Embed Size (px)

Citation preview

1

2

3

Suggested Citation:

Ismal, R., and Abduh, M. (2013). Depositors’ withdrawal behavior in Indonesian Islamic Banks.

Australian Journal of Islamic Banking and Finance, Vol. 2 No.1., pp.1-20.

(I have not received the printed copy from the publisher, just received the scanned

cover and table of contents from a colleague. Therefore, below is the final version

of the article submitted for publication to the Australian Journal of Islamic

Banking and Finance)

4

Depositors’ Withdrawal Behavior in Indonesian Islamic Banks

Rifki Ismal

Lecturer

Faculty of Economics,

University of Indonesia, Depok, Indonesia

Muhamad Abduh

IIUM Institute of Islamic Banking and Finance,

International Islamic University Malaysia, Kuala Lumpur, Malaysia

Abstract

Purpose – This paper aims to investigate factors determining depositors’ withdrawal behavior

based on the empirical survey of the Indonesian Islamic banking industry.

Design/methodology/approach – This paper conducts a direct survey towards Islamic banking

depositors in Indonesia. Particularly, it uses a combination of open and close questions assessing

information about depositors’ withdrawal behavior under different circumstances. Then, it

analyzes such primary data with statistical tool to find information and factors determining

depositors’ withdrawal behavior.

Findings – Firstly, the paper finds the general factors causing depositors to take their money

which is if the Islamic banks do not comply with Sharia. Secondly, it finds the specific factors,

which are: (i) the willingness to adjust the tenor of deposits, (ii) the need of funds for transactions

and, (iii) less payment of return sharing on deposits than the previous period. Further, it is also

found that depositors tend to deposit funds in Islamic banks rather than Islamic windows and

most of them have income of less than Rp5 million per month. Meanwhile, with regard to

interaction with the sources of information, news in the newspapers and news on the TV are the

dominant ones influencing the depositors banking behavior. However, in the daily life, they

interact intensively with internet. As such, this paper recommends Islamic banks to keep

complying with Sharia and maintaining the robust performance in order to be able to pay positive

and competitive return sharing on deposits. Further, they need to intensify internet banking

facilities to conduct intensive communication with depositors, facilitate the depositors’

transactions and monitor their schedule of withdrawals to manage deposit withdrawals.

Originality/value – This paper conducts an empirical research on deposit withdrawals and

provides useful recommendations for Islamic banks in Indonesia to manage the potential deposit

withdrawal. The best of authors’ knowledge, this is the first paper trying to analyze the deposits’

withdrawal in Indonesian Islamic banking emphasizing on the psychological aspects of

depositors to withdraw money and their interaction with the banks and media.

Paper type: Research paper

Keywords: Withdrawal risk, Islamic banking, Indonesia

5

1. Background

Islamic banking and finance is experiencing a rapid acceleration worldwide. According to the

report released by The Banker Magazine which conducted a worldwide survey of the

development of Islamic financial institutions during 2009, the assets held by Islamic commercial

banks and Islamic windows of the conventional banks rose 28.6% from USD639 billion in 2008

to USD822 billion in 20091. Whereby, the conventional banks’ assets posted only 6.8% annual

growth within the same period2. This is a two digit growth shown by the industry despite the

severe impact of the global financial crisis 2008-2009.

In the case of Indonesia, the development of Islamic banking can be traced from the

establishment of Bank Muamalat Indonesia, the first Islamic bank, in 1992. Even though

Indonesia is a country with the largest Muslim population in the world, the establishment of its

first Islamic bank in 1992 was actually ten years behind Malaysia and Turkey, and almost twenty

years behind Dubai which established its first Islamic commercial bank in 1975 namely, Dubai

Islamic bank.

Nonetheless, the Indonesian Islamic banking industry has been growing promisingly in

the last two decades with the rate of growth between 50-60%. It can be seen from the

performance of several Islamic banking indicators such as the number of Islamic commercial

banks (BUS), Islamic windows (UUS), Islamic rural banks and, their branches. Moreover, the

total assets, total financing, as well as total deposits managed by Islamic banking industry also

show a significant growth.

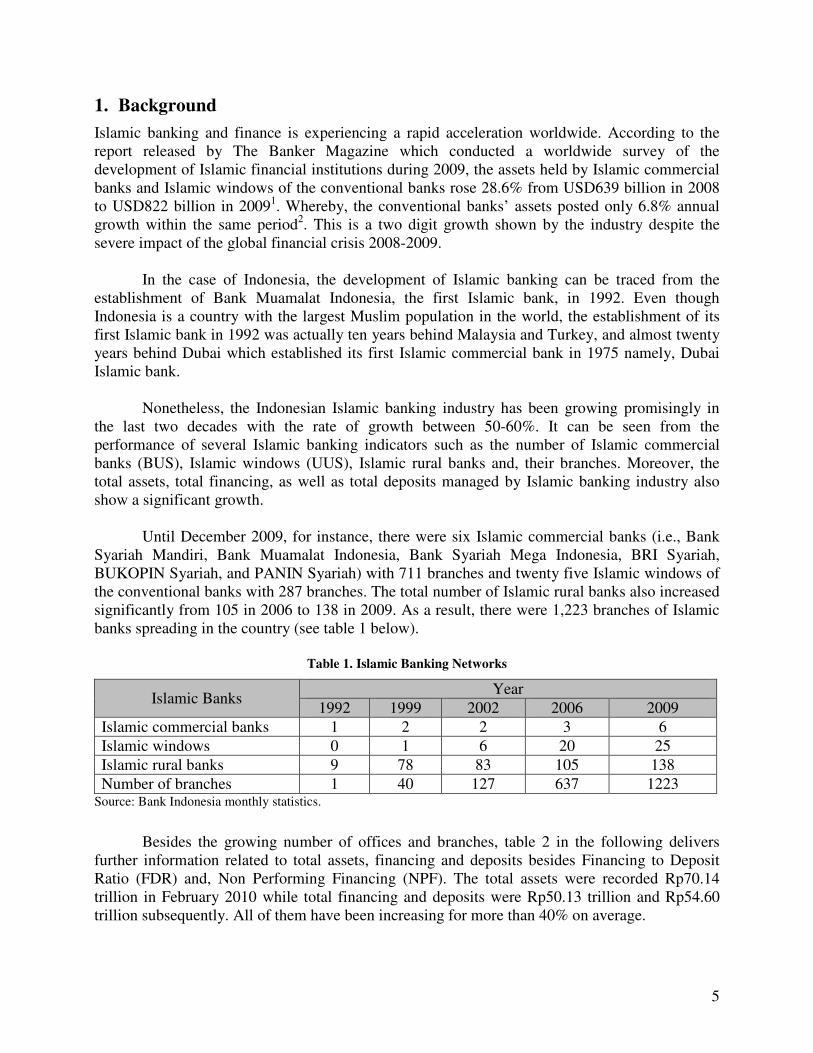

Until December 2009, for instance, there were six Islamic commercial banks (i.e., Bank

Syariah Mandiri, Bank Muamalat Indonesia, Bank Syariah Mega Indonesia, BRI Syariah,

BUKOPIN Syariah, and PANIN Syariah) with 711 branches and twenty five Islamic windows of

the conventional banks with 287 branches. The total number of Islamic rural banks also increased

significantly from 105 in 2006 to 138 in 2009. As a result, there were 1,223 branches of Islamic

banks spreading in the country (see table 1 below).

Table 1. Islamic Banking Networks

Islamic Banks Year

1992 1999 2002 2006 2009

Islamic commercial banks 1 2 2 3 6

Islamic windows 0 1 6 20 25

Islamic rural banks 9 78 83 105 138

Number of branches 1 40 127 637 1223 Source: Bank Indonesia monthly statistics.

