Embed Size (px)

Citation preview

Institutional Equities

Coromandel International

2QF

Y20

Res

ult U

pdat

e

Reuters: CORF.NS; Bloomberg: CRIN IN

Upgrading to Accumulate on revised earnings, TP Coromandel International (CRIN) positively surprised the street with better than expected 2QFY20 results despite the delayed monsoon. During the post-results conference call CRIN management sounded upbeat on future prospects in nutrients and crop protection chemicals businesses. The company was especially positive on the 2HFY20E outlook based on an extended Kharif season and prospects for a robust Rabi cropping season supported by near full reservoir levels and expectations of a normal northeast monsoon. Based on these factors, we are upgrading our rating on CRIN from Sell to Accumulate after raising our TP 23.4% to Rs468 using 14x PE on revised Sept 21E EPS (0.34% up from CMP).

Raising earnings by 19.4%/24.9%/21.5 over FY20-22E: This is based on i) revised assumptions on CPC business growth and margins as well as ii) improved unit margins for nutrients business and iii) lower interest costs following the sharp 42% reduction in debt as a result of 23% fall in subsidy receivables and 22% fall in inventories.

2QFY20 results conference call take-away: Coromandel management sounded positive on growth prospects in both Nutrients and CPC segments after posting good results that beat street and our expectations. The company’s prospects in 2QFY20 were boosted by adequate rainfall and improving trend in acreage sown in August-September, which made up for the delayed monsoon and weak sowing trend in July. The 0.1 mn tonne additional train for phosphoric acid (PA) was completed in September and is running from this month. As a result, the Vizag unit is now 100% on captive PA, while the need for imports has now reduced to 0.55 mn tonne. This increase in captive PA production will result in additional value addition of US$100-120/tonne. Management also expects better prospects for the CPC business based on 4 new products launched YTD FY20 and further new launches in the offing across technical grades as well as formulations, especially in the B2C segment.

Subsidy and receivables: Subsidy receivable is down from Rs23.93bn to Rs18.48bn and the company has received subsidy payments worth Rs7.2bn vs. Rs2.2bn a year ago. As a result, gross debt has declined by 42% to Rs17.25bn. Core interest expense before the IND-AS impact has shown a decline. However, this benefit has been partly offset by the additional interest on lease liability applicable this year as a result of lease accounting changes. Notwithstanding this, we expect the company to benefit from the lower interest expense on the reduced borrowings.

Capex: The capex over FY20E is estimated at Rs5bn. This includes Rs2bn on the phosphoric acid capacity expansion and Rs1.2bn on CPC. The balance amount is towards normal maintenance capex.

CPC business: The plan going forward is to set up multipurpose plants for technical grades and formulations as well as securing raw materials and technology for key technical grades from potential innovator partners from Japan, China or Germany with whom the company is in discussions. The company is aiming at new launches on its own and through co-marketing tie ups based on its own R&D initiatives and those sourced from innovator partners. Management is also looking to strengthen the company’s presence in B2C in the overseas market. The company is expecting CPC segment revenues for FY20 to be flat YoY while maintaining margins at par with 2QFY20 levels. The operations at Sarigam have stabilized after resuming in the middle of 2Q. CRIN admitted that Mancozeb sales is likely to be under pressure because of weak dispatches YTD and it is unlikely to pick up in the near term.

ACCUMULATE

Sector: Chemicals

CMP: Rs466

Target Price: Rs468

Upside: 0.34%

Amit Agarwal Research Analyst [email protected] +91-22-6273 8145

Key Data

Current Shares O/S (mn) 292.6

Mkt Cap (Rsbn/US$bn) 136.3/1.9

52 Wk H / L (Rs) 520/337

Daily Vol. (3M NSE Avg.) 199,917

Price Performance (%)

1-M 6-M 1-Y

CRIN 11.7 6.6 20.0

Nifty Index (0.0) (1.2) 13.3

Source: Bloomberg

Exhibit 1: 2QFY20 Result

25 October 2019

Y/E March (Rs Mn) 2QFY19 2QFY20 Ch YoY % 1QFY20 Ch QoQ % 2QFY20E Var. (%)

Net sales 50,083 48,580 -3 21,307 128 43,661 11

Cost of goods 36,369 35,215 -3 14,217 148 30,005 17

Employee benefits expenses 1,063 1,128 6 1,107 2 1,117 1

Other expenses 5,988 5,107 -15 4,030 27 6,630 -23

EBITDA 6,663 7,130 7 1,953 265 5,909 21

EBITDAM (%) 13.30 14.68 137 9.17 551 13.53 114

Depreciation and amortization 263 417 59 305 37 333 25

Other income 98 95 -3 100 -5 108 -12

Interest expenses 696 664 -5 796 -17 848 -22

Exceptional income/ (exp) (197) -

-

Profit before tax 5,605 6,145 10 952 546 4,836 27

Tax expenses 1,944 1,110 -43 326 240 1,132 -2

Share of JV and assoc. +/- (5) 4

(2)

3

Adj.Consol. PAT 3,853 5,039 31 624 707 3,708 36

NPM (%) 7.69 10.37 268 2.93 744 8.49 188

EPS 13.18 17.23 31 2.14 -93 12.68 36

Source: Company, Nirmal Bang Institutional Equities Research

Institutional Equities

2 Coromandel International

Investment Rationale:

We have raised earnings for FY20E -FY22E post the decent 2QFY20 results that beat market expectations. We have also raised TP by 23.4% from Rs379 to Rs468 based on a PE of 14x FY21E September (10% discount to 5-year median PE). Based on the new TP we have upgraded the rating on CRIN from Sell to Accumulate.

Exhibit 2: Change in our estimates

Revised estimate Earlier estimate % Revision

Rs Mn FY20E FY21E FY22E FY20E FY21E FY22E FY20E FY21E FY22E

Nutrient Revenue 111,562 120,640 127,884 107,275 116,012 121,818 4.0 4.0 5.0

CPC Revenue 16,555 19,997 22,406 13,960 16,068 18,490 18.6 24.5 21.2

Total Revenue 128,117 140,637 150,290 121,235 132,080 140,308 5.7 6.5 7.1

EBITDA 14,950 16,306 17,493 14,008 14,516 15,640 6.7 12.3 11.8

EBITDA margin (%) 11.67 11.59 11.64 11.55 10.99 11.15 - - -

Nutrient EBIT 11,169 11,578 12,333 10,860 10,475 11,226 2.8 10.5 9.9

CPC EBIT 1,946 2,768 3,149 1,636 2,141 2,778 18.9 29.3 13.3

Total EBIT 13,115 14,346 15,482 12,496 12,615 14,004 5.0 13.7 10.6

EBIT margin 10.24 10.20 10.30 10.31 9.55 9.98 - - -

PAT 8,760 9,457 10,148 7,337 7,571 8,353 19.4 24.9 21.5

EPS 29.86 32.17 34.44 25.00 25.75 28.35 19.4 24.9 21.5

TP

468

379

23.4

Source: Nirmal Bang Institutional Equities Research

The positives for the stock have been largely priced in following the stock’s sharp surge post results and the 22.08% rise over the last 1 year.

Our target multiple of 14x at a 10% discount to 5 year median PE, in our view captures the risk reward in the stock based on our assessment of positives and concerns.

