Embed Size (px)

Citation preview

See important disclosures, including any required research certifications, beginning on page 33

China Consumer Discretionary

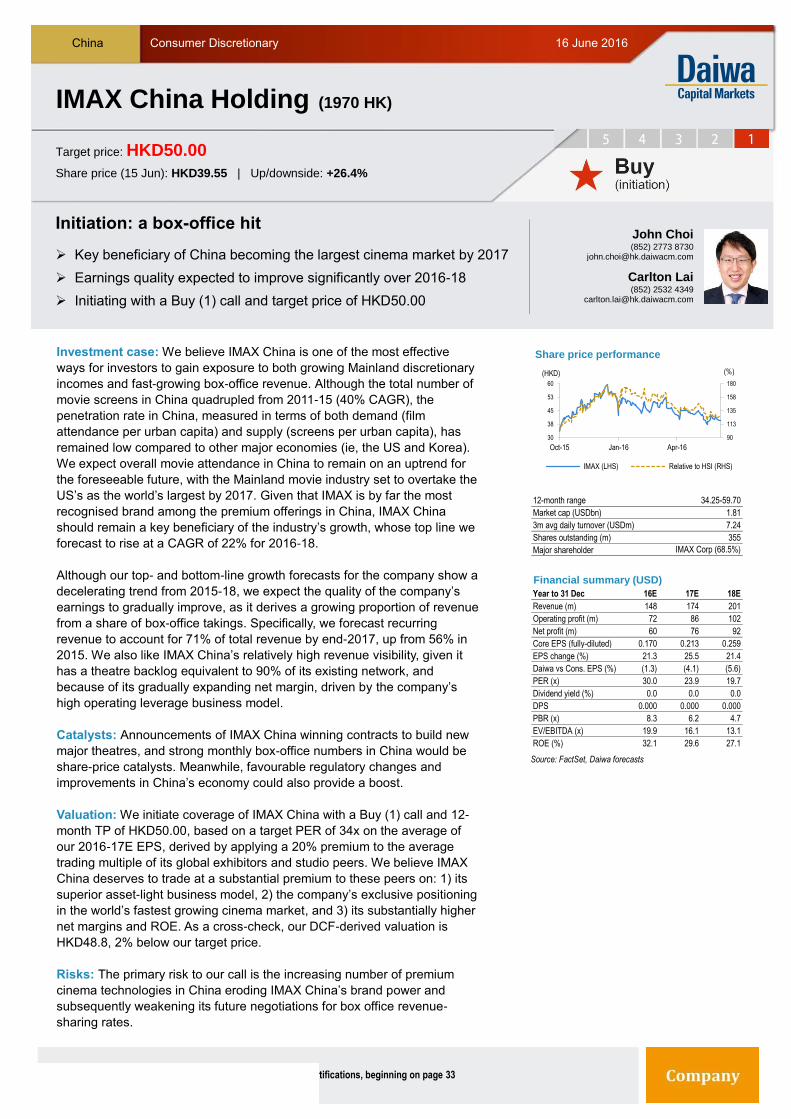

Investment case: We believe IMAX China is one of the most effective

ways for investors to gain exposure to both growing Mainland discretionary

incomes and fast-growing box-office revenue. Although the total number of

movie screens in China quadrupled from 2011-15 (40% CAGR), the

penetration rate in China, measured in terms of both demand (film

attendance per urban capita) and supply (screens per urban capita), has

remained low compared to other major economies (ie, the US and Korea).

We expect overall movie attendance in China to remain on an uptrend for

the foreseeable future, with the Mainland movie industry set to overtake the

US’s as the world’s largest by 2017. Given that IMAX is by far the most

recognised brand among the premium offerings in China, IMAX China

should remain a key beneficiary of the industry’s growth, whose top line we

forecast to rise at a CAGR of 22% for 2016-18.

Although our top- and bottom-line growth forecasts for the company show a

decelerating trend from 2015-18, we expect the quality of the company’s

earnings to gradually improve, as it derives a growing proportion of revenue

from a share of box-office takings. Specifically, we forecast recurring

revenue to account for 71% of total revenue by end-2017, up from 56% in

2015. We also like IMAX China’s relatively high revenue visibility, given it

has a theatre backlog equivalent to 90% of its existing network, and

because of its gradually expanding net margin, driven by the company’s

high operating leverage business model.

Catalysts: Announcements of IMAX China winning contracts to build new

major theatres, and strong monthly box-office numbers in China would be

share-price catalysts. Meanwhile, favourable regulatory changes and

improvements in China’s economy could also provide a boost.

Valuation: We initiate coverage of IMAX China with a Buy (1) call and 12-

month TP of HKD50.00, based on a target PER of 34x on the average of

our 2016-17E EPS, derived by applying a 20% premium to the average

trading multiple of its global exhibitors and studio peers. We believe IMAX

China deserves to trade at a substantial premium to these peers on: 1) its

superior asset-light business model, 2) the company’s exclusive positioning

in the world’s fastest growing cinema market, and 3) its substantially higher

net margins and ROE. As a cross-check, our DCF-derived valuation is

HKD48.8, 2% below our target price.

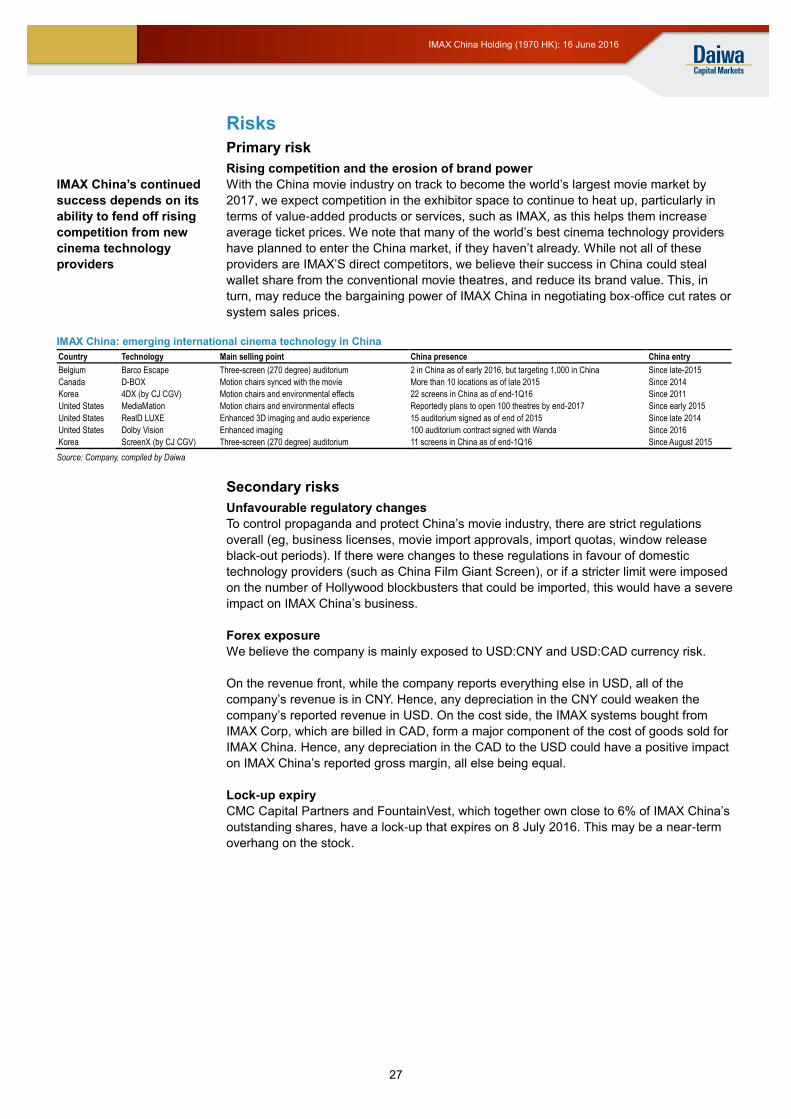

Risks: The primary risk to our call is the increasing number of premium

cinema technologies in China eroding IMAX China’s brand power and

subsequently weakening its future negotiations for box office revenue-

sharing rates.

16 June 2016

IMAX Chi na Hol ding

Initiation: a box-office hit

Key beneficiary of China becoming the largest cinema market by 2017

Earnings quality expected to improve significantly over 2016-18

Initiating with a Buy (1) call and target price of HKD50.00

Source: FactSet, Daiwa forecasts

IMAX China Holding (1970 HK)

Target price: HKD50.00

Share price (15 Jun): HKD39.55 | Up/downside: +26.4%

John Choi(852) 2773 8730

Carlton Lai(852) 2532 4349

90

113

135

158

180

30

38

45

53

60

Oct-15 Jan-16 Apr-16

Share price performance

IMAX (LHS) Relative to HSI (RHS)

(HKD) (%)

12-month range 34.25-59.70

Market cap (USDbn) 1.81

3m avg daily turnover (USDm) 7.24

Shares outstanding (m) 355

Major shareholder IMAX Corp (68.5%)

Financial summary (USD)

Year to 31 Dec 16E 17E 18E

Revenue (m) 148 174 201

Operating profit (m) 72 86 102

Net profit (m) 60 76 92

Core EPS (fully-diluted) 0.170 0.213 0.259

EPS change (%) 21.3 25.5 21.4

Daiwa vs Cons. EPS (%) (1.3) (4.1) (5.6)

PER (x) 30.0 23.9 19.7

Dividend yield (%) 0.0 0.0 0.0

DPS 0.000 0.000 0.000

PBR (x) 8.3 6.2 4.7

EV/EBITDA (x) 19.9 16.1 13.1

ROE (%) 32.1 29.6 27.1

2

IMAX China Holding (1970 HK): 16 June 2016

Table of contents

A huge appetite for movies ...................................................................................... 6

China’s entertainment segment: still nascent .....................................................................6

FAQ: How many theatres can IMAX ultimately open in China? ..........................................9

What’s different about IMAX? ............................................................................................9

FAQ: Will cinemas still be relevant in 5 years, given the major advances in home-theatre

technology? ..................................................................................................................... 10

“High-Definition” revenue visibility .......................................................................13

Shifting business models ................................................................................................. 13

Key assumptions for IMAX China box-office revenue ...................................................... 14

FAQ: How does China’s film quota affect IMAX China? ................................................... 17

Enhanced earnings quality .....................................................................................22

A prime reason for multiple expansion ............................................................................. 22

Valuation and Risks ................................................................................................24

Stock looks oversold ........................................................................................................ 24

Risks ................................................................................................................................ 27

Appendix: management/shareholder structure ....................................................28

3

IMAX China Holding (1970 HK): 16 June 2016

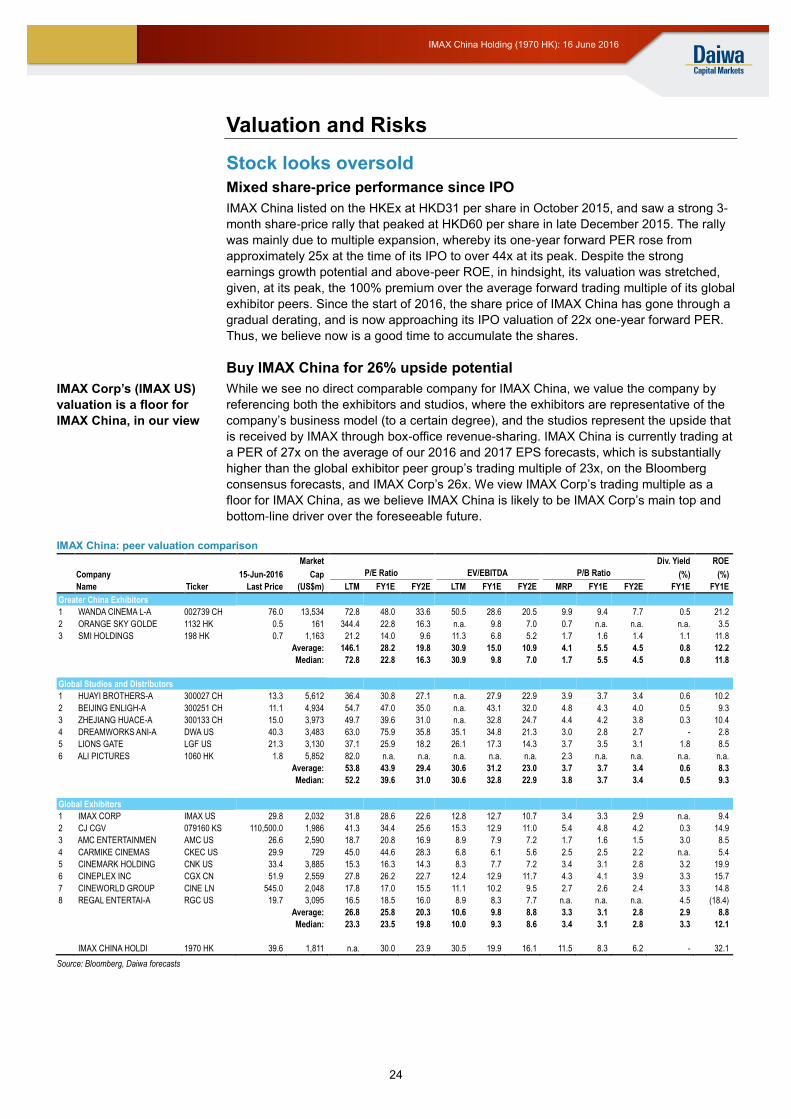

How do we justify our view?

Growth outlook Valuation Earnings revisions

Growth outlook IMAX China: adjusted operating profit and net profit

With a theatre backlog (ie, theatres for which contracts

have been signed but are not yet built) equivalent to 90%

of its existing theatre network, IMAX China’s revenue

visibility is fairly high, in our view. We forecast a project

theatre-network CAGR of 27% over 2015-18, and a total

revenue CAGR of 22%, given its growing number of

revenue-sharing agreements vs. sales-type agreements

(selling equipment upfront).

As a result, we expect the company’s earnings quality to

improve throughout 2016-18 and its adjusted net margin to

expand from 37% for 2015 to 46% by end-2018, driven

largely by improved operating leverage.

Source: Company, Daiwa forecasts

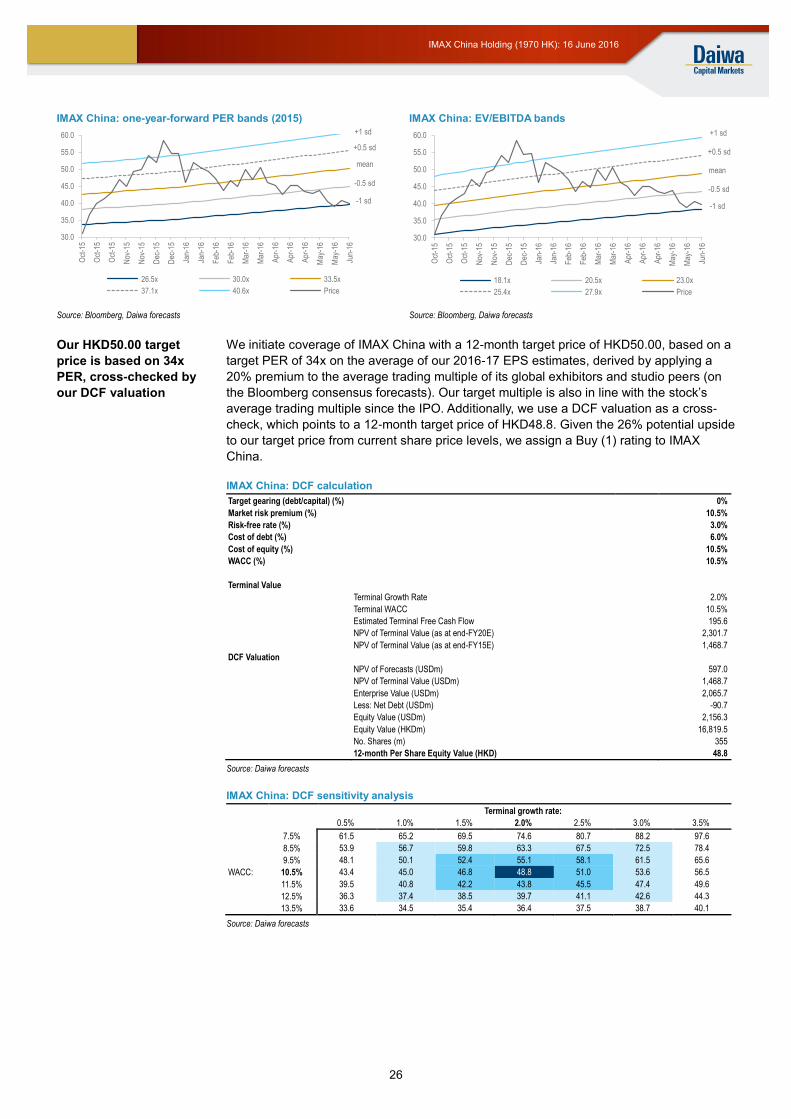

Valuation IMAX China: 1-year forward PER bands

The stock is trading currently at a significant premium to its

global exhibitor and studio peers, which we think is justified

by its: 1) superior asset-light business model, 2) exclusive

positioning in the world’s fastest-growing cinema market,

and 3) substantially higher net margin and ROE.

