Embed Size (px)

Citation preview

Banking Sector Outlook

2020-21

Economy

❖ BWR expects GDP to contract by 9.5% in FY21

❖ Except agriculture, all other sectors to report contraction in FY21

❖ BWR expects Centre’s fiscal deficit to reach 7% of GDP in FY21 due to shortage in revenue collections

Banking

❖ Credit growth to see a major slump in FY21 owing to prolonged pandemic situation

❖ Asset quality of banks is expected to deteriorate further, however, this deterioration will be elongated due to restructuring

❖ Profitability of banks will take a hit due to higher provisioning and lower credit growth

❖ PSBs to require capital to the tune of Rs 1-1.25 lakh crores upto 31 March 2022

Emerging Trends

❖ Manufacturing sector is witnessing a gradual recovery

❖ Digital banking is becoming the new normal in India and is a critical enabler for growth

❖ Evolution of co-lending model is expected to transform credit delivery in the times to come

❖ Innovative structured finance transactions across asset classes to aid growth of financial institutions

BRICKWORK RATINGS www.brickworkratings.com

Executive Summary

2

To read the full

report click here

Economic Trends

Banking Sector Trends

Emerging Trends

Brickwork Ratings

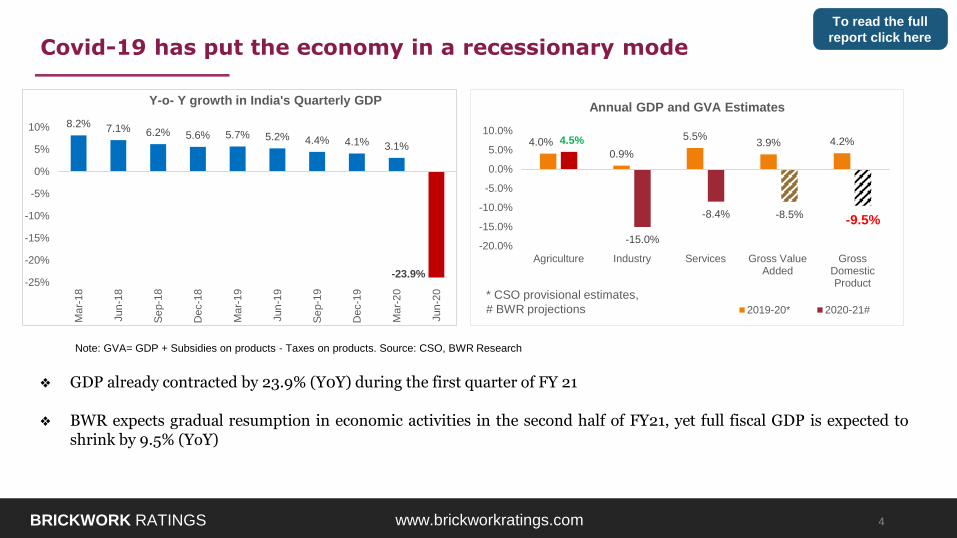

❖ GDP already contracted by 23.9% (Y0Y) during the first quarter of FY 21

❖ BWR expects gradual resumption in economic activities in the second half of FY21, yet full fiscal GDP is expected toshrink by 9.5% (YoY)

BRICKWORK RATINGS www.brickworkratings.com

Covid-19 has put the economy in a recessionary mode

Note: GVA= GDP + Subsidies on products - Taxes on products. Source: CSO, BWR Research

