Embed Size (px)

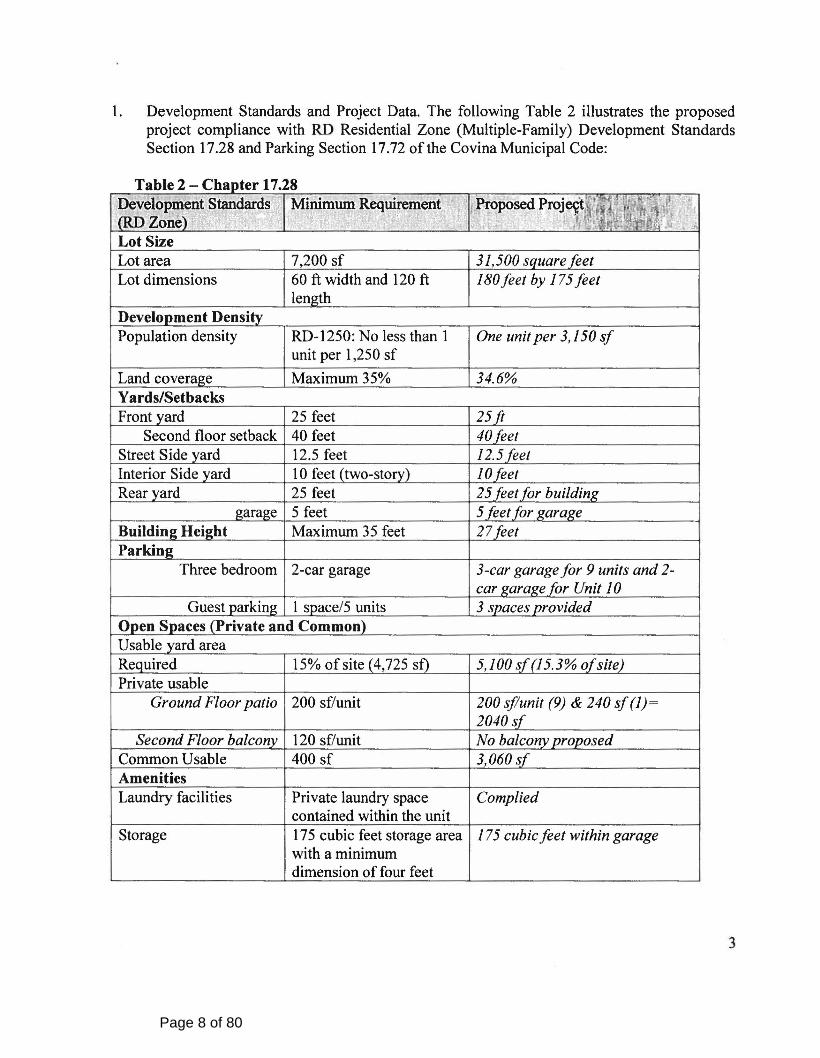

Citation preview

City Council/CSA/CPFA/CHA Agenda Tuesday February 16, 2021

REGULAR MEETING AGENDA

125 E. College Street, Covina, California

Council Chamber of City Hall/Virtual Meeting

Tuesday, February 16, 2021

IMPORTANT NOTICE

This meeting is being conducted utilizing teleconferencing and electronic means consistent with

State of California Executive Order N-29-20 dated March 17, 2020, regarding the COVID-19

pandemic. In accordance with the Executive Order N-29-20, the Council Chamber will be closed

to the public. As always, the public may view the meeting live on the City’s website at

www.covinaca.gov or on local cable television, Spectrum channel 29 and Frontier Channel 42.

To view from the website, hover over the Departments & Services tab until the drop-down menu

appears and click on City Council Video Library under the City Council header. A live banner

will appear at the start of the meeting.

Meeting Assistance Information: In compliance with the Americans with Disabilities Act, if you

need special assistance to participate in this meeting, please contact the City Clerk’s Office at

[email protected] or 626-384-5430. Notification 48 hours prior to the meeting will enable

the City to make reasonable arrangements to ensure accessibility to this meeting.

Submission of Public Comments: For those wishing to make public comments on non-agenda

and agenda items you may submit comments via email or by phone.

Email: Please submit your comments to [email protected] by 6:00 p.m., Tuesday,

February 16, 2021. Please enter “PUBLIC COMMENT” (and the agenda item number if

applicable) in the subject line. Public Comments will be forwarded to Council for review prior

to the meeting.

Phone: Please email your name and number to [email protected] prior to the close of the public comment period or the close of the comment period for the specific agenda item you wish to provide comment on. Please enter “PUBLIC COMMENT” (and the agenda item number if applicable) in the subject line. Staff will call you at the appropriate time.

CITY COUNCIL/SUCCESSOR AGENCY TO THE COVINA

REDEVELOPMENT AGENCY/COVINA PUBLIC FINANCING

AUTHORITY/COVINA HOUSING AUTHORITY

JOINT MEETING—CLOSED SESSION

6:30 PM

City Council/CSA/CPFA/CHA Agenda Tuesday February 16, 2021

CALL TO ORDER

ROLL/CALL Council/Agency/Authority Members: Walter Allen, III, Patricia Cortez, John C. King, Mayor Pro

Tem/Vice-Chair Jorge A. Marquez and Mayor/Chair Victor Linares

PUBLIC COMMENTS For those wishing to make public comments on closed session items please submit your comments by email to [email protected] by 6:00 p.m., Tuesday, February 16, 2021. Please enter “PUBLIC COMMENT – Closed Session” in the subject line. Public Comments will be forwarded to Council for review prior to the meeting. State Law prohibits the Council/Agency/Authority Members from taking action on any item not on the agenda. Individual speakers are limited to five minutes each, unless, for good cause, the Mayor/Chairperson amends the time limit.

CLOSED SESSION The City Council/Successor Agency to the Covina Redevelopment Agency/Covina Public Financing

Authority/Covina Housing Authority will adjourn to closed session for the following: A. Government Code § 54957.6 – CONFERENCE WITH LABOR NEGOTIATORS

Agency

Designated

Representatives:

Anita Agramonte, Administrative Services Director

Suzanne Stone, Human Resources Manager

Employee

Organizations:

American Federation of State, County and Municipal

Employees (AFSCME); Police Association of Covina (PAC);

Police Management Group (PMG); and Police Supervisors of

Covina (PSC)

B. Government Code § 54957.6 – CONFERENCE WITH LABOR NEGOTIATORS

Agency

Designated

Representatives:

Anita Agramonte, Administrative Services Director

Suzanne Stone, Human Resources Manager

Unrepresented

Employees:

Mid-Management, Supervisory and Professional, and

Confidential and technical Employees; and Executive

Employees (excluding the City Manager)

RECESS

CITY COUNCIL/SUCCESSOR AGENCY TO THE COVINA

REDEVELOPMENT AGENCY/COVINA PUBLIC FINANCING

AUTHORITY/COVINA HOUSING AUTHORITY

JOINT MEETING—OPEN SESSION

7:30 PM

RECONVENE AND CALL TO ORDER

ROLL CALL

City Council/CSA/CPFA/CHA Agenda Tuesday February 16, 2021

PLEDGE OF ALLEGIANCE

Led by Councilmember Allen

INVOCATION

Given by Covina Police Chaplain Chuck Cannizzaro

PRESENTATIONS - NONE.

PUBLIC COMMENTS For those wishing to make public comments on non-agenda and agenda items you may submit comments

via email or by phone. Email: Please submit your comments to [email protected] by 6:00 p.m., Tuesday, February 16, 2021.

Please enter “PUBLIC COMMENT” (and the agenda item number if applicable) in the subject line. Public

Comments will be forwarded to Council for review prior to the meeting.

Phone: Please email your name and number to [email protected] prior to the close of the public comment period or the close of the comment period for the specific agenda item you wish to provide comment on. Please enter “PUBLIC COMMENT” (and the agenda item number if applicable) in the subject line. Staff will call you at the appropriate time. State Law prohibits the Council/Agency/Authority Members from taking action on any item not on the agenda. Individual speakers are limited to five minutes each, unless, for good cause, the Mayor/Chairperson amends the time limit.

COUNCIL/AGENCY/AUTHORITY COMMENTS Council/Agency/Authority Members wishing to make any announcements of public interest or to request

that specific items be added to future Council/Agency/Authority agendas may do so at this time.

CITY MANAGER COMMENTS

CONSENT CALENDAR All matters listed under consent calendar are considered routine, and will be enacted by one motion. There

will be no separate discussion on these items prior to the time the Council/Agency/Authority votes on them,

unless a member of the Council/Agency/Authority requests a specific item be removed from the consent

calendar for discussion. CC 1. Minutes

Staff Recommendation:

Approve the Minutes of the February 2, 2021, Regular Meeting of the City Council/Successor Agency to the Covina Redevelopment Agency/Covina Public Financing Authority/Housing Authority. 2021 02 02 Minutes CC DRAFT

CC 2. Payment of Demands

Staff Recommendation:

Approve Payment of Demands in the amount of $2,422,831.89. Agenda Report - Payment of Demands Jan 15 - Jan 28, 2021 - Pdf

City Council/CSA/CPFA/CHA Agenda Tuesday February 16, 2021

CC 3. Monthly Investment Report of the Treasurer to the City Council and Successor Agency

to the Covina Redevelopment Agency for January 2021

Staff Recommendation:

Receive and File. Agenda Report - Monthly Investment Report Ended January 31, 2021 - Pdf

CC 4. Citywide Bus Stop Improvement Project - Final Acceptance and Filing Notice of

Completion

Staff Recommendation:

1. Accept the work performed by E.C. Construction Co.;

2. Authorize the City Clerk to file a Notice of Completion for the Citywide Bus Stop

Improvement Project; and

3. Adopt Resolution CC 2021-07 to amend the Fiscal Year 2021-2025 Capital

Improvement Program to increase funding by $135,731 for the Citywide Bus Stop

Improvement Project and appropriate the necessary funds from available Proposition

A Local Return Fund Balance. Agenda Report - Citywide Bus Stop Improvement Project NOC - Pdf

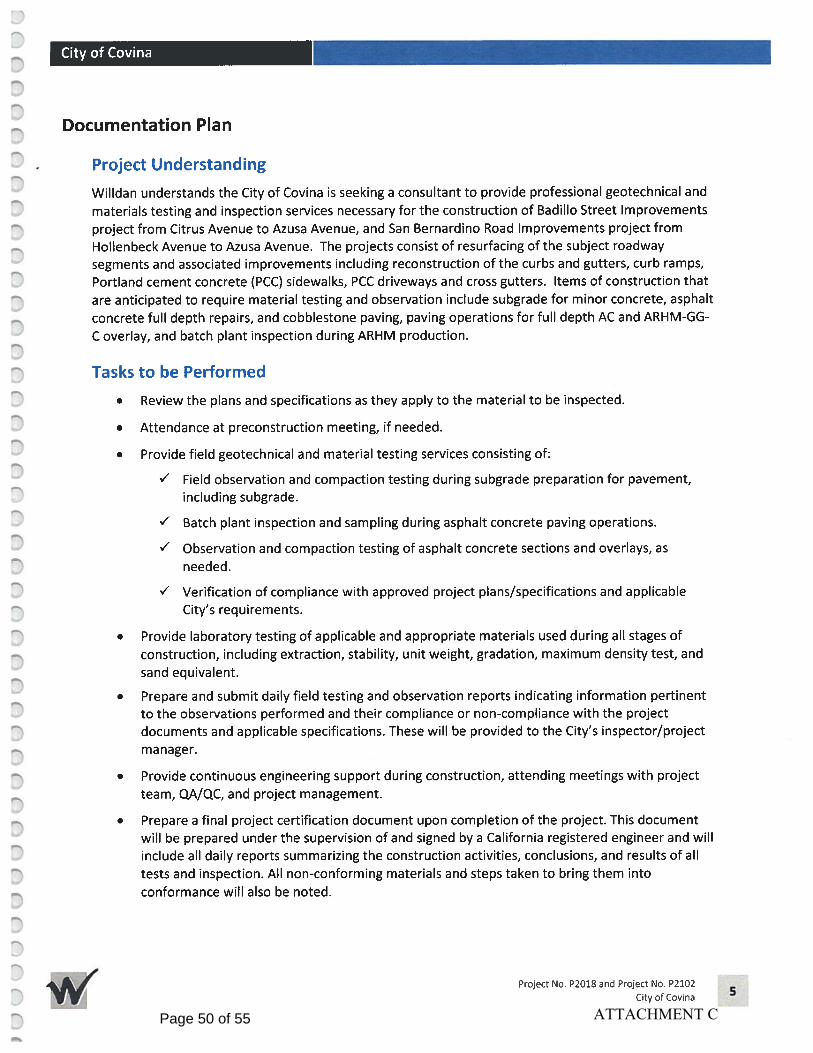

CC 5. Badillo Street Improvements & San Bernardino Road Rehabilitation Project – Award

of Contract to Sequel Contractors Inc. for an Amount Not-to-Exceed $1,653,130

Staff Recommendation:

1. Approve plans and specifications for the Badillo Street Improvements & San

Bernardino Road Rehabilitation Project;

2. Award the Contract for the Badillo Streets Improvements & San Bernardino Road

Rehabilitation Project to Sequel Contractors Inc. as the lowest responsive and

responsible bidder in an amount not-to-exceed $1,653,130 and authorize the City

Manager to execute the Contract; and

3. Authorize a contingency amount of 10%, or $165,313, for any unforeseen

construction expenses. Agenda Report - Badillo St Improvements & San Bernardino Rd Rehab Project –

Award of Contract - Sequel Contractors Inc - Pdf CC 6. Approval of Resolution CC 2021-08 to Submit an Application Under the Statewide

Park Development and Community Revitalization Program

Staff Recommendation:

Adopt Resolution CC 2021-08 approving the submittal of an application for state

grant funds under the Proposition 68 Statewide Park Development and Community

Revitalization Program for Wingate Park. Agenda Report - Resolution CC 2021-08 Statewide Park Development and

