Embed Size (px)

Citation preview

Lessons from the Credit Crunch – a look at how new

financing structures and techniques are going to

impact restructurings in the next downturn

Ken Baird and Simon Brodie

15 March 2008

Financial guarantees

Monolines – what are they?

Monoline:

a specialist institution that provides insurance for financial obligations

agrees to pay interest and principal on securities, if SPV defaults

Seller of protection

Minimal levels of risk; large amounts

Eurotunnel restructuring / MBIA – I

Part of Eurotunnel debt was securitised

Fixed-Link Finance 1

Fixed-Link Finance 2

MBIA wrapped debt of both FLF 1 and FLF 2

MBIA objective: to eliminate/minimise any draw on its

financial guarantees

Eurotunnel restructuring / MBIA – II

Safeguard plan provided for:

issue of hybrid securities plus cash

ability of holder of debt to elect to receive cash instead of hybrid

securities and cash

MBIA directed trustee to elect to receive cash at the earliest

possible opportunity

lack of certainty that dividends would cover interest expense

risk of call on MBIA to cover payments due on an ongoing basis and

at maturity

Citibank v MBIA

Credit derivatives

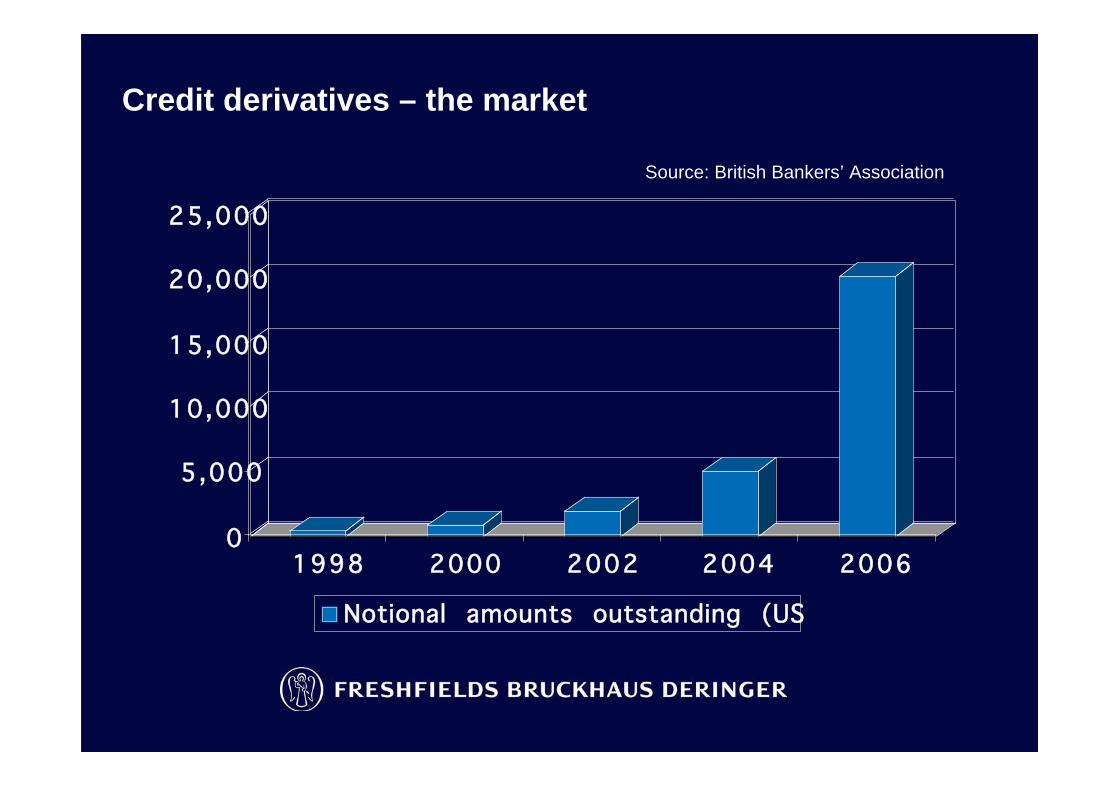

Credit derivatives – the market

0

5,000

10,000

15,000

20,000

25,000

1998 2000 2002 2004 2006

Notional amounts outstanding (USS$ bn)

Source: British Bankers’ Association

Uses and types of credit derivatives

Transfer of credit risk

Used by financial institutions and others

to hedge default risk

trading and market-making

for active portfolio and asset management

Historically, protection purchased on investment gradenames; now increasingly on sub-investment grade names

