Embed Size (px)

Citation preview

Jakarta Property Market Report

Research &

Forecast Report

Q4 2015

Accelerating success.

2 Research & Forecast Report | Q4 2015 | Highlight | Colliers International

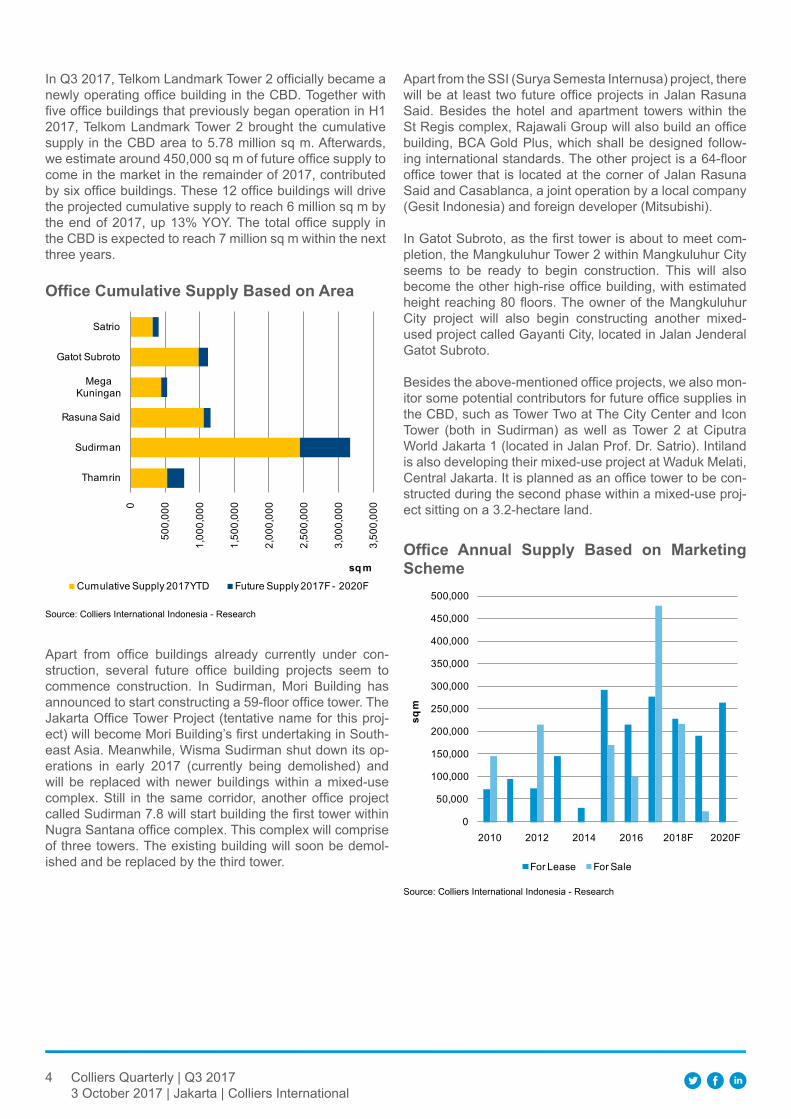

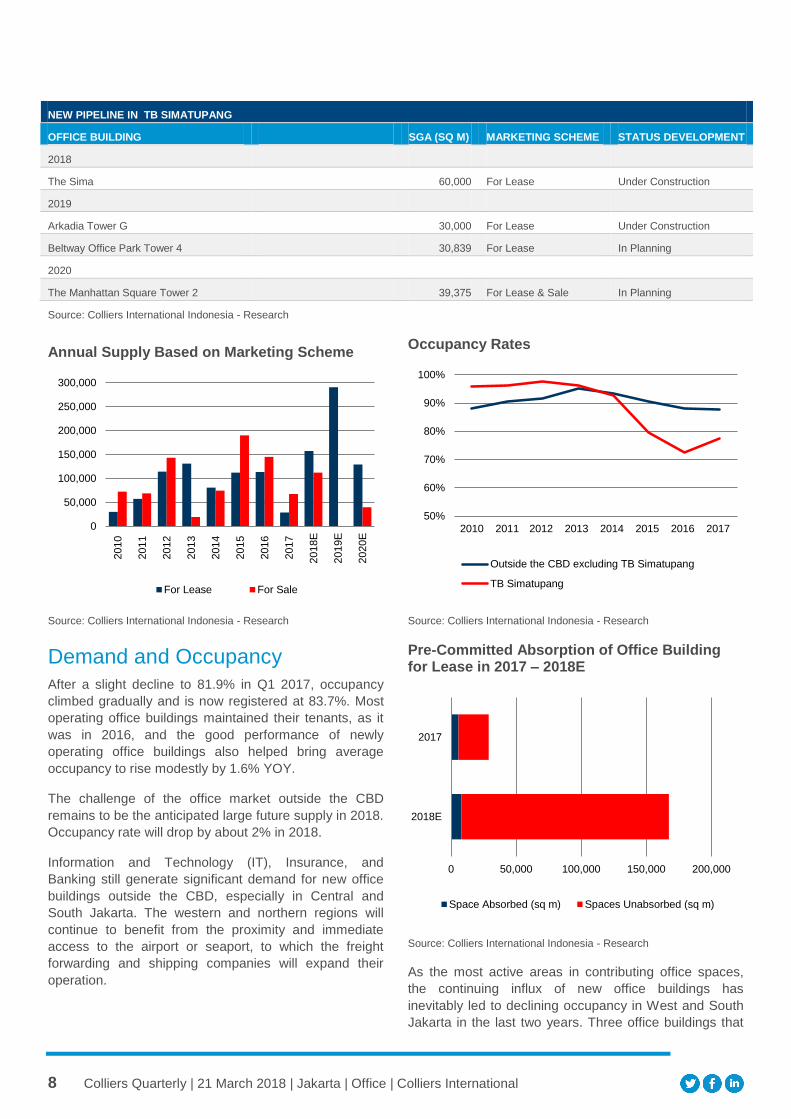

Office SectorThe sq m of office space actually completed in 2015 was less than previously projected in early 2015 because developers delayed the completion of their projects in light of the predicted oversupply of space. The actual figure was 77% (462,553 sq m) of that projected for the CBD and 91% (302,506 sq m) of that projected outside the CBD. The abundance of supply and modest office space inquiries have led to a “tenant market” situation where YoY occupancy has already dropped from 95.7% to 89.4% in the CBD and 93.2% to 87.9% in outside the CBD. The YoY average asking base rental rate was also down by 4.4% (IDR332,309 / sq m / month) in the CBD. In contrast, average asking base rents outside the CBD rose by 6.7% YoY to IDR238,381 / sq m / month due to the influx of new buildings in TB Simatupang quoting higher rental rates.

Apartment SectorThe number of completed apartment units which came on the market in 2015 was only 47% of our initial projection of a total 29,758 units made at the beginning of last year. The apparent reason for the delays by developers are slower than projected sales. Looking ahead, the market will receive around 82,000 units in the next four years, which will increase the cumulative supply of apartment units in Jakarta by around 50% to more than 239,000 in 2019. The average apartment asking price grew 13.5% YoY in Rupiah terms during 2014 - 2015, lower than the 20.5% annual growth during 2010 - 2013. Average asking prices per sq m were recorded at IDR47.2 million in the CBD, IDR35.4 million in South Jakarta and IDR22.9 million in other non-prime areas.

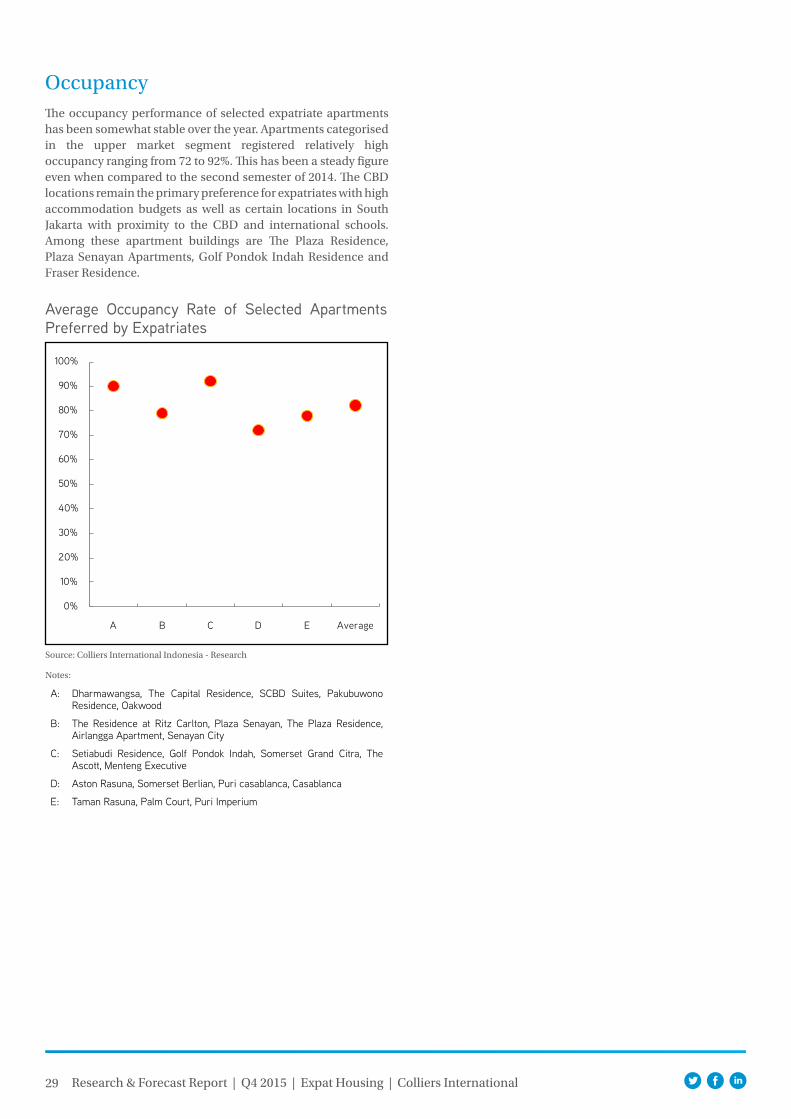

HighlightExpat HousingSince the beginning of 2015, the expatriate housing market has increasingly become a tenant market as reflected in the 25% drop in enrolment at international schools during the same period. One of the reasons for the shrinking expatriate population is the difficulty experienced by some multinational companies in obtaining working permits. The plummet in the global oil prices has further shrunk the demand for expat housing since the oil and gas industry has been the primary demand generator. In light of current market conditions, landlords of expatriate housing have become more accommodating and cooperative in entertaining additional requests from lessees and are attuned to the needs and trends in the market.

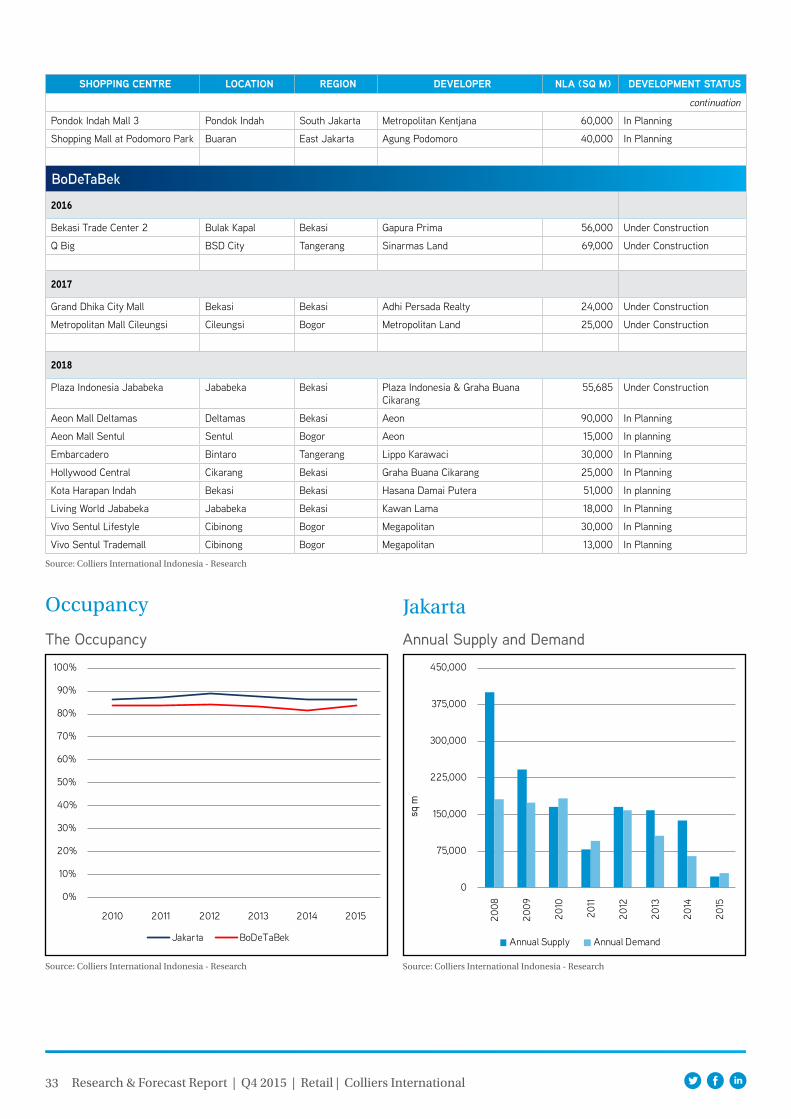

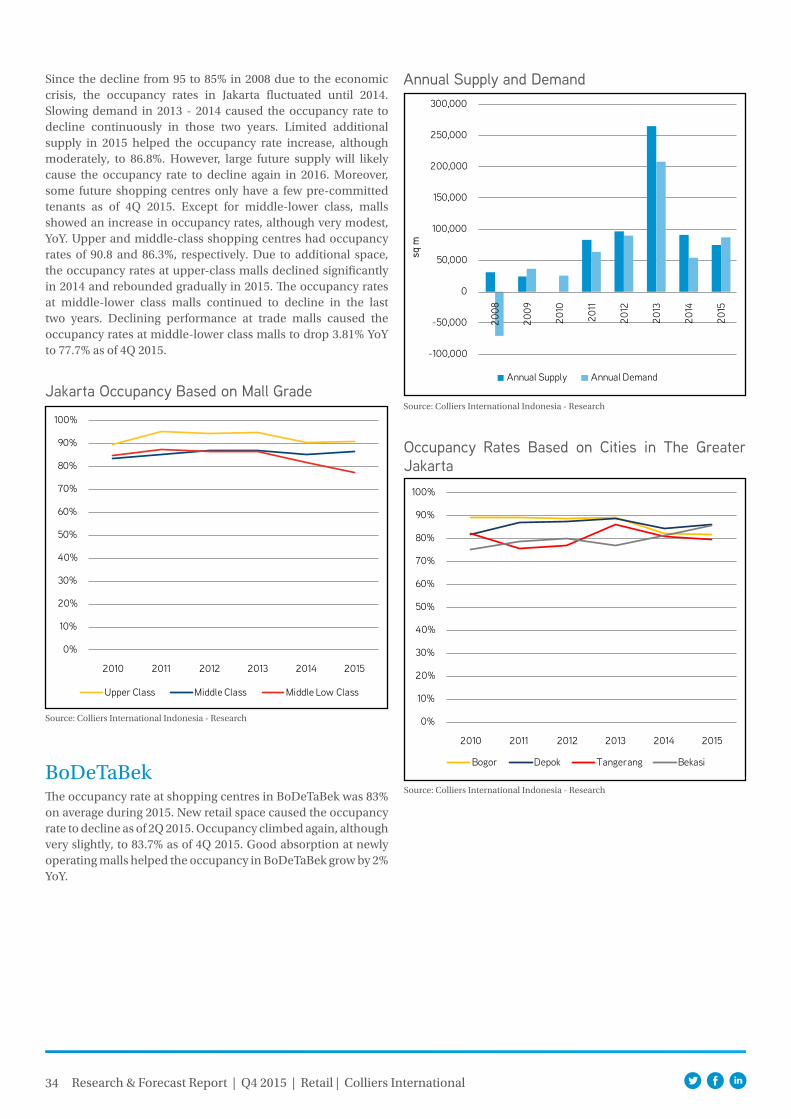

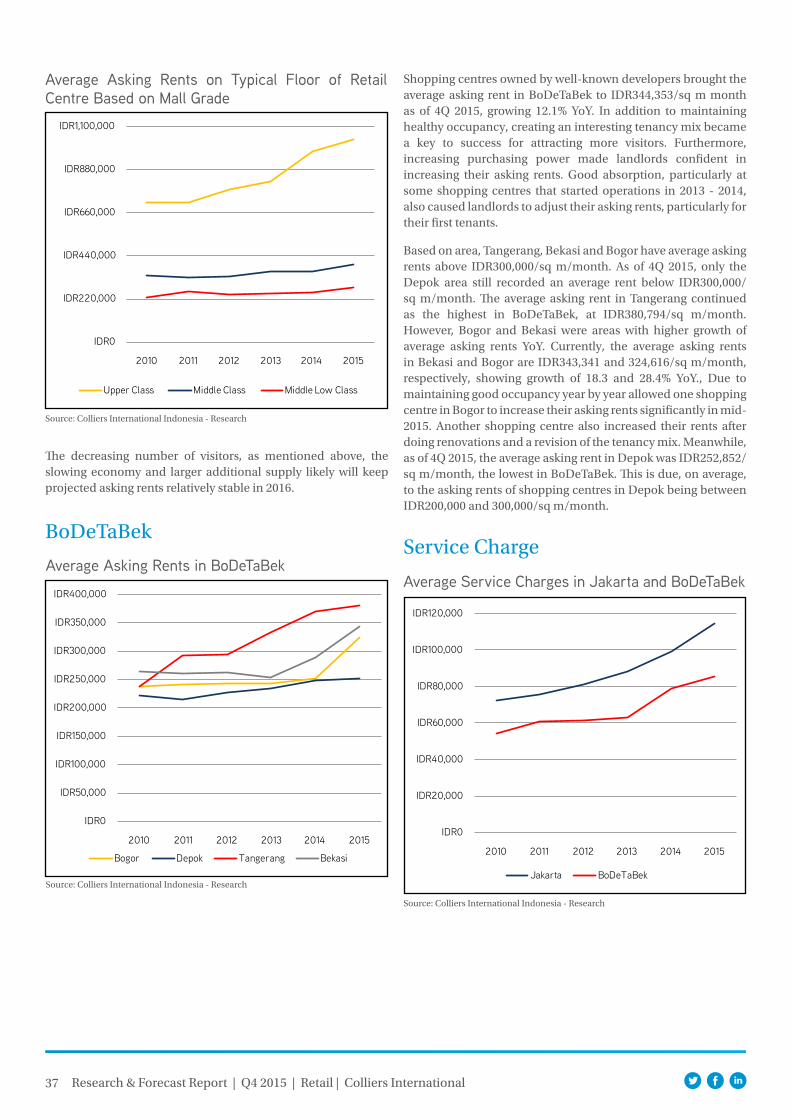

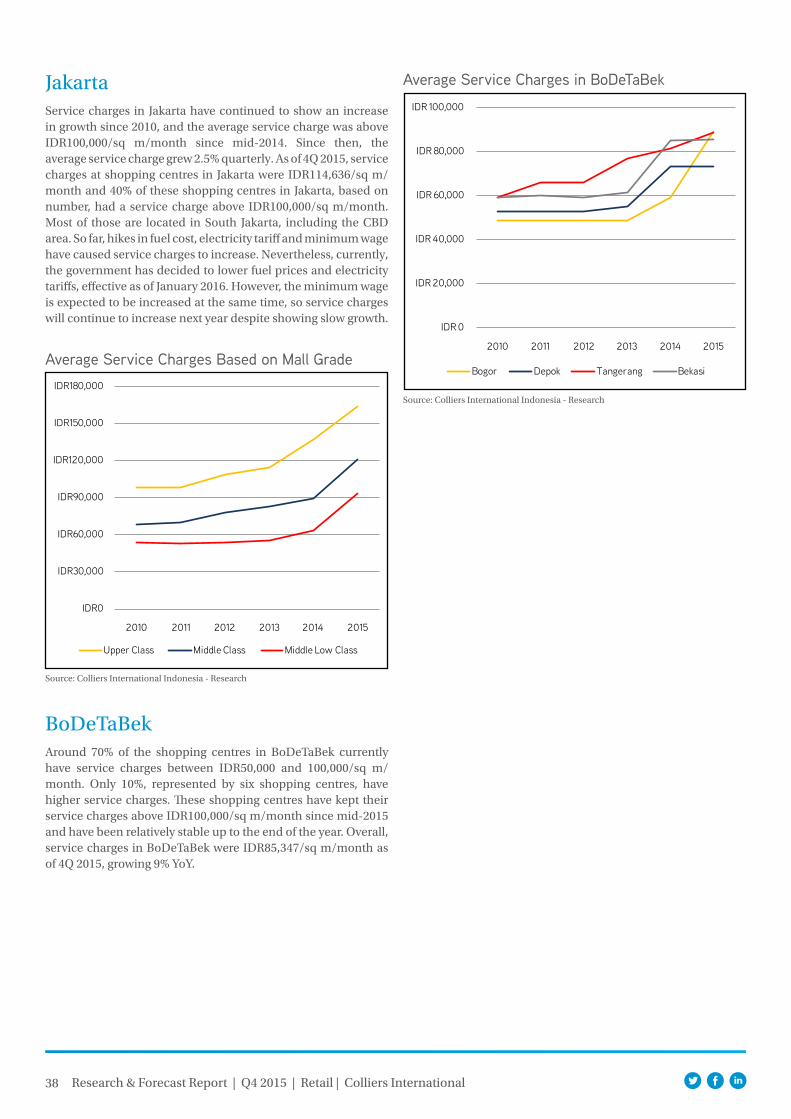

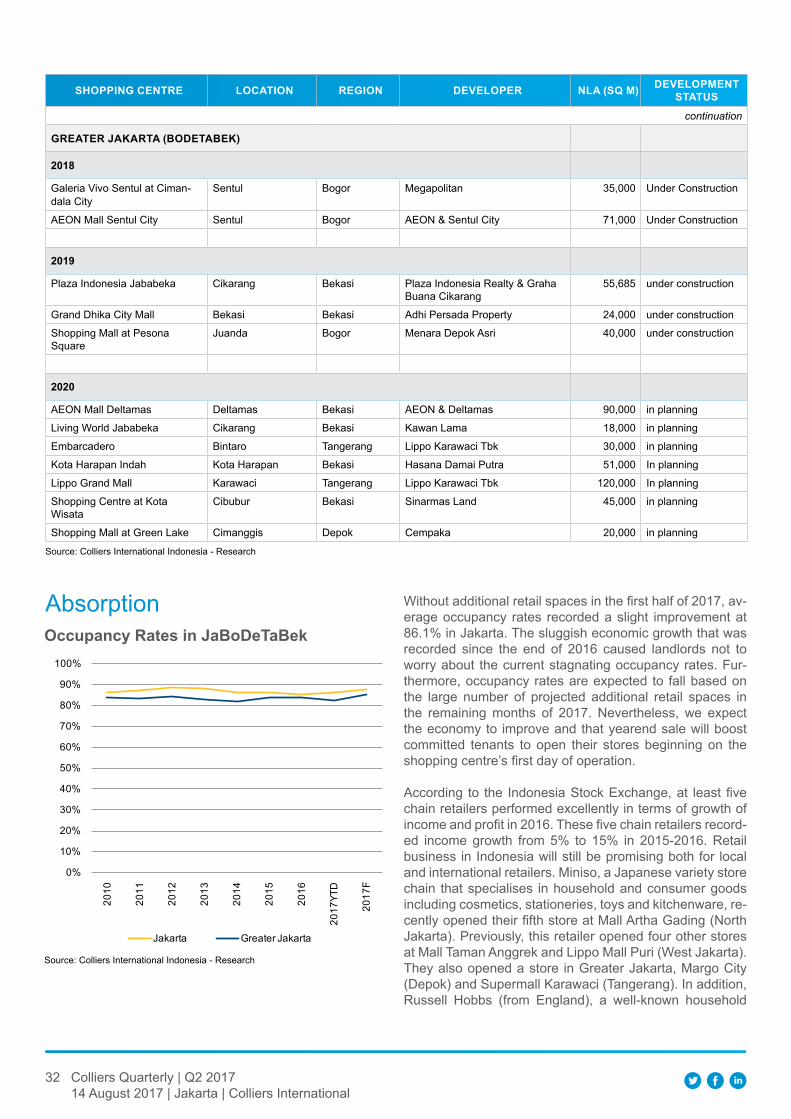

Retail SectorTwo shopping malls have confirmed a rescheduling of their openings until early 2016 and One Belpark therefore was the only new shopping centre completed in DKI Jakarta in 2015 adding 23,650 sq m of new retail space to DKI’s cumulative supply in of 4.45 million sq m. Going forward, DKI Jakarta is expected to witness 12 new shopping centres totalling of 444,000 sq m opening in 2016 – 2018. Similarly, only one shopping centre, Aeon Mall BSD, began operating in BoDeTaBek in 2015 bringing the cumulative supply to 2.34 million sq m in this area. More than 585,000 sq m of new retail spare will be available in BoDeTaBek during 2016 – 2018. The occupancy rate in DKI Jakarta stabilised at 86.8% while in BoDeTaBek it was registered at 83.0%. The average rental rate for all classes of shopping centres in DKI Jakarta was IDR535,285 / sq m / month, growing at 5.5% YoY, while a higher growth of 12.1% YoY was experienced by shopping centres in the BoDeTaBek which recorded the average rental rate at IDR344,353 / sq m/ month.

