Embed Size (px)

Citation preview

LIABILITY OF A HOLDING COMPANY FOR THE DEBTS OF ITS INSOLVENT SUBSIDIARY

By

Johanna Barbara Cilliers

B A LLB H Dip Co Law L L M

Submitted in fulfilment of the requirements for the degree of

Doctor of Philosophy

from the University of Western Australia

Law School

University of Western Australia

Year of submission: 2002

PREFACE

I gratefully acknowledge a grant received from the University of Western

Australia, which was applied towards the research for this thesis.

My supervisor, Professor Jim O'Donovan, has offered invaluable guidance and

assistance which I sincerely appreciate and for which I would like to thank him.

I would also like to thank m y family, especially m y husband, both for acting as

a sounding-board and for his encouragement and motivation.

I declare that the thesis is my own composition, substantially completed during

the course of enrolment in this degree at the University of Western Australia

and has not previously been accepted for a degree at this or another institution.

INDEX

1 INTRODUCTION

1.1 Separate entity principle and limited liability 1

1.2 Extension of limited liability to corporate groups 6

1.2.1 Automatic extension inappropriate 6

1.2.2 Risk of creditor prejudice 8

1.2.3 Creditors are less efficient risk-bearers 14

1.3 Scope of investigation 16

1.3.1 Comparison with other jurisdictions 16

1.3.2 Limitation of topic 18

1.3.3 Roadmap 23

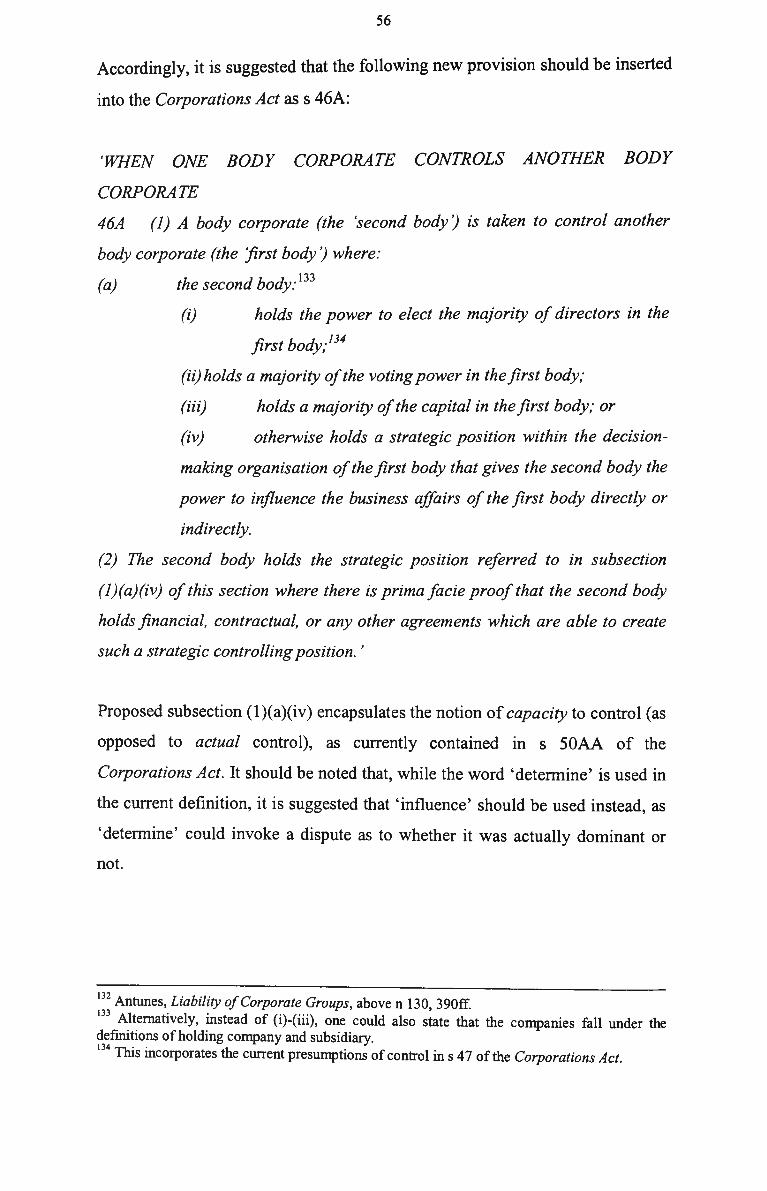

2 THE MEANING OF CONTROL AND THE REGULATION OF CORPORATE GROUPS

2.1 Background 25

2.2 Various applications of the control concept 28

2.2.1 Subsidiary/holding company relationship 29

2.2.1.1 Test of controlling the composition of the board 30

2.2.1.2 Voting control test 31

2.2.2 Consolidated accounts 35

2.2.3 Related party transactions 38

2.2.4 Cross share-holdings 41

2.3 Evaluation of position of group creditors 44

2.3.1 CASAC recommendations 45

45 2.3.1.1 Regulation by general control test

2.3.1.2 Wholly-owned groups to choose whether enterprise principles 46

apply

2.3.2 Critique of CAS AC recommendations 49

2.3.2.1 Regulation by general control test 49

(a) Replacement of 'holding/subsidiary' with 'control' 50 (b) Preferred definition of 'control' 52

2.3.2.2 Wholly-owned groups to choose whether enterprise principles 57

apply

60

61

3 PIERCING THE CORPORATE VEIL

3.1 Background

3.2 Fraud

3.2.1 Limited to exceptional cases 61

3.3.2 Further restriction on lifting the veil 66

3.3 Agency

3.3.1 Extent of control 70

3.3.2 Authorisation to contract 72

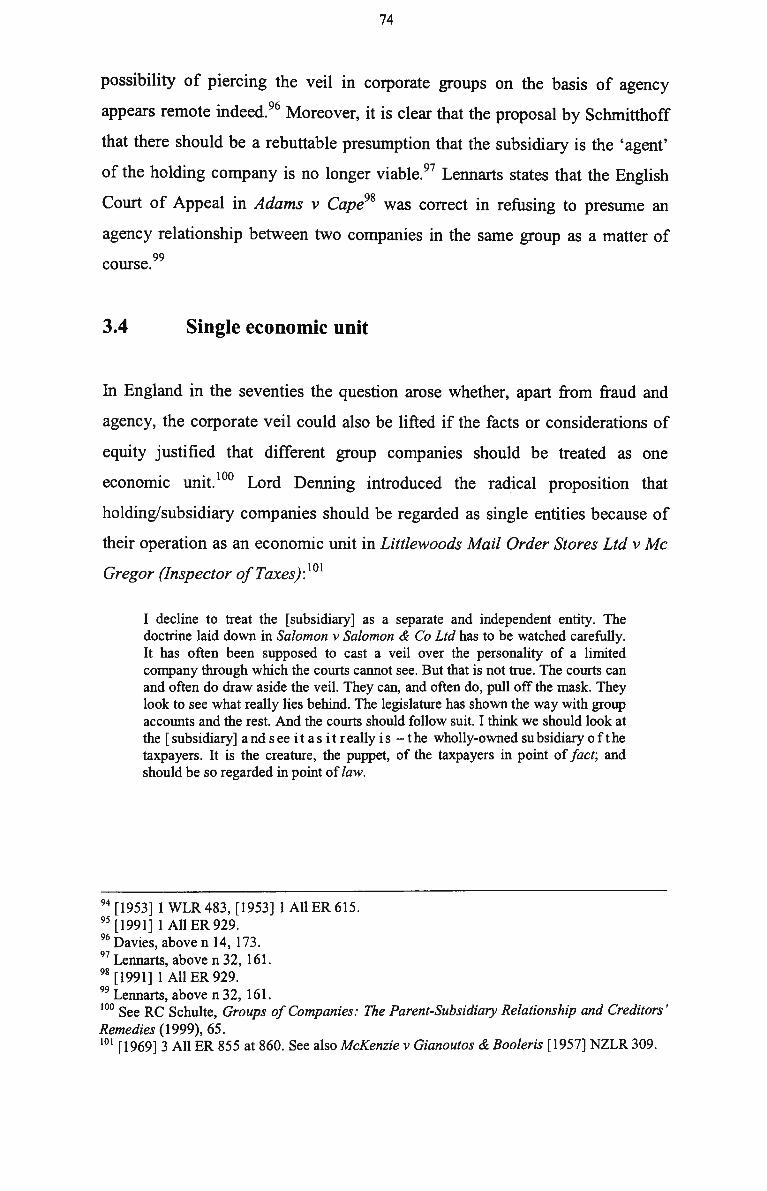

3.4 Single economic unit 74

3.5 Evaluation of position of group creditors 95

4 DIRECTORS' DUTIES: GENERAL PRINCIPLES

4.1 Background 98

4.2 Fiduciary duty to act in interests of company 99

4.2.1 Objective test laid down in Charterbridge 100

4.2.2 Subjective test laid down in Walker v Wimborne 102

4.2.3 Implied recognition of Charterbridge test after Walker v 105 Wimborne

4.2.4 Express recognition of Charterbridge test after Walker v 109 Wimborne

4.3

4.3.1

4.3.2

4.3.3

4.4

4.4.1

4.4.2

4.4.3

4.4.4

4.5

4.5.1

4.5.2

4.5.3

Nominee directors: notion of 'dual loyalty'

