Embed Size (px)

Citation preview

This article was downloaded by: [Radboud Universiteit Nijmegen], [Erwin Van DerKrabben]On: 09 December 2011, At: 02:18Publisher: RoutledgeInforma Ltd Registered in England and Wales Registered Number: 1072954 Registeredoffice: Mortimer House, 37-41 Mortimer Street, London W1T 3JH, UK

European Planning StudiesPublication details, including instructions for authors andsubscription information:http://www.tandfonline.com/loi/ceps20

Industrial Land and Property Markets:Market Processes, Market Institutionsand Market Outcomes: The Dutch CaseErwin Van Der Krabben a b & Edwin Buitelaar ca Institute for Management Research, Radboud UniversityNijmegen, Nijmegen, NL—, 6500 HK, The Netherlandsb School of the Built Environment, University of Ulster, Belfast, UKc Environmental Assessment Agency, The Hague, The Netherlands

Available online: 09 Dec 2011

To cite this article: Erwin Van Der Krabben & Edwin Buitelaar (2011): Industrial Land and PropertyMarkets: Market Processes, Market Institutions and Market Outcomes: The Dutch Case, EuropeanPlanning Studies, 19:12, 2127-2146

To link to this article: http://dx.doi.org/10.1080/09654313.2011.633822

PLEASE SCROLL DOWN FOR ARTICLE

Full terms and conditions of use: http://www.tandfonline.com/page/terms-and-conditions

This article may be used for research, teaching, and private study purposes. Anysubstantial or systematic reproduction, redistribution, reselling, loan, sub-licensing,systematic supply, or distribution in any form to anyone is expressly forbidden.

The publisher does not give any warranty express or implied or make any representationthat the contents will be complete or accurate or up to date. The accuracy of anyinstructions, formulae, and drug doses should be independently verified with primarysources. The publisher shall not be liable for any loss, actions, claims, proceedings,demand, or costs or damages whatsoever or howsoever caused arising directly orindirectly in connection with or arising out of the use of this material.

Industrial Land and Property Markets:Market Processes, Market Institutionsand Market Outcomes: The Dutch Case

ERWIN VAN DER KRABBEN∗,∗∗ & EDWIN BUITELAAR†

∗Institute for Management Research, Radboud University Nijmegen, Nijmegen, NL—6500 HK,

The Netherlands, ∗∗School of the Built Environment, University of Ulster, Belfast, UK, †Environmental

Assessment Agency, The Hague, The Netherlands

(Received July 2009; accepted September 2010)

ABSTRACT Outcomes of land and property markets may be understood by studying the effects of(interventions in) market processes and market institutions. Many studies have paid attention tothe meaning of institutions for land and property development processes. The standpoint of thispaper is that changes in the institutional order of the market may be considered to arrive at moredesirable market outcomes. It will be argued that institutional economic theory offers a valuabletheoretical approach to bring forward possible interventions in this institutional order. Thistheoretical approach to land and property development processes is applied to analyse onespecific market outcome, the spatial layout of industrial parks in the Netherlands. Starting fromthe analysis of the oversupply of industrial land and the deterioration of existing industrial parks,the paper focuses on possible interventions to change the institutional order that should lead tomore favourable market outcomes. For the present submarket for industrial land (building plots),a number of interventions are discussed to internalize the externalities that occur in this marketand to increase the number of suppliers. Additional interventions are proposed to create a “new”submarket for new leasehold industrial property, which is almost absent in the case of industrialestates.

1. Introduction

Urban spatial structures are the result of developments taking place on land and property

markets. The outcome of land and property development processes can be understood by

analysing market mechanisms. Welfare economic theory focuses on the way buyers and

sellers respond to changes in prices and to disruptions of the price mechanism. Since

land and property markets are, by their typical characteristics never perfect (i.e. hetero-

geneous goods, incomplete information, externalities, public goods), the price mechanism

Correspondence Address: Erwin van der Krabben, Institute for Management Research, Radboud University

Nijmegen Postbus 9108, NL—6500 HK Nijmegen, The Netherlands. Email: [email protected]

European Planning Studies Vol. 19, No. 12, December 2011

ISSN 0965-4313 Print/ISSN 1469-5944 Online/11/122127–20 # 2011 Taylor & Francishttp://dx.doi.org/10.1080/09654313.2011.633822

Dow

nloa

ded

by [

Rad

boud

Uni

vers

iteit

Nijm

egen

], [

Erw

in V

an D

er K

rabb

en]

at 0

2:18

09

Dec

embe

r 20

11

often does not work well (see, for instance, van der Krabben & Lambooy, 1993; Evans,

2004; Needham, 2006a). These features are then the rationale for government interven-

tions such as land-use regulations, direct government investments, subsidies, etc. To

welfare economists, “the task of land-use planning is to take care of the goods, which

the market will not provide, undersupplies (Webster, 1998) (e.g. public transport in

remote rural areas) or oversupplies (e.g. office buildings)” (Buitelaar, 2007, p. 4). Those

interventions often work out well. However, “one of the implicit assumptions of this

welfare economic approach is the idea that when the market fails and the government

intervenes, the latter will do so perfectly and without costs” (Buitelaar, 2007, p. 4).

Many have argued that, in addition to market failures, there are public or government

failures as well (Levacic, 1991; Lai, 1997, 2007; Webster, 1998; Pennington, 2000;

Lai & Hung, 2008).

However, this discussion of the failure of the market versus the failure of the govern-

ment does not bring us much further (see also Buitelaar, 2003, 2007). In welfare econ-

omics, every situation that is not optimal is qualified as inefficient or as a “failure”. But

because these optima are hardly ever reached, there is only failure, which significantly

devaluates failure as a concept for judging the allocation of resources. In addition,

reality is often too complex to fit within the neat dichotomy of “the government” versus

“the market”. It is not fruitful to regard the government and planning on one side and

the market on the other as counterparts, since they are not mutually exclusive. The

market is structured by the government who makes the rules that facilitate exchange. In

addition, the government can and often is a market actor.

The present paper aims to conceptualize the relations between market processes and

market institutions on the one hand and market outcomes with respect to land and property

markets on the other hand. The paper is built on the assumption that changing the insti-

tutional order may lead to a different market outcome. The term “institutional order”

not only involves government interventions. It concerns both the rules of the game

(especially the property rights regime) and the set of players that are in the game. It pro-

vides a broader perspective—so it will be argued in this paper—to understanding and

improving markets and market outcomes. In addition, in line with Coase (1960), we

believe, it is more productive to compare real-life or feasible alternatives than to relate

reality to an unattainable optimum.

Many studies have already paid attention to the meaning of institutions for land and

property development processes, taking institutional economic theory (Coase, 1960) as

the basis for analysis. Those studies show, for instance, to what extent transaction costs

matter for land and property development (Buitelaar, 2007), the relation between

deficiencies in the property rights regime and externalities (Webster & Lai, 2003;

Needham, 2006a; van der Krabben, 2009), and why and under which conditions insti-

tutional change and continuity takes place (Needham & Louw, 2006; Buitelaar et al.,

2007). In the perspective of this theoretical tradition, applied to planning studies and

the analysis of land and property development, Lai and Hung (2008) have emphasized

the need to test empirically the relation between institutional order, planning interventions

and market outcomes. The aim of this paper is to contribute to this Coasian Planning

Research Agenda (after Lai & Hung, 2008).

One of the benefits of welfare economics is the attention for market outcomes (the allo-

cation of resources, in our case land). In most of these contributions there is more attention

for the market processes. This paper’s objectives are, on the one hand, to explain the

2128 E. van der Krabben & E. Buitelaar

Dow

nloa

ded

by [

Rad

boud

Uni

vers

iteit

Nijm

egen

], [

Erw

in V

an D

er K

rabb

en]

at 0

2:18

09

Dec

embe

r 20

11

relationship between market institutions and processes and outcomes, and on the other

hand, to analyse how market outcomes can be changed by different types of interventions

in/changes of the institutional order. Starting from a more general analysis of the relations

between institutional order and market outcomes, based on institutional economics

(Section 2), we will then focus on one specific market outcome: the spatial layout of indus-

trial parks in the Netherlands. Many have argued that the outcomes of this segment of the

land and property market are not satisfactory (we will discuss this in Section 3). There

seems to be two problems that are interrelated. One is the abundance of newly developed

industrial sites on offer and the other is the deteriorating existing stock. In this paper,

we will analyse how this market outcome is related to the market institutions (Section 4).

And in addition, we explore how changes in the institutional order may lead to more

favourable market outcomes (Section 5). Finally, Section 6 reflects both on the theoretical

standpoint of the paper and the results of our “thought experiment”.