We value IMAX China at a target PER of 34x on the

average of our 2016-17E EPS, derived by applying a 20%

premium to the average trading multiple of the company’s

global exhibitors and movie studio peers. A PER of 34x is

in line with the stock’s average trading PER since its IPO in

October 2015.

Source: Bloomberg, Daiwa forecasts

Earnings revisions IMAX China: Bloomberg-consensus EPS forecast revisions

The Bloomberg-consensus EPS revisions have been

largely on an uptrend for both 2016 and 2017, likely due to

the company’s incremental theatre signings.

Our EPS forecasts for 2016-18 are 1-6% below consensus,

largely a result of our lower revenue forecasts, as we

assume the proportion of sales-type contracts will decline

(implying less upfront revenue). We expect the company to

win more revenue-sharing agreements, which would

provide it with increased recurring revenue.

Source: Bloomberg

0%

20%

40%

60%

0

10

20

30

40

50

60

70

80

90

100

110

2012 2013 2014 2015 2016E 2017E 2018E

Adjusted operat ing profit (USDm) Adjusted net pro fit (USDm)

Adj. operating margin (%) Adj. net marg in (%)

30.0

35.0

40.0

45.0

50.0

55.0

60.0

Oct

-15

Oct

-15

Oct

-15

Nov

-15

Nov

-15

Dec

-15

Dec

-15

Jan-

16

Jan-

16

Feb

-16

Feb

-16

Mar

-16

Mar

-16

Apr

-16

Apr

-16

Apr

-16

May

-16

May

-16

Jun-

16

26.5x 30.0x 33.5x

37.1x 40.6x Price

+0.5 sd

-0.5 sd

mean

-1 sd

+1 sd

0.15

0.16

0.17

0.18

0.19

0.20

0.21

0.22

0.23

0.24

30-O

ct-1

5

30-N

ov-1

5

31-D

ec-1

5

31-J

an-1

6

29-F

eb-1

6

31-M

ar-1

6

30-A

pr-1

6

31-M

ay-1

6

2016E 2017E

4

IMAX China Holding (1970 HK): 16 June 2016

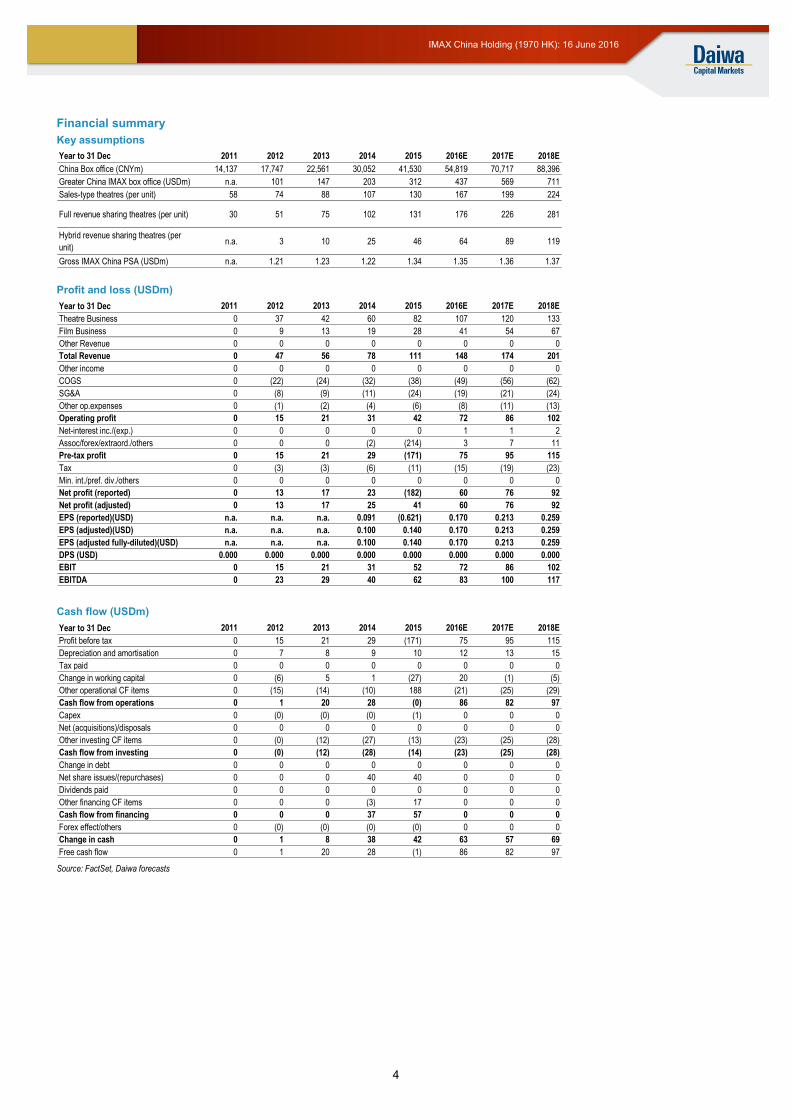

Financial summary

Key assumptions

Profit and loss (USDm)

Cash flow (USDm)

Source: FactSet, Daiwa forecasts

Year to 31 Dec 2011 2012 2013 2014 2015 2016E 2017E 2018E

China Box office (CNYm) 14,137 17,747 22,561 30,052 41,530 54,819 70,717 88,396

Greater China IMAX box office (USDm) n.a. 101 147 203 312 437 569 711

Sales-type theatres (per unit) 58 74 88 107 130 167 199 224

Full revenue sharing theatres (per unit) 30 51 75 102 131 176 226 281

Hybrid revenue sharing theatres (per

unit)n.a. 3 10 25 46 64 89 119

Gross IMAX China PSA (USDm) n.a. 1.21 1.23 1.22 1.34 1.35 1.36 1.37

Year to 31 Dec 2011 2012 2013 2014 2015 2016E 2017E 2018E

Theatre Business 0 37 42 60 82 107 120 133

Film Business 0 9 13 19 28 41 54 67

Other Revenue 0 0 0 0 0 0 0 0

Total Revenue 0 47 56 78 111 148 174 201

Other income 0 0 0 0 0 0 0 0

COGS 0 (22) (24) (32) (38) (49) (56) (62)

SG&A 0 (8) (9) (11) (24) (19) (21) (24)

Other op.expenses 0 (1) (2) (4) (6) (8) (11) (13)

Operating profit 0 15 21 31 42 72 86 102

Net-interest inc./(exp.) 0 0 0 0 0 1 1 2

Assoc/forex/extraord./others 0 0 0 (2) (214) 3 7 11

Pre-tax profit 0 15 21 29 (171) 75 95 115

Tax 0 (3) (3) (6) (11) (15) (19) (23)

Min. int./pref. div./others 0 0 0 0 0 0 0 0

Net profit (reported) 0 13 17 23 (182) 60 76 92

Net profit (adjusted) 0 13 17 25 41 60 76 92

EPS (reported)(USD) n.a. n.a. n.a. 0.091 (0.621) 0.170 0.213 0.259

EPS (adjusted)(USD) n.a. n.a. n.a. 0.100 0.140 0.170 0.213 0.259

EPS (adjusted fully-diluted)(USD) n.a. n.a. n.a. 0.100 0.140 0.170 0.213 0.259

DPS (USD) 0.000 0.000 0.000 0.000 0.000 0.000 0.000 0.000

EBIT 0 15 21 31 52 72 86 102

EBITDA 0 23 29 40 62 83 100 117

Year to 31 Dec 2011 2012 2013 2014 2015 2016E 2017E 2018E

Profit before tax 0 15 21 29 (171) 75 95 115

Depreciation and amortisation 0 7 8 9 10 12 13 15

Tax paid 0 0 0 0 0 0 0 0

Change in working capital 0 (6) 5 1 (27) 20 (1) (5)

Other operational CF items 0 (15) (14) (10) 188 (21) (25) (29)

Cash flow from operations 0 1 20 28 (0) 86 82 97

Capex 0 (0) (0) (0) (1) 0 0 0

Net (acquisitions)/disposals 0 0 0 0 0 0 0 0

Other investing CF items 0 (0) (12) (27) (13) (23) (25) (28)

Cash flow from investing 0 (0) (12) (28) (14) (23) (25) (28)

Change in debt 0 0 0 0 0 0 0 0

Net share issues/(repurchases) 0 0 0 40 40 0 0 0

Dividends paid 0 0 0 0 0 0 0 0

Other financing CF items 0 0 0 (3) 17 0 0 0

Cash flow from financing 0 0 0 37 57 0 0 0

Forex effect/others 0 (0) (0) (0) (0) 0 0 0

Change in cash 0 1 8 38 42 63 57 69

Free cash flow 0 1 20 28 (1) 86 82 97

5

IMAX China Holding (1970 HK): 16 June 2016

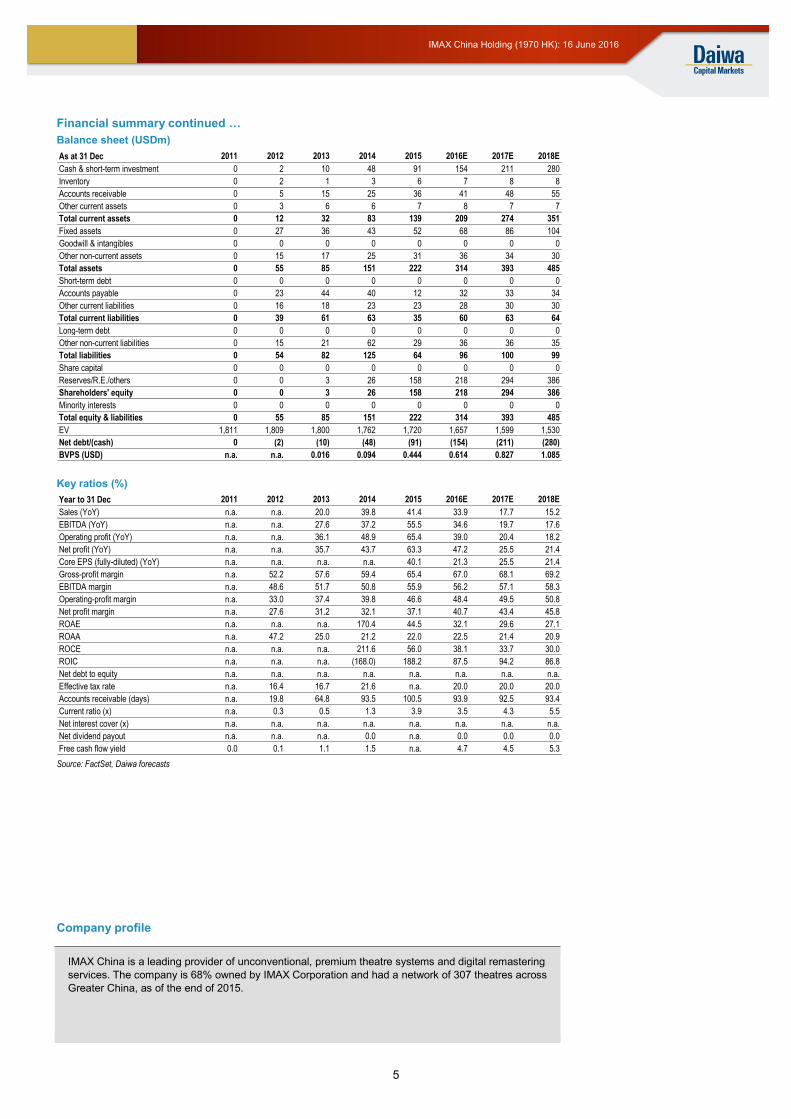

Financial summary continued …

Balance sheet (USDm)

Key ratios (%)

Source: FactSet, Daiwa forecasts

As at 31 Dec 2011 2012 2013 2014 2015 2016E 2017E 2018E

Cash & short-term investment 0 2 10 48 91 154 211 280

Inventory 0 2 1 3 6 7 8 8

Accounts receivable 0 5 15 25 36 41 48 55

Other current assets 0 3 6 6 7 8 7 7

Total current assets 0 12 32 83 139 209 274 351

Fixed assets 0 27 36 43 52 68 86 104

Goodwill & intangibles 0 0 0 0 0 0 0 0

Other non-current assets 0 15 17 25 31 36 34 30

Total assets 0 55 85 151 222 314 393 485

Short-term debt 0 0 0 0 0 0 0 0

Accounts payable 0 23 44 40 12 32 33 34

Other current liabilities 0 16 18 23 23 28 30 30

Total current liabilities 0 39 61 63 35 60 63 64

Long-term debt 0 0 0 0 0 0 0 0

Other non-current liabilities 0 15 21 62 29 36 36 35

Total liabilities 0 54 82 125 64 96 100 99

Share capital 0 0 0 0 0 0 0 0

Reserves/R.E./others 0 0 3 26 158 218 294 386

Shareholders' equity 0 0 3 26 158 218 294 386

Minority interests 0 0 0 0 0 0 0 0

Total equity & liabilities 0 55 85 151 222 314 393 485

EV 1,811 1,809 1,800 1,762 1,720 1,657 1,599 1,530

Net debt/(cash) 0 (2) (10) (48) (91) (154) (211) (280)

BVPS (USD) n.a. n.a. 0.016 0.094 0.444 0.614 0.827 1.085

Year to 31 Dec 2011 2012 2013 2014 2015 2016E 2017E 2018E

Sales (YoY) n.a. n.a. 20.0 39.8 41.4 33.9 17.7 15.2

EBITDA (YoY) n.a. n.a. 27.6 37.2 55.5 34.6 19.7 17.6

Operating profit (YoY) n.a. n.a. 36.1 48.9 65.4 39.0 20.4 18.2

Net profit (YoY) n.a. n.a. 35.7 43.7 63.3 47.2 25.5 21.4

Core EPS (fully-diluted) (YoY) n.a. n.a. n.a. n.a. 40.1 21.3 25.5 21.4

Gross-profit margin n.a. 52.2 57.6 59.4 65.4 67.0 68.1 69.2

EBITDA margin n.a. 48.6 51.7 50.8 55.9 56.2 57.1 58.3

Operating-profit margin n.a. 33.0 37.4 39.8 46.6 48.4 49.5 50.8

Net profit margin n.a. 27.6 31.2 32.1 37.1 40.7 43.4 45.8

ROAE n.a. n.a. n.a. 170.4 44.5 32.1 29.6 27.1

ROAA n.a. 47.2 25.0 21.2 22.0 22.5 21.4 20.9

ROCE n.a. n.a. n.a. 211.6 56.0 38.1 33.7 30.0

ROIC n.a. n.a. n.a. (168.0) 188.2 87.5 94.2 86.8

Net debt to equity n.a. n.a. n.a. n.a. n.a. n.a. n.a. n.a.

