Embed Size (px)

Citation preview

OFFERING CIRCULAR

Grupo Comercial Chedraui, S.A.B. de C.V. 133,793,545 Shares

________________________________________________________

Offering Price: Ps. 34.00 per Share

We are offering 119,385,898 shares of our Series B, Class I shares of common stock (the “Shares”) and the selling shareholder is offering 14,407,647 of our Shares in a combined offering consisting of (a) an initial public offering of 60,207,095 Shares in Mexico to the general public and (b) an international offering of 73,586,450 Shares in the United States to qualified institutional buyers as defined under Rule 144A under the Securities Act of 1933, as amended (the “Securities Act”) in transactions exempt from registration thereunder and in other countries outside of Mexico to certain non-U.S. persons in reliance on Regulation S under the Securities Act. Shares being offered in the combined offering may be reallocated among the Mexican offering and the international offering. See “Plan of Distribution.”

The initial purchasers and the Mexican underwriters have options, exercisable for 30 days from the date of this offering circular, to purchase, up to 20,069,032 Shares from us to cover over-allotments, if any. See “Plan of Distribution.”

No public market currently exists for the Shares. We have applied to register the Shares in Mexico with the Registro Nacional de Valores (the “RNV”) maintained by the Comisión Nacional Bancaria y de Valores (the “CNBV”) and to list the Shares for trading on the Bolsa Mexicana de Valores, S.A.B de C.V. (the “BMV”) under the symbol “CHDRAUI”. The registration of the Shares in the RNV is expected to be obtained on or before the closing of the Global Offering as required under the Ley del Mercado de Valores (the “Mexican Securities Market Law”). Registration of the Shares in the RNV does not imply any certification as to the investment quality of the Shares, our solvency or the accuracy or completeness of the information contained in this offering circular and such registration does not ratify or validate acts or omissions, if any, undertaken in contravention of applicable law.

Investing in the Shares involves risks. See “Risk Factors” beginning on page 16.

The Shares have not been and will not be registered under the Securities Act. The Shares may not be offered and sold within the United States or to U.S. persons, except to qualified institutional buyers in reliance on the exemption from registration provided by Rule 144A under the Securities Act and to certain non-U.S. persons in offshore transactions in reliance on Regulation S under the Securities Act. You are hereby notified that sellers of the Shares may be relying on the exemption from the provisions of Section 5 of the Securities Act provided by Rule 144A. See “Transfer Restrictions” for a description of the restrictions regarding the purchase and transfer of the Shares.

Delivery of the Shares in book-entry form will be made on or about May 5, 2010, through the book-entry system of S.D. Indeval Institución para el Depósito de Valores, S.A. de C.V. (“Indeval”) in Mexico City, Mexico.

Sole Global Coordinator

Citi

Joint Bookrunners

Citi Credit Suisse

The date of this offering circular is April 29, 2010.

i

TABLE OF CONTENTS NOTICE TO INVESTORS................................... ii SELECTED CONSOLIDATED FINANCIAL NOTICE TO NEW HAMPSHIRE RESIDENTS ....... iii INFORMATION........................................... 39 SERVICE OF PROCESS AND ENFORCEMENT OF MANAGEMENT’S DISCUSSION AND CIVIL LIABILITIES ....................................... iv ANALYSIS OF FINANCIAL CONDITION AND AVAILABLE INFORMATION............................. iv RESULTS OF OPERATIONS ......................... 42 FORWARD-LOOKING STATEMENTS ................ v BUSINESS .................................................... 62 PRESENTATION OF CERTAIN FINANCIAL MANAGEMENT ............................................ 94 INFORMATION............................................. vii PRINCIPAL AND SELLING SHAREHOLDERS... 99 GLOSSARY OF TERMS AND DEFINITIONS ........ ix RELATED PARTY TRANSACTIONS................ 100 SUMMARY ...................................................... 1 DESCRIPTION OF OUR CAPITAL STOCK AND THE GLOBAL OFFERING ................................. 9 BYLAWS ................................................... 101 SUMMARY FINANCIAL DATA.......................... 12 TAXATION................................................... 107 RISK FACTORS................................................ 16 PLAN OF DISTRIBUTION............................... 112 USE OF PROCEEDS .......................................... 27 TRANSFER RESTRICTIONS ........................... 117 CAPITALIZATION ............................................ 28 VALIDITY OF THE SHARES........................... 118 DILUTION ....................................................... 29 INDEPENDENT AUDITORS ............................ 119 DIVIDENDS AND DIVIDEND POLICY................ 30 INDEX TO CONSOLIDATED FINANCIAL EXCHANGE RATES.......................................... 31 STATEMENTS ............................................ F-1 THE MEXICAN SECURITIES MARKET.............. 32 ANNEX A— UNAUDITED INTERIM FINANCIAL INFORMATION........................................... A-1 ANNEX B—SIGNIFICANT DIFFERENCES BETWEEN MEXICAN FRS AND IFRS......... B-1

You should rely only on the information contained in this offering circular. We have not authorized anyone to provide you with information that is different. This offering circular may only be used where it is legal to sell these Shares. The information in this document may only be accurate as of the date on the front cover of this offering circular. We are not making an offer of these Shares in any jurisdiction where such an offer is not permitted.

THIS OFFERING CIRCULAR IS SOLELY THE RESPONSIBILITY OF GRUPO COMERCIAL CHEDRAUI, S.A.B. DE C.V. AND HAS NOT BEEN REVIEWED OR AUTHORIZED BY THE CNBV. APPLICATION HAS BEEN MADE TO REGISTER THE SHARES IN MEXICO WITH THE RNV MAINTAINED BY THE CNBV, WHICH IS A REQUIREMENT UNDER THE MEXICAN SECURITIES MARKET LAW. SUCH REGISTRATION IS EXPECTED TO BE OBTAINED ON OR BEFORE THE CLOSING OF THE GLOBAL OFFERING, AND DOES NOT IMPLY ANY CERTIFICATION AS TO THE INVESTMENT QUALITY OF THE SHARES, OUR SOLVENCY OR THE ACCURACY OR COMPLETENESS OF THE INFORMATION CONTAINED IN THIS OFFERING CIRCULAR AND SUCH REGISTRATION DOES NOT RATIFY OR VALIDATE ACTS OR OMISSIONS, IF ANY, UNDERTAKEN IN CONTRAVENTION OF APPLICABLE LAW. IN MAKING AN INVESTMENT DECISION, ALL INVESTORS, INCLUDING ANY MEXICAN CITIZEN WHO MAY ACQUIRE SHARES FROM TIME TO TIME, MUST RELY ON THEIR OWN EXAMINATION OF GRUPO COMERCIAL CHEDRAUI, S.A.B. DE C.V.

ii

NOTICE TO INVESTORS

The Mexican offering is being made in the United Mexican States (“Mexico”) pursuant to a prospectus in Spanish with the same date as this offering circular. The Mexican prospectus, which has been filed with and will be reviewed and approved by the CNBV, and this offering circular contain substantially the same information, in all material respects, except that the Mexican prospectus includes other information required by regulation in Mexico. The international offering is being made in the United States and elsewhere outside Mexico solely on the basis of information contained herein.

We are relying upon an exemption from registration under the Securities Act for an offer and sale of securities that do not involve a public offering. By purchasing the Shares, you will be deemed to have made the acknowledgments, representations and agreements described under “Transfer Restrictions” in this offering circular. We are not, and the initial purchasers and selling shareholder are not, making an offer to sell the Shares in any jurisdiction except where such an offer or sale is permitted. You should understand that you will be required to bear the financial risks of your investment for an indefinite period of time.

We have submitted this offering circular solely to a limited number of institutional investors in the United States and to certain investors outside the United States and Mexico so that they can consider a purchase of the Shares. We have not authorized the use of this offering circular for any other purpose. This offering circular may not be copied or reproduced in whole or in part. This offering circular may be distributed and its contents disclosed only to prospective investors to whom it is provided. By accepting delivery of this offering circular, you agree to these restrictions. See “Transfer Restrictions.”

This offering circular is based on information provided by us and other sources that we believe to be reliable. We, the initial purchasers and the selling shareholder cannot assure you that this information is accurate or complete. This offering circular summarizes certain documents and other information and we refer you to them for a more complete understanding of what we discuss in this offering circular.

We are not making any representation to any purchaser regarding the legality of an investment in the Shares by such purchaser under any legal investment or similar laws or regulations. You should not consider any information in this offering circular to be legal, financial, business or tax advice. You should consult your own counsel, accountant, business advisor and tax advisor for legal, financial, business and tax advice regarding any investment in the Shares.

We reserve the right to withdraw this offering of the Shares at any time and we and the initial purchasers reserve the right to reject any commitment to subscribe for the Shares in whole or in part and to allot to any prospective investor less than the full amount of Shares sought by that investor. The initial purchasers and certain related entities may acquire for their own account a portion of the Shares.

