Embed Size (px)

Citation preview

EXAMINING THE RELATIONSHIP BETWEEN BUDGETING AND

PROFITABILITY IN SUGAR FACTORIES IN KENYA

A CASE STUDY OF MUMIAS SUGAR COMPANYLIMITED.

BY

REV. KITERE WILSON AGGREY OGAMA

REG.No. MBA199401521DF

A RESEARCH THESIS SUBMITTED TO THE SCHOOL OF POST-GRADUATE

STUDIES RESEARCH AND EVALUATION CENTRE IN PARTIAL

FULFILLMENT OF THE REQUIREMENTS FOR THE

AWARD OF THE DEGREE OF MASTERS IN BUSINESS

ADMINISTRATION (FINANCE AND ACCOUNTING)

OF KAMPALA INTERNATIONAL UNIVERSITY.

SEPTEMBER 2007

I~ POSTGRADUATE t~\

~ LIBRARY ~J

DECLARATION< UBRARy

/* DATE:

I hereby declare that this work is a result of my own effort and has ne~e4 been

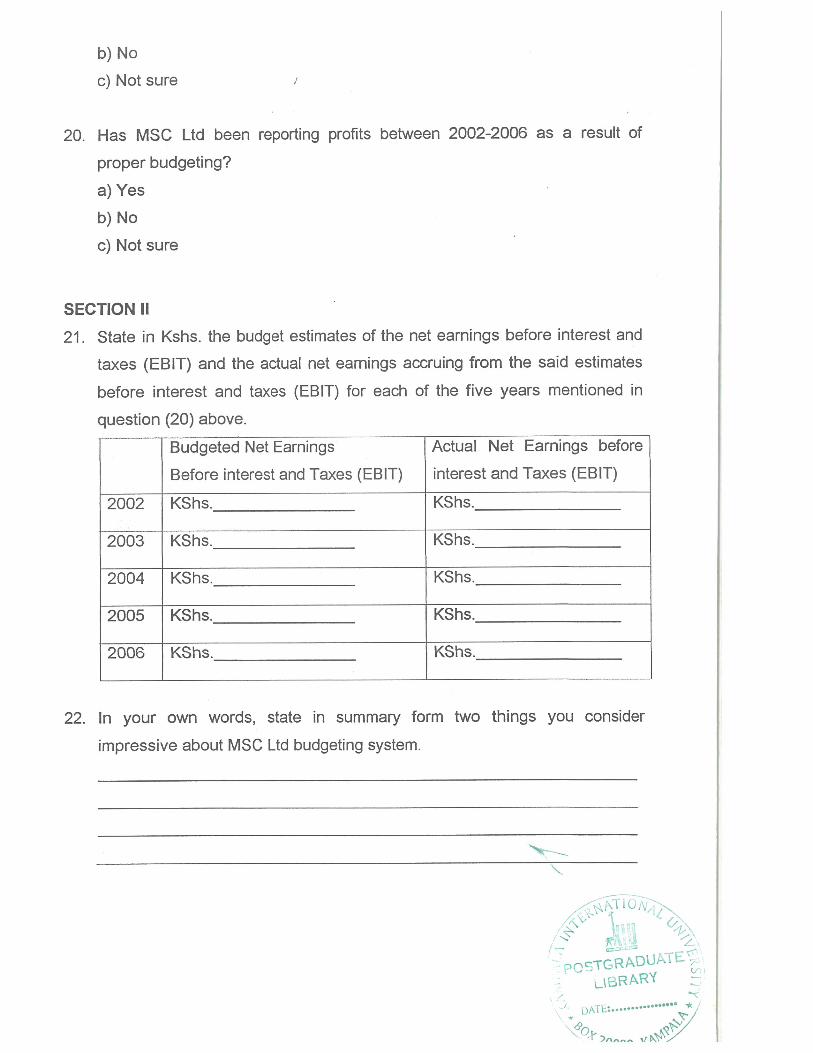

submitted for an award in any other university or institution of higher learning. ‘~“ ~

Signed __________________________________

Rev. Kitere Wilson Aggrey Ogama

Date ____ ~ (~~7

APPROVAL

This work has been done under’my supervision as a university supervisor, and

submitted with my approval.

Signed______________________

Supervisor

Date____________

W ~-\-~

DEDICATION ~ POSTGRADUATE ~~ LIBRARy ~?~2.* DATE:.._....

This book is dedicated to my father, David Masinde, my mother Norah~~nb~~*

(though deceased) for the condition they made in pursuit of my education.

May the Almighty God bless them.

Also dedicated to my wife Juliana Nafoyo Kitere for the financial and spiritual

support and my beloved friends, Timothy Wekesa Karandini,

Christabel.W.Karandinj, the Christian community of Kenya Assemblies of God

and Mabanga church who have been supportive throughout the study outside my

mother country.

Thank you.

Acknowledgement

The researcher wishes to acknowledge and show recognition to all those

individuals and the management of Kampala International University for making it

possible for him to carry out this study and complete it successfully.

First and foremost, to my supervisor Dr. Isaac Kayonga for being actively involved

in positive criticism, encouragement and guidance throughout the study. This

made the researcher more confident and encouraged to accomplish the study

with high morale.

Furthermore, I wish to appreciate the contribution rendered by his colleagues at

Kampala International University in terms of financial and material support and

advice. May the Lord reward them abundantly.

I further pay tribute to the respondents of Mumias Sugar Company limited and

the members of the community for being very cooperative and giving honest

answers to the researcher that facilitated the successful completion of the

research.

Last but not least, I wish to thank lecturers, Dr. Nyaboga Benjamin and Dr. John

Opio for their encouragement and support during this hard struggle to achieve

success in his studies.

Rev. Kitere Wilson Aggrey Ogama

September 2007

Table of Contents

CHAPTER ONE: INTRODUCTION

1.0 Introduction i

1.1 Background i

1.2 Statement of the problem 3

1.3 Purpose of the study 4

1.4 Objectives of the study 4

1.5 Research questions 5

1.6 Hypothesis 5

1.7 Scope of the study 5

1.8 Significance of the study 5

1.9 Theoretical Framework 7

CHAPTER TWO: REVIEW OF LITERATURE

2.0 Introduction 10

2.1 The meaning of budgeting at MSC Ltd 10

2.2 The Advantages of budgeting and profitability in MSC Ltd 13

2.3 The administration of budgeting process and profitability in

MSC Ltd 16

2.4 Master budget preparation and profitability in MSC Ltd 20

2.5 Profit 30

CHAPTER THREE: METHODOLOGY

3.1 Introduction 32

3.2 Research design 32

3.3 Study Population 32

3.4 Sampling Design 33

3.5 Study area 34

3.6 Data collection instruments 35

3.7 Data collection procedures 35

//~ ~‘~pOSTGRADUAT~~ LIBRARY~ PAGE~ DATE *

4~ ~

3.8 Data Processing and analysis .36

3.9 Validityof the research...j 36

3.10 Data Presentation 36

CHAPTER FOUR: DATA PRESENTATION, ANALYSIS & INTERPRETATION

4.0 Introduction 38

CHAPTER FIVE: DISCUSSIONS, CONCLUSIONS & RECOMMENDATIONS

5.0 Introduction 70

5.1 Discussions of findings 70

5.2 Conclusions 73

5.3 Recommendations 74

5.4 Areas of future research 77

References 78

Appendix

I

List of tables“~ L8R1~~~

Table 1.1 ............... Showing the number of respondents selected from MS~ bt4F.

—.Table 1.2 Respondents’ knowledge about relationship betwe~9flOfl ‘~ ~

budgeting and profitability at MSC Ltd.

Table 1.3 Respondents’ knowledge about advantages of budgeting atMSC Ltd.

Table 1.4 Respondents’ understanding whether MSC Ltd administersbudgeting and profitability.

Table 1.5 Respondents’ response concerning their participation inbudgeting at MSC Ltd.

Table 1.6 Respondents’ understanding whether MSC Ltd has abudget committee, budget directors, budget manual.

Table 1.7 Respondents’ understanding whether MSC Ltd has abudget period.

Table 1.8 Respondents’ understanding of a master budget.

Table 1.9 Respondents’ understanding of MSC Ltd preparation ofsales budget.

Table 1.10 Respondents’ understanding of MSC Ltd preparation ofproduction budget.Table 1.11 Respondents’ understanding of MSC Ltd preparation ofdirect labour budget.

Table 1.12 Respondents’ understanding of preparation of cost of salesbudget at MSC Ltd.

Table 1.13 Respondents’ understanding of MSC Ltd preparation ofending inventory budget.

Table 1.14 Respondents’ understanding of preparation of manufacturingbudget at MSC Ltd.

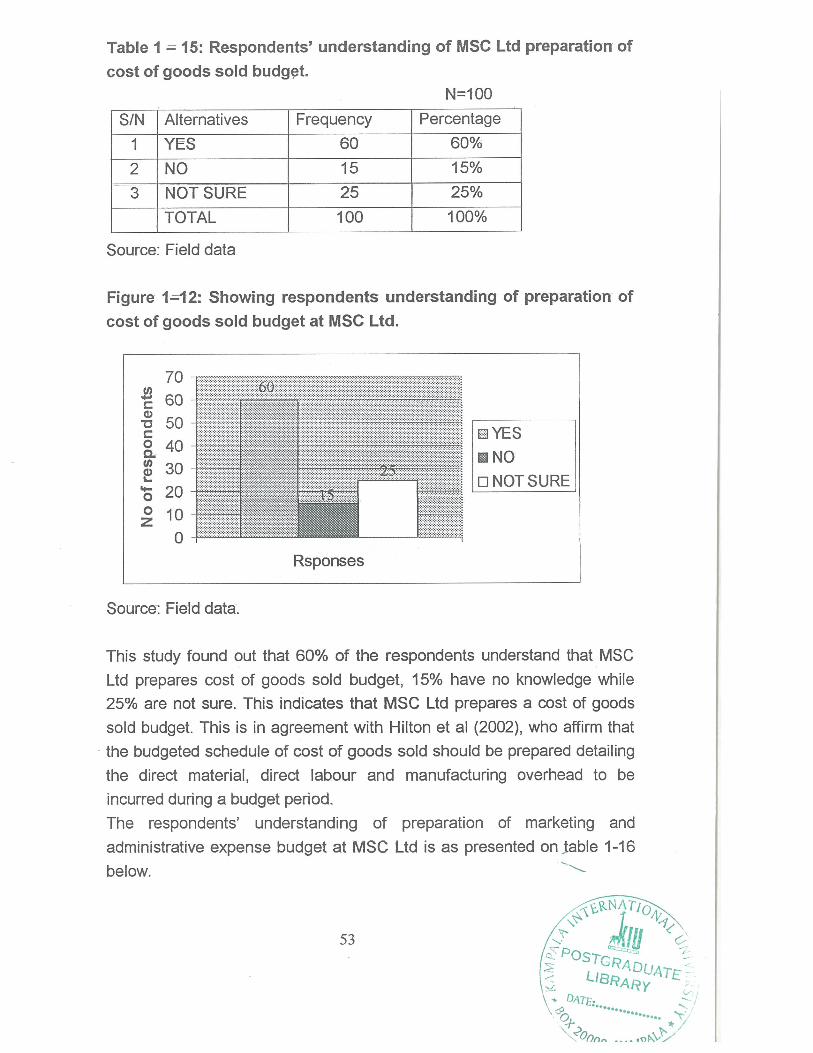

Table 1.15 Respondents’ understanding of MSC Ltd preparation of costof goods sold budget.

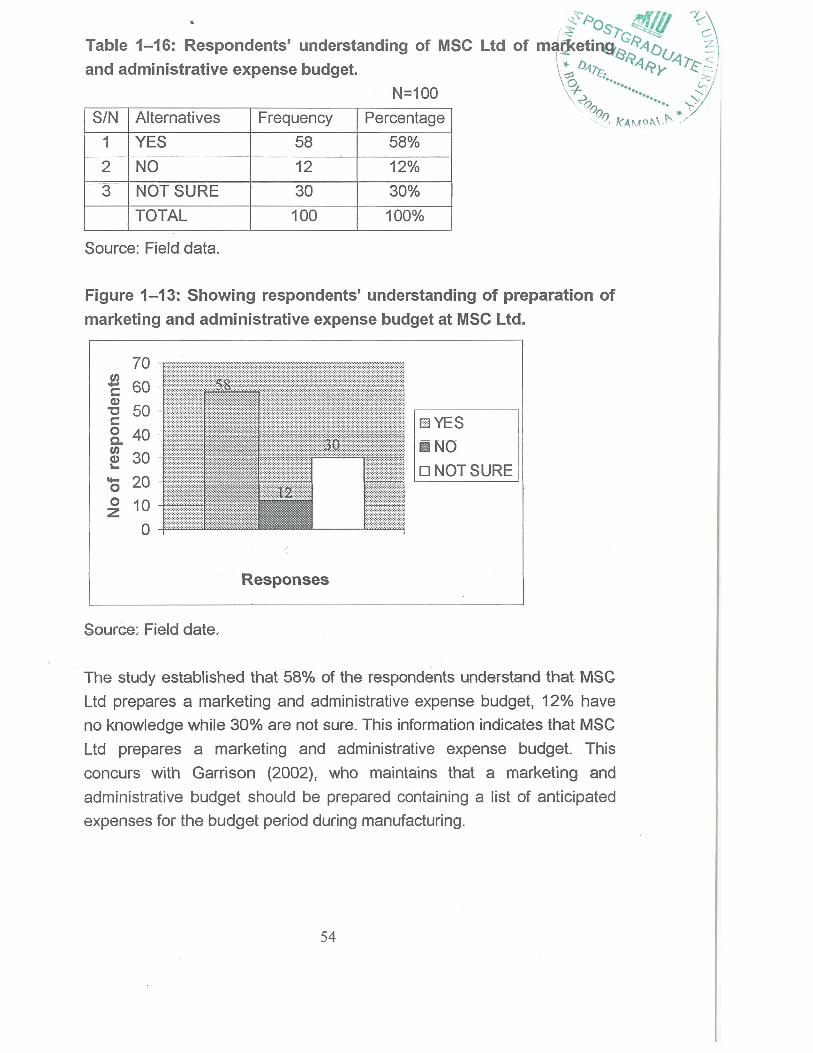

Table 1.16 Respondents’ understanding of MSC Ltd preparation ofmarketing and administrative expenses budget.

VII

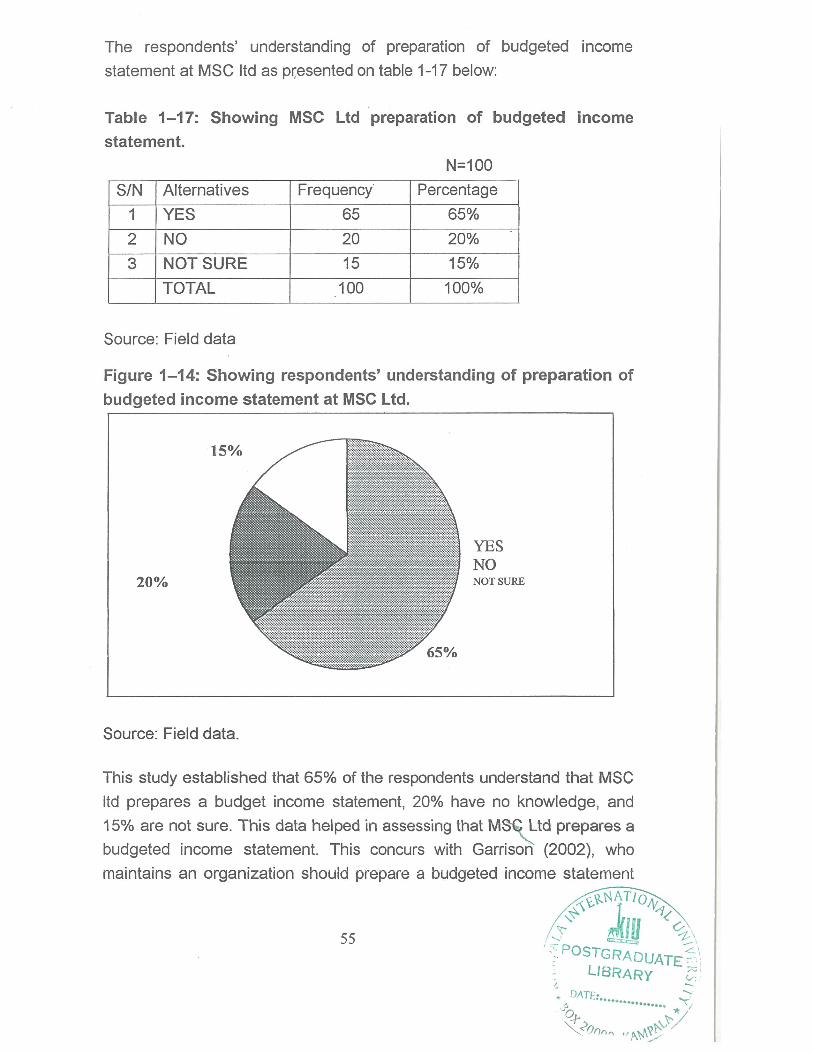

Table 1.17 showing MSC Ltd preparation of budgeted income statement.

