Embed Size (px)

Citation preview

Does The Practice of Islamic Credit Card

Islamic ?Subject: Tafsir & Hadith Ekonomi &

Bisnis Economics Department of Universitas Muhammadiyah Yogyakarta

1. Introduction2. Conventional vs. Islamic Credit

Card: An Overview3. Islamic Credit Card in Indonesia4. Problem, Opportunities and

Challenges

Outline

Introduction Credit card is one of the latest banking gadgets.

It facilitates people to make transaction without carrying cash.

Most goods and services can be bought either online or at the usual “brick and mortar” sales outlets by using this card. Normally, the merchant pays around 2.5% - 3% to the bank as a processing fee. In addition, clients are given grace period in order to pay the loan free from charge of late payment.

This convenience has led the widespread of credit card.

However, for Muslim customers, the usage of conventional credit card which involves practice of riba when there is late payment has brought a conflict with their belief.

Therefore, there is a need for a payment instrument which has function as credit card but comply with the Islamic principles.

The problem is: does the practice of Islamic credit card Islamic?

……………..…………………cont

Billah (2007) explained that credit card known as plastic money is an essential mode. In today s society, people ’own credit card for many reasons. Such as, to obtain credit facility, cash advance, and easy payment.

Credit card is different from a debit card that credit card does not remove money directly from user account after every transaction as it does with debit card. Credit card is different from charge card too. Charge card require from card holder to buy full amount of balance by the due date. In contrast credit card allows the card holder to arrange their payment monthly at the cost of interest.

What Does it Mean by Credit Card?

Bakhshi (2006) stated that credit card offers a line of credit to the user who can spend up to a pre-arrange ceiling level. Credit card has identification information written on it such as a signature or picture and authorized person to charge purchase and services to his account, which one will billed periodically.

The credit card is inventive system that involves all aspect of cryptography (secret code). Moreover, it has a microprocessor built into the card itself.

……………..…………………cont

There are many types of credit card issues based on the income and the services which are provided by the companies. Standard cards are available to anyone over 18, subject to the application being accepted platinum gold or black are issue for higher credit limit and have lower interest rates. Premium are offered for people who consider to be a better credit risk, also available to people who have a specified minimum income level quit high normally.

Sometime many cards offer extra benefits such as travel insurances, product guarantees and preferential loan rates. There is another type of credit card issued on behalf of charities and other organizations like football clubs and universities. This kind of card the company will generally make a donation to the charity or affinity group with no addition charge to the cardholder.

……………..…………………cont

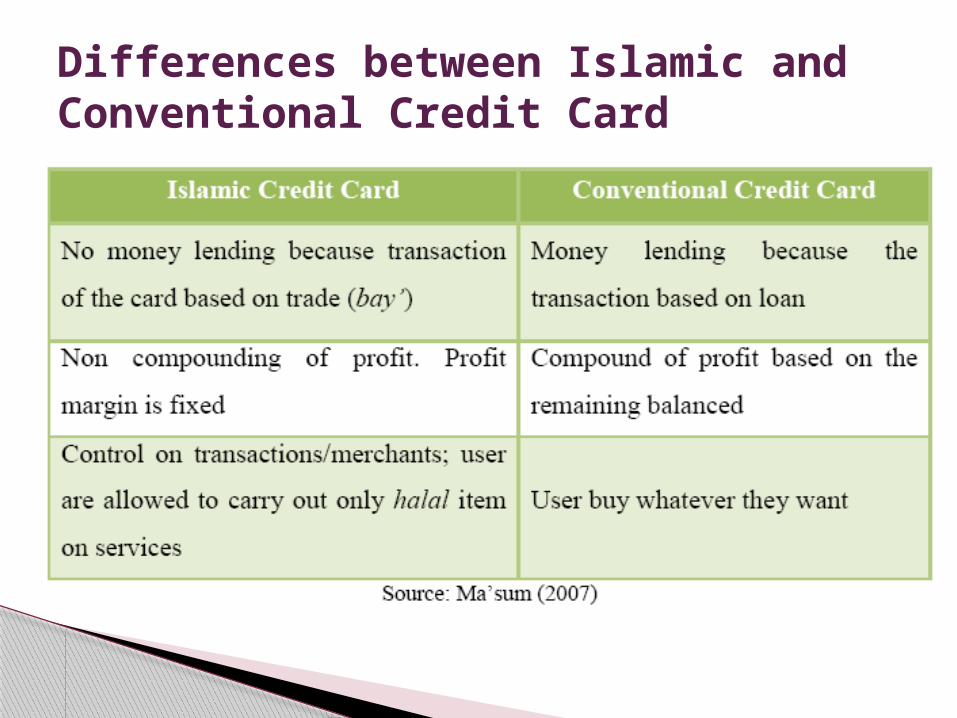

Massey on Ferdian et. al (2008) defined Islamic credit card as a payment that meet with at least three criteria of Islamic principle. First, card must meet the shariah requirement on lending. It must ditch the three essential prohibitions in the Islamic finance which are riba, gharar and maysir.

Secondly, an Islamic credit card must have certainty to be accepted worldwide it should use payment scheme like visa or master card. Beside that it should provide some available facilities such as CVV number for transaction and held amounts. Furthermore, the merchant charge and issuer’s fee should not be withheld. Thirdly, an Islamic credit card should not animate behavior that considers haraam.

What Does it Mean by Islamic Credit Card?

