Embed Size (px)

Citation preview

1

October 2015 ‧2015 年 10 月

ONC Corporate Disputes and Insolvency Quarterly

We are pleased to share with you our first ONC Corporate Disputes and Insolvency Quarterly

eNewsletter. This newsletter will be published quarterly (in the middle of every October,

January, April and July) to inform our clients, colleagues and friends about recent cases on

corporate disputes and insolvency. Apart from Hong Kong cases, discussion will also extend

to authorities from the U.K. and other parts of the Commonwealth. This first issue is relatively

long. However, future issues will be shorter as they are supposed to cover only a quarter’s

worth of new cases.

The cases are reported in a succinct manner and we endeavor to highlight the most

important legal points in the cases. It is of course no substitute for reading the full judgments

and should not be relied upon as definitive advice on any legal points.

Your comments and suggestions are most welcome.

ONC Lawyers

October 2015

我們欣然宣布,《ONC 企業糾紛及清盤案例季報》正式面世。這份刊物將每逢十月、一月、

四月及七月中刊發,為客戶、同業及各界友好匯報近期的企業糾紛及清盤案例。除了香港案

例,我們也會討論英國及其他英聯邦地區的案例。今期創刊號的篇幅較長,往後各期的季報只

會匯報當季的新案例,篇幅會較短。

本季報將精簡地匯報案件,因此只會重點講述案中最重要的法律要點,不能代替完整判詞,亦

不能倚賴作任何法律觀點的正式意見。

如對本季報有任何意見或建議,歡迎與我們聯絡。

柯伍陳律師事務所

2015 年 10 月

2

Factors for the court to consider in exercising discretion to approve scheme of arrangement involving foreign companies

1. Re LDK Solar Co Ltd [2015] 1 HKLRD 458

LDK Solar Co Ltd (“LDK Solar”) and its direct wholly-owned subsidiary, LDK Silicon &

Chemical Technology Co Ltd (“LDK Silicon”) were both incorporated in the Cayman Islands.

LDK Silicon Holding Co Ltd (“LDK Silicon Holding”), a company incorporated in Hong Kong,

was the wholly-owned subsidiary of LDK Silicon.

Due to financial distress, LDK Solar applied to the Grand Court of the Cayman Islands for its

own winding-up and appointment of joint provisional liquidators (“JPLs”). The JPLs reached

an agreement with the majority creditors in the form of various restructuring proposals

involving agreement governed by Hong Kong law and creditors incorporated in Hong Kong.

The schemes were approved by the required majority of creditors in class meetings.

At issue was whether the court had jurisdiction to sanction schemes of arrangement for

foreign companies and if so, whether such jurisdiction should be exercised.

Citing Re Drax Holdings Ltd [2004] 1 BCLC 10 with approval, Justice Lam considered that

the three core requirements in the context of winding up an unregistered company were only

relevant to the exercise of discretion of the court, rather than the existence of its jurisdiction.

Further, Justice Lam opined that the court can exercise its jurisdiction to approve a scheme if

it is satisfied that there is sufficient connection with Hong Kong, while the other two

requirements might not be relevant. In determining whether a sufficient connection has been

established, the judge held that this is a matter of judgment to be made in view of the

evidence as well as the object and purpose of the jurisdiction invoked.

A principal concern in the present case was whether there were connecting factors with the

jurisdiction so that the Hong Kong Schemes, if approved, would have a substantial effect. It

was noted that some of the claims were governed by Hong Kong law and a debt can only be

discharged under the law governing the debt. As such, if the restructuring is not sanctioned

in Hong Kong, there is a risk that the creditors might be able to enforce the debts in Hong

Kong. Further, given the fact that the Hong Kong schemes formed part of a larger cross-

border restructuring, Justice Lam was satisfied that in sanctioning the Hong Kong schemes,

comity would be fostered. In light of all the evidence, the Court concluded that the

connections with Hong Kong were sufficient to justify the exercise of the jurisdiction of the

court to sanction the schemes.

3

法院在行使酌情權批准涉及外國公司的

債務償還安排計劃時所考慮的因素

1. Re LDK Solar Co Ltd [2015] 1 HKLRD 458

LDK Solar Co Ltd(「LDK Solar」)及其直接全資附屬公司 LDK Silicon & Chemical

Technology Co Ltd (「LDK Silicon」)均為開曼群島註冊公司,而在香港註冊的 LDK

Silicon Holding Co Ltd(「LDK Silicon Holding」)是 LDK Silicon 的全資附屬公司。

LDK Solar 因財政困難而向開曼群島大法院申請自行清盤及委任聯合臨時清盤人。聯合臨時清

盤人與大多數債權人達成協議,採納多項涉及受香港法律管轄的協議及在香港註冊為法團的債

權人的重組建議。上述債務償還安排計劃在類別債權人會議中獲得所須的大多數債權人批准。

案件的爭議是:法院是否具有司法管轄權批准外國公司的債務償還安排計劃?如有,是否應行

使該司法管轄權?

林雲浩法官引用並認同 Re Drax Holdings Ltd [2004] 1 BCLC 10 一案,認為把非香港註冊公

司清盤的三個核心要求是關乎法院行使酌情權,而非關乎法院的司法管轄權存在與否。此外,

林官認為,如果法院信納有關公司與香港有充分關連,亦可行使其司法管轄權批准債務償還安

排計劃,其餘兩項要求並非必須。在判斷是否有充分關連時,法官裁定應從證據以及所援引的

司法管轄權的目標和目的來作出判斷。

本案的主要關注點是,有關公司與香港是否有關連因素,令香港的債務償還安排計劃一經批准

將具有實質作用。法院注意到,部分債權受香港法律管轄,而債務只能根據管轄該債務的法律

解除。因此,假如重組計劃在香港不獲批准,將有被債權人強制執行在香港的債務的風險。此

外,由於香港債務償還安排計劃是更大規模的跨境重組計劃的一部分,林官信納批准香港計劃

符合國際互讓原則。基於所有現有證據,法院裁定有關公司與香港有充分關連,法院有恰當的

理由行使司法管轄權批准債務償還安排計劃。

4

Does a minority shareholder have common law right to intervene and defend actions on behalf of the company?

2. Myers Management Consulting Limited v Topmix International Company Limited

[2015] HKEC 1319

The plaintiff obtained a default judgment against the defendants. When the judgment debt fell

due and was unpaid, the plaintiff presented a petition to wind up the defendant companies.