Traditional approach

Pragmatic approach

Notion of 'dual loyalty' similar to Charterbridge test

Duty of care, skill and diligence

Scope of duty

Statutory formulation of duty

Overlap with fiduciary duty

Overlap with insolvent trading provisions

Evaluation of position of group creditors

Fiduciary duty to act in interests of company

Nominee directors

Duty of care, skill and diligence

112

113

114

118

121

121

126

130

133

134

134

136

137

5 DIRECTORS' DUTIES: CAPITA SELECTA

5.1 Background 139

5.2 Particular difficulties in intra-group transactions 139

5.2.1 Downstream, lateral and upstream transactions 139

5.2.2 Restructuring a group 142

5.2.3 Uncommercial transactions 146

5.3 Duty to take into account interests of creditors 153

5.3.1 Extension of duty 153

5.3.2 Insolvency as condition established 155

5.3.3 Concept of'insolvency'delineated 157

5.3.4 Duty to future creditors 159

5.3.5 No direct duty to creditors 162

5.4 Statutory duty to act in interests of company 164

5.4.1 Interests of the company and proper purpose 164

5.4.2 Specific provision for corporate groups 167

5.5 Evaluation of position of group creditors 173

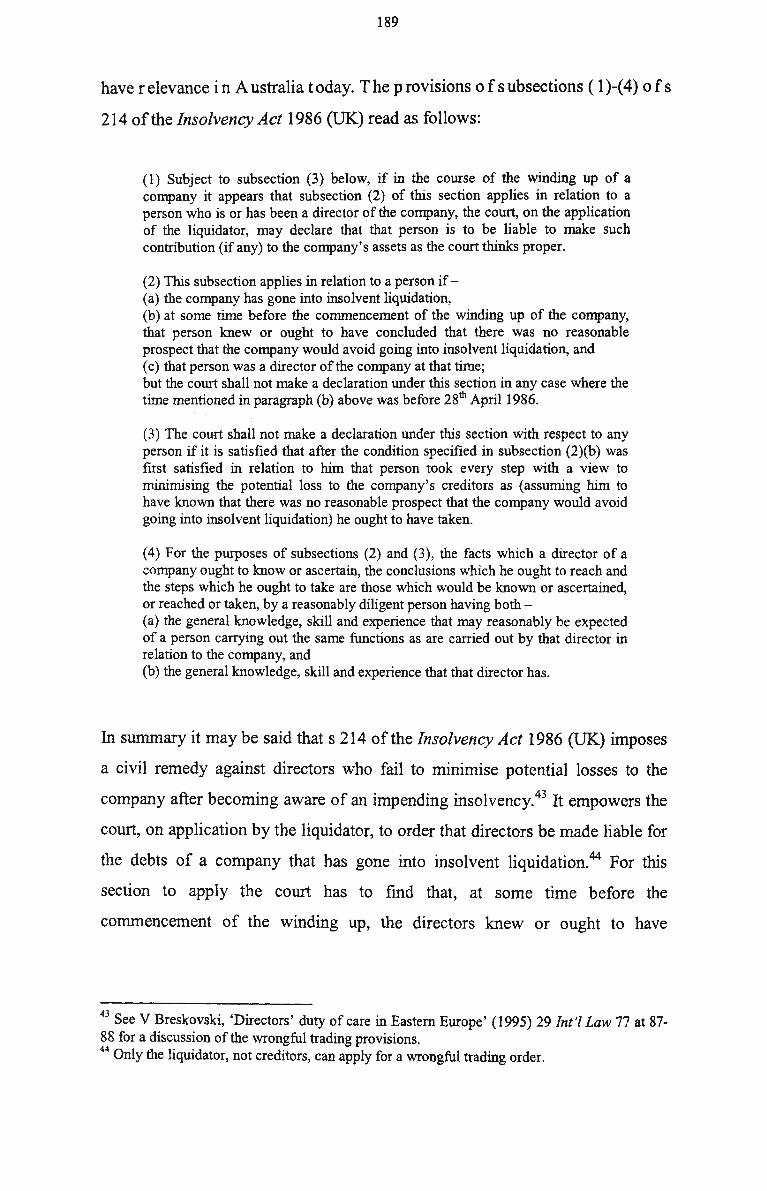

6 INSOLVENT TRADING: HOLDING COMPANY AS SHADOW DIRECTOR

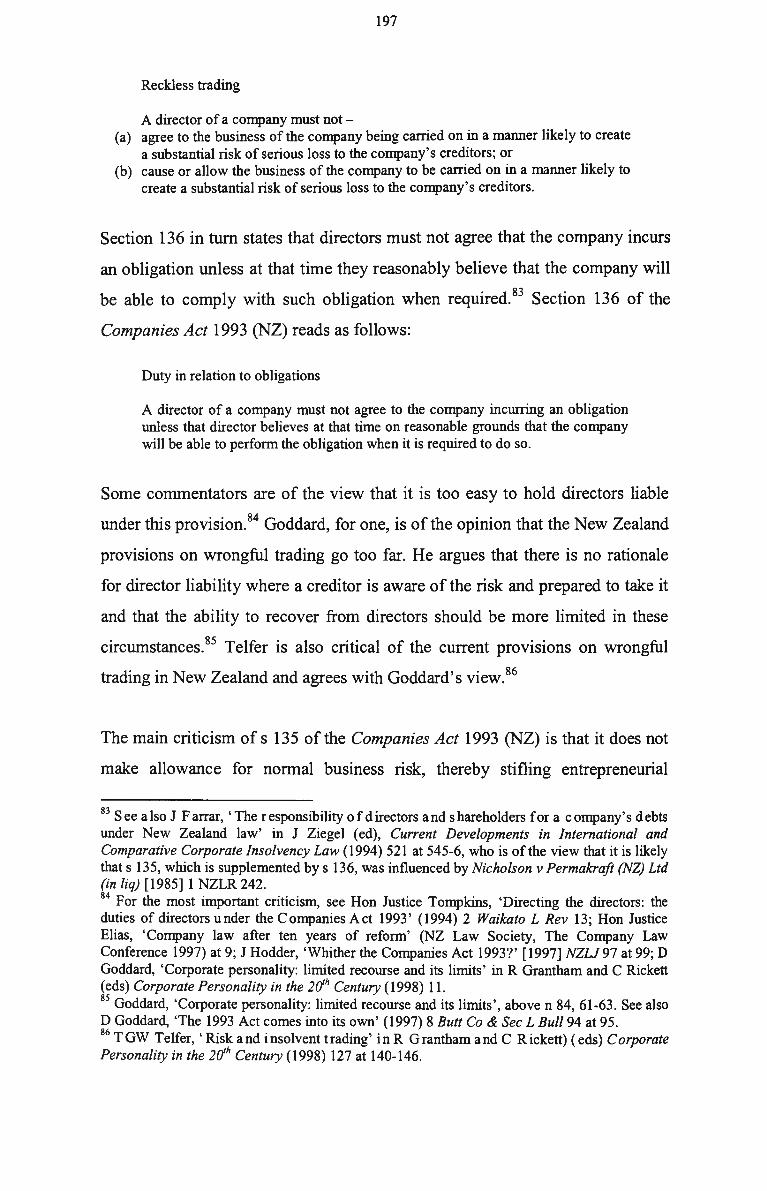

6.1 Background 182

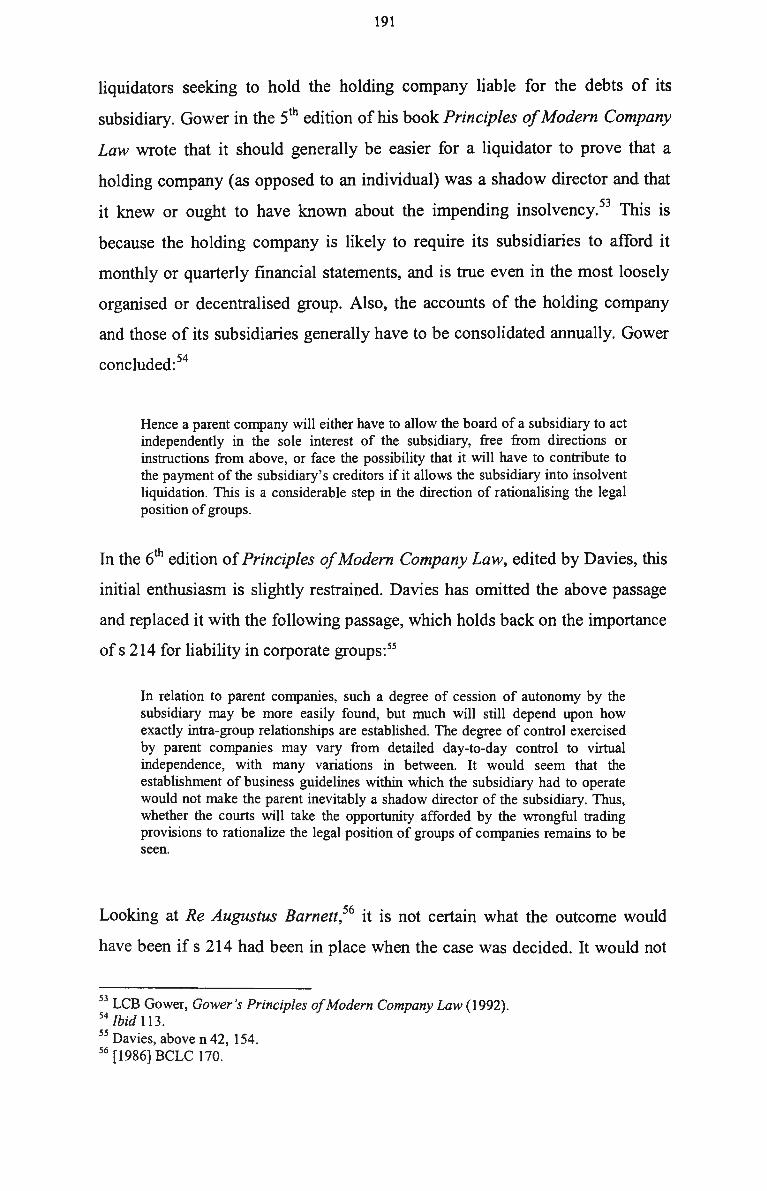

6.2 Addressing the problem 188

6.2.1 Position in the United Kingdom 188

6.2.2 Position in Australia 192

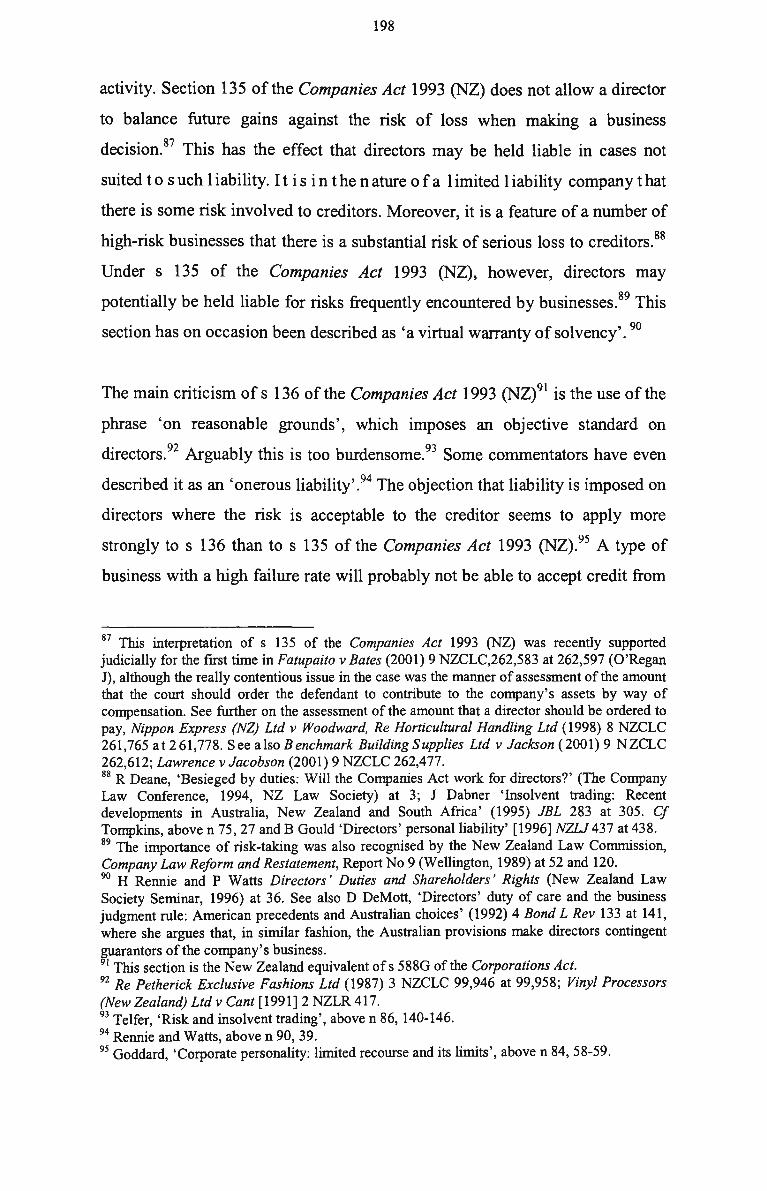

6.2.3 Position in New Zealand 196

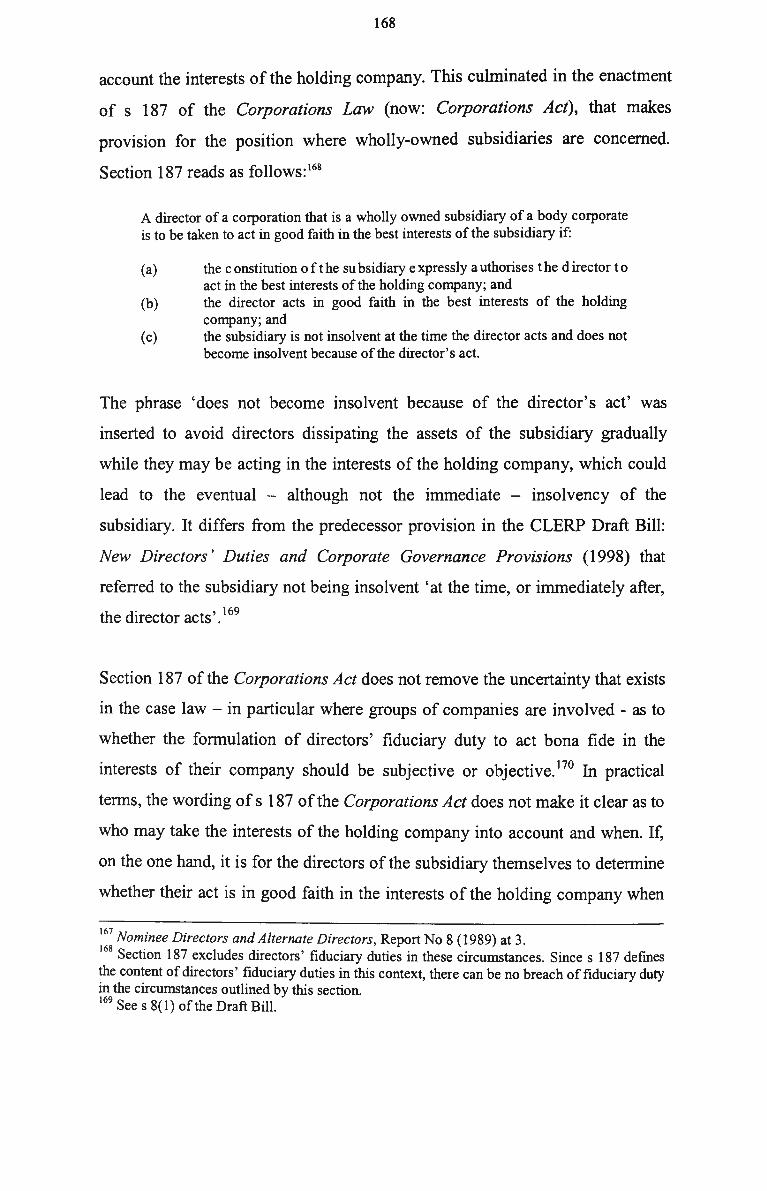

.3 Liability of holding company 199

6.4 Evaluation of position of group creditors 218

6.4.1 Meaning of 'directors of the body' 218

6.4.2 Meaning of 'accustomed to act' 221

6.4.3 Meaning of directions or instructions' 222

7 INSOLVENT TRADING: HOLDING COMPANY AS SHAREHOLDER

7.1 Background 225

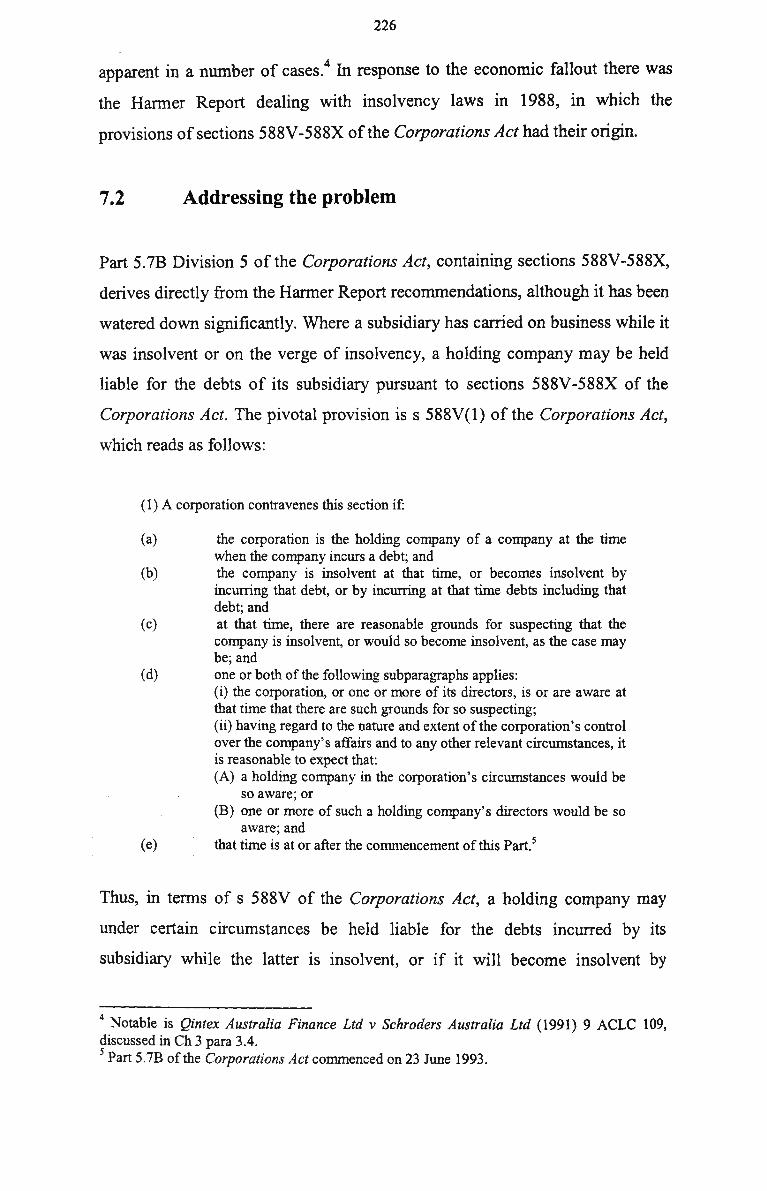

7.2 Addressing the problem 226

7.3 Liability of holding company 230

7.3.1 Criteria to be satisfied for contravention 230

7.3.1.1 'Incurs a debt' 233 (a) General 233 (b) Narrow approach - directors may easily escape liability 235 (c) Flexible approach - more difficult for directors to 238

