Embed Size (px)

Citation preview

Investor presentation

January 2011

Nordic Mining ASA | N-0250 Oslo | Norway | Tel +47 22 94 77 90 | Fax +47 22 94 77 01 | Org. no 989 796 739 | [email protected]

E ��������� ��� ���������� �� ���� ��� �������� ��� ������

1

Disclaimer

This presentation (the “Presentation”) has been prepared solely for information purposes in connection with the contemplated issue of shares in Nordic Mining ASA (“NOM” or the “Company”) and is being furnished by NOM to a limited number of parties (the “Recipients”) who have a potential interest in subscribing shares in the Company.

The Presentation is strictly confidential and any disclosure, use, copying and circulation of this Presentation is prohibited without the consent from the Company. gThe information contained in this Presentation does not constitute or form part of, and should not be construed as, an offer or invitation to subscribe for or purchase the securities discussed herein in any jurisdiction. Neither this Presentation nor any part of it shall form the basis of, or be relied upon in connection with any offer, or act as an inducement to enter into any contract or commitment whatsoever. No representation or warranty is given, express or implied, as to the accuracy of the information contained in the Presentation.

This Presentation contains certain forward-looking statements relating to the business, financial performance and results of the Company and/or the industry in which it operates Forward-looking statements concern future circumstances and results and other statements that are not historical facts The forward-lookingwhich it operates. Forward looking statements concern future circumstances and results and other statements that are not historical facts. The forward looking statements, contained in this Presentation, including assumptions, opinions and views of the Company or cited from third party sources are solely opinions and forecasts which are uncertain and subject to risks. A multitude of factors can cause actual events to differ significantly from any anticipated development. Neither the Company, Carnegie (the "Advisor") nor any of its parent or subsidiary undertakings or any such person’s officers or employees guarantee that the assumptions underlying such forward-looking statements are free from errors and omissions nor does any of them accept any responsibility for the future accuracy of the opinions expressed in this Presentation or the actual occurrence of the forecasted developments.

Th i f ti t i d h i h b d t i t th R i i t i ki th i l ti th C d d t t t t i llThe information contained herein has been prepared to assist the Recipients in making their own evaluation on the Company and does not purport to contain all information that they may desire. In all cases, the Recipients should conduct their own investigation and analysis of the Company, its business, prospects, results of operations and financial condition as well as any other information the Recipients may deem relevant. The Advisor has not independently verified any of the information set forth herein, including any statements with respect to projections or prospects of the Company or the assumptions on which such statements are based, and does not undertake any obligation to do so. Neither the Company nor the Advisor makes any representation or warranty, express or implied, as to the accuracy or completeness of this Presentation or of the information contained herein and neither of such parties (including without limitation their directors, employees, representatives and advisors) shall have any liability for the information contained in, or any omissions from, this Presentation, nor f f th itt l t i l i ti t itt d t th R i i t (i l di ith t li it ti it di t l t ti dfor any of the written, electronic or oral communications transmitted to the Recipients (including without limitation its directors, employees, representatives and advisors).

Neither the receipt of this Presentation by any Recipients, nor any information contained herein or supplied herewith or subsequently communicated in written, electronic or oral form to any person in connection with the contemplated issue of shares in the Company constitutes, or shall be relied upon as constituting, the giving of investment advise by the Advisor or anyone else to any such person. Each person should make their own independent assessment of the merits of investing in the Company and should consult their own professional advisors. By receiving this Presentation you acknowledge and agree that you will be solely g p y p y g y g g y yresponsible for your own assessment of the market and the market position of the Company and that you will conduct your own analysis and be solely responsible for forming your own opinion of the potential future performance of the Company’s business.

The Presentation is at the date hereof. Neither the delivery of this Presentation nor any further discussions in relation to the Company or the contemplated issue of shares with any of the Recipients shall, under any circumstances, create any implication that there has been no change in the affairs of the Company since the date of this Presentation.