Differences between Islamic and Conventional Credit Card

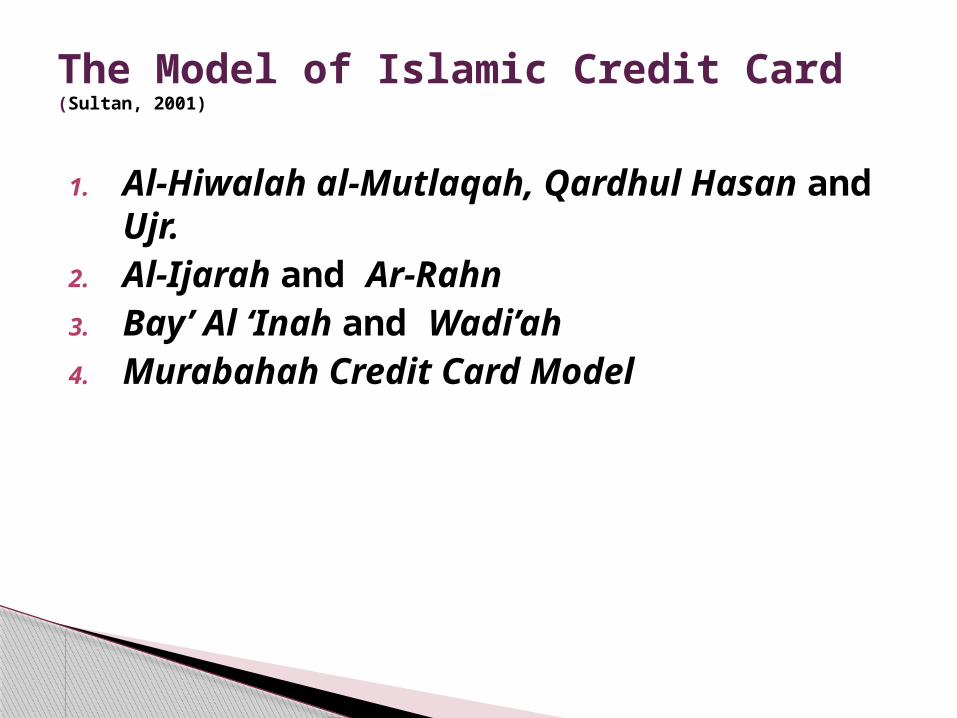

1. Al-Hiwalah al-Mutlaqah, Qardhul Hasan and Ujr.

2. Al-Ijarah and Ar-Rahn3. Bay’ Al ‘Inah and Wadi’ah 4. Murabahah Credit Card Model

The Model of Islamic Credit Card (Sultan, 2001)

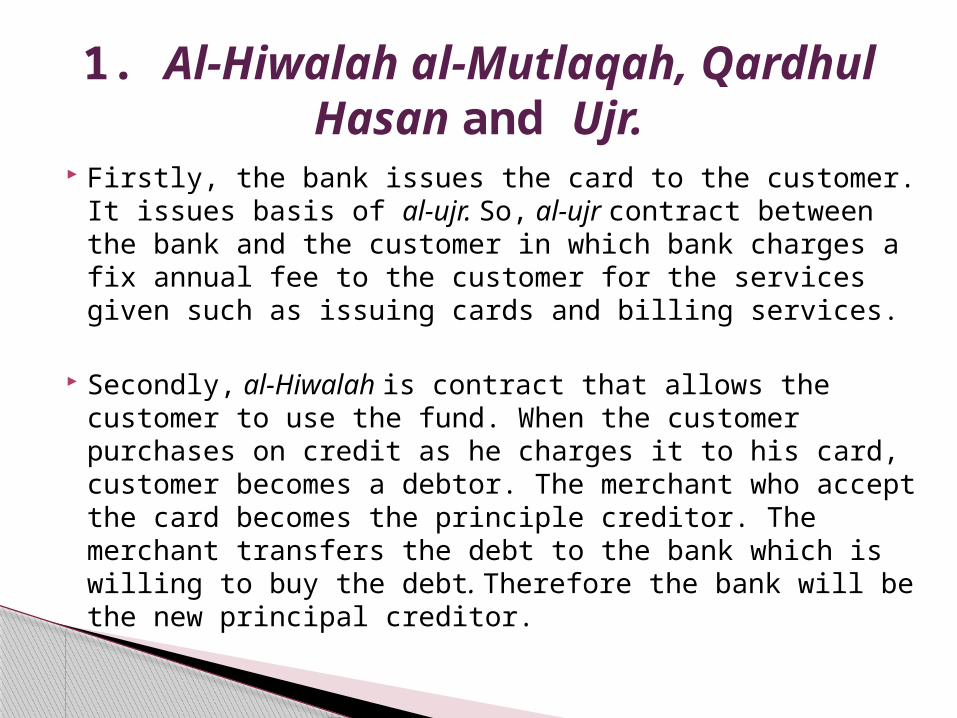

Firstly, the bank issues the card to the customer. It issues basis of al-ujr. So, al-ujr contract between the bank and the customer in which bank charges a fix annual fee to the customer for the services given such as issuing cards and billing services.

Secondly, al-Hiwalah is contract that allows the customer to use the fund. When the customer purchases on credit as he charges it to his card, customer becomes a debtor. The merchant who accept the card becomes the principle creditor. The merchant transfers the debt to the bank which is willing to buy the debt. Therefore the bank will be the new principal creditor.

