Embed Size (px)

Citation preview

- 1 -

Agency Cost and Dividend:

Evidence from Anti-Takeover Legislation

Bill Francis

Lally School of Management and Technology of Rensselaer Polytechnic Institute

110 8th Street - Pittsburgh Building, Troy, NY, U.S.A., 12180, [email protected],

518-276-3908

Iftekhar Hasan

Lally School of Management and Technology of Rensselaer Polytechnic Institute

110 8th Street - Pittsburgh Building, Troy, NY, U.S.A., 12180, [email protected],

518-276-2525

Kose John

Stern School of Business, New York University

44 West 4th Street, Suite 9-190, New York, 10012, [email protected] ,

212-998-0337

Liang Song∗

Lally School of Management and Technology of Rensselaer Polytechnic Institute

110 8th Street - Pittsburgh Building, Troy, NY, U.S.A., 12180, [email protected],

518-892-8098

∗ Correspondence Author

- 2 -

Agency Cost and Dividend: Evidence from Anti-Takeover Legislation

Bill Francis, Iftekhar Hasan, Kose John, Liang Song

Abstract

The paper uses an exogenous shock-passage of Anti-Takeover Laws as proxies of

increased agency cost to investigate the relation between managerial entrenchment and

dividend policy for a large number of U.S. industrial firms over the period 1981-1993.

Consistent with conventional wisdom suggests that managers have a strong preference

against dividends payments since paying dividends reduces cash subject to managerial

discretion, this paper finds that firms with entrenched managers are less likely to pay

dividends, specifically; firms have fewer propensities to pay dividends and lower

dividend payout ratio after passage of Anti-Takeover Laws. This paper adds to the

existing literature by using an exogenous shock-passage of Anti-Takeover Laws

(Bertrand and Mullainathan 2003; Cheng, Nagar et al. 2005) as proxies of increased

agency cost to avoid the problem - endogenous measure of managerial entrenchment

and our results are consistent in various robustness checks.

Keywords: payout policy, corporate governance, agency conflicts.

- 3 -

I. Introduction

Agency theory (Jensen 1986; Morck, Shleifer et al. 1990; Lang, Stulz et al. 1991)

argues that in corporations with diffused ownership, managers are often found to

pursue their own goals instead of maximizing shareholder wealth when they are not

closely monitored. This conflict of interests is manifest when managers are entrenched.

They make value-destroying acquisitions (Jensen 1986; Morck, Shleifer et al. 1990;

Lang, Stulz et al. 1991); choose capital structures not in favor of shareholders’

interests (Jensen and Meckling 1976; Stulz 1988) and even make decisions in favor of

their own compensation (Fahlenbrach 2003). It is obvious to predict that managers

prefer to cut or lower dividend payout if they become more entrenched based on

Agency Theory since paying dividend reduces the amount of cash at managers’

disposal, therefore they will get better capital market monitoring or do fewer

inefficient investments. As Easterbrook and Jensen point out, a policy of paying

dividends reduces firms’ agency costs by improving the monitoring and risk-raking

incentives of managers (Easterbrook 1984; Jensen 1986).

However, empirical results about the relation between entrenched managers and

dividend payout policy are still mixed. One school of researches is consistent with the

theoretical prediction based on Agency Theory. For example, (La Porta,

Lopez-de-Silane et al.(2000) examine a cross-section of 4,000 companies from around

the world, which operate in 33 countries with different levels of shareholder protection,

and therefore different strength of minority shareholder rights and finds that stronger

minority shareholder rights are associated with higher dividends.

- 4 -

The other strand of researches gets the opposite results using firm level measures

of managerial entrenchment. Pan (2007) find that firms with entrenched managers, as

measured by the governance index (the G index) developed by Paul, Joy et al.(2003),

are more likely to pay dividends. Officer (2007) provides evidence that firms with

weak governance, as measured by board characteristics and so on, have significantly

higher dividend initiation announcement abnormal returns than other firms. Fenn and

Liang (2001) and Hu and Kumar (2004) find that the likelihood and level of dividend

payouts is increasing when factors such as managerial stock-option holding,

managerial and outside blockholder ownership, CEO compensation policy, and board

independence indicate a high likelihood of managerial entrenchment and high agency

cost.

One problem that arises in any analysis of managerial entrenchment effect

measured by firm level variables on dividend payout policy is endogeneity. Thus,

corporate governance may be driven by, rather than a determinant of, differences in

firms’ dividend payout policy. As a result, higher dividend payout ratio firms may

have stronger firm level corporate governance measures since managers in those firms

don’t have enough cash flow to do fewer inefficient investments and have to get better

capital market monitoring. Consistent with it, Chidambaran, Palia et al.(2006) finds

that firms choose governance endogenously by investigating a broader measure of

governance, including board of directors, pay-performance sensitivity, shareholder

rights, institutional ownership and CEO turnover. This paper adds to the existing

literature by using an exogenous shock-passage of Anti-Takeover Laws (Bertrand and

- 5 -

Mullainathan 2003; Cheng, Nagar et al. 2005) as proxies of increased agency cost to

investigate how managerial entrenchment is related to firms’ payout policies and

avoids the problem - endogenous measure of managerial entrenchment.

I measure entrenchment by passage of Anti-Takeover Legislation and take the

view that Anti-Takeover Laws make it more difficult for a potential raider to take

control a firm and further allocate extensive power to the incumbent management

since managers do not need to worry about the possibility to be replaced after firms

are taken over by outsiders, in other words, outside market discipline for managers

decreases after passage of Anti-Takeover Legislation. So they provide a natural testing

ground for Agency Theory to explain firms’ payout policy.

Overall, this paper uses an exogenous shock-passage of Anti-Takeover Laws

(Bertrand and Mullainathan 2003; Cheng, Nagar et al. 2005) as proxies of increased

agency cost to investigate the relation between managerial entrenchment and dividend

policy for a large number of U.S. industrial firms over the period 1981-1993. The

paper finds that firms with entrenched managers are less likely to pay dividends,

specifically; firms have fewer propensities to pay dividends and lower dividend

payout ratio after passage of Anti-Takeover Laws. This result is consistent with

conventional wisdom suggests that managers have a strong preference against

dividends payments since paying dividends reduces cash subject to managerial

discretion, therefore imposing additional discipline on firm managers and reducing

their ability to pursue their own objectives. The results from this analysis can be

briefly summarized as follows.

