Embed Size (px)

Citation preview

© Copyright Business Monthly 2018. All rights reserved. No part of this magazine may be reproduced without the prior written consent of the editor. The opinions expressed in Business Monthly do not necessarily reflect the views of the American Chamber of Commerce in Egypt.

OCTOBER 2018VOLUME 3 5 | IS SUE 1 0

Investor Focus18 Road to Recovery Is Egypt’s apparel industry a potentialcash cow?

Regional Focus40 Investing in EGX vs. TadawulChoosing your best bet

Inside12 Editor’s Note14 Viewpoint

8• Business Monthly - OCTOBER 2018

The Newsroom16 In BriefAn analytical view of the topmonthly news

Market Watch48 Not a Bear Market … Yet

American Impact 44 Shadow BankingIs the global economy approachinganother crisis?

© Copyright Business Monthly 2018. All rights reserved. No part of this magazine may be reproduced without the prior written consent of the editor. The opinions expressed in Business Monthly do not necessarily reflect the views of the American Chamber of Commerce in Egypt.

OCTOBER 2018VOLUME 3 5 | IS SUE 1 0

10• Business Monthly - OCTOBER 2018

Public and private sector join forcesto lessen the dependency on printmoney

Cover Design: Nessim N. Hanna

Cover Story34 Egypt as a CashlessSociety

In Depth22 The Long-Awaited IPOProgramEgypt’s equity financing future

The Chamber

54 Events

63 Exclusive Offers

64 Media LiteAn irreverent glance

at the press

Executive Life50 A Beautiful Investment Investing in Egypt’s art scene

At a Glance26 Investing in EgyptA market overview

Many lives, at least in my opinion, can be summarized in the strugglebetween the need to evolve and the comfort zone. The humankind isconditioned to have both, one to help us connect continents and theother to keep us from slipping off a cliff, each triumphing at point in time.

One of my favorite stories of this struggle is that of Pharaoh Akhenaten. He challengedthe norm of the Egyptian society by depicting his reign in a vastly different way from therulers who came before him. He changed the religion of ancient Egypt from polytheisticto monotheistic, and moved the capital from Luxor where it has always been to the middleof the desert. Legend has it that he chose this location because the sun rises exactlybetween two hills, representing the power of the god Aten. He promoted a different kindof art, life, and philosophy. Alas, as you visit his kingdom today in the outskirts of Al Minya,you will only find a little more than a patch of desert. What Akhnaten missed was the com-fort zone of his people. The culture wasn’t ready, and as soon as he passed away his sonmoved the capital back and the people went to the cultural practices they were comfort-able with.For Egypt, this struggle today can be seen in the country’s pursuit of a cashless society.

With government plans, private sector initiatives, more FinTechs than Egypt has ever had,the near future is looking more and more paperless. However, cultural readiness and com-mon perceptions remain a huge hurdle to overcome. Continuing on the financial track, the Egyptian government is following through on its

2016 announced plans to list state-owned companies. We speak to experts on the expectedpotential and looming challenges, especially in light of the emerging markets crisis. Despite the volatility witnessed in Egypt’s stock exchange, foreign investment is well on

the rise. However, as Saudi Arabia reformed its regulations, encouraging foreign invest-ment in Tadawul, its international standing rose to compete with that of Egypt. Thismonth’s Regional Focus compares the figures and performance of both stock exchanges. Shifting to other investment angles, Egyptian apparel brands are back on the interna-

tional wagon. However, the industry is still plagued with significant challenges that hamperits growth locally and internationally. Business Monthly delves into the sector’s profitabil-ity analyzing its investment potential.Not all investment ventures are dry and figure-based. This month we chose to look into

the investment activity of Egypt’s contemporary art scene. Hidden in Cairo’s nooks andcrannies are galleries making millions per sale, which begs the question: Are we missing outon significantly appreciating assets?Last but not least, we did things a bit differently this month. We swapped one of our in-

depth articles for a detailed visual presentation of the different factors that shape thepotential of new investments, covering everything from cultural readiness, labor compet-itiveness, business environment, to technology penetration. Tell us if you would like to seemore of this.

Cultural Evolution

Director of Publications & ResearchKhaled F. Sewelam

Editor-in-ChiefNadine Abou el Atta

Contributing EditorTamer HafezLeah BremerKate Durham

Consulting EditorsBertil G. Peterson

Contributing WritersMahinaz el BazJulian NabilMenna Farouk

Senior Art DirectorNessim N. Hanna

Senior Graphic DesignerEmy Emile

Graphic DesignerVerina Maher

Advertising & Business DevelopmentDirectorAmany Kassem

Advertising CoordinatorLamia Seleit

Circulation CoordinatorDina Karara

PhotographersKarim el SharnoubySaid Abdelmessih

Production SupervisorHany Elias

Market Watch AnalystAmr Hussein Elalfy

Chamber News ContactsNada Abdalla, Azza Sherif,Susanne Winkler

U.S. address: 1615 H Street, NW • Washington, D.C. 20062Please forward your comments or suggestions to the Egypt editorial office:

Business Monthly American Chamber of Commerce in Egypt33 Soliman Abaza Street, Dokki 12311 • Cairo • EgyptTel: (20-2) 3338-1050 • Fax: (20-2) 3338-0850E-mail: [email protected]/bmonthly

CTP and printing: Sahara Printing Company, SAE – Nasr City Free Zone

NADINE ABOU EL ATTAEDITOR-IN-CHIEF

Editor’s Note

12• Business Monthly - OCTOBER 2018

@BusinessMonthlyEg @BusinessMonthly @BusinessMonthly

U.S-Egypt relations are witnessing an upward trend. We just came back from amini-doorknock, highlighted by a business dinner in honor of President AbdelFattah al Sisi in New York. The meeting was attended by 21 distinguishedbusiness leaders representing some of the top U.S. companies, both working and

interested to work in Egypt. President Sisi articulated the case of Egypt and hit on all theright notes, he touched upon economic reforms, social inclusion, security, stability,citizenship, and continuing the reform agenda.

The feedback from corporate America was beyond positive, unlike previous meetingswhere optimism was guarded by caution. Not this time.

Further boosting Egypt’s positive image, we heard the meeting with President Trumpwent even better than the previous one. In Washington DC the positive sentiment regardingEgypt’s successful economic reforms by far takes priority as opposed to any concerns. In factthe message is keep doing what you are doing right. International financial organizations areimpressed by Egypt’s ability to weather the emerging markets storm, in one strikingcomment: “It’s too good to be true” notwithstanding the imperative need and urgency forsectoral reform, which are needed more so than ever.

Interestingly enough, no serious concerns regarding government debt were raised, as longas it is getting lower in percentage to GDP, not necessarily in absolute terms. October willwitness the periodical review of rating agencies and donor organizations, along with annualWEF Competitiveness ranking. It will be interesting to see the outcome.

Egypt still has a challenging time ahead, hot money flight, emerging markets stress, therising price of oil, and the challenge of attracting foreign direct investments, which is yet tohappen. In many ways it could be a blessing in disguise, prompting the government to pushfurther to unlock the ill-famed bureaucracy.

A sentiment that seems to gain traction within Egypt’s decision-making circles is againperceived as a bastion of stability in a treacherous region, and has a role to play in manydifferent fronts, be it the Israeli-Palestine presumed peace initiative, the Libya file, or EastMediterranean economic coalition. Egypt foreign relations are back on track.

On a final note, the Egypt-U.S. relations are highlighted by the release of $195 million inmilitary aid in August, the visit of Melania Trump in October, the 40th celebration of CampDavid, and the honorary medal awarded to late President Sadat, and the resumption of thestrategic dialogue between the ministries of foreign affairs and defense in both countries,along with the unequivocal support from the U.S. on our war on terror.

For a change we come back this time with a positive note.TAREK TAWFIK

President, AmCham Egypt

Strength in Partnership

Viewpoint

14• Business Monthly - OCTOBER 2018

THE NEWSROOMIN BRIEF

16• Business Monthly - OCTOBER 2018

Tourism Revenue up 77 Percent

Software Piracy Down

Egypt's tourism revenue jumped 77 percent in the firsthalf of 2018 to around $4.8 billion compared with thesame period last year, a government official toldReuters in late August. The recovery is partly attrib-uted to the flotation of the Egyptian pound, whichhalved the currency’s value, making the country a moreattractive holiday destination through cheaper hotelprices. He added the number of visitors jumped in thefirst half of the year to 5 million, a 41 percent year-on-year growth. “Indicators suggest the sector will earnabout $9 billion by the end of this year,” the officialsaid, adding there were expectations of greater trafficfrom Western Europe, Italy, Germany and Ukrainetowards the end of the year. Last year the governmentpocketed $7.6 billion off the tourism sector, which haslong been considered a pillar of Egypt’s economy and akey foreign currency earner.

The software piracy rate in Egypt hasdropped two percent in 2017, to 59percent, according to a bi-annualreport by U.S.-based BusinessSoftware Alliance. The value of unli-censed software in Egypt declinedfrom $157 million in 2015 to $64 mil-lion in 2017. The report ranks Egyptseventh on the Middle East and

fourth place in Africa. Egypt’s figuresstand to further improve after parlia-ment in July approved the nation’sfirst-ever cybercrimes law, which isexpected to limit the ability to down-load pirated software off the internet.This is made possible as the regulationfor the first time allows the court touse digital evidence to prosecute a

case. Under the law, offenders includethose who operate any informationsystem, such as a website, account, oremail, that encourages cybercrime.Those convicted can face up to a yearin prison and fees up to EGP 100,000,depending on whether the defendantwas a distributer or solely a user ofpirated software.

•17Business Monthly - OCTOBER 2018

In Brief

New Assiut Investment UpdateNew Assiut city is set to receive EGP247 million in investments in fiscal year(FY) 2018/2019 atop the EGP 4.1 billionit has received to date. The New UrbanCommunities Authority (NUCA) hasreleased a report highlighting invest-ment figures for the construction ofNew Assiut city, an extension of Assiutgovernorate which is 386 kilometerssouth of Cairo. It is built over 30,000feddans, of them, 6,600 feddans areallocated to real estate development.This land is earmarked for a maximumof 71,000 residential units, of which12,700 will be built by NUCA.Developers have already completed11,280 units, with an additional 648units under construction. Meanwhile, 15commercial centers have been complet-ed, with 22 still under construction.

Infrastructure has also made significantprogress, with underground pipeworkalready complete, and the electricitygrid work 95 percent finished. Laggingare road paving, at only 50 percent com-pletion, as well as cultivation works,which are 75 percent complete. This cityis part of an ambitious plan to build newcities on the outskirts of every majorgovernorate in Egypt, including theNew Administrative Capital and NewAlamein City.

