Embed Size (px)

Citation preview

FRIDAY NOVEMBER 13, 2020

CO-SPONSOR S

BENEFAC TOR

PRESENTER: CHRISTOPHER HOYT

FRIDAY, NOVEMBER 13, 2020

PROGRAM AGENDAVirtual doors open

7:45 to 8:00

Retirement Assets for First and Second Marriages: Let the Fun Begin (Part 2)

9:50 to 11:10

Break

11:10 to 11:20

So, You Wanna Be a Philanthropist, including Proposed New Rules for Donor Advised Funds

11:20 to 12:30

Seminar Concludes

12:30

Break

9:42 to 9:50Opening remarks and speaker introduction

8:00 to 8:12

Washington Update

8:12 to 8:17

Estate Planning for Retirement Assets after the

SECURE Act

8:17 to 9:17

Retirement Assets for First and Second Marriages: Let the Fun

Begin (Part 1)

9:17 to 9:42

PRESENTING SPONSORS

BENEFACTOR

BOK FINANCIALFENNEMORE.

FINEMARK NATIONAL BANK & TRUSTFRAZER RYAN GOLDBERG & ARNOLD LLP

DIAMOND

CONTENTSJewish Community Foundation

Arizona Community FoundationPAGES 4-7

01Estate Planning for Retirement Assets after the SECURE ActPAGES 126-138

04

2020 Tax & Legal Planning Committee and Underwriters

PAGES 8-40

02Retirement Assets for First and Second Marriages:Let the Fun BeginPAGES 139-179

05

Chris Hoyt’s Presentation SlidesPAGES 41-125

03So, You Wanna Be a Philanthropist, including Proposed New Rules for Donor Advised FundsPAGES 180-209

06

SEE YOU NEXT YEAR2021 Tax & Legal Seminar

Friday, November 5

Building a permanent source of financial support for a vibrant, enduring Jewish community.

pihsredaeL lanoisseforP

Richard Kasper

Sheryl Quen Director of Grants and Communications

Donna Corcoran Director of Finance and Operations

Rachel Rabinovich Director of Special Projects

LIFE & LEGACYTM Program Director

Andrea Cohen Director of Youth Philanthropy

Ernie Muntner Administrative Assistant

Board of Directors

Lee Eisinberg, Chair

Francine Coles

Bradley Dimond

Nora Feinberg

Alan Gold

Neil Goldstein

Richard Gottlieb

Victoria Corwin Harris

Neal Kurn, Honorary Director

Rebecca Light

Deborah Miller

Andrew Plattner

Virginie Polster

Sandy Rife

Robert Roos, Immediate Past Chair

Sadie Rosenthal

Donald Schon

12701 North Scottsdale Road, Suite 202 | Scottsdale, Arizona 85254

FOR PROFESSIONAL ADVISORS

Building a permanent source of financial support for a vibrant, enduring Jewish community.

History of the Jewish Community Foundation of Greater PhoenixThe Jewish Community Foundation of Greater Phoenix was established in 1972 with the vision of ensuring that future generations will inherit a thriving Jewish community.

We work with individuals, families and organizations to create personal charitable legacies rooted in Jewish tradition and values, to grow and sustain a vibrant, enduring Jewish community.

We are proud of the strong relationships we have built with financial and estate planning professionals, who share a common belief in the value of charitable giving. These professionals often are among our best referral sources, because of the trust and confidence they have earned from their clients. Likewise, donors often consult us when they need a referral for qualified professional services.

Because of the value we place on these important relationships, the Foundation offers a number of services to the professional advisory community.

GiftLawGiftLaw is a free electronic resource, which complements the services of the Foundation’s experienced staff, and is accessible through our website. It offers planned giving calculations, the latest information on IRS private letter rulings, and well-researched, expert articles on current trends. Weekly updates are delivered via email, ensuring that you never miss news and analysis that may be critical to your practice.

Tax & Legal SeminarThe region's most respected program for financial planning, tax and estate planning professionals, the annual Tax & Legal Seminar presents nationally recognized speakers on the latest trends and developments in tax, estate planning, and charitable giving. Attendees receive up to four hours of well-priced continuing education credits and the opportunity to network with hundreds of professionals who register annually.

This program has been presented by the Jewish Community Foundation since 1993, and in partnership with the Arizona Community Foundation since 2001.

Professional Advisory CommitteeProfessionals in the fields of law, accounting, financial and insurance services meet over breakfast four to five times annually. Committee members learn about stimulating topics of mutual interest, and are exposed to the Foundation’s work and the work of our community partners. Committee members have an opportunity to discuss recent developments in their own professional practices with a trusted group of professional peers.

Professional ConsultationThe Jewish Community Foundation offers personal advice and information to suit the individual needs of your clients, including custom illustrations of the charitable and financial implications of your clients’ various tax and charitable planning options. We are glad to be a confidential resource to you and your clients, at your convenience.

Phone: 480.699.1717 | Fax: 480.699.1807 | Email: [email protected] | www.jcfphoenix.org

FOR PROFESSIONAL ADVISORS

Building a permanent source of financial support for a vibrant, enduring Jewish community.

History of the Jewish Community Foundation of Greater PhoenixThe Jewish Community Foundation of Greater Phoenix was established in 1972 with the vision of ensuring that future generations will inherit a thriving Jewish community.

We work with individuals, families and organizations to create personal charitable legacies rooted in Jewish tradition and values, to grow and sustain a vibrant, enduring Jewish community.

We are proud of the strong relationships we have built with financial and estate planning professionals, who share a common belief in the value of charitable giving. These professionals often are among our best referral sources, because of the trust and confidence they have earned from their clients. Likewise, donors often consult us when they need a referral for qualified professional services.

Because of the value we place on these important relationships, the Foundation offers a number of services to the professional advisory community.

GiftLawGiftLaw is a free electronic resource, which complements the services of the Foundation’s experienced staff, and is accessible through our website. It offers planned giving calculations, the latest information on IRS private letter rulings, and well-researched, expert articles on current trends. Weekly updates are delivered via email, ensuring that you never miss news and analysis that may be critical to your practice.

Tax & Legal SeminarThe region's most respected program for financial planning, tax and estate planning professionals, the annual Tax & Legal Seminar presents nationally recognized speakers on the latest trends and developments in tax, estate planning, and charitable giving. Attendees receive up to four hours of well-priced continuing education credits and the opportunity to network with hundreds of professionals who register annually.

This program has been presented by the Jewish Community Foundation since 1993, and in partnership with the Arizona Community Foundation since 2001.

Professional Advisory CommitteeProfessionals in the fields of law, accounting, financial and insurance services meet over breakfast four to five times annually. Committee members learn about stimulating topics of mutual interest, and are exposed to the Foundation’s work and the work of our community partners. Committee members have an opportunity to discuss recent developments in their own professional practices with a trusted group of professional peers.

Professional ConsultationThe Jewish Community Foundation offers personal advice and information to suit the individual needs of your clients, including custom illustrations of the charitable and financial implications of your clients’ various tax and charitable planning options. We are glad to be a confidential resource to you and your clients, at your convenience.

Phone: 480.699.1717 | Fax: 480.699.1807 | Email: [email protected] | www.jcfphoenix.org

The Arizona Community Foundation has over 40 years of experience partnering with individuals, families, and organizations who wish to give back to their community. We make sure our donors have the expert guidance and flexible options that best suit their style of giving.

We partner with professional advisor firms across the state to provide personal service and helpful resources to meet their clients’ charitable goals. Some of the services we offer to our partners and their clients include:

Our network of professional advisor partners is always growing. If you’re interested in connecting with us, give us a call at 602.381.1400.

Tax planning. ACF will work directly with you and your clients to understand charitable interests, overall strategy, and goals for giving, while also ensuring their choices maximize available tax benefits.

Donor advised funds. With this cost-effective alternative to a private foundation, your clients can take advantage of available tax deductions when they contribute cash, stock, or appreciated assets to their named fund while making grant recommendations that align with their goals.

Local connections. With six affiliate offices across the state, ACF has a strong and comprehensive network of local resources to help your clients identify nonprofit organizations and projects that align with their charitable goals and interests.

Dedicated support. Your clients will receive a dedicated relationship manager who serve as their main point of contact to ensure that their charitable goals are accomplished. ACF will work directly with them to support local, national, or international causes.

Education events. ACF hosts a wide range of convenings and events on important social, cultural, and community topics for donors and community members. We also host seminars for professional advisors with opportunities to earn continuing education credit.

Investment management. When charitable assets meet a certain threshold, donors may continue to work with their existing wealth advisor to manage the investment of assets held in ACF funds.

We rely on our Professional Advisory Board to provide the Arizona Community Foundation with strategic planning, guidance, and oversight.

BOARD OF DIRECTORSStephen O. Evans, chair Robbin M. Coulon, Esq., vice chairLeezie Kim, Esq., secretaryRufus Glasper, Ph.D., CPA, treasurer Benito AlmanzaJim AmeduriLon BabbyNoreen BishopMark C. Bohn, Esq.Tony BolazinaDanny BryantGwen CalhounJavier Cárdenas, MD.Shelley Cohn, immediate past chair

Marianne Cracchiolo MagoAnn Drummond MelsheimerMark Feldman Charley FreericksPatricia Garcia DuarteXavier GutierrezNeil H. Hiller, Esq.Heidi Jannenga, PT, DPT, ATC/LLeonardo LooTammy McLeodJacob MooreRichard MorrisonDon OpatrnyEssen OtuMi-Ai ParrishBarbara A. Poley Eve Ross, JD

Lisa UriasRon Butler, past chairJack Davis, past chairWilliam J. Hodges, CPA/PFS, past chairMarilyn Harris, past chairRichard H. Silverman, past chairGerald Bisgrove, past chairRobert M. Delgado, past chairBennett Dorrance, past chairRichard B. Snell, past chairNeal Kurn, Esq., past chairRichard H. Whitney, Esq., past chairBert Getz, chairman emeritusSteve G. Seleznow, president & CEO

2020 PROFESSIONAL ADVISORY BOARD

Russell S. Goldstein, CFP®, CAP®, chairTrish Stark, vice chairYaser Ali, Esq.Ellen Steele Allare, CLU®, ChFC®, past chair emeritusStephen BarberMacAuley BeloneyBrenda A. Blunt, CPAMark C. Bohn, CPA, Esq., past chair emeritusLinda H. Bowers, JD, AEP®, CFP®, CEPA®, past chairRussell J. Bucklew, CFP®, JDSergio CàrdenasDavid L. Case, Esq.Stephen S. Case, Esq., past chair emeritusTheresa E. Chacopulos, CFP®Beth S. Cohn, Esq.Kathie J. Gummere, Esq., JD

Brent M. Gunderson, Esq.Carrie L. Hall, CLU®, CFP®William J. Hodges, CPA, past chair emeritusScott M. Horn, CPACharles J. Inderieden, CPA, PFSLindsey A. Jackson, Esq.Lynton M. Kotzin, CPA, CFA®Gregory M. Kruzel, Esq., past chair emeritusNeal H. Kurn, Esq., emeritusT. James Lee, Esq.W. John Lischer, emeritusMiranda Lumer, Esq.Thomas Maguire, CPAJeffrey M. Manley, Esq.Denise E. McClain, Esq., immediate past chairT. Troy McNemar, Esq.Jonathon M. Morrison, Esq.Mahes Prasad, AIF