1. Al-Hiwalah al-Mutlaqah, Qardhul Hasan and Ujr.

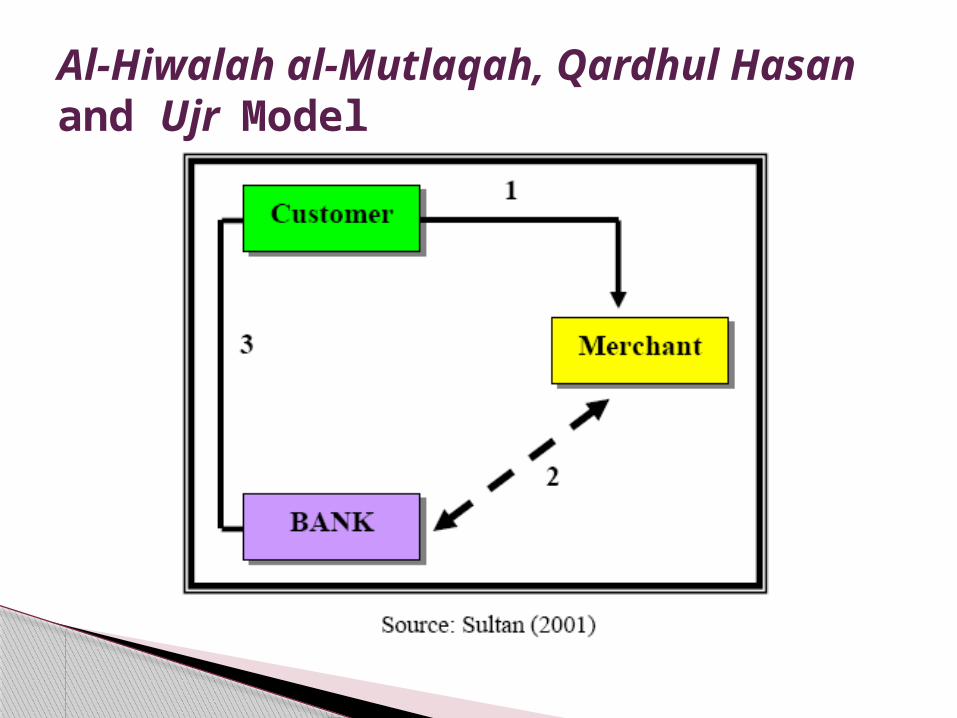

Al-Hiwalah al-Mutlaqah, Qardhul Hasan and Ujr Model

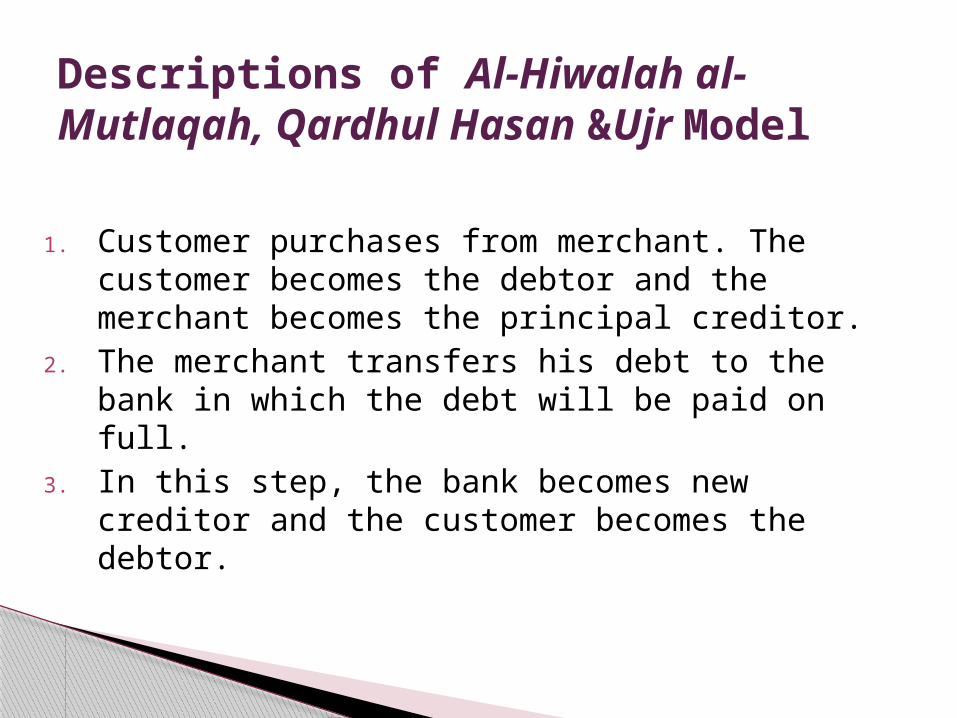

1. Customer purchases from merchant. The customer becomes the debtor and the merchant becomes the principal creditor.

2. The merchant transfers his debt to the bank in which the debt will be paid on full.

3. In this step, the bank becomes new creditor and the customer becomes the debtor.

Descriptions of Al-Hiwalah al-Mutlaqah, Qardhul Hasan &Ujr Model

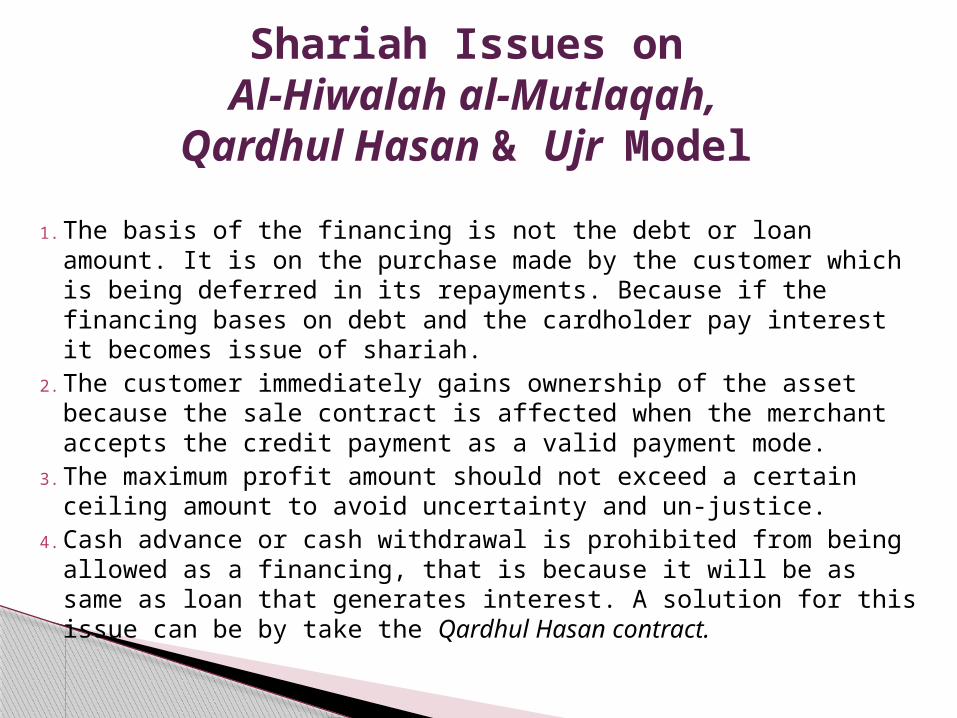

1.The basis of the financing is not the debt or loan amount. It is on the purchase made by the customer which is being deferred in its repayments. Because if the financing bases on debt and the cardholder pay interest it becomes issue of shariah.

2.The customer immediately gains ownership of the asset because the sale contract is affected when the merchant accepts the credit payment as a valid payment mode.

3.The maximum profit amount should not exceed a certain ceiling amount to avoid uncertainty and un-justice.

4.Cash advance or cash withdrawal is prohibited from being allowed as a financing, that is because it will be as same as loan that generates interest. A solution for this issue can be by take the Qardhul Hasan contract.