Exhibit 3: Valuation

Sep 21E EPS Rs 33.31

Premium/(Disc) -0.1

5 yr Median PE (x) 15.6

Target PE 10% dis on 5 Yr Median (x) 14.04

Target Price Rs 468

CMP Rs 466

Upside % 0.34

Source: Nirmal Bang Institutional Equities Research

Institutional Equities

3 Coromandel International

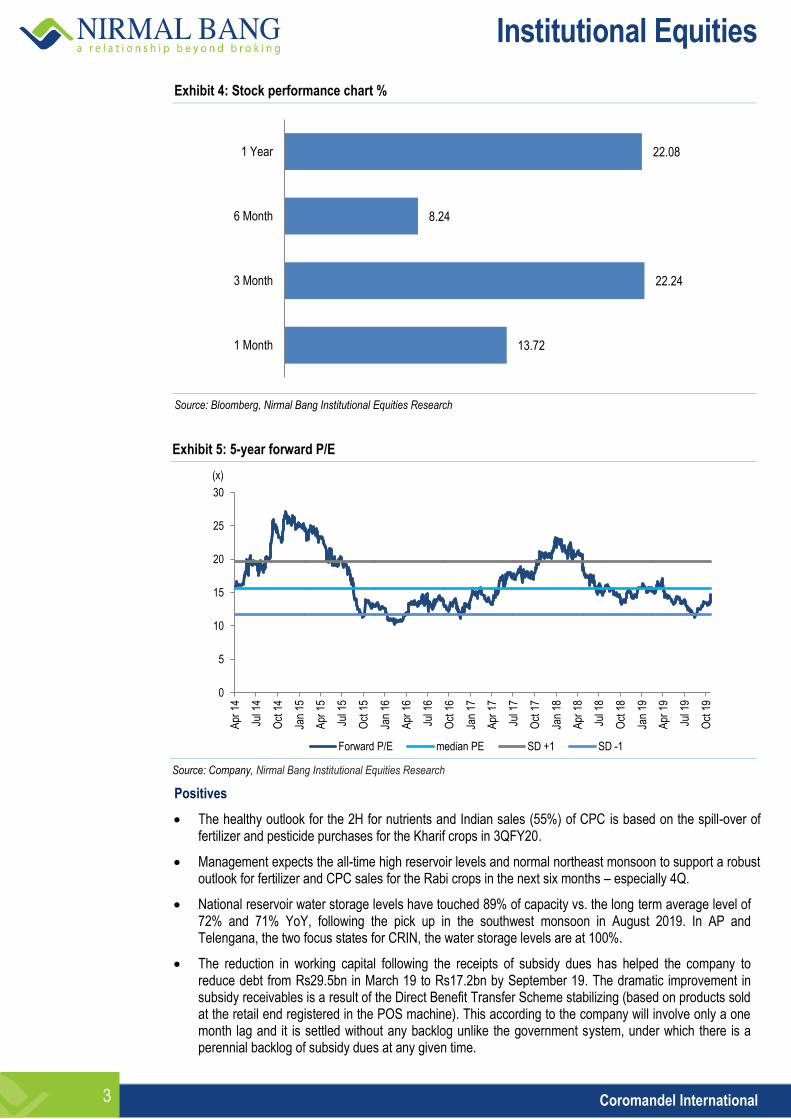

Exhibit 4: Stock performance chart %

Source: Bloomberg, Nirmal Bang Institutional Equities Research

Exhibit 5: 5-year forward P/E

Source: Company, Nirmal Bang Institutional Equities Research

Positives

The healthy outlook for the 2H for nutrients and Indian sales (55%) of CPC is based on the spill-over of fertilizer and pesticide purchases for the Kharif crops in 3QFY20.

Management expects the all-time high reservoir levels and normal northeast monsoon to support a robust outlook for fertilizer and CPC sales for the Rabi crops in the next six months – especially 4Q.

National reservoir water storage levels have touched 89% of capacity vs. the long term average level of 72% and 71% YoY, following the pick up in the southwest monsoon in August 2019. In AP and Telengana, the two focus states for CRIN, the water storage levels are at 100%.

The reduction in working capital following the receipts of subsidy dues has helped the company to reduce debt from Rs29.5bn in March 19 to Rs17.2bn by September 19. The dramatic improvement in subsidy receivables is a result of the Direct Benefit Transfer Scheme stabilizing (based on products sold at the retail end registered in the POS machine). This according to the company will involve only a one month lag and it is settled without any backlog unlike the government system, under which there is a perennial backlog of subsidy dues at any given time.

13.72

22.24

8.24

22.08

1 Month

3 Month

6 Month

1 Year

0

5

10

15

20

25

30

Apr

14

Jul

14

Oct

14

Jan

15

Apr

15

Jul

15

Oct

15

Jan

16

Apr

16

Jul

16

Oct

16

Jan

17

Apr

17

Jul

17

Oct

17

Jan

18

Apr

18

Jul

18

Oct

18

Jan

19

Apr

19

Jul

19

Oct

19

Forward P/E median PE SD +1 SD -1

(x)

Institutional Equities

4 Coromandel International

The increase in MSP for key crops as well as AP and Telengana government schemes to provide subsidy worth Rs13500 for farmers for buying agri-inputs support a positive outlook for fertilizer and CPC demand.

Exhibit 6: Trend in working capital and debt

Rs Mn FY16 FY17 FY18 FY19 1HFY20

Subsidy Receivable 23,671 25,570 26,269 23,935 18,488

Inventory 23,458 17,246 22,625 32,414 25,414

Gross Debt 26,267 22,284 27,284 29,545 17,255

Net Debt 19,486 15,382 17,651 23,670 15,781

Source: Company, Nirmal Bang Institutional Equities Research

Exhibit 7: Trend in cashflows and returns

Rs Mn FY16 FY17 FY18 FY19 1HFY20

Operating Cashflow before Working Capital Ch. 7,693 7,282 10,173 9,865 25,191

Working Capital Ch. -7,509 1,870 -7,540 -4,601 -8,374

Operating Cashflow after Working Capital Ch. 184 9,152 2,633 5,264 16,817

Free Cashflow -430 8,366 2,953 -707 15,286

ROCE (%) 10.94 14.42 16.00 14.14 15.66

ROIC (%) 12.60 16.63 18.95 16.57 16.63

Source: Company, Nirmal Bang Institutional Equities Research

Exhibit 8: Total live storage in 120 important reservoirs in India

BCM % of storage capacity at full reservoir level

17th Oct 2019 151.83 89

17th Oct 2018 121.55 71

10 year storage average 122.00 72

Source: Ministry of Fertilizer, Nirmal Bang Institutional Equities Research

Concerns

Dependence on monsoon is a key risk that could impact demand outlook for both nutrient and CPC segments. This makes it difficult to make year on year forecasts; at best one could make estimates assuming normal monsoon and stable farmer incomes and factor in the downside risk in the valuations. Also, we would be a bit cautious on the working capital cycle as volatility in global input prices could result in material movement in inventory and trade receivables.

The CPC business especially for technicals has become very competitive while rising input costs and availability of critical raw materials pose a challenge, especially given the curtailment of production of agrochemicals in China and the ongoing US-China Tariff war.

Health, safety concerns and regulatory surveillance are added challenges for the CPC segment.

The company has 65-70% of its CPC revenues coming from technicals and Mancozeb is a key product in its portfolio. The rising input costs and weak outlook for Mancozeb prices will put pressure on CPC margins in the short term until the company is able to ramp the share of higher value molecules and formulations as well as increase the share of the B2C segment.

The company’s plan to expand the CPC business in future could entail the potential increase in receivable and inventory which could increase the working capital requirements.

