Embed Size (px)

Citation preview

©

Your success is our success

Emkay

Emkay Research is also available on www.emkayglobal.com, Bloomberg EMKAY<GO>, Reuters and DOWJONES. DBS Bank Ltd, DBS Vickers Securities (Singapore) Pte Ltd,its respective connected and associated corporations and affiliates are the distributors of the research reports, please refer to the last page of the report on Restrictions on Distribution. In Singapore, this research report or research analyses may only be distributed to Institutional Investors,Expert Investors or Accredited Investors as defined in the Securities and Futures Act, Chapter 289 of Singapore ED: ANISH MATHEW SA: DHANANJAY SINHA

India Equity Research | Oil & Gas

December 3, 2018

Initiating Coverage

Gulf Oil Lubricants India Refer to important disclosures at the end of this report

A Well-Oiled Growth Machine at a Compelling Valuation

CMP Target Price

Rs 738 Rs 1,150 as of (December 3, 2018) 12 months

Rating Upside

BUY 55.8 %

Change in Estimates

EPS Chg FY19E/FY20E (%) -/-

Target Price change (%) NA

Target Period (Months) 12

Previous Reco NA

Emkay vs Consensus

EPS Estimates

FY19E FY20E

Emkay 36.0 44.0

Consensus - -

Mean Consensus TP (12M) Rs 957

Stock Details

Bloomberg Code GOLI IN

Face Value (Rs) 2

Shares outstanding (mn) 50

52 Week H/L 1,100 / 618

M Cap (Rs bn/USD bn) 37 / 0.53

Daily Avg Volume (nos.) 34,656

Daily Avg Turnover (US$ mn) 0.4

Shareholding Pattern Sep '18

Promoters 72.7%

FIIs 8.0%

DIIs 5.9%

Public and Others 13.4%

Price Performance

(%) 1M 3M 6M 12M

Absolute 4 (10) (16) (28)

Rel. to Nifty (1) (3) (17) (32)

We initiate coverage on Gulf Oil Lubricants India (GOLI), with a Buy rating and a target

price of Rs1,150 (over 50% upside). We value GOLI at 22x FY21E EPS on the back of

18% EPS CAGR and 30%+ ROE during FY18-21.

GOLI recorded a robust 3-year volume CAGR of 12% despite major economy-wide

disruptions such as the demonetization and GST. In 1HFY19, core growth accelerated

further to 27% yoy, with all segments growing in double digits.

While 1HFY19 margins were impacted by rise in base oil prices, a weak rupee and higher

share of B2B-insti-OEM volumes, recent softening of base oil, steady rupee, proactive

pricing and overall premiumization, should aid margin recovery going forward.

Relative price chart

Source: Bloomberg This report is solely produced by Emkay Global. The following person(s) are responsible for the production of the recommendation:

Sabri Hazarika

+91-022-66121282

Ankur Chauhan

+91-022-66242491

-40

-30

-20

-10

0

10

700

780

860

940

1020

1100

Dec-17 Jan-18 Apr-18 May-18 Jul-18 Sep-18 Nov-18

%Rs

Gulf Oil Lubricant (LHS) Rel to Nifty (RHS)

Strong volume growth trajectory leading to market share gains: In the past three

years, GOLI’s volume CAGR stood at a strong 12%, in line with its target to do 2-3x industry

growth. This was despite major economy-wide disruptions such as the demonetization and

GST implementation. In 1HFY19, core volume growth accelerated to 27% yoy with all

segments, namely motorcycle (MCO), passenger car (PCMO), CV/diesel (CVO/DEO) and

industrial oils reporting double-digit growth, driven by a low base, OEM tie ups and

distribution expansion. In the Bazaar segment, GOLI’s market share is estimated to have

grown from under 7%, 2-3 years ago to almost 8% currently (~0.5% increase annually).

We expect the lube market to grow at 4-5% and see GOLI’s volume growth at

25%/15%/13% yoy for FY19/20/21, with FY20/21 run-rate likely having upside risks.

Margins likely to recover with proactive pricing, premiumization and softer base oil

prices: GOLI’s EBITDA/liter (margin) has grown at a 9% CAGR in the past five years until

FY18. FY17 was the only year in this period when margins were impacted due to de-

monetization playing the spoil sport. In FY18, there was 8%/13%/17% increase in net

realization/gross margin/EBITDA margin. FY19 is weaker on the margin front, with

EBITDA/liter in 1H down 7% yoy due to high oil/base oil prices, a weak rupee, and

increased share of low-margin B2B-insti-OEM sales that were driving volume growth. We,

however, expect margins to recover going forward due to softening of base oil prices, a

steady rupee, and the effect of price hikes (last taken in July). Against a 2% decline in

EBITDA/liter expected in FY19, we estimate a 3% growth each in FY20/21.

Initiating coverage with a Buy rating and a TP of Rs1,150: We estimate an EPS CAGR

of 18% during FY18-21 building in 18% volume and 2% EBITDA/liter CAGR assumptions.

We value GOLI at a conservative 22x FY21E EPS of Rs52 to arrive at our target price of

Rs1,150, providing over 50% upside. GOLI’s return ratios are likely to remain steady at

over 30%. We initiate coverage on the stock with a Buy rating. The key risks are acute

competitive pressure and adverse base oil price and currency movements.

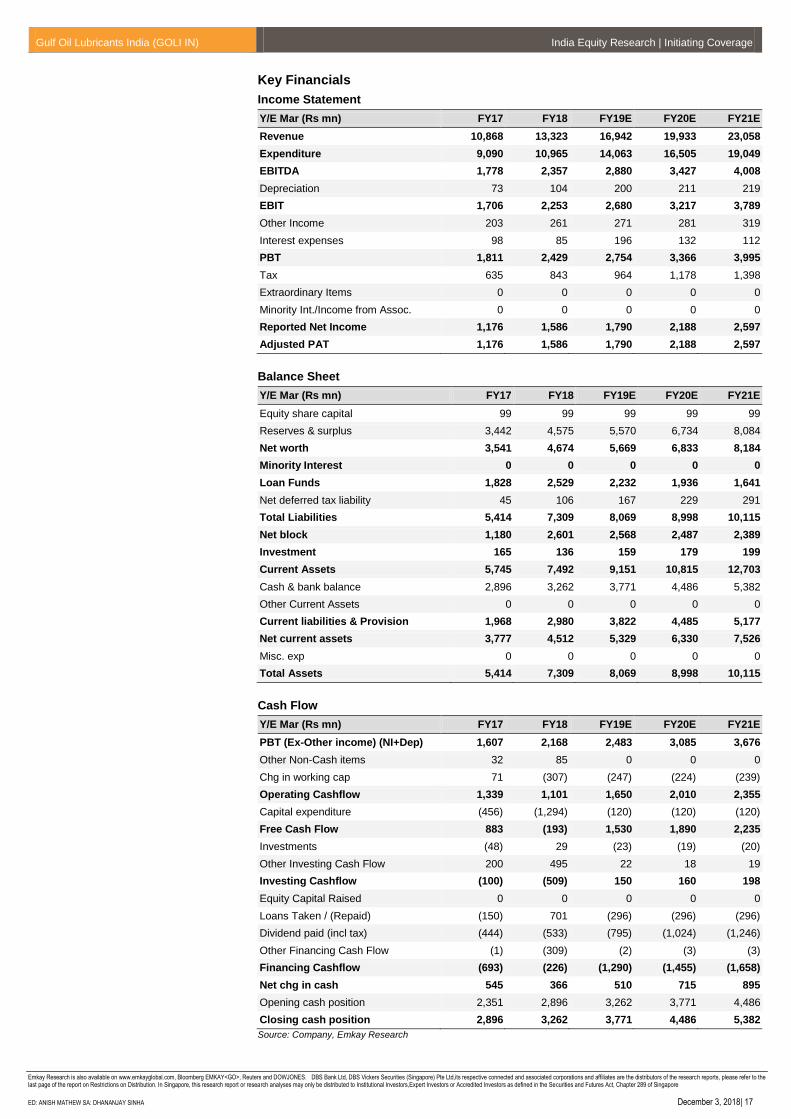

Financial Snapshot

(Rs mn) FY17 FY18 FY19E FY20E FY21E

Revenue 10,868 13,323 16,942 19,933 23,058

EBITDA 1,778 2,357 2,880 3,427 4,008

EBITDA Margin (%) 16.4 17.7 17.0 17.2 17.4

APAT 1,176 1,586 1,790 2,188 2,597

EPS (Rs) 23.7 31.9 36.0 44.0 52.3

EPS (% chg) 17.0 34.7 12.9 22.2 18.7

ROE (%) 39.0 38.6 34.6 35.0 34.6

P/E (x) 31.4 23.3 20.6 16.9 14.2

EV/EBITDA (x) 20.0 15.3 12.2 10.0 8.2

P/BV (x) 10.4 7.9 6.5 5.4 4.5

Source: Company, Emkay Research

Gulf Oil Lubricants India (GOLI IN) India Equity Research | Initiating Coverage

Emkay Research is also available on www.emkayglobal.com, Bloomberg EMKAY<GO>, Reuters and DOWJONES. DBS Bank Ltd, DBS Vickers Securities (Singapore) Pte Ltd,its respective connected and associated corporations and affiliates are the distributors of the research reports, please refer to the last page of the report on Restrictions on Distribution. In Singapore, this research report or research analyses may only be distributed to Institutional Investors,Expert Investors or Accredited Investors as defined in the Securities and Futures Act, Chapter 289 of Singapore

ED: ANISH MATHEW SA: DHANANJAY SINHA December 3, 2018 | 2

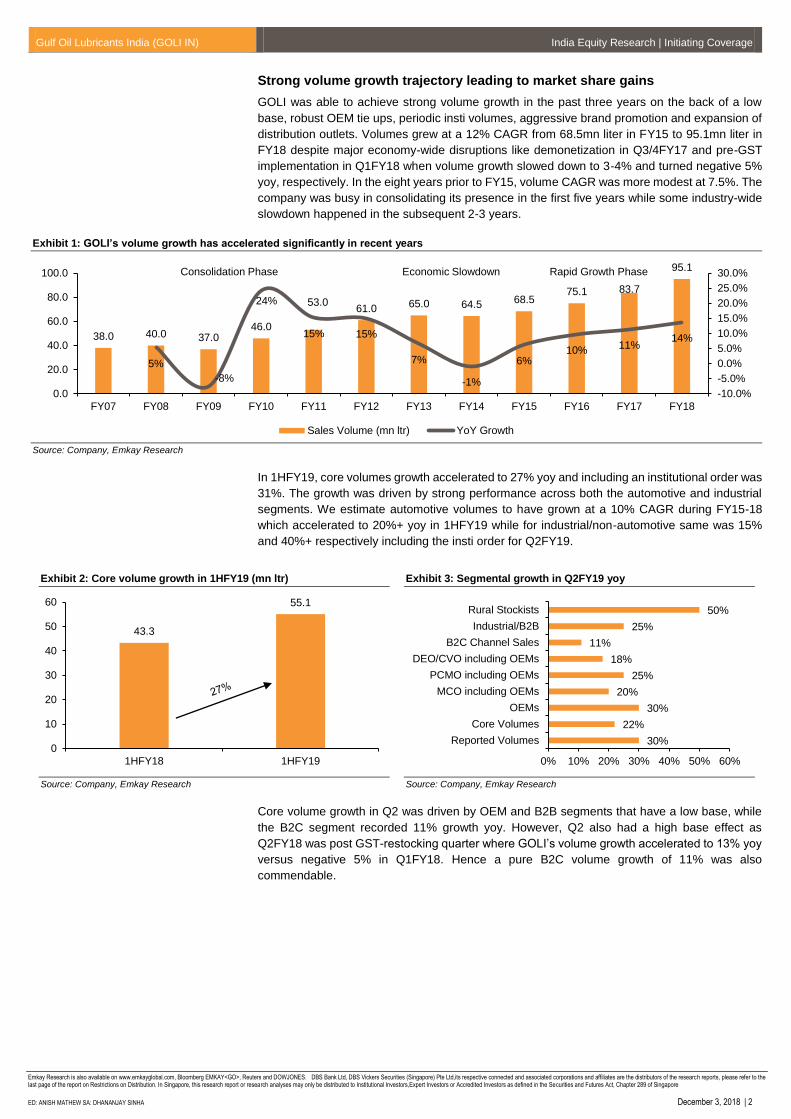

Strong volume growth trajectory leading to market share gains

GOLI was able to achieve strong volume growth in the past three years on the back of a low

base, robust OEM tie ups, periodic insti volumes, aggressive brand promotion and expansion of

distribution outlets. Volumes grew at a 12% CAGR from 68.5mn liter in FY15 to 95.1mn liter in

FY18 despite major economy-wide disruptions like demonetization in Q3/4FY17 and pre-GST

implementation in Q1FY18 when volume growth slowed down to 3-4% and turned negative 5%

yoy, respectively. In the eight years prior to FY15, volume CAGR was more modest at 7.5%. The

company was busy in consolidating its presence in the first five years while some industry-wide

slowdown happened in the subsequent 2-3 years.

Exhibit 1: GOLI’s volume growth has accelerated significantly in recent years

Source: Company, Emkay Research

In 1HFY19, core volumes growth accelerated to 27% yoy and including an institutional order was

31%. The growth was driven by strong performance across both the automotive and industrial

segments. We estimate automotive volumes to have grown at a 10% CAGR during FY15-18

which accelerated to 20%+ yoy in 1HFY19 while for industrial/non-automotive same was 15%

and 40%+ respectively including the insti order for Q2FY19.

Exhibit 2: Core volume growth in 1HFY19 (mn ltr)

Source: Company, Emkay Research

Exhibit 3: Segmental growth in Q2FY19 yoy

Source: Company, Emkay Research

Core volume growth in Q2 was driven by OEM and B2B segments that have a low base, while

the B2C segment recorded 11% growth yoy. However, Q2 also had a high base effect as

Q2FY18 was post GST-restocking quarter where GOLI’s volume growth accelerated to 13% yoy

versus negative 5% in Q1FY18. Hence a pure B2C volume growth of 11% was also

commendable.