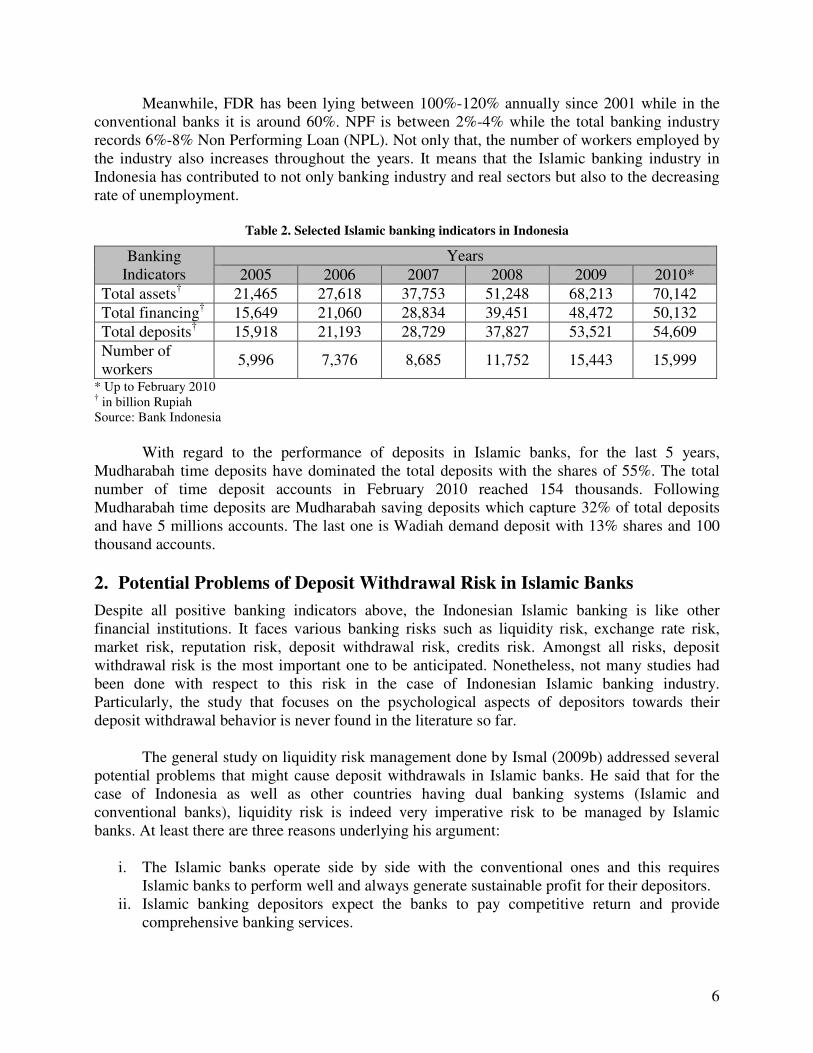

Besides the growing number of offices and branches, table 2 in the following delivers

further information related to total assets, financing and deposits besides Financing to Deposit

Ratio (FDR) and, Non Performing Financing (NPF). The total assets were recorded Rp70.14

trillion in February 2010 while total financing and deposits were Rp50.13 trillion and Rp54.60

trillion subsequently. All of them have been increasing for more than 40% on average.

6

Meanwhile, FDR has been lying between 100%-120% annually since 2001 while in the

conventional banks it is around 60%. NPF is between 2%-4% while the total banking industry

records 6%-8% Non Performing Loan (NPL). Not only that, the number of workers employed by

the industry also increases throughout the years. It means that the Islamic banking industry in

Indonesia has contributed to not only banking industry and real sectors but also to the decreasing

rate of unemployment.

Table 2. Selected Islamic banking indicators in Indonesia

Banking

Indicators

Years

2005 2006 2007 2008 2009 2010*

Total assets† 21,465 27,618 37,753 51,248 68,213 70,142

Total financing† 15,649 21,060 28,834 39,451 48,472 50,132

Total deposits† 15,918 21,193 28,729 37,827 53,521 54,609

Number of

workers 5,996 7,376 8,685 11,752 15,443 15,999

* Up to February 2010 † in billion Rupiah

Source: Bank Indonesia

With regard to the performance of deposits in Islamic banks, for the last 5 years,

Mudharabah time deposits have dominated the total deposits with the shares of 55%. The total

number of time deposit accounts in February 2010 reached 154 thousands. Following

Mudharabah time deposits are Mudharabah saving deposits which capture 32% of total deposits

and have 5 millions accounts. The last one is Wadiah demand deposit with 13% shares and 100

thousand accounts.

2. Potential Problems of Deposit Withdrawal Risk in Islamic Banks

Despite all positive banking indicators above, the Indonesian Islamic banking is like other

financial institutions. It faces various banking risks such as liquidity risk, exchange rate risk,

market risk, reputation risk, deposit withdrawal risk, credits risk. Amongst all risks, deposit

withdrawal risk is the most important one to be anticipated. Nonetheless, not many studies had

been done with respect to this risk in the case of Indonesian Islamic banking industry.

Particularly, the study that focuses on the psychological aspects of depositors towards their

deposit withdrawal behavior is never found in the literature so far.

The general study on liquidity risk management done by Ismal (2009b) addressed several

potential problems that might cause deposit withdrawals in Islamic banks. He said that for the

case of Indonesia as well as other countries having dual banking systems (Islamic and

conventional banks), liquidity risk is indeed very imperative risk to be managed by Islamic

banks. At least there are three reasons underlying his argument:

i. The Islamic banks operate side by side with the conventional ones and this requires

Islamic banks to perform well and always generate sustainable profit for their depositors.

ii. Islamic banking depositors expect the banks to pay competitive return and provide

comprehensive banking services.

7

iii. During the global financial crisis 2008-2009 especially when the conventional banks

offered attractive (higher) return on deposits, Islamic banks appeared into a dilemma. It is

because such high interest return on deposit caused a higher expected return on Islamic

deposits while the business was in downturn. This might lead into a displaced commercial

risk and at the end is the deposit withdrawal risk.

His study on liquidity risk is very close with the topic of deposit withdrawal risk.

However, he did not explore the psychological aspects of depositors and the interaction of

depositors with the media as communication tools between Islamic banks and depositors. With

regard to studying on deposit withdrawal, this paper attempts to answer the question of how

Islamic banking depositors behave towards some essential issues such as Sharia compliant issue,

rate of return on Islamic deposits, interaction with various media and, responses of depositors

with the rumor about financial crises that could probably lead to deposit withdrawals.

3. Depositors’ Behavior in Withdrawing Money from Islamic Banks

Hitherto, researches about depositors’ behavior to withdraw money in Islamic banks are rarely

found particularly the specific research which accommodates depositors’ attributes to withdraw

money from Islamic deposits. But, there are many researches which utilize macro economic

variables to explain volatility of deposits in the conventional banks.

Some literatures related to the study of deposit withdrawals in the conventional banking

institution are presented in this section (see table 3). First of all was the study of deposit behavior

done by Lauchlin Currie, the former analyst of United States Treasury Department. He said that

demand deposits were susceptible to all forces that affected the volume of media of exchange of

the community, whereas time deposits were affected more by factors that affected saving and

investing (Currie, 2004). He further said that:

“The remarkable stability of the deposits of mutual savings banks throughout the depression suggests

that the decline shown in commercial bank time deposits was not so much a reflection of the

entrenchment on savings for living expenses as it was attributable to withdrawals because of loss of

confidence.”

In fact, the situation when depositors loose his confidence on banks and hence take their

funds from banks is determined by several factors. For example, when studying about

individuals’ behavior on deposit withdrawal based on rumors of financial crisis, Takemura and

Kozu (2009) found that depositors, who believed in media as sources of information such as

weekly/monthly magazines, internet, and conducted conversations within the social community,

would be more susceptible in trusting banks. Most of them are likely to withdraw their deposits

from banks because of negative rumors in media or social community.

The other research done by Yada et al (2009) focused on the individuals’ deposit behavior

after they heard rumors about financial crisis. They found that individuals with the following

characteristics: high annual incomes, less known about deposit insurance, self employed or

working in a family business, are most likely to withdraw money from banks because of the

rumors of financial crisis. This was what they found in Japanese Banks.