Effective tax rate n.a. 16.4 16.7 21.6 n.a. 20.0 20.0 20.0

Accounts receivable (days) n.a. 19.8 64.8 93.5 100.5 93.9 92.5 93.4

Current ratio (x) n.a. 0.3 0.5 1.3 3.9 3.5 4.3 5.5

Net interest cover (x) n.a. n.a. n.a. n.a. n.a. n.a. n.a. n.a.

Net dividend payout n.a. n.a. n.a. 0.0 n.a. 0.0 0.0 0.0

Free cash flow yield 0.0 0.1 1.1 1.5 n.a. 4.7 4.5 5.3

Company profile

IMAX China is a leading provider of unconventional, premium theatre systems and digital remastering

services. The company is 68% owned by IMAX Corporation and had a network of 307 theatres across

Greater China, as of the end of 2015.

6

IMAX China Holding (1970 HK): 16 June 2016

A huge appetite for movies

China’s entertainment segment: still nascent

Movie-going: second most-preferred leisure activity

We believe IMAX China is one of the most effective ways for investors to capture the

upside in the rise of Mainland consumer spending. Despite slowing economic growth in

China, we believe it is inevitable that the purchasing power of the average Mainland

consumer will continue to rise over the foreseeable future. Driven by the country’s

increasing urbanisation and growing wealth, the average disposable income per capita in

China rose by over 50% from 2011, to around CNY22,000 in 2015. At the current pace, it is

on track to meet McKinsey’s forecast of a doubling in the per capita disposable income

between 2010 and 2020.

Among the growth of household incomes in China, the millennials (otherwise known as

Generation Y) should enjoy the most buoyant income growth, and this is also typically the

demographic that spends the most on clothes and entertainment. In terms of entertainment

options, we believe movie-going remains one of the most affordable, easily accessible and

time-tested entertainment for youngsters. According to a report by Alibaba Pictures and

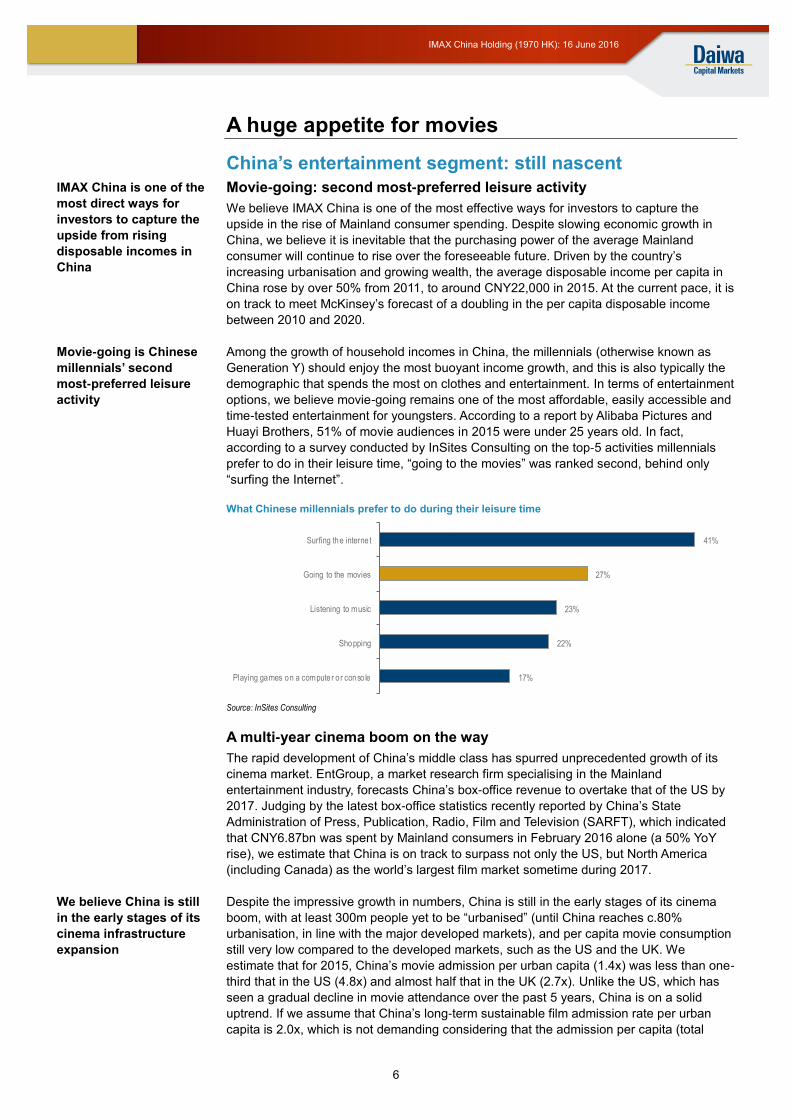

Huayi Brothers, 51% of movie audiences in 2015 were under 25 years old. In fact,

according to a survey conducted by InSites Consulting on the top-5 activities millennials

prefer to do in their leisure time, “going to the movies” was ranked second, behind only

“surfing the Internet”.

What Chinese millennials prefer to do during their leisure time

Source: InSites Consulting

A multi-year cinema boom on the way

The rapid development of China’s middle class has spurred unprecedented growth of its

cinema market. EntGroup, a market research firm specialising in the Mainland

entertainment industry, forecasts China’s box-office revenue to overtake that of the US by

2017. Judging by the latest box-office statistics recently reported by China’s State

Administration of Press, Publication, Radio, Film and Television (SARFT), which indicated

that CNY6.87bn was spent by Mainland consumers in February 2016 alone (a 50% YoY

rise), we estimate that China is on track to surpass not only the US, but North America

(including Canada) as the world’s largest film market sometime during 2017.

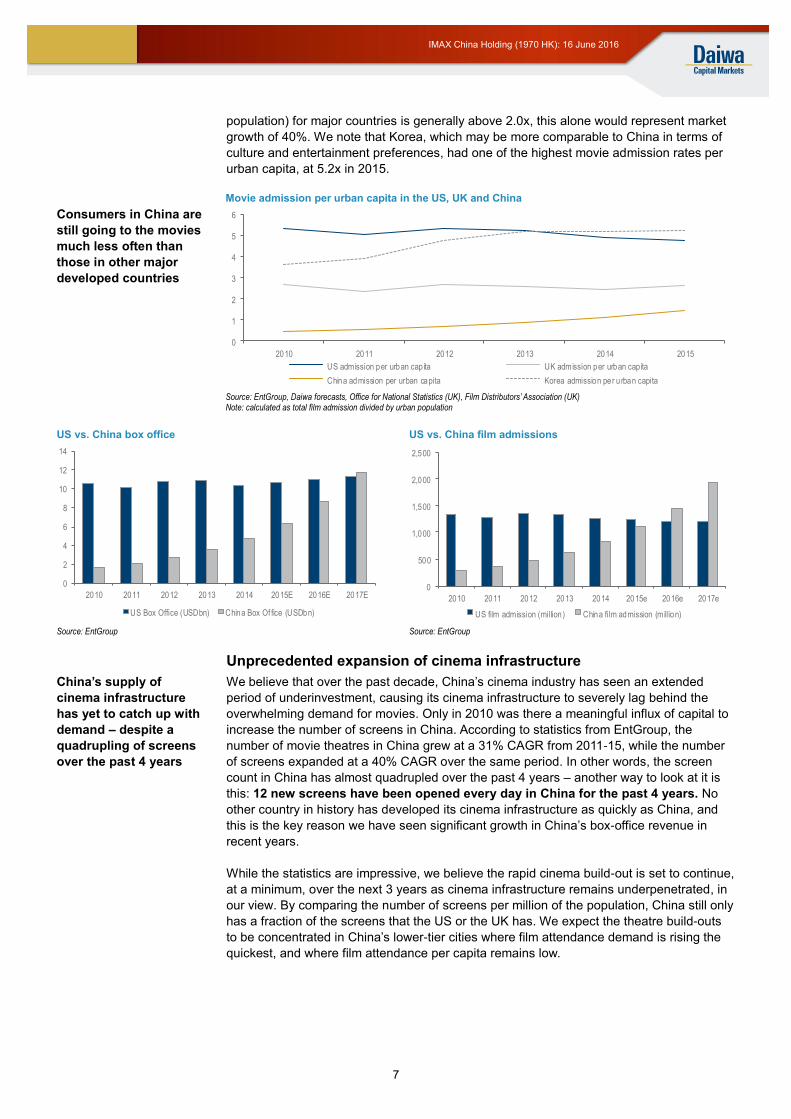

Despite the impressive growth in numbers, China is still in the early stages of its cinema

boom, with at least 300m people yet to be “urbanised” (until China reaches c.80%

urbanisation, in line with the major developed markets), and per capita movie consumption

still very low compared to the developed markets, such as the US and the UK. We

estimate that for 2015, China’s movie admission per urban capita (1.4x) was less than one-

third that in the US (4.8x) and almost half that in the UK (2.7x). Unlike the US, which has

seen a gradual decline in movie attendance over the past 5 years, China is on a solid

uptrend. If we assume that China’s long-term sustainable film admission rate per urban

capita is 2.0x, which is not demanding considering that the admission per capita (total

17%

22%

23%

27%

41%

Playing games on a computer or conso le

Shopping

Listening to music

Going to the movies

Surfing the internet

IMAX China is one of the

most direct ways for

investors to capture the

upside from rising

disposable incomes in

China

Movie-going is Chinese

millennials’ second

most-preferred leisure

activity

We believe China is still

in the early stages of its

cinema infrastructure

expansion

7

IMAX China Holding (1970 HK): 16 June 2016

population) for major countries is generally above 2.0x, this alone would represent market

growth of 40%. We note that Korea, which may be more comparable to China in terms of

culture and entertainment preferences, had one of the highest movie admission rates per

urban capita, at 5.2x in 2015.

Movie admission per urban capita in the US, UK and China

Consumers in China are

still going to the movies

much less often than

those in other major

developed countries

Source: EntGroup, Daiwa forecasts, Office for National Statistics (UK), Film Distributors’ Association (UK)

Note: calculated as total film admission divided by urban population

US vs. China box office US vs. China film admissions

Source: EntGroup Source: EntGroup

Unprecedented expansion of cinema infrastructure

We believe that over the past decade, China’s cinema industry has seen an extended

period of underinvestment, causing its cinema infrastructure to severely lag behind the

overwhelming demand for movies. Only in 2010 was there a meaningful influx of capital to

increase the number of screens in China. According to statistics from EntGroup, the

number of movie theatres in China grew at a 31% CAGR from 2011-15, while the number

of screens expanded at a 40% CAGR over the same period. In other words, the screen

count in China has almost quadrupled over the past 4 years – another way to look at it is

this: 12 new screens have been opened every day in China for the past 4 years. No

other country in history has developed its cinema infrastructure as quickly as China, and

this is the key reason we have seen significant growth in China’s box-office revenue in

recent years.

While the statistics are impressive, we believe the rapid cinema build-out is set to continue,

at a minimum, over the next 3 years as cinema infrastructure remains underpenetrated, in

our view. By comparing the number of screens per million of the population, China still only

has a fraction of the screens that the US or the UK has. We expect the theatre build-outs

to be concentrated in China’s lower-tier cities where film attendance demand is rising the

quickest, and where film attendance per capita remains low.

0

1

2

3

4

5

6

2010 2011 2012 2013 2014 2015

US admission per urban cap ita UK admission per urban cap ita

China admission per urban capita Korea admission per u rban capita

0

2

4

6

8

10

12

14

2010 2011 2012 2013 2014 2015E 2016E 2017E

US Box Office (USDbn) China Box Of fice (USDbn)

0

500

1,000

1,500

2,000

2,500

2010 2011 2012 2013 2014 2015e 2016e 2017e

US film admission (million) China film admission (million)

China’s supply of

cinema infrastructure

has yet to catch up with

demand – despite a

quadrupling of screens

over the past 4 years

8

IMAX China Holding (1970 HK): 16 June 2016

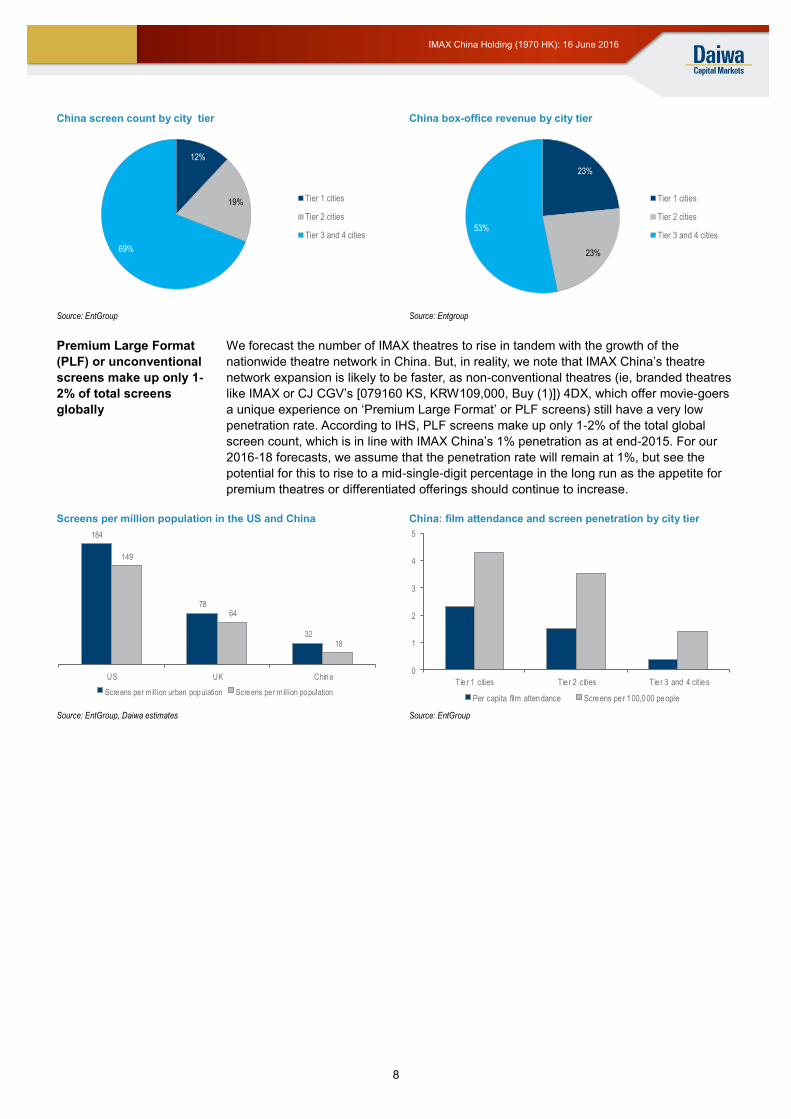

China screen count by city tier China box-office revenue by city tier

Source: EntGroup Source: Entgroup

We forecast the number of IMAX theatres to rise in tandem with the growth of the

nationwide theatre network in China. But, in reality, we note that IMAX China’s theatre

network expansion is likely to be faster, as non-conventional theatres (ie, branded theatres

like IMAX or CJ CGV’s [079160 KS, KRW109,000, Buy (1)]) 4DX, which offer movie-goers

a unique experience on ‘Premium Large Format’ or PLF screens) still have a very low

penetration rate. According to IHS, PLF screens make up only 1-2% of the total global

screen count, which is in line with IMAX China’s 1% penetration as at end-2015. For our

2016-18 forecasts, we assume that the penetration rate will remain at 1%, but see the

potential for this to rise to a mid-single-digit percentage in the long run as the appetite for

premium theatres or differentiated offerings should continue to increase.