3 Research & Forecast Report | Q4 2015 | Highlight | Colliers International

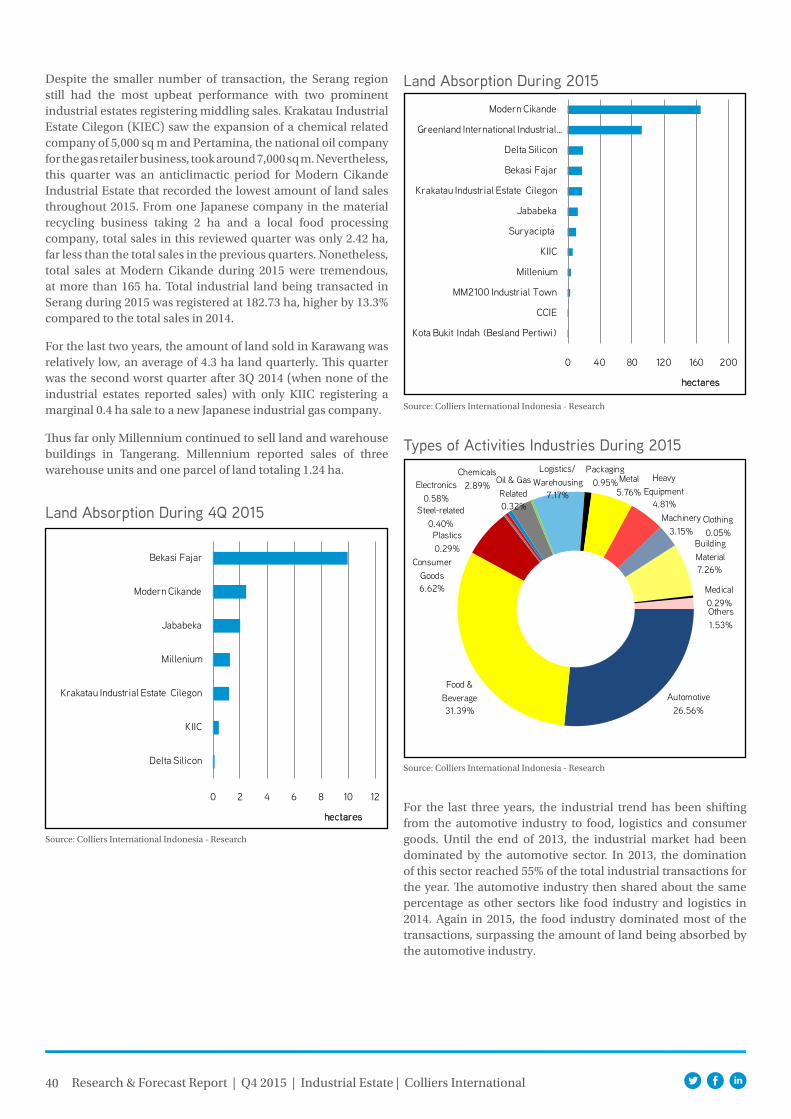

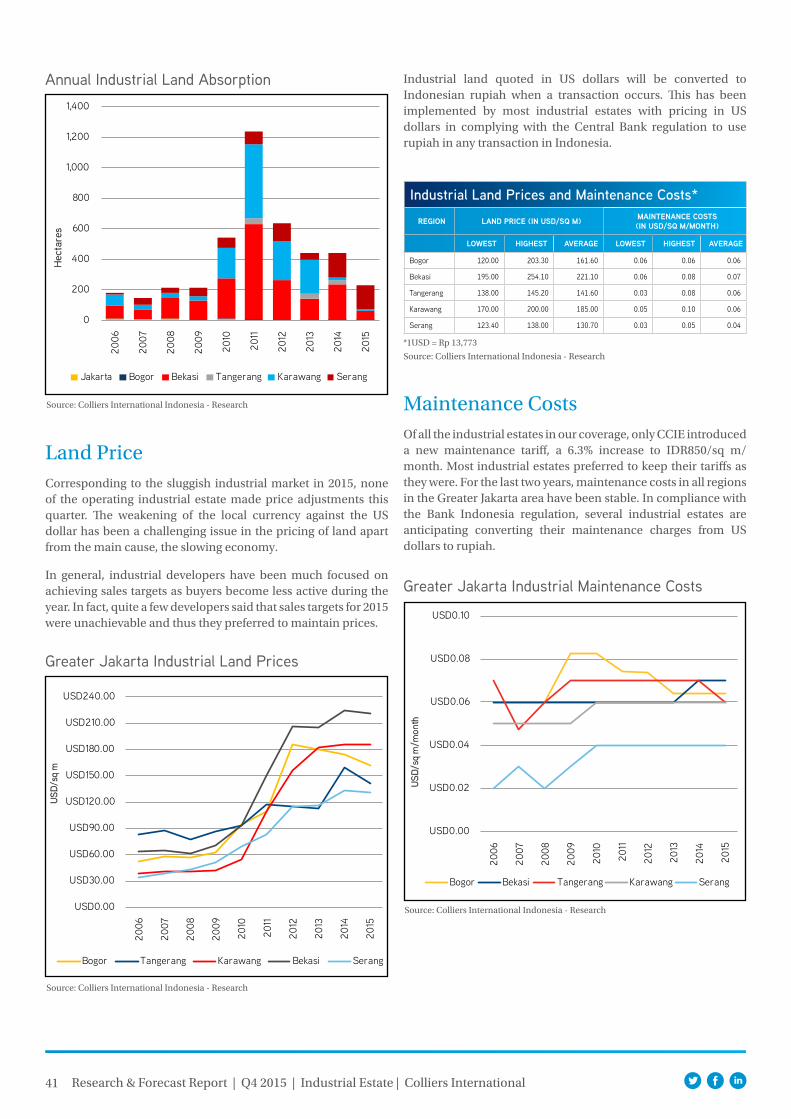

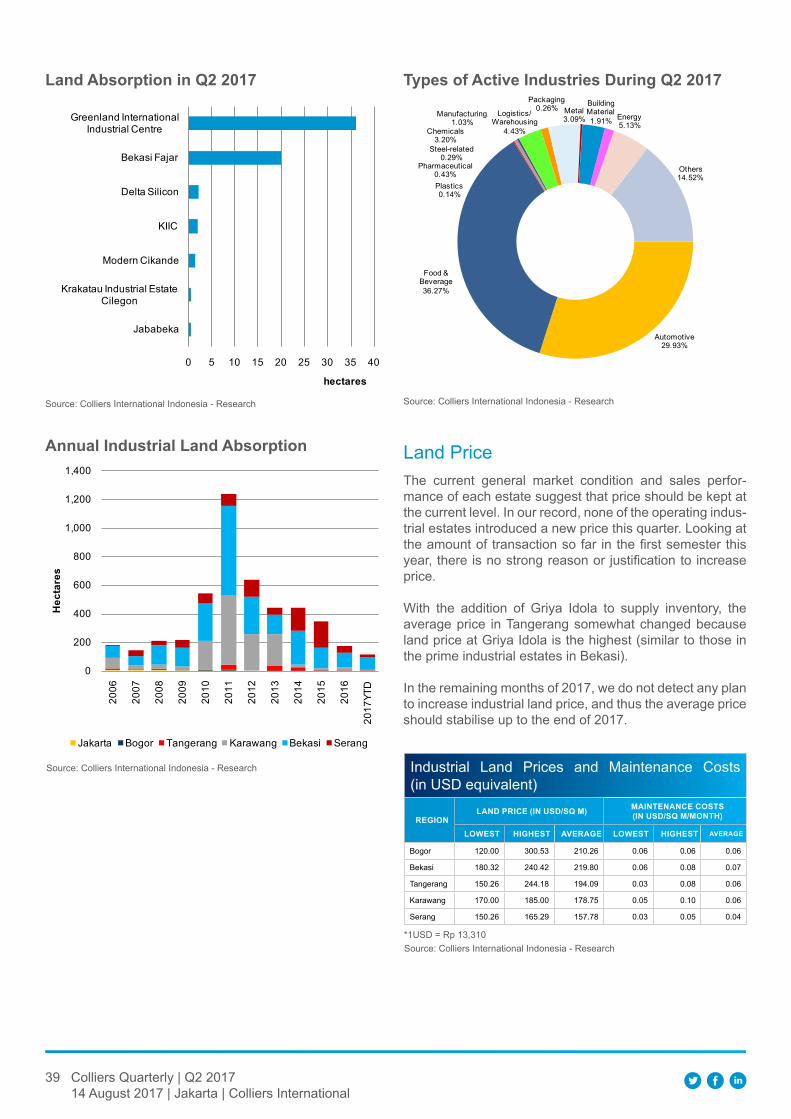

Industrial SectorDuring 2015, only one industrial estate in Bekasi added to the supply of industrial land with 20 additional hectares. Nevertheless, a large amount of additional industrial land is expected to be available over the next two years in Jabodetabek, Serang and Karawang. Total land sales for the whole of 2015 were 347.51 ha or about 79% of the total sales in 2014. Of this, almost 50% of industrial land sales was underpinned by substantial sales concluded at Modern Cikande Industrial Estate. None of the operating industrial estates made price adjustments this quarter. Quite a few developers said that their sales targets for 2015 were unachievable and thus they preferred to maintain the current prices.