- 6 -

First, univariate analysis shows that dividend payer percentage, dividend payout

ratio and dividend propensity are decreasing when managers are more entrenched and

there is a strong impact of Anti-Takeover legislation on firms’ dividend payout policy.

Second, the likelihood of dividend payout significantly declines after an increase

in the level of entrenchment, proxied by passage of Anti-Takeover Legislation. In

particular, in logit regressions that estimate firms’ divided payout probability, the

dummy variable that represents passage of Anti-Takeover Legislation, has a

significant negative coefficient, suggesting that firms will cut or lower their dividend

payout compared to those firms incorporated in the stats where Anti-Takeover

Legislation does not pass.

Finally, we provide evidence that firms’ dividend payout ratio also significantly

decreases after managerial entrenchment becomes more severe using

difference-in-difference approach.

The remainder of this paper is structured as follows. Section II reviews some

previous dividend research. Section III gives a brief introduction of Anti-Takeover

Legislation and its impact. Section IV describes our methodology and sample. Section

V states empirical results. Section VI does some robustness test. Section VII

concludes.

II. Agency Conflicts and Payout Policy Theory

While finance academics have long wondered why firms pay dividends when cash

distributions in the form of dividends are tax disadvantaged relative to retention or

- 7 -

stock repurchase (Black 1976). Despite a large body of literature on dividends and

payout policy, researchers have not yet to reach a consensus on why firms pay

dividends and what determines the payout ratio. Theories based on signaling

hypothesis (Aharony and Swary 1980), tax clienteles (Michaely, Thaler et al. 1995) or

catering (Malcolm and Jeffrey 2004) are not always consistent with the existing

empirical results. Michaely and Allen (2002) and Baker, Powell et al.(2002) provide

detailed surveys of existing work on payout policy.

One strand of this recent literature relates payout policy to managerial

entrenchment (Erik and Juergen 2000; La Porta, Lopez-de-Silane et al. 2000; Hu and

Kumar 2004; Pan 2007). The relation between dividend policy and agency cost is

central to the debate about the agency costs of free-cash-flow (Easterbrook 1984;

Jensen 1986). To be specific, managers dislike dividend payout and want to cut or

lower it while they could since a policy of paying dividends reduces firms’ agency

costs by improving the monitoring and risk-raking incentives of managers

(Easterbrook 1984), as well as reducing the amount of cash flow at managers’

disposal.

It is very likely that managers will manipulate firms’ payout policy since the

existing empirical literature have found amounts of results that managers make

decisions in favor of themselves like value-destroying acquisitions (Jensen 1986;

Morck, Shleifer et al. 1990; Lang, Stulz et al. 1991); choosing capital structures not in

favor of shareholders’ interests (Jensen and Meckling 1976; Stulz 1988) and even

making decisions in favor of their own compensation (Fahlenbrach 2003).

- 8 -

One model of the relation between corporate governance and dividend policy is

the outcome model proposed by La Porta, Lopez-de-Silane et al. (2000). In the

outcome model, the payment of dividends is the result of effective governance-

well-governed. Firms pay dividends because strong governance makes expropriation

from shareholders more difficult and shareholders successfully pressure managers to

distribute excess cash. La Porta, Lopez-de-Silane et al. (2000) findings on payout

levels and other results support their outcome agency model of dividends by

examining a cross-section of 4,000 companies from around the world, which operate

in 33 countries with different levels of shareholder protection, and therefore different

strength of minority shareholder rights.

Another substitute model in La Porta, Lopez-de-Silane et al. (2000) argues that

dividend payments are a substitute for other characteristics that are consistent with

strong governance because poorly-governed firms need an alternate means of

establishing a reputation for acting in the interests of shareholders if they intend to

raise capital form public markets in the future. While it is almost a tautology that more

dividend payout will increase firm level corporate governance directly by reducing

free cash flow inside the firm or indirectly by having to access more to outside capital

market and get better capital market monitoring or discipline. So there is no surprise

that some existing literature (Paul, Joy et al. 2003; Officer 2007; Pan 2007) using firm

level corporate governance measures get the result that those firms with higher firm

level corporate governance have higher dividend payout ratio. They can not rule out

- 9 -

the possibility of endogeneity that those firms with higher dividend payout ratio have

higher firm level corporate governance.

Our paper presents evidence on the role of corporate governance in influencing

firms’ dividend payout. It differs from existing literature in several important ways.

First, we use an exogenous shock-passage of Anti-Takeover Laws (Bertrand and

Mullainathan 2003; Cheng, Nagar et al. 2005) as proxies of increased agency cost to

investigate the relation between managerial entrenchment and dividend policy and

avoid endogeneity problem of the existing literature using firm level variables to

measuring managerial entrenchment effect. Second, we use difference-in-difference

approach to find a control group of sample firms, so our results are more robust. We

find that firms decrease dividend payout after managers become more entrenched. In

particular, firms have less propensity to pay dividend and lower or cut dividend ratio

when corporate governance discipline from outside capital market declines measured

by passage of Anti-Takeover Legislation.

III. Anti-Takeover Laws

A. Description

The main proxy for managerial entrenchment in the paper is passage of

Anti-Takeover Legislation. More detailed description about Anti-Takeover laws can

be found in several researches (Karpoff and Malatesta 1989; Comment and Schwert

1995; Bertrand and Mullainathan 2003); we will give a brief discussion as follows.

Williams Act, a federal statute designed to protect investors from unannounced

- 10 -

takeovers, passed in 1968. Based on that, the first generation state laws passed in a lot

of states, but they were deemed unconstitutional in 1982. To address these concerns,

the second generation state laws passed in 1980’s. In the 1990s, the third generation

laws test current limits, attempting to make Anti-Takeover legislation more stringent.

In our study, we focus on the second generation state Anti-Takeover Laws, which

increased the difficulty of a successful takeover for firms incorporated in those states.