2. The Relation Between “Institutional Order and Market Outcomes”

Williamson uses the market as the starting point, by saying that “in the beginning there

were markets” (Williamson, 1975). This implies that if no hierarchies are constructed,

the market will automatically operate. However, this does not sufficiently acknowledge

that markets are institutions in themselves that are socially constructed (Hodgson,

2004). Markets are not simply there, but are created. Mainstream economics offers

well-known explanations why markets fail to appear, but when they are there, it seems

that markets have emerged as a natural given: “if there is a good, then there is a

market; and the classification of goods is part of the analyst’s natural endowment”

(Loasby, 2000, p. 299). However, Loasby argues, “markets are themselves goods (. . .)

and we can enquire into their costs and benefits” (Loasby, 2000, p. 300). Evolutionary

economics claims that markets are created, because the most effective way of overcoming

the obstacles to trade is not to proceed transaction by transaction, but to make substantial

investments in the creation of a system of conventions and rules, assuming there is enough

trade to make this worthwhile (Casson, 1982, p. 164, cited in Loasby, 2000). Each market

is created by actors, within the institutional framework they operate, usually “by those who

expect to be large-scale transactors on one or both sides of that market, and who therefore

expect to gain a large enough share of the benefits to justify bearing an even greater share

of the costs” (Loasby, 2000, p. 301). Likewise, Anderson and Catignon (2008, p. 401)

argue that new markets do not emerge, nor do they appear: “(t)hey are made by the

activities of firms. New markets are created when firms correctly sense (by accident or

by design) a latent need and communicate their solution to that need: markets spring

into being when economic actors shift resources to that firm’s solution”.

Some go further by emphasizing the explicit role of the state within the market. Polanyi

argues the following about laissez-faire in Britain in the nineteenth century: “The road to

the free market was opened and kept open by an enormous increase in continuous, cen-

trally organized and controlled interventionism. The introduction of free markets, far

from doing away with the need for control, regulation and intervention, enormously

increased their range. Administrators had to be constantly on the watch to ensure the

free working of the system. Thus, even those who wished most inherently to free the

state from all unnecessary duties, and whose whole philosophy demanded the restriction

of the state activities, could not but entrust the self-same state with the new powers,

Industrial Land and Property Markets 2129

Dow

nloa

ded

by [

Rad

boud

Uni

vers

iteit

Nijm

egen

], [

Erw

in V

an D

er K

rabb

en]

at 0

2:18

09

Dec

embe

r 20

11

organs, and instruments required for the establishment of laissez faire. Laissez-faire was

planned” (Polanyi, 1957, pp. 140–141).

More generally speaking, markets are institutions that are socially constructed. This is

also emphasized by thefollowing two definitions. “Markets are institutions that exist to

facilitate exchange, that is, they exist in order to reduce the cost of carrying out exchange

transactions.” (Coase, 1988, p. 7). “A market is an institution in which a significant number

of commodities of a particular, reasonably well-defined type are regularly exchanged.”

(Hodgson, 2002, p. 44).

The key institutions in markets are property rights. When we talk of a market in land, it

is not so much the land that is exchanged, but the right to use land in a specific way (e.g.

freehold, leasehold, fishing rights) and for a specific period (e.g. in perpetuity, for a long

lease, per year) (Alchian & Demsetz, 1973). We have to recognize that a property right is

something established by law or custom. Moreover, it has to be possible to enforce the

obligation implied by that right, if necessary by force: otherwise, it can be a dead letter.

That also is regulated by law or custom (Bromley, 1991).

Apart from acknowledging that markets are institutional and are socially constructed, it

is important to recognize that the relation between actors and institutions is reciprocal in

nature: actors are also influenced by market institutions. And therefore, the way markets

are institutionalized has an effect on market outcomes, since it is the people within the

market (the buyers, the sellers and the government) that produce that outcome.

If the outcome is unsatisfactory changing market institutions might help to come to a

better outcome. The institutions can be changed so as to change the behaviour of

actors—although this is not always successful—and therefore the market outcome. There

are two ways of reorganizing the market: a priori and a posteriori interventions.1 This

needs to be explained. Welfare economists that follow Pigou (1920) would argue that

when the market fails the government should intervene to correct these failures. The

government responds to the market from the outside and is more or less exogenous. In

the institutional economist tradition,2 the market is organized and reorganized by govern-

ments that create and change property rights structures so as to facilitate and improve

exchange. Government actions are an integral part of the market and are hence endogenous.

In this paper, we will explore the second option by looking at how market outcomes can be

explained through an analysis of the institutional order and how changes in the institutional

order can lead to a change in the market outcome.

3. Industrial Parks in the Netherlands: Undesired Market Outcomes

There is a growing dissatisfaction with the market outcomes of industrial land development

in the Netherlands.3 Many have recently criticized the current landscape of industrial parks

(MinEZ, 2004; Ruimtelijk Planbureau, 2006; VROM-Raad, 2006; THB, 2008) and the

Dutch Cabinet has announced several policy measures to deal with it (TK, 2008), some

of which have been implemented already. Unsatisfactory outcomes of industrial land and

property development are not exclusively Dutch. Particularly in the UK, substandard

developments in this market segment have received attention as well (Fothergill et al.,

1987; Henneberry, 1988, 1996; Tsolacos, 1997; Jones, 2005). Problems with brownfields—

perhaps the most visible examples of industrial property obsolescence—and brownfield

policies have received a lot of attention both in European and American planning and

real-estate literature (Alker et al., 2000; Meyer & Lyons, 2000; Simons & Jaouhari, 2001;

2130 E. van der Krabben & E. Buitelaar

Dow

nloa

ded

by [

Rad

boud

Uni

vers

iteit

Nijm

egen

], [

Erw

in V

an D

er K

rabb

en]

at 0

2:18

09

Dec

embe

r 20

11

McCarthy, 2002; Alberini et al., 2005; Gorman, 2005; Heberle & Wernstedt, 2006). Other

studies have paid attention to the impact of industrial land-use policy on market outcomes

(Cook, 1989; Zhu, 2000) and investment cycles in industrial real estate (Giussani et al.,

1992). STOGO (2007) has analysed industrial parks’ planning policies in Belgium (Flanders),

France, Germany and the UK. What we can learn from this study is that the deterioration of

industrial properties is an important spatial planning issue in all those countries, that the

oversupply of land is an issue in Germany as well, while in Belgium and the UK the opposite

occurs and that in all three countries urban containment policies, dedicated new industrial land,

have been implemented. The public sector dominance exists in Belgium, France and

Germany as well, while in the UK, there is a strong private sector involvement. Though we

focus on the Dutch case, a similar analysis with a similar analytical framework could be

of use for other countries as well.

The undesired outcomes of the Dutch industrial land and property market can be cate-

gorized as follows. First, many of the existing industrial parks that have been developed

after World War II now face serious problems of deterioration of private property and

reduced quality of public space. The national database of industrial estates shows that

33% of the total area on existing industrial estates has been labelled as “deteriorated”

by the municipalities involved, which means that investments are necessary to bring the

functional and/or spatial quality of the site to an acceptable level (IBIS, 2008).4 Table 1

shows that the deteriorated industrial parks are not only restricted to the category of

industrial parks that have been developed before 1990, but that a substantial part of the

industrial parks that have been developed after 1990 face problems of deterioration as

well. Further analysis learns that almost 40% of the deteriorated industrial parks have

been developed after 1990 (IBIS, 2008).

Whatever the problem has caused, strategies to “solve” the problems have not been very

successful so far (THB, 2008). THB (2008) shows that, between 1990 and 2006, annually

only 200–300 ha of obsolete industrial parks have gone through a process of improvement

or regeneration on a total of 16,000 ha that need to be improved (THB, 2008). Total public

sector investments amount to 6.35 billion euros. The national government’s ambitions for

2009–2013 are to improve and regenerate 1600 ha per year (TK, 2008). Table 2 shows,

however, that only for 4% of the industrial parks revitalization plans have been prepared,

while for 8% of these plans have been prepared to redevelop the location for other uses. It

means that for the larger part of the deteriorated industrial parks no strategies to solve or

Table 1. Deteriorated industrial parks: by development period and by region (The

Netherlands)a

After 2002 (%) Between 1991 and 2002 (%) Before 1991 (%)

North 0 5 5East 6 21 34West 22 34 32South 6 22 28

Source: IBIS (2008); reworked: authors.a“North” consists of provinces Groningen, Friesland, Drenthe; “East” consists of provinces Overijssel and

Gelderland; “West” consists of provinces Noord-Holland, Zuid-Holland, Utrecht and Flevoland; “South” consists

of provinces Zeeland, Brabant and Limbur.

Industrial Land and Property Markets 2131

Dow

nloa

ded

by [

Rad

boud

Uni

vers

iteit

Nijm

egen

], [

Erw

in V

an D

er K

rabb

en]

at 0

2:18

09

Dec

embe

r 20

11

reduce the problems have been developed yet.5 And even when there are strategies, it is

not clear whether these have succeeded in turning around economic obsolescence.