38.0 40.0 37.046.0

53.061.0 65.0 64.5 68.5

75.1 83.7

95.1

5%

-8%

24%

15% 15%

7%

-1%

6%10%

11%14%

-10.0%

-5.0%

0.0%

5.0%

10.0%

15.0%

20.0%

25.0%

30.0%

0.0

20.0

40.0

60.0

80.0

100.0

FY07 FY08 FY09 FY10 FY11 FY12 FY13 FY14 FY15 FY16 FY17 FY18

Sales Volume (mn ltr) YoY Growth

Consolidation Phase Economic Slowdown Rapid Growth Phase

43.3

55.1

0

10

20

30

40

50

60

1HFY18 1HFY19

30%

22%

30%

20%

25%

18%

11%

25%

50%

0% 10% 20% 30% 40% 50% 60%

Reported Volumes

Core Volumes

OEMs

MCO including OEMs

PCMO including OEMs

DEO/CVO including OEMs

B2C Channel Sales

Industrial/B2B

Rural Stockists

Gulf Oil Lubricants India (GOLI IN) India Equity Research | Initiating Coverage

Emkay Research is also available on www.emkayglobal.com, Bloomberg EMKAY<GO>, Reuters and DOWJONES. DBS Bank Ltd, DBS Vickers Securities (Singapore) Pte Ltd,its respective connected and associated corporations and affiliates are the distributors of the research reports, please refer to the last page of the report on Restrictions on Distribution. In Singapore, this research report or research analyses may only be distributed to Institutional Investors,Expert Investors or Accredited Investors as defined in the Securities and Futures Act, Chapter 289 of Singapore

ED: ANISH MATHEW SA: DHANANJAY SINHA December 3, 2018 | 3

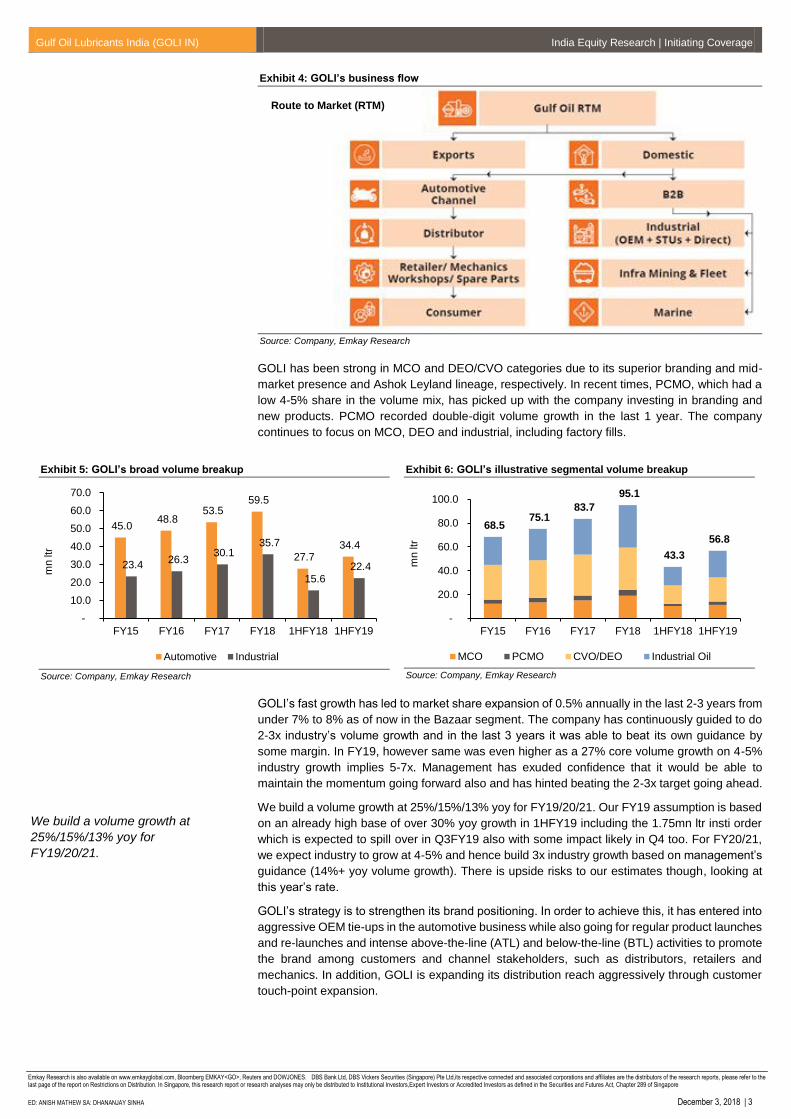

Exhibit 4: GOLI’s business flow

Source: Company, Emkay Research

GOLI has been strong in MCO and DEO/CVO categories due to its superior branding and mid-

market presence and Ashok Leyland lineage, respectively. In recent times, PCMO, which had a

low 4-5% share in the volume mix, has picked up with the company investing in branding and

new products. PCMO recorded double-digit volume growth in the last 1 year. The company

continues to focus on MCO, DEO and industrial, including factory fills.

Exhibit 5: GOLI’s broad volume breakup

Source: Company, Emkay Research

Exhibit 6: GOLI’s illustrative segmental volume breakup

Source: Company, Emkay Research

GOLI’s fast growth has led to market share expansion of 0.5% annually in the last 2-3 years from

under 7% to 8% as of now in the Bazaar segment. The company has continuously guided to do

2-3x industry’s volume growth and in the last 3 years it was able to beat its own guidance by

some margin. In FY19, however same was even higher as a 27% core volume growth on 4-5%

industry growth implies 5-7x. Management has exuded confidence that it would be able to

maintain the momentum going forward also and has hinted beating the 2-3x target going ahead.

We build a volume growth at 25%/15%/13% yoy for FY19/20/21. Our FY19 assumption is based

on an already high base of over 30% yoy growth in 1HFY19 including the 1.75mn ltr insti order

which is expected to spill over in Q3FY19 also with some impact likely in Q4 too. For FY20/21,

we expect industry to grow at 4-5% and hence build 3x industry growth based on management’s

guidance (14%+ yoy volume growth). There is upside risks to our estimates though, looking at

this year’s rate.

GOLI’s strategy is to strengthen its brand positioning. In order to achieve this, it has entered into

aggressive OEM tie-ups in the automotive business while also going for regular product launches

and re-launches and intense above-the-line (ATL) and below-the-line (BTL) activities to promote

the brand among customers and channel stakeholders, such as distributors, retailers and

mechanics. In addition, GOLI is expanding its distribution reach aggressively through customer

touch-point expansion.

45.0 48.8

53.5 59.5

27.7 34.4

23.4 26.3

30.1 35.7

15.6 22.4

-

10.0

20.0

30.0

40.0

50.0

60.0

70.0

FY15 FY16 FY17 FY18 1HFY18 1HFY19

mn ltr

Automotive Industrial

68.5 75.1

83.7

95.1

43.3

56.8

-

20.0

40.0

60.0

80.0

100.0

FY15 FY16 FY17 FY18 1HFY18 1HFY19

mn ltr

MCO PCMO CVO/DEO Industrial Oil

We build a volume growth at

25%/15%/13% yoy for

FY19/20/21.

Route to Market (RTM)

Gulf Oil Lubricants India (GOLI IN) India Equity Research | Initiating Coverage

Emkay Research is also available on www.emkayglobal.com, Bloomberg EMKAY<GO>, Reuters and DOWJONES. DBS Bank Ltd, DBS Vickers Securities (Singapore) Pte Ltd,its respective connected and associated corporations and affiliates are the distributors of the research reports, please refer to the last page of the report on Restrictions on Distribution. In Singapore, this research report or research analyses may only be distributed to Institutional Investors,Expert Investors or Accredited Investors as defined in the Securities and Futures Act, Chapter 289 of Singapore

ED: ANISH MATHEW SA: DHANANJAY SINHA December 3, 2018 | 4

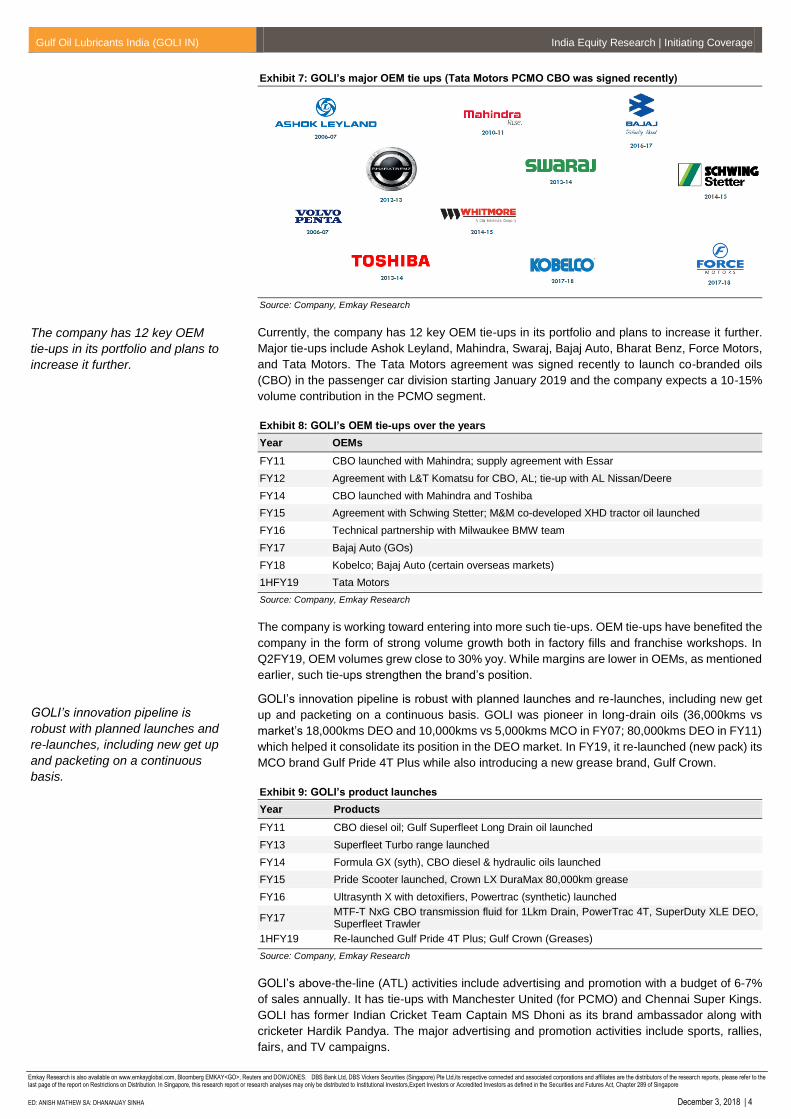

Exhibit 7: GOLI’s major OEM tie ups (Tata Motors PCMO CBO was signed recently)

Source: Company, Emkay Research

Currently, the company has 12 key OEM tie-ups in its portfolio and plans to increase it further.

Major tie-ups include Ashok Leyland, Mahindra, Swaraj, Bajaj Auto, Bharat Benz, Force Motors,

and Tata Motors. The Tata Motors agreement was signed recently to launch co-branded oils

(CBO) in the passenger car division starting January 2019 and the company expects a 10-15%

volume contribution in the PCMO segment.

Exhibit 8: GOLI’s OEM tie-ups over the years

Year OEMs

FY11 CBO launched with Mahindra; supply agreement with Essar

FY12 Agreement with L&T Komatsu for CBO, AL; tie-up with AL Nissan/Deere

FY14 CBO launched with Mahindra and Toshiba

FY15 Agreement with Schwing Stetter; M&M co-developed XHD tractor oil launched

FY16 Technical partnership with Milwaukee BMW team

FY17 Bajaj Auto (GOs)

FY18 Kobelco; Bajaj Auto (certain overseas markets)

1HFY19 Tata Motors

Source: Company, Emkay Research

The company is working toward entering into more such tie-ups. OEM tie-ups have benefited the

company in the form of strong volume growth both in factory fills and franchise workshops. In

Q2FY19, OEM volumes grew close to 30% yoy. While margins are lower in OEMs, as mentioned

earlier, such tie-ups strengthen the brand’s position.

GOLI’s innovation pipeline is robust with planned launches and re-launches, including new get

up and packeting on a continuous basis. GOLI was pioneer in long-drain oils (36,000kms vs

market’s 18,000kms DEO and 10,000kms vs 5,000kms MCO in FY07; 80,000kms DEO in FY11)

which helped it consolidate its position in the DEO market. In FY19, it re-launched (new pack) its

MCO brand Gulf Pride 4T Plus while also introducing a new grease brand, Gulf Crown.

Exhibit 9: GOLI’s product launches

Year Products

FY11 CBO diesel oil; Gulf Superfleet Long Drain oil launched

FY13 Superfleet Turbo range launched

FY14 Formula GX (syth), CBO diesel & hydraulic oils launched

FY15 Pride Scooter launched, Crown LX DuraMax 80,000km grease

FY16 Ultrasynth X with detoxifiers, Powertrac (synthetic) launched

FY17 MTF-T NxG CBO transmission fluid for 1Lkm Drain, PowerTrac 4T, SuperDuty XLE DEO, Superfleet Trawler

1HFY19 Re-launched Gulf Pride 4T Plus; Gulf Crown (Greases)

Source: Company, Emkay Research

GOLI’s above-the-line (ATL) activities include advertising and promotion with a budget of 6-7%

of sales annually. It has tie-ups with Manchester United (for PCMO) and Chennai Super Kings.

GOLI has former Indian Cricket Team Captain MS Dhoni as its brand ambassador along with

cricketer Hardik Pandya. The major advertising and promotion activities include sports, rallies,

fairs, and TV campaigns.

The company has 12 key OEM

tie-ups in its portfolio and plans to

increase it further.

GOLI’s innovation pipeline is

robust with planned launches and

re-launches, including new get up

and packeting on a continuous

basis.