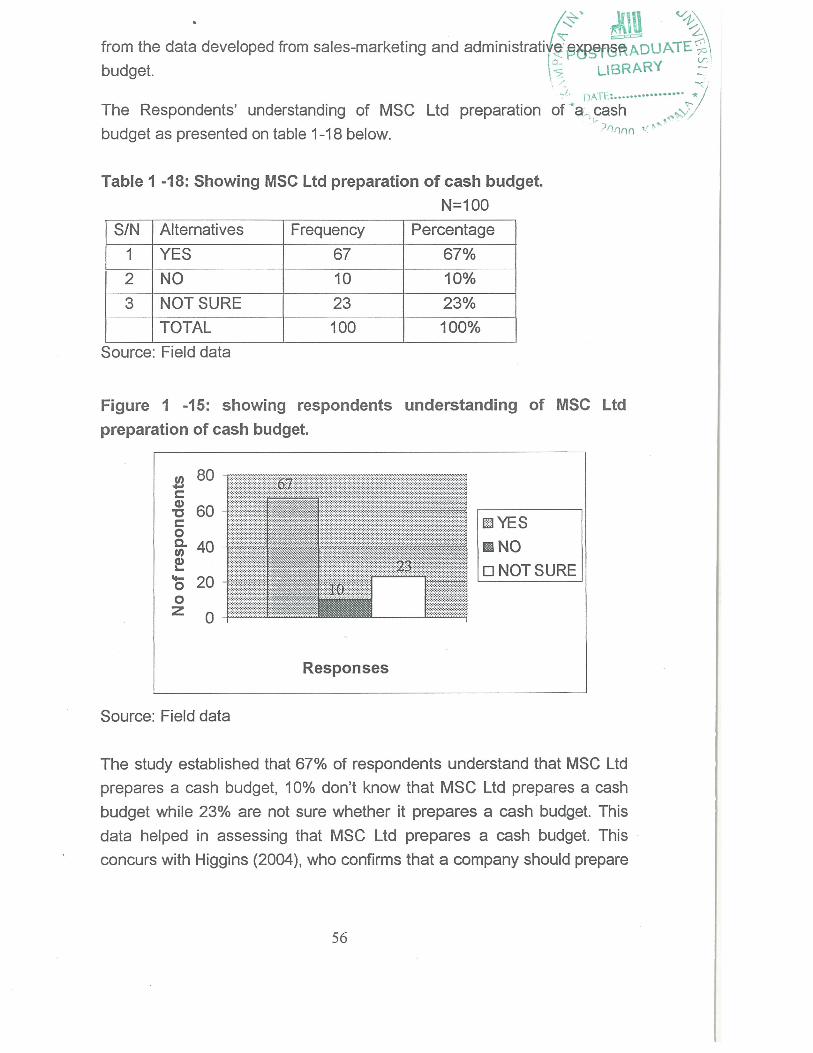

Table 1.18 showing MSC Ltd preparation of cash budget

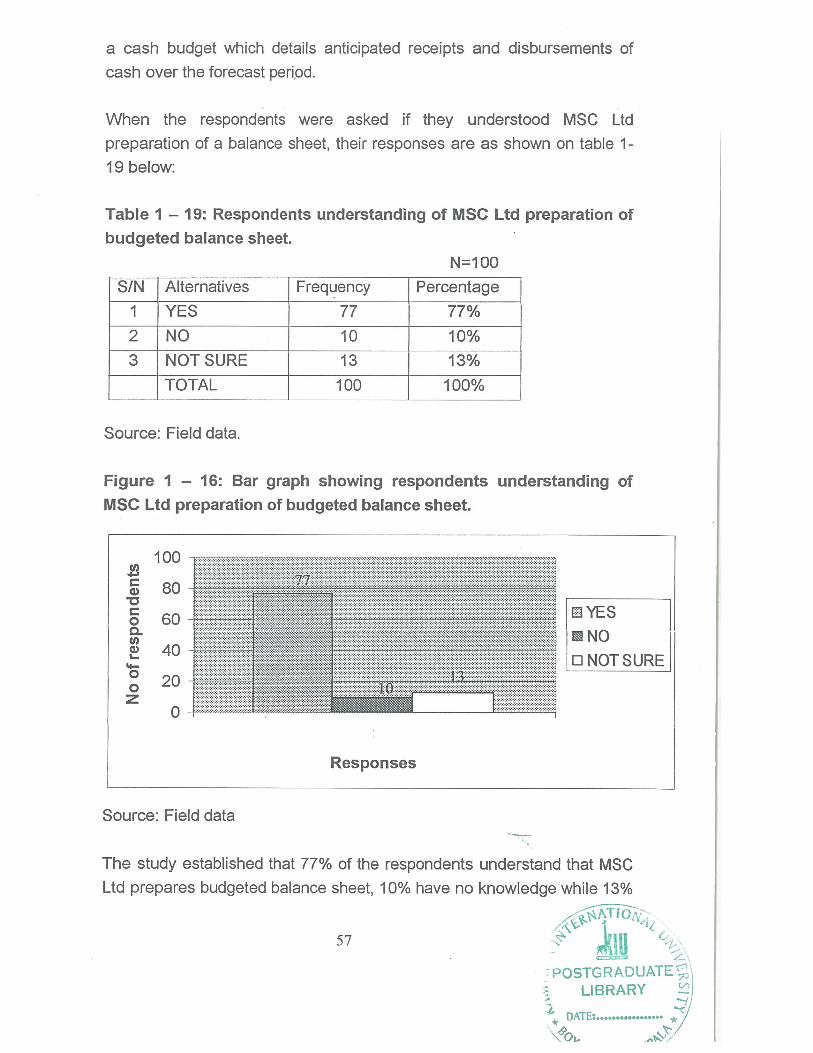

Table 1.19 Respondents’ understanding of MSC Ltd preparation ofbudgeted balance sheet.

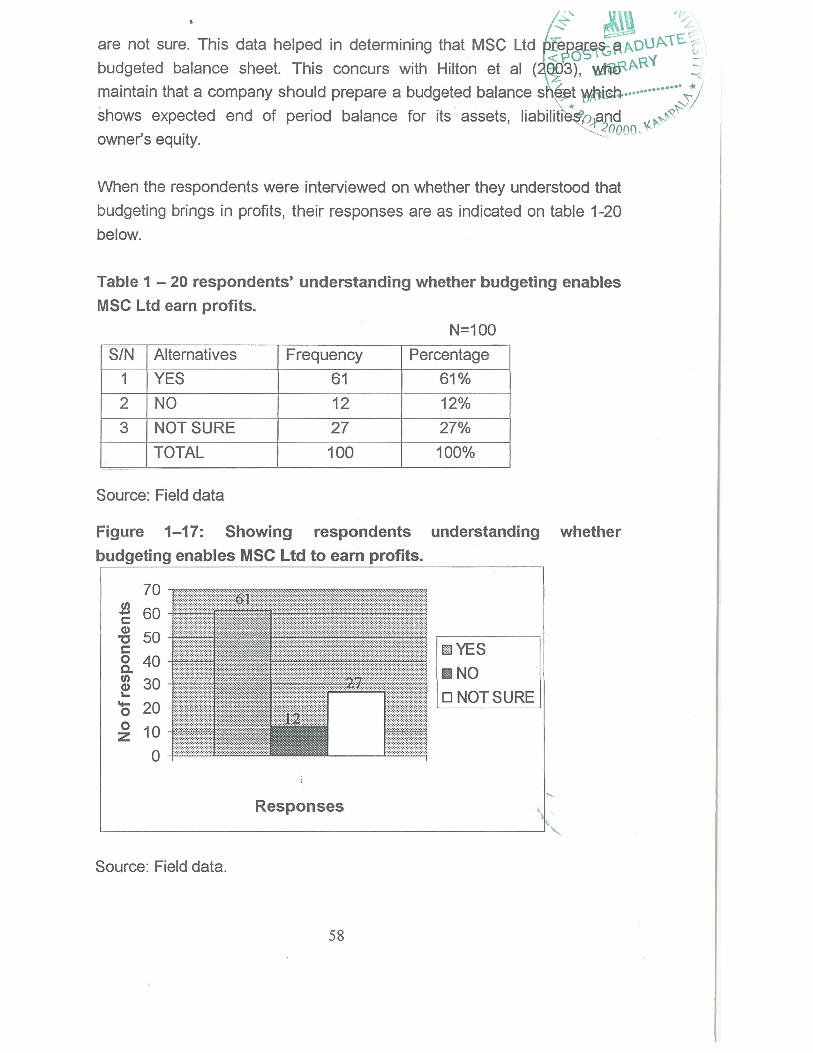

Table 1.20 Respondents’ understanding whether budgeting enablesMSC Ltd earn profits.

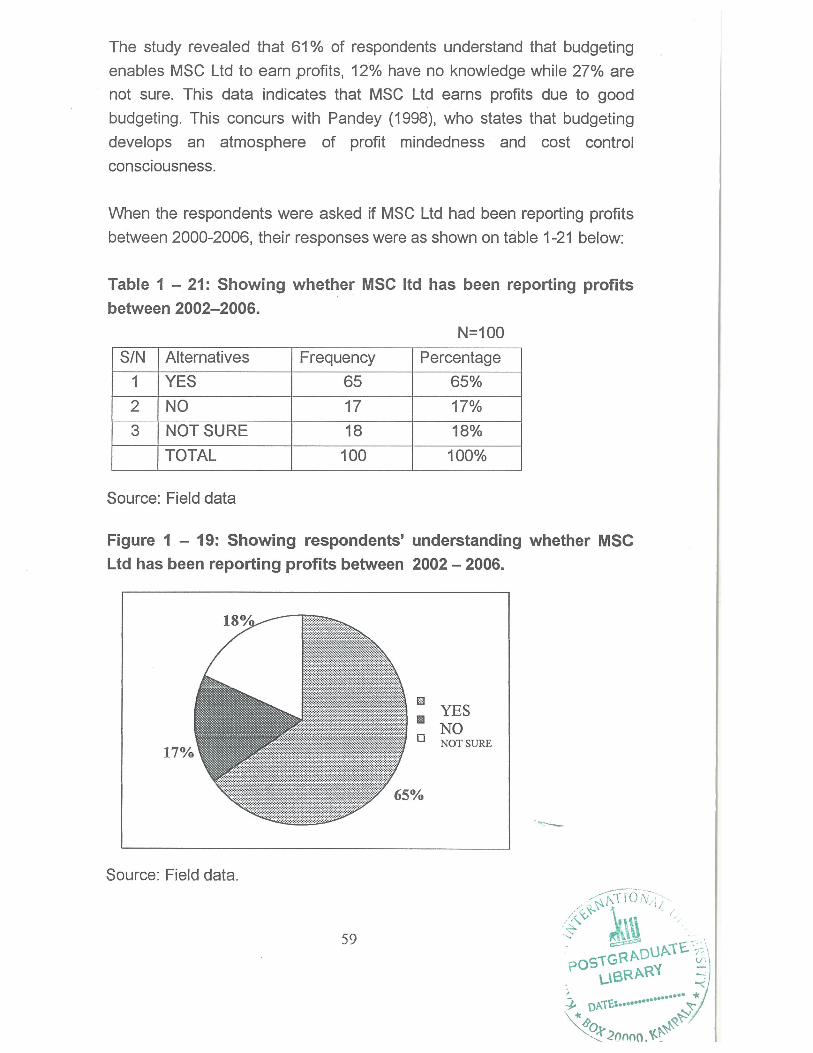

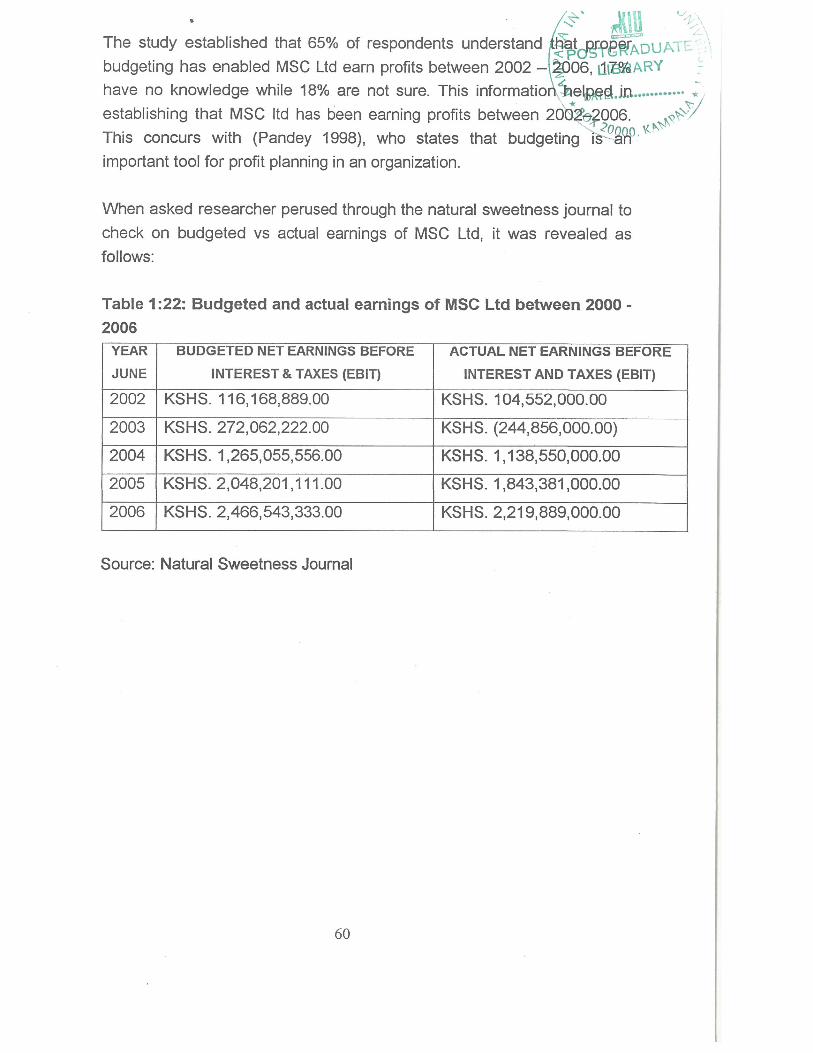

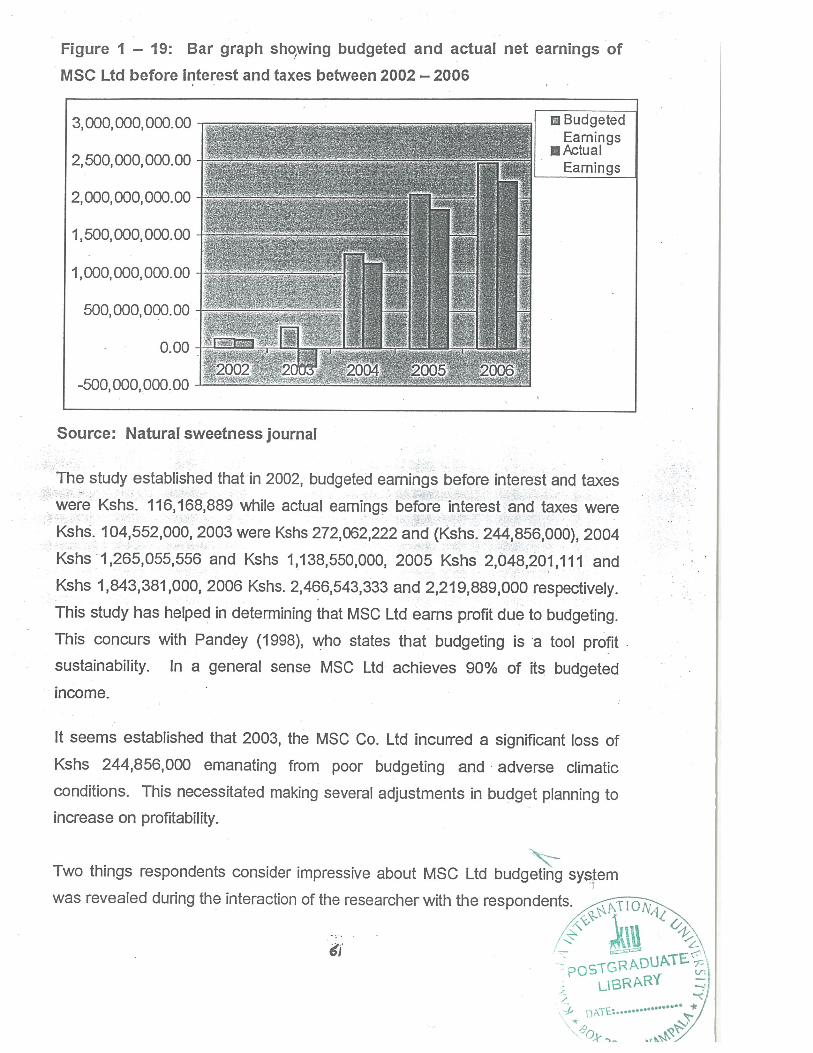

Table 1.21 showing whether MSC Ltd has been• reporting profitsbetween 2002-2006.Table 1.22 showing budgeted and actual earnings before interest andtaxes at MSC Ltd between 2002-2006.

Table 1.23 respondents’ response pointing to zero base method,preparation of budget in June and qualified staff.

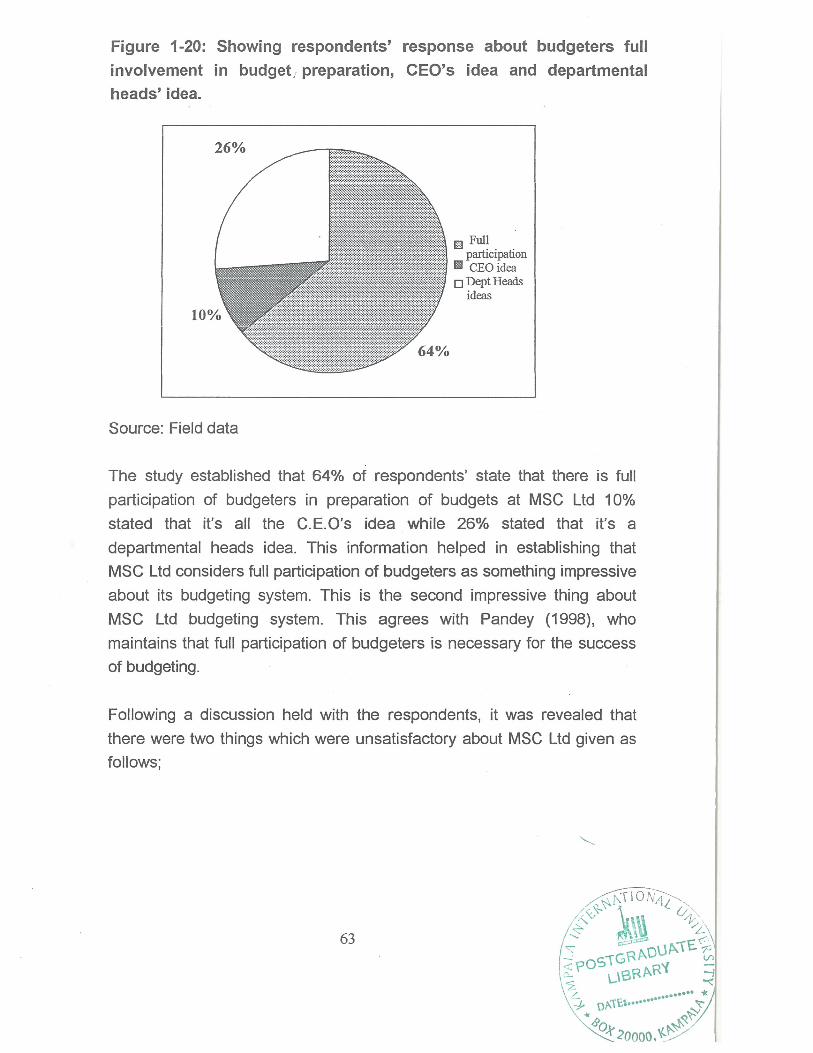

Table 1.24 Respondents’ response pointing to full participation ofbudgeters, CEO’s sales and departmental needs idea.

