Embed Size (px)

Citation preview

Underwriting

Objectives

Underwriting, Principles and types1

Application Form and Documentation2

Rules and Regulations3

Underwriting Process Flow4

The possibility of any adverse deviation from a desired outcome that is expected or hoped from any occurrence

What is underwriting?• Underwriting is the process of

– Examining, accepting or rejecting insurance risks, and – Classifying those selected, in order to charge the appropriate

premium for each.

• The purpose of underwriting is to spread the risk among a pool of insured in a manner that is equitable for the insureds and profitable for the insurer.

RiskRisk

Technical Underwriters

Broad Classification of underwriters

Field cum primary Underwriter

Underwriters

• Agents & the Agency development managers.

• They come in personal contact with the client and have an excellent opportunity to assess the risk.

• It is essential that the they should help to screen out bad risk.

• The person actually concluding the contract of insurance there by committing the contractual liability and obligations.

• He is required to be vigilant while scrutinizing each and every document submitted and ensure that the basic underwriting requirements are abided by.

What does an Underwriter do?• The underwriter is an employee of the

insurer who-

UnderwriterUnderwriter

BB

CC

DD

AAEvaluates risk

Accepts Applications

Declines Applications

Determines appropriate premium

The decision to provide insurance coverage or not is

commonly referred to as an underwriting

decision

These decisions greatly affect the success or failure of an insurance company

Underwriting is considered to be sound if each risk is evaluated accurately, classified properly, approved for an appropriate premium amount, or denied accurately

Why is sound underwriting important?• Sound underwriting is beneficial to the insurance

company, the insured and the insurance sales persons:– Helps insurance companies remain competitive and financially

strong.– An insurer’s profit primarily determined by controlling expenses,

accurately pricing products and exercising sound judgment in underwriting

– An insurer must charge premium amounts that correspond to the risk that each proposed insured represents.

– Sound underwriting benefits sales agent because they can use an insurer’s sound underwriting practices as a selling point to demonstrate the company’s focus on fairness to policy owners and its commitment to financial strength.

SoundSoundUnderwritingUnderwriting

What are the objectives of Underwriting?• Effective underwriting enables insurers to issue policies that are:

Basic concept underlying life insurance pricing is to ensure that the premium amounts charged for a cover is based only on factors affecting the policy’s costs. As the underwriter receives each application for insurance, he evaluates the degree of risk presented by the proposed insured and charges a fair premium to insure the risk.

When the agent delivers the policy, the customer may choose not to accept it, if the premium or the coverage is different from what was expected.To be acceptable to the buyer, a policy must satisfy three basic requirements.

1. The policy must provide benefits that meet the buyer’s needs.

2. The coverage provided by the policy must be affordable to the buyer.

3. The premium charged for the coverage must be competitive in the marketplace.

Equitable to Equitable to policy-owners, policy-owners,

Deliverable by Deliverable by agents agents

What are the objectives of Underwriting?

Just like insured should be charged premium amounts that are appropriate for the level of risk they present, insurance companies should also be compensated for the level of risk they accept on each policy.

All insurance companies, require sound underwriting to help assure favorable financial results.

Although underwriters are only indirectly involved in establishing a company’s premium structure, underwriters’ decisions are crucial in producing actual mortality results that correspond to the actuaries’ mortality projections, and, thus, produce profitable business.

Profitable to the Profitable to the insurance insurance company.company.

Insurance Products

Risk Premium

Savings Premium

Typical Endowment Plan

Risk Premium

Typical Term Plan

[Rs. 5]

[Rs. 20]

[Sum Assured: Rs. 100]

[5 Year]

[Rs. 25] [Rs. 5]

“Utmost Good Faith” (Uberimma fides )

• “ A Duty voluntarily to disclose, accurately and fully all material facts pertaining to risk proposed, whether requested or not. ”

Anti Selection• Any action by the applicant which obstructs the

underwriter from selecting and classifying risk fairly

• How does one Antiselect ???– Non-disclosure– Misleading information– Avoiding medical tests– Legally the insurer can repudiate claim and even confiscate

premium.

Moral hazard• Moral hazard is the prospect that a party insulated from

risk may behave differently than it would if it were fully exposed to the risk.

• Moral hazard arises because an individual or institution does not bear the full consequences of its actions or may want to bring about an unnatural outcome to an other wise normal life.

1. Occupation

2. Avocation

3. Hobbies

4. Residence

5. Moral Hazard

1. Insurable Interest

2. Income Protection

3. Persistency

4. Net Worth

1. Build

2. Habits

3. Personal Medical History

4. Family Medical History

Risk Factors in Life Insurance• The various risk factors to be assessed prior to

underwriting decision are:1. Medical2. Financial 3. Personal

Life Insurance Risk Factors

321

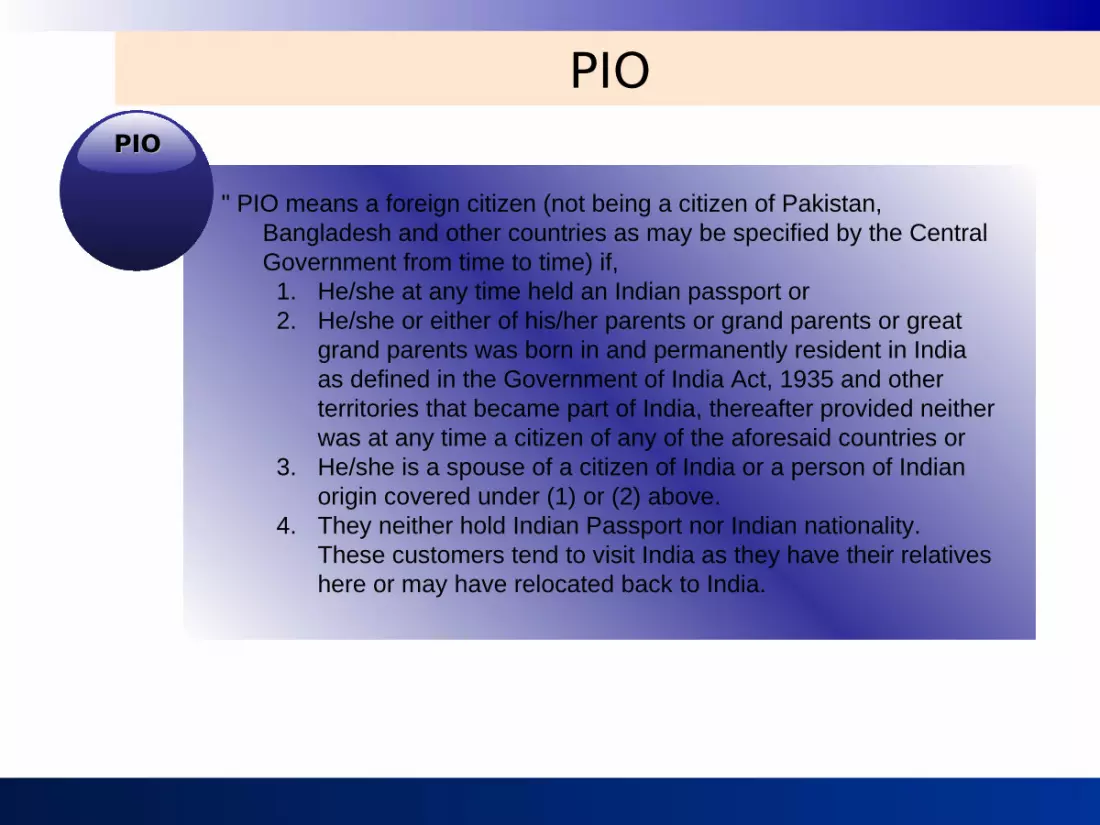

Some Product rules• Product not offered to NRI/PIOs/Foreign Nationals (residing

in India)• Term products, Term riders and Hospitalization products are not

offered to NRI /PIOs/Foreign Nationals• Product not offered to Illiterate• Term plans, Term Riders Accident & Health products are not offered

to Illiterates.• Product not offered to Class 5• Riders and Accident & Health products are not offered to Individuals

belonging to occupation class 5.• Products where back date is not allowed• Unit Linked covers, Accident & Health products and Term plans and

product with term rider are products where back date is not allowed.• Product not available to Housewife • Term plans, Term riders are not available to Housewife.• Products not available to Juveniles less than age 18• Any riders, term plans, ShubhLife, Health products, Nirvana plus,

Assure Security and growth plans.

Some Product rules• ADB and ADDL cannot be offered simultaneously• Whenever CI rider has been opted, the premium cannot be

paid through CC authorization or SI instruction.• No riders can be attached to term plans• Regulatory Rule: - Total rider premium should not exceed

30% of basic premium: - Such cases have to be pended for reduction in sum assured of riders.

• For HP, the ADB benefit cannot be more than 2 times the Term benefit. The total FADD benefit cannot be more than the Term benefit.

• NRIs as well PIOs can be offered HP subject to AHC rider minimum i.e. Rs.100/-as well as Term benefit minimum.

Filling in the application form

Rules relating to application form filling• The application form is the basis of each and every

contract and as such is, in the majority of cases, the most important source of information available to the underwriter. Each question contained within the form has its relevance in assessing the risk being presented while a cover is being applied for. Hence it is very essential that all the details are captured correctly and to the fullest

• All details in the application form as well other documents submitted should be completed in all respects (no blanks acceptable).

• Any overwriting, correction or cancellation in the Application form and other documents including Amendment form has to countersigned by the Insured/Applicant (same signature as on the last page of the application form).

Rules relating to application form filling• Questions, in the application form and other documents,

should not be answered as NA or Not Applicable. If the answer is in negative, should be answered as NIL (Exception: Female life Questions where Insured is male.)

• Combined Life application form, HP and FIH forms, only the first part of Health Declaration is to be filled up to the specified simplified limits of corresponding plans, but both parts of the Health declaration has to be filled beyond the limits.

• However if there is any adverse health declaration, than both parts of Health declaration has to be filled even within the simplified limits.

Application Form

Important information in an application form

Application form• Name: This not only gives the identity of the applicant but

also can reveal their ethnic origin, indicate if they are famous or even infamous, and would suggest Insured’s lifestyle, travel, pastimes, etc.

• Points to be noted– Specify the full name of the proposed insured corresponding to the

age proof submitted by the client.– Insured/Applicant's name must be written in block letters using blue /

black ink as Surname-------------First Name---------------Middle Name

– In case of married female, if the name has been changed after marriage, Maiden Name Declaration (full name of the Insured prior to Marriage) has to be completed in the application form.