Screens per million population in the US and China China: film attendance and screen penetration by city tier

Source: EntGroup, Daiwa estimates Source: EntGroup

12%

19%

69%

Tier 1 cities

Tier 2 cities

Tier 3 and 4 cities

23%

23%

53%

Tier 1 cities

Tier 2 cities

Tier 3 and 4 cities

184

78

32

149

64

18

US UK China

Screens per million urban population Screens per million population

0

1

2

3

4

5

Tier 1 cities Tier 2 cities Tier 3 and 4 cit ies

Per capita film attendance Screens per 100,000 people

Premium Large Format

(PLF) or unconventional

screens make up only 1-

2% of total screens

globally

9

IMAX China Holding (1970 HK): 16 June 2016

FAQ: How many theatres can IMAX ultimately open in China?

Short answer: 1,000 screens by 2022 looks feasible

In 4 years, the number of theatre screens in China quadrupled to 24,317 by the end of

2015, representing a CAGR of 40%. While this breakneck pace of cinema infrastructure

expansion is likely to slow due to the higher base in 2016, we forecast a new screen

CAGR of 20% over 2016-18, reaching 42,000 screens by 2018. However, at 18 screens

per million population in China, the penetration rate still lags greatly behind that of the US,

UK and Korea, at 149, 64 and 45 screens, respectively. Even if we conservatively assume

that China will ultimately match the UK’s penetration rate over the long term (less than half

of the US’s), this would imply a potential screen count of 88,064 screens, on the population

number for 2015, or 262% growth from the 2015 screen count.

Excluding the backlog, the 2015 penetration rates for IMAX screens in North America and

China were 1.1% and 1.3%, respectively, of the total screen count in each country. Taking

the average of 1.2% on the 88,064 screens, this implies that the potential screen count for

IMAX in China is 1,057 screens. We note that this is in line with management’s announced

“long-term target” of 1,000 IMAX screens in China. At the earliest, we estimate IMAX China

will be able to hit this target by 2022.

What’s different about IMAX?

The “IMAX Experience” vs. competitors

To watch a movie in an IMAX auditorium, movie-goers have to pay a premium on top of the

average movie ticket. In 2014, the average movie ticket price (non-IMAX or non-PLF) in

China was USD5.8, while the average ticket price for IMAX movies was USD11.0, a 90%

premium. What consumers are paying for is a thoroughly upgraded movie-going

experience, billed as the ‘IMAX Experience’.

The IMAX Experience generally comprises:

IMAX Digital Media Remastering (DMR) conversion: this is a highly automated,

proprietary process that digitally converts digital films or legacy 35mm films into a

larger resolution IMAX format.

Advanced high-resolution digital projectors: all the IMAX theatres that are part of

IMAX China’s network use IMAX digital xenon projection systems, which were first

rolled out by IMAX Corporation in 2008. These projectors are designed to deliver

superior, brighter and higher contrast images than a conventional projector.

Non-conventional theatre screens: an IMAX screen is typically one that spans wall-

to-wall and floor-to-ceiling (IMAX screens can be as large as 20 x 30 meters). The

screen is also curved and coated with a proprietary technology.

Proprietary theatre geometry: the shape of an IMAX auditorium is designed to

maximise the immersion effect experienced by the audience, by substantially enlarging

the field of view compared with what they get in a conventional theatre.

Specialised theatre acoustics and sound systems: IMAX claims that its acoustics

result in a 4-fold reduction in background noise compared to a conventional theatre. Its

sound-system components also deliver expansive sound and can pinpoint the

origination of sound to any specific spot in an IMAX theatre.

IMAX faces competition mainly from 3 other PLF providers in China: China Film Giant

Screen (not listed), Wanda’s (not rated) own X-Land cinemas, and to a lesser extent, CJ

CGV’s 4DX auditoriums. We believe China Film Giant Screen and X-Land are the closest

competitors, as both their target customers are looking for an enhanced movie experience

(through larger screens and upgraded sound systems), but at cheaper price than IMAX.

IMAX is able to charge a

90% premium for its

upgraded movie-going

experience

10

IMAX China Holding (1970 HK): 16 June 2016

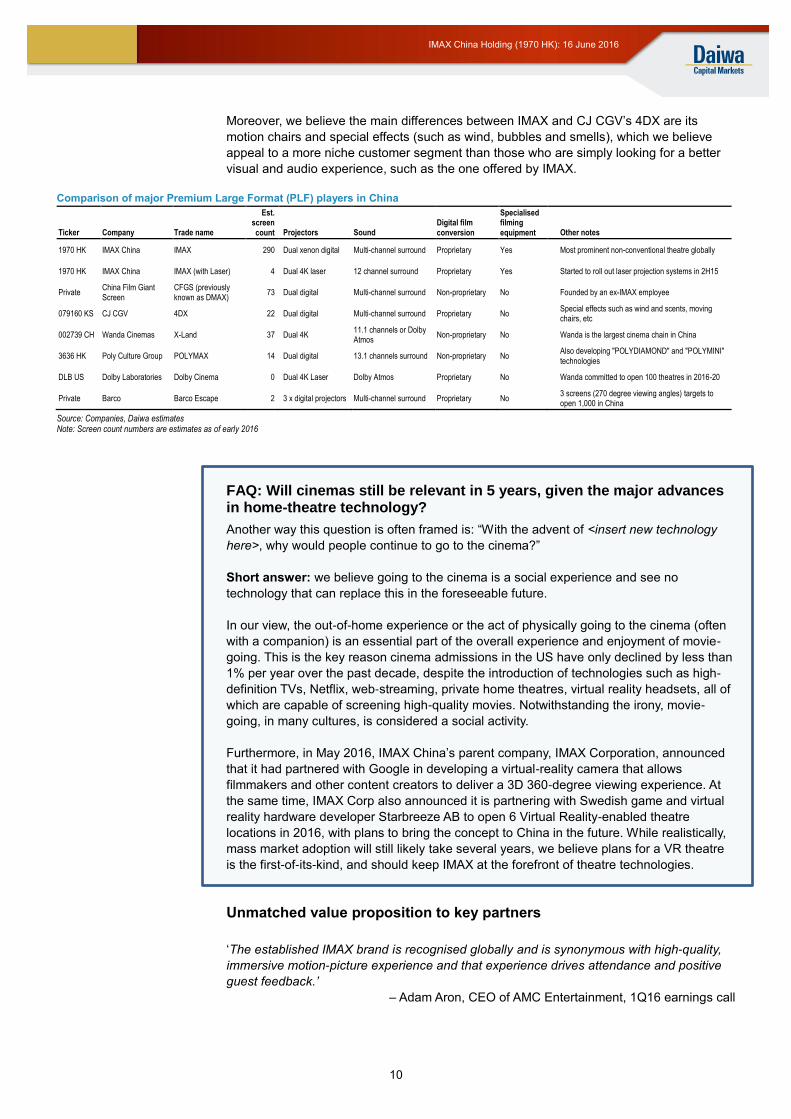

Moreover, we believe the main differences between IMAX and CJ CGV’s 4DX are its

motion chairs and special effects (such as wind, bubbles and smells), which we believe

appeal to a more niche customer segment than those who are simply looking for a better

visual and audio experience, such as the one offered by IMAX.

Comparison of major Premium Large Format (PLF) players in China

Ticker Company Trade name

Est. screen count Projectors Sound

Digital film conversion

Specialised filming equipment Other notes

1970 HK IMAX China IMAX 290 Dual xenon digital Multi-channel surround Proprietary Yes Most prominent non-conventional theatre globally

1970 HK IMAX China IMAX (with Laser) 4 Dual 4K laser 12 channel surround Proprietary Yes Started to roll out laser projection systems in 2H15

Private China Film Giant Screen

CFGS (previously known as DMAX)

73 Dual digital Multi-channel surround Non-proprietary No Founded by an ex-IMAX employee

079160 KS CJ CGV 4DX 22 Dual digital Multi-channel surround Proprietary No Special effects such as wind and scents, moving chairs, etc

002739 CH Wanda Cinemas X-Land 37 Dual 4K 11.1 channels or Dolby Atmos

Non-proprietary No Wanda is the largest cinema chain in China

3636 HK Poly Culture Group POLYMAX 14 Dual digital 13.1 channels surround Non-proprietary No Also developing "POLYDIAMOND" and "POLYMINI" technologies

DLB US Dolby Laboratories Dolby Cinema 0 Dual 4K Laser Dolby Atmos Proprietary No Wanda committed to open 100 theatres in 2016-20

Private Barco Barco Escape 2 3 x digital projectors Multi-channel surround Proprietary No 3 screens (270 degree viewing angles) targets to open 1,000 in China

Source: Companies, Daiwa estimates Note: Screen count numbers are estimates as of early 2016

FAQ: Will cinemas still be relevant in 5 years, given the major advances in home-theatre technology?

Another way this question is often framed is: “With the advent of <insert new technology

here>, why would people continue to go to the cinema?”

Short answer: we believe going to the cinema is a social experience and see no

technology that can replace this in the foreseeable future.

In our view, the out-of-home experience or the act of physically going to the cinema (often

with a companion) is an essential part of the overall experience and enjoyment of movie-

going. This is the key reason cinema admissions in the US have only declined by less than

1% per year over the past decade, despite the introduction of technologies such as high-

definition TVs, Netflix, web-streaming, private home theatres, virtual reality headsets, all of

which are capable of screening high-quality movies. Notwithstanding the irony, movie-

going, in many cultures, is considered a social activity.

Furthermore, in May 2016, IMAX China’s parent company, IMAX Corporation, announced

that it had partnered with Google in developing a virtual-reality camera that allows

filmmakers and other content creators to deliver a 3D 360-degree viewing experience. At

the same time, IMAX Corp also announced it is partnering with Swedish game and virtual

reality hardware developer Starbreeze AB to open 6 Virtual Reality-enabled theatre

locations in 2016, with plans to bring the concept to China in the future. While realistically,

mass market adoption will still likely take several years, we believe plans for a VR theatre

is the first-of-its-kind, and should keep IMAX at the forefront of theatre technologies.

Unmatched value proposition to key partners

‘The established IMAX brand is recognised globally and is synonymous with high-quality,

immersive motion-picture experience and that experience drives attendance and positive

guest feedback.’

– Adam Aron, CEO of AMC Entertainment, 1Q16 earnings call

11

IMAX China Holding (1970 HK): 16 June 2016

Despite the likely increase in competitors that offer premium cinema technologies in China,

we expect IMAX China’s order book to be largely unaffected and remain strong going

forward. Through its first-mover advantage in China, as well as the company’s strong

brand reputation in the country, we believe IMAX China has created a virtuous cycle of

theatre network expansion that is hard to substitute.

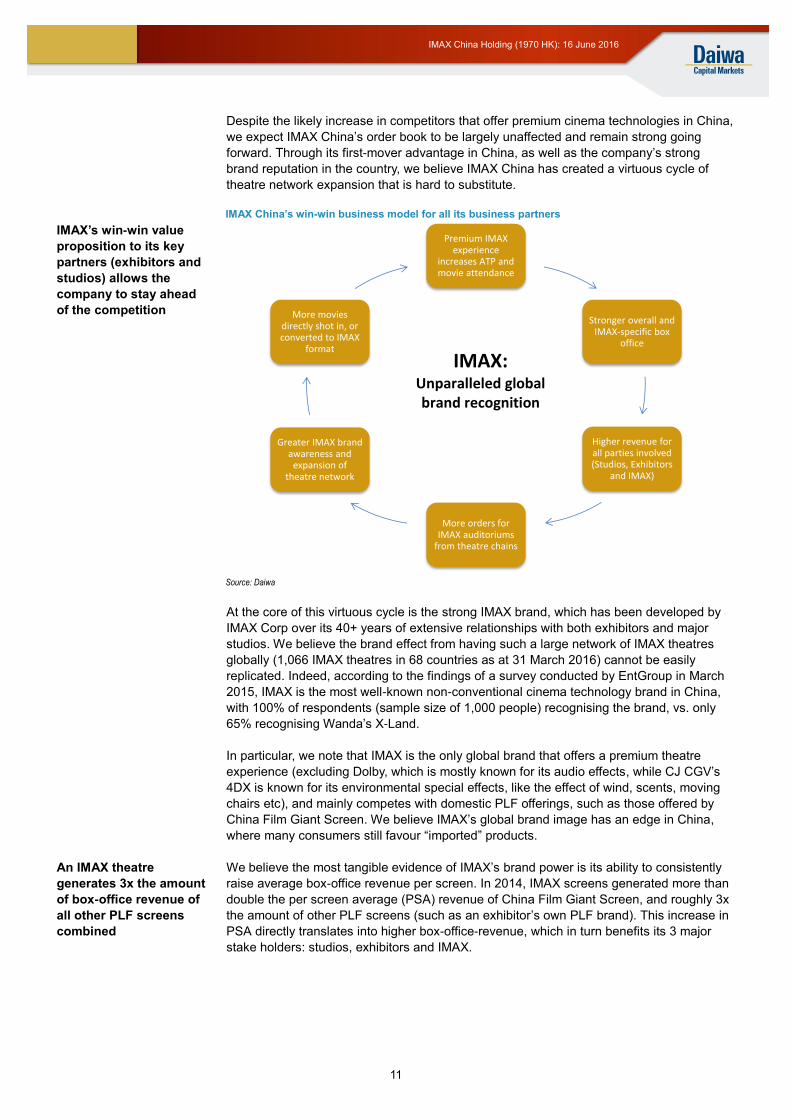

IMAX China’s win-win business model for all its business partners

IMAX’s win-win value

proposition to its key

partners (exhibitors and

studios) allows the

company to stay ahead

of the competition

Source: Daiwa

At the core of this virtuous cycle is the strong IMAX brand, which has been developed by

IMAX Corp over its 40+ years of extensive relationships with both exhibitors and major

studios. We believe the brand effect from having such a large network of IMAX theatres

globally (1,066 IMAX theatres in 68 countries as at 31 March 2016) cannot be easily

replicated. Indeed, according to the findings of a survey conducted by EntGroup in March

2015, IMAX is the most well-known non-conventional cinema technology brand in China,

with 100% of respondents (sample size of 1,000 people) recognising the brand, vs. only

65% recognising Wanda’s X-Land.

In particular, we note that IMAX is the only global brand that offers a premium theatre

experience (excluding Dolby, which is mostly known for its audio effects, while CJ CGV’s

4DX is known for its environmental special effects, like the effect of wind, scents, moving

chairs etc), and mainly competes with domestic PLF offerings, such as those offered by

China Film Giant Screen. We believe IMAX’s global brand image has an edge in China,

where many consumers still favour “imported” products.