Large variety of products

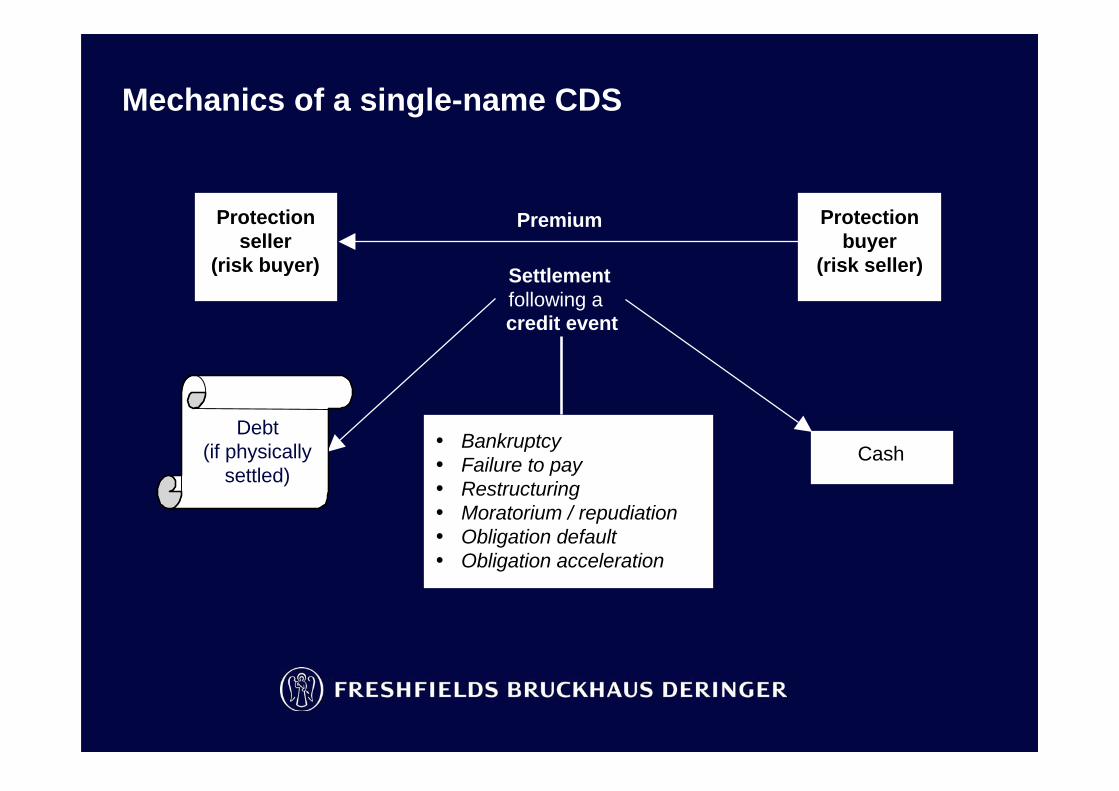

Mechanics of a single-name CDS

Cash

Settlement

following a

Debt

(if physically

settled)

• Bankruptcy

• Failure to pay

• Restructuring

• Moratorium / repudiation

• Obligation default

• Obligation acceleration

credit event

Protection

seller

(risk buyer)

Protection

buyer

(risk seller)

