Embed Size (px)

Citation preview

Award Scheme on Instruction Design

2019/2020

Consolidated

Statement of Financial Position

C103

Form 6 Accounting

Lesson Plan (Unit)

2019/2020 C103

1

A. Introduction

Learning the Accounting subject is never easy for our students. They do not have real life

experiences in most aspects of Accounting. Some students find the subject challenging and

fun, like puzzles, while others find the subject tedious and discouraging. Our best option is to

try to relate skills and techniques learnt in the subject with their daily life whenever possible;

And make teaching and learning as supportive as we can.

When designing the teaching and learning of the subject and this particular topic, we have

used cooperative learning setting. Students of different ability sit in groups of 4. Studies

showed that cooperative learning in general increase student achievement, student self-

esteem as well as promoting other positive outcomes (Slavin, 1980).

The use of tangible objects in learning abstract ideas is one of the main strategies used in the

teaching and learning of this topic. Studies show that using tangible objects guides children in

the acquisition of knowledge (Evangelou, et al., 2010) and help them learn abstract ideas and

symbol relations (Balter, 1999).

Formative assessment tools are used through the teaching and learning of the topic. This is

endorsed by the school-wide assessment reform to use assessment as a tool for learning,

rather than a tool of giving grades. Studies show that formative assessments benefit students

by making students aware of the gap between their desired goal and their current knowledge

and skills (Boston, 2002). It also promotes self-evaluation where students can develop a

stronger sense of self-improvement.

In this document, a discussion of the detailed design of teaching and learning the topic of

Consolidation Statement of Financial Position for group companies is laid out. Lesson plans

for the 10 lessons are shown, followed by a evaluation and recommendation part.

2019/2020 C103

2

Table of Contents A. Introduction ............................................................................................................ 1

B. Design of Teaching and Learning ............................................................................ 3

Learning Objectives ......................................................................................... 3

1.1 Overall learning objectives of the subject .............................................. 3

1.2 Learning objectives of the topic ............................................................. 3

Students’ Background ...................................................................................... 5

Main Design Features ...................................................................................... 6

Teaching Focus ................................................................................................. 7

Difficult Points .................................................................................................. 7

Assessment ...................................................................................................... 8

Teaching Aids ................................................................................................... 9

Information Technology Application .............................................................. 10

8.1 Consolidation Spreadsheet .................................................................. 10

8.2 Kahoot! Check-up Exercise ................................................................... 10

C. Teaching Schedule ................................................................................................. 11

D. Detailed Lesson Plans ........................................................................................... 12

Lesson 1-2 ...................................................................................................... 12

Lesson 3-4 ...................................................................................................... 32

Lesson 5-6 ...................................................................................................... 41

Lesson 7-8 ...................................................................................................... 50

Lesson 9-10 .................................................................................................... 59

E. Evaluation.............................................................................................................. 59

Lesson Execution ............................................................................................ 59

Accomplishment of Learning Objectives ....................................................... 62

F. Recommendations ................................................................................................ 64

G. Appendix ............................................................................................................... 66

Appendix 1 – Question 8.2 (Lesson 1-2) ............................................................... 66

Appendix 2 – Question 8.1 (Lesson 1-2) ............................................................... 67

Appendix 3 – Question 3 (Lesson 5-6) .................................................................. 68

Appendix 5 – Question 5 (Lesson 7-8) .................................................................. 70

Appendix 6 – Consolidation Spreadsheet (screen shot) (Lesson 7-8) .................. 71

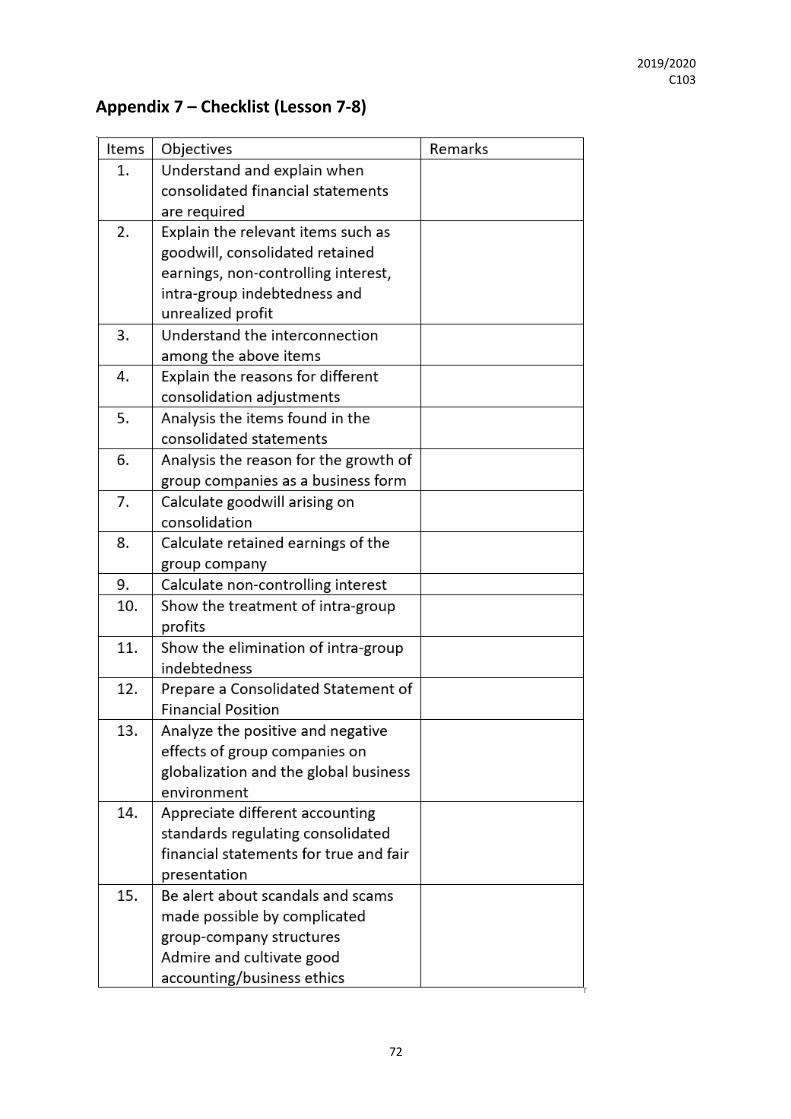

Appendix 7 – Checklist (Lesson 7-8) ..................................................................... 72

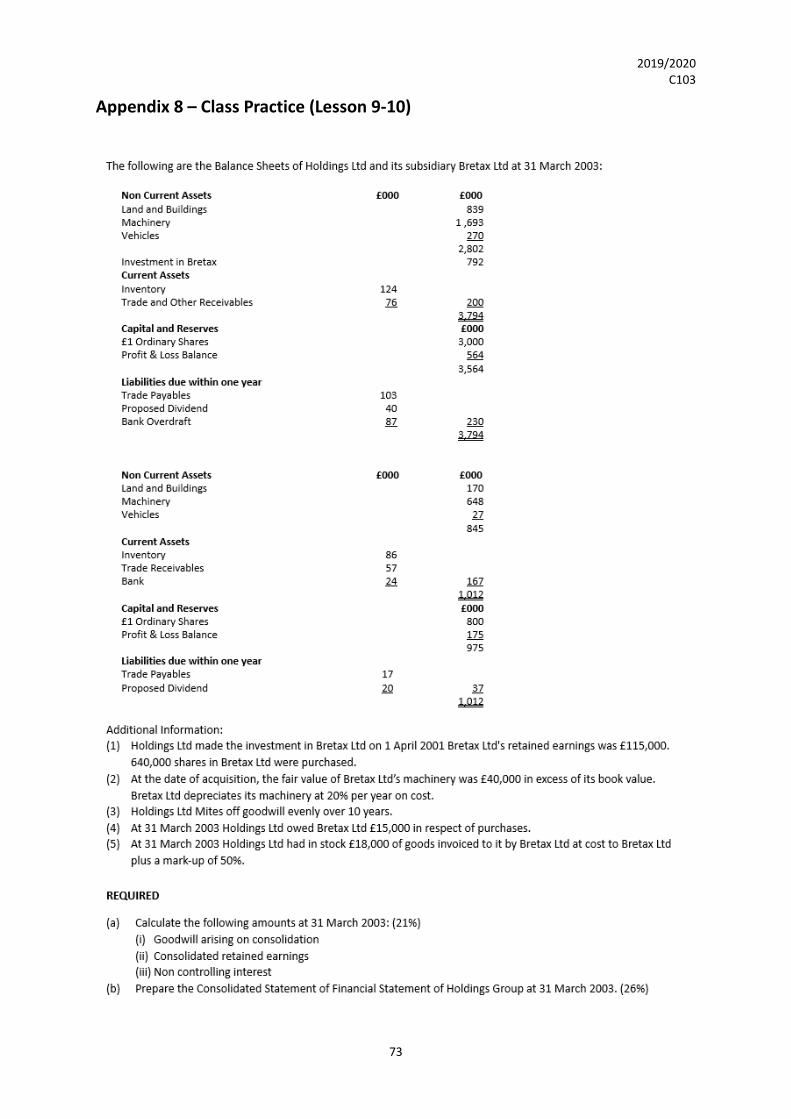

Appendix 8 – Class Practice (Lesson 9-10) ............................................................ 73

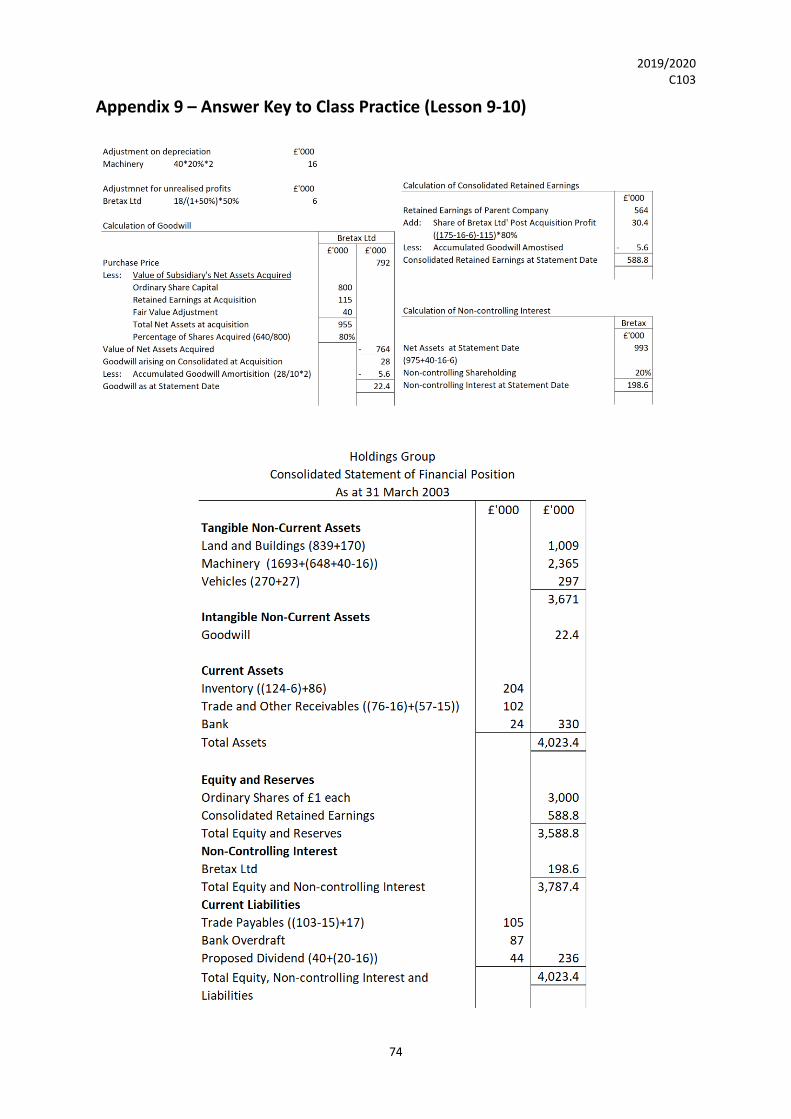

Appendix 9 – Answer Key to Class Practice (Lesson 9-10) .................................... 74

H. Reference .............................................................................................................. 75

2019/2020 C103

3

B. Design of Teaching and Learning

Learning Objectives

1.1 Overall learning objectives of the subject

The overall objectives of the subject is to make students to have a good knowledge and

understanding of the principles, concepts and techniques of accounting. It lays a secure

foundation for further study of Accounting and related fields.

After completion of the syllabus of the year, students will be equipment with the knowledge

and skills in attempting public examinations for the Pearson Edexcel International Advanced

Level Accounting, the LCCI Level 3 Accounting and Level 3 Advanced Business Calculations.

1.2 Learning objectives of the topic

This topic is a very advanced topic for Form 6 level accounting students. It is about the

preparation of financial statements for group companies, which requires solid understanding

and various pre-requisite knowledge. After completion of the topic, students are able to:

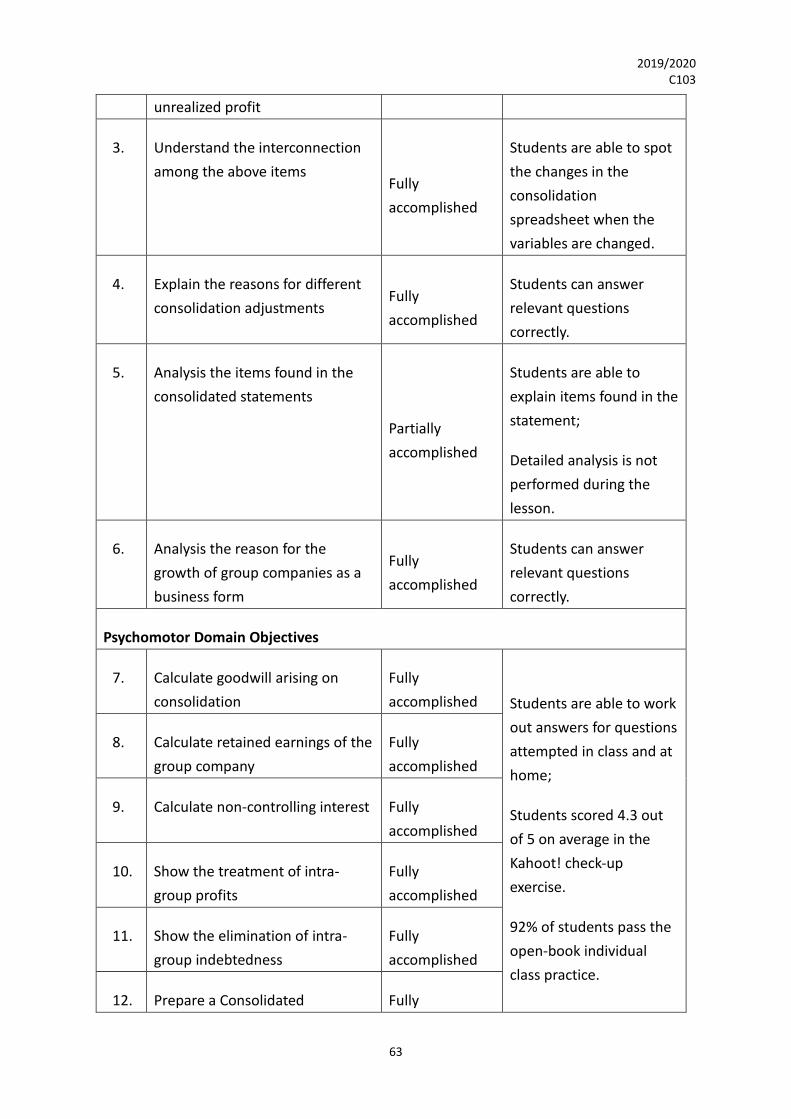

1.2.1 Cognitive Domain

✓ Understand and explain when consolidated financial statements are required

✓ Explain the relevant items such as goodwill, consolidated retained earnings, non-

controlling interest, intra-group indebtedness and unrealized profit

✓ Understand the interconnection among the above items

✓ Explain the reasons for different consolidation adjustments

✓ Analysis the items found in the consolidated statements

✓ Analysis the reason for the growth of group companies as a business form

1.2.2 Psychomotor Domain

✓ Calculate goodwill on consolidation

✓ Calculate retained earnings of the group company

✓ Calculate non-controlling interest

✓ Show the treatment of intra-group profits

✓ Show the elimination of intra-group indebtedness

✓ Prepare a Consolidated Statement of Financial Position

2019/2020 C103

4

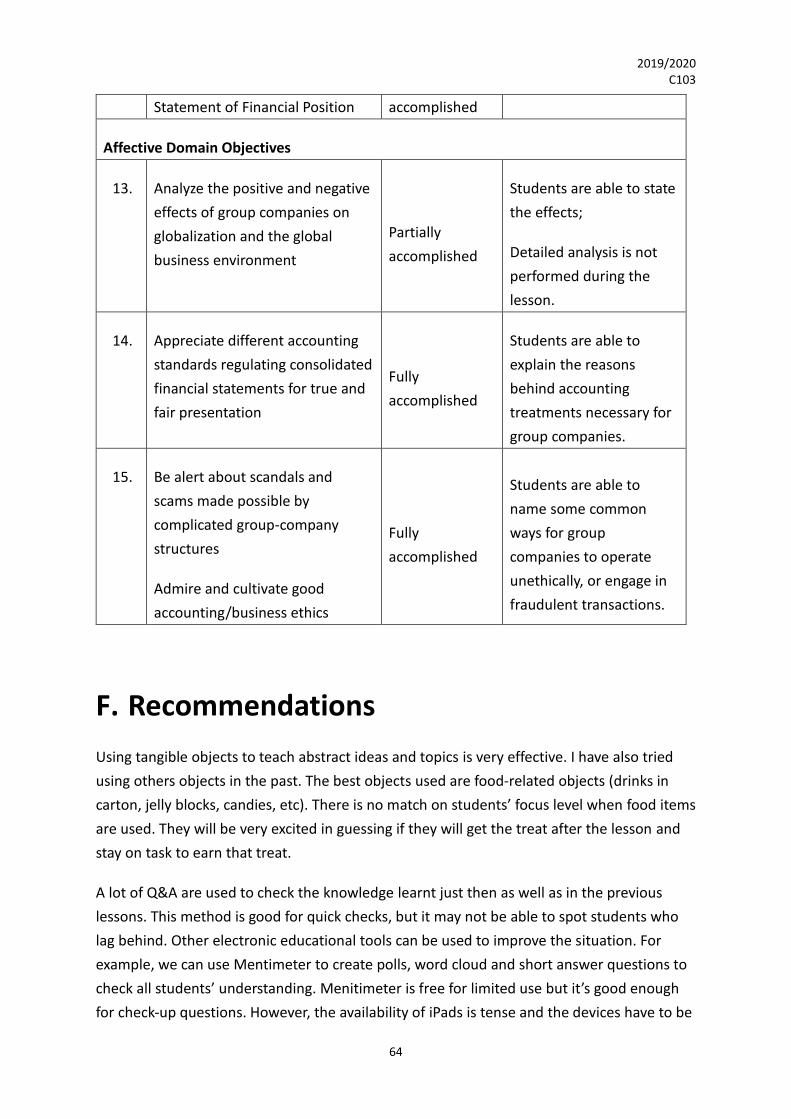

1.2.3 Affective Domain

✓ Analyze the positive and negative effects of group companies on globalization and

the global business environment

✓ Appreciate different accounting standards regulating consolidated financial

statements for true and fair presentation

✓ Be alert about scandals and scams made possible by complicated group-company

structures

✓ Admire and cultivate good accounting/business ethics

2019/2020 C103

5

Students’ Background

The class involved is a form 6 class in the Business stream (in-depth division). The Business

stream in our school offers a comprehensive curriculum in different business-related subjects

in senior secondary years. Starting from form 4, students will study Accounting, Economics

and Business, along with other general subjects. Upon completion of form 4, they will choose

between in-depth division and broad division. The in-depth division aims at A-Level public

examinations in Accounting and Economics.

This year’s form 6 students are pioneers of the in-depth/broad division arrangement. There

are 25 students in the class involved. It is the second year that I have been teaching this class

and a strong bond has been built in the teaching and learning of the subject. Students in this

class is generally regarded as active in class and enthusiastic in learning. My experience of

teaching this class tells that they have inquisitive minds, love challenges, not afraid of making

mistakes and are willing to share their thoughts.

Cooperative learning is used for this subject with teaching the class. Students are arranged in

groups of 4 according to their academic performance of the subject. Each group consist of a

strong student, 2 middle ranged students and a weak student. Cooperative learning has been

quite a success in this class. Students developed a habit of simultaneously sharing their

thoughts in their group when a question is asked. Members help each other in completing

tasks in class. This helps in dealing with learning differences for the weaker ones as well as in

consolidating ideas for the stronger ones. When there are challenging parts, I generally give

hints to two groups only (eg A & B) and make sure they get the idea correctly. Other groups

(C, D, E & F) then have to ask the groups (A & B) with the hints if they need help. I will join the

latter groups and listen to what they learnt to make sure the message to correct.

During the school suspension period, lessons are conducted regularly online. Students have

to attend two sessions of online lecture of 1.5 hours a week. This keep them in the learning

mode and they do not have to spend much time in picking up the pace after school resumption.

2019/2020 C103

6

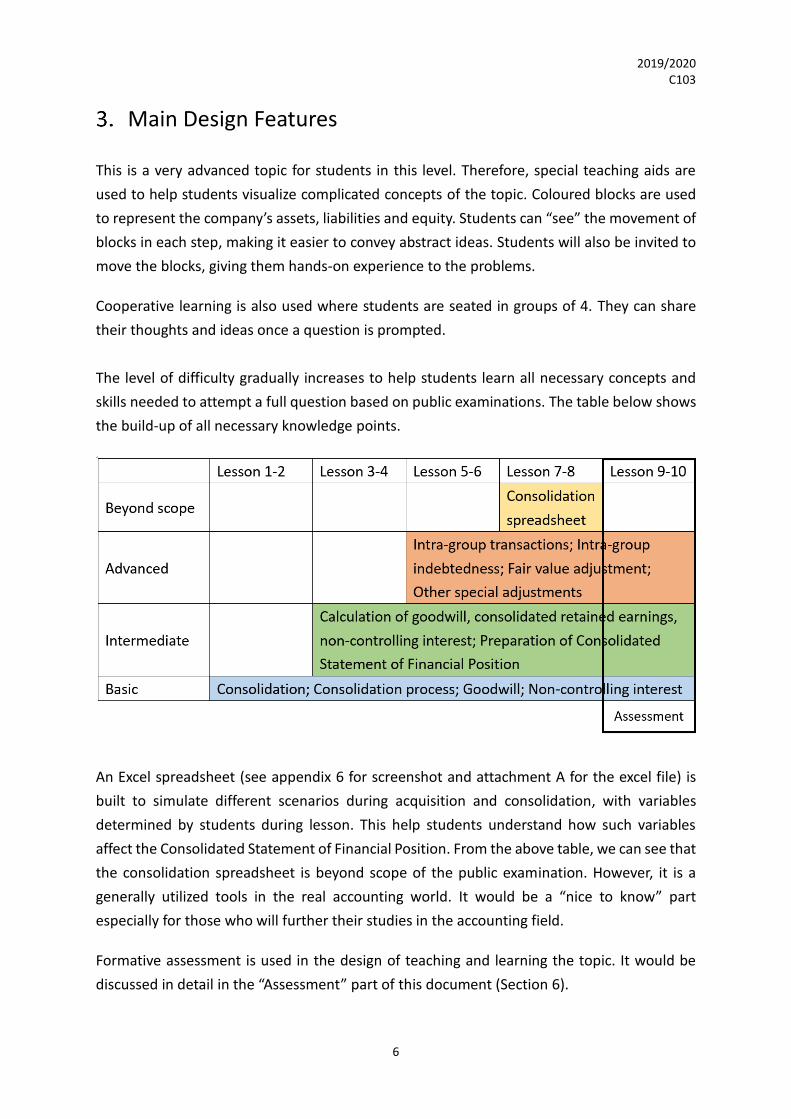

Main Design Features

This is a very advanced topic for students in this level. Therefore, special teaching aids are

used to help students visualize complicated concepts of the topic. Coloured blocks are used

to represent the company’s assets, liabilities and equity. Students can “see” the movement of

blocks in each step, making it easier to convey abstract ideas. Students will also be invited to

move the blocks, giving them hands-on experience to the problems.