Second, there seems to be an oversupply of new industrial land that has been made

available for industrial use and rapid increase (Table 3; Figure 1). Table 3 indicates

that, as a result of local and regional government strategies aimed at making sure that

there is sufficient industrial land “in stock” at all times to be able to accommodate,

attract and maintain employment (see Section 4), the amount of available industrial

land in all regions may be expected to be sufficient for the next 10–20 years (or even

much longer, taking into account the reduced demand for industrial land since the begin-

ning of the economic crisis (see also Olden, 2010). Related to this, there are discussions in

the Netherlands that focus on the negative externalities of this on the landscape (problems

of urban sprawl). The Ministry for Spatial Planning considers the abundant development

of industrial land a problem: “The open Dutch landscape is under pressure. Along motor-

ways and the outskirts of cities in particular, seemingly haphazard development fills the

once wide horizon. This gives the landscape a fragmented and urbanized character,

which we refer to as landscape cluttering. (. . .) Though the term is difficult to define,

everyone knows more or less what it involves: the open landscape is being taken over

by ‘business blocks’, greenhouses, windmills, breaker’s yards, transmitter masts, moto-

cross sites, camping grounds, tree nurseries, etc.” (MinVROM, 2007, p. 1, translation

ours). Although it cannot be derived from Table 3 and Figure 1 that too much land has

Table 2. Revitalization and redevelopment plans for industrial parks (The Netherlands;

figures 2007)

Number of industrialestates

Share in total number of industrialestates (%)

Revitalization plan (industrial use) 115 4.0Redevelopment plan (residential use) 114 3.9Redevelopment plan (mixed use) 121 4.2No plan available 2556 88.0

Total 2906 100.0

Source: PBL (2009).

Table 3. Supply-demand ratio industrial land, per province (The Netherlands)

Supply (available land)Demand (sold industrial

land) Supply—demand ratio

1994 2000 2007 1994 2000 2007 1994 2000 2007

Total number of hectaresNorth 2698 2513 2350 123 267 193 5% 11% 8%East 1995 2486 2594 213 280 181 11% 11% 7%West 3210 3369 4169 256 286 200 8% 9% 5%South 4068 3253 2714 367 507 267 10% 16% 10%

Total 11,971 11,621 11,827 959 1340 841 8% 12% 7%

Source: IBIS (2008); reworked: authors.

2132 E. van der Krabben & E. Buitelaar

Dow

nloa

ded

by [

Rad

boud

Uni

vers

iteit

Nijm

egen

], [

Erw

in V

an D

er K

rabb

en]

at 0

2:18

09

Dec

embe

r 20

11

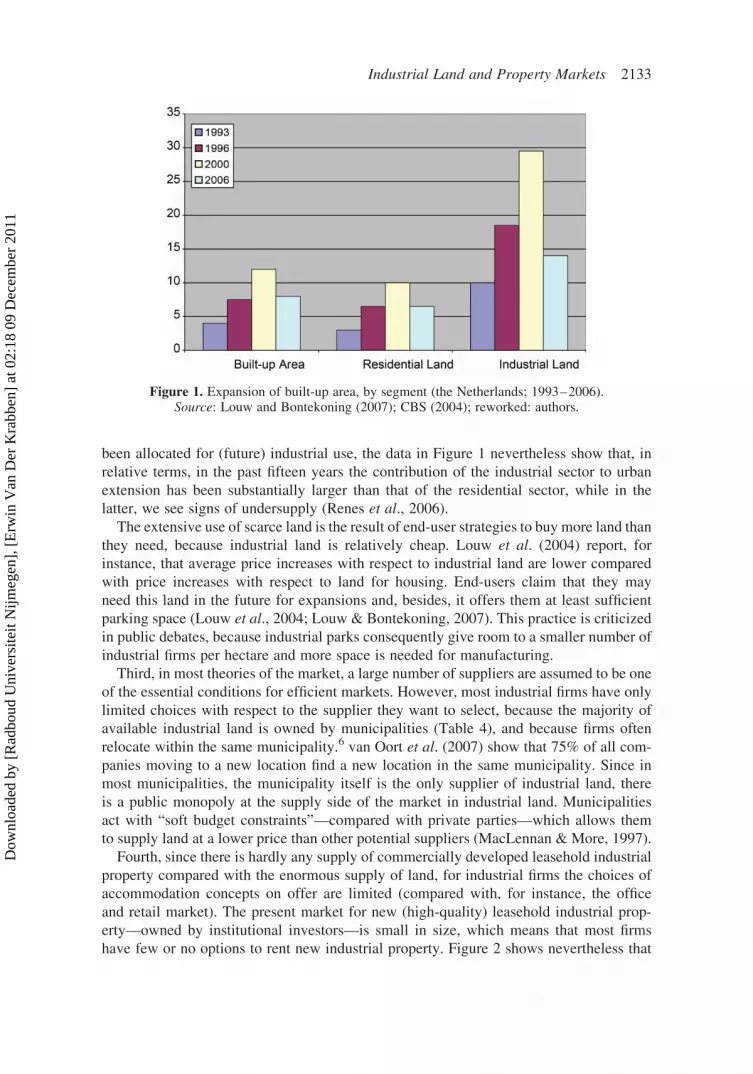

been allocated for (future) industrial use, the data in Figure 1 nevertheless show that, in

relative terms, in the past fifteen years the contribution of the industrial sector to urban

extension has been substantially larger than that of the residential sector, while in the

latter, we see signs of undersupply (Renes et al., 2006).

The extensive use of scarce land is the result of end-user strategies to buy more land than

they need, because industrial land is relatively cheap. Louw et al. (2004) report, for

instance, that average price increases with respect to industrial land are lower compared

with price increases with respect to land for housing. End-users claim that they may

need this land in the future for expansions and, besides, it offers them at least sufficient

parking space (Louw et al., 2004; Louw & Bontekoning, 2007). This practice is criticized

in public debates, because industrial parks consequently give room to a smaller number of

industrial firms per hectare and more space is needed for manufacturing.

Third, in most theories of the market, a large number of suppliers are assumed to be one

of the essential conditions for efficient markets. However, most industrial firms have only

limited choices with respect to the supplier they want to select, because the majority of

available industrial land is owned by municipalities (Table 4), and because firms often

relocate within the same municipality.6 van Oort et al. (2007) show that 75% of all com-

panies moving to a new location find a new location in the same municipality. Since in

most municipalities, the municipality itself is the only supplier of industrial land, there

is a public monopoly at the supply side of the market in industrial land. Municipalities

act with “soft budget constraints”—compared with private parties—which allows them

to supply land at a lower price than other potential suppliers (MacLennan & More, 1997).

Fourth, since there is hardly any supply of commercially developed leasehold industrial

property compared with the enormous supply of land, for industrial firms the choices of

accommodation concepts on offer are limited (compared with, for instance, the office

and retail market). The present market for new (high-quality) leasehold industrial prop-

erty—owned by institutional investors—is small in size, which means that most firms

have few or no options to rent new industrial property. Figure 2 shows nevertheless that

Figure 1. Expansion of built-up area, by segment (the Netherlands; 1993–2006).Source: Louw and Bontekoning (2007); CBS (2004); reworked: authors.

Industrial Land and Property Markets 2133

Dow

nloa

ded

by [

Rad

boud

Uni

vers

iteit

Nijm

egen

], [

Erw

in V

an D

er K

rabb

en]

at 0

2:18

09

Dec

embe

r 20

11

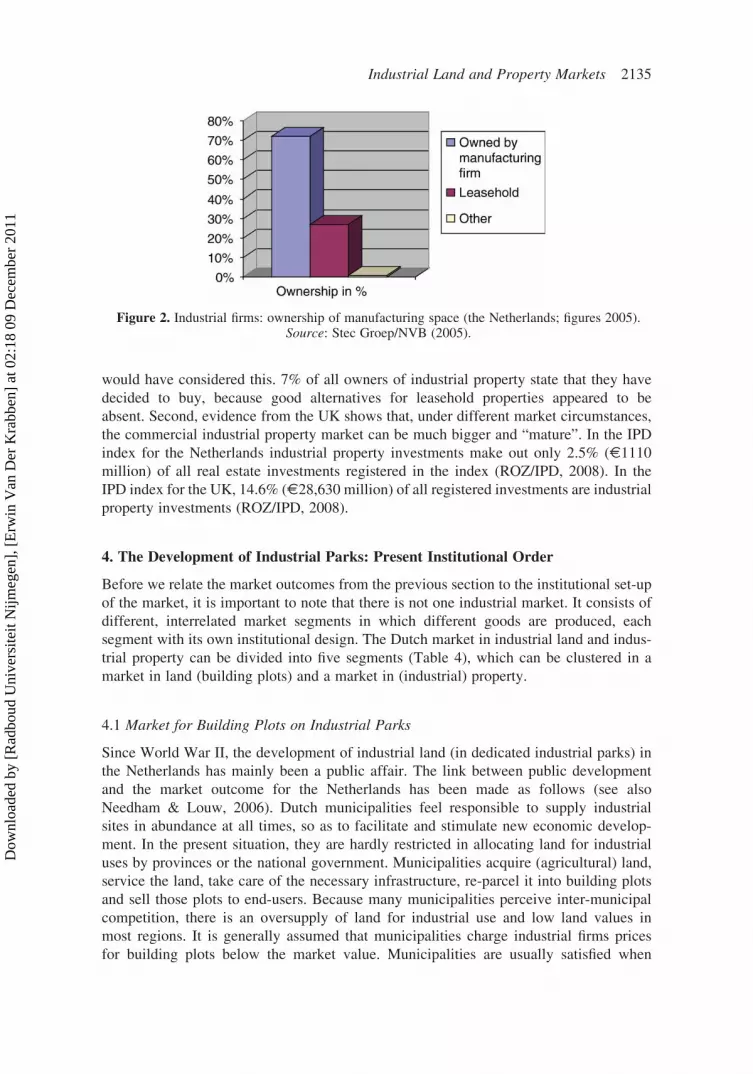

27% of all manufacturing firms rent property. However, only 8% of all leasehold industrial