Angelica F. Prescod, AAMSNeil E. Robbins, CLU®, ChFC®James W. Ryan, Esq., past chair emeritusAbbie S. Shindler, Esq.Christopher P. Siegle, Esq.Verne Smith, CLU®, ChFC®Mary Taylor Huntley, CFP®Michael J. Tucker, Esq.Benjamin Voelker, CFP®, CPWA®Angela Walker-Weber, Esq.David K. Walser, CPA, PFSCharles W. Whetstine, Esq.Kris Yamano, JD, MBAPaul E. Yates, FSA, CLU®

We offer special thanks to our Seminar Chair: Teresa Coin, Esq., Chair BOK Financial

Brenda A. Blunt, CPA, CGMA Eide Bailly, LLPDieter G. Bollmann First Financial Equity CorporationLinda H. Bowers, JD, AEP®, CFP®, CEPA®, Past Chair Northern TrustAdam M. Brooks, CFP®, Past Chair ABLE Financial Group, LLCKelley L. Cathie, Esq. Braun Siler Kruzel PCSusan M. Ciupak, Esq. First International Bank and TrustBeth S. Cohn, Esq. Jaburg & Wilk, P.C.John B. Even, Esq. Schmitt Schneck Casey Even & Williams PCRylan Folts One Charles Private Wealth Services, LLCJ. Noland Franz, Esq. Buchalter, a Professional CorporationTerri A. Hardy BonhamsVictoria C. Harris, CPA, Past Chair Hunter Hagan & Company, Ltd.Stephen Hart, CPA Stephen Hart PLLCDaniel L. Hulsizer, JD, CPA Warner Angle Hallam Jackson & Formanek PLCErin B. Itkoe, CPA/PFS, CFP® Tarbox Family OfficeLindsey A. Jackson, JD FineMark National Bank and TrustBrad Jepson, CFP®, CTFA, ChFC Northern Trust Elena Kohn ArtFortune LLCKimberly C. Kur, JD, CAP® Arizona Community FoundationJustin Lines Copper Canyon Law LLCMiranda K. Lumer, JD MidFirst BankDenise E. McClain, Esq., Past Chair Abbot Downing

James Sean McGettigan, CPA/PFS, CFP®, CGMA Stoker OstlerDeborah W. Miller, Esq. Immediate Past Chair Deborah W. Miller PLLCPaul R. Nothman, CPA McGrath Nothman, PCShawn Parker, CPC, QPA MGKSKristel K. Patton, Esq. Empowered Legacy PlanningDebra J. Polly, Esq. Sherman & Howard L.L.C.Christy Ray, JD, LLM First International Bank and TrustEliza Daley Read Mangum, Wall, Stoops & Warden, PLLCT.J. Ryan, Esq. Frazer Ryan Goldberg & Arnold LLPJeff A. Schlichting, CPA Eide Bailly, LLPDarin Shebesta, CFP®, AIF® Jackson/Roskelley Wealth Advisors, Inc.Abbie S. Shindler, Esq. Buchalter, a Professional CorporationChristopher P. Siegle, Esq. J.P. MorganLisa L. Sullivan, AEP®, CSOP®, CTFA, CWS® TrustBankAllyson J. Teply, Esq. Sacks Tierney P.A.Michelle Margolies Tran, Esq. Clark Hill PLCStephanie F. Tribe, Esq. Fennemore.Jeanne Vatterott-Gale, Esq. Hunt & GaleThomas C. Waite, CFP®, CWS® Schwab Private Client Investment Advisory, Inc.Pamela Wheeler, EA Past Chair Henry+HorneTrevor S. Whiting, JD, LLM, MBA Dana Whiting Law, PLLCFarrah H. Whitworth, CPA Globe CorporationKeith Wibel, CFA® Capital Insight Partners, LLCKris Yamano, JD, MBA BMO Private BankPaul E. Yates, FSA, CLU® Cohn Financial Group

2020 PLANNING COMMITTEEThank you to the committee of dedicated legal, accounting, financial planning

professionals, and life underwriters who volunteer their time and expertise to both the Arizona Community Foundation and the Jewish Community

Foundation. You are vital to the success of this annual seminar.

We gratefully acknowledge these contributors for their generous support of the 2020 Tax & Legal Seminar

Brenda A. Blunt, CPA, CGMALinda H. Bowers, JD, CFP®, AEP®, CEPA®

Susan M. Ciupak, JDTeresa Coin, Esq.

Jay Franz

Terri A. HardyVictoria C. Harris, CPA

Erin B. Itkoe, CFP®, CPA/PFSDenise E. McClain, JDKristel K. Patton, Esq.

Chris Siegle, Esq. Michelle Margolies Tran

Thomas C. Waite CFP® CWS®Farrah H. Whitworth, CPA

Keith Wibel, CFA

FRIENDS

Benefit Financial Services GroupBerk Law Group

BMO Wealth ManagmentCohn Financial Group

Deborah W. Miller, PLLCFirst Financial Equity Corporation

First Western TrustHolland & Knight

Hunt & GaleJackson/Roskelley Wealth Advisors, Inc.

Jewish Tuition OrganizationJohn Event of Schmitt Schneck Casey Even &

Williams, PC Dan P. Kammrath

Mack Business Appraisals, LLCJames Sean McGettigan, CPA/PFS, CFP®,

CGMA

McGrath Nothman, PCMcNemar Law Offices, P.C.Sherman & Howard L.L.P.

South Park AdvisorsStephen Hart PLLC

Strategic Wealth Advisors, LLCT&T Estate Services, LLC

SUPPORTERS

PATRONSAASK-Aid to Adoption for Special Kids

ABLE Financial GroupArizona Bank & Trust

Boyer Bohn, p.c.Braun Siler Kruzel PC

Dana Whiting Law, PLLC

Hunter Hagan & Company, Ltd. Jaburg|WilkJ.P. Morgan

Jennings, Strouss, & Salmon, PLCLohman Company, PLLC

Midfirst Bank

MRA AssociatesRSM US LLP

Sacks TierneyStoker Ostler Wealth AdvisorsVersant Capital Management

Warner Angle Hallam Jackson & Formanek PLC

BENEFACTOR

BOK FINANCIAL FENNEMORE.

FINEMARK NATIONAL BANK & TRUST

FRAZER RYAN GOLDBERG & ARNOLD LLP

DIAMONDBESSEMER TRUST

DYER BREGMAN & FERRIS, PLLCHENRY+HORNE

KOTZIN VALUATION PARTNERS, LLC

NORTHERN TRUSTTARBOX FAMILY OFFICE

TRUSTBANK

PLATINUMEIDE BAILLY LLP

ESTATE MANAGEMENT SERVICESMGKS

TFO PHOENIX, INC. ZIA TRUST, INC.

GOLD

480.699.1717jcfphoenix.org

Making a gift through your will, trust, retirement accounts, life insurance, or other assets, transforms your communityforever. A planned gift through the Jewish Community Foundation is an easy way to impact the community and the

their charitable goals, connect to the causes they care about, and create a vibrant Jewish community.Learn more about planting the seeds for those who will come after you. Plan your charitable legacy today.

How Will You Assure Jewish Tomorrows?Make Plans Today to Pass on Your Values

Partner with charitable experts to do more for your clients. Call or click: 602.381.1400 or azfoundation.org

“Working with ACF has been one of the true highlights of my 38 years in the investment industry.”James P. Marten, CIMAGlobal Institutional Consultant, Wealth Management Advisor, Merrill Lynch

Abbot Downing, a Wells Fargo business, provides products and services through Wells Fargo Bank, N.A., and its various affiliates and subsidiaries. Wells Fargo Bank, N.A. is the banking affiliate of Wells Fargo & Company.

© 2020 Wells Fargo Bank, N.A. All rights reserved. Member FDIC. WCR-0920-00348

WWW.ABBOTDOWNING.COMA Wells Fargo Business

To learn more, contact Denise McClain, Director at [email protected] or 480–887–4210.

ABBOT DOWNING IS PLEASED TO SUPPORT THE 2020 VIRTUAL TAX AND LEGAL SEMINAR

Abbot Downing helps build lasting legacies for

ultra-high-net-worth clients, family offices, foundations,

and endowments. We collaborate with clients and

their advisors to manage the full impact of wealth.

The result is a finely crafted strategy designed to

deliver desired results and a meaningful legacy for

future generations.

Drawing on the global resources of Wells Fargo,

Abbot Downing offers clients access to

opportunities not widely available, including:

• ASSET MANAGEMENT

• LEGACY AND WEALTH PLANNING

• INSTITUTE FOR FAMILY CULTURE

• TRUST, FIDUCIARY, AND ADMINISTRATIVE

SERVICES

• PRIVATE BANKING

• FOUNDATIONS AND ENDOWMENTS

PROUD TO BE PART OF ARIZONA’S PAST,

PRESENT AND FUTURE

www.bok� nancial.com | Jason Ray | 480.596.4353

BOK Financial® is a trademark of BOKF, NA. Member FDIC. Equal Housing Lender . ©2020 BOKF, NA.

PERSONALLY DEDICATEDTO CREATING POSSIBILITIES

SO YOU CAN THRIVE.Fennemore’s team of Trusts, Estates & Wealth

Preservation attorneys go beyond the expected to help clients achieve their goals.

Partner with counselors who create possibilities for future generations.

Proud supporters of the Arizona Community Foundation and Jewish Community Foundation’s Tax and Legal Seminar.

Visit us at FennemoreCraig.com.

David McCarvilleAttorney

Stephanie TribeAttorney

Jim LeeAttorney

Steve GoodAttorney

Thomas AldousAttorney

FINEMARK IS HONORED TO SUPPORT THE 2020 TAX AND LEGAL SEMINAR

To learn more, please contact Lindsey Jackson at [email protected] or 480-607-4882.

www.finemarkbank.comMember FDIC • Equal Housing Lender Trust and investment services are not FDIC insured, are not guaranteed by the bank and may lose value.

GAINEY RANCH7600 E. Doubletree Ranch Road, Suite 100

Scottsdale, AZ 85258

480-607-4860

DC RANCH20909 N. 90th Place, Suite 102

Scottsdale, AZ 85255

480-333-3950

▪ Asset Management ▪ Trust Administration

▪ Estate Settlement ▪ Financial Planning

▪ Banking ▪ Lending

FineMark National Bank & Trust delivers exceptional client service and offers customized solutions to help individuals and families reach their goals and build lasting legacies for generations to come. FineMark’s comprehensive wealth management services include:

ARIZONA TRUST & INVESTMENT TEAMTIM NGUYEN ASHLEY WITTNEBEN CHRIS HIGHMARK LINDSEY JACKSON MICHAEL BARNES JENNIFER GARCIA

BEFORE YOU SEL EC T AW E ALTH MANAGEMENT F IRM,

GIV E THEM THIS TEST.

Q. Is the firm privately or publicly held?

Q. What percentage of the firm’s revenue is generated by its wealth management business?

Q. Do the owners and employees invest their own wealth alongside that of clients?

Q. Are client relationship managers paid for sales or service?

Q. Are portfolio managers paid based on assets under management or on long-term performance?

Our answers are clear and concise: we are privately owned and independent; we only focus on private wealth management; our interests are aligned because our clients, owners, and employees invest side-by-side; our relationship managers are rewarded for their client service, not sales; and our portfolio managers are measured on long-term performance, not assets under management. These key principles have guided our firm since its founding. Bessemer Trust is a multifamily o∞ce that has served individuals and families of substantial wealth for more than 110 years. Through comprehensive investment management, wealth planning, and family o∞ce services, we help clients achieve peace of mind for generations.

To learn more about Bessemer Trust, please contact Jeff Glowacki, Western Region Head, at 213-330-8570, or visit Bessemer.com.