Cooperative learning is also used where students are seated in groups of 4. They can share

their thoughts and ideas once a question is prompted.

The level of difficulty gradually increases to help students learn all necessary concepts and

skills needed to attempt a full question based on public examinations. The table below shows

the build-up of all necessary knowledge points.

An Excel spreadsheet (see appendix 6 for screenshot and attachment A for the excel file) is

built to simulate different scenarios during acquisition and consolidation, with variables

determined by students during lesson. This help students understand how such variables

affect the Consolidated Statement of Financial Position. From the above table, we can see that

the consolidation spreadsheet is beyond scope of the public examination. However, it is a

generally utilized tools in the real accounting world. It would be a “nice to know” part

especially for those who will further their studies in the accounting field.

Formative assessment is used in the design of teaching and learning the topic. It would be

discussed in detail in the “Assessment” part of this document (Section 6).

2019/2020 C103

7

Teaching Focus

Key knowledge points to be learnt in this topic are already laid out in the Learning Objectives

part (section 1). However, the teaching focus lies in making students aware of “why” such

accounting treatments are necessary.

In the recent 10 years, public examinations have changed to a more diversified approach

where students are required to have skills that are transferrable among different topics. Thus,

rather than just learning the “how (working out the question)”, our focus is more on learning

the “why (the reason behind the how)”.

The “why” approach enables students to have solid background knowledge of the topic and

equipment them with the skill to tackle any non-typical question types. It also enable students

to see the beauty of the well-development accounting system that governs the number game

of the commercial world.

Difficult Points

As mentioned above, this topic is a very advanced one for students in this level (Form 6). The

difficulty mainly lies in the fact that consolidation and group-company financial statements

are never part of students’ life. Even if students are given real world consolidated financial

statements to read, the process is behind the scenes and will not be shown. It is not like other

topics in our accounting course where practical uses and daily life examples are ample even

in their level.

For this reason, more effort has to be made on conveying abstract ideas using real object

teaching aids, and focusing on the reasons (“why” approach) of the accounting treatments

learnt.

2019/2020 C103

8

Assessment

In the academic year 2019-2020, our school is undergoing a reform in assessment methods.

The proportion of marks taken up by summative assessments (tests and exams) is significantly

reduced. Formative assessments are encouraged to take different forms. The aim of this

reform is to (1) lessen students from the pressure of taking too many tests, (2) increase

teaching and learning time and (3) utilize assessment as a tool for learning.

In the design of teaching and learning of this topic, several assessments are given:

(1) Check-up exercise on calculations of goodwill, consolidated retained earnings and non-

controlling interest (lesson 3-4)

(2) Kahoot! check-up exercise on intra-group items (lesson 5-6)

(3) Homework on preparation of consolidated statement of financial position (lesson 5-6)

(4) Consolidation spreadsheet adjustment (bonus; lesson 7-8)

(5) Open-book individual class practice on the topic (lesson 9-10)

Although these assessments perform the function of checking students’ knowledge, the aim

is to spot areas of common mistakes to be rectified immediately. Students are encouraged to

learn the topic when taught, but not only before tests and exams.

Students’ notebooks are also collected regularly and graded on the quality of their notes made.

Discussions and performance in lessons also contributes towards participation marks. This

comprehensive assessment method aims at enhancing student’s learning effectiveness and

promoting better results.

2019/2020 C103

9

Teaching Aids

Teaching aids used in teaching the topic includes the following:

• Colour blocks (specially designed and adapted for teaching the topic) (lesson 1-2)

• Kahoot! check-up exercise (lesson 5-6)

• Consolidation spreadsheet (lesson 7-8)

• iPads for each student (lesson 5-6, 7-8)

• Checklist of the knowledge points

• Class practice worksheets

• Textbook – Turbo LCCI Level 3: Accounting (K.Y.Ng, 2010)

• Powerpoint slides

• Format sheets

• Question worksheets (Question 3, 4, 5)

2019/2020 C103

10

Information Technology Application

8.1 Consolidation Spreadsheet

An Excel spreadsheet is built to simulate different scenarios during take-over, with variables

determined by students during lesson. This help students understand how such variables

affect the consolidated statement of Financial Position.

The consolidation spreadsheet is shared online during lesson (refer to detailed lesson plan for

lesson 7-8). Multiple users viewing and editing is enabled. In the first part, students can see in

their iPads changes made by the teacher in real time. In the second part, students are asked

to play with the variables and see for themselves how such changes affect the statement. In

the third part, students are encouraged to make adjustment to the consolidation spreadsheet

to accommodate an extra requirement, and to submit online for a bonus. Submitted works

are also made available for other students for viewing.

Excel spreadsheet is a very useful tool, especially for accounting/business students. Most

students are not used to the powerful functions of spreadsheets. They use it but is only limited

to the very basic functions. We would like to encourage them to learn more Excel skills and

tailor Excel spreadsheet to their own use.

8.2 Kahoot! Check-up Exercise

Kahoot! is a game-based learning platform. It enables learning with engagement and fun.

Students participates using iPads provided by the school. In the design of teaching and

learning for the topic, we have used a 5-quesitons quiz for the game. For each question,

students have to answer a multiple question within the one-minute time limit. The

background music adds to the tense and competitive atmosphere. The distribution of

students’ answers is shown immediately after each question. This enables teacher to explain

common misconceptions on the spot. Students’ scores are accumulated according to (1)

correct choice, (2) time needed to make the correct choice, and (3) the streak bonus. This also

coincide with the requirement of our accounting course that ask for accuracy and speed.

Students are also encouraged to log on to the Kahoot! accounts at home and re-attempt

questions that they got wrong answers. This help to further consolidate the knowledge points

learnt during class.

2019/2020 C103

11

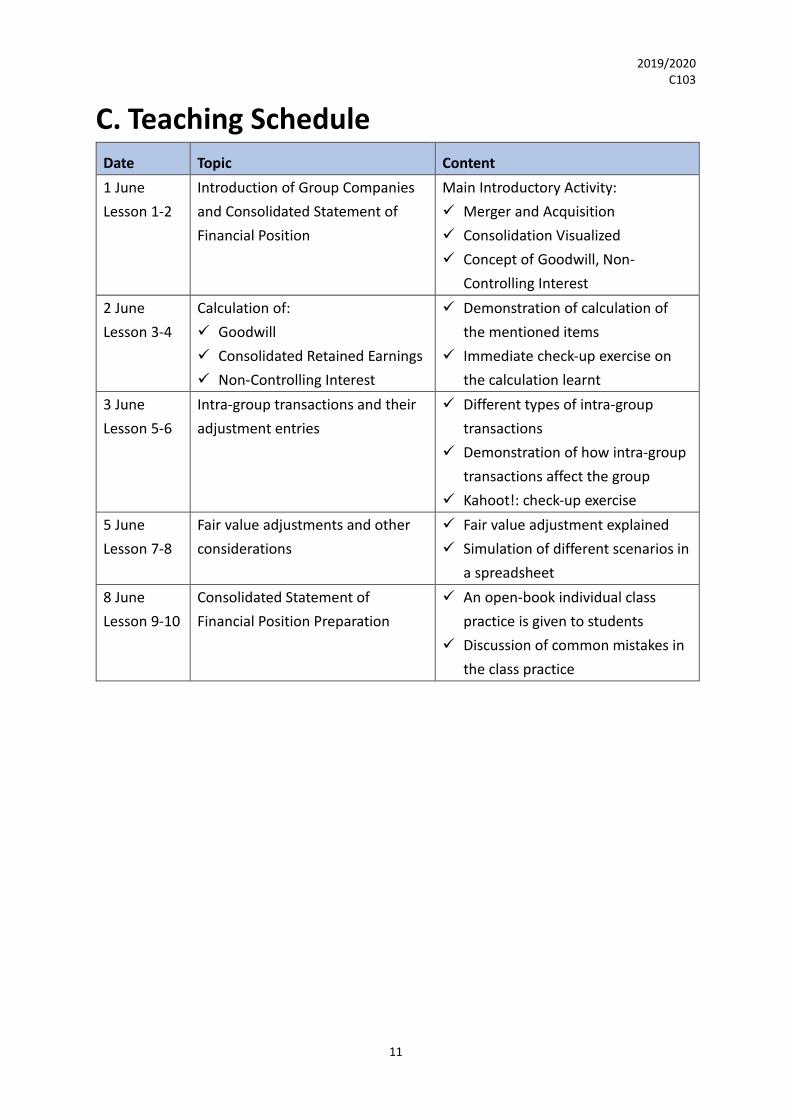

C. Teaching Schedule Date Topic Content

1 June

Lesson 1-2

Introduction of Group Companies

and Consolidated Statement of

Financial Position

Main Introductory Activity:

✓ Merger and Acquisition

✓ Consolidation Visualized

✓ Concept of Goodwill, Non-

Controlling Interest

2 June

Lesson 3-4

Calculation of:

✓ Goodwill

✓ Consolidated Retained Earnings

✓ Non-Controlling Interest

✓ Demonstration of calculation of

the mentioned items

✓ Immediate check-up exercise on

the calculation learnt

3 June

Lesson 5-6

Intra-group transactions and their

adjustment entries

✓ Different types of intra-group

transactions

✓ Demonstration of how intra-group

transactions affect the group

✓ Kahoot!: check-up exercise

5 June

Lesson 7-8

Fair value adjustments and other

considerations

✓ Fair value adjustment explained

✓ Simulation of different scenarios in

a spreadsheet

8 June

Lesson 9-10

Consolidated Statement of

Financial Position Preparation

✓ An open-book individual class

practice is given to students

✓ Discussion of common mistakes in

the class practice

2019/2020 C103

12

D. Detailed Lesson Plans

Lesson 1-2

Date: 1 June 2020 Lesson 1-2 Duration: 80 minutes

Objectives

Must know

• Definition of control, goodwill, non-controlling interest

• Journal entry of acquisition

• General process of preparing a consolidated statement of financial

position

Should know

• The reason for the need of consolidated financial statements

• General rule of when goodwill, non-controlling interest will arise

• Calculation of goodwill, non-controlling interest right after acquisition

Nice to know

• Features and benefit vs drawbacks of different type of business

expansion

• Factor affecting determination of purchase price in an acquisition

Sequence Key Points Remarks

Lead-in Show “Merger and Acquisition” on screen. Students

should be able to mention that the Chinese

translation is “收購與合併”. Ask students if they

know the difference between the two.

Give students time for discussion and set up the

main teaching aids in front of them.

Students should be able to answer that:

Merger is the combination of two companies, where

a new company will be formed and their assets,

liabilities and capital are joined together.

10 mins

2019/2020 C103

13

Acquisition is the situation where a larger company

take over a smaller one. The latter usually ceases to

exist.

Ask students to suggest reasons for mergers and

acquisition. Students should be able to mention

reasons like: for expansion of market share,

diversification to other industries, for enjoying

economies of scale, etc.

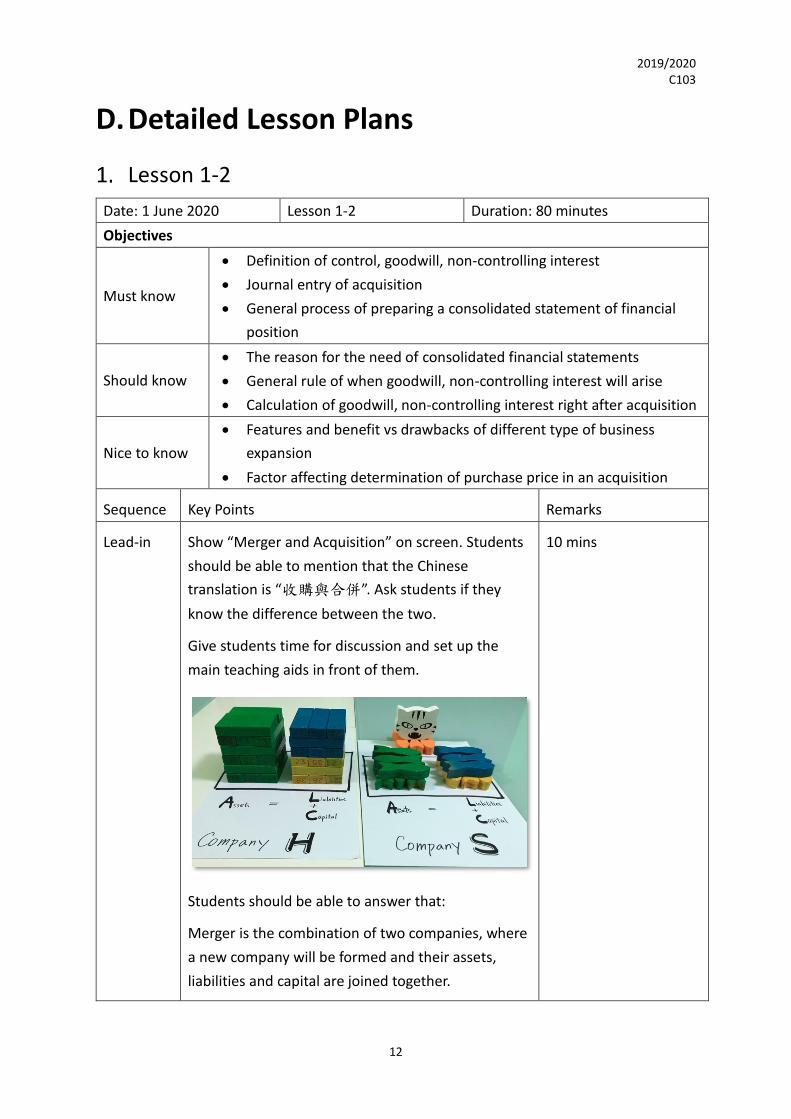

Explain to students the settings in front of them.

There are two companies: Company H (owned by us)

and Company S (owned by Mr Cat). The blocks

represent the assets, liabilities and capital of each

company. They are placed in a way to show the

accounting equation of each company.

Company H Company S

A 18 L 9

A 6 L 3

C 9 C 3

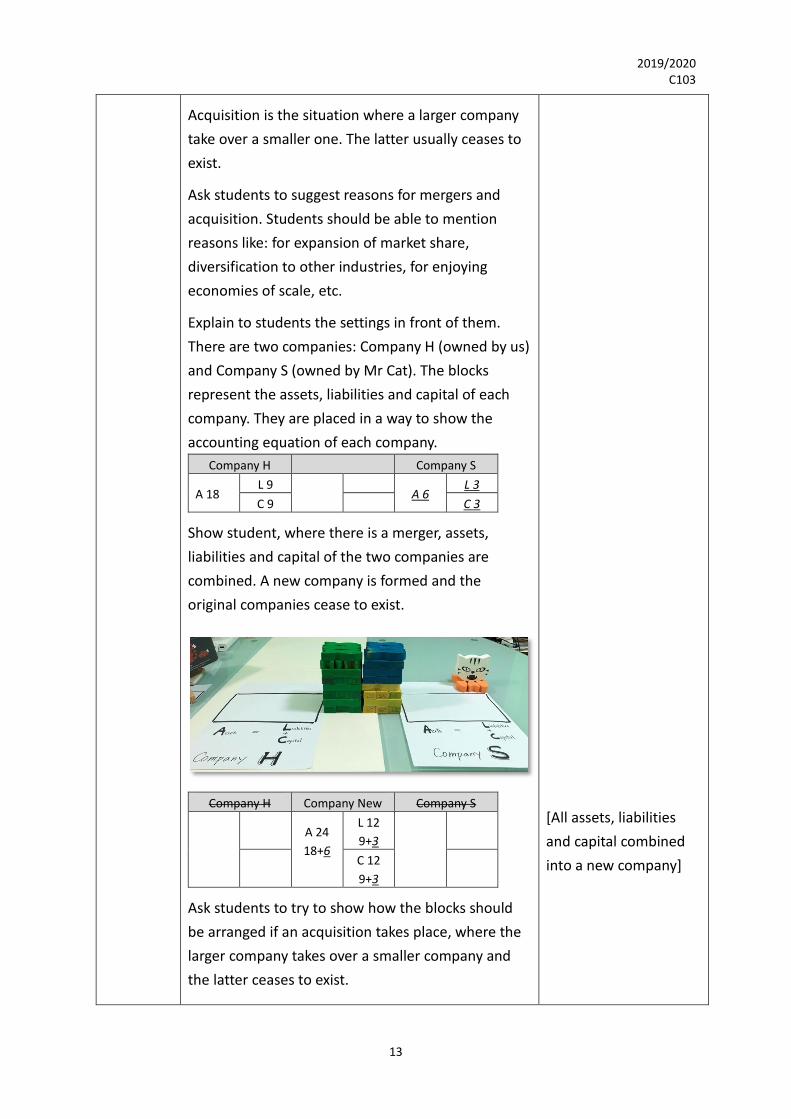

Show student, where there is a merger, assets,

liabilities and capital of the two companies are

combined. A new company is formed and the

original companies cease to exist.

Company H Company New Company S

A 24

18+6

L 12

9+3

C 12

9+3

Ask students to try to show how the blocks should

be arranged if an acquisition takes place, where the

larger company takes over a smaller company and

the latter ceases to exist.

[All assets, liabilities

and capital combined

into a new company]

2019/2020 C103

14

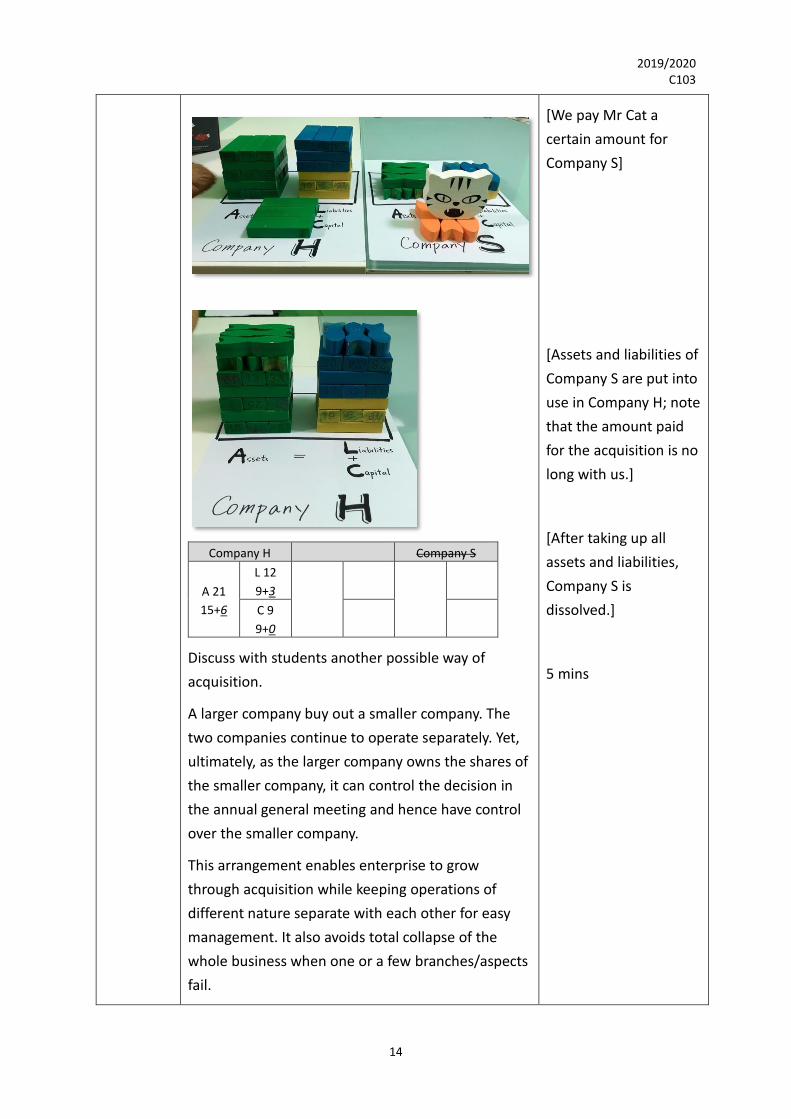

Company H Company S

A 21

15+6

L 12

9+3

C 9

9+0

Discuss with students another possible way of

acquisition.

A larger company buy out a smaller company. The

two companies continue to operate separately. Yet,

ultimately, as the larger company owns the shares of

the smaller company, it can control the decision in

the annual general meeting and hence have control

over the smaller company.

This arrangement enables enterprise to grow

through acquisition while keeping operations of

different nature separate with each other for easy

management. It also avoids total collapse of the

whole business when one or a few branches/aspects

fail.

[We pay Mr Cat a

certain amount for

Company S]

[Assets and liabilities of

Company S are put into

use in Company H; note

that the amount paid

for the acquisition is no

long with us.]

[After taking up all

assets and liabilities,

Company S is

dissolved.]

5 mins

2019/2020 C103

15

When a company owns the controlling share of

another company (50% or more), the two companies

together are called a company group.

Cite famous group company examples to students:

Walt Disney Company owns ESPN, Marvel

Entertainment, Pixar Animation, etc;

Google’s parent company is Alphabet Inc.

Ask students to give a few examples of group

companies they know.

Discuss with students that these related yet

separately operating companies are required to

prepare separate sets of financial statements, as well

as a combined set of statements for the group, called

the consolidated financial statements. It is because,

the holding company, acting as the head of the

group, actually controls the subsidiary companies,

making all these companies ONE big enterprise in

reality. Showing a combined (consolidated) set of

statement is the only way to shows the situation of

the group in a true and fair way.

[If they have difficulties

giving examples, help

them with hints like

Sands Macao, Bank of

China, etc]

[Mention that this type

of acquisition is what

we are going to

investigate in this topic]

2019/2020 C103

16

Develop-

ment

Show the words “Consolidated Statement of

Financial Position” on screen.

Tell the students that we are going to use 5 scenarios

to learn the basics of a consolidated statement of

financial position. We will repeat the below process

for each of the 5 scenarios:

Details of the scenario given;

2 minute group discussion time (or less for later

scenarios)

Volunteer in showing with the blocks how the

consolidated statement of financial position should

be prepared

Floor assistance if the attempt is incorrect

Explanation of new terms (by students)

Mini conclusion (by students or teacher)

1 minute note taking time

2019/2020 C103

17

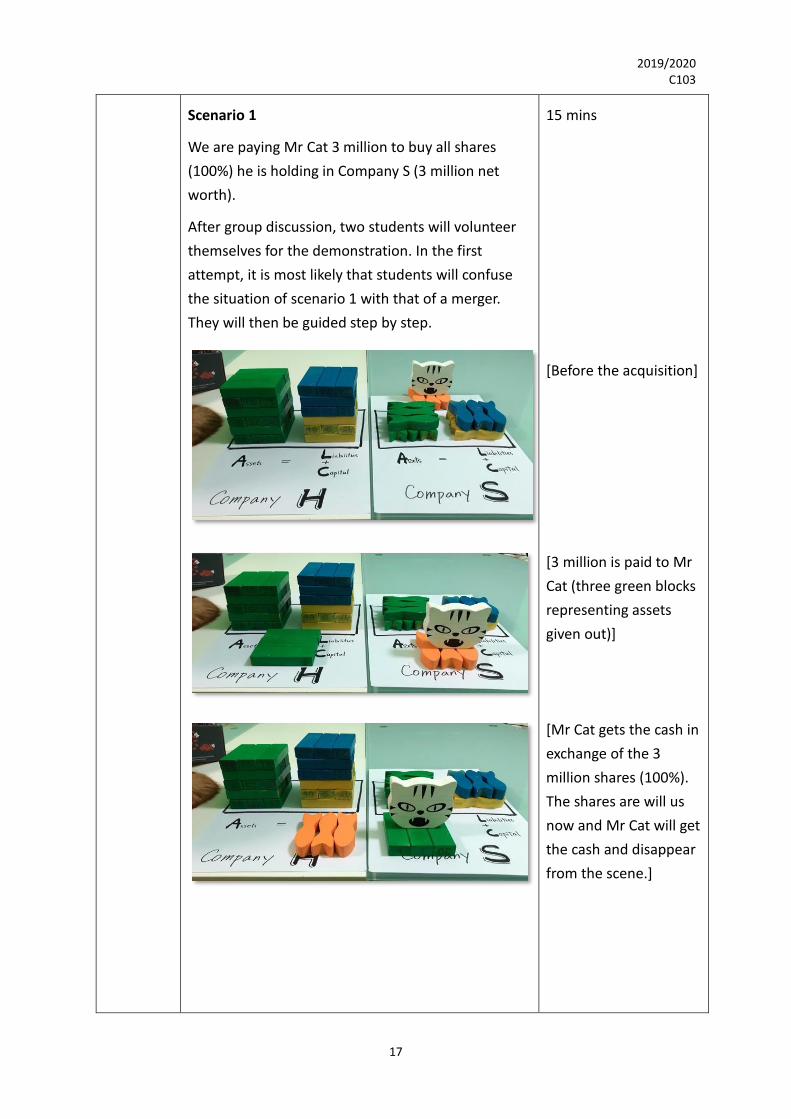

Scenario 1

We are paying Mr Cat 3 million to buy all shares

(100%) he is holding in Company S (3 million net

worth).