Gulf Oil Lubricants India (GOLI IN) India Equity Research | Initiating Coverage

Emkay Research is also available on www.emkayglobal.com, Bloomberg EMKAY<GO>, Reuters and DOWJONES. DBS Bank Ltd, DBS Vickers Securities (Singapore) Pte Ltd,its respective connected and associated corporations and affiliates are the distributors of the research reports, please refer to the last page of the report on Restrictions on Distribution. In Singapore, this research report or research analyses may only be distributed to Institutional Investors,Expert Investors or Accredited Investors as defined in the Securities and Futures Act, Chapter 289 of Singapore

ED: ANISH MATHEW SA: DHANANJAY SINHA December 3, 2018 | 5

Exhibit 10: GOLI’s marketing, branding and promotional activities

Source: Company, Emkay Research

Exhibit 11: Advertisement & Promotion and Selling & Marketing Expenses

Rs mn FY15 FY16 FY17 FY18

A&P 556 672 701 873

Sales % 5.8% 6.7% 6.5% 6.6%

Rs mn FY15 FY16 FY17 FY18

S&M 605 730 542 906

Sales % 6.3% 7.2% 5.0% 6.8%

Source: Company, Emkay Research

Exhibit 12: GOLI’s promotional activities over the years

Year Promotions

FY11 Brand promotions in airports; Pride 4T Plus promotions; Kisan Mela in Maharashtra; Motorsports & MRF event

FY12 MS Dhoni endorses Gulf; Shop branding; Signages; Motorsports; Customer events; Cricket (IPL/CSK); Below the line activities

FY13 Aston Martin team promotion; MS Dhoni based promotions; Motorsports (rallies); Cricket; Posters; Fairs; Promotion of long drain CBOs

FY14 Cricket (IPL) related promotions; Bike rally; Bollywood related promotions; Industrial fairs

FY15 Aston Martin team promotion; Cricket (incl. IPL/CSK), bike fest, car & bike racing; MS Dhoni is brand ambassador; Advertising (TV, social

media, outdoor campaigns)

FY16 MS Dhoni key brand ambassador; Associations with cricket (Pune IPL team), football (ManU); 2W, car rally; Social media campaigns; OEM

oils promotion; Attendance in Industrial fairs

FY17 LeMans Endurance Race 2017, Gulf Monsoon Scooter Rally (GMSR), IPL 360deg campaign (Pune team), ManU promotions, Vento Cup 2016

FY18 World Superbike; Pressure moves you campaign with ManU; GMSR - Bhopal; Gulf Fan Academy

1HFY19 IPL; Idhu Namma Pride; TV campaign with MS Dhoni

Source: Company, Emkay Research

The lubricant market, particularly in the replacement category, is impacted by channel

stakeholders such as distributors, retailers and mechanics who are major influencers in purchase

decisions of the end customer. The replacement market is the key to B2C and has the highest

margins. GOLI has engaged actively with incentivizing distributors, retailers and mechanics

through awards, shop makeover, training programs, attractive commissions etc., leading to a

favorable view of its products among these parties.

Exhibit 13: GOLI’s BTL activities

Year Retailers & Mechanics

FY12 Awarding distributors

FY13 Non-Stop Express launched to deepen distribution; Pilots for rural penetration

FY15 Gulf Rural Stockist program launched for MCO and TO

FY16 Select garages for Gulf Carstops; Industrial customer offsites

FY17 Bike & Carstop initiatives, Unnati Retailer Loyalty Program

FY18 BTL campaigns for Truckers

1HFY19 Gulf Master Mechanic

Source: Company, Emkay Research

Gulf Oil Lubricants India (GOLI IN) India Equity Research | Initiating Coverage

Emkay Research is also available on www.emkayglobal.com, Bloomberg EMKAY<GO>, Reuters and DOWJONES. DBS Bank Ltd, DBS Vickers Securities (Singapore) Pte Ltd,its respective connected and associated corporations and affiliates are the distributors of the research reports, please refer to the last page of the report on Restrictions on Distribution. In Singapore, this research report or research analyses may only be distributed to Institutional Investors,Expert Investors or Accredited Investors as defined in the Securities and Futures Act, Chapter 289 of Singapore

ED: ANISH MATHEW SA: DHANANJAY SINHA December 3, 2018 | 6

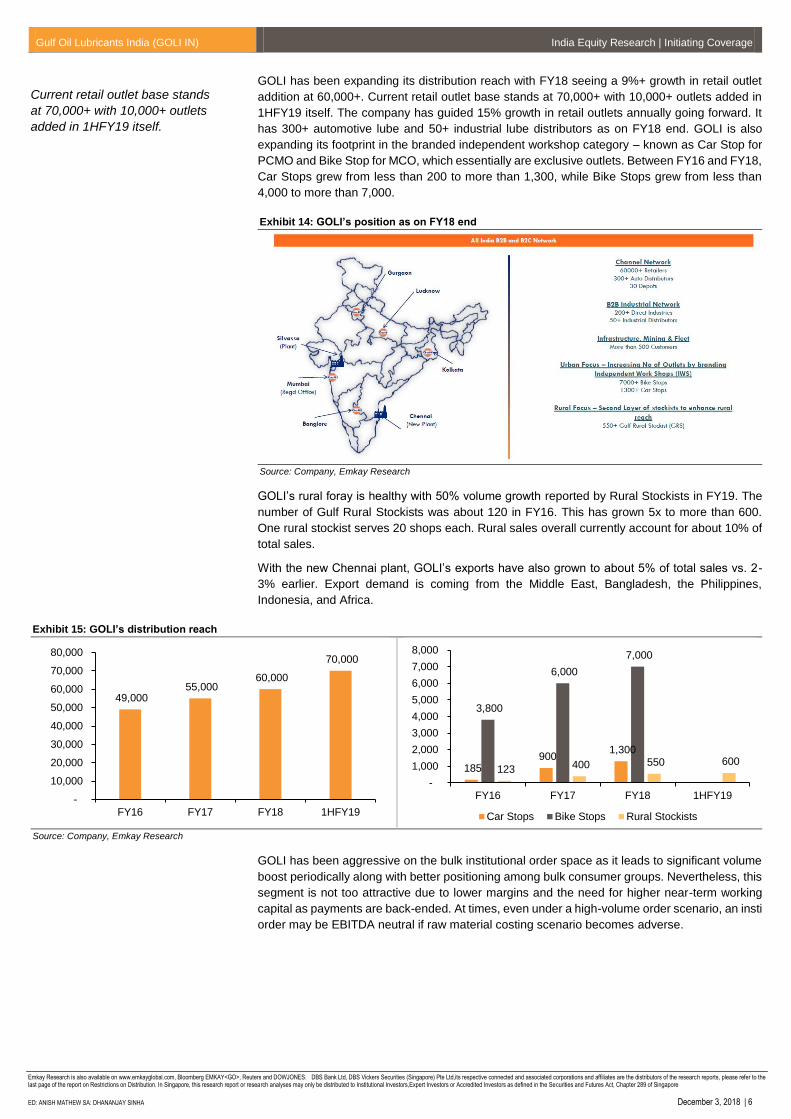

GOLI has been expanding its distribution reach with FY18 seeing a 9%+ growth in retail outlet

addition at 60,000+. Current retail outlet base stands at 70,000+ with 10,000+ outlets added in

1HFY19 itself. The company has guided 15% growth in retail outlets annually going forward. It

has 300+ automotive lube and 50+ industrial lube distributors as on FY18 end. GOLI is also

expanding its footprint in the branded independent workshop category – known as Car Stop for

PCMO and Bike Stop for MCO, which essentially are exclusive outlets. Between FY16 and FY18,

Car Stops grew from less than 200 to more than 1,300, while Bike Stops grew from less than

4,000 to more than 7,000.

Exhibit 14: GOLI’s position as on FY18 end

Source: Company, Emkay Research

GOLI’s rural foray is healthy with 50% volume growth reported by Rural Stockists in FY19. The

number of Gulf Rural Stockists was about 120 in FY16. This has grown 5x to more than 600.

One rural stockist serves 20 shops each. Rural sales overall currently account for about 10% of

total sales.

With the new Chennai plant, GOLI’s exports have also grown to about 5% of total sales vs. 2-

3% earlier. Export demand is coming from the Middle East, Bangladesh, the Philippines,

Indonesia, and Africa.

Exhibit 15: GOLI’s distribution reach

Source: Company, Emkay Research

GOLI has been aggressive on the bulk institutional order space as it leads to significant volume

boost periodically along with better positioning among bulk consumer groups. Nevertheless, this

segment is not too attractive due to lower margins and the need for higher near-term working

capital as payments are back-ended. At times, even under a high-volume order scenario, an insti

order may be EBITDA neutral if raw material costing scenario becomes adverse.

49,000 55,000

60,000

70,000

-

10,000

20,000

30,000

40,000

50,000

60,000

70,000

80,000

FY16 FY17 FY18 1HFY19

185 900

1,300

3,800

6,000

7,000

123 400 550 600

-

1,000

2,000

3,000

4,000

5,000

6,000

7,000

8,000

FY16 FY17 FY18 1HFY19

Car Stops Bike Stops Rural Stockists

Current retail outlet base stands

at 70,000+ with 10,000+ outlets

added in 1HFY19 itself.

Gulf Oil Lubricants India (GOLI IN) India Equity Research | Initiating Coverage

Emkay Research is also available on www.emkayglobal.com, Bloomberg EMKAY<GO>, Reuters and DOWJONES. DBS Bank Ltd, DBS Vickers Securities (Singapore) Pte Ltd,its respective connected and associated corporations and affiliates are the distributors of the research reports, please refer to the last page of the report on Restrictions on Distribution. In Singapore, this research report or research analyses may only be distributed to Institutional Investors,Expert Investors or Accredited Investors as defined in the Securities and Futures Act, Chapter 289 of Singapore

ED: ANISH MATHEW SA: DHANANJAY SINHA December 3, 2018 | 7

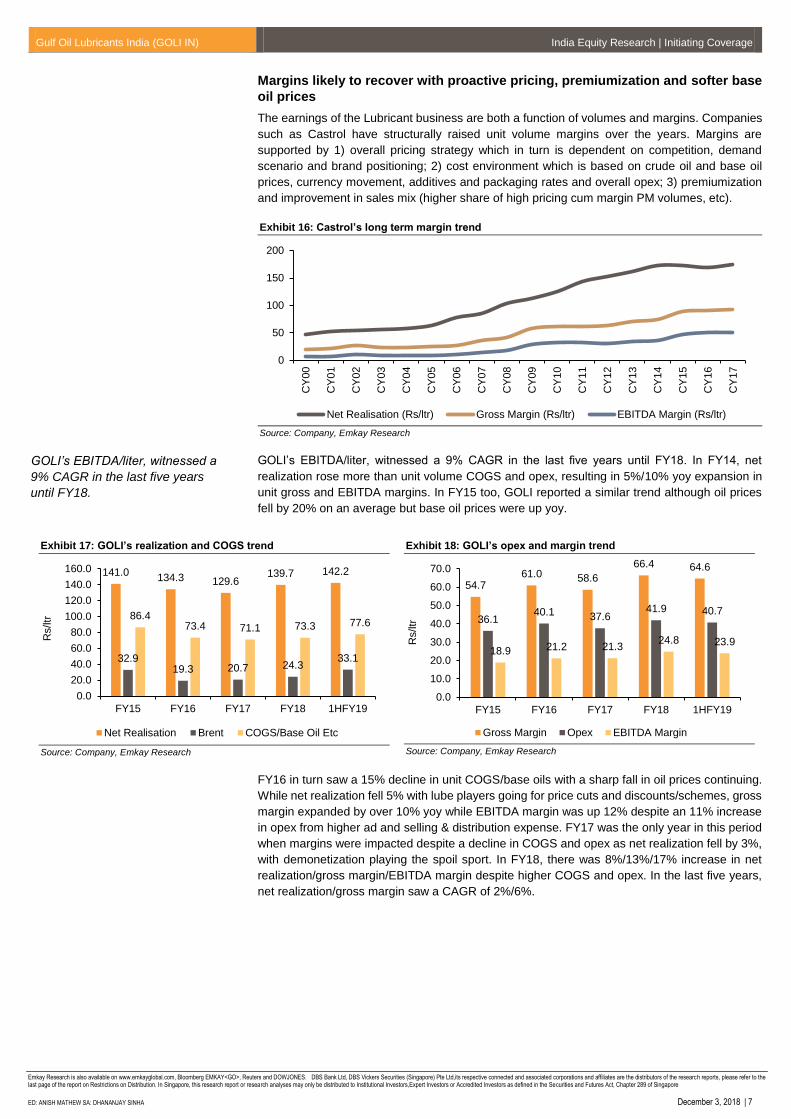

Margins likely to recover with proactive pricing, premiumization and softer base

oil prices

The earnings of the Lubricant business are both a function of volumes and margins. Companies

such as Castrol have structurally raised unit volume margins over the years. Margins are

supported by 1) overall pricing strategy which in turn is dependent on competition, demand

scenario and brand positioning; 2) cost environment which is based on crude oil and base oil

prices, currency movement, additives and packaging rates and overall opex; 3) premiumization

and improvement in sales mix (higher share of high pricing cum margin PM volumes, etc).

Exhibit 16: Castrol’s long term margin trend

Source: Company, Emkay Research

GOLI’s EBITDA/liter, witnessed a 9% CAGR in the last five years until FY18. In FY14, net

realization rose more than unit volume COGS and opex, resulting in 5%/10% yoy expansion in

unit gross and EBITDA margins. In FY15 too, GOLI reported a similar trend although oil prices

fell by 20% on an average but base oil prices were up yoy.

Exhibit 17: GOLI’s realization and COGS trend

Source: Company, Emkay Research

Exhibit 18: GOLI’s opex and margin trend

Source: Company, Emkay Research

FY16 in turn saw a 15% decline in unit COGS/base oils with a sharp fall in oil prices continuing.

While net realization fell 5% with lube players going for price cuts and discounts/schemes, gross

margin expanded by over 10% yoy while EBITDA margin was up 12% despite an 11% increase

in opex from higher ad and selling & distribution expense. FY17 was the only year in this period

when margins were impacted despite a decline in COGS and opex as net realization fell by 3%,

with demonetization playing the spoil sport. In FY18, there was 8%/13%/17% increase in net

realization/gross margin/EBITDA margin despite higher COGS and opex. In the last five years,

net realization/gross margin saw a CAGR of 2%/6%.