4.0%0.9%

5.5%3.9% 4.2%4.5%

-15.0%

-8.4% -8.5%-9.5%

-20.0%

-15.0%

-10.0%

-5.0%

0.0%

5.0%

10.0%

Agriculture Industry Services Gross ValueAdded

GrossDomesticProduct

Annual GDP and GVA Estimates

2019-20* 2020-21#

* CSO provisional estimates,

# BWR projections

8.2% 7.1% 6.2% 5.6% 5.7% 5.2% 4.4% 4.1% 3.1%

-23.9%-25%

-20%

-15%

-10%

-5%

0%

5%

10%

Ma

r-1

8

Jun

-18

Se

p-1

8

Dec-1

8

Ma

r-1

9

Jun

-19

Se

p-1

9

Dec-1

9

Ma

r-2

0

Jun

-20

Y-o- Y growth in India's Quarterly GDP

4

To read the full

report click here

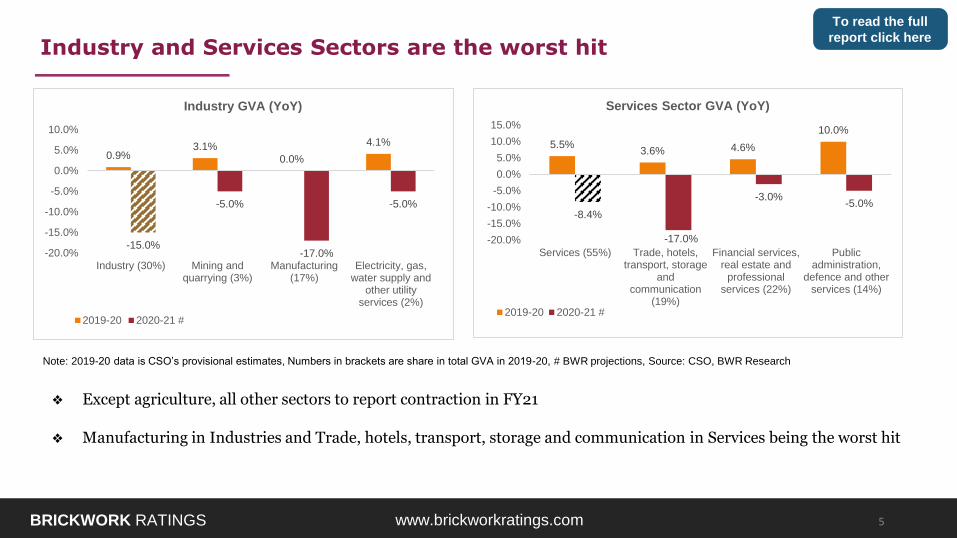

❖ Except agriculture, all other sectors to report contraction in FY21

❖ Manufacturing in Industries and Trade, hotels, transport, storage and communication in Services being the worst hit

BRICKWORK RATINGS www.brickworkratings.com

Industry and Services Sectors are the worst hit

Note: 2019-20 data is CSO’s provisional estimates, Numbers in brackets are share in total GVA in 2019-20, # BWR projections, Source: CSO, BWR Research

0.9%3.1%

0.0%

4.1%

-15.0%

-5.0%

-17.0%

-5.0%

-20.0%

-15.0%

-10.0%

-5.0%

0.0%

5.0%

10.0%

Industry (30%) Mining andquarrying (3%)

Manufacturing(17%)

Electricity, gas,water supply and

other utilityservices (2%)

Industry GVA (YoY)

2019-20 2020-21 #

5.5%3.6% 4.6%

10.0%

-8.4%

-17.0%

-3.0%-5.0%

-20.0%

-15.0%

-10.0%

-5.0%

0.0%

5.0%

10.0%

15.0%

Services (55%) Trade, hotels,transport, storage

andcommunication

(19%)

Financial services,real estate and

professionalservices (22%)

Publicadministration,

defence and otherservices (14%)

Services Sector GVA (YoY)

2019-20 2020-21 #

5

To read the full

report click here

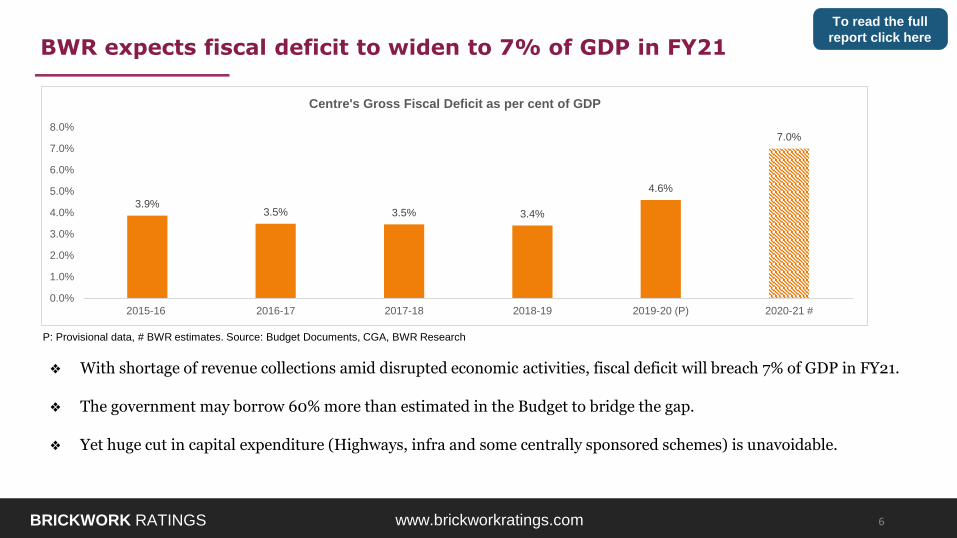

❖ With shortage of revenue collections amid disrupted economic activities, fiscal deficit will breach 7% of GDP in FY21.

❖ The government may borrow 60% more than estimated in the Budget to bridge the gap.

❖ Yet huge cut in capital expenditure (Highways, infra and some centrally sponsored schemes) is unavoidable.