The second generation laws can be divided into three types: (1) Control Share

Acquisition (CSA), (2) Fair Price (FP) and (3) Business Combination (BC). Although

these laws have some differences in various states, they share some similar themes.

The similarity of Anti-Takeover Laws in various states allows us not to care about the

difference of role from Anti-Takeover Laws of various states.

B. Impact of Laws

Passage of Anti-Takeover Legislation has played an important role in deterring

takeovers, which further increases agency cost (Jensen 1986). Mass of cases tested

these laws as they passed, indicating that corporate raiders understood the implications.

Laws received extensive coverage by both popular press and legal practitioners. The

existing literature (Karpoff and Malatesta 1989; Morck, Shleifer et al. 1990; Bertrand

and Mullainathan 1999a; Bertrand and Mullainathan 1999b; Bertrand and

Mullainathan 2003) have done amounts of outstanding researches using

Anti-Takeover Legislation as a testing ground and argue that these legislations

increase the power of existing managers, which means that managers would not

- 11 -

maintain the same levels of operational efficiency as before while outside market

discipline decreases and agency cost increases. Although some scholars such as Stein

(1988) do not agree that agency cost increases after passage of Anti-Takeover

Legislation. Cheng, Nagar et al. (2005) argues that Stein’s arguments are flawed. So

we can get the conclusion that agency cost of the firms incorporated in the states

where Anti-Takeover laws have been passed increases and managers in those firms

become more entrenched than before. And we can use passage of Anti-Takeover

legislation as a testing ground to investigate the relation between managerial

entrenchment and dividend policy.

IV. Empirical Methodology and Sample Construction

A. Difference-in-Difference Approach

The goal of this paper is to understand whether cross-sectionally, the propensity to

pay dividends and the dividend payout ratio are related to the degree of managerial

entrenchment, controlling for other firm characteristics. We use the same

difference-in-difference methodology as Bertrand and Mullainathan (1999b). Our

control group for any given year is the set of states, which did not pass Anti-Takeover

Laws at that time, even if they will pass the law later, it makes our control group not

very small since it is very clear that most of companies are incorporated in the states

passing laws. Table I summarizes state Anti-Takeover Legislation.

[Insert TALBE I]

- 12 -

To use difference-in-difference approach, we define a dummy variable Treat one

if a firm is incorporated in a state, which passed Anti-Takeover laws, otherwise zero.

We also define a dummy variable Post as one after passage of the Anti-Takeover law

for a certain company and zero otherwise. Bertrand and Mullainathan (2003) uses the

passage of Business Combination Laws to represent Anti-Takeover Law passage time

and they argue that Business Combination Laws were the most stringent of the three

laws. In this way, we define the dummy variable Post for each firm that takes a value

of unity in the year when Business Combination Laws passed and call this approach

Business Combination Law Approach.

Cheng, Nagar et al. (2005) uses passage of the first Anti-Takeover Law to

represent Anti-Takeover Law passage time. They argue that the passages of various

Anti-Takeover Laws were stimulated by one another and further investors will have

anticipated the passage of next law upon knowing the passage of the previous law. So

they believe it is the first law that has the most influence on investors since the

enactment of subsequent laws in a certain state is eased by passage of the first piece of

Anti-Takeover laws. So based on this way, the dummy variable Post for each firm

takes a value of unity in the year when the corresponding state’s first Anti-Takeover

law passed and we call this approach the First Passed Law Approach. In this paper, we

only present the result based on the Business Combination Law Approach. When we

use the First Law Approach to do robustness test, we got qualitatively same empirical

results.

- 13 -

B. Sample Selection

Our sampling procedure parallels those of Fama and French (2001). Specifically,

we restrict analysis to nonfinancial and nonutility (hereafter, industrial firms) on

CRSP and Compustat, defined as firms with SIC codes outside the intervals

4900-4949 and 6000-6999. We consider only NYSE, NASDAQ, and AMEX firms

that have securities with CRSP share codes 10 or 11 to ensure those firms are publicly

traded and those are incorporated in the U.S. according to Compustat. We exclude

firms with book equity (BEt) below $250,000 or total assets (Assett) below $500,000.

We focus on our sample firms for calendar year t, 1981-1993 and include those firms

with fiscal year-ends in t. Since the first second-generation Anti-Takeover Law in our

sample passed in 1984 and the last one passed in 1990, we extend our sample coverage

three years before and after that period to include all possible related influence by

Anti-Takeover Laws. Firms’ state of incorporation are collected from Compustat,

which refers to the state of incorporation in 1994 if the firm is still running or the last

state of incorporation if the firm was dead before 1994 (Bertrand and Mullainathan

1999a).

To remain in the final sample, each firm-year observation must have information

available to derive the following variables (details provided in the appendix):

1. Dividend Dummy (DIVt).

2. NYSE Percentile (NYPt).

3. Market-to-Book Ratio (Vt/At).

4. Growth Rate of Assets (dAt/At)

- 14 -

5. Profitability (Et/At)

We impose additional Compustat data availability conditions when conducting

some of our tests and related analyses (details provided where appropriate).

C. Sample Statistics

The final sample contains 1,469 firms, and an overall total of 11,524 firm year

observations over the period 1981-1993. Table II presents descriptive statistics of key

variables and control variables for the sample and table III presents variable

correlation matrix.

[Insert TALBE II]

[Insert TALBE III]

V. Empirical Results

Fama and French (2001) identify four firm characteristics as important

determinants of a firm’s likelihood to pay dividends - firm size, investment

opportunities, growth rate and profitability. DeAngelo, DeAngelo et al.(2006) find

that firms are more likely to pay dividends when they enter into the mature stage of

their lifecycle. Using the ratio of retained earnings to total capital as a proxy for a

firm’s lifecycle stage, they show that the variables REt/TEt and REt/TAt have strong

explanatory power in estimating a firm’s likelihood to pay dividends. (Baker and

Wurgler (2004) propose a new dividend theory. They argue that managers cater to

investor demand for dividends by paying dividends when investors place a premium

- 15 -

on dividend-paying stocks, and vice versa. They measure dividend premium as equal

weighted dividend premium (EWt) and value weighted dividend premium (VWt)1.