Outline

1. Company background and overview

2. Engebø - Titanium project

3. Keliber - Lithium project

4. Gudvangen Stein - Anorthosite production

5. Summary

3

Strategic position in high-end mineralsCompany background and overview

Ni, PGM

Engebøfjellet (100%) Titanium Rutile/Garnet

Resource estimate 383 mill. tons

Mineable ore estimate 250 mill. tons

Lifetime 50 years

Will be Europe’s largest producerof natural rutile (TiO2)

Mo

Si

Gudvangen Stein (100%) Anorthosite

Resource estimate >500 mill. tons

Mineable ore estimate >400 mill. tons

Keliber Oy (68%) Lithium

Resource estimate >3 mill. tons

Mineable ore estimate >1.8 mill. tonsMineable ore estimate >400 mill. tons

Current production 200 000 tpaLifetime >10 years

Will be Europe’s first producer oflithium carbonate

Mine in operation – upside potentialin new applications

Aggregates,sand and gravel

Coal Iron ore

Industrial metals & mineralsLow-end

Industrial metals & mineralsHigh-end

Preciousmetals

Diamonds

Future projects; High-purity quartz deposit in western Norway being analyzed – Molybdenum project at Kleivan/Vest-Agder Norway -Nickel, PGE project in Finnmark Norway

Why Nordic Mining?

Company background and overview

• Global push in demand for strategic resources (minerals and metals)

• Norway and the Nordic region is underexplored and contain world class depositsNorway and the Nordic region is underexplored and contain world class deposits

• Excellent logistics from the Nordic region to EU, Middle East and US east coast

L t h fl t ti l th h tt ti i d t i l d l t• Long term cash flow potential through attractive industrial developments

Mining exploration in Nordic countriesg p

5

Solid team and shareholder structure

Company background and overview

Ivar S. Fossum, CEO20 i f t iti i

Largest shareholdersManagement teamAs per 15 December 2010

Number of20 years experience from management positions in Hydro, Yara and FMC Technologies

Lars K. Grøndahl, CFOMore than 20 years experience from industrial

Rank Name of shareholderNumber of shares

%

1 DAG DVERGSTEN AS 8 469 145 6,7 %

2 SKAGEN VEKST 7 915 000 6,3 %

3 HOLBERG NORGE 7 118 400 5,7 %More than 20 years experience from industrial management positions, i.a. Aker Group, Scancem Group and Heidelberg Cement

Ottar Nakken, VP CommercialF Vi P id t H d A i N th A i d

4 FINNISH INDUSTRY INVESTMENT LTD. 6 000 000 4,8 %

5 JP MORGAN CHASE BANK NORDEA 5 040 454 4,0 %

6 NORDNET BANK AB 3 836 941 3,1 %

7 DYBVAD CONSULTING 3 539 788 2,8 %

8 MP PENSJON 3 270 000 2 6 %Former Vice President Hydro Agri North America and COO of Jebsen Management

Paul I. Norkyn, VP Mining OperationsFormer R&D Manager in Titania (Kronos Group), 30 years

8 MP PENSJON 3 270 000 2,6 %

9 GRØNDAHL LARS K. 2 544 851 2,0 %

10 SOLON AS 2 242 333 1,8 %

11 SNATI AS 2 201 628 1,8 %

12 NORDEA BANK PLC FINL CLIENTS 1 831 066 1,5 %Former R&D Manager in Titania (Kronos Group), 30 years experience from the Titania, Sydvaranger, Bleikvassli and Grong mining operations

Mona Schanche, Exploration Manager

13 DNO INVEST AS 1 806 442 1,4 %

14 DYBVAD AUDSTEIN 1 798 184 1,4 %

15 VPF NORDEA SMB 1 747 000 1,4 %

Top 15 shareholders 59 361 232 47,3 %

Resource geologist from University in Trondheim, former project geologist in Titania (Kronos Group)

Share price 14.01.11 NOK 1.75

Others 66 108 859 52,7 %

Total 125 470 091 100,0 %

6

Market cap. 14.01.11 MNOK 220

1. Company background and overview

Outline

p y g

2. Engebø - Titanium project

3. Keliber - Lithium project3. Keliber Lithium project

4. Gudvangen Stein - Anorthosite production

5 Summary5. Summary

7

Engebø, a unique titanium rutile project

Engebø titanium project

• Will be Europe’s largest producer of natural l ( d d )