The Interveners, holding 50% of the shares in each of the defendants, applied to be added

as interveners in order to defend on behalf of the defendants in the actions and to set aside

the default judgment. Instead of relying on the statutory framework provided under s.732(3)

of the Companies Ordinance (Cap 622) (“CO”), the Interveners chose to resort to their

common law rights to intervene, the existence of which was disputed by the plaintiff.

Although no precedent of such cases were found and cited to the court, after a detailed

examination of the wordings of the CO, the court concluded that the CO confirms the

existence of the common law right of aggrieved shareholders to intervene in proceedings on

behalf of the companies. In particular, ss.732(6), 733(2)(b) and 736(1) of the CO explicitly

refer to the common law right to intervene in proceedings. Section 736(6) expressly states

that the statutory provisions do not affect “any common law right of a member of a

company…to…intervene in any proceedings to which the company is a party.”

Further, the court noticed a number of suspicious circumstances, in light of which the court

held that the Interveners had a real prospect of success. The default judgment was therefore

set aside. On 17 August 2015, leave to appeal was granted. So watch out for the appeal!

5

The Liquidator’ power to require production of documents under s.221(3) is narrower than his power of private examination under s.221(1) of Cap 32

3. Re China Medical Technologies Inc. (No 2) [2015] 2 HKLRD 27

In these winding-up proceedings, the provisional liquidators (“PLs”) applied under s.221(3) of

the Companies (Winding Up and Miscellaneous Provisions) Ordinance (Cap 32) for an order

against Tsang, a former director and chief officer of the subject Company to produce all

documents in relation to divorce proceedings involving Tsang, all bank statements for

accounts held in his name and all documents and bank statements of companies controlled

by him, upon finding that Tsang failed to make disclosure in two connected party transactions.

The PLs were of the view that such documents would shed light on transactions involving the

Company.

Section 221(3) provides that the court “may require [any officer of the company] to produce

any books and papers in his custody or power relating to the company…” The PLs argued

that “relating to the company” should be given the same meaning as “concerning the

promotion, formation, trade, dealings, affairs, or property of the company” in s.221(1), which

set out the matters on which a person could be examined on oath. Harris J declined to order

the production of documents sought and held that regard must be given to the fact that

different language was used in s.221(1) and (2) on the one hand and (3) on the other. The

interpretation of the PLs therefore went beyond that which the language bore and the

personal papers sought could not fairly be said to relate to the Company.

6

The criteria for granting and continuing a receivership order over a public company

4. Re Birmingham International Holdings Limited [2015] HKEC 1793

Birmingham International Holdings Ltd (the “Company”) was incorporated in Cayman Islands.

Its shares are listed on Hong Kong Stock Exchange. The Company is in a parlous state,

mainly due to the misconduct of Mr. Yeung, who is a significant shareholder of the Company.

Due to serious disagreement amongst the directors, receivers were appointed. Yeung

applied to have the receivership order discharged.

The court held that in a case where a public company is in a parlous state, the court should

adopt a forward-looking and constructive approach and decide what is best for the Company

and the shareholders as a whole without delay. The court found that the receivers were

making progress, doing a good job in keeping the Company afloat and taking actions to

recover its losses from the wrongdoers. Further, it has been uncovered that funds of the

Company were misappropriated by Yeung and another Yeung aligned director. Legal

proceedings have been commenced against Yeung and the two companies, which received

the misappropriated assets of the Company. If the order is discharged, it would allow Yeung

to meddle with the running of the Company, resulting in more litigation and probably hinder

the legal actions against him.

In light of all the circumstances, the order is continued.

7

對公眾公司發出及維持接管令的準則

4. Re Birmingham International Holdings Limited [2015] HKEC 1793

Birmingham International Holdings Ltd(「該公司」)在開曼群島註冊,其股份在香港聯合交

易所上市。該公司因為一名重要股東楊先生的不當行為而處於紛亂狀態,由於董事之間嚴重意

見分歧,法院就該公司委任了接管人。楊先生申請解除接管令。

法院認為,假如一間公眾公司處於紛亂狀態,法院應該從速採取前瞻性及具建設性的方針,決

定怎樣做才對公司及股東整體最好。法院認為接管人為該公司取得進展,令該公司能維持下

去,並採取行動向犯過者追討該公司的損失。此外,楊先生及另一名與他同一陣營的董事被發

現挪用公款,他和兩間接收被挪用資產的公司正被控告。假如解除接管令,楊先生便可以干涉

該公司的運作,引起更多訴訟,更可能妨礙對他提出的法律訴訟。

鑒於上述情況,法院裁定接管令維持有效。

8

Winding-up of listed company under s.212 of the Securities and Futures Ordinance in the interest of the public

5. Re China Metal Recycling (Holdings) Ltd (No 3) [2015] 2 HKLRD 415

On application of the Securities and Futures Commission (“SFC”), the Court of First Instance

ordered that China Metal Recycling (Holdings) Limited (the “Company”), a Hong Kong-listed

company, be wound up in the public interest. The said petition was the first public interest

petition of this sort.

The SFC alleged that the affairs of the Company involved a carefully planned and

sophisticated round robin funds flow scheme spanning Hong Kong, Macao, the Mainland and

the US. The scheme dated back to the time of the Company’s IPO prospectus in 2009 and

became larger and more complex in the subsequent years. As a result of the scheme, the

Company’s revenue and profit were greatly inflated.

Granting the petition, Harris J first considered the objectives and functions of the SFC, as set

out in ss.4 and 5 of the SFO and confirmed that it was clearly in the public interest that the

SFC sought orders from the court to advance and achieve those regulatory objectives.

Although the economic interests of creditors and minority shareholders were relevant

considerations, the principal concern was the interests of the investing public and the

integrity of the market.

The court identified that the dissemination of false or misleading financial information by the

Company was in contravention of ss. 298, 300 and 384 of the SFO, as well as section 342F

of the Old Companies Ordinance (Cap 32). Further, it was held that the more serious and

extensive the contravention is, the more stringent the remedy necessary to address it. In a

case where a listing was obtained by wholly dishonest fabrication of accounts, the

appropriate order would almost invariably be a winding-up order.

Given that the fraud was carefully planned, implemented on a massive scale and the

activities were not isolated wrongful acts, the court concluded that the present case fell firmly

in the category of cases in which the courts took the view that a winding-up order was

appropriate.