Shariah Issues on Al-Hiwalah al-Mutlaqah,

Qardhul Hasan & Ujr Model

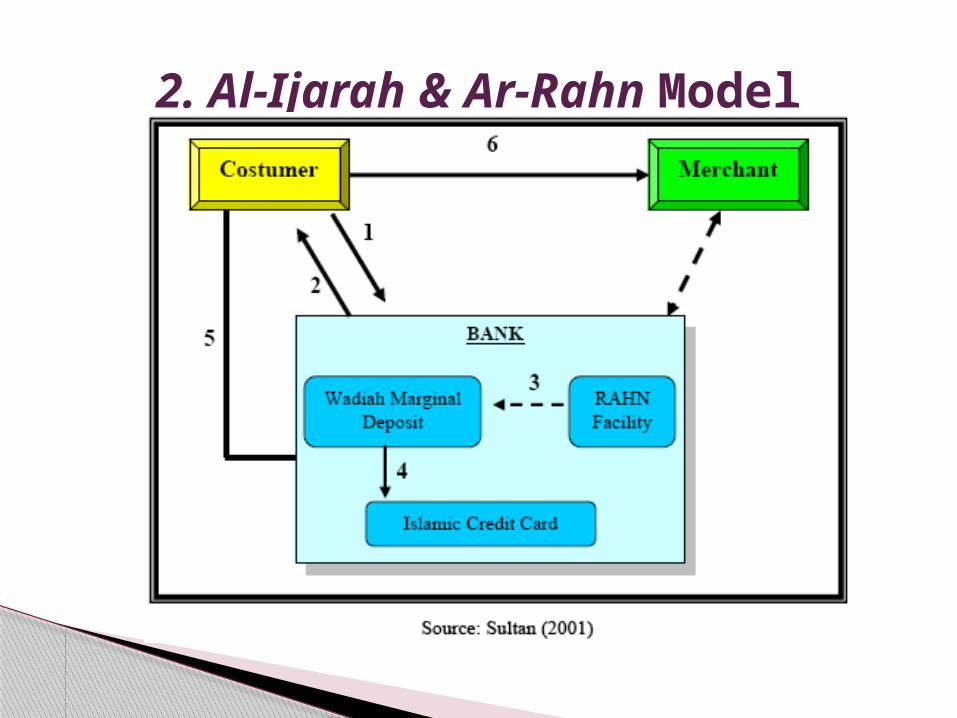

2. Al-Ijarah & Ar-Rahn Model

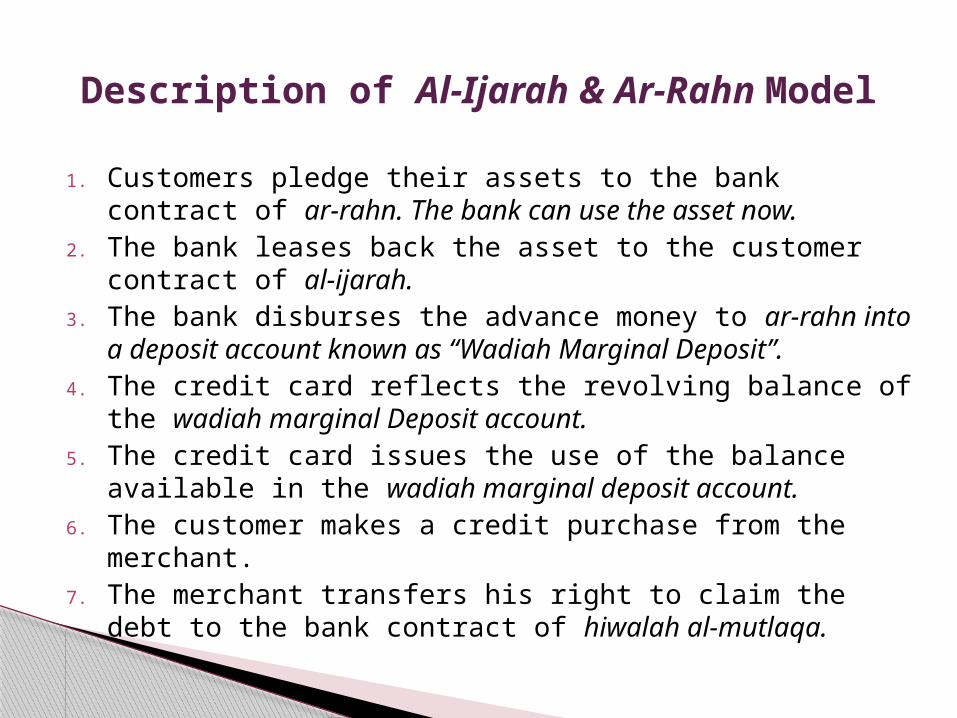

1. Customers pledge their assets to the bank contract of ar-rahn. The bank can use the asset now.

2. The bank leases back the asset to the customer contract of al-ijarah.

3. The bank disburses the advance money to ar-rahn into a deposit account known as “Wadiah Marginal Deposit”.

4. The credit card reflects the revolving balance of the wadiah marginal Deposit account.

5. The credit card issues the use of the balance available in the wadiah marginal deposit account.

6. The customer makes a credit purchase from the merchant.

7. The merchant transfers his right to claim the debt to the bank contract of hiwalah al-mutlaqa.

Description of Al-Ijarah & Ar-Rahn Model

1. The bank can lease out the asset which is a pledged to the lessee who is the originally a pledged asset.

2. In ijarah contract, the bank becomes the leasor and the customer becomes the lessee. Therefore, banks will have to bear the cost of maintenance of the asset. However, in ar-rahn the customer is responsible for the maintenance of the asset. It means the cost of the asset will fall back to the customer.