8

The next research done by Gilkeson and Ruff (1996) studied the early liquidity withdrawals

in American Banks. They found that early liquidity withdrawals from depositors were mainly

motivated by reinvestment incentives. However, after three years, Gilkeson et al (1999) found the

different results than Gilkeson and Ruff (1996). They discovered that early withdrawals were

significantly sensitive to changes in interest rates and the need for liquidity rather than higher

return on investment.

Meanwhile, literatures related to the Islamic banking depositors’ withdrawal behavior are

for example Ahmed (2003) and Ahmed (2002). Ahmed (2003), by using some mathematical

notations and logic, concluded that asset preservation in terms of minimizing the risk of loss due

to a lower rate of return was an important factor explaining depositors’ withdrawal behavior. In

another paper, Ahmed (2002) arranged a survey involving 468 respondents and covered three

different countries, which are: Bahrain, Bangladesh, and Sudan. The result was summarized in

the following:

o Depositors would withdraw funds if there were rumors about the poor performance of

Islamic banks.

o In the short run, the lower rate of return would not force depositors to withdraw funds. But

in the long run, it might lead significant number of depositors to take their funds from

Islamic banks.

o Depositors would shift their funds to other banks because of the non Sharia compliant

Islamic banks.

o Depositors would shift their funds to other banks if they found out that some parts of the

banks’ incomes came from interest incomes.

Table 3. Selected Literatures Regarding the Depositors’ Behavior on Deposit Withdrawals

Auhtor(s)

(Year) Country Type of bank Findings

Currie (2004) USA Conventional

banking

Loss of confidence on banks would lead depositors

to withdraw funds.

Gilkeson and

Ruff (1996) USA

Conventional

banking

Early deposit withdrawals were motivated by

reinvestment incentives.

Gilkeson,

List, and

Ruff (1999)

USA Conventional

banking

1. The early deposit withdrawals were significantly

sensitive to changes in interest rates.

2. Most of early withdrawals were triggered by

depositors' liquidity needs rather than higher

returns on investment.

9

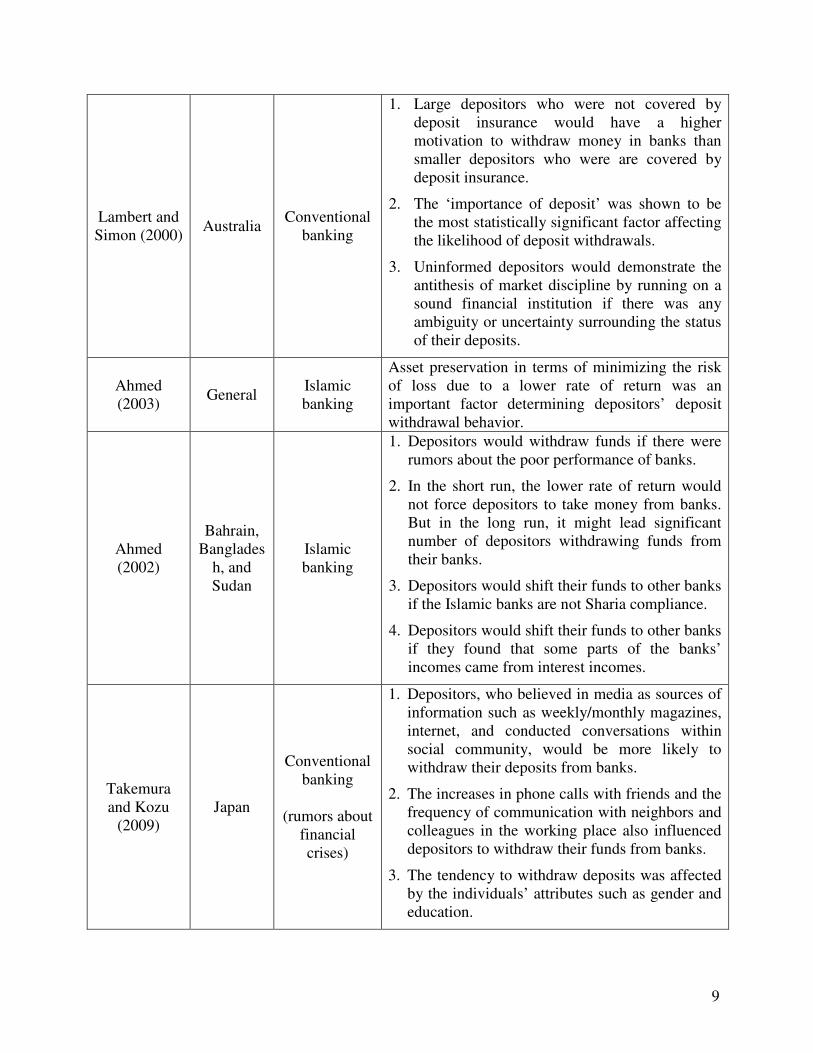

Lambert and

Simon (2000) Australia

Conventional

banking

1. Large depositors who were not covered by

deposit insurance would have a higher

motivation to withdraw money in banks than

smaller depositors who were are covered by

deposit insurance.

2. The ‘importance of deposit’ was shown to be

the most statistically significant factor affecting

the likelihood of deposit withdrawals.

3. Uninformed depositors would demonstrate the

antithesis of market discipline by running on a

sound financial institution if there was any

ambiguity or uncertainty surrounding the status

of their deposits.

Ahmed

(2003) General

Islamic

banking

Asset preservation in terms of minimizing the risk

of loss due to a lower rate of return was an

important factor determining depositors’ deposit

withdrawal behavior.

Ahmed

(2002)

Bahrain,

Banglades

h, and

Sudan

Islamic

banking

1. Depositors would withdraw funds if there were

rumors about the poor performance of banks.

2. In the short run, the lower rate of return would

not force depositors to take money from banks.

But in the long run, it might lead significant

number of depositors withdrawing funds from

their banks.

3. Depositors would shift their funds to other banks

if the Islamic banks are not Sharia compliance.

4. Depositors would shift their funds to other banks

if they found that some parts of the banks’

incomes came from interest incomes.

Takemura

and Kozu

(2009)

Japan

Conventional

banking

(rumors about

financial

crises)

1. Depositors, who believed in media as sources of

information such as weekly/monthly magazines,

internet, and conducted conversations within

social community, would be more likely to

withdraw their deposits from banks.

2. The increases in phone calls with friends and the

frequency of communication with neighbors and

colleagues in the working place also influenced

depositors to withdraw their funds from banks.

3. The tendency to withdraw deposits was affected

by the individuals’ attributes such as gender and

education.