After group discussion, two students will volunteer

themselves for the demonstration. In the first

attempt, it is most likely that students will confuse

the situation of scenario 1 with that of a merger.

They will then be guided step by step.

15 mins

[Before the acquisition]

[3 million is paid to Mr

Cat (three green blocks

representing assets

given out)]

[Mr Cat gets the cash in

exchange of the 3

million shares (100%).

The shares are will us

now and Mr Cat will get

the cash and disappear

from the scene.]

2019/2020 C103

18

Make students aware that the journal entry for

buying the shares of another company being:

Dr Investment 3M

Cr Bank 3M

Explain to students that when we work on the

consolidated statement of financial position, we are

indeed converting the “Investment” into the assets

and liabilities we control. In scenario 1, the 3 million

investment is the ownership of 3 million (100%)

shares of Company S, which in turn represent the 3

million capital of Company S. The capital in turn

represents 6 million assets and 3 million liabilities of

Company S. That said, the 3 million investment will

be converted into 6 million assets and 3 million

liabilities.

Lay out such relationship in the way shown below.

[We pay cash to acquire

something. It is

represented by the

brown blocks. Ask

students what the

brown blocks should be

called (Investment).]

[The relationship

mentioned is very

important. Make sure

that students have

good understanding on

this part before moving

on.]

2019/2020 C103

19

The consolidated statement of financial position is as

follows.

Students will most likely put the 3 million capital of

Company S in the consolidated statement as well.

Emphasize to students that the only transaction

taken place is “Dr Investment Cr Bank”. Nothing else

has taken place, hence the group shouldn’t have

more capital.

Draw students’ attention to the 3 important points

to be learnt in this basic scenario. Ask them to write

down these key points in their notebooks.

Company H Consolidation Company S

A 18

(Inv. 3)

L 9 A 21

(15+6)

L 12

(9+3) A 6

L 3

C 9 C 9

(9+0) C 3

[Important point in this

scenario: (1) in

consolidation,

investment is converted

into the assets and

liabilities of Company S

we control. (2) There

should be no change in

Capital right after

acquisition If there is

no issue of shares]

[Important point: (3)

Company H and

Company S continue to

exist and have to

prepare separately

their individual

financial statements.]

2019/2020 C103

20

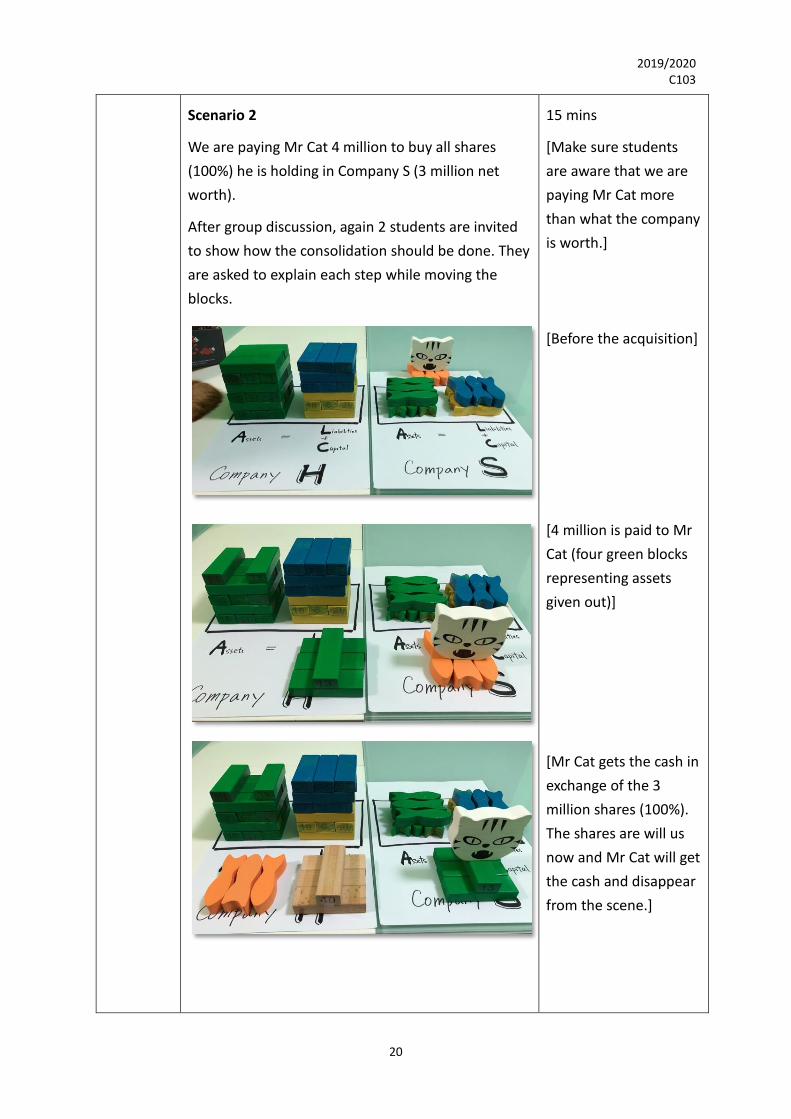

Scenario 2

We are paying Mr Cat 4 million to buy all shares

(100%) he is holding in Company S (3 million net

worth).

After group discussion, again 2 students are invited

to show how the consolidation should be done. They

are asked to explain each step while moving the

blocks.

15 mins

[Make sure students

are aware that we are

paying Mr Cat more

than what the company

is worth.]

[Before the acquisition]

[4 million is paid to Mr

Cat (four green blocks

representing assets

given out)]

[Mr Cat gets the cash in

exchange of the 3

million shares (100%).

The shares are will us

now and Mr Cat will get

the cash and disappear

from the scene.]

2019/2020 C103

21

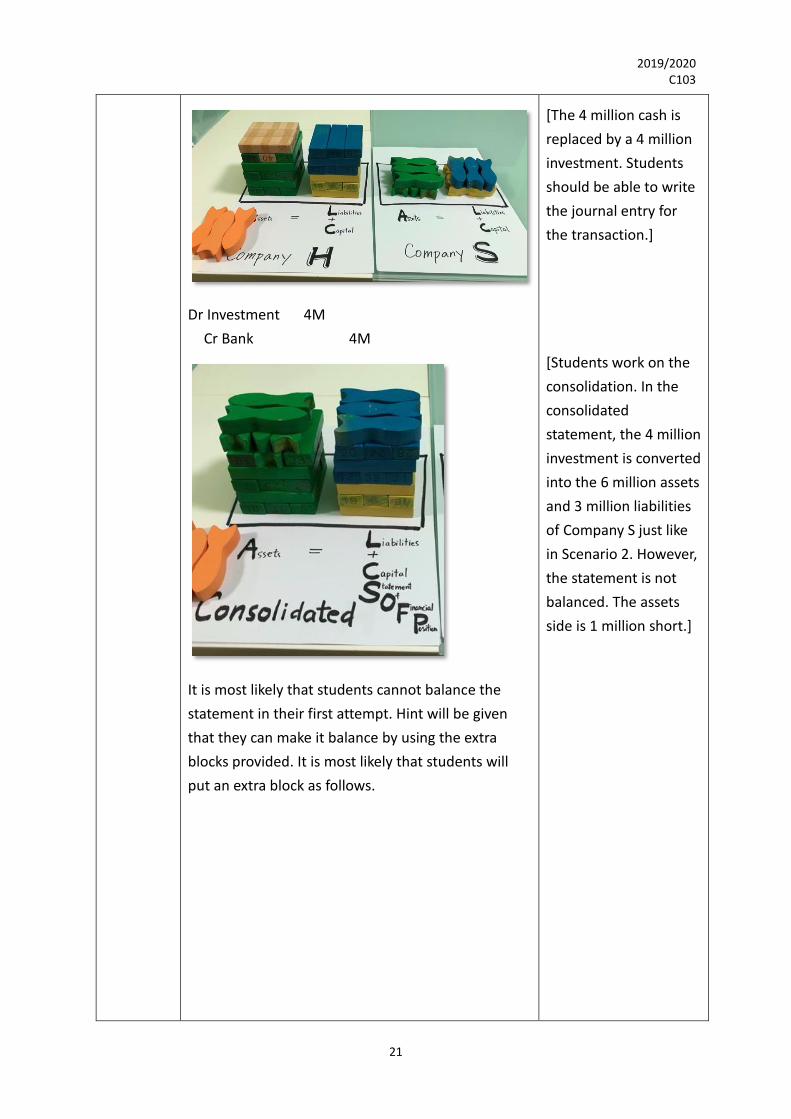

Dr Investment 4M

Cr Bank 4M

It is most likely that students cannot balance the

statement in their first attempt. Hint will be given

that they can make it balance by using the extra

blocks provided. It is most likely that students will

put an extra block as follows.

[The 4 million cash is

replaced by a 4 million

investment. Students

should be able to write

the journal entry for

the transaction.]

[Students work on the

consolidation. In the

consolidated

statement, the 4 million

investment is converted

into the 6 million assets

and 3 million liabilities

of Company S just like

in Scenario 2. However,

the statement is not

balanced. The assets

side is 1 million short.]

2019/2020 C103

22

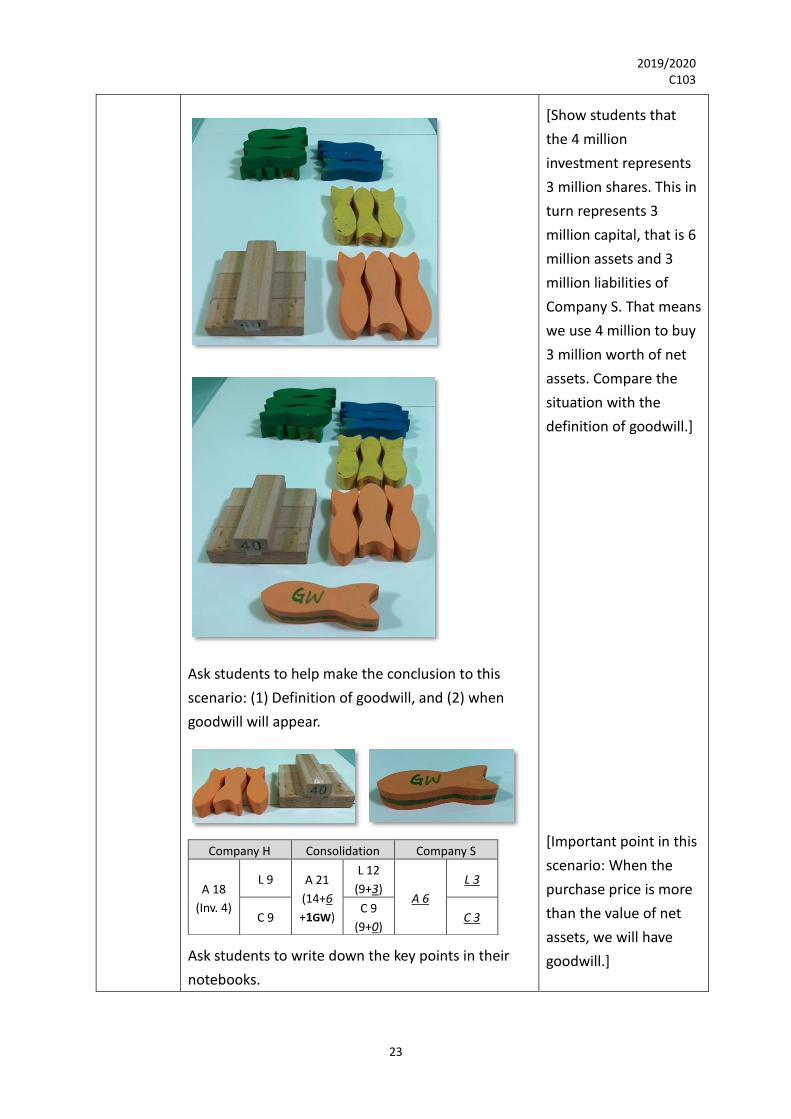

Question to student: what does this extra block

represent? With the marking on the block, students

should be able to guess it as “Goodwill”.

Invite students to give the definition of Goodwill,

which they have previously learnt. [The excess of

purchase price of a company over the value of its net

assets]

2019/2020 C103

23

Ask students to help make the conclusion to this

scenario: (1) Definition of goodwill, and (2) when

goodwill will appear.

Ask students to write down the key points in their

notebooks.

Company H Consolidation Company S

A 18

(Inv. 4)

L 9 A 21

(14+6

+1GW)

L 12

(9+3) A 6

L 3

C 9 C 9

(9+0) C 3

[Show students that

the 4 million

investment represents

3 million shares. This in

turn represents 3

million capital, that is 6

million assets and 3

million liabilities of

Company S. That means

we use 4 million to buy

3 million worth of net

assets. Compare the

situation with the

definition of goodwill.]

[Important point in this

scenario: When the

purchase price is more

than the value of net

assets, we will have

goodwill.]

2019/2020 C103

24

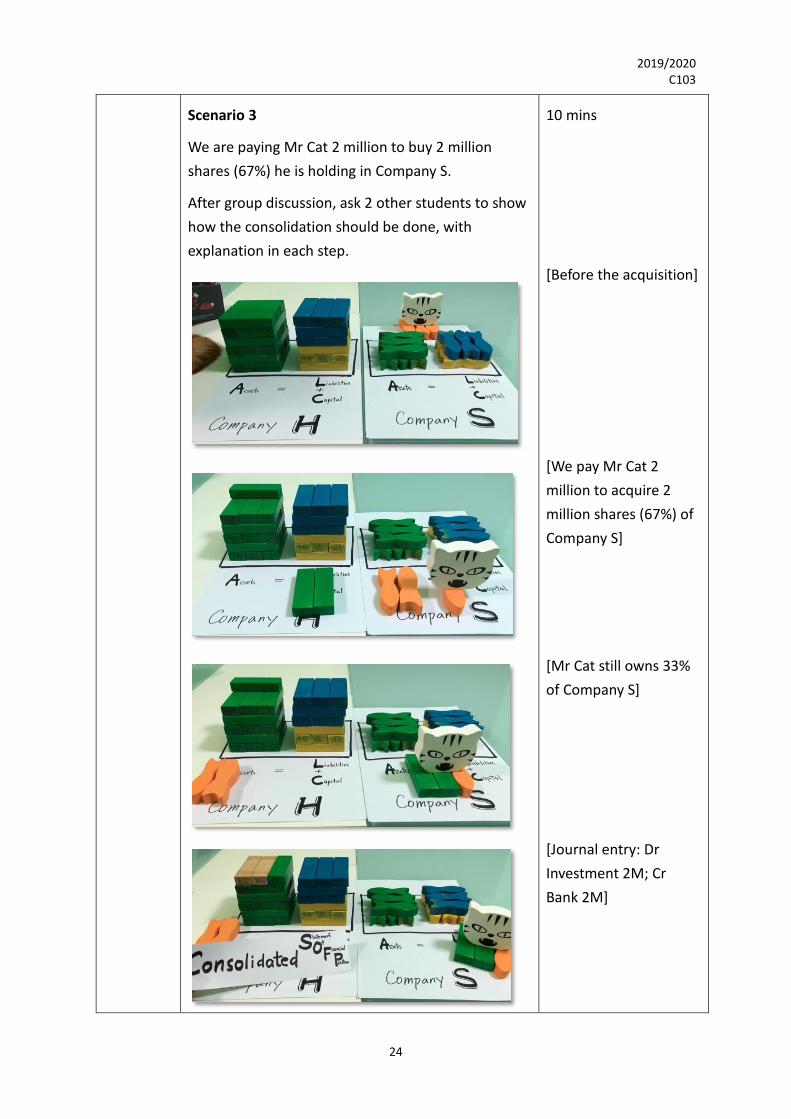

Scenario 3

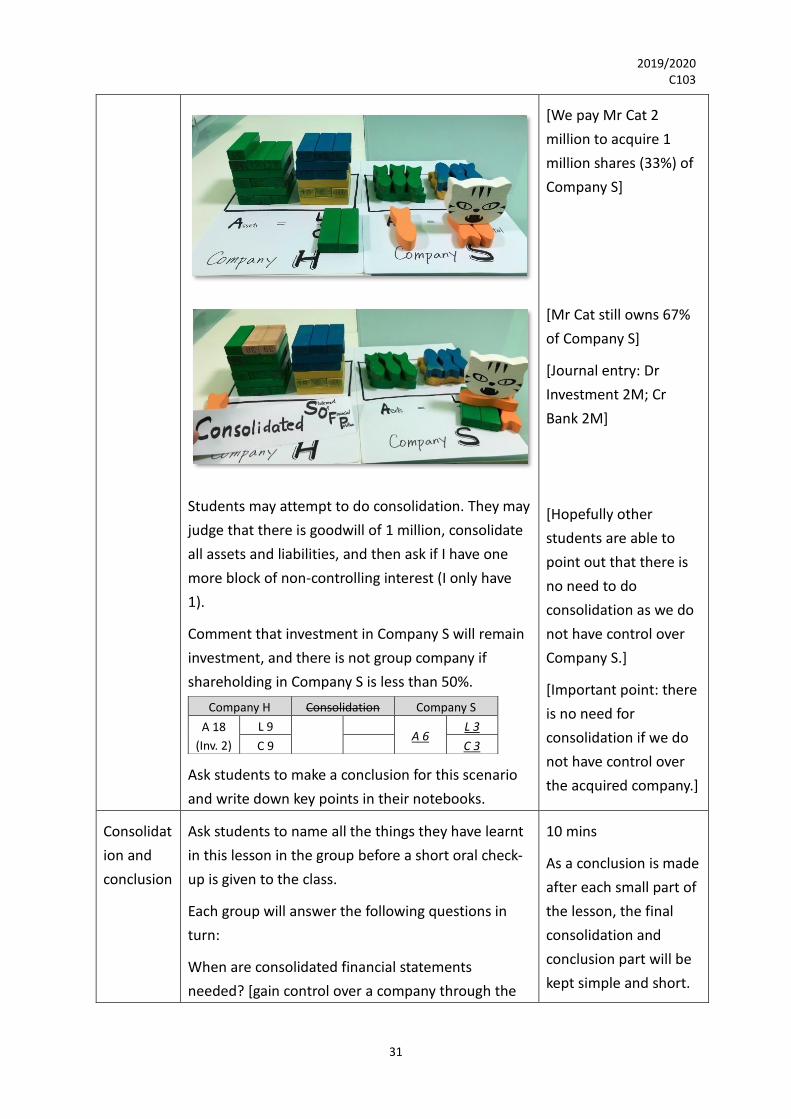

We are paying Mr Cat 2 million to buy 2 million

shares (67%) he is holding in Company S.

After group discussion, ask 2 other students to show

how the consolidation should be done, with

explanation in each step.

10 mins

[Before the acquisition]

[We pay Mr Cat 2

million to acquire 2

million shares (67%) of

Company S]

[Mr Cat still owns 33%

of Company S]

[Journal entry: Dr

Investment 2M; Cr

Bank 2M]

2019/2020 C103

25

When working on the consolidated statement, it is

very likely that students will put 4 million assets and

2 million liabilities of Company S (which is 67% of the

company) to make it balanced as follows.

Question to students: Do you still remember what

we have discussed about “Control”?

Students should recall our earlier discussion that,

when shareholding is 50% or more, we can control

all assets and liabilities of the acquired company.

Question to students: Should be consolidate all

assets and liabilities or just 67% of it?

It is possible that students put the block

representing “Goodwill” to make the statement

balance.

[All assets and liabilities

should be consolidated]

[When all assets and

liabilities are

consolidated, the

statement is not

balanced. Give hint to

students that they can

use the extra blocks.]

2019/2020 C103

26

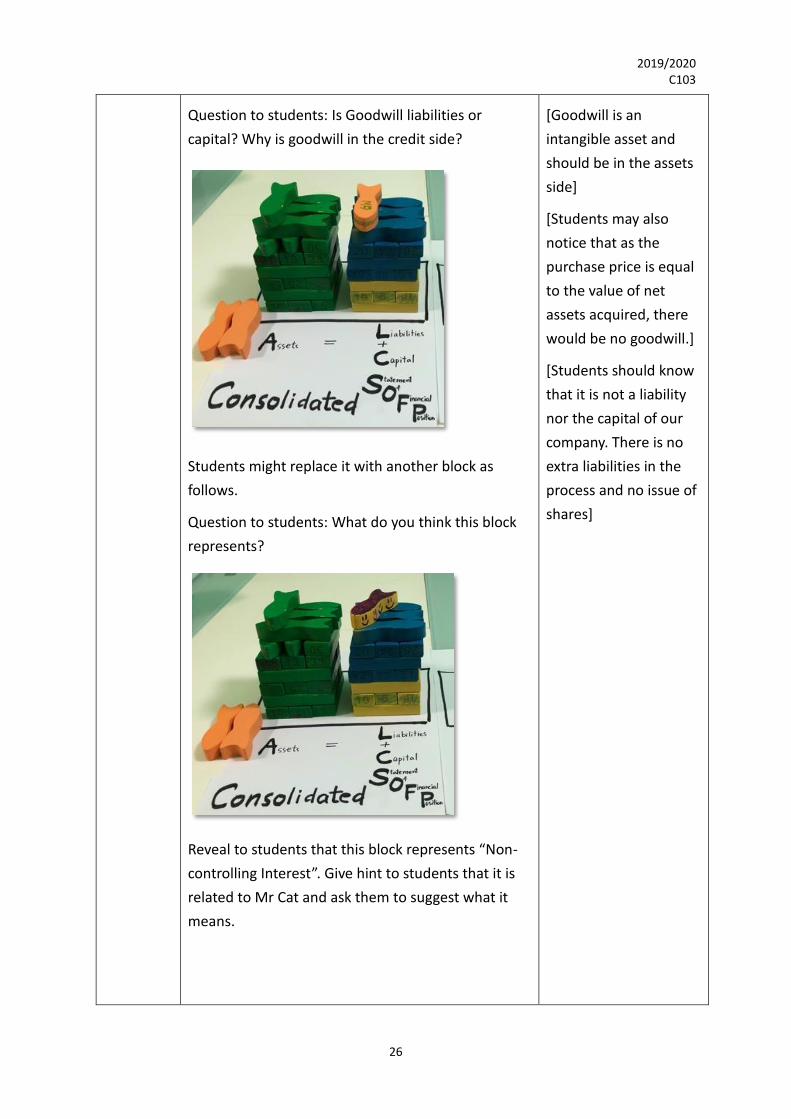

Question to students: Is Goodwill liabilities or

capital? Why is goodwill in the credit side?

