Embed Size (px)

Citation preview

ORI GINA L A R TI C L E

Taxonomy: racism versus fiscal conservatism in votingon segregationist provisions in Alabama’s constitution

Michael Reksulak Æ William F. Shughart II

Published online: 15 January 2008

� Springer Science + Business Media, LLC 2007

Abstract On Election Day 2004, a razor-thin majority of Alabama’s voters

rejected a proposed amendment to remove overtly segregationist language from the

state constitution. Opponents had contended that approval would have opened the

legislative door to significantly higher taxes. We employ the results from two earlier

special elections to analyze the outcome. In 2000, voters supported repealing a

constitutional provision prohibiting interracial marriages. Three years later, Ala-

bamians were asked to reveal their preferences with respect to additional taxation.

The evidence suggests that opposition to higher taxes rather than bigotry was

decisive in the rejection of Amendment 2 in 2004.

Keywords Constitutional choice � Voting � Taxation

JEL Classification D72 � H4

The first and most important step to improve the educational conditions in

Alabama would be the convening of a Constitutional Convention to revise our

present antiquated fundamental law. (Governor Emmet O’Neal, 1914).1

M. Reksulak (&)

School of Economic Development, Georgia Southern University, P.O. Box 8152, Statesboro, GA

30460-8152, USA

e-mail: [email protected]

W. F. Shughart II

Department of Economics, University of Mississippi, University, MS 38677-1848, USA

1 Emmet O’Neal, Educational Reform and a New Constitution (Montgomery: Brown Printing Co., 1914),

pp. 5–6; quoted in Thomson (2003).

123

Constit Polit Econ (2008) 19:61–80

DOI 10.1007/s10602-007-9031-3

Can there be a loonier way to run state and local government? Can there be a

less efficient way to govern? Can there be any doubt Alabama needs a new

constitution? (Editorial in the Birmingham News, 2004).2

1 Introduction

The State of Alabama has had six constitutions in its 186-year history. The current

one, in force since 1901,3 has the dubious distinction of being the longest US state

constitution and—with 287 sections—one of the wordiest constitutions in the

western world. It has been amended more than 777 times (as of July 2007)4 and

counting—ballooning, by our reckoning, to more than 350,000 words.

The historical record suggests that the constitution of 1901 had two major

objectives: to deny the franchise to Alabama’s African-American citizens, rights

which had been guaranteed by the constitution adopted in 1868 while the state was

occupied by victorious Union troops and in the midst of post-Civil War

Reconstruction, and to curtail as much as possible governmental powers of

taxation.5 The 1875 constitution was a first step in this direction, providing for low

taxes, authorizing a minimum of government services and protecting the political

supremacy of Alabama’s property owners. In the opinion of the landowner class,

however, the constitution of 1875 did not go far enough in curtailing the rights of

black (and, in general, poor) voters. The 1901 constitution was a successful attempt

to remedy this situation. The state’s planters and merchants—the ‘‘Bourbon

Democrats’’ (McMillan 1955)—lobbied effectively for even stricter limits on

government’s power to tax and for the implementation of burdensome tests for

prospective voters, practically ensuring that black Alabamians would have no

further access to the ballot box.

Those favoring rewriting the 1875 document ‘‘asked for the disenfranchisement

of the Negro in the name of ‘white supremacy’ and an honest electorate’’ (ibid.,

p. 260). A majority of the 155 all-white and all-male delegates to the constitutional

convention exhibited considerable gusto in evaluating several alternative means

tests as well as educational requirements previously imposed in other Confederate

states that would assuredly disenfranchise blacks while not running afoul of legal

precedent and the Fourteenth Amendment to the United States Constitution. They

2 Bob Blalock, ‘‘Blame Constitution for Much of what Ails State,’’ Birmingham News, Vol. 117, No. 211

(14 November 2004), p. 2C.3 The present Alabama document was preceded by the constitutions of 1819, 1861, 1865, 1868 and 1875.

See URL: http://www.legislature.state.al.us/misc/history/constitutions/constitutions.html4 See URL: http://www.legislature.state.al.us/CodeOfAlabama/Constitution/1901/Constitution1901_toc.htm5 This discussion is based in part on Malcolm Cook McMillan’s (1955) authoritative history of

Alabama’s constitutional development and on information provided by the Alabama Department of

Archives & History at the following URL: http://www.alabamamoments.state.al.us; accessed 04

September 2006.

62 M. Reksulak, W.F. Shughart II

123

finally proposed a constitution that seriously disadvantaged persons of low means

and limited education seeking to exercise their constitutional right to vote.6

The 1901 constitution was adopted after Alabama voters ratified it, with 108,613

voters reported to have voted ‘‘Yes’’, while 81,734 voted ‘‘No’’. Charges of vote-

rigging abounded and election returns in, especially, those ‘‘black belt’’ counties with

African-American majorities gave much credence to those accusations (Jackson

1994). Attempts to change the constitution once again commenced within a decade,

when it became clear to those in positions of political power that its restrictions on

governing, specifically fiscal ones, proved to be almost insurmountable.

Two avenues exist for those wanting to modify the basic law in Alabama. A

complete rewriting of the constitution requires approval by a majority of the voters,

following compliance with a plethora of executive and legislative requirements

contained in the 1901 constitution itself. Many attempts, the most recent one

initiated by Governor Robert R. Riley (R) in 2003, to draft a new state constitution

have failed for a variety of reasons. Another method is to change the constitution

incrementally, each requiring a vote by the legislature and ratification by the eligible

voters. Incremental revision has led to the aforementioned prevalence of amend-

ments in the Alabama Constitution.

The restrictions imposed by the 1901 document were, by and large, intended to

remove power from local governments and to concentrate it in the state’s capital at

Montgomery. In addition to its impact on voting rights—which has, in the

meantime, been superseded by federal court decisions—the constitution of 1901 has

had profound influence on the economic development of the state. Local pro-growth

initiatives can only be undertaken if constitutionally approved—i.e., by amendment.

Home rule by counties is verboten. Analyses by ‘‘Alabama Citizens for Constitu-

tional Reform’’ show that, as a consequence, approximately two-fifths of the bills

considered by the Alabama Legislature have local significance only, and more than

two-thirds of the amendments to the constitution apply to a single county or city.

Examples of the 1901 constitution’s narrowly tailored and often comical provisions

are plentiful and include ‘‘Amendment 520: Excavating Human Graves in Madison

County’’, ‘‘Amendment 601: Compensation of Judge of Probate of Barbour

County’’ and ‘‘Amendment 756: Enforcement of Traffic Laws in Shelby County’’.

6 John B. Knox of Calhoun County, elected President of the Constitutional Convention, chose to frame

the issue as follows on Wednesday, May 22, 1901, the second day of the convention:

It is contended in defense of this provision, that while, in effect, it will exclude the great mass of

ignorant negro voters it does not, in terms, exclude them, and applies generally to all classes of

voters, without reference to their race, color or previous condition of servitude; that all negroes

who were voters prior to January 1st, 1867, of whom, it is claimed, there were quite a number,

could vote, and the descendants, whether slaves or not, of these free negroes were entitled to vote,

and that these were quite numerous. And on the other hand, that white people born in other

countries—emigrants, who cannot read and write, could not vote, nor could white people who

were unable to vote in the State in which they lived prior to 1867, unless they were able to read

and write. If it be said that this exception permits many more white people to vote than negroes,

the answer was that this would be equally true of any proper qualifications which might be

proposed. It would be true of an educational qualification, and it would be true of a property

qualification, the validity of which has never been questioned. (Source: Alabama Legislature,

http://www.legislature.state.al.us/misc/history/constitutions/1901/proceedings/1901_proceedings_

vol1/day2.html; accessed 04 September 2006).