10

Yada et.al

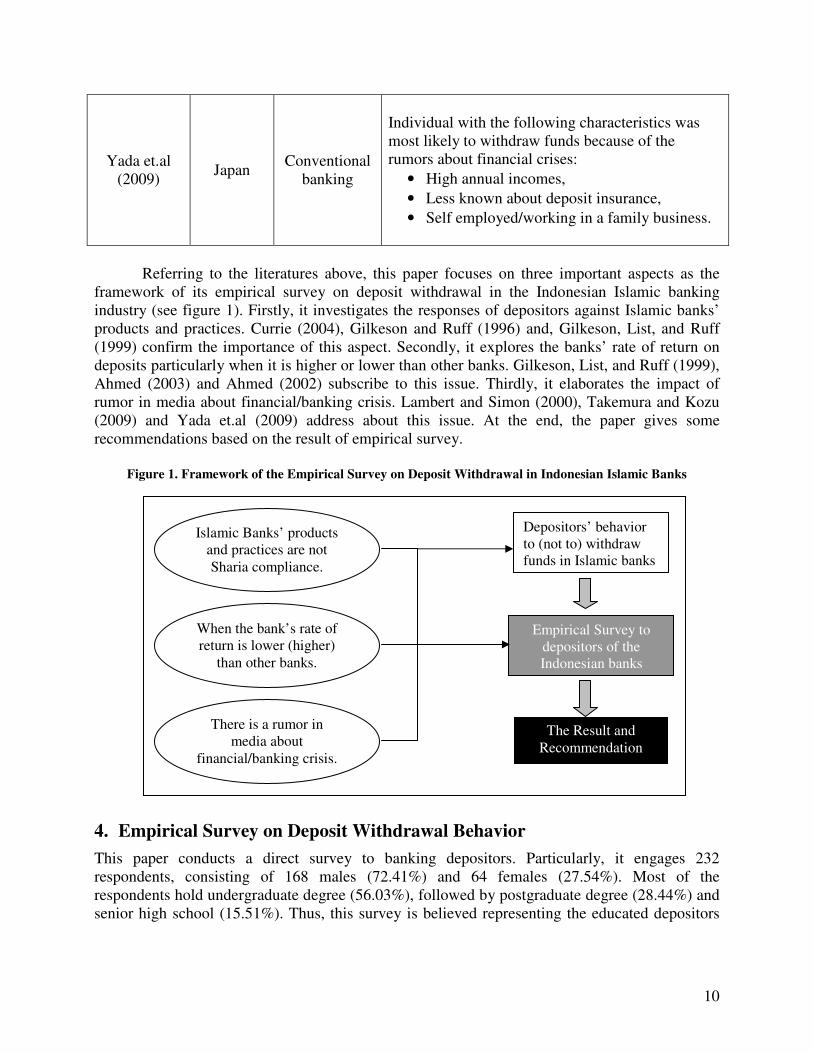

(2009) Japan

Conventional

banking

Individual with the following characteristics was

most likely to withdraw funds because of the

rumors about financial crises:

• High annual incomes,

• Less known about deposit insurance,

• Self employed/working in a family business.

Referring to the literatures above, this paper focuses on three important aspects as the

framework of its empirical survey on deposit withdrawal in the Indonesian Islamic banking

industry (see figure 1). Firstly, it investigates the responses of depositors against Islamic banks’

products and practices. Currie (2004), Gilkeson and Ruff (1996) and, Gilkeson, List, and Ruff

(1999) confirm the importance of this aspect. Secondly, it explores the banks’ rate of return on

deposits particularly when it is higher or lower than other banks. Gilkeson, List, and Ruff (1999),

Ahmed (2003) and Ahmed (2002) subscribe to this issue. Thirdly, it elaborates the impact of

rumor in media about financial/banking crisis. Lambert and Simon (2000), Takemura and Kozu

(2009) and Yada et.al (2009) address about this issue. At the end, the paper gives some

recommendations based on the result of empirical survey.

Figure 1. Framework of the Empirical Survey on Deposit Withdrawal in Indonesian Islamic Banks

4. Empirical Survey on Deposit Withdrawal Behavior

This paper conducts a direct survey to banking depositors. Particularly, it engages 232

respondents, consisting of 168 males (72.41%) and 64 females (27.54%). Most of the

respondents hold undergraduate degree (56.03%), followed by postgraduate degree (28.44%) and

senior high school (15.51%). Thus, this survey is believed representing the educated depositors

Islamic Banks’ products

and practices are not

Sharia compliance.

When the bank’s rate of

return is lower (higher)

than other banks.

There is a rumor in

media about

financial/banking crisis.

Empirical Survey to

depositors of the

Indonesian banks

The Result and

Recommendation

Depositors’ behavior

to (not to) withdraw

funds in Islamic banks

11

with good knowledge in banking and high frequency of dealing with banks especially Islamic

banks.

The following sub sections present the result of the empirical survey with regard to: (a)

general factors leading to deposit withdrawals, (b) specific factors leading to deposit withdrawals,

(c) analysis of type of depositors’ banks, (d) analysis of depositors’ incomes and amount of

deposits and, (e) the impact of media as sources of information.

4. 1. General Factors Leading to Deposit Withdrawals

The survey finds that depositors give much faith on the compliance of Islamic banking products

and operations with Sharia principles and practices. This factor is confirmed by 57.49% of total

respondents and implies that depositors have high expectation to Islamic banks to have Islamic

products and operate based on Sharia principles and practices. Whenever depositors find Islamic

banks violate Sharia principles and practices, it is most likely that they will take their money out

from the banks (deposit withdrawals). This group of depositors is commonly called religious

depositors (see table 4).

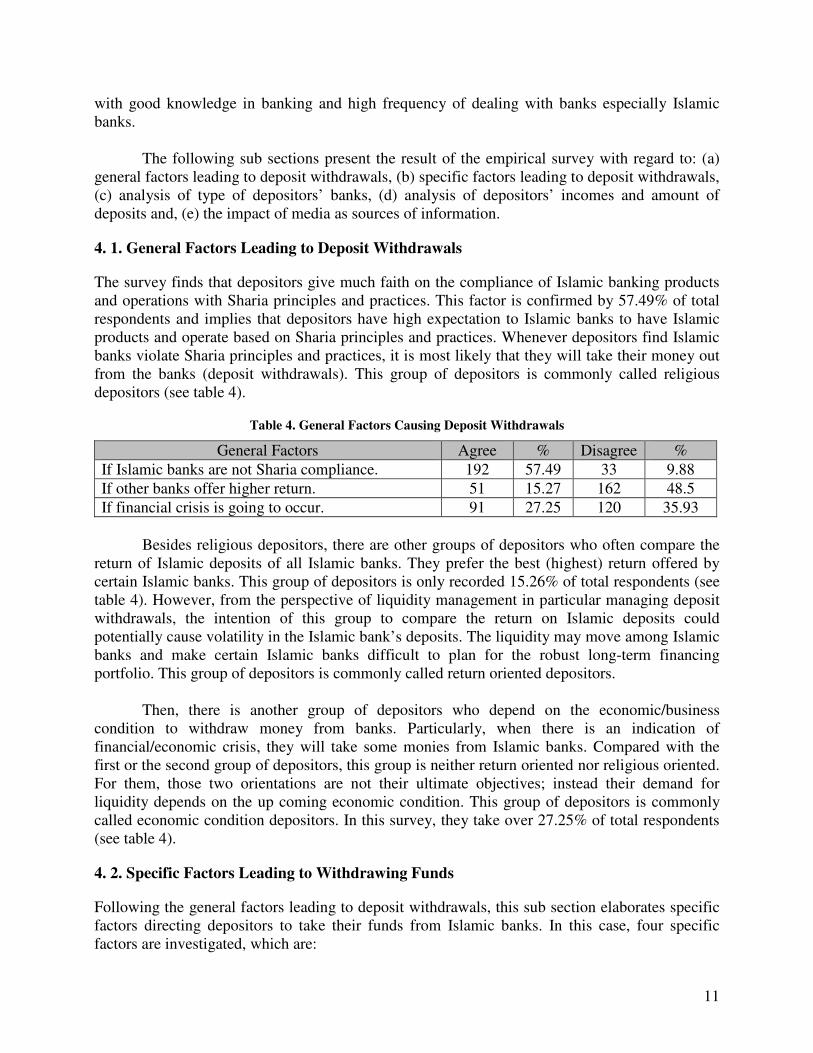

Table 4. General Factors Causing Deposit Withdrawals

General Factors Agree % Disagree %

If Islamic banks are not Sharia compliance. 192 57.49 33 9.88

If other banks offer higher return. 51 15.27 162 48.5

If financial crisis is going to occur. 91 27.25 120 35.93

Besides religious depositors, there are other groups of depositors who often compare the

return of Islamic deposits of all Islamic banks. They prefer the best (highest) return offered by

certain Islamic banks. This group of depositors is only recorded 15.26% of total respondents (see

table 4). However, from the perspective of liquidity management in particular managing deposit

withdrawals, the intention of this group to compare the return on Islamic deposits could

potentially cause volatility in the Islamic bank’s deposits. The liquidity may move among Islamic

banks and make certain Islamic banks difficult to plan for the robust long-term financing

portfolio. This group of depositors is commonly called return oriented depositors.

