Embed Size (px)

Citation preview

Prepared by Papias Njaala CPA Review

BUDGETARY PLANNINGMeaning of BudgetingBudgeting is the process of expressing a plan into monetary terms. A plan is adesign of a desired future and of effective ways of bringing it about. It isprepared in order to fulfill long-term goals of an organization. Normally theorganization is required to prepare long-term plans, which will fulfill itsmission.

Long-term Goals/ObjectivesLong-term goals are set taking into consideration both internal and externalenvironment. The internal environment consists of internal resources such asemployees, machines and finance whereas external environment relates to thefactors over which the organization has no control. They include governmentpolicies and decisions, competition, social environment, economic environmentetc.

Meaning of a BudgetA budget is a plan of action expressed in monetary terms and which is used tocoordinate the activities of the organization and their implementation. Informulating the budget, the mission, long-term goals/objectives, strategies andpolicies of the organization are taken into consideration.

Reasons for Preparing Budgets(a) To aid the planning of operationsThe plans, which have been formulated, must be translated into monetary terms.This translation will help the managers to determine how the conditions on thecoming period might change and their financial implications and which stepsshould be taken in order to respond to these changed conditions. Therefore, ithelps managers to anticipate problems before they occur.

(b) CommunicationThrough the budget, top management communicates its expectations to lower levelmanagement so as to enable them coordinate their activities to achieve thoseexpectations. This communication is done in the actual act of preparing it.

(c) Performance EvaluationThe budget provides a useful tool of informing managers on how well their actualperformance has been compared to the budget.

(d) AuthorizationOnce a budget is passed by proper authorities (normally by Board of Directors orsimilar body) it authorizes relevant officials to collect and spend funds in thelines of that budget.

(e) ControlThe budget helps managers to manage and control the activities for which they areresponsible. When actual results are compared with the budget, managers canascertain costs which are not in line with the budget and which requires their

1

Prepared by Papias Njaala CPA Review

attention. The reasons for deviations are investigated and appropriate correctiveaction is taken.

(f) CoordinationThe budget facilitates the activities of various segments of the organization tobe brought together and reconciled into a common plan. Without this coordination,each segmental manager would make his/her own decision, which may not be in linewith the best interest of the whole organization. Budgeting compels managers toexamine the relationship between their operations and those of other departments.For example, Sales Department can not budget to sell the volume of output, whichis above the Production Department’s ability to produce and vice versa.

(g) MotivationThe budget can be used to influence managerial behaviour and motivating managersto perform in line with organizational objectives. However, this will be possibleonly if individuals are allowed to participate actively in preparing the budget.Otherwise a budget will act as a threat/pressure device rather than a challenge.

ADMINISTRATION OF THE BUDGETING PROCESSIn a large OrganizationIn large organizations, the responsibility of preparing the budget of theorganization is vested in the hands of the Budgeting Committee. This committeeconsists of senior officials of the organization and is normally under thechairmanship of the Chief Executive Officer. Other members of the Committee maybe representatives of various departments, for example Sales Department,Purchases Department, Production Department, and Administration Department etc.The Budgeting Committee is required to ensure that it prepares the budget, whichwill be presented to the Board of Directors (or similar body) for approval. Thiscommittee therefore, approves departmental budgets and then prepares the budgetfor the whole organization. This is done after evaluating the possible results ofimplementing the budget. Then it is forwarded to the Board of Directors (orsimilar body).

The whole budgeting process is coordinated by a Budget Coordinator who isresponsible for the following: Issuing the budget time table Issuing the budget manual and other information Putting together all departmental (segmental) budgets into a single budget for

the whole organization. This will be presented to the Budget Committee.

NB: The coordination of the budgeting process is normally done by the seniormember of the Finance Department.

In a Small OrganizationNormally, the head of Finance (or Accounting) Department prepares the budget fora small organization. After the preparation of the budget, it is discussed by themanagement and approved. In case the small organization in question has a boardof directors (or similar body), the budget must be approved by it, after being

2

Prepared by Papias Njaala CPA Review

discussed by the management. However, many small organizations do not have boardsof directors (or similar bodies). Stages in the Budgeting Process(i) Communicating Details The initial step in the budgeting process is to communicate details of the budgetpolicy and guidelines to those who are responsible for preparation of budgets.This is done by the Budget Coordinator. (ii) Determining the Budget-limiting FactorAfter receiving the details of the budget policy, each segment of theorganization is required to determine the budget-limiting factor, whichdetermines the attainable volume of activity of that department/segment.

(iii) Preparation of the Sales BudgetThis is the base for the preparation of all other budgets. However, theproduction capacity or the financial capacity to purchase (as the case may be) istaken into consideration while preparing the Sales Budget.

(iv) Preparation of other Departmental/Segmental BudgetsManagers who are responsible for meeting the budgeted performance should preparethe budgets for areas for which they responsible. The preparation of segmentalbudgets is a bottom up process.

(v) Negotiation of Budgets with SuperiorsThe superior will then incorporate all budgets from their subordinates with hisown budget and then submit the budget to the next higher level. The figuresappearing in the budget are the result of bargaining/negotiation process betweenmanagers and their superiors.

(vi) Coordination and Review of BudgetsAs the individual budgets go up the organization hierarchy in the bargainingprocess, they must be compared in order to make sure that they are consistent toeach other. Those budgets which are not consistent to each other, must bemodified so as to make them consistent and compatible with other conditions,constraints and plans, which are beyond the manager’s knowledge and /or control.The manager concerned must be informed on the modifications made and theirreasons.

(vii) Acceptance of the BudgetWhen all budgets are consistent to each other, a Master Budget is prepared. Themaster budget is the budget summarizing all other budgets. After the approval ofthe master budget, the budgets are then passed down through the organization tothe relevant responsibility centres. The manager of each responsibility centre isrequired to carry out the plans contained in each relevant budget.

3

Prepared by Papias Njaala CPA Review

(viii) Understanding Budgetary Control InformationEach manager must understand the budgetary control information and the aim ofbudgetary information.

How to Determine the Volume of OperationDetermining the Volume of Operation of the Business OrganizationFor a business-oriented organization, there are many constraints, which may set alimit above, which the organization will not operate. The organization may not beable to sell every thing. It can sell what the market can purchase. Even if themarket is unlimited the organization will not be able to sell more than what theinternal resources can produce/purchase. Those internal resources (including thecapacity available, skilled manpower, finance, warehouse etc) may be insufficientto produce the quantity (volume) which is demanded by the market.

Each departmental (segmental) budget will be prepared taking into consideration agiven constraint. Each departmental constraint is referred to as Budget LimitingFactor. There is one budget-limiting factor for the whole organization and thisis referred to as a Principal Budgeting Factor. Determining the Volume of Operation of a Non-profit Making OrganizationFor a non-profit making organization the Principal Budgeting Factor is usuallythe funds expected to be available to finance the selected programmes. Normallythe non-profit making organization identifies the costs to be incurred in thecoming year in order to carry out the planned activities, and then it will lookfor sources of funds to finance those activities. When funds, which are expectedto be available, are not sufficient then the organization will reduce itsactivities to the level of funds expected to be available.

Problems and Dangers of BudgetingBudgeting is an important process for the anticipating problems before theyoccur. However, the budgeting process suffers the following problems and dangers: Sometimes it is very difficult and time consuming to seek support and involve

all levels of management. It is difficult to develop meaningful forecasts and plans, especially the

sales budget which is the base for all other budgets. It is difficult to train all persons to be involved in the budgeting process

and winning their participation. It is difficult to formulate objectives, policies, procedures and standards in

a realistic manner. It is sometimes difficult to cope with changes which were not forecasted and

hence not budgeted for, when preparing the budget. Using the budget in the rigid manner.

Once the budget has been prepared, it must be used intelligently taking intoconsideration changes, which might take place. When the budget is used in therigid manner efficiency and effectiveness will not be achieved because it willnot go with changes taking place after its formulation.

Behavioural Aspects of Budgetary Control Systems

4

Prepared by Papias Njaala CPA Review

Budgetary control systems are concerned with influencing the behaviours ofindividuals and groups within an organization so as to achieve objectives of thatorganization. Therefore, techniques applied in the budgetary control system mustbe established carefully otherwise the budgetary control system will not help theorganization to achieve its objectives.

The following are some of the human behavioural problems: (i) The budget considered as a threat/pressure deviceWhen trying to influence employees to work harder in order to attainorganizational objectives through a budget, they may consider a budget as athreat/pressure device.

(ii) Poor relationship between individualsFinance people who undertake budgetary control exercises can be seen as budgetpolicemen by managers hence leading to poor relationship between Finance peopleand managers. This leads to loss of interest in budgetary reports prepared byFinance people.

(iii) Disguising of responsibilityPoor managers may blame the budget for their failure to achieve objectives,especially if there was no participation in the budget preparation process. Theymay urge that the budget was not realistic.

(iv) DepartmentalismFor fear of getting lesser funds next year, departments may spend up to the lastcent allocated to them. In this way, the needs of departments are put before theorganizational needs.

(v) Budget as a tool of minimizing costsManagers might concentrate on minimizing costs and hence overlook other measuresof performance enhancement, for example productivity improvement.

Those problems can be minimized through the following ways: (i) Encouraging participation during the budget preparation process(ii) Accountants should assume an educational role. They should educate managerson the importance of accounting controls information.(iii) Accounting budgetary reports should incorporate other variables besidescosts.

The Budget of the Business OrganizationA business organization can either be a manufacturing or merchandisingorganization. The budget of the business organization has two main parts, namelyoperating budget and finance budget. When these two budgets are put together weget a master budget. The master budget is the summary of all budgets receivedfrom all departments.

