Embed Size (px)

Citation preview

JSPM Vol 4 Issue 1

DISSATISFACTION WITH PERFORMANCE MANAGEMENT SYSTEM IN A BANK; POSSIBLE REASONS AND REMEDIES

Sana Iqbal, Center for Advanced Studies in Engineering, Islamabad, Pakistan. [email protected].

Nadeem I Kureshi, Center for Advanced Studies in Engineering, Islamabad, Pakistan. [email protected].

Citation: Iqbal, S. and Kureshi, N. I. (2016). Dissatisfaction with Performance Management System in a bank; Possible Reasons and Remedies, Journal of Strategy and Performance Management, 4(1), 4-23.

ABSTRACT Performance Management has been one of the most criticized yet widely implemented HR functional strategy that serves the sole purpose of ensuring the achievement of organizational objectives through the inimitable asset of an organization i.e. Human Resources. This study encompasses the case of National Bank of Pakistan (NBP) with regard to its performance management system called “Annual Performance Appraisal” (APA); detailing its initiation objectives back in 2000; how it evolves through the last decade; operational minutiae of its implementation while identifying the loopholes in the system. Going through the history of APA in NBP and perceptual opinions of our interviewees, distinct and unusually hyped non-popularity of the system is apparent; which was then explored through a data-collection instrument i.e. open-ended face-to-face/telephonic interview in terms of identifying most apparent reasons for this dislike of appraisals prevalent among the employed masses of the Bank, regardless of their position and performance. It has been seen that the system is plagued by different nature of problems ranging from Rater’s related problems like biasness (both at conscious & unconscious level), psychological blocks and rating errors to System and Format related issues like criterion problems and lack of proper training and guidance about the system itself, all of which leaves the performance management at the Bank ineffective and unpopular with the employees. Through the conducted interviews and application of concepts of Performance Management, different remedies are being suggested for the Bank to solve the identified issues like planning a frequent feed-back providence program, trainings, format and generic system related changes etc. which can lead NBP to build up on an effective linkage between individual performance and the overall strategy of the organization through translating these individual performance data into meaningful signals of performance of the Bank (Smith & Goddard, 2002).

!4

JSPM Vol 4 Issue 1

Keywords: Performance Management; Appraisal; Performance Management in Public Sector; Ineffective Performance Management System; Problems of Performance Management.

INTRODUCTION

The art and science of Human Resource Management (HRM) is as old as the human race itself or at least to the time when humans have started to work together to achieve something for the greater collective good, leading to their own individual welfare in turn. From hunting the game through building of pyramids to designing of sophisticated computer applications, all require coordinated effort from a group of individuals; thus, utilization of managerial skills and strategies which initially were more of at an unconscious level. Soon as these strategies were identified, explored, experimented with and formally jotted down for ready reference of all concerned; there have been many managerial fads being added to the list; few of which seriously influenced and altered irreversibly our needs, point of views and preoccupations with the field. Performance management is safely one such case with an on-the-record life history of more than six to seven decades, which eventually boomed during late 80’s and 90’s (Smith & Goddard, 2002).

Performance is, informally speaking, the combination of all efforts, may be physical or mental or both, carried out by an individual that can go and fit somewhere in the bigger picture, might it be a team’s collective performance, an organizational output, or a whole societal development. But this term is surely a very complex issue, not only because of the components that make it up and that are required to be considered when understanding it; but also because of the heterogeneity of its measures (9), that can be as diverse as the range of objectives for performance, personality differences of the performers, influencing factors and nevertheless the variety of stakeholders involved. In short, these efforts of individual beings need to be aligned, ignited, maintained, measured, developed and rewarded accordingly, in order to precisely tailor and brought it up to the exact needs of the organization, thus, leading to a mutually symbiotic win-win situation; and this is where the concept of Performance Management came in action.

Performance Management is actually an umbrella term, encompassing the concepts of performance measurement, performance appraisal and performance development; but it is often used synonymous with any or all of these notions. The concept, which has progressively broadened to the extent that it is now a concern of strategic management of an entire organization (Smith & Goddard, 2002), is characterized as “an integrated set of planning and review procedures which cascade down through the organization to provide a link between each individual and the overall strategy of the organization” (Rogers, 1990), and if fully implemented in its true sense, stood out as a high-commitment HRM-strategy leading to more insider ownership and stronger firm performance (Buck et al., 2003). Pollitt (1999) described the process of performance management as composed of basic five

!5

JSPM Vol 4 Issue 1

procedures: Setting objectives; assigning responsibility; measuring performance; feedback of information to decision making; and external accountability. The following figure, adopted by Smith & Goddard (2002), further depicts the framework:

Upon study of successful public and private sector organizations, these performance management systems, together with performance appraisals, are seen as important components resulting in their success (Lacho et al., 1991). Performance Management and Performance Appraisal, though are different generically as shown above, but for the purpose of this study, are taken as synonyms keeping in view the term used in the organization under consideration i.e. The Bank, a public sector banking organization. Now before going into the detailed literature review explaining different aspects of this performance management process, especially considering the growth of this system as taken place in the Bank and how the available body of knowledge supports or contradicts with the implemented changes and managerial strategies implemented by Bank; a relevant but brief introduction of the Bank will enable the readers to built the necessary context for effective understanding the upcoming case-study.

Introduction of the Bank

What was started as an effort to financially support to jute crop and other agriculture related products of Pakistan is now the largest commercial Bank of the country; the Bank was established in 1949 out of a special ordinance to be a financial institute that can extend credit or provide necessary finances to the farmers. With time, the Bank expanded its operations to cotton yielding areas and other important agriculture products, and afterwards came into play in full-fledged commercial banking.