Then, there is another group of depositors who depend on the economic/business

condition to withdraw money from banks. Particularly, when there is an indication of

financial/economic crisis, they will take some monies from Islamic banks. Compared with the

first or the second group of depositors, this group is neither return oriented nor religious oriented.

For them, those two orientations are not their ultimate objectives; instead their demand for

liquidity depends on the up coming economic condition. This group of depositors is commonly

called economic condition depositors. In this survey, they take over 27.25% of total respondents

(see table 4).

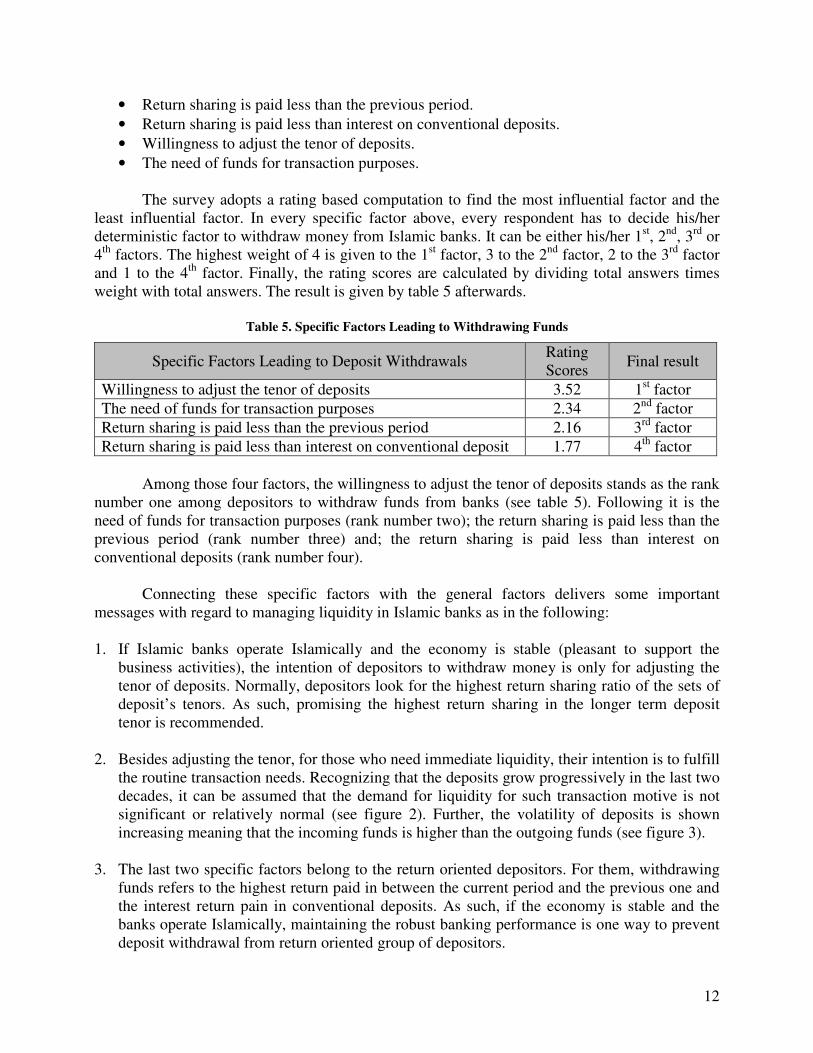

4. 2. Specific Factors Leading to Withdrawing Funds

Following the general factors leading to deposit withdrawals, this sub section elaborates specific

factors directing depositors to take their funds from Islamic banks. In this case, four specific

factors are investigated, which are:

12

• Return sharing is paid less than the previous period.

• Return sharing is paid less than interest on conventional deposits.

• Willingness to adjust the tenor of deposits.

• The need of funds for transaction purposes.

The survey adopts a rating based computation to find the most influential factor and the

least influential factor. In every specific factor above, every respondent has to decide his/her

deterministic factor to withdraw money from Islamic banks. It can be either his/her 1st, 2

nd, 3

rd or

4th

factors. The highest weight of 4 is given to the 1st factor, 3 to the 2

nd factor, 2 to the 3

rd factor

and 1 to the 4th

factor. Finally, the rating scores are calculated by dividing total answers times

weight with total answers. The result is given by table 5 afterwards.

Table 5. Specific Factors Leading to Withdrawing Funds

Specific Factors Leading to Deposit Withdrawals Rating

Scores Final result

Willingness to adjust the tenor of deposits 3.52 1st factor

The need of funds for transaction purposes 2.34 2nd

factor

Return sharing is paid less than the previous period 2.16 3rd

factor

Return sharing is paid less than interest on conventional deposit 1.77 4th

factor

Among those four factors, the willingness to adjust the tenor of deposits stands as the rank

number one among depositors to withdraw funds from banks (see table 5). Following it is the

need of funds for transaction purposes (rank number two); the return sharing is paid less than the

previous period (rank number three) and; the return sharing is paid less than interest on

conventional deposits (rank number four).

Connecting these specific factors with the general factors delivers some important

messages with regard to managing liquidity in Islamic banks as in the following:

1. If Islamic banks operate Islamically and the economy is stable (pleasant to support the

business activities), the intention of depositors to withdraw money is only for adjusting the

tenor of deposits. Normally, depositors look for the highest return sharing ratio of the sets of

deposit’s tenors. As such, promising the highest return sharing in the longer term deposit

tenor is recommended.

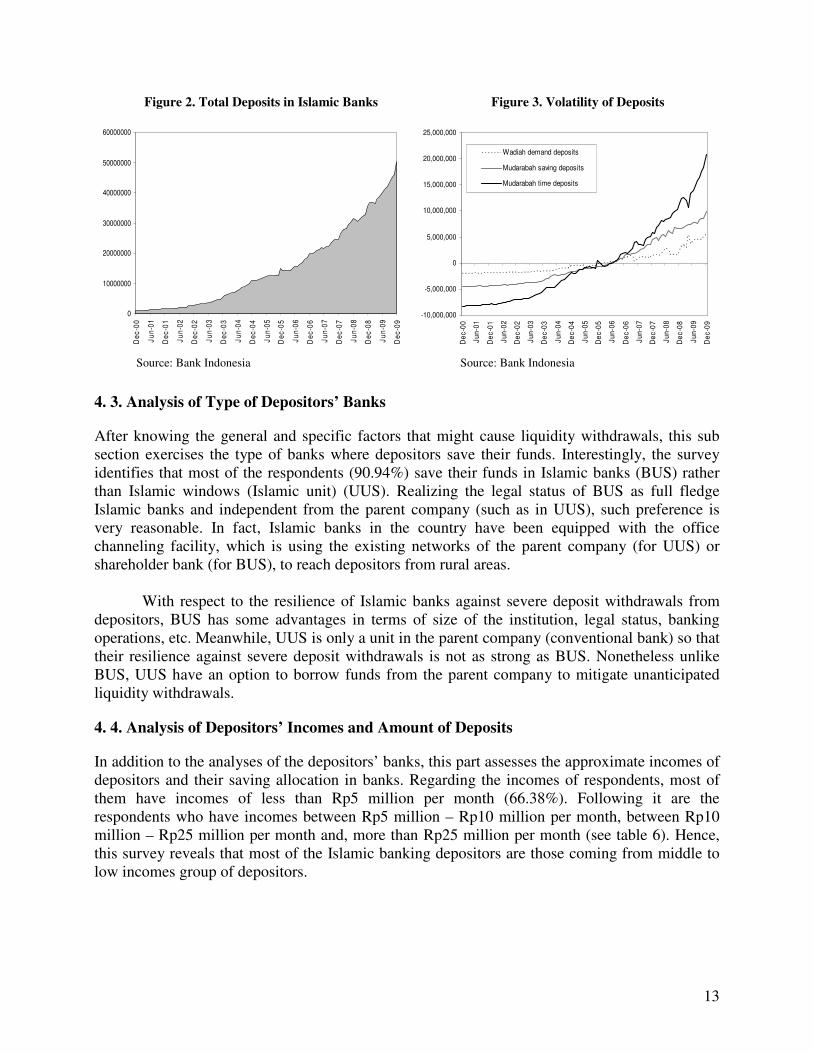

2. Besides adjusting the tenor, for those who need immediate liquidity, their intention is to fulfill

the routine transaction needs. Recognizing that the deposits grow progressively in the last two

decades, it can be assumed that the demand for liquidity for such transaction motive is not

significant or relatively normal (see figure 2). Further, the volatility of deposits is shown

increasing meaning that the incoming funds is higher than the outgoing funds (see figure 3).