You must comply with all applicable laws and regulations in force in the jurisdiction to which you are subject and you must obtain any consent, approval or permission required by you for the purchase, offer or sale of the Shares under the laws and regulations in force in the jurisdiction to which you are subject or in which you make such purchase, offer or sale, and none of we, the initial purchasers or the selling shareholder will have any responsibility therefor.

In making an investment decision, you must rely on your own examination of us and the terms of this offering, including the merits and risks involved. Neither the U.S. Securities and Exchange Commission (the “SEC”) nor any other securities commission or other regulatory authority has approved or disapproved the Shares or determined if this offering circular is truthful, accurate, adequate or complete. Any representation to the contrary is a criminal offense. No public market currently exists for the Shares.

Notwithstanding anything in this offering circular to the contrary, except as reasonably necessary to comply with applicable securities laws, you (and each of your employees, representatives or other agents) may disclose to any and all persons, without limitation of any kind, the U.S. federal income tax treatment and tax structure of the offering and all materials of any kind (including opinions or other tax analyses) that are provided to you relating to such tax treatment and tax structure. For this purpose, “tax structure” is limited to facts relevant to the U.S. federal income tax treatment of the offering.

iii

NOTICE TO NEW HAMPSHIRE RESIDENTS

NEITHER THE FACT THAT A REGISTRATION STATEMENT OR AN APPLICATION FOR A LICENSE HAS BEEN FILED UNDER CHAPTER 421-B OF THE NEW HAMPSHIRE REVISED STATUTES WITH THE STATE OF NEW HAMPSHIRE NOR THE FACT THAT A SECURITY IS EFFECTIVELY REGISTERED OR A PERSON IS LICENSED IN THE STATE OF NEW HAMPSHIRE CONSTITUTES A FINDING BY THE SECRETARY OF STATE THAT ANY DOCUMENT FILED UNDER RSA 421-B IS TRUE, COMPLETE AND NOT MISLEADING. NEITHER ANY SUCH FACT NOR THE FACT THAT AN EXEMPTION OR EXCEPTION IS AVAILABLE FOR A SECURITY OR A TRANSACTION MEANS THAT THE SECRETARY OF STATE HAS PASSED IN ANY WAY UPON THE MERITS OR QUALIFICATIONS OF, OR RECOMMENDED OR GIVEN APPROVAL TO, ANY PERSON, SECURITY, OR TRANSACTION. IT IS UNLAWFUL TO MAKE, OR CAUSE TO BE MADE, TO ANY PROSPECTIVE PURCHASER, CUSTOMER, OR CLIENT ANY REPRESENTATION INCONSISTENT WITH THE PROVISIONS OF THIS PARAGRAPH.

___________________

INFORMATION FOR INVESTORS IN CERTAIN COUNTRIES

For information for investors in certain countries, see “Transfer Restrictions” and “Plan of Distribution.”

iv

SERVICE OF PROCESS AND ENFORCEMENT OF CIVIL LIABILITIES

Upon consummation of the Global Offering, we will be deemed a sociedad anónima bursátil de capital variable (variable capital public stock corporation) organized under the laws of Mexico. As of the date of this offering, we are a sociedad anónima de capital variable (variable stock corporation) organized under the laws of Mexico. Most of our directors, executive officers, controlling persons, and experts named herein are non-residents of the United States and substantially all of the assets of such non-resident persons and substantially all of our assets are located outside the United States. As a result, it may not be possible for investors to effect service of process within the United States or in any other jurisdiction outside Mexico upon such persons or us or to enforce against them or us in courts of any jurisdiction outside Mexico judgments predicated upon the laws of any such jurisdiction, including any judgment predicated substantially upon the civil liability provisions of United States federal and state securities laws. We have appointed CT Corporation System, as an agent to receive service of process with respect to any action brought against us in any federal or state court in the State of New York arising from this offering. There is doubt as to the enforceability in Mexican courts, in original actions or in actions for enforcement of judgments obtained in courts of jurisdictions outside Mexico, of civil liabilities arising under the laws of any jurisdiction outside Mexico, including any judgment predicated solely upon United States federal or state securities laws. We have been advised by our special Mexican counsel that no treaty is currently in effect between the United States and Mexico that covers the reciprocal enforcement of foreign judgments. In the past, Mexican courts have enforced judgments rendered in the United States by virtue of the legal principles of reciprocity and comity, consisting of the review in Mexico of the United States judgment in order to ascertain whether Mexican legal principles of due process and public policy (orden público) have been complied with, without reviewing the merits of the subject matter of the case. See “Risk Factors―Risks Related to the Shares.”

AVAILABLE INFORMATION

We are not subject to the reporting requirements of the Securities Exchange Act of 1934, as amended the “Exchange Act”). For so long as any of the Shares remain outstanding and are “restricted securities” within the meaning of Rule 144(a)(3) under the Securities Act, we agree to furnish upon the request of any shareholder of the Shares, to the holder or beneficial owner or to each prospective purchaser designated by any such holder of the Shares or interests therein who is a “qualified institutional buyer” within the meaning of Rule 144A(a)(1), information required by Rule 144A(d)(4) under the Securities Act, unless we either maintain the exemption from reporting under Rule 12g3-2(b) of the Securities Act or furnish the information to the SEC in accordance with Section 13 or 15 of the Exchange Act. Any such request may be made to us in writing at our main offices located at Privada de Antonio Chedraui Caram #248, Colonia Encinal, 91180, Xalapa, Veracruz, Mexico, Attention: Chief Financial Officer. We are also required periodically to furnish certain information, including quarterly and annual reports, to the CNBV and to the BMV, which will be available in Spanish for inspection through the BMV’s website at www.bmv.com.mx.

v

FORWARD-LOOKING STATEMENTS

This offering circular contains forward-looking statements. Examples of such forward-looking statements include, but are not limited to: (i) statements regarding our results of operations and financial position; (ii) statements of plans, objectives or goals, including those related to our operations; and (iii) statements of assumptions underlying such statements. Words such as “aim,” “anticipate,” “believe,” “could,” “estimate,” “expect,” “forecast,” “guidance,” “intend,” “may,” “plan,” “potential,” “predict,” “seek,” “should,” “will” and similar expressions are intended to identify forward-looking statements but are not the exclusive means of identifying such statements.

By their very nature, forward-looking statements involve inherent risks and uncertainties, both general and specific, and risks exist that the predictions, forecasts, projections and other forward-looking statements will not be achieved. We caution investors that a number of important factors could cause actual results to differ materially from the plans, objectives, expectations, estimates and intentions expressed or implied in such forward-looking statements, including the following factors:

• competition in our industry and markets;

• limitations on our ability to open new stores and operate them profitably;

• increases in supplier prices;

• product liability claims;

• limitations on our access to sources of financing on competitive terms;

• our ability to service our debt;

• performance of financial markets and our ability to refinance our financial obligations as needed;

• restrictions on foreign currency convertibility and remittance outside Mexico;

• changes in consumer spending habits;

• changes in overall economic conditions in Mexico and the United States;

• our ability to execute our corporate strategies;

• our ability to enhance or expand our store network;

• failure of our information technology (“IT”) systems, including data and communications systems;

• changes in exchange rates, market interest rates or the rate of inflation;

• the effect of changes in accounting principles, new legislation, intervention by regulatory authorities, government directives and monetary or fiscal policy in Mexico; and

• the risk factors discussed under “Risk Factors” beginning on page 16.

Should one or more of these factors or uncertainties materialize, or should underlying assumptions prove incorrect, actual results may vary materially from those described herein as anticipated, believed, estimated, expected, forecast or intended.

Prospective investors should read the sections of this offering circular entitled “Summary,” “Risk Factors,” “Management’s Discussion and Analysis of Financial Condition and Results of Operations” and “Business” for a more complete discussion of the factors that could affect our future performance and the markets in which we operate.

vi

In light of these risks, uncertainties and assumptions, the forward-looking events described in this offering circular may not occur. These forward-looking statements speak only as to the date of this offering circular and we undertake no obligation to update or revise any forward-looking statement, whether as a result of new information or future events or developments. Additional factors affecting our business emerge from time to time and it is not possible for us to predict all of these factors, nor can we assess the impact of all such factors on our business or the extent to which any factor, or combination of factors, may cause actual results to differ materially from those contained in any forward-looking statement. Although we believe the plans, intentions and expectations reflected in or suggested by such forward-looking statements are reasonable, we cannot assure you that those plans, intentions or expectations will be achieved. In addition, you should not interpret statements regarding past trends or activities as assurances that those trends or activities will continue in the future. All written, oral and electronic forward-looking statements attributable to us or persons acting on our behalf are expressly qualified in their entirety by this cautionary statement.

vii

PRESENTATION OF CERTAIN FINANCIAL INFORMATION

Unless otherwise specified or the context otherwise requires, references in this offering circular to “the Company,” “Grupo Chedraui,” “the issuer,” “we,” “us” and “our” are references to Grupo Comercial Chedraui, S.A.B. de C.V. and its subsidiaries.

