Embed Size (px)

Citation preview

Decimal Trading and Market Impact

Sugato Chakravarty

Purdue University, West Lafayette, IN 47907 Tel: (765) 494 6427

E-mail: [email protected]

Stephen P. Harris Bridge Information Systems

Tel: (314) 468-8292 E-mail: [email protected]

Robert A. Wood University of Memphis, Memphis, TN 38152

Tel: (901) 755-8322 E-mail: [email protected]

Version 2.1: March 29, 2001

Abstract

Using high-frequency data and a carefully constructed 1-1 matched sample of control (non decimal) stocks, we isolate the effects of decimalization for a sample of NYSE-listed common stocks trading in decimals. We find that decimalization has resulted in significantly lower quoted and effective bid/ask spreads and that the most popular quoted spread is 1 cent. The available depths at the best bid and ask prices are also significantly lower. Together, these spread-depth results deliver a mixed verdict on market liquidity after decimalization. We find that decimalization has resulted in significant increases (decreases) in relatively smaller size (larger size) trades and trading volume. The frequency of quote updates and autoquotes in decimal stocks following decimalization has also increased significantly. Regional stock exchanges also appear to be significantly more active in competing for order flow. Our results have important research and policy implications.

JEL classification: Keywords: decimalization, bid/ask spread, trading, stock exchange

Acknowledgements: Please direct all comments to Chakravarty. We thank Robert Battalio, Tarun Chordia, Bill Christie, Mike Cooper, Amy Edwards, Gene Finn, Melinda Gigante-Carlson, Michael Goldstein, Robert Jennings, Ananth Madhavan, Tim McCormick, Eric Sirri, George Sofianos, Robert Wood Jr., and Robert Van Ness, for comments on earlier drafts, Wonil Hwang and Dan Zhou for research assistance, and Stephen Harris of Bridge Information Systems for providing some of the data. An earlier version of this paper was titled “The Effect of Decimal Trading on Market Liquidity.” Sadly, we alone are responsible for any remaining errors.

Decimal Trading and Market Impact

Abstract

Using high-frequency data and a carefully constructed 1-1 matched sample of control (non decimal) stocks, we isolate the effects of decimalization for a sample of NYSE-listed common stocks trading in decimals. We find that decimalization has resulted in significantly lower quoted and effective bid/ask spreads and that the most popular quoted spread is 1 cent. The available depth at the best bid and offer prices is also significantly lower. These spread-depth results together deliver a mixed verdict on market liquidity after decimalization. We find that decimalization has resulted in significant increases (decreases) in relatively smaller size (larger size) trades and trading volume. The frequency of bid/ask quote updates and autoquotes in decimal stocks following decimalization has also increased significantly. Regional stock exchanges also appear to be significantly more active in competing for order flow. Our results have important research and policy implications.

JEL classification: Keywords: decimalization, bid/ask spread, trading, stock exchange

3

“The theory is straightforward: As prices are quoted in smaller and smaller increments, there are more opportunities and less costs for dealers and investors to improve the bid or offer on a security. As more competitive bidding ensues, naturally the spread becomes smaller. And this means better, more efficient prices for investors.”

Arthur Levitt, Chairman SEC. March, 2000.

1. Introduction

Between August 28, 2000, and January 29, 2001, the New York Stock Exchange (NYSE),

through a series of incremental steps, began trading and quoting all its listed securities in

increments of a penny. Decimalization had finally arrived in Wall Street! A two-hundred-year

tradition of trading in fractions was now officially history.

According to the NYSE, the reduction in minimum price increment to sixteenths, in June

1997, was but an interim step in a move toward the decimalization of prices and price

increments (Jones and Lipson (2000)). And while it is tempting to think of decimalization as

merely a continuation in the process of tick size reduction, it is actually much more than just

that. While the move to sixteenths resulted in a doubling of the price points or “ticks”, the

move to decimals (from sixteenths) results in a six-fold increase in ticks.1 Also, a unique, and

potentially dangerous, aspect of decimalization is that for as little as 1 cent per share (as

compared to about 6.25 cents a share under sixteenths), intermediaries could step in front of

public limit orders in what amounts to “front running.” If the stock heads down after this

purchase, these investors could simply sell to the public limit orders and be none the worse for

it. It is, therefore, conceivable that the supply of liquidity from the investing public in the form

1 A report by the Securities Industry Association (SIA) and SRI Consulting group, prepared in early 2000, before the first phase of the decimal pilot, reveals that the minimum price variation of a penny was expected to have a more significant impact on share volume and the number of trades and quotes than during the previous switch over to sixteenths: specifically, that the move to decimals was expected to result in a 139% increase in trades, an 80% increase in quotes and a 9% increase in share volume.

4

of public limit orders may also dry up. Conversely, with decimalization it will be easier for

institutional investors to jump in front of the queue with limit orders, supplying liquidity rather

than demanding it (thereby acting as pseudo-dealers) and, in the process, earning the spread

rather than paying it. Which effect will ultimately dominate is unclear.

The NYSE's board approved conversion to decimal pricing in June 1997 with the goal of

making prices more easily understood by investors, reducing spreads and bringing the United

States into conformity with international practices. The importance of liquid markets is of

paramount importance to both suppliers and demanders of capital as well as regulators

entrusted with the mandate of maintaining a fair and orderly market. While there is little

debate that prices are easily understood under the decimal system where one does not have to

pause momentarily and wonder if 5/8 is greater than 9/16, for example, whether or not this has

actually impacted market liquidity (and its various facets) is an empirical issue and is a focus of

the current paper.

Many stock exchanges have recently reduced their minimum ticks. And despite such

changes being studied extensively, both theoretically and empirically, its appropriateness

remains an open question.2 Of particular relevance to the current paper is Bacidore’s (1997)

investigation into the impact on market quality associated with Toronto Stock Exchange’s

switching to decimal trading on April 15, 1996. He finds that for stocks whose minimum tick

was reduced from one-eighth dollar to five cents, such reduction decreased spreads, while

2Examples of theoretical research include Grossman and Miller (1988), Brown, Laux and Schachter (1991),

Hart (1993), Chordia and Subrahmanyam (1995), Peake (1995), Battalio and Holden (1996), Bernhardt and Hughson (1996), Kandel and Marx (1996), Cordella and Foucault (1996), O’Connell (1997), Harris (1994, 1997), Seppi (1997), and Anshuman and Kalay (1998). Examples of empirical research include Crack (1994), Ahn, Cao and Choe (1996), Bacidore (1997), Bessembinder (1997), Huson, Kim and Mehrotra (1997), Porter and Weaver (1997) and Ahn, Cao and Choe (1998), Ronen and Weaver (1998), Bollen and Whaley (1998), Ricker (1998), Goldstein and Kavajecz (2000), Jones and Lipson (2000)).

5

liquidity was not adversely affected and trading volume did not increase. For stocks whose

minimum tick size declined from 5 cents to 1 cent, the reduction had little impact on market

quality. Goldstein and Kavajecz (2000) investigate the impact of reducing the tick size from

eighths to sixteenths on the NYSE (on June 24, 1997) on the liquidity of the market. Their main

finding is that the quoted spreads and the corresponding depths, as well as depth in the limit

order book itself, declined post sixteenths.3 Finally, Jones and Lipson (2000) investigate the

impact of the tick size reduction to sixteenths on execution costs of a sample of institutional

trades. They conclude that smaller tick sizes may actually reduce market liquidity.

We use tick-by-tick (TAQ) data from the NYSE to investigate the impact of decimal

trading on the various facets of market liquidity. Our investigation period comprises October 2,

2000, to January 26, 2001 (the decimal period) and July, 2000 (the pre-decimal benchmark

period). The ending date of our analysis corresponds to the last trading date of the decimal

pilot program. Private communications with market participants confirm that significant

“learning” was taking place in the first few weeks of commencement of the decimal pilot as

traders freely experimented with the new system. We, therefore, choose to report results from

week 6 onwards (relative to the start of Phase I decimal pilot in August 28, 2000) to provide

enough time for market participants to have found an equilibrium trading pattern.