2,079 Unused Government Assets Egypt has 2,079 state-owned assets ofempty plots, buildings, and factorystructures in 15 governorates, PrimeMinister, Mostafa Madbouly,announced during a press event. Thecabinet is still discussing the optimalutilization of the assets. According to

Madbouly, they will either be includedin Egypt’s recently-announced sover-eign wealth fund, if they pass certain cri-teria; used for different projects; or soldin open auctions to pay off the debtsaccumulated by different governmententities. The findings were based on thework of a specialized committee thatwas formed a year ago to consolidate thegovernment’s assets nationwide. LastJuly, Parliament assessed the govern-ment’s unused assets at EGP 1 trillion.Their recommendation, at the time,was that they should all be put under thesovereign wealth fund. This, theyargued, would allow each asset to befully utilized as some of Egypt’s bestinvestment experts run the fund. This isthe first time that the government hasmade an official nationwide, cross min-isterial, record of all of the government’sunused assets.

Petroleum Consumption on the Rise

Consumption of petroleum products in Egypt isexpected to reach 35.5 million tons by the end offiscal year 2018/2019, a 10.24 percent increase overthe previous fiscal year. That was the estimation ofTarek el Molla, minister of petroleum and mineralresources, when speaking to Al Shorouk newspa-per in September. This comes as the government isworking on reducing butane consumption by 4.87percent, capping it at 3.9 million tons compared to4.1 million last fiscal year. However, it is allowingconsumption of other petroleum products to fluc-tuate based on supply and demand. El Molla pre-dicted that gasoline consumption will increase by5.63 percent to reach 7.5 million tons by the end ofthis fiscal year. Meanwhile, diesel consumption willgrow 8.88 percent to reach 14.7 million tons, whilethe highest consumption forecast goes to mazut,which is set to increase by 25.3 percent to reach 9.4million tons. For the past three years, the govern-ment has been resorting to raising prices of fuelproducts annually in an attempt to force people touse less expensive public transportation.

18• Business Monthly - OCTOBER 2018

Investor Focus

Egypt’s homegrown apparel industry is undergoing a revival that is pushing itonto the international stage. Can domestic manufacturers overcome challenges tothe “Made in Egypt” brand?

By Menna A. Farouk

Road to RecoveryEgypt’s Apparel Industry

•19

Twenty years ago, Hani Guweida built a business in Cairo based on selling importedapparel to domestic retailers. By 2014, the entrepreneur abandoned that strategy infavor of bringing 100 percent locally-produced products to the market.

“We realized how promising Egypt’s apparel market is, taking into consideration the high-quality materials we have and the country’s strategic location,” says Guweida, chief executiveofficer of Town Team Company for Readymade Garments. “We managed to establish a factoryin Tanta, and we are now building another manufacturing plant in El Sadat City.” Despite such expansion, several challenges undermining growth not just for Guweida’s com-

pany, but throughout a sector considered vital to the Egyptian economy. “The scarcity oftrained workers and the high production costs,” he says, citing the two main areas of concern.“We are still trying to overcome them.”Guweida is among hundreds of apparel manufacturers who face soaring prices for raw mate-

rials, and a lack of machinery and qualified workers, as well as the widespread perception thatimported clothes are better.

Robust IndustryAccording to the Readymade Garments Export Council, the apparel industry contributes 3 per-cent to Egypt’s gross domestic product, represents 15 percent of non-oil exports, and employs33 percent of the industrial labor force.The council reported in January that Egypt’s exports in this sector rose 13 percent in 2017

to $1.4 billion, compared to $1.3 billion a year earlier, the first increase in three years. Previousexports declined year-on-year by 3 percent in 2016 and 8 percent in 2015, according to thecouncil’s data. Meanwhile, imports of readymade garments declined 55 percent from January through

August due to the devaluation of the Egyptian pound, the Ministry of Trade and Industry statedin an October 2017 press release.Last year, the U.S. topped the list of Egyptian apparel importers, receiving knit apparel worth

$380 million and woven apparel worth $348 million, according to the Office of the U.S. TradeRepresentative. On the other hand, China had the lion’s share of apparels exported to the U.S. with $27.04

billion worth of products. Vietnam came in second with $11.56 billion, followed byBangladesh at 5.06 billion and India at $3.7 billion, as per data released by the Office ofTextiles and Apparel in the U.S. Department of Commerce.

Market EdgeThose interviewed stress the industry’s potential. “There is an increasing supply of workers,declining wages in comparison with other countries, and the availability of fertile land forgrowing long-staple cotton, which rarely exists elsewhere,” says Magdy Tolba, chairman ofCairo Cotton Center, a supplier of high-quality knitted apparel to Europe and the United States.Tolba adds that multinational companies have robust confidence in the apparel produced in

Egypt, citing his company’s contracts with Macy’s, Gap Inc., Liz Claiborne, Levi Strauss, Nike,Adidas, Marks & Spencer, Calvin Klein.The float of the Egyptian pound in 2016 laid the foundation for an export-friendly economy.

“Locally made products have become more affordable for consumers abroad, giving a largeboost to the industry,” he says.Taking into account the encouraging market conditions in Egypt, Tolba says, his company is

launching an international trademark inspired by the movement to promote Egyptian products.“The 100 percent Egyptian brand will go international and be sold across the world,” he adds,offering no further details.Furthermore, Egypt enjoys a competitive edge that has lured investors. Yehia Zananeri, chair-

man of the Association of Readymade Garments Producers, believes Egypt’s apparel industryhas drawn both local and foreign investors, which is encouraging expansion. “Egypt has a very

Business Monthly - OCTOBER 2018

Investor Focus

Investor Focus

20• Business Monthly - OCTOBER 2018

strategic location, being proximate toEurope, the Middle East, and Africa.This enables the country to export eas-ily to several countries. It also hassome of the best materials in theworld,” he adds.Nevertheless, Zananeri emphasizes

that Egypt still must make efforts tocompete. Turkey benefits from a simi-lar geographic advantage and has cap-italized on its location near Europeand the Middle East to surpass Egyptin apparel exports. Turkey’s exports of clothing reached

$17 billion by the end of 2017, up 3percent, according to a report by theTurkish Exporters’ Assembly, whileEgypt’s exports of apparel paled incomparison at $1.4 billion.Experts cite Turkey’s qualified and

educated workforce, adequate invest-ment in technology, world-class quali-ty, adherence to environmental andhealth regulations, and competitivedesign as the country’s major advan-tages over Egypt.In order to boost its apparel indus-

try, the Turkish government increasedthe number of private foundationsand universities that specialize in fash-ion design. In addition, it raised thenumber of fashion exchange opportu-nities with European countries.In cooperation with the private sec-

tor, the Turkish government also start-ed to organize design competitions,fashion shows at high schools andshopping malls, and a fashion week inits capital.

Challenges to GrowthAll those interviewed acknowledgedthe challenges that persist despite gov-ernment support and the potential ofthe apparel industry. SayyedMahmoud, the owner of a small shopat Wekalet el Balah, a marketplaceknown for its affordability, says prob-lems include the poor machines usedin manufacturing, a lack of trainedworkers, rising prices of raw materialsdue to the exchange rate, and highproduction costs. “Although the country has a strong

apparel industry with a long and

reputable history, it does not produceadequate apparel products to coverthe local market. Most clothing wehave is from China, Italy, the U.S.,among others,” Mahmoud says.He adds that quality domestic

readymade garments do exist, empha-sizing that Egypt has some of the finestraw materials in the world. "Whatdamages the image of ready-made gar-ments in Egypt is random workshopsthat are not monitored by the govern-ment, do not apply international stan-dards, and produce poor-quality prod-ucts," he says. “Such low-qualityapparel has reinforced the perceptionthat locally made products are notworth the money.”As a result, local products can’t

compete with international brands,says Waleed el Masry, another shopowner in Wekalet el Balah.“Marketing is also added to the list ofreasons,” he says. “We do not knowhow to market our products abroad.You know what? Chinese ready-madegarments are very low-quality.However, there is demand for them.People prefer to buy any foreign thingrather than a locally made product.”El Masry adds that with the devalu-

ation of the Egyptian pound, the pur-chasing power of Egyptians dramati-cally declined. “There is barely anylocal demand for clothes,” he says.“Prices of clothes have soared.”

Government EffortsIn recent years, the government hasstarted to pay more attention to theapparel industry. In July 2017, itsigned an agreement worth $1.7 bil-lion with the United NationsIndustrial Development Organizationand the Italian Agency forDevelopment Cooperation to improvethe quality of cotton.Moreover, the government

launched a mass campaign under theslogan “Made in Egypt” promotinglocal commodities, including gar-ments. They further complementedthe decision by imposing tariffson hundreds of imported goods,including 40 percent on clothing.

In September, the Ministry of Tradeand Industry signed a protocol ofcooperation with EG-Gate, a platformdeveloped to offer marketing servicesto local manufacturers to digitallypromote Egyptian products.According to the protocol, onlinestores will be set up for Egyptian com-panies on the EG-Gate platform.Enas Abbass, a marketing expert

and public relations consultant, saidthe first thing the government has todo is address the widespread percep-tion about the quality of local prod-ucts. “This can be done through mas-sive media campaigns,” she explains.“Secondly, the government has toimprove the quality of Egypt’s apparelproducts, intensify monitoring of theirproduction, before launching onlineand offline marketing campaigns.”Moreover, Abbass says Egyptian

apparel brands should be displayed atlarge shopping malls in the countryalongside international brands to give theimpression they are on equal footing.

Investment PotentialIn addition to government efforts,Egyptian fashion designers are spread-ing the word about their country’sapparel industry. Several brands arebecoming known on the internationalstage over the past decade, includingMarie Louis, Shahira Lasheen, Zak,Rana Madkour Designs, and SarahBahaa Designs.“This proves how strong Egypt’s

apparel industry is and the potential forit to be stronger. We can go internation-al, but we just need a sound governmentstrategy that supports local manufactur-ing, addresses the challenges, and focus-es on marketing,” says Ahmed elShami, an economist and professor offeasibility studies at Ain ShamsUniversity. “It seems the government isadamant about that, but this will takesome time to be felt on the ground. Thepassion is there and the government’scurbs on imports are being implement-ed. Egypt is heading toward a develop-ment in the apparel market and theindustry is expected to rebound and seeunprecedented growth.”■

•21Business Monthly - OCTOBER 2018

Investor Focus

As the government takes steps toward launching its long-awaited IPO program, experts weigh in on implementation.

By Mahinaz el Baz

InDepth

After years of deliberation, Egyptis finally ready to list its state-ownedcompanies in the stock exchange. Oflate, it has taken steps to prepare forInitial Public Offerings (IPO) for anumber of governmentally ownedcorporations in different sectors. Theplan was officially announced in 2016and is partially building on the lastpublic offering of state-owned com-panies, which took place in 2015.The IPO program intends to list 23

public sector companies on theEgyptian Exchange (EGX). Themove is in line with the government’sproposed national budget for fiscalyear (FY) 2018/2019. Plans includeoffering EGP 100 billion worth ofshares in state-owned companies,according to a March statement bythe Ministry of Finance. The IPOprogram is expected to be imple-mented over 24-30 months.