!6

Formulation of Strategy

Instruments designed to encourage appropriate organizational responses

Development of Performance Measurement instrument

Performance Measurement

Performance Development

Performance Appraisal

Application of interpretive analytical

technique

JSPM Vol 4 Issue 1

Era Wise History of the Bank

The following timeline bullets depict the division of Bank’s life history into regimes based on the overall intentions of Bank operations and focus, keeping in view the dynamics of the respective timeslots:

• The Era of Expansion (1949-1960) • The Era of Decline (1961-1972) • The Era of Commercialization (1973-1981) • The Era of Aggressive Business (1982-1990) • The Era of Modernization (1990-1996) • The Era of Denationalization & Cost Minimization (1996-2002) • The Era of Changes and Experimentation (2003-2009) • The Era of Technologization (2010-Todate)

Organizational Objectives & Strategy of the Bank

The Bank, in line with revisiting of its basic area of operations like from an Agricultural Bank to a modern commercial and consumer bank, continue to revise the vision, mission, long-terms objectives and core values in order to provide its employees with an inspiring and motivating vision of the future direction of their efforts, along with letting them know about which values to adhere to while improving their performances.

The Vision

“To be recognized as a Leader and a Brand synonymous with Trust, Highest Standard of Service Quality, International Best Practices and Social Responsibility.”

The Mission

The Bank will aspire to the values that make it truly the Nation’s Bank by:

• Institutionalizing a merit and performance culture.

• Creating a distinctive brand identity by providing the highest standards of services.

• Adopting the best international management practices.

• Maximizing the Shareholder’s value.

• Discharging our responsibility as a good corporate citizen of Pakistan and in countries where we operate.

Long-Term Goal

“To enhance Profitability and Maximization of Bank’s share through increasing leverage of existing customer base and diversified range of Products.”

!7

JSPM Vol 4 Issue 1

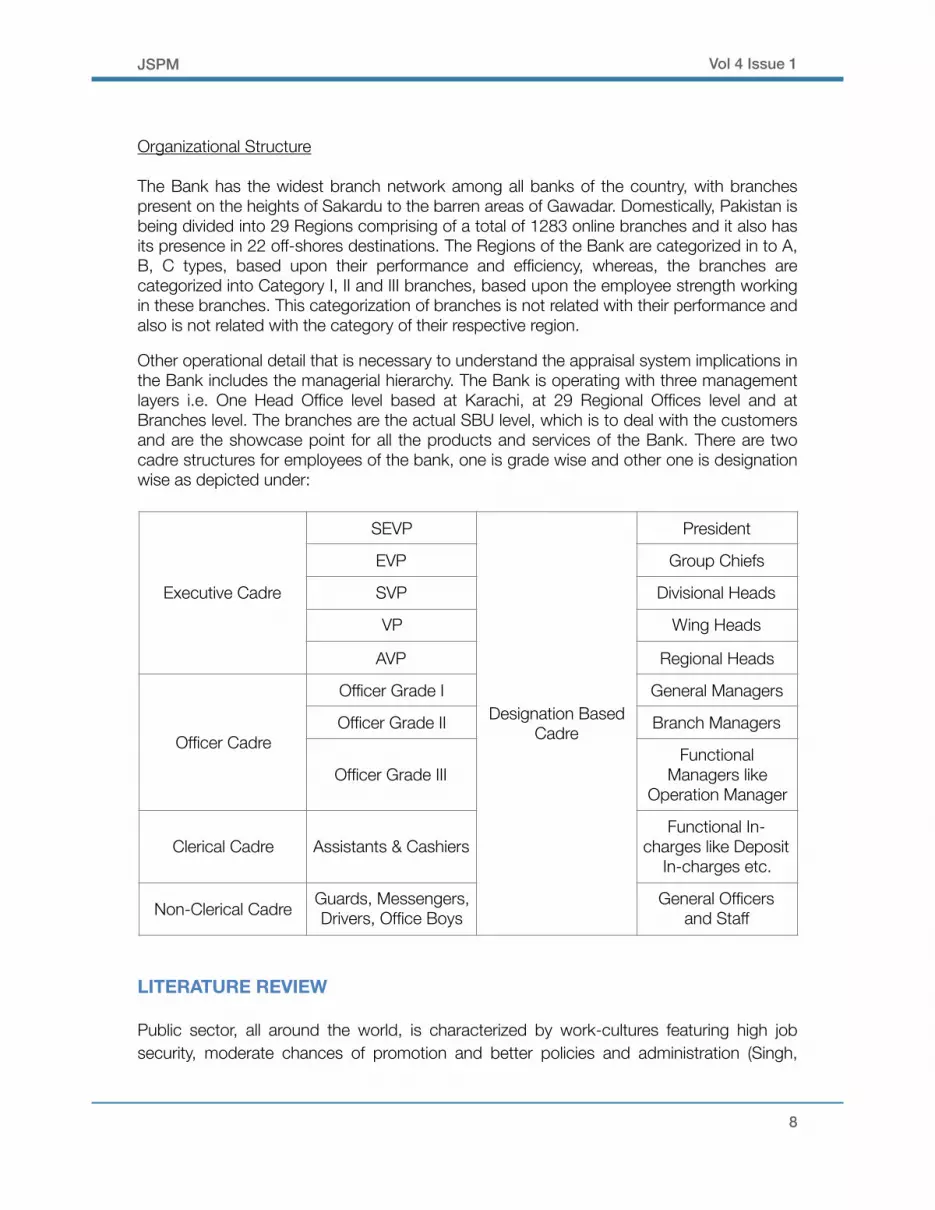

Organizational Structure

The Bank has the widest branch network among all banks of the country, with branches present on the heights of Sakardu to the barren areas of Gawadar. Domestically, Pakistan is being divided into 29 Regions comprising of a total of 1283 online branches and it also has its presence in 22 off-shores destinations. The Regions of the Bank are categorized in to A, B, C types, based upon their performance and efficiency, whereas, the branches are categorized into Category I, II and III branches, based upon the employee strength working in these branches. This categorization of branches is not related with their performance and also is not related with the category of their respective region.

