Embed Size (px)

Citation preview

BI3221 Multinational BusinessManagement

Section: 405

Prepared by:

Shenyuan Qiu

473-5195

Katchaporn 461-

4619

Yaoyao 462-

5249

Giao Quynh Thi Vo

463-5259

Xue Tang

455-1051

Suttikit N.

461-0616

Rit Subsomboon

461-8511

Teera R.

461-5171

Minwoo Park 461-1186

1

Introduction

This paper is going to show you how 7-Eleven would enterVietnam market, beginning from main and capital cities inVietnam.

This paper is consisted by three parts: 1) introduction andcompany analysis of 7-Eleven; 2) industry and competitiveanalysis; 3) international strategic plans.

In the first part, we show how 7-Eleven is running now, whathappened to it in the past and what its future aim is andwhy it is going to Vietnam market based on SWOT analysis.

The second part defines the competencies to 7-Elevenentering Vietnam by Porter’s Five Forces Model. And it givesus key competitors’ analysis globally and domestically.

The last part is a plan how 7-Eleven will enter Vietnambased on international strategy by master franchising. Theorganization structure will be shown by a chart andelaborated. Then, the human resource process will bedetailed based on ethnocentric company policy.

In the appendix, a brief introduction of whole Vietnameconomy situation is given.

2

Company Analysis

Background of 7-Eleven

The Story of Convenience Shopping7-Eleven pioneered the convenience storeconcept way back in 1927 at theSouthland Ice Company in Dallas,Texas. In addition to selling blocksof ice to refrigerate food, anenterprising ice dock employee beganoffering milk, bread and eggs on Sundays and evenings whengrocery stores were closed. This new business idea producedsatisfied customers and increased sales, and convenienceretailing was born!

The company's first convenience outlets were known as Tote'mstores since customers "toted" (orcarry) away their purchases, and someeven sported genuine Alaskan totempoles in front. In 1946, Tote'm became7-Eleven to reflect the stores' new,extended hours - 7 a.m. until 11 p.m., seven days aweek. The company's corporate name was changed from TheSouthland Corporation to 7-Eleven, Inc. in 1999.

Today, 7-Eleven is the undisputed leader in convenienceretailing with more than 27,900 stores operating in the U.S. and 17other countries and total sales of more than $36 billion in 2003.

Business Operations

3

More than 5,800 7-Eleven and otherconvenience stores are operated andfranchised by 7-Eleven, Inc. in theUnited States and Canada, and theyserve approximately six millioncustomers each day.

Each store focuses on meeting the needs of busy shoppers byproviding a broad selection of fresh, high-quality products and services ateveryday fair prices, along with speedy transactions and a clean, safe, friendlyshopping environment.

Proprietary Products7-Eleven is known internationallyfor Big Gulp fountain soft drinks,Big Bite hot dogs, Slurpeebeverages, and Café Select freshbrewed coffee. The stores haveexpanded their food service offeringswith a proprietary line of deli items and baked goods, which are prepared and delivered fresh daily.

7-Eleven also offers convenient services based on each neighborhood's individual needs, including automated money orders, copiers, fax and automatic teller machines, long-distance phone cards and lottery tickets, where available.

Global Convenience

4

Approximately 3,200 of the company's 5,300 stores in the United States are operated by franchisees, and an additional485 are operated by licensees. 7-Eleven, Inc., its licenseesand affiliates operate more than 27,900 7-Eleven and other convenience stores in Japan, Australia, Mexico, Taiwan, Singapore, Canada, the Philippines, Sweden, Denmark, South Korea, Thailand, Norway, Turkey, Malaysia, China and the U.S. territories of Puerto Rico and Guam.

IYG Holding Company, a wholly owned subsidiary of Ito-YokadoCo., Ltd. and Seven-Eleven Japan Co., Ltd., has owned a majority interest in 7-Eleven since 1991. Seven-Eleven Japanoperates more than 10,000 7-Eleven stores in Japan and Hawaii under an area license agreement with 7-Eleven, Inc.

In 2005, 7-Eleven, Inc. celebrated its 78th birthday.

Company Milestones

Over 78 years, 7-Eleven has accomplished a number ofmilestones. Here is an overview:

1927

The Southland Ice Company is founded in Oak Cliff,TexasTote’m stores introduced

192 Tote’m stores begin selling gasoline

5

81946

7-Eleven® store name introduced because the stores areopen 7 a.m. until 11 p.m.

1949

“Owl & Rooster” television commercial introduced: firstfor a convenience store chain

1952

100th store opening

1954

First store opened outside of Texas (Florida)

1958

First cold weather store opened in the northeast(Virginia)

1960

500th store opening

1963

1,000th store opening7-Eleven purchases Speedee Mart in California andenters into franchisingFirst 24-hour operation introduced (Austin, TX and LasVegas, NV)

1964

Coffee-to-go introduced in Long Island, NY

1966

Slurpee® frozen beverage introduced

1968

First domestic area license signed

1969

“Oh Thank Heaven for 7-Eleven” campaign introducedFirst Canadian store opened

1971

First $1,000,000,000 sales yearFirst store opens in MexicoFirst entry into the European market (England &Scotland)Self-serve gasoline introduced

1974

First store opens in Japan

6

1979

First $1,000,000,000 sales quarter

1980

7-Eleven International opens 1,000th store

1984

Super Big Gulp® is introduced (44-ounce fountain softdrink)ATMs introduced to convenience stores7-Eleven International opens 2,500th store

1988

Oscar Mayer Big Bite® Hot Dogs (proprietary brand)introduced7-Eleven International opens 5,000th store

1991

Revitalization of 7-Eleven beginsDeli Central™ introduced (proprietary sandwiches)World Ovens® pastry introduced (proprietary bakeryitems)

1993

7-Eleven International opens 7,500th store

1995

Company opens its 15,000th store

1996

7-Eleven Mexico celebrates its 25th Anniversary7-Eleven International opens 10,000th store

1997

Café Select® coffees introducedRetail Information System rollout begins

1998

Café Cooler™ introduced (proprietary frozen cappuccino)Financial Services Centers introduced

1999

The Southland Corporation changes name to 7-Eleven,Inc.Früt Cooler™ introduced (proprietary low-fat smoothie-like fruit drink)7-Eleven International opens 12,500th store

2000

20,000th store opens (Tokyo)7-Eleven International opens its 15,000th store

7

7-Eleven is re-listed on the New York Stock Exchange2001

Vcom™ kiosk, the next generation of financial servicecenters, is introduced in Texas and Florida7-Eleven raises more than $2 million for the Red Crossto assist victims of the September 11 terrorist attacksStore of the Future Lab opens in Dallas, TX

2002

7-Eleven achieves $10,000,000,000 in revenue7-Eleven Celebrates its 75th AnniversaryFirst sugar-free Slurpee drink introduced nationallySlurp & Gulp Introduced7-Eleven Australia celebrates its 25th Anniversary7-Eleven begins rollout of Vcom kiosks in 1,000 of its7-Eleven stores in the United States

2003

7-Eleven International opens its 20,000th storeSeven-Eleven Japan observes 30th anniversary as 7-Eleven's first overseas licensee7-Eleven introduces its first proprietary import beer -Santiago7-Eleven offers nationally its own stored value cardcalled the 7-Eleven Convenience CardCompany opens its 25,000th store – celebration notingmilestone held in July at a downtown Chicago storegrand opening

2004

7-Eleven offers Atkins and other controlled-carbohydrates products7-Eleven launches new online Vendor/SupplierApplication process in March7-Eleven opens stores in Beijing, China, in April7-Eleven sells Cityplace headquarters building in April7-Eleven introduces new Franchise Agreement in March7-Eleven becomes first retailer to offer its ownprepaid wireless program, called 7-Eleven Speak Out™wireless

8

Management Team7-Eleven, Inc., founded in 1927 inDallas, Texas, is the world's largestoperator, franchisor and licensor ofconvenience stores with more than 27,900units worldwide, including 5,800 in theUnited States and Canada, the c-storeretail pioneer serves six millioncustomers a day.