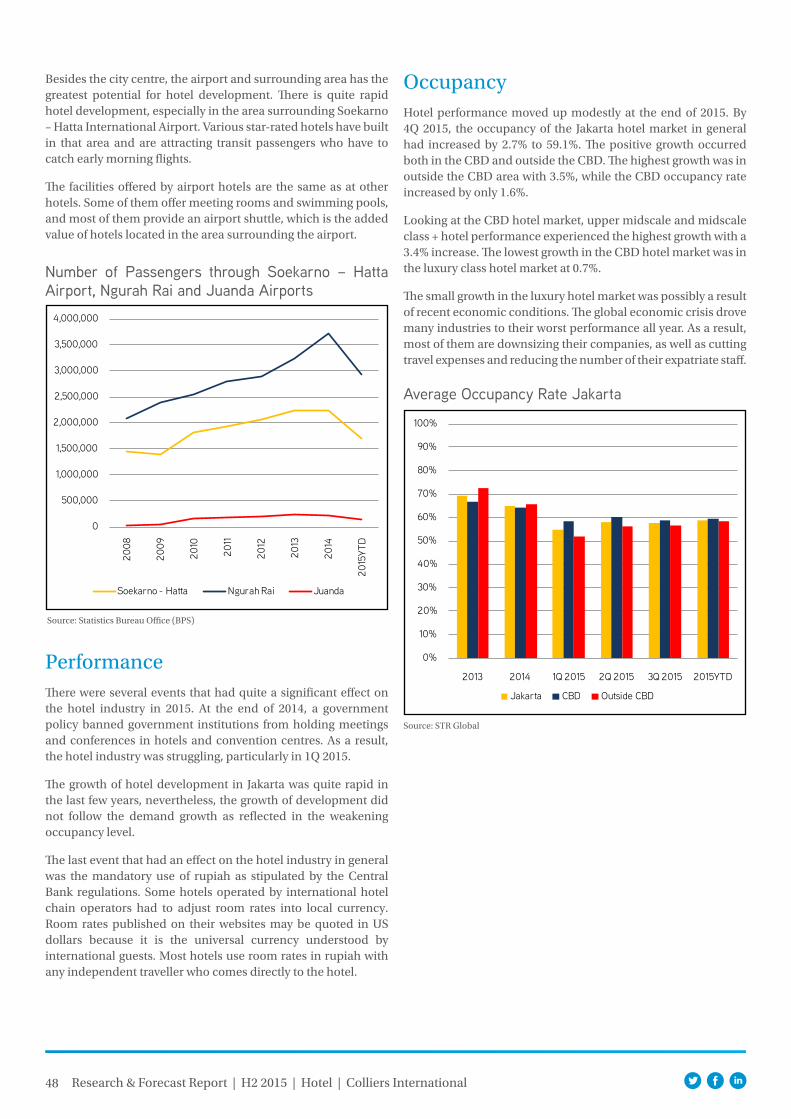

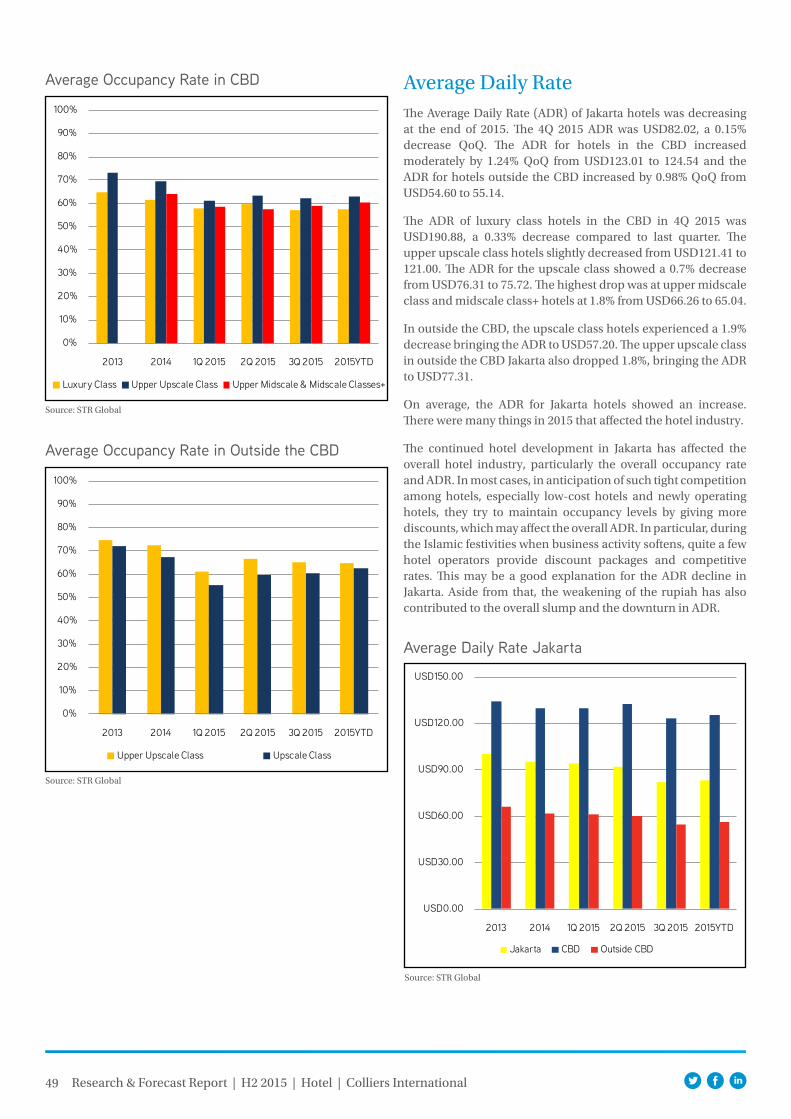

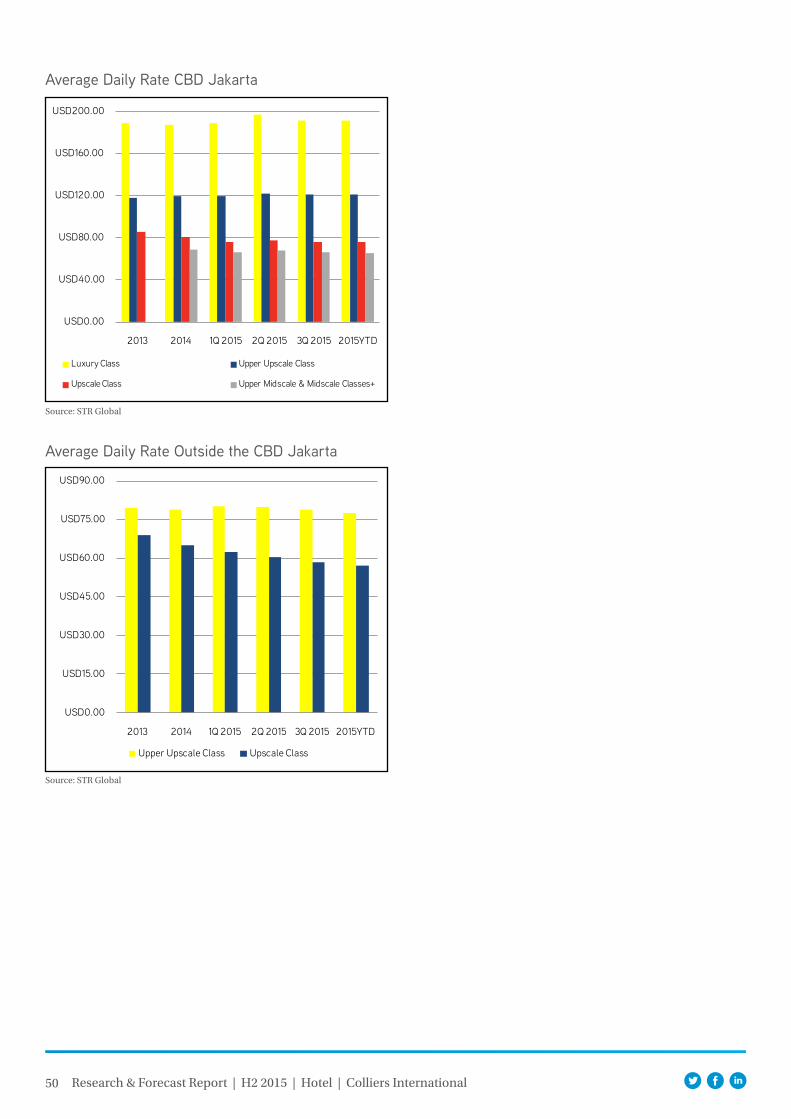

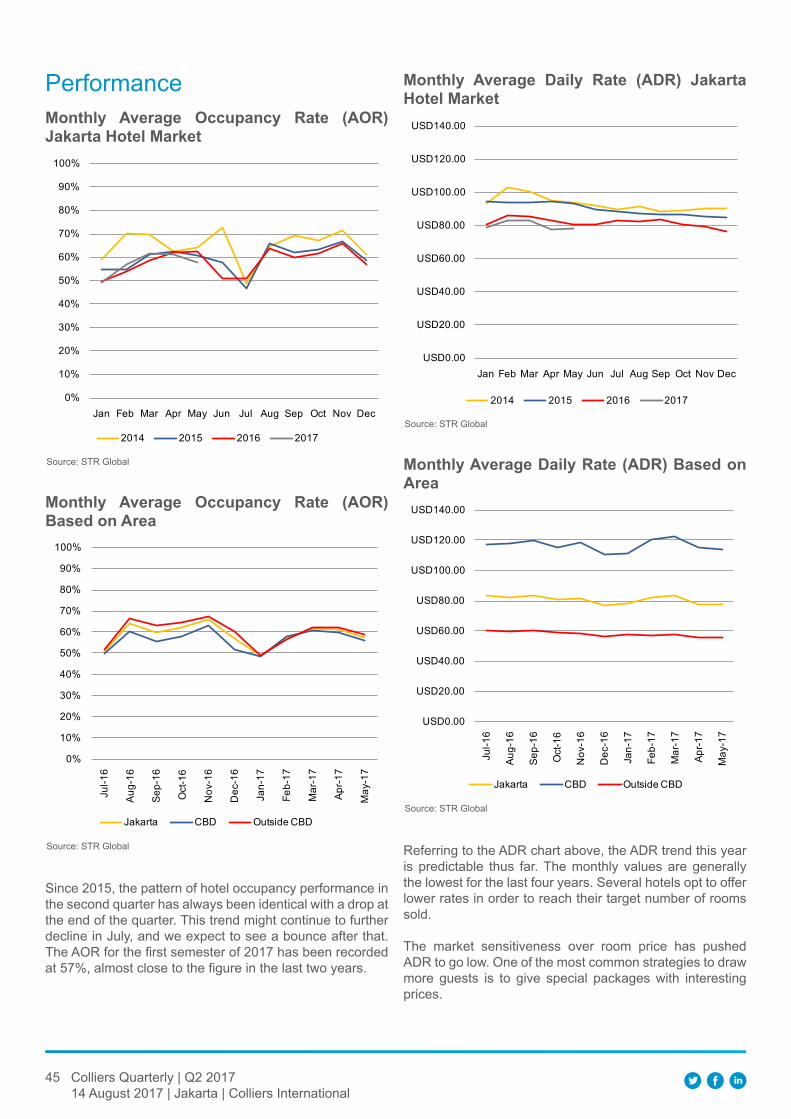

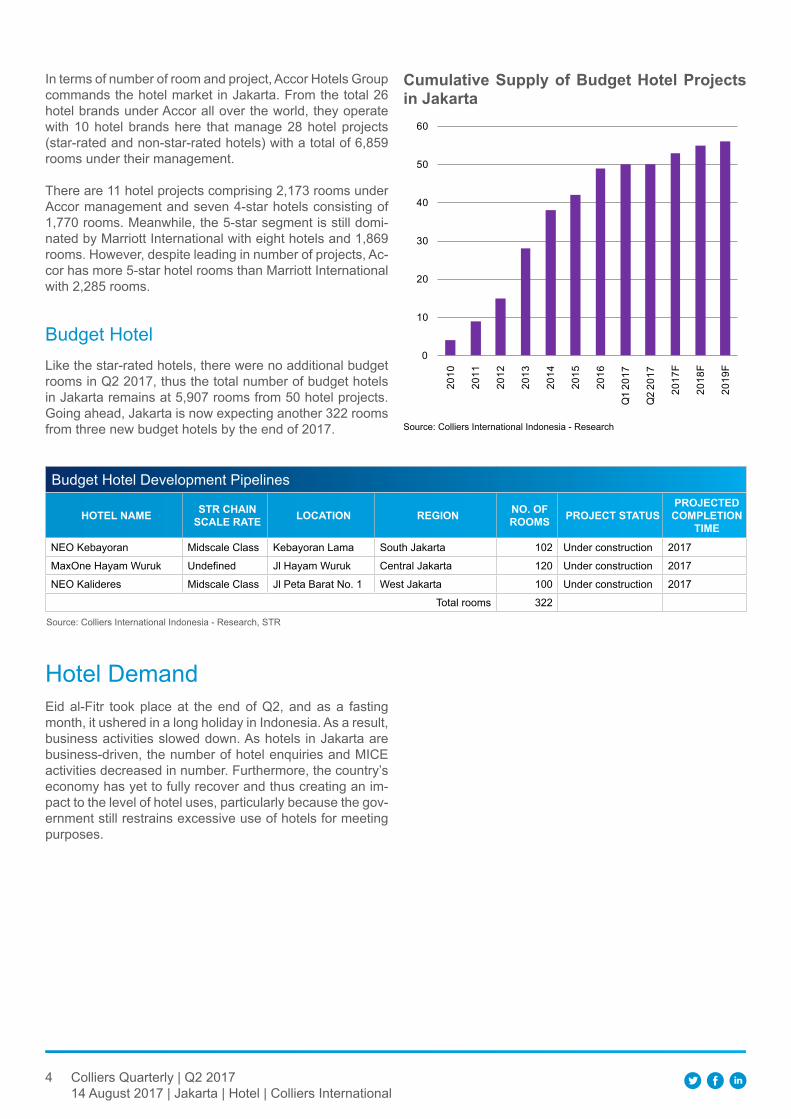

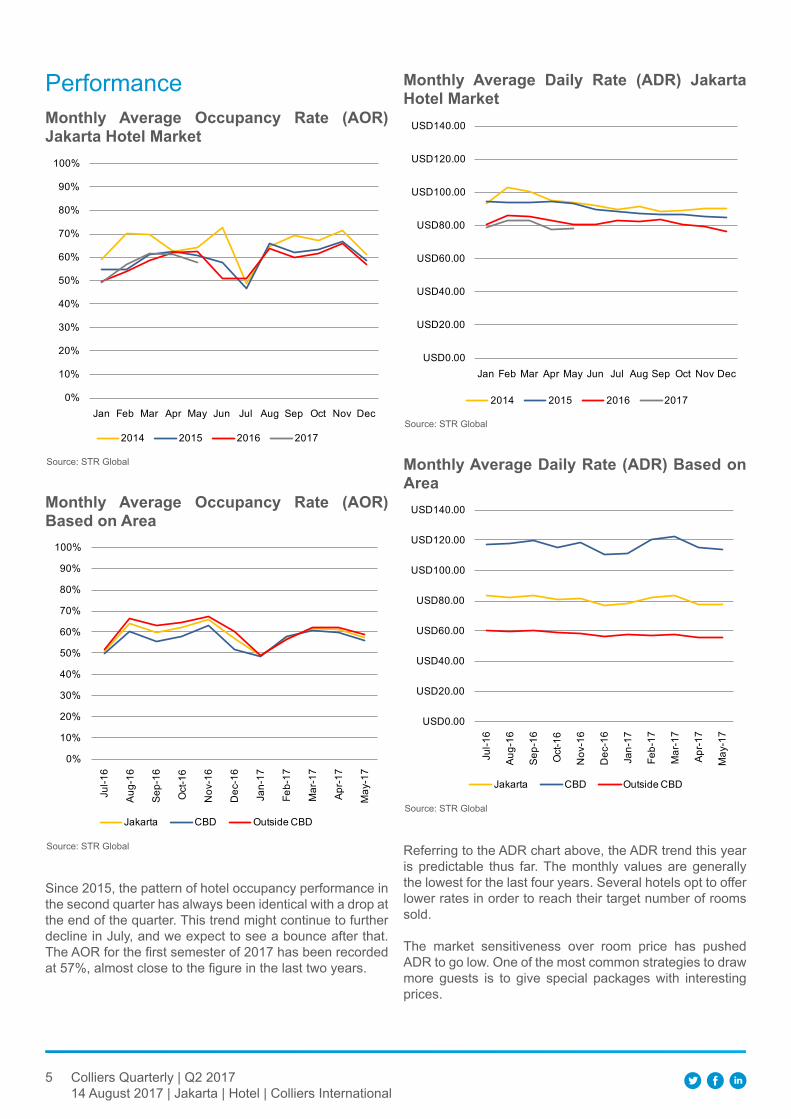

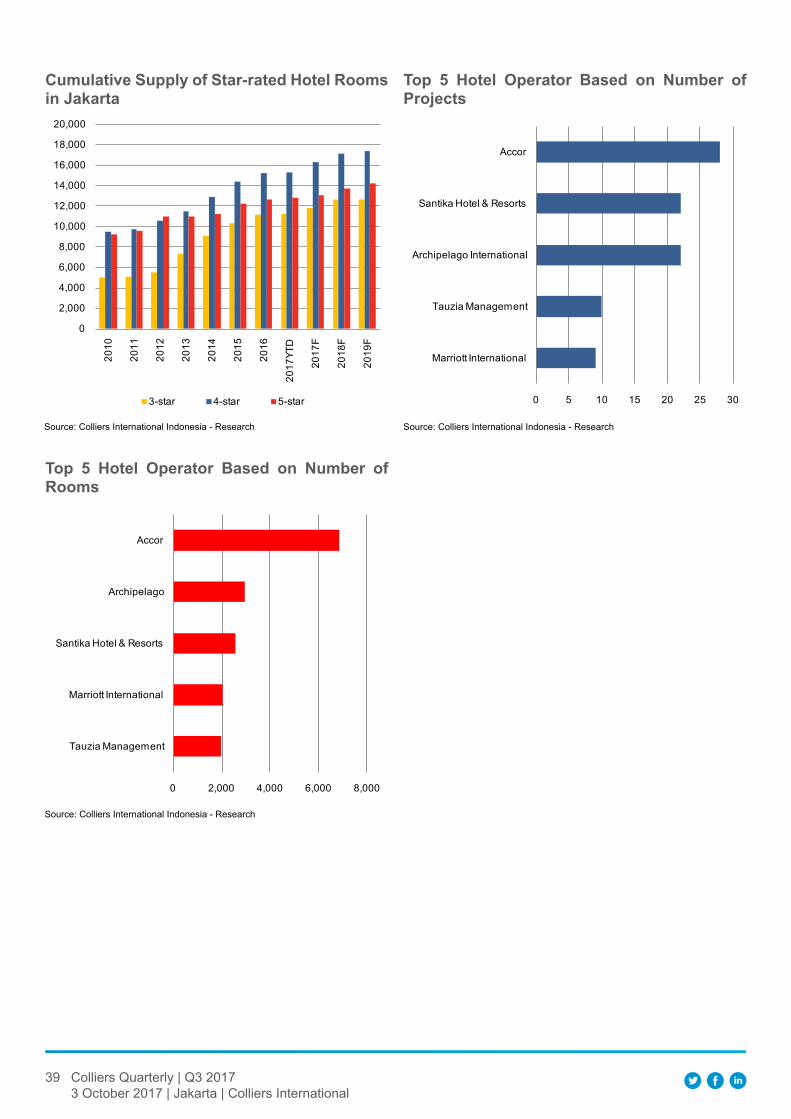

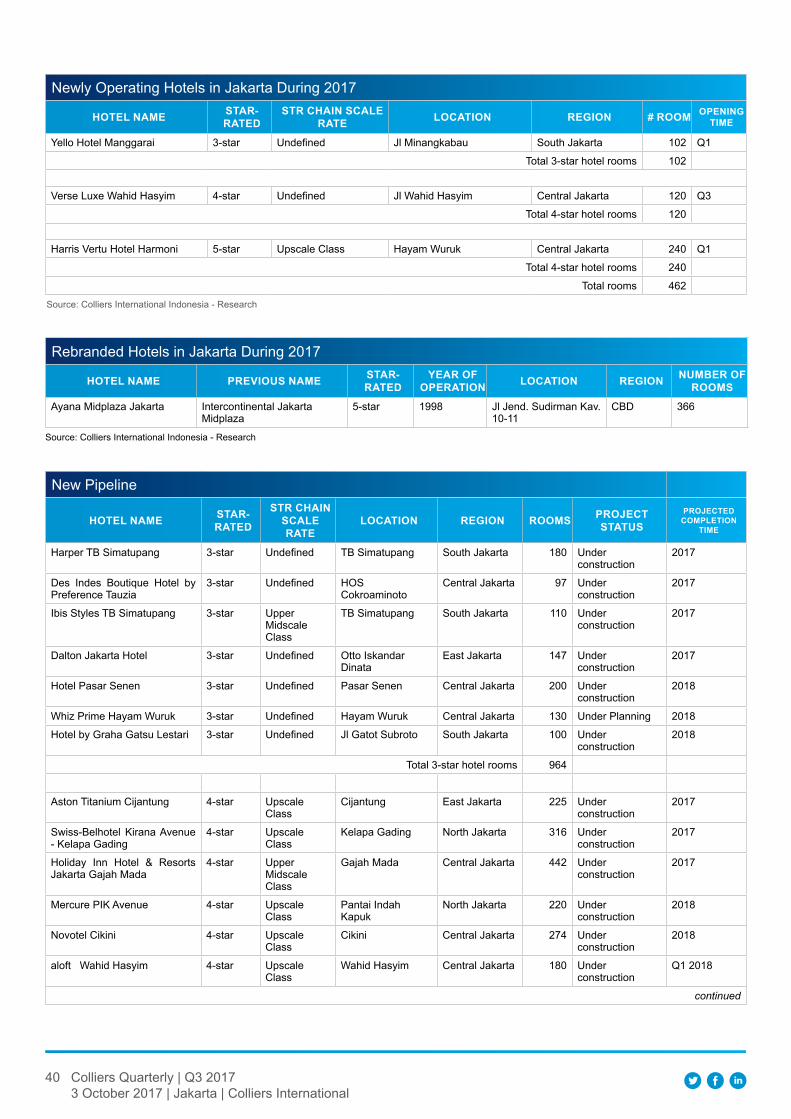

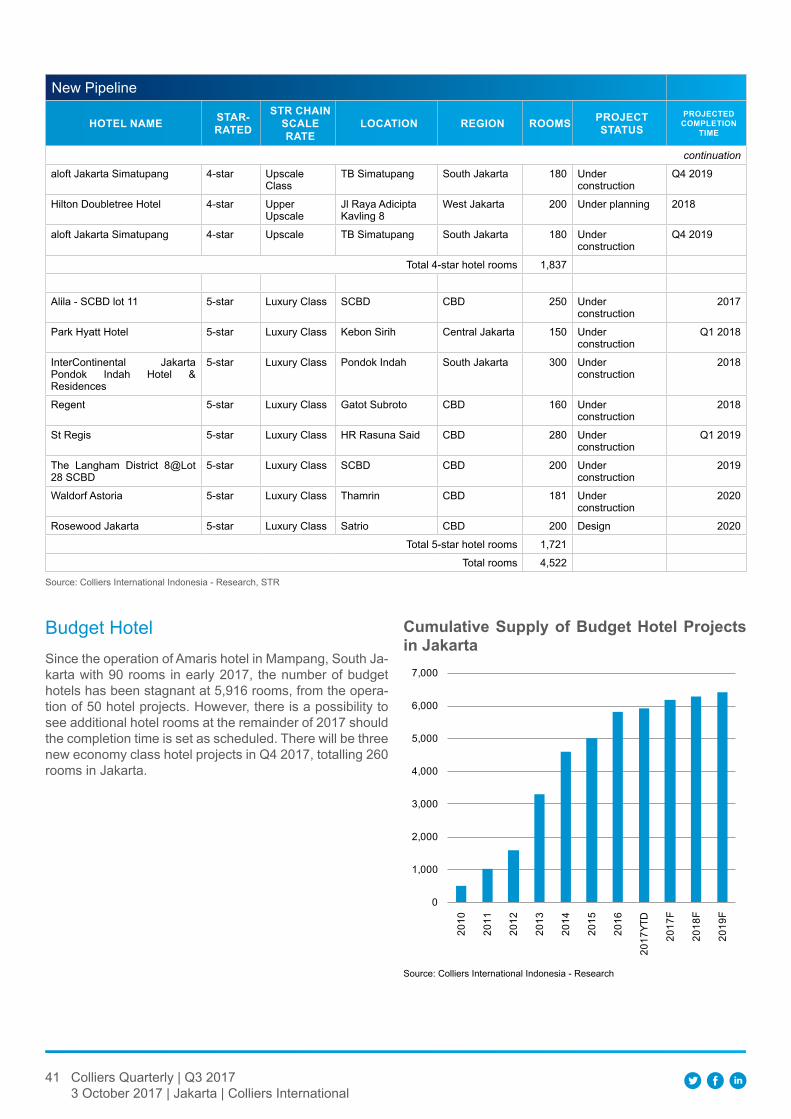

Hotel SectorBy the end of 2015, the total room supply of star-rated hotels in DKI Jakarta was 37,648 rooms in 179 hotels. Jakarta is anticipating a substantial amount of new hotel rooms during 2016 – 2018 with additional 10,509 rooms in 51 new hotels. The overall Average Occupancy Rate in DKI Jakarta was recorded at 59.1% which was lower than the 2014 figure of 64.8%. This was the result of the reduced number of corporate guests from the Indonesian government after the regulation that officially banned civil servants from having meeting in hotels. Likewise the Average Daily Rate also dropped YoY from USD95.04 in 2014 to USD82.02 in 2015

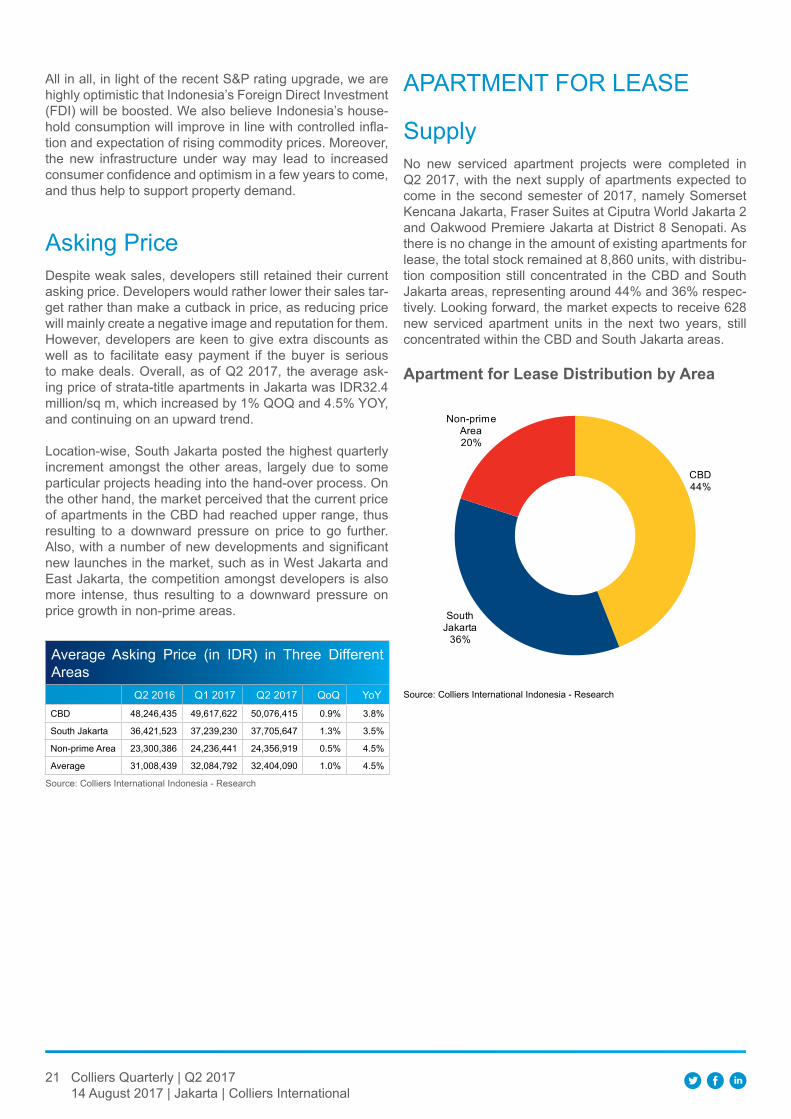

OFFICE SECTOROffice Spaces Offered For Lease

Supply

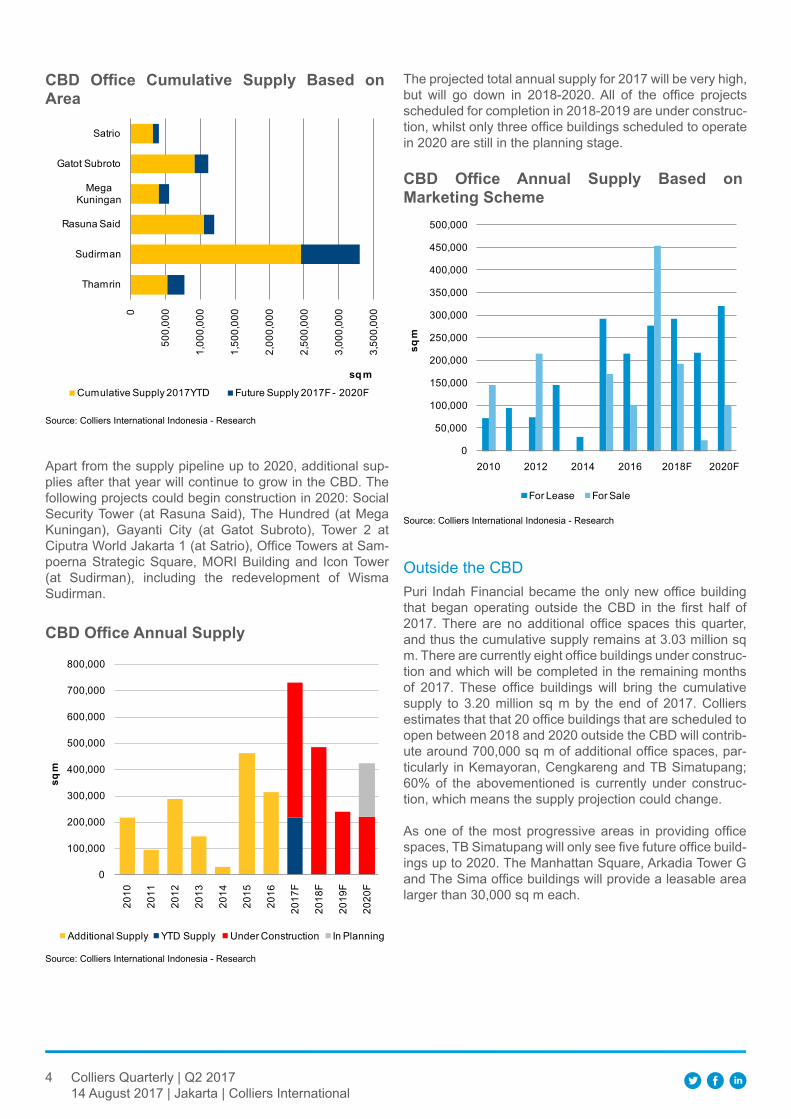

CBD

CBD Office Cumulative Supply

Source: Colliers International Indonesia - Research

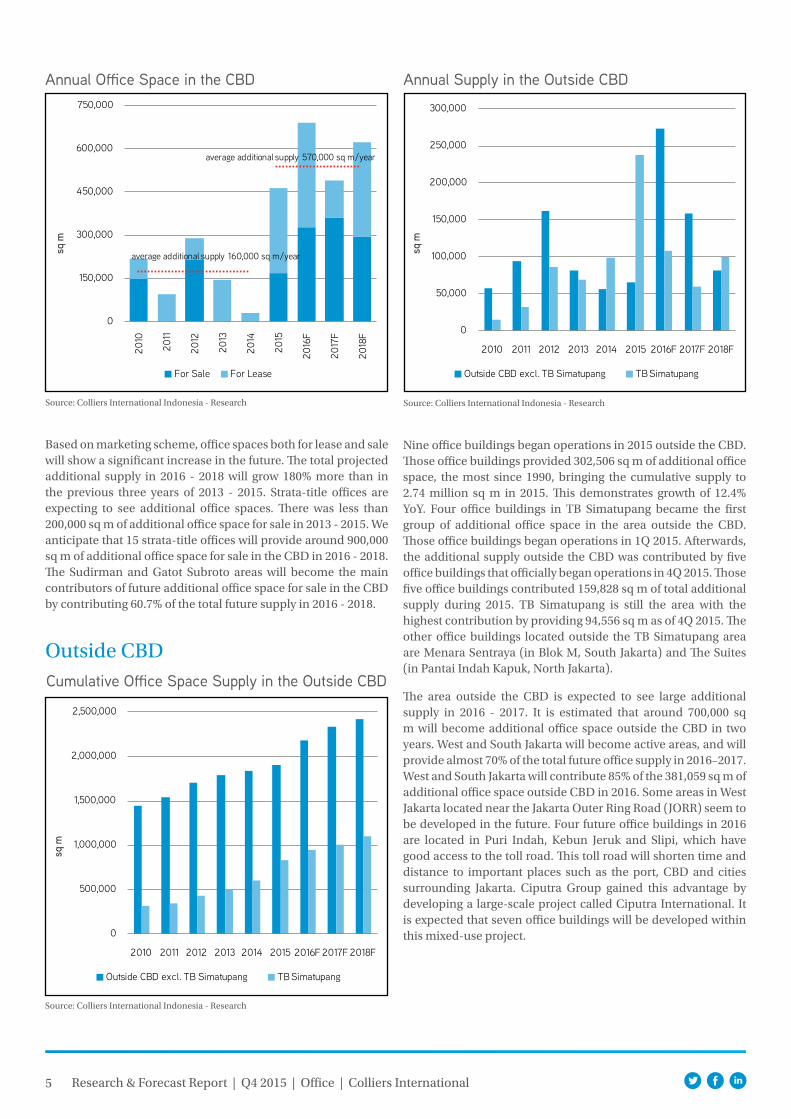

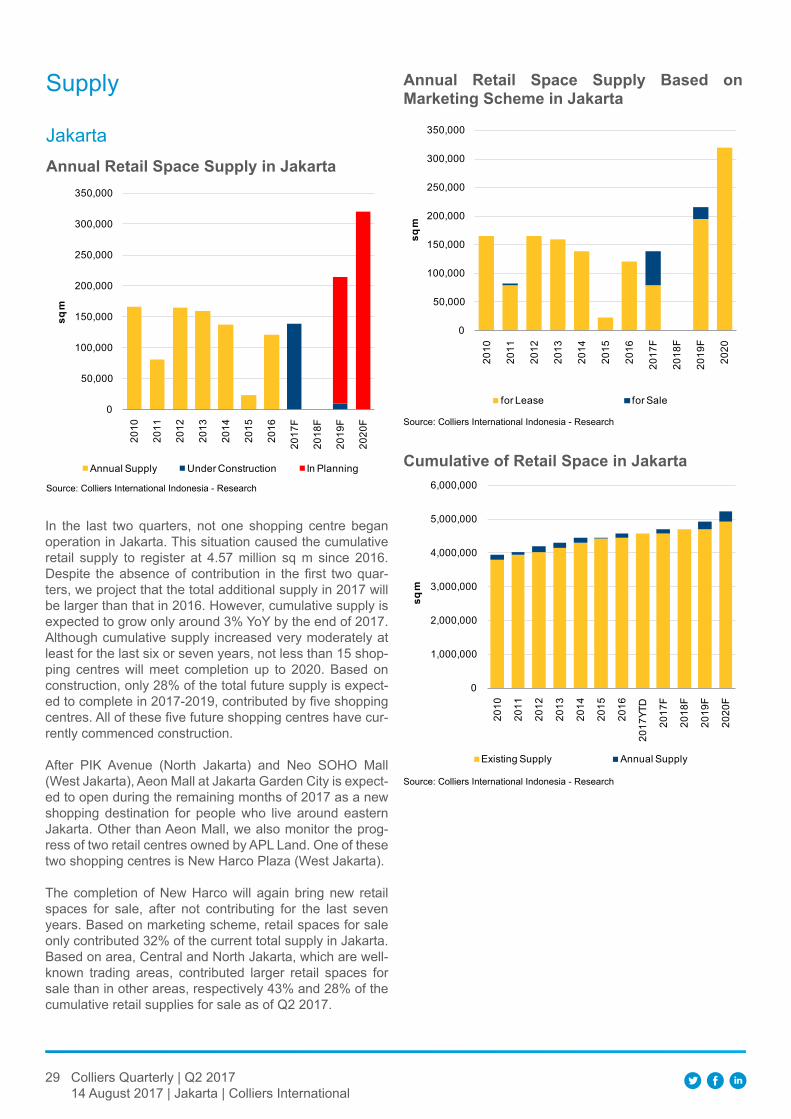

Eight office buildings began operating during 2015 and brought 462,533 sq m of new supply to the CBD. Four office buildings, namely, Gran Rubina (in Rasuna Said), Noble House (in Mega Kuningan), Sahid Sudirman Centre and AIA Central (in Sudirman) were the first to be launched. Later, four other office buildings, namely, Wisma Mulia 2 (in Gatot Subroto), Muamalat Tower (previously called Satrio Square and located in Satrio Street), BTPN Tower (in Mega Kuningan) and Gama Tower (previously called Rasuna Tower and then renamed Cemindo Tower and now called Gama Tower) located in Rasuna

Said, began operations and brought 200,595 sq m of additional office space as of 4Q 2015. Two office buildings in Sudirman and Gatot Subroto that were previously expected to begin operations in 2015, have confirmed the delay of their operations until early 2016. Delaying the launch of these office buildings caused the updated additional supply to be lower than the projection at the end of 2014, which was expected to reach around 600,000 sq m.

The eight office buildings brought the cumulative supply to 5.18 million sq m, rowth of 8.5% YoY. The CBD will see a larger additional supply in 2016. All office buildings that are projected to begin operations next year will seemingly be completed. This will be added to by the delayed office buildings from 2015, so the projected additional supply will reach around 700,000 sq m in 2016. As of 4Q 2015, most of the future office buildings have shown significant construction work. In addition, in 2016, future office buildings slated for 2017 - 2018 will start construction work. Some high-rise projects with large office buildings are also reported to be showing progress on construction. Given the high updated plot ratio, four future office buildings will provide office space of more than 90,000 sq m. Those office buildings are currently showing significant progress in their construction work. Overall, 27 office buildings are expected to begin operations and bring an average of 600,000 sq m of additional supply per year to the CBD in 2016 - 2018. In addition, the CBD is expected to see more skyscraper office buildings. In 2019, the CBD will see three new office buildings larger than 100,000 sq m. One of them is called Indonesia Satu. This project is being built by redeveloping the demolished shopping centre in Thamrin. It is expected that this office building will provide around 150,000 sq m and begin operations in 2019.

Turmoil in economic growth will likely cause landlords and developers to reschedule their building completion time, particularly those office buildings that were still in the planning stages in 2015. Other than that, landlords and developers will carefully launch their new projects to avoid tight competition among future office buildings. However, this time may be an appropriate momentum to develop office buildings while estimating that economic growth will likely rebound in the next two years. It already happened in 2010 - 2012 when Indonesia faced the economic crisis of 2008.

0

1,500,000

3,000,000

4,500,000

6,000,000

7,500,000

2010

2011

2012

2013

2014

2015

2016

F

2017

F

2018

F

sq m

Existing Supply Annual Supply

5 Research & Forecast Report | Q4 2015 | Office | Colliers International

Annual Office Space in the CBD

Source: Colliers International Indonesia - Research

Based on marketing scheme, office spaces both for lease and sale will show a significant increase in the future. The total projected additional supply in 2016 - 2018 will grow 180% more than in the previous three years of 2013 - 2015. Strata-title offices are expecting to see additional office spaces. There was less than 200,000 sq m of additional office space for sale in 2013 - 2015. We anticipate that 15 strata-title offices will provide around 900,000 sq m of additional office space for sale in the CBD in 2016 - 2018. The Sudirman and Gatot Subroto areas will become the main contributors of future additional office space for sale in the CBD by contributing 60.7% of the total future supply in 2016 - 2018.