Institutional Equities

5 Coromandel International

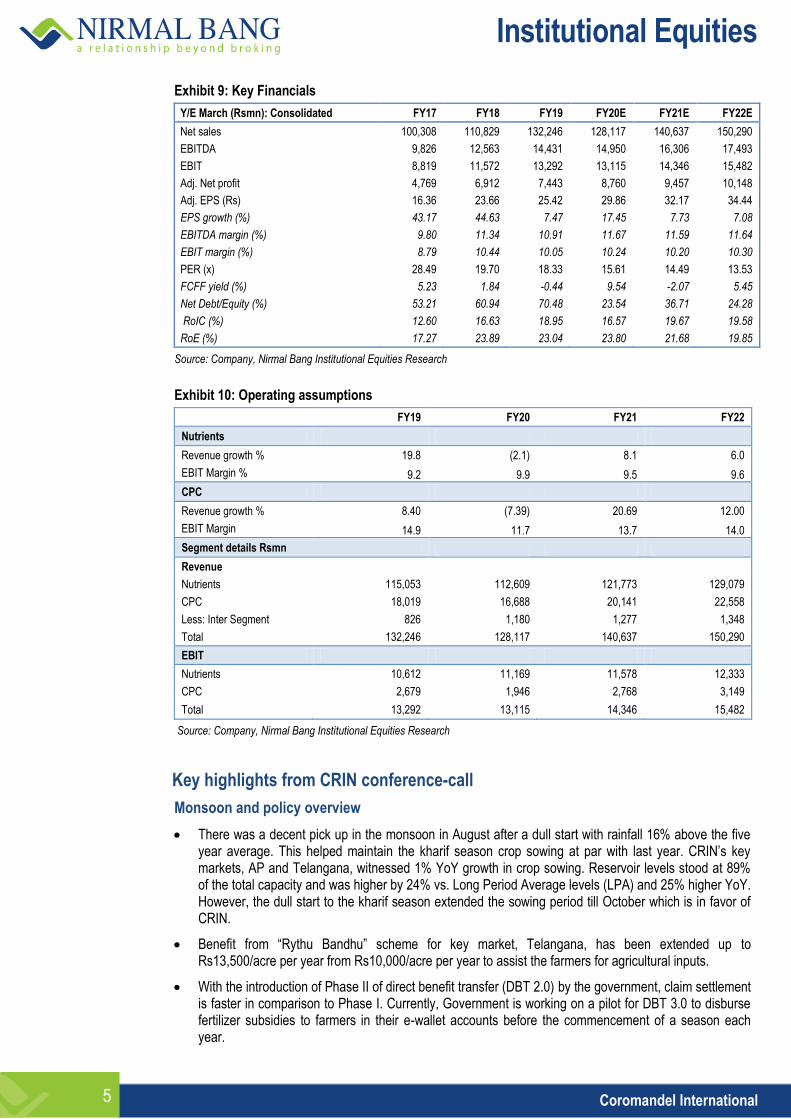

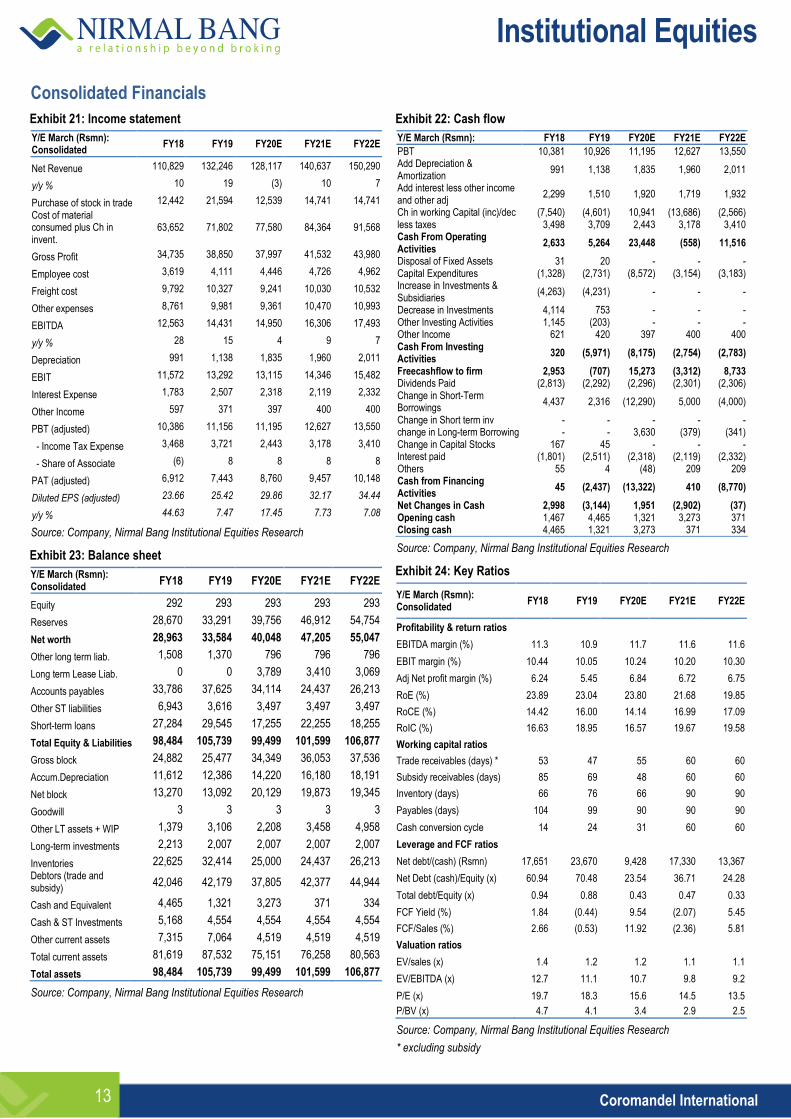

Exhibit 9: Key Financials

Y/E March (Rsmn): Consolidated FY17 FY18 FY19 FY20E FY21E FY22E

Net sales 100,308 110,829 132,246 128,117 140,637 150,290

EBITDA 9,826 12,563 14,431 14,950 16,306 17,493

EBIT 8,819 11,572 13,292 13,115 14,346 15,482

Adj. Net profit 4,769 6,912 7,443 8,760 9,457 10,148

Adj. EPS (Rs) 16.36 23.66 25.42 29.86 32.17 34.44

EPS growth (%) 43.17 44.63 7.47 17.45 7.73 7.08

EBITDA margin (%) 9.80 11.34 10.91 11.67 11.59 11.64

EBIT margin (%) 8.79 10.44 10.05 10.24 10.20 10.30

PER (x) 28.49 19.70 18.33 15.61 14.49 13.53

FCFF yield (%) 5.23 1.84 -0.44 9.54 -2.07 5.45

Net Debt/Equity (%) 53.21 60.94 70.48 23.54 36.71 24.28

RoIC (%) 12.60 16.63 18.95 16.57 19.67 19.58

RoE (%) 17.27 23.89 23.04 23.80 21.68 19.85

Source: Company, Nirmal Bang Institutional Equities Research

Exhibit 10: Operating assumptions

FY19 FY20 FY21 FY22

Nutrients

Revenue growth % 19.8 (2.1) 8.1 6.0

EBIT Margin % 9.2 9.9 9.5 9.6

CPC

Revenue growth % 8.40 (7.39) 20.69 12.00

EBIT Margin 14.9 11.7 13.7 14.0

Segment details Rsmn

Revenue

Nutrients 115,053 112,609 121,773 129,079

CPC 18,019 16,688 20,141 22,558

Less: Inter Segment 826 1,180 1,277 1,348

Total 132,246 128,117 140,637 150,290

EBIT

Nutrients 10,612 11,169 11,578 12,333

CPC 2,679 1,946 2,768 3,149

Total 13,292 13,115 14,346 15,482

Source: Company, Nirmal Bang Institutional Equities Research

Key highlights from CRIN conference-call

Monsoon and policy overview

There was a decent pick up in the monsoon in August after a dull start with rainfall 16% above the five year average. This helped maintain the kharif season crop sowing at par with last year. CRIN’s key markets, AP and Telangana, witnessed 1% YoY growth in crop sowing. Reservoir levels stood at 89% of the total capacity and was higher by 24% vs. Long Period Average levels (LPA) and 25% higher YoY. However, the dull start to the kharif season extended the sowing period till October which is in favor of CRIN.

Benefit from “Rythu Bandhu” scheme for key market, Telangana, has been extended up to Rs13,500/acre per year from Rs10,000/acre per year to assist the farmers for agricultural inputs.

With the introduction of Phase II of direct benefit transfer (DBT 2.0) by the government, claim settlement is faster in comparison to Phase I. Currently, Government is working on a pilot for DBT 3.0 to disburse fertilizer subsidies to farmers in their e-wallet accounts before the commencement of a season each year.

Institutional Equities

6 Coromandel International

Upcoming irrigation projects in CRIN’s key markets AP and Telangana are expected to cover a combined 4 lakh hectares of land. This will likely help improve the agricultural prospects by pushing farmers to change the cropping pattern from core cereals or pulses towards more agricultural input products like paddy and maize.

Industry overview:

Phosphatic fertilizers industry sales grew to 6.1mn tonne from 6.08mn tonne last year. The increase has come from south-10%, west- 5% and north- 2%, while central and east had deficit of 25% and 7%, respectively.