The company's success is due in part to the 7-Elevenmanagement team, a talented group of individuals who havebeen able to effectively evaluate challenges and quicklyrespond to opportunities.

9

Customers & Products

Why choose Vietnam

Vietnam is a young, changing, and active country. During thelast ten years, Vietnam’s economy improved very fast. It wasthought as the best one in Asia by many economists. Vietnamattracts lots of foreign direct investments, which goesbeyond its GDP of last year 8% while using foreigninvestment as the standard.

When foreigners visit Vietnam, we find that there is noconvenient stores available there, let alone 24-houroperation. It is a brand new idea to have 24-hour convenientstores for Vietnamese. If we say there is at least a fewcompetitions, we believe that it is from local people cannotaccept the new living style right away. And this problemcould be solved by penetration and foreign consumers’mobilization because most visitors in Vietnam expect a 24-hour convenient store.

On the other hand, the traditional stores and localconvenient stores cannot satisfy people any more. Whenpeople feel hungry or want some medicine in case ofemergency after midnight, they cannot get any services orhelp since lack of convenient stores around them. Thus, wesee there is a diet need of 24-hour convenient stores inVietnam.

Fast economic development with relatively more stablesociety gives higher living standards to Vietnamese, whichis a precious chance to us as well. Vietnam is our nexttarget market; we are going to bring more convenient andmodern living style and culture to Vietnamese.

Customers

10

7-Eleven group is one of the most famous and successfulmultinational company which runs business with franchisingand licensing. In Vietnam, because of its particular type ofinternational business and strategies, it has several targetgroups of customers that are mainly divided into businesscustomers and end-consumers.

When 7-Eleven group plays in the role of franchiser, thereare three types of customers:

1. Vietnamese who want to be the owners of theconvenience stores that have an efficient andacceptable pattern of the improved ones;

2. Vietnamese who are already the owners of the localgrocery shops, but they want to improve theperformances and efficiency of theirshops by being franchisees under thebrand of 7- Eleven;

3. The biggest group of end-consumers is localVietnamese and expatriates who work and live inVietnam.

When 7-Eleven group plays in the role of the conveniencestores, the customers of these shops are ultimate consumerswho use the products. They will play this role byestablishing their own stores in Vietnam. These stores arepresented to be the sampling stores to show the efficiencyand performance to local people who are in the first twogroups of customers. (This will be the plan to advertise theshop, too)

Finally, 7-Eleven groups will be the franchiser in Vietnam.In this part, their business customers are the large andwell-known company who run their business in many areas ofVietnam. This type of customer seems to be similar to apartner in other contracts because 7-Eleven group uses this

11

one to be the leader of the outlets in this geographicalarea. It has the right to evaluate and control performance,standard and efficiency of the outlets in the area(Vietnam).

These target groups will be use in the urban, communityareas and business centers in the first step that they beginto run business in Vietnam. The next step, they willincrease outlets in the rural area by focusing on the firsttarget group hopefully.

12

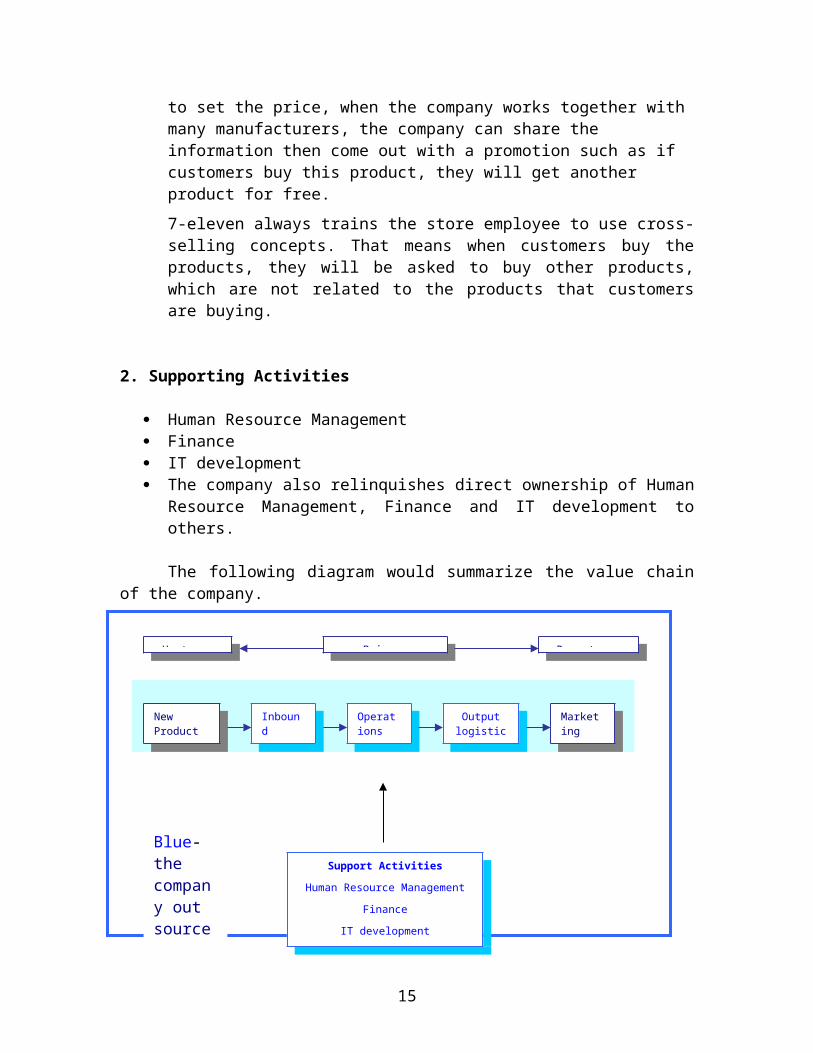

Generic Strategy Based on ValueChain AnalysisTo develop competitive advantage and formulating the mostappropriate generic strategy, understanding activities ofthe firms is very important. To understand activities of thefirm, it is useful to separate its activities into valuechain analysis initiated by Michael E. Porter.

Main Activities of 7-Eleven

1. Primary Activities

New Product Development

We call this first activity in the value chain asproduct selection. Although 7-Eleven does not producephysical goods itself (this will be discussed later inthe outsourcing topic), 7-Eleven does not allow thefirms that 7-Eleven outsource to produce the productsto make critical decisions about order quantities orshelf placement. Rather, the retailer will use the dataon customer purchasing patterns to make decision.

7-Eleven is capable of getting such data by two ways.The first is from outside vendor. Secondly, the companywill look into customer buying pattern. Then, thecompany will distinguish products, which are the fast-moving item and slow-moving item.

After getting the data, the company will formatcustomer purchasing behavior data. This will give thefirm a mix of product and customer wants.