BRICKWORK RATINGS www.brickworkratings.com

BWR expects fiscal deficit to widen to 7% of GDP in FY21

P: Provisional data, # BWR estimates. Source: Budget Documents, CGA, BWR Research

6

3.9%3.5% 3.5% 3.4%

4.6%

7.0%

0.0%

1.0%

2.0%

3.0%

4.0%

5.0%

6.0%

7.0%

8.0%

2015-16 2016-17 2017-18 2018-19 2019-20 (P) 2020-21 #

Centre's Gross Fiscal Deficit as per cent of GDP

To read the full

report click here

Economic Trends

Banking Sector Trends

Emerging Trends

Brickwork Ratings

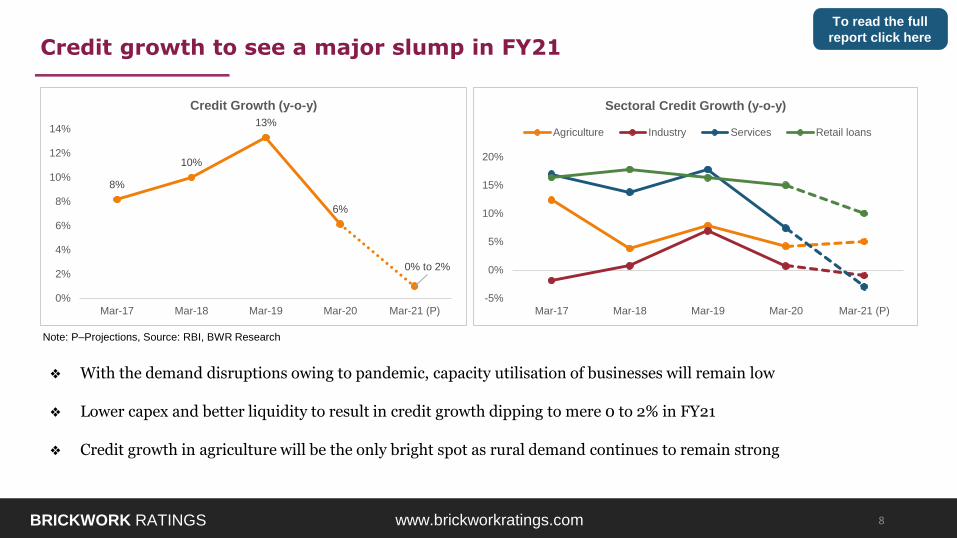

❖ With the demand disruptions owing to pandemic, capacity utilisation of businesses will remain low

❖ Lower capex and better liquidity to result in credit growth dipping to mere 0 to 2% in FY21

❖ Credit growth in agriculture will be the only bright spot as rural demand continues to remain strong

BRICKWORK RATINGS www.brickworkratings.com

Credit growth to see a major slump in FY21

Note: P–Projections, Source: RBI, BWR Research

8%

10%

13%

6%

0% to 2%

0%

2%

4%

6%

8%

10%

12%

14%

Mar-17 Mar-18 Mar-19 Mar-20 Mar-21 (P)

Credit Growth (y-o-y)

-5%

0%

5%

10%

15%

20%

Mar-17 Mar-18 Mar-19 Mar-20 Mar-21 (P)

Sectoral Credit Growth (y-o-y)

Agriculture Industry Services Retail loans

8

To read the full

report click here

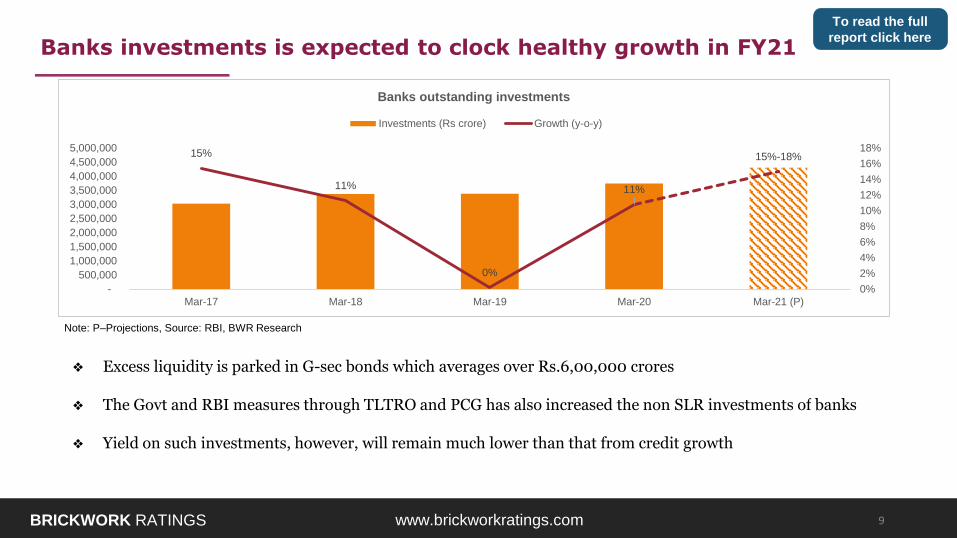

❖ Excess liquidity is parked in G-sec bonds which averages over Rs.6,00,000 crores

❖ The Govt and RBI measures through TLTRO and PCG has also increased the non SLR investments of banks

❖ Yield on such investments, however, will remain much lower than that from credit growth