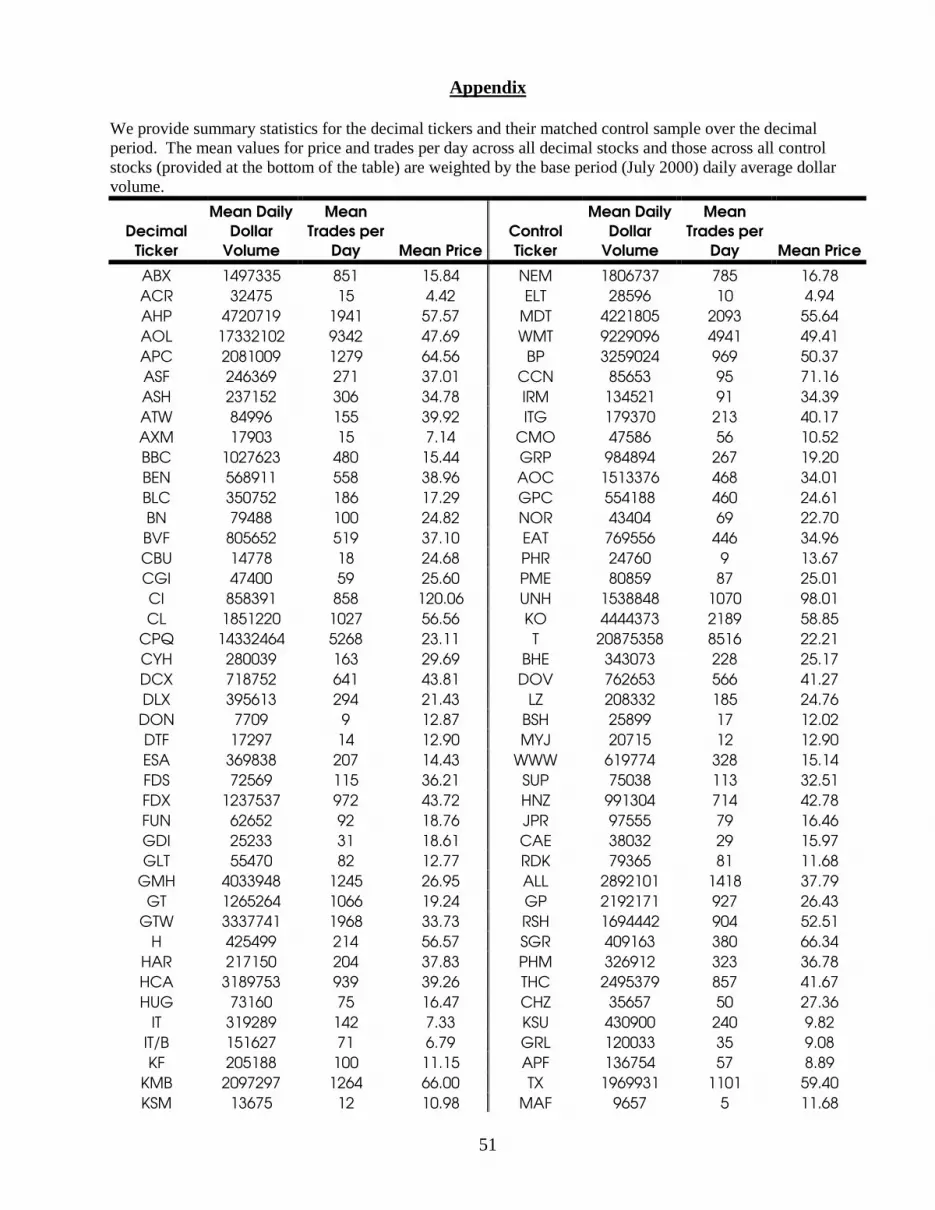

Our decimal sample consists of 87 common stocks listed in the NYSE and included in

the decimal pilot in any of the three phases before full conversion. To isolate the effects of

decimalization independent of market trends, we also construct a portfolio of control stocks

matched 1-1 with the decimal stocks in our sample. Essentially, at the time of selection, each

control stock was “similar” to its matched decimal stock on a number of dimensions with the

3In related work, Ball and Chordia (1998) show that the tick size of US stocks is large compared to the

“true” spreads for large, liquid stocks, and advocate a move to decimalization with a tick size of one cent.

6

important distinction that it was still trading in sixteenths over the decimal period. The details

of the selection of the control stocks are provided later.

Our main results for decimal stocks over the decimal period can be summarized as

follows.

Regional exchange competition parameters

��We find significant increases (of about 14%) in frequency of quote adjustment (or quote

flickering) and in autoquotes4 in decimal stocks among regional stock exchanges after

decimalization. The increase in quote adjustments and autoquotes remains significant

after controlling for factors other than decimalization through our sample of matched

control stocks.

��There are significant increases in time during which the regional exchanges possess

either the best bid and/or the best offer (BBO5) following decimalization in the decimal

stocks.

��About 29% of the BBO quote changes in decimal stocks occur at a penny and almost 80%

of the quote changes occur at a nickel or less. In comparison, about 75% of all (bid or

ask) quote changes in control stocks occur at 1/16ths and a further 19% of the quote

changes occur at 1/8ths. The NYSE also appears to be leading the way in the greatest

number of 1- through 5-cent quote changes (i.e., in the updating of the best bid or the

best ask or both) among all exchanges.

4 Autoquote is a bid ask quote generated automatically by computers in regional exchanges positioned just outside the prevailing highest price to buy and the lowest price to sell (otherwise known as the best bid and offer or BBO). The presence of autoquotes usually mean that the regional specialists are willing to be market participants for orders but not by paying as aggressive a price as the BBO. 5 The BBO is an important measure of an exchange’s dominance as a liquidity supplier and as a source of price discovery.

7

Liquidity related parameters

��Quoted spreads in the decimal stocks declined (compared to the non event period) an

average of 35% compared to about 9% in the control stocks. This decline in decimal

stocks remains significant after controlling for factors other than decimalization.

Specifically, we find that decimalization itself results in quoted spreads in decimal stocks

declining by an average of about 3.8 cents. Also, the most frequently quoted spread

among the decimal stocks was 1 cent.

��Effective spreads (measured as twice the absolute difference between the trade price and

the prevailing BBO midpoint) declined an average of 11% in the decimal stocks

compared to a 2% increase in effective spreads in control stocks. Decimalization itself

is responsible for a reduction of about 2.7 cents in effective spreads.

��Effective spreads also display most significant decline in relatively smaller trade sizes,

ranging from a decline of 28% in trade sizes of less than 500 shares, to a 20% decline in

trade sizes of 1,000-4,999 shares. Its decline for large size trades is comparatively

modest. For example, the decline in effective spreads for trade sizes of at least 10,000

shares is about 3.5%. In comparison, the control stocks either show a significantly

modest decrease or a significant increase in effective spreads in the corresponding trade

size categories. The effect of decimalization itself appears to have had no significant

impact on the reduction in effective spreads associated with 10,000-share (or greater)

trades.

��Bid and ask depths (trade sizes for which the corresponding quotes are guaranteed) in

decimal stocks declined an average of about 62% compared to an increase of about 19%

8

in control stocks.6 Decimalization itself is associated with an average decline in depth of

about 7,560 shares.

Transaction related parameters

��We find that that while both trades and trading volume have increased in relatively

smaller size trades (less than 1,000 shares) in decimal stocks following decimals, the

relatively larger size trades (greater than 1,000 shares) have declined significantly both

in frequency and in trading volume.

��We find no evidence of any significant changes in volatility in decimal stocks following

decimalization.

��We find evidence of significant increases in runs (or trends) in BBO quotes and

simultaneously fewer quote reversals in decimal stocks, compared to the control stocks.

These results have important policy implications as the debate on decimalization

continues. Foremost among them is the concern on available liquidity. Proponents of

decimalization argue that decimals allow for more efficient price discovery without adversely

affecting the supply of liquidity. Opponents, however, argue that decimals will result in less

liquid and high volatility markets. Our results provide a mixed verdict on the issue of liquidity

and volatility. Overall, our results suggest that we have moved to a new phase in security

transactions – one in which participants will have to learn new rules to play the game

effectively. Whether or not they do so, will determine, in large part, the success of

decimalization in keeping prices efficient and markets liquid. At the very least, information

6 Our spread and depth-related results are consistent with earlier work surrounding the conversion to sixteenths in 1997 (see, for example, Goldstein and Kavajecz (2000)).

9

about the available supply and demand schedule outside the BBO will be have to be made

available to market participants. There is evidence that the NYSE is already heading in that

direction.7 Other implications of our study are discussed in the conclusion.

The plan for the remainder of the paper is as follows. Section 2 discusses related

research. Section 3 provides a brief history of decimal pricing. Section 4 describes the data

methodology. Section 5 provides results related to bid/ask spreads. Section 6 provides

transactional results. Section 7 provides a discussion of some of the implications of our results.

The Appendix provides details of the decimal stocks in our sample and their corresponding

matched control stocks.

2. Related Research

Many stock exchanges have recently reduced their minimum ticks. And despite such

changes being studied extensively, both theoretically and empirically, its appropriateness

remains an open question. On the theoretical front, one stream of research has investigated the

issue of the optimal tick size and posits that the minimum tick results from market friction

arising from Bertrand competition among the liquidity providers (Anshuman and Kalay (1998)

Bernhardt and Hughson (1996), Kandel and Marx (1996)). Another stream models the idea that

minimum tick size coordinates negotiation (Brown, Laux and Schachter (1991) and Cordella and

Foucault (1996)). A third stream of theoretical literature investigates the relationship between

tick size and payment for order flow (Chordia and Subrahmanyam (1995) and Battalio and

Holden (1996)). A fourth group of researchers (see, for example, Hart (1993), Peake (1995),

7 For example, the NYSE, beginning March 19, 2001, has started disseminating “depth indications” on eight of its stocks. Its purpose is to show investors that there is a meaningful number of shares of a given stock available beyond the best price being bid and offered for the stock (WSJ, March 15, 2001, C1).