9

根據《證券及期貨條例》第 212 條

基於公眾利益把上市公司清盤

5. Re China Metal Recycling (Holdings) Ltd (No 3) [2015] 2 HKLRD 415

經證券及期貨事務監察委員會(「證監會」)申請,原訟法庭基於公眾利益命令在香港上市的

中國金屬再生資源(控股)有限公司(「該公司」)清盤。這是首宗以公眾利益為理由而提出

的清盤呈請。

證監會指該公司涉及橫跨香港、澳門、中國內地及美國進行精心策劃而複雜的循環現金流計

劃。該計劃早於 2009 年該公司的首次公開發售招股章程開始,其後數年變得日益龐大和複

雜。由於該計劃的緣故,該公司的收入及利潤大幅膨漲。

夏利士法官批准呈請時,首先考慮了《證券及期貨條例》第 4 及第 5 條列明的證監會目標及職

能,確定證監會請求法院頒令以促進及達成有關監管目標,明顯符合公眾利益。雖然債權人及

小股東的經濟利益是相關的考慮因素,但主要的關注點是公眾投資者的利益及市場的穩健性。

法院指出,該公司散播虛假或具誤導性的財務資料,違反《證券及期貨條例》第 298、300 及

384 條以及前《公司條例》(第 32 章)第 342F 條。此外,法院裁定,違規的情況越嚴重、

牽涉的範圍越廣,便需要越嚴厲的補救方法來處理。若一間公司是以完全不誠實地虛構的帳目

來取得上市地位,適當的命令幾乎必定是清盤令。

由於案中涉及經精心策劃、大規模進行的欺詐行為,有關活動並非個別不當行為,法院表示此

案正正是法院認為適合頒下清盤令的案件種類。

10

Can unpaid solicitors’ fees be admitted as proof for voting purpose under r.125 of Cap 32H?

6. Re Grande Holdings Ltd (No.1) [2015] 1 HKLRD 743

In this case, the provisional liquidators of Grande Holdings Ltd (the “Company”) admitted the

proof of debt of Sidley Austin LLP for voting purposes at the first meeting of creditors. The

fees were based on time spent and hourly rates charged. A creditor of the Company sought

to reverse the liquidators’ decision, arguing that the fees claimed were “unliquidated” debt

under r.125 of the Companies (Winding-up) Rules (Cap 32H) and consequently their proof

should not be admitted.

The liquidators’ decision to admit the proof of debt was reversed. Harris J was of the view

that for a claim of solicitors’ fee that have not been judicially assessed or agreed, a client had

a right to challenge the reasonableness of the fees charged; and the solicitor’s right to be

paid was for a reasonable sum, not a liquidated sum. In addition, there was no evidence as

to whether or not the Company objected to the fees billed.

11

The threshold requirement for misfeasance proceedings against liquidators

7. Re Shun Kai Finance Co Ltd [2015] 2 HKLRD 264

In 2003, Shun Kai Finance Company Limited (the “Company”) went into liquidation on the

petition of a judgment creditor Japan Leasing (Hong Kong) Limited (“Japan Leasing”). In

2006, the liquidator of the Company settled the legal proceedings against Japan Leasing with

the sanction of the court.

A shareholder of the Company alleged that the settlement was at a significant undervalue.

She, therefore, commenced, among others, misfeasance proceedings under s.276 of the

Companies (Winding Up and Miscellaneous Provisions) Ordinance (Cap 32) against the

liquidator.

The Court of Appeal affirmed the decisions of the Court of First Instance, holding that the

reference to “it appears” in s.276(1) indicated that there was a threshold requirement which

must be surmounted before the court was obliged to “examine into the conduct” of the

liquidator. The Court of Appeal clarified that the appropriate standard for an action under

s.276 should be a prima facie case, rather than an arguable case. Therefore, it must be

shown that there existed sufficient basis, which warranted an inquiry under s.276.

The Court of Appeal further emphasized that the court would not interfere with the liquidator’s

commercial decision unless there was some lack of good faith, error in law or principle, or

some real and substantive ground for doubting the prudence of the liquidator. The action was

dismissed, as the complaints were insufficient to cast doubt on the liquidator’s good faith and

prudence in reaching the settlement.

12

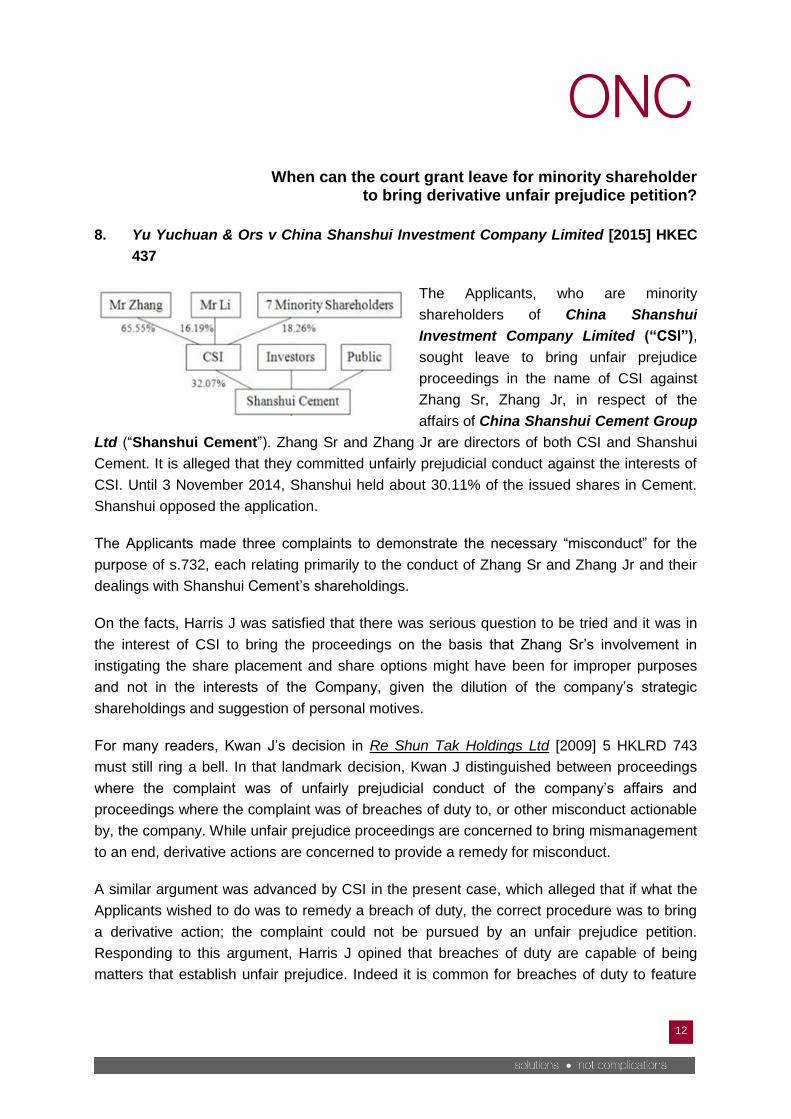

When can the court grant leave for minority shareholder to bring derivative unfair prejudice petition?