Inbound Logistics and Operations

13

The firm lets others to produce the products for thefirm instead of producing by itself. For example, thecompany makes a close relationship with Frito-Lay sincesnack food is one of the most profitable product linesfor the firm, not only for 7-Eleven but also otherconvenience stores. 7-Eleven allows Frito-Lay todistribute its products directly to the stores.

Moreover, 7-Eleven also shares its information with aselected group of suppliers, allowing them to producesome products that are unique for 7-Eleven. Forexample, 7-Eleven worked with Hershey and Coca-Cola andcame up with Twizzler-flavoured products, which arenormally, called Slurpee drink.

The activities that we are going to discuss are thecore activities that 7-Eleven should concentrate on.Briefly, these activities are quiterelated to merchandising concept,which is to buy and sell goods by advertisingor displaying.

Outbound Logistics

Outbound logistics is warehousing and distribution offinished goods. From our analysis, there are two means:

Firstly, outbound logistics of 7-Eleven means thecompany that produce products for 7-Eleven todistribute products directly to its stores such asFrito-Lay.

The second is combined distribution centre.7-Elevenworks with its distributors to distribute productespecially fresh goods such as sandwiches and milk.

Marketing and sales 7-eleven promotes its products mostly through advertising. Although the company dose not have a right

14

to set the price, when the company works together with many manufacturers, the company can share the information then come out with a promotion such as if customers buy this product, they will get another product for free. 7-eleven always trains the store employee to use cross-selling concepts. That means when customers buy theproducts, they will be asked to buy other products,which are not related to the products that customersare buying.

2. Supporting Activities

Human Resource Management Finance IT development The company also relinquishes direct ownership of Human

Resource Management, Finance and IT development toothers.

The following diagram would summarize the value chainof the company.

Why does the company outsource other companies?

15

New Product Developm

Inbound Logist

Operations

Outputlogistic

s

Marketing and

Upstream Primary Downstream

Support Activities

Human Resource Management

Finance

IT development

Blue- the company out sources

Before 1991, 7-Eleven had been losing both profit and marketshare. There were probably two main reasons. Firstly, theconvenience store industry was highly competitive. As themajor Oil Company tried to add mini-marts to their gasstations, the convenience store industry was becomingcrowed. Second, 7-Eleven was trying to do many things andwas not good at any of them, controlling most of theactivities in the value chain. The company, for instance,made it own candy and ice. It even owned the cows thatproduced the milk. Actually, as a nature of the company, itshould had focused on merchandising but it tried to doeverything. The company did lose both profit and marketshare due to high cost.

Consequently, the company needs outsourcing because it canbe better at every activity. It should concentrate onmerchandising. When the company uses outsourcing, it canreduce the cost and increase profit. That means company isimplementing low cost strategy. The company does deliverproducts equal to its competitors but it is capable ofproducing products more efficiently. That is, it can lowerthe cost of their production by outsourcing.

How does outsourcing help 7-Eleven to achieve LowCost Strategy?

The activities that the firm lets others do can help thecompany to reduce its cost, as the company cannot do thoseactivities as good as others. If the company insists to dothose activities by itself, the company would suffer from ahigh cost. It is clearly shown that before 1991, 7-Elevenwas not successful because of this reason. When the companyoutsources others to do, the company can use the capabilityto concentrate on core activity, which is merchandising.

Comparing the revenue and profit that the company can getnow with pre-1991, we find that when the company changed thepolicy to outsource other company to do some activities that

16

7-Eleven is worse, it can be a leader in the market of thisindustry.

Another example is, when the company outsources, usingcombined distribution centre, the company is capable ofreducing its costs from more than 15 percent of revenues to10 percent.

17

Company’s distinctive competencies

We think that the first activity in the value chain is theactivity that the company can perform best in accordancewith the following resources and capabilities.

Resources

Retail information system is the main resource that thecompany has.

This system will provide store managers with a model to helpthem make a decision to order right products at a righttime. Store managers should know which products are fast-moving products or slow-moving products. For fast-movingitems, the company would keep such items in stock with alarge volume.

The system also has weather pattern to help store managersto forecast if and how many certain products will bedemanded on the next day such as selling more hot coffeeduring colder days. Therefore, they would know the buyingtrends of each product and they can know which products theyought to stock and order. By this way, the company caneasily maximize store sales.

CapabilitiesThe system that the company uses cannot go well if thecompany does not have good staff and workers.

Although the system above can facilitate the company to makebetter decision on new products more easily, it isimpossible to rely only on the system. The skills of workers

18

are very important. The task is not easy, however.Consequently, 7-Eleven concentrates much on training forstore managers including classroom and on-the-job training.

The above resources and capabilities can help the company toachieve low cost strategy as the company can perform thefirst activity in the value chain better than others.

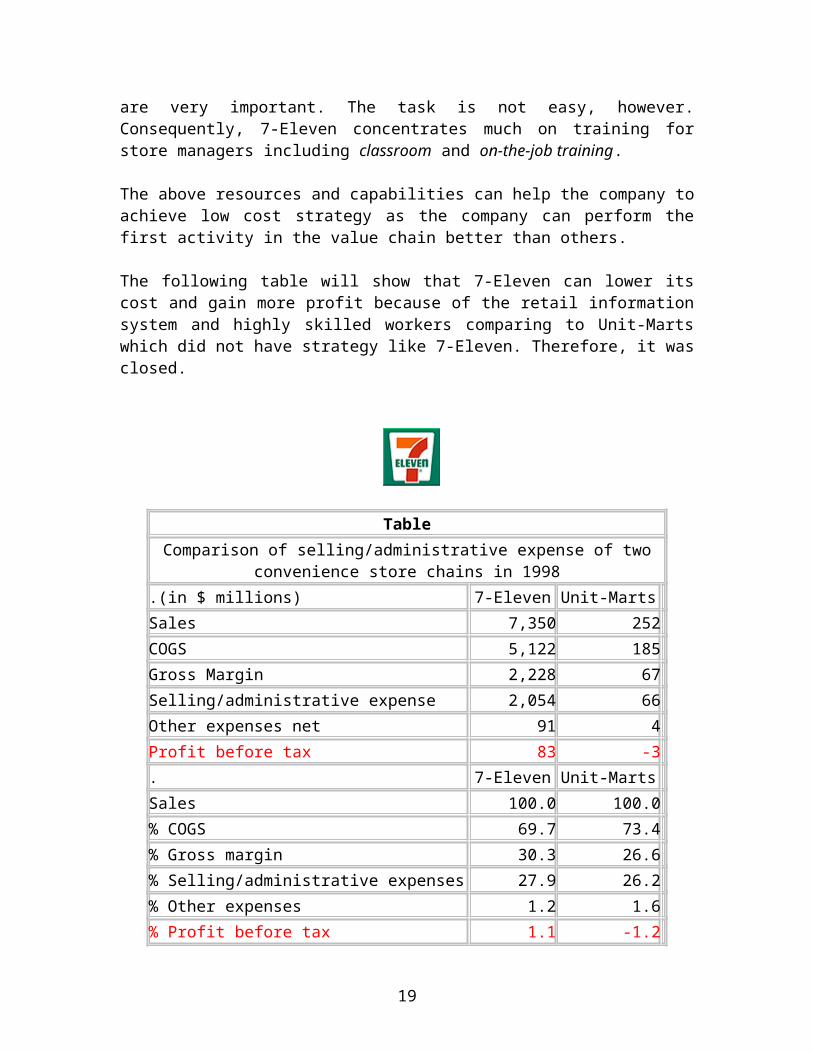

The following table will show that 7-Eleven can lower itscost and gain more profit because of the retail informationsystem and highly skilled workers comparing to Unit-Martswhich did not have strategy like 7-Eleven. Therefore, it wasclosed.