Students might replace it with another block as

follows.

Question to students: What do you think this block

represents?

Reveal to students that this block represents “Non-

controlling Interest”. Give hint to students that it is

related to Mr Cat and ask them to suggest what it

means.

[Goodwill is an

intangible asset and

should be in the assets

side]

[Students may also

notice that as the

purchase price is equal

to the value of net

assets acquired, there

would be no goodwill.]

[Students should know

that it is not a liability

nor the capital of our

company. There is no

extra liabilities in the

process and no issue of

shares]

2019/2020 C103

27

After students’ response, explain that we have

acquired 67% of the shares of Company S and gained

control over all assets and liabilities. That is why we

consolidate all assets and liabilities into the

consolidated statement. However, we do not own

everything of the consolidated items. “Non-

controlling Interest” represents the part of the

assets and liabilities of the consolidated assets and

liabilities that we do not own.

Ask students to help make the conclusion to this

scenario: (1) Explanation of non-controlling interest,

and (2) when non-controlling interest will appear.

2019/2020 C103

28

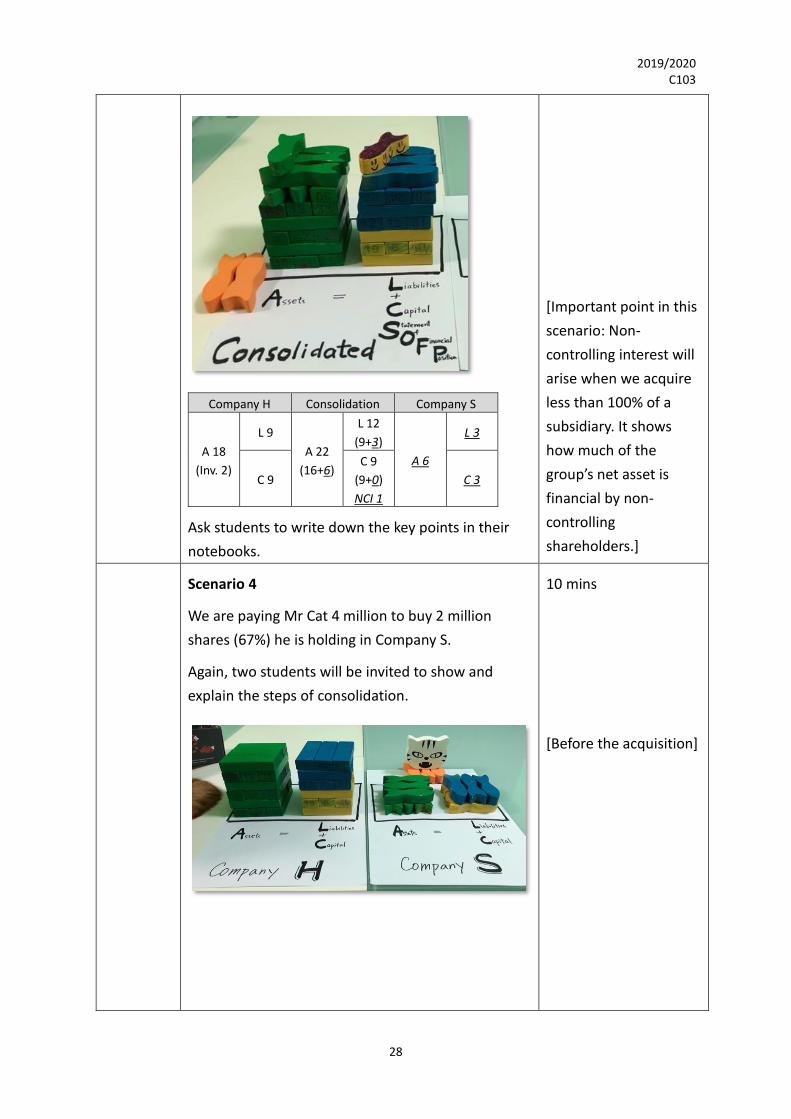

Ask students to write down the key points in their

notebooks.

Company H Consolidation Company S

A 18

(Inv. 2)

L 9

A 22

(16+6)

L 12

(9+3)

A 6

L 3

C 9

C 9

(9+0)

NCI 1

C 3

[Important point in this

scenario: Non-

controlling interest will

arise when we acquire

less than 100% of a

subsidiary. It shows

how much of the

group’s net asset is

financial by non-

controlling

shareholders.]

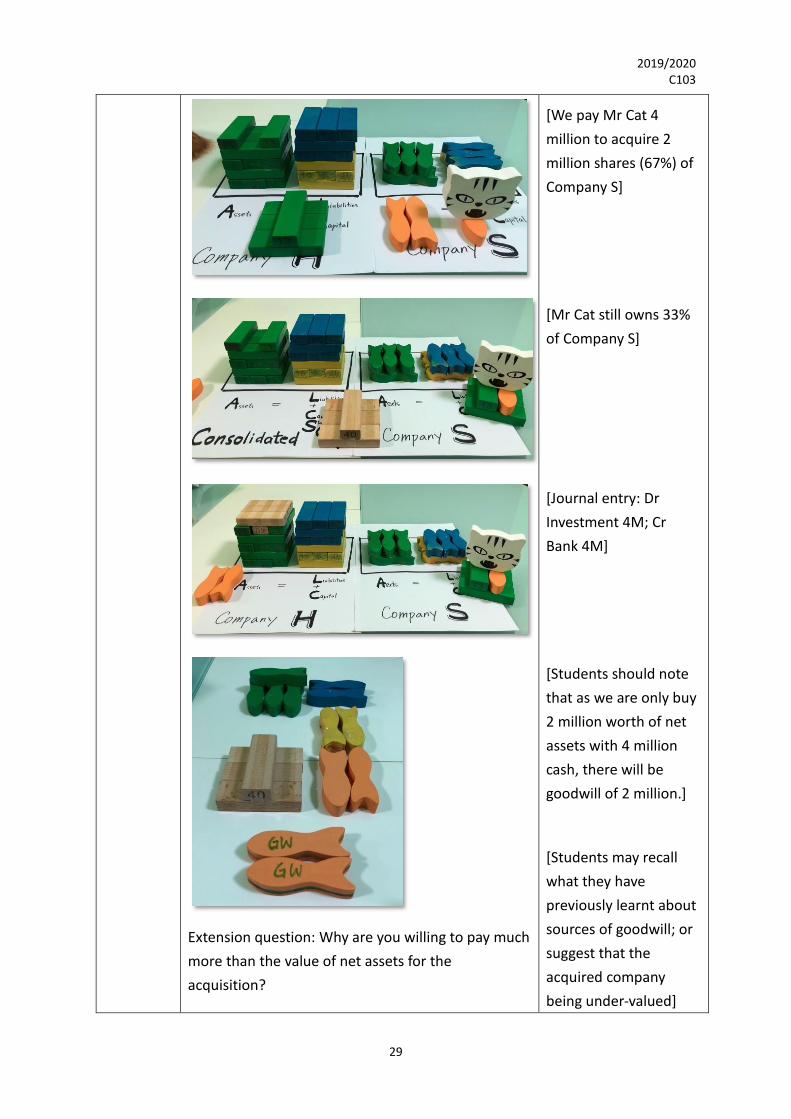

Scenario 4

We are paying Mr Cat 4 million to buy 2 million

shares (67%) he is holding in Company S.

Again, two students will be invited to show and

explain the steps of consolidation.

10 mins

[Before the acquisition]

2019/2020 C103

29

Extension question: Why are you willing to pay much

more than the value of net assets for the

acquisition?

[We pay Mr Cat 4

million to acquire 2

million shares (67%) of

Company S]

[Mr Cat still owns 33%

of Company S]

[Journal entry: Dr

Investment 4M; Cr

Bank 4M]

[Students should note

that as we are only buy

2 million worth of net

assets with 4 million

cash, there will be

goodwill of 2 million.]

[Students may recall

what they have

previously learnt about

sources of goodwill; or

suggest that the

acquired company

being under-valued]

2019/2020 C103

30

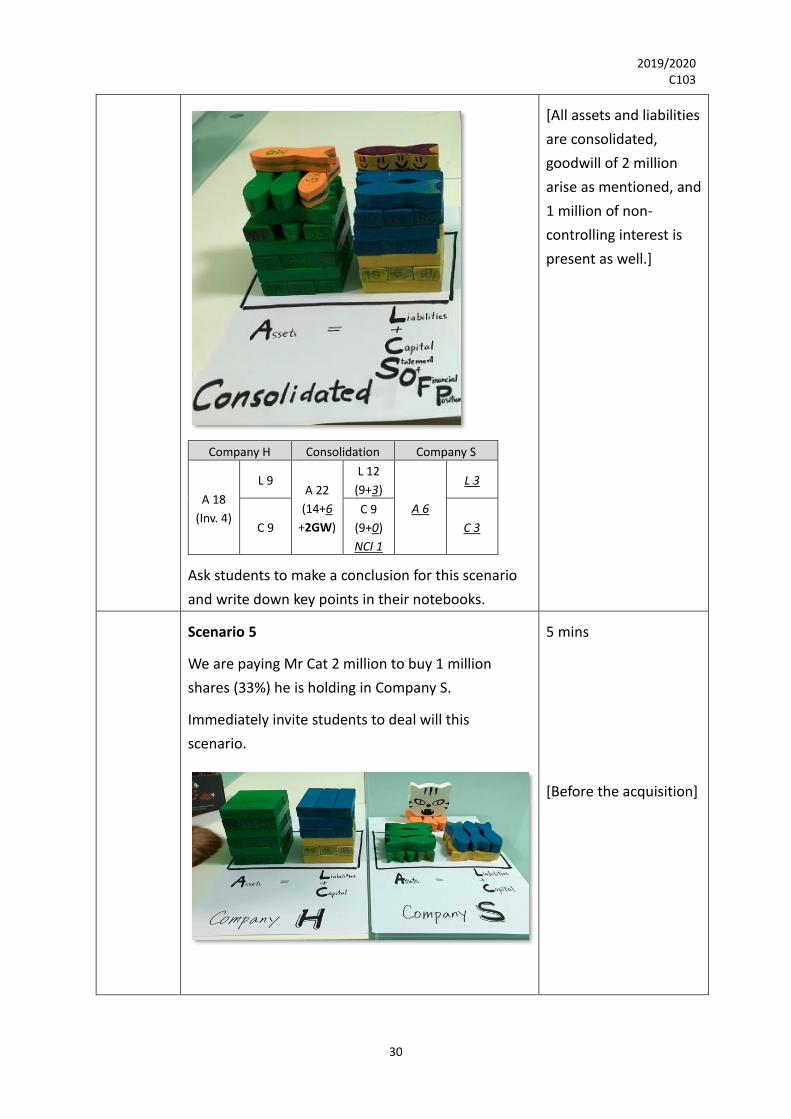

Ask students to make a conclusion for this scenario

and write down key points in their notebooks.

Company H Consolidation Company S

A 18

(Inv. 4)

L 9 A 22

(14+6

+2GW)

L 12

(9+3)

A 6

L 3

C 9

C 9

(9+0)

NCI 1

C 3

[All assets and liabilities

are consolidated,

goodwill of 2 million

arise as mentioned, and

1 million of non-

controlling interest is

present as well.]

Scenario 5

We are paying Mr Cat 2 million to buy 1 million

shares (33%) he is holding in Company S.

Immediately invite students to deal will this

scenario.

5 mins

[Before the acquisition]

2019/2020 C103

31

Students may attempt to do consolidation. They may

judge that there is goodwill of 1 million, consolidate

all assets and liabilities, and then ask if I have one

more block of non-controlling interest (I only have

1).

Comment that investment in Company S will remain

investment, and there is not group company if

shareholding in Company S is less than 50%.

Ask students to make a conclusion for this scenario

and write down key points in their notebooks.

Company H Consolidation Company S

A 18

(Inv. 2)

L 9

A 6

L 3

C 9 C 3

[We pay Mr Cat 2

million to acquire 1

million shares (33%) of

Company S]

[Mr Cat still owns 67%

of Company S]

[Journal entry: Dr

Investment 2M; Cr

Bank 2M]

[Hopefully other

students are able to

point out that there is

no need to do

consolidation as we do

not have control over

Company S.]

[Important point: there

is no need for

consolidation if we do

not have control over

the acquired company.]

Consolidat

ion and

conclusion

Ask students to name all the things they have learnt

in this lesson in the group before a short oral check-

up is given to the class.

Each group will answer the following questions in

turn:

When are consolidated financial statements

needed? [gain control over a company through the

10 mins

As a conclusion is made

after each small part of

the lesson, the final

consolidation and

conclusion part will be

kept simple and short.

2019/2020 C103

32

acquisition of more the 50% shareholding]

What is the journal entry in our books when we pay

5 million to acquire 3 million worth of shares? [Dr

Investment 5 million; Cr Bank 5 million]

What is goodwill? What is the amount of goodwill in

the case above? [Goodwill is the excess of purchase

price of a company over the value of net assets

acquired; 2 million]

What will arise in the consolidated statement of

financial statement if we acquire more that 50% but

less than 100% of a company? [Non-controlling

interest]

If we acquired 80% of the shares of a company, how

many % of assets and liabilities do we consolidate

into our consolidated statement? Why? [100%;

because we have control over all assets and liabilities

even though we do not own them all.]

How about if we only acquire 20% of the company?

How many % do we consolidate? [No consolidation

is needed as we have not gained control over the

company.]

Lesson 3-4

Date: 2 June 2020 Lesson 3-4 Duration: 80 minutes

Objectives

Must know

• Definition of Goodwill, Consolidated Retained Earnings and Non-

controlling Interest

• Calculation of Goodwill, Consolidated Retained Earnings and Non-

controlling Interest

Should know • Suggested format for the calculation of the items mentioned

Nice to know

• Why goodwill should be amortised

• What other items exist in the different between retained earnings of

the subsidiary at acquisition and statement date

Sequence Key Points Remarks

2019/2020 C103

33

Lead-in Recap what is learnt in the previous lesson.

Ask students to explain the following in the context

of consolidated financial statements:

1. Control: when the acquiring company has more

than 50% shareholding of the acquired company,

there is control over it and the consolidated

financial statements has to be prepared.

2. Goodwill: arises when the purchase consideration

is in excess of the value of net assets.

3. Non-controlling interest: in the consolidated

statement of financial position, all assets and

liabilities are consolidated into the group

statement as there is control. However, part of

these assets and liabilities are owned by

shareholders other than that of our group. Non-

controlling interest shows the part of the group

which in financed by other parties.

10 mins

These are important

basics of the topic.

Students have to have

clear concepts on the

items before moving

forward.

Develop-

ment

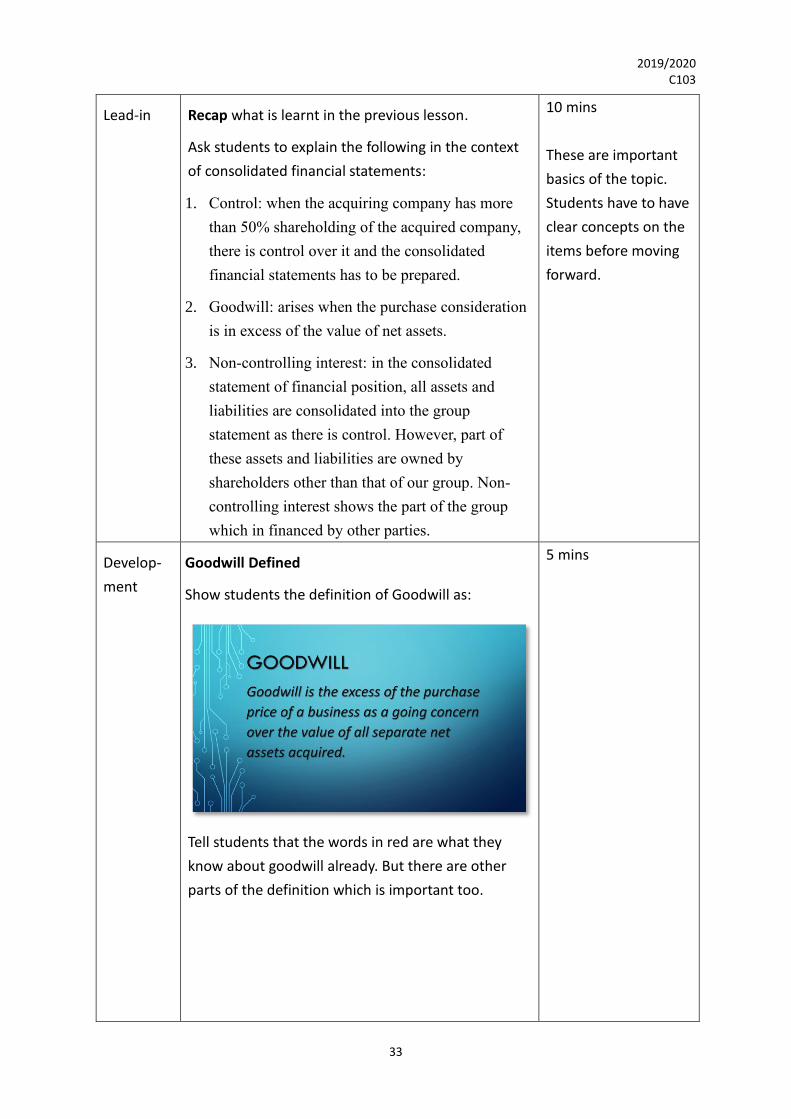

Goodwill Defined

Show students the definition of Goodwill as:

Tell students that the words in red are what they

know about goodwill already. But there are other

parts of the definition which is important too.

5 mins

2019/2020 C103

34

Goodwill arise only when we buy a business that

continues to run. It indicates that the business is

worth more than the value of its net assets.

If we purchase the net assets only, the value of the

net assets will be the amount we pay for the

purchase (historical cost concept). There is no

goodwill involved.

When we purchase less than 100%, take note that

in the calculation of goodwill, we compare the

purchase price with the proportional value of the

net assets of the business acquired.

2019/2020 C103

35

Goodwill calculation

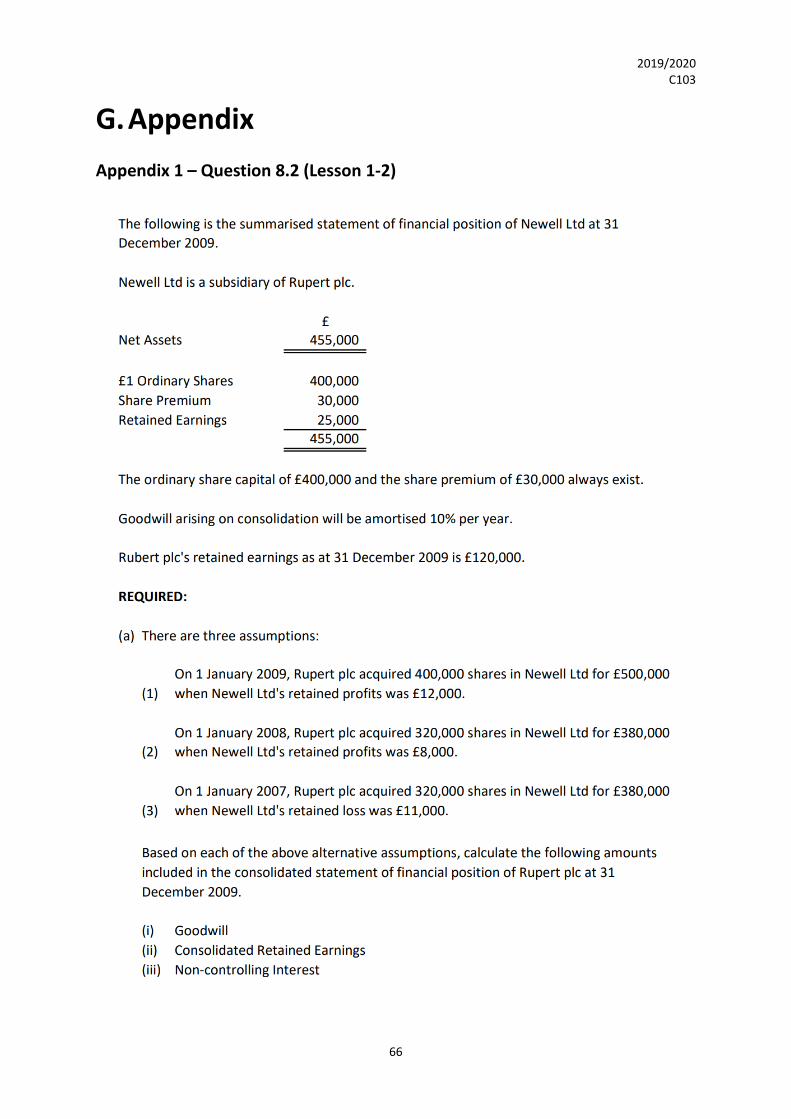

With the information given in Question 8.2 in the

textbook (see appendix 1), ask students to work out

the goodwill for each of the 3 assumptions, showing

detailed calculation process and the reasoning

behind.

Students are most likely to have doubts on what

goodwill amortization is; and the use of retained

profits/losses given. Hints will be given to two

groups only and students are expected to spread the

explanation across the class.

After the hints, students should be able to get to the

following answers

Assump-tion

Process and calculations (in thousands pounds)

1 (Purchase price – equity as at acquisitionx100% shareholding) with 1 year goodwill amortistion

[500-(400+30+12)]x(1-10%)= 52.2

2 (Purchase price – equity as at acquisitionx80% shareholding) with 2 years goodwill amortistion

[380-(400+30+8)x80%]x(1-20%)= 23.68

3 (Purchase price – equity as at acquisition(retained loss is negative)x100% shareholding) with 3 years goodwill amortistion

[350-(400+30-11)x80%]x(1-30%)= 10.36

Choose a group with the most organized answer and

show to the class.

15 mins

Hint 1: Goodwill

amortization is the

reduction of the value

of goodwill through

years. (10% per year

as given; pay

attention to the years

past after acquisition.

Hint 2: When calcu-

lating goodwill as at

the acquisition date,

we will compare the

purchase price with

the value of net assets

acquired as at acqui-

sition date. Net assets

equal equity. Retained

profits/l osses given

help in getting the

equity (net assets) as

at acquisition.

2019/2020 C103

36

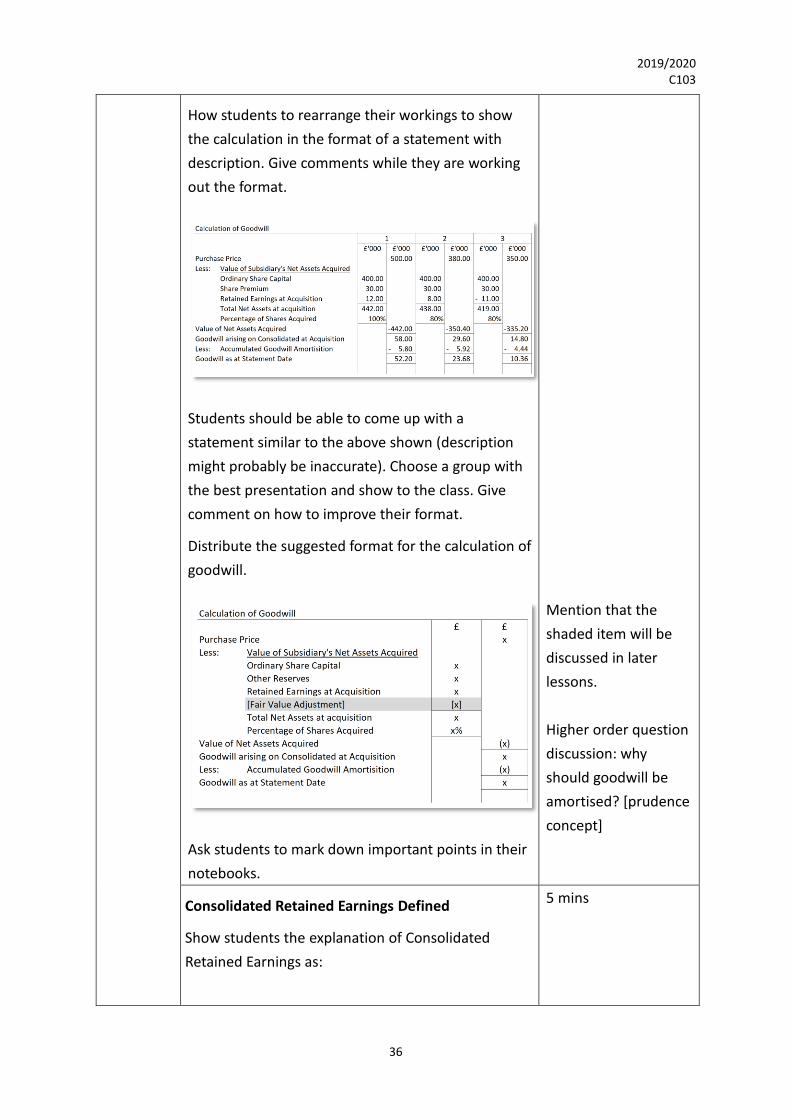

How students to rearrange their workings to show

the calculation in the format of a statement with

description. Give comments while they are working

out the format.