8. Yu Yuchuan & Ors v China Shanshui Investment Company Limited [2015] HKEC

437

The Applicants, who are minority

shareholders of China Shanshui

Investment Company Limited (“CSI”),

sought leave to bring unfair prejudice

proceedings in the name of CSI against

Zhang Sr, Zhang Jr, in respect of the

affairs of China Shanshui Cement Group

Ltd (“Shanshui Cement”). Zhang Sr and Zhang Jr are directors of both CSI and Shanshui

Cement. It is alleged that they committed unfairly prejudicial conduct against the interests of

CSI. Until 3 November 2014, Shanshui held about 30.11% of the issued shares in Cement.

Shanshui opposed the application.

The Applicants made three complaints to demonstrate the necessary “misconduct” for the

purpose of s.732, each relating primarily to the conduct of Zhang Sr and Zhang Jr and their

dealings with Shanshui Cement’s shareholdings.

On the facts, Harris J was satisfied that there was serious question to be tried and it was in

the interest of CSI to bring the proceedings on the basis that Zhang Sr’s involvement in

instigating the share placement and share options might have been for improper purposes

and not in the interests of the Company, given the dilution of the company’s strategic

shareholdings and suggestion of personal motives.

For many readers, Kwan J’s decision in Re Shun Tak Holdings Ltd [2009] 5 HKLRD 743

must still ring a bell. In that landmark decision, Kwan J distinguished between proceedings

where the complaint was of unfairly prejudicial conduct of the company’s affairs and

proceedings where the complaint was of breaches of duty to, or other misconduct actionable

by, the company. While unfair prejudice proceedings are concerned to bring mismanagement

to an end, derivative actions are concerned to provide a remedy for misconduct.

A similar argument was advanced by CSI in the present case, which alleged that if what the

Applicants wished to do was to remedy a breach of duty, the correct procedure was to bring

a derivative action; the complaint could not be pursued by an unfair prejudice petition.

Responding to this argument, Harris J opined that breaches of duty are capable of being

matters that establish unfair prejudice. Indeed it is common for breaches of duty to feature

13

amongst complaints in unfair prejudice petitions. There is, consequently, an overlap between

the subject matter of the two different types of proceedings. As such, the “proceedings”

available under section 733 of the Companies Ordinance (Cap 622) to deal with

“misconduct” can also include an unfair prejudice petition.

Leave was therefore granted to the Applicants to commence derivative proceedings by way

of unfair prejudice petition on the condition that the parallel common law derivative action

discontinued.

14

The role and function of interim receivers of shares in a company

9. 張才奎所託管中國山水投資有限公司股份相關員工、李延民所託管中國山水投資有限公

司股份相關員工 and 張才奎、李延民 HCA 1661/2014, HCA 1766/2014, HCA

2191/2014, HCA 623/2015, HCA 939/2015, HCA 1564/2015

By the decision dated 20 May 2015, Godfrey Lam J granted the application for the

appointment of interim receivers of certain shares in China Shanshui Investment Company

Limited (“CSI”), to which the plaintiffs claim to be beneficially entitled. In a subsequent

decision, Godfrey Lam J gave direction to the receivers that without obtaining further

directions of the court, the receivers do not seek to alter the composition of the board of

directors of China Shanshui Cement Group Ltd (“Shanshui Cement”).

The receivers applied to the court for direction as to how to vote at Shanshui Cement’s

incoming EGM, which is to consider and if thought fit to pass the resolution to remove all but

one existing directors and appoint seven new directors. If directions are granted, the

composition of the board of directors of Shanshui Cement will be fundamentally changed and

CSI will be left with no nominees on the board.

First of all, the court found that the function of a court appointed receiver is not so much to

restore profitability, rather it is to “hold the ring” between warring litigants until the disputed

issues are finally determined. Further, it was noted that a company is a trading entity and the

court will be in a difficult position to select those who are appropriate to conduct the

commercial affairs of a company. As such, the court should only interfere if it is absolutely

essential to do so. On the facts, the court found that what the receivers seek to achieve was

to restore the proper management of Shanshui Cement and hence its profitability. They were

not just protecting the value of a parcel of shares but also indirectly managing CSI and

Shanshui Cement.

Further, the court considered that the concerns relied on by the receivers, namely the

misconduct, incompetency of the existing directors, at best form serious issues to be tried.

Their factual bases were seriously contested. After all, the receivers’ proposal was not in the

interest of CSI and a complete “change of control” on the board could give rise to serious

financial consequences to Shanshui Cement. The application for direction was declined.

15

Where a company has mortgaged its property to its full value to a bank, the bank’s loans to the company after a winding-up petition

has been presented are not void as a post-petition disposition

10. Super Speed Ltd (in liquidation) v Bank of Baroda [2015] 2 HKLRD 965

Marshel Exports Limited (in liquidation) v Bank of Baroda [2015] 2 HKLRD 965

Super Speed Limited and Marshel Exports Limited (collectively, the “Companies”) were both

customers of Bank of Baroda (the “Bank”). The Companies granted legal charge/mortgage

over their properties in favor of the Bank to secure all monies in respect of general banking

facilities and interest.

Two petitions for the winding-up of the Companies were presented on 3 August 2012 (the

“Petition Date”) and the Companies were subsequently wound up. The Bank was informed

that the winding-up petitions had been presented. Nonetheless, the Bank continued to

advance loans to the Companies after the Petition Date.

The liquidators of the Companies contended that the post-petition loans were void under

s.182 of the Companies (Winding Up and Miscellaneous Provisions) Ordinance (Cap 32) and

were liable to be set aside.