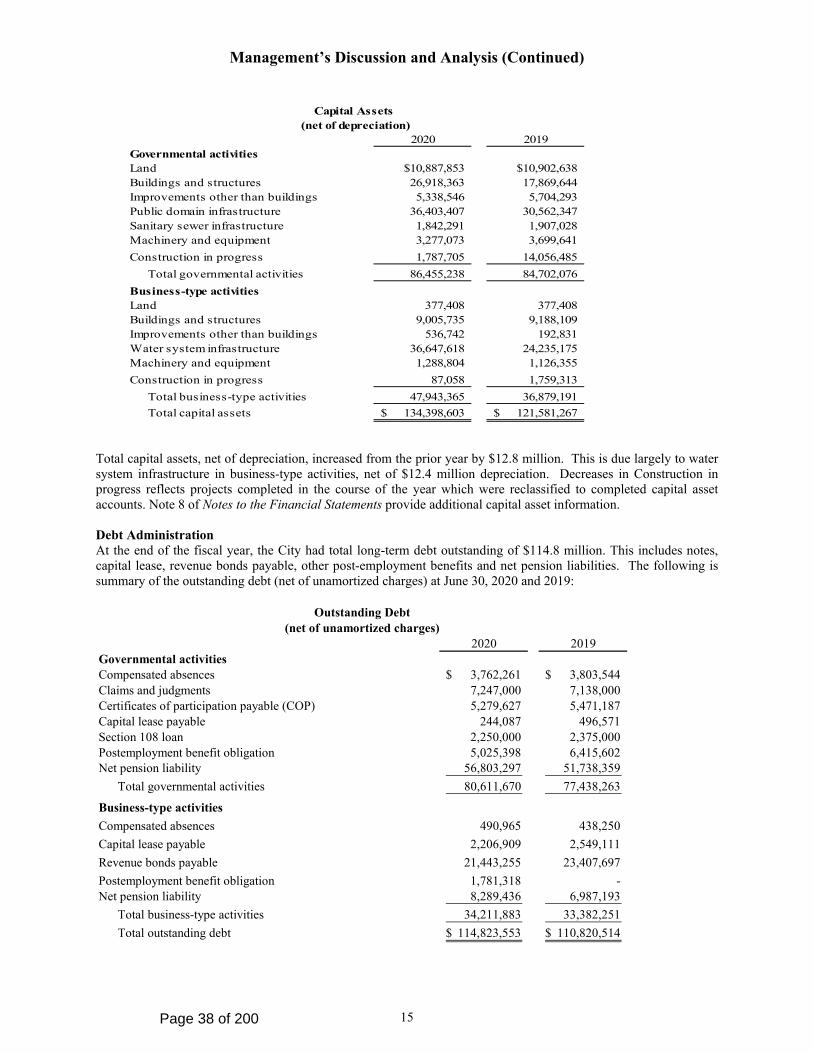

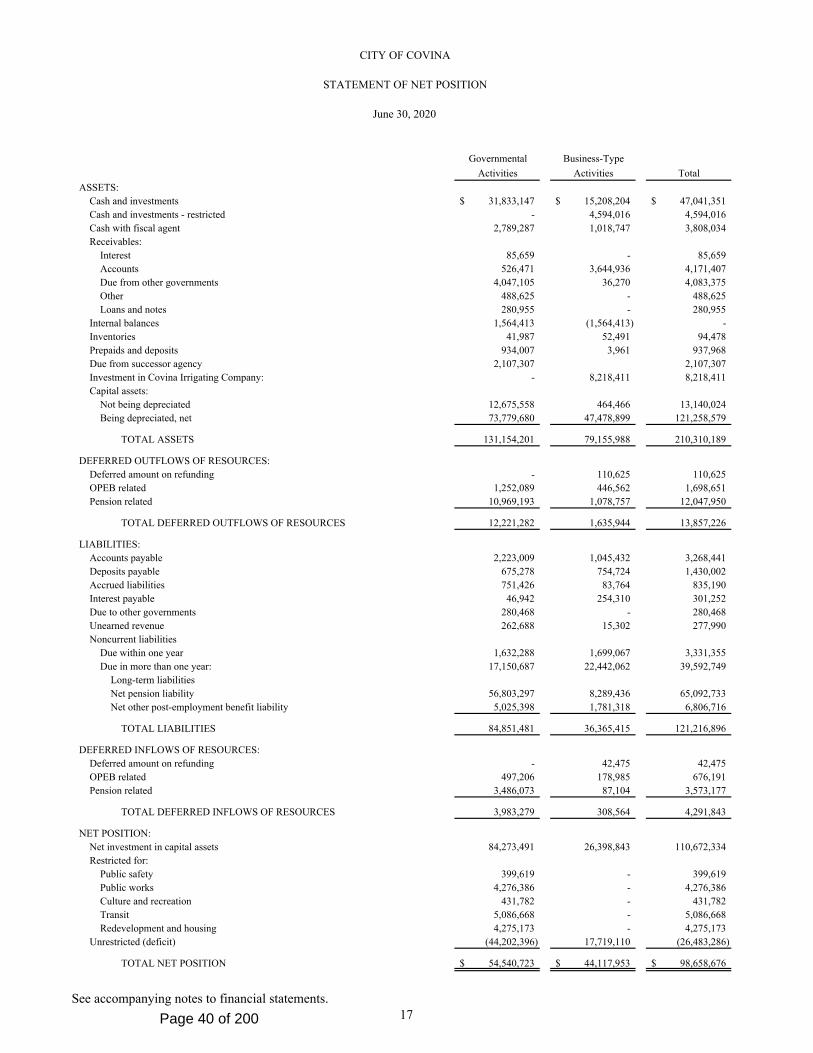

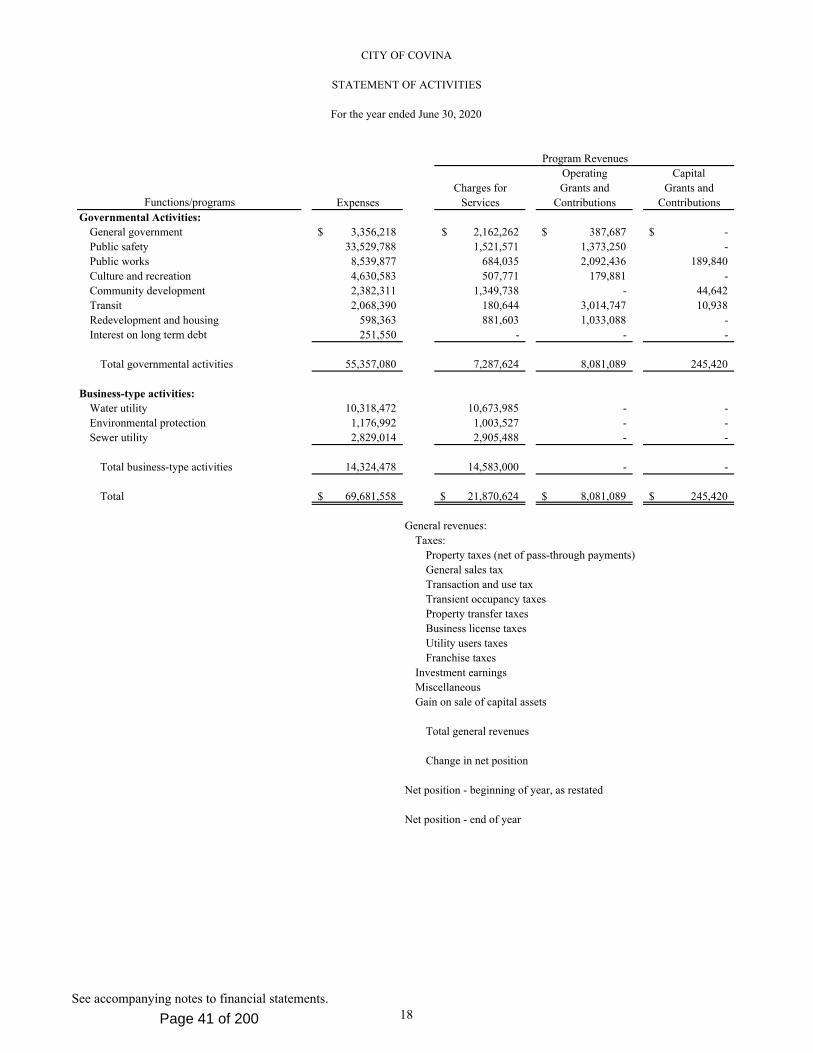

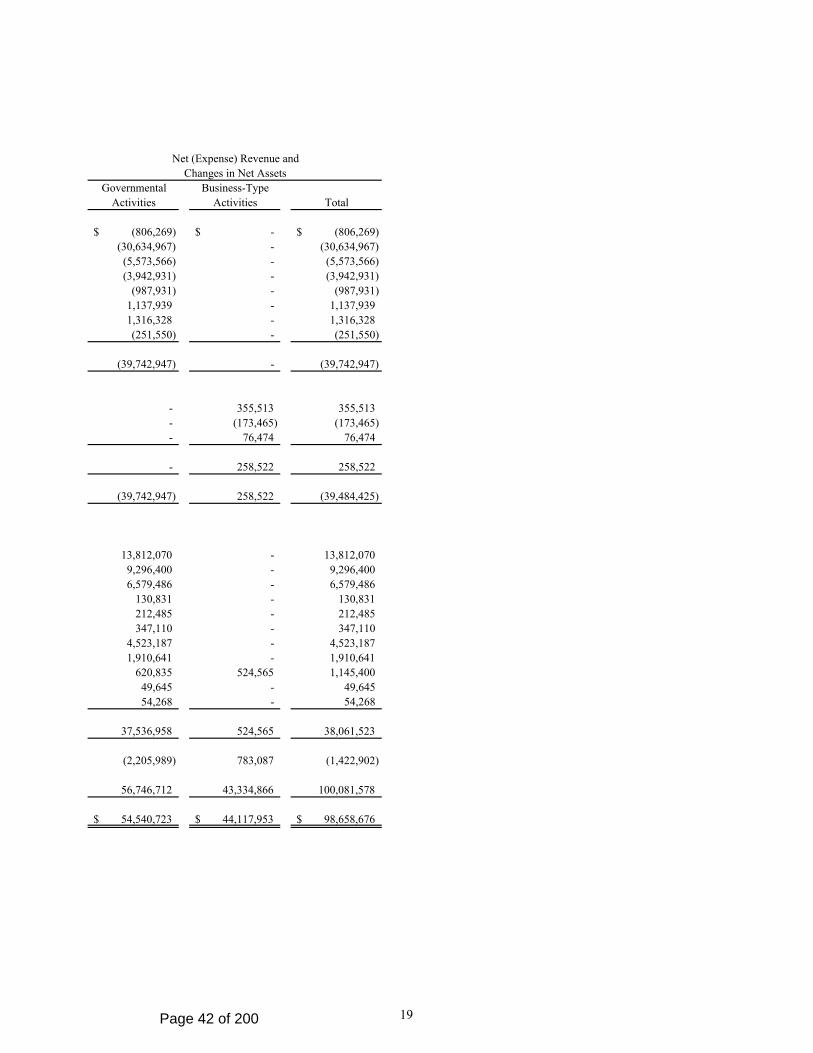

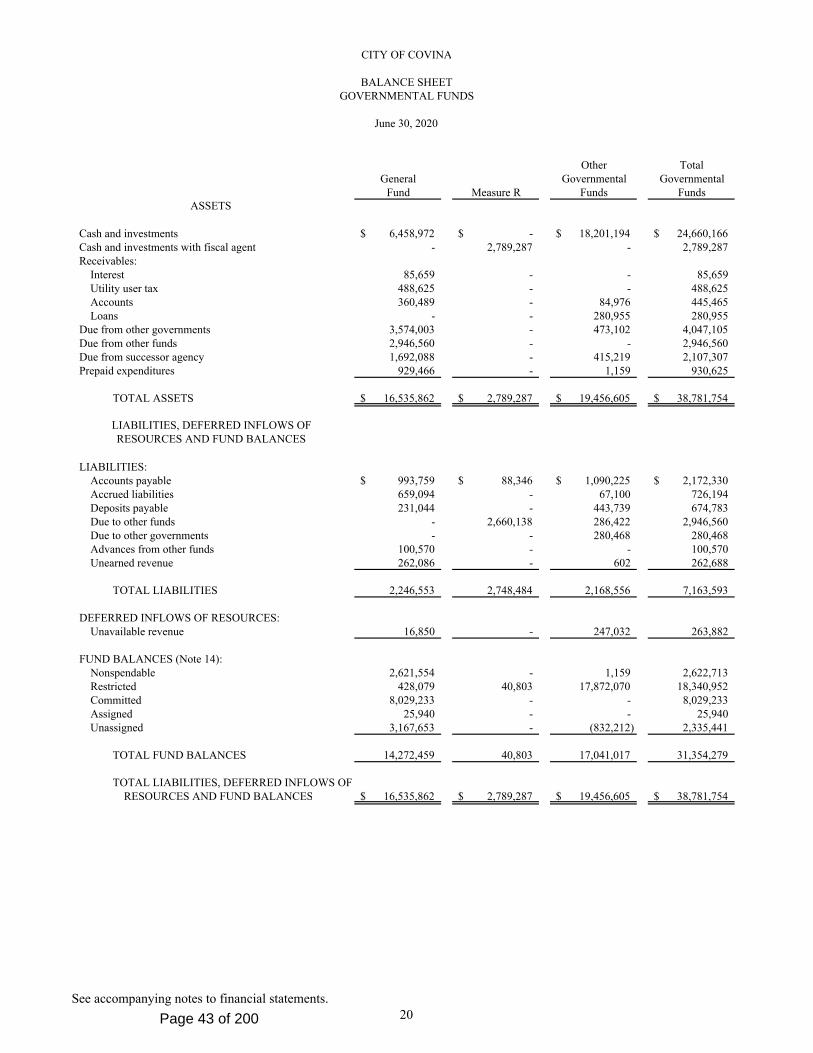

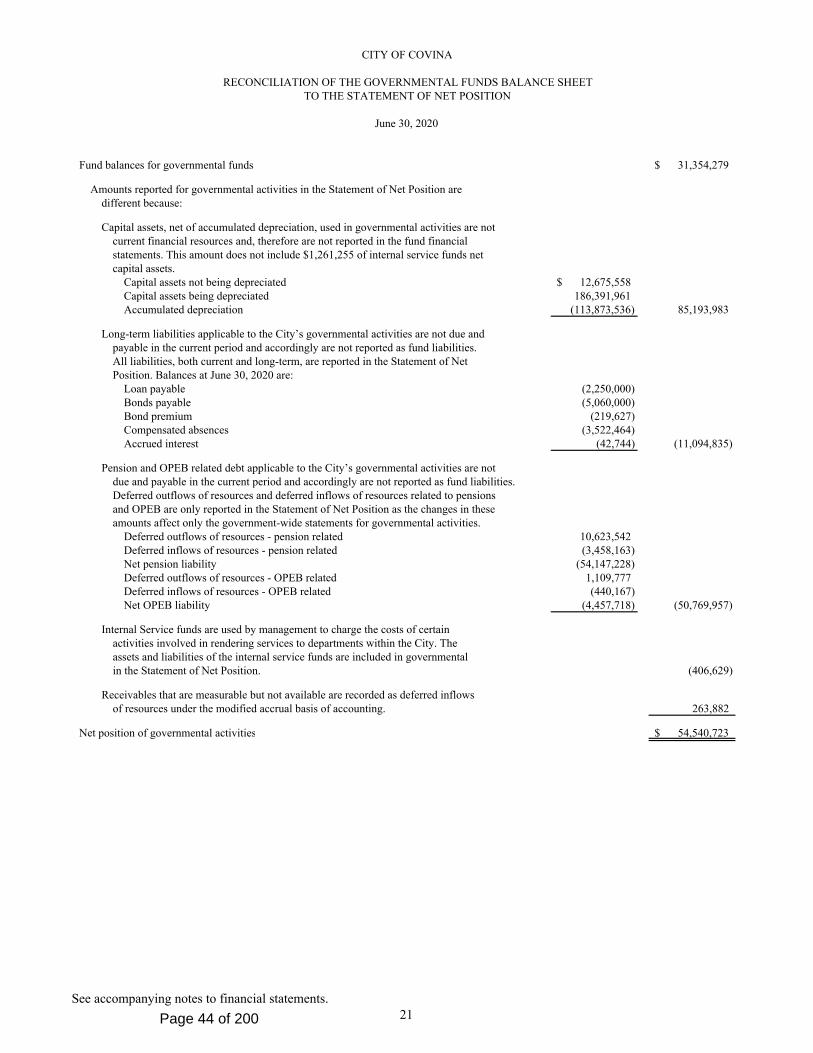

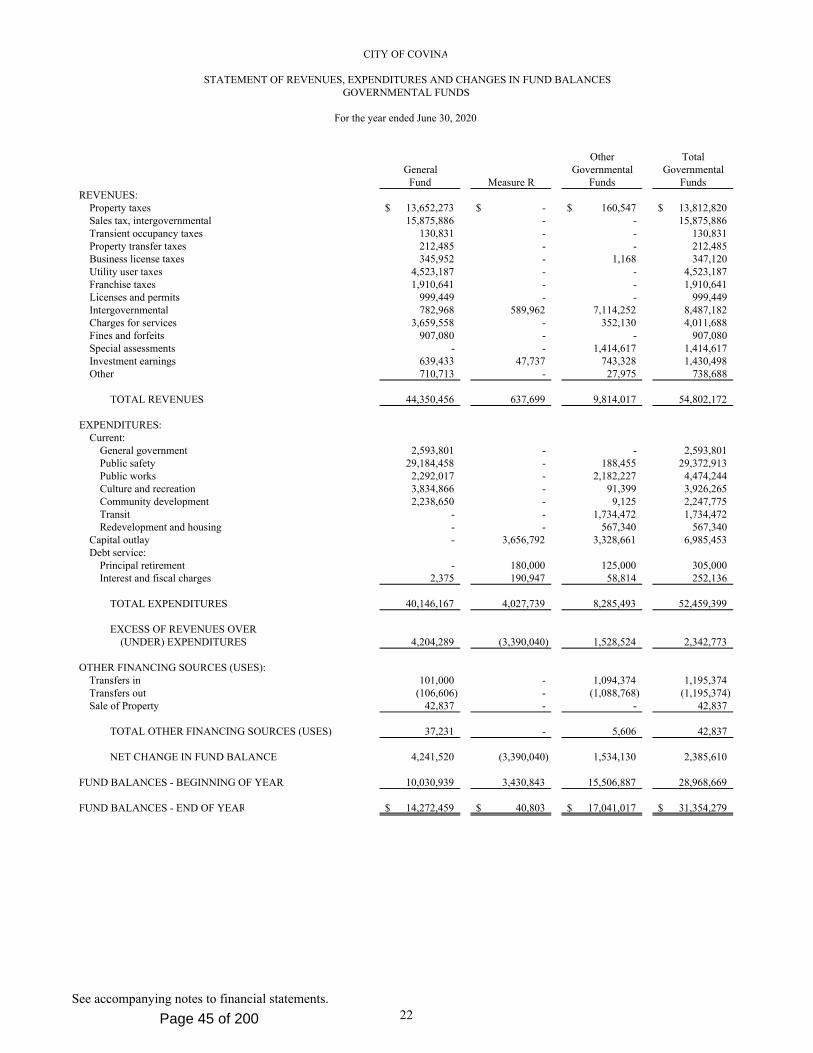

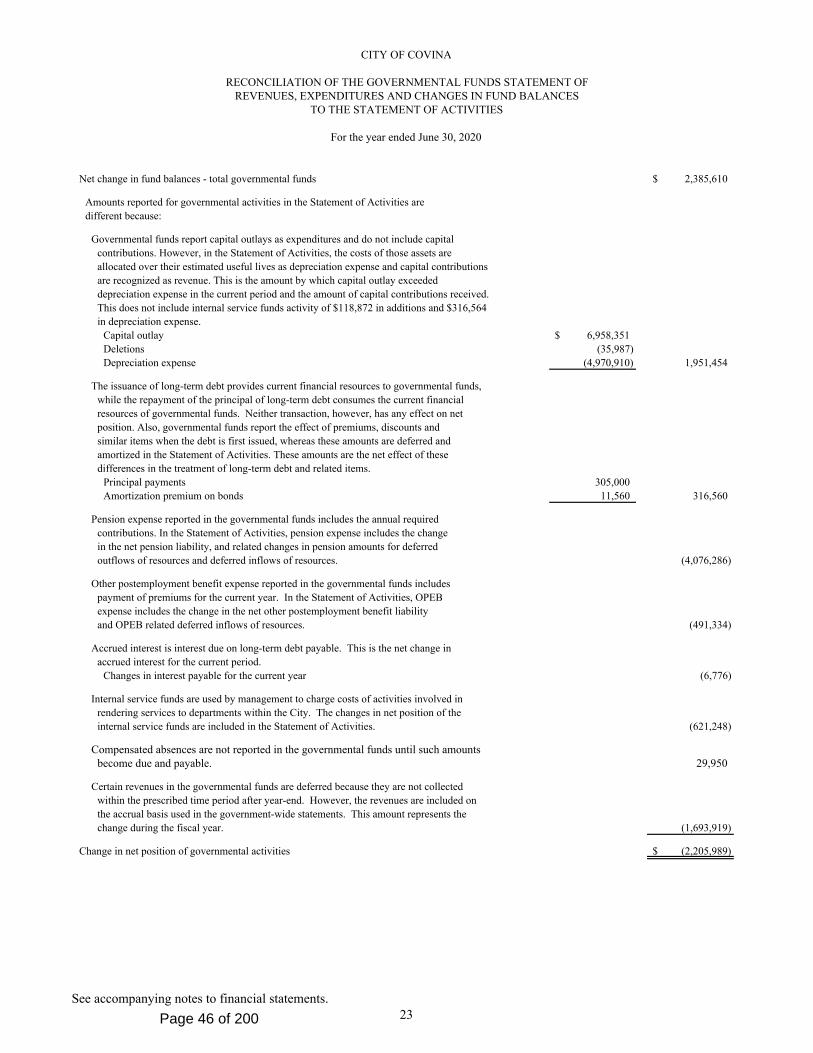

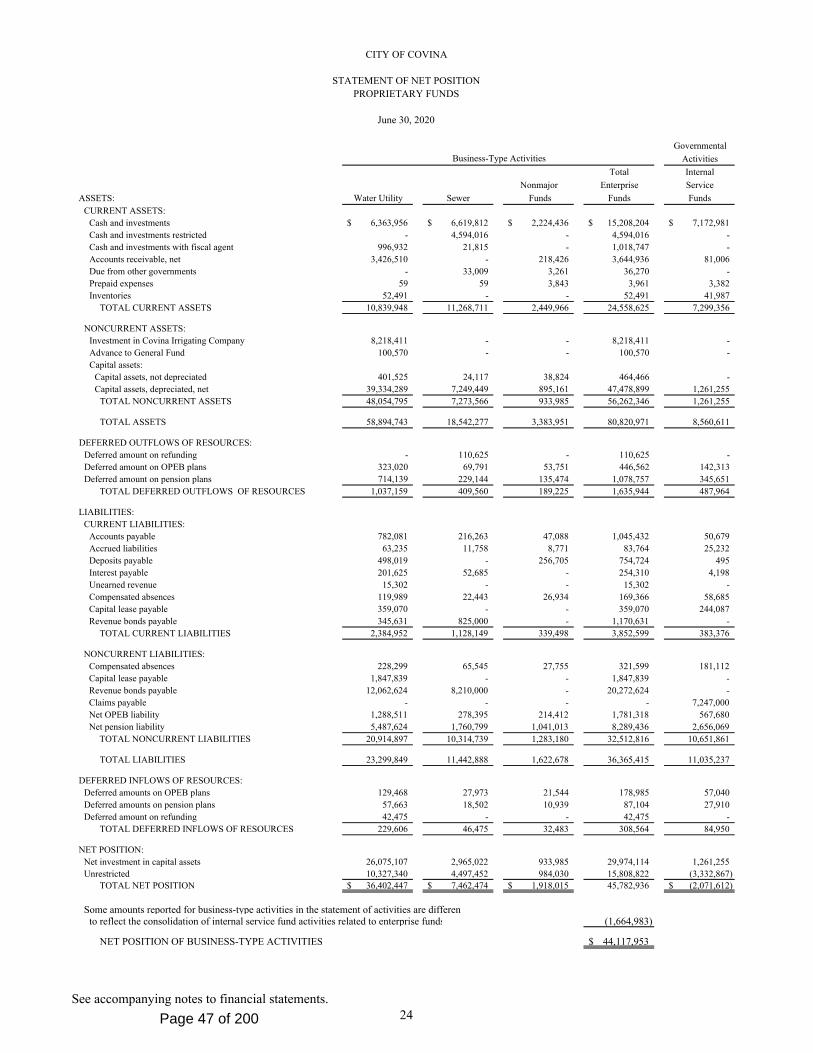

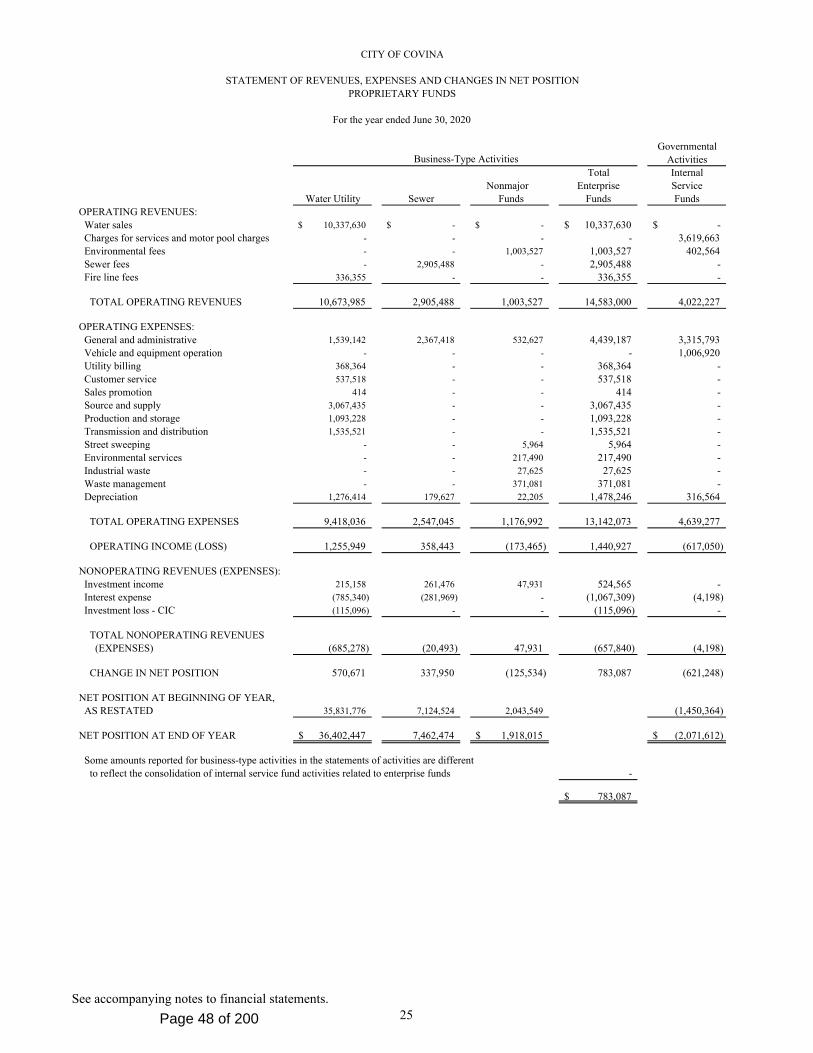

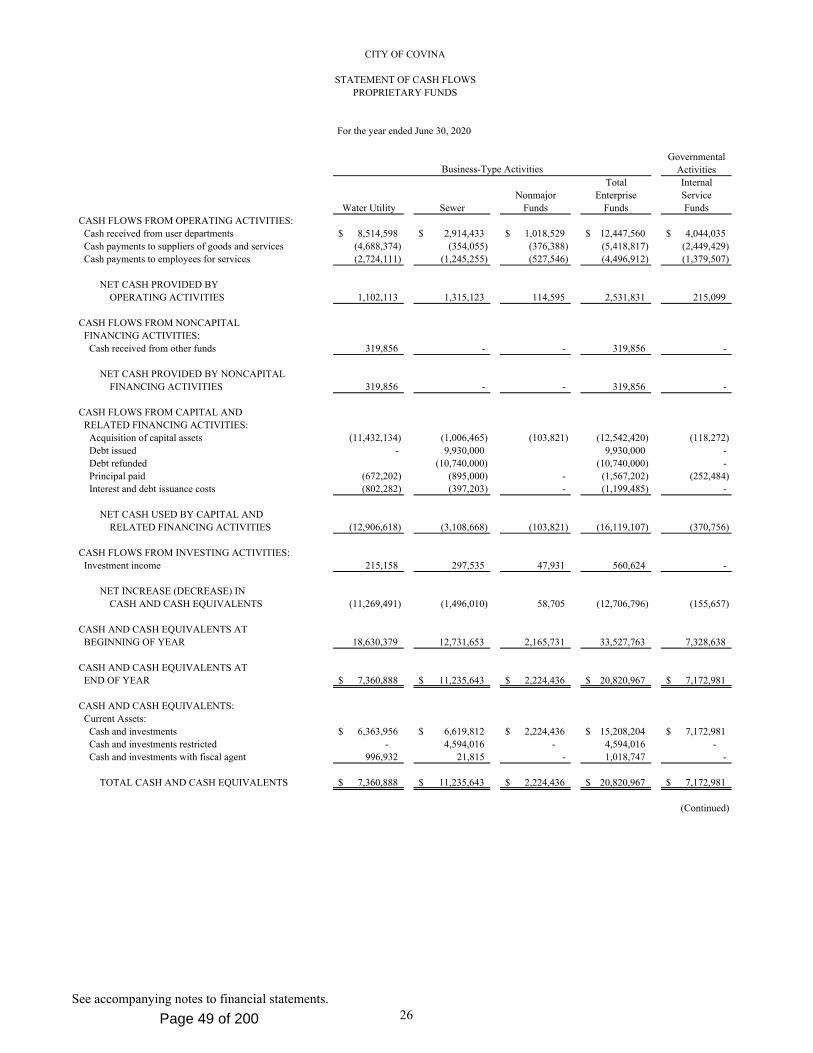

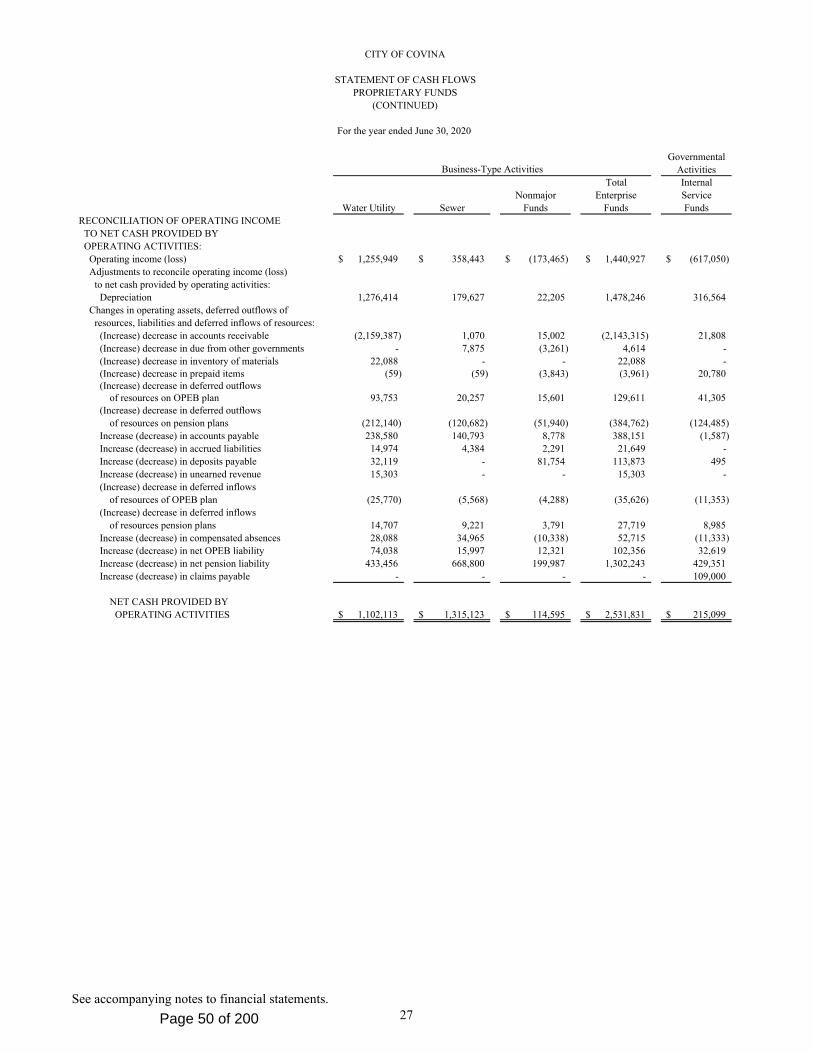

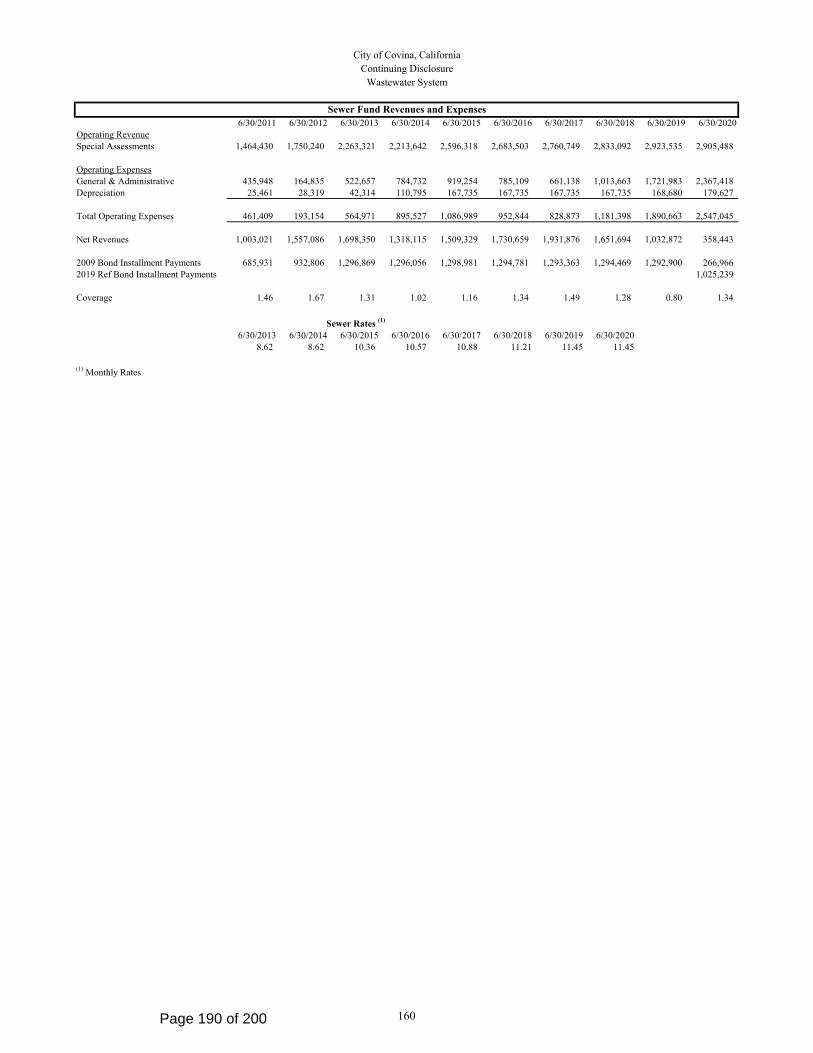

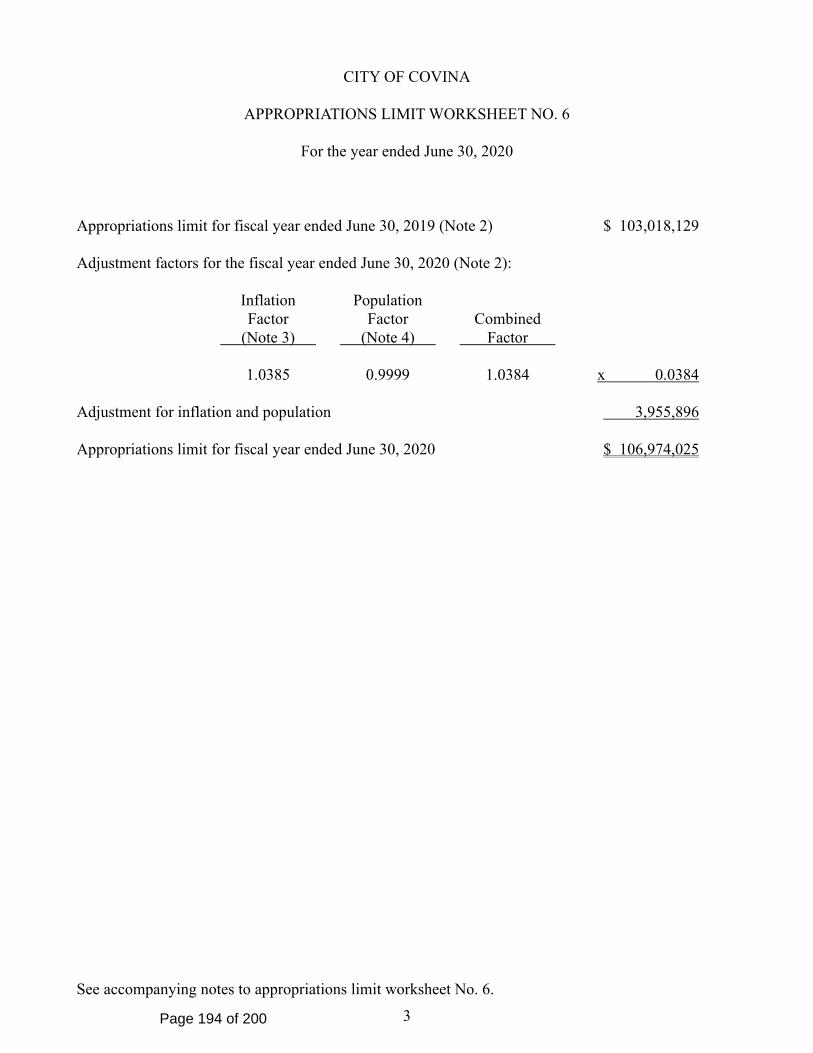

Community Revitalization Program - Pdf CC 7. Comprehensive Annual Financial Report (CAFR) for Fiscal Year Ended June 30, 2020

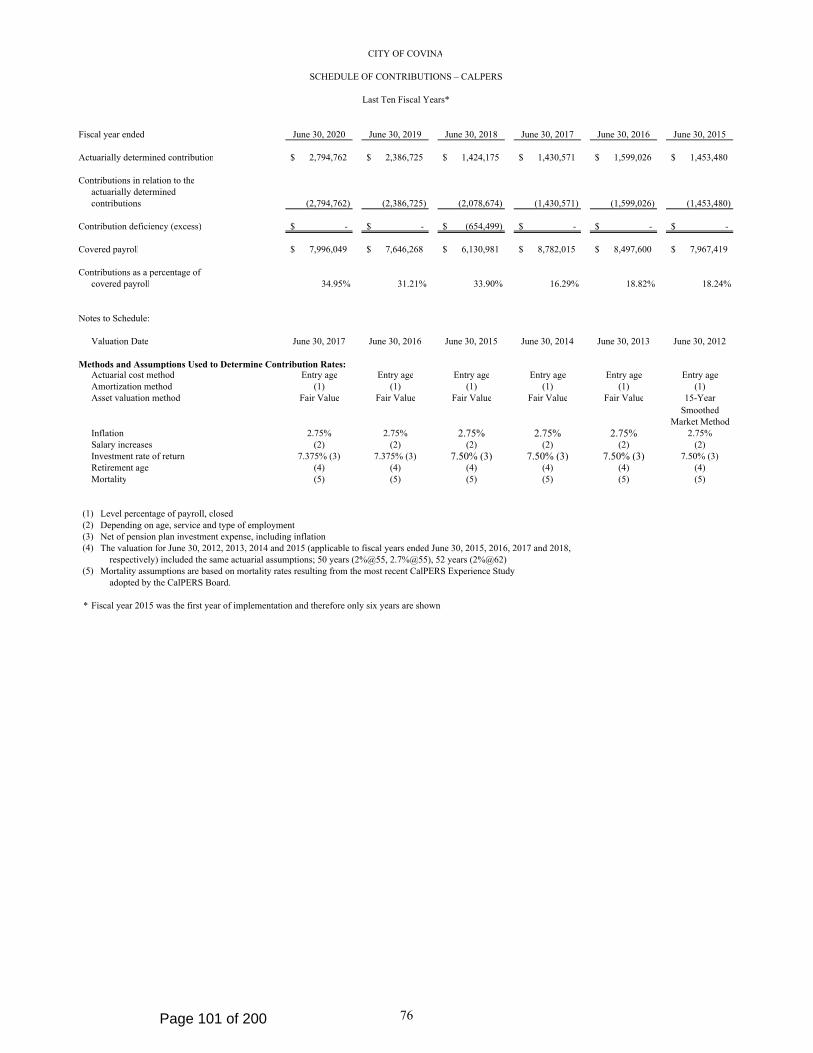

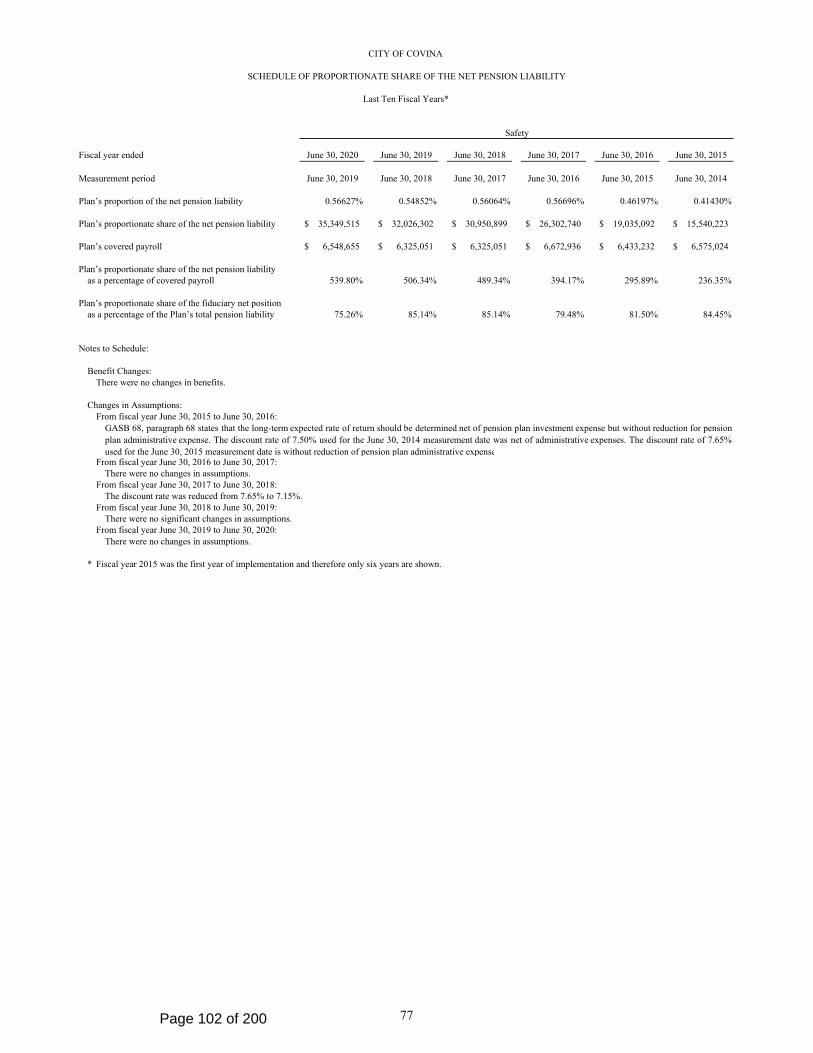

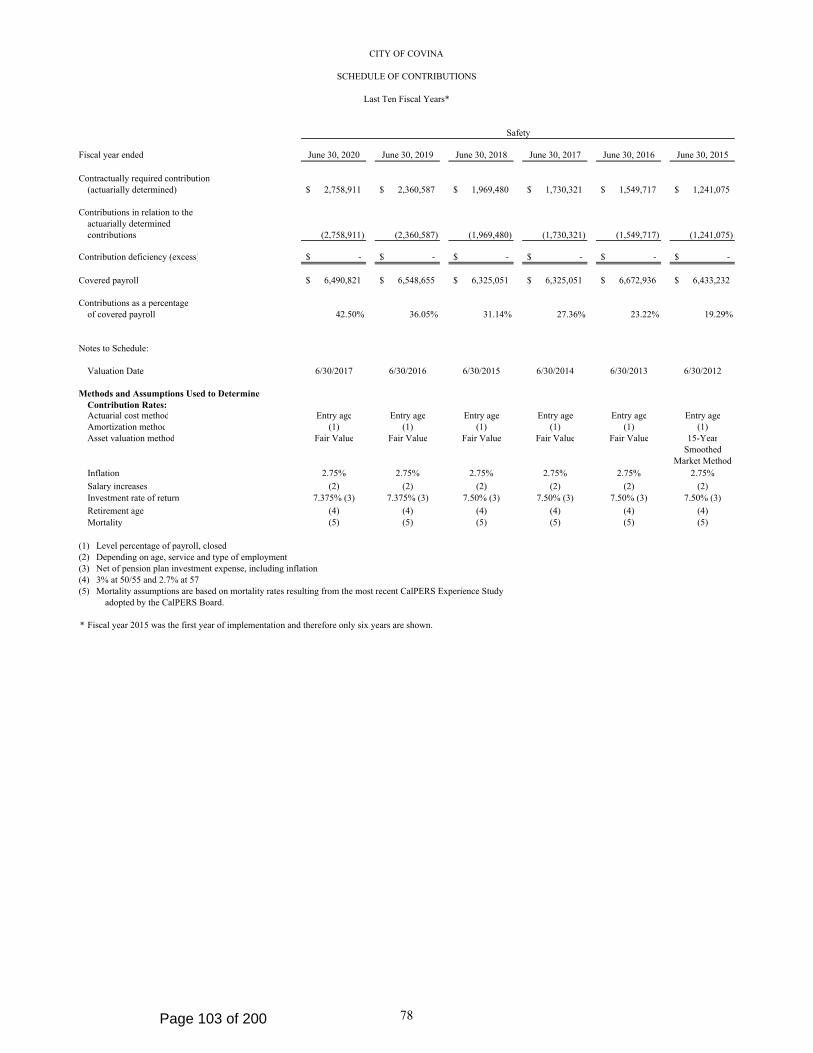

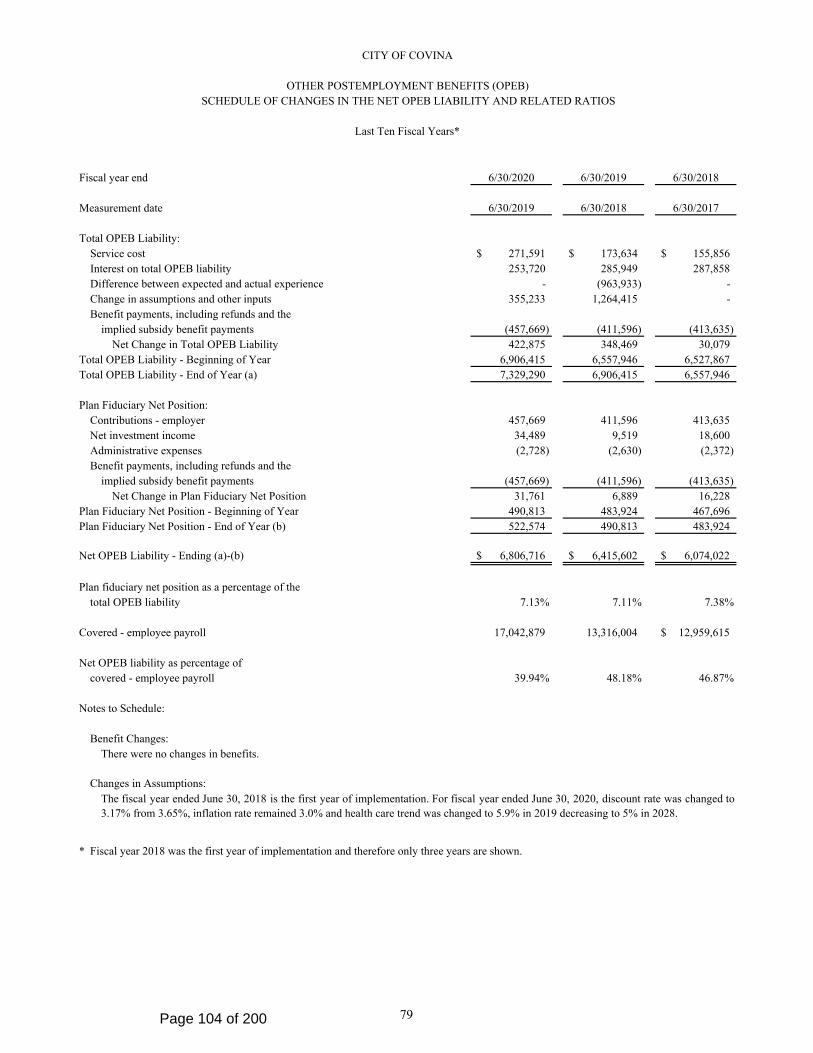

Staff Recommendation:

Receive and file the following reports for Fiscal Year ended June 30, 2020:

City Council/CSA/CPFA/CHA Agenda Tuesday February 16, 2021

• the Comprehensive Annual Financial Report (CAFR) and related Auditor

Communications

• the Independent Accountants' Report on Agreed-Upon Procedures Applied to

Appropriations Limit Agenda Report - CAFR FY Ended June 30, 2020 - Pdf

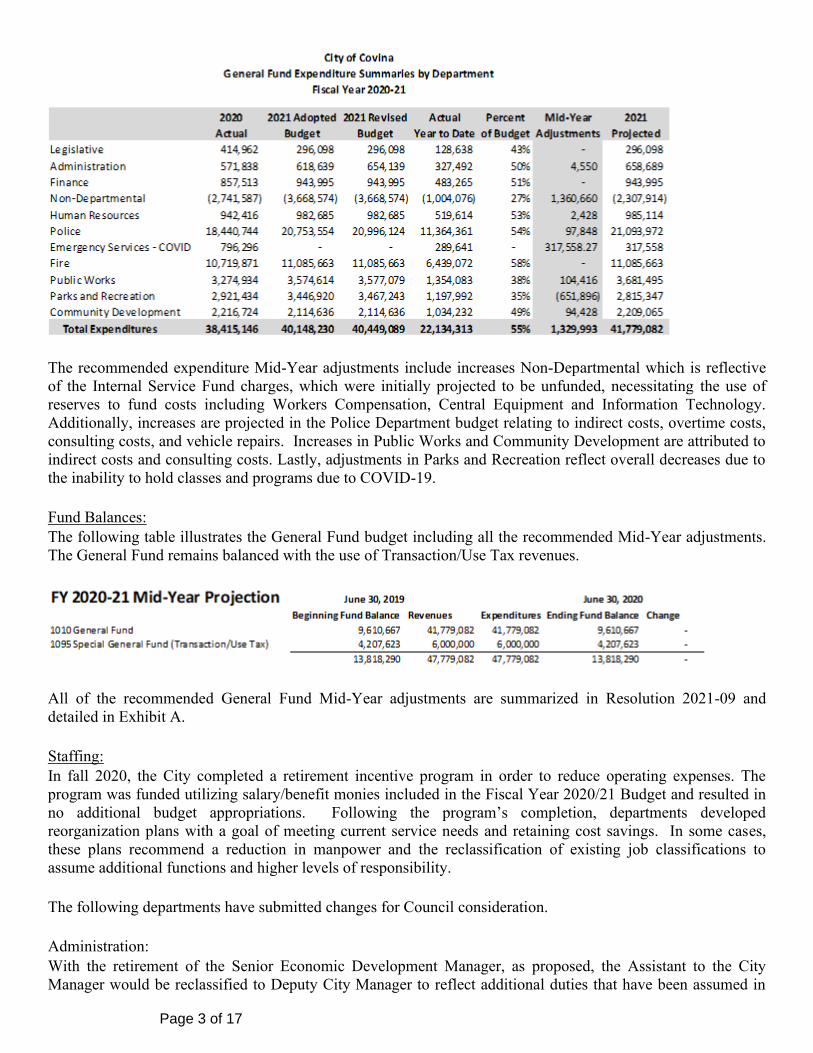

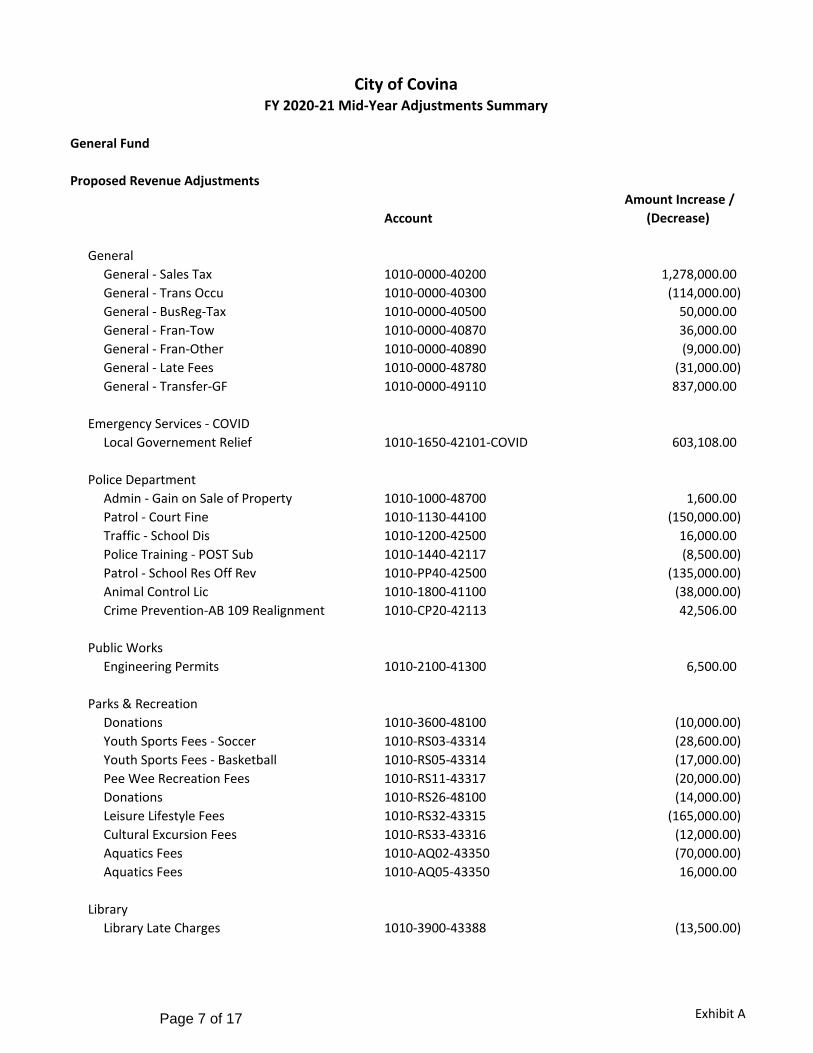

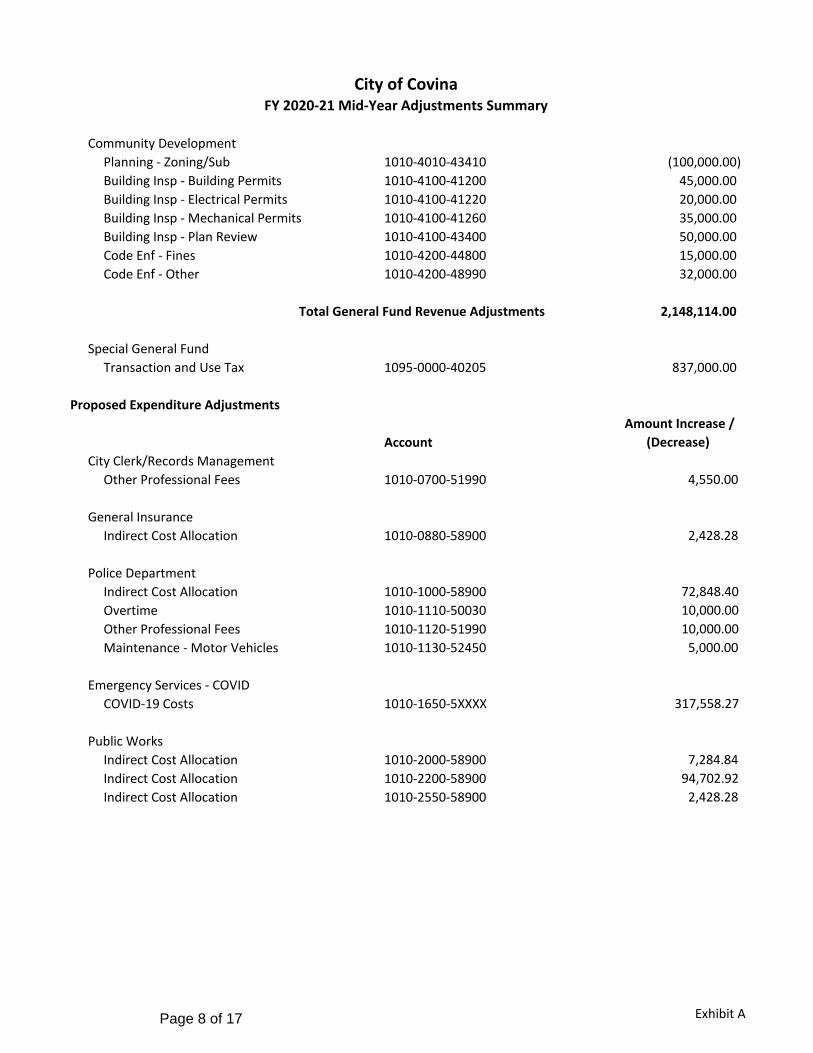

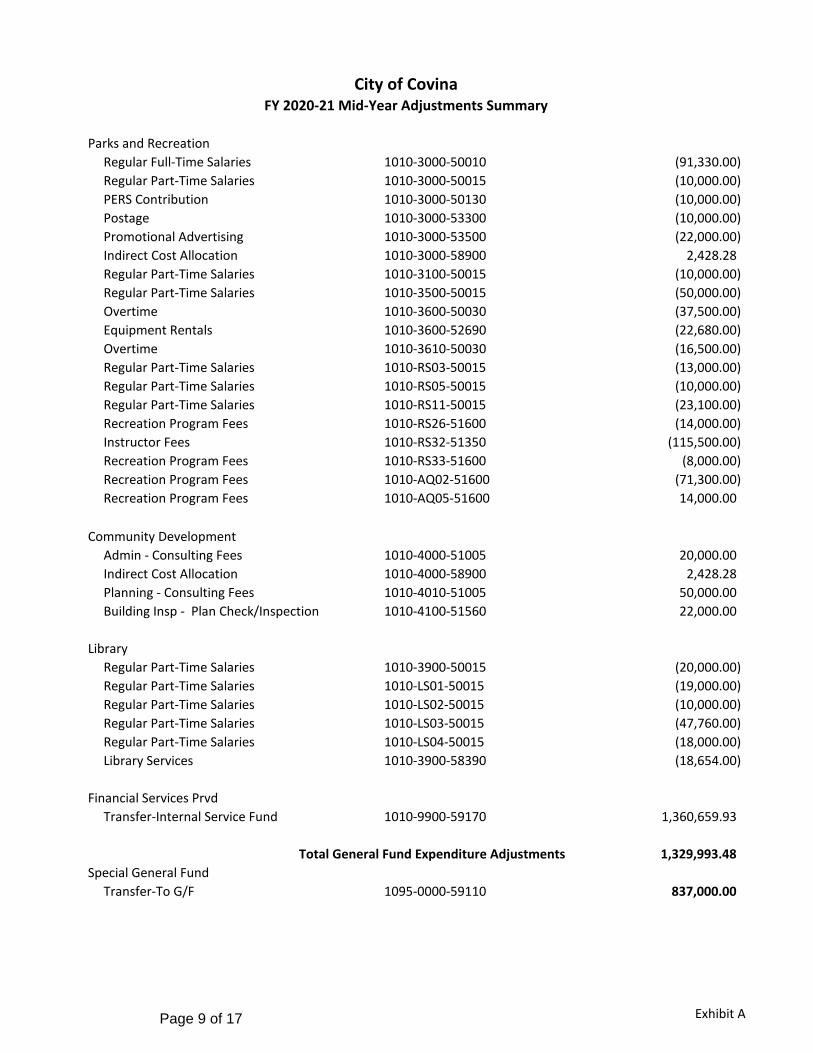

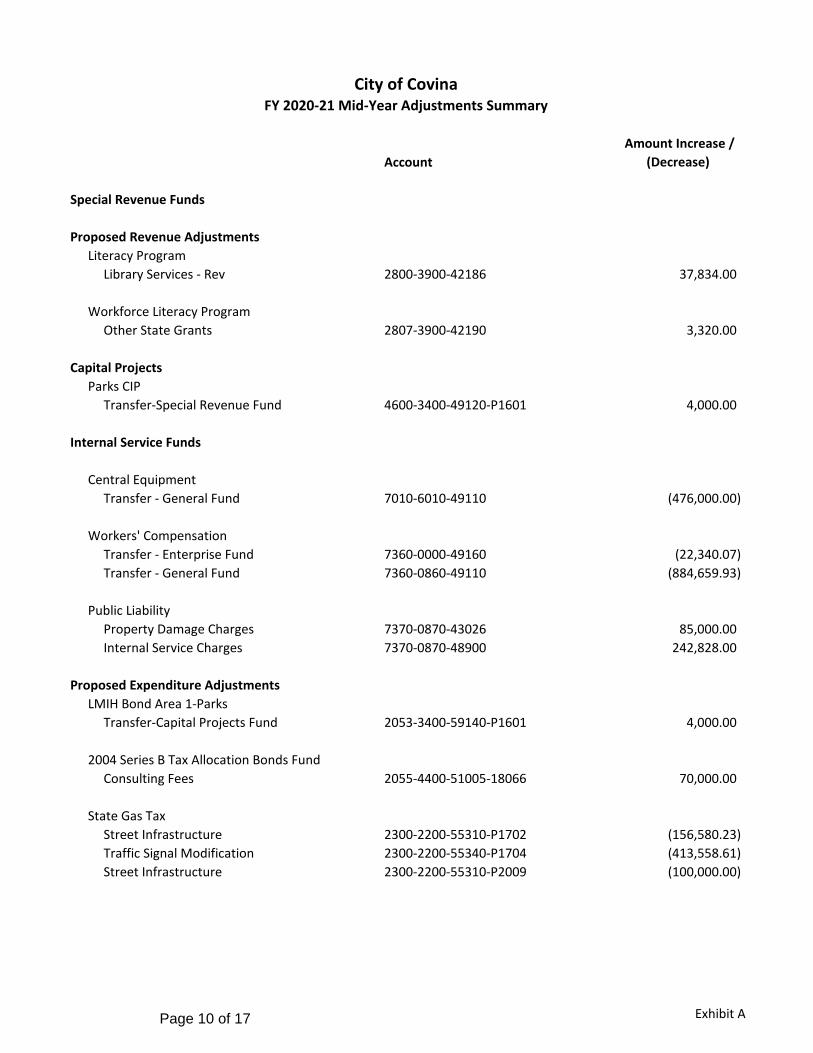

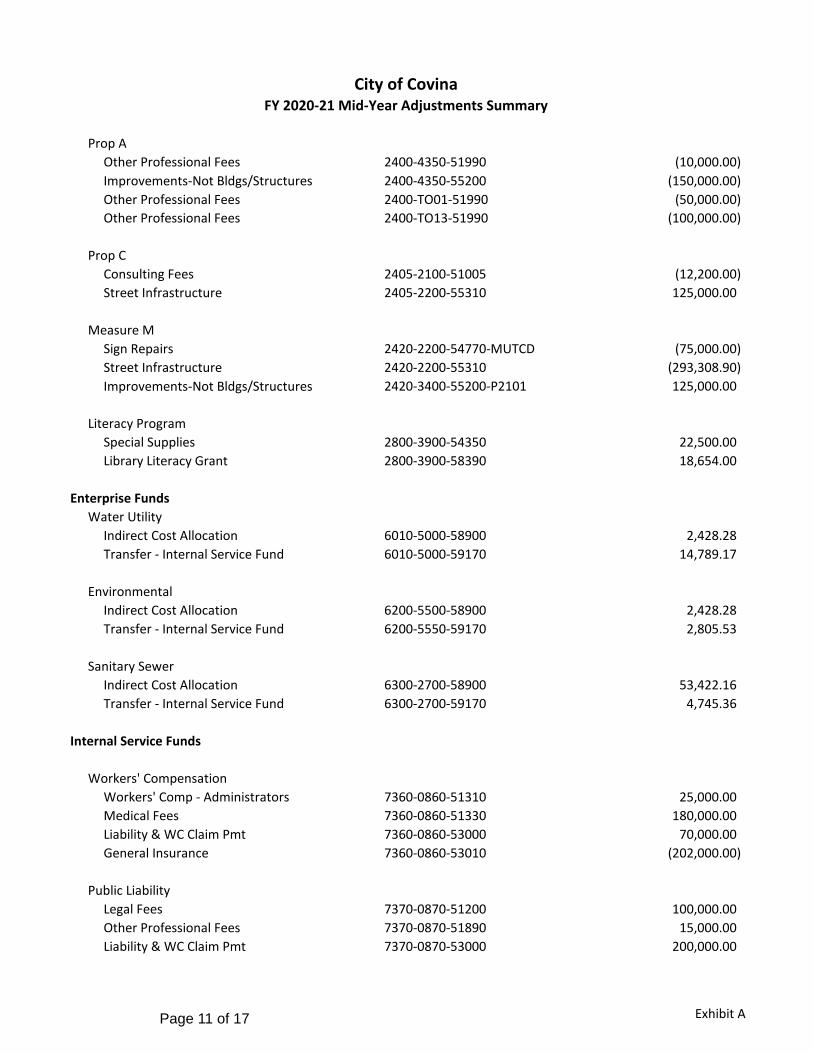

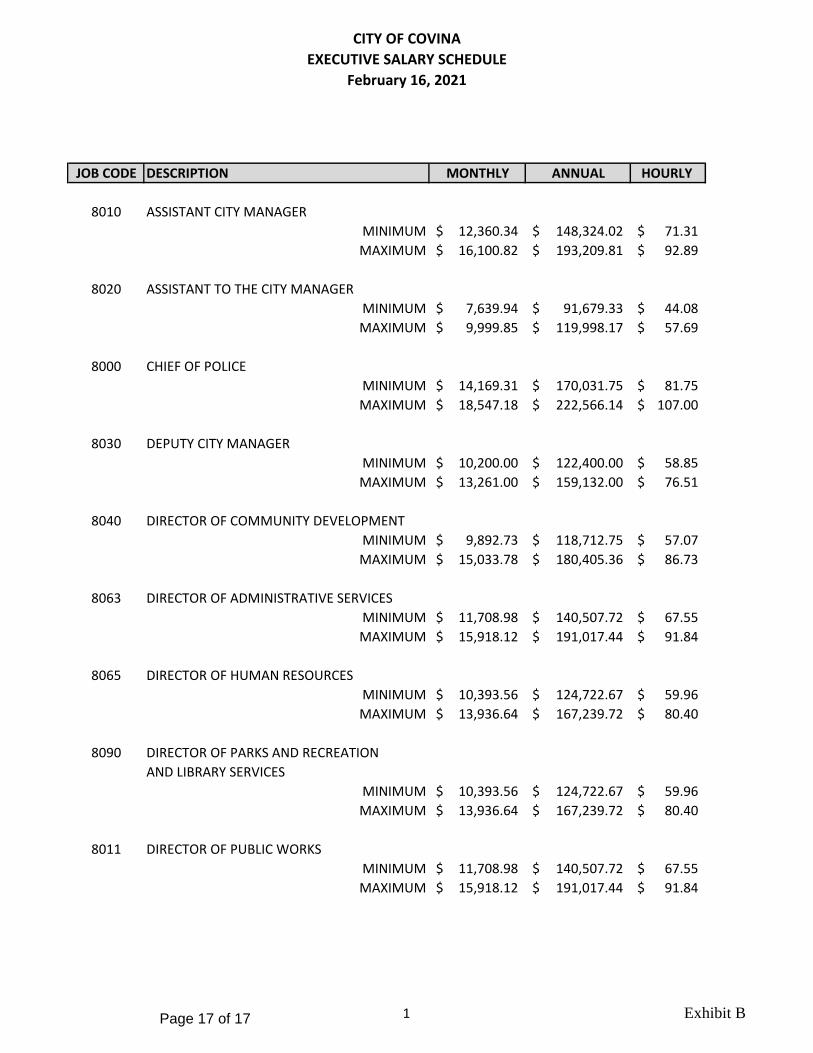

CC 8. Fiscal Year 2020-21 Mid-Year Budget Update and Adjustments Resolution CC 2021-

09

Staff Recommendation:

Staff recommends that the City Council take the following actions:

1. Adopt Resolution CC 2021-09 authorizing budget adjustments for Fiscal Year

2020-21 and receive and file the Fiscal Year 2020-21 Mid-Year Budget

Update; and

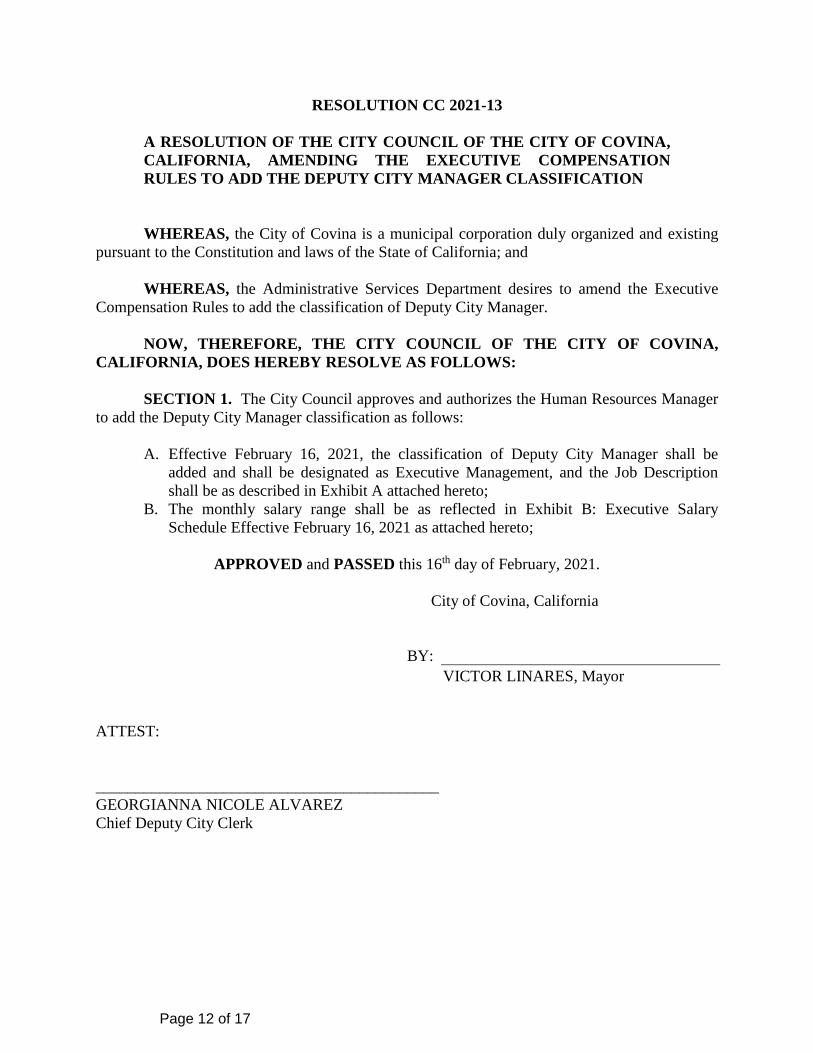

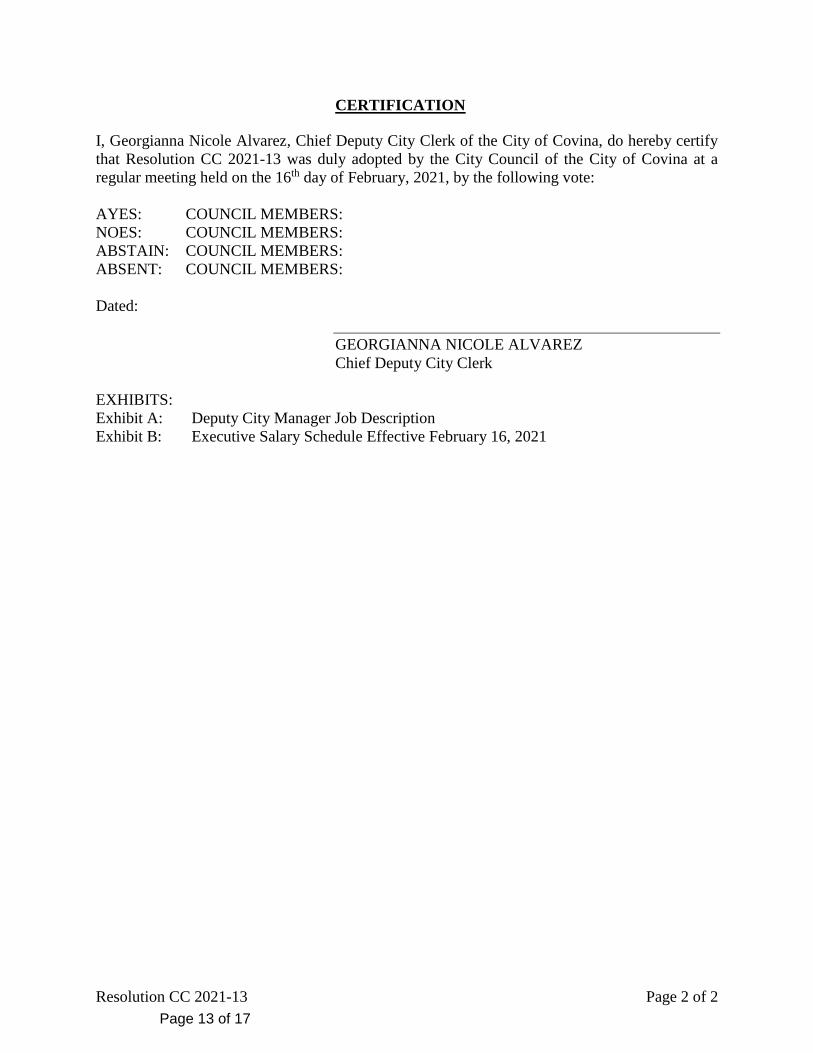

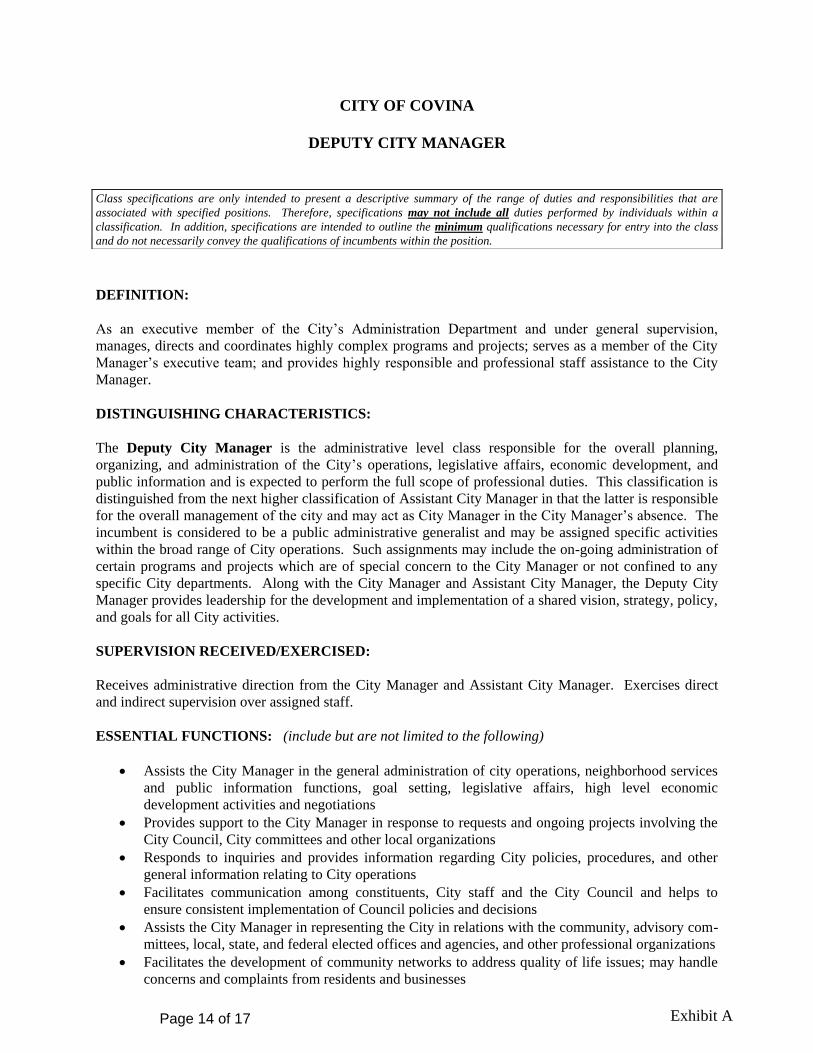

2. Adopt Resolution CC 2021-13 amending the Executive Compensation Rules

to add the Deputy City Manager Classification. Agenda Report - Resolution CC 2020-14 FY 2019-20 Mid Year Adjustments - Pdf

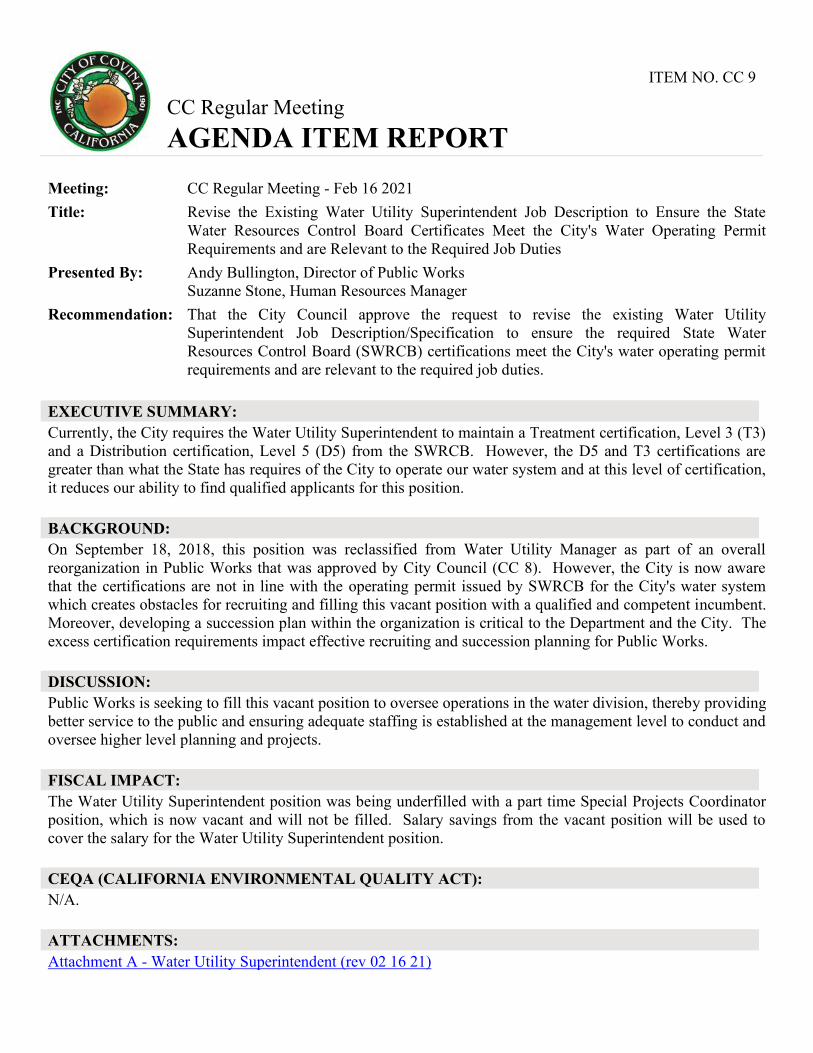

CC 9. Revise the Existing Water Utility Superintendent Job Description to Ensure the State

Water Resources Control Board Certificates Meet the City's Water Operating Permit

Requirements and are Relevant to the Required Job Duties

Staff Recommendation:

That the City Council approve the request to revise the existing Water Utility

Superintendent Job Description/Specification to ensure the required State Water

Resources Control Board (SWRCB) certifications meet the City's water operating

permit requirements and are relevant to the required job duties. Agenda Report - Water Utility Superintendent - Pdf

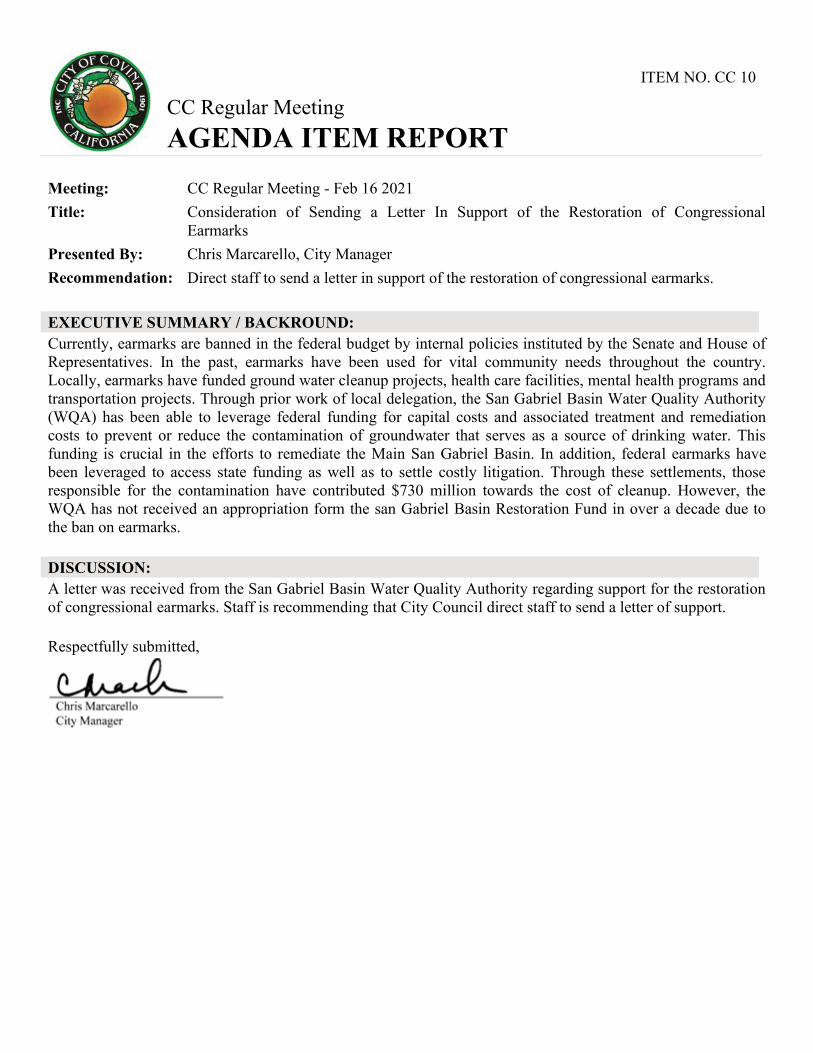

CC 10. Consideration of Sending a Letter In Support of the Restoration of Congressional

Earmarks

Staff Recommendation:

Direct staff to send a letter in support of the restoration of congressional earmarks. Agenda Report - Letter of Support - Congressional Earmarks - Pdf

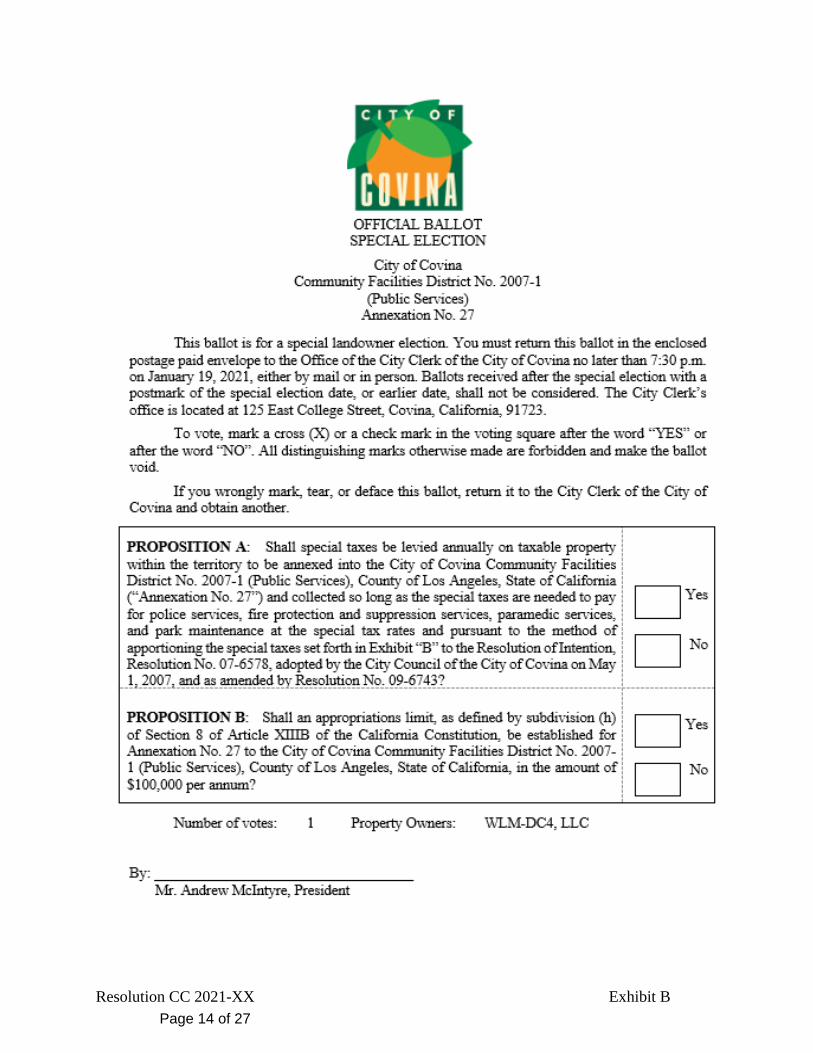

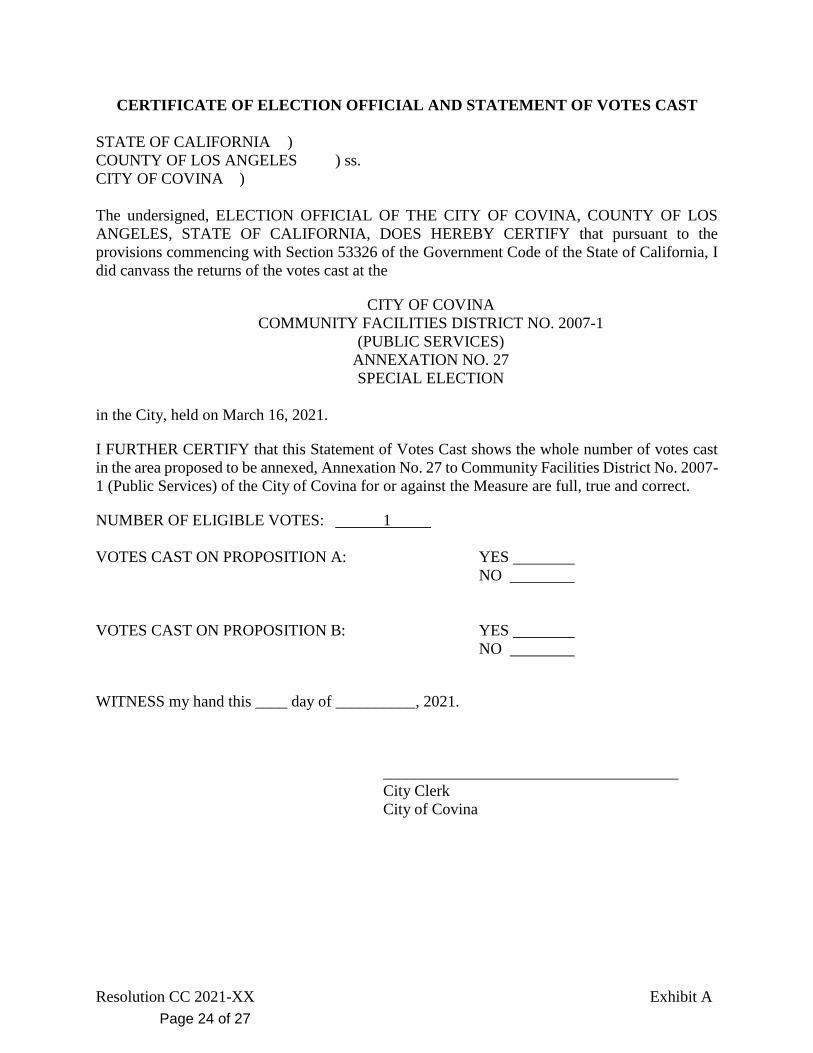

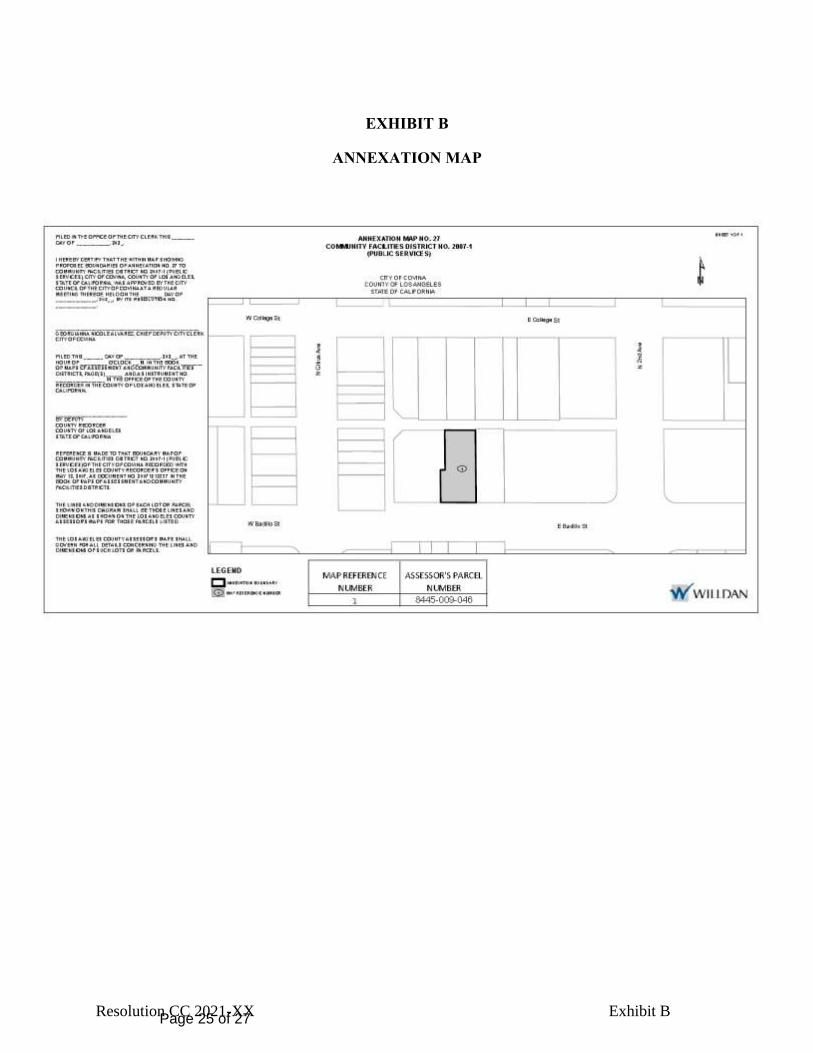

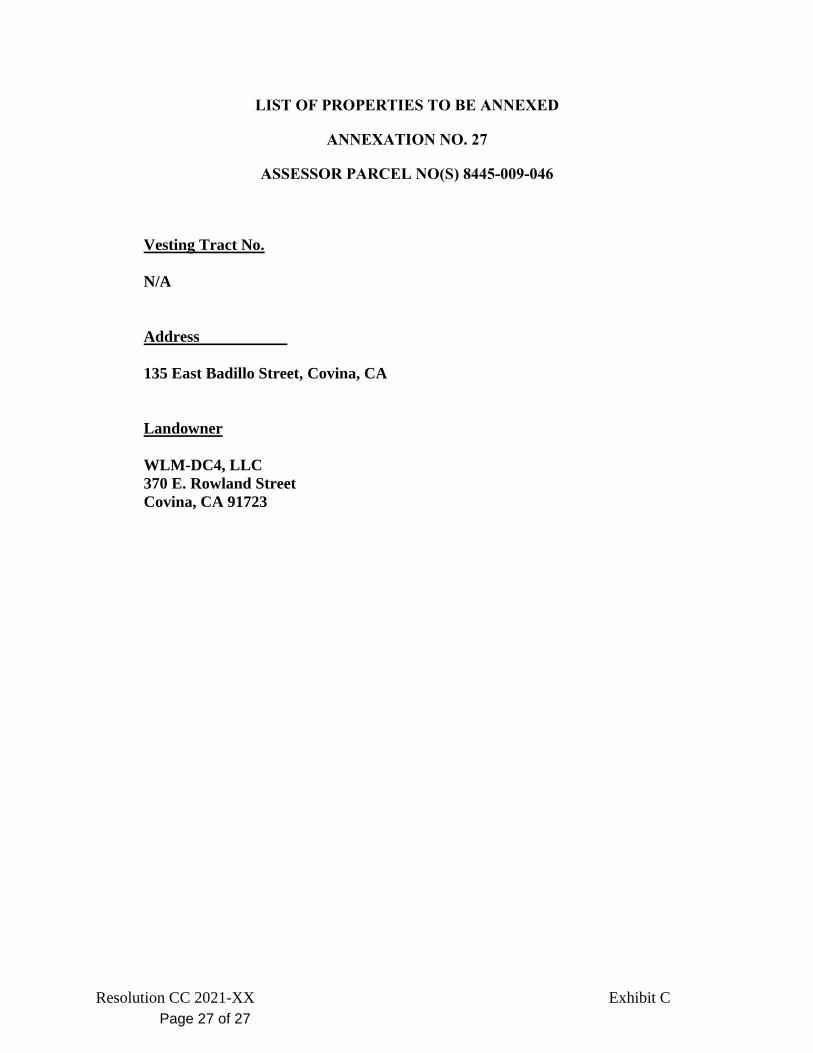

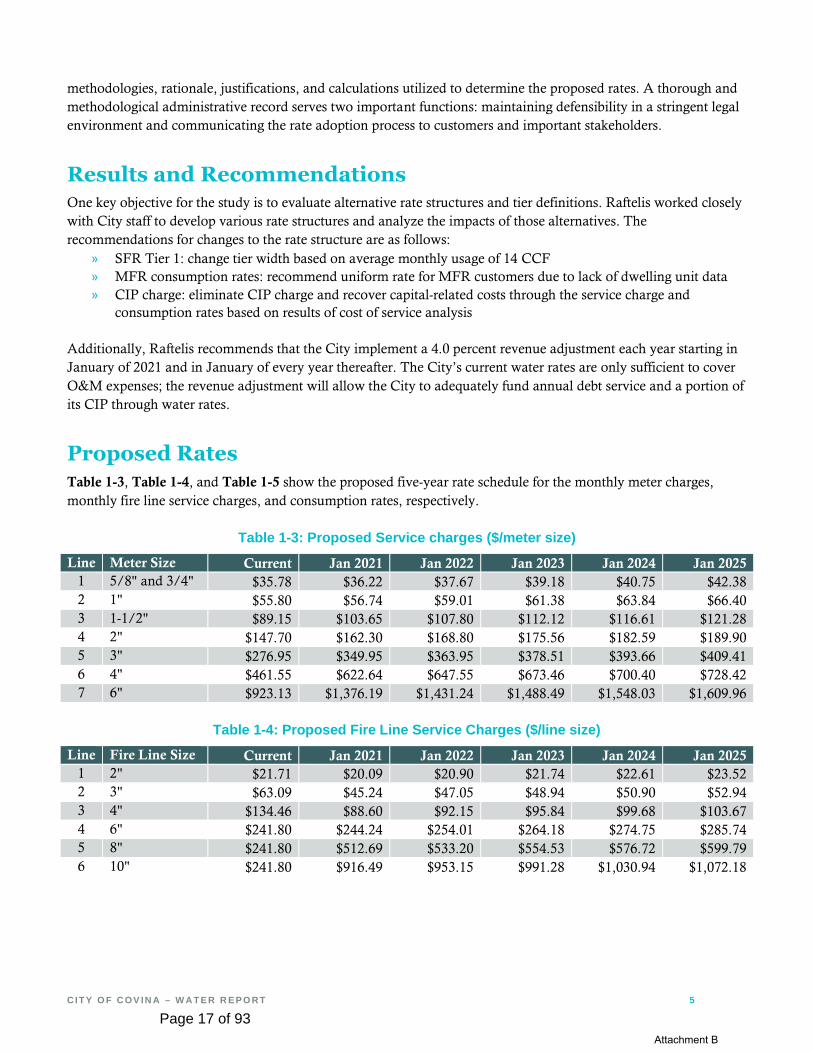

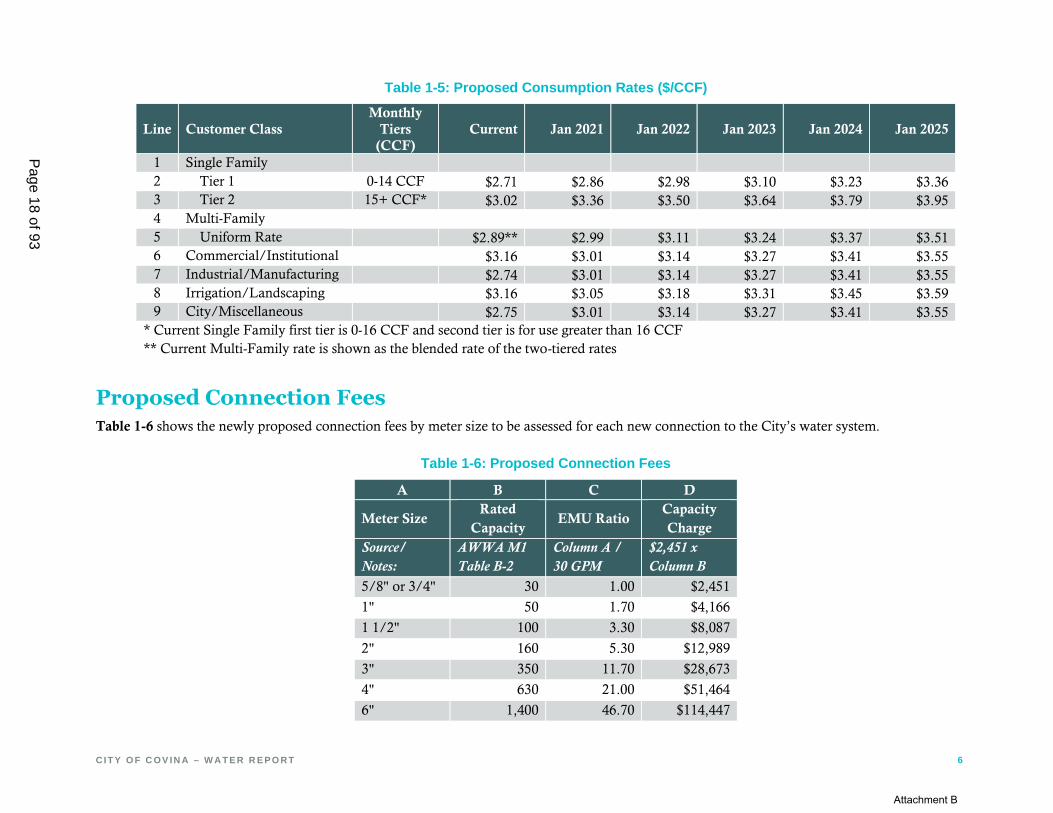

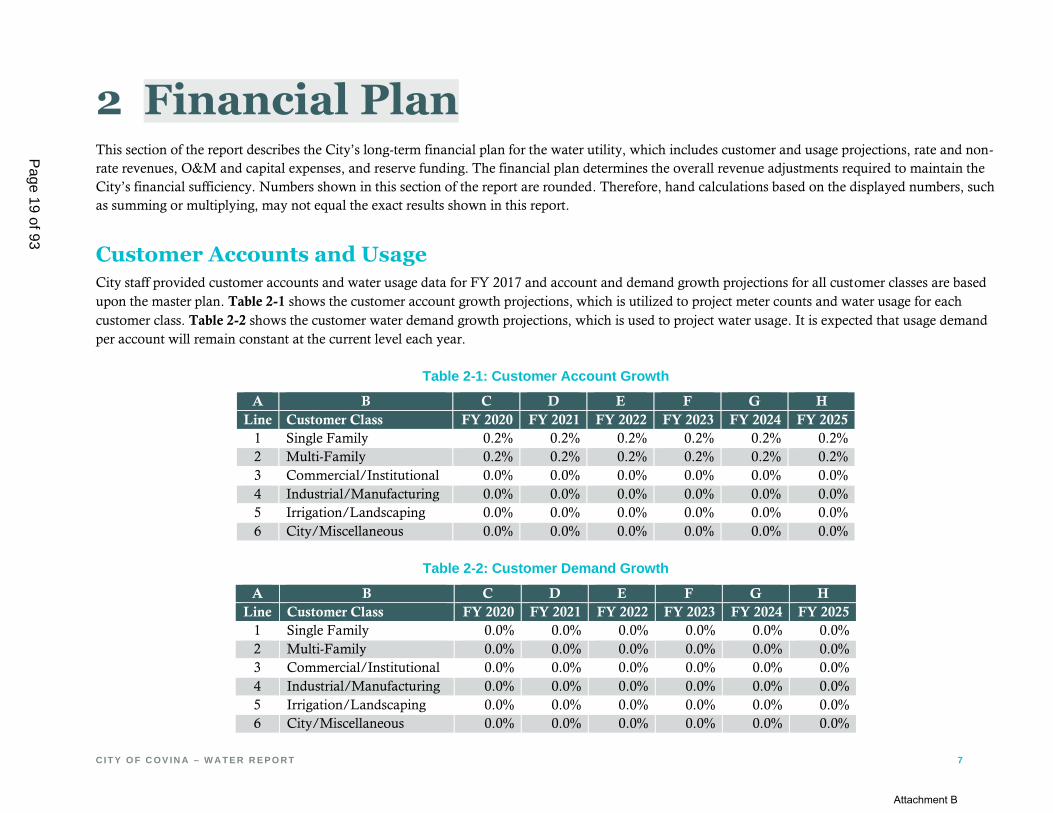

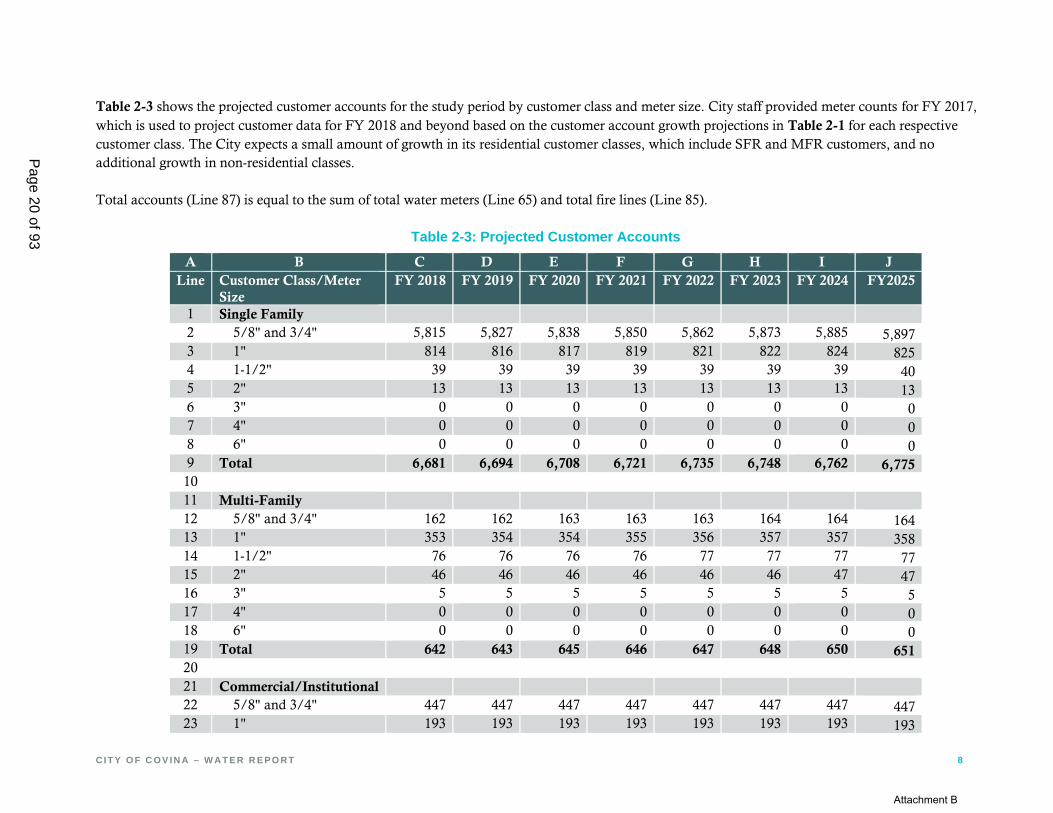

CONTINUED PUBLIC HEARING CPH 1. Consideration of Resolutions CC 2021-xx, CC 2021-xx, and CC 2021-xx,

Authorizing Annexation of Territory to City of Covina Community Facilities

District No. 2007-1 (Public Services) (Annexation No. 27), and to Call and Hold

a Special Election (135 E. Badillo Street, Covina)

Staff Recommendation:

1. City Council to open the public hearing and consider public testimony; and

2. Continue the public hearing to the meeting of March 16, 2021. Agenda Report - CFD Annexation 27 - Pdf

City Council/CSA/CPFA/CHA Agenda Tuesday February 16, 2021

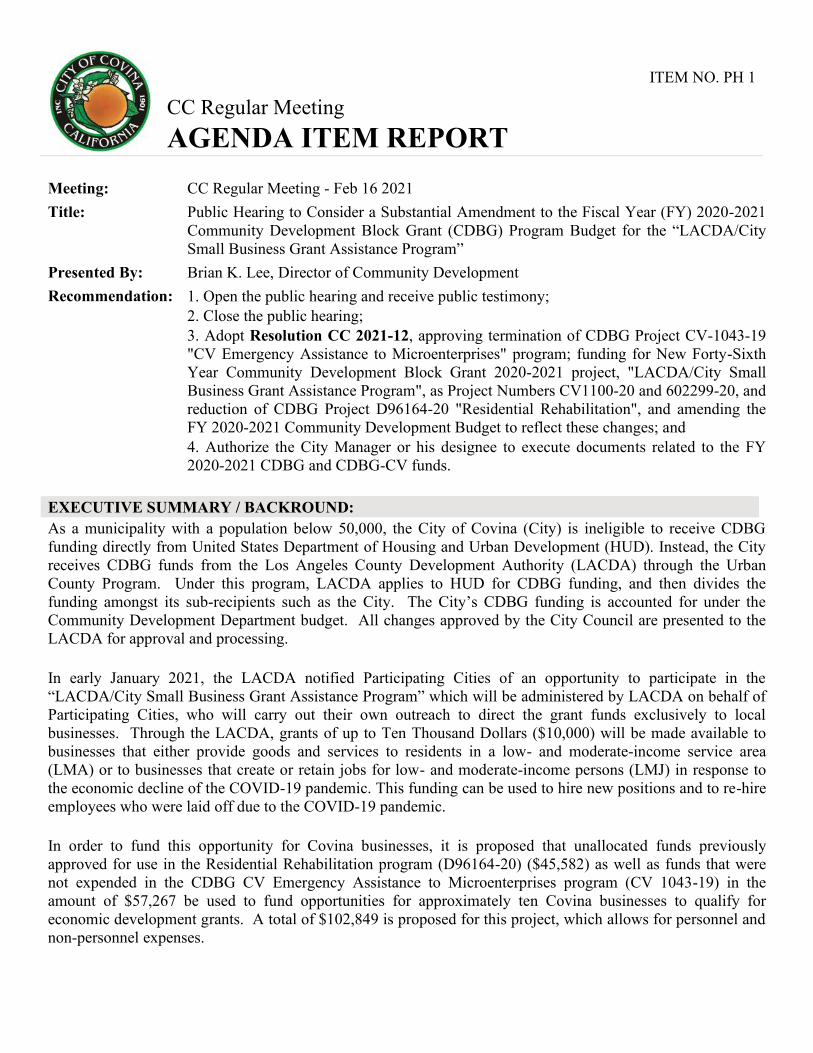

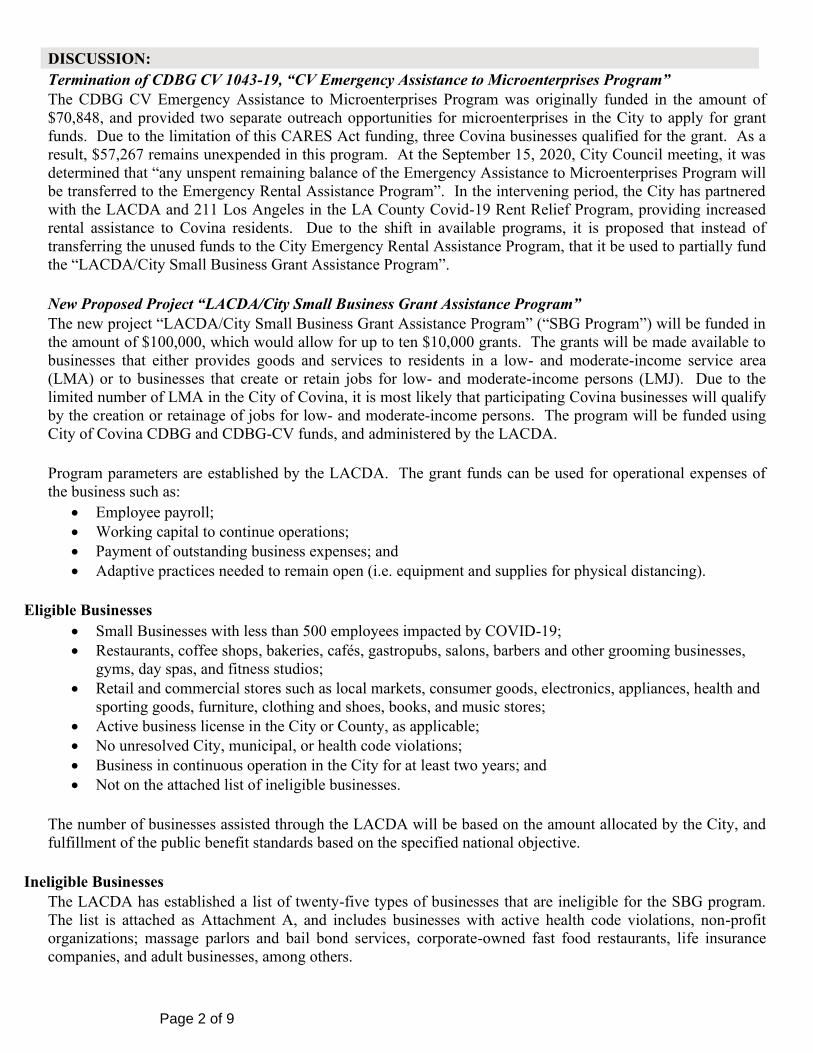

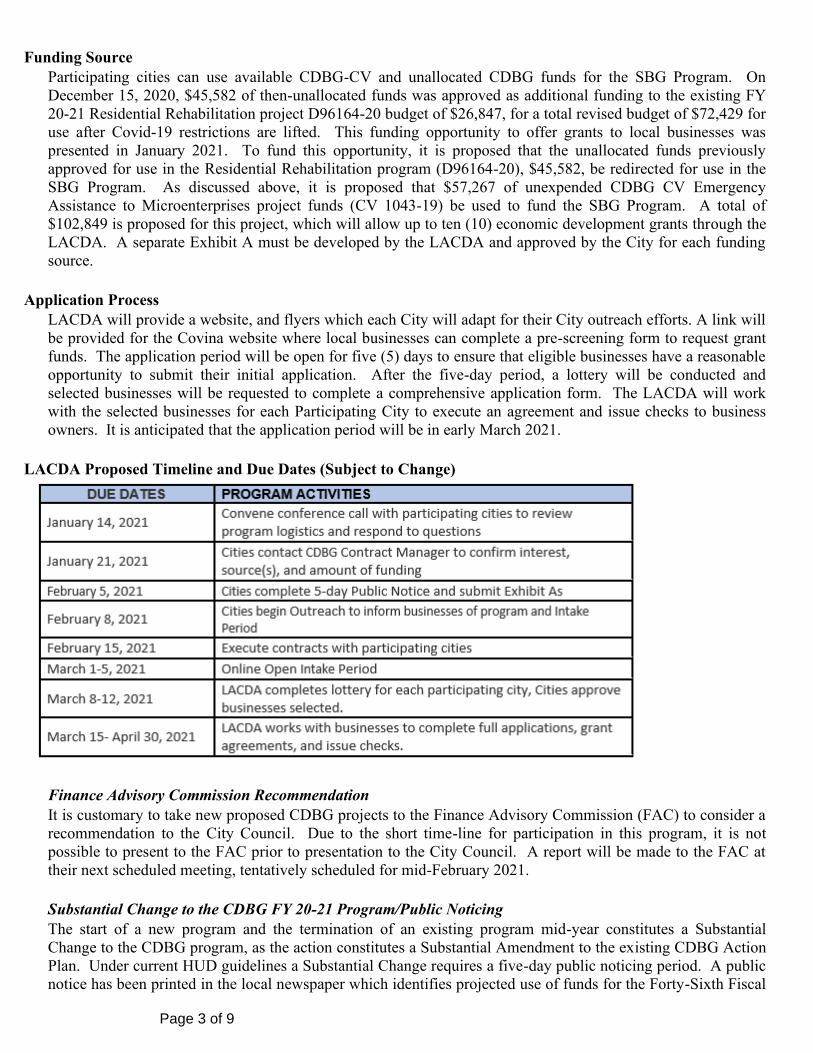

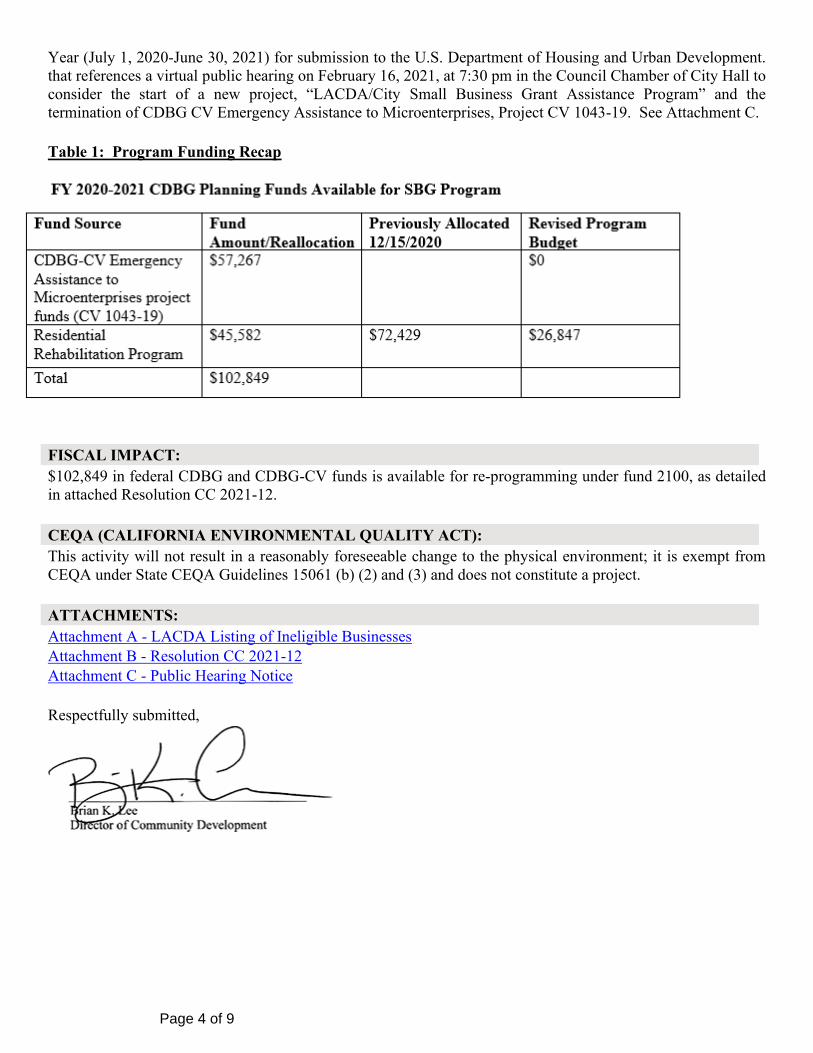

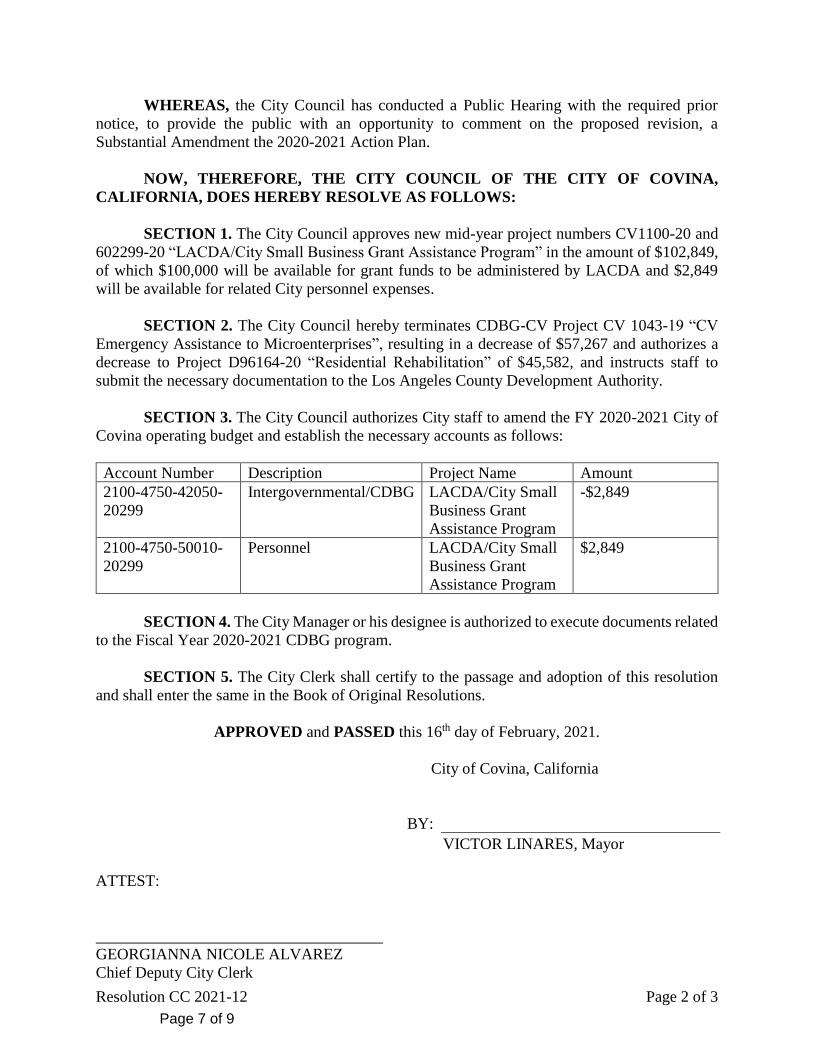

PUBLIC HEARINGS PH 1. Public Hearing to Consider a Substantial Amendment to the Fiscal Year (FY)