Students should be able to come up with a

statement similar to the above shown (description

might probably be inaccurate). Choose a group with

the best presentation and show to the class. Give

comment on how to improve their format.

Distribute the suggested format for the calculation of

goodwill.

Ask students to mark down important points in their

notebooks.

Mention that the

shaded item will be

discussed in later

lessons.

Higher order question

discussion: why

should goodwill be

amortised? [prudence

concept]

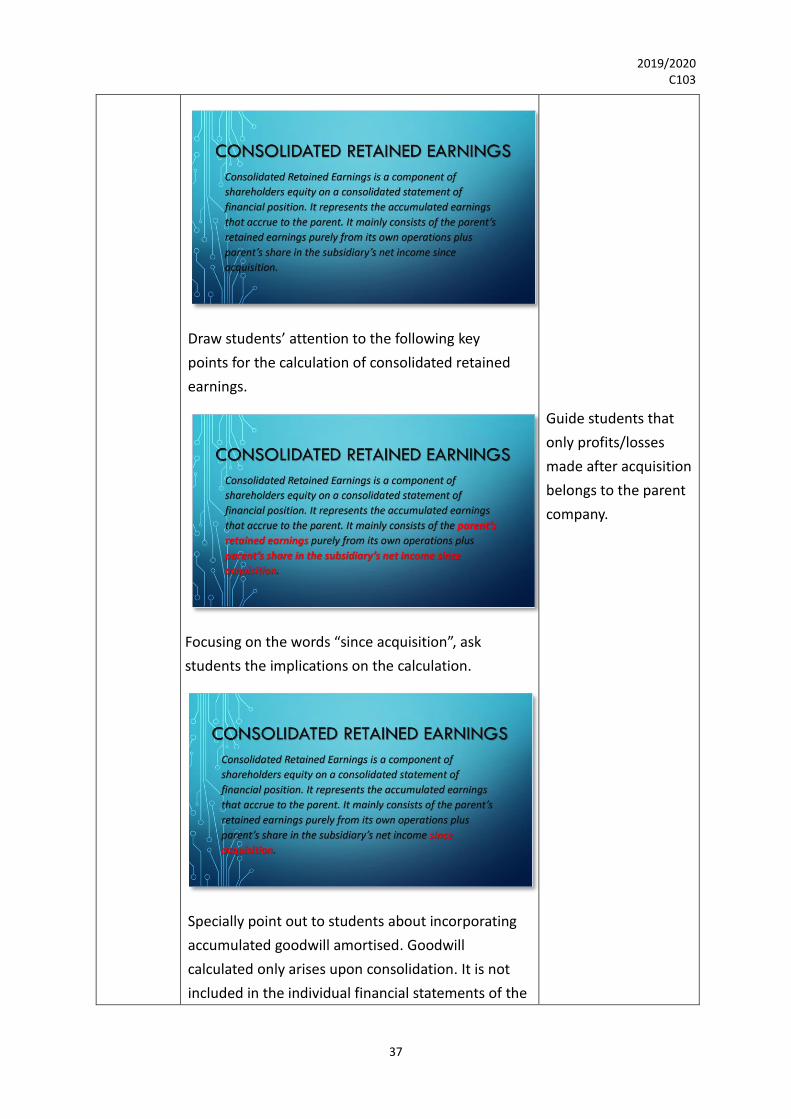

Consolidated Retained Earnings Defined

Show students the explanation of Consolidated

Retained Earnings as:

5 mins

2019/2020 C103

37

Draw students’ attention to the following key

points for the calculation of consolidated retained

earnings.

Focusing on the words “since acquisition”, ask

students the implications on the calculation.

Specially point out to students about incorporating

accumulated goodwill amortised. Goodwill

calculated only arises upon consolidation. It is not

included in the individual financial statements of the

Guide students that

only profits/losses

made after acquisition

belongs to the parent

company.

2019/2020 C103

38

holding company and the subsidiary. Thus, goodwill

amortization is an expense arising in the

consolidation process. This should be reflected as an

adjustment of consolidated retained earnings.

Consolidated Retained Earnings Calculation

Distribute the format for the calculation of

Consolidated Retained Earnings.

Continue with Question 8.2, ask students to work

out the consolidated retained earnings, showing

workings where necessary.

Students are most likely to have doubts on share of

subsidiary’s post acquisition profit; and how to

adjust for accumulated goodwill amortised. Again,

hints will be given to two groups only and students

are expected to spread the explanation across the

class.

After the hints, students should be able to get to the

following answers.

Assump-tion

Calculation of the share of subsidiary’s post acquisition profit (in thousands pounds)

1 (25-12)x100% = 13 2 (25-8)x80% = 13.6 3 (25-(-11))x80% = 28.8

Ask students to mark down important points in their

15 mins

Mention that the

shaded item will be

discussed in later

lessons.

Hint 1: post

acquisition profit is

the profit made by

the subsidiary since

acquisition. It is the

difference between

the retained earnings

at acquisition and

statement date.

Hint 2: adjustment for

accumulated goodwill

amortised in

consolidated retained

earnings is the figure

calculated in the

goodwill calculation.

Higher order question

discussion: Is post

acquisition profit the

2019/2020 C103

39

notebooks. only item that

changes retained

earnings of the

subsidiary? [No;

dividend; transfer to

reserves; other uses]

What to do with these

items? [Let students

consider this question

at home]

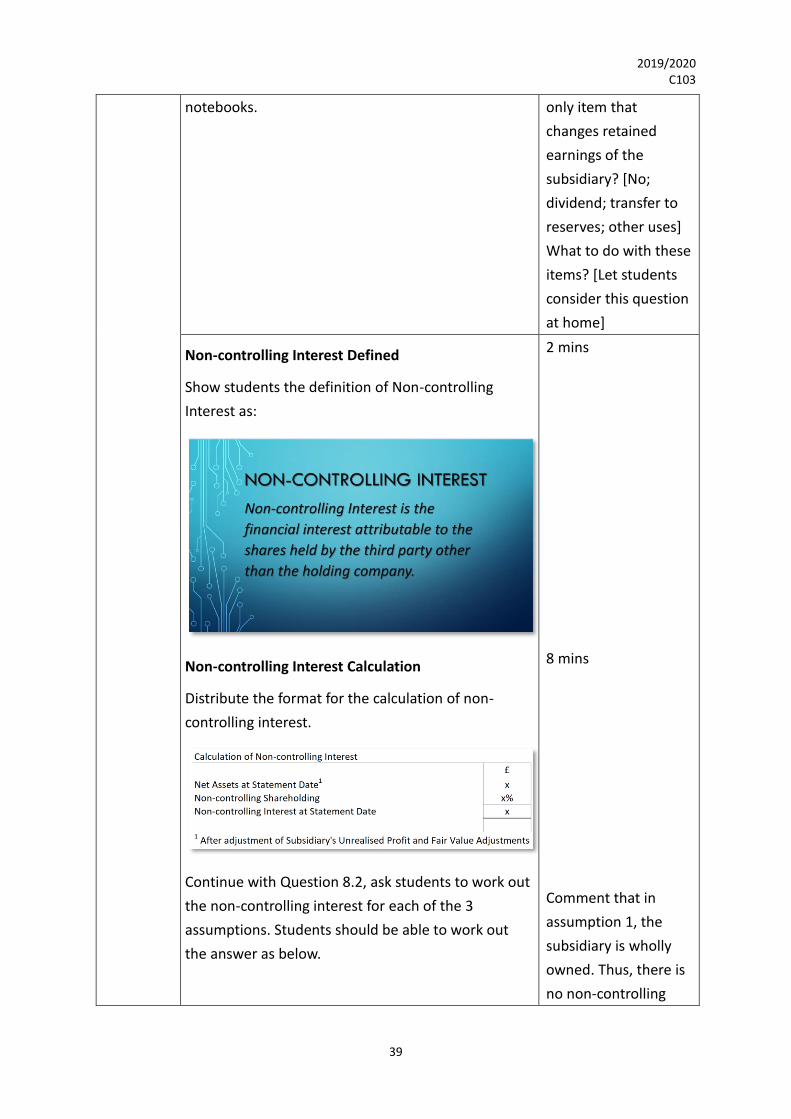

Non-controlling Interest Defined

Show students the definition of Non-controlling

Interest as:

Non-controlling Interest Calculation

Distribute the format for the calculation of non-

controlling interest.

Continue with Question 8.2, ask students to work out

the non-controlling interest for each of the 3

assumptions. Students should be able to work out

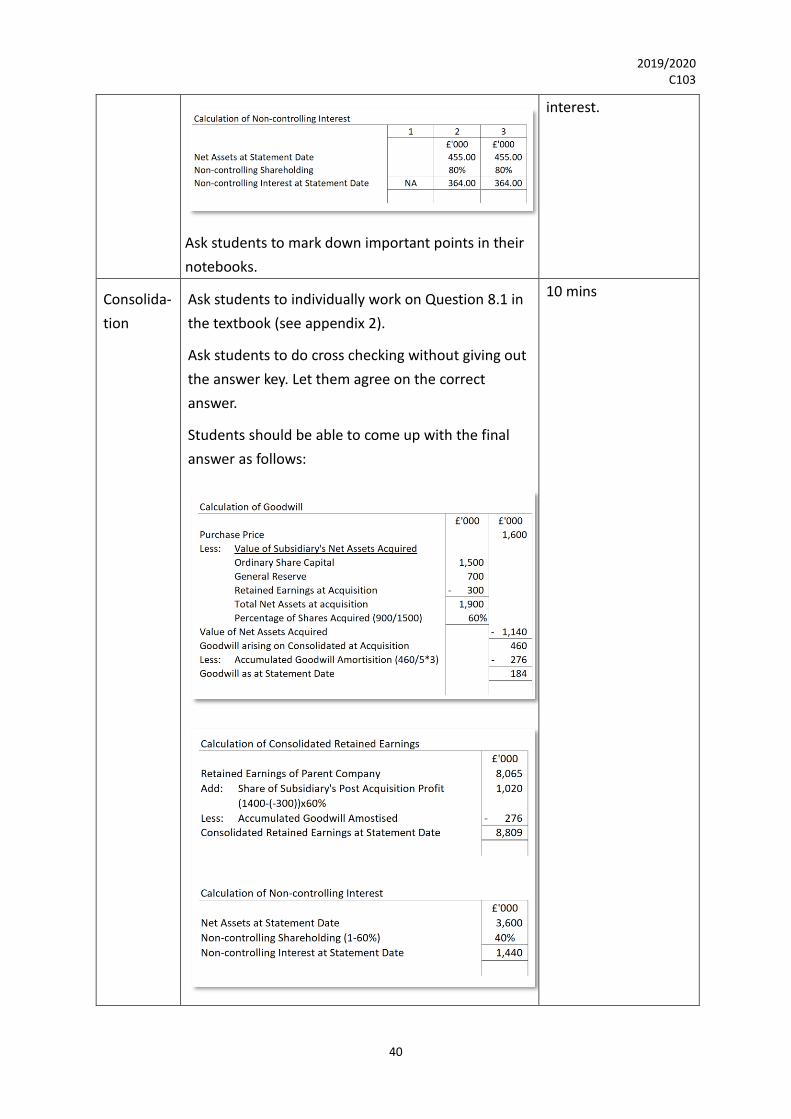

the answer as below.

2 mins

8 mins

Comment that in

assumption 1, the

subsidiary is wholly

owned. Thus, there is

no non-controlling

2019/2020 C103

40

Ask students to mark down important points in their

notebooks.

interest.

Consolida-

tion

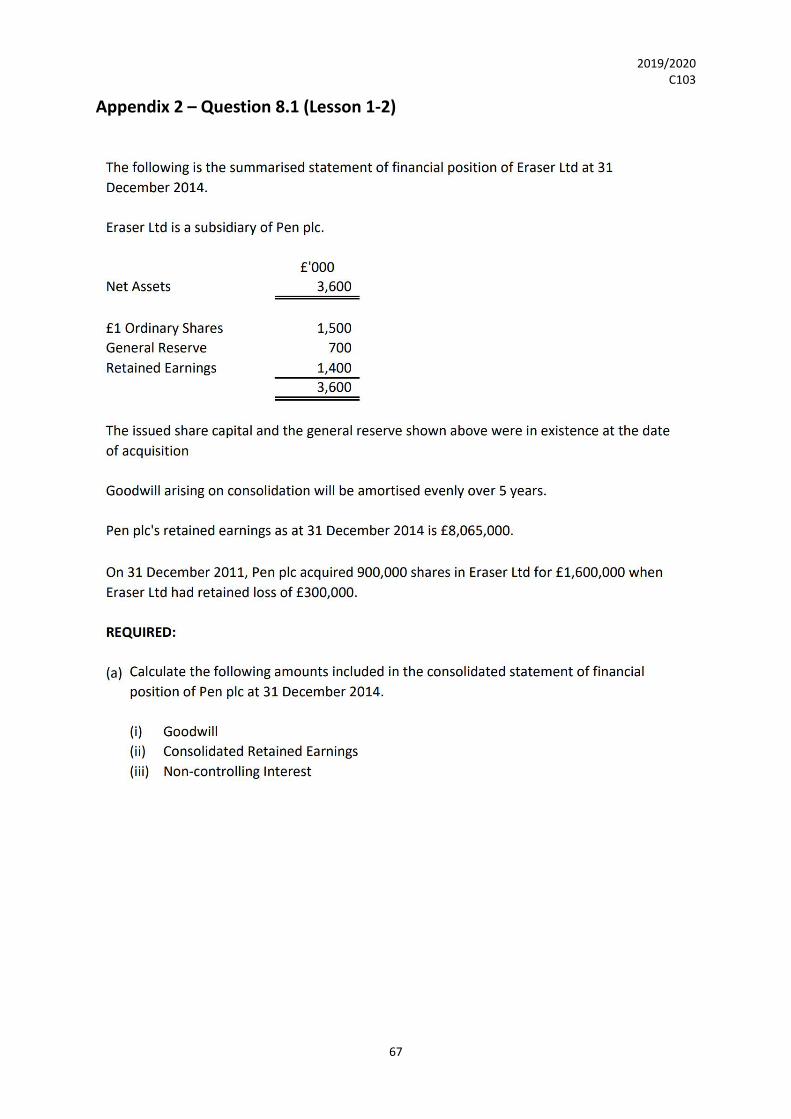

Ask students to individually work on Question 8.1 in

the textbook (see appendix 2).

Ask students to do cross checking without giving out

the answer key. Let them agree on the correct

answer.

Students should be able to come up with the final

answer as follows:

10 mins

2019/2020 C103

41

Conclu-

sion

Give students 2 minutes group discussion time to

recap on the new things they have learnt.

For each group in turn, ask them to name one item

until all the following are covered:

1. Definition of goodwill/consolidated retained

earnings/non-controlling interest

2. Retained earnings at acquisition date is used in

the calculation of goodwill

3. Goodwill amortised will be adjusted in

consolidated retained earnings

4. Only post acquisition profit goes into the

consolidated retained earnings

5. Non-controlling interest takes the net worth

multiplied by non-controlling shareholding

10 mins

Lesson 5-6

Date: 3 June 2020 Lesson 5-6 Duration: 80 minutes

Objectives

Must know

• Preparation of consolidated statement of financial position

• Treatment of Intra-group transactions

• Treatment of Intra-group indebtedness

• Treatment of negative goodwill arising on consolidation

Should know • Reasons behind the need for elimination of intra-group unrealized

profit and indebtedness

Nice to know

• How holding companies gain indirect control over subsidiaries

through layered shareholding

• How fraudulent transactions are created in group companies

• Process and effects of subsidiary declaring dividends

Sequence Key Points Remarks

Lead-in Game of Control

In pairs, students play the “Game of Control”. One

student is the leader, who commands the actions

and postures of the follower. The follower is allowed

5 mins

2019/2020 C103

42

to act on her own will when there is no command

from the leader.

Ask students to relate the game play to the topic

“group companies”.

Students should be able to answer points like:

✓ the relationship between the players of the

game resembles that of the holding company

and its subsidiary

✓ the companies are individual entities

operating separately

✓ the holding company can control the action

of its subsidiaries, and the subsidiaries have

to act according to the commands.

Extend the idea by saying that “Think about our

relationship in class. You all are there participating in

this game because you are kind of under my control.

I command the leaders to give commands to the

followers. The holding company can control its direct

subsidiaries, and at the same time control lower

level subsidiaries as well through indirect control.”

All these companies are also part of the group

company, and consolidation is needed for all in such

case.

Comment that subsidiary companies do not have

total freedom on their operations. They must do

what the holding company instruct them to do.

Develop-

ment

Distribute a LCCI 3rd Level Accounting past paper

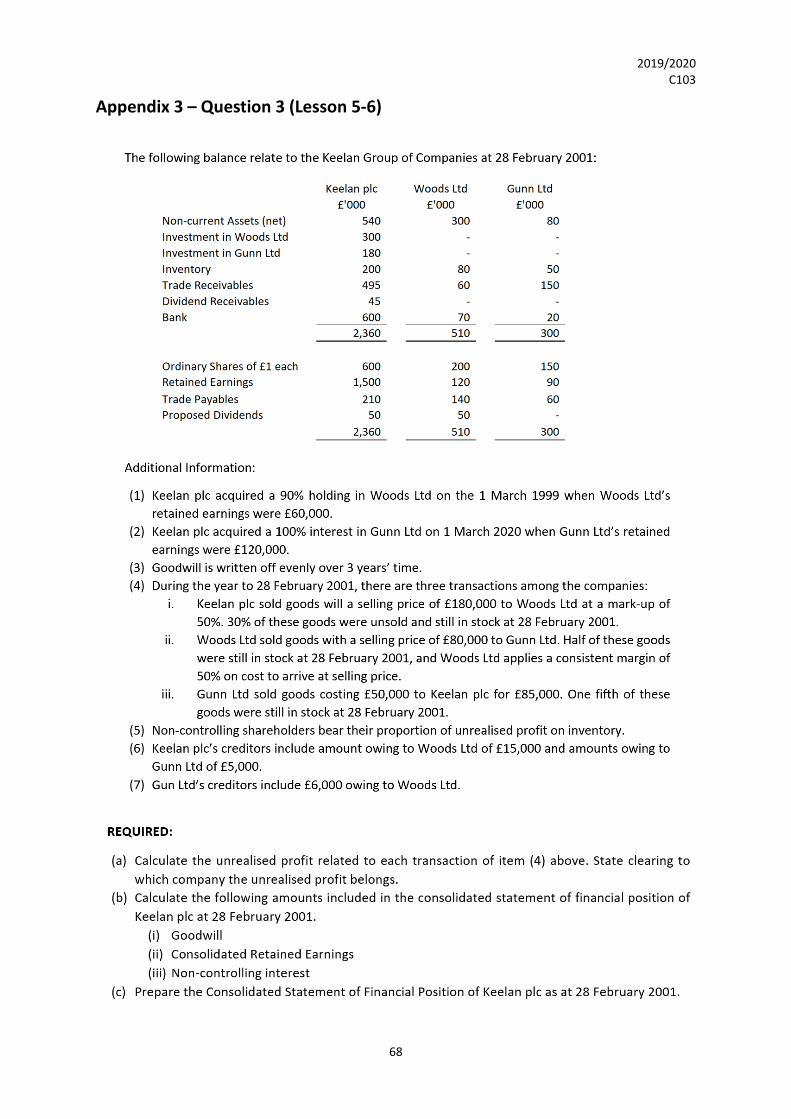

question “Question 3” (see appendix 3).

New concepts explained

Read the whole question with students. Ask them to

point out about things that are new to them. They

should mention the intra-group transactions and

intra-group indebtedness (though they may not use

these terms yet). Ask students to read page 119 of

the textbook for information. Give them 3 minutes

10 mins

This question

incorporates what

students have learnt

about goodwill,

consolidated retained

earnings and non-

controlling interest. It

explore on new

2019/2020 C103

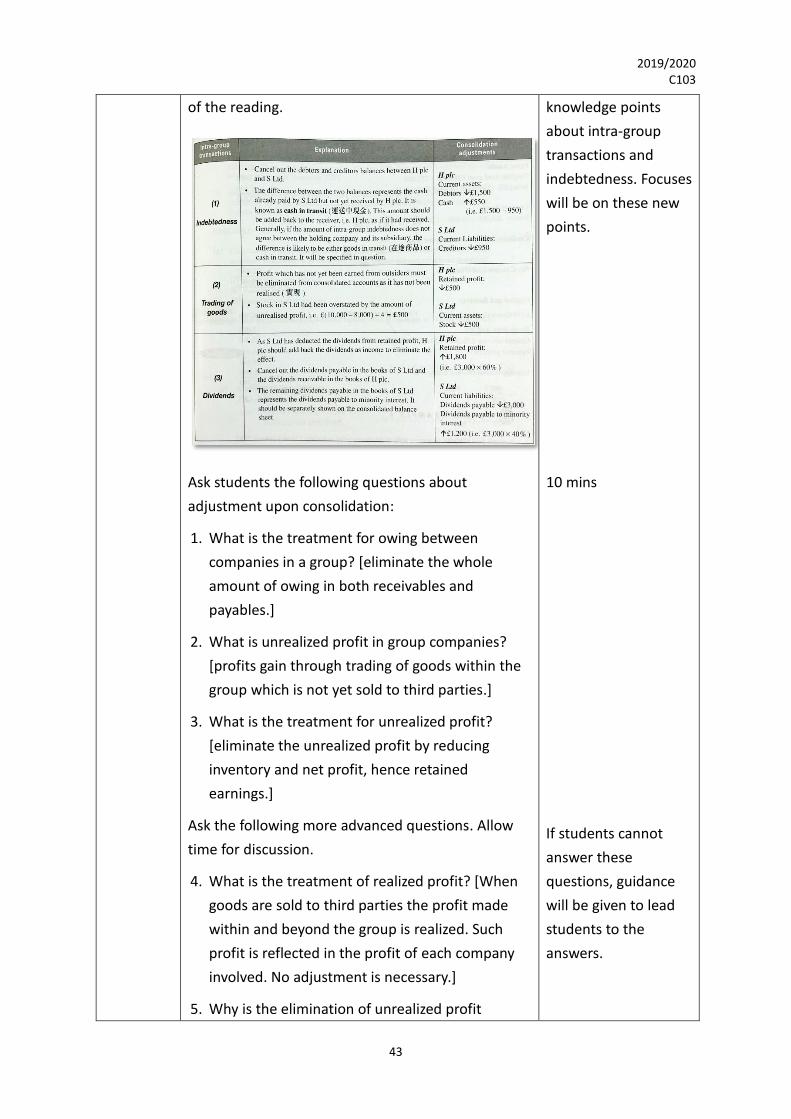

43

of the reading.