0

50

100

150

200

CY

00

CY

01

CY

02

CY

03

CY

04

CY

05

CY

06

CY

07

CY

08

CY

09

CY

10

CY

11

CY

12

CY

13

CY

14

CY

15

CY

16

CY

17

Net Realisation (Rs/ltr) Gross Margin (Rs/ltr) EBITDA Margin (Rs/ltr)

141.0134.3 129.6

139.7 142.2

32.919.3 20.7 24.3

33.1

86.473.4 71.1 73.3 77.6

0.0

20.0

40.0

60.0

80.0

100.0

120.0

140.0

160.0

FY15 FY16 FY17 FY18 1HFY19

Rs/ltr

Net Realisation Brent COGS/Base Oil Etc

54.761.0 58.6

66.4 64.6

36.140.1 37.6

41.9 40.7

18.9 21.2 21.324.8 23.9

0.0

10.0

20.0

30.0

40.0

50.0

60.0

70.0

FY15 FY16 FY17 FY18 1HFY19

Rs/ltr

Gross Margin Opex EBITDA Margin

GOLI’s EBITDA/liter, witnessed a

9% CAGR in the last five years

until FY18.

Gulf Oil Lubricants India (GOLI IN) India Equity Research | Initiating Coverage

Emkay Research is also available on www.emkayglobal.com, Bloomberg EMKAY<GO>, Reuters and DOWJONES. DBS Bank Ltd, DBS Vickers Securities (Singapore) Pte Ltd,its respective connected and associated corporations and affiliates are the distributors of the research reports, please refer to the last page of the report on Restrictions on Distribution. In Singapore, this research report or research analyses may only be distributed to Institutional Investors,Expert Investors or Accredited Investors as defined in the Securities and Futures Act, Chapter 289 of Singapore

ED: ANISH MATHEW SA: DHANANJAY SINHA December 3, 2018 | 8

Exhibit 19: Base oil pricing trend & outlook

Source: Company, Emkay Research

Exhibit 20: Oil price and currency trend and current run-rate

Source: Bloomberg, Emkay Research

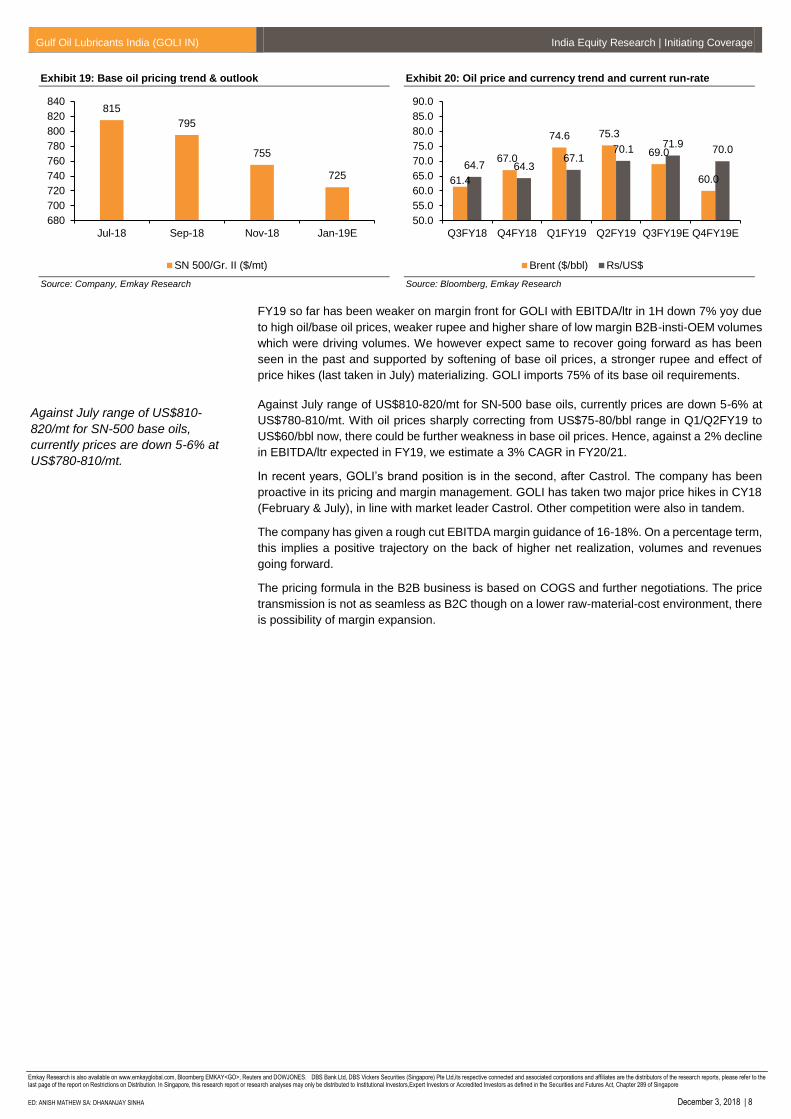

FY19 so far has been weaker on margin front for GOLI with EBITDA/ltr in 1H down 7% yoy due

to high oil/base oil prices, weaker rupee and higher share of low margin B2B-insti-OEM volumes

which were driving volumes. We however expect same to recover going forward as has been

seen in the past and supported by softening of base oil prices, a stronger rupee and effect of

price hikes (last taken in July) materializing. GOLI imports 75% of its base oil requirements.

Against July range of US$810-820/mt for SN-500 base oils, currently prices are down 5-6% at

US$780-810/mt. With oil prices sharply correcting from US$75-80/bbl range in Q1/Q2FY19 to

US$60/bbl now, there could be further weakness in base oil prices. Hence, against a 2% decline

in EBITDA/ltr expected in FY19, we estimate a 3% CAGR in FY20/21.

In recent years, GOLI’s brand position is in the second, after Castrol. The company has been

proactive in its pricing and margin management. GOLI has taken two major price hikes in CY18

(February & July), in line with market leader Castrol. Other competition were also in tandem.

The company has given a rough cut EBITDA margin guidance of 16-18%. On a percentage term,

this implies a positive trajectory on the back of higher net realization, volumes and revenues

going forward.

The pricing formula in the B2B business is based on COGS and further negotiations. The price

transmission is not as seamless as B2C though on a lower raw-material-cost environment, there

is possibility of margin expansion.

815

795

755

725

680

700

720

740

760

780

800

820

840

Jul-18 Sep-18 Nov-18 Jan-19E

SN 500/Gr. II ($/mt)

61.4

67.0

74.6 75.3

69.0

60.0

64.7 64.367.1

70.171.9

70.0

50.0

55.0

60.0

65.0

70.0

75.0

80.0

85.0

90.0

Q3FY18 Q4FY18 Q1FY19 Q2FY19 Q3FY19E Q4FY19E

Brent ($/bbl) Rs/US$

Against July range of US$810-

820/mt for SN-500 base oils,

currently prices are down 5-6% at

US$780-810/mt.

Gulf Oil Lubricants India (GOLI IN) India Equity Research | Initiating Coverage

Emkay Research is also available on www.emkayglobal.com, Bloomberg EMKAY<GO>, Reuters and DOWJONES. DBS Bank Ltd, DBS Vickers Securities (Singapore) Pte Ltd,its respective connected and associated corporations and affiliates are the distributors of the research reports, please refer to the last page of the report on Restrictions on Distribution. In Singapore, this research report or research analyses may only be distributed to Institutional Investors,Expert Investors or Accredited Investors as defined in the Securities and Futures Act, Chapter 289 of Singapore

ED: ANISH MATHEW SA: DHANANJAY SINHA December 3, 2018 | 9

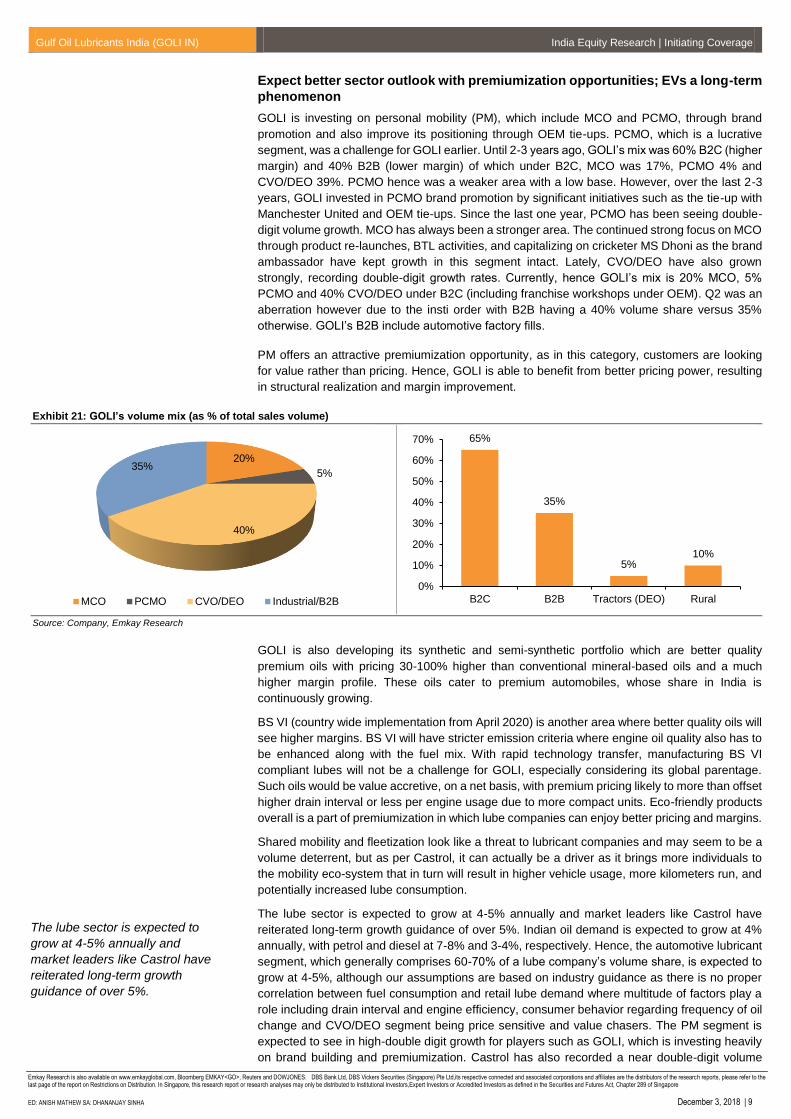

Expect better sector outlook with premiumization opportunities; EVs a long-term

phenomenon

GOLI is investing on personal mobility (PM), which include MCO and PCMO, through brand

promotion and also improve its positioning through OEM tie-ups. PCMO, which is a lucrative

segment, was a challenge for GOLI earlier. Until 2-3 years ago, GOLI’s mix was 60% B2C (higher

margin) and 40% B2B (lower margin) of which under B2C, MCO was 17%, PCMO 4% and

CVO/DEO 39%. PCMO hence was a weaker area with a low base. However, over the last 2-3

years, GOLI invested in PCMO brand promotion by significant initiatives such as the tie-up with

Manchester United and OEM tie-ups. Since the last one year, PCMO has been seeing double-

digit volume growth. MCO has always been a stronger area. The continued strong focus on MCO

through product re-launches, BTL activities, and capitalizing on cricketer MS Dhoni as the brand

ambassador have kept growth in this segment intact. Lately, CVO/DEO have also grown

strongly, recording double-digit growth rates. Currently, hence GOLI’s mix is 20% MCO, 5%

PCMO and 40% CVO/DEO under B2C (including franchise workshops under OEM). Q2 was an

aberration however due to the insti order with B2B having a 40% volume share versus 35%

otherwise. GOLI’s B2B include automotive factory fills.

PM offers an attractive premiumization opportunity, as in this category, customers are looking

for value rather than pricing. Hence, GOLI is able to benefit from better pricing power, resulting

in structural realization and margin improvement.

Exhibit 21: GOLI’s volume mix (as % of total sales volume)

Source: Company, Emkay Research

GOLI is also developing its synthetic and semi-synthetic portfolio which are better quality

premium oils with pricing 30-100% higher than conventional mineral-based oils and a much

higher margin profile. These oils cater to premium automobiles, whose share in India is

continuously growing.

BS VI (country wide implementation from April 2020) is another area where better quality oils will

see higher margins. BS VI will have stricter emission criteria where engine oil quality also has to

be enhanced along with the fuel mix. With rapid technology transfer, manufacturing BS VI

compliant lubes will not be a challenge for GOLI, especially considering its global parentage.

Such oils would be value accretive, on a net basis, with premium pricing likely to more than offset

higher drain interval or less per engine usage due to more compact units. Eco-friendly products

overall is a part of premiumization in which lube companies can enjoy better pricing and margins.

Shared mobility and fleetization look like a threat to lubricant companies and may seem to be a

volume deterrent, but as per Castrol, it can actually be a driver as it brings more individuals to

the mobility eco-system that in turn will result in higher vehicle usage, more kilometers run, and

potentially increased lube consumption.

The lube sector is expected to grow at 4-5% annually and market leaders like Castrol have

reiterated long-term growth guidance of over 5%. Indian oil demand is expected to grow at 4%

annually, with petrol and diesel at 7-8% and 3-4%, respectively. Hence, the automotive lubricant

segment, which generally comprises 60-70% of a lube company’s volume share, is expected to

grow at 4-5%, although our assumptions are based on industry guidance as there is no proper

correlation between fuel consumption and retail lube demand where multitude of factors play a

role including drain interval and engine efficiency, consumer behavior regarding frequency of oil

change and CVO/DEO segment being price sensitive and value chasers. The PM segment is

expected to see in high-double digit growth for players such as GOLI, which is investing heavily

on brand building and premiumization. Castrol has also recorded a near double-digit volume

20%

5%

40%

35%

MCO PCMO CVO/DEO Industrial/B2B

65%

35%

5%10%

0%

10%

20%

30%

40%

50%

60%

70%

B2C B2B Tractors (DEO) Rural

The lube sector is expected to

grow at 4-5% annually and

market leaders like Castrol have

reiterated long-term growth

guidance of over 5%.

