont.)

The offering price:• Determining the correct offering price is an

underwriter’s hardest task.• The issuing firm faces a potential cost if the offering

price is set too high or too low.Underpricing:• Underpricing is a common occurrence and it clearly

helps new shareholders earn a higher return on the shares they buy.

• In the case of an IPO, underpricing reduces the proceeds received by the original owners.

The Announcement of New Equity and the Value of the Firm

• The market value of existing equity drops on the announcement of a new issue of common stock.

• Reasons include– Managerial Information

Since the managers are the insiders, perhaps they are selling new stock because they think it is overpriced.

– Debt CapacityIf the market infers that the managers are issuing

new equity to reduce their debt-to-equity ratio due to the specter of financial distress the stock price will fall.

– Falling Earnings

The Cost of Issuing Securities

1. Spread or underwriting discount2. Other direct expenses3. Indirect expenses4. Abnormal returns5. Underpricing6. Green Shoe option

The Costs of Public Offerings

Costs of Going Public in Canada: 1984--97 Fees 6.00 % Underpricing 7.88 % TOTAL 13.88 %

•The above figures understate the total cost because they ignore indirect expenses or the overallotment option.

Rights

• An issue of common stock offered to existing shareholders is called a rights offering.

• Prior to the 1980 Bank Act, chartered banks were required to raise equity exclusively through rights offerings.

• If a preemptive right is contained in the firm’s articles of incorporation, the firm must offer any new issue of common stock first to existing shareholders.

• This allows shareholders to maintain their percentage ownership if they so desire.

Mechanics of Rights Offerings

• The management of the firm must decide:– The exercise price (the price existing shareholders

must pay for new shares).– How many rights will be required to purchase one

new share of stock.

• These rights have value:– Shareholders can either exercise their rights or sell

their rights.

Rights Offering Example

• Popular Delusions, Inc. is proposing a rights offering. There are 200,000 shares outstanding trading at $25 each. There will be 10,000 new shares issued at a $20 subscription price.

• What is the new market value of the firm?• What is the ex-rights price?• What is the value of a right?

Rights Offering Example

• What is the new market value of the firm?• There are 200,000 outstanding shares at $25 each.There

will be 10,000 new shares issued at a $20 subscription price.

shares 20$shares 000,10

share 25$shares 000,200000,200,5$

Rights Offering Example

• What is the ex-rights price?• There are 110,000 outstanding shares of a firm

with a market value of $5,200,000.• Thus the value of an ex-rights share is:

7619.24$shares 000,210000,200,5$

• Thus the value of a right is $0.2381 = $25 – $24.7619

Theoretical Value of a Right

The theoretical value of a right during the rights-on period is:

R0 = (M0 – S) / (N +1)

Where,M0 = Common share price during the rights-on period

S = Subscription priceN = Number of rights required to buy one new share

Value of a Right after Ex-Rights Date

• When the stock goes ex-rights, its price drops by the value of one right.

Me = M0 – R0

Re = (Me – S) / N

Where,Me is the common share price during the ex-rights period.

Cost of Rights Offerings

• Until the early 1980s, rights offerings were the most popular method of raising new equity in Canada for seasoned issuers because of lower flotation costs.

• In the late 1980s and early 1990s, with the rise of POP, bought deals replaced rights offers as the prevalent form of equity issue.

The Private Equity Market

• The previous sections assumed that a company is big enough, successful enough, and old enough to raise capital in the public equity market.

• There are many firms that have not reached this stage and cannot use the public equity market.

• For start-up firms and firms in financial trouble, the public equity market is often not available.

Private Placements

• Avoid the costly procedures associated with the registration requirements that are a part of public issues.

• The OSC and SEC restrict private placement issues of no more than a couple of dozen knowledgeable investors including institutions such as insurance companies and pension funds.

• The biggest drawback is that the securities cannot be easily resold.

Venture Capital• The limited partnership is the dominant form of

intermediation in this market.• There are five types of suppliers of venture capital:

1. Old-line wealthy families.2. Private partnerships and corporations.3. Large industrial or financial corporations with established

venture-capital subsidiaries.4. The federal government (through crown-related firms).5. Individuals, typically with incomes in excess of $100,000

and net worth over $1,000,000. Often these “angels” have substantial business experience and are able to tolerate high risks.

Stages of Financing

1. Seed-Money Stage: Small amount of money to prove a concept or develop a

product.2. Start-Up

Funds are likely to pay for marketing and product refinement.3. First-Round Financing

Additional money to begin sales and manufacturing.

4. Second-Round FinancingFunds earmarked for working capital for a firm that is

currently selling its product but still losing money.5. Third-Round Financing

Financing for a firm that is at least breaking even and contemplating expansion; a.k.a. mezzanine financing.

6. Fourth-Round FinancingFinancing for a firm that is likely to go public within six

months; a.k.a. bridge financing.

Summary and Conclusions

• Larger issues have proportionately much lower costs of issuing equity than small ones.

• Firm-commitment underwriting is far more prevalent for large issues than is best-effort underwriting. Smaller issues probably use best effort because of the greater uncertainty.

• Rights offering are cheaper than general cash offers.• Shelf registration is a new method of issuing new debt

and equity.• Venture capitalists are an increasingly important

influence in start-up firms and subsequent financing.

Buy- Back of Shares and Redemption of Preference shares Concepts, accounting treatment,

Income tax applications.

An old lady, with shabby looks waspicking up something from the sea shore

but the people, scared of her, did not allowtheir children to go near her.

What was she picking?Why were the people scared of her?

Did she pick up Shells or Stones?

Think, before having a lookat the next slide.

She picked up broken pieces of glassWhy did she pick up these?

So that these pieces should not harm

the children.

Judge not by the looks or colour!!!!!

Meaning of Redemption

• Pay back the capital before winding up either by cash or conversion of preference shares into equity shares or pay cash to such share holders.

Buy- Back of shares-Meaning

• Take back the equity shares from market or shareholders by paying cash and reduce equity shares available in the share market. It is also known as a stock repurchase.

• , cash is exchanged for a reduction in the number of shares outstanding. The firm either retires the shares or keeps them as treasury stock, available for re issuance.

Methods of re-purchase of sharesin the USA

• 1. Open market share purchase: 95% of repurchase is done through this

methodDaily re-purchase of shares from market is

limitedThe company may not openly announce that

it will re-purchase shares from open market

2. Fixed price tender offer• Single purchase price and number of

shares sought are mentioned.• Person would like to sell to the company

should come with offer of the price and number of shares that he offers to the company.