2020-2021 Community Development Block Grant (CDBG) Program Budget for

the “LACDA/City Small Business Grant Assistance Program”

Staff Recommendation:

1. Open the public hearing and receive public testimony;

2. Close the public hearing;

3. Adopt Resolution CC 2021-12, approving termination of CDBG Project CV-1043-

19 "CV Emergency Assistance to Microenterprises" program; funding for New Forty-

Sixth Year Community Development Block Grant 2020-2021 project, "LACDA/City

Small Business Grant Assistance Program", as Project Numbers CV1100-20 and

602299-20, and reduction of CDBG Project D96164-20 "Residential Rehabilitation",

and amending the FY 2020-2021 Community Development Budget to reflect these

changes; and

4. Authorize the City Manager or his designee to execute documents related to the FY

2020-2021 CDBG and CDBG-CV funds. Agenda Report - Amendment to FY 2020-21 CDBG Program Budget for

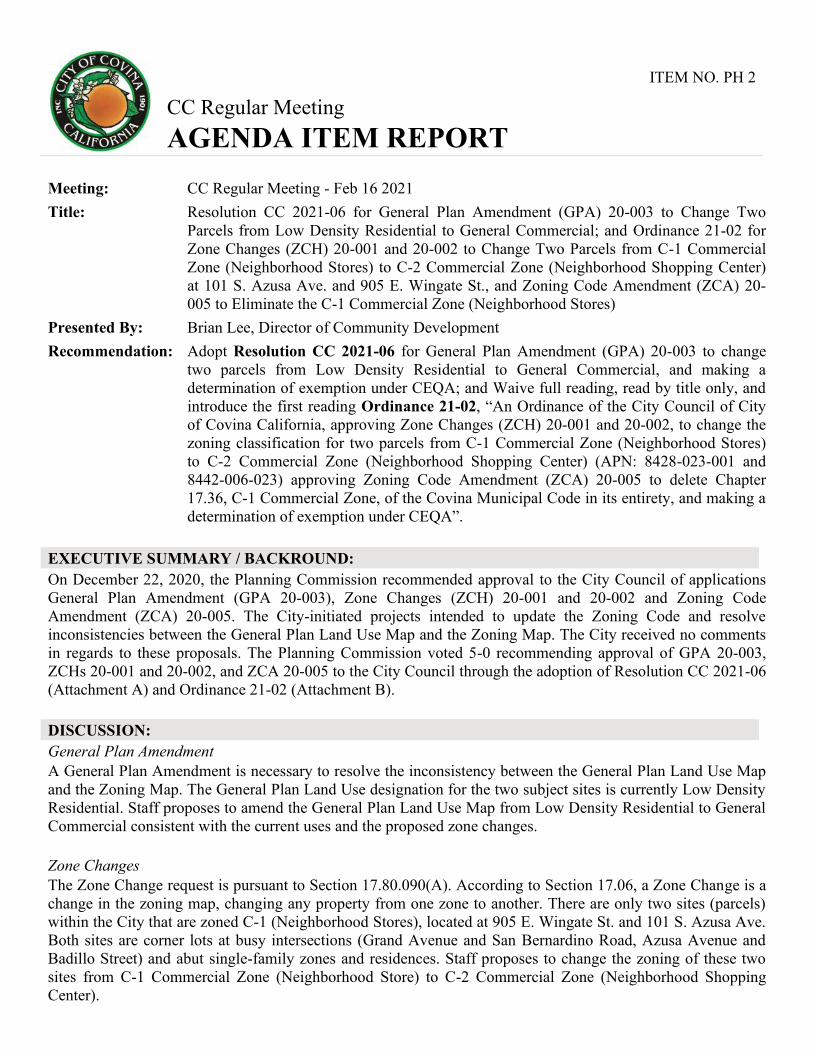

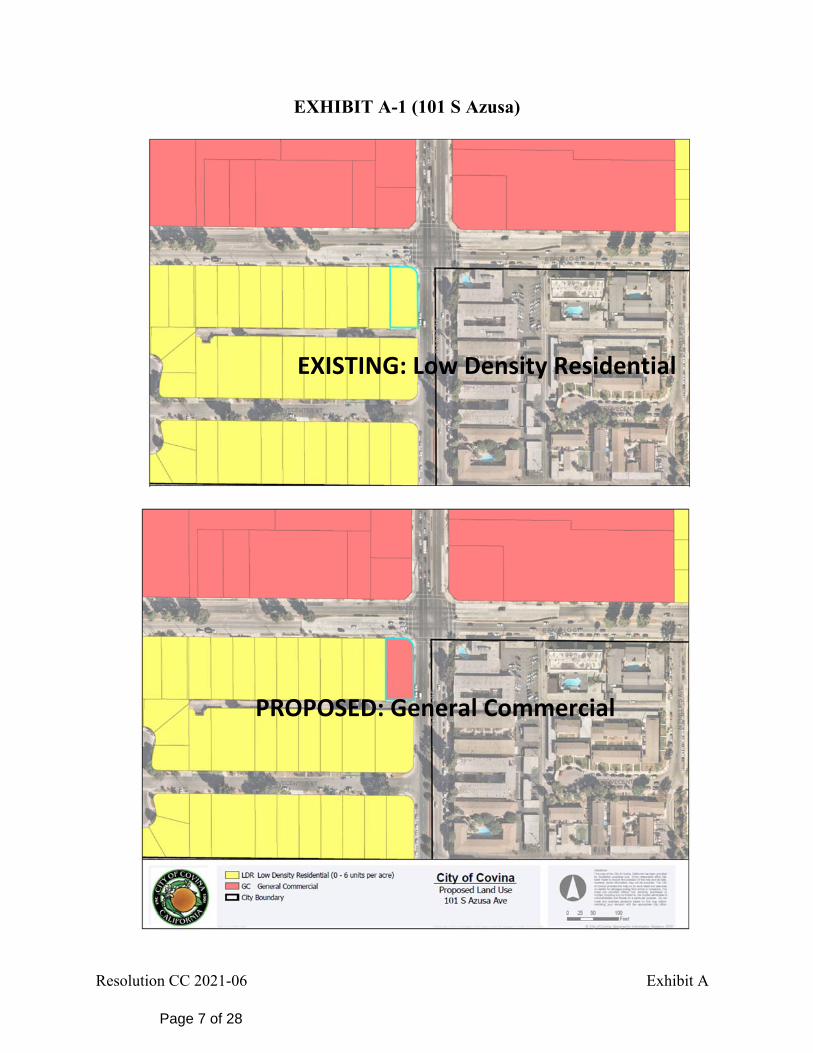

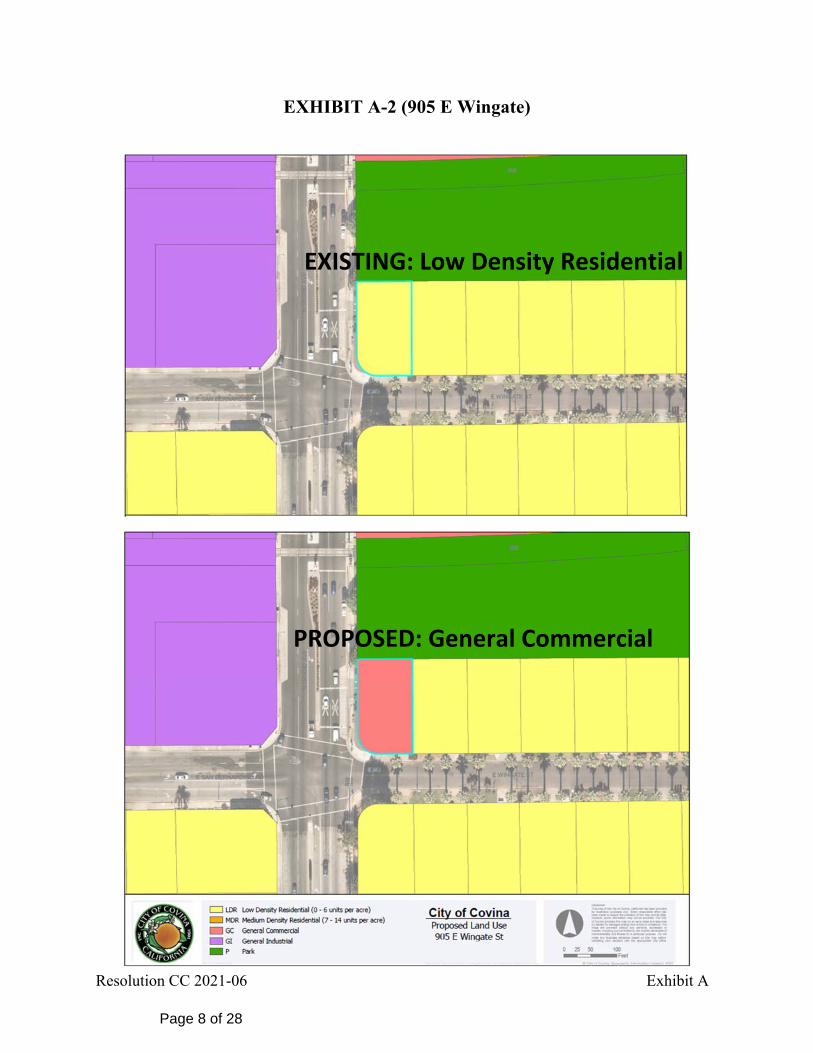

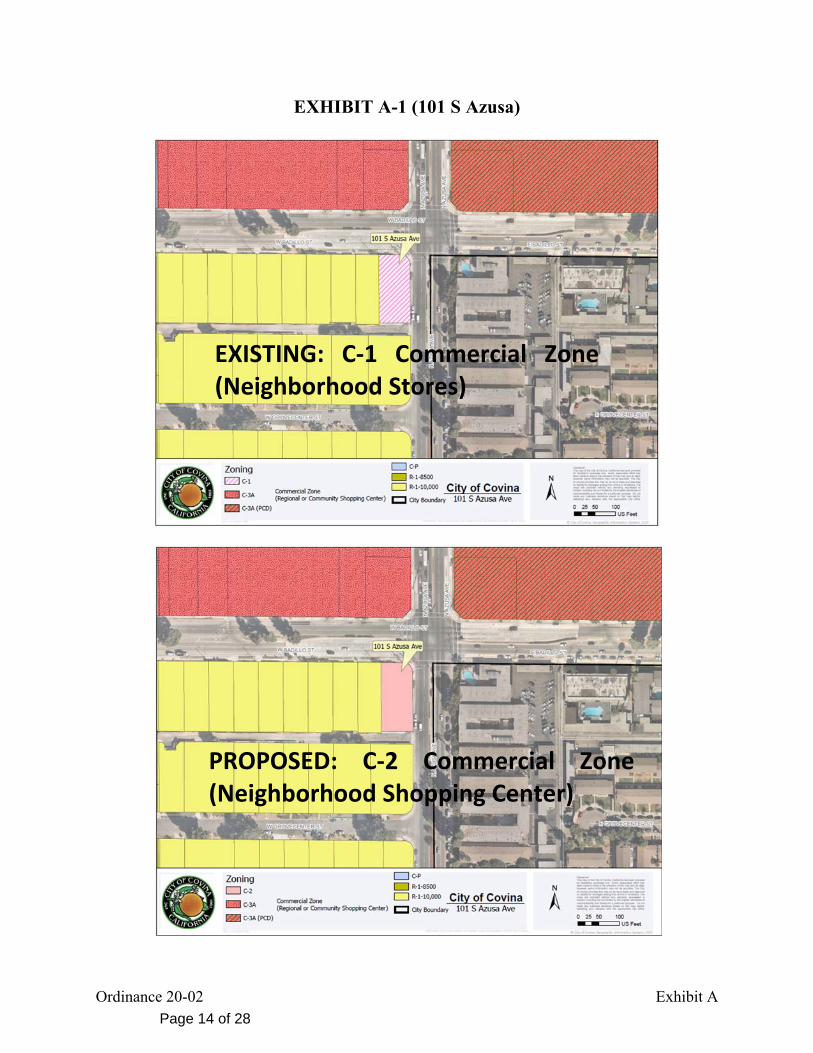

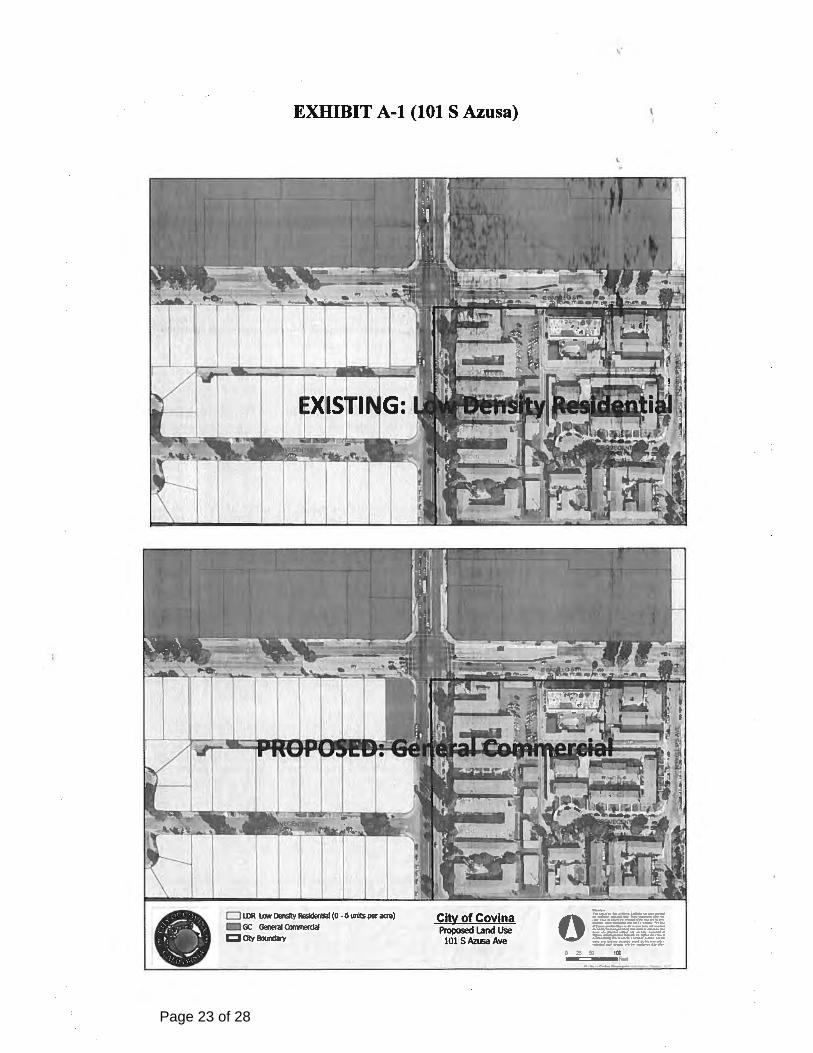

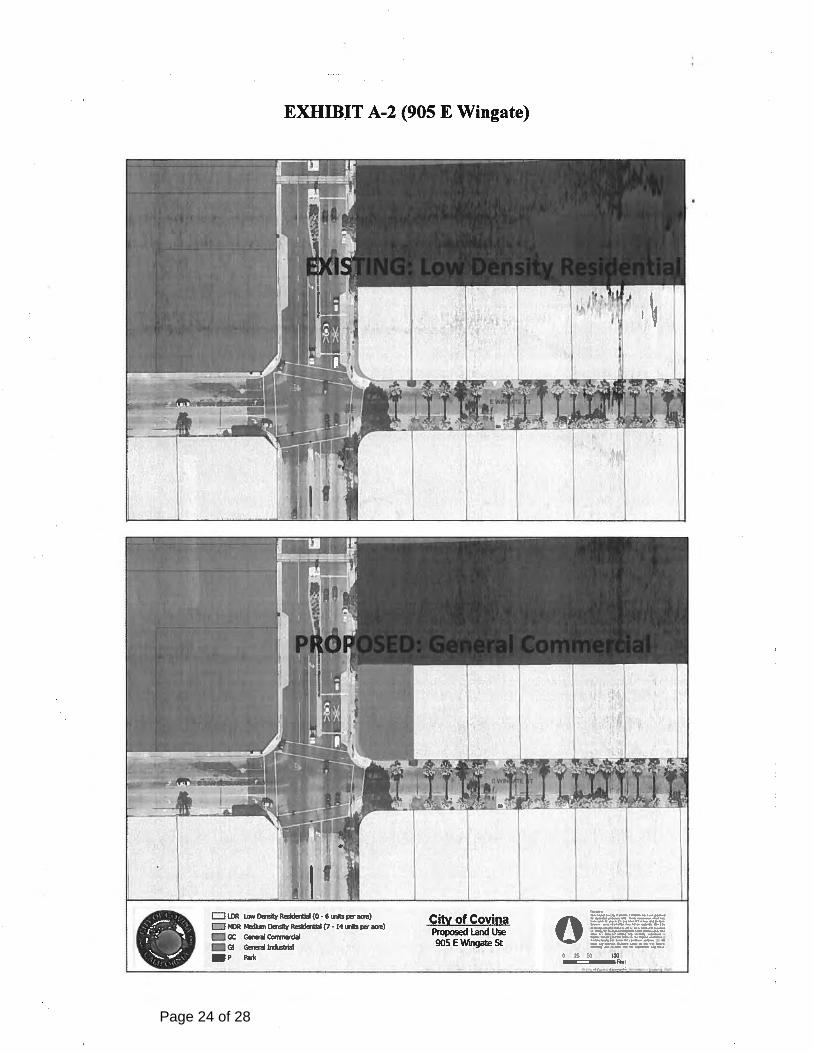

“LACDA/City Small Business Grant Assistance Program” - Pdf PH 2. Resolution CC 2021-06 for General Plan Amendment (GPA) 20-003 to Change

Two Parcels from Low Density Residential to General Commercial; and

Ordinance 21-02 for Zone Changes (ZCH) 20-001 and 20-002 to Change Two

Parcels from C-1 Commercial Zone (Neighborhood Stores) to C-2 Commercial

Zone (Neighborhood Shopping Center) at 101 S. Azusa Ave. and 905 E. Wingate

St., and Zoning Code Amendment (ZCA) 20-005 to Eliminate the C-1

Commercial Zone (Neighborhood Stores)

Staff Recommendation:

Adopt Resolution CC 2021-06 for General Plan Amendment (GPA) 20-003 to change

two parcels from Low Density Residential to General Commercial, and making a

determination of exemption under CEQA; and Waive full reading, read by title only,

and introduce the first reading Ordinance 21-02, “An Ordinance of the City Council

of City of Covina California, approving Zone Changes (ZCH) 20-001 and 20-002, to

change the zoning classification for two parcels from C-1 Commercial Zone

(Neighborhood Stores) to C-2 Commercial Zone (Neighborhood Shopping Center)

(APN: 8428-023-001 and 8442-006-023) approving Zoning Code Amendment (ZCA)

20-005 to delete Chapter 17.36, C-1 Commercial Zone, of the Covina Municipal Code

in its entirety, and making a determination of exemption under CEQA”. Agenda Report - PH GPA 20-003, ZCH 20-001 and 002, ZCA 20-005 Wingate &

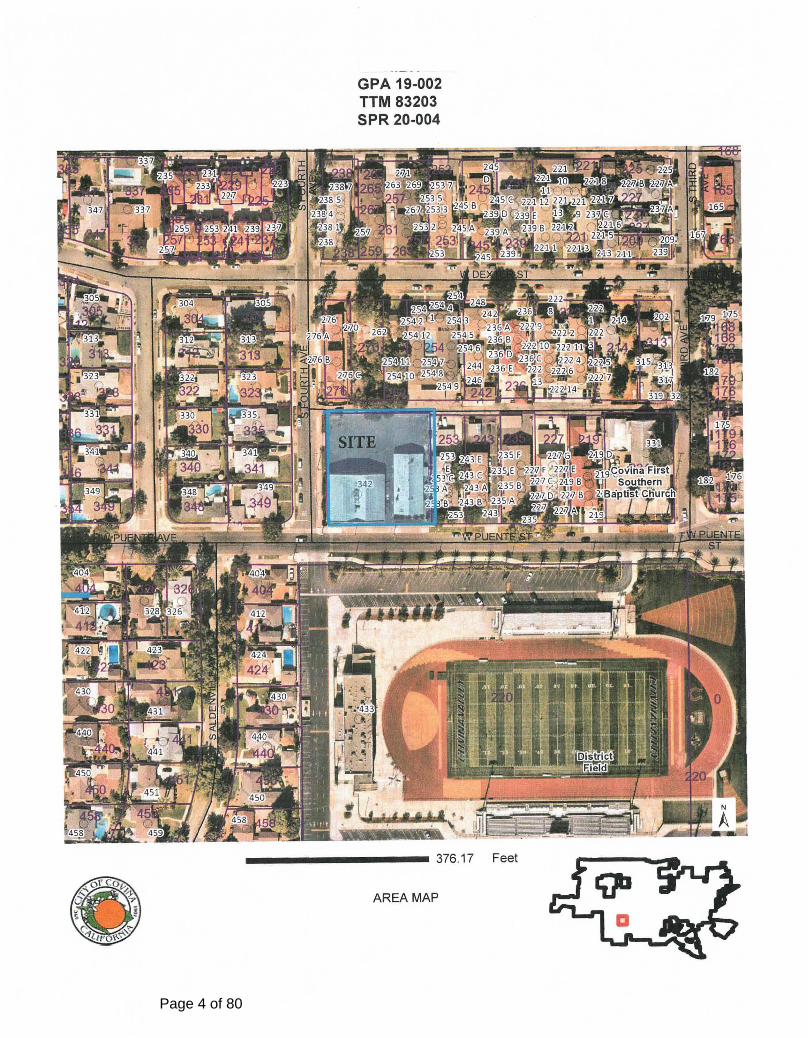

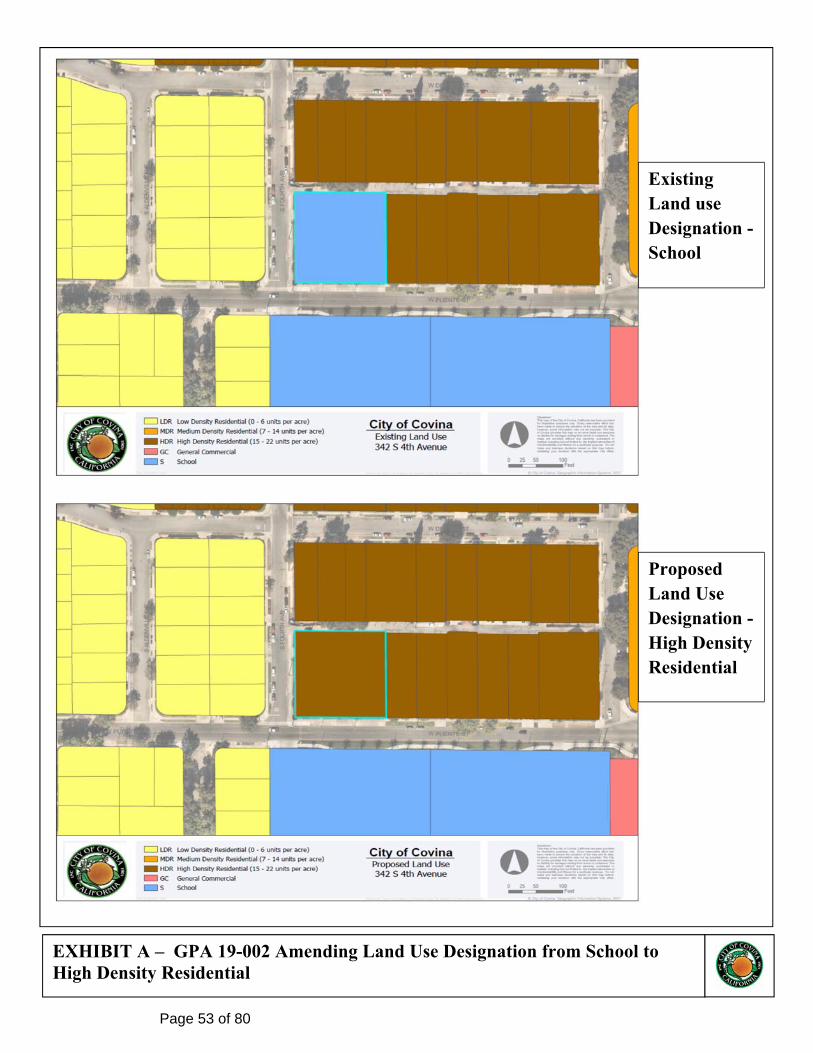

Azusa - Pdf PH 3. Resolution CC 2021-10, Approving a Mitigated Negative Declaration (MND) as