BRICKWORK RATINGS www.brickworkratings.com

Banks investments is expected to clock healthy growth in FY21

15%

11%

0%

11%

15%-18%

0%

2%

4%

6%

8%

10%

12%

14%

16%

18%

-

500,000

1,000,000

1,500,000

2,000,000

2,500,000

3,000,000

3,500,000

4,000,000

4,500,000

5,000,000

Mar-17 Mar-18 Mar-19 Mar-20 Mar-21 (P)

Banks outstanding investments

Investments (Rs crore) Growth (y-o-y)

Note: P–Projections, Source: RBI, BWR Research

9

To read the full

report click here

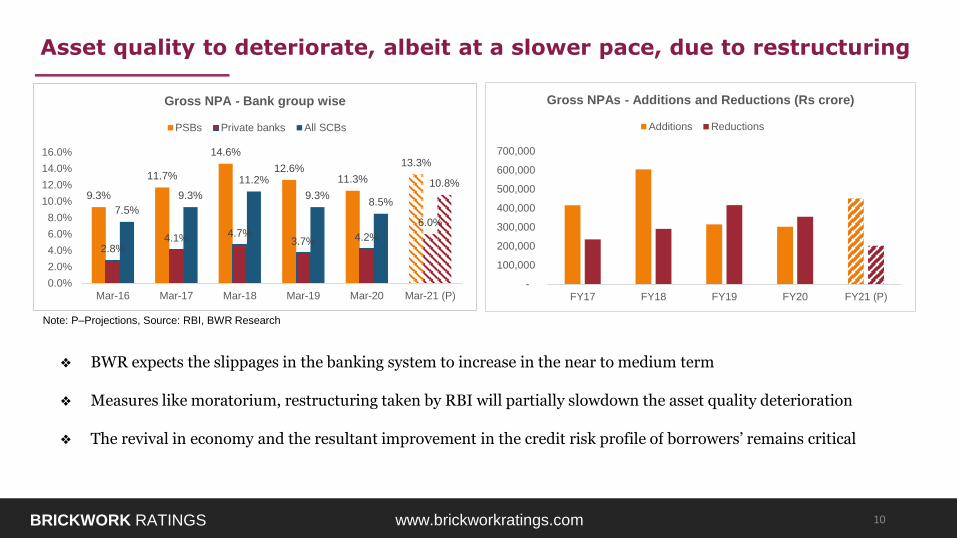

❖ BWR expects the slippages in the banking system to increase in the near to medium term

❖ Measures like moratorium, restructuring taken by RBI will partially slowdown the asset quality deterioration

❖ The revival in economy and the resultant improvement in the credit risk profile of borrowers’ remains critical

BRICKWORK RATINGS www.brickworkratings.com

Asset quality to deteriorate, albeit at a slower pace, due to restructuring

9.3%

11.7%

14.6%

12.6%11.3%

13.3%

2.8%4.1% 4.7%

3.7% 4.2%

6.0%7.5%

9.3%

11.2%

9.3%8.5%

10.8%

0.0%

2.0%

4.0%

6.0%

8.0%

10.0%

12.0%

14.0%

16.0%

Mar-16 Mar-17 Mar-18 Mar-19 Mar-20 Mar-21 (P)

Gross NPA - Bank group wise

PSBs Private banks All SCBs

Note: P–Projections, Source: RBI, BWR Research

-

100,000

200,000

300,000

400,000

500,000

600,000

700,000

FY17 FY18 FY19 FY20 FY21 (P)

Gross NPAs - Additions and Reductions (Rs crore)

Additions Reductions

10

BRICKWORK RATINGS www.brickworkratings.com

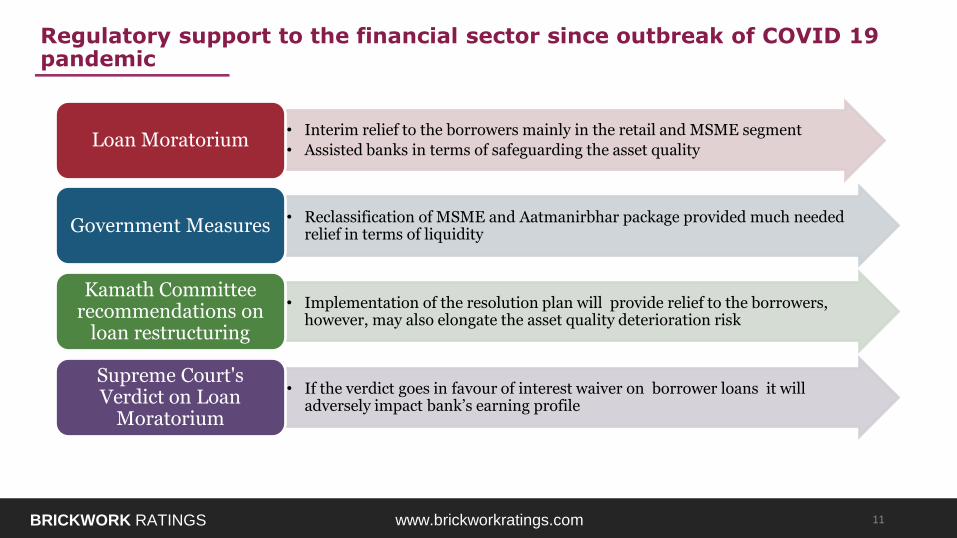

Regulatory support to the financial sector since outbreak of COVID 19 pandemic

• Interim relief to the borrowers mainly in the retail and MSME segment

• Assisted banks in terms of safeguarding the asset qualityLoan Moratorium

• Reclassification of MSME and Aatmanirbhar package provided much needed relief in terms of liquidityGovernment Measures