Financial Statements

This offering circular includes our annual audited consolidated financial statements as of December 31, 2007, 2008 and 2009 and for the years then ended, together with the notes thereto (the “Audited Financial Statements”) beginning on page F-1.

See Annex A for a discussion of our results for the three-month periods ended March 31, 2010 and 2009 and our unaudited interim financial information as of and for the three-month periods ended March 31, 2010 and 2009.

The financial information in this offering circular has been prepared in accordance with Mexican Financial Reporting Standards (“Mexican FRS” or “MFRS”, individual standards referred to herein as Normas de Información Financiera, or “NIFs” or “Bulletins”), which differ in certain significant respects from International Financial Reporting Standards (“IFRS”). See “Significant Differences Between Mexican FRS and IFRS” for a description of certain principal differences between Mexican FRS and IFRS as they relate to us.

EBITDA

References to “EBITDA” are to earnings before interest expense, income taxes, depreciation and amortization. EBITDA is not a financial measure computed under Mexican FRS or IFRS. We calculate EBITDA as operating income (loss) plus depreciation and amortization expense. EBITDA should not be construed as an alternative to (i) net income as an indicator of our operating performance, or (ii) cash flow from operations as a measure of our liquidity. See “Management’s Discussion and Analysis of Financial Condition and Results of Operations—EBITDA.”

Accounting Principles

Prior to January 1, 2008, Mexican FRS Bulletin B-10, “Recognition of the Effects of Inflation on Financial Information,” outlined the inflation accounting methodology mandatory for all Mexican companies reporting under Mexican FRS. The presentation of financial information in period-end, or constant, currency units was intended to eliminate the distorting effect of inflation on the financial information and to permit comparisons across periods in comparable monetary units. Our Audited Financial Statements for periods ending on dates on or prior to December 31, 2007 were prepared giving effect to Bulletin B-10 and thus are reported in constant period-end pesos as of December 31, 2007 to adjust for the inter-period effects of inflation by applying factors derived from the Mexican National Consumer Price Index (Índice Nacional de Precios al Consumidor, or “NCPI”), an inflation index determined by the Mexican Central Bank, Banco de México. Effective January 1, 2008, NIF B-10, “Effects of Inflation” replaced the prior Bulletin B-10 and we are no longer required to use inflation accounting for periods beginning in 2008, unless the economic environment in which we operate qualifies as “inflationary,” as defined by Mexican FRS. There was no significant volatility in the rate of inflation in Mexico in 2009 and 2008. The value of the UDI was Ps. 3.93 at December 31, 2007, Ps. 4.18 at December 31, 2008 and Ps. 4.34 at December 31, 2009. Accordingly, the economic environment in Mexico for the three-year periods preceding December 31, 2009 and 2008 did not qualify as inflationary, for which reason we did not account for the effects of inflation as of and for the periods ended December 31, 2009 and 2008. As a result, amounts in this offering circular for financial information for dates or periods beginning on or after January 1, 2008 is presented in nominal terms; however, such amounts reflect inflationary effects recognized up to December 31, 2007. See Note 3(c) to our Audited Financial Statements included herein for a summary of the effects of adoption of NIF B-10.

Currency and Other Information

Unless otherwise stated, the financial information appearing in this offering circular is presented in Mexican pesos. In this offering circular references to “pesos” or “Ps.” are to Mexican pesos and references to “U.S. dollars,” “dollars” or “U.S.$” are to United States dollars.

viii

This offering circular contains translations of certain peso amounts into U.S. dollars at specified rates solely for the convenience of the reader. These translations should not be construed as representations that the peso amounts actually represent such U.S. dollar amounts or could be converted into U.S. dollars at the rate indicated. Unless otherwise indicated, U.S. dollar amounts that have been translated from pesos have been so translated at an exchange rate of Ps.12.25 per U.S. dollar, the rate published on Thursday, April 29, 2010 in the Mexican Official Gazette of the Federation (Diario Oficial de la Federación, or the “Official Gazette”) by Banco de México. See “Exchange Rates” for information regarding rates of exchange between the peso and the U.S. dollar for the periods specified therein.

Totals in some tables in this offering circular may differ from the sum of individual amounts in those tables due to rounding.

References to spreads refer to percentage amounts representing the difference between two interest rates or transaction values, as the context requires.

In this offering circular, where information is presented in thousands, millions or billions of pesos or thousands, millions or billions of dollars, amounts of less than one thousand, one million, or one billion, as the case may be, have been truncated unless otherwise specified. All percentages have been rounded to the nearest percent, one-tenth of one percent or one-hundredth of one percent, as the case may be. In some cases, amounts and percentages presented in tables in this offering circular may not add up due to such rounding adjustments or truncating.

Unless otherwise specified, all units of area shown in this offering circular are expressed in terms of square meters.

Industry and Market Data

Market data and other statistical information (other than with respect to our financial results and performance) used throughout this offering circular are based on independent industry publications, government publications, reports by market research firms or other published independent sources, including: Asociación Nacional de Tiendas de Autoservicio y Departamentales, A. C. (“ANTAD”), a private association that, among other things, measures the commercial activity, growth and quality of services provided by their member stores (which include department stores, convenience stores, discount stores and drug stores); The Nielsen Company (“Nielsen”); Asociación Mexicana de Agencias de Investigación de Mercado y Opinión Pública, A.C. (“AMAI”); Planet Retail Ltd. (“Planet Retail”), a provider of on-line business information services including retail rankings, retail profiles and grocery retailing; Consejo Nacional de Población (“CONAPO”) a government entity dedicated to publishing information on Mexico’s population; and Instituto Nacional de Estadística, Geografía e Informática (“INEGI”), Mexico’s National Institute of Statistics, Geography and Computer Sciences.

Some data are also based on our estimates, which are derived from our review of internal surveys and analyses, as well as independent sources. Although we believe these sources are reliable, we have not independently verified the information and cannot guarantee its accuracy or completeness. In addition, these sources may use different definitions of the relevant markets than those we present. Data regarding our industry are intended to provide general guidance but are inherently imprecise. Though we believe these estimates were reasonably derived, you should not place undue reliance on estimates, as they are inherently uncertain.

Other Information Presented

The standard measure of area in Mexico is the square meter, while in the United States the standard measure is the square foot. Unless otherwise specified, all units of area shown in this offering circular are expressed in terms of square meters. One square meter is equal to approximately 10.76 square feet.

References to Super Chedraui

In January of 2010, we initiated a gradual renaming of our Super Che stores to Super Chedraui in order to take advantage of the Chedraui brand recognition. On January 15, 2010, we opened a new store in Ecatepec de Morelos, Estado de Mexico, which was our first store to be named Super Chedraui. We intend for all our new stores in this format to be opened as Super Chedraui, however existing Super Che stores will be renamed as they are renovated. References in this offering circular to “Super Chedraui” refer to both our Super Che and Super Chedraui stores.

ix

GLOSSARY OF TERMS AND DEFINITIONS

Unless otherwise specified, references in these definitions to financial statement line items are references to those line items as set forth in our Audited Financial Statements.

“Banorte” means Banco Mercantil del Norte, S.A., Institución de Banca Múltiple, Grupo Financiero Banorte.

“CAGR” means the compounded annual growth rate in any given period.

“CINIF” means the Consejo Mexicano para la Investigación y Desarrollo de Normas de Información Financiera S.C., which is the Mexican Board for Research and Development of Financial Information Standards.

“Inventory Days” means, for any fiscal year, the average number of days a company holds its inventory before selling it and is calculated as the value of the inventory at period end multiplied by 365 divided by cost of sales for such period.

“Invested Capital” means property and equipment-net plus Net Working Capital as of December 31 of any given year.

“Invex” means Banco Invex, S.A. Institución de Banca Múltiple, Invex Grupo Financiero.

“Days Payables” means, for any fiscal year, the average number of days a company takes to pay its suppliers and is calculated as an amount equal to accounts payable at period end multiplied by 365 divided by cost of sales for such period.

“GDP” means gross domestic product.

“Net Working Capital” is calculated as accounts and notes receivables-net, plus inventories-net, minus trade notes and accounts payable.

“Principal Competitors” means Walmart de México, S.A.B. de C.V. (“Walmex”), Organización Soriana, S.A.B. de C.V., (“Soriana”) and Controladora Comercial Mexicana, S.A.B. de C.V. (“Comerci”).

“ROIC” means return on invested capital, which is a common measure of profitability over investment in our industry. We calculate ROIC as (i) operating income for any period, multiplied by an amount equal to one minus the Statutory Tax Rate, divided by (ii) Invested Capital as of the end of such period.

“Same-Store Sales” means the sales of our retail stores, operating throughout both financial periods being compared. If a retail store has not operated during the entire prior 13-month period prior to a relevant period end date, we exclude its sales from our calculation of same-stores sales data. For example, if a new retail store was opened on July 1, 2008 and operated throughout the last six months of 2008, (i) our “Same-Store Sales” data would exclude the sales of that retail store until August 1, 2009 and (ii) we would account for the sales of that new retail store during that 13-month period as sales from a newly opened retail store. Our calculations of Same-Store Sales data may differ from same-store sales calculations of other retailers.