Operating Budget5

Prepared by Papias Njaala CPA Review

Operating budget of the manufacturing organization will have the following: Sales Budget Production Units Budget Cost of Raw Materials Usage Budget Cost of Raw Materials Purchase Budget Direct Labour Budget Production Overheads Budget Closing Stock Budget Cost of Sale Budget sometimes taken as one budget Gross Profit Budget Administration Cost Budget Marketing Cost Budget

A merchandizing organization’s operating budget will be slightly different fromthat of the manufacturing organization. This difference is due to the fact thatits activities relate to purchasing and selling. It does not produce what itsells. Therefore, its operating budget will include the following: Sales Budget Purchases Budget Closing Stock Budget Cost of Sale Budget sometimes taken as one budget Gross Profit Budget Administration Cost Budget Marketing Cost Budget

Finance BudgetThe Finance Budget for the manufacturing organization is similar to that of themerchandizing organization. It includes the following: Cash Budget Capital Budget Proforma Income Statement/Budgeted Income Statement. Proforma Balance Sheet/Budgeted Balance Sheet

Cash BudgetA Cash Budget shows the expected cash inflows and expected cash outflows. It willtherefore, exclude the following: Non-cash items included in the expenses, for example, depreciation expense,

amortization of goodwill and the like. Accrued items

However, all deferred items must be included in the Cash Budget

Capital BudgetCapital Budget shows how a fixed asset is going to be purchased and financed andthe financial implications of acquiring it.

Proforma Balance Sheet/Budgeted Balance Sheet.Proforma Balance Sheet/Budgeted Balance Sheet shows the expected financialposition of an organization at a given date. It shows the expected resources andway of financing the acquisition of those expected resources. Those expected

6

Prepared by Papias Njaala CPA Review

resources comprise of fixed assets and current assets. Fixed assets includeplant, motor vehicles, buildings, furniture and the like. Current assets includestocks (or inventory), debtors (or accounts receivable), prepayments, cash andthe like.

ExampleSofi Company’s Budget Committee is in the budgeting session for the coming year.The following details are to be taken into consideration during the budgetingsession:

A minimum cash equal to 500,000/= should always be maintained.

Inventory levels should be equal to 25 % and 20 % of finished goods and rawmaterials respectively of sales needs and production needs of the next quarter.

Creditors for raw materials will be paid within discount period in order to takeadvantage of 2 % cash discount. As such creditors will be paid in the quarter ofpurchase except for 20 % of purchase, which will be paid in the next quarter.

Collections from debtors will be as follows: 20 % collected in the quarter of sale 60 % collected in the next quarter 18 % collected in the third quarter 2 % will be possible bad debts.

1 % of wages incurred in the quarter will accrue and it will be paid in the nextquarter.

All overheads will be paid as follows: Quarter 1 2 3 4Payments 20 % 40 % 20 % 20 %These expenses will exclude depreciation expenses.

Desired inventories will be as follows: Raw materials 15,000 kgs Finished goods 8,000 units

The budget coordinator has been able to obtain the following summaries: (1) The expected financial position at the end of this year is as follows: Cash100,000/= Debtors (net)1,600,000/= Stock: Raw materials (14,000 kgs) 1,456,000/= : Finished goods (6,000 units)2,382,000/=

7

Prepared by Papias Njaala CPA Review

Plant23,000,000/= Motor vehicles10,000,000/= Creditors2,100,000/= Accrued Wages50,000/= Dividends provision3,000,000/= Share Capital30,000,000/= Retained Earnings3,388,000/=

(2) In the coming year the costs of raw materials will not change and theefficiency in the use of materials will not change too.

(3) Sales will be as follows: Quarter 1 2 34 Units 40,000 50,000 60,000 80,000 Price 500/= 480/= 480/= 480/=

(4) Each finished unit requires 2 kgs of raw materials.

(5) Average rate of direct labour will be 48/= per labour hour and the finishedunit will require 2 hours.

(6) Factory overhead will be applied to production at a rate of 40/= per hour.

(7) Administration overheads will amount to 10,500,000/= excluding depreciationexpense.

(8) Depreciation will be charged at 20 % of book value.

(9) The company is liable to pay tax on income at a rate of 30 %, and dividend ifsufficient profit is generated, equal to 12 %.

(10) In the case of a deficit the company can borrow at an interest rate of 20 %and it can lend excess cash only for the periods not exceeding three months and interest rate for 3 months is 12 %

Required:

8

Prepared by Papias Njaala CPA Review

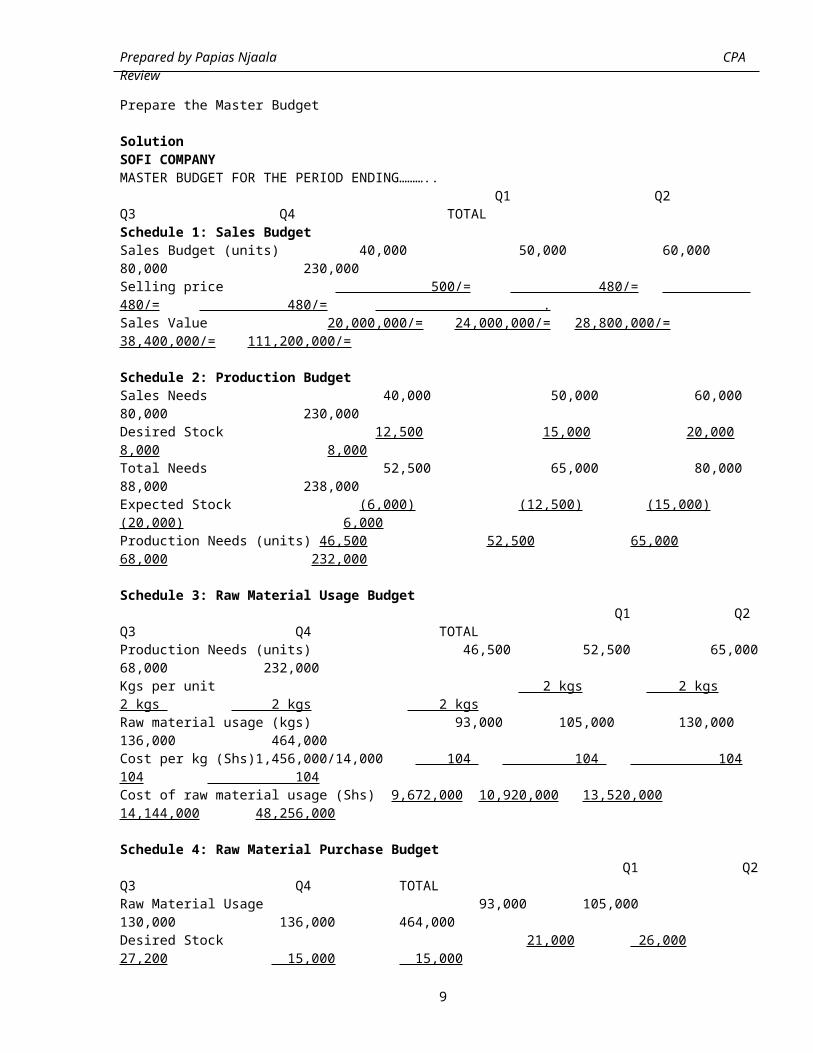

Prepare the Master Budget

SolutionSOFI COMPANYMASTER BUDGET FOR THE PERIOD ENDING……….. Q1 Q2 Q3 Q4 TOTALSchedule 1: Sales BudgetSales Budget (units) 40,000 50,000 60,000 80,000 230,000Selling price 500/= 480/= 480/= 480/= .Sales Value 20,000,000/= 24,000,000/= 28,800,000/= 38,400,000/= 111,200,000/=

Schedule 2: Production BudgetSales Needs 40,000 50,000 60,000 80,000 230,000Desired Stock 12,500 15,000 20,000 8,000 8,000Total Needs 52,500 65,000 80,000 88,000 238,000Expected Stock (6,000) (12,500) (15,000) (20,000) 6,000Production Needs (units) 46,500 52,500 65,000 68,000 232,000

Schedule 3: Raw Material Usage Budget Q1 Q2 Q3 Q4 TOTALProduction Needs (units) 46,500 52,500 65,000 68,000 232,000Kgs per unit 2 kgs 2 kgs 2 kgs 2 kgs 2 kgsRaw material usage (kgs) 93,000 105,000 130,000 136,000 464,000Cost per kg (Shs)1,456,000/14,000 104 104 104 104 104Cost of raw material usage (Shs) 9,672,000 10,920,000 13,520,000 14,144,000 48,256,000

Schedule 4: Raw Material Purchase Budget Q1 Q2 Q3 Q4 TOTALRaw Material Usage 93,000 105,000 130,000 136,000 464,000Desired Stock 21,000 26,000 27,200 15,000 15,000