Racism versus fiscal conservatism 63

123

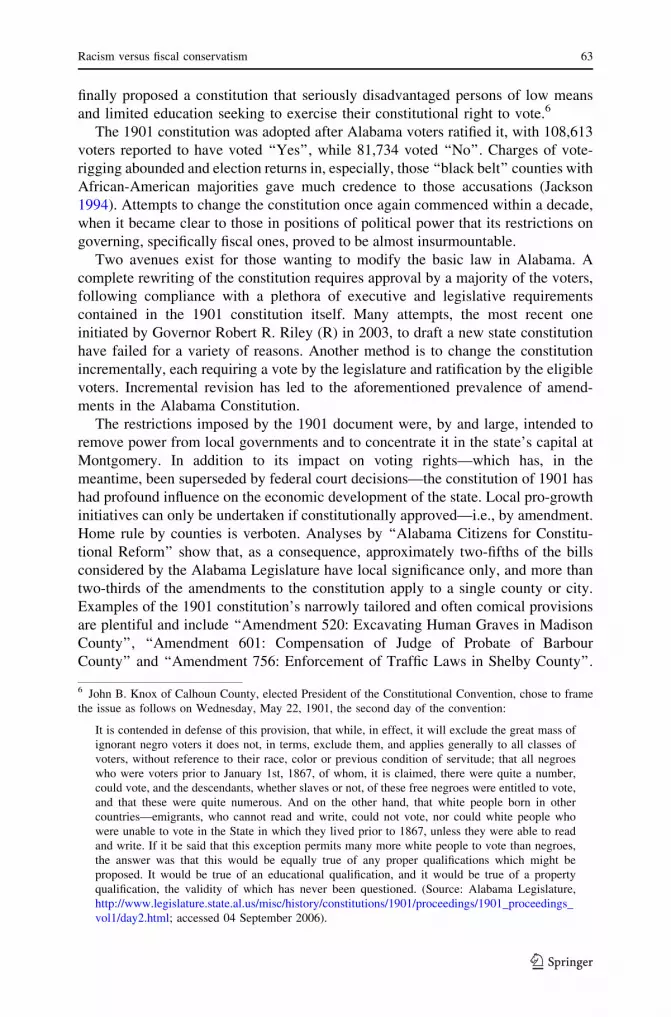

Certain changes in the Alabama tax code must be approved by constitutional

amendment as well. The upshot is one of the highest degrees of tax-earmarking in

the country, with approximately 87% of Alabama’s revenue being assigned to

specific purposes (Ormond 2004). Given the difficulties in adjusting the tax code,

Alabama has one of the lowest maximum tax rates on personal income in the nation

(see Table 1) and allows complete deduction of federal tax payments in computing

state taxable income, but also has the lowest threshold for income tax payments,

starting at $4,600 for a family of four. It is for these reasons that, after taking office

in 2003, Governor Riley felt compelled to propose an all-encompassing ‘‘Alabama

Table 1 State maximum tax rates on personal income as of January 1, 2006

State Maximum tax rate State Maximum tax rate

Alabama 5.0 Montanaa 6.9

Alaska No state income tax Nebraskaa 6.84

Arizona 5.04 Nevada No state income tax

Arkansasa 7.0 New Hampshire Only dividends and interest

income are taxed

Californiaa 9.3 New Jersey 8.97

Colorado 4.63 New Mexico 5.3

Connecticut 5.0 New York 6.85

Delaware 5.95 North Carolina 8.25

Florida No state income tax North Dakota 5.54

Georgia 6.0 Ohioa 7.185

Hawaii 8.25 Oklahoma 6.25

Idahoa 7.8 Oregona 9.0

Illinois 3.0 Pennsylvania 3.07

Indiana 3.4 Rhode Island 25% of federal tax liability

Iowaa 8.98 South Carolinaa 7.0

Kansas 6.45 South Dakota No state income tax

Kentucky 6.0 Tennessee Only dividends and interest

income are taxed

Louisiana 6.0 Texas No state income tax

Mainea 8.5 Utah 7.0

Maryland 4.75 Vermonta 9.5

Massachusettsa 5.3 Virginia 5.75

Michigana 3.9 Washington No state income tax

Minnesotaa 7.85 West Virginia 6.5

Mississippi 5.0 Wisconsin 6.75

Missouri 6.0 Wyoming No state income tax

a These 15 states have statutory provision for automatic adjustment of tax brackets, personal exemption

or standard deductions to the rate of inflation. Massachusetts, Michigan, Nebraska and Ohio index the

personal exemption amounts only

Source: Federation of Tax Administrators (http://www.taxadmin.org/fta/rate/ind_inc.html)

64 M. Reksulak, W.F. Shughart II

123

Excellence Initiative Fund’’ in order to address a $675 million projected budget

deficit for fiscal year 2004.

It is the 2003 vote on the constitutional amendment to implement the Riley tax

plan as well as the result of an earlier referendum that enables us to analyze

questions surrounding Alabama’s narrow affirmation of segregationist constitutional

language in 2004. The earlier vote, in 2000, resulted in the removal of a section of

the constitution prohibiting interracial marriages.

Although the state constitution of 1901 is widely seen as both a nuisance to

politicians and citizens alike and an impediment to Alabama’s economic progress

(see Fig. 1), the frequency of its amendment turns out to be a treasure trove for

political economists. Astronomers and economists share the dubious distinction of

not being able to set up controlled scientific experiments on a large scale. In the case

of the economists it is ethical constraints as well as monetary ones that often prove

the most forbidding: they frequently are compelled to draw conclusions from the

data they have rather than the data they would wish for. Every once in a while,

however, it turns out that such experiments have, indeed, been conducted

unintentionally. The succession of votes on an unambiguously racially divisive

issue (2000) and on a straightforward fiscal matter (2003) permits us to address the

question whether or not the 2004 vote—rejecting the removal of segregationist

language from the Alabama constitution—should be taken as evidence for the

continued prevalence of bigotry among the state’s citizenry. The results of our

analysis suggest that economic considerations rather than racism were decisive in

the voter’s rejection of Amendment 2 in 2004.

Section 2 recounts the histories of the proposed constitutional amendments in

2000, 2003 and 2004. We discuss our empirical models and data sources in Sect. 3.

Section 4 presents the regression results for the three referendums; Sect. 5

concludes.

Fig. 1 The burden imposed by Alabama’s 1901 constitution. Note: Courtesy of The Mobile Register2000� All rights reserved. Reprinted with permission

Racism versus fiscal conservatism 65

123

2 Proposed constitutional amendments

House Bill 587 was first read in the Alabama legislature on April 13, 2003. It was

proposed by Representative James E. Buskey (D) and co-sponsored by Represen-

tative Ken Guin (D), currently the House Majority Leader. The bill passed

the House with 91 ‘‘Yea’’ votes (out of a possible 105) on May 14 and it passed the

Senate with 29 ‘‘Yea’’ votes (out of 35) on the 16th of June. The amendment to the

constitution authorized by the bill and put before the voters on Election Day 2004

read as follows:

Shall the following Amendment be adopted to the Constitution of Alabama?

Proposed Statewide Amendment No. 2

Proposing an amendment to the Constitution of Alabama of 1901, to repeal

portions of Section 256 and Amendment 111 relating to separation of schools

by race and repeal portions of Amendment 111 concerning constitutional

construction against the right to education, and to repeal Section 259,

Amendment 90, and Amendment 109 relating to the poll tax. (Proposed by

Act 2003–203).7

Specifically, the amendment would remove, among other language, the following

sentence from Alabama’s constitution: ‘‘Separate schools shall be provided for

white and colored children, and no child of either race shall be permitted to attend a

school of the other race.’’ Importantly, the authors of the bill also proposed

eliminating a half-sentence disputing a constitutional right to education: ‘‘but

nothing in this Constitution shall be construed to as creating or recognizing any right

to education or training at public expense, nor as limiting the authority and duty of

the legislature, in furthering or providing for education, to require and impose

conditions or procedures deemed necessary to the preservation of peace and order.’’

Another section of the proposed amendment would repeal the poll tax exemption for

veterans of foreign wars. The poll tax itself had been one building block in earlier

attempts to deter individuals of insufficient means from voting.

