Embed Size (px)

Citation preview

> Benetton Group2002 Annual Report

>Benetton G

roup 2002 Annual R

eport

Benetton Group S.p.A.Villa MinelliPonzano Veneto [Treviso] - ItalyShare Capital: Euro 236,026,454.30 fully paid-inTax ID/Treviso Company register: 00193320264

> Benetton Group2002 Annual Report

James Mollison photographs

Aqulmina and Mahjabina at the

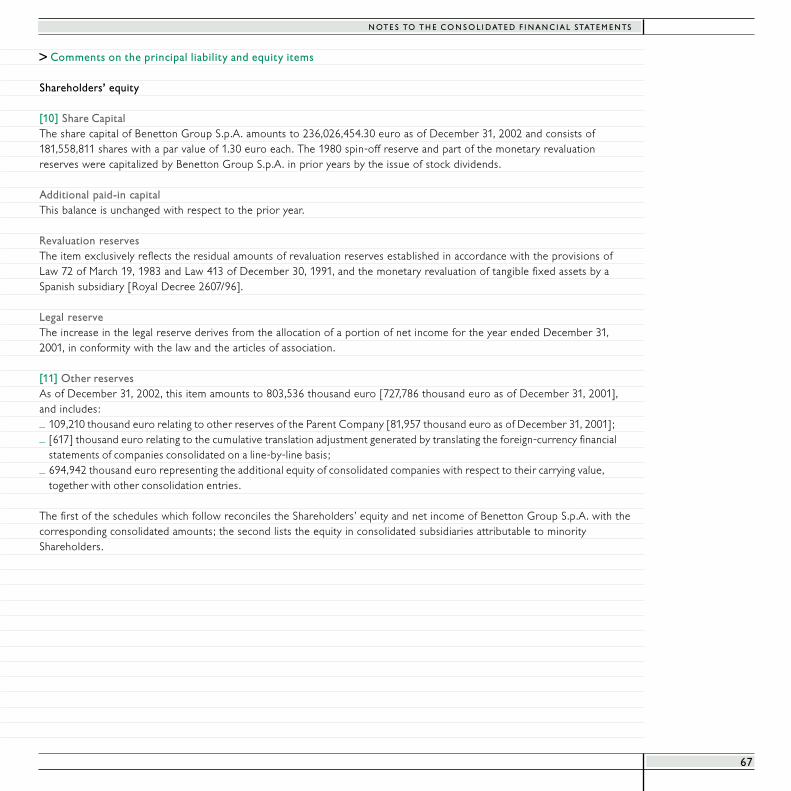

Pol-I-Charki Repatriation Camp

for returning Afghan refugees.

I N D E X

4

The Benetton Group

9 Directors and other officers

10 Letter to our Shareholders

13 Financial highlights

14 Directors’ report

Strategic focusBrands and marketsCapital expenditures

16 TechnologyCommunication

17 Supplementary informationSale of the Nordica, Rollerblade and Prince brandsFinancial managementTreasury shares

18 Performance of Benetton shares19 Ownership of the Company

20 Relations with the Parent Company and its subsidiariesCorporate Governance

25 DirectorsShares held by Directors and Statutory auditors

27 Principal organizational and corporate changesSignificant events since year-endOutlook for 2003

28 Group resultsConsolidated statement of income

31 Financial situation - highlights

5

I N D E X

35 Consolidated financial statements

36 Balance sheets reclassified according to financial criteria

38 Statements of income reclassified to cost of sales

40 Balance sheet - Assets

42 Balance sheet - Liabilities, Shareholders’ equity and Memorandum accounts

44 Statements of income

46 Statements of changes in Shareholders’ equity

47 Statements of changes in minority interests

48 Statements of cash flow

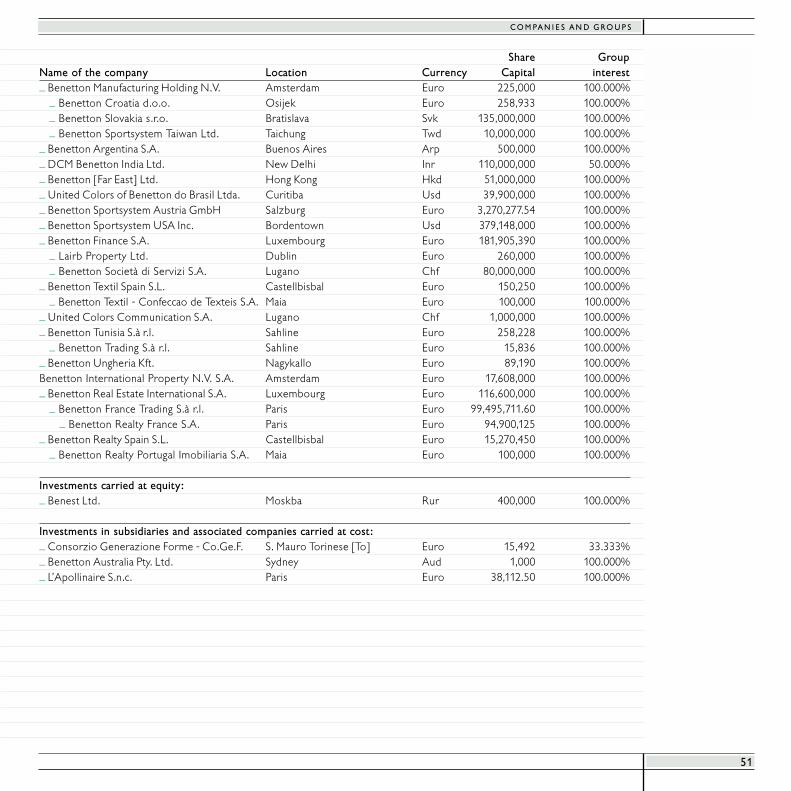

50 Companies and groups included within the consolidation area as of December 31, 2002

52 Notes to the consolidated financial statements

Activities of the GroupForm and content of the consolidated financial statements

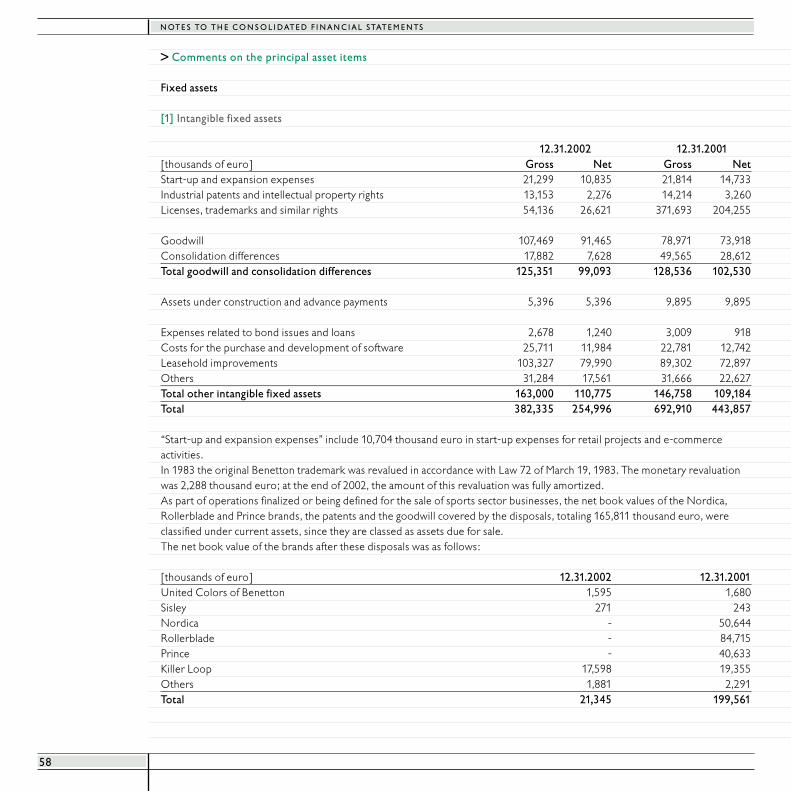

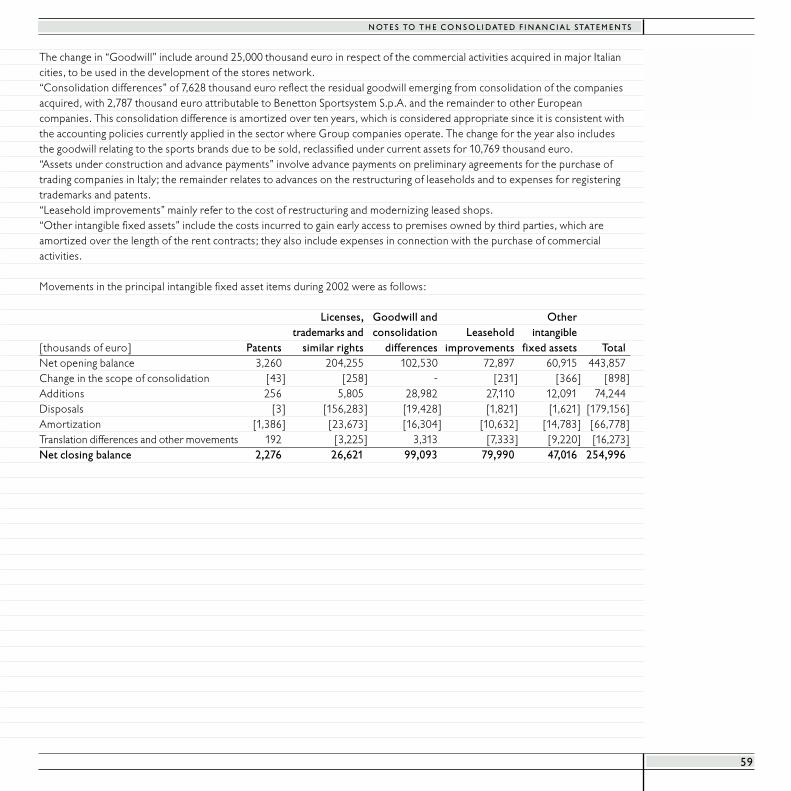

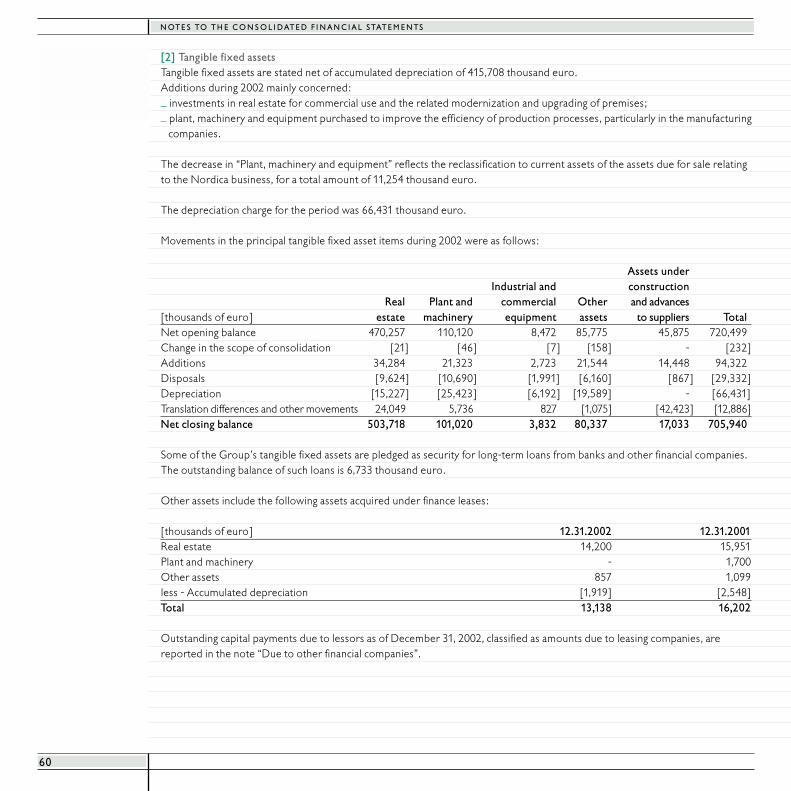

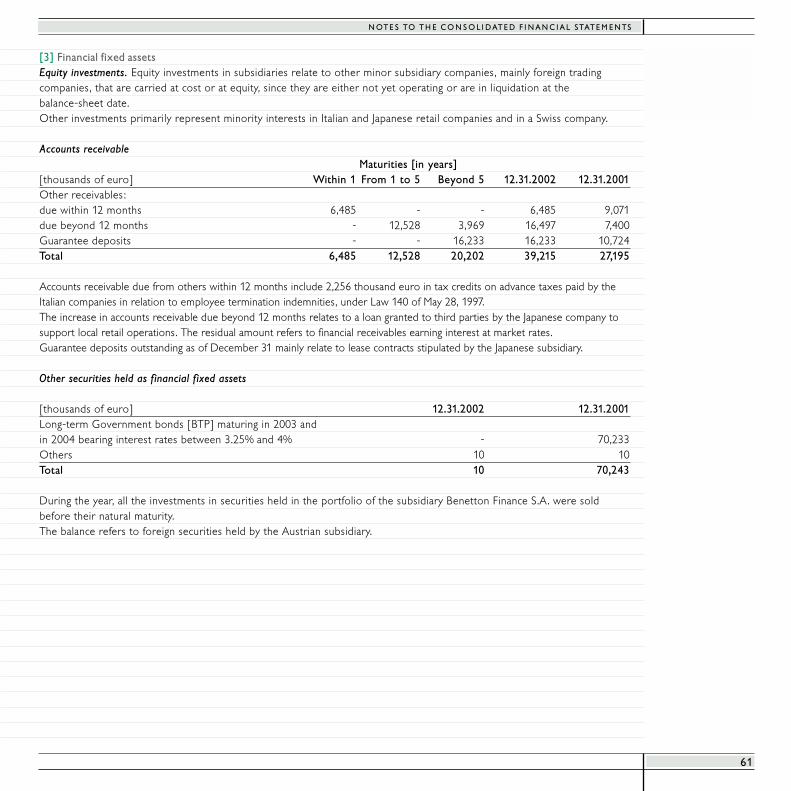

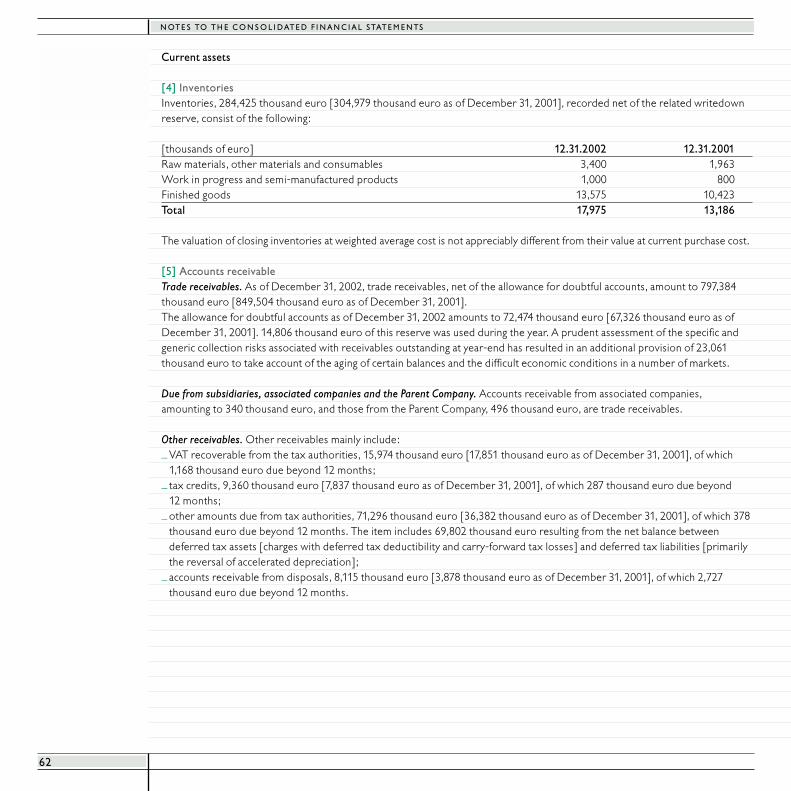

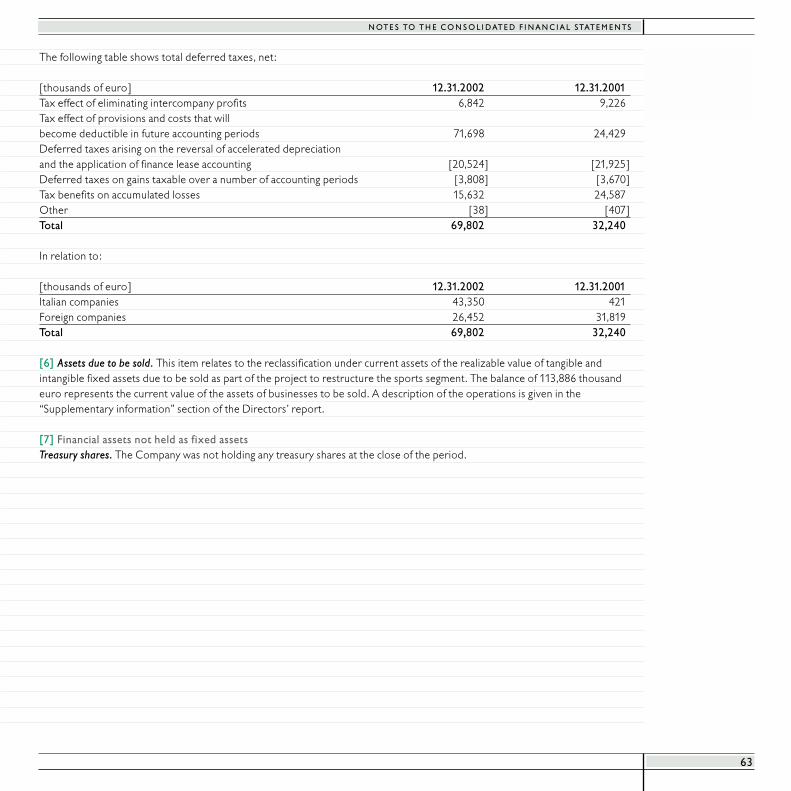

53 Principles of consolidation54 Accounting policies56 Supplementary information58 Comments on the principal asset items67 Comments on the principal liability and equity items74 Memorandum accounts75 Comments on the principal statement of income items

83 Independent Auditors’ report

Basmina is photographed at the Pol-I-Charki

Repatriation Camp for returning refugees

in Afghanistan.