escape liability (d) Voluntary and involuntary debts 240

7.3.1.2 'Insolvent' 243

7.3.1.3 'Reasonable grounds for suspecting' 247

7.3.2 Defences 250

7.3.2.1 Reasonable grounds to expect insolvency 251

7.3.2.2 Reliance on another 256

7.3.2.3 Illness or some other good reason 257

7.3.2.4 Reasonable steps to prevent incurring a debt 264

7.4 Evaluation of position of group creditors 265

7.4.1 Disadvantages as a result of intermingling 265

7.4.2 Other disadvantages 266

8 CONTRIBUTION AND POOLING: THE CURRENT POSITION

8.1 Background 272

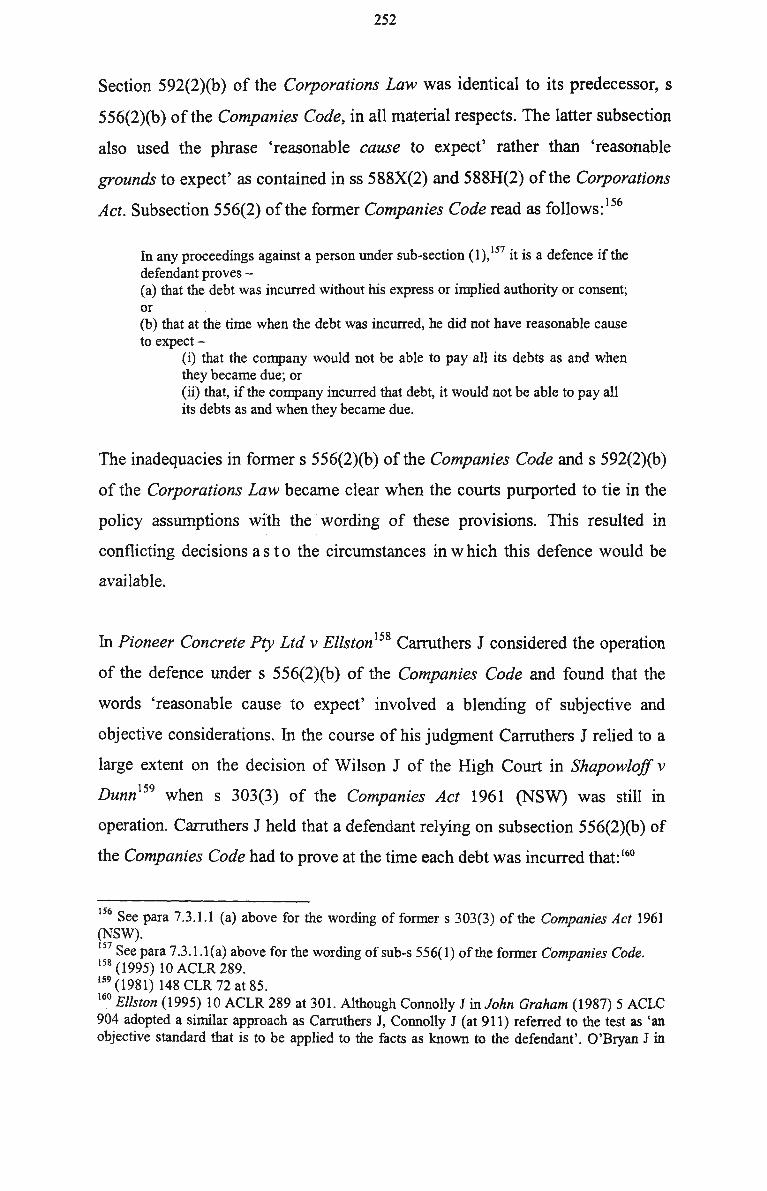

8.2 Indirect pooling by the regulator 274

8.2.1 Shortcomings of Deeds of Cross Guarantee vis-a-vis creditors 276

8.2.1.1 Multiple insolvencies 276

8.2.1.2 Release from obligations 280 (a) Revocation 280 (b) Sale 281

8.2.2 Shortcomings of Deeds of Cross Guarantee vis-a-vis directors 282

8.2.2.1 Breach of fiduciary duty 282 (a) Committal 283 (b) Revocation 285

8.2.2.2 Breach of insolvent trading provisions of the Corporations Act 286

8.3 Indirect pooling by the courts 287

8.3.1 Schemes of arrangement and compromises/arrangements with 287 creditors

8.3.2 Other avenues 292

8.3.2.1 Rights of contribution and subrogation under inter-company 292 guarantees

8.3.2.2 Section 447A of the Corporations Act 296

8.3.2.3 Section 510 of the Corporations Act 303

8.4 Evaluation of position of group creditors 312

8.4.1 Indirect pooling by the regulator 312

8.4.2 Indirect pooling by the courts 315

9 CONTRIBUTION AND POOLING: THE CASAC RECOMMENDATIONS FOR A MODIFIED NEW ZEALAND MODEL

9.1 Background 318

9.2 Harmer Report recommendations 320

9.2.1 Contribution 320

9.2.2 Pooling 323

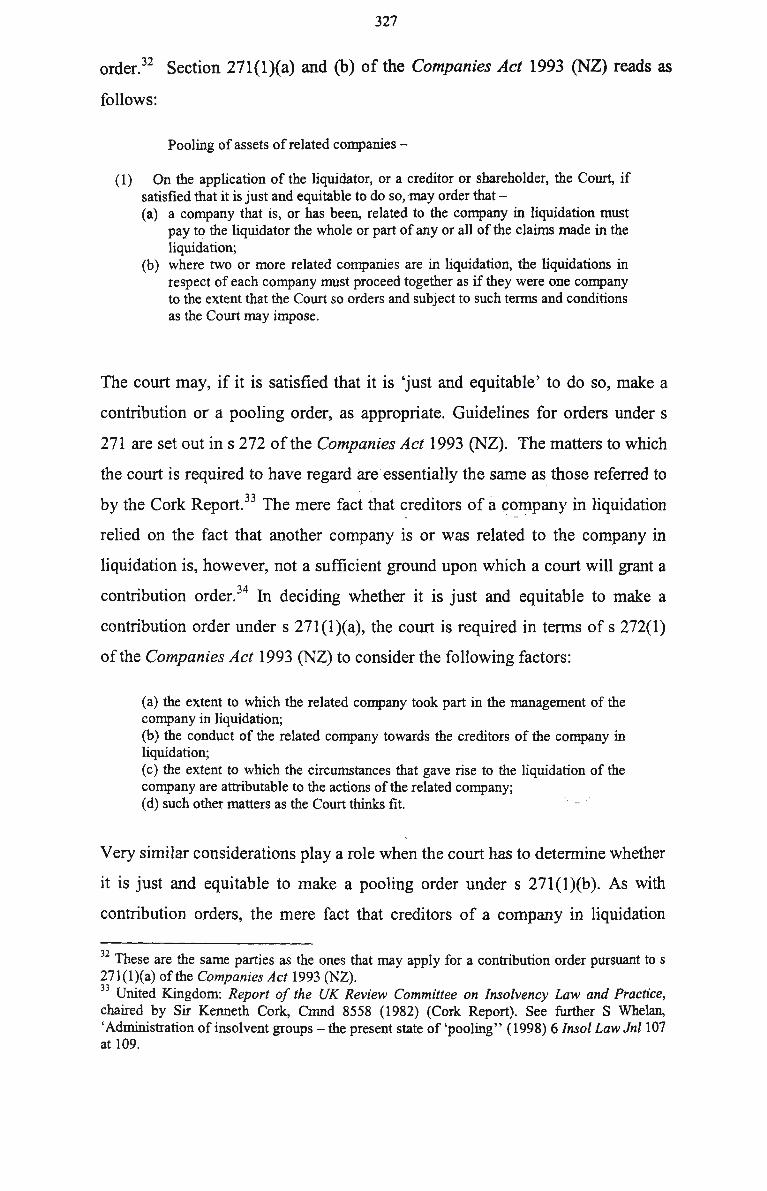

9.3 Legislative provisions relating to contribution and 325 pooling in New Zealand

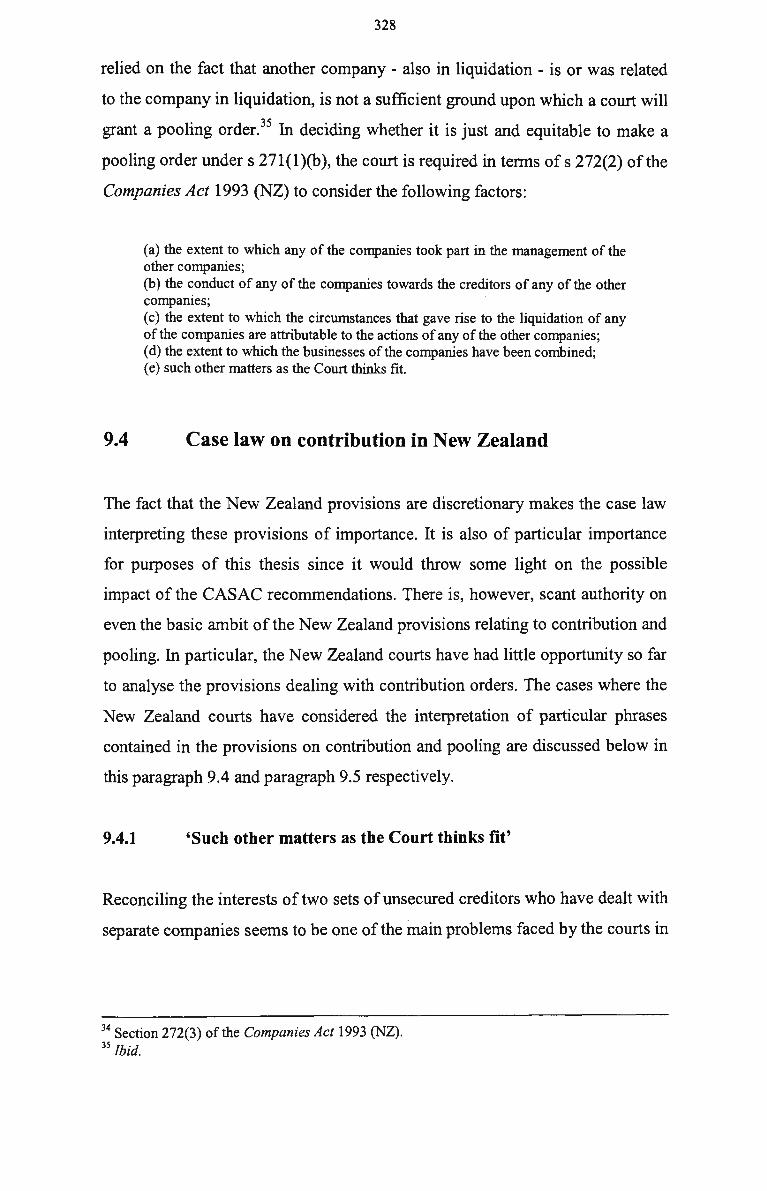

9.4 Case law on contribution in New Zealand 328

9.4.1 'Such other matters as the Court thinks fit' 328

9.4.2 'Just and equitable' 330

9.5 Case law on pooling in New Zealand 334

9.5.1 'As if they were one company' 334

9.5.2 'Just and equitable' 337

9.6 Evaluation of position of group creditors 341

9.6.1 CASAC recommendations 341

9.6.1.1 Contribution orders 341

9.6.1.2 Pooling orders 343

9.6.2 Critique of CASAC recommendations 346

9.6.2.1 Uncertainty exists also in respect of pooling orders 346

9.6.2.2 Uncertainty exacerbated by confusing contribution and pooling 348

9.6.2.3 Summary 351

10 PROPOSALS

10.1 Inadequacy of existing law 352

10.1.1 Piercing the corporate veil 353

10.1.2 Directors'duties 354

10.1.3 Insolvent trading 355

10.1.4 Contribution and pooling 356

10.2 Proposed model 358

10.2.1 Pooling: To be used as a last resort 358

10.2.2 Contribution: Presumption of abuse based on control 361

10.2.2.1 Liability based on status versus liability based on fault 361

10.2.2.2 Substantive aspects 364

10.2.2.3 Procedural aspects 368

10.2.2.4 Contribution with a difference 374

10.2.2.5 Advantages of proposed model 378

10.3 Conclusion 381

SUMMARY 383

TABLE OF CASES 384

BIBLIOGRAPHY 395

ABBREVIATIONS 416

1

1.1

1.2

1.2.1

1.2.2

1.2.3

1.3

1.3.1

1.3.2

1.3.3

INTRODUCTION

Separate entity principle and limited liability

Extension of limited liability to corporate groups

Automatic extension inappropriate

Risk of creditor prejudice

Creditors are less efficient risk-bearers

Scope of investigation

Comparison with other jurisdictions

Limitation of topic

Roadmap

1

6

6

8

14

16

16

18

23

1 INTRODUCTION

1.1 Separate entity principle and limited liability

Anthropomorphism, prevalent in religion and politics since the Middle

Ages, also found its way into law.1 In the eighteenth century the

anthropomorphic idea inspired lawyers to regard every company as an

'artificial body' or legal persona, which was in turn the impetus for the

development of the principle of separate legal personality of a company.2

This principle and the other principles of our company and insolvency law

were developed in England in the nineteenth century, culminating fin de

siecle in the doctrine of limited liability in respect of companies. The

twentieth century evidenced the phenomenon of group activity in the sense

of the conduct of various businesses by a holding company through a

number of subsidiaries. Thus, as the Cork Report pointed out: 'It is not

surprising, therefore, that some of the basic principles of company and

insolvency law fit uneasily with the modern commercial realities of group

enterprise.'3

Consider the following scenario. Company A is the holding company of the

A B C Group.4 Company A and company B, a wholly owned subsidiary of

company A, have the same directors. Creditors of company B suffer losses

as a result of company B 's actions. They institute action not only against

company B, but also against company A. W h e n the creditors settle the

particular dispute with company B, the latter has no assets left and is

virtually insolvent. However, it becomes clear that a few similar actions lie

ahead. Company A decides to restructure the A B C Group. As part of the

restructuring company B is liquidated and company C is incorporated with

1 CT Carr, The General Principles of the Law of Corporations (1905) 150-155. 2 JB Cilliers 'Similar Company Names: A Comparative Analysis and Suggested Approach - Part I' (1998) 61 THRHR 132; JB Cilliers, The Prohibition of and Protection Against the Use of Identical and Similar Company Names in Company Law: A Comparative Study (1996), 1. 3 United Kingdom: Report of the UK Review Committee on Insolvency Law and Practice chaired by Sir Kenneth Cork, Cmnd 8558 (1982) (Cork Report), para 1922. 41 n Australia t he t erms ' holding c ompany' a nd ' parent' (or ' parent c ompany') a re used interchangeably. For the sake of consistency the term 'holding company' is used throughout this thesis, unless a quotation is used or reference is made to authority which itself makes use of the term 'parent'.

2

the financial assistance of company A to continue company B's activities.

As anticipated, company B's creditors institute a second series of actions

against company A.

Startling though it may be, as the law currently stands there is generally no

basis on which to hold company A or its directors (who acted on its behalf)

liable in this hypothetical scenario, whether by piercing the corporate veil

between the different group companies or otherwise. Company A is allowed

to continue trading without the risk of being held liable for the claims by

company B's creditors. Company A is legally entitled to use the corporate

structure to ensure that the liability of particular activities falls on another

group member. Since company B is in insolvent liquidation and company C

did not exist at the time it is claimed the losses were suffered, there is no

remedy available for the creditors.

The rule that shareholders and directors are not generally liable for the debts

of their company has become almost synonymous with the principle of

separate legal personality.5 However, incorporated companies existed and

operated long before the general introduction of limited liability. The

limitation of its members' liability was not a consistent feature of a

company incorporated as a separate legal person - it was only generally

introduced when the change of law was considered a matter of social and

economic necessity.6 But the separate legal entity principle, which was

reaffirmed in Salomon v Salomon & Co Ltd,1 was taken to have been

Limited liability is not an inevitable, but rather a natural, consequence of separate legal personality. It is possible to register an unlimited company: s 112 and s 113 of the Corporations Act 2001 (Cth) (Corporations Act). The Corporations Law was replaced by the Corporations Act on 15 July 2001. Reference is made to the Corporations Law where applicable in this thesis, for example, where previous case law is discussed. Unless otherwise indicated, however, the provisions of the Corporations Law and the Corporations Act discussed in this thesis may for all practical purposes be regarded as similar. 6 See D K Avgitides, Groups of Companies - The Liability of the Parent Company for the Debts of its Subsidiary, (1996), 43. 7 [1897] A C 22 (Salomon v Salomon), reversing sub nom Broderip v Salomon [1895] 2 Ch 323. For a discussion oi Salomon v Salomon, see L Sealy, 'Modern insolvency law and Mr Salomon' (1998) 16 C&SU 176 at 176-77; Avgitides, above n 6, 147-150. For a more extended discussion of corporate personality, see the various contributions in R Grantham and C Rickett (eds), Corporate Personality in the 2(fh Century, (1998) and the Federal Law Review, 'Special issue on corporate law: a century of Salomon'' (1999) 27 Fed L Rev 173-

3

extended so that the liability of shareholders and directors would be limited

as a general rule. From this it follows that ordinarily a holding company is

not liable for the debts of its subsidiary.8

Arguably, in Salomon v Salomon9 a radical proposition by Lord Macnaghten

extended the separate legal entity principle unnecessarily to include limited

liability. First his Lordship laid down clearly the concept of separate

corporate personality when he stated:10

The company is at law a different person altogether from the subscribers to the memorandum; and though it may be that after incorporation the business is precisely the same as it w as before, and the same persons are managers, and the same hands receive the profits, the company is not in law the agent of the subscribers or trustee for them.

However, Lord Macnaghten then continued by saying that '[n]or are the

subscribers as members liable, in any shape or form, except to the extent

and in the manner provided by the Act'.11 Since then the separate legal

entity and limited liability principles have been 'fused' and viewed as the 1*)

same. Thus, although it developed as a sort of 'afterthought', the rule of

limited liability became generally entrenched as part of the principle that a

company is a separate legal entity and has since become one of the linchpins

of modern company law.

Lord Denning pointed out that the doctrine laid down in Salomon v 1 "\

Salomon 'has often been supposed to cast a veil over the personality of a

limited company through which the courts cannot see'.14 This doctrine will

be adhered to unless the existence of special circumstances justify the lifting

321. As Avgitides, above n 6, points out at 13-44, English law had accepted long before this case that a non-human entity could in law be the subject of rights and duties. This was borne out by the legislative reforms five decades earlier, culminating in the Companies Act 1844 (UK). 8 But see, eg, s 588V of the Corporations Act. 9 [1897] A C 22. 10 Ibid 5\. uIbid. 12 H G Henn and JR Alexander, Laws of Corporations and Other Business Enterprises (1983), 19. 13 [1897] A C 22. 14 Littlewoods Mail Order Stores Ltd v Mc Gregor (Inspector of Taxes) [1969] 3 All ER 855 at 860.

4

of the veil of incorporation b y the court or specific 1 egislative previsions

enable the corporate veil to be pierced.15 The principle that a company is a

separate legal entity is also firmly entrenched in Australia, where it has been

extended to companies carrying on business in corporate groups.