properties is let by professional institutional investors (mainly logistics real estate). For the

remaining 92% of the leasehold industrial properties, landlords are often small companies

that have become landlords more or less by coincidence.7 It means that only about 2% of

all industrial property is owned and let by institutional investors (Stec Groep/NVB, 2005).

We have only indirect evidence that the lack of high-end leasehold industrial property

should be considered as a problem. First, a survey among industrial firms in the Nether-

lands shows that a relatively large number of firms would be interested in leasehold

industrial property: 28% of all companies would have considered a leasehold, if available

(Stec Groep/NVB, 2005). From the larger companies (more than 100 employees), 70%

Table 4. Market segments industrial land and property market

Market segmentsMarket size andcharacteristics Supply Demand

LandMarket for

building plotson industrialestates

Large market;limitedavailability insome regions;

Mainlymunicipalities(localmonopolies);

Manufacturing firms;Service sector and consumerservices sector firms (as faras allowed bymunicipalities);

Local markets,limited regionalcompetition;

Small share ofprivatedevelopers;

Mainly relocating firms,already located in samemunicipality;

PropertyMarket for new

rented industrialproperties

Small market; Institutionalinvestors;

Mainly limited to logisticssector firms;

Specialized realestate investmentfunds;

Latent need othermanufacturing firms (?);

Market for newindustrialproperties, forsale

Non-existent market; – Latent need manufacturingfirms (?);

Market forsecond-handrented industrialproperties

Large market;available onexisting industrialestates;

Manufacturing firms,moving to a newlocation;

Manufacturing firms, lookingfor (temporary)manufacturing or storagespace;

Mainly low-qualityproperties; lowrent levels;

(Small) investmentcompanies;

Small firms, starting newbusinesses;

High vacancy rates;Market for

second-handindustrialproperties, forsale

Small market; Manufacturing firms,moving to a newlocation;

Manufacturing firms, lookingfor (temporary)manufacturing or storagespace;

Small firms, starting newbusinesses;

2134 E. van der Krabben & E. Buitelaar

Dow

nloa

ded

by [

Rad

boud

Uni

vers

iteit

Nijm

egen

], [

Erw

in V

an D

er K

rabb

en]

at 0

2:18

09

Dec

embe

r 20

11

would have considered this. 7% of all owners of industrial property state that they have

decided to buy, because good alternatives for leasehold properties appeared to be

absent. Second, evidence from the UK shows that, under different market circumstances,

the commercial industrial property market can be much bigger and “mature”. In the IPD

index for the Netherlands industrial property investments make out only 2.5% (E1110

million) of all real estate investments registered in the index (ROZ/IPD, 2008). In the

IPD index for the UK, 14.6% (E28,630 million) of all registered investments are industrial

property investments (ROZ/IPD, 2008).

4. The Development of Industrial Parks: Present Institutional Order

Before we relate the market outcomes from the previous section to the institutional set-up

of the market, it is important to note that there is not one industrial market. It consists of

different, interrelated market segments in which different goods are produced, each

segment with its own institutional design. The Dutch market in industrial land and indus-

trial property can be divided into five segments (Table 4), which can be clustered in a

market in land (building plots) and a market in (industrial) property.

4.1 Market for Building Plots on Industrial Parks

Since World War II, the development of industrial land (in dedicated industrial parks) in

the Netherlands has mainly been a public affair. The link between public development

and the market outcome for the Netherlands has been made as follows (see also

Needham & Louw, 2006). Dutch municipalities feel responsible to supply industrial

sites in abundance at all times, so as to facilitate and stimulate new economic develop-

ment. In the present situation, they are hardly restricted in allocating land for industrial

uses by provinces or the national government. Municipalities acquire (agricultural) land,

service the land, take care of the necessary infrastructure, re-parcel it into building plots

and sell those plots to end-users. Because many municipalities perceive inter-municipal

competition, there is an oversupply of land for industrial use and low land values in

most regions. It is generally assumed that municipalities charge industrial firms prices

for building plots below the market value. Municipalities are usually satisfied when

Figure 2. Industrial firms: ownership of manufacturing space (the Netherlands; figures 2005).Source: Stec Groep/NVB (2005).

Industrial Land and Property Markets 2135

Dow

nloa

ded

by [

Rad

boud

Uni

vers

iteit

Nijm

egen

], [

Erw

in V

an D

er K

rabb

en]

at 0

2:18

09

Dec

embe

r 20

11

they can cover their costs of making the land available and provide the necessary

infrastructure works. As a consequence, private developers usually do not show much

interest in the development of industrial land and/or industrial parks, neither to sell

plots of land to end-users (industrial firms), nor to develop leasehold industrial property

(and to sell the property subsequently to an institutional investor). Moreover, the present

situation takes away the incentive for industrial firms to build sustainable accommo-

dation or redevelop their industrial property, since there is enough cheap and “fresh”

land available elsewhere.

Manufacturing firms make their own arrangements with building companies to develop

their own properties. Public development is also common in other segments of the Dutch

land market, however, not as dominant as in the case of industrial estates. The underlying

reason seems to be a chicken and egg problem. Are municipalities involved the way they

are because private developers are not so much interested in developing sites for industrial

use? Or are private developers not interested because of the heavy involvement of local

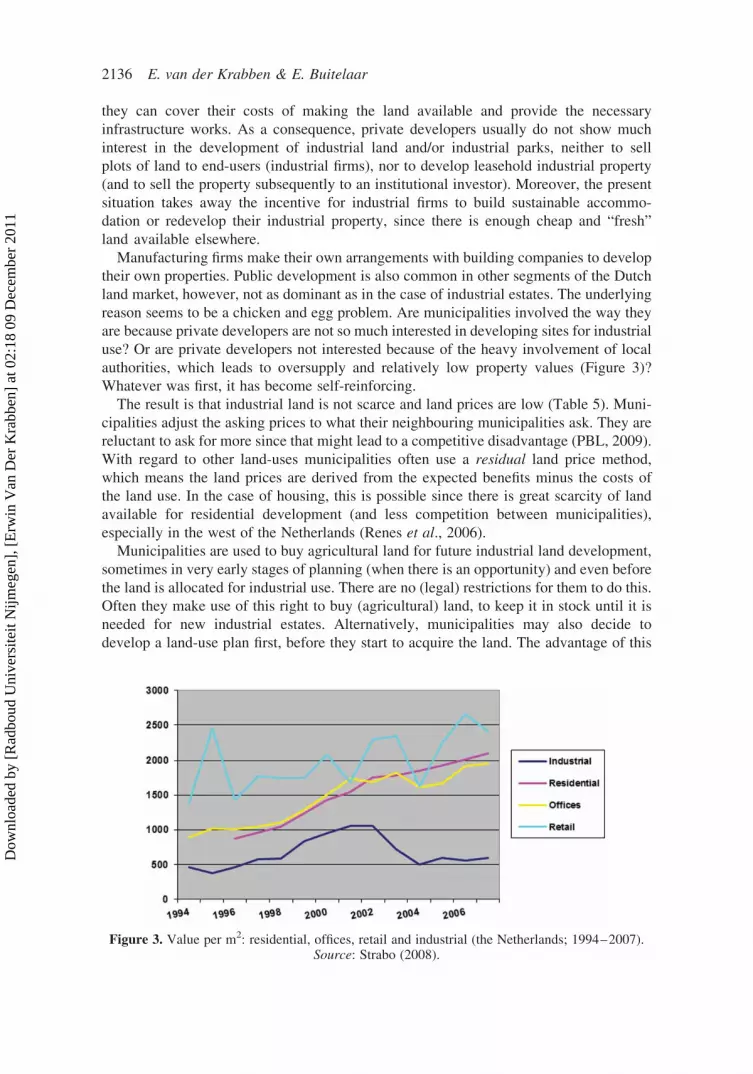

authorities, which leads to oversupply and relatively low property values (Figure 3)?