Anthony Chan J, sitting as the trial judge, found that the properties of the Companies were

charged to their full values at all material times. Thus, there could not be any reduction of the

equity in the properties by reason of the post-petition loans. On appeal, Kwan J upheld the

decision and confirmed that s.182 of CWUMPO has no application where the disposition has

no impact on the creditors’ benefit or interest.

16

SFC successfully applied for court order against directors for causing a listed company to make an unjustified payment,

even though the directors made no personal gains

11. SFC v Yin Yingneng Richard & Others [2015] HKEC 86

First China Financial Network Holdings Limited (the “Company”), a Hong Kong listed

company, acquired a financial information services company from Fame Treasure Limited

(the “Seller”). After the completion of the acquisition, the Company issued an announcement

stating that there was before completion a mutual understanding and agreement between it

and the Seller that a dividend of RMB18.7 million would be distributed to the Seller. The

Securities and Futures Commission (“SFC”) alleged that the purported prior understanding

and agreement did not exist and as such, the directors of the Company were not entitled to

distribute the sum. The SFC took out a petition under section 214 of the Securities and

Futures Ordinance (Cap 571) for orders including a compensation order against the three

current and former directors.

The court ruled against all three directors, holding that no honest director could have acted

as they did. Of the three, one of the directors was also a shareholder of the Seller and

therefore stood to personally gain from the arrangement. The other two directors argued that

their lack of personal gain should act in their favor. However, it was dismissed by the court

and a compensation order was imposed upon all three directors.

17

證監會成功向法院申請就董事

安排上市公司作出不當付款而頒令

,儘管董事沒有個人得益

11. SFC v Yin Yingneng Richard & Others [2015] HKEC 86

在香港上市的首華財經網絡集團有限公司(「該公司」)向健禮有限公司(「賣方」)收購了

一間財經資訊服務公司。收購完成後,該公司發出公告,表示雙方在交易完成前已達成共識及

協議,賣方將獲發人民幣 1,870 萬元的股息。證券及期貨事務監察委員會(「證監會」)指所

謂的事先共識和協議根本不存在,因此該公司的董事無權分配該款項。證監會根據《證券及期

貨條例》(第 571 章)第 214 條提出呈請,要求頒令三名現任及前任董事作出賠償等。

法院裁定三名董事全部敗訴,認為一名誠實的董事不可能作出他們所作的行為。三名董事中,

其中一名同時是賣方的股東,因此在有關安排中涉及個人利益;其餘兩名董事亦指自己並無個

人得益,應獲勝訴。然而,法院並不接納,並頒令全部三名董事作出賠償。

18

The ability to bring a derivative action in relation to a foreign company is a substantive matter of foreign law

12. Charles Zhi v SRK Consulting Ltd & Ors [2015] HKEC 1814

The plaintiff is a shareholder of Siberian Mining Group Company Ltd (the “Company”), which

was incorporated in the Cayman Islands. For some reason, the plaintiff brought a common

law derivative action based on the “fraud on the minority” exception against D4 and other

defendants. D4 sought to strike out the action and challenged the plaintiff’s locus standi.

The court noted that when such a challenge is made, the burden lies firmly on the plaintiff to

produce evidence to establish the requisite prima facie case. The plaintiff has to establish not

only that there exists a viable cause of action vested in the Company which, if made good,

would establish a fraud on the minority, but also control of the Company by the alleged

wrongdoers. The plaintiff, however, failed to adduce credible evidence.

Moreover, the court observed that “the ability to bring derivative actions in Hong Kong is a

matter for the law of the place of incorporation of the company” and the derivative actions

brought on behalf of a Cayman Islands company require leave of the Cayman court. As no

leave had been obtained from the Cayman court, the court was bound to strike out the action

against D4.

19

Limits on the court’s power to assist foreign liquidators

13. Singularis Holdings Ltd v PricewaterhouseCoopers [2015] 2 WLR 971

Singularis Holdings Limited (“Singularis”) was a company incorporated in the Cayman

Islands and was wound up by the Grand Court of the Cayman Islands.

PricewaterhouseCoopers (“PwC”), which was registered in Bermuda, were the auditors of

Singularis. Being unable to obtain certain documents from PwC under the law of Cayman

Islands, the liquidators of Singularis applied to the Bermudan Court for orders against PwC

for the production of PwC’s audit work papers under s.195 of the Bermuda Companies Act

1981 (“section 195”). However, this provision only applies to companies that are wound up

by the Bermudan Court.

In the first instance, the Bermuda Supreme Court granted the disclosure order by applying

section 195, on the basis that the court has common law power to assist foreign liquidators.

PwC appealed and the decision was set aside. The liquidators appealed to the Privy Council,

which was unsuccessful.

The Privy Council reaffirmed the principle of “modified universalism”, i.e. a common law

power to assist a foreign winding up proceedings so far as the court properly can, which

does extend to assisting a foreign court of insolvency jurisdiction by ordering the production

of information which is necessary for the administration of a foreign winding up. This power,

however, is subject to certain limits.

Importantly, it was noted that such power is limited to only enabling liquidators to do what

they would be entitled to do under the laws by which they are appointed and it’s only

available when necessary for the performance of the officeholder’s function. Moreover, any

order must be consistent with the substantive law and public policy of the assisting court.

The Privy Council held that the Bermuda Court of Appeal was correct in finding that the

disclosure order should be set aside on the ground that the Cayman Court had no jurisdiction

to make a similar order. The Privy Council also ruled that it was wrong to apply section 195,

because the Bermuda Court does not have the power to impose a statutory regime in

circumstances where the statute does not apply.

20

The case illustrates the approaches the court would take in addressing unfair prejudice suffered by the shareholders

14. Re Asia Television Ltd [2015] 1 HKLRD 607

ATV held a domestic free television program service licence (the “Licence”). Wong Ching

(“Wong”), a Mainland businessman, acquired the shareholdings in Panfair, Dragon Viceroy

and China Light and thus controlled 52.42% of the shares of ATV. But Wong did not satisfy

the residence requirement under the Broadcasting Ordinance (Cap 562). To circumvent the

residency restriction, Wong sold his shareholdings in the three companies to BK. As a result,

Wong and BK became the ultimate majority shareholder of ATV. P held the remaining shares

in ATV.

A chain of incidents then ensued. Eventually, P presented an unfair prejudice petition under

s.168A of the Companies (Winding Up and Miscellaneous Provisions) Ordinance (Cap 32),

seeking orders for the appointment of managers over ATV and the sale by Panfair of its

shares in ATV to an independent third party, so as to change the control of the majority

shareholder at board level.