• Implementation of the resolution plan will provide relief to the borrowers, however, may also elongate the asset quality deterioration risk

Kamath Committee recommendations on

loan restructuring

• If the verdict goes in favour of interest waiver on borrower loans it will adversely impact bank’s earning profile

Supreme Court's Verdict on Loan

Moratorium

11

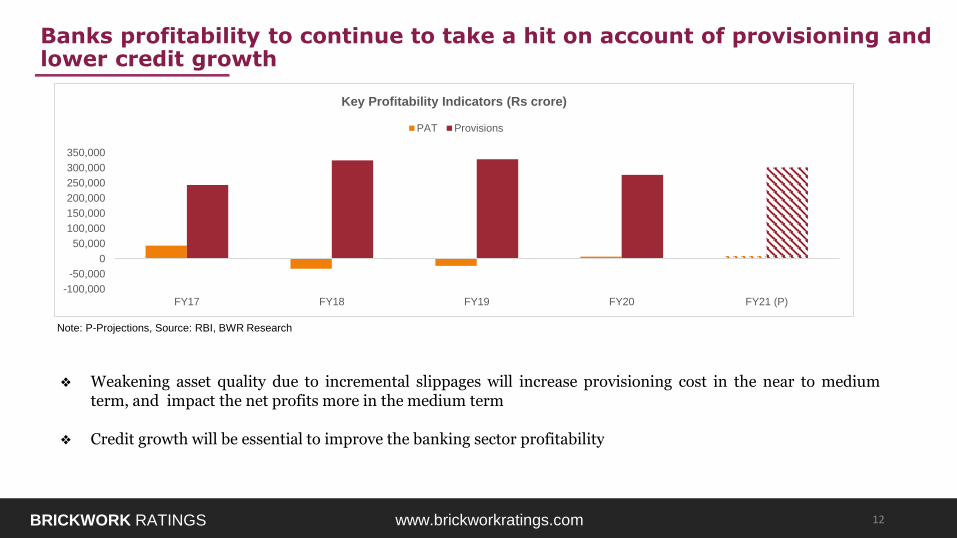

❖ Weakening asset quality due to incremental slippages will increase provisioning cost in the near to mediumterm, and impact the net profits more in the medium term

❖ Credit growth will be essential to improve the banking sector profitability

BRICKWORK RATINGS www.brickworkratings.com

Banks profitability to continue to take a hit on account of provisioning and lower credit growth

Note: P-Projections, Source: RBI, BWR Research

-100,000

-50,000

0

50,000

100,000

150,000

200,000

250,000

300,000

350,000

FY17 FY18 FY19 FY20 FY21 (P)

Key Profitability Indicators (Rs crore)

PAT Provisions

12

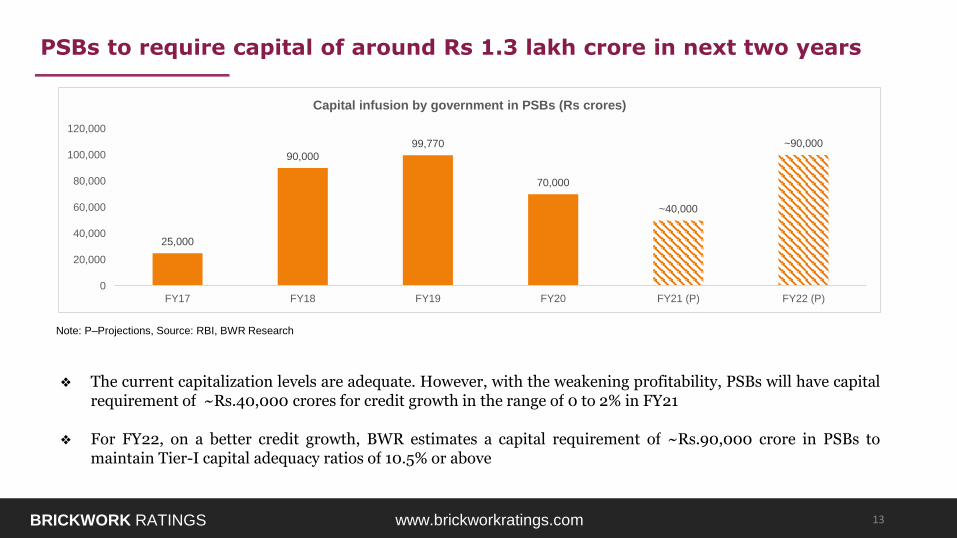

❖ The current capitalization levels are adequate. However, with the weakening profitability, PSBs will have capitalrequirement of ~Rs.40,000 crores for credit growth in the range of 0 to 2% in FY21