– Name Mismatch: In case name of the Insured has been changed or there is a mismatch in the name, as given in the application form vis-à-vis age proof submitted, a gazette copy has to be provided as proof of the name change.

Application form• Address: Apart from its role in communicating with the

applicant, the address can give some idea of the financial status of the applicant, especially if he or she lives in an area, which is well known. In conjunction with other features such as occupation and marital status, it can lead to further enquiries regarding lifestyle.

• Points to be noted– Ensure that both the Residential & Business addresses are mentioned

in full.– For NRI or PIO residing abroad, the foreign address can be mentioned

as residential address.– Address Proof required of the Temporary or Permanent from AML

perspective– Both the permanent & current address proofs required if both

are different as per application form.

Application form• Marital Status: A useful indicator for the need for cover & of

the level of acceptable sum assured.

• Points to be noted– For the Male Insured, based on marital status, BPE test will be

called at the age 35 and above.– For age between 35 – 40 year above 100,000 Sum assured

RBT is required and for age 40 years RBT will be called in all sum assured

Application form• Date of birth: This information is essential for premium rate

calculation. It is also important in determining if the sum proposed exceeds routine non-medical limits & is important in assessing the significance of certain medical impairments e.g. Asthma.

• Points to be noted– Date of Birth mentioned in the application form should match with that

on the standard/Non standard Age proof submitted. – DOB Mismatch:

• If there is mismatch of the Age as per the DOB mentioned in Application form vis-a vis non standard age proof submitted, and if the Age as per DOB mentioned in the Application form is lower, alternate Standard age proof will be required or higher age premium and higher age SIS can to be submitted with reconfirmation of the DOB in a GAF.

• However, if the Age as per DOB mentioned in the Application form is higher, the same can be accepted, if the corresponding premium and SIS has been submitted.

Application form• Nationality Check nationality and residential status:

– Nationality should be specified correctly since based on nationality and residential status (Nationality of the Proposed Insured other than Indian or residing for more than 180 days out of India), Specific NRI/PIO rules will be applied for the case.

For PIOs /Juveniles & housewife having foreign resident Parent or Husband, respectively, the residential status should be clearly mentioned in a separate GAF.

Application form• Occupation

– The obvious advantage of knowing the applicant's occupation is being able to assess any associated accident and/or health risk and, for disability coverage to classify the occupation for rating purposes.

– Occupation are classified in to five different categories as per the risk they bring along with them (described in occupation section).

– The information can also be useful to assess whether the sum proposed and premiums payable are reasonable, given the applicant's likely financial status and income.

– If the occupation is ‘Driver’, a special mention should be made regarding the type of vehicle and the nature of the goods being transported (Hazardous/Non Hazardous) and in other occupations appropriate Occupation Questionnaire should be provided.

Application form• Applicant and Nominee details

If applicant is different as compared to Insured, all the details as mentioned earlier needs to captured.

For HUF and Keyman cover, the same has to be specified in the Applicant name details and the date of Incorporation of the HUF or company has to be provided.

As per Section 39 of Insurance Act, 1938 the holder of a policy on his own life, may either at the time of taking out the policy or any time during the term of the policy before maturity, nominate the person or persons to whom the money secured by the policy shall be paid in the event of death of the Life Assured, for the disbursement to the Legal heirs (beneficiaries).

As per the company rules, direct relatives e.g. Father, Mother, Wife, Children, brother, sister, grandparents can be designated as Nominee for the cover

Application form• Following can be nominated, subject to a satisfactory declaration

from the client. – Aunt– Uncle– Cousin– Nephew– Niece

• Any other Nomination would not be allowed.• Name, age and relationship of the Nominees should be specified.• Nomination is not allowed in all cases where Applicant & Insured

are not the same (e.g. Juvenile cases, Housewives, Students above 18 years)

• Although nomination is not compulsory, it is preferable to declare nominee for the ease of payout at the claim stage.

• Although multiple nominees can be allowed, assigning percentage for the various nominees is not allowed.

• A minor (less than 18 years of age) can be a Nominee but not an Appointee.

Application form• Appointee and Contingent policyholder:

– When a nominee is a minor (below age 18 yrs), the applicant (Payor) of the policy should appoint an appointee.

– In juvenile policies, contingent policy holder name with age and relationship should be provided, The CPH should an adult. If the CPH is not among the relatives as mentioned above, an explanation has to be provided.

– CPH signature has to be mandatory be provided.– Applicant cannot be the contingent policyholder.

Application form• Hazardous risk questions:

– Details of any hazardous pursuits, frequent flying or working in armed force should be answered ‘Yes’ or ‘No’, N.A is not accepted.

– If any previous cover has been rated up or declined or postponed, the same should be specified and details have to provided.

– If answer to Hazardous risk Questions like working in Arm force or working as Pilot is ‘Yes’, the corresponding questionnaire should be enclosed

• Aviation/ Armed Forces question:– Many hazardous sports and pastimes require a high level of physical

fitness, whilst others such as sub-aqua diving or private aviation can require participants to undergo periodical medical in order to meet licensing requirements.

– The special questionnaires have to be provided, as it is essential in the assessment of risk to obtain considerably more information than would normally be available from a standard application form.

Application form• Insurance Covers with other companies:

– Should clearly state the Insured’s or Applicant’s insurance cover giving relevant policy details.

– In case policy with TATA-AIG the policy number should be provided.– If the Proposed Insured does not have any insurance, other than the

current policy for which he/she is applying then “NIL” has to be written in the column provided.

– Previous cover detail is used determine to eligibility of the maximum cover to carry out Financial underwriting

– If any previous policy with any other Insurance has been declined, Postponed or rated up, details of the same must be provided.

Application form• Questions for smoking, alcohol and build

– The proposed insured or the applicant should clearly specify the type and no.of cigarettes smoked or type and quantity of tobacco consumed along with details of how many years, since consumed.

– If there is alcohol consumption, the amount and type of Alcohol consumed, and how frequently & since how many years need to be specified.

– Build need to be specified correctly.

• Points to be noted:– Ht should be specified in cms and Wt in Kg.– If there is large discrepant Build, Medical examination may be called based on

the same.– If there is significant change in Build with in last 12 months, the same should

be mentioned along with the reason for the same. – In Juveniles, the Height and Weight of the child should be captured correctly

and accurately. Even small discrepancy, in Build of child, may lead to rejection of case.

– If the Ht and Wt of the child has been measured in presence of Doctor, the same should be captured in a GAF, duly attested and signed by the physician (Reg. No. of Doctor should be provided) and the same can be submitted at the time of application itself.

Application form• Health Questions

– Health declaration Questions are mandatory including the family history Questions and if there any positive health declaration, the details of the same should be provided.

• Points to be noted– In case the client discloses any personal Impairment – further

Questionnaires, Medical examination or medical test, personal reports or APS may be called.

Application form• Date Back option questions:

– Dating back or Back Dating is an option that allows the assured to get the benefits of lower age by commencing the policy from a date earlier than the date on which the proposal form was signed. Application date and date back can’t be the same.

– Birth date and date back date cannot be the same.– In case of juvenile (less than 1 year) back date is not allowed.– In case of term riders, term plans, 20TROP, UL & Health first back

date is not allowed. – For ShubhLife, date back allowed for a maximum of 6 months within

the same financial year.– Date backing is allowed up to 12 months for Nirvana Plus-WSM cases.– The back date should not be more than 6 months from the application

date.– Premium to be collected from Date back date.

Application form• Signature:

– Signature of the Proposed Insured and/or applicant and signature of the agent has to be provided.

– For Juvenile cases, applicant only has to sign the application form. In cases where Insured is Adult (> age 18) and applicant is different (Parent or Husband), signature of both the applicant and Insured would be required.

– Vernacular declaration is required to be counter-signed by the agent or the person explaining the contents of the application form along with his identity details.

– If agent is the proposed insured/applicant, application form is to be duly attested by the RDM/ADM.

– Corrections done in the agent related information should be countersigned by the RDM/ADM.

Application form• Signature (Continued):

– In HUF and Keyman cover, the signature of the Karta with the Karta stamp, and Signature of Authorized signatory along with stamp would be required in addition to Signature of proposed insured.

– For Illiterate Right thumb in Females and Left thumb in Males.– The place of signing the application form has to be within India.– When the agent has filled the application form on behalf of the

Applicant, a declaration has to be provided to the effect by the agent as well as Applicant.

– Also a declaration has to be provided by the agent, regarding the submission of the KYC and AML documents in non Health or Term plans

Customer Signature

• Following are the list of proofs that require self attestation : – Age Proof – Address/Residential Proof – MOA/AOA – Attended Physician's statement – Personal Medical reports/Prescription papers / Hospital Discharge card – Income documents like ITR ; Salary Slip or certificate ; Bank

Statements ; CA Certificate ; Asset & Liability statement ; PnL ; Balance Sheet etc. If income documents are multiple pages or compilation of several documents then attestation or signature should be on relevant pages only i.e. certification page , stake holder's detail page ,Balance Sheet /P&L details page.

Please note: Effective 1st June 2008, it is MANDATORY for all

supplementary proofs submitted to be signed by the customer.

Some common errors relating to application forms

Height and weight details not provided. Other details correctly filled in.

Age Proof

Age Proof Guidelines• Classification based on the Sum Assured* and Products

Sum Assured*

(Rs)

0 – 8,00,000 / Health First up to 4 Units

8,00,001 – 30,00,000 > 30,00,000 / Health First more

than 4 Units

Type of Product

All products All products All products.

Type of acceptable Age proofs

List A List B List C

*Sum Assured will include Basic plan along with Term and Critical illness riders and Total Permanent Disability with TALIC and will include all the policies on the Life of that individual with TATA AIG Life.

For SA band 8.0 Lacs to 30.0 Lacs for all products we will require List B only. We shall not call for List C for Term/ Health products and covers more then 8 lacs and having Term/Critical illness riders

Acceptable Age Proofs- List “A”• Driving License – a document that is issued by the Issuing Authority (It

should have completed more than 2 years since it has been issued and for an Expired Driving License it should be not more than 2 years since expiry)

• Pan Card – a document issued by the Income Tax authorities• Ration Card (Date of issue of the Ration card is required.) – Issued by the

municipal authority for every family.• Voter ID card – issued by Government • The Certificate issued by the Village Panchayat, providing details of

the name and date of birth and duly stamped.• LIC policies where the age is shown as admitted, will be accepted• TALIC Agents License / ID card.• Health Scheme (CGHS) certificate with details of Age/DOB on it, will be

accepted for all Central Government employees.• ESIS card• PF statement from employers, which states the name and date of birth.• Only discharge card from the Nursing home/Hospital specifying the DOB

for age upto 5 yr. will be acceptable. However, it is mandatory to submit name of the child or an amendment form in which applicant (Payor) gives declaration that the age proof belongs to the proposed insured for age 0-5 year.