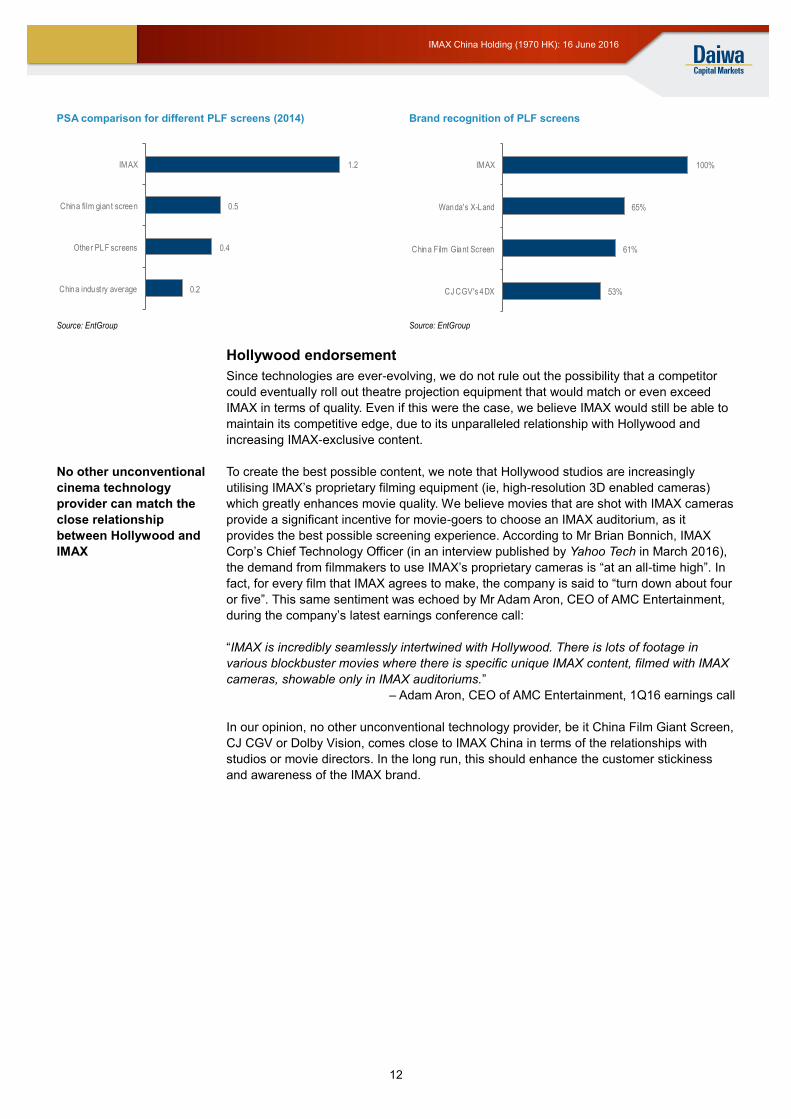

We believe the most tangible evidence of IMAX’s brand power is its ability to consistently

raise average box-office revenue per screen. In 2014, IMAX screens generated more than

double the per screen average (PSA) revenue of China Film Giant Screen, and roughly 3x

the amount of other PLF screens (such as an exhibitor’s own PLF brand). This increase in

PSA directly translates into higher box-office-revenue, which in turn benefits its 3 major

stake holders: studios, exhibitors and IMAX.

Premium IMAX experience

increases ATP and movie attendance

Stronger overall and IMAX-specific box

office

Higher revenue for all parties involved (Studios, Exhibitors

and IMAX)

More orders for IMAX auditoriums

from theatre chains

Greater IMAX brand awareness and

expansion of theatre network

More movies directly shot in, or converted to IMAX

format

An IMAX theatre

generates 3x the amount

of box-office revenue of

all other PLF screens

combined

IMAX: Unparalleled global brand recognition

12

IMAX China Holding (1970 HK): 16 June 2016

PSA comparison for different PLF screens (2014) Brand recognition of PLF screens

Source: EntGroup Source: EntGroup

Hollywood endorsement

Since technologies are ever-evolving, we do not rule out the possibility that a competitor

could eventually roll out theatre projection equipment that would match or even exceed

IMAX in terms of quality. Even if this were the case, we believe IMAX would still be able to

maintain its competitive edge, due to its unparalleled relationship with Hollywood and

increasing IMAX-exclusive content.

To create the best possible content, we note that Hollywood studios are increasingly

utilising IMAX’s proprietary filming equipment (ie, high-resolution 3D enabled cameras)

which greatly enhances movie quality. We believe movies that are shot with IMAX cameras

provide a significant incentive for movie-goers to choose an IMAX auditorium, as it

provides the best possible screening experience. According to Mr Brian Bonnich, IMAX

Corp’s Chief Technology Officer (in an interview published by Yahoo Tech in March 2016),

the demand from filmmakers to use IMAX’s proprietary cameras is “at an all-time high”. In

fact, for every film that IMAX agrees to make, the company is said to “turn down about four

or five”. This same sentiment was echoed by Mr Adam Aron, CEO of AMC Entertainment,

during the company’s latest earnings conference call:

“IMAX is incredibly seamlessly intertwined with Hollywood. There is lots of footage in

various blockbuster movies where there is specific unique IMAX content, filmed with IMAX

cameras, showable only in IMAX auditoriums.”

– Adam Aron, CEO of AMC Entertainment, 1Q16 earnings call

In our opinion, no other unconventional technology provider, be it China Film Giant Screen,

CJ CGV or Dolby Vision, comes close to IMAX China in terms of the relationships with

studios or movie directors. In the long run, this should enhance the customer stickiness

and awareness of the IMAX brand.

0.2

0.4

0.5

1.2

China indust ry average

Other PLF screens

China film giant screen

IMAX

53%

61%

65%

100%

CJ CGV's 4DX

China Film Giant Screen

Wanda's X-Land

IMAX

No other unconventional

cinema technology

provider can match the

close relationship

between Hollywood and

IMAX

13

IMAX China Holding (1970 HK): 16 June 2016

“High-Definition” revenue visibility

Shifting business models

One of the key attributes that has drawn us to IMAX China is the company’s strong

revenue visibility. Particularly in the face of rising macro uncertainty, we prefer companies

with predictable cash flows and sustainable business growth. Given that the bulk of IMAX

China’s revenue (approx. 75% in 2015) is generated by its theatre systems business,

which is largely equivalent to the growth of its theatre network expansion, we believe an

important figure to track is its theatre pipeline, or backlog. Fortunately, IMAX China does

generally keep investors informed of major contract wins through announcements and

during quarterly results. As at 13 June 2015, IMAX China had over 307 IMAX theatres in

operation across Greater China, with an estimated backlog of 280 theatres. Even though

the backlog represents installations anywhere from 1 to 5 years in the future, the

commitments are binding on the exhibitors. The remaining c.25% of its total revenue is a

function of box-office revenue, paid by the studios.

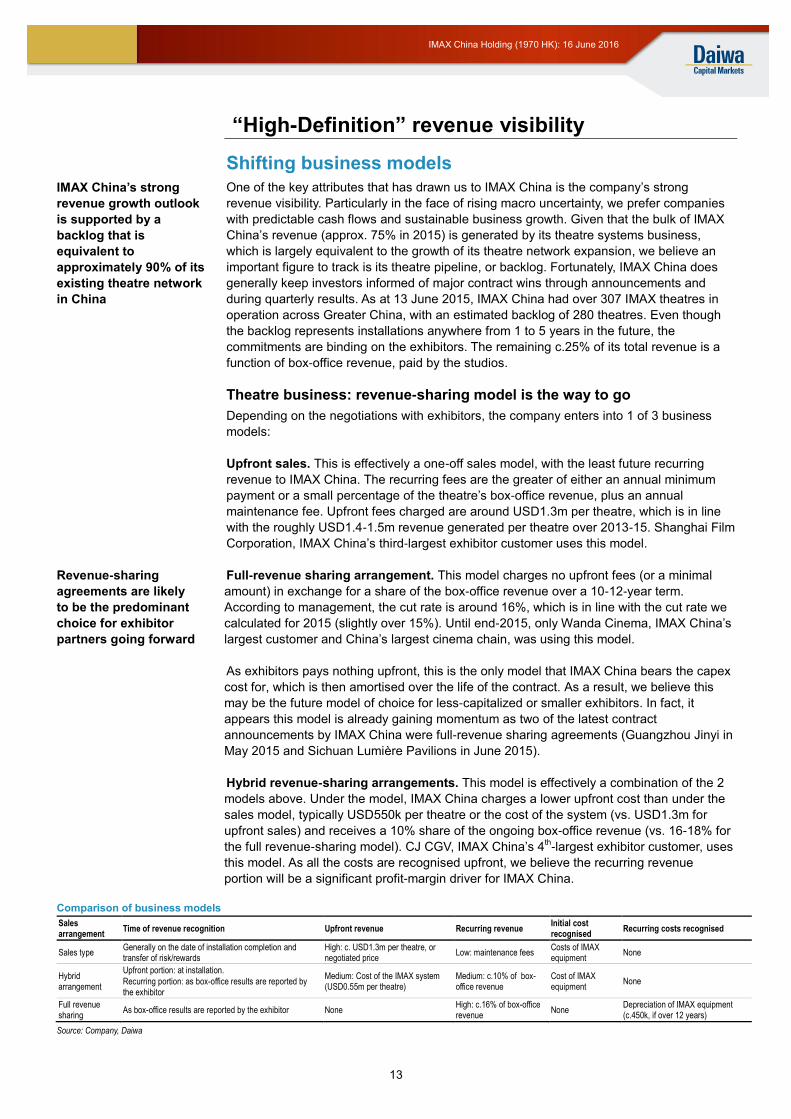

Theatre business: revenue-sharing model is the way to go

Depending on the negotiations with exhibitors, the company enters into 1 of 3 business

models:

Upfront sales. This is effectively a one-off sales model, with the least future recurring

revenue to IMAX China. The recurring fees are the greater of either an annual minimum

payment or a small percentage of the theatre’s box-office revenue, plus an annual

maintenance fee. Upfront fees charged are around USD1.3m per theatre, which is in line

with the roughly USD1.4-1.5m revenue generated per theatre over 2013-15. Shanghai Film

Corporation, IMAX China’s third-largest exhibitor customer uses this model.

Full-revenue sharing arrangement. This model charges no upfront fees (or a minimal

amount) in exchange for a share of the box-office revenue over a 10-12-year term.

According to management, the cut rate is around 16%, which is in line with the cut rate we

calculated for 2015 (slightly over 15%). Until end-2015, only Wanda Cinema, IMAX China’s

largest customer and China’s largest cinema chain, was using this model.

As exhibitors pays nothing upfront, this is the only model that IMAX China bears the capex

cost for, which is then amortised over the life of the contract. As a result, we believe this

may be the future model of choice for less-capitalized or smaller exhibitors. In fact, it

appears this model is already gaining momentum as two of the latest contract

announcements by IMAX China were full-revenue sharing agreements (Guangzhou Jinyi in

May 2015 and Sichuan Lumière Pavilions in June 2015).

Hybrid revenue-sharing arrangements. This model is effectively a combination of the 2

models above. Under the model, IMAX China charges a lower upfront cost than under the

sales model, typically USD550k per theatre or the cost of the system (vs. USD1.3m for

upfront sales) and receives a 10% share of the ongoing box-office revenue (vs. 16-18% for

the full revenue-sharing model). CJ CGV, IMAX China’s 4th-largest exhibitor customer, uses

this model. As all the costs are recognised upfront, we believe the recurring revenue

portion will be a significant profit-margin driver for IMAX China.

Comparison of business models

Sales arrangement

Time of revenue recognition Upfront revenue Recurring revenue Initial cost recognised

Recurring costs recognised

Sales type Generally on the date of installation completion and transfer of risk/rewards

High: c. USD1.3m per theatre, or negotiated price

Low: maintenance fees Costs of IMAX equipment

None

Hybrid arrangement

Upfront portion: at installation.

Recurring portion: as box-office results are reported by the exhibitor

Medium: Cost of the IMAX system (USD0.55m per theatre)

Medium: c.10% of box-office revenue

Cost of IMAX equipment

None

Full revenue sharing

As box-office results are reported by the exhibitor None High: c.16% of box-office revenue

None Depreciation of IMAX equipment (c.450k, if over 12 years)

Source: Company, Daiwa

IMAX China’s strong

revenue growth outlook

is supported by a

backlog that is

equivalent to

approximately 90% of its

existing theatre network

in China

Revenue-sharing

agreements are likely

to be the predominant

choice for exhibitor

partners going forward

14

IMAX China Holding (1970 HK): 16 June 2016

Film business: capturing the upside of a studio’s success

Apart from generating revenue from exhibitors, IMAX China also shares a portion of the

revenue collected by the studios, mainly for the DMR conversion process and the

exhibition of their films on IMAX’s theatre network. The revenue sharing rate is 9.5% for

Hollywood films and 12.5% for converted-IMAX Chinese films currently.

We believe the film business is a substantial gross- and net-margin driver for IMAX China

as this business has a very high operating leverage. We note that the cost of converting

the films into the IMAX format (DMR process) is fixed: USD150,000 for a 2D film and

USD200,000 for a 3D film. Hence, IMAX China’s revenue share with the studios would

also increase with China’s growing box-office revenue, but with almost no additional

associated costs. Theoretically, this could allow for a continuous improvement in IMAX

China’s operating leverage as long as the China box-office revenue keeps increasing.

Key assumptions for IMAX China box-office revenue

In 2015, roughly 47% of IMAX China’s total revenue was linked to its China box-office

performance. Due to the likely increase in revenue-sharing business models going forward,

we expect the proportion of recurring revenue for IMAX China to rise from 56% in 2015 to

71% in 2018E.

While for many companies, revenue is simply a function of quantity (akin to the number of

theatres in China) and the average price (akin to the average movie ticket price), we note

that a third variable also comes into play for box-office sales – the quality of the film slate

(or movie pipeline) – one that is admittedly hard to forecast or control. According to

Deloitte, much of annual movie box-office revenue (roughly 40%) is driven by just the top-5

blockbusters alone (based on US box-office analysis). Hence, if box-office revenue is weak

in any given year, the revenue of exhibitors, studios and IMAX could be negatively

affected.

Diversifying the swing factor (quality of the movie slate)

For IMAX China, we believe this swing factor will not have a noticeable impact on the

company’s top line over the near term as: 1) unlike the US, China’s movie attendance

remains on a solid uptrend and there are still many more years of growth to come, in our

view; and 2) the movies that are shown at IMAX theatres in China are even more

diversified than those in the US, as the company is increasing the number of Chinese-

language films that it runs.

We believe the key variables in the film slate that can affect IMAX China in terms of

revenue are the quality of the individual movies (box-office performance), the genre of

movies (action-oriented or super-hero movies typically attract higher attendance to IMAX

theatres) and the impact of regulations such as release windows (ie, the time frames within

which certain movies can be released) and film quotas (which includes the quality of the

movies actually chosen to be imported).

Viewing preferences of US and China audiences are not the same

While IMAX China has a much heavier reliance on Hollywood movies than other exhibitors

in China (75% of IMAX China’s box-office revenue in 2015 was accounted for by

Hollywood movies, vs. around 45% for a typical exhibitor in China), we assume that strong

box-office performance in the US immediately translates into similarly strong performance

for IMAX China. Although the likelihood of this happening tends to be high, we note that

there can be variability due to differences in release schedules and consumer behaviour.

We believe that the most important factor that can skew the box-office performance of a

film is the Chinese government’s restrictions on release windows, which favour

domestically produced films in order to protect the local film industry. Typically, there are 5

months of the year, namely February (Chinese New Year), July, August (summer holidays),

October (national holiday), and December (winter holidays) that are black-out periods for

Theoretically, the film

business could allow for

perpetual operating

leverage, as long as the

box office keeps rising

Restrictions on release

windows and differences

in consumer tastes

result in the US and

China box-office

performances differing

15

IMAX China Holding (1970 HK): 16 June 2016

Hollywood quota films being released in China. In 2015, for all 5 of these months, over

70% of China’s box-office receipts came from domestic films.

Due to the restrictions on release windows, and the additional time required for

government screening and approval, Hollywood movies are usually released in China

weeks or months after being released in the US. According to our research, for the 34

imported movies released in 2015, the median delay days between the US and China was

37 days while 2 movies were actually released ahead of the US (Jurassic World by 2 days

and Seventh Son by 21 days).

As Hollywood produces roughly 500 films every year, but only 34 of them can be imported

into China in any given year, it is important that the China Film Group Corporation (the sole

authorised importer of films in China) imports the right (blockbuster) Hollywood movies that

appeal to the masses. Fortunately, empirical data suggests that the Hollywood movies

China has imported over the past 3 years have indeed been among the top performers in

the global box office.