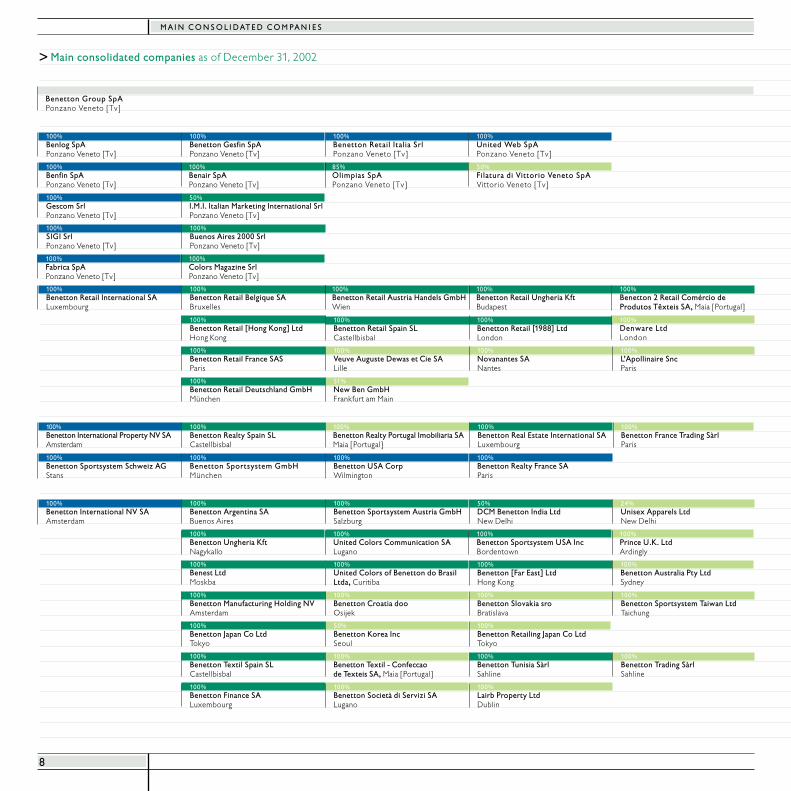

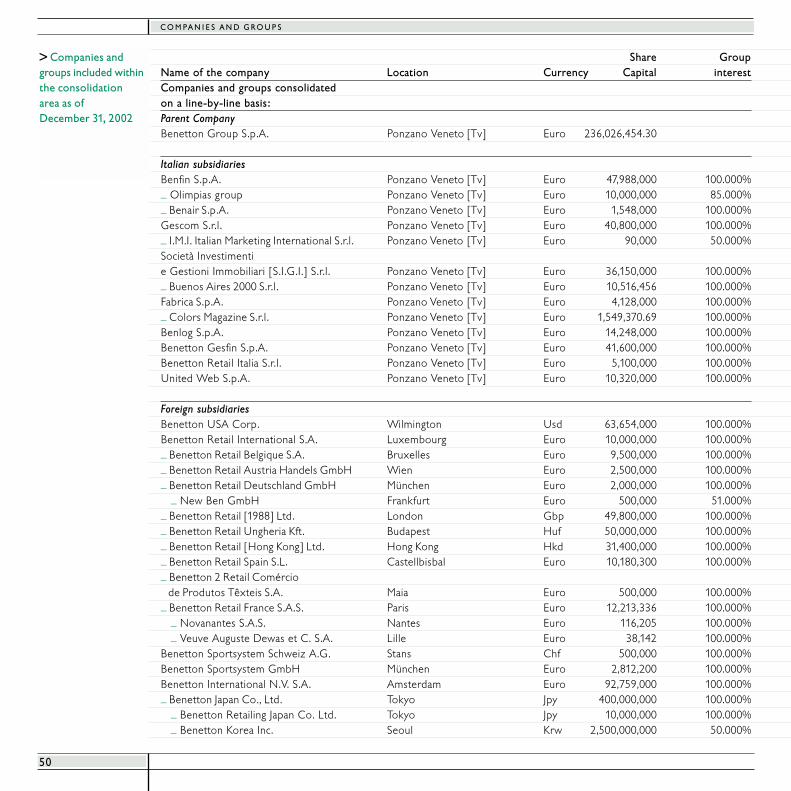

M A I N C O N S O L I D AT E D C O M PA N I E S

8

Benetton Group SpAPonzano Veneto [Tv]

100%Benlog SpAPonzano Veneto [Tv]

100%Colors Magazine SrlPonzano Veneto [Tv]

100%Benetton Retail Belgique SABruxelles

100%Benetton Sportsystem Schweiz AGStans

100% Benetton Croatia dooOsijek

100%United Colors of Benetton do BrasilLtda, Curitiba

100%Benetton Sportsystem GmbHMünchen

50%DCM Benetton India LtdNew Delhi

100%Benetton Textil Spain SLCastellbisbal

100% Benetton Textil - Confeccaode Texteis SA, Maia [Portugal]

100%Benetton [Far East] LtdHong Kong

100% Benetton Retail [1988] LtdLondon

100%Benetton Retail Austria Handels GmbHWien

100%Benetton Tunisia SàrlSahline

100%Benetton Trading SàrlSahline

100% Benetton Finance SALuxembourg

100%Lairb Property LtdDublin

100%Benetton USA CorpWilmington

100%Benetton Argentina SABuenos Aires

100% Benetton Sportsystem Austria GmbHSalzburg

100% Benetton Retail Deutschland GmbHMünchen

100%Benetton Manufacturing Holding NVAmsterdam

100% Benetton Japan Co LtdTokyo

100%Benetton Società di Servizi SA Lugano

100%Benair SpAPonzano Veneto [Tv]

100%Benetton Gesfin SpAPonzano Veneto [Tv]

100%Benetton Retail Italia SrlPonzano Veneto [Tv]

85%Olimpias SpAPonzano Veneto [Tv]

100%United Web SpAPonzano Veneto [Tv]

50%Filatura di Vittorio Veneto SpAVittorio Veneto [Tv]

100%Benfin SpAPonzano Veneto [Tv]

100%Fabrica SpAPonzano Veneto [Tv]

100%Benetton Retail International SALuxembourg

100%Benetton International NV SAAmsterdam

100% Benetton Slovakia sroBratislava

51% New Ben GmbHFrankfurt am Main

100% Denware LtdLondon

100%Benetton Australia Pty LtdSydney

50% Benetton Korea IncSeoul

100%Benetton Retailing Japan Co LtdTokyo

100%Gescom SrlPonzano Veneto [Tv]

50%I.M.I. Italian Marketing International SrlPonzano Veneto [Tv]

100% Benetton Retail Ungheria KftBudapest

100%Benetton Retail France SASParis

100% Veuve Auguste Dewas et Cie SALille

100% Novanantes SANantes

100% L’Apollinaire SncParis

100% Benetton 2 Retail Comércio deProdutos Têxteis SA, Maia [Portugal]

100%Benetton Sportsystem Taiwan LtdTaichung

100%Benest LtdMoskba

100%Benetton International Property NV SAAmsterdam

100%Benetton Realty Spain SLCastellbisbal

100%Benetton Realty Portugal Imobiliaria SAMaia [Portugal]

24%Unisex Apparels LtdNew Delhi

100%Buenos Aires 2000 SrlPonzano Veneto [Tv]

100%SIGI SrlPonzano Veneto [Tv]

> Main consolidated companies as of December 31, 2002

100% Benetton Retail [Hong Kong] LtdHong Kong

100% Benetton Retail Spain SLCastellbisbal

100%Benetton Realty France SAParis

100%Benetton Real Estate International SALuxembourg

100%Benetton France Trading SàrlParis

100%Benetton Ungheria KftNagykallo

100%Benetton Sportsystem USA IncBordentown

100%United Colors Communication SA Lugano

100%Prince U.K. LtdArdingly

9

S O M M A R I O

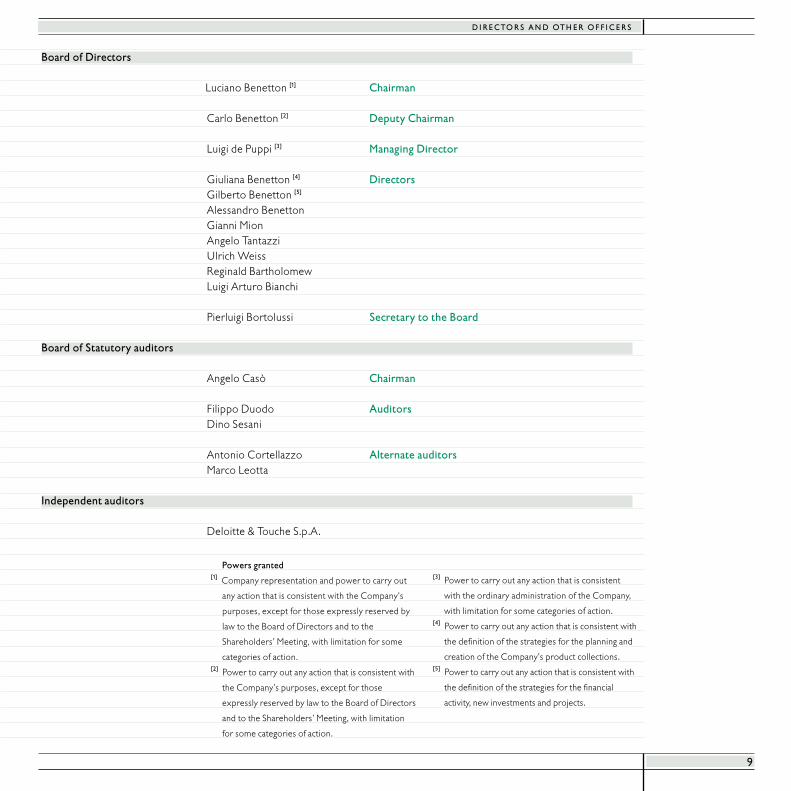

Board of Directors

Luciano Benetton [1] Chairman

Carlo Benetton [2] Deputy Chairman

Luigi de Puppi [3] Managing Director

Giuliana Benetton [4] DirectorsGilberto Benetton [5]

Alessandro BenettonGianni MionAngelo TantazziUlrich WeissReginald BartholomewLuigi Arturo Bianchi

Pierluigi Bortolussi Secretary to the Board

Board of Statutory auditors

Angelo Casò Chairman

Filippo Duodo AuditorsDino Sesani

Antonio Cortellazzo Alternate auditorsMarco Leotta

Independent auditors

Deloitte & Touche S.p.A.

D I R E C TO R S A N D OT H E R O F F I C E R S

Powers granted[1] Company representation and power to carry out

any action that is consistent with the Company’s

purposes, except for those expressly reserved by

law to the Board of Directors and to the

Shareholders’ Meeting, with limitation for some

categories of action.[2] Power to carry out any action that is consistent with

the Company’s purposes, except for those

expressly reserved by law to the Board of Directors

and to the Shareholders’ Meeting, with limitation

for some categories of action.

[3] Power to carry out any action that is consistent

with the ordinary administration of the Company,

with limitation for some categories of action.[4] Power to carry out any action that is consistent with

the definition of the strategies for the planning and

creation of the Company’s product collections.[5] Power to carry out any action that is consistent with

the definition of the strategies for the financial

activity, new investments and projects.

L ET T E R TO O U R S H A R E H O L D E R S

10

> Letter to our Shareholders

Dear Shareholders,

The Benetton Group decided to make a break with the past in 2002 by ending its experience in the sports equipment business, whoseresults over the years had failed to provide the same level of satisfaction as the casual sector. The program for the division’s disposal wasstarted during the year and completed in the early part of 2003.

With regard to the core business of clothing, our system confirms its ability to be competitive and generate value: although net income for2002 was affected by extraordinary items deriving mostly from the sale of the sports sector, this did not harm Shareholders’ returns.

We have spent the past two years on gradually improving our organizational structure. As regards distribution, we are investing in thenetwork in partnership with over 2,000 distributors: we are rapidly expanding our flagship stores, while also concentrating on transformingour traditional retail outlets from small to medium-size.

The fact that we can rely on the energy of such a large group of entrepreneurs, ready to invest with increasing commitment in our brand,confirms the validity of our business model, where innovation, hi-tech and system speed are the basis of our philosophy.

I would like to emphasize the business’s firm commitment, unique among its major international competitors, to maintain productionmainly in Italy and Europe. This is a demonstration of excellence, which focuses on those values of design and quality, greatly appreciated bythe ever more complex and sophisticated needs of the global market.

It is superfluous to dwell on the international crisis and the gloomy outlook for markets and consumption. However, I should like toemphasize our vigorous determination in dealing with this situation: in fact, I have always said that it is during times of greatest difficulty thatthose who are most prepared are able to grasp the best opportunities.

Luciano BenettonChairman Benetton Group

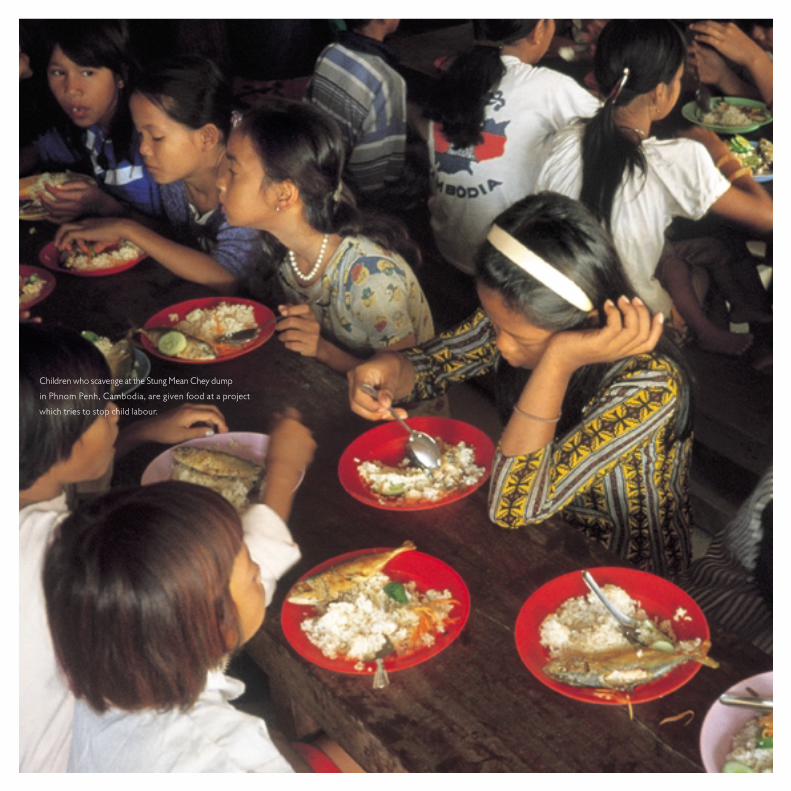

Children who scavenge at the Stung Mean Chey dump

in Phnom Penh, Cambodia, are given food at a project

which tries to stop child labour.

F I N A N C I A L H I G H L I G H TS

12

> 2002 revenuesby activity [%]

> 2002 revenuesby geographicalarea [%]

> Net revenues [millions of euro]

> Total capitalexpenditures andself-financing [millions of euro]

casualwear 79.6%

sportswear and equipment 14.2%

manufacturing and other 6.2%

euro area 68.9%

asia 8.9%

the americas 9.6%

other 12.6%

2002

2001

2000

1999

1998

1,992

2,098

2,018

1,982

1,980

net revenues

312

311

191

375

266

332

374

311

349

170

total capital expenditures

self-financing

1998

1999

2000

2001

2002

13

F I N A N C I A L H I G H L I G H TS

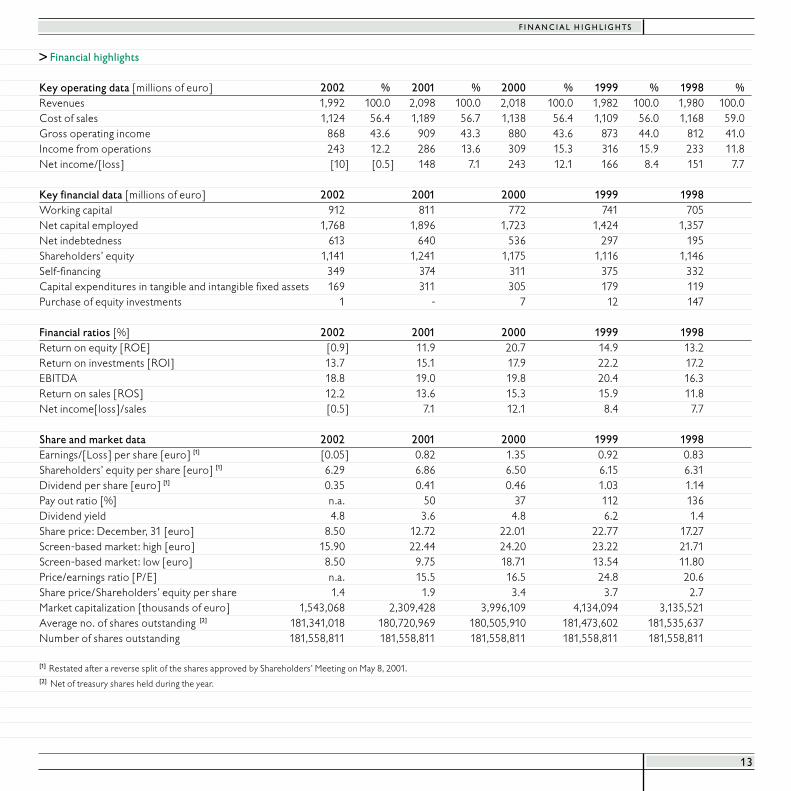

> Financial highlights

Key operating data [millions of euro] 2002 % 2001 % 2000 % 1999 % 1998 %Revenues 1,992 100.0 2,098 100.0 2,018 100.0 1,982 100.0 1,980 100.0Cost of sales 1,124 56.4 1,189 56.7 1,138 56.4 1,109 56.0 1,168 59.0Gross operating income 868 43.6 909 43.3 880 43.6 873 44.0 812 41.0Income from operations 243 12.2 286 13.6 309 15.3 316 15.9 233 11.8Net income/[loss] [10] [0.5] 148 7.1 243 12.1 166 8.4 151 7.7

Key financial data [millions of euro] 2002 2001 2000 1999 1998Working capital 912 811 772 741 705Net capital employed 1,768 1,896 1,723 1,424 1,357Net indebtedness 613 640 536 297 195Shareholders’ equity 1,141 1,241 1,175 1,116 1,146Self-financing 349 374 311 375 332Capital expenditures in tangible and intangible fixed assets 169 311 305 179 119Purchase of equity investments 1 - 7 12 147

Financial ratios [%] 2002 2001 2000 1999 1998Return on equity [ROE] [0.9] 11.9 20.7 14.9 13.2Return on investments [ROI] 13.7 15.1 17.9 22.2 17.2EBITDA 18.8 19.0 19.8 20.4 16.3Return on sales [ROS] 12.2 13.6 15.3 15.9 11.8Net income[loss]/sales [0.5] 7.1 12.1 8.4 7.7

Share and market data 2002 2001 2000 1999 1998Earnings/[Loss] per share [euro] [1] [0.05] 0.82 1.35 0.92 0.83Shareholders’ equity per share [euro] [1] 6.29 6.86 6.50 6.15 6.31Dividend per share [euro] [1] 0.35 0.41 0.46 1.03 1.14Pay out ratio [%] n.a. 50 37 112 136Dividend yield 4.8 3.6 4.8 6.2 1.4Share price: December, 31 [euro] 8.50 12.72 22.01 22.77 17.27Screen-based market: high [euro] 15.90 22.44 24.20 23.22 21.71Screen-based market: low [euro] 8.50 9.75 18.71 13.54 11.80Price/earnings ratio [P/E] n.a. 15.5 16.5 24.8 20.6Share price/Shareholders’ equity per share 1.4 1.9 3.4 3.7 2.7Market capitalization [thousands of euro] 1,543,068 2,309,428 3,996,109 4,134,094 3,135,521Average no. of shares outstanding [2] 181,341,018 180,720,969 180,505,910 181,473,602 181,535,637Number of shares outstanding 181,558,811 181,558,811 181,558,811 181,558,811 181,558,811

[1] Restated after a reverse split of the shares approved by Shareholders’ Meeting on May 8, 2001.[2] Net of treasury shares held during the year.