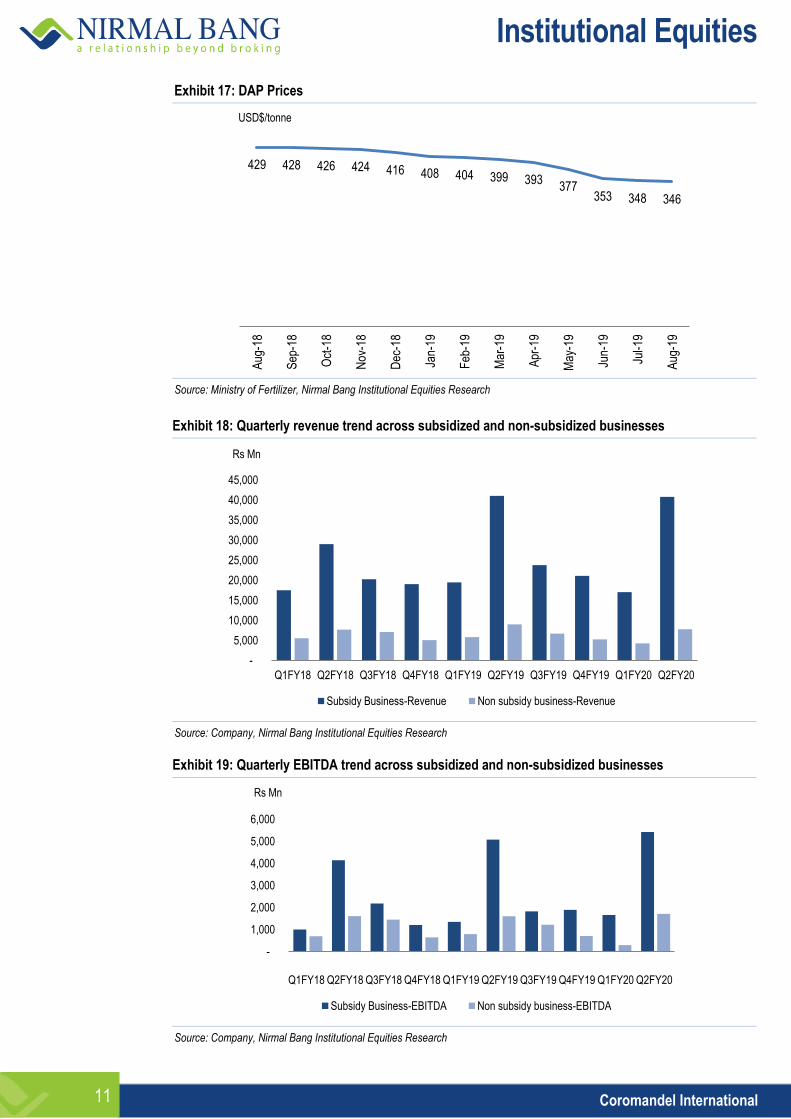

Raw material prices in the fertilizer segment are showing a softening trend. Phos acid prices for 3Q were at USD$625 per tonne compared to 2Q prices last year of USD $655 per tonne. Industry has passed on the benefit of stable currency and softer raw material prices to the consumer and overall MRP has been brought down by 4% to 10%.

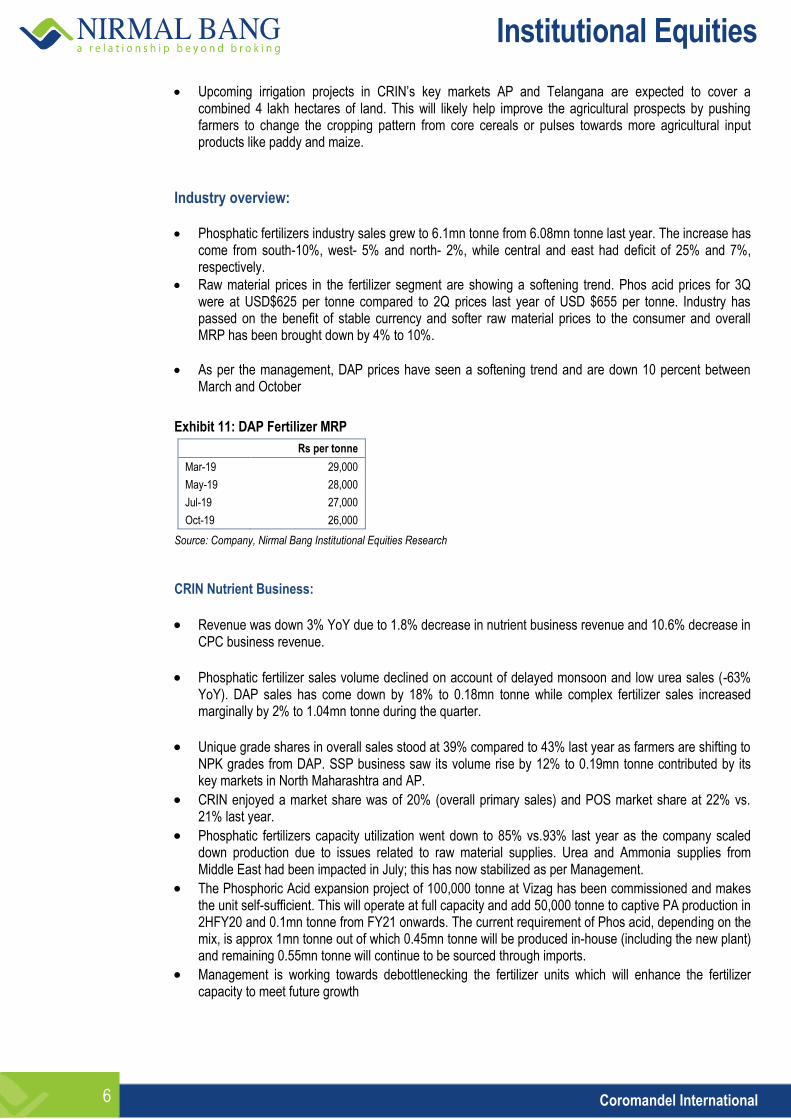

As per the management, DAP prices have seen a softening trend and are down 10 percent between March and October

Exhibit 11: DAP Fertilizer MRP

Rs per tonne

Mar-19 29,000

May-19 28,000

Jul-19 27,000

Oct-19 26,000

Source: Company, Nirmal Bang Institutional Equities Research

CRIN Nutrient Business:

Revenue was down 3% YoY due to 1.8% decrease in nutrient business revenue and 10.6% decrease in CPC business revenue.

Phosphatic fertilizer sales volume declined on account of delayed monsoon and low urea sales (-63% YoY). DAP sales has come down by 18% to 0.18mn tonne while complex fertilizer sales increased marginally by 2% to 1.04mn tonne during the quarter.

Unique grade shares in overall sales stood at 39% compared to 43% last year as farmers are shifting to NPK grades from DAP. SSP business saw its volume rise by 12% to 0.19mn tonne contributed by its key markets in North Maharashtra and AP.

CRIN enjoyed a market share was of 20% (overall primary sales) and POS market share at 22% vs. 21% last year.

Phosphatic fertilizers capacity utilization went down to 85% vs.93% last year as the company scaled down production due to issues related to raw material supplies. Urea and Ammonia supplies from Middle East had been impacted in July; this has now stabilized as per Management.

The Phosphoric Acid expansion project of 100,000 tonne at Vizag has been commissioned and makes the unit self-sufficient. This will operate at full capacity and add 50,000 tonne to captive PA production in 2HFY20 and 0.1mn tonne from FY21 onwards. The current requirement of Phos acid, depending on the mix, is approx 1mn tonne out of which 0.45mn tonne will be produced in-house (including the new plant) and remaining 0.55mn tonne will continue to be sourced through imports.

Management is working towards debottlenecking the fertilizer units which will enhance the fertilizer capacity to meet future growth

Institutional Equities

7 Coromandel International

CRIN CPC business:

Revenue from CPC segment declined by 10.6% YoY to Rs5.1bn due to the following factors:

The Sarigam unit started operation in late July after a prolonged outage due to the fire mishap in January this year. This curtailed the output from this unit to just 45 days

Mancozeb is seeing pricing pressure as well as some shipping problem in the international market, which impacted the CPC revenue.

Pymetrozin plant has been commissioned for pilot testing at Dahej.

The management mentioned that it has created separate B2B and B2C verticals in for the overseas markets to grow its B2C sales and is working on its product mix to help both its domestic and international markets.

The company stated that the WDG facility for Mancozeb is ready and will support Mancozeb sales in export markets once the registration is complete.

The company expects new launches to support growth in the CPC business over 2H FY20 and beyond.