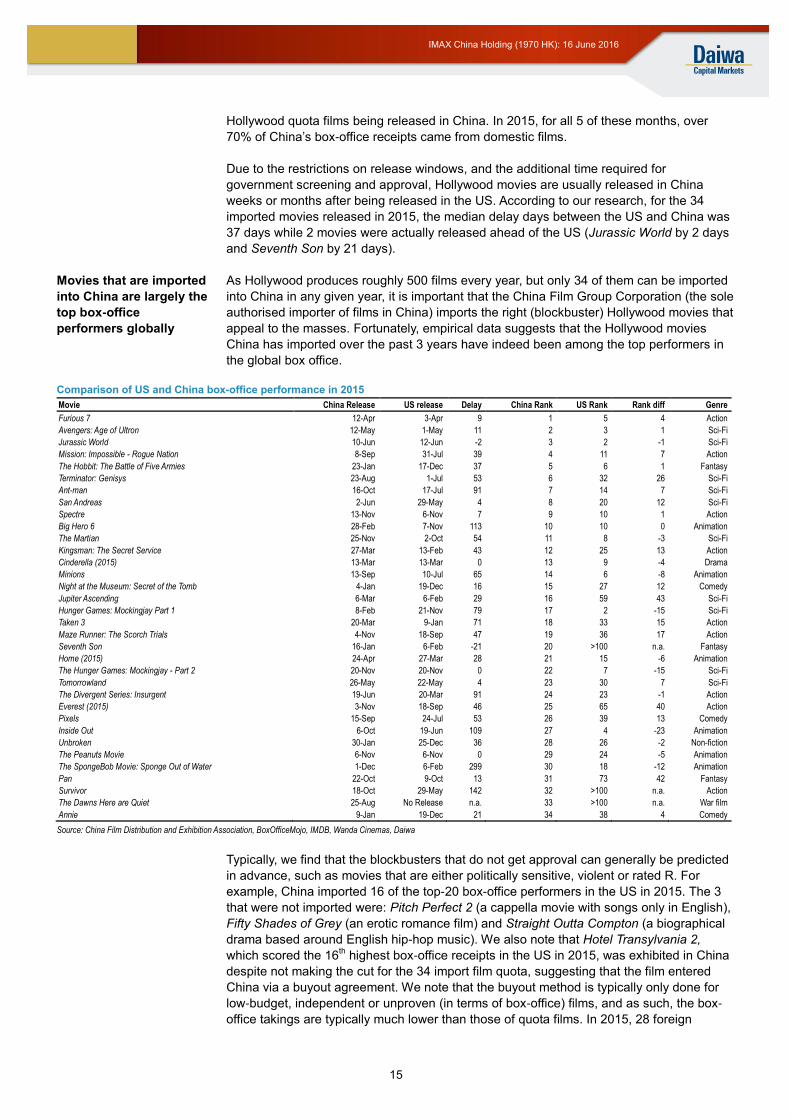

Comparison of US and China box-office performance in 2015

Movie China Release US release Delay China Rank US Rank Rank diff Genre

Furious 7 12-Apr 3-Apr 9 1 5 4 Action

Avengers: Age of Ultron 12-May 1-May 11 2 3 1 Sci-Fi

Jurassic World 10-Jun 12-Jun -2 3 2 -1 Sci-Fi

Mission: Impossible - Rogue Nation 8-Sep 31-Jul 39 4 11 7 Action

The Hobbit: The Battle of Five Armies 23-Jan 17-Dec 37 5 6 1 Fantasy

Terminator: Genisys 23-Aug 1-Jul 53 6 32 26 Sci-Fi

Ant-man 16-Oct 17-Jul 91 7 14 7 Sci-Fi

San Andreas 2-Jun 29-May 4 8 20 12 Sci-Fi

Spectre 13-Nov 6-Nov 7 9 10 1 Action

Big Hero 6 28-Feb 7-Nov 113 10 10 0 Animation

The Martian 25-Nov 2-Oct 54 11 8 -3 Sci-Fi

Kingsman: The Secret Service 27-Mar 13-Feb 43 12 25 13 Action

Cinderella (2015) 13-Mar 13-Mar 0 13 9 -4 Drama

Minions 13-Sep 10-Jul 65 14 6 -8 Animation

Night at the Museum: Secret of the Tomb 4-Jan 19-Dec 16 15 27 12 Comedy

Jupiter Ascending 6-Mar 6-Feb 29 16 59 43 Sci-Fi

Hunger Games: Mockingjay Part 1 8-Feb 21-Nov 79 17 2 -15 Sci-Fi

Taken 3 20-Mar 9-Jan 71 18 33 15 Action

Maze Runner: The Scorch Trials 4-Nov 18-Sep 47 19 36 17 Action

Seventh Son 16-Jan 6-Feb -21 20 >100 n.a. Fantasy

Home (2015) 24-Apr 27-Mar 28 21 15 -6 Animation

The Hunger Games: Mockingjay - Part 2 20-Nov 20-Nov 0 22 7 -15 Sci-Fi

Tomorrowland 26-May 22-May 4 23 30 7 Sci-Fi

The Divergent Series: Insurgent 19-Jun 20-Mar 91 24 23 -1 Action

Everest (2015) 3-Nov 18-Sep 46 25 65 40 Action

Pixels 15-Sep 24-Jul 53 26 39 13 Comedy

Inside Out 6-Oct 19-Jun 109 27 4 -23 Animation

Unbroken 30-Jan 25-Dec 36 28 26 -2 Non-fiction

The Peanuts Movie 6-Nov 6-Nov 0 29 24 -5 Animation

The SpongeBob Movie: Sponge Out of Water 1-Dec 6-Feb 299 30 18 -12 Animation

Pan 22-Oct 9-Oct 13 31 73 42 Fantasy

Survivor 18-Oct 29-May 142 32 >100 n.a. Action

The Dawns Here are Quiet 25-Aug No Release n.a. 33 >100 n.a. War film

Annie 9-Jan 19-Dec 21 34 38 4 Comedy

Source: China Film Distribution and Exhibition Association, BoxOfficeMojo, IMDB, Wanda Cinemas, Daiwa

Typically, we find that the blockbusters that do not get approval can generally be predicted

in advance, such as movies that are either politically sensitive, violent or rated R. For

example, China imported 16 of the top-20 box-office performers in the US in 2015. The 3

that were not imported were: Pitch Perfect 2 (a cappella movie with songs only in English),

Fifty Shades of Grey (an erotic romance film) and Straight Outta Compton (a biographical

drama based around English hip-hop music). We also note that Hotel Transylvania 2,

which scored the 16th highest box-office receipts in the US in 2015, was exhibited in China

despite not making the cut for the 34 import film quota, suggesting that the film entered

China via a buyout agreement. We note that the buyout method is typically only done for

low-budget, independent or unproven (in terms of box-office) films, and as such, the box-

office takings are typically much lower than those of quota films. In 2015, 28 foreign

Movies that are imported

into China are largely the

top box-office

performers globally

16

IMAX China Holding (1970 HK): 16 June 2016

movies were imported via the buyout method, but only 5 managed to earn more than

CNY100m at the box office.

Importantly, of 2015’s top-10 movies at the box office in the US, all 10 were shown in

China. While most of the movies performed well in both countries in terms of box-office

rankings, there were a couple of exceptions. For example, 2 movies in China’s top-10 at

the box office had a ranking difference of over 10 spots compared with the US; namely

Terminator Genisys appeared to be a much bigger hit in China than in the US, coming in at

6th highest at the box office in China vs. only 32 in the US, while San Andreas came in at

8th position in China, but was ranked 20

th in the US.

A more recent example of how big China and US viewing preferences can differ: the

Warcraft movie, which was launched in the US on 10 June 2016, has been a clear flop,

having generated only USD28.4m over 5 days, according to BoxOfficeMojo (production

budget of approximately USD160m). In contrast, the Warcraft movie was launched in

China 2 days earlier (on 8 June 2016) but generated USD156m in 5 days, and appears set

to overtake Furious 7 as the highest grossing Hollywood film in China. While we believe it

is unlikely that there will be many other movies that would see a contrasting movie

reception of this magnitude (since the key reason for the movie’s success is that roughly

half of the game’s 5m players are from China), we believe it illustrates the complexity in

predicting box office successes.

After analysing box-office performance trends in China, we have observed 2 traits that

increase the likelihood of a strong box-office slate:

1) Action and sci-fi movies. It appears that Chinese movie goers prefer 2 genres the

most: action and science fiction (sci-fi) movies. Among the top-20 Hollywood movies in

China in 2015, 14 were either action or sci-fi movies vs. only 11 in the US. We note

that action and sci-fi movies are most often the candidates for an IMAX-formatted

movie, particularly for IMAX 3D.

2) Franchise films or super-hero movies. Over the past several years, we have

noticed that many of the top box-office performers in China have been typically part of

a renowned global franchise (like the Fast and Furious series) or super-hero movies

(from Marvel and DC Comics etc).

Action and sci-fi genres

as well as major

franchise films typically

do well at the box office

in China

17

IMAX China Holding (1970 HK): 16 June 2016

FAQ: How does China’s film quota affect IMAX China?

Short answer: unless the Chinese Government cuts the film import quota significantly (ie,

by more than 30%), we see no significant impact on IMAX China in terms of risk or reward.

Under China’s censorship rules and regulations, the number of films imported (mostly

Hollywood films) into China is restricted by a film quota. In general, only 20 Hollywood films

may be imported in to China per year; but in 2012, the Chinese Government signed an

agreement with the World Trade Organization to permit an additional 14 3D or IMAX format

films to be imported, on top of the previous quota of 20 Hollywood films. This amounts to

34 Hollywood films that IMAX China can work with every year. However, the 2012

agreement for an additional 14 3D or IMAX films is set to expire at the end of 2016 and is

subject to renegotiation.

Given the significant growth of China’s box-office takings (in turn benefiting the government

and social welfare through a 3.3% business tax and a 5% tax for the national special fund

for the film industry’s development), we believe the chance that this additional quota will

not be renewed is extremely slim. On the contrary, we see upside to the quota given the

appetite of Chinese movie-goers.

In terms of revenue growth or profitability, we believe the film quota itself does not

adversely affect IMAX China. Of the 34 Hollywood films that were imported into China in

2015, 23 were shown in IMAX, meaning the quota was around 30% under-utilised by

IMAX. Additionally, 23 films in a year averages just under 2 IMAX films per month. Given

that the average life cycle for a film is roughly 2 weeks in China, 23 films should already be

sufficient to utilise the IMAX theatre network efficiently, since there is typically only 1 IMAX

screen per location in China.

In reality, the Chinese Government has tight control over the release windows for

Hollywood films. Typically, Hollywood films are locked out of peak movie-going seasons,

such as December, when the best release windows are reserved for domestically

produced films. This means that during some months of the year, 3 or 4 Hollywood films

can be fighting for 1 IMAX screen per location. Hence, in the absence of a regulatory

change regarding the release windows for Hollywood films, we see limited upside from

having a significantly greater quota or even having the quota removed altogether.

2016 Hollywood slate is good, but 2017 could be even better

Judging by the first 4 months of box-office numbers, the strong appetite for movie-going

has carried into 2016, with total box-office receipts rising by 28% YoY to CNY17.6bn.

However, when broken down by domestic films and imported films, all of the incremental

growth was driven by domestic films, with a 54% YoY increase in box-office revenue, while

imported films actually recorded a 4% YoY decline. We believe the relatively poor

performance of imported films was a result of several domestic mega blockbusters, with 3

local films dominating the top-5 at the box office. Notably, Stephen Chow’s The Mermaid

was the first domestically produced film that exceeded CNY3bn at the box-office and so far

in 2016, has generated more than twice the box-office revenue of the second best film,

Zootopia, a Hollywood film. Journey to the West: Conquering Demons and From Vegas to

Macau III took number 3 and 4 spots in terms of box-office receipts.

Unfortunately, of the 3 domestic blockbusters, only Journey to the West: Conquering

Demons was shown in IMAX format. Hence, the lack of IMAX for the record-breaking

movie The Mermaid, likely dragged down IMAX China’s box-office performance. Although

the company did collect box-office receipts of CNY83.4m in Greater China in 1Q16,

representing a 33% YoY increase, we believe most of the growth was a result of its theatre

network expansion, which expanded by 31% YoY to 312 theatres. We believe a more

China domestic films

have dominated the top

box-office in 2016

18

IMAX China Holding (1970 HK): 16 June 2016

representative figure is the IMAX Greater China per screen average, which dropped from

USD295,400 to USD290,000 in 1Q16, a sign that the quality of the film slate declined.

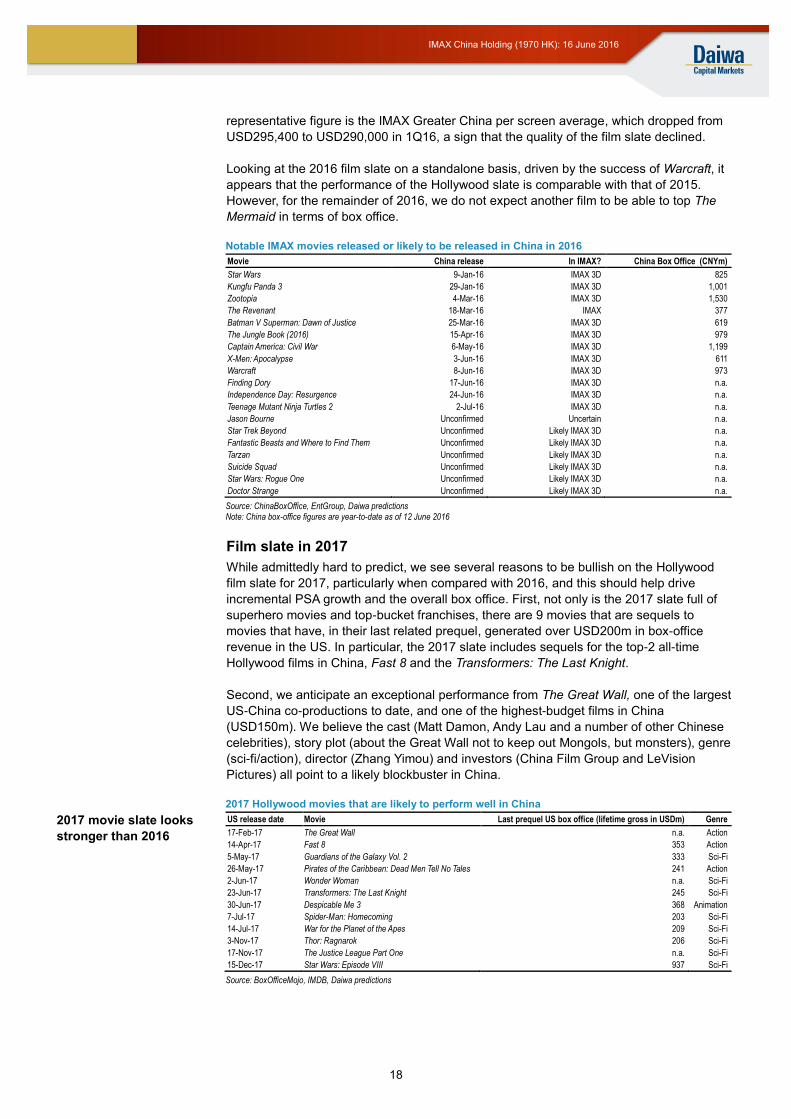

Looking at the 2016 film slate on a standalone basis, driven by the success of Warcraft, it

appears that the performance of the Hollywood slate is comparable with that of 2015.