• If offer from public exceeds than shares sought it may buy on pro rata basis.

Method-3. Dutch auction share repurchases • Range of prices that the company would

like to re-purchase are mentioned in the offer. Shareholders can indicate their prices within the rage prescribed.

• Lowest bidder to highest price bidder are chosen

• The company has right to cancel the entire offer if a few take holders.

4.Equal access buy-backs

• All share holders have given equal opportunity to sell shares to the company.

5.Selective buy-backs• In broad terms, a selective buy-back is one in

which identical offers are not made to every shareholder, for example, if offers are made to only some of the shareholders in the company. The scheme must first be approved by all shareholders, or by a special resolution (requiring a 75% majority) of the members in which no vote is cast by selling shareholders or their associates. Selling shareholders may not vote in favour of a special resolution to approve a selective buy-back

Employees’ stock option re-purchase

• A company may also buy back shares held by or for employees or salaried directors of the company or a related company. This type of buy-back, referred to as an employee share scheme buy-back, requires an ordinary resolution

On-market buy-backs and minimum holding buy-back

• A listed company may also buy back its shares in on-market trading on the stock exchange, following the passing of an ordinary resolution.The stock exchange’s rules apply to on-market buy-backs.

• A listed company may also buy unmarketable parcels of shares from shareholders (called a minimum holding buy-back). This does not require a resolution but the purchased shares must still be cancelled.

Contradicting sections on Buy- back of shares in India

• Section 77 of the Companies Act does not allow a company to buy its own shares until the winding up of companies.

• but the subsequent Section 77A permits buyback subject to certain conditions. What is the rationale behind?

Section-77 of the Companies Act

• Most of the sections in the Companies Act tries to protect the interest of the outsiders who had lent money in the form of debentures or loans or deposits by restricting company not to pay unless outsiders(loan vendors) are paid fully.

• Share holders are paid last and has taken maximum risk in the company.

Other sections to protect the interest of outsiders

• Section 80 of the Companies Act 1956:-Redemption of preference shares:-Preference shares can be redeemed out of fresh

issue of shares or divisible profits which are normally available for the declaration of dividend or both(Partly by fresh issue of shares and divisible profits)

Preference shares can not be redeemed out of fresh issue of Debentures. Why?

Debentures can not be issued to redeem preference shares

• Debentures are loan funds from outsiders which will reduce long term solvency of the existing debenture holders of the company.More debt will reduce credit worthiness further.

• If further shares are issued for redemption of preference shares, one type of own funds go out and another type of own funds come to the company which do not affect credit worthiness of existing debenture holders. Law tries to protect the existing debenture holders.It is the reason Section 77 says own capital can not be returned before making payment to debenture holders.

Rules for redemption of preference shares

• Section-80 of the Companies Act:Rule 1:Only fully paid preference shares can be redeemed-

Why?When preference shares are issued, it was assured that

all money ie to the extent of nominal value of shares will be received by the company.It is a statutory liability of every shareholders to pay fully to the extent of nominal value of shares. The debenture holders are given security not only on the present assets but also future assets that will be realised from partly paid up preference shares.There is a legal obligation on the part of the company to receive the balance of amount from preference share holders before winding up.

Rule-2

• No company can issue any preference shares, shall issue any preference shares which is irredeemable or redeemable beyond 20 years

Rule-3

• Preference shares can be redeemed either by fresh issue of shares or out of divisible profits or both.-Why?

• Divisible profits is profits which are freely available for the declaration of dividend to shareholders. Only such profits which are free from all clutches can be used for redemption. How is it done? What is the logic?

What is the mechanism of using revenue profit to CRR account?

• Revenue profits which are free for dividend have to be converted into Capital profit.The converted capital profit is known as Capital Redemption Reserve fund.Capital redemption funds(CRR) are used to capitalise proft into fully paid up bonus shares. It means revenue profit becomes shares which will be with the firm for ever and gives effective protection to existing Debenture holders.

• Journal entry:• Profit and loss Account Debit• Capital Redemption Account credit• It means reduce revenue profit and increase Capital profit.

otherwise share holders will ask the company to declare dividend out of revenue profit.

If there is no revenue profits?

• Go for fresh issue of shares. It can be equity or preference.It should not be debentures or loan funds.

If free reserves usedFor redemption

CRR toFully paid upBonus shares

Bonus shares to Equity shares

Revenue profit to Be transferred to

CRR account

Steps fromLeft to right

Redemption of Preference shares

If fresh issue of sharesIssued for redemption with

CRR

Cash received to the extend of Nominal value of shares

Premium on issue to be accounted separately

+ CRR

=

Nominal value ofRedeemable preference shares

Note

Divisible profits orProfits for redemption

1.Profit and loss Account2.Reserves

3.Investment fluctuation Reserve

4.Dividend equalisation reserve

1.Security premium2.Capital Redemption

Reserve Account3.Development rebate reserve

4. Capital profits/reserve6. Statutory reserve

7. Profits prior to Incorporation

Not divisible/Capital profits

Kept in the company for ever(Married)

Can be used for any purpose(bachelor)

If loss occurred due to sale of Any asset

Set off such capital with Capital reserve

If not enoughSet off against revenueProfit. the balance is

DIVISIBLE PROFITS

Premium on redemption

To be set off against existing security premium account and new

Security premium on fresh issue of shares

If not enough

Reduce such deficit with revenue profits Then calculate divisible profits.

Amalgamationcost of acquisition of the asset of old company deemed to be the

cost of acquisition of the new company(continuing company

conversion of bonds or debentures, debenture-stock the cost of acquisition of the asset to the assessee shall be

deemed to be that part of the cost of debenture, debenture- stock or deposit certificates in relation to which such asset is acquired

by the assessee.

If Section 2(1B) is fulfilled it does not attract capital gain as per Income tax Act to share holders. Section 2(1B) states that all

assets and liabilities to be transferred to the new company and the new company should be an Indian company. At least 75% of

share holders should be the shareholders of the new company(acquiring company)

Demerger

• The cost of acquisition of the shares in the resulting company shall be the amount which bears to the cost of acquisition of shares, held by the assessee in the demerged company.

• No capital gain to the share holder who exchange shares if all conditions are fulfilled.

Buy back of shares( Sec.77A)• Why buy back of shares introduced in

India?• In late 1996-1999 Indian share market did

not move. People hesitate to buy and people were not interested in sell shares as they felt that share market might go up. It is one of the mechanism to make the market to be vibrant in such situation.How?