0

150,000

300,000

450,000

600,000

750,000

2010

2011

2012

2013

2014

2015

2016

F

2017

F

2018

F

sq m

For Sale For Lease

average additional supply 570,000 sq m/year

average additional supply 160,000 sq m/year

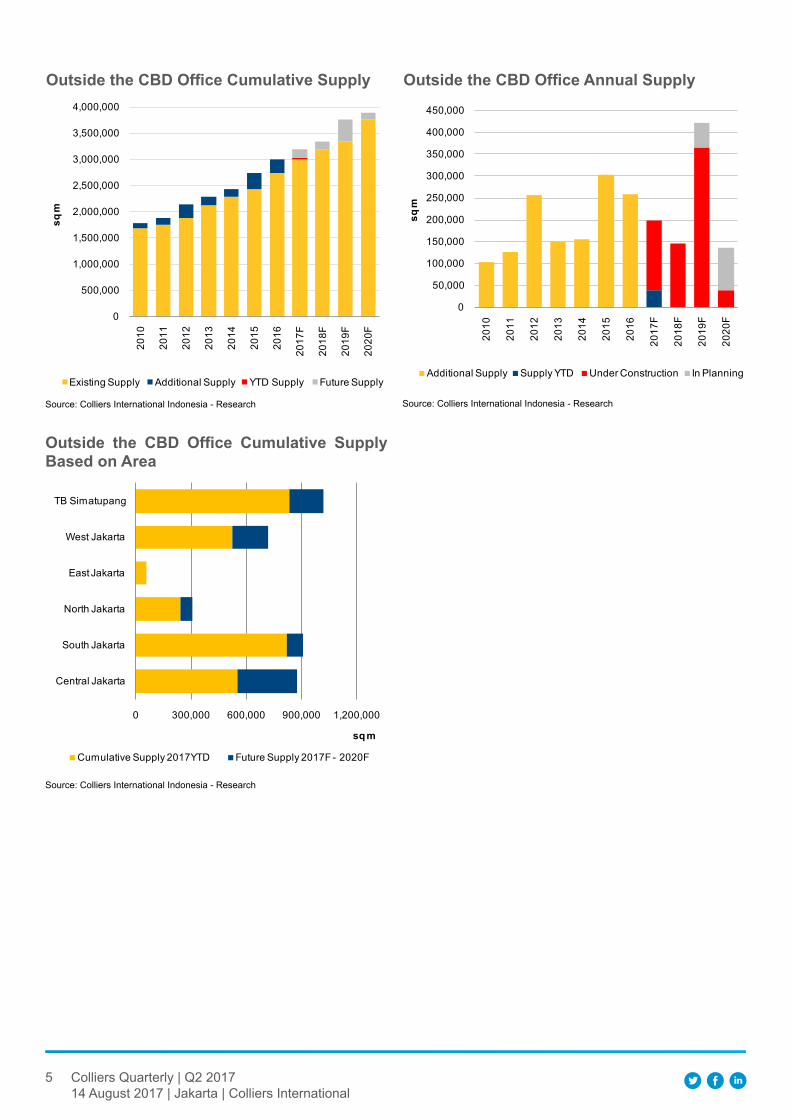

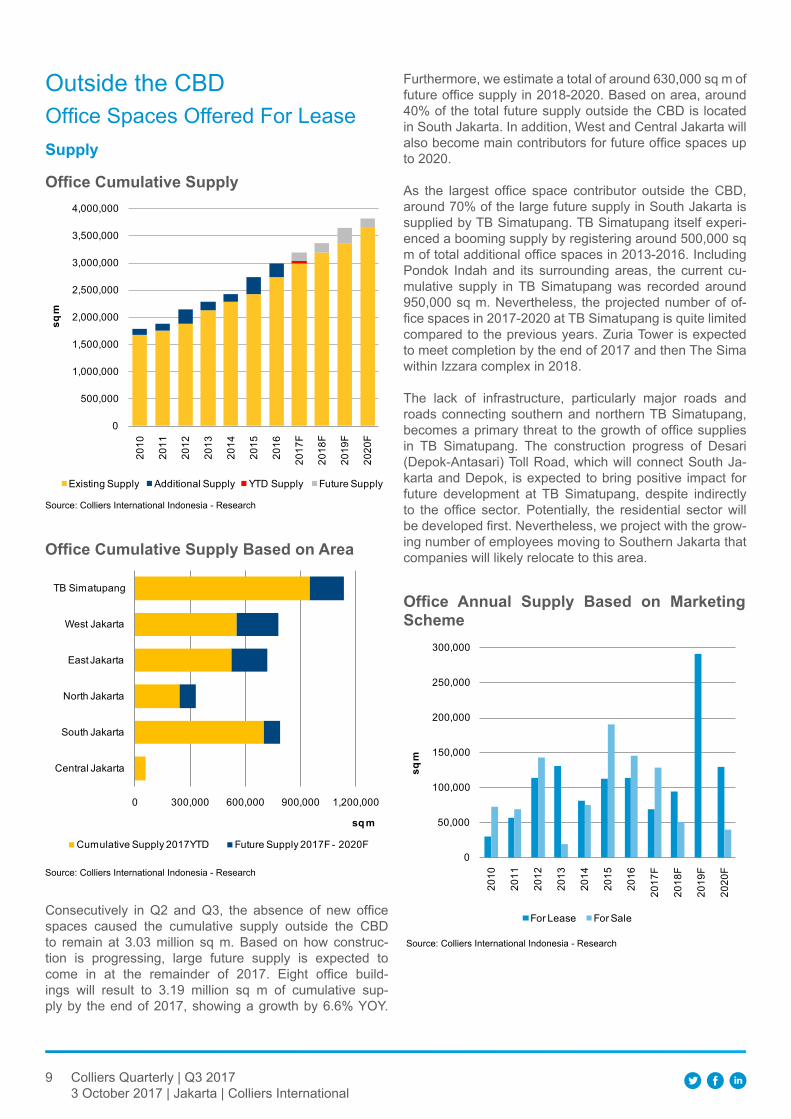

Outside CBDCumulative Office Space Supply in the Outside CBD

Source: Colliers International Indonesia - Research

Annual Supply in the Outside CBD

Source: Colliers International Indonesia - Research

Nine office buildings began operations in 2015 outside the CBD. Those office buildings provided 302,506 sq m of additional office space, the most since 1990, bringing the cumulative supply to 2.74 million sq m in 2015. This demonstrates growth of 12.4% YoY. Four office buildings in TB Simatupang became the first group of additional office space in the area outside the CBD. Those office buildings began operations in 1Q 2015. Afterwards, the additional supply outside the CBD was contributed by five office buildings that officially began operations in 4Q 2015. Those five office buildings contributed 159,828 sq m of total additional supply during 2015. TB Simatupang is still the area with the highest contribution by providing 94,556 sq m as of 4Q 2015. The other office buildings located outside the TB Simatupang area are Menara Sentraya (in Blok M, South Jakarta) and The Suites (in Pantai Indah Kapuk, North Jakarta).

The area outside the CBD is expected to see large additional supply in 2016 - 2017. It is estimated that around 700,000 sq m will become additional office space outside the CBD in two years. West and South Jakarta will become active areas, and will provide almost 70% of the total future office supply in 2016–2017. West and South Jakarta will contribute 85% of the 381,059 sq m of additional office space outside CBD in 2016. Some areas in West Jakarta located near the Jakarta Outer Ring Road (JORR) seem to be developed in the future. Four future office buildings in 2016 are located in Puri Indah, Kebun Jeruk and Slipi, which have good access to the toll road. This toll road will shorten time and distance to important places such as the port, CBD and cities surrounding Jakarta. Ciputra Group gained this advantage by developing a large-scale project called Ciputra International. It is expected that seven office buildings will be developed within this mixed-use project. 0

500,000

1,000,000

1,500,000

2,000,000

2,500,000

2010 2011 2012 2013 2014 2015 2016F 2017F 2018F

sq m

Outside CBD excl. TB Simatupang TB Simatupang

0

50,000

100,000

150,000

200,000

250,000

300,000

2010 2011 2012 2013 2014 2015 2016F 2017F 2018F

sq m

Outside CBD excl. TB Simatupang TB Simatupang

6 Research & Forecast Report | Q4 2015 | Office | Colliers International

Outside CBD Cumulative Supply Based on Area

Source: Colliers International Indonesia - Research

0

500,

000

1,000

,000

1,500

,000

2,00

0,00

0

2,50

0,00

0

3,00

0,00

0

3,50

0,00

0

Central Jakarta

South Jakarta

North Jakarta

East Jakarta

West Jakarta

sq mExisting Supply 2015 Future Supply 2016 - 2018

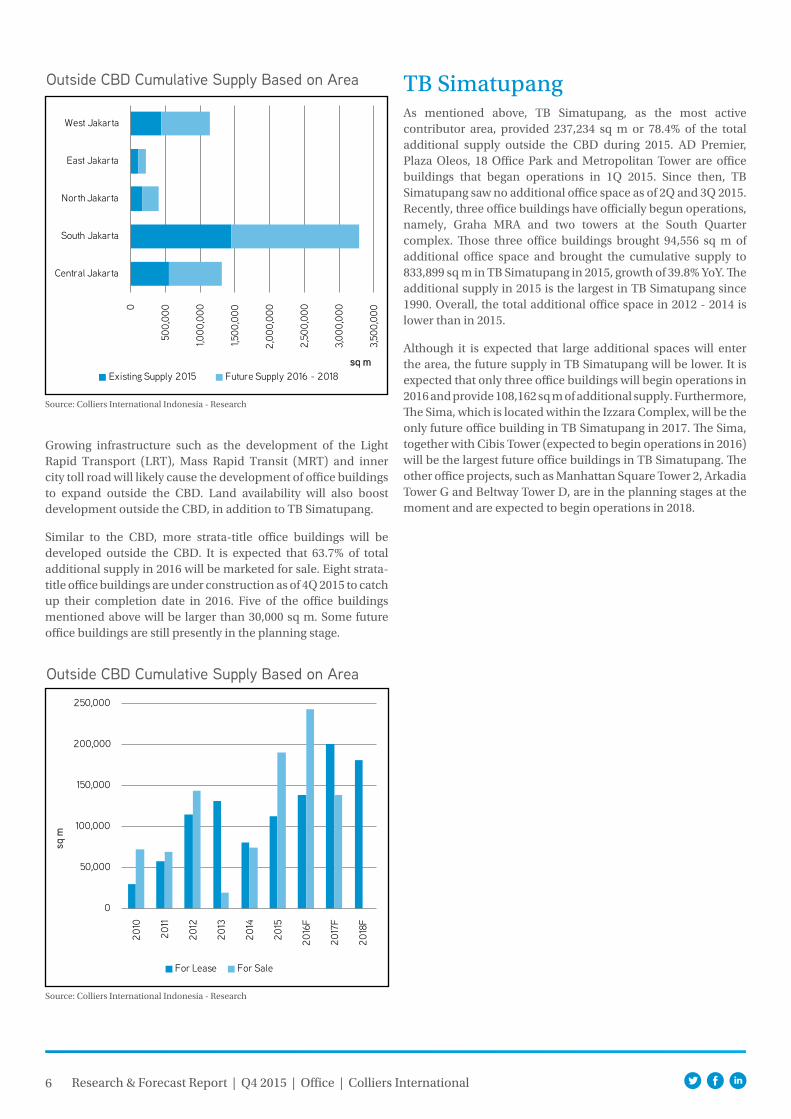

Growing infrastructure such as the development of the Light Rapid Transport (LRT), Mass Rapid Transit (MRT) and inner city toll road will likely cause the development of office buildings to expand outside the CBD. Land availability will also boost development outside the CBD, in addition to TB Simatupang.

Similar to the CBD, more strata-title office buildings will be developed outside the CBD. It is expected that 63.7% of total additional supply in 2016 will be marketed for sale. Eight strata-title office buildings are under construction as of 4Q 2015 to catch up their completion date in 2016. Five of the office buildings mentioned above will be larger than 30,000 sq m. Some future office buildings are still presently in the planning stage.

Outside CBD Cumulative Supply Based on Area

Source: Colliers International Indonesia - Research

0

50,000

100,000

150,000

200,000

250,000

2010

2011

2012

2013

2014

2015

2016

F

2017

F

2018

F

sq m

For Lease For Sale

As mentioned above, TB Simatupang, as the most active contributor area, provided 237,234 sq m or 78.4% of the total additional supply outside the CBD during 2015. AD Premier, Plaza Oleos, 18 Office Park and Metropolitan Tower are office buildings that began operations in 1Q 2015. Since then, TB Simatupang saw no additional office space as of 2Q and 3Q 2015. Recently, three office buildings have officially begun operations, namely, Graha MRA and two towers at the South Quarter complex. Those three office buildings brought 94,556 sq m of additional office space and brought the cumulative supply to 833,899 sq m in TB Simatupang in 2015, growth of 39.8% YoY. The additional supply in 2015 is the largest in TB Simatupang since 1990. Overall, the total additional office space in 2012 - 2014 is lower than in 2015.

Although it is expected that large additional spaces will enter the area, the future supply in TB Simatupang will be lower. It is expected that only three office buildings will begin operations in 2016 and provide 108,162 sq m of additional supply. Furthermore, The Sima, which is located within the Izzara Complex, will be the only future office building in TB Simatupang in 2017. The Sima, together with Cibis Tower (expected to begin operations in 2016) will be the largest future office buildings in TB Simatupang. The other office projects, such as Manhattan Square Tower 2, Arkadia Tower G and Beltway Tower D, are in the planning stages at the moment and are expected to begin operations in 2018.