Premium

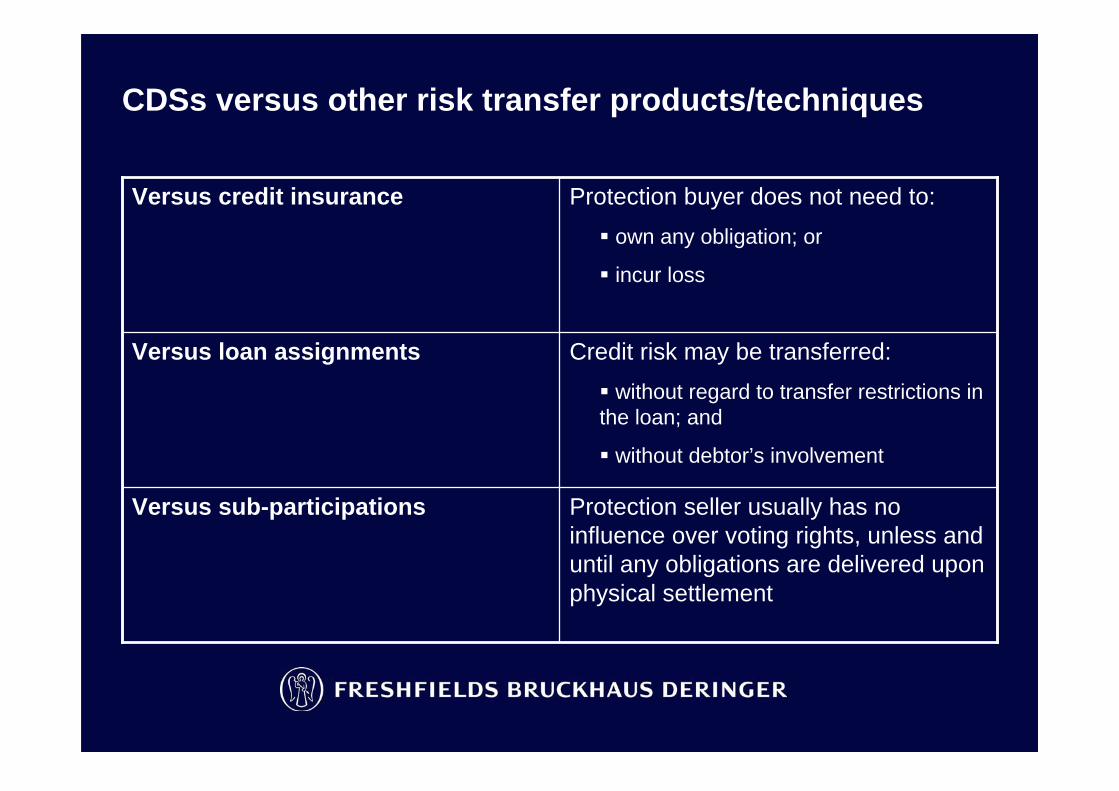

CDSs versus other risk transfer products/techniques

Protection seller usually has no

influence over voting rights, unless and

until any obligations are delivered upon

physical settlement

Versus sub-participations

Credit risk may be transferred:

without regard to transfer restrictions in

the loan; and

without debtor’s involvement

Versus loan assignments

Protection buyer does not need to:

own any obligation; or

incur loss

Versus credit insurance

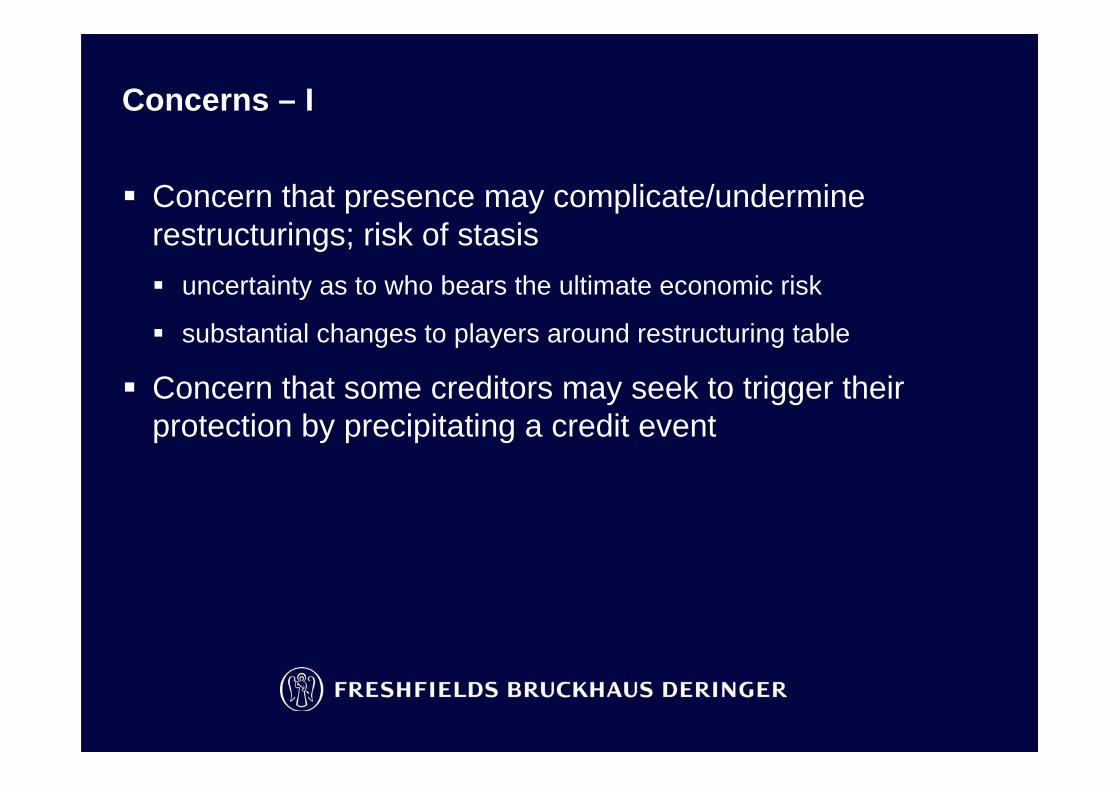

Concerns – I

Concern that presence may complicate/undermine

restructurings; risk of stasis

uncertainty as to who bears the ultimate economic risk

substantial changes to players around restructuring table

Concern that some creditors may seek to trigger their

protection by precipitating a credit event

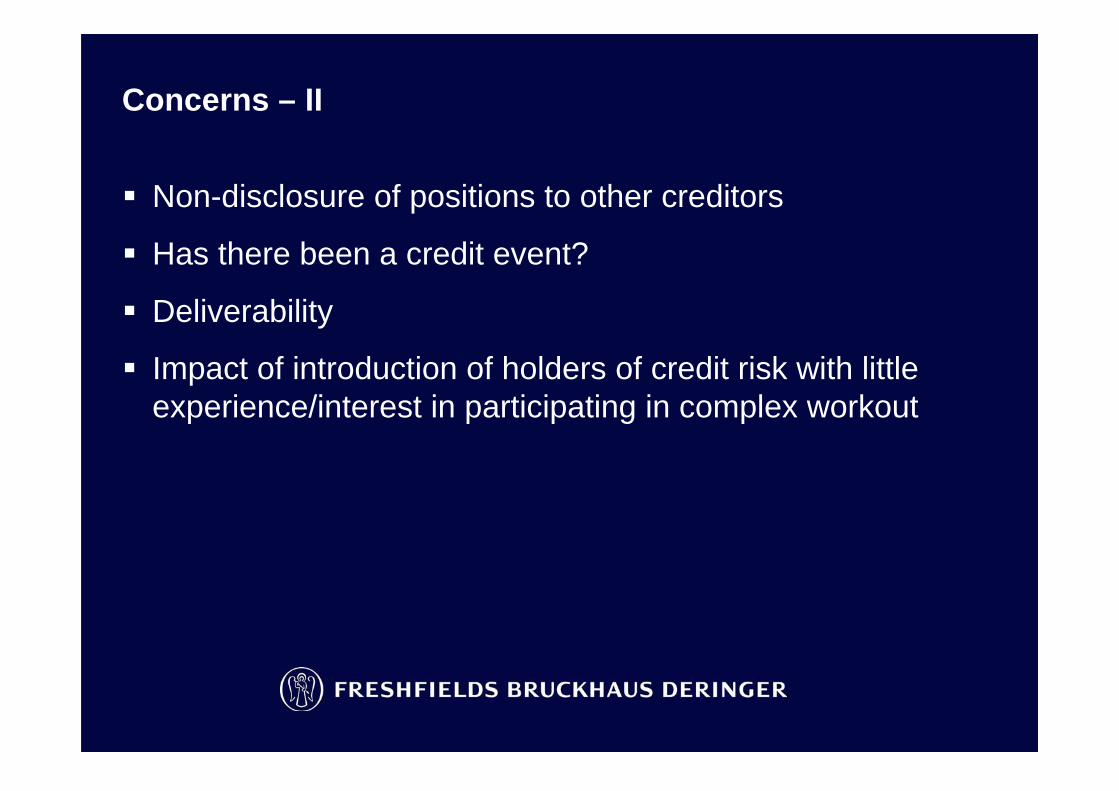

Concerns – II

Non-disclosure of positions to other creditors

Has there been a credit event?

Deliverability

Impact of introduction of holders of credit risk with little

experience/interest in participating in complex workout

Mitigating factors – I

Protection buyers may only have partial cover, retaining an

economic interest in the debtor

Even if protection buyer is substantially covered, CDS

might not directly impact on conduct of workout group

information barriers

reputational concerns

Mitigating factors – II

Impact of cash settlement rather than physical settlement

no transfer of debt

but physical settlement for LCDSs

Protection sellers may just sell on

Early discussions/negotiations with key creditors may helpidentify issues and minimise disruption