However, for the remainder of 2016, we do not expect another film to be able to top The

Mermaid in terms of box office.

Notable IMAX movies released or likely to be released in China in 2016

Movie China release In IMAX? China Box Office (CNYm)

Star Wars 9-Jan-16 IMAX 3D 825

Kungfu Panda 3 29-Jan-16 IMAX 3D 1,001

Zootopia 4-Mar-16 IMAX 3D 1,530

The Revenant 18-Mar-16 IMAX 377

Batman V Superman: Dawn of Justice 25-Mar-16 IMAX 3D 619

The Jungle Book (2016) 15-Apr-16 IMAX 3D 979

Captain America: Civil War 6-May-16 IMAX 3D 1,199

X-Men: Apocalypse 3-Jun-16 IMAX 3D 611

Warcraft 8-Jun-16 IMAX 3D 973

Finding Dory 17-Jun-16 IMAX 3D n.a.

Independence Day: Resurgence 24-Jun-16 IMAX 3D n.a.

Teenage Mutant Ninja Turtles 2 2-Jul-16 IMAX 3D n.a.

Jason Bourne Unconfirmed Uncertain n.a.

Star Trek Beyond Unconfirmed Likely IMAX 3D n.a.

Fantastic Beasts and Where to Find Them Unconfirmed Likely IMAX 3D n.a.

Tarzan Unconfirmed Likely IMAX 3D n.a.

Suicide Squad Unconfirmed Likely IMAX 3D n.a.

Star Wars: Rogue One Unconfirmed Likely IMAX 3D n.a.

Doctor Strange Unconfirmed Likely IMAX 3D n.a.

Source: ChinaBoxOffice, EntGroup, Daiwa predictions Note: China box-office figures are year-to-date as of 12 June 2016

Film slate in 2017

While admittedly hard to predict, we see several reasons to be bullish on the Hollywood

film slate for 2017, particularly when compared with 2016, and this should help drive

incremental PSA growth and the overall box office. First, not only is the 2017 slate full of

superhero movies and top-bucket franchises, there are 9 movies that are sequels to

movies that have, in their last related prequel, generated over USD200m in box-office

revenue in the US. In particular, the 2017 slate includes sequels for the top-2 all-time

Hollywood films in China, Fast 8 and the Transformers: The Last Knight.

Second, we anticipate an exceptional performance from The Great Wall, one of the largest

US-China co-productions to date, and one of the highest-budget films in China

(USD150m). We believe the cast (Matt Damon, Andy Lau and a number of other Chinese

celebrities), story plot (about the Great Wall not to keep out Mongols, but monsters), genre

(sci-fi/action), director (Zhang Yimou) and investors (China Film Group and LeVision

Pictures) all point to a likely blockbuster in China.

2017 Hollywood movies that are likely to perform well in China

2017 movie slate looks

stronger than 2016

US release date Movie Last prequel US box office (lifetime gross in USDm) Genre

17-Feb-17 The Great Wall n.a. Action

14-Apr-17 Fast 8 353 Action

5-May-17 Guardians of the Galaxy Vol. 2 333 Sci-Fi

26-May-17 Pirates of the Caribbean: Dead Men Tell No Tales 241 Action

2-Jun-17 Wonder Woman n.a. Sci-Fi

23-Jun-17 Transformers: The Last Knight 245 Sci-Fi

30-Jun-17 Despicable Me 3 368 Animation

7-Jul-17 Spider-Man: Homecoming 203 Sci-Fi

14-Jul-17 War for the Planet of the Apes 209 Sci-Fi

3-Nov-17 Thor: Ragnarok 206 Sci-Fi

17-Nov-17 The Justice League Part One n.a. Sci-Fi

15-Dec-17 Star Wars: Episode VIII 937 Sci-Fi

Source: BoxOfficeMojo, IMDB, Daiwa predictions

19

IMAX China Holding (1970 HK): 16 June 2016

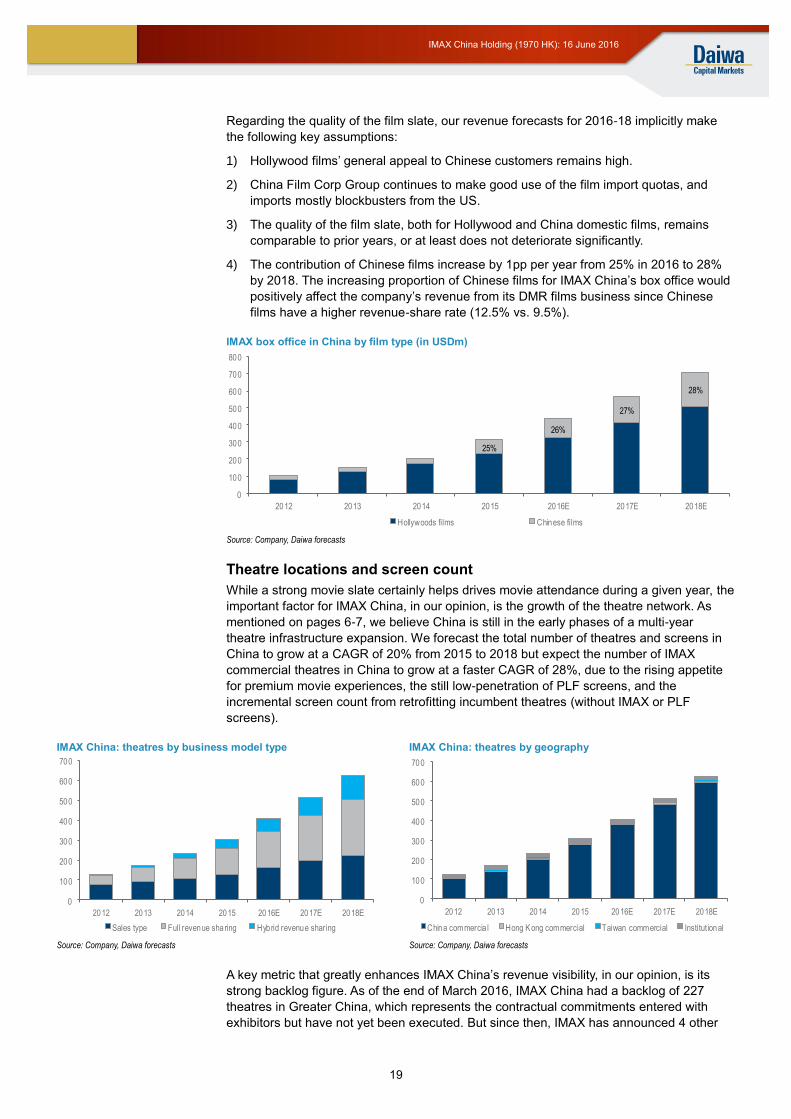

Regarding the quality of the film slate, our revenue forecasts for 2016-18 implicitly make

the following key assumptions:

1) Hollywood films’ general appeal to Chinese customers remains high.

2) China Film Corp Group continues to make good use of the film import quotas, and

imports mostly blockbusters from the US.

3) The quality of the film slate, both for Hollywood and China domestic films, remains

comparable to prior years, or at least does not deteriorate significantly.

4) The contribution of Chinese films increase by 1pp per year from 25% in 2016 to 28%

by 2018. The increasing proportion of Chinese films for IMAX China’s box office would

positively affect the company’s revenue from its DMR films business since Chinese

films have a higher revenue-share rate (12.5% vs. 9.5%).

IMAX box office in China by film type (in USDm)

Source: Company, Daiwa forecasts

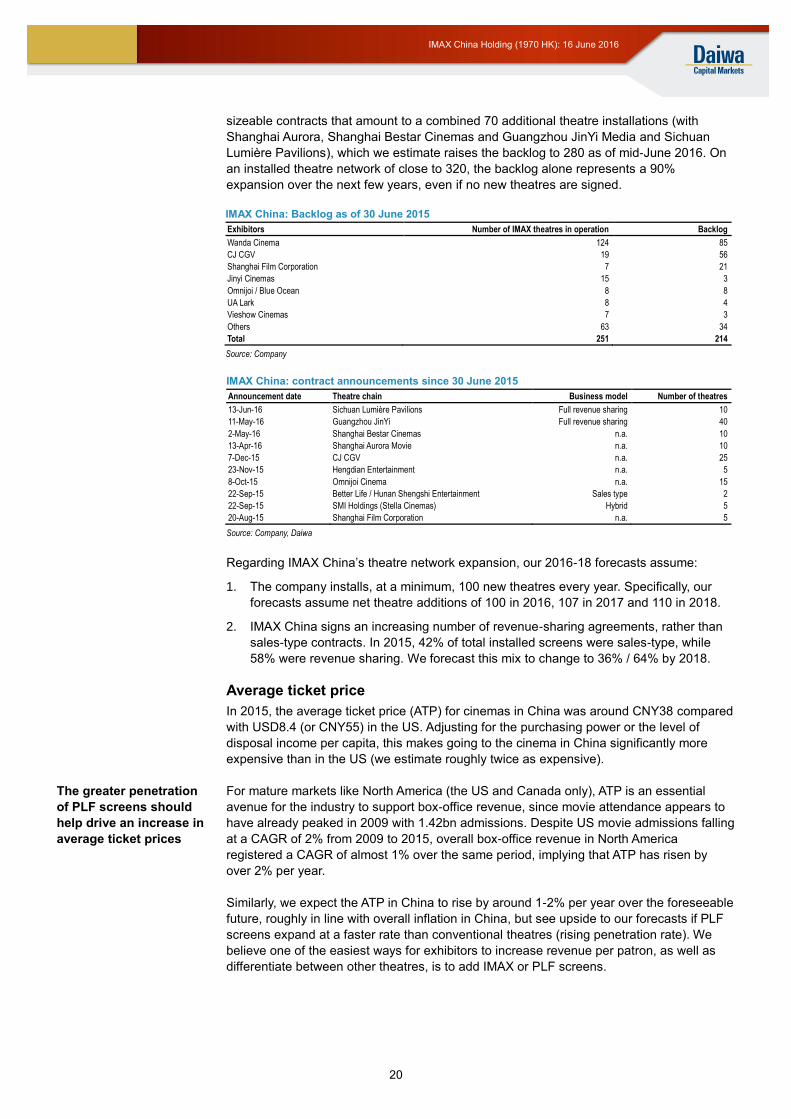

Theatre locations and screen count

While a strong movie slate certainly helps drives movie attendance during a given year, the

important factor for IMAX China, in our opinion, is the growth of the theatre network. As

mentioned on pages 6-7, we believe China is still in the early phases of a multi-year

theatre infrastructure expansion. We forecast the total number of theatres and screens in

China to grow at a CAGR of 20% from 2015 to 2018 but expect the number of IMAX

commercial theatres in China to grow at a faster CAGR of 28%, due to the rising appetite

for premium movie experiences, the still low-penetration of PLF screens, and the

incremental screen count from retrofitting incumbent theatres (without IMAX or PLF

screens).

IMAX China: theatres by business model type IMAX China: theatres by geography

Source: Company, Daiwa forecasts Source: Company, Daiwa forecasts

A key metric that greatly enhances IMAX China’s revenue visibility, in our opinion, is its

strong backlog figure. As of the end of March 2016, IMAX China had a backlog of 227

theatres in Greater China, which represents the contractual commitments entered with

exhibitors but have not yet been executed. But since then, IMAX has announced 4 other

25%

26%

27%

28%

0

100

200

300

400

500

600

700

800

2012 2013 2014 2015 2016E 2017E 2018E

Hollywoods films Chinese films

0

100

200

300

400

500

600

700

2012 2013 2014 2015 2016E 2017E 2018E

Sales type Full revenue sharing Hybrid revenue sharing

0

100

200

300

400

500

600

700

2012 2013 2014 2015 2016E 2017E 2018E

China commercia l Hong Kong commercial Taiwan commercial Institut ional

20

IMAX China Holding (1970 HK): 16 June 2016

sizeable contracts that amount to a combined 70 additional theatre installations (with

Shanghai Aurora, Shanghai Bestar Cinemas and Guangzhou JinYi Media and Sichuan

Lumière Pavilions), which we estimate raises the backlog to 280 as of mid-June 2016. On

an installed theatre network of close to 320, the backlog alone represents a 90%

expansion over the next few years, even if no new theatres are signed.

IMAX China: Backlog as of 30 June 2015

Exhibitors Number of IMAX theatres in operation Backlog

Wanda Cinema 124 85

CJ CGV 19 56

Shanghai Film Corporation 7 21

Jinyi Cinemas 15 3

Omnijoi / Blue Ocean 8 8

UA Lark 8 4

Vieshow Cinemas 7 3

Others 63 34

Total 251 214

Source: Company

IMAX China: contract announcements since 30 June 2015

Announcement date Theatre chain Business model Number of theatres

13-Jun-16 Sichuan Lumière Pavilions Full revenue sharing 10

11-May-16 Guangzhou JinYi Full revenue sharing 40

2-May-16 Shanghai Bestar Cinemas n.a. 10

13-Apr-16 Shanghai Aurora Movie n.a. 10

7-Dec-15 CJ CGV n.a. 25

23-Nov-15 Hengdian Entertainment n.a. 5

8-Oct-15 Omnijoi Cinema n.a. 15

22-Sep-15 Better Life / Hunan Shengshi Entertainment Sales type 2

22-Sep-15 SMI Holdings (Stella Cinemas) Hybrid 5

20-Aug-15 Shanghai Film Corporation n.a. 5

Source: Company, Daiwa

Regarding IMAX China’s theatre network expansion, our 2016-18 forecasts assume:

1. The company installs, at a minimum, 100 new theatres every year. Specifically, our

forecasts assume net theatre additions of 100 in 2016, 107 in 2017 and 110 in 2018.

2. IMAX China signs an increasing number of revenue-sharing agreements, rather than

sales-type contracts. In 2015, 42% of total installed screens were sales-type, while

58% were revenue sharing. We forecast this mix to change to 36% / 64% by 2018.

Average ticket price

In 2015, the average ticket price (ATP) for cinemas in China was around CNY38 compared

with USD8.4 (or CNY55) in the US. Adjusting for the purchasing power or the level of

disposal income per capita, this makes going to the cinema in China significantly more

expensive than in the US (we estimate roughly twice as expensive).

For mature markets like North America (the US and Canada only), ATP is an essential

avenue for the industry to support box-office revenue, since movie attendance appears to

have already peaked in 2009 with 1.42bn admissions. Despite US movie admissions falling

at a CAGR of 2% from 2009 to 2015, overall box-office revenue in North America

registered a CAGR of almost 1% over the same period, implying that ATP has risen by

over 2% per year.

Similarly, we expect the ATP in China to rise by around 1-2% per year over the foreseeable

future, roughly in line with overall inflation in China, but see upside to our forecasts if PLF

screens expand at a faster rate than conventional theatres (rising penetration rate). We

believe one of the easiest ways for exhibitors to increase revenue per patron, as well as

differentiate between other theatres, is to add IMAX or PLF screens.