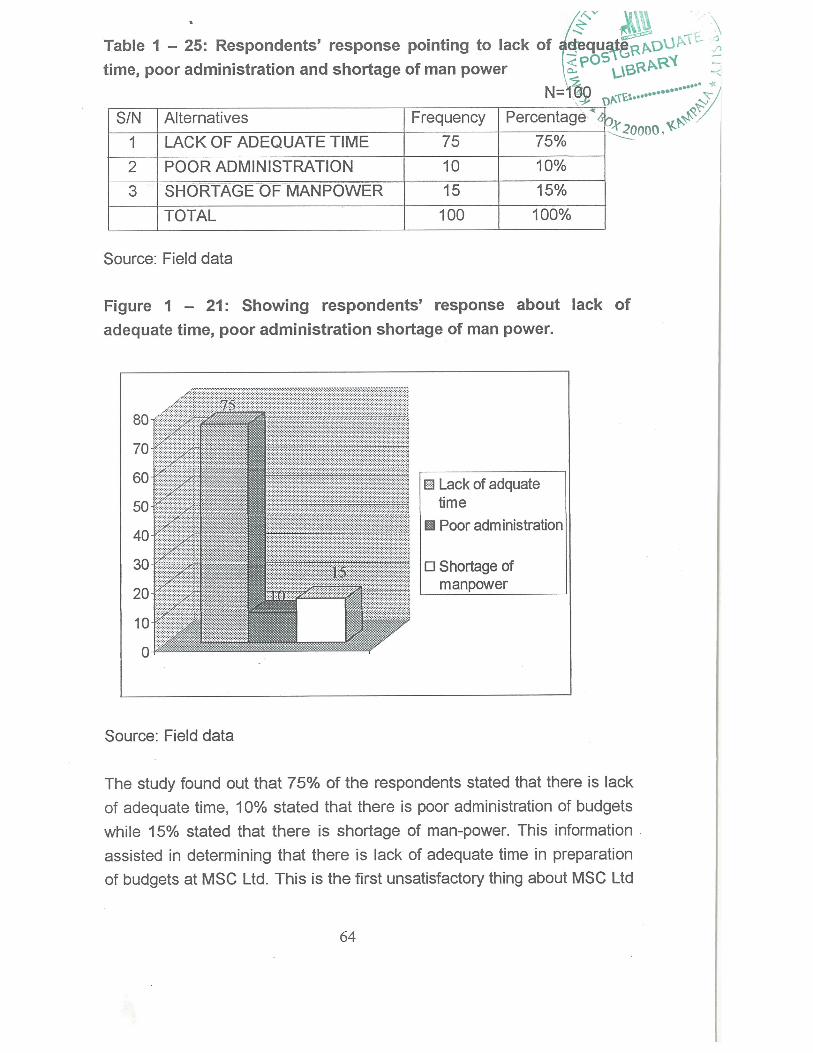

Table 1.25 respondents’ response pointing to lack of adequate time,poor administration and shortage of manpower.

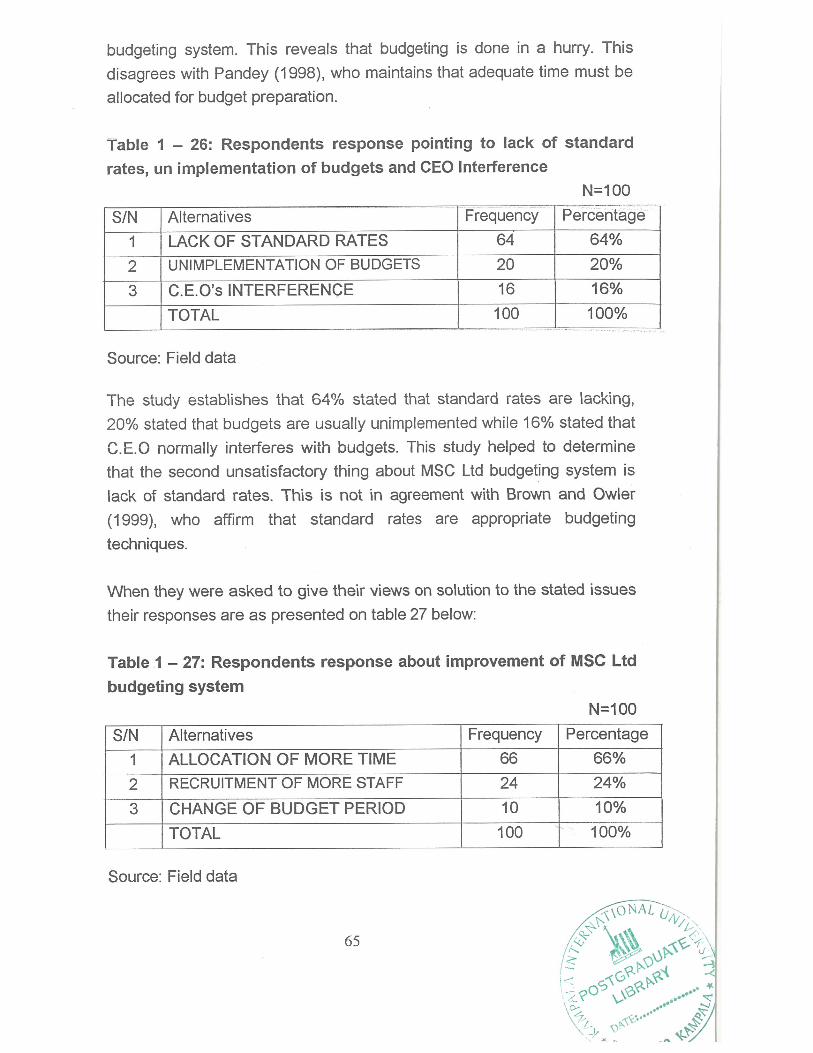

Table 1.26 respondents’ response pointing to lack of standard rates,unimplementation of budgets and CEO’s interference.

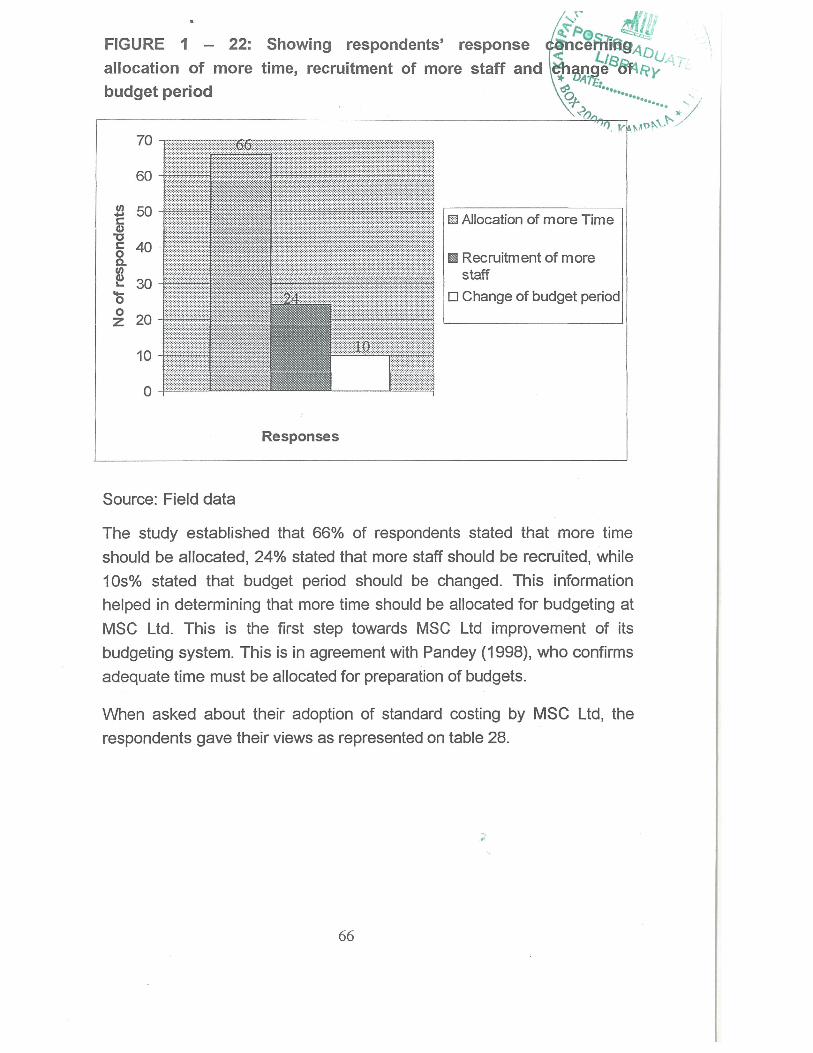

Table 1.27 respondents’ response about improvement of MSC Ltdbudgeting system pointing to allocation of more time, recruitment of more staffand change of budget period.

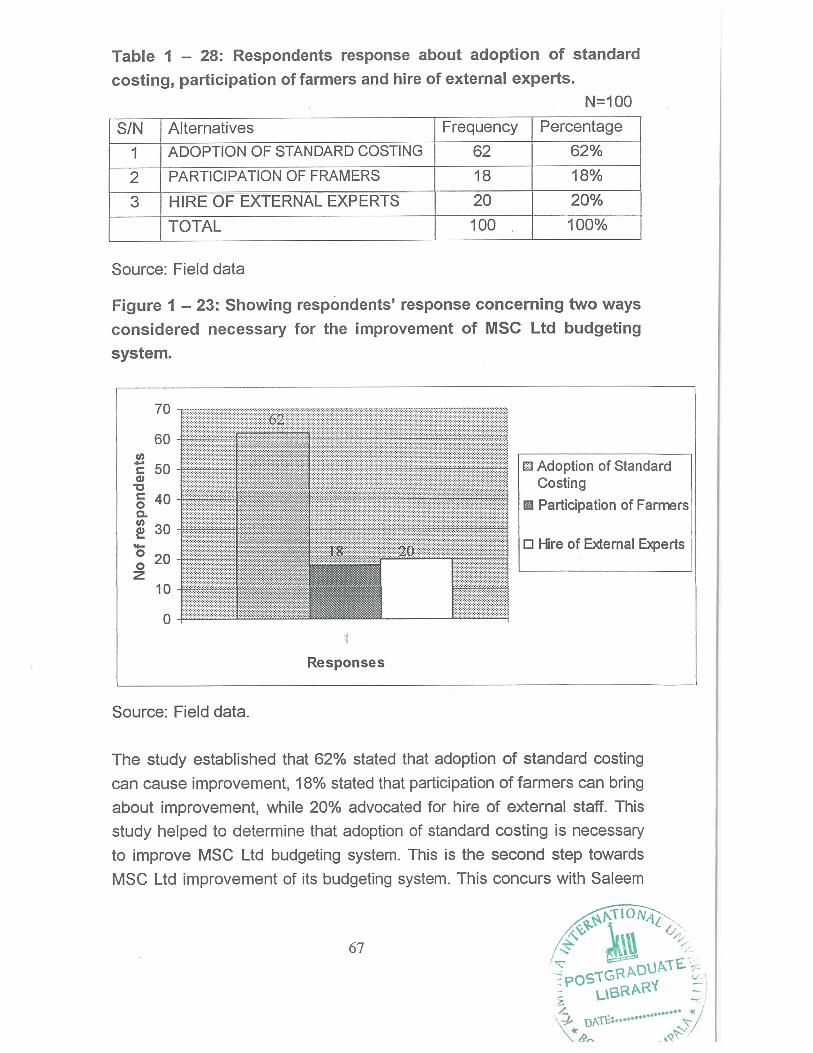

Table 1.28 respondents’ response pointing toadoption of standard costing, participation of farmers and hire of external staff.

viii

POSTGRADUATELIBRARY

DATE:........•.nn.fl * -!

r~4(IUList of Figures ~~~OSTGF?ADuATE~

~Figures / -~

Fig 1.1 showing master budget

Fig 1.2 showing planning inflows and outflows of an enterprise

Fig 1.3 showing respondents’ knowledge about meaning of budgeting atMSC Ltd.

Fig 1.4 showing respondents knowledge about advantages of budgeting.

Fig 1.5 showing respondents’ understanding concerning administration ofbudgeting.

Fig 1.6 showing respondents’ understanding whether MSC Ltd has budgetcommittees, budget directors, budget manual.

Fig 1.7 showing respondents understanding whether MSC Ltd has abudget period.

Fig 1.8 showing respondents’ understanding of a master budget.

Fig 1.9 showing respondents’ understanding of MSC Ltd preparation ofproduction budget.

Fig 1.10 showing respondents’ understanding of direct material budget atMSC Ltd.

Fig 1.11 showing respondents’ understanding of direct labour budget.

Fig 1.12 showing respondents’ understanding of preparation of cost ofsales budget at MSC Ltd.

Fig 1.13 showing respondents’ understanding of preparation of marketingand administrative expenses budget at MSC Ltd.

Fig 1.14 showing respondents’ understanding of preparation of budgetedincome statement at MSC Ltd.

Fig 1.15 showing respondents’ understanding of MSC Ltd preparation ofcost budget.

Fig 1.16 showing respondents’ understanding of MSC Ltd preparation of abalance sheet.

Fig 1.17 showing respondents’ understanding whether budgeting enablesMSC Ltd to earn profits.

Fig 1.18 showing respondents’ understanding whether MSC Ltd has beenreporting profits between 2002-2006.

Fig 1.19 showing budgeted and actual earnings of MSC Ltd before interestand taxes between 2002-2006.

Fig 1.20 showing respondents’ response pointing to budgeters’ fullparticipation, CEO’s idea and departmental heads idea about preparation ofbudgets.

Fig 1.21 showing respondents’ response pointing to lack of adequate time,poor administration and shortage of manpower for preparation of budgets atMSC Ltd.

Fig 1.22 showing respondents’ response pointing to allocation of time,recruitment of more staff and change period for preparation of budgets at MSCLtd.

Fig 1.23 showing pointing to adoption of standard costing, participation offarmers and hire of external staff for preparation of budgets at MSC Ltd.

‘~ POSTGRADUATELIBRARY

DATE *

Acronyms!Abbreviations

1. CSR — Corporate Social Responsibility

2. MSC — Mumias Sugar Company

3. LTD — Limited

4. KSB — Kenya Sugar Board

5. W.W.F — World Wide Fund

6. CEO — Chief Executive Officer•

7. KRA — Kenya Revenue Authority

- Ill

LIBRARY .~‘)

DATE: fle•en.

~

CHAPTER ONE

INTRODUCTION

1.1. Background of the Study

Budgeting in the 21st century is considered a pilgrimage to corporate

image, vision and mission. It is a tool that ignites management toward

overall goal of profit sustainability and a pivot on which other factors revolt.

Horngren and Foster (1997), state that budgeting is becoming increasingly

important, growing in prominence in the operations of both profit seeking

and non-profit seeking organizations. Because of perpetual changing

technology and management information systems globally, academicians,

strategists and stakeholders are being challenged to consider budgeting

as a contemporary factor on which other organizational factors cluster.

On the basis of this, there is great need to undertake a comprehensive

study of Mumias Sugar Company Limited (MSC ltd) budgeting strategies

and to examine how this helps management in p~ofit sustainability. The

thrust of this study is to examine whether budgeting paradigm is

appropriate to MSC Ltd and whether there is a positive linkage between

budgeting and profitability in the organization. Affirmatively, it is significant

to understand the theoretical framework of budgeting and worth still to

validate this with profitability at MSC Ltd.

Wangara (2006) states that MSC Ltd is the largest sugar factory in Kenya

and produces 65% of the locally consumed sugar. It has the most

competitive remuneration package among all sugar factories within the

Republic of Kenya. It falls under group “B” according t~the ranking of

factories in the industrial sector. MSC ltd is the key of Kenya as far as

production of sugar for local consumption and export purposes are

concerned.

~POSTGRADUATE~ LIBRARY

DATF ••

//~~ ~

MSC Ltd has won several awards. It earned awards as best company iV~ ~~jp~TE~\

environmental management and marketing in 2006. The CEO, Dr. Evan~ LiBR1’~ _.1)

Kidero was declared CEO of the year during the same period. In 2005~~ ~ • /

MSC ltd earned best management awards performance and was ranked n~

most respected company in East Africa in Agricultural services

management. During the same period it acquired ISO 91001/ 2000

enabling it to sell its products anywhere in the world. In 2004 MSC ltd was

ranked the best company in corporate governance in the country. In 2002

MSC ltd earned the best award in human resource management. The

organization is outstanding in the provision of corporate social

responsibility (CRS) in the country through support of education,

construction of roads, support of Agriculture and sports and games.

During the periods stated above (2002 — 2006), the company had a lot of

retrenchments. This was attributed to adverse weather conditions,

importation of cheap sugar, dysfunctional management, and poor

budgeting, particularly 2003 which was the exit of the management of the

white CEO. In the same year the profitability of the company went into

negativity and Profit recovery was realized in 2004 — 2006, the period

during which MSC ltd reported the highest profits since its inauguration in

1973. This profitability was attributed to the entry of an African CEO who

was vision driven and mission oriented.

MSC Ltd is a subsidiary of BOOKER TATE international company based

in the United Kingdom. It is situated in western Kenya and it is about 53

km from Busia boarder toward the eastern direction from Busia town of

Kenya.

Oringe (2006) states that MSC Ltd has a vision, mission, and values.

VISION: To be a leading Kenyan manufacturing company that

efficiently and profitably prqduces and markets sugar and related products

to world class standards.

MISSION: To satisfy customer needs for sugar and other products

through efficient and innovative production and marketing practices while

meeting the diverse expectations of all stakeholders.

VALUES:

> To consistently offer quality products and services to customers, being a

customer driven company.

> To encourage team work and positive contribution from motivated and

innovative work force.

> To contact business with employees, customers and other stakeholders in

an honest, fair and caring manner.

> To have an equal opportunity employer guided by international labour

organization conventions.

> To practice fair competition.

> To at all times observe good corporate governance.

> To uphold excellence in performance as the basis of employee rewards.

~> To be caring and supportive to the local community.

> To embrace internationally accepted health, safety and environmental

practices in operations.

1.2 PROBLEM STATEMENT

There was no proper budgeting in relation to profitability at MSC Ltd

between 2002-2006 as pointed out by employees within the organization.

This scenario seems to adversely affect profitability, which is evidenced by

the employees’ outcry owing to rampant retrenchment schemes that have

seen so many workers out of the company between 2002-2006. Being

~POSTGRADUATE ~~ LIBRARY

DATE

/‘S~7~ HI ~‘

part of the MSC Ltd stakeholders, no definite explanation has b~~n give W

to them as contributing ~o this anomaly. Whereas those ~ ~RADUATEIBRARY —

retrenched are given their terminal benefits, the remaining emplo~e~A~e\ * ..flflflS........ *

living in fear and unaware of their fate. Some employees attrib~~this“~

situation to poor profitability due to poor budgeting, while some feel botn

profitability and budgeting are in place but the move is particularly tribal

and aimed at clearing a specific species.

Although there are five other sugar factories in Kenya that have a similar

problem, the researcher chose MSC Ltd in particular because it is the

largest sugar factory in the country and produces 65% of Kenya’s locally

consumed sugar. This study looked at budgeting and how this influences

profitability at MSC Ltd. The comprehensive study of MSC will be

representative of all other sugar factories in Kenya. MSC Ltd is also the

focal point of the government of Kenya and a backbone of Kenya Sugar

Board Authority. The problems manifested with poor budgeting seemed to

be declining in profitability which resulted in employee retrenchment to

reduce costs in order to increase profitability at.MSC Ltd. This and other

related factors have precipitated the study.

1.3 PURPOSE OF THE STUDY

The purpose of the study was to examine the relationship between

Budgeting and profitability among sugar factories in Kenya so as to reveal

its advantages and exhibit management and maintenance of a master

budget in order to create effectiveness and efficiency by correcting

negative deviations that were anticipated.

1.4.0 OBJECTIVES

1. To establish the meaning of budgeting in relation to profitability at

MSC Ltd.

To examine the advantages of budgeting in relation to profitability

at MSC Ltd.

To examine the administration of the budgeting process and

profitability in MSC Ltd.

To determine whether MSC Ltd prepares a master budget to

increase profitability.

1.5.0 RESEARCH QUESTIONS

• What is the meaning of budgeting in relation to profitability at MSC

Ltd?