Opponents of the amendment quickly seized the ‘‘right to education’’ language to

vigorously campaign against it. They asserted that approval would implicitly

recognize such a right and, as a result, would lead to major tax increases in order to

finance public education in Alabama. The amendment’s proponents argued that this

conclusion was nonsensical given the existing constitutional limitations on

government’s taxing powers. After the defeat of the amendment by the electorate

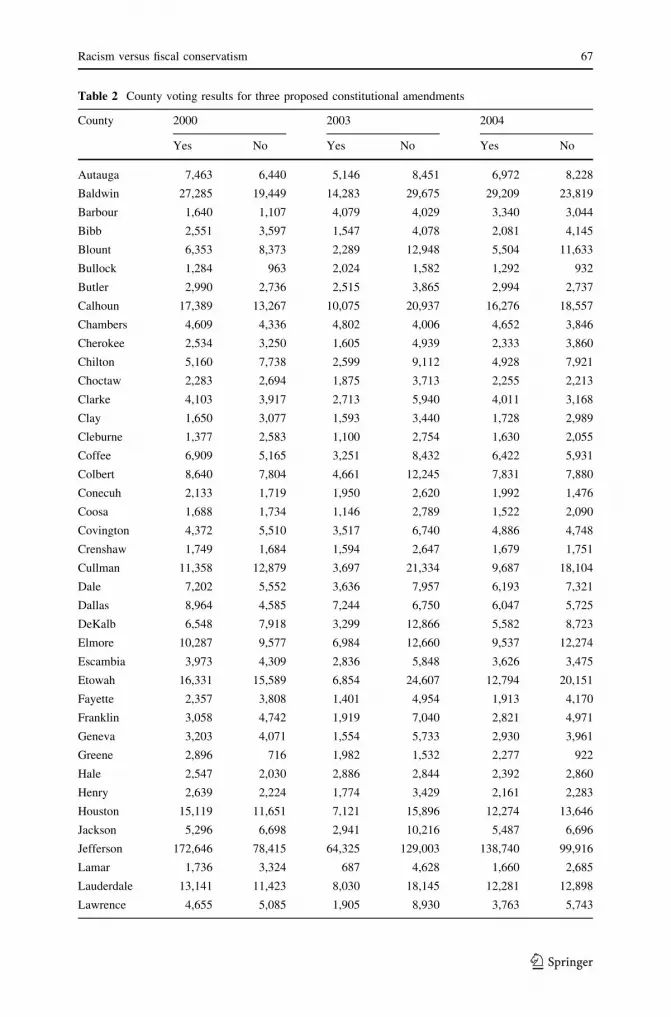

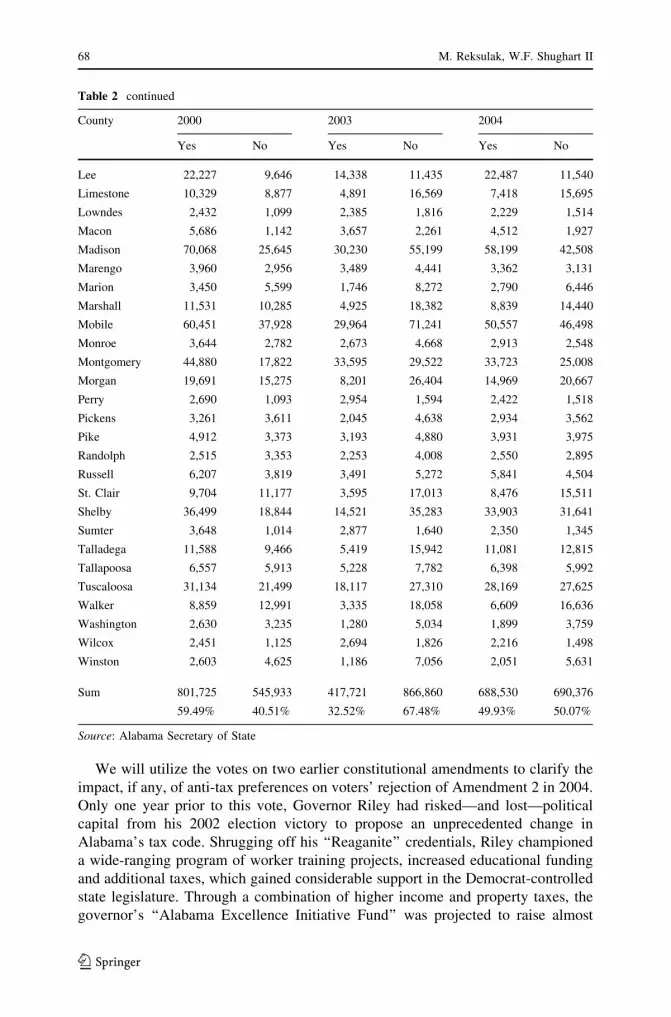

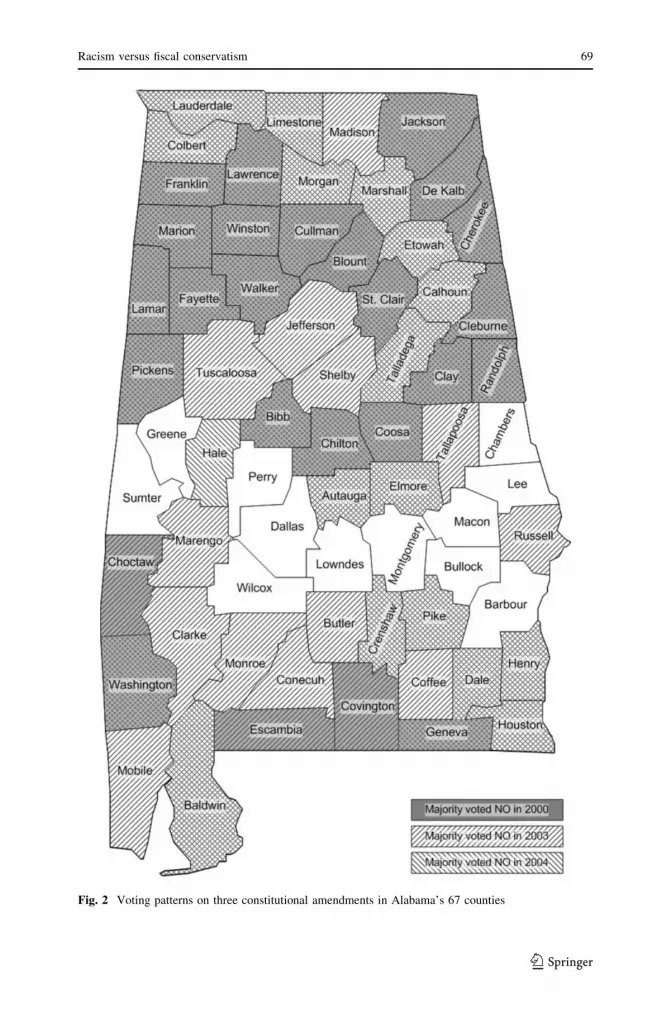

(Table 2 lists the electoral outcomes for all three amendments discussed here; Fig. 2

provides a graphical representation), the soul-searching started in newspaper

editorials and everyday discussions across the state. The ‘‘Old South’’ label was

attached to Alabama anew. Questions were raised as to how bigotry could still be so

prevalent at the beginning of the 21st century and what that would augur for the

future. Others pointed to the possible tax consequences identified by the

amendment’s opponents and dismissed the inference of racial bias.

7 Election Division, Office of the Secretary of State, State of Alabama, http://www.sos.state.al.us/

Elections/2004/2004ProposedAmendmts.aspx; accessed 08 December 2007.

66 M. Reksulak, W.F. Shughart II

123

Table 2 County voting results for three proposed constitutional amendments

County 2000 2003 2004

Yes No Yes No Yes No

Autauga 7,463 6,440 5,146 8,451 6,972 8,228

Baldwin 27,285 19,449 14,283 29,675 29,209 23,819

Barbour 1,640 1,107 4,079 4,029 3,340 3,044

Bibb 2,551 3,597 1,547 4,078 2,081 4,145

Blount 6,353 8,373 2,289 12,948 5,504 11,633

Bullock 1,284 963 2,024 1,582 1,292 932

Butler 2,990 2,736 2,515 3,865 2,994 2,737

Calhoun 17,389 13,267 10,075 20,937 16,276 18,557

Chambers 4,609 4,336 4,802 4,006 4,652 3,846

Cherokee 2,534 3,250 1,605 4,939 2,333 3,860

Chilton 5,160 7,738 2,599 9,112 4,928 7,921

Choctaw 2,283 2,694 1,875 3,713 2,255 2,213

Clarke 4,103 3,917 2,713 5,940 4,011 3,168

Clay 1,650 3,077 1,593 3,440 1,728 2,989

Cleburne 1,377 2,583 1,100 2,754 1,630 2,055

Coffee 6,909 5,165 3,251 8,432 6,422 5,931

Colbert 8,640 7,804 4,661 12,245 7,831 7,880

Conecuh 2,133 1,719 1,950 2,620 1,992 1,476

Coosa 1,688 1,734 1,146 2,789 1,522 2,090

Covington 4,372 5,510 3,517 6,740 4,886 4,748

Crenshaw 1,749 1,684 1,594 2,647 1,679 1,751

Cullman 11,358 12,879 3,697 21,334 9,687 18,104

Dale 7,202 5,552 3,636 7,957 6,193 7,321

Dallas 8,964 4,585 7,244 6,750 6,047 5,725

DeKalb 6,548 7,918 3,299 12,866 5,582 8,723

Elmore 10,287 9,577 6,984 12,660 9,537 12,274

Escambia 3,973 4,309 2,836 5,848 3,626 3,475

Etowah 16,331 15,589 6,854 24,607 12,794 20,151

Fayette 2,357 3,808 1,401 4,954 1,913 4,170

Franklin 3,058 4,742 1,919 7,040 2,821 4,971

Geneva 3,203 4,071 1,554 5,733 2,930 3,961

Greene 2,896 716 1,982 1,532 2,277 922

Hale 2,547 2,030 2,886 2,844 2,392 2,860

Henry 2,639 2,224 1,774 3,429 2,161 2,283

Houston 15,119 11,651 7,121 15,896 12,274 13,646

Jackson 5,296 6,698 2,941 10,216 5,487 6,696

Jefferson 172,646 78,415 64,325 129,003 138,740 99,916

Lamar 1,736 3,324 687 4,628 1,660 2,685

Lauderdale 13,141 11,423 8,030 18,145 12,281 12,898

Lawrence 4,655 5,085 1,905 8,930 3,763 5,743

Racism versus fiscal conservatism 67

123

We will utilize the votes on two earlier constitutional amendments to clarify the

impact, if any, of anti-tax preferences on voters’ rejection of Amendment 2 in 2004.