D I R E C TO R S ’ R E P O RT

14

> Directors’ report

Strategic focusIn 2002 the strategic decision to focus Benetton’s activity on the core business of casual clothing and sportswear resulted in anextensive reorganization of the sports equipment division, with the objective of bringing the Nordica, Prince and Rollerbladebrands to a substantial break-even and starting a program for their disposal, duly completed in the early part of 2003. The new policy also involves strengthening the management team, to which all operational responsibilities will be delegated.In numerical terms, the steep decrease in turnover in the sports sector hurt the Group’s overall performance: total sales in 2002amounted to approximately 2.0 billion euro, down from 2.1 billion in 2001. The program for the disposal of the sports equipment business resulted in the booking of extraordinary and non-recurringcosts. While these had a limited impact on financial flows, they were the main reason for the small loss for the year of some 10million euro.

Brands and marketsThe main objective for all the Group’s brands in 2002 was the consolidation of a “made in Europe” standard of quality. This wasbased on typically Italian style, passion and creativity, without competing solely on the basis of costs.Moreover, the commitment to operational planning and stylistic design of collections made it possible to react with increasingspeed to market requirements, and to give each brand an even stronger and more distinctive identity. United Colors of Benetton reasserted its global yet “inclusive” brand image, supported by a unique, strong and recognizablemessage, which consistently focuses on a humane concept of the world, excluding nothing and no-one.Sisley chose to emphasize its fashionable but very price-competitive nature, partly thanks to a high-impact advertising message,where glamour and intelligent provocation skillfully intermingle. In the sports clothing business, Playlife and Killer Loop primarily focused on consolidating the network of single-brand stores and on enhancing their presence in European specialized chains. There was a rapid expansion in the worldwide network of flagship megastores, which represent the best international showcasefor the Benetton style and benefit its image throughout the network: at the end of 2002 there were 150 megastores locatedacross the world. In particular, we continued consolidating the Group’s presence in strategic commercial areas, like Europe and Japan, andinvesting in developing markets such as those in Eastern Europe, or those with future potential such as China, where Shanghai,its most modern and elegant city, was chosen as the location for the first Benetton megastore in this country. In collaboration with the network of 2,000 manager-partners, the program also went ahead to transform the traditional retailoutlets, both as regards a shift from small to medium-size stores, and in terms of service quality, design and atmosphere.As for licenses, the objective for the year was to focus on adding new product corners under license, within the megastores, and to make new agreements for completing the Benetton total look. We particularly mention the agreements with Sector[watches], Marazzi [ceramics] and Sara Lee [hosiery].

Capital expendituresTotal capital expenditures made during the year came to approximately 170 million euro, including miscellaneous purchases[mainly of software and concessions, licenses and brands]. The Group spent around 120 million euro on the acquisition of commercial enterprises and buildings, and on upgrades andimprovements to sales space. This was in addition to the approximately 610 million euro invested in previous years and includes,among others, the acquisition of the following premises: Bilbao [Spain], Boulevard Haussmann and Champs-Elysées [France],Siena and Caltanissetta [Italy]. Technological renewal and upgrades involved operational and production investments amounting to some 30 million euro,which were spent on improving operations and production by the manufacturing facilities in Italy and abroad.

15

S O M M A R I OD I R E C TO R S ’ R E P O RT

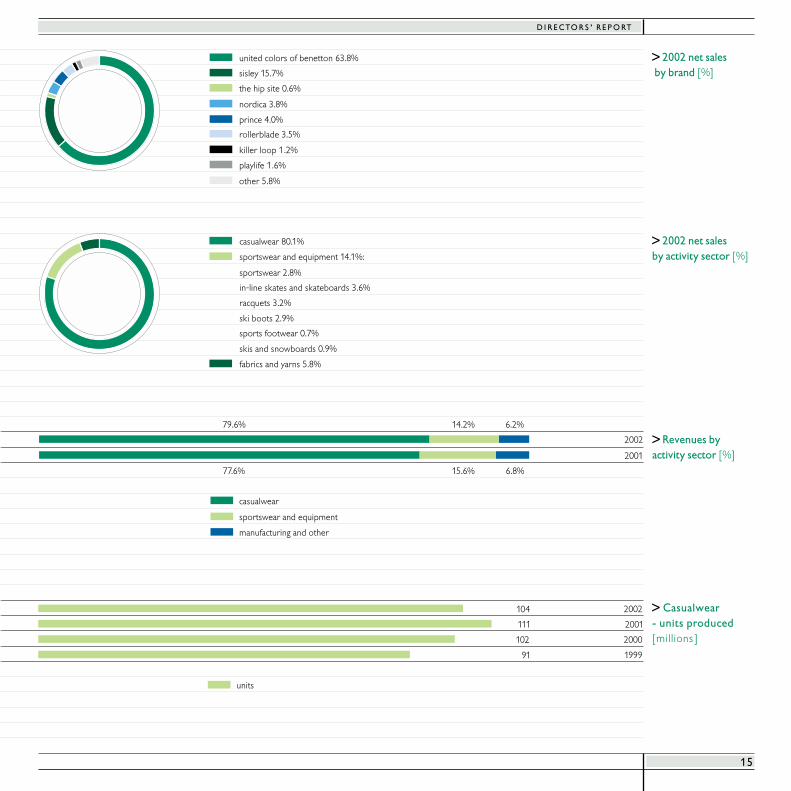

> 2002 net salesby brand [%]

> 2002 net sales by activity sector [%]

> Revenues by activity sector [%]

> Casualwear - units produced [millions]

casualwear 80.1%

sportswear and equipment 14.1%:

sportswear 2.8%

in-line skates and skateboards 3.6%

racquets 3.2%

ski boots 2.9%

sports footwear 0.7%

skis and snowboards 0.9%

fabrics and yarns 5.8%

united colors of benetton 63.8%

sisley 15.7%

the hip site 0.6%

nordica 3.8%

prince 4.0%

rollerblade 3.5%

killer loop 1.2%

playlife 1.6%

other 5.8%

2002

2001

casualwear

79.6% 14.2% 6.2%

77.6% 15.6% 6.8%

sportswear and equipment

manufacturing and other

91

102

111

104

units

1999

2000

2002

2001

D I R E C TO R S ’ R E P O RTO M M A R I O

16

Technology The Benetton Group was able to strengthen its organizational structure during 2002 thanks to the transformation of its networksystem into an improved, original “network of networks” model. This system consists of production, commercial, logistics and supply networks, all of which are in constant communication withone another. A three-year technological and organizational innovation project was started during the year for the purposes ofmanaging this system. This will involve integrating company computer systems to improve the speed and quality of the entirestructure, accompanied by reduced complexity and costs. The SAP system, first introduced in the finance area and gradually extended to the commercial, production and logistics sectors,will enable a high level of centralized control, a streamlining of information flows, a drastic reduction in the “time-to-the-market”and improved management efficiency and effectiveness in the clothing business.With regard to production, the Castrette center coordinates a series of other manufacturing clusters in Europe, which, in turn,manage networks of qualified local partners. This is a unique system which, during a time of globalization, guarantees consistencyof quality at European level, as well as benefiting related businesses and the local economies. This also involved enhancing the level of integration of certain manufacturing divisions, with a view to improving management ofexternal partners who supply fabrics and raw materials.The logistics network, in turn, saw completion of the first phase in the upgrade of the Castrette distribution center. This involvedimplementing technology aimed at supporting the new requirements for integration, flexibility, capacity and rapid productdelivery to customers.

CommunicationThe 2002 Oscar awarded to Danis Tanovic’s No Man’s Land for best foreign film, gained prestigious international recognition forthe work of Fabrica. During the month of September, to mark the first anniversary of the attack on the World Trade Center, Fabrica and ColorsMagazine [which celebrates its 10th anniversary] organized the Visions of Hope Exhibition in New York involving portraits ofpersons from all over the world who, with their eyes closed, express their idea of hope for the future. During the second half of the year, Fabrica formulated a global communications plan dedicated to food. The project, which waslaunched at the beginning of 2003, comprised three main initiatives: a global communications campaign on hunger incollaboration with the World Food Programme, a special edition of Colors and a book edited by Electa on the anthropologicaland artistic aspects of food.

17

S O M M A R I O

Supplementary information

Sale of the Nordica, Rollerblade and Prince brands. The decision to sell the sports equipment business forms part of thestrategy of focusing activities on the core business of clothing. In January 2003 the Benetton Group reached an agreement withthe Tecnica group for the sale of business activities relating to the Nordica brand. The sale became effective as from February 1,2003. The overall price for the transaction was calculated based on the valuation of all business components, such as for exampleexisting plant, machinery and inventory as of January 31, 2003. The value of the intellectual property alone, including the Nordicatrademark, was set at 38 million euro. Under this agreement, Benetton Group S.p.A. acquires 10% of Tecnica S.p.A.’s sharecapital with a guaranteed put [sale] option to be exercised as from February 1, 2008 and a call option for repurchase by TecnicaS.p.A. to be exercised between February 1, 2006 and January 31, 2008. This acquisition is valued at around 15 million euro.In March 2003, the Benetton Group, through the American company Benetton Sportsystem USA Inc., signed a bindingpreliminary agreement for the sale of the Rollerblade brand to Prime Newco, a member of the Tecnica group, the purchaser of the Nordica brand. The price established for the Rollerblade brand alone amounted to 20 million euro, payable uponcompletion of the sale, scheduled for May 31, 2003. On this date, subject to separate valuation, other components of thebusiness and the entire interest in the Swiss subsidiary, Benetton Sportsystem Schweiz A.G., will also be transferred. Asadditional consideration with regard to the transfer of know-how, the Group will receive 1.5% of the Rollerblade brand sales forthe next five years, with a minimum guaranteed payment of 5 million euro; the Group is entitled to the operating profit for thefirst five months of 2003.At the end of March the Group also formalized the sale of the Prince and Ektelon brands to Lincolnshire Management Inc., a U.S.private equity fund with existing interests in the sports equipment sector through its investment in Riddel Sport Group Inc. The price established for the sale of the Prince and Ektelon brands and the associated intangible fixed assets will amount to 36.5million euro, to be paid in two installments of 26.5 million euro [generating interest] in January 2004 and 10 million euro uponcompletion of the sale scheduled for April 30, 2003, at which time the other components, subject to separate valuation, will betransferred at book value. This agreement completes the Benetton Group’s departure from the sports equipment sector.Net sales, costs and the operating loss for 2002, relating to the sports equipment business being sold, amounted to 228, 260 and 32 million euro respectively. The corresponding figures for 2001 amounted to 252, 304 and 52 million euro respectively.

Financial management. The Group has always been attentive to trends in the financial markets, especially of interest andexchange rates. It handles financial risks by constantly monitoring its exchange and interest rate positions, which it actively manages in keepingwith budget objectives. In the interests of maintaining a healthy balance between bank loans and bond exposure, on July 26, 2002, Benetton GroupS.p.A. issued a floating-rate, 300 million euro bond with a three-year maturity. Organized by Caboto IntesaBci, MCC S.p.A.,Mediobanca S.p.A. and Schroder Salomon Smith Barney, the operation featured an issue price of 99.857 and a coupon payingthree-month Euribor plus 0.5%.

Treasury shares. During the first six months of 2002, Benetton Group S.p.A. sold at an average price of 13.887 euro all the1,594,650 shares that it had acquired in 2001 for a total of 22.8 million euro [average purchase price of 14.305 euro per share]. During the second half of the year, the Company purchased 154,953 shares at an average price of 10.388 euro for a total amountof 1.6 million euro; all the shares were later sold at an average price of 10.422 euro.During the period, Benetton Group S.p.A. neither bought nor sold any shares or quotas in parent companies, either directly orindirectly or through subsidiaries, trustees or other intermediaries.

D I R E C TO R S ’ R E P O RT

D I R E C TO R S ’ R E P O RT

18

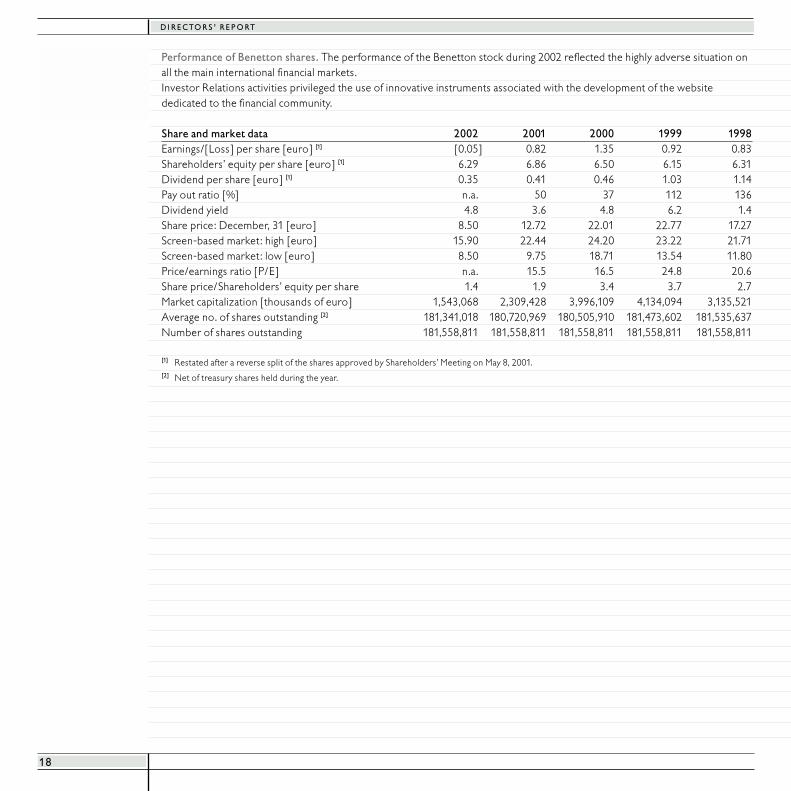

Performance of Benetton shares. The performance of the Benetton stock during 2002 reflected the highly adverse situation onall the main international financial markets. Investor Relations activities privileged the use of innovative instruments associated with the development of the websitededicated to the financial community.

Share and market data 2002 2001 2000 1999 1998Earnings/[Loss] per share [euro] [1] [0.05] 0.82 1.35 0.92 0.83Shareholders’ equity per share [euro] [1] 6.29 6.86 6.50 6.15 6.31Dividend per share [euro] [1] 0.35 0.41 0.46 1.03 1.14Pay out ratio [%] n.a. 50 37 112 136Dividend yield 4.8 3.6 4.8 6.2 1.4Share price: December, 31 [euro] 8.50 12.72 22.01 22.77 17.27Screen-based market: high [euro] 15.90 22.44 24.20 23.22 21.71Screen-based market: low [euro] 8.50 9.75 18.71 13.54 11.80Price/earnings ratio [P/E] n.a. 15.5 16.5 24.8 20.6Share price/Shareholders’ equity per share 1.4 1.9 3.4 3.7 2.7Market capitalization [thousands of euro] 1,543,068 2,309,428 3,996,109 4,134,094 3,135,521Average no. of shares outstanding [2] 181,341,018 180,720,969 180,505,910 181,473,602 181,535,637Number of shares outstanding 181,558,811 181,558,811 181,558,811 181,558,811 181,558,811

[1] Restated after a reverse split of the shares approved by Shareholders’ Meeting on May 8, 2001.[2] Net of treasury shares held during the year.

19

D I R E C TO R S ’ R E P O RT

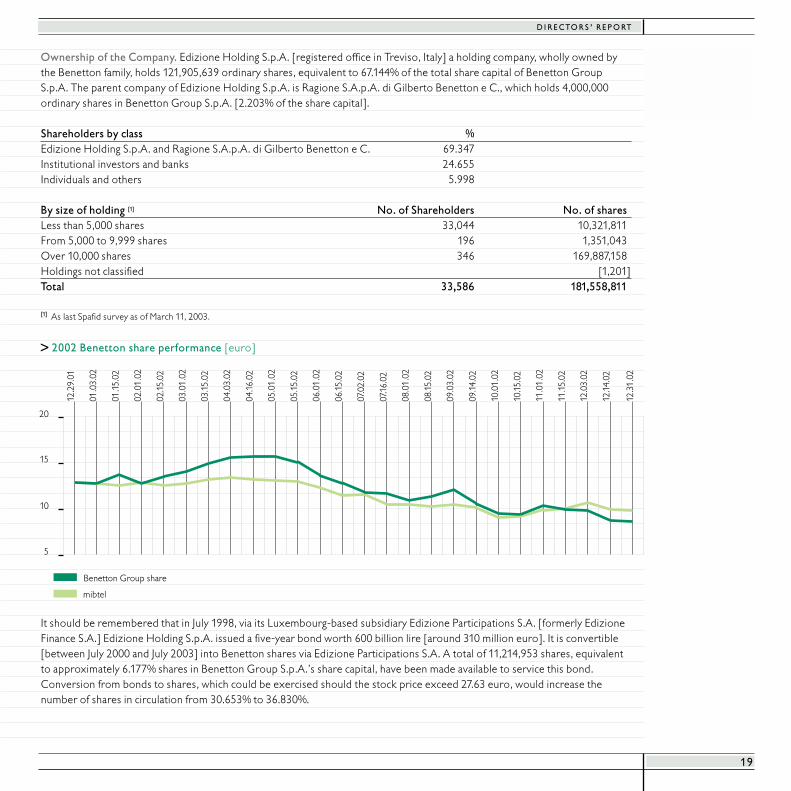

Ownership of the Company. Edizione Holding S.p.A. [registered office in Treviso, Italy] a holding company, wholly owned bythe Benetton family, holds 121,905,639 ordinary shares, equivalent to 67.144% of the total share capital of Benetton GroupS.p.A. The parent company of Edizione Holding S.p.A. is Ragione S.A.p.A. di Gilberto Benetton e C., which holds 4,000,000ordinary shares in Benetton Group S.p.A. [2.203% of the share capital].

Shareholders by class %Edizione Holding S.p.A. and Ragione S.A.p.A. di Gilberto Benetton e C. 69.347Institutional investors and banks 24.655Individuals and others 5.998

By size of holding [1] No. of Shareholders No. of sharesLess than 5,000 shares 33,044 10,321,811From 5,000 to 9,999 shares 196 1,351,043Over 10,000 shares 346 169,887,158Holdings not classified [1,201]Total 33,586 181,558,811

[1] As last Spafid survey as of March 11, 2003.

> 2002 Benetton share performance [euro]

It should be remembered that in July 1998, via its Luxembourg-based subsidiary Edizione Participations S.A. [formerly EdizioneFinance S.A.] Edizione Holding S.p.A. issued a five-year bond worth 600 billion lire [around 310 million euro]. It is convertible[between July 2000 and July 2003] into Benetton shares via Edizione Participations S.A. A total of 11,214,953 shares, equivalentto approximately 6.177% shares in Benetton Group S.p.A.’s share capital, have been made available to service this bond.Conversion from bonds to shares, which could be exercised should the stock price exceed 27.63 euro, would increase thenumber of shares in circulation from 30.653% to 36.830%.