3. The last two specific factors belong to the return oriented depositors. For them, withdrawing

funds refers to the highest return paid in between the current period and the previous one and

the interest return pain in conventional deposits. As such, if the economy is stable and the

banks operate Islamically, maintaining the robust banking performance is one way to prevent

deposit withdrawal from return oriented group of depositors.

13

Figure 2. Total Deposits in Islamic Banks Figure 3. Volatility of Deposits

0

10000000

20000000

30000000

40000000

50000000

60000000D

ec

-00

Ju

n-0

1

De

c-0

1

Ju

n-0

2

De

c-0

2

Ju

n-0

3

De

c-0

3

Ju

n-0

4

De

c-0

4

Ju

n-0

5

De

c-0

5

Ju

n-0

6

De

c-0

6

Ju

n-0

7

De

c-0

7

Ju

n-0

8

De

c-0

8

Ju

n-0

9

De

c-0

9

-10,000,000

-5,000,000

0

5,000,000

10,000,000

15,000,000

20,000,000

25,000,000

De

c-0

0

Ju

n-0

1

De

c-0

1

Ju

n-0

2

De

c-0

2

Ju

n-0

3

De

c-0

3

Ju

n-0

4

De

c-0

4

Ju

n-0

5

De

c-0

5

Ju

n-0

6

De

c-0

6

Ju

n-0

7

De

c-0

7

Ju

n-0

8

De

c-0

8

Ju

n-0

9

De

c-0

9

Wadiah demand deposits

Mudarabah saving deposits

Mudarabah time deposits

Source: Bank Indonesia Source: Bank Indonesia

4. 3. Analysis of Type of Depositors’ Banks

After knowing the general and specific factors that might cause liquidity withdrawals, this sub

section exercises the type of banks where depositors save their funds. Interestingly, the survey

identifies that most of the respondents (90.94%) save their funds in Islamic banks (BUS) rather

than Islamic windows (Islamic unit) (UUS). Realizing the legal status of BUS as full fledge

Islamic banks and independent from the parent company (such as in UUS), such preference is

very reasonable. In fact, Islamic banks in the country have been equipped with the office

channeling facility, which is using the existing networks of the parent company (for UUS) or

shareholder bank (for BUS), to reach depositors from rural areas.

With respect to the resilience of Islamic banks against severe deposit withdrawals from

depositors, BUS has some advantages in terms of size of the institution, legal status, banking

operations, etc. Meanwhile, UUS is only a unit in the parent company (conventional bank) so that

their resilience against severe deposit withdrawals is not as strong as BUS. Nonetheless unlike

BUS, UUS have an option to borrow funds from the parent company to mitigate unanticipated

liquidity withdrawals.

4. 4. Analysis of Depositors’ Incomes and Amount of Deposits

In addition to the analyses of the depositors’ banks, this part assesses the approximate incomes of

depositors and their saving allocation in banks. Regarding the incomes of respondents, most of

them have incomes of less than Rp5 million per month (66.38%). Following it are the

respondents who have incomes between Rp5 million – Rp10 million per month, between Rp10

million – Rp25 million per month and, more than Rp25 million per month (see table 6). Hence,

this survey reveals that most of the Islamic banking depositors are those coming from middle to

low incomes group of depositors.

14

Table 6. Range of Incomes of Respondents

Incomes of Depositors Number %

Less than Rp 5 million per month 154 66.38

Between Rp 5 – 10 million per month 47 20.26

Between Rp 10 – 25 million per month 19 8.19

More than Rp 25 million per month 12 5.17

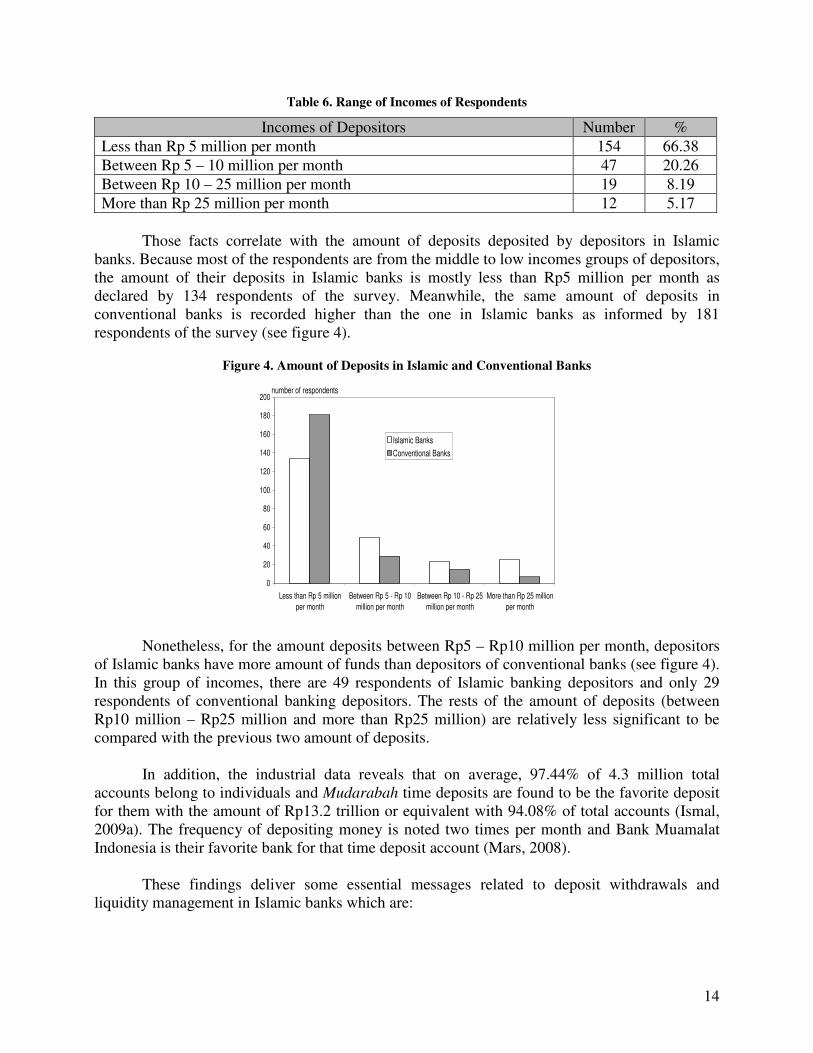

Those facts correlate with the amount of deposits deposited by depositors in Islamic

banks. Because most of the respondents are from the middle to low incomes groups of depositors,

the amount of their deposits in Islamic banks is mostly less than Rp5 million per month as

declared by 134 respondents of the survey. Meanwhile, the same amount of deposits in

conventional banks is recorded higher than the one in Islamic banks as informed by 181

respondents of the survey (see figure 4).

Figure 4. Amount of Deposits in Islamic and Conventional Banks

0

20

40

60

80

100

120

140

160

180

200

Less than Rp 5 million

per month

Between Rp 5 - Rp 10

million per month

Between Rp 10 - Rp 25

million per month

More than Rp 25 million

per month

Islamic Banks

Conventional Banks

number of respondents

Nonetheless, for the amount deposits between Rp5 – Rp10 million per month, depositors

of Islamic banks have more amount of funds than depositors of conventional banks (see figure 4).