Adequately Prepared in Accordance with California Environmental Quality Act

(CEQA), the Required Findings Under CEQA and the Mitigation Monitoring

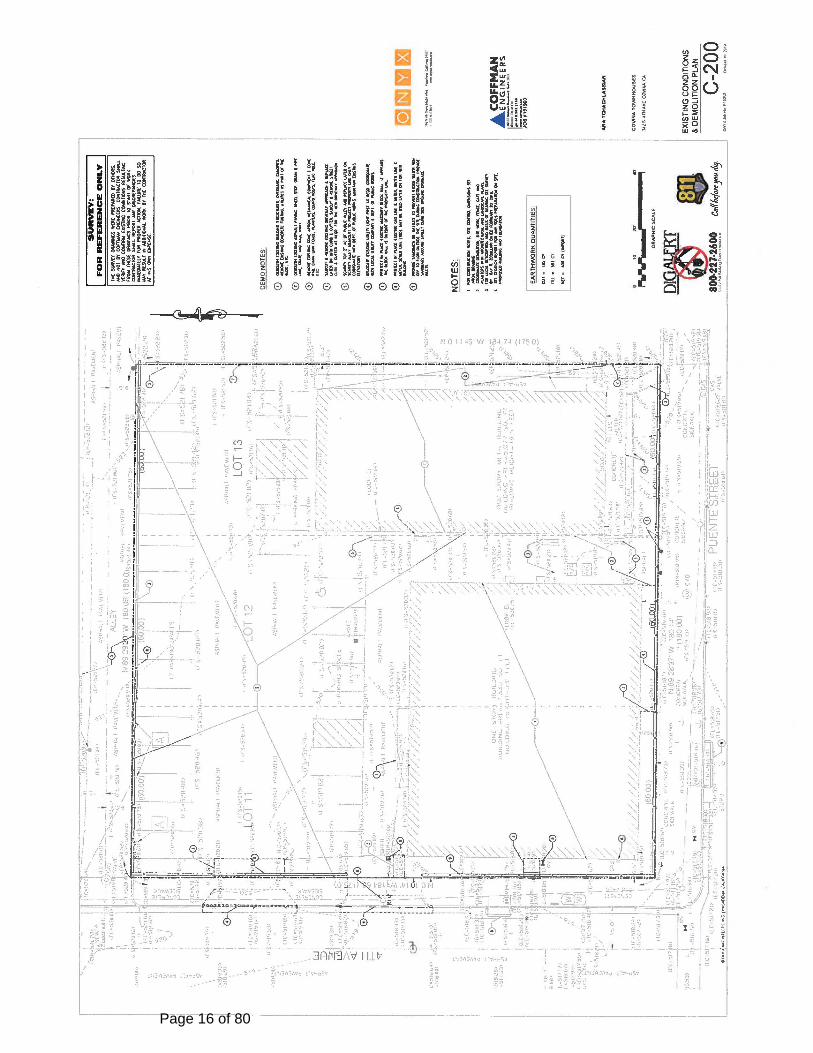

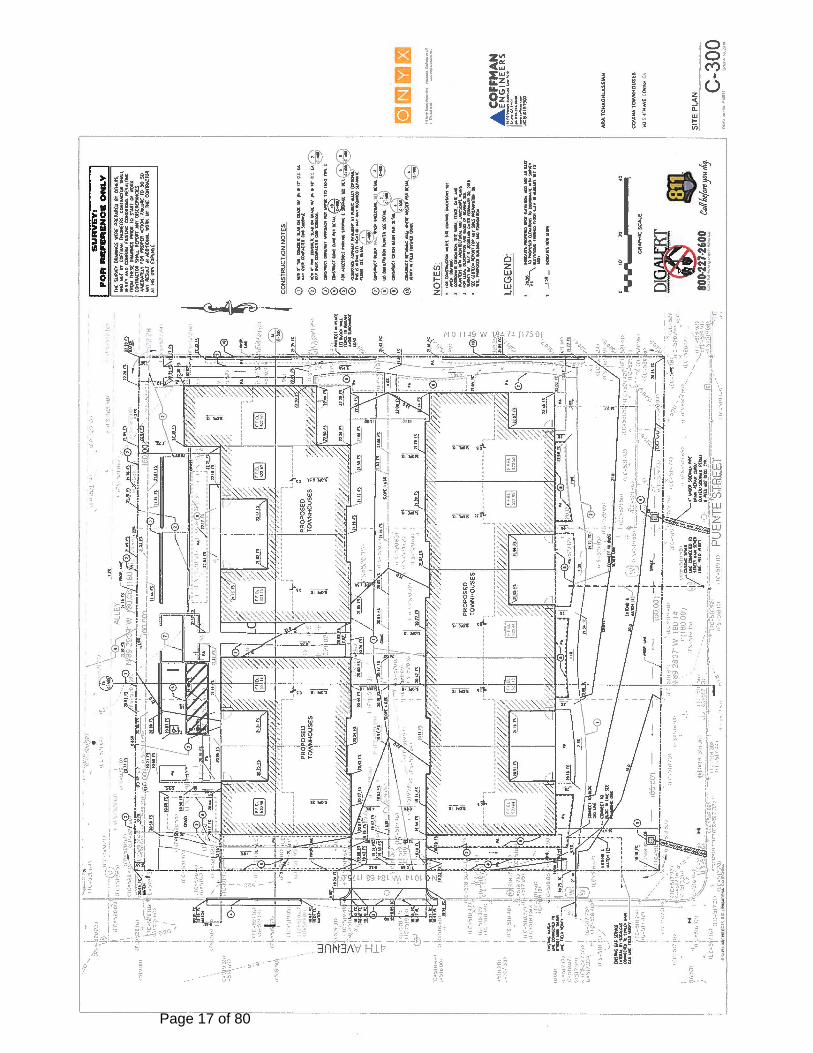

and Reporting Program for GPA 19-00, TTM 83202 and SPR 20-004, and

Approving General Plan Amendment (GPA) 19-002, Amending the Land Use

City Council/CSA/CPFA/CHA Agenda Tuesday February 16, 2021

Map of the Covina General Plan to Change the Land Use Designation from

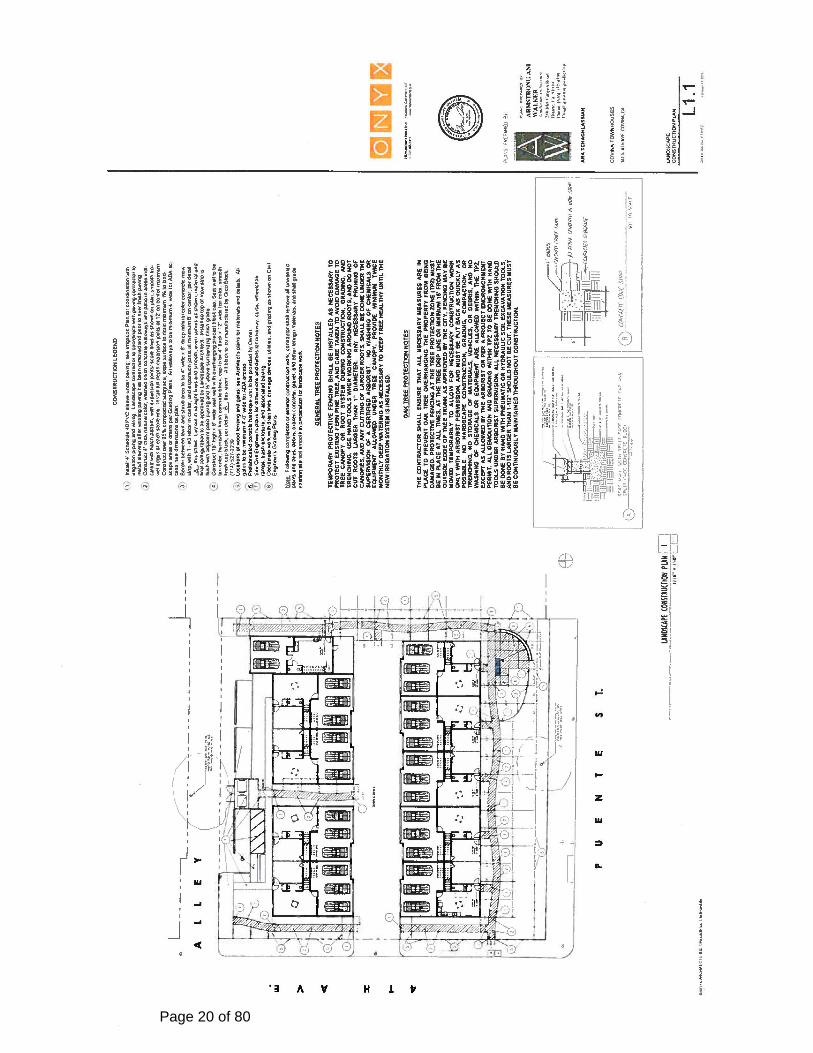

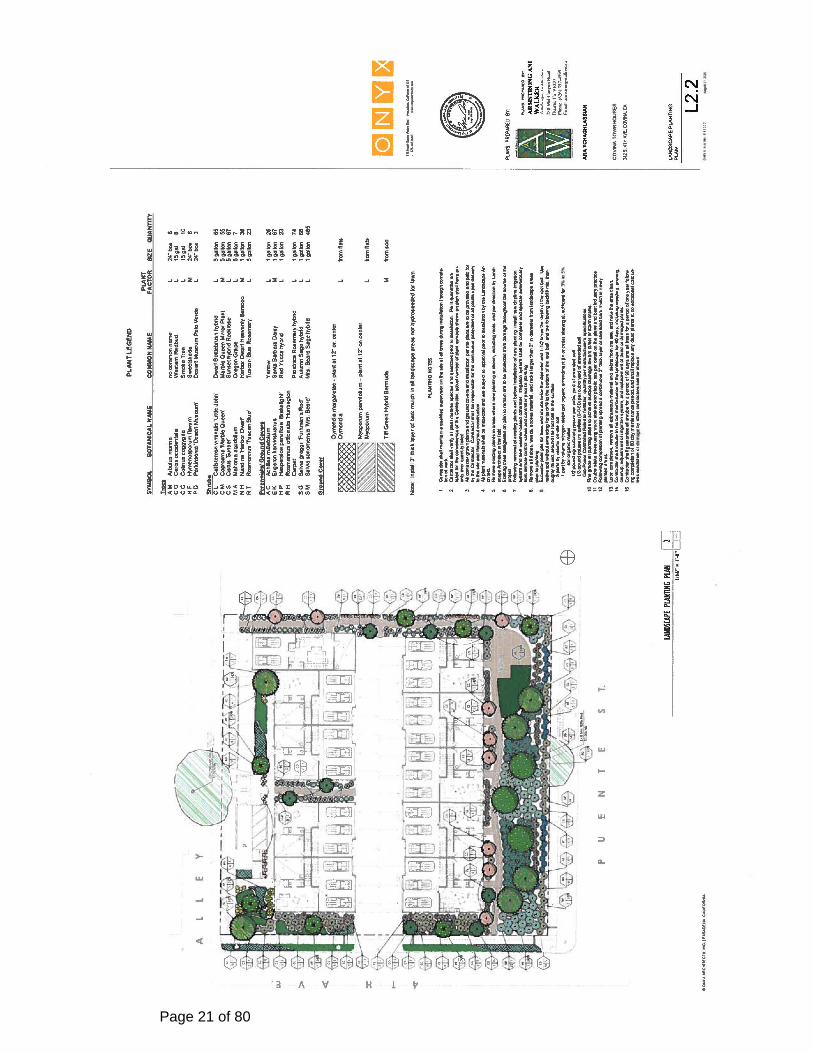

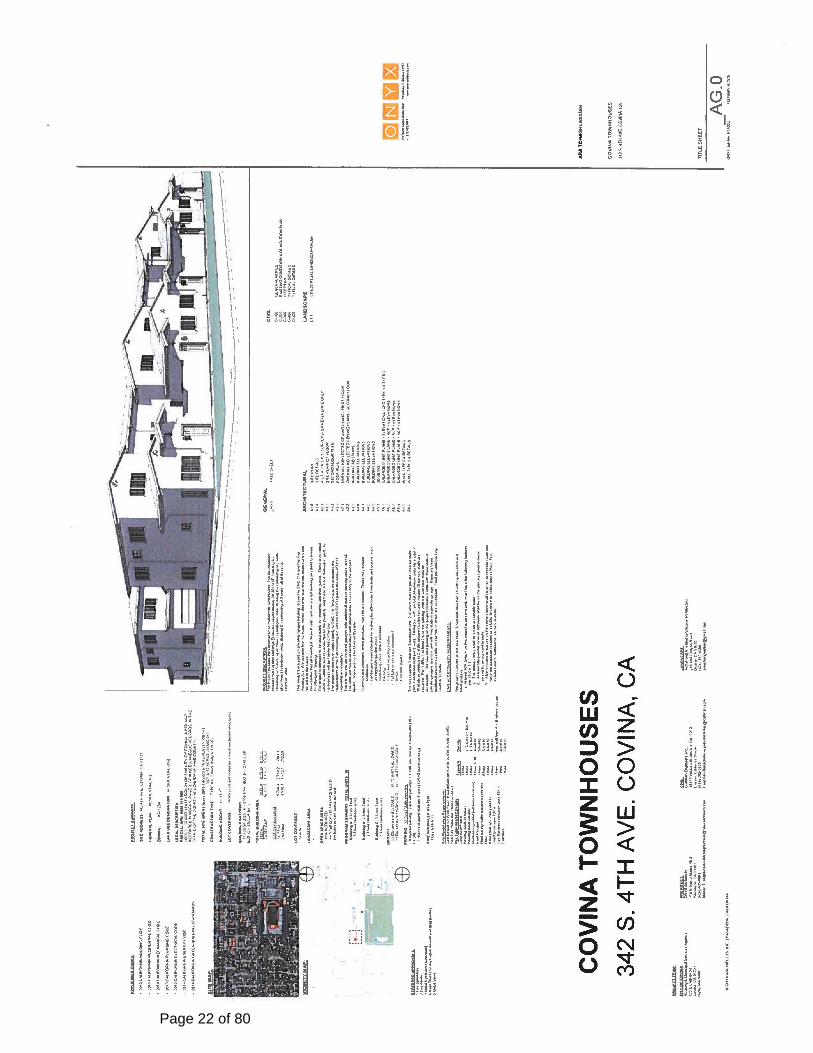

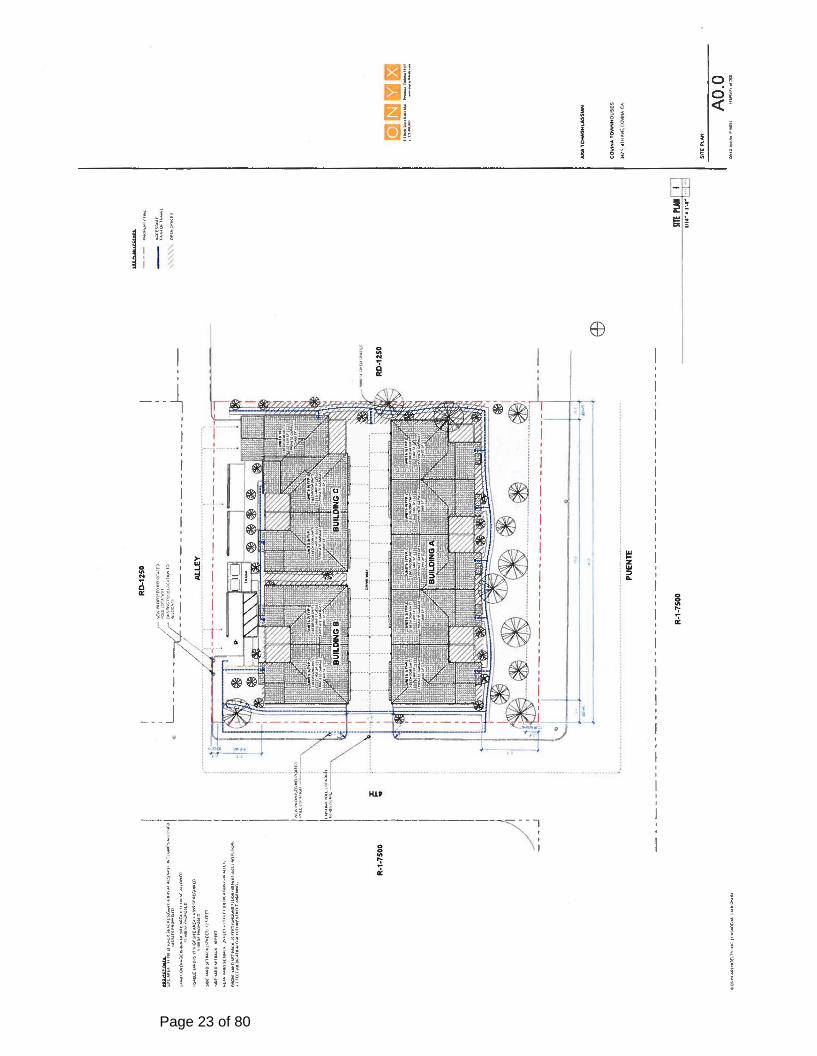

School to High Density Residential for a 0.72-Acre Property, Located at 342

South Fourth Avenue – APN: 8444-010-900; and Resolution CC 2021-11,

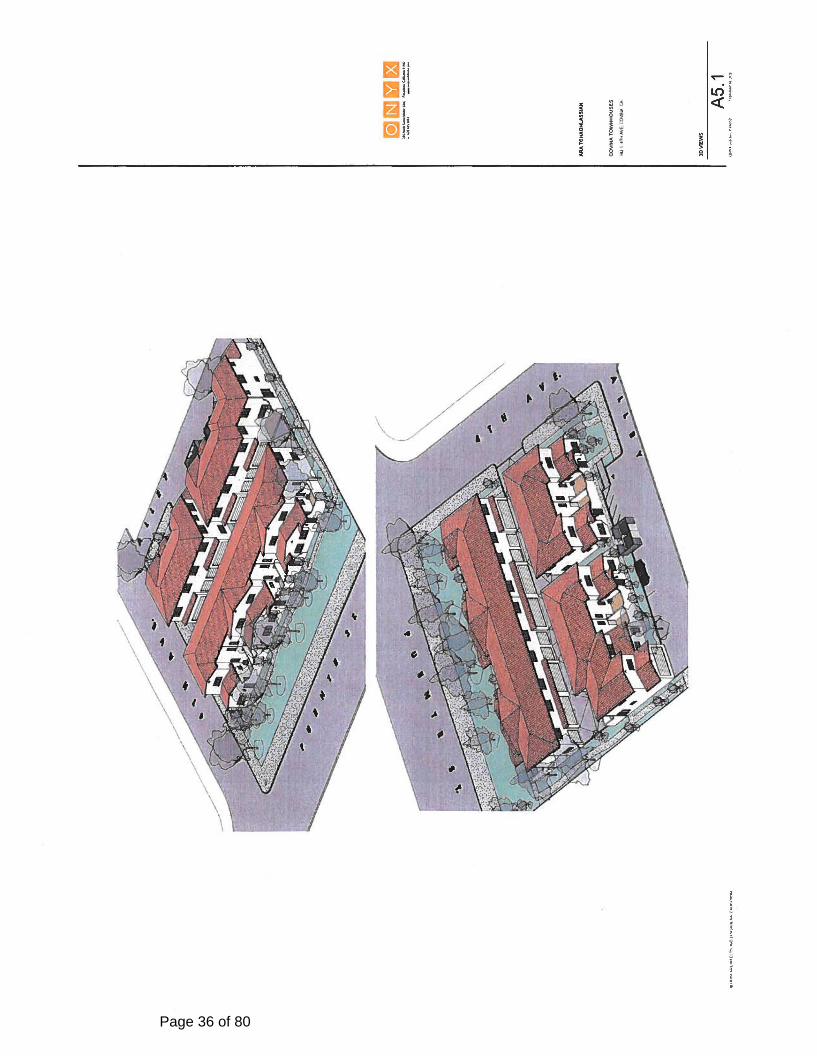

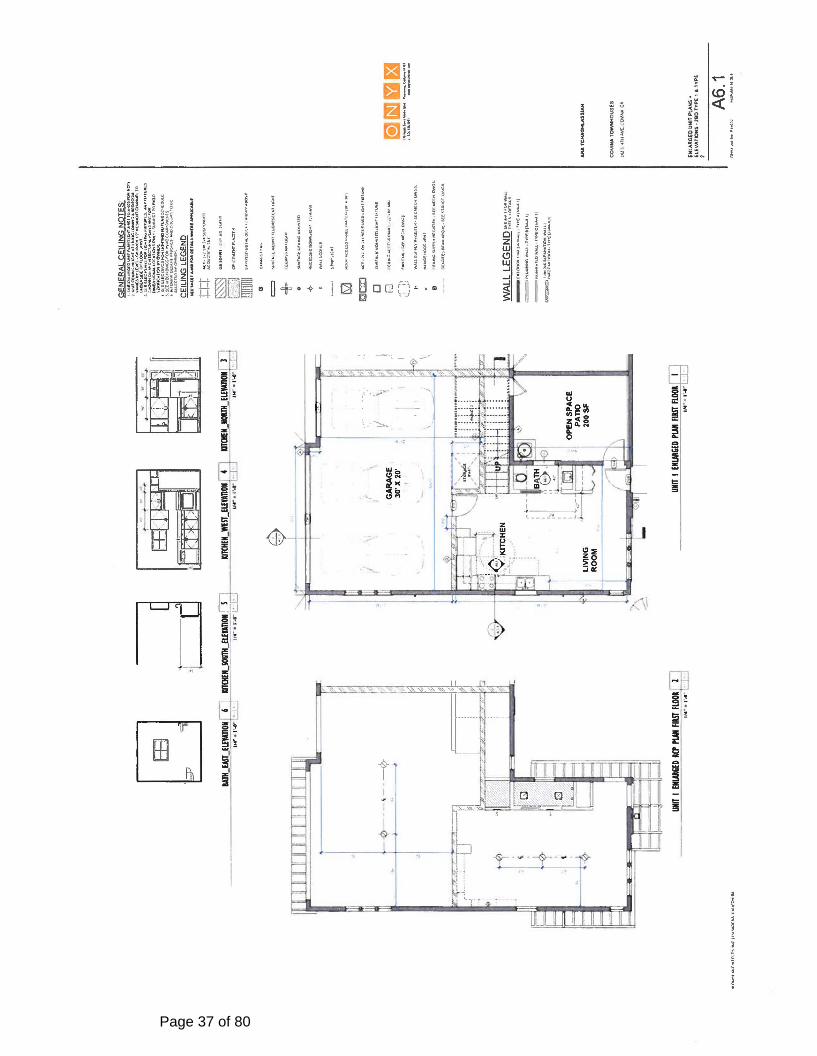

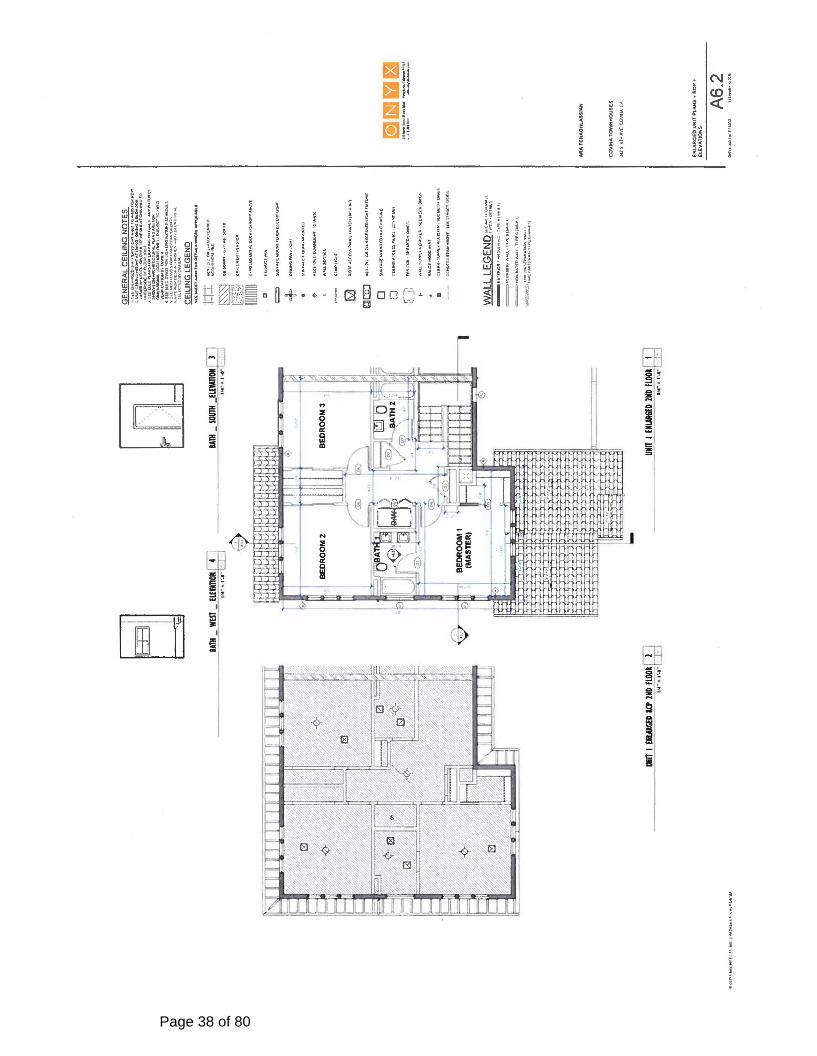

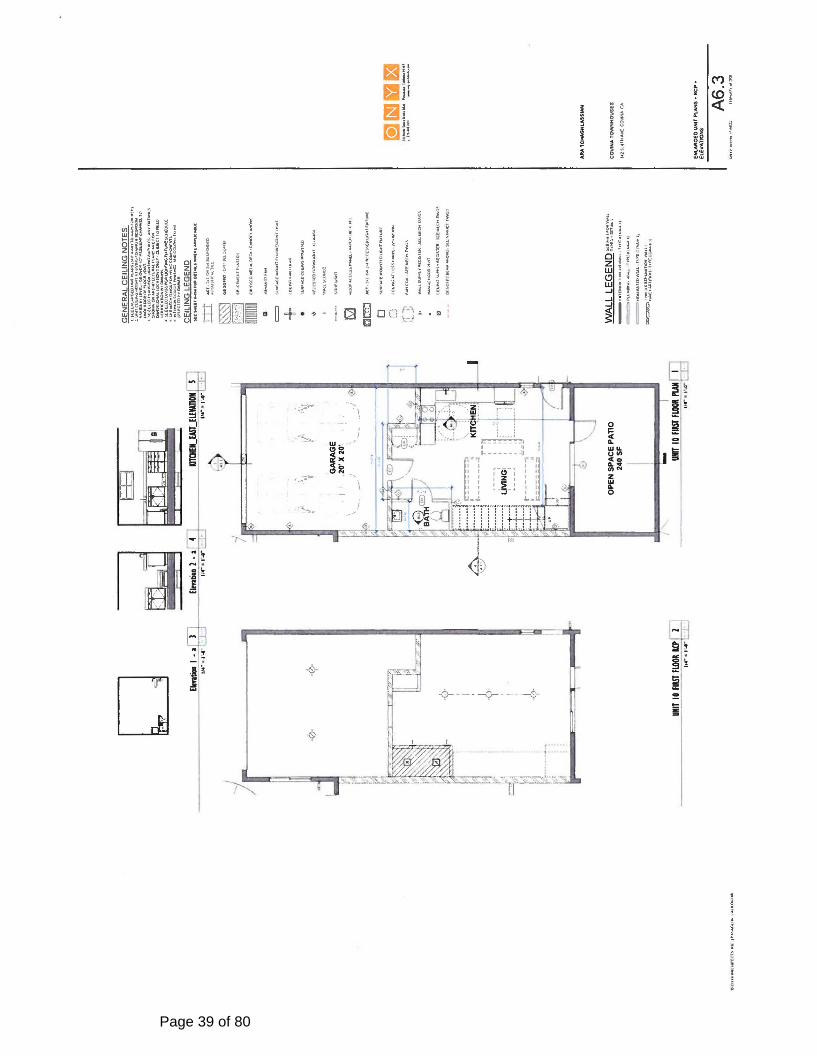

Approving Tentative Tract Map (TTM) 83203 and Site Plan Review (SPR) 20-

004, a Residential Subdivision for Condominium Purpose and the Development

of the Property for 10-Unit Townhouses on Approximately 0.72 Acres of Land

Zoned RD Residential Zone (Multiple-Family), Located at 342 South Fourth

Avenue – APN: 8444-010-900

Staff Recommendation:

Adopt Resolution CC 2021-10 approving a Mitigated Negative Declaration (MND)

as adequately prepared in accordance with California Environmental Quality Act

(CEQA), the required findings under CEQA and the Mitigation Monitoring and

Reporting Program for GPA 19-00, TTM 83202 and SPR20-004, and approving

General Plan Amendment (GPA) 19-002, amending the Land Use Map of the Covina

General Plan to change the Land Use designation from School to High Density

Residential for a 0.72-acre property, located at 342 South Fourth Avenue – APN:

8444-010-900; and Adopt Resolution CC 2021-11, approving Tentative Tract Map

(TTM) 83203 and Site Plan Review (SPR) 20-004, a residential subdivision for

condominium purpose and the development of the property for 10-unit townhouses on

approximately 0.72 acres of land zoned RD Residential Zone (Multiple-Family),

located at 342 South Fourth Avenue – APN: 8444-010-900. Agenda Report - PH Resolutions CC 2021-10 & 2021-11 342 S Fourth Ave - Pdf

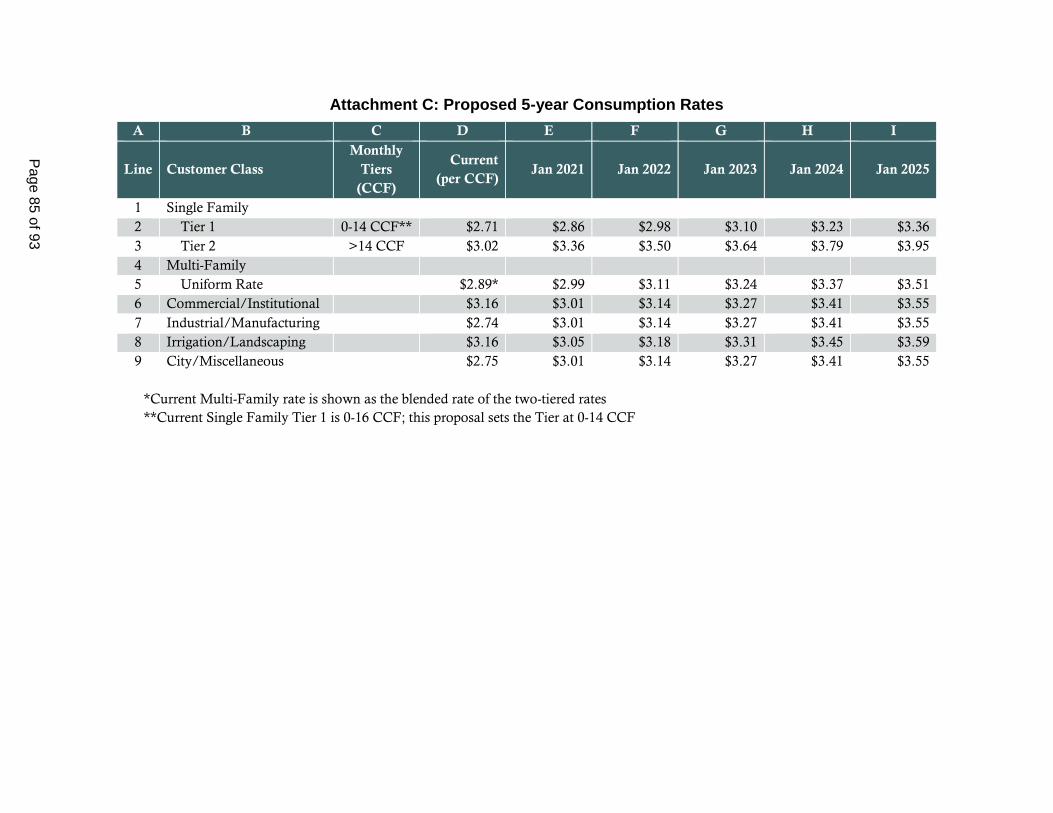

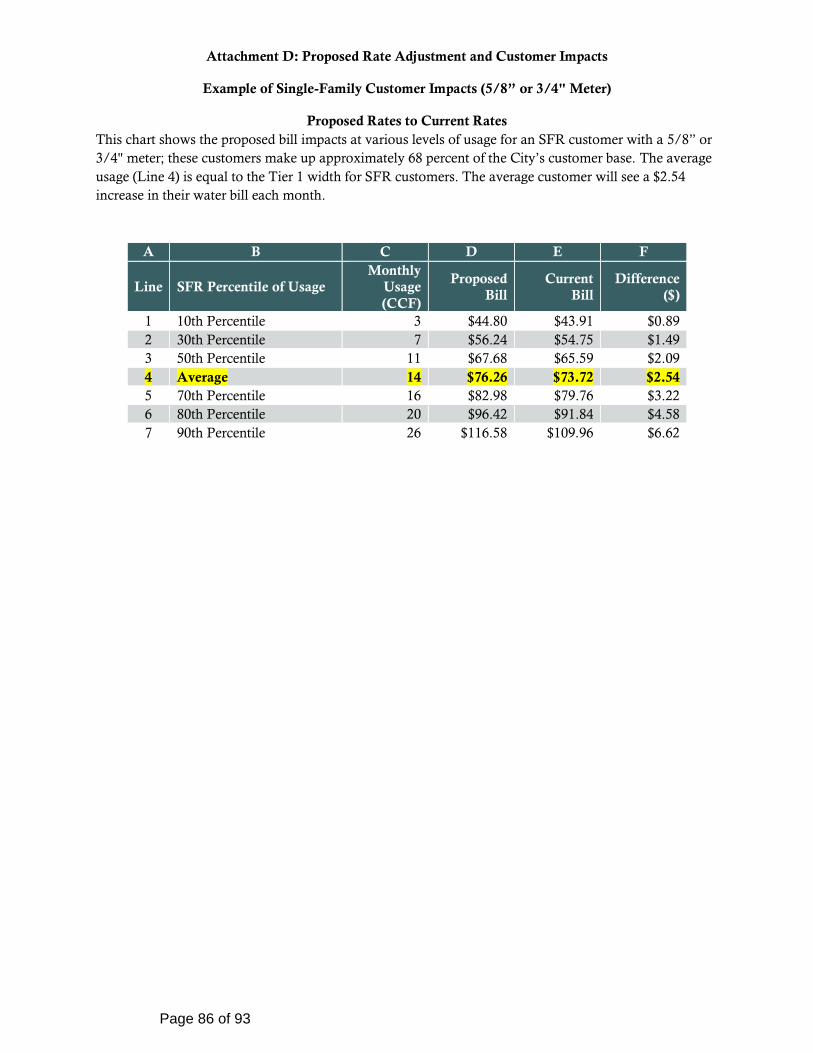

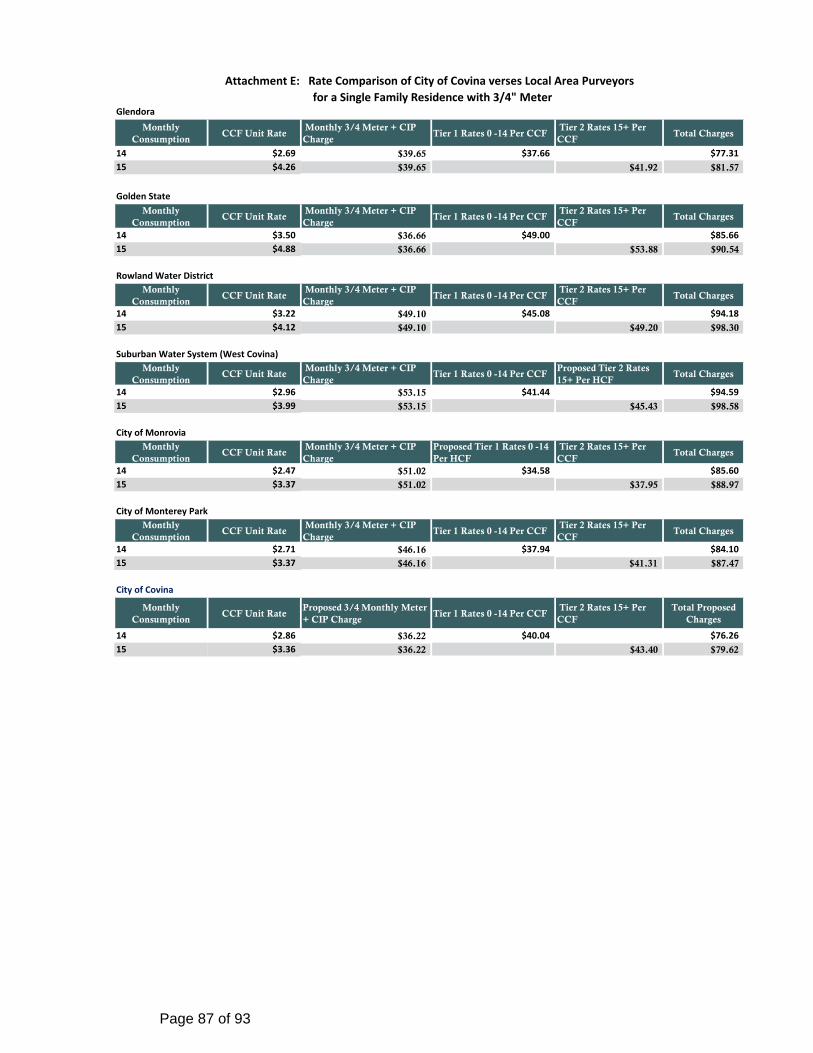

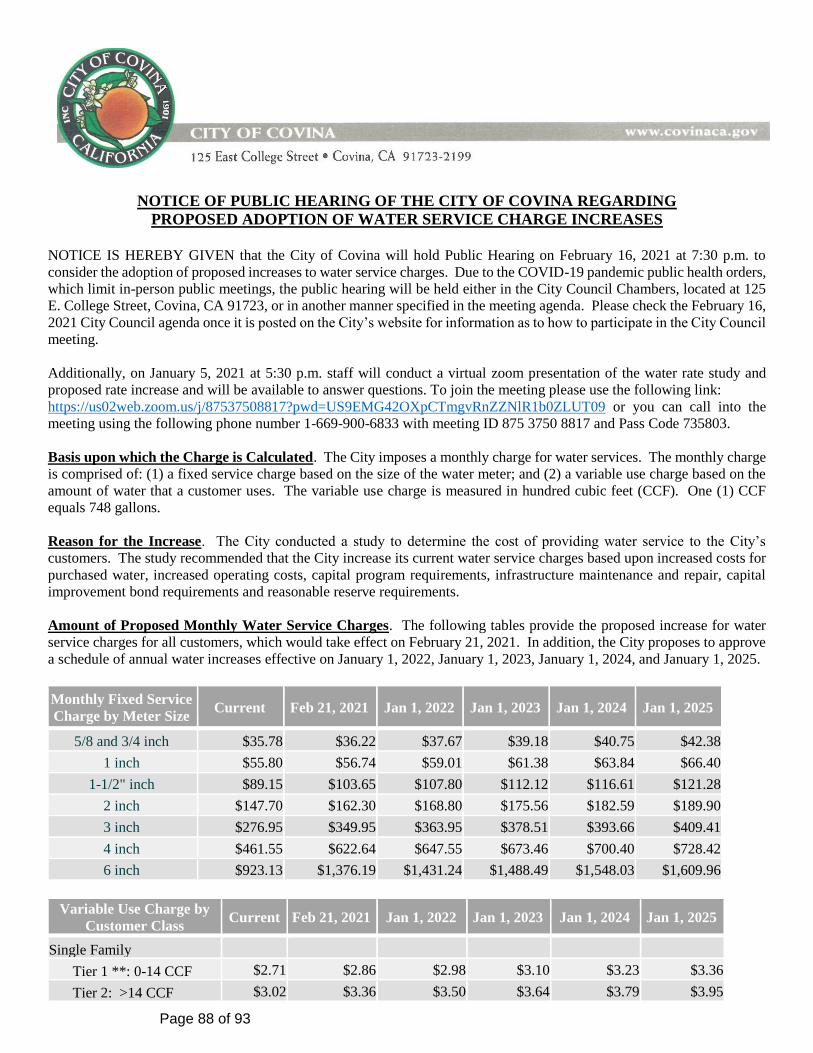

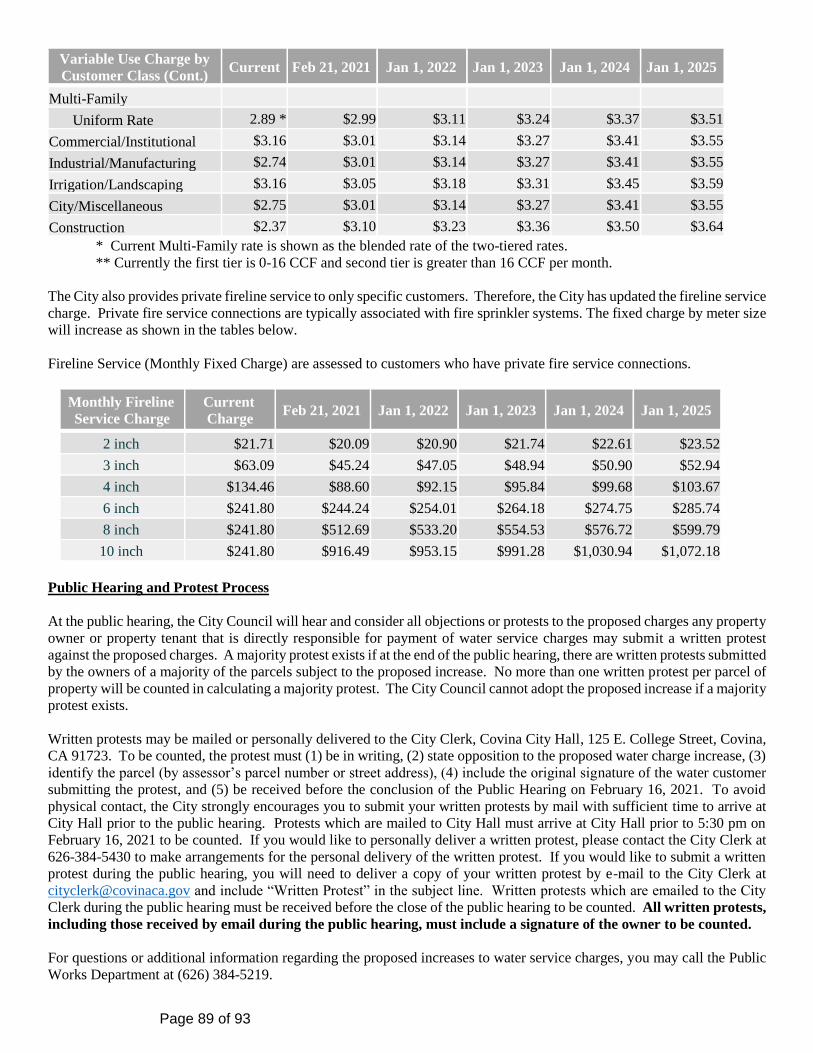

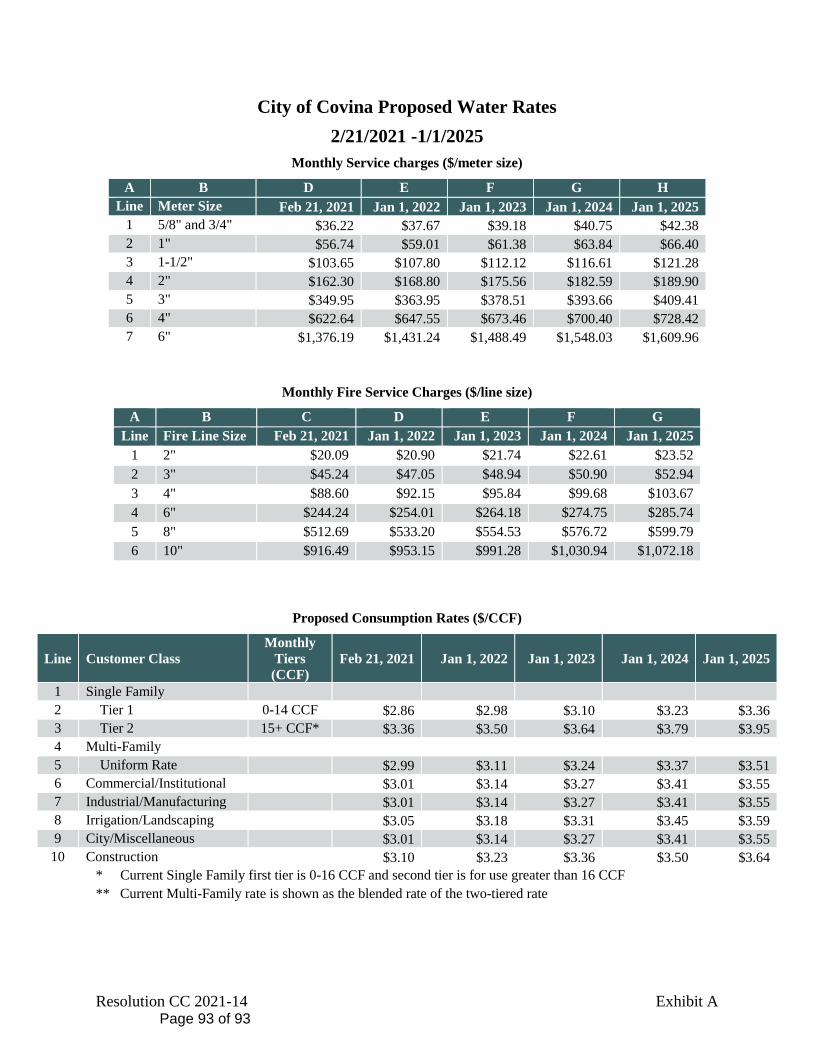

PH 4. Public Hearing for Consideration of Adopting Resolution CC 2021-14 Amending

Existing Water Rates

Staff Recommendation:

1. That the City Council conduct the Public Hearing and if it is determined that a

majority protest does not exist adopt Resolution CC 2021-14 establishing a new five-

year schedule of water rates within the areas serviced by the City’s Water Division to

address wholesale water cost increases and future water system capital improvement

needs; and

2. Close Public Hearing and adopt new five-year schedule of water rates within the

areas serviced by the City’s Water Division. Agenda Report - Resolution CC 2021-14 Amending Existing Water Rates - Pdf

CONTINUED BUSINESS - NONE.

NEW BUSINESS - NONE.

ADJOURNMENT

The Covina City Council/Successor Agency to the Covina Redevelopment Agency/Covina Public

Financing Authority/Covina Housing Authority will adjourn to its next regular meeting of the

Council/Agency/Authority scheduled for Tuesday, March 2, 2021, at 6:30 p.m. for closed session

and at 7:30 p.m. for open session inside the Council Chamber at City Hall, located at 125 East

College Street, Covina, California, 91723.

City Council/CSA/CPFA/CHA Agenda Tuesday February 16, 2021

The Covina City Clerk’s Office does hereby declare that, in accordance with California Government Code Section 54954.2(a), the agenda for the Tuesday, February 16, 2021, meeting was posted on February 11, 2021, on the City’s website and near the front entrances of: 1) Covina City Hall, 125 East College Street, Covina; and 2) the Covina Public Library, 234 N. Second Avenue, Covina.

If you challenge in court any discussion or action taken concerning an item on this agenda, you may be limited to raising only

those issues you or someone else raised during the meeting or in written correspondence delivered to the City at or prior to the

City’s consideration of the item at the meeting.

MATERIALS RELATED TO AN ITEM ON THIS AGENDA, AND SUBMITTED TO THE CITY COUNCIL AFTER

PUBLICATION OF THE AGENDA, ARE AVAILABLE TO THE PUBLIC IN THE CITY CLERK’S OFFICE AT 125 E.

COLLEGE STREET, COVINA.

COUNCIL/CSA/CPFA/CHA MINUTES Page 1 of 6 Tuesday, February 2, 2021

MINUTES OF FEBRUARY 2, 2021

REGULAR MEETING OF THE COVINA CITY COUNCIL/SUCCESSOR AGENCY TO

THE COVINA REDEVELOPMENT AGENCY/COVINA PUBLIC FINANCING

AUTHORITY/COVINA HOUSING AUTHORITY HELD IN THE COUNCIL CHAMBER

OF CITY HALL, 125 EAST COLLEGE STREET, COVINA, CALIFORNIA/VIRTUAL

MEETING

This meeting was conducted utilizing teleconferencing and electronic means consistent with State

of California Executive Order N-29-20 dated March 17, 2020, regarding the COVID-19 pandemic.

CLOSED SESSION – None.

CALL TO ORDER

Mayor Linares called the Council/Agency/Authority meeting to order at 7:30 p.m. with all

Councilmembers present.

Mayor Linares announced that no closed session was held and that the meeting was being

conducted in a virtual setting using Zoom and that members of the public may view and listen to

the meting live on the City’s website at covinaca.gov or on cable television Spectrum channel 29

or Frontier channel 42.

ROLL CALL

Councilmembers Present: Walter Allen, III, Patricia Cortez, John C. King, Mayor Pro

Tem/Vice-Chair Jorge A. Marquez, Mayor/Chair Victor Linares.

Councilmembers Absent: None.

Elected Members Present: City Clerk Mary Lou Walczak.

Elected Members Absent: City Treasurer Geoffrey Cobbett.

Staff Members Present: City Manager Chris Marcarello, City Attorney Candice K. Lee,

Police Chief John Curley, Administrative Services Director Anita Agramonte, Community

Development Director Brian Lee, Parks & Recreation/Library Services Director Lisa Evans,

Public Works Director Andy Bullington, Assistant to the City Manager Angel Carrillo, and Chief

Deputy City Clerk Nicole Alvarez.

PLEDGE OF ALLEGIANCE

Mayor Pro Tem Marquez led the Pledge of Allegiance.

INVOCATION

Councilmember John King gave the invocation.

ITEM NO. CC 1

COUNCIL/CSA/CPFA/CHA MINUTES Page 2 of 6 Tuesday, February 2, 2021

PRESENTATIONS

A. Police Chief Curley Retirement Acknowledgement

City Manager Marcarello gave a brief presentation, highlighting the career of Police Chief Curley.

City Manager Marcarello congratulated Police Chief Curley on a well-deserved retirement. City

Council, Director of Government Affairs Brian Johsz, on behalf of Athens Services, Vernon Police

Chief Tony Miranda on behalf of the Los Angeles County Police Chiefs Association, Phil Ramirez,

on behalf of the Covina Police Volunteers, Los Angeles County Assistant Fire Chief Mike Inman,

Covina Police Captain Povero and Covina Police Captain Walczak on behalf of the Police

Management Group, provided heartfelt comments as they recalled their memories with Police

Chief Curley, wished him well on his new position with Foothill Transit, and thanked Police Chief

Curley’s wife and daughters for their sacrifice.

Police Chief Curley was presented with two plaques: one plaque was presented by Phil Ramirez,

on behalf of the Covina Police Volunteers, in appreciation for his guidance and leadership with

the volunteer program; and the other plaque was presented by Mayor Linares, on behalf of City

Council, which memorialized his time here at the City of Covina.

Police Chief Curley said a few words regarding his retirement and expressed his thanks and

appreciation for all those he has worked with and his friends and family that have supported him.

Two videos were shared: the first video highlighted Police Chief Curley’s career with the City of

Covina; and the second video was of coworkers, colleagues and community members thanking

him for his many years of dedicated service to the City of Covina, congratulating him on his

retirement, and wishing him well.

Councilmember King provided words of admiration to Police Chief Curley.

Police Chief Curley’s daughter, on behalf of her and her sister, commented that their dad has been

great at balancing his home life and work life and it’s clear that he excels in all areas of his life

and expressed how very proud they are of their dad.

Police Chief Curley’s wife, Bobbi, expressed her pride in her husband and thanked City Manager

Marcarello, City Council, Honorable Mayor, the Covina Police Department, and the community

for all their support.

PUBLIC COMMENTS

Public comments were provided via email which were read aloud by Chief Deputy City Clerk

Alvarez and City Clerk Walczak. The comments are summarized below.

Phyllis Meadow commented on Police Chief Curley’s retirement, wished him many successful,

healthy and productive years, and gave him sincere thanks for his many years of service.

Evan Clark requested that City Council represent all community members regardless of their

religious beliefs, to support religious freedom, religious diversity and inclusivity, and to reject

sectarian gifts.

COUNCIL/CSA/CPFA/CHA MINUTES Page 3 of 6 Tuesday, February 2, 2021

Brienne Bennett commented against invocations and requested that City Council represent all

community members regardless of their religious beliefs, to support religious freedom, religious

diversity and inclusivity.

Sabrina Loesh commented against religion and religious reference in City Council meetings.

Jonathan Hawes requested that City Council call out the crimes of Andre Quintero and Team El

Monte’s embezzlement of $10 million form the El Monte Promise Foundation scholarship fund

and protect the vulnerable residents.

Jolie Key commented in support of opening up Council meetings to all belief and non-belief

systems, or to separate from religion completely.

Arul Teimouri commented against invocations and distribution of religious books to members of

the council and questioned if it is acceptable to give gifts to members of the Council.

Neil Polzin implored City Council to implement a $4/hour increased wage for essential workers

including grocery workers and restaurant and other food workers/servers; requested that Council

add additional restrictions to Covina and at the very minimum send a clear message that Covina

stands with public health mandates; expressed his hope that the Mayor would wear a mask to

Council meetings; and asked the City Attorney to review and offer recommendations to correct

the clear endorsement of religion.

Lauren Polzin commented against offering bibles in the role of a city official.

CITY MANAGER COMMENTS

City Manager Marcarello informed that the Covina Police Department has resumed overnight

parking enforcement but will be taking a phased approach with issuing warnings first, and how to

purchase parking permits. City Manager Marcarello commented regarding the roll-out of vaccines.

COUNCIL/AGENCY/AUTHORITY COMMENTS

Councilmember Allen gave another shout out to Police Chief Curley for being iconic.

Councilmember Allen commented regarding the public comments provided tonight and clarified

that City Council were not given bibles as the public comments suggested, but were given candy

regarding a pantry that gives food out to the homeless.

Councilmember Cortez also commented regarding the public comments made tonight and clarified

that City Council did not pass out bibles, but chocolates.

Councilmember King agreed with Councilmember Cortez’ comments and indicated that different

groups/different cultures have come in to share many different things with City Council and City

Council has always treated everyone with the utmost respect and do not treat anyone differently

because of their beliefs or their approach.

Mayor Pro Tem Marquez also confirmed the items given were chocolates and indicated he’ll reach

out to the City Attorney and City Manager regarding invocations.

COUNCIL/CSA/CPFA/CHA MINUTES Page 4 of 6 Tuesday, February 2, 2021

Mayor Linares commented that today is about Police Chief Curley and the great police chief he

has been and he tipped his hat off to him and thanked him once again for his service. Mayor Linares

commented that he has spoken to a lot of senior residents and that City Council, staff and the City

Manager have been working hard to work with some health care providers to have a site in Covina

where they can get COVID testing and hopefully vaccines. Mayor Linares expressed his thanks to

Covina resident Barbara Baker for her help and huge support in helping Covina residents make

appointments to get vaccines. He thanked the residents for their support and urged the residents to

stay safe in light of the Super Bowl.

CONSENT CALENDAR

A motion was made by Mayor Pro Tem Marquez, seconded by Councilmember King, to approve

Consent Calendar items CC 1 – 6 as presented.

Motion approved by roll call vote for Consent Calendar items CC 1 – 6 as follows:

AYES: ALLEN, CORTEZ, KING, MARQUEZ, LINARES

NOES: NONE

ABSTAIN: NONE

ABSENT: NONE

CC 1. City Council/Successor Agency to the Covina Redevelopment Agency/Covina Public

Financing Authority/Covina Housing Authority approved the Minutes of the January

19, 2021, Regular Meeting of the City Council/Successor Agency to the Covina

Redevelopment Agency/Covina Public Financing Authority/Housing Authority. CC 2. City Council/Successor Agency to the Covina Redevelopment Agency approved the

Payment of Demands in the amount of $2,995,137.77.

CC 3. City Council accepted the work performed by SKY JTC Corporation; and authorized

the City Clerk to file a Notice of Completion for the Metrolink Parking Station

Improvements Project. CC 4. City Council authorized the reorganization of the Administrative Services Department

Finance Division and took the following actions:

A. Adopted Resolution CC-2021-05 to Amend the Mid-Management,

Supervisory and Professional, and Confidential and Technical Employees

Compensation Rules to Reinstate the Finance Manager classification,

including Job Description and Salary Schedule and reclassify the current

Accounting Supervisor to the Finance Manager position.

B. Reclassified the current Management Analyst to the Senior Management

Analyst position.

C. Reclassified the current Accountant to the Senior Accountant position.

D. Replaced the Part Time Account Clerk II with a Part Time Administrative

Technician position. CC 5. City Council rejected all Bids received for the Covina Park Walking / Bike Trail

Project; and authorized staff to re-advertise the project for bids. CC 6. City Council adopted Resolution CC 2021-03 appropriating donations from The

Champion Family Foundation in the amount of $10,000 for police equipment and

installation and increased the Police Department Fiscal Year budget 2020-21 by the

same amount.

COUNCIL/CSA/CPFA/CHA MINUTES Page 5 of 6 Tuesday, February 2, 2021

PUBLIC HEARINGS – None.

CONTINUED BUSINESS

CB 1. Authorization to File Validation Action and Authorization of Issuance of Pension

Obligation Bonds The agenda report was presented by Administrative Services Director Agramonte.

Kevin Hale from Orrick provided a brief overview of the validation process.

There were no public comments.

A motion was made by Councilmember King, seconded by Councilmember Cortez, to:

1. Adopt Resolution CC 2021-04 of the City of Covina providing for the issuance of one or

more series of City of Covina taxable Pension Obligation Bonds and authorizing a Trust

Agreement, a validation action and other matters relating thereto; and

2. Authorize the City to issue Pension Obligation Bonds to refund its CalPERS Unfunded

Accrued Liability in an amount not to exceed $74 million and to pay associated costs of

issuance; and

3. Authorize the City to file judicial validation proceedings related the issuance of such

Pension Obligation Bonds.

Motion approved by roll call vote for Continued Business item CB 1 as follows:

AYES: ALLEN, CORTEZ, KING, MARQUEZ, LINARES

NOES: NONE

ABSTAIN: NONE

ABSENT: NONE

CB 2. Consideration of Survey Feedback from FM3 Research Inc. Related to the Public

Opinion Community Survey on Cannabis and General Community Topics

Staff Recommendation:

That the City Council review feedback from the public opinion community survey and

provide additional direction.

A PowerPoint presentation regarding the City of Covina Community and Cannabis Issues Survey

was presented by FM3 Research Senior Vice President Rick Sklarz.

Discussion and questions included question development, population sample size, survey format

to include individual or multiple issues, and knowledge of sample group.

Assistant to the City Manager Carrillo gave a report on behalf of the ad-hoc committee, including

a list of steps for Council’s consideration and further direction.

A public comment was received via email from Dennis Kies which was read by Chief Deputy City

Clerk Alvarez. The comment is summarized below.