Gulf Oil Lubricants India (GOLI IN) India Equity Research | Initiating Coverage

Emkay Research is also available on www.emkayglobal.com, Bloomberg EMKAY<GO>, Reuters and DOWJONES. DBS Bank Ltd, DBS Vickers Securities (Singapore) Pte Ltd,its respective connected and associated corporations and affiliates are the distributors of the research reports, please refer to the last page of the report on Restrictions on Distribution. In Singapore, this research report or research analyses may only be distributed to Institutional Investors,Expert Investors or Accredited Investors as defined in the Securities and Futures Act, Chapter 289 of Singapore

ED: ANISH MATHEW SA: DHANANJAY SINHA December 3, 2018| 10

growth in this segment despite being the market leader and hence commanding a bigger share.

The CVO/DEO segment is expected to grow at 3-4% industry-wide though for GOLI same would

be higher and closer to double digit due to a low base and growing OEM profile. The industrial

lubricant sector’s growth is dependent on overall economic activities including manufacturing,

infrastructure, mining, and marine. Being a B2B business, margins are lower in the CVO/DEO

segment compared with the B2C automotive business. However, due to its low base and rapid

expansion, GOLI has been able to record high-double digit growth in this space as well. Hence,

we believe that compared with the industry’s volume growth of 4-5%, GOLI can do a steady-

state volume growth of 13-15% which we are building in FY20/21.

Exhibit 22: Castrol’s outlook on EVs

Source: Castrol, Emkay Research

Globally, EVs are perceived as a threat to the oil industry in general and lubricant sector in

particular. Due to the rising clamor toward electric and hybrid vehicles, long-term growth outlook

of the lube sector has faced concerns, which is cited as a reason for multiple de-rating. Going

forward, lube companies have highlighted the focus on advanced mobility solutions and an

exposure to the EV ecosystem. GOLI already has a minor battery business where it imports and

sells two-wheeler batteries although it plans to expand this business. The company sees a

demand-supply mismatch in quality battery segment and expects robust growth in this segment.

Exhibit 23: GOLI’s battery branded Gulf Pride

Source: Industry, Emkay Research

Nevertheless in a country like India EVs is a longer-term phenomenon as the vehicle penetration

itself is very low compared with global developed country standards, and consumer preference

is for high-fuel efficiency petrol and diesel cars (where filling time is low). Even CNG, which is

much cheaper and is pushed by the government, is yet to make an important mark outside a few

key areas such as Delhi and Mumbai. The EV eco-system will need significant investments and

will be back-ended and the affordability of the higher-priced EVs is also a question.

Compared with the industry’s

volume growth of 4-5%, GOLI can

do a steady-state volume growth

of 13-15% which we are building

in FY20/21

In a country like India EVs is a

longer-term phenomenon as the

vehicle penetration itself is very

low compared with global

developed country standards

Gulf Oil Lubricants India (GOLI IN) India Equity Research | Initiating Coverage

Emkay Research is also available on www.emkayglobal.com, Bloomberg EMKAY<GO>, Reuters and DOWJONES. DBS Bank Ltd, DBS Vickers Securities (Singapore) Pte Ltd,its respective connected and associated corporations and affiliates are the distributors of the research reports, please refer to the last page of the report on Restrictions on Distribution. In Singapore, this research report or research analyses may only be distributed to Institutional Investors,Expert Investors or Accredited Investors as defined in the Securities and Futures Act, Chapter 289 of Singapore

ED: ANISH MATHEW SA: DHANANJAY SINHA December 3, 2018| 11

According to Castrol, EVs could possibly take more than 20 years to even have a 20% share of

the total vehicle sales in India under an evolving scenario in which the conventional vehicle

universe will continue to expand. Based on Castrol’s estimates, against a ~30mn vehicle

population currently (cars) with negligible non-ICE vehicles (EVs, CNG, etc), under an evolving

scenario, the Internal Combustion Engine (ICE) vehicle universe should grow to 230-240mn by

CY40, while the EV population would not be more than 10mn. Only if ICE is altogether banned

(which is highly unlikely) can EVs attain a major mass of the ~150mn vehicles under the given

scenario. Castrol also expects vehicle population to grow by 50% in the next five years to

300mn+ including 2W which would aid lube consumption.

GOLI believes, if at all, EVs would not impact the DEO and industrial oils category being limited

to only PM even under an optimistic case. For a lube player DEO and industrial comprises almost

60% of volume share which would keep growing at 2-3x on an industry level over the longer

term. Hence overall industry growth would remain at 1.5-2% even beyond CY35-40. GOLI

expects to better this at 2-3% long term volume CAGR. We therefore find EV-led concerns

overdone for the lubricant sector and expect the sector to continue in its growth trajectory.

According to Castrol, EVs could

possibly take more than 20 years

to even have a 20% share of the

total vehicle sales in India under

an evolving scenario

Gulf Oil Lubricants India (GOLI IN) India Equity Research | Initiating Coverage

Emkay Research is also available on www.emkayglobal.com, Bloomberg EMKAY<GO>, Reuters and DOWJONES. DBS Bank Ltd, DBS Vickers Securities (Singapore) Pte Ltd,its respective connected and associated corporations and affiliates are the distributors of the research reports, please refer to the last page of the report on Restrictions on Distribution. In Singapore, this research report or research analyses may only be distributed to Institutional Investors,Expert Investors or Accredited Investors as defined in the Securities and Futures Act, Chapter 289 of Singapore

ED: ANISH MATHEW SA: DHANANJAY SINHA December 3, 2018| 12

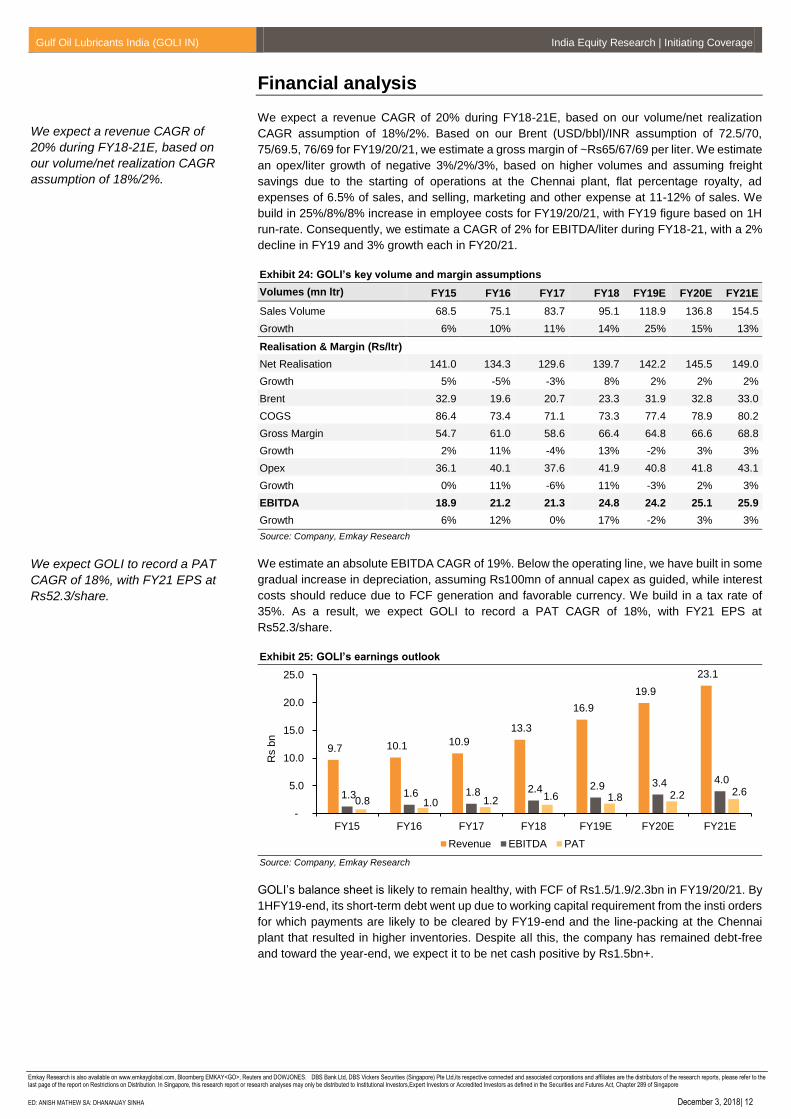

Financial analysis

We expect a revenue CAGR of 20% during FY18-21E, based on our volume/net realization

CAGR assumption of 18%/2%. Based on our Brent (USD/bbl)/INR assumption of 72.5/70,

75/69.5, 76/69 for FY19/20/21, we estimate a gross margin of ~Rs65/67/69 per liter. We estimate

an opex/liter growth of negative 3%/2%/3%, based on higher volumes and assuming freight

savings due to the starting of operations at the Chennai plant, flat percentage royalty, ad

expenses of 6.5% of sales, and selling, marketing and other expense at 11-12% of sales. We

build in 25%/8%/8% increase in employee costs for FY19/20/21, with FY19 figure based on 1H

run-rate. Consequently, we estimate a CAGR of 2% for EBITDA/liter during FY18-21, with a 2%

decline in FY19 and 3% growth each in FY20/21.

Exhibit 24: GOLI’s key volume and margin assumptions

Volumes (mn ltr) FY15 FY16 FY17 FY18 FY19E FY20E FY21E

Sales Volume 68.5 75.1 83.7 95.1 118.9 136.8 154.5

Growth 6% 10% 11% 14% 25% 15% 13%

Realisation & Margin (Rs/ltr)

Net Realisation 141.0 134.3 129.6 139.7 142.2 145.5 149.0

Growth 5% -5% -3% 8% 2% 2% 2%

Brent 32.9 19.6 20.7 23.3 31.9 32.8 33.0

COGS 86.4 73.4 71.1 73.3 77.4 78.9 80.2

Gross Margin 54.7 61.0 58.6 66.4 64.8 66.6 68.8

Growth 2% 11% -4% 13% -2% 3% 3%

Opex 36.1 40.1 37.6 41.9 40.8 41.8 43.1

Growth 0% 11% -6% 11% -3% 2% 3%

EBITDA 18.9 21.2 21.3 24.8 24.2 25.1 25.9

Growth 6% 12% 0% 17% -2% 3% 3%

Source: Company, Emkay Research

We estimate an absolute EBITDA CAGR of 19%. Below the operating line, we have built in some

gradual increase in depreciation, assuming Rs100mn of annual capex as guided, while interest

costs should reduce due to FCF generation and favorable currency. We build in a tax rate of

35%. As a result, we expect GOLI to record a PAT CAGR of 18%, with FY21 EPS at

Rs52.3/share.

Exhibit 25: GOLI’s earnings outlook

Source: Company, Emkay Research

GOLI’s balance sheet is likely to remain healthy, with FCF of Rs1.5/1.9/2.3bn in FY19/20/21. By

1HFY19-end, its short-term debt went up due to working capital requirement from the insti orders

for which payments are likely to be cleared by FY19-end and the line-packing at the Chennai

plant that resulted in higher inventories. Despite all this, the company has remained debt-free

and toward the year-end, we expect it to be net cash positive by Rs1.5bn+.

9.7 10.1 10.9

13.3

16.9

19.9

23.1

1.3 1.6 1.8 2.4 2.9 3.4 4.0

0.8 1.0 1.2 1.6 1.8 2.2 2.6

-

5.0

10.0

15.0

20.0

25.0

FY15 FY16 FY17 FY18 FY19E FY20E FY21E

Rs b

n

Revenue EBITDA PAT

We expect a revenue CAGR of

20% during FY18-21E, based on

our volume/net realization CAGR

assumption of 18%/2%.

We expect GOLI to record a PAT

CAGR of 18%, with FY21 EPS at

Rs52.3/share.

Gulf Oil Lubricants India (GOLI IN) India Equity Research | Initiating Coverage

Emkay Research is also available on www.emkayglobal.com, Bloomberg EMKAY<GO>, Reuters and DOWJONES. DBS Bank Ltd, DBS Vickers Securities (Singapore) Pte Ltd,its respective connected and associated corporations and affiliates are the distributors of the research reports, please refer to the last page of the report on Restrictions on Distribution. In Singapore, this research report or research analyses may only be distributed to Institutional Investors,Expert Investors or Accredited Investors as defined in the Securities and Futures Act, Chapter 289 of Singapore

ED: ANISH MATHEW SA: DHANANJAY SINHA December 3, 2018| 13

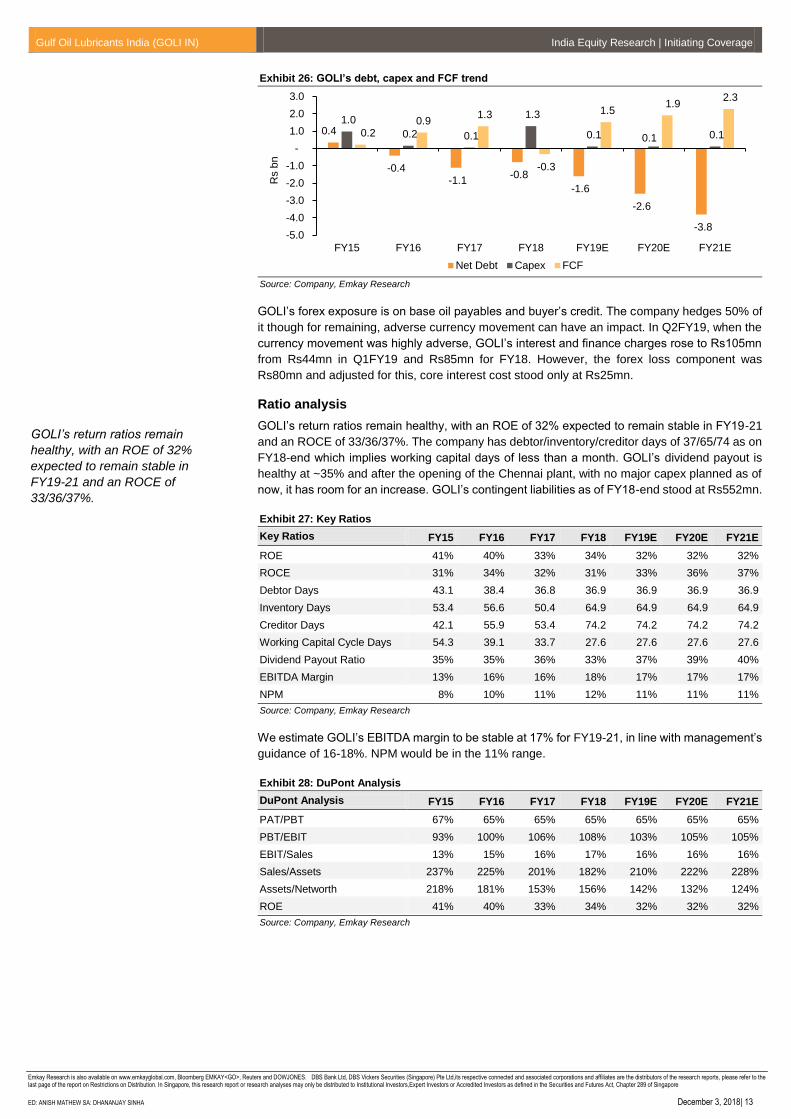

Exhibit 26: GOLI’s debt, capex and FCF trend

Source: Company, Emkay Research

GOLI’s forex exposure is on base oil payables and buyer’s credit. The company hedges 50% of

it though for remaining, adverse currency movement can have an impact. In Q2FY19, when the

currency movement was highly adverse, GOLI’s interest and finance charges rose to Rs105mn

from Rs44mn in Q1FY19 and Rs85mn for FY18. However, the forex loss component was

Rs80mn and adjusted for this, core interest cost stood only at Rs25mn.