5

10

15

20

Benetton Group share

12.2

9.01

01.0

3.02

mibtel

01.1

5.02

02.0

1.02

02.1

5.02

03.0

1.02

03.1

5.02

04.0

3.02

04.1

6.02

05.0

1.02

05.1

5.02

06.0

1.02

06.1

5.02

07.0

2.02

07.1

6.02

08.0

1.02

08.1

5.02

09.0

3.02

09.1

4.02

10.0

1.02

10.1

5.02

11.0

1.02

11.1

5.02

12.0

3.02

12.1

4.02

12.3

1.02

D I R E C TO R S ’ R E P O RT

20

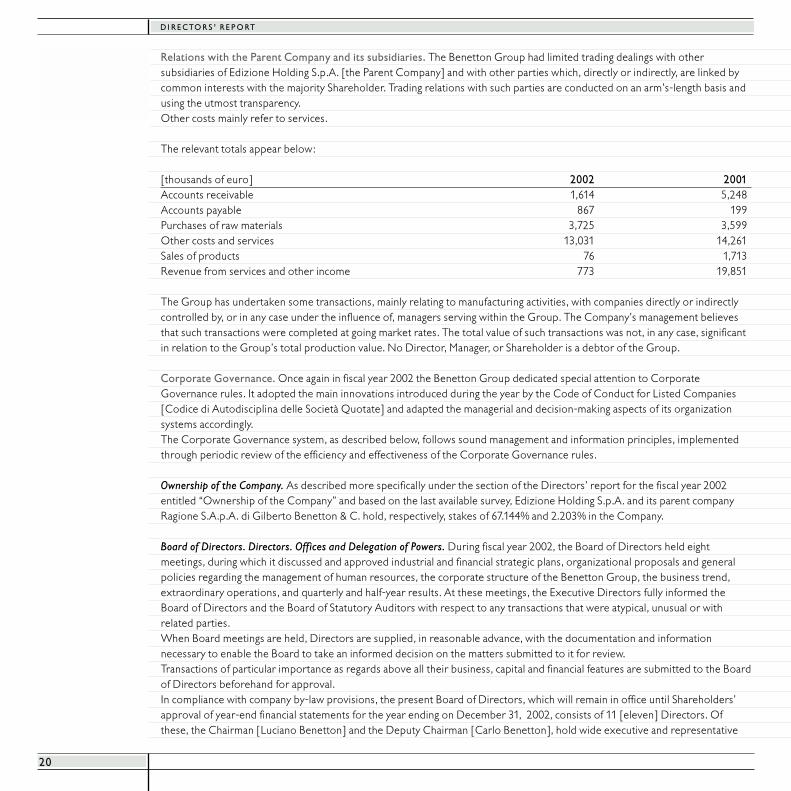

Relations with the Parent Company and its subsidiaries. The Benetton Group had limited trading dealings with othersubsidiaries of Edizione Holding S.p.A. [the Parent Company] and with other parties which, directly or indirectly, are linked bycommon interests with the majority Shareholder. Trading relations with such parties are conducted on an arm’s-length basis andusing the utmost transparency.Other costs mainly refer to services.

The relevant totals appear below:

[thousands of euro] 2002 2001Accounts receivable 1,614 5,248Accounts payable 867 199Purchases of raw materials 3,725 3,599Other costs and services 13,031 14,261Sales of products 76 1,713Revenue from services and other income 773 19,851

The Group has undertaken some transactions, mainly relating to manufacturing activities, with companies directly or indirectlycontrolled by, or in any case under the influence of, managers serving within the Group. The Company’s management believesthat such transactions were completed at going market rates. The total value of such transactions was not, in any case, significantin relation to the Group’s total production value. No Director, Manager, or Shareholder is a debtor of the Group.

Corporate Governance. Once again in fiscal year 2002 the Benetton Group dedicated special attention to CorporateGovernance rules. It adopted the main innovations introduced during the year by the Code of Conduct for Listed Companies[Codice di Autodisciplina delle Società Quotate] and adapted the managerial and decision-making aspects of its organizationsystems accordingly. The Corporate Governance system, as described below, follows sound management and information principles, implementedthrough periodic review of the efficiency and effectiveness of the Corporate Governance rules.

Ownership of the Company. As described more specifically under the section of the Directors’ report for the fiscal year 2002entitled “Ownership of the Company” and based on the last available survey, Edizione Holding S.p.A. and its parent companyRagione S.A.p.A. di Gilberto Benetton & C. hold, respectively, stakes of 67.144% and 2.203% in the Company.

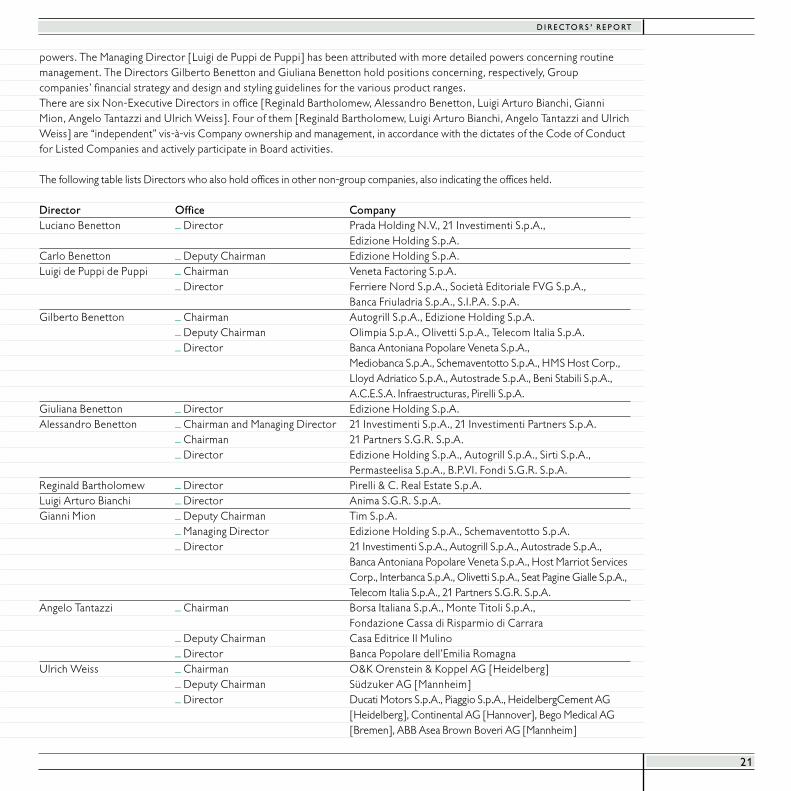

Board of Directors. Directors. Offices and Delegation of Powers. During fiscal year 2002, the Board of Directors held eightmeetings, during which it discussed and approved industrial and financial strategic plans, organizational proposals and generalpolicies regarding the management of human resources, the corporate structure of the Benetton Group, the business trend,extraordinary operations, and quarterly and half-year results. At these meetings, the Executive Directors fully informed theBoard of Directors and the Board of Statutory Auditors with respect to any transactions that were atypical, unusual or withrelated parties.When Board meetings are held, Directors are supplied, in reasonable advance, with the documentation and informationnecessary to enable the Board to take an informed decision on the matters submitted to it for review.Transactions of particular importance as regards above all their business, capital and financial features are submitted to the Boardof Directors beforehand for approval.In compliance with company by-law provisions, the present Board of Directors, which will remain in office until Shareholders’approval of year-end financial statements for the year ending on December 31, 2002, consists of 11 [eleven] Directors. Ofthese, the Chairman [Luciano Benetton] and the Deputy Chairman [Carlo Benetton], hold wide executive and representative

21

D I R E C TO R S ’ R E P O RT

powers. The Managing Director [Luigi de Puppi de Puppi] has been attributed with more detailed powers concerning routinemanagement. The Directors Gilberto Benetton and Giuliana Benetton hold positions concerning, respectively, Groupcompanies’ financial strategy and design and styling guidelines for the various product ranges.There are six Non-Executive Directors in office [Reginald Bartholomew, Alessandro Benetton, Luigi Arturo Bianchi, GianniMion, Angelo Tantazzi and Ulrich Weiss]. Four of them [Reginald Bartholomew, Luigi Arturo Bianchi, Angelo Tantazzi and UlrichWeiss] are “independent” vis-à-vis Company ownership and management, in accordance with the dictates of the Code of Conductfor Listed Companies and actively participate in Board activities.

The following table lists Directors who also hold offices in other non-group companies, also indicating the offices held.

Director Office CompanyLuciano Benetton _ Director Prada Holding N.V., 21 Investimenti S.p.A.,

Edizione Holding S.p.A.Carlo Benetton _ Deputy Chairman Edizione Holding S.p.A.Luigi de Puppi de Puppi _ Chairman Veneta Factoring S.p.A.

_ Director Ferriere Nord S.p.A., Società Editoriale FVG S.p.A., Banca Friuladria S.p.A., S.I.P.A. S.p.A.

Gilberto Benetton _ Chairman Autogrill S.p.A., Edizione Holding S.p.A._ Deputy Chairman Olimpia S.p.A., Olivetti S.p.A., Telecom Italia S.p.A._ Director Banca Antoniana Popolare Veneta S.p.A.,

Mediobanca S.p.A., Schemaventotto S.p.A., HMS Host Corp., Lloyd Adriatico S.p.A., Autostrade S.p.A., Beni Stabili S.p.A., A.C.E.S.A. Infraestructuras, Pirelli S.p.A.

Giuliana Benetton _ Director Edizione Holding S.p.A.Alessandro Benetton _ Chairman and Managing Director 21 Investimenti S.p.A., 21 Investimenti Partners S.p.A.

_ Chairman 21 Partners S.G.R. S.p.A._ Director Edizione Holding S.p.A., Autogrill S.p.A., Sirti S.p.A.,

Permasteelisa S.p.A., B.P.VI. Fondi S.G.R. S.p.A.Reginald Bartholomew _ Director Pirelli & C. Real Estate S.p.A.Luigi Arturo Bianchi _ Director Anima S.G.R. S.p.A.Gianni Mion _ Deputy Chairman Tim S.p.A.

_ Managing Director Edizione Holding S.p.A., Schemaventotto S.p.A._ Director 21 Investimenti S.p.A., Autogrill S.p.A., Autostrade S.p.A.,

Banca Antoniana Popolare Veneta S.p.A., Host Marriot Services Corp., Interbanca S.p.A., Olivetti S.p.A., Seat Pagine Gialle S.p.A.,Telecom Italia S.p.A., 21 Partners S.G.R. S.p.A.

Angelo Tantazzi _ Chairman Borsa Italiana S.p.A., Monte Titoli S.p.A., Fondazione Cassa di Risparmio di Carrara

_ Deputy Chairman Casa Editrice Il Mulino_ Director Banca Popolare dell’Emilia Romagna

Ulrich Weiss _ Chairman O&K Orenstein & Koppel AG [Heidelberg] _ Deputy Chairman Südzuker AG [Mannheim]_ Director Ducati Motors S.p.A., Piaggio S.p.A., HeidelbergCement AG

[Heidelberg], Continental AG [Hannover], Bego Medical AG[Bremen], ABB Asea Brown Boveri AG [Mannheim]

D I R E C TO R S ’ R E P O RT

22

Compensation Committee and Committee for Proposed Appointments of Directors. For fiscal year 2002, compensation forindividual Directors was established by the Board of Directors, as indicated in the Note to the consolidated financial statementof the Benetton Group, following the determination of the aggregate compensation for the Board of Directors by theShareholders at the General Meeting in accordance with the By-laws. The Board of Directors, in compliance with the Code of Conduct for Listed Companies, set up a Compensation Committeewith the tasks indicated by the Code. The members of the Compensation Committee are Reginald Bartholomew, Ulrich Weissand Gianni Mion, all of whom are non-executive Directors. Directors are appointed on the basis of just one list that is held at the Company’s registered offices prior to the Shareholders’Meeting, accompanied by a comprehensive outline of the personal and professional qualifications of the persons on the list. Given the Company’s present ownership structure, the Board of Directors has still not deemed it appropriate to establish aCommittee for Proposed Appointments of Directors.

Internal Auditing. Internal Audit Committee. Already in 2001 the Board of Directors set up the Internal Audit Committee, formed by the Directors Ulrich Weiss, Luigi Arturo Bianchi, and Angelo Tantazzi, all of whom are non-executive Directors andindependent from company ownership and management.The Internal Audit Committee has the following tasks:_ make proposals for the establishment of an internal audit department responsible for the internal audit and to determine the

duties of this department; _ review periodic reports from, and the executive plan of, the persons responsible for the internal audit, as well as to promote

actions for the improvement of the internal audit system;_ report to the Board of Directors, at least every six months, in connection with its approval of year-end financial statements

and the interim report, on the activities carried out and on the adequacy of the internal audit;_ monitor compliance with, and periodic revision of, corporate governance rules;_ verify, together with the head of the administrative function and the internal auditor, the adequacy of accounting principles;_ assess, together with the head of the administrative function and the internal auditor, proposals submitted by independent

auditing firms for assignment of the independent audit, making a recommendation for assignment of the task that the Board ofDirectors has to submit to the Shareholders’ Meeting;

_ evaluate the results presented in the independent auditor’s report.

During fiscal year 2002 the Committee performed its tasks under the chairmanship of Mr. Ulrich Weiss, in compliance with therules of operation adopted by the Committee.The functionality and adequacy of the internal audit system were assured by the Managing Director. Organization andinformation systems were found to be able to assure, also as regards subsidiaries, monitoring of the administrative andaccounting system and of the central and decentralized organizational structure. Work continued on mapping of risks concerningall Group companies’ businesses, as did operational and budget control of individual businesses and auditing of internal auditingsystems by outside auditors. Non-executive Directors, the Board of Statutory Auditors, and the independent auditing firm allreceived adequate information in this respect.In order to improve the effectiveness and efficiency of its internal auditing system, in early fiscal year 2003 the Companyintroduced the Internal Auditor position.

Handling of confidential information. All confidential information is managed by the Managing Director, upon consultation withthe Chairman. Together, the Managing Director and the Chairman also ensure that controls are carried out with regard to theclassification of confidential information in accordance with current legislation. The Managing Director supervises legal compliance with respect to proper disclosure of information relating to the Companyand, to this end, arranges and co-ordinates all suitable action by the various internal structures.

Scavengers, Dong and Mao,

from Stung Mean Chey dump in

Cambodia hold their polaroids.

D I R E C TO R S ’ R E P O RT

24

The Board of Directors approves all press releases relating to resolutions on the year’s financial statements, the interim report,and the quarterly report, as well as extraordinary decisions or operations that are subject to the approval of the Board ofDirectors. All communications to and relations with the press, institutional investors and individual Shareholders are conducted by the Mediaand Communications Department and the Investor Relations Department, respectively.During fiscal year 2002, implementing the “Regulation for Markets Organized and Managed by Borsa Italiana S.p.A.” [Regolamentodei Mercati Organizzati e Gestiti da Borsa Italiana S.p.A.], the Board of Directors officially adopted the “Code of Conduct forInternal Dealing”. This is designed to regulate obligations of notification and disclosure concerning transactions undertaken infinancial instruments issued by Benetton Group S.p.A. by those persons defined by the Code as “important persons”.The notification obligations imposed by the Code on the “important persons” envisage tighter timing and involve widercategories of subjects and securities than does the Regulation of Borsa Italiana S.p.A. Since Benetton Group S.p.A. shares arealso listed on the Frankfurt stock exchange, the Code of Conduct also implements the obligations of notification and disclosureenvisaged by the Wertpapierhandelsgesetz – WpHG law [Securities Trading Act], Section 15a, introduced by the 4thFinanzmarktförderungs [Fourth Financial Markets Promotion Act].

Relations with Institutional Investors and with other Shareholders. The Investor Relations Department ensures correctmanagement of relations with financial analysts, institutional investors and individual Italian and foreign Shareholders. Amongother activities, this department co-ordinates activities with financial experts.

Code of Ethics. During fiscal year 2002, the Board of Directors, coming into line with the most advanced standards of corporategovernance, officially adopted the “Code of Ethics”. This is designed to instill correctness, equity, integrity, loyalty andprofessional rigour into operations, conduct and ways of working into both relationships inside the Group and those withpersons and entities outside the Company. The Code places a central focus on compliance with the laws and regulations of thecountries where the Group is active, as well as on compliance with company procedures.This document is available on the Website www.benetton.com in the Investor Relations section.

25

D I R E C TO R S ’ R E P O RT

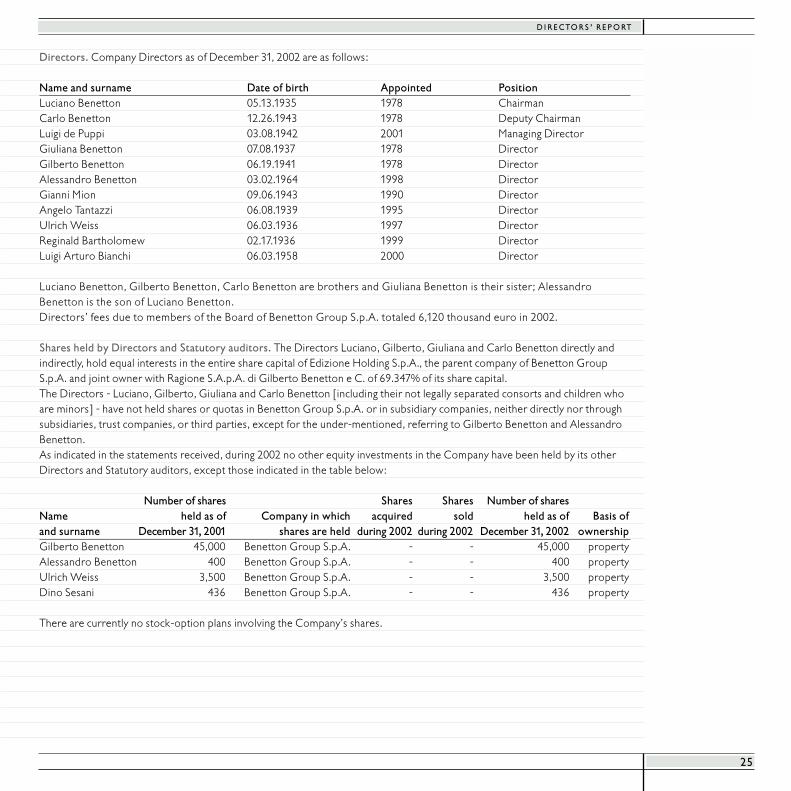

Directors. Company Directors as of December 31, 2002 are as follows:

Name and surname Date of birth Appointed PositionLuciano Benetton 05.13.1935 1978 ChairmanCarlo Benetton 12.26.1943 1978 Deputy ChairmanLuigi de Puppi 03.08.1942 2001 Managing DirectorGiuliana Benetton 07.08.1937 1978 DirectorGilberto Benetton 06.19.1941 1978 Director Alessandro Benetton 03.02.1964 1998 DirectorGianni Mion 09.06.1943 1990 DirectorAngelo Tantazzi 06.08.1939 1995 DirectorUlrich Weiss 06.03.1936 1997 DirectorReginald Bartholomew 02.17.1936 1999 DirectorLuigi Arturo Bianchi 06.03.1958 2000 Director

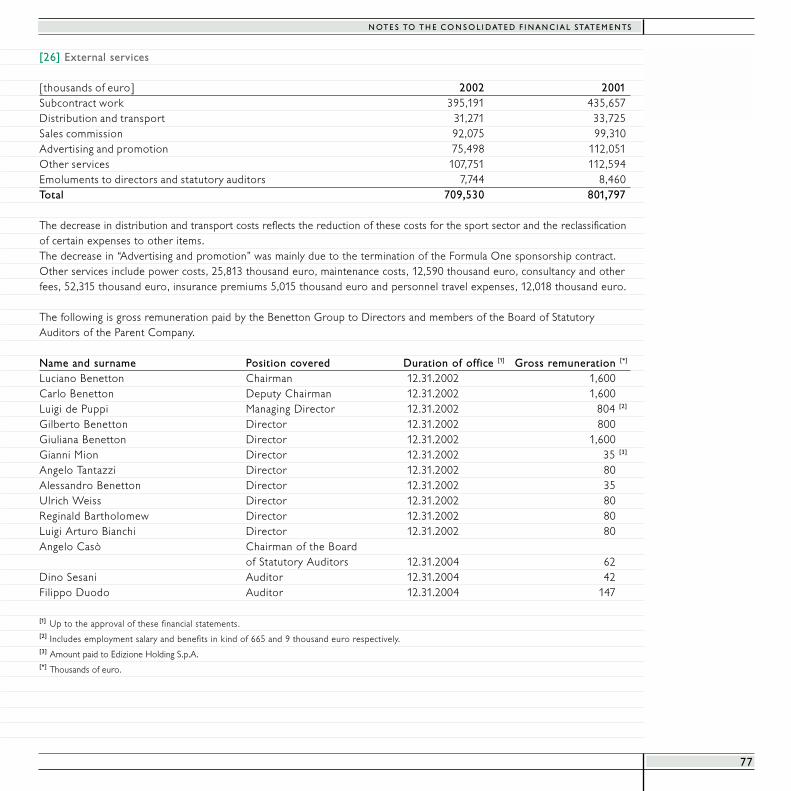

Luciano Benetton, Gilberto Benetton, Carlo Benetton are brothers and Giuliana Benetton is their sister; AlessandroBenetton is the son of Luciano Benetton.Directors’ fees due to members of the Board of Benetton Group S.p.A. totaled 6,120 thousand euro in 2002.