How?• When shares were issued at premium, the

company earned capital profits. If shares are quoted in the market less than nominal value or a little above nominal value the company has a chance to re-purchase such shares from market at low price and cancel such shares from the share capital. The remaining share holders value go up because net worth of the firm remain almost the same to the remaining number of shares.

• to allow promoters to get a better hold on the company.

• To wit, if the existing promoters in the saddle are having 20 per cent of the shares and the company announces a 20 per cent buyback in which obviously the promoters will not participate, the bottomline would be their stake now going up to 25 per cent (20 divided by 80).

• There cannot be a simpler and less expensive way of beefing up one's control in a company. In fact the promoters gain at the expense of the company whose cash is used in bankrolling this exercise.

Buy back and Companies Act

• Section-77A(since 1999)• Sources for buy back1. Free reserves(divisible profit)2. The security premium account3. Fresh issue of shares(ESOP other

securities)

Maximum Buy back

• Upto 25% of total paid up share capital and free reserves.

Other conditions• 1. Debt equity ratio should not be more than 2:1

after buy back• (all secured and unsecured debts are included)• 2. All the shares other securities are fully paid

up( It is same like redemption of preference shares)

• 3. Such securities are to be listed on recognised stock exchange

• 4. If free reserves used the amount used for such purpose to be transferred to Capital Redemption Reserve Account.

Buy-Back from whom?

• 1. Existing security holders on a proportional basis

• 2. From open market• 3. ESOP• 4.If listed securities smaller than such buy

back, as prescribed by Stock exchange.

Thank you

Help your father/mother in cooking

Do your house hold workWithout giving excuses.

Disclosure Requirements under Schedule VI

of Companies Act 1956

Section 211. Form and contents of balance sheet and profit and loss account:

1. Every balance sheet of a company shall give a true and fair view of the state of affairs of the company as at the end of the financial year and shall, subject to the provisions of this section, be in the form set out in Part I of Schedule VI, or as near thereto as circumstances admit or in such other form as may be approved by the Central Government either generally or in any particular case; and in preparing the balance sheet due regard shall be had, as far as may be, to the general instructions for preparation of balance sheet under the heading "Notes" at the end of that Part :

2. Every profit and loss account of a company shall give a true and fair view of the profit or loss of the company for the financial year and shall, subject as aforesaid, comply with the requirements of Part II of Schedule VI, so far as they are applicable thereto :

PARTS OF SCHEDULE VI

1. Part I & II – Form of Balance Sheet & Requirements as to Profit and Loss A/c

2. Part III – Interpretation of certain terms for the purpose of Part I & II e.g. Provision, Reserve, Capital Reserve, Liability, Quoted Investment etc.

3. Part IV - Balance Sheet Abstract and Company's General Business Profile

Section 117 of Companies Bill 2009 : Financial Statement

1. The financial statement shall give a true and fair view of the state of affairs of the company or companies as at the end of the financial year, comply with the accounting standards notified under section 119 and shall be in such form as may be prescribed.

3. Where a company has one or more subsidiaries, it shall prepare a consolidated financial statement of all the subsidiaries in the same form and manner as that of its own which shall also be laid before the annual general meeting of the company along with the laying of its financial statement under sub-section (2).

PART I – BALANCE SHEET (A & B)

A Company shall disclose the following in the notes to accounts:

A. Share Capital - For each class of Share Capital:

(a) the number and amount of shares authorized; (b) the number of shares issued, subscribed and fully paid, and subscribed but not fully

paid; (c) par value per share; (d) a reconciliation of the number of shares outstanding at the beginning and at the end of

the period; (e) the rights, preferences and restrictions attaching to that class including restrictions on

the distribution of dividends and the repayment of capital; (f) shares in the company held by its holding company or its ultimate holding company or

by its subsidiaries or associates; (g) shares in the company held by any shareholder holding more than 5 percent shares; (h) shares reserved for issue under options and contracts/commitments for the sale of

shares/disinvestment, including the terms and amounts; (i) Separate particulars for a period of five years following the year in which the shares have

been allotted/bought back, in respect of: Aggregate number and class of shares allotted as fully paid up pursuant to contract (s)

without payment being received in cash. Aggregate number and class of shares allotted as fully paid up by way of bonus

shares (Specify the source from which bonus shares are issued). Aggregate number and class of shares bought back. (j) Terms of any security issued along with the earliest date of conversion in descending order

starting from the farthest such date.

Some Important aspects of Share Capital:

1. The Authorised share capital should be higher than Issued, Subscribed & paid up capital.

2. The criteria of minimum paid-up capital Rs. 1 Lac and Rs. 5 lacs in case of Private and Public Co. respectively should be complied.

3. If the new shares has been issued during the year, it should be compared with the secretariate compliance report (in case paid up capital is more than Rs. 10 lacs).

4. The share application money of which allotment is pending should not be shown in share capital and should be shown separately in between capital and reserves including contracts/ commitments and the terms thereof.

5. The ‘Capital Suspense A/c’ should be shown under Share Capital with there related contracts / commitments.

B. Reserves & Surplus:

(i) Reserves and Surplus shall be classified as: (a) Capital Reserves; (b) Capital Redemption Reserves; (c) Securities Premium Reserve; (d) Debenture Redemption Reserve; (e) Revaluation Reserve; (f) Other Reserves – (specify the nature of each reserve and the amount in respect

thereof); (g) Surplus i.e. balance in statement of Profit & Loss disclosing allocations and

appropriations such as dividend paid, bonus shares and transfer to/from reserves. (Additions and deductions since last balance sheet to be shown under each of the specified heads)

(ii) A reserve specifically represented by earmarked investments shall be termed as a ‘fund’ (basically known as ‘Reserve Fund’).

(iii) The balance of ‘Surplus’ after deducting debit balance of profit and loss account shall be shown under the head ‘Surplus’ even if the resulting figure is in the negative. Similarly, the balance of ‘Reserves and Surplus’, after adjusting negative balance of surplus, if any, shall be shown under the head ‘Reserves and Surplus’ even if the resulting figure is in the negative.

Some Important aspects of Reserves & Surplus:

1. The Reserve for Doubtful Debt is not a provision for doubtful debt, hence it should be shown in the reserves instead of deducting from ‘Sundry Debtors’ (it means it is the appropriation of profit and not the provisions).

2. No dividend should be declared out of the capital reserve.

3. The debit balance in profit & loss a/c should be deducted from free reserve only.

4. If the accumulated losses is more than 50% of its Net worth, then auditors report should be referred to.

5. If the company transfers amount of reserve for the purpose of claiming any tax benefit, then it should be shown separately.