KEY ADVANTAGES:

High grade product (can deliver up to 97% titanium dioxide)

Natural rutile is the preferred titaniumrutile (Titanium dioxide TiO2)

• 50 years mine life

• NPV > USD 350 million

Confirmed attractive deposit:

Natural rutile is the preferred titanium feedstock over the different ilmenite sources

Low on radioactive elements (high radioactive content is a problem with many• Confirmed attractive deposit:

International interest from industrial and financial companies incl. funding/ownership proposal

radioactive content is a problem with many of the other rutile deposits)

Located next to deep sea port

Short distance to large European market

8

market

MoU signed with long term industrial partners on rutile and garnet

A well defined deposit Engebø titanium project

D ill dDrilled

Pl d

Resource classJORC

Million tons TiO2% @ 3% cut-off

Indicated 31 7 3 77

Planned

Exploration and analysis

• 15,000 meters/50 holes

• 1,129 surface samplesIndicated 31.7 3.77

Inferred 122.6 3.75

• >50,000 sample analysis

• Block model – ordinary kriging

9

Proven resource, class upgrade by drilling

Efficient mine plan; first open pit, then underground

Engebø titanium project

Open pit: 10 - 15 years

Total mineable ore : 45 million tons

Underground: 35 years

Total mineable ore : 200 million tons

Products: Rutile and garnet

50 years mine lifeReduced visual impact

10

Underground mining by Longwall stopingStandard open pit/glory hole design

Existing infrastructure, well known technology

Engebø titanium project

Proven process steps• Crushing and grinding• Millingg• Magnetic separation• Gravity separation• Flotation• Dewatering and drying• High intensity dry separation

Production- Ore: 3 – 6 mill. ton/y- Rutile: 70 – 100,000 ton/y- Garnet: ca. 100,000 ton/y

Employees 150 - 170

11

Employees 150 170

Environmentally friendly products, expanding markets

Engebø titanium project

Rutile (Titanium dioxide/TiO2)• Superior properties • Broad range of application areas

Garnet • Advanced abrasive mineral • Health legislation on silica drives demand

Main markets: Main markets:

Broad range of application areas Health legislation on silica drives demand

Health care

Consumer/Pigments

Aircraft

Industry/Aerospace

Main markets:

Sandblasting

Waterjet cuttingIndustry/Aerospace

Green tech Various filtration and abrasives

Price range: 300 – 500 USD/tonIncreasing price premium for natural rutile *

*

Engebø garnet has tested favourably with

12Source: IBMA, Roskill, USGS

g g yexisting top quality waterjet products

Long sea freights underpin new production in Europe

Engebø titanium project

Il iIlmenite

Ilmenite + Rutile

Rutile

Canada22%Vietnam

Ukraine 5%

India5%

Other3%

Major TiO2 feedstock producers

Iluka AusQIT Can

Feedstock distribution

Ti feedstock producers

Ti feedstocks

Zimbabwe

South Africa%China

Norw ay 8%

USA 5%

5%TiWest AusDuPont USTicor SANamakwa SAKronos USIrshansk Ucr

42 %

29 %

15 %

14 %

Ti feedstocks

Norway8%

13Source: IndMin

20%

Australia 19%

China8%Volnogorsk Ucr

29 %

Ilmenite Slag Synrutile Rutile

E������� ��������� ����������� �� 30� �� ��� ����� �����

European titanium majors are future customers

Engebø titanium project

• Huntsman Tioxide Greatham UK

Large pigment plants for high-grade feedstock:

• Huntsman Tioxide Greatham UK

• Kronos Inc. Ghent BelgiumLeverkusen Germany

• Tronox Rotterdam Netherland

Substantial commercial interest confirmed by i t t l d ldi d d

• Cristal Stallingborough UK

pigment, metal and welding rod producers

Several European customers can each take Engebø’s annual production

Simple logistics improves working capitalSimple logistics improves working capital, storage and planning