Ask students the following questions about

adjustment upon consolidation:

1. What is the treatment for owing between

companies in a group? [eliminate the whole

amount of owing in both receivables and

payables.]

2. What is unrealized profit in group companies?

[profits gain through trading of goods within the

group which is not yet sold to third parties.]

3. What is the treatment for unrealized profit?

[eliminate the unrealized profit by reducing

inventory and net profit, hence retained

earnings.]

Ask the following more advanced questions. Allow

time for discussion.

4. What is the treatment of realized profit? [When

goods are sold to third parties the profit made

within and beyond the group is realized. Such

profit is reflected in the profit of each company

involved. No adjustment is necessary.]

5. Why is the elimination of unrealized profit

knowledge points

about intra-group

transactions and

indebtedness. Focuses

will be on these new

points.

10 mins

If students cannot

answer these

questions, guidance

will be given to lead

students to the

answers.

2019/2020 C103

44

necessary? What happen if such elimination is

not required by accounting standards? [If

elimination of unrealized profit is not required,

group companies can “create” unlimited amount

of profit by selling and buying frequently within

the group or setting unrealistically high mark-up.

Profits and inventory will be inflated, and

financial statement would not be true and fair.

Elimination takes away effects of such

transactions aiming to mislead financial

statement users.]

6. Why is the elimination of intra-group

indebtedness necessary? What happen if such

elimination is not required by accounting

standards? [if elimination of intra-group

indebtedness is not required, companies in a

group can inflate the size of the group indefinitely

by lending and borrowing within the group. Such

lending and borrowing has no substance as one

cannot borrow money from oneself. Elimination

of intra-group indebtedness makes such inflation

impossible.]

Ask students to mark down important points in their

notebooks.

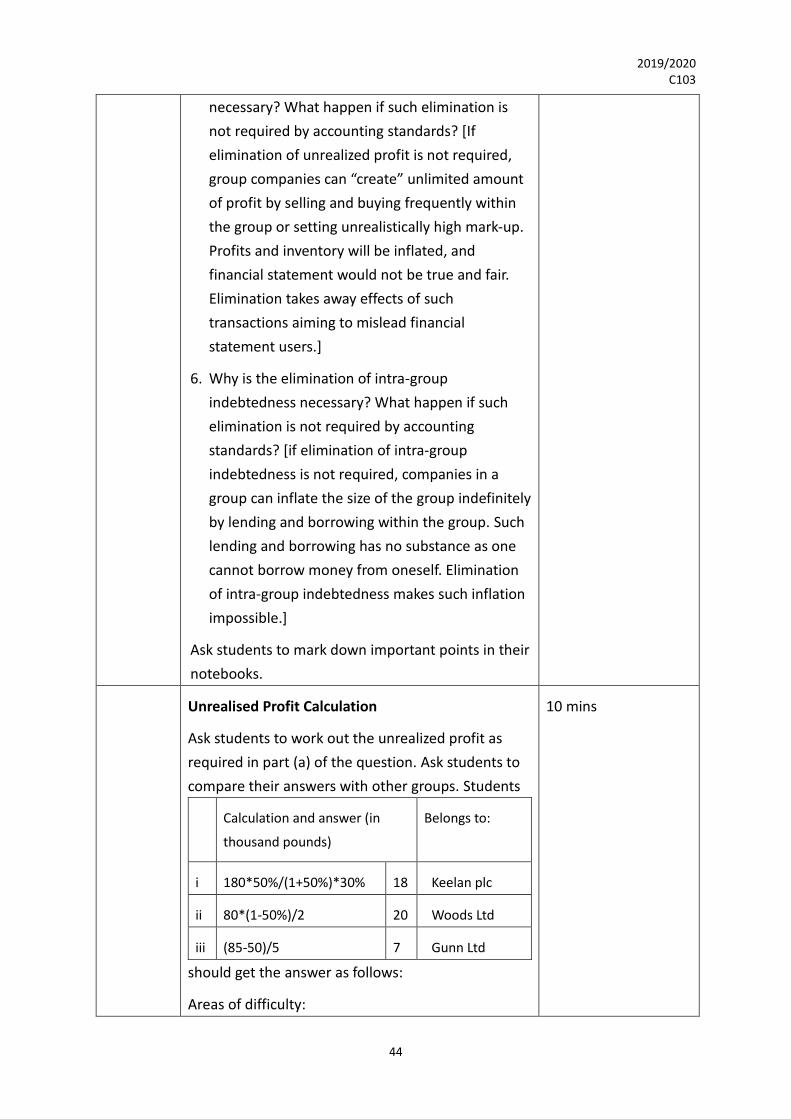

Unrealised Profit Calculation

Ask students to work out the unrealized profit as

required in part (a) of the question. Ask students to

compare their answers with other groups. Students

should get the answer as follows:

Areas of difficulty:

Calculation and answer (in

thousand pounds)

Belongs to:

i 180*50%/(1+50%)*30% 18 Keelan plc

ii 80*(1-50%)/2 20 Woods Ltd

iii (85-50)/5 7 Gunn Ltd

10 mins

2019/2020 C103

45

1. Students might easily mix up mark-up and

margin. Mark-up is “profit compared to cost”

while margin is “profit compared to selling price”.

2. Unrealised profit is not the whole amount of

profit made in the transaction. It is the

proportion of profit carried by the inventory that

still remind in the group.

3. The unrealized profit belongs to the company

selling the goods.

Ask students to mark down important points in their

notebooks.

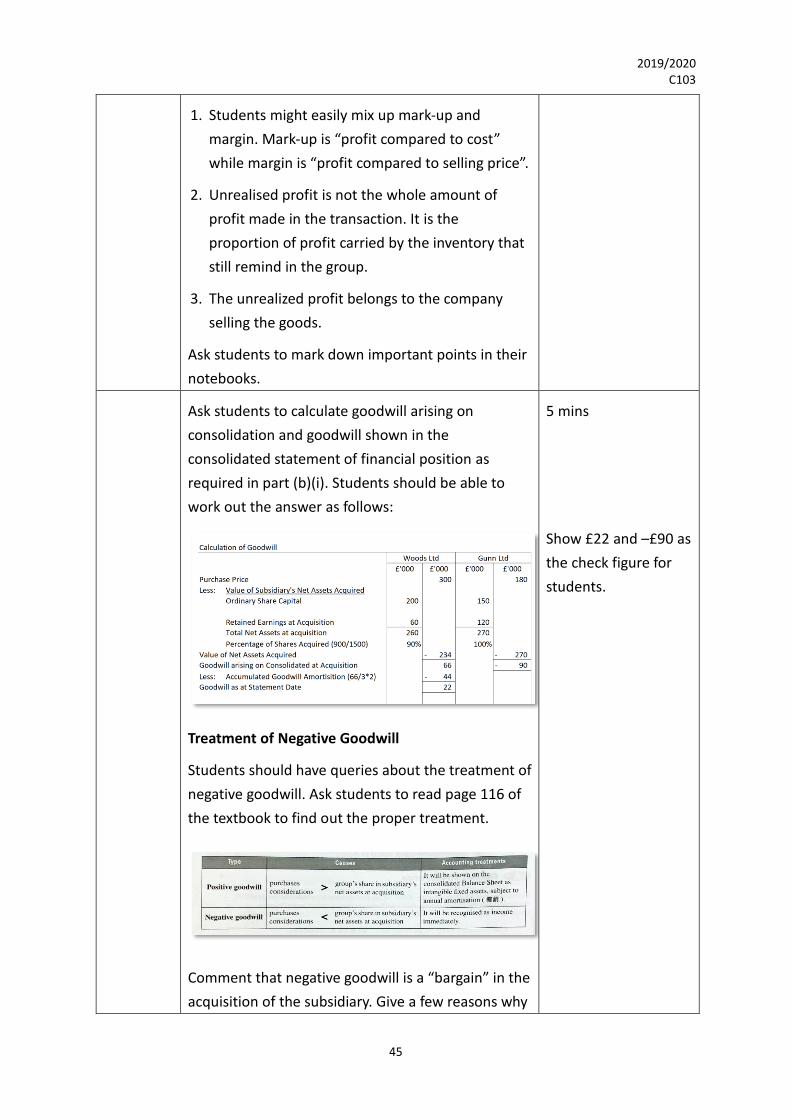

Ask students to calculate goodwill arising on

consolidation and goodwill shown in the

consolidated statement of financial position as

required in part (b)(i). Students should be able to

work out the answer as follows:

Treatment of Negative Goodwill

Students should have queries about the treatment of

negative goodwill. Ask students to read page 116 of

the textbook to find out the proper treatment.

Comment that negative goodwill is a “bargain” in the

acquisition of the subsidiary. Give a few reasons why

5 mins

Show £22 and –£90 as

the check figure for

students.

2019/2020 C103

46

such a bargain is obtained. Negative goodwill is

recognized as income in the year of acquisition, thus

an addition to retained earnings of the parent

company.

Ask students to mark down important points in their

notebooks.

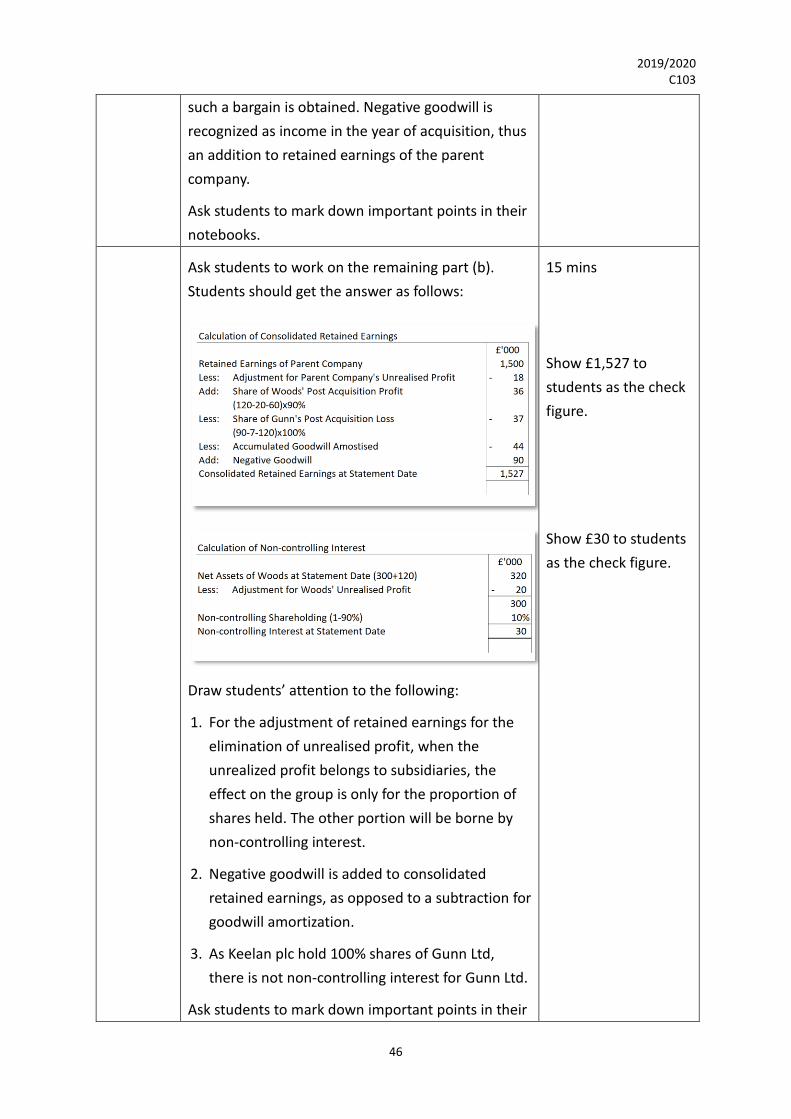

Ask students to work on the remaining part (b).

Students should get the answer as follows:

Draw students’ attention to the following:

1. For the adjustment of retained earnings for the

elimination of unrealised profit, when the

unrealized profit belongs to subsidiaries, the

effect on the group is only for the proportion of

shares held. The other portion will be borne by

non-controlling interest.

2. Negative goodwill is added to consolidated

retained earnings, as opposed to a subtraction for

goodwill amortization.

3. As Keelan plc hold 100% shares of Gunn Ltd,

there is not non-controlling interest for Gunn Ltd.

Ask students to mark down important points in their

15 mins

Show £1,527 to

students as the check

figure.

Show £30 to students

as the check figure.

2019/2020 C103

47

notebooks.

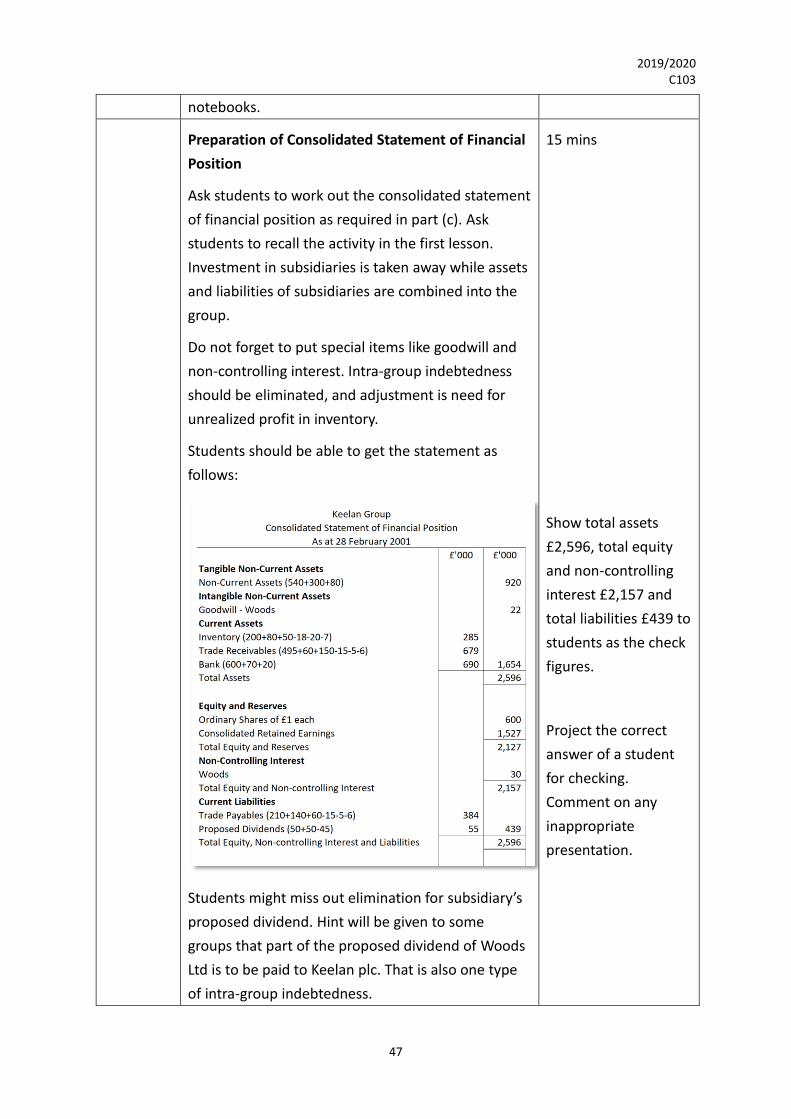

Preparation of Consolidated Statement of Financial

Position

Ask students to work out the consolidated statement

of financial position as required in part (c). Ask

students to recall the activity in the first lesson.

Investment in subsidiaries is taken away while assets

and liabilities of subsidiaries are combined into the

group.

Do not forget to put special items like goodwill and

non-controlling interest. Intra-group indebtedness

should be eliminated, and adjustment is need for

unrealized profit in inventory.

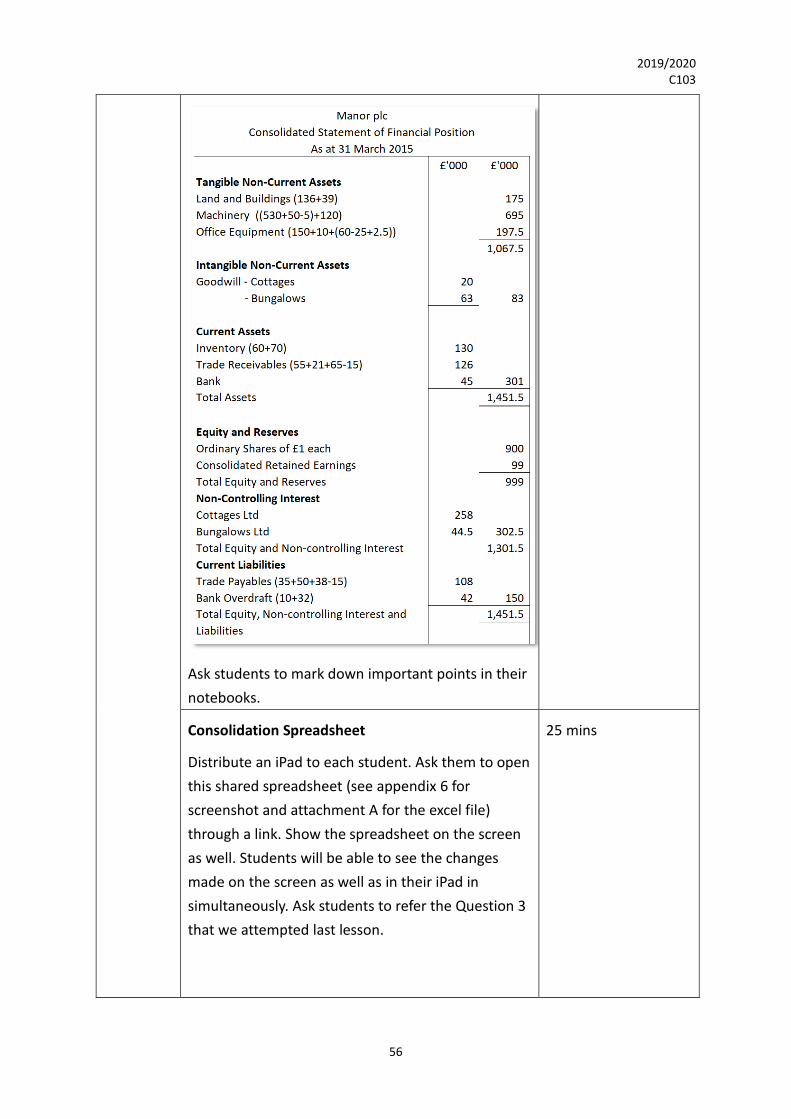

Students should be able to get the statement as

follows:

Students might miss out elimination for subsidiary’s

proposed dividend. Hint will be given to some

groups that part of the proposed dividend of Woods

Ltd is to be paid to Keelan plc. That is also one type

of intra-group indebtedness.

15 mins

Show total assets

£2,596, total equity

and non-controlling

interest £2,157 and

total liabilities £439 to

students as the check

figures.

Project the correct

answer of a student

for checking.

Comment on any

inappropriate

presentation.

2019/2020 C103

48

As an advanced-level question, ask students to

consider the process and effect of a subsidiary

declaring dividends on the parent company and the

consolidated statement. Discussion will be made in

the next lesson.

Consolida-

tion and

Conclusion

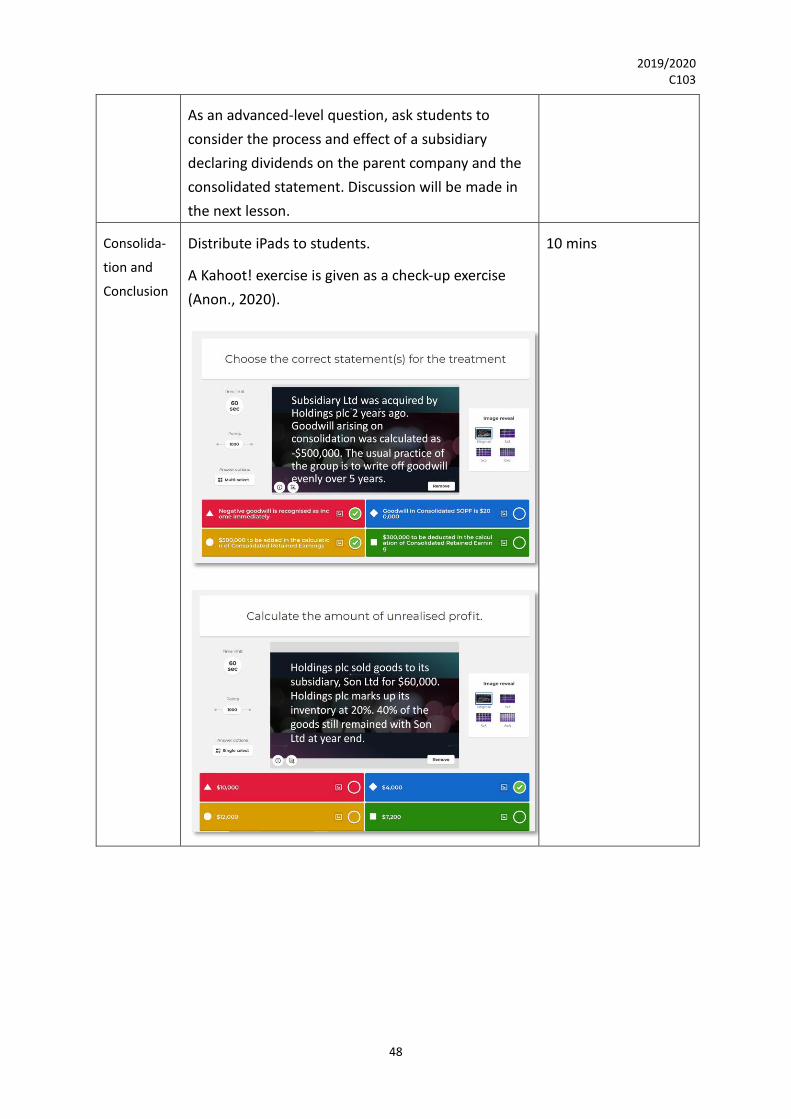

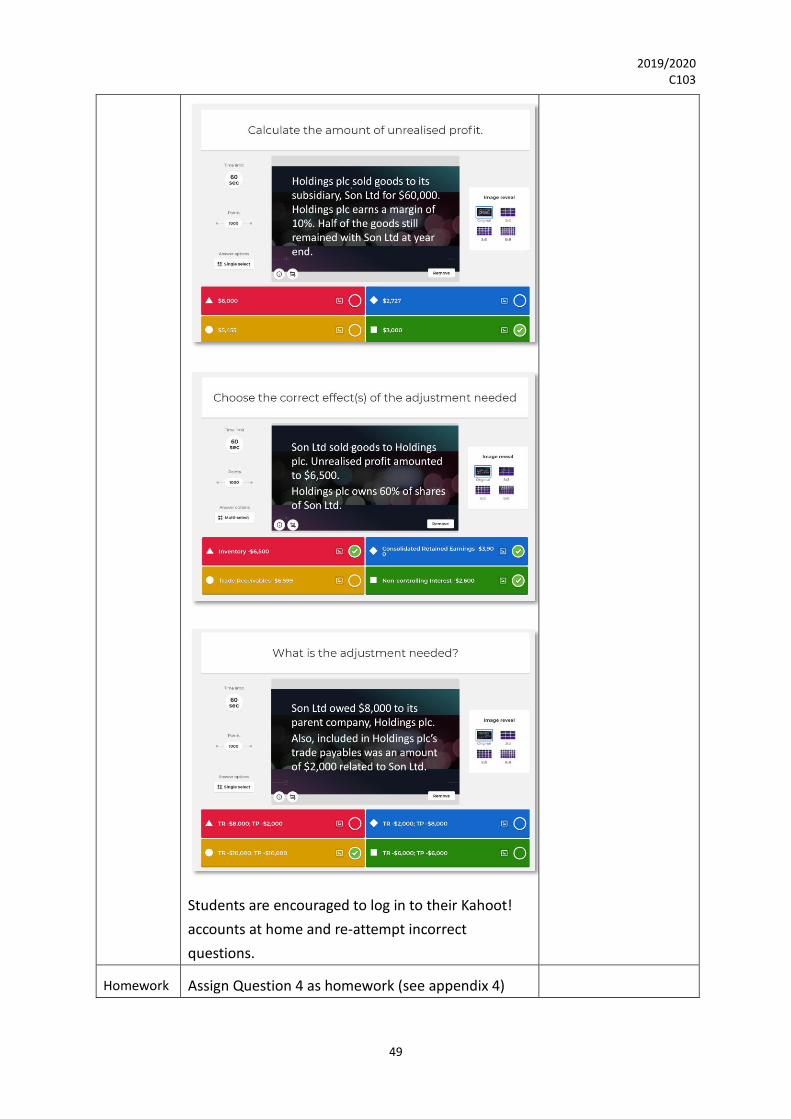

Distribute iPads to students.