9

Prepared by Papias Njaala CPA Review

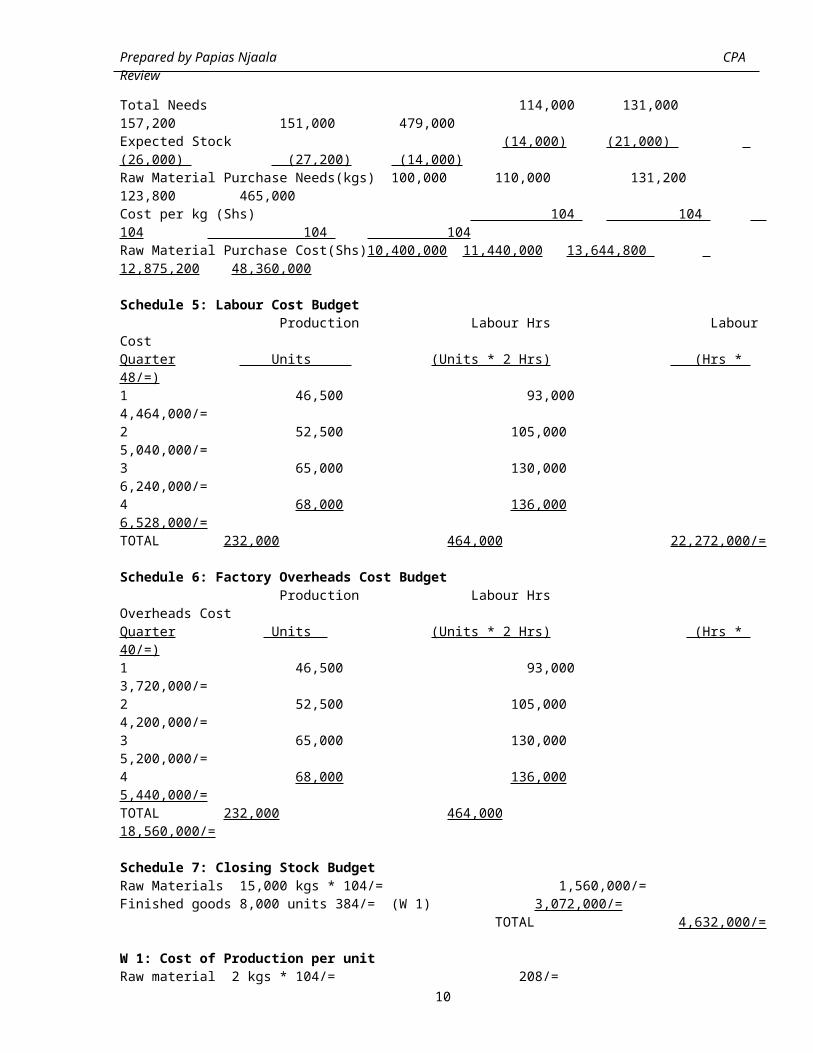

Total Needs 114,000 131,000 157,200 151,000 479,000Expected Stock (14,000) (21,000) (26,000) (27,200) (14,000)Raw Material Purchase Needs(kgs) 100,000 110,000 131,200 123,800 465,000Cost per kg (Shs) 104 104 104 104 104Raw Material Purchase Cost(Shs)10,400,000 11,440,000 13,644,800 12,875,200 48,360,000

Schedule 5: Labour Cost Budget Production Labour Hrs Labour CostQuarter Units (Units * 2 Hrs) (Hrs * 48/=)1 46,500 93,000 4,464,000/=2 52,500 105,000 5,040,000/=3 65,000 130,000 6,240,000/=4 68,000 136,000 6,528,000/=TOTAL 232,000 464,000 22,272,000/=

Schedule 6: Factory Overheads Cost Budget Production Labour Hrs Overheads CostQuarter Units (Units * 2 Hrs) (Hrs * 40/=)1 46,500 93,000 3,720,000/=2 52,500 105,000 4,200,000/=3 65,000 130,000 5,200,000/=4 68,000 136,000 5,440,000/=TOTAL 232,000 464,000 18,560,000/=

Schedule 7: Closing Stock BudgetRaw Materials 15,000 kgs * 104/= 1,560,000/=Finished goods 8,000 units 384/= (W 1) 3,072,000/= TOTAL 4,632,000/=

W 1: Cost of Production per unitRaw material 2 kgs * 104/= 208/=

10

Prepared by Papias Njaala CPA Review

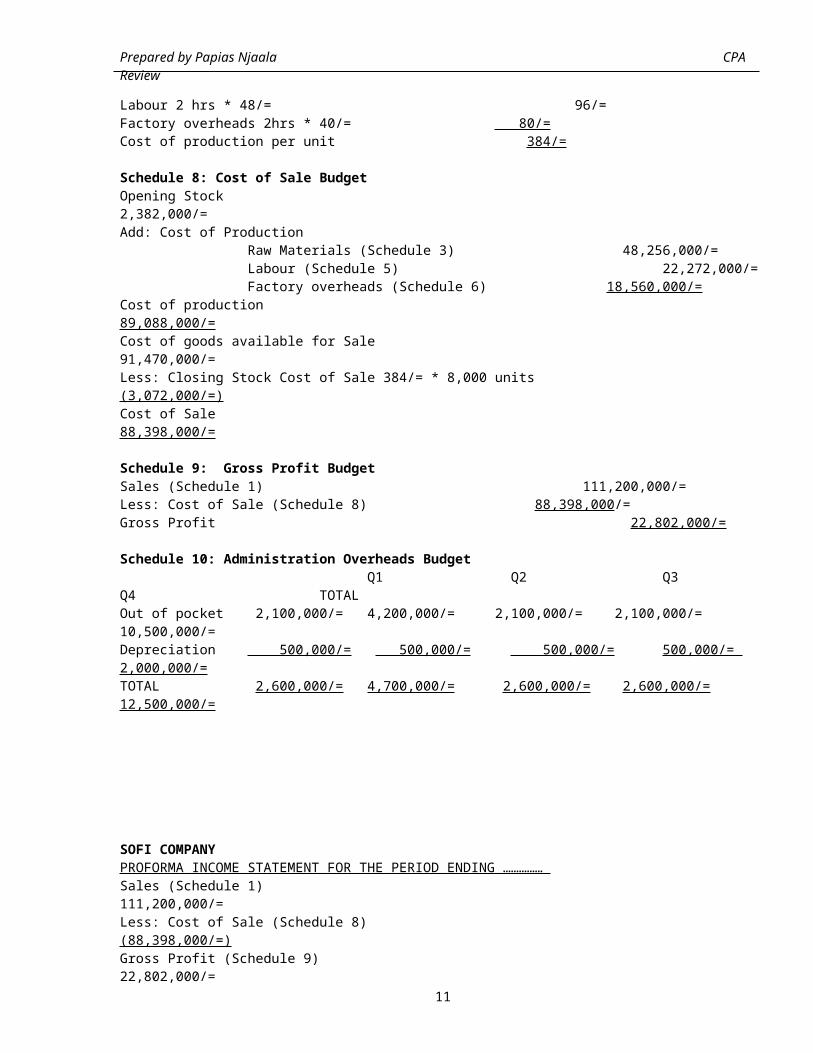

Labour 2 hrs * 48/= 96/=Factory overheads 2hrs * 40/= 80/=Cost of production per unit 384/=

Schedule 8: Cost of Sale BudgetOpening Stock 2,382,000/=Add: Cost of Production Raw Materials (Schedule 3) 48,256,000/= Labour (Schedule 5) 22,272,000/= Factory overheads (Schedule 6) 18,560,000/=Cost of production 89,088,000/=Cost of goods available for Sale 91,470,000/=Less: Closing Stock Cost of Sale 384/= * 8,000 units (3,072,000/=)Cost of Sale 88,398,000/=

Schedule 9: Gross Profit BudgetSales (Schedule 1) 111,200,000/=Less: Cost of Sale (Schedule 8) 88,398,000/=Gross Profit 22,802,000/=

Schedule 10: Administration Overheads Budget Q1 Q2 Q3 Q4 TOTALOut of pocket 2,100,000/= 4,200,000/= 2,100,000/= 2,100,000/= 10,500,000/=Depreciation 500,000/= 500,000/= 500,000/= 500,000/= 2,000,000/=TOTAL 2,600,000/= 4,700,000/= 2,600,000/= 2,600,000/= 12,500,000/=

SOFI COMPANYPROFORMA INCOME STATEMENT FOR THE PERIOD ENDING …………… Sales (Schedule 1) 111,200,000/=Less: Cost of Sale (Schedule 8) (88,398,000/=)Gross Profit (Schedule 9) 22,802,000/=

11

Prepared by Papias Njaala CPA Review

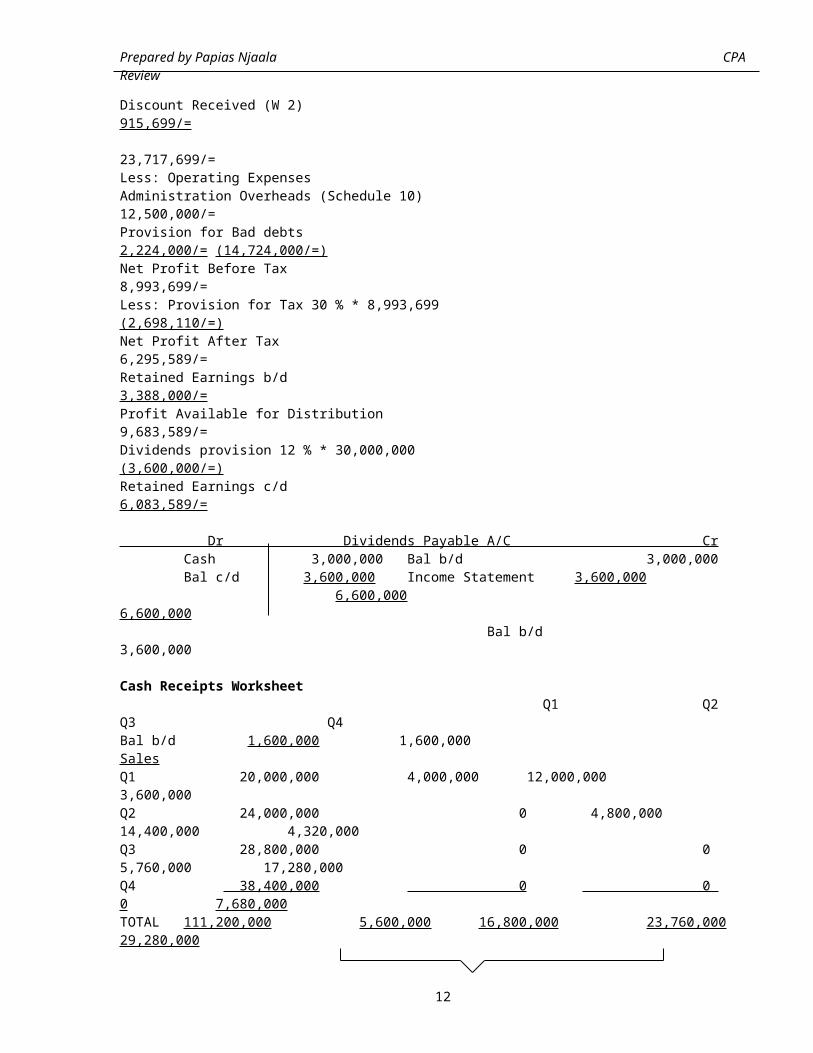

Discount Received (W 2) 915,699/= 23,717,699/=Less: Operating ExpensesAdministration Overheads (Schedule 10) 12,500,000/=Provision for Bad debts 2,224,000/= (14,724,000/=)Net Profit Before Tax 8,993,699/=Less: Provision for Tax 30 % * 8,993,699 (2,698,110/=)Net Profit After Tax 6,295,589/=Retained Earnings b/d 3,388,000/=Profit Available for Distribution 9,683,589/=Dividends provision 12 % * 30,000,000 (3,600,000/=)Retained Earnings c/d 6,083,589/=