3. Ar-Rahn contract should sign first before the ijarah contract; otherwise it would violate the principle of “Al-Ghunm bil Ghurm”.

4. n this transaction, the structure looks as a loan which makes the profit that the bank makes interest (riba).

5. here are too many contracts making it quite difficult with the legal documentation and contract signing.

Shariah Issues on Al-Ijarah & Ar-Rahn Model

3. Bay’ Al ‘Inah & Wadi’ah Model

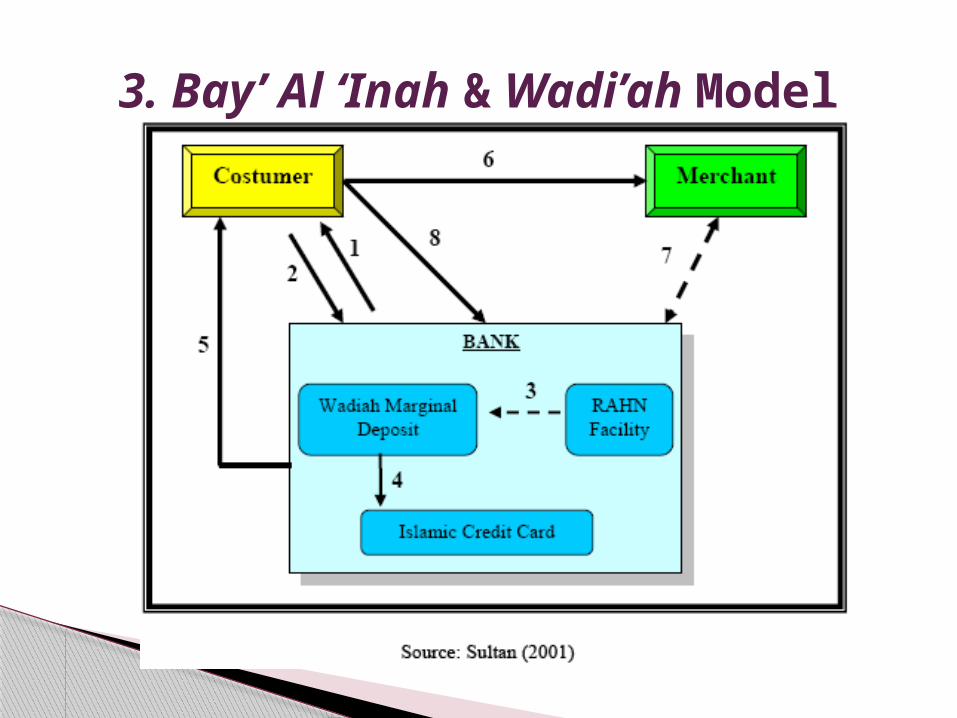

1. The bank sells its asset to the customer on a deferred repayment basis.

2. The bank buys back the asset on cash at lower price; whereas bank gets profit from the different amount customer which has cash advanced.

3. The bank buys out the cash proceeded from the buy back into marginal deposit which becomes the credit limit for the customer.

4. An Islamic credit card will be created for the customer 5. The credit card is issued for the customer to be used. 6. The customer makes the purchasing from the merchant. 7. The merchant transfers his right to claim the debt to the bank (contract of hiwalah al-mutlaqah).