10

O’Connell (1997) and Ricker (1998)) argues that with smaller ticks, competition between

liquidity suppliers should reduce the bid/ask spread—thereby increasing liquidity and

benefiting liquidity demanders. Finally, a fifth group (Grossman and Miller (1988), Harris

(1994, 1997), and Seppi (1997)) makes the opposite argument that a finer tick size would lower

spreads but also lower the quoted depth (and, hence, market liquidity) due to the decline in the

marginal profitability of supplying liquidity. This may reduce the incentive of liquidity

suppliers to supply liquidity in such markets.

The current paper, however, appeals to the empirical research that investigates the

effects of actual tick size reduction in financial markets. These include the September 1992

reduction in minimum tick size for stocks priced under five dollars for AMEX stocks (Crack

(1994) and Ahn, Cao and Choe (1996)); the April 1996 reduction in tick size from eighths to a

nickel in the Toronto Stock Exchange (Bacidore (1997), Huson, Kim and Mehrotra (1997), Porter

and Weaver (1997) and Ahn, Cao and Choe (1998)); the May 1997 changeover of AMEX stocks

to sixteenths (Ronen and Weaver (1998)); the June 1997 changeover of NYSE stocks to sixteenths

(Bollen and Whaley (1998), Ricker (1998), Goldstein and Kavajecz (2000), and Jones and Lipson

(2000)). Additionally, Bessembinder (1997) examines Nasdaq stocks that change on an

individual basis to (or from) sixteenths. Overall, the focus of almost all of the empirical research

is to examine trades, the inside bid/ask quotes (or, the best bid and offer or BBO) and the

corresponding bid and offer sizes; and the effective spreads around tick-size reduction. Some

have also examined the impact of institutional trades on spreads. The overall conclusion of

these studies is that a reduction in tick sizes has caused spreads to decline and has made it

costlier for institutions to trade.

11

3. Brief History of Decimal Pricing

The move toward decimal pricing began in 1996 – significantly before the conversion to

sixteenths. At that point, a congressional subcommittee was formed to study the issue.

Hearings were held and legislation was proposed that would direct the SEC to require that

securities be traded in dollars and cents rather than in traditional fractions. During the 105th

Congress, Finance and Hazardous Materials Subcommittee Chairman Mike Oxley proposed

H.R. 1053, the Common Cents Stock Pricing Act of 1997. His bill required U.S. exchanges to

price stocks in dollars and cents, rather than in government set fractions. This set the tone for

the initiatives that followed. The National Association of Securities Dealers (NASD) has been a

strong proponent of the marketplace's shift to decimals. The NASD, in cooperation with the

Securities Industry Association (SIA), the SEC, and other equity and options markets have been

working to ensure a successful transition to decimals. Some of the benefits that decimalization

is expected to provide include savings for investors through narrower spreads and easily

understood numbers.

4. Data and Methodology

4.1 The Sample Stocks

The stocks in the decimal pilot were chosen based on several criteria developed by the

NYSE, along with a securities-industry committee. These criteria include stocks having varying

levels of daily trading activity, that trade on multiple exchanges, are part of an index, are

underlying issues for multiply listed options; and may have corporate action pending. To avoid

introducing confounding effects, we eliminate all preferred and convertible preferred stocks,

closed end funds, ADRs, stocks that may have merged, stocks with abnormally low average

12

daily trading volume over the study period, and stocks with no trading in at least one day over

the decimal and/or control periods. We also exclude all common stocks below $5 and above

$150, and those stocks in the decimal pilot that moved from Nasdaq to NYSE during the period

of the study. Finally, decimal stocks, which were delisted due to merger, or for other reasons,

during the study period, were also excluded. Our final sample comprises 87 NYSE-listed

common stocks selected for trading in decimals under the three phases of the decimal pilot.

These include 4 stocks from Phase I, 39 stocks from Phase IIA and 44 stocks from Phase IIB.8

Even though we report results corresponding to NYSE-listed stocks only, we repeated

the analysis for the eligible AMEX-listed stocks in the various phases of the decimal pilot, as

well. We do not report them here since they do not add any new insights.

We obtain tick-by-tick transaction and quote data for each stock in our sample over

October 2, 2000, and January 26, 2001, in the post-decimals phase, and over July 2000 as the non-

event benchmark period. It should be noted that while the overall period after decimalization

that is studied is from October to January, it is only the phase I and IIA stocks that entered the

sample on October 2 and remained till January 26, 2001. Phase IIB stocks entered the sample

only on December 11 and remained till January 26, 2001.

The quote data was extensively error filtered and all quotes with missing values, with

negative and zero spreads, and with quoted spreads greater than $2, were eliminated. This

removed less than 1% of the quotes.9 Transactions prices were also examined (and filtered) for

8 The main reason for the existence of Phase IIB was that all of the Phase IIA stocks were assigned to the same specialist firm and the NYSE wanted to involve other specialist firms before general conversion took place at the end of January 2001. 9 The comparison of trades and quotes also requires that data from CTA and CQS be merged by time.

For various technical reasons (see Blume and Goldstein (1997), Hasbrouck and Soesbee (1992)), not only can the time stamps be in error, but also the very sequencing of trades in the same stock can be wrong. We considered using the Blume and Goldstein (1997) formula to adjust our quote time stamps the same

13

potential errors. The appendix provides a breakdown of the specific decimal tickers included in

our study.

4.2 Selection of Control Stocks

Investigating the impact of decimalization on the pilot stocks after and before the event is

valid under the assumption that the market remains constant over the examination period. In the

presence of market trends, however, it is impossible to tell if an effect is due to decimalization or

due to market trends. One way to isolate the effect of decimalization, independent of market

trends, is to examine a matching sample of stocks, identical to the control stocks in every way,

except that they do not trade in decimals. We, therefore, compile a matching sample of NYSE-

listed control stocks for the decimal stocks in our sample, using the following exhaustive criteria.

Specifically, for each stock in the decimal sample, the selection criterion for a matching

stock in the control group is

��(option availability). Decimal stocks that have options got matching control stocks that also have options, and vice versa.

��(similar price). The price of each control stock had to be no more than 20% above

or below the price of its corresponding decimal stock. This limit was increased somewhat for lower priced stocks. For stocks trading under $3, the limit was expanded to 35%. In many cases, a control stock had a price within a dollar or two of its decimal partner.

��(similar traded volume). The average traded volume of each control stock was

no more than 20% above or below the average traded volume of its corresponding decimal stock. In practice this limit was set lower than 20% and if no satisfactory matches were found it was increased.

��(similar volatility). The volatility of the decimalized stocks generally ranged

from 20 - 80, with a few outliers. The control stocks were selected to have a

trading day. But the quote adjustment algorithm Blume and Goldstein develop is based upon 10-year old data contained in the NYSE TORQ database. Extensive improvements in trade recording systems have been implemented in the intervening years and there is currently a sense that adjusting quote time stamps is no longer appropriate.

14

volatility within 25% of that of their decimal partners. In a few cases this limit had to be widened to find a suitable match.

��(similar market capitalization). The market capitalization of each control stock

was selected to be within a 50% range of that of the corresponding decimal stock in most cases. This range had to be expanded in a few cases to find a match.

��The three-month relative strength to the S&P 500 Index, between a decimal stock

and its chosen control stock, should have been similar.

��Additionally, recent price performance was considered. A stock that had been rising strongly in recent months was not given a control stock whose price had been falling sharply and vice versa.

��Control stock selected from same industry as decimal stock, if possible.

��Each NYSE decimal stock was given a control stock that also traded on the

NYSE.

It should be noted, however, that for each phase, control stocks were selected shortly

before the date of decimalization. Due to normal stock market fluctuations, the prices, trading

volume and volatilities of stocks that were similar when the selection was made could have been

much less similar by the end of the study period. They also could have been different during the

benchmark period of July 2000. The appendix provides a breakdown of the control stocks

matched with the corresponding NYSE-listed decimal stock.

5. Decimalization and Bid and Ask Quotes

We present the results of our analysis based on the NYSE-listed decimal stocks in our

sample and the matched control stock sample, both before decimalization (over July, 2000) and

after decimalization (from October, 2, 2000 through January 26, 2001).