ATLANTA BOSTON CHICAGO DALLAS DENVER GRAND CAYMAN GREENWICH HOUSTON LOS ANGELES MIAMI

NAPLES NEW YORK PALM BEACH SAN FRANCISCO SEATTLE STUART WASHINGTON, D.C. WILMINGTON WOODBRIDGE

Estate Planning | Probate | Trust Administration

Disputed Inheritances | Undue Influence and Exploitation Litigation

Nursing Home Abuse and Wrongful Death | Guardianships

Conservatorships | Special Needs Planning | Veterans Disability

We provide legal services in the following areas and are available for

collaborations or referrals

3411 N. 5th Ave., Suite 300, Phoenix, AZ 85013Phone: (602) 254-6008 | www.dbfazlaw.com

Providing legal services to the community for over 50 years.

Northern Trust banks are members FDIC. © 2016 Northern Trust Corporation.

WEALTH PLANNING \ BANKING \ TRUST & ESTATE SERVICES \ INVESTING \ FAMILY OFFICE

Managing the complexities of wealth can be a challenge, even for the savviest of individuals and their advisors. When you partner with Northern Trust, you can draw on the expertise of highly experienced financial professionals who can help your clients consider, clarify and prioritize their financial needs across their entire lifetime – and beyond. We call it Life Driven Wealth Management.

For more than a century, Northern Trust has helped professional advisors address the complex financial needs of their high-net-worth clients. We are committed to creating a partnership that complements your expertise, builds trust, deepens relationships and brings value to both you and your clients.

FOR MORE INFORMATION CONTACT:

Stephen Barber, Senior Wealth Strategist2398 East Camelback Road, Suite 1100, Phoenix, AZ 85016

602-468-2553 or [email protected]

Doug Diehl, Senior Wealth Strategist14624 North Scottsdale Road, Suite 250, Scottsdale, AZ 85254

480-365-6708 or [email protected]

EXPERIENCE THE RIGHT PARTNERSHIP™

northerntrust.com/wealthadvisor

www.tbaz.com

Phoenix 2375 E Camelback Rd, Ste 155 Phoenix, Arizona

Scottsdale 14631 N Scottsdale Rd, Scottsdale, ArizonaOcotillo 4913 S Alma School Rd, Ste 5 Chandler, Arizona

602-957-2006

FOCUS INTEGRITY RESILIENCE

John Chichester Sr Wealth Stratetist

Phil HotchkissCWS

Sandra HudsonCEO

Lisa SullivanCOO

Greg FursethCFO

Jena Lugo Trust Officer

Gregg Balderrama Sr Portfolio Manager

Jay Nova Sr Portfolio Manager

What inspires you, inspires us.602.264.5844 | eidebailly.com

DOINGDREAMING

Wealth planning shouldn’t distract clients from the moments that matter most. Eide Bailly’s Wealth Planning Team works closely with industry advisors to offer well-rounded solutions and a holistic perspective. Together, we can offer the support clients need to feel confident in their future and live in the moment.

6530 North 16th Street, Phoenix, AZ 85016

P | 602.944.1515www.mgks.com

RETIREMENT SOLUTIONS FOR YOUR BUSINESSWe offer a free initial consultation and retirement plan design analysis

aimed at achieving optimal results for the stakeholders in your business.

ALAN GOLD, CPARUSSELL J. SNOW, ENROLLED ACTUARY

HENRY DESPAIN, APA, QPA, ERPASHAWN T. PARKER, CPC, QPA, ERPA

MGKSACTUARIES - CONSULTANTS - ADMINISTRATORS

Helping Families by Connecting Wealth and Purpose®.It’s what we do.

WEALTH PLANNING | INVESTMENT ADVICE | TAX | FINANCIAL EDUCATION | ESTATE PLANNING

602.466.2611 | www.tfophoenix.com

TFO Phoenix, Inc. is registered as an investment advisor with the SEC and only transacts business in states where it is properly registered, or is excluded or exempted from registration requirements. SEC registration does not constitute an endorsement of the firm by the Commission nor does it indicate that the advisor has attained a particular level of skill or ability.

The Advisors’ Trust Company®Zia Trust, Inc.

Dave Long, J.D.Vice President and Senior Trust Officer

Josh Moore, M.S. Trust Officer

Rachel Zaslow, J.D.Trust Officer

Our Arizona fiduciary team offers skilled trust administration, estate settlement services, and more to families and individuals across the state.

We work with clients and their professional advisors to establish, implement, and accomplish the family estate plan.

We work alongside your clients’ investment advisors

11811 N. Tatum Blvd, Ste. 1062Phoenix, AZ 85028602.633.7999 www.ziatrust.com

SEE YOU NEXT YEAR!2021 Tax & Legal SeminarSteve Akers is Managing Director and Senior Fiduciary Counsel at Bessemer Trust. In this role, he serves as Chair of the firm’s Estate Planning Committee and works closely with clients in the Southwest region regarding their estate and trust planning issues.

Steve serves as President of The American College of Trust and Estate Counsel (ACTEC) and is a member of the Advisory Committee to the University of Miami Philip E. Heckerling Institute on Estate Planning, where he is a frequent speaker. He has previously served as Chair of the American Bar Association Section of Real Property, Trust & Estate Law and as Chair of the State Bar of Texas Real Estate, Probate & Trust Law Section.

Steve earned a JD from the University of Texas School of Law and a BS in chemical engineering from Oklahoma State University.

FRIDAY, NOVEMBER 5, 2021

Investment products and services are offered through Wells Fargo Advisors Financial Network, LLC (WFAFN), Member SIPC. ABLE Financial Group, LLC is a separate entity from WFAFN. ABLE Financial Group and WFAFN are not tax or legal advisors. 06/17

8737 E. Via de Commercio, Suite 100Scottsdale AZ 85258

TEL 480-258-6104 Toll Free 888-258-6108www.ablefinancialgroup.com

Creating Strategies Designed to Deliver Results

WE BELIEVE IN TRUE,COMPREHENSIVE,

AND HOLISTICPLANNING

Making sure your clients are prepared.

We work closely with CPA’s & Attorneys by providing your clients with unbiased and independent advice and solutions regarding:

First Vice President Financial Advisor Associate Financial AdvisorLarry Van Quathem Lane Reynolds Pearson Davis

Adam M. Brooks, CFP® Lee C. EisinbergManaging Partner Managing Partner

Call us today for a free consultation!

• Investment Management• Tax Minimization Strategies• Estate Planning Investment Strategies• Legacy Planning• Business Succession Planning• Converting Proceeds from the Sale of a Business Into Retirement Income• Wealth Transfer Planning and Family Dynamics• Retirement Income Planning and Strategies

WealthAdvisoryServices

Products offered through Wealth Advisory Services and Heartland Re�rement Plan Servicesare not FDIC insured, are not bank guaranteed and may lose value.

Andrew RoodveldtSenior Wealth Advisor, VP(602) [email protected]

Nadia Cunningham, JDWealth Advisor, [email protected]

Brooks Crandell, JDWealth Advisor, [email protected]

Experienced representation today to protect your assets for tomorrow.

Your personal and professional assets are only as valuable as the degree to which they are protected. Our adept estate planning, administration and business planning attorneys have been practicing in the Valley for over 33 years and have 100+ years of combined experience in protecting clients’ wealth, trus ts, estates and business endeavors.

Find out what we can do for you today to ensure a better tomorrow.

Estate Planning • Estate Administration • Business Planning • Estate, Trust, and Business Dispute Resolution

14811 North Kierland Boulevard, Suite 500 | Scottsdale, AZ 85254 | 480.951.8044 bskazlaw.com

www.DanaWhitingLaw.com

“An investment in knowledgepays the best interest.” - Benjamin Franklin

Maahew S. Dana Trevor S. WhitingESQ LLM CPA ESQ LLM MBA

Serving Arizona and the nation’s families for 200 years, with planning and executing the most creative plans. Proud sponsor of the 2020 Tax and Legal Seminar.

Chris Siegle J.P. Morgan Private Bank 480.367.3279 [email protected]

Julie GoldenJ.P. Morgan Private [email protected]

In the United States, bank deposit accounts, such as checking, savings and bank lending, may be subject to approval. Deposit products and related services are offered by JPMorgan Chase Bank, N.A. Member FDIC.

JPMorgan Chase Bank, N.A. and its affiliates (collectively “JPMCB”) offer investment products, which may include bank-managed accounts and custody, as part of its trust and fiduciary services. Other investment products and services, such as brokerage and advisory accounts, are offered through J.P. Morgan Securities LLC (“JPMS”), a member of FINRA and SIPC. JPMCB and JPMS are affiliated companies under the common control of JPMorgan Chase & Co. Products not available in all states.

INVESTMENT PRODUCTS: • NOT FDIC INSURED • NO BANK GUARANTEE • MAY LOSE VALUE

Business & Succession PlanningEstate Planning

• Corporate and Business Transactions

• Real Estate Transactions• Probate and Trust

Administration• Closely Held Business

Planning • Tax• Estate Planning

Beth S. Cohn, Esq.

State Bar of Arizona Certified Tax

SpecialistCertified Public

Accountant

Lisa Paine, Esq.

Estate PlanningBusiness Attorney

Stephanie Fierro, Esq.

Transactions Business

Estate Planning Attorney

Nikki Wilk, Esq.

Business & Probate Attorney

3200 N. Central Avenue Phoenix, AZ 85012602·248·1000 jaburgwilk.com

To achieve your financial goals, chose partners who will help you seize every opportunity. Jennings Strouss has a deep understanding of tax, estate planning, estate administration, and probate. When you work with us, you’ll have a team of legal experts who are dedicated to your vision for success.

Jennings Strouss is honored to support the Jewish Community Foundation/Arizona Community Foundation 2020 Tax and Legal Seminar.

HELPING YOU PREPARE FORTHE FUTURE

One E. Washington Street, Suite 1900Phoenix, AZ 85004-2554

jsslaw.com

William A. ClarkeEstate Planning, Estate Administration, and Probate 602.262.5886 [email protected]

Richard C. Smith Tax 602.262.5972 [email protected]

Otto S. Shill, III Tax and Employee Benefits 602.262.5956 [email protected]

Stapley Center | 1630 South Stapley Drive, Suite 108 | Mesa, Arizona 85204-6658480.355.1100 | www.lohmancompany.com

LOHMAN COMPANY, PLLCCertified Public Accountants & Business Consultants

At Lohman Company, we believe the most important part of a professional service relationship is “service.” If you erase that, what’s the point? You want a CPA who communicates clearly, is there when you need them, and always keeps their pencil sharp.

You want Lohman Company.

WE’RE MORE THAN SHARPWe’re User Friendly

Mary C. Jordan, CPA, Partner

LOHMAN COMPANY IS A PROUD PATRON OF THE ARIZONA COMMUNITY FOUNDATION AND JEWISH COMMUNITY FOUNDATION

TAX & LEGAL SEMINAR

480-384-5750 ▪ midfirstprivatebank.com20645 N. Pima Rd. #220 ▪ Scottsdale, AZ 85255

Member FDIC

Miranda Lumer Arizona Regional Manager

Jesper Hahn Portfolio Manager

Sal Bretts Fiduciary Advisor

Craig Hagen Wealth Advisor

Proud supporters of the Jewish Community Foundation and the Arizona Community Foundation

We study changing tax laws so you don’t have to.

RSM US LLP is the U.S. member firm of RSM International, a global network of independent audit, tax and consulting firms. Visit rsmus.com/aboutus for more information regarding RSM US LLP and RSM International.

RSM and our dedicated team of tax advisors constantly

monitor the latest regulations and laws. With extensive

middle market experience, we’re able to tailor solutions

to your specific challenges. And our global resources

help your company advance with confidence.

rsmus.com

Providing forward-thinking wealth management and investment strategies since 2004.