Other operational detail that is necessary to understand the appraisal system implications in the Bank includes the managerial hierarchy. The Bank is operating with three management layers i.e. One Head Office level based at Karachi, at 29 Regional Offices level and at Branches level. The branches are the actual SBU level, which is to deal with the customers and are the showcase point for all the products and services of the Bank. There are two cadre structures for employees of the bank, one is grade wise and other one is designation wise as depicted under:

LITERATURE REVIEW

Public sector, all around the world, is characterized by work-cultures featuring high job security, moderate chances of promotion and better policies and administration (Singh,

Executive Cadre

SEVP

Designation Based Cadre

President

EVP Group Chiefs

SVP Divisional Heads

VP Wing Heads

AVP Regional Heads

Officer Cadre

Officer Grade I General Managers

Officer Grade II Branch Managers

Officer Grade IIIFunctional

Managers like Operation Manager

Clerical Cadre Assistants & CashiersFunctional In-

charges like Deposit In-charges etc.

Non-Clerical Cadre Guards, Messengers, Drivers, Office Boys

General Officers and Staff

!8

JSPM Vol 4 Issue 1

2000) along with far complex lines of accountability (Smith, 1990), yet low adaptability and high resistance to innovation/change. Unexpectedly, it appears that the concept of performance appraisal had marked public-sector work entities at almost the same instance as it penetrates the corporate sector (Holloway, 1999). The reason of this unusualness may be because of the stimulation of growth of appraisal systems occurred due to devolution of accountability and the resultant need to develop explicit models of performance measurement and accountability (OECD, 1996).

The primary objectives meant to be achieved out of implementation of formal appraisal system in an organization includes, according to England & Parle (1987), employee feedback, reward distribution, and a Skill Gap Analysis, yet, the systems that are successfully implemented in any one public sector organization may not be suitable for others, probably because of one or more of reasons like persuasion of different organizational goals, operating in different markets or demographical area, facing different level of costs & budgetary constraints, utilization of resources at different managerial excellence level and due to presence of measurement difficulties etc. (Smith, 1988). This leads to the need of having a unique, carefully customized performance appraisal system by a specific organization, that exactly applicable to its needs and is compatible with the strategic direction of a firm/company. Thus, this makes performance management one of the toughest-to-successfully-perform HR function, especially in large organizations with employees being highly sensitive to the outcomes of the system like that of The Bank.

The Bank is a public sector bank of Pakistan, displaying all the typical characteristic of a ‘public-sector’ organization and involves the related dynamics especially when it comes to functions like performance appraisal or so. Formal Performance Appraisal system in it modern form was initiated no longer than 13 years back in The Bank, and though it has a very brief history with most of sedative time where it couldn’t as such evolve at some noticeable rate; Appraisal have been one of the biggest bone of contention for both the Management and the employees of the Bank.

Out of two types of performance appraisal i.e. systematic (organizational based) and informal (team based) appraisals (Mathis & Jackson, 1988) both of which are equally important, the concepts of any systematic performance management system were literally unknown to the Bank if we go just a decade back. Informal appraisal were, though, present at unconscious level stemming out of personalized managerial styles of team leads/managers, but these efforts were unfortunately neither recognized by Management nor by the employees because of the reasons like lack of monetary impacts as well as for being not standardized i.e. not being in black and white. Prior to the beginning of this millennium, Annual Confidential Reports were written for each individual employee by his/her immediate supervisor. These ACRs impacts only the promotions, while the salaries of the employees were revised along the pre-decided patterns or standard same-for-all percentages based

!9

JSPM Vol 4 Issue 1

upon the external economic pressures like inflation or the overall performance of the Bank, which was obviously dragged through the vested powers from the Government Fund-based and non-funded businesses.

With the gradually worsening performance levels and more pronouncing competition from other banks, The Bank get on some serious thinking notes to adapt a more market based managerial strategy in order to motivate human resources of the Bank, capitalize on their potential and to create a more conducive work environment so as to cope the emerging challenges of financial sector, and to enforce the principles of merit, accountability, justice and transparency, which is the mission and core values of the organization. Historically, the renowned methods and models that can be utilized in order to build a high performance culture within organizations include developing on quality of Work life, organizational development practices, socio-technical systems, management by objectives, new payout systems, collateral organizations and TQM (Schneider, Brief and Guzzo, 1996). The Bank had opted to utilize Management by Objectives (MBO), through the usage of some Annual Job Objectives (AJOs) against each job/designation that are to be decided through mutual discussion and consent by both the captive of the seat and his/her immediate supervisor. These Job objectives would be representing the outline which pertains to what a person performing a particular job would do in the coming year or so and these will be precisely aligned with the overall annual goals of the branch/region or organization as a whole. These objectives as were intended to be settled through mutual consent of subordinate and supervisor, therefore, would be open to both parties, who are meant to meet on regular basis i.e. on quarterly basis to follow up on the performance against the already decided objectives, being the actual theme of MBO.

Management by Objectives which is inherently related to Performance appraisals (Lacho et al., 1991), is often implemented to pave the way toward a culture of pay-for-performance and to gain a highly receptive view by respondents (Moore & Staton, 1981 in Lacho et al., 1991), therefore, The Bank intends to achieve the following benefits/purposes through successful implementation of MBO:

• Placing the right person for the right job (the job-personality match). • Developing need based training system (trainings, at that time, were generic,

inconsistent and not need-based). • Career Planning for the employees (especially the functional career planning i.e. to

create field experts like credit specialists, foreign exchange experts, General Banking masters etc.)