6. As per the NBFC norms, 20% of net profit should be transfer to ‘special reserve A/c’ before making the distribution to shareholders as a dividend or bonus shares.

C. Secured & Unsecured Loans:

(i) Long-term borrowings shall be classified as: (a) Bonds/debentures. (b) Term loans from banks. from other parties. (c) Deferred payment liabilities. (d) Public deposits. (e) Loans and advances from subsidiaries/holding company/associates/business ventures. (f) Other loans and advances (specify nature). (ii) Borrowings shall further be sub-classified as secured and unsecured. Nature of security

shall be specified separately in each case. (iii) Where loans have been guaranteed by directors or others, a mention thereof shall be made

and also the aggregate amount of such loans under each head. (iv) Bonds/debentures (along with the rate of interest and particulars of redemption or conversion,

as the case may be) stated in descending order of maturity or conversion, starting from farthest redemption or conversion date, as the case may be. Where bonds/debentures are redeemable by installments, the date of maturity for this purpose must be reckoned as the date on which the first installment becomes due.

(v) Particulars of any redeemed bonds/ debentures which the company has power to reissue. (vi) Terms of repayment of term loans and other loans. (vii) Period and amount of default in repayment of dues, providing break-up of principal and

interest shall be specified separately in each case.

Long-term provisions The amounts shall be classified as: (a) Provision for employee benefits. (b) Others (specify nature).

Some Important aspects of Secured Loans :

1. The nature of security should be specified in each and every case.

2. The secured loans should be matched with the entries in the Register of charge u/s 125.

3. Interest accrued and due should be indicated under appropriate sub-heads. The interest accrued but not due should be shown in current liability.

D. Current Liabilities and Provisions:

1. Short-term borrowings (Due for less than 1 year)

(i) Short-term borrowings shall be classified as: (a) Loans repayable on demand from banks. from other parties (in case of MSMEs, if the due is exceeding 3 months,

then amount including interest as per the act should be shown separately). (b) Loans and advances from subsidiaries/holding

company/associates/business ventures. (c) Demand deposits. (d) Other loans and advances (specify nature).

(ii) Borrowings shall further be sub-classified as secured and unsecured. Nature of security shall be specified separately in each case.

(iii) Where loans have been guaranteed by directors or others, a mention thereof shall be made and also the aggregate amount of loans under each head.

(iv) Period and amount of default in repayment of dues, providing break-up of principal and interest shall be specified separately in each case.

2. Other current liabilities

The amounts shall be classified as: (a) Current maturities of long-term debt; (b) Current maturities of finance lease obligations; (c) Other payables (specify nature); (d) Interest accrued but not due on borrowings; (e) Interest accrued and due on borrowings; (f) Unearned revenue; (g) The following amounts shall be shown separately: Unpaid dividends* Unpaid application money received for allotment of securities and due for refund* Unpaid matured deposits* Unpaid matured debentures* Interest accrued on above* *In the above cases, any amount is transferred to Investor Education and Protection

fund as per the companies act should be verified and check whether the same is paid within the prescribed limit.

3. Short-term provisions

The amounts shall be classified as: (a) Provision for employee benefits. (b) Others (specify nature) e.g . Provision for expenses, proposed dividend etc. etc..

E. FIXED ASSETS: (Least Liquidity Asset to be arrange first & vice versa)

1. Tangible assets

(i) Classification shall be given as: (a) Land. (b) Buildings. (c) Plant and Equipment. (d) Furniture and Fixtures. (e) Vehicles. (f) Office equipment. (g) Others (specify nature).

(ii) Assets under lease shall be separately specified under each class of asset.

(iii) A reconciliation of the gross and net carrying amounts of each class of assets at the beginning and end of the reporting period showing additions, disposals, acquisitions and other movements and the related depreciation and impairment losses/reversals shall be disclosed separately.

2. Intangible assets

(i) Classification shall be given as: (a) Goodwill. (b) Brands /trademarks. (c) Computer software. (d) Mastheads and publishing titles. (e) Mining rights. (f) Copyrights, and patents and other intellectual property rights, services and operating rights. (g) Recipes, formulae, models, designs and prototypes. (h) Licenses and franchise. (i) Others (specify nature).

(ii) A reconciliation of the gross and net carrying amounts of each class of assets at the beginning and end of the reporting period showing additions, disposals, acquisitions and other movements and the related amortization and impairment losses/reversals shall be disclosed separately.

Some Important aspects of Fixed Assets :

1. In case of land, whether it is freehold or leasehold should be indicated.

2. The original cost and accumulated depreciation should be correctly displayed.

3. If the assets are purchased on foreign currency, the exchange difference should be transfer to profit and loss A/c and not to capitalise with the fixed assets (As per the AS-11 & amendment in Companies Accounting Standard rule).

4. If the fixed assets have been revalued or reduce on re-structuring of the company during the year, the same should be disclosed by way of note for a period of 5 years in notes to accounts forming part of balance sheet.

5. If the company sales the fixed assets, to check the auditor’s report whether it affects the going concern of the company.

E. Investments (Also termed as Non-Current Investment):

Non-current investments shall be classified as: (a) Investment property; (b) Investments in Government or trust securities; (c) Investments in units, debentures or bonds; (d) Other non-current investments (specify nature)

The investments held-to-maturity shall be stated separately.

The following shall also be disclosed: (a) Aggregate amount of quoted investments and market value thereof; (b) Aggregate amount of unquoted investments; (c) Aggregate amount of partly paid-up investments; (d) The names of bodies corporate (indicating separately the names of subsidiaries, associates and other business ventures) in whose securities, investments have been made and the nature and extent of the investments so made in each such body corporate (Whether investment company or other than

investment).

In case of investment in subsidiary company, one have to check whether requirement of consolidated balance is required as per AS 21.

If there is some unutilised money towards the issues, then it should be shown separately.

E. Current Assets & Loans and Advances:

1. Long-term loans and advances

(i) Long-term loans and advances shall be classified as: (a) Capital Advances; (b) Security Deposits; (c) To directors / subsidiaries / associates / business ventures loans and

advances to specify separately; (d) Others (specify nature)- loans and advances to specify separately.

(ii) The above shall also be separately sub-classified as: (a) To the extent secured, considered good; (b) Others, considered good; (c) Doubtful.

(iii) Allowance for bad and doubtful loans and advances shall be disclosed under the relevant heads separately.