Whatever was first, it has become self-reinforcing.

The result is that industrial land is not scarce and land prices are low (Table 5). Muni-

cipalities adjust the asking prices to what their neighbouring municipalities ask. They are

reluctant to ask for more since that might lead to a competitive disadvantage (PBL, 2009).

With regard to other land-uses municipalities often use a residual land price method,

which means the land prices are derived from the expected benefits minus the costs of

the land use. In the case of housing, this is possible since there is great scarcity of land

available for residential development (and less competition between municipalities),

especially in the west of the Netherlands (Renes et al., 2006).

Municipalities are used to buy agricultural land for future industrial land development,

sometimes in very early stages of planning (when there is an opportunity) and even before

the land is allocated for industrial use. There are no (legal) restrictions for them to do this.

Often they make use of this right to buy (agricultural) land, to keep it in stock until it is

needed for new industrial estates. Alternatively, municipalities may also decide to

develop a land-use plan first, before they start to acquire the land. The advantage of this

Figure 3. Value per m2: residential, offices, retail and industrial (the Netherlands; 1994–2007).Source: Strabo (2008).

2136 E. van der Krabben & E. Buitelaar

Dow

nloa

ded

by [

Rad

boud

Uni

vers

iteit

Nijm

egen

], [

Erw

in V

an D

er K

rabb

en]

at 0

2:18

09

Dec

embe

r 20

11

strategy is that they can make use of their compulsory purchase powers. However, they

also risk paying a higher price. Property developers can also buy agricultural land or

land allocated for industrial use whenever they like, but they do not have the same infor-

mation about the future land-use plan as the municipality and they do not have the same

legal instruments as the municipality. And even if they have the information, the expected

land value of land allocated for industrial uses does not provide a great incentive for

private developers to buy the land.

Information from the national industrial parks database shows that 73% of all available

building plots on industrial parks is owned and developed by municipalities, while private

developers and semi-public regional development companies own, respectively, 13% and

14% (Table 6).

The development model for privately developed industrial estates is usually identical to

the public development model: building plots are sold to manufacturing firms.

4.2 Property Market Segments

Additionally, four other (existent and potential) market segments can be identified. First, a

small market for new leasehold industrial properties exist, mainly owned by institutional

investors in the logistics sector. Institutional investors show only minor interest in acquir-

ing industrial properties (as in most other countries). The share of industrial properties in

their real estate portfolios amounts only to 2.5% (against 43% residential, 28% retail, 24%

offices and more than 2% mixed use, see IVBN, 2006). Second, in principle, there might

Table 5. Prices per square metre serviced land for residential and industrial uses in 2007

per province (The Netherlands)a

Land prices for housing Land prices for industrial estates

2007 Increase 2003–2007 (%) 2007 Increase 2003–2007 (%)

Groningen 182 25 42 22Friesland 178 28 46 19Drenthe 180 20 58 18Overijssel 266 6 69 216Flevoland 227 30 80 26Gelderland 400 30 145 51Utrecht 638 28 202 4Noord—Holland 552 40 123 29Zuid—Holland 529 40 217 25Noord—Brabant 225 33 69 34Limburg 354 14 88 24Netherlands 348 26 104 17

Source: IBIS/Kadaster; reworked: authors.aNote that the data should be interpreted with care. Both categories contain the prices that individual buyers

(industrial firms, private developers and households) pay to the municipality, that is, in the case municipalities

own the land, service it and sell it off. The prices for industrial land are based on a national database (IBIS), for

which the data are provided by the municipalities. These data are the averages per province of the maximum

asking prices (so no transaction prices) of all municipalities in the province. The transaction prices are likely to be

lower as a result of negotiations and additional conditions. The land prices for housing are the average transaction

prices of serviced land that goes from the municipalities to private developers and individual households.

Industrial Land and Property Markets 2137

Dow

nloa

ded

by [

Rad

boud

Uni

vers

iteit

Nijm

egen

], [

Erw

in V

an D

er K

rabb

en]

at 0

2:18

09

Dec

embe

r 20

11

be a market for new freehold industrial properties (as in the housing sector). However, at

present, this market does not exist and we do not assume that this market segment will

develop significantly in the future. The reason for this is that we expect that it cannot

compete with the market for building plots (end users developing their own premises).

Third, there is a large market for second-hand leasehold industrial properties. The lease-

hold industrial property stock mainly consists of second-hand properties, quite often still

owned by manufacturing firms that used to have the property previously in use. We

suspect that for many owners of those properties, a leasehold construction is the best

they can get. They might prefer to sell, but the interest in buying those properties is

very limited. And finally, there is a market for second-hand industrial properties for

sale. The transferability of industrial properties is limited: only circa 600 transactions

per year, for the whole of the country (Strabo, 2008). Most second-hand properties are

usually let to other industrial firms, instead of sold (because the demand to buy those

properties is small).

5. Analysing and Changing the Present Institutional Order

What can be derived from the previous section is that neither industrial land nor industrial

property is valued highly. It is therefore that the price mechanism in these two market seg-

ments is not working well: there is hardly a market in industrial property and the industrial

land market is dominated by local authorities that supply land cheaply and in abundance,

hence generating negative externalities. But it is also vice versa: because these markets are

ill-defined, the good (land and property) gets a low value. In this section, we make sugges-

tions to improve the working of both market segments.

5.1 Internalizing Externalities

Both the urban sprawl problems (see Section 3) and the pace in which the deterioration of

existing industrial estates takes place can be seen as negative externalities. In Section 3, it

has been argued that the present structure of the industrial land market leads to the allo-

cation of more land for industrial use than necessary. In economic terms, we consider

this contribution to urban sprawl as an externality. Likewise, the increased deterioration

of existing industrial properties can also be seen as an externality caused by the develop-

ment of new industrial parks (because it takes away the incentive for industrial firms to

Table 6. Available land on industrial parks: public, private and semi-public development,

by region (The Netherlands; figures 2007)

Municipality Private developer Public–private partnership/semi-public

Available land (in hectares)North 1987 (87%) 204 (9%) 106 (4%)East 1782 (76%) 241 (10%) 327 (14%)West 2639 (70%) 550 (15%) 578 (15%)South 1514 (63%) 435 (18%) 473 (20%)Netherlands total 7922 (73%) 1430 (13%) 1484 (14%)

Source: IBIS (2008); reworked: authors.

2138 E. van der Krabben & E. Buitelaar

Dow

nloa

ded

by [

Rad

boud

Uni

vers

iteit

Nijm

egen

], [

Erw

in V

an D

er K

rabb

en]

at 0

2:18

09

Dec

embe

r 20

11

redevelop their properties).8 In property rights theory, externalities are considered to be

problems of undeveloped markets/institutions: “(t)hey arise when resources have a

value, but are ill-defined in terms of property rights and as a result of proprietary

ambiguity, remain unpriced and inefficiently allocated” (Webster & Lai, 2003, p. 103).

The solution to an externality problems is then “to assign property rights, and the effi-

ciency of any particular solution depends on the externality costs saved less the costs of

creating institutions that create the property rights” (Webster & Lai, 2003, p. 104).9

The main obstacle to the internalization of externalities is probably the difficulty to price

them. What are the costs of urban sprawl and what are the costs of the deterioration of both

private properties and public space caused by the abundant supply of cheap “fresh” indus-

trial land elsewhere? Though not easy to solve, there are different ways to deal with this.

First, (public or private) developers could be obliged to pay a fixed redevelopment fee

when developing a new industrial park (based on some kind of national government

measure), meant to finance (part of) the restructuring costs of obsolete industrial parks.

Municipalities within a region may come to an agreement about the size of this fee.10

The residual claimants11 of new industrial parks are made partly responsible of existing

parks and the regeneration thereof. Most likely, the costs of the development of industrial

parks will increase. However, to cover those costs, developers can increase building plot

prices for end-users (as long as it is a general rule, for all new developments). Second,

since Dutch planning tradition allows strong interventions by the national government,

a national government policy measure could be to introduce new regulation with

respect to the contents of local land-use plans (to increase spatial and building quality

in such a way that externalities with regard open spaces are reduced) or to encourage muni-

cipalities to develop industrial parks in existing urban areas only, as part of an urban rede-

velopment project (brownfield target). When property rights over the externalities are

addressed and defined, it will make public and private developers more reluctant to

develop industrial parks in “vulnerable” areas, assuming that the costs to minimize the

(effects of the) externality problems are substantial.

One of the indirect effects of both suggested interventions will be that for industrial

firms that relocate to a new location real-estate costs (and thus overall production costs)

increase, while they are usually not able to pass this on to their clients. Even though

there is some room for an increase in real-estate costs, this means that the price of the

externality cannot be increased infinitely12 Another indirect effect will be that the compe-

titiveness of properties on existing industrial parks improves, encouraging industrial firms

to invest in their existing properties, and probably preventing or postponing relocation to

a new industrial park.