Acceptable Age Proofs- List “A”• Baptism certificate, Municipal Birth Certificate with DOB & Name of the

proposed Insured will be acceptable. However in case where the name of the child is missing in the age proof, it is mandatory to submit an amendment form in which applicant gives declaration that the age proof belongs to the proposed insured and clearly stating the name and DOB (acceptable only upto age 5 years).

• S.L.C. or Higher Secondary Mark list, School / College certificate/Certified extract from school or college/Progress Cards will be acceptable. The certified extracts have to be provided on the letter head of the institution duly signed, stamped by the Principal.

• Certified extract from Service register in case of Govt. Employee & Employee of Quasi Government & Institutions belonging to Public Ltd. Cos. provided, conclusively evidence of age was produced at the time of recruitment of employees. Certified extract to be obtained on the Cos. letter pad and Cos. seal and countersigned by insured.

• ID cards of only TATA Employees, Government/Semi government employees clearly stating the DOB will be accepted as standard age proof

• Passport• Marriage Certificate of a Christian issued by a Roman Catholic Church• ID card issued by Defense Dept.• Domicile Certificate• Copy of Family extract page 2 of the Gram Panchayat, which gives

details of Name, Age, Date of Birth and relationship to the head of the Family *• Bonafide school certificate stating the date of birth**.

Acceptable Age Proofs- List “B”• Driving License – a document that is issued by the Issuing Authority (It

should have completed more than 2 years since it has been issued and for an Expired Driving License it should be not more than 2 years since expiry. (Learner’s license will not be accepted as Age proof)

• Pan Card – a document issued by the Income Tax authorities. • Only discharge card from the Nursing home/Hospital specifying the DOB

for age upto 5 yr. will be acceptable. However, it is mandatory to submit name of the child or an amendment form in which applicant (Payor) gives declaration that the age proof belongs to the proposed insured for age 0-5 year.

• Baptism certificate, Municipal Birth Certificate with DOB & Name of the proposed Insured will be acceptable. However in case where the name of the child is missing in the age proof, it is mandatory to submit an amendment form in which applicant gives declaration that the age proof belongs to the proposed insured and clearly stating the name and DOB (acceptable only upto age 5 years).

• S.L.C. or Higher Secondary Mark list, School / College certificate/Certified extract from school or college/Progress Cards will be acceptable. The certified extracts have to be provided on the letter head of the institution duly signed, stamped by the Principal.

• Certified extract from Service register in case of Govt. Employee & Employee of Quasi Government & Institutions belonging to Public Ltd. Cos. provided, conclusively evidence of age was produced at the time of recruitment of employees. Certified extract to be obtained on the Cos. letter pad and Cos. seal and countersigned by insured.

• ID cards of only TATA Employees, Government/Semi government employees clearly stating the DOB will be accepted as standard age proof

Acceptable Age Proofs- List “B”• Passport• Marriage Certificate of a Christian issued by a Roman Catholic

Church• ID card issued by Defense Dept.• Domicile Certificate• Copy of Family extract page 2 of the Gram Panchayat, which gives

details of Name, Age, Date of Birth and relationship to the head of the Family.

• LIC Policy –• The LIC policies and the premium receipts, which indicates the age,

admitted based on the following codes only will be accepted as Standard age proof. The codes are

• P: Passport • S: School Certificate • C: College Certificate • M: Municipal Birth Certificate • B: Baptism Certificate • I: Defense ID card • J: Domicile Certificate • E.g. LIC Policy which indicates Age, admitted: Yes (P), will be accepted as

standard age proof. • Policies with the above abbreviations only, will be accepted as Standard age

Proof.• Bonafide school certificate stating the date of birth.

Acceptable Age Proofs- List “C”• Only discharge card from the Nursing home/Hospital specifying the DOB

for age upto 5 yr. will be acceptable. However, it is mandatory to submit name of the child or an amendment form in which applicant (Payor) gives declaration that the age proof belongs to the proposed insured for age 0-5 year.

• Baptism certificate, Municipal Birth Certificate with DOB & Name of the proposed Insured will be acceptable. However in case where the name of the child is missing in the age proof, it is mandatory to submit an amendment form in which applicant gives declaration that the age proof belongs to the proposed insured and clearly stating the name and DOB (acceptable only upto age 5 years).

• S.L.C. or Higher Secondary Mark list, School / College certificate/Certified extract from school or college/Progress Cards will be acceptable. The certified extracts have to be provided on the letter head of the institution duly signed, stamped by the Principal.

• Certified extract from Service register in case of Govt. Employee & Employee of Quasi Government & Institutions belonging to Public Ltd. Cos. provided, conclusively evidence of age was produced at the time of recruitment of employees. Certified extract to be obtained on the Cos. letter pad and Cos. seal and countersigned by insured.

• ID cards of only TATA Employees, Government/Semi government employees clearly stating the DOB will be accepted as standard age proof

• Passport• Marriage Certificate of a Christian issued by a Roman Catholic

Church

Acceptable Age Proofs- List “C”• ID card issued by Defense Dept.• Domicile Certificate• Copy of Family extract page 2 of the Gram Panchayat,

which gives details of Name, Age, Date of Birth and relationship to the head of the Family. (Attached is the copy family extract)– LIC Policy –

• The LIC policies and the premium receipts, which indicates the age, admitted based on the following codes only will be accepted as Standard age proof. The codes are

• P: Passport • S: School Certificate • C: College Certificate • M: Municipal Birth Certificate • B: Baptism Certificate • I: Defense ID card • J: Domicile Certificate • E.g. LIC Policy which indicates Age, admitted: Yes (P), will be accepted

as standard age proof. • Policies with the above abbreviations only, will be accepted as

Standard age Proof.– Bonafide school certificate stating the date of birth.

Acceptable Age Proofs• NOTE:

• All I.D must clearly show date of birth. (I.D. showing age only will not be acceptable).

• Age proofs in Vernacular (regional) language should be translated and attested by the Br. Manager.

Format for School CertificateSchool Certificate

This is certify that Shri / Kumari : --------------Son / Daughter of shri/Mr------------------------- Village ----------------- P.O ------------ Dist/Tahsil.------- State-----------------was a bonafide student Of our institution -----------------------during the session-----------------------------------------------. His/Her date of birth as per the school admission register number (if available).-------------------- Date: Signature of the headmaster Signature of the insured/ applicant _______________________________________________________________________________ I undersigned hereby confirm that the above institution/school is existing in the given location and is currently functional Branch Operation Manager/ Gazetted officer Date: ________________________________________________________________________

Points to be noted• The copy of age proof submitted has to be signed by the

Life Assured.• Pan card and Driving License are acceptable for Sum

Assured 8 - 30 lacs .i.e. as soon as Sum assured (Basic plan along with Term and Critical illness riders and Total Permanent Disability) 8 lacs through single or multiple policies, list B will be applicable except when customer has opted for Term plan or Health Products or where plans has Term or critical illness riders in any of the plan opted with TALIC.

• Driving License provided, should have been issued more than 2 years ago, at the point of application.

• An expired passport can be used as Age proof document (however not as photo ID proof)

• The Affidavit cannot be submitted as an age proof

Points to be noted• When two substandard documents have been submitted

as Age proof and Photo ID proof and there is mismatch in the age as mentioned in the two documents and customer has opted for lower age as mentioned in the Application form, the Applicant can – provide a a alternative std age proof document or – can take higher age as per higher age giving document

submitted, confirming the same by a GAF and – pay higher age premium and provide SIS for the higher Age

in conventional plan or just provide higher age SIS for ULIP plans.

Points to be noted• However, if the Age as per DOB mentioned in the

Application form is higher, the same can be accepted, if the corresponding premium and SIS has been submitted.

• Age proofs in Vernacular (regional) language should be translated and attested by the Br. Manager.

• DOB declared by school/college should be on the letterhead of the institution, bearing its stamp & signed by the Principal/Headmaster (exception of letterhead in rural cases).

Sales Presenter and Goal Finder/DnA

Sales Illustration - SIS• SIS has to be submitted in all cases. • The SIS has to be of the same version and same set and

all the pages have to be submitted. • SIS should be signed by applicant/Insured in pages where

signature column is provided.• It may or may not have signature of the Applicant on all

the pages; however it needs to have signature of the Applicant (and Insured, if different from applicant and age > 18 yrs).

• The following areas are important:1. Name,

2. Age

3. Gender (if CI rider has been opted)

4. Payment opted

5. Plan opted

6. Rider details

7. Term

8. Sum Assured

9. Premium

In addition to these, for Unit Linked Insurance Plans, the premium multiple and fund allocation is also important.

Sales Illustration- FormatCustomer Specific Details

Policy Specific Details

DnA Sales Tool• DnA Sales Tool is mandatory in all Unit linked cases,

however they are not required Bancassuarnce and Broker channel & DM Channel .

• The following information should be captured:– Clients Personal Information– Family Members/ Dependents– Policy Owners Signature– Agents Signature– Clients Chosen Plan– Client's Risk/Return Attitude. (At least one option should be

ticked)

D n A- Format

Forms and Questionnaires

General Amendment Form• This form is used to make any changes/clarification called

for in the application form prior to the issue of the policy.

• All the details should be mentioned clearly in the general amendment form and the form has to be signed by the applicant and the agent, duly dated.

Financial Questionnaire• Financial Questionnaire is an important declaration

provided by the Applicant, giving details of the financial status of the insured.

• Part II of the Financial Questionnaire is mandatory for Business class and self employed, where all the Business details for the Applicant have to be filled up.

• For non earning individuals like juveniles or housewives, financials details of the applicant or the Payor have to be provided and incase the Insured is adult, signature of both insured and Payor is required, otherwise it has to be duly signed by the applicant.

Financial Questionnaire• Modified abbreviated form of financial questionnaire can

be utilized for covers for individuals who are premier or power vantage customers of premier banks only.

• Part II of the modified financial questionnaire has to be filled by the Relationship manager of the bank providing the relationship details.

• Annual Income section of the Financial Questionnaire should reflect the actual earned income of the applicant or the payor.

Important parts of the financial questionnaire

• Intent of taking cover• Previous cover details including Individual on which the covers is

taken, kind of cover, Insurance company, sum assured and premium.

• Pan No.• Nature of occupation, salaried or Business.• Last 3 years annual income.• Income from other source, details.• Various assets including properties and investments and liability.• Lifestyle questions• Juvenile Questions giving details on life cover on the sibling of the

insured.• Business ownership details.• Account details of the Business.• Part III of the Financial Questionnaire has to be filled by the

agent.