Dennis Kies expressed his concerns over the recent “City of Covina Community Issues” survey.

COUNCIL/CSA/CPFA/CHA MINUTES Page 6 of 6 Tuesday, February 2, 2021

Mayor Linares clarified that today City Council is not taking any action on marijuana in the City

of Covina and that City Council is only receiving feedback from the ad-hoc committee and survey.

Mayor Linares also advised that there will be community outreach.

Discussion included, ad-hoc committee perspective, appreciation for ad-hoc committee and FM3

Research team, concern for public safety, five steps recommended by the ad-hoc committee,

gathering more information, community outreach, and local control.

A motion was made by Councilmember Cortez, seconded by Councilmember King, to take the

following steps:

1. Community outreach – Conduct up to four information and outreach sessions to gain

additional feedback on cannabis programs and uses;

2. Review cannabis programs developed in other communities – Evaluate entitlement

processes, land use constraints and operating guidelines and draft local program guidelines;

3. Public safety review – Engage with police stakeholders in other communities where

cannabis programs have been adopted;

4. Federal regulatory environment – Engage with Federal representatives to evaluate potential

legislative efforts to amend existing regulations; and

5. Joint discussion with Planning Commission – Conduct a joint study session to review

public opinion survey feedback and evaluate cannabis uses.

Motion approved by roll call vote for Continued Business item CB 2 as follows:

AYES: ALLEN, CORTEZ, KING, MARQUEZ, LINARES

NOES: NONE

ABSTAIN: NONE

ABSENT: NONE

NEW BUSINESS – None.

ADJOURNMENT

At 9:59 p.m., the meeting of the Covina City Council/Successor Agency to the Covina

Redevelopment Agency/Covina Public Financing Authority/Covina Housing Authority was

adjourned to its next regular meeting of the Council/Agency/Authority on Tuesday, February 16,

2021, at 6:30 p.m. for closed session and 7:30 p.m. for open session in the Council Chamber of

City Hall located at 125 East College Street, Covina, CA 91723.

Respectfully Submitted:

__________________________________________

Georgianna Nicole Alvarez, CMC, CPMC

Chief Deputy City Clerk

Approved this 2nd day of February, 2021:

_____________________________________

Victor Linares, Mayor/Chair

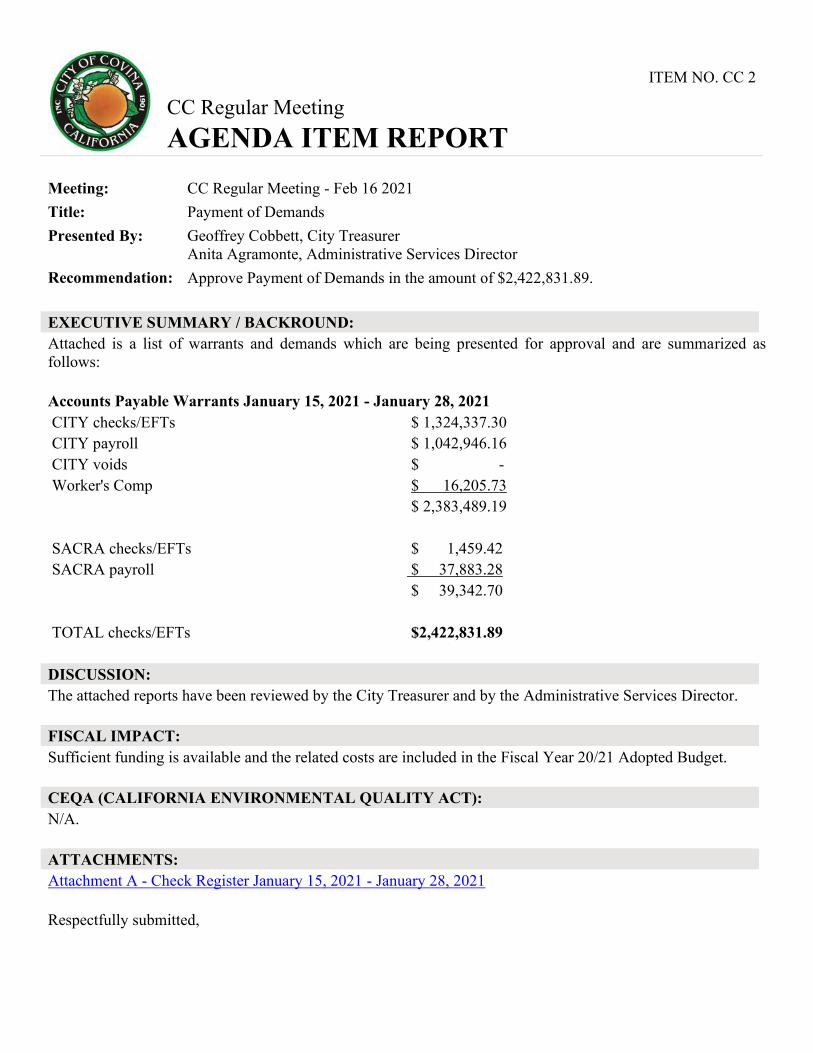

CC Regular Meeting AGENDA ITEM REPORT

ITEM NO. CC 2

Meeting: CC Regular Meeting - Feb 16 2021 Title: Payment of Demands Presented By: Geoffrey Cobbett, City Treasurer

Anita Agramonte, Administrative Services Director Recommendation: Approve Payment of Demands in the amount of $2,422,831.89. EXECUTIVE SUMMARY / BACKROUND: Attached is a list of warrants and demands which are being presented for approval and are summarized as follows: Accounts Payable Warrants January 15, 2021 - January 28, 2021 CITY checks/EFTs $ 1,324,337.30 CITY payroll $ 1,042,946.16 CITY voids $ - Worker's Comp $ 16,205.73 $ 2,383,489.19 SACRA checks/EFTs $ 1,459.42 SACRA payroll $ 37,883.28 $ 39,342.70 TOTAL checks/EFTs $2,422,831.89 DISCUSSION: The attached reports have been reviewed by the City Treasurer and by the Administrative Services Director. FISCAL IMPACT: Sufficient funding is available and the related costs are included in the Fiscal Year 20/21 Adopted Budget. CEQA (CALIFORNIA ENVIRONMENTAL QUALITY ACT): N/A. ATTACHMENTS: Attachment A - Check Register January 15, 2021 - January 28, 2021 Respectfully submitted,

Page 2 of 6

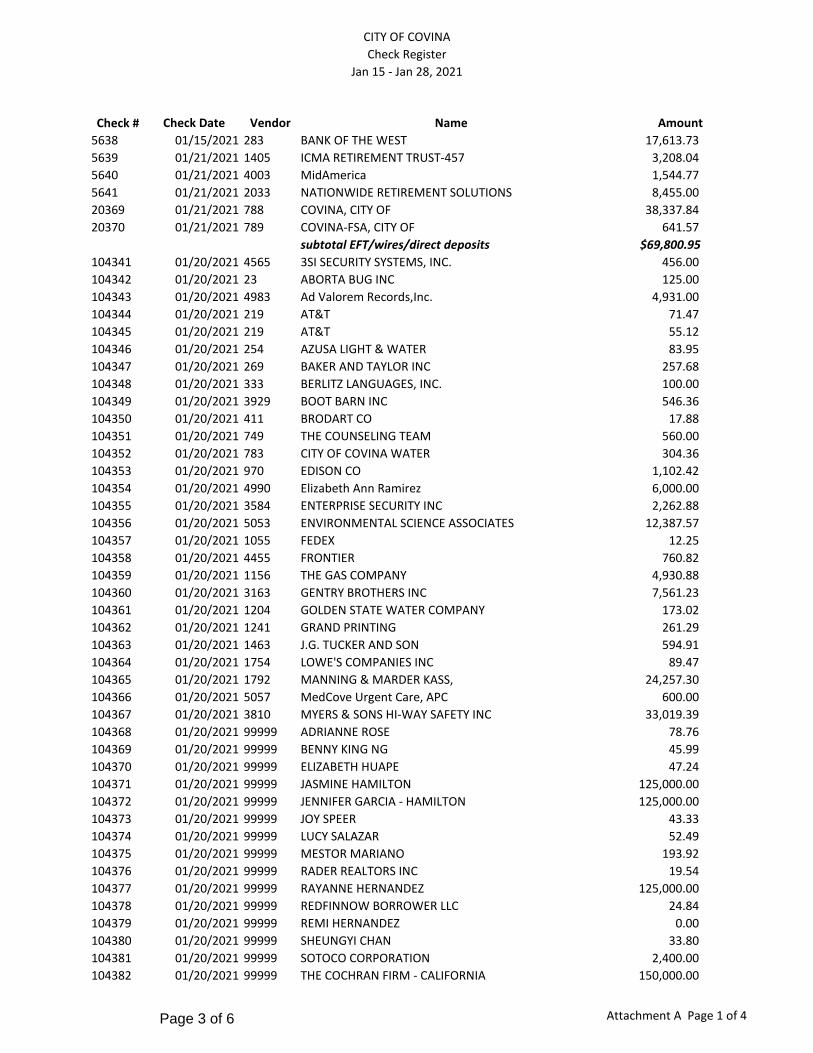

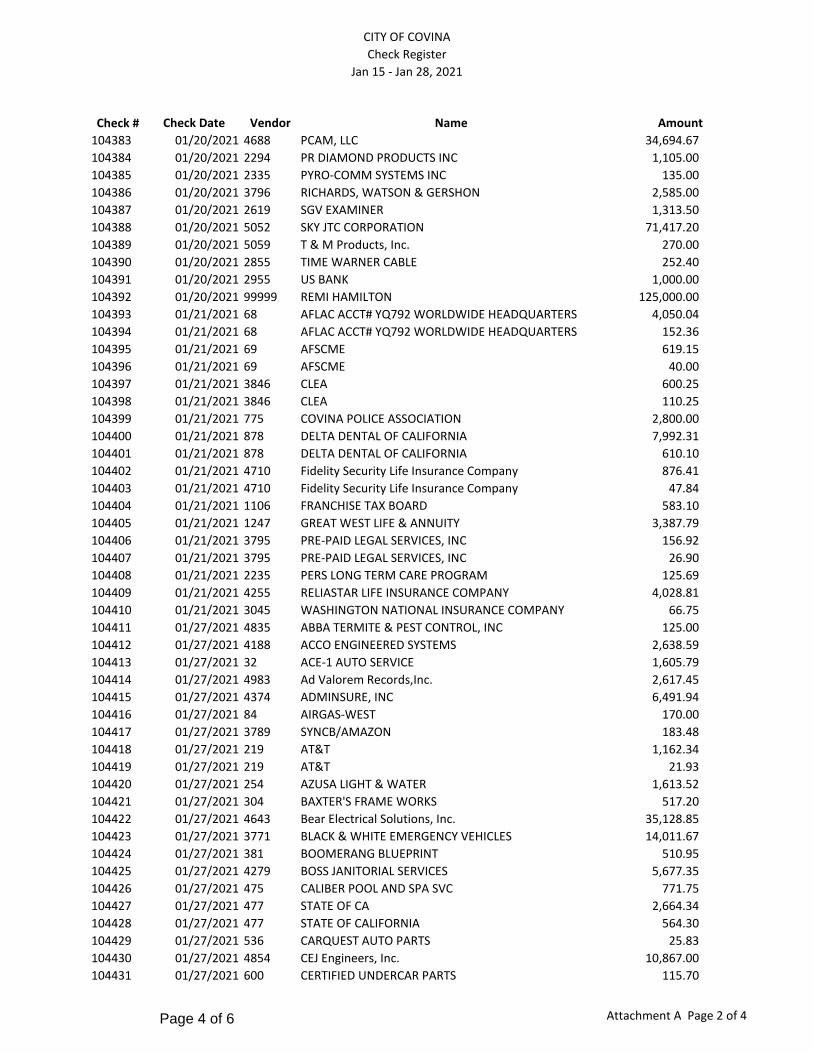

CITY OF COVINA

Check Register

Jan 15 - Jan 28, 2021

Check # Check Date Vendor Name Amount

5638 01/15/2021 283 BANK OF THE WEST 17,613.73

5639 01/21/2021 1405 ICMA RETIREMENT TRUST-457 3,208.04

5640 01/21/2021 4003 MidAmerica 1,544.77

5641 01/21/2021 2033 NATIONWIDE RETIREMENT SOLUTIONS 8,455.00

20369 01/21/2021 788 COVINA, CITY OF 38,337.84

20370 01/21/2021 789 COVINA-FSA, CITY OF 641.57

subtotal EFT/wires/direct deposits $69,800.95

104341 01/20/2021 4565 3SI SECURITY SYSTEMS, INC. 456.00

104342 01/20/2021 23 ABORTA BUG INC 125.00

104343 01/20/2021 4983 Ad Valorem Records,Inc. 4,931.00

104344 01/20/2021 219 AT&T 71.47

104345 01/20/2021 219 AT&T 55.12

104346 01/20/2021 254 AZUSA LIGHT & WATER 83.95

104347 01/20/2021 269 BAKER AND TAYLOR INC 257.68

104348 01/20/2021 333 BERLITZ LANGUAGES, INC. 100.00

104349 01/20/2021 3929 BOOT BARN INC 546.36

104350 01/20/2021 411 BRODART CO 17.88

104351 01/20/2021 749 THE COUNSELING TEAM 560.00

104352 01/20/2021 783 CITY OF COVINA WATER 304.36

104353 01/20/2021 970 EDISON CO 1,102.42

104354 01/20/2021 4990 Elizabeth Ann Ramirez 6,000.00

104355 01/20/2021 3584 ENTERPRISE SECURITY INC 2,262.88

104356 01/20/2021 5053 ENVIRONMENTAL SCIENCE ASSOCIATES 12,387.57

104357 01/20/2021 1055 FEDEX 12.25

104358 01/20/2021 4455 FRONTIER 760.82

104359 01/20/2021 1156 THE GAS COMPANY 4,930.88

104360 01/20/2021 3163 GENTRY BROTHERS INC 7,561.23

104361 01/20/2021 1204 GOLDEN STATE WATER COMPANY 173.02

104362 01/20/2021 1241 GRAND PRINTING 261.29

104363 01/20/2021 1463 J.G. TUCKER AND SON 594.91

104364 01/20/2021 1754 LOWE'S COMPANIES INC 89.47

104365 01/20/2021 1792 MANNING & MARDER KASS, 24,257.30

104366 01/20/2021 5057 MedCove Urgent Care, APC 600.00

104367 01/20/2021 3810 MYERS & SONS HI-WAY SAFETY INC 33,019.39

104368 01/20/2021 99999 ADRIANNE ROSE 78.76

104369 01/20/2021 99999 BENNY KING NG 45.99

104370 01/20/2021 99999 ELIZABETH HUAPE 47.24

104371 01/20/2021 99999 JASMINE HAMILTON 125,000.00

104372 01/20/2021 99999 JENNIFER GARCIA - HAMILTON 125,000.00

104373 01/20/2021 99999 JOY SPEER 43.33

104374 01/20/2021 99999 LUCY SALAZAR 52.49

104375 01/20/2021 99999 MESTOR MARIANO 193.92

104376 01/20/2021 99999 RADER REALTORS INC 19.54

104377 01/20/2021 99999 RAYANNE HERNANDEZ 125,000.00

104378 01/20/2021 99999 REDFINNOW BORROWER LLC 24.84

104379 01/20/2021 99999 REMI HERNANDEZ 0.00

104380 01/20/2021 99999 SHEUNGYI CHAN 33.80

104381 01/20/2021 99999 SOTOCO CORPORATION 2,400.00

104382 01/20/2021 99999 THE COCHRAN FIRM - CALIFORNIA 150,000.00

Attachment A Page 1 of 4Page 3 of 6

CITY OF COVINA

Check Register

Jan 15 - Jan 28, 2021

Check # Check Date Vendor Name Amount

104383 01/20/2021 4688 PCAM, LLC 34,694.67

104384 01/20/2021 2294 PR DIAMOND PRODUCTS INC 1,105.00

104385 01/20/2021 2335 PYRO-COMM SYSTEMS INC 135.00

104386 01/20/2021 3796 RICHARDS, WATSON & GERSHON 2,585.00

104387 01/20/2021 2619 SGV EXAMINER 1,313.50

104388 01/20/2021 5052 SKY JTC CORPORATION 71,417.20

104389 01/20/2021 5059 T & M Products, Inc. 270.00

104390 01/20/2021 2855 TIME WARNER CABLE 252.40

104391 01/20/2021 2955 US BANK 1,000.00

104392 01/20/2021 99999 REMI HAMILTON 125,000.00

104393 01/21/2021 68 AFLAC ACCT# YQ792 WORLDWIDE HEADQUARTERS 4,050.04

104394 01/21/2021 68 AFLAC ACCT# YQ792 WORLDWIDE HEADQUARTERS 152.36

104395 01/21/2021 69 AFSCME 619.15

104396 01/21/2021 69 AFSCME 40.00

104397 01/21/2021 3846 CLEA 600.25

104398 01/21/2021 3846 CLEA 110.25

104399 01/21/2021 775 COVINA POLICE ASSOCIATION 2,800.00

104400 01/21/2021 878 DELTA DENTAL OF CALIFORNIA 7,992.31

104401 01/21/2021 878 DELTA DENTAL OF CALIFORNIA 610.10

104402 01/21/2021 4710 Fidelity Security Life Insurance Company 876.41

104403 01/21/2021 4710 Fidelity Security Life Insurance Company 47.84

104404 01/21/2021 1106 FRANCHISE TAX BOARD 583.10

104405 01/21/2021 1247 GREAT WEST LIFE & ANNUITY 3,387.79

104406 01/21/2021 3795 PRE-PAID LEGAL SERVICES, INC 156.92

104407 01/21/2021 3795 PRE-PAID LEGAL SERVICES, INC 26.90

104408 01/21/2021 2235 PERS LONG TERM CARE PROGRAM 125.69

104409 01/21/2021 4255 RELIASTAR LIFE INSURANCE COMPANY 4,028.81

104410 01/21/2021 3045 WASHINGTON NATIONAL INSURANCE COMPANY 66.75

104411 01/27/2021 4835 ABBA TERMITE & PEST CONTROL, INC 125.00

104412 01/27/2021 4188 ACCO ENGINEERED SYSTEMS 2,638.59

104413 01/27/2021 32 ACE-1 AUTO SERVICE 1,605.79

104414 01/27/2021 4983 Ad Valorem Records,Inc. 2,617.45

104415 01/27/2021 4374 ADMINSURE, INC 6,491.94

104416 01/27/2021 84 AIRGAS-WEST 170.00

104417 01/27/2021 3789 SYNCB/AMAZON 183.48

104418 01/27/2021 219 AT&T 1,162.34

104419 01/27/2021 219 AT&T 21.93

104420 01/27/2021 254 AZUSA LIGHT & WATER 1,613.52

104421 01/27/2021 304 BAXTER'S FRAME WORKS 517.20

104422 01/27/2021 4643 Bear Electrical Solutions, Inc. 35,128.85

104423 01/27/2021 3771 BLACK & WHITE EMERGENCY VEHICLES 14,011.67

104424 01/27/2021 381 BOOMERANG BLUEPRINT 510.95

104425 01/27/2021 4279 BOSS JANITORIAL SERVICES 5,677.35

104426 01/27/2021 475 CALIBER POOL AND SPA SVC 771.75

104427 01/27/2021 477 STATE OF CA 2,664.34

104428 01/27/2021 477 STATE OF CALIFORNIA 564.30

104429 01/27/2021 536 CARQUEST AUTO PARTS 25.83

104430 01/27/2021 4854 CEJ Engineers, Inc. 10,867.00

104431 01/27/2021 600 CERTIFIED UNDERCAR PARTS 115.70

Attachment A Page 2 of 4Page 4 of 6

CITY OF COVINA

Check Register

Jan 15 - Jan 28, 2021

Check # Check Date Vendor Name Amount

104432 01/27/2021 649 CINTAS CORP #693 434.36

104433 01/27/2021 4714 CIR, Inc. 17,449.61

104434 01/27/2021 654 CITRUS CAR WASH 89.95

104435 01/27/2021 700 COLLEY FORD 1,097.11

104436 01/27/2021 703 COMBINED GRAPHICS 52.92

104437 01/27/2021 749 THE COUNSELING TEAM 600.00

104438 01/27/2021 766 ATHENS SERVICES 5,371.38

104439 01/27/2021 849 DAPEER ROSENBLIT & LITVAK LLP 11,944.00

104440 01/27/2021 3701 DEPARTMENT OF JUSTICE 147.00

104441 01/27/2021 885 DEPT OF MOTOR VEHICLES 88.00

104442 01/27/2021 4886 DG Collision LLC 1,263.34

104443 01/27/2021 4292 DUDEK 240.00

104444 01/27/2021 962 SUPERIOR COURT OF CALIFORNIA, CNTY OF LA 69.00

104445 01/27/2021 962 SUPERIOR COURT OF CALIFORNIA, CNTY OF LA 4,777.50

104446 01/27/2021 970 EDISON CO 110.27

104447 01/27/2021 970 EDISON CO 473.64

104448 01/27/2021 4965 Environment Planning Development Solutions, Inc. 33,377.97

104449 01/27/2021 4682 Evan Brooks Associates, Inc. 3,112.50

104450 01/27/2021 1055 FEDEX 13.99

104451 01/27/2021 4860 Francisco Clemente 992.25

104452 01/27/2021 4455 FRONTIER 107.02

104453 01/27/2021 1156 THE GAS COMPANY 93.04

104454 01/27/2021 4883 Glendora Employment Agency, Inc 1,513.89

104455 01/27/2021 5042 GoGov, Inc. 20,160.00

104456 01/27/2021 4650 GOLDEN BELL PRODUCTS, INC. 11,500.00

104457 01/27/2021 1235 GRAINGER 602.76

104458 01/27/2021 1275 HAAKER EQUIPMENT CO 1,295.96

104459 01/27/2021 1361 HOLLIDAY ROCK CO INC 123.48

104460 01/27/2021 1364 HOME DEPOT CREDIT SERVICES 1,329.65

104461 01/27/2021 3988 LANDSCAPE WAREHOUSE 84.66

104462 01/27/2021 5039 Image Property Services LLC 3,692.29

104463 01/27/2021 4349 Intelli-Tech 3,193.00

104464 01/27/2021 1441 INTERSTATE BATTERY SYSTEM OF EAST SAN GABRIEL 61.17

104465 01/27/2021 4077 INTERWEST CONSULTING GROUP INC 12,603.75

104466 01/27/2021 1463 J.G. TUCKER AND SON 115.65

104467 01/27/2021 3749 JCL TRAFFIC SERVICES 108.57

104468 01/27/2021 1498 JNL CREATIONS 385.88

104469 01/27/2021 1505 JOHNNY'S POOL SERVICE 220.26

104470 01/27/2021 1571 KING BOLT CO 69.41

104471 01/27/2021 1612 LA CNTY DEPT OF PUBLIC WORKS 8,695.08

104472 01/27/2021 1617 LOS ANGELES COUNTY CLERK 225.00

104473 01/27/2021 1619 LA CNTY SHERIFF'S DEPT 1,323.50

104474 01/27/2021 1698 LEXIPOL LLC 2,700.00

104475 01/27/2021 1792 MANNING & MARDER KASS, 14,816.25

104476 01/27/2021 4874 MARIA E. VELOSCO BEDRAN 1,889.42

104477 01/27/2021 4717 Merchants Landscape Services, Inc. 19,081.00

104478 01/27/2021 4833 Michael R. Hillmann 3,445.00

104479 01/27/2021 1933 MISSION LINEN SUPPLY 22.88

104480 01/27/2021 4360 MOORE IACOFANO GOLTSMAN, INC. 332.50

Attachment A Page 3 of 4Page 5 of 6

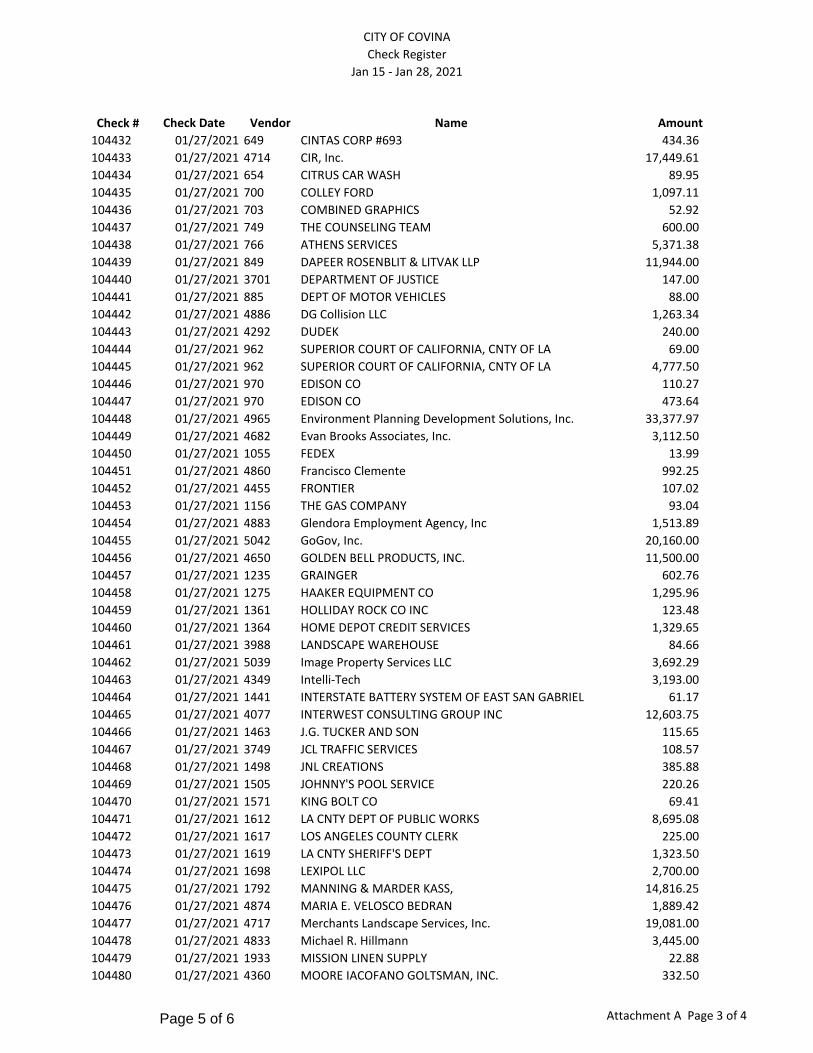

CITY OF COVINA

Check Register

Jan 15 - Jan 28, 2021

Check # Check Date Vendor Name Amount

104481 01/27/2021 2091 O REILLY AUTO PARTS 319.06

104482 01/27/2021 4824 Occu-Med, Ltd. 591.00

104483 01/27/2021 2104 OFFICE DEPOT 76.93

104484 01/27/2021 99999 DAWN A. SMITH 2,404.88

104485 01/27/2021 99999 DOMINIQUE PEREZ 2,850.00

104486 01/27/2021 99999 JOLANDA CHRISTIANSEN 25.00

104487 01/27/2021 99999 SUNBELT CONTROLS 45.00

104488 01/27/2021 99999 THERESA MULLALY 240.00

104489 01/27/2021 99999 WINFRIED BIGGS 25.00

104490 01/27/2021 4662 OverDrive, Inc 6,000.00

104491 01/27/2021 2163 PACIFIC PARKING SYS INC 1,100.00

104492 01/27/2021 2255 PHONE SUPPLEMENTS 1,026.49

104493 01/27/2021 2309 PROFESSIONAL ACCOUNT MANAGEMENT LLC 3,738.22

104494 01/27/2021 2345 QUILL 78.94

104495 01/27/2021 2415 REPUBLIC MASTER CHEFS 419.97

104496 01/27/2021 3796 RICHARDS, WATSON & GERSHON 28,568.73

104497 01/27/2021 4350 RKA Consulting Group 433.75

104498 01/27/2021 4857 Robert Andrew Nava 7,952.00

104499 01/27/2021 2510 S & S WORLDWIDE INC 18.64

104500 01/27/2021 2542 SAN GABRIEL VALLEY WATER ASSOCIATION 25.00

104501 01/27/2021 2581 SCHOLASTIC INC. EDUCATION 6,141.44

104502 01/27/2021 2719 SPARKLETTS 25.26

104503 01/27/2021 4928 Springstead & Associates, Inc. 4,000.00

104504 01/27/2021 2757 STEVEN ENTERPRISES INC 1,126.33

104505 01/27/2021 2804 TAG AMS INC 175.00

104506 01/27/2021 2852 THREE VALLEY MUN WATER DISTR 5,200.82

104507 01/27/2021 2855 TIME WARNER CABLE 35.24

104508 01/27/2021 2903 TRI-XECUTEX CORP 265.95

104509 01/27/2021 4813 JOHNSON CONTROLS FIRE PROTECTION LP 1,308.91

104510 01/27/2021 2935 UNDERGROUND SERVICE ALERT 83.82

104511 01/27/2021 4764 UniFirst Corporation 741.09

104512 01/27/2021 2966 V & V MANUFACTURING 28.61

104513 01/27/2021 4065 VERIZON BUSINESS SERVICES 2,678.96

104514 01/27/2021 3052 WATERLINE TECHNOLOGIES INC 320.38

104515 01/27/2021 3621 WAXIE ENTERPRISES INC 1,737.19

104516 01/27/2021 3078 THOMSON REUTERS - WEST PAYMENT CENTER 376.96

104517 01/27/2021 3137 Y TIRE SALES 2,358.83

104518 01/27/2021 3152 YWCA 961.93

subtotal checks 1,255,995.77$

voids (prior to current mo.) -$

payroll (1/21/2021) 1,080,829.44$

workers' compensation 16,205.73$

TOTAL checks/EFTs $2,422,831.89

Attachment A Page 4 of 4Page 6 of 6

CC Regular Meeting AGENDA ITEM REPORT

ITEM NO. CC 3

Meeting: CC Regular Meeting - Feb 16 2021 Title: Monthly Investment Report of the Treasurer to the City Council and Successor Agency to

the Covina Redevelopment Agency for January 2021 Presented By: Geoffrey Cobbett, City Treasurer

Anita Agramonte, Administrative Services Director Recommendation: Receive and File. EXECUTIVE SUMMARY / BACKROUND: Pursuant to Government Code Section 53600 et seq. and Section 4.0 of the City of Covina’s Investment Policy, a monthly investment report must be provided to the City Council and City Manager, containing detailed information of all securities, investments of the City. DISCUSSION: The attached monthly report for the City reflects the portfolio balances for the month ended January 31, 2021. The report is in conformity with the City’s Investment Policy as well as Government Code 53607. There are

sufficient funds to meet the pooled expenditure requirements for all City funds for the next 6 months. FISCAL IMPACT: None to receive and file. CEQA (CALIFORNIA ENVIRONMENTAL QUALITY ACT): None. ATTACHMENTS: Attachment A - Monthly Investment Report - signed Attachment A-1 - Total Investment Portfolio Attachment A-2 - Investment Transaction Summary Attachment A-3 - City LAIF Statement Attachment A-4 - Successor Agency LAIF Statement Respectfully submitted,

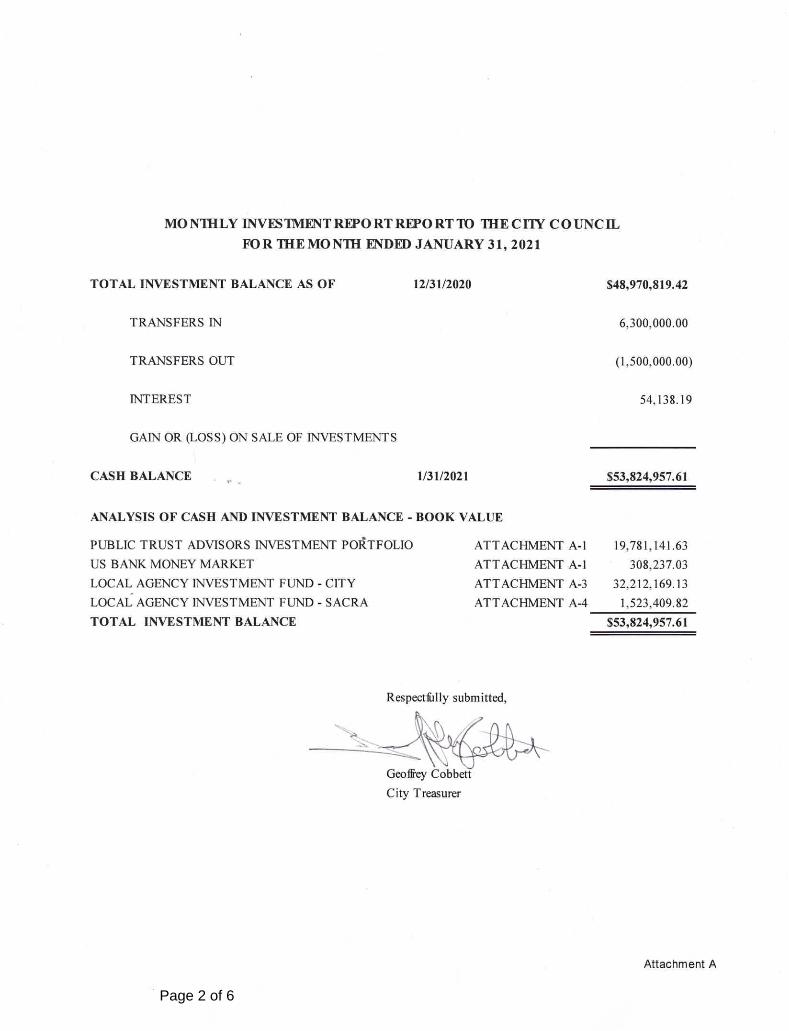

MONTHLY INVIBTNIENTREPORTREPORTTO THE CITY COUNCIL

FOR THE MO NTI-I ENDED JANUARY 31, 2021

TOTAL INVESTMENT BALANCE AS OF 12/31/2020 $48,970,8l9.42

TRANSFERS IN 6.300.000.00

TRANSFERS OUT (l.500.000.00)

INTEREST 54.13X.l9

GAIN OR (LOSS) ON SALE OF INVESTMENTS

CASH BALANCE‘ _

I/31/2021 $53,824,957.6I

ANALYSIS OF CASH AND INVESTMENT BALANCE - BOOK VALUE

PUBLIC TRUST ADVISORS NVESTMENT PORTFOLIO ATTACHNTENT A-1 19,78l,14l.63

US BANK MONEY MARKET ATTACHMENT A-1 308.237.03LOCAL AGENCY INVESTMENT FUND - CITY ATTACI-DVIENT A-3 32.212.169.13LOCALAGENCY INVESTMENT FUND - SACRA ATTACHMENT A-4 1.523.409.82TOTAL INVESTMENT BALANCE $S3,824,957.6l

Respect?xlly submitted,

Geo?iey CobbéttCity Treasurer

Attachment A

Page 2 of 6

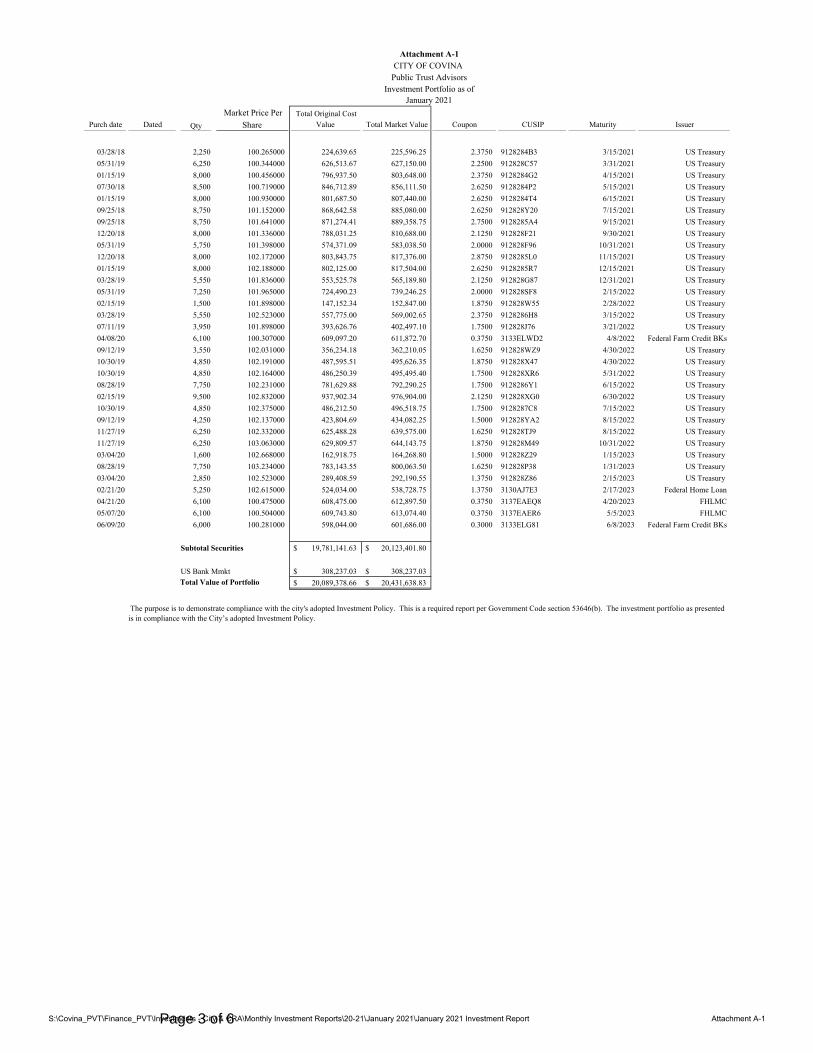

Purch date Dated Qty

Market Price Per

Share Total Original Cost

Value Total Market Value Coupon CUSIP Maturity Issuer

03/28/18 2,250 100.265000 224,639.65 225,596.25 2.3750 9128284B3 3/15/2021 US Treasury

05/31/19 6,250 100.344000 626,513.67 627,150.00 2.2500 912828C57 3/31/2021 US Treasury

01/15/19 8,000 100.456000 796,937.50 803,648.00 2.3750 9128284G2 4/15/2021 US Treasury

07/30/18 8,500 100.719000 846,712.89 856,111.50 2.6250 9128284P2 5/15/2021 US Treasury

01/15/19 8,000 100.930000 801,687.50 807,440.00 2.6250 9128284T4 6/15/2021 US Treasury

09/25/18 8,750 101.152000 868,642.58 885,080.00 2.6250 912828Y20 7/15/2021 US Treasury

09/25/18 8,750 101.641000 871,274.41 889,358.75 2.7500 9128285A4 9/15/2021 US Treasury

12/20/18 8,000 101.336000 788,031.25 810,688.00 2.1250 912828F21 9/30/2021 US Treasury

05/31/19 5,750 101.398000 574,371.09 583,038.50 2.0000 912828F96 10/31/2021 US Treasury

12/20/18 8,000 102.172000 803,843.75 817,376.00 2.8750 9128285L0 11/15/2021 US Treasury

01/15/19 8,000 102.188000 802,125.00 817,504.00 2.6250 9128285R7 12/15/2021 US Treasury

03/28/19 5,550 101.836000 553,525.78 565,189.80 2.1250 912828G87 12/31/2021 US Treasury

05/31/19 7,250 101.965000 724,490.23 739,246.25 2.0000 912828SF8 2/15/2022 US Treasury

02/15/19 1,500 101.898000 147,152.34 152,847.00 1.8750 912828W55 2/28/2022 US Treasury

03/28/19 5,550 102.523000 557,775.00 569,002.65 2.3750 9128286H8 3/15/2022 US Treasury

07/11/19 3,950 101.898000 393,626.76 402,497.10 1.7500 912828J76 3/21/2022 US Treasury

04/08/20 6,100 100.307000 609,097.20 611,872.70 0.3750 3133ELWD2 4/8/2022 Federal Farm Credit BKs

09/12/19 3,550 102.031000 356,234.18 362,210.05 1.6250 912828WZ9 4/30/2022 US Treasury

10/30/19 4,850 102.191000 487,595.51 495,626.35 1.8750 912828X47 4/30/2022 US Treasury

10/30/19 4,850 102.164000 486,250.39 495,495.40 1.7500 912828XR6 5/31/2022 US Treasury

08/28/19 7,750 102.231000 781,629.88 792,290.25 1.7500 9128286Y1 6/15/2022 US Treasury

02/15/19 9,500 102.832000 937,902.34 976,904.00 2.1250 912828XG0 6/30/2022 US Treasury

10/30/19 4,850 102.375000 486,212.50 496,518.75 1.7500 9128287C8 7/15/2022 US Treasury

09/12/19 4,250 102.137000 423,804.69 434,082.25 1.5000 912828YA2 8/15/2022 US Treasury

11/27/19 6,250 102.332000 625,488.28 639,575.00 1.6250 912828TJ9 8/15/2022 US Treasury

11/27/19 6,250 103.063000 629,809.57 644,143.75 1.8750 912828M49 10/31/2022 US Treasury

03/04/20 1,600 102.668000 162,918.75 164,268.80 1.5000 912828Z29 1/15/2023 US Treasury

08/28/19 7,750 103.234000 783,143.55 800,063.50 1.6250 912828P38 1/31/2023 US Treasury

03/04/20 2,850 102.523000 289,408.59 292,190.55 1.3750 912828Z86 2/15/2023 US Treasury

02/21/20 5,250 102.615000 524,034.00 538,728.75 1.3750 3130AJ7E3 2/17/2023 Federal Home Loan

04/21/20 6,100 100.475000 608,475.00 612,897.50 0.3750 3137EAEQ8 4/20/2023 FHLMC

05/07/20 6,100 100.504000 609,743.80 613,074.40 0.3750 3137EAER6 5/5/2023 FHLMC

06/09/20 6,000 100.281000 598,044.00 601,686.00 0.3000 3133ELG81 6/8/2023 Federal Farm Credit BKs

Subtotal Securities 19,781,141.63$ 20,123,401.80$

US Bank Mmkt 308,237.03$ 308,237.03$

20,089,378.66$ 20,431,638.83$ Total Value of Portfolio

The purpose is to demonstrate compliance with the city's adopted Investment Policy. This is a required report per Government Code section 53646(b). The investment portfolio as presented is in compliance with the City’s adopted Investment Policy.