5.2 How to Change Suppliers?

One way of characterizing the market for industrial land in the Netherlands (and indeed in

many other European countries as well) is to say that the production of industrial land is

treated by municipalities as a (semi-)public good. Property rights economist Barzel argues

that the market fails to take care of these because the property rights over these goods are

ill-defined, and therefore lie in the so-called public domain (Barzel, 1997). Public goods

(i.e. open access goods) are goods that are unpriced, not necessarily because they do

not have a value, but because of the high costs of assigning property rights, the lack of

political will or the technological unfeasibility to make them tradable. The result of this

Industrial Land and Property Markets 2139

Dow

nloa

ded

by [

Rad

boud

Uni

vers

iteit

Nijm

egen

], [

Erw

in V

an D

er K

rabb

en]

at 0

2:18

09

Dec

embe

r 20

11

proprietary ambiguity is that these resources remain unpriced and are therefore

inefficiently allocated (Webster & Lai, 2003). What follows from this is that solving

this proprietary ambiguity and taking them out of the public domain, would result in a

better developed and operating market, which is expected to result in more efficient use

and allocation of resources.

A prerequisite for a competitive market is the privatization of property rights. But not

every good is or can become a private good. What are the economic conditions for

privatizing goods? Figure 4 (based on Webster & Lai, 2003) shows a typology of goods

ranging from pure private goods (A) to pure public goods (D). It shows two basic criteria:

(non-) excludability in supply and (non-) rivalry in consumption. Excludability refers to

the right of the owner to consume the goods or resource exclusively, which hence excludes

all others. Rivalry refers to the situation where there is competition between suppliers and

between users. Lindblom (2001) says about the scarcity condition: “If a performance

object is not scarce, offering it will induce no response. [. . .] If available without

constraint—if everyone has all of each that he wants—no one would offer any for sale,

and no one would buy.” So constraints—rules—can make goods scarcer, which leads to

higher value and price.

There is no public domain problem with goods of type A. In case the consumption of

such goods is rival, it makes them scarce resources. This scarcity leads to a point where

the value of these resources exceeds the costs of assigning exclusive property rights.

This is, for instance, the case with new houses, which are pure private goods because

they are scarce and because private property rights have been assigned. So, these goods

could be made exclusionary and captured from the public domain. Goods of type C are

rival, but non-excludable. Actually few rival goods are non-excludable. If they are, the

reasons might be institutional (including cultural and political reasons) or technological.

It is, therefore, a transitional category, meaning that all the economic conditions for pri-

vatization are there, institutional or political inertia impair this. (Access to) road infrastruc-

ture is also for a long time considered as rival, but non-excludable, but belongs now to this

transitional category. For, congestion has made well-passable roads a rival good, while

innovative toll systems are being developed to make them excludable as well. Category

D consists of pure public goods. Although in practice there are examples of such goods,

they are also rare. As we saw with type C, almost every good can be made excludable.

In addition, many goods that are presumed to be non-rival are (becoming) rival (and are

Figure 4. Typology of public goods.Source: Webster and Lai (2003).

2140 E. van der Krabben & E. Buitelaar

Dow

nloa

ded

by [

Rad

boud

Uni

vers

iteit

Nijm

egen

], [

Erw

in V

an D

er K

rabb

en]

at 0

2:18

09

Dec

embe

r 20

11

therefore transitional as well). For instance, clean air and fresh water, which are tradition-

ally not seen as scarce goods, are becoming scarce. Type B goods (which can also be

transitional) are excludable but non-rival. McNutt (2000, p. 930) regards club goods as

type B resources, as people can be excluded (e.g. by requiring a membership), but are

not rival like the road capacity within a gated community.

We could also say that industrial land in the Netherlands is a type B good.13 Exclusive

property rights are assigned over plots of industrial land, but its use is apparently not scarce

enough to attract many private developers. Different interventions in the institutional order

can be considered to improve “rivalry” on the industrial land market. The THB has

suggested to increase scarcity with respect to the supply of building plots on industrial

parks, by reducing the (municipal) plans for new industrial parks. This can be done in

two ways. The first is to limit supply by a stricter regulation of the number and size of

industrial parks (command-and-control). To achieve this, the responsibility for the plan-

ning of new industrial parks should be transferred from the municipalities to the provinces

(THB, 2008). It is assumed, probably correctly, that consequently building plot prices will

go up, which might attract more private developers to develop industrial land. Though

the result might be a larger variety of suppliers, this intervention is not without limits.

Tsolacos (1997), for instance, has reported that a shortage of industrial land appeared to

be a serious threat to economic growth in the South East of England.

Second, local public supply of land should be reduced since it distorts the working of the

price mechanism. Owing to the earlier mentioned perception of inter-municipal compe-

tition and the “soft budget constraints” of public organizations municipalities offer land

against prices below what industrial firms are able to pay. Private developers would only

supply land if the benefits outweigh the costs. Obviously, prices would go up which is dis-

advantageous for the industrial firms that want to buy building plots. But the price would

be a better mechanism to trade-off the preferences of the demanders (the manufacturing

firms) and those of the suppliers (the private developers). This would also affect the

market for industrial property (Section 5.2). However, preventing private monopolies

(instead of public) at the supply side would be an important concern to allow the market

to function as efficient as possible.

5.3 High-end Leasehold Property

The market for industrial property consists of four different segments (Section 4), but we

assume here that industrial firms will show most interest in increased opportunities for

high-standard leasehold properties. In Section 3, we have referred to a survey by Stec

Groep/NVB (2005) showing that 7% of all owners of industrial property would have pre-

ferred a leasehold construction, if available. Though a small percentage, it nevertheless

implies a substantial (potential) annual demand for commercial properties. Between

1986 and 2009, the size of newly constructed industrial property has varied between 3.3

and 9 million m2 per year (NVB, 2010). It would imply that the potential annual demand

for commercial industrial property might vary between 230,000 and 630,000 m2 per

year.14 Apparently, the right economic conditions are lacking to fulfil this potential

demand. We briefly look at the possibilities to change those conditions.

The first condition is that there must be sufficient suppliers. In principle, Dutch and

foreign institutional investors and investment funds can fill this gap, since investments

in commercial industrial property are to a large extent similar to investments in alternative

Industrial Land and Property Markets 2141

Dow

nloa

ded

by [

Rad

boud

Uni

vers

iteit

Nijm

egen

], [

Erw

in V

an D

er K

rabb

en]

at 0

2:18

09

Dec

embe

r 20

11

property segments. Higher land and property values are key to that. The above-mentioned

suggestions with respect to the industrial land market may lead to that.

The second condition is that sufficient market information must be available to investors,

to reduce uncertainty and improve transparency. Part of this transparency is already

provided through the ROZ/IPD index, the (inter)national benchmark for commercial

property investments (ROZ/IPD, 2008).

The third condition is that the transferability of industrial property should be improved.

Since building standardization processes with respect to industrial property are less

developed compared with the residential, office and retail market—industrial firms

often prefer tailor-made buildings—suppliers of industrial property usually face larger

re-letting risks. Needham (2006b) has suggested that the conditions in tenancy contracts

with respect to subletting (which is usually excluded) must be held responsible for the,

on average, rather short contract terms for industrial property (5–10 years contracts),

instead of sometimes 20 to 25 years contracts for industrial property in the UK. Changing

those conditions—there are no legal restrictions—might help to increase the attractiveness

of leasehold property for industrial firms.

Table 7 summarizes the suggested interventions related to the undesired market out-

comes that have been identified in this paper.

6. Concluding Remarks

The central theme of this paper has been the relation between market processes and market

institutions on the one hand and market outcomes with respect to land and property

Table 7. Undesired market outcomes and suggested interventions

Undesired market outcomes Type of market failure Suggested interventions

1. Deterioration of industrialproperties and industrial parks

Misprized externalitiesin industrial landmarket

Pricing of externalities:Developers of industrial parkpay redevelopment feeStrict quality requirements fornew industrial parks

2. Oversupply of industrial land Inelastic price response; Regional co-ordination ofindustrial park planning;

Misprized externalitiesin industrial landmarket

Pricing of externalities:Costs of urban sprawl

3. Low building plot prices andlimited number of suppliers ofindustrial land

Non-competitive market Regional co-ordination ofindustrial parks planning;

Reduction of the rights ofmunicipalities to developindustrial parks

4. Absence of market for high-standard leasehold industrialproperty

Non-competitivemarket;

Pricing of externalities(combination of 1 and 2);

Misprized externalitiesin industrial landmarket

Change conditions in tenancycontracts;

Regional co-ordination of high-end industrial parks planning

2142 E. van der Krabben & E. Buitelaar

Dow

nloa

ded

by [

Rad

boud

Uni

vers

iteit

Nijm

egen

], [

Erw

in V

an D

er K

rabb

en]

at 0

2:18

09

Dec

embe

r 20

11

markets on the other hand. We have systematically analysed for the Netherlands the out-

comes of the industrial land and property market, the relationship between the market

outcome and its institutional order and the changes that could be made with respect to

the institutional design of the market so as to allow it to function more smoothly and offer-

ing possibilities to improve the outcome.