Harris J noted that Wong took an active role in directing ATV’s affairs and he appointed 6

directors, including JS, to the board. Further, under the disguise of a consulting agreement

between Wong and JS, Wong in fact exercised de facto control over ATV. The

Communications Authority therefore intended to recommend that the Licence not be

renewed when it expired on 30 November 2015.

Ruling in favor of P, Harris J stated that unfairness might consist of a breach of the rules or in

using the rules in a manner which equity would regard as contrary to good faith. The articles

of the company and any shareholders agreement would form the criteria by reference to

which unfairness was to be assessed, as would a director’s failure to comply with his or her

fiduciary duties. Once unfair prejudice was proved, the court had a wide discretion in

determining the relief to be granted to do what was fair and equitable. It was held that, in the

present case, what needed to be remedied was the conduct which had led to the Authority’s

recommendation of non-renewal of the Licence and this could only be done by removing

control from the hands of the Wong aligned directors. As such, Harris J ordered that

managers be appointed over ATV and Panfair’s shares in ATV be sold to an independent

third party.

21

Can dishonest directors plead illegality when being sued by the company?

15. Jetivia SA & Anor v Bilta (UK) Limited (in liquidation) & Ors [2015] UKSC 23

Bilta (UL) Limited (“Bilta”) is an English company which was ordered to be wound up on the

application of HM Revenue & Customs. Through its liquidators, Bilta brought proceedings

against its two former directors, a Swiss company, Jetivia SA, and its chief executive.

In summary, Bilta alleged that, between April and July 2009, the two directors caused Bilta to

engage in fraudulent trading. As a result of the fraud, Bilta had a claim for damages against

the directors. The directors maintained in response that Bilta was, through its directors and

shareholders, party to the illegality, which precluded it from pursuing the claim.

The key question for the UK Supreme Court was whether the company is barred from suing

the directors for losses caused by their breach of fiduciary duty by virtue of the ex turpi

doctrine, also known as the “illegality defence”.

The Supreme Court firmly rejected the contention, holding that the dishonest directors, and

their associate, cannot rely on their own wrongdoings to escape liability. In particular, the

court held that “where a company has been the victim of wrong-doing by its directors, or of

which its directors had notice, then the wrong-doing, or knowledge, of the directors cannot be

attributed to the company as a defence to a claim against the directors by the company’s

liquidators, in the name of the company and/or on behalf of its creditors.”

Further, the Supreme Court found that section 213 of the Insolvency Act 1986 (equivalent to

section 275 of the Companies (Winding-up and Miscellaneous Provisions) Ordinance (Cap

320)) has extra-territorial effect. Hence, it was held that a contribution could be sought from

Jetivia and its chief executive.

22

Can directors rely on exculpatory clauses in the company’s constitution to be relieved of liability for their wrongful acts?

16. Weavering Macro Fixed Income Fund Limited (in Liquidation) v Stefan Peterson

and Hans Ekstrom (unreported, CICA, 12 February 2015)

Weavering Macro Fixed Income Fund Limited (the “Fund”) was founded by Magus Peterson.

The directors were his brother and step-father. The Fund’s investment activities were

contracted out to an investment manager, an entity owned by Peterson. The Fund collapsed

in 2009 and subsequently went into liquidation.

The directors were unaware of the fraud being perpetrated by Peterson. In fact, the court

found that they exercised no supervision over the running of the Fund whatsoever.

Unlike the position in England and Hong Kong, exculpatory clauses, which operated to

contractually relieve directors of liability for their actions, are permissible in the Cayman

Islands. In fact, the Fund’s constitutional document provided an indemnity for the directors

which covered liability for any wrongful or negligent acts or omissions unless it was due to

“wilful neglect or default”.

The Cayman Islands Grand Court found that the negligence amounted to “wilful neglect or

default” and so held that the directors could not avail themselves of the indemnity. The

directors appealed. While affirming the original findings of breach of duty by the directors, the

Court of Appeal found that the directors had acted in the belief that they were complying with

their duties, and accordingly held that while they had been negligent in the performance of

their duties, they had not acted in “wilful neglect or default”. The earlier judgment against the

directors was set aside.

Readers are reminded that under the Hong Kong Companies Ordinance (Cap 622), a

company is prohibited from indemnifying directors for breach of due care and skill to the

company.

23

Recent Singaporean decision brings clarity to the liquidator’s power to assign the fruits of a cause of action

17. Re Vanguard Energy Pte Ltd [2015] SGHC 144

Vanguard Energy Pte Ltd (“Vanguard”) had filed three actions in the High Court prior to

being placed into compulsory winding up on 21 November 2014, and had also identified

various other potential claims (the “Claims”). Given that Vanguard had insufficient assets, the

liquidators were unwilling to proceed with the Claims without an indemnity or funding from a

third party. Three shareholders of Vanguard, one was a director, and the other two were

former directors, offered to fund the litigation to allow Vanguard to proceed with the Claims.

The High Court was requested to consider the application for approval of the terms of an

assignment of proceeds agreement (the “Assignment Agreement”), which provided for the

sale of the rights to certain proceeds of the Claims, capped at the amount of funding

provided by the assignees.

Section 272(2)(c) of the Singapore Companies Act empowers the liquidator to “sell the

immovable and movable property and things in action of the company”. In holding that the

fruits of a cause of action could be sold under section 272(2)(c), the High Court was

persuaded by the English and Australian authorities in which it had been held that the share

of the fruits of an action may be regarded as property of the company which may be sold

under the liquidator’s statutory power of sale, especially since the relevant provisions in both

jurisdictions were similar to section 272(2)(c).

Further, the court found that a liquidator’s sale of the fruits of a cause of action is immune

from the doctrine of maintenance and champerty because section 272(2)(c) is a statutory

exception to that doctrine. In any event, the Assignment Agreement did not offend the

doctrine, as the assignees had a genuine commercial interest in the litigation and the

liquidators retained substantial control of the litigation and the assignees would not be in a

position to influence the outcome of the litigation.

24

The common law “double derivative” action remains available

18. Bhullar v Bhullar [2015] EWHC 1943

The claimant, Inder, was a minority shareholder in the parent company, BL, alongside with

his brother Jat, and their mother Rajinder. BL wholly owned two subsidiaries, namely BDL

and BBL. Jat and Rajinder were directors of BL and the subsidiaries. Crucially, Inder was not

a shareholder in the subsidiaries and could not rely on the statutory derivative claim regime,

which is only available to registered shareholders in companies, to pursue his claim. As such,

Inder applied for permission to continue a common law double derivative claim comprising

two allegations of wrongdoings by Jat.