Biltmore Center at 24th Street & Camelback Road (602) 635-3760 versantcm.com

Proud sponsor of the 2020 Tax & Legal Seminar.

BMO Wealth Management is a brand name that refers to BMO Harris Bank N.A. and certain of its affiliates that provide certain investment, investment advisory, trust, banking, securities, insurance and brokerage products and services. Investment products are: NOT FDIC INSURED – NOT BANK GUARANTEED – NOT A DEPOSIT – MAY LOSE VALUE. © 2020 BMO Financial Group.

Grace Y. Lau

Chartered Financial Analyst ® Managing Principal

1643 E Bethany Home Road, Phoenix, AZ 85016

Email: [email protected] Phone: 602-997-8882 Fax: 602-997-8887

Website: www.bfsg-az.com

wealthoffers

opportunities

“Logic will get you from A to B. Imagina on will take you everywhere.”

Albert Einstein, Inventor

(Cr + Ep) x CI30 = Cf(G)(Crea vity + Experience) x Collabora on30 years = Cohn Financial Group

There is a formula for successfully serving affluent clients.We’ve solved it. That’s why leading advisors con�nue topartner with us for sophis�cated life insurance solu�ons.As a member of M Financial Group, we work with thena�on’s top legal and tax advisors to offer innova�vesolu�on to the high net worth and corporate markets.We provide objec�ve life insurance audits and marketstudies, and are one o�he few advisors in the U.S.specializing in private placement solu�ons for individualsand businesses. To nd out how Cohn Financial Groupcan help you formulate the right solu�ons for your clients,call us.

Paul Yates, CLU, FSAArea Vice President

Cohn Financial Group602.468.9667 (o) / 503.927.7843 (c)

5090 N. 40th St., Suite 180, Phoenix, AZ 85018www.cfgllc.com

Trust Where You Bank“You really find out a lot when your back

is against the wall. First Western Trust was there for me; they gave hope to me

and my family when we needed it the most... I want a bank you can Trust; First

Western Trust is that bank for me.”

— Tom L.

Private & Commercial BankingPlanning, Trust & Investment Management

myfw.com | (602) 224-7600

IT’S OUR GOAL TOHELP YOU REACH YOUR

FINANCIAL GOALS

EXPERIENCED FINANCIALADVISORS READY TO HELP YOU

Dieter Bollmann, VP Investments7373 N. Scottsdale Rd., Suite D-120 • Scottsdale, AZ 85253

Direct: (480) 778-2085E-mail: [email protected]

Website: www.ffec.com/dbollmann

Holland & Knight is proud to sponsor the

2020 Tax & Legal SeminarOur law firm supports the Jewish Community Foundation and the Arizona Community Foundation in their efforts to provide a premier educational forum for financial and estate planning professionals in Arizona. We are honored to help our clients identify and implement strategies to achieve wealth, tax, charitable and business succession goals.

Copyright © 2020 Holland & Knight LLP All Rights Reserved

www.hklaw.com

Shari A. Levitan, Partner Boston, MA | 617.854.1405

YEARS 20

CERTIFIED SPECIALISTS Arizona Board of Legal Specialization

256 South 2nd Avenue, Suite E • Yuma, Arizona 85364PHONE (928) 783-0103 • FAX (928) 783-2788

www.azyumalaw.com

ESTATE AND TRUST LAW

GERALD W. HUNTis admitted to practice in:

• Arizona • Oregon • Colorado • Texas • Wyoming • Washington • District of • Alaska Columbia

JEANNEVATTEROTT-GALE

is admitted to practice in: • Arizona • California • Missouri

Jackson/Roskelley Wealth Advisors is not a registered broker/dealer and is independent of

Services, Inc. Member FINRA/SIPC. Investment advisory services offered through Raymond James Financial Services Advisors, Inc. and Jackson/Roskelley Wealth Advisors, Inc.

Darin Shebesta, CFP®, AIF® 480-213-3430

9590 E Ironwood Square Dr, Ste 110

www.JFAwealth.com

Wealth Advisors to Professional Advisors

Comprehensive

Charitable

IT’S OUR GOAL TOHELP YOU REACH YOUR

FINANCIAL GOALS

EXPERIENCED FINANCIALADVISORS READY TO HELP YOU

Dieter Bollmann, VP Investments7373 N. Scottsdale Rd., Suite D-120 • Scottsdale, AZ 85253

Direct: (480) 778-2085E-mail: [email protected]

Website: www.ffec.com/dbollmann

KNOWLEDGE TO PROSPER

Local focus, team approach.Wealth and estate planning with a

Connected View.

Private Banking • Investment ManagementWealth Planning • Mortgage

Commercial Banking • Trusts & Estates

Member FDICNMLS ID: 477166

Scottsdale7025 North Scottsdale Road

Suite 100Scottsdale, AZ 85253

Phoenix2425 East Camelback Road

Suite 100Phoenix, AZ 85016

Dan ThompsonRegional President

480.596.1800

myfw.com

Trusts • Probate • BusinessTrusts • Probate • Business

www.johneven.com

47

Mack Business Appraisals has been providing trusted business valuation services to thousands of companies and their trusted legal and accounting advisors since the early 1990s.

• Estate and Succession Planning Valuation Specialists

• Credentialed, Experienced and Trusted Advisors

• Accurate and Defensible Business Valuations

Call us today at 623-340-6770 for a no-cost consultation!

John G. Mack, ASA, MCBA, ABAR

24654 N. Lake Pleasant Pkwy | Suite 103-522 Peoria, Arizona 85383

ESTATE PLANNING VALUATION EXPERTISE DELIVERED

ON-BUDGET AND ON-TIME

M AC K B U S I N E S S A P P R A I S A L S .CO M

McGrath Nothman PC

Certified Public Accountants

11000 N Scottsdale Road Suite 220Scottsdale AZ 85254

480-951-1040 www.McGrathCPA.net

Let Our Experience Countfor You!

Sherman & Howard’s Tax & Probate team advises clients on

how to protect their families, preserve their

wealth, safeguard their companies,

and achieve their personal, business,

and tax goals.

www.shermanhoward.com480.624.2710

A Century of Service

TAILORING WEALTH PLANNING STRATEGIES FOR GENERATIONS TO COME

Sherman & Howard’s Tax & Probate team

personal, business, and tax goals.

In 1999, we set out to build a boutique wealth management firm that focused strictly on the client’s needs. Twenty years later, our team has over seven decades of combined experi-ence and has been recognized locally and nationally for its

client centric work.

Our firm’s guiding principles remain true:

Personalized Service - Every client’s objectives are different. We do not manage by "model" or one size fits all portfolios.

Long Term Relationships - Our goal is to be our clients’ partner, someone who helps them achieve their goals now and in the future.

Consultative Educational Approach - Our unique educational approach allows our clients to determine their level of involvement.

Objective Fee-Only Advice - As fiduciaries, we work on a fee-only basis and do not accept commissions. We give advice based on our clients’ needs, not ours.

Integrated Services - We help coordinate every aspect of our clients’ finances and maintain ongoing relationships and communications with other team professionals.

Find out how working with a small, family runbusiness can benefit your clients. Contact us today!

480.998.1798 | www.xpertadvice.comLaurie Bagley CFA John Bagley CFP, CPA, MBA Jim Schwartz CFP, RICP

We are proud to support the 2020 Tax & Legal Seminar

benefiting the Arizona Community Foundation and the Jewish Community Foundation.

Our motto has always been “whatever it takes” to assist our

clients in the duties of estate planning and settlement with real

and personal property, and to achieve it all with just one phone call.

Specializing in:

────

Personal property inventory and Appraisals

────

Sale or distribution of personal property

────

Shipping, storage, & outside services

────

T&T ESTATE SERVICES

TAMMY O’NEAL & TERRY O’NEAL A.S.A.

Accredited Senior Appraiser, A.S.A.

623.486.4310

Residential & CommercialTrust Real Estate

Your business. Our knowledge. One team.

Proud Supportersof the

2020 Tax & Legal Seminar.

CHARLOTTE, NC | ROCHESTER, NY | PHOENIX, AZ

www.southparkval.com

9/10/2020

1

RREETTIIRREEMMEENNTT AACCCCOOUUNNTTSS:PPLLAANNNNIINNGG FFOORR IINNHHEERRIITTEEDD AACCCCOOUUNNTTSS AANNDD FFOORR MMAARRIITTAALL RRIIGGHHTTSS

TAX and LEGAL SEMINARJewish Community Foundation / Arizona Community Foundation

November 13, 2020

CHRISTOPHER R. HOYTUniversity of Missouri - Kansas City

School of Law

Legislative Changes

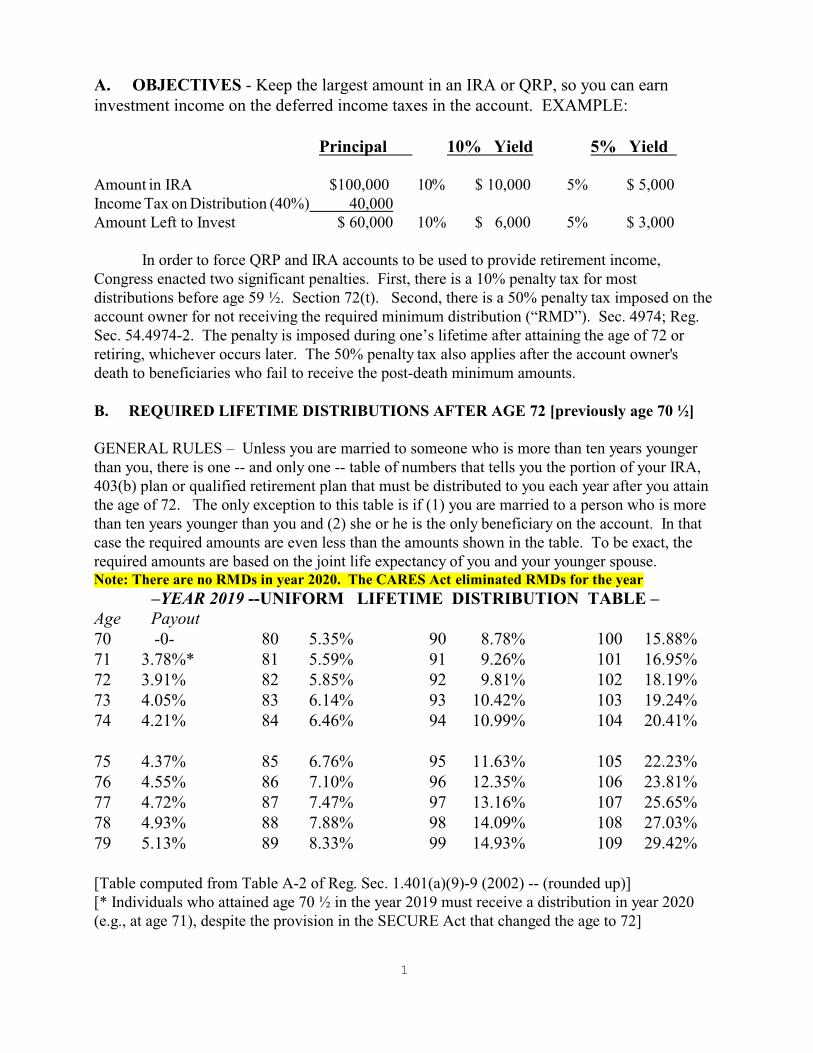

• CARES Act (March 2020) – The Coronavirus Aid, Relief, and Economic Security Act – the $2.2 trillion legislation to provide relief from the economic damage triggered by the coronavirus Covid-19

• SECURE Act – (December 2019) – The Setting Every Community Up for Retirement Enhancement Act –made major changes to the laws governing retirement accounts

Slides section 03

9/10/2020

2

CCoorroonnaavviirruuss AAiidd,, RReelliieeff,, aanndd EEccoonnoommiicc SSeeccuurriittyy ((CCAARREESS)) AAcctt

CChhaannggeess tthhaatt AAffffeecctt RReettiirreemmeenntt AAccccoouunnttss

• No RMDs required in the year 2020This includes accounts of people over age 70 ½ and people of all ages who have inherited retirement accounts

• 401(k) plans: Employees who have been diagnosed with Covid-19 (including a spouse or a dependent) or who have lost income from a layoff, business closure, quarantine, reduced hours, or inability to work because of child care:

* Hardship distribution possible. (Under age 59 ½, no 10% penalty)

It is still taxable income, but can avoid tax if repay in 3 years* Loan from plan possible: maximum increased to $100,000

.