Only one year prior to this vote, Governor Riley had risked—and lost—political

capital from his 2002 election victory to propose an unprecedented change in

Alabama’s tax code. Shrugging off his ‘‘Reaganite’’ credentials, Riley championed

a wide-ranging program of worker training projects, increased educational funding

and additional taxes, which gained considerable support in the Democrat-controlled

state legislature. Through a combination of higher income and property taxes, the

governor’s ‘‘Alabama Excellence Initiative Fund’’ was projected to raise almost

Table 2 continued

County 2000 2003 2004

Yes No Yes No Yes No

Lee 22,227 9,646 14,338 11,435 22,487 11,540

Limestone 10,329 8,877 4,891 16,569 7,418 15,695

Lowndes 2,432 1,099 2,385 1,816 2,229 1,514

Macon 5,686 1,142 3,657 2,261 4,512 1,927

Madison 70,068 25,645 30,230 55,199 58,199 42,508

Marengo 3,960 2,956 3,489 4,441 3,362 3,131

Marion 3,450 5,599 1,746 8,272 2,790 6,446

Marshall 11,531 10,285 4,925 18,382 8,839 14,440

Mobile 60,451 37,928 29,964 71,241 50,557 46,498

Monroe 3,644 2,782 2,673 4,668 2,913 2,548

Montgomery 44,880 17,822 33,595 29,522 33,723 25,008

Morgan 19,691 15,275 8,201 26,404 14,969 20,667

Perry 2,690 1,093 2,954 1,594 2,422 1,518

Pickens 3,261 3,611 2,045 4,638 2,934 3,562

Pike 4,912 3,373 3,193 4,880 3,931 3,975

Randolph 2,515 3,353 2,253 4,008 2,550 2,895

Russell 6,207 3,819 3,491 5,272 5,841 4,504

St. Clair 9,704 11,177 3,595 17,013 8,476 15,511

Shelby 36,499 18,844 14,521 35,283 33,903 31,641

Sumter 3,648 1,014 2,877 1,640 2,350 1,345

Talladega 11,588 9,466 5,419 15,942 11,081 12,815

Tallapoosa 6,557 5,913 5,228 7,782 6,398 5,992

Tuscaloosa 31,134 21,499 18,117 27,310 28,169 27,625

Walker 8,859 12,991 3,335 18,058 6,609 16,636

Washington 2,630 3,235 1,280 5,034 1,899 3,759

Wilcox 2,451 1,125 2,694 1,826 2,216 1,498

Winston 2,603 4,625 1,186 7,056 2,051 5,631

Sum 801,725 545,933 417,721 866,860 688,530 690,376

59.49% 40.51% 32.52% 67.48% 49.93% 50.07%

Source: Alabama Secretary of State

68 M. Reksulak, W.F. Shughart II

123

Fig. 2 Voting patterns on three constitutional amendments in Alabama’s 67 counties

Racism versus fiscal conservatism 69

123

$600 million more than necessary to close a projected $675 million budget gap for

fiscal year 2004. Timber companies and large landowners would have seen their

property taxes increase manifold.

Riley also proposed to raise, from a national record low of $4,600 for a family of

four, the threshold for payment of income taxes to $20,000 over 4 years. The voters

were asked to approve the following text of the amendment in a special election

held on September 9, 2003:

Shall the following Amendment be adopted to the Constitution of Alabama?

Proposed Statewide Amendment Number One (1)

Proposing an amendment to the Constitution of Alabama of 1901, establishing

the Alabama Excellence Initiative Fund which may be used to fund programs

including, but not limited to, the furtherance of excellence in public education,

college scholarships, health care benefits for senior citizens and job training

programs to attract new high paying jobs and otherwise provide for distributing

state tax revenues; to adjust income and property taxes; to establish the General

Fund Rainy Day Account; to provide for the replenishment of the General Fund

Rainy Day Account and the Education Trust Fund Rainy Day Account.

(Proposed by Act No. 2003–78).8

Although property taxes would have increased substantially, it was estimated at

the time that almost 67% of all families in Alabama would either have seen their tax

bills fall or remain unchanged if the amendment was adopted (Webster and Webster

2004). The electorate nevertheless soundly rejected the constitutional amendment,

with only 32.5% of those voting favoring Governor Riley’s plan. In the sequel,

general fund expenditures were cut by 5.3% across the board in 2004, and most

programs saw budget reductions of about 18% (Ormond 2004). If nothing else,

Alabamians had demonstrated a significant aversion to higher taxes, notwithstand-

ing the myriad pro-growth arguments made in favor of it.

Measuring preferences for racial bias is difficult to do, mainly because perceived

or actual peer pressure will often lead to disingenuous replies when the issue is

assessed by surveys or opinion polls. The legislators of the State of Alabama,

however, conducted an experiment of their own, when they asked the people to vote

8 Source: Election Division, Office of the Secretary of State, State of Alabama, http://www.sos.state.al.us/

Elections/2003/SCAElection.aspx; accessed 08 December 2007. The governor’s package consisted of

numerous legislatively approved changes to existing constitutional language relating to taxes and public

education. The relevant provisions were: 101—To limit credits allowed insurance companies; 102—Toclarify the definition of taxable income; 103—Relating to the Teacher Tenure Act; 105—Board ofEducation to create program for payments to teachers and for scholarships; 106—Relating to the FairDismissal Act; 107—To increase the rates of mortgage and deed recording taxes; 108—To increase ratesof the utility gross receipts & utility service use taxes; 109—To increase the tax on cigarettes; 110—Stateto pay tuition of any qualified student for higher and postsecondary education; 111—Pertaining toFoundation Program of public schools to update funding formulas/disbursement; 112—To amend Tea-cher Accountability Act; 113—To prohibit public funds from being passed through from one entity toanother by Legislature; 114—School Fiscal Management and Responsibility Act; 115—To repeal thededuction for federal income taxes; 116—Relating to individual and corporate income tax to providefunding for public education; 117—To provide for sharing the cost of health insurance premiums by stateemployees and retirees; 118—To eliminate the lubricating oil tax and exemption from sales and use tax;

and 119—To update the method of determining current use valuation of property.

70 M. Reksulak, W.F. Shughart II

123

on an amendment to the constitution which would remove an ‘‘anti-miscegenation’’

section from it. That vote is even more significant for the purpose of measuring

racial prejudice per se, because it was apparent that its approval would have no

impact in terms of the level of taxation—or any other measurable economic effect.

The amendment put before Alabama’s voters on Election Day 2000 read:

Shall the following Amendment be adopted to the Constitution of Alabama?

Proposed Statewide Amendment Number 2

Proposing an amendment to the Constitution of Alabama of 1901, to abolish

the prohibition of interracial marriages. (Proposed by Act No. 1999–321).9

If approved by the voters, the amendment would strike from Section 102 of the

constitution’s text language consisting of a glaring expression of racism, namely,

‘‘The legislature shall never pass any law to authorize or legalize any marriage

between any white person and a negro, or descendant of a negro.’’ However, the

change to the constitution proposed in 2000 was evidently little more than a gesture

that would not have affected the status quo. All miscegenation laws had been

rendered void by the Supreme Court’s decision in Loving v. Virginia, 388 U.S. 1

(1967).10 It was, therefore, considered by many to be a symbolic act (Knigge and

Moody 2003). Nearly 60% of those voting (59.5%, to be precise) approved of the

amendment. The general outcome was hailed throughout the state as a sign of

Alabama shedding its stained image, personified by the infamous picture of

Governor George Wallace blocking two African-American students from entering

the University of Alabama and by the scenes of peaceful civil rights marchers being

bloodied by state troopers on Selma’s Edmund Pettus Bridge on March 7, 1965.