Dr Dividends Payable A/C Cr Cash 3,000,000 Bal b/d 3,000,000 Bal c/d 3,600,000 Income Statement 3,600,000 6,600,000 6,600,000 Bal b/d 3,600,000

Cash Receipts Worksheet Q1 Q2 Q3 Q4Bal b/d 1,600,000 1,600,000SalesQ1 20,000,000 4,000,000 12,000,000 3,600,000Q2 24,000,000 0 4,800,000 14,400,000 4,320,000Q3 28,800,000 0 0 5,760,000 17,280,000Q4 38,400,000 0 0 0 7,680,000TOTAL 111,200,000 5,600,000 16,800,000 23,760,000 29,280,000

12

Prepared by Papias Njaala CPA Review

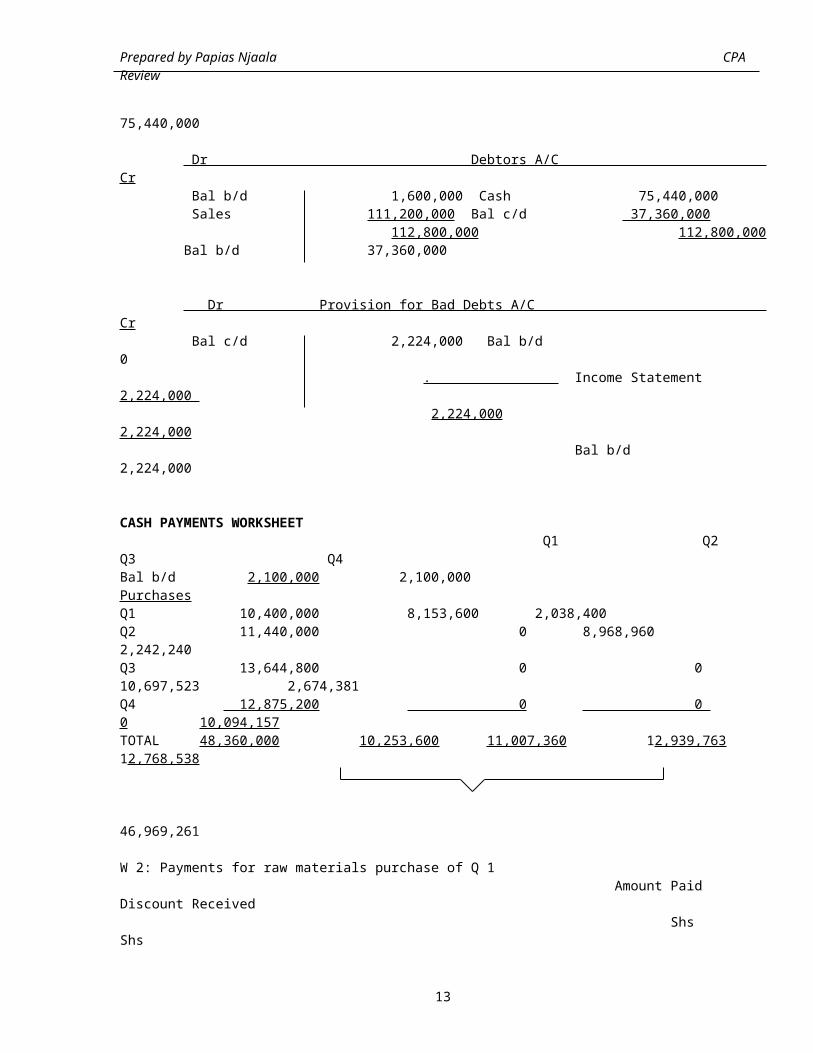

75,440,000

Dr Debtors A/C Cr Bal b/d 1,600,000 Cash 75,440,000 Sales 111,200,000 Bal c/d 37,360,000 112,800,000 112,800,000 Bal b/d 37,360,000

Dr Provision for Bad Debts A/C Cr Bal c/d 2,224,000 Bal b/d 0 . Income Statement 2,224,000 2,224,000 2,224,000 Bal b/d 2,224,000

CASH PAYMENTS WORKSHEET Q1 Q2 Q3 Q4Bal b/d 2,100,000 2,100,000PurchasesQ1 10,400,000 8,153,600 2,038,400 Q2 11,440,000 0 8,968,960 2,242,240 Q3 13,644,800 0 0 10,697,523 2,674,381Q4 12,875,200 0 0 0 10,094,157TOTAL 48,360,000 10,253,600 11,007,360 12,939,763 12,768,538

46,969,261 W 2: Payments for raw materials purchase of Q 1 Amount Paid Discount Received Shs Shs

13

Prepared by Papias Njaala CPA Review

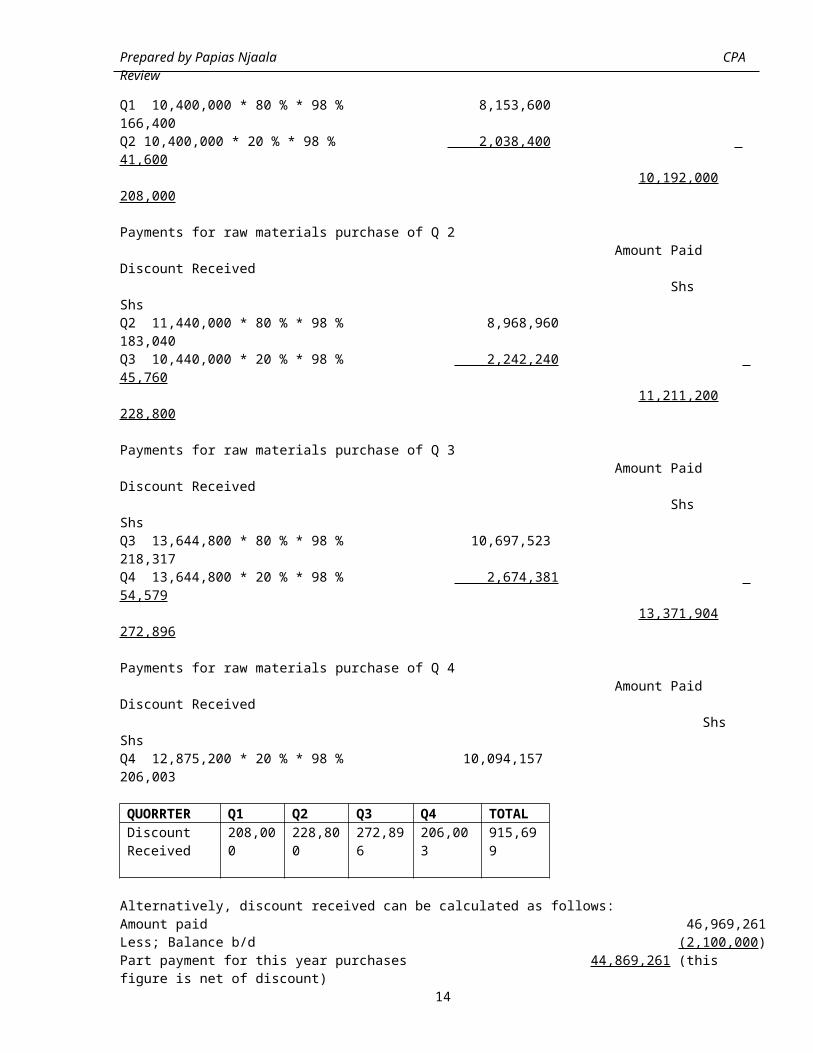

Q1 10,400,000 * 80 % * 98 % 8,153,600 166,400Q2 10,400,000 * 20 % * 98 % 2,038,400 41,600 10,192,000 208,000

Payments for raw materials purchase of Q 2 Amount Paid Discount Received Shs ShsQ2 11,440,000 * 80 % * 98 % 8,968,960 183,040Q3 10,440,000 * 20 % * 98 % 2,242,240 45,760 11,211,200 228,800

Payments for raw materials purchase of Q 3 Amount Paid Discount Received Shs ShsQ3 13,644,800 * 80 % * 98 % 10,697,523 218,317Q4 13,644,800 * 20 % * 98 % 2,674,381 54,579 13,371,904 272,896

Payments for raw materials purchase of Q 4 Amount Paid Discount Received Shs ShsQ4 12,875,200 * 20 % * 98 % 10,094,157 206,003

QUORRTER Q1 Q2 Q3 Q4 TOTALDiscount Received

208,000

228,800

272,896

206,003

915,699

Alternatively, discount received can be calculated as follows:Amount paid 46,969,261Less; Balance b/d (2,100,000)Part payment for this year purchases 44,869,261 (this figure is net of discount)