Table Comparison of selling/administrative expense of two

convenience store chains in 1998.(in $ millions) 7-Eleven Unit-MartsSales 7,350 252COGS 5,122 185Gross Margin 2,228 67Selling/administrative expense 2,054 66Other expenses net 91 4Profit before tax 83 -3. 7-Eleven Unit-MartsSales 100.0 100.0% COGS 69.7 73.4% Gross margin 30.3 26.6% Selling/administrative expenses 27.9 26.2% Other expenses 1.2 1.6% Profit before tax 1.1 -1.2

19

SWOT

Strengths:

A very good reputation;

A reliable and fresh assortment of high-qualityproducts;

Speedy transactions;

Everyday fair prices;

24-hour opening;

Helping society to deal with unemployment and someother social issues;

A clean, safe and friendly environment in which toshop;

A stable company;

Provides Franchisees with a proprietary retail computersystem that gives them valuable store information in anaccurate, timely manner.

Weaknesses:

Large franchise fee which is averaging approximately$70,000;

Opportunities:

Tariff of Vietnam is lowering year by year. Vietnam'sweighted average tariff rate in 2004 was 13.7 percent,down from the 17.4 percent for 2001 reported in the2005 Index, based on World Bank data;

21

More purchasing power, according to much higher GDP andGDP per capita;

Fiscal burden is getting lower because of GDP increased2.6 percentage. The top corporate tax is 29% in 2003.

Threats:

Culture conflict. Vietnamese may not accept this kindof modern convenience store at first;

Inflation rate is high. From 1995 to 2004,Vietnam's weighted average annual rate ofinflation was 5.98 percent, up from the 2.96percent from 1994 to 2003 reported in the2005 Index;

Limited foreign employees. All enterprises operating inVietnam are limited to employing foreign nationals atthe lesser of: (1) a maximum rate of 3 percent of theirtotal work force; or (2) 50 persons."

Restrictions on foreign exchange accounts and moneytransferring. The International Monetary Fund reportsthat both residents and non-residents may hold foreignexchange accounts, subject to restrictions andgovernment approval for resident accounts held abroad.Payments and transfers face restrictions, includingrequirements for government approval over establishedamounts. Most transactions in money market and capitalinstruments, derivatives, commercial credits, anddirect investments either are prohibited or requiregovernment approval. Foreigners may not own land butcan lease it from the government;

Government intervention and corruption. The World Bankreports that the government consumed 6.9 percent of GDPin 2003. In the same year, based on data from theInternational Monetary Fund, Vietnam received 12.12

22

percent of its total revenues from state-ownedenterprises and government ownership of Property.According to the Economist Intelligence Unit, however, Vietnam has over 5,000 state-ownedenterprises, and the "state-owned sector generates 41%of industrial output?" The state is involved infinance, telecommunications, energy, and manufacturing.Based on the apparent unreliability of the figure forgovernment consumption, corruption is very serious.

23

Industry and CompetitiveAnalysis

Competitor Analysis

Domestic Competitor

Vietnam’s mass grocery retail sectors, which generated US$87 million in sales 2003, is set to experience significantgrowth, with sales forecast to increase by more than 100% by2007, rising to around US$175 million.

The retail food sector in Vietnam has until recently beencharacterized almost exclusively by numerous wet markets,corner grocery and sundry shops ("mom and pop stores") andtemporary stalls that are ubiquitous in Vietnamese citiesand towns. Estimates are that Ho Chi Minh City alone has6,000 small private shops selling groceries and sundries andas many as 2,000 wet markets. A similar situation prevailsin Hanoi. Despite their market domination, domestic foodproducts are for the most part of inferior quality. With afew notable exceptions, these products are attractive toVietnamese consumers because of the lower price and closinglocation with their houses. Moreover, the corner shops arealready become their purchasing tradition and keep from onegeneration to another.

Thus, the domestic competitors of 7-Eleven are made up withmany small individual convenience stores and localtraditional grocery stores in Vietnam. As almost all of thedomestic competitors are composed with many small individualconvenience stores which situated in neighborhood areasacross Vietnam, so their main strategic intent is to retain

24

its business position and market share in each of theirareas.

The generic strategy that most of domestic competitors fromVietnam adopt is the Low Cost Strategy. It is due to the factthat Vietnamese consumers prefer to buy goods or to consumefrom the convenience stores which provide the lowest sellingprice to them. With the fact that each of small individualconvenience store trying to provide the lowest price as theycan, so it can be expected that they will tend to use theoffensive competitive strategy of direct attack of lowpricing to fight and fend off their rivals within the samearea.

And as for the domestic competitors current position, eventhough they are all in the growing retail market of Vietnamwhich seem to be profitable to them but due to the lack ofmany competitive factors such as good financing andmanagement, so they are all in the stagnant state. If thesituation continues to go on, these small individualconvenience stores (domestic competitor) willlose their standing in the growing retail market.

Global Competitor (Family Mart)

As for the global competitor, the chosen global competitoris Family Mart. It is due to the fact that Family Mart iswell-known and has been actively expanding its businesswithin Pan-Pacific area. And if 7-Eleven wanted to invest inVietnam region, it may have to compete with Family Martwhich has already established its wide based within thisregion. The Family Mart’s basic strategic intent is to bewell known company for quality products in retailingindustry which will establish good ties to its consumers.And the end result that Family Mart desires is its storeswill be competitive with high consumer loyalty.

The generic strategies that Family Mart will adopt are boththe low cost strategy and differentiation strategy by

25

proving higher quality of product, broad product line andetc in order to gain its competitive advantage over itscompetitors in the global market. In order for the FamilyMart to be even more successful, it will also implement inoffensive strategies of direct attack by establishing higherquality for its products and stores. Other than the directattack, Family Mart also using end-run offensives strategyin which Family Mart will target untapped markets around theglobe. As for the defensive strategy aspect, the Family Martis also going to use counter-parry strategy as it has a planto enter US market (7-Eleven home based) to capture some ofthe US market share. And if it were to do so, it would be abig threat to 7-Eleven.

At the present moment, Family Mart is having 11,501 storesaround the globe especially in the Pan-Pacific region andstill keeping increasing. In addition, in 2005 Family Martis also having net income of 120 millions USD which growsteadily from previous years; they are able to increasetheir earning steadily. Furthermore Family Mart is alsohaving a good foundation in home country, Japan, whichconstitutes of 6,424 stores. With the above situations, itcan be concluded that Family Mart is having high marketshare around the globe in total especially when consideringonly within Pan-Pacific region.

26

Porter’s Five Forces Model

1. Internal Rivalry

1.1 Industry Growth A big population and growing disposable income fuelledby strong economic growth and an increasing volume oftourist spending resulted in retail sales growth by ahealthy 9.1% in current value terms over 2002 to reachVND241312 billion in 2003 and continues to grow. In agrowing market, firms do not need to fight for marketshare and are able to improve revenues simply becauseof the expanding market. Even though the rapid growthbrought many firms to the retail sector, those firmsfocused on large size grocery stores not small sizeconvenience stores.

1.2 Brand Identity Household-owned retail shops can be found everywhere inVietnam. Wet markets and independent grocers still playa traditional role in selling food to meet daily basicneeds while modern outlets are mainly used for non-fooditems. Since most of food items are sold through wetmarkets and independent grocers and they are in form ofhousehold-owned shops, these shops do not have certainbrand identifications.