❖ For FY22, on a better credit growth, BWR estimates a capital requirement of ~Rs.90,000 crore in PSBs tomaintain Tier-I capital adequacy ratios of 10.5% or above

BRICKWORK RATINGS www.brickworkratings.com

PSBs to require capital of around Rs 1.3 lakh crore in next two years

Note: P–Projections, Source: RBI, BWR Research

25,000

90,000

99,770

70,000

~40,000

~90,000

0

20,000

40,000

60,000

80,000

100,000

120,000

FY17 FY18 FY19 FY20 FY21 (P) FY22 (P)

Capital infusion by government in PSBs (Rs crores)

13

Economic Trends

Banking Sector Trends

Emerging Trends

Brickwork Ratings

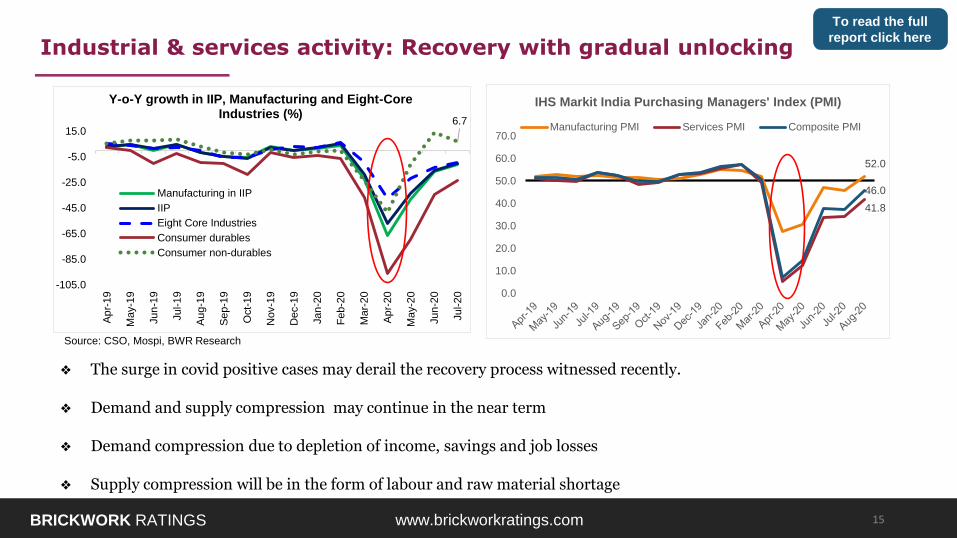

❖ The surge in covid positive cases may derail the recovery process witnessed recently.

❖ Demand and supply compression may continue in the near term

❖ Demand compression due to depletion of income, savings and job losses

❖ Supply compression will be in the form of labour and raw material shortage

BRICKWORK RATINGS www.brickworkratings.com

Industrial & services activity: Recovery with gradual unlocking

Source: CSO, Mospi, BWR Research

6.7

-105.0

-85.0

-65.0

-45.0

-25.0

-5.0

15.0

Ap

r-19

Ma

y-1

9

Jun

-19

Jul-1

9

Au

g-1

9

Se

p-1

9

Oct-

19

Nov-1

9

Dec-1

9

Jan

-20

Feb-2

0

Ma

r-20

Ap

r-20

Ma

y-2

0

Jun

-20

Jul-2

0

Y-o-Y growth in IIP, Manufacturing and Eight-CoreIndustries (%)

Manufacturing in IIP

IIP

Eight Core Industries

Consumer durables

Consumer non-durables

52.0

41.8

46.0

0.0

10.0

20.0

30.0

40.0

50.0

60.0

70.0

IHS Markit India Purchasing Managers' Index (PMI)