8. The customer settles his outstanding balances which make his line of the credit to be revolved.

Description of Bay’ Al ‘Inah & Wadi’ah Model

1. There are a lot of issues surrounding al-’inah contract that makes ‘inah structure becomes unviable.

2. The amount of money that customer will be paid from “cash sell back” as a wadiah in his saving account to forms his credit limit and the profit shall be based on using of such fund which will generate interest (riba).

Shariah Issues on Bay’ Al ‘Inah & Wadi’ah Model

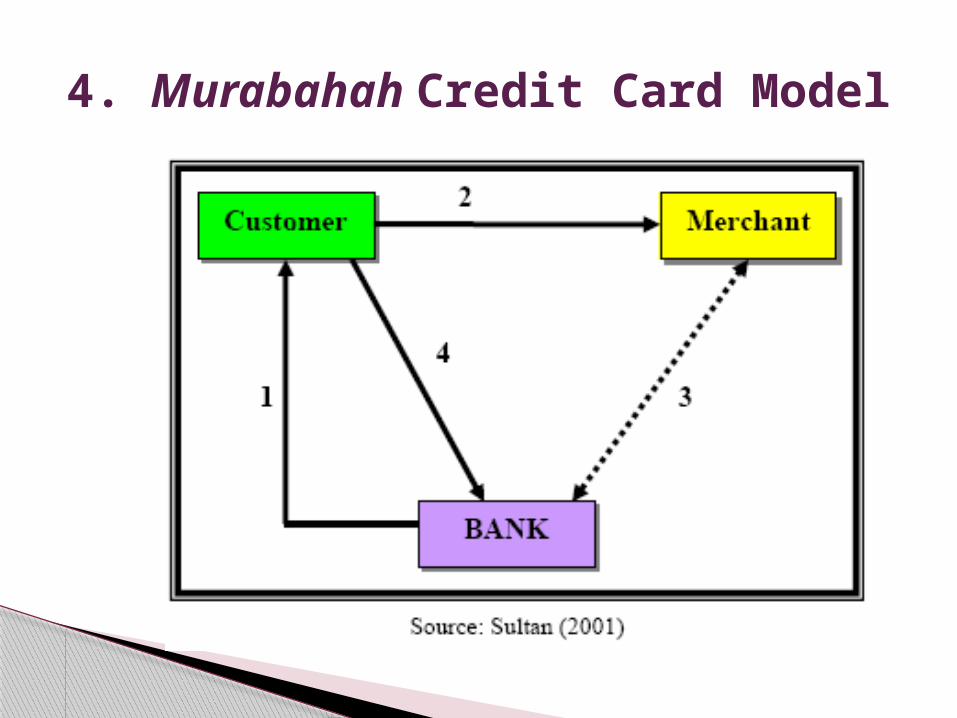

4. Murabahah Credit Card Model

1. The bank appoints the customer as a purchasing agent on behalf of the bank. In murabah contract, the seller requires to be in the ownership of the asset which will be sold even for a moment.

2. The customer makes a credit purchased from the merchant on behalf of the bank. So, the bank is the owner of the asset.

3. The bank as the owner of the asset remits payment to the merchant.

4. The customer then makes the purchasing from the bank and makes his repayment on a deferred basis.

Description of Murabahah Credit Card Model

1. Murabaha is a contract between the buyer and the seller. Thus, the seller must be a legal owner of the asset. This is because it will be used to justify the profit margin.

2. The seller must disclose the cost price. That is because this contract is a part of the trust sale.

3. The customer shall give an extension to the repayment period to the bank.

4. The seller must be a valid owner of the asset. That is way the bank appoints the customer as a form of legal trick which is debatable.

Shariah Issues on Murabahah Model

Dewan Syariah Nasional Majelis Ulama Indonesia (National Syariah Council) with the issuance of fatwa No: 54/DSN-MUI/X/2006 concerning “Syariah Card”. On this fatwa, the council stated that Islamic credit card or Syariah Card is built based on three contracts: kafalah (guarantee), qardh (loan) and ijarah. Thus, all Islamic credit cards issued in this country must follow contracts which are already prepared.

The Practice of Islamic Credit Card in Indonesia

a. Shariah Credit Card has the same function with credit card that has a lawful relationship a between parties in any established jurisdiction, based on the principles of shariah.

b. The parties involved are the card issuer (mushdir al-bithaqah), card holder (hamil al-bithaqah) and card acceptance/ merchant (tajir or qabil a-bithaqah).

c. Membership fee (rususm al-„udhwiyah) is the payment for using the services of card issuer.

The general rules of Islamic (Shariah) Credit Card in Indonesia are (syafrudin, 2007):

d. Merchant fee refers to the fee given by the merchant to the card issuer as the payment (ujrah) of being the agent service (samsarah), marketing (taswiq) and billing payment (tahsil al-dayn).

e. Cash withdrawal fee is the payment for using the facility of cash withdrawal (rusum sahb al-nuqud).

f. Ta‟widh is compensation payment for the card issuer resulting from card holder late payment.

g. The late charge fee is the late payment cost to be charged to the cardholder which will be given to charity.