1.3 Concentration Up until now, modern retail outlets have been mainlyconcentrated in developed cities and they do not coverthe entire country. Only household-owned retail shopscan be found in rural areas and they are not opened 24hours a day.

2. Entry Barriers

27

1.1 Government Policy Investors face underdeveloped and cumbersome legal andfinancial systems, an unwieldy bureaucracy, non-transparent regulations, high start-up costs, arcaneland acquisition and transfer regulations andprocedures. Issuance of investment licenses andimplementation of projects often is a lengthy processduring which the investment environment in areas suchas taxes and procedures frequently changes.

1.2 Access to Distribution Vietnam still has a poorly developed infrastructurewhich causes difficult access to distribution. Everyfirm entering Vietnamese retail industry needs toensure its access to distribution channels.

1.3 Capital Requirements

Due to the underdeveloped government policy and poorlydeveloped infrastructure of Vietnam, any foreign firmentering Vietnam will need high start-up capital.Convenience store chains with strong financial powerare limited e.g. 7-Eleven, Family Mart.

3. Substitutes Threat

1.1 Relative Price and Performance of Substitutes Relative price and performance of commodity productsare similar. Consumers tend to choose conveniencerather than price or performance in purchasingcommodity products.

1.2 Switching Costs Switching retail outlets cost zero virtually. But itwill cost time to move to another outlet.

1.3 Buyers’ Tendency to Substitute

28

Buyers do not tend to substitute retail outlets whenthey purchase commodity products because most ofcommodity products are low-involvement products.

4. Supplier Power

1.1 Differentiation of InputsCommodity products are standardized products. Thus,inputs by suppliers are similar and have just a littleor no differentiation. This fact is interpreted assuppliers’ low bargaining power.

1.2 Substitute Inputs Since commodity products are manufactured by manyfirms, it would not be difficult to substitutesuppliers.

1.3 Level of Supplier Integration by Main Firms Suppliers of commodity products manufacture severalkinds of products (narrow range) while conveniencestores carry a moderate number of items. Thus, it isdifficult for suppliers of commodity productsmanufacturers to integrate forward to retail sector.

5. Buyer Power

1.1 Buyer concentration Buyers are fragmented and no buyer hasany particular influence on product pricebecause every person needs commodityproducts. There is no buyer concentration inretail sector in Vietnam.1.2 Switching Cost Switching cost is virtually for standardized products(commodity products). Consumers only need time to moveto another retail outlet.

29

1.3 Price Sensitivity Commodity products price sensitivity in developingcountries is higher than in developed countries becausedisposable income in developed countries is higher.Commodity products are easily substituted by consumers.As a result, consumers are very price sensitive.

30

International Strategic Plans

Multinational strategy: International strategy

While 7-Eleven group operates the franchising activities, itis standardized. There is only little need for adaptationand development in its services and 7-Eleven group also canlet its master franchisees in each country manage theseadaptation and development in term of promotion,advertisement, and local products in an outlet. On the otherhand, the company focuses on the other side that is toachieve the economies of scale, cost reduction, and locationadvantage.

Because of this, the company has decided to use theinternational strategy to be its multinational strategy. Aswe present before, the company will find the large localcompany, which becomes its master franchisee in Vietnam, tomake a contract with and let this firm manage operation,adaptation and development in term of promotion,advertisement, and local products in an outlet in the areaof permission. The headquarter of 7-Eleven will communicateand monitor the performances in Vietnam through itsinternational division without foreign subsidiary, but thecompany will deal with the master franchisee to establishthe special division in its firm (without real asset) whichhas a duty to link the communication and cooperation between7-Eleven group and its master franchisee. This method willmake the smooth and efficient communication.

Advantages:

1. Low initial cost;

2. There is only one responsible manager who deals withthe contact. (Less confusion);

31

3. The firm can create co-brand easily.

Problems that may occur:

1. The company loses the control;

2. It takes longer time for responses from headquarter ineach communication.

The reason for using International Strategy:

To decide our participation strategy in Vietnam market, wehave to consider various problems.

Global market

Recently, the global consumers’ needs are getting similarand converging especially the consumer goods. Due to ourfranchising store’s main products are consumer goods suchlike beverages, snacks and commodity, Best of all, 7-ElevenFranchisees receive assistance and support along the way.

On the other hand, 7-Eleven® is among the world's premiereconvenience store retailers with a long and proud historythat dates back over 75 years. We have been a leader in thefranchise industry for over 40 years. The 7-Eleven FranchiseSystem is like no other in the country. It is a provenretail operation with a world-famous trademark, and the 7-Eleven Franchise System has received a number of accoladesfor its business performance and franchising opportunities.That means we will still use our quality brand name inVietnam market.

It is absolutely a good chance for us to attract Vietnamgrocery owners to join in our franchising system within areasonable average initial cash investment.

Costs

32

The 7-Eleven Franchisee is responsible for ordering, buyingand maintaining inventory; hiring and training employees, aswell as payroll, cash variation, supplies, certain repairs,maintenance and other controllable in-store expenses.

Since this is the first time for us to enter Vietnam, toreduce the conflict between two countries, we decided to usemaster-franchising system to handle the different cultureproblems, which is means we just have to communicate withonly one local company and it will help us to settle everyfranchising procedures and provide feedback to us.

Both two operating process help us to save a lot ofinvestment and time, and it really helps us to save ourdevelopment cost.

Government

Although the new commercial law of Vietnam is more favor forforeign investors, but for franchising, this is the firsttime Vietnamese commercial laws deal with this issue. Thatwhy we will use master-franchising system to avoid suchcomplicate political problems. Depend on their specificlocal knowledge and local relationship, it will help us tooperate our franchising system more efficiency and minimizethe government intervention.

Competition

We will be the first mover of franchising convenience storein Vietnam. Before that, the main competitors for us arelocal corner groceries, vendors and some foreign mini-supermarkets. Even they are offering lower price, we willfocus on standardize management for our franchisees andprovide widely distribution for local consumers, which alsohelp us to ensure our competitive advantage.

33

Based on above factors, we know we can serve the Vietnam’scustomers as we have done in other countries. Because we canuse our world-famous brand name and efficiently control ourrunning costs, we decided to use International strategy. Butto better manage our franchising system in Vietnam, all ofsupport activities will be concentrated at the US homecountry.

34

Participation Strategy: Master-Franchising

Master-FranchisingMaster-Franchising is an effective way of enteringVietnamese market since it offers a very large return oninvestment with lowest risk. As the first part said, 7-Eleven headquarter is looking for a big company whose credtand financing must be very good and is involved in severalor many industries. On the other hand, it may controlsuppliers or have the ability to be the supplier for 7-Eleven convenience stores. 7-Eleven is going to grant it tofind more local franchisees in Vietnam. So the model issimilar to what Thailand CP Company is doing.

The products sold at 7-Eleven are commodity products whichare standardized and are low-involvement products. For thiskind of products, price competitiveness and productadaptation are key success factors. Thesub-franchisee/master franchisee, the domestic company, haslow cost of production and purchasing because of itseconomies of scale and well-established supplier network;furthermore, the product adaptation is not needed. Marketingeffort made by the franchisee with its accumulated marketknowledge would be also beneficial.