14

Prepared by Papias Njaala CPA Review

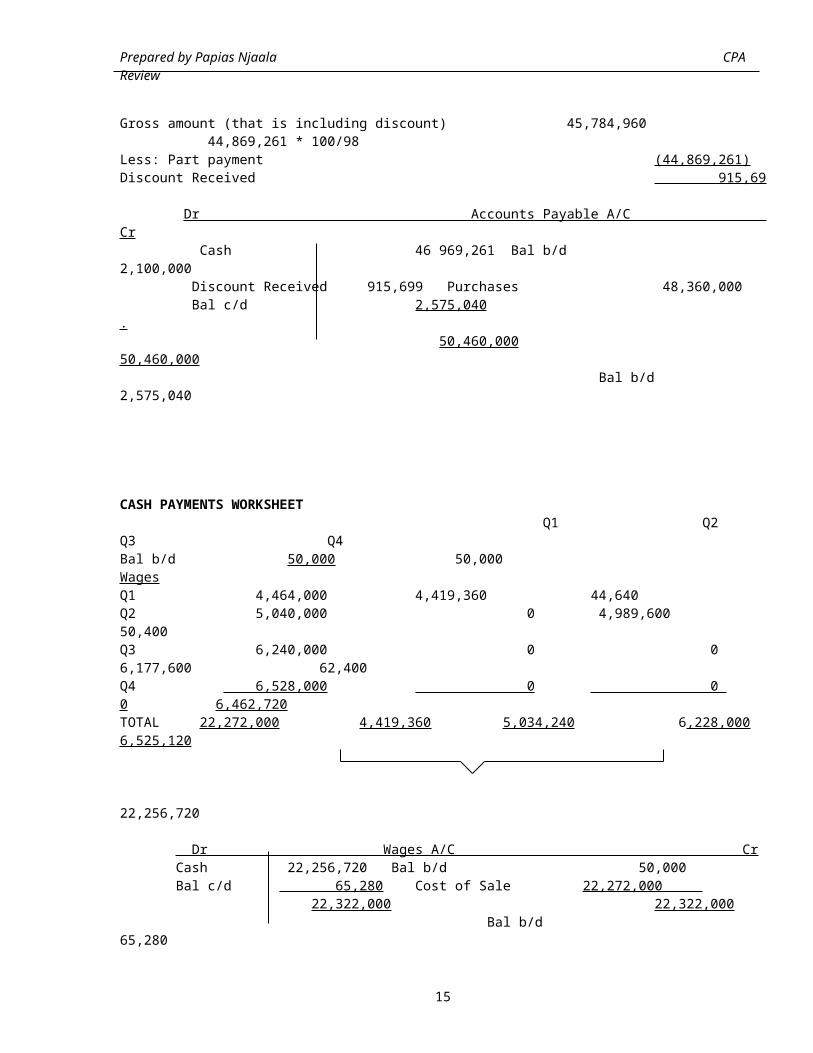

Gross amount (that is including discount) 45,784,960 44,869,261 * 100/98 Less: Part payment (44,869,261) Discount Received 915,69

Dr Accounts Payable A/C Cr Cash 46 969,261 Bal b/d 2,100,000 Discount Received 915,699 Purchases 48,360,000 Bal c/d 2,575,040 . 50,460,000 50,460,000 Bal b/d 2,575,040

CASH PAYMENTS WORKSHEET Q1 Q2 Q3 Q4Bal b/d 50,000 50,000WagesQ1 4,464,000 4,419,360 44,640 Q2 5,040,000 0 4,989,600 50,400 Q3 6,240,000 0 0 6,177,600 62,400Q4 6,528,000 0 0 0 6,462,720TOTAL 22,272,000 4,419,360 5,034,240 6,228,000 6,525,120

22,256,720

Dr Wages A/C Cr Cash 22,256,720 Bal b/d 50,000 Bal c/d 65,280 Cost of Sale 22,272,000 22,322,000 22,322,000 Bal b/d 65,280

15

Prepared by Papias Njaala CPA Review

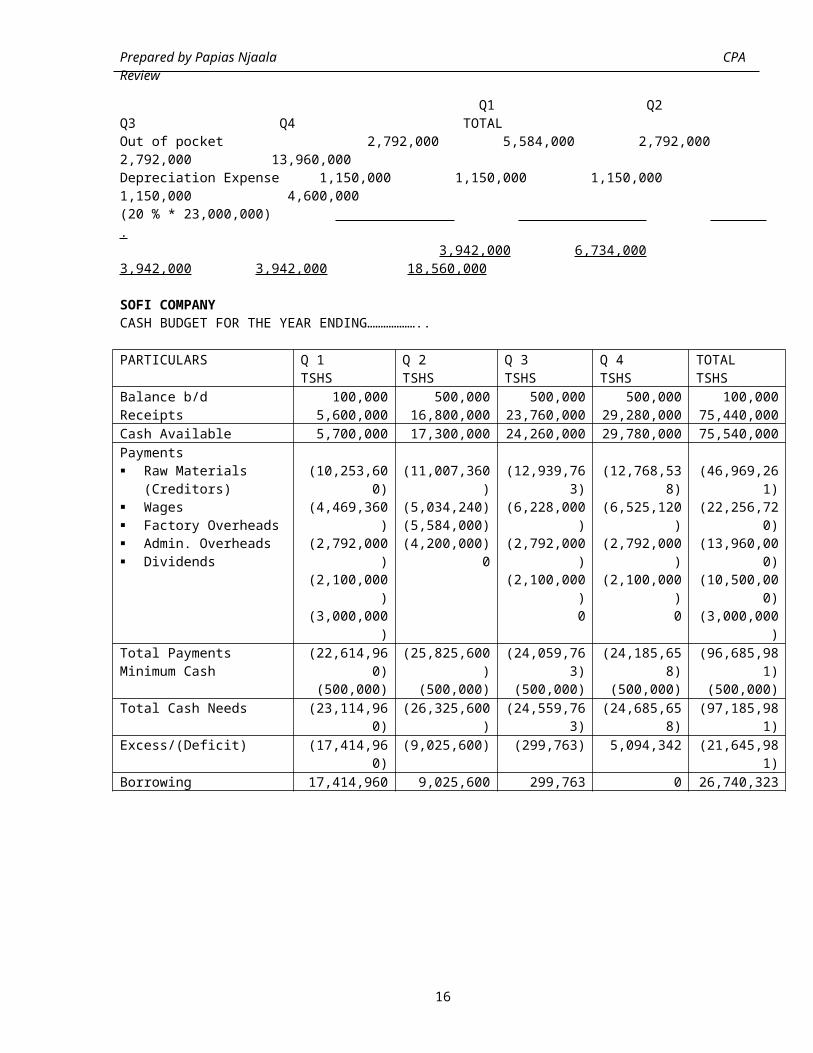

Q1 Q2 Q3 Q4 TOTALOut of pocket 2,792,000 5,584,000 2,792,000 2,792,000 13,960,000Depreciation Expense 1,150,000 1,150,000 1,150,000 1,150,000 4,600,000(20 % * 23,000,000) . 3,942,000 6,734,000 3,942,000 3,942,000 18,560,000

SOFI COMPANYCASH BUDGET FOR THE YEAR ENDING………………..

PARTICULARS Q 1TSHS

Q 2TSHS

Q 3TSHS

Q 4TSHS

TOTALTSHS

Balance b/dReceipts

100,0005,600,000

500,00016,800,000

500,00023,760,000

500,00029,280,000

100,00075,440,000

Cash Available 5,700,000 17,300,000 24,260,000 29,780,000 75,540,000Payments Raw Materials

(Creditors) Wages Factory Overheads Admin. Overheads Dividends

(10,253,600)

(4,469,360)

(2,792,000)

(2,100,000)

(3,000,000)

(11,007,360)

(5,034,240)(5,584,000)(4,200,000)

0

(12,939,763)

(6,228,000)

(2,792,000)

(2,100,000)0

(12,768,538)

(6,525,120)

(2,792,000)

(2,100,000)0

(46,969,261)

(22,256,720)

(13,960,000)

(10,500,000)

(3,000,000)

Total PaymentsMinimum Cash

(22,614,960)

(500,000)

(25,825,600)

(500,000)

(24,059,763)

(500,000)

(24,185,658)

(500,000)

(96,685,981)