The launches in 1HFY20 include four formulations – Mythri, Arithri, Fornax SC and Fornax granule

Exhibit 12: Product Mix

Brands under FUNGICIDE

Brand Name Technical

Aaroosh Propineb 70% WP

Agni Tricyclazole 75% WP

Azogro Azoxystrobin 23% SC

Benofit Benomyl 50% WP

Colastro Metiram 55% + Pyraclostrobin 5% WP

Corazole EC Hexaconazole 5% EC

Corazole SC Hexaconazole 5% SC

Hexastop Thiophanate Methyl 70% WP

Jatayu Chlorothalonil 75% WP

Kapeni Carbendazim 12%+ Mancozeb 63% WP

Marlett Mancozeb 75% WP

Odin Dimethomorph

Propicron Propiconazole 25% EC

Sten Carbendazim 50% WP

Brands under HERBICIDE

Brand Name Technical

Cormix Metsulfuron Methyl 10% + Chlorimuron Ethyl 10% WP

Eezykill Pendimethalin 30% EC

Fervent Imazethapyr 10% SL

Glycor Glyphosate 41% SL

Grometri Metribuzin 70% WP

Killshot Ammonium Salt of Glyphosate 71% SG

Pilot Pretilachlor 50% EC

Pyramox Imazamox 35% + Imazethapyr 35% WG

Skipper Clodinafop Propargyl 15% WP

Weedax Paraquat dichloride 24% SL

Brands under INSECTICIDE

Institutional Equities

8 Coromandel International

Brand Name Technical

Aayudh Carbosulfan 25% EC

Ajanta Profenofos 50% EC

Ajanta super Profenofos 40% EC + Cypermethrin 4% EC

Benzer Emamectin Benzoate 5% SG

Canister Bifenthrin 10% EC

Catchh Chlorpyriphos 50% + Cypermethrin 5% EC

Cyperkill Cypermethrin 25% EC

Cythion Malathion 50% EC

Endurer Hexythiazox 5.45% EC

Ferotia Diafenthiuron 50% WP

Integer Chlorpyrifos 50% EC

Josh SP Cartap Hydrochloride 50% SP

Marvex Super Dichlorvos 76% EC

Ninja Buprofezin 25% SC

Optra Thiomethoxam 25% WG

Ortain Acephate 75% SP

Parry Ratna Cartap Hydrochloride 4% G

Parryfos / Monophos Monocrotophos 36% SL

Parrymida Imidacloprid 17.8% SL

Permasect Permethrin 25% EC

Phendal Phenthoate 50 % EC

Salvo Gr Fipronil 0.3% G

Salvo SC Fipronil 5% SC

Scuba Acetamprid 20% SP

Trishul Chlorpyriphos 20% EC

Brand under Bio Stimulants

Brand Name Technical

Fantac Plus Mixture of Amino acids and vitamins

Source: Company, Nirmal Bang Institutional Equities Research

Subsidy:

On the subsidy front, total outstanding subsidy on September 2019 was Rs18.48bn vs. Rs26.26bn last year. This includes among others, Rs7.3bn of past POS acknowledgment, Rs2bn of September POS acknowledgement and Rs5bn balance claims.