What are the advantages of budgeting at MSC Ltd?

• Does MSC Ltd administer a budgeting process and profitability?

• Does MSC Ltd prepare a master budget to increase profitability?

1.6.0 HYPOTHESIS

There is strong relationship between Budgeting and profitability among

sugar factories in Kenya.

1.7.0 SCOPE OF THE STUDY

The study focuses on examining the relationship between budget planning

and profitability at MSC Ltd. MSC Ltd is situated 53 km on the eastern

direction of Busia town —Kenya. The research is limited to 5 years. It is to

examine the budgeting phenomenon of MSC Ltd between 2002-2006.

This is the period during which retrenchments were rampant at MSC Ltd

pointing to poor profitability as a result of poor budgeting.

1.8.0 SIGNIFICANCE OF THE STUDY

The study was urgent and critical in examining the budget planning

process and assessing profitability of MSC LTD.

~ POSTGRADUATE’~ LIBRARy

flATE•*

/s~” I (A

It was widely believed by staff and the community around MS~.1td th~!!~ POSTGRADUATEthe company was not progressing well; it was needed that wó\~stab1L~RARY ~5why this trend was so, and devise ways and means of making it~

The findings of the study may be of benefit to a number of stakeholders in

Kenya:

Sugar factories in Kenya may evaluate their profitability in light of

budgeting paradigm3 improving their efficiency and productivity in their

business.

Investors may be able to ascertain the profitability of sugar factories

through budgeting in order to make wise and proper investment decisions

thereby realizing profits through assessing profitability of entrepreneurial

activities.

Kenya Sugar Board Authority (KSB) may be able to provide necessary

professional advice not only to MSC Ltd but also to all other sugar

factories in Kenya plus revenue authorities, particularly, Kenya Revenue

Authority (KRA)

Future researchers shall use the findings of this study as future references

as they carryout their studies on budgeting for profitability at MSC Ltd and

other manufacturing concerns in Kenya and outside.

Future researchers shall use the study in widening the scope and faculty

of knowledge on performance improvement of factories in production of

sugar and other products.

MSC LTD would use this study to improve profitability through budgeting

and make necessary adjustment in resource mobilization, allocation and

utilization so as to increase productivity.

The organization of MSC LTD stood to lose all the above benefits if the

study did not take place; there would be poor planning, losses as a result

of poor budgeting, hasty decision making and limited information on the

topic that was investigated. It was, therefore, urgent and critical that the

study be conducted, it was also feasible in terms of financial and material

resources that were at his disposal.

1.9.0 THEORETICAL FRAMEWORK

This study is based on the planning and control theory of Fayol as

advanced by Welsch et. a! (2001). This theory states that the future

destiny of the enterprise can be manipulated; hence it can be planned and

controlled by management. The concept of comprehensive profit planning

and control rests firmly upon the planning and control theory; that is, the

primary success factor in an enterprise is the competence of management

to plan and control enterprise activities. Management earns its bread and

butter only if it can plan and control in ways that determine the long-range

destiny of the enterprise.

The foundation of profit planning and control, then, is that management

must have confidence in its ability to establish a realistic objective and to

devise efficient strategies to attain those objectives. Management can plan

and control the long-range destiny of the enterprise by making a

continuing stream of well-conceived decisions.

Gomez et. a! (2002), state that planning is a process that helps

management set objectives for the future and map out activities and

means that will make it possible to achieve those objectives. The purpose

of the elements of planning is to provide a blueprint for management

action.

\V’

I ‘(‘\I.

In the words of Griffin (2002), strategic plans are the plans de~~*~Liachieve strategic goals. More precisely, a strategic plan is a g&ieral p~1~4i?y ~

* °A1Eoutlining decisions of resource allocation, priorities, and acti~j, st~f5~

4-,necessary to reach strategic goals. These plans are set by the bo~Ift~~

directors and top management; generally have an extended time horizon

and address questions of scope, resource deployment, competitive

advantage, and synergy.

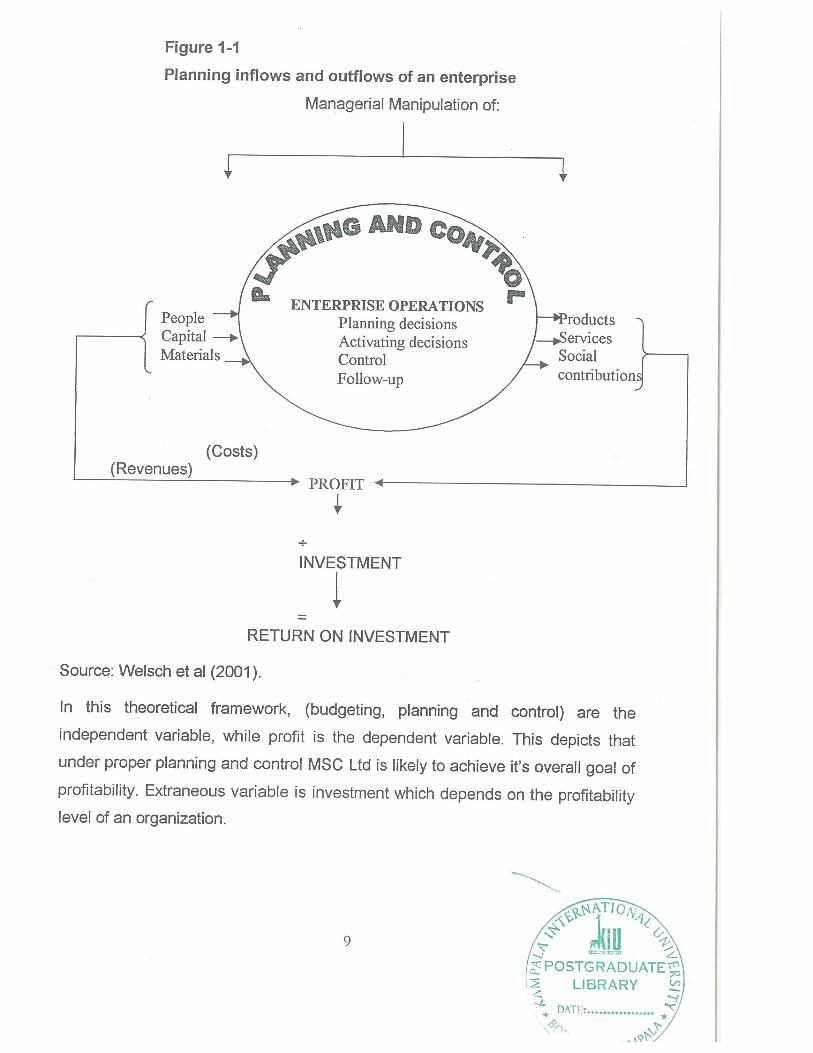

Figure 1-1

Planning inflows and oufflows of an enterprise

Managerial Manipulation of:

Source: Welsch et al (2001).

INVESTMENT

1~RETURN ON INVESTMENT

In this theoretical framework, (budgeting, planning and control) are the

independent variable, while profit is the dependent variable. This depicts that

under proper planning and control MSC Ltd is likely to achieve it’s overall goal of

profitability. Extraneous variable is investment which depends on the profitability

level of an organization.

4r

‘4,

.~-& IHE! ~<R~1IU1~—•~ ~

CHAPTER T~O (~P0sTGRADuATE~

i~ LIBR~~yLITERATURE REVIEW *ATE:

2.0 INTRODUCTION

This chapter looks at the meaning of budgeting at MSC Ltd, advantages of

budgeting at MSC Ltd, administration of budgeting, master budget

preparation and profit. Information is presented as per research questions.

2.1 The meaning of Budgeting at MSC LTD

According to Pandey (1998), a budget is a comprehensive and

coordinated plan, expressed in financial terms, for the operations and

resources of an enterprise for some specific period in the future. It is a

plan of management’s intentions of attaining specified objectives. A

budget is a mechanism to plan for the firms operations or activities. The

two aspects of every operation are; revenues and expenditures. The

budget must plan for and quantify revenues and expenses related to a

specific operation. Planning should not only be done for revenues and

expenses, but the resources necessary to carryout operations should also

be planned. The planning of the resources will include planning for assets

and sources of funds.

He further states that a budget is the planning of the firm’s expectations in

the future. Planning involves the control and manipulation of relevant

variables —controllable and non-controllable, and reduces the impact of

uncertainty, It makes management active to influence~the environment in

the interest of the enterprise. A budget expresses the plan in formal terms

and helps to realize the firm’s expectations. It is a comprehensive plan in

the sense that all activities and operations are considered when it is

prepared. It is a budget for the enterprise as a whole. Budgets are indeed

prepared for various segments of the enterprise, but they are a component

10

of the total budget or the master budget. The comprehensive or master

budget is prepared after coordinating budgets for various segments of the

enterprise. If budgets for various segments of the enterprise are not

prepared jointly and in harmony with each other, the master budget will

loose much of its importance and may even prove to be harmful in

realizing the firm’s expectations.

He continues to maintain that for operational purposes, a budget is always

quantified in financial terms. Initially the budget may be developed in

terms of varieties of quantities, but finally they may be expressed in the

money unit. For example, purchase and production budgets will involve

units of raw materials and finished goods respectively, the labour hours

and the sales budget will involve territories and customers to be served.

But a coordinated and comprehensive budget can be developed only

when all these budgets are expressed in some common denominator; the

money unit undoubtedly serves as the common denominator.

He further emphasizes that time dimension must be added to a budget. A

budget is meaningful only when it is related to a specified period of time;

the budget estimates will be relevant only for some specific period. For

example, a production target of 1,000,000 units or a profit target of

$5,000,000 has no meaning unless it is stated in concrete terms. But to

achieve these qualitative expectations of the firm, the short-term

objectives or goals, expressed in quantitative terms must be related to the

time period within which they have to be achieved.

Garrison and Noreen (2002), state that a budget is a detailed plan

outlining the acquisition and use of financial and other resources over

some given period. It represents a plan for the future expressed in formal

quantitative terms.

,4~’ dL ~They further state that a budget is a detailed plan for the acquI~ J~4~ADuATE ~

use of financial and other resources over specified period. It ~sen~~f~*R’I’DATEplan for the future expressed in formal quantitative terms.Oi.

‘2Ofr~fl y~’

Williamson (2002), asserts that budget and budgetary control are a set of

knowledge and skills from which we can derive significant benefit no

matter whether we are the largest organization in the world or the poorest

individual. The act of budgeting imbues us with a sense àf discipline that

we cannot gain from anywhere else. The budget system is a feed forward

in that by using it we attempt to anticipate what we will do, what is going to

happen during the budget period. A budget is a statement setting out the

monetary or numerical aspects of an organization’s plans for the coming

year.

According to Khan and Jam (2001), budgets are an important tool of profit

planning. Budgets as a tool of planning, is closely related to the broader

system of planning in an organization. Planning involves the specification

of the basic fundamental policies that will guide it. A budget is a

comprehensive and coordinated plan expressed in financial terms, for the

operations and resources of an enterprise for some specific period in the

future.

Owler and Brown (1999), state that a budget is a plan quantified in

monetary terms, prepared and approved prior to definite period of time,

usually showing planned income to be generated and or expenditure to be

incurred during that period and the capital to be employed to attain a given

objective.

According to Hilton et al (2003), a budget is a detailed plan, expressed in

quantitative terms, that specifies how an organization will acquire and use

resources during a particular period of time.

12

2.2 The advantages of budgeting and profitability at MSC Ltd

According to Pandey (1998), budgeting is a management tool; it is a way

of managing. Budgeting is a feed-forward process; it makes an evaluation

of the variables likely to affect future operations of the enterprise. It

predicts the future with reasonable precision and removes uncertainty to a

greater extent. Budgeting facilitates control by providing definite

expectations in the planning phase that can be used as a frame of

reference for judging the subsequent performance. Undoubtedly,

budgeted performance is a more relevant standard for comparison than

past performance, since past performance is based on historical factors,

which are constantly changing.

He also maintains that budgeting improves the quality of communication.

The enterprise objectives, budget goals, plans, authority and responsibility

and procedures to implement plans are clearly written and communicated

through budgets to all individuals in the enterprise. This results in better

understanding and harmonious relations among managers and

subordinates.

He further affirms that budgeting helps to optimize the use of the firm’s

resources —capital and human; it aids in directing the total efforts of the

firm into the most profitable channels.

Similarly, he states that budgeting develops an atmosphere of profit

mindedness and cost consciousness. Budgeting leads to cost control and

increases profitability in an organization. It is an important tool for profit

planning in an organization. It thus implies that an organization without

proper budgeting strategy is like a ship on the sea without a captain.

Anytime the ship may sink with all the cargo aboard and in the twinkling of

an eye everything may go underground.

According to Homgren and Foster (1997), planning

watchword for business managers an.d for every individual

often, “executives practice management by crisis”. E

interfere with planning. Operations drift along until the

catches the firms or individuals in undesirable situations that should have

been anticipated and avoided. Budgets compel managers to look ahead

and be ready for changing conditions. This forced planning is the greatest

contribution of budgeting to management.

They further assert that, budgeting is an integral part of strategy and

tactics. Strategy is a broad form that usually means selection of overall

objectives. Tactics are general means for attaining strategic goals.

Similarly they argue that strategy analysis may include consideration of

such questions as the following;

1. What are the overall goals or objectives of the organization?

2. What trends will affect our markets? How are we affected by the

economy, the industry and our competitors?

3. What are the best ways to invest in our research design,

production, distribution, marketing, and administrative activities?

4. What forms of organizational structure serve us best?

5. What fundamental financial structure is desirable?

6. What are the risks of alternative strategies, and what are our

contingency plans if our preferred pans fail?

Affirmatively they maintain that budgeting is a basis for judging actual

results, budgeted performance is generally a better criteria than past

performance. Budgeting involves coordination which is the meshing and

balancing of all factors and all of the departments and functions so that the

company can meet organizational objectives. Coordination implies, for

example, that purchasing officers integrate their plans with production

requirements and that production officers use sales budget as a basis for

__ \j:~S~R~DUATE~’

Ll:ARYweN. 00

planning personnel needs and machinery use. Top managers want

systems designed so that the self-interests of all managers do not conflict

with the interests of the organization.

Arguably they state that budgets help management to coordinate in

several ways;

1. The existence of a well-laid plan is the major step toward achieving

coordination. Executives are forced to think of the relationship

among individual operations and the company as a whole.

2. Budgets help to restrain the empire-building efforts of executives.

Budgets broaden a manager’s thinking to include more than just his

or her department and remove bias —conscious or unconscious in

favour or his or her departments.

3. Budgets help to search out weaknesses in the organizational

structure. The formulation and administration of budgets identify

problems in communication in fixing responsibility and in working

relationships.

They further continue to maintain there ground by stressing that budgets

help managers but budgets need help. That is, top management must

understand and enthusiastically support the budget and all aspects of the

control system and that administration of budgets should not be rigid.

Changing conditions call for changes in plans. The budget must receive

respect, but it should not prevent a manager from taking prudent action. A

department’s need may commit to the budget, but matters might develop

so that some special repairs or a special advertising outlay would best

serve the interests of the firm. That managers should feel free to request

permission for outlays or the budget itself should provide enough flexibility

to permit reasonable discretion in deciding how best to get the job done.

Hilton et. al (2003), state that for any organization to be effective, each

manager throughout the organization must be aware ofiFiè plans made by

//~~ .1other managers. The budgeting process pulls together the~

manager in an organization. Budgeting is thus a vehicle thrc~jgh ~ ~ARYDATE “i

communication is channeled throughout the organizatT~n. An

organization’s resources are limited, and budgets provide one

allocate resources among competing uses.

They further confirm that a budget is a plan, and plans are subject to

change. Nevertheless, a budget serves as a useful benchmark with which

actual results can be compared.

Saleem (2001), states that budgeting increases the morale and thus, the

productivity of the employees by seeking their meaningful participation in

the formulation of plans and policies, bringing a harmony between

individual goals and the enterprise objectives more effectively.

According to Owler and Brown (1999), budgeting permits to focus

management attention on significant matters through budgetary reports;

thus, it facilitates management by exception and thereby saves

management time and energy considerably. Management is enabled to

direct much attention on weak and or non performing areas.

2.3 The Administration of budgeting process and profitability at MSC Ltd

Pandey (1998), states that budget preparation is a line function while the

organization and administration of budgeting is a staff function. The line

executives have the responsibility of deciding what the plans (budgets) are

to be. It is not the function of the staff organization to decide what the

plans are to be for areas of responsibility other than its own. The primary

responsibility of the staff organization is to assist line executives in

preparing budgets by providing data and technical advice and coordinating

the budgets of various departments.

He- also affirms that a joint effort of all managers is needed to prepare

budgets. All should participate in setting goals, developing plans and

formulating policies. Generally, the administration of budgeting may be

delegated to a budget committee. The member of a budget committee

consists of executive from each department. Frequently members from

production, sales, and finance are included in the budget committee. The

budget director is the overall in-charge of the budget committee. The

overall director may be the controller or the chief accountant or an

independent person. Sometimes the membership of the budgets

committee may be confined to the budget director, the financial manager,

the managing director and the economist. Special budget committee may

also be formed —such as a production —budget committee or sales budget

committee.

He further outlines the major functions of the budget committee as

outlined below;

1. To provide general guidelines for preparing budgets.

2. To offer technical advice

3. To receive and coordinate individual budgets

4. To suggest changes

5. To reconcile divergent views

6. To coordinate budgetary activities

7. To approve budgets with or without revisions

8. To scrutinize budget reports later on.

He also states that a budget committee in fact, is a management

committee. It brings together activities of all departments in a coordinated

way and controls those activities in an effective manner.

Similarly he states that the overall responsibility of the budget committee

lies on the budget director or the budget officer. He is responsible of

drawing up a detailed timetable for the preparation of budgets and making

necessary adjustments and calculations to consolidate individual budgets

into a maser budget. The budget director is usually the controller or the

LIBRARy ~:* DATE.

/~V ~ c

chief accountant. He should be unbiased and objective in his

He is a staff expert, who provides technical assistance to fi’e Iirt~BR1~~~

executives. He should keep good rapport with his managers and

not enforce his advice upon them.

Affirmatively he maintains that it is usually desirable to express objectives,

goals, procedures, organizational structure and authority and responsibility

in writing. These matters are explicitly set out in a budget manual. The

budget manual is a written set of instructions and pertinent information

that serves as a rulebook and a reference for the implementation of a

budget programme. It tells what to do, how to do it, when to do it and

which form to do it on.

In a similar strand, he clarifies that time dimension must be added to a

budget. A budget is meaningful only when it is related to a specific period

of time; the budget estimates will be relevant only for some specific period.

A typical budget spans over a period of one year, which may be

subdivided into quarterly or sometimes monthly budgets.

Garrison and Noreen (2002), state that a standing budget committee will

usually be responsible for overall policy matters relating to the budget

program and for coordinating the preparation of the budget itself. This

committee generally consists of the president; vice presidents in charge of

various functions such as sales; production and purchasing and the

controller. Difficulties and disputes between segments of the organization

in matters relating to the budget are resolved by the budgets committee. In

addition, the budget committee approves the final budget and receives

periodic report on the progress of the company in attaining budgeted

goals.