The general rules of Islamic (Shariah) Credit Card in Indonesia are (syafrudin, 2007):

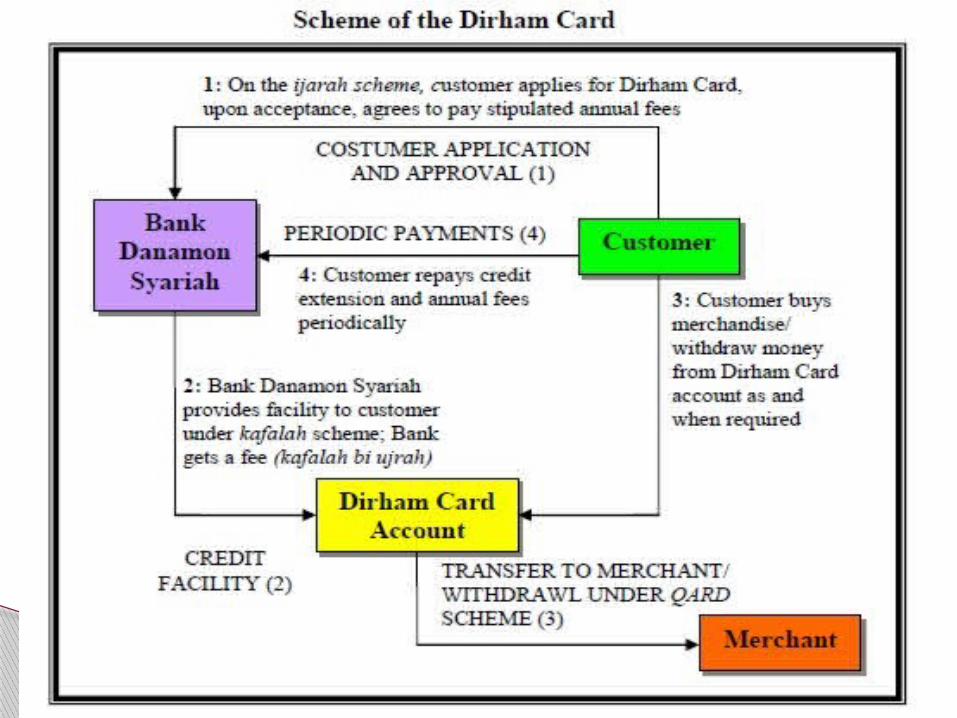

Dirham Card is an Islamic credit card which is a collaborate product between Bank Danamon and Master Card with all networks or merchants thought the world to provide payment services to card holders.

Dirham Card uses three contracts: kafalah, qardh and ijarah.

The 1st Indonesian Islamic CC “Dirham Card” (PT Bank Danamon Tbk)

On the ijarah scheme, the card issuer acts as the provider of payment and service system for the card holder. For the provision of this service, the card holder is charged a membership fee. Meanwhile, in the kafalah transaction scheme, Bank Danamon Syariah as card issuer, acts as the guarantor (kafil) for the card holders against the merchants, of all obligations to pay (dayn) which arise from the transactions between card holder and merchant, and/or cash withdrawal from banks other than the ATM of the bank issuing the card.

Based on kafalah, the card issuer can accept a fee (ujr kafalah). Under the qardh scheme, the card issuer acts as the lender (muqridh) to the card holder (muqtaridh) through the cash withdrawal from the bank or ATM of the card issuing the bank. The card holder is therefore obliged to return the same amount of funds he withdrew at the time.

Some customers argue that the Dirham Card is more expensive than the conventional credit card. By using the Dirham Card, the customer must pay 10% form the limit credit amount at the beginning of transaction as “a goodwill investment”. Whereby, the limit credit amount which is decided by Bank Danamon Syariah is Rp5 million until Rp40 million. The cardholders are compulsory to have a saving in Bank Danamon Syariah at least Rp500.000,-. If the cardholder pays over the due date,

Issues of the Dirham Card

They will be imposed two kinds of compounds. Those are a ta‟widh and a 3% form the balance account as the late charge fee. In addition, customers must pay a monthly fee, (3.25 – 3.5) % and this fee is as same as the amount of interest in the conventional credit card.

In Indonesia, Islamic credit cards face some problems regarding the problem of high costs and the strategy of promotions. People are still not understanding well about the concept of Islamic credit cards. They only can compare with conventional credit card whether Islamic credit card gives more advantages or not. Therefore, in launching the Islamic credit card, resolute attention must be paid to the promotional agenda to extend that it should be pompous and grand not merely to create awareness but also should attempt to bring in immediate “coverts”.

Islamic Credit Cards in Indonesia: Problems, Opportunities and Challenges

Sultan (2001) argues that this is because, if promotional campaigns are focused merely to create awareness, the idea enters into the “black box” of the customer and takes a long time to trigger them to go and get one of those cards. Thus, the campaign should be focused to prompt the customers to get is on impulse and let them do the mouth-to-mouth campaign for the issuer, which eventually is cost-effective for the issuer. Towards that end, a mass media advertisement campaign might just not be it. It must be followed by road shows, reward campaign, door-to-door campaigns by the direct sales team members and also Islamic credit card clinics.

Although Islamic credit cards in Indonesia do not face the shariah issues regarding to its contract because kafalah, qard and ijarah are contracts which are already accepted globally by the Muslim scholars, it still face the shariah issue regarding the opinion that Islamic credit cards are not different with conventional credit cards.

This is because the Islamic credit card still includes “implicit” riba in its scheme. The bank only changes the interest with the term of “administration cost”. So, the implementation of “administration cost” is like interest charge in conventional credit cards, but with the different term.