However, investors are skepti-cal as to whether this IPOprogram will benefit Egypt’seconomic prospects. “Weshould ask ourselves animportant question. Whydoes the government actu-ally list the state-owned compa-nies?” saysMo h am e dReda,

CEO of SOLID Capital Egypt, aninvestment bank. “If the answer is topump the profits directly into thebudget to reduce its deficit, then itshould halt this program.” Redabelieves the rationalpurpose of theIPO program is torestructure unsuc-cessful public com-panies. This goalcan beachieved byintroducingother suc-c e s s f u lc o m p a -nies tot h eEGX in

order to increase their overall capitaland profit, which will be invested insustaining the reform of the unsuc-cessful companies. “I believe that the program is a

very critical one,” says Omar elShenety, managing director ofMultiples Group, an investmentbank. “On one hand, it aims at listingsome of the government-owned com-panies to generate cash to reduce thebudget deficit. On the other hand,listing the government entities isaimed at improving governance andprofessional management at thosecompanies.” Economic consultant Reham el

Desoki explains that “increasing thenumber of state-owned listed compa-nies will enhance the performance of

the stock market by giving itmore depth and [growing] market

capitalization. The bigger the mar-ket capitalization, the cheaper thefinancing methods.”Moreover, IPOs could contribute

to economic growth by forcing state-owned entities to become more effi-cient, Jenik Radon, a lawyer andadjunct professor at the School ofInternational and PublicAffairs at ColumbiaUniversity, told Egypt Oil& Gas magazine inSeptember 2017. “Making

Equity Financing and Egypt’sLong-Awaited IPO Program

22• Business Monthly - OCTOBER 2018

an enterprise more efficient, prof-itable, and expanding a good enter-prise by investment—through morecapital—would obviously grow theeconomy,” he said. “In the end, theissue is making enterprises more effi-cient, which means more business,more taxes.”

The Plan’s Two PhasesThe Ministry of Finance plans toimplement the IPO program overtwo phases. The first will include sell-ing additional shares of already-listedAlexandria Mineral Oils Company(AMOC) and Eastern Company,Finance Minister Mohamed Maaitannounced in September at the EuroMoney Conference. Abu QirFertilizers, Alexandria Container andCargo Handling (ACCH), andHeliopolis Company for Housing andDevelopment (HHD) will follow bythe end of the year.The government hopes to raise as

much as EGP 25 billion from the fiveIPOs, with EGP 10 billion going tothe state’s coffers, according toMaait.Eastern Company and AMOC will

pilot the program; the two compa-nies will introduce a new wave oftheir shares to the EGX. Eastern andHHD were originally slated to pilotthe program, but Public BusinessSector Minister, Hisham Tawfik, told

Bloomberg in a June interview thatAMOC had replaced HDD for anOctober slot. Furthermore, Maaithad announced in September that afurther 20 percent of AMOC will beoffered on the EGX. The Ministryexpects that the offering will gener-ate around EGP 2.8 billion, Reutersreported.As for AMOC, the company

showed a 24 percent year-on-yearincrease in profit to EGP 1.05 billionfor the nine-month period ending inMarch. To secure eligibility to issueglobal depository receipts (GDRs),the government is considering float-ing some of its shares on the NasdaqDubai exchange after it is listed onthe London Stock Exchange Eastern Company, a subsidiary of

the Chemical Industries HoldingCompany, is an Egypt-based jointstock company. It produces 94 per-cent of all cigarettes sold in Egypt,and exports to 30 countries, accord-ing to an August Ahram Onlinereport.“The Eastern Company is a monop-

olistic company that controls domes-tic tobacco production. Demand forits products is exceptional, thus it

gains remarkable profits annually. As aresult, investors would definitely wel-come investing in such a company’s[stock,]” says Reda. In 2017 the compa-ny recorded EGP 13.4 billion in sales,according to an official statement.However, according to Reda, with

65 percent of its production spent onraw materials, primarily importedtobacco, the company is vulnerableto any change in foreign exchangerates. The company needs EGP 600million annually to buy raw materials.Reda believes the five companies

are the optimal choices for the firstphase of the IPO program. They arecharacterized by strong financial per-formance, positive future insights,and increasing demand for theirstock on the EGX. El Shenety agrees, saying the gov-

ernment chose companies that wouldsatisfy the appetite of investors. “Atthe end of the day, investors want to

Business Monthly - OCTOBER 2018 •23

InDepth

see companies with good financialstatements, solid track records, andreasonable forecasts,” he continues,“so the government had to focus onsome of the good companies andinstitutions it has.”Preparations for the program’s sec-

ond phase are on track as well, withmore state-owned companies sched-uled to tap into the equity markets in2019, Maait says, adding that the listof potential companies is still underconsideration.For the second phase of the IPO pro-

gram, Reda says, “Enppi is at the top ofthe list. It has diversified activities and astrong financial position in the market.Maybe by then the government willdecide to introduce national banks tothe EGX in the second phase--Banquedu Caire, for instance.”

ImplementationHurdlesIn principle, the IPO initiative couldbe a good program, yet the devil liesin the details when it comes to execu-tion, how proceeds will be used, andhow companies will cope, el Shenetyexplains. “I believe these are the cri-teria that can define the success andusefulness of the program.”According to Reda, the program

was delayed by conflicts amongstakeholders deciding what compa-nies should be listed. In addition, tocontradicting plans due to the multi-ple government entities involved.“The ongoing IPO program is moreorganized,” he says. “The Ministry ofFinance is the only official entityresponsible for the program.” In the pre-IPO phase, el Shenety

explains that “a lot of organizationaldevelopment efforts have to be done,including restructuring of these compa-nies as well as building a solid corporategovernance system that would matchthe requirements of publicly listed com-

panies. The downside internally couldbe related to manpower, where somelayoffs may result from restructuringand this is a sensitive topic.”According to Reda, public compa-

nies introduced to the EGX will besubject to governance, disclosure,and transparency practices. “Havinga proper business plan, a clear vision,and an elastic structure are key ele-ments in sustaining the success of theprogram and increasing the ability tofinance new projects,” he says. Challenges can change due to the

dynamic nature of both the econom-ic and financial markets. Those inter-viewed argue the potential challengesthat might face the ongoing programare different than the previous chal-lenges that caused the earlier delaysin launching the program.

The stock market has not beendoing well lately, with disappointingtrade volumes. “For the IPO programto succeed, there must be externalinvestors participating and injectingfresh funds in the market,” says elShenety. “This is the wish of every-one, but it is not clear whether thiswill happen. The looming emergingmarket crisis could definitely affectthe IPO program. I believe lots ofefforts on promotion and fundraisingin the international markets for theseIPOs are critical.”Reda, on the other hand, believes

the main challenges are high interestrates, which cause lower levels of liq-uidity and erode purchasing power.“The government should considercutting rates to achieve IPO programgoals,” he says.

Moreover, there is regional pres-sure from the Saudi IPO program.The Saudi financial market is seventimes larger than Egypt’s and couldattract foreign investments not onlyfrom Egypt, but also from other mar-kets in the Gulf, Reda explains.

From her side, el Desoki believes“the more transparent the program,the less public criticism it will face.Transparency increases investor con-fidence.”

To assure success of the govern-ment’s IPO program, Reda explainsthat three key elements must be met.“I call it the success triangle: timing,pricing, and promotion,” he says.“First, the government should choosethe best time for listing state-ownedcompanies. Secondly, price the stocksfairly. Third, promote the stocks oflisted companies to attract both for-eign and domestic investments.”

Deciding to InvestDividing the program into two phaseswas important to boost investor confi-dence. The first phase of increasingthe free float and selling additionalshares of the two already-listed com-panies, AMOC and the EasternCompany, will prepare the market forthe second phase, according to Reda. “The main purpose of including

listed state-owned companies in theIPO program is to expand the privatesector’s stake,” el Desoki says. “Thiswill support improving the financialperformance of these companies.”Furthermore, economic and financial

experts agreed that any counseling ser-vice should be based on financial andtechnical analyses. “For the first phase,investors have a clear vision, since thecompanies already are listed,” says Reda.“However, it is going to be more compli-cated in the second phase. It will mainlydepend on the availability of data foreach company.”El Shenety believes the stock mar-

ket can be a lucrative investmentchannel with new listings. “It will giveinvestors a bigger set of opportunitiesto look at. I would recommend thatthey look at these opportunities andallocate part of their portfolios tothese new listings,” he says. “Thebelief is that the biggest gains happenin the first few days, and I think thiswill affect the view of individualinvestors.” ■

24• Business Monthly - OCTOBER 2018

InDepth

“The belief is that the biggest gains happenin the first few days, and I think this willaffect the view of individual investors.”

Egypt100

Morocco71

Jordan65

Kuwait52

Bahrain44

UAE17

Saudi Arabia

Rank is out of 137.Source: Global Competitiveness Index 2017-2018

30

Lebanon105

Competitiveness of Regional Players

26• Business Monthly - OCTOBER 2018

At a Glance

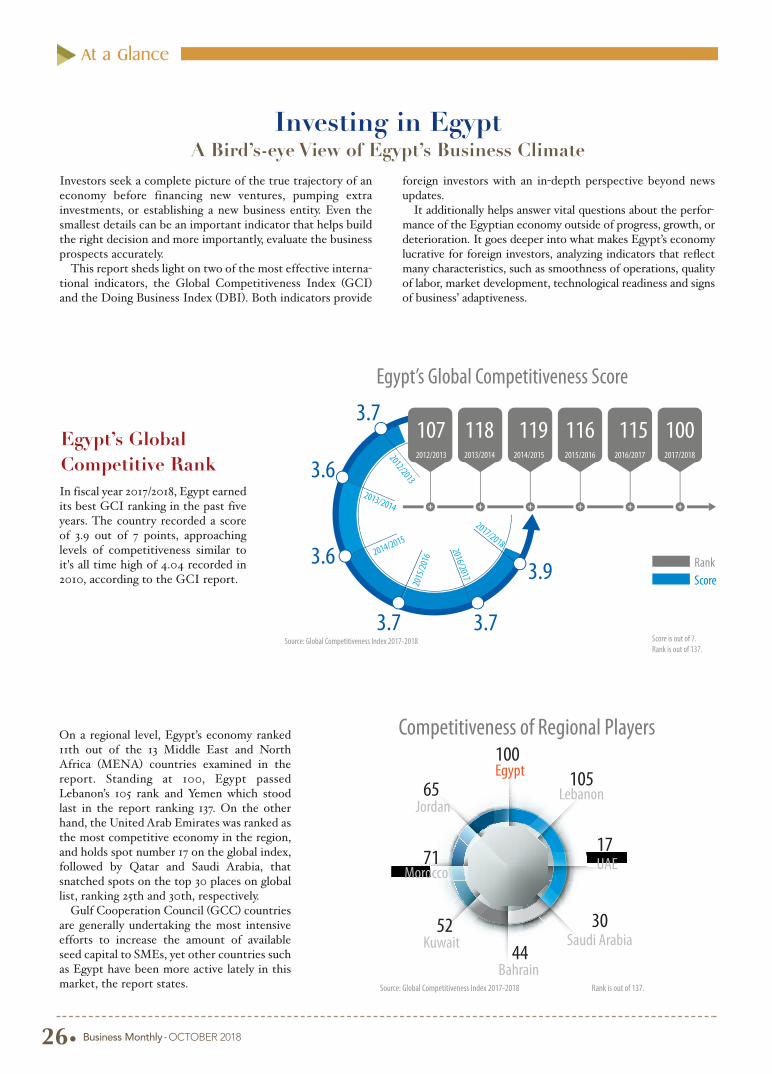

Investing in EgyptA Bird’s-eye View of Egypt’s Business Climate

Egypt’s GlobalCompetitive Rank

Investors seek a complete picture of the true trajectory of aneconomy before financing new ventures, pumping extrainvestments, or establishing a new business entity. Even thesmallest details can be an important indicator that helps buildthe right decision and more importantly, evaluate the businessprospects accurately.This report sheds light on two of the most effective interna-