Asset Liability Statement• All parts of asset liability statement should be duly filled up.• Important areas these statements are:

1. Name of the bank should be specified.

2. Last 3 years annual income details

3. Various categories of Asset and liabilities

4. Name of the bank with whom the investments are made should be specified.

5. Net worth of the Individual.

6. Statement should be duly dated & signed by the Applicant/Payor.

7. In case of bancassurance channel, it has to be duly signed by the Relationship manager and Bank manager, along with the applicant. (HSBC certified asset liability is not acceptable)

8. In case of Non bancassurance channel case, it has to be duly dated and signed by the Chartered accountant (CA), duly stamped. Also name of the CA firm with name of the main partner or proprietor and CA registration no. has to be provided, along with applicant signature.

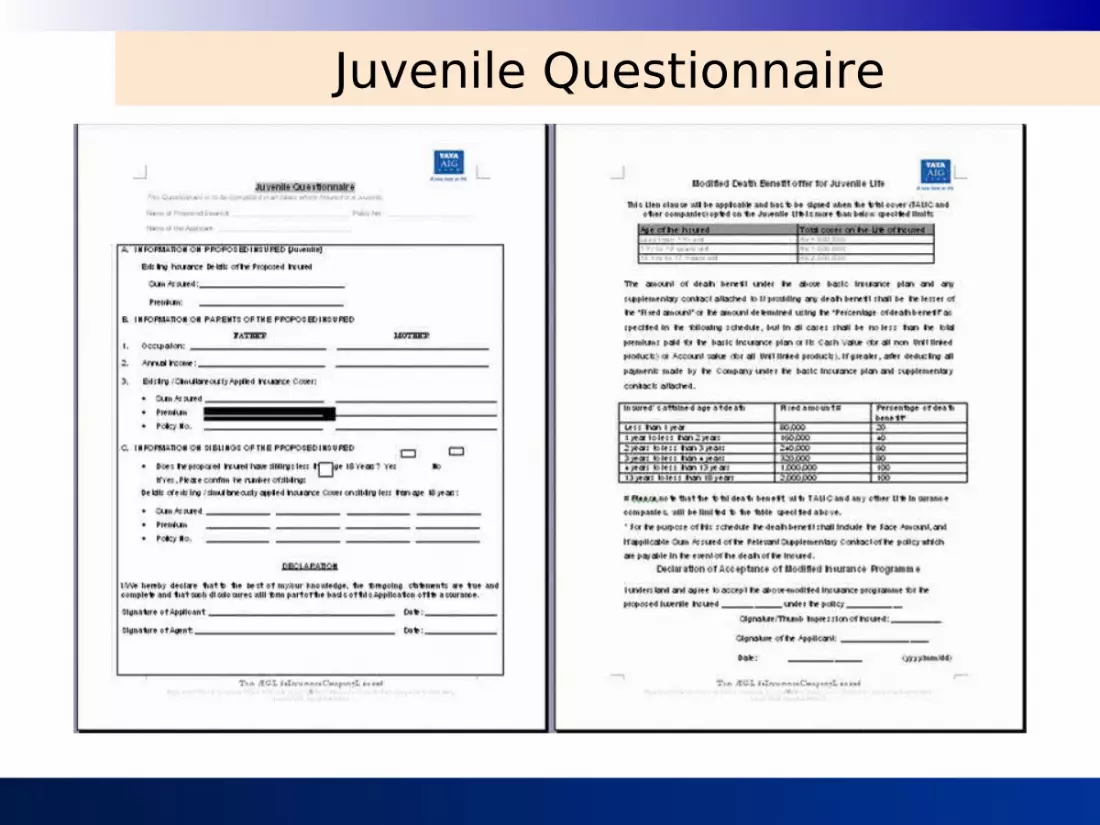

Juvenile Questionnaire• Juvenile Questionnaire is to be mandatorily filled in all juvenile cases.

Important areas of Juvenile Questionnaire are:• Current and previous cover details• Annual income and existing or applied cover details of both the

parents.• Details if Insured has any siblings less than age 18 and details of the

cover on their life.• Based on these details, decision of the maximum cover that can be

granted on the life of the juvenile is decided.• Part II of Juvenile Questionnaire has to be signed by the applicant,

when the total TALIC cover on the child exceeds the limit of:

Age bands Total Sum assured0 to 12 years Rs 1,000,000

13 to 17 years Rs 2,000,000

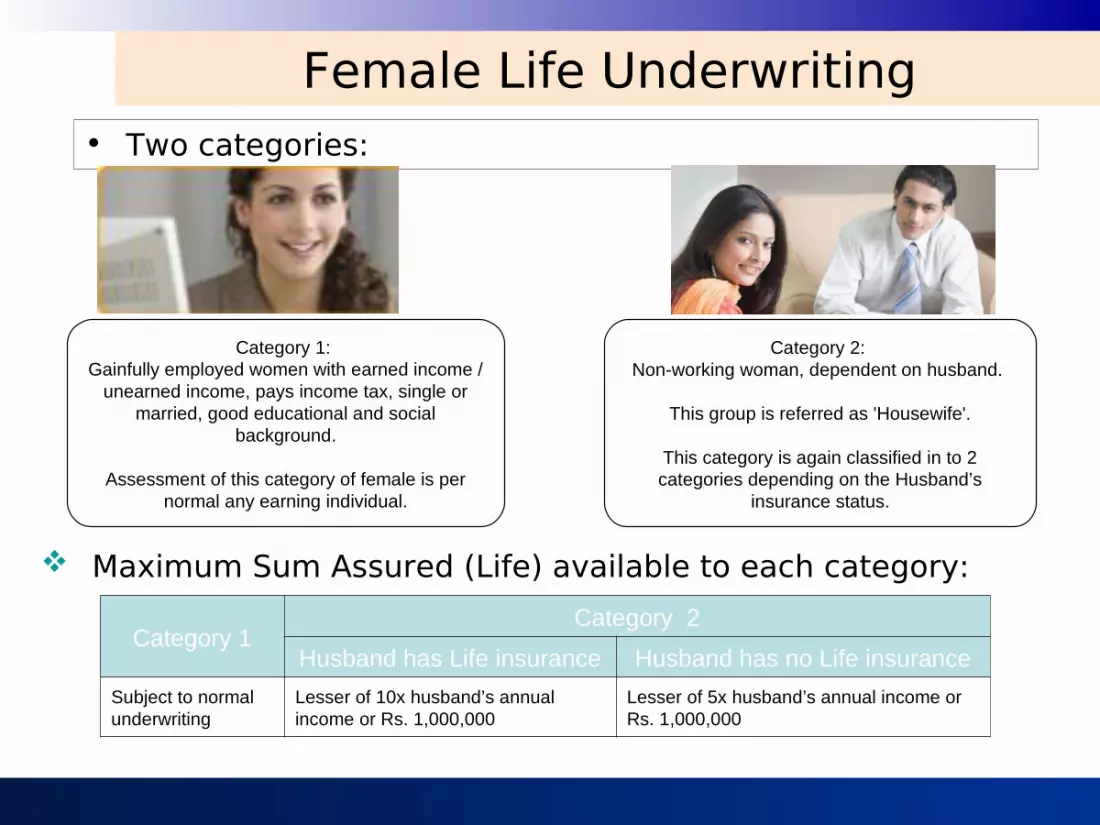

Housewife Questionnaire• Housewife questionnaire has to be submitted in housewife

cases. It provides details about the Profile of the Housewife Annual income of Husband of the Insured. Existing or applied cover on the life of Husband.• If the cover of the Housewife is more than 10 lacs, proof of

Husband’s income and proof of cover on his life has to be provided.

Payment• Through Credit card or ECS :

1. Incase of payment to be made through credit card, we require the front side of credit card copy along with the Credit card authorization form

2. Incase of Auto premium payment through ECS we require the original forms to submit to the POS dept and not the Xerox.

3. Incase of Debit card instruction, only debit card copy is sufficient.

Payment• Through Standing Instruction (SI) :

1. Should contain the S.V (Signature verified) stamp OR HSBC Stamp.

2. Should contain signature of authorized HSBC employee with HSBC stamp in the allotted space below "For bank use only".

3. Should contain the HSBC employee's signing number.4. If there is any alteration in the account number, policy

number, policy name or amount, should be countersigned.

Payment• Towards a bounced instrument

1. Payment towards bounced instrument should be in cash/demand draft.

2. If the payment is for SI or CC bounce cases, then the cashier would only accept that modal premium in cash/cheque.

3. For any payment against bounced cheque, maximum amount accepted in cash would be 49,999 and the balance should be presented by Demand Draft.

A general amendment form is required from the applicant when he wants to change the mode of payment from SI or CC to cash or cheque, confirming the same.

Payment• Transfer of funds request:

– Transfer of funds can be requested via letter/GAF duly signed and mentioning the policy no. from the customer.

– The Customer can request for transfer of funds in his capacity of an Insured or Payor.

– It can be transfer of funds from one policy to another or for a particular policy if a refund cheque has been send back by the applicant.

• Transfer of Funds can be done only in the following two scenarios:

From an existing policy of the Customer, his children or spouse (which is closed, declined, postponed or withdrawn) with our company to a new application being

submitted by the customer.

From an existing policy of the Customer, his children or wife (which is closed, postponed, declined) with our company to another of his earlier inforce policy for adjustment against

his due premium.

Medical Underwriting

Medical Underwriting• Medical Limit- Total Sum Assured for Medical Underwriting

This includes the amount of Basic Life (Permanent or Term) + Term Rider + Critical illness rider + ½Sum Assured of Payor Benefit Rider of all TALIC policies

(provided there are no fully underwritten Health products) + Top up Sum Assured.

• Medical Limit- Total Sum Assured for Medical Underwriting– Where along with conventional life covers, A&H product is

also applied for, the medical limit would be defined as for • If the HP applied for is simplified, than medical limit would be Total

permanent disability benefit+ CI or cancer benefit+ CI benefits of Health first plan for all TALIC plans

• Fully underwritten life and A&H -Basic Life (Permanent or Term) + Term Rider + Critical illness rider + Top up Sum assured + ½Sum Assured of Payor Benefit Rider + Term Benefit (>4 Lac) +Total permanent disability benefit+ CI or Cancer benefit + Health First CI benefit (for all TALIC policies)

Factors affecting Medical Underwriting

7 7 FactorsFactors

F1F1

F6F6

F2F2

F3F3

F7F7Age

Gender

Build

Lifestyle Habits

F5F5 F4F4Family Medical

History Personal Medical

History

Factors affecting Medical Underwriting• Individually each of these items can have a significant effect

on mortality and where an adverse response is given, may lead to further medical evidence being requested.