• Ensuring enhanced individual productivity (by personalizing accountability to a more individual level rather than the prevalent group accountability).

• Monitoring and measuring achievements both at individual and corporate level (in order to ensure that credit is given where it is due).

• Identifying the high performers (in order to identify future managers and to lead the way towards effective succession planning).

• Increasing the job satisfaction, motivation and loyalty with the Bank.

!10

JSPM Vol 4 Issue 1

These uses of Formal AJOs decided through MBO, at that point of time, if materialized may have changed the Bank’s future for better but lack of follow-ups, zero trickledown effect, technical blankness of actual system-users and juvenile backup for implementation create unbreakable hurdles towards the achievement of above mentioned conditional goals. Simultaneously, the Performa used for these activities seriously lack written guidelines and provide the filler (in this case, both appraise and appraiser) with no support how to go-on with the activity. This vagueness when coupled with low technical expertise of the teams with regard to the newly implemented Management by Objectives and most importantly with zero ongoing feedback process i.e. no quarter or even half-year meetings, almost fails the intended aim of the implementation (Cayer et al., 1988).

Keeping in view the failure of the old implemented system, Management of the Bank decided to revive its performance management mechanisms after few years, where a better updated version of AJOs was adopted via building on the same framework of MBO, where the flaw of vagueness was catered through inculcating the concept of SMART goals (Specific, Measurable, Attainable, Realistic, and Timely objectives to be settled for each appraise). These attributes were to be ensured by the supervisor, while determining next year’s targets for the employee. These targets are generated from two dimensions of banking i.e. financial and non-financial targets, which are to be precisely rated in terms of their characteristics like quantity, quality, timeliness of achievement, compliance to the standard procedures and cost effectiveness.

These performance appraisals are often used for three basic purposes: administrative decisions i.e. promotions, placement of right resource at right place and allocation of monetary rewards; employee development i.e. training need assessments and identification of other developmental needs; and internal personnel research (Barrett, 1966 in Singh et al., 1981). Management of the Bank also started to use appraisals as the basis of these decisions i.e. in making both individual related and organization related decisions (William et al. 1977), through tying the scores of an individual employee, which lead to formation of a conclusive picture of how that specific person is performing in relative terms to the people around him/her, with the decision of next year’s promotions. This conditioning of one over the other made field staff to feel the seriousness of the management in this regard, yet, weak follow up made the implementation slow and deviant.

The long awaited pay for performance finally was implemented in The Bank initially for AVPs and above, followed by inclusion of officer cadre as well, in line with the theoretical findings of Camilleri et al., (2007), where the senior and middle management employees are to be rated based on pay-for-performance scheme where regular feedback is provided to employees about their performance. This was the first time when a full-fledge appraisal system was implemented in the Bank and employees were meant to be rated on pre-decided objectives related to the specific job designation/duties of an employee. Upon examination of performance appraisal systems in public sector, it has been observed that these systems emphasized personality traits and fall back in emphasizing developmental roles (Dayal, 1979 in Singh et al., 1981). Therefore, the objectives upon which employees were to be rated, that were now termed as KPIs (Key Performance Indicators) were consciously meant to be job-specific. These ratings are done on graphic rating scales and then, compared on a forced distribution campbell-curve.

!11

JSPM Vol 4 Issue 1

These rating scales and normal distribution curve, though are used most often in evaluating employees (England and Parie, 1987), ignited the retaliation from employees. Most of this resistance is due to inaccurate ratings given by supervisors, both in higher or lower terms, mostly out of being inappropriately trained (Newstrom, 1974), having the tendency to play safe (Niazi, 1976), posed with little or no penalties for inaccurate ratings (Meyer et al., 1965), and being overall resistant to judging people (Dayal, 1969) as is very apparent in Asian societies (Wright, 2004), where supervisors tend to rate their subordinates higher in order to encourage future cooperation and support or to avoid conflicts and confrontation (Lacho et al., 1991).

These problems fall in three basic categories i.e. psychological blocks, criterion related problems and conscious or unconscious distortion of facts (Dalton & Mcfarland, 1968 in Singh et al., 1981). Along with these pitfalls, employees usually feel that operational side of appraisal systems i.e. its guidelines, form format/design and content and performance criteria/standards stood out to be most ineffective components in their respective organizations (Cayer et al., 1988). These aspects and all others eventually lead to perceptual differences between appraisers and appraisee which are considered to be very important in the success chances of a performance appraisal system (Wright, 2004), and in determining the long-term effectiveness of the system (Longenecker & Nykodym, 1996). These perceptions are what lead the system implemented by The Bank into a failure, despite the fact that there have been many experiments and application of theoretically proven practices, as is clear after study of the above mentioned literature. Thus, this become pronounced that there are some other reasons that result in this system being disliked by the employees of the Bank and to such an extent that they even don’t allow it the chances of having evolved with time and most are vocal in suggesting discontinuation of this HR function, not caring about what the existing body of knowledge tell about the benefits and essentiality of a formal performance management system for an organization.

PROBLEM STATEMENT

Why is Performance Appraisal System unpopular among the employees of The Bank? What are the possible reasons for this unpopularity specifically from an insider’s point of view?

Research Objectives

Keeping in view the above mentioned review of related researches and the identified area of this case taking The Bank as the focused organization, the following are the alleged aims for undertaken study:

• Study the performance appraisal system in the form as implemented by The Bank.

• Identify the problems that result in ineffectiveness of the system and seriously haunt the satisfaction of the employees of the Bank with the system.