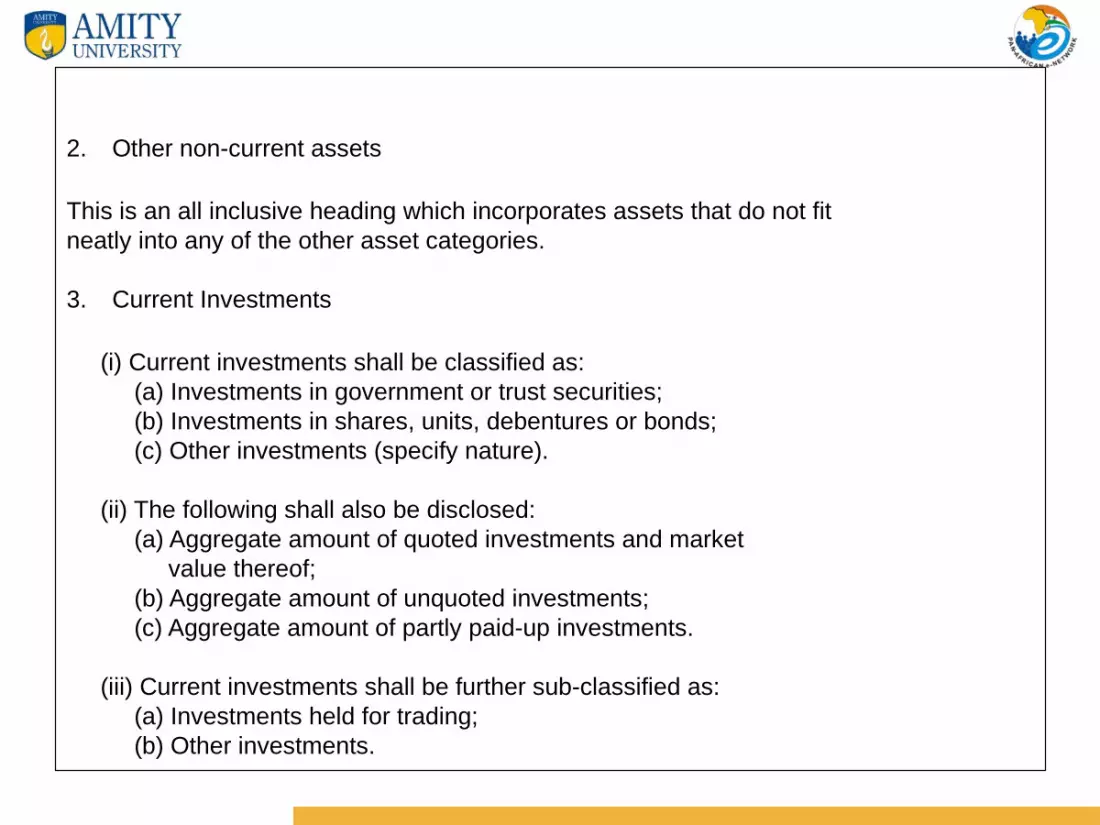

2. Other non-current assets

This is an all inclusive heading which incorporates assets that do not fitneatly into any of the other asset categories.

3. Current Investments

(i) Current investments shall be classified as: (a) Investments in government or trust securities; (b) Investments in shares, units, debentures or bonds; (c) Other investments (specify nature).

(ii) The following shall also be disclosed: (a) Aggregate amount of quoted investments and market value thereof; (b) Aggregate amount of unquoted investments; (c) Aggregate amount of partly paid-up investments.

(iii) Current investments shall be further sub-classified as: (a) Investments held for trading; (b) Other investments.

4. Inventories

(i) Classification shall be made as: (a) Raw material; (b) Work-in-progress; (c) Finished goods; (d) Stock-in-trade; (e) Stores and spares; (f) Loose tools; (g) Others (specify nature). (ii) Goods-in-transit shall be disclosed under the relevant sub-head of inventories.

5. Trade Receivables

(i) The amounts shown under ‘Trade Receivables’ shall include the amounts due in respect of goods sold or services rendered in the normal course of business. (ii) Trade receivables shall also be classified as: (a) To the extent secured, considered good; (b) Others, considered good; (c) Doubtful.

(iii) Allowance for bad and doubtful debts shall be disclosed under the relevant heads separately.