They further state that operating budgets are ordinarily set to cover a one

year period. The one-year period should correspond to the company’s

18

fiscal year so that the budget figures can be compared with the actual

results. This approach has the advantage of requiring periodic review and

reappraisal of budget data throughout the year. This approach keeps the

managers focused on the future at least one year ahead.

They continue to affirm that operating budgets are ordinarily set to cover a

one-year period. The one-year period should correspond to the company’s

fiscal year so that the budget figures can be compared with the actual

results. Many companies divide their budget period into four quarters. The

first quarter is then subdivided into months, and monthly budget figures

established. The last three quarters are carried in the budget at quarterly

totals only. As the year progresses, the figures for the second quarter are

broken down into monthly amounts, then the third quarter figures are

broken down and so forth. This approach has the advantage of requiring a

constant review and reappraisal of budget data. He also states that

continuous or perpetual budgets are becoming very popular. A continuous

or perpetual budget is one that covers a 12-month period but which is

constantly adding a new month on the end as the current month is

completed. This approach to budgeting is superior to other approaches in

that it keeps management thinking and planning a full 12-months ahead.

Thus, it stabilizes the planning horizon.

According to Hilton et. a! (2003), a budget committee, consisting of key

senior executives often is appointed to advise the budget director during

the preparation of the budget. The authority to give final approval to the

master budget usually belongs to the Board of Directors, or The Board of

Trustees in many non-profit organizations. Usually a board has a

subcommittee whose task is to examine the proposed budget carefully

and recommend approval or any changes deemed necessary. By

exercising its authority to make changes in the budget and grant final

approach, the Board of Directors or the Board of Tru~.~es can wield

considerable influence on the overall direction the organization takes.

19

.~\~‘•‘“•

They further explain that larger organizations usually designate~a bud’ ~jdirector or chief budget officer who specifies the process by ~hf~ .Ii~4tDUATE~1

data are gathered, collects information, and prepares the mastéj j~get.

They continue to state that to communicate budget proced L~’

deadlines to employees through the organization, the budget director

develops and disseminates a budget manual. The budget manual

indicates who is responsible for providing various types, of information,

when the information is required, and what form of information is to take.

For example, the budget manual for a large manufacturing firm might

specify that each regional sales director is to send an estimate of the

following years sales, by product manual also states who should receive

each schedule when the master budget is complete.

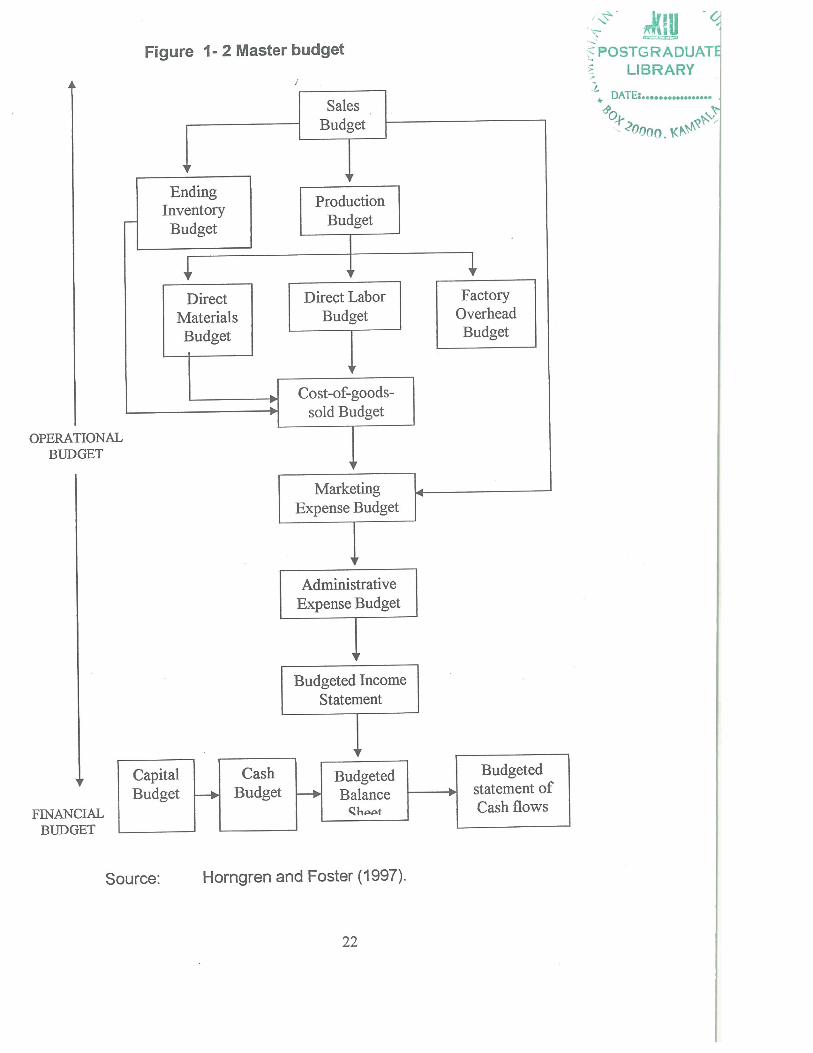

2.4 Master budget preparation and profitability at MSC Ltd.

Pandey (1998), clarifies that a comprehensive budgeting involves the

preparation of a master budget with a complete package of the component

budgets. The three important components of the master budget include:

operating budgets, financial budgets, and capital budgets.

According to Garrison and Noreen (2002), the master budget is a network

consisting of many separate budgets that are independent.

Edmonds et at (2000), state that the master budget consists of a series of

detailed schedules and budgets that describe the company’s overall

financial plans for the accounting period. The three major budget

categories are; operating budgets, capital budgets and financial statement

budgets. The budgeting process normally begins with the preparation of

the operating budgets. Preparation of the master budget begins with the

sales forecast. The detailed budgets for inventory purchases and

operating expenses are developed on the basis of projected sales.

20

Information contained in the operating budgets is used to prepare the

financial statement budgets. Again, the number of financial statement

budgets also called proforma statements, depend on the nature and

needs of the budget entity.

They continue to maintain that the budgeting process normally begins with

the preparation of the operation budgets. An operating budget is prepared

by individual sections within a company and becomes part of thecompany’s master budget.

According to Hilton et al (2003), a master budget or profit plan is acomprehensive set of budgets covering all phases of an organization’s

operations for a specified period of time.

Horngren and Foster (1997), state that the preparation of the master

budget is fundamentally nothing more than the preparation of familiar

financial statements. Preparation of a master budget involves preparing

necessary schedules, namely; sales budget, production budget, direct

material budget, direct labor budget, factory overhead budget, ending

inventory budget, cost-Of-goods sold budget, and marketing and

administrative expense budget; budgeted income statement, the cash

budget, and budgeted balance sheet.

21 ~

If ~~posTG0~~~ ~\~ LIBR2..4. ~

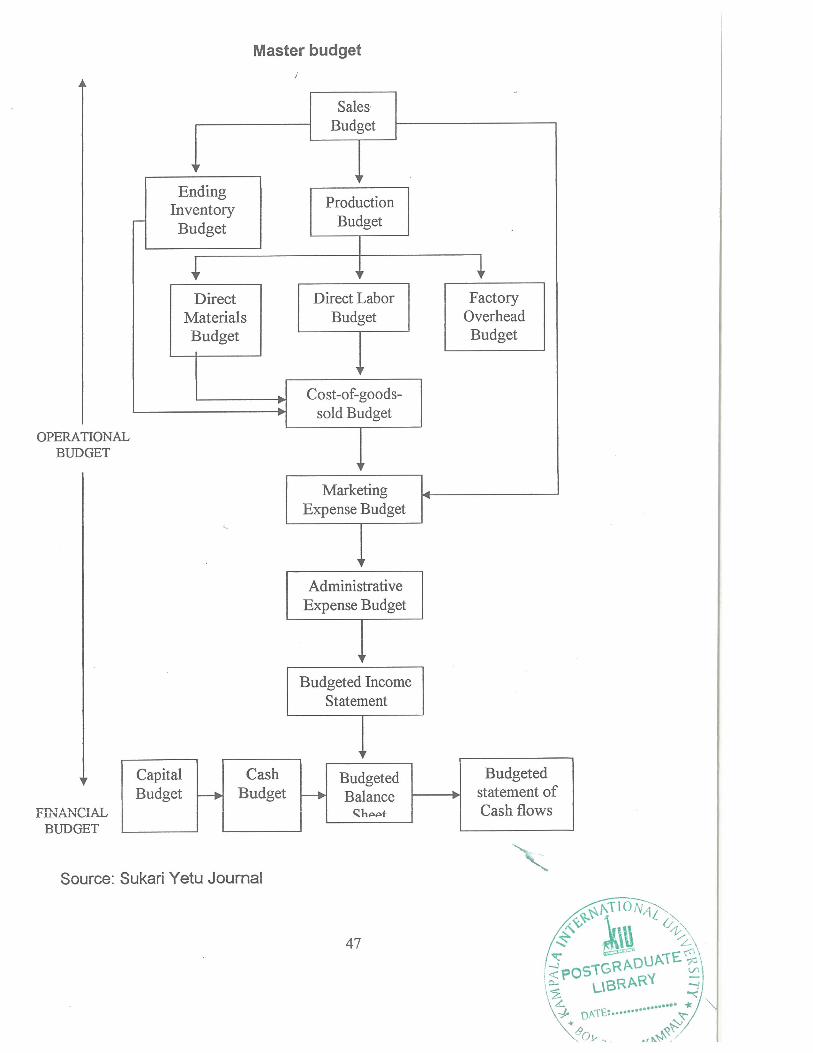

Figure 1-2 Master budget

,: ~ -

~POSTG RADUAT~ LIBRARY

DATE:.................

OPERATIONALBUDGET

FiNANCIALBUDGET

Source: Horngren and Foster (1997).

Administrative IExpense Budge~J

Budgeted IncomeStatement

22

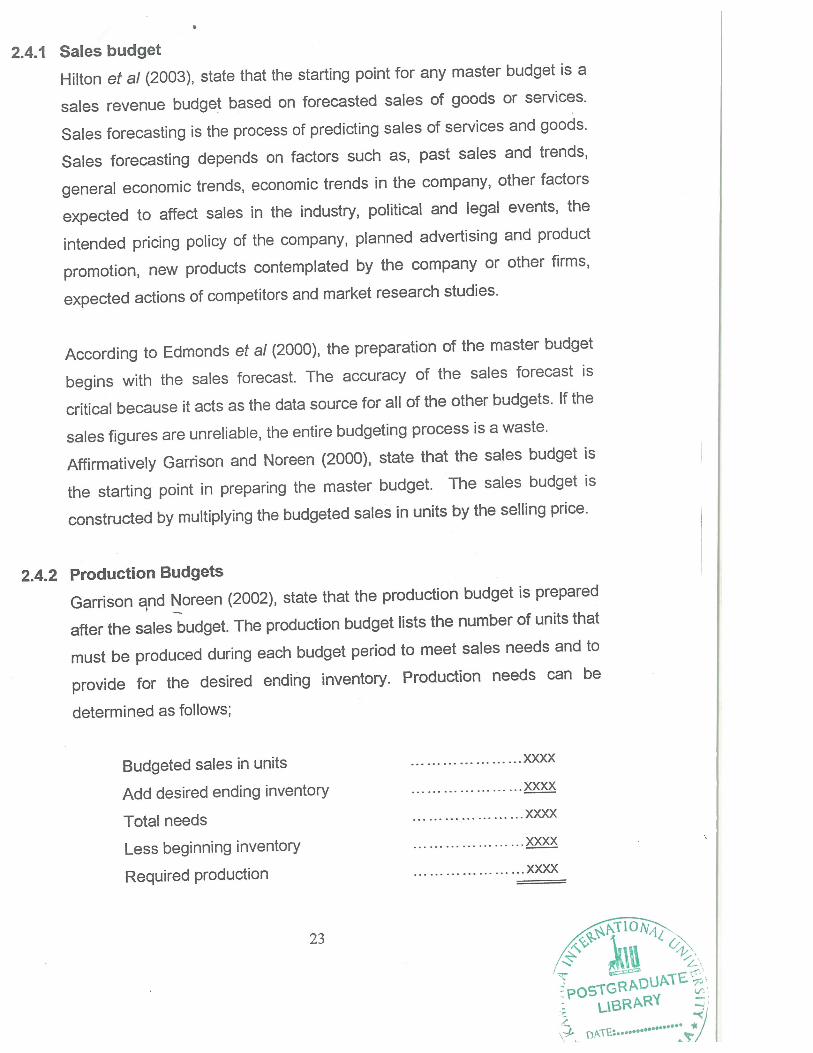

2.4.1 Sales budget

Hilton et a! (2003), state that the starting point for any master budget is a

sales revenue budget based on forecasted sales of goods or services.

Sales forecasting is the process of predicting sales of services and goods.

Sales forecasting depends on factors such as, past sales and trends,

general economic trends, economic trends in the company, other factors

expected to affect sales in the industry, political and legal events, the

intended pricing policy of the company, planned advertising and product

promotion, new products contemplated by the company or other firms,

expected actions of competitors and market research studies.

According to Edmonds et a! (2000), the preparation of the master budget

begins with the sales forecast. The accuracy of the sales forecast is

critical because it acts as the data source for all of the other budgets. If the

sales figures are unreliable, the entire budgeting process is a waste.

Affirmatively Garrison and Noreen (2000), state that the sales budget is

the starting point in preparing the master budget. The sales budget isconstructed by multiplying the budgeted sales in units by the selling price.

2.4.2 Production BudgetsGarrison qnd Noreen (2002), state that the production budget is prepared

after the sales budget. The production budget lists the number of units that

must be produced during each budget period to meet sales needs and to

provide for the desired ending inventory. Production needs can be

determined as follows;

Budgeted sales in units xxxx

Add desired ending inventory xxxx

Total needs XXXX

Less beginning inventory xxxx

Required production xxxx

23

UBRP’~ •

;~. ü~tE ••••~~•~•

Pandey (1998), affirms that production budget is prepared after

budget. It is based on sales forecasts to prepare the production’~

the sales forecasts for each product are combined with ir

the beginning level and the expected level of ending inventories of

finished products. The units of budgeted products may be calculated as

follows;

Budgeted Production Units = Sales Estimate + Expected Ending

Inventory - Beginning inventory

Hilton ef a! (2003), maintain that production budget shows the number of

services or goods that are to be produced during a budget period.

Production budget is ascertained by the following formula;

Sales in units + Desired inventory of finished goods = Total units required:

Total units required — Expected beginning inventory of finished goods =

Units to be produced.

2.4.3 Direct Material Budget

Hilton et al (2003), state that direct material budget shows the number of

units and the cost of material to be purchased and used during a budget

period. It is calculated by the following formula;

Raw material required for production + Desired ending inventory or

raw material = Total material required; Total material required —

expected beginning inventory of raw material Raw material to be

purchased.

Edmonds et al (2000), assert that meeting the sales demand requires

having enough inventory to cover expected sales and future sales

between recorder points. Accordingly, the total amount of inventory

needed for each month equals the amount of budgeted sales plus the

desired ending inventory. The total amount of inventory needed can be

24

*

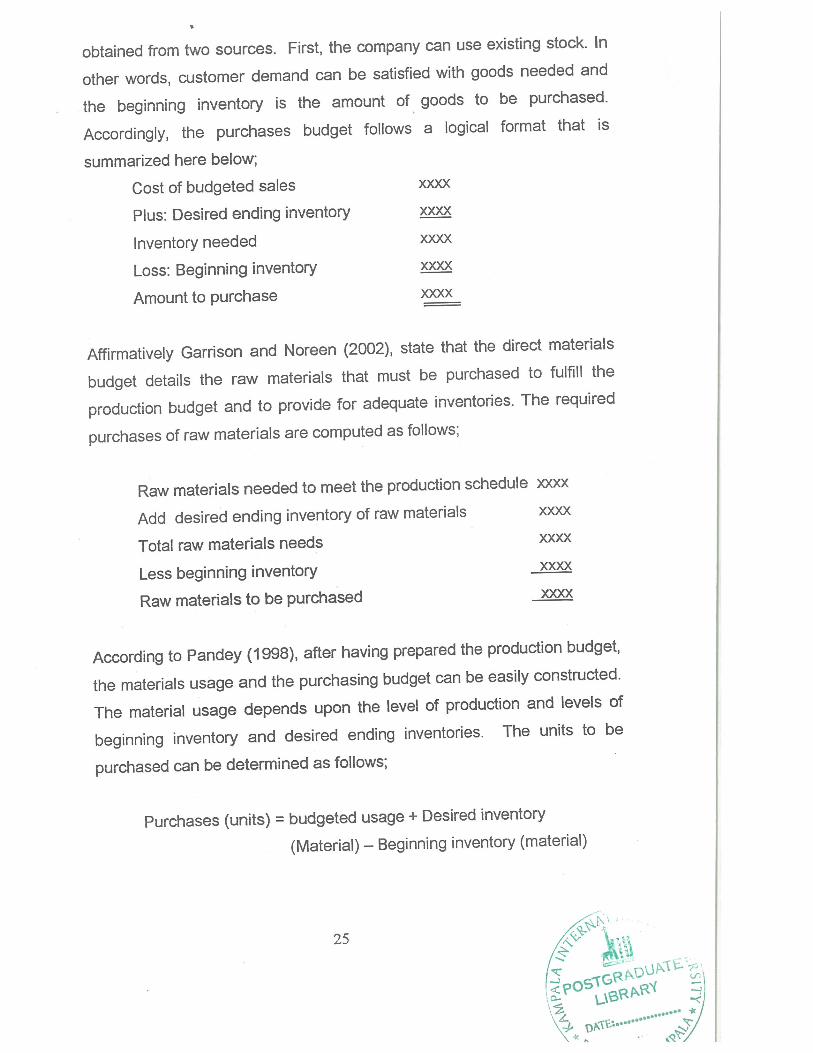

obtained from two sources. First, the company can use existing stock. In

other words, customer demand can be satisfied with goods needed and

the beginning inventory is the amount of goods to be purchased.

Accordingly, the purchases budget follows a logical format that is

summarized here below;

Cost of budgeted sales xxxx

Plus: Desired ending inventory xxxx

Inventory needed xxxx

Loss: Beginning inventory xxxx

Amount to purchase xxxx

Affirmatively Garrison and Noreen (2002), state that the direct materials

budget details the raw materials that must be purchased to fulfill the

production budget and to provide for adequate inventories. The required

purchases of raw materials are computed as follows;

Raw materials needed to meet the production schedule xxxx

Add desired ending inventory of raw materials xxxx

Total raw materials needs xxxx

Less beginning inventory xxxx

Raw materials to be purchased xxxx

According to Pandey (1998), after having prepared the production budget,

the materials usage and the purchasing budget can be easily constructed.

The material usage depends upon the level of production and levels of

beginning inventory and desired ending inventories. The units to be

purchased can be determined as follows;

Purchases (units) = budgeted usage + Desired inventory(Material) — Beginning inventory (material)

25

r ,~

2.4.4 Direct Labour Budget - LPOSTGRADUATE~/ LIBRARY ~

Pandey (1998), states that a direct labour schedule can also be Ø~epaneti.............. ~j/from data given in the production budget. The direct labour hour~~

spent depend on the units to be produced and the labour hours required

per unit of production.