!12

JSPM Vol 4 Issue 1

• Suggesting possible solutions against the identified problem, out of the theoretical concepts of Performance Management.

• Giving out the solutions that can be implemented while incurring minimal cost and that can yield maximum benefit for the Bank via enhancing the productivity of the system.

METHODS & MEASURES

This case study is intended to be explorative and descriptive in nature, thus, falls in the category of social research (Babbie 2001; Neuman 2003). In order to carry out with the necessary explorations and building up of the case, a flexible preliminary exploratory research is coupled with qualitative interviewing technique in order to get primary data about the selected organization. The data collection instrument is an open ended highly flexible interview technique, being administered both face-to-face as well as telephonically, loosely moderated by the interviewer in order to ensure the inclusion of all relevant aspects of the performance management as is present in the selected organization i.e. The Bank.

Five respondents out of a population of 16542 employees (as of 31.05.2013) of The Bank were chosen via using purposive sampling technique where four face-to-face and one telephonic interview were conducted and moderated in order to collect relevant information to build this case upon. Interviewees are from managerial positions in The Bank and all have relevant exposure and in depth knowledge regarding the appraisal system of the Bank.

The unit of analysis for this case study is individuals, time horizon was one-shot (cross-sectional), while the study setting was non-contrived i.e. natural with minimum external intervention. Afterwards, the collected information is qualitatively analyzed and associated with existing researches and theoretical concepts in order to identify key problems and their possible remedies.

FINDINGS OF THE INTERVIEWS

During the interviews at very different time-frames and regional location, the study came to reveal one thing straight forwardly that Performance Appraisal System is not at all famous among the employees of the Bank, and this initiative of the Bank’s management is not welcomed by different field functionaries, even including those who were rated higher than others. This made one wonder about the reasons, yet the thought was not so surprising, as throughout the world, Performance appraisals and rating employees are criticized and not liked by most of the employed masses. But one of the key discussed point of the interview is the opinion of three out of five interviewees, that according to them, most of the employees of The Bank prefer the old ACR system over this new APRs thing, as this is generally against what is expected out of majority of employees in the world that a timely, open and accurate feedback is indeed widely acknowledged as one of biggest motivator

!13

JSPM Vol 4 Issue 1

for employees (Pulakos, 2004). This aspect is further discussed along with other identified reasons of prevalent low satisfaction among employees with appraisal system in The Bank, which are described as under:

1. According to the interviewees, the major reason for this dislike-ness of APRs is the dissonance created out of knowing what their respective bosses are rating them rather than what they thought they deserve; as compared to no knowledge of their rating in ACR format. But in my opinion, this cognitive dissonance in employees is not out of knowledge of their rating; rather it is out of the discrepancy that exists between what they think of the rating they deserve and what they get out of the pen of their immediate supervisor. This discrepancy definitely needs to be resolved in order to make APR more worthwhile implementation in the organization (Wright, 2004).

2. The second major reason for this unpopularity lies in what can be the sole ground of above mentioned cognitive dissonance i.e. the biasness of the supervisors, both at intentional or unintentional level (Singh et al., 1981). This biasness, often tagged as favoritism by the employees of the Bank, play havoc with the equity perception that is a must for effective implementation of any such appraisal mechanism. Yet, it is not always the intended favoritism which haunts the effectiveness of the system, few very famous rating errors and tendencies to rate according to a pre-planned pattern i.e. effects like Halo-effect, Leniency error, or average or exaggerated rating, further deepen the problems. Most Branch Managers, according to the interviewees, rate all the employees of their branch as an A (outstanding worker), irrespective of their actual performance mostly to avoid personal conflicts between themselves and their subordinates (Lacho et al., 1991). This leads to tall bell curves and does not allow the normal distribution of the scores, and eventually distorts the actual results of system.

3. The current Performa of the APA used in The Bank does not ask for evidences to justify the ratings that a rater is giving to a specific employee, even annual appraisal usually lack reliable data that makes the rating more justifiable, which almost makes it impossible to gain accurate appraisal results just out of the usage of inappropriate rating format (Smith & Kendall, 1963). These evidences, if inculcated in the system, would give appraisees precise feedback on what goes wrong that leads to lower than expected ratings, and would also somewhat cater the biasness problem of the system.

4. The biggest problem that lowers the effectiveness graph of APA system at The Bank is the absence of ongoing feedback which is the most prominent characteristic of MBO. In The Bank, though the policy states that employee and his/her supervisor should meet at regular intervals, at least on quarterly basis, in order to discuss and analyze the performance of the employee against decided and delegated targets, but in practice no such meetings are formally arranged. Supervisors and employee do not usually meet for the feedback purpose, therefore, resultantly employees, who are to be rated at the end of the year, remain blank throughout the time about how they are actually performing, is it up to the expectations of the management, are my efforts aligned with the direction of my

!14

JSPM Vol 4 Issue 1

targets and how the usual dynamics of the current business world impact my performance and achievement of my annual goals. These uninformed employees, though are performing to the best of their will, may be at the end of the year rated otherwise of their expectation, thus generating dissonance in them, and this also damages the actual aim of the performance appraisal and management system i.e. the increase in the performance effectiveness towards the achievement of organizational goals (Boswell & Boudreau, 2000).

5. Union activity and labor associations are, apparently, pretty active in The Bank thus, enjoys high persuasive powers. This, in one way or the other, impeded the evolution of APA system in the Bank, as the demanded perfection at very first step can sometimes inhibit the implementation of a potentially useful process at the very start, without allowing the system to grow, mature and self-rectify.