Shares held by Directors and Statutory auditors. The Directors Luciano, Gilberto, Giuliana and Carlo Benetton directly andindirectly, hold equal interests in the entire share capital of Edizione Holding S.p.A., the parent company of Benetton GroupS.p.A. and joint owner with Ragione S.A.p.A. di Gilberto Benetton e C. of 69.347% of its share capital. The Directors - Luciano, Gilberto, Giuliana and Carlo Benetton [including their not legally separated consorts and children whoare minors] - have not held shares or quotas in Benetton Group S.p.A. or in subsidiary companies, neither directly nor throughsubsidiaries, trust companies, or third parties, except for the under-mentioned, referring to Gilberto Benetton and AlessandroBenetton.As indicated in the statements received, during 2002 no other equity investments in the Company have been held by its otherDirectors and Statutory auditors, except those indicated in the table below:

Number of shares Shares Shares Number of sharesName held as of Company in which acquired sold held as of Basis ofand surname December 31, 2001 shares are held during 2002 during 2002 December 31, 2002 ownershipGilberto Benetton 45,000 Benetton Group S.p.A. - - 45,000 propertyAlessandro Benetton 400 Benetton Group S.p.A. - - 400 propertyUlrich Weiss 3,500 Benetton Group S.p.A. - - 3,500 propertyDino Sesani 436 Benetton Group S.p.A. - - 436 property

There are currently no stock-option plans involving the Company’s shares.

James Mollison photographs the

“homes” of some of the families who

live in the Stung Mean Chey dump

and whose children work there

selling rubbish.

27

S O M M A R I O

Principal organizational and corporate changes. The process of reorganizing and rationalizing the corporate structure wasvirtually completed during 2002, involving a concentration of equity investments in the sub-holding companies of the Retail, RealEstate and Manufacturing sectors.The demerger of Benetton International N.V. S.A. was completed with the creation of two new companies, BenettonInternational Property N.V. S.A., and Benetton International N.V. S.A., both with operational headquarters in Luxembourg.The former holds all the real-estate related equity investments, while the latter owns the interests in the service and manufacturingcompanies. As part of this process, Benetton Retail Netherlands N.V., a company incorporated in the Netherlands andcontrolled by Benetton International N.V. S.A., changed its corporate purpose and name to Benetton Manufacturing HoldingN.V. The latter then acquired certain equity investments in companies from the manufacturing sector, again because of the needto concentrate these interests under the same sub-holding company.The process of reorganizing the corporate structure also involved the company Benetton Finance S.A., which transferred theactivities managed by its Lugano office to Benetton Società di Servizi S.A., another subsidiary incorporated in Switzerland. In France, the concentration of equity investments in retail companies under Benetton Retail France S.A.S. was finalized. InPortugal, Benetton Textil - Confeccao de Texteis S.A. was set up through a spin-off from Benetton S.A., which changed its nameto Benetton Realty Portugal Imobiliaria S.A. in relation to the real estate portion of the business.New Ben GmbH was set up to enhance the Group’s commercial presence on the German market. This company is held 51% byBenetton Retail Deutschland GmbH and 49% by third parties. The company’s business will involve both the management ofretail outlets in Germany, and the supply of agency services to Benetton Group S.p.A.Moreover, a Permanent Establishment of Benetton Real Estate International S.A. was set up in Vilnius - Lithuania, in order tomanage the real estate investment made in Lithuania, which will result in the opening of a new retail business in 2003. In Italy, there were certain operations involving the manufacturing sector: the companies Tessitura Travesio S.p.A. and ColoramaS.r.l. were merged into Olimpias S.p.A.; in addition, Olimpias S.p.A. sold its interest in Color Service S.r.l. to third parties. The required capital payments were made to cover both new investments and the economic-financial needs of the followingcompanies: Benetton Retail Belgique S.A., Benetton Retail [Hong Kong] Ltd., Benetton Retail [1988] Ltd., Benetton Retail SpainS.L., Benetton Realty Spain S.L., and DCM Benetton India Ltd. As part of the process of redefining commercial strategies on the Chinese market, new arrangements for distribution werestarted in China, while the liquidation process of the Chinese-incorporated company of Beijing Benetton Fashion Co. Ltd. wascompleted.

Significant events since year-end. As previously explained under “Supplementary information”, the Nordica business was soldat the end of January. During the month of March two agreements were signed for the sale of Rollerblade and Prince, completingthe Benetton Group’s departure from the sports equipment sector.With effect from February 1, 2003, Benetton Group S.p.A. also acquired a 10% interest in the share capital of Tecnica S.p.A. witha guaranteed “put” option, and a “call” option on the part of Tecnica S.p.A. In the area of manufacturing activities, a new company is currently being set up in Tunisia under the name of BenettonManufacturing Tunisia S.à r.l. as part of the project to delocalize production.

Outlook for 2003. The forecasts for 2003 confirm the difficult situation economically and on international markets.Consumption, including in the textile clothing sector, reported an uncertain trend during the first few months of the year. Giventhis background, the Group is being cautious about its sales, although, on the basis of current information, it should be able toconfirm its 2002 performance in the casual sector in terms of both turnover and margins.Net income for 2003, compared with normalized net income for the previous year, is expected to rise; the Group’s netindebtedness will come down significantly.

D I R E C TO R S ’ R E P O RT

D I R E C TO R S ’ R E P O RT

28

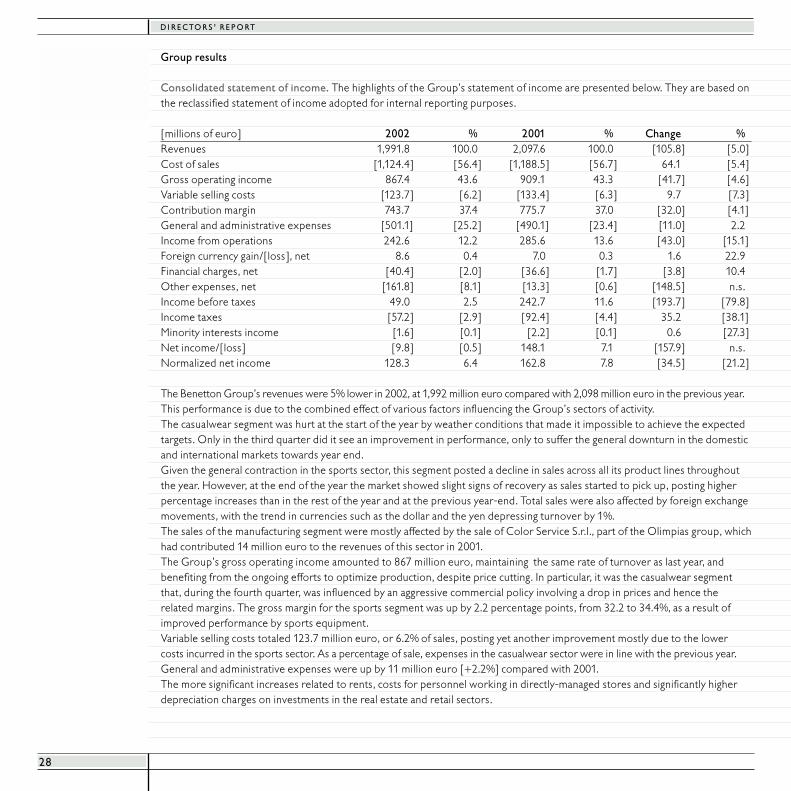

Group results

Consolidated statement of income. The highlights of the Group’s statement of income are presented below. They are based onthe reclassified statement of income adopted for internal reporting purposes.

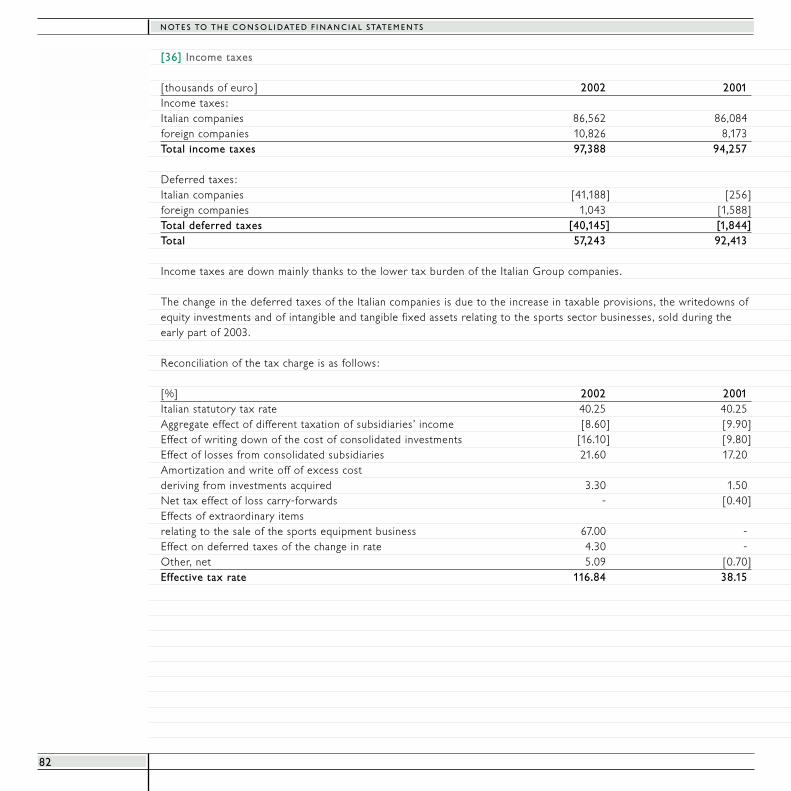

[millions of euro] 2002 % 2001 % Change %Revenues 1,991.8 100.0 2,097.6 100.0 [105.8] [5.0]Cost of sales [1,124.4] [56.4] [1,188.5] [56.7] 64.1 [5.4]Gross operating income 867.4 43.6 909.1 43.3 [41.7] [4.6]Variable selling costs [123.7] [6.2] [133.4] [6.3] 9.7 [7.3]Contribution margin 743.7 37.4 775.7 37.0 [32.0] [4.1]General and administrative expenses [501.1] [25.2] [490.1] [23.4] [11.0] 2.2Income from operations 242.6 12.2 285.6 13.6 [43.0] [15.1]Foreign currency gain/[loss], net 8.6 0.4 7.0 0.3 1.6 22.9Financial charges, net [40.4] [2.0] [36.6] [1.7] [3.8] 10.4Other expenses, net [161.8] [8.1] [13.3] [0.6] [148.5] n.s.Income before taxes 49.0 2.5 242.7 11.6 [193.7] [79.8]Income taxes [57.2] [2.9] [92.4] [4.4] 35.2 [38.1]Minority interests income [1.6] [0.1] [2.2] [0.1] 0.6 [27.3]Net income/[loss] [9.8] [0.5] 148.1 7.1 [157.9] n.s.Normalized net income 128.3 6.4 162.8 7.8 [34.5] [21.2]

The Benetton Group’s revenues were 5% lower in 2002, at 1,992 million euro compared with 2,098 million euro in the previous year. This performance is due to the combined effect of various factors influencing the Group’s sectors of activity. The casualwear segment was hurt at the start of the year by weather conditions that made it impossible to achieve the expectedtargets. Only in the third quarter did it see an improvement in performance, only to suffer the general downturn in the domesticand international markets towards year end.Given the general contraction in the sports sector, this segment posted a decline in sales across all its product lines throughoutthe year. However, at the end of the year the market showed slight signs of recovery as sales started to pick up, posting higherpercentage increases than in the rest of the year and at the previous year-end. Total sales were also affected by foreign exchangemovements, with the trend in currencies such as the dollar and the yen depressing turnover by 1%.The sales of the manufacturing segment were mostly affected by the sale of Color Service S.r.l., part of the Olimpias group, whichhad contributed 14 million euro to the revenues of this sector in 2001.The Group’s gross operating income amounted to 867 million euro, maintaining the same rate of turnover as last year, andbenefiting from the ongoing efforts to optimize production, despite price cutting. In particular, it was the casualwear segmentthat, during the fourth quarter, was influenced by an aggressive commercial policy involving a drop in prices and hence therelated margins. The gross margin for the sports segment was up by 2.2 percentage points, from 32.2 to 34.4%, as a result ofimproved performance by sports equipment.Variable selling costs totaled 123.7 million euro, or 6.2% of sales, posting yet another improvement mostly due to the lowercosts incurred in the sports sector. As a percentage of sale, expenses in the casualwear sector were in line with the previous year. General and administrative expenses were up by 11 million euro [+2.2%] compared with 2001. The more significant increases related to rents, costs for personnel working in directly-managed stores and significantly higherdepreciation charges on investments in the real estate and retail sectors.

29

S O M M A R I O

Advertising and sponsorship costs amounted to about 102 million euro compared with 112.6 million euro in 2001. The decreaseis mainly attributable to the sports sector. In the casualwear segment, a portion of the costs that used to go toward Group brandbuilding was devoted to product promotion in support of the development and management of the megastore network. Income from operations, totaling some 242.6 million euro, came to 12.2% of sales, 1.4 percentage points lower than in theprevious year. Income from operations in the casualwear segment was still significantly affected by general expenses relating toretail expansion, while the operating loss in the sports sector improved by 5.1% as percentage of sales. The overall result of foreign exchange management was a net gain of 8.6 million euro; this reflected the policy of hedgingexchange risks and was principally influenced by currency market fluctuations during the period. In particular, there was asignificant variation in the dollar and the yen with respect to the beginning of the year. Net financial charges, which increased from 1.7 to 2.0% of sales, were influenced by the sale and maturity of some investments insecurities bearing particularly good rates. The Group’s average net indebtedness was substantially unchanged with respect to theprevious period, despite the investment in support of retail operations, while the end-of-period indebtedness showed a markedimprovement.Other charges were mostly due to restructuring operations involving the sports segment. Plans for the sale of the businessesmade it necessary to adjust the value of all components in the sports equipment sector to their disposal value and to takeaccount of the related divestment costs. The tax rate was influenced by the major impact of partially tax undeductible extraordinary items, deriving from the valuation attheir realizable value of intangible and tangible fixed assets pertaining to the sports sector.The net loss of 9.8 million euro particularly reflected the aforementioned extraordinary operations. The 2001 financial year hadclosed with net income of 148.1 million euro.Without these extraordinary items, Group net income in 2002 would have amounted to approximately 128 million euro.

Revenues by geographical area are as follows:

[millions of euro] 2002 % 2001 % Change %Euro area 1,372.0 68.9 1,441.0 68.7 [69.0] [4.8]The Americas 191.8 9.6 213.6 10.2 [21.8] [10.2]Asia 177.2 8.9 195.8 9.3 [18.6] [9.5]Other areas 250.8 12.6 247.2 11.8 3.6 1.5Total 1,991.8 100.0 2,097.6 100.0 [105.8] [5.0]

The euro-zone continues to be the Group’s main market of reference. The “Other areas” are showing an opposing trend.

Performance by activity. The Group’s activities are traditionally divided into three sectors to provide the basis for effectiveadministration and adequate decision-making by company management, and to supply accurate and relevant information aboutcompany performance to financial investors.

The business sectors are as follows:_ casualwear sector, representing the Benetton brands [United Colors of Benetton, Undercolors and Sisley], which also

incorporates complementary products, such as accessories and footwear, as well as figures for the retail business;_ the sportswear and equipment sector, with the Playlife, Nordica, Prince, Rollerblade and Killer Loop brands;_ the manufacturing and other sectors, including sales of raw materials, semi-finished products, industrial services and revenues

and expenses from real estate activity.

D I R E C TO R S ’ R E P O RT

D I R E C TO R S ’ R E P O RT

30

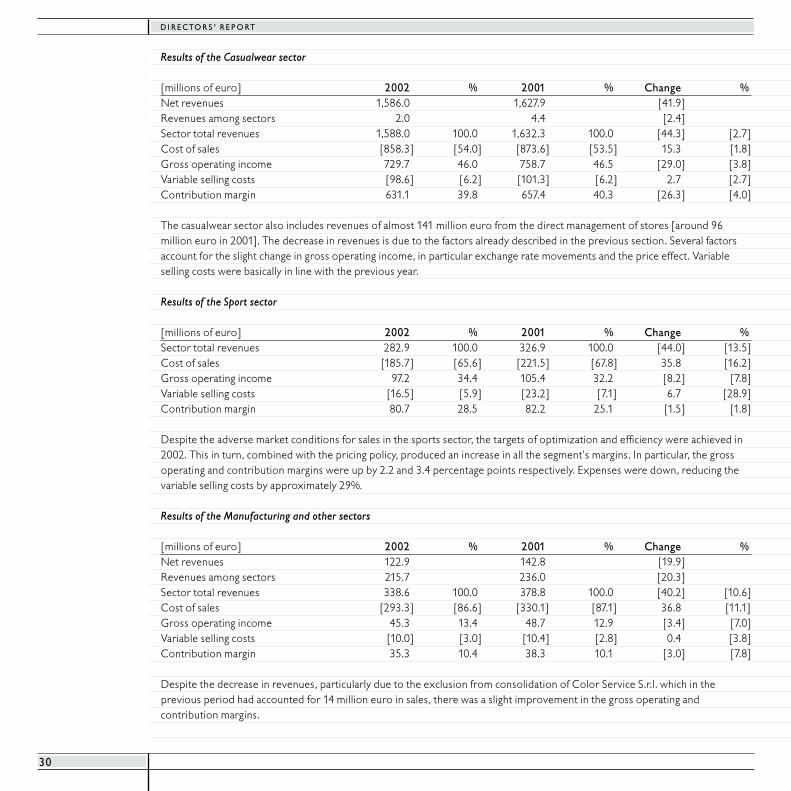

Results of the Casualwear sector

[millions of euro] 2002 % 2001 % Change %Net revenues 1,586.0 1,627.9 [41.9]Revenues among sectors 2.0 4.4 [2.4]Sector total revenues 1,588.0 100.0 1,632.3 100.0 [44.3] [2.7]Cost of sales [858.3] [54.0] [873.6] [53.5] 15.3 [1.8]Gross operating income 729.7 46.0 758.7 46.5 [29.0] [3.8]Variable selling costs [98.6] [6.2] [101.3] [6.2] 2.7 [2.7]Contribution margin 631.1 39.8 657.4 40.3 [26.3] [4.0]

The casualwear sector also includes revenues of almost 141 million euro from the direct management of stores [around 96million euro in 2001]. The decrease in revenues is due to the factors already described in the previous section. Several factorsaccount for the slight change in gross operating income, in particular exchange rate movements and the price effect. Variableselling costs were basically in line with the previous year.