Hoberg and Prabhala (2005) argues that of idiosyncratic risk (Riskt) is more important

variable than dividend premium mentioned above.

In the analysis that follows, we control for these firm characteristics, and examine

whether my proxy form managerial entrenchment, passage of Anti-Takeover

Legislation, has any additional explanatory power in explaining firms’ propensity to

pay dividends. we start with comparing dividend payout pattern before and after

passage of Anti-Takeover legislation, and then run logit regressions to estimate the

firms’ propensity to pay dividends, finally, we use difference-in-difference approach

to estimate dividend payout ratio. The key variable in multivariate test is Treat*Post

dummy variable.

A. Change of Dividend Pattern before and after Laws

Figure I shows the change in dividend payout pattern for the firms incorporated in

the states passed Anti-Takeover Legislation over the time period three years before

and three years after passage of the law. The year of passage of Anti-Takeover

Legislation is considered time 0. Dividend payout ratio (DivRatio) is defined as total

amount of dividend (Compustat item #21) scaled by earnings (Compustat item #18).

To construct DivRatio variable, we only include firms with positive earnings. To

mitigate the effect of outliers, we eliminate observations with a dividend payout ratio

1 In multivariate analysis, we only present results using variables REt/TEt and EWt, when we replace those with REt/TAt and VWt, our results do not qualitatively change.

- 16 -

greater than one. Dividend propensity measures the difference between firms’ real

dividend payout status and expected dividend payout status (details provided in the

appendix). We begin with two sided two-sample t-test to assess the difference in the

payout policy of firms three years before and after passage of Anti-Takeover

Legislation and plot the trend of dividend payout.

[Insert Figure I]

We observe that dividend payer percentage, dividend payout ratio and dividend

propensity are decreasing before the year 0 and increasing after the year 0 from Panel

B, Panel C ad Panel D. Our two sided two-sample t-test in Panel A shows that

dividend payout ratio and dividend propensity is decreasing in mean value. So we can

come to the conclusion that passage of Anti-Takeover Legislation has a strong impact

on firms’ dividend payout policy and on average, firms ‘s dividend payout declines

when managerial entrenchment are more severe.

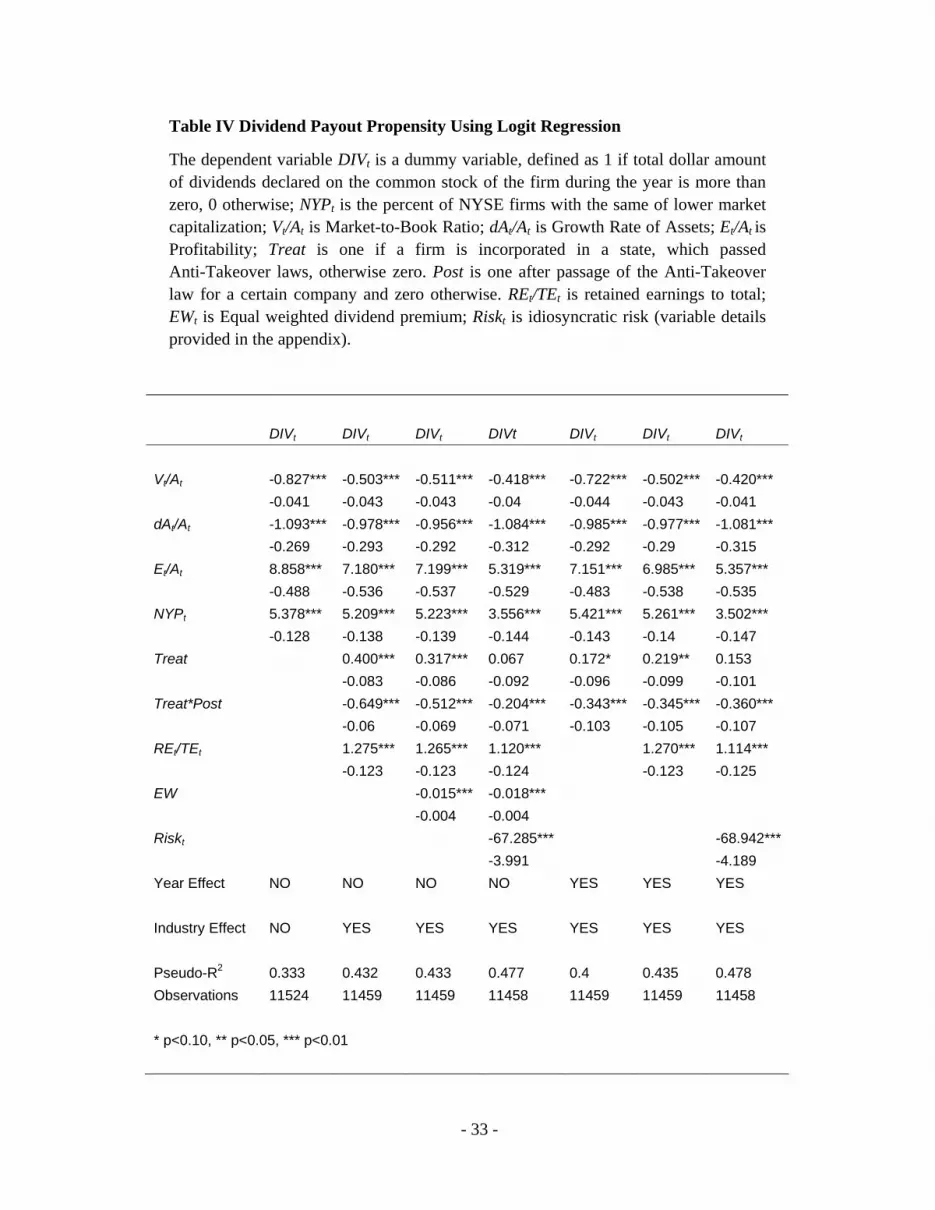

B. Dividend Payout Possibility Using Logit Regression

To control additional firm characteristics, we also do a multivariate analysis. The

likelihood of being a payer is predicted with the Logit model. All Logit regressions are

performed in the panel data format. Table IV presents regression results.

[Insert TALBE IV]

We observe that dividend payout is less likely when managers are more

entrenched after passage of Anti-Takeover Legislation. The result is robust even if we

add more control variables, industry effect and year effect into the regression equation.