“Southwestern United States” means the following states of the United States of America: California, Arizona, Nevada and New Mexico.

“Statutory Tax Rate” means 28%, or the statutory tax rate in effect in Mexico during the period from January 1, 2007 through December 31, 2009. As of January 1, 2010 the statutory tax rate in Mexico is 30%.

“Supplier Financing” means, for any fiscal year, an amount equal to Days Payables divided by Inventory Days.

“TIIE” means Tasa de Interés Interbancaria de Equilibrio (or Mexican Interbank Equilibrium Interest Rate).

“UDIs” means Unidades de Inversión, a peso equivalent unit of account indexed for Mexican inflation on a daily basis, as measured by changes in the NCPI.

(This page intentionally left blank)

1

EXECUTIVE SUMMARY

This summary highlights selected information from this offering circular and may not contain all the information that is important to you. For a more complete understanding of us, our business and this offering, you should read this entire offering circular, including the “Risk Factors” and our Audited Financial Statements appearing elsewhere in this offering circular.

Overview

We are a leading Mexican multi-format retailer with operations in Mexico and the United States. Through our stores located in over 20 states throughout Mexico, we sell a variety of food items, including basic groceries and perishables, as well as non-food items, including consumer electronics, white goods (e.g., major household appliances), furniture, small appliances, apparel, cellular phones and other goods. We also operate stores in Southwestern United States selling perishables and other grocery items, primarily to Hispanic, and in particular Mexican-American, customers. As of December 31, 2009, we operated 142 retail stores in Mexico under two retail store formats, Chedraui and Super Chedraui and 21 stores in the United States under the El Super format, with a total selling area of approximately 967,160 square meters (10.4 million square feet). We believe that the Chedraui brand name has historically been associated with a broad assortment of products at affordable prices for the lower-to middle-income segments of the Mexican population; and the El Super brand name has had a similar association for the Hispanic, and in particular the Mexican-American community, in Southwestern United States for over 12 years. We believe our strategy of offering the most competitive prices, combined with our broad product offering has been a key strategic differentiator and an important factor in the growth of our businesses. In recent years, we have maintained a successful track record of consistent profitability and growth. From 2005 to 2009, we more than doubled our number of stores, from 69 to 163, by opening or acquiring 94 new stores, of which 29 were acquired from Carrefour, S.A. de C.V. (“Carrefour”) in Mexico in 2005 and seven were acquired from Grupo Gigante, S.A.B. de C.V. (“Grupo Gigante”) in the United States in 2008. In addition, our consolidated net revenues have increased from Ps.27.7 billion in 2005 to Ps.47.9 billion in 2009, implying a 14.7% Revenue CAGR, and our consolidated EBITDA increased from Ps.1.6 billion to Ps.3.2 billion over the same period yielding a 18.9% EBITDA CAGR.

We operate three distinct lines of business: Mexican Retail, U.S. Retail and Real Estate. Our Mexican retail business operates under two store formats which target different market niches and segments of the population, including 109 hyper-market stores under the name Chedraui that carry a breadth of products and brands in cities with populations of at least 100,000 inhabitants. In 2005, we opened our smaller format stores, Super Che, which are generally concentrated in smaller cities and towns with populations of at least 25,000. Over the past four years, we opened 33 Super Che stores, which we recently decided to gradually rename Super Chedraui in order to take advantage of our brand recognition. Our Chedraui and Super Chedraui retail stores are mainly located in southern and central Mexico, including Mexico City. Our Chedraui stores, which accounted for 75.2% of our consolidated revenues for 2009, range from 3,226 square meters (approximately 34,724 square feet) to 11,592 square meters (approximately 124,775 square feet), with an average of 7,408 square meters (approximately 79,739 square feet) and contain 57,000 stock-keeping units (“SKUs”) on average. Super Chedraui stores, which accounted for 8.4% of our consolidated revenues for 2009, range from 1,737 square meters (approximately 18,696 square feet) to 2,481 square meters (approximately 26,705 square feet), with an average of 2,069 square meters (approximately 22,173 square feet) and contain over 29,000 SKUs on average.

Our U.S. retail operations target the Hispanic, and more specifically the Mexican-American, communities, in California, Nevada and Arizona through our 21 El Super stores, which accounted for 15.4% of our consolidated revenues in 2009. Our El Super stores range from 2,811 square meters (approximately 30,257 square feet) to 7,536 square meters (approximately 81,116 square feet), averaging 4,353 square meters (approximately 46,855 square feet) and contain 5,000 SKUs on average. Our U.S. Retail Operations, held through Bodega Latina Corporation (“Bodega Latina”), are independently managed and self-funded from our operations in Mexico. Grupo Chedraui holds a 66.2% ownership interest in Bodega Latina, with the remainder held by minority shareholders, none of whom hold more than a 5.5% interest.

2

Our real estate operations are responsible for the administration of our owned and leased real estate assets in Mexico, the development of existing and projected stores and shopping centers, and the expansion, construction and remodeling of our stores in Mexico. Real estate revenues account for only 1% of our consolidated revenues in 2009, however, contributed 11% to our total EBITDA.

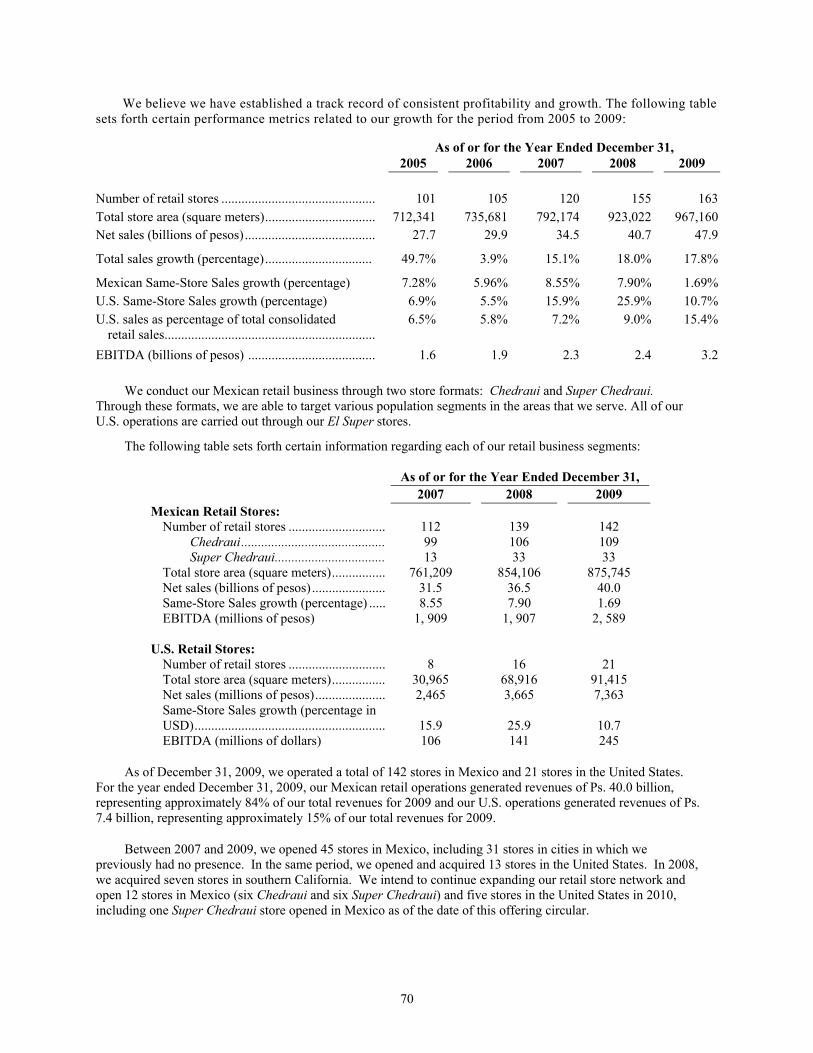

The following table sets forth key financial and operating data for each of our segment markets:

As of or for the year ended December 31, 2007 2008 2009 Retail Business in Mexico Number of retail stores(1) 112 139 142 Selling area (square meters) (1) 761,209 854,106 875,745 Net sales (millions of pesos) 31,515 36,506 40,033 Same-Store Sales growth (%) 8.55 7.90 1.69 EBITDA (millions of pesos) 1,909 1,907 2,589 Retail Business in the United States

Number of retail stores(1) 8 16 21 Selling area (square meters)(1) 30,965 68,916 91,415 Net sales (millions of pesos) 2,465 3,665 7,363 Same-Store Sales growth (%) 15.9 25.9 10.7 EBITDA (millions of pesos) 106 141 245 Real Estate Business Gross leasable area (square meters) (1)

256,805 278,591 267,368

Average monthly revenue, pesos per square meter

131 139 171

Total revenue (millions of pesos) 473 487 505 Occupancy rate (%) 94% 92% 93% EBITDA (millions of pesos) 270 345 340 Consolidated Business Net retail sales (millions of pesos) 33,979 40,171 47,396 Total retail selling area (square meters) (1)

792,174 923,022 967,160

Total revenue (millions of pesos) 34,452 40,658 47,901 Revenue growth (%) 15.1% 18.0% 17.8% EBITDA (millions of pesos) 2,285 2,393 3,174 EBITDA growth (%) 18.0% 4.7% 32.6% EBITDA margin (%) 6.6% 5.9% 6.6%

________________________________________

(1) As of December 31. Not a weighted average.