(500,000)Total Cash Needs (23,114,96

0)(26,325,600

)(24,559,76

3)(24,685,65

8)(97,185,98

1)Excess/(Deficit) (17,414,96

0)(9,025,600) (299,763) 5,094,342 (21,645,98

1)Borrowing 17,414,960 9,025,600 299,763 0 26,740,323

16

Prepared by Papias Njaala CPA Review

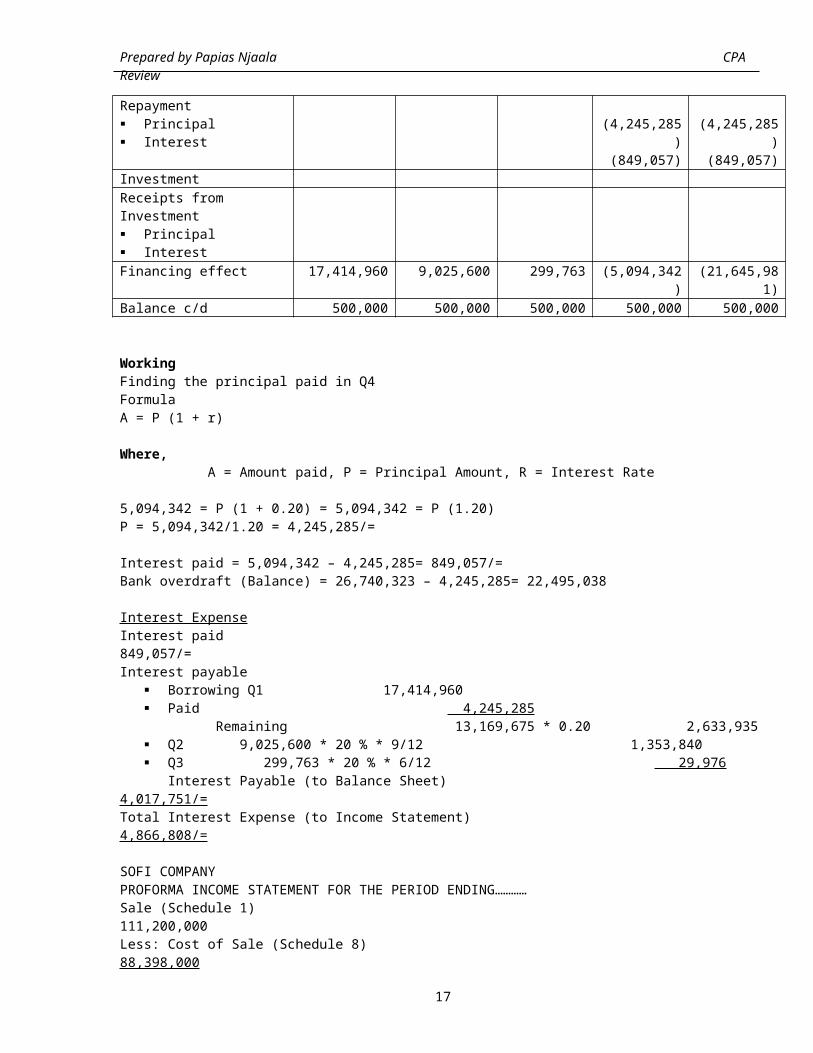

Repayment Principal Interest

(4,245,285)

(849,057)

(4,245,285)

(849,057)InvestmentReceipts from Investment Principal InterestFinancing effect 17,414,960 9,025,600 299,763 (5,094,342

)(21,645,98

1)Balance c/d 500,000 500,000 500,000 500,000 500,000

WorkingFinding the principal paid in Q4FormulaA = P (1 + r)

Where, A = Amount paid, P = Principal Amount, R = Interest Rate

5,094,342 = P (1 + 0.20) = 5,094,342 = P (1.20)P = 5,094,342/1.20 = 4,245,285/=

Interest paid = 5,094,342 – 4,245,285= 849,057/=Bank overdraft (Balance) = 26,740,323 – 4,245,285= 22,495,038

Interest ExpenseInterest paid 849,057/=Interest payable

Borrowing Q1 17,414,960 Paid 4,245,285

Remaining 13,169,675 * 0.20 2,633,935 Q2 9,025,600 * 20 % * 9/12 1,353,840 Q3 299,763 * 20 % * 6/12 29,976

Interest Payable (to Balance Sheet) 4,017,751/=Total Interest Expense (to Income Statement) 4,866,808/=

SOFI COMPANYPROFORMA INCOME STATEMENT FOR THE PERIOD ENDING…………Sale (Schedule 1) 111,200,000Less: Cost of Sale (Schedule 8) 88,398,000

17

Prepared by Papias Njaala CPA Review

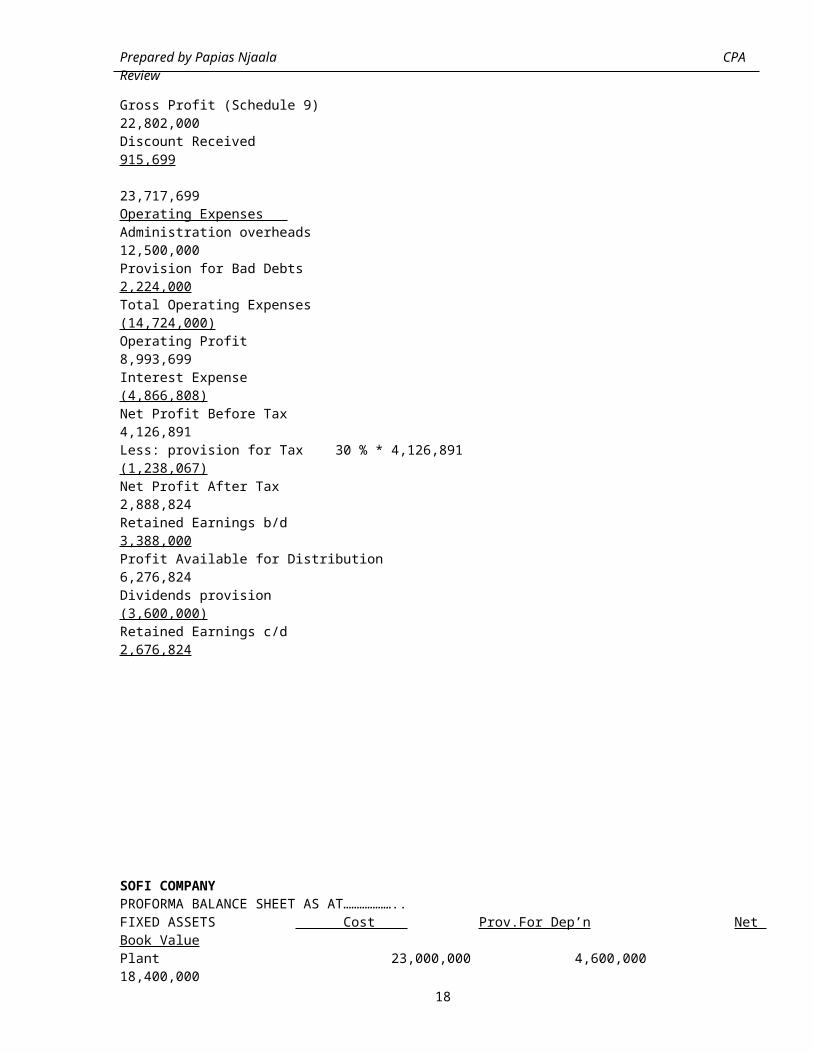

Gross Profit (Schedule 9) 22,802,000Discount Received 915,699 23,717,699Operating Expenses Administration overheads 12,500,000Provision for Bad Debts 2,224,000Total Operating Expenses (14,724,000)Operating Profit 8,993,699Interest Expense (4,866,808)Net Profit Before Tax 4,126,891Less: provision for Tax 30 % * 4,126,891 (1,238,067)Net Profit After Tax 2,888,824Retained Earnings b/d 3,388,000Profit Available for Distribution 6,276,824Dividends provision (3,600,000)Retained Earnings c/d 2,676,824

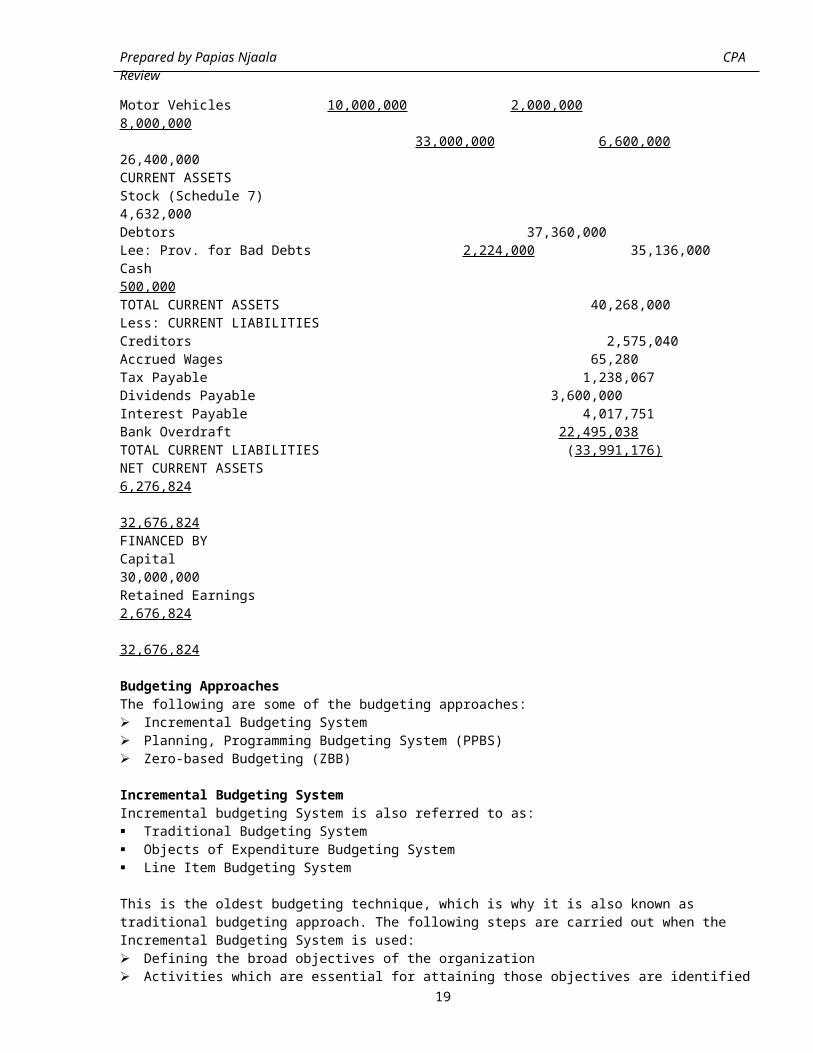

SOFI COMPANYPROFORMA BALANCE SHEET AS AT………………..FIXED ASSETS Cost Prov.For Dep’n Net Book ValuePlant 23,000,000 4,600,000 18,400,000

18

Prepared by Papias Njaala CPA Review

Motor Vehicles 10,000,000 2,000,000 8,000,000 33,000,000 6,600,000 26,400,000CURRENT ASSETSStock (Schedule 7) 4,632,000Debtors 37,360,000Lee: Prov. for Bad Debts 2,224,000 35,136,000Cash 500,000TOTAL CURRENT ASSETS 40,268,000Less: CURRENT LIABILITIESCreditors 2,575,040Accrued Wages 65,280Tax Payable 1,238,067Dividends Payable 3,600,000Interest Payable 4,017,751Bank Overdraft 22,495,038TOTAL CURRENT LIABILITIES (33,991,176)NET CURRENT ASSETS 6,276,824 32,676,824FINANCED BYCapital 30,000,000Retained Earnings 2,676,824 32,676,824

Budgeting ApproachesThe following are some of the budgeting approaches: Incremental Budgeting System Planning, Programming Budgeting System (PPBS) Zero-based Budgeting (ZBB)

Incremental Budgeting SystemIncremental budgeting System is also referred to as: Traditional Budgeting System Objects of Expenditure Budgeting System Line Item Budgeting System

This is the oldest budgeting technique, which is why it is also known as traditional budgeting approach. The following steps are carried out when the Incremental Budgeting System is used: Defining the broad objectives of the organization Activities which are essential for attaining those objectives are identified

19

Prepared by Papias Njaala CPA Review

Expenditure items of each activity are identified and costs are determined.