Some commentators questioned that rosy conclusion by pointing to the 40% of

voters who had marked their ballots in favor of continuing to outlaw interracial

marriages (Altman and Klinkner 2005).

The referendums on the constitutional amendments in 2000 and 2003 provide us

with the tools to dissect the vote in 2004. In the next section, we will use the

information supplied by the outcomes of those earlier ballots to scrutinize more

carefully the result of the 2004 referendum, in which Alabamians narrowly voted

not to rescind segregationist language calling for separate public schools for the

state’s black and white children.

3 Empirical model and data

We analyze the three different votes across the 67 counties in Alabama. The results

of the constitutional referendums were obtained from the Secretary of State’s office.

We measure the outcomes as the percentage of voters selecting ‘‘No’’ on each of the

9 Source: Election Division, Office of the Secretary of State, State of Alabama, http://www.sos.state.al.us/

Elections/2000/2000PropStateAmendmts.aspx; accessed 08 December 2007.10 The unanimous majority opinion delivered by Chief Justice Earl Warren held that the Commonwealth

of Virginia’s statute prohibiting marriages between persons solely on the basis of racial classifications

violated both the Equal Protection and Due Process clauses of the Fourteenth Amendment. Source: Find

Law at URL: http://laws.findlaw.com/us/388/1.html; accessed 04 September 2006.

Racism versus fiscal conservatism 71

123

ballots. The variables are labeled V2000NOPERC, V2003NOPERC and

V2004NOPERC, respectively. We also collected data on socioeconomic variables

that have been shown to impact voters’ choices. These include the percentage of the

county population that is African-American (BLACKPERC), the fraction of the

population over 25 with at least a bachelor’s degree (BAPERC25PLUS), county

income per capita in 1999 (PCAPITAINCOME99) and the percentage of the

population above the age of 55 (PERCABOVE55). Moreover, given the education

and timber-related debates surrounding, specifically, the 2003 and 2004 votes, we

also utilize the per capita employment in education per county (PERCAPITAEM-

PLOYEDUC) as well as a variable measuring the economic dependence of a given

county on industries directly connected to timber (TIMBERDEPPERC). The

observations on variables other than the election results were collected from the

2000 US Census. The timber variable was calculated using a methodology described

in a recent analysis of timber dependency in Alabama (Howze et al. 2003).

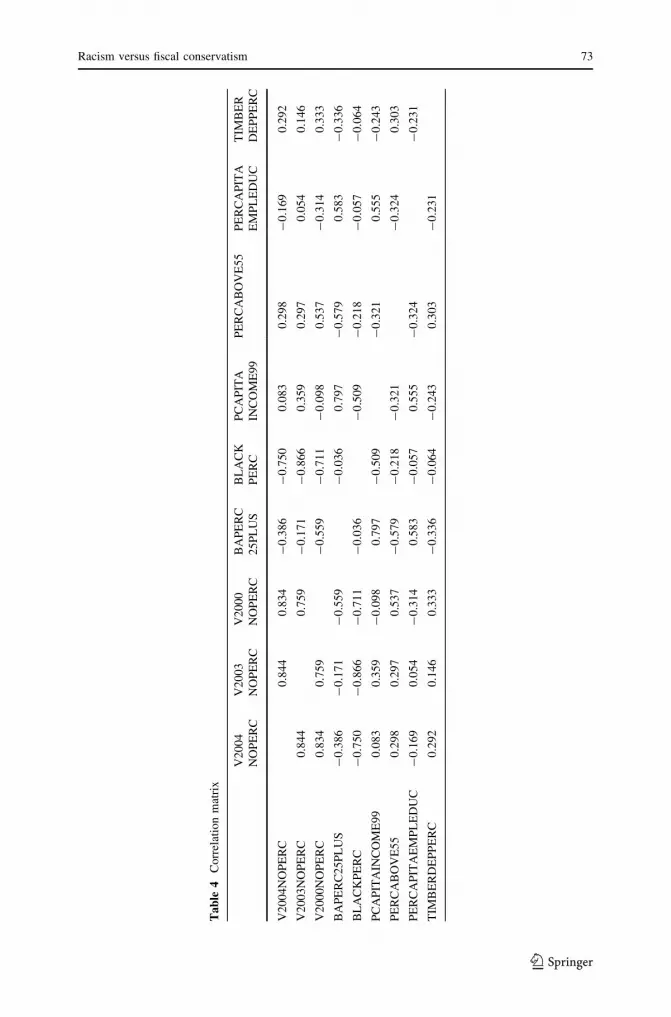

Descriptive statistics for all variables are reported in Table 3 and correlation

coefficients among them are shown in Table 4.

With respect to the 2000 and the 2004 votes, it is likely a priori that the larger the

percentage of African-American voters in a given county, the greater the support

will be for the removal of racist constitutional language. As members of the group

that is most directly affected by such provisions, they would have a strong incentive

to vote for repeal. The effect of this variable on the 2003 vote, the tax vote, is

somewhat ambiguous but also likely to raise the odds of approval. According to

census statistics—and borne out by our data for the State of Alabama—poverty is

still correlated with one’s race in the ‘‘Old South’’. Thus, since the governor’s

proposal had promised additional funding for worker-training and other social

programs, we expect a negative correlation between BLACKPERC and the fraction

of no votes on that amendment.

The percentage of people age 25 and above with at least a bachelor’s degree

should have a strongly negative effect on the number of no votes on all three

amendments. In instances of officially endorsed racism, the literature has shown a

pattern such that more educated members of the populace—independent of

geographic area—are more inclined to favor repealing remnants of the Confederacy

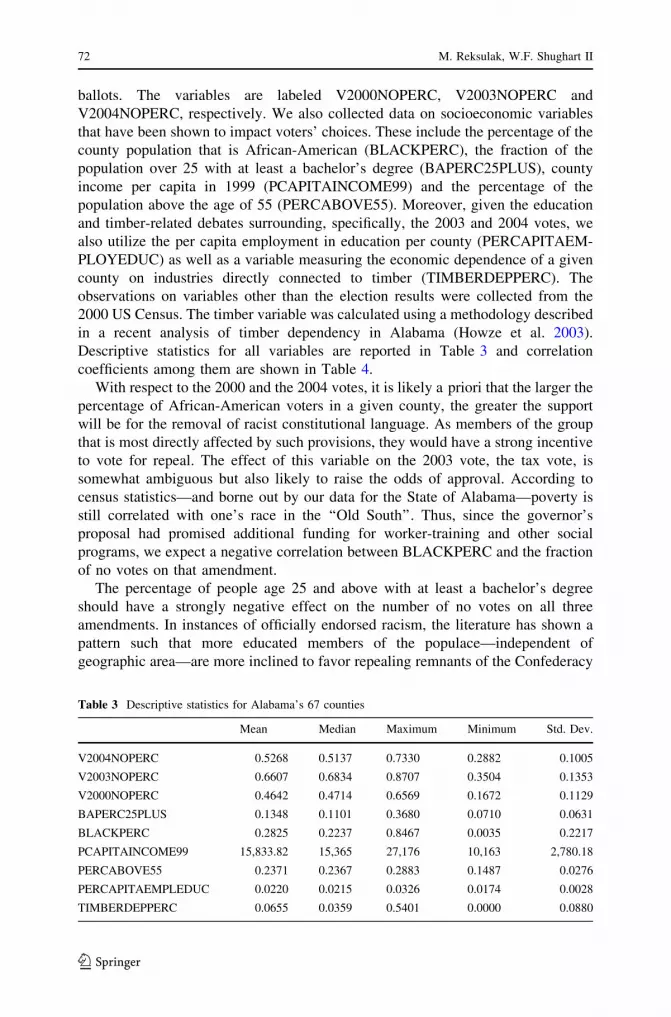

Table 3 Descriptive statistics for Alabama’s 67 counties

Mean Median Maximum Minimum Std. Dev.