RREEQQUUIIRREEDD MMIINNIIMMUUMM DDIISSTTRRIIBBUUTTIIOONNSS**LLIIFFEETTIIMMEE DDIISSTTRRIIBBUUTTIIOONNSS**

THREE CHANGES FOR LIFETIME RMDs:1. New RMD Age : 72

(for people who attain age 70 ½ after 2019)(Despite new age 72, charitable QCD still 70 ½)

2. RMDs are not required in year 2020 - CARES-- from either your own IRA or an inherited IRA

3. New life expectancy tables (beginning in 2021)Annual RMD amounts will decline by

between 0.3% and 0.5% each year (varies by age)

9/10/2020

3

RREEQQUUIIRREEDD MMIINNIIMMUUMM DDIISSTTRRIIBBUUTTIIOONNSS**LLIIFFEETTIIMMEE DDIISSTTRRIIBBUUTTIIOONNSS –– YYEEAARR 22001199**

Age of Account Owner Required Payout72 3.91%75 4.37%80 5.35%85 6.76%90 8.75%95 11.63%

100 15.88%

RREEQQUUIIRREEDD MMIINNIIMMUUMM DDIISSTTRRIIBBUUTTIIOONNSS**LLIIFFEETTIIMMEE DDIISSTTRRIIBBUUTTIIOONNSS –– YYEEAARR 22002211++ **

Age of Account Owner Required Payout72 3.67%75 4.07%80 4.95%85 6.25%90 8.27%95 11.24%

100 15.71%

9/10/2020

4

RREEQQUUIIRREEDD MMIINNIIMMUUMM DDIISSTTRRIIBBUUTTIIOONNSS**LLIIFFEETTIIMMEE DDIISSTTRRIIBBUUTTIIOONNSS**

A. THREE CHANGES FOR LIFETIME RMDs:

1. New RMD Age : 72 (for people who attain age 70 ½ after 2019)(Despite new age 72, charitable QCD still 70 ½)

2. No RMDs required in year 20203. New life expectancy tables (beginning in 2021)

Annual RMD amounts will decline bybetween 0.3% and 0.5% each year (varies by age)

B. WORKING INDIVIDUALS OVER AGE 70 ½ CAN MAKE TAX-DEDUCTIBLE CONTRIBUTIONS TO A TRADITIONAL IRA (Year 2020 maximum: $7,000)

WWaanntt ttoo mmaakkee cchhaarriittaabbllee ggiiffttss ffrroomm yyoouurr IIRRAA ((““QQCCDD””))??TThheenn NNEEVVEERR mmaakkee aa ttaaxx--ddeedduuccttiibbllee ccoonnttrriibbuuttiioonn

ttoo yyoouurr IIRRAA aafftteerr aattttaaiinniinngg aaggee 7700 ½½

New last sentence added to end of Sec 408(d)(8)(A):The amount of distributions not includible in gross income by reason of the preceding sentence for a taxable year (determined without regard to this sentence) shall be reduced (but not below zero) by an amount equal to the excess of—• (i) the aggregate amount of deductions allowed to the taxpayer under

section 219 for all taxable years ending on or after the date the taxpayer attains age 70 ½, over

• (ii) the aggregate amount of reductions under this sentence for alltaxable years preceding the current taxable year.

.

9/10/2020

5

WWaanntt ttoo mmaakkee cchhaarriittaabbllee ggiiffttss ffrroomm yyoouurr IIRRAA ((““QQCCDD””))??TThheenn NNEEVVEERR mmaakkee aa ttaaxx--ddeedduuccttiibbllee ccoonnttrriibbuuttiioonn

ttoo yyoouurr IIRRAA aafftteerr aattttaaiinniinngg aaggee 7700 ½½

LEGISLATIVE INTENT • To get a tax benefit from a charitable gift, a taxpayer must generally itemize

deductions (state taxes, mortgage interest, etc)• Only 11% of tax returns itemized deductions in 2018• A working senior could (a) contribute $7,000 to an IRA and then (b)

distribute $7,000 that same year to charities, and indirectly deduct charitable gifts via IRA contributions

ADMINISTRATIVE and BOOKEEPING HEADACHES• People in their 80s and 90s will need to keep all tax records after age 70 ½

and then make cumulative computations

.

WWaanntt ttoo mmaakkee cchhaarriittaabbllee ggiiffttss ffrroomm yyoouurr IIRRAA ((““QQCCDD””))??TThheenn NNEEVVEERR mmaakkee aa ttaaxx--ddeedduuccttiibbllee ccoonnttrriibbuuttiioonn

ttoo yyoouurr IIRRAA aafftteerr aattttaaiinniinngg aaggee 7700 ½½ EXAMPLE• I. Work’s RMD both for this year and next year is $5,000• She donates each year’s RMD to charity; would be QCD• She is employed. This year she deducts $7,000 for IRA.

Next year she does not deduct any IRA contribution• How much can she EXCLUDE from income for QCD?

Year Donate Exclude Taxable This year $5,000 -0- $5,000*Next year $5,000 $3,000 $2,000** Taxpayer can claim an itemized charitable deduction

.

9/10/2020

6

WWaanntt ttoo mmaakkee cchhaarriittaabbllee ggiiffttss ffrroomm yyoouurr IIRRAA ((““QQCCDD””))??TThheenn NNEEVVEERR mmaakkee aa ttaaxx--ddeedduuccttiibbllee ccoonnttrriibbuuttiioonn

ttoo yyoouurr IIRRAA aafftteerr aattttaaiinniinngg aaggee 7700 ½½

STRATEGIES• If ever want to make a QCD, don’t contribute after age 70 ½ • Working seniors can contribute to plan at work (401(k), etc.)• Working seniors can contribute to a Roth IRA

• Footnote: Employed upper-income taxpayers can’t even make tax-deductible contributions to an IRA if there is a plan at work (e.g., 401(k) ). No tax deduction is permitted in year 2020 if AGI is over $75,000 ($124,0000 on married

.

SSeettttiinngg EEvveerryy CCoommmmuunniittyy UUpp ffoorr RReettiirreemmeenntt EEnnhhaanncceemmeenntt ((SSEECCUURREE)) AAcctt

CHANGES TO THE LAW:• Make it easier for 401(k) plans to offer annuities

-- Convert assets into reliable income in retirement • RMDs to begin at age 72 (up from age 70 ½) • Permit working individuals over age 70 ½ to make contributions to a

traditional IRA • Other changes to retirement plans and 529 plans• Kill the Stretch IRA. QRP and IRA accounts would generally have to be

liquidated by the end of the 10th year after death. There would be no RMDs in years 1 through 9.

.

9/10/2020

7

Setting Every Community Up for Retirement Enhancement (SECURE) Act

OTHER CHANGES TO RETIREMENT and 529 PLANS:• 529 plan account owners may withdraw up to $10,000 tax-

free (per beneficiary) to pay qualified education loans• 529 plans can be used for apprenticeships (old: schools only)• No 10% penalty on up to $5,000 distributed from a

retirement plan to a person under age 59 ½ within one year of a birth or adoption (though is still taxable income)

• “Kiddie tax” – parent’s rate (repeal T & E tax rates). Amend 2018?

.

DDiissttrriibbuuttiioonnss ffrroomm IInnhheerriitteedd RReettiirreemmeenntt AAccccoouunnttss AArree TTaaxxaabbllee IInnccoommee

IInnccoommee IInn RReessppeecctt ooff AA DDeecceeddeenntt ““IIRRDD”” ––§§669911

• No stepped up basis for retirement assets• Distributions from inherited retirement accounts are

usually taxable income to the beneficiaries.

9/10/2020

8

UUSSUUAALL OOBBJJEECCTTIIVVEE::DDeeffeerr ppaayyiinngg iinnccoommee ttaaxxeess

iinn oorrddeerr ttoo ggeett ggrreeaatteerr ccaasshh ffllooww

Principal 10% Yield

• Pre-Tax Amount $ 100,000 $ 10,000• Income Tax

on Distribution (40%) 40,000

• Amount Left to Invest $ 60,000 $ 6,000

Stretch IRA• “Stretch IRA” means an inherited retirement account

(e.g., IRA), where payments are gradually made over the beneficiary’s life expectancy

• Until the enactment of the SECURE Act, it was fairly easy for any beneficiary who inherited a retirement account to receive distributions until the age of 83 (or older for beneficiaries who inherited at an older age)

• New rules apply beginning in year 2020• Compare rules of the present, past & future

9/10/2020

9

Distributions After Death(for decedents who die in 2020 and later)

Maximum time period to empty account:

• Ten years (No RMD until year #10)[the account needs to be empty by December 31 of the tenth year after the year of the decedent’ death, or else there is a 50% penalty on the balance]

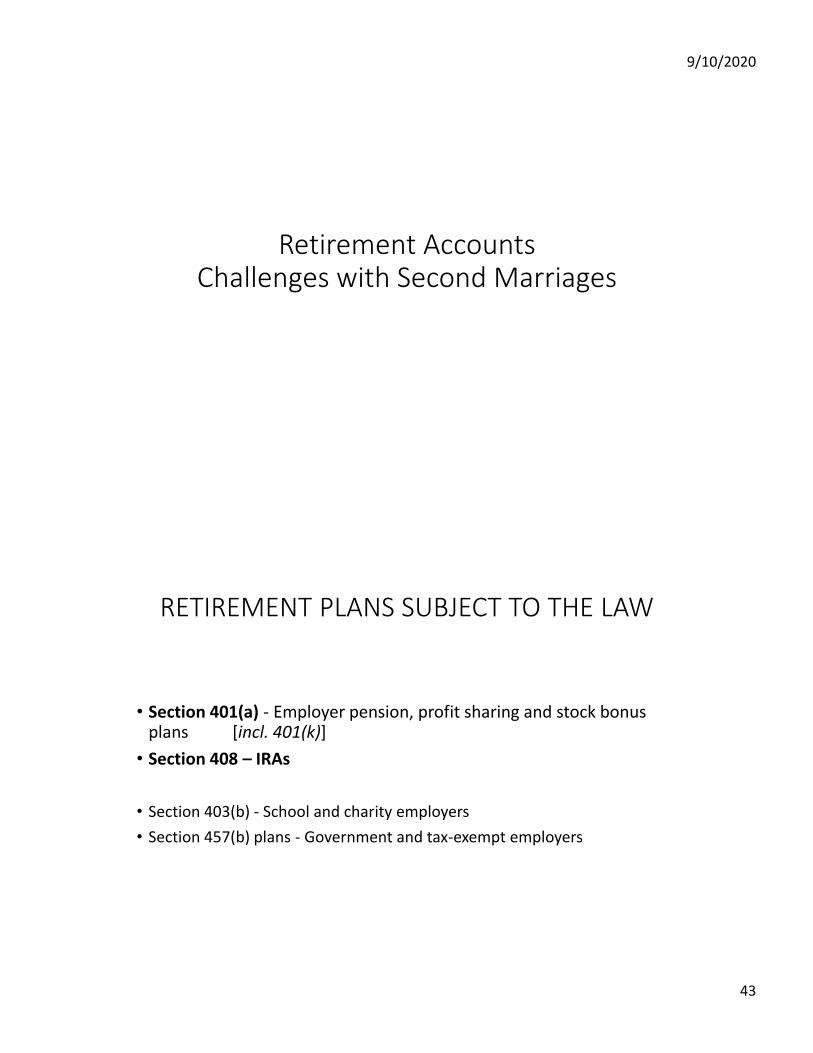

RREETTIIRREEMMEENNTT AACCCCOOUUNNTTSS IINN MMAARRRRIIAAGGEESS::TTYYPPEESS OOFF QQRRPPss

•Section 401(a) - Employer pension, profit sharing and stock bonus plans[incl. 401(k)]