TB Simatupang

7 Research & Forecast Report | Q4 2015 | Office | Colliers International

Source: Colliers International Indonesia - Research

Office Buildings Newly Operating in 2015

Office Building PrOject lOcatiOn Sga (Sq m) marketing Scheme

cBd

Sahid Sudirman Center Sudirman 138,500 For Lease & Sale

Generali Office Park (Gran Rubina Tower 1) Rasuna Said 31,438 For Sale

Noble House Office Tower Mega Kuningan 45,000 For Lease

AIA Center (Menara Selaras) Sudirman 47,000 For Lease

Gama Tower (Cemindo Tower) Rasuna Said 60,995 For Lease

Muamalat Tower (Satrio Square) Satrio 24,600 For Lease

BTPN Tower (Bahana Office Tower) Mega Kuningan 50,000 For Lease

Wisma Mulia 2 Gatot Subroto 65,000 For Lease

OutSide cBd

Menara Sentraya Blok M 52,072 For Sale

The Suites Pantai Indah Kapuk 13,200 For Sale

18 Office Park TB Simatupang 40,000 For Lease & Sale

Plaza Oleos TB Simatupang 39,778 For Lease & Sale

AD Premier TB Simatupang 18,900 For Lease

Metropolitan Tower TB Simatupang 44,000 For Lease & Sale

Graha MRA TB Simatupang 13,000 For Lease

South Quarter Tower 1 TB Simatupang 40,778 For Sale

South Quarter Tower 2 TB Simatupang 40,778 For Lease

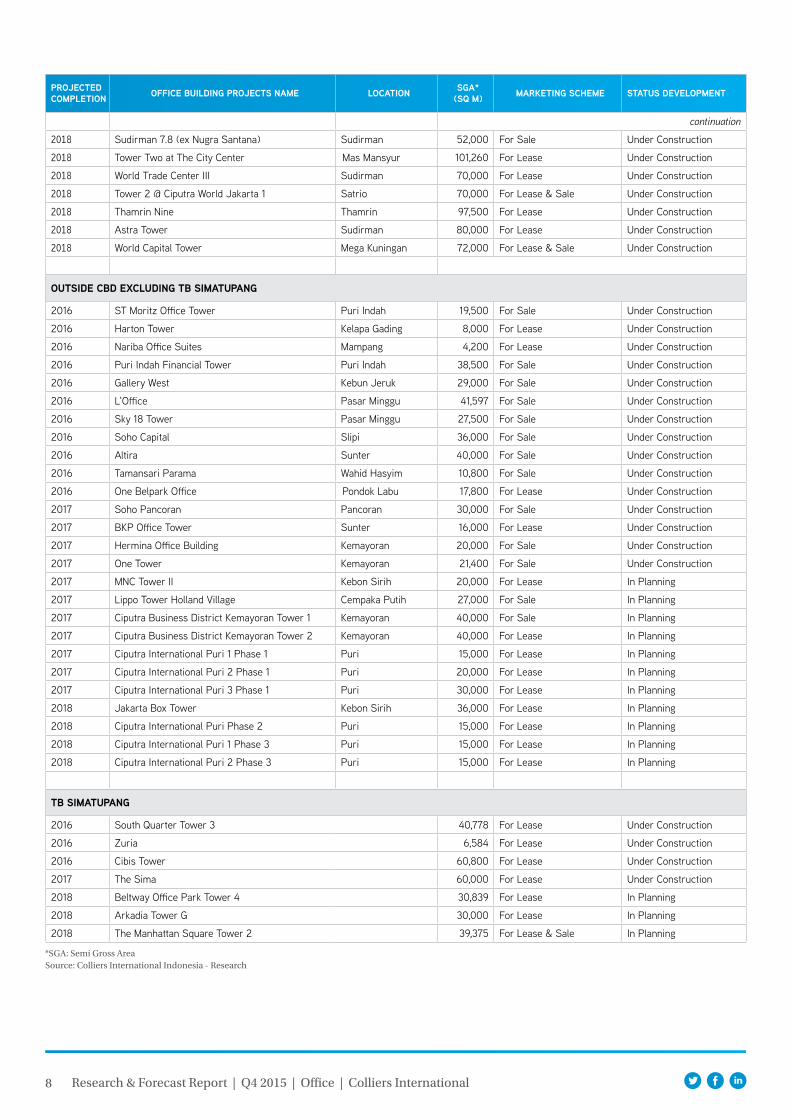

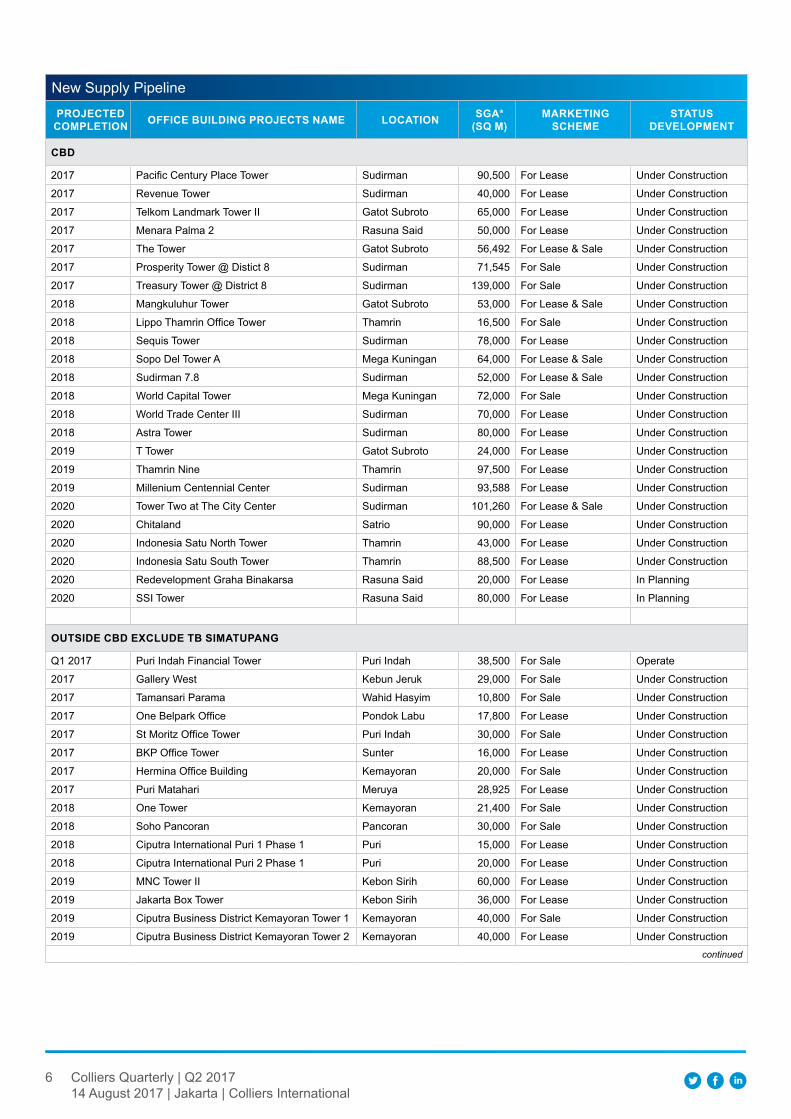

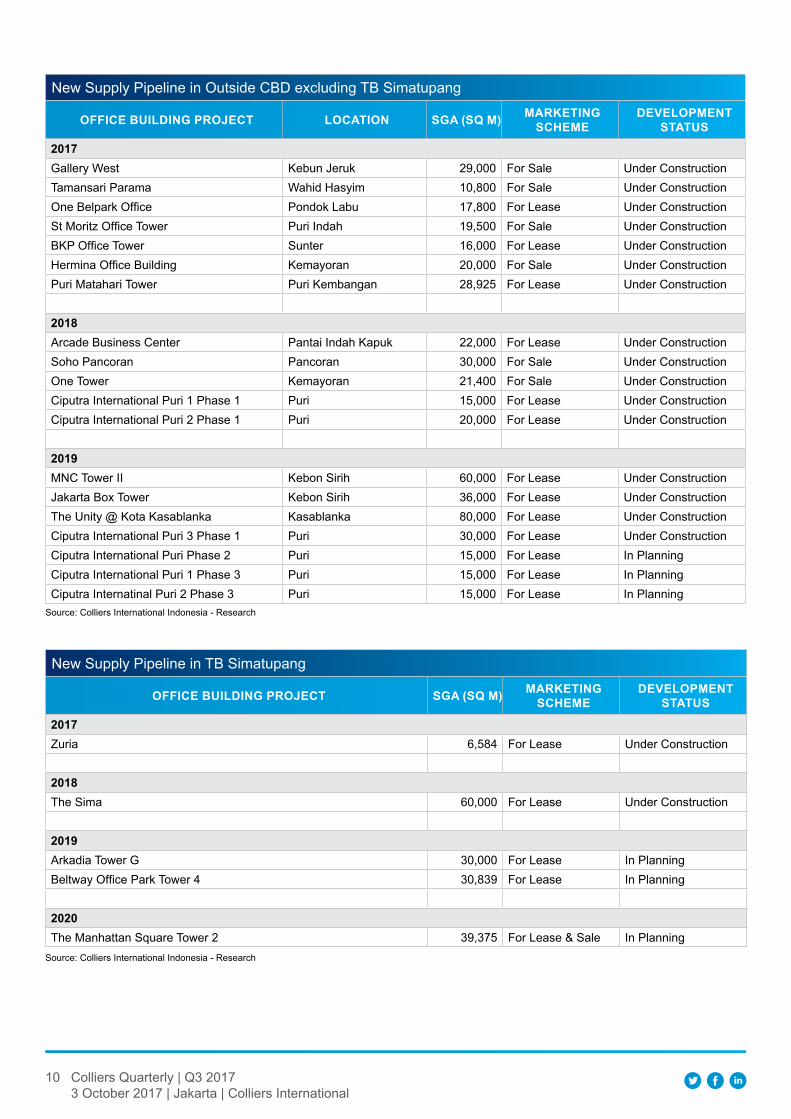

New Supply Pipeline

PrOjected cOmPletiOn Office Building PrOjectS name lOcatiOn Sga*

(Sq m) marketing Scheme StatuS develOPment

2016 Sinarmas MSIG Sudirman 75,000 For Lease Under Construction

2016 Telkom Landmark Tower II Gatot Subroto 65,000 For Lease Under Construction

2016 Convergence Rasuna Said 36,367 For Lease & Sale Under Construction

2016 International Financial Center 2 Sudirman 50,000 For Lease Under Construction

2016 Menara Pertiwi Mega Kuningan 41,456 For Sale Under Construction

2016 Capital Palace (Office Tower @ ST Regis) Gatot Subroto 90,511 For Lease Under Construction

2016 Menara Palma 2 Rasuna Said 50,000 For Lease Under Construction

2016 Centennial Tower Gatot Subroto 100,000 For Sale Under Construction

2016 Ciputra World Jakarta 2 Satrio 70,000 For Lease & Sale Under Construction

2016 Satrio Tower Satrio 31,604 For Lease Under Construction

2016 The Tower Gatot Subroto 56,492 For Sale Under Construction

2016 T Tower (BJB Tower) Gatot Subroto 24,000 For Lease & Sale Under Construction

2017 Lippo Thamrin Office Tower Thamrin 16,500 For Sale Under Construction

2017 Mangkuluhur Tower Gatot Subroto 53,000 For Lease & Sale Under Construction

2017 Prosperity Tower @ District 8 SCBD, Sudirman 71,545 For Sale Under Construction

2017 Treasury Tower @ District 8 SCBD, Sudirman 139,000 For Sale Under Construction

2017 Sopo Del Tower A Mega Kuningan 80,000 For Lease & Sale Under Construction

2017 Sopo Del Tower B Mega Kuningan 40,000 For Lease Under Construction

2017 Office Tower Lot.10 SCBD (PCPD Tower) SCBD, Sudirman 90,500 For Lease Under Construction

2018 Sequis Tower Sudirman 78,000 For Lease Under Construction

continued

8 Research & Forecast Report | Q4 2015 | Office | Colliers International

*SGA: Semi Gross AreaSource: Colliers International Indonesia - Research

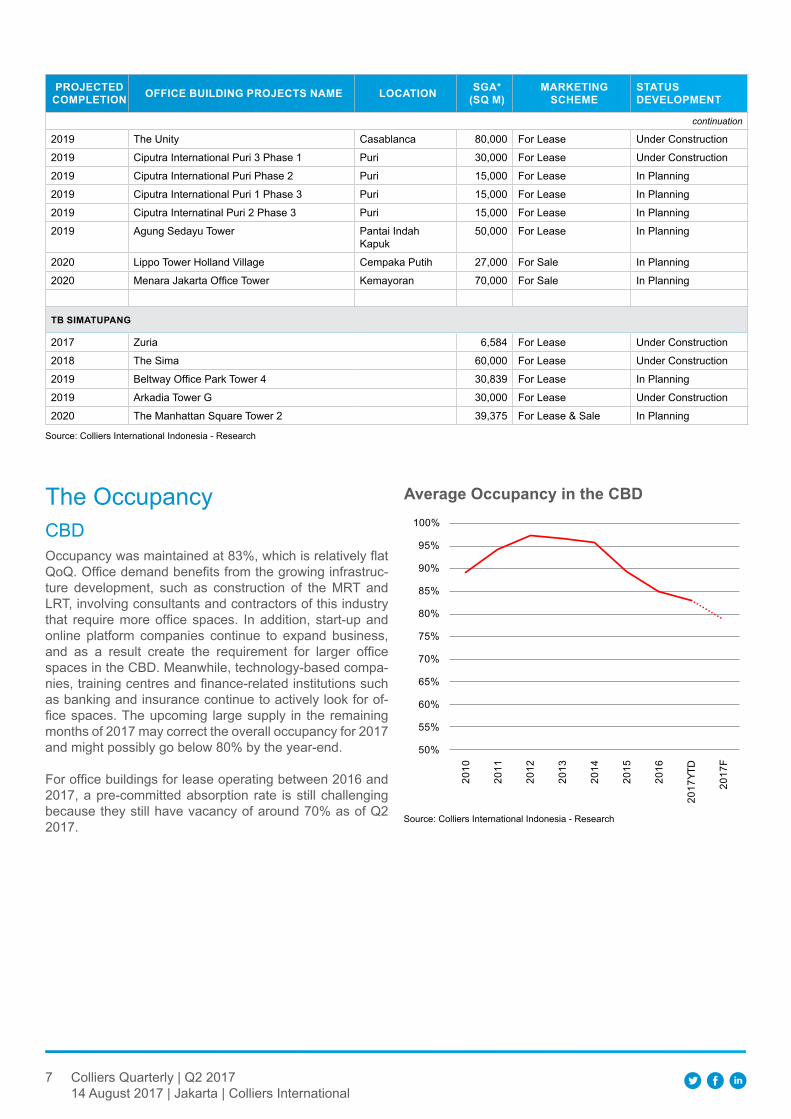

PrOjected cOmPletiOn Office Building PrOjectS name lOcatiOn Sga*

(Sq m) marketing Scheme StatuS develOPment

continuation

2018 Sudirman 7.8 (ex Nugra Santana) Sudirman 52,000 For Sale Under Construction

2018 Tower Two at The City Center Mas Mansyur 101,260 For Lease Under Construction

2018 World Trade Center III Sudirman 70,000 For Lease Under Construction

2018 Tower 2 @ Ciputra World Jakarta 1 Satrio 70,000 For Lease & Sale Under Construction

2018 Thamrin Nine Thamrin 97,500 For Lease Under Construction

2018 Astra Tower Sudirman 80,000 For Lease Under Construction

2018 World Capital Tower Mega Kuningan 72,000 For Lease & Sale Under Construction

OutSide cBd eXcluding tB SimatuPang

2016 ST Moritz Office Tower Puri Indah 19,500 For Sale Under Construction

2016 Harton Tower Kelapa Gading 8,000 For Lease Under Construction

2016 Nariba Office Suites Mampang 4,200 For Lease Under Construction

2016 Puri Indah Financial Tower Puri Indah 38,500 For Sale Under Construction

2016 Gallery West Kebun Jeruk 29,000 For Sale Under Construction

2016 L'Office Pasar Minggu 41,597 For Sale Under Construction

2016 Sky 18 Tower Pasar Minggu 27,500 For Sale Under Construction

2016 Soho Capital Slipi 36,000 For Sale Under Construction

2016 Altira Sunter 40,000 For Sale Under Construction

2016 Tamansari Parama Wahid Hasyim 10,800 For Sale Under Construction

2016 One Belpark Office Pondok Labu 17,800 For Lease Under Construction

2017 Soho Pancoran Pancoran 30,000 For Sale Under Construction

2017 BKP Office Tower Sunter 16,000 For Lease Under Construction

2017 Hermina Office Building Kemayoran 20,000 For Sale Under Construction

2017 One Tower Kemayoran 21,400 For Sale Under Construction

2017 MNC Tower II Kebon Sirih 20,000 For Lease In Planning

2017 Lippo Tower Holland Village Cempaka Putih 27,000 For Sale In Planning

2017 Ciputra Business District Kemayoran Tower 1 Kemayoran 40,000 For Sale In Planning

2017 Ciputra Business District Kemayoran Tower 2 Kemayoran 40,000 For Lease In Planning

2017 Ciputra International Puri 1 Phase 1 Puri 15,000 For Lease In Planning

2017 Ciputra International Puri 2 Phase 1 Puri 20,000 For Lease In Planning

2017 Ciputra International Puri 3 Phase 1 Puri 30,000 For Lease In Planning

2018 Jakarta Box Tower Kebon Sirih 36,000 For Lease In Planning

2018 Ciputra International Puri Phase 2 Puri 15,000 For Lease In Planning

2018 Ciputra International Puri 1 Phase 3 Puri 15,000 For Lease In Planning

2018 Ciputra International Puri 2 Phase 3 Puri 15,000 For Lease In Planning

tB SimatuPang

2016 South Quarter Tower 3 40,778 For Lease Under Construction

2016 Zuria 6,584 For Lease Under Construction

2016 Cibis Tower 60,800 For Lease Under Construction

2017 The Sima 60,000 For Lease Under Construction

2018 Beltway Office Park Tower 4 30,839 For Lease In Planning

2018 Arkadia Tower G 30,000 For Lease In Planning

2018 The Manhattan Square Tower 2 39,375 For Lease & Sale In Planning

9 Research & Forecast Report | Q4 2015 | Office | Colliers International

Source: Colliers International Indonesia - Research

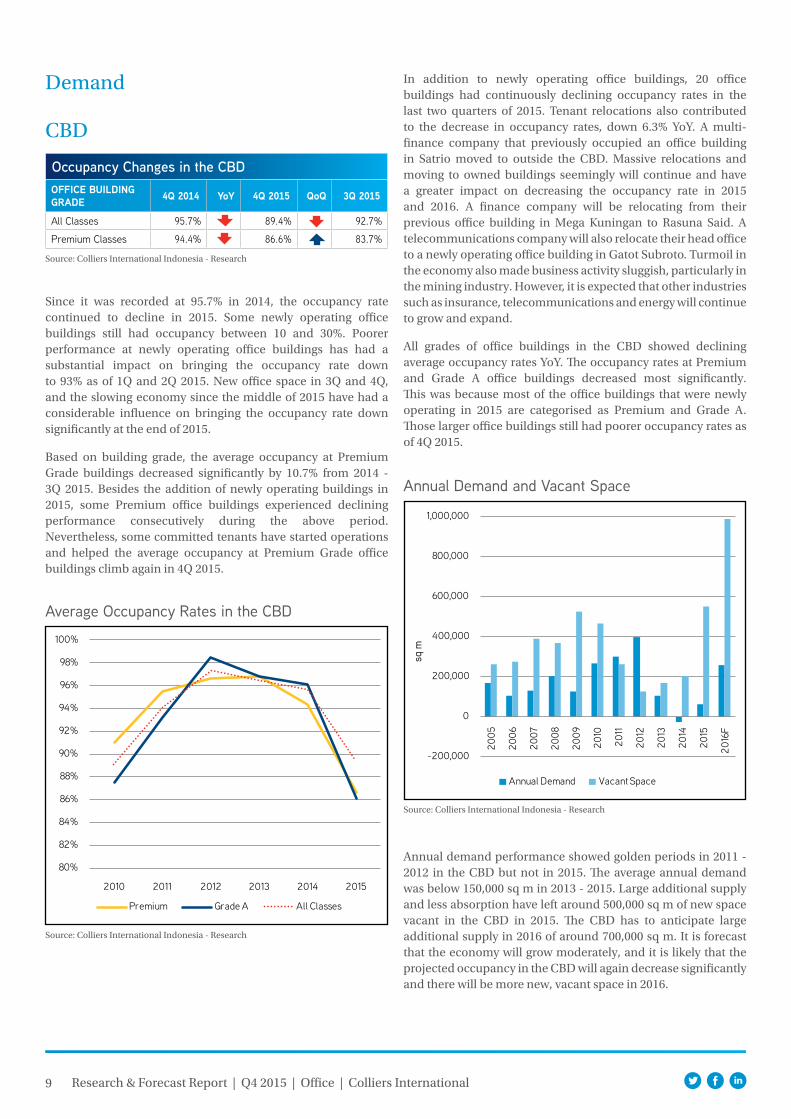

Occupancy Changes in the CBDOffice Building grade 4q 2014 YoY 4q 2015 qoq 3q 2015

All Classes 95.7% 89.4% 92.7%

Premium Classes 94.4% 86.6% 83.7%

Demand

CBD

Since it was recorded at 95.7% in 2014, the occupancy rate continued to decline in 2015. Some newly operating office buildings still had occupancy between 10 and 30%. Poorer performance at newly operating office buildings has had a substantial impact on bringing the occupancy rate down to 93% as of 1Q and 2Q 2015. New office space in 3Q and 4Q, and the slowing economy since the middle of 2015 have had a considerable influence on bringing the occupancy rate down significantly at the end of 2015.

Based on building grade, the average occupancy at Premium Grade buildings decreased significantly by 10.7% from 2014 - 3Q 2015. Besides the addition of newly operating buildings in 2015, some Premium office buildings experienced declining performance consecutively during the above period. Nevertheless, some committed tenants have started operations and helped the average occupancy at Premium Grade office buildings climb again in 4Q 2015.

Annual Demand and Vacant Space

Source: Colliers International Indonesia - Research

Average Occupancy Rates in the CBD

Source: Colliers International Indonesia - Research

80%

82%

84%

86%

88%

90%

92%

94%

96%

98%

100%

2010 2011 2012 2013 2014 2015

Premium Grade A All Classes

In addition to newly operating office buildings, 20 office buildings had continuously declining occupancy rates in the last two quarters of 2015. Tenant relocations also contributed to the decrease in occupancy rates, down 6.3% YoY. A multi-finance company that previously occupied an office building in Satrio moved to outside the CBD. Massive relocations and moving to owned buildings seemingly will continue and have a greater impact on decreasing the occupancy rate in 2015 and 2016. A finance company will be relocating from their previous office building in Mega Kuningan to Rasuna Said. A telecommunications company will also relocate their head office to a newly operating office building in Gatot Subroto. Turmoil in the economy also made business activity sluggish, particularly in the mining industry. However, it is expected that other industries such as insurance, telecommunications and energy will continue to grow and expand.

All grades of office buildings in the CBD showed declining average occupancy rates YoY. The occupancy rates at Premium and Grade A office buildings decreased most significantly. This was because most of the office buildings that were newly operating in 2015 are categorised as Premium and Grade A. Those larger office buildings still had poorer occupancy rates as of 4Q 2015.

Annual demand performance showed golden periods in 2011 - 2012 in the CBD but not in 2015. The average annual demand was below 150,000 sq m in 2013 - 2015. Large additional supply and less absorption have left around 500,000 sq m of new space vacant in the CBD in 2015. The CBD has to anticipate large additional supply in 2016 of around 700,000 sq m. It is forecast that the economy will grow moderately, and it is likely that the projected occupancy in the CBD will again decrease significantly and there will be more new, vacant space in 2016.

-200,000

0

200,000

400,000

600,000

800,000

1,000,000

2005

2006

2007

2008

2009

2010

2011

2012

2013

2014

2015

2016

F

sq m

Annual Demand Vacant Space

10 Research & Forecast Report | Q4 2015 | Office | Colliers International

Commitments to Space at Office Buildings for Lease in 2015 - 2016

Source: Colliers International Indonesia - Research

Source: Colliers International Indonesia - Research

TB Simatupang

0 100,000 200,000 300,000 400,000

2015

2016F

sq mSpace Absorbed Space Unabsorbed

Source: Colliers International Indonesia - Research

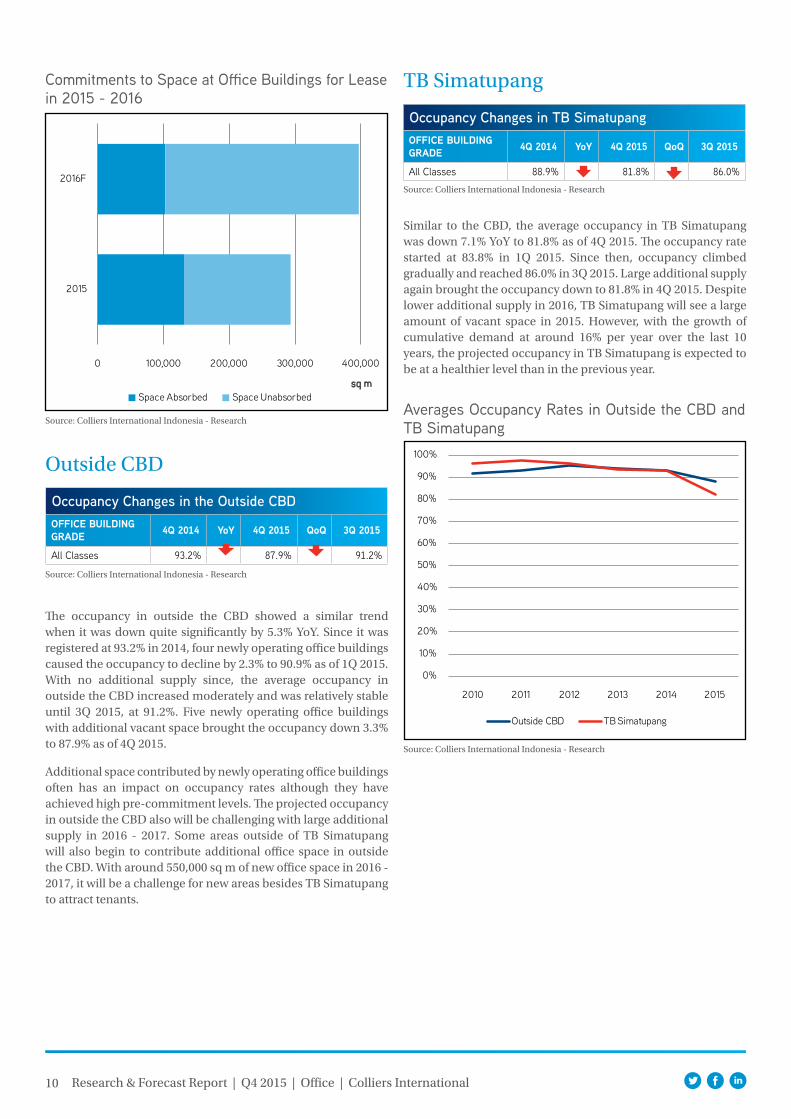

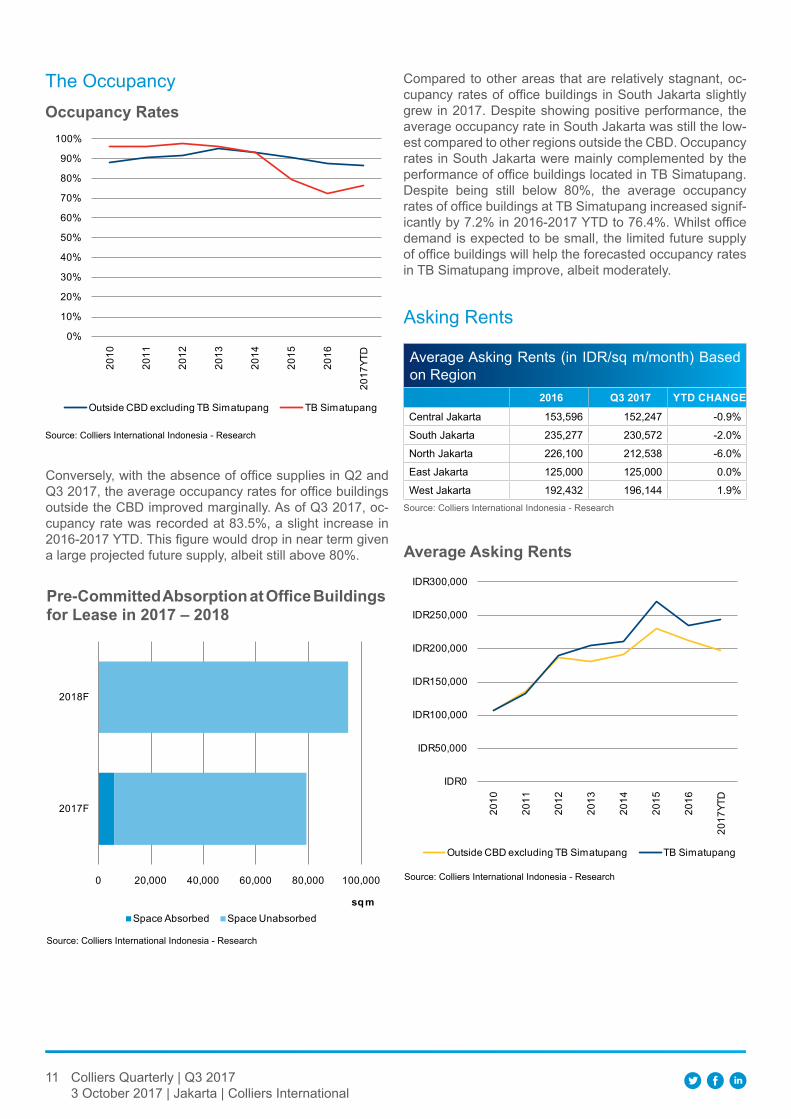

Occupancy Changes in the Outside CBDOffice Building grade 4q 2014 YoY 4q 2015 qoq 3q 2015

All Classes 93.2% 87.9% 91.2%

Outside CBD

Occupancy Changes in TB SimatupangOffice Building grade 4q 2014 YoY 4q 2015 qoq 3q 2015

All Classes 88.9% 81.8% 86.0%

Averages Occupancy Rates in Outside the CBD and TB Simatupang

Source: Colliers International Indonesia - Research

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

2010 2011 2012 2013 2014 2015

Outside CBD TB Simatupang

Similar to the CBD, the average occupancy in TB Simatupang was down 7.1% YoY to 81.8% as of 4Q 2015. The occupancy rate started at 83.8% in 1Q 2015. Since then, occupancy climbed gradually and reached 86.0% in 3Q 2015. Large additional supply again brought the occupancy down to 81.8% in 4Q 2015. Despite lower additional supply in 2016, TB Simatupang will see a large amount of vacant space in 2015. However, with the growth of cumulative demand at around 16% per year over the last 10 years, the projected occupancy in TB Simatupang is expected to be at a healthier level than in the previous year.

The occupancy in outside the CBD showed a similar trend when it was down quite significantly by 5.3% YoY. Since it was registered at 93.2% in 2014, four newly operating office buildings caused the occupancy to decline by 2.3% to 90.9% as of 1Q 2015. With no additional supply since, the average occupancy in outside the CBD increased moderately and was relatively stable until 3Q 2015, at 91.2%. Five newly operating office buildings with additional vacant space brought the occupancy down 3.3% to 87.9% as of 4Q 2015.

Additional space contributed by newly operating office buildings often has an impact on occupancy rates although they have achieved high pre-commitment levels. The projected occupancy in outside the CBD also will be challenging with large additional supply in 2016 - 2017. Some areas outside of TB Simatupang will also begin to contribute additional office space in outside the CBD. With around 550,000 sq m of new office space in 2016 - 2017, it will be a challenge for new areas besides TB Simatupang to attract tenants.

11 Research & Forecast Report | Q4 2015 | Office | Colliers International

Committed Space at Office Buildings for Lease in 2015 - 2016 in the Outside CBD

Source: Colliers International Indonesia - Research

Average Asking Rental Rates for Office Occupation in the CBD

Source: Colliers International Indonesia - Research

0 50,000 100,000 150,000 200,000 250,000

TB Simatupang

Outside CBD excl. TB Simatupang

sq mSpace Absorbed Space Unabsorbed

Asking Rents

USD0.00

USD10.00

USD20.00

USD30.00

USD40.00

IDR0

IDR100,000

IDR200,000

IDR300,000

IDR400,000

2010 2011 2012 2013 2014 2015

IDR Aggregate USD

Average Asking Rental Rates for Office Occupation in the CBD at Premium and Grade A Office Buildings

Source: Colliers International Indonesia - Research

USD0.00

USD10.00

USD20.00

USD30.00

USD40.00

USD50.00

IDR0

IDR100,000

IDR200,000

IDR300,000

IDR400,000

IDR500,000

2010 2011 2012 2013 2014 2015

IDR Aggregate USD

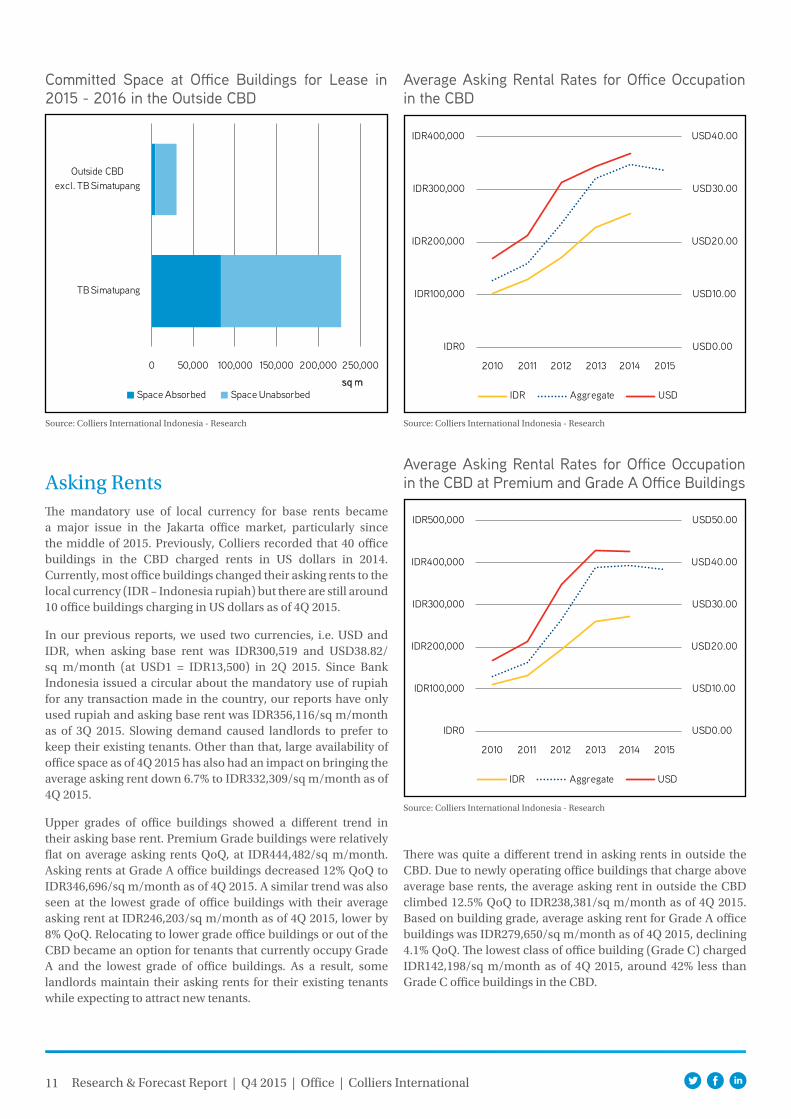

The mandatory use of local currency for base rents became a major issue in the Jakarta office market, particularly since the middle of 2015. Previously, Colliers recorded that 40 office buildings in the CBD charged rents in US dollars in 2014. Currently, most office buildings changed their asking rents to the local currency (IDR – Indonesia rupiah) but there are still around 10 office buildings charging in US dollars as of 4Q 2015.

In our previous reports, we used two currencies, i.e. USD and IDR, when asking base rent was IDR300,519 and USD38.82/sq m/month (at USD1 = IDR13,500) in 2Q 2015. Since Bank Indonesia issued a circular about the mandatory use of rupiah for any transaction made in the country, our reports have only used rupiah and asking base rent was IDR356,116/sq m/month as of 3Q 2015. Slowing demand caused landlords to prefer to keep their existing tenants. Other than that, large availability of office space as of 4Q 2015 has also had an impact on bringing the average asking rent down 6.7% to IDR332,309/sq m/month as of 4Q 2015.

Upper grades of office buildings showed a different trend in their asking base rent. Premium Grade buildings were relatively flat on average asking rents QoQ, at IDR444,482/sq m/month. Asking rents at Grade A office buildings decreased 12% QoQ to IDR346,696/sq m/month as of 4Q 2015. A similar trend was also seen at the lowest grade of office buildings with their average asking rent at IDR246,203/sq m/month as of 4Q 2015, lower by 8% QoQ. Relocating to lower grade office buildings or out of the CBD became an option for tenants that currently occupy Grade A and the lowest grade of office buildings. As a result, some landlords maintain their asking rents for their existing tenants while expecting to attract new tenants.