Credit derivatives – an overall assessment

Many issues yet to be tested

Credit derivatives clearly could have a major impact in

some cases

Mitigating factors suggest that in many cases problems will

not be acute

Restructurings will be more complex – more issues to be

aware of and to manage

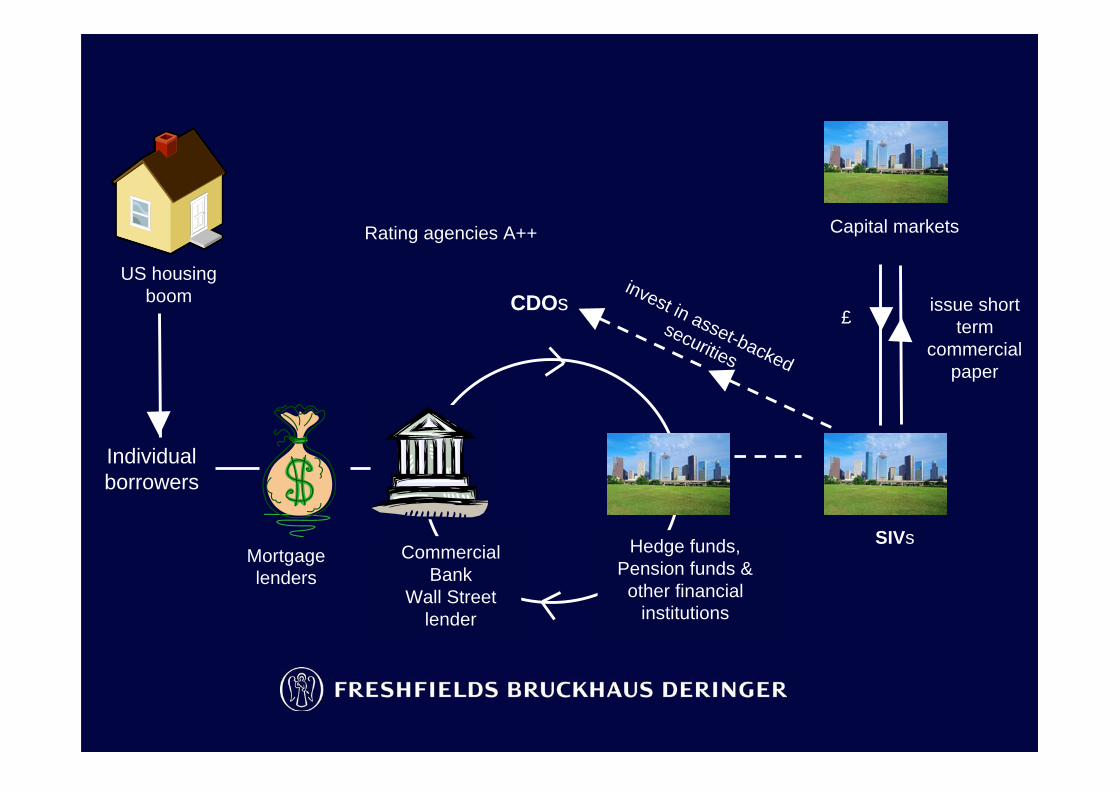

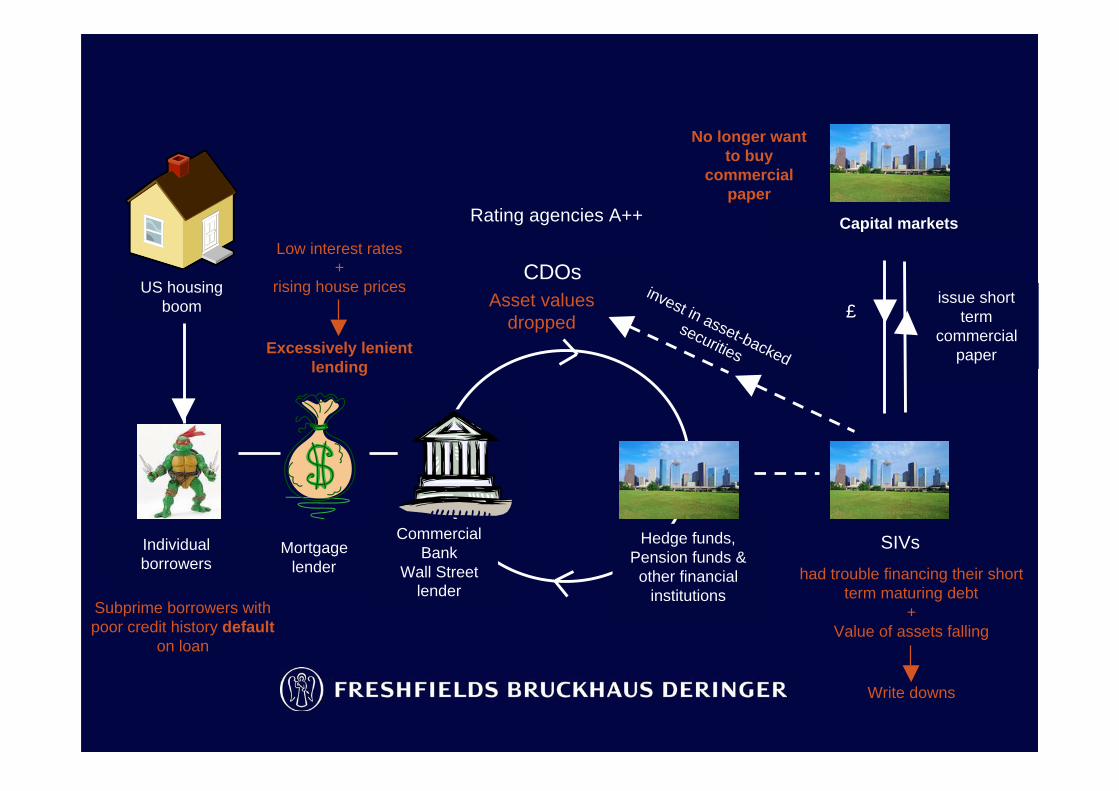

Background to the crunch

US housing

boom

Individual

borrowers

Mortgage

lenders

SIVs

issue short

term

commercial

paper

Capital markets

CDOsinvest in asset-backed

securities

Commercial

Bank

Wall Street

lender

Hedge funds,

Pension funds &

other financial

institutions

£

Rating agencies A++

US housing

boom

Mortgage

lender

SIVs

issue short

term

commercial

paper

Capital markets

CDOsinvest in asset-backed

securities

Commercial

Bank

Wall Street

lender

Hedge funds,

Pension funds &

other financial

institutions

£

Individual

borrowers

No longer want

to buy

commercial

paper

Asset values

dropped

Low interest rates

+

rising house prices

Excessively lenient

lending

Subprime borrowers with

poor credit history default

on loan

had trouble financing their short

term maturing debt

+

Value of assets falling

Write downs

Rating agencies A++

Cheyne Finance Plc

Structured investment vehicle - heavily invested in mortgage-backed

securities

Liquidated its assets as a result of the credit crunch

September 2007 - receivers appointed over business and assets

The ‘pay as you go’ approach

Court to determine proper construction of priorities clause in securitydocumentation

Held:

Receivers to apply monies by paying first debts of the senior creditors asand when they fall due

Rejected ‘pari passu’ approach – involved making full provisioning forpayment of all senior debts in precedence to payment on time and in fullof debts as when they fell due

Became clear this approach would require a high level of asset salesbefore maturity

At a discount

Depleting balance sheet

Unable to pay late-maturing debts

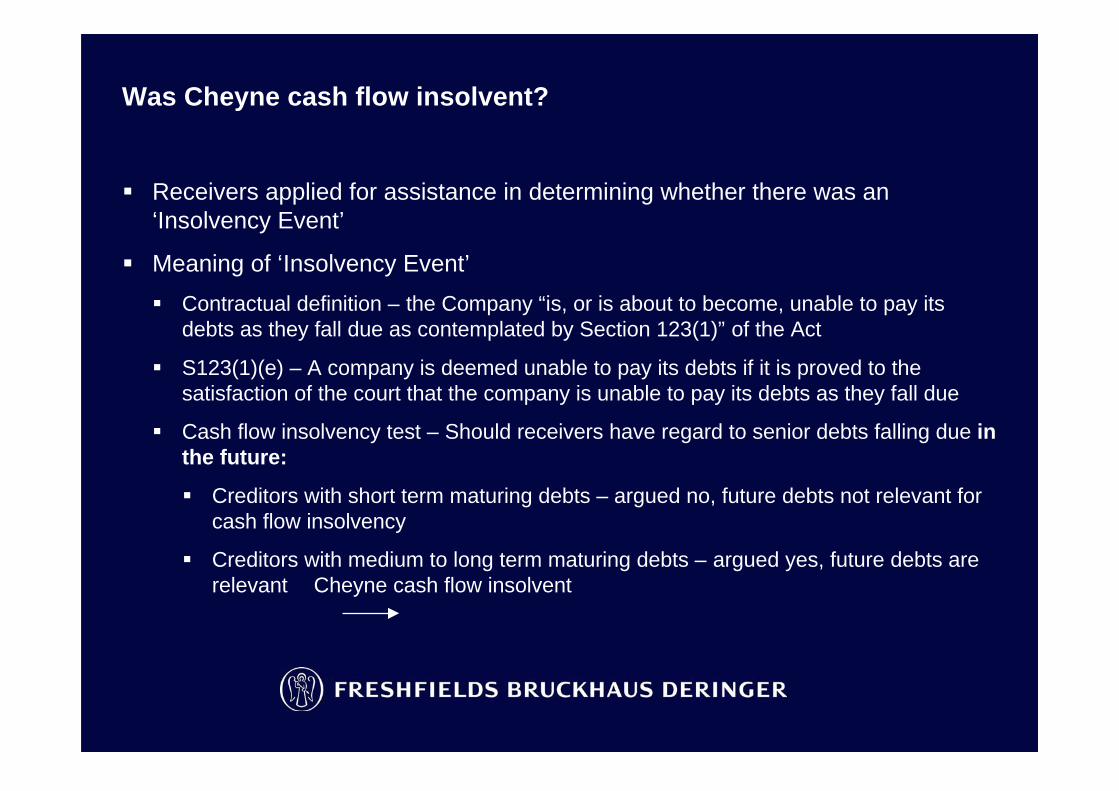

Was Cheyne cash flow insolvent?

Receivers applied for assistance in determining whether there was an

‘Insolvency Event’

Meaning of ‘Insolvency Event’

Contractual definition – the Company “is, or is about to become, unable to pay its

debts as they fall due as contemplated by Section 123(1)” of the Act

S123(1)(e) – A company is deemed unable to pay its debts if it is proved to the

satisfaction of the court that the company is unable to pay its debts as they fall due

Cash flow insolvency test – Should receivers have regard to senior debts falling due in

the future:

Creditors with short term maturing debts – argued no, future debts not relevant for