6. Further, the technical knowhow of employees and their supervisors regarding such HR related concepts, is below average, thus the requisite mindset to actually implement the system via understanding the importance of the process with reference to its role in the broader picture is lacking at The Bank. This also leads to miscellaneous miscommunication between management and employees, thus failing the benefits to materialize. Further, necessary trainings for both the appraisee and appraisers are lacking, giving wider way to ineffectiveness, biases and failure to the system.

7. The fixing of the percentages who are to be placed in A, B, C, D and E sometimes mislead the rater to alter the ratings just to maintain the normality of the graph, and thus, may not depict the actual performance level of the employee, just because of using of wrong rating methodology (Smith & Kendall, 1963).

8. Upon scrutiny of the procedures as per the available information, one will have this feeling that there exist strong levels of procedural justice prevalent in the Bank. What creates the problem in satisfaction level of the employee is the perceived distributive injustice, which needs to be catered thoroughly in order to get an evenly motivated workforce for the Bank (Vigoda, 2000 in Krajewski et al., 2007).

SUGGESTIONS AND DISCUSSION

Keeping the above mentioned list of factors that are apparently resulting in leaving appraisals as the most aching tooth of the employees and lower the popularity graph of the system at The Bank, along with the studied literature from existing researches and concepts of the field, following are few acceptable and implementable suggestions for the organization so as to allow it to keep this under-implementation concept of key HR issues in business:

1. The dissonance factor discussed above can be compensated to a larger extent by focusing on the on-going feedback i.e. keeping a track of the progress of each individual against his targets on regular basis at least quarterly, and through sharing the progress and results with appraisee, resulting in making the system more objective (Singh et al., 1981). This ongoing feedback will on one hand, increase the

!15

JSPM Vol 4 Issue 1

efficiency and probability of achievement of targets by the individual due to timely control and rectification of strategies, and on the other increase the appraisal acceptance rate among the employees through giving idea to them about how their individual performances are being viewed by their appraisers and let them see if there are any differences of perception or evaluation specification between their self evaluation and the evaluation of the same performance by the appraiser who is mostly the immediate supervisor. This on-going and regular feedback should start from the target setting meeting at the start of New Year and should run till the target dates of the last target, and is the actual essence of Management by Objectives, which is fruitless without such monitoring activity (Lacho et al., 1991). This concept is practical in The Bank, because performing regions in terms of meeting their annual targets already do practice this mechanism when it comes to their business targets. The general structure or pattern of this feedback mechanism and to make performance management more speedier and rigorous (Dwiredi, 2001) can be as follows:

!16

Defining the Targets at Companywide level at Strategic Policy Committee or BOD level (for Year 2) timed at the last quarterly meeting of Year 1

Dividing the Company Targets into Regional targets at an all Region meeting conducted at HO Level and clearly delegating these to the concerned Region Head along with strategizing the performance against these Targets (for Year 2) timed at the end of October of Year 1

Dividing the Regional Targets into Branch targets at an all Branches meeting at Region Office Level and clearly delegating these to the concerned Branch Manager along with strategizing the performance against these Targets (for Year 2) timed at the end of November of Year 1

Dividing the Branch Targets into Individual targets at one or multiple intra-Branch meetings at Branch level and clearly delegating these to the concerned employee along with strategizing the performance against these Targets (for Year 2) timed at the first week of January of Year 2

Four Quarterly Meetings at all the above mentioned levels by measuring the performance against the quarterly targets sourced out of Annual Targets rated with the appraise and appraiser together on the standard Performa to be used in APA at the end of Year 2

APA meeting the end of Year 2 or start of Year 3 to rate the appriasee commensurate/inline with the quarterly rating and performance which can now be predicted by both the appriasee as well as appraiser

JSPM Vol 4 Issue 1

2. Formulation of formal job-descriptions and standardization of performance criteria will help in both strong alignment of individual job-goals with the goals of the organization, thus, strong strategy alliance, as well as in making the system more objective and acceptable as the acceptability of these results directly depends upon how individual targets are settled along with the extent to which these are realistic (Singh et al., 1981). These will pave the way to prioritization of tasks and addressing of any ambiguity and conflict through informing employees about their specific goals (Camilleri et al., 2007).

3. The biasness of the appraisers can be controlled via taking various steps like: ▪ Training of the appraiser regarding goal setting, performance monitoring

and personal interaction skills (Harris, 1988) along with the practice of how to conduct APA sessions and how to point out the unconscious biasness as well as the strategies to control these (Lacho et al., 1991). These sessions will build the ability of the rater to rate the subordinates successfully and accurate (Decotis, 1978), as well as making them more accountable towards the system itself (Singh et al., 1981).

▪ The targets should be job relevant and SMART, which are to be converted to objective numbers where possible. The standards of achievement of each numerical target can be very easily set against percentages, which let most subjectivity out of the process. The description of the circumstances prevailing during the appraised period and the difficulty level of the targets should be considered.

▪ Awareness sessions for the appriasee and the appraiser. ▪ Open door policy for both appraiser and appraise, which can lead to a feel

that no subjectivity can be done against them (EEOC vs IBM Corp., 1984 in Lacho et al., 1991).

▪ Switch to multi-person appraisal mode can be good option as more persons become involve into the system, discrimination and biasness is least likely to occur (Lacho et al., 1991). This is also favored by Lawler (1967) and Campbell et al. (1977).

4. The current one pager Performa and the used appraisal method show many problems therefore, consideration of revising these can do the trick. The current appraisal method used in The Bank is Graphic Rating Scale (GRS) method, where management just simply does checks on the performance levels of their staff along a continuum of 1 to 5 scale, without any evidence; what can be more use is BARS (Behaviorally Anchored Rating Scale) or a balance score-card approach which are a combination of GRS and Critical Incident Method, where the management not only rate the employee against a continuum but also provide examples out of the behavior of appraisee in terms of the incidents that have appeared during the period under appraisal so as to justify the rating, which would be more worthwhile and give specific feedback for the appraisee (Flanagan & Burns, 1975).