5.1. Daily Quote Frequency

From a theoretical standpoint, bid/ask quotes are updated when market conditions

change. These may be related to adverse selection, liquidity pressure or a combination of the

15

two. Suffice it to say that frequent updating of quotes would be indicative of a volatile market

overall where the search for an efficient price for that security is actively being pursued,

compared to a market with relatively infrequent quote adjustments. A market with frequently

changing quotes is also a trading venue where the “best” possible price for a trade execution

may be harder to determine and, hence, may be open to gaming and other strategic behavior by

professional investors for personal gain.

Table 1 presents the daily average quote frequency of the NYSE-listed decimal and

control stocks in our sample, both after (panel A) and before (panel B) decimalization, across the

five regional stock exchanges in addition to the NYSE and NASDAQ. While the non-event

period finds average daily quote adjustment frequencies that are statistically similar between

decimal and control stocks in almost all of the regional exchanges, the picture changes

significantly over the decimal period. Here we see significant increases in quote adjustment

frequencies in all five regional exchanges, both with respect to the control stocks and with

respect to the non-event period. Overall, table 1 shows that there was an increase of 14% in

quote adjustments in decimal stocks after decimalization relative to a decrease of 11% in quote

adjustments in control stocks over the same period.

To focus on the change in quote frequencies in decimal stocks due to the act of

decimalization itself, we compute the net difference in daily average quote frequencies by

subtracting the daily average (quote frequency) of each control stock from its matched decimal

stock in our sample. The average of these differences over each exchange and over each period

(pre decimal and post decimal) is then computed. The table reports this difference in the pre-

decimal average from the post-decimal average for each exchange. Overall, these numbers

confirm that the act of decimalization itself appears to have caused a significant increase in

quote frequency in all regional stock exchanges. The main markets like NYSE and NASDAQ,

16

however, do not display this tendency, where quote frequencies after decimalization stay about

the same as those before decimals. What these results imply towards the overall market

liquidity is unclear and is examined in greater detail in following sections.

An extreme case of quote adjustment is known as quote flickering where quotes changes

occur so rapidly that the eye cannot discern the changes. Not surprisingly, some traders are

uncomfortable in a market with quote flickering since it is extremely difficult to get a sense of

the true value of the stock at a given point in time. Our results (not reported) indicate that

quote flickering (as high as 4 per second in some stocks post decimals) is likely to be a

significant issue in a world of decimal trading.

5.2 Prevalence and distribution of the Best Bid and Offer (BBO) among Regional Stock Exchanges

In a competitive dealer market, multiple dealers post quotes simultaneously and there

exists at any point in time, a set of bid and ask quotes that represent the highest price to buy

and the lowest price to sell. This is known as the best bid and offer (BBO). In a continuous

auction market, such as the NYSE and AMEX, a specialist posts quotes in stocks, comprising of

a combination of own interest as well as the interest of the public limit orders competing

directly with the specialist. Such competition can also come from the regional stock exchanges,

posting quotes simultaneously in those stocks. In short, BBOs are generated by public limit

orders originating both in the primary market as well in the regional stock exchanges, and

dictate which exchange at any point in time has the best bid and offer quotes. The fraction of

time that any particular exchange has the BBO is an indication of its dominance in terms of a

supplying liquidity as well as price discovery – the two most important roles of a modern

financial exchange.

To examine the issue of BBO dominance, we compute the frequency of BBOs using the

17

quoted bids and asks and the corresponding bid and ask depths offered by the exchanges at

those prices. If two exchanges have the same bid, for example, but one has a larger quoted size

at the bid, it is awarded the BBO. If both have the same bid price and quoted size, then the BBO

is awarded to that exchange with the oldest bid quote. Note that this procedure strongly favors

the NYSE since by virtue of its dominant position the NYSE almost always has the maximum

size offered.

Table 2 presents the frequency of BBO observations and the corresponding percent of

total trading time that a BBO is in effect across the regional exchanges for decimal and control

stocks both during the decimal period and during the pre event period. While the percentage of

BBO times held by regional exchanges in decimal stocks increases significantly after

decimalization, the percentage of the BBO times held by most regionals in control stocks also

increases over the same period. Simultaneously, the percentage of BBO times held by NYSE

declines significantly in decimal stocks from 86% to 79% and in control stocks from 87% to 81%.

To isolate the effect of decimalization on BBO times in the regional exchanges, the net

difference in decimal stocks is calculated as the difference between the daily average frequency

of BBO observations of each decimal stock and its paired control stock. The average of these

differences over each exchange and over each (pre decimal and post decimal) period is then

computed. The table reports the difference in the pre-decimal average from the post-decimal

average. The results indicate that after controlling for other factors, decimalization appears to

have significantly increased the ability of most regionals to price-compete with the NYSE. An

important implication of this finding for academics is that research involving spreads, which

have traditionally considered only NYSE quotes as a representation of the market as a whole,

will henceforth need to consider regional and third-market quotes.

5.2 Frequency distribution of changes in the best bids and the best asks (BBOs)

18

In this section, we investigate the frequency of changes in the best bids and the best

offers (BBOs). The purpose is to see if all penny increments are being hit after decimalization or

are the BBO quote changes loading up only on certain penny increments. Specifically, we find

the number of times the best prevailing bid (for example) changes by 1 cent, 2 cents, and so on,

and simultaneously the number of times the best prevailing ask changes by the same

increments, for all the decimal and control stocks in our sample and over the decimal period.

Table 3 explores the frequency distribution of the sum of changes in both the best bids

and the best asks, in cents, and presents the corresponding cumulative percent, of all such

changes at the bid and at the ask. Note that while about 75% of quote changes in the control

stocks occur at 1/16ths and a further 18% at 1/8ths, about 29% of the changes in decimal stocks

occur at one penny, while about 80% of the changes occur at 5 cents or less. Clearly, even

though the cumulative changes in the bid and offer quotes between decimal and control stocks

at an 1/8th or less are almost identical, all penny-ticks in between appear to be hit by the

decimal stocks and, especially comforting to the supporters of decimal pricing is the fact that,

quote increments of 5 cents or less appear to be used actively by the market in the decimal

stocks. The latter may also indicate that 1/8 and 1/16 minimum tick sizes may have

represented barriers to price competition, which have been ameliorated with decimal pricing.

5.3 Distribution of bid and ask quotes and quote changes among regional exchanges

Given the significant usage of increments of 5 cents or less in the BBOs noted in Table 3,

a natural question to investigate is for possible clustering in BBO quotes ending in numbers 0-9.

A related question is to ask which regional exchanges are responsible for this narrowing of the

BBOs. Panel A of table 4 provides a frequency distribution of all bid and ask quotes ending in

numbers 0-9. We find evidence of clustering in that quotes ending in 4, 5, 9 and 0 appear to be

favored over quotes ending in the remaining numbers in all regional and national exchanges.

19

Panel B of table 4 examines 1-5 cents quote changes (at the best bid and at the best ask) by the

regional exchanges for NYSE-listed decimal stocks over the sample period. The reported

numbers, for each exchange, are computed as the sum of all ask changes and bid changes of 1

through 5 cents expressed as a percentage of all changes at a given cent. From Panel B, we see

that NYSE has by far the greatest number of 1-5 cent changes, while Nasdaq is competitive in all

five-cent categories. The Pacific comes in third in all except the 3-cent category. The NYSE and

NASDAQ also appear to have disproportionately high frequencies of 5-cent quote changes.

Overall, it appears that all the regional exchanges are actively contending for quote changes,

even though the NYSE is still leading the way.

5.4 Quoted and Effective bid/ask spreads

A traditional measure of market liquidity has been the quoted bid-ask spread that

captures the ex ante transactions cost (see O’Hara (1995), Huang and Stoll (1996) and

Bessembinder (1997)). Peterson and Fialkowski (1994) and others have, however, argued that

the quoted bid-ask spread is no longer an accurate measure of transaction costs when trades are

executed inside the prevailing quoted spread. They also show that when the posted (quoted)

spread widens, only about 10-22% of the increase in posted spreads appears in the effective

spread, where the effective bid-ask spread associated with a trade is defined as twice the

absolute difference between the transaction rice and the midpoint of the prevailing quoted bid-

ask spread (BBO). The effective spread, which measures the ex post transaction cost, is thus

favored by some.

We begin our investigation into spreads by examining, in Table 5A, the distribution of

all quoted spreads originating from the national and regional exchanges in terms of odd and

even ticks for decimal and control stocks, following decimalization. Even ticks are spreads of 2,

4,…cents, while odd ticks are covered by 1,3, 5,…..cent spreads. While decimal stocks show an

20

almost even split between even and odd ticks in every exchange, the control stocks, over the

same period, show a preponderance towards even ticks in Boston, Chicago and Philadelphia

and towards odd ticks in Cincinnati and Pacific. About 61% of all quotes from the NASDAQ

are at even-ticks while 45% of all quotes at the NYSE are at even-ticks.