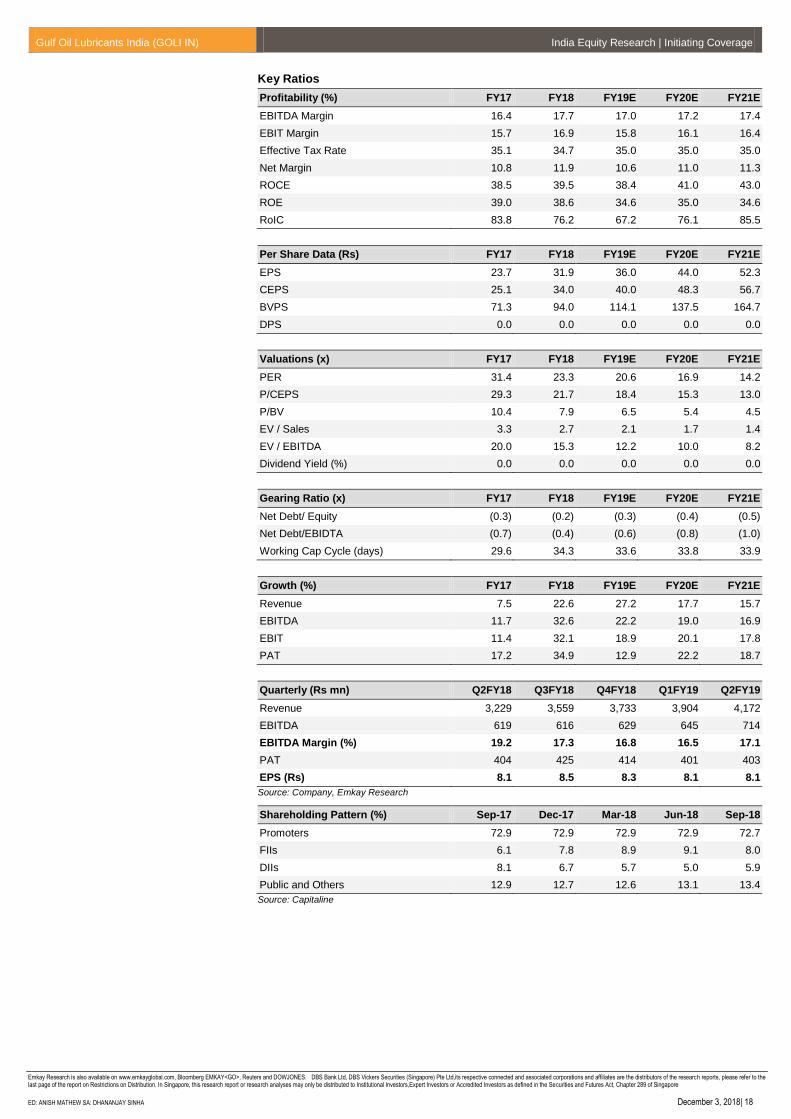

Ratio analysis

GOLI’s return ratios remain healthy, with an ROE of 32% expected to remain stable in FY19-21

and an ROCE of 33/36/37%. The company has debtor/inventory/creditor days of 37/65/74 as on

FY18-end which implies working capital days of less than a month. GOLI’s dividend payout is

healthy at ~35% and after the opening of the Chennai plant, with no major capex planned as of

now, it has room for an increase. GOLI’s contingent liabilities as of FY18-end stood at Rs552mn.

Exhibit 27: Key Ratios

Key Ratios FY15 FY16 FY17 FY18 FY19E FY20E FY21E

ROE 41% 40% 33% 34% 32% 32% 32%

ROCE 31% 34% 32% 31% 33% 36% 37%

Debtor Days 43.1 38.4 36.8 36.9 36.9 36.9 36.9

Inventory Days 53.4 56.6 50.4 64.9 64.9 64.9 64.9

Creditor Days 42.1 55.9 53.4 74.2 74.2 74.2 74.2

Working Capital Cycle Days 54.3 39.1 33.7 27.6 27.6 27.6 27.6

Dividend Payout Ratio 35% 35% 36% 33% 37% 39% 40%

EBITDA Margin 13% 16% 16% 18% 17% 17% 17%

NPM 8% 10% 11% 12% 11% 11% 11%

Source: Company, Emkay Research

We estimate GOLI’s EBITDA margin to be stable at 17% for FY19-21, in line with management’s

guidance of 16-18%. NPM would be in the 11% range.

Exhibit 28: DuPont Analysis

DuPont Analysis FY15 FY16 FY17 FY18 FY19E FY20E FY21E

PAT/PBT 67% 65% 65% 65% 65% 65% 65%

PBT/EBIT 93% 100% 106% 108% 103% 105% 105%

EBIT/Sales 13% 15% 16% 17% 16% 16% 16%

Sales/Assets 237% 225% 201% 182% 210% 222% 228%

Assets/Networth 218% 181% 153% 156% 142% 132% 124%

ROE 41% 40% 33% 34% 32% 32% 32%

Source: Company, Emkay Research

0.4

-0.4 -1.1

-0.8

-1.6

-2.6

-3.8

1.0

0.2 0.1

1.3

0.1 0.1 0.1 0.2 0.9

1.3

-0.3

1.5 1.9

2.3

-5.0

-4.0

-3.0

-2.0

-1.0

-

1.0

2.0

3.0

FY15 FY16 FY17 FY18 FY19E FY20E FY21E

Rs b

nNet Debt Capex FCF

GOLI’s return ratios remain

healthy, with an ROE of 32%

expected to remain stable in

FY19-21 and an ROCE of

33/36/37%.

Gulf Oil Lubricants India (GOLI IN) India Equity Research | Initiating Coverage

Emkay Research is also available on www.emkayglobal.com, Bloomberg EMKAY<GO>, Reuters and DOWJONES. DBS Bank Ltd, DBS Vickers Securities (Singapore) Pte Ltd,its respective connected and associated corporations and affiliates are the distributors of the research reports, please refer to the last page of the report on Restrictions on Distribution. In Singapore, this research report or research analyses may only be distributed to Institutional Investors,Expert Investors or Accredited Investors as defined in the Securities and Futures Act, Chapter 289 of Singapore

ED: ANISH MATHEW SA: DHANANJAY SINHA December 3, 2018| 14

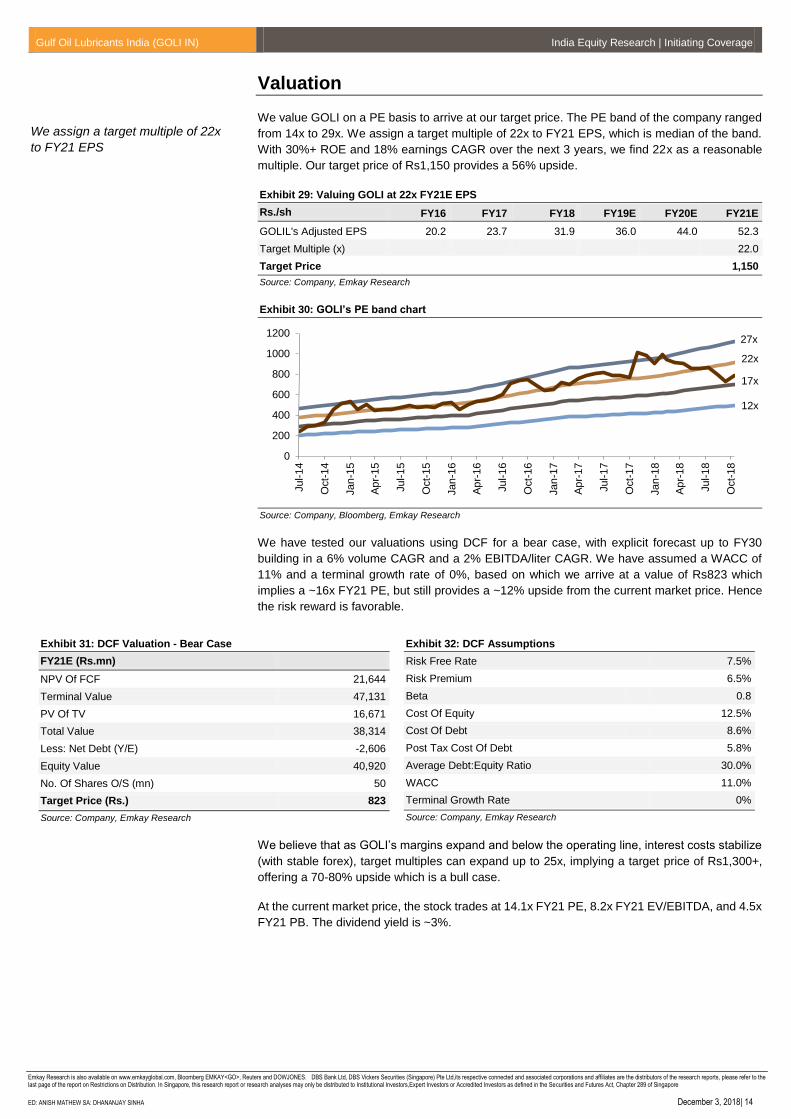

Valuation

We value GOLI on a PE basis to arrive at our target price. The PE band of the company ranged

from 14x to 29x. We assign a target multiple of 22x to FY21 EPS, which is median of the band.

With 30%+ ROE and 18% earnings CAGR over the next 3 years, we find 22x as a reasonable

multiple. Our target price of Rs1,150 provides a 56% upside.

Exhibit 29: Valuing GOLI at 22x FY21E EPS

Rs./sh FY16 FY17 FY18 FY19E FY20E FY21E

GOLIL's Adjusted EPS 20.2 23.7 31.9 36.0 44.0 52.3

Target Multiple (x) 22.0

Target Price 1,150

Source: Company, Emkay Research

Exhibit 30: GOLI’s PE band chart

Source: Company, Bloomberg, Emkay Research

We have tested our valuations using DCF for a bear case, with explicit forecast up to FY30

building in a 6% volume CAGR and a 2% EBITDA/liter CAGR. We have assumed a WACC of

11% and a terminal growth rate of 0%, based on which we arrive at a value of Rs823 which

implies a ~16x FY21 PE, but still provides a ~12% upside from the current market price. Hence

the risk reward is favorable.

Exhibit 31: DCF Valuation - Bear Case

FY21E (Rs.mn)

NPV Of FCF 21,644

Terminal Value 47,131

PV Of TV 16,671

Total Value 38,314

Less: Net Debt (Y/E) -2,606

Equity Value 40,920

No. Of Shares O/S (mn) 50

Target Price (Rs.) 823

Source: Company, Emkay Research

Exhibit 32: DCF Assumptions

Risk Free Rate 7.5%

Risk Premium 6.5%

Beta 0.8

Cost Of Equity 12.5%

Cost Of Debt 8.6%

Post Tax Cost Of Debt 5.8%

Average Debt:Equity Ratio 30.0%

WACC 11.0%

Terminal Growth Rate 0%

Source: Company, Emkay Research

We believe that as GOLI’s margins expand and below the operating line, interest costs stabilize

(with stable forex), target multiples can expand up to 25x, implying a target price of Rs1,300+,

offering a 70-80% upside which is a bull case.

At the current market price, the stock trades at 14.1x FY21 PE, 8.2x FY21 EV/EBITDA, and 4.5x

FY21 PB. The dividend yield is ~3%.