80% freight reduction, single shipments

10 vs 50 USD/ton freight (current freight is10 vs. 50 USD/ton freight (current freight is 10% of feedstock price)

14

Supply/demand pattern in Europe secures off-take of rutile

Commercial partnerships established on all products

Engebø titanium project

Commercial partnerships established on all products

Rutile(titanium dioxyde)

MoU signed with major pigment producer Cristal Global, product development and off-takeSep 2010

G tMoU signed with international player in industrial

i l d l t di t ib ti d ff t kGarnet minerals, development, distribution and off-takeFeb 2010

Host minerals

MoU signed with ARCADIS, on soil improvement

MoU signed with concrete producer on product trials and off-take2009/2010

15

MoU signed with global pigment major Cristal Global

Engebø titanium project

MoU signed with global pigment major, Cristal Global

Key facts Cristal Global

• Owned by TASNEE, a privatelisted company in SaudiArabia

• No two in the world intitanium pigments

• 8 production facilities in 6countries on 5 continents

• Appr. 4,000 employees

16

Engebø titanium project

Good profitability – with significant potential

CAPEX: MUSD 210

p y g p

$140

$160

RevenueKey figures

Annual revenue: MUSD 100 – 200

EBITDA-margin: >50%

NPV @ 10% WACC: >MUSD 350

Payback time: <5 years$ 9 $81 $84$15

$32 $33 $35 $37 $39 $42 $44 $46

$40

$60

$80

$100

$120

$

ay ac e 5 yea s

Mine life: 50 years

Large return on equity with typical 60+% loan financing

$33

$68 $70 $72 $74 $77 $79 $81 $84$15

$0

$20

$40

2014 E 2015 E 2016 E 2017 E 2018 E 2019 E 2020 E 2021 E 2022 E

TiO2 revenues (mill.) Garnet revenues (mill.) Aggregates revenue

500

550

800900

1000

Large upside in increased recoverySignificant upside in price of rutile

300

350

400

450

NPV

MU

SD300400500600700800

NP

V, M

US

D Target

Base caseBase case

Realistic

200

250

55 % 60 % 65 %% Recovery

0100200

5% 7% 9%Annual rutile price increase

Based on 55% recoveryBased on 5% annual rutile price increase

Base case

17

Further upside potential- Further growth in markets for garnet (currently assuming selling only 20% of output)- Off-take of waste rock and tailing material, e.g. for construction fundament and filling

Based on 5% annual rutile price increase

Significant work completed, near term milestones

Engebø titanium project

Significant work completed, near term milestones

• Over 40 MNOK invested in pre-studies, analysis and verification

• Most comprehensive Environmental Impact Assessment (EIA) in Norwegian mining industry: 34 different special reports, 12 research institutions

• Two rounds of public hearing completed

• Local/regional politicians in favour of project

• Due for final permits: - Industrial area permit (Municipality)• Due for final permits: Industrial area permit (Municipality)- Waste disposal permit (State)

Pilot plant

production

Pre-feasibility

study

Bankable feasibilitystudy

Resourcemodel and

classification

Construction

and

commissioning

Official

permits

2011 2012 2013 / 2014

18

Permitting process moving forwardEngebø titanium project

EIA program resolved by municipality Nov 07

EIA analysis and Industrial area plan development 08/09 √

√

√Second hearing of industrial area plan completed.