Manufacturing PMI Services PMI Composite PMI

15

To read the full

report click here

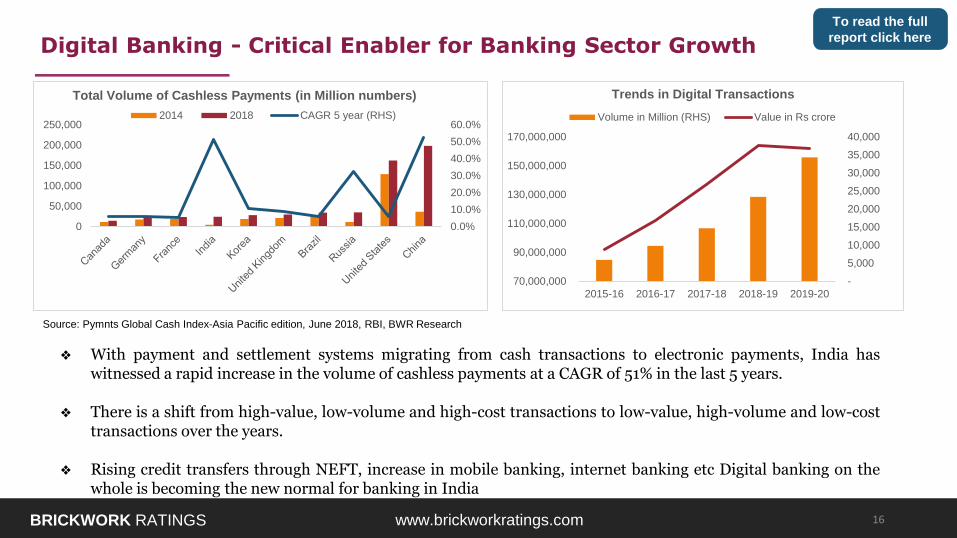

❖ With payment and settlement systems migrating from cash transactions to electronic payments, India haswitnessed a rapid increase in the volume of cashless payments at a CAGR of 51% in the last 5 years.

❖ There is a shift from high-value, low-volume and high-cost transactions to low-value, high-volume and low-costtransactions over the years.

❖ Rising credit transfers through NEFT, increase in mobile banking, internet banking etc Digital banking on thewhole is becoming the new normal for banking in India

BRICKWORK RATINGS www.brickworkratings.com

Digital Banking - Critical Enabler for Banking Sector Growth

Source: Pymnts Global Cash Index-Asia Pacific edition, June 2018, RBI, BWR Research

0.0%

10.0%

20.0%

30.0%

40.0%

50.0%

60.0%

0

50,000

100,000

150,000

200,000

250,000

Total Volume of Cashless Payments (in Million numbers)

2014 2018 CAGR 5 year (RHS)

-

5,000

10,000

15,000

20,000

25,000

30,000

35,000

40,000

70,000,000

90,000,000

110,000,000

130,000,000

150,000,000

170,000,000

2015-16 2016-17 2017-18 2018-19 2019-20

Trends in Digital Transactions

Volume in Million (RHS) Value in Rs crore

16

To read the full

report click here

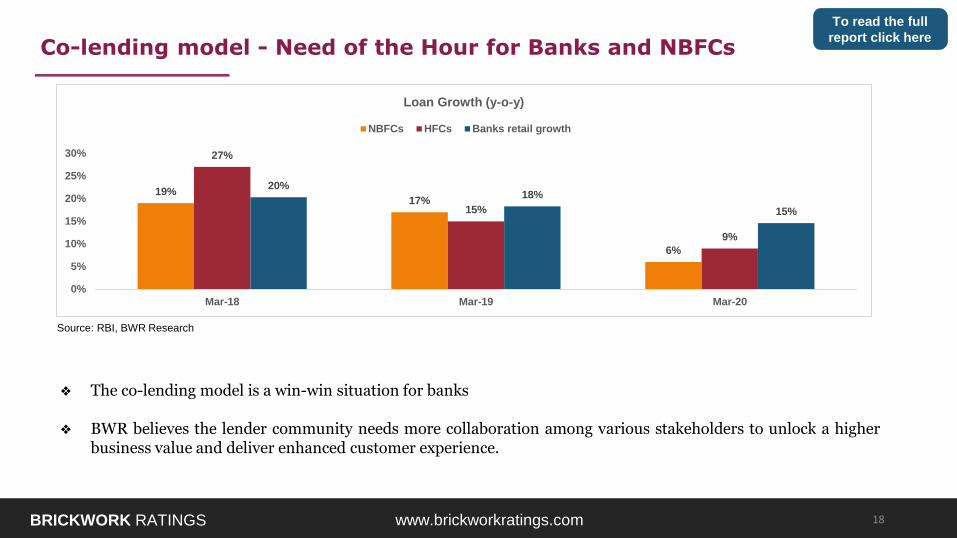

❖ The co-lending model is a win-win situation for banks

❖ BWR believes the lender community needs more collaboration among various stakeholders to unlock a higherbusiness value and deliver enhanced customer experience.

BRICKWORK RATINGS www.brickworkratings.com

Co-lending model - Need of the Hour for Banks and NBFCs

Source: RBI, BWR Research

19%17%

6%

27%

15%

9%

20%18%

15%

0%

5%

10%

15%

20%

25%

30%

Mar-18 Mar-19 Mar-20

Loan Growth (y-o-y)