cash flow insolvency

Creditors with medium to long term maturing debts – argued yes, future debts are

relevant Cheyne cash flow insolvent

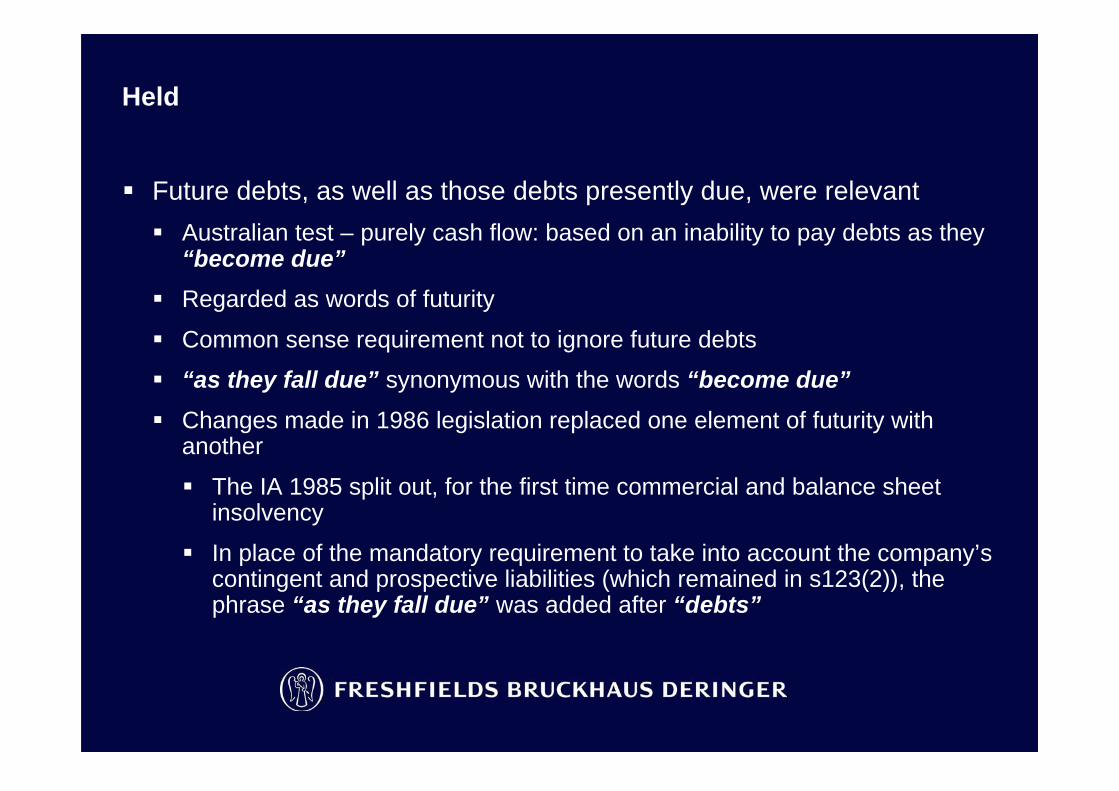

Held

Future debts, as well as those debts presently due, were relevant

Australian test – purely cash flow: based on an inability to pay debts as they“become due”

Regarded as words of futurity

Common sense requirement not to ignore future debts

“as they fall due” synonymous with the words “become due”

Changes made in 1986 legislation replaced one element of futurity withanother

The IA 1985 split out, for the first time commercial and balance sheetinsolvency

In place of the mandatory requirement to take into account the company’scontingent and prospective liabilities (which remained in s123(2)), thephrase “as they fall due” was added after “debts”

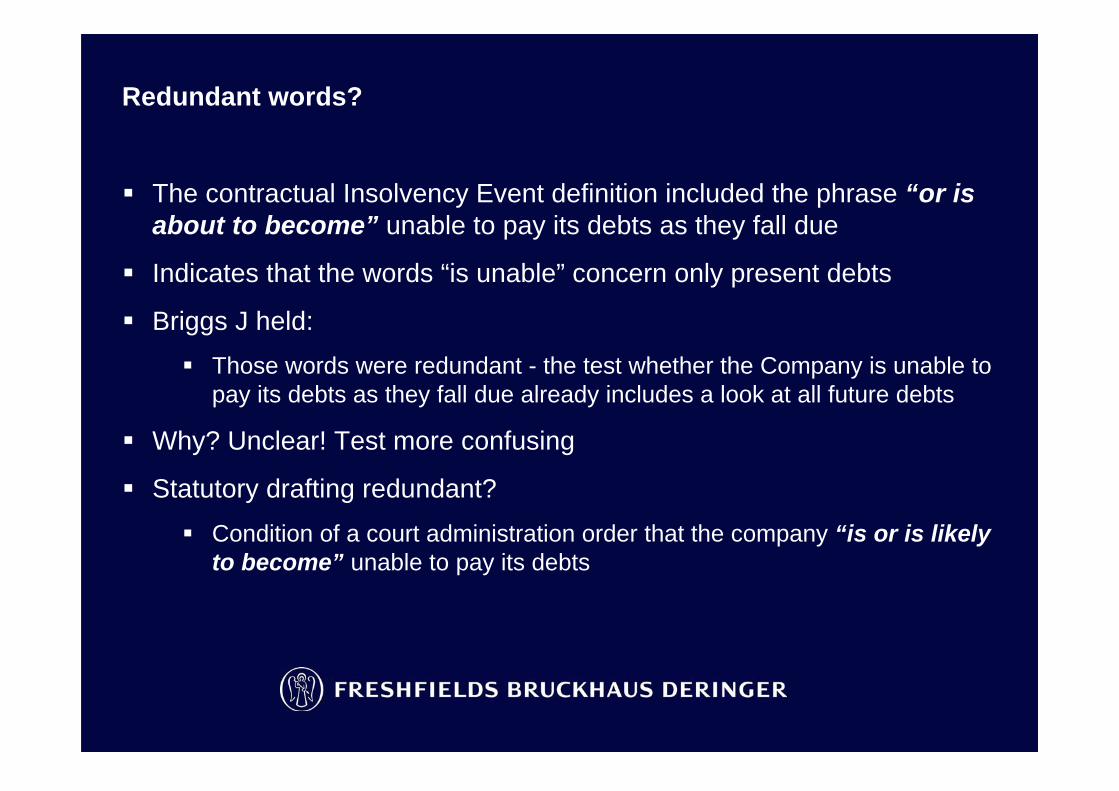

Redundant words?