The greater penetration

of PLF screens should

help drive an increase in

average ticket prices

21

IMAX China Holding (1970 HK): 16 June 2016

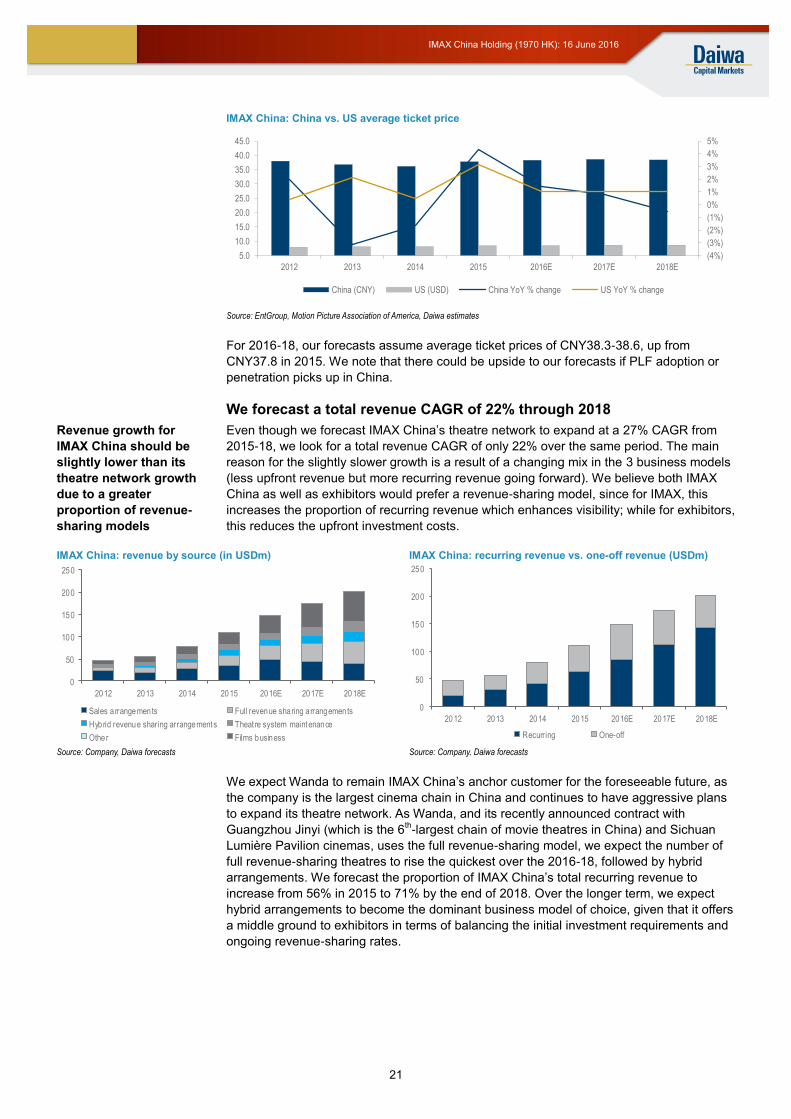

IMAX China: China vs. US average ticket price

Source: EntGroup, Motion Picture Association of America, Daiwa estimates

For 2016-18, our forecasts assume average ticket prices of CNY38.3-38.6, up from

CNY37.8 in 2015. We note that there could be upside to our forecasts if PLF adoption or

penetration picks up in China.

We forecast a total revenue CAGR of 22% through 2018

Even though we forecast IMAX China’s theatre network to expand at a 27% CAGR from

2015-18, we look for a total revenue CAGR of only 22% over the same period. The main

reason for the slightly slower growth is a result of a changing mix in the 3 business models

(less upfront revenue but more recurring revenue going forward). We believe both IMAX

China as well as exhibitors would prefer a revenue-sharing model, since for IMAX, this

increases the proportion of recurring revenue which enhances visibility; while for exhibitors,

this reduces the upfront investment costs.

IMAX China: revenue by source (in USDm) IMAX China: recurring revenue vs. one-off revenue (USDm)

Source: Company, Daiwa forecasts Source: Company, Daiwa forecasts

We expect Wanda to remain IMAX China’s anchor customer for the foreseeable future, as

the company is the largest cinema chain in China and continues to have aggressive plans

to expand its theatre network. As Wanda, and its recently announced contract with

Guangzhou Jinyi (which is the 6th-largest chain of movie theatres in China) and Sichuan

Lumière Pavilion cinemas, uses the full revenue-sharing model, we expect the number of

full revenue-sharing theatres to rise the quickest over the 2016-18, followed by hybrid

arrangements. We forecast the proportion of IMAX China’s total recurring revenue to

increase from 56% in 2015 to 71% by the end of 2018. Over the longer term, we expect

hybrid arrangements to become the dominant business model of choice, given that it offers

a middle ground to exhibitors in terms of balancing the initial investment requirements and

ongoing revenue-sharing rates.

(4%)

(3%)

(2%)

(1%)

0%

1%

2%

3%

4%

5%

5.0

10.0

15.0

20.0

25.0

30.0

35.0

40.0

45.0

2012 2013 2014 2015 2016E 2017E 2018E

China (CNY) US (USD) China YoY % change US YoY % change

0

50

100

150

200

250

2012 2013 2014 2015 2016E 2017E 2018E

Sales arrangements Full revenue sharing arrangements

Hybrid revenue sharing arrangements Theat re system maintenance

Other Films business

0

50

100

150

200

250

2012 2013 2014 2015 2016E 2017E 2018E

Recurring One-off

Revenue growth for

IMAX China should be

slightly lower than its

theatre network growth

due to a greater

proportion of revenue-

sharing models

22

IMAX China Holding (1970 HK): 16 June 2016

Enhanced earnings quality

A prime reason for multiple expansion

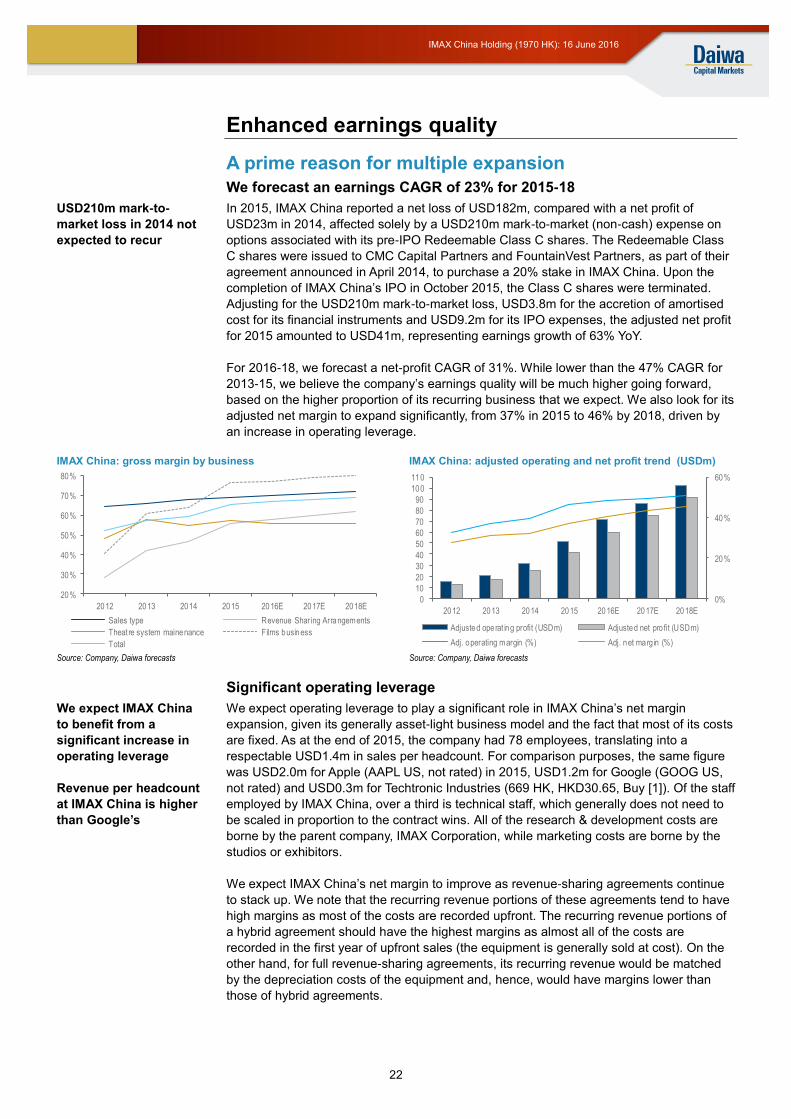

We forecast an earnings CAGR of 23% for 2015-18

In 2015, IMAX China reported a net loss of USD182m, compared with a net profit of

USD23m in 2014, affected solely by a USD210m mark-to-market (non-cash) expense on

options associated with its pre-IPO Redeemable Class C shares. The Redeemable Class

C shares were issued to CMC Capital Partners and FountainVest Partners, as part of their

agreement announced in April 2014, to purchase a 20% stake in IMAX China. Upon the

completion of IMAX China’s IPO in October 2015, the Class C shares were terminated.

Adjusting for the USD210m mark-to-market loss, USD3.8m for the accretion of amortised

cost for its financial instruments and USD9.2m for its IPO expenses, the adjusted net profit

for 2015 amounted to USD41m, representing earnings growth of 63% YoY.

For 2016-18, we forecast a net-profit CAGR of 31%. While lower than the 47% CAGR for

2013-15, we believe the company’s earnings quality will be much higher going forward,

based on the higher proportion of its recurring business that we expect. We also look for its

adjusted net margin to expand significantly, from 37% in 2015 to 46% by 2018, driven by

an increase in operating leverage.

IMAX China: gross margin by business IMAX China: adjusted operating and net profit trend (USDm)

Source: Company, Daiwa forecasts Source: Company, Daiwa forecasts

Significant operating leverage

We expect operating leverage to play a significant role in IMAX China’s net margin

expansion, given its generally asset-light business model and the fact that most of its costs

are fixed. As at the end of 2015, the company had 78 employees, translating into a

respectable USD1.4m in sales per headcount. For comparison purposes, the same figure

was USD2.0m for Apple (AAPL US, not rated) in 2015, USD1.2m for Google (GOOG US,

not rated) and USD0.3m for Techtronic Industries (669 HK, HKD30.65, Buy [1]). Of the staff

employed by IMAX China, over a third is technical staff, which generally does not need to

be scaled in proportion to the contract wins. All of the research & development costs are

borne by the parent company, IMAX Corporation, while marketing costs are borne by the

studios or exhibitors.

We expect IMAX China’s net margin to improve as revenue-sharing agreements continue

to stack up. We note that the recurring revenue portions of these agreements tend to have

high margins as most of the costs are recorded upfront. The recurring revenue portions of

a hybrid agreement should have the highest margins as almost all of the costs are

recorded in the first year of upfront sales (the equipment is generally sold at cost). On the

other hand, for full revenue-sharing agreements, its recurring revenue would be matched

by the depreciation costs of the equipment and, hence, would have margins lower than

those of hybrid agreements.

20%

30%

40%

50%

60%

70%

80%

2012 2013 2014 2015 2016E 2017E 2018E

Sales type Revenue Sharing Arrangements

Theat re system mainenance Films business

Total

0%

20%

40%

60%

0

10

20

30

40

50

60

70

80

90

100

110

2012 2013 2014 2015 2016E 2017E 2018E

Adjusted operat ing profit (USDm) Adjusted net pro fit (USDm)

Adj. operating margin (%) Adj. net marg in (%)

USD210m mark-to-

market loss in 2014 not

expected to recur

We expect IMAX China

to benefit from a

significant increase in

operating leverage

Revenue per headcount

at IMAX China is higher

than Google’s

23

IMAX China Holding (1970 HK): 16 June 2016

Chinese films to improve utilisation and margins

Lastly, we expect the utilisation rate of IMAX theatres to improve over time, which should

help expand margins. We see 2 types of utilisation rates relevant to IMAX China:

1) Theatre utilisation, ie, the number of admissions per auditorium. In our opinion, this is

not under the control of IMAX China as it is largely a result of the film-slate quality and

the operational effectiveness of the exhibitor, and

2) Strategic timing of movie releases. This pertains to the scheduling of movie

releases in China to ensure that there is always IMAX content playing at IMAX

theatres. We note that according to IMAX China’s agreements with exhibitors,

exhibitors can play non-IMAX films at IMAX auditoriums, but only if IMAX China cannot

provide IMAX content at any given time. As IMAX China plans to convert more

Chinese-language films, we believe this will improve the utilisation of IMAX China’s

theatres as: 1) Chinese films are not restricted by the blackout window release

periods, and 2) there is generally be more fresh content playing at IMAX theatres,

which should improve overall theatre attendance.

On 15 June 2016, IMAX Corporation and IMAX China announced that, along with their

partner China Media Capital, they established a USD50m film fund to co-finance

approximately 15 Mandarin-language tentpole films (films that are predicted to be a sure-

fire top blockbuster) over the next 3 years. We believe this fund could help accelerate the

expansion of IMAX China’s Chinese language content pipeline, as well as boost its

relationship with Chinese studios and directors.

A cash-cow business with dividend potential

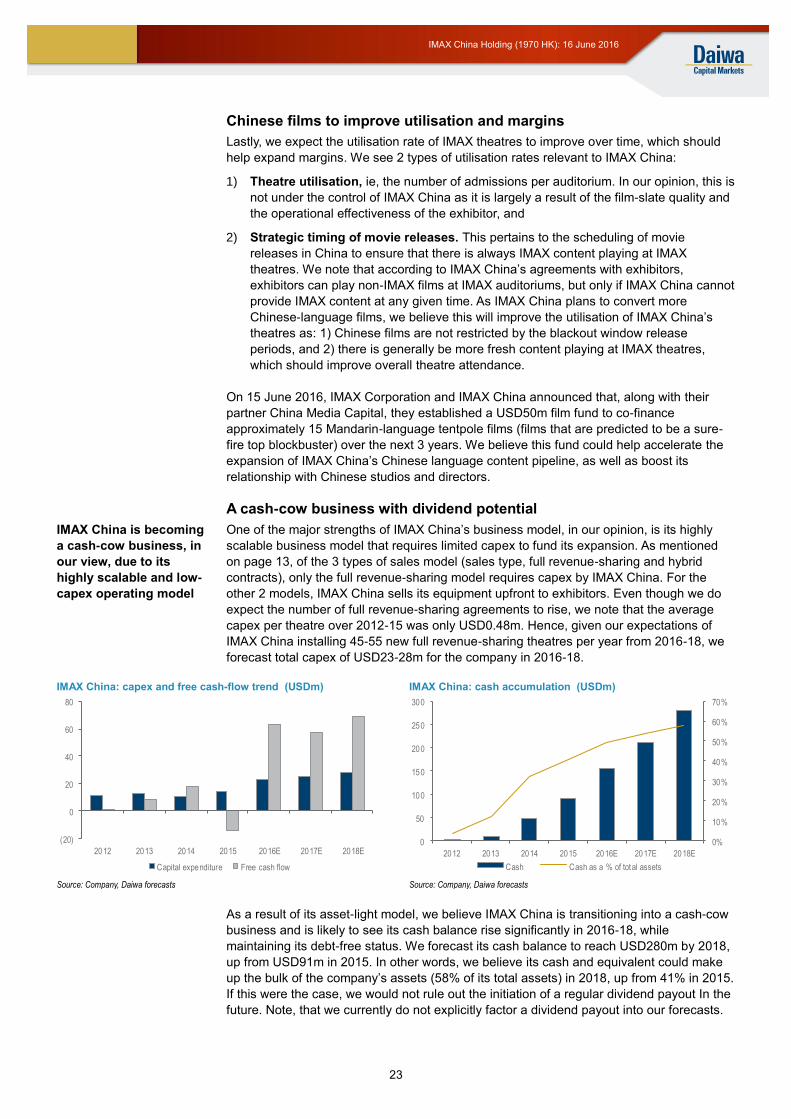

One of the major strengths of IMAX China’s business model, in our opinion, is its highly

scalable business model that requires limited capex to fund its expansion. As mentioned

on page 13, of the 3 types of sales model (sales type, full revenue-sharing and hybrid

contracts), only the full revenue-sharing model requires capex by IMAX China. For the

other 2 models, IMAX China sells its equipment upfront to exhibitors. Even though we do

expect the number of full revenue-sharing agreements to rise, we note that the average

capex per theatre over 2012-15 was only USD0.48m. Hence, given our expectations of

IMAX China installing 45-55 new full revenue-sharing theatres per year from 2016-18, we

forecast total capex of USD23-28m for the company in 2016-18.