tional indicators, the Global Competitiveness Index (GCI)and the Doing Business Index (DBI). Both indicators provide

foreign investors with an in-depth perspective beyond newsupdates.It additionally helps answer vital questions about the perfor-

mance of the Egyptian economy outside of progress, growth, ordeterioration. It goes deeper into what makes Egypt’s economylucrative for foreign investors, analyzing indicators that reflectmany characteristics, such as smoothness of operations, qualityof labor, market development, technological readiness and signsof business’ adaptiveness.

In fiscal year 2017/2018, Egypt earnedits best GCI ranking in the past fiveyears. The country recorded a scoreof 3.9 out of 7 points, approachinglevels of competitiveness similar toit's all time high of 4.04 recorded in2010, according to the GCI report.

On a regional level, Egypt’s economy ranked11th out of the 13 Middle East and NorthAfrica (MENA) countries examined in thereport. Standing at 100, Egypt passedLebanon’s 105 rank and Yemen which stoodlast in the report ranking 137. On the otherhand, the United Arab Emirates was ranked asthe most competitive economy in the region,and holds spot number 17 on the global index,followed by Qatar and Saudi Arabia, thatsnatched spots on the top 30 places on globallist, ranking 25th and 30th, respectively.Gulf Cooperation Council (GCC) countries

are generally undertaking the most intensiveefforts to increase the amount of availableseed capital to SMEs, yet other countries suchas Egypt have been more active lately in thismarket, the report states.

2012/2013

2012/2013 2013/2014 2014/2015 2015/2016 2016/2017 2017/2018

3.7

3.6

3.6

3.7 3.7

3.9

2013/2014

2014/2015

2015

/201

6

2016/2017

2017/2018

107 118 119 116 115 100

Source: Global Competitiveness Index 2017-2018 Score is out of 7.Rank is out of 137.

RankScore

Egypt’s Global Competitiveness Score

•27Business Monthly - OCTOBER 2018

At a Glance

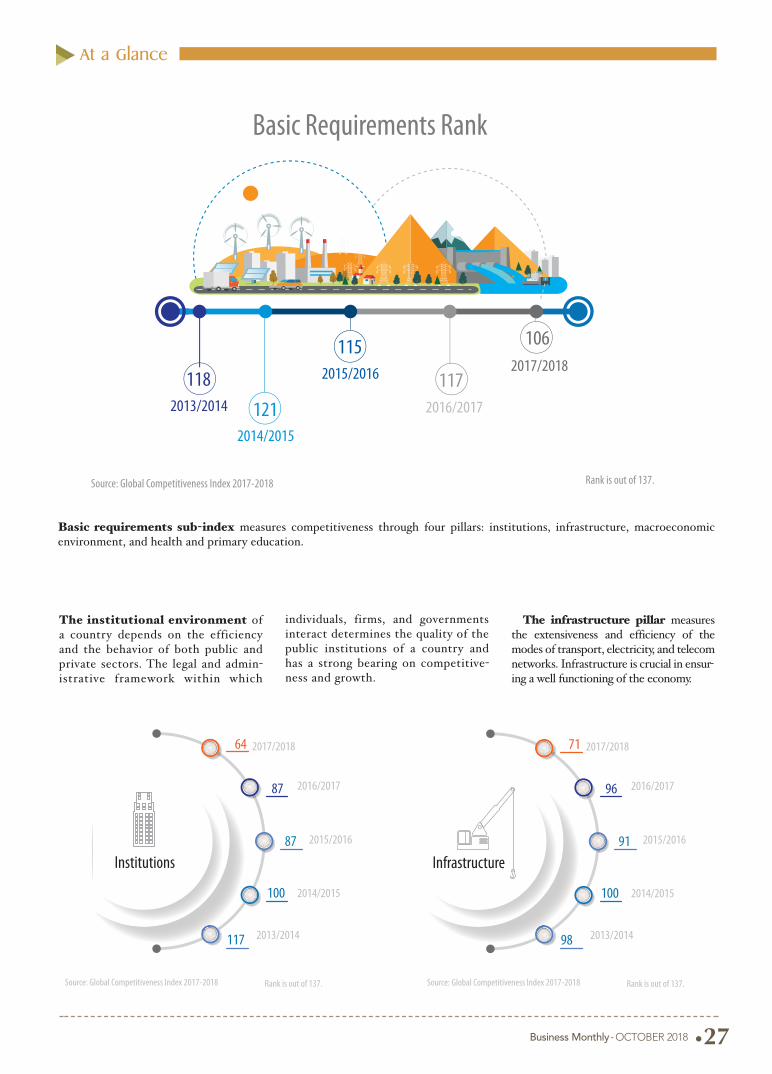

Basic requirements sub-index measures competitiveness through four pillars: institutions, infrastructure, macroeconomicenvironment, and health and primary education.

2013/2014

2014/2015

2015/2016

2016/2017

2017/2018118

121

115

117

106

Basic Requirements Rank

Rank is out of 137.Source: Global Competitiveness Index 2017-2018

Infrastructure

98

100

91

96

71 2017/2018

2016/2017

2015/2016

2014/2015

2013/2014

Source: Global Competitiveness Index 2017-2018 Rank is out of 137.

The institutional environment ofa country depends on the efficiencyand the behavior of both public andprivate sectors. The legal and admin-istrative framework within which

individuals, firms, and governmentsinteract determines the quality of thepublic institutions of a country andhas a strong bearing on competitive-ness and growth.

The infrastructure pillar measuresthe extensiveness and efficiency of themodes of transport, electricity, and telecomnetworks. Infrastructure is crucial in ensur-ing a well functioning of the economy.

Institutions

117

100

87

87

64 2017/2018

2016/2017

2015/2016

2014/2015

2013/2014

Source: Global Competitiveness Index 2017-2018 Rank is out of 137.

28• Business Monthly - OCTOBER 2018

At a Glance

140

141

137

134

132 2017/2018

2016/2017

2015/2016

2014/2015

2013/2014

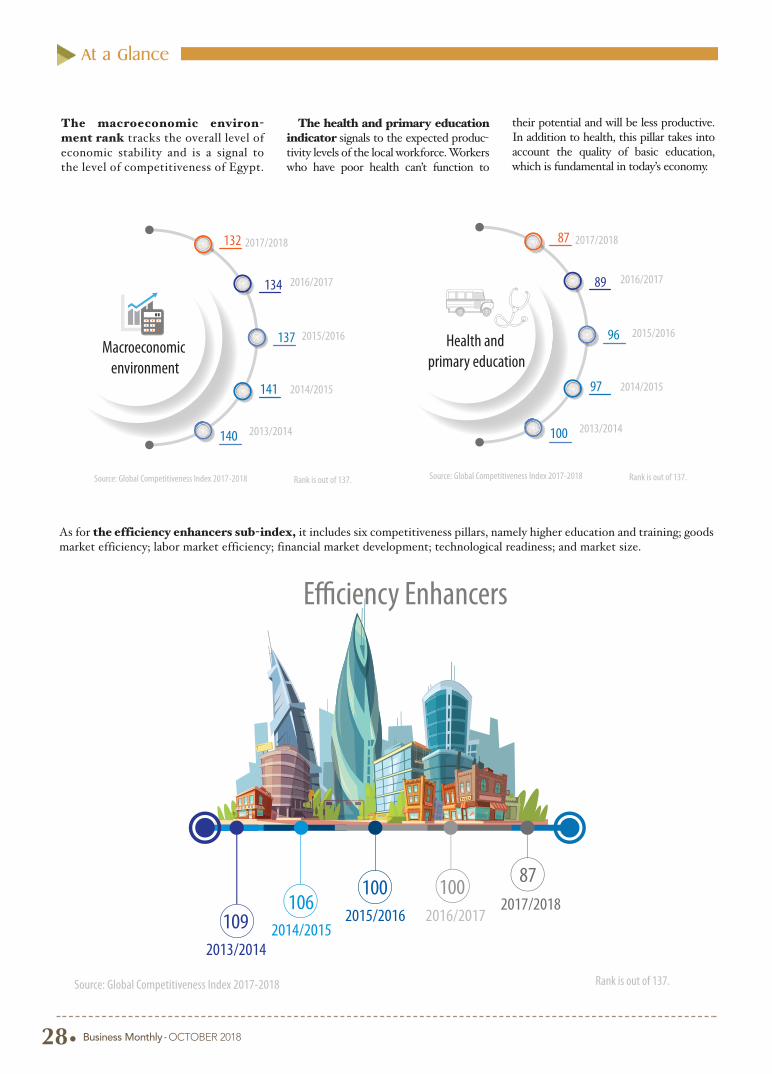

Macroeconomic environment

Source: Global Competitiveness Index 2017-2018 Rank is out of 137.

Health and primary education

100

97

96

89

87 2017/2018

2016/2017

2015/2016

2014/2015

2013/2014

Source: Global Competitiveness Index 2017-2018 Rank is out of 137.

The macroeconomic environ-ment rank tracks the overall level ofeconomic stability and is a signal tothe level of competitiveness of Egypt.

The health and primary educationindicator signals to the expected produc-tivity levels of the local workforce. Workerswho have poor health can’t function to

their potential and will be less productive.In addition to health, this pillar takes intoaccount the quality of basic education,which is fundamental in today’s economy.