• However, in combination with other items such as occupation, they can help to build up a picture of the proposed insured which may give the underwriter a better insight into the risk presented.

• For example a proposed insured with a stressful occupation may be prone to drink or smoke to excess.

• Similarly, an under average family history in combination with overweight and or smoking may lead to further investigations that individually those items may not be warranted.

Tools for medical underwriting• Medical Reports (Insurance/personal)

– Based on the findings on the Medical reports, a decision can be taken about the health status of the Proposed Insured.

• Attending Physician’s Statement – Often some of the Past health details of the Insured would

be available with Attending Physician of the proposed insured only and hence APS would become very important certain such cases.

• Medical Check-up Questionnaire– Whenever, the proposed Insured has undergone medical

test or check up, the Medical check up Questionnaire will have to be provided along with copy of reports.

• Specific Disease Questionnaires• Discharge Report

Medical Limits for India

Medical Limits for India

Medical Limits for India• Points to be noted• Please note that Random Medical examination may be called for

certain Non Medical cases randomly based on certain percentages.

• RBT (not called randomly but based on certain criteria) is mandatory for certain specified occupation, Single male aged 40 & above OR aged 35 & above if S.A. > Rs.1 lac and all term plans and Health protector plan with Term benefit more than 4 lakhs.

• Please note that that during Medical test, the Insured (and in Juvenile cases, Applicant) has to sign the Medical test form and has to submit Xerox copy of their Photo identity proof (Signature, during ME, has to be in same format as used in the Application form).

• Based on Disclosed History, certain additional requirements can be called for

• (For any past history of significant Illness, Hospitalization or operation or medical test carried out, it would be advisable to submit beforehand all the relevant papers like Discharge summary or copy of reports, for faster processing of cases).

Medical Table- Health First• The Non medical limit is 2 units subject to a maximum age of 55

years. Age 56 and beyond are subject to Medical requirements. • The Medical requirements table for the FIH product is:

9. ME, BPC, ECG-R, APS OR MEDICAL RECORDS, PFT OR CXR, ECG-EX

8. ME (AIA), Blood (BPC + PSA), ECG-R, APS or Med Records (if available), PFT or CXR, Abdominal Ultrasound, ECG-EX

7. ME

6. ME (AIA), BPC, ECG-R, APS or Med Records (if available), PFT or CXR, Abdominal Ultrasound

5. ME (AIA), BPC, ECG-R, APS or Med Records, PFT or CXR

4. ME, BPC, ECG-R

3. ME, BPB

2. ME, BPA

1. Blood or Saliva test (HIV)

0. Non Medical

HIV Testing Limit Rs 800,000. All Term cover to have HIV testing Medical Examination [ME] to be performed by AIA Panel Doctors.

9444417-20

443338-16

333335-7

222203-4

222002

200000-1

56 + 51 - 5546 - 5036 - 4518 - 35Units

Age

Medical Limits for India -FIH.

9. ME, BPC, ECG-R, APS OR MEDICAL RECORDS, PFT OR CXR, ECG-EX

8. ME (AIA), Blood (BPC + PSA), ECG-R, APS or Med Records (if available), PFT or CXR, Abdominal Ultrasound, ECG-EX

7. ME

6. ME (AIA), BPC, ECG-R, APS or Med Records (if available), PFT or CXR, Abdominal Ultrasound

5. ME (AIA), BPC, ECG-R, APS or Med Records, PFT or CXR

4. ME, BPC, ECG-R

3. ME, BPB

2. ME, BPA

1. Blood or Saliva test (HIV)

0. Non Medical

HIV Testing Limit Rs 800,000. All Term cover to have HIV testing Medical Examination [ME] to be performed by AIA Panel Doctors.

9444417-20

443338-16

333335-7

222203-4

222002

200000-1

56 + 51 - 5546 - 5036 - 4518 - 35Units

Age

Medical Limits for India -FIH.

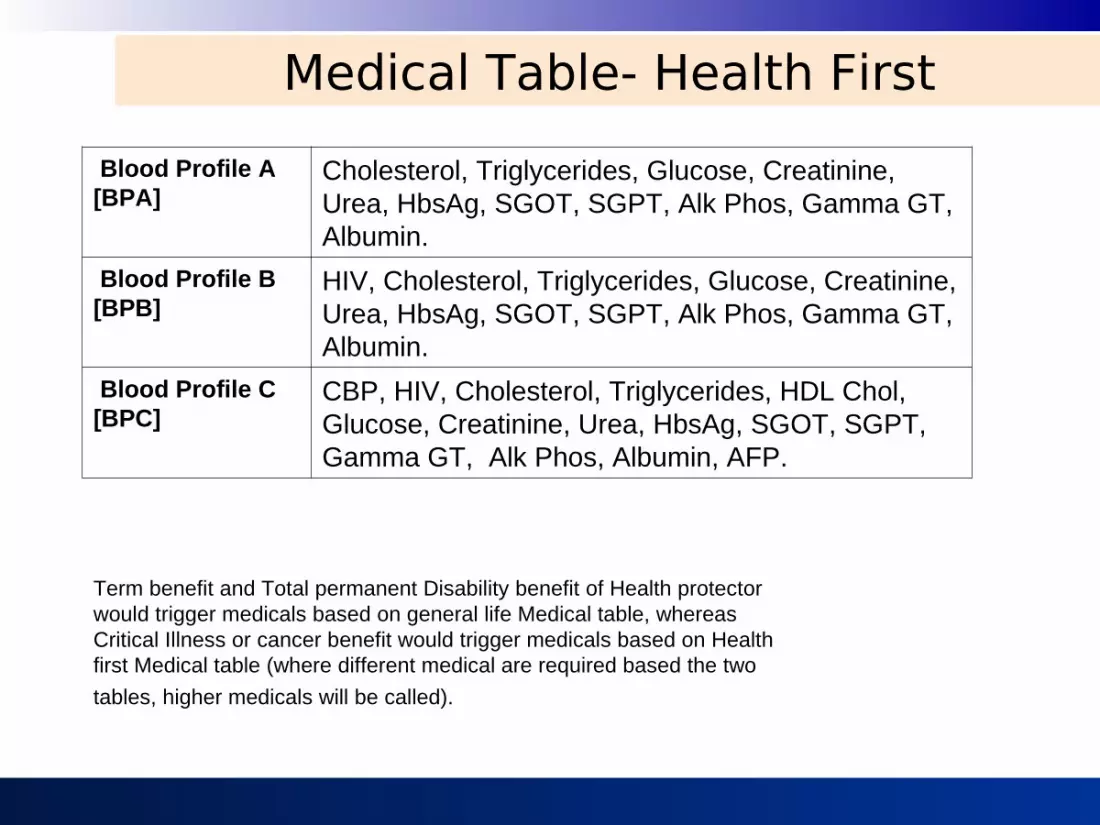

Medical Table- Health First Blood Profile A [BPA]

Cholesterol, Triglycerides, Glucose, Creatinine, Urea, HbsAg, SGOT, SGPT, Alk Phos, Gamma GT, Albumin.

Blood Profile B [BPB]

HIV, Cholesterol, Triglycerides, Glucose, Creatinine, Urea, HbsAg, SGOT, SGPT, Alk Phos, Gamma GT, Albumin.

Blood Profile C [BPC]

CBP, HIV, Cholesterol, Triglycerides, HDL Chol, Glucose, Creatinine, Urea, HbsAg, SGOT, SGPT, Gamma GT, Alk Phos, Albumin, AFP.

Term benefit and Total permanent Disability benefit of Health protector would trigger medicals based on general life Medical table, whereas Critical Illness or cancer benefit would trigger medicals based on Health first Medical table (where different medical are required based the two tables, higher medicals will be called).

Medical requirements for specific diseases• High Blood pressure or Hypertension: Specific Medicals +

Hypertension Questionnaire.• Diabetes Mellitus type II: Specific Medicals + Diabetes

Questionnaire.• Asthma: Asthma Questionnaire with or without

medicals• Thyroid problem: Medical + Latest Personal thyroid

Function reports + Attending Physician statement for thyroid problem

• History of jaundice in last 5 years: Hepatitis Questionnaire with or without medicals

• History of Mental Illness: Mental disorder Questionnaire.

Medical requirements for specific diseases• History of Respiratory problem: Specific medicals with

Attending Physician attending Respiratory disorder Questionnaire.

• History of Back or neck problem: Past reports + back Neck disorder Questionnaire.

• History of Growth, swelling, cyst or cancer: Medicals + Past reports including Histopath reports+ Attending Physician statement + Tumor Questionnaire.

• History of Heart problem: Medicals + Personal reports + Attending physician statement + Congenital Heart Disorder Qn.( if since birth) or Ischemic Heart disease Questionnaire. (if low blood supply to Heart problem)

• History of Injury: Injury Questionnaire.

Financial Underwriting

Objective of financial underwriting• The main purpose of Insurance cover is to facilitate and

allow only the replacement of the financial loss due to any untoward incident.

• In general, while offering a cover to a individual one has to remember that the gain due to death or Illness or disability should not be more than the continued normal survival of the Insured.

• So, financial Underwriting is done to ensure that that the level of cover proposed, corresponds with and is appropriate to the personal or business circumstances of the customer

Objective of financial underwriting• Traditionally, the following reasons are given for financial

underwriting:– Ensure a valid Insurable Interest.– Ensure that there is no intention or temptation on the part of

the insured or the other party to bring about the claim earlier than anticipated by the insurer.

– Ensure the sum assured and contract proposed is consistent with the customer’s needs, lifestyle and ability to pay the premiums throught the contract term.

– Overall to ensure that no moral hazard is generated by offering the cover to the individual Insured.

Steps of financial underwritingAAInsurable interest for

the cover

CCPremium Paying Capacity.

First step of establishing financial eligibility is to ensure that there is Insurable interestto ensure that there is Insurable interest in offering the cover

A person has an "insurable interest" in something when loss or damage to it would cause that person to suffer a financial loss or certain other kinds of losses.

A basic requirement for all types of insurance is the person who buys a policy must have an insurable interest in the subject of the insurance.

Subsequent step would be establishing Financial eligibilityFinancial eligibility

The final step is establishing Premium paying capacity. Financial eligibility and Paying Capacity can be assessed by the current annual income of the proposed.

Life Income Multiple calculation.