Table 5B refines the examination of quoted spreads by investigating the distribution of

BBO spreads (in cents) for decimal and control stocks following decimalization. It is notable

that decimal stocks have a higher frequency of spreads at six cents or less compared to the

control stocks (49.4% versus 44.9%). Even for spreads up to 13 cents, decimal stocks dominate

the control stocks (75.3% versus 73.8%). Not surprisingly, the difference (in cumulative

frequencies) between decimal and control stocks disappears at spreads of 19 cents or higher.

Overall, there is evidence that 1-5 cent spreads are being quoted actively by the market makers.

Tables 6A and 6B provide information on the quoted and the effective bid/ask spreads

on the NYSE-listed decimal stocks and the corresponding control sample over the sample

period and over the non-event benchmark period of July 2000. Both the quoted and effective

bid/ask spreads are calculated on the basis of the best bid and offer (BBO) prices available at

the time of trade. Thus, autoquotes, which simply bracket an existing BBO, are automatically

eliminated from consideration. Such autoquotes, however, have other purposes and are

discussed later in section 5.6. We compute spreads of stock portfolios formed on the basis of the

average daily dollar volume of trade of stocks over the non-event benchmark period. Stocks in

portfolio 1 (5) comprise the smallest (largest) dollar volume stocks. The reported spreads in

Table 6A (and in Panel A of Table 6B) for each dollar volume portfolio are computed by

weighting, for a given stock within a given day, by the time each spread is outstanding, and

weighted across stocks, by their daily average non-event dollar trading volume.

Table 6A reveals that the decrease in quoted spreads for decimal stocks is significant

21

across all five dollar volume portfolios, and ranges from 21% for the portfolio 1 to 36% in

portfolio 4, while the (dollar-volume weighted) average over all portfolios is also about 35%.

The corresponding changes in the control stock portfolios range from a 0% increase to a 10%

decrease, with an overall average of 9% decrease. Thus, decimalization appears to have

significantly reduced quoted spreads, in comparison to control stocks.

To isolate the effect of decimalization on the quoted spreads of decimals stocks, the net

difference in quoted spreads in decimal stocks is calculated as the difference between the daily

average quoted spread of each decimal stock and its paired control stock in a particular size

rank. For each portfolio, the average of these differences over each (pre decimal and post

decimal) period is then computed. The table reports the difference in the post-decimal and pre-

decimal averages. These reveal that decimalization itself may have resulted in quoted spreads

declining by an average of about 3.8 cents.

Table 6B Panel A reports the effective spreads of portfolios, once again classified by their

average daily non event dollar volume. The reduction in effective spreads in decimal stocks

ranges from 4% to 15% among the five portfolios with the greatest reductions occurring in the

higher dollar volume portfolios. The overall (dollar volume weighted average) decrease is about

11%. In contrast, the control portfolios show significant increases in effective spreads in almost

all portfolio size categories with an overall (dollar volume weighted average) increase of about

1.5%. Once again, a net difference variable is reported to isolate the effect of decimalization on

the effective spreads of decimal stocks. The net difference for the small portfolios (1 and 2) is

statistically insignificant from zero while those for the remaining portfolios are negative and

statistically significant. Overall, decimalization itself appears to be responsible for a reduction

of about 2.7 cents in effective spreads.

To get a sense of the relationship between effective spreads and trade size, we further

22

compute the effective spreads corresponding to trades in each of five trade size categories: all

trades less than 500 shares (small trades), all trades between 500 and 999 shares (medium1

trades), all trades between 1,000 and 4,999 shares (medium2 trades), all trades between 5000 and

9999 shares (medium3 trades), and all trades of 10000 shares or greater (large trades). Panel B of

Table 6B presents the average effective spreads (in cents) in each trade size category, for decimal

and control stocks, before and after decimalization.

We see that while the spreads in each trade size category are statistically similar between

decimal and control stocks over the pre-decimal period, there are significant declines in

effective spreads in every trade size category in decimal stocks after decimalization.

Specifically, the spread decreases monotonically from 28% in small trades to about 3% in large

size trades. In contrast, within control stocks, effective spreads appear to have increased in the

larger trade size categories and show relatively insignificant declines in the two remaining

smaller trade size categories, compared to effective spreads associated with corresponding size

trades in decimal stocks. The net difference variable indicates that decimalization itself has

resulted in reduction of effective spreads ranging from 2.08 – 2.81 cents in all but the largest

trade size category. For large size trades, however, the net difference variable is negative but

not statistically significant at the 10% level, indicating no significant effect of decimalization on

effective spread reduction.

In summary, decimalization appears to have significantly reduced both quoted and

effective spreads. Our conclusion holds even after accounting for effects other than

decimalization, through the net difference variable, and are consistent with those reported in

Goldstein and Kavajecz (2000) and Jones and Lipson (2001) following the conversion to

sixteenths. Decimalization appears to have enabled relatively smaller size trades to obtain

better prices and execute deeper inside the quoted spreads, compared to larger size trades.

23

5.5 Changes in bid and ask depths

Following Harris (1990), it is now widely accepted that a complete characterization of

market liquidity encompasses both the bid/ask spreads and the corresponding bid and ask

depths. When liquidity is defined along these two dimensions, it is entirely likely that a

reduction in liquidity could occur through a reduction in the bid and/or ask depth even though

the bid/ask spread itself remains unchanged. Having examined spreads in the prior section,

we now turn to the depths to see if we could say anything conclusive about market liquidity

following decimalization.

Related to the magnitude of the quoted bid and ask depths themselves, it is reasonable

to expect that quoted depths will reduce, the closer a bid or offer is to the equilibrium price,

consistent with the shape of the supply-demand curves. Further, the likelihood of a quote

becoming stale increases as the spread narrows, so the option cost implicit in quotes will

increase correspondingly.10 Finally, the advantage of being at the front of the queue decreases

as the tick size decreases and the spread narrows.

Table 7 provides information on the bid and ask depths of the decimal and control

stocks both before and after decimalization. As in the case of spreads, we report depths based

on the five portfolios (1-5) formed on the basis of the average daily dollar volume of trade of the

sample stocks over the benchmark period. Consistent with the spread table, the reported

depths in Table 7 for each dollar volume portfolio are computed by averaging across stocks in a

10 Consider, for example, a stock trading at 20 - 20 1/8 where a trader has posted a limit order to sell at 20 1/8. If the quote then jumps to 20 1/4 - 20 3/8 while the limit order is left unchanged, one could buy the stale limit order at 20 1/8 and immediately resell it at 20 1/4 ("picking it off"). With decimal trading, if a stock is quoted at 20 - 20.01, a 20.01 sell limit order could be picked off with a much smaller upward spread movement. Thus, the likelihood of the option being excercised against the limit-order provider is greater with decimal trading, but the expected value of the payoff price is smaller. The net effect of these two counteracting forces is indeterminate. Yet this influence could discourage the placement of limit orders in a decimal environment.

24

portfolio, by their non-event daily average dollar trading volume.

We see that both the bid and ask depths decreased significantly during the decimal

period compared to the pre event period. Specifically, the decline in depths among the five

decimal stock portfolios ranges from 15% to 79%. The higher dollar volume stock portfolios

appear to experience a greater decline in depths than the less active lower dollar volume stock

portfolios. In contrast, the control stock portfolios, over the same period, show an overall

increase in depths (by about 19%). There is also no clear trend between depth change and size

portfolios. Once again, the net difference variable isolates the impact of decimalization on the

depths of decimal stocks following decimalization. From here, we see that decimalization has

lead to a reduction in depth of about 7,560 shares.

In summary, after controlling for market trends (other than decimalization), there

appears to be a significant decline in bid and ask depths at the BBO. Goldstein and Kavajecz

(2000), in comparison, report an average quote depth decline of about 48% following conversion

to sixteenths. While a decline in quoted and effective spreads indicates an increase in market

liquidity, a simultaneous decrease in the corresponding bid and ask depths (i.e., the

corresponding order sizes that these quotes are valid for) implies a drop in liquidity. The

overall effect is therefore uncertain, although the observation that trading volume in upstairs

markets and in automated equity-matching systems like POSIT has increased significantly since

decimalization would suggest that institutional trading costs, and the cost of executing large

size trades through conventional channels, have, in fact, increased.