Institutional Equities

9 Coromandel International

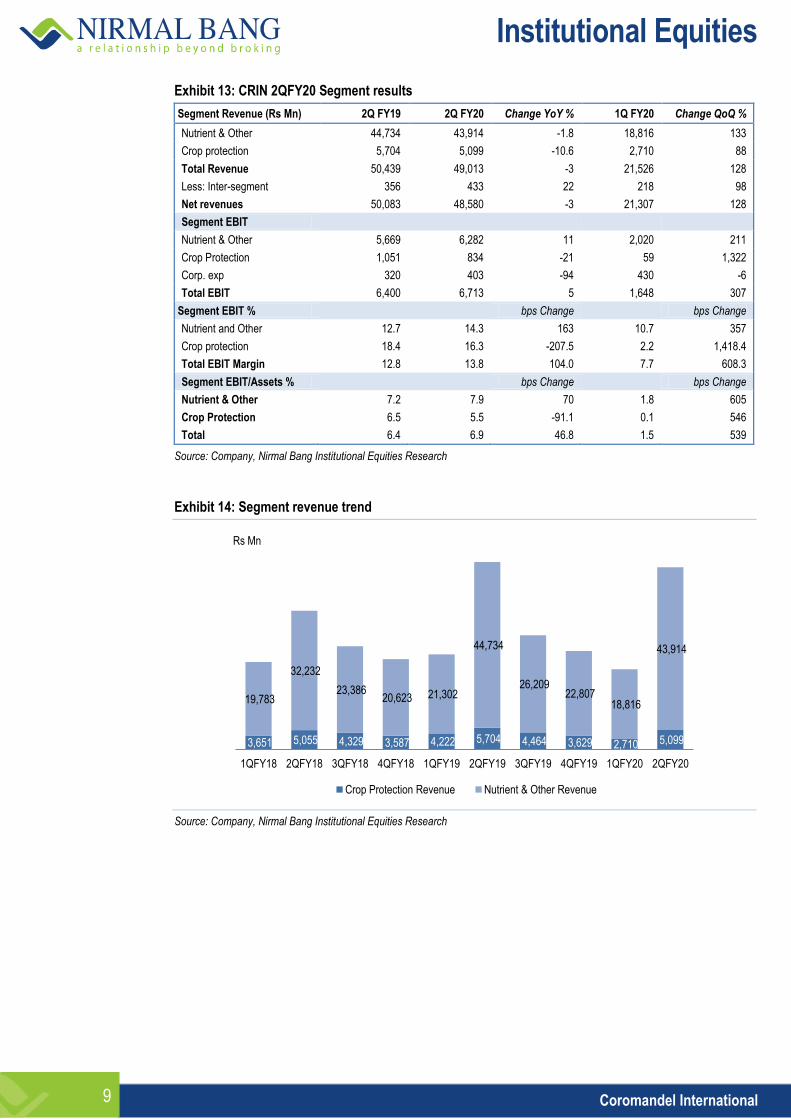

Exhibit 13: CRIN 2QFY20 Segment results

Segment Revenue (Rs Mn) 2Q FY19 2Q FY20 Change YoY % 1Q FY20 Change QoQ %

Nutrient & Other 44,734 43,914 -1.8 18,816 133

Crop protection 5,704 5,099 -10.6 2,710 88

Total Revenue 50,439 49,013 -3 21,526 128

Less: Inter-segment 356 433 22 218 98

Net revenues 50,083 48,580 -3 21,307 128

Segment EBIT

Nutrient & Other 5,669 6,282 11 2,020 211

Crop Protection 1,051 834 -21 59 1,322

Corp. exp 320 403 -94 430 -6

Total EBIT 6,400 6,713 5 1,648 307

Segment EBIT %

bps Change

bps Change

Nutrient and Other 12.7 14.3 163 10.7 357

Crop protection 18.4 16.3 -207.5 2.2 1,418.4

Total EBIT Margin 12.8 13.8 104.0 7.7 608.3

Segment EBIT/Assets %

bps Change

bps Change

Nutrient & Other 7.2 7.9 70 1.8 605

Crop Protection 6.5 5.5 -91.1 0.1 546

Total 6.4 6.9 46.8 1.5 539

Source: Company, Nirmal Bang Institutional Equities Research

Exhibit 14: Segment revenue trend

Source: Company, Nirmal Bang Institutional Equities Research

3,651 5,055 4,329 3,587 4,222 5,704 4,464 3,629 2,710 5,099

19,783

32,232

23,386 20,623 21,302

44,734

26,209 22,807

18,816

43,914

1QFY18 2QFY18 3QFY18 4QFY18 1QFY19 2QFY19 3QFY19 4QFY19 1QFY20 2QFY20

Rs Mn

Crop Protection Revenue Nutrient & Other Revenue

Institutional Equities

10 Coromandel International

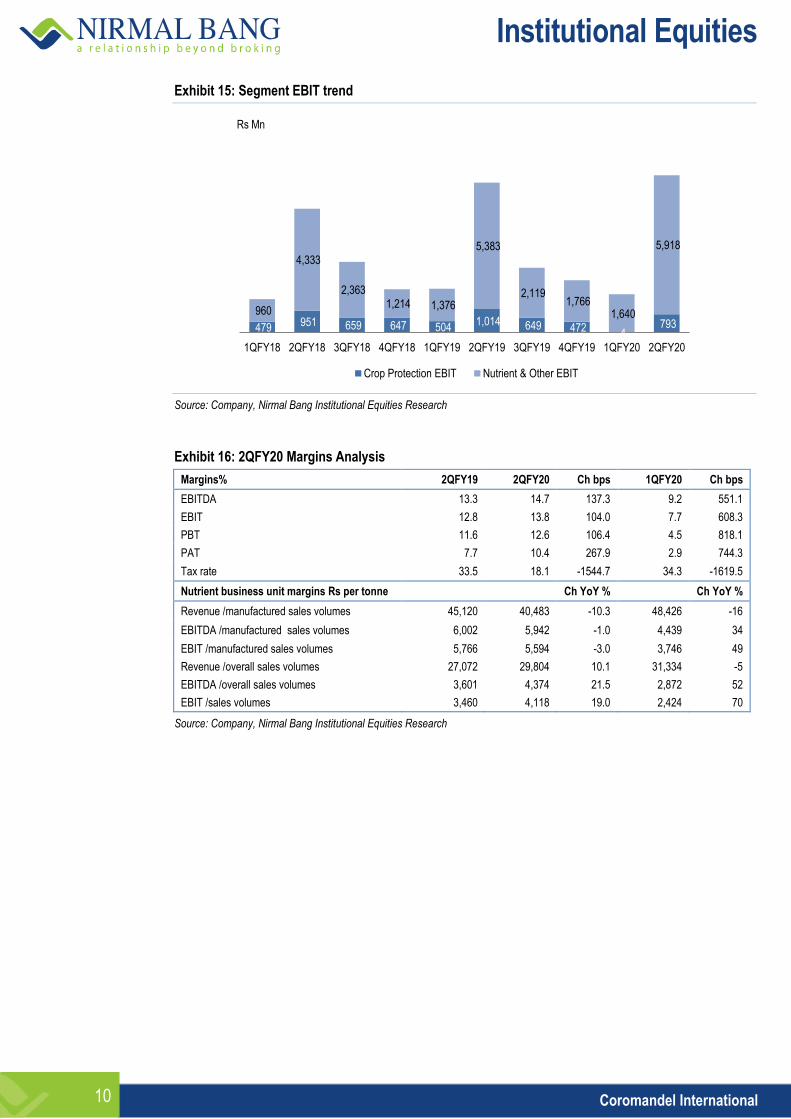

Exhibit 15: Segment EBIT trend

Source: Company, Nirmal Bang Institutional Equities Research

Exhibit 16: 2QFY20 Margins Analysis

Margins% 2QFY19 2QFY20 Ch bps 1QFY20 Ch bps

EBITDA 13.3 14.7 137.3 9.2 551.1

EBIT 12.8 13.8 104.0 7.7 608.3

PBT 11.6 12.6 106.4 4.5 818.1

PAT 7.7 10.4 267.9 2.9 744.3

Tax rate 33.5 18.1 -1544.7 34.3 -1619.5

Nutrient business unit margins Rs per tonne

Ch YoY %

Ch YoY %

Revenue /manufactured sales volumes 45,120 40,483 -10.3 48,426 -16

EBITDA /manufactured sales volumes 6,002 5,942 -1.0 4,439 34

EBIT /manufactured sales volumes 5,766 5,594 -3.0 3,746 49

Revenue /overall sales volumes 27,072 29,804 10.1 31,334 -5

EBITDA /overall sales volumes 3,601 4,374 21.5 2,872 52

EBIT /sales volumes 3,460 4,118 19.0 2,424 70

Source: Company, Nirmal Bang Institutional Equities Research

479 951 659 647 504 1,014 649 472 4

793 960

4,333

2,363 1,214 1,376

5,383

2,119 1,766

1,640

5,918

1QFY18 2QFY18 3QFY18 4QFY18 1QFY19 2QFY19 3QFY19 4QFY19 1QFY20 2QFY20

Rs Mn

Crop Protection EBIT Nutrient & Other EBIT

Institutional Equities

11 Coromandel International

Exhibit 17: DAP Prices

Source: Ministry of Fertilizer, Nirmal Bang Institutional Equities Research

Exhibit 18: Quarterly revenue trend across subsidized and non-subsidized businesses

Source: Company, Nirmal Bang Institutional Equities Research

Exhibit 19: Quarterly EBITDA trend across subsidized and non-subsidized businesses

Source: Company, Nirmal Bang Institutional Equities Research

429 428 426 424 416 408 404 399 393 377

353 348 346

Aug

-18

Sep

-18

Oct

-18

Nov

-18

Dec

-18

Jan-

19

Feb

-19

Mar

-19

Apr

-19

May

-19

Jun-

19

Jul-1

9

Aug

-19

USD$/tonne

-

5,000

10,000

15,000

20,000

25,000

30,000

35,000

40,000

45,000

Q1FY18 Q2FY18 Q3FY18 Q4FY18 Q1FY19 Q2FY19 Q3FY19 Q4FY19 Q1FY20 Q2FY20

Rs Mn

Subsidy Business-Revenue Non subsidy business-Revenue

-

1,000

2,000

3,000

4,000

5,000

6,000

Q1FY18

Q2FY18

Q3FY18

Q4FY18

Q1FY19

Q2FY19

Q3FY19

Q4FY19

Q1FY20

Q2FY20

Rs Mn

Subsidy Business-EBITDA Non subsidy business-EBITDA

Institutional Equities

12 Coromandel International

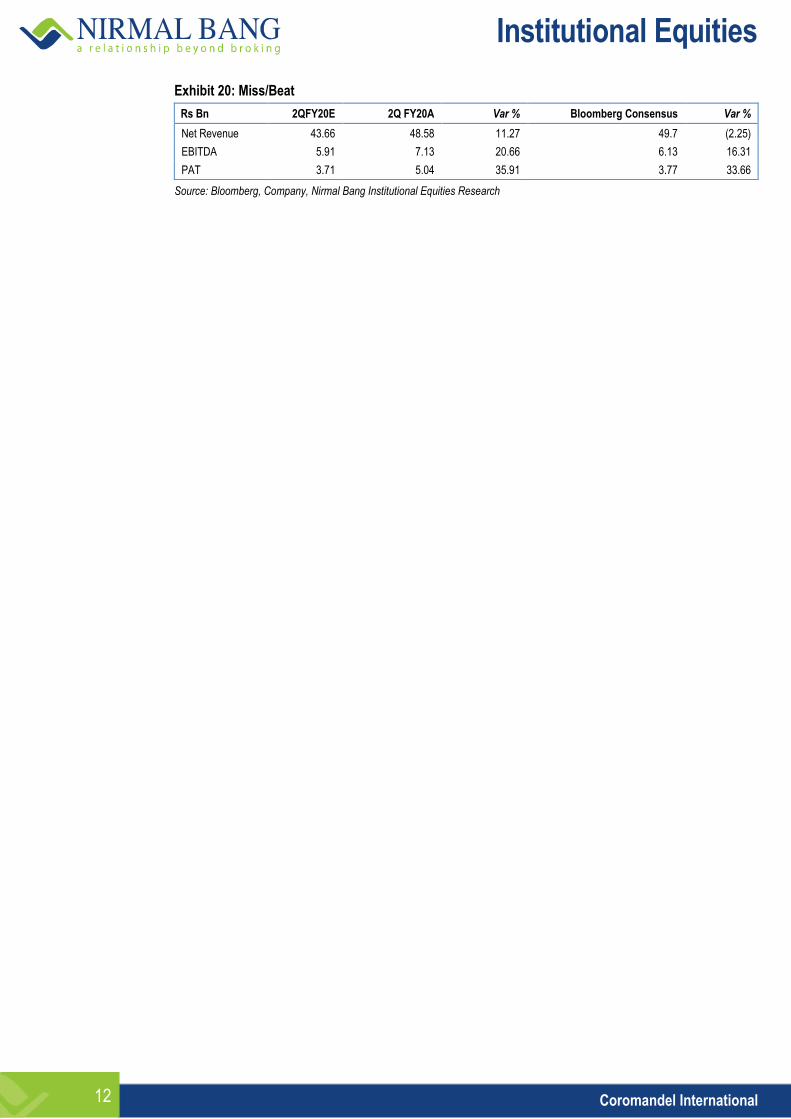

Exhibit 20: Miss/Beat

Rs Bn 2QFY20E 2Q FY20A Var % Bloomberg Consensus Var %

Net Revenue 43.66 48.58 11.27 49.7 (2.25)

EBITDA 5.91 7.13 20.66 6.13 16.31

PAT 3.71 5.04 35.91 3.77 33.66

Source: Bloomberg, Company, Nirmal Bang Institutional Equities Research

Institutional Equities

13 Coromandel International

Consolidated Financials

Exhibit 21: Income statement

Y/E March (Rsmn): Consolidated

FY18 FY19 FY20E FY21E FY22E

Net Revenue 110,829 132,246 128,117 140,637 150,290

y/y % 10 19 (3) 10 7

Purchase of stock in trade 12,442 21,594 12,539 14,741 14,741

Cost of material consumed plus Ch in invent.