Attachment A-1CITY OF COVINA

Public Trust AdvisorsInvestment Portfolio as of

January 2021

S:\Covina_PVT\Finance_PVT\Investments - City & CRA\Monthly Investment Reports\20-21\January 2021\January 2021 Investment Report Attachment A-1Page 3 of 6

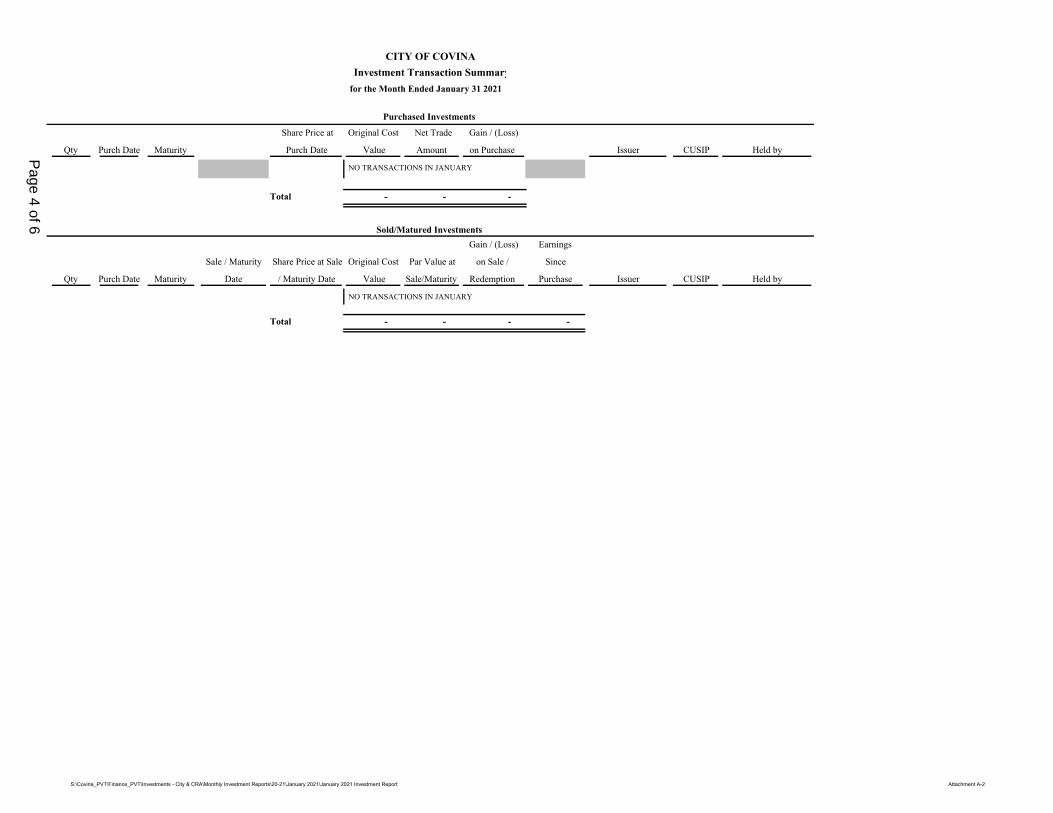

Qty Purch Date Maturity

Share Price at

Purch Date

Original Cost

Value

Net Trade

Amount

Gain / (Loss)

on Purchase Issuer CUSIP Held by

NO TRANSACTIONS IN JANUARY

Total - - -

Qty Purch Date Maturity

Sale / Maturity

Date

Share Price at Sale

/ Maturity Date

Original Cost

Value

Par Value at

Sale/Maturity

Gain / (Loss)

on Sale /

Redemption

Earnings

Since

Purchase Issuer CUSIP Held by

NO TRANSACTIONS IN JANUARY

Total - - - -

CITY OF COVINAInvestment Transaction Summary

for the Month Ended January 31 2021

Purchased Investments

Sold/Matured Investments

S:\Covina_PVT\Finance_PVT\Investments - City & CRA\Monthly Investment Reports\20-21\January 2021\January 2021 Investment Report Attachment A-2

Page 4 of 6

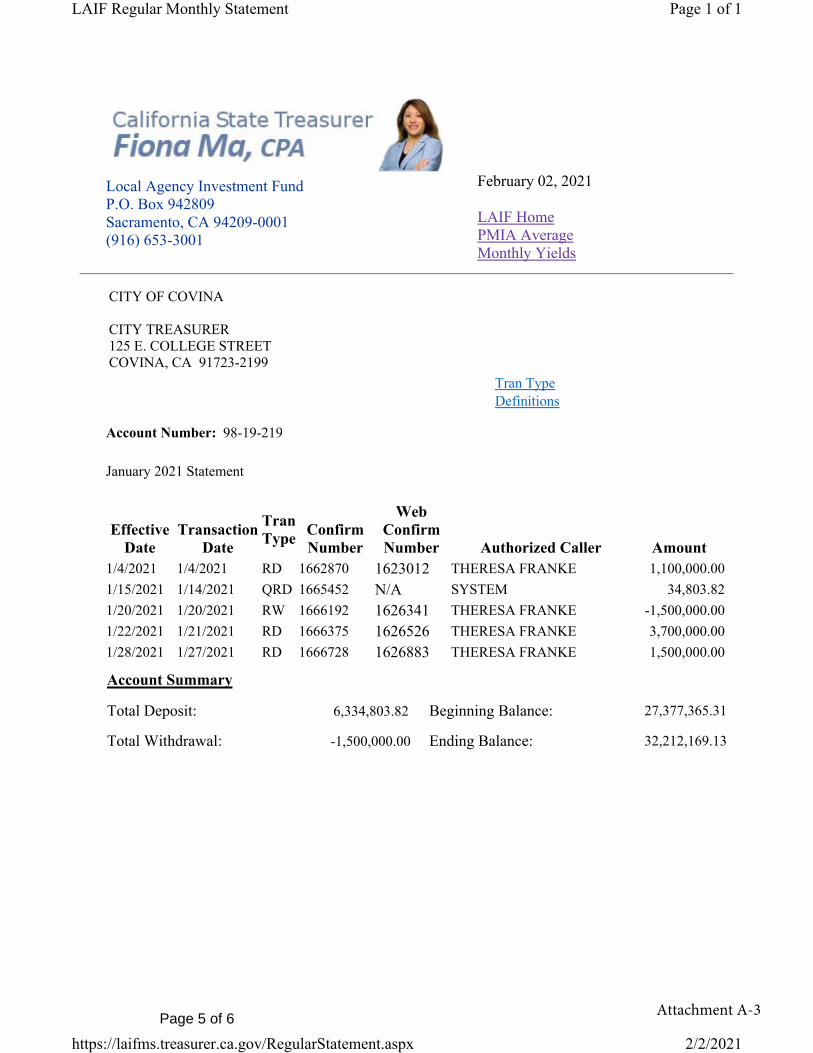

Local Agency Investment Fund P.O. Box 942809Sacramento, CA 94209-0001(916) 653-3001

February 02, 2021

LAIF HomePMIA Average Monthly Yields

CITY OF COVINA

CITY TREASURER 125 E. COLLEGE STREET COVINA, CA 91723-2199

Account Number: 98-19-219

January 2021 Statement

Tran Type Definitions

Effective Date

Transaction Date

TranType Confirm

Number

Web Confirm Number Authorized Caller Amount

1/4/2021 1/4/2021 RD 1662870 1623012 THERESA FRANKE 1,100,000.00 1/15/2021 1/14/2021 QRD 1665452 N/A SYSTEM 34,803.82 1/20/2021 1/20/2021 RW 1666192 1626341 THERESA FRANKE -1,500,000.00 1/22/2021 1/21/2021 RD 1666375 1626526 THERESA FRANKE 3,700,000.00 1/28/2021 1/27/2021 RD 1666728 1626883 THERESA FRANKE 1,500,000.00

Account Summary

Total Deposit: 6,334,803.82 Beginning Balance: 27,377,365.31

Total Withdrawal: -1,500,000.00 Ending Balance: 32,212,169.13

Page 1 of 1LAIF Regular Monthly Statement

2/2/2021https://laifms.treasurer.ca.gov/RegularStatement.aspx

Attachment A-3Page 5 of 6

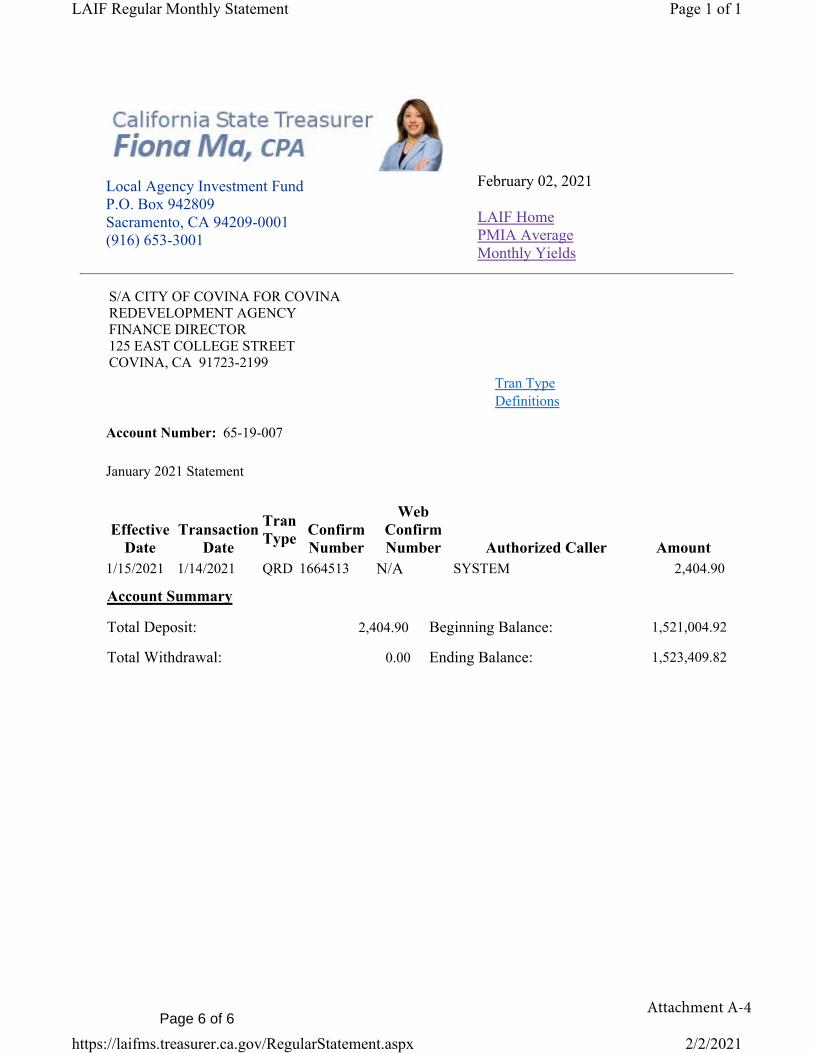

Local Agency Investment Fund P.O. Box 942809Sacramento, CA 94209-0001(916) 653-3001

February 02, 2021

LAIF HomePMIA Average Monthly Yields

S/A CITY OF COVINA FOR COVINA REDEVELOPMENT AGENCY FINANCE DIRECTOR 125 EAST COLLEGE STREET COVINA, CA 91723-2199

Account Number: 65-19-007

January 2021 Statement

Tran Type Definitions

Effective Date

Transaction Date

Tran Type Confirm

Number

Web Confirm Number Authorized Caller Amount

1/15/2021 1/14/2021 QRD 1664513 N/A SYSTEM 2,404.90

Account Summary

Total Deposit: 2,404.90 Beginning Balance: 1,521,004.92

Total Withdrawal: 0.00 Ending Balance: 1,523,409.82

Page 1 of 1LAIF Regular Monthly Statement

2/2/2021https://laifms.treasurer.ca.gov/RegularStatement.aspx

Attachment A-4Page 6 of 6

CC Regular Meeting AGENDA ITEM REPORT

ITEM NO. CC 4

Meeting: CC Regular Meeting - Feb 16 2021 Title: Citywide Bus Stop Improvement Project - Final Acceptance and Filing Notice of

Completion Presented By: Andy Bullington, Director of Public Works Recommendation: 1. Accept the work performed by E.C. Construction Co.;

2. Authorize the City Clerk to file a Notice of Completion for the Citywide Bus Stop Improvement Project; and 3. Adopt 2021CCResolution -07 2021Year Fiscal the amend to -2025 Capital Improvement Program to increase funding by $135,731 for the Citywide Bus Stop Improvement Project and appropriate the necessary funds from available Proposition A Local Return Fund Balance.

EXECUTIVE SUMMARY: Accept the work performed by E.C. Construction Co. and authorize the City Clerk to file a Notice of Completion (Attachment A) for the Citywide Bus Stop Improvement Project. Adopt Resolution CC 2021-07 (Attachment B) to amend the FY2021-2025 to increase funding by $135,731 for the Citywide Bus Stop Improvement Project and appropriate the necessary funds from available Proposition A Fund Balance. BACKGROUND: On September 3, 2019, the City Council approved a budget appropriation of $700,000 for the Citywide Bus Stop Improvement Project from the Proposition A fund balance to upgrade 98 City of Covina bus stops with safety enhancements, ADA accessibility, and modern amenities in order to improve the user experience for local bus riders. The culmination of these efforts targets the ultimate replacement of all existing City bus stop amenities transitalong located other Works Publiccomplement to projects - and arterials oriented neighborhoods. On December 17, 2019, staff requested that the City Council reject all initial bids submitted on December 3, 2019 for the Citywide Bus Stop Improvement Project in response to the City receiving two bids, one from Gentry Brothers, Inc. in the amount of $1,076,700 and the other from AP Construction, Inc. in the amount of $1,839,335, with the lowest bid amount approximately 65% higher than the Engineer's estimate of $650,000. The City Council approved the rejection of all bids and authorized staff to rebid the transit shelter component of the project while concurrently working with prospective vendors to directly procure all other street furniture and appurtenances in an effort to expedite project completion. Following a new public bidding process initiated in January 2020 to install 35 new transit shelters and perform additional sitework within pertinent bus stop zones, the City received two bids, one from E.C. Construction Co. in the amount of $657,060 and the other from AP Construction, Inc. in the amount of $1,331,350. As such, a contract was awarded on February 4, 2020 for the Citywide Bus Stop Improvement Project to E.C. Construction Co. as the lowest responsive and responsible bidder in an amount not-to-exceed $657,060 with a contingency amount of $65,706 also approved to supplement any unforeseen site conditions during construction. All work

including the installation of 35 new steel bus shelters outfitted with solar lighting units as well as the repair of approximately 11,000 square feet of concrete sidewalk located within the bus stop zones has been completed and a final inspection of all locations was performed by City staff in late January 2021. DISCUSSION: During construction, the need for additional work, not included in the original scope of work, was identified by the City. As a result, the City Engineer reviewed and approved the following change orders, increasing the overall contract in the amount of $720,370.26: Change Order No. 1 Change Order No. 1 increased the overall contract amount by $24,085 due to ADA Improvements and Concrete Sitework at various bus stops – Quantity Adjustments Based on Field Measurements. Change Order No. 2 Change Order No. 2 increased the overall contract amount by $4,884.69 pursuant to a redesign of the COVINA metal insert located on each bus shelter Change Order No. 3 Change Order No. 3 increased the overall contract amount by $29,228 as a result of additional concrete sidewalk and curb / gutter repairs needed at various bus stop locations for safety precautions Change Order No. 4 Change Order No. 4 increased the overall contract amount by $5,112.57 to perform additional sitework at Citrus Ave and Arrow Highway after discovering subsurface railway ties in the Right-of-Way. FISCAL IMPACT: An appropriation of $1,052,095 to the Department of Public Works, Transportation Proposition A, Buildings and Structures budget (account no. 2400-TO01-55100-P2014) was approved by the City Council on February 4, 2020. As a result of the project carrying over into FY 2021, project contingency and ancillary funds in the amount of $135,731 for equipment, force labor and contract expenses were not carried over; as such, City staff is requesting that Resolution CC 2021-07 be approved in order to reallocate project funds in FY 2021 to the Citywide Bus Stop Improvement Project. Moreover, the following table presents a summary of available funding sources and actual construction, City labor and procurement costs: Citywide Bus Stop Improvement Project Approved Budget $1,052,950.00 Construction Contract – E.C. Construction Co. (+ contingency) $722,766.00 Total Contract Expenditures (including 4 Change Orders) <$720,370.26> Remaining Contract Balance $2,395.74 Other Citywide Bus Stop Project Expenditures in FY20 & FY21 Project Advertising - Reproduction & Bids <$1,705.88> Design and Bid Documents - Robert Nava Design <$10,800.00> 87 Trash Receptacles - Victor Stanley, Inc. <$126,239.44> 24 Steel Benches - Keystone Ridge Designs <$25,019.62> 45 Pole-mounted Solar Lights - Urban Solar <53,587.31>

Page 2 of 6

61 Bus Benches, Refurbish and Paint - Hawk Industry <$12,200.00> Other Miscellaneous Expenses (supplies, etc.) <1,127.80> City Labor and Ancillary Expenses <$99,503.95> Total - Other Citywide Bus Stop Project Expenditures <$330,184.00> Current Project Funds Available in FY21 $557,343.44 Existing Project Expenditures / Encumbrances in FY21 <$693,074.00> Funding Allocation Needed in FY21 for Project Completion $135,731.00 CEQA (CALIFORNIA ENVIRONMENTAL QUALITY ACT): This project has been determined to be categorically exempt under CEQA in accordance with Title 14, Chapter 3, Class 1, Sections 15301 and 15302. This exemption includes the minor alteration of existing public facilities involving negligible or no expansion of use beyond that existing at the time of the lead agency's determination. The project involves negligible or no expansion of an existing use. ATTACHMENTS: Attachment A - NOC - Citywide Bus Stop Improvement Project Attachment B - Resolution CC 2021-07 Respectfully submitted,

Page 3 of 6

ATTACHMENT A

RECORDING REQUESTED BY AND WHEN RECORDED MAIL TO:

NAME City of Covina

STREET ADDRESS 125 E College Street

CITY Covina

STATE CA

ZIP CODE 91723

SPACE ABOVE THIS LINE FOR RECORDER’S USE

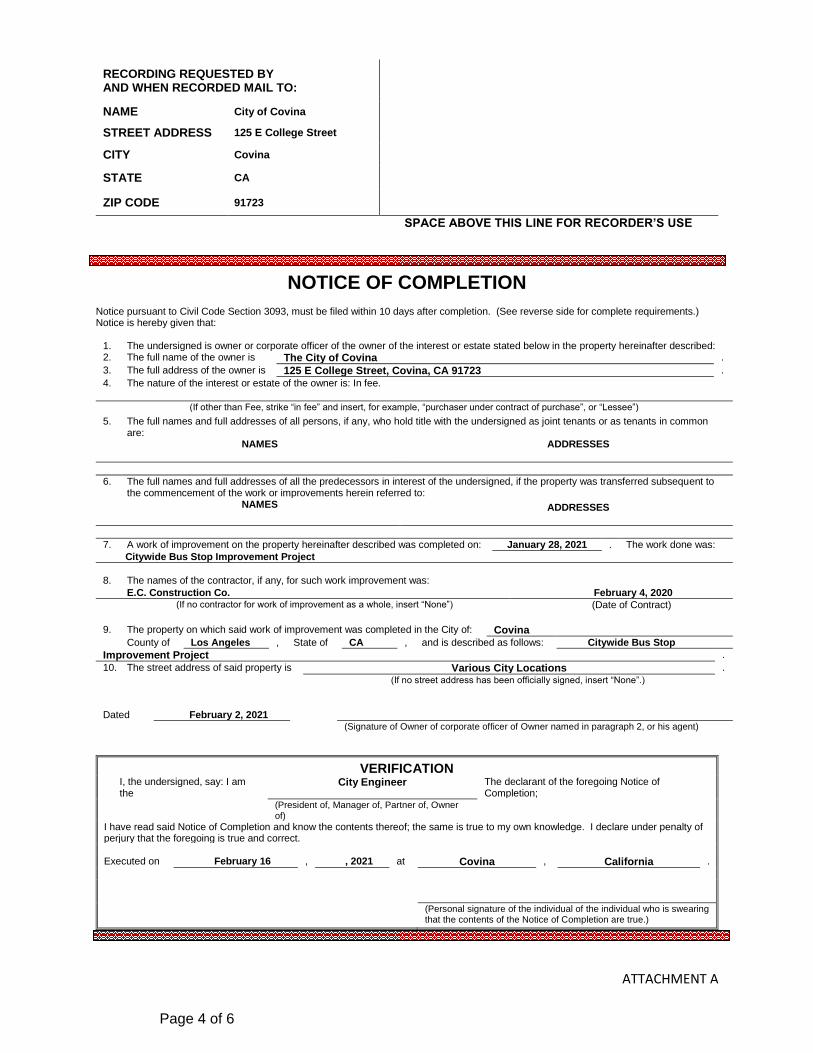

NOTICE OF COMPLETION Notice pursuant to Civil Code Section 3093, must be filed within 10 days after completion. (See reverse side for complete requirements.) Notice is hereby given that:

1. The undersigned is owner or corporate officer of the owner of the interest or estate stated below in the property hereinafter described: 2. The full name of the owner is The City of Covina .

3. The full address of the owner is 125 E College Street, Covina, CA 91723 .

4. The nature of the interest or estate of the owner is: In fee.

(If other than Fee, strike “in fee” and insert, for example, “purchaser under contract of purchase”, or “Lessee”)

5. The full names and full addresses of all persons, if any, who hold title with the undersigned as joint tenants or as tenants in common are:

NAMES ADDRESSES

6. The full names and full addresses of all the predecessors in interest of the undersigned, if the property was transferred subsequent to

the commencement of the work or improvements herein referred to: NAMES

ADDRESSES

7. A work of improvement on the property hereinafter described was completed on: January 28, 2021 . The work done was:

Citywide Bus Stop Improvement Project

8. The names of the contractor, if any, for such work improvement was:

E.C. Construction Co. February 4, 2020 (If no contractor for work of improvement as a whole, insert “None”) (Date of Contract)

9. The property on which said work of improvement was completed in the City of: Covina County of Los Angeles , State of CA , and is described as follows: Citywide Bus Stop

Improvement Project .

10. The street address of said property is Various City Locations .

(If no street address has been officially signed, insert “None”.)

Dated February 2, 2021

(Signature of Owner of corporate officer of Owner named in paragraph 2, or his agent)

VERIFICATION I, the undersigned, say: I am

the City Engineer The declarant of the foregoing Notice of

Completion;

(President of, Manager of, Partner of, Owner of)

I have read said Notice of Completion and know the contents thereof; the same is true to my own knowledge. I declare under penalty of perjury that the foregoing is true and correct. Executed on February 16 , , 2021 at Covina , California .

(Personal signature of the individual of the individual who is swearing that the contents of the Notice of Completion are true.)

Page 4 of 6

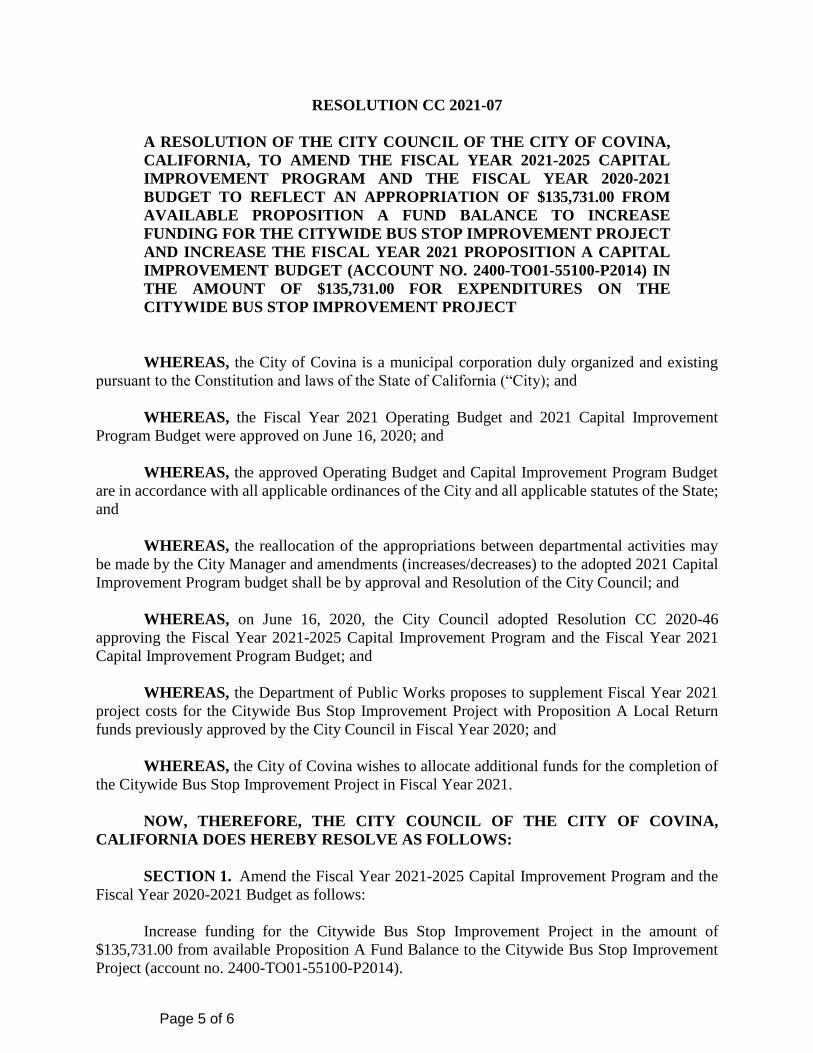

RESOLUTION CC 2021-07

A RESOLUTION OF THE CITY COUNCIL OF THE CITY OF COVINA,

CALIFORNIA, TO AMEND THE FISCAL YEAR 2021-2025 CAPITAL

IMPROVEMENT PROGRAM AND THE FISCAL YEAR 2020-2021

BUDGET TO REFLECT AN APPROPRIATION OF $135,731.00 FROM

AVAILABLE PROPOSITION A FUND BALANCE TO INCREASE

FUNDING FOR THE CITYWIDE BUS STOP IMPROVEMENT PROJECT

AND INCREASE THE FISCAL YEAR 2021 PROPOSITION A CAPITAL

IMPROVEMENT BUDGET (ACCOUNT NO. 2400-TO01-55100-P2014) IN

THE AMOUNT OF $135,731.00 FOR EXPENDITURES ON THE

CITYWIDE BUS STOP IMPROVEMENT PROJECT

WHEREAS, the City of Covina is a municipal corporation duly organized and existing

pursuant to the Constitution and laws of the State of California (“City); and

WHEREAS, the Fiscal Year 2021 Operating Budget and 2021 Capital Improvement

Program Budget were approved on June 16, 2020; and

WHEREAS, the approved Operating Budget and Capital Improvement Program Budget

are in accordance with all applicable ordinances of the City and all applicable statutes of the State;

and

WHEREAS, the reallocation of the appropriations between departmental activities may

be made by the City Manager and amendments (increases/decreases) to the adopted 2021 Capital

Improvement Program budget shall be by approval and Resolution of the City Council; and

WHEREAS, on June 16, 2020, the City Council adopted Resolution CC 2020-46

approving the Fiscal Year 2021-2025 Capital Improvement Program and the Fiscal Year 2021

Capital Improvement Program Budget; and

WHEREAS, the Department of Public Works proposes to supplement Fiscal Year 2021

project costs for the Citywide Bus Stop Improvement Project with Proposition A Local Return

funds previously approved by the City Council in Fiscal Year 2020; and

WHEREAS, the City of Covina wishes to allocate additional funds for the completion of

the Citywide Bus Stop Improvement Project in Fiscal Year 2021.

NOW, THEREFORE, THE CITY COUNCIL OF THE CITY OF COVINA,

CALIFORNIA DOES HEREBY RESOLVE AS FOLLOWS:

SECTION 1. Amend the Fiscal Year 2021-2025 Capital Improvement Program and the

Fiscal Year 2020-2021 Budget as follows:

Increase funding for the Citywide Bus Stop Improvement Project in the amount of

$135,731.00 from available Proposition A Fund Balance to the Citywide Bus Stop Improvement

Project (account no. 2400-TO01-55100-P2014).

Page 5 of 6

Resolution CC 2021-07 Page 2 of 2

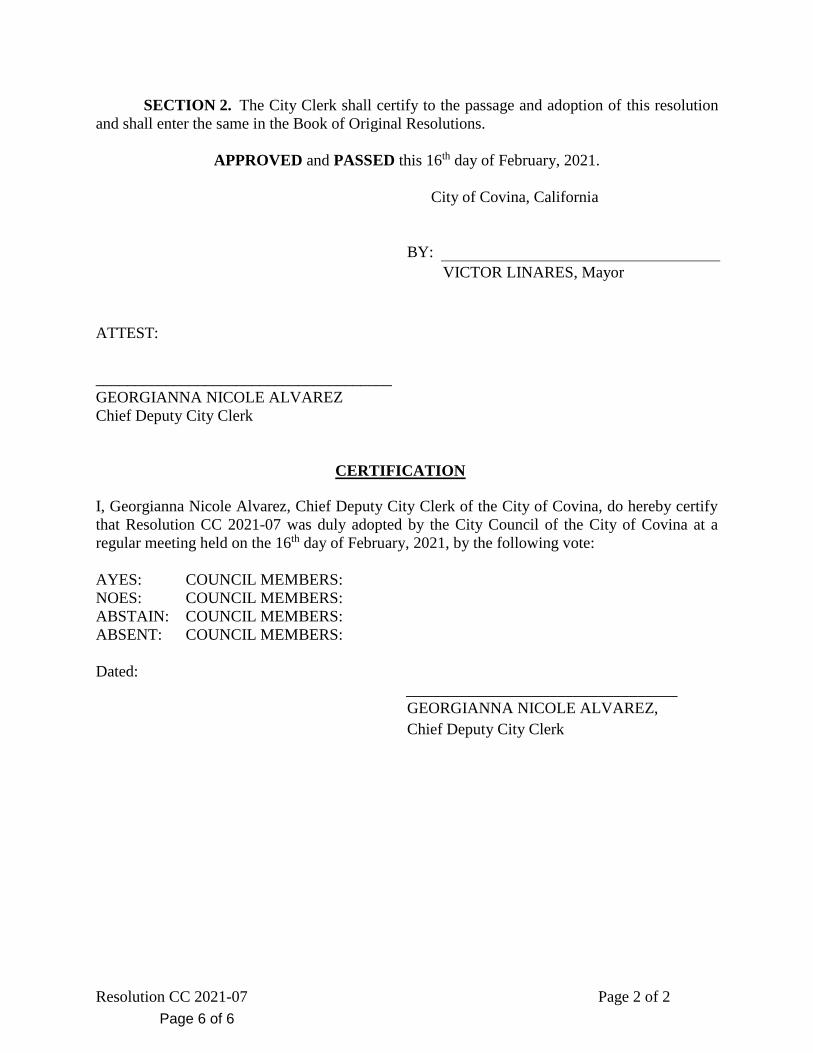

SECTION 2. The City Clerk shall certify to the passage and adoption of this resolution

and shall enter the same in the Book of Original Resolutions.

APPROVED and PASSED this 16th day of February, 2021.

City of Covina, California

BY:

VICTOR LINARES, Mayor

ATTEST:

______________________________________

GEORGIANNA NICOLE ALVAREZ

Chief Deputy City Clerk

CERTIFICATION

I, Georgianna Nicole Alvarez, Chief Deputy City Clerk of the City of Covina, do hereby certify

that Resolution CC 2021-07 was duly adopted by the City Council of the City of Covina at a

regular meeting held on the 16th day of February, 2021, by the following vote:

AYES: COUNCIL MEMBERS:

NOES: COUNCIL MEMBERS:

ABSTAIN: COUNCIL MEMBERS:

ABSENT: COUNCIL MEMBERS:

Dated:

__________________________________

GEORGIANNA NICOLE ALVAREZ,

Chief Deputy City Clerk

Page 6 of 6

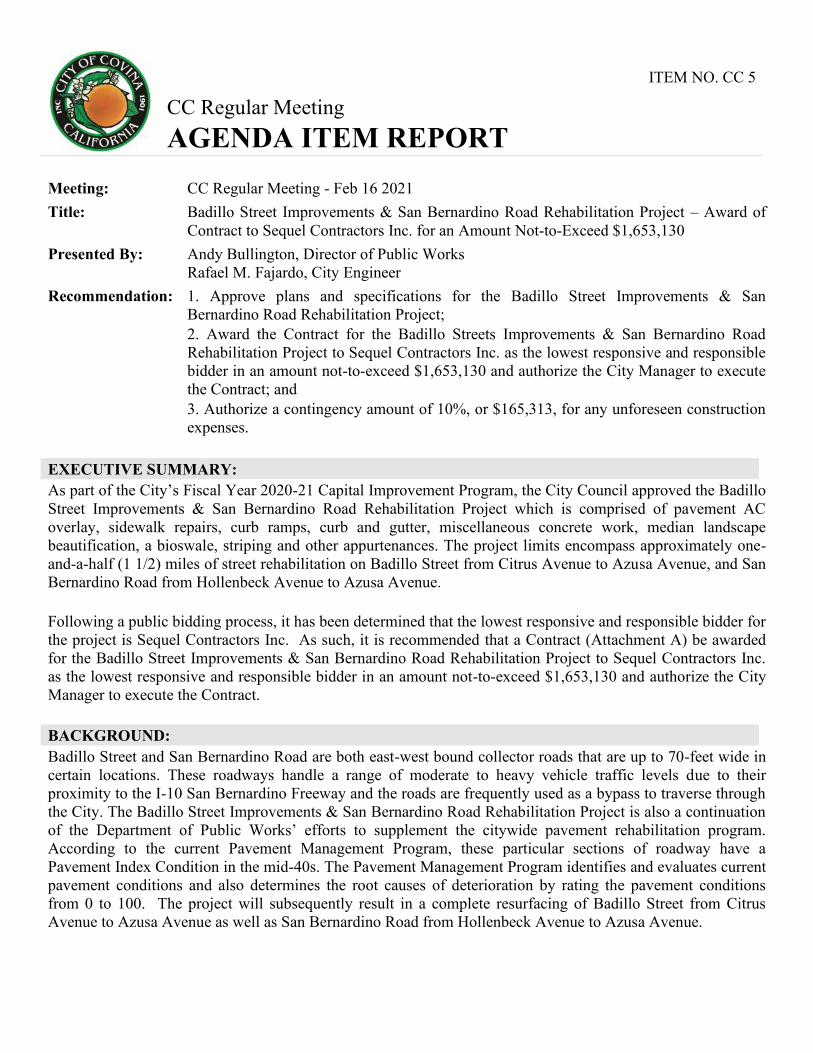

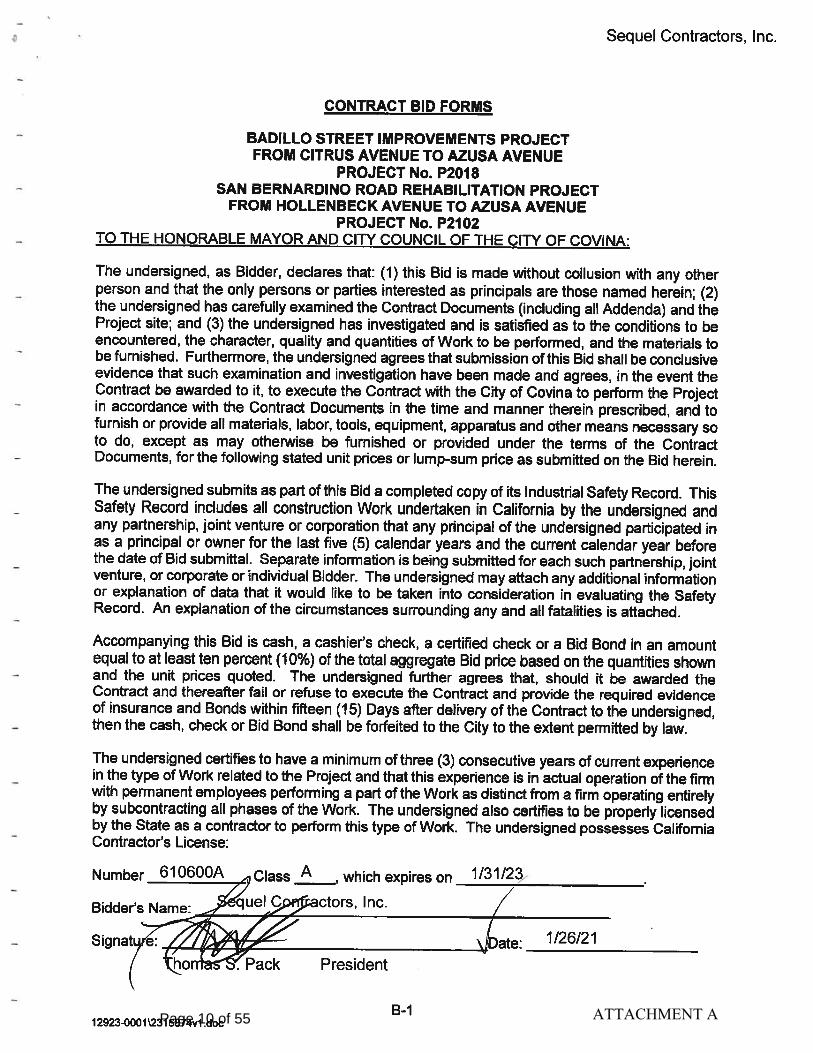

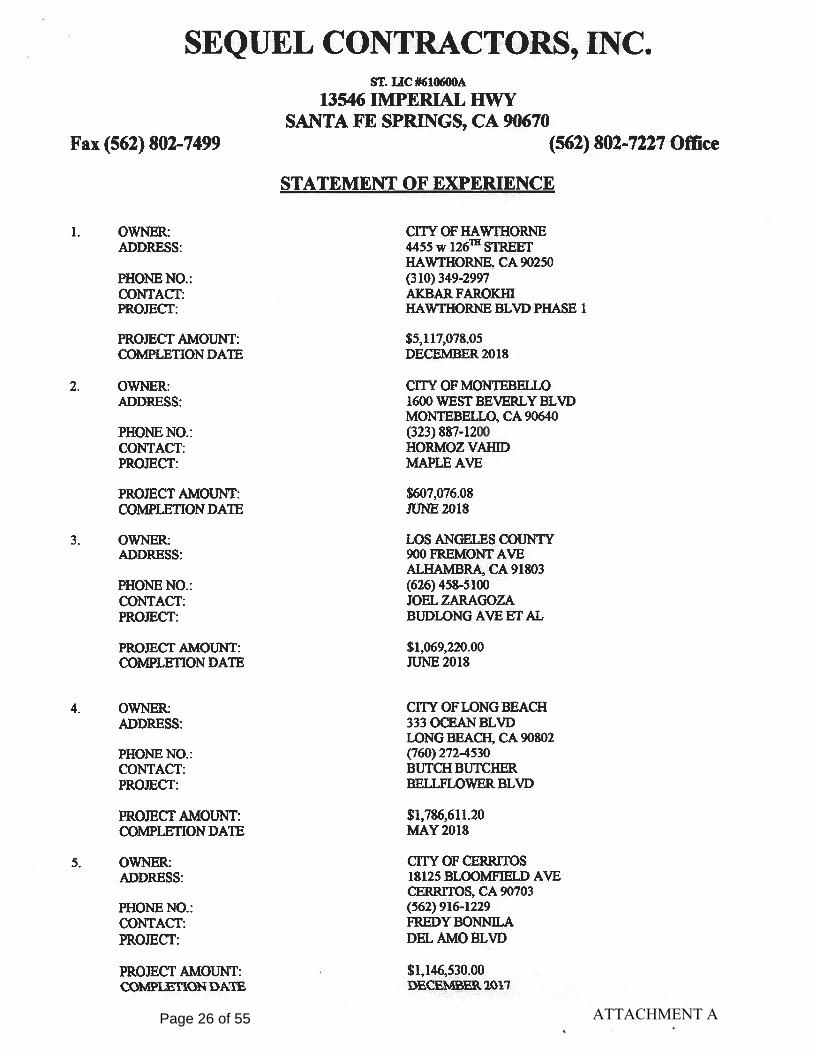

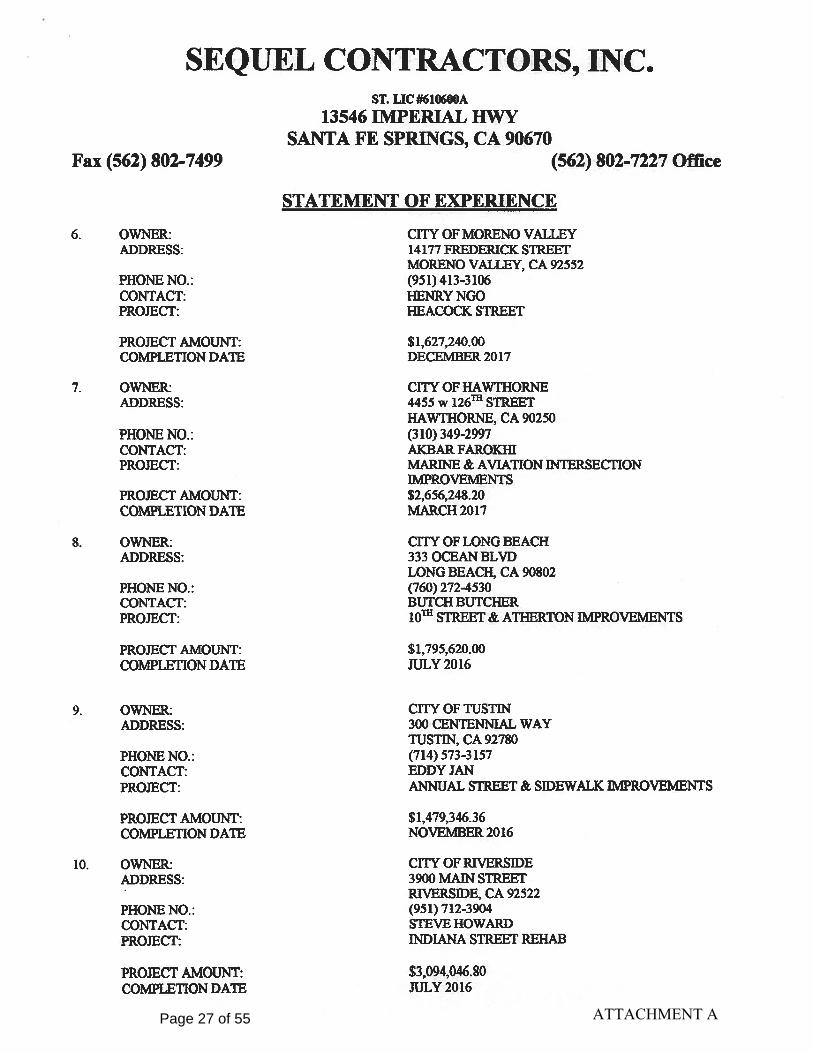

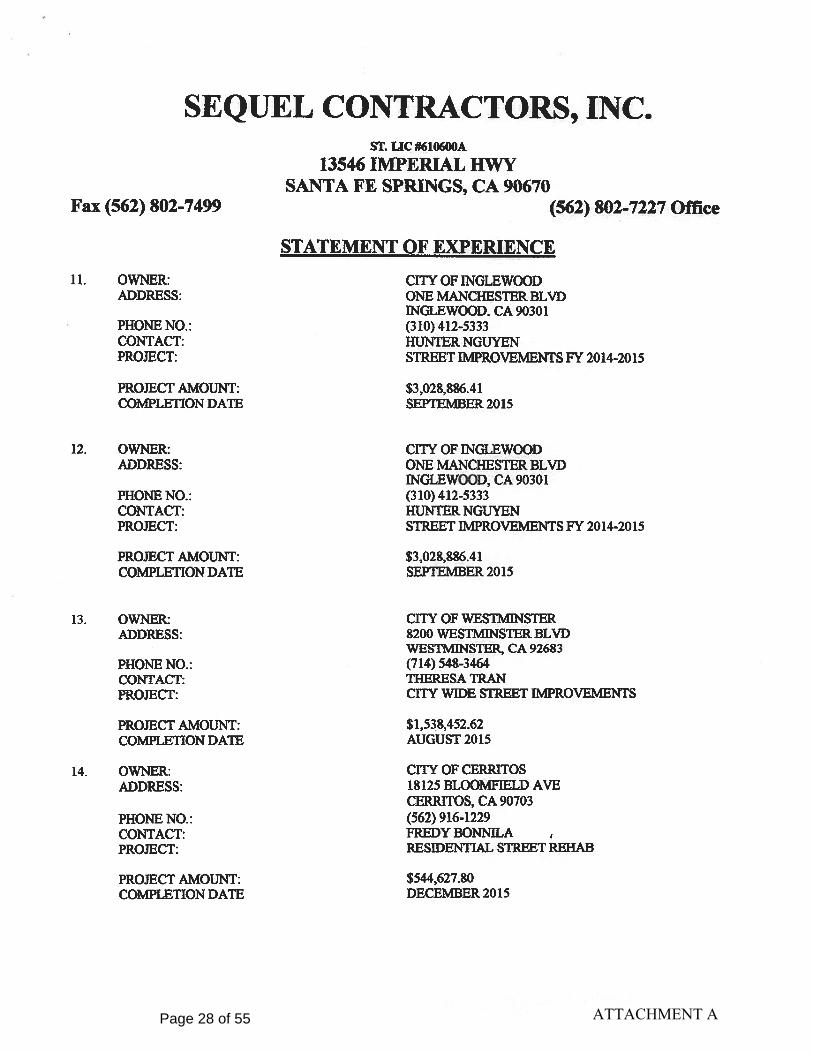

CC Regular Meeting AGENDA ITEM REPORT

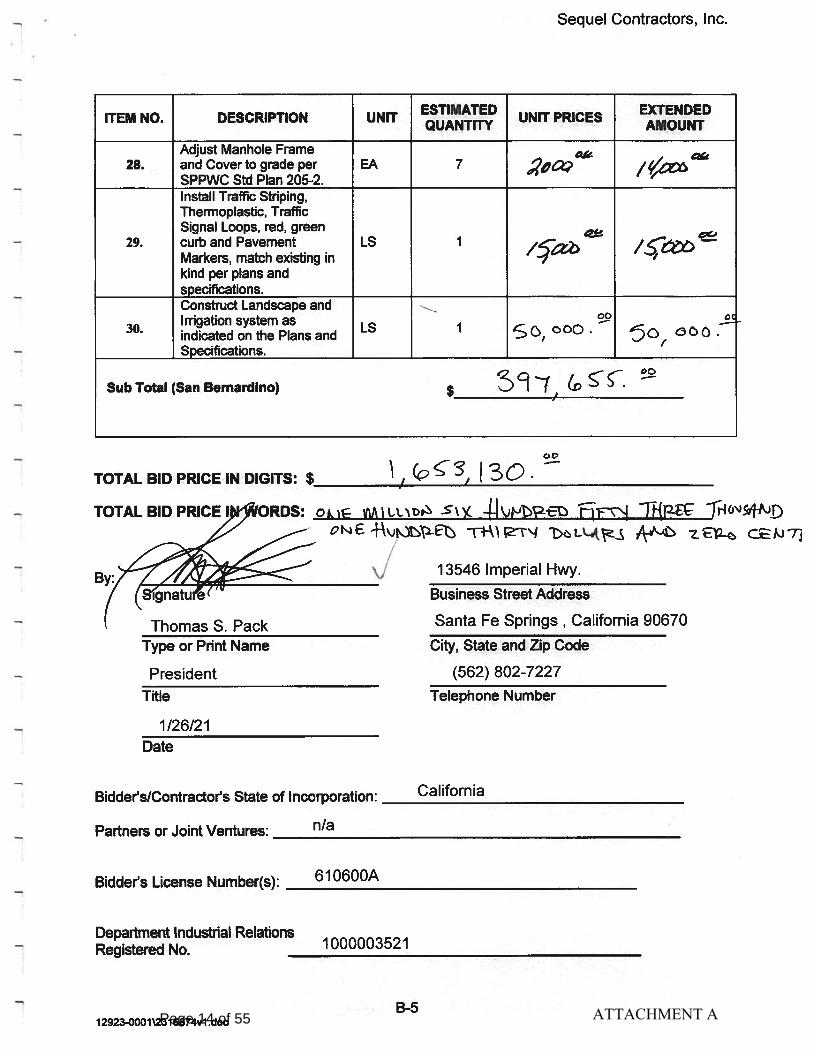

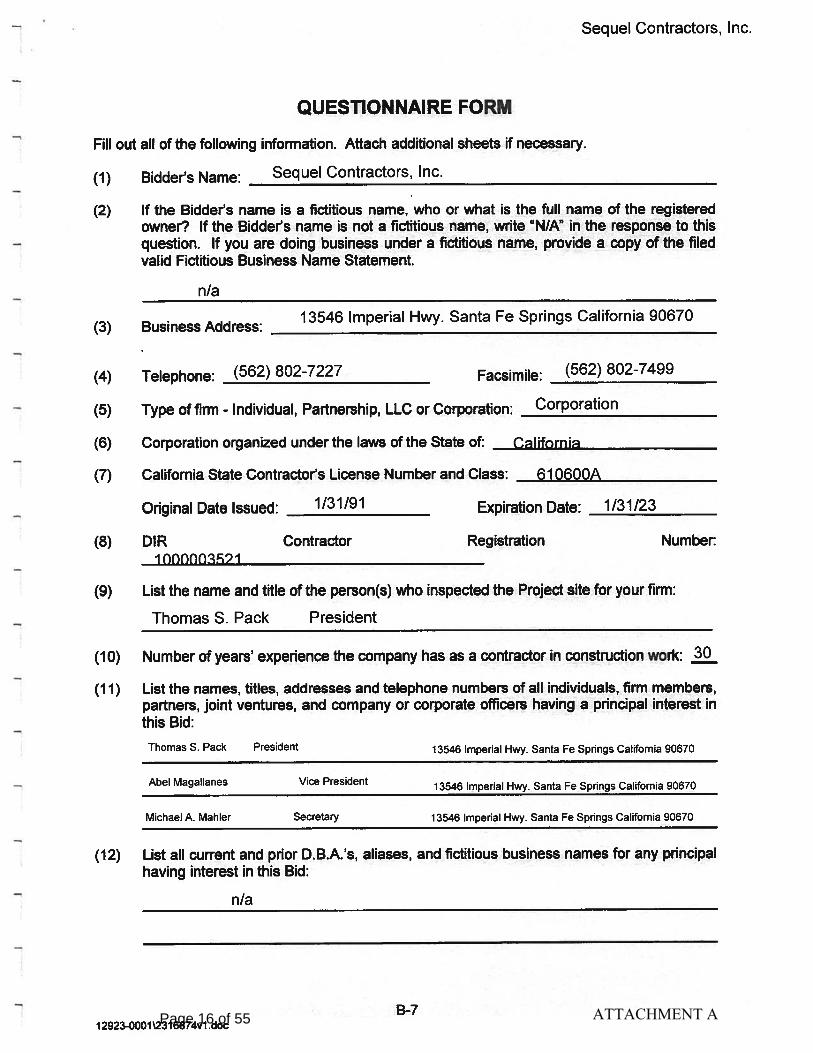

ITEM NO. CC 5

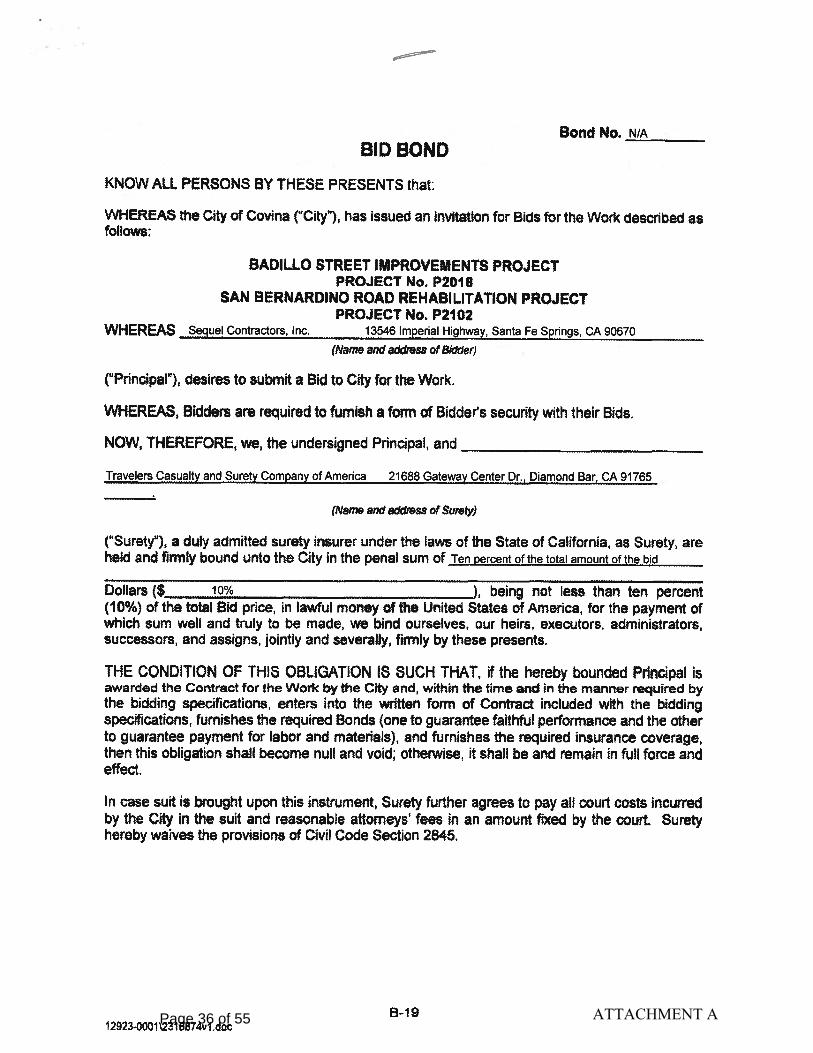

Meeting: CC Regular Meeting - Feb 16 2021 Title: Badillo Street Improvements & San Bernardino Road Rehabilitation Project – Award of

Contract to Sequel Contractors Inc. for an Amount Not-to-Exceed $1,653,130 Presented By: Andy Bullington, Director of Public Works

Rafael M. Fajardo, City Engineer Recommendation: 1. Approve plans and specifications for the Badillo Street Improvements & San

Bernardino Road Rehabilitation Project; 2. Award the Contract for the Badillo Streets Improvements & San Bernardino Road Rehabilitation Project to Sequel Contractors Inc. as the lowest responsive and responsible bidder in an amount not-to-exceed $1,653,130 and authorize the City Manager to execute the Contract; and 3. Authorize a contingency amount of 10%, or $165,313, for any unforeseen construction expenses.

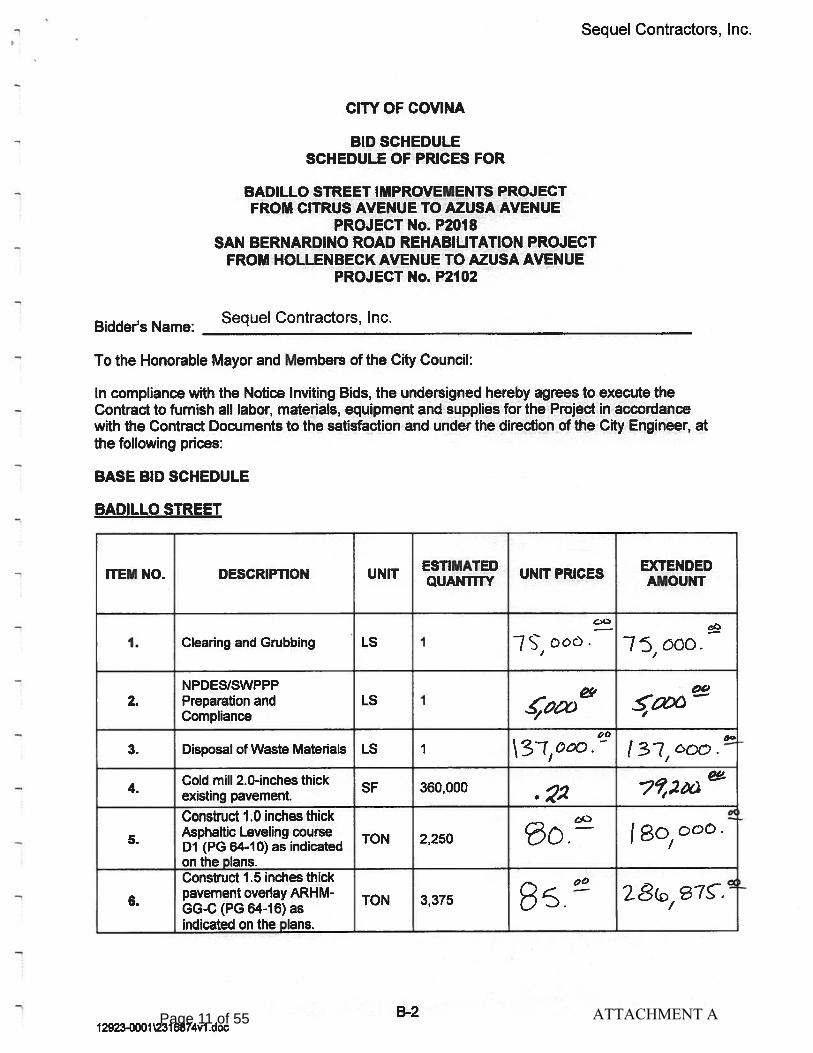

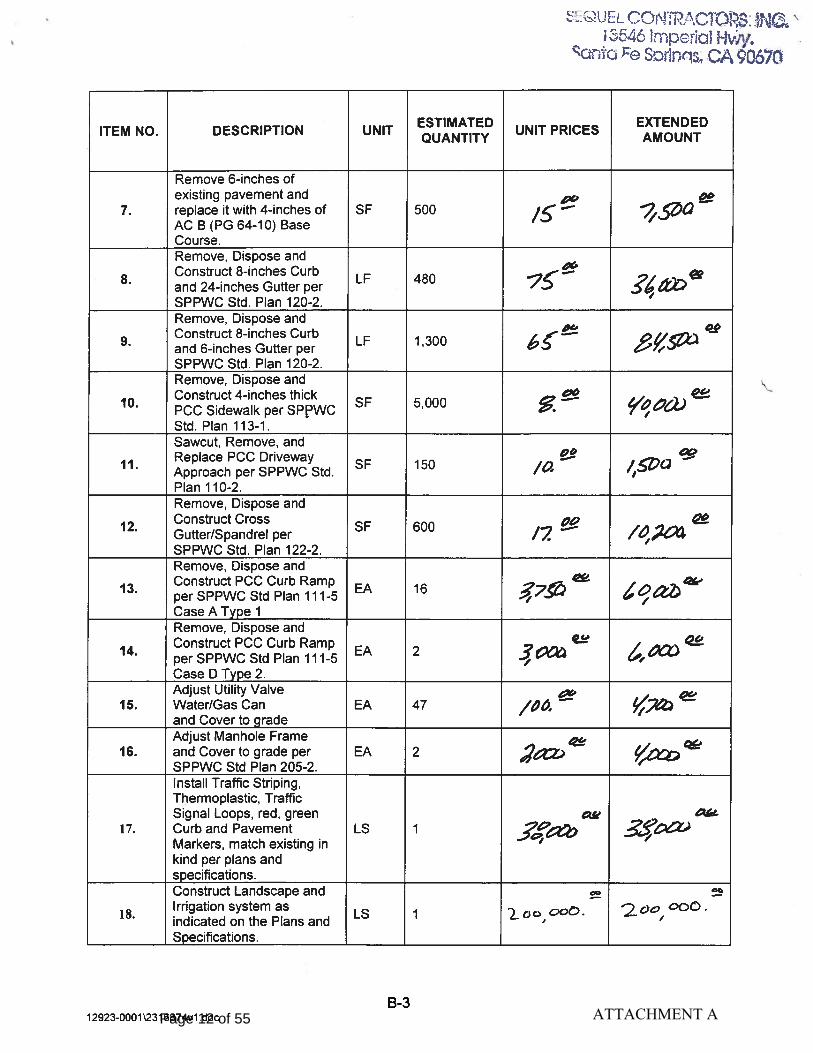

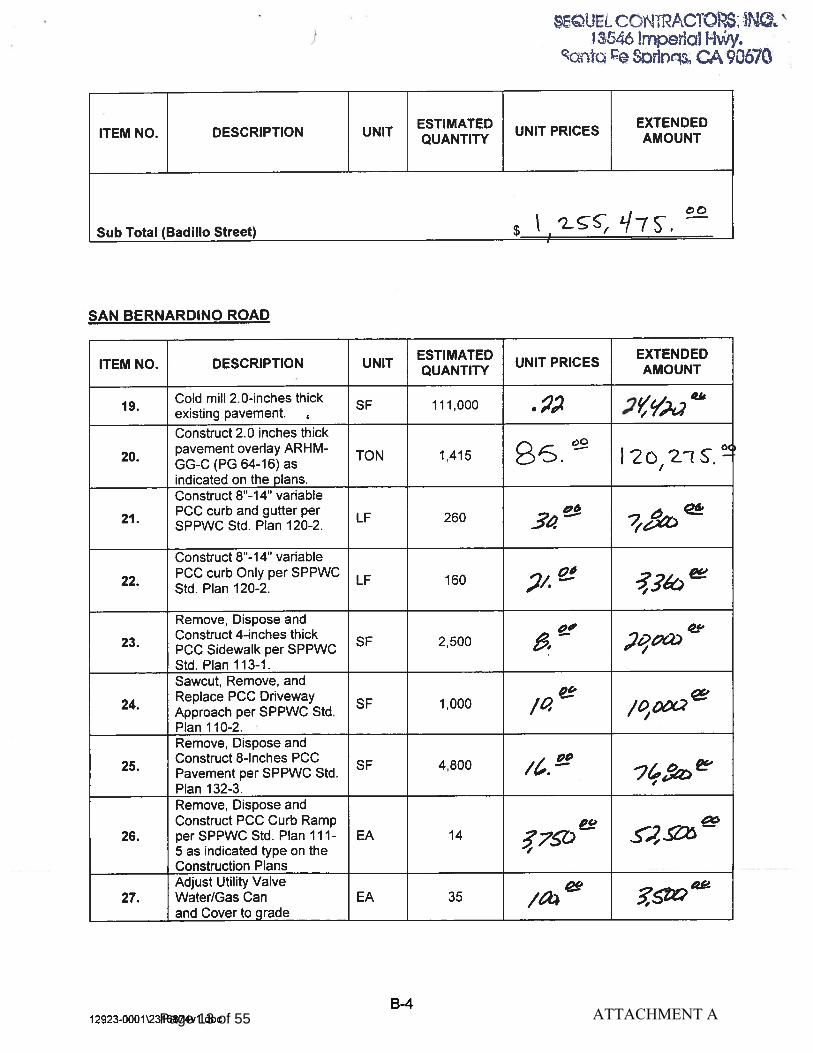

EXECUTIVE SUMMARY: As part of the City’s Fiscal Year 2020-21 Capital Improvement Program, the City Council approved the Badillo Street Improvements & San Bernardino Road Rehabilitation Project which is comprised of pavement AC overlay, sidewalk repairs, curb ramps, curb and gutter, miscellaneous concrete work, median landscape beautification, a bioswale, striping and other appurtenances. The project limits encompass approximately one-and-a-half (1 1/2) miles of street rehabilitation on Badillo Street from Citrus Avenue to Azusa Avenue, and San Bernardino Road from Hollenbeck Avenue to Azusa Avenue. Following a public bidding process, it has been determined that the lowest responsive and responsible bidder for the project is Sequel Contractors Inc. As such, it is recommended that a Contract (Attachment A) be awarded for the Badillo Street Improvements & San Bernardino Road Rehabilitation Project to Sequel Contractors Inc. as the lowest responsive and responsible bidder in an amount not-to-exceed $1,653,130 and authorize the City Manager to execute the Contract. BACKGROUND: Badillo Street and San Bernardino Road are both east-west bound collector roads that are up to 70-feet wide in certain locations. These roadways handle a range of moderate to heavy vehicle traffic levels due to their proximity to the I-10 San Bernardino Freeway and the roads are frequently used as a bypass to traverse through the City. The Badillo Street Improvements & San Bernardino Road Rehabilitation Project is also a continuation of the Department of Public Works’ efforts to supplement the citywide pavement rehabilitation program.

According to the current Pavement Management Program, these particular sections of roadway have a Pavement Index Condition in the mid-40s. The Pavement Management Program identifies and evaluates current pavement conditions and also determines the root causes of deterioration by rating the pavement conditions from 0 to 100. The project will subsequently result in a complete resurfacing of Badillo Street from Citrus Avenue to Azusa Avenue as well as San Bernardino Road from Hollenbeck Avenue to Azusa Avenue.

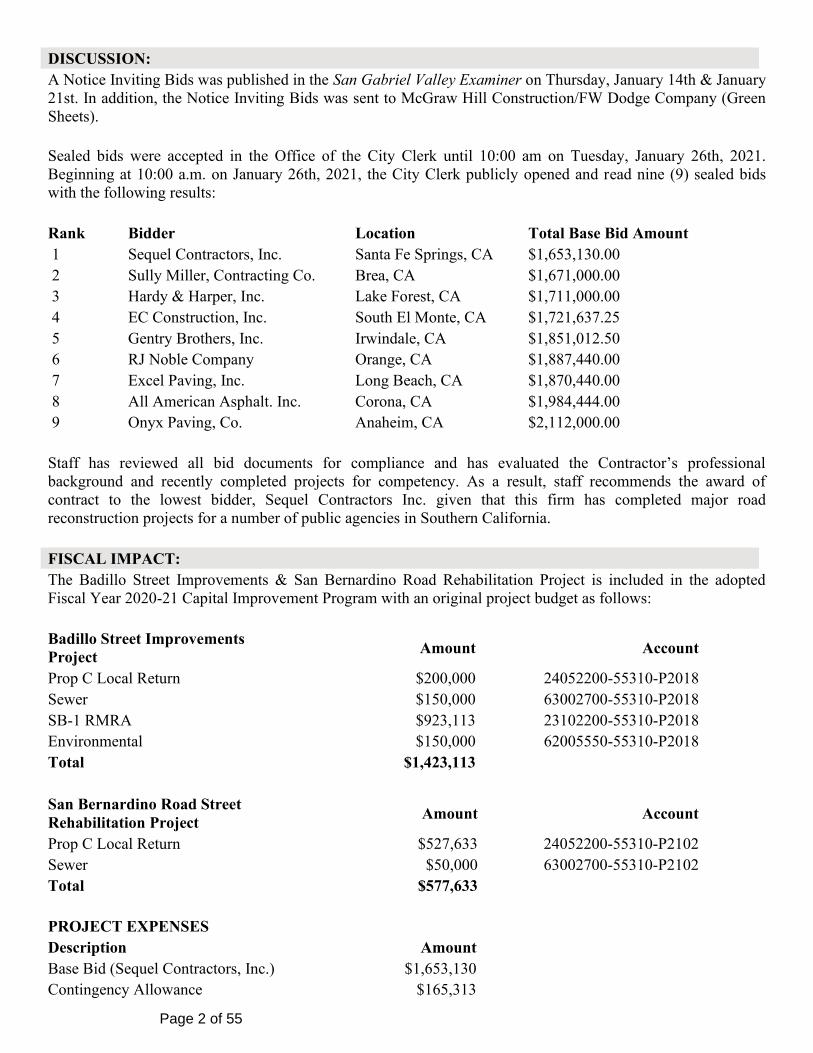

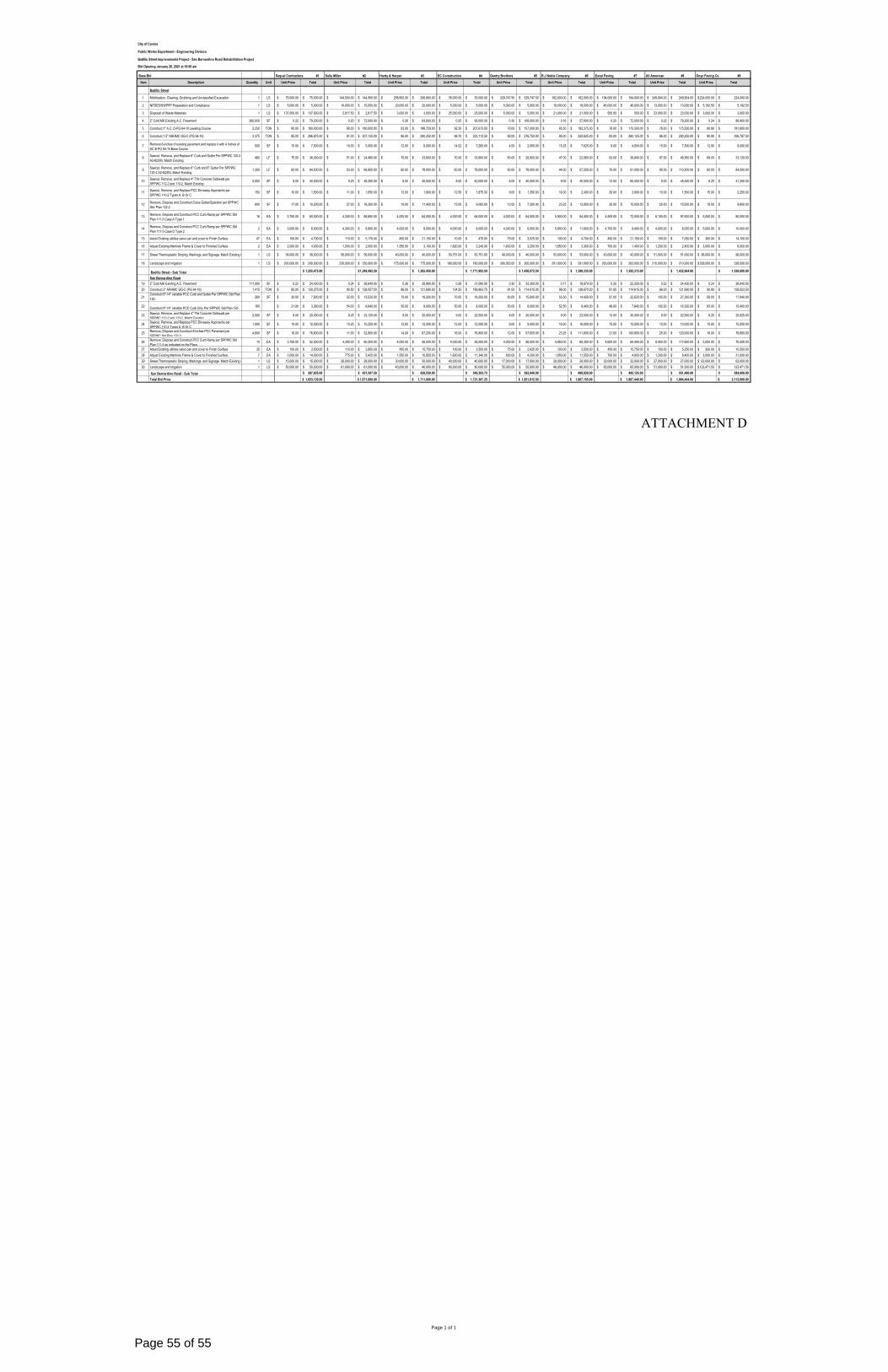

DISCUSSION: A Notice Inviting Bids was published in the San Gabriel Valley Examiner on Thursday, January 14th & January 21st. In addition, the Notice Inviting Bids was sent to McGraw Hill Construction/FW Dodge Company (Green Sheets). Sealed bids were accepted in the Office of the City Clerk until 10:00 am on Tuesday, January 26th, 2021. Beginning at 10:00 a.m. on January 26th, 2021, the City Clerk publicly opened and read nine (9) sealed bids with the following results: Rank Bidder Location Total Base Bid Amount 1 Sequel Contractors, Inc. Santa Fe Springs, CA $1,653,130.00 2 Sully Miller, Contracting Co. Brea, CA $1,671,000.00 3 Hardy & Harper, Inc. Lake Forest, CA $1,711,000.00 4 EC Construction, Inc. South El Monte, CA $1,721,637.25 5 Gentry Brothers, Inc. Irwindale, CA $1,851,012.50 6 RJ Noble Company Orange, CA $1,887,440.00 7 Excel Paving, Inc. Long Beach, CA $1,870,440.00 8 All American Asphalt. Inc. Corona, CA $1,984,444.00 9 Onyx Paving, Co. Anaheim, CA $2,112,000.00 Staff has reviewed all bid documents for compliance and has evaluated the Contractor’s professional

background and recently completed projects for competency. As a result, staff recommends the award of contract to the lowest bidder, Sequel Contractors Inc. given that this firm has completed major road reconstruction projects for a number of public agencies in Southern California. FISCAL IMPACT: The Badillo Street Improvements & San Bernardino Road Rehabilitation Project is included in the adopted Fiscal Year 2020-21 Capital Improvement Program with an original project budget as follows: Badillo Street Improvements Project Amount Account

Prop C Local Return $200,000 24052200-55310-P2018 Sewer $150,000 63002700-55310-P2018 SB-1 RMRA $923,113 23102200-55310-P2018 Environmental $150,000 62005550-55310-P2018 Total $1,423,113 San Bernardino Road Street Rehabilitation Project Amount Account

Prop C Local Return $527,633 24052200-55310-P2102 Sewer $50,000 63002700-55310-P2102 Total $577,633 PROJECT EXPENSES Description Amount Base Bid (Sequel Contractors, Inc.) $1,653,130 Contingency Allowance $165,313

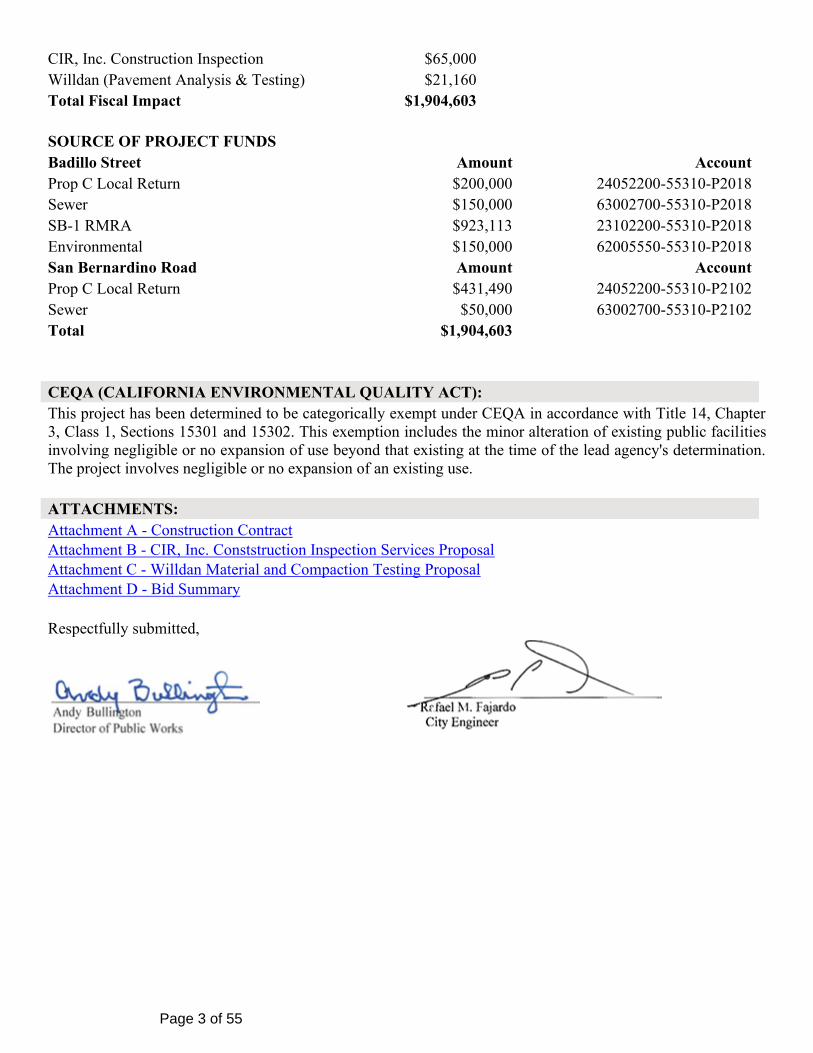

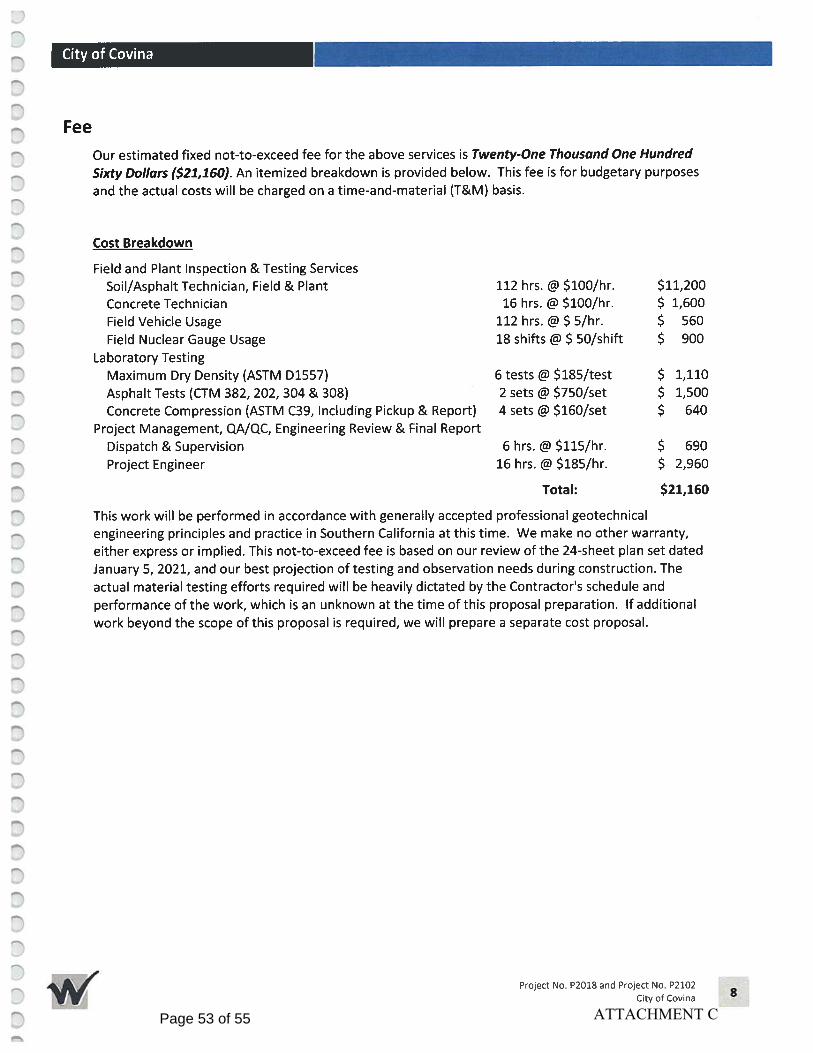

Page 2 of 55

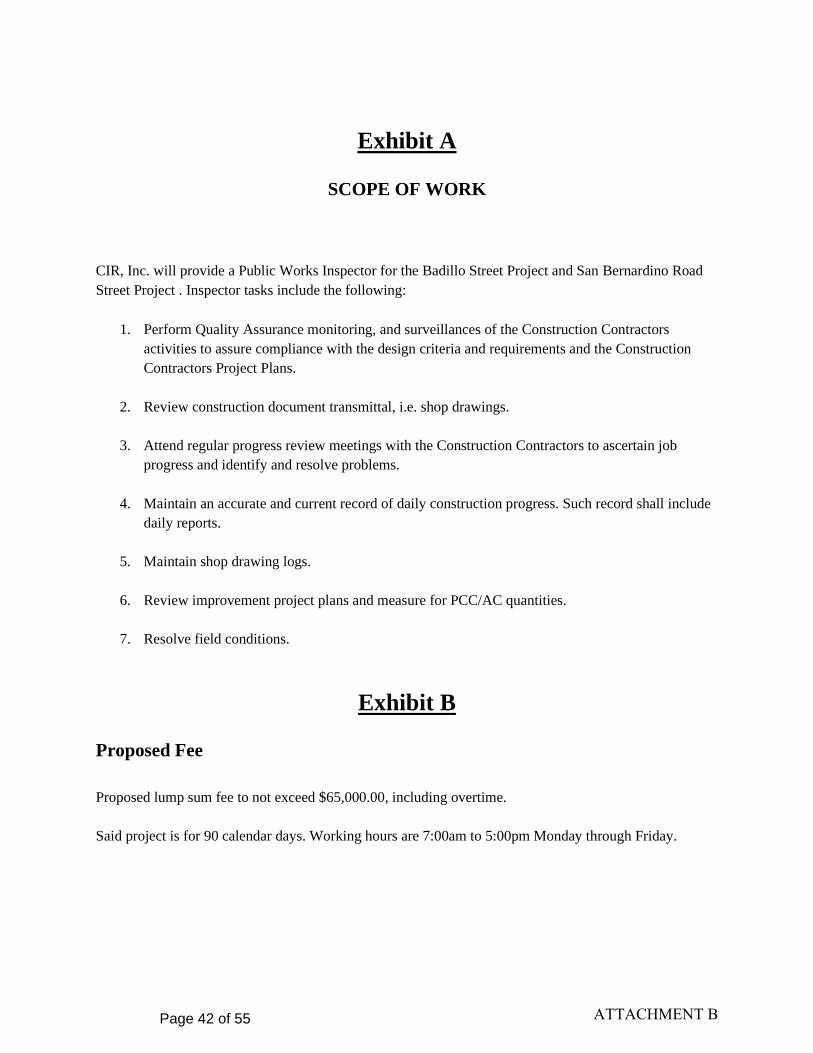

CIR, Inc. Construction Inspection $65,000 Willdan (Pavement Analysis & Testing) $21,160 Total Fiscal Impact $1,904,603 SOURCE OF PROJECT FUNDS Badillo Street Amount Account Prop C Local Return $200,000 24052200-55310-P2018 Sewer $150,000 63002700-55310-P2018 SB-1 RMRA $923,113 23102200-55310-P2018 Environmental $150,000 62005550-55310-P2018 San Bernardino Road Amount Account Prop C Local Return $431,490 24052200-55310-P2102 Sewer $50,000 63002700-55310-P2102 Total $1,904,603 CEQA (CALIFORNIA ENVIRONMENTAL QUALITY ACT): This project has been determined to be categorically exempt under CEQA in accordance with Title 14, Chapter 3, Class 1, Sections 15301 and 15302. This exemption includes the minor alteration of existing public facilities involving negligible or no expansion of use beyond that existing at the time of the lead agency's determination. The project involves negligible or no expansion of an existing use. ATTACHMENTS: Attachment A - Construction Contract Attachment B - CIR, Inc. Conststruction Inspection Services Proposal Attachment C - Willdan Material and Compaction Testing Proposal Attachment D - Bid Summary Respectfully submitted,

Page 3 of 55

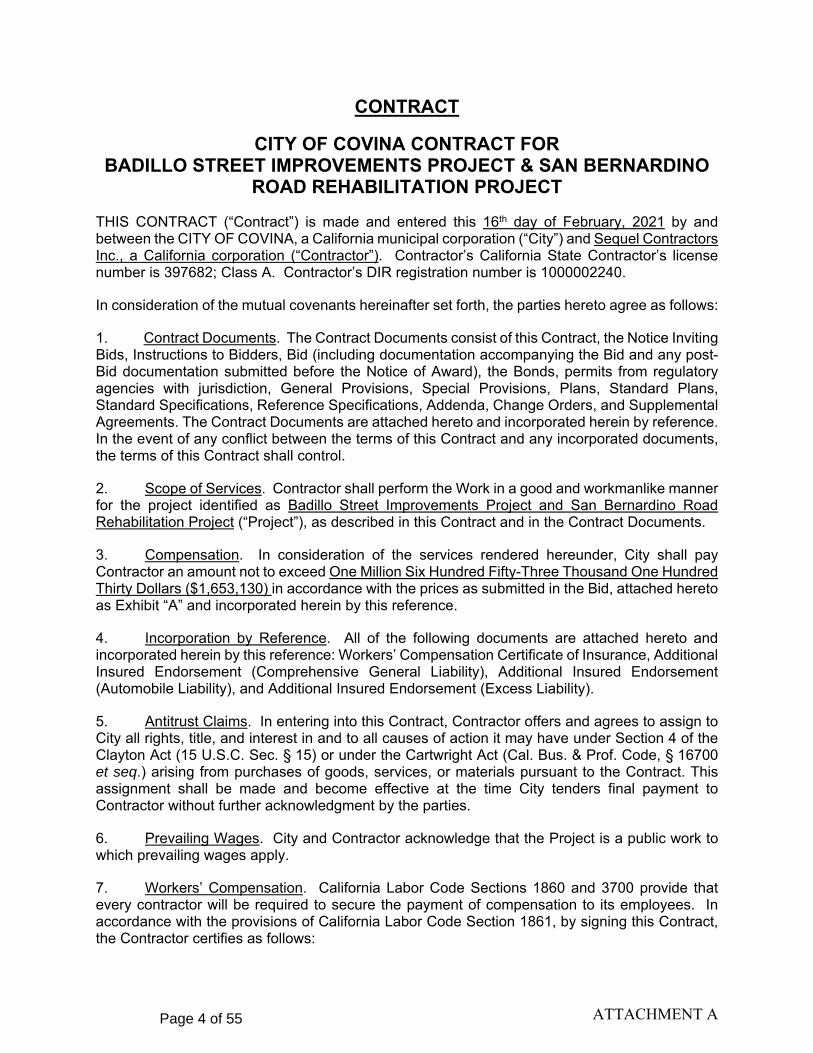

CONTRACT

CITY OF COVINA CONTRACT FOR BADILLO STREET IMPROVEMENTS PROJECT & SAN BERNARDINO

ROAD REHABILITATION PROJECT

THIS CONTRACT (“Contract”) is made and entered this 16th day of February, 2021 by and between the CITY OF COVINA, a California municipal corporation (“City”) and Sequel Contractors Inc., a California corporation (“Contractor”). Contractor’s California State Contractor’s license number is 397682; Class A. Contractor’s DIR registration number is 1000002240.

In consideration of the mutual covenants hereinafter set forth, the parties hereto agree as follows:

1. Contract Documents. The Contract Documents consist of this Contract, the Notice Inviting Bids, Instructions to Bidders, Bid (including documentation accompanying the Bid and any post-Bid documentation submitted before the Notice of Award), the Bonds, permits from regulatory agencies with jurisdiction, General Provisions, Special Provisions, Plans, Standard Plans, Standard Specifications, Reference Specifications, Addenda, Change Orders, and Supplemental Agreements. The Contract Documents are attached hereto and incorporated herein by reference. In the event of any conflict between the terms of this Contract and any incorporated documents, the terms of this Contract shall control.

2. Scope of Services. Contractor shall perform the Work in a good and workmanlike manner for the project identified as Badillo Street Improvements Project and San Bernardino Road Rehabilitation Project (“Project”), as described in this Contract and in the Contract Documents.

3. Compensation. In consideration of the services rendered hereunder, City shall pay Contractor an amount not to exceed One Million Six Hundred Fifty-Three Thousand One Hundred Thirty Dollars ($1,653,130) in accordance with the prices as submitted in the Bid, attached hereto as Exhibit “A” and incorporated herein by this reference.

4. Incorporation by Reference. All of the following documents are attached hereto and incorporated herein by this reference: Workers’ Compensation Certificate of Insurance, Additional Insured Endorsement (Comprehensive General Liability), Additional Insured Endorsement (Automobile Liability), and Additional Insured Endorsement (Excess Liability).

5. Antitrust Claims. In entering into this Contract, Contractor offers and agrees to assign to City all rights, title, and interest in and to all causes of action it may have under Section 4 of the Clayton Act (15 U.S.C. Sec. § 15) or under the Cartwright Act (Cal. Bus. & Prof. Code, § 16700 et seq.) arising from purchases of goods, services, or materials pursuant to the Contract. This assignment shall be made and become effective at the time City tenders final payment to Contractor without further acknowledgment by the parties.

6. Prevailing Wages. City and Contractor acknowledge that the Project is a public work to which prevailing wages apply.

7. Workers’ Compensation. California Labor Code Sections 1860 and 3700 provide that every contractor will be required to secure the payment of compensation to its employees. In accordance with the provisions of California Labor Code Section 1861, by signing this Contract, the Contractor certifies as follows:

ATTACHMENT APage 4 of 55

“I am aware of the provisions of Section 3700 of the Labor Code which require every employer to be insured against liability for workers’ compensation or to undertake self-insurance in accordance with the provisions of that Code, and I will comply with such provisions before commencing the performance of the Work of this Contract.”