V2004NOPERC 0.5268 0.5137 0.7330 0.2882 0.1005

V2003NOPERC 0.6607 0.6834 0.8707 0.3504 0.1353

V2000NOPERC 0.4642 0.4714 0.6569 0.1672 0.1129

BAPERC25PLUS 0.1348 0.1101 0.3680 0.0710 0.0631

BLACKPERC 0.2825 0.2237 0.8467 0.0035 0.2217

PCAPITAINCOME99 15,833.82 15,365 27,176 10,163 2,780.18

PERCABOVE55 0.2371 0.2367 0.2883 0.1487 0.0276

PERCAPITAEMPLEDUC 0.0220 0.0215 0.0326 0.0174 0.0028

TIMBERDEPPERC 0.0655 0.0359 0.5401 0.0000 0.0880

72 M. Reksulak, W.F. Shughart II

123

Tab

le4

Corr

elat

ion

mat

rix

V2

00

4

NO

PE

RC

V2

00

3

NO

PE

RC

V2

00

0

NO

PE

RC

BA

PE

RC

25

PL

US

BL

AC

K

PE

RC

PC

AP

ITA

INC

OM

E9

9

PE

RC

AB

OV

E5

5P

ER

CA

PIT

A

EM

PL

ED

UC

TIM

BE

R

DE

PP

ER

C

V2

00

4N

OP

ER

C0

.844

0.8

34

-0

.38

6-

0.7

50

0.0

83

0.2

98

-0

.169

0.2

92

V2

00

3N

OP

ER

C0

.844

0.7

59

-0

.17

1-

0.8

66

0.3

59

0.2

97

0.0

54

0.1

46

V2

00

0N

OP

ER

C0

.834

0.7

59

-0

.55

9-

0.7

11

-0

.098

0.5

37

-0

.314

0.3

33

BA

PE

RC

25

PL

US

-0

.386

-0

.171

-0

.559

-0

.036

0.7

97

-0

.57

90

.583

-0

.33

6

BL

AC

KP

ER

C-

0.7

50

-0

.866

-0

.711

-0

.03

6-

0.5

09

-0

.21

8-

0.0

57

-0

.06

4

PC

AP

ITA

INC

OM

E9

90

.083

0.3

59

-0

.098

0.7

97

-0

.509

-0

.32

10

.555

-0

.24

3

PE

RC

AB

OV

E5

50

.298

0.2

97

0.5

37

-0

.57

9-

0.2

18

-0

.321

-0

.324

0.3

03

PE

RC

AP

ITA

EM

PL

ED

UC

-0

.169

0.0

54

-0

.314

0.5

83

-0

.057

0.5

55

-0

.32

4-

0.2

31

TIM

BE

RD

EP

PE

RC

0.2

92

0.1

46

0.3

33

-0

.33

6-

0.0

64

-0

.243

0.3

03

-0

.231

Racism versus fiscal conservatism 73

123

in state documents and state houses (as has been the case in votes on Confederate

flag symbols).11 Given the dire financial straits in which Alabama found itself in

2003, and considering that state employees tend to have more years of schooling

and were most likely to be affected personally by the looming spending cuts

required in case that the constitutional amendment were to fail, our a priori

expectation is that a higher level of education leads to fewer no votes, ceteris

paribus.

We include average income per capita in a county (PCAPITAINCOME99) for

two reasons. Such a variable, arguably, would not be indicative of racial bias (either

way). On the other hand, self-interest and self-conception will usually incline high-

income taxpayers to be more hostile to additional taxation, not the least because

those in this stratum of society already shoulder a disproportionate share of the tax

burden. High-income Alabamians almost surely would be opposed to the provision

contained in Governor Riley’s ‘‘Alabama Excellence Initiative Fund’’ that would

repeal the allowable state income tax deduction for federal tax payments. Similarly,

timber interests would have expected—as explained above—significant increases in

taxes and, hence, would also have been more likely to oppose the initiative. This

reasoning should permit us to distinguish, in the 2004 referendum, whether or not

economic considerations may have had a decisive effect.

Considering the consequences of the age of the electorate in the analysis of

voting decisions is a well-established practice. For the issue at hand, it is likely that

older constituents hold more traditional views of race relations. Conversely, being—

on average—more reliant on the state’s welfare system, the elderly are usually

disposed towards supporting additional funding for social services, even if that

includes a rise in general taxes. Thus, a priori, we expect more votes against

removing segregationist provisions from the constitution the older the population of

a county and fewer no votes on the tax amendment. This does, however, leave us

with no basis for predicting the influence of median age on the constitutional

questions that came before the voters in 2004, which raised both issues.

The relative importance of public education in a given county is measured by the

per capita employment in this sector. Taking into account the considerable potential

inflow of monies earmarked for education-related funding, a stronger impetus for not

rejecting the 2004 vote is a priori expected to be found with respect to this variable.

We hypothesize that the foregoing socioeconomic variables will contribute

explanatory power to the outcomes of each of the three amendments discussed here.

If, in addition, one conjectures that earlier referendum results (in 2000 and in 2003)

themselves have an impact on the 2004 vote, then the appropriate econometric

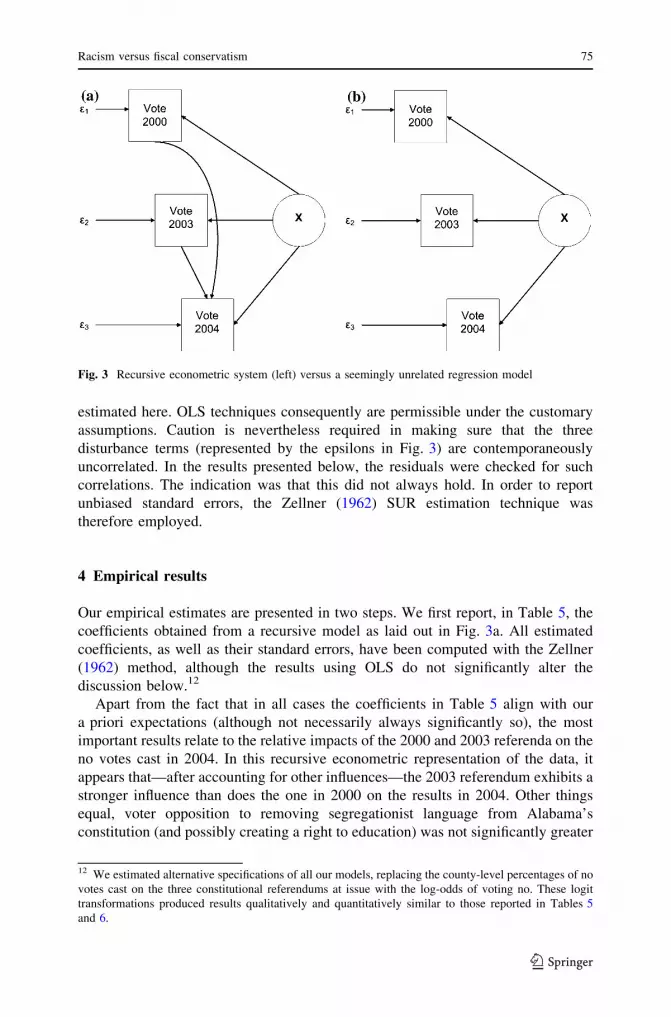

model is the one shown in Fig. 3a. Gujarati (1995: 680–682) and Kennedy (2004:

169) describe the characteristics of these so-called recursive systems. The seemingly

unrelated regression model illustrated in part b of Fig. 3, by contrast, does not

suggest such a direct link between 2004 and the previous votes. (X stands for the

matrix of independent variables in both panels).

In either case, however, only a unidirectional dependency exists. There are no

feedback loops either in our maintained hypotheses or in the econometric models

11 For a history of the controversy over the state flag in Mississippi, see Karahan and Shughart (2004).

74 M. Reksulak, W.F. Shughart II

123

estimated here. OLS techniques consequently are permissible under the customary

assumptions. Caution is nevertheless required in making sure that the three

disturbance terms (represented by the epsilons in Fig. 3) are contemporaneously

uncorrelated. In the results presented below, the residuals were checked for such

correlations. The indication was that this did not always hold. In order to report

unbiased standard errors, the Zellner (1962) SUR estimation technique was

therefore employed.