The contractual Insolvency Event definition included the phrase “or is

about to become” unable to pay its debts as they fall due

Indicates that the words “is unable” concern only present debts

Briggs J held:

Those words were redundant - the test whether the Company is unable to

pay its debts as they fall due already includes a look at all future debts

Why? Unclear! Test more confusing

Statutory drafting redundant?

Condition of a court administration order that the company “is or is likely

to become” unable to pay its debts

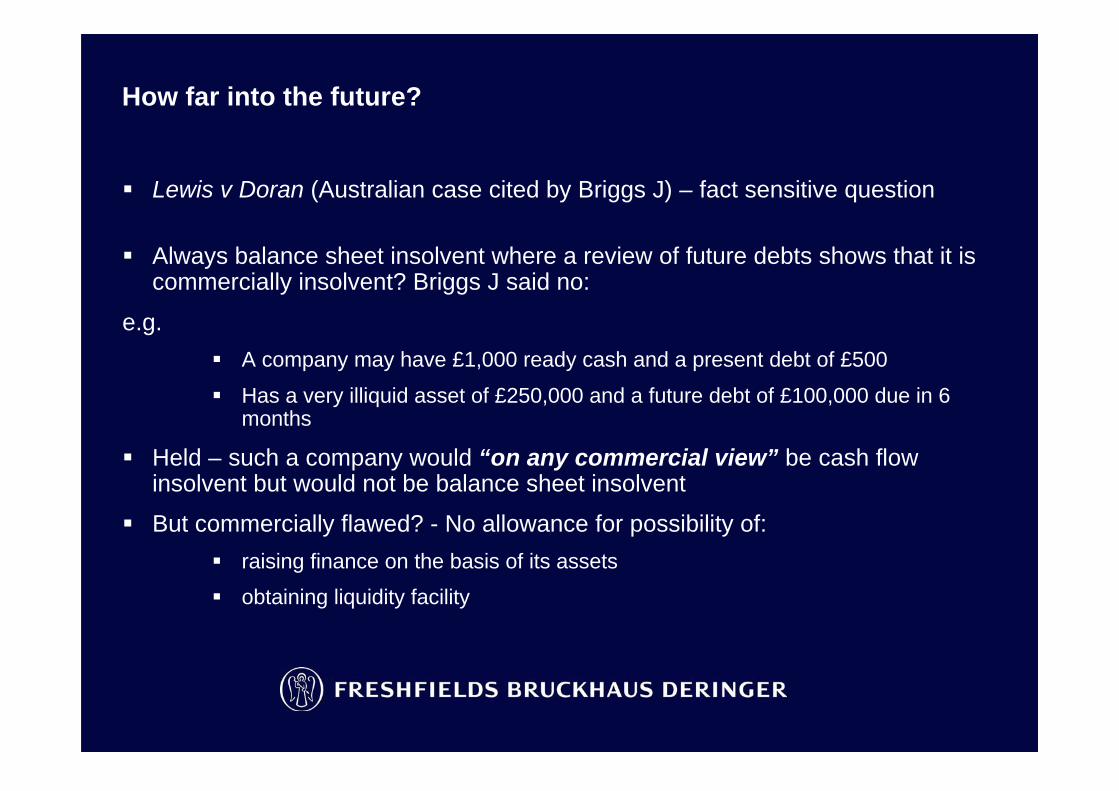

How far into the future?

Lewis v Doran (Australian case cited by Briggs J) – fact sensitive question

Always balance sheet insolvent where a review of future debts shows that it iscommercially insolvent? Briggs J said no:

e.g.

A company may have £1,000 ready cash and a present debt of £500

Has a very illiquid asset of £250,000 and a future debt of £100,000 due in 6months

Held – such a company would “on any commercial view” be cash flowinsolvent but would not be balance sheet insolvent

But commercially flawed? - No allowance for possibility of:

raising finance on the basis of its assets

obtaining liquidity facility

Implications – creditor’s new friend

Need careful consideration of contractual drafting – reference to s123(1)(e) maynow be breached earlier than both parties had expected!

Result: creditors may put pressure on debtors by suggesting a default eventhas occurred by referring to debts falling due in the future

Tool in restructuring or workouts:

to increase their leverage

to extract fees in return for waiver of the ‘default’

Used by those with an interest in company default

creditors may have bought credit or loan default swaps which trigger paymentswhen a company fails

The Future

Decision – good commercial decision, bad legal decision?

Makes test far harder to apply – confusion with balance sheet test

Application to trading companies? Limit Cheyne to facts/SIVs?

Creditors seeking financial information – Re COLT?

© Freshfields Bruckhaus Deringer 2008

This material is for general information only and is not intended to provide legal

advice.

LON2387739