Finalisation of Industrial area plan and EIA June 09

EIA analysis and Industrial area plan development 08/09

Sep 10

√

√

√g p p

“Remark” received from Directorate of Fisheries √

Positive resolution from Sogn og Fjordane County √

p

Sep 10

Sep 10

Discussion and resolution by technical committee

Discussion/resolvement by the county governor

Jan 11

Feb 11

R l ti b Di i d

Grant of waste disposal permit from the Norwegian

Resolution bythe Naustdal Municipality board

Discussion and resolution byMinistry of Environment

19

Grant of waste disposal permit from the NorwegianClimate and Pollution Agency

Criteria established for deep sea tailings disposal

Engebø titanium project

Resource group:

• SINTEF

NIVA• NIVA

• Norges Naturvernforbund

• Havforskningsinstituttetg

• Bellona

• Klif

• NGU

• DNV

• Multiconsult AS• Multiconsult AS

• NTNU

20Engebø fulfils all criteria outlined in the report

Engebø titanium project

Good dialogue with governmental politicians

21

Firda, January 3 2011

1. Company background and overview

Outline

p y g

2. Engebø - Titanium project

3. Keliber - Lithium project3. Keliber Lithium project

4. Gudvangen Stein - Anorthosite production

5 Summary5. Summary

22

Keliber, prosperous opportunities in high-grade lithium Keliber lithium project

FinlandFinland

Kaustinen

• First producer of lithium carbonate in Europe

• Li - key element in mobile power and energy

KEY ADVANTAGES:

High +99.9% purity Li-product• Li - key element in mobile power and energy storage

• Positive project NPV with existing resource base

g 99 9% pu ty p oduct

Excellent quality to be used for battery applications, the fastest growing lithium segment

i l i h i l f f h• Ongoing exploration is evidencing significant upside potential based on additional deposits

• Discussions with industrial partners for high-end battery materials and other advanced

Processing plant with potential for further refining directly to battery chemicals

Strong lithium/battery/electric vehicle (EV) focus in Finland

23

applications ongoing Attractive independent supply alternative

Large growth market driven by automotive demand

Keliber lithium project

Consumption of Lithium Price of Lithium carbonate

1 000 000

1 200 000

r 12

14

200 000

400 000600 000

800 000

1 000 000

Tonn

es p

er y

ea

2

4

6

8

10

USD

/ kg

0

200 000

2006 2010 2016 2020

T

Minimum demand Maximum demand Expected supply

0

2

Jan.04

Jan.05

Jan.06

Jan.07

Jan.08

Jan.09

Market price standard lithium carbonateBattery grade lithium carbonate premium company estimate

Electrification of transport sectorLithium carbonate consumption

Battery grade lithium carbonate premium, company estimate

Continuous Other, 1%

Pharmaceuticals, 1%

Batteries, 37%Glass, 14%

Glass-ceramics, 6%

casting, 6%Other, 1%

Aluminium, 18%

Ceramics, 16%

24____________________Sources: MiR, NREL, IndMin, Roskill, Mark Lines, J.P.Morgan

Lithium is core material and brings unique properties to batteriesLi-battery market forecasted to grow 15% p.y.

Abundant resource base for long-term production

Keliber lithium project

First phase production from proven deposit at Länttä

Expansion possibilities in regional lithium resources

Mining concession and permits for processing and environment in place

Approx. 50 drill holes of a total of 5,500 meters

• Several identified prosperous depositswithin 20 km range from processing site

• Promising exploration results and new discoveries

Exploration work by Keliber and GTK (Geological Survey of Finland)

Current resource estimate is in process of being revised according to JORC code

in 2010 field season

• Drilling program ongoing; well-defined additionaldeposits identified and expansion of resourceestimation ongoingg

Probable direction of the revision:- Verification of mineable ore in open pit- Upgrade of volume in Measured and

Indicated categories (JORC code)I d ill f d d (Li O %)

a o o go g

• Good probability for significant (min. 3 – 5x)increase of minable ore volume in low costopen pit resources

- Increased mill feed grade (Li2O-%)

Länttä deposit

25

Process plant

Advanced and awarded processing methodKeliber lithium project

Ore mining, crushing, milling and flotation

Spodumene concentration and conversion

Chemical plant; Li-carbonate production

Capacity: 4 000 tpy battery grade lithiumCapacity: 4,000 tpy battery grade lithiumcarbonate

By-products: Tantalum concentrate,

quartz/feldspar concentrates,

crushed rock aggregatescrushed rock aggregates

Production: 18 – 20 months fromconstruction start-up

• Processing method developed in cooperationwith Outotec; process guarantees

• Keliber awarded Finnish innovation prize forprocessing method and environmentallyfriendly profile