As for the efficiency enhancers sub-index, it includes six competitiveness pillars, namely higher education and training; goodsmarket efficiency; labor market efficiency; financial market development; technological readiness; and market size.

Source: Global Competitiveness Index 2017-2018 Rank is out of 137.

2013/20142014/2015

2015/2016 2016/20172017/2018

109106

100 100 87

•29Business Monthly - OCTOBER 2018

At a Glance

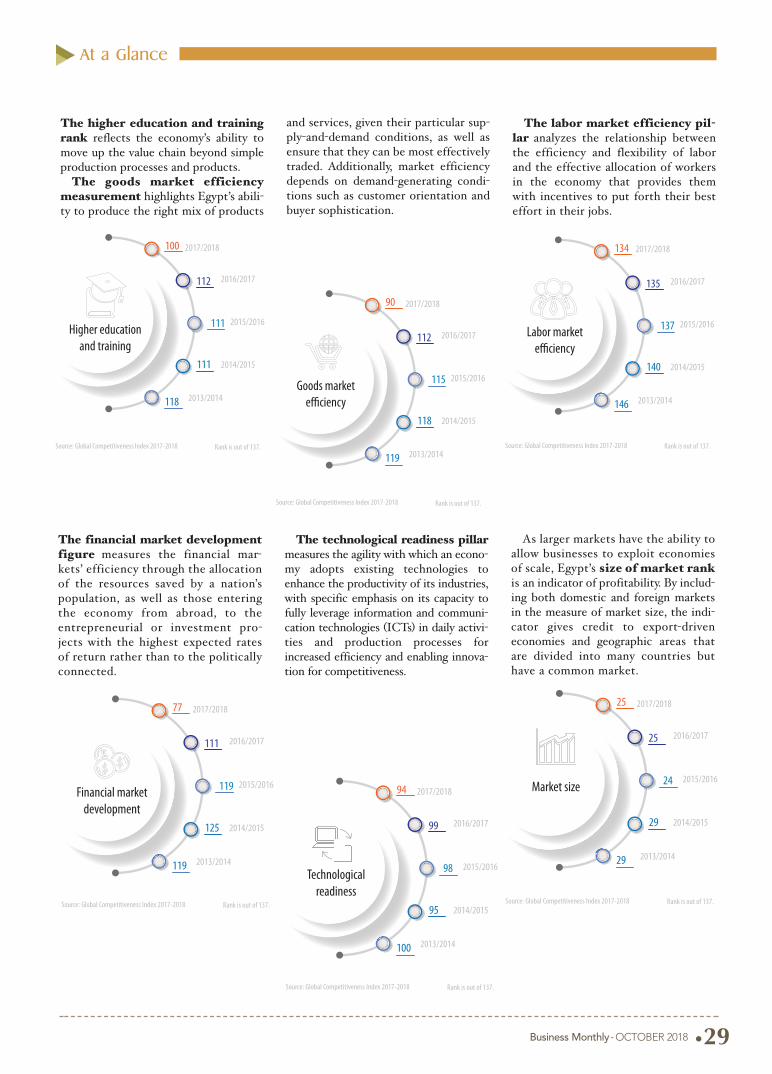

The higher education and trainingrank reflects the economy’s ability tomove up the value chain beyond simpleproduction processes and products.

The goods market efficiencymeasurement highlights Egypt’s abili-ty to produce the right mix of products

and services, given their particular sup-ply-and-demand conditions, as well asensure that they can be most effectivelytraded. Additionally, market efficiencydepends on demand-generating condi-tions such as customer orientation andbuyer sophistication.

The labor market efficiency pil-lar analyzes the relationship betweenthe efficiency and flexibility of laborand the effective allocation of workersin the economy that provides themwith incentives to put forth their besteffort in their jobs.

Source: Global Competitiveness Index 2017-2018 Rank is out of 137.

118

111

111

112

100 2017/2018

2016/2017

2015/2016

2014/2015

2013/2014

Higher education and training

Source: Global Competitiveness Index 2017-2018 Rank is out of 137.

119

118

115

112

90 2017/2018

2016/2017

2015/2016

2014/2015

2013/2014

Goods market

Source: Global Competitiveness Index 2017-2018 Rank is out of 137.

146

140

137

135

134 2017/2018

2016/2017

2015/2016

2014/2015

2013/2014

Labor market

Source: Global Competitiveness Index 2017-2018 Rank is out of 137.

119

125

119

111

77 2017/2018

2016/2017

2015/2016

2014/2015

2013/2014

Financial market development

Source: Global Competitiveness Index 2017-2018 Rank is out of 137.

100

95

98

99

94 2017/2018

2016/2017

2015/2016

2014/2015

2013/2014

Technological readiness

Source: Global Competitiveness Index 2017-2018 Rank is out of 137.

29

29

24

25

25 2017/2018

2016/2017

2015/2016

2014/2015

2013/2014

Market size

The financial market developmentfigure measures the financial mar-kets’ efficiency through the allocationof the resources saved by a nation’spopulation, as well as those enteringthe economy from abroad, to theentrepreneurial or investment pro-jects with the highest expected ratesof return rather than to the politicallyconnected.

The technological readiness pillarmeasures the agility with which an econo-my adopts existing technologies toenhance the productivity of its industries,with specific emphasis on its capacity tofully leverage information and communi-cation technologies (ICTs) in daily activi-ties and production processes forincreased efficiency and enabling innova-tion for competitiveness.

As larger markets have the ability toallow businesses to exploit economiesof scale, Egypt’s size of market rankis an indicator of profitability. By includ-ing both domestic and foreign marketsin the measure of market size, the indi-cator gives credit to export-driveneconomies and geographic areas thatare divided into many countries buthave a common market.

30• Business Monthly - OCTOBER 2018

At a Glance

Source: Global Competitiveness Index 2017-2018 Rank is out of 137.

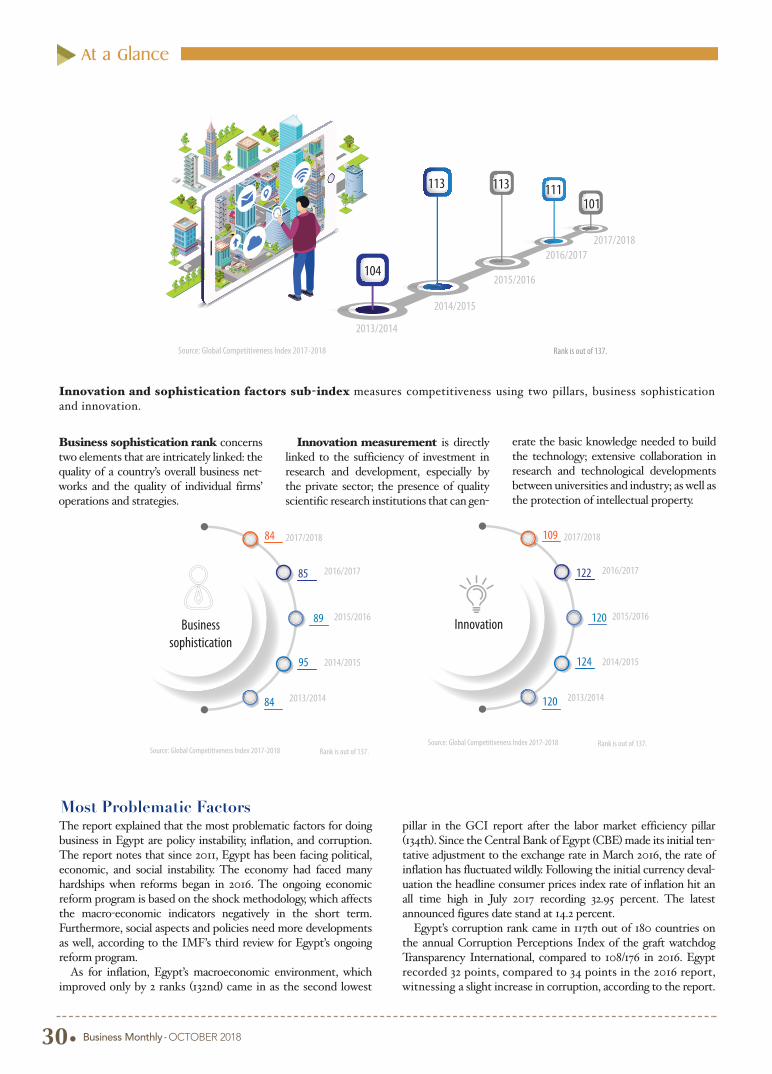

84

95

89

85

84 2017/2018

2016/2017

2015/2016

2014/2015

2013/2014

Business sophistication

Source: Global Competitiveness Index 2017-2018 Rank is out of 137.

120

124

120

122

109 2017/2018

2016/2017

2015/2016

2014/2015

2013/2014

Innovation

Business sophistication rank concernstwo elements that are intricately linked: thequality of a country’s overall business net-works and the quality of individual firms’operations and strategies.

Innovation measurement is directlylinked to the sufficiency of investment inresearch and development, especially bythe private sector; the presence of qualityscientific research institutions that can gen-

erate the basic knowledge needed to buildthe technology; extensive collaboration inresearch and technological developmentsbetween universities and industry; as well asthe protection of intellectual property.

Most Problematic FactorsThe report explained that the most problematic factors for doingbusiness in Egypt are policy instability, inflation, and corruption.The report notes that since 2011, Egypt has been facing political,economic, and social instability. The economy had faced manyhardships when reforms began in 2016. The ongoing economicreform program is based on the shock methodology, which affectsthe macro-economic indicators negatively in the short term.Furthermore, social aspects and policies need more developmentsas well, according to the IMF’s third review for Egypt’s ongoingreform program.As for inflation, Egypt’s macroeconomic environment, which

improved only by 2 ranks (132nd) came in as the second lowest

pillar in the GCI report after the labor market efficiency pillar(134th). Since the Central Bank of Egypt (CBE) made its initial ten-tative adjustment to the exchange rate in March 2016, the rate ofinflation has fluctuated wildly. Following the initial currency deval-uation the headline consumer prices index rate of inflation hit anall time high in July 2017 recording 32.95 percent. The latestannounced figures date stand at 14.2 percent.Egypt’s corruption rank came in 117th out of 180 countries on

the annual Corruption Perceptions Index of the graft watchdogTransparency International, compared to 108/176 in 2016. Egyptrecorded 32 points, compared to 34 points in the 2016 report,witnessing a slight increase in corruption, according to the report.

Innovation and sophistication factors sub-index measures competitiveness using two pillars, business sophisticationand innovation.

2017/20182016/2017

2015/2016

2014/2015

2013/2014

101111113113

104

Source: Global Competitiveness Index 2017-2018 Rank is out of 137.