0

200

400

600

800

1000

1200

Jul-1

4

Oct-

14

Jan

-15

Ap

r-15

Jul-1

5

Oct-

15

Jan

-16

Ap

r-16

Jul-1

6

Oct-

16

Jan

-17

Ap

r-17

Jul-1

7

Oct-

17

Jan

-18

Ap

r-18

Jul-1

8

Oct-

18

12x

17x

22x

27x

We assign a target multiple of 22x

to FY21 EPS

Gulf Oil Lubricants India (GOLI IN) India Equity Research | Initiating Coverage

Emkay Research is also available on www.emkayglobal.com, Bloomberg EMKAY<GO>, Reuters and DOWJONES. DBS Bank Ltd, DBS Vickers Securities (Singapore) Pte Ltd,its respective connected and associated corporations and affiliates are the distributors of the research reports, please refer to the last page of the report on Restrictions on Distribution. In Singapore, this research report or research analyses may only be distributed to Institutional Investors,Expert Investors or Accredited Investors as defined in the Securities and Futures Act, Chapter 289 of Singapore

ED: ANISH MATHEW SA: DHANANJAY SINHA December 3, 2018| 15

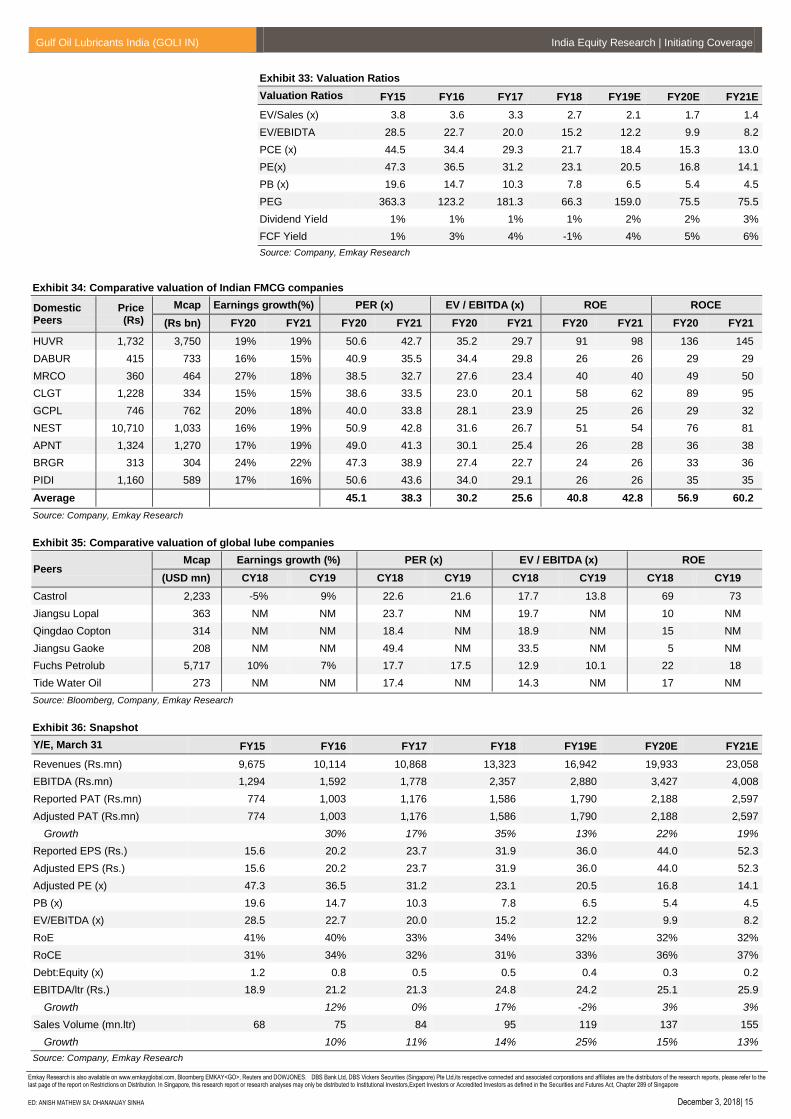

Exhibit 33: Valuation Ratios

Valuation Ratios FY15 FY16 FY17 FY18 FY19E FY20E FY21E

EV/Sales (x) 3.8 3.6 3.3 2.7 2.1 1.7 1.4

EV/EBIDTA 28.5 22.7 20.0 15.2 12.2 9.9 8.2

PCE (x) 44.5 34.4 29.3 21.7 18.4 15.3 13.0

PE(x) 47.3 36.5 31.2 23.1 20.5 16.8 14.1

PB (x) 19.6 14.7 10.3 7.8 6.5 5.4 4.5

PEG 363.3 123.2 181.3 66.3 159.0 75.5 75.5

Dividend Yield 1% 1% 1% 1% 2% 2% 3%

FCF Yield 1% 3% 4% -1% 4% 5% 6%

Source: Company, Emkay Research

Exhibit 34: Comparative valuation of Indian FMCG companies

Domestic Peers

Price (Rs)

Mcap Earnings growth(%) PER (x) EV / EBITDA (x) ROE ROCE

(Rs bn) FY20 FY21 FY20 FY21 FY20 FY21 FY20 FY21 FY20 FY21

HUVR 1,732 3,750 19% 19% 50.6 42.7 35.2 29.7 91 98 136 145

DABUR 415 733 16% 15% 40.9 35.5 34.4 29.8 26 26 29 29

MRCO 360 464 27% 18% 38.5 32.7 27.6 23.4 40 40 49 50

CLGT 1,228 334 15% 15% 38.6 33.5 23.0 20.1 58 62 89 95

GCPL 746 762 20% 18% 40.0 33.8 28.1 23.9 25 26 29 32

NEST 10,710 1,033 16% 19% 50.9 42.8 31.6 26.7 51 54 76 81

APNT 1,324 1,270 17% 19% 49.0 41.3 30.1 25.4 26 28 36 38

BRGR 313 304 24% 22% 47.3 38.9 27.4 22.7 24 26 33 36

PIDI 1,160 589 17% 16% 50.6 43.6 34.0 29.1 26 26 35 35

Average 45.1 38.3 30.2 25.6 40.8 42.8 56.9 60.2

Source: Company, Emkay Research

Exhibit 35: Comparative valuation of global lube companies

Peers Mcap Earnings growth (%) PER (x) EV / EBITDA (x) ROE

(USD mn) CY18 CY19 CY18 CY19 CY18 CY19 CY18 CY19

Castrol 2,233 -5% 9% 22.6 21.6 17.7 13.8 69 73

Jiangsu Lopal 363 NM NM 23.7 NM 19.7 NM 10 NM

Qingdao Copton 314 NM NM 18.4 NM 18.9 NM 15 NM

Jiangsu Gaoke 208 NM NM 49.4 NM 33.5 NM 5 NM

Fuchs Petrolub 5,717 10% 7% 17.7 17.5 12.9 10.1 22 18

Tide Water Oil 273 NM NM 17.4 NM 14.3 NM 17 NM

Source: Bloomberg, Company, Emkay Research

Exhibit 36: Snapshot

Y/E, March 31 FY15 FY16 FY17 FY18 FY19E FY20E FY21E

Revenues (Rs.mn) 9,675 10,114 10,868 13,323 16,942 19,933 23,058

EBITDA (Rs.mn) 1,294 1,592 1,778 2,357 2,880 3,427 4,008

Reported PAT (Rs.mn) 774 1,003 1,176 1,586 1,790 2,188 2,597

Adjusted PAT (Rs.mn) 774 1,003 1,176 1,586 1,790 2,188 2,597

Growth 30% 17% 35% 13% 22% 19%

Reported EPS (Rs.) 15.6 20.2 23.7 31.9 36.0 44.0 52.3

Adjusted EPS (Rs.) 15.6 20.2 23.7 31.9 36.0 44.0 52.3

Adjusted PE (x) 47.3 36.5 31.2 23.1 20.5 16.8 14.1

PB (x) 19.6 14.7 10.3 7.8 6.5 5.4 4.5

EV/EBITDA (x) 28.5 22.7 20.0 15.2 12.2 9.9 8.2

RoE 41% 40% 33% 34% 32% 32% 32%

RoCE 31% 34% 32% 31% 33% 36% 37%

Debt:Equity (x) 1.2 0.8 0.5 0.5 0.4 0.3 0.2

EBITDA/ltr (Rs.) 18.9 21.2 21.3 24.8 24.2 25.1 25.9

Growth 12% 0% 17% -2% 3% 3%

Sales Volume (mn.ltr) 68 75 84 95 119 137 155

Growth 10% 11% 14% 25% 15% 13%

Source: Company, Emkay Research

Gulf Oil Lubricants India (GOLI IN) India Equity Research | Initiating Coverage

Emkay Research is also available on www.emkayglobal.com, Bloomberg EMKAY<GO>, Reuters and DOWJONES. DBS Bank Ltd, DBS Vickers Securities (Singapore) Pte Ltd,its respective connected and associated corporations and affiliates are the distributors of the research reports, please refer to the last page of the report on Restrictions on Distribution. In Singapore, this research report or research analyses may only be distributed to Institutional Investors,Expert Investors or Accredited Investors as defined in the Securities and Futures Act, Chapter 289 of Singapore

ED: ANISH MATHEW SA: DHANANJAY SINHA December 3, 2018| 16

Company description

Gulf Oil Lubricants India Ltd (GOLI) is 72.7% owned by Gulf Oil International, a Hinduja group

company. The parent company has rights to the Gulf brand in all countries except Portugal,

Spain, and the US. GOLI was demerged as a pure-play lubricant company from Gulf Oil

Corporation in CY15. GOLI is No.2 in the private/non-OMCs space with an 8% Bazaar and 5%

overall market share.

GOLI’s key segments are automotive and industrial lubricants and its product line includes

engine oils, gear oils, transmission fluids, brake fluids, and fork oil under automotive and

hydraulic oils, compressor oils, cutting oils, and rust preventives under the industrial category,

which includes marine oils. GOLI’s marquee brands are Gulf Formula GX, Tec, Ultrasynth and

MAX in PCMO, Gulf Pride in MCO/2W, Gulf Supreme, Superduty, Superfleet, Super Diesel and

Master in CVO, Gulf XHD in tractors and Gulf Supreme in 3W/CNG. GOLI also has exposure to

the tender business of transport corporations, government entities, defense, etc. In terms of

pricing, GOLI claims to be a 10‐15% discount provider compared with the market leader Castrol.

It has two blending plants — one in Silvassa with a capacity of 90mn liters and a second one in

Chennai with a capacity of 50mn liters that was recently commissioned with a capex of Rs 1.8bn.

The Chennai plant is operating at 50% capacity utilization and has helped GOLI consolidate and

cater the South Indian market in addition to giving export volumes. The Silvassa plant’s capacity

utilization is ~85%. As of FY18-end, GOLI had 60,000+ retailers, 300+ automotive distributors,

30 depots, 200+ direct industrial customers under B2B, 50+ industrial distributors, and 500+

customers in the infra mining space. The company’s headquarters is in Mumbai.

GOLI also has a battery business in which it markets imported 2W batteries and the company is

aiming to significantly scale it up. Mr. Ravi Chawla is the MD and Mr Manish Gangwal is the

CFO. Mr. Sanjay Hinduja is the Chairman of the Board, which comprises three independent

directors and a non‐independent non‐executive director. The company reported revenues of

Rs13bn and a PAT of Rs1.6bn in FY18. The current market capitalization stands at Rs37bn.

Key risks

Adverse oil price and base oil pricing scenario: raw material cost fluctuation could impact

margins if retail pricing is sticky. This will include additives and packaging.

Currency risks: since base oil and additives are dollar-denominated and retail products are

rupee-denominated, currency risk is inherent in the business with a depreciating INR/USD

adverse affecting margins.

Competitive risk: predatory and destructive pricing by competitors, crowding out of new

players. Intense promotional activities can lead to a jump in advertising and other expenses.

Other risks: plant outage, industrial relations, adverse taxation, JV and related party risks.

Higher drain intervals: the structural decline in lube consumption due to efficient and smaller

engines and long drain oils by lubricant players. However, long drain oils are generally

value-accretive for a lube supplier.

Technological changes: the advent of EVs and the clamor around it. Although, as

discussed earlier, in India EVs are a much longer-term phenomenon. Channel disruptions,

with online market places offering substantial discounts.

Gulf Oil Lubricants India (GOLI IN) India Equity Research | Initiating Coverage

Emkay Research is also available on www.emkayglobal.com, Bloomberg EMKAY<GO>, Reuters and DOWJONES. DBS Bank Ltd, DBS Vickers Securities (Singapore) Pte Ltd,its respective connected and associated corporations and affiliates are the distributors of the research reports, please refer to the last page of the report on Restrictions on Distribution. In Singapore, this research report or research analyses may only be distributed to Institutional Investors,Expert Investors or Accredited Investors as defined in the Securities and Futures Act, Chapter 289 of Singapore

ED: ANISH MATHEW SA: DHANANJAY SINHA December 3, 2018| 17

Key Financials

Income Statement

Y/E Mar (Rs mn) FY17 FY18 FY19E FY20E FY21E

Revenue 10,868 13,323 16,942 19,933 23,058

Expenditure 9,090 10,965 14,063 16,505 19,049

EBITDA 1,778 2,357 2,880 3,427 4,008

Depreciation 73 104 200 211 219

EBIT 1,706 2,253 2,680 3,217 3,789

Other Income 203 261 271 281 319

Interest expenses 98 85 196 132 112

PBT 1,811 2,429 2,754 3,366 3,995

Tax 635 843 964 1,178 1,398

Extraordinary Items 0 0 0 0 0

Minority Int./Income from Assoc. 0 0 0 0 0

Reported Net Income 1,176 1,586 1,790 2,188 2,597

Adjusted PAT 1,176 1,586 1,790 2,188 2,597

Balance Sheet

Y/E Mar (Rs mn) FY17 FY18 FY19E FY20E FY21E

Equity share capital 99 99 99 99 99

Reserves & surplus 3,442 4,575 5,570 6,734 8,084

Net worth 3,541 4,674 5,669 6,833 8,184

Minority Interest 0 0 0 0 0

Loan Funds 1,828 2,529 2,232 1,936 1,641

Net deferred tax liability 45 106 167 229 291

Total Liabilities 5,414 7,309 8,069 8,998 10,115

Net block 1,180 2,601 2,568 2,487 2,389

Investment 165 136 159 179 199

Current Assets 5,745 7,492 9,151 10,815 12,703

Cash & bank balance 2,896 3,262 3,771 4,486 5,382

Other Current Assets 0 0 0 0 0

Current liabilities & Provision 1,968 2,980 3,822 4,485 5,177

Net current assets 3,777 4,512 5,329 6,330 7,526

Misc. exp 0 0 0 0 0

Total Assets 5,414 7,309 8,069 8,998 10,115

Cash Flow

Y/E Mar (Rs mn) FY17 FY18 FY19E FY20E FY21E

PBT (Ex-Other income) (NI+Dep) 1,607 2,168 2,483 3,085 3,676

Other Non-Cash items 32 85 0 0 0

Chg in working cap 71 (307) (247) (224) (239)

Operating Cashflow 1,339 1,101 1,650 2,010 2,355

Capital expenditure (456) (1,294) (120) (120) (120)

Free Cash Flow 883 (193) 1,530 1,890 2,235

Investments (48) 29 (23) (19) (20)