Moreover, in this country the extension of the separate legal entity principle

was also adopted so that, among other things, creditors of a particular

subsidiary m a y only look to that subsidiary for payment of monies owed,

and not to any of the other companies in the group.

The fact that holding companies also enjoy limited liability is largely

responsible for claims that creditors of group companies are inadequately

protected. Under general law limited liability allows holding companies,

which by definition control their subsidiary companies, to undertake risky

projects through their subsidiaries with finance from external creditors. If

the subsidiary becomes insolvent, the creditors are not repaid, while the

holding company may c ontinue to flourish because it is not liable for the

debts of its subsidiary. It would therefore appear that creditors are not

adequately protected against possible abuse of control in a group situation,

especially where insolvency intervenes.

1 7

In Re Southard & Co Ltd a holding company placed its wholly-owned

subsidiary in a creditors' voluntary liquidation through an extraordinary

general meeting of shareholders. The holding company subsequently sought

an order for the compulsory winding up of the subsidiary. The question that

arose was whether the order should be refused on the ground that a minority

of unsecured creditors opposed the petition. The court refused the winding-

Technically speaking there is a difference between piercing the corporate veil and lifting the corporate veil. See further the discussion in I Ramsay and D Noakes, 'Piercing the corporate veil in Australia' (2001) 19 C&SLf 250 at 251-252. The distinction between the meaning of the two terms is not widely recognised in Australia, with the courts sometimes using them as alternatives. The terms are used interchangeably in this thesis. 16 Walker v Wimborne (1976) 137 C L R 1; Industrial Equity Ltd v Blackburn (1977) 137 C L R 567. This thesis applies to both formal and informal groups. A n example of an informal group may be found in Walker v Wimborne, where the companies were only associated and did not formally fall within the definition of holding and subsidiary company of the Corporations Act. 17 [1979] 1 WLR1198.

5

up order since the holding company had not proved that the assets of its

subsidiary would be realised more expeditiously and more economically if

the company were wound up compulsorily.18 However, the right of the

holding company to place its subsidiary in voluntary liquidation was not

challenged. In this regard Templeman LJ in an oft-quoted passage restated:19

English company law possesses some curious features, which may generate some curious results. A parent company may spawn a number of subsidiary companies, all controlled directly or indirectly by shareholders of the parent company. If one of the subsidiary companies, to change the metaphor, turns out to be the runt of the litter and declines into insolvency to the dismay of its creditors, the parent company and the other subsidiary companies may prosper to the joy of the shareholders, without any liability for the debts of the insolvent subsidiary.

Although Roman law had traces of limited liability and group trading, the

modern limited liability company in the common law developed in the mid-

nineteenth century in England from where it spread to other j urisdictions

such as the United States of America (United States).21 Generally, the object

of using the corporate form was to facilitate the raising of capital, but it is

arguable that from the earliest times the predominant motive was to obtain

the advantage of limited liability.22 In the United States Anderson v Abbott22

confirmed that the main purpose of incorporation was insulation from

creditors.24 This was reiterated by the Master of the Rolls in Commissioners

of Inland Revenue v Sansom25 where he stated:26

[T]he great reason why so many people form their businesses into limited companies and others invest their money in them is in order that they may be under no personal liability in respect of the transactions of those companies, and that is a perfectly legitimate object..,

18 Ibid 1206 (Buckley LJ). 19 Ibid 120$. 20 See W Buckland, Roman Law and Common Law (1965) 54; S Williston, 'History of the Law of Business Corporations Before 1800 (pt 2)' (1888) 2 HarvLRev 149 at 164. 21 P W Ireland, 'The Rise of the Limited Liability Company' (1984) 12 Int J Soc Law 239; Avgitides, above n 6, 13-44. 22 Ireland, above n 21, 248; A Freiberg, 'Abuse of the Corporate Form: Reflections from the Bottom of the Harbour' (1987) 10 UNSWLJ 67 at 90. Cf A Hicks, 'Corporate form: Questioning the unsung hero' (1997) JBL 306 at 315-6. 23 321 U S 349 (1944), 361 (Douglas J). 24 On the history of limited liability in the United States, see E M Dodd, 'The evolution of limited liability in American industry: Massachusetts' (1948) 61 Harv LRev 1351. 25 [1921] 3 K B 492. 26 Ibid 500 (Lord Sterndale M R ) .

6

1.2 Extension of limited liability to corporate groups

1.2.1 Automatic extension inappropriate

Limited liability has been described as 'the greatest single discovery of

modern times' and 'by far the most effective legal invention ...made in the

nineteenth century'.27 It has also been said that '[ejven steam and electricity

are far less important than the limited liability corporation, and they would 98

be reduced to comparative impotence without it.' But it does not

necessarily mean that a blanket extension of this principle to corporate

groups is justified.29 The main problem is that, in the nineteenth century

when the principle of separate legal personality was laid down, the practice

of companies trading as a group had not been e stablished. The separate

legal entity principle only regulated the affairs of a single company and

made no provision for companies carrying on business as part of a group.

The holding company/subsidiary relationship came into existence some time

after the notion of limited liability had become popular and the latter was

' President Eliot of Harvard, quoted in W W Cook, 'Watered stock - Commissions - Blue sky laws - Stock without par value' (1921) 19 Mich L Rev 583. Cf however, W P Hackney and T G Benson, 'Shareholder liability for inadequate capital' (1982) 43 Uof Pitt L Rev 837 at 841 and S M Bainbridge, 'Abolishing veil piercing' (2001) 26 Iowa J Corp L 479 who quote President Nicholas Murray of Columbia University as having said in 1911: 'I weigh m y words when I say that in m y judgment the limited liability corporation is the greatest single discovery of modern times ... Even steam and electricity are far less important than the limited liability corporation, and they would be reduced to comparative impotence without it'. See further A Muscat, The Liability of the Holding Company for the Debts of its Insolvent Subsidiaries (1996) 153 and the authorities referred to there. 28 N M Butler, 'Why should we change our form of Government', quoted in JC Bonbright and G C Means, The Holding Company- Its Public Significance and its Regulation (1932) at 3. 29 See, eg, R Nathan, 'Controlling the puppeteers: reform of parent-subsidiary laws in N e w Zealand' (1986) 3 Canterbury L Rev 1 at 25, who is of the view that 'the extension of limited liability to corporate shareholders has the undesirable consequence of fostering inefficient investment in rather marginal and questionable undertakings.' 30 JE Antunes, 'The liability of poly-corporate enterprises' (1999) 13 Conn J Int'l L 197 at 208. For a discussion of reasons for corporate groups, see I Ramsay and G Stapledon, Corporate Groups in Australia (1998) 14-16. 31 F Wooldridge, Groups of Companies - The Law and Practice in Britain, France and Germany (1981) 1.

7

automatically extended to corporate groups without taking into account the

different considerations involved.32

Professor Blumberg, a leading authority on corporate groups in the United

States, argues that, while in a single corporation the shareholder has to be

insulated from liability by way of limited liability, this is not necessary in a

group situation. The shareholders of the holding company already have the

privilege of limited liability. In this regard he states:34

The courts, dazzled by the concept of the corporation as a separate entity, the same rule was applied apparently unthinkingly and automatically to the parent corporation, achieving a different unanticipated end ...[L]imited liability for corporate groups, one of the most important legal rules in economic society appears to have emerged as an historical accident.

The majority of commentators agree with the view that one should not

extend the concepts of legal personality and limited liability uncritically to

holding companies.35 It is submitted that there is ample justification for this

view. W h e n a company becomes part of a corporate group a double layer of

protection is called into use. Individual shareholders will still enjoy limited

liability if the holding company is held liable for the debts of another

company in the group. Also, by incorporating again - by making use of a

subsidiary - individuals w h o invested in the company originally and enjoyed

limited liability are n o w not even liable for their original investment.

Liability is therefore being limited twice (or many times) over.

A n extension of the concept of limited liability would ignore the fact that

completely different considerations apply, depending on whether one is

32 In England, the Limited Liability Act 1855 (18 & 19 Vict, c 133) introduced general limited liability. For the historical background, see H A Shannon, 'The coming of general limited liability' (1931-1932) 11 Economic History 267; Avgitides, above n 6, 13-44. 33 Hereinafter referred to as 'Blumberg'. 34 See PI Blumberg, The Law of Corporate Groups: Problems in the Bankruptcy or Reorganization of Parent and Subsidiary Corporations Including the Law of Corporate Guarantees (1985) (Corporate Groups: Bankruptcy) 3 99-452. Cf Berkey v Third Ave Ry 244 NY 84, 155 NE 58 (1926). 35 Antunes, 'The liability of poly-corporate enterprises', above n 30, at 213-214. Muscat, above n 27, 158 and 161. 36 Muscat, above n 27, 195. See further J Farrar, 'Legal issues involving corporate groups' (1998) 16C<ft£L/184atl89.

8

dealing with the liabilities of sole independent corporations or with mere

parts of a corporate group whose activities fall squarely under the control of

the holding company. W h e n one attempts to apply the principle of a

company's separate legal existence to conglomerates, a legal minefield

fraught with problems is exposed, so that the strict application of this

principle requires re-evaluation in an environment where group trading is

commonplace.37 The indiscriminate application of limited liability to

corporate groups has led to 'untenable distortions' and 'grossly unfair

results'.38 The best proof that the automatic extension of the principle in

Salomon v Salomon39 is not appropriate where corporate groups are

involved is the growing number of cases in which it is alleged that the result

of the application of this rule is inequitable. These cases range across the

whole spectrum of the law and will probably increase, since enterprises

operating in industrial sectors usually expand by making use of subsidiaries

to limit their exposure for torts.40

1.2.2 Risk of creditor prejudice

Limited 1 iability is generally j ustified o n the b asis that i t i s e conomically

efficient.41 A number of reasons are given in support of the argument that

C Schmitthoff, 'Introduction' in C M Schmitthoff and F Wooldridge (eds) Groups of Companies (1991) ix; JE Antunes, Liability of Corporate Groups - Autonomy and Control in Parent-Subsidiary Relationships in US, German and EU Law: An International and Comparative Perspective (1994) (Liability of Corporate Groups) 4. 38 Antunes 'The liability of poly-corporate enterprises', above n 30, 213-214. 39 [1897] A C 22.

Illustrations of catastrophes involving large multinational corporate groups are the Bhopal disaster in India, the A m o c o Cadiz channel oil spill in France, and the chemical accidents involving Sandoz in Switzerland and Hoffmann-La Roche in Italy. Recent examples of corporate collapses in Australia include Ansett Holdings Ltd, HIH Insurance Ltd, One.Tel Ltd and Harris Scarfe Holdings Ltd. See further C C H , Collapse Incorporated - Tales, Safeguards & Responsibilities of Corporate Australia (2001). See also F Varess, 'The buck will stop at the board? A n examination of directors' (and other) duties in light of the HIH collapse' (2002) 16 Comm LQ 12.

If the principle that a company is a separate legal entity is strictly adhered to in a group context, a risk for creditors exists in that assets and liabilities can be moved around in the group. One of the most important justifications of limited liability for corporate groups - ie that risk can be allocated efficiently as creditors can determine what risk is involved and act accordingly - is thereby negated: See H Hansmann and R Kraakman, 'Toward Unlimited Shareholder Liability for Corporate Torts' (1991) 100 Yale LJ 1879; R E Meiners, JS Mofsky and R D Tollison, 'Piercing the Veil of Limited Liability' (1979) 4 Delaware J Corp L 351 at 361; Freiberg, 'Abuse of the Corporate Form: Reflections from the Bottom

9

limited liability is more efficient as a general rule than unlimited liability.