•31Business Monthly - OCTOBER 2018

At a Glance

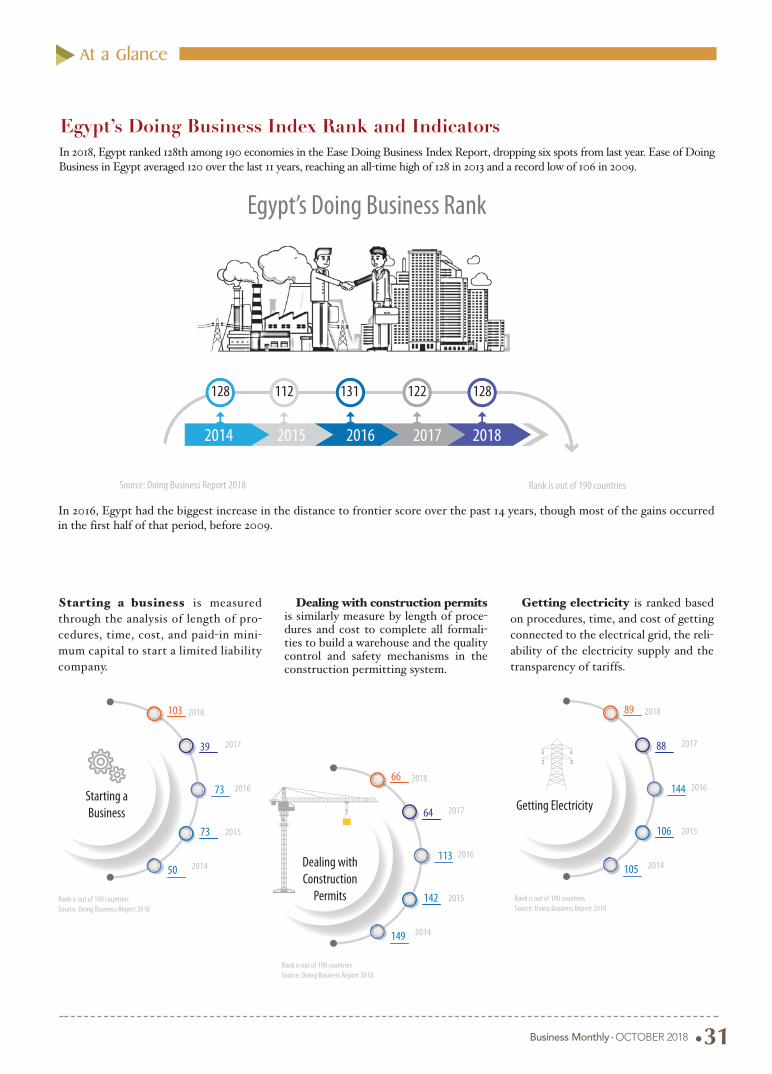

Egypt’s Doing Business Index Rank and IndicatorsIn 2018, Egypt ranked 128th among 190 economies in the Ease Doing Business Index Report, dropping six spots from last year. Ease of DoingBusiness in Egypt averaged 120 over the last 11 years, reaching an all-time high of 128 in 2013 and a record low of 106 in 2009.

In 2016, Egypt had the biggest increase in the distance to frontier score over the past 14 years, though most of the gains occurredin the first half of that period, before 2009.

Source: Doing Business Report 2018 Rank is out of 190 countries

Egypt’s Doing Business RankEgypt’s Doing Business Rank

2015 2016 2017 20182014

128 112 131 122 128

Rank is out of 190 countriesSource: Doing Business Report 2018

50

73

73

39

103 2018

2017

2016

2015

2014

Starting a Business

Rank is out of 190 countriesSource: Doing Business Report 2018

149

142

113

64

66 2018

2017

2016

2015

2014

Dealing withConstruction

Permits Rank is out of 190 countriesSource: Doing Business Report 2018

105

106

144

88

89 2018

2017

2016

2015

2014

Getting Electricity

Starting a business is measuredthrough the analysis of length of pro-cedures, time, cost, and paid-in mini-mum capital to start a limited liabilitycompany.

Dealing with construction permitsis similarly measure by length of proce-dures and cost to complete all formali-ties to build a warehouse and the qualitycontrol and safety mechanisms in theconstruction permitting system.

Getting electricity is ranked basedon procedures, time, and cost of gettingconnected to the electrical grid, the reli-ability of the electricity supply and thetransparency of tariffs.

Rank is out of 190 countriesSource: Doing Business Report 2018

156

152

157

162

160 2018

2017

2016

2015

2014

Enforcing Contracts

32• Business Monthly - OCTOBER 2018

At a Glance

Rank is out of 190 countriesSource: Doing Business Report 2018

148

149

151

162

167 2018

2017

2016

2015

2014

Paying Taxes

Rank is out of 190 countriesSource: Doing Business Report 2018

83

99

155

168

170 2018

2017

2016

2015

2014

Trading acrossBorders

Paying taxes is measured through thepayments, time, and total tax rate for afirm to comply with all tax regulations aswell as post-filing processes.

Trading across borders rankdepends on the time and cost to exportthe product of comparative advantageand import automotive parts.

Enforcing contracts pillar isbased on the time and cost to resolve acommercial dispute and the quality ofjudicial processes.

Registering property index is basedon procedures, time, and cost to transfera property and the quality of the landadministration system.

Getting credit rank is based onthe quantification of the movable col-lateral laws and credit informationsystems.

Protecting minority investors ismeasured by analyzing minority sharehold-ers’ rights in related-party transactions andin corporate governance.

Rank is out of 190 countriesSource: Doing Business Report 2018

105

84

111

109

119 2018

2017

2016

2015

2014

Registering Property

Rank is out of 190 countriesSource: Doing Business Report 2018

86

71

79

82

90 2018

2017

2016

2015

2014

Getting Credit

Rank is out of 190 countriesSource: Doing Business Report 2018

147

135

122

114

81 2018

2017

2016

2015

2014

Protecting Minority Investors

Rank is out of 190 countriesSource: Doing Business Report 2018

146

126

119

109

115 2018

2017

2016

2015

2014

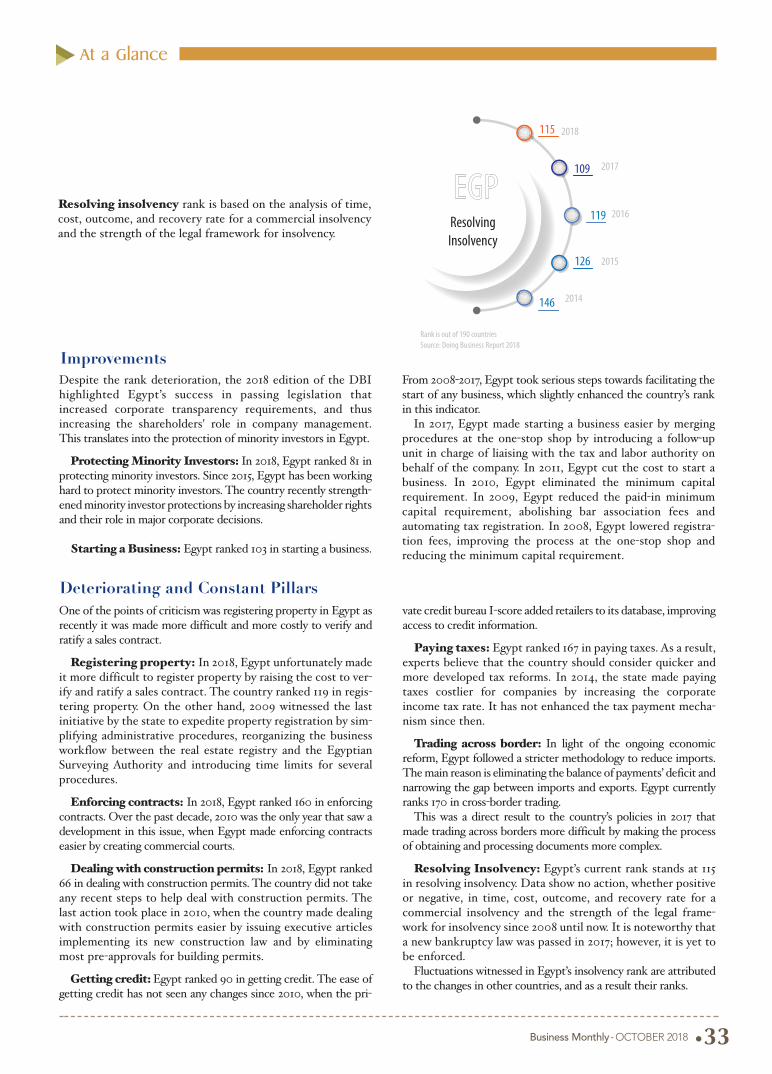

Resolving Insolvency

Resolving insolvency rank is based on the analysis of time,cost, outcome, and recovery rate for a commercial insolvencyand the strength of the legal framework for insolvency.

ImprovementsDespite the rank deterioration, the 2018 edition of the DBIhighlighted Egypt’s success in passing legislation thatincreased corporate transparency requirements, and thusincreasing the shareholders' role in company management.This translates into the protection of minority investors in Egypt.

Protecting Minority Investors: In 2018, Egypt ranked 81 inprotecting minority investors. Since 2015, Egypt has been workinghard to protect minority investors. The country recently strength-ened minority investor protections by increasing shareholder rightsand their role in major corporate decisions.

Starting a Business: Egypt ranked 103 in starting a business.

From 2008-2017, Egypt took serious steps towards facilitating thestart of any business, which slightly enhanced the country’s rankin this indicator.In 2017, Egypt made starting a business easier by merging

procedures at the one-stop shop by introducing a follow-upunit in charge of liaising with the tax and labor authority onbehalf of the company. In 2011, Egypt cut the cost to start abusiness. In 2010, Egypt eliminated the minimum capitalrequirement. In 2009, Egypt reduced the paid-in minimumcapital requirement, abolishing bar association fees andautomating tax registration. In 2008, Egypt lowered registra-tion fees, improving the process at the one-stop shop andreducing the minimum capital requirement.

Deteriorating and Constant PillarsOne of the points of criticism was registering property in Egypt asrecently it was made more difficult and more costly to verify andratify a sales contract.

Registering property: In 2018, Egypt unfortunately madeit more difficult to register property by raising the cost to ver-ify and ratify a sales contract. The country ranked 119 in regis-tering property. On the other hand, 2009 witnessed the lastinitiative by the state to expedite property registration by sim-plifying administrative procedures, reorganizing the businessworkflow between the real estate registry and the EgyptianSurveying Authority and introducing time limits for severalprocedures.

Enforcing contracts: In 2018, Egypt ranked 160 in enforcingcontracts. Over the past decade, 2010 was the only year that saw adevelopment in this issue, when Egypt made enforcing contractseasier by creating commercial courts.