3

Our Business Model

Our mission statement, which is to deliver to all possible locations, the products our customers prefer at the best prices, is the main driver behind our business model and the key reason underpinning our continued strong financial performance. We believe this simple but powerful strategy results in a successful business model that positions us well to take full advantage of both Mexican and U.S. growth opportunities. The fundamentals are as follows:

Lowest Price: Our focus is to always offer all our products at the lowest price in the markets in which we operate. We believe this commitment to the lowest price clearly differentiates us from our competitors. While certain of our competitors focus on targeted or seasonal promotions and sales, we seek to offer a consistent message of every-day lowest prices for each product we sell. We believe our strategy and price positioning is widely recognized in the industry. In order to always provide our customers with their preferred products at the lowest price, we engage in extensive price comparison efforts in Mexico at both national and local levels to guarantee our competitive position among retailers and specialty stores. This process is supported by innovative technology and quick response capacity at a local level, which is led by empowered store managers. By engaging in these price comparisons on behalf of our customers, we believe we have been successful in providing our customers with a one-stop shopping experience in which they are comfortable purchasing a broad assortment of merchandise without independently undertaking local price and merchandise comparisons. As a result of this strategy, we believe we successfully offer our customers their preferred products at the best price, which enhances customer loyalty as reflected by our growing customer base.

Our wide selection of products: We believe our retail stores offer a broad selection of value-based, competitively-priced brand name and private label goods. Our Chedraui stores contain above-industry an average of 57,000 SKUs. Our Super Chedraui format carries an average of 29,000 SKUs and our El Super stores in the United States carry an average of 5,000 SKUs. Our objective is to carry not only leading brands, but also a full range of brands and products within each product category, including value items for our target market at each store location. Our assortment of merchandise, consisting of both imported and domestic brand-name products, is tailored to each store and is responsive to such store’s climate, region and client preference and socioeconomic level. In addition, our logistics system and strategically located modern and custom-built distribution centers enable us to readily and efficiently meet the merchandising demands of our stores.

Customer experience: As part of our core strategy, we focus on offering superior customer service in our stores by maintaining clean stores, with clearly labeled departments, products and prices, that we believe are more comfortable than those of our Principal Competitors. We believe we offer our customers an attractive shopping environment. We have a policy of continuously evaluating whether we need to remodel our stores based on the age of our equipment, construction improvement needs and our local competitors’ stores. This remodeling policy assures that we are able to provide our customers with clean, well-labeled and sizeable stores, supported by the appropriate number of trained employees to provide superior customer service, further enhancing the shopping experience. In addition, in order to increase traffic to our stores in Mexico, we offer a variety of services to our customers, such as extended warranties through Garex, wire transfers through Cartera Dinámica, and the ability to make bill payments to certain government and private entities.

Our Strengths

We believe that the following key competitive strengths differentiate us and are critical to our continuing success:

Unique Position as the “Lowest Price” Mexican Retailer with a Broad Product Assortment Compared to Other Competitors

Our simple but powerful pricing strategy is based on always offering all our products at the lowest prices in the markets in which our stores operate. Unlike many of our competitors, who price their products based on target margins, we engage in central, company-wide and local pricing comparison and price our products accordingly. As a result, we make approximately 1,900 price adjustments daily on a company-wide level. In addition, individual store managers are empowered to implement real-time price adjustments based on the prices offered by local competitors resulting in approximately 85,200 daily price adjustments made at a local level. We believe we have been

4

successful in executing and communicating this strategy through our slogan “En Chedraui, Cuesta Menos” (At Chedraui, It Costs Less) and our quick and effective responses to changes in prices, which we believe has also contributed to an increase in customer loyalty as well as our overall customer base. Each of our retail stores is connected by a customized and integrated communications network that allows the transmission of information 24-hours a day in order to provide real-time information between our stores, corporate offices and distribution centers in Mexico. We believe we are also recognized for our broad product assortment, which is based on specific demographics and regional and local customer preferences. In particular, our high-quality perishable section is one of our distinguishing factors vis-à-vis our competitors. Our shopping area is also greater than that of similar competitors and we believe offers a more attractive shopping environment. In addition, we continuously evaluate whether we need to remodel our stores based on the age of our equipment, construction improvement needs and our local competitors’ stores. This remodeling policy assures that we are able to provide our customers with clean, sizeable stores, with clearly labeled departments, products and prices, which are supported by superior customer service, further enhancing the shopping experience. Each of these factors supports our distinct position in the Mexican retail market as the lowest-priced retailer that also offers a broad product assortment and superior customer experience as compared to other low-price competitors.

Proven Track Record and Strong Platform for Future Growth.

Our current network of stores is a result of both consistent organic growth and the successful integration of acquisitions, such as Carrefour’s Mexican operations, which added 29 stores, and certain Gigante stores in the United States, which added seven stores. Those 29 Carrefour stores increased our number of stores in Mexico by 45% and represented approximately 40% of our net sales in 2005. We believe the Mexican market continues to offer significant organic growth potential given the low levels of formal retail penetration relative to the U.S., European and other Latin American markets. Furthermore, low retail penetration in our core southwestern and southeastern Mexican markets presents attractive new store potential in our existing markets. In addition, we believe the Mexican retail market offers additional consolidation opportunities. Hence, we believe this market environment presents attractive growth opportunities in both our current, as well as potential new markets, specifically in northern Mexico. We continue to dedicate time and resources to developing a strong growth platform as evidenced by our expansion plan begun in 2007. In addition, we believe that the capacity of our existing distribution centers and improved IT systems infrastructure, which results from our significant investments over the last few years, supports our planned growth. Moreover, we believe our Super Chedraui format, introduced in 2005 under the name Super Che, has been successful at serving smaller cities and should allow us to enter the approximately 70 cities in Mexico of at least 25,000 inhabitants that typically are not only highly fragmented but also underserved by large retailers. Due to our established retail platform, including our strong presence in southeastern Mexico, and our growth strategy, we believe we are well positioned to benefit from other favorable market conditions such as population and economic growth as well as an increase in disposable income of our target market.

We believe El Super stores enjoy strong positioning within the Hispanic, and in particular the Mexican-American, communities in Southwestern United States. We have focused on personalized service as well as an emphasis on the Mexican culture and Spanish language within our stores, which we believe has contributed to our strong reputation for quality customer service and has increased customer loyalty. We believe there are additional opportunities within these communities and through our expansion plan, we intend to reinforce our presence in Southwestern United States and capitalize on our existing presence and strong reputation to expand our operations to other regions with significant Hispanic populations.

Market Leader in Southeastern Mexico Benefiting from Strong Presence and Strategic Store Locations.

We are the leading retailer in Mexico’s southeastern region with approximately 39% of the market share,

according to Nielsen and we have a strong presence in over 20 states. We believe we have successfully established and defended this leading position in southeast Mexico during the past 40 years. We believe we are Mexico’s fourth leading food and general merchandise retailer on a national basis, and that we lead the market in southeastern Mexico, which has enhanced our bargaining position with our suppliers. Within southeastern Mexico, we believe we benefit not only from our scale but also from the strategic location of our stores, which has resulted in a proven record of long-term Same-Store Sales growth. We also believe the

5

success of our new store strategy is evidenced by the closure of only three stores in our 40 years of operation. Furthermore, we believe that in many states the strategic location of our stores would be difficult to replicate due to the lack of available retail space in key locations. We believe these factors, combined with our strong brand recognition and reputation, create substantial barriers to entry for our competitors. Also, given that we own 68% of the stores we operate in Mexico, we believe we are not significantly exposed to lease re-negotiation risks, and at the same time, we can benefit from potential appreciation of the underlying economic value of our real estate assets, which provides us with an additional competitive advantage. Efficient Operation, Focus on Low Cost and Efficient Inventories Supported by Cutting Edge IT and Distribution Platforms.

One of the pillars of our strategy is our ability to efficiently manage costs and inventories while increasing sales. Given our competitive pricing policy, we focus on reducing each store’s working capital and investing capital needs in a cost-efficient way, while maintaining high sales volume and superior store quality. Our efficient supply chain network, supported by continued investments in IT, allows us to optimize our working capital requirements through high inventory rotation and reduce our inventory related costs, such as shrinkage. In addition, our strategically located, modern and custom-built distribution centers, and our logistics system, enable us to readily meet the merchandising demands of our stores. In recent years, we have also made significant investments in technology systems focused primarily on supporting our pricing strategy, improving inventory and operational efficiency and optimizing human resources. Innovative technologies currently under implementation include SAP, Manhattan, Intactix, Reflexis and People Soft, among others. We believe that continued upgrading of our operations allows us to further increase efficiency, reduce expenses and provide the necessary product and sales information to enhance merchandising decisions at each store.