According to Garrison and Noreen (2002), the direct labour budget is also

developed from the production budget. Direct labour requirements must

be computed so that the company will know whether sufficient labour time

is available to meet production needs. By knowing in advance just what

will be needed in the way of labour time throughout the budget year, the

company can develop plans to adjust the labour force as the situation may

require. Firms that neglect to budget run the risk of having to hire and

layoff at awkward times. To compute direct labour requirements, the

number of units of finished product to be produced each period (month,

quarter, and so on) is multiplied by the number of direct labour hours

required to produce a single unit. Many different types of labour may be

involved. If so, then computations should be by type of labour needed.

Hilton et. a! (2003), affirm that the direct labour budget shows the number

of hours and the cost of the direct labour to be used during a budget

period.

2.4.5 Manufacturing —Overhead budget

Hilton et a! (2003), state that the manufacturing overhead budget shows

the cost of overhead expected to be incurred in the production process

during the budget period.

26

Affirmatively, Garrison and Noreen (2000), agree that the manufacturing

overhead budget provides a schedule of all costs of production including

direct materials and direct labour.

2.4.6 Ending Finished Goods Inventory Budget

Garrison and Noreen (2002), state that the carrying cost of unsold units is

computed on the ending finished goods inventory budget.

Williams et a! (2002), maintain that in a merchandising company, inventory

consists of all goods owned and held for sale to customers. Inventory is

expected to be converted into cash within the company’s operating cycle.

In the balance sheet, inventory is listed immediately after accounts

receivables, because it is just one step farther removed from conversion

into cash than customer receivables.

2.4.7 Cost-of-goods-sold Budget

Hilton et a! (2003), state that the budgeted schedule of cost of goods

manufactured and sold details the direct material, direct labour, and

manufacturing overhead costs to be incurred and shows the cost of goods

to be sold during a budget period.

2.4.8 Marketing and Administrative expense budget

According to Garrison and Noreen (2002), the selling and administrative

expense budget lists the budgeted expenses for areas other than

manufacturing. In large organizations, this budget would be a completion

of many smaller, individual budgets submitted by department heads and

other persons responsible for selling and administrative expenses. For

example, the marketing manager in a large organization would submit a

budget detailing the advertising expenses for each budget period.

27 /~,/~- ___

~POSTGRADUATELIBRARY

~ DATE .._,__...

IThey affirm that the selling and administrative expense budget~

list of anticipated expenses for the budget period that will be ir~urre~I~~” .~)areas other than manufacturing. The budget will be made up ~f

smaller, individual budgets submitted by various persons h~In~0 ~

responsibility for cost control in selling and administrative matters, If the

number of expense items is very large, separate budgets may be needed

for the selling and administrative functions.

2.4.9 Budgeted Income Statement

Garrison and Noreen (2002), state that a budgeted income statement can

be prepared from the data developed from sales-marketing and

administrative expense budget. The budgeted income statement is one of

the key schedules in the budgeted process. It is the document that tells

how profitable operations are anticipated to be in the forthcoming period.

After it has been developed, it stands a benchmark against which

subsequent company performance can be measured.

According to Hilton et. a! (2003), the budgeted income statement shows

the expected revenue and expenses for a budget period, assuming that

planned operations are carried out.

Edmonds et. a! (2000), affirm that the budgeted income statement

provides insights into the new stores expected profitability. If expected

profitability is unsatisfactory, management may decide to abandon the

project or to alter planned activity.

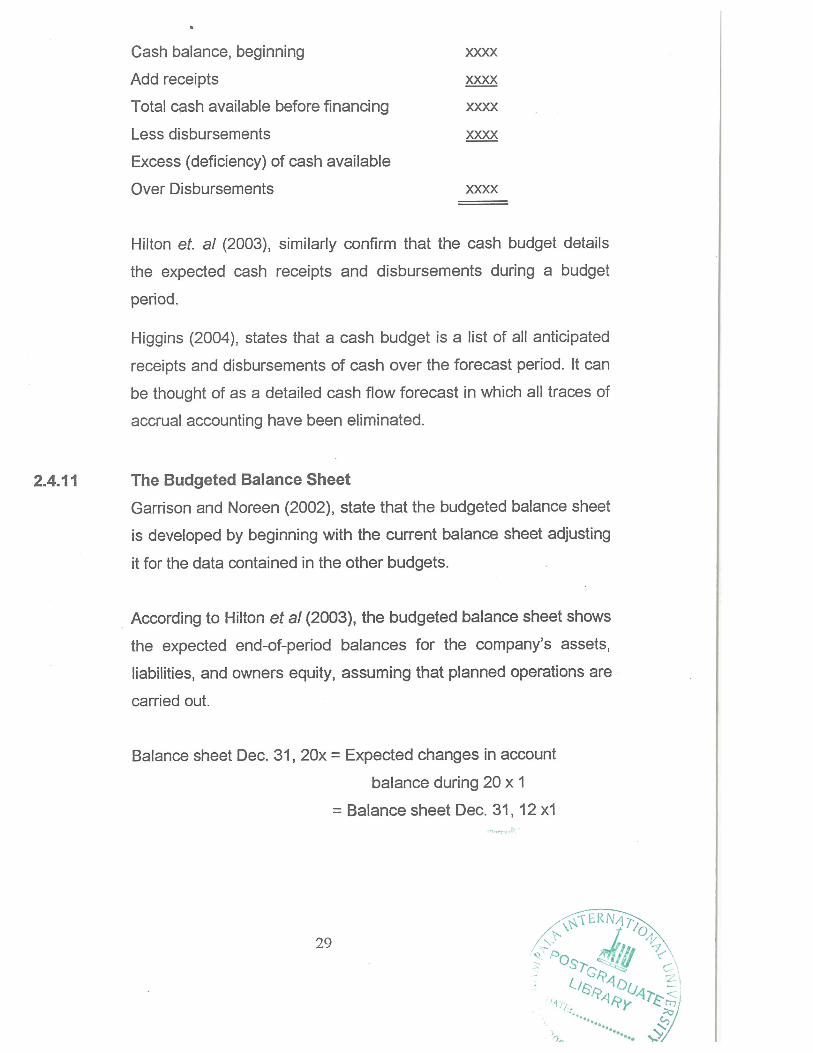

2.4.10 The Cash Budget

Garrison and Noreen (2002), affirm that a cash iudget pulls together

much of the data developed in the previous steps. The cash budget is

composed of; receipt section, the disbursement section, the cash excess

or deficiency section, and the financing section. The cash excess or

deficiency section is computed as follows;

28

Cash balance, beginning xxxx

Add receipts xxxx

Total cash available before financing xxxx

Less disbursements xxxx

Excess (deficiency) of cash available

Over Disbursements XXJO(

Hilton et. a! (2003), similarly confirm that the cash budget details

the expected cash receipts and disbursements during a budget

period.

Higgins (2004), states that a cash budget is a list of all anticipated

receipts and disbursements of cash over the forecast period. It can

be thought of as a detailed cash flow forecast in which all traces of

accrual accounting have been eliminated.

2.4.11 The Budgeted Balance Sheet

Garrison and Noreen (2002), state that the budgeted balance sheet

is developed by beginning with the current balance sheet adjusting

it for the data contained in the other budgets.

According to Hilton et a! (2003), the budgeted balance sheet shows

the expected end-of-period balances for the company’s assets,

liabilities, and owners equity, assuming that planned operations are

carried out.

Balance sheet Dec. 31, 20x = Expected changes in accountbalance during 20 x I

= Balance sheet Dec. 31, 12 xl

29

2.5 Profit

According to Crystal and Lipsy (1997), a firm’s profits are the

between the revenue it receives from selling its outputs and its’

producing that output. Firms seek profits by producing and

products. The materials and factor services used in the production

process are called inputs and the productions that emerge are called

outputs.

The main objective of a business is to maximize its profits. The conditions

for profit maximization are practiced and implementable in a wide range of

different business situations. Basically, for profit to be at a maximum, there

has to be equality incremental costs and incremental revenues, (equality

of marginal costs and marginal revenues) which is achievable through

budgeting.

Saleem (2001), states that profit is the difference between selling price

and cost of production.

Khan and Jam (2001), state that budgets are an important tool of profit

planning, are closely related to the broader system of planning in an

organization. Planning involves the specification of the basic objectives

that the organization will pursue and fundamental policies that will guide it.

According to Garrison and Noreen (2002), a budget is a step taken by

business organizations to achieve their desired levels of profits. This

process is generally called planning. Profit planning is accomplished

through the preparation of a number of budgets, which when brought

together, form an integrated business plan known as the master budget.

The master budget is an essential management tool that communicates

management’s plans throughout the organization, allocates resources,

and coordinates activities.

30

Edmonds et a! (2000), state that planning is critical to the operations of a

profitable business. The area of planning that is associated with financial

matters is commonly called budgeting; which involves coordinating the

finances of all areas of the business. The planning or budgeting area of an

organization is responsible for the profits an organization makes or

achieves.

Wangara (2007), editor of Natural Sweetness, the in-house Journal of

Mumias Sugar Company, profits out that the profitability of an organization

is interwoven in a proper budgeting planning. The expectations of an

organization during a given financial period are set out and quantified in

financial terms in a planning format called budgeting. The relationship

between budgeting and profitability is so strong and intertwined in nature

that one cannot exist without the other. Organizations that anticipate

profitability must have a sound budgeting staff.

Otieno (2007), Chief Executive Officer of Kenya Sugar Board Authority

and Member of Editorial committee of Sukari Yetu, a quarterly journal for

the Kenya Sugar industry, states that budgeting is a critical path to an

organization’s profitability. Organizations that do not achieve profitability

are those whose budgeting environment exhibits a lot of weakness and

where top officials consider budgeting a management preserve. The

potentiality of an organization to achieve profitability lies primarily in a goal

budgeting planning and management should therefore coordinate all

activities thereby allowing all stakeholders take a participative role in the

planning process of an enterprise.

~

~ LIBRARY .1~?

* DATE... *

~

11

JCHAPTER THREE /

/ ~METHODOLOGY ~

DATE:—‘p

3.0 INTRODUCTION ~l~f) ~

This chapter discusses the methodology used in the study. It expounds on

research design, study population, sampling design, study area, data

collection instruments, data collection procedures, data processing and

analysis, validity of the research and limitations of the study.

The task of collecting data commenced after getting a letter of introduction

from the director of postgraduate school, research and evaluation centre

of Kampala International University on 12/0112007. On deciding the types

of methods to be used in data collection, the researcher used both primary

and secondary data collection methods.

The choice of respondents was based on understanding is a vital tool for

profit sustainability. More importantly the involvement of all stakeholders is

pivotal for the achievement of the objectives and goals of MSC Ltd.

3.2 RESEARCH DESIGN

This study employed descriptive survey method to examine therelationship between budgeting planning and profitability at MSC Ltd. This

design was considered because of its ease to collect original data from the

population. This design was used by selecting a representative sample

from all the departments at MSC Ltd that included departmental head line

managers, superintendents, supervisors and general staff.

3.3 STUDY POPULATION

MSC Ltd has 1949 regular employees. 100 questionnaires were prepared

and administered to 100 employees that included heads of departments,

32

line managers, superintendents, supervisors and general staff to examine

the relationship between budgeting, planning and profitability at MSC Ltd.

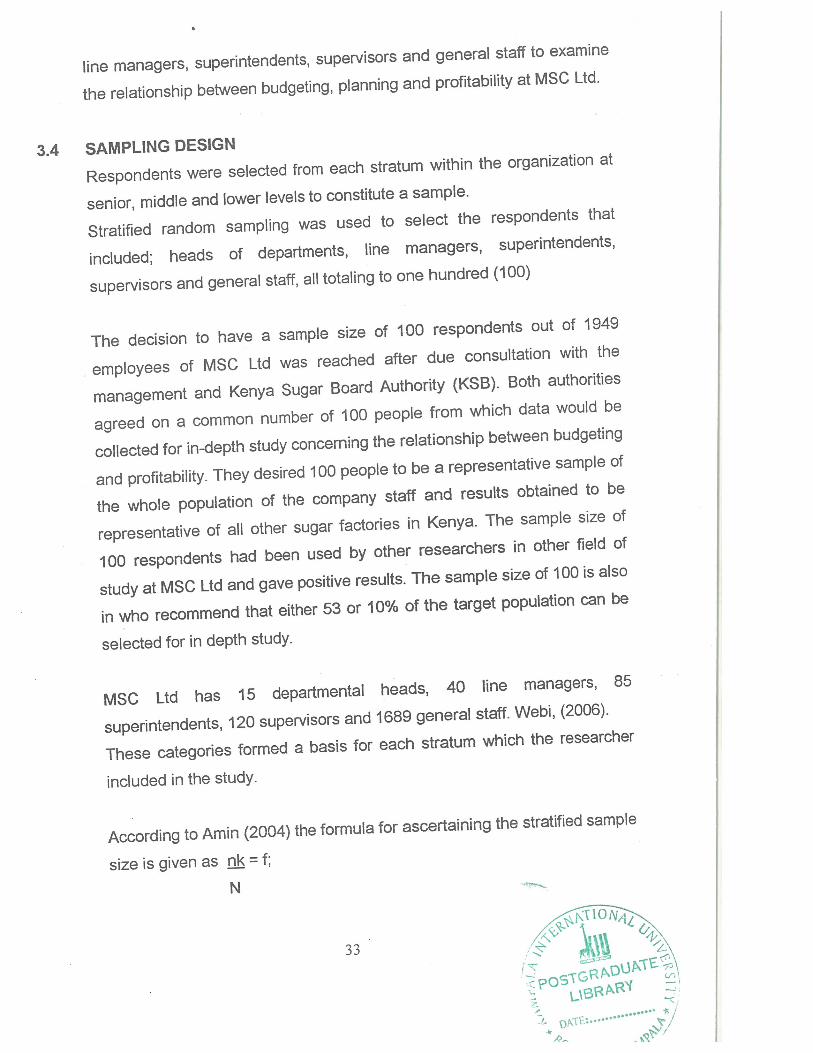

3.4 SAMPLING DESIGNRespondents were selected from each stratum within the organization at

senior, middle and lower levels to constitute a sample.

Stratified random sampling was used to select the respondents that

included; heads of departments, line managers, superintendents,

supervisors and general staff, all totaling to one hundred (100)

The decision to have a sample size of 100 respondents out of 1949

employees of MSC Ltd was reached after due consultation with the

management and Kenya Sugar Board Authority (KSB). Both authorities

agreed on a common number of 100 people from which data would be

collected for in-depth study concerning the relationship between budgeting

and profitability. They desired 100 people to be a representative sample of

the whole population of the company staff and results obtained to berepresentative of all other sugar factories in Kenya. The sample size of

100 respondents had been used by other researchers in other field of

study at MSC Ltd and gave positive results. The sample size of 100 is also

in who recommend that either 53 or 10% of the target population can beselected for in depth study.

MSC Ltd has 15 departmental heads, 40 line managers, 85superintendents, 120 supervisors and 1689 general staff. Webi, (2006).

These categories formed a basis for each stratum which the researcher

included in the study.

According to Amin (2004) the formula for ascertaining the stratified sample

size is given as ~ = f;N

33

L

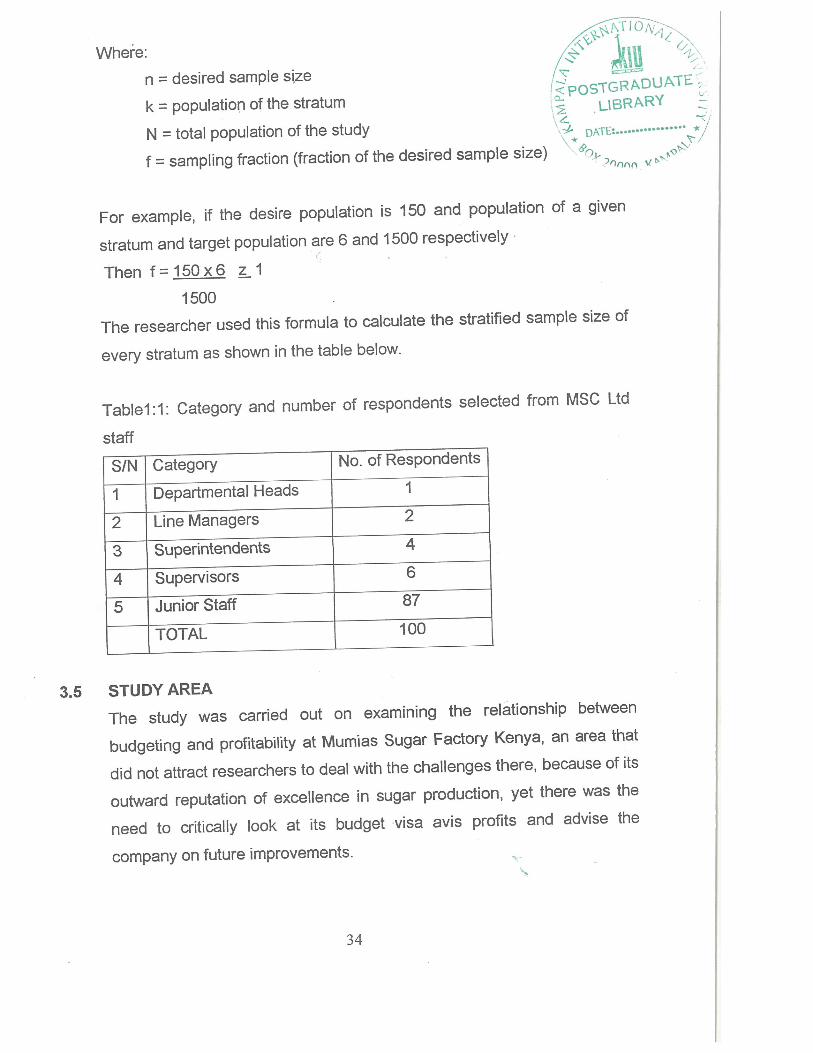

Where:

n = desired sample size

k = population of the stratum (~‘posTGRATE ~

N = total population of the study DATE• *1”*

f = sampling fraction (fraction of the desired sample size) ~ )lflnfl.v~.

For example, if the desire population is 150 and population of a given

stratum and target population are 6 and 1500 respectively•

Then f150x6 zI1500

The researcher used this formula to calculate the stratified sample size of

every stratum as shown in the table below.

Tablel :1: Category and number of respondents selected from MSC Ltd

staff

rSIN Category No. of Respondents ILi Departmental Heads I

Line Managers 2

~ SuperintendentS 4

F~ SupervisOrs 6Junior Staff 87

TOTAL 100

3.5 STUDY AREA

The study was carried out on examining the relationship between

budgeting and profitability at Mumias Sugar Factory Kenya, an area that

did not attract researchers to deal with the challenges there, because of its

outward reputation of excellence in sugar production, yet there was the

need to critically look at its budget visa avis profits and advise the

company on future improvements.