Another obstacle of entering Vietnamese market directly isthe Vietnamese government policy. Investors faceunderdeveloped and cumbersome legal and financial systems,an unwieldy bureaucracy, non-transparent regulations, highstart-up costs, arcane land acquisition and transferregulations and procedures. Thus it is much easier to enterwith a large domestic partner who has well-establishedlinkage with the government officials who could help tosmooth the progress of operation in Vietnam. Neverthelesslicensing also has some risks such as limited form ofparticipation or franchisee becoming competitors. To avoidthese risks, it is recommended that the franchiser should

35

try to keep options to buy into partner exist or provisionto take royalties in stock.

Rationale for not choosing alternative entry modes:Exporting:

The costs that 7-Eleven has to pay for exporting such astransportation, tariff, etc. are very high. Hence, theycannot achieve economies of scale which is very importancein this type of industry.

Moreover, the products that are produced in US are moreexpensive than Vietnam due to the high labor cost.Therefore, when it is imported to Vietnam, it cannot competewith domestic products which are much cheaper and similar inquality.

The most importance thing that 7-Eleven cannot use exportingas its strategy is the useful life of products.Because most of products which are sold at 7-Eleven are perishable and the time that is requiredto ship the products from US to Vietnam is quitelong.

International Strategic Alliance:

Since the cultural values of Vietnamese and American aretotally difference. If 7-Eleven find one company in Vietnamto co-operate, the cultural conflict may occur.

7-Eleven is a large and well-known multinational companyover the world. It is difficult to find a company which hascomparable size to 7-Eleven in Vietnam. Thus, the “elephant-and-ant” complex might be happened. It will lead to theresult that 7-Eleven will dominate and control thestrategies, management of the alliance since 7-Eleven is thelarger company. As the result, the co-operation cannotmaintain for a long time.

36

Foreign Direct Investment:

If 7-Eleven want to do direct investment in Vietnam, it hasto spend a lot of money to invest in capital, physicalfacility or manufacturing, etc. There will be so adventureand cost a lot to 7-Eleven since most of Vietnamese belongto uncertainty avoidance group. They will not accept a newbrand immediately, so that 7-Eleven has to take a long timeto increase its brand equity. Thus, it may take long time tobreak even.

The tax that Vietnam will charge on 7-Eleven is higher thandomestic firm. So that, 7-Eleven cannot compete withdomestic firms due to the higher costs.

Moreover, foreign investors face underdeveloped andcumbersome legal and financial systems, an unwieldybureaucracy, non-transparent regulations, high start-upcosts, arcane land acquisition and transfer regulations andprocedures.

37

Part IV c)

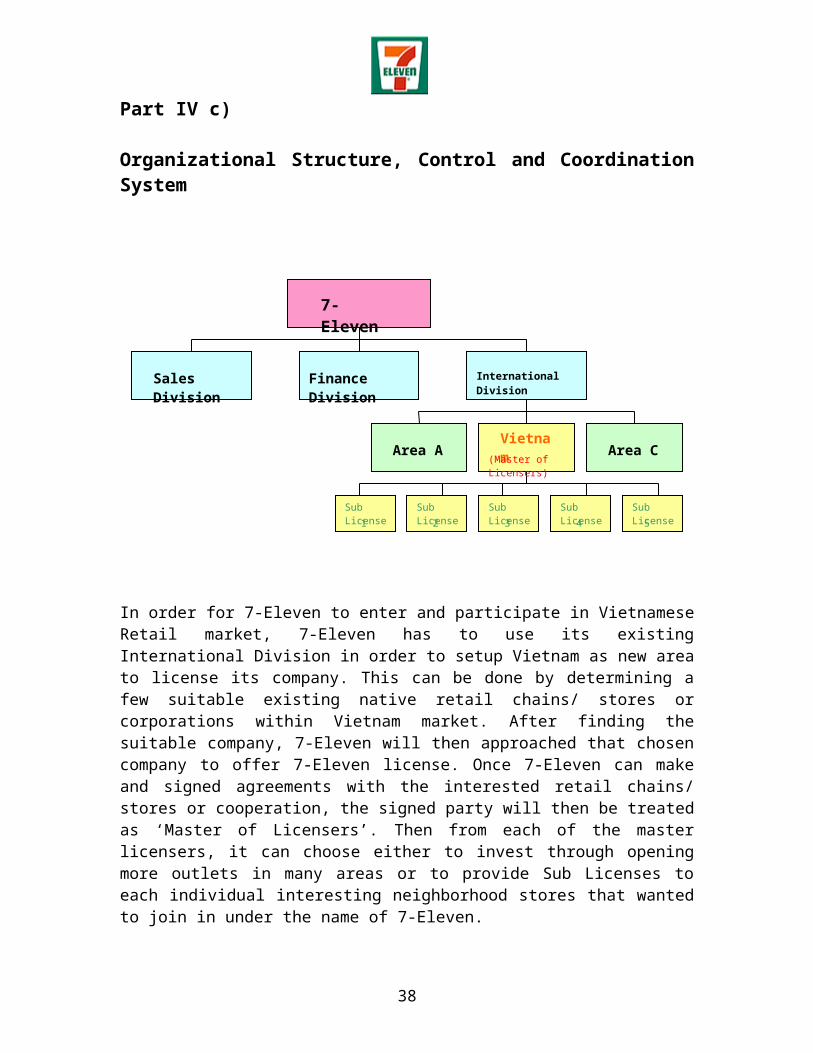

Organizational Structure, Control and CoordinationSystem

In order for 7-Eleven to enter and participate in VietnameseRetail market, 7-Eleven has to use its existingInternational Division in order to setup Vietnam as new areato license its company. This can be done by determining afew suitable existing native retail chains/ stores orcorporations within Vietnam market. After finding thesuitable company, 7-Eleven will then approached that chosencompany to offer 7-Eleven license. Once 7-Eleven can makeand signed agreements with the interested retail chains/stores or cooperation, the signed party will then be treatedas ‘Master of Licensers’. Then from each of the masterlicensers, it can choose either to invest through openingmore outlets in many areas or to provide Sub Licenses toeach individual interesting neighborhood stores that wantedto join in under the name of 7-Eleven.

7-Eleven

Sales Division

Finance Division

International Division

Area A Area CVietnam(Master of

Licensers)

Sub License

Sub License

Sub License

Sub License1 2 3 4 5

Sub License

38

After 7-Eleven made agreement with masters of licenser, 7-Eleven will then provide an early training program on theway to operate and manage convenience stores in order towell governed under the name of 7-Eleven to each of themasters of licenser. In addition to the training programoffered, 7-Eleven will also be providing the service ofField Consultant in order to help and give advice to each ofthe masters of licenser on certain aspects. Under thisprogram, it is a way too well coordinate betweenthe licenser and licensees under the brandname of 7-Eleven.

As for the responsibility of each of the master offranchisers, the masters themselves have to responsible inordering, buying and maintaining their own inventory. Theyalso have to govern the function of Human ResearchManagement such as hiring people for the job by themselves.This means that the Vietnamese masters of licenser willcontrol themselves in financing, marketing activities andetc while 7-Eleven, the licenser, will have less controlover this structure; 7-Eleven can only provide guidelines toits licensees on how to well manage.

39

Human Resource Management Strategy

Company policy: Ethnocentric

The international strategy emphasizes globalization on theupstream end of the value-chain – produce and sell globalproducts with minimal local adaptation and with centralizedcontrol in the home country. Given 7-Eleven is going to finda sun-franchisee or master franchisee in Vietnam. So themain task of 7-Eleven headquarter should be communicatingwell with master franchisee. To achieve this aim, we aregoing to use ethnocentric as our company policy.