Historically Strong Financial Performance.

We have a track record of consistent growth, profitability and cash flow generation. We have been able to

maintain a 20.3% Revenue CAGR from 2000 through 2009, while opening a total of 114 new stores throughout the same period. We believe our focus on growth is proved by our top line performance. Our net sales for 2009 were Ps.47.9 billion, which represented increases of 17.8% and 39.0% over our net sales in 2008 and 2007, respectively. We believe our Revenue CAGR of 17.0% between 2006 and 2009 is well above that of our Principal Competitors, which registered an average growth of 6.3% over the same period. Our EBITDA for 2009 was Ps.3.2 billion, which represented increases of 32.7% and 38.9% over our EBITDA in 2008 and 2007, respectively. We believe our EBITDA CAGR of 18.7% between 2006 and 2009 is also well above that of our Principal Competitors, which registered an average EBITDA growth of 6.7%. We believe our Supplier Financing results for 2009, 2008 and 2007 of 181.5%, 193.4% and 198.0%, respectively, exceeded our publicly-traded competitors’ average by 59%, 68% and 63% for 2009, 2008 and 2007, respectively. As a result of our strong operating performance and working capital management, we believe we have also consistently generated above average ROIC in 2009, 2008 and 2007 of 11.5%, 9.0%, and 9.6%, respectively. In addition, we believe our strong financial performance and cash generation has enabled us to reduce our indebtedness following our acquisition of Carrefour in Mexico in 2005, resulting in an attractive capital structure of 1.3x to 1.2x debt to EBITDA ratio as of December 31, 2009 with additional leverage capacity if required for future capital expenditures or strategic acquisitions. Moreover, we do not have significant credit risk as nearly 95% of our sales are in cash or cash equivalents, such as debit and credit card and electronic market vouchers sales, and we do not offer consumer financing at our stores.

We believe the success of our business model also relies on our focus on efficient working capital, cash

management and asset returns. We believe our strong ROIC is a result of our strong store operating performance together with superior Supplier Financing ratios, high inventory rotations and efficient capital deployment. In order to maintain attractive ROIC, we intend to continue to focus on efficient capital expenditure and cash flow generation.

6

Experienced Management Team Supported by a Committed and Well-Trained Workforce.

Our senior management team has an average of 14 years of experience in the retail industry and we believe has the depth, expertise and motivation to execute our growth strategy, as proven by its capacity to open new stores as well as successfully integrate the Carrefour and Gigante operations from our recent acquisitions. Under our management, the Carrefour stores experienced a 43% increase in sales through 2009 and sales per square meter have improved from Ps.6,135 per square meter in 2005 to Ps. 8,803 per square meter in 2009, which represents a 9.4% CAGR. In addition, we believe our management team is responsible for the transformation of the seven stores acquired from Grupo Gigante, six of which had been operating at a loss at the time of their acquisition in August 2008. By August of 2009, all seven of the acquired Gigante stores were profitable. We believe that creating a culture based on both teamwork and strong economic incentives has also produced a loyal management team dedicated to achieving our corporate goals. We believe the team’s experience has enabled us to anticipate and respond effectively to industry trends and competition, better understand our customer base and build strong business relationships. Furthermore, we believe that our goal-oriented culture and incentive programs have also contributed to developing a motivated work-force that is focused on building solid relationships with customers while maintaining high operating and financial performance by delivering quality personalized service, increasing sales, lowering inventories, growing profitability and achieving operational efficiency. Moreover, we have invested in our employees through Universidad Chedraui, our in-house training and certification program. We believe our efforts have resulted in a competent, well-trained and loyal work-force. Through our training programs, variable compensation schemes, promotions and relocations, we seek to align the goals of the Company, its management and our employees. Our Strategy Our strategy emphasizes strengthening our position as a leading retailer in Mexico, which offers the lowest prices in the market, while continuing to grow in Mexico and the United States and focus on our key business strengths. The key elements of our strategy are the following:

Continue Expanding our Store Network in Mexico.

We believe that our compelling retail store formats, our focus on ROIC and cash generation and our successful track record of opening stores provide us with a strong foundation for continued organic growth. From the beginning of 2007, when we operated 105 stores, through year-end 2009, we opened 58 new stores, which represents a 55% increase to our operations during that period. Our strategic expansion in Mexico includes focusing on larger as well as smaller cities through our Chedraui and Super Chedraui formats. We believe there are significant growth opportunities to expand into Mexico’s northern region, where we currently have a limited presence, as well as Mexico’s smaller cities (with populations of approximately 25,000 inhabitants), which according to CONAPO represent approximately an additional 15.4 million of potential customers through 2030 that are currently underserved by modern retailers. We intend to use our smaller Super Chedraui format to target these smaller cities. In addition, further market consolidation is expected to create growth opportunities through potential acquisitions of both national and regional players that can complement our existing retail platform. We therefore intend to both pursue an organic growth plan in existing as well in new domestic markets in order to continue achieving national coverage, and to evaluate potential consolidation opportunities. Our aggressive growth strategy is supported by our technology and logistics capability, and underpinned by the capacity at our distribution centers which we believe can support approximately an additional 160 stores over our current operation.

Improve Sales and Market Position by Continuing to Focus on our Business Strengths.

We intend to capitalize on our business strengths, including our unique position as a low-priced Mexican retailer committed to providing its customers with a broad assortment of quality merchandise and a superior shopping experience. We intend to continue to promote our “Lowest Price” pricing strategy and to improve our product offering in order to increase sales and customer loyalty from our current customers as well as from new customers. We recognize that the retail business is highly competitive and therefore also seek to increase our average total ticket spending by offering a combination of quality products, assorted merchandise and an

7

attractive “one-stop” shopping environment in clean, well-labeled, sizeable and comfortable stores. To this end, we plan to continue to remodel our stores, including six stores in 2010. We also intend to further increase brand recognition and customer loyalty by expanding the use of our logo across all formats in Mexico and the United States to leverage the strength of the Chedraui brand across formats and markets. By taking advantage of our strong retail platform, purchasing power, economies of scale, private label development and customer services, we seek to continue to offer our customers the best prices while maintaining competitive margins.

Continue to Focus on Maintaining Attractive Returns on Investment Capital While Executing our Growth Strategy.

Chedraui enjoys strong return on invested capital (ROIC) as a result of our robust operating performance and our superior Supplier Financing ratios. Our ROIC reached 11.5% in 2009, second only to Walmex among our Principal competitors. In order to maintain attractive ROIC, we intend to continue to focus on efficient inventory management and capital deployment while maximizing cash flow generation. We will also seek to further these goals by implementing best practices and efficient IT systems to maintain high inventory rotation and reduced operating costs and shrinkage. In addition, although our business strategy revolves around our “Lowest Price” pricing strategy, and not the achievement of specific operating margins, we believe that we can improve margins by increasing scale and operating leverage opportunities and continuing to successfully implement our pricing strategy.

Continue to Fully Integrate Operations Utilizing a Highly Developed Information Technology and Systems Platform.

We believe that we have made significant investments in maintaining and updating our technology infrastructure, systems applications and business solutions. In collaboration with various third-party providers, we are in the process of a company-wide roll-out of a new information technology system, which incorporates certain worldwide best practices into our current processes to facilitate the implementation of our growth strategy. Moreover, we expect that these and other highly advanced systems, including SAP, People Soft, Reflexis, Intactix and Manhattan and other customized applications, will result in additional operating efficiencies and margin improvement initiatives. Operating efficiencies, for example, would include streamlining daily operations to improve our real-time responses to local market prices, reductions in inventory and out-of-stock days, decline in obsolete product or shrinkage, optimization of product distribution and on-time delivery. By continuing to integrate these applications, we hope to be better positioned to adopt and implement the best business practices across our formats and markets.

Grow in the U.S. Retail Market.

We have established ourselves as a Mexican food retailer with operations in Southwestern United States, where we currently operate 21 retail stores in cities with large Hispanic, and more specifically, Mexican-American, populations in southern California, Arizona and Nevada. With more than 12 years of successful operations in Southwestern United States, we have acquired significant experience and knowledge of the U.S. retail market. We have focused on perishable and Latin American products targeted to Hispanic, and in particular Mexican-American, consumers and believe the Mexican-American retail market is a niche that presents important growth opportunities, given the growing size and increasing purchasing power of this group of consumers. We also believe we have successfully taken advantage of these opportunities, by differentiating ourselves with an every day low price strategy: a specific product offering based on Mexican-Americans’ preferences and a superior customer service with Spanish speaking employees. We have also significantly increased our scale through the acquisition of seven Gigante stores in 2008. We intend to continue to target the Hispanic populations and focus on the Mexican-American communities in the areas surrounding Los Angeles, Tucson, Phoenix, Las Vegas and other select U.S. cities.