•Section 408 – IRAs•Section 403(b) - School and charity employers•Section 457(b) plans - Government and tax-exempt

employers

9/10/2020

10

DDiissttrriibbuuttiioonnss AAfftteerr DDeeaatthh

Company policy may require faster liquidation• Employer might require account of

deceased employee to liquidated in just one year

• No such problem with IRAs• Beneficiary of employer plan account can

compel transfer to an inherited IRA

DDiissttrriibbuuttiioonnss AAfftteerr DDeeaatthh((ffoorr ddeecceeddeennttss wwhhoo ddiiee iinn 22002200 aanndd llaatteerr))

Maximum time period to empty account:

• Ten years (No RMD until year #10), or• Remaining life expectancy of an “eligible

designated beneficiary” (RMD every year)-- surviving spouse

9/10/2020

11

MARRIED COUPLES: RETIREMENT ASSETS

Surviving spouse has an option that no other beneficiary has:a rollover of deceased spouse’s retirement assets to her or his own new IRA (creditor protection, too!)

Other beneficiaries cannot do a rollover. Main option: liquidate over ten years

LLEEAAVVEE MMOONNEEYY IINN DDEECCEEDDEENNTT’’SS AACCCCOOUUNNTT??RReeqquuiirreedd DDiissttrriibbuuttiioonnss iiff tthhee

SSuurrvviivviinngg SSppoouussee iiss tthhee SSoollee BBeenneeffiicciiaarryy

•Spouse can recalculate life expectancy• IRAs only: Spouse can elect to treat IRA as

her own •Decedent died before age 72 ?

• No required distribution until year the deceased spouse would have been age 72

9/10/2020

12

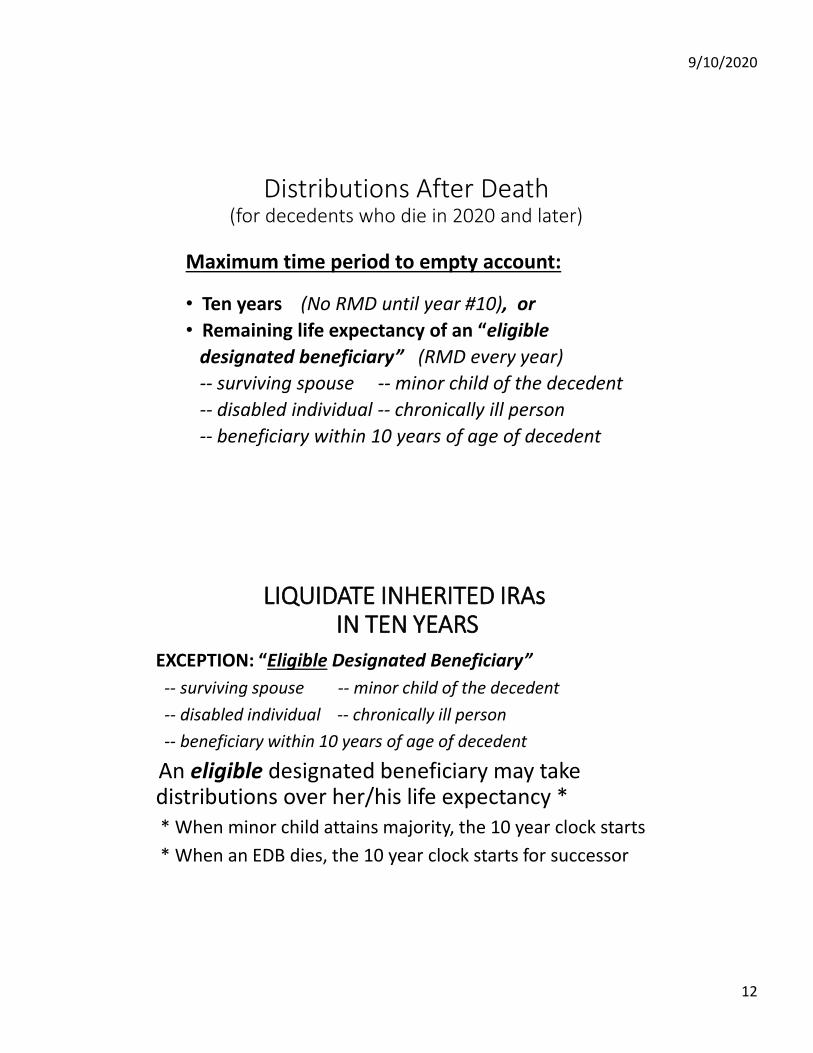

Distributions After Death(for decedents who die in 2020 and later)

Maximum time period to empty account:

• Ten years (No RMD until year #10), or• Remaining life expectancy of an “eligible

designated beneficiary” (RMD every year)-- surviving spouse -- minor child of the decedent-- disabled individual -- chronically ill person-- beneficiary within 10 years of age of decedent

LLIIQQUUIIDDAATTEE IINNHHEERRIITTEEDD IIRRAAssIINN TTEENN YYEEAARRSS

EXCEPTION: “Eligible Designated Beneficiary” -- surviving spouse -- minor child of the decedent-- disabled individual -- chronically ill person-- beneficiary within 10 years of age of decedent

An eligible designated beneficiary may take distributions over her/his life expectancy ** When minor child attains majority, the 10 year clock starts* When an EDB dies, the 10 year clock starts for successor

9/10/2020

13

DDiissttrriibbuuttiioonnss AAfftteerr DDeeaatthh((ffoorr ddeecceeddeennttss wwhhoo ddiiee iinn 22002200 aanndd llaatteerr))

Maximum time period to empty account:

• Ten years (No RMD until year #10), or• Remaining life expectancy of an “eligible

designated beneficiary”, or• Five Years, or • “Ghost life expectancy”

RREEQQUUIIRREEDD MMIINNIIMMUUMM DDIISSTTRRIIBBUUTTIIOONNSS** DDEEFFIINNIITTIIOONNSS **

• Required Beginning Date (“RBD”)April 1 in year after attain age 72

• Designated Beneficiary (“DB”)A human being. An estate or charitycan be a beneficiary of an account, but not a DB.

• Determination DateSeptember 30 in year after death.

9/10/2020

14

RREEQQUUIIRREEDD DDIISSTTRRIIBBUUTTIIOONNSS IIFF TTHHEERREE IISS EEVVEENN JJUUSSTT OONNEE

NNOONN--DDEESSIIGGNNAATTEEDD BBEENNEEFFIICCIIAARRYY

Death Before RBD Death After RBDRemaining life

FIVE expectancy of YEARS someone who is

decedent’s age at death Roth IRA: Just 5 years

AACCTTIIOONNSS TTHHAATT CCAANN BBEE TTAAKKEENN BBEEFFOORREE TTHHEE DDEETTEERRMMIINNAATTIIOONN DDAATTEE

• Disclaimers• Full distribution of share• Divide into separate accounts

For example, separate accounts when: • one beneficiary is an EDB and another is not• one beneficiary is a charity & can’t pay by 9/30

9/10/2020

15

RREEQQUUIIRREEDD DDIISSTTRRIIBBUUTTIIOONNSS IIFF TTHHEERREE IISS EEVVEENN JJUUSSTT OONNEE

NNOONN--DDEESSIIGGNNAATTEEDD BBEENNEEFFIICCIIAARRYY

Death Before RBD Death After RBDRemaining life

FIVE expectancy of YEARS someone who is

[No RMD until year #5] decedent’s age at death [Each year has an RMD][“ghost life expectancy”]

RREEQQUUIIRREEDD MMIINNIIMMUUMM DDIISSTTRRIIBBUUTTIIOONNSS**GGhhoosstt LLiiffee EExxppeeccttaannccyy**

Age of Beneficiary Life Expectancy 72 Too soon! 5 year liquidation !73 April & later is after RBD74 6.4% 15.6 more years 75 6.8% 14.876 7.1% 14.0 77 7.5% 13.378 7.9% 12.678 8.4% 11.9 80 8.9% 11.2

9/10/2020

16

DDiissttrriibbuuttiioonnss AAfftteerr DDeeaatthh((ffoorr ddeecceeddeennttss wwhhoo ddiiee iinn 22002200 aanndd llaatteerr))

Maximum time period to empty account:

• Ten years (No RMD until year #10), or• Remaining life expectancy of an “eligible

designated beneficiary”, or If on Sept 30:• Five Years, or << Charity is beneficiary• “Ghost life expectancy” << Charity is beneficiary

LLIIQQUUIIDDAATTEE IINNHHEERRIITTEEDD IIRRAAss IINN TTEENN YYEEAARRSS

EFFECTIVE DATES:* Rules apply for decedents dying after December 31, 2019* For decedents who died before 2020, beneficiaries can continue to receive payments over remaining life expectancy.• However, upon the death of that beneficiary, the 10 year clock starts ticking.• EXAMPLE: A 60 year old beneficiary inherited an IRA in 2019 when he had a

life expectancy to age 85 (for 25 years). That beneficiary dies 2 years later at age 62. The inherited IRA must be empty in the 10th year after death [rather than the year that the individual would have been age 85]

.

9/10/2020

17

Distributions After Death“ life expectancy“

Oversimplified: Half of population will die before that age, and half will die after

RREEQQUUIIRREEDD MMIINN.. DDIISSTTRRIIBBUUTTIIOONNSS**LLIIFFEE EEXXPPEECCTTAANNCCYY TTAABBLLEE**

““SSTTRREETTCCHH IIRRAASS -- LLAAWW BBEEFFOORREE 22002200””

Age of Beneficiary Life Expectancy 30 1.9% 53.3 more years 40 2.3% 43.650 2.9% 34.260 4.0% 25.270 5.3% 18.7 80 8.9% 11.290 17.5% 5.7

9/10/2020

18

RREEQQUUIIRREEDD MMIINNIIMMUUMM DDIISSTTRRIIBBUUTTIIOONNSSEExxaammppllee:: DDeeaatthh aatt aaggee 8800??

NNEEWW LLAAWW:: TTEENN YYEEAARRSS ((iiff >>1100 yyeeaarr yyoouunnggeerr))

Age of Beneficiary Life Expectancy 30 10 years 40 1050 1060 1070 5.3% 18.7 80 8.9% 11.290 8.9% 5.7 * [11.2 yrs]

LLIIQQUUIIDDAATTEE IINNHHEERRIITTEEDD IIRRAAss IINN TTEENN YYEEAARRSS

STRATEGIES:• Lotsa beneficiaries! Share the love! Spread the wealth!