The above steps are carried out in the first year. In the following year items established in the previous year are not questioned. The budget will aim at providing sufficient cash to sustain the previous level of expenditure plus the budget for new items. The previous year expenditure is adjusted to take into consideration the inflation factor.

Advantages(i) It is simple, hence allowing comparatively inexperienced people to operate it.(ii) It is easy to understand (iii) It facilitates easy statistical comparison from year to year. This is possible due to the fact that budget items for the previous year are maintained without being questioned.

Disadvantages(i) It takes last year expenditure as it is and therefore it does not question the validity of existing (last year) budget items. The items with more benefits may be ignored.

(ii) The budgetee is not required to justify the entire budget. He is only required to justify new items in the budget. Therefore if funds are not enough, new budget items are likely to be rejected even though they may have more benefits than old (or existing) items.

(iii) Ignoring the volume of activity.The budget of the last year is taken as it is but adjusted for the effect of inflation. The last year budget may be appropriate taking into consideration the volume of activity of that year but may it may not correspond with the volume of activity desired for this year.

(iv) Perpetuation of the previous inefficiencyPrevious expenditures may include inefficiency. Adding the funds to the previous year budget items (adjusting for the effect of inflation) may perpetuate past inefficiency to the future.

(v) No input-output relationshipThis budget approach does not consider the input-output relationship. Therefore, it can not be used for controlling purposes.

Planning, Programming Budgeting System (PPBS)When using the Planning, Programming Budgeting System the following questions should be answered: - What should be done this year out of multi-year organizational goals? How much should be done? When should it be done?

20

Prepared by Papias Njaala CPA Review

The following steps are carried out when the Planning, Programming Budgeting System (PPBS) is used: Determining the overall objectives of the organization Specifying objectives of various programmes Organizing the programme structure.

The programme structure provides the linkage of resources and activities toobjectives.

Undertaking programme analysis which includes: Measuring the output in terms of objectives Determining the total costs of the programme for several future periods Analyzing alternatives and selecting those, which will lead to the

attainment of objectives? Implementing and reviewing the selected alternatives.

When using the PPBS, allocation of resources is based on the evaluation of programmes and their alternatives basing on the cost-benefit analysis. Therefore,programmes that offer greater benefit will be allocated the grater amount of resources.

Since PPBS bases on the approved programmes, it offers an input-output relationship. Therefore it is a good tool of planning and controlling.

Advantages(i) PPBS forces the management to identify the activities, functions or programmes to be provided, there by establishing a basis for evaluating their worthiness.

(ii) PPBS provides information that will enable the management to assess the effectiveness of its plans.

(iii) Facilitates more effective allocation of resources.

(iv) Good tool for planning and controlling.

Disadvantages(i) It needs highly skilled and properly trained staff.(ii) It is costly in terms of time and other resources.

Zero-based Budgeting System (ZBB)If the great part of an organization’s costs is discretionary, zero-based budgeting system is ideal for such an organization.

The following differences of the discretionary costs, committed costs and engineered costs are important for clear understanding of zero-based budgeting.

Discretionary Costs

21

Prepared by Papias Njaala CPA Review

These are costs, which an organization can do without or can postpone undertakingthe activities which result into their occurrence. These are costs whose value isa matter of policy. Examples of discretionary costs are training costs, advertising costs, research & development costs.

Committed CostsThese are costs, which an organization can not do without. Their incurrence is not the matter of policy. They are influenced by the capacity. Examples of a committed costs are salaries to key personnel, rent, and insurance.

Engineered CostsThese are costs, which will directly be influenced by the volume of activity. These are variable in nature and include direct material and direct labour.

If the great part of the organization’s costs is comprised of the discretionary costs and it has no enough funds to cover all costs, it is going to postpone a part of discretionary costs.

Under the ZBB System the budgetee is required to justify the expenditure for eachitem whether it is existing (or old) or new. Therefore old and new budget items compete for allocation of resources on the basis of cost-benefit comparison.The budgetee is required to answer the following questions for each budget item: Should we perform this function at all? What should be the level of performance? Is this level actually required? Should this operation be performed in this way? This involves finding possible alternatives of undertaking the operations. How much should it cost?

The following steps are carried out when ZBB system is used: (i) Breaking the entire organization into small units capable of preparing budgets. These are not necessarily functional departments.

(ii) Preparation of decision packages.Each decision unit will prepare the decision package. Decision packages are budget items which will indicate the objectives for the expenditure, feasibility assessment, alternatives for performing the same function and tangible and intangible benefits.

(iii) Ranking the decision packages.Decision packages prepared by decision units will be ranked depending on their costs and benefits.

(iv) Establishing a cut-off pointAfter ranking the decision packages a cut-off point will be made and the decisionpackages above the cut-off point will be allocated resources. All decision packages below the cut-off point will not be allocated resources regardless whether they are new or existing.

22

Prepared by Papias Njaala CPA Review

Advantages(i) Better way of allocating resources.ZBB questions every budget item thus resulting into better way of allocating scarce resources by eliminating activities, which will contribute less to the success of the organization.

(ii) It provides basis for measuring achievements.(iii) ZBB leads to increased staff involvement, which may lead to improved motivation and grater interest in the job.(iv) It opens up the debate, which leads to evaluation of plans and optimal allocation of resources.

Disadvantages(i) It involves a lot of paper work(ii) It is very time-consuming because old issues are evaluated afresh each year.(iii) Some budgetees hate to justify every item in the budget.

NB: In practice, these approaches are not mutually exclusive. Normally, each approach tend to overlap the other, hence a combination of the techniques is normally adopted.

Manpower Budget taking into consideration AbsenteeismWhen an organization prepares its manpower budget it normally takes into consideration expected level of absenteeism.

The man power budget is prepared for planning of requirements for the budget period. It takes into consideration the output to be produced during the period, the expected level of efficiency and the rate of absenteeism.

ExampleMoshi Company Ltd is in the budget preparation session for the year ending 31st December 2006. The budget coordinator of the company managed to extract the following data:

Production is estimated to be as follows: Product A 10,350 unitsProduct B 6,875 units

(i) Raw Materials usage per unit of a finished good: Product A Product BMaterial X 2 kgs 1 kg Material Y 1 kg 2 kgsMaterial Z 3 kgs 2 kgs

(ii) Raw Materials cost per unitMaterial X 25/= Material Y 20/=Material Z 30/=

23

Prepared by Papias Njaala CPA Review

(iii) Labour requirements per unit of output Department 1 Department 2 Product A

Unskilled labour 4 hours 2 hoursSkilled labour 1 hour 1 hour

Product BUnskilled labour 5 hours 3

hoursSkilled labour 1 hour 2

hours

(iv) Labour rate per hour: Unskilled labour TShs 20/= Skilled labour TShs 30/=

(v) From past experience and taking into consideration new controls put in place by the management, absenteeism rates are estimated to be as following: Unskilled labour 2%

Skilled labour 1%

(vi) Production Overheads Variable production overheads are absorbed at the following rates:

Department 1 TShs 10/= per direct labour hourDepartment 2 TShs 8/= per direct labour hour.

Fixed production overheads are absorbed at a rate of TShs 5/= per direct labour hour. Other overheads (all fixed) amount to TShs 1,200,000/= p.a.

Beginning and ending inventories will be as follows: Anticipated

TargetBeginning Inventories Ending Inventories

Materials:X 1,000 kgs

1,200 kgsY 500 kgs

500 kgsZ 2,000 kgs

1,100 kgs

Finished GoodsProduct A 100 units

450 unitsProduct B 1,200 units

500 units

24

Prepared by Papias Njaala CPA Review

Required: Prepare the following budgets for the period ending 31st December, 2005:

(a) Raw Material usage Budget (b) Raw Material Purchase Budget (c) Labour Budget (d) Variable Production Overheads Budget (e) Fixed Production Overheads Budget.