• New test batch in process

Award winning processing method based on proven technology potential for

26

Award winning processing method based on proven technology - potential for refining directly into higher margin battery chemicals

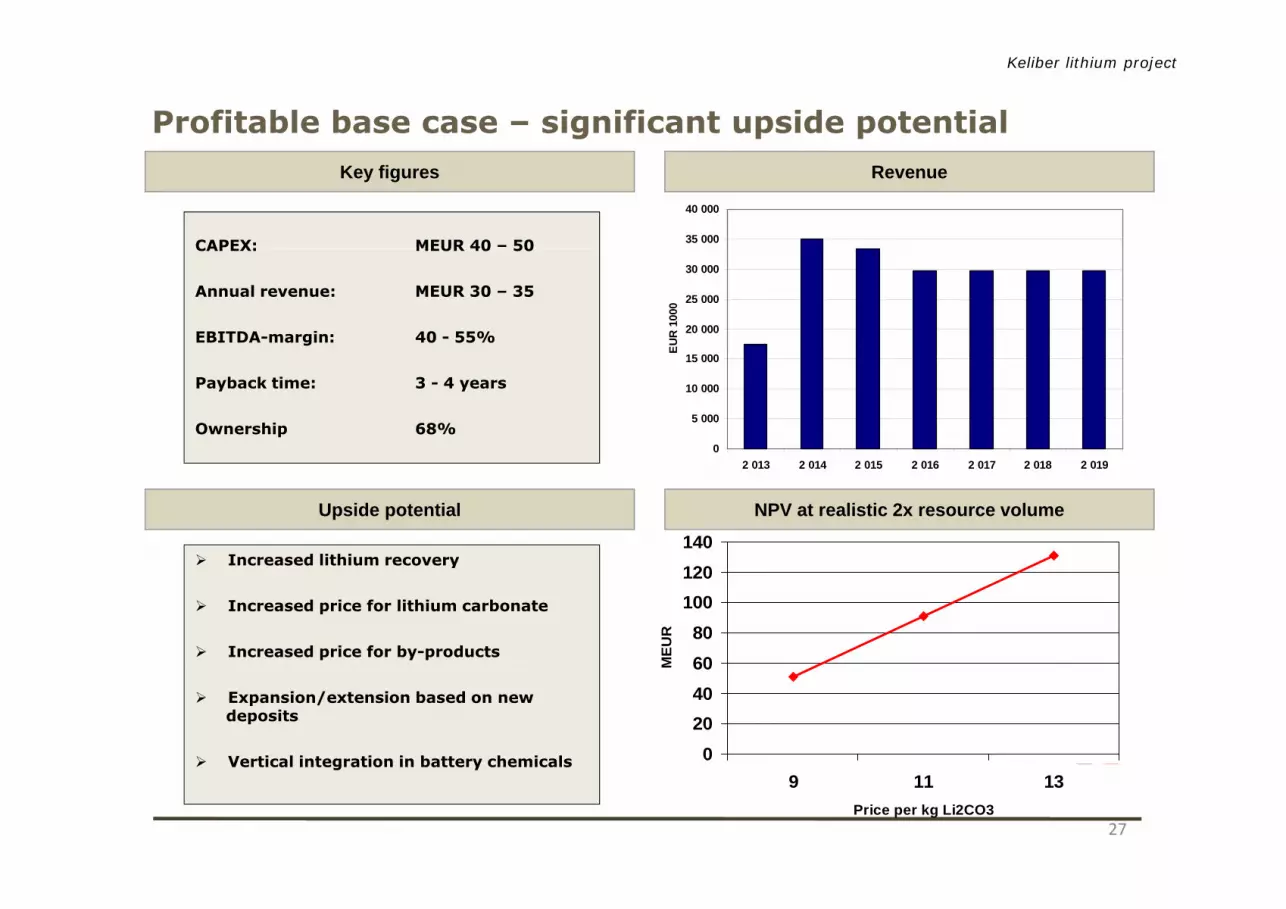

Profitable base case – significant upside potential

Keliber lithium project

CAPEX: MEUR 40 – 50

RevenueKey figures

35 000

40 000

CAPEX: MEUR 40 50

Annual revenue: MEUR 30 – 35

EBITDA-margin: 40 - 55%20 000

25 000

30 000

EUR

1000

Payback time: 3 - 4 years

Ownership 68%0

5 000

10 000

15 000

E

NPV at realistic 2x resource volumeUpside potential

2 013 2 014 2 015 2 016 2 017 2 018 2 019

Increased lithium recovery140

Increased lithium recovery

Increased price for lithium carbonate

Increased price for by-products6080

100120

MEU

R

Expansion/extension based on newdeposits

Vertical integration in battery chemicals 0204060M

27

Vertical integration in battery chemicals9 11 13

Price per kg Li2CO3

1. Company background and overview

Outline

p y g

2. Engebø - Titanium project

3. Keliber - Lithium project3. Keliber Lithium project

4. Gudvangen Stein - Anorthosite production

5 Summary5. Summary

28

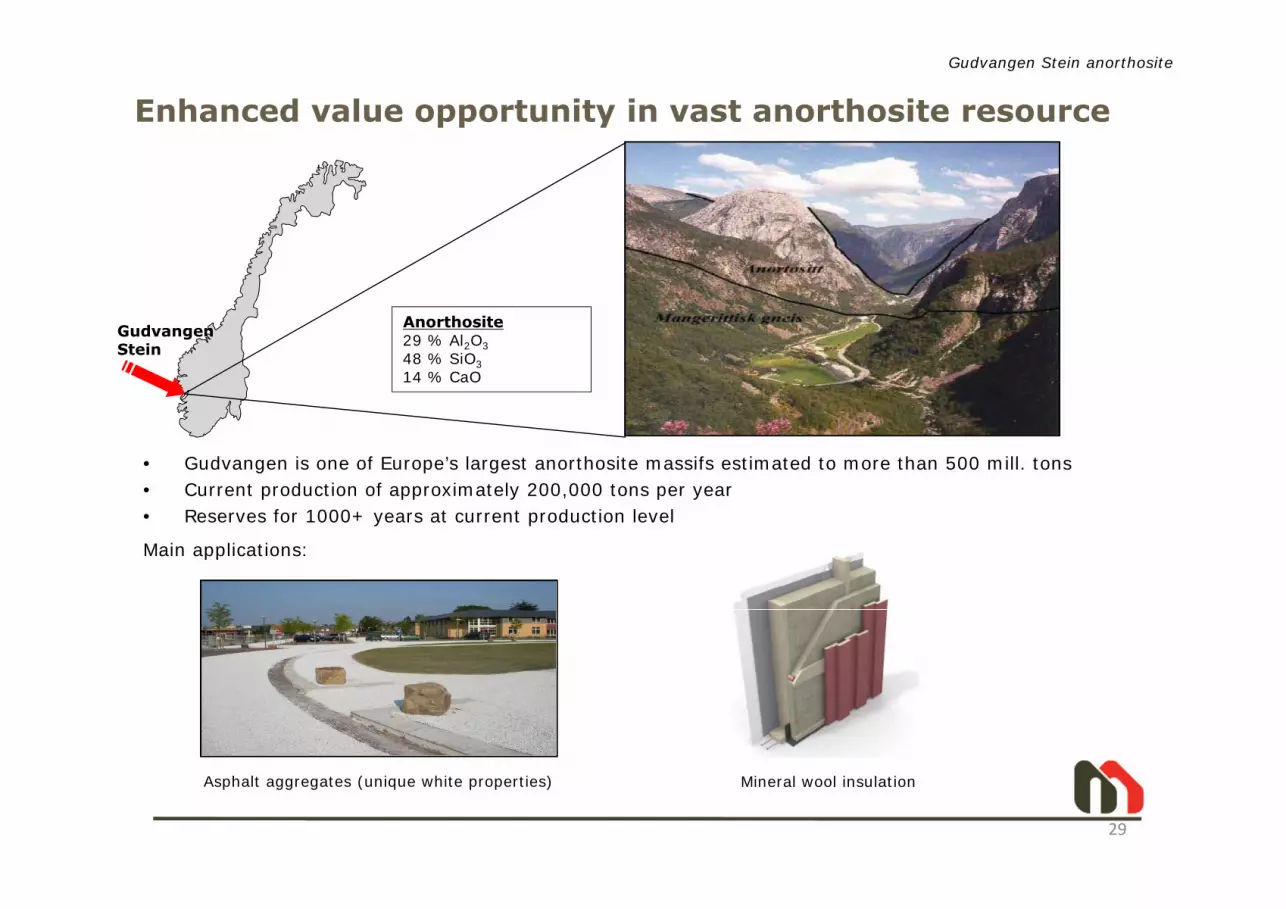

Enhanced value opportunity in vast anorthosite resource

Gudvangen Stein anorthosite

Anorthosite 29 % Al2O3

Gudvangen Stein 48 % SiO3

14 % CaO

Stein