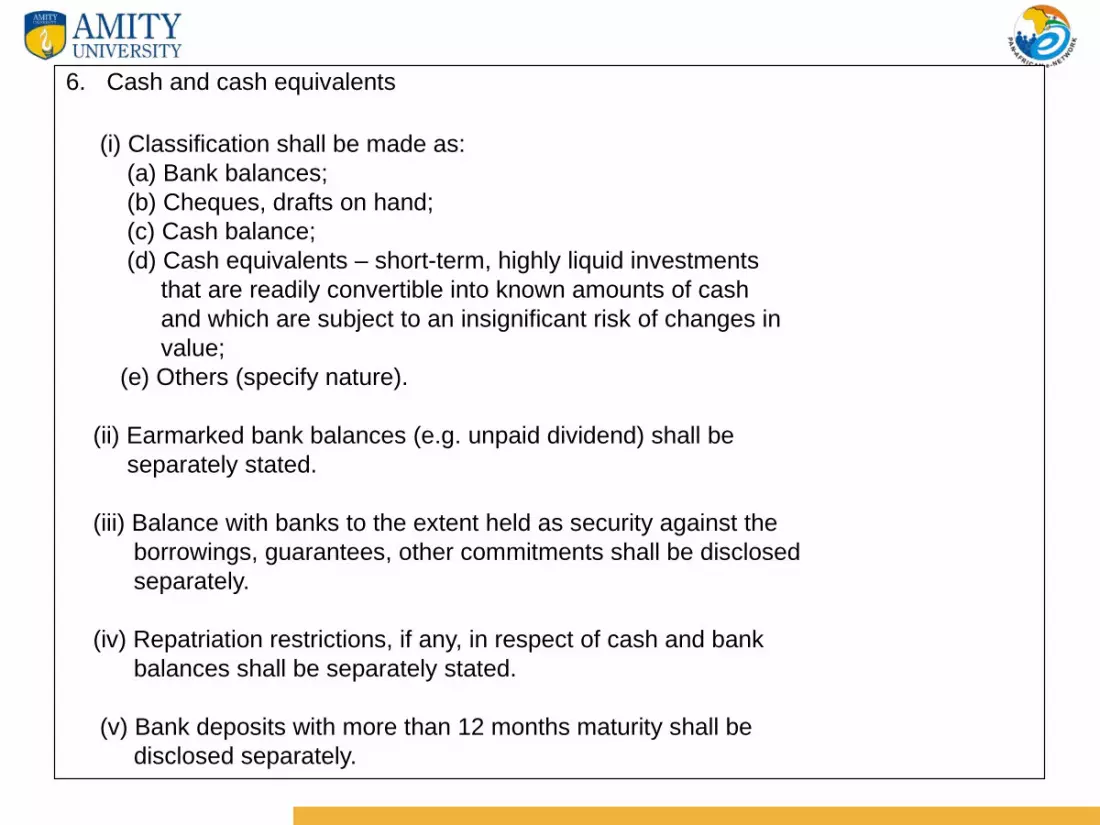

6. Cash and cash equivalents

(i) Classification shall be made as: (a) Bank balances; (b) Cheques, drafts on hand; (c) Cash balance; (d) Cash equivalents – short-term, highly liquid investments that are readily convertible into known amounts of cash and which are subject to an insignificant risk of changes in value; (e) Others (specify nature).

(ii) Earmarked bank balances (e.g. unpaid dividend) shall be separately stated.

(iii) Balance with banks to the extent held as security against the borrowings, guarantees, other commitments shall be disclosed separately.

(iv) Repatriation restrictions, if any, in respect of cash and bank balances shall be separately stated.

(v) Bank deposits with more than 12 months maturity shall be disclosed separately.

7. Short-term loans and advances

(i) Loans and advances shall be classified separately as: (a) To subsidiaries/associates/business ventures; (b) To others (specify nature).

(ii) The above shall also be sub-classified as: (a) To the extent secured, considered good; (b) Others, considered good; (c) Doubtful.

(iii) Allowance for bad and doubtful loans and advances shall be disclosed under the relevant heads separately.

8. Other current assets (specify nature).

Some Important aspects of Current Assets & Loans and advances :

1. The mode of valuation as per AS 2 should be separately stated wherever practicable.

2. Interest accrued on investments held in current assets should be separately stated

3. The maximum balance in respect of due from directors should be stated.

4. In case of unutilised monies in respect of issue made on current investment should be separately stated.

5. The types & nature of account in schedule bank should be given.

6. In case of non-scheduled banks, the name of the banks and maximum balance during the year should be stated.

7. In case loans given to the companies under same management, the maximum amount due from them should be separately stated.

8. The opinion of BOD should be obtained regarding the valuation on realisation of current assets, loans and advances should have at least the value at which they are stated.

E. MISCELLANEOUS EXPENDITURE:

1. The balance should be shown to the extent not written off or adjusted.

2. In case of debit balance in profit and loss a/c and that could not be adjusted with the earlier year’s free reserve or even if adjusted the negative value comes, then it should be shown under miscellaneous expenditure.

3. To check out whether intangible assets hitherto shown under this head is now required to be shown under the head Fixed Assets in view of AS26.

F. CONTINGENCIES AND COMMITMENTS:

1. Contingencies (to the extent not provided for):

(i) Contingencies shall be classified as:

(a) Tax contingencies and law suits (except those where the likelihood of an outflow of resources is remote); (b) Guarantees; (c) Other money for which the company is contingently liable (except those where the likelihood of an outflow of resources is remote).

2. Commitments: (i) Commitments shall be classified as: (a) Estimated amount of contracts remaining to be executed on capital account and not provided for; (b) Uncalled liability on shares and other investments partly paid; (c) Other commitments (specify nature).

3. The amount of dividends proposed to be distributed to equity holders for the period and the related amount per share shall be disclosed separately. Arrears of fixed cumulative dividends shall also be disclosed separately.

New Schedule VI(In the Offing)

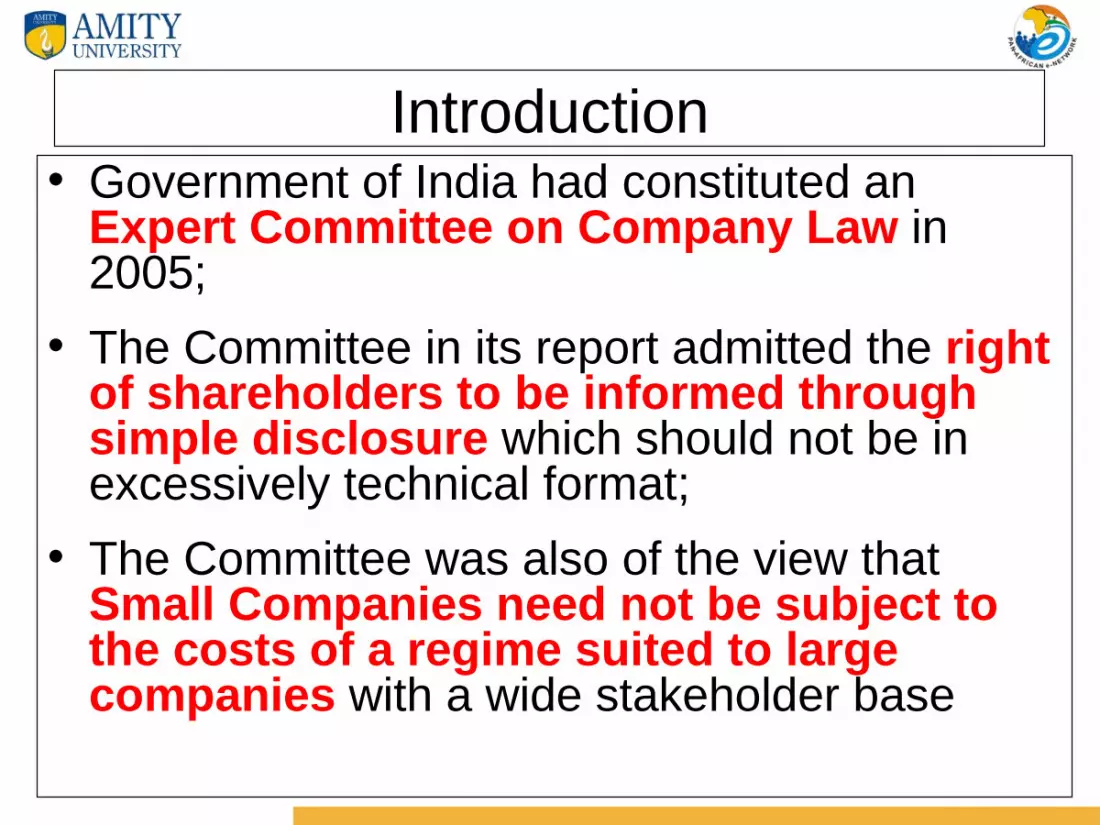

Introduction• Government of India had constituted an

Expert Committee on Company Law in 2005;

• The Committee in its report admitted the right of shareholders to be informed through simple disclosure which should not be in excessively technical format;

• The Committee was also of the view that Small Companies need not be subject to the costs of a regime suited to large companies with a wide stakeholder base

ICAI’s Role• Ministry of Corporate Affairs had requested the

ICAI to review Schedule VI in order to simplify the same;

• The ICAI was also requested to prescribe a SARAL Schedule VI for small and medium sized companies;

• To carry out the exercise, the Institute had constituted a Study Group:1. To formulate the suggestions on Schedule VI;

and 2. For prescribing SARAL Schedule VI for small

and medium sized companies.