Master franchisee will be granted and authorized by 7-Elevengroup. The task of the master franchisee is to find manymore franchisees in Vietnam and to be the supplier of 7-Eleven convenience stores in Vietnam. At the same time, themaster franchisee has to report to headquarter which is inU.S. monthly on financing, logistics, supply and demand andother relevant important information. On this point, masterfranchisee has to do a good job on communicating withheadquarter and know 7-Eleven culture very well. Thus, weare going to send an expatriate manager from home country –U.S. to Vietnam to help master franchising.

Therefore, ethnocentric company policy or culture would givethe master franchisee a very detail culture. The expatriateis a messenger also from a certain extent for 7-eleven.

On the other hand, the world is getting smaller and similar.So does Vietnam. Vietnamese has a large demand on globalproducts which are mainly consumer products. According to aconvenience store’s nature, most products in 7-Eleven havevery similar characters, which leads to easier control for7-Eleven master franchisee in Vietnam and headquarter. Thisis the other reason why 7-Eleven needs to use ethnocentric.

40

In sum, ethnocentric would help 7-Eleven headquarter to havebetter communication with the sub-franchisee to improve bothsides’ understand. Additionally, ethnocentric may help thegroup save more money on controlling.

41

Human Resource Management Process:

Since 7-Eleven is a very large company which has world wideoutlets, a lot of people are needed to provide the service.And the standard of the service is very significant for itsbusiness and that is the reason why human resourcemanagement is a must.

However, we decided to enter the Vietnam’s market through a“Master Franchising” as the reason mentioned above so theresponsible of this part of management is shifted to theVietnamese firm who will be willing to buy the license.

Recruitment:The employees have to be home-country nationals since theyhave to stand at the cashier and talk with the Vietnamesecustomers so Vietnamese language will be very important.They have to be friendly and honest. Apart from sellingproduct the company is selling the 24 hours services as wellso the friendly and relaxing environment is a countedfactor. Being honest is need for people who have to stand atthe counter and receive money. And when the employees arelocal, the manager has to be a local as well and it is forthe sake of communication.

Selection: The selecting manager is definitely based on the followings:

1. Technical and Managerial skill – it will be the firsttime of 24 hours convenience store in Vietnam and thatleads to many challenges so our licensee needs anexpert;

2. Personality traits – being a leader surely needs aleadership and other qualifications that can makesubordinate trust.

Training and development:

42

It will mainly focus on how the standard of the service willbe sustainable. Development and try to differentiate fromcompetitors is needed so that the company can create thevalue-add to the service.

Performance appraisal& Compensation:

This will depend on how the sub-franchisee company wouldgrant because the franchising will not cover on performanceappraisal and compensation of the firm. However, it has tobe according to the Vietnamese Labor laws so in case there’sanything happen, the headquarter in United State will notsuffer.

43

Reference

Parboteeah, K. Praveen & Cullen, John B. (2005) MultinationalManagement: A strategic approach, 3rd Ed, Thomson South-Western;Ohio

URL:<http://news.rednet.com.cn/Articles/2004/06/575568.HTM>

URL:<http://www.7-Eleven.com/default.asp>

URL:<http://www.quickmba.com/strategy/porter.shtml>

URL:<http://www.euromonitor.com/Retailing_in_Vietnam>

URL:<http://www.heritage.org/research/features/index/country.cfm?ID=Vietnam>

URL:<http://www.vir.com.vn/Client/VIR/index.asp?url=content.asp&doc=8906>

URL:<http://www.heritage.org/research/features/index/country.cfm?id=Vietnam>

URL:<http://www.7-Eleven.com/franchising/franchising.asp>

URL:<http://www.peoi.org>

44

URL:<http://www.fabcleaning.com.au/franch_codes.htm>

45

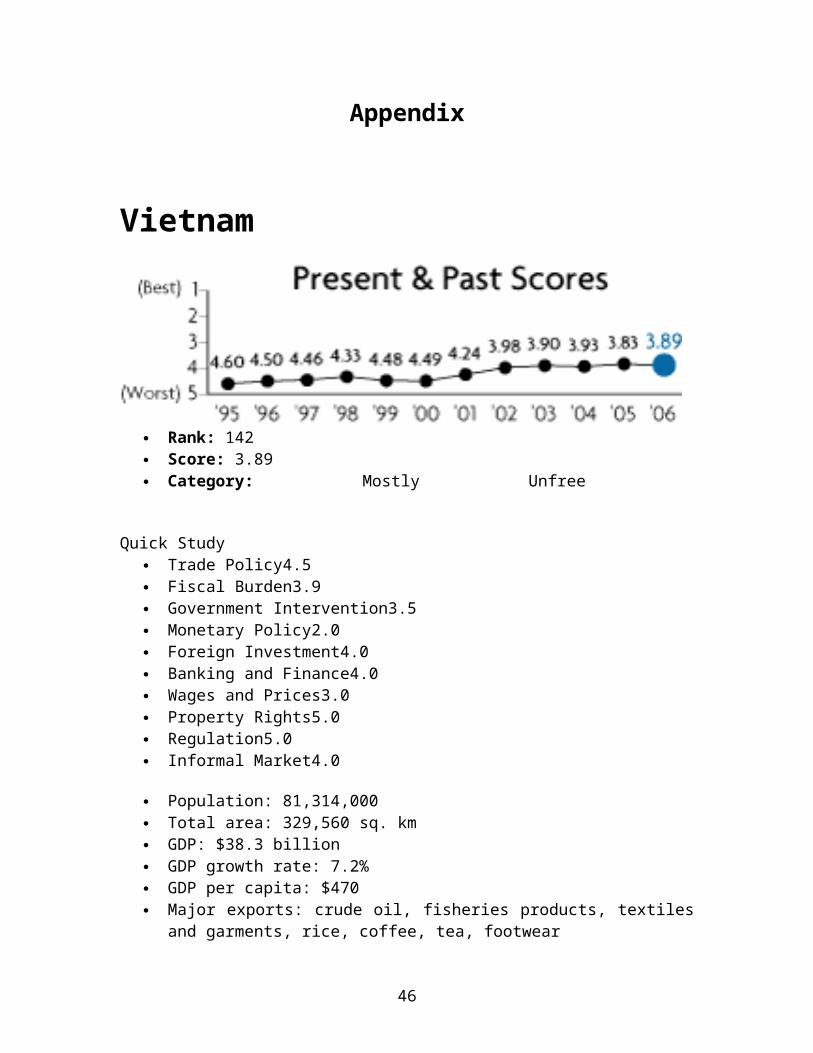

Appendix

Vietnam

Rank: 142 Score: 3.89 Category: Mostly Unfree

Quick Study Trade Policy4.5 Fiscal Burden3.9 Government Intervention3.5 Monetary Policy2.0 Foreign Investment4.0 Banking and Finance4.0 Wages and Prices3.0 Property Rights5.0 Regulation5.0 Informal Market4.0

Population: 81,314,000 Total area: 329,560 sq. km GDP: $38.3 billion GDP growth rate: 7.2% GDP per capita: $470 Major exports: crude oil, fisheries products, textiles

and garments, rice, coffee, tea, footwear

46

Exports of goods and services: $23.9 billion Major export trading partners: US 21.8%, Japan 13.7%,