First, it is argued that it reduces the agency costs involved in supervising

management and the wealth of other shareholders.43 Secondly, it is argued

that it contributes to the efficient operation of securities markets by

providing an incentive to managers to act in shareholders' interests by

promoting the free transfer of shares. Limited liability is also justified on the

basis that it fosters effective diversification by shareholders, lowering their

individual risk and reducing the cost of capital. Furthermore, it is argued

that limited liability benefits society in general by facilitating ideal

investment decisions by management.44

Blumberg points out that many of the justifications for limited liability have

limited or no application as far as holding companies and their wholly

owned subsidiaries are concerned.45 The argument that agency costs are

lower does not apply to holding companies with wholly owned subsidiaries,

as a holding company has strong incentives to monitor the managers of its

wholly owned subsidiaries and there are no other shareholders involved

whose wealth must be monitored. The argument that limited liability

provides an incentive to managers to act in shareholders' interests by

promoting the free transfer of shares does not apply where the holding

company is the only shareholder. The justification that limited liability

allows shareholders to diversify in an efficient manner, enabling them to

minimise their individual risk, is to a lesser extent applicable to holding

companies. This is because holding companies are generally less risk-averse

than individual shareholders, as they have a double layer of protection.46

of the Harbour', above n 20, 77-78; Companies and Securities Advisory Committee (CASAC), Report on Reform of the Law Governing Corporate Financial Transactions, (Burrows Committee Report) (1991) 1. 42 F Easterbrook and D Fischel, The Economic Structure of Corporate Law (1991), 41-44. 43 Agency costs are the costs of monitoring and assessing management. 44 For a comprehensive explanation, see F Easterbrook and D Fishel, 'Limited liability and the corporation' (1985) 52 Univ Chicago Law Rev 90; P Halpern, M Trebilcock and S Turnbull, 'An economic analysis of limited liability in corporation law' (1980) 30 UT Faculty LR 299. 45 P Blumberg, 'Limited liability and corporate groups' (1986) 11 J Corp Law 573 at 623-626. See also Bainbridge, above n 27, 529fF. 46 K Hofstetter, 'Multinational enterprise parent liability: efficient legal regimes in a world market environment' (1990) 15 North Car J Int'l L & Comm 299 at 307. See further IM

10

Blumberg admits, however, that some of the justifications for limited

liability are applicable to partly owned subsidiaries.47 Although his analysis

demonstrates that the case for limited liability is diminished as far as

wholly-owned subsidiaries are concerned, it does not prove that it would be

more efficient to remove limited liability from holding companies. Indeed,

this is a question that has been troubling lawyers for a very long time. In this

regard the n o w famous debate between Professors Landers and Posner as

to whether limited liability should apply to so-called 'multi-tiered'

corporations in bankruptcy that took place in the United States in the 1970's

is relevant.50 This debate is revisited in Chapter 10.

Landers opposed limited liability of group companies, arguing that creditors

of a single corporation were not exposed to the same dangers as creditors of

group companies.52 In a group there was a great incentive for group

controllers to move assets between different companies, so that profits to the

group, rather than to individual companies in the group, were maximised.

Due to the likelihood of intra-group movement of assets, it may be too

expensive for creditors to obtain information regarding the financial position

of the relevant company.53 Creditors could thus easily be misled as to which

company in the group owned what assets. Complex group structures may be

Ramsay, 'Allocating liability in corporate groups: an Australian perspective' (1999) 13 Conn J Int'lL 329 at 341-343; I Ramsay and D Noakes, 'Piercing the corporate veil in Australia' (2001) 19 C&SLJ 250 at 263. 47 Blumberg, 'Limited liability and corporate groups', above n 45, 573. 48 K Yeung, 'Corporate groups: legal aspects of the management dilemma' [1997] LMCLQ 208 at 256-263. 49 Hereinafter referred to as 'Landers' and 'Posner' respectively. ,0 This debate was started by JM Landers, 'A unified approach to parent, subsidiary, and affiliate questions in bankruptcy' (1975) 42 Univ Chicago Law Rev 589. R A Posner challenged this in 'The right of creditors of affiliated corporations' (1976) 43 Univ Chicago Law Rev 499. Landers had an opportunity to reply to Posner in 'Another word on parent, subsidiaries and affiliates in bankruptcy' (1976) 43 Univ Chicago Law Rev 527. 51 See Ch 10 para 10.2.3.

Landers, 'A unified approach to parent, subsidiary, and affiliate questions in bankruptcy', above n 50, 639-40 did, however, state an exception to this principle, namely in cases where a creditor could prove that he relied on the creditworthiness of a particular member of the group.

In other words, the directors would m ake management decisions for the benefit of the group as a whole, rather than looking after the interests of a specific subsidiary company, so that the subsidiary may never become profitable.

11

used to conceal the true financial position of individual group companies

from creditors. Furthermore, the directors could make management

decisions for the benefit of the group as a whole, rather than look after the

interests of a specific subsidiary company, so that the subsidiary might

never become profitable. Basically, Landers argued that the abuses of

limited liability in corporate groups were so rife that creditors should be

excused from having to prove that an abuse occurred. Landers contended

that, because limited liability shifted the risk of business failure to creditors,

for which they were under-compensated, limited liability was inefficient in

corporate groups.54

In stark contrast to Landers, Posner supported limited liability for group

companies. H e claimed that creditors were fully compensated for the risk

they had to bear, which was reflected in their profit margin. Posner argued

that creditors should contract to protect themselves against subsequent

action by a corporation that adversely affected their prospects of being

repaid. H e denied the claim that a holding company had the incentive to

maximise the profits of the group rather than individual companies. Instead

he claimed that, when the profits of each individual company were

maximised, the profits of the group would likewise be maximised.56 Posner

argued that abuses were not as prevalent as portrayed by Landers, who only

considered reported case law on bankruptcy. This, according to Posner, was

not a true reflection of everyday business transactions involving creditors.

Posner said that it was d eceptive to look only a t these cases, because the

incorrect impression could be created that invariably the purpose of carrying

54 Landers, 'Another word on parent, subsidiaries and affiliates in bankruptcy', above n 50, 529. 55 Landers was primarily concerned with the increase in misappropriation risk: Landers, 'A unified approach to parent, subsidiary, and affiliate questions in bankruptcy', above n 50, 595-596. 'Misappropriation risk'provides increased opportunities for asset shifting from shareholders to creditors. It should be distinguished from 'enterprise risk', which is the irreducible variability in the earnings of the business. Although Posner did consider misappropriation risk, he appeared to be more concerned with the allocation of enterprise risk: Posner, 'The right of creditors of affiliated corporations', above n 5 0,5 07-509 and 515-516. Their approaches conflict, because the desirability of enterprise risk allocation by making use of limited liability m a y substantially increase misappropriation risk in corporate groups. 56 Posner did not supply any reasons in support of his claim.

12

on business in a group was to mislead creditors. H e also claimed that

liability of a holding company for its subsidiaries' debts would increase the

cost of credit, as creditors of one company would have to examine the

creditworthiness of all the other group companies.57

Although this controversy is still unresolved,58 it may be argued that

Posner's claim that creditors are fully compensated for the risk that they

have to bear can only be true in an ideal market where all information is

available to creditors and where there are no transaction costs.59 The reality

is that high transaction costs m a y prevent the proper re-allocation of risks.

The costs involved for creditors in obtaining sufficient information about

their credit risk m a y be out of proportion to the amount involved. There is

also empirical evidence, at least in the United States, to the effect that it is

very rare for trade creditors to extract negative pledges. ' Furthermore, it is

very difficult for individual creditors to co-operate in a collective action.

They m a y therefore lack the necessary incentive to act jointly to prevent

opportunistic behaviour by the company to their detriment.62

From the exposition above it appears that the removal of limited liability

may be justified in certain circumstances to ensure that holding companies

do not transfer the risk of business failure to the creditors of their subsidiary

companies without compensation.63 The transfer of assets between different

57 Posner, 'The right of creditors of affiliated corporations', above n 50, 513-514. See C W Frost, 'Organizational form, misappropriation risk, and the substantive

consolidation of corporate groups' (1993) 44 Hastings LJ 449 at 467ff. Blumberg, Corporate Groups: Bankruptcy, above n 34, 448-52 sided with Landers, while Hansmann and Kraakman, above n 41, at 1919-1921 sided with Posner. See further D W Leebron, 'Limited liability, tort victims, and creditors' (1991) 91 Columb L Rev 1565 and R A Posner, Economic Analysis of Law (1992) at 406-09 (revisiting the debate). 59 Yeung, above n 48, 256-263.

K Hofstetter, 'Parent responsibility for subsidiary corporations: evaluating European trends' (1990) 39 ICLQ 576. J C Coffee,' Shareholders versus managers: the strain in the corporate web' (1986) 85

Mich LRev\. See also Bond Brewing Holdings Ltd v National Australia Bank Ltd (1990) 1 A C S R 445; R Grantham, 'The judicial extension of directors' duties to creditors' [1991] JBL 1 at 3 and the authorities cited there.

I Ramsay, 'Holding company liability for the debts of an insolvent subsidiary: a law and economics perspective' (1994) 17 UNSWLJ 520 at 523.

D D Prentice, 'Groups of companies: the English experience' in KJ Hopt (ed) Groups of Companies in European Law - Legal and Economic Analyses on Multinational Enterprises

63

13

group companies m a y enhance the efficiency of the group and should

therefore not as a matter of course be prohibited. Such transfers may,

however, prejudice creditors' interests where there are insufficient assets to

satisfy their claims. The legal protection of creditor interests m a y therefore

be justified where the transaction costs are prohibitive, so as to preclude

them from protecting themselves by contract against actions that m a y reduce

the assets of the particular company.64 The theory that creditors can protect

themselves by charging higher interest rates for higher levels of risk does

not ring true where the costs involved for the creditor to obtain the

necessary information regarding the level of risk are disproportionate to the

amount involved in the transaction.65 The removal of limited liability in the

context of corporate groups across the board may, however, not be justified,

as creditors will then need to assess the credit risk of all group companies.

This will increase the cost of credit66 and may serve to discourage

entrepreneurial activity.

It is relevant that creditors of an insolvent company are faced with what is fZQ

known as a 'moral hazard'. This may be explained as follows. Excessive

risk-taking by shareholders is exacerbated at the onset of insolvency. The

existence of limited liability means that a holding company is only liable to

the amount of its shareholding in its subsidiary if the latter becomes

insolvent. The holding company as shareholder (via its directors) is

therefore prepared to engage in risky investments as it has nothing to lose.

Most of its funds have already been dissipated and there is a remote chance

that, if it continues the business of the company, insolvency m a y even be

prevented so that the holding company does not lose its original investment

(1982) 102 at 106. See further Ramsay, 'Allocating liability in corporate groups: an Australian perspective', above n 46, 366-367. 54 Yeung, above n 48, 256-263. 65 Ramsay, 'Allocating liability in corporate groups: an Australian perspective', above n 46, 363-364. 66 Posner, 'The right of creditors of affiliated corporations', above n 50, 516-517; Cork Report, above n 3, para 1946. 67 Cork Report, above n 3, para 1940. 68 Yeung, above n 48, 256-263; Coffee, above n 61, 61-62. 69 L Lin, 'Shift of fiduciary duty upon corporate insolvency: proper scope of directors' duty to creditors' (1993) 46 Vand L Rev 1485 at 1489-93.

14

in the subsidiary.70 It is thus in the interests of the holding company that the

subsidiary should continue trading when it is insolvent, even though it is

obviously more risky for the subsidiary's creditors.71 It is therefore often

said that, because of the principle of limited liability, a holding company has

a perverse incentive to allow the subsidiary to continue trading while it is

insolvent.

1.2.3 Creditors are less efficient risk bearers

Leaving aside the question of the risk of creditor prejudice, a related

question is whether, on policy grounds, limited liability should in any event

be extended to corporate groups. It is sometimes argued that the application

of limited liability to corporate groups, irrespective of the control of the

holding company over the subsidiary, is inefficient on the ground that the

holding company is a more efficient bearer of risk of business failure than

the creditors of the subsidiary.72 This argument is even more controversial

than the argument relating to the risk of creditor prejudice that formed the

subject of the debate between Landers and Posner. It entails that the power

of the holding company to control the affairs of its subsidiaries should lead

to a positive duty to act on the part of the holding company, in order to

prevent detriment to the creditors of its subsidiaries.74

The Australian legislature has, however, embraced the notion that holding

companies are superior risk bearers by enacting ss 588V-588X of the

Corporations Act.15 This thesis therefore proceeds upon the assumption that

holding companies are the most efficient risk-bearers in the context of

corporate groups. Section 588V shifts the risk of loss that results from

insolvent trading by an insolvent subsidiary from its creditors or its directors

Coffee, above n 61, 61. 71 Ibid 61-62.