In Section 2, we have tried to make clear that institutional economic theory offers a solid

basis for this task, because it provides rules how to choose for interventions in the insti-

tutional order (the definition and allocation of property rights and/or the reduction of trans-

action costs). Three remarks must be made with respect to the theoretical position taken in

this paper. First, we have brought forward arguments that institutional economic theory

offers explanations regarding the relation between the institutional order and market out-

comes that go further than the welfare economic treatment of “government” on the one

hand and “market” on the other hand. Second, this paper holds no proof that the proposals

to change market institutions in order to change market outcomes, based on theoretical

considerations, will work out well. As for every theoretical approach, these proposals

must still be tested empirically. Three “effects” are particularly uncertain: the attractive-

ness for the development industry to invest in industrial property (under different market

conditions), the extent to which industrial firms will increase maintenance investments in

existing property when prices of building plots on new industrial parks will go up, and the

extent to which industrial firms are willing to pay for higher quality properties and more

flexibility. Third, the argument for interventions in property rights regimes (instead of

the welfare economic-based government interventions) must not be confused with a liber-

tarian approach—less government, more market—to spatial planning. We do not suggest

“more market”, but a better functioning one. A market needs serious government control

to be able to function efficiently. We have tried to make clear that various interventions in

market institutions can be considered to change market outcomes.

We conclude with some remarks regarding the outcomes of the case study of the devel-

opment of industrial parks in the Netherlands. The case study has been based on empirical

evidence (secondary data analysis) of undesired market outcomes. We have classified

them as “undesired”, based on economic arguments and because they are not in line

with the national spatial policy goals. These market outcomes do not necessarily imply

that individual industrial firms face severe efficiency problems. There is not much

empirical proof of efficiency problems for individual firms, nor is there much evidence

of firms complaining about it. Contrarily, the characteristics of the present market

guarantee industrial firms usually cheap and sufficient building plots on dedicated indus-

trial parks and the possibility to buy additional land for future expansions.

The suggestions made in the paper to intervene in market institutions are based both on

theoretical arguments and on the current political debate in the Netherlands with respect to

the issue. This political debate focuses particularly on the problems of deterioration, the

externalities that occur and on the necessary interventions in this market. Regarding the

necessary interventions, there seems to be a certain consensus (in the political debate)

that the industrial land and property market will benefit from more market, less govern-

ment (MinVROM, 2008; THB, 2008).

Finally, we believe that the market outcomes in the Netherlands do not differ so much

from other (Western European) countries. The main distinction between the Netherlands

and other countries, perhaps, is the (political) attention that is given to the subject (which

seems to be less in other countries).

Industrial Land and Property Markets 2143

Dow

nloa

ded

by [

Rad

boud

Uni

vers

iteit

Nijm

egen

], [

Erw

in V

an D

er K

rabb

en]

at 0

2:18

09

Dec

embe

r 20

11

Notes

1. Here we look particularly at the government as a regulator and legislator not as market actor (e.g. a land

developer) comparable to any other market actor. We recognize that we cannot speak of “the govern-

ment”, but that it consists of a variety of public bodies. In our case study we will particularly distinguish

between the local, regional and national level.

2. This counts for both old institutional economics and new institutional economics (Buitelaar, 2007).

3. In this paper, we distinguish between industrial land (land that has been made available for industrial

use), industrial properties (properties/buildings that are in use by industrial firms) and industrial parks

(areas that have been designated for industrial use and give room to a certain number of firms with

their properties). Industrial land is, in most cases, only available at dedicated industrial parks. Some

of the industrial parks may also contain commercial functions (offices, retail) and may then come

close to what we would call a business park. The empirical work in this paper refers to all industrial

parks (some of which are still under development) that have been defined as such in a national database

that we have used. Those parks have in common that the primary use is industrial.

4. Note that info in IBIS is provided by municipalities. There is some discussion about the rightness of the

data, because municipalities are believed sometimes to exaggerate the problem of deteriorated industrial

parks for strategic reasons (i.e. to receive more national governments grants).

5. We do not know which percentage of those plans have already been implemented.

6. On 1 January 2007, 84% of all available land on industrial estates was owned by municipalities. Only

16% of the available building plots was owned by private companies (PBL, 2009).

7. This does not mean that those properties do not meet with industrial firms’ demand. However, we

suppose that the quality of the major part of those properties is relatively poor. This is supported by evi-

dence from rent levels on the industrial property market, which are low (for 42% of leasehold industrial

property, rent levels are even below E50 per m2, per year) (Stec Groep/NVB, 2005).

8. It is hard to prove whether these developments can really be seen as externalities (which is the case with

most externalities). However, at least the externalities argument seems to be supported by the national

Taskforce Report and the Cabinet’s response to it (THB, 2008; TK, 2008).

9. For instance, it may be more efficient to assign property rights to the inconvenience caused by an airport

and leave the solution to negotiations between the airport and its neighbours, than to regulate this by

some kind of government intervention. In case of well-assigned property rights to such nuisance, the

airport can negotiate with its neighbours about, e.g. financial compensation, the reduction of nuisance

or, in an extreme situation, decide to move to another location if the size of the financial compensation

would be insurmountable for the airport. If the negotiations do not lead to an agreement, the parties involved

can go to court.

10. We are aware of at least one example of such a regional agreement in the Netherlands. A number of

municipalities in the Achterhoek (in the eastern part of the country) have agreed to pay a redevelopment

fee for every hectare of newly developed industrial land. The fees go to a regional fund that will co-

finance restructuring projects for existing industrial parks.

11. Barzel (1997, p. 3) defines the principle of residual claimancy as follows: “(t)he residual claimant to, say,

an apartment house is its economic owner in that he is able to gain (here by exchange) from an increase

in the value of the building, whereas he loses from a reduction in that value. Being its owner, he is

motivated to take any action that will, net of its cost, increase the value of the property”.

12. Earlier research showed that on average the investments in land and property are only 1.8% of the total

investments by industrial firms.

13. The analysis in Sections 2 and 3 shows that industrial land is not a pure type B good, but is in fact treated

by municipalities as such.

14. In the Dutch perspective, the size of this potential demand is substantial. In comparison, the size of newly

constructed office space varies between 750,000 and 1,500,000 m2 per year, while the size of newly

constructed retail space amounts to circa 250,000 m2 per year.

References

Alberini, A., Longo, A., Tonin, S., Trombetta, F. & Turvani, M. (2005) The role of liability, regulation and

economic incentives in brownfield remediation and redevelopment: Evidence from surveys of developers,

Regional Science and Urban Economics, 35(4), pp. 327–351.

2144 E. van der Krabben & E. Buitelaar

Dow

nloa

ded

by [

Rad

boud

Uni

vers

iteit

Nijm

egen

], [

Erw

in V

an D

er K

rabb

en]

at 0

2:18

09

Dec

embe

r 20

11

Alchian, A. A. & Demsetz, H. (1973) The property rights paradigm, Journal of Economic History, 33(1),

pp. 16–27.

Alker, S., Joy, V., Roberts, P. & Smith, N. (2000) The definition of brownfield, Journal of Environmental

Planning and Management, 43(1), pp. 49–69.

Anderson, E. & Catignon, H. (2008) Firms and the creation of new markets, in: C. Menard & M. M. Shirly (Eds).

Handbook of New Institutional Economics, pp. 401–431 (Berlin/Heidelberg: Springer).

Barzel, Y. (1997) Economic Analysis of Property Rights (Cambridge, MA: Cambridge University Press).

Bromley, D. W. (1991) Environment and Economy: Property Rights and Public Policy (Oxford: Blackwell).

Buitelaar, E. (2003) Neither market nor government. Comparing the performance of user rights regimes, Town

Planning Review, 74(3), pp. 315–330.

Buitelaar, E. (2007) The Cost of Land Use Decisions. Applying Transaction Cost Economics to Planning &

Development (Oxford: Blackwell).

Buitelaar, E., van der Heijden, R. & Argiolu, R. (2007) Managing traffic by privatisation of road capacity: A

property rights approach, Transport Reviews, 27(4), pp. 699–713.

Casson, M. (1982) The Entrepreneur: An Economic Theory (Oxford: Martin Robertson).

CBS (2004) Investeringen in vaste activa in de nijverheid (Voorburg: Centraal Bureau Voor de Statistiek).

Available at www.statline.nl (accessed 1 June 2010).

Coase, R. H. (1960) The problem of social cost, Journal of Law and Economics, 3(1), pp. 1–44.