5.6 Autoquoting behavior of regional exchanges

In this section, we examine the dynamic behavior of quotes originating from the NYSE

and the regional stock exchanges between decimal and control stocks, before and after

decimalization. The issue of dynamic quote behavior itself has been addressed by various

25

researchers in the context of increased fragmentation of U.S. equity orders and in the context of

price discovery (see, for example, Garbade and Silber (1979), Shapiro (1993) and Hasbrouck

(1995)). The NYSE and the regional exchanges are electronically linked and all trades and

quotes are disseminated by a central transmission authority (the Consolidated Tape Association

(CTA)). Although the regional exchanges sometimes establish the BBO, frequently they will

choose to extract themselves from active quote competition in listed stocks by programming a

computer to intercept all NYSE/AMEX quotes and immediately generate a new quote of their

own by adding a delta to the ask and subtracting a delta from the bid, with 100 shares bid and

100 shares offered (the bid and ask depths). The mechanism(s) by which the regional quotes

default to the BBOs, widened by a small arbitrary amount, are known as “autoquotes”. Thus,

an autoquote is effectively a non-quote whereby regional specialists signal that they are willing

to supply liquidity but not at the best prices. Trades occur on the regional exchanges during

periods of autoquoting, but those trades must match or better the existing BBO. Our algorithm

identifies an autoquote as any regional or third-market quote that brackets the existing NYSE or

AMEX quote.

With the advent of decimalization it is reasonable to anticipate an increase in posting

quotes off the BBO by serious liquidity providers. With the possible elimination of the barrier

to price competition that was provided by a minimum tick size of sixteenths, it follows that

liquidity providers who wish to earn more than a 1-2 cent spread will be forced to post quotes

off the BBO following decimalization. With the thin book that naturally results from such tight

spreads, significant buy/sell programs could easily march up/down the book and hit limit

orders away from the minimum tick size. Thus, some regional exchange specialists are

increasingly autoquoting to supply liquidity with sophisticated algorithms to determine quote

prices and sizes. These autoquotes are, however, not for 100 shares bid and 100 shares offered

26

but for quantities greater than 100 shares on either (or both) side. We attempt to capture this

behavior by reporting autoquotes over both 100-share depths (the regular autoquotes) and

greater than 100-share depths (the smart autoquotes).

Table 8 reports the percentage of time the NYSE-listed decimal and control stocks are

(regular and smart) autoquoted before and after decimalization in the various regional

exchanges. The reported numbers are a simple percentage of all autoquotes (in each regular or

smart autoquote category) from a given regional over all quotes from the regionals and the

NYSE. While tests reveal that the percentage of regular autoquoting is statistically similar

between decimal and control stocks in the pre event period, post decimalization finds that

regular autoquoting has increased significantly in decimal stocks compared to the control stocks

in almost all the regional exchanges. Cincinnati, Pacific and Chicago have the highest increases

of autoquoting in decimal stocks, while there is decline in autoquoting in the control stocks in

two of these exchanges.

To isolate the effect of decimalization itself on autoquoting behavior, we provide the net

difference in (regular or smart) autoquotes, calculated as the difference in daily average

autoquote frequency between each decimal stock and its matched control stock. The averaging

is now done over each exchange and over each (pre decimal and post decimal) period. The

table reports the difference in post and pre-decimal average. While Boston and Chicago show

evidence of significant increase in autoquotes as a result of decimalization, for the rest,

including NYSE and NASDAQ, the increase is statistically insignificant at the 10% level. From

Panel B, the net increase in smart autoquotes as a result of decimalization is positive and

statistically significant in all but the Pacific and Philadelphia stock exchanges.

Overall, it appears that (with few exceptions), the regional exchanges are ready to

participate in quote competition in the decimal stocks following decimalization, as evidenced

27

by overall net increases in both regular and smart autogquoting.

6. Decimalization and Transaction-related Variables

6.1 Trades and trading volume

An issue of interest to regulators and practitioners is the relative behavior of institutions

compared to individual investors. It is generally perceived that institutions are “smart” or

informed traders while individuals are uninformed investors. Evidence that institutional

investors are more likely to use larger trade sizes than individuals, appears in Chakravarty

(2001). Support that large trade sizes are more likely to be from informed traders than small

trade sizes appears in Easley and O’Hara (1987). To investigate the relative activity of large

(informed) trades versus small (uninformed) trades around decimalization, we investigate the

frequency of trades and trading volume in the five trade size categories described earlier: small,

medium1, medium2, medium3 and large.

Table 9 reports results both for decimal and control stocks over the benchmark period

and the decimal pilot period. Panel A presents the average daily trading volume results

classified by trade size; panel B provides the corresponding daily average trade frequency

statistics.

From table 9, we see an increase in average daily trading volume in almost all trade size

categories in decimal stocks following decimalization. Interestingly, the control stocks show an

even greater increase in every trade size category. Average daily trades show a decline in three

of the five categories in the decimal stocks while the control stocks show a significant increase in

each trade size category following decimalization.

To isolate the effects of decimalization, we report the net difference in trade volume (or

28

trade frequency) in decimal stocks is calculated as the difference between the daily average

volume (or trade frequency) of each decimal stock and its paired control stock in a particular

trade size category. The average of these differences over each category and over each (pre

decimal and post decimal) period is then computed. The table reports the difference in the

post-decimal average and the pre-decimal average. These numbers indicate that while both

trades and trading volume have increased in relatively lower size trades (less than 1,000 shares)

in decimal stocks following decimals, the relatively larger size trades (greater than 1,000 shares)

have declined significantly both in frequency and in trading volume. Decimalization appears to

have dampened the market for large size trades.

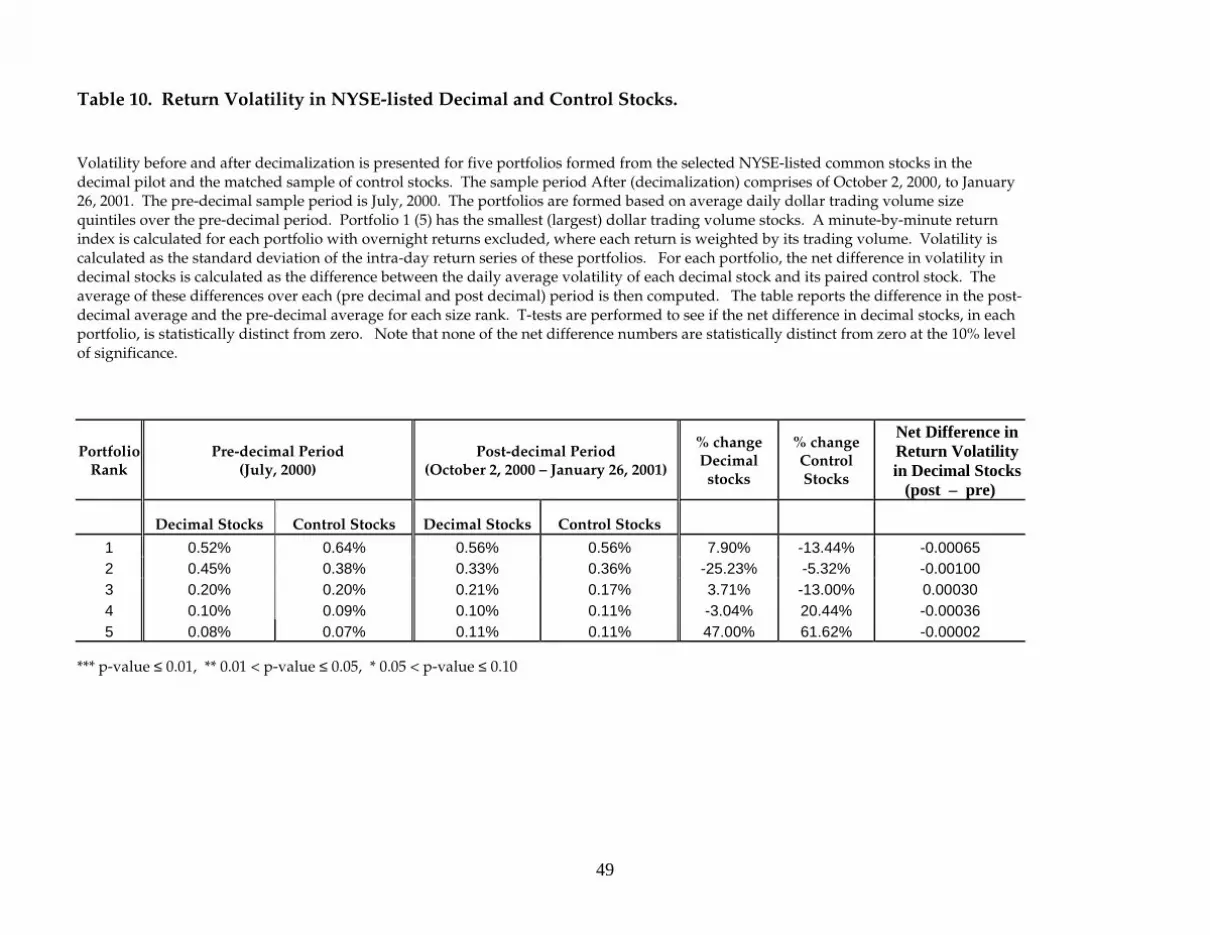

6.2 Volatility

In this section we examine volatility, before and after decimalization, and between

decimal and control stocks. Our investigation is motivated by a desire to investigate if market

risk in decimal stocks has increased significantly (relative to the control stocks) following

decimalization. If it is the case that the aggregate liquidity in the limit order book has shrunk

post-decimals, we would expect a greater price impact (or higher volatility) for a trade of a

given size.