5. Multi-facet appraisals would also be helpful for The Bank, as currently an employee is judged on two generic and open ended facets i.e. Job KPIs and Behavioral skills. These facets can be increased and made specific to Job-Specific Targets,

!17

JSPM Vol 4 Issue 1

Compliance to the set standards of performance, Communication Skills, Developing of the successor, Customer Dealership, Discipline, Professionalism, Learning and critical/analytical approach etc. These facets if explained precisely and comprehensively gives the rater a good opportunity to rate the appraisee more thoroughly, while minimizing the chances of biasness (Scott et al., 1975).

6. The forced distribution curve is a controversial and debatable ranking method, but keeping in view the fact that same is implemented successfully in other companies, therefore, this study would not suggest its total eradication or substitution. What is nessesary is to give out the awareness to the appraisers both at Regional and Branch level that it’s the performance of an employee which should drive his or her rating and not the mere normality of the graph/curve as a determinant if the appraisee should be rated as high performing or low-performing employee; and not the other way around. Through the interviews, I had this feel that people at The Bank get seriously confused and impacted due to this maintenance of normality to an extent that this eventually grew into the most important driver of the ratings they are giving out the people working under them. Keeping these scenarios in mind, I would rather suggest that this strictness of normality in this forced distribution curve should be loosened up to an extent where the manager/appraiser can convincingly justify any out-of-the-normality skewness if become apparent in their curve.

7. Change of name of the performance management system is suggested keeping in view that this may deal with associated escalations of dislike, and will encourage the employees to at least try out the new system before making any opinion about it.

8. A culture based change is suggested to be gradually implemented in The Bank of keeping individual salaries, appraisal ratings and related data strictly confidential to other un-authorized personnel like colleagues etc. This confidentiality is currently been tried at HR departments (personnel side) with many crack-holes. This need of confidentiality is to be inculcated in the minds of the employees which is obviously a gradual process that can be kicked off to start through a formal policy of action against the employee who is found/reported discussing his/her personnel appraisal data with others or the quoting face of any such discussion.

9. These appraisals should be kept tied with monetary benefits/rise of the employee, as without this the seriousness of both the appraiser and appraisee to this long, time-consuming, tiring, and costly activity can become on stake.

10. Benchmarking the performance of a whole Region against its own previous performances or with the performance of the similar yet better performing Regions, and measuring the performance as a group and not on individual level may also be experimented with in order to have Bank with an ultimate performance measuring system solution.

!18

JSPM Vol 4 Issue 1

11. So as to deal with external and union pressures, making the appraisal system with the characteristics like specific written instruction, job-specific behavioral performance criteria, basing the appraisal source on formal job-analyses, sharing of the results with appraisee, will enable the Bank to have a strong footing as well as ending with successful defending (Lacho et al., 1991).

CONCLUSION

Performance Management System, once implemented needs to be controlled and followed up, as such an affecting change, especially with regard to the point of view of an individual employee, require a slow, gradual and time-taking process of cultural change that required the up gradation of mental setups of a huge work force especially in the context of The Bank. The Bank should fasten its seat belt and keep on working on the issue discussed in the report before it is too late to. High level of communication, control over union activity, the culture of merit to be inculcated at the very basic level, strong departmental liaison and Management support can do the trick for the Bank. Viewing the identified problems through a systematic ‘whole-approach’ can also benefit the solution implementation process, because sometimes, the problem with these appraisals stems out of organizational reluctance to change any complimenting/supplementing system, which is closely related with appraisal system like streamlining of promotion and reward policies, decision making style, team culture etc (Singh et al., 1981). All discussion aside, the basic factor that should remain in focus by the Management of the Bank is the field level implementation of the policies they make at strategic level of the organization, because a beautifully planned policy with zero implementation proves out to be no-good at all, neither for the Management, nor for the field functionaries and nor for the organization itself.

REFERENCES

Boice, Deborah F. & Kleiner, Brian H. (1997), “Designing effective Performance Appraisal Systems”, Vol. 46, No. 6, pp. 197-201, MCB University Press.

Boswell, W. R., & Boudreau, J. W. (2000), “Employee Satisfaction with Performance Appraisals and Appraisers: the Role of Perceived Appraisal Use”, Vol.11, No. 3, pp 283-299, Human Resource Development Quarterly.

Buck et al. (2003), “Insider Ownership, Human Resource Strategies and Performance in a Transition Economy”, Vol.34, No.6, pp 530-549, Journal of Internal Business Studies

Camilleri et al. (2007), “Organizational Commitment, Public Service, Motivation and Performance

!19

JSPM Vol 4 Issue 1

within the Public Sector”, Vol.31, No.2, pp 241-274, Public Productivity and Management Review.

Campbell et al., (1970) “Managerial Behavior, Performance and Appraisal”, McGraw Hill Book Co., New York City.

Cayer et al. (1988), “Conquering Evaluation Fear”, Vol.33, pp 97-107, Personnel Administrator.

Daval, I., (1969) ''Some Issues in Performance Appraisal", Vol. 32 Personnel Administration.

Decotis, T. et al., (1978), "The Performance Appraisal Process? A Model and Certain Testable Propositions", Academy of Management Review

Dubnick, Melvon (2005), “Accountability and the Promise of Performance: In Search of the Mechanisms”, Vol.28, No.3, pp 376-417, Public Productivity and Management Review.

Dwiredi, R.S. (2001), “Developing a Culture of High Performance: Some Research Findings and Experiences”, Vol. 37, No.1, pp 31-57, Indian Journal of Industrial Relations.