BB

Maximum cover based on HLV Multiple• Life Insurance Need/Maximum cover that can be offered

= Substantiated Annual income X Human Life value multiple based on age (as given below)

• This Maximum cover, mentioned above, gives the Total cover that can be availed on the life of insured (Cover with TALIC and Non TALIC covers).

• Human Life value indicates today's value of Insured’s future earning.

• This formula helps to determine Insured’s economic value for his loved ones.

• Normally any Individual is never offered a cover more than Maximum cover, mentioned above.

Premium Paying Capacity• Premium paying capacity is the percentage of Insured’s

annual Income that can be contributed for all the covers paid by him. (It includes TALIC and Non TALIC covers as well as premium paid by Insured for the covers on life his Family members).

• In general, we can allow 30 to 50 % of premium paying capacity, depending on the plan opted by the insured.

• Spouse or father of the Insured can support his/her premium paying capacity.

• Premium paying capacity calculation is not carried out for single premium cases.

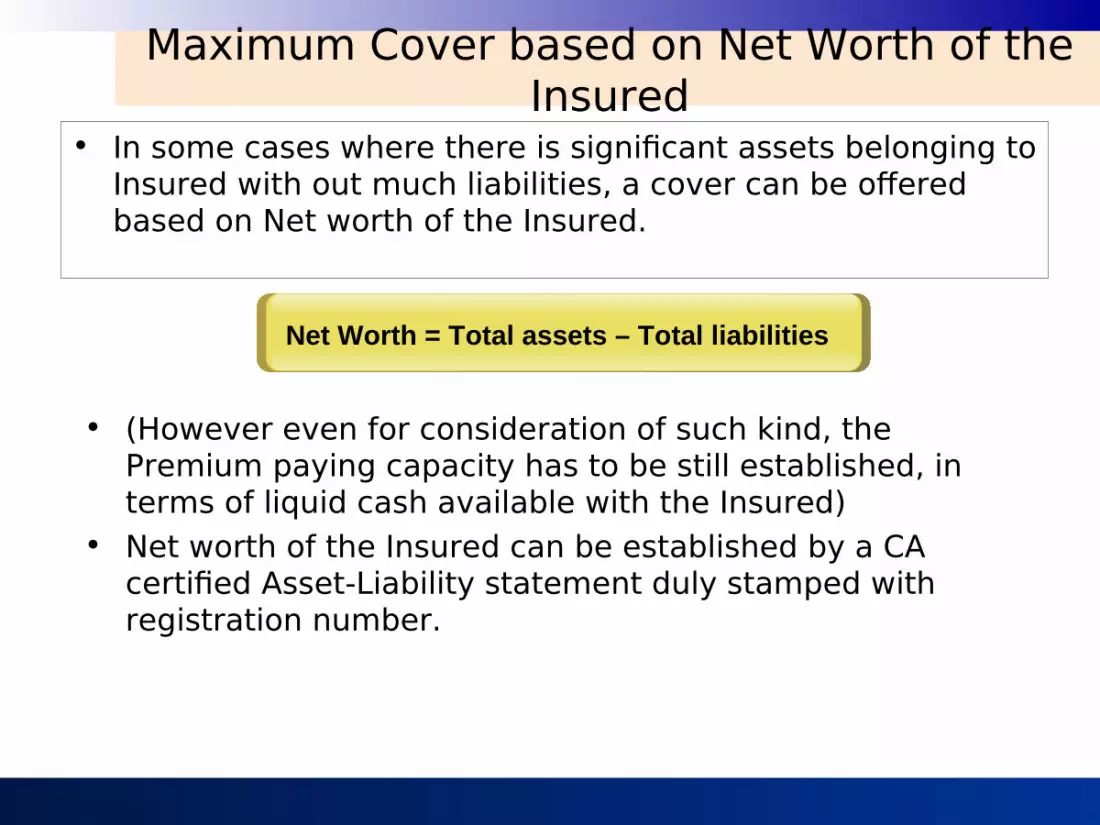

Maximum Cover based on Net Worth of the Insured

• In some cases where there is significant assets belonging to Insured with out much liabilities, a cover can be offered based on Net worth of the Insured.

Net Worth = Total assets – Total liabilities

• (However even for consideration of such kind, the Premium paying capacity has to be still established, in terms of liquid cash available with the Insured)

• Net worth of the Insured can be established by a CA certified Asset-Liability statement duly stamped with registration number.

Financial Assessment of Riders

Age

Accident rider multiple &

Maximum Accident cover

Critical illness benefit &

Maximum Critical illness cover

Disability benefit &Maximum Disability

benefit

16-45 yrs 15X Annual Income 5X Annual Income 5X Annual Income

46 yrs and above 10X Annual Income 5X Annual Income 5X Annual Income

Maximum issue limit 10,000,000 1,000,000 10,000,000

Financial Limits• Total Sum Assured for Financial Underwriting:

This includes the amount of Basic SA of all policies with TALIC (including pure term plans) + Term rider of all policies with TALIC + CI rider of all the policies with TALIC +1/2 of Payor benefit rider+ Top up sum assured + Non simplified Health

Protector {Term benefit (if more than 4 lacs) + CI benefit + TPD Benefit + Accident Benefit} + Basic cover of all policies with other companies

Financial Limit RequirementUp to Rs. 2,500,000/- Application Form

Rs. 2,500,001/- to 5,000,000/-

Financial Questionnaire

Rs. 5,000,001/- to 10,000,000/-

o Financial Questionnaire o Asset and Liability Statement [Refer annexure]

& Surrogates/Std Financials

Rs 10,000,001 and above

o Financial Questionnaire o Std Financials along with surrogates & Asset –

Liability statement

• Financial Requirement grid:

Documents for verification of financial status of applicant

• Latest financial document has to be provided.• If there is discrepancy in the profile of the customer vis-à-

vis the cover opted for, financial document will have to be provided, to justify the cover and premium paying capacity.

• Salary certificate provided has to company letter head duly signed by the authorized signatory of the company.

• Asset- Liability statement, balance sheet, P/L account and CA certificate certifying the annual income of the applicant, has to be signed by the CA, duly stamped along with registration number.

• When the annual turnover of the company is more than Rs 40 lac, audited accounts have to be provided.

• For non proprietorship firm/company, stake of the Insured/applicant in the company/firm has to be provided.

List of standard income proofs• Income Tax Returns /Form 16 of past three years

• Evidence of Salary earned (e.g. salary slips) of past 6 months

• P&L Account and Balance sheets duly certified by the CA of past three years. (If audited company financial statements are not yet available, then obtaining most recent management accounts (profit and loss statements and balance sheets) or provisional statements - signed by life assured and stamped and signed by company accountant or auditor - can be utilized.)

List of documents in lieu of income proofs• List of surrogate assets is given below that can be

accepted in lieu of standard income proofs, to verify financial capacity – Asset & liability statement duly signed by the applicant and

certified by his CA/Bank manager. (copy attached)• It is important to know what the life assureds net worth is (assets –

liabilities). • Life assured could have Rs10, 000,000 in fixed deposit, but

liabilities of Rs 20,000,000.– Bank Statements for the past 6 months

(The only problem with normal current account statements is that balances normally fluctuate due to regular (almost daily) deposits and withdrawals. Hence more value is given to saving account as compared to current account. Statement should include ongoing balance to check if balance is relatively consistent, or even increasing.)

List of documents in lieu of income proofs– Investment Proofs/Deposits in Government Bonds/Long Term Bank

Deposits/ Portfolio Report • Proofs of the same will be required.

– Copy of the Rent Agreement– Letter from the local revenue department specifying the agricultural

income /Copy of Sat Barah Utara/Copy of Patwari Report.– Form J giving details of the earning through agriculture.– Mortgages held with reputable providers such as Personal/Home Loan

statements for the past 6 months– Last six months payment statement from the concerned financing

institution can be used to give an indication of income. – Details of Property /Car Ownership (non Hypothecated cars) document

• Relevant papers should be provided if the asset is purchased in the name of the applicant.

Financial assessment- premier status of the bank customers

• Applicable for Banking Relationship Customers only• Applicable to the defined Privileged Customers of Approved

banks only.• Rules will be applicable to customer who have relationship

strength exclusive of premium paid for the policy applied for

• Completed Revised Financial Questionnaire & Bank endorsement of the Privilege status on Bank Letterhead by the Bank Manager

• Anti-Money Laundering Documents (as per current AML policy) has to be provided in addition to the above requirement.

• It is applicable to Investment Products only• Occupation class I to V• Not applicable to Housewife / Retired individuals

Financial assessment- premier status of the bank customers

• Covers to Children of such Privileged customers may be offered based on case to case consideration

• Limits are based on total Cover on life (cover with Tata-AIG and with other companies)

• Riders will be offered based on normal underwriting rules • Amount of cover needs to be justified financially. It means

that although there is relaxation in terms of documentation, there will still be Financial underwriting be carried out in all such cases.

With the satisfaction of the above mentioned criteria and up to the below mentioned limits for different categories of customers, we

can offer such high covers with simplified Documentation of Revised Financial Questionnaire and Anti Money Laundering

Documents

Regulations for premier banks

Bank HSBC bank Premier Customer

Premier customer

Salaried Businessman

Relationship type

Investments/Loans Investments/Loans

No. Of Years > 2 years 6 months –2 years

0 - 6 months > 2 years 6 months –2 years

0 - 6 months

Maximum Sum assured allowed

Up to 2 crore Up to 1.5 crore

Up to 75 lacs Up to 1.5 crore

Up to 1.25 crore

Up to 50 lacs

Requirement 1.Financial Questionnaire (revised) 2. Bank Endorsement 3.Relationship proof (bank statements/investment proof as AML requirement)

1.Financial Questionnaire (revised) 2. Bank Endorsement 3.Relationship proof (bank statements/investment proof as AML requirement)

Regulations for premier banks

Sector HSBC Power Vantage Customers

Premier customer

Salaried Businessman

Relationship type

Investments/Loans Investments/Loans

No. Of Years 6 months –2 years

0 - 6 months 6 months –2 years

0 - 6 months

Maximum Sum assured allowed

Up to 50 Lacs Up to 35 lacs Up to 40 Lacs Up to 30 lacs

Requirement 1.Financial Questionnaire (revised) 2. Bank Endorsement 3.Relationship proof (bank statements/investment proof as AML requirement)

1.Financial Questionnaire (revised) 2. Bank Endorsement 3.Relationship proof (bank statements/investment proof as AML requirement)