Coase, R. H. (1988) The Firm, the Market and the Law (Chicago, IL: University of Chicago Press).

Cook, G. (1989) Local authorities and industrial property markets, Property Management, 7(1), pp. 3–12.

Evans, A. W. (2004) Economics, Real Estate & the Supply of Land (Oxford: Blackwell Publishing).

Fothergill, S., Monk, S. & Perry, M. (1987) Property and Industrial Development (London: Hutchinson).

Giussani, B., Hsia, M. & Tsolakos, S. (1992) A comparative analysis of the major determinants of office rental

values in Europe, Journal of Property Valuation and Investment, 11(1), pp. 157–173.

Gorman, H. S. (2005) Brownfields in historical context, Environmental Practice, 5(1), pp. 21–24.

Heberle, L. & Wernstedt, K. (2006) Understanding brownfields regeneration in the US, Local Environment,

11(5), pp. 479–497.

Henneberry, J. (1988) Conflict in the industrial property market, Town Planning Review, 59(3), pp. 241–262.

Henneberry, J. (1996) Property Market Structure and Behaviour: The Interaction of Use and Investment Sectors

and its Impact on Urban and Regional Development (London: The Cutting Edge, RICS Research).

Hodgson, G. M. (2002) The legal nature of the firm and the myth of the firm-market hybrid, International Journal

of the Economics of Business, 9(1), pp. 37–60.

Hodgson, G. M. (2004) The Evolution of Institutional Economics: Agency, Structure and Darwinism in American

Institutionalism (London: Routledge).

IBIS (2008) IBIS Werklocaties (Den Haag: MinVROM).

IVBN (2006) De vastgoedbeleggingsmarkt in Nederland in 2006 (Voorburg: IVBN).

Jones, C. (2005) A regional perspective on the impact of the privatisation of the UK public industrial property

stock, Environment and Planning C: Government and Policy, 23(1), pp. 123–139.

van der Krabben, E. (2009) A property rights approach to externality problems: Planning based on compensation

rules, Urban Studies, 46(13), pp. 2869–2890.

van der Krabben, E. & Lambooy, J. (1993) A theoretical framework for the functioning of the Dutch property

market, Urban Studies, 30(8), pp. 1381–1397.

Lai, L. W. C. (1997) Property rights justifications for planning and a theory of zoning, Progress in Planning,

48(3), pp. 161–246.

Lai, L. W. C. (2007) The problem of social cost: The Coase theorem and externality explained, Town Planning

Review, 78(3), pp. 335–368.

Lai, L. W. C. & Hung, C. W. Y. (2008) The inner logic of the Coase theorem and a Coasian planning research

agenda, Environment and Planning B: Planning and Design, 35(2), pp. 207–226.

Levacic, R. (1991) Markets and government: An overview, in: G. Thompson, J. Frances, R. Levacic & J. Mitchell

(Eds) Markets, Hierarchies & Networks: The Coordination of Social Life, pp. 35–47 (London: Sage).

Lindblom, C. E. (2001) The Market System. What it is, How it Works and What to Make of It (New Haven, CT:

Yale University Press).

Loasby, B. J. (2000) Market institutions and economic evolution, Journal of Evolutionary Economics, 10(3),

pp. 297–309.

Louw, E. & Bontekoning, Y. (2007) Planning of industrial land in the Netherlands: Its rationales and conse-

quences, Tijdschrift voor Economische en Sociale Geografie, 98(1), pp. 121–129.

Industrial Land and Property Markets 2145

Dow

nloa

ded

by [

Rad

boud

Uni

vers

iteit

Nijm

egen

], [

Erw

in V

an D

er K

rabb

en]

at 0

2:18

09

Dec

embe

r 20

11

Louw, E., Needham, B., Olden, H. & Pen, C. J. (2004) Planning van bedrijventerreinen (Den Haag: Sdu uitgevers).

MacLennan, D. & More, A. (1997) The future of Social Housing; key economic questions, Housing Studies,

12(4), pp. 531–547.

MacLennan, D. & More, A. (1997) The future of Social Housing: Key economic questions, Housing Studies,

12(4), pp. 531–547.

McCarthy, L. (2002) The brownfield dual land-use policy challenge: Reducing barriers to private development

while connecting reuse to broader community goals, Land Use Policy, 19(4), pp. 287–296.

McNutt, P. (2000) Public goods and club goods, in: B. Bouckaert & G. de Geest (Eds) Encyclopedia of Law and

Economics, Vol. I: The History and Methodology of Law and Economics, pp. 927–951 (Cheltenham: Edward

Elgar).

Meyer, P. B. & Lyons, T. S. (2000) Lessons from private sector brownfield redevelopers, Journal of the American

Planning Association, 66(1), pp. 46–57.

MinEZ (2004) Actieplan bedrijventerreinen (Den Haag: Ministerie Economische Zaken).

MinVROM (2007) Een structuurvisie voor de “Panorama’s en de snelwegzone”, Brief aan Tweede Kamer der

Staten Generaal, The Hague.

MinVROM (2008) Landscape Cluttering. Available at www.vrom.nl/pagina.html?id=37396 (accessed 1 June

2010).

Needham, B. (2006a) Planning, Law and Economics: The Rules We Make for Using Land (London: Routledge

Taylor & Francis Group).

Needham, B. (2006b) Een andere taakverdeling. Privaatrechtelijke regels voor bedrijventerreinen, S&RO, 87(3),

pp. 40–43.

Needham, B. & Louw, E. (2006) Institutional economics and policies for changing land markets: The case of

industrial estates in the Netherlands, Journal of Property Research, 23(1), pp. 75–90.

NVB (2010) Thermometer Bedrijjfsruimten (Voorburg: Nederlandse Vereniging van Bouwondernemers).

Olden, H. (2010) Uit voorraad leverbaar. De overgewaardeerde rol van bouwrijpe grond als vestigingsfactor

bij de planning van bedrijventerreinen (Utrecht: GeoMedia).

van Oort, F., Ponds, R., van Vliet, J., van Amsterdam, H., Declerck, S., Knoben, J., Pellenbarg, P. & Weltevreden, J.

(2007) Achtergronden: Verhuizing van bedrijven en groei van werkgelegenheid (Rotterdam: NAi Uitgevers).

Pennington, M. (2000) Planning and the Political Market (London: Athlone Press).

Pigou, A. C. (1920) The Economics of Welfare (London: MacMillan).

PBL (Planbureau Voor de Leefomgeving) (2009) De toekomst van bedrijventerreinen: van uitbreiding naar

herstructurering (Den Haag: PBL).

Polanyi, K. (1957) The Great Transformation (Boston, MA: Beacon Press).

Renes, G., Thissen, M. & Segeren, A. (2006) Betaalbaarheid van koopwoningen en het ruimtelijk beleid

(Rotterdam: NAi Uitgevers).

ROZ/IPD (2008) Vastgoed Jaarindex 2007. Available at www.rozindex.nl (accessed 1 June 2010).

Ruimtelijk Planbureau (2006) Bloeiende bermen. Vestedelijking langs de snelweg (Rotterdam: NAi Uitgevers).

Simons, R. & Jaouhari, A. E. (2001) Local government intervention in the brownfields arena, Economic

Development Commentary, 25(3), pp. 12–18.

Stec Groep/NVB (2005) Bedrijfsruimtegebruikers in beeld (Voorburg: NVB).

STOGO (2007) Beleid voor bedrijventerreinen in Vlaanderen, Duitsland, Verenigd Koninkrijk en Frankrijk

(Utrecht: STOGO).

Strabo (2008) Vastgoedtransactie Informatiesysteem. Available at www.strabo.nl

THB (2008) Kansen voor Kwaliteit, een ontwikkelingstrategie voor bedrijventerreinen (Den Haag: Advies van de

Taskforce (her)ontwikkeling bedrijventerreinen aan Minister van VROM en Minister van EZ).

TK (2008) Kabinetsreactie Taskforce (her)ontwikkeling bedrijventerreinen, Tweede Kamer 2007–2008, The

Hague, pp. 31253–31258.

Tsolacos, S. (1997) A case study of industrial property development in South Hampshire, Journal of Property

Research, 14(3), pp. 211–236.

VROM-Raad (2006) Werklandschappen: een regionale strategie voor bedrijventerreinen (Den Haag: VROM-

Raad).

Webster, C. J. (1998) Public choice, Pigovian and Coasian Planning Theory. Urban Studies, 35(1), pp. 53–75.

Webster, C. J. & Lai, L. W. C. (2003) Property Rights, Planning and Markets: Managing Spontaneous Cities

(Cheltenham: Edward Elgar).

Williamson, O. E. (1975) Markets and Hierarchies (New York: The Free Press).

Zhu, J. M. (2000) The impact of industrial land use policy on industrial change, Land Use Policy, 17(1), pp. 21–28.

2146 E. van der Krabben & E. Buitelaar