Example: Children and grandchildren, rather than just children• Lifetime Roth IRA conversions, if current income tax rate is likely to be less than

future tax rates• Are any beneficiaries “eligible designated beneficiaries”?• Charitable bequests

* Have pre-tax dollars used for charitable purposes, especially if estate will be subject to federal or state estate taxes

* Charitable remainder trusts (more on this later)

.

9/10/2020

19

IIRRAAss PPAAYYAABBLLEE TTOO TTRRUUSSTTSSGeneral Rule: Trust is not DB

Exception: “Look-through” trust if four conditions are met. Reg. § 1.409(a)(9)-4, Q&A 5 & 6

• (1) The trust is a valid trust under state law• (2) The trust is irrevocable (or will become irrevocable on death)• (3) The beneficiaries are identifiable from the trust instrument,• (4) A document is given to the plan administrator. Either:

(a) a copy of the entire trust instrument or (b) a certified list of all of the beneficiaries of the trust

IIRRAAss PPAAYYAABBLLEE TTOO TTRRUUSSTTSS

General Rule: Trust is not DBException: “Look-through” trust if four

conditions are met. Reg. § 1.409(a)(9)-4, Q&A 5 & 6

Types:-- “accumulation trusts”-- “conduit trusts”

9/10/2020

20

CCOONNDDUUIITT TTRRUUSSTTSS • Defined: Where the governing instrument provides

that all amounts distributed from the retirement account to the trustee while the primary beneficiary is alive will, upon receipt by the trustee, be paid directly from the trust to that beneficiary. Reg. § 1.409(a)(9)-5, Q&A 7(c)(3), Example 2.

• Advantage of a conduit trust: The conduit beneficiary is considered to be the sole beneficiary of that trust. The RMD computation ignores beneficiaries who will receive retirement plan $$ after the conduit beneficiary dies.

AACCCCUUMMLLAATTIIOONN TTRRUUSSTTSS • Defined: A trust where the trustee has the power to

either distribute or retain distributions that the trustee receives from a retirement plan account. Reg. §1.409(a)(9)-5, Q&A 7(c)(1)

• If retained, the income tax rate will likely be 37%• Effect of remainder beneficiaries: Except for a

“mere potential successor”, all possible beneficiaries must be considered for the RMD computation. PLR 200228025 (Apr. 18, 2002)

• Potential negative impact when some beneficiaries are EDBs and others aren’t?

9/10/2020

21

IIRRAAss PPAAYYAABBLLEE TTOO TTRRUUSSTTSS

•Payable to a “minimum RMD” trust?• Is the IRA itself a “trusteed IRA”?•Payable to a conduit trust? •Payable to an accumulation trust?

““MMiinniimmuumm RRMMDD”” TTrruusstt

•Review the terms of the trust!Does the trust instrument state (oversimplified):“distribute only the minimum RMD required by law”? If so, there would be zero distributions in years 1 through 9 and 100% would be distributed in year #10. An income tax disaster!

• If appropriate, consider modification of the trust instrument, or decanting

• Most states permit modification to achieve the settlors’ tax objectives when laws change. UTC § 416

9/10/2020

22

CCOONNDDUUIITT TTRRUUSSTTSS

• Unless the beneficiary is an eligibledesignated beneficiary, the retirement account will be fully liquidated in ten years. The beneficiary will personally own all of the retirement assets.

• So what are the advantages of naming a conduit trust as the beneficiary, compared to simply naming the individual as the beneficiary on the IRA/retirement plan beneficiary form?

AACCCCUUMMLLAATTIIOONN TTRRUUSSTTSS • Trusts pay the highest income tax rate: 37%.

Will the beneficiaries be in a much lower income tax bracket?

• If so, will the benefits of the trust outweigh the much higher income tax cost?

• Benefits include: * Asset protection * Professional management* Restricted withdrawals by spendthrift beneficiaries

9/10/2020

23

AACCCCUUMMLLAATTIIOONN TTRRUUSSTTSS

• In general, there should a real need for a trust. If the beneficiaries are stable, mature adults who will pay substantially lower income tax rates than the trust’s 37% income tax rate, the rules are simpler if they are named as the beneficiaries of the account.

• If a trust will be a beneficiary of a retirement account, adopt specific strategies for the receipt of retirement assets. Those assets are pure taxable income that could be taxed at the highest 37% rate.

(Individuals don’t pay that 37% rate unless taxable income is over $500,000+ single ($600,000+ married joint))

TTwwiinn TTEEAA PPOOTT TTrruusstt SSyysstteemm℠℠AAllaann GGaassssmmaann,, CChhrriissttoopphheerr DDeenniiccoolloo aanndd BBrraannddoonn KKeettrroonn

Concept: • If an estate has both taxable IRD assets and

tax-free assets (e.g., assets that have a stepped-up income tax basis),

• Then the greatest amount of wealth will be transferred to the heirs and beneficiaries if the IRD will be taxed at the lowest possible income tax rate.

9/10/2020

24

TTwwiinn TTEEAA PPOOTT TTrruusstt SSyysstteemm℠℠AAllaann GGaassssmmaann,, CChhrriissttoopphheerr DDeenniiccoolloo aanndd BBrraannddoonn KKeettrroonn

• A trust arrangement for beneficiaries (e.g., children) who are in very different income tax brackets.

• A pot trust is named as the beneficiary of the retirement accounts. Trustee has discretion to give different amounts to different beneficiaries.

• The pot trust is a look-through accumulation trust. Yes, IRA is liquidated in ten years. Trustee distributes most taxable retirement income to low tax-rate beneficiaries.

• A separate pot trust distributes tax-free principal to high-tax rate beneficiaries. Equalizes after-tax dollars to all.

• Caution: Take steps to avoid “merger” of the two trusts

Beneficiary Deemed Owner Trust (BDOT)• A “grantor trust,” where the income of the trust is taxed to

the beneficiary under §678(a)• The beneficiary is usually in a lower income tax bracket than

the trust’s 37%. Trust distributes cash to pay tax.• Beneficiary is given a withdrawal power over the taxable

income of the trust. But no withdrawal power over the principal. This provides asset protection and other benefits for the assets retained in the trust.

Not perfect, of course. Wouldn’t want to have a withdrawal power for a substance abuser or when trying to qualify for public assistance with a special-needs beneficiary

• Comprehensive article by Ed Morrow: Google search: SSRN BDOT

9/10/2020

25

IIRRAAss PPAAYYAABBLLEE TTOO TTRRUUSSTTSS TTHHAATT BBEENNEEFFIITT BBOOTTHH EEDDBBss aanndd nnoonn--EEDDBBSS

ISSUE: Does naming an accumulation trust for a spouse (e.g., QTIP trust), minor child, etc. as an IRA beneficiary require liquidation of the IRA in 10 years, if there are also beneficiaries who are not eligible designated beneficiaries?GENERALLY YES: Under current tax regulations, all beneficiaries of an accumulation trust are considered when computing RMDs. Regs bias to faster payout.

IRAs PAYABLE TO TRUSTS THAT BENEFIT BOTH EDBs and non-EDBS

EXAMPLE: An accumulation trust states (oversimplified): “pay to my second wife (an EDB) for life, remainder to my children from my first marriage (adult children are not EDBs)”

An IRA payable to such a trust must be liquidated within ten years after the decedent’s death.Consider alternatives. Conduit trust? Percent outright to spouse (who can rollover) and percent to kids?

9/10/2020

26

IIRRAAss PPAAYYAABBLLEE TTOO TTRRUUSSTTSS TTHHAATT BBEENNEEFFIITT BBOOTTHH EEDDBBss aanndd nnoonn--EEDDBBSS

ISSUE: Naming an accumulation trust for a spouse(e.g., QTIP trust), minor child, etc. as an IRA beneficiary requires liquidation of the IRA in 10 years. EXCEPTION:• Accumulation trust for disabled & chronically illPLANNING:• Conduit trust for other type of EDB

AACCCCUUMMLLAATTIIOONN OORR CCOONNDDUUIITT TTRRUUSSTT FFOORR DDIISSAABBLLEEDD OORR CCHHRROONNIICCAALLLLYY IILLLL

EXCEPTION IN STATUTE: A retirement account payable to a trust (either accumulation or conduit) that benefits a disabled or chronically ill beneficiary could qualify for stretch life-expectancy payouts. Upon the death of that beneficiary, the ten year rule would apply.

Statute only provides an exemption for trust beneficiaries who are disabled or chronically ill.

There is no comparable provision for other EDBs:surviving spouse, minor child, person within ten years age

9/10/2020

27

CCoonndduuiitt TTrruussttss ffoorr EElliiggiibbllee DDeessiiggnnaatteedd BBeenneeffiicciiaarriieess

Conduit trusts for EDBs permit RMDs to be made over the EDB’s life expectancy, without considering the potential impact of contingent or remainder beneficiaries who are not EDBs.Conduit trusts can still make sense for:• A surviving spouse (though a rollover is better)• A person not more than ten years younger• A minor child (but have flexibility after majority age)

MMAANNDDAATTOORRYY DDIISSTTRRIIBBUUTTIIOONNSS[[AAssssuummee iinnhheerriitt IIRRAA aatt aaggee 8800 aanndd ddiiee aatt 9944]

EXAMPLE: D. John Mustard owned three IRAs when he died this year at age 93. His surviving spouse, Honey, turned age 80 the year after his death. Each IRA had a different beneficiary: • An accumulation trust for Honey, remainder to his children

from his first marriage• A conduit trust for Honey, remainder to his children from his

first marriage• Honey was the sole beneficiary ( rollover is possible )

9/10/2020

28

MMAANNDDAATTOORRYY DDIISSTTRRIIBBUUTTIIOONNSS[[AAssssuummee iinnhheerriitt IIRRAA aatt aaggee 8800 aanndd ddiiee aatt 9944]]

ROLL - Accumulation ConduitAGE OVER Trust Trust . 80 4.95% -0-% 8.93%

85 6.25 % -0- % 12.35%

90 8.26% 100.00% << 10 years, since it is 91 8.77% empty an accumulation trust92 9.26% empty 20.41%

MMAANNDDAATTOORRYY DDIISSTTRRIIBBUUTTIIOONNSS[[AAssssuummee iinnhheerriitt IIRRAA aatt aaggee 8800 aanndd ddiiee aatt 9944]

Conduit Trust for Surviving Spouse?