To study volatility, we use the same five (quintile) portfolios of decimal and control

stocks separately, based on the average daily dollar trading volume over the non-event period

(and discussed earlier). We form a minute-by-minute return series for the stocks within these

portfolios, where each return is weighted by its corresponding share volume. Portfolio returns

are then formed by weighting each stock in a portfolio by its pre event average daily dollar

volume. Overnight returns are discarded. Volatility for portfolio returns is calculated daily and

the average volatility across days is reported.

Table 10 does not reveal a clear pattern of volatility increases or decreases across the

29

dollar volume portfolios. There is, however, evidence that volatility appears to have gone up in

the smallest (7.9%) and largest quintile (47%) portfolios of decimal stocks following

decimalization. In comparison, the corresponding control stock portfolios show a decrease of

about 13% and an increase of about 62%, respectively. The remaining portfolios indicate both

increases and decreases for both decimal and control stocks.

As always, the net difference variable attempts to isolate the effects of decimalization on

decimal stocks. The results indicate that in four of the five portfolios there is a decline in

volatility in decimal stocks following decimalization although none are significant at the 10%

level.

In summary, there is no evidence of any significant pattern of volatility changes

following decimalization.

6.3 Runs and Reversals in Quote Adjustments

There is concern amongst practitioners in Wall Street that decimal pricing may lead to

more runs in price and less price reversals, thereby exposing the limit orders of individual

investors to greater stale price risks, which may, in turn, leave them at the mercy of being

picked off by professional investors. Thus, an investor could easily step in front (by a penny) of

a standing limit order in a rising market or sell into a standing limit order in a falling market

(see also footnote 10). In either situation, the liquidity supplier would be faced with losses in

her position. If this situation leads some limit order traders to avoid submitting such orders, the

overall liquidity and depth of the markets are in jeopardy. Brown and Holden (1999) model

“mispricing” risk of limit orders and show how market adjusted (or smart) limit orders can

mitigate this risk.

To examine the issue of price runs versus reversals, we define a simple metric to

measure such phenomena. Specifically, we examine the prevailing BBO quote midpoint

30

sequence and define an increase in quote midpoint by +1 and a decrease by –1. A simple run of

length 1 is defined as (+1+1) or a (-1-1). Similarly, a run of length 2 is defined as (+1+1+1) or (-1-

1-1), and so on. A reversal is defined very simply as triples of BBO quote changes, where the

direction of the quote midpoint is reversed, as in (+1-1+1) or (-1+1-1). While relatively crude, it

provides us with a framework to study the issue.11

Table 11 Panel A documents quote reversals, both in terms of the frequency of quote

reversals and the corresponding percentage of all non-zero quote changes, among decimal and

control stocks, both in the pre event period and during the decimal pilot. While the frequency

of quote reversals between the decimal and control stock sample over the pre event period is

statistically similar, about 25% (34%) of all non-zero quote changes were reversals in the

decimal (control) stock sample. This difference is statistically distinct at reasonable levels of

significance. Thus, quotes appear to be reversed less frequently in decimal stocks following

decimalization.

Panel B provides the frequency (and the corresponding cumulative percentage) of runs

in quote adjustments between decimal and control stocks before and after decimalization.

While the pre-decimal run length frequency at run lengths up to 25 are statistically similar

between the decimal and control stocks, following decimalization we find statistically

significantly greater run lengths among decimal stocks over the control stock sample for almost

all reasonable run lengths reported in the table.

In summary, our results underscore the significant increase in quote trends in the

market following decimalization and provide support to the argument that decimalization may

have increased stale price risk of the liquidity supplying limit order traders, who stand a greater

11 For robustness, we replicated our work using changes in transaction prices in place of quote midpoint changes and obtained qualitatively similar results.

31

chance of being picked off for a loss. The broader implications of our finding here are discussed

in the following section.

7. Discussion of Results

Using tick-by-tick transaction and quote data over the pre-decimal period of July 2000,

and the decimal period of October 2, 2000, through January 26, 2001, we study the impact of

decimalization on NYSE and AMEX-listed common stocks. To ensure that our results are not

influenced by market trends over the decimal period, we carefully construct a sample of control

stocks matched 1-1 with each decimal stock in our sample. We study the effects of

decimalization, both with respect to the non-event period and with regard to the control sample

of stocks.

Even though it is tempting to think of decimalization as just another decrease in

minimum tick size, it is, in reality, much more than just that. The mantra is that the minimum

tick must make it an economic cost for someone to step up in front of another liquidity supplier.

While this was true even up to the conversion to sixteenths, it may not be true anymore where it

takes just one penny to step ahead of a standing limit order. And if it is almost costless to step

ahead, as one fund manager puts it, “……mutual funds may stop using limit orders and simply

pay fees to brokers to buy and sell at the prevailing market price. Most stocks already are

traded that way on the nation's exchanges.” In this backdrop, we study the impact of

decimalization on market liquidity parameters, price competition (through quotes) of regional

exchanges vis-à-vis the NYSE and/or AMEX, and transaction related parameters.

We find mixed evidence on market liquidity following decimalization. Specifically,

while both the quoted and effective bid/ask spreads show significant decline, the

32

corresponding bid and ask depths also display a significant decline. Thus, while better prices

now exist to buy and sell, the quantities that can be purchased or sold at those improved prices

have also declined significantly. Our finding of significantly smaller spreads post

decimalization bodes well for retail traders trading smaller size trades. Anecdotal evidence,

however, suggests that institutional investors are, in fact, experiencing significantly higher costs

to execute block trades (in decimal stocks) following decimalization and automated trading

systems like POSIT, which let users confidentially find the natural buyer or seller of a trade

during the market day, has experienced a tremendous increase in trading volume in recent

months.12

We find evidence of significantly increased competition coming from the regional

exchanges in terms of bid/ask quote adjustment frequencies, BBO times, and percentage of

autoquotes. Decimalization may have increased the ability of the regionals and Nasdaq third-

market dealers to aggressively price-compete with the main listing exchanges like the NYSE.

Interestingly, however, the NYSE appears to be still leading the way in terms of 1-5 cent

changes in bids and offers among all exchanges.

Finally, using a simple metric to capture runs and reversals in bid/ask quotes, we find

evidence of significantly greater frequency of trending quotes (and significantly lower quote

reversals) in decimal stocks. One implication of the latter result is the possibility of the

existence of greater stale price or mispricing risk in public limit orders, which could then be

picked off by relatively professional investors, thereby inflicting losses on these liquidity

suppliers. If this is pervasive, there is concern that placement of limit orders (and, by extension,

the supply of liquidity) may begin to dry up in the market. In fact, Bacidore et al. (2001) report

12 The Toronto Stock Exchange also displayed a similar drop off in market liquidity and a resulting increase in trading costs following their conversion to decimals in 1996.

33

that, following decimalization, traders appear to have decrease their use (and size) of traditional

limit orders and are canceling orders more frequently.

One way for investors to protect themselves from being “penny-jumped” is to place

smart limit orders, which could be adjusted automatically to reflect changing market conditions

by a computer algorithm. Brown and Holden (1998) provide a comparative analysis of liquidity

supply through market and quote adjusted limit orders to minimize mispricing risk.

Fortunately, there is evidence that such mechanisms may already be in place. Recently, a

brokerage subsidiary of CS First Boston began offering its clients the opportunity to trade with

limit orders that are adjusted automatically by the brokerage to reflect changing market

conditions. It is likely that more such opportunities will be available to investors in the near

future.

34

References

Ahn, H., Cao, C.Q., and H. Choe, 1996, Tick size, spread and volume, Journal of Financial Intermediation, 5, 2-22.

Ahn, H., Cao, C.Q., and H. Choe, 1998, Decimalization and competition among stock markets:

evidence from the Toronto Stock Exchange cross-listed securities, Journal of Financial Markets, 1, 51-87.