Regulations for premier banks

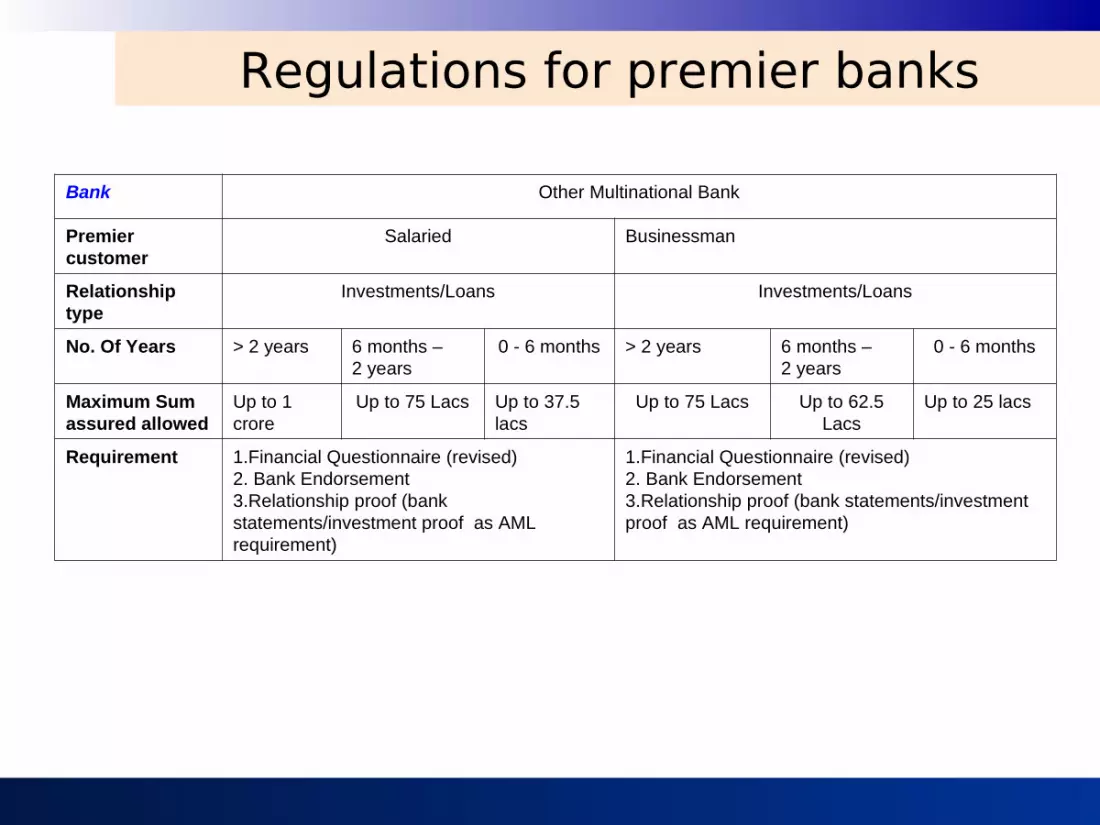

Bank Other Multinational Bank

Premier customer

Salaried Businessman

Relationship type

Investments/Loans Investments/Loans

No. Of Years > 2 years 6 months –2 years

0 - 6 months > 2 years 6 months –2 years

0 - 6 months

Maximum Sum assured allowed

Up to 1 crore

Up to 75 Lacs Up to 37.5 lacs

Up to 75 Lacs Up to 62.5 Lacs

Up to 25 lacs

Requirement 1.Financial Questionnaire (revised)2. Bank Endorsement 3.Relationship proof (bank statements/investment proof as AML requirement)

1.Financial Questionnaire (revised)2. Bank Endorsement 3.Relationship proof (bank statements/investment proof as AML requirement)

Rules relating to proof of source of income• Based on AML guidelines, depending on the premium paid

for all the TALIC policies as Insured, Applicant or just Payor, further proof of Source of income will be called for as per below mentioned norms.Total Aggregate Premium with TALIC (excluding the Service tax)

Proof required

Equal to more than Rs 2,500,000

Std Financial document. Other documents e.g. documents substantiating proceeds from an existing insurance policy but not forming part of standard income proof may be used as additional source of income proof

Less than Rs 2,500,000 Std or Non Std Financial document (which may be supported by actual source of the money paid for the premium) or Non Std or Surrogate Financial document

Less than Rs 100,000 No Proof of Source of Income required

Standard Financial Evidence- Proof of source of income

Proof of Source of Income (Document) Guidelines

Latest ITR (Latest)

Allow 50 % of Net Annual income as maximum Total premium paying capacity

Latest last one month Salary slip

Latest Appointment / Contract Letter (latest)

Latest Form No 16 (latest)

CA certified Asset Liability Statement as of date in the format specified by TALIC

50% of Total Liquid Assets*** would be considered as maximum premium paying capacity (Liquid assets as per below specified list).

Latest CA certified Profit & Loss account 50% of Net Profit would be considered as maximum premium paying capacity for individual. 50% of the individuals share in Net Profit of the Company / Partnership firm would be considered as maximum premium paying capacity

Agricultural Income: Saat Bara Utara / Tehsildar /revenue officer certificate

50% of the total Annual Income would be considered as maximum premium paying capacity for individual.

Salary credits in Bank statements 50% of the Annualized salary credits would be considered as maximum premium paying capacity.

Surrogate Financial Evidence- Proof of source of income

Proof of Source of Income (Document)

Guidelines

Bank Statements of last 3 months 50% of Average of last 03 months bank balance would be considered as maximum premium paying capacity where Saving / Current (proprietorship) Account is provided as a proof of source of income *If the statement shows salary credits, the same will be extrapolated to derive his annual income, 50% of which will be allowed as his maximum premium paying capacity

Mutual Portfolio Statement & Bank Deposits

50% of current market value of mutual fund portfolio / Bank Deposits/ Investments would be considered as maximum premium paying capacity.

Bank Certification Bank can certify the Liquid static Assets (Mutual funds, Fixed Deposits etc), only with them or invested through them. The Certification has to include actual breakup of the investments. Certification of the average balance of Saving Account/ current account has to be backed with actual bank statements.

Single Premium Products

Guidelines

50% of Total Liquid assets would be considered as maximum premium paying capacity.

If Large flows of Income from genuine source (like proceeds sale of shares, properties, Mutual funds or receiving of Bonus / retirement funds) are known than, basis the customer declaration and proof of the same, larger Single Premiums can be given**

Guidelines for Single Premium Products:

• * For bank account statement containing only one transaction, the transaction has to be at least 3 months old i.e. the closing balance has to be static for the preceding 3 months. For account transactions, which are mostly cash in nature, & large cash transaction or cheque deposits with no narration, further proof of source of Income would be required.

• ** If bank statements have narration like Mutual funds redemption, dividends, Bonus, salary credits, then further proof will not be required for AML. If source of Funds is another bank / institute then proof of that funds will have to be provided.

• *** Liquid Assets: Cash in Hand & Bank, Stocks, Certificate of Deposits & investments (as per def of liquid)

• **** For salary income net salary (after deduction of tax) will be considered

• Basis any discrepancies in the documents provided further proof of source of income can be called for as per underwriter’s discretion on case-to-case basis.

Special Underwriting for Selected products• Health First:

– Up to 4 units of Health First, Financial underwriting is simplified i.e. no Financial underwriting is carried out.

– From 5 units onwards, Coverage units calculation is carried out based on following formula

– No. of Units = Annual income/ 50,000– I.e. if a individual is earning Rs 300,000, he can avail of 6

Units.– Housewife is offered maximum cover of 4 units. – Students are offered maximum cover of 2 units.

• Invest Assure Gold financial underwriting: – For IA Gold minimum multiple stands revised .– For all cases of IA Gold one can opt for 5 times premium

multiple irrespective of the age

Simplified Underwriting

Simplified Products• Nirvana Plus - up to sum assured Rs.4, 00,000/-• Nirbhay Life - up to sum assured Rs. 4, 00,000/- for Banc

assurance and Rs.2, 00,000/- for all other channels.• Star Kid - up to sum assured Rs.10,00,000/- through

different policies (Through a given policy only maximum of 4 lacs can be applied for)

• Invest Assure extra and care up to limits of 20 lacs and 10 lacs respectively.

The above mentioned all 3 products are completely

simplified, sourced through one page simplified application form

Simplified Process• Mahalife Gold • 21Year Money Saver Plan • Life Plus • Health Protector• Health First

– For Mahalife gold, 21 Year money saver plan and for Life plus the Simplified process limits are

– For age 0 – 35 years = SA 10, 00, 000/-– For age 36 – 45 years = SA 4, 00,000/-– For age 46 and above = fully underwritten.

Important points to be considered• Products Mahalife Gold, 21 years Money Saver plan and

Life plus has to be sourced through common life application form only.

• For age 46 and above complete application form has to be filled i.e. step 10 of the application form has to be filled.

Riders • The following riders can be attached with the said plans

and will be treated as Simplified. – ABD– ADDL– ADDS– WP– PB

• Note: - Cases with CI and Term rider will be treated as fully underwritten (i.e. step 10 mandatory in common life application form), irrespective of the Sum assured and age.

Simplified limits for Health First and Health Protector

• Health First– 18-45 years - 4 units– 46-55 years- 2 units– 56-60 years- 1 unit.

• Health Protector– ADB rider - Rs. 8,00 ,000/-– TPD rider Rs. 8, 00,000/- – CI/ Cancer rider -Rs. 8,00,000/-– Term rider - Rs. 4,00,000/-– FADD rider - Rs. 4,00,000/-– AHC rider - Rs. 10,000/-

• Any rider if exceeds its simplified limits, becomes fully underwritten and completely filled application (step 7 and 8 for FIH and HP application form) form is required.

• Any adverse Health declaration in the Application form even within simplified process limits will mandate filling up of the entire application, as per the fully underwritten process and will be subjected to full underwriting.

Rural Business• Micro Insurance – All 3 products up to sum assured Rs.50,

000/-(including previous policies with TALIC)• 5TN1 product - Age 18 to 55, sum assured Rs.50, 000/-

(including previous policies with TALIC)

‘The relationship, which exists between persons carrying on business in common, with a view to profit other than as a member of a corporate body'.

Business Insurance- Partnership• Each partner owns a share of capital or goodwill in the

partnership and is similarly responsible for a share of the liabilities.

• An individual partnership agreement may specify otherwise, but usually local legislation states that:– Profits, assets and liabilities are shared equally, and– A partnership is dissolved upon death

PartnershipPartnership

Business Insurance- Partnership• In the event of a death the partnership is at risk in that the

interests of the deceased might pass into the hands of a third party that may either not understand or contribute to the profitable running of the partnership.