Results of the Sport sector

[millions of euro] 2002 % 2001 % Change %Sector total revenues 282.9 100.0 326.9 100.0 [44.0] [13.5]Cost of sales [185.7] [65.6] [221.5] [67.8] 35.8 [16.2]Gross operating income 97.2 34.4 105.4 32.2 [8.2] [7.8]Variable selling costs [16.5] [5.9] [23.2] [7.1] 6.7 [28.9]Contribution margin 80.7 28.5 82.2 25.1 [1.5] [1.8]

Despite the adverse market conditions for sales in the sports sector, the targets of optimization and efficiency were achieved in2002. This in turn, combined with the pricing policy, produced an increase in all the segment’s margins. In particular, the grossoperating and contribution margins were up by 2.2 and 3.4 percentage points respectively. Expenses were down, reducing thevariable selling costs by approximately 29%.

Results of the Manufacturing and other sectors

[millions of euro] 2002 % 2001 % Change %Net revenues 122.9 142.8 [19.9]Revenues among sectors 215.7 236.0 [20.3]Sector total revenues 338.6 100.0 378.8 100.0 [40.2] [10.6]Cost of sales [293.3] [86.6] [330.1] [87.1] 36.8 [11.1]Gross operating income 45.3 13.4 48.7 12.9 [3.4] [7.0]Variable selling costs [10.0] [3.0] [10.4] [2.8] 0.4 [3.8]Contribution margin 35.3 10.4 38.3 10.1 [3.0] [7.8]

Despite the decrease in revenues, particularly due to the exclusion from consolidation of Color Service S.r.l. which in theprevious period had accounted for 14 million euro in sales, there was a slight improvement in the gross operating andcontribution margins.

31

S O M M A R I O

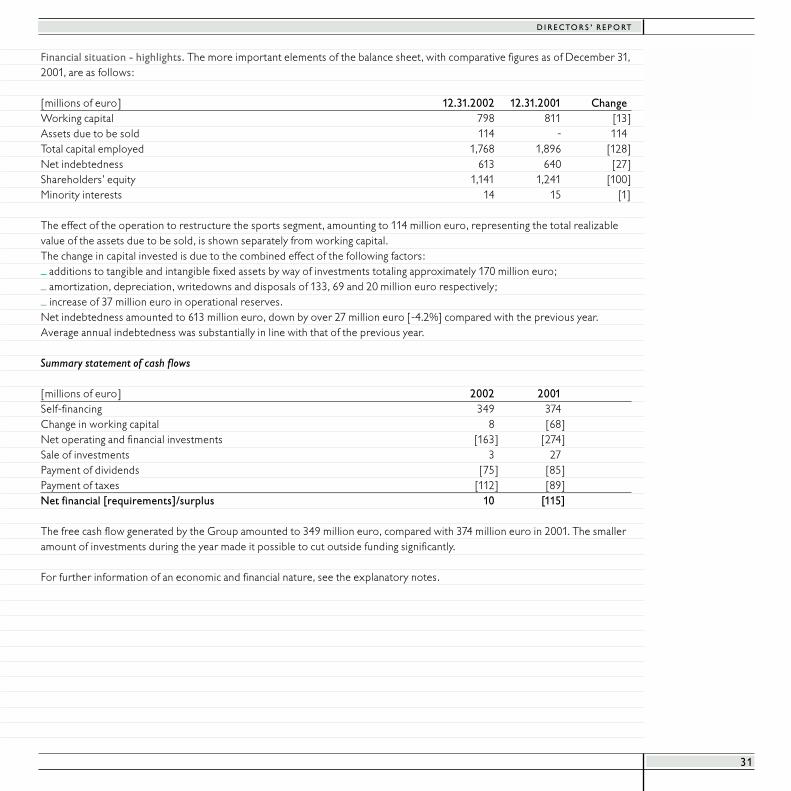

Financial situation - highlights. The more important elements of the balance sheet, with comparative figures as of December 31,2001, are as follows:

[millions of euro] 12.31.2002 12.31.2001 ChangeWorking capital 798 811 [13]Assets due to be sold 114 - 114Total capital employed 1,768 1,896 [128]Net indebtedness 613 640 [27]Shareholders’ equity 1,141 1,241 [100]Minority interests 14 15 [1]

The effect of the operation to restructure the sports segment, amounting to 114 million euro, representing the total realizablevalue of the assets due to be sold, is shown separately from working capital. The change in capital invested is due to the combined effect of the following factors:_ additions to tangible and intangible fixed assets by way of investments totaling approximately 170 million euro;_ amortization, depreciation, writedowns and disposals of 133, 69 and 20 million euro respectively;_ increase of 37 million euro in operational reserves.Net indebtedness amounted to 613 million euro, down by over 27 million euro [-4.2%] compared with the previous year.Average annual indebtedness was substantially in line with that of the previous year.

Summary statement of cash flows

[millions of euro] 2002 2001Self-financing 349 374Change in working capital 8 [68]Net operating and financial investments [163] [274]Sale of investments 3 27Payment of dividends [75] [85]Payment of taxes [112] [89]Net financial [requirements]/surplus 10 [115]

The free cash flow generated by the Group amounted to 349 million euro, compared with 374 million euro in 2001. The smalleramount of investments during the year made it possible to cut outside funding significantly.

For further information of an economic and financial nature, see the explanatory notes.

D I R E C TO R S ’ R E P O RT

D I R E C TO R S ’ R E P O RT

32

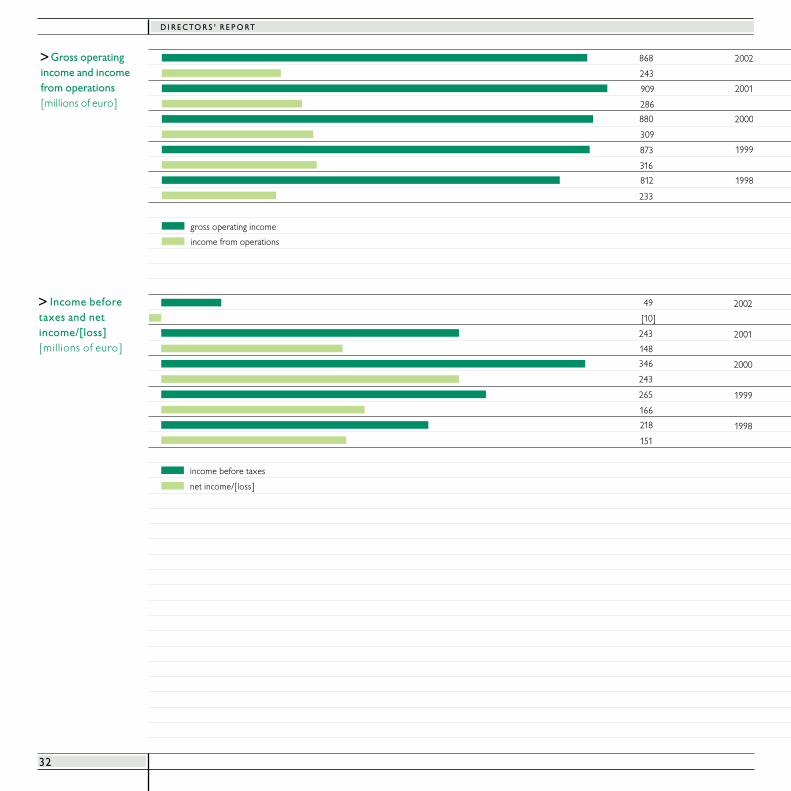

> Gross operatingincome and incomefrom operations [millions of euro]

> Income beforetaxes and netincome/[loss] [millions of euro]

880

309

873

316

812

233

286

909

243

868

gross operating income

income from operations

346

243

265

166

218

151

148

243

[10]

49

income before taxes

net income/[loss]

1998

1999

2000

2001

2002

1998

1999

2000

2001

2002

33

D I R E C TO R S ’ R E P O RT

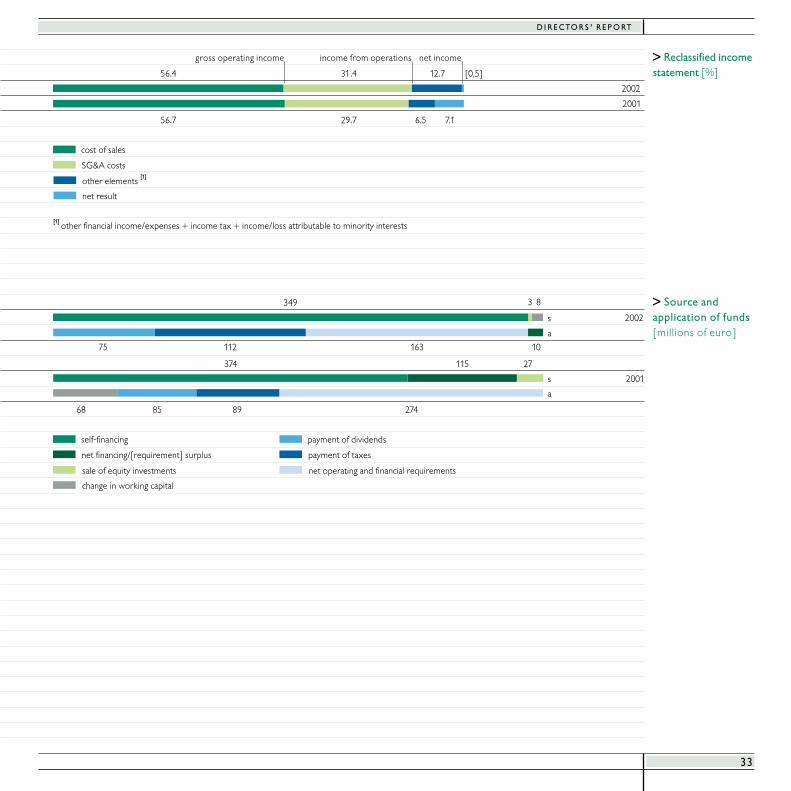

> Reclassified incomestatement [%]

> Source andapplication of funds [millions of euro]

[0,5]12.756.4 31.4

7.16.556.7 29.7

cost of sales

SG&A costs

other elements [1]

net result

[1] other financial income/expenses + income tax + income/loss attributable to minority interests

374

68 85 89 274

349

75 112 163 10

s 2002

2001

a

s

a

3 8

115 27

self-financing

net financing/[requirement] surplus

sale of equity investments

change in working capital

payment of dividends

payment of taxes

net operating and financial requirements

2001

2002

gross operating income income from operations net income

Children queue up for class at the

Ashuqan and Arifan School in Kabul

where they receive free bread.

> Benetton Group2002 consolidated financial statementsand related notes

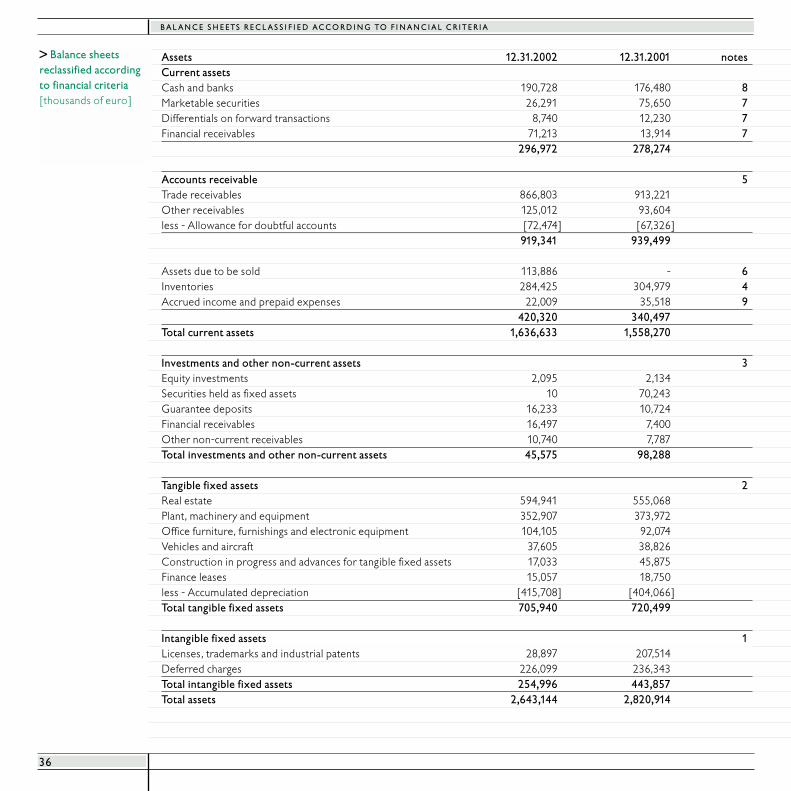

B A L A N C E S H E ETS R E C L AS S I F I E D AC C O R D I N G TO F I N A N C I A L C R I T E R I A

36

Assets 12.31.2002 12.31.2001 notesCurrent assetsCash and banks 190,728 176,480 8Marketable securities 26,291 75,650 7Differentials on forward transactions 8,740 12,230 7Financial receivables 71,213 13,914 7

296,972 278,274

Accounts receivable 5Trade receivables 866,803 913,221Other receivables 125,012 93,604less - Allowance for doubtful accounts [72,474] [67,326]

919,341 939,499

Assets due to be sold 113,886 - 6Inventories 284,425 304,979 4Accrued income and prepaid expenses 22,009 35,518 9

420,320 340,497Total current assets 1,636,633 1,558,270

Investments and other non-current assets 3Equity investments 2,095 2,134Securities held as fixed assets 10 70,243Guarantee deposits 16,233 10,724Financial receivables 16,497 7,400Other non-current receivables 10,740 7,787Total investments and other non-current assets 45,575 98,288

Tangible fixed assets 2Real estate 594,941 555,068Plant, machinery and equipment 352,907 373,972Office furniture, furnishings and electronic equipment 104,105 92,074Vehicles and aircraft 37,605 38,826Construction in progress and advances for tangible fixed assets 17,033 45,875Finance leases 15,057 18,750less - Accumulated depreciation [415,708] [404,066]Total tangible fixed assets 705,940 720,499

Intangible fixed assets 1Licenses, trademarks and industrial patents 28,897 207,514Deferred charges 226,099 236,343Total intangible fixed assets 254,996 443,857Total assets 2,643,144 2,820,914

> Balance sheets reclassified accordingto financial criteria [thousands of euro]

37

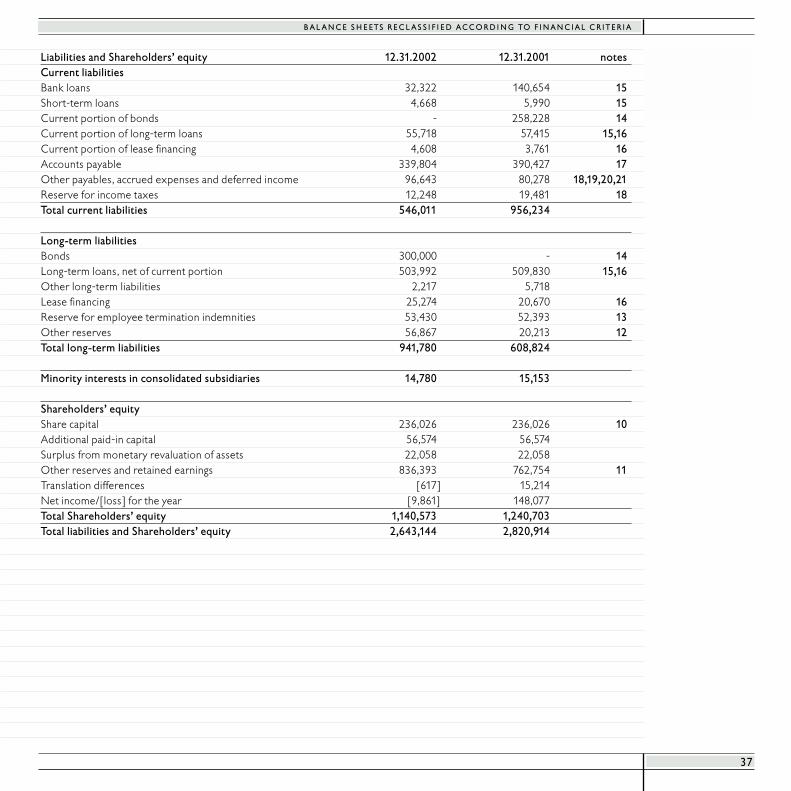

B A L A N C E S H E ETS R E C L AS S I F I E D AC C O R D I N G TO F I N A N C I A L C R I T E R I A

Liabilities and Shareholders’ equity 12.31.2002 12.31.2001 notesCurrent liabilitiesBank loans 32,322 140,654 15Short-term loans 4,668 5,990 15Current portion of bonds - 258,228 14Current portion of long-term loans 55,718 57,415 15,16Current portion of lease financing 4,608 3,761 16Accounts payable 339,804 390,427 17Other payables, accrued expenses and deferred income 96,643 80,278 18,19,20,21Reserve for income taxes 12,248 19,481 18Total current liabilities 546,011 956,234

Long-term liabilitiesBonds 300,000 - 14Long-term loans, net of current portion 503,992 509,830 15,16Other long-term liabilities 2,217 5,718Lease financing 25,274 20,670 16Reserve for employee termination indemnities 53,430 52,393 13Other reserves 56,867 20,213 12Total long-term liabilities 941,780 608,824

Minority interests in consolidated subsidiaries 14,780 15,153

Shareholders’ equityShare capital 236,026 236,026 10Additional paid-in capital 56,574 56,574Surplus from monetary revaluation of assets 22,058 22,058Other reserves and retained earnings 836,393 762,754 11Translation differences [617] 15,214Net income/[loss] for the year [9,861] 148,077Total Shareholders’ equity 1,140,573 1,240,703Total liabilities and Shareholders’ equity 2,643,144 2,820,914