1. A conduit trust with several beneficiaries permits an EDB to receive distributions over remaining life expectancy, rather than just ten years

(There are RMDs every year, though)

2. A surviving spouse can annually recompute remaining life expectancy

9/10/2020

29

MMAANNDDAATTOORRYY DDIISSTTRRIIBBUUTTIIOONNSS[[AAssssuummee iinnhheerriitt IIRRAA aatt aaggee 8800 aanndd ddiiee aatt 9944]]

ROLL - Accumulation ConduitAGE OVER Trust Trust . 80 4.95% -0-% 8.93%

85 6.25% -0- % 12.35%

90 8.26% 100.00% 17.54%91 8.77% empty 18.87%92 9.26% empty 20.41%

CCoonndduuiitt TTrruussttss ffoorr EElliiggiibbllee DDeessiiggnnaatteedd BBeenneeffiicciiaarriieess

Conduit trusts for EDBs permit RMDs to be made over the EDB’s life expectancy, without considering the potential impact of contingent or remainder beneficiaries who are not EDBs.Conduit trusts can still make sense for:• A surviving spouse (though a rollover is better)• A person not more than ten years younger• A minor child (but have flexibility after majority age)

9/10/2020

30

IIRRAAss PPAAYYAABBLLEE TTOO TTRRUUSSTTSS

•Payable to a “minimum RMD” trust?• Is the IRA a “trusteed IRA”?•Payable to a conduit trust? •Payable to an accumulation trust?• If appropriate, consider modification of the trust instrument, or decanting

LLIIQQUUIIDDAATTEE IINNHHEERRIITTEEDD IIRRAAss IINN TTEENN YYEEAARRSS

IMPLICATIONS FOR CHARITIESDonors more likely to consider•Outright bequests•Retirement assets to tax-exempt CRT

• Child: income more than 5 years; then charity• Spouse & children (no estate tax marital deduction)

9/10/2020

31

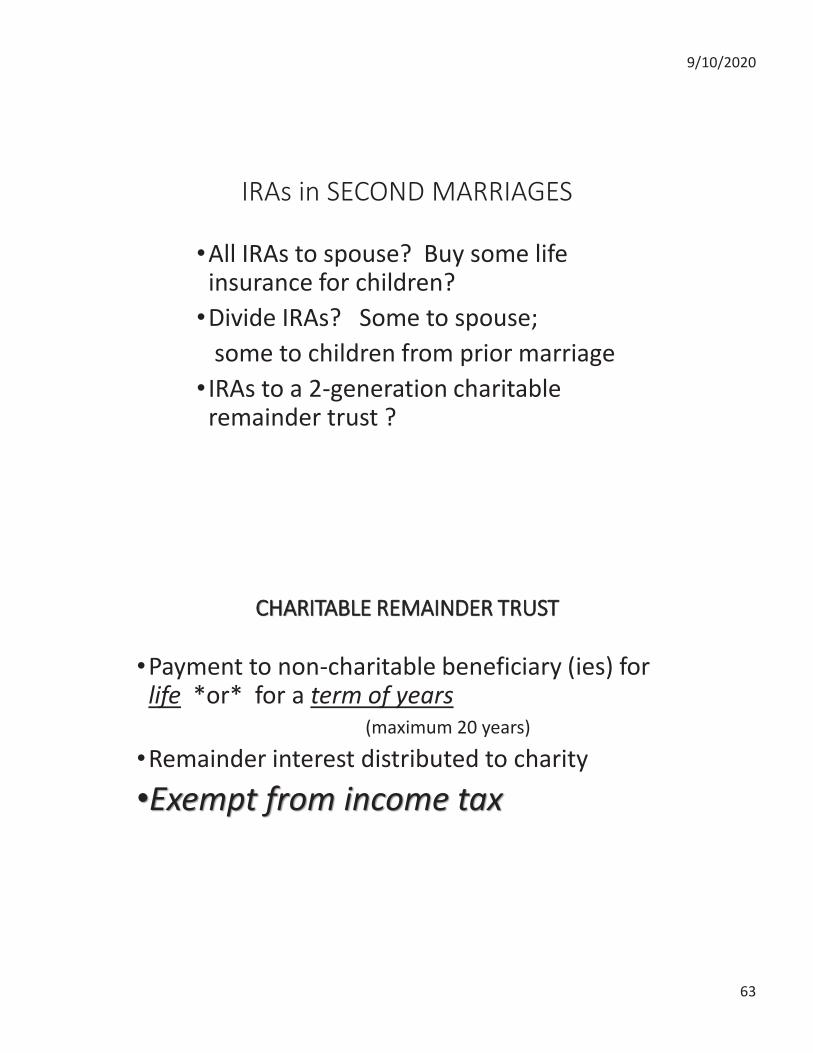

CCHHAARRIITTAABBLLEE RREEMMAAIINNDDEERR TTRRUUSSTT

•Payment to non-charitable beneficiary (ies) for life *or* for a term of years

(maximum 20 years)

•Remainder interest distributed to charity•Exempt from income tax

2-GENERATION CHARITABLE REMAINDER UNITRUST

•Typically pays 5% to elderly surviving spouse for life, then 5% to children for life, then liquidates to charity

•Like an IRA, a CRT is exempt from income tax•Can be like a QTIP trust for IRD assets [but no

estate tax marital deduction]

9/10/2020

32

TThheeoorryy:: TTaaxx aaddvvaannttaaggee ooff iinnccoommee ttaaxx ddeeffeerrrraall !!

Move IRD tax-free after death from one tax exempt trust (e.g., the IRA) to another tax-exempt trust (the CRT). It can be done! PLR 199901023. No taxable income to beneficiaries until they receive distributions from CRT

[ compare: a charitable lead trust is NOT tax-exempt; don’t name a CLT as an IRA beneficiary !]

Can a CRT Produce More Family Wealth Than a Ten Year Liquidation?

Yes. It is possible. But usually not likely.• It can happen with long-term CRUTS (e.g., 40 or 50 years) and

beneficiaries who pay high income tax rates• Outcomes vary with investment returns and tax rates

9/10/2020

33

CCaann aa CCRRTT PPrroodduuccee MMoorree FFaammiillyy WWeeaalltthh TThhaann aa TTeenn YYeeaarr LLiiqquuiiddaattiioonn??

5% CRUT -- Investments earn 5% -- Tax rate: 40%5% Annual

Income Consume Save

CRT $1,000,000 $50,000 $30,000 $20,000

Income tax -400,000 Income tax >>> -$8,000

Net annual investment $12,000

After-tax $600,000 Purchase $600k life insurance? <50 years?

CCaann aa CCRRTT PPrroodduuccee MMoorree FFaammiillyy WWeeaalltthh TThhaann aa TTeenn YYeeaarr LLiiqquuiiddaattiioonn??

5% CRUT -- Investments earn 5% -- Tax rate: 20%5% Annual

Income Consume Save

CRT $1,000,000 $50,000 $40,000 $10,000

Income tax -200,000 Income tax >>> -$2,000

Net annual investment $8,000

After-tax $800,000 <50 years?

9/10/2020

34

Can a CRT Produce More Family Wealth Than a Ten Year Liquidation?

Yes. It is possible. But usually not likely.• It can happen with long-term CRUTS (e.g., 40 or 50 years) and

beneficiaries who pay high income tax rates• Outcomes vary with investment returns and tax rates• How often have you seen outcomes over 40 or 50 years

actually match the projections & assumptions that had been made 40 or 50 years earlier? (Me? Never)

• A CRT is best for someone with charitable intentions who also wants to benefit family. It should not be foisted on people who have no charitable intent.

PLANNING and LEGAL HURDLESA. Choosing the trustee and the charityB. Choosing the Best Type of CRT

- CRAT, CRUT, FLIPCRUT, or NIMCRUTC. How Long ? Term of Years? For Life?D. CRT Requirements That Can Pose ChallengesE. Extra Requirements for CRATsF. Asset protection issues G. Four-tier system for taxation of beneficiaries [WIFO]H. What do you say if a client or a charity suggest

“a charitable gift annuity” instead of a CRT ?

9/10/2020

35

Choosing the trustee and the charity

Charity• Stable; likely to exist when CRT endsTrustee• Competent to administer CRT• What is the minimum asset size to justify the costs of

administering the trust?• Some charities are willing to do $100,000 CRT if they

are named as the remainder beneficiary(but maybe not for a long term of 40 or 50 years)

CChhoooossiinngg tthhee BBeesstt TTyyppee ooff CCRRTT -- CCRRAATT,, CCRRUUTT,, FFLLIIPPCCRRUUTT,, oorr NNIIMMCCRRUUTT --

Charitable Remainder Annuity Trust (“CRAT”) - A trust that pays a fixed dollar amount (at least 5% and no more than 50% of the value of the property contributed to the trust) each year to one or more income beneficiaries for life (or for a fixed term of years -- maximum 20) and on liquidation distributes to a charity.

Charitable Remainder Unitrust (“Standard CRUT”) - A trust that pays a fixed percentage (at least 5% and no more than 50% ) of the value of the trust’s assets each year (redetermined annually) to one or more income beneficiaries for life (or for a fixed term of years -- maximum 20) and on liquidation distributes to a charity.

9/10/2020

36

CCRRTT RReeqquuiirreemmeennttss TThhaatt CCaann PPoossee CChhaalllleennggeess

1. Annual payouts between 5% and 50%2. Minimum 10% charitable deduction3. Avoid multiple donors to a single CRT4. Private foundation self-dealing rules apply to CRTs5. Problematic assets (partnership interests, debt-encumbered, etc)

6. Was trust actually administered in accordance with its terms

MMiinniimmuumm 1100%% cchhaarriittaabbllee ddeedduuccttiioonn• The value of the charity’s remainder interest

of a CRT must be at least 10 percent of the initial net fair market value of all property placed in the trust

• [computed using the Section 7520 discount rates in effect at the time of contribution. ]

• If a contribution is made to a trust that fails the 10 percent requirement, the trust will not qualify as a tax-exempt CRT.

9/10/2020

37

MMiinniimmuumm 1100%% cchhaarriittaabbllee ddeedduuccttiioonnOversimplified, there are two ways that the present value of a charity’s remainder interest in a CRT can be less than 10 percent of the value of the property contributed to the trust. • The first is if the stated payout rate is too

high (e.g., “for the next 20 years, distribute to my child 30% of the trust’s assets each year”).

• The solution is to lower the CRT’s payout rate, but it cannot be lowered below 5%.

MMiinniimmuumm 1100%% cchhaarriittaabbllee ddeedduuccttiioonnThe second way is if the projected term of the trust is too long. • The 10 percent requirement limits the

projected term of a CRUT to a maximum of roughly 55 years.

• For example, in 2019 if there was only one beneficiary of a CRUT, then the 10 percent test was met only if the beneficiary was at least age 27. If there were two beneficiaries who were the same age (e.g., husband and wife), then each had to be at least age 38.

9/10/2020

38

MMiinniimmuumm 1100%% cchhaarriittaabbllee ddeedduuccttiioonnWhat can an estate planner do if the beneficiaries are so young that a CRT fails the 10 percent test? • One strategy is to create multiple CRTs. For example, if a

client has three children who are triplets and each is age 27, there could be three CRTs (one per child) rather than a single CRT.

• Wait 5 years to liquidate IRA (death before RBD)? Can draft CRT for person age 22? Estate tax issue?

• Another option is to have a CRT for a term of years.

TTeerrmm--ooff--YYeeaarrss CCRRTT::AAnnnnuuaall PPaayymmeennttss DDeecclliinnee wwiitthh HHiigghh %% CCRRUUTT

• One advantage of a Stretch IRA is that each year’s RMD percentage increases, leading to rising payments over time

• Helps with inflation and psychology

9/10/2020

39

TTeerrmm--ooff--YYeeaarrss CCRRTT::AAnnnnuuaall PPaayymmeennttss DDeecclliinnee wwiitthh HHiigghh %% CCRRUUTT

• One advantage of a Stretch IRA is that each year’s RMD percentage increases, leading to rising payments over time

• Helps with inflation and psychology• If a CRT provides that the distribution percentage is “the

highest rate permitted by law”, payments from a term-of-years CRT will likely decline every year

• Example: A CRUT pays 11%, but only earns 7% -- every future year’s payment will fall by 4%

MMiinniimmuumm 1100%% cchhaarriittaabbllee ddeedduuccttiioonn

The “Sweet Spot”: A 5% CRUT•With a 5% payout (the lowest distribution rate permitted

by law), both the CRUT assets and the annual distributions can grow if the trustee can earn more than 5%

•The benefit to the family of a 5% CRUT is greatest with a long-term trust (maximum projected term of about 55 years) compared to a term-of-years CRT.

9/10/2020

40

CCRRTT RReeqquuiirreemmeennttss TThhaatt CCaann PPoossee CChhaalllleennggeess

1. Annual payouts between 5% and 50%2. Minimum 10% charitable deduction3. Avoid multiple donors to a single CRT4. Private foundation self-dealing rules

apply to CRTs5. Problematic assets (partnership interests,