- 17 -

Dividend pay out propensity is increasing in firm profitability and size and decreasing

in firm investment opportunities and growth rate, which is consistent with (Fama and

French (2001). Dividend pay out probability is increasing in firm retained earnings,

which is consistent with DeAngelo, DeAngelo et al.(2006) and decreasing in dividend

premium and idiosyncratic risk which is consistent with Hoberg and Prabhala (2005).

They argue that idiosyncratic risk is more important variable than dividend premium.

C. Dividend Payout Ratio Using Difference-in-Difference Approach

Although univariate results provide some evidence on the relation between

dividend payout ratio and managerial entrenchment, they do not control for other firm

characteristics that can be correlated with corporate governance as well as payout. To

address the issue, we employ difference-in-difference approach using a set of

firm-level controls described in the previous section. The dependent variable Dividend

payout ratio (DivRatio) is defined as total amount of dividend (Compustat item #21)

scaled by earnings (Compustat item #18). To construct DivRatio variable, we only

include firms with positive earnings. To mitigate the effect of outliers, we eliminate

observations with a dividend payout ratio greater than one. To make our dependent

variable more normal distributed, we eliminate firms with zero dividend payments

over the whole sample period. Table V presents regression results.

[Insert TALBE V]

We observe that dividend payout ratio is lower when managers are more

entrenched after passage of Anti-Takeover Legislation, even if compared to the

- 18 -

control group of firms incorporated in the states where Anti-Takeover Legislation

does not pass. Dividend pay out propensity is increasing in firm size and retained

earnings and decreasing in growth rate and idiosyncratic risk. The significant negative

coefficient of firm profitability shows that dividend payment is increasing in the lower

proportion compared to the increase of firms’ earning. The explanatory effect of firm

investment opportunities on firms’ payout ratio is not always significant.

VI. Robustness Test

A. Substitute Effect from Repurchase

Another possible explanation that dividend payout is decreasing when managers

become more entrenched is the Substitution Hypothesis proposed by Gustavo and

Roni (2002). They argue that firms have gradually substituted repurchases. To address

this concern, we plot the change in repurchase payout and total payout pattern for the

firms incorporated in the states passed Anti-Takeover Legislation over the time period

three years before and three years after passage of the law in figure II. The year of

passage of Anti-Takeover Legislation is considered time 0.

[Insert Figure II]

Panel A and B shows that repurchase payer percentage and repurchase ratio are

also decreasing when managerial entrenchment become more severe (variable

definition detail is provided in appendix). When we consider both dividend payout and

repurchase payout together, we can observe that total payout payer percentage and

total payout ratio have the same declining trend in our sample period from Panel C and

- 19 -

D. So we can get the conclusion that Substitution Hypothesis can not explain that

dividend payout decline after passage of Anti-Takeover Legislation, at least in our

sample period.

VII. Conclusions

We investigate the relationship between managerial entrenchment and dividend

policy for a large number of firms over the period 1981-1993. In particular, we study

the relation between a firm’s propensity to pay dividends, dividend payout ratio and

the degree of managerial entrenchment, proxied by an exogenous shock-passage of

Anti-Takeover Legislation. We find that, consistent with the conventional wisdom,

entrenched managers are less likely to pay dividends and pay less dividend. This paper

argues that other papers in this domain get the opposite results since their firm level

measures of managerial entrenchment are endogenous and we use an exogenous

shock-passage of Anti-Takeover legislation and avoid this endogeniety problem.

Logit regressions show a strong negative relation between dummy variable of

passage of Anti-Takeover Legislation, proxies for the degree of entrenchment, and its

propensity to pay dividends, after controlling for other firm characteristics, i.e., firm

size, investment opportunities, growth rate, profitability, retained earnings, dividend

premium and idiosyncratic risk. Difference-in-deference approach shows a significant

negative relation between dummy variable of passage of Anti-Takeover Legislation,

and dividend payout ratio. These results hold up well under a series of robustness

checks.

- 20 -

Our result is consistent with the recent findings in international context using

country level investor protection as a proxy for managerial entrenchment, dividends

are lower and cash holdings are higher in countries with weak investor protection (La

Porta, Lopez-de-Silane et al. 2000; Dittmar, Mahrt-Smith et al. 2003).

- 21 -

Reference

Aharony, J. and I. Swary (1980). "Quarterly Dividend and Earnings Announcements and Stockholders' Returns: An Empirical Analysis." The Journal of Finance: 1-12. Baker, H. K., G. E. Powell, et al. (2002). "Revisiting the dividend puzzle: Do all of the pieces now fit?" Review of Financial Economics 11(4): 241. Baker, M. and J. Wurgler (2004). "A Catering Theory of Dividends." Journal of Finance 59(3): 1125. Baker, M. P. and J. A. Wurgler (2002). Why are Dividends Disappearing? An Empirical Analysis, SSRN. Bertrand, M. and S. Mullainathan (1999a). "Is There Discretion in Wage Setting? A Test Using Takeover Legislation." RAND Journal of Economics 30: 535-554. Bertrand, M. and S. Mullainathan (1999b). "Corporate Governance and Executive Pay: Evidence from Takeover Legislation." Working Paper. Bertrand, M. and S. Mullainathan (2003). "Enjoying the Quiet Life? Managerial Behavior Following Antitakeover Legislation." Journal of Political Economy 111: 1043-1043. Black, F. (1976). "The dividend puzzle." Journal of Portfolio Management 2: 5-8. Cheng, S., V. Nagar, et al. (2005). "Identifying Control Motives in Managerial Ownership: Evidence from Antitakeover Legislation." The Review of Financial Studies 18(2): 637-672. Chidambaran, N. K., D. Palia, et al. (2006). Does Better Corporate Governance 'Cause' Better Firm Performance? SSRN. Comment, R. and G. W. Schwert (1995). "Poison or placebo? Evidence on the deterrence and wealth effects of modern antitakeover measures." Journal of Financial Economics 39(1): 3. DeAngelo, H., L. DeAngelo, et al. (2006). "Dividend policy and the earned/contributed capital mix: a test of the life-cycle theory." Journal of Financial Economics 81(2): 227. Dittmar, A., J. Mahrt-Smith, et al. (2003). "International Corporate Governance and Corporate Cash Holdings." Journal of Financial and Quantitative Analysis 38: 111-133. Easterbrook, F. H. (1984). "Two Agency-Cost Explanations of Dividends." American Economic Review 74(4): 650.