4 Empirical results

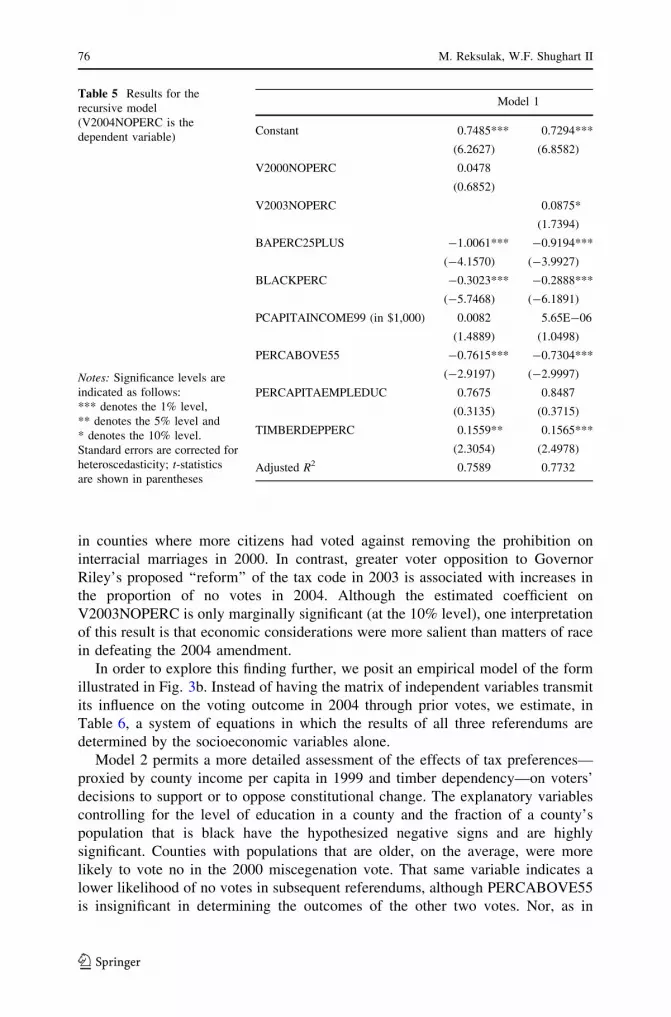

Our empirical estimates are presented in two steps. We first report, in Table 5, the

coefficients obtained from a recursive model as laid out in Fig. 3a. All estimated

coefficients, as well as their standard errors, have been computed with the Zellner

(1962) method, although the results using OLS do not significantly alter the

discussion below.12

Apart from the fact that in all cases the coefficients in Table 5 align with our

a priori expectations (although not necessarily always significantly so), the most

important results relate to the relative impacts of the 2000 and 2003 referenda on the

no votes cast in 2004. In this recursive econometric representation of the data, it

appears that—after accounting for other influences—the 2003 referendum exhibits a

stronger influence than does the one in 2000 on the results in 2004. Other things

equal, voter opposition to removing segregationist language from Alabama’s

constitution (and possibly creating a right to education) was not significantly greater

Fig. 3 Recursive econometric system (left) versus a seemingly unrelated regression model

12 We estimated alternative specifications of all our models, replacing the county-level percentages of no

votes cast on the three constitutional referendums at issue with the log-odds of voting no. These logit

transformations produced results qualitatively and quantitatively similar to those reported in Tables 5

and 6.

Racism versus fiscal conservatism 75

123

in counties where more citizens had voted against removing the prohibition on

interracial marriages in 2000. In contrast, greater voter opposition to Governor

Riley’s proposed ‘‘reform’’ of the tax code in 2003 is associated with increases in

the proportion of no votes in 2004. Although the estimated coefficient on

V2003NOPERC is only marginally significant (at the 10% level), one interpretation

of this result is that economic considerations were more salient than matters of race

in defeating the 2004 amendment.

In order to explore this finding further, we posit an empirical model of the form

illustrated in Fig. 3b. Instead of having the matrix of independent variables transmit

its influence on the voting outcome in 2004 through prior votes, we estimate, in

Table 6, a system of equations in which the results of all three referendums are

determined by the socioeconomic variables alone.

Model 2 permits a more detailed assessment of the effects of tax preferences—

proxied by county income per capita in 1999 and timber dependency—on voters’

decisions to support or to oppose constitutional change. The explanatory variables

controlling for the level of education in a county and the fraction of a county’s

population that is black have the hypothesized negative signs and are highly

significant. Counties with populations that are older, on the average, were more

likely to vote no in the 2000 miscegenation vote. That same variable indicates a

lower likelihood of no votes in subsequent referendums, although PERCABOVE55

is insignificant in determining the outcomes of the other two votes. Nor, as in

Table 5 Results for the

recursive model

(V2004NOPERC is the

dependent variable)

Notes: Significance levels are

indicated as follows:

*** denotes the 1% level,

** denotes the 5% level and

* denotes the 10% level.

Standard errors are corrected for

heteroscedasticity; t-statistics

are shown in parentheses

Model 1

Constant 0.7485*** 0.7294***

(6.2627) (6.8582)

V2000NOPERC 0.0478

(0.6852)

V2003NOPERC 0.0875*

(1.7394)

BAPERC25PLUS -1.0061*** -0.9194***

(-4.1570) (-3.9927)

BLACKPERC -0.3023*** -0.2888***

(-5.7468) (-6.1891)

PCAPITAINCOME99 (in $1,000) 0.0082 5.65E-06

(1.4889) (1.0498)

PERCABOVE55 -0.7615*** -0.7304***

(-2.9197) (-2.9997)

PERCAPITAEMPLEDUC 0.7675 0.8487

(0.3135) (0.3715)

TIMBERDEPPERC 0.1559** 0.1565***

(2.3054) (2.4978)

Adjusted R2 0.7589 0.7732

76 M. Reksulak, W.F. Shughart II

123

Table 5, does employment in education seem to matter, even in 2003 when,

arguably, public school teachers and administrators stood to gain personally from

supporting the governor’s ‘‘Alabama Excellence Initiative Fund’’. Alabamians who

were more highly educated and black tended to vote in favor of all three proposed

constitutional amendments: the estimated coefficients on these two variables are

consistently negative and significant at the 1% level.

The most interesting estimation results again relate to income and timber

dependency. The level of a county’s income per capita is not a statistically significant

factor in explaining the fraction of votes cast against repealing the constitutional

prohibition on interracial marriages in 2000. That same variable enters with a positive

sign and is different from zero at the 1% level of significance in 2003, when Alabama’s

voters decisively rejected the governor’s tax package amendment. Other things being

equal, the higher the average per capita income in a given county, the greater the

percentage of votes cast against the Riley plan. Furthermore, this same relationship

appears to hold in 2004, although the marginal effect is weaker (p = 0.13), perhaps

because some voters did not believe that creating a constitutional right to education

would have adverse fiscal consequences, or because the amendment’s companion

proposal to remove segregationist language from the constitution clouded the issue. It

may also be the case that its impact is somewhat overshadowed by the influence of

timber dependency, which—in 2004—significantly increases the number of no votes.

In any case, both higher per capita incomes and timber dependency on the margin,

Table 6 Results for SUR model of all three referenda

Independent variables Model 2

V2000NOPERC V2003NOPERC V2004NOPERC

Constant 0.6634*** 0.5904*** 0.7722***

(7.0821) (4.4844) (6.7868)

BAPERC25PLUS -0.9118*** -1.4960*** -1.0430***

(-4.2717) (-5.3226) (-4.2785)

BLACKPERC -0.3778*** -0.3539*** -0.3258***

(-9.4783) (-6.3485) (-6.7590)

PCAPITAINCOME99 (in $1,000) -0.0020 0.0291*** 0.0078

(-0.3817) (4.3448) (1.3467)

PERCABOVE55 0.2628 -0.2409 -0.7255***

(1.0649) (-0.7661) (-2.6546)

PERCAPITAEMPLEDUC -1.5319 1.2445

(-0.5253) (0.5073)

TIMBERDEPPERC 0.0362 0.1216*

(0.4527) (7.8074)

Adjusted R2 0.8433 0.8226 0.7557

Note: See Table 5

Racism versus fiscal conservatism 77

123

once more, raise the percentage of no votes cast on an amendment that, at least in the

eyes of its detractors, foreshadowed higher taxes.