Australia 7.2%, China 6.5% Major imports: refined petroleum, steel, cloth,

computer and electronic goods Imports of goods and services: $28.6 billion Major import trading partners: China 13.6%, Taiwan

11.4%, Japan 11.2%, South Korea 11.0%, Singapore 10.3% Foreign direct investment (net): $1.4 billion 2003 Data (in constant 2000 US dollars)

The Communist Party of Vietnam continues to balance one-party political rule with economic decentralization. Graftremains rampant, but government officials have beenincreasingly vigilant in investigating bribery andcorruption cases to maintain legitimacy. Vietnam's humanrights record remains poor, and the rule of law needs to bestrengthened. Because of the judicial system's lack oftransparency, arbitration is becoming more popular amonglocal and foreign firms. The 11th Plenum of the CentralCommittee, held in January 2005, continued to affirmVietnam's "socialist-oriented market economy" on its path tojoin the World Trade Organization (WTO). As of June 2005,Vietnam had reached bilateral agreements with Japan andSouth Korea concerning trade deregulation of industrialgoods. Although Vietnam had concluded negotiations withEuropean Union and Latin American countries, it still neededto reach agreement with the United States, China, Canada,and Australia among other countries before joining the WTO.The government continues to experiment with different formsof private ownership and equitization schemes with itsstate-owned enterprises. It also is pushing forwardenterprise laws that would subject state and private firmsto uniform regulation in an effort to attract foreigninvestment and meet conditions for accession to the WTO.Vietnam's trade policy score is 0.5 point better this year;however, its fiscal burden of government score is 0.1 pointworse, and its monetary policy score is 1 point worse. As a

47

result, Vietnam's overall score is 0.06 point worse thisyear.

Trade Policy Score: 4.5

According to the World Bank, Vietnam's weighted averagetariff rate in 2004 was 13.7 percent, down from the 17.4percent for 2001 reported in the 2005 Index, based on WorldBank data. The U.S. Trade Representative reports that"Vietnam has made significant progress in reducing the useof [non-tariff barriers]" but continues to prohibit numerousgoods and apply quantitative restrictions and licensingrequirements to others. Based on the lower tariff rate, aswell as a revision of the trade factor methodology,Vietnam's trade policy score is 0.5 point better this year.

Fiscal Burden Score: 3.9

Vietnam's top income tax rate is 40 percent. The topcorporate tax rate is 28 percent. In 2003, according to theAsian Development Bank, government expenditures as a shareof GDP increased 2.6 percentage points to 29 percent,compared to a 2 percentage point increase in 2002. On net,Vietnam's fiscal burden of government score is 0.1 pointworse this year.

Government Intervention Score: 3.5

The World Bank reports that the government consumed 6.9percent of GDP in 2003. In the same year, based on data fromthe International Monetary Fund, Vietnam received 12.12percent of its total revenues from state-owned enterprisesand government ownership of property. According to the

48

Economist Intelligence Unit, however, Vietnam has over 5,000state-owned enterprises, and the "state-owned sectorgenerates 41% of industrial output?" The state is involvedin finance, telecommunications, energy, and manufacturing.Based on the apparent unreliability of the figure forgovernment consumption, 1 point has been added to Vietnam'sgovernment intervention score.

Monetary Policy Score: 2.0

From 1995 to 2004, Vietnam's weighted average annual rate ofinflation was 5.98 percent, up from the 2.96 percent from1994 to 2003 reported in the 2005 Index. As a result,Vietnam's monetary policy score is 1 point worse this year.

Foreign Investment Score: 4.0

"Despite two decades of market reforms," reports theEconomist Intelligence Unit, "Vietnam remains a difficultbusiness environment. Relative political and economicstability must be weighed against poor physicalinfrastructure, government red tape and corruption,unevenness of skills and other obstacles to foreigninvestment." According to the U.S. Trade Representative,"the 卐 xtensive investment licensing process’s characterizedby stringent and time-consuming requirements that arefrequently used to protect domestic interests, limitcompetition, and allocate foreign investment rights amongvarious countries? [A]ll enterprises operating in Vietnam[are limited] to employing foreign nationals at the lesserof: (1) a maximum rate of 3 percent of their total workforce; or (2) 50 persons." The International Monetary Fundreports that both residents and non-residents may holdforeign exchange accounts, subject to restrictions andgovernment approval for resident accounts held abroad.

49

Payments and transfers face restrictions, includingrequirements for government approval over establishedamounts. Most transactions in money market and capitalinstruments, derivatives, commercial credits, and directinvestments either are prohibited or require governmentapproval. Foreigners may not own land but can lease it fromthe government.

Banking and Finance Score: 4.0

According to the Economist Intelligence Unit, "As of March2005, there were five state-run commercial banks, 38 jointstock commercial banks, four joint-venture banks, 29 foreignbank branches and 46 foreign bank representative offices?Vietnam's 卐 ig four' state commercial banks are the VietnamBank for Agriculture and Rural Development (BARD),Vietcombank (VCB), Incombank (ICB) and the Bank forInvestment and Development of Vietnam (BIDV)? [These fourbanks] plus the Bank for Housing Development of Cuu LongRiver Delta together accounted for nearly 75% of thefinancial system's total assets." The same source reportsthat "Vietnam has allowed 100%-foreign-owned banks sinceOctober 1st 2004." The government still affects theallocation of credit. "[State bank] lending practicesfrequently favour state-owned firms over private companies,"reports the EIU. "Bank lending is still treated in some waysas an arm of government policy, with banks directed to offerpreferential interest rates and debt relief to farmers, andstill often enjoying a cosy relationship with large state-owned enterprises." According to First Initiative, "Foreigncompetitors have spurred local firms, particularly thestate-owned market leader, which controls close to half ofthe insurance market, to become more competitive."

Wages and Prices Score: 3.0

50

The government controls prices to stem inflation. "Thegovernment continues to set rates for electricity,telecommunications, petrol, water, and fares for train andair travel," reports the Economist Intelligence Unit. "Inmost of these areas, the rates have traditionally beenhigher for foreigners, although harmonization is underway."In addition, "The government made significant adjustments toprice controls in the telecoms sector effective January 6th2003? In March 2005, the government began to implementprocedures to limit the price of pharmaceuticals." Vietnamhas a minimum wage.

Property Rights Score: 5.0

"Interference in the legal process and the bribing of judgesto serve particular interests is common," reports theEconomist Intelligence Unit. "Contractual arrangements arebacked by the force of law but the legal system iscomplicated. Contractual disputes often involve a prolongedperiod of negotiation preceding any attempt to resolve thematter in court." Moreover, "Because of the lack of faith inthe Vietnamese legal system, many foreign investors includeclauses in their contracts allowing disputes to be dealtwith by the Singapore Court of Arbitration." The Economistreports that the state owns all the land and grants land-userights to farmers, businesses, and homeowners.

Regulation Score: 5.0

The U.S. Department of Commerce reports that "The evolvingnature of regulatory regimes and commercial law, combinedwith overlapping jurisdiction among government ministries,often result in a lack of transparency, uniformity andconsistency in government policies and decisions oncommercial projects. Many firms operating in Vietnam,

51

foreign and domestic, find corruption to be a major sourceof difficulty." According to The Economist, the government"passed a law in 2000 making it easier to set [smallbusinesses] up." However, medium-size businesses find ithard to grow because they "cannot readily get access to landor capital."

Informal Market Score: 4.0

Transparency International's 2004 score for Vietnam is 2.6.Therefore, Vietnam's informal market score is 4 this year.

52