Ramsay, 'Holding company liability for the debts of an insolvent subsidiary: a law and economics perspective', above n 62, 540-541. See the discussion in para 1.2.2 above.

74 Yeung, above n 48, 256-263.

See also I Ramsay, Transcript of Symposium held at Connecticut in 1998, published in (1999) 13 Conn JInt'l L 397 at 471-4. For a detailed discussion of s 588V, see Ch 7.

15

to the holding company. Sections 588V-588X provide that a holding

company m a y be held liable for debts incurred by a subsidiary under certain

circumstances. This will be the case when the holding company (or one or

more of its directors) was aware of, or could reasonably be expected to be

aware of, grounds for suspecting that the subsidiary was insolvent and failed

to take all reasonable steps to prevent the subsidiary from incurring the debt.

It is not necessary to prove that the holding company was actively involved

in the affairs of the subsidiary.76 In its defence the holding company may,

however, prove that it expected or that it had reasonable grounds to expect

that the subsidiary was solvent and would remain solvent at the relevant 77

time.

It is submitted that Ramsay is correct, at least theoretically, when he states

that these provisions are advantageous to ensure that the most efficient risk

bearers,78 namely the holding companies, as opposed to the subsidiary's

creditors or directors, bear the risk of business failure.79 It is conceded that

sophisticated creditors m a y be better placed than individual shareholders to

monitor management, because they have specialised knowledge and do not

suffer from what has become known as the 'free rider' problem. This

entails that shareholders are often reluctant to incur expenses in instituting

proceedings against management because they are unable to exclude other

shareholders w h o have not contributed to the legal costs from participating

in the benefits obtained. At the same time it must be acknowledged that a

holding c ompany i s in a b etter position than b oth individual shareholders

and creditors to monitor the affairs of its subsidiaries. The fact is, however,

that in practice holding companies emerge unscathed.

76 J Hill, 'Corporate groups, creditor protection and cross guarantees: Australian perspectives' (1995) 24 Can BusUl2\ at 237. 77 Section 588X of the Corporations Act. 78 This statement was made in the context of public companies. 791 Ramsay, 'Holding company liability for the debts of an insolvent subsidiary: a law and economics perspective', above n 62, 523. 80 See further on the 'free riding' problem Bainbridge, above n 27, 491.

16

1.3 Scope of investigation

1.3.1 Comparison with other jurisdictions

Countries other than Australia have employed different techniques in an

attempt to overcome the separate legal entity principle in corporate group

insolvencies. To effect this the corporate entity is not necessarily

disregarded, but priorities are adjusted by taking into account principles of

equity. In N e w Zealand, for example, the courts have a wide discretion to

deal with group companies in liquidation. The N e w Zealand courts are

allowed to make 'contribution orders' on broad grounds where a related

company is liquidated and there is also provision for so-called 'pooling o i m

orders' in respect of related companies in liquidation. Apart from ordering

that a related company should contribute to the assets available for winding

up, the court can - where there is more than one related company in

liquidation - wind up the companies as if they were one on the basis that it is

just and equitable to do so.

The basic legal principle in New Zealand, like in Australia, is that each

company in a group is a separate legal entity. This entails that the directors

of a particular company in the group have to take into account the interests

of their own company before the interests of the group as a whole. In

practice, however, this is not always the case. The concept of requiring a

company to contribute to the assets of a related company which is in the

process of being wound up, and the idea of winding up different companies

as if they were one company, is out of line with the separate legal entity

principle. Instead, it acknowledges the concept of so-called 'enterprise'

liability, discussed in Chapter 2.82

The United States has a concept similar to the pooling of assets in New

Zealand, but goes a bit further. In the United States there is a bankruptcy

See Ch 9 para 9.3 for a discussion of the concept of a 'related' company under the N e w Zealand law.

17

principle of substantive consolidation that allows the assets and liabilities of

various corporations to be consolidated in one entity against which all

claims are instituted.83 Another principle of the United States bankruptcy

law, equitable subordination, confers jurisdiction on a court to defer certain

inter-corporate claims84 if it is just and equitable to do so.85 In applying this

principle, the courts scrutinise the conduct of the parties and the financial

arrangements giving rise to the debt. A n inter-corporate claim will not easily

be deferred - something like fraud or mismanagement has to be established

before deferral of the inter-corporate claim will be ordered. If it is deferred,

the external creditors are given priority.

In May 2000 CASAC released its Corporate Groups Final Report, making

radical recommendations for reform of the law of insolvency in the context

of corporate groups.86 C A S A C paid particular attention to the position in

N e w Zealand and the United States, recommending, inter alia, that the N e w

Zealand law on pooling orders in liquidations should be adopted. This

necessitates an investigation of the current position and most recent

developments across the Tasman in this country. In addition, where

appropriate, the position in the United States is also periodically referred to,

being one of the countries at the forefront of legal responses to the problems

encountered with corporate groups. In the search for an equitable solution to

the problem of winding up a group of companies, the position in the United

Kingdom, from which the Australian corporate law system originates, is

also taken into account. Although reference is occasionally made to other

jurisdictions as authority or by way of illustration, it should be pointed out

82 See Ch 2 para 2.1. 83 See, in general, Blumberg, Corporate Groups: Bankruptcy, above n 34, chapter 10. 84 Typically, an inter-corporate claim is a debt owed to the holding company by its subsidiary. 85 For a further discussion on equitable subordination under United States law, see, eg, JD Cox, TL Hazen and F H O'Neal, Corporations (1997) para 7.10 (pp 123-126). 86 (Final Report). See also the C A S A C Discussion Paper on Corporate Groups (December 1998) and the C A S A C Corporate Groups Draft Proposals (October 1999). On 11 March 2002 C A S A C became known as the Corporations and Markets Advisory Committee ( C A M A C ) as a result of the Financial Services Reform Act 2001.

18

that this work is not an exhaustive comparative analysis - the focus is on the

Australian law.

1.3.2 Limitation of topic

The main area to be investigated in this thesis is how creditors may enjoy

sufficient protection when they are dealing with companies forming part of

a group where one or more of the companies are faced with insolvency. It

should be noted that this study has been undertaken from a law and

economics perspective, although a number of analytical frameworks do exist

within which the question of the liability of a holding company for the debts

of its insolvent subsidiary has been examined, notably a sociological

89

viewpoint.

W h e n observing the corporation through an economics lens, as has been

done in this thesis, the corporation may be seen simply as a "nexus of

contracts ... a financing device ... [that] is not otherwise distinctive".90

W h e n viewing the corporation from a sociological vantage point, however,

the corporation may be seen as "a central institution ... [and as] an

institution it is a particular historical pattern of rights and duties, of powers

and responsibilities".91 In other words, adopting a sociological perspective

on law entails treating it as an aspect of social life in an attempt to

This thesis does not deal with issues of extra-territoriality and international law related to regulating cross-border corporate groups.

A corporate group would comprise a holding company and its subsidiaries, including any intermediate subsidiaries in a corporate chain.

See also L Johnson, 'Individual and collective sovereignty in the corporate enterprise' (1992) 92 Colum L Rev 2215. For further alternative analytical frameworks in which the liability of a holding company for the debts of its insolvent subsidiary have been examined, see, eg, the contributions utilising Teubner's autopoetic theory in D Sugarman and G Teubner (eds), Regulating Corporate Groups in Europe (1990). '° FH Easterbrook & D R Fischel, The Economic Structure of Corporate Law (1991) at 10, 12. S ee further on a s ociological a pproach t owards c ompany 1 aw, S W heeler ' Company Law' in PA Thomas, Socio-Legal Studies (1997) at 279ff. 91 R N Bellah et al, The Good Society (1991) 97.

19

understand the larger social environment and the place of the law within it

systematically and empirically.92

Indications are that, if the institution of groups of companies were viewed

from a sociological perspective, the solution of where liability should fall in

corporate groups would probably entail some form of group liability, as

opposed to liability only of the particular company or companies involved.

This is because, when the institution of the modern company rose to

prominence in the 1800s, it fitted into society on the basis of a natural

person or individual holding shares in this legal entity - the company - to

shield it from liability. However, in the twentieth century, the emphasis has

shifted to the group where one company holds shares in another company

and the dominant purpose is the raising and management of capital on a

wider, often trans-national, scale, such capital representing the whole

enterprise or business. Before one could reach a conclusion on the liability

in corporate groups from a sociological perspective, however, further

empirical studies would have to be conducted. Embarking on a discussion of

the problem of the liability of a holding company for the debts of its

subsidiary and the related question of how such liability should be regulated

from a sociological perspective falls outside the scope of this thesis.

It should be noted that this thesis focuses on trade creditors, lessors and

banks that have lent on an unsecured basis, and does not deal with the

position of involuntary creditors, such as tort creditors or employees, to

which different considerations apply.95 A number of reasons exist for

92 R Cotterrell (ed), Sociological Perspectives on Law, Vol I: Classical Foundations (2001) xi; R Cotterrell (ed), Sociological Perspectives on Law, Vol II: Contemporary Debates (2001) xi-xiii. 93 See R Cotterrell, The Sociology of Law: An Introduction (1992) 130. 94 For examples of related empirical studies, see I Ramsay and M Blair, 'Ownership concentration, institutional investment and corporate governance: an empirical investigation of 100 Australian companies' (1993) 19 MULR 153; and IM Ramsay and G P Stapledon, Corporate Groups in Australia (1998). 95 O n the position of involuntary creditors, see, eg, H Hansmann and R Kraakman, above n 41; D Wishart, he personal liability of directors in tort' (1992) C&SLI 363; R Carroll, Corporate parents and tort liability' in M Gillooly (ed), The Law Relating to Corporate Groups (1993) 91; R B Thompson, 'Unpacking limited liability: direct and vicarious liability of corporate participants for torts of the enterprise' (1994) 47 VandL Rev I; R

20

distinguishing between tort creditors and contract creditors. The main

distinguishing feature between tort creditors and contract creditors is the

involuntary nature of the relationship between the tort victim and the

96 tortfeasor. This is important for a number of reasons.

First, disclosure requirements and other procedures that protect shareholder

and contract creditors' interests are rendered ineffective to a large extent.

This is because in the typical scenario a tort victim will not have knowledge

of or access to information to assess the risk of harm or the ability of a

subsidiary to pay compensation.97 Secondly, there is often no continuing

relationship between the parties. While, in the case of contract creditors,

there m a y be long-term interests to be served by a holding company

agreeing to meet its subsidiary's obligations, in the case of tort creditors no

such interest is likely to exist.98 The third reason for distinguishing between

tort and contract creditors provides an even stronger argument in favour of

differential treatment of them by the law. This is that tort victims are

frequently less able to predict the likelihood or the nature of the loss or

injury that m a y be inflicted upon them and to implement appropriate steps to

protect their position, for example, by insurance.99

The emphasis in this thesis is on the problems that may arise because a

subsidiary is subject to the control of its holding company, with certain

consequences for the subsidiary as a separate legal entity, its directors and

creditors. Although the significance of factors such as economic integration

and financial interdependence in the context of control is recognised, the

focus of this thesis is on legal control which, in a sense, m a y be said to

Carroll, 'Shadow director and other third party liability for corporate activity' in I Ramsay, Corporate Governance and the Duties of Company Directors (1997) 162; P Edmundson and P Stewart 'Liability of a holding company for negligent injuries to an employee of a subsidiary: C S R v Wren' (1998) 6 Torts U 123; R Grantham, R and C Rickett, 'Directors' 'tortious' liability: contract, tort or company law?' (1999) 62 MLR 133; K Wnepper, 'Piercing the corporate veil: a comparison of contract versus tort claimants under Oregon law' (1999) 78 Or LR 347.

R Carroll, Corporate parents and tort liability' in M Gillooly (ed), The Law Relating to Corporate Groups (1993) 91 at 93-95. 97 Ibid 94. 9*Ibid. "Ibid.

21

incorporate these factors. The focus of the thesis is on cases in which control

is in a holding company, rather than in an individual, a trust or another non

corporate association or entity.