The court, first, considered whether it did in fact have jurisdiction in relation to a double

derivative claim in light of the statutory regime introduced for normal derivative claims in the

Companies Act. Following the earlier decision of Universal Project Management Services Ltd

v Fort Gillicker Ltd [2013] Ch 551, the court found that its jurisdiction in relation to common

law double or multiple derivative claims had survived the introduction of the statutory regime.

The court then went on to consider whether permission to continue derivative claim should

be granted. After a detailed consideration of all the relevant issues, the court was satisfied

that permission to continue a derivative action in respect of one claim should be granted.

Finally, the court considered whether Inder should be indemnified out of the assets of BBL

and BDL for his costs in pursuing the derivative claims against Jat on their behalf. On the

facts of the case and considering in particular that there was likely to be a negotiation

between Inder and Jat as to a formal split of the business, the court chose to depart from the

usual principles of making a pre-emptive order of a costs indemnity to a claimant who was

granted permission to pursue the derivative claim.

Unlike English Companies Act, the statutory derivative action regime under Hong Kong

Companies Ordinance (Cap 622) not only applies to proceedings brought by a member of a

company, but also provides for double or multiple derivative actions.

25

Does acquisition of a minority shareholder’s shares by the majority amount to unfairly prejudicial conduct?

19. Arbuthnott v Bonnyman and Ors [2015] EWCA Civ 536

The appellant, along with others, was a founder shareholder of a company governed by

articles of association and a shareholders’ agreement (the “SA”). The SA provided that if a

founder majority agreed to pursue an exit, the shareholder would agree to sell his shares on

the same terms as those offered to the other shareholders. When the appellant and other

founding members approached retirement, members intending to continue with the business

offered to purchase all of the shares in the company. All retiring members accepted, except

the appellant. The remaining members then altered the company’s articles of association to

enable the buyout to proceed without the appellant’s consent. The appellant presented an

unfair prejudice petition under section 994 of the Companies Act 2006.

Dismissing the appeal, the court looked at the terms of the SA as to exit strategy and the

articles of association together. It held, on the facts, that amendments to the articles were no

more than a “tidying-up” exercise with no evidence of bad faith or improper motive and that

the amendment to allow the buyout to proceed was not inconsistent with original

arrangements between the founding members.

The acquisition of the shares in the company by the majority of members was in accordance

with and contemplated by the original commercial bargain struck between the shareholders.

It was not now open to the minority shareholder to seek to rewrite that bargain to achieve a

new deal. The Court of Appeal emphasized that a member of a company will not normally be

entitled to complain that the conduct of the company’s affairs is unfair if it is consistent with

the agreement between the shareholders. The appeal was dismissed.

26

The establishment of 2nd core requirement is not a necessary precursor to the jurisdiction to wind up a foreign company

20. Perfect Direct Ltd v Dejin Resources Group Co Ltd [2015] HKEC 1234

Dejin Resources Group Co Limited (the “Company”) was incorporated in the BVI. Its shares

are listed on the Hong Kong Stock Exchange. The Company is registered as a non-Hong

Kong company. In 2010, the Company issued two series of convertible notes. The Petitioner

is one of the noteholders. When the notes matured in 2013, the Company was not able to

pay the Petitioner the amount due. As a consequence, the Petitioner applied to wind up the

Company on the ground of insolvency.

The Company contended that the three core requirements in Re Yung Kee Holdings Ltd

[2014] 2 HKLRD 313 must be satisfied before the court has jurisdiction to wind up a foreign

company. It was alleged that neither the 2nd nor 3rd core requirements have been satisfied.

But it was accepted by the Company that jurisdiction may exist despite the 3rd core

requirement not being established. But it contended that there is no such flexibility over the

2nd core requirement.

The court first clarified, citing Re China Medical Technologies Inc [2014] 2 HKLRD 997, that

the three core requirements went to the question of discretion rather than the question of

jurisdiction. Further, the court held that it was not inevitably necessary to establish the 2nd

core requirements in order to exercise the jurisdiction to wind up a foreign company. The

judge referred to the comments of Harris J in Re Pioneer Iron and Steel Group Co Ltd [2013]

HKEC 317 that “the core requirements constitute guidance as to the circumstances in which

the discretion should be exercised and their application can be moderated if the

circumstances clearly call for it.” As such, the question must be considered on the basis of

the entirety of the company’s overall connection to Hong Kong.

On the facts, the court was satisfied that there was sufficient connection to justify the

exercise of the jurisdiction, such as the Company being listed and having its principal place

of business in Hong Kong. In addition, the court was convinced that the 2nd and the 3rd core

requirements were in fact established.

However, the petition was dismissed at the end as the court found that there was a bona fide

dispute on substantial ground.

27

Is estoppel preventing company taking limitation defence binding on liquidator?

21. Re Leco Watch Case Manufactory Ltd [2015] 2 HKLRD 87

The Applicant and Mr. Yau were long-time friends and business associates. The Applicant

claimed that on 1 June 2005, he made a loan to Mr. Yau’s company (the “Company”), which

was agreed orally and evidenced only by a cheque for HK$580,000. Despite numerous

requests for repayment, Mr. Yau always replied “let’s discuss later”. Subsequently, the

Company went into voluntary winding-up and the Applicant lodged a proof of debt with the

Liquidator on 25 January 2013, which was rejected. The Applicant applied to reverse the

Liquidator’s decision.

The court held that if a person makes a loan without specifying when or in what

circumstances it has to be repaid, he must require payment within 6 years or the right to

recover money is lost. However, the Company is estopped from relying on a limitation

defence, because Mr. Yau promised the Applicant orally from time to time that the Company

would settle the loan. Further, the court held that the estoppel was binding on the Liquidator.

The Applicant was entitled to be repaid the money advanced and, but for the requests to wait,

it was reasonable to assume he would have acted to obtain repayment. Admitting his proof of

debt is not unjustly prejudicial to the interests of other creditors.

The Liquidator’s adjudication was reversed.