63,652 71,802 77,580 84,364 91,568

Gross Profit 34,735 38,850 37,997 41,532 43,980

Employee cost 3,619 4,111 4,446 4,726 4,962

Freight cost 9,792 10,327 9,241 10,030 10,532

Other expenses 8,761 9,981 9,361 10,470 10,993

EBITDA 12,563 14,431 14,950 16,306 17,493

y/y % 28 15 4 9 7

Depreciation 991 1,138 1,835 1,960 2,011

EBIT 11,572 13,292 13,115 14,346 15,482

Interest Expense 1,783 2,507 2,318 2,119 2,332

Other Income 597 371 397 400 400

PBT (adjusted) 10,386 11,156 11,195 12,627 13,550

- Income Tax Expense 3,468 3,721 2,443 3,178 3,410

- Share of Associate (6) 8 8 8 8

PAT (adjusted) 6,912 7,443 8,760 9,457 10,148

Diluted EPS (adjusted) 23.66 25.42 29.86 32.17 34.44

y/y % 44.63 7.47 17.45 7.73 7.08

Source: Company, Nirmal Bang Institutional Equities Research

Exhibit 23: Balance sheet

Y/E March (Rsmn): Consolidated

FY18 FY19 FY20E FY21E FY22E

Equity 292 293 293 293 293

Reserves 28,670 33,291 39,756 46,912 54,754

Net worth 28,963 33,584 40,048 47,205 55,047

Other long term liab. 1,508 1,370 796 796 796

Long term Lease Liab. 0 0 3,789 3,410 3,069

Accounts payables 33,786 37,625 34,114 24,437 26,213

Other ST liabilities 6,943 3,616 3,497 3,497 3,497

Short-term loans 27,284 29,545 17,255 22,255 18,255

Total Equity & Liabilities 98,484 105,739 99,499 101,599 106,877

Gross block 24,882 25,477 34,349 36,053 37,536

Accum.Depreciation 11,612 12,386 14,220 16,180 18,191

Net block 13,270 13,092 20,129 19,873 19,345

Goodwill 3 3 3 3 3

Other LT assets + WIP 1,379 3,106 2,208 3,458 4,958

Long-term investments 2,213 2,007 2,007 2,007 2,007

Inventories 22,625 32,414 25,000 24,437 26,213

Debtors (trade and subsidy)

42,046 42,179 37,805 42,377 44,944

Cash and Equivalent 4,465 1,321 3,273 371 334

Cash & ST Investments 5,168 4,554 4,554 4,554 4,554

Other current assets 7,315 7,064 4,519 4,519 4,519

Total current assets 81,619 87,532 75,151 76,258 80,563

Total assets 98,484 105,739 99,499 101,599 106,877

Source: Company, Nirmal Bang Institutional Equities Research

Exhibit 22: Cash flow

Y/E March (Rsmn): FY18 FY19 FY20E FY21E FY22E

PBT 10,381 10,926 11,195 12,627 13,550 Add Depreciation & Amortization

991 1,138 1,835 1,960 2,011

Add interest less other income and other adj

2,299 1,510 1,920 1,719 1,932

Ch in working Capital (inc)/dec (7,540) (4,601) 10,941 (13,686) (2,566) less taxes 3,498 3,709 2,443 3,178 3,410 Cash From Operating Activities

2,633 5,264 23,448 (558) 11,516

Disposal of Fixed Assets 31 20 - - - Capital Expenditures (1,328) (2,731) (8,572) (3,154) (3,183) Increase in Investments & Subsidiaries

(4,263) (4,231) - - -

Decrease in Investments 4,114 753 - - - Other Investing Activities 1,145 (203) - - - Other Income 621 420 397 400 400 Cash From Investing Activities

320 (5,971) (8,175) (2,754) (2,783)

Freecashflow to firm 2,953 (707) 15,273 (3,312) 8,733 Dividends Paid (2,813) (2,292) (2,296) (2,301) (2,306) Change in Short-Term Borrowings

4,437 2,316 (12,290) 5,000 (4,000)

Change in Short term inv - - - - - change in Long-term Borrowing - - 3,630 (379) (341) Change in Capital Stocks 167 45 - - - Interest paid (1,801) (2,511) (2,318) (2,119) (2,332) Others 55 4 (48) 209 209 Cash from Financing Activities

45 (2,437) (13,322) 410 (8,770)

Net Changes in Cash 2,998 (3,144) 1,951 (2,902) (37) Opening cash 1,467 4,465 1,321 3,273 371 Closing cash 4,465 1,321 3,273 371 334