Dealing with construction permits: In 2018, Egypt ranked66 in dealing with construction permits. The country did not takeany recent steps to help deal with construction permits. Thelast action took place in 2010, when the country made dealingwith construction permits easier by issuing executive articlesimplementing its new construction law and by eliminatingmost pre-approvals for building permits.

Getting credit: Egypt ranked 90 in getting credit. The ease ofgetting credit has not seen any changes since 2010, when the pri-

vate credit bureau I-score added retailers to its database, improvingaccess to credit information.

Paying taxes: Egypt ranked 167 in paying taxes. As a result,experts believe that the country should consider quicker andmore developed tax reforms. In 2014, the state made payingtaxes costlier for companies by increasing the corporateincome tax rate. It has not enhanced the tax payment mecha-nism since then.

Trading across border: In light of the ongoing economicreform, Egypt followed a stricter methodology to reduce imports.The main reason is eliminating the balance of payments’ deficit andnarrowing the gap between imports and exports. Egypt currentlyranks 170 in cross-border trading.This was a direct result to the country’s policies in 2017 that

made trading across borders more difficult by making the processof obtaining and processing documents more complex.

Resolving Insolvency: Egypt’s current rank stands at 115in resolving insolvency. Data show no action, whether positiveor negative, in time, cost, outcome, and recovery rate for acommercial insolvency and the strength of the legal frame-work for insolvency since 2008 until now. It is noteworthy thata new bankruptcy law was passed in 2017; however, it is yet tobe enforced. Fluctuations witnessed in Egypt’s insolvency rank are attributed

to the changes in other countries, and as a result their ranks.

•33Business Monthly - OCTOBER 2018

At a Glance

34•Business Monthly - OCTOBER 2018

Cover Story

As the government attempts to make Egypt a cashless economy by pushing its agencies toaccept only payments made online and cards, challenges persist.

By Tamer Hafez

Coming SoonA Cashless Society

•35Business Monthly - OCTOBER 2018

Cover Story

“Despite having an increasingly stronger position in thelocal market since 2012, 85 percent of Jumia’s cus-tomers in Egypt choose the ‘pay on delivery’ option,”says Hisham Safwat, Egypt’s CEO of Jumia, an e-com-

merce website operating in 21 other African countries. “E-com-merce is supposed to help increase cashless transactions. Yetdespite our best efforts [periodic promotions and discountswhen paying online] buyers just want to pay in cash.” Egyptians love using cash, even when buying something offthe internet. A 2018 McKinsey report noted that only 2 percentof Egypt’s payment transactions were cashless in 2017. Last year,cashless transactions accounted for 4.4 percent of Egypt’s GDP,according to the report. This comes at a time when the government is pushing to makeEgypt a cashless society to create a more stable financial system,as all transactions would be recorded in the banking system.This is vital as such transactions would help achieve the goals ofthe country’s Vision 2030 plan, Hala el Saeed, minister of plan-ning, follow-up and administrative reform, noted during a con-ference in August. Such a system would include cashless pay-ment options for government agencies, individuals, and busi-nesses, making them faster, safer, and simpler. Yet many believe that neither Egypt’s society nor infrastruc-ture is ready for cashless payments on a national level. Such pay-ments would not solve imminent or nagging problems for locals,such as the fear of being conned. In addition, infrastructureneeds major updates to withstand extra loads. “To push aheadwith infrastructure investments and force civil servants to dothings differently on a national level needs a serious and strongcommitment from the government,” says Mohamed Shawky,deputy head of the customs clearance officers committee in theAlexandria Chamber of Commerce.

Perception 1.0 For many Egyptians, the idea of not paying for goods and ser-vices with paper notes is alien. “I generally don’t like to use cred-it cards because I need to feel how muchmoney I am paying for a product

or service, and not justgive the seller a card and type

in some numbers,” says KhadigaAmr, a 51-year-old university professor.

Meanwhile, factory manager Yassin el Gammal,35, avoids using his card in general as he fears his

information could be stolen. “The only exception is the ATMmachine, as it is owned by the bank,” says el Gammal.Such attitudes constitute a major obstacle for the govern-ment. “As banks, our biggest challenge has always been theparts of society that believe banks are evil,” says Adnan elSharkawy, former head of the Egyptian Real Estate Bank.

“These people deliberately avoid banks. No matter what youdo, they still won’t be banked.” He cites the example of thosewho withdraw all their salary as soon as it is deposited. “Eventhough they are banked on paper, in reality they are no differentfrom unbanked individuals,” says Sharkawy. “Those people cannever go cashless without strong campaigns to make thembelieve in the [banking] system.” This distrust dates back to the 1990s, according to TarekHelmy, a board member at Suez Canal Bank. “There can be nodenying that confidence in the system was lacking with thebankruptcy of a few high-profile non-bank investment firms,which were not supervised by the Central Bank of Egypt,” hesays. “Now, however, it is a completely different world.” A major factor in the successful shift to cashless transactionsin other countries stems from fear of being mugged or robbed,Sharkawy points out. One such example is Sweden, where about1 percent of the value of payments nationwide is done in papermoney and coins, according to Riksbank, Sweden’s CentralBank. "We wanted to minimize the risk of robberies, and it'squicker with the customers when they pay by card," VictoriaNilsson, who manages two bakeries in Sweden, told the BBC inSeptember 2017. Enabling such a switch is an array of consistentand strong legislations, such as banning the use of currency onbuses.In Egypt, however, being safe from mugging is not a high pri-ority. Yamen Sobhy, a 40-year-old civil engineer, bought his newcar with cash. He took the money from selling his old car, with-drew his savings, went to a second bank to withdraw a loan hehad previously secured, and took his brother to the car show-room, where they paid in cash.

Cashless GroundworkDespite cultural barriers and limited infrastructure, Egyptshould have a lot of potential when it comes to adopting cashlesstransactions because of its predominantly young population, saythose interviewed. According to a report by CanadianHootsuite, in 2017 there were 49.23 million—out of a popula-tion of nearly 100 million—already online. That is a 41 percentincrease compared to 2016, stated the report. However, most Egyptians don’t use smartphones to access theinternet. As of July, smartphone penetration remains low at 34.2percent of all mobile users, according to the ministry of commu-nications report “ICT Indicators in Brief”Another factor that could make people stop using papermoney on a daily basis is access to financial services and usabletools. According to CBE Governor, Tarek Amer, during a Julyinterview with The Egyptian Economist magazine, the numberof bank accounts equals 33 percent of the 60 million people eli-gible to have them. However, as it is common practice forEgyptians to have multiple bank accounts, the actual number of

banked unique individuals is likely less.“I believe that 10 million uniqueEgyptians have at least one bankaccount,” says Shawky. The CBE doesn’t publish figures onhow many bank accounts exist or howmany individuals are banked. However,according to the 2018 McKinsey Report,there were 22.95 million debit, credit, andprepaid cards in circulation as of 2017, ofwhich only 3.5 percent of debit cards and1.4 percent of credit cards were used tomake a purchase in the year. While all canbe used to pay for goods and services,only the 2.8 million credit cards in circu-lation can be used online. Nevertheless,the report highlighted that these figuresrepresent a 17 percent increase in com-parison to the number of available cardsa year earlier.

Building the SystemFor the government, the first step tobuild a cashless society was to createthe National Council for Payments(NCP), which has a higher authoritythan ministries and is headed by thePresident Abdel Fattah al Sisi, accord-ing to Helmy. Established in February2017, the NPC has a mandate toreduce the use of banknotes outside thebanking system as well as develop anational payment system that wouldachieve financial inclusion.The NCP has met only three times,most recently in September. Accordingto a press release after that meeting,Amer said the CBE was working on a“general framework for a transition toa less cash-based society” with the firstconcrete announcements to be made bythe end of 2018. The release furthernoted the CBE will have cybercrimetraining for those overseeing the newsystem. It added that Finance Minister,Mohamed Maait, has completed con-version of payroll to e-payments for allcivil servants, while the InteriorMinistry is researching the issuance of anew national identification cards withsmart chips, opening the door for usingID cards to gain access to governmentservices, including subsidies. Such tools require cooperation

among the private sector, CBE, andMinistry of Information andCommunication Technology (MCIT).“This is one crucial factor, in my view,as there is a definite mutual need forbanking and ICT infrastructures towork together,” says Mohamed elItriby, chairman of Banque Misr. He explains the main role of the CBEis to ensure the security and soundnessof the transactions as the nation movesfrom banknotes and checks to onlineand cashless transactions. Meanwhile,the MCIT and private sector are neededto help banks get services online as wellas offer more ways to access the inter-net. Sharkawy of the customs clearanceunion believes the introduction of 4Ghigh-speed internet helped facilitate theintegration as it ensured real-timeupdates whenever a transaction wasexecuted, which is vital for security.“Having a 100 percent reliable infra-structure is step one,” he continues,“you can’t rush this step.” Lobna Helal, the deputy CBE gover-nor, explained during an August confer-ence that the bank’s strategy is to buildfinTech tools and services that potentialusers would find useful, enticing themto make the switch. “We want people toput their money in banks,” she said.“Then they would want to pay foreverything using their cards, and thiswould push businesses to offer this pay-ment option.” She noted that a seniorstaff delegation from the CBE andbanks traveled to Sweden to learn fromits experiences.

National-Scope Projects One of the first projects under the CBEumbrella was implementation of a cash-less payment system in 2017 thatincludes ATM machines and convertingsalary payments for 5 million govern-ment employees from cash to bankaccount transfers, accessible via debitcards. In addition, the project saw 10government universities equipped tocollect education fees using debit andcredit cards. In March, HelwanUniversity announced a partnershipwith the National Bank of Egypt, Visa,

and e-Finance to allow students to paytuition using mobile-oriented toolsincluding NBEPay and mVisa. A furtherpart includes equipping farmers withsmart cards to pay for their subsidizedseeds and fertilizer.“These projects are excellent exam-ples of the government working withthe private sector on the paymentfront,” Saeed said during a Februaryconference organized by the EgyptianFederation of Industries. Another major government project isconverting the Egyptian CustomsAuthority (ECA) payment system fromaccepting only cash to requiring onlinepayments starting 2019. The projectwas announced in November 2017.Currently, payment in banknotes andchecks is allowed for amounts underEGP 100,000. Larger amounts must bepaid through the ECA website. If that isimpossible, cash payments would beaccepted with a fee added.Moreover, under development at theCBE are upgrades to the mobile pay-ment system for better regulation andtransparency, according to AymanHussein, CBE sub-governor for pay-ment systems and business technology.This is in addition to the developmentof a system that allows cashless inter-governmental payments, he adds. In thelong term, the CBE is working on creat-ing a unified payment card that wouldbe used in any transaction with the gov-ernment. According to Maait, talking tothe press in September, as of next April,any citizen not paying the governmentusing a payment card will be fined EGP10,000 plus 10 percent of what is owed.The system should be up and runningby January and include prepaid cardsissued at government agencies. It isunclear whether these agencies willaccept commercial credit and debitcards. The private sector has also beeninvesting cashless-transaction projects.In October 2017, the CommercialInternational Bank and Careem-Egyptagreed to develop a digital wallet for theride-sharing firm’s drivers for quicktransfer of payments with the company

Cover Story

36•Business Monthly - OCTOBER 2018

as well as clients who have a compatibleelectronic tool. Furthermore, inOctober, AlexBank signed a memoran-dum of understanding with theNational Council for Women to offerdigital payment services and toolsto encourage

womento have bank accounts, asa step towards formalizingtheir business under theone-man-show companylaw or micro-enterpriseslaw implemented since fis-cal year 2017/2018. Amonth later, in November,Vodafone Egypt signed anagreement with AlexBank tosupport the mobile moneytransfers.