Risks Related to Our Business

For a discussion of certain considerations that should be taken into account in deciding whether to invest in the Shares, see “Risk Factors” beginning on page 16.

8

Recent Developments

On January 15, 2010, we opened one new Super Chedraui in Ecatepec de Morelos, Estado de Mexico, Mexico. Our board of directors also made the decision to close two of our Super Chedraui stores in March 2010. The decision to close the Super Chedraui stores of Tacambaro, Michoacan and San Pablo, Tlaxcala was based on the stores’ inability over the past three years to generate the target sales volumes.

In addition, on March 8, 2010, we executed a binding letter of intent, pursuant to which we plan to acquire three stores in Baja California, Mexico from Centro Comercial Californiano, S.A. de C.V. for an amount equal to Ps.500 million, plus the cost of inventory. The consummation of the transaction is subject to customary conditions and the negotiation and execution of definitive documentation.

We recently agreed to provide certain minority shareholders representing approximately 20% of the capital stock of Bodega Latina, the entity that operates our El Super stores in the United States, the right to sell a portion of their shares in Bodega Latina to us each year. Following the announcement of our proposed global offering, several minority shareholders in Bodega Latina advised us that they believed our proposed offering would violate certain terms of an agreement among shareholders of Bodega Latina. Although we believe these claims were without merit, we agreed to resolve our differences by amending the agreement among shareholders of Bodega Latina. The amended agreement will allow certain minority shareholders of Bodega Latina to sell to us a portion of their Bodega Latina shares each year, allowing us to further consolidate our investment in Bodega Latina. We will be required in 2010 to repurchase at a set price up to US$14 million of Bodega Latina shares, representing up to approximately 6% of the capital stock of Bodega Latina, and up to an additional US$10 million worth of shares of Bodega Latina in each subsequent year at a variable price. In subsequent years the per share purchase price will be based on an average of an EBITDA-multiple and a revenue-multiple applied to Bodega Latina's most recent fiscal year end results. The future purchase price is based on our own EBITDA and revenue multiples, and we therefore believe the result will be non-dilutive, although no assurances can be given. This agreement will remain in place until all the shares of the minority shareholders have been repurchased.

Grupo Comercial Chedraui, S.A.B. de C.V. is a variable capital public corporation (sociedad anónima bursátil de capital variable) organized under the laws of Mexico. Our principal executive offices are located at Privada de Antonio Chedraui Caram #248, Colonia Encinal, 91180, Xalapa, Veracruz, Mexico. Our telephone number at that address is +52 22-8842-1100. Our website is located at www.chedraui.com.mx. Any information contained on, or accessible through, our website is not incorporated by reference herein and shall not be considered part of this offering circular.

9

THE GLOBAL OFFERING

The following is a brief summary of certain terms of this offering. For a more complete description of the Shares, see “Description of our Capital Stock and Bylaws.”

Issuer........................................................ Grupo Comercial Chedraui, S.A.B. de C.V.

The selling shareholder............................ The selling shareholder is offering 14,407,647 Shares as part of the Mexican Offering. For more information regarding our principal shareholders and the selling shareholder, see “Principal and Selling Shareholders.”

Offering price per Share .......................... The initial offering price is Ps.34.00 per Share, equivalent to U.S. $2.78 per Share based on the exchange rate of Ps.12.25 per U.S. dollar on April 29, 2010.

Shares offered .......................................... 133,793,545 Shares of our Series B, Class I common stock, no par value, of which we are offering 119,385,898 Shares and the selling shareholder is offering 14,407,647 Shares.

The Mexican Offering ............................. As part of our primary public offering in Mexico, we are offering 45,799,448 Shares and the selling shareholder is offering 14,407,647 Shares in Mexico to the general public in a secondary offering. See “Plan of Distribution.”

The International Offering....................... We are offering 73,586,450 Shares in the United States to qualified institutional buyers (“QIBs”) in reliance on Rule 144A under the Securities Act and in other countries outside Mexico, to non-U.S. persons in reliance on Regulation S under the Securities Act.

The Global Offering ................................ 133,793,545 Shares are being offered in the international and Mexican offerings, together with an additional 20,069,032 Shares, assuming the exercise of the over-allotment options in full. See “Plan of Distribution.”

Reallocations ........................................... The number of Shares to be offered pursuant to the international offering and the Mexican offering is subject to reallocation among the initial purchasers and the Mexican underwriters. See “Plan of Distribution.”

Shares outstanding after the Global Offering ...................................................

936,838,320 Shares (assuming no exercise by the initial purchasers or the Mexican underwriters of the options granted by us to the initial purchasers and the Mexican underwriters to purchase additional Shares in the Global Offering).

Use of proceeds ....................................... The net proceeds to us from the sale of the Shares being offered in the Global Offering by us will be Ps.3,911 million, assuming the over-allotment option is not exercised and after deducting commissions and estimated offering expenses. We intend to use the net proceeds to fund our ongoing store expansion plan and for general corporate purposes. See “Use of Proceeds.”

We will not receive any of the proceeds from the sale of Shares by the selling shareholder.

10

Listing...................................................... An application has been filed to register the Shares with the RNV maintained by the CNBV, and to list the Shares on the Mexican Stock Exchange. Upon consummation of the Global Offering, such registration and listing will have been effected. Prior to the Global Offering, there has been no trading market for the Shares in Mexico, the United States or elsewhere. We cannot assure you that a trading market will develop or will continue if developed.

Mexican Stock Exchange symbol............ “CHDRAUI”

Payment, settlement and delivery ............ Settlement of the Shares will be made on May 5, 2010 through the book-entry, settlement and custody system of Indeval.

Voting rights ............................................ All of our Shares have voting rights in our general shareholders’ meetings. Each Share grants full voting rights to its holder. See “Description of our Capital Stock and Bylaws” for a discussion of your voting rights.

Control Trust ........................................... Certain of our existing shareholders have created a control trust, where Banco Nacional de México, S.A., integrante de Grupo Financiero Banamex, División Fiduciaria, acts as trustee (the “Control Trust”). Pursuant to the Control Trust, these existing shareholders have transferred to the Control Trust shares, representing 95.73% of our Series B, Class II, common stock shares outstanding prior to consummation of the Global Offering. In general terms, the Control Trust provides for uniform voting of the shares maintained through the Control Trust and includes provisions relating to transfer of shares and trust rights by beneficiaries. See “Principal and Selling Shareholders” for a description of the Control Trust.

Transfer restrictions................................. The international offering is being made in accordance with Rule 144A and Regulation S. The Shares have not been and will not be registered under the Securities Act or with any securities regulatory authority of any U.S. state or other jurisdiction and, accordingly, may not be offered, sold, pledged or otherwise transferred or delivered within the United States or to, or for the account or benefit of, U.S. persons (as defined in Regulation S) except as set forth in “Transfer Restrictions.” As a result of these restrictions, investors are advised to consult legal counsel prior to making any reoffering, resale, pledge or transfer of the Shares.

Lock-up period ........................................ We, the selling shareholder and other principal shareholders have agreed that they will not, subject to certain exceptions, for a period of 180 days from the date of this offering circular, without the prior written consent of the initial purchasers, issue, sell or transfer, any shares of our capital stock or any securities convertible into or exchangeable for, or that represent the right to receive, shares of our capital stock. See “Plan of Distribution.”

11

Over-allotment options ............................ We have granted to the initial purchasers and the Mexican underwriters options, exercisable within 30 days of the date of this offering circular, to purchase up to 20,069,032, at the initial offering price thereof, to cover over-allotments, if any.

Dividends................................................. See “Dividends and Dividend Policy” for further information.

Taxation................................................... Under Mexican law, dividends paid by us to holders of our Shares who are not residents of Mexico for tax purposes are not subject to any Mexican withholding or other similar tax but generally will be subject to corporate taxes if not paid from a net after-tax profits account. We currently intend that any dividends we pay will come from such account. See “Taxation” for a discussion of certain U.S. federal and Mexican tax consequences of holding and disposing of the Shares.

Risk factors .............................................. See “Risk Factors” and the other information in this offering circular for a discussion of factors you should carefully consider before deciding to invest in the Shares.