• Gudvangen is one of Europe’s largest anorthosite massifs estimated to more than 500 mill. tons• Current production of approximately 200,000 tons per year• Reserves for 1000+ years at current production level

Main applications:pp

29

Mineral wool insulationAsphalt aggregates (unique white properties)

Significant opportunities in product development

Gudvangen Stein anorthosite

• Glass related industriesNew products by simpleGlass related industries

• Ceramics• Filler (paint)• Abrasives

by simple processing

Same plant used for several products

• Aluminium feedstock

Sales

New small scale plant for high value products

CAPEX processing plant 5 – 7 MUSD

Product price range 100 – 400 USD/ton

Up to approx. 50 000 ton/y

Long term energy advantage

MN

OK

g gy g

2 year paydown on plant

30

Trial and testing campaigns ongoing with international industrial partners

Ongoing research program with IFE/Gassnova,mineral enhancement and CO binding

Gudvangen Stein anorthosite

mineral enhancement and CO2 binding

AnorthositeNatural gas

5 mill. tpa

CO2

0 5 ill tCarbonatisation

29 % Al2O348 % SiO3 14 % CaO

0.5 mill. tpaprocess

Silica

2.45 mill. tpa

Calcium carbonate

0 7 mill tpa

Alumina

1.5 mill. tpa Tailings

X mill. tpa

31

0.7 mill. tpa800’ tpa Al met.

p

High purity quartz in Western Norway

• Hydrothermal quartz deposit

• Low in critical elements such as Ti, Al, Fe, P, Na, K, Li and B

• Under exploration

Mineral resources at seafloor

• Norway has front-end exploration technology

• Norway is world leader on deep sea operations

• Nordic Mining aim to be a long term pioneer in exploration for mineralson the Norwegian continental shelf

Financing strategy for large projects

Summary and discussion

• Financing strategy well anchored with

ProjectsNordic Mining ASA

g gylarge shareholders

• Step-wise approach based on company/project milestone achievements

• Financing based on commercial solutions(off-take agreement, industrial partnership orsimilar)

• Forward sales?

• Flexibility for financing at top level ordirectly in projects/subsidiaries

• Forward sales?

• Loans from banks and other credit institutions

• Supplier credits and equipment leasing

• Priority to expand institutional/industrialshareholding

• Equity, tentatively estimated in the range of40%

34

Summary

Summary and discussion

y

Large resources of high-end forward looking strategic minerals:

Titanium, lithium and anorthosite

Stable price development compared to commodity metals and minerals

European deficit and demand for strategic minerals

P t ti l t i i f dPotential triggers going forward

Political approval for Engebø development

Upgrade of lithium mineral resources

Industrial cooperation agreement for Keliber (lithium)

Successful industrial testing of new anorthosite concentrates

Industrial market agreements for anorthosite concentrates

Large value potential compared to current company value

35