NBFCs HFCs Banks retail growth

18

To read the full

report click here

BRICKWORK RATINGS www.brickworkratings.com

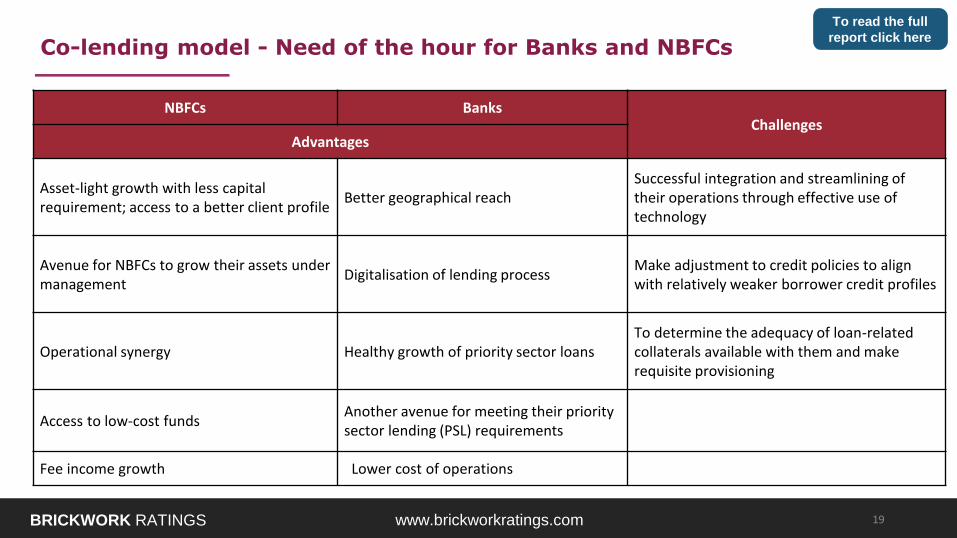

Co-lending model - Need of the hour for Banks and NBFCs

NBFCs BanksChallenges

Advantages

Asset-light growth with less capital requirement; access to a better client profile

Better geographical reachSuccessful integration and streamlining of their operations through effective use of technology

Avenue for NBFCs to grow their assets under management

Digitalisation of lending processMake adjustment to credit policies to align with relatively weaker borrower credit profiles

Operational synergy Healthy growth of priority sector loansTo determine the adequacy of loan-related collaterals available with them and make requisite provisioning

Access to low-cost fundsAnother avenue for meeting their priority sector lending (PSL) requirements

Fee income growth Lower cost of operations

19

To read the full

report click here

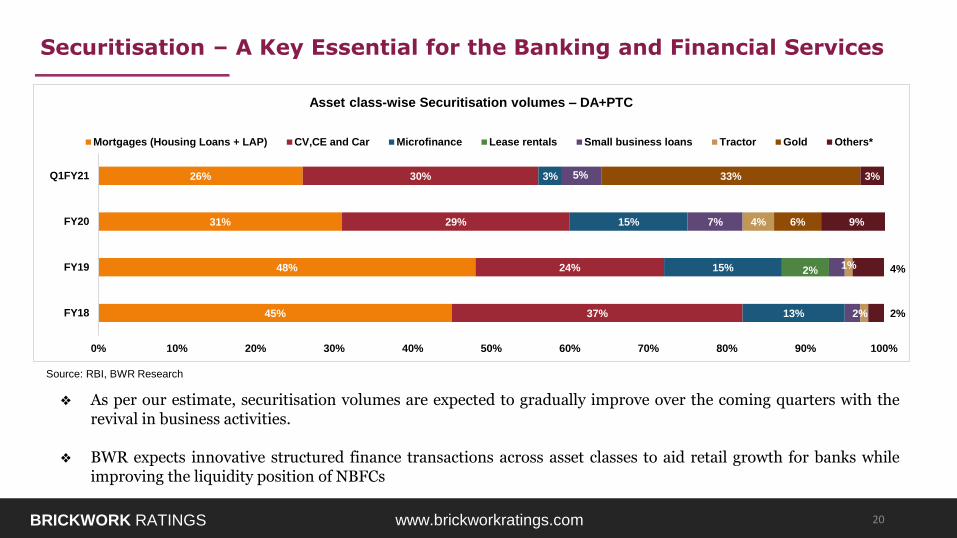

❖ As per our estimate, securitisation volumes are expected to gradually improve over the coming quarters with therevival in business activities.

❖ BWR expects innovative structured finance transactions across asset classes to aid retail growth for banks whileimproving the liquidity position of NBFCs

BRICKWORK RATINGS www.brickworkratings.com

Securitisation – A Key Essential for the Banking and Financial Services

Source: RBI, BWR Research

45%

48%

31%

26%

37%

24%

29%

30%

13%

15%

15%

3%

2%

2%

7%

5%

1%

4% 6%

33%

2%

4%

9%

3%

0% 10% 20% 30% 40% 50% 60% 70% 80% 90% 100%

FY18

FY19

FY20

Q1FY21

Asset class-wise Securitisation volumes – DA+PTC

Mortgages (Housing Loans + LAP) CV,CE and Car Microfinance Lease rentals Small business loans Tractor Gold Others*

20

❖ Economic activities likely to gain pace from the third quarter of FY 21

❖ Credit growth to remain subdued in FY 21, but may pick up in the next fiscal with pick up in economy

❖ Co-lending model expected to transform credit delivery in the times to come

❖ Digital banking is becoming the new normal in India and is a critical enabler for growth

BRICKWORK RATINGS www.brickworkratings.com

To Conclude…

21

To read the full

report click here

To read the full

report click here