28

Hong Kong Court of Appeal confirmed that ad valorem fees were payable on the conversion of compulsory

liquidation to creditors’ voluntary winding-up

22. Re MF Global Hong Kong Ltd [2015] 2 HKLRD 325

In October 2012, Harris J ordered the compulsory liquidations of MF Global Hong Kong

Limited and MF Global Holdings Hong Kong Limited (collectively the “Companies”) be

converted to creditors’ voluntary winding-up. The orders provided for the appointment of the

then provisional liquidators (the “PLs”) as liquidators of the Companies and for the

realizations made by the PLs up to the date of the conversion to be paid to them as

liquidators “without any deduction being made in respect of ad valorem fees”. The Official

Receiver appealed.

Relying on Re Lehman Brothers Securities Asia Ltd (No 2) [2010] 1 HKLRD 58, the PLs

argued that having been appointed under s.193 of the Companies (Winding Up and

Miscellaneous Provisions) Ordinance (Cap 32) (‘CWUMPO”), the PLs were not “liquidators”

within the meaning of s.2(1) of the CWUMPO.

Allowing the appeal, the Court of Appeal reconsidered the interpretation of s.2(1) of the

CWUMPO in Lehman Brothers (No 2) and decided that such interpretation should no longer

be adopted. Barma JA accepted that the difference between the position of provisional

liquidator in the periods before and after the making of the winding up order is such that

s.2(1) shall include all three types of post-winding up provisional liquidators. Notwithstanding

that the PLs were initially appointed under s.193, following the making of the winding-up

orders in respect of the Companies, they held their office as a post-winding up PLs by virtue

of s.194(1)(aa). As such, they are caught by the provisions pertaining to ad valorem fees.

29

Only in exceptional circumstances will the court appoint independent auditor after deciding to grant leave but before derivative action is actually on foot

23. Kan Sau Lan v Kin Lee Construction Co Ltd [2015] 1 HKLRD 1015

The plaintiff is a shareholder and director of the defendant Company. She applied for leave

to bring a statutory derivative action on behalf of the Company. In addition, she applied for an

order that an independent auditor be appointed to investigate and report to the court on the

Company’s financial position. The Company did not oppose the plaintiff being granted leave

to bring a derivative action, but opposed the appointment of an independent auditor.

The court noted that the exercise of the power of appointment by the court under s.737(2) of

the Companies Ordinance (Cap 622) would depend on which types of proceedings the court

was dealing with. Section 737(1)(a) referred to the actual derivative proceedings instituted by

a member after obtaining leave of the court to do so; or proceedings already on foot involving

the company which a member had obtained leave to intervene in. On the other hand,

s.737(1)(b) referred to an application for leave for the purposes of s.732(1),(2) or (3).

The present case was still at the stage of s.737(1)(b). In deciding whether it was necessary

to appoint an independent investigator at this stage, the court would consider whether the

obtainment of such an investigation report was reasonably necessary to (a) assist the court

in arriving at a correct decision of either granting or refusing leave or (b) enable the applicant

to adequately frame at least a prima facie case in the writ to be issued if leave was granted.

Only in exceptional circumstances would the court exercise the power of appointment after

deciding to grant leave but before derivative action was actually on foot.

The court found that the plaintiff was able to frame her case with reasonable precision. There

was no necessity at this stage to appoint an independent auditor to make the wide ranging

investigation sought. When the derivative action was properly instituted pursuant to the leave

granted, the court would arrive at the situation envisaged in s.737(1)(a). The court would

then consider whether it was just and convenient for the fair disposal of the derivative action

to order such an investigation.

The plaintiff’s application for leave to bring the statutory derivative action was allowed. The

application for the appointment of an independent auditor was dismissed.

30

“Value judgment” engaged, even when the funder is of commercial character

24. Re Company A HCCW 384/2006

The Liquidators of 7 Companies applied for leave to enter a funding agreement. The

intended funder is a Cayman incorporated fund. The funder has no other interest in the

proposed proceedings but that under the funding agreement.

Harris J observes that there is no direct authority in Hong Kong on “the extent to which, if at

all, the commercial character of the funder effects an assessment of whether or not the

proposed funding agreement infringes the common law rules against maintenance and

champerty.”

It is recognized that it is objectionable if the funding litigation is for the purposes of making a

profit rather than enforcing a right. But Harris J refers to the judgment of Ribeiro PJ in Unruh

v Seeberger [2007] 10 HKCFAR 31 and confirms that in determining whether a particular

arrangement infringes the rules against maintenance and champerty the court must weigh all

the considerations and no one consideration is necessarily determinative.

In the present case, Harris J is satisfied that the Liquidators remain in control of the intended

litigation and there is limited risk of the funder being able to pressure the Liquidators or the

lawyers to conduct the litigation improperly. His Lordship also recognizes that it is desirable

that the claim be pursued and there is no other practical way to fund the litigation.

Order sought is granted.

31

即使訴訟資金提供者屬商業性質仍採用「價值判斷」

24. Re Company A HCCW 384/2006

七間公司的清盤人向法院申請准許訂立一份為訴訟籌資的協議。資金提供者是一個在開曼群島

註冊的基金,它除了在籌資協議下有利益外,在案件中並無其他利益。

夏利士法官注意到,香港並無案例直接訂明「資金提供者的商業性質是否影響對於建議的籌資

協議是否違反普通法禁止助訟及包攬訴訟的規則的評估以及(如有)影響的程度。」

法院認同,如果為訴訟提供資金的目的是牟利而非強制執行一項權利,那是不妥當的。但夏利

士法官引述李義法官在 Unruh v Seeberger [2007] 10 HKCFAR 31 一案的裁決,確認在判斷某

項安排是否違反禁止助訟及包攬訴訟的規則時,法院必須衡量所有考慮因素,沒有任何一項考

慮因素是必然具決定性的。

在本案中,夏利士法官信納擬進行的訴訟仍然由清盤人控制,而且資金提供者能夠迫使清盤人

或律師不當地進行訴訟的風險有限。法官亦認同清盤人宜提出有關申索,而且並無其他切實可

行的方法能為訴訟提供資金。

因此,法院發出清盤人請求的命令。

For enquiries, please contact our Litigation & Dispute Resolution Department:

E: [email protected] T: (852) 2810 1212 W: www.onc.hk F: (852) 2804 6311

19th Floor, Three Exchange Square, 8 Connaught Place, Central, Hong Kong

Important: The law and procedure on this subject are very specialised and complicated. This article is just a very

general outline for reference and cannot be relied upon as legal advice in any individual case. If any advice or assistance is needed, please contact our solicitors.

Published by ONC Lawyers © 2015