- 22 -

Erik, L. and W. Juergen (2000). Does the Governed Corporation Perform Better? Governance Structures and Corporate Performance in Germany, Center of Finance and Econometrics, University of Konstanz. Fahlenbrach, R. (2003). Shareholder Rights and CEO Compensation, SSRN. Fama, E. F. and K. R. French (2001). "Disappearing dividends: changing firm characteristics or lower propensity to pay?" Journal of Financial Economics 60(1): 3. Fenn, G. W. and N. Liang (2001). "Corporate Payout Policy and Managerial Stock Incentives." Journal of Financial Economics 60(1): 45. Gustavo, G. and M. Roni (2002). "Dividends, Share Repurchases, and the Substitution Hypothesis." Journal of Finance 57(4): 1649. Hoberg, G. and N. Prabhala (2005). "Disappearing Dividends: The Importance of. Idiosyncratic Risk and the Irrelevance of Catering." Working Paper. Hu, A. and P. Kumar (2004). "Managerial Entrenchment and Payout Policy." Journal of Financial and Quantitative Analysis 39: 759-790. Jensen, M. C. (1986). "Agency Cost of Free Cash Flow, Corporate Finance, and Takeovers." American Economic Review 76: 323-329. Jensen, M. C. and W. H. Meckling (1976). "Theory of the Firm: Managerial Behavior, Agency Costs and Ownership Structure." Journal of Financial Economics 3(4): 305. Karpoff, J. M. and P. H. Malatesta (1989). "The wealth effects of second-generation state takeover legislation." Journal of Financial Economics 25(2): 291. La Porta, R., F. Lopez-de-Silane, et al. (2000). "Agency Problems and Dividend Policies Around the World." The Journal of Finance, 55: 1-33. Lang, L. H. P., R. Stulz, et al. (1991). "A Test of the Free Cash Flow Hypothesis: The Case of Bidder Teturns." Journal of Financial Economics 29(2): 315. Malcolm, B. and W. Jeffrey (2004). "A Catering Theory of Dividends." Journal of Finance 59(3): 1125. Michaely, R. and F. Allen (2002). Payout Policy, SSRN. Michaely, R., R. H. Thaler, et al. (1995). "Price Reactions to Dividend Initiations and Omissions: Overreaction or Drift?" Journal of Finance 50(2): 573.

- 23 -

Morck, R., A. Shleifer, et al. (1990). "Do Managerial Objectives Drive Bad Acquisitions?" The Journal of Finance, 45(1): 31-48. Officer, M. S. (2007). "Dividend Initiations, Corporate Governance, and Agency Costs." Working Paper. Pan, C. H. (2007). Why are Firms With Entrenched Managers More Likely to Pay Dividends? SSRN. Paul, G., I. Joy, et al. (2003). "Corporate Governance And Equity Prices." The Quarterly Journal of Economics 118(1): 107. Stein, J. C. (1988). "Takeover Threats and Managerial Myopia." Journal of Political Economy 96(1): 61. Stulz, R. (1988). "Managerial control of voting rights: Financing policies and the market for corporate control." Journal of Financial Economics 20: 25.

- 24 -

Appendix:

Variable Definitions:

1. Total Asset (Assett). (Compustat item #6);

2. Book Equity (BEt). Defined as shareholders’ equity (Compustat item #216) [or total

liabilities (Compustat item #181), or common equity (Compustat item #60) +preferred

stock carrying value (Compustat item #130)] – preferred stock liquidating value

(Compustat item #10) [or preferred stock redemption value (Compustat item #56), or

preferred stock carrying value (Compustat item #130);

3. Market Equity (MEt). Defined as fiscal year end market price (Compustat item #199)

* common shares outstanding (Compustat item #25)

4. Dividend Dummy (DIVt). Defined as 1 if total dollar amount of dividends

(Compustat item #21) declared on the common stock of the firm during the year is

positive, 0 otherwise;

5. NYSE Percentile (NYPt). Defined as the percent of NYSE firms with the same of

lower market capitalization;

6. Market-to-Book Ratio (Vt/At). Defined as (Assett – BEt+ MEt)/ Assett;

7. Growth Rate of assets (dAt/At). Defined as (Assett-Assett-1)/Assett;

8. Profitability (Et/At). Defined as [income before extraordinary items (Compustat item

#18)+interest expense (Compustat item #15) + deferred taxes (Compustat item #50) if

available]/Assett;

9. Retained earnings to total capital (REt/TEt). Defined as Retained Earnings

(Compustat item #36)/ MEt;

- 25 -

10. Retained earnings to total capital (REt/TAt). Defined as Retained Earnings

(Compustat item #36)/ Assett;

11. Equal weighted dividend premium (EWt) and value weighted dividend premium

(VWt) are from (Baker and Wurgler 2004);

12. Idiosyncratic risk (Riskt). Defined as the standard deviation of residuals from a

regression of its excess returns (raw returns less the riskless rate) on the Fama and

French factors HML, SMB, and MKT;

13. Dividend propensity. Defined as the difference between Dividend Dummy (DIVt)

and expected probability of dividend payout. The expected probability of dividend

payout is calculates by the formula:

Pr (DIVt=1) =logit (-0.14+4.26 NYPt-0.81 Vt/At -1.07 dAt/At +15.57 Et/At) (1)

The coefficients of this formula are averages across years of Fama-MacBeth logit

regressions of the probability that a firm with given characteristics is a dividend payer

from 1963-1977, in the Compustat sample (Baker and Wurgler 2002);

14. Dividend payout ratio (DivRatio). Defined as total amount of dividend (Compustat

item #21) scaled by earnings (Compustat item #18);

15. Repurchase payout ratio. Defined as total amount of repurchase (the expenditure

on the purchase of common and preferred stocks (Compustat item # 115) minus any

reduction in the value (redemption value) of the net number of preferred shares

outstanding (Compustat item # 56)) scaled by earnings (Compustat item #18);

16. Total payout ratio. Defined as sum of dividend and repurchase scaled by earnings

(Compustat item #18).