There was quite a different trend in asking rents in outside the CBD. Due to newly operating office buildings that charge above average base rents, the average asking rent in outside the CBD climbed 12.5% QoQ to IDR238,381/sq m/month as of 4Q 2015. Based on building grade, average asking rent for Grade A office buildings was IDR279,650/sq m/month as of 4Q 2015, declining 4.1% QoQ. The lowest class of office building (Grade C) charged IDR142,198/sq m/month as of 4Q 2015, around 42% less than Grade C office buildings in the CBD.

12 Research & Forecast Report | Q4 2015 | Office | Colliers International

Average Asking Rental Rates for Office Occupation in Outside the CBD

Source: Colliers International Indonesia - Research

USD0.00

USD5.00

USD10.00

USD15.00

USD20.00

USD25.00

USD30.00

IDR0

IDR50,000

IDR100,000

IDR150,000

IDR200,000

IDR250,000

IDR300,000

2010 2011 2012 2013 2014 2015

IDR Aggregate USD

Average Asking Rental Rates for Office Occupation in TB Simatupang

Source: Colliers International Indonesia - Research

USD0.00

USD5.00

USD10.00

USD15.00

USD20.00

USD25.00

USD30.00

IDR0

IDR50,000

IDR100,000

IDR150,000

IDR200,000

IDR250,000

IDR300,000

2010 2011 2012 2013 2014 2015

IDR Aggregate USD

Service Charges

Range of Service Charges in Jakarta

Source: Colliers International Indonesia - Research

IDR0

IDR30,000

IDR60,000

IDR90,000

IDR120,000

IDR150,000

Tham

rin

Sudi

rman

Rasu

na S

aid

Meg

a Ku

ning

an

Gato

t Sub

roto

Satr

io

Cent

ral J

akar

ta

Sout

h Ja

kart

a

Nor

th J

akar

ta

East

Jak

arta

Wes

t Jak

arta

TB S

imat

upan

g

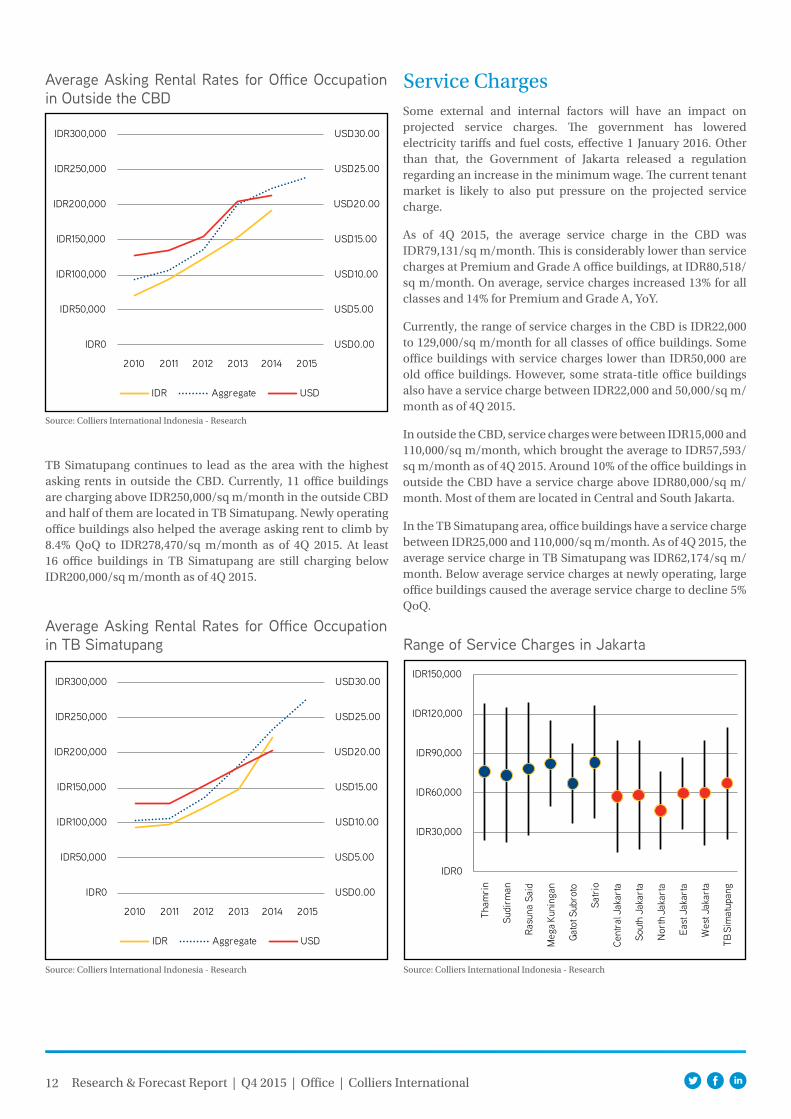

TB Simatupang continues to lead as the area with the highest asking rents in outside the CBD. Currently, 11 office buildings are charging above IDR250,000/sq m/month in the outside CBD and half of them are located in TB Simatupang. Newly operating office buildings also helped the average asking rent to climb by 8.4% QoQ to IDR278,470/sq m/month as of 4Q 2015. At least 16 office buildings in TB Simatupang are still charging below IDR200,000/sq m/month as of 4Q 2015.

Some external and internal factors will have an impact on projected service charges. The government has lowered electricity tariffs and fuel costs, effective 1 January 2016. Other than that, the Government of Jakarta released a regulation regarding an increase in the minimum wage. The current tenant market is likely to also put pressure on the projected service charge.

As of 4Q 2015, the average service charge in the CBD was IDR79,131/sq m/month. This is considerably lower than service charges at Premium and Grade A office buildings, at IDR80,518/sq m/month. On average, service charges increased 13% for all classes and 14% for Premium and Grade A, YoY.

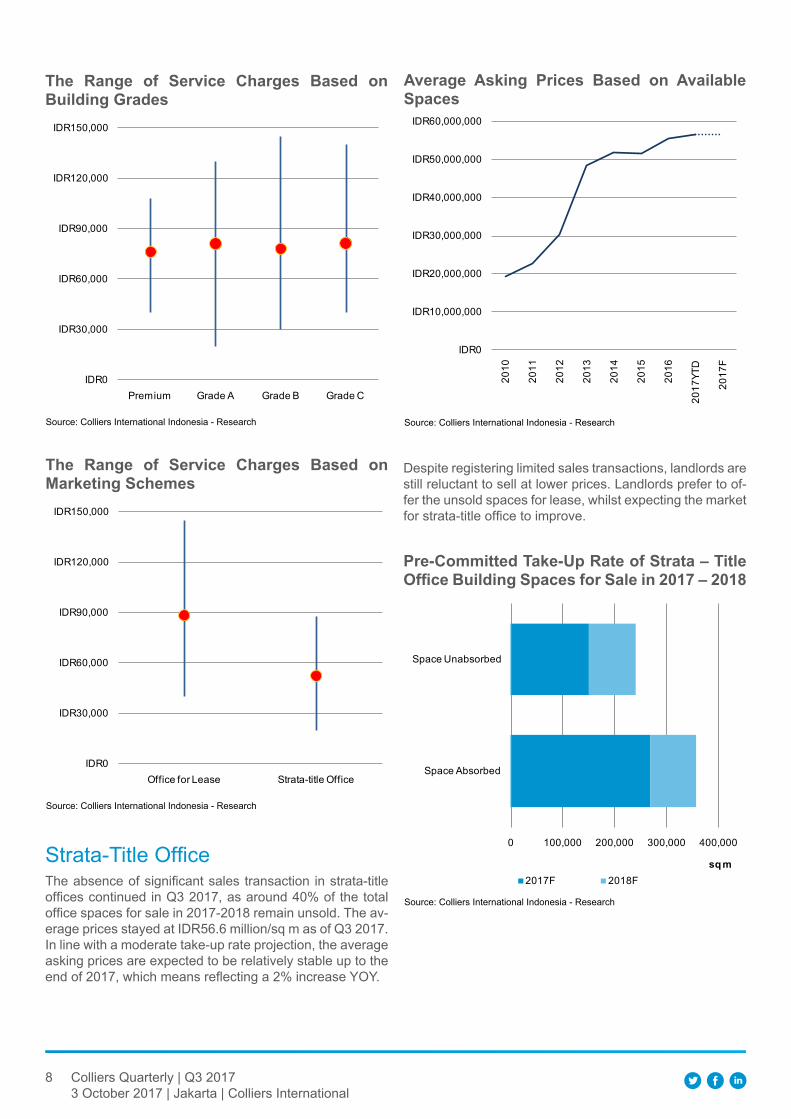

Currently, the range of service charges in the CBD is IDR22,000 to 129,000/sq m/month for all classes of office buildings. Some office buildings with service charges lower than IDR50,000 are old office buildings. However, some strata-title office buildings also have a service charge between IDR22,000 and 50,000/sq m/month as of 4Q 2015.

In outside the CBD, service charges were between IDR15,000 and 110,000/sq m/month, which brought the average to IDR57,593/sq m/month as of 4Q 2015. Around 10% of the office buildings in outside the CBD have a service charge above IDR80,000/sq m/month. Most of them are located in Central and South Jakarta.

In the TB Simatupang area, office buildings have a service charge between IDR25,000 and 110,000/sq m/month. As of 4Q 2015, the average service charge in TB Simatupang was IDR62,174/sq m/month. Below average service charges at newly operating, large office buildings caused the average service charge to decline 5% QoQ.

13 Research & Forecast Report | Q4 2015 | Office | Colliers International

Two strata-title office buildings for sale, namely Sahid Sudirman Centre and Gran Rubina, began operations in 1Q 2015 in the CBD. By offering 169,938 sq m of new office space for sale, those buildings brought the cumulative supply of strata-title offices to 986,767 sq m. Since then, the CBD saw no additional office space for sale by 4Q 2015. The CBD will see almost one million square metres of additional office space for sale in the three years ahead. Six office buildings are expected to begin operations and bring 328,315 sq m of new office space for sale in 2016. Half of those future office buildings in 2016 will be larger than 50,000 sq m. Gatot Subroto will become the greatest contributor area by providing 55% of the total additional office space for sale in 2016. Sudirman will still contribute the most office space for sale in 2016 - 2018. Four strata-title office buildings will bring 363,805 sq m of additional space for sale in Sudirman during that period.

Five office buildings officially began operations in 2015 in outside the CBD. TB Simatupang still continues as the main contributor area since 2014. Three newly operating office buildings that provided 124,778 sq m of additional office space for sale brought the cumulative supply to 214,354 sq m as of 4Q 2015. Despite being the main contributor of office space in TB Simatupang in 2014 - 2015, South Quarter, which began operations in 4Q 2015, will become the latest strata-title office building for sale in TB Simatupang. This is due, at least until the end of 2015, to landlords and developers having not yet launched or announced the development of new strata-title office buildings in TB Simatupang.

Apart from TB Simatupang, Menara Sentraya (in South Jakarta) and The Suites (in North Jakarta) began operating and brought 65,272 sq m of new office space for sale in outside the CBD as of 4Q 2015. Those two office buildings brought the cumulative supply to 467,626 sq m in 2015. It is expected that 13 future office buildings will bring around 380,000 sq m of additional office space for sale in 2016 - 2017 in outside the CBD; 60% of that future supply will be contributed by eight office buildings in 2016.

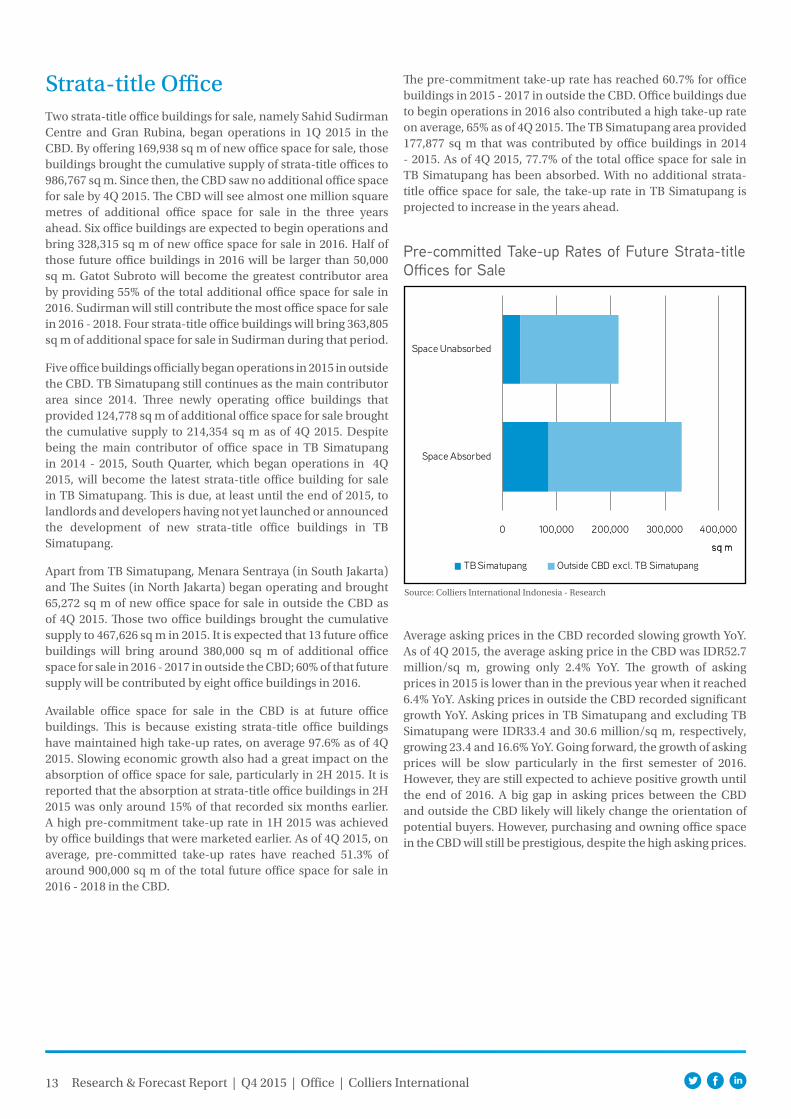

Available office space for sale in the CBD is at future office buildings. This is because existing strata-title office buildings have maintained high take-up rates, on average 97.6% as of 4Q 2015. Slowing economic growth also had a great impact on the absorption of office space for sale, particularly in 2H 2015. It is reported that the absorption at strata-title office buildings in 2H 2015 was only around 15% of that recorded six months earlier. A high pre-commitment take-up rate in 1H 2015 was achieved by office buildings that were marketed earlier. As of 4Q 2015, on average, pre-committed take-up rates have reached 51.3% of around 900,000 sq m of the total future office space for sale in 2016 - 2018 in the CBD.

The pre-commitment take-up rate has reached 60.7% for office buildings in 2015 - 2017 in outside the CBD. Office buildings due to begin operations in 2016 also contributed a high take-up rate on average, 65% as of 4Q 2015. The TB Simatupang area provided 177,877 sq m that was contributed by office buildings in 2014 - 2015. As of 4Q 2015, 77.7% of the total office space for sale in TB Simatupang has been absorbed. With no additional strata-title office space for sale, the take-up rate in TB Simatupang is projected to increase in the years ahead.

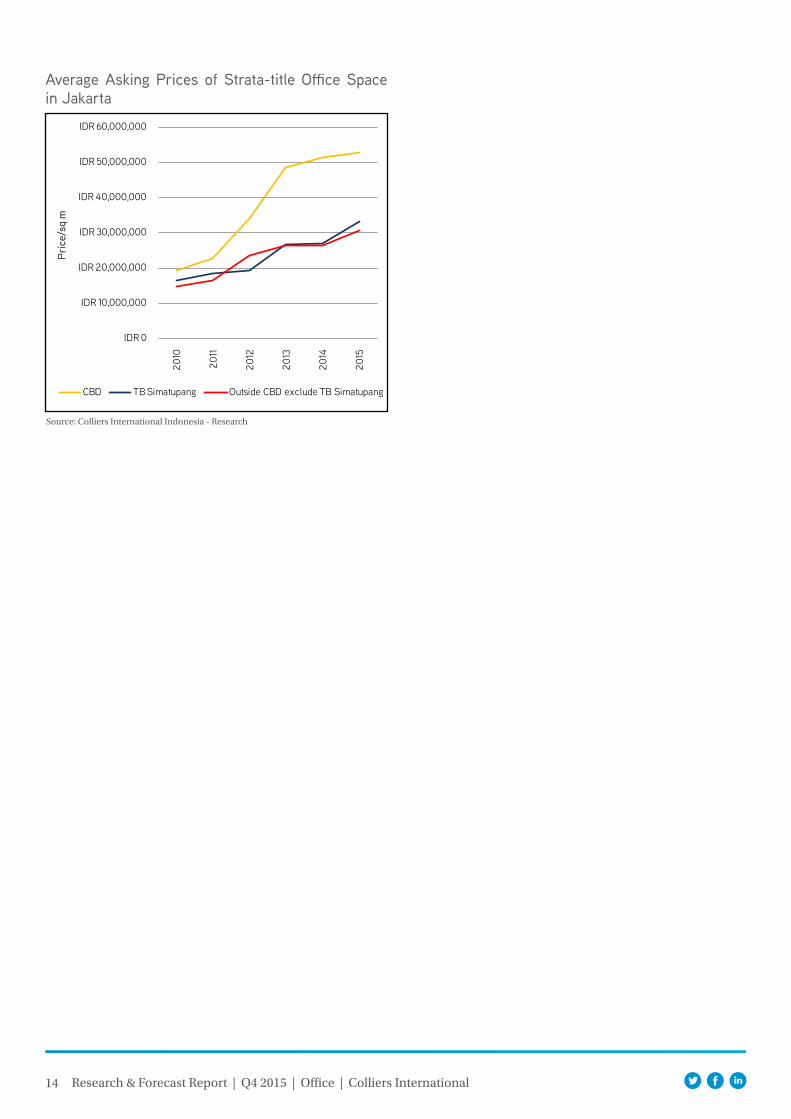

Average asking prices in the CBD recorded slowing growth YoY. As of 4Q 2015, the average asking price in the CBD was IDR52.7 million/sq m, growing only 2.4% YoY. The growth of asking prices in 2015 is lower than in the previous year when it reached 6.4% YoY. Asking prices in outside the CBD recorded significant growth YoY. Asking prices in TB Simatupang and excluding TB Simatupang were IDR33.4 and 30.6 million/sq m, respectively, growing 23.4 and 16.6% YoY. Going forward, the growth of asking prices will be slow particularly in the first semester of 2016. However, they are still expected to achieve positive growth until the end of 2016. A big gap in asking prices between the CBD and outside the CBD likely will likely change the orientation of potential buyers. However, purchasing and owning office space in the CBD will still be prestigious, despite the high asking prices.

Strata-title Office

Pre-committed Take-up Rates of Future Strata-title Offices for Sale

Source: Colliers International Indonesia - Research

0 100,000 200,000 300,000 400,000

Space Absorbed

Space Unabsorbed

sq m

TB Simatupang Outside CBD excl. TB Simatupang

14 Research & Forecast Report | Q4 2015 | Office | Colliers International

Average Asking Prices of Strata-title Office Space in Jakarta

Source: Colliers International Indonesia - Research

IDR 0

IDR 10,000,000

IDR 20,000,000

IDR 30,000,000

IDR 40,000,000

IDR 50,000,000

IDR 60,000,000

2010

2011

2012

2013

2014

2015

Pri

ce/s

q m

CBD TB Simatupang Outside CBD exclude TB Simatupang

Apartment SectorApartment for Strata-title

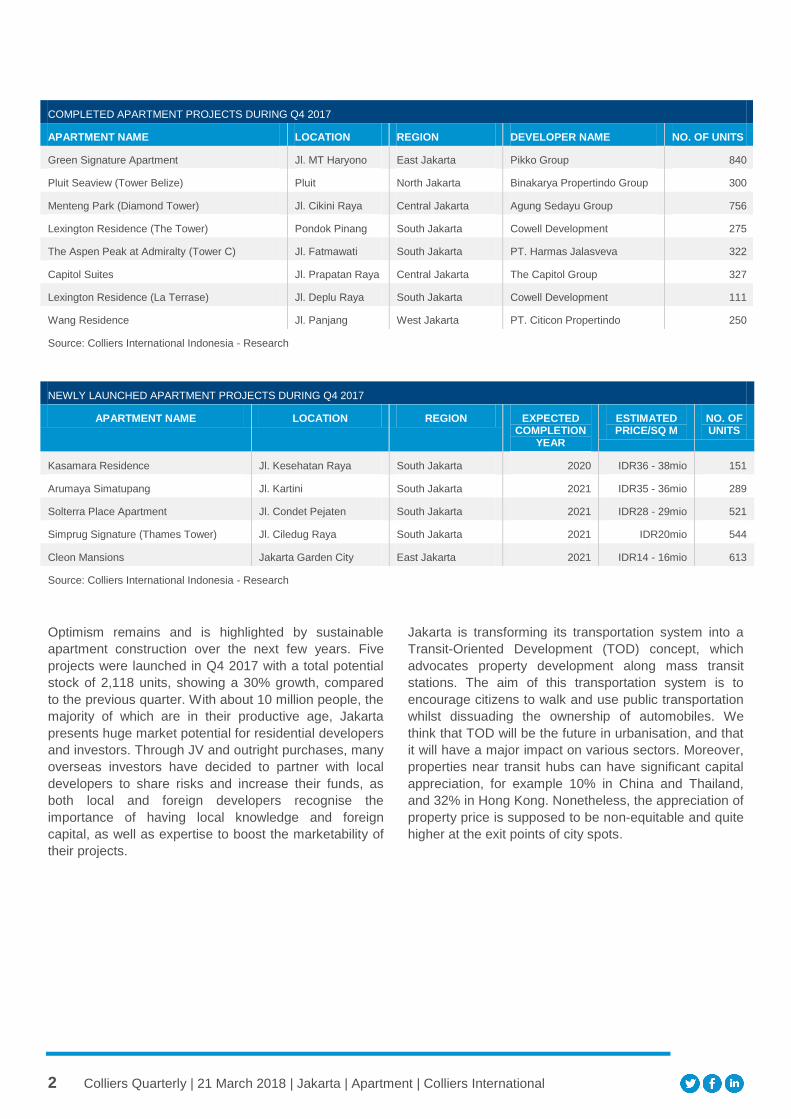

SupplyWith a total of 11 completed apartment projects consisting of 4,549 new units, the cumulative supply of apartments in Jakarta

Projects Newly Completed in 4Q 2015name Of develOPment lOcatiOn regiOn develOPer unitS

Setiabudi Sky Garden (tower 2) Jl. Karbela Selatan CBD Jakarta Setiabudi International 160

Capitol Park Apartment (Tower Emer-ald)

Jl. Salemba Raya, Menteng Central Jakarta PT. Wikaraga Sapta Utama (Sinarmas Land)

727

The Mansion at Dukuh Golf Residence (Aurora Tower)

Jl. Benyamin Sueb Kemayoran Central Jakarta Agung Sedayu Group 502

The Mansion at Dukuh Golf Residence (Bellavista Tower)

Jl. Benyamin Sueb Kemayoran Central Jakarta Agung Sedayu Group 574

Callia Residence Jl. Perintis Kemerdekaan North Jakarta Duta Anggada Realty 560

The Oak Tower (2 Towers) Jl. Perintis Kemerdekaan North Jakarta PT. Mahardhika Propertindo (Duta Putra Group)

821

La Maison Barito Jl. Barito South Jakarta Duta Anggada Realty 80

Niffaro Apartment (Ebony Tower) Jl. Kalibata Raya South Jakarta PT. Putra Indonesia Bersama 288

Royal Olive Residence (2 towers) Jl. Buncit Raya South Jakarta PT. AD Realty 500

Kencana Residence Jl. Sultan Iskandar Muda South Jakarta Margahayu Land 173

The Windsor (Tower 2) Jl. Puri Indah West Jakarta PT Antilope Madju Puri Indah 164

Source: Colliers International Indonesia - Research

increased by 3% QoQ and 9.7% YoY, bringing the total existing supply at the end of 2015 to 156,907 units. Central Jakarta has the largest share (39.6%) of newly completed projects this quarter, followed by North and South Jakarta with 30.2% and 22.9% respectively. Most of the newly completed projects are brand-new developments, including The Mansion at Dukuh Golf Residence (Aurora and Bellavista Tower), Callia Residence, The Oak Tower, La Maison Barito, Royal Olive Residence and Kencana Residence. The other four projects are the extensions (i.e. additional tower) of the existing projects.

The annual supply in 2015 was a little higher at 3% compared to the average supply in the last five years. However, only 47% of our initial projection of a total 29,758 units at the beginning of the year have confirmed the hand-over schedule. Most delayed projects have a similar argument that they are still in the grace period and will deliver the projects during the first semester of 2016. As a result, there will be a substantial number of new units should all the projects be completed on time

next year. Looking ahead, the market will receive around 82,000 units in the next four years, which will bring the inventory of apartment units in Jakarta to more than 239,000 in 2019.

Our initial supply projection for 2016 was 22,210 units. With the delay in completion of quite a few units in 2015, the total annual projected supply for 2016 will be quite significant (35,205 units).