• They may therefore sell the interest to a competitor. • A written agreement often called a buy and sell or

partnership agreement is essential so that the interests of a deceased may be acquired by the surviving associate(s).

• This is an undertaking entered into which legally obliges the estate of a deceased partner to offer for sale his/her interest to the surviving partner(s).

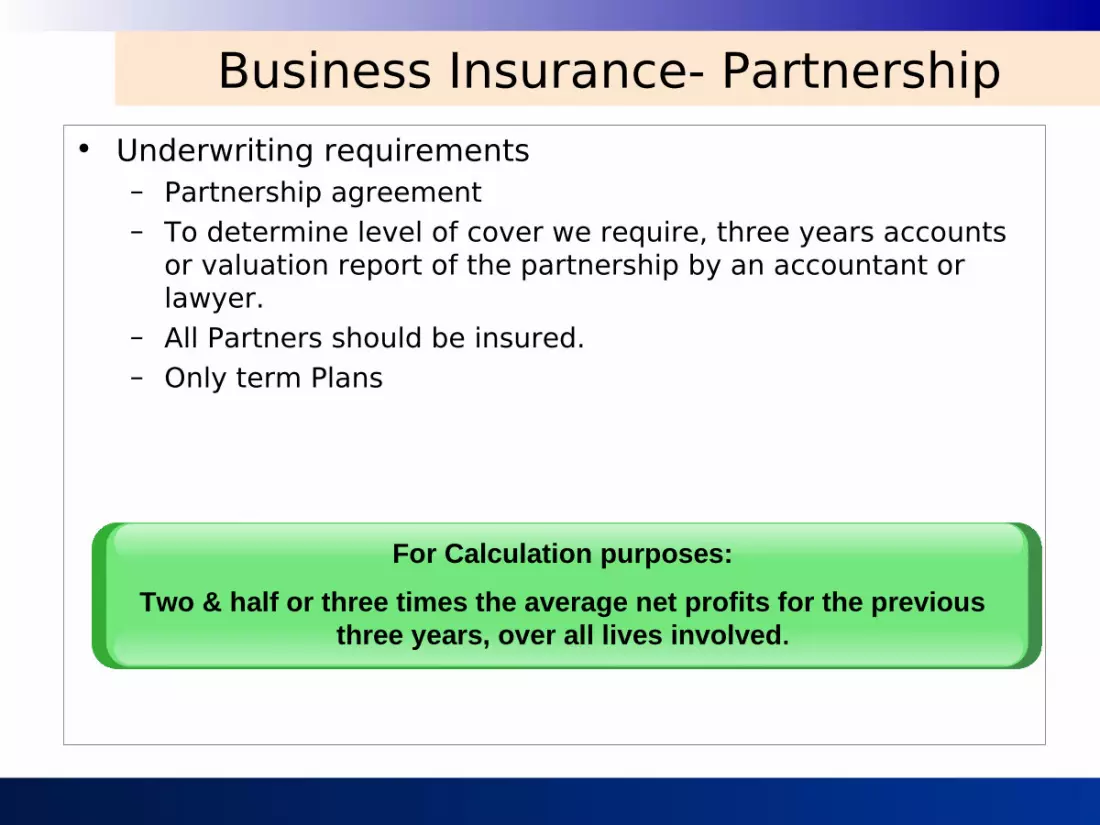

Business Insurance- Partnership• Underwriting requirements

– Partnership agreement– To determine level of cover we require, three years accounts

or valuation report of the partnership by an accountant or lawyer.

– All Partners should be insured.– Only term Plans

For Calculation purposes:

Two & half or three times the average net profits for the previous three years, over all lives involved.

Business Insurance- Key Person• Why is Key Person Insurance necessary?

– The knowledge and abilities of a key person are unique and extremely valuable. Loss of this person could cause financial loss to the company.

– Should the unfortunate happen, the business will require time and finance to find and then adequately train a replacement.

– Business may have been secured because of the key-person's reputation or personal relationships would otherwise not have been extended to the company.

Business Insurance- Key Person• Why is Key Person Insurance necessary?

– Future business development could be significantly affected by the loss of that valued person.

– Suppliers may also not extend credit when the key-person dies

– Relationship with the work force may be affected.

It is therefore the value of his contribution and the financial consequences to the business on death that is being insured.

Business Insurance- Key Person• Rules Relating to Key Person Insurance:

– The key-person must be a full time employee of the company and actively involved in the day to day running of the company.

– The sum assured for employees is limited to 10 - 15 times salary for ages 25 - 40 and 12 times for 41 or over.

– For owners of the business, the total cover (all sources) available to all the Key Persons is limited to 3 times average gross profit or 6 times average net profit.

– A maximum of 5 Key Persons per company may be insured

Business Insurance- Key Person• Underwriting Requirements for a Key Person Insurance

Cover:– Application Form signed by Insured & the authorized person

on behalf of the company– Age proof of the Insured– Medical Reports as required for the Cover proposed– Board Resolution of the Company allowing for the purchase of

a Key-man contract on the Key-man's life and the name of the person authorized to sign on behalf of the company

– Justification for the Face Amount proposed– Justification as to why the Key-man is a Key-man– Questionnaire regarding the Key-man

Business Insurance- Key Person• Underwriting Requirements for a Key Person Insurance

Cover:– Keyman Endorsement– Profit & Loss Account and Balance sheet of the Company for

the last 3 years– Income Tax Returns of the Company for the last 3 years– Personal Income Tax returns of the proposed Key-man– Memorandum/Articles of Association of the Company

The replacement cost basis• Age 25-40 yrs., use 15X

multiple of salary• Age 41yrs & over, use 12X

multiple of salary

The loss of profits basis• Multiple of profits, we use

three times average gross profit or six times average net profit.

For Calculation purposes:

These two methods include the amount of cover for all the key persons in total, under that company.

Business Insurance- Key Person• The premium notice is sent to the Company, since the

company is the owner rather than the life insured.• Details of the company are captured in the applicant part

of the Application form, including the Date of Incorporation in the Birth date part of the Applicant details.

• Nominee part in the application is to be left blank.• There must be two signatures in the application form:

– Signature of life proposed, and– Signature of the official representative of the company

Business Insurance- Key Person• Whenever a Key Man insurance application is to be

received an endorsement has to be also submitted along with the app. form duly signed by Official Representative of the Company.

• No Riders are allowed to a Keyman.• Only Term Insurance policy will be offered for Key man

Insurance cover.• As per IRDA guidelines, no alteration( increase) in the sum

assured is allowed after the policy is issued of Key Man /Partnership cases.

Employer- Employee Insurance• A benefit provided to the employees of a company or an

organization as a perk benefit.• Employee and/or the Employer needs to complete the

form.• The employer must issue first premium cheque. • However, renewal payment for premiums can be made

through cheque issued by employee or employer. • Cashier will be verifying that the employer has issued the

cheque received for the first premium.• The letter of undertaking will be required on the company’s

(Employer) letterhead as per the prescribed format and should bear the company’s seal and signatures of the authorized signatory.

Employer- Employee Insurance• The policy under the employer-employee scheme can be

purchased only on the life of the employee only on the life of the employee and the benefits should be passed on to the nominees/ rightful heirs of the employee either directly or through the company.

• The company does not have rights on the benefits of the plan.

• The existing underwriting rules and guidelines will be applicable to the policies submitted under Employer-Employee scheme.

• This benefit should be available to the employees of the company (as per its HR policy).Cover cannot be offered under this scheme by a company, to a

individual who has more than 5% stake in the same company.

Scheme 1• Employer is the applicant and policyholder.

Employer:

Pays the premiumsIs the applicant and policy holder and passes the benefits to the

relative of the employee

Employee:

Is the insured

Please note: This Scheme has been scrapped with immediate effect due to regulatory reasons.

Scheme 2• Employee is the applicant and policyholder.

Employer:

Pays the premiums

Employee:

Is the insured and policy holder.His nominee will get the death

benefits of the policy.

Specific requirements for Scheme-2• The Insured (Employee) only has to sign the application

form.• All correspondence during the processing of the policy will

be addressed to the insured (employee) and the address would be of the Applicant (Employer).

• The PIP document will be dispatched to the address of the Applicant (Employer).

• The Renewal Premium has to be paid by the applicant (Employer) and a reconciliation statement is required with such payment showing the details of the policy number, Premium Amount and Name of the Employee.

• Any plan can be offered under this scheme.

Draft letter of undertaking for Scheme-1

Draft letter of undertaking for Scheme-2

A Hindu Undivided Family (HUF), which is also known as Joint Hindu Family is governed by the Hindu Law. HUF is presumed to be joint in food, worship and estate.

This includes wife of the Karta, wives and

unmarried daughters of co-parcenars.

All male descendents of a common male ancestor. Male children of the co-parcenars

acquire interest in the family by birth and are admitted to the benefits of the family but are

not liable to the commitment of the HUF during their minority.

Every co-parcenars has joint possession and joint interest in the HUF property.

Hindu Undivided Family (HUF)• An HUF consists of:

– All persons lineally descendent from a common ancestor and have not separated, their Wives & unmarried daughters.

HUFHUF

The head/senior most male member of the family. He is

responsible for all the affairs of the family. He

represents the HUF as the Manager.

Co-parcenarsKarta Female

Members

Hindu Undivided Family (HUF)• Neither the Karta of the HUF nor any member thereon can

take out policies on their own lives for their own benefits or for the benefits of their dependants and finance them to the detriment of HUF funds.

• Therefore if policy is financed through HUF funds, the policy would always belong to the HUF entirely and as such the policy money would be payable only to the Karta who represents the HUF as the Manager.

• Hence financial eligibility for a cover under HUF is based on the Income under HUF only.

Hindu Undivided Family (HUF)• Policy is for the benefit of the HUF and it forms a part of the HUF fund.• Premium must be paid out of the HUF fund.• Policy proceeds form a part of the HUF fund.• Applicant for the life insurance policy must always be the Karta of the HUF.• The application form must be signed by the Karta along with the stamp of

the HUF.• HUF deed or HUF ITR may have to be submitted to establish the status of

HUF.• Addendum to HUF must be submitted along with the application form.• Neither the Karta of the HUF nor any member can take out policies on

his/her own life for own benefits or for the benefits of his/her dependents and pay premium from the HUF fund.

• Policy exclusively belongs to the HUF. Therefore, Nomination is not allowed.• Assignment may be allowed. Only the Karta can effect the assignment

either for valuable consideration or for natural love & affection by way of gift, among members of the family.

• No Loans or Surrender can be availed except for legal necessity or benefit of the HUF. In this event, a consent letter signed by the members of the HUF must be obtained.