In this group of incomes, there are 49 respondents of Islamic banking depositors and only 29

respondents of conventional banking depositors. The rests of the amount of deposits (between

Rp10 million – Rp25 million and more than Rp25 million) are relatively less significant to be

compared with the previous two amount of deposits.

In addition, the industrial data reveals that on average, 97.44% of 4.3 million total

accounts belong to individuals and Mudarabah time deposits are found to be the favorite deposit

for them with the amount of Rp13.2 trillion or equivalent with 94.08% of total accounts (Ismal,

2009a). The frequency of depositing money is noted two times per month and Bank Muamalat

Indonesia is their favorite bank for that time deposit account (Mars, 2008).

These findings deliver some essential messages related to deposit withdrawals and

liquidity management in Islamic banks which are:

15

i) Most of the depositors of Islamic banks are retail depositors from middle to low incomes

groups of depositors and have the amount of deposits of less than Rp5 million per month. It is

believed that constructing an optimal portfolio financing of the funds coming from so many

retail depositors with small amount of deposits is much difficult than the funds coming from

big depositors with high amount of deposits and clear schedule of withdrawals.

ii) Such retail depositors, as they have small amount of deposits, tend to have high frequency of

deposit withdrawals. Information from this survey as well as from the industry should alert

the Islamic banking industry about the potential problem of withdrawal risk. Especially, the

potential of short-term deposit termination from these groups of depositors.

iii) Most of the depositors of Islamic banks have two accounts, in Islamic banks and conventional

banks. Interestingly, for the less than Rp5 million deposits, depositors locate most of them in

conventional banks. This can be interpreted that they still position Islamic banks indifferently

with conventional banks. Further, they use Islamic banks for transaction purposes rather than

investment purposes.

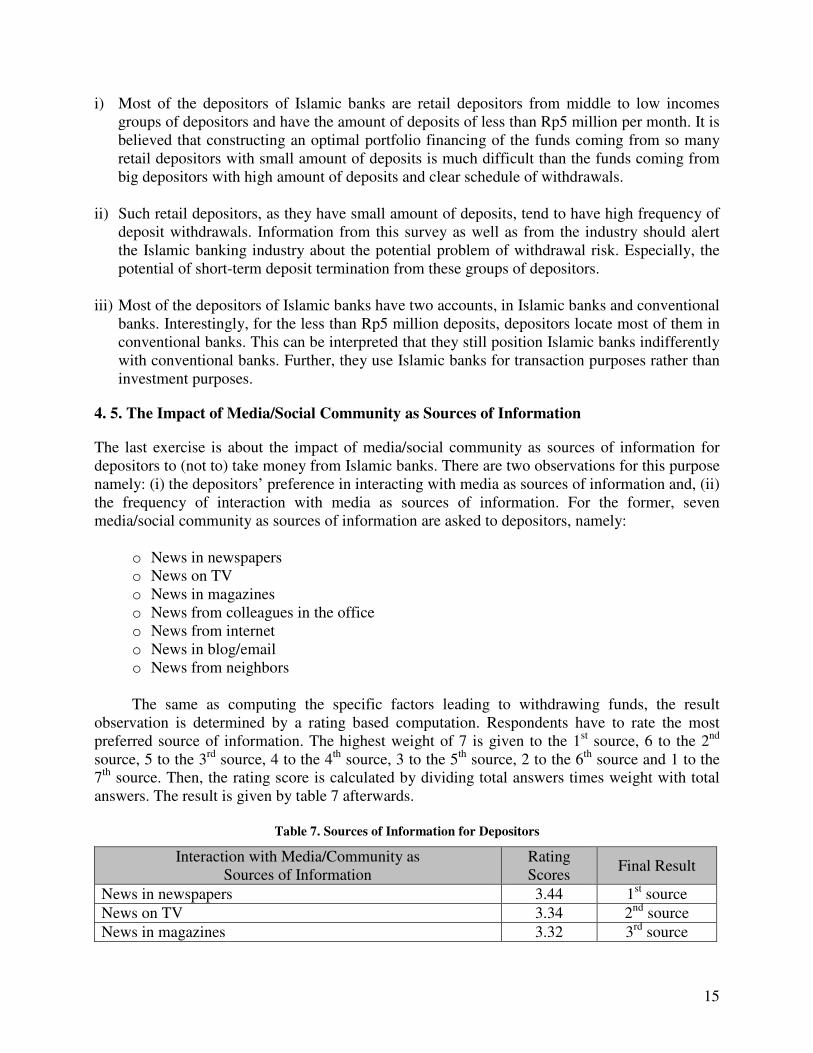

4. 5. The Impact of Media/Social Community as Sources of Information

The last exercise is about the impact of media/social community as sources of information for

depositors to (not to) take money from Islamic banks. There are two observations for this purpose

namely: (i) the depositors’ preference in interacting with media as sources of information and, (ii)

the frequency of interaction with media as sources of information. For the former, seven

media/social community as sources of information are asked to depositors, namely:

o News in newspapers

o News on TV

o News in magazines

o News from colleagues in the office

o News from internet

o News in blog/email

o News from neighbors

The same as computing the specific factors leading to withdrawing funds, the result

observation is determined by a rating based computation. Respondents have to rate the most

preferred source of information. The highest weight of 7 is given to the 1st source, 6 to the 2

nd

source, 5 to the 3rd

source, 4 to the 4th

source, 3 to the 5th

source, 2 to the 6th

source and 1 to the

7th

source. Then, the rating score is calculated by dividing total answers times weight with total

answers. The result is given by table 7 afterwards.

Table 7. Sources of Information for Depositors

Interaction with Media/Community as

Sources of Information

Rating

Scores Final Result

News in newspapers 3.44 1st source

News on TV 3.34 2nd

source

News in magazines 3.32 3rd

source

16

News from colleagues in the office 3.16 4th

source

News from internet 3.12 5th

source

News in blog/email 2.99 6th

source

News from neighbors 2.97 7th

source

The table expresses that, depositors prefer interacting with electronic media to interact

with people. Among those seven media/social community as sources of information, the top three

are: news in newspapers (the 1st rank), news on TV (the 2

nd rank) and, news in magazines (the 3

rd

rank). The rests are: news from colleagues in the office (the 4th

rank), news from internet (the 5th

rank), news in blog/email (the 6th

rank), and news from neighbors (the 7th

rank).