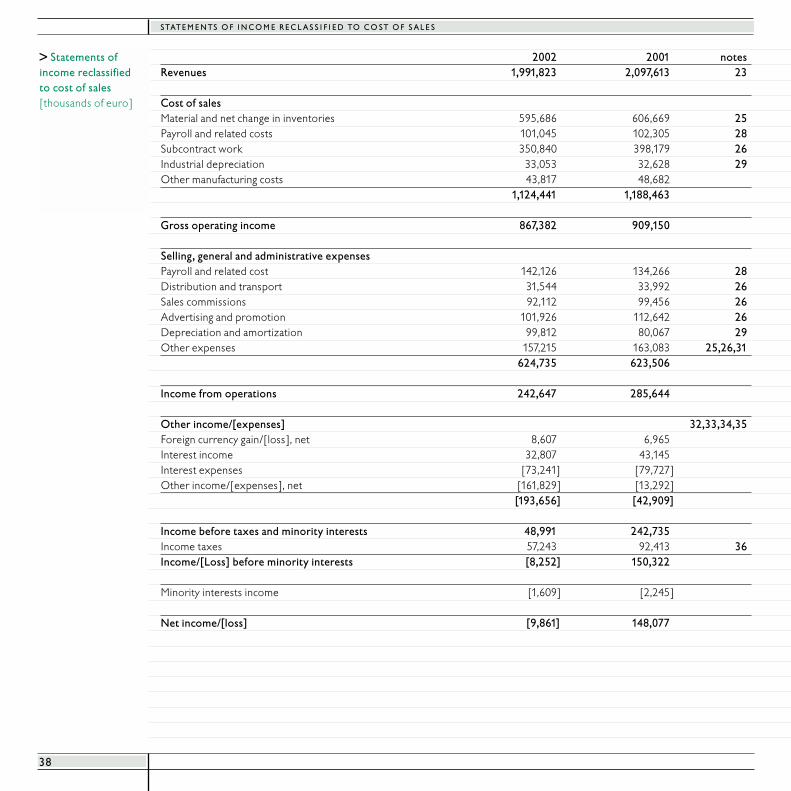

STAT E M E N TS O F I N C O M E R E C L AS S I F I E D TO C O ST O F S A L E S

38

2002 2001 notesRevenues 1,991,823 2,097,613 23

Cost of salesMaterial and net change in inventories 595,686 606,669 25Payroll and related costs 101,045 102,305 28Subcontract work 350,840 398,179 26Industrial depreciation 33,053 32,628 29Other manufacturing costs 43,817 48,682

1,124,441 1,188,463

Gross operating income 867,382 909,150

Selling, general and administrative expensesPayroll and related cost 142,126 134,266 28Distribution and transport 31,544 33,992 26Sales commissions 92,112 99,456 26Advertising and promotion 101,926 112,642 26Depreciation and amortization 99,812 80,067 29Other expenses 157,215 163,083 25,26,31

624,735 623,506

Income from operations 242,647 285,644

Other income/[expenses] 32,33,34,35Foreign currency gain/[loss], net 8,607 6,965Interest income 32,807 43,145Interest expenses [73,241] [79,727]Other income/[expenses], net [161,829] [13,292]

[193,656] [42,909]

Income before taxes and minority interests 48,991 242,735Income taxes 57,243 92,413 36Income/[Loss] before minority interests [8,252] 150,322

Minority interests income [1,609] [2,245]

Net income/[loss] [9,861] 148,077

> Statements ofincome reclassified to cost of sales [thousands of euro]

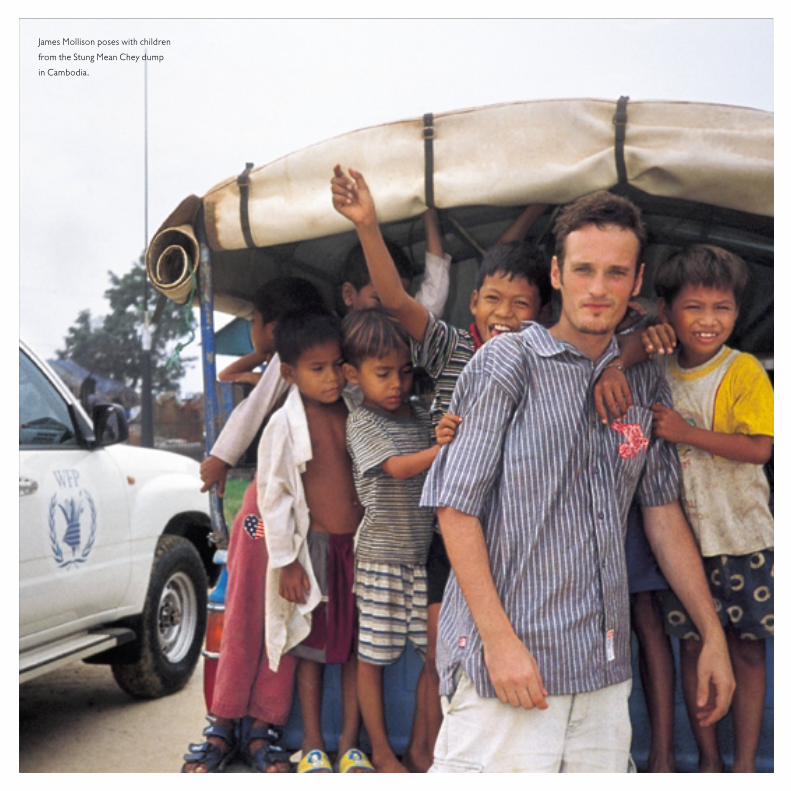

James Mollison poses with children

from the Stung Mean Chey dump

in Cambodia.

B A L A N C E S H E ET - AS S ETS

40

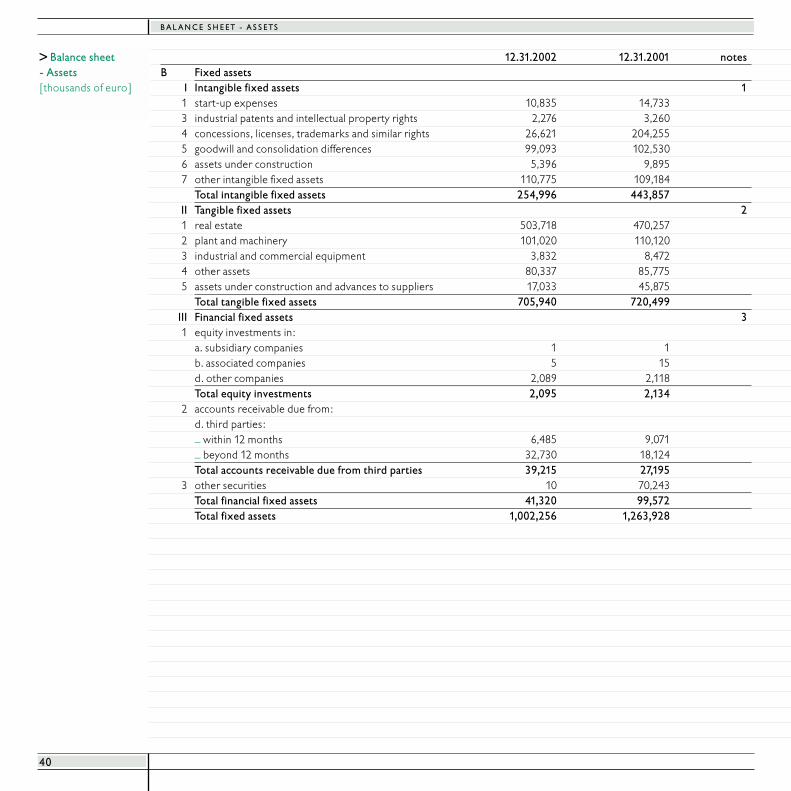

12.31.2002 12.31.2001 notesB Fixed assets

I Intangible fixed assets 11 start-up expenses 10,835 14,7333 industrial patents and intellectual property rights 2,276 3,2604 concessions, licenses, trademarks and similar rights 26,621 204,2555 goodwill and consolidation differences 99,093 102,5306 assets under construction 5,396 9,8957 other intangible fixed assets 110,775 109,184

Total intangible fixed assets 254,996 443,857II Tangible fixed assets 21 real estate 503,718 470,2572 plant and machinery 101,020 110,1203 industrial and commercial equipment 3,832 8,4724 other assets 80,337 85,7755 assets under construction and advances to suppliers 17,033 45,875

Total tangible fixed assets 705,940 720,499III Financial fixed assets 31 equity investments in:

a. subsidiary companies 1 1b. associated companies 5 15d. other companies 2,089 2,118Total equity investments 2,095 2,134

2 accounts receivable due from:d. third parties:_ within 12 months 6,485 9,071_ beyond 12 months 32,730 18,124Total accounts receivable due from third parties 39,215 27,195

3 other securities 10 70,243Total financial fixed assets 41,320 99,572Total fixed assets 1,002,256 1,263,928

> Balance sheet - Assets[thousands of euro]

41

B A L A N C E S H E ET - AS S ETS

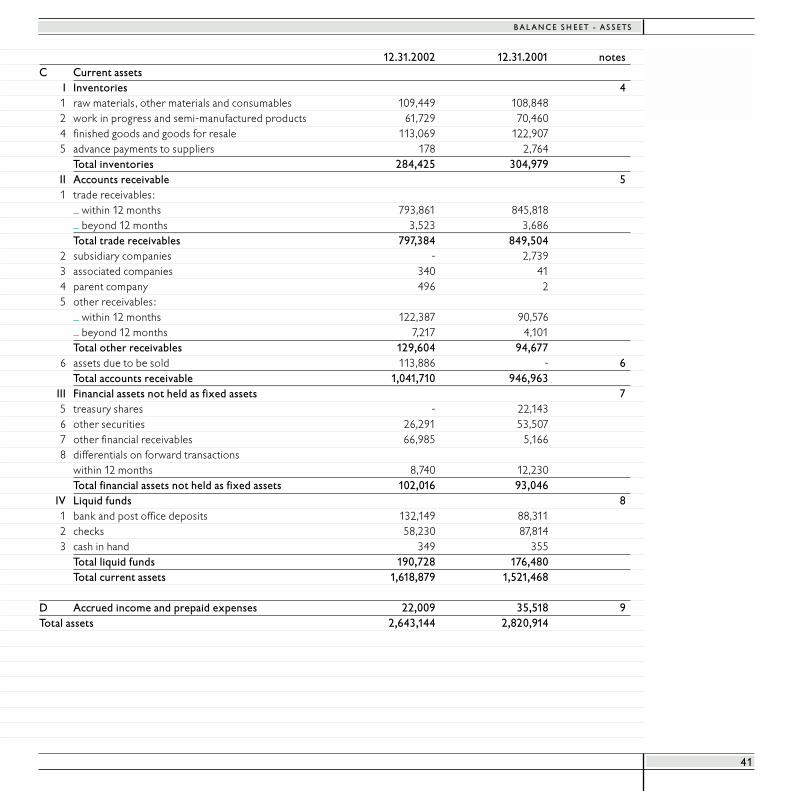

12.31.2002 12.31.2001 notesC Current assets

I Inventories 41 raw materials, other materials and consumables 109,449 108,8482 work in progress and semi-manufactured products 61,729 70,4604 finished goods and goods for resale 113,069 122,9075 advance payments to suppliers 178 2,764

Total inventories 284,425 304,979II Accounts receivable 51 trade receivables:

_ within 12 months 793,861 845,818_ beyond 12 months 3,523 3,686Total trade receivables 797,384 849,504

2 subsidiary companies - 2,7393 associated companies 340 414 parent company 496 25 other receivables:

_ within 12 months 122,387 90,576_ beyond 12 months 7,217 4,101Total other receivables 129,604 94,677

6 assets due to be sold 113,886 - 6Total accounts receivable 1,041,710 946,963

III Financial assets not held as fixed assets 75 treasury shares - 22,1436 other securities 26,291 53,5077 other financial receivables 66,985 5,1668 differentials on forward transactions

within 12 months 8,740 12,230Total financial assets not held as fixed assets 102,016 93,046

IV Liquid funds 81 bank and post office deposits 132,149 88,3112 checks 58,230 87,8143 cash in hand 349 355

Total liquid funds 190,728 176,480Total current assets 1,618,879 1,521,468

D Accrued income and prepaid expenses 22,009 35,518 9Total assets 2,643,144 2,820,914

B A L A N C E S H E ET - L I A B I L I T I E S A N D S H A R E H O L D E R S ’ E Q U I T Y

42

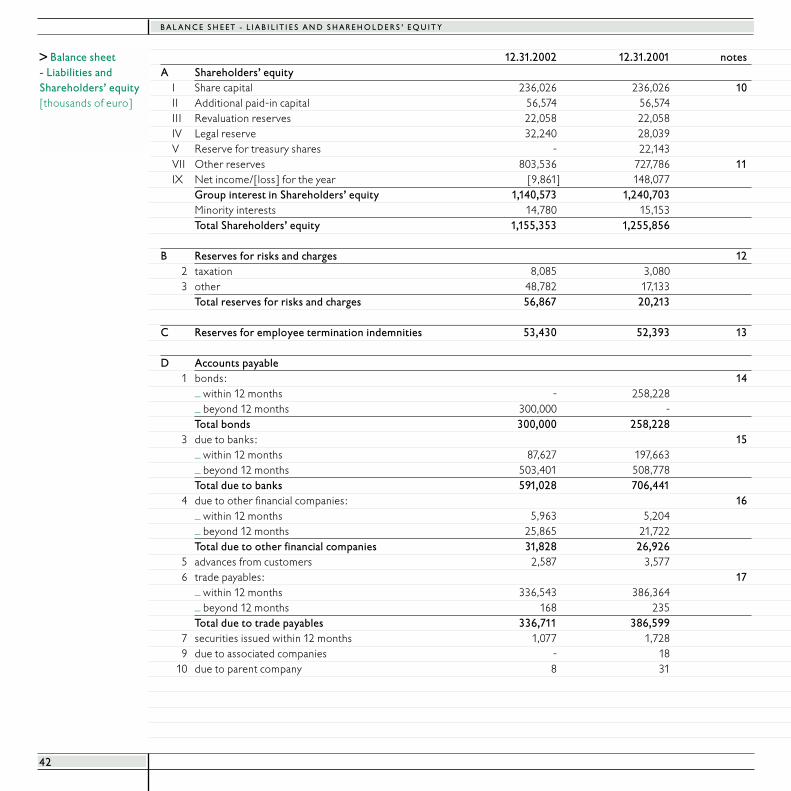

12.31.2002 12.31.2001 notesA Shareholders’ equity

I Share capital 236,026 236,026 10II Additional paid-in capital 56,574 56,574III Revaluation reserves 22,058 22,058IV Legal reserve 32,240 28,039V Reserve for treasury shares - 22,143VII Other reserves 803,536 727,786 11IX Net income/[loss] for the year [9,861] 148,077

Group interest in Shareholders’ equity 1,140,573 1,240,703Minority interests 14,780 15,153Total Shareholders’ equity 1,155,353 1,255,856

B Reserves for risks and charges 122 taxation 8,085 3,0803 other 48,782 17,133

Total reserves for risks and charges 56,867 20,213

C Reserves for employee termination indemnities 53,430 52,393 13

D Accounts payable1 bonds: 14

_ within 12 months - 258,228_ beyond 12 months 300,000 -Total bonds 300,000 258,228

3 due to banks: 15_ within 12 months 87,627 197,663_ beyond 12 months 503,401 508,778Total due to banks 591,028 706,441

4 due to other financial companies: 16_ within 12 months 5,963 5,204_ beyond 12 months 25,865 21,722Total due to other financial companies 31,828 26,926

5 advances from customers 2,587 3,5776 trade payables: 17

_ within 12 months 336,543 386,364_ beyond 12 months 168 235Total due to trade payables 336,711 386,599

7 securities issued within 12 months 1,077 1,7289 due to associated companies - 18

10 due to parent company 8 31

> Balance sheet - Liabilities and Shareholders’ equity[thousands of euro]

43

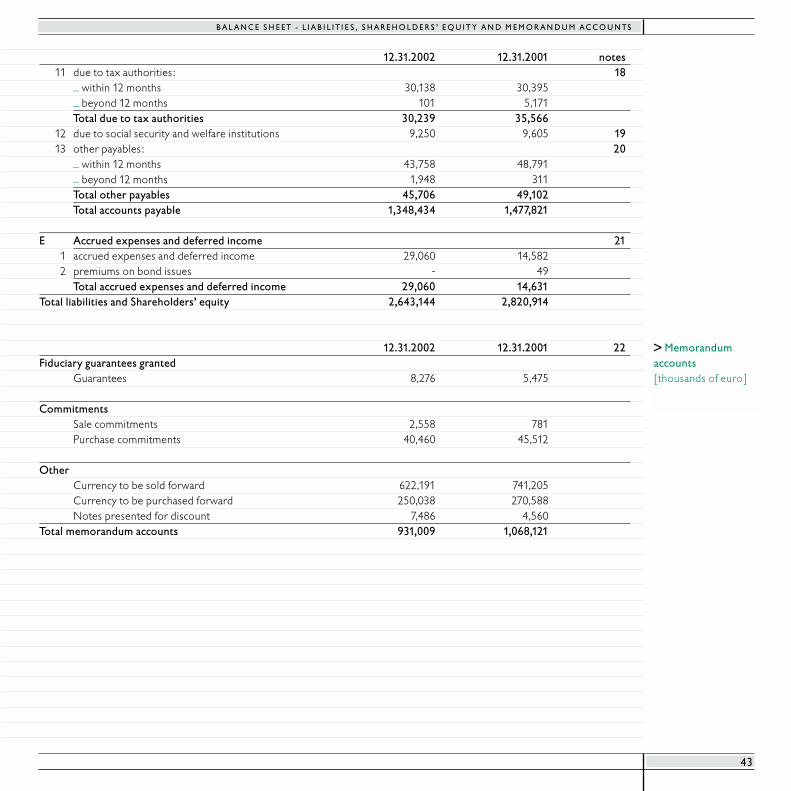

B A L A N C E S H E ET - L I A B I L I T I E S , S H A R E H O L D E R S ’ E Q U I T Y A N D M E M O R A N D U M AC C O U N TS

12.31.2002 12.31.2001 notes11 due to tax authorities: 18

_ within 12 months 30,138 30,395_ beyond 12 months 101 5,171Total due to tax authorities 30,239 35,566

12 due to social security and welfare institutions 9,250 9,605 1913 other payables: 20

_ within 12 months 43,758 48,791_ beyond 12 months 1,948 311Total other payables 45,706 49,102Total accounts payable 1,348,434 1,477,821

E Accrued expenses and deferred income 211 accrued expenses and deferred income 29,060 14,5822 premiums on bond issues - 49

Total accrued expenses and deferred income 29,060 14,631Total liabilities and Shareholders’ equity 2,643,144 2,820,914

12.31.2002 12.31.2001 22Fiduciary guarantees granted

Guarantees 8,276 5,475

CommitmentsSale commitments 2,558 781Purchase commitments 40,460 45,512

OtherCurrency to be sold forward 622,191 741,205Currency to be purchased forward 250,038 270,588Notes presented for discount 7,486 4,560

Total memorandum accounts 931,009 1,068,121

> Memorandumaccounts [thousands of euro]