A Kahoot! exercise is given as a check-up exercise

(Anon., 2020).

10 mins

2019/2020 C103

49

Students are encouraged to log in to their Kahoot!

accounts at home and re-attempt incorrect

questions.

Homework Assign Question 4 as homework (see appendix 4)

2019/2020 C103

50

Lesson 7-8

Date: 5 June 2020 Lesson 7-8 Duration: 80 minutes

Objectives

Must know

• Explain what fair value adjustment is and its treatment in the

process consolidation

• Calculation of adjustment of depreciation due to fair value

adjustment

• Effects of fair value adjustment in the consolidated statement of

financial position

• Be able to show positive bank balance and bank overdraft in the

statement of financial position in the proper way

Should know

• Understand why fair value adjustment is needed

• Distinguish between assets revaluation and fair value adjustment

during consolidation

Nice to know

• State and explain the risk of revaluing assets upon consolidation

• Understand the use of a consolidation spreadsheet

• Build a consolidation spreadsheet to show the process of

consolidation

Sequence Key Points Remarks

Lead-in Recap with students what we have learnt about

consolidation so far.

Students should be able to mention: calculation of

goodwill, consolidated retained earnings, non-

controlling interest; the treatment of intra-group

transactions and indebtedness.

Ask students “If the value of the acquired company is

substantially misjudged, eg. The value should be

much higher or lower”, what should we do?”

Students would probably suggest that the acquired

company revalue their assets and liabilities before

the acquisition according to accounting standards.

Follow up their suggestion by asking how such

revaluation should be done.

5 mins

Also comment that if

the value is just a

slight variation from

the fair value, it can

be ignored according

2019/2020 C103

51

[Assets revalued upwards should be debited and

revaluation reserve created correspondingly. Assets

revalued downwards should be written off/make

provisions and recognize as expenses immediately.]

Commented that their suggestion is correct, but it is

also possible that the revaluation is not done in the

individual company level. It can be done only in the

consolidated level. Ask students to go back to the

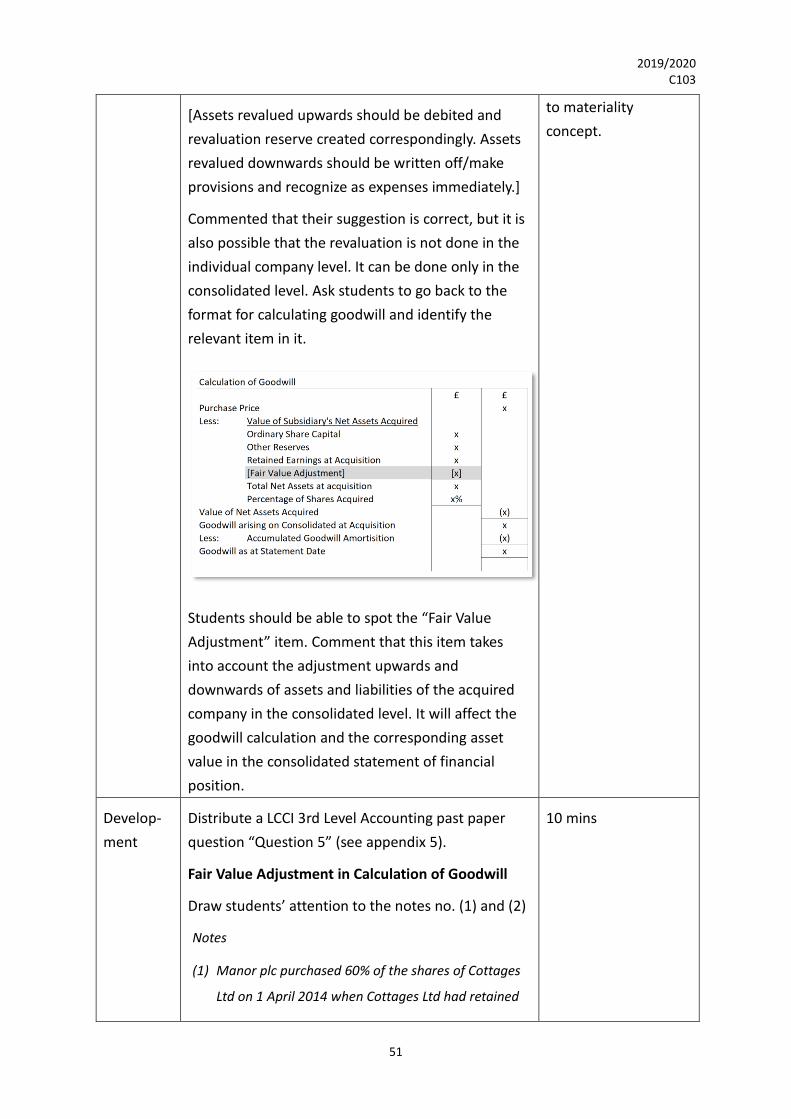

format for calculating goodwill and identify the

relevant item in it.

Students should be able to spot the “Fair Value

Adjustment” item. Comment that this item takes

into account the adjustment upwards and

downwards of assets and liabilities of the acquired

company in the consolidated level. It will affect the

goodwill calculation and the corresponding asset

value in the consolidated statement of financial

position.

to materiality

concept.

Develop-

ment

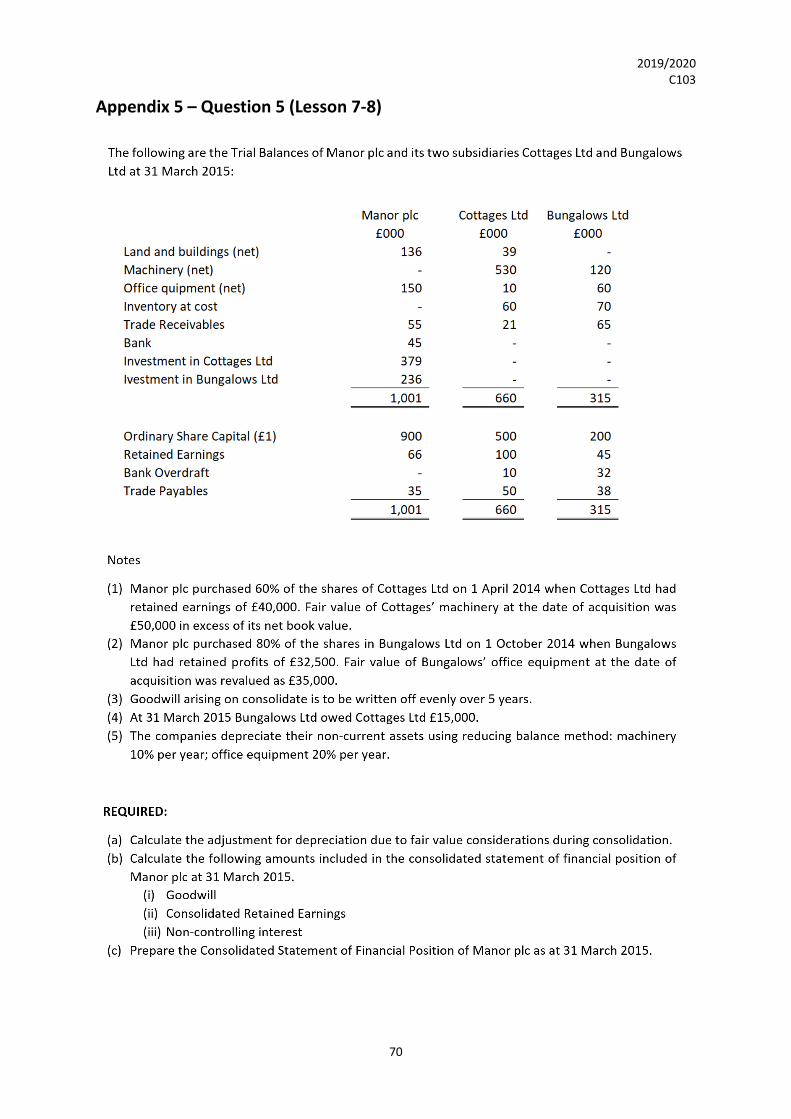

Distribute a LCCI 3rd Level Accounting past paper

question “Question 5” (see appendix 5).

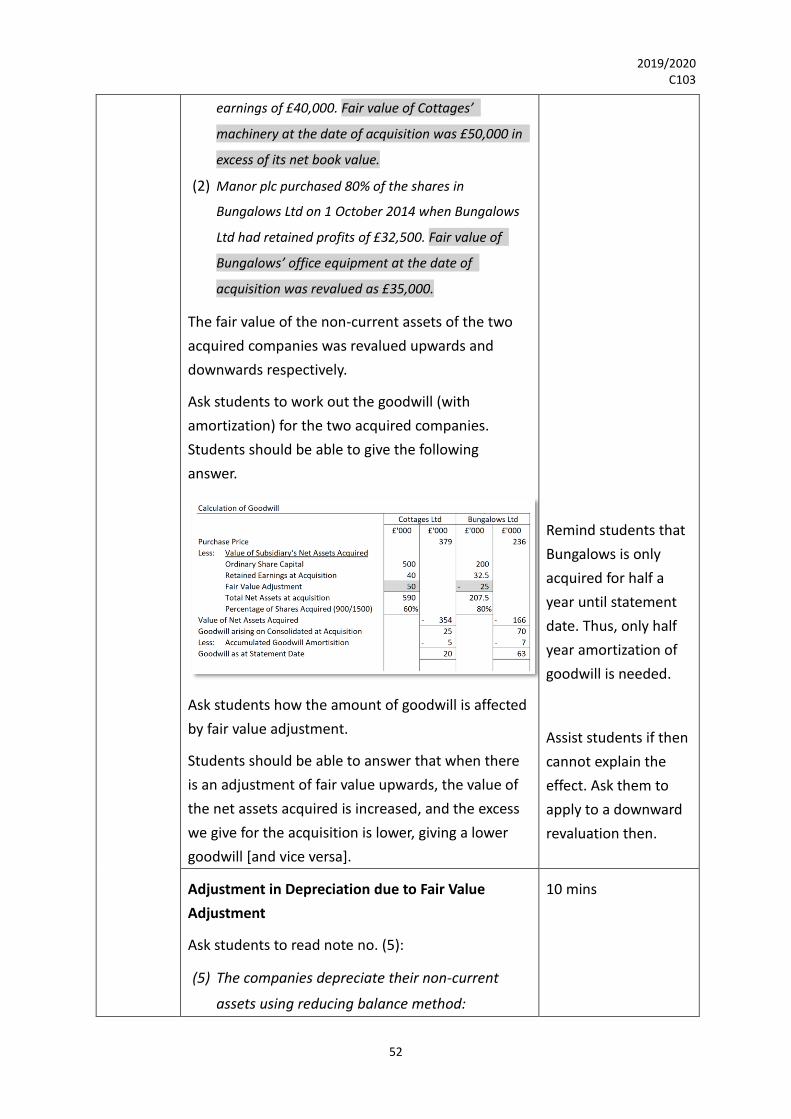

Fair Value Adjustment in Calculation of Goodwill

Draw students’ attention to the notes no. (1) and (2)

Notes

(1) Manor plc purchased 60% of the shares of Cottages

Ltd on 1 April 2014 when Cottages Ltd had retained

10 mins

2019/2020 C103

52

earnings of £40,000. Fair value of Cottages’

machinery at the date of acquisition was £50,000 in

excess of its net book value.

(2) Manor plc purchased 80% of the shares in

Bungalows Ltd on 1 October 2014 when Bungalows

Ltd had retained profits of £32,500. Fair value of

Bungalows’ office equipment at the date of

acquisition was revalued as £35,000.

The fair value of the non-current assets of the two

acquired companies was revalued upwards and

downwards respectively.

Ask students to work out the goodwill (with

amortization) for the two acquired companies.

Students should be able to give the following

answer.

Ask students how the amount of goodwill is affected

by fair value adjustment.

Students should be able to answer that when there

is an adjustment of fair value upwards, the value of

the net assets acquired is increased, and the excess

we give for the acquisition is lower, giving a lower

goodwill [and vice versa].

Remind students that

Bungalows is only

acquired for half a

year until statement

date. Thus, only half

year amortization of

goodwill is needed.

Assist students if then

cannot explain the

effect. Ask them to

apply to a downward

revaluation then.

Adjustment in Depreciation due to Fair Value

Adjustment

Ask students to read note no. (5):

(5) The companies depreciate their non-current

assets using reducing balance method:

10 mins

2019/2020 C103

53

machinery 10% per year; office equipment 20%

per year.

Ask students to think about why depreciation policy

is given and what the use of it is.

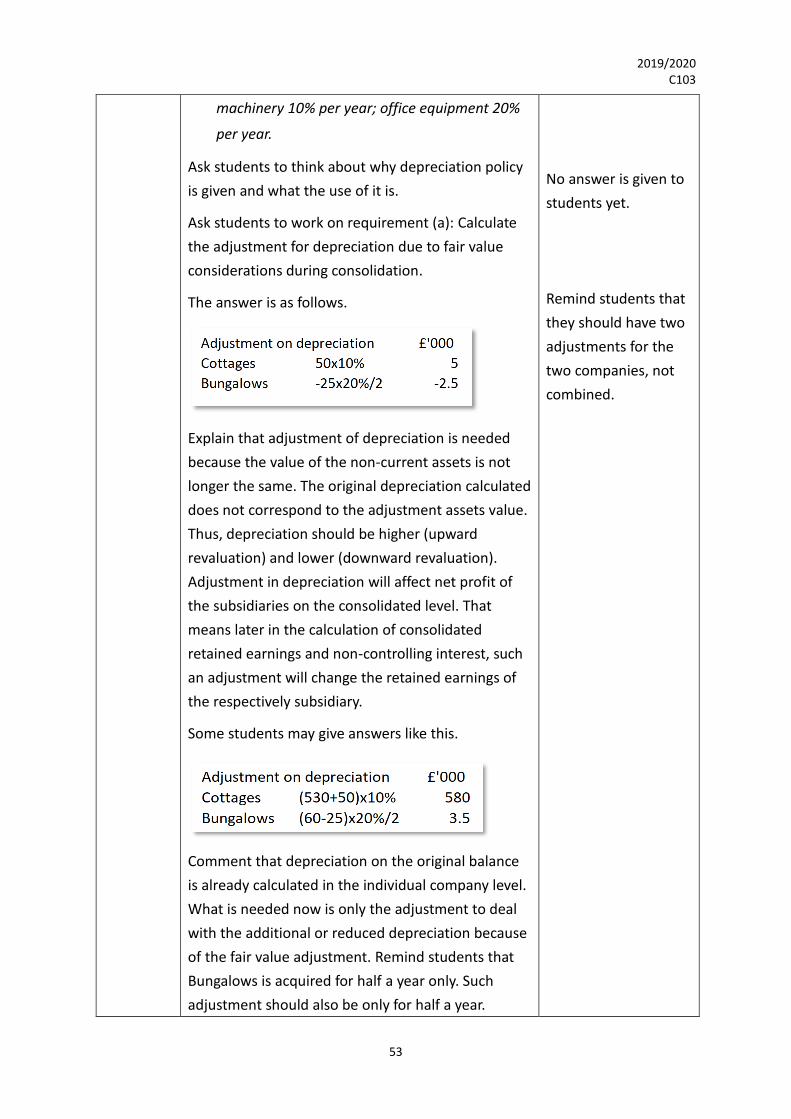

Ask students to work on requirement (a): Calculate

the adjustment for depreciation due to fair value

considerations during consolidation.

The answer is as follows.

Explain that adjustment of depreciation is needed

because the value of the non-current assets is not

longer the same. The original depreciation calculated

does not correspond to the adjustment assets value.

Thus, depreciation should be higher (upward

revaluation) and lower (downward revaluation).

Adjustment in depreciation will affect net profit of

the subsidiaries on the consolidated level. That

means later in the calculation of consolidated

retained earnings and non-controlling interest, such

an adjustment will change the retained earnings of

the respectively subsidiary.

Some students may give answers like this.

Comment that depreciation on the original balance

is already calculated in the individual company level.

What is needed now is only the adjustment to deal

with the additional or reduced depreciation because

of the fair value adjustment. Remind students that

Bungalows is acquired for half a year only. Such

adjustment should also be only for half a year.

No answer is given to

students yet.

Remind students that

they should have two

adjustments for the

two companies, not

combined.

2019/2020 C103

54

Ask students to mark down important points in their

notebooks.

Retained Earnings and Non-Controlling Interest

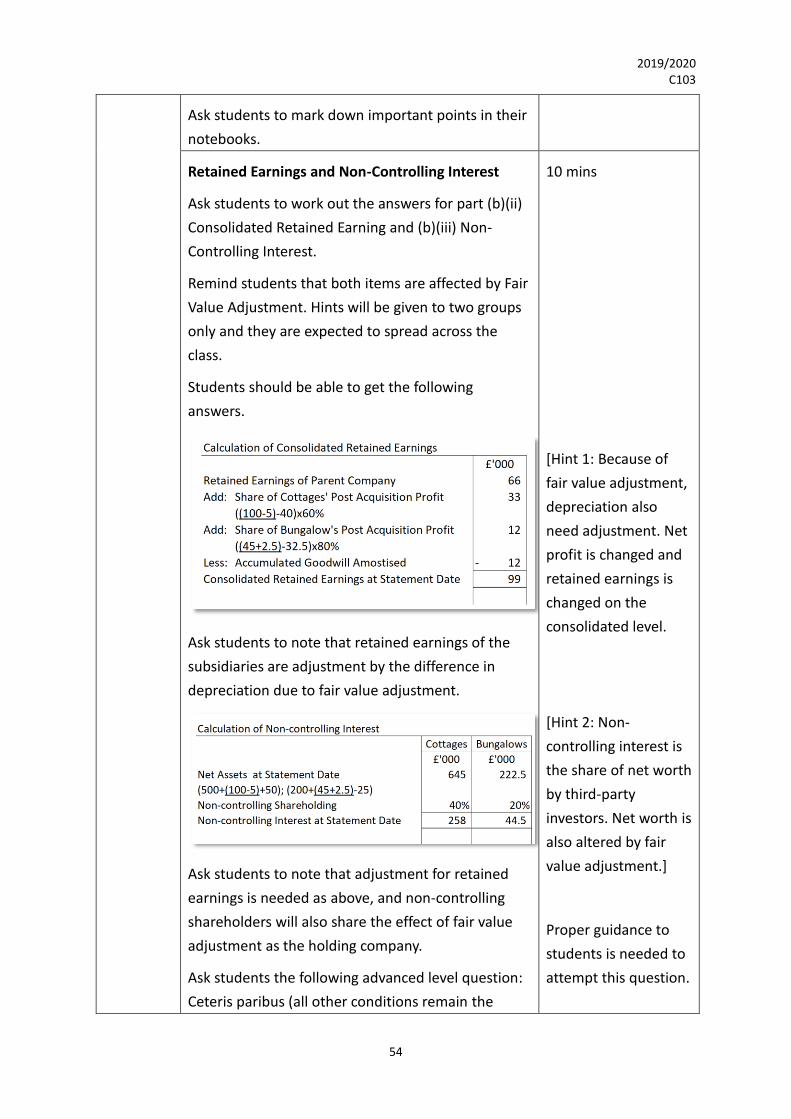

Ask students to work out the answers for part (b)(ii)

Consolidated Retained Earning and (b)(iii) Non-

Controlling Interest.

Remind students that both items are affected by Fair

Value Adjustment. Hints will be given to two groups

only and they are expected to spread across the

class.

Students should be able to get the following

answers.

Ask students to note that retained earnings of the

subsidiaries are adjustment by the difference in

depreciation due to fair value adjustment.

Ask students to note that adjustment for retained

earnings is needed as above, and non-controlling

shareholders will also share the effect of fair value

adjustment as the holding company.

Ask students the following advanced level question:

Ceteris paribus (all other conditions remain the

10 mins

[Hint 1: Because of

fair value adjustment,

depreciation also

need adjustment. Net

profit is changed and

retained earnings is

changed on the

consolidated level.

[Hint 2: Non-

controlling interest is

the share of net worth

by third-party

investors. Net worth is

also altered by fair

value adjustment.]

Proper guidance to

students is needed to

attempt this question.

2019/2020 C103

55

same), what will be different if Cottages Ltd was

acquired for 3 years already?

Correct answers include:

(1) Goodwill amortization will be 3 years instead of

1 year.

(2) Adjustment on depreciation should be 3 years

instead of 1 year. (The case in complicated by

the fact that reducing balance method is used

for the calculation)

(3) Adjustment for retained earnings of Cottages

Ltd in the calculation of Consolidated Retained

Earnings and Non-controlling Interest will

change accordingly.

Ask students to mark down important points in their

notebooks.

Ask students to work out the Consolidated

Statement of Financial Position as required in part

(c).

Give students minimal assistant in this part. Students

will try to balance the statement and find out the

problems by themselves. Students would have

problem mainly in these areas:

(1) Non-current assets should be adjusted by the

fair value adjustment and the corresponding

depreciation adjustment.

(2) If fair value adjustment is positive (revalue

upwards), depreciation is under-charged.

Adjusting depreciation in this case would have a

negative effect. If fair value adjustment is

negative (revalue downwards), depreciation is

over-charged. Adjusting depreciation in this

case would have a positive effect.

(3) Bank and bank overdraft should be treated

separately, but not offset again each other.

15 mins

2019/2020 C103

56

Ask students to mark down important points in their

notebooks.