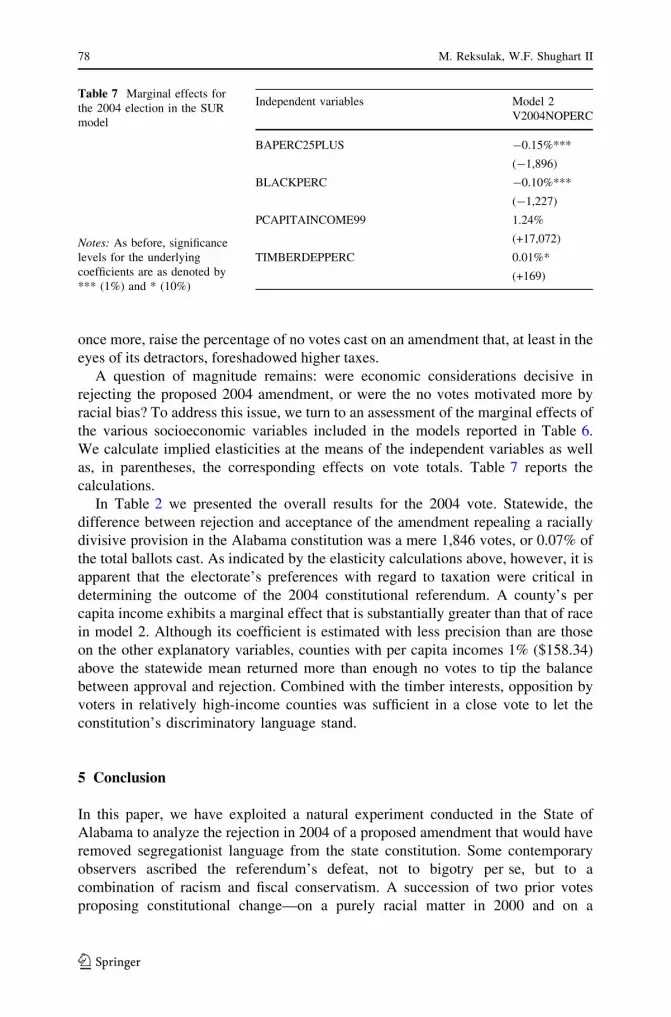

A question of magnitude remains: were economic considerations decisive in

rejecting the proposed 2004 amendment, or were the no votes motivated more by

racial bias? To address this issue, we turn to an assessment of the marginal effects of

the various socioeconomic variables included in the models reported in Table 6.

We calculate implied elasticities at the means of the independent variables as well

as, in parentheses, the corresponding effects on vote totals. Table 7 reports the

calculations.

In Table 2 we presented the overall results for the 2004 vote. Statewide, the

difference between rejection and acceptance of the amendment repealing a racially

divisive provision in the Alabama constitution was a mere 1,846 votes, or 0.07% of

the total ballots cast. As indicated by the elasticity calculations above, however, it is

apparent that the electorate’s preferences with regard to taxation were critical in

determining the outcome of the 2004 constitutional referendum. A county’s per

capita income exhibits a marginal effect that is substantially greater than that of race

in model 2. Although its coefficient is estimated with less precision than are those

on the other explanatory variables, counties with per capita incomes 1% ($158.34)

above the statewide mean returned more than enough no votes to tip the balance

between approval and rejection. Combined with the timber interests, opposition by

voters in relatively high-income counties was sufficient in a close vote to let the

constitution’s discriminatory language stand.

5 Conclusion

In this paper, we have exploited a natural experiment conducted in the State of

Alabama to analyze the rejection in 2004 of a proposed amendment that would have

removed segregationist language from the state constitution. Some contemporary

observers ascribed the referendum’s defeat, not to bigotry per se, but to a

combination of racism and fiscal conservatism. A succession of two prior votes

proposing constitutional change—on a purely racial matter in 2000 and on a

Table 7 Marginal effects for

the 2004 election in the SUR

model

Notes: As before, significance

levels for the underlying

coefficients are as denoted by

*** (1%) and * (10%)

Independent variables Model 2

V2004NOPERC

BAPERC25PLUS -0.15%***

(-1,896)

BLACKPERC -0.10%***

(-1,227)

PCAPITAINCOME99 1.24%

(+17,072)

TIMBERDEPPERC 0.01%*

(+169)

78 M. Reksulak, W.F. Shughart II

123

standalone tax matter in 2003—provided an opportunity to disentangle the influence

of these different factors in 2004.

A closer look at the 2000 decision illuminates the astonishing extent to which

racial bias is still prevalent in some areas of the state. After all, as Table 2

demonstrates, in 25 (or almost 40%) of Alabama’s 67 counties, popular majorities

then opposed repealing the state’s unenforceable constitutional ban on interracial

marriage. Our purpose here was to investigate whether such apparent racial

intolerance played a role in 2004. The evidence in this paper suggests that economic

considerations—specifically an aversion to higher taxes—were more important than

race in explaining why Alabama’s voters rejected Amendment 2.

The reasoning underlying this conclusion is as follows. Other things being the

same, the level of income per capita in a county is not a statistically significant

determinant of the fraction of votes cast against repealing a state constitutional

prohibition on interracial marriages in 2000. That same variable is positive and

significantly different from zero at the 1% level in 2003, when Alabama’s voters

decisively rejected a constitutional amendment to implement Governor Riley’s

‘‘Alabama Excellence Initiative Fund’’, a tax reform initiative intended to close a

looming state budget deficit. Other things being equal, the higher the average per

capita income in a given county, the greater the fraction of votes cast against the

Riley plan. What is more important, this same relationship holds in 2004, when

Alabama’s voters narrowly rejected an amendment that would have repealed

constitutional language providing for separate public schools for blacks and whites,

but at the same time also would have removed a provision denying a constitutional

right to education. The marginal effect of per capita income is weaker in 2004 than

in 2003, perhaps because some voters did not believe that creating a constitutional

right to education would have adverse fiscal consequences, or because the

amendment’s companion proposal to remove segregationist language from the

constitution clouded the issue. In any case, economic variables such as higher

income and timber dependency, raise the percentage of no votes cast on an

amendment that, at least in the eyes of its detractors, foreshadowed higher taxes.

There are two obvious lessons: When the objective is to sanitize a state

constitution of the remnants of Jim Crow, proponents of this course of action are put

on notice to carefully draft the remedy in such a way as to forestall arguments that

the change implies higher tax bills. Opponents of constitutional ethnic-cleansing

operations, on the other hand, now have a blueprint, grounded in the specter of tax

increases, for stopping similar amendments from succeeding. As demonstrated in

2000, Alabamians seem to be quite willing to purge their constitution of racist

provisions. They are also extremely hostile to higher taxes, as demonstrated in 2003.

Given the opportunity to vote on both issues simultaneously, fiscal conservatism

narrowly trumps racial conciliation.

Acknowledgements We benefited from comments on earlier drafts by Michael Belongia, Frank

Stephenson, and Lewis Smith. Seminar participants at the annual meeting of the Southern Economic

Association as well as at research seminars at the University of Mississippi and Georgia Southern

University also facilitated improvements to this paper. As is customary, however, the authors take full

responsibility for any and all errors.

Racism versus fiscal conservatism 79

123

References

Altman, M., & Klinkner, P. A. (2005). Is the ‘old racism’ really dead? Harvard-MIT Data Center and

Hamilton College, Working Paper.

Gujarati, D. N. (1995). Basic econometrics (3rd ed.). New York: McGraw-Hill.

Howze, G. R., Robinson, L. J., & Norton, J. F. (2003). Historical analysis of timber dependency in

Alabama. Southern Rural Sociology, 19(2), 1–39.

Jackson, H. H. III. (1994). Supremacy and the stolen vote: Bourbon democrats solidified power in 1901

with the highly suspect election approving a new constitution. The Mobile Register, 11 December.

Karahan, G. R., & Shughart, W. F. II. (2004). Under two flags: Symbolic voting in the state of

Mississippi. Public Choice, 118(1–2), 105–124.

Kennedy, P. (2004). A guide to econometrics (4th ed.). Cambridge: MIT Press.

Knigge, P., & Moody, B. (2003). The 2000 ‘anti-miscegenation’ vote in Alabama: Is the ‘old south’ really

that old? Auburn University, Working Paper.

McMillan, M. C. (1955). Constitutional development in Alabama, 1798–1901: A study in politics, thenegro, and sectionalism. Chapel Hill: University of North Carolina Press.

Ormond, B. A. (2004). State responses to budget crises in 2004: Alabama. Urban Institute, Working

Paper, February.

O’Neal, E. (1914). Educational reform and a new constitution. Montgomery: Brown Printing Co.

Thomson, H. B. (2003). The struggle in Alabama for constitutional reform. Jones Law Review,

http://www.accessmylibrary.com/coms2/summary_0286-12456701_ITM.

Webster, G. R., & Webster, R. H. (2004). Taxing issues: Geography, politics and the 2003 tax reform

referendum in Alabama. Southeastern Geographer, 44(2), 190–215.

Zellner, A. (1962). An efficient method of estimating seemingly unrelated regressions and tests of

aggregation bias. Journal of American Statistical Association 57(298), 348–368.

80 M. Reksulak, W.F. Shughart II

123