Endo, Koshi (1998), “’Japanization’ of Performance Appraisal System: A Historical Comparison of American and Japanese Systems”, Vol.1, No.2, 247-262, Oxford Journals

England, R. E., and Parle, W. M. (1987), "Non-Managerial Performance Appraisal Practices in Large American Cities”, Vol.47, No.6, pp 498-504, Public Administration Review.

Flangan, J.C. & Burns, Robert K., (1975) "The Employee Performance Record: A New Appraisal and Development Tool", Harvard Business Review.

Harris, C. (1988), "A Comparison of Employee Attitudes Towards Two Performance Appraisal Systems." Vol.17, No.4, pp 443-455, Public Personnel Management.

Holloway, J. (1999), “Managing Performance. In: Rose A and Lawton A (eds). Public Services Management”, pp 238-259, Prentice Hall: London.

Information retrieved from Face to face and telephonic interviews of The Bank employees.

Information retrieved from http://www.the Bank.com.pk/AboutUs/index.aspx.

!20

JSPM Vol 4 Issue 1

Krajewski et al. (2007), “Is Personality Related to Assessment Center Performance? That Depends on How Old You Are”, Vol.22, No.1, pp 21-33, Journal of Business and Psychology.

Lacho et al. (1991), “Performance Appraisal in Local Government: A Current Update”, Vol. 153, No. 1, pp 281-296, Public Productivity and Management Review.

Lawler, E.E. (1967), "The Multi-trait Multi-rater Approach to Measuring Managerial Job Performance", Vol. 51, Journal of Applied Psychology

Longenecker, C. O. & Nykodym, N. (1996), “Public Sector Performance Appraisal Effectiveness: A Case Study”, Vol.25, No.2, pp 151-165, Public Personnel Management.

Meyer, H.H., Kay, E. & French, J.R.P. (1965), "Split Roles in Performance Appraisal", Vol.43, Harvard Business Review

The Bank Annual Report for the year 2010.

The Bank Instruction and President Office Circulars for the respective years on the under study topics.

Newstrom, J.D. (1974), "Smooth the Way for Your Own Performance Appraisal", No. 5, Vol.19, Supervisory Management.

Niazi, A.A. (1976), "Performance Appraisal: An Approach", Indian Management.

Organization for Economic Cooperation and Development (1996), “Performance Management in Government” OECD: Paris.

Pollitt, C. (1999), “Integrating Financial Management and Performance Management”, OECD: Paris.

Pulakos, Elaine D. (2004), “Performance Management; A Roadmap for Developing, Implementing and Evaluating Performance Management Systems”, SHRM Foundation.

Rivenbark, William C. and Kelly, Janet M. (2006), “Performance Budgeting in Municipal Government”, Vol.30, No.1, pp 35-46, Public Productivity and Management Review.

Rizwi, S. Fawad Ali & Khan, Ashfaque H. (2002), “Post-liberalization Efficiency and Productivity of the Banking Sector in Pakistan”, Vol.40, No.4, pp 605-632, The Pakistan Development Review.

!21

JSPM Vol 4 Issue 1

Rogers, S. (1990), “Performance Management in Local Government”, Longman: London.

Saqib, Muhammad et al. (2012), “A Brief Review of Performance Appraisal Practices and its Implementation at Government Office in Pakistan”, Vol. 3, No. 10, Institute of Interdisciplinary Business Research.

Schneider, B., Brief, A.P. and Guzzo, R.A. (1996), "Creating a Climate and Culture for Sustainable Organizational Change", Vol 7, No.19, Organizational Dynamics.

Scott et al. (1975), "The Influence of Variations in Performance Profiles on the Performance Evaluation Process: An Examination of the Validity of the Criterion", Vol.14, Organizations Behavior and Human Performance.

Singh et al. (1981), “Performance Appraisal System: A Critical Analysis”, Vol.16, No.3, pp 315-343, Indian Journal of Industrial Relations.

Singh, K. (2000), “A Study of Work Culture in Selected Indian Organizations”, (Unpublished Ph. D. Thesis), University of Delhi, Delhi.

Smith, P. (1988), “Assessing Competition among Local Authorities in England and Wales”, Vol.4, pp 235-251, Financial Accounting and Business Management.

Smith, P.C. & Goddard, M. (2002), “Performance Management and Operational Research: A Marriage made in Heaven?”, Vol. 53, No. 3, pp 247-255, The Journal of the Operational Research Society.

Smith, P.C. & Kendall, L.M. (1963), "Retranslation of Expectation: An Approach to the Construction of Unambiguous Anchors for Rating Scales", Journal of Applied Psychology.

Smith, Peter (1990), “The Use of Performa Indicators in the Public Sector”, Vol. 153, No. 1, pp 53-72, Journal of the Royal Statistical Society.

Ullah, Imdad (2011), “Internship Report”, CECOS, University of Science and Technology, Peshawar, Pakistan

Vance et al. (1992), “An Examination of the Transferability of Traditional Performance Appraisal Principles across Cultural Boundaries”, Vol.32, No.4, pp 313-326, Management International Review

!22

JSPM Vol 4 Issue 1

Varman, P. Mahendra (2005), “Impact of Self-Help Groups on Formal Banking Habits”, Vol.40, No.17, pp 1705-1713, Economic and Political Weekly.

Williams, et al., "International Review of Staff Appraisal Practices: Current Trends and Issues", Vol.1, No.6, Public Personnel Management.

Wright, Robert P. (2004), “Mapping Cognition to Better Understand Attitudinal and Behavioral Responses in Appraisal Research”, Vol.25, No.3, pp 339-374, Journal of Organizational Behavior.

!23