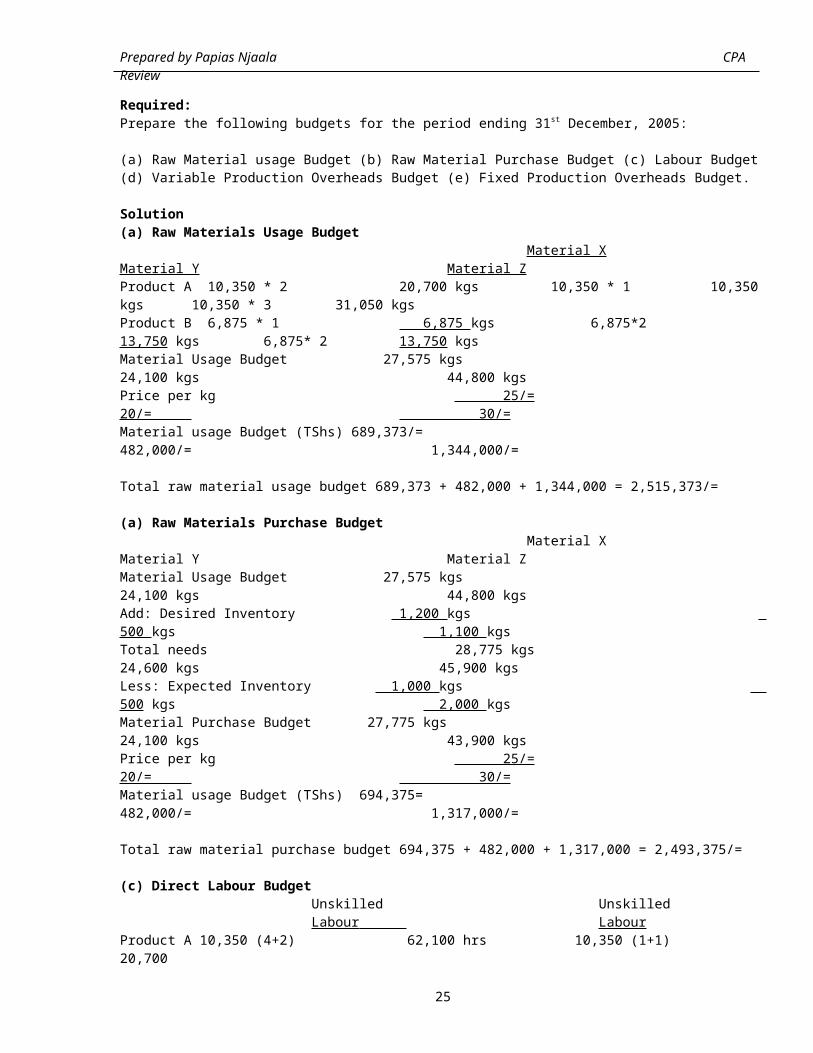

Solution(a) Raw Materials Usage Budget Material X Material Y Material ZProduct A 10,350 * 2 20,700 kgs 10,350 * 1 10,350 kgs 10,350 * 3 31,050 kgsProduct B 6,875 * 1 6,875 kgs 6,875*2 13,750 kgs 6,875* 2 13,750 kgsMaterial Usage Budget 27,575 kgs 24,100 kgs 44,800 kgsPrice per kg 25/= 20/= 30/=Material usage Budget (TShs) 689,373/= 482,000/= 1,344,000/=

Total raw material usage budget 689,373 + 482,000 + 1,344,000 = 2,515,373/=

(a) Raw Materials Purchase Budget Material X Material Y Material ZMaterial Usage Budget 27,575 kgs 24,100 kgs 44,800 kgsAdd: Desired Inventory 1,200 kgs 500 kgs 1,100 kgsTotal needs 28,775 kgs 24,600 kgs 45,900 kgsLess: Expected Inventory 1,000 kgs 500 kgs 2,000 kgsMaterial Purchase Budget 27,775 kgs 24,100 kgs 43,900 kgsPrice per kg 25/= 20/= 30/=Material usage Budget (TShs) 694,375= 482,000/= 1,317,000/=

Total raw material purchase budget 694,375 + 482,000 + 1,317,000 = 2,493,375/=

(c) Direct Labour BudgetUnskilled Unskilled Labour Labour

Product A 10,350 (4+2) 62,100 hrs 10,350 (1+1) 20,700

25

Prepared by Papias Njaala CPA Review

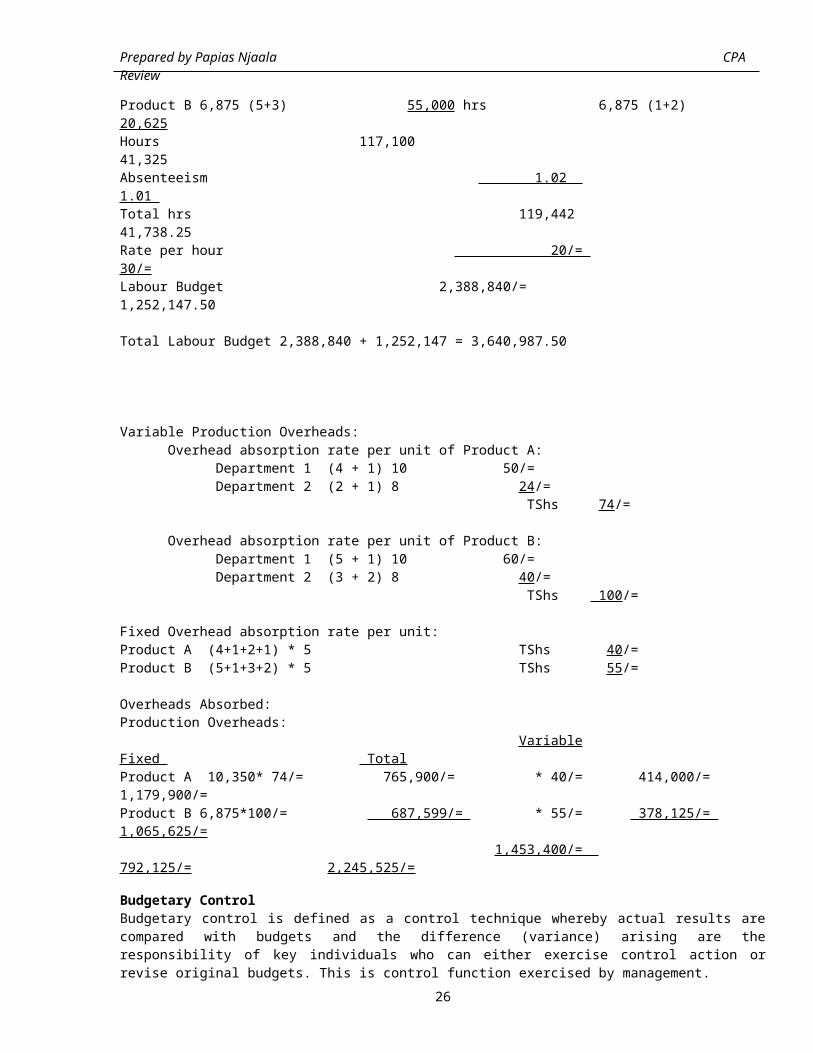

Product B 6,875 (5+3) 55,000 hrs 6,875 (1+2) 20,625Hours 117,100 41,325Absenteeism 1.02 1.01 Total hrs 119,442 41,738.25Rate per hour 20/= 30/=Labour Budget 2,388,840/= 1,252,147.50

Total Labour Budget 2,388,840 + 1,252,147 = 3,640,987.50

Variable Production Overheads: Overhead absorption rate per unit of Product A:

Department 1 (4 + 1) 10 50/=Department 2 (2 + 1) 8 24/= TShs 74/=

Overhead absorption rate per unit of Product B:Department 1 (5 + 1) 10 60/=Department 2 (3 + 2) 8 40/= TShs 100/=

Fixed Overhead absorption rate per unit:Product A (4+1+2+1) * 5 TShs 40/=Product B (5+1+3+2) * 5 TShs 55/=

Overheads Absorbed:Production Overheads: Variable Fixed TotalProduct A 10,350* 74/= 765,900/= * 40/= 414,000/= 1,179,900/=Product B 6,875*100/= 687,599/= * 55/= 378,125/= 1,065,625/= 1,453,400/= 792,125/= 2,245,525/=

Budgetary ControlBudgetary control is defined as a control technique whereby actual results arecompared with budgets and the difference (variance) arising are theresponsibility of key individuals who can either exercise control action orrevise original budgets. This is control function exercised by management.

26

Prepared by Papias Njaala CPA Review

The preparation of budgets relate to the responsibilities of executives to therequirement of policy and the continuous comparison of actual with budgetedresults either to secure by individual action the objectives of that policy or toprovide basis for revisions.

Main Features of Budgetary Control Control by responsibility – delegation of authority and accountability The continuous comparison of actual/budgeted figures i.e. monitoring of

budgets at frequent intervals. Management action required for the significant adverse variances (i.e.

Management by Exception) The attainment of objectives The revision of the policy where necessary, e.g. where basic assumption change

Budgetary Control involves the following:Establishment of budgets and the continuous comparison of actual with budgets forachievement of targets and responsibility accounting involves the revision ofbudgets in the light of changed circumstances. Effective budgetary controlorganization consists of: Installation of Budget Centres

Budget centres should be clearly demarcated to facilitate the formulation ofvarious budgets.

Budget Education Briefing of employees and managers on the usefulness and limitations ofbudgetary control should be done regularly.

Formulation of Budget CommitteeFinance and Budget Committee should be formed under the chairmanship of theChief Executive Officer and a team of top management constituting themembership of the committee. The Head of Finance is the Secretary to theCommittee. The main functions of the committee are: To formulate broad policies of management relating to the budgetary system. To provide budget guidelines and directives for preparation, submission and

review of budgets To approve the Master Budget To review budget To suggest prompt corrective action To foster cooperation among members

Budget Manual To facilitate communication and cooperation among members it is essential toprepare written standardized procedures/routines by means of a budget manual.

Budget manual is defined as a document which spells out responsibilities orpersons engaged in the routine of and the forms and records required forbudgetary control. It spells out various steps in the preparation of different

27

Prepared by Papias Njaala CPA Review

budgets including submission, review, approval and final adoption. It containsaccounts codes for items of expenditure and revenue included in the budget.

Determination of Budget Period A budget may cover any time period (weekly, monthly, quarterly, semi-annually andannually). In any case, the longer the span of budget the less reliable it is. Ashort term budget is more reliable and show specific plans and tactics. Thebudget period should vary with managers’ objectives and the use of budgeting inplanning. The time period depends on sales, production, manufacturing, processingcycle, stability, risk, accuracy of input data, type of product line seasonality,inventory turnover, availability of resources and government regulations.

.

28