Objectives• Simplification of presentation;• Evaluate existing format with respect to

unwanted and outdated disclosures;• Harmonize and converge with global

disclosure requirements;• To minimize disclosure requirements for

Small and Micro Companies

Updates Now• The study group recommended the drafts of

“Simplified Schedule VI” and “SARAL Schedule VI” considering IFRS and Other reporting practices;

• The Corporate Laws Committee of the Institute considered the drafts of both the Schedules and finalized the same;

• The drafts are being sent to the Ministry of Corporate Affairs and other Specified Bodies for comments

Structure of New Schedule VI

• Saral Schedule VI for SMCs: Divided into Parts I & II

• Simplified Schedule VI for Non-SMCs: Divided into Parts I, II & III

SMC Conditions

Key Changes• Formats prescribed for Profit and Loss

account and Cash flow Statement;• However, Cash Flow Statement not

required for SMCs

Key Changes:

Rounding of figures appearing in Financial statements (appears to be mandatory)

Key Changes• Schedule VI and Accounting Standards

flexibility;• The disclosure requirements specified

in Schedule are in addition to and not in substitution of the disclosure requirements specified in the Accounting Standards prescribed under the Companies Act, 1956

Key Changes

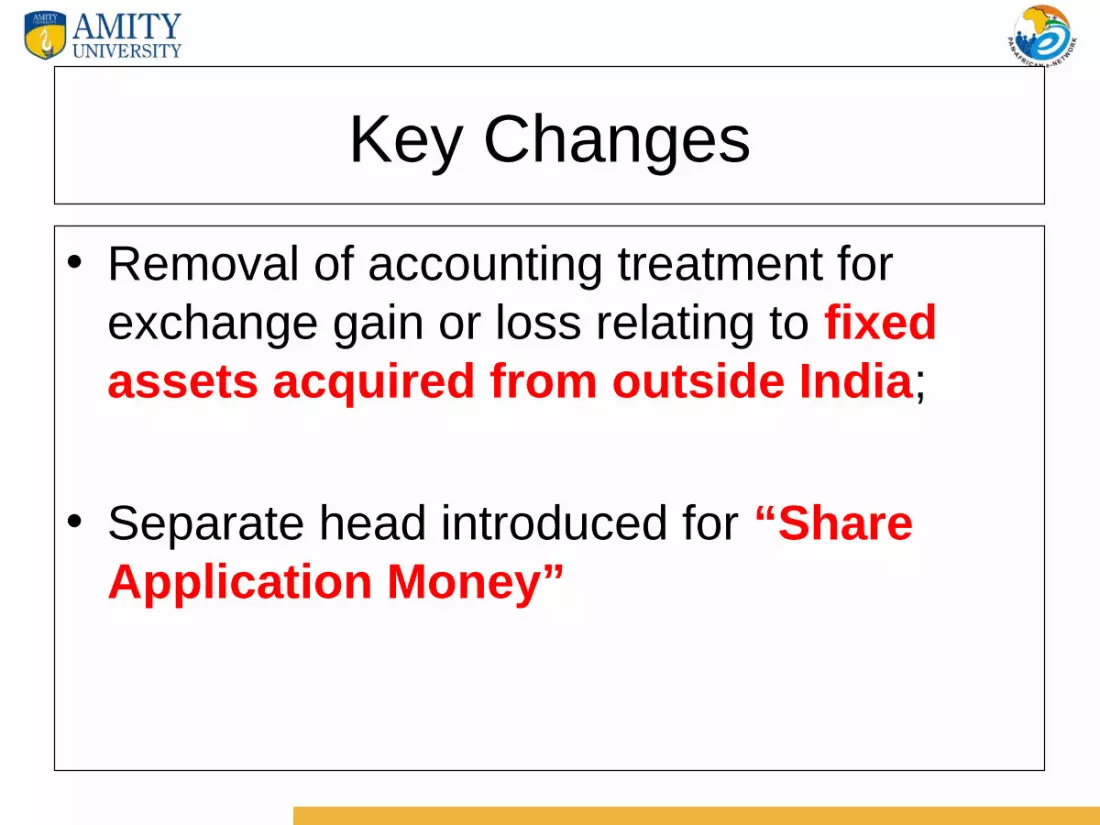

• Removal of accounting treatment for exchange gain or loss relating to fixed assets acquired from outside India;

• Separate head introduced for “Share Application Money”

Key Changes

• Schedules to the financial statements to form part of notes accounts;

Key Changes

• Presentation changes in balance sheet almost on the same lines as of IAS 1;

Key Changes• Additional Disclosure in respect of Share

Capital;• For Instance:

– Reconciliation of number of shares outstanding at the beginning of shares with shares at the end of period.

– Shares in the company held by any share holder holding more than 5 %

Key Changes

• Reserves and surplus:

Debit balance of profit and loss account should be shown under surplus; and

Negative balance of surplus after adjusting against reserve should be shown under reserve and surplus, even if resultant figure is negative.