As the thesis does not consider the position of minority shareholders, partly-

owned subsidiaries are only dealt with for the purposes of considering

creditors' entitlements.100 The thesis is furthermore confined to corporations

that are affiliated in a way that depends significantly on share ownership,

namely vertical corporate groups, consisting of a holding company and one

or more subsidiaries.101 Apart from the fact that vertical groups are more

prevalent, the question of liability in any event does not generally arise in

horizontal groups, because of their non-hierarchical linkage. Group

accounting and taxation matters also fall outside the scope of this thesis.

In search of an answer to the question how to balance entrepreneurial

investment, on the one hand, with creditor protection, on the other, the Cork

Report in the United Kingdom highlighted two principal issues in the 1 (WX

possible reforms of insolvency law for corporate groups in 1982. The first

issue highlighted by the Cork Report is how the claims of the other

companies in the group should be treated in the insolvent liquidation of one

company in the group. This is inextricably linked with the principle of pari

passu, according to which like claims are to be treated alike, or creditors of

the same standing should receive equal treatment. The general

recommendation made in the Cork Report regarding the principle oi pari

passu, namely that 'any inter-company indebtedness which appears to

100 For more on shareholder protection, see the contributions of M Gillooly, 'Outside shareholders in corporate groups' at 159 and P Redmond, 'Problems for insiders' at 208 in M Gillooly (ed), The Law Relating to Corporate Groups (1993). 101 This is as opposed to so-called 'horizontal' groups, where corporations are affiliated purely by contracts or interlocking directorates. For a discussion of the distinction between vertical and horizontal groups, see, eg, M A Eisenberg, 'Corporate groups' in M Gillooly (ed), The Law Relating to Corporate Groups, (1993) at 1. 102 See Antunes, Liability of Corporate Groups, above n 37, 235. 103 Above n 3.

22

represent the long-term capital structure of a subsidiary should be

subordinated to the claims of external creditors', was not implemented.

In its Final Report, CASAC recommended that the Corporations Law (now

Corporations Act) should not be amended to allow courts to subordinate

intra-group claims in the insolvency of a group company. ' Although

equitable subordination along these lines is not negated outright as a

possible solution, it is excluded by the scheme of the Corporations Act

and would warrant a thorough investigation before the viability of

implementing it in Australia could be properly considered. In this light,

coupled with the fact that numerous general doctrines and statutory

provisions already exist in Australian law which could be invoked to

produce similar results to equitable subordination, it m a y be argued that 108

there is scarcely any need for such a doctrine in this country. Equitable

subordination is therefore not discussed further in this thesis.

The other issue highlighted by the Cork Report is whether any of the other

companies in the group should be held liable for the debts of an insolvent

group company. This involves liability to external creditors and is also

known as 'the corporate liability rule'. The Cork Report was of the view that

the corporate liability rule was so important that it warranted a full-scale

review. It considered that the matter of groups raised issues that were

outside its terms of reference, which were confined to insolvency law. A s a

result no specific recommendations were made as far as the liability of

For a further discussion on equitable subordination under English law, see, eg, R Schulte, 'Corporate groups and the equitable subordination of claims on insolvency' (1997) 18 Co Law 2.

C A S A C Final Report, above n 86, Recommendation 24. In this regard s 555 of the Corporations Act provides: 'Except as otherwise provided by

this Act, all debts and claims proved in a winding up rank equally and, if the property of the company is insufficient to meet them in full, they must be paid proportionately'. Although this pari passu principle is subject to specific statutory exceptions, s 555 does not admit any general law exceptions.

It is conceded that equitable subordination could be introduced by an express provision in the Corporations Act. Section 563C recognises debt subordination by means of an agreement or declaration by a creditor of a company. However, there is at present no capacity for a court to order equitable subordination of a lender's claim. See further J O'Donovan, Lender Liability (2000) para 11.80.

23

holding companies was concerned. It is the purpose of this thesis to

examine the corporate liability rule, while only referring to the principle of

pari passu to the extent that is necessary.

1.3.3 Roadmap

Since the concept 'control' plays such a crucial role in the relationship

between holding companies and their subsidiaries, its meaning is considered

at the outset in Chapter 2, before considering the safeguards available for

group creditors under the current regime.110 In Chapter 3 the protection for

creditors under the doctrine of piercing the corporate veil is analysed, while

Chapters 4 and 5 consider the scope of directors' duties in corporate groups.

In particular, the issue of whether directors may disregard their duties to

their individual companies in favour of acting for the benefit of the group

and what implications this has for creditors, is considered.

Especially significant in the context of the protection o f creditors are the

provisions of the Corporations Act under which a holding company may be

held liable for insolvent trading by its subsidiary. Chapters 6 and 7 deal with

the liability of the holding company for insolvent trading in its capacity as

shadow director and in its capacity as shareholder respectively. Although

108 D B Robertson, 'The lender-borrower relationship and the subordination of lender's claims - Part III' (1991) JBFLP 219 at 230. 109 As far as liability to external creditors in corporate groups is concerned, five principal policy options were suggested to the Committee in charge of the Cork Report, above n 3. The five options outlined in the Cork Report, above n 3, are: (1) that each group company should be jointly and severally liable for the external debts of all the other companies in the group; (2) that group responsibility should arise only by way of a voluntary contracting-in procedure; (3) that group responsibility should be qualified by a contracting-out procedure; that liability should be imposed on one or more of the other companies in the group in the event of a proven departure from a predetermined code of conduct; and (5) that 1 iability should be imposed on one or more group members by a decision of the court in the course of the insolvency of another group member, where the court has a wide discretion but is required to have regard to certain guidelines. For further comment on these five options, see C A S A C Final Report, above n 86, para 6.30. 110 In this thesis the historical setting of the problem posed has not been reviewed since it has on previous occasions been done extensively. See, eg, Antunes, Liability of Corporate Groups, above n 37, 13-111; Avgitides, above n 6, 13-44. For a critical account of the role of limited liability to commercial expansion historically see, eg, B C Hunt, The Development of the Business Corporation in England, J800-1867, (1936). For a different, morally grounded, perspective of Salomon v Salomon see, eg, G R Rubin, 'Aron Salomon and his circle' in J Adams, Essays for Clive Schmitthoff, (1983) at 99ff.

24

contribution and pooling as such have not formally been recognised in

Australia, both the regulator and the courts have done so indirectly, as

discussed in Chapter 8. The recent C A S A C recommendations relating to

contribution and pooling are dealt with in Chapter 9, before an exposition of

m y proposals follows in Chapter 10.

2 THE MEANING OF CONTROL AND THE REGULATION OF CORPORATE GROUPS

2.1 Background 25

2.2 Various applications of the control concept 28

2.2.1 Subsidiary/holding company relationship 29

2.2.1.1 Test of controlling the composition of the board 30

2.2.1.2 Voting control test 31

2.2.2 Consolidated accounts 35

2.2.3 Related party transactions 38

2.2.4 Cross share-holdings 41

2.3 Evaluation of position of group creditors 44

2.3.1 CASAC recommendations 45

2.3.1.1 Regulation by general control test 45

2.3.1.2 Wholly-owned groups to choose whether enterprise principles 46

apply

2.3.2 Critique of CAS AC recommendations 49

2.3.2.1 Regulation by general control test 49 (a) Replacement of 'holding/subsidiary' with 'control' 50 (b) Preferred definition of 'control' 52

2.3.2.2 Wholly-owned groups to choose whether enterprise principles 57

apply

2 THE MEANING OF CONTROL AND THE

REGULATION OF CORPORATE GROUPS

2.1 Background

There are two major types of regulatory strategies posed as a solution to what

has been described as 'one of the great unsolved problems of modern company

law',1 namely, in what circumstances a holding company m a y be held liable for

the debts of its subsidiary. The two regulatory strategies are the traditional

entity law approach and the revolutionary enterprise approach. In addition, and

falling between the entity approach and the enterprise approach, lies an

intermediate approach, also known as the dualist approach.

According to the entity approach a holding company should not be held liable

for the debts of its subsidiary, because they are separate legal entities. Only in

exceptional circumstances will this rule be set aside and the corporate veil

lifted.4 Underlying this approach is the idea of corporate autonomy. By

contrast, in terms of the enterprise approach, the holding company should be

held liable for all the debts of its subsidiary, because it controls the latter.5

Enterprise liability entails an automatic application of the opposite rule to

limited liability that applies in the entity approach, namely, that there is

1 C M Schmitthoff, 'Introduction' in C M Schmitthoff and F Wooldridge (eds), Groups of

Companies (1991) ix. 2 The enterprise approach is followed in the European Union. The entity law approach is followed in many countries, including Australia, the U K , N e w Zealand and the United States. In the United States, however, the legislature, assisted by the courts, increasingly make use of single enterprise principles in the context of corporate groups: PI Blumberg, 'The increasing recognition of enterprise principles in determining parent and subsidiary corporation liabilities' (1996) 28 Conn L Rev 295. See also PI Blumberg, The Multinational Challenge to Corporation Law, Oxford University Press, 1993, at 100-107. The selective introduction of single enterprise principles into United States corporate law has been made possible mainly because the courts have held that controlling shareholders owe duties of fairness to minority shareholders: see, eg, JD Cox, T L Hazen and F H O'Neal, Corporations (1997) para 11.10 (pp 250-258). 3 The best example of this strategy is the German model. This is blown in Germany as the

'Konzernrecht'. 4 See C h 3 for a discussion of the lifting of the corporate veil. 5 Under the enterprise approach the group of related companies is treated as one economic enterprise. See further A A Berle, 'The theory of enterprise entity' (1947) 47 Columb L Rev 343.

26

unlimited liability of the holding company. Underlying this approach is the

notion of corporate control.6 The dualist approach distinguishes between

preserving the subsidiary's autonomy and legitimising the holding company's

control. In a contractual group7 the holding company's control is legitimised,

while in a factual group8 the subsidiary's autonomy is preserved.

In contractual groups the de jure (legal) control of the holding company is

embodied in a special contract known as a 'contract of domination'. The law

expressly recognises that holding companies control their subsidiaries. In

exchange for this control the holding company is obliged to make good all the

annual losses of the subsidiary or is held jointly liable for the debts of the

subsidiary. B y comparison, in the factual groups, the control by the holding

company of the subsidiary is only de facto (effective). This entails that the

entity approach basically applies so that, in exercising its control over the

subsidiary, the holding company has to act in the best interests of the

subsidiary. The holding company is only obliged to compensate for losses that

occurred as a result of its controlling influence over the subsidiary.

As in other common law countries, the whole system of Australian corporate

law is based on the classical legal model of the individual autonomous

company, where an entity law approach is followed. This model proceeds upon

the assumption that the company is an independent economic and legal entity

where individual widely dispersed shareholders are interested in the best return

on their investment and where those managing the company are interested in

acting in the best interests of the company. The fact that each individual

shareholder has only very small voting power ensures harmony between

individual interests. This, in turn, ensures that the interests of other groups of

persons such as creditors are at the same time protected, though indirectly.9

See also JE Antunes, 'The liability of polycorporate enterprises' (1999) 13 ConnJInt'l L 197 at 217-218.

Under German law this is known as 'Vertragskonzerne'. Under German law this is known as 'Faktische Konzerne'.

9 H Wiedemann, "The German experience with the law of affiliated enterprises' in Klaus J Hopt (ed) Groups of Companies in European Law - Legal and Economic Analyses on Multinational Enterprises, Volume II, (1982) 21-22.

27

However, as soon as one shareholder, or a group of shareholders acting in

concert, acquires a majority of shares so that it can control the company, this

harmony is endangered. The reason for this is that these shareholders may

abuse their influence in furtherance of their own interests and to the detriment

of other relevant groups of persons. The dangers are exacerbated in two

instances. The first instance is where the number of shares held by a

shareholder is increased, culminating in the case of a single shareholder

company or a wholly owned subsidiary. The second instance is where the

controlling shareholder becomes active in an economic activity external to the

company, that is, where the shareholder is an entrepreneur such as another

company. The chances for abuse are therefore the greatest in the case of a

holding/subsidiary company relationship, particularly in the case of a wholly

owned subsidiary.10

Contrary t o w hat u sually happens i n t he c ase o f a n i ndividual s hareholder, a

corporate shareholder will most likely make use of its controlling power to

continue to seek its o w n economic interests within the controlled company and

at the expense of the controlled company.11 In other words, because the