Anshuman, V., and A. Kalay, 1998, Market making rents under discrete prices, Review of

Financial Studies, 11, 81-109. Bacidore, J.M., 1997, The Impact of Decimalization on Market Quality: An Empirical

Investigation of the Toronto Stock Exchange, Journal of Financial Intermediation, 6, 92-120. Bacidore, J.M., R. H. Battalio, and R.H. Jennings, 2001, Order submission strategies, liquidity

supply, and trading in pennies on the New York Stock Exchange, NYSE working paper. Ball, C., and T. Chordia, 1998, True spreads and equilibrium prices, working paper, Vanderbilt

University. Battalio, R., and C. Holden, 2001, A simple model of payment for order flow, internalization,

and total trading cost, Journal of Financial Markets, 4, 33-71. Bernhardt, D., and E. Hughson, 1996, Discrete pricing and the design of dealership markets,

Journal of Economic Theory, 71, 148-182. Bessembinder, H., 1997, The degree of price resolution and equity trading costs, Journal of

Financial Economics, 45, 9-34. Blume, M.E., and M.A. Goldstein, 1997, Quotes, Order Flow, and Price Discovery, Journal of

Finance, 52, 221-244. Bollen, N. P. B., and R.E. Whaley, 1998, Are “teenies” better? Journal of Portfolio Management, 25,

10-24. Brown, S., P. Laux, and B., Schachter, 1991, On the existence of an optimal tick size, Review of

Futures Markets, 10, 50-72. Brown, D.P., and C. Holden, 1998, The design of limit orders under a hybrid mechanism with

endogenous depth, working paper, Indiana University. Chakravarty, S., 2001, Stealth trading: Which traders’ trades move stock prices? Forthcoming

Journal of Financial Economics. Chordia, T., and A. Subrahmanyam, 1995. Market making, the tick size, and payment-for-order

35

flow: theory and evidence, Journal of Business 68, 543-575. Cordella, T., and T. Foucault, 1996, Minimum price variation, time priority and quote dynamics,

working paper, Universitat Pompeu Fabra. Crack, T. F., 1994, Tinkering with ticks: choosing minimum price variation for U.S. equity

markets, working paper, MIT. Easley, D., and M. O’Hara, 1987, Price, trade size and information in securities’ markets, Journal

of Financial Economics, 19, 69-90. Garbade, K.D., and W. L. Silber, 1979, Dominant and satellite markets: A study of dually-

traded securities, Review of Economics and Statistics, 61, 455-460. Glosten, L.R., and L.E. Harris, 1988, Estimating the components of the bid ask spread, Journal of

Financial Economics, 21, 123-142. Garfinkel, J.A., and M. Nimalendran, 1995, Market structure and trader anonymity: an analysis

of insider trading, working paper, University of Florida, Gainesville. Goldstein, M.A., K.A. Kavajecz, 2000, Eights, sixteenths and market depth: changes in tick size

and liquidity provision on the NYSE, Journal of Financial Economics, 56, 125-149. Grossman, S.J., M.H. Miller, 1988, Liquidity and market structure, Journal of Finance, 43, 617-633. Harris, L.E., 1990, Liquidity, trading rules, and electronic trading systems, Monograph Series in

Finance and Economics, New York University. Harris, L. E., 1994, Minimum price variations, discrete bid ask spreads, and quotation sizes,

Review of Financial Studies, 7, 149-178. Harris, L. E., 1997, Decimalization: a review of the arguments and evidence, working paper,

University of Southern California. Hart, M., 1993, Decimal stock pricing: dragging the securities industry into the twenty-first

century, Loyola of Los Angeles Law Review, 26, 883-890. Hasbrouck, J., and D. Sosebee, 1992, Orders, trades, reports and quotes at the New York Stock

Exchange, working paper, New York Stock Exchange. Hasbrouck, J., 1995, One security, many markets: determining the contributions to price

discovery, Journal of Finance, 50, 1175-1199. Huang, R.D., and H.R. Stoll, 1996, Dealer versus auction markets: a paired comparison of

execution costs on NASDAQ and the NYSE, Journal of Financial Economics, 41, 313-357. Huson, M., Kim, Y., and V. Mehrotra, 1997, Decimal quotes, market quality, and competition

36

for order flow: evidence from the Toronto Stock Exchange, working paper, University of Alberta.

Jones, C. M., and M.L. Lipson, 2000, Sixteenths: direct evidence on institutional execution costs,

forthcoming Journal of Financial Economics, Kandel, E., and L. Marx, 1996, Nasdaq market structure and spread patterns, working paper,

University of Rochester. Lee, C. M. C., and M.A. Ready, 1991, Inferring trade direction from intraday data, Journal of

Finance, 46, 733-746. Madhavan, A., M. Richardson and M. Roomans, 1997, Why do security prices fluctuate? A

transaction-level analysis of NYSE stocks, Review of Financial Studies, 10, 1035-1064. Madhavan, A., and S. Smidt, 1991, A Bayesian model of intraday specialist pricing, Journal of

Financial Economics, 30, 99-134. O’Connell, V., 1997, Conversion to decimal system in stocks could prove a boon to small

investors. Wall Street Journal, June 6, C1. O’Hara, M., 1995, Market Microstructure Theory, Blackwell Publishers. Peake, J.W., 1995, Brother can you spare a dime: let’s decimalize U.S. equity markets In:

Schwartz, R.A. (Ed.), Global Equity Markets: Technological, Competitive and Regulatory Challenges. Irwin Professional, Chicago.

Peterson, M. and D. Fialkowski, 1994, Posted versus effective spreads, Journal of Financial

Economics, 35, 269-292. Porter, D., and D. Weaver, 1997, Decimalization and market quality, Financial Management, 26, 5-

26. Ricker, J.P., 1998, Breaking the eighth: sixteenths on the New York Stock Exchange, working

paper. Ronen, T., and D.G. Weaver, 1998, Teenies’ anyone: the case of the American Stock Exchange,

working paper, Rutgers University. Seppi, D.J., 1997, Liquidity provision with limit orders and a strategic specialist, Review of

Financial Studies, 10, 103-150. Shapiro, J., 1993, Recent competitive developments in U.S. equity markets, NYSE working

paper, 93-02.

37

Table 1. Daily Average Quote Updating Frequency of NYSE-listed Decimal Stocks Across Regional Exchanges. This table presents the daily average quote frequency in each regional exchange for selected NYSE-listed decimal stocks and the corresponding matched sample of control stocks, before decimalization (July, 2000) and after decimalization (between October 22, 2000 and January 26, 2001). The reported numbers, for a given exchange, are weighted averages of daily averages (across stocks), where the weights are the average daily dollar trading volume of stocks over the non-event benchmark period of July 2000. The net difference in daily average quote frequency in decimal stocks is calculated as the difference between the daily average (quote frequency) of each decimal stock and its paired control stock. The average of these differences over each exchange and over each period is then computed. The table reports the difference in the post-decimal average and the pre-decimal average. T-tests (of equality of means) are performed to see if the net differences in decimal stocks are statistically distinct from zero.

Pre-decimal Period (July, 2000)

Post-decimal Period (October 2, 2000 – January 26,

2001)

% Change Decimal Stocks

(post – pre)

% Change Control Stocks

(post – pre)

Net Difference in

Quoted Spreads in Decimal Stocks

(post – pre ) Exchanges Decimal Stocks Control Stocks Decimal Stocks Control Stocks

Boston 374 346 541 285 44.7 -17.6 175.9*** Chicago 287 298 701 286 144.3 -4.0 151.1*** NYSE 1,769 1,511 1,515 1,809 -14.4 19.7 -13.6 Pacific 394 462 705 350 78.9 -24.2 119.5*** Nasdaq 1,659 1,682 1,201 1,033 -27.6 -38.6 52.4* Philadelphia 468 418 795 416 69.9 -0.5 127.0*** Cincinnati 273 401 495 380 81.3 -5.2 119.0** Average 751 735 854 654 13.7 -11.0 *** p-value ≤ 0.01, ** 0.01 < p-value ≤ 0.05, * 0.05 < p-value ≤ 0.10

38

Table 2. Time of Existence of the Best Bid and Offer Prices (BBO) by Regional Exchanges for NYSE-listed Decimal Stocks

This table presents the frequency and the corresponding percent of total trading time that a given exchange held the best bid and the times that the same exchange held the best offer. The sample comprises of selected NYSE-listed stocks in the decimal pilot and a matched sample of control stocks. The examination period is between October 2, 2000, and January 26, 2001 (decimal period). Results are also provided for the same stocks over July 2000, the pre-decimal benchmark period. The net difference in decimal stocks is calculated as the difference between the daily average (frequency of BBO observations) of each decimal stock and its paired control stock. The average of these differences over each exchange and over each (pre decimal and post decimal) period is then computed. The table reports the difference in the post-decimal average and the pre-decimal average. T-tests (of equality of means) are performed to see if the net differences in decimal stocks are statistically distinct from zero.

Pre-decimal Period (July, 2000)

Post-decimal Period (October 2, 2000 --- January 26, 2001)

%change in Number of BBO Obs

(post – pre)

%change in Number of BBO Obs

(post – pre)

Net Difference in the

Number of BBO Obs in Decimal Stocks

(post – pre) Exchange Number

of BBO Obs

% of Total Seconds

Number of BBO

Obs

% of Total Seconds

Number of BBO

Obs

% of Total Seconds

Number of BBO

Obs

% of Total Seconds

Decimal Stocks Control Stocks Decimal Stocks Control Stocks Decimal Stocks

Control Stocks