16 Research & Forecast Report | Q4 2015 | Apartment | Colliers International

Apartments Newly Introduced or Launched in 4Q 2015

name Of develOPment lOcatiOn regiOn eXPected cOmPletiOn time

aSking Price/Sq m* nO. Of unitS

Apartemen South East Capital (Cattleya Tower) Jl. Bina Marga, Cipayung East Jakarta 2020 IDR14,000,000 823

Newly Launched/Introduced Projects per Quarter (2013 – 2015)

Source: Colliers International Indonesia - Research

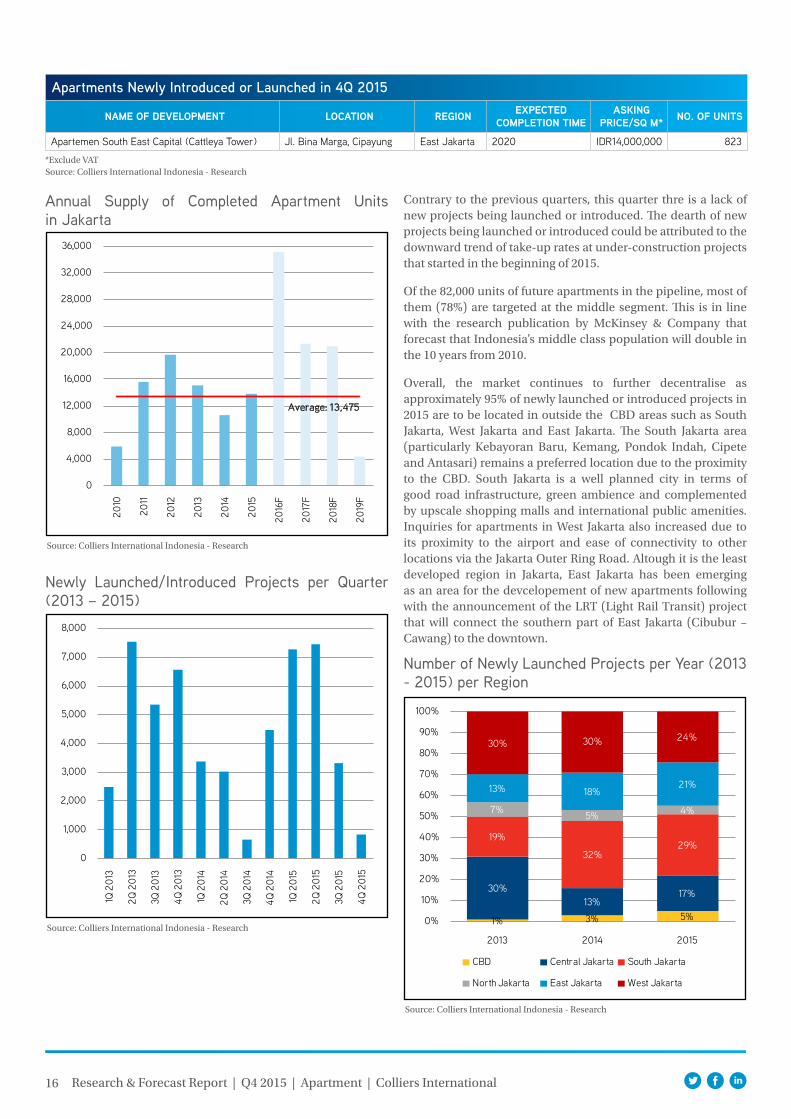

Contrary to the previous quarters, this quarter thre is a lack of new projects being launched or introduced. The dearth of new projects being launched or introduced could be attributed to the downward trend of take-up rates at under-construction projects that started in the beginning of 2015.

Of the 82,000 units of future apartments in the pipeline, most of them (78%) are targeted at the middle segment. This is in line with the research publication by McKinsey & Company that forecast that Indonesia’s middle class population will double in the 10 years from 2010.

Overall, the market continues to further decentralise as approximately 95% of newly launched or introduced projects in 2015 are to be located in outside the CBD areas such as South Jakarta, West Jakarta and East Jakarta. The South Jakarta area (particularly Kebayoran Baru, Kemang, Pondok Indah, Cipete and Antasari) remains a preferred location due to the proximity to the CBD. South Jakarta is a well planned city in terms of good road infrastructure, green ambience and complemented by upscale shopping malls and international public amenities. Inquiries for apartments in West Jakarta also increased due to its proximity to the airport and ease of connectivity to other locations via the Jakarta Outer Ring Road. Altough it is the least developed region in Jakarta, East Jakarta has been emerging as an area for the devcelopement of new apartments following with the announcement of the LRT (Light Rail Transit) project that will connect the southern part of East Jakarta (Cibubur – Cawang) to the downtown.

*Exclude VATSource: Colliers International Indonesia - Research

Annual Supply of Completed Apartment Units in Jakarta

Source: Colliers International Indonesia - Research

0

4,000

8,000

12,000

16,000

20,000

24,000

28,000

32,000

36,000

2010

2011

2012

2013

2014

2015

2016

F

2017

F

2018

F

2019

F

Average: 13,475

0

1,000

2,000

3,000

4,000

5,000

6,000

7,000

8,000

1Q 2

013

2Q 2

013

3Q 2

013

4Q 2

013

1Q 2

014

2Q 2

014

3Q 2

014

4Q 2

014

1Q 2

015

2Q 2

015

3Q 2

015

4Q 2

015

Number of Newly Launched Projects per Year (2013 - 2015) per Region

Source: Colliers International Indonesia - Research

1% 3% 5%

30%13%

17%

19%

32%29%

7% 5% 4%

13% 18%21%

30% 30% 24%

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

2013 2014 2015

CBD Central Jakarta South Jakarta

North Jakarta East Jakarta West Jakarta

17 Research & Forecast Report | Q4 2015 | Apartment | Colliers International

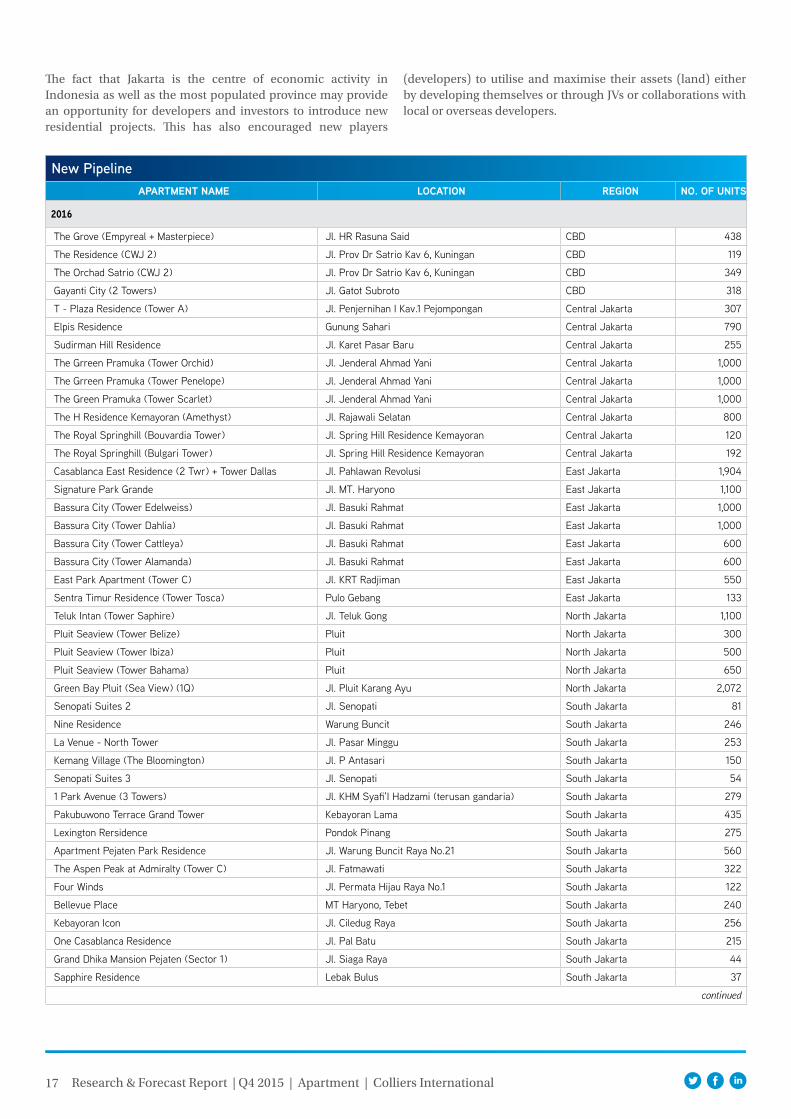

New PipelineaPartment name lOcatiOn regiOn nO. Of unitS

2016

The Grove (Empyreal + Masterpiece) Jl. HR Rasuna Said CBD 438

The Residence (CWJ 2) Jl. Prov Dr Satrio Kav 6, Kuningan CBD 119

The Orchad Satrio (CWJ 2) Jl. Prov Dr Satrio Kav 6, Kuningan CBD 349

Gayanti City (2 Towers) Jl. Gatot Subroto CBD 318

T - Plaza Residence (Tower A) Jl. Penjernihan I Kav.1 Pejompongan Central Jakarta 307

Elpis Residence Gunung Sahari Central Jakarta 790

Sudirman Hill Residence Jl. Karet Pasar Baru Central Jakarta 255

The Grreen Pramuka (Tower Orchid) Jl. Jenderal Ahmad Yani Central Jakarta 1,000

The Grreen Pramuka (Tower Penelope) Jl. Jenderal Ahmad Yani Central Jakarta 1,000

The Green Pramuka (Tower Scarlet) Jl. Jenderal Ahmad Yani Central Jakarta 1,000

The H Residence Kemayoran (Amethyst) Jl. Rajawali Selatan Central Jakarta 800

The Royal Springhill (Bouvardia Tower) Jl. Spring Hill Residence Kemayoran Central Jakarta 120

The Royal Springhill (Bulgari Tower) Jl. Spring Hill Residence Kemayoran Central Jakarta 192

Casablanca East Residence (2 Twr) + Tower Dallas Jl. Pahlawan Revolusi East Jakarta 1,904

Signature Park Grande Jl. MT. Haryono East Jakarta 1,100

Bassura City (Tower Edelweiss) Jl. Basuki Rahmat East Jakarta 1,000

Bassura City (Tower Dahlia) Jl. Basuki Rahmat East Jakarta 1,000

Bassura City (Tower Cattleya) Jl. Basuki Rahmat East Jakarta 600

Bassura City (Tower Alamanda) Jl. Basuki Rahmat East Jakarta 600

East Park Apartment (Tower C) Jl. KRT Radjiman East Jakarta 550

Sentra Timur Residence (Tower Tosca) Pulo Gebang East Jakarta 133

Teluk Intan (Tower Saphire) Jl. Teluk Gong North Jakarta 1,100

Pluit Seaview (Tower Belize) Pluit North Jakarta 300

Pluit Seaview (Tower Ibiza) Pluit North Jakarta 500

Pluit Seaview (Tower Bahama) Pluit North Jakarta 650

Green Bay Pluit (Sea View) (1Q) Jl. Pluit Karang Ayu North Jakarta 2,072

Senopati Suites 2 Jl. Senopati South Jakarta 81

Nine Residence Warung Buncit South Jakarta 246

La Venue - North Tower Jl. Pasar Minggu South Jakarta 253

Kemang Village (The Bloomington) Jl. P Antasari South Jakarta 150

Senopati Suites 3 Jl. Senopati South Jakarta 54

1 Park Avenue (3 Towers) Jl. KHM Syafi'I Hadzami (terusan gandaria) South Jakarta 279

Pakubuwono Terrace Grand Tower Kebayoran Lama South Jakarta 435

Lexington Rersidence Pondok Pinang South Jakarta 275

Apartment Pejaten Park Residence Jl. Warung Buncit Raya No.21 South Jakarta 560

The Aspen Peak at Admiralty (Tower C) Jl. Fatmawati South Jakarta 322

Four Winds Jl. Permata Hijau Raya No.1 South Jakarta 122

Bellevue Place MT Haryono, Tebet South Jakarta 240

Kebayoran Icon Jl. Ciledug Raya South Jakarta 256

One Casablanca Residence Jl. Pal Batu South Jakarta 215

Grand Dhika Mansion Pejaten (Sector 1) Jl. Siaga Raya South Jakarta 44

Sapphire Residence Lebak Bulus South Jakarta 37

continued

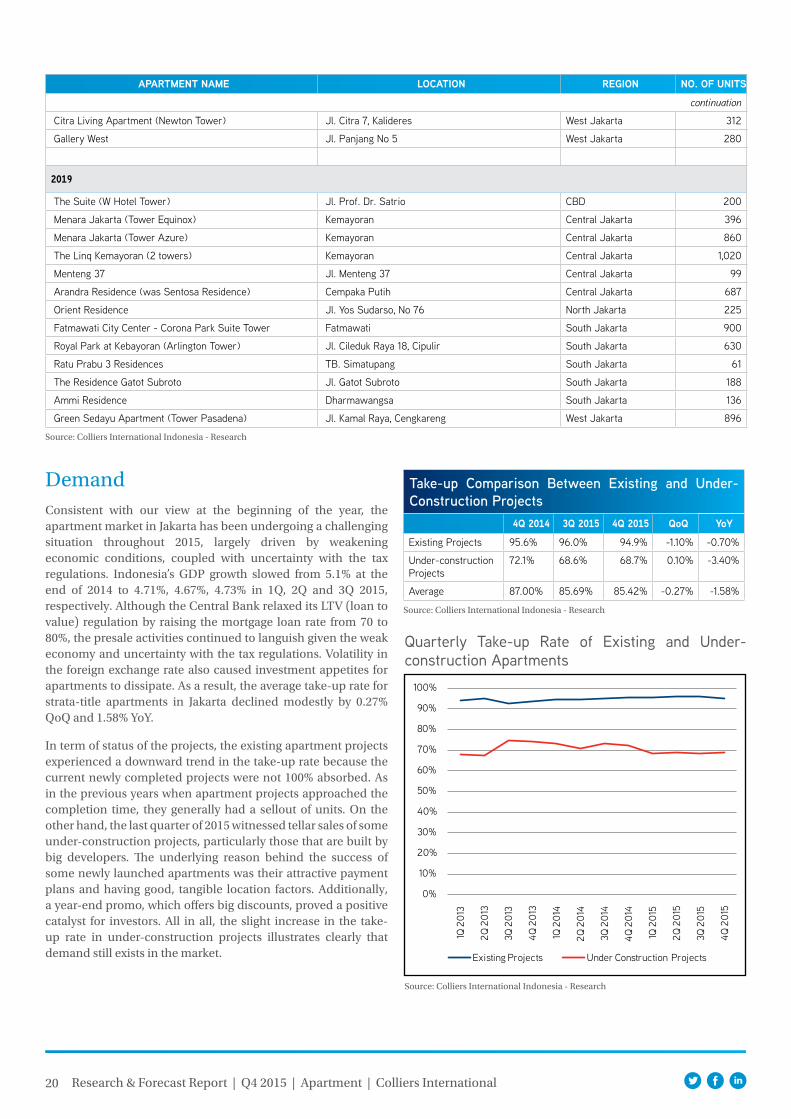

The fact that Jakarta is the centre of economic activity in Indonesia as well as the most populated province may provide an opportunity for developers and investors to introduce new residential projects. This has also encouraged new players

(developers) to utilise and maximise their assets (land) either by developing themselves or through JVs or collaborations with local or overseas developers.

18 Research & Forecast Report | Q4 2015 | Apartment | Colliers International

aPartment name lOcatiOn regiOn nO. Of unitS

continuation

Woodland Park (Mahogany Tower) Jl. Pahlawan Kalibata South Jakarta 218

St Moritz (The New Ambassador Suite Tower) Jl. Puri Indah Kembangan West Jakarta 200

Gianetti Apartment Jl. Kebon Jeruk Raya, Kemanggisan West Jakarta 500

Metro Park Residence Kebon Jeruk West Jakarta 1,451

St. Moritz (New Presidential Tower) Jl. Puri Indah West Jakarta 159

The Nest Apartment Jl. Raden Saleh Raya, Meruya Utara West Jakarta 1,100

Green Park View (Tower G) Jl. Daan Mogot West Jakarta 1,200

Belmont Residence (TowerAthena) Jl. Meruya Ilir West Jakarta 193

Puri Mansion Apartment (Tower Amethyst) Jl. Lingkar Luar Barat, Puri Kembangan West Jakarta 900

Madison Park Tanjung Duren West Jakarta 1,200

Veranda Jl. Pesanggrahan Raya, Kembangan West Jakarta 174

19 Avenue Apartment 9 (Tower A) Daan Mogot West Jakarta 338

2017

Domaine Jl. Jend. Sudirman Kav 1 CBD 186

Rosewood Residences Satrio CBD 160

Verde Two (Tower East) Jl. Rasuna Said CBD 182

Anandamaya Residences (3 towers) Jl. Jend Sudirman CBD 500

Sudirman Suites Jl. Sudirman CBD 380

Menteng Park Jl. Cikini Raya No.79 Central Jakarta 756

Holland Village Cempaka Putih Central Jakarta 400

Royal Suites Kemayoran Central Jakarta 450

The Green Pramuka (Tower Nerine) Jl. Jenderal Ahmad Yani Central Jakarta 1,000

Green Signature Apartment Jl. MT. Haryono East Jakarta 800

Podomoro Park Jl. I Gusti Ngurah Rai, Klender East Jakarta 3,000

Sentra Timur Residence (Tower Brown) Pulo Gebang East Jakarta 605

Bassura City (Tower Jasmine) 2 tower Jl. Basuki Rahmat East Jakarta 2,000

Bassura City (Tower Heliconia) Jl. Basuki Rahmat East Jakarta 700

Regatta London Tower Jl. Pantai Mutiara North Jakarta 186

La Terrasse Jl. Deplu Raya No.12 South Jakarta 111

Kemang Penthouse Kemang South Jakarta 262

The Foresque Pasar Minggu, Ragunan South Jakarta 660

The Langham Residences Senopati South Jakarta 57

Antasari Heights (One Otium Residence) Jl. Pangeran Antasari No.8 South Jakarta 360

The Batik @ Pejaten Jl. Siaga Raya South Jakarta 137

La Foret Vivante Jl. Limo, Permata Hijau South Jakarta 253

Selatan 8 (Tower Sultan) Kebayoran Lama South Jakarta 336

The Hamilton Jl. KHM Syafi'I Hadzami South Jakarta 112

LA City Apartment (Tower A) Jl. Raya Lenteng Agung, Jagakarsa South Jakarta 980

District 8 (Tower Eternity) Jl. Senopati South Jakarta 400

District 8 (Tower Infinity) Jl. Senopati South Jakarta 280

Izzara Apartment (South and North Tower) TB. Simatupang South Jakarta 542

Puri Orchad (3 Tower) Jl Raya Adicipta West Jakarta 3,000

Maqna Residence Jl. Meruya Ilir No. 88 West Jakarta 312

Vittoria Residence (3 tower) Jl. Daan Mogot West Jakarta 1,100

Wang Residence Jl. Panjang No 18 West Jakarta 250

Taman Anggrek Residence (6 towers) Tanjung Duren West Jakarta 3,000

continued

19 Research & Forecast Report | Q4 2015 | Apartment | Colliers International

aPartment name lOcatiOn regiOn nO. Of unitS

continuation

19 Avenue Apartment (Tower B) Daan Mogot West Jakarta 416

Sycamore Suite Puri Botanical, Joglo West Jakarta 125

2018

Verde Two (Tower West) Jl. Rasuna Said CBD 152

Lavie Jl. Denpasar Raya CBD 302

South Hill Jl. Denpasar Raya CBD 611

Le' Parc Jl. Thamrin CBD 100

Regent Residences (tower 1) Semanggi CBD 100

The Hundred Residence Mega Kuningan CBD 100

The Elements Epicentrum (2 Towers) Rasuna Said CBD 372

Capitol Suites Jl. Prapatan Raya Central Jakarta 327

Holland Village (Phase II) Cempaka Putih Central Jakarta 230

Sahid Garden Residence Ciracas East Jakarta 476

Gold Coast Apartment (Atlantic Tower) Pantai Indah Kapuk North Jakarta 568

Regatta Apartment (Tower New York) Pantai Mutiara North Jakarta 186

Sedayu City (Tower Melbourne) Jl. Pegangsaan Dua Raya North Jakarta 912

Sedayu City (Tower Darwin) Jl. Pegangsaan Dua Raya North Jakarta 936

The Kensington Royal Suites (4 Tower) Kelapa Gading North Jakarta 790

Jaya Ancol Seafront - Oceana Tower Pademangan, Ancol North Jakarta 524

Gold Coast Apartment (Bahama Tower) Pantai Indah Kapuk North Jakarta 600

Gold Coast Apartment (Carribean Tower) Pantai Indah Kapuk North Jakarta 600

Gold Coast Apartment (Honolulu Tower) Pantai Indah Kapuk North Jakarta 600

Grand Marina Ancol Ancol North Jakarta 672

The Aspen Peak at Admiralty (Tower D) Jl. Fatmawati South Jakarta 322

Casa Grande Residence 2 (Tower Angelo) Jl. Casablanca South Jakarta 350

Casa Grande Residence 2 (Tower Bella) Jl. Casablanca South Jakarta 350

Casa Grande Residence 2 (Tower Chianti) Jl. Casablanca South Jakarta 350

Pondok Indah Residences (3 Towers) Pondok Indah South Jakarta 880

Selatan 8 (Tower Prabu) Jl. Raya Ulujami South Jakarta 344

45 Antasari (2 Tower) Antasari South Jakarta 1,924

Arzuria Apartment Jl. Tendean South Jakarta 210

Pakubuwono Spring (2 towers) Jl. Teuku Nyak Arief No.9 South Jakarta 545

Branz Simatupang (2 tower) TB. Simatupang South Jakarta 381

Synthesis Residence Kemang (3 towers) Jl. Ampera Raya No.17 South Jakarta 1,100

The Ease Brawijaya Jl. Taman Brawijaya III Kebayoran Baru South Jakarta 54

Ciputra International Puri Indah (Tower Amsterdam) Jl. Lingkar Luar Barat West Jakarta 412

Grand Madison Park Tanjung Duren West Jakarta 300

Citra Lake Suites (Tower Rosewood) Jl. Raya Kresek West Jakarta 104

Citra Lake Suites (Tower Greenwood) Jl. Raya Kresek West Jakarta 126

Citra Lake Suites (Tower Oakwood) Jl. Raya Kresek West Jakarta 117

Citra Lake Suites (Tower Sherwood) Jl. Raya Kresek West Jakarta 122

Aerium Taman Permata Buana (2 towers) Taman Permata Buana West Jakarta 491

Ciputra International Puri Indah (Tower Barcelona) Jl. Lingkar Luar Barat West Jakarta 335

Puri Mansion Apartment (Tower Crystal) Jl. Lingkar Luar Barat, Puri Kembangan West Jakarta 700

West Vista (2 towers) Jl. Lingkar Luar Barat No.8, Duri Kosambi West Jakarta 2,840

Citra Living Apartment (Somerset Tower) Jl. Citra 7, Kalideres West Jakarta 312

Citra Living Apartment (Orchad Tower) Jl. Citra 7, Kalideres West Jakarta 312

continued

20 Research & Forecast Report | Q4 2015 | Apartment | Colliers International

aPartment name lOcatiOn regiOn nO. Of unitS

continuation

Citra Living Apartment (Newton Tower) Jl. Citra 7, Kalideres West Jakarta 312

Gallery West Jl. Panjang No 5 West Jakarta 280

2019

The Suite (W Hotel Tower) Jl. Prof. Dr. Satrio CBD 200

Menara Jakarta (Tower Equinox) Kemayoran Central Jakarta 396

Menara Jakarta (Tower Azure) Kemayoran Central Jakarta 860

The Linq Kemayoran (2 towers) Kemayoran Central Jakarta 1,020

Menteng 37 Jl. Menteng 37 Central Jakarta 99

Arandra Residence (was Sentosa Residence) Cempaka Putih Central Jakarta 687

Orient Residence Jl. Yos Sudarso, No 76 North Jakarta 225

Fatmawati City Center - Corona Park Suite Tower Fatmawati South Jakarta 900

Royal Park at Kebayoran (Arlington Tower) Jl. Cileduk Raya 18, Cipulir South Jakarta 630

Ratu Prabu 3 Residences TB. Simatupang South Jakarta 61

The Residence Gatot Subroto Jl. Gatot Subroto South Jakarta 188

Ammi Residence Dharmawangsa South Jakarta 136

Green Sedayu Apartment (Tower Pasadena) Jl. Kamal Raya, Cengkareng West Jakarta 896

Source: Colliers International Indonesia - Research

DemandConsistent with our view at the beginning of the year, the apartment market in Jakarta has been undergoing a challenging situation throughout 2015, largely driven by weakening economic conditions, coupled with uncertainty with the tax regulations. Indonesia’s GDP growth slowed from 5.1% at the end of 2014 to 4.71%, 4.67%, 4.73% in 1Q, 2Q and 3Q 2015, respectively. Although the Central Bank relaxed its LTV (loan to value) regulation by raising the mortgage loan rate from 70 to 80%, the presale activities continued to languish given the weak economy and uncertainty with the tax regulations. Volatility in the foreign exchange rate also caused investment appetites for apartments to dissipate. As a result, the average take-up rate for strata-title apartments in Jakarta declined modestly by 0.27% QoQ and 1.58% YoY.