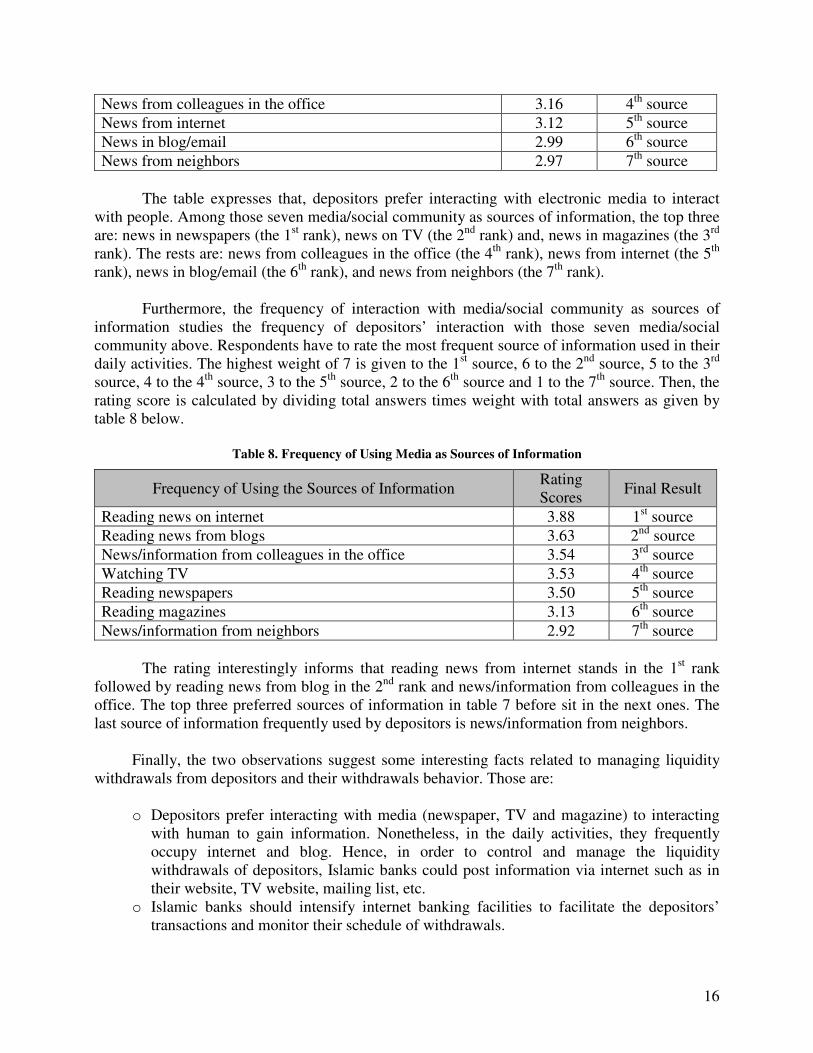

Furthermore, the frequency of interaction with media/social community as sources of

information studies the frequency of depositors’ interaction with those seven media/social

community above. Respondents have to rate the most frequent source of information used in their

daily activities. The highest weight of 7 is given to the 1st source, 6 to the 2

nd source, 5 to the 3

rd

source, 4 to the 4th

source, 3 to the 5th

source, 2 to the 6th

source and 1 to the 7th

source. Then, the

rating score is calculated by dividing total answers times weight with total answers as given by

table 8 below.

Table 8. Frequency of Using Media as Sources of Information

Frequency of Using the Sources of Information Rating

Scores Final Result

Reading news on internet 3.88 1st source

Reading news from blogs 3.63 2nd

source

News/information from colleagues in the office 3.54 3rd

source

Watching TV 3.53 4th

source

Reading newspapers 3.50 5th

source

Reading magazines 3.13 6th

source

News/information from neighbors 2.92 7th

source

The rating interestingly informs that reading news from internet stands in the 1st rank

followed by reading news from blog in the 2nd

rank and news/information from colleagues in the

office. The top three preferred sources of information in table 7 before sit in the next ones. The

last source of information frequently used by depositors is news/information from neighbors.

Finally, the two observations suggest some interesting facts related to managing liquidity

withdrawals from depositors and their withdrawals behavior. Those are:

o Depositors prefer interacting with media (newspaper, TV and magazine) to interacting

with human to gain information. Nonetheless, in the daily activities, they frequently

occupy internet and blog. Hence, in order to control and manage the liquidity

withdrawals of depositors, Islamic banks could post information via internet such as in

their website, TV website, mailing list, etc.

o Islamic banks should intensify internet banking facilities to facilitate the depositors’

transactions and monitor their schedule of withdrawals.

17

o Islamic banks should do intensive communication via internet with their depositors to

manage the liquidity withdrawals

5. Policy Recommendations

Based on the result of empirical survey above, there are some policy recommendations to

be implemented by Islamic banks and all related parties in order to properly manage deposit

withdrawals. Such policy recommendations are:

a) Islamic banks should keep maintaining the compliance with Sharia particularly with

respect to their banking products and banking operations. This is very important

recommendation to keep maintaining the trust and positive expectation of depositors to

the banks.

b) Islamic banks should have a robust portfolio financing in order to be able to pay positive

and competitive return on Islamic deposits and a conversion of UUS to BUS is

recommended as depositors prefer BUS to deposit their funds to UUS.

c) Intensive communication with retail depositors needs to be established to successfully

manage the deposit withdrawals from depositors.

d) Particularly, communication via newspapers, TV and internet is so recommended as most

of depositors deal with those media to search information about their Islamic banks.

6. Conclusion and Areas for Future Research

Islamic banking is a growing industry worldwide unexceptionally in Indonesia. In fact, the

country has had a promising Islamic banking industry in the last two decades. However, the same

as other financial institutions, Islamic banks in Indonesia face some risks and one of the

important risks to be anticipated is withdrawal risk. There are limited literatures studying this

type of risk and the paper attempts to study the withdrawal behavior of depositors in Indonesian

Islamic banks.

The paper finds that in general depositors consider the compliance of Islamic banks with

Sharia principles and practices as the most important factor determining deposit withdrawals.

Then, there are three specific factors determining deposit withdrawals namely: (i) if the return

sharing is paid less than the previous period; (ii) if the return sharing is paid less than interest on

conventional deposits and; (iii) the willingness of depositors to adjust the tenor of deposits.

Further, the paper finds that Islamic banks (BUS) is preferred than Islamic windows

(UUS) and most of depositors of Islamic banks come from middle to low incomes groups of

depositors. Then, in terms of effective communication with depositors, sharing news via

newspapers, TV and internet is the most effective way to do.

For the future research, it would be more informative if corporate depositors are included

in the survey and analysis since this paper only concentrates on individual depositors. This would

hopefully give more comprehensive analysis on the management of deposit withdrawals in

Islamic banks. The other idea is to use the more sophisticated statistical tools for the analysis

such as applying logit/probit model, Bayesian approach and, dynamic model to give more

information on this issue. A cross country research on this issue is also recommended to study the

18

similarities and differences of the deposits withdrawals and to find the best solution to improve

the current practices of deposit withdrawals in Islamic banking industry.

Notes

1 The Banker. (2010). http://top500islamic.thebanker.com/index. Access date 21st April 2010.

2 Arabian Business. (2010). http://www.arabianbusiness.com. Access date 21

st April 2010.

References

Ahmed, Habib. (2002), A microeconomic model of an Islamic bank, Research paper No. 59,

Islamic Research and Training Institute, Islamic Development Bank.

Ahmed, Habib. (2003), “Withdrawal risk in Islamic banks, market discipline and bank stability”,

Paper presented at the International Conference on Islamic Banking: Risk Management,

Regulation and Supervision, Jakarta, Indonesia.

Currie, Lauchlin. (2004), “The behavior of deposits”, Journal of Economic Studies, 31(¾), 340-

346. Based on Lauchlin Currie’s speech at the Chicago Forum of the American Institute of

Banking, February 24, 1938.

Gilkeson, James H., and Craig K. Ruff. (1996), “Valuing the Withdrawal Option in Retail CD

Portfolios”, Journal of Financial Services Research, 10, 333-358.

Gilkeson, James H., List, John A., and Ruff, Craig K. (1999), “Evidence of early withdrawal in

time deposits portfolios”, Journal of Financial Services Research, 15:2, 103-122.

Ismal, Rifki. (2009a), “Withdrawal risk, bankruptcy, and revenue sharing equilibrium ratio in

Islamic banks”, Paper presented at the International Research Conference on Global Financial

Crisis and the Resilience of Islamic Financial Services, Manama, Bahrain.

Ismal, Rifki. (2009b), “Industrial Analysis of Liquidity Risk Management in Islamic Bank”,

Journal of Islamic Banking and Finance, 26 (2), International Association of Islamic Bank,

Karachi, Pakistan.

Lambert, R. B. and Simon, A. (2000), “An ideal regulatory model for dealing with retail financial

institution runs and failures”, Journal of Financial Regulation and Compliance, 8 (4), 309-

325.

Mars, Research Specialist. (2008), The Study of the Market and Islamic Banking Depositors

Behaviors 2008, PT. Mars Indonesia, Jl. Paus 89G Rawamangun Jakarta.

Takemura, Toshihiko and Kozu, Takashi. (2009), “An empirical analysis on individuals deposit

withdrawal behaviors using data collected through a web-based survey”, Eurasian Journal of

Business and Economics, 2 (4), 27-41.

Yada, K., Washio, T., Ukai, Y., and Nagaoka, H. (2009), “Modeling bank runs in financial

crises”, Rev Socionetwork Strat, 3: 19-31.