- 26 -

Figure I Dividend Payout Pattern versus Time

Figure I show the change in Dividend Payout Pattern for the firms three years before and three years after passage of Anti-Takeover legislation. The year of passage of Anti-Takeover Legislation is considered time 0. Dividend payout ratio (DivRatio) is defined as total amount of dividend scaled by earnings. We only include firms with positive earnings and eliminate observations with a dividend payout ratio greater than one. Dividend propensity measures the difference between firms’ real dividend payout status and expected dividend payout status (details provided in the appendix).

Panel A

Relative Year -3 -2 -1 0 1 2 3 Total Firm Number 595 648 721 1234 1065 958 887 Payer Number 364 373 386 488 478 468 452 Payer Percent (%) 61.18 57.56 53.54 39.55 44.88 48.85 50.96

Before After DifferenceRelative Year -3 -2 -1 1 2 3 Dividend Propensity -0.074 -0.076 -0.115 -0.173 -0.159 -0.134 -5.62** Dividend Ratio 0.216 0.208 0.191 0.166 0.194 0.208 -2.27*

* p<0.05, ** p<0.01

Panel B

- 27 -

Panel C

Panel D

- 28 -

Figure II Repurchase and Total Payout Pattern versus Time

Figure II show the change in Repurchase Payout and Total Payout Pattern for the firms three years before and three years after passage of Anti-Takeover legislation. The year of passage of Anti-Takeover Legislation is considered time 0. Repurchase ratio is defined as total amount of repurchase scaled by earnings. Total payout ratio is defined as sum of dividend and repurchase scaled by earnings (details provided in the appendix).We only include firms with positive earnings and eliminate observations with a dividend payout ratio greater than one to make sample consistent with Figure I.

Panel A

Panel B

- 29 -

Panel C

Panel D

- 30 -

Table I State Anti-Takeover Legislation

Table I describes various Anti-Takeover legislation passage times in various states, which is obtained from Bertrand and Mullainathan (1999b).

Business Combination Law Fair Price Law Control Share Acquisition Law Arizona 1987 Arizona 1987 Arizona 1987 Connecticut 1989 Connecticut 1984 Hawaii 1985 Delaware 1988 Georgia 1985 Idaho 1988 Georgia 1988 Idaho 1988 Indiana 1986 Idaho 1988 Illinois 1984 Kansas 1988 Illinois 1989 Indiana 1986 Louisiana 1987 Indiana 1986 Kentucky 1989 Maryland 1988 Kansas 1989 Louisiana 1985 Massachusetts 1987 Kentucky 1987 Maryland 1983 Michigan 1988 Maine 1988 Michigan 1984 Minnesota 1984 Maryland 1989 Mississippi 1985 Mississippi 1991 Massachusetts 1989 Missouri 1986 Missouri 1984 Michigan 1989 New Jersey 1986 Nebraska 1988 Minnesota 1987 New York 1985 Nevada 1987 Missouri 1986 North Carolina 1987 North Carolina 1987 Nebraska 1988 Ohio 1990 Oklahoma 1987 New Jersey 1986 Pennsylvania 1989 Oregon 1987 New York 1985 South Carolina 1988 Pennsylvania 1989 Ohio 1990 South Dakota 1990 South Carolina 1988 Pennsylvania 1989 Tennessee 1988 South Dakota 1990 Rhode Island 1990 Virginia 1985 Tennessee 1988 South Carolina 1988 Washington 1990 Utah 1987 South Dakota 1990 Wisconsin 1985 Virginia 1988 Tennessee 1988 Wisconsin 1991 Virginia 1988 Wyoming 1990 Washington 1990 Wisconsin 1987 Wyoming 1989

- 31 -

Table II Descriptive Statistics

Table II presents descriptive statistics for the sample of 1,469 firms and an overall total of 11,524 firm year observations over the period 1981-1993. DIVt is a dummy variable, defined as 1 if total dollar amount of dividends declared on the common stock of the firm during the year is more than zero, 0 otherwise; NYPt is the percent of NYSE firms with the same of lower market capitalization; Vt/At is Market-to-Book Ratio; dAt/At is Growth Rate of Assets; Et/At is Profitability; Treat is one if a firm is incorporated in a state, which passed Anti-Takeover Laws, otherwise zero. Post is one after passage of the Anti-Takeover law for a certain company and zero otherwise. REt/TEt is retained earnings to total; REt/TAt is retained earnings to total capital; EWt is equal weighted dividend premium and VWt is value weighted dividend premium; Riskt is idiosyncratic risk (variable details provided in the appendix).

Variable Obs Mean Std. Dev. Min Max Key Variables DIVt 11524 0.521 0.500 0.000 1.000 Et/At 11524 0.048 0.157 -3.564 0.524 Vt/At 11524 1.859 2.458 0.275 84.229 NYPt 11524 0.332 0.301 0.050 1.000 dAt/At 11524 0.077 0.266 -11.004 0.989 treat 11524 0.858 0.349 0.000 1.000 treat*post 11524 0.505 0.500 0.000 1.000 Control Variables

REt/TEt 11524 0.234 1.386 -68.316 16.034

REt/TAt 11524 0.149 0.778 -24.235 3.539

EWt 11524 -34.038 7.862 -50.130 -23.530

VWt 11524 -9.834 6.478 -26.200 -1.020

Riskt 11523 0.031 0.022 0.000 0.497

- 32 -

Table III Variable Correlation Matrix

Table III presents variable correlation matrix for the sample of 1,469 firms and an overall total of 11,524 firm year observations over the period 1981-1993. DIVt is a dummy variable, defined as 1 if total dollar amount of dividends declared on the common stock of the firm during the year is more than zero, 0 otherwise; NYPt is the percent of NYSE firms with the same of lower market capitalization; Vt/At is Market-to-Book Ratio; dAt/At is Growth Rate of Assets; Et/At is Profitability; Treat is one if a firm is incorporated in a state, which passed Anti-Takeover laws, otherwise zero. Post is one after passage of the Anti-Takeover law for a certain company and zero otherwise. REt/TEt is retained earnings to total; REt/TAt is retained earnings to total capital; EWt is Equal weighted dividend premium and VWt is value weighted dividend premium; Riskt is idiosyncratic risk (variable details provided in the appendix).