34

3.6 DATA COLLECTION INSTRUMENTS

The researcher used both primary and secondary data in this study. Theprimary data collection instruments that were used in this study were

mainly research questionnaires. The researcher presented them to

various respondents at MSC Ltd to be filled and returned to him. The

sample population comprised of 100 respondentS, all employees of MSC

Ltd.

The secondary data collection instruments were company journals, MSC

Ltd budgeted statements and annual reports and Kenya Sugar Boardannual reports and journals that were included in the study.

These instruments were a vital source of information which the researcher

used in the study on examining the relationship between budgeting andprofitability at MSC Ltd.

The questionnaires were both open and closed ended. The open endedquestions required respondents to fill in their opinions while the closed

ended questions required respondents to choose the most appropriate

alterative. The choice of using questionnaires in this study, particularly the

closed ended ones, is because they are easier to analyse since they are

in an immediate usable form, they are easier to administer because each

item is followed by alternative answers and because the are economical in

terms of time and money. (Mugenda G.M.& M.O, 2003)

3.7 DATA COLLECTION PROCEDURES

The researcher took an introduction letter from the school of PostGraduate Studies and evaluation centre of Kampala International

University on 12th January to the Chief Executive Officer MSC Ltd seeking

for his approval to interview various officers in the organization concerning

the relationship between budgeting planning and profitability.

35

I,

Upon approval, schedule was prepared and questionnaires pr~testec~jU ~\before administering them ~o the chosen respondents to estab~s~i0l~J DUATE’~LRAF?y

effective questionnaires were in collecting information from resp6~n~f~ts.

Thereafter, questionnaires were given to respondents to fill at thh~wnf,l,nI.~ v~~’?~

free time.

Both primary and secondary data was collected using questionnaires,

Kenya Sugar Board Authority and MSC Ltd journals.

After receiving back the questionnaires, data was processed, statistically

treated, results interpreted and arranged in order and finally analyzed.

3.8 DATA PROCESSING AND ANALYSIS

The researcher developed questionnaires with both closed and open

ended questions. The questionnaires were presented to MSC Ltd in

person. After being filled, they were sorted out and results were compared

and analyzed accordingly.

The researcher used the computer program SPSS (statistical package for

social science) to process and analyze data. The data was manually

entered and stored in the SPSS worksheet and by the advantage of

statistical tests excel analytical tools, information was generated through

graphical presentations and statistical inferences.

3.9 VALIDITY OF THE RESEARCH

The researcher increased validity and reliability of results by including the

use of triangulation, for example, using several methodologies in the

research.

36

The research instruments, for example, questionnaires were pre-tested on

30 participants before being taken to the field to be filled by differentrespondents.

The researcher ensured that required respondents fully participated inanswering questionnaires in order to increase reliability of results. In a

similar strand, the researcher made sure good representation of the

respondents in terms of age, gender, departments, and positions held was

taken into consideration.

In a nutshell, this study was valid because key personalities at MSC Ltdparticipated in answering questionnaires honestly. The friendly

atmosphere the researcher created to the management of MSC Ltd

attracted good quality and validity of this study.

3.10 DATA PRESENTATION

The data was presented using tables, pie charts and graphs and wasinterpreted by use of percentages to make meaning.

CHAPTER FOUR

PRESENTATION, ANALYSIS AND INTERPRETATION OF

4.0 INTRODUCTION

This chapter looks at the research presentation, analysis andinterpretation of the research findings concerning the relationship betweenbudgeting, planning, and profitability at Mumias Sugar Company Limited(MSC LTD).

Questionnaires were distributed to respondents that included Heads ofdepartments, line managers, Superintendents, Supervisors and generalstaff. 100 questionnaires were distributed and all were answered andreturned representing 100% of the respondents. These questionnaireswere open and closed ended. They had two sections: section one requiredrespondents to tick against the most appropriate alternative and sectiontwo required respondents to fill in their opinions in the open-endedquestions.

The findings were as follows:-

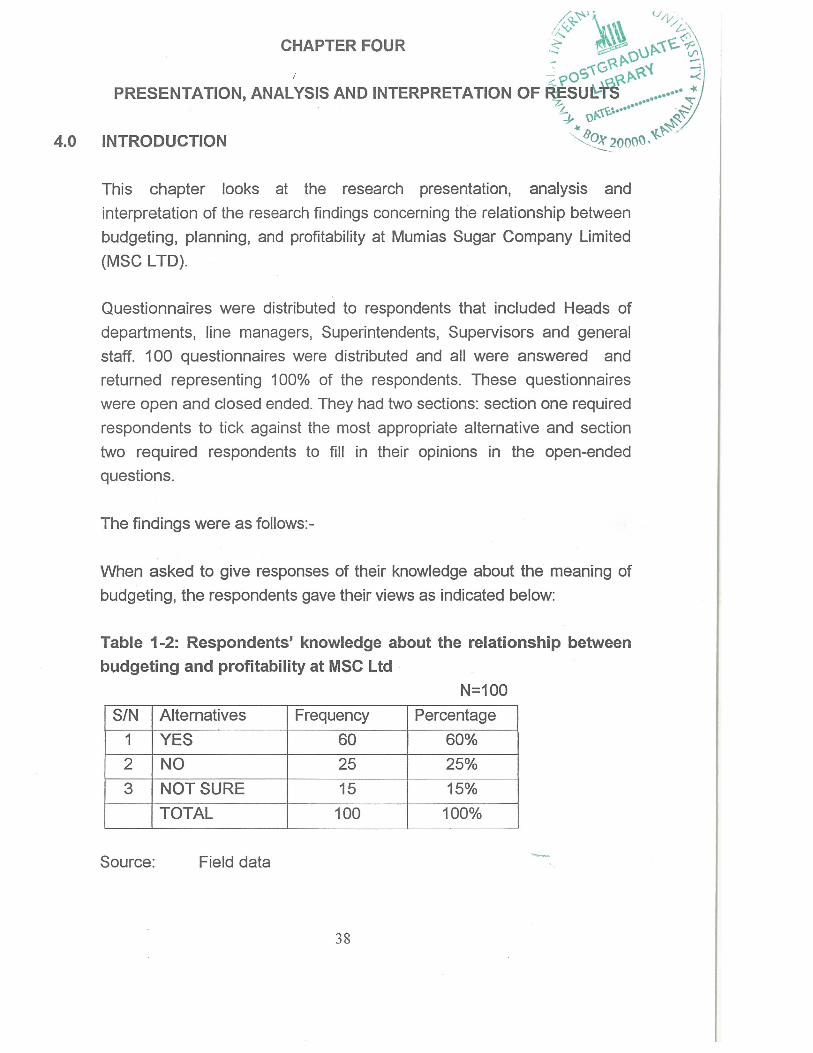

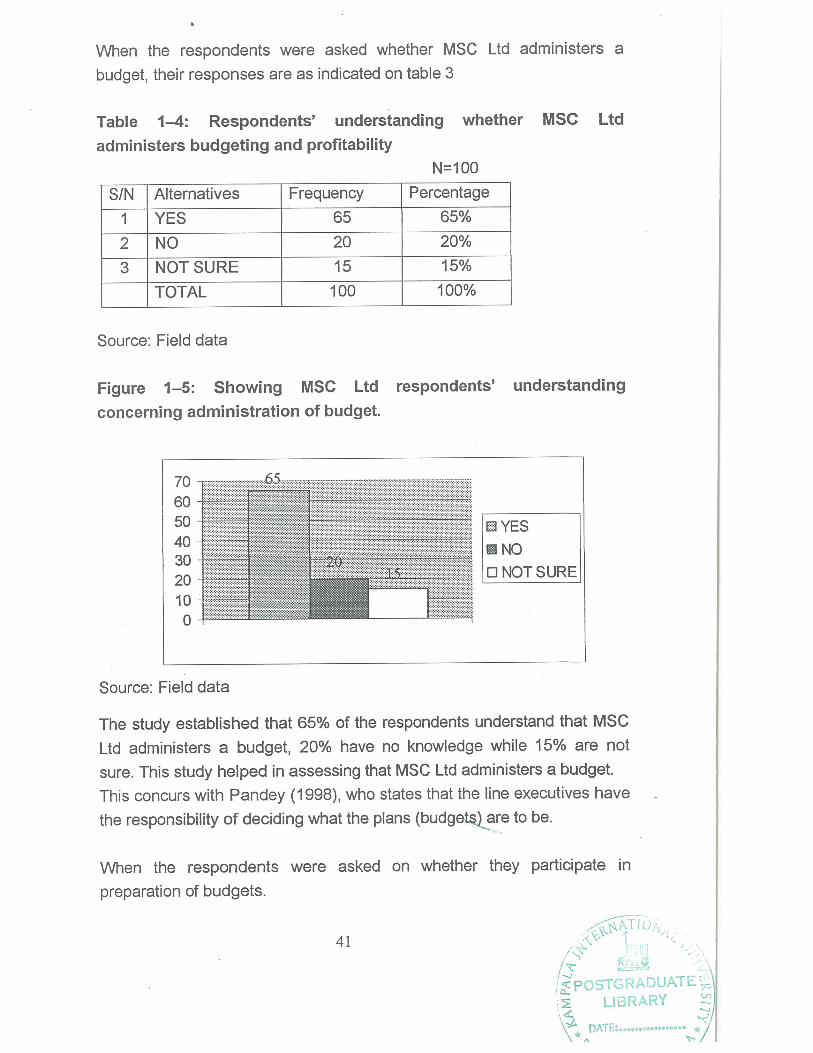

When asked to give responses of their knowledge about the meaning ofbudgeting, the respondents gave their views as indicated below:

Table 1-2: Respondents’ knowledge about the relationship betweenbudgeting and profitability at MSC Ltd

N=1 00S/N Alternatives Frequency Percentage

I YES 60 60%2 NO 25 25%3 NOT SURE 15 15%

TOTAL 100 100%

Source: Field data

38

S

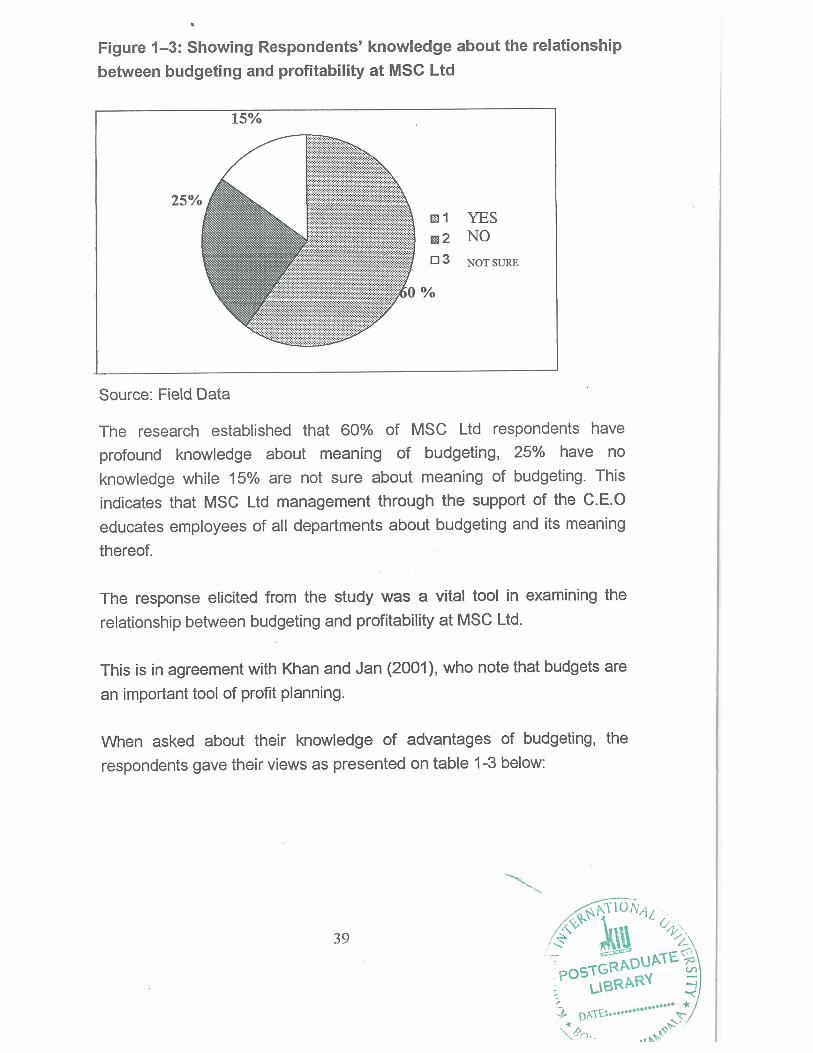

Figure 1—3: Showing Respondents’ knowledge about the relationshipbetween budgeting and profitability at MSC Ltd

The research established that 60% of MSC Ltd respondents haveprofound knowledge about meaning of budgeting, 25% have noknowledge while 15% are not sure about meaning of budgeting. Thisindicates that MSC Ltd management through the support of the C.E.Oeducates employees of all departments about budgeting and its meaningthereof.

The response elicited from the study was a vital tool in examining therelationship between budgeting and profitability at MSC Ltd.

This is in agreement with Khan and Jan (2001), who note that budgets arean important tool of profit planning.

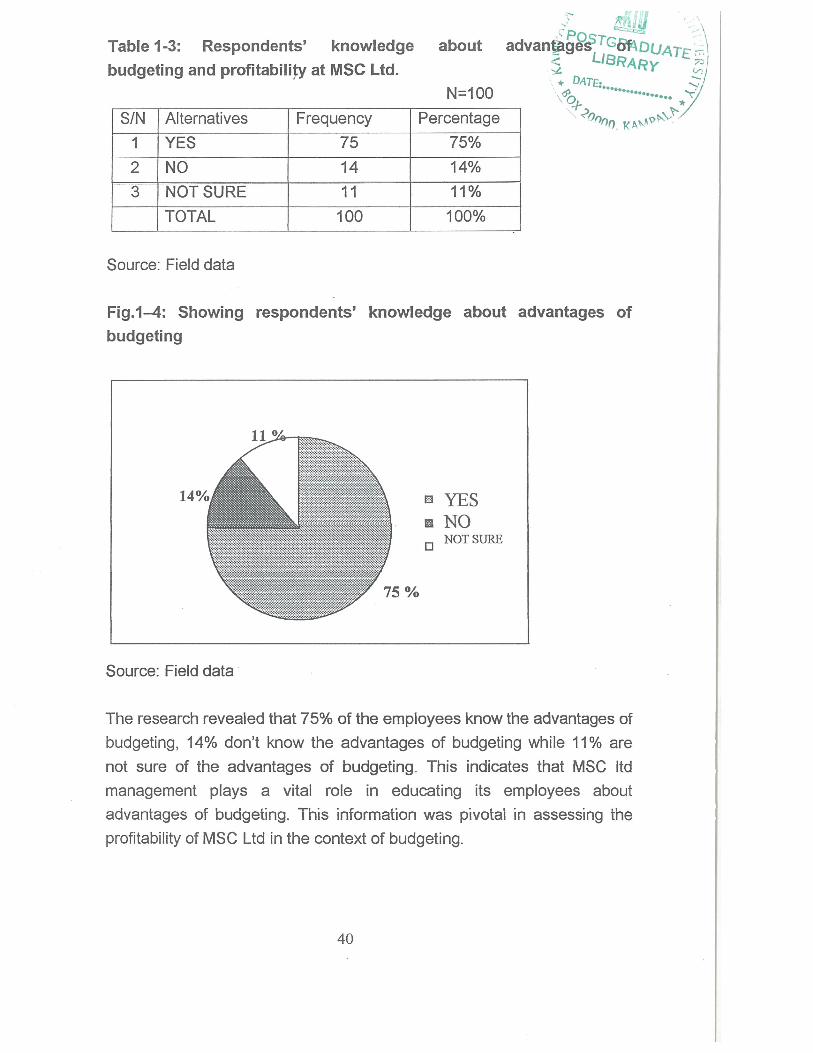

When asked about their knowledge of advantages of budgeting, therespondents gave their views as presented on table I -3 below:

Source: Field Data

39

Source: Field data

Fig.1—4: Showingbudgeting

Source: Field data

about~~ L..I~F?ARy ~I* D,1TE ~JI

N=1 00 •

______________ _____________ ~ ~

respondents’ knowledge about advantages of

The research revealed that 75% of the employees know the advantages ofbudgeting, 14% don’t know the advantages of budgeting while 11 % arenot sure of the advantages of budgeting. This indicates that MSC ltdmanagement plays a vital role in educating its employees aboutadvantages of budgeting. This information was pivotal in assessing theprofitability of MSC Ltd in the context of budgeting.

Table 1-3: Respondents’ knowledgebudgeting and profitability at MSC Ltd.

SIN Alternatives Frequency PercentageI YES 75 75%2 NO 14 14%3 NOTSURE 11 11%

TOTAL 100 100%

El YES~NO

NOT SURE

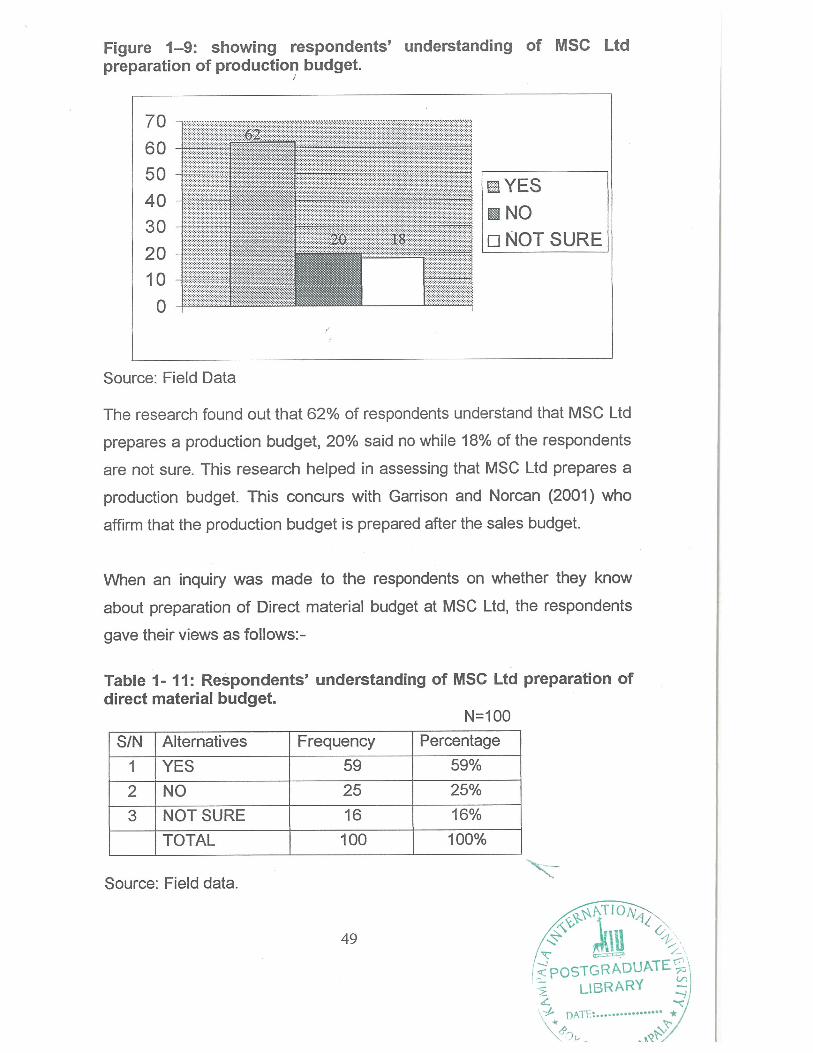

40

- •. .- —

• ..— — — I. —

I. •~

• _—•• _._

..- I • I I •

• _•

. •

— — • ..— lee —

- •• •—

- •

— I

• —••— — •I —

• — — I — • _• - • I•~

• .•. ._ ..: • —

- •• I • I~ • •

- •• •-

— —._ I ••~ —~

.—•__ • I I •I~

~T1Q,S,.