Other Investing Cash Flow 200 495 22 18 19

Investing Cashflow (100) (509) 150 160 198

Equity Capital Raised 0 0 0 0 0

Loans Taken / (Repaid) (150) 701 (296) (296) (296)

Dividend paid (incl tax) (444) (533) (795) (1,024) (1,246)

Other Financing Cash Flow (1) (309) (2) (3) (3)

Financing Cashflow (693) (226) (1,290) (1,455) (1,658)

Net chg in cash 545 366 510 715 895

Opening cash position 2,351 2,896 3,262 3,771 4,486

Closing cash position 2,896 3,262 3,771 4,486 5,382

Source: Company, Emkay Research

Gulf Oil Lubricants India (GOLI IN) India Equity Research | Initiating Coverage

Emkay Research is also available on www.emkayglobal.com, Bloomberg EMKAY<GO>, Reuters and DOWJONES. DBS Bank Ltd, DBS Vickers Securities (Singapore) Pte Ltd,its respective connected and associated corporations and affiliates are the distributors of the research reports, please refer to the last page of the report on Restrictions on Distribution. In Singapore, this research report or research analyses may only be distributed to Institutional Investors,Expert Investors or Accredited Investors as defined in the Securities and Futures Act, Chapter 289 of Singapore

ED: ANISH MATHEW SA: DHANANJAY SINHA December 3, 2018| 18

Key Ratios

Profitability (%) FY17 FY18 FY19E FY20E FY21E

EBITDA Margin 16.4 17.7 17.0 17.2 17.4

EBIT Margin 15.7 16.9 15.8 16.1 16.4

Effective Tax Rate 35.1 34.7 35.0 35.0 35.0

Net Margin 10.8 11.9 10.6 11.0 11.3

ROCE 38.5 39.5 38.4 41.0 43.0

ROE 39.0 38.6 34.6 35.0 34.6

RoIC 83.8 76.2 67.2 76.1 85.5

Per Share Data (Rs) FY17 FY18 FY19E FY20E FY21E

EPS 23.7 31.9 36.0 44.0 52.3

CEPS 25.1 34.0 40.0 48.3 56.7

BVPS 71.3 94.0 114.1 137.5 164.7

DPS 0.0 0.0 0.0 0.0 0.0

Valuations (x) FY17 FY18 FY19E FY20E FY21E

PER 31.4 23.3 20.6 16.9 14.2

P/CEPS 29.3 21.7 18.4 15.3 13.0

P/BV 10.4 7.9 6.5 5.4 4.5

EV / Sales 3.3 2.7 2.1 1.7 1.4

EV / EBITDA 20.0 15.3 12.2 10.0 8.2

Dividend Yield (%) 0.0 0.0 0.0 0.0 0.0

Gearing Ratio (x) FY17 FY18 FY19E FY20E FY21E

Net Debt/ Equity (0.3) (0.2) (0.3) (0.4) (0.5)

Net Debt/EBIDTA (0.7) (0.4) (0.6) (0.8) (1.0)

Working Cap Cycle (days) 29.6 34.3 33.6 33.8 33.9

Growth (%) FY17 FY18 FY19E FY20E FY21E

Revenue 7.5 22.6 27.2 17.7 15.7

EBITDA 11.7 32.6 22.2 19.0 16.9

EBIT 11.4 32.1 18.9 20.1 17.8

PAT 17.2 34.9 12.9 22.2 18.7

Quarterly (Rs mn) Q2FY18 Q3FY18 Q4FY18 Q1FY19 Q2FY19

Revenue 3,229 3,559 3,733 3,904 4,172

EBITDA 619 616 629 645 714

EBITDA Margin (%) 19.2 17.3 16.8 16.5 17.1

PAT 404 425 414 401 403

EPS (Rs) 8.1 8.5 8.3 8.1 8.1

Source: Company, Emkay Research

Shareholding Pattern (%) Sep-17 Dec-17 Mar-18 Jun-18 Sep-18

Promoters 72.9 72.9 72.9 72.9 72.7

FIIs 6.1 7.8 8.9 9.1 8.0

DIIs 8.1 6.7 5.7 5.0 5.9

Public and Others 12.9 12.7 12.6 13.1 13.4

Source: Capitaline

Gulf Oil Lubricants India (GOLI IN) India Equity Research | Initiating Coverage

Emkay Research is also available on www.emkayglobal.com, Bloomberg EMKAY<GO>, Reuters and DOWJONES. DBS Bank Ltd, DBS Vickers Securities (Singapore) Pte Ltd,its respective connected and associated corporations and affiliates are the distributors of the research reports, please refer to the last page of the report on Restrictions on Distribution. In Singapore, this research report or research analyses may only be distributed to Institutional Investors,Expert Investors or Accredited Investors as defined in the Securities and Futures Act, Chapter 289 of Singapore

ED: ANISH MATHEW SA: DHANANJAY SINHA December 3, 2018| 19

Emkay Rating Distribution

BUY Expected total return (%) (Stock price appreciation and dividend yield) of over 25% within the next 12-18 months.

ACCUMULATE Expected total return (%) (Stock price appreciation and dividend yield) of over 10% within the next 12-18 months.

HOLD Expected total return (%) (Stock price appreciation and dividend yield) of upto 10% within the next 12-18 months.

REDUCE Expected total return (%) (Stock price depreciation) of upto (-) 10% within the next 12-18 months.

SELL The stock is believed to underperform the broad market indices or its related universe within the next 12-18 months.

Completed Date: 03 Dec 2018 17:16:24 (SGT) Dissemination Date: 03 Dec 2018 17:17:24 (SGT)

Sources for all charts and tables are Emkay Research unless otherwise specified.

GENERAL DISCLOSURE/DISCLAIMER BY EMKAY GLOBAL FINANCIAL SERVICES LIMITED (EGFSL): Emkay Global Financial Services Limited (CIN-L67120MH1995PLC084899) and its affiliates are a full-service, brokerage, investment banking, investment management and financing group. Emkay Global Financial Services Limited (EGFSL) along with its affiliates are participants in virtually all securities trading markets in India. EGFSL was established in 1995 and is one of India's leading brokerage and distribution house. EGFSL is a corporate trading member of Bombay Stock Exchange Limited (BSE), National Stock Exchange of India Limited (NSE), MCX Stock Exchange Limited (MCX-SX). EGFSL along with its subsidiaries offers the most comprehensive avenues for investments and is engaged in the businesses including stock broking (Institutional and retail), merchant banking, commodity broking, depository participant, portfolio management, insurance broking and services rendered in connection with distribution of primary market issues and financial products like mutual funds, fixed deposits. Details of associates are available on our website i.e. www.emkayglobal.com EGFSL is registered as Research Analyst with SEBI bearing registration Number INH000000354 as per SEBI (Research Analysts) Regulations, 2014. EGFSL hereby declares that it has not defaulted with any stock exchange nor its activities were suspended by any stock exchange with whom it is registered in last five years, except that NSE had disabled EGFSL from trading on October 05, October 08 and October 09, 2012 for a manifest error resulting into a bonafide erroneous trade on October 05, 2012. However, SEBI and Stock Exchanges have conducted the routine inspection and based on their observations have issued advice letters or levied minor penalty on EGFSL for certain operational deviations in ordinary/routine course of business. EGFSL has not been debarred from doing business by any Stock Exchange / SEBI or any other authorities; nor has its certificate of registration been cancelled by SEBI at any point of time. EGFSL offers research services to clients as well as prospects. The analyst for this report certifies that all of the views expressed in this report accurately reflect his or her personal views about the subject company or companies and its or their securities, and no part of his or her compensation was, is or will be, directly or indirectly related to specific recommendations or views expressed in this report. Other disclosures by Emkay Global Financial Services Limited (Research Entity) and its Research Analyst under SEBI (Research Analyst) Regulations, 2014 with reference to the subject company(s) covered in this report EGFSL and/or its affiliates may seek investment banking or other business from the company or companies that are the subject of this material. Our salespeople, traders, and other professionals may provide oral or written market commentary or trading strategies to our clients that reflect opinions that are contrary to the opinions expressed herein, and our proprietary trading and investing businesses may make investment decisions that may be inconsistent with the recommendations expressed herein. In reviewing these materials, you should be aware that any or all of the foregoing, among other things, may give rise to real or potential conflicts of interest including but not limited to those stated herein. Additionally, other important information regarding our relationships with the company or companies that are the subject of this material is provided herein. This report is not directed to, or intended for distribution to or use by, any person or entity who is a citizen or resident of or located in any locality, state, country or other jurisdiction where such distribution, publication, availability or use would be contrary to law or regulation or which would subject EGFSL or its group companies to any registration or licensing requirement within such jurisdiction. Specifically, this document does not constitute an offer to or solicitation to any U.S. person for the purchase or sale of any financial instrument or as an official confirmation of any transaction to any U.S. person. Unless otherwise stated, this message should not be construed as official confirmation of any transaction. No part of this document may be used by private customers in United Kingdom. All material presented in this report, unless specifically indicated otherwise, is under copyright to Emkay. None of the material, nor its content, nor any copy of it, may be altered in any way, transmitted to, copied or distributed to any other party, without the prior express written permission of EGFSL . All trademarks, service marks and logos used in this report are trademarks or registered trademarks of EGFSL or its Group Companies. The information contained herein is not intended for publication or distribution or circulation in any manner whatsoever and any unauthorized reading, dissemination, distribution or copying of this communication is prohibited unless otherwise expressly authorized. Please ensure that you have read “Risk Disclosure Document for Capital Market and Derivatives Segments” as prescribed by Securities and Exchange Board of India before investing in Indian Securities Market. In so far as this report includes current or historic information, it is believed to be reliable, although its accuracy and completeness cannot be guaranteed.

This publication has not been reviewed or authorized by any regulatory authority. There is no planned schedule or frequency for updating research publication relating to any issuer.

Please contact the primary analyst for valuation methodologies and assumptions associated with the covered companies or price targets Disclaimer for U.S. persons only: This research report is a product of Emkay Global Financial Services Limited (Emkay), which is the employer of the research analyst(s) who has prepared the research report. The research analyst(s) preparing the research report is/are resident outside the United States (U.S.) and are not associated persons of any U.S. regulated broker-dealer and therefore the analyst(s) is/are not subject to supervision by a U.S. broker-dealer, and is/are not required to satisfy the regulatory licensing requirements of Financial Institutions Regulatory Authority (FINRA) or required to otherwise comply with U.S. rules or regulations regarding, among other things, communications with a subject company, public appearances and trading securities held by a research analyst account. This report is intended for distribution to "Major Institutional Investors" as defined by Rule 15a-6(b)(4) of the U.S. Securities and Exchange Act, 1934 (the Exchange Act) and interpretations thereof by U.S. Securities and Exchange Commission (SEC) in reliance on Rule 15a 6(a)(2). If the recipient of this report is not a Major Institutional Investor as specified above, then it should not act upon this report and return the same to the sender. Further, this report may not be copied, duplicated and/or transmitted onward to any U.S. person, which is not the Major Institutional Investor. In reliance on the exemption from registration provided by Rule 15a-6 of the Exchange Act and interpretations thereof by the SEC in order to conduct certain business with Major Institutional Investors.

Gulf Oil Lubricants India (GOLI IN) India Equity Research | Initiating Coverage

Emkay Research is also available on www.emkayglobal.com, Bloomberg EMKAY<GO>, Reuters and DOWJONES. DBS Bank Ltd, DBS Vickers Securities (Singapore) Pte Ltd,its respective connected and associated corporations and affiliates are the distributors of the research reports, please refer to the last page of the report on Restrictions on Distribution. In Singapore, this research report or research analyses may only be distributed to Institutional Investors,Expert Investors or Accredited Investors as defined in the Securities and Futures Act, Chapter 289 of Singapore

ED: ANISH MATHEW SA: DHANANJAY SINHA December 3, 2018| 20

GENERAL DISCLOSURE/DISCLAIMER BY DBS BANK LTD AS DISTRIBUTOR OF THE RESEARCH REPORT This report is solely intended for the clients of DBS Bank Ltd,its respective connected and associated corporations and affiliates only and no part of this document may be (i) copied, photocopied or duplicated in any form or by any means or (ii) redistributed without the prior written consent of DBS Bank Ltd. The research set out in this report is based on information obtained from sources believed to be reliable, but we (which collectively refers to DBS Bank Ltd, its respective connected and associated corporations, affiliates and their respective directors, officers, employees and agents (collectively, the “DBS Group”) have not conducted due diligence on any of the companies, verified any information or sources or taken into account any other factors which we may consider to be relevant or appropriate in preparing the research. Accordingly, we do not make any representation or warranty as to the accuracy, completeness or correctness of the research set out in this report. Opinions expressed are subject to change without notice. This research is prepared for general circulation. Any recommendation contained in this document does not have regard to the specific investment objectives, financial situation and the particular needs of any specific addressee. This document is for the information of addressees only and is not to be taken in substitution for the exercise of judgement by addressees, who should obtain separate independent legal or financial advice. The DBS Group accepts no liability whatsoever for any direct, indirect and/or consequential loss (including any claims for loss of profit) arising from any use of and/or reliance upon this document and/or further communication given in relation to this document. This document is not to be construed as an offer or a solicitation of an offer to buy or sell any securities. The DBS Group, along with its affiliates and/or persons associated with any of them may from time to time have interests in the securities mentioned in this document. The DBS Group, may have positions in, and may effect transactions in securities mentioned herein and may also perform or seek to perform broking, investment banking and other banking services for these companies. Any valuations, opinions, estimates, forecasts, ratings or risk assessments herein constitutes a judgment as of the date of this report, and there can be no assurance that future results or events will be consistent with any such valuations, opinions, estimates, forecasts, ratings or risk assessments. The information in this document is subject to change without notice, its accuracy is not guaranteed, it may be incomplete or condensed, it may not contain all material information concerning the company (or companies) referred to in this report and the DBS Group is under no obligation to update the information in this report. This publication has not been reviewed or authorized by any regulatory authority in Singapore, Hong Kong or elsewhere. There is no planned schedule or frequency for updating research publication relating to any issuer.