DIVt Et/At Vt/At NYPt dAt/At treat Treat*Post REt/TEt REt/TAt EWt VWt Riskt DIVt 1.000 Et/At 0.274 1.000 Vt/At -0.137 -0.273 1.000 NYPt 0.524 0.250 0.027 1.000

dAt/At 0.009 0.338 0.052 0.108 1.000 treat 0.086 0.042 -0.009 0.143 0.007 1.000

Treat*Post -0.095 -0.048 0.012 0.023 -0.034 0.412 1.000

REt/TEt 0.210 0.197 -0.061 0.103 0.106 0.020 -0.061 1.000

REt/TAt 0.342 0.616 -0.314 0.244 0.163 0.027 -0.077 0.437 1.000

EWt -0.115 -0.058 -0.005 -0.039 -0.009 -0.009 0.481 -0.066 -0.073 1.000

VWt -0.126 -0.081 0.010 -0.032 -0.036 -0.008 0.499 -0.070 -0.077 0.751 1.000

Riskt -0.494 -0.340 0.060 -0.482 -0.150 -0.091 0.112 -0.265 -0.362 0.089 0.149 1.000

- 33 -

Table IV Dividend Payout Propensity Using Logit Regression

The dependent variable DIVt is a dummy variable, defined as 1 if total dollar amount of dividends declared on the common stock of the firm during the year is more than zero, 0 otherwise; NYPt is the percent of NYSE firms with the same of lower market capitalization; Vt/At is Market-to-Book Ratio; dAt/At is Growth Rate of Assets; Et/At is Profitability; Treat is one if a firm is incorporated in a state, which passed Anti-Takeover laws, otherwise zero. Post is one after passage of the Anti-Takeover law for a certain company and zero otherwise. REt/TEt is retained earnings to total; EWt is Equal weighted dividend premium; Riskt is idiosyncratic risk (variable details provided in the appendix).

DIVt DIVt DIVt DIVt DIVt DIVt DIVt Vt/At -0.827*** -0.503*** -0.511*** -0.418*** -0.722*** -0.502*** -0.420*** -0.041 -0.043 -0.043 -0.04 -0.044 -0.043 -0.041 dAt/At -1.093*** -0.978*** -0.956*** -1.084*** -0.985*** -0.977*** -1.081*** -0.269 -0.293 -0.292 -0.312 -0.292 -0.29 -0.315 Et/At 8.858*** 7.180*** 7.199*** 5.319*** 7.151*** 6.985*** 5.357*** -0.488 -0.536 -0.537 -0.529 -0.483 -0.538 -0.535 NYPt 5.378*** 5.209*** 5.223*** 3.556*** 5.421*** 5.261*** 3.502*** -0.128 -0.138 -0.139 -0.144 -0.143 -0.14 -0.147 Treat 0.400*** 0.317*** 0.067 0.172* 0.219** 0.153 -0.083 -0.086 -0.092 -0.096 -0.099 -0.101 Treat*Post -0.649*** -0.512*** -0.204*** -0.343*** -0.345*** -0.360*** -0.06 -0.069 -0.071 -0.103 -0.105 -0.107 REt/TEt 1.275*** 1.265*** 1.120*** 1.270*** 1.114*** -0.123 -0.123 -0.124 -0.123 -0.125 EW -0.015*** -0.018*** -0.004 -0.004 Riskt -67.285*** -68.942*** -3.991 -4.189 Year Effect NO NO NO NO YES YES YES Industry Effect NO YES YES YES YES YES YES Pseudo-R2 0.333 0.432 0.433 0.477 0.4 0.435 0.478 Observations 11524 11459 11459 11458 11459 11459 11458 * p<0.10, ** p<0.05, *** p<0.01

- 34 -

Table V Dividend Payout Ratio Using Difference-in-Difference Approach

The dependent variable Dividend payout ratio (DivRatio) is defined as total amount of dividend (Compustat item #21) scaled by earnings (Compustat item #18). To construct DivRatio variable, we only include firms with positive earnings. To mitigate the effect of outliers, we eliminate observations with a dividend payout ratio greater than one; Model 2 is truncated regression and others are ordinary least square regression; NYPt is the percent of NYSE firms with the same of lower market capitalization; Vt/At is Market-to-Book Ratio; dAt/At is Growth Rate of Assets; Et/At is Profitability; Treat is one if a firm is incorporated in a state, which passed Anti-Takeover laws, otherwise zero. Post is one after passage of the Anti-Takeover law for a certain company and zero otherwise. REt/TEt is retained earnings to total; Riskt is idiosyncratic risk (variable details provided in the appendix).

1 2 3 4 5 DivRatio DivRatio DivRatio DivRatio DivRatio Vt/At 0.001 0.032*** 0.006 0.01 0.011* -0.003 -0.005 -0.007 -0.007 -0.006 dAt/At -0.344*** -0.709*** -0.124*** -0.117*** -0.124*** -0.019 -0.034 -0.018 -0.017 -0.017 Et/At -0.885*** -1.887*** -2.013*** -1.952*** -1.958*** -0.068 -0.113 -0.091 -0.091 -0.09 NYPt 0.220*** 0.149*** 0.069** 0.080*** 0.046* -0.008 -0.012 -0.029 -0.029 -0.027 Treat 0.038*** 0.062*** -0.008 -0.012 Treat*Post -0.018*** -0.020*** -0.016** -0.015** -0.016** -0.006 -0.008 -0.007 -0.007 -0.007 REt/TEt 0.047*** 0.045*** -0.01 -0.01 Riskt -2.307*** -0.341 Year Effect NO NO YES YES YES Industry Effect NO NO YES YES YES R-Squared 0.177 0.702 0.704 0.709 Log likelihood 2013.0763 Observations 6121 5235 6121 6121 6121 * p<0.10, ** p<0.05, *** p<0.01