/~• N~ib/~pOSTGRADUATE~\~ LIBRARY ~I

DATE ,...,.,..o.a

A

I.

a —

.

IA

= — • 1= —

I

Percentage

65%20%15%

100%II

I II ••

I..

/-~‘ [mu ~

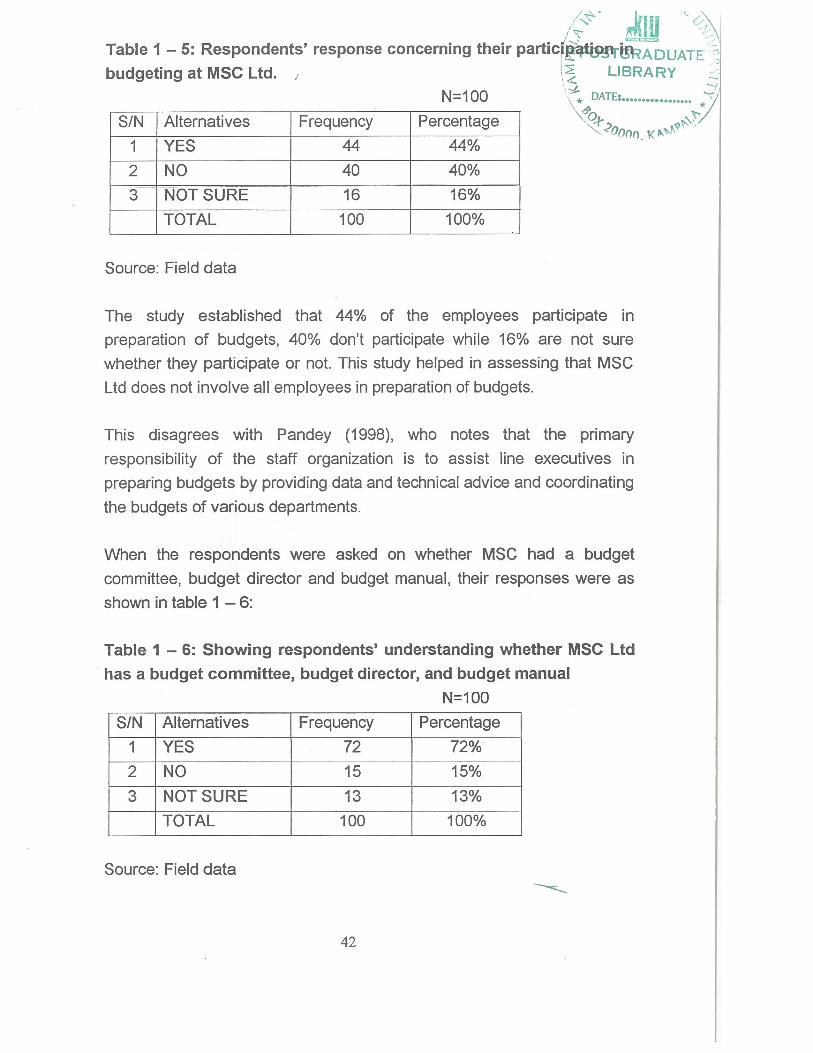

Table 1 —5: Respondents’ response concerning their~budgeting at MSC Ltd. / LIBRARY ~•

N1 00 * DATE:

~SIN Alternatives Frequency Percentage

I YES 44 44%2 NO 40 40%3 NOT SURE 16 16%

TOTAL 100 100%

Source: Field data

The study established that 44% of the employees participate inpreparation of budgets, 40% don’t participate while 16% are not surewhether they participate or not. This study helped in assessing that MSCLtd does not involve all employees in preparation of budgets.

This disagrees with Pandey (1998), who notes that the primaryresponsibility of the staff organization is to assist line executives inpreparing budgets by providing data and technical advice and coordinatingthe budgets of various departments.

When the respondents were asked on whether MSC had a budgetcommittee, budget director and budget manual, their responses were asshown intablel —6:

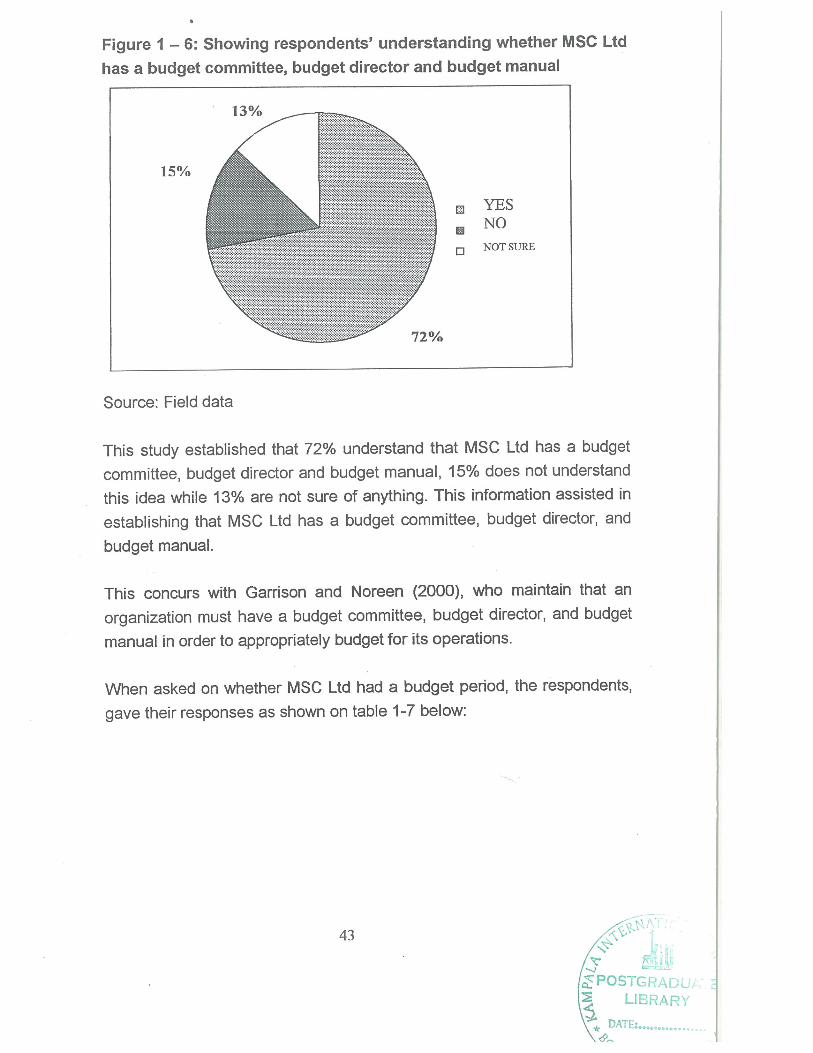

Table I — 6: Showing respondents’ understanding whether MSC Ltdhas a budget committee, budget director, and budget manual

N=100SIN Alternatives Frequency Percentage

I YES 72 72%2 NO 15 15%3 NOT SURE 13 13%

TOTAL 100 100%

Source: Field data

42

Figure 1 —6: Showing respondents’ understanding whether MSC Ltdhas a budget committee, budget director and budget manual

Source: Field data

This study established that 72% understand that MSC Ltd has a budgetcommittee, budget director and budget manual, 15% does not understandthis idea while 13% are not sure of anything. This information assisted inestablishing that MSC Ltd has a budget committee, budget director, andbudget manual.

This concurs with Garrison and Noreen (2000), who maintain that anorganization must have a budget committee, budget director, and budgetmanual in order to appropriately budget for its operations.

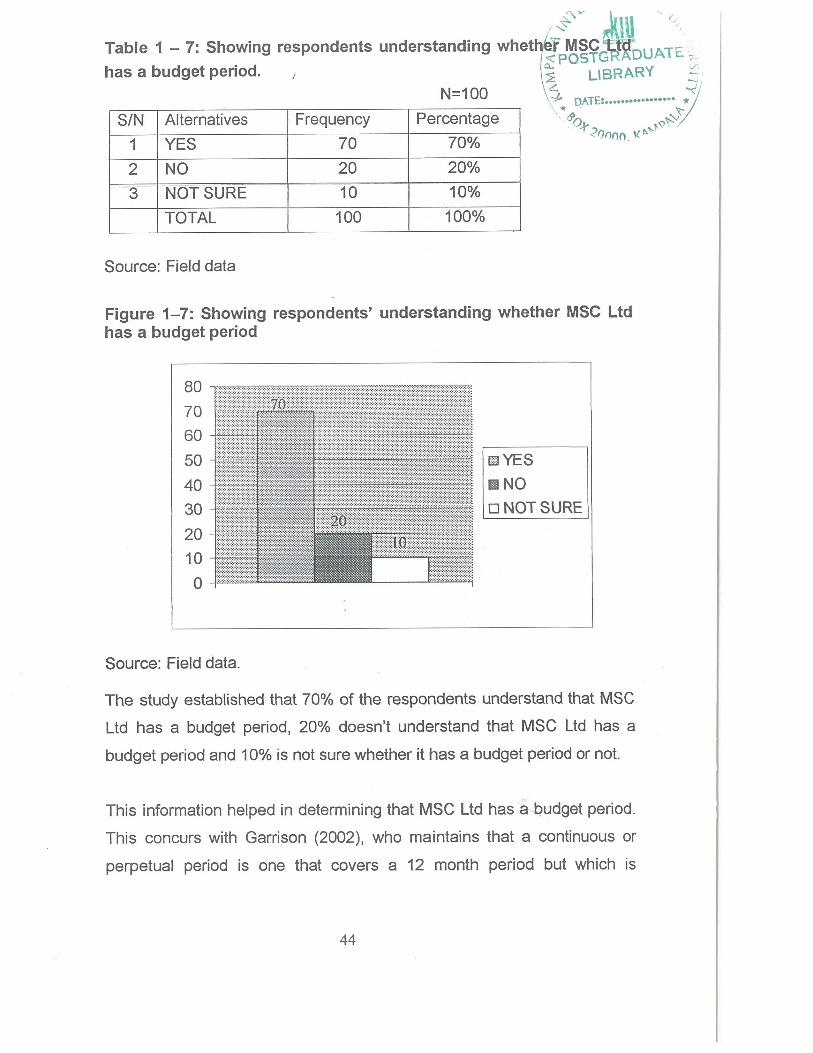

When asked on whether MSC Ltd had a budget period, the respondents,gave their responses as shown on table 1-7 below:

15%

YES~NO

NOT SURE

43

I —~

(~POSTGRADULIBRARY

DATE•

F.

I I II •

.- I

— . ._ —

=

I

I

I

II

II

Percentage70%

20%10%

100%

.111~pOSTG ~DUATE-,

IBRARY4“~ DATE. * I

2fTh~~ ‘.c~

. — =1 —. — I,, .

— — I •I~ •~ II I’. ..—

I 11=1=11=1 I., .

— - I• •~

I— — I I

— _. ..— I— •II

= I—. I — I 11= I’ II

. - I II I - . I I

I~ I— I— II I — — I — I- II I

.

.

I — — I I~ —

44

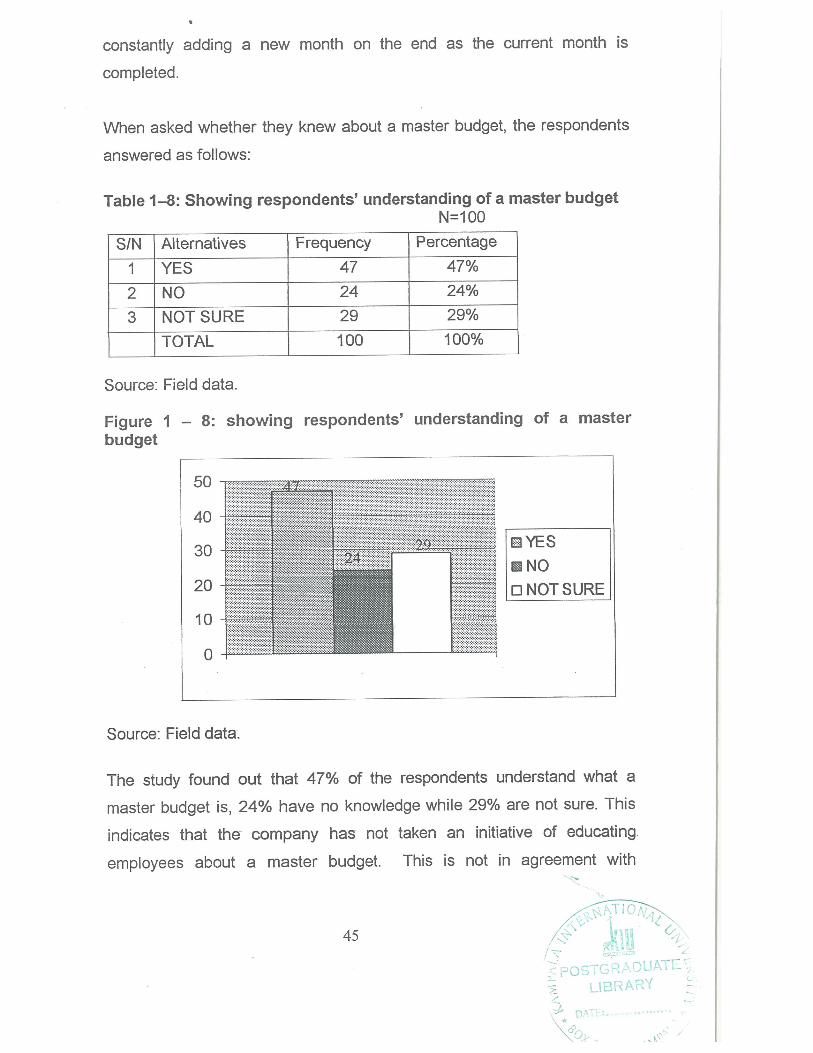

- _.. . — th on the end as the current month is

• .——.

— —I

--._ • •

I• •~

- • • .et, the respondents

. . •

I,

- I •I~ • • -....t, — — •

• —— • •_ - • — • ~I -

— I. —— • •I—

45

• ——

poSTGRADU~~TE/

3 LiBRA~L DAT~~

\L)fr

Percentage47%24%29%100%

I

I •I~

.

— I •~ —

— I •~ —

• I

.

I.

I. ••

I - I. •~ I- — •

Edmonds et al (2000), who affirm that a master budget consists ~ a serieS~ -ç<poSTGR~~ -

of detailed schedules and budgets that describe the compa ~s ovej~fl~ARY-q

financial plans for the accounting period. ~ o~-ri~

)flf~(~~~

A master budget comprises of a sales budget, production budget, direct

material budget, direct labour budget, ending inventory budget,

manufacturing overhead budget, cost of goods sold budget, marketing and

administrative expense budget, budgeted income statement budget, cash

budget and budgeted balance sheet. These are the budgets that the study

looked to examine the relationship between budgeting and profitability at

MSC Ltd.

46

Master budget

OPERATIONALBUDGET

FINANCIALBUDGET

Source: Sukan Yetu Journal

“P

ProductionBudget

4,Direct Labor

Budget

4,Factory

OverheadBudget

AdministrativeExpense Budget

Budgeted IncomeStatement

N

47

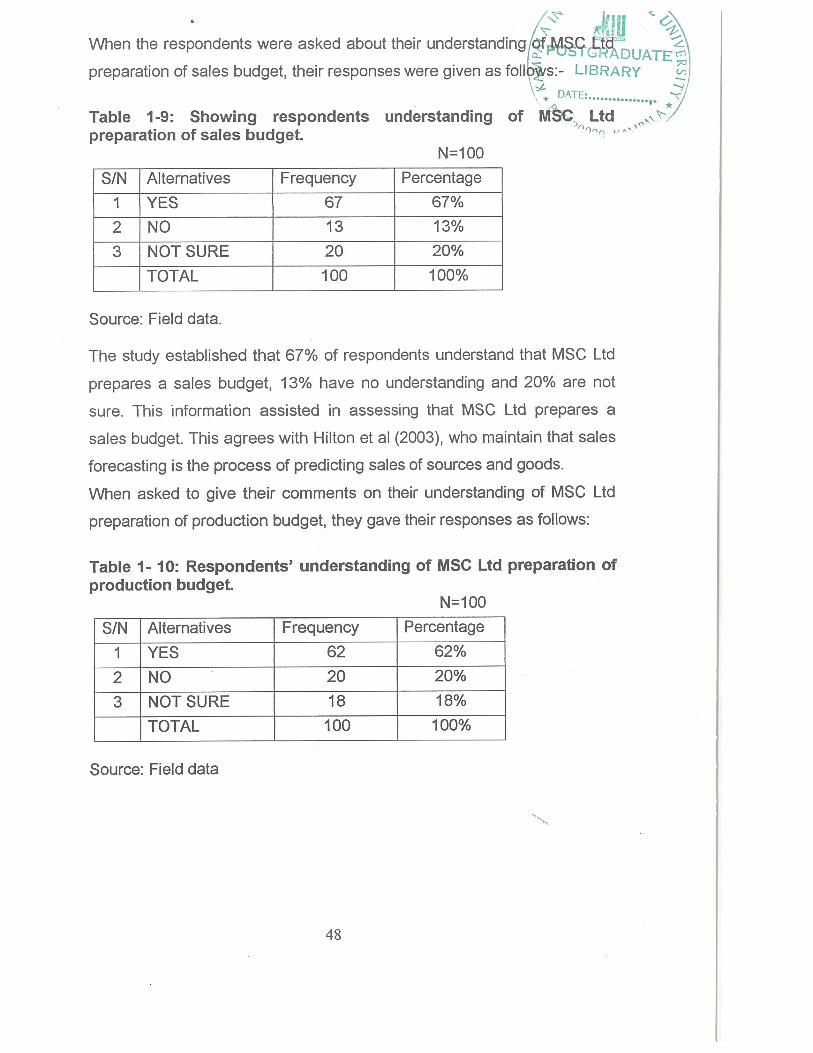

/~ fr~ ~-~C)\When the respondents were asked about their~

preparation of sales budget, their responses were given as foll~,s:- LIBRARY~ DATES

-~ ~ *1

understanding of MSC, Ltd ~~ ,, ~.

Table 1-9: Showing respondentspreparation of sales budget.

N=1 00

SIN Alternatives Frequency PercentageI YES 67 67%2 NO 13 13%3 NOT SURE 20 20%

TOTAL 100 100%

Source: Field data.

The study established that 67% of respondents understand that MSC Ltd

prepares a sales budget, 13% have no understanding and 20% are not

sure. This information assisted in assessing that MSC Ltd prepares a