FinTech Downscaling These large projects are complement-ed by small-scale businesses that aremerging and tailoring technology andfinancial services (finTech) to encourageindividual companies and laymen toswitch to cashless transactions. “The

wave of innova-tion sweepingthrough theworld of finan-cial technolo-gy promisesn o t h i n gshort of arevolution[…] It willc h a n g ethe natureof money,shake thefoundationsof centralbanking, anddeliver nothingless than a democ-ratic revolution forall who use financialservices,” said Mark

Carney, the Governor ofBank of England last January. The Egyptian government

understood the best way to create acashless society was integrating cashlesspayment options within startups fromday one. To that end, in September2017, the Ministry of Investment andInternational Cooperation along withthe U.N. Development Program andinvestment bank EFG-Hermeslaunched Fekretak Sherketak (YourIdea, Your Company) accelerator, anentity that works with entrepreneurs onturning their business plans into star-tups. Projects supported by EFG-Hermes include fintech tools that makethem cashless enterprises. Barclays Bank and Flat6Labs, anentrepreneurship support organization,established finTech focused 1864Accelerator in May 2016. It is a 14-week program that focuses on commer-cializing finTech ideas. Supporting thesecompanies as well is the AUC VentureLab Fintech accelerator, established bythe American University in Cairo andthe Commercial International Bank. Inaddition, Payfort incubator, an organi-zation that works on growing youngstartups, is known as a finTech factory.It is a subsidiary of Amazon that

Cover Story

•37Business Monthly - OCTOBER 2018

launched in 2016 and serves theMENA region through its Cairo office.However, the incubator accepts onlybusinesses that can benefit Payfort. This rise of accelerators and incuba-tors signals strong potential forfinTechs in Egypt and that local entre-preneurs are willing, and have theskills, to capitalize on the anticipatedboom. “FinTech is one of the mostprominent spaces in the startup com-munity in Egypt,” says KennedyKitheka, Seedstars managing directorin Egypt. “Early entrants are gainingtraction, and stronger, more structuredconcepts are popping up. The model ofFawry [Egypt’s first finTech, estab-lished in 2009], has demonstrated thevalidity of such business models.”Despite this growth, many believe fin-tech is still hampered by Egypt’s lowlevel of financial inclusion. “FinTechstartups usually have small markets iftheir services are not targeted towardimproving financial inclusion,” saysAbdelrahman Elsharawy, co-founder ofVapulus, a finTech firm specializing inonline payment software and hardware.

Informal EconomyConundrum Another major factor in deciding howcashless can Egypt ultimately becomerests with informal businesses. “I am afan of businesses that are cropping upon social media. They are inexpensiveand offer unique products and services.I stopped going to brand namesbecause they are too boring and expen-sive,” says Sara Sobhy, a 41-year-oldmiddle manager at a real estate firm.This is despite the inconvenience ofhaving to withdraw cash from an ATMwhenever she needs to buy somethingfrom unregistered online businesses. “Iwould like for them to offer paymentby credit card, but if not, it wouldn’t bea deal breaker,” she adds. To offer a cashless payment option,informal businesses need to register

with the state before opening a corpo-rate bank account and apply for acredit card license. However, the feasi-bility of such businesses is based on thepremise of avoiding government paper-work and hassle to reduce costs as wellas expedite the startup phase. “It wasperhaps the easiest and quickest deci-sion I ever took to become a profes-sional photographer. I just took somepictures, posted them on social mediaand mentioned that I am a freelancephotographer,” says Wael Saleh (nothis real name). Now, whatever he ispaid is not reported to the state, despitecharging several thousand pounds perevent and securing at least one gig aweek. Yet he is starting to rethink his statusas an informal professional, as itbecomes increasingly uncomfortablecarrying wads of cash. “I offer clientsthe option to pay me via a bank trans-fer, but nearly no one is doing it,” hesays. “I believe that if they can pay mewith a credit card, it would definitelybe much better for both of us.”However, the hassles he expects to facewhen registering still outweigh the ben-efits. “I am in a holding pattern, so tospeak. If my business gets any bigger, Imay have to register,” he says.

Problematic InfrastructureA major challenge to going cashless ona large scale is the tech infrastructure.A case in point is the repetitive net-work crashes that plague the ECAsince the law forced companies to payon the website. “We have been tryingto work with online payments for afew months, and it’s actually worse forus because the network keeps crashing,and we are left unable to pay due cus-toms for days,” says Shawky of thecustoms clearance officers committee.

“I [spoke] to people on the inside, andthey said it was because the network isoverloaded with requests.” This ishurting their business and raising costs,as paying in banknotes or checks addsan administration fee that can’t bepassed on to clients. Currently, no gov-ernment agency accepts credit cardpayments. Another potential obstacle is Egypt’sinconsistent legal infrastructure. “Oneimportant thing we need to consider isthat banks are heavily regulated.Meanwhile, tech companies are notheavily regulated,” says Itriby. “To cre-ate a cashless society, there has to be alegal convergence, or balance, betweenthe two sectors.” That has proved achallenge thus far as the CBE is heavilyregulating banks, for better or worse.A case in point is that mobile moneytransfers haven’t been a runaway suc-cess, in part because of restrictions ontransferred amounts, according toexperts. Currently, out of all smart-phones in Egypt, 9.5 million are sub-scribed to mobile money services.According to Hussein, they belong to 8million unique users. However, he isoptimistic such transfers will eventual-ly gain traction. For some, having a hybrid legal sys-tem and strong oversight to balancesecurity with flexibility should provestraightforward because the FinancialRegulatory Authority has a strongtrack record of regulating non-bankfinancial institutions. The key questionprobably will be how much the CBE isinvolved in fintech. Regardless, going completely cash-less is likely to take years, if notdecades. “I think my granddaughterwill not use cash at all,” says Amr, theuniversity professor and reluctant carduser. “My sons, who are in their 30s,already use cards when buying devices,and sometimes for groceries or out-ings. Their culture is noticeably differ-ent from mine.” ■

38• Business Monthly - OCTOBER 2018

Cover Story

“Even though they are banked on paper, inreality they are no different from unbankedindividuals.”

“I generally don’t like to use credit cardsbecause I need to feel how much money I amspending.”

•39Business Monthly - OCTOBER 2018

Cover Story

Even as stock market volatilityspreads from developed toemerging economies world-wide, investors are turning

their attention to countries like Egyptthat have undertaken financial sectorreforms. At the same time, Saudi Arabiais becoming a potent competitor sinceit began implementation of its Vision2030 initiative by gradually opening itsmarket further to foreign investors,removing most restrictions on partici-pation in Tadawul, its stock exchange. A recent Bloomberg article described

emerging-market stocks as one of thesafest places for investors as they are“cheaper today than they were beforethe U.S. presidential election, comparedwith U.S. and developed-market equi-ties. The lower valuations and growingearnings estimates may give the comfortinvestors need in times of turbulence.” Foreign investments in the Egyptian

Exchange (EGX) leaped from EGP 1.6billion before the floatation of thepound in late 2016 to EGP 25 billion inApril 2017 and EGP 73 billion ($4.1 bil-lion) by the end of last year, EGXChairman Mohamed Farid said inDecember. For Saudi Arabia, Tadawul’sreports show the total value of sharespurchased by foreigners reached SAR34.6 ($9.23 billion) in 2017, in compari-son to the slightly less SAR 33.91 billion($9 billion) in a year earlier.

EGX LuresIn line with economic reform measuresundertaken by the Egyptian govern-ment as part of the InternationalMonetary Fund loan program, the EGXhas embarked on a plan designed toimprove the capital market, includingincreasing its daily volume and tradingthrough a number of new measures. Anexample of which is targeting youngerinvestors. “Those who are 40 years oldand younger make up 75-80 percent ofthe population, yet only 30 to 34 per-cent of them are investors, we need toincrease this percentage,” Farid said dur-ing the Euromoney 2018 Conference inSeptember. To achieve greater partici-pation, the EGX wants to introduceincremental savings, an approach usedin many capital markets for long-terminvestments, he added.Amr Hussein el Alfy, head of

research at SHUAA Securities,believes raising awareness is the keyto attracting young people, sayinguniversities should do more toexpose undergraduates to economicsand finance. To that end, Faridannounced the EGX is working withthe Ministry of Education on afinance curriculum, including invest-ing in the stock market.Another obstacle is making mar-

kets more exciting. “Egypt’s stockexchange model is still plain vanilla,

with investors being able to makemoney in bull markets on the way up(being long),” el Alfy explains. Withthe long position, the investor buys astock with the expectation that itwill rise in value, and thus benefitfrom its upward price movement.Some experts, including el Alfy,

believe short-selling activity couldcomplement the long-position strat-egy that dominates the EGX.Therefore, the stock exchange hasbeen studying the implementation ofshort selling, which involves shed-ding shares at higher prices thenreacquiring them later at lowerprices.

The Financial RegulatoryAuthority told Reuters it would final-ize rules for short selling by the endof September, adding, “We will beready for implementation in early2019, then wait for an official deci-sion to start using it.”Furthermore, the EGX plans to

introduce derivatives, includingfutures that allow buying and sellingof stocks at a specified price anddate, which investors use to hedgetheir risk. “This will take 12-18months to be finalized because ofinformation technology require-ments, such as developing tradingand management systems,” Faridexplained.

Regional Focus

40• Business Monthly - OCTOBER 2018

As part of ongoing reform efforts, Saudi Arabia is opening its stock exchange to foreign investors,a move that could make the EGX less attractive.

By Julian Nabil

EGX vs. Saudi’s TadawulWhere should you invest?

•41

Adding futures to the mix wouldboost liquidity and provide investorswith more tools. “This will all add to themarket depth and drive more efficiency,in my opinion, and attract new types ofinvestors,” says el Alfy.Also in the works is restructuring

some indices to focus on certain sectorsbased on an international standard. “Wewant to add a total return index to allowpeople to see actual returns associatedwith the market and not only pricereturns,” said Farid.Total return indices track the gains of