12

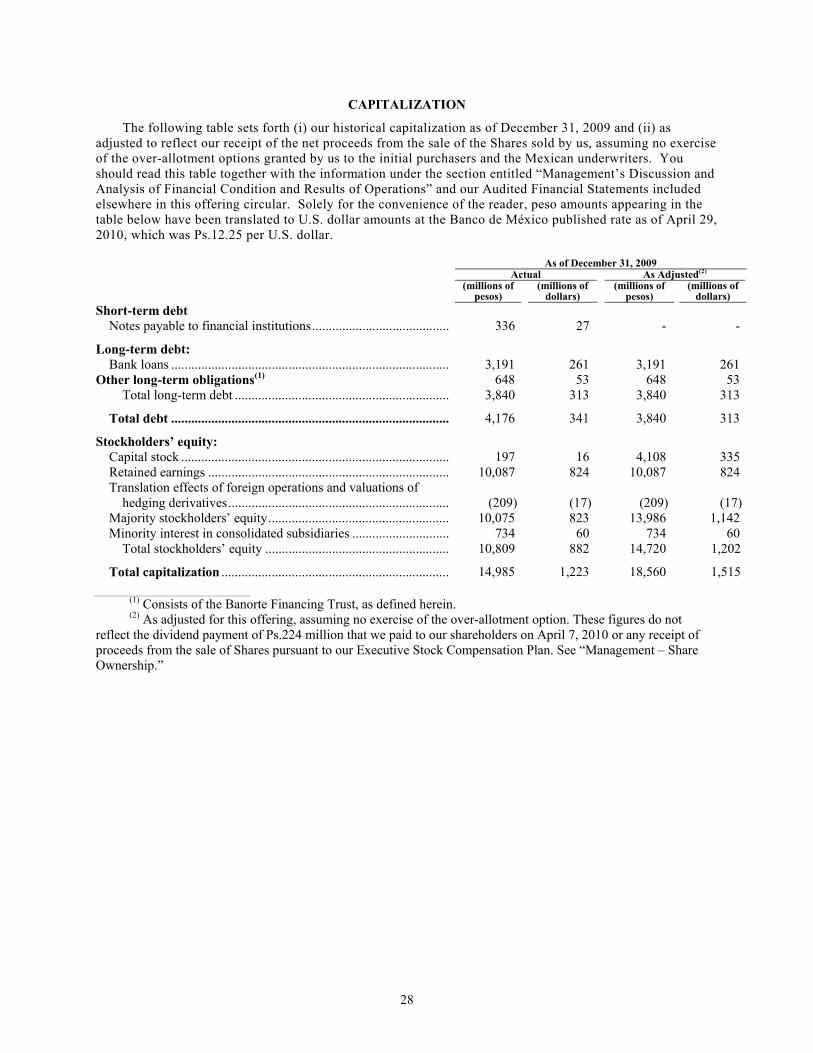

SUMMARY CONSOLIDATED FINANCIAL INFORMATION

The following tables present our summary consolidated financial information and operating data as of the dates and for each of the periods indicated. This information is qualified in its entirety by reference to, and should be read together with, “Presentation of Certain Financial and Other Information,” “Management’s Discussion and Analysis of Financial Condition and Results of Operations” and the Audited Financial Statements included elsewhere in this offering circular. The consolidated balance sheet data as of December 31, 2007, 2008 and 2009 and the income statement data for the years ended December 31, 2007, 2008 and 2009, are derived from the Audited Financial Statements appearing elsewhere in this offering circular.

Our Audited Financial Statements have been prepared in accordance with Mexican FRS, which differ in significant respects from IFRS. See “Significant Differences Between Mexican FRS and IFRS” for a description of certain principal differences between Mexican FRS and IFRS as they relate to us.

The exchange rate used in translating pesos into U.S. dollars in calculating the convenience translations included in the following tables is determined by reference to the rate published by the Banco de México in the Official Gazette on December 31, 2009, which was Ps.13.07 per U.S. dollar. The exchange rate translations contained in this offering circular should not be construed as representations that the peso amounts actually represent the U.S. dollar amounts presented or could be converted into U.S. dollars at the rate indicated as of the dates mentioned herein or at any other rate.

See Annex A for a discussion of our results for the three-month periods ended March 31, 2010 and 2009 and our unaudited interim financial information as of and for the three-month periods ended March 31, 2010 and 2009.

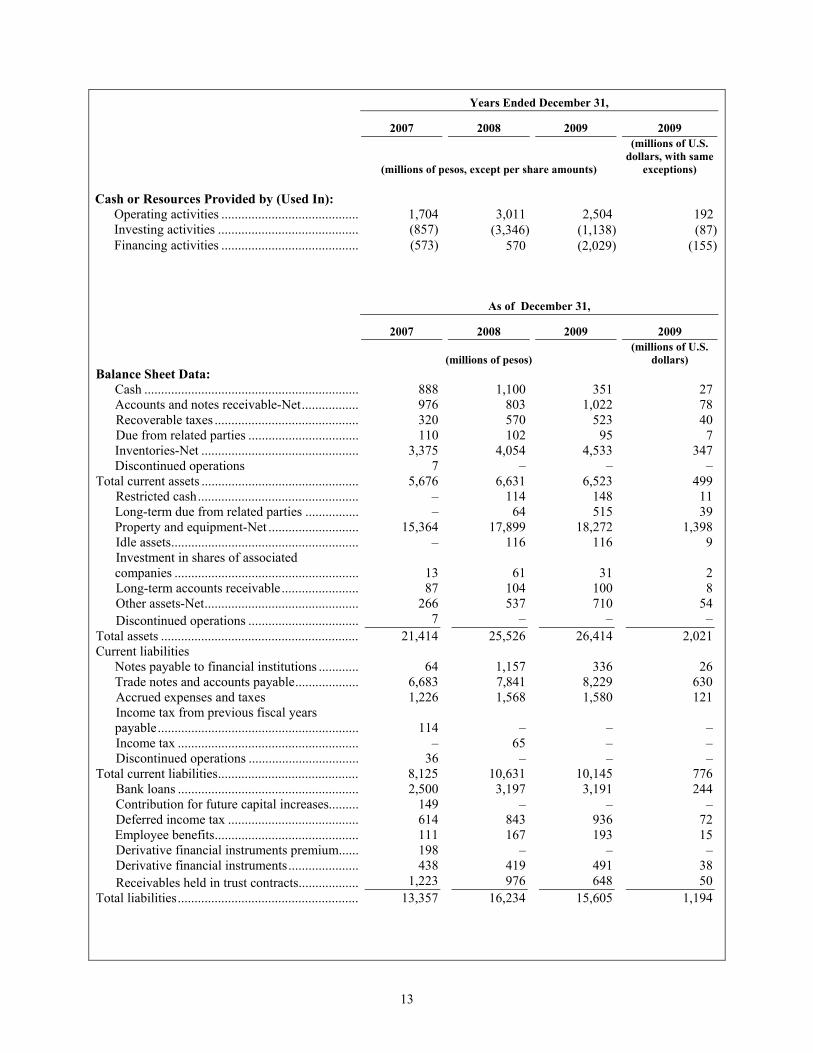

Years Ended December 31,

2007 2008 2009 2009

(millions of pesos, except per share amounts)

(millions of U.S. dollars, with same

exceptions) Income Statement Data: Revenues Net sales .......................................................... 34,452 40,658 47,901 3,665 Cost of sales .................................................... 27,147 32,174 37,535 2,872 Gross profit ........................................................... 7,305 8,483 10,366 793 Operating expenses ............................................... 5,563 6,620 7,879 603 Operating income.................................................. 1,742 1,864 2,487 190 Other (income) expenses – Net............................. (44) 3 (11) (1) Net comprehensive financing cost ........................ 500 615 767 59 Interest expenses ............................................. 816 689 677 52

Interest income................................................ (105) (123) (111) (8) Exchange gain................................................. (4) (70) (1) (.08) Monetary position gain ................................... (362) – – – Valuation of derivative ................................... 155 118 202 15

Participation in the results of associate

companies .......................................................(19)

(39) – – Non-ordinary item................................................. 114 – – – Income before income taxes ................................. 1,192 1,285 1,731 132 Income taxes ......................................................... 627 371 337 26 Income before discontinued operations 565 914 1,394 107 Discontinued operations ....................................... 26 – – – Consolidated net income ................................. 539 914 1,394 107 Net income of majority stockholders .............. 524 924 1,349 103 Net income (loss) of minority stockholders .... 15 (11) 45 3 Basic earnings per common share................... 15 26 35 3

13

Years Ended December 31,

2007 2008 2009 2009

(millions of pesos, except per share amounts)

(millions of U.S. dollars, with same

exceptions) Cash or Resources Provided by (Used In): Operating activities ......................................... 1,704 3,011 2,504 192 Investing activities .......................................... (857) (3,346) (1,138) (87) Financing activities ......................................... (573) 570 (2,029) (155) As of December 31,

2007 2008 2009 2009

(millions of pesos) (millions of U.S.

dollars) Balance Sheet Data: Cash ................................................................ 888 1,100 351 27 Accounts and notes receivable-Net................. 976 803 1,022 78

Recoverable taxes ........................................... 320 570 523 40 Due from related parties ................................. 110 102 95 7

Inventories-Net ............................................... 3,375 4,054 4,533 347 Discontinued operations 7 – – – Total current assets ............................................... 5,676 6,631 6,523 499

Restricted cash................................................ – 114 148 11 Long-term due from related parties ................ – 64 515 39 Property and equipment-Net ........................... 15,364 17,899 18,272 1,398