Key Changes

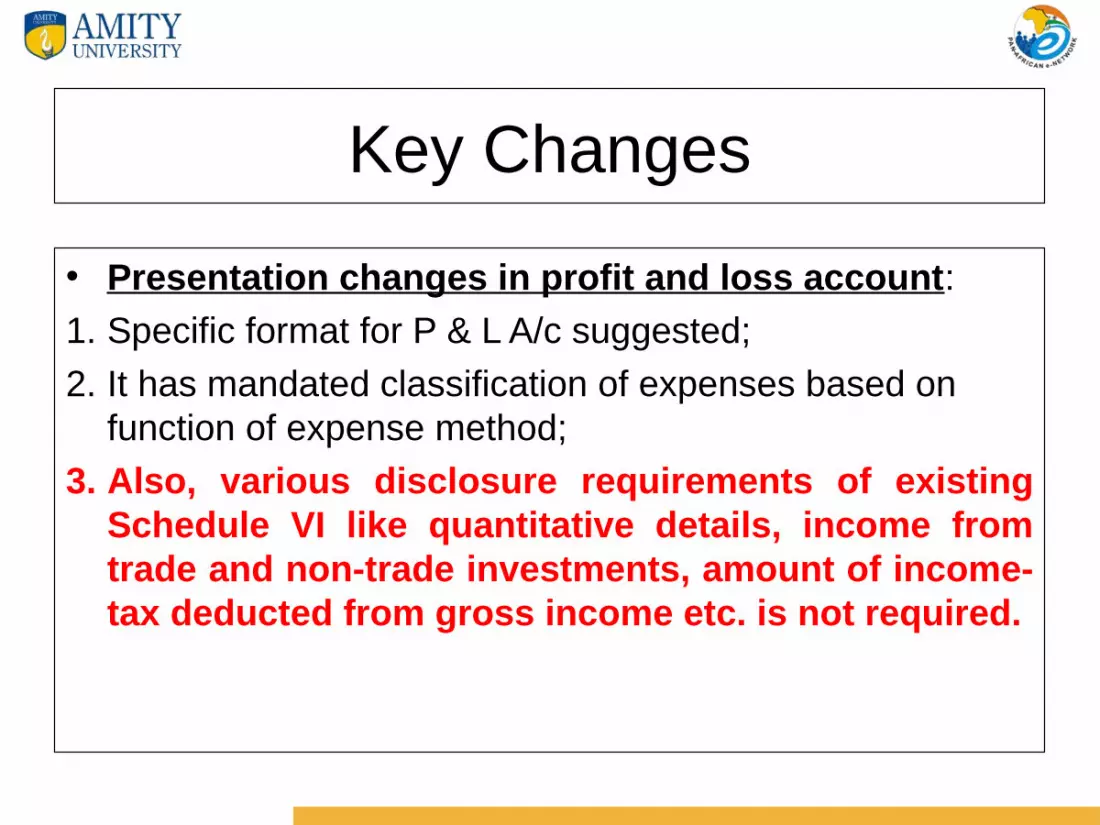

• Presentation changes in profit and loss account: 1. Specific format for P & L A/c suggested;2. It has mandated classification of expenses based on

function of expense method;3. Also, various disclosure requirements of existing

Schedule VI like quantitative details, income from trade and non-trade investments, amount of income-tax deducted from gross income etc. is not required.

Materiality• Any item for which the expense exceed

1% of the revenues from operations of the Company or Rs. 50,000 (for SMCs) or Rs. 1,00,000 (for Non SMCs), whichever is higher, shall be shown as a separate and distinct item;

• Result from discontinued operations to be disclosed separately in line with AS 24.

Key Changes

• Significant reduction in redundant and irrelevant information:

1.capacity details, 2.expenditure/ income in foreign currency, 3.details of debts/advances due from

companies under same management etc.

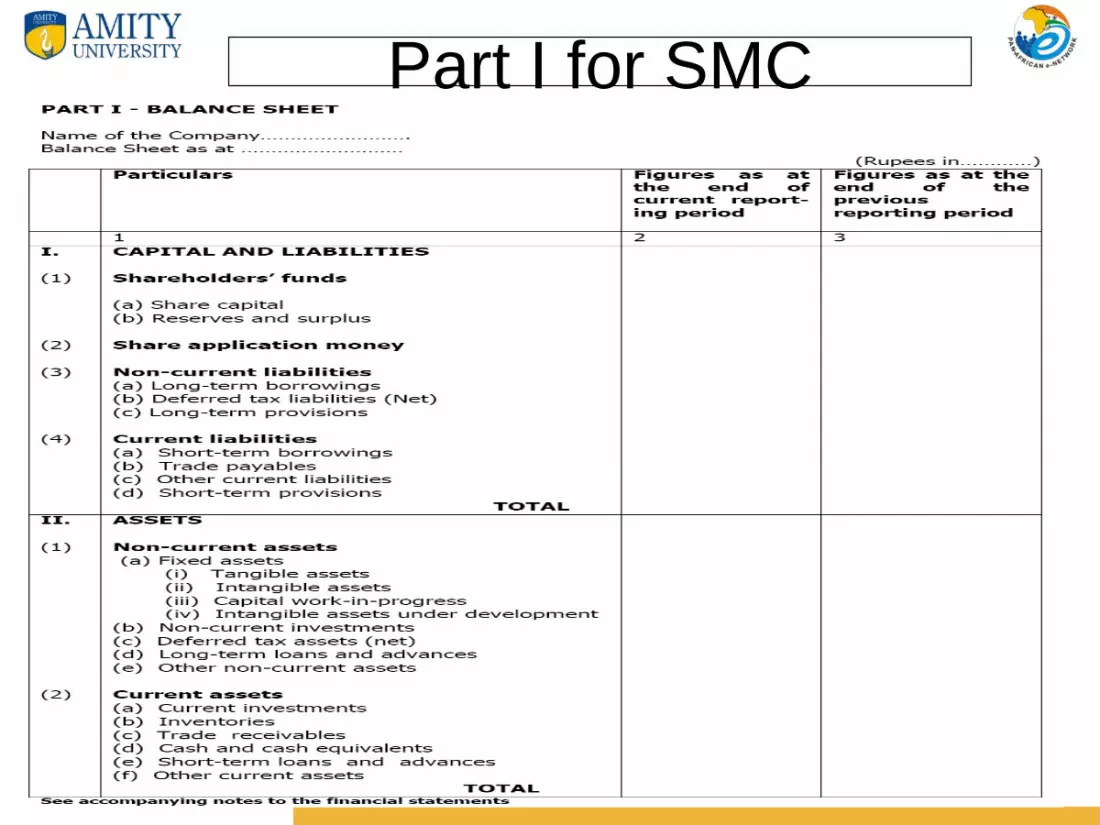

Part I for SMC

Part II for SMC

Part I for Non-SMCs

Part II for Non-SMCs

Part III for Non-SMCs• Cash Flow Statement: Almost on the same

lines as AS 3

Thank You

Copyright @ Amity University

Please forward your query To: [email protected]: [email protected]