Source: Company, Nirmal Bang Institutional Equities Research

Exhibit 24: Key Ratios

Y/E March (Rsmn): Consolidated

FY18 FY19 FY20E FY21E FY22E

Profitability & return ratios

EBITDA margin (%) 11.3 10.9 11.7 11.6 11.6

EBIT margin (%) 10.44 10.05 10.24 10.20 10.30

Adj Net profit margin (%) 6.24 5.45 6.84 6.72 6.75

RoE (%) 23.89 23.04 23.80 21.68 19.85

RoCE (%) 14.42 16.00 14.14 16.99 17.09

RoIC (%) 16.63 18.95 16.57 19.67 19.58

Working capital ratios

Trade receivables (days) * 53 47 55 60 60

Subsidy receivables (days) 85 69 48 60 60

Inventory (days) 66 76 66 90 90

Payables (days) 104 99 90 90 90

Cash conversion cycle 14 24 31 60 60

Leverage and FCF ratios

Net debt/(cash) (Rsmn) 17,651 23,670 9,428 17,330 13,367

Net Debt (cash)/Equity (x) 60.94 70.48 23.54 36.71 24.28

Total debt/Equity (x) 0.94 0.88 0.43 0.47 0.33

FCF Yield (%) 1.84 (0.44) 9.54 (2.07) 5.45

FCF/Sales (%) 2.66 (0.53) 11.92 (2.36) 5.81

Valuation ratios

EV/sales (x) 1.4 1.2 1.2 1.1 1.1

EV/EBITDA (x) 12.7 11.1 10.7 9.8 9.2

P/E (x) 19.7 18.3 15.6 14.5 13.5

P/BV (x) 4.7 4.1 3.4 2.9 2.5

Source: Company, Nirmal Bang Institutional Equities Research

* excluding subsidy

Institutional Equities

14 Coromandel International

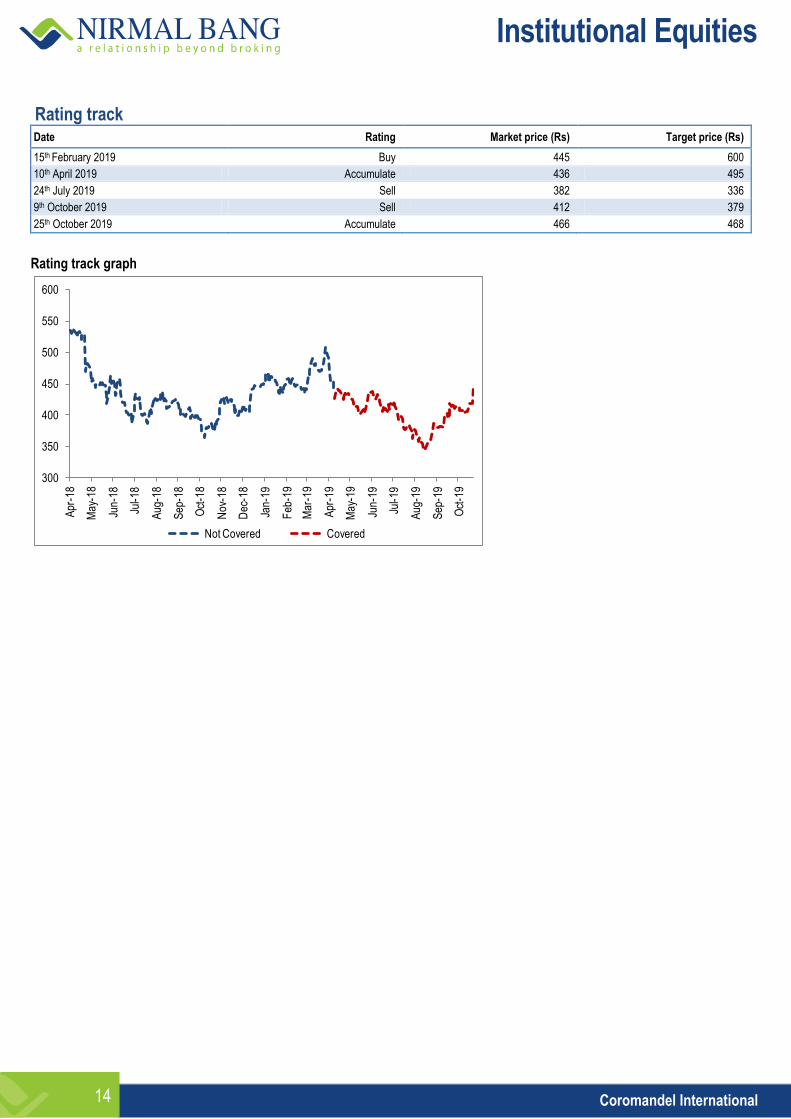

Rating track Date Rating Market price (Rs) Target price (Rs)

15th February 2019 Buy 445 600

10th April 2019 Accumulate 436 495

24th July 2019 Sell 382 336

9th October 2019 Sell 412 379

25th October 2019 Accumulate 466 468

Rating track graph

300

350

400

450

500

550

600

Apr

-18

May

-18

Jun-

18

Jul-1

8

Aug

-18

Sep

-18

Oct

-18

Nov

-18

Dec

-18

Jan-

19

Feb

-19

Mar

-19

Apr

-19

May

-19

Jun-

19

Jul-1

9

Aug

-19

Sep

-19

Oct

-19

Not Covered Covered

Institutional Equities

15 Coromandel International

DISCLOSURES

This Report is published by Nirmal Bang Equities Private Limited (hereinafter referred to as “NBEPL”) for private circulation. NBEPL is a registered Research Analyst under SEBI (Research Analyst) Regulations, 2014 having Registration no. INH000001436. NBEPL is also a registered Stock Broker with National Stock Exchange of India Limited and BSE Limited in cash and derivatives segments. NBEPL has other business divisions with independent research teams separated by Chinese walls, and therefore may, at times, have different or contrary views on stocks and markets. NBEPL or its associates have not been debarred / suspended by SEBI or any other regulatory authority for accessing / dealing in securities Market. NBEPL, its associates or analyst or his relatives do not hold any financial interest in the subject company. NBEPL or its associates or Analyst do not have any conflict or material conflict of interest at the time of publication of the research report with the subject company. NBEPL or its associates or Analyst or his relatives do not hold beneficial ownership of 1% or more in the subject company at the end of the month immediately preceding the date of publication of this research report. NBEPL or its associates / analyst has not received any compensation / managed or co-managed public offering of securities of the company covered by Analyst during the past twelve months. NBEPL or its associates have not received any compensation or other benefits from the company covered by Analyst or third party in connection with the research report. Analyst has not served as an officer, director or employee of Subject Company and NBEPL / analyst has not been engaged in market making activity of the subject company. Analyst Certification: I, Amit Agarwal, research analyst and the author of this report, hereby certify that the views expressed in this research report accurately reflects my personal views about the subject securities, issuers, products, sectors or industries. It is also certified that no part of the compensation of the analyst was, is, or will be directly or indirectly related to the inclusion of specific recommendations or views in this research. The analyst is principally responsible for the preparation of this research report and has taken reasonable care to achieve and maintain independence and objectivity in making any recommendations.

Institutional Equities

16 Coromandel International

Disclaimer

Stock Ratings Absolute Returns

BUY > 15%

ACCUMULATE -5% to15%

SELL < -5%

This report is for the personal information of the authorized recipient and does not construe to be any investment, legal or taxation advice to you. NBEPL is not soliciting any action based upon it. Nothing in this research shall be construed as a solicitation to buy or sell any security or product, or to engage in or refrain from engaging in any such transaction. In preparing this research, we did not take into account the investment objectives, financial situation and particular needs of the reader.

This research has been prepared for the general use of the clients of NBEPL and must not be copied, either in whole or in part, or distributed or redistributed to any other person in any form. If you are not the intended recipient you must not use or disclose the information in this research in any way. Though disseminated to all the customers simultaneously, not all customers may receive this report at the same time. NBEPL will not treat recipients as customers by virtue of their receiving this report. This report is not directed or intended for distribution to or use by any person or entity resident in a state, country or any jurisdiction, where such distribution, publication, availability or use would be contrary to law, regulation or which would subject NBEPL & its group companies to registration or licensing requirements within such jurisdictions.

The report is based on the information obtained from sources believed to be reliable, but we do not make any representation or warranty that it is accurate, complete or up-to-date and it should not be relied upon as such. We accept no obligation to correct or update the information or opinions in it. NBEPL or any of its affiliates or employees shall not be in any way responsible for any loss or damage that may arise to any person from any inadvertent error in the information contained in this report. NBEPL or any of its affiliates or employees do not provide, at any time, any express or implied warranty of any kind, regarding any matter pertaining to this report, including without limitation the implied warranties of merchantability, fitness for a particular purpose, and non-infringement. The recipients of this report should rely on their own investigations.

This information is subject to change without any prior notice. NBEPL reserves its absolute discretion and right to make or refrain from making modifications and alterations to this statement from time to time. Nevertheless, NBEPL is committed to providing independent and transparent recommendations to its clients, and would be happy to provide information in response to specific client queries.

Before making an investment decision on the basis of this research, the reader needs to consider, with or without the assistance of an adviser, whether the advice is appropriate in light of their particular investment needs, objectives and financial circumstances. There are risks involved in securities trading. The price of securities can and does fluctuate, and an individual security may even become valueless. International investors are reminded of the additional risks inherent in international investments, such as currency fluctuations and international stock market or economic conditions, which may adversely affect the value of the investment. Opinions expressed are subject to change without any notice. Neither the company nor the director or the employees of NBEPL accept any liability whatsoever for any direct, indirect, consequential or other loss arising from any use of this research and/or further communication in relation to this research. Here it may be noted that neither NBEPL, nor its directors, employees, agents or representatives shall be liable for any damages whether direct or indirect, incidental, special or consequential including lost revenue or lost profit that may arise from or in connection with the use of the information contained in this report.

Copyright of this document vests exclusively with NBEPL.

Our reports are also available on our website www.nirmalbang.com

Access all our reports on Bloomberg, Thomson Reuters and Factset.

Team Details:

Name Email Id Direct Line

Rahul Arora CEO [email protected] -

Girish Pai Head of Research [email protected] +91 22 6273 8017 / 18

Dealing

Ravi Jagtiani Dealing Desk [email protected] +91 22 6273 8230, +91 22 6636 8833

Pradeep Kasat Dealing Desk [email protected] +91 22 6273 8100/8101, +91 22 6636 8831

Michael Pillai Dealing Desk [email protected] +91 22 6273 8102/8103, +91 22 6636 8830

Nirmal Bang Equities Pvt. Ltd.

Correspondence Address

B-2, 301/302, Marathon Innova,

Nr. Peninsula Corporate Park,

Lower Parel (W), Mumbai-400013.

Board No. : 91 22 6273 8000/1; Fax. : 022 6273 8010