In addition, some Indonesian Muslim scholars reject the issuing of Islamic credit card because the credit card is same as a debt, whereas the debt is one thing which is not recommended in Islam. In Islam-economy (2009), it is explained that this refers to many traditions narrated by Bukhari whose contents people who have debts always tell lie and are never kept their word. Therefore, the Prophet Muhammad p.b.u.h. himself always prays to avoid the debt and in Qur’an, al-Baqarah:280, Allah SWT says that:

“if the debtor is in straitened circumstances, then postponement to ease; and that ye remit the debt as alms giving would be better for you if ye did but know”.

Actually, the debt is allowed in a very forced situation and the added debt must be repaid as soon as possible. Whatever types of transaction used in Islamic credit cards, the substance remains to advise people in debt. So, this underlies why Islamic credit cards may not be a shariah.

Moreover, the presence of Islamic credit card can encourage people to consume more. This is because the function of Islamic credit cards is same as other credit cards.

Faber and O’Guinn (1988) explained that the most obvious reasons for credit problems are come from people unprepared to meet their existing credit obligations. Moreover, due to the increasing of credit card debts, the inflation of America became doubled in the mid-December 1997. This was because credit cards spurred people to continue their consumption of un-needed goods only to avoid loss of credit card fee burden.

Nevertheless, Islamic credit cards have some benefits for Muslims especially in the urgent conditions. For example, if someone wants to buy an airline’s ticket at a lower price now, but he does not have enough account in his debit card and he can expect that he will receive some incomes in the next month, he can transact by using the Islamic credit card.

First, he does not loss the opportunity to get the lower price of his ticket. Second, he can avoid a riba. Third, he can participate in the developing of the economy riba free which is very necessary to increase the economy of ummah

With regard to the consumerism matter, the Islamic bankers can maximize their policy which can avoid that. Mechanism to offer Islamic credit cards only for persons who have certain level of income should be applied. Thus the use of the card can be supported with the ability to pay. Furthermore, this policy can reduce credit risks faced by any Islamic banks which issue Islamic credit cards (Ferdian, et,al, 2008).

Islam encourages yudfa „asyaddu adh-dhararyn, the intention is that the transaction may be allowed initially banned on the grounds when there are no other choices and to take things on the less dangerous. For example, Muslims can buy books at the online store which is the payment method is using credit cards if there are no other stores providing those books. But, if they can find a one store which is selling that book, this store should be prioritized.

Finally, Islamic credit cards must be developed properly and the attitude of the customers must be controlled well when they use this product. Muslims must have a scale of priorities in their daily life which is appropriating with Islam. They must classify their needs wisely according to the level of maqasid al-shariah: dharuriyat (primary), hajjiyat (secondary) and tahsiniyah (tertiary). Thus, the developing of Islamic credit cards in Malaysia and Indonesia can be done well and can fulfill the maqasid al-shariah of the ummah themselves.

Al-Suwaylim, Sami ibn Ibrahim. 2008. “Tawarruq Banking Products”. Accessed on December 18, 2009. [Available at http://isra.my/media-centre/downloads.html?task=finish&cid=88&catid=20&m=0]

Antara. 2007. “Bank Danamon Launches Dirham Card”. Viewed on March 10, 2010. <http://www.antara.co.id/en/print/?i=1184819311>

Asst. Prof. Dr. Rusni Hassan, a shariah advisor on HSBC Amanah Malaysia Berhad

Bibliography

Bakhshi, Adil Manzoor. 2006. “Developing of Financial Model for Islamic Credit Card for UK”. Viewed on March 12, 2010. < http://www.kantakji.com/fiqh/Files/Finance/223.pdf>

Billah, Mohd. Ma’sum. “Islamic Credit Card in Practice”. Viewed March 13, 2010. <http://www.islamicmortgages.co.uk/index.php?id=262>

Bouheraoua, Sa’id. 2009. “Tawarruq In The Banking System: A Critical Analytical Study Of Juristic Views On The Topic”. Accessed on December 18, 2009. [Available at http://isra.my/media-centre/downloads.html?task=finish&cid=86&catid=20&m=0]

Dali, Nuradli Ridzwan Shah Bin Mohd and Hanifah Abdul Hamid. 2007. “A Study on Islamic Credit Cards Holders”. Proceeding of National Conference on Islamic Finance (NCiF 2007) Organized by the Faculty of Business Management and Accountancy, University Darul Imam Malaysia

Faber, RJ and O’Guinn, TC. 1988. “Compulsive Consumption and Credit Abuse”. Journal of Consumer Policy, Vol. 11: 97-109

Farook, Sayd. 2009. “Innovating Islamic Plastic: A Value Added Socially Responsible Alternative”. Journal of Oxford Islamic Finance Dar Al-Istithmar

Ferdian, Ilham Reza, et., al. 2008. “The Practice of Islamic Credit Cards: A Comparative Look between Bank Danamon Indonesia’s Dirham Card and Bank Islam Malaysia’s BI Card”. Proceeding of IAEI International Conference, Surabaya, Indonesia

HSBC Amanah. 2009. “HSBC Amanah Malaysia Achieves More Than 50,000 Islamic Credit Cards”. News Release on September 4, 2009

Islam-Economy. 2009. “Islamic Credit Card, between Allowed and Forbidden”. Viewed on March 8, 2010. <http://islam-economy.blogspot.com/2009/10/islamic-credit-card-between-allowed-and.html>

Safruddin. 2007. “Shariah Credit Card – the Structure and Usage”. Viewed on March 10, 2010. <http://safruddin.wordpress.com/2007/08/04/dirham-card-kartu-kredit-syariah-pertama-di-indonesia/>

Sultan, Syed Alwi Mohamed. 2001. Islamic Credit Card: A Framework of Implementation in Malaysia. Thesis Collection of International Islamic University Malaysia