In term of status of the projects, the existing apartment projects experienced a downward trend in the take-up rate because the current newly completed projects were not 100% absorbed. As in the previous years when apartment projects approached the completion time, they generally had a sellout of units. On the other hand, the last quarter of 2015 witnessed tellar sales of some under-construction projects, particularly those that are built by big developers. The underlying reason behind the success of some newly launched apartments was their attractive payment plans and having good, tangible location factors. Additionally, a year-end promo, which offers big discounts, proved a positive catalyst for investors. All in all, the slight increase in the take-up rate in under-construction projects illustrates clearly that demand still exists in the market.

Source: Colliers International Indonesia - Research

Take-up Comparison Between Existing and Under-Construction Projects

4q 2014 3q 2015 4q 2015 qoq YoY

Existing Projects 95.6% 96.0% 94.9% -1.10% -0.70%

Under-construction Projects

72.1% 68.6% 68.7% 0.10% -3.40%

Average 87.00% 85.69% 85.42% -0.27% -1.58%

Quarterly Take-up Rate of Existing and Under-construction Apartments

Source: Colliers International Indonesia - Research

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

1Q 2

013

2Q 2

013

3Q 2

013

4Q 2

013

1Q 2

014

2Q 2

014

3Q 2

014

4Q 2

014

1Q 2

015

2Q 2

015

3Q 2

015

4Q 2

015

Existing Projects Under Construction Projects

21 Research & Forecast Report | Q4 2015 | Apartment | Colliers International

Source: Colliers International Indonesia - Research

Average Take-up Rate in Three Regions4q 2014 3q 2015 4q 2015 qoq YoY

CBD 97.5% 96.8% 93.8% -3.0% -3.7%

South Jakarta 92.6% 86.1% 86.6% 0.5% -6.1%

Non-prime area 83.4% 84.0% 83.7% -0.3% 0.4%

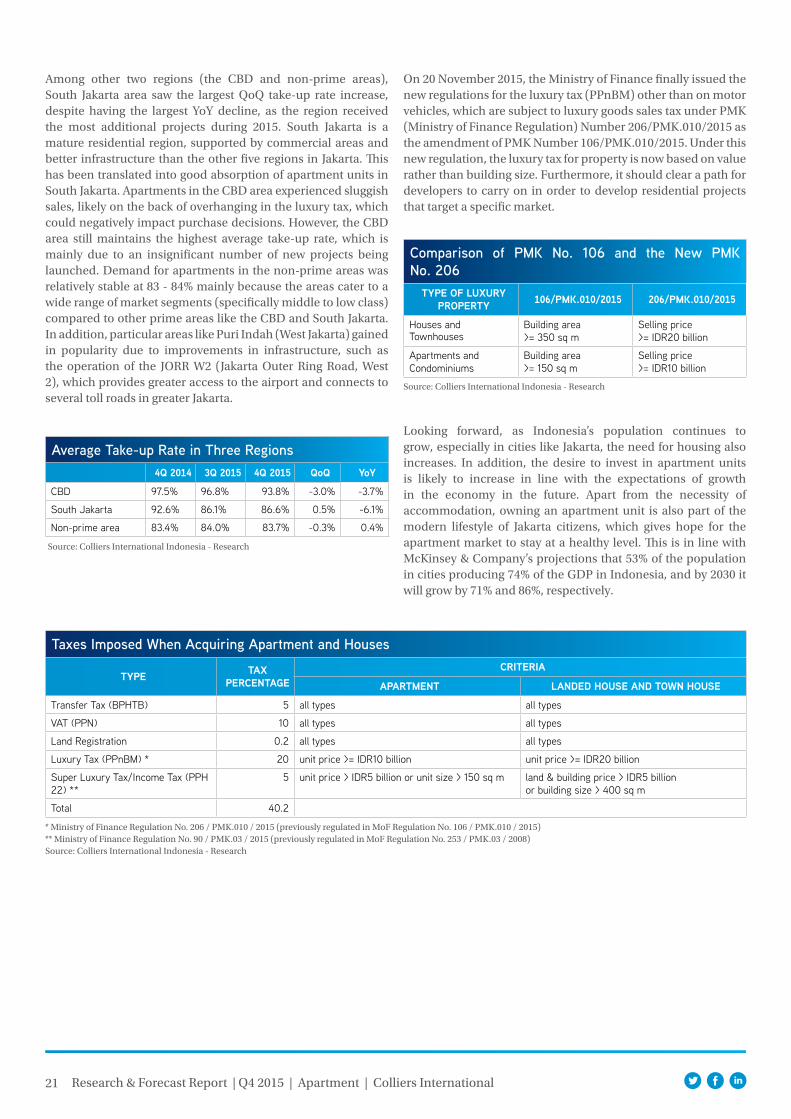

On 20 November 2015, the Ministry of Finance finally issued the new regulations for the luxury tax (PPnBM) other than on motor vehicles, which are subject to luxury goods sales tax under PMK (Ministry of Finance Regulation) Number 206/PMK.010/2015 as the amendment of PMK Number 106/PMK.010/2015. Under this new regulation, the luxury tax for property is now based on value rather than building size. Furthermore, it should clear a path for developers to carry on in order to develop residential projects that target a specific market.

Among other two regions (the CBD and non-prime areas), South Jakarta area saw the largest QoQ take-up rate increase, despite having the largest YoY decline, as the region received the most additional projects during 2015. South Jakarta is a mature residential region, supported by commercial areas and better infrastructure than the other five regions in Jakarta. This has been translated into good absorption of apartment units in South Jakarta. Apartments in the CBD area experienced sluggish sales, likely on the back of overhanging in the luxury tax, which could negatively impact purchase decisions. However, the CBD area still maintains the highest average take-up rate, which is mainly due to an insignificant number of new projects being launched. Demand for apartments in the non-prime areas was relatively stable at 83 - 84% mainly because the areas cater to a wide range of market segments (specifically middle to low class) compared to other prime areas like the CBD and South Jakarta. In addition, particular areas like Puri Indah (West Jakarta) gained in popularity due to improvements in infrastructure, such as the operation of the JORR W2 (Jakarta Outer Ring Road, West 2), which provides greater access to the airport and connects to several toll roads in greater Jakarta.

Source: Colliers International Indonesia - Research

Comparison of PMK No. 106 and the New PMK No. 206

tYPe Of luXurY PrOPertY 106/Pmk.010/2015 206/Pmk.010/2015

Houses and Townhouses

Building area >= 350 sq m

Selling price >= IDR20 billion

Apartments and Condominiums

Building area >= 150 sq m

Selling price >= IDR10 billion

Looking forward, as Indonesia’s population continues to grow, especially in cities like Jakarta, the need for housing also increases. In addition, the desire to invest in apartment units is likely to increase in line with the expectations of growth in the economy in the future. Apart from the necessity of accommodation, owning an apartment unit is also part of the modern lifestyle of Jakarta citizens, which gives hope for the apartment market to stay at a healthy level. This is in line with McKinsey & Company’s projections that 53% of the population in cities producing 74% of the GDP in Indonesia, and by 2030 it will grow by 71% and 86%, respectively.

Taxes Imposed When Acquiring Apartment and Houses

tYPe taX Percentage

criteria

aPartment landed hOuSe and tOWn hOuSe

Transfer Tax (BPHTB) 5 all types all types

VAT (PPN) 10 all types all types

Land Registration 0.2 all types all types

Luxury Tax (PPnBM) * 20 unit price >= IDR10 billion unit price >= IDR20 billion

Super Luxury Tax/Income Tax (PPH 22) **

5 unit price > IDR5 billion or unit size > 150 sq m land & building price > IDR5 billion or building size > 400 sq m

Total 40.2

* Ministry of Finance Regulation No. 206 / PMK.010 / 2015 (previously regulated in MoF Regulation No. 106 / PMK.010 / 2015)** Ministry of Finance Regulation No. 90 / PMK.03 / 2015 (previously regulated in MoF Regulation No. 253 / PMK.03 / 2008)Source: Colliers International Indonesia - Research

22 Research & Forecast Report | Q4 2015 | Apartment | Colliers International

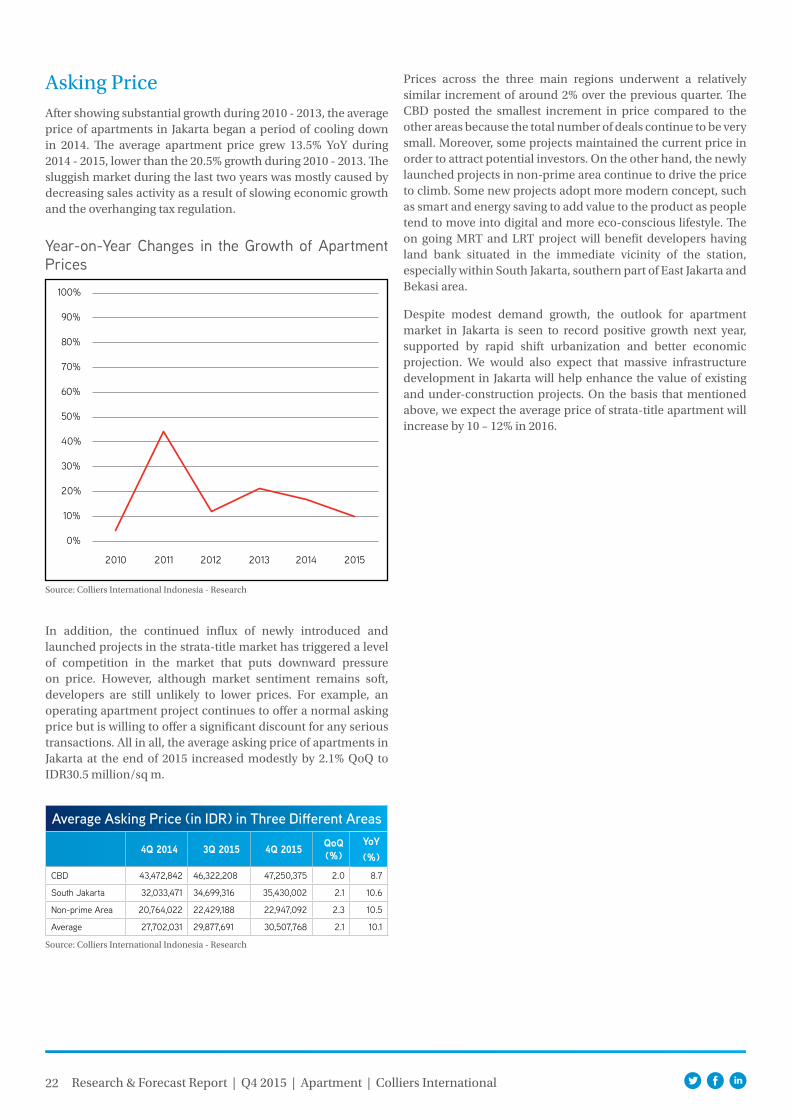

Asking PriceAfter showing substantial growth during 2010 - 2013, the average price of apartments in Jakarta began a period of cooling down in 2014. The average apartment price grew 13.5% YoY during 2014 - 2015, lower than the 20.5% growth during 2010 - 2013. The sluggish market during the last two years was mostly caused by decreasing sales activity as a result of slowing economic growth and the overhanging tax regulation.

Year-on-Year Changes in the Growth of Apartment Prices

Source: Colliers International Indonesia - Research

In addition, the continued influx of newly introduced and launched projects in the strata-title market has triggered a level of competition in the market that puts downward pressure on price. However, although market sentiment remains soft, developers are still unlikely to lower prices. For example, an operating apartment project continues to offer a normal asking price but is willing to offer a significant discount for any serious transactions. All in all, the average asking price of apartments in Jakarta at the end of 2015 increased modestly by 2.1% QoQ to IDR30.5 million/sq m.

Source: Colliers International Indonesia - Research

Average Asking Price (in IDR) in Three Different Areas

4q 2014 3q 2015 4q 2015 qoq (%)

YoY (%)

CBD 43,472,842 46,322,208 47,250,375 2.0 8.7

South Jakarta 32,033,471 34,699,316 35,430,002 2.1 10.6

Non-prime Area 20,764,022 22,429,188 22,947,092 2.3 10.5

Average 27,702,031 29,877,691 30,507,768 2.1 10.1

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

2010 2011 2012 2013 2014 2015

Prices across the three main regions underwent a relatively similar increment of around 2% over the previous quarter. The CBD posted the smallest increment in price compared to the other areas because the total number of deals continue to be very small. Moreover, some projects maintained the current price in order to attract potential investors. On the other hand, the newly launched projects in non-prime area continue to drive the price to climb. Some new projects adopt more modern concept, such as smart and energy saving to add value to the product as people tend to move into digital and more eco-conscious lifestyle. The on going MRT and LRT project will benefit developers having land bank situated in the immediate vicinity of the station, especially within South Jakarta, southern part of East Jakarta and Bekasi area.

Despite modest demand growth, the outlook for apartment market in Jakarta is seen to record positive growth next year, supported by rapid shift urbanization and better economic projection. We would also expect that massive infrastructure development in Jakarta will help enhance the value of existing and under-construction projects. On the basis that mentioned above, we expect the average price of strata-title apartment will increase by 10 – 12% in 2016.

23 Research & Forecast Report | Q4 2015 | Apartment | Colliers International

Apartment For Lease

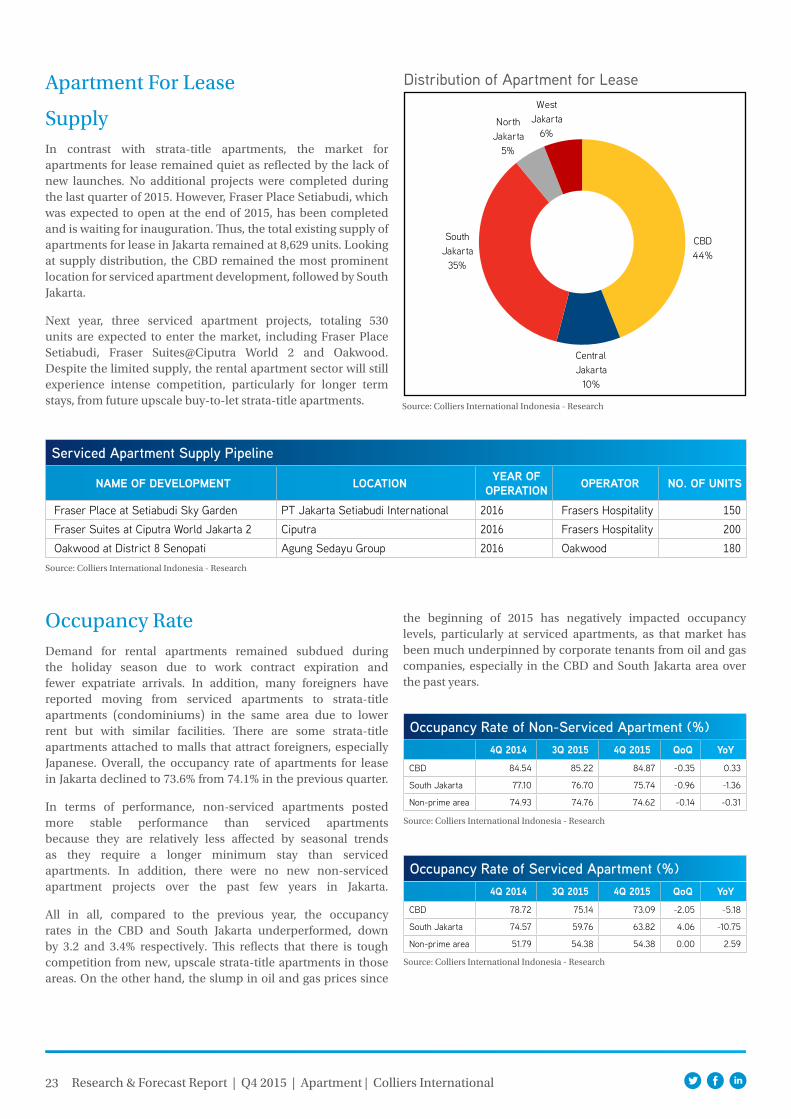

SupplyIn contrast with strata-title apartments, the market for apartments for lease remained quiet as reflected by the lack of new launches. No additional projects were completed during the last quarter of 2015. However, Fraser Place Setiabudi, which was expected to open at the end of 2015, has been completed and is waiting for inauguration. Thus, the total existing supply of apartments for lease in Jakarta remained at 8,629 units. Looking at supply distribution, the CBD remained the most prominent location for serviced apartment development, followed by South Jakarta.

Next year, three serviced apartment projects, totaling 530 units are expected to enter the market, including Fraser Place Setiabudi, Fraser Suites@Ciputra World 2 and Oakwood. Despite the limited supply, the rental apartment sector will still experience intense competition, particularly for longer term stays, from future upscale buy-to-let strata-title apartments.

Distribution of Apartment for Lease

Source: Colliers International Indonesia - Research

Source: Colliers International Indonesia - Research

Serviced Apartment Supply Pipeline

name Of develOPment lOcatiOn Year Of OPeratiOn OPeratOr nO. Of unitS

Fraser Place at Setiabudi Sky Garden PT Jakarta Setiabudi International 2016 Frasers Hospitality 150 Fraser Suites at Ciputra World Jakarta 2 Ciputra 2016 Frasers Hospitality 200 Oakwood at District 8 Senopati Agung Sedayu Group 2016 Oakwood 180

Occupancy RateDemand for rental apartments remained subdued during the holiday season due to work contract expiration and fewer expatriate arrivals. In addition, many foreigners have reported moving from serviced apartments to strata-title apartments (condominiums) in the same area due to lower rent but with similar facilities. There are some strata-title apartments attached to malls that attract foreigners, especially Japanese. Overall, the occupancy rate of apartments for lease in Jakarta declined to 73.6% from 74.1% in the previous quarter.

In terms of performance, non-serviced apartments posted more stable performance than serviced apartments because they are relatively less affected by seasonal trends as they require a longer minimum stay than serviced apartments. In addition, there were no new non-serviced apartment projects over the past few years in Jakarta.

All in all, compared to the previous year, the occupancy rates in the CBD and South Jakarta underperformed, down by 3.2 and 3.4% respectively. This reflects that there is tough competition from new, upscale strata-title apartments in those areas. On the other hand, the slump in oil and gas prices since

Source: Colliers International Indonesia - Research

CBD44%

Central Jakarta

10%

South Jakarta

35%

North Jakarta

5%

West Jakarta

6%

the beginning of 2015 has negatively impacted occupancy levels, particularly at serviced apartments, as that market has been much underpinned by corporate tenants from oil and gas companies, especially in the CBD and South Jakarta area over the past years.

Occupancy Rate of Non-Serviced Apartment (%)4q 2014 3q 2015 4q 2015 qoq YoY

CBD 84.54 85.22 84.87 -0.35 0.33

South Jakarta 77.10 76.70 75.74 -0.96 -1.36

Non-prime area 74.93 74.76 74.62 -0.14 -0.31

Source: Colliers International Indonesia - Research

Occupancy Rate of Serviced Apartment (%)4q 2014 3q 2015 4q 2015 qoq YoY

CBD 78.72 75.14 73.09 -2.05 -5.18

South Jakarta 74.57 59.76 63.82 4.06 -10.75

Non-prime area 51.79 54.38 54.38 0.00 2.59

24 Research & Forecast Report | Q4 2015 | Apartment | Colliers International

Looking forward, decreasing occupancy rates at apartments for lease are expected to continue due to intense competition from strata-title apartments, although there are only a few new serviced apartment projects that will be added to the market in the future. As such, we predict that the average occupancy level of apartments for lease will be corrected to 72 - 74% in the upcoming years.

Source: Colliers International Indonesia - Research

Average Occupancy Rate of Apartment for Lease Based on Region (%)

4q 2014 3q 2015 4q 2015 qoq YoY CBD 81.4 79.5 78.2 -1.3 -3.2

South Jakarta 76.6 73.1 73.2 0.1 -3.4

Non-prime area 69.6 70.0 69.9 -0.1 0.3

Rental RatesThe rental rates for serviced and non-serviced apartments in the CBD area were relatively stable. A minor adjustment occurred during the quarter mainly due to the correction of the rupiah value against the US dollar. On the other hand, some apartments in South Jakarta have renovated their units, causing rents to rise slightly.

During 4Q 2015, the average asking rental rate in the CBD was IDR361,290/sq m/month, moderately down by less than 1% compared to the previous quarter. The average asking rental rate in South Jakarta including the non-prime area was IDR221,310/sq m/month, which represents an increase of 4.2% compared to the previous quarter.

Source: Colliers International Indonesia - Research

Average Rental Rate of Apartment for Lease Based on Region

3q 2015 4q 2015 YoY CBD 362,471 361,290 -0.3%

South Jakarta (Inc. Non-Prime area) 212,478 221,310 4.2%

Based on our survey, most non-serviced apartments did not increase the rent in order to attract tenants, while several serviced apartment buildings, mostly those operated by international hotel chains, signalled an increase in the rental rate. We expect that the average rental rate will continue to increase in the years ahead, albeit at a slower pace compared to previous years. Yearly inflation adjustment is the most common reason that management will raise the rental rate next year, by 3 to 5%.

OutlookThe apartment sector remained firm during 2015 despite several factors that managed to slow growth over the past two years, including the regulation on LTV in 2013, a high interest rate and tax regulations. Currently, investors are generally opting to place their money into projects with a proven track record, a proven concept and a good location.

The middle-class projects are expected to face more headwinds next year compared to other classes as the impact of a slowing economy as well as tight competition among the under-construction projects is likely to weaken apartment absorption. Developers may cope with these drawbacks by offering more incentives, such as more installments (up to six years), balloon payments or other marketing gimmicks to attract potential investors.

However, brisker Indonesian economic activities are expected, likely in the second semester next year, given the following considerations: 1) the realisation of government spending is expected to increase, so that its contribution to economic growth will be more significant; and 2) the implementation of several economic packages is likely to make macroeconomic improvements.

Furthermore, some of the easing measures announced in the last quarter of 2015 including new luxury tax regulations, assignment of a special economic zone and the removal of double taxation for REIT transactions will probably take some time to start having a real positive impact on the market.

Residential Expatriate Housing SectorExpatriate HousingThe expatriate housing market has been experiencing a tough condition in general since the beginning of 2015. Anecdotal evidence reflecting the situation can be seen with some international schools that underwent a downturn in school enrollment by as much as 25%, compared to last year. Other factors are the difficulty for multinational companies to get working permit approval for their middle-level expatriates. Top level management has been less affected by the slow immigration process, however many KITAS that are issued have a “transfer of knowledge” stipulation in line with the Indonesian government’s aim to expedite the transfer of higher level positions from expert expatriates to local staff.

In an attempt to foster an investment climate, on 23 October 2015, the Ministry of Manpower replaced the previous regulation (Minister of Manpower Regulation No. 16 / 2015) on foreign workers with the much more expat-friendly Regulation No. 35 / 2015. The regulation issued in October came in the face of criticism from both domestic and international companies over tightened restrictions limiting expatriate staffing levels and complicating work permit requirements. The old regulation (No. 16 / 2015) required short-term work permits for those who travel to Indonesia for meetings, obligated foreign-domiciled directors to have work permits and imposed the obligation for employers to hire at least 10 local workers for each foreign worker (“ten to one” rule). These have been removed from the latest regulations. Nevertheless, in general, expatriates still complain about difficulties in getting KITAS (work permit) which can take up to six months, when previously it took only two.

In light of the current market conditions, landlords of expatriate standard housing have become more accommodating and cooperative in entertaining additional requests from the lessees and they are commercially attuned to the needs and trends of the market. Common additional requests are mainly related to the length of lease, renovations, improvements and inquiries about inclusive features of the house. They are generally becoming more flexible in negotiating extensions when leases expire. Landlords used to be quite rigid concerning lease extensions and renewal commonly included a 10 - 15% rent increase. Currently, this situation has changed and many landlords now welcome renewal applications that generally need to be negotiated three to six months before expiration without a rent increase. Moreover, the lease terms often have been reduced from a minimum of two years to only one year, since the work permits that are currently being issued are only valid for one year and must be renewed every year. In terms of rental rate, most landlords are largely willing to consider discounts ranging from 5 to 10% for a standard expatriate house. In some cases, some owners of multiple units with many vacancies are willing to decrease the rent by up to 30% instead of leaving the house empty.

In order to comply with global franchise commitments, hotel chain operators that manage serviced apartments have less flexibility and have restrictions when asked to adjust the rental rate. Similar to home owners, however, service apartment operators may be more flexible in terms of leasing time frame, extras included in the contract and services provided. Options for a lease term can be six months, three months, two weeks or even in some cases, a daily rate.

26 Research & Forecast Report | Q4 2015 | Apartment | Colliers International

Housing Rental Rates in Several Expatriate Areas

eXPatriate hOuSing BY area Size (Sq m)rental range (uSd/unit/mOnth)minimum maXimum

Menteng 4 - 5 Bedrooms House 500 - 1,200 4,500 13,500

Kuningan 4 - 5 Bedrooms House 500 - 900 4,050 10,800

Pondok Indah 4 - 5 Bedrooms House 450 - 1,000 4,050 13,500

Kebayoran Baru 4 - 5 Bedrooms House 600 - 1,500 4,500 13,500 3 - 4 Bedrooms Townhouse/complex 250 - 700 3,150 7,650

Permata Hijau 4 - 5 Bedrooms House 400 - 1,500 4,050 10,800 3 - 4 Bedrooms Townhouse/complex 220 3,150