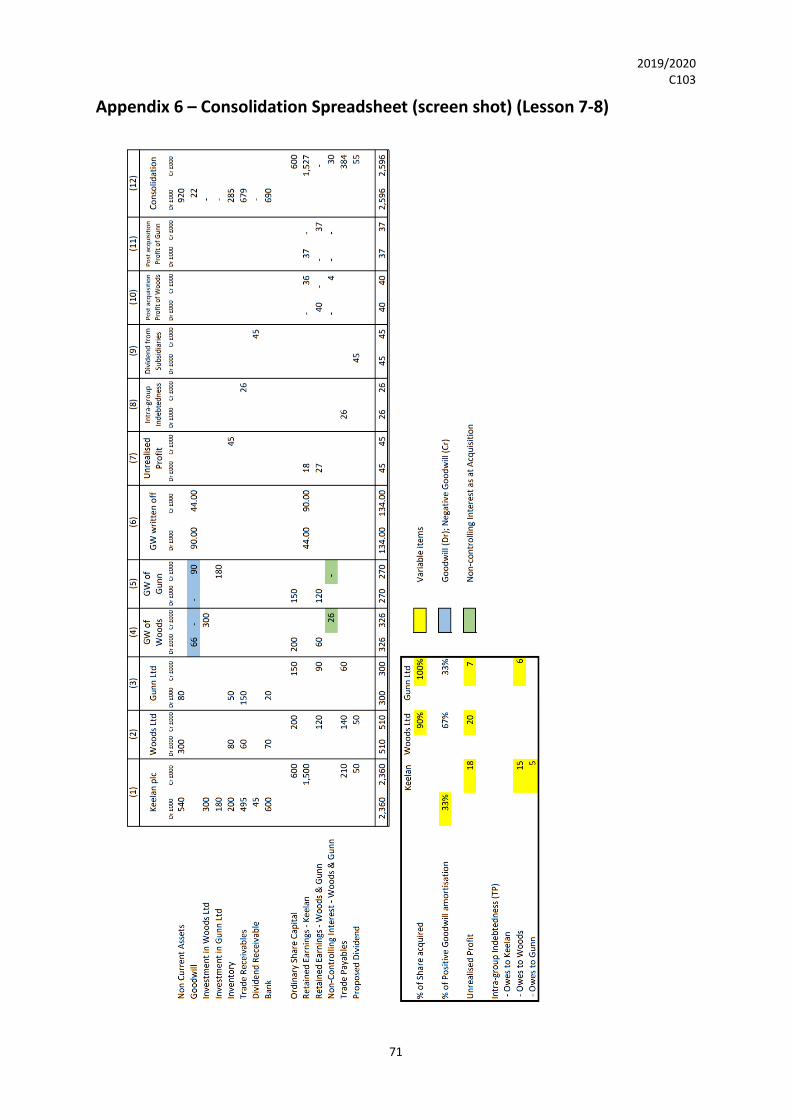

Consolidation Spreadsheet

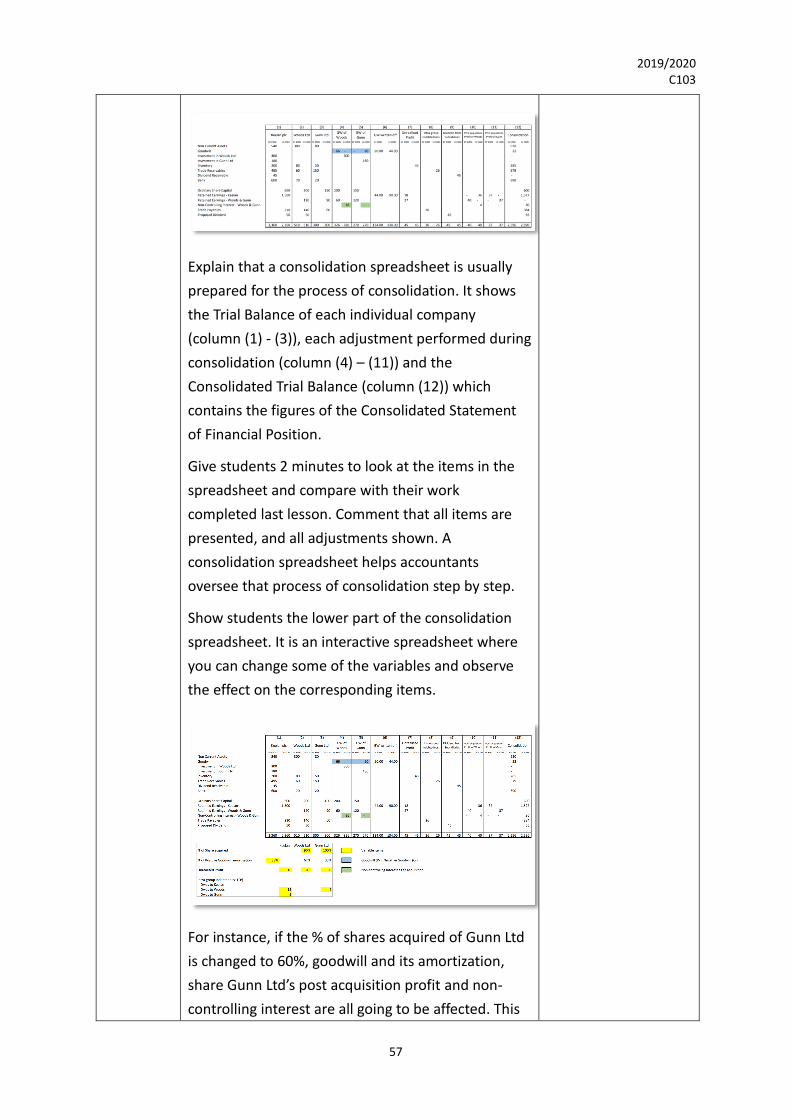

Distribute an iPad to each student. Ask them to open

this shared spreadsheet (see appendix 6 for

screenshot and attachment A for the excel file)

through a link. Show the spreadsheet on the screen

as well. Students will be able to see the changes

made on the screen as well as in their iPad in

simultaneously. Ask students to refer the Question 3

that we attempted last lesson.

25 mins

2019/2020 C103

57

Explain that a consolidation spreadsheet is usually

prepared for the process of consolidation. It shows

the Trial Balance of each individual company

(column (1) - (3)), each adjustment performed during

consolidation (column (4) – (11)) and the

Consolidated Trial Balance (column (12)) which

contains the figures of the Consolidated Statement

of Financial Position.

Give students 2 minutes to look at the items in the

spreadsheet and compare with their work

completed last lesson. Comment that all items are

presented, and all adjustments shown. A

consolidation spreadsheet helps accountants

oversee that process of consolidation step by step.

Show students the lower part of the consolidation

spreadsheet. It is an interactive spreadsheet where

you can change some of the variables and observe

the effect on the corresponding items.

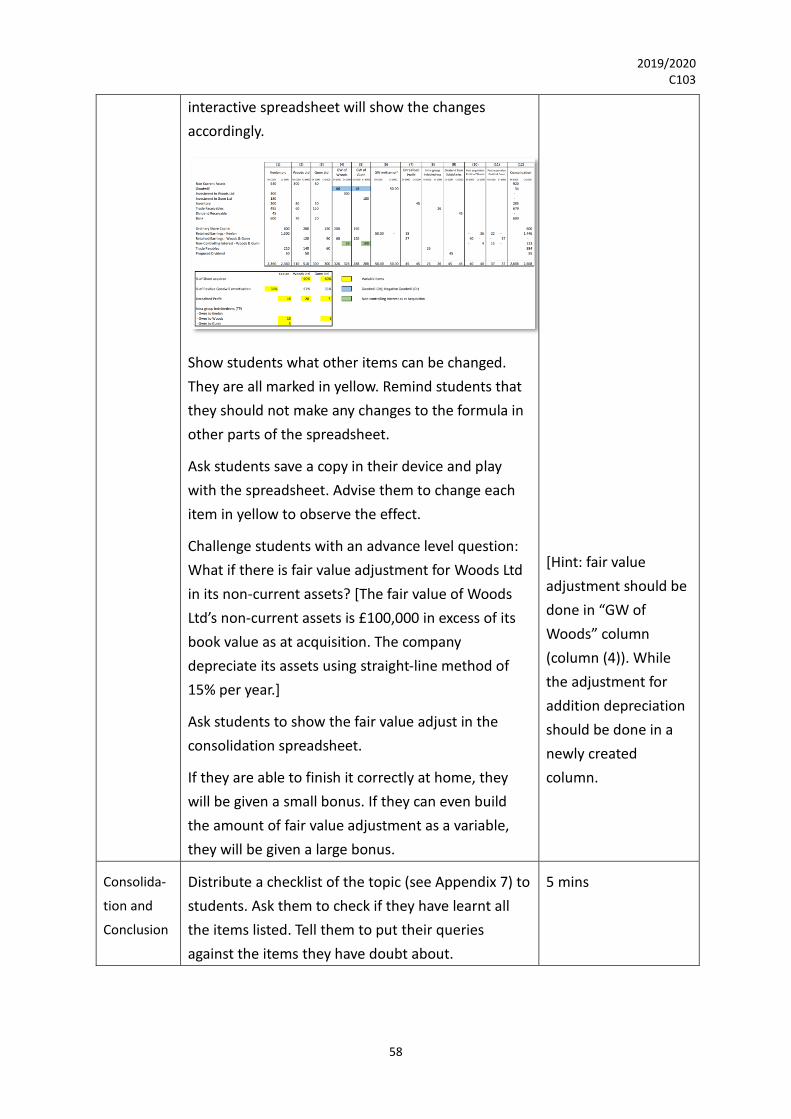

For instance, if the % of shares acquired of Gunn Ltd

is changed to 60%, goodwill and its amortization,

share Gunn Ltd’s post acquisition profit and non-

controlling interest are all going to be affected. This

2019/2020 C103

58

interactive spreadsheet will show the changes

accordingly.

Show students what other items can be changed.

They are all marked in yellow. Remind students that

they should not make any changes to the formula in

other parts of the spreadsheet.

Ask students save a copy in their device and play

with the spreadsheet. Advise them to change each

item in yellow to observe the effect.

Challenge students with an advance level question:

What if there is fair value adjustment for Woods Ltd

in its non-current assets? [The fair value of Woods

Ltd’s non-current assets is £100,000 in excess of its

book value as at acquisition. The company

depreciate its assets using straight-line method of

15% per year.]

Ask students to show the fair value adjust in the

consolidation spreadsheet.

If they are able to finish it correctly at home, they

will be given a small bonus. If they can even build

the amount of fair value adjustment as a variable,

they will be given a large bonus.

[Hint: fair value

adjustment should be

done in “GW of

Woods” column

(column (4)). While

the adjustment for

addition depreciation

should be done in a

newly created

column.

Consolida-

tion and

Conclusion

Distribute a checklist of the topic (see Appendix 7) to

students. Ask them to check if they have learnt all

the items listed. Tell them to put their queries

against the items they have doubt about.

5 mins

2019/2020 C103

59

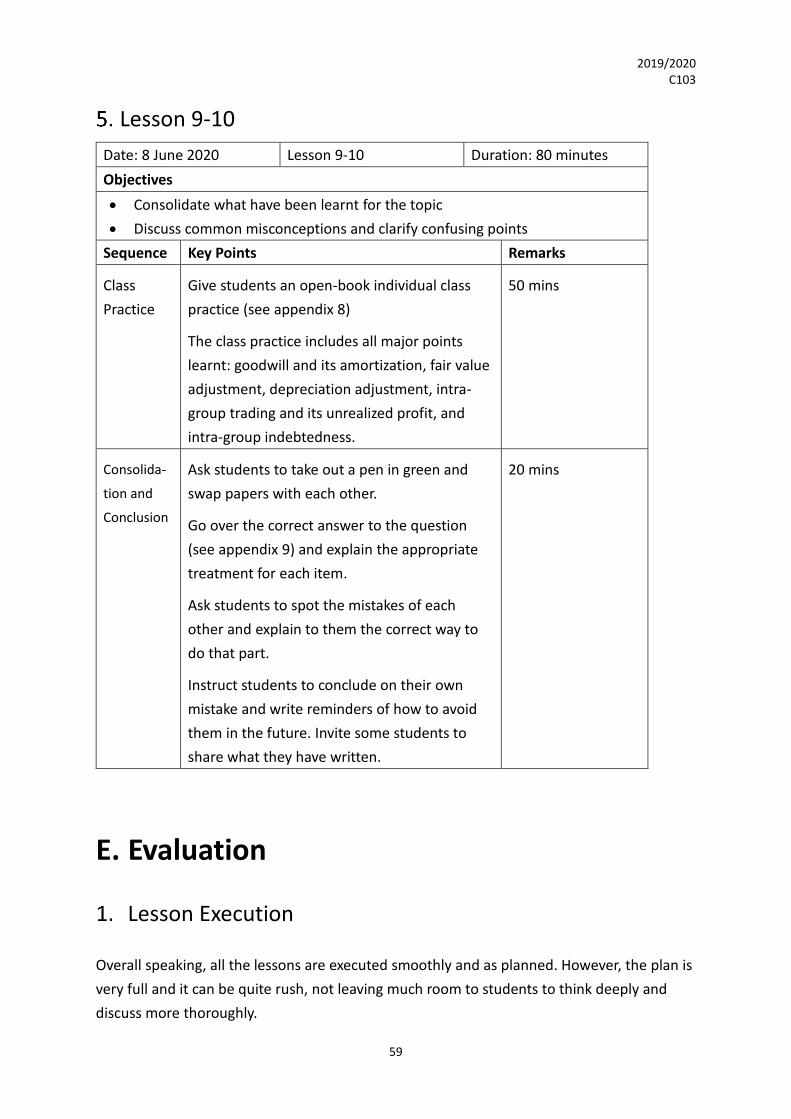

Lesson 9-10

Date: 8 June 2020 Lesson 9-10 Duration: 80 minutes

Objectives

• Consolidate what have been learnt for the topic

• Discuss common misconceptions and clarify confusing points

Sequence Key Points Remarks

Class

Practice

Give students an open-book individual class

practice (see appendix 8)

The class practice includes all major points

learnt: goodwill and its amortization, fair value

adjustment, depreciation adjustment, intra-

group trading and its unrealized profit, and

intra-group indebtedness.

50 mins

Consolida-

tion and

Conclusion

Ask students to take out a pen in green and

swap papers with each other.

Go over the correct answer to the question

(see appendix 9) and explain the appropriate

treatment for each item.

Ask students to spot the mistakes of each

other and explain to them the correct way to

do that part.

Instruct students to conclude on their own

mistake and write reminders of how to avoid

them in the future. Invite some students to

share what they have written.

20 mins

E. Evaluation

Lesson Execution

Overall speaking, all the lessons are executed smoothly and as planned. However, the plan is

very full and it can be quite rush, not leaving much room to students to think deeply and

discuss more thoroughly.

2019/2020 C103

60

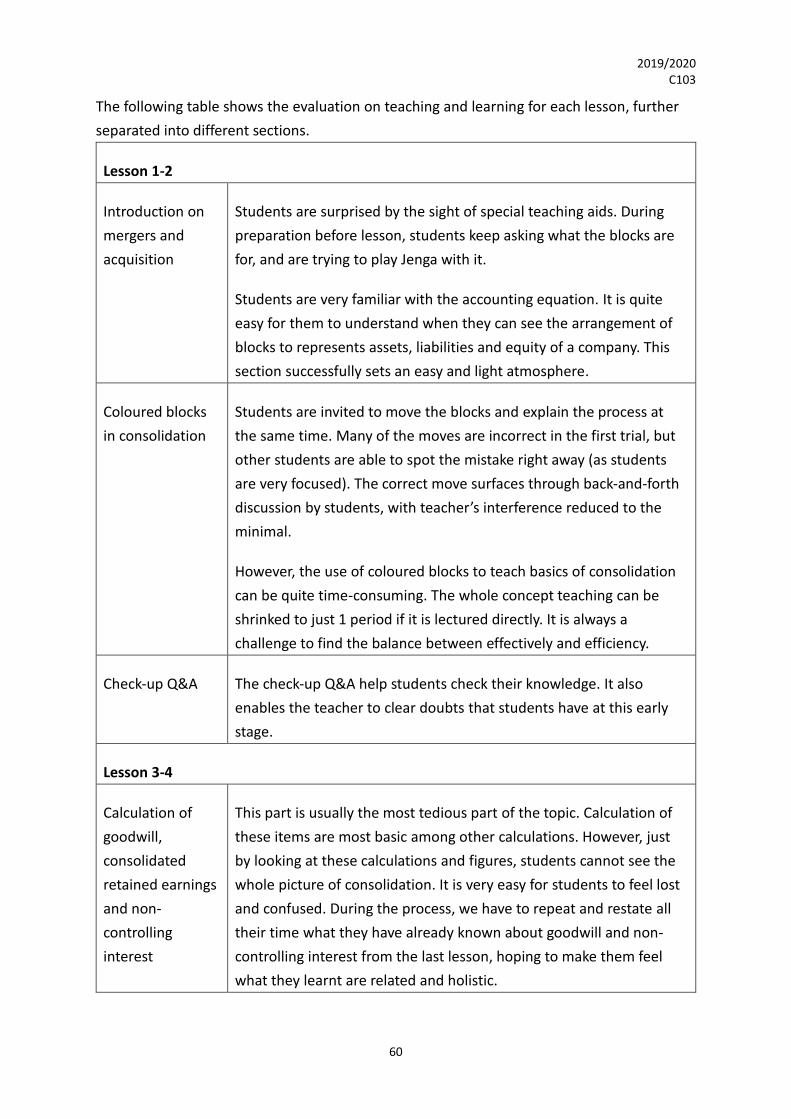

The following table shows the evaluation on teaching and learning for each lesson, further

separated into different sections.

Lesson 1-2

Introduction on

mergers and

acquisition

Students are surprised by the sight of special teaching aids. During

preparation before lesson, students keep asking what the blocks are

for, and are trying to play Jenga with it.

Students are very familiar with the accounting equation. It is quite

easy for them to understand when they can see the arrangement of

blocks to represents assets, liabilities and equity of a company. This

section successfully sets an easy and light atmosphere.

Coloured blocks

in consolidation

Students are invited to move the blocks and explain the process at

the same time. Many of the moves are incorrect in the first trial, but

other students are able to spot the mistake right away (as students

are very focused). The correct move surfaces through back-and-forth

discussion by students, with teacher’s interference reduced to the

minimal.

However, the use of coloured blocks to teach basics of consolidation

can be quite time-consuming. The whole concept teaching can be

shrinked to just 1 period if it is lectured directly. It is always a

challenge to find the balance between effectively and efficiency.

Check-up Q&A The check-up Q&A help students check their knowledge. It also

enables the teacher to clear doubts that students have at this early

stage.

Lesson 3-4

Calculation of

goodwill,

consolidated

retained earnings

and non-

controlling

interest

This part is usually the most tedious part of the topic. Calculation of

these items are most basic among other calculations. However, just

by looking at these calculations and figures, students cannot see the

whole picture of consolidation. It is very easy for students to feel lost

and confused. During the process, we have to repeat and restate all

their time what they have already known about goodwill and non-

controlling interest from the last lesson, hoping to make them feel

what they learnt are related and holistic.

2019/2020 C103

61

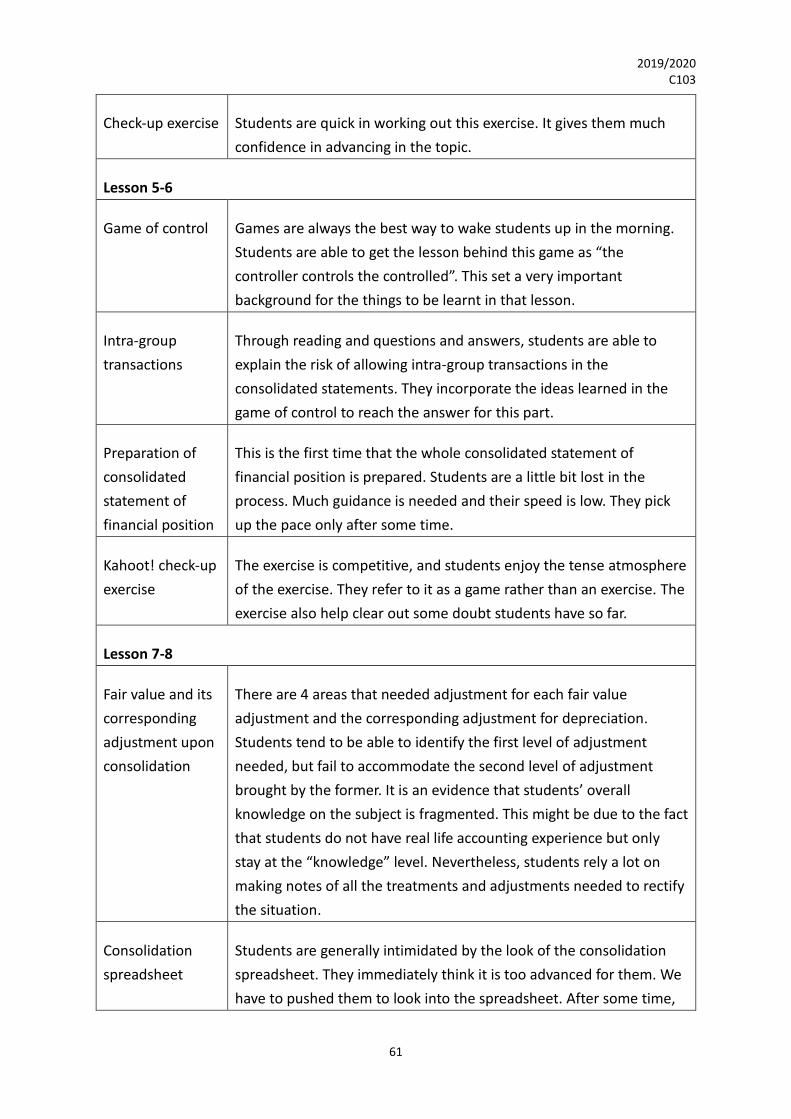

Check-up exercise Students are quick in working out this exercise. It gives them much

confidence in advancing in the topic.

Lesson 5-6

Game of control Games are always the best way to wake students up in the morning.

Students are able to get the lesson behind this game as “the

controller controls the controlled”. This set a very important

background for the things to be learnt in that lesson.

Intra-group

transactions

Through reading and questions and answers, students are able to

explain the risk of allowing intra-group transactions in the

consolidated statements. They incorporate the ideas learned in the

game of control to reach the answer for this part.

Preparation of

consolidated

statement of

financial position

This is the first time that the whole consolidated statement of

financial position is prepared. Students are a little bit lost in the

process. Much guidance is needed and their speed is low. They pick

up the pace only after some time.

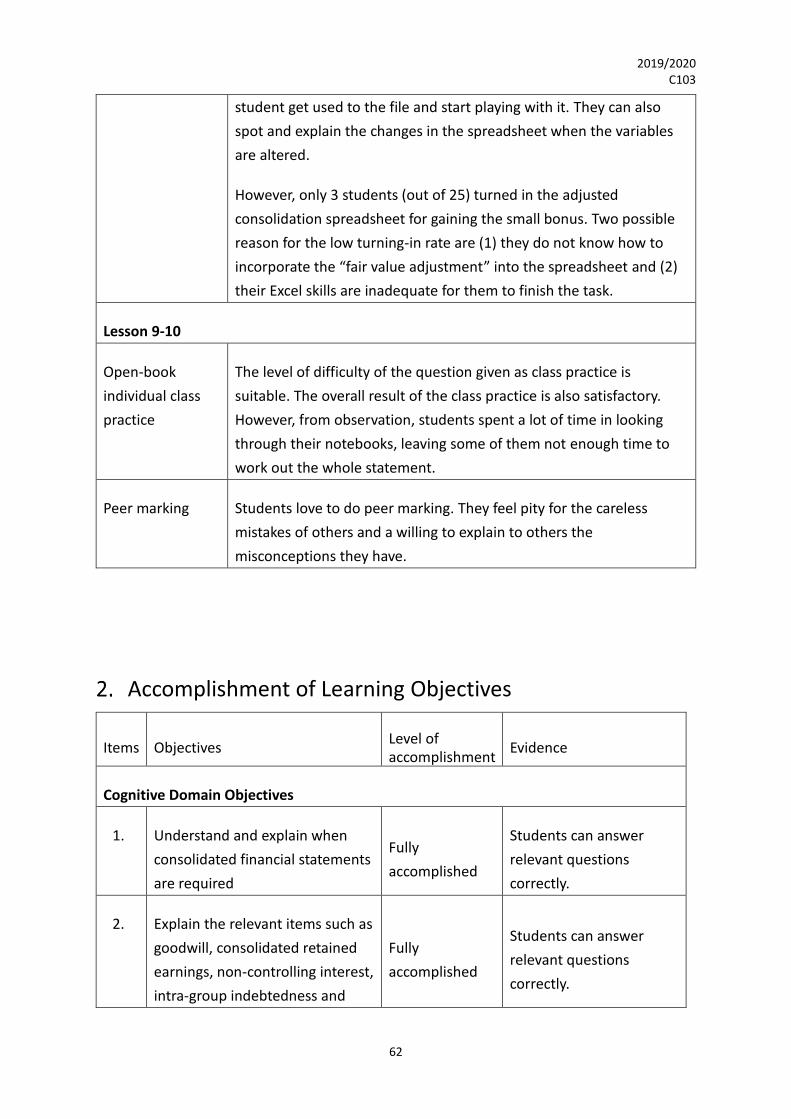

Kahoot! check-up

exercise