STAT E M E N TS O F I N C O M E

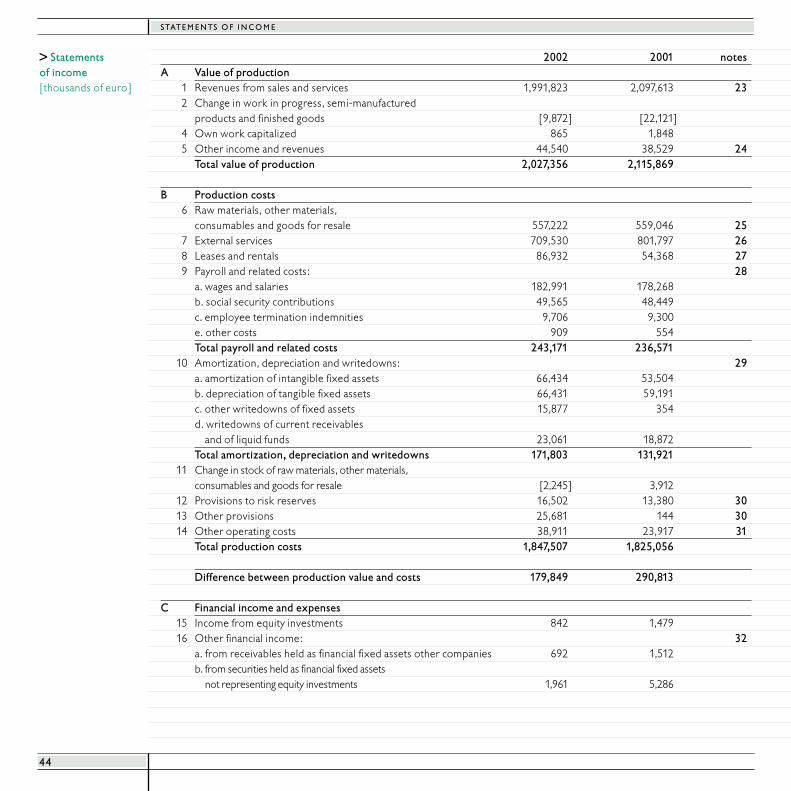

44

2002 2001 notesA Value of production

1 Revenues from sales and services 1,991,823 2,097,613 232 Change in work in progress, semi-manufactured

products and finished goods [9,872] [22,121]4 Own work capitalized 865 1,8485 Other income and revenues 44,540 38,529 24

Total value of production 2,027,356 2,115,869

B Production costs6 Raw materials, other materials,

consumables and goods for resale 557,222 559,046 257 External services 709,530 801,797 268 Leases and rentals 86,932 54,368 279 Payroll and related costs: 28

a. wages and salaries 182,991 178,268b. social security contributions 49,565 48,449c. employee termination indemnities 9,706 9,300e. other costs 909 554Total payroll and related costs 243,171 236,571

10 Amortization, depreciation and writedowns: 29a. amortization of intangible fixed assets 66,434 53,504b. depreciation of tangible fixed assets 66,431 59,191c. other writedowns of fixed assets 15,877 354d. writedowns of current receivables

and of liquid funds 23,061 18,872Total amortization, depreciation and writedowns 171,803 131,921

11 Change in stock of raw materials, other materials, consumables and goods for resale [2,245] 3,912

12 Provisions to risk reserves 16,502 13,380 3013 Other provisions 25,681 144 3014 Other operating costs 38,911 23,917 31

Total production costs 1,847,507 1,825,056

Difference between production value and costs 179,849 290,813

C Financial income and expenses15 Income from equity investments 842 1,47916 Other financial income: 32

a. from receivables held as financial fixed assets other companies 692 1,512b. from securities held as financial fixed assets

not representing equity investments 1,961 5,286

> Statements of income [thousands of euro]

45

STAT E M E N TS O F I N C O M E

2002 2001 notesc. from securities included among current assets

not representing equity investments 1,988 6,134d.financial income other than the above:_ subsidiary companies 130 158_ other companies 147,229 134,709Total financial income other than the above 147,359 134,867Total other financial income 152,000 147,799

17 Interest and other financial expenses 33from other companies 188,416 180,759Total financial income and expenses [35,574] [31,481]

D Changes in value of financial assets18 Revaluations:

c. of securities included among current assets not representing equity investments 26 65

19 Writedowns:a. of equity investments 11 260b. of financial fixed assets not representing equity investments - 1c. of securities included among current assets

not representing equity investments 11 1,684Total writedowns 22 1,945Total changes in value of financial assets 4 [1,880]

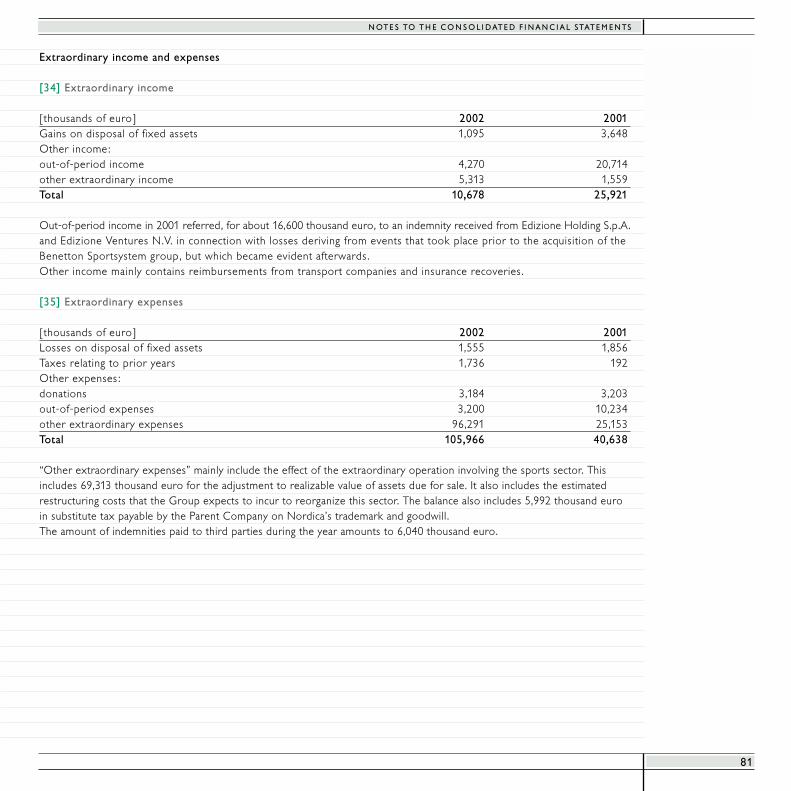

E Extraordinary income and expenses20 Income: 34

_ gains on disposals 1,095 3,648_ other 9,583 22,273Total income 10,678 25,921

21 Expenses: 35_ losses on disposals 1,555 1,856_ taxes relating to prior years 1,736 192_ other 102,675 38,590Total expenses 105,966 40,638Total extraordinary income and expenses [95,288] [14,717]

Results before income taxes 48,991 242,735

22 Income taxes 57,243 92,413 36Income/[Loss] before minority interests [8,252] 150,322

Income/[Loss] attributable to minority interests [1,609] [2,245]26 Net income/[loss] for the year [9,861] 148,077

STAT E M E N TS O F C H A N G E S I N S H A R E H O L D E R S ’ E Q U I T Y

46

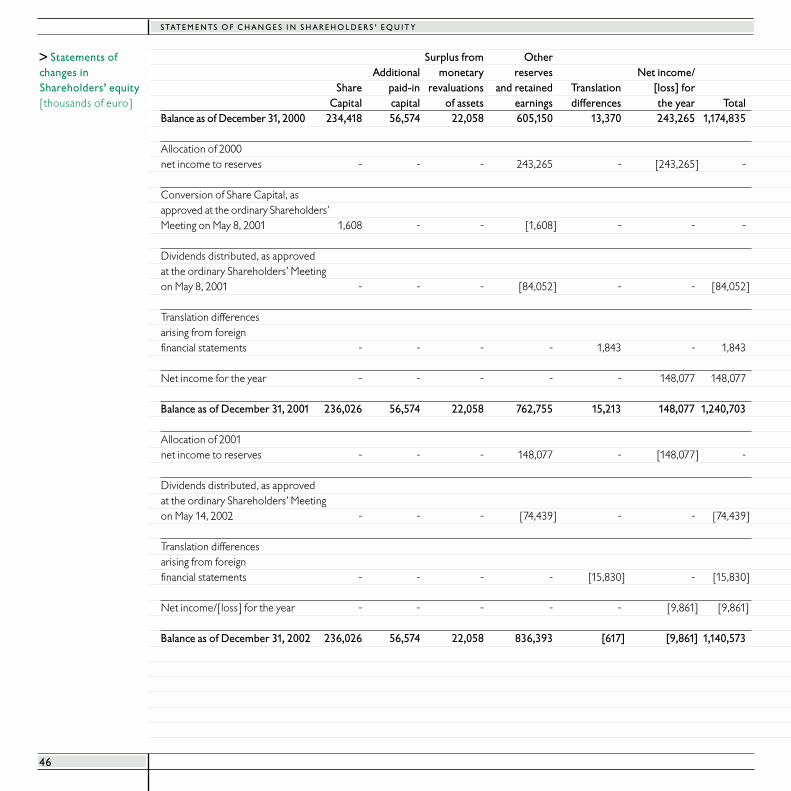

Surplus from OtherAdditional monetary reserves Net income/

Share paid-in revaluations and retained Translation [loss] forCapital capital of assets earnings differences the year Total

Balance as of December 31, 2000 234,418 56,574 22,058 605,150 13,370 243,265 1,174,835

Allocation of 2000net income to reserves - - - 243,265 - [243,265] -

Conversion of Share Capital, asapproved at the ordinary Shareholders’ Meeting on May 8, 2001 1,608 - - [1,608] - - -

Dividends distributed, as approved at the ordinary Shareholders’ Meeting on May 8, 2001 - - - [84,052] - - [84,052]

Translation differences arising from foreign financial statements - - - - 1,843 - 1,843

Net income for the year - - - - - 148,077 148,077

Balance as of December 31, 2001 236,026 56,574 22,058 762,755 15,213 148,077 1,240,703

Allocation of 2001net income to reserves - - - 148,077 - [148,077] -

Dividends distributed, as approved at the ordinary Shareholders’ Meeting on May 14, 2002 - - - [74,439] - - [74,439]

Translation differences arising from foreign financial statements - - - - [15,830] - [15,830]

Net income/[loss] for the year - - - - - [9,861] [9,861]

Balance as of December 31, 2002 236,026 56,574 22,058 836,393 [617] [9,861] 1,140,573

> Statements ofchanges in Shareholders’ equity [thousands of euro]

47

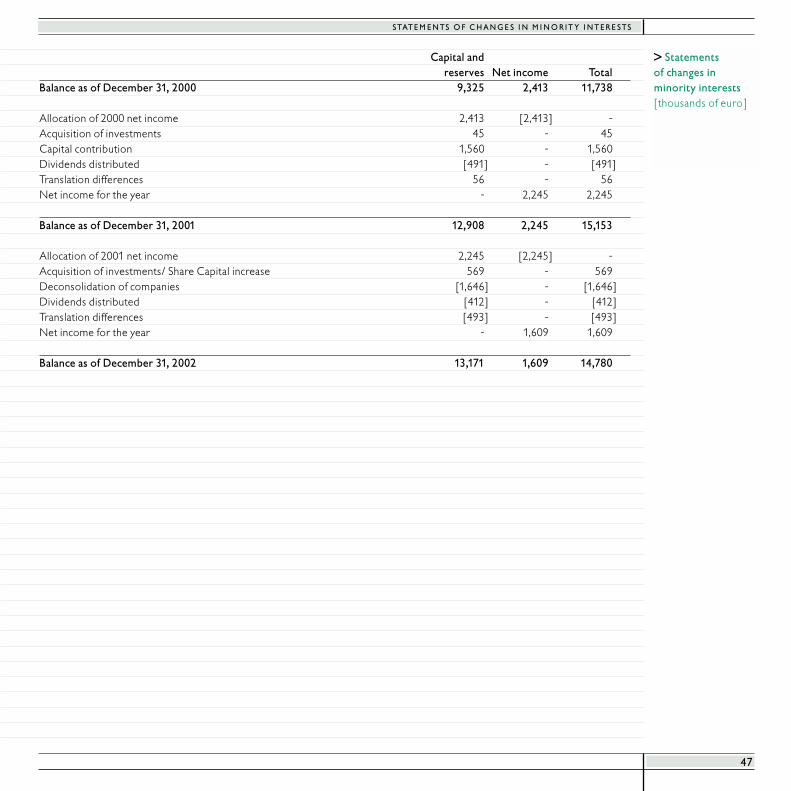

STAT E M E N TS O F C H A N G E S I N M I N O R I T Y I N T E R E STS

Capital andreserves Net income Total

Balance as of December 31, 2000 9,325 2,413 11,738

Allocation of 2000 net income 2,413 [2,413] -Acquisition of investments 45 - 45Capital contribution 1,560 - 1,560Dividends distributed [491] - [491]Translation differences 56 - 56Net income for the year - 2,245 2,245

Balance as of December 31, 2001 12,908 2,245 15,153

Allocation of 2001 net income 2,245 [2,245] -Acquisition of investments/ Share Capital increase 569 - 569Deconsolidation of companies [1,646] - [1,646]Dividends distributed [412] - [412]Translation differences [493] - [493]Net income for the year - 1,609 1,609

Balance as of December 31, 2002 13,171 1,609 14,780

> Statements of changes in minority interests [thousands of euro]

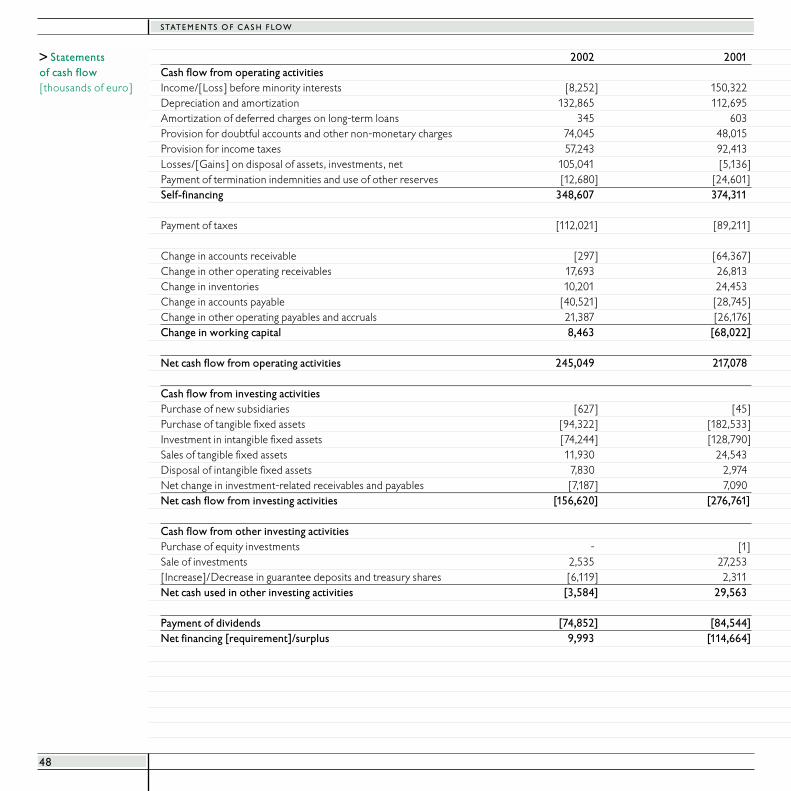

STAT E M E N TS O F C AS H F LOW

48

2002 2001Cash flow from operating activitiesIncome/[Loss] before minority interests [8,252] 150,322Depreciation and amortization 132,865 112,695Amortization of deferred charges on long-term loans 345 603Provision for doubtful accounts and other non-monetary charges 74,045 48,015Provision for income taxes 57,243 92,413Losses/[Gains] on disposal of assets, investments, net 105,041 [5,136]Payment of termination indemnities and use of other reserves [12,680] [24,601]Self-financing 348,607 374,311

Payment of taxes [112,021] [89,211]

Change in accounts receivable [297] [64,367]Change in other operating receivables 17,693 26,813Change in inventories 10,201 24,453Change in accounts payable [40,521] [28,745]Change in other operating payables and accruals 21,387 [26,176]Change in working capital 8,463 [68,022]

Net cash flow from operating activities 245,049 217,078

Cash flow from investing activitiesPurchase of new subsidiaries [627] [45]Purchase of tangible fixed assets [94,322] [182,533]Investment in intangible fixed assets [74,244] [128,790]Sales of tangible fixed assets 11,930 24,543Disposal of intangible fixed assets 7,830 2,974Net change in investment-related receivables and payables [7,187] 7,090Net cash flow from investing activities [156,620] [276,761]

Cash flow from other investing activitiesPurchase of equity investments - [1]Sale of investments 2,535 27,253[Increase]/Decrease in guarantee deposits and treasury shares [6,119] 2,311Net cash used in other investing activities [3,584] 29,563

Payment of dividends [74,852] [84,544]Net financing [requirement]/surplus 9,993 [114,664]

> Statements of cash flow[thousands of euro]

49

STAT E M E N TS O F C AS H F LOW

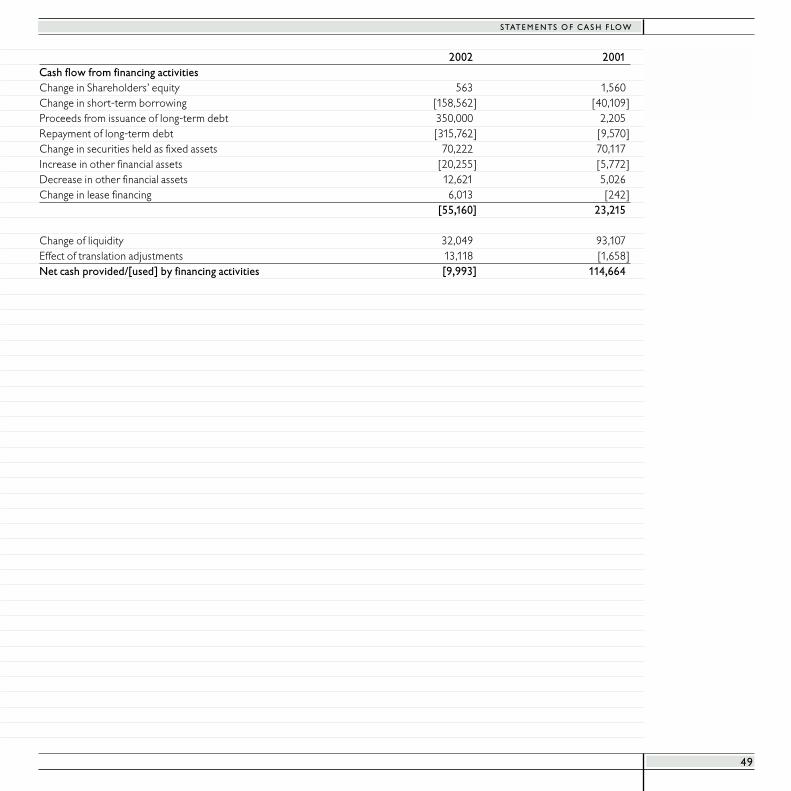

2002 2001Cash flow from financing activitiesChange in Shareholders’ equity 563 1,560Change in short-term borrowing [158,562] [40,109]Proceeds from issuance of long-term debt 350,000 2,205Repayment of long-term debt [315,762] [9,570]Change in securities held as fixed assets 70,222 70,117Increase in other financial assets [20,255] [5,772]Decrease in other financial assets 12,621 5,